Submitted:

02 August 2023

Posted:

03 August 2023

You are already at the latest version

Abstract

The perceived poor performance of publicly traded companies on their sustainability commitments and the quality of sustainability reporting has prompted stakeholders to consider the economic, environmental, and social impacts of corporate activities. Economic activities have led to various threats in the form of climate change, pollution, greenhouse gas emissions, natural disasters, and other issues that have negatively impacted the environment and stakeholders. Companies are expected to report to stakeholders on their sustainability performance, but reality proves that present reporting falls below stakeholders’ expectations mainly due to its still voluntary nature. The present study aims to provide a literature review of the relationship between sustainability reporting and the role of companies governance, especially observing if climate change requirements and energy-needed changes are being accounted. Results highlight mixed evidence for the influence of board governance attributes, providing interesting insights for research advancement. The study has practical implications for businesses, regulators, governments, and other stakeholders in their policy deliberations and investment decisions. Further empirical studies are recommended to re-examine sustainability reporting using the variables identified as important factors and gaps in this study and other board characteristics to improve the generalizability of the results.

Keywords:

Sustainability Reporting

; Climate Change

; Energy Requirements

; Companies

; Boards

; Governance

; Literature Review

1. Introduction

Weather exchange requirements, stakeholders’ stress, consumers awareness [1,2], legal impositions, or managers' consciousness, the continued environmental degradation puts pressure on the dominant economic version constructed over fossil and scarce assets and on the linear manufacturing and intake fashions [3]. But the transition to a sustainable course is a long-time period, non-linear process, worrying massive adjustments being the result of external or inner pressures [1,2,4,5]. Corporations that comply with company sustainability necessities may do it as a result of mandatory [6] or voluntary [7] motives, being that still in the general public of nations sustainability reporting remains voluntary [8]. Being processes of systematic trade, they'll even result from outside pressures from society or imposed competitive pressures from the market or societal niches [4]. For certain, transitions impose disruption, conflict, resistance, social instability, and non-linear dynamics, forcing monetary sectors or societal systems to transport out of equilibrium, however additionally offering a pathway to recognize large-scale and suited system exchange in the relative quick-term [3].

In the transition to a sustainable desirable world, firms must comply with sustainability practices. If government policies or regulations pressure firms to comply with sustainability rules, to prevent the future costs of social and environmental corporate irresponsibility, nowadays, several firms are willing to co-operate with sustainability schemes voluntarily [2]. As businesses evolve, their managers and governance team become more aware of climate change issues and impositions, turning sustainability reporting more prevalent [2,5]. Sustainability reporting might work as an efficient means of propagating a firm’s position on sustainable development, enhancing its competitive advantage. Besides, it might work as an effective tactic that improves accountability and supports ongoing CSR (corporate social responsibility) and ESG (environmental, social, and governance) strategies [9,10]. At the time this article is being written, sustainability reporting occurring is still voluntary, resulting in companies rarely disclosing them independently of the development stage and growth, of the firm and the country [8]. With the new directive, it would be interesting to account for its effectiveness in a few years. For now, we know that the board of directors end playing a crucial role due to the heterogeneity existing among board members, and the literature has been exploring how specific board characteristics might influence the sustainability reporting quality [11]. Besides, little is known about sustainability reporting and climate change energy requirements, and what the governance role is in these releases.

There are already available standards for reporting effectively. GRI (Global Reporting Initiative) is an independent, international organization that helps businesses and other organizations take responsibility for their impacts, by providing them with a global common language to communicate those impacts (https://www.globalreporting.org/). But how do organizations comply with these standards nowadays? How does the management or governance team deals with these issues? How is the energy part included in sustainability reporting? According to earlier research [12,13,14], CEOs are typically willing to share important corporate social responsibility (CSR) information that increases stakeholder participation. More significantly, according to [15], new chief executive officers (CEOs) are more inclined to release environmental information. However, when a woman holds the position of CEO, the results are not always positive. Investors respond favorably to revealing environmental information when a female CEO is in charge, according to a study conducted in Singapore [16]. However, a study from India found that when a female CEO holds the post, there is a drop in the disclosure of environmental information [17]. Thus, there are different literature views in this regard.

Looking into the previous literature, we already find several empirical and theoretical works exploring board characteristics' effects on sustainability reporting (SR). Gender has been declared as being one of these main characteristics able to impact sustainability reporting practices and quality. But there are also opposite results found in the literature about the influence of gender in sustainability reporting. However, we do not find, as far as we are aware, a bibliometric and bibliographic analysis of governance influence in sustainable reporting by firms where climate change is highlighted through energy statements. As such, our work tries to inform about the effect of governance (management/boards) in still voluntarily disclosure of sustainability reports, from different perspectives. This is done by using the SCOPUS bibliographic database. Our search for the interest keywords returned 39 articles which will be deeply analyzed. Policy implications are to be presented from both bibliographic and bibliometric analysis, and we further contribute to the existing literature by providing important avenues for future research on the topic.

The rest of the article develops as follows. Section 2 presents basic concepts and ideas which relate sustainability reporting with climate change and energy, focusing on the governance role in this disclosure. Section 3 states the methodology followed, whereas Section 4 presents the results of the bibliometric analysis of the 39 documents retrieved and the policy implications derived. Section 5 exposes the bibliographic analysis done and presents some policy implications derived from here. Section 6 presents and discusses future research avenues considering the entire sample of documents offering guidance to important aspects of climate change and energy-related issues to be necessarily disclosed considering its future impact, and finally, section 7 concludes this work.

2. Sustainability Reporting

A sustainability report (SR) is an assertion outlining how a business will make its operations more sustainable, as well as how near it's miles to meeting key targets. It units out an organization’s ESG desires, highlighting the movement needed to meet goals relating to environmental, social, and moral issues.

2.1. Sustainability Reporting, Climate Change, and Energy

SR is considered a defining benchmark of ESG. It’s a transparent means of detailing a business’ environmental and social responsibility. Two attributes that are hastily turning into prerequisites for securing shareholder investment and client advocacy. The reason for SR isn’t entirely about outward perceptions and popularity-constructing, even though. It additionally offers a powerful means of identifying risks and possibilities, allowing corporations to implement adjustments that reply to converting environmental and social best practice requirements. Provided SR are far-reaching, covering all bases will be the key to their success. It should contain a sustainability vision statement, key action points of a business (to reach sustainable development), examples of measures implemented to improve ESG and sustainability, goals and objectives related to the ESG strategy, outlining the risks and opportunities these goals present, and the steps required to accomplish them, indicate key performance indicators qualitatively and quantitatively, governance structures and implementation, and ending with a valuable CEO statement that demonstrates the pledge to improve ESG practices.

Within the GRI Standards, the concept of impact refers to the influence that an organization has or may have on the economy, environment, and people, including any effects on their human rights, resulting from the organization's activities or business relationships. These effects can encompass both actual and potential outcomes, whether positive or negative, short-term or long-term, deliberate or unintentional, and reversible or irreversible. These impacts serve as an indication of the organization's contribution, whether positive or negative, to the advancement of sustainable development. The effects of an organization on the economy pertain to its influence on economic structures at local, national, and global levels. One way an organization can impact the economy is through its competition practices, procurement practices, and tax payments to governments. When it comes to the environment, an organization's effects involve the impact on living organisms and non-living elements such as air, land, water, and ecosystems. The use of energy, land, water, and other natural resources by an organization can have an impact on the environment. The influence an organization has on the economy can be seen in its effects on economic structures at local, national, and global levels. An organization can impact the economy through its competition practices, procurement practices, and tax payments to governments. In terms of the environment, an organization's effects involve the impact on living organisms and non-living elements such as air, land, water, and ecosystems. The utilization of energy, land, water, and other natural resources by an organization can have an impact on the environment. The interconnectedness of the economy, environment, and people is undeniable. Any organization's actions that affect the economy and environment will invariably have repercussions on individuals and their human rights. Similarly, positive impacts can also give rise to negative consequences, and vice versa. Take, for instance, an organization's positive environmental efforts that may inadvertently harm people and their human rights.

On the consolidated set of GRI standards, it is observable that Topic Standard disclosures include: GRI 302: Energy (Disclosure 302-1 Energy consumption within the organization; Disclosure 302-2 Energy consumption outside of the organization; Disclosure 302-3 Energy intensity) and GRI 305: Emissions (Disclosure 305-1 Direct (Scope 1) GHG emissions; Additional sector recommendations; Disclosure 305-2 Energy indirect (Scope 2) GHG emissions; Disclosure 305-3 Other indirect (Scope 3) GHG emissions; Disclosure 305-4 GHG emissions intensity). The question is do organizations already report in accordance? In the context of energy and emissions reporting, the baseline is the projected energy consumption or emissions in the absence of any reduction activity.

On 5 January 2023, in the European Union (EU), the Corporate Sustainability Reporting Directive (CSRD) entered into force. It modernizes and strengthens the rules concerning the social and environmental information that companies must report. Therefore, a broader set of large companies, as well as listed SMEs, will now be required to report on sustainability (approximately 50 000 companies in total; [18]). As defined by [19]: “Corporate Sustainability Reporting represents a potential mechanism to generate data and measure progress and the contribution of companies towards global sustainable development objectives as it can help companies and organizations measure their performance in all dimensions of sustainable development, set goals, and support the transition towards a low carbon, resource efficient, and inclusive green economy.” However, firms are expecting to gain something additional with these measures in the long-term [2], either competitive advantage like increased stock value [20], to achieve proactive leadership [1], enhancing trust [5], conforming to customer demands and expectations [1,2], or to gain reputation [21,22,23]. Additionally, The World Business Council for Sustainable Development (WBCSD) defines sustainability reports as “public reports by companies to provide internal and external stakeholders with a picture of corporate position and activities on economic, environmental and social dimensions” ([24], p.7). Thus, these are broad reports which extend beyond environmental concerns—including social, equity, and gender. In sum, “such reports attempt to describe the company's contribution toward sustainable development” ([24], p.7).

