Submitted:

05 July 2023

Posted:

07 July 2023

You are already at the latest version

Abstract

The mobile payment has been emerging as an alternative to cash and credit cards and is rapidly evolving around the world. This study integrated the general model of innovation diffusion theory (IDT) with the technology acceptance model (TAM) to examine the impact of near-field-communication (NFC) mobile payment environment on the restaurant operating performance (ROP). This paper used convenience sampling to distribute questionnaires to restaurant owners and managers in order to investigate the impact of NFC mobile payment environment on ROP. A total of 279 valid questionnaires were collected. The empirical results show that sales growth, cost saving, flexibility, accessibility and trust & safety had significantly positive impacts on ROP. After considering the restaurant size as a moderator for analysis, there are only two constructs- accessibility and trust & safety had significant impacts on ROP. This empirical finding could provide restaurateurs with a reference to improve ROP by increasing the mobile payment environment.

Keywords:

Mobile payment environment

; Restaurateur

; Restaurant operating performance

; Restaurant size

; Innovation diffusion theory (IDT)

; Technology acceptance model (TAM)

1. Introduction

From Internet to personal banking to powerful apps, people are increasingly using mobile devices to manage our daily environment. Bittman et al. [1] indicated that the mobile phone is one of the most quickly spread devices in the past of technical revolution. Therefore, Near-Field-Communication (NFC) mobile payment environment which would pay for transactions via smartphone devices are getting more popular. However, from the perspective of business owners, do the NFC mobile payments create the relative advantage or increase comparative operation obstacles in current fast-paced environments? There is a paucity of empirical research to study the NFC environment impacts on the small-business performance, such as food and beverage businesses. However, more and more of customers have used to the environment that pay with their mobile devices. The existing literature focused on the customer viewpoints to investigate the determinants of customer behavioral intentions for NFC mobile payment, neglecting the merchant’s perspective. Hence, this paper aims to integrate the general model of innovation diffusion theory (IDT) with the technology acceptance model (TAM) to examine the impact of NFC mobile payment environment on the restaurant operating performance (ROP) from the restaurateur’s perspective.

The global mobile payment market size was valued at $2.32 trillion in 2022 and is projected to experience significant growth, reaching $18.84 trillion by 2030, with an estimated increase to $2.98 trillion in 2023 [2]. This prediction shows the importance of NFC in the new era of smartphones. There are more and more advanced environments that allow easy installation of NFC mobile payment. Moreover, the convenient environment of mobile phones has gradually shifted people’s focus from traditional desktop computers to mobile phones. The state-of-the-art technology including the maturity of cloud computing technology, the revolution of smartphones and communications technology had made the mobile payment environment become an emerging trend around the world that quickly replaced cash and even credit cards. During the COVID-19 lockdown, there was a notable surge in the adoption of mobile payments as consumers sought to minimize the risk of infection associated with traditional cash payments [3]. Even after the lifting of lockdown measures, the use of mobile payments continued to rise steadily. According to reports published by Capgemini and The Royal Bank of Scotland [4], the global volume of non-cash transactions, which includes transactions facilitated through mobile applications, is expected to increase from 17% in 2021 to 28% in 2026. This growth can be attributed, in part, to the ongoing endorsement of mobile payments by the business and retail sectors, which have recognized the numerous advantages they offer, such as cost reduction and increased consumer expenditure on products and services [3].

However, according to the report of The Wall Street Journal [5], the mobile payment operators had observed that the small-business restaurateurs intended to receive cash instead of other types of payment in the restaurant compared to other traditional stores. This complex installation procedure might probably block the restaurateurs from adopting mobile payment environments. Begonha et al. [6] suggested that NFC mobile payment environment might provide a more convenient and cost-effective alternative for merchants that originally do not accept credit card payments. Researchers suggested that the food and beverage enterprises would be able to enhance consumer loyalty and faithfulness by introducing a technology-operating model leading to well quality and efficiency improvement and making service profit chain for performance growth [7,8,9].

The majority of restaurants in Taiwan are unlisted companies as well as not easy to obtain secondary data for financial performance. This paper aims to utilize the survey method: (1) to examine the moderating effects of the size of restaurants on the relationship between mobile payment environment and restaurant operations performance (ROP); (2) to identify the influential factors of the NFC mobile payment environment on ROP through the combination of IDT and TAM.

2. Literature review

2.1. Mobile payment environment definition and literature review

Au and Kauffman [10] defined a mobile payment environment as a mobile device that initiates authorization for any payments and confirms the exchange property value in give-and-take for goods and services. Mallat [11] defined a mobile payment environment as carrying out funds transfer or payment transactions with a mobile device through a third party or direct payment to the third party who will pay the receiving party. Ghezzi et al. [12] recap the concept of a mobile payment environment as an electronic payment procedure in which at least one part of the transaction is conducted using a mobile phone capable of securely handling a financial transaction over a mobile network, or via various wireless technologies, such as NFC or Bluetooth. Mobile payment environment can be divided as remote payment and NFC payment-short-range contactless technologies [13]. The technology and platforms used by these two forms of payments are different. A remote payment environment is an e-commerce online transaction, in which consumers use their mobile phone to make payments and complete the shopping procedures on the Internet through credit cards, IC cards, or electronic coupons. NFC payments environment use a mobile phone as the payment tool, which is used in physical store to complete payment transaction in a connected or offline mode [13]. NFC lets two devices positioned in a very short distances of each other to exchange data. Both devices ought to be equipped with an NFC chip [14]. NFC has already been recognized by some scholars as the future trend of mobile payment environments [15]. This is because the advantages of NFC environment are low power, accessibility, and simple communication equipment [16]; also NFC technology does not require complex device pairing. Therefore, it provides many benefits to food and beverage operators and consumers [17,18]. Hayashi [19] pointed out that the environment using NFC mobile payment is 15 to 30 seconds faster than usual card swiping. This is because the time spent on the NFC device is short, simple operating method and secures message transfer; this type of payment technology is most convenient and suitable for fast-paced restaurants and travel environment [16,20]. Getz and Robinson [21] also mentioned that it is possible to use NFC mobile payment environment to raise consumer satisfaction towards the restaurant. Slade et al. [22] argued that mobile payment related research is still in its early stage, even though there has been a relative increase in mobile payment research over the past few years [23]. However, as compared to the extensive e-commerce research (e.g. online bank, mobile bank etc.), the mobile payment environment is a relatively new area of research [24] with most of the research focused on the consumer perspectives [25,26,27,28]. There are quite few studies to understand the environment that merchants use for mobile payment, and the method they acquire to implement this new payment vehicle [29]. Not to mention that little research examines the influential factors in the mobile payment environment from the restaurateurs’ perspective [30].

2.2. The impact of mobile payment environment to operations performance

Niedritis et al. [31] indicated that effective business processes ensure the achievement of the enterprise’s goals. The performance measurement should be performed from different perspectives. Performance is the extent to which the organization’s goal is achieved [32]. To meet an organization’s goal and to create the organization’s value, an organization needs to establish performance measurement scheme and create a revenue-generated environment. Fredendall and Robbins [33] believe that the purpose of an organization’s existence is to achieve its predetermined goal, performance is to measure the extent to which the organization’s goal is achieved, and managing performance is thus the achievement rate for a business’s strategic goal. Organizations effectively make an empowering environment, or latently adapt to the environment through asset distribution, the methods taken to accomplish the association's objective is an essential record to survey if a business activity has been fruitful [34]. That is, the mission of the manager of a business is to develop an environment that increases the organizational performance, creates maximum efficiency with the least investment. Qiu [35] believes that the subjects of performance evaluation is not an individual of the organization, it should be the overall organizational performance. Performance evaluation is the systematic process about how an organization achieves its goals.

