Submitted:

09 June 2023

Posted:

12 June 2023

You are already at the latest version

Abstract

This study aims to assess and identify the role of disruptive/digital technologies in financial innovation strategies as part of social innovations at both firm and country level. There are few studies of this type that "cross-examine" technical/social innovative capacity at the firm level vs. the same innovative capacity at the level of the world's major countries. Our proposed study brings some novel elements to the literature on this topic. First, the study synthesizes the factors/variables explaining technical/social innovative capacity as ranked by the GCI (Global Competitiveness Index) and GII (Global Innovation Index) at the country level and then correlates these variables with the factors explaining innovative capacity for the 50 companies in the BCG (Boston Consulting Group) ranking. Second, the study identifies three "driving forces" (digital technologies, managers and the market) as the main variables determining financial innovativeness at firm level. Third, based on the "cross" analysis of the information/data provided by the BCG study vs. the GII and GCI studies, the study suggests some ways to delineate and quantify financial innovation as part of social innovation (e.g., it is argued that 80% of the social innovation achieved annually by a firm relates to the financial relationships engaged by the firm with various categories of stakeholders). Finally, the study is also important from a pragmatic point of view as it suggests/proposes a number of principles that can be considered by managers for building a KM (knowledge management) and continuous innovation strategy. From a theoretical perspective, the study provides a starting point for further research aimed at explaining firm-level financial innovation through the massive use of disruptive technologies.

Keywords:

disruptive technology

; financial innnovation

; social innovation

; MNCs

1. Introduction

From the 1990 to the present, the entire business environment in the global economy has entered a phase of instability and/or successive and increasing change, due to political, technological, social, ecological, cultural and other factors. Since the 1970, Drucker [1] partially anticipated the new realities that were to emerge in the world economy, in that major transformations in technology, industrial structures, education and public policy would generate a chaotic environment for all firms that operate transnationally. This idea has been confirmed by the existences since the 1990; and the Great Global Recession of 2008-2010 came as further confirmation [2] of the unprecedented instability of the business environment. The stability of stock markets, financial markets at the international level, visible from 2020 until today, can be explained by the fact that systemic trust has remained relatively stable in the main countries of the world as well as at the global level, between firms/institutions and different international organisations ([3]).More recently, other major events at the global level (the trade war between the US and China, the social crisis caused by Covid 19, the war triggered by Russia in Ukraine, etc.) show us more and more clearly that we live in a risk society. [4] [5]. In 2021, the Global Risks Report ranks epidemics among the top global risks with potentially significant impact, whereas after 2010, the main risk was considered financial failure. [6].

In the context described, given the unstable nature of the capitalist system, innovation can become a creative response to trends and transformations taking place in the economic and social environment [7] [8] [9] [10]. Added to this is the technological opportunity created by progressive research in areas such as advanced manufacturing, robotics and digital technologies and their implementation in different socio-economic areas. In contrast, the turbulence that spread throughout the economy during the economic crisis of 2008 [2] affected the innovative behaviour of firms [11] [12], especially as a result of delaying access to financial resources, all the more so as the nature of innovation projects makes their financing different from the financing of ordinary assets [13].

This study proposes an analysis of the relationship between innovative capacity at country level (according to GII and GCI) vs. innovative capacity at firm/company level (according to BCG) taking into account that any entity can make extensive use of various disruptive technologies. In a turbulent and/or chaotic business environment, the use of digital technologies as part of disruptive technologies can assistance firms to improve their technical and social innovative capacity, and thus better respond to the challenges of going through a downswing in the cyclical evolution of business. More specifically, this study aims to identify the clearest and most substantiated principles that would support firms to implement financial innovation (as a major part of social innovation) through the extensive use of disruptive technologies.

A more in-depth analysis of what we call social innovations, and in particular disruptive social innovations, is needed, taking into account existing conceptualisations of disruptive innovation in general. Continuous innovative activity at firm level assumes, by definition, the acquisition and processing of new knowledge by skilled employees who are motivated to learn persistently. The paper published in 1995 by Nonaka and Takeuchi argues how tacit and explicit knowledge held by employees in firms is transformed into innovations and patents, respectively, but it is particularly concerned with technical innovations [14]. By explicit knowledge we mean knowledge that exists in books, manuals and can be easily transferred to others. By tacit knowledge we mean knowledge of an intuitive nature, based on experience and which is more difficult to transfer to others.

The structure of our proposed research includes a literature review section, followed by a research design section. In this third section of the study we formulate some hypotheses of the study and carry out an in-depth analysis of the factors/variables explaining the competitive position and/or innovative capacity according to the GCI and GII rankings for the main countries of the world. Subsequently, in section 4 of the study we present the company approached as a "hub" and the financial relationships it engages with various stakeholders, relationships that can be managed efficiently based on digital technologies. In the final part of the study, we present 3 "driving forces" for financial innovation using disruptive technologies at the firm level and analyse the main variables/factors that explain financial/social innovative capacity for the 50 companies included in the BCG ranking.

2. Literature review

One of the main ideas of Schumpeter's thought explains economic cyclicality as the result of innovation, which in turn is shaped by economic dynamics [15]. In Schumpeter's view [16]entrepreneurs successively bring technical, organisational or other novelties to the market and society, which means technical and social innovations. The competition between entrepreneurs and continuous innovation generates under certain conditions the emergence of a new industry, which means "creative destruction" ([17]; ([18]).

In the 1980s, Drucker argued quite well that social innovations are at least as important as technical innovations [19]. Thus, from the 1980s to the present day we discuss technical innovations (mainly concerning products and technologies) and social innovations (mainly concerning market relations and organization). In 1997, Christensen (C.M. Christensen, 1997) proposed the concept of "disruptive innovation" as equivalent to "creative destruction"; subsequently, dozens of volumes and articles have been written on disruptive innovations/technologies and their role for the economic progress of countries/firms [20,21,22,23,24]; [25]). In direct connection with disruptive innovation the concept of open innovation has developed more recently [26,27], which essentially refers to the orientation of the firm towards various stakeholders to build alliances, partnerships and other business networks through the use of digital technologies leading to a cumulative effect on the sources for continuous innovation. Some studies highlight the role of digital technologies in enhancing sustainable development in various countries/regions of the world, in balancing gender ratios, in managing various organizations, in holding social positions, etc. [28,29,30,31] Other studies explore, as appropriate, the role of digital/disruptive technologies for GDP growth at country level, for process optimisation at company level, as well as on the changes these technologies bring to society; times of crisis in society/economy seem to be better managed through ICT-enabled advances. [8,13,32,33,34,35,36]. In short, it can be concluded that episodes of crisis transform the environment and the innovative behaviour of firms. Thus, while the pre-crisis model of creative accumulation better explains the results, in the post-crisis period the model of creative destruction seems to dominate. Moreover, the manufacturing sector, the main generator of technological innovations, tends to matter less in value creation and employment, while the services sector is more likely to compete through non-technological innovations.

3. Research Design

3.1. Hypotheses and phases

In our study, we aimed to identify/argue the relationship between disruptive technology and financial innovations and to suggest some principles for the realization of financial innovation by firms; such principles would also be of theoretical/conceptual interest in that they would become a starting point for other similar studies. Most studies [31,37] on financial innovation through the use of disruptive technologies refer either to firms in high-tech sectors of the manufacturing industry (Pharmaceuticals, ITC, etc.) or to firms in more knowledge intensive services (KIS) sectors. There are few studies that propose financial evaluation by technologies from both a country and a firm perspective and that, in addition, propose a synthetic analysis of the factors/principles that explain the innovative capacity of an entity (whether it is a firm in the manufacturing industry or KIS). Another important aspect to achieve the aim of our research is the identification of a unified classification of innovation types/categories. In the sense invoked, according to the Oslo Manual under the auspices of the OECD[38] and the European Commission, there are four types/categories of innovations: product innovations, process innovations, marketing innovations and organisational innovations (OECD, 2005). As we will show later (point 5.2 in section 5 of the study), financial innovation at the level of any firm refers in particular to marketing innovations and organisational innovations (even if it is not possible to clearly delimit/dissociate between the 4 types of innovations mentioned, the way in which protection can be obtained for an element of novelty in the firm and the industry sector in which the firm is located).

At the basis of our study we state the following research hypotheses:

H1: There is no statistical, correlation and/or direct association between technical and social innovative capacity at the MNC level;

H2: Financial innovative capacity, with or without the help of disruptive technologies, at the firm level accounts for about 80% of the social innovations that are made by such entities;

H3: Countries that have a good international competitive position, i.e. are part of the group of innovative countries, have a number of MNCs and/or SMEs that are each significant in terms of resources allocated to R&D and technical, social and financial innovation results.

In order to achieve this proposed objective, we have proceeded through several steps specific to such research:

We have listed a number of 3-4 hypotheses on which the whole study would be based;

We have selected the GCI (Global Competitiveness Index) ranking [39,40] for the period 2009-2019 in an attempt to get a first picture of the competitiveness/innovative capacity of the world's major countries. This first picture based on the GCI gives us, at the same time, elements of interest for our study on the innovative capacity existing in the firms of these countries (since some sub-pillars such as: social capital, cooperation in labour employer relation, university industry collaboration in R$D, extent of staff training give us important information for innovation in firms).

We selected the GII (Global Innovation Index) ranking [41,42] for the period 2010-2020 to see which of the world's major countries have an innovative capacity above the average of the entire group of countries analysed by this annual ranking. Even the choice of this ranking was determined by the fact that some of the sub-indexes (e.g. gross expenditure on R&D, global R&D companies; ICT access, ICT use, GERD performed by business enterprise, etc.) also provide valuable information on the innovative capacity of firms in these countries. The inclusion in our study of GCI and GII at slightly postponed times has been foreseen for informal comparisons that can be formulated already at this stage of the study (year 2010 vs. 2009, respectively year 2020 vs. 2019), in order to connect these comparisons later with the microeconomic perspective on innovative, technical and/or other capacities in the main countries of the world.

We have chosen the study provided by BCG (Boston Consulting Group) for the period 2004-2022 and which highlights 50 of the most innovative companies in the world (27-USA; 15-Asia; 8-Europe) and for which, based on the Annual Report of each organization, we have highlighted in Annex 1 technical and social innovative capacity together with some information on size, financial performance, etc.The data on the 50 MNCs in the BCG study were then statistically ordered by different tools trying to identify association relationships between companies, sectors in which they are located and countries of affiliation.

In the fifth part of the research, we have recurred to our own analysis in which we "cross-reference" (mix) the main data provided by the international literature, the GCI study and the GII study, including the BCG study in an attempt to suggest our own way of assessing financial innovations as part of the social innovations that are carried out by firms. Also at this stage, in the final part of the research we have outlined a number of "n" principles that can be considered for strategic thinking on social innovation at firm level in different countries of the world. The same principles for financial/social innovation are also of interest from a theoretical perspective as they provide a "common denominator" for future studies that aim to argue the relationship between disruptive technologies and innovative capacity at the firm/country level.

3.2. Implications of GCI for financial innovation in firms

By "implications of the GCI for financial innovation" we mean that this ranking provides some useful, although partial, information for understanding and subsequently assessing (section 5 of the study, Main Findings) innovative capacity at the firm level. Our assessment focuses on MNCs, as the realities of the last 3 decades in the global economy lead to the conclusion that this category of organisations in particular have become the main vectors for technical and social innovation. As argued by [43] medium and large firms have become essential for R&D&innovation, job creation, exports, revenues, productivity and other critical indicators for competition in different markets. At the same time, our assessment, reasoning and conclusions may also include, where appropriate, firms in the SME category (in high-tech sectors such as IT, telecommunications, etc. firms with a significant number of employees can quickly become highly innovative).

