Submitted:

15 August 2023

Posted:

16 August 2023

You are already at the latest version

Abstract

This study investigated the factors affecting consumers’ acceptance to use cashless payment services in Malaysia through the construction of the Cashless Society Acceptance (CSA) model. The Technology Readiness Index 2.0 and Unified Theory of Acceptance and Use of Technology 2 were employed to create the CSA model. A total of 434 questionnaires were collected from Malaysian consumers, aged 18 years and above. The results show that Perceived Usefulness, Perceived Ease of Use, and Discomfort have the most significant influence on the consumers’ acceptance of cashless payment services with R-square of 71.4%.

Keywords:

cashless payment

; enablers

; barriers

; Malaysia

; UTAUT 2

; TRI 2

1. Introduction

Consumers have developed a variety of new habits due to COVID-19, many of which are expected to stay such as digital lifestyles of consumers. Nationwide lockdowns and movement controls to avoid the spread of the virus have increased the growth of e-Commerce massively in the world. In addition to that, with the advancement of technology, it increases the digital lifestyles of consumers. There are many types of cashless payment methods such as online transfer, contactless card and mobile payments, e-wallets and QR payments. The most pressing sense why we need to adopt a cashless society today is the ongoing pandemic which has made non-contact a norm.

The cashless society theory correlates to the purchasing behaviour of the society through digital transactions, typically aided by banking cards or electronic devices (Balakrishnan et al., 2021). In some developing countries, cash is still the undisputed king of payments. According to Financier Worldwide Magazine (May, 2021), the future of money is seen as a digital paradise by many. E-payment is a successful way people adopt in developed countries. It is considered as an essential part of e-Commerce that saves consumers’ time, effort and money. (Ragaventhar et al., 2016) defined cashless society as the “situation of economic state where financial transactions are not conducted with money in the form of physical banknotes or coins, but rather through the transfer of information between transacting parties”. So, it is important for us to determine the factors affecting consumers’ acceptance to use cashless payment services.

2. Background

2.1. Cashless in Southeast Asia and Malaysia

According to Mandy (2021), nearly two-third of consumers in Southeast Asia (64%) have attempted to go cashless. According to the report, cash remains widely used by consumers in this region as 45% of the consumers perceive cash as their most preferred payment method. Malaysia’s highest payment method is still by cash with 43%. From the article, it is clear that with the growth of digital payment experiences Southeast Asia's transition to a cashless society is gaining momentum. Over half of consumers in Southeast Asia (52%) also cited having lesser opportunities to pay with cash compared to before the pandemic. This is proven when the countries faced movement order restrictions and nationwide lockdowns, including Malaysia (59%). Contactless cards are fairly popular in Southeast Asia where 95% of the consumer are aware of it but only 65% of them are using it. Mobile contactless payments are less prevalent in Southeast Asia but continue to gain traction in markets where they are available. QR codes are also particularly widespread in Malaysia where 93% of the consumers are aware of it but only 50% of them are using it (Mandy, 2021).

In Malaysia, the government is undertaking a long-term plan for reaching a cashless society. Bank Negara Malaysia (BNM) targeted to enhance the rate of electronic payments by 78% within the next 10 years (Bank Negara Malaysia, 2020). The financial report year 2020 also stressed that electronic payments in Malaysia significantly increased by 14% in comparison to the year 2019 financial year, however 50% of the country’s financial transactions were cash based. This clearly shows that, consumers face uncertainty in using cashless payment systems. According to Yuen (2019), around 20% of the total payment in Malaysia involved electronic wallets. In addition to that, Visa, the world’s leader in digital payments has announced in their year 2022 study on Visa Consumer Payment Attitudes that majority of the Malaysian consumers (55%) can stay for more than a week without using cash. This stays 13% higher compared to 2021.

The Covid pandemic has encouraged the Malaysian consumers to use digital payments over cash. Around 28% of the respondents stressed that they are likely not to use cash in most places after the pandemic. Besides that, the preferences among the consumers on merchants that accept cashless payment options instead of cash increased tremendously. This includes the automated app payments (64%), self-service checkouts (64%), and biometric payments through fingerprint or facial authentication (60%). The study also stressed that around 74% of the respondents are entering into the cashless society. The respondents agreed that Malaysian consumers could move into cashless society by 2025. The study also revealed that there is a growth in cashless payment adoption, especially via QR payments (60%), mobile wallets (54%), and contactless cards (51%) (The Star, 2022).

2.2. Unified Theory of Acceptance and Use of Technology (UTAUT 2) Model and the Technology Readiness Index (TRI 2.0) Model

Two acceptance models were referred in this study to determine the consumers’ acceptance towards cashless society, i.e., the Unified Theory of Acceptance and Use of Technology (UTAUT 2) model and the Technology Readiness Index (TRI 2.0) model. The UTAUT 2 model was synthesized by Venkatesh et al. (2007) corresponding to the TAM and Theory of Planned Behaviour (TPB) model. This model classifies four primary factors and moderators associated with the prediction of behavioural patterns of intent and actual technology usage in organizational situations (Venkatesh et al., 2016). The major drawbacks of the UTAUT 2 model are its lack of inclusion of attitude as a direct element of intention; inconsideration of self-efficiency as a direct element of intention; incongruent relationship between intention and behavioural patterns, whereby external factors are not assessed (Moghavvemi et al., 2013). On the other hand, TRI model was developed in 2000 by Parasuraman and Colby, fundamentally functioning as a gauging tool in evaluating the technological acceptance of consumers situated in North America. The enablers and inhibitors for this model includes the measure of optimism, innovativeness, discomfort, and insecurity (Pires et al., 2011). Based on the literature review, although majority of the previous studies have used the UTAUT 2 or TRI 2.0 model or both, unfortunately there were a number of important factors that were excluded in the previous studies such as the status symbol, lack of awareness (Rena et al., 2013), and compatibility (Wiese, 2017).

