Submitted:

10 July 2023

Posted:

11 July 2023

You are already at the latest version

Abstract

Previous research has paid little attention to the relationship between corporate governance and brand equity in the tourism industry. This study aims to investigate the moderating effect of corporate governance (CG) on the relationship between brand equity (BE) and corporate profit-ability (CP) with ten control variables including five company characteristics and five macroeconomic variables. Financial data is retrieved from the Taiwan Economics Journal Database (TEJ), covering a total of 196 records from 32 listed companies for 16 years. Results indicate that BE has a significantly positive impact on CP in Taiwanese-listed tourism companies, and that CG moderates the relationship between BE and CP. These findings could help management executives enhance profitability by deepening BE and CG in the tourism industry. Managerial implications are also discussed.

Keywords:

Corporate Governance

; Brand Equity

; Profitability

; Listed Tourism Companies

1. Introduction

A reputable brand and right brand orientation are key factors for success in the tourism industry [1,2,3,4,5]. Brands create not only value for the company but also an impression for customers to determine the quality and attributes of products and services [6,7,8]. Bharadwaj et al. [9] found that 85% of business travelers and 76% of leisure travelers prefer well-known hotel brands and asserted that the reason for these preferences was to reduce risk.

The performance appraisals of brand managers are closely associated with companies’ financial performance. Therefore, many previous studies have centered on measuring the “brand-finance index” [10].

Previous studies concerning BE had largely focused on customers or markets, and used customer loyalty, customer satisfaction, or market share indices as the independent variables [11,12,13,14,15,16,17,18,19]. Few studies have combined BE with the financial aspects of a company, such as profitability, operating performance, and financial performance. By bridging this gap, the empirical findings of this paper may therefore help Taiwanese tourism companies gain a better understanding of the importance of BE. To achieve the future goal of internationalization, tourist companies can draw from their understanding of BE to engage in brand adjustment or enhance BE by increasing advertising budgets or expanding advertising channels.

However, when management executives addressed on the BE enhancement, how to manage the risk is also another important issue. Few studies included corporate governance (CG) variables in their brand-finance index models. This paper aims to elucidate whether CG moderates the relationship between brand equity (BE) and corporate profitability (CP).

Corporate governance has gradually gained international attention following the Asian Financial Crisis in 1997, the Enron scandal in 2001, and WorldCom’s bankruptcy crisis in 2003 [20]. A series of corporate embezzlement cases that occurred in Taiwan in 1998 prompted the Taiwanese government to ratify regulations to enforce the establishment of independent director committees and audit committees in the listed companies in the Taiwan Stock Exchange (TWSE) and Gre Tai Securities Market (GTSM) [21]. A survey conducted by McKinsey & Company highlighted that Asian corporate investors are willing to allocate 20% of their stock premiums to investment targets with favorable CG performance [21].

The Taiwanese tourism industry is currently flourishing. TWSE/GTSM-listed companies are expanding and showing interest in international development. CG reduces the risk of financial fraud and malfeasance and facilitates stable corporate development. While the massive development of the tourism industry in Taiwan, both dimensions of profit and risk are needed to pay attention. Therefore, this paper examines the impact of BE and CG on the CP for TWSE/GTSM-listed tourism companies.

To assist such companies in establishing favorable CG systems and promote the sound development of the stock market, the Financial Supervisory Commission issued the Corporate Governance Best Practice Principles for TWSE/GTSM Listed Companies, establishing six major principles and urging the compliance of affected companies: (1) these principles are established an effective corporate governance framework; (2) protect the rights and interests of shareholders; (3) strengthen the powers of the board of directors; (4) fulfill the function of supervisors; (5) respect the rights and interests of stakeholders; (6) enhance information transparency. An increasing number of TWSE/GTSM-listed companies have subsequently begun to take notice of the importance of CG to the company and its investors. The Taiwanese company gradually paid attention to the CG issue. The independent directors in Taiwanese listed companies have assumed the immense responsibility of handling affairs concerning the company’s audit and remuneration committees. Major investment decisions must first be approved by no less than half of the audit committee and two-thirds of the board of directors before they can be assigned to professional managers for implementation.

Although a series of embezzlement and corruption cases occurred in the years after 1990, a number of managers and researchers have continued to center their efforts on CG [20,21]. However, most applicable studies are centered on Western financial industries [21,22,23,24,25]. Previous research has pointed out that cultural differences significantly influence management. The power distances between different corporate positions are far greater in Western than in Eastern countries. Companies in the West advocate the allocation of authority and respect the right to express personal opinions; that is, they trend towards individualism. By comparison, Eastern countries prefer collectivism in that people seek integration into and protection by groups, even if they are required to violate personal principles. Strategies formulated by companies in the East are more conservative and have a stronger preference for uncertainty avoidance than those formulated in the West, which prefer to pursue risk[26]. This paper aims to analyze the CG of tourism companies in Taiwan, including an investigation of how to enhance CP by modifying director board size (DSIZE), the percentage of independent directors (ID), and the percentage of director stock holding (DHOLDING). Our findings may assist both managers in the industry and future researchers to better understand issues relating to CG.

2. Literature Review

2.1. Brand Equity

A brand may be a name, label, advertisement, or company. Regardless of form, brands have in common that they possess “uniqueness.” According to the study of Kotler and Armstrong [27], brands not only exhibit uniqueness but also contain the core values of the creator and the concepts they wish to deliver to consumers. Brands promote products, services, or company identity and offer consumers guidance in selecting their preferred product or service. Brands thus help differentiate similar products or services offered by different companies [19].

When different brands offering similar products or services emerge in the market, consumers are presented with options and providers encounter competition, leading to the rise of brand management behavior. Providers adopt various approaches, such as advertising, organizing promotional activities, innovating products, providing product warranties, or offering after-sales services, to attract consumers, stimulate their willingness to purchase, and ultimately sell branded products [4,5,11,31,34].

Previous studies have proposed a number of definitions for BE based on the dimensions of market, consumer, and finance [35]. Table 1 shows definitions of BE based on the diversified literature since the concept of BE was introduced in 1991.

A literature review indicates that although BE definitions have been segregated, they were all based on the associations between customer and company. Definitions proposed by different studies contain different perspectives and dimensions of BE. This paper adopted the tourism industry as the observed sample and focused on analyzing the correlation between market orientation and CP. Therefore, the BE definition proposed by Bailey and Ball [36] was adopted as the operating definition of this paper; indicating that “BE is the associative value between brands and customers/hotel owners, the effects of these associations on customers/hotel owners and subsequent financial performance of the brand.”

A literature review of the definitions of BE shows that these definitions can be broadly characterized into three categories: customer-oriented, market-oriented, and finance-oriented, each with its specific measurement approaches. For the customer category, researchers have suggested using a questionnaire survey approach to measure the indices of brand perception, brand association, brand loyalty, repurchase intention, and willingness to pay [17,19]. For the market category, it has been argued that advertising had a significantly positive impact on BE, mediated by brand association and perceived quality. Therefore, market input and output data and indices, including advertising expenditure (AVE), market share, and premium effects, are recommended to measure BE [12,13,14,15,16,18].