There are different perspectives about performance measurement indicators among different scholars. The objective measurement using the secondary data for listed companies is one commonly used method. Miller and Friesen [36] proposed various performance evaluation indicators to include investment returns, cash flow, market share stability, price-to-book ratios and employee productivity. Woo and Willard [37] suggested that there are 14 types of performance measurement index including investment returns, sales returns, sales income, cash flow, investment etc. Walker and Ruekert [38] used three index, financial performance, growth, and profitability, as benchmark to measure overall operations performance of a company. Richard and Johnson [39] suggested that objective measurement in business performance could use employee turnover rate, employee productivity, and return on equity, as a basis.

The second perspective for performance measurement is using the subjective assessment, commonly for unlisted small-and-medium enterprises. Gunday et al. [40] brought up the survey method in performance measurement. Moideenkutty et al. [41] highlighted that the use of questionnaire could reflect respondents’ feelings, which is the subjective performance measurement. Amin et al. [42] also used the questionnaire method as subjective measurement of business performance. Subjective measurement method as compared to objective measurement method enables a higher probability to get more information about the organization they served [40,41,42]. Due to the fact that this research sample focused on the unlisted restaurants, therefore, the ROP used the questionnaire for measuring business performance as proposed by Gunday et al. [40].

2.3. Theoretical model and research hypotheses

Pal et al. [43] use a keyword searching method to review a total of 50 pieces of literature about mobile payment environment and mobile banks in recent years, most of the papers attempt to utilize a theoretical model to investigate the determinants of consumers’ intention of mobile payment. Kim et al. [44] claimed that it would be better to use TAM than the unified theory of acceptance and use of technology (UTAUT) proposed by Venkatesh et al. [45] as a theory basis for research about mobile payment environments. Andersson [46] also pointed out that most research used these two theories, TAM and IDT respectively to explore the drivers of consumers’ uses for new information technology environments.

Davis [47] developed the TAM theory to explain the decision-making factors in accepting information technology environment, with a particular focus on technology use behavior. The implication is that individual level of willingness to accept the new technology environment is dependent on the individual perceived usefulness and perceived ease of use for this technology. Szajna [48], and Wu and Wang [49] suggested that TAM needed to integrate with other variables in order to increase model’s explanation power.

IDT proposed by Rogers [48] is used to explain diffusion behavior [50]. New innovation needs to undergo specific communications channels and is accepted by users as time went on, this is so-called diffusion behavior. Five cognitive constructs of the innovation are (1) relative advantage; (2) compatibility; (3) complexity or accessibility; (4) trialability (the degree the users may be tried to use before adoption); (5) observability. Tornatzky and Klein [52] carried out research on 57 papers about innovative diffusion, and found that there were only three innovative characteristics that had a significant influence on consumers’ decision-making for adopting innovation. Therefore, some research related to innovation adoption only focused on these three variables that influenced adoption behaviors [51,53]. The three variables were: comparative advantage, compatibility, and accessibility.

Moore and Benbasat [53] conducted semi-structured interviews with managers whose environments had adopted information technology innovation, and had obtained 143 valid questionnaires. They used exploratory factor analysis, and extracted into six factors for mobile payment environment adoption. They were: sales growth, cost reduction, flexibility, accessibility, trust & safety, and network externalities. The literature also pointed out that relative advantage construct included the sub-constructs of sales growth and cost saving. Sheikh et al. [54] used the questionnaire method from 278 marketing managers to validate the positive impact of relative advantage on the performance of textile business in Pakistan. The NFC-Mobile payment environment would benefit for eliminating to use cash, offering fast speed and convenience, exchange of secure data between devices in environment with high volume of payments, such as restaurants [16,24]. Both merchants and consumers benefit from operation time reduction, with feasible cost savings and productivity gains [24]. According to the survey conducted by the Statista [55], the worldwide mobile payment revenue in 2015 was US$450 billion and is expected to exceed US$ 1 trillion in 2019, thus becoming one of the most important environments for conducting mobile transactions.

Hence, this paper establishes the following hypothesis:

H1: Relative advantage

environment- sales growth has a positive influence on ROP.

H2: Relative advantage

environment- cost saving has a positive influence on operations performance.

As compared to traditional e-commerce, the most important quality about mobile payment environment is flexibility. It is the ability to use mobile network functions at any time and any place, providing more services and functions for the users [56,57]. Flexibility is also recognized as one of the most important factors for the success of mobile commerce environment [58]. Moore and Benbasat [53] pointed out that the attractive factor for mobile payment users also included flexibility. H3 is established as below:

H3: Flexibility

has a positive influence on ROP.

Research has proven that accessibility is a very important aspect in influencing consumers to use new technology [47,51,59,60]. As the mobile payment environment can provide a greater scope of payment capability, consumers intended to use mobile payment [44]. Dahlberg et al. [61] also claimed that accessibility is the most important factor in mobile payment environment.

H4:

Accessibility has a positive influence on ROP.

In spite of the fact that innovation advancements realized numerous advantages for buyers, however, there are still a few factors that could hinder customers' acknowledgment towards the technology innovation. Past literature indicated that new technology often comes with certain risks [62]. Security is one of the key factors in acceptance of new technology environment [63]. Whether consumers are willing to use the Internet to conduct transaction, primary consideration is given to transaction security [64]. That is, the more secure the online transaction environment, the more the consumer is willing to use on-line transactions. Chang et al. [65] suggested that consumers and merchants’ payment services rely heavily upon a secure and reliable payment environment, even if it is easy to use. According to research by Bast [66], restaurants that use NFC mobile payment environments also heavily rely on system security. This paper establishes the following hypothesis:

H5:

An environment with trust & safety has a positive influence on ROP.

Melitz and Ottaviano [67] and Rumelt [68] revealed that company size is an important moderator for company’s operational performance, and as compared to small-and-medium businesses, large companies have advantages in terms of market, management, and financial resources [69]. Therefore, according to past literature [70,71], this research hypothesizes that the size of company would have different influences to the relationship between five constructs and ROP as below,

H6a:

Company size moderates the relationship between sales growth and ROP.

H6b:

Company size moderates the relationship between cost saving and ROP.

H6c:

Company size moderates the relationship between flexibility and ROP.

H6d:

Company size moderates the relationship between accessibility and ROP.

H6e:

Company size moderates the relationship between trust & safety and ROP.