Based on this ranking (GCI) we conducted a comparative analysis at the time of 2009 and respectively 2019, trying to identify what are the main correlations and significant associations between the different sub-pillars of the ranking, as well as the extent to which these sub-pillars support the understanding of technical and social innovative activity at the firm level (from a microeconomic analysis perspective). As is well known, the GCI ranking is based on 12 main pillars (Institution, Infrastructure, ICT adoption, Macroeconomic stability, Product market, Business dynamism, Innovation capability, etc. ); countries are grouped by main ranking and by sub-pillars, based on a "score" expressed on a scale of 0-100 (relative position of countries). In our analysis we have selected a number of 7 variables that should show us, cumulatively, the innovative capacity at country level (social_capital, health_primary_education, higher_education_training,extent_of_staff_training, cooperation_in_labour_employer_relations, state_of_cluster_development, university_industry_collaboration_in_RD). A second selection condition was given by the need to "cover" most of the 12 main pillars with the 7 variables and which refer, at the same time, directly or indirectly, to R&D and innovation activity in firms. A total of 24 main countries of the world have been selected (countries that are in the top positions in the ranking both at the time of 2009 and at the time of 2019; Switzerland, USA, Japan, Singapore, South Korea, Germany, Denmark, France, Netherlands, UK, etc.; countries that are important in the global economy but have a more prudent/modest position in the ranking; countries such as Argentina, Brazil, China, India, Mexico, South Africa, etc.).

We present below the correlation matrix in SPSS for 2009 (Table 1) and for 2019 (Table 2). In the first half of the tables are the pairwise correlations between the 7 variables included in the analysis for the two years (sub-pillars). In the second half of the table are the significance coefficients calculated for the correlation coefficients obtained (having different values in 2019 vs 2009).

In both tables we have used some unitary underlining, respectively:

- -

- In each table, we have marked in bold the significant correlations between the 7 variables (this means statistically significant correlations; some sub-pillars help us to further understand the factors explaining the innovative capacity of the companies in the BCG ranking);

- -

- We have marked in bold and italics in each table the sig. coefficients of significance greater than 0.05 between the 7 variables, which indicate that there are no statistically significant correlations.

Taking into account the previous mentions, some conclusions of interest for our study can be drawn (which will then be correlated with the information shown by the GII ranking and the situation of the 50 companies in the BCG ranking):

- The situation of insignificant correlations between the 7 variables has changed significantly during the decade under analysis, i.e. in 2009 there were five correlations of this type, and in 2019 there were only two correlations of this type:

- ✓

- At the time of 2009 the realities of the following variables were insignificant:

- -

- Social capital variable and Cooperation in_labour_employer_relations, State_of_cluster_development, University_industry_collaboration_in_R&D;

- -

- health_primary_education if extent_of_staff_training, State_of_cluster_development;

- -

- higher_education_training if State_of_cluster_development;

- -

- extent_of_staff_training and State_of_cluster_development;

- -

- State_of_cluster_development and Univeristy_industry_collaboration_in_R&D.

- ✓

- At the time of 2009 a smaller number of the following variables were insignificant:

- -

- health_life_expectancy and extent_of_staff_training;

- -

- cooperation_in_labour_employer_relation, respectively Multistakeholder_collaboration.

In addition, it is easy to notice that the association between variables recording insignificant correlations is completely different at the two moments of analysis (this means that different pillars of the GCI component advanced/evolved differently from one country to another and led to changes in position at both pillar and ranking level in 2019 vs 2009).

- b.

- The situation of significant correlations between the 7 variables has changed significantly during the decade under analysis, i.e. in 2009 there were three correlations of this type, and in 2019 there were four correlations of this type:

- ✓

- At the time of 2009, there were significant differences between the following variables:

- -

- health primary_education si higher_education_training (0.748);

- -

- extent_of_staff_training if Cooperation_in_labour_employer_relations (0.791);

- -

- extent_of_staff_training if Univeristy_industry_collaboration_in_R&D (0,800).

- ✓

- At the time of 2019 there were significant realities between the following variables:

- -

- extent_of_staff_training if Cooperation_in_labour_employer_relations (0.799);

- -

- extent_of_staff_training if Multistakeholder_collaboration (0.932);

- -

- Cooperation_in_labour_employer_relation if Multistakeholder_collaboration (0.738);

- -

- State_of_cluster_development if Multistakeholder_collaboration (0.735).

In the following, we summarize in Table 1 and 2 the "Correlation Matrix" for previously reported issues at the time of 2009 and 2019 respectively.

From the data presented in Table 1 and Table 2, it is easy to see that the association between variables with significant correlations has changed significantly during the decade under analysis, 2019 vs. 2009. At the time of 2019, there were four statistically significant correlations between the seven variables compared to only three such correlations at the beginning of the period. These statistical correlation changes between the different variables/factors about which the GCI provides information derive from changes in overall ranking and/or ranking of the plilars in the competitive position component. Such changes in terms of the ranking provided by the GCI for the world's leading countries will then be analysed "cross-referenced" with the main conclusions provided by the GII ranking (including performing an informal analysis, by main influencing factors, of some deductible aspects for the year 2020 vs 2019 and 2010 vs 2009 respectively) and the main conclusions provided by the BCG ranking for the 50 MNCs considered to be the most innovative in the world.

Next, based on the information provided by the same GCI ranking we calculate and present synthetically the KMO and the Bartlett sphericity test (Table 3 and Table 4), as well as the Initial Eigenvalues associated to each factor before extraction, after extraction and after rotation (Table 5 and Table 6).

Table 3 and Table 4 present two indicators relevant to our study, namely the KMO (Kaiser-Meyer-Olkin) and the Bartlett sphericity test. The KMO varies between 0 and 1. A value close to 0 indicates that the sum of partial correlations is relatively high compared to the sum of correlations and factor analysis is not indicated while a value close to 1 indicates that factor analysis should produce distinct and reliable factors. A value above 0.5 is considered acceptable (http://cda.psych.uiuc.edu/psychometrika_highly_cited_articles/kaiser_1974.pdf). In this case the value is 0.627, so an acceptable value.

Bartlett's test of sphericity is highly significant, the sig value is less than 0.01, which means that the correlation matrix R is not an identical matrix. There are links between variables that could be included in our analysis based on the GCI ranking.

In the following table, applying the same tests based on data provided by the GCI at the time of 2019 leads to slightly higher values than at the time of 2009.

Table 5 and Table 6 centralize the Initial Eigenvalues associated with each factor before extraction, after extraction and after rotation. Before extraction, 7 factors were identified corresponding to the 7 variables included in the analysis. The initial values associated to each factor also show the weight of the explained variants. For example, at the time of 2009, the first factor explains 53.86% of the total variance and the second factor 17.623%. It can be seen that the first two factors together explain 71.48% of the total variance. After extraction, at the same time 2009 only 2 factors remained as can be seen in Table 5 (SPSS extracts only factors that have values above 1). It can be seen that for the extracted factors the values are identical to those before extraction. In the last part of the table are the eigenvalues after rotation. Before and after rotation the first factor and the second factor keep their values.