Based on a sample of UK companies’ sustainability reports for the period between 2014 and 2018, [25] study the sustainability report descriptions, focusing on the issues of forward-looking, risk, and sustainability-specific contents. Using a computational linguistic technique, the authors conclude that the core issues that regulate the content of sustainability reports are “external governance-related factors, including the voluntary adoption of sustainability reporting assurance, the choice of assurance provider, stakeholder engagement and ownership concentration; internal governance factors, including board quality and the existence of a sustainability committee; and reporting behavior including the publication of standardized Global Reporting Initiative sustainability reports and financial reporting quality” ([25], p.738). [10] investigate the sustainable development goals (SDGs) on corporate reports for the 50 largest listed companies on the Nigerian stock exchange, covering the period from 2016 to 2018, considering the content analysis to assess the SDGs activities of the sample companies. Additionally, they distributed a questionnaire to the financial managers of the respective companies, as well as to the Governance audit companies and the Sustainability department. The results show that corporate organizations do not make a great effort to contribute to the performance of the SDGs, which led the authors to conclude that Nigerian companies show a low concern regarding the disclosure of the SDGs, as demonstrated in the indicators of the reports of business.

The 17 SDGs of the 2030 Agenda were introduced, and this led to a rise in public awareness of the most pressing global sustainability challenges. The academic community is seeing an increase in studies on the adoption, engagement, and disclosure of the SDGs, which include introducing global goals and incorporating them into non-financial reporting systems [26]. Businesses are increasingly adopting SR as a powerful tool in company strategy and policy, typically voluntarily, even though we have lately helped to expand mandates. Corporate governance, social responsibility, environmental awareness, and economic efficiency are all covered in sustainability reporting. Corporate SR is becoming more popular on a global scale as a voluntary reporting tool to increase stakeholders' confidence.

2.2. Reported Board Characteristics Effects

Looking into the previous literature, we already find several empirical and theoretical works exploring Board Characteristics' effects on SR. Gender has been declared as being one of these main characteristics able to impact SR practices and quality. But there are also opposite results found in the literature about the influence of gender in sustainability reporting. However, we do not find, as far as we are aware, a bibliometric and bibliographic analysis of gender influence in SR by firms, despite the inconclusive results reported in the literature, able to highlight the already achieved results and provide light for future research needs.

One of the most significant dimensions of corporate governance mechanisms for social, environmental, and voluntary disclosure of corporate activities is gender diversity [8,27]. Once the company commits to carrying out social and environmental activities by providing sustainability reports the entire society can find these activities, which enhance corporate performance [8,28]. [29] examines the association between SR and earnings management, considering the moderating effect of board gender diversity on this relationship, in the context of listed firms from the East Africa Community, and the 2011-2021 period. The results show a negative relationship between SR and earnings management, suggesting that revealing economic, environmental, and social performance enhances earnings quality and that gender diversity indeed moderates this relationship. Consequently, increasing the number of women on the board of directors will reduce the earnings management practices and will promote greater gender equity, meeting the Sustainable Development Goals (SDGs), particularly, SDG number five –gender equality. [30] indicate that the corporate social responsibility (CSR) committee presence positively influences sustainable development goals (SDG) disclosure and shows that gender diversity does indeed have a significant positive moderating effect on the relationship between the presence of CSR committee and SDG disclosure considering a sample of enterprises from Argentina, Brazil, Chile, Colombia, Mexico, and Peru. [31] also find that gender-diverse boards are positively associated with sustainability reporting and the involvement of an external assurance provider, with a sample of 366 large Asian and African companies.

Diversity of the board of directors is explored under the heterogeneity of its members as educational background [32,33,34], tenor [33], age, nationality, religious background, task skills, relational skills, and political preferences [35,36,37,38], expertise and experience [39], and board characteristics such as board size, board independence, CEO Duality, board meetings, and committee [11]. Diversity respects the composition of the board and the diverse attributes of combination, characteristics, and expertise of each board member, reflected in board processes and decision-making [40]. When we discuss gender diversity, we are usually referring to the ratio of female directors to the total number of boards of directors [14].

As pointed out by [41] and [11], being the board of directors composed of heterogeneous individuals in terms of ethnicity, gender, geographical background, and technological knowledge, they reveal different preferences for and concerning environmental aspects. For [41] board size, independence, and gender diversity could improve the quality of sustainability reporting in the Asia-Pacific region. More recently, [11] found that sustainability report disclosure can mediate the board of directors' effect on tenure and nationality diversity’s effect on the firm value in India. The authors also include other directors’ diversity factors like gender, age, tenure, educational level, and nationality. Other authors have also evidenced a good relationship between corporate governance practices and environmental and social disclosure [42,43]. Moreover, diversity in terms of unique skills, experience, and knowledge of directors can enhance the board’s information to management [44]. It is even argued in the literature that gender diversity on the board of directors can reduce the information asymmetry between management and shareholders [45].

Given the requirement for a fair business assessment to boost the company's performance, the gender diversity of the board of directors is essential for excellent and effective corporate governance [46,47]. If all board members and executive boards are aware of the steps in managing sustainability challenges in the organization, the board of directors will be more committed [8]. Female directors can bring perspectives, experiences, and work styles that are distinct and different from those of male directors, which can raise the depth and breadth of conversations and boost the quality of decisions [48]. Additionally, according to [39], having more women on boards of directors can improve financial performance. The gender balance of the board of directors might result in a variety of viewpoints when making decisions that have to do with sustainability and human concerns. According to [49,50,51], gender diversity on the board of directors, and particularly the board of directors, motivates businesses to engage in socially responsible behavior and advance sustainable policies. Increased excellent company governance can offer significant market value. According to [52] the market value of the company is correlated with gender diversity on the board of directors. According to [53], increasing gender diversity can lower business risk, boost performance, and close the pay gap for senior management.

Female CEOs enhance CSR disclosure, according to a Pakistani study [54,55]. But according to a different study conducted in a developed country like Italy [56], women CEOs were unable to implement gender policy disclosure, which is contrary to their nature as CEOs. However, we anticipate a female CEO to be equally as successful as a male CEO in carrying out the CEO role's skills, particularly when a stand-alone sustainability report structure is used. The point made by [14] is corroborated by data from earlier research, which show that choosing stand-alone reporting increases stakeholders' access to information [57,58].

Gender diversity and CSR disclosure have been the subject of numerous research [54,55,59,60,61]. Most studies examining the relationship between gender diversity and CSR, or environmental disclosure found a favorable correlation. Gender, for instance, enhances CSR disclosure, according to a Pakistani study [54,55]. Additionally, another study [61] used a Malaysian context to argue that gender diversity and CSR disclosure have a favorable relationship. Additionally, a different study that looked at gender diversity and the Carbon Disclosure Project (CDP) score/index found a favorable correlation between the two [59]. Another study [60] found the inverse correlation between gender diversity and environmental, social, and governance (ESG) disclosure in a Latin American context. The choice of report format and gender board diversity, however, has not been investigated in any studies. According to results that favor stand-alone reports over integrated reporting, the report format is a function of environmental and social performance disclosure [57]. [14] feel that gender board diversity has a similar impact on the choice of sustainability report format due to the good impact it has on sustainability disclosure.

Finally, the proportion of women on boards and its impact on CSR have been examined in many studies [62,63]. Because female directors contribute an ethical perspective to choices regarding environmental and social issues, the study's findings specifically demonstrated that having female directors on the board enhances voluntary disclosure of CSR reports [63]. Similar findings supported the actions taken by female directors to raise the bar for CSR reporting [64]. According to the author of a Sri Lankan study, more female directors are positively correlated with sustainability disclosure, which is in line with [65]'s conclusions [66]. [35] study of 9,744 business years showed that having at least three female directors has a positive impact on CSR disclosure. According to [67], female directors have distinct governance variables that may increase the amount of CSR disclosure listed.

3. Methodology

To carry out a bibliometric and bibliographic analysis, as a research method that offers an unbiased criterion to evaluate the research spanning in a specific topic [68], and that facilitates the identification of new directions for future research [69], we use the SCOPUS database (https://www.scopus.com/search/). The reason to choose this database is based on previous studies, such as the ones of [70,71], who conclude that SCOPUS offers higher measures than other alternatives, such as the Web of Science. As well, [72] argue that SCOPUS is the favorite database for many researchers. The Scopus research was done on 25th July 2023.