For the finance category, Aaker [11] suggested that the stock market reflects the investors’ views on future trends and brand prospects. The author calculated share prices to determine the market value of companies. Tangible assets were excluded from market value to determine intangible assets, and value created from BE-related R&D and industrial factors (e.g., laws and industrial concentration) were excluded from the intangible assets to determine to BE. Other researchers have proposed determining replacement cost to evaluate the brand value, such as using Tobin’s Q ratio of shareholders’ equity to replacement cost; an increased value denotes a high BE [11,18,42]. Several studies also suggested using future returns to calculate BE directly, as these outcomes represent the value that BE can create for a company. For example, the Discounted Cash Flow Method uses net earnings and the primary reference indices and takes into account asset duration and inflation rate. This method directly converts future brand value into present values [11,43].

For the tourism industry, Oak and Dalbor [44] adopted the Thompson Financial Spectrum to analyze data concerning hotels in the United States collected from the COMPUSTAT database. The researchers selected institution investor holding percentage (IIHP) as the dependent variable, advertising cost as the independent variable, and size, share price, year of operation, stock turnover rate (STOR), debt ratio (DEBT), and operating performance as the control variables. Linear regression analysis showed that the advertising cost had a significant and positive impact on IIHP, and it was concluded that institutional investors prefer hotels with increased BE as investment targets. The present study selected TWSE/GTSM-listed tourism companies as the sample population. Therefore, the advertising expenditures were selected as the proxy variable for BE.

2.2. Corporate Profitability

Companies exist to turn a profit, and CP is an index of profitability. Profitability directly affects whether a company is able to continue operations, create returns, provide earnings to shareholders, and attract investors. Common CP indices include return on assets (ROA); return on equity (ROE); earnings before interest, taxes, depreciation, and amortization (EBITDA); and earnings per share (EPS) [45,46].

EPS refers to the earnings or losses of a company’s ordinary shares within a specific accounting period. EPS is often used to evaluate profitability trends and stock investment risks, or adopted as a reference for investment decisions [47]. A number of previous studies selected EPS as a proxy variable for CP [48,50]. Meanwhile, BE is significantly and positively correlated with stock returns. In the overall stock market, brands reduce cash flow variability, enhance shareholders’ equity, and facilitate corporate financial performance [10]. Therefore, the study establishes the following hypothesis based on the literature review:

H1: Brand equity has a significantly positive impact on corporate profitability.

2.3. Corporate Governance

CG is an extensive mechanism for ensuring the fairness of shareholders’ equity and protecting the rights of external shareholders from being exploited by company managers or major shareholders with voting rights [25]. Wang [18] defined an array of CG variables comprising DSIZE, ID, percentage of managing directors (MD), DHOLDING, percentage of external shareholder holdings (EHOLDING), and degree of deviation between control right and cash flow right (DEV), and noted that CG significantly and positively influences the corporate value and financial performance. Previous studies also suggested that CG variables be incorporated into accounting-based valuation models to comprehensively evaluate corporate financial performance and corporate value [20].

Agrawal and Knoeber [54] suggested that corporate governance should take note of the characteristics of companies and the structure of shareholders of the Top 800 companies in the Forbes index to raise corporate value and performance. Al-Najjar [22]analyzed the tourism industry in Middle Eastern countries and found that profitability increases with DSIZE and that a decreased DSIZE could better reflect share price performance. However, views concerning the influence of DSIZE and CP/financial performance remain inconsistent, and a number of researchers have argued that DSIZE is negatively correlated to corporate value [55,56,57]. Wang [18] selected TWSE/GTSM-listed tourism-related companies as the research targets and collected annual report data for 2008–2011 from the Taiwan Economic Journal (TEJ) and the Market Observation Post System (MOPS). He chose selected intellectual assets (Tobin’s Q) as the independent variable, corporate value (price per share, PPS) as the dependent variable, and six CG proxy variables as the moderator variables for multiple regression analysis. Findings showed that DSIZE had a positive moderating effect on the relationship between intellectual assets and corporate value. Therefore, the following hypothesis was formulated:

H2: Director board size has moderating effect on the relationship between brand equity and corporate profitability.

Ahmed and Duellman [59] found that the stringency of accounting reviews increased with ID. Vafeas [59] examined the data of 262 companies in the US between 1994 and 2000 and found that the quality and transparency of the company’s financial statements increased with ID, thus benefiting their financial performance. However, other researchers have argued that independent directors may tend to boycott or reject a portion of the proposals presented by the board of directors for mitigating the risk of investment. Such actions also decrease investment and expansion opportunities, which negative impact on corporate profitability [23.54]. Wang [18] asserted that ID has a positive moderating effect on the relationship between intellectual assets and corporate value. Therefore, the following hypothesis was formulated:

H3: The percentage of independent directors has moderating effect on the relationship between brand equity and corporate profitability.

Bradley [60] suggested that when managers as inside directors could consolidate company authority, assist the organization to smoothly implement the policies, reduce the likelihood of misinterpretation of the policies, and integrate the board of directors and management. They concluded that when managers as inside directors would positively influence operating performance. Jensen and Meckling [61] found that the losses assumed by managers increase with the number of shares they hold, which led them to lead to more stringent and careful behavior during decision-making because their interests are aligned with those of the company. Core et al. [23] analyzed 405 observed data of 205 US-based listed companies over three years and found that managers as inside directors yielded to the controlling power of the company dominated by insider directors. For realizing self-interest, those managers may attempt to gain full control of those companies. This behavior not only greatly reduces the company’s CG capability but also significantly and negatively impacts corporate financial performance. Jensen and Ruback [63] argued that once managers own a specific percentage of company shares, they are more likely to engage in anti-takeover behaviors to reinforce their own authority and prevent dilution, such as rejecting merger and acquisition opportunities or capital increase strategies that may be beneficial to the company. Therefore, the following hypothesis was formulated:

H4: Percentage of managers as inside directors has moderating effect on the relationship between brand equity and corporate profitability.

Two factions of academics have engaged in a long-standing dispute concerning about DHOLDING. Jensen and Meckling [61] introduced the convergence of interest hypothesis, arguing that the corporate value increases concurrently with the concentration of equity among a small group of directors because directors’ self-interest becomes jeopardized when the company operates at a loss. To prevent loss, they assume the responsibility of reviewing every corporate decision in hopes to enhance corporate performance and profitability and maximize self-interest. In contrast, Crutchley et al. [62] examined the initial public offerings (IPO) of 242 US-based companies in 1993 and 1994 and found that the stability of board of directors increased with DHOLDING, leading to improved corporate supervision. DHOLDING can thus be regarded as positively affecting corporate value. However, Jensen and Ruback [63] opposed this argument by proposing the ‘entrenchment’ hypothesis. The authors suggested that the voting rights and tangible authority of directors increase concurrently with DHOLDING, causing the board of directors to lose their mediation and supervision functions and those directors who with authority would trend towards self-interest, and threaten the interest of other small shareholders. Thus, they argued that DHOLDING thus negatively affected corporate performance and corporate value. Fang et al. [64] analyzed the statistics of the National Bureau of Economics Research (NBER), including 39,469 listed companies in the American Express (Amex), New York Stock Exchange (NYSE), and National Association of Securities Dealers Automated Quotations (NASDAQ), and found that the over-concentration of equity among a few directors produced information asymmetry, leading to deceit small shareholders or market investors and deprive their interest. The researchers also maintained that DHOLDING has a negative influence on corporate value. Therefore, the following hypothesis was formulated:

H5: Percentage of director stock holding has moderating effect on the relationship between brand equity and corporate profitability.