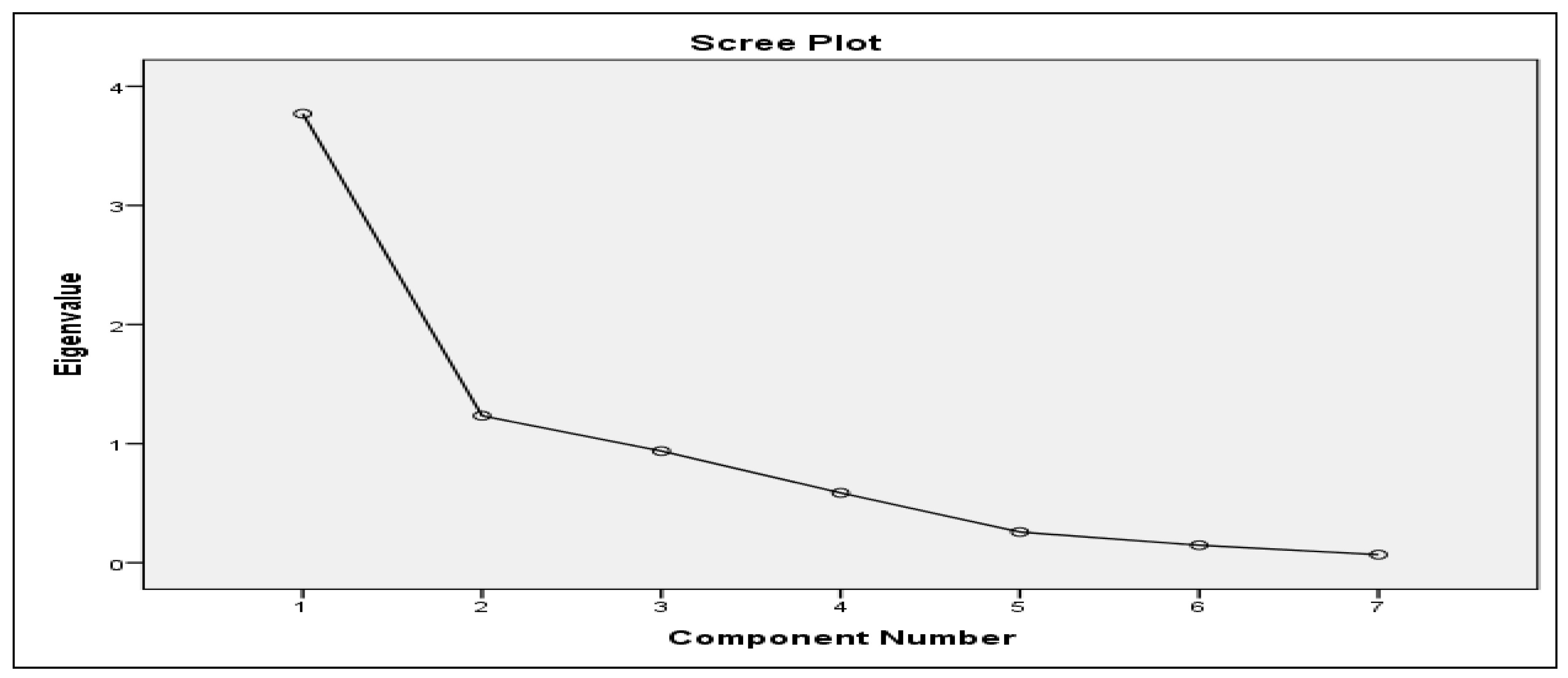

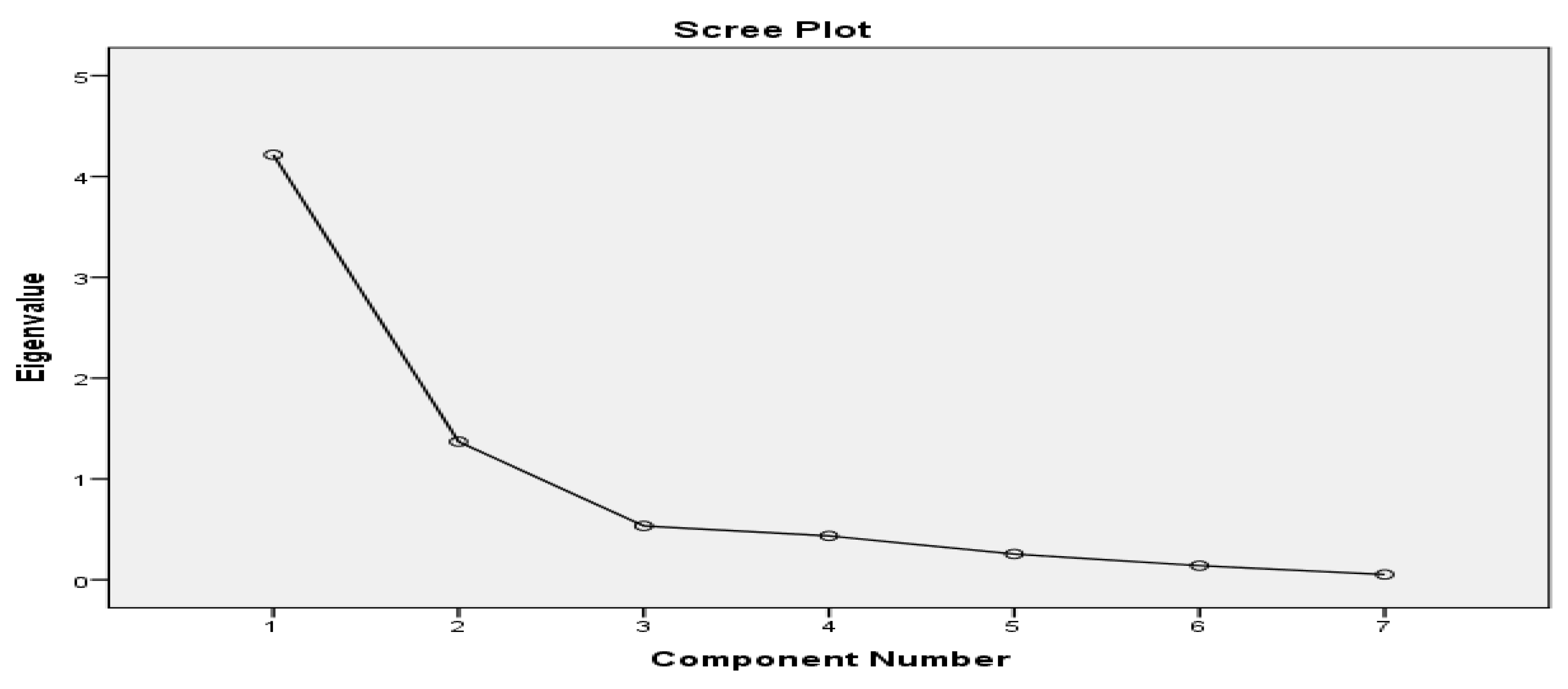

A more synthetic version of the analysis on the 7 variables at the time 2019 vs 2009 can be obtained by plotting the Scree plot for the year 2009 (Figure 1) and 2019 (Figure 2).

From Figure 1 and Figure 2 it can be deduced that the main points of inference occur in variables 2 and 3 which means that education, employee training and R&D investment are the main factors explaining innovative capacity at country level. This preliminary conclusion has significance for the objective of our research, and we will then analyse whether or not various elements related to education, training and R&D are reflected in the methodology applied by BCG to establish the ranking of the 50 globally innovative companies.

The next step the authors used is to analyze the variables that were assigned in the first factor to see if there is some common theme. It can be seen that between the variable State_of_cluster_development2009, which has the highest loadings distributed in component 2 and the variable Cooperation_in_labour_employer_relations2009 there is a certain relationship. Therefore, the variables allocated to the first component at the time of 2009 seem to fall under the same theme, namely education. All of them are related to the same aspect, as follows: higher_education_training2009,Univeristy_industry_collaboration_in_RD2009,extent_of_staff_training2009, Cooperation_in_labour_employer_relations2009, healt_primary_education2009, social_capital2009 .

Table 11 shows the matrix of rotated components, for the year 2009, then in Table 12 the same data for the year 2019.

Factor loadings less than 0.5 have been removed from the table. We can see that there are two components and most of the variables are distributed in the first component, except for 2 variables: Cooperation_in_labour_employer_relations and State_of_cluster_development which have been distributed in the second component. The variables have been presented in the table in the order in which they were entered. A descending sort by load size places the variable higher_education_training first, followed by Univeristy_industry_collaboration_in_RD.

Factor loadings less than 0.4 have been removed from the table. We can see that there are two components and 4 variables (extent_of_staff_training2019, Cooperation_in_labour_employer_relation2019, State_of_cluster_development2019, Multistakeholder_collaboration2019) are distributed in the first and 3 variables (social_capital2019, healt_life_expectancy2019, mean_years_of_schooling2019) are distributed in the 2nd component.

The Multistakeholder_collaboration2019 variable is ranked first by the upload size. Therefore, it can be inferred that, although there have been some changes on the variables/factors explaining the innovative capacity of countries in 2019 vs 2009, education, staff training and collaboration with various categories of stakeholders remain essential for innovative capacity at country level. Finally, the last stage of the authors' analysis of the importance of the variables/factors on which the GCI ranking is based is presented at the time of 2019, as shown in Table 13.

It can be seen that there have been some changes in 2019 in the distribution of variables by components compared to 2009; however, the conclusion remains that social capital, education, staff training, R&D activity and collaboration with various categories of stakeholders remain the main factors conditioning the innovative capacity of countries. As we will see later (evaluation based on the 50 Top BCG ranking[44]), employee education, investment in R&D, firms' orientation towards open networks for innovation, staff training, organisational culture and/or social capital, collaboration between management and employees/trade unions, etc. are the main factors determining innovative capacity at firm level. It is, however, extremely difficult to argue which would be the "common factors" that simultaneously explain innovative capacity at firm and country level.

Next we conduct an analysis based on the Global Innovation Index (GII) to further assess innovative capacity at the country level and the theoretical/hypothetical relationship between such rankings vs. innovative capacity at the firm level. Later (section 5 of the study, Main findings), when we perform an in-depth analysis based on the BCG survey of the 50 most innovative companies internationally, we will try to "disentangle/separate" social/financial innovation from overall firm-level innovative capacity. Also in the above sense, based on the information provided by the GCI and GII we will then try to "cross-check" the results we arrive at on financial innovativeness as part of social innovation, both at firm and country level.

3.3. Implications of GII for financial innovation in firms

In order to understand and assess financial innovative capacity at the firm level (BCG Innovation Study), we further recurre to an assessment of innovative capacity (technical and social) at the level of major countries of the world. For this purpose we will use the data provided by the GII ranking.

We use a data set of Global Innovation Index (GII), sub-indexes and components for 2010, and 2020; in the following table we summarize the main variables selected for analysis. In our study, we have chosen to assess the relationship between GII and firm-level innovative capacity at 2020 vs. 2010 in order to have a broader picture (4 years if GII and GCI are cumulated) of the factors/variables determining technical, social and other types of innovation at country/firm level.

In order to determine the paternity of evolution, i.e. the central tendency and the variability of the components, we used a quantitative analysis using descriptive statistics. In the first step, we identified global patterns of evolution for all countries included in the index calculation. In the second step, we selected countries that scored above the world average on the GII and determined the central tendency and variability for these groups of countries. For the group of countries that scored above the world average, we performed a correlation analysis.

Table 15 summarises descriptive statistics for the GII and selected components in 2010, both for all countries included in the index calculation and for the group of countries scoring above the world average.

Overall, the trend in innovation performance (GII) in 2010 remains somewhat constant, with a relatively normal distribution of values. The best performers are countries such as Switzerland, Sweden, Singapore, Hong Kong (SAR), China, Finland, Denmark, United States of America, Canada, Netherlands, United Kingdom, Iceland, Germany, Ireland, Israel, New Zealand, Korea, Rep, Luxembourg, Norway, Austria, Japan, Australia, France, Estonia, Belgium, Hungary, Qatar, etc. , while the lowest performers are associated with countries such as Senegal, Swaziland, Venezuela, Cameroon, Tanzania, Pakistan, Uganda, Mali, Malawi, Rwanda, Nicaragua, Cambodia, Bolivia, Madagascar, Zambia, Syrian Arab Republic, Tajikistan, Cote d'Ivoire, Benin, Zimbabwe, Burkina Faso, Ethiopia, Niger, Yemen, Sudan, Algeria, etc.a. As we will see later (section 5, BCG ranking starting point study), there are several European countries such as Sweden, Estonia, Belgium, Hungary, France, Finland, Denmark, etc. that are in good positions in the GII vs GCI ranking, but do not have large/representative MNCs to include companies from these countries in the BCG ranking. How can this situation be explained? Also in the sense mentioned, there are countries such as Qatar, Canada, New Zealand etc. that do not have representative companies in the top tier of innovation category that is summarised by the BCG study.

Among the selected components, the best scores were obtained in the Infrastructure pillar on components such as ICT access, Creative outputs (ICTs and business model creation, ICTs and organisational model creation). As regards Business sophistication, notable performances were obtained GERD performed by business enterprises, GERD financed by business enterprise), but the importance of inter-firm cooperation through strategic alliances or joint ventures in innovation was rather low. The central trend towards the Human capital and research pillar is also rather moderate, with a dispersed distribution of values across the board. The central tendency towards high-tech exports as a means of knowledge diffusion is also low, with a dispersed distribution of values.

In the group of countries performing above the world average in innovation, the central trend is relatively constant, but with a more dispersed distribution of variables. In this group, there is a noticeable trend towards a much stronger focus on infrastructure (through components such as ICT access, ICT use), Business sophistication (GERD performed by business, GERD financed by business enterprise), Creative outputs (ICTs and business model creation, ICTs and organisational model creation). Also noteworthy is the increasing trend of knowledge diffusion, through high-tech exports and ICT services exports. However, the trend towards attracting external sources for research and development (GERD financed by abroad) is less pronounced than the worldwide trend.

Table 16 illustrates the correlation matrix for the group of countries scoring above the world average in the GII, highlighting a number of significant influences that various components/variables have on innovation.

In 2010, in the group of countries scoring above the world average, innovation performance is positively and significantly associated with gross expenditure on R&D, infrastructure (ICT access, ICT use) and business sophistication. Also, a significant influence has been had by the creation of business and organisational models through the use of ICT, which are positively associated with R&D financed and carried out by firms and with access to ICT (which predominantly means common social innovations of which some may later prove to be disruptive in society). An insignificant influence was exerted by R&D financed by abroad. As regards joint ventures and strategic alliances, there is a positive association with the use of ICT and R&D activity carried out within firms, positively influencing overall innovation performance. Thus, based on the 2010 GII data, it is quite clear that some factors/variables related to the innovative capacity of an entity (gross expenditure on R&D, with infrastructure (ICT access, ICT use) and with business sophistication, business model, alliances and open innovation in R&D activity, etc.) are simultaneously found at the level of countries and/or firms that are considered to be innovative. However, it is extremely difficult to quantify and argue to what extent the existing technical or social innovative capacity in firms conditions/determines the same innovative capacity in countries A, B, C, etc. This is because, according to the Forbes rankings for both 2010 and more recently in 2022 [45], at the time of 2022 there were at least 2000 important/significant companies globally, yet the vast majority of them are far from making the BCG ranking, even if they also have quite good achievements on technical and social innovations. During the last decade we analysed (2010-2020) there have been major changes in the number of companies and countries of origin that are included in the various international rankings (Forbes 2022; Fortune 2022; etc.). However, the dominance of US innovative capacity at country and firm level remains; more recently China and companies originating from this country have improved their international competitive capacity. In a few cases we find companies that have a turnover of USD 2-10 billion or more (Gold Fields-South Africa; Grifols-Spain; Cencosud-Chile; Dexus-Australia; Ayala Corporation-Philippines; Fertiglobe-United Arab Emirates, etc.), have a good position in Forbes 2022 and come from countries that do not have an above average position in the GCI and GII. Simply put, the world's leading developed countries with relatively high GDP per capita dominate R&D activity (funding by firms as well as by government) and perform better annually in terms of number of patents, social innovations, financial innovations, etc..

Table 17 summarises descriptive statistics for the GII and selected components in 2020, both for all countries included in the index calculation and for the group of countries scoring above the world average.