3. Method

3.1. Research framework and methodology

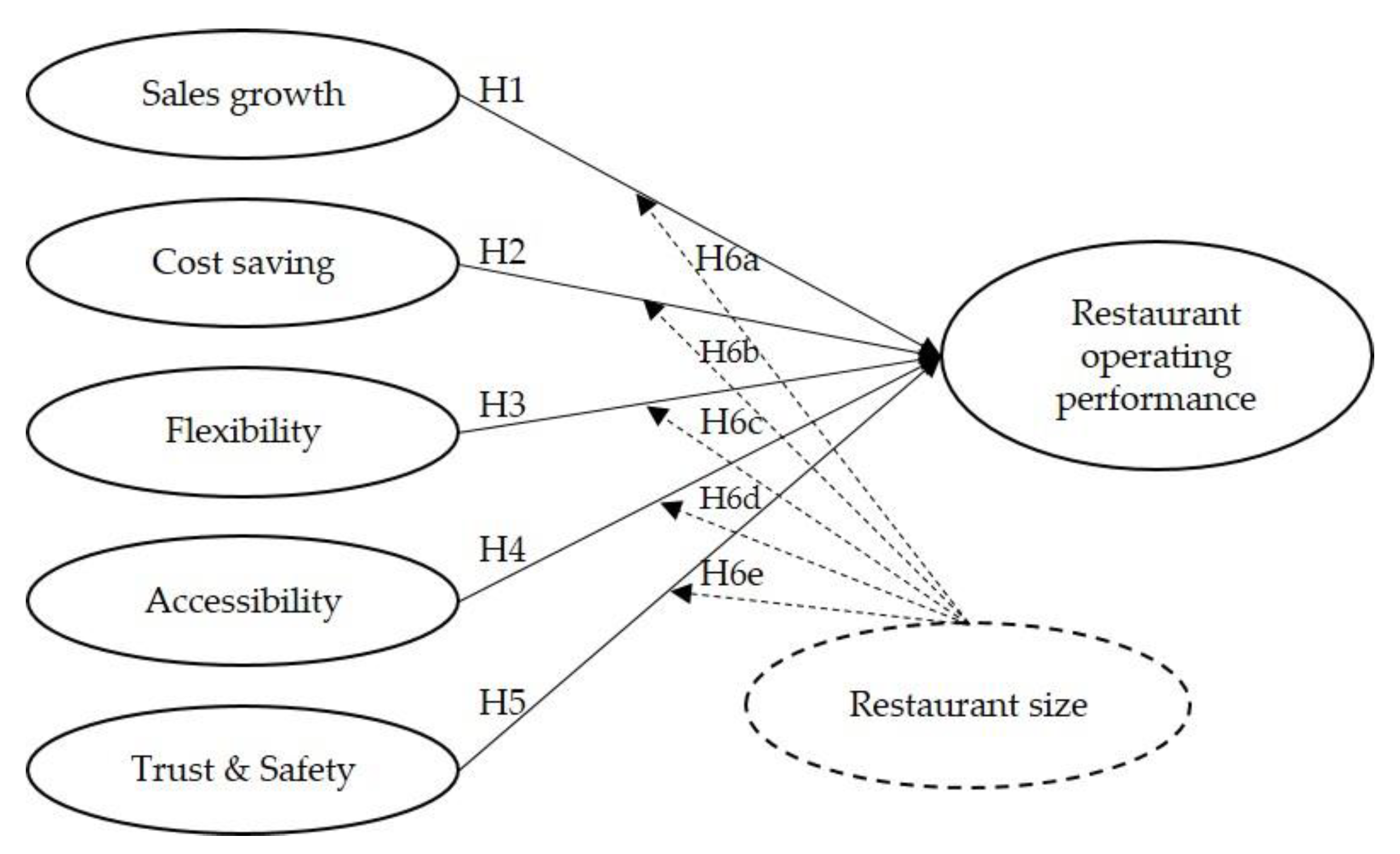

This paper combined TAM and IDT, and added two important variables (flexibility and trust & safety) as research framework in Figure 1 to examine the determinants of NFC mobile payment to ROP. We adopted two constructs (perceived usefulness and perceived ease of use) from TAM, while the other constructs (relative advantage and accessibility) are from IDT. Meanwhile, we combined questionnaire items from construct “perceived ease of use” from TAM and “accessibility” from IDT into one construct. This paper refers to two works from Mallat and Tuunainen [72], and Moore and Benbasat [53] and mainly focused on examining the drivers and barriers for merchants using NFC mobile payment environments not including compatibility, trial ability and observability from IDT.

This research first invited eight experts from industry and academia to examine the validity of the questionnaire. The pretest is distributed to 52 restaurant owners as the basis of reliability test. After the items’ modification from the experts’ opinion and pilot test responses, a total of 279 valid questionnaires from restaurants’ owners and managers were collected. This survey uses the Likert-type 5-point scale as measurement tool, with 1 for strongly disagree to 5 representing strongly agree. We distributed this questionnaire to the in-store managers or owners of catering businesses that already had mobile payment systems. The job position of the respondents, managerial title or cashier, was confirmed prior to sending the survey. After confirmation, an electronic survey will be sent, and participants are asked to help to pass the survey to other restaurateurs who have set-up mobile payment systems. Managerial staff are selected as participants because they are more aware of how businesses are run, and would therefore be able to provide an accurate evaluation [73]. In addition, cashiers are the key frontline personnel operating the mobile payment system; they can also provide an objective response to the survey questions.

After the survey dimensions were established and translation of the survey items were completed, this research invited a total of eight experts from businesses and academia as non-samples to test the validity of the survey. Suggestions from the experts were provided based on the correctness, appropriateness, relevance, coverage, and wordings of the questions for each dimension. After the majority of the master assessments were gathered and incorporated, the proposals given by the specialists were utilized to overhaul the study inquiries in a semantic way, to affirm that the substance of the review was opportune and simple to round out.

3.2. Reliability test of pretest questionnaire

The pilot survey was released via the Internet and distributing 54 copies of pretest questionnaire. After deducting two copies of invalid questionnaires, a total of 52 valid questionnaires were obtained. SPSS 23.0 was used to conduct a reliability test for the questionnaire. Cronbach’s α value was used to measure and test the internal consistency of each independent and dependent variable. Moideenkutty [41] pointed out that it is acceptable for all dimensions with Cronbach’s α value larger than 0.6. The Cronbach’s α for all of the dimensions of this research was between 0.675 and 0.911. This shows that there was consistency and reliability for each dimension of this survey in Table 1.

4. Results

4.1. Descriptive Statistics

This survey was distributed to 300 respondents. After deducting incomplete invalid samples, a total of 279 valid questionnaires were obtained. SPSS 23.0 was used to analyze descriptive statistics as shown in Table 2.

The ratio of male to female respondents is similar, with 50.9% male and 49.1% female. Education-level wise, university stands the most at 33.7%, followed second by college at 25.4%, then high school education level at 24.4% and middle school education level is the least at 0.7%. 31.2% of the respondents aged between 36 to 40 years old stand the most, followed by 19.4% of the respondents aged between 31 to 25 years old, the least were respondents of below 25 years old at 2.5%. Food and beverage-related work experience between 3 to 6 years stands the most at 21.5%, followed by those with 6 to 9 years of work experience at 20.1%, the least were those with 12 to 15 years of work experience at 10.8%. Respondents who were management level stands at 58.1%, business operators stand at 40.5%.

The descriptive statistics for each question and dimension are summarized in Table 3.

For the construct of sales growth, the average score is 3.928, and the standard deviation is 0.772. In this dimension, question 3 “Your company’s product is suitable for mobile payment”, the average score is 4.407, which is higher than the overall average value indicating the restaurant industries suitable for mobile payment environment. The second dimension “cost savings”, the overall average score is 3.79, and the standard deviation is 0.768. In this dimension, the scores of the top three questions were: question #10 “The use of the mobile phone for payment is effective,” question #14 “Mobile payment is useful,” and question #9 “The use of mobile payment speeds up the payment process.” This shows that respondents agree that using mobile payment at restaurants is effective. Dimension three: flexibility, the overall average score is 3.857, and the standard deviation is 0.792. In this dimension, three questions are approaching four points. This shows that respondents intend to agree that NFC mobile payment is helpful for flexibility. Dimension four: accessibility, the overall average is 3.946, and the standard deviation is 0.805. In this dimension, only question 21 “the use of mobile payment is easy” and question 20 “it is easy to understand mobile payment” the average value surpasses 4 points, the overall value is high. This shows that respondents think that the use of mobile payment is easy and it is easy to understand. Dimension five: trust & safety, the overall value is 3.82, the standard deviation is 0.887. This shows that the selected restaurant operators intentionally agree that currently mobile payment operation environment is secure. For the dimension ‘ROP’, the average value is 4.064, the standard deviation is 0.708. In this dimension, all of the questions have an average value of four points. This shows that respondents agree that the restaurants at which they work at have a greater performance value than others in the same industry.