Denis [24] reviewed studies concerning CG in the last 25 years and found that an increase in EHOLDING benefited CG probability and indicated that EHOLDING could improve financial performance. However, Demsetz and Lehn [65] analyzed the shareholding structure, corporate assets, corporate values, and financial performance of 511 US-based listed companies and found that EHOLDING has non-significant inference on financial performance. To validate the effects of EHOLDING on corporate profitability, the following hypothesis was formulated:

H6: Percentage of external shareholder holdings has moderating effect on the relationship between brand equity and corporate profitability.

Controlling shareholders or directors can participate in company decisions using a minimum number of shares through the company’s pyramid structure or cross-ownership. Board directors can secure a set in the company and gain voting rights with the help of family members or substitutes, thereby increasing their controlling rights in the company. To measure the disparity between those directors’ authority and investment, the model selected DEV as our observational variable. DEV includes two parts, control rights and cash-flow rights [66]. DEV refers to control rights minus cash-flow rights. The agency problem becomes more evident as DEV increases. That is, controlling shareholders or directors are more likely to formulate unfavorable decisions for other shareholders by exercising their voting rights or exploiting information asymmetry to maximize self-interest [52,66,67,68]. Therefore, the following hypothesis was formulated:

H7: The deviation degree between control right and cash flow right has moderating effect on the relationship between brand equity and corporate profitability.

3. Methods

3.1. Control Variable Selection

A number of studies have found that the size of a corporation directly affects company funds and the funds available for BE. Therefore, corporate size (SIZE) was selected as a control variable. The tourism industry contains many sub-industries, making it difficult to determine SIZE by measuring the number of employees or the number of guestrooms in a company. In the present paper, total assets (log-transformed) were selected as a proxy variable [15,31,69]. A number of previous studies indicated that DEBT has a direct negative impact on CP. Companies that exhibit low DEBT may be ineffective in leveraging their assets, which may decrease CP. However, excessively high DEBT denotes that the company has a risky asset structure [44]. Therefore, DEBT was selected as a control variable in this paper. IIHP is usually higher than the percentage of small shareholders holding and the investment targets, and strategies of IIHP influence stock price. Previous studies also indicated that Asian corporate investors are willing to allocate 20% of their premiums to investment targets with favorable CG performance variables [21,44]. Therefore, IIHP was selected as a control. STOR represents the popularity of particular stocks. An increased STOR value indicates that the transaction of a particular stock has increased in the market and that stock prices are likely to change drastically, that is, a major event within the company is likely to occur shortly [44,70]. Therefore, this paper assumed that STOR is closely related to stock market events, and it was therefore selected as a control variable.

Since data from TWSE/GTSM-listed tourism companies were analyzed over a period of 16 years, a number of common macroeconomic indices used in previous studies were also selected as control variables. These consisted of the unemployment rate (UE), USD exchange rate (USDE), Gross Domestic Product growth rate (GDPG), inflation rate (IR), and money supply growth rate (MSG) [71,72,73].

3.2. Research Framework

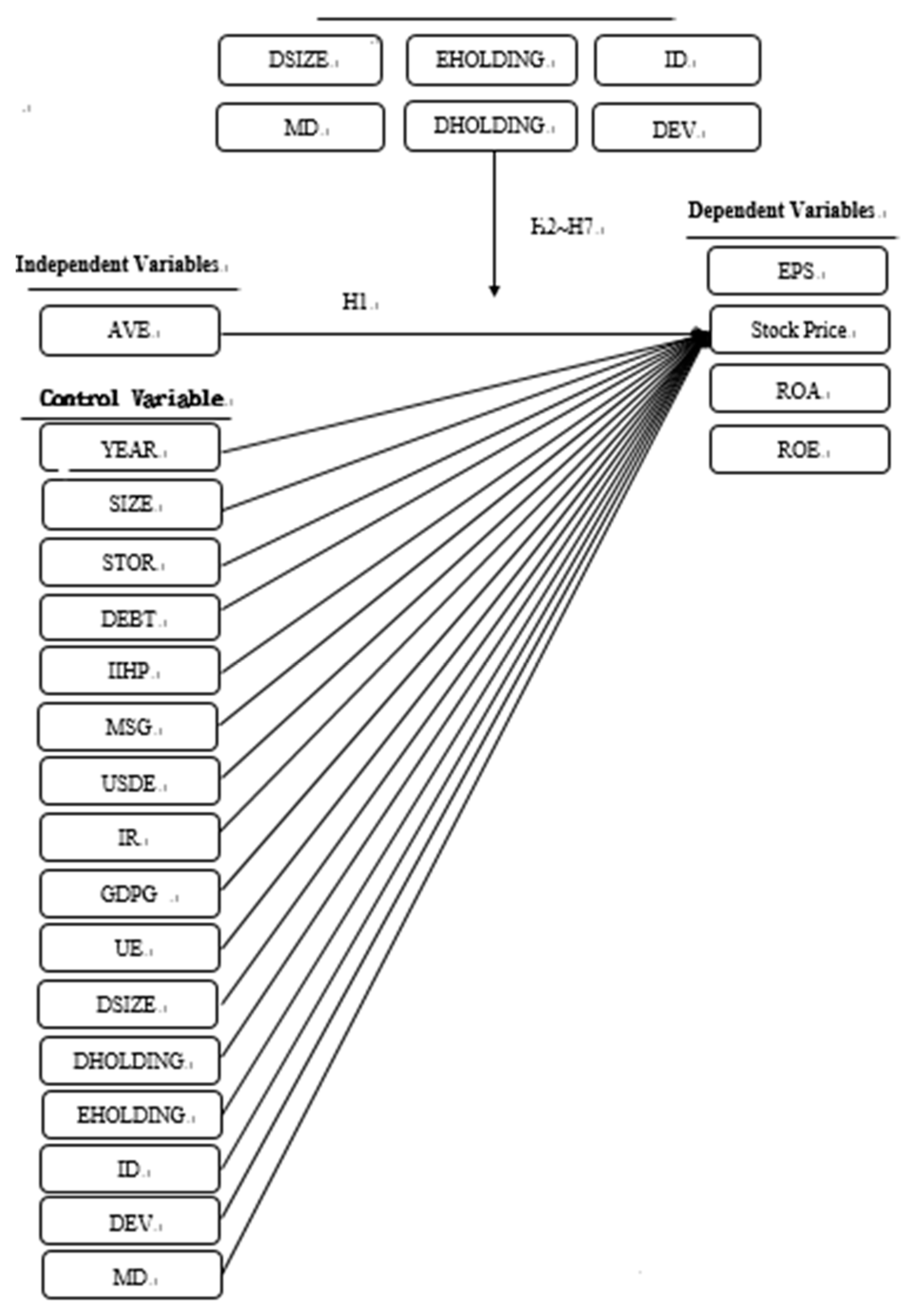

The research framework is illustrated in Figure 1. For the independent variable, AVE was selected as a proxy variable for BE. EPS, Stock Price, ROA, and ROE were selected as the dependent variables. YEAR, SIZE, STOR, DEBT, IIHP, MSG, USDE, IR, GDPG, UE, SIZE, DHOLDING, EHOLDING, ID, DEV, and MD were selected as the control variables. DSIZE, DHOLDING, EHOLDING, ID, DEV, and MD were selected as the moderator variables of CG to test whether CG moderates the relationship between BE and CP.

3.3. Research Subjects and Data Collection

Data of 32 TWSE/GTSM listed tourism companies over a 16-year period were collected from the TEJ. A total of 196 datasets were obtained.