The trend for the Global Innovation Index in 2020 remains somewhat constant, close to the trend recorded in 2010 in terms of value distribution. The best performers are Switzerland, Sweden, United States of America (the), United Kingdom (the), Netherlands (the), Denmark, Finland, Singapore, Germany, Republic of Korea, Hong Kong, China, France, Israel, China, Ireland, Japan, Canada, Luxembourg, Austria, Norway, Iceland, Belgium, Australia, Estonia, Czech Republic, New Zealand, Malta, Cyprus, Italy, Spain, Portugal, while the lowest performances are associated with countries such as Bolivia, Guatemala, Ghana, Pakistan, Tajikistan, Cambodia, Malawi, Côte d'Ivoire, Lao People's Democratic Republic, Uganda, Bangladesh, Madagascar, Nigeria, Burkina Faso, Cameroon, Zimbabwe, Algeria, Zambia, Mali, Mozambique, Togo, Benin, Ethiopia, Niger, Myanmar, Guinea, Yemen, etc.a. Of the selected components, the best scores were obtained in the Infrastructure pillar (on components such as ICT access, ICT use), Business sophistication (GERD financed by business enterprise), Creative outputs (ICTs and business model creation, ICTs and organisational model creation), while the central trend towards the Human capital and research pillar is still rather moderate, with a dispersed distribution of values across all situations. Also notable is the central trend of increasing high-tech exports, as a means of knowledge diffusion, but still with a dispersed distribution of values; this time among the leaders are Malaysia, Vietnam, the Philippines, the Republic of Korea, China and Singapore, together with the Czech Republic, France, Germany, etc. Together with other conclusions that can be drawn, it follows that the GCI and GII rankings are still largely dominated by the developed countries of the world by 2020. In a few cases we will find in 2020 companies that are globally significant ([41,42]) but come from countries that are well below the average GII ranking. Therefore, we see that there is a certain conditionality/correlation between existing technical and social capacity at firm/company level vs. innovative capacity and/or competitive position at country level. In the next part of the study (section 5) we address the same topic, but from the microeconomic perspective of analysing financial innovations as part of social innovations at the firm/country level.

In the group of countries performing above the world average in GII, the central trend is relatively constant, but with a more dispersed distribution of variables. In this group, there is a perceptible trend towards a much stronger focus on infrastructure (through components such as ICT access, ICT use), Business sophistication (GERD financed by business enterprise), Creative outputs (ICTs and business model creation, ICTs and organisational model creation); at the same time, the central trend towards the Human capital and research pillar, although still moderate and rather spread, is more consistent than the global trend. The orientation towards attracting external sources for research and development (GERD financed by abroad) should also be highlighted, with Israel, the Czech Republic, Austria, Iceland, Belgium, Sweden, Finland, etc. leading the way. Japan, Malaysia, China, Thailand, India, etc. have shown less interest in this direction. Last but not least, mobile app creation is showing a more consistent, albeit still dispersed, upward trend than the global trend.

In 2020, the innovation performance of the 53 countries scoring above the world average was positively and significantly associated mainly with resources invested in R&D activity, infrastructure, R&D activity carried out by firms and especially the creation of new organisational models under the impact of ICT. (United States of America , Sweden, Finland, Netherlands , Estonia, United Kingdom, Denmark, Germany, Switzerland, Norway, Israel, Canada, Iceland, Singapore, Luxembourg, Belgium). The creation of these new organisational models is positively and significantly associated with ICT use, cooperation through joint ventures and strategic alliances, and R&D activities carried out by firms. The conclusions that can be drawn from the GCI and GII rankings over the last 10 years largely confirm Porter's concept of "The five forces" shaping competition at the level of industrial sectors and/or countries [46].

In contrast to 2010, the role of strategic alliances, but especially R&D financed by abroad, has increased. High-tech and medium-tech production is mainly supported by in-house R&D, and high-tech exports are positively associated with R&D financed by firms. Moreover, in 2020, the role, albeit still modest, of mobile technologies is being felt, which is positively associated with cooperation through JVs and strategic alliances.

Up to this point, our assessments have predominantly focused on the macro-economic perspective of country/firm level innovation processes through the use of disruptive technologies. In the following sections of the study we aim to focus the analysis on the same topic from a microeconomic perspective, i.e. with reference to the realities in different categories of firms (especially MNCs). In the innovative sense, we then aim to "intersect" the two perspectives of analysis in order to reach some clearer conclusions on the role/importance of disruptive/digital technologies in the case of financial innovations made by firms.

4. Financial innovations by disruptive technology

As we argue in our study, there is no clear/unambiguous distinction between "financial innovation" vs other types of "social innovation" in the entire international literature. Previously we listed some of the world's leading countries that are significantly above the GII average at both 2010 (Table 16) and 2020 (Table 18). Comparing the information provided by the GCI and the GII (for about a decade of analysis of the two rankings), it can be deduced that the world's leading countries with higher annual nominal GDP per capita will also have a better position with regard to innovative capacity in general. Innovative capacity in such leading countries of the world is, however, determined by a complex of factors (values, institutions, government policies, government and/or firm-funded R&D investments, university education, competition between firms, scientific competition, etc.), even for smaller countries (Sweden, Denmark, Finland, Spain, Portugal, Italy, etc.) that do not have MNCs to be included in the BCG ranking of the most innovative companies. Some important questions arise that are related to the basic idea of our study: "In all or most of these countries do we find MNCs and SMEs that are technically, socially and financially innovative? Do such firms excel or not on all three innovation dimensions?" "Do such firms excel or not on all four types of innovation, i.e. product, process, marketing and organisation?". It is difficult to formulate clear and reasoned answers to such questions because, globally, there are about 2000 companies (Fortune 2000-2022) that are in various rankings and have a significant innovative capacity, even if very differently from one organisation to another. In our study, we included in the analysis only 50 companies considered to be the most innovative from 2004-2022, according to the BCG (Boston Consulting Group) study, and they are analysed together in Annex 1. Also in the sense mentioned, we admit that there are relatively clear/consistent statistical data for the innovative capacity of the main countries of the world (studies such as GII, Global Competitiveness Report, WIPO [47] etc. ), but there are only few studies on the same subject on MNCs coming from different countries as location of headquarters.

Over the past 3 decades, disruptive technologies have emerged as a common element/vector for knowledge acquisition, exploitation and transformation into patents and various types of social innovation [48,49] both at the level of firms, other organizations and countries. Any firm and/or other type of organisation, regardless of size or country of origin, has the opportunity to use digital and other disruptive technologies (robots, satellites, biotechnologiesetc.) to improve its organisational, production and market processes ().

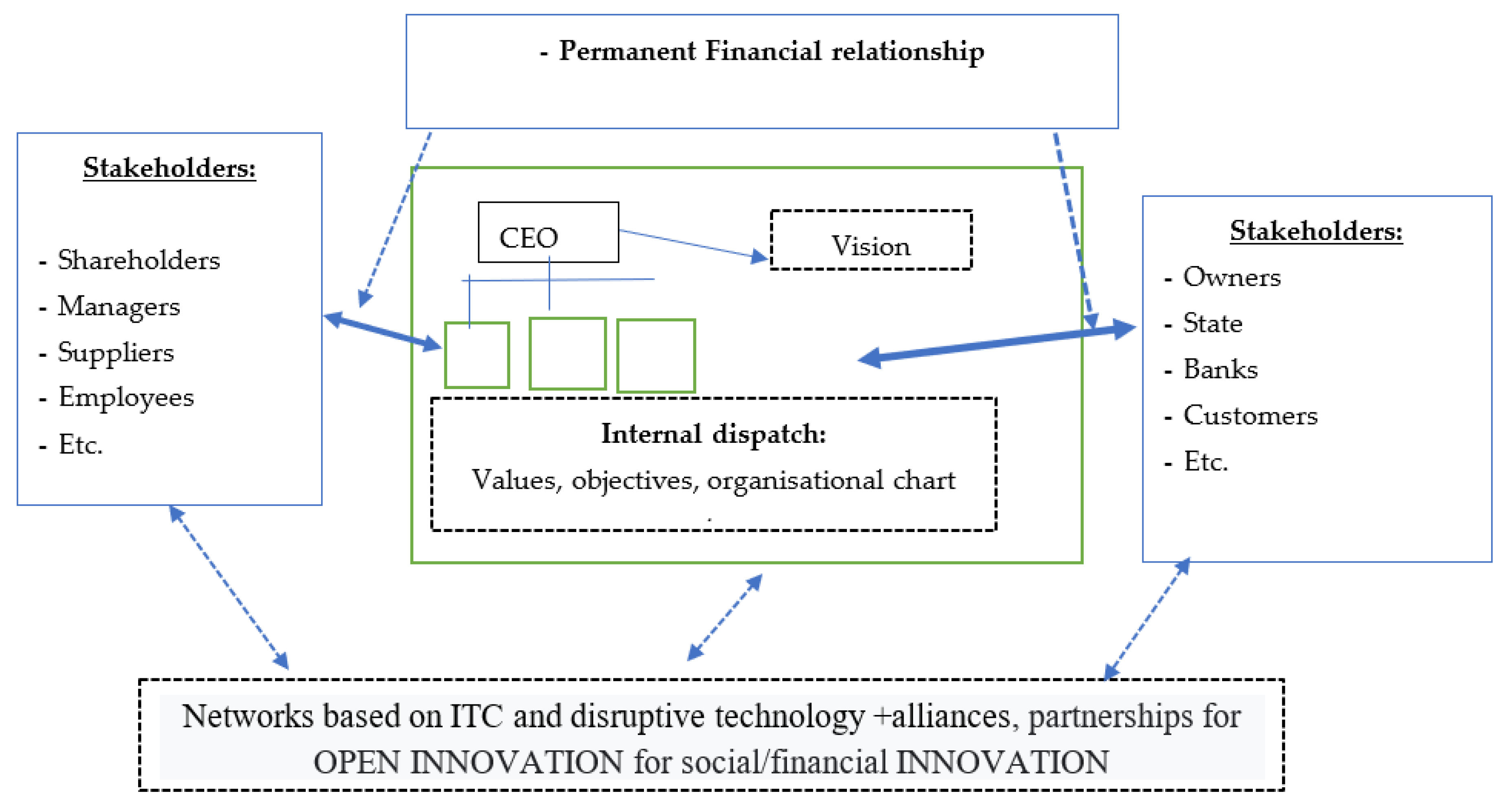

Any firm can be approached as a socio-economic system, i.e. a hub that is in permanent connection with certain stakeholders (investors, shareholders, managers, suppliers, employees, customers, banks, insurers, state institutions, universities, other firms, etc.). Current relations with the vast majority of stakeholders involve financial relations (i.e. with investors, shareholders, managers, suppliers, employees, customers, banks, etc.). Any firm, regardless of size, needs to manage capital and cash flows extremely preventively, in order not to end up making "book profit" and at the same time being in financial crisis [50] These ongoing relationships with various other entities require the widest possible use of digital and other types of technology, and at the same time require financial innovations as part of social innovations [21]. In Figure 3 we present the firm approached as a hub in its relations with various stakeholders

In so far as we approach the firm as a "hub"/open socio-economic system, depending on the field in which it is located (manufacturing industry, knowledge intensive services, other fields), it follows that a large part of the relationships it engages in with other entities also involve and/or require financial flows. Since a large part of the relationships that any firm (MNCs and SMEs), in any country, engages in materialize as financial relationships, it can be considered empirically, according to Pareto's principle, that 80% of the social innovations that a firm/organization is able to achieve annually are in fact financial innovations. Therefore, any technological input that a firm uses to improve its innovative capacity, both technical and social, is highly beneficial and is reflected in the financial innovations achieved annually by firms. This is even though we do not have studies measuring/quantifying a firm's financial innovative capacity as part of its social innovative capacity. In turbulent/haotic times, argues [51], the CEO of any company should consider that "Financial Strength" is far more important than revenue and profit; this was true in the 1980s and has become much more evident after 2008 and up to the present.