2.3. Theoretical Implications and Hypotheses Affecting the Acceptance to Use Cashless Payment Services

2.3.1. Perceived Ease of Use

User attitude and behaviour desire to embrace and use a technology are influenced by perceived ease of use (Chawla et al., 2020). It has been established that a customer's choice to buy is influenced by perceived ease of use (PE). As a result, prior shopping experiences may impact a consumer's perception of e-wallet ease of use. Many clients viewed their e-wallet software experience as basic (Hamid et al., 2016). As a result, perceived ease of use refers to how straightforward it is to navigate a website and complete an online transaction using a technology (Grover et al., 2017). Technology is more profitable for online users; in other words, if a technology is easier to use, it will become the preferred form of payment for clients. Therefore, the first hypothesis is thus formulated as follows:

H1:

Perceived ease of use positively influences the acceptance of cashless payment services

2.3.2. Perceived Usefulness

Perceived usefulness is defined as customers' perceptions based on previous experience. According to Davis (1993), the term perceived usefulness is defined as an individual's view of the use of new technology that will increase or improve their present performance (Davis, 2011). Besides, perceived usefulness is also identified as one of the two important variables in the technological adoption model (UTAUT 2). The perceived usefulness element has a direct impact on both the attitude toward system use and the behavioural intention to utilize the system; it is also significantly influenced by the perceived ease of use attribute (Bradley, 2009). A study in Iran reported perceived usefulness to have a direct impact on the usage of mobile banking, principally resonating to the demographics of the respondents, whereby majority of them were young adults and educated. It can be deduced that the inclination towards user acceptance of mobile banking is associated to age and educational factors, as people of these age group are less resistance towards change and development (Mohammadi, 2015). Therefore, hypothesis two is formulated as follows:

H2:

Perceived Usefulness positively influences the acceptance of cashless payment services

2.3.3. Optimism

Optimism is defined as a product or service that will fulfil a user's needs (Parasuraman et al., 2015), and research suggests that optimism is a motivating factor in the desire to utilise technology (McLean et al., 2020). The optimism factor was also explored by Parasuraman et al. (2015) in their TRI 2.0 model which intricately justified the elements encompassing driving and inhibiting factors of the technology readiness of the society. From this study, it was deduced that optimism is a enablers factor of technology acceptance; a person optimistic towards the notion of technology, easily accepts and integrates it into their daily life, similar to individuals with innovative traits (Parasuraman et al., 2015). Because technology optimists often foresee ideas and matters to go their way and trust that great things will occur to them more readily than bad things, they have an instinctive optimistic perception of new technologies owing to their self-confidence in their ability to grasp new technologies (Nagdev et al., 2021). Therefore, hypothesis three is formulated as follows:

H3:

Optimism positively influences the acceptance of cashless payment services

2.3.4. Compatibility

The fit of cashless payment services with user demands, as well as the possibility to test out new services have a beneficial influence on adoption attitudes (Yang et al., 2021). Compatibility also significantly affects the behavioural pattern of individuals, whereby it provides substantial advantages in assessing their behavioural intent as well. In simple terms, it can be said that the lifestyle compatibility of an individual plays an important role in the adoption of a cashless society and this study shows compatibility is a positive factor of cashless adoption (Yang et al., 2021). with compatibility having a direct influence on user acceptance of m-payment via perceived utility and simplicity of use. Therefore, hypothesis four is thus formulated as follows:

H4:

Compatibility positively influences the acceptance of cashless payment services

2.3.5. Enjoyment

The definition of pleasure or fun is perceived delight (Kiwanuka, 2015). This is an incentive to embrace a technology because it is pleasurable or fun. Perceived satisfaction is a key factor in deciding whether or not to utilise a system or service (Kiwanuka, 2015). Technology will minimise levels of worry, anxiety, and danger, which will encourage consumers to adopt the new technology if they are having a good time. Previous research by Chin et al. (2015) on the effect of perceived enjoyment on the usage intention and adoption of a single channel e-payment platform amongst Malaysians. The main hypothesis associated with this attribute was enjoyment is coupled with the usage intention of consumers, besides being co-dependent with perceived usefulness and ease of use. This study involved 389 respondents; 60.4% of the respondents were male; 45.2% of the respondents were between 26 to 40 years old; 62.7% had access to instruments facilitating cashless transactions, such as bank cards, internet, and mobile devices. However, from the study, it was deduced that the relationship between enjoyment and customer’s intention of e-payment usage was heavily influenced by the usefulness and ease of use. As a result, when customers believe that the single platform e-payment system is very fun, simple to use, and beneficial, they are more likely to utilize it (Chin et al., 2015). Therefore, hypothesis five is thus formulated as follows:

H5:

Enjoyment positively influences the acceptance of cashless payment services

2.3.6. Status Symbol

Status symbols are vital to individuals, particularly as it preserves a social class through incorporating digital media in their daily lives (Sen, 2020). A study on the digital economy in India was conducted by Sen, (2019). According to the study participants have contributed to the development of a favourable attitude toward the use of digital media. The status symbol element has emerged, and it addresses the requirement for participants to use digital media in their career or in their personal lives to retain a social class. This has, in fact, functioned as a positive motivation for most participants to become aware of the benefits of digitalisation, which has motivated them to become active participants in the digital economy. According to Sen (2019), the women participants mentioned this category 59 times. This category has been pronounced 64 times more frequently by men. Participants are mostly influenced by comments from friends, family, and colleagues, and they are also required to employ digital means, which are not just motivated by a need for a status symbol. Many of the participants have been discovered to be engaged in digitization in order to retain their social position as well as because it is a mandate in their professional grounds. (Sen, 2019). Therefore, hypothesis six is formulated as follows:

H6:

Status Symbol positively influences the acceptance of cashless payment services

2.3.7. Innovativeness

A study by Humbani et al. (2018) on the acceptance of customers towards a cashless society hypothesised that the adoption of mobile payment services is favourably influenced by consumer innovation in this area. Interestingly, the findings from their study showed that innovation has no effect on the adaptivity of mobile-based payment services in contrary to their proposed hypothesis (Humbani et al., 2018). Furthermore, a considerable body of literature exists on the innovativeness attribute corresponding to the consumer adoption of cashless transactions in Malaysia by Rahman et al. (2020). The postulated hypotheses of the conceptual model, i.e., innovativeness significantly influences the adoption rate were evaluated in this study using a self-administered questionnaire. This was executed amongst 500 Malaysian customers who had previously purchased goods and services online via online banking, non-cash transactions, and other online transactions. Findings from this study indicated that innovativeness indeed affected the adoption of a cashless society in Malaysia (Rahman et al., 2020). Therefore, hypothesis seven is thus formulated as follows:

H7:

Innovativeness positively influences the acceptance of cashless payment services

2.3.8. Lack of Awareness

According to the self-awareness idea, people are more inclined to adopt when they believe their existing behaviours and actions do not meet the society's expectations (Duval et al., 1972). This means that people will adjust their conduct if certain environmental signals make them understand that their present position is not in any way consistent with social norm. Consumer knowledge of the system is critical in getting them to accept the new technology in the case of cashless payment. When customers realise, they are falling behind the rest of society in terms of cashless payment systems, they will assess themselves to determine whether there is a problem (Duval et al., 1972). They will search for methods to eventually accept the system if they believe the problem can be solved by changing specific parts of their actions and behaviours. However, if the problem cannot be minimised according to their assessment, they will blame society's strict standards, a lack of appropriate communication, or technology as a cause of the problem. As a result of this state, customers avoid self-awareness, which has an impact on their willingness to accept innovation (Silvia et al., 2001). According to the original self-awareness hypothesis, which is backed by the current one, the system must be something that individuals can achieve easily. Therefore, hypothesis eight is thus formulated as follows:

H8:

Lack of Awareness negatively influences the acceptance of cashless payment services

2.3.9. Discomfort

A sense of being overwhelmed by technology and a perceived lack of control over it is characterized as discomfort. Users that have a high level of discomfort feel out of control and overwhelmed by technology (Kim et al., 2018). As a result, they regard technology as more challenging. Previous study has backed up these findings (Kim et al., 2018)., stating that excessive degrees of discomfort with technology might result in unfavourable views. Therefore, hypothesis nine is thus formulated as follows:

H9:

Discomfort negatively influences the acceptance of cashless payment services

2.3.10. Perceived Risk

Perceived risk is a mix of uncertainty with the seriousness of the consequence involved (Bauer, 1960). The user behaviour on hazards is explained by the perceived risk hypothesis. Negative causalities may highlight from user activities, resulting in a well-established notion in consumer behaviour, namely perceived risk. Meanwhile, perceived risk is a natural perception of unreliability in relation to the potential for undesirable usage of a service or product (Nguyen et al., 2018). Seminal contributions focusing on the significance of perceived risk and its influence on the adoption of electronic payments was studied by Nguyen et al (2018). The study involved 200 respondents from the Ho Chi Minh city; 53% were females; 40% were from the 16 to 22 age group; 44% of the total respondents had a university level education background; 40% were e-payment users. The dangers of online transactions and the security challenges of e–payment systems are defined as perceived risk in this study. From this study, it was concluded that perceived risk did significantly impact other inhibiting factors such as trust, perceived ease of use and usefulness, associated with the adoption of electronic payments in Vietnam and Taiwan (Nguyen et al., 2018). Therefore, hypothesis ten is thus formulated as follows:

H10:

Perceived risk negatively influences the acceptance of cashless payment services

3. Methodology

3.1. Research Model

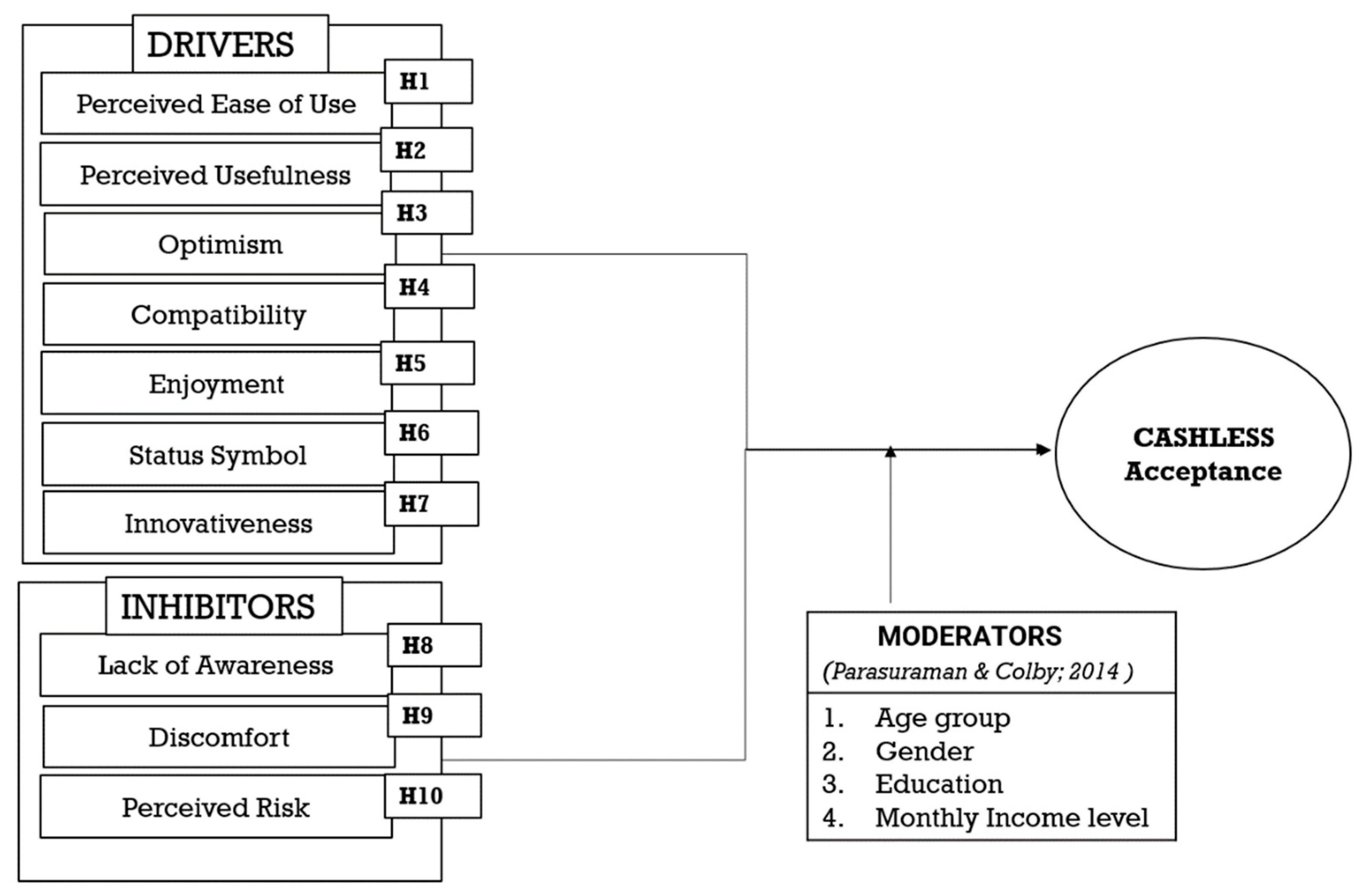

This study was designed predominantly to determine, evaluate, and analyse the driving and inhibiting factors influencing the perceived acceptance of consumers in transitioning towards a cashless society. It is also an approach facilitating the acceptance of cashless transaction services to harmonize and authenticate the determining factors of cashless payment services acceptance in Malaysia. Fig.1 depicts the theoretical framework of Cashless Society Acceptance Model (CSA) along with the dependent, independent, and mediating factors together with its hypotheses.

Fundamentally, the execution of this research is heavily dependent on the utilisation of the updated TRI 2.0 and UTAUT 2 framework. The technology readiness index (TRI 2.0) was developed by Parasuraman et al (2000), encompassing of 36 aspects intended for the measurement of the structure and its key components. TRI 2.0 essentially evaluates the perspective of an individual towards the advancements of technology, as a whole (Parasuraman et al., 2015). In contrary, the unified theory of acceptance and used of technology (UTAUT 2) was developed by (Venkatesh et al., 2012) with a sole objective of justifying the intention of users in utilising information systems while analysing their usage patterns (Venkatesh et al., 2016).