3.4. Research Tools and Data Analysis Methods

Prior to regression analysis, a Shapiro-Wilk test for normality was performed on the dependent variables, with a significance level of p < 0.05. A Box-Cox transform can be used to adjust variables in case of non-normality [74]. A panel regression analysis was performed to analyze two models: a fixed effect model, wherein the effects of time series on the various samples were fixed values, and a random effect model, wherein the effects of time series on the various samples were random values within a normal distribution. A Hausman test was used to test which modeling approach provided a better fit to the data [75,76,77]. This test indicated that for every model considered in this paper, the fixed effect structure was preferable.

The Panel Regression equation can be expressed as follows:

Where the dependent variables, which included EPS, Stock Price, ROA, and ROE on each respective model. This model selected AVE as the proxy variable for BE. Furthermore, SIZE, DEBT, IIHP, STOR, ID, DSIZE, DHOLDING, EHOLDING, DEV, and MD had been used in the model as control variables. ID×AVE, DSIZE×AVE, DHOLDING×AVE, EHOLDING×AVE, DEV×AVE, and MD×AVE are the interaction of those CP observational variables and AVE. i is the ith TWSE/GTSM-listed tourism company, where i=1, 2,3…32. t is the year, where t=1, 2, 3…16 to represent data for 16 years, respectively. β0t is the intercept and μit is the error (normally distributed).

4. Results

4.1. Descriptive Statistics

The descriptive statistics for the independent, dependent, control, and moderator variables of the 196 TWSE/GTSM-listed tourism companies are tabulated in Table 2. Among the macroeconomic variables of Taiwan, the average annual money supply growth for the observed 16 years was roughly 7.7%, the average GDP growth was 3.5%, the average inflation was 10.1%, NT Dollar was 31.7 to the US Dollar, and the unemployment rate was roughly 4.3% of the overall working population.

In terms of the control variables, TWSE/GTSM-listed tourism companies spend an average of NT $500,000 a year on AVE, with a maximum of NT $8.98 million and a minimum of NT $0 (e.g., Holiday Garden, and Hotel Royal). These statistics suggest that BE value and AVE investment differed exponentially among companies. This resulted in a standard deviation of NT $1.35 million, further highlighting the importance of the topic investigated in this paper.

Average DEBT was 39.2% and average IIHP was 41.6%. The smallest DSIZE was 3 and the largest was 16, with a standard deviation of 39.3%. These statistics indicate that the DSIZE of the various companies were relatively similar. The average ID was 13%. In a company with a DSIZE of 6.8, the number of independent directors is less than one, suggesting that the board of directors of many tourism companies in Taiwan have yet to appoint independent directors. Ahmed and Duellman [58] found that the stringency of accounting reviews and the quality of finance statements increase with ID and that ID thus positively influences corporate performance.

4.2. Panel Regression Results

Panel Regression outcomes are tabulated in Table 3. Four models using EPS, PPS, ROA, and ROE as the dependent variables were analyzed, respectively. As noted above, all models used the fixed effect variable structure based on significant Hausman test results (p-value < 0.05).

Model 1 shows that AVE, SIZE, STOR, and DSIZE had significantly positively influenced EPS. These results were consistent with those of Madden et al. [10] and supported H1. Among moderator variables, DSIZE×AVE and DEV×AVE significantly and positively influenced EPS, suggesting that DSIZE and DEV have a significant and negative moderating effect on the relationship between BE and CP. That is, the influence of AVE on EPS diminishes with an increase in DSIZE or DEV degradation. These results are consistent with those of Wang [18] and support the entrenchment hypothesis proposed by Jensen and Ruback [63], who suggested that core agency problems and information asymmetry are more likely to occur with increased DEV and when directors with control rights are inadequately supervised, threatening the other shareholders. Furthermore, ID×AVE significantly and positively influenced EPS. ID can enhance supervision on the board of directors, reduce core agency problems, and eliminate the risk to minority shareholders. When the board of directors is able to make fair decisions, that would enlarge the effects of BE on CP.

Model 2 demonstrates that YEAR, SIZE, and IIHP significantly and positively influenced the stock price, while DEBT had a significantly negative influence. Among macroeconomic indices, the coefficient of inflation was -24.854, suggesting that inflation significantly and negatively influences CP, which means that company stock price decreases with the severity of inflation. Due to the occurrence of inflation denotes that the purchasing power of currency has dropped, or rather that the amount of investment money in circulation has dropped, thus stagnating investment market activity. Stock prices inevitably drop when the market lacks activity [53]. The coefficient of ID was -4.110, suggesting that ID has a significantly negative impact on CP. [54] suggested that independent directors may boycott company investment and merger and acquisition plans to mitigate operating risk, causing the company to become more conservative, which may also cause the company to lose many opportunities to profit or expand. These losses are eventually reflected in the company’s stock price. DHOLDING×AVE significantly and negatively influenced the stock price, which is consistent with the ‘entrenchment’ hypothesis [64]. MD×AVE has a significantly positive influence on stock price, suggesting the positive moderation of MD on the relationship between AVE and stock price. This is because when directors at the same time serve as managers, they are able to eliminate the communication barrier between the board of directors and CEO, then facilitate the implementation and fulfillment of company visions, core values, and brand strategies, thereby enhancing the effects of BE on CP [18].

Model 3 shows that SIZE, IIHP, and STOR significantly and positively influenced ROA, similar to model 2. DEBT maintained a significant and negative influence on ROA. DHOLDING significantly and positively influenced ROA with a coefficient of 0.309. These results were consistent with the ‘convergence of interest’ hypothesis proposed by [62]. The hypothesis posits that when DHOLDING increases, directors become more stringent during decision-making because their self-interest is closely related to the company’s operating conditions. Therefore, the likelihood of a company operating at a loss decreases with increased stringency of directors during decision-making, consequently achieving favorable performance. Among moderator variables, DHOLDING and DEV have negative moderating effects on the relationship between AVE and ROA, however, MD has a positive moderating effect. These results support H4, H5, and H7.

Model 4 indicates that SIZE, DEBT, STOR, and IIHP had significantly influenced ROE, similar to their effect on ROA in Model 3. Additionally, YEAR had a positive effect on ROE, though it had a non-significant impact on ROA. Notably, the inflation rate and unemployment rate achieve had a significant and negative influence on ROE. Increased inflation and unemployment rate implying that the overall macro economy is in recession lead to increased currency devaluation and the unemployed population. The ROE of companies during bear markets is naturally lower than during bulls. Therefore, market sentiment is a key influence on CP. All moderator variables are in contrast to the ROA model, except for DSIZE had a significant and positive influence on CP. This suggests that increased DSIZE allows directors to formulate favorable strategic decisions through collective thinking, maximizing the unit shareholders’ equity of their investment to create return [18].

5. Discussion

5.1. Discussion and Managerial Implications

The findings of our study indicate that AVE, macroeconomic variables, and CG affected the profitability of TWSE/GTSM-listed tourism companies. In addition, a number of CG variables have a moderating effect on the effects of BE on CP. based on this, the managerial implication had been discussed in the following.

5.1.1. Well-planned advertisement expenditure budget

The descriptive statistics indicated that a number of companies did not include AVE as an annual budget item among the 32 TWSE/GTSM-listed tourism samples. The study suggests that these companies take AVE into account in the next year’s annual budget. The literature review and empirical findings showed that BE is an indispensable asset in the service industry. Brands have become a key factor concerning consumers’ preferences for products or services. Moreover, BE has a significantly positive influence on CP. Therefore, budgeting for AVE enables the tourism companies to interact with consumers through advertisement and marketing, deepening consumers’ impressions of a tourism product as well as effectively establishing BE continuously. When consumers require a product or service in the future, they will recall the brand and select products or services under the brand, thereby enhancing CP [6,7,8].

