Submitted:

22 April 2023

Posted:

23 April 2023

You are already at the latest version

Abstract

This research study aims to explore how during COVID-19, the adoption of online banking is impacted by various factors such as perceived usefulness, perceived ease of use, perceived security, and trust. The data were collected using the primary questionnaire with 98 respondents. The study investigates the direct effect using the PLS-SEM method, and the indirect effects are analyzed using mediation analysis. The study indicates that perceived security is an important factor that impacts the adoption of online banking by self-help groups in India. Trust in online banking without allaying the fears of banking online does not lead to the adoption of technology. Perceived ease of use and ease of usage directly impact the adoption of online banking by the members of self-help groups in India. The study is the first-ever study to measure the indirect impact of trust on the intention to use online banking by the members of self-help groups in India This study has far-reaching implications for policymakers and banks. To increase the adoption of online banking, it is important to allay the fears of security among the members of self-help groups in India.

Keywords:

Online banking

; Digital security

; Technology implementation

1. Introduction

COVID-19 has once again highlighted the need to use technology in banking to promote financial inclusion and poverty reduction. In March 2019, COVID-19 was declared an epidemic, leading to a global crisis. Nations worldwide declared COVID-19 and imposed various restrictions in the form of work from home. In this scenario, information technology and digital banking emerged as a panacea. Despite the vision adopted by the state of India to achieve 100 percent digital banking, the percentage of people using technology for banking has not increased as per expectations. This paper aims to analyze the factors that impact small entrepreneurs' use of digital banking in rural India. Despite several initiatives by the banks in India to promote digital banking, the hinterlands and usage of digital banking by the poor diaspora are extremely limited due to cyber security risks. Using (the TAM) Technology of Acceptance Model, the study aims to measure the impact of various attitudes such as perceived usefulness, perceived ease, and perceived security of users on the adoption of digital banking by the self-help group members. COVID-19-related lockdown and the thrust of the Indian state on the adoption of technology for banking will promote the use of digital banking. With the increasing cyber mafia, financial fraud has become more professionalized. Phishing is one of the significant types of fraud that has emerged in modern India. It is a crime in which fraudsters attempt to steal account credentials. This study, for the first time, aims to measure the impact of technology on perceived trust, ease of use, security, and intention of use. This theory highlights five factors: perceived ease of use, perceived usage, perceived security, trust, and usage. The study hypothesizes that perceived ease of use, perceived usage, and perceived security, perceived trust and usage of technology. A total of 98 respondents were selected by purposive random sampling and direct interviews were conducted using a questionnaire. The PLS-SEM method was used for analysis (Herman Wold, 1980). This study will help the Government, banks, and policymakers to chalk out strategies for adopting digital banking. With the advent of affordable devices, the internet, and mobile technology, the adoption of technology in banking should be driven through appropriate social intermediation initiatives. However, the research on the acceptance of technology by semi-informal financial sectors like group lending is minimal.

2. Literature

In the field of information systems (IS), various kinds of intention models have been used to predict user behavior. (Liao Cheung et al., 2002), in his research has highlighted the factors that impact the perceived usefulness of a product and service, including willingness to use and security, to name a few. (R. Agarwal, E. Karahanna,, 2000), (E. Karahanna, D.W. Straub, 1999), (D. Straub, M. Keil, W. Brenner,, 1997), (V. Venkatesh, F.D. Davis, 2000) in their research study have highlighted the importance of perceived ease of use, perceived usefulness as the factors impacting the acceptance of technology. These studies emphasize that despite the increasing proliferation of the internet and e-commerce, customers are reluctant to provide information on digital channels and are thus wary of using digital media for banking. These studies, for the first time, besides beliefs, highlighted the importance of trust to enable consumers to accept technology such as digital banking. (Fishbein, 1975) propounded the theory of reasoned action that has been used extensively in predicting behavior across varied domains. According to the theory of reasoned action (TRA), a person's behavior is determined by behavioral intention (BI). This behavioral intention is further defined by the attitude of the members and the subjective norms. This implies that a person's behavior is motivated by an individual's attitude toward the consequences of that behavior. (TAM), The Technology Acceptance Model further adopts the (TRA) Theory of Reasoned Action to explain an individual's internet or technology acceptance behavior. (Davis, F.D., 1986), propounded the (TAM) Theory of Acceptance Model and explored the impact of external factors on the internal beliefs and attitudes of the respondents. (TAM) The theory of the Acceptance Model propagates that the members' beliefs, which include the perceived usefulness and perceived ease of use, impact the acceptance behaviors received usefulness refers to the proposition that the use of the information system improves the performance of a community or an entity. Perceived ease of use refers to the extent to which the users believe the system is easy to use. In this study, we intend to use the (TAM) Theory of Acceptance Model to measure the impact of perceived usefulness and ease of use on the behavior of the members of the community.

- Trust in online banking

Mainly economic behavior is explored through the lens of the competitive theory, and there is a lack of literature that discusses economic behavior through the lens of cooperative theory. In the case of self-help groups, generally, the members act in a collaborative environment (Alderson Wroe, 1965). Trust is a hygiene factor for economic exchange (Sonja Grabner Krauter & Rita Faullant, 2008) and is at the heart of all relationships (Robert M. Morgan and Shelby D. Hunt, 1994). It is defined as the assurance regarding the performance and derivation of the benefits from a contract. It acts as a source of insurance and makes commerce possible in the intangible electronic environment (Dr Regina Connolly & Frank Bannister, 2007). (Mcknight, D. & Chervany, Norman, 2001), in their research have highlighted that trust can be of four types – disposition to trust, institution-based trust, trusting belief, and trusting intention. A disposition towards trust in which an individual continuously demonstrates a readiness to rely on others. Institutional trust refers to the perception that the institution's atmosphere is conducive to trusting behavior. The notion that a person possesses favorable attributes is a trusting belief. People have a trusting intent when they are willing to rely on others. (P. Ratnasingham, 1998) highlights that trust is crucial in the internet banking environment. In the online banking environment, where the parties are not physically present, uncertainty and risk are inherent. Broadly, the internet banking environment is highly uncertain, and trust is vital in promoting loyalty and technology usage. It is related to the reliability of the spoken words regarding the performance of a contract. Trust has various dimensions, including competency. Trust is a willingness of a party to be vulnerable to the actions of another party without considering the motivation or ability of a peer or the other members of the community or group. It is often defined as the predictability of the person or member. As per the literature, this predictability leads to cooperation (Lewis , 2001). Trust is considered a cognitive component (Anderson and Narus, 1990). Trust is discussed through competency, benevolence (Strickland, 1958), honesty, and ability (Mayer et al., 1995), (Hsiu-FenLin, 2011). Honesty is the belief that the other person will perform the promise (Suh and Han , 2002). As per the literature, safety and privacy profoundly impact the trust of the members or users in an online environment (Lee and Turban, 2001). According to the Theory of Planned Behavior, the intention to use technology is determined by the intention to use, and the intention to use is determined by the subjective norms and attitudes toward behavior. And the attitude comprises the perceived usefulness and the ease of perceived use. Perceived usefulness refers to the degree to which the user expects that the technology system requires less effort to use (Davis et al., 1989). Trust refers to a person's belief depending on another person (Mayer et al., 1995).