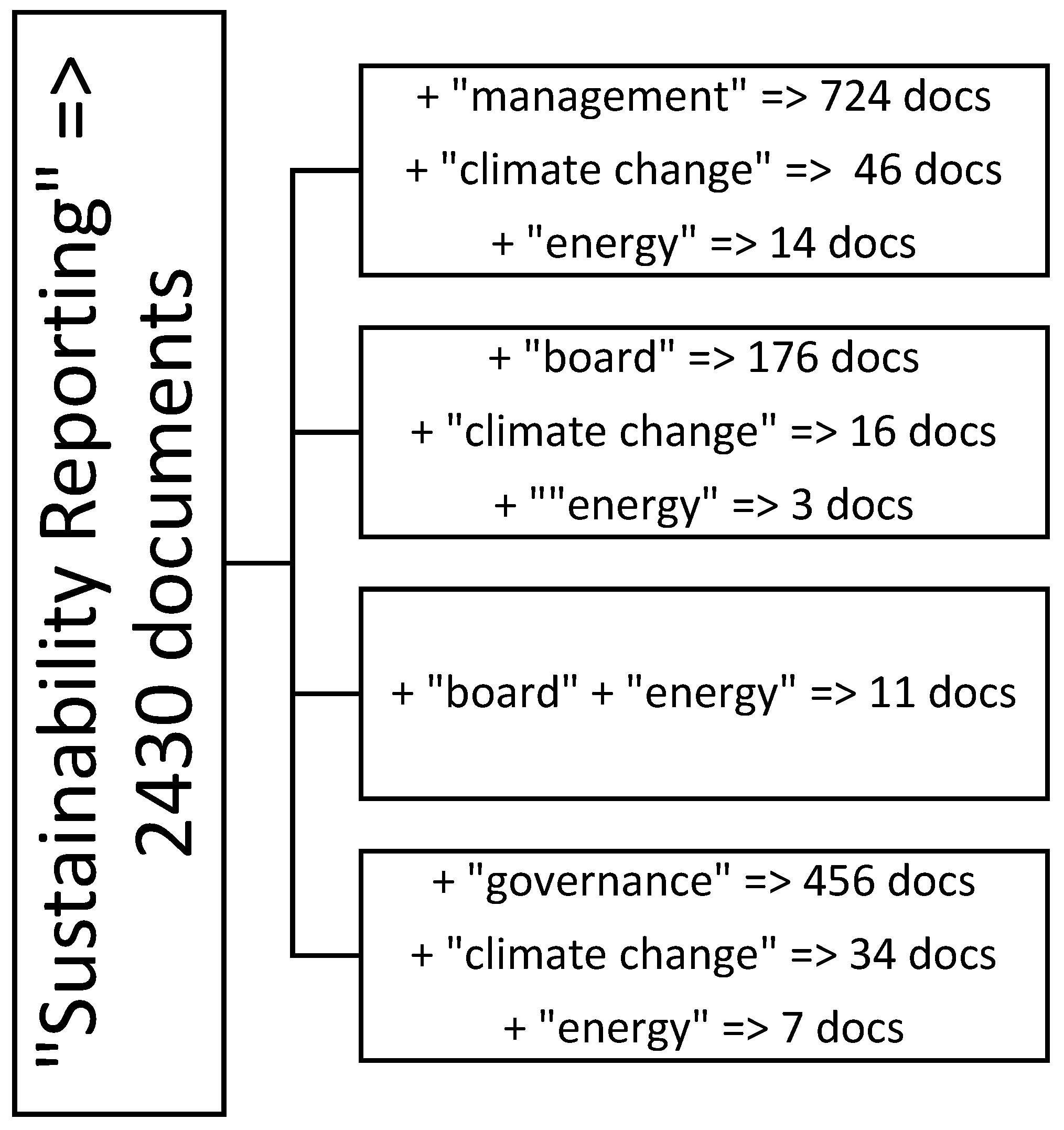

Figure 1 describes the search methodology used and the number of documents that emerged from the adopted criteriums.

Starting with the search criteria TITLE-ABS-KEY (sustainability reporting), 2430 documents have been retrieved. After, we used as criteria TITLE-ABS-KEY ("sustainability reporting" AND "management" AND “climate change” AND “energy”), to remain with only 14 publications. Three other searches were done, leaving us with 14, 16 (not considering “energy”), 11, and 7 documents respectively, while using keywords one by one additionally. These will be named search criteria 1, search criteria 2, search criteria 3, and search criteria 4, respectively. The search was done considering the entire period of publications available, which will be analyzed next in bibliometric and bibliographic terms. All these documents were articles, reviews, conference proceedings, or book chapters, and after merging all the references for each search criteria, and cleaning the repetitions, we end up with a final sample of 39 documents to be analyzed. All these are presented in Table 1.

4. Results: Analysis of Bibliometric Data

Table 1 presents the 39 documents over time and the number of citations. The interest in the theme increased from 2014 onwards, but the years where most of the documents have been published were 2022 and 2023. The year 2023 already counts with 10 documents published, which is justified by the recent theme which started being explored more recently. The first document was published in 2005. There has been a total of 661 citations, with the most cited article being the one from [73], titled “Inter-linking issues and dimensions in sustainability reporting”, published by the Journal of Cleaner Production, which has received 370 citations.

It is not easy to present a usual bibliographic analysis with the 39 documents identified in Table 1, considering that these result from 4 distinct searches. Therefore, we will just present the possible bibliometric analysis considering that we have collected information about authors' affiliations at the time of the publication, the countries/sample analyzed, and information regarding the affiliations, and type of document. This information is to be presented in Figures 2 to 5.