5.1.2. Reinforcing CG

CG is the aspect most often overlooked in this regard, yet it plays a key role in enhancing corporate value. As an example, WorldCom, a company founded at the end of the 20th century, later became the world’s largest communications company through continuous mergers and acquisitions. It was once ranked seventh in the Fortune Global 500. However, the E-commerce industry in the United States took a downturn at the beginning of the 21st century, and WorldCom’s financial situation began to deteriorate. The company’s Chief Finance Officer conspired with a number of accounts and created a fake account named “communication line cost” as a fixed asset to create favorable financial statements without the CG auditing. The scandal was uncovered by KPMG in 2002, and the case was submitted to the United States Securities and Exchange Commission. After the public exposure of the scandal, investor confidence dissipated and WorldCom’s share prices dropped by 75%. Within two days, only 0.3% of peak share prices remained. The company eventually filed for bankruptcy, and the parties involved were successfully prosecuted [79]. The United States is commonly recognized as the most robust capital market in the world with a fair and transparent supervisory system. However, accounting fraud cases continue to emerge. Therefore, companies should reinforce CG to prevent the circulation of negative news that may cause market investors or creditors to lose confidence or the company brand to lose reputability, which could cause company funds to dissipate overnight, obstruct corporate development, or cause irreversible damage. Therefore, CG is beneficial for the company, investment market, and consumer.

The minimum value of the ID of the observed sample in this study was 0, suggesting that a number of the investigated companies failed to implement CG policies. This descriptive statistic recommends that these companies establish or adjust their board of directors, adjust DSIZE, appoint independent directors, enhance DHOLDING, and reallocate internal holding/cross-shareholding structures as soon as possible. According to the empirical results, DSIZE has a negative moderating effect on the effects of BE on CP. ID reduces the risk of corporate decisions, benefits comprehensive corporate development, and enhances CP. Increased DHOLDING denotes an increased consistency between the interests of the directors and the company, which encourages directors to make the most beneficial decisions for the company to enhance self-interest, which is consistent with the convergence of interest hypothesis [61]. By reconfiguring internal holding structures, companies can reduce DEV, the likelihood of core agency problems caused by the reduced board of directors, and the risk of fraud. Consequently, market investors’ confidence in the company may be reinforced. Moreover, the effects of BE on CP increase with a reduction in DEV.

In summary, TWSE/GTSM-listed tourism companies should endeavor to establish or improve their BE through advertisement rather than engaging in traditional price competition or reducing costs. Brands provide added value to products and services, which incentivizes consumers to select the branded products or services of a company, thereby enhancing its profitability [5,11,31,32,34]. Moreover, reinforcing CG can magnify the effects of BE on CP, assisting companies in their efforts to increase corporate performance [18,42].

6. Conclusions

This study investigated the moderating effect of corporate governance on the relationship between BE and CP in terms of EPS, stock price, ROA and ROE in Taiwanese-listed tourism companies. Six corporate control variables (total asset, years of operation, debt ratio, operating performance, stock turnover rate and institutional investors’ holding rate) and five macroeconomic control variables (unemployment rate, USD exchange rate, Gross Domestic Product growth rate, inflation rate, and money supply growth rate) to construct a multiple regression model. This paper used data from the Taiwan Economics Journal, covering a total of 196 records from 32 companies for the observed periods. The empirical results validate the research hypothesis through panel regression. AVE has a significantly positive impact on EPS. Therefore, H1 is supported. Regarding the impact of control variables, the empirical results indicate that YEAR, SIZE, STOR, and IIHP positively influence; however that DEBT had a negative effect on CP. Among the macroeconomic variables, IR and UE negatively influenced CP, suggesting that CP is reduced when the market is in recession (i.e., increased inflation and unemployment). DSIZE had a negative moderating effect on the relationship between AVE and EPS as well as a positive moderating effect on the relationship between AVE and ROA. Therefore, H2 is supported. In addition, DHOLDING had a positive moderating effect on the relationship between AVE and EPS, but a negative one on the relationships between AVE and stock price as well as the relationships between AVE and ROA. Roychowdhury [79] found that managers adjust employee allotment or buy back treasury stock to reinforce market investors’ confidence and prevent share price drops. In effect, they manipulate EPS to maintain EPS at a specific value. The outcomes of the EPS model differed from those of the other models, yet supported H5. No significant effects were found for EHOLDING; therefore, H6 was rejected. These results are similar to those proposed by Demsetz and Lehn [65], who analyzed 511 US-based companies. The authors argued that external shareholders typically focus on company earnings and net profit and rarely participate in company decision-making, thus failing to noticeably influence corporate value. ID had a positive moderating effect on the relationship between AVE and EPS; therefore, H3 was supported. DEV×AVE negatively influenced EPS, ROA, and ROE; therefore, H7 was supported. Finally, MD×AVE significantly and positively influenced EPS, ROA, and ROE; therefore, H4 was supported. Table 4 illustrates the results.

This paper examined data over a 16-year period. Future studies might expand the data collection period to obtain results with increased explanatory power. Furthermore, this paper examined TWSE/GTSM-listed tourism companies. Taiwan is an island economy with a smaller economic and industrial scale than other countries. Future studies could include samples from similar industries (e.g., the aviation industry) to obtain more generalized results.

References

- Ambler, T., Bhattacharya, C. B., Edell, J., Keller, K. L., Lemon, K. N., & Mittal, V. (2002). Relating brand and customer perspectives on marketing management. Journal of Service Research, 5(1), 13-25. [CrossRef]

- Brady, M. K., Bourdeau, B. L., & Heskel, J. (2005). The importance of brand cues in intangible service industries: an application to investment services. Journal of Services Marketing, 19(6), 401-410. [CrossRef]

- Jiang, W., Dev, C. S., & Rao, V. R. (2002). Brand extension and customer loyalty: Evidence from the lodging industry. Cornell Hotel and Restaurant Administration Quarterly, 43(4), 5-16. [CrossRef]

- Kayaman, R., & Arasli, H. (2007). Customer based brand equity: evidence from the hotel industry. Managing Service Quality: An International Journal, 17(1), 92-109. [CrossRef]

- Leone, R. P., Rao, V. R., Keller, K. L., Luo, A. M., McAlister, L., & Srivastava, R. (2006). Linking brand equity to customer equity. Journal of Service Research, 9(2), 125-138. [CrossRef]

- Anderson, E. W., & Mittal, V. (2000). Strengthening the satisfaction-profit chain. Journal of Service Research, 3(2), 107-120. [CrossRef]

- Christopher, M., Payne, A., & Ballantyne, D. (2013). Relationship marketing: Taylor & Francis.

- Kapferer, J.-N. (1997). Strategic brand management: creating and sustaining brand equity long term, 2. Auflage, London.

- Bharadwaj, S. G., Varadarajan, P. R., & Fahy, J. (1993). Sustainable competitive advantage in service industries: a conceptual model and research propositions. Journal of Marketing, 83-99.

- Madden, T. J., Fehle, F., & Fournier, S. (2006). Brands matter: An empirical demonstration of the creation of shareholder value through branding. Journal of The Academy of Marketing Science, 34(2), 224-235. [CrossRef]

- Aaker, D. A. (2009). Managing Brand Equity: Simon and Schuster.