Hypothesis 1.

Trust positively impacts the perceived security in online banking

Hypothesis 2.

Perceived usefulness has a direct impact on the trust of online banking

- Perceived ease of use and perceived usefulness

Perceived ease of use and perceived usefulness refer to the perception of the user regarding the ease of use of technology and perceived usefulness of technology. As per the theory, these two factors impact the user behavior intention (Bitkina and Kim et al. , 2022). The research model incorporates the critical constructs from the Theory of Technology Acceptance Model, i.e., the trust regarding the exchanging the information, and integrates it through the TRA (Theory of Reasoned Action). From the literature, it is established that perceived usefulness positively impacts the members' purchase intention. PEOU (Perceived Ease of Use) refers to the extent to which the user expects that the use of technology will require less effort. And PU (Perceived Usefulness) refers to the perception that the adoption of technology will enhance the performance of the members of the community. In our research, we have looked at the benefits of digital banking in saving time, making banking available at any location, at any time, and saving costs. Perceived ease of use refers to the reduction in the effort involved. In the context of digital banking, usage by self-help group members refers to the convenience and ease of banking. In this research paper, we propagate that the Perceived ease of use increases perceived usefulness. (Davis, 1989) proposed that behavioral intention comprises perceived usage and perceived ease of use. Theory of Reasoned Action (TRA) decomposes the (Technology Acceptance Model) construct of attitude into "perceived usage" and "perceived ease of usage." And perceived ease of use and trust increase the perceived usage of digital banking. The Theory of Acceptance Model (TAM) employs (PEOU) Perceived ease of use to describe internal control factors and does not consider the external factors. At the same time, the (Theory of Planned Behavior) considers the impact of situation-specific factors. But in this paper, since the main aim is to explain the underlying phenomenon and not the prediction, the Technology Acceptance Model (TAM) has been used, not the Theory of Planned Behavior (TPB).

Hypothesis 3.

Perceived ease of use directly impacts trust in digital banking

Hypothesis 4.

Perceived usage directly impacts the intention to use digital banking

Hypothesis 5.

Perceived ease of use directly impacts the intention to use digital banking

Hypothesis 6.

Trust directly impacts the intention to use digital banking

- Perceived Security

Perceived security refers to the perception of security in the trust, flow of information, and members' satisfaction. The study highlights that security and privacy concerns harm the members' trust. Moreover, the research highlights that security is a perception rather than a reality for average users. The intention to use is impacted by trust, flow, and satisfaction (Gao et al., 2015) In an external environment of the digital informational interface, the users cannot ensure whether the system is secure or not. Thus, we propagate that perceived security influences the technology adoption behavior of individual users (Ye, C. et al., 2008).

Moreover, this hypothesis further highlights that the capability of the information provider to provide information impacts the user's perception of security. Thus, we hypothesize that perceived security positively impacts the intention to use technology in digital banking. Also, perceived security affects the users' trust in the integrity and security of the digital banking environment.

Hypothesis 7.

Perceived security directly impacts the intention to use digital banking Intention to use technology

As per the literature, the adoption of technology is an individual's behavior. The attitude towards that behavior impacts the adoption of technology. As per the Theory of Reasoned Action (TRA) (Fishbein, 1975), technology usage is driven by behavioral intention and attitude, which can be cognitive and affective. Most of the studies use the theoretical lens of the Theory of Technology Acceptance Model (TAM), which highlights that the users adopt and use a technology that has utility for them (Brown et al. 2002), (Bhattacharjee & Premkumar, 2004).

Hypothesis 8.