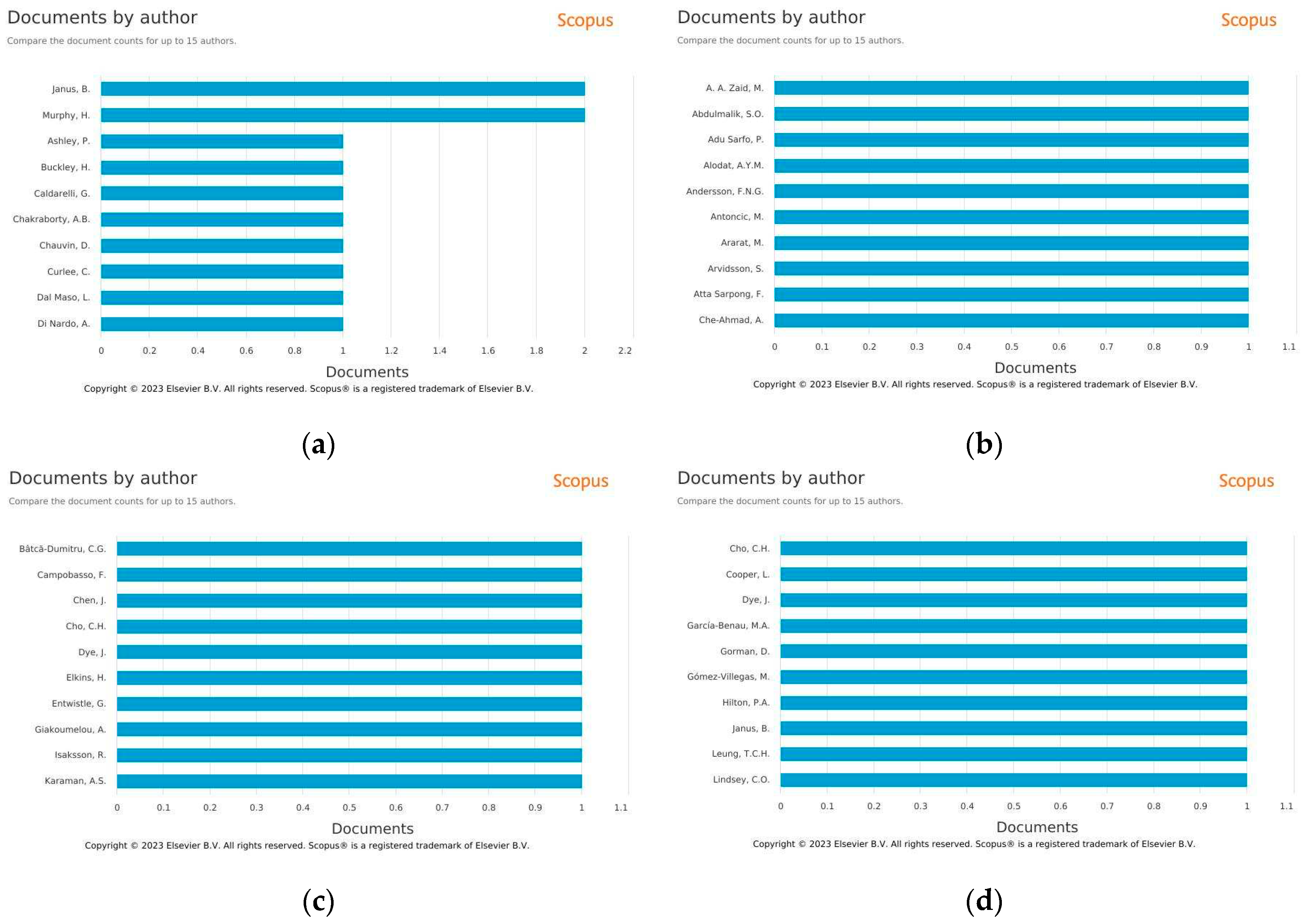

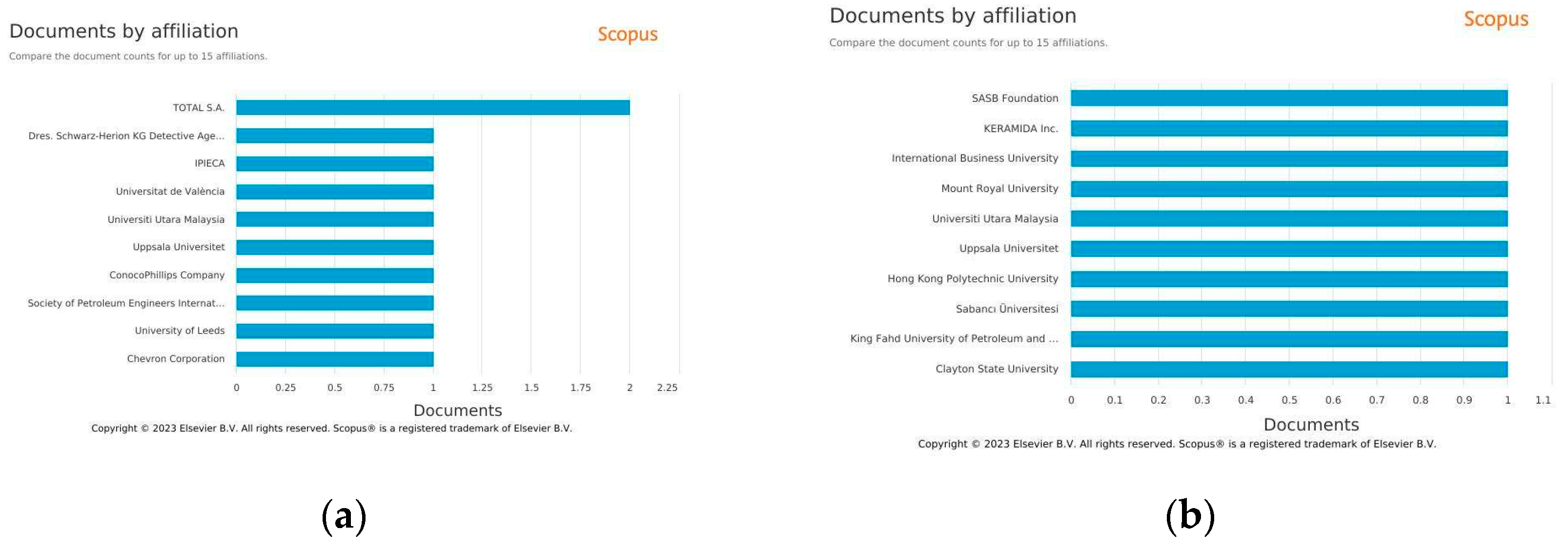

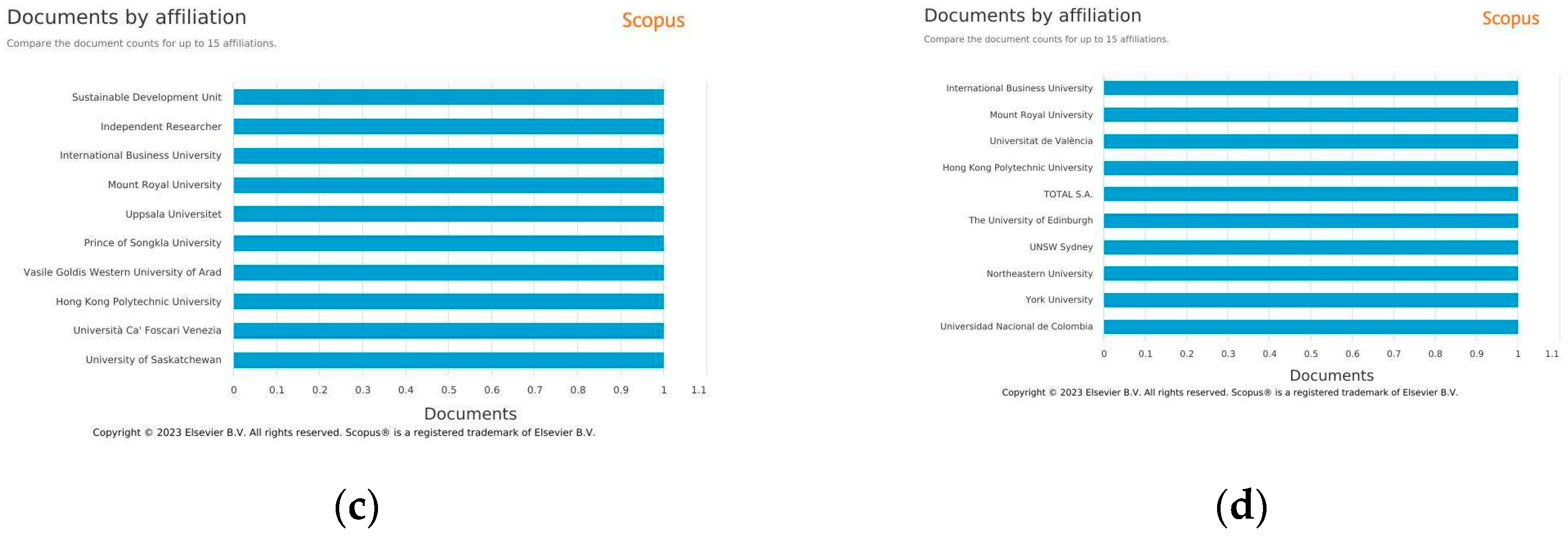

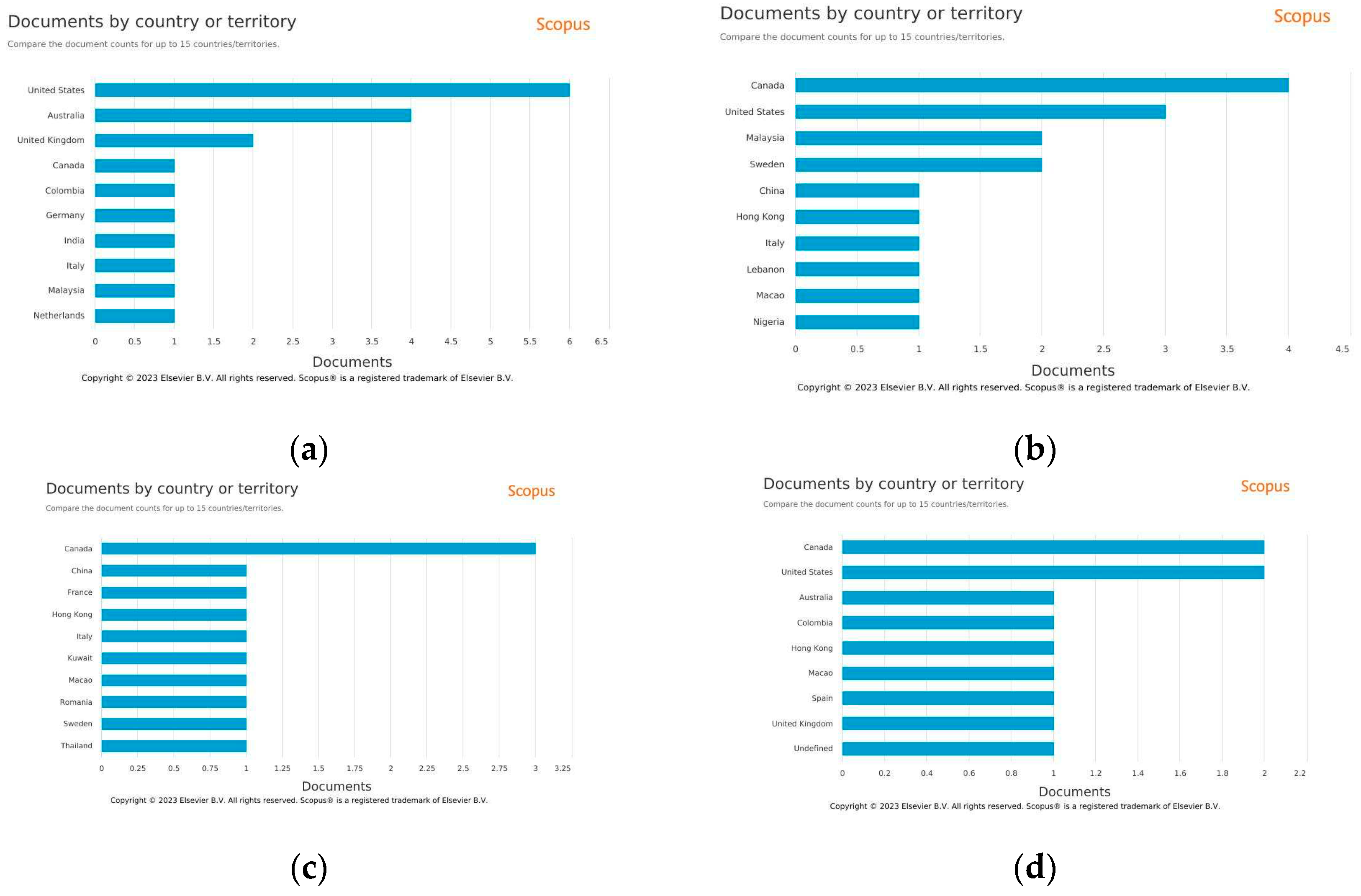

As easily observed in Figure 2, panel (a), only Janus, B. and Murphy, H. have published 2 articles each, while the rest of the authors have just published 1. Figure 3 presents the search documents by affiliation. Total S.A. is the affiliation with the highest number of documents among the 39. All the other institutions present 2 to-1 documents each at maximum, not denoting a trend as to affiliations. Finally, Figure 4 presents the documents by country/territory. As expected the country with the highest number of documents is the United States with 6 documents, followed by Australia with 4, and the United Kingdom with 2 (Figure 4, panel (a)). Regarding search criteria 2 (b), we have Canada leading with 4 documents, followed by the United States with 3, and Malaysia and Sweden both with 2 documents. Moreover, Canada leads with 3 documents in search criteria 3 and with 2 jointly with the United States in search criteria 4.

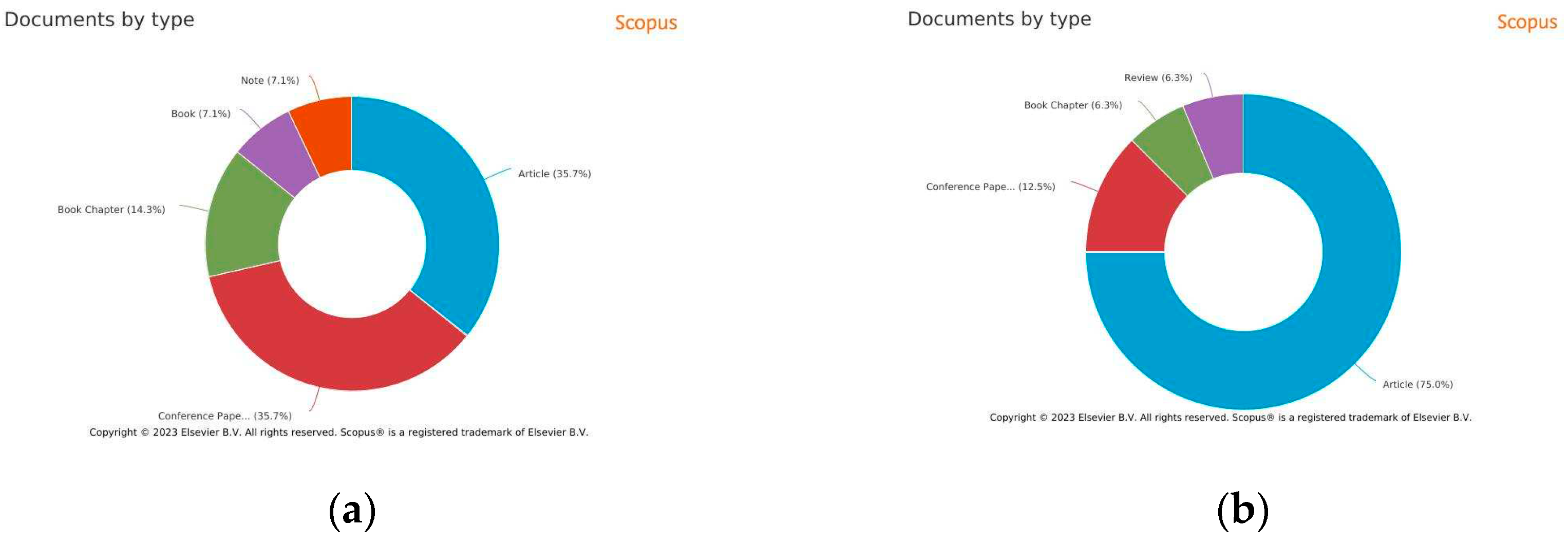

Comparing document types among search criteria, we have that in search 1, 35.7% of the documents are articles with an equal percentage of conference papers. In search criteria 2, articles dominate with 75% of the sample respecting these, whereas in search 3 from the 11 retrieved documents, 81.8% are articles. Finally, in the last search criterion 4, 57.1% of the 7 documents retrieved correspond to articles, 28.6% to book chapters, and 14.3% to conference papers.