- Chaudhuri, A. (2002). How brand reputation affects the advertising-brand equity link. Journal of Advertising Research, 42(3), 33-43. [CrossRef]

- Chauvin, K. W., & Hirschey, M. (1993). Advertising, R&D expenditures and the market value of the firm. Financial Management, 128-140. [CrossRef]

- Davcik, N. S., & Sharma, P. (2015). Impact of product differentiation, marketing investments and brand equity on pricing strategies: A brand level investigation. European Journal of Marketing, 49(5/6), 760-781. [CrossRef]

- Eng, L. L., & Keh, H. T. (2007). The effects of advertising and brand value on future operating and market performance. Journal of Advertising, 36(4), 91-100. [CrossRef]

- Jagpal, S. (2008). Fusion for profit: how marketing and finance can work together to create value: Oxford University Press.

- Keller, K. L. (1993). Conceptualizing, measuring, and managing customer-based brand equity. Journal of Marketing, 1-22.

- Wang, M.-C. (2015). Value Relevance of Tobin’s Q and Corporate Governance for the Taiwanese Tourism Industry. Journal of Business Ethics, 130(1), 223-230. [CrossRef]

- Winters, L. C. (1991). Brand equity measures: some recent advances. Marketing Research, 3(4), 70.

- Chen, C., Chang, C., Wang, L., & Lee, W. (2005). The Ohlson valuation framework and value-relevance of corporate governance: an empirical analysis of the electronic industry in Taiwan. NTU Management Review, 15(2), 123-142.

- Yeh, Y.-H., Lee, T.-S., & Ko, C. (2002). Corporate governance and rating system. Taipei: Sun Bright Co.

- Al-Najjar, B. (2014). Corporate governance, tourism growth and firm performance: Evidence from publicly listed tourism firms in five Middle Eastern countries. Tourism Management, 42, 342-351. [CrossRef]

- Core, J. E., Holthausen, R. W., & Larcker, D. F. (1999). Corporate governance, chief executive officer compensation, and firm performance. Journal of Financial Economics, 51(3), 371-406. [CrossRef]

- Denis, D. K. (2001). Twenty-five years of corporate governance research… and counting. Review of Financial Economics, 10(3), 191-212. [CrossRef]

- La Porta, R., Lopez-de-Silanes, F., Shleifer, A., & Vishny, R. (2000). Investor protection and corporate governance. Journal of financial economics, 58(1), 3-27. [CrossRef]

- Hofstede, G. (1993). Cultural constraints in management theories. The Academy of Management Executive, 7(1), 81-94. [CrossRef]

- Kotler, P., & Armstrong, G. (2010). Principles of Marketing. Pearson Education.

- Srivastava, R. K., & Shocker, A. D. (1991). Brand equity: a perspective on its meaning and measurement: Marketing Science Institute.

- Pitta, D. A., & Prevel Katsanis, L. (1995). Understanding brand equity for successful brand extension. Journal of Consumer Marketing, 12(4), 51-64. https://www.msi.org/reports/brand-equity-a-perspec... [CrossRef]

- Feldwick, P. (1996). Do we really need ‘brand equity’? Journal of Brand Management, 4(1), 9-28.

- Hanson, B., Mattila, A. S., O'Neill, J. W., & Kim, Y. (2009). Hotel Rebranding and Rescaling Effects on Financial Performance. Cornell Hospitality Quarterly, 50(3), 360-370.

- Kapferer, J.-N. (1997). Strategic brand management: creating and sustaining brand equity long term, 2. Auflage, London.

- Leone, R. P., Rao, V. R., Keller, K. L., Luo, A. M., McAlister, L., & Srivastava, R. (2006). Linking brand equity to customer equity. Journal of Service Research, 9(2), 125-138.

- O'Neill, J. W., & Mattila, A. S. (2010). Hotel brand strategy. Cornell Hospitality Quarterly, 51(1), 27-34.

- Wood, L. (2000). Brands and brand equity: definition and management. Management Decision, 38(9), 662-669. [CrossRef]

- Bailey, R., & Ball, S. (2006). An exploration of the meanings of hotel brand equity. Service Industries Journal, 26(1), 15-38. [CrossRef]

- Keller, K. L. (1993). Conceptualizing, measuring, and managing customer-based brand equity. Journal of Marketing, 1-22.

- Winters, L. C. (1991). Brand equity measures: some recent advances. Marketing Research, 3(4), 70.

- Chaudhuri, A. (2002). How brand reputation affects the advertising-brand equity link. Journal of Advertising Research, 42(3), 33-43.

- Davcik, N. S., & Sharma, P. (2015). Impact of product differentiation, marketing investments and brand equity on pricing strategies: A brand level investigation. European Journal of Marketing, 49(5/6), 760-781.

- Eng, L. L., & Keh, H. T. (2007). The effects of advertising and brand value on future operating and market performance. Journal of Advertising, 36(4), 91-100.

- Wang, M.-C. (2013). Value relevance on intellectual capital valuation methods: the role of corporate governance. Quality & Quantity, 47(2), 1213-1223. [CrossRef]

- O’Neill, J. W. (2003). ADR rule of thumb validity and suggestions for its application. Cornell Hotel and Restaurant Administration Quarterly, 44(4), 7-16. [CrossRef]

- Oak, S., & Dalbor, M. C. (2010). Do institutional investors favor firms with greater brand equity? An empirical investigation of investments in US lodging firms. International Journal of Contemporary Hospitality Management, 22(1), 24-40.

- Fox, D. R., & McCully, C. P. (2009). Concepts and methods of the US national income and product accounts. NIPA Handbook.

- O'Neill, Saunders, C. B., & McCarthy, A. D. (1989). Board members, corporate social responsiveness and profitability: Are tradeoffs necessary? Journal of Business Ethics, 8(5), 353-357.

- Zahra, S. A., & Stanton, W. W. (1988). The implications of board of directors composition for corporate strategy and performance. International Journal Of Management, 5(2), 229-236.

- Aupperle, K. E., Carroll, A. B., & Hatfield, J. D. (1985). An empirical examination of the relationship between corporate social responsibility and profitability. Academy of Management Journal, 28(2), 446-463.

- Khan, Z. H., Alin, T. S., & Hussain, M. A. (2011). Price prediction of share market using artificial neural network (ANN). International Journal of Computer Applications, 22(2), 42-47. [CrossRef]

- Nizar Al-Malkawi, H.-A. (2007). Determinants of corporate dividend policy in Jordan: an application of the Tobit model. Journal of Economic and Administrative Sciences, 23(2), 44-70.

- Madden, T. J., Fehle, F., & Fournier, S. (2006). Brands matter: An empirical demonstration of the creation of shareholder value through branding. Journal of The Academy of Marketing Science, 34(2), 224-235.