Perceived usage directly impacts the perceived ease of usage

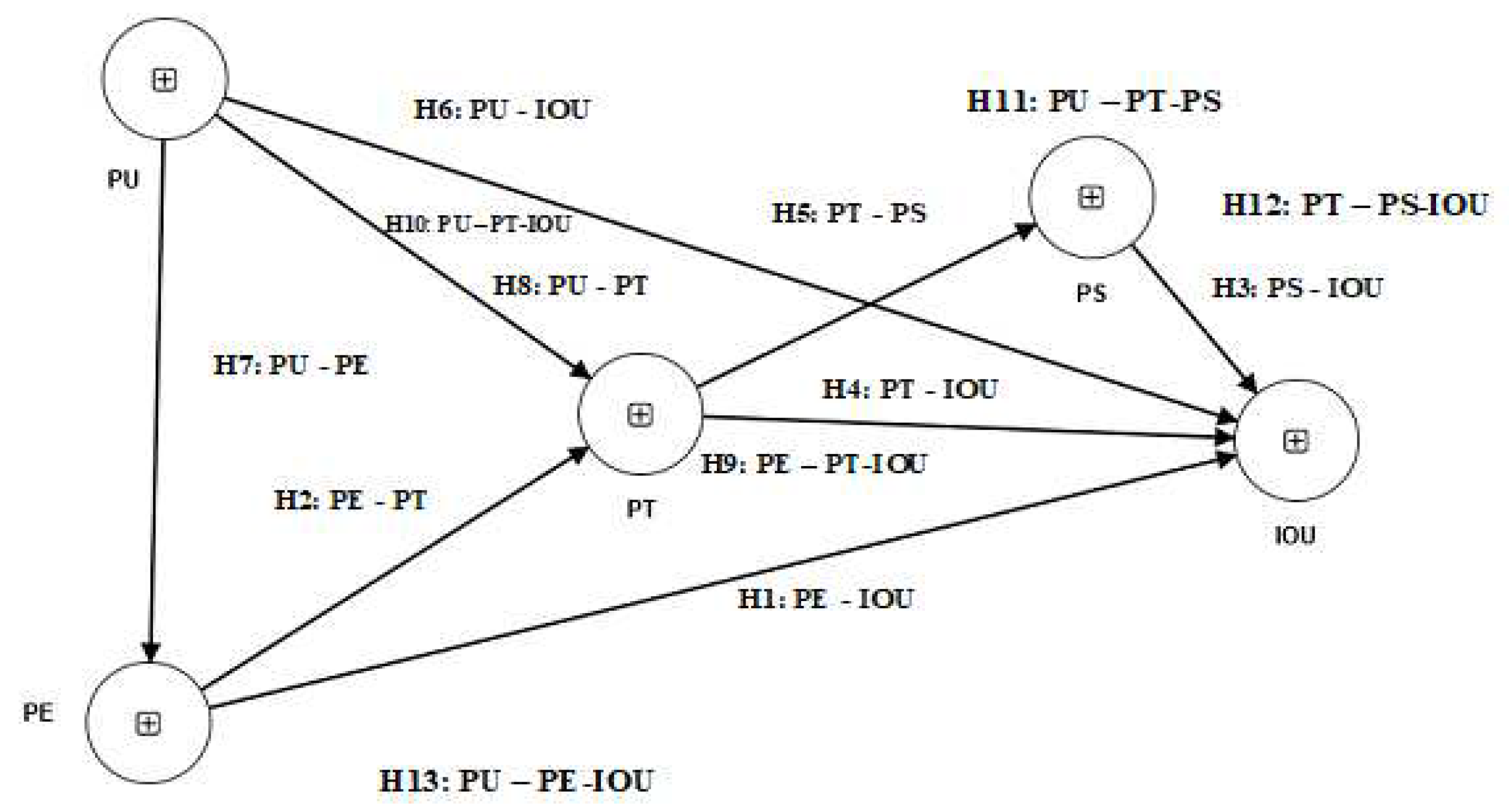

- Research Model

The research model for this study investigates the factors that impact the usage of online banking by the members of the community. As shown in Figure 1, the research model adapted the four determinant constructs (i.e., perceived ease of use, perceived usage, perceived security, and trust) in understanding the purchase intention. All the constructs in the measurement model are reflective, (Cheryl Jarvis Burke et al., 2003), (Edwards and Bagozzi, 2000), ( Podsakoff et al, 2012). In reflective indicators, the indicators are the consequence of the image of the destination. And the indicators flow from the construct to the indicators. In this model of Theory of Reasoned Action (TRA), three variables, i.e., (1) attitudes toward behavior or how people behave rationally through perceived ease of use, perceived usage, and perceived security, which could be instrumental (behavior perceived usefulness) and experimental (anticipated negative and positive feelings) (2) determinant of behavior, which refers to Trust (3) Behavior, i.e., usage. The dependent variable in this model is behavior, which refers to the usage of technology for banking by the members of the self-help groups. (Fishbein, M., & Ajzen, I, 2010), have defined behavior as action, target, context, and time. Target behavior of banking (action & target), online (context) usually (when). In this study, the mediation (Kenny, 1986) analysis has been used for analysis, (Cepeda et al. , 2017 ), (Hair et al. , 2017 ), (Memon et al., 2018), (Nitzl et al, 2016), (Sarstedt et al., 2020), (Zhao et al., 2010).

Besides that, there are various hypothesis that have been tested as part of mediation analysis. The hypothesis is given as follows:

H9.

Perceived trust mediates the relationship between perceived ease of use and intention to use

H10.

Perceived trust mediates the relationship between perceived usage and intention to use technology

H11.

Perceived trust mediates the relationship between perceived usage and perceived security

H12.

Perceived security mediates the relationship between perceived trust and intention to use technology

H13.

Perceived ease of use mediates the relationship between perceived usage and intention to use technology

2.1. Methodology

For the research, we used a questionnaire comprising different scales supported by the literature. The paper uses a Likert Scale, ranging from 1 (strongly disagree) to 5 (strongly agree). In this questionnaire, the items were adopted from the literature. In this study, five constructs, namely (1) Perceived ease of use, (2) Perceived usage, (3) Perceived security, (4) Trust (5) Intention to usage, are used. The first construct in the study is, Perceived ease of use as a construct comprises four significant indicators, namely, (1) Digital banking is reliable as a system of banking, (2) Digital banking fulfills the commitment that it assumes, (3) Digital banking delivers the promise (4) I trust digital banking, (Loonam et al., 2008 ). The second construct in the study is, Perceived usage, which comprises indicators such as (1) Digital banking saves time, (2) Digital banking is accessible anywhere, (3) Digital banking is available at all times, (4) Digital banking saves time, (Davis et al., 1989), (Akturan & Tezcan 2012), (Kaur and Malik , 2019), (Vukovic et al., 2019). Perceived security as a construct comprises indicators such as (1) Your operations are protected from any threat while using digital banking; (2) My personal information is kept confidential while using digital banking (3) My sensitive information is secure while using digital banking (4) Transactions conducted through digital banking are secure, (Khalilzadeh et al., 2017). Perceived ease of use is a construct that comprises various indicators such as (1) Digital banking is extremely convenient, (2) Digital banking is extremely easy, (3) Learning to use digital banking is easy (Venkatesh & Davis, 2000), (Bashir and Madhavaiah, 2015), (Rahi et al., 2016), (Wang et al., 2003). Trust as a construct comprises various indicators such as (1) Digital banking is reliable as a system of banking, (2) Digital banking fulfills the commitment that it assumes, (3) Digital banking delivers the services promised (McKnight et al., 1998), (Komiak et al., 2004), (Ennew & Sekhon, 2007), (Yousafzai et al., 2010) and

Table 1.

Questionnaire.

| Construct | Indicators |

| Perceived Trust | (1) Digital Banking is reliable as a system of banking |

| (2) Digital banking fulfill the commitments that it assumes | |

| (3) Digital banking delivers the services promised | |

| (4) I trust digital banking | |

| Perceived Security | (1) Your operations are protected from any digital banking threats (offense; attack; theft of money, documents, information, passwords, etc.) |

| (2) My personal information is kept confidential while using digital banking | |

| (3) My sensitive information is secure while using digital banking | |

| (4) Transactions conducted through digital banking are secure. | |

| Perceived usage | (1) Digital banking saves time |

| (2) Digital banking is accessible anywhere | |

| (3) Digital banking is available at all times | |

| (4) Digital banking saves cost | |

| Perceived ease of use | (1) Digital banking is extremely convenient |

| (2) Digital banking is extremely easy | |

| (3) Learning to use digital banking is easy | |

| Intention to use | (1) I use digital banking regularly |

| (2) I recommend digital banking to others | |

| (3) I use digital banking for my banking needs |

(Jarvenpaa et al, 2000). Usage as a construct comprises various indicators such as (1) I use digital banking regularly, (2) I recommend digital banking to others (3) I use digital banking for my banking needs. Error! Reference source not found. shows the questionnaire with a description of indicators.

The hypotheses constructed within TAM (Technology Acceptance Model) are tested using the questionnaire-based approach using PLS-SEM (Structural Equation Modeling) (Wold, 1985). (Babin & Boles, 1998) has shown that SEM (Structural Equation Modeling) is highly regarded by academicians. PLS-SEM is aimed at maximizing the explained variance of the endogenous constructs while minimizing the overall term (Claudia et al., 2014). This method is suitable for data with non-normality and mediation analysis (Hair et al., 2017), (Sarstedt M et al., 2017). This PLS SEM-based method is also preferable over covariance-based structural modeling and ordinary least squares (OLS) regressions in case of non normality and small sample sizes (Hair et al., 2011), (Claudia et al., 2014). This method is critical and significant for exploring new relationships in the structural model (Hair et al., 2019), (Jose Benitez et al., 2010 ). SmartPLS v4 software, (Joseph et al. , 2019 ). This software is used for the calculation of the measurement and structural model. The measurement model was assessed in the first step, and the structural model was evaluated in the second step.

2.2. Data Collection Process

The details are given in the table:

Table 1.