Table 2 presents the subject area of the documents collected by search criteria. Energy is the field where more articles have been written. It should be noted that the subject area is that of the Journal where the article has been published. Business, Management and Accounting is the next subject area where the highest number of documents in our search has been published. Curiously, the subject areas of Environmental Science and Economics, Econometrics and Finance are journal subject areas where a residual number of documents is published. Considering that sustainability reporting, climate change, and energy have huge consequences in these areas, it would be interesting if journals within the field started publishing more articles, especially if we are dealing with institutions whose impact on the economy, environment, and financial system is huge. Thus, as another recommendation up to this moment, we would recommend the exploration of these effects in economic and financial terms to increase the number of documents published within the subject area journal.

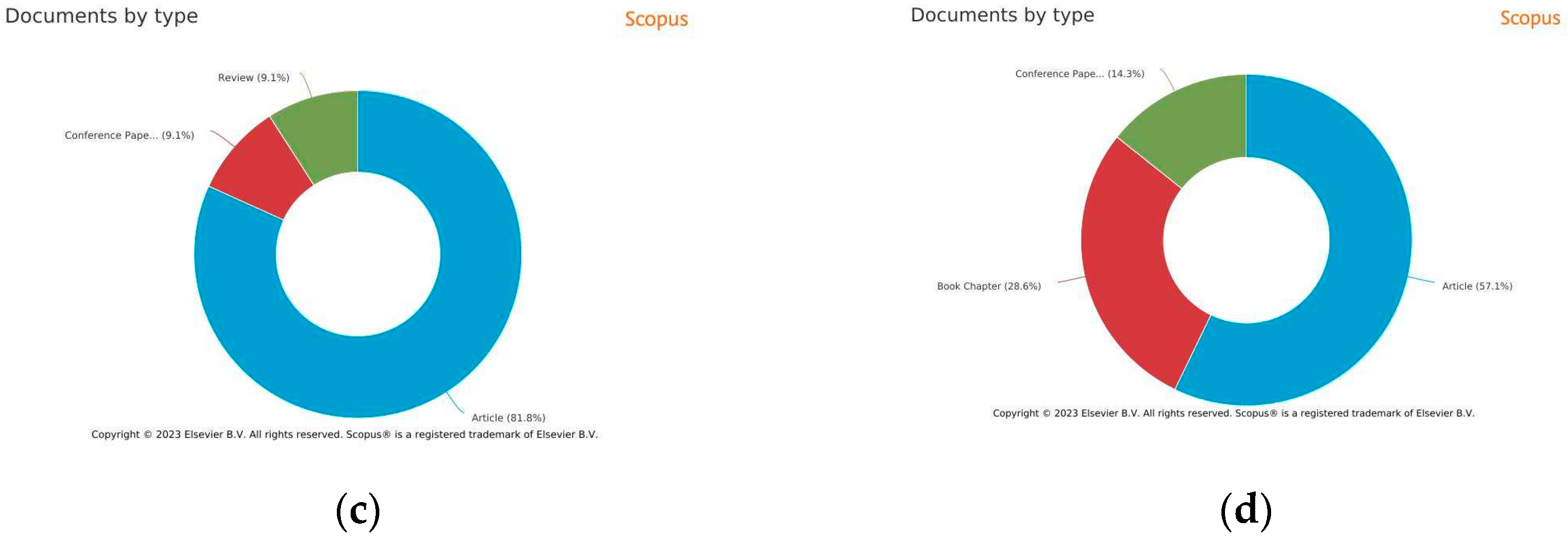

To be more specific and present results using also the keywords which are used in each of the 39 documents, Figure 6 presents a word cloud using these same keywords. From these keywords sustainability reporting, climate change, and sustainability are those more repeated in terms of keywords. It is interesting to notice that few documents that consider financial sustainability, financialization, and performance, leaving room for more applications in research terms. It is also anticipated that most of the methodologies used by authors in these documents samples are content analysis or qualitative tools, provided the hardness it is to perform empirical analysis using solely the available data we have. Therefore, this leaves room for the need to perform empirical analysis, which will be more suitable in a few years from now considering the sustainability reporting imposition. Even so, [74]'s (2023) literature review of 27 articles concludes from the results that a large majority of the papers examined used empirical methods. Moreover, the findings reveal that the most commonly used keywords were climate change, carbon reporting/disclosure, corporate greenhouse gas disclosure, and corporate climate change disclosure, conforming to our data presented in Figure 6. In terms of future research directions, the analyzed papers suggest exploring the indirect effects of factors such as board diversity, professional shareholders, audit committees, green innovation, and the cost of capital on climate change disclosures.

Despite the proven usefulness of SR there exists evidence for the United States that the complete advancement of society will be enhanced by disclosing sustainability information in financial reports and obtaining professional assurance. The rationale behind this is that this will lead to more balanced and healthier progress for society as a whole [75]. Indeed, increased regulation in Asia, growing prevalence in Europe, and rising interest from US investors signify the importance of sustainability information in decision-making. The sustainability disclosure community aims to streamline reporting standards for greater efficiency, encouraging companies to report. Executive involvement and oversight of ESG disclosures can further bolster sustainability efforts. Ideally, sustainability reporting will become more integrated into mainstream financial disclosures, rather than being confined to separate annual reports [76].

[77]'s (2022) findings support the idea that having women on corporate boards can positively influence a company's social responsibility efforts and the extent to which they report on sustainability. Additionally, the results indicate that when there is representation of women on boards, there is a greater likelihood of implementing policies related to climate change, business ethics, and health and safety. This study highlights the value of women's participation on corporate boards in the GCC region, as it improves board effectiveness and governance. The findings also encourage companies and policymakers in GCC countries to increase the number of women on corporate boards, as it can enhance a company's reputation and attract foreign investors.

It is easy to observe that considering board management and SR, researchers are actively exploring the effects of gender on SR, but as stated previously the mandatory decrees demanding SR have only been released at the beginning of 2023. Still, there is a lot of data to be explored within the context of European countries in the following years to analyze if the rules are effectively being implemented, if gender quotas are being respected, and if the effects of gender diversity produce the same results as those already reported in the literature using voluntary disclosure of sustainability reports. The same is true for other worldwide countries, especially establishing the difference between developed and developing countries, with different financial systems, between big, medium, and small enterprises, and between listed and non-listed firms. A special case of research would be that of family firms in different environments considering that they possess other issues and characteristics like intergenerational conflicts that may impede the necessary sustainable evolution, where there is still lacking research, as far as it was possible to infer.

Corporate sustainability is now closely associated with the intersection of environmental, social, and governance (ESG) issues. Businesses are incorporating sustainability into their operations, whether focused on Planet, People, Profit, or the triple bottom line. However, the extent to which companies integrate ESG principles varies widely, from basic acknowledgment of corporate social responsibility to comprehensive programs that impact the entire supply chain. [78] provides an overview of U.S. industrial sustainability reports, evaluating 44 publicly traded American corporations across eleven industries. Reports were assessed based on a standard set of criteria covering environmental, social, governance, and other relevant topics. Sector-specific summaries are included for industry benchmarking. The first part of the evaluation featured a study on sustainability reports published by forty-four Fortune 500 corporations. The top four companies from each industrial sector were selected for analysis. Sustainability indicators were compared to a set of evaluation criteria developed by the author, focusing on environmental, social, governance, and transparency topics. These criteria were based on the Global Reporting Initiative standards. Each company received individual grades, allowing for industry sector-specific comparisons. In the second part of the survey, the same evaluation criteria were used to assess smaller corporations in the same eleven industry sectors. This new group of forty-four companies was chosen based on their annual revenues, specifically selecting the four lowest revenue-generating Fortune 500 companies from each sector. The sustainability reporting of these smaller companies was compared to the large companies surveyed in part one. The similarities, differences, and observations about the entire sample of eighty-eight companies are presented, and huge differences are revealed, suggesting more companies-dimension assessment as to sustainability reporting is still needed.

5. Discussion

Sustainability reporting, in terms of materiality, focuses on environmental management and strives to decrease greenhouse gas emissions through efficient actions [79]. Although the practice of managing sustainability risks is still developing, there are now standards and metrics related to environmental, social, and governance (ESG) factors that can assist companies in their strategic planning, decision-making, and risk management processes.