- La Porta, R., Lopez-de-Silanes, F., Shleifer, A., & Vishny, R. (2002). Investor protection and corporate valuation. Journal of finance, 1147-1170. [CrossRef]

- Chen, N.-F., Roll, R., & Ross, S. A. (1986). Economic forces and the stock market. Journal of Business, 383-403. [CrossRef]

- Agrawal, A., & Knoeber, C. R. (1996). Firm performance and mechanisms to control agency problems between managers and shareholders. Journal of Financial and Quantitative Analysis, 31(03), 377-397. [CrossRef]

- Abbott, L. J., Parker, S., & Peters, G. F. (2004). Audit committee characteristics and restatements. Auditing: A Journal of Practice & Theory, 23(1), 69-87. [CrossRef]

- Eisenberg, T., Sundgren, S., & Wells, M. T. (1998). Larger board size and decreasing firm value in small firms. Journal of Financial Economics, 48(1), 35-54. [CrossRef]

- Yermack, D. (1996). Higher market valuation of companies with a small board of directors. Journal Of Financial Economics, 40(2), 185-211. [CrossRef]

- Ahmed, A. S., & Duellman, S. (2007). Accounting conservatism and board of director characteristics: An empirical analysis. Journal of Accounting and Economics, 43(2), 411-437. [CrossRef]

- Vafeas, N. (2005). Audit committees, boards, and the quality of reported earnings. Contemporary accounting research, 22(4), 1093-1122. [CrossRef]

- Bradley, K. (1997). Intellectual capital and the new wealth of nations. Business Strategy Review, 8(1), 53-62. [CrossRef]

- Jensen, M. C., & Meckling, W. H. (1976). Theory of the firm: Managerial behavior, agency costs and ownership structure. Journal of Financial Economics, 3(4), 305-360. [CrossRef]

- Crutchley, C. E., Garner, J. L., & Marshall, B. B. (2002). An examination of board stability and the long-term performance of initial public offerings. Financial Management, 63-90. [CrossRef]

- Jensen, M. C., & Ruback, R. S. (1983). The market for corporate control: The scientific evidence. Journal of Financial Economics, 11(1), 5-50. [CrossRef]

- Fang, V. W., Tian, X., & Tice, S. (2014). Does stock liquidity enhance or impede firm innovation? Journal of Finance, 69(5), 2085-2125.

- Demsetz, H., & Lehn, K. (1985). The structure of corporate ownership: Causes and consequences. Journal of Political Economy, 93(6), 1155-1177. [CrossRef]

- Su, K., Li, L., & Wan, R. (2017). Ultimate ownership, risk-taking and firm value: evidence from China. Asia Pacific Business Review, 23(1), 10-26. [CrossRef]

- Claessens, S., Djankov, S., Fan, J. P., & Lang, L. H. (2002). Disentangling the incentive and entrenchment effects of large shareholdings. Journal of Finance, 57(6), 2741-2771. [CrossRef]

- Leuz, C., Nanda, D., & Wysocki, P. D. (2003). Earnings management and investor protection: an international comparison. Journal of Financial Economics, 69(3), 505-527. [CrossRef]

- O’Neill, J. W., & Xiao, Q. (2006). The role of brand affiliation in hotel market value. Cornell Hotel and Restaurant Administration Quarterly, 47(3), 210-223.

- Datar, V. T., Naik, N. Y., & Radcliffe, R. (1998). Liquidity and stock returns: An alternative test. Journal of Financial Markets, 1(2), 203-219. [CrossRef]

- Gligor, M., & Ausloos, M. (2008). Convergence and cluster structures in EU area according to fluctuations in macroeconomic indices. Journal of Economic Integration, 297-330. [CrossRef]

- Kandir, S. Y. (2008). Macroeconomic variables, firm characteristics and stock returns: evidence from Turkey. International Research Journal of Finance and Economics, 16(1), 35-45.

- Singh, T., Mehta, S., & Varsha, M. (2011). Macroeconomic factors and stock returns: Evidence from Taiwan. Journal Of Economics And International Finance, 3(4), 217.

- Razali, N. M., & Wah, Y. B. (2011). Power comparisons of shapiro-wilk, kolmogorov-smirnov, lilliefors and anderson-darling tests. Journal Of Statistical Modeling and Analytics, 2(1), 21-33.

- Ahn, S. C., & Low, S. (1996). A reformulation of the Hausman test for regression models with pooled cross-section-time-series data. Journal of Econometrics, 71(1), 309-319. [CrossRef]

- Hausman, J. A. (1978). Specification Tests in Econometrics. Econometrica. 46 (6): 1251–1271. [CrossRef]

- Nakamura, A., & Nakamura, M. (1981). On the relationships among several specification error tests presented by Durbin, Wu, and Hausman. Econometrica: Journal of the Econometric Society, 1583-1588. [CrossRef]

- Brickey, K. F. (2003). From Enron to WorldCom and beyond: Life and crime after Sarbanes-Oxley. Washington University Law Quarterly, 81.

- Roychowdhury, S. (2006). Earnings management through real activities manipulation. Journal of Accounting and Economics, 42(3), 335-370. [CrossRef]

Figure 1.

EPS: earnings per share; ROA: return on assets; ROE: return on equity; AVE: advertising expenditure; SIZE: No. of employees; DEBT: debt ratio; STOR: stock turnover rate; IIHP: institutional investor holding percentage; MSG: money supply growth rate; IR: inflation rate; GDPG: GDP growth rate; UE: unemployment rate; USDE: USD exchange rate; DSIZE: director board size; DHOLDING: percentage of director stock holding; EHOLDING: percentage of outside shareholdings; ID: percentage of independent directors; DEV: degree of deviation between control rate and cash flow rate; MD: percentage of inside director.

Figure 1.

EPS: earnings per share; ROA: return on assets; ROE: return on equity; AVE: advertising expenditure; SIZE: No. of employees; DEBT: debt ratio; STOR: stock turnover rate; IIHP: institutional investor holding percentage; MSG: money supply growth rate; IR: inflation rate; GDPG: GDP growth rate; UE: unemployment rate; USDE: USD exchange rate; DSIZE: director board size; DHOLDING: percentage of director stock holding; EHOLDING: percentage of outside shareholdings; ID: percentage of independent directors; DEV: degree of deviation between control rate and cash flow rate; MD: percentage of inside director.

Table 1.

The Definitions of Brand Equity (BE).

| Year | Researcher | Definition | Results |

|---|---|---|---|

| 1991 | Srivastava and Shocker[28] | BE is the aggregation of all accumulated attitudes and behavior patterns in the extended minds of consumers, distribution channels and influence agents, which will enhance future profits and long-term cash flow | Brand name and label were not taken into account. |

| 1991 | Winters[19] | BE involves the value added to a product by consumers' associations and perceptions of a particular brand name | Price was taken into account and involved in the measurement of BE. |

| 1993 | Keller[17] | BE represents a condition in which the consumer is familiar with the brand and recalls all associations with the brand, such as label color scheme, brand values, jingle, and even purchase experience. | A consumer-centered definition was proposed. |

| 1995 | Pitta and Katsanis[29] | BE increases the probability of brand choice, leads to brand loyalty, and insulates the brand from a measure of competitive threats. | Market competition was taken into account. |

| 1996 | Feldwick[30] |

|

The definition of BE was simplified and categorized. |

| 2006 | Bailey and Ball[36] | The BE of hotels is the associative value between brands and customers/hotel owners, the effects of these associations on customers/hotel owners and subsequent financial performance of the brand. | A definition of BE in hotel industry was proposed. |

| 2009 | Aaker[11] | BE is a multidimensional concept that includes brand loyalty, brand awareness, perceived quality, brand associations, and other related brand assets. | This is currently the most complete and widely used definition. |

Table 2.