Descriptive Statistics for the sample.

| Profile | Particulars | Frequency |

|---|---|---|

| Age | 20-24 | 5 |

| 25-29 | 14 | |

| 30-34 | 17 | |

| 35-39 | 15 | |

| 40-44 | 12 | |

| 45-49 | 22 | |

| 50-54 | 7 | |

| 55-59 | 5 | |

| 60-64 | 1 | |

| Gender | Females | 20 |

| Males | 78 |

As per Table 1, in our dataset, there are 98 members. The majority of the members are between 25 to 49. In the given dataset, there is no issue of univariate data normality. All the skewness and kurtosis values are between -2 and +2. From the multivariate normality analysis, it becomes apparent that Mardia's Multivariate skewness (β= 97.28; p <0.00) and multivariate kurtosis ( β=407.55 ; p <0.00) suggest the multivariate non-normality. This is another reason for using the PLS-SEM, as it can adequately handle nonnormal data (Hair et al. , 2019 ).

3. Results

3.1. Normality Test

(Zhang & Yuan, 2018), suggested a web-based calculator test for multivariate normality in the data (Mardia, 1970). For accurate model prediction, multivariate normality is one of the criteria. Our data show univariate normality as indicated by the test of Skewness and Kurtosis (George & Mallery, 2010), (Field, 2009). Nonnormality was found in the data while testing multivariate normality through Skewness and Kurtosis. The nonnormality of data and lack of distributional assumption is another reason for using the PLS-SEM analysis (Hair et al., 2012b) (Nitzl et al. , 2016 ). PLS-SEM shows higher robustness in situations of abnormality (Sarstedt et al., 2016b), (Sarstedt et al., 2017b) (Efron, B, 1987).

3.2. Common Method Bias

Common method bias is when data is derived from a single source (Avolio et al., 1991). This could be a source of the problem and lead to validity issues in the data (Podsakoff et al., 2012). The study mitigated the case of common method bias in the data (CMB) by using the procedural design and statistical test (Reio, 2010). The questionnaire was designed so that the questions were specific and targeted to a particular audience. For statistical control, the study used the VIF (Variance Inflation Factor) method to test for collinearity (Kock, 2015), (Podsakoff et al., 2003), (Burton Jones, 2009), (Vishwanathan & Kayande, 2012). A pilot study was undertaken with 30 respondents to ensure that the responses were accurate (Hulland et al., 2018). As per the results, the VIF (Variance Inflation Factor) ranged between 1 to 3.73 for all the latent constructs, which is below the conservative threshold of 5 and slightly above 3.3, suggesting that CMB (Common Method Bias) is not an issue for the study

3.3. Assessment of the Reflective Constructs

As per the research prescription, the outer loadings of indicators were examined. The outer loadings for all the indicators for the five constructs are above 0.7 (Hair et al. , 2010 ). Figure 1. shows the final structural model used for PLS-SEM hypothesis testing. The first step in evaluating the PLS-SEM model is to assess the outer model. It involves evaluating the relationship between the constructs and the indicators (Hair et al., 2014). To measure and assess the model, the study aims to estimate its internal consistency reliability, indicator validity, convergent validity, and discriminant validity (Bernstein, 2017). The first step is to evaluate the reliability of internal consistency. The first criterion to measure the indicator reliability is to estimate the Cronbach Alpha. This indicator has a value bound between 0 and 1. Values > 0.60 are considered acceptable for early-stage research, and values greater than 0.70 and more significant than 0.80 are deemed appropriate. Values higher than 0.90 are not desirable, which implies that the same indicator is being measured or the indicators are highly correlated. This indicator focuses solely on the correlation of the indicators. The other measures are composite reliability and Rho values to test the indicator reliability. Cronbach Alpha is the lower bound, and the composite reliability is the upper bound of the true internal consistency and reliability. The Cronbach alpha is the most conservative indicator of internal consistency, while the composite reliability is the most liberal indicator. The Rho value is the indicator between the Cronbach alpha and the composite reliability. The inference statistics for the Rho value are more significant than 0.70 and lower than 0.90. The AVE (Average Variance) criterion was used in the study to assess convergent validity. To determine the convergent validity, AVE (Average Variance) values, as suggested by Hair et al. (2017), were computed, and all the values were above the threshold value of 0.50. (Fornell & Larcker, 1981) suggests that discriminant validity implies that the latent variables account for more variance explained by its indicator variables than shared with other constructs (Campbell & Fiske, 1959). The Fornell and Larcker criterion and HTMT (Heterotrait Monotrait ratio) were used to determine the discriminant validity (Fornell & Larcker, 1981). As per the Fornell & Larcker criterion (Fornell & Larcker, 1981), the square root of AVE (Average Variance) is higher than the construct's correlation with the other constructs. Thus, there is no issue of discriminant validity in the data. Heterotrait Monotrait Ratio (HTMT) (Henseler et al., 2015) values are all above the threshold value of 0.85, which shows no discriminant validity issue in the data. So, the issues of convergent and discriminant validity are dealt with by different measurements based on the indicator values given in the study. Figure 2 below shows the measurement model. The results of indicator reliability, internal consistency, and convergent validity are shown in Table 2. And the results of discriminant validity are shown in Table 3.

3.4. Assessment of structural model

In the next step after testing the reliability and validity of the measurement model, the next step is to analyze the structural model to validate the hypothesis (Hair et al., 2017). Further, the VIF (Variance Inflation Factor) was calculated to test the multicollinearity of the model. The results show that all the tolerance values are below the threshold value of 5. The direct and indirect hypothesis are tested using the PLS SEM methodology. In this structural model, the results of hypothesis testing for direct and indirect effects are presented in Table 4. There is a significant relationship between perceived ease of use and intention to use (β1 = 0.326; t = 2.418; p<0.008) at 1% significance level; perceived ease of use and perceived trust (β2 = 0.230; t = 1.681; p<0.046) at 10% significance level. Also, the relationship between perceived security and intention to use is not significant (β3=0.174; t=1.391; p =0.082) at 10% significance level. Moreover, the relationship between the perceived trust and intention to use is insignificant (β4 = 0.055; t = 0.756; p <0.225) is not significant at 10%; but relationship of perceived trust with perceived security the relationship is significant (β5 = 0.774; t = 12.559; p < 0.00) at 1%. The relationship between perceived usage and intention to use is significant (β6 = 0.389; t = 3.552; p<0.00) at 1%. The relationship between perceived usage and perceived trust is significant (β8 = 0.583; t=4.664; p<0.00) is significant at 1%. And the relationship between perceived usage and perceived ease of usage is significant at 1% (β9 = 0.855; t=19.35; p<0.00).

To assess the quality of the structural model, the explained variance through the coefficient of determination (R2), effect size (f2), and predictive relevance (Q2_predict) were calculated. The model exhibits reasonable predictive relevance. Perceived ease of usage explains 62.2% of the predictive relevance in perceived trust. Perceived ease of usage explain 79.4% of the predictive relevance in usage. Thus, the model has substantial predictive relevance, as all the values of R2 are above the threshold value of 0.26 (Cohen, J., 1988). Also, the f2 value shows enough predictive relevance, as most of the values are above the threshold of 0.15 (medium), and at least four are above (0.35). Table shows the results of the structural model. The predictive relevance was calculated using Stone-Geisser Q2 (Stone, M, 1974), (Geisser, S., 1974). The Q2_predict value is greater than 0 for intention to use (0.734), perceived security (0.661), perceived ease of use (0.734), and perceived trust (0.601). This clarifies that the model is predictively valid (Shmueli et al., 2019), (Chin et al., 2020).