5.1. Bibliographic Sample Analysis

From a sector perspective, SR has been explored within the education sector [79,80], the water sector [81], the oil and gas sector [82,83,84,85,86], the logistics sector [87], and the health sector [88]. [89] highlights the usefulness of the industry-specific framework provided by the Sustainability Accounting Standards Board for corporate SR. This framework has demonstrated the ability to link sustainability with financial performance, thereby improving returns for shareholders while considering risks and opportunities. The growing interest of shareholders in ESG issues and data allows for better analysis of company performance and allocation of economic capital. Investor-focused ESG reporting can benefit corporations, shareholders, and society as a whole, encouraging companies to be more responsible global citizens and fostering sustainable economic growth. Ultimately, businesses have the potential to drive the transition to a stronger and more resilient global economy [89]. [88] offer perspective from the Sustainable Development Unit. This unit is responsible for implementing and monitoring sustainable policies in the National Health Service, a large and complex healthcare system. They work to integrate sustainability practices throughout the organization. Sustainability reporting is essential for oil and gas companies. It allows them to outline how they address crucial matters like climate change and energy through their long-term plans and ongoing initiatives. In addition to enhancing external trust and confidence, the reporting process, which involves engagement with stakeholders, data collection, analysis, communication, and results, offers extensive opportunities for enhancing performance [84]. [86] concluded that oil companies are increasingly embracing Carbon Management practices. This involves addressing various challenges such as estimating greenhouse gas (GHG) emissions, taking into account external factors, future allocations, and limits, promoting low-carbon development, and implementing mitigation measures. Globally, there are new developments in energy, fuel consumption, and emissions taxes. Nations are implementing controls on emission inventories and forecasts for national planning purposes. This paper covers the development of GHG inventory and prediction, GHG accounting and information systems, climate protection policies, protocols, scientific assessments, sustainability reporting, and the potential benefits to stakeholders and the industry. It also addresses new regulatory requirements, sustainability, economic development, climate change, carbon management opportunities for service providers, and other climate change-related issues including scientific complexity, government policies, international debates, and competitive pressures. Carbon Management is becoming a reality for oil companies, and it is advantageous for organizations to adopt a proactive approach to be competitive, effective, and credible. This approach will yield first-mover benefits, foster innovation, and technology development, and influence global financial systems. The paper [86] aimed to share experiences and address actions for tomorrow. After sixteen years we are still debating sustainability issues, which are becoming more and more important nowadays.

Globally, the disclosure of greenhouse gas emissions and energy usage has significantly increased. This is largely due to a rise in sustainability reporting, growing concerns about climate change, and the implementation of new legislation and taxes. Various stakeholders such as audit committees, management, and internal and external auditors, all have a potential role concerning these disclosures. [90]'s research specifically focuses on the role of internal auditors. Through 29 interviews with senior audit committee members, senior accountants, in-house internal auditors, and partners specializing in internal audit, the authors aimed to understand the current and future roles of internal auditors in greenhouse gas and energy reporting. They also examined the level of involvement of audit committee members in such reporting. Findings align with certain corporate governance theories, but no single theory can fully explain the results obtained.

Climate change is discussed in [91]’s chapter from the perspective of socially responsible investing. Many analysts increasingly analyze the financial risks and benefits connected with climate change when analyzing a firm, as well as the corporate response to climate change at various levels of governance. Because such evaluation is dependent on accurate information, three initiatives to promote climate change openness are discussed. Furthermore, social investment experts have impressed on firm management their concern for climate change as a corporate duty through dialogue and shareholder resolutions. Because of increased sensitivity to the interaction of social, environmental, and financial aspects, socially responsible investment analysts have been able to better appreciate the potential risk implications of climate change. Indeed, GRI standards are discussed already for a long time. Companies may face direct consequences from extreme weather events and climate change, such as damage to physical assets, higher insurance claims, or loss of core business. firms that make a point of qualifying reductions for trading credit, as well as firms that focus on cost savings connected to excellent energy management, may profit financially. The GRI aims to encourage businesses all around the globe to utilize a consistent framework for reporting on sustainability concerns. The GRI publishes Sustainability Reporting Guidelines, which comprise basic reporting concepts and essential indicators. Social investment analysts use their connections to corporations to raise a variety of corporate responsibility concerns [91].

[73] infer, by analyzing three companies' (2 from Mexico and 1 from the US) sustainability reports, to which degree they address economic, ecological, and social issues. From the intra-linkages found they recommend the time dimension to be analyzed to ensure sustainable development. Thus, the analysis through time by using panel data becomes imperative with the need for deeper sector, country, and region assessment of sustainability reporting. [92] proposed a measurement of the materiality of ESG reported by Latin American listed companies (65 in 2017 and 67 in 2018) from different economic activity sectors. Their article opens the debate as to whether disclosed information responds to the stakeholder's needs or if it just serves the company's interests, suggesting complementing their qualitative study with the analysis of stakeholders’ engagement processes in the context.

[93] applied content, ratio, statistical data, and regression analysis methods using data from 49 Czech Republic and 40 Slovak Republic companies' annual financial reports for the year 2014. Results indicate that few companies report environmental and social issues comprehensively. Company size drives upward the relative share of environmental and social disclosure in the total disclosure, whereas company affiliation to a high-profile industry increases the relative share of environmental disclosure. Moreover, the total amount of information disclosed increases economic, environmental, and social disclosure, and the authors found that reporting considering IFRS increases social disclosure practices. Previously, [94]'s conceptual paper creates a sustainability index for manufactured products. This index could allow businesses to better measure, manage and use their available resources, while also allowing a better firm performance. More recently, [95] analyze the responses of Canadian residents to a survey to find that respondents globalized sustainability reporting standards and the creation of Sustainability Standards Boards, aligned with worldwide citizen’s responses. These are meant to help for a better sustainable future world and thus should be pursued.

[96] present a literature review of SR and ESG disclosure, and their effects on firm performance. Conclusions point to an increased trend in publishing from 2010 and that most studies are applied to developed economies such as Italy, England, the USA, and China. Sustainability and sustainability reporting are pointed as prominent research themes, whereas greenwashing and climate change were found to be less focused by the existing research. The focus of the existent research has been placed on ESG disclosure, SR, and firm performance considering firm value and leverage, with a considerable amount of studies including board and gender diversity, with inconclusive results but the majority linking SR and firm performance negatively. [97] surveyed top management teams of firms listed in the Stockholm stock exchange, They found that the management of climate-change risks seems to be a residual issue for most firms, with low active engagement of both managers and boards of directors. Thus, companies are advised to revise theoretical and empirical thoughts of climate-risk management and climate risks' role in the newer policy setting. Previously, [98] study reviewed the definition and identification of materiality. Four screening methods were proposed, being that of GRI’s Sustainability Disclosure database the one recommended considering its balanced disclosure of topics like management, economic, environmental, and social sustainability.

[99] finds that accountants are giving a more significant role in climate change risk disclosure, but still, there is a lack of appropriate care for climate change issues. [100] presents a report on the primary drivers of corporate action on sustainability. Conclusions enforce the idea that peer pressure is more effective than treaties, laws, or regulations for companies' involvement. The author highlights that the term climate change remains a contentious issue and that companies would be wise if they would refer to and report all sustainability-related actions. [101] inclusively outlines the basis in the EU treaties for the reform of EU company law, pointing to the risks of continued unsustainability. It highlights the need to change legislation in Europe to force SR by companies, showing them also how to conform to the requirements. Indeed, at the beginning of 2023, these sustainability reports for European companies started being mandatory. [83] point out that firms in environmentally sensitive industries, such as the oil and gas sector, are more scrutinized for ESG performance, mainly if related to climate change. They collected a sample of 30 oil and gas sustainability reports and ESG reports for 19 financial institutions in Alberta and performed a content analysis. Conclusions point to a lack of standardization regarding ESG investor demands and company disclosure. [102] tried to infer if financial and ESG practices affect European energy equipment and services industry companies. No causality was found between market capitalization and ESG performance. The authors conclude that the investment decisions of stakeholders are done based on the information provided by financial reports, the early phase of regulation regarding sustainability reporting. Thus, companies are advised to increase the quality and availability of CSR for investors.

5.2. The Role of Governance

[82] placed their attention on the risk disclosure of companies in the energy sector. For that they used manual content analysis and regressions to explore the features of the board of directors and audit committee on risk disclosure in SR, concluding a positive effect of their size, and that of the independence of the board of directors. The authors used a sample of 65 international companies in the energy sector. In the same year, [103] explored the determinants influencing the voluntary Italian public interest entities adoption of the Task Force on climate change disclosure using logistic regressions. Results point out that board size, ESG risks integration, and company size influence managers' decisions to adopt the guidelines. Also applying logistic regression models, [104] analyzed the effects of sustainability reporting and gender diversity on ASEAN-listed companies between 2010 and 2019. They used seven key performance indices from the GRI standards, to indicate a positive impact of energy used, water management, work safety, and gender diversity, but a negative effect of carbon emissions and waste management on corporate performance. With a similar methodology, [21] considered a random sample of 500 emerging Chinese enterprises to examine disparities in environmental, social, and governance reporting during 2018-2019. They adopted binary logistic regressions and Chi-square tests to find that international institutional ownership increases the disclosure of climate change. Also, independent non-executive directors are found to improve reporting quality and commitment to sustainable development goals, suggesting to Asian companies to increase independent directors and gender diversity. The presence of female directors is found to significantly influence disclosure emphasis on energy-saving initiatives.