In order to get a better understanding on the consumers acceptance towards Cashless Services to achieve Cashless Society, a significant contribution in fulfilling the gaps in literature on both the perception of consumers on cashless acceptance and the availability of models to assess the cashless acceptance of Malaysian consumers need to be carried out. This is principally achieved through the combination of the model and factors from UTAUT 2, TRI 2.0 and few external factors are included in the Cashless Society Acceptance (CSA) model to have a better view on the enablers and barriers of going cashless. Figure 1 shows the formulation of a Cashless Society Acceptance (CSA) model. CSA can be viewed as an overall result of a combination of enablers and inhibitors that collectively determine a consumers’ acceptance towards cashless services to achieve cashless society. CSA model comprises 10 components that belongs to the enablers and inhibitors. Perceived Ease of Use, Perceived Usefulness and enjoyment are the enablers of UTAUT 2 (Vengkatesh et al., 2012). Optimism and innovativeness are enablers of TRI 2.0, while discomfort and perceived risk are the inhibitors of TRI 2.0. (Parasuraman et al., 2014). The additional enablers include compatibility (Wiese et al., 2017), status symbol (Rena et al., 2013) and lack of awareness (Oliveria et al., 2017).

This study includes additional features from prior research that have been identified as major enablers and inhibitors of customers' acceptance of cashless payment systems. In order to recognise the differences in individual consumers' acceptance of mobile payment services and the widening scope of the elements of new technology adoption studies, this study incorporates other variables from prior studies that have been reported as significant enablers and inhibitors of consumers' acceptance of cashless payment services. Compatible (Liébana-Cabanillas et al., 2015) and (Mallat, 2007), status symbol (Rena et al., 2013), enjoyment (Vengkatesh et al., 2012), perceived ease of use (Vengkatesh et al., 2012), and perceived usefulness (Vengkatesh et al., 2012) Lack of awareness (Oliveriaet al., 2017) is one of the extra inhibitors mentioned in the framework as below. Based on Table 1, the CSA model was developed with 7 enablers, i.e., perceived ease of use, perceived usefulness, optimism, compatibility, perceived enjoyment, status symbol, and innovativeness: 3 inhibitors, i.e., lack of awareness, discomfort, and perceived risk. The mediating variables correspond to the demographics of the user, that is elements such as their age group (18-65 years old), gender (Female, Male) education background (High school, tertiary, post-graduate), and income (Less than 3K MYR, 3K-10K MYR, more than 10K MYR). Its dependent variable however is the measure of cashless acceptance towards a cashless society. Figure 1 depicts the theoretical framework of the CSA model.

3.2. Instrument

For this study, the data analysed was collected online via bulk emails and social media sites like Facebook and Google. The sample size of this research was 434 respondents, consuming approximately six months. This quantitative questionnaire comprised of two primary sections, that is Part A and Part B. Part A predominantly solicited the demographic information of respondents, i.e., age (continuous), gender (dichotomous), education background (ordinal), income (ordinal), frequency of weekly usage (ordinal), and types of digital payment services used (dichotomous). Dichotomous is basically attributes with only two comparative variables, ordinal is attributes with two or more comparative variables, and continuous is attributes with more than five comparative variables.

Subsequently, Part B encompasses elements principally specifying individual enablers, inhibitors, and dependent variables. These are measured or ranked corresponding to the four-point Likert scale, whereby 1 = Strongly Disagree and 4 = Strongly Agree. The validation of the questionnaire will be performed by a faculty member with core competence in the quantitative analysis and financial technology division. Prior to launching the pilot study, this process was repeated three times for consistency, improvement, and improving the efficacy (Sullivan et al., 2016). The pilot study was conducted amongst 30 people, the Mage obtained was 24.2, SDage obtained was 0.88; no significant issues were detected during the pilot study, thus approved for mass distribution.

3.3. Respondents

The final survey questionnaire was disseminated online and also offline. Specifically, the link to the questionnaire survey was shared via Google drive and Facebook. 434 responses were received. A preliminary investigation revealed that 66.3% of the total respondents were classified to be within 25 to 50 years of age. The demographic characteristics of the respondents are shown in Table 2.

As much as 120 respondents in this research were male and the other 138 respondents were female, the female respondents outnumbering the male respondents by 7%. The percentage of respondents below 25 years old was 24.8%; the percentage of respondents 25 to 50 years old is 66.2%; the percentage of respondents beyond 51 years old was 9%. Focusing on the educational aspect, majority of the respondents had a tertiary level education background, making up 66.7% of the total respondent. This was closely followed by the respondents with a post-graduate education background, at 32.6% and respondents with a secondary level education background, at 0.8%. The percentage of income per month below RM 3,000 was 28.3%, whereas for the income range of RM 3,000 to RM 10,000 the percentage was 62.4%. As much as 9.3% have an income range beyond RM 10,000 per month.

The percentage of respondent that used cashless transaction at least four to nine times a week was determined to be 32.9%; 52.7% used cashless transactions less than three times a week and the remaining 14.3% also used cashless transactions but a frequency beyond ten times a week. Based on the statistical analysis, it was also evident that a great percentage of the total respondents, that is 82.2% used digital payments, with 50.7% from the total being users of more than one particular service or app. The most popular digital payment service among respondents was identified to be GrabPay, followed by Maybank QR Pay, JomPay and finally Boost.