Table 5.

Results of structural model with bootstrapping procedure (Insert here).

| Path | Beta | Std Err | T stat | LLCI | ULCI | Remark | R2 | F2 | Q2predict |

| PE-IOU | 0.326 | 0.135 | 2.418*** | 0.108 | 0.551 | Supported | 0.794 | 0.110 | 0.734 |

| PE-PT | 0.230 | 0.137 | 1.681** | 0.020 | 0.466 | Supported | 0.622 | 0.038 | |

| PS-1OU | 0.174 | 0.125 | 1.391** | -0.021 | 0.386 | Supported | 0.029 | ||

| PT-IOU | 0.055 | 0.073 | 0.756 | -0.057 | 0.178 | Not supported | 0.005 | ||

| PT-PS | 0.774 | 0.062 | 12.559*** | 0.649 | 0.850 | Supported | 0.599 | 1.494 | 0.661 |

| PU-IOU | 0.389 | 0.109 | 3.552*** | 0.200 | 0.569 | Supported | 0.141 | ||

| PU-PE | 0.855 | 0.044 | 19.355*** | 0.759 | 0.907 | Supported | 0.731 | 2.716 | 0.734 |

| PU-PT | 0.583 | 0.125 | 4.664*** | 0.368 | 0.776 | Supported | 0.242 | 0.601 |

Table 6.

Results of Mediation analysis with bootstrapping procedure.

| Path | Beta | Std Err | T stat | LLCI | ULCI | Remark |

| PE-PT-IOU | 0.013 | 0.019 | 0.651 | -0.006 | 0.061 | Not Supported |

| PU-PT-IOU | 0.032 | 0.028 | 0.721 | -0.028 | 0.120 | Not Supported |

| PU-PT-PS | 0.451 | 0.103 | 4.373*** | 0.279 | 0.615 | Supported |

| PT-PS-IOU | 0.135 | 0.098 | 1.371 | -0.011 | 0.310 | Not Supported |

| PU-PE-IOU | 0.279 | 0.272 | 2.373*** | 0.095 | 0.479 | Supported |

Note: *p<0.05, *p<0.10; PE- Perceived ease of use; IOU- Intention to use; PT – Perceived trust; PS – Perceived security; PU – Perceived usage.

3.5. Mediation Analysis

In this study, the transmittal approach has been used to evaluate the mediation effect (Rungtusanatham et al., 2014), (Preacher & Hayes, 2008). Through this approach, we want to measure the indirect effect of the independent variable on the dependent variable through a mediator using the methodology suggested by the early researchers (Zhao et al., 2010), (Wood et al., 2008). In this study, a bootstrapping method with 5,000 subsamples was used to estimate the indirect effect using the 95 percent bias-corrected confidence interval (Hair et al. , 2017 ), (Bollen & Stine, 1990), (Shrout & Bolger, 2002). Further, the decision tree proposed by (Nitzl et al., 2016). The results of the PLS-SEM analysis are shown in the form of mediation analysis in Table 6. The results of the mediation analysis show that the indirect pathway running from perceived ease of use to intention of use through perceived trust is not significant (β9 = 0.013; t = 0.651; p <0.257). And, the indirect pathway between perceived usage and intention to use, through perceived trust is insignificant (β10 = 0.032; t=0.721; p<0.235) and is not significant at even 10%. But the pathway from perceived usage to perceived security through perceived trust is significant at 1% (β11 = 0.451; t = 4.373; p < 0.000) and the pathway from perceived usage to intention to use through perceived ease of use is significant at 1% significance level (β12 = 0.279; t = 2.379; p < 0.009) and the pathway from perceived usage to intention to use through perceived ease of use is significant at 5% significance level (β13 = 0.135; t = 1.371; p >0.000). The mediation is complementary partial mediation.

4. Conclusion

The data analysis shows that perceived ease of use and perceived security lead to the intention to use technology for banking. But perceived trust does not lead to the intention to use technology. Perceived security has a significant role in promoting the intention to use technology in banking. And the data analysis establishes that perceived usage leads to perceived ease of use, which leads to the intention to use technology in online banking. Without cognitive security , trust per se does not lead to the intention to use technology for online banking. Perceived security leads to the intention to use technology for banking. There is need to undertake social intermediation initiatives to educated the users regarding the digital or cyber security issued to ensure safe usage of the technology. In current scenario the usage is purely based on perceived ease of usage. There is need to develop cognitive attitude regarding security issued related to digital banking to promote safe usage. This approach based on security will lead to trust and better utilization of digital technology for banking while reducing cyber frauds. Trust without addressing the security concerns of the users will not promote adoption of technology.

References

- Agitaputri, 1998. Robin Hill Sample Size. Interpersonal Computing & Technology: An electronic journal for the 21st century, Volume 6, pp. 3-4.

- Akturan, U., & Tezcan, N, 2012. Mobile banking adoption of the youth market. Marketing intelligence and Planning, 30(4), pp. 444-459. [CrossRef]

- Alderson Wroe, 1965. Dynamic Marketing Behavior. Homewood II: Richard D. Irwin.

- Andrew Burton Jones, 2009. Minimizing Method Bias Through Programmatic Research. MIS Quarterly, 33(3), pp. 449-491. [CrossRef]

- Anshuman et al., 2021. Does SMS advertising still have relevance to increase consumer purchase intention? A hybrid PLS-SEM-neural network modelling approach. Computers in Human Behavior, pp. 1-16. [CrossRef]

- Avolio, B. J. et al., 1991. Identifying Common Methods Variance With Data Collected From A Single Source: An Unresolved Sticky Issue. Journal of Management, 17(3), pp. 571-581. [CrossRef]

- Babin, J. B., & Boles, J. S, 1998. The Effects of Perceived Co-Worker Involvement and Supervisor Support onService Provider Role Stress,. Journal of Retailing, 72(1), pp. 57-75. [CrossRef]

- Bashir I and Madhavaiah C, 2015. Consumer attitude and behavioural intention towards Internet banking adoption in India. Journal of Indian Business Research, 7(1), pp. 67-102. [CrossRef]

- Bernstein, N. a., 2017. Psychometric Theory. USA : McGrawHill.

- Bhattacherjee, A., & Premkumar, G, 2004. Understanding Changes in Belief and Attitude toward Information technology usage : A theoretical model and longitudnal test. MIS Quarterly, 28(2), pp. 229-254. [CrossRef]

- Bitkina and Kim et al., 2022. Measuring user perceived characterstics for banking services : Proposing a methodology. International Journal of Environmental Research and Public Health, pp. 1-15. [CrossRef]

- Brown, S. A., Massey, A. P., Montoya-Weiss, M. M., &, 2002. Do I Really Have to? User Acceptance of Mandated Technology. European Journal of Information Systems, 11(4), pp. 283-295. [CrossRef]

- Campbell, D. T., & Fiske, D. W, 1959. Convergent and discriminant validation by the multitrait multimethod matrix. Psychological bulletin, 56(2), pp. 81-105. [CrossRef]

- Cepeda et al., 2017. Mediation analysis in PLS SEM : Guidelines and Empirical Examples. H. Latan & R. Noonan (Eds.), Partial Least Squares Path Modeling: Basic Concepts, Methodological Issues and Applications, pp. 173-195.