We mentioned earlier (section 3.1.), about the 4 types of innovation according to the existing OECD[38] classification (product, process, marketing and organisational). The use of digital/disruptive technologies supports the firm's effort to bring elements of novelty in any of the 4 directions/types of innovation. However, some differentiations can be made by categories of firms, depending on the domain in which they are located (but not on the countries they belong to), respectively:

-Firms in high-tech and medium-high-tech sectors are more likely to achieve technical, product and process/technological innovations/inventions; the field does not limit innovation in these entities on marketing and organisational issues;

-Firms in medium-low-tech and low-tech sectors are more likely to achieve social innovation, i.e. on marketing and organisational issues; the area in which they are located partially limits the achievement of product and process innovation (but there may be many exceptions to this rule);

-Firms in various service sectors are more likely to achieve social innovations, i.e. on marketing and organisational issues; also, the area in which they are located partially limits the achievement of product and process innovations (but there may be many exceptions to this rule);

5. Main Findings

5.1. Driving forces for financial Innovation

From a historical perspective, social innovations such as the newspaper, the insurance system, hire-purchase, labour relations or the pension system have fundamentally changed the Western economy/society, Drucker points out [19] It is obvious, however, that social innovations of any kind cannot be protected by patent, as is the case with a technical innovation. In Annex 1 we have summarised together the technical innovative capacity given by the number of patents of the 50 companies in the BCG study[44], and the social innovative capacity for the same companies (reflected by the number of trademarks, industrial designs, etc. registered with various state agencies, as appropriate). Some of the social innovations, i.e. trademarks, trade names, industrial designs, logos, symbols, etc. can be protected by firms through registrations with the agencies under which patents are usually granted (national agencies such as USPTO in the case of the US, EPO in the case of Europe, etc.). Even in such cases where the law offers some protection for any element of novelty brought by a firm, some social innovations will become sources of orientation for competitors and will gradually be taken over by other firms. Only in the case of social innovations made by the firm on the basis of tacit knowledge held by employees, which are dependent on the values they believe in and are more difficult to transform into explicit knowledge (i.e. know-how, ways of solving a problem, mental models, etc.) can one hope for longer protection of such elements of novelty.

There are, as we argue below, at least three driving forces that directly support any firm to achieve social innovations in general (only some of which will also prove to be disruptive social innovations). As the case may be, it is likely that the result of the cumulative action of the three driving forces will be a mix/combination of technical innovation and social innovation. In other words, only each firm can correctly assess on which direction of action it should focus its resources in order to overcome the specific crisis of the period 2021-2022 through social innovation. As we have shown above, most of the social innovations made by firms will be found on the market and/or in society as financial innovations.

The three types of driving forces for financial/social innovation are:

- ✓

- Firstly, the technologies already existing in society, especially digital technologies (but not the only ones), are a real catalyst for companies to maintain their position in the market, improve performance, etc. This means massive recourse to digital technologies, which requires skilled employees, investments, own intranet systems, permanent connections with customers/suppliers and other stakeholders, etc. This trend of increasing use of digital technologies started in the 1990s, became more pronounced in the context of the Great Recession of 2008 and has become essential for the survival of firms from 2020 onwards. Computer networks, communication networks and satellites have made e-commerce possible, which in turn has fundamentally changed social and business relations in modern society. In the age of e-commerce, Drucker argues, even small, locally operating firms must be managed transnationally if they are to survive [48]. The new IT&C systems that firms are developing are leading to changes in processes within the firm and in its relationship with the outside world, changes that significantly alter the organisational culture. Almost every employee in firms and other organisations in modern society can gradually make small improvements in the performance of job tasks when using elements of digital technology. In other words, digital/disruptive technology supports employees at all levels of the organisation chart to contribute directly to the realisation of social innovations by firms. For some of the social/financial innovations achieved to be disruptive, there needs to be a 'mindset' across the culture of the organisation that aims to systematically take advantage of the benefits given by digital technologies [20] There is no known 'recipe' or mechanism by which firms should proceed to achieve disruptive social/financial innovation. Each firm needs to define and identify its own direction in which it should focus, to act systematically to understand the constraints and opportunities given by the market on the product/service offered. Only then, after understanding what has real value for its customers [50], can the firm choose a favourable combination of existing technologies that will support its continuous innovation effort.

- ✓

- Another driver forcing companies to resort to technical and social innovations is the competition in the market itself. Simply put, the market, with all its imperfections, offers constraints as well as opportunities for any business organisation. Particularly in the context of a global recession such as the current one, it is essential for companies to understand in depth what is of value to the customers to whom the product/service offered is addressed. More importantly, the very values to which customers (end consumers) relate are changing rapidly in a global and increasingly interdependent society. The values, preferences, consumption habits, time-sharing of each individual and social conditioning imposed by governments are all changing in a social climate defined by uncertainties. What directions for action can firms see in this new social climate?

So, for the whole period after 2008 and up to the present, the market and what the customer considers to be of value as a product/service has become the key element for companies to relate to. The general allocation of funds to R&D and obtaining patents and various trademarks, designs etc. must be "doubled" by a systematic CEO effort to make disruptive innovations and especially disruptive financial innovations. Ownership of a large portfolio of patents by leading companies in high-tech and medium-tech sectors seems no longer sufficient to overcome the current global recession. The question arises as to whether some of the patents held by such companies will be transformed into low-end disruptive products/services. For companies in low-tech and service industries, the use of digital technologies, investment in their own IT&C systems, seems to be the best way to adapt the product/service to the new requirements of low-end disruptive markets.

Thirdly, managers and particularly the CEO and his team have become, perhaps more than a decade ago, the essential vector or "driving-force" for firms (in any economic sector) that have a distinct strategy for achieving disruptive technical and social innovation. This CEO strategy/vision also requires skilled employees who are willing to continuously learn, to accumulate new explicit and tacit knowledge. In fact, the role of professional managers became essential with the emergence of large corporations, first in the US from 1880 to the present. The emergence of managerial capitalism was an economic phenomenon of American origin that then spread to Europe and Japan [52].During the post-war period, the importance and role of professional managers has increased in all major countries of the world (including China in the last four decades). Since the 1980s, as digital technologies have become ubiquitous in society, the tasks to be performed by CEOs and the skills required have increased greatly in complexity.

In Figure 4 below we present the three "driving forces" that together support the systematic effort of firms to achieve social innovation, of which the vast majority (about 80%) will be financial.

In relation to the three "driving forces" suggested by us in Figure 4, two or more variants (marked by us with a question mark in the figure) emerge, quite obviously, as a solution of connection/intersection between the support given by technologies and what the market considers to be of value to consumers. As can be easily deduced from the figure, the first variant of "intersection" or connection, usually accessible, can be more easily intuited, by managers in established companies in a given market. As it can be seen, the "option I for financial innovation" is given by the combination of the benefits brought by technologies and new market disruption, as an immediate direction of action for the managers of firms; only in the second place, the mix of the two elements can also be done in relation to "low-end market disruption". The financial relationships that the firm engages in with various categories of stakeholders (argued in section 4 of the study, Figure 3), together with the values, knowledge and training of the firm's human resources will determine over time the financial/social innovation capacity of the organisation. Through the policies applied, investments in R&D, the quality of education and the quality of the infrastructure built, governments can support this direction of action in innovative firms (even if no distinction is made between technical and social innovation through such policies). On the other hand, when the support given by ICT would intersect with the value given by the market in any other location in the three-dimensional plane (of analysis) it becomes much more difficult for any manager to intuit at what point the "intersection" between the two might take place. As noted from the figure, along this line of action and/or intuitive assessment of social innovation opportunities, managers should first build their KM/innovation strategy on the basis of going through steps such as associating, questioning, observing, networking and experimenting [26]. Therefore, a different vision, thinking differently, is needed for managers to be able to intuit what would be the "Option II for financial innovation" action to achieve social innovations of which most of them will turn out to be financial innovations. In this case, depending on the vision and intuition of managers, any kind of intersection between technologies and the two types of markets becomes possible which then confirms or disproves the disruptive nature of any innovation (be it social, financial or other). It is not the size of a firm that limits an organisation's innovative capacity, Drucker argues, but the kind of developed culture and entrepreneurship that can be learned over time through practice [50].

5.2. Financial innovation of MNCs and SMEs

Our assessments of financial innovation globally to this point in the study lead us to conclude that any type of organization, i.e. MNCs, SMEs, universities, public institutions, etc. can achieve significant, modest or more significant social innovations through extensive use of digital/disruptive technologies. This means that any of the tens of millions of firms globally can have an effective KM, MRU and continuous innovation strategy. There are no studies that highlight/synthesise the technical and social innovative capacity for millions of firms in Europe, America, Asia and other regions of the world. Specifically in the case of our study we restrict ourselves to a more in-depth analysis of innovative capacity at the level of 50 major companies that have been monitored by BCG over the last approximately 2 decades.

The BCG study is based on a questionnaire methodology that is applied annually to top executives of leading companies in both industry and services globally (the questionnaire is structured on 4 dimensions: Global Mindshare; Industry Peer View; Industry Disruption; Value Creation). The very structure of the BCG questionnaire used to determine each year which are the most innovative companies in the world takes into account the strategies and/or disruptive innovations achieved by the companies, as well as the practices and platforms used by innovative companies. The BCG methodology lists 3 pillars for practices (Portfolio management, Funnel management, Project management) and 8 pillars for platforms (Idea to impact process, Talent and culture, Organization setup and ecosystems, Performance management and metrics, Innovation governance, Innovation domains, Innovation ambition). Some of the 50 companies (depending on the score obtained on each pillar) will be considered more committed innovators and others less committed to innovation (as an explicit top management strategy). In the same sense, we find that the content of the 11 pillars of the BGC methodology is only partially matched by the content of the various pillars of the GCI and GII rankings (the application of KM and systematic innovation is to a large extent dependent on the CEO's vision, the company culture, the cyclical evolution of the business and other similar factors; only to a certain extent the innovative capacity of the country of origin can influence/determine the innovation orientation of the companies). In Table 19 we present the BCG ranking for 2022, and in Table 20 we present the BCG ranking for 2023; in our substantive analysis, we will only deepen the ranking for 2022 for which we have the extended assessment in annex no. 1 of the study.

The same BCG study of the most innovative companies globally for 2023 is shown in the table below:

The comparative analysis of Table 19 and Table 20 shows that there is a very robust competition between internationally known MNCs and that there are annual changes in positions (companies dropping out of the ranking and coming in; changes in the actual position of those remaining, etc.). In 2023, companies such as Saudi Aramco or PetroChina have recently entered (so companies from countries with a more modest position in the GII can enter this ranking; in the same sense, although it is a developing country by GDP per capita, it has improved its competitive position in the last decade, and an increasing number of companies are starting to find themselves in various international rankings).

In manufacturing industry there is a separation of industries into four broad sectors: High-Technology, Medium-High-Technology, Medium-Low-Technology and Low-Technology [54,55] As regards the services sector, depending on the intensity of technology use, the Knowledge Intensive Services (KIS) sector has a special place; in this sector we include: High-tech Knowledge - Intensive - Services (HTKIS); Knowledge - intensive - market services (KIMS); Knowledge - intensive - financial services (KIFS); Other knowledge -intensive -services (OKIS) [55]. In the category other services, which are less knowledge-intensive, we will classify areas/sectors such as tourism, road transport, retail, etc.; they are classified under the Eurostat less knowledge-intensive services (LKIS) [55].