3.4. Data Analysis

The data gathered is evaluated in the last stage, which consists of two primary steps: data analysis and model comparison. Statistical Package for Social Sciences (SPSS) 21 was used to characterise the sample using descriptive statistics such as mean (M), mode, standard deviation (SD), frequency, and so on. An IBM SPSS@AMOS version 25 was utilised to validate the Cashless Society Acceptance Model (CSA), as well as to identify the major enablers and inhibitors, as well as its predictive potential. Confirmatory factor analyses (CFA) and AMOS with maximum likelihood estimation (MLE) were performed in the same order. The model was tested for reliability, parameter estimation, and hypothesis testing using AMOS. A 0.7 loading threshold was used as a criteria for examining factor loadings. With a 0.7 and 0.5 cut-off point for AVE, Cronbach's alpha (CA), Composite Reliability (CR), and Average Variance Extracted (AVE) were also studied. Finally, discriminant validity was determined using the Fornell-Larcker criterion (David Alarcón et al., 2015), which examines the squared correlations across assessments of potentially overlapping domains. The reliability and validity of all the criteria were determined using a variety of methods. All of the goods and their loadings are listed in Table 3. Items with loadings less than 0.7 were deleted, and eight of them, as indicated in bold in Table 3, were omitted from further analysis.

4. Results and Discussion

This section presents the results and discussion, beginning with the reliability evaluation and moving on to the proposed model and its hypothesis.

4.1. Reliability Evaluation

The degree to which an instrument can produce dependable results on similar topics under similar settings and can be integrated with the precision of particular measures is referred to as reliability (Sapian et al., 2021). Looking at the composed reliability (CR), attributes with an alpha rating of 0.6 to 0.7 is considered adequate, and an alpha of higher than 0.8 is considered excellent. However, if it is more than 0.95, it does not necessarily imply that it is excellent, but it may indicate that the variable is redundant (Hulin et al., 2001).

From the previous section, it was established that several methods were employed for the evaluation of the data obtained. Additionally, items with factor loading rates below 0.7 were eradicated from the conceptualised theoretical framework of the CSR model. Table 4 demonstrates the CR evaluation comprising parameters such as the CA, CR, and AVE as an alternative for the measure of the degree of reliability. Based on the table below, eight variables key in identifying the impact of cashless transactions on payment method performances were accepted, irrespective of UTAUT 2 or TRI 2.0 models. The Cronbach’s Alpha (CA) for perceived ease of use was 0.826; perceived usefulness was 0.815; optimism was 0.861; compatibility was 0.717; enjoyment was 0.863; status symbol was 0.911; lack or no awareness was 0.903; discomfort was 0.892. All of the items included in the questionnaires for this study were dependable, with CA values of at least 0.7 or greater. CA essentially is a test used to determine if indicators for latent variables have convergent validity, if yes then classified as reliable. The highest CA as shown in Table 3 was the status symbol with a CA of 0.911 and lowest being compatibility with a CA of 0. 717. Similarly, most of the CR values were more than 0.5, ranging from 0.59 to 0.89, indicating that all of the measurements were indeed reliable. Finally, the AVE for each component was greater than or equal to 0.60, implying the reliability of the factors.

4.1. Goodness-of-Fit of the Framework

Comparative Fit Index (CFI), Root mean square error of approximation (RMSEA), Tucker-Lewis index (TLI) and Normed Fit Index (NFI),) were used to assess the framework's goodness-of-fit, as recommended by (Hair et al., 2006). (Xia et al., 2019). CFI, TLI, and NFI values should all be larger than 0.9, while RMSR should be greater than 0.07 and RMSEA should be less than 0.80 or equivalent to show a satisfactory match. As a consequence, the measurement model's results are an excellent fit. CFI = 0.925; NFI = 0.900; TLI = 0.905; RMSEA = 0.78; RMSR = 1.31 were the fit indices. The study found that the framework's 71.4 R-Square is explained by all eight (8) components.