- Cheryl Jarvis Burke et al., 2003. A Critical Review of Construct Indicators and Measurement Model Specification in Marketing and Consumer Research. Journal of Consumer Research, 30(2), pp. 199-218. [CrossRef]

- Chou et al., 1991. Scaled test statistics and robust standard errors for Non Normal data in covariance structure. British Journal of Mathematical and Statistical Psychology, 44(2), pp. 347-357. [CrossRef]

- Claudia et al., 2014. A comparative study of CB-SEM and PLS-SEM for theory development in family firm research. Journal of Family Business Strategy, 5(1), pp. 116-128. [CrossRef]

- Cohen, J., 1988. Statistical Power Analysis for the Behavioral Sciences (2nd ed.). Hillsdale, New Jersey : Lawrence Erlbaum Associates, Publishers. [CrossRef]

- D. Straub, M. Keil, W. Brenner,, 1997. Testing the technology acceptance model across cultures: a three country study. Information and Management, 33(1), pp. 1-11. [CrossRef]

- Davis F.D., 1989. erceived usefulness, perceived ease of use, and user acceptance of information technology. MIS Quarterly, 13(3), pp. 319-340. [CrossRef]

- Davis FD, Bagozzi, RP and Warshaw PR, 1989. User acceptance of computer technology : A comparison of two theoretical models. Management Science, 35(8), pp. 982-1003. [CrossRef]

- Davis, F.D., 1986. A Technology Acceptance Model for Empirically Testing New End-User Information Systems: Theory and Results.. Sloan, Massachusetts : Sloan School of Management, Massachusetts Institute of Technology..

- Dr Regina Connolly & Frank Bannister, 2007. Consumer Trust in Internet Shopping in Ireland: Towards the Development of a More Effective Trust Measurement Instrument. Journal of Information technology, Volume 22, pp. 102-118. [CrossRef]

- E. Karahanna, D.W. Straub, 1999. he psychological origins of perceived usefulness and ease of use,. Information and Management, 35(4), pp. 237-250. [CrossRef]

- E. Karahanna, D.W. Straub, n.d. The psychological origins of commerce, Internet Research: Electronic Networking Appli-.

- Edwards J.R. and Bagozzi R.P, 2000. On the nature and direction of relationships between cosntructs and measures. Psychological methods, Volume 52, pp. 155-74. [CrossRef]

- Efron, B, 1987. Better bootstrap confidence intervals. Journal of the American Statistical Association, 82(397), pp. 171-185. [CrossRef]

- Ennew C and Sekhon H, 2007. Measuring trust in financial services : the trust index. Consumer Policy Review, Volume 17, pp. 62-8.

- F.D. Davis, 1989. Perceived usefulness, perceived ease of use and user acceptance of information technology. MIS Quarterly, 13(3), pp. 319-340. [CrossRef]

- Faul F et al., 2009. Statistical power analysis using G* Power 3.1 : Tests for correlation and regression analysis. Behavior Research Methods, 41(4), pp. 418-432. [CrossRef]

- Field A, 2009. Discovering statistics using SPSS. London : SAGE. [CrossRef]

- Fishbein, M., & Ajzen, I, 2010. Predicting and changing behavior: The reasoned action approach.. New York : Psychology Press.

- Fishbein, M. &. A. I., 1975. Belief, attitude, intention and behavior: An introduction to theory and research. Reading : MA Addison Wesley.

- Fornell, C. G., & Larcker, D. F., 1981. Evaluating structural equation model with unobservable variables and measurement error. Journal of Marketing Resaerch, 18(1), pp. 39-50. [CrossRef]

- Fornell, C., & Larcker, D. F., 1981. Structural Equation Models with Unobservable Variables and Measurement Error: Algebra and Statistics.. Journal of Marketing Research, Volume 18, pp. 382-388. [CrossRef]

- Gao, L.; Waechter, K.A.; Bai, X, 2015. Understanding consumers’ continuance intention towards mobile purchase: A theoretical farmework and empirical study. Computer Human Behaviour, Volume 53, pp. 249-262. [CrossRef]

- Gay, L. R., & Diehl, P. L, 1992. Research Methods for Business and Management. In Hill, R. (1998) (Ed.), What Sample Size Is “Enough’ in Internet Survey Research”? Interpersonal Computing and Technology:. An Electronic Journal for the 21st Century..

- Geisser, S., 1974. A Predictive Approach to the Random Effect Model. Biometrika, Volume 64, pp. 101-107. [CrossRef]

- George D. & Mallery M, 2010. SPSS for Windows Step by Step : A Simple Guide and Reference. Boston : Pearson.

- Hair et al., 2010. Multivariate data analysis. New Jersey : Prentice hall.

- Hair et al., 2017. A Primer on Partial Least Squares Structural Equation Modelling (PLS SEM), Chapter 7. Thousands Oaks, CA : Sage.

- Hair et al., 2019. When to use and how to report the results of PLS-SEM. European Business Review, pp. 1-24. [CrossRef]

- Hair et al., 2011. PLS SEM : Indeed a silver bullet. The Journal of Marketing Theory and Practice, 19 (2), pp. 139-151. [CrossRef]

- Hair et al., 2014. A primer on partial least squares structural equation modeling (PLS-SEM). Thousands Oaks : Sage publication.

- Hair et al., 2017. A Primer on Partial Least Squares Structural Equation Modelling (PLS SEM). Thousand Oaks California: Sage Publisher.

- Hair, J.F. et al., 2012b. An assessment of the use of partial least squares structural equation modeling in marketing research. Journal of the Academy of Marketing Science, Volume 40, pp. 414-433. [CrossRef]

- Hair, J.F., Hult, G.T.M., Ringle, C.M. and Sarstedt, M., 2017. A Primer on Partial Least Squares Structural Equation Modeling (PLS-SEM).. Thousand Oaks, CA : Sage Publications Inc.

- Henseler, J et al., 2015. A new criterion for assessing discriminant validity in variance-based structural equation modeling. Journal of the Academy of Marketing Science,, 43 (1), pp. 115-135. [CrossRef]

- Herman Wold, 1980. Model construction and evaluation when theoretical knowledge is scarce. In J. Kmenta and J. B. Ramsey. Evaluation of econometric models, pp. 47-74.