4.2. Moderated Regression Results

In order to investigate the relationship between relative advantage, flexibility, accessibility, trust and safety toward ROP, linear multiple regression is first used. Researchers suggested that the regression model is better than the structure equation model (SEM) in the exploratory studies [74,75]. Meanwhile, Bryne [76] indicated that each of three SEM software, such as AMOS, PLS and LISREL, differs in the way they treat missing data and many methods available to users to handle with incomplete data. Meanwhile, different software produced different types of fit indices. However, the regression analysis using SPSS program is properly direct and easier to use [74,75]. The moderated regression model is further used to examine the moderating effect of restaurant size between independent variables and ROP. The regression model explained 52 percent of the variation in the dependent variable, ROP, as indicated by the adjusted-R²=0.52 in Table 4. Variance inflation factor (VIF) range is between 3.313 and 4.639. Since the VIF value for the various dimensions is smaller than 10 [77], it is known that there are no serious collinearity problems between various dimensions. Five factors had a significant effect on ROP. These include sales growth (b=0.453; p<0.000); cost saving (b=-0.236; p=0.009); flexibility (b=0.117; p=0.098); accessibility (b=0.184; p=0.035); trust & safety (b=0.286; p<0.000).

The standardized beta values suggest that sales growth has the greatest impact on ROP. Trust & safety, accessibility and flexibility were also determined to be a significantly positive impact on ROP. However, cost savings are negatively related, this means that the lower the costs the worse the ROP. This can be due to the food and beverage industry being a labor-intensive industry, excessive cost reduction will result in poor service quality. This will lead to reluctance to visit again by the consumers, which in turn results in poor performance. Therefore, costs should be controlled within a reasonable level.

4.3. Moderation effect

Moderated regression was conducted using interaction terms between independent variables and moderating variables. Model 1 is the main-effects model in Table 5. The size of the restaurant is added as a moderator, however, after the multi-collinearity test (see Table 5, Model 2), the VIF value of the interaction term of sales growth by restaurant size and the interaction term of cost saving by restaurant size are 36.649 and 48.269 indicating high collinearity between these two interaction terms. Therefore, these two interaction terms for sales x restaurant size and cost saving x restaurant size, are deleted.

The model 3 in Table 6 was revised to three interaction terms because of the elimination of collinearity problems. The adjusted-R² is 0.526 of model 3 in Table 6 indicating that this regression model explained 52.6 percent of the variation in the dependent variable, ROP. After accounting for differences in restaurant size as a moderator, the accessibility and trust & safety in ROP vary on the basis of restaurant size. Two interactions are statistically significant. The interaction term of accessibility and restaurant size has a positive impact on ROP. This indicates that as the restaurant size is larger, the easier use of the NFC mobile payment in the restaurant leads to better ROP. It validates that larger-size restaurants need more efficient equipment to expedite or simplify complex processes. Another interaction term of trust & safety and restaurant size presents a negative impact on ROP. This indicates that when too many personnel operate the mobile payment system, this may pose risks to the checkout process. Consumers will distrust this transaction method, resulting in poor ROP.

5. Discussion

As shown in model 1 in Table 7, besides cost saving shown with a negative correlation, the remaining four dimensions are positively correlated. The hypothetical empirical result of this research is shown in Table 7. This result is similar to the result by Mallat and Tuunainen [72], who mentioned that although businesses understand the benefits brought about by NFC mobile payment, but the costs for the initial system setup stage are high, and business operators were not able to predict the time required to reduce costs greatly, this might be one factor that resulted in a negative correlation in this research for the dimension on cost saving. Another possible reason might be due to the fact that restaurant is an industry that requires heavy manpower; excessive cost reduction will result in poor service quality, thus, influencing fewer operations performance.

In terms or moderating effect, as shown in model 3 in Table 7, in summary, the hypothesis of the moderation effect of restaurant size between accessibility and ROP and trust & safety and ROP was supported. This result is partially consistent with the works from the literature. Melitz and Ottaviano [67] indicated that larger enterprises have a relative advantage over smaller companies in terms of market power, management processes and financial resources. However, from the safety and trust perspectives, the larger company might expose its security risk in the mobile payment processes.

6. Conclusion, Implications and limitations

6.1. Conclusion

This study integrated IDT with TAM to examine the impact of NFC mobile payments on ROP. This research invited eight experts from industry and academia to test the validity of the questionnaire. Reliability testing of the questionnaires was conducted through the distribution of 52 hard copies of the valid questionnaire. This paper used convenience sampling to distribute questionnaires to restaurant owners and managers instead of customers in order to investigate the impact of NFC mobile payment on ROP. A total of 279 valid questionnaires were collected. Multiple regression analysis is used to explore the relationship between independent and dependent variables. The research results show that respondents believe the five dimensions (sales growth, cost saving, flexibility, accessibility and trust & safety) have a significant influence on ROP, but the cost-saving dimension has a significantly negative impact on ROP. After considering the restaurant size as a moderator for analysis, there are two constructs ‘accessibility’ and ‘trust & safety’ that had significantly positive impacts on ROP.

6.2. Theoretical implications

Early research on mobile payments, mostly focus on the ubiquity and personal traits of the system and services [77]. This research is based on the integration of IDT and TAM theories, added to two recognized key variables (flexibility, trust & safety). Through empirical research of restaurateurs and catering managers on the impacts of mobile payment on operations performance, this research proves that the features of NFC mobile payment including relative advantages, flexibility, accessibility and trust & safety can effectively increase the performance of restaurant operations. These empirical results provide the theoretical implications of the integration IDT and TAM and the other two constructs (flexibility and trust & safety) could explain the impact of NFC mobile payment on the operational performance in the restaurant industry. This result is consistent with the result of a research conducted by Mallat and Tuunainen [72] through a questionnaire survey and semi-structured interview. For the NFC payment environment in Taiwan, the empirical results of this research can provide relevant researchers to further develop and improve the theoretical model of NFC mobile payment. This can also provide a more specific and effective payment system for restaurant managers.

Meanwhile, this research examines the moderation effect of the size of the restaurant to mobile payment on operations performance. Analysis shows that only the interaction term of accessibility and restaurant size has a significantly positive moderation effect, and another interaction term of trust & safety and restaurant size has a significantly negative moderation effect. This result is different from the research results of Melitz and Ottaviano [67], and Rumelt [68]. From the management perspective, the possible reason for inference is that the bigger companies have more diversified partners, such as financial institutions and telecom operators, leading to involve complex processes to mitigate the payment process risk through more investment. Hence, as the size of the company is larger, more investment yields less operations performance.

6.3. Practical implications

As all industries expedite the introduction of mobile payment application, on top of the government’s vigorous promotion, mobile payment application has continuously sprung up in various fields in Taiwan over the past year. But the data of this research shows that the average point for each dimension has not reached the 4-point level. This indicates that mobile payment is the future trend, but from the business operators’ perspective, they have not been getting the return or reward that they deserve. They do not get to enjoy the benefit of mobile payment. Therefore, based on the analysis results, this research provides some managerial practice recommendations as decision-making references for mobile payment service providers.

These findings show that trust & safety is the second most important construct toward operational performance. Quite a few pieces of the literature suggested that when consumers are operating NFC mobile payment, the security of the transaction is the most concerned matter [62,63,64,65,66]. Users including managers and customers generally believe that there are unknown risks present in mobile payment. Besides the current type of verification vehicle, mobile payment service providers can also consider other types of verification mechanisms like biometrics (iris, fingerprint) to confirm the proceeding of the transaction. This would strengthen consumer confidence in regard to security concerns, and help to increase their willingness to use. In regard to protection measures for system stability and data safety, there is a need to be extra cautious to avoid the leak of personal data or system instability. Any of these events will cause distrust in the users, businesses have to make sure they meet the responsibility of doing a good job in these checks.