Based on the data in Table 19, Table 20 and Appendix 1, we present below a more in-depth analysis of the situation of the 50 companies in the BCG 2022 ranking. This analysis highlights the following issues:

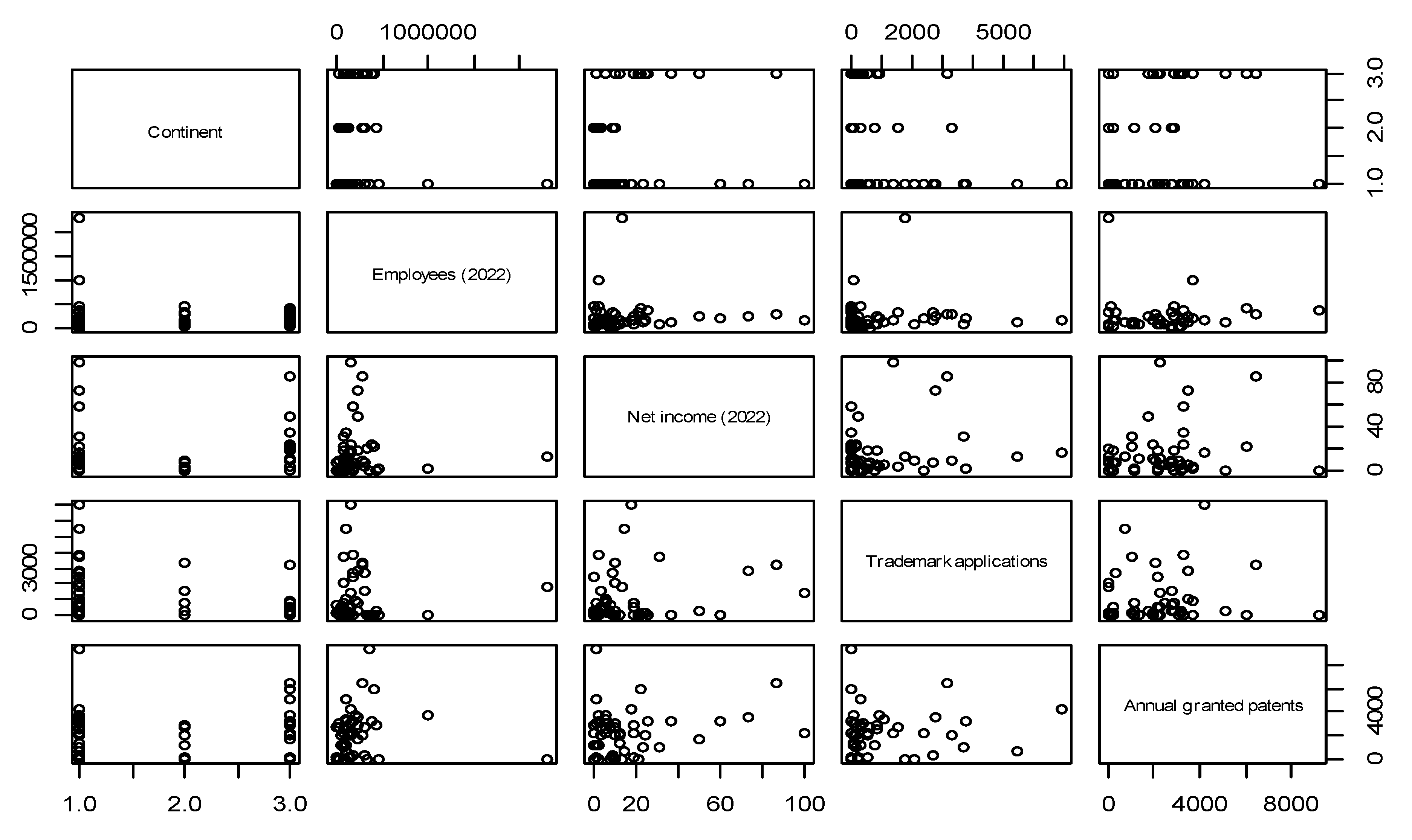

It is possible to perform a pairwise comparison between variables to identify the type of link that might exist between the 50 companies (based on geographical location, number of employees, net income, registered trademarks, patents obtained by each entity as summarised in Annex 1). In Figure 5 we present the summary of the statistical evaluation of this comparison between the 50 companies.

The data in appendix no. 1 show a rather large dispersion of the variables taken into account (examples: from about 400 employees at Moderna to about 420 thousand employees at Bosch; from a symbolic profit of 0.1 billion at Zalando to a profit of almost 100 billion USD at Apple; from 40 social innovations at Zalando to over 1500 social innovations at other companies; from 10 patents per year at Moderna to over 6000 patents per year at Samsung), which is reflected in the distribution of companies in the previous figure.

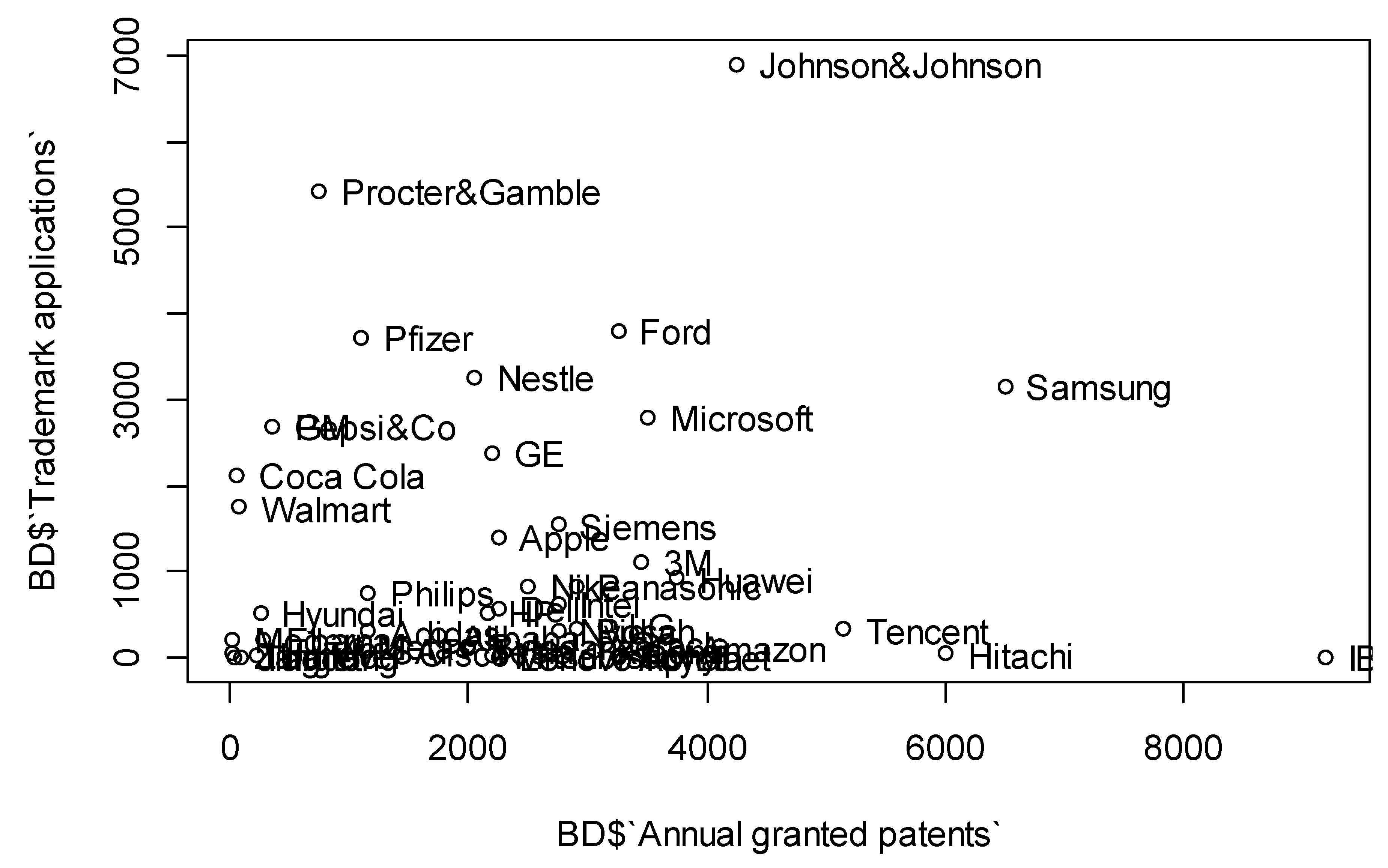

If we select only the number of patents (as equivalent for technical innovations) vs. the number of trademarks, trade names, logos, etc. (as equivalent for social innovations), the distribution of the 50 firms is shown in Figure 6.

From what has been presented up to this point regarding the distribution of the 50 companies in the BCG ranking, only a few preliminary conclusions can be formulated with respect to the objective of our research (the "cross" analysis of innovative capacity from firms to the countries of origin, in the conditions of extensive use of disruptive technologies; these technologies constituting a "driving force" according to the arguments made in point 5.1.). So far, on the basis of the BCG ranking for 2022, taking into account also the analysis based on the GCI (point 3.2) and the GII (point 3.3) we find that there are some common "driving forces" to explain the innovative capacity both at firm and country level. This is because some of the pillars of the BCG methodology (e.g. Global Mindshare, Value Creation, etc.), as well as most of the 8 elements that form the basis of the strategies applied by innovative firms (Practices and Platforms), have as their country-level equivalent education, training, stakeholder relations, government policies and other variables that explain innovative capacity from a macro-economic perspective.