4.2. Hypothesis Testing

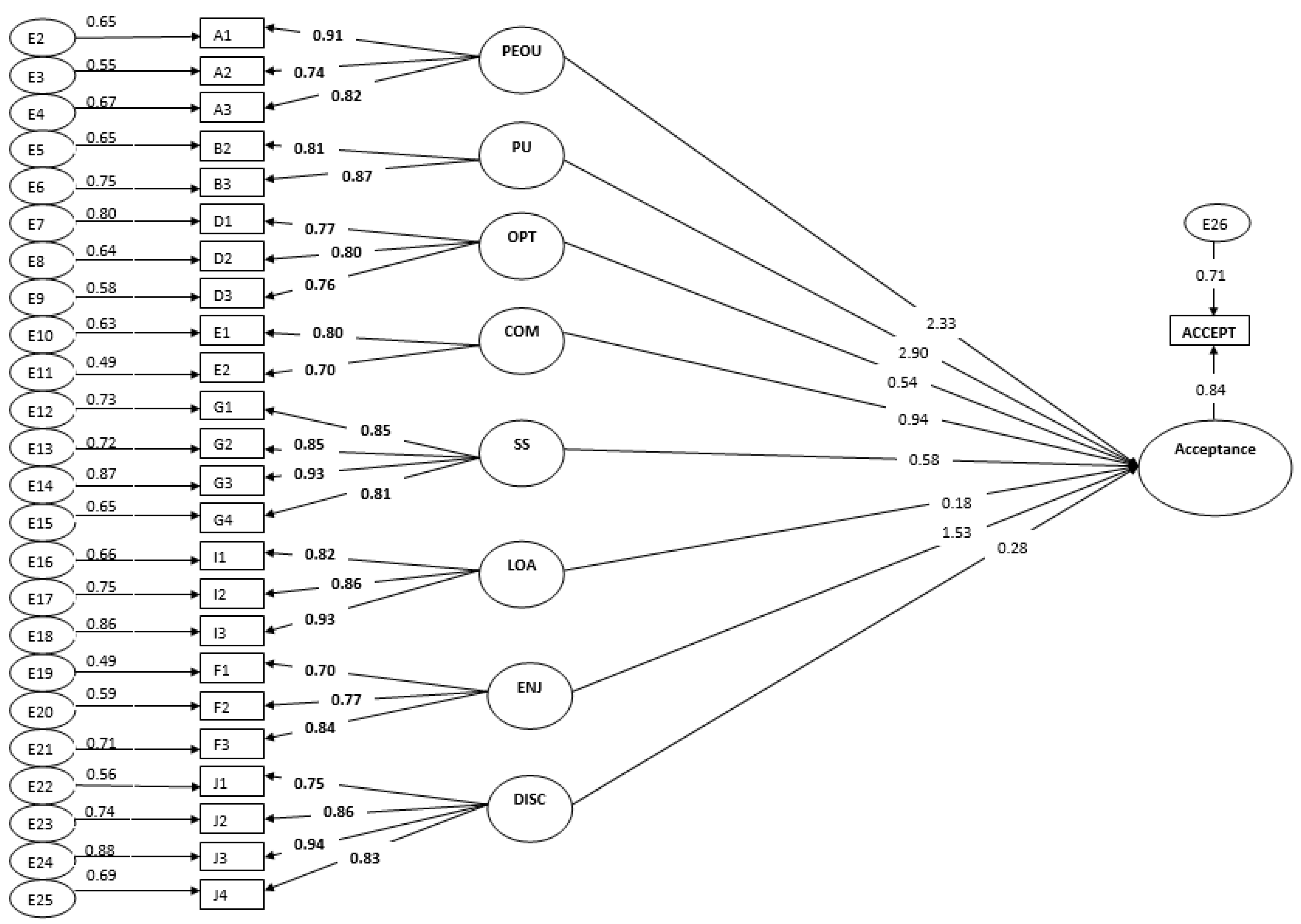

Table 5 shows the findings of the AMOS software, as well as the path coefficients and prediction power for the Cashless Acceptance – Acceptance Model, as well as the hypothesis assessment outcomes. Both Figure 2 and Table 5 support H1, H2, and H9, and the effects were assessed to be substantial. Based on studies from Malaysia (Mun et al., 2007), South Korea (Kim et al., 2008), and India, the emergence of substantial impacts for Perceived Ease of Use and Perceived Usefulness was partially expected (Singh et al., 2020). It is widely acknowledged that simple and helpful technology systems (and others) are more appealing to customers. Given that most respondents in this study are educated and often utilise cashless payment services, they may possess the necessary knowledge and confidence to use digital payment services. Because of their abilities and competence, individuals are already accustomed with using cashless payments, which explains the effect of these two variables on user acceptance. Discomfort's findings are consistent with prior research Kim (2010) and Verkijika (2018), and it was discovered to have a major negative influence on consumers' willingness to become cashless. The findings show that the majority of respondents felt that monitoring credit balances and setting up digital payments on a mobile phone is time consuming, and that carrying about electronic equipment such as laptops and smartphones makes it difficult to become cashless. This makes sense since it is natural for humans to avoid putting too much effort into setting up and transporting digital gadgets.

Note: PEOU: Perceived Ease of Use; PU: Perceived Usefulness; OPT: Optimism, COM: Compatibility; SS: Status Symbol; LOA: Lack of Awareness; ENJ: Enjoyment; DISC: Discomfort

The lack of awareness had no effect on the acceptance of turning cashless by users. The findings show that the majority of respondents disagree that a lack of knowledge about the availability, use, and benefits of cashless payment systems has an impact on user acceptability. This makes sense since it is normal for humans to be wary of new technology in the year 2021, particularly for Millennials, who are generally between the ages of 24 and 50 and so refer to a generation raised in a cashless environment. Similarly, other factors like as optimism have no substantial influence on user acceptability. The majority of respondents do not believe that payments can be effectively performed only through cashless payment services, nor do they believe that digital payment is the way of the future. It is also possible that cashless payment systems give little flexibility. In addition, Enjoyment, Status Symbol and Compatibility also did not have any significant impact on the user acceptance of going cashless. The respondents disagree that cashless payments and the mean to use cashless payment services does not fit the current lifestyle. Moreover, respondents do not find it fun, enjoyable or provides them satisfaction of using any cashless payment services.