Indeed, we may find already several different literature reviews surrounding the theme of SR and management team or board roles. [105] explore quality science and management roles to solve CSR challenges. Results point out that CSR measurement frameworks are limited and not appropriate to measure the company’s ecological footprint. The main pointed problem is the lack of primary data for this assessment. They include CSR stakeholders, sustainability managers, company leadership, and boards in their literature review. [106] examine the relationship between board governance mechanisms and sustainability reporting quality in Malaysia presenting a literature review and concluding for a positive effect of governance attributes. Even so, important empirical research ideas have also been presented in this regard. [87] explore the relationship between green logistics performance and sustainability reporting using the corporate governance moderating role, with a sample from 177 countries between 2007 and 2016. Results suggest that ineffective boards of directors ensure a stronger link between logistics performance and sustainability reporting. Results should be validated for other industries, whereas other institutional factors and regulatory frameworks of nations should also be included. Country-level research should also be enhanced. [107] study if the audit committee effectiveness influences reporting practices of GHG emissions of publicly listed Malaysian companies (43 companies GHG disclosures between 2016 and 2019). Regression results indicate that audit committee effectiveness is vital, leading to a better corporate disclosure practice. [108] used a sample of Turkish companies from 2010-2019 to conclude that the presence of women on boards increases the likelihood of voluntary climate change disclosures. However, they do not find a positive relationship between climate change reporting and women’s board representation. The authors suggest board reforms, with an increased percentage of women on board committees to ensure greater management of sustainability risks and increased responses to stakeholders' demands in economic contexts where legislators continue finding irrelevant the introduction of climate change reforms.

As clearly stated previously, there is already a vast amount of research dealing with board or corporate governance members' characteristics and effects on SR, especially the effects of gender. For [109], it will be critical to understand how gender is portrayed in sustainability communication when ESG is developing as a popular reporting framework for sustainability by capturing extra-financial disclosures. Through an examination of the visual imagery used to support sustainability claims, this article attempts to examine how gender is represented in these textual genres of a sample of Indian companies that are among the top Nifty 100 Enhanced ESG Index participants. Their qualitative research shows that despite increased exposure and evidence that they are rejecting gender norms, women nonetheless exhibit the tradition and modernity dilemma that feminist theorists have identified. In the author's conclusion, they demonstrate how the portrayal of women might be improved by adopting the principles of equality and inclusion: developing feminine strengths, preserving the good qualities of girls and women, emphasizing female bonding, and inclusiveness for all. They suggest practices and training to enable such a progressive mindset, which will eventually show in communication.

[110] found an absolute imbalance in terms of gender diversity on the boards considering 25 Indian IT companies. Among the explored reasons the authors point 6 which was the most relevant, namely 1. Due to the difficulties and risks associated with this industry, women who have excelled in technological education are reluctant to accept leadership roles in IT businesses, 2. Due to health difficulties and family obligations, women are unable to devote the necessary time to managing corporate boards of IT companies. 3. Women's employment opportunities are constrained by joint families and the patriarchal Indian system, 4. Because men never want to be led by women in IT firms, women with liberal outlooks and merit are not considered candidates, 5. The upskilling programs offered by IT organizations to their female employees lack the necessary focus to advance women into leadership roles. 6. The excess share requirement for directorship set forth by listed public firms prevents women from being considered for executive roles. Thus, the country's culture exerts an interesting impact that should be considered in future empirical studies, both in comparative terms and individually.

[111] purpose is to look at the important company traits that affect the adoption of sustainability reporting practices. A Logit model is used in the study, which is based on a sample of 366 significant Asian and African businesses that have addressed the SDGs in their sustainability reports that were released in 2017. According to the findings, large businesses in low- and middle-income nations that used SDGs tend to have traits including a greater market-to-book value (Tobin's q) and a larger use of external assurance for their reports. The findings also demonstrate a favorable correlation between the adoption of SDG reporting and the presence of female and younger directors in the company's management structure. In contrast to other studies, the use of sustainability reporting is not strongly influenced by the industry sector. To ensure that they are working in the best interests of the company and its stakeholders while growing their engagement in sustainability projects, the boards of directors of significant Asian and African corporations face problems, which are supported in this article. Similar conclusions have been reached by [112] while using the same sample (Table 3). As well, [21] emphasize the need for policymakers and practitioners in Asian nations to take into consideration raising the number of independent non-executive directors (INEDs) and gender diversity in emerging Chinese enterprises (ECEs). For the authors, ESG reporting should be improved, supporting the conclusions of earlier international research that suggested such governance methods. As opposed to [111] results, [113] findings evidence that companies in the chemical, pharmaceutical, and technology sectors are more likely to publish a sustainability report. These results imply that governance traits, business characteristics, and industry sectors can predict whether companies will provide standalone sustainability reports in a disclosure environment with little to no regulation, at least in Pakistan. Previously, [114] stated that SDG reporting has an impact on performance in contentious businesses as well as environmentally delicate ones. Thus, addressing SDGs is a value-enhancing tool for businesses in contentious and environmentally sensitive industries in Europe. With the same sample, [115] state that the adoption of SDG practices and external assurance of sustainability reporting is strengthened by an increase in the proportion of female directors on the Board of Directors. Furthermore, their research shows that businesses in environmentally sensitive and highly consumer-focused industries are more likely to implement SDG reporting and external assurance to boost their reputation and lessen public awareness of the overall environmental impact of their operations.

According to [14], female CEOs who play a dual function have little influence over whether integrated reporting or stand-alone sustainability reporting is preferable. The study also demonstrates the lack of significance of females on boards with two or fewer members and gender board diversity (% of women over total board size). However, stand-alone sustainability reporting is considerably and favorably impacted when there are three or more female board members. Female independent directors are also more likely to favor stand-alone reporting over integrated reporting. Because female CEOs are more likely to implement stand-alone sustainability reporting, policymakers must encourage sensitive environmental enterprises to hire more female CEOs than male CEOs. Moreover, [116]'s results, it is advised that women's presence on corporate boards of directors is one of the most important aspects of corporate governance since they may be more conscious of environmental issues and more concerned with lowering perceived risks.

According to [117] companies' disclosure of sustainability reports is influenced by their low leverage, high-profile traits, and whether they have a growing variety of female directors. Occasionally, decisions made by women tend to be more socially conscious and will benefit stakeholders and sustainable practices more than those made by men. Consequently, it is anticipated that a higher proportion of women serving on boards of directors will be able to assist with the difficulties faced by senior management. The favorable impact of gender diversity on sustainability reports disclosure demonstrates that organizations can gain from gender diversity in terms of SDG reporting as well as corporate performance. As a result, it is assumed that the government can lessen inequity in the proportion of female directors on corporate boards. This is so because it has been shown that having more women on boards of directors increases commitment to sustainability policies, particularly in developing nations like Indonesia.

Companies that adhere to the Global Reporting Initiative's (GRI) sustainability reporting guidelines and whose sustainability performance disclosures (SPD) do so are more profitable [118]. The result that gender diversity has no impact on GRI-based sustainability reporting in Uganda was explained by [119] by the fact that there are more males (about 77%) employed in manufacturing firms as compared to 33% of females employed in such firms, justifying the lack of females positions on these boards as well. Besides, [119] report that human resources with knowledge, experience, and skills in sustainability-related issues improve SPD. But also, the importance of a Sustainability Committee (SC) has been highlighted in the literature [26]. [26] study's findings are pertinent, by explaining how a SC plays a crucial role in shaping SDG disclosure and regulating its relationship with board gender diversity. The SC's creation encourages the dissemination of more information to stakeholders on the efforts companies are making to integrate the SDGs into their corporate agenda. The creation of an SC also provides women with the opportunity to strategically coordinate their efforts to encourage the board to better serve stakeholders' requirements through increased openness about SDG commitment. The study of [120] demonstrates how Indonesian businesses frequently work to promote justice, peace, equality for women, and the attainment of excellent health. Companies disclose more CSR actions in line with the SDGs of decent health, quality education, access to clean water and sanitation, economic growth, and cooperation in their sustainability reports from 2017 to 2019. The findings of this analysis can be utilized to persuade businesses to pay more attention to SDG indicators that have not been met and work to implement CSR in a way that supports the SDGs and connects them to their daily operations.

[121] findings suggest that the presence of women on the board of directors (BoD) positively impacts the extent of disclosure of social information, with a critical mass (the smallest number of women needed to affect the decision-making process about the extent of disclosure of social information) of 4 women or more (with an increase of 9.95%). The similarity between male and female board members, which can be explained by the functional training and sector experience being measured based on the similarity/homogeneity between them, made it so that the functional training and director's experience in the company's sector of activity were not significant. Additionally, the functional training and councilwomen's experience in the company's sector of activity based on critical mass was also not significant.

The stakeholder approach is supported by empirical studies, which show that companies are more likely to publish sustainability reports if their audit committees are bigger, their boards are made up of more women, and their institutional ownership is higher. The findings show that audit committee independence, foreign ownership, concentrated ownership, and management ownership have a negative impact on the decision of the corporations to report on sustainability. Overall, the influence of board composition on the choice of SR is marginal, but the influence of ownership structure and audit committee characteristics is considerable and inconsistent. The decision to voluntarily disclose is also influenced by the firm's age, size, financial capability, and growth potential [113]. However, [122], in the investigated mining businesses, declare that effective operations are considered as being fundamentally driven by compliance with regulations and permissions, as well as additional considerable pressure in the form of community acceptability, or the social license to operate.

Considering a different output, although associated with SR, [123] findings prove that the choice to disclose carbon emissions is closely tied to the CSR report's assurance and release. Firms’ high-quality sustainability reports help to increase their credibility and influence stakeholders' perceptions of their company. Results also indicate that the presence of a CSR committee is significantly related to carbon disclosures, and they emphasize the significance of the CSR committee as the only driver for better environmental behavior (or carbon management) by significantly affecting the reduction of emissions. Reported findings in the literature also show that board independence and nationality play a key role in enhancing carbon disclosure [124].

[125] have selected the following from a list of probable determinants of required CSR disclosure in business annual reports: corporate ownership, financial performance, board size, corporate visibility, and gender diversity. Regression models have been used to evaluate the connections between independent variables and mandated CSR disclosure (environment, human resource, product, consumer, and community involvement). The empirical evidence from this study supports the notion that CSR disclosure is required in developing nations. This study backs up the assertion that businesses in emerging nations seem to favor giving. The findings of the study suggest that the stakeholder theory is the most pertinent one to explain the requirements for CSR disclosure. At the expense of shareholders, obligatory CSR disclosure modifies corporate behavior and creates positive externalities for society. [125]'s data also indicate that the effect of research factors on the requirement for CSR disclosure is minimal. As a result, the requirement for CSR disclosure is significantly impacted by government ownership.