It is known from past literature and information that NFC mobile payment is one of the trends in future payment method development [79]. But cash and credit card are still the major forms of payment. Currently, the use of NFC mobile payment is not as simple as making payments using cash or credit card. For a new type of payment method, it will certainly undergo comparison by consumers or frontline operating employees with past usage habits. If a better usage experience is not achieved, consumers will not be willing to use the new payment method, and frontline-operating staff will also refuse to use it. This will be a huge obstacle in the promotion of the method. Therefore, the mobile payment service providers should start from simplifying the operating procedures, reducing operating time for the users, and reducing barriers to learning or use [80]. In any innovation, it must start with a good consumer payment experience, thus, raised payment convenience, and reduced the pain for users. Operators must provide a high quality mobile payment system, so that the consumers can use it anytime and anywhere. Mobile payment can then be a part of the regular activities in daily living, and it will allow profits for operators at the same time. Promoting mobile payments is going to be a lot easier only when either side can profit from this.

Finally, this research suggests that one can make use of the backend big data of the mobile payment, to combine with the advertising activities promoted by the food and beverage businesses on the APP. This will lower the advertisement costs for the businesses, and consumers can receive firsthand discount ads information and boost consumption. On the other hand, when consumers continue to use mobile payment, financial industry can also earn a profit on the payment fees, and the three parties benefited.

This paper also provides the policy makers some suggestions. (1) Regarding the reason affecting the construction of mobile payment, there is the cost factor. There are: newly added tax when business operators generated invoices, the fees charged by third party payment industry, high construction costs, and more in Taiwan. The lack of an appropriate fee-charging model for adopting mobile payment is one of the primary problems that need to resolve first. (2) On the technical side, the problem is failure to integrate the end system for mobile payment. Methods to integrate QR-code, and sensor and other forms should be actively sought after. Currently, mobile payment service providers are developing their own special tools for designated stores. Consumers often see three or four types of POS machines placed on the cashier counter upon entering these stores. If the consumer experiences poor performing sensor moments during mobile payment several times, they would end up using a payment method that they are more accustomed to.

Taiwan’s mobile payment penetration rate is behind China, India, and even countries like Africa. Although the government has developed mobile payment, and has been listed as one of the primary policy objectives, but it is still far from the 2025 goal of attaining 90% penetration rate as set by the Financial Supervisory Commission Taiwan [81]. The goal would not be met, unless the operators’ demand to those problems are addressed and resolved.

6.4. Research limitations and future research

The study considers the perspectives of restaurant owners and management level staff to investigate the impacts of five constructs and one moderator on performance in restaurants. Other hospitality industries, such as hotels, and other retailers may also be worth studying for comparisons. Limitations of this paper include that this research uses TAM and IDT to explore the applicability of mobile payments for food and beverage restaurant operators. However, there are still some variables that have a direct or indirect influence on them, for example, eat-in or take away, price of meal, and more. Future research would include more variables, allowing research inferences to get closer to real situations.

It is also suggested to collect more samples from the perspectives of merchants and customers for future research, and investigate if there are other factors affecting merchants to set up mobile payment systems. At the same time, a questionnaire survey with the consumers to understand the gap between the two sides is also an alternative to develop an improvement plan. This can in turn accelerate the penetration rate of mobile payment in Taiwan. Gefen et al. (2000) [82] pointed out that under the theoretical basis of this research, comparing structural equation modeling (SEM) and regression analysis, SEM has better explanatory power than regression analysis. However, researchers suggested that the regression model is better than the SEM in the exploratory studies [74,75]. The regression analysis using SPSS program is properly direct and easier to use [74,75]. It is suggested that future studies can use SEM with different software as an analytical tool, enhancing explanatory power for variables.

The respondents are the same for the independent and dependent variables of the two dimensions. Systematic bias caused by measurement methods may affect the conclusion. Therefore, it is suggested that future research can match consumers and industry operators to respond, avoiding situations where common method variance (CMV) may occur.

References

- Bittman, M.; Brown, J.E.; Wajcman, J. The cell phone, constant connection and time scarcity in Australia. Soc. Indic. Res. 2009, 93, 229–233. [Google Scholar] [CrossRef]

- Mobile payment market size, share & COVID-19 impact analysis, by payment type (proximity payment and remote payment), by industry (media & entertainment, retail & E-commerce, BFSI, automotive, medical & healthcare, transportation, consumer electronics, and others), and regional forecast, 2023-2030, Fortune Business Insights. Available online: https://www.fortunebusinessinsights.com/industry-reports/mobile-payment-market-100336 (accessed on 4 July 2023).

- Alrawad, M.; Lutfi, A.; Almaiah, M.A.; Elshaer, I.A. Examining the influence of trust and perceived risk on customers intention to use NFC mobile payment system. Journal of Open Innovation: Technology, Market, and Complexity 2023, 100070. [Google Scholar] [CrossRef]

- Capgemini, Winning with SMBs: Optimizing technology and data to drive deep engagement, RBS World Payments Report; 2022, Available online:. Available online: https://www.capgemini.com/insights/research-library/world-payments-report/ (accessed on 4 Jul 2023).

- Mobile-payments firms order up new strategy: restaurants. Available online: https://blogs.wsj.com/digits/2014/08/11/mobile-payments-firms-order-up-new-strategy-restaurants-2/?mod=ST1 (accessed on 4 Jul 2023).

- Begonha, D.B.; Hoffmann, A.; Melin, P. M-payments: Hang up, try again. Credit Card Management 2002, 15, 40–40. [Google Scholar]

- Heskett, J.L.; Sasser Jnr, W.E.; Schlesinger, L.A. The service profit chain: How leading companies link profit and growth to loyalty, satisfaction and value; Free Press: New York, USA, 1997. [Google Scholar]

- Loveman, G.W. Employee satisfaction, customer loyalty, and financial performance-An empirical examination of the service profit chain in retail banking. J. Serv. Res-US 1998, 1, 18–31. [Google Scholar] [CrossRef]

- Kamakura, W.A.; Mittal, V.; De Rosa, F.; Mazzon, J.A. Assessing the service-profit chain. Market. Sci. 2002, 21, 294–317. [Google Scholar] [CrossRef]

- Au, Y.A.; Kauffman, R.J. The economics of mobile payments: Understanding stakeholder issues for an emerging financial technology application. Electron. Commer. R. A. 2008, 7, 141–164. [Google Scholar] [CrossRef]

- Mallat, N. Exploring consumer adoption of mobile payments–A qualitative study. J. Strategic Inf. Syst. 2007, 16, 413–432. [Google Scholar] [CrossRef]

- Ghezzi, A.; Renga, F.; Balocco, R.; Pescetto, P. Mobile payment applications: offer state of the art in the Italian market. Info 2010, 12, 3–22. [Google Scholar] [CrossRef]

- Khalilzadeh, J.; Ozturk, A.B.; Bilgihan, A. Security-related factors in extended UTAUT model for NFC based mobile payment in the restaurant industry. Comput. Hum. Behav. 2017, 70, 460–474. [Google Scholar] [CrossRef]

- Everything you need to know about NFC and mobile payments. Available online: https://www.cnet.com/how-to/how-nfc-works-and-mobile-payments/ (accessed on 9 Sep 2014).