- Hsiu-FenLin, 2011. An empirical investigation of mobile banking adoption: The effect of innovation attributes and knowledge-based trust. International Journal of Information Management, 31(3), pp. 252-260. [CrossRef]

- Hulland et al., 2018. Marketing survey research best practices: Evidence and recommendations from a review of JAMS article. Journal of the Academy of Marketing Sciences, 46(1), pp. 92-108. [CrossRef]

- James C. Anderson and James A. Narus, 1990. A Model of Distributor Firm and Manufacturer Firm Working Partnerships. Journal of Marketing, 54(1), pp. 42-58. [CrossRef]

- Jarvenpaa et al, 2000. Consumer trust in internet store. Information Technology and Management, Volume 1, pp. 45-71. [CrossRef]

- John Hulland et al., 2018. Marketing Survey research best practices : Evidence and recommendations from a review of JAMS article. Journal of the Academy Marketing Sciences, Volume 46, pp. 92-108. [CrossRef]

- Jose Benitez et al., 2010. How to perform and report an impactful analysis using partial least squares: Guidelines for confirmatory and explanatory IS Model. Information and Management, pp. 1-16. [CrossRef]

- Joseph et al., 2019. When to use and how to report the results of PLS-SEM. European Business Review, pp. 1-24. [CrossRef]

- Joseph F. Hair et al., 2019. When to use and how to report the results of PLS SEM. European Business Review, 31(1), pp. 1-24. [CrossRef]

- K.A. Bollen, R. Stine, 1990. Direct and indirect effects: classical and bootstrap estimates of variability. Sociological Methodology, 20(1), pp. 115-140. [CrossRef]

- K.J. Preacher and A.F. Hayes, 2008. Asymptotic and resampling strategies for assessing and comparing indirect effects in multiple mediator models. Behavior Research Methods, 40(3), pp. 879-891. [CrossRef]

- Kaur A and Malik G, 2019. Examining factors influencing Indian customers intentions and adoption of internet banking: Extending TAM with electronic service quality. Innovative Marketing, 15(2), pp. 42-57. [CrossRef]

- Kenny, B. R. a. D., 1986. The Moderator - Mediator Variable Distinction in Social Pyschological Research : Conceptual, Strategic, and Statistical Considerations. Journal of Personality and Social Psychology, 51 (6), pp. 1173-1182. [CrossRef]

- Khalilzadeh, J et al., 2017. Security-related factors in extended UTAUT model for NFC based mobile payment in the restaurant industry. Computer Human Behavior, Volume 70, pp. 460 -474. [CrossRef]

- Komiak et al., 2004. Understanding consumer trust in agent mediated electronic commerce. Web mediated Electronic Commerce and Traditional Commerce, 5(1-2), pp. 181-207. [CrossRef]

- Lee and Turban, 2001. A Trust Model for Consumer Internet Shopping. International Journal of Electronic Commerce, 6(1), pp. 75-91. [CrossRef]

- Lewis A Friedland, 2001. Communication, Community, and Democracy: Toward a Theory of the Communicatively Integrated Community. Communication Research, pp. 358-391. [CrossRef]

- Liao Cheung et al., 2002. Internet-based e-banking and consumer attitudes: an empirical study. Information and Management, 39(4), pp. 283-295. [CrossRef]

- Loonam, Mary, and Deirdre O’Loughlin, 2008. Exploring E-service Quality: A Study of Irish Online Banking.. Marketing Intelligence & Planning, pp. 759-80. [CrossRef]

- Mardia K.V., 1970. Measures of multivariate skewness and kurtosis with applications. Biometrika, pp. 519-530. [CrossRef]

- Mayer et al., 1995. An Integrative Model of Organizational Trust. The Academy of Management Review, 20(3), pp. 709-734. [CrossRef]

- McKnight et al., 1998. Initial trust formation in new organizational relationships. The Academy of Management Review, 23(3), pp. 473-90. [CrossRef]

- Mcknight, D. & Chervany, Norman, 2001. Trust and Distrust definition : One bite at time. Trust in Cyber Societies, Volume 2246, pp. 27-54. [CrossRef]

- Melody A Hertzog, 2008. Considerations in determining sample size for pilot studies. Research in Nursing & Health, Volume 31, pp. 180-191. [CrossRef]

- Memon et al., 2018. Mediation Analysis : Issues and recommendation. Journal of Applied Structural Equation Modeling, 2 (1), pp. i - ix. [CrossRef]

- Ned Kock, 2015. Common method bias in PLS-SEM: A full collinearity assessment approach. International Journal of e collaboration, 11(4), pp. 1-10. [CrossRef]

- Nitzl et al., 2016. Mediation analysis in partial least squares path modeling: Helping researchers discuss more sophisticated models. Industrial Management Data Systems, pp. 1849-1864. [CrossRef]

- Nitzl et al, 2016. Mediation Analyses in Partial Least Squares Structural Equation Modeling : Helping Researchers discuss more sophisticated model. Industrial Management and Data Systems, 119 (9), pp. 1849-1864. [CrossRef]

- Nitzl, C, Roldan, J.L. and Cepeda, 2016. Mediation analysis in partial least squares path modeling: Helping researchers discuss more sophisticated models. Industrial management & data systems, 116(9), pp. 1849-1864. [CrossRef]

- P. Ratnasingham, 1998. The importance of trust in electronic commerce. Internet Research : Electronic Networking Applications and Policy, 8(4), pp. 313-321. [CrossRef]

- P.E. Shrout, N. Bolger, 2002. Mediation in experimental and nonexperimental studies: new procedures and recommendations. Psychological Methods, 7(4), pp. 422-445. [CrossRef]

- Philip M Podsakoff et al, 2012. Sources of method bias in social science research and recommendations on how to control it. Annual review of psychology, Volume 63, pp. 539-569. [CrossRef]

- PL Alreck and RB Settle, 2002. The hurried consumer: Time-saving perceptions of Internet and catalogue shopping. Journal of Database Marketing and Customer Strategy Management, Volume 10, pp. 25-35. [CrossRef]

- Podsakoff, P.M. et al., 2003. Common method biases in behaviorial research : A critical review of literature and recommended remedies. Journal of Applied Psychology, 88(5), pp. 879-903. [CrossRef]

- R. Agarwal, E. Karahanna,, 2000. Time flies when you’re having computer technology: a comparison of two theoretical. IS Quarterly, 24(4), pp. 665-694. [CrossRef]

- R.E. Wood et al., 2008. Mediation testing in management research: a review and proposals. Organizational Research Methods, 11(2), pp. 270-295. [CrossRef]

- Rahi, Samar & Ghani, Mazuri & Ngah, Abdul., 2016. Investigating the role of UTAUT and e service quality in internet banking adoption setting. The TQM Journal, 31(3), pp. 491-506. [CrossRef]

- Reio, T. G., 2010. The Threat of Common Method Variance Bias to Theory Building. Human Resource Development Review,, 9(4), pp. 405-411. [CrossRef]

- Robert M. Morgan and Shelby D. Hunt, 1994. The Commitment-Trust Theory of Relationship Marketing. Journal of Marketing, 58(3), pp. 20-38. [CrossRef]

- Roger C. Mayer et al., 1995. An Integrative Model of Organizational Trust. Academy of Management Review, 20(3), pp. 709-734. [CrossRef]

- Rungtusanatham et al., 2014. Theorizing, testing and concluding for mediation in SCM research: Tutorial and procedural recommendations. Journal of Operations Management, 32(3), pp. 99-113. [CrossRef]

- Sarstedt et al., 2016b. Estimation issues with PLS and CBSEM : Where the bias lies. Journal of Business Research, 69(10), pp. 3998-4010. [CrossRef]

- Sarstedt et al., 2020. Beyond a Tandem Analysis of SEM and PROCESS : Use of PLS SEM for Mediation Analysis. International Journal of Marketing Research, 62 (3), pp. 288-299. [CrossRef]

- Sarstedt M et al., 2017. Partial Least Squares Structural Equation Modeling. In : Homburg C Klarmann, M and Vomberg A (Eds). Handbook of Market Research, New York et al. New York: Springer.