With a few exceptions [126], deep diversity components at all organizational levels do not get much attention. [126] findings show that having more women serve on organizational boards benefits the organization's overall gender diversity and other diversity-related factors. For boards of directors, corporate management, and regulators interested in enhancing corporate governance and diversity policies in New Zealand organizations, the outcomes of a focus on complete diversity have significant ramifications.

As may be shown, there is currently no established association in the literature between women serving on boards of directors and voluntary information disclosure, and there is conflicting empirical evidence. It is advised that the evidence in other publicly traded companies, as well as medium- and small-sized businesses, be investigated to generalize the findings. Most studies include publicly traded companies that are registered in specific financial markets and that voluntarily disclosed the sustainability report. It would be useful if in the future, with the ongoing mandatorily release of SR by companies a specific database gathering this data would become available.

It should be remembered that various CSR metrics or dimensions may be more important to some directors than others. Cultural and legal distinctions have not been specifically considered in previous studies, and therefore the findings should not be extrapolated to businesses with different legal and cultural traditions from the sample, as highlighted by [121]. Additionally, [113] findings for Pakistan point to the need for its authorities to rethink their approach and call for completely independent audit committees because of the unfavorable correlation between audit committee independence and sustainability reporting decisions. Thus, other BoD characteristics should be included in the analysis of the effectiveness of SR, and it can be as mediating role exerted into the relationship between gender and SR practices.

According to research, older and larger companies are more likely to publish sustainability reports (e.g., [113]). Regulators ought to support small, medium-sized, and emerging businesses to adopt sustainable business practices. The empirical findings also show that companies in the chemical, pharmaceutical, and technology sectors are actively involved in sustainability reporting [113], but others find no sector influence [31,111]. If in the [113] study it appears that companies working in other industries are not under any pressure to provide sustainability information from stakeholders, the business sector can make use of these results to manage sustainability performance, respond to social and environmental hazards, and fulfill the expanding information needs of stakeholders. Comparing different sectors worldwide is still lacking research in the face of these conflicting results.

The results of some country-specific studies might not apply to other emerging, developing, and developed economies because they don't all have the same company structures, capital allocations, or investment climates. A comparable study should also be carried out in the finance industry to generate fresh insights. The use of qualitative research techniques could also aid in conducting a thorough assessment of the efficiency of corporate boards and audit committees in SR.

Regarding the geographical restriction, studies concentrating on other nations can add to the discussions of empirical studies presented in this article and can use previous research findings to compare and contrast their conclusions. When it comes to the usage of document analysis, the sustainability reports that are utilized are public information reports that businesses offer to stakeholders to demonstrate their advancements; as a result, it is required that they are as strong and comprehensive as feasible. However, we feel there is still lacking research exploring if sustainability reporting conforms to the imposed rules. Additionally, it is critical that stakeholders and investors regard this information as reliable and that businesses refrain from viewing this reporting with cynicism to guarantee the value relevance of SDG reporting. Investors, stakeholders, activist groups, and others cannot view SDG reporting as a symbolic gesture; it is only meant to resolve legitimacy concerns and comply with stakeholder pressure [114]. Additionally, to boost firm transparency activities, the government should assist in providing guidelines that are still not being fully applied by businesses. It might also show appreciation to those businesses that have backed the Sustainable Development Goals [120].

In some of these countries, individual knowledge might appropriately be generalized for other developing or developed countries that have a similar economic structure. Still, a lack of geographical comparison is identified, both empirically and theoretically. Also, some of these articles do not relate financial theories to the empirical studies developed, and a complete overview of the conformation of each of these authors' results to the existing theories is still needed to be developed. Moreover, sometimes, data from businesses in one or three industries served as the basis for research findings on mandated or voluntary CSR and SR disclosure elements. Therefore, generalizing the results statistically could be deceptive. Also, a document-based source of data is usually preferred because the research aimed to compare the data across firms at the same time. Other media, such as company websites and social networking marketing, are used by businesses to publicize their CSR initiatives, whose examination is still lacking research.

Some of the identified authors' results cannot be generalized because it only includes data from one year of disclosure. Thus, extensive-time databases are needed to analyze the evolution through time. As far as possible, we recommend that future studies again try to update the results presented thus far with at least a cover period of 3 recent years, but preferably with a data span of more than 10 years for us to be able to analyze the evolution through time, as well, of SR and its relationship with gender diversity. Additionally, future studies employing various methodological techniques, such as interviews to specify BoD's thoughts on the firm's features and the level of mandated CSR disclosure, could consider external stakeholders' perceptions, corporate governance, and leverage. In this vein, [126] were the first to contend that there is a synergistic relationship between gender diversity goals and deep diversity goals (race, age, sexual orientation, disability, and ethnicity) and that neither gender diversity goals nor deep diversity goals can be met without the other. This study does a content analysis of the diversity-related disclosures made by 152 NZX-listed businesses using a 30-item diversity disclosures index. The authors found that when examining diversity-related disclosures in annual and sustainability reports, NZX-listed businesses mostly only discuss board gender diversity. Thus, more studies including other factors besides gender diversity should emerge.

To improve the generalizability of [124]'s board diversity findings, future studies might consider bigger samples. Second, [124]'s study developed a board diversity index using the Australian Board Diversity Index methodology. Other aspects of variety, like ethnicity, may be studied by academics. Using a variety of theoretical frameworks that include five dimensions—board nationality, gender, independence, tenure, and age—within enterprises with variable decarbonization performance and industry carbon impact, analyze the relationship between carbon disclosure and board diversity. Future research may also look at how addressing SDGs in sustainability reports affects alternative market outcomes like capital costs, company reputation, stakeholders' views of legitimacy, and other things outside performance [114].

In the already existent empirical literature, some control variables may have been left out, and due to that the proposed regression models might have certain flaws. Empirical studies on the subject should include more controls as those accounting for business size, leverage, risk, R&D intensity, physical and final resources, and ownership concentration when estimating regressions. Moreover, macroeconomic, and cultural contexts [117] can also exert influence. Although European nations are innovators and leaders in addressing sustainability strategies, these are still underexplored. Thus, we advise that future research broaden the evidence presented to other regions, looking at, for instance, other continents or regions, as well as the impact of the institutional context (examples include transparency, corruption, and a country's orientation to socially responsible issues, among others).

Finally, the empirical results presented in most of the studied documents cannot be generalized to small and medium-sized organizations (SMEs) because the samples are usually made up of the largest global listed corporations. Future research on this relationship in the context of SMEs would be interesting. Additionally, the context of family firms with their specific characteristics could be explored since from Table 3 we observe that only one study up to this moment has explored this enterprise context of family-owned firms [127], where usually women have more difficulties to stand out in managing roles.

6. Conclusions

This study was based on a bibliometric analysis of 39 documents, that should be repeated in a few years to notice if some of the suggestions have already been explored and what has contributed to the understanding of the relationship between climate change and energy, boards, and sustainability reporting. It was found mixed results regarding the relationships explored in this literature review. Especially, it is pointed out a clear lack of studies that consider solely energy-related issues reported under sustainability reports, as climate change risks are still unexplored issues. A lot more is found in the literature about gender effects on sustainability reporting. With time, the association between board members' characteristics and sustainability reporting increased, but there is still a lack of relevant empirical studies which associate some of these characteristics with sustainability reporting, mainly because the involved data is still scarce. More cross-country or cross-sector analysis studies are necessary to provide more useful insights as to the reason why opposite findings are also reported.

The findings of the current bibliometric and bibliographic analysis allow us to conclude that to achieve gender equality, firms can expand the chances for women to serve on corporate boards of directors and other critical positions following their skills and expertise. This is supported by the considerable impact of gender diversity on SR disclosure reported in the literature. Moreover, increasing the presence of independent non-executive directors and gender diversity enhances ESG reporting as does external institutional ownership.

Some important implications are derived from our analysis. Given that reporting frameworks primarily focus on "the past" while sustainability requires strategic, long-term thinking, various research methods or data sources, such as interviews with sustainability committees or key stakeholders, could be used to provide a broader view and better understanding of the effectiveness of the implemented sustainability activities and practices. In addition, internal and external economic drivers for the adoption of sustainable practices might be investigated, including those for enhancing SDGs, which may come about because of increased profitability and production efficiency. Also, reporting on gender issues is found to focus narrowly on women, but a broader intersectional and gender perspective is needed. From the literature review it was also possible to infer that even though many businesses had programs in place that catered to women, they typically did not explain why they were required. This makes it difficult for the reader to determine whether the activities were worthwhile or even successful [128]. As well, the generalizability of the results to other nations may be constrained using a single country with listed enterprises. Future research might compare the effects of gender on board and the choice of report style in both emerging and advanced economies [14,29] and analyze each of the ESG dimensions individually [129]. Finally, the bibliographic analysis is based solely on the SCOPUS database, in the future, similar studies should also consider other bibliographic data sources.

Author Contributions

Conceptualization, M.M.; methodology, M.M., E.V., and D.M.; validation, M.M., D.M., E.V. and M.N.; formal analysis, M.M.; writing—original draft preparation, M.M., E.V., D.M. and M.N.; writing—review and editing, M.M., E.V., D.M. and M.N. All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding.

Data Availability Statement

No new data were created.

Acknowledgments

In this section, you can acknowledge any support given which is not covered by the author contribution or funding sections. This may include administrative and technical support, or donations in kind (e.g., materials used for experiments).

Conflicts of Interest

The authors declare no conflict of interest.

References

- Öberseder, M.; Schlegelmilch, B.B.; Murphy, P.E. CSR practices and consumer perceptions. J Bus Res 2013, 66, 1839–1851. [Google Scholar] [CrossRef]