- Ondrus, J.; Pigneur, Y. An assessment of NFC for future mobile payment systems. In International Conference on the Management of Mobile Business; IEEE: Toronto, Ont., Canada, 2007; pp. 43–50. [Google Scholar]

- Leong, L.Y.; Hew, T.S.; Tan, G.W.H.; Ooi, K.B. Predicting the determinants of the NFC-enabled mobile credit card acceptance: A neural networks approach. Expert Syst. Appl. 2013, 40, 5604–5620. [Google Scholar] [CrossRef]

- Egger, R. The impact of near field communication on tourism. J. Hosp. Tour. Tech. 2013, 4, 119–133. [Google Scholar] [CrossRef]

- Pesonen, J.; Horster, E. Near field communication technology in tourism. Tourism Management Perspectives 2012, 4, 11–18. [Google Scholar] [CrossRef]

- Hayashi, F. Mobile payments: What’s in it for consumers? Economic Review-Federal Reserve Bank of Kansas City 2012, 35.

- Alliance, S.C. Proximity mobile payments: Leveraging NFC and the contactless financial payments infrastructure; Smart Card Alliance: Mercer, NJ, 2007. [Google Scholar]

- Getz, D.; Robinson, R.N.S. Foodies and their travel preferences. Tourism Anal. 2014, 19, 659–672. [Google Scholar] [CrossRef]

- Slade, E.L.; Williams, M.D.; Dwivedi, Y.K. Extending UTAUT2 to explore consumer adoption of mobile payments. UK Academy for Information Systems Conference Proceedings, 2013, 36.

- Dahlberg, T.; Guo, J.; Ondrus, J. A critical review of mobile payment research. Electron. Commer. R. A. 2015, 14, 265–284. [Google Scholar] [CrossRef]

- Oliveira, T.; Thomas, M.; Baptista, G.; Campos, F. Mobile payment: Understanding the determinants of customer adoption and intention to recommend the technology. Comput. Hum. Behav. 2016, 61, 404–414. [Google Scholar] [CrossRef]

- Choi, J.; Seol, H.; Lee, S.; Cho, H.; Park, Y. Customer satisfaction factors of mobile commerce in Korea. Internet Res. 2008, 18, 313–335. [Google Scholar] [CrossRef]

- Wei, T.T.; Marthandan, G.; Chong, A.Y.- L.; Ooi, K.B. What drives Malaysian m-commerce adoption? An empirical analysis. Ind. Manage. Data Syst. 2009, 109, 370–88. [Google Scholar] [CrossRef]

- Wu, X.; Chen, Q.; Zhou, W.; Guo, J. A review of Mobile Commerce consumers' behaviour research: consumer acceptance, loyalty and continuance (2000-2009). Int. J. Mob. Commun. 2010, 8, 528–560. [Google Scholar] [CrossRef]

- Zhou, T. An empirical examination of initial trust in mobile banking. Internet Res. 2011, 21, 527–40. [Google Scholar] [CrossRef]

- Salo, J.; Sinisalo, J.; Karjaluoto, H. Intentionally developed business network for mobile marketing: a case study from Finland. J. Bus. Ind. Mark. 2008, 23, 497–506. [Google Scholar] [CrossRef]

- Cobanoglu, C.; Yang, W.; Shatskikh, A.; Agarwal, A. Are consumers ready for mobile payment? An examination of consumer acceptance of mobile payment technology in restaurant industry. Hospitality Review 2015, 31, Article 6. [Google Scholar]

- Niedritis, A.; Niedrite, L.; Kozmina, N. Performance measurement framework with formal indicator definitions. International Conference on Business Informatics Research, Springer: Berlin, Heidelberg, 2011; 44–58. [Google Scholar] [CrossRef]

- Hatten, K.J.; Hatten, M.L. Strategic groups, asymmetrical mobility barriers and contestability. Strateg. Manage. J. 1987, 8, 329–342. [Google Scholar] [CrossRef]

- Fredendall, L.D.; Robbins, T.L. Organizational culture and quality practices in six sigma. Acad. Manage. Proc. 2006, 1, 1–6. [Google Scholar] [CrossRef]

- Wang, J.H.; Cheng, C.C.; Hsu, J.L. A study on the acceptance and operating performance of self-service electronic ordering service for catering industry- integrating views of the customers and operators. Journal of Performance and Strategy Research 2012, 9, 63–84. [Google Scholar]

- Qiu, C.T. Public policy: Basic. Chu Liu Publishing: Taipei, Taiwan, 2000.

- Miller, D.; Friesen, P.H. Innovation in conservative and entrepreneurial firms: Two models of strategic momentum. Strategic Manage. J. 1982, 3, 1–25. [Google Scholar] [CrossRef]

- Woo, C.Y.; Willard, G. Performance representation in business policy research: discussion and recommendation. In 23rd annual national meetings of the academy of management, Dallas, TX, USA, 1983.

- Walker Jr, O.C.; Ruekert, R.W. Marketing's role in the implementation of business strategies: a critical review and conceptual framework. J. marketing 1987, 51, 15–33. [Google Scholar] [CrossRef]

- Richard, O.C.; Johnson, N.B. Strategic human resource management effectiveness and firm performance. Int. J. Hum. Resource Manag. 2001, 12, 299–310. [Google Scholar] [CrossRef]

- Gunday, G.; Ulusoy, G.; Kilic, K.; Alpkan, L. Effects of innovation types on firm performance. Int. J. Prod. Econ. 2011, 133, 662–676. [Google Scholar] [CrossRef]

- Moideenkutty, U.; Al-Lamki, A.; Sree Rama Murthy, Y. HRM practices and organizational performance in Oman. Pers Rev 2011, 40, 239–251. [Google Scholar] [CrossRef]

- Amin, M.; Khairuzzaman Wan Ismail, W.; Zaleha Abdul Rasid, S.; Daverson Andrew Selemani, R. The impact of human resource management practices on performance: Evidence from a Public University. The TQM Journal 2014, 26, 125–142. [Google Scholar] [CrossRef]

- Pal, A.; Herath, T.; De, R.; Rao, H.R. Factors facilitating adoption of mobile payment services over credit/debit cards: An investigation after the demonetization policy shock in India. Proceedings of the Pacific Asia Conference on Information Systems. AIS e-Library: Tokyo, Japan, 2018, 337. [CrossRef]

- Kim, C.; Mirusmonov, M.; Lee, I. An empirical examination of factors influencing the intention to use mobile payment. Comput. Hum. Behav. 2010, 26, 310–322. [Google Scholar] [CrossRef]

- Venkatesh, V.; Morris, M.G.; Davis, G.B.; Davis, F.D. User acceptance of information technology: toward a unified view. MIS Quart. 2003, 27, 425–478. [Google Scholar] [CrossRef]

- Andersson, L. Challenges of introducing and implementing mobile payments: A Qualitative study of the Swedish mobile payment application WyWallet. 2016.

- Davis, F.D. Perceived usefulness, perceived ease of use, and user acceptance of information technology. MIS Quart. 1989, 13, 319–340. [Google Scholar] [CrossRef]

- Szajna, B. Empirical evaluation of the revised technology acceptance model. Manage. Sci. 1996, 42, 85–92. [Google Scholar] [CrossRef]

- Wu, J.H.; Wang, S.C. What drives mobile commerce?: An empirical evaluation of the revised technology acceptance model. Inform. Manage. 2005, 42, 719–729. [Google Scholar] [CrossRef]

- Rogers, E.M. Diffusion of Innovations, 3th ed.; 1983; The Free Press: New York, USA. [Google Scholar]

- Agarwal, R.; Prasad, J. A conceptual and operational definition of personal innovativeness in the domain of information technology. Inform. Syst. Res. 1998, 9, 204–215. [Google Scholar] [CrossRef]

- Tornatzky, L.G.; Klein, K.J. Innovation characteristics and innovation adoption-implementation: a meta-analysis of findings. IEEE T. Eng. Manage. 1982, 29, 28–45. [Google Scholar] [CrossRef]

- Moore, G.C.; Benbasat, I. Development of an instrument to measure the perceptions of adopting an information technology innovation. Inform. Syst. Res. 1991, 2, 192–222. [Google Scholar] [CrossRef]

- Sheikh, A.A.; Shahzad, A.; Ishak, A.K. The effects of e-marketing uses, market orientation, relative advantage and trading partners pressure on the performance of textile business in Pakistan: A mediated-moderation analysis. Journal of Economic & Management Perspectives 2016, 10, 562–580. [Google Scholar]

- Global mobile payment revenue 2015-2019. Available online: https://www.statista.com/statistics/226530/mobile-payment-transaction-volume-forecast/ (accessed on 4 July 2023).