- Sarstedt Ringle et al., 2017b. Treating unobserved heterogeneity in PLS-SEM: a multi method approach in Noonan R and Latan H (Ed). Partial Least Squares Structural Modeling : Basic Concepts, Methodological Issues and Applications, pp. 197-217.

- Saunders, M., Lewis, P. and Thornhill, A., 2009. Research Methods for Business Students. New York : Pearson.

- Shmueli, G., Sarstedt, M., Hair, J.F., Cheah, J.-H., Ting, H., Vaithilingam, S. and Ringle, C.M, 2019. Predictive model assessment in PLS-SEM: guidelines for using PLSpredict. European Journal of Marketing, 53(11), pp. 2322-2347. [CrossRef]

- Sonja Grabner Krauter & Rita Faullant, 2008. Consumer acceptance of internet banking: the influence of internet trust. International Journal of Bank Marketing, 26 (7 ), pp. 483-504. [CrossRef]

- Stone, M, 1974. Cross-Validatory Choice and Assessment of Statistical Predictions.. Journal of the Royal Statistical Society. Series B (Methodological),, 36(2), pp. 111-147. [CrossRef]

- Strickland, L. H, 1958. Surveillance and trust. Journal of Personality, Volume 26, pp. 200-215. [CrossRef]

- Suh and Han, 2002. Effect of trust on customer acceptance of Internet banking. Electronic Commerce Research and Applications, Issue 3-4, pp. 247-263. [CrossRef]

- V. Venkatesh, F.D. Davis, 2000. A theoretical extension of the technology acceptance model four longitudinal field studies. Management Science, 46(2), pp. 186-204. [CrossRef]

- Venkatesh, V., & Davis, F. D., 2000. A theoretical extension of the technology acceptance model: Four longitudinal field studies.. Management Sciences, Volume 46, pp. 186-204. [CrossRef]

- Vishwanathan & Kayande, 2012. Commentary on Common Method Bias in Marketing : Cause, Mechanisms and Procedural Methods. Journal of Retailing, 88(4), pp. 556-562. [CrossRef]

- Vukovic M. et al., 2019. Technology acceptance model for internet banking acceptance in split. Business Systems Research : International Journal of Society for Advancing Innovation and Research in Economy, 10(2), pp. 124-140. [CrossRef]

- W. Chin, J.-H. Cheah, Y. Liu, H. Ting, X.-J. Lim and T.H. Cham, 2020. Demystifying the role of causal-predictive modeling using partial least squares structural equation modeling in information systems research. Industrial Management & Data Systems, 120(12), pp. 2161-2209. [CrossRef]

- Wang et al., 2003. Determinants of User Acceptance of Internet Banking: An Empirical Study. International Journal of Service Industry Management, 14(5), pp. 501-513. [CrossRef]

- Wold, H.O.A, 1985. Partial least squares”, in Kotz, S. and Johnson, N.L. (Eds). Encyclopedia of Statistical Sciences, pp. 581-591. [CrossRef]

- X. Zhao, J.G. Lynch, Q. Chen, 2010. Reconsidering Baron and Kenny: myths and truths about mediation analysis. Journal of Consumer Research, 37(2), pp. 197-206. [CrossRef]

- Yao et al., 2015. Wine brand category choice and confucianism: A purchase motivation comparison of caucasian, Chinese and Korean consumers. Advances in national brand and private label marketing, pp. 19-33. [CrossRef]

- Ye, C. et al., 2008. The Role of Innovation and Wealth in the Net Neutrality Debate. J. Am. Soc. Inf. Sci. Technol., Volume 59, pp. 2115-2132. [CrossRef]

- Yousafzai S.M. et al., 2010. Explaining internet banking behavior : theory of reasoned action, theory of planned behavior or technology acceptance model. Journal of Applied Social Psychology, 40(5), pp. 1172-202. [CrossRef]

- Zhang, Z., & Yuan, K. H, 2018. Practical statistical power analysis using Webpower and R.. China, beijing : ISDSA Press. [CrossRef]

- Zhao et al., 2010. Reconsidering Baron and Kenny : Myths and Truths about Mediation Analysis. Journal of Consumer Research, 37(3), pp. 197-206. [CrossRef]

Figure 1.

Research Model.

Figure 2.

Measurement Model for Technology Acceptance Model.

Table 2.

Results of the Measurement model.

| Construct | Item | Scale | Loading/Weight | AVE/t-value | Composite reliability (rho_a) | Cronbach's Alpha | Composite reliability (rho_c) |

|---|---|---|---|---|---|---|---|

| Perceived Usage | PU1 | Reflective | 0.843 | 0.740 | 0.886 | 0.883 | 0.919 |

| PU2 | 0.859 | ||||||

| PU3 | 0.854 | ||||||

| PU4 | 0.884 | ||||||

| Perceived ease of use | PE1 | Reflective | 0.913 | 0.830 | 0.900 | 0.898 | 0.936 |

| PE2 | 0.898 | ||||||

| PE3 | 0.922 | ||||||

| Perceived Trust | PT1 | Reflective | 0.929 | 0.841 | 0.938 | 0.937 | 0.955 |

| PT2 | 0.903 | ||||||

| PT3 | 0.918 | ||||||

| PT4 | 0.917 | ||||||

| Perceived Security | PS1 | Reflective | 0.905 | 0.796 | 0.914 | 0.914 | 0.940 |

| PS2 | 0.896 | ||||||

| PS3 | 0.893 | ||||||

| PS4 | 0.874 | ||||||

| Intention to Use | IOU1 | Reflective | 0.942 | 0.866 | 0.924 | 0.923 | 0.951 |

| IOU2 | 0.929 | ||||||

| IOU3 | 0.922 |

Table 3.

Discriminant Validity.

| IOU | PEOU | PS | PT | PU | |

|---|---|---|---|---|---|

| IOU | 0.931 | ||||

| PEOU | 0.847 | 0.911 | |||

| PS | 0.827 | 0.852 | 0.892 | ||

| PT | 0.730 | 0.728 | 0.774 | 0.917 | |

| PU | 0.859 | 0.854 | 0.854 | 0.780 | 0.860 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Copyright: This open access article is published under a Creative Commons CC BY 4.0 license, which permit the free download, distribution, and reuse, provided that the author and preprint are cited in any reuse.