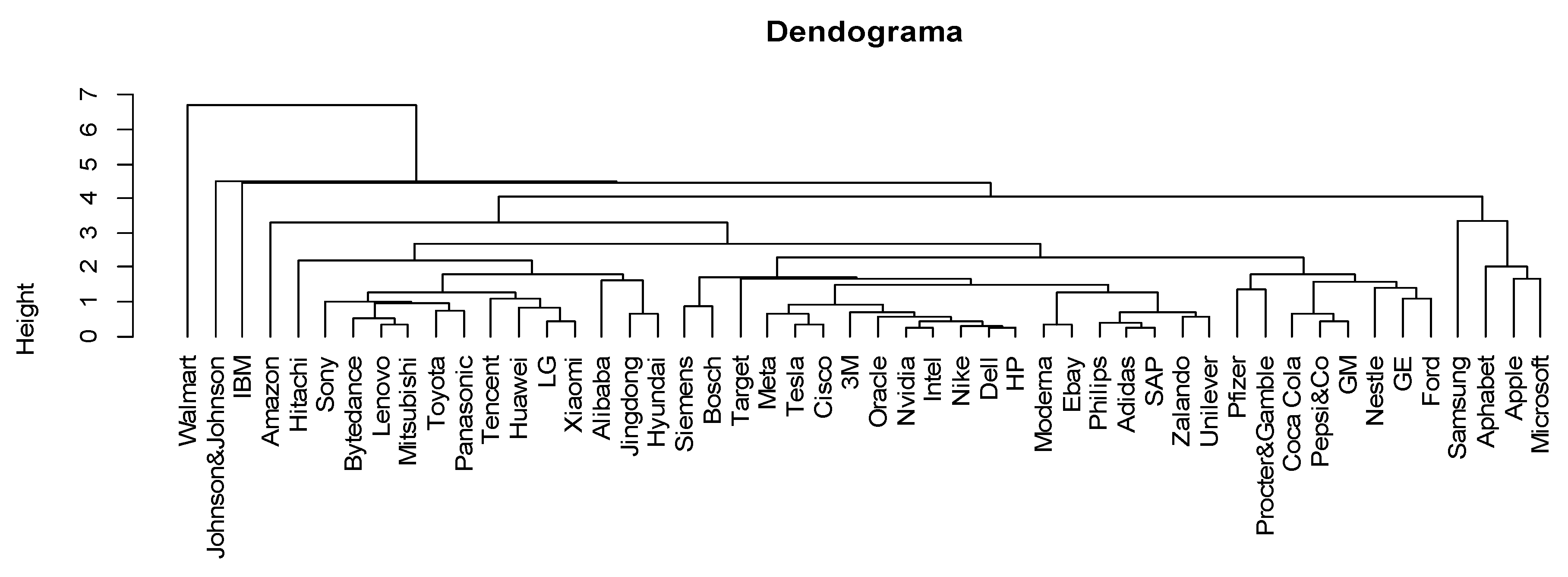

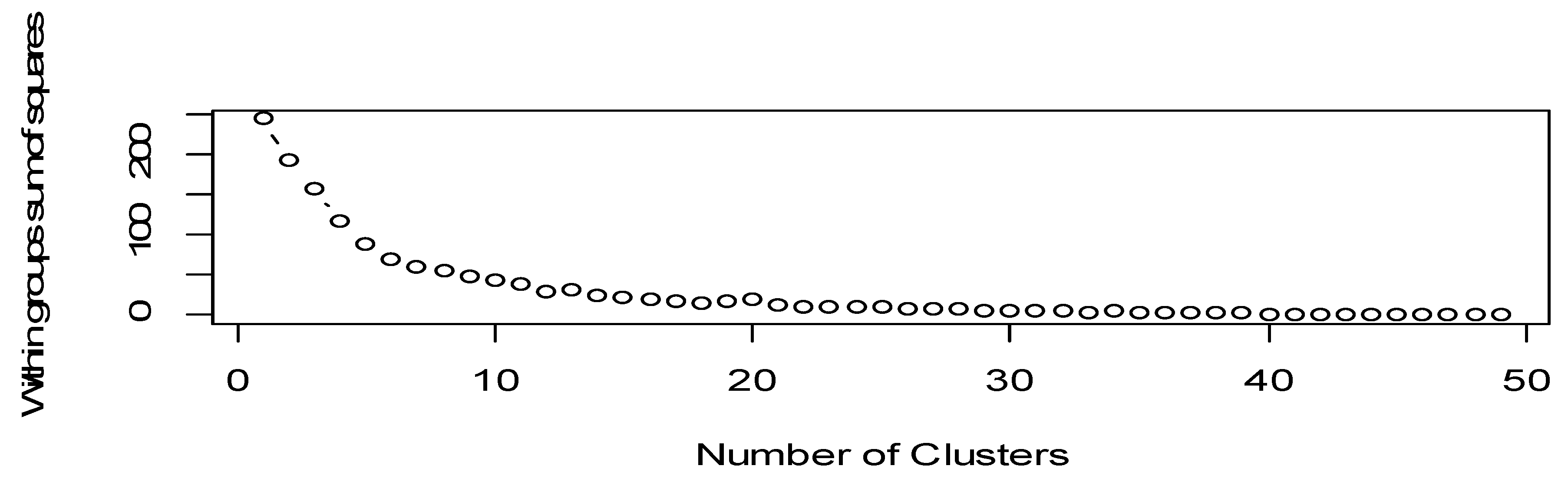

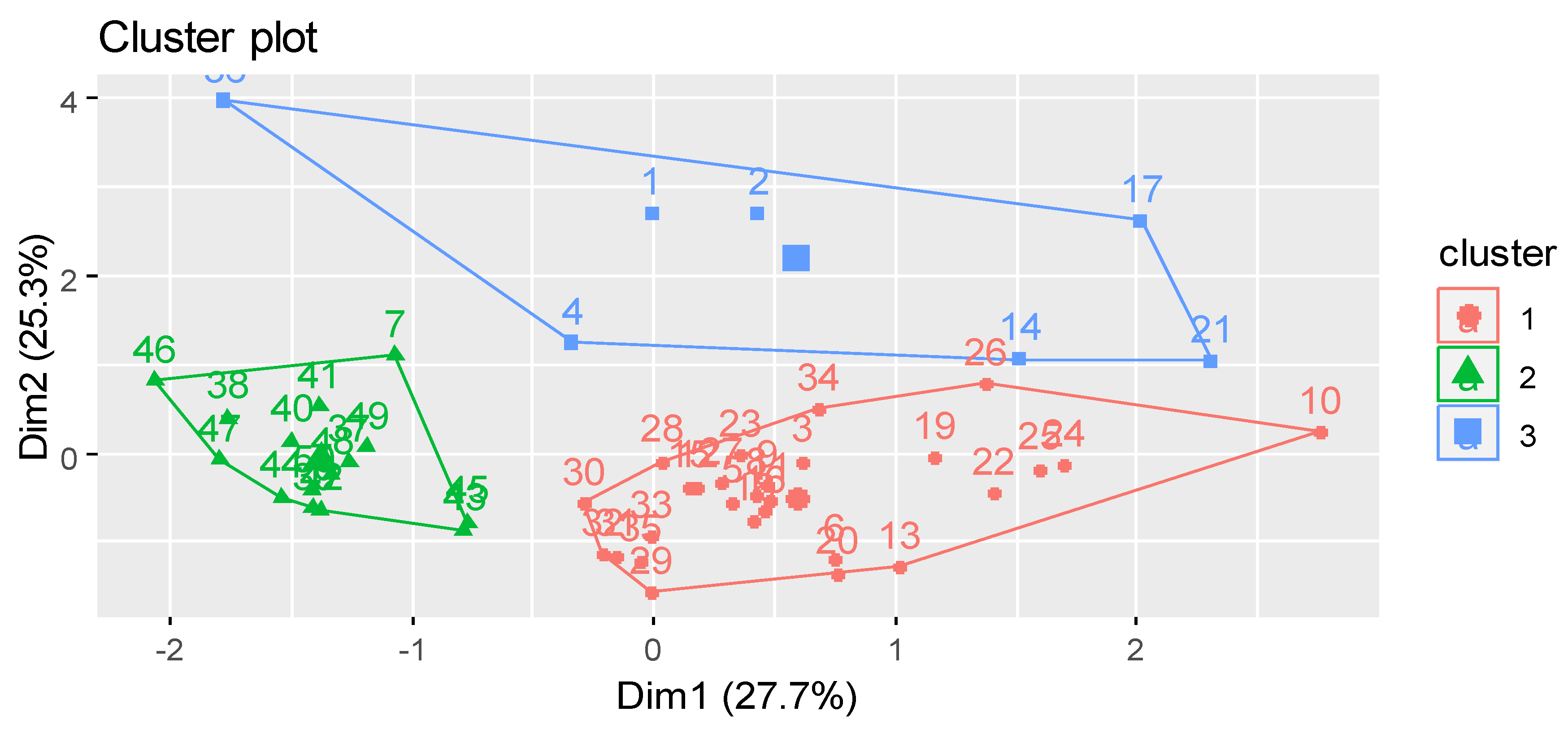

Next, in order to identify the extent to which there are certain sub-clusters (small clusters that have similar characteristics based on 2-3 variables considered) within the entire sample of 50 companies we will proceed to plot the dendogram (Figure 7), the scree plot to determine the number of clusters (Figure 8). Theoretically there are two extreme situations (all 50 firms are differentiated and no sub-clusters can be established; all 50 firms are similar and form a single cluster).

Based on the data in Figure 7 and Figure 8, it follows, depending on the variables considered, the optimal number of clusters would be between 3 to 5 different sub-cluster firms.

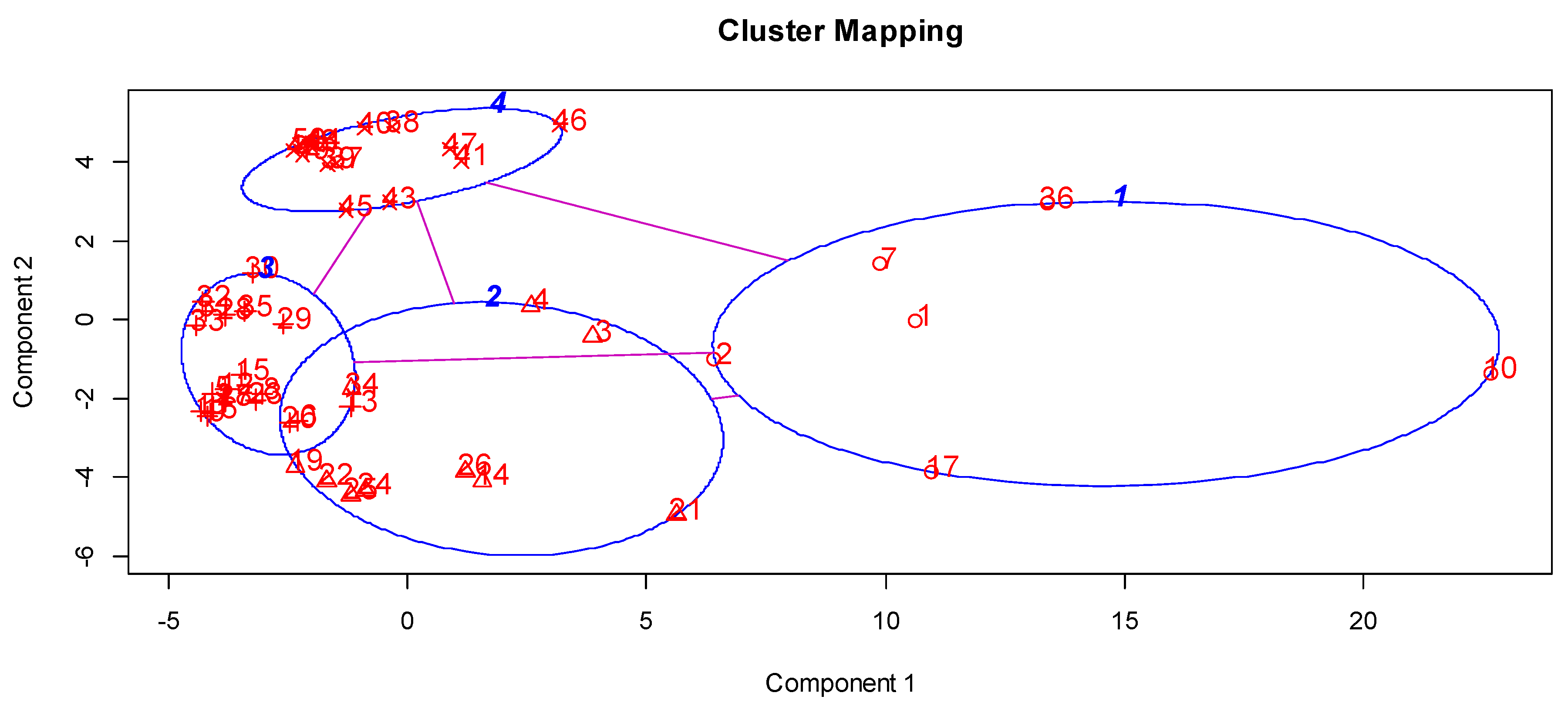

In order to highlight more clearly the number of subgroups (distinct clusters that can be constituted for the entire BCG sample), we have resorted to the presentation of Cluster Mapping (Figure 9) and Cluster Plot (Figure 10).

From the Figure 9 and Figure 10, it is easy to deduce that 3-4 sub-clusters can be formed, depending on the variables by which the firms are compared to each other; each sub-cluster/cluster would however have a different number of firms from which it is made up (from about 5 firms to 20 firms per cluster).