The Definitions of Brand Equity (BE).

| Variables | Min | Max | Mean | Standard Deviation |

|---|---|---|---|---|

| EPS (NTD) | -6.94 | 15.69 | 1.59 | 3.77 |

| Stock Price (NTD) | 2.41 | 1875.63 | 89.10 | 186.24 |

| ROA (%) | -53.76 | 22.92 | 2.14 | 12.66 |

| ROE (%) | -156.95 | 67.28 | 1.03 | 27.89 |

| AVE (NTD) | .00 | 8893598.00 | 507720.91 | 1351807.57 |

| Year (NTD) | 2.00 | 58.00 | 28.07 | 14.29 |

| SIZE | 11.74 | 16.32 | 14.44 | 1.04 |

| DEBT (%) | 7.59 | 86.48 | 39.21 | 18.16 |

| STOR (%) | .75 | 2611.69 | 112.52 | 218.46 |

| IIHP (%) | .00 | 87.88 | 41.60 | 25.43 |

| MSG (%) | -4.12 | 20.47 | 7.70 | 4.86 |

| IR (%) | -.07 | 16.53 | 10.12 | 6.05 |

| GDPG (%) | -1.57 | 10.63 | 3.48 | 2.97 |

| UE (%) | 2.99 | 5.85 | 4.30 | .60 |

| USDE (NTD) | 29.46 | 34.58 | 31.67 | 1.59 |

| DSIZE (people) | 3.00 | 16.00 | 6.89 | 2.70 |

| DHOLDING (%) | .16 | 67.87 | 25.10 | 14.45 |

| EHOLDING (%) | .00 | 53.86 | 16.35 | 11.33 |

| ID (%) | .00 | 60.00 | 12.99 | 17.69 |

| DEV (%) | .00 | 35.01 | 3.60 | 6.98 |

| MD (%) | .00 | 75.00 | 18.04 | 14.24 |

| DSIZE×AVE | .00 | 78809004.00 | 4462570.35 | 12414209.96 |

| DHOLDING×AVE | .00 | 411862523.38 | 14964438.82 | 52087607.02 |

| EHOLDING×AVE | .00 | 230344188.20 | 9610816.02 | 29840041.24 |

| ID×AVE | .00 | 444679900.00 | 14886405.04 | 53704949.44 |

| DEV×AVE | .00 | 179997186.40 | 5958092.17 | 24635207.22 |

| MD×AVE | .00 | 444679900.00 | 13750456.87 | 51756351.40 |

* EPS: earnings per share; ROA: return on assets; ROE: return on equity; AVE: advertising expenditure; SIZE: measuring the number of employees; DEBT: debt ratio; STOR: stock turnover rate; IIHP: institution investor holding percentage; MSG: money supply growth rate; IR: inflation rate; GDPG: gross domestic product growth rate; UE: unemployment rate; USDE: USD exchange rate; DSIZE: director board size; DHOLDING: the percentage of director stock holding; EHOLDING: percentage of external shareholder holdings; ID: the percentage of independent directors; DEV: degree of deviation between control rate and cash flow rate; MD: percentage of managers as inside director.

Table 3.

Panel Regression Analysis.

| Coefficients | Model 1 | Model 2 | Model 3 | Model 4 |

| DV | EPS | Stock Price | ROA | ROE |

| AVE | 4.71e-06 * | 5.84e-05 | -7.76e-06 | -2.54e-05 |

| YEAR | .206 | 25.819 * | 1.327 | 4.890 * |

| SIZE | 159.136*** | 125.183 *** | 5.537 *** | 13.194 *** |

| DEBT | -.004 | -1.636 *** | -.153 *** | -.808 *** |

| STOR | .003 *** | -.015 | .017 *** | .517 *** |

| IIHP | .032 | 5.521 *** | .321 *** | .673 *** |

| MSG | -.023 | -1.773 | -.074 | -.111 |

| IR | -.089 | -24.854 * | -1.368 | -4.495 ** |

| GDPG | .040 | 2.219 | -.155 | -.646 |

| UE | -.230 | -32.472 | -1.999 | -7.713 ** |

| USDE | -.110 | .777 | -1.317 | -2.578 |

| DSIZE | .465 ** | 13.046 | -.029 | -2.112 |

| DHOLDING | .023 | .670 | .309 *** | .410 * |

| EHOLDING | -.002 | -2.825 * | .061 | .202 |

| ID | .010 | -4.110 ** | .073 | .030 |

| DEV | -.001 | -1.623 | .350 | 1.143 |

| MD | .021 | -.803 | .062 | .102 |

| DSIZE×AVE | -6.09e-07 *** | 1.06e-06 | 1.41e-06 | 5.22e-06 * |

| DHOLDING×AVE | 6.74e-08 * | -7.35e-06 * | -4.15e-07 * | -9.43e-07 |

| EHOLDING×AVE | -2.47e-08 | -1.20e-06 | -2.44e-08 | -4.90e-07 |

| ID×AVE | 1.24e-07 * | 6.96e-07 | -6.54e-08 | -5.67e-09 |

| DEV×AVE | -8.59e-08 ** | -3.49e-06 | -6.45e-07 ** | -1.65e-06 ** |

| MD×AVE | -6.85e-07 | 4.62e-06 * | 3.63e-07 ** | 8.80e-07 ** |

| Adjusted R2 | 0.025 | 0.029 | 0.051 | 0.046 |

* p<.1; ** p<.05 **; *** p<.01; * EPS: earnings per share; ROA: return on assets; ROE: return on equity; AVE: advertising expenditure; SIZE: No. of employees; DEBT: debt ratio; STOR: stock turnover rate; IIHP: institutional investor holding percentage; MSG: money supply growth rate; IR: inflation rate; GDPG: GDP growth rate; UE: unemployment rate; USDE: USD exchange rate; DSIZE: director board size; DHOLDING: percentage of director stock holding; EHOLDING: percentage of outside shareholdings; ID: percentage of independent directors; DEV: degree of deviation between control rate and cash flow rate; MD: percentage of inside director.

Table 4.

Summary of Panel Regression Result.

| Model | Model 1 | Model 2 | Model 3 | Model 4 |

| DV | EPS | Stock Price | ROA | ROE |

| AVE | + | Ns | ns | ns |

| YEAR | ns | + | ns | + |

| SIZE | + | + | + | + |

| DEBT | ns | - | - | - |

| STOR | + | Ns | + | + |

| IIHP | ns | + | + | + |

| MSG | ns | ns | ns | ns |

| IR | ns | - | ns | - |

| GDPG | ns | ns | ns | ns |

| UE | ns | ns | ns | - |

| USDE | ns | ns | ns | ns |

| DSIZE | + | ns | ns | ns |

| DHOLDING | ns | ns | + | + |

| EHOLDING | ns | - | ns | ns |

| ID | ns | - | ns | ns |

| DEV | ns | ns | ns | ns |

| MD | ns | ns | ns | ns |

| DSIZE×AVE | - | ns | ns | + |

| DHOLDING×AVE | + | - | - | ns |

| EHOLDING×AVE | ns | ns | ns | ns |

| ID×AVE | + | ns | ns | ns |

| DEV×AVE | - | ns | - | - |

| MD×AVE | ns | + | + | + |

*” + ” means positive effect, “ - “ means positive effect, “ ns ”means non-significant effect. Note 2: EPS: earnings per share; ROA: return on assets; ROE: return on equity; AVE: advertising expenditure; SIZE: No. of employees; DEBT: debt ratio; STOR: stock turnover rate; IIHP: institutional investor holding percentage; MSG: money supply growth rate; IR: inflation rate; GDPG: GDP growth rate; UE: unemployment rate; USDE: USD exchange rate; DSIZE: director board size; DHOLDING: percentage of director stock holding; EHOLDING: percentage of outside shareholdings; ID: percentage of independent directors; DEV: degree of deviation between control rate and cash flow rate; MD: percentage of inside director.

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Copyright: This open access article is published under a Creative Commons CC BY 4.0 license, which permit the free download, distribution, and reuse, provided that the author and preprint are cited in any reuse.