- May, P. Mobile commerce: opportunities, applications, and technologies of wireless business (Vol. 3). Cambridge University Press: New York, USA, 2001.

- Anckar, B.; D’Incau, D. Value creation in mobile commerce: Findings from a consumer survey. J. Inform. Tech. Theor. Appl. 2002, 4, 43–65. [Google Scholar]

- Xu, G.; Gutierrez, J.A. An exploratory study of killer applications and critical success factors in M-commerce. J. Electron. Commerce Org. 2006, 4, 63–79. [Google Scholar] [CrossRef]

- Karnouskos, S. Mobile payment: a journey through existing procedures and standardization initiatives. IEEE Commun. Surv. Tut. 2004, 6, 44–66. [Google Scholar] [CrossRef]

- Zmijewska, A.; Lawrence, E.; Steele, R. Classifying m-payments–a user-centric model. In Proceedings of the Third International Conference on Mobile Business. https://epress. lib. uts. edu. au/research/handle/10453/7311 (dostęp: 01.06. 2013). [Google Scholar]

- Dahlberg, T.; Mallat, N.; Penttinen, E.; Sohlberg, P. What characteristics of mobile payment solutions make them valuable to consumers. In Proceedings of the Global Information Technology Management Conference, New York, USA; 2002. [Google Scholar]

- Schierz, P.G.; Schilke, O.; Wirtz, B.W. Understanding consumer acceptance of mobile payment services: An empirical analysis. Electron. Comer. R. A. 2010, 9, 209–216. [Google Scholar] [CrossRef]

- Wang, Y.S.; Wang, Y.M.; Lin, H.H.; Tang, T.I. Determinants of user acceptance of internet banking: An empirical study. Int. J. Serv. Ind. Manag. 2003, 14, 501–519. [Google Scholar] [CrossRef]

- Liao, Z.; Cheung, M.T. Internet-based e-banking and consumer attitudes: An empirical study. Infor. Manage. 2002, 39, 283–295. [Google Scholar] [CrossRef]

- Chang, Y.F.; Chen, C.S.; Zhou, H. Smart phone for mobile commerce. Comp. Stand. Inter. 2009, 31, 740–747. [Google Scholar] [CrossRef]

- Bast, E. Exploring technology acceptance aspects of an NFC enabled mobile shopping system: Perceptions of German grocery consumers. PhD Thesis, Auckland University of Technology, New Zealand, 2011. [Google Scholar]

- Melitz, M.J.; Ottaviano, G.I.P. Market size, trade, and productivity. Rev. Econ. Stud. 2008, 75, 295–316. [Google Scholar] [CrossRef]

- Rumelt, R.P. Towards a strategic theory of the firm. Resources, Firms, and Strategies: A Reader in the Resource-based Perspective, Oxford University Press: New York, USA, 1997, 131-145.

- Beck, T.; Demirguc-Kunt, A.S.L.I.; Laeven, L.; Levine, R. Finance, firm size, and growth. J. Money Credit Bank. 2008, 40, 1379–1405. [Google Scholar] [CrossRef]

- Jang, S.S.; Kim, J. Revisiting the financing behavior of restaurant firms: The firm-size perspective. Int. J. Hosp. Manag. 2009, 28, 177–179. [Google Scholar] [CrossRef]

- Park, K.; Kim, J. The firm growth pattern in the restaurant industry: Does Gibrat’s law hold? Int. J. Tourism Sci. 2010, 10, 49–63. [Google Scholar] [CrossRef]

- Mallat, N.; Tuunainen, V.K. Exploring merchant adoption of mobile payment systems: an empirical study. e Ser. J. 2008, 6, 24–57. [Google Scholar] [CrossRef]

- Choi, T.Y.; Eboch, K. The TQM paradox: relations among TQM practices, plant performance, and customer satisfaction. J. Oper. Manag. 1998, 17, 59–75. [Google Scholar] [CrossRef]

- Nunkoo, R.; Gursoy, D. Residents’ support for tourism: An identity perspective. Ann. Tourism Res. 2012, 39, 243–268. [Google Scholar] [CrossRef]

- Nunkoo, R.; Ramkissoon, H. Structural equation modelling and regression analysis in tourism research. Curr. Issues Tour. 2012, 15, 777–802. [Google Scholar] [CrossRef]

- Bryne, B.M. Structural equation modeling with AMOS: Basic concepts, applications and programming. Lawrence Erlbaum Associates Inc: New Jersey, NJ, 2001.

- Hair, J.F.; Black, W.C.; Babin, B.J.; Anderson, R.E. Multivariate data analysis (7th ed.). New York, IL: Prentice Hall. 1992. [Google Scholar]

- Jarvenpaa, S.L.; Lang, K.R. Managing the paradoxes of mobile technology. Inform. Syst. Manage. 2005, 22, 7–23. [Google Scholar] [CrossRef]

- Tavilla, E. Opportunities and challenges to broad acceptance of mobile payments in the United States. Fed. Bank Bo. 2012, 2–19. [Google Scholar]

- Chen, W.Y. Create a comprehensive wisdom and good neighbors. Taiwan Econ. Forum 2017, 16, 62–78. [Google Scholar]

- Financial supervisory commission, R.O.C. Fintech development strategy white paper. Taipei, Taiwan. 2016.

- Gefen, D.; Straub, D.; Boudreau, M.C. Structural equation modeling and regression: Guidelines for research practice. Comm. Assoc. Inform. Syst. 2000, 4, 1–77. [Google Scholar] [CrossRef]

Figure 1.

The Research Framework.

Table 1.

Validity Test.

| Construct | Cronbach’s α | No of Item |

|---|---|---|

| Sales growth | 0.911 | 7 |

| Cost saving | 0.860 | 7 |

| Flexibility | 0.675 | 3 |

| Accessibility | 0.927 | 5 |

| Trust & safety | 0.908 | 4 |

| ROP | 0.869 | 4 |

Note: ROP means restaurant operational performance.

Table 2.

Descriptive statistics.

| Item | Class | Number (people) | Percent (%) |

|---|---|---|---|

| Gender | Male | 142 | 50.9 |

| Female | 137 | 49.1 | |

| Age | < 25 years | 7 | 2.5 |

| 26-30 years | 50 | 17.9 | |

| 31-35 years | 54 | 19.4 | |

| 36-40 years | 87 | 31.2 | |

| 41-45 years | 45 | 16.1 | |

| 46-50 years | 17 | 6.1 | |

| > Over 51 years | 19 | 6.8 | |

| Education Level | Junior high school | 2 | .7 |

| Senior high school | 68 | 24.4 | |

| Junior college | 71 | 25.4 | |

| University | 94 | 33.7 | |

| Masters | 37 | 13.3 | |

| Doctorate/PHD | 7 | 2.5 | |

| Years of Operation | ≦3 | 44 | 15.8 |

| 3 ~6 | 60 | 21.5 | |

| 6 ~9 | 56 | 20.1 | |

| 9 ~12 | 35 | 12.5 | |

| 12 ~15 | 30 | 10.8 | |

| ≧15 | 54 | 19.4 | |

| Organizational Type | Other | 3 | 1.1 |

| Chain operation | 123 | 44.1 | |

| Independent operation | 153 | 54.8 | |

| Job Titles | Cashier | 2 | 0.7 |

| First-line supervisor | 1 | 0.4 | |

| Restaurateur | 113 | 40.5 | |

| Manager | 162 | 58.1 | |

| Chief | 1 | 0.4 |

Table 3.