The data presented by us previously (sections 2,3 and 4 of the study), together with those shown at this point of the study, lead us to some preliminary conclusions, namely:

- ✓

- This fully confirms hypotheses H1 and H2 formulated by us at the beginning of the study (point 3.1), in the sense that there is no direct association/conditioning/influence relationship between the financial/social innovative capacity vs. the technical innovative capacity of a firm. As a confirmation of H2 it follows that, whether or not using disruptive technologies extensively, the financial innovations obtained annually can be empirically evaluated as representing about 80% of the social innovations that are achieved by such entities. On the other hand, with regard to hypothesis H3 formulated by us, it appears that this is only partially confirmed, based on "cross-checking" between the BCG studies and the GII and GCI reports, as there are hundreds of thousands of other innovative firms that are not included in any international innovation ranking. However, at the same time hypothesis H3 is partially confirmed because the world's leading countries that dominate the GCI and GII rankings have firms in the BCG survey, the Forbes survey and other international rankings at the same time.

- ✓

- The existing innovative capacity of the world's leading countries (both financial and technical innovation) is reflected in the existence of a number of firms that are large enough to enter various international innovation rankings. Even when looking at the 2000 firms in the Forbes ranking [45] it appears that this ranking is far dominated by American MNCs, then Asian MNCs and then European MNCs. Simply put, the number of European firms that are sufficiently competitive and innovative has decreased significantly in terms of representation in the BCG survey and/or representation in other international rankings.

- ✓

- There is a fairly strong conditioning from countries to firms on the innovative capacity achieved annually, as countries and various international entities (EU, OECD) directly influence R&D activity through regulations and funds allocated to firms. This means that, theoretically, we will find medium and large firms coming from countries at the middle of the GCI and GII rankings that are not included in the BCG study, but have significant annual financial or technical innovation achievements.

- ✓

- Conversely, the existence of technical and social innovation capacity at firm level does not automatically/implicitly reflect on innovation capacity at country level.

- ✓

- Leading US-based companies in various international rankings [45] have a real monopoly on international technical and social innovation. Companies that make it into the BCG rankings and come from European countries are finding it increasingly difficult to maintain their innovative position internationally (Europe is far ahead of the US and even Japan and China more recently).

- ✓

- With the use of digital/disruptive technologies, any company in industry, commerce, tourism can be considered innovative at international level even if it does not get its own annual patents (such as Wallmart, Zalando, Jingdong etc.) it can still be extremely innovative in its relationship with the market, its customers, its organisational structures etc.It is not by chance that tourism companies such as Marriott and Hilton have been found in various BCG rankings as being among the most innovative in terms of funds allocated to digital technologies and networking with various stakeholders (Marriott was also in 2019 in a similar ranking by Forbes).

- ✓

- The majority of marketing and organisational innovations made annually by firms (whether or not they belong to countries considered to be innovative) will take the form of social innovations of which about 80% will be found as financial innovations.

- ✓

- Internationally, there has been a trend in recent decades to set up "international/global born companies", which means that investors from one or more countries raise capital and set up successful start-ups to operate from scratch in various foreign markets. [56,57]. In the same vein, we recall "fintech" investments/firms [58] whereby the owners aim to create from scratch a successful start-up in high-tech sectors of the global economy. Such internationally newly created firms, through the strategies applied and the results obtained, seem to deviate from the criteria for gaining competitive advantage that were outlined by M. Porter.

Therefore, it is necessary to conclude that digital technologies are currently generating new paradoxes in the theory of competitive advantage and classical organizational theory. From the perspective of our study, this means that it is not possible to assess globally and/or by large sectors of the economy the number and importance of financial innovations made by firms with disruptive technologies. Such an assessment is only possible to be made by managers in firms that have KM and social innovation strategies.

5.3. Principles for Financial Innovation

Following the issues/arguments we have raised in the first sections of the research (section 2, 3 and 4), as well as the clear and argued distinction between financial innovation and social innovation, a number of theoretical principles can be formulated that could be considered by firms (MNCs and SMEs) to base their strategies on innovation, KM, MRU, etc.

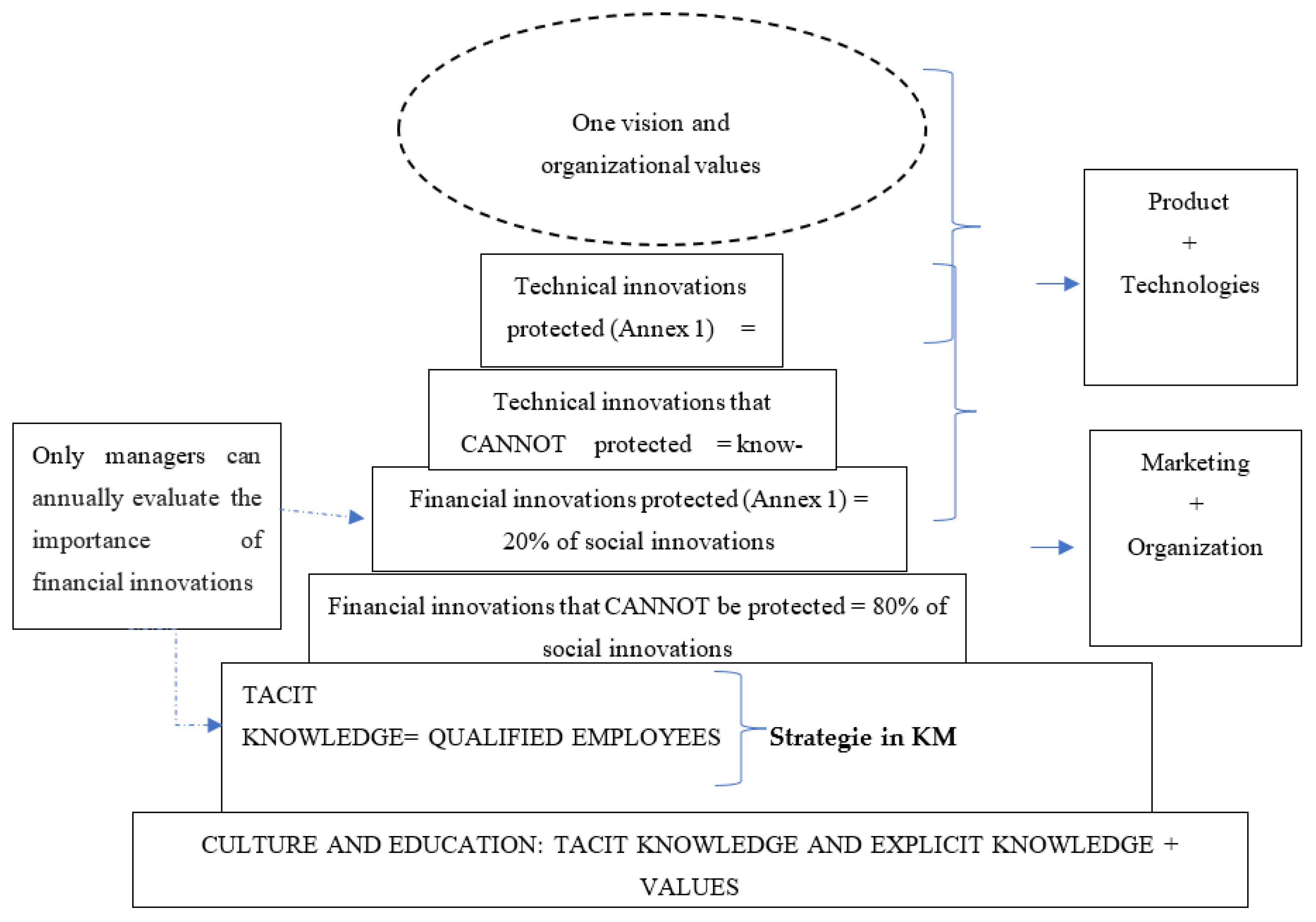

First of all, we stress that to improve financial innovation in companies with the help of digital technologies, there must be 2-3 key values at the core of the organisational culture and a single vision at top management level (in relation to product, technologies, market and organisation). It should be concluded in advance that the realisation of technical innovations by firms that are protected by patenting (as shown in Annex 1) is not directly conditioned by the realisation of financial innovations as part of social innovations (which may or may not be protected by registration with a state agency). At the same time, it appears that the competitive position of a company operating in the manufacturing industry is mainly determined by the stock of tacit knowledge of employees, such as know-how (technical innovations that can be protected). The financial innovations that can be protected by companies (according to Annex 1) are empirically estimated, according to the Pareto principle, to represent about 20% of the total social innovations made annually by organizations. Therefore, the largest share of social innovations achieved annually by a firm, i.e. 80% of the total, will be found as financial innovations that cannot be protected by registration with a state agency. To a large extent (but not totally), both categories of financial innovations refer to innovations related to the market and the organisation of the firm. The whole "pyramid construction" that explains financial innovation at the firm level is based on existing values, culture and education at the country/firm level, as shown in Figure 11.

In addition to what has been shown in this section of the study, we list below a number of 10 principles that are de facto at the core of financial innovation activities over the last 2 decades at the global level:

- ✓

- Principle 1 (P1): Using disruptive technologies

A first principle is that any business (MNCs and SMEs), as well as other types of organisations, can and should make extensive use of disruptive/digital technologies to improve their financial innovation capacity as part of their social innovations. One of the directions of innovation strategy is towards open innovation by setting up various business networks for innovation.

- ✓

- Principle 2 (P2): Applying strategies in KM

Every company should have a clear and distinct strategy for KM and continuous innovation. The focus of this strategy should be on technical and/or social innovation, depending on the field/sector in which the company operates. The best theoretical approaches can be taken towards social innovation in relation to different stakeholders.

- ✓

- Principle 3 (P3): Stakeholder orientation

Any company has, by the very nature of its daily activity, a certain volume of financial relations with a group of stakeholders (suppliers, customers, employees, shareholders, public institutions, etc.). These day-to-day financial relationships are nowadays carried out through various solutions offered by ITC and other disruptive technologies. The strengthening of financial stakeholder relationships needs to be continuously monitored and improved as new tools and disruptive technologies emerge, especially from the Artificial Intelligence (AI) category.

- ✓

- Principle 4 (P4): Multiplying financial innovations

When a company/organisation has a KM strategy and systematically uses various digital/disruptive technologies it can exploit the multiplier effect of an innovation. This means that a financial innovation based on digital technologies achieved in one direction of action (e.g. in relation to suppliers) can then be extended/duplicated very quickly in another direction of action/interest of the firm (e.g. in relation to customers/consumers). According to Drucker's arguments customers and the market should be the most important source of inspiration for the firm in its attempt to achieve financial innovation by acquiring new knowledge and managing this knowledge through the use of various technologies [50].

- ✓

- Principle 5 (P5): Customer/market orientation

The most important element/factor that should be at the heart of a continuous innovation strategy in the financial sector using various technologies remains the customer and the market, including other competitors. In other words, the customer and the market has become over the last three decades the "core" element of any strategy applied by firms in KM and continuous innovation. Continuous innovation of the "financial innovation" type remains the most important part of the social innovation undertaken/achieved by firms; the former cannot be "broken/dissociated" from the broader framework of social innovation [19]. Whatever the size of the firm and whatever the area of location, the starting/foundation point of KM strategy and continuous innovation is given by the values that customers/consumers believe in. Only by starting from this point and building ICT-based networks for open innovation can firms strengthen their competitive position and innovative capacity in a given market. It is only the satisfied customer that determines the outcome and/or existence of a firm [50].

- ✓

- Principle 6 (P6): Financial innovation is partially associated with the business area

Most financial innovation will be related to process, marketing and organisational innovation. However, the chances of achieving such innovations are conditioned by the location of firms in large sectors (from high-tech to low-tech).

- ✓

- Principle 7 (P7): Disruptive technologies diminish the importance of size