The Descriptive Statistics of Constructs and Items.

| Item | Mean | SD |

|---|---|---|

| Sales growth | 3.928 | .772 |

| 1. Mobile payments are compatible with other payment options used in our company. | 3.996 | .923 |

| 2. Mobile payments are compatible with our company’s work routines. | 3.878 | 1.035 |

| 3. Our company’s products are applicable to be paid for with mobile payments. | 4.047 | .990 |

| 4. We wish that our customers use mobile payments. | 3.918 | 1.027 |

| 5. Companies that offer mobile payments are forerunners. | 3.878 | 1.049 |

| 6. Offering mobile payments enhances our company’s image among customers. | 3.910 | .942 |

| 7. Offering mobile payments increases our appreciation by other companies in our business. | 3.871 | .912 |

| Cost saving | 3.790 | .768 |

| 8. Mobile payments decrease our company’s costs. | 3.459 | 1.114 |

| 9. Paying with a mobile phone speeds up payments. | 4.036 | .944 |

| 10. Paying with a mobile phone is efficient. | 4.125 | .903 |

| 11. Mobile payments free resources for other purposes. | 3.577 | 1.172 |

| 12. Mobile payments make the processing of complaints easier. | 3.530 | 1.017 |

| 13. Mobile payments help the staff to concentrate on more important tasks. | 3.703 | .986 |

| 14. Mobile payments are useful. | 4.097 | .783 |

| Flexibility | 3.857 | .792 |

| 15. Mobile payments increase impulse purchases. | 3.728 | 1.034 |

| 16. Mobile payment benefits include the ability of customers to pay independent of time. | 3.910 | .875 |

| 17. Mobile payment benefits include the ability of customers to pay independent of place. | 3.932 | .929 |

| Accessibility | 3.946 | .805 |

| 18. It is easy for the personnel to learn to use the mobile payment system. | 3.935 | .895 |

| 19. It is easy for the personnel to process mobile payments. | 3.957 | .920 |

| 20. Mobile payments are easy to understand. | 4.007 | .898 |

| 21. It is easy to pay with a mobile phone. | 4.122 | .848 |

| 22. It is easy to instruct customers on how to use mobile payments. | 3.710 | .909 |

| Trust & safety | 3.82 | .887 |

| 23.Cooperation partners, such as financial institutions and telecom operators are trustworthy. | 3.961 | .934 |

| 24. Mobile payments are secure. | 3.753 | 1.003 |

| 25. Mobile phones are reliable enough for payment transactions. | 3.756 | .970 |

| 26. Mobile networks are reliable enough for payment transactions. | 3.810 | .950 |

| Performance | 4.064 | .708 |

| 27. Compared with your industry as a whole, how would you rate your organization’s performance in terms of public image and goodwill? | 4.151 | .772 |

| 28. Compared with your industry as a whole, how would you rate your organization’s performance in terms of growth rate of sales or revenues? | 4.011 | .798 |

| 29. Compared with your industry as a whole, how would you rate your organization’s performance in terms of product or service quality? | 4.057 | .803 |

| 30. Compared with your industry as a whole, how would you rate your organization’s performance in terms of employee productivity? | 4.036 | .790 |

Table 4.

The regression results (N=279).

| Independent variables | β | p-Value | VIF | |

|---|---|---|---|---|

| Sales growth | .453 | *** | .000 | 3.313 |

| Cost saving | -.236 | *** | .009 | 4.639 |

| Flexibility | .117 | * | .098 | 2.869 |

| Accessibility | .184 | ** | .035 | 4.378 |

| Trust & safety | .286 | *** | .000 | 2.672 |

| R2= .529, Adjusted R2 = .520, F-value = 61.227 | ||||

Dependent variable: Restaurant operating performance; * p < 0.1, ** p < 0.05, *** p < 0.01.

Table 5.

The moderated regression (N=279).

| Variable name | Dependent variable: ROP | |||||

|---|---|---|---|---|---|---|

| Model 1 | Model 2 | |||||

| ß | VIF | ß | VIF | |||

| Sales growth | 0.453 | *** | 3.313 | .499 | *** | 3.613 |

| Cost saving | -0.236 | *** | 4.639 | -.247 | *** | 5.938 |

| Flexibility | 0.117 | * | 2.869 | .104 | 2.915 | |

| Accessibility | 0.184 | ** | 4.378 | .161 | * | 4.691 |

| Trust & safety | 0.286 | *** | 2.672 | .298 | *** | 2.932 |

| Interactions | ||||||

| Sales growth x restaurant size | .298 | 36.649 | ||||

| Cost saving x restaurant size | -.161 | 48.269 | ||||

| Flexibility x restaurant size | .042 | 1.498 | ||||

| Accessibility x restaurant size | .099 | 9.290 | ||||

| Trust & safety x restaurant size | -.308 | ** | 10.806 | |||

| R2 | 0.529 | 0.543 | ||||

| Adj R2 | 0.52 | 0.526 | ||||

| F | 61.227 | 39.595 | ||||

| df | (5, 273) | (8, 270) | ||||

Dependent variable: Restaurant operating performance. * p < 0.1, ** p < 0.05, *** p < 0.01.

Table 6.

The moderated regression after deletion of collinear variables.

| Variable name | dependent variable:ROP | |||||

|---|---|---|---|---|---|---|

| Model 1 | Model 3 | |||||

| ß | VIF | ß | VIF | |||

| Sales growth | 0.453 | *** | 3.313 | .478 | *** | 3.372 |

| Cost saving | -0.236 | *** | 4.639 | -.236 | *** | 4.667 |

| Flexibility | 0.117 | * | 2.869 | .103 | ** | 2.914 |

| Accessibility | 0.184 | ** | 4.378 | .163 | 4.422 | |

| Trust & safety | 0.286 | *** | 2.672 | .307 | * | 2.717 |

| Interactions | ||||||

| Flexibility x restaurant size | .020 | 1.317 | ||||

| Accessibility x restaurant size | .108 | * | 2.448 | |||

| Trust & safety x restaurant size | -.169 | ** | 2.592 | |||

| R2 | 0.529 | 0.54 | ||||

| Adj R2 | 0.52 | 0.526 | ||||

| F | 61.227 | 39.595 | ||||

| df | (5, 273) | (8, 270) | ||||

Note: ROP: Restaurant operating performance; * p < 0.1, ** p < 0.05, *** p < 0.01.

Table 7.

The empirical results of the research hypothesis.

| Variable name | Model 1 | Model 3 | ||||

|---|---|---|---|---|---|---|

| ß | Decision | ß | Decision | |||

| Sales growth | .453 | *** | H1 Supported | .478 | *** | |

| Cost saving | -.236 | *** | H2 Supported | -.236 | *** | |

| Flexibility | .117 | * | H3 Supported | .103 | ** | |

| Accessibility | .184 | ** | H4 Supported | .163 | ||

| Trust & safety | .286 | *** | H5 Supported | .307 | * | |

| Interactions | ||||||

| Flexibility x restaurant size | .020 | H6c Rejected | ||||

| Accessibility x restaurant size | .108 | * | H6d Supported | |||

| Trust & safety x restaurant size | -.169 | ** | H6e Supported | |||

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Copyright: This open access article is published under a Creative Commons CC BY 4.0 license, which permit the free download, distribution, and reuse, provided that the author and preprint are cited in any reuse.