Majority also finds cashless payment services does not enhance their status neither make them look professional or cool in using cashless payments because of an insecure feeling of privacy issues using cashless payments. Concern about discomfort issues have been reported by many Z. Sahnoune (2015) and J. Kang et al. (2017) and our results show that respondents may not accept cashless payments services due to discomfort issues. Finally, this sample's overall predictive power of being able to take cashless payments is 71.4 percent higher than the Indonesian scholars' estimated variance of 14.6 percent (I. Trinugroo, 2017). The data show that Malaysians of all ages and cities are still falling behind in accepting cashless payment methods.

5. Conclusion, Implication, Limitation and Future Work

This study aimed to identify the enablers and inhibitors affecting users’ acceptance in going cashless. The Cashless Society Acceptance – Acceptance Model was devised based on two well-known models, namely, UTAUT 2 and TRI 2.0. The response for this study included 434 Malaysian respondents between the ages of 18 and 64, gathered using self-administered surveys. Results from this study indicated that aspects such as the perceived ease of use, perceived usefulness and discomfort have significant direct affects in users’ acceptance in going cashless, with a predictive power 71.4%. Being cashless acceptance, however, does not necessarily indicate the acceptance of cashless payment services as shown by the insignificant result.

5.1. Implications

Based on the findings from this study, this research was determined to have one major implication: that is stemming from the development of the Cashless Society Acceptance-Acceptance model, as well as the identification of the enablers and inhibitors to a cashless society, which will consequently be useful to other researchers who want to learn more about this issue, in the future.

5.2. Limitations and Recommendations

There were several limitations from this approach of study on a cashless society in Malaysia. Despite the fact that the respondents in this research ranged in age from 18 to 64, the respondents were identified to be mostly urban educated. A cashless society seeks to cover the vast majority of the population; as a result, future studies might duplicate the research design to include Malaysians from other socioeconomic strata, particularly those from smaller towns or with lower levels of education. Furthermore, additional respondents from the B40 category should be enlisted since low income may be a barrier to digital payment adoption. This may enable the government to work with service providers to provide greater financial support to low-income people in the form of promotions or special packages.

Another implication is the use of self-administered questionnaires, which can lead to problems like social desirability and inaccurate reporting. Surveys are a quick and simple approach to obtain information on digital payment users' perceptions; however, focus groups or interviews might be used to further understand the enablers and inhibitors. Face-to-face encounters with respondents, particularly those with a lesser educational background, are seen to be more successful in data collecting than self-administered surveys, which do not allow for any clarification of any uncertainties. In fact, focus groups or interviews allow researchers to go further into the themes, as well as the enablers and inhibitors, in order to better understand the motivations behind the acceptance or rejection of digital payment systems.

Conclusively, as a result of the ongoing corona virus epidemic, adoption of cashless payment services has grown in the nation, and potentially worldwide, in the previous years. Malaysia, for example, has ramped up its efforts by implementing movement control orders, effectively "forcing" individuals to stay at home. As a result, there has been an increase in the usage of food and grocery delivery services, which helps to reduce the risk of the virus spreading. This circumstance, perhaps, will stimulate the use of digital payment systems such as e-wallets in the future.

References

- Kadar HH, B.; Sameon SS, B.; Din MB, M.; Rafee PA, B.A. Malaysia towards cashless society. International Symposium of Information and Internet Technology; Springer: Cham, 2018; pp. 34–42. [Google Scholar]

- Din MB, M.; Rafee PA, B.A. Malaysia towards cashless society. Proceedings of the 3rd international symposium of information and internet technology (SYMINTECH 2018. 565; Springer, 2019; p. 34. [Google Scholar]

- Humbani, M.; Wiese, M. A cashless society for all: Determining consumers’ readiness to adopt mobile payment services. Journal of African Business 2018, 19, 409–429. [Google Scholar] [CrossRef]

- Parasuraman, A.; Colby, C.L. An updated and streamlined technology readiness index:TR 2.0. Journal of Service Research 2014, 18, 59–74. [Google Scholar] [CrossRef]

- Parasuraman, A. Technology readiness index (TRI): A multiple-item scale to measure readiness to embrace new technologies. Journal of Service Research 2000, 2, 307–320. [Google Scholar] [CrossRef]

- Fripp, C. http://www.htxt.co.za/ 2014/10/23/south-africas-mobile-penetration-is-133/. 2014. Available online: http://www.htxt.co.za/ 2014/10/23/south-africas-mobile-penetration-is-133/.

- GSMA. (2016). State of the industry report on mobile money.

- Ajzen, I. (1991). The theory of planned behavior. Organizational Behavior and Human Decision Processes, 50, 179–211. [CrossRef]

- De Kerviler, G.; Demoulin NT, M.; Zidda, P. Adoption of in-store mobile payment: Are perceived risk and convenience the only drivers? Journal of Retailing and Consumer Services 2016, 31, 1–39. [Google Scholar] [CrossRef]

- Jacob, N.A.; Antony, G.V. A critical review of information-security threats faced by Indian banks. International Journal of Advanced Research in Computer Science and Management Studies 2016, 4, 7–13. [Google Scholar]

- Jaradat MI, R.M.; Al Rababaa, M.S. Assessing key factors that have an influence on the acceptance of mobile commerce, based on modified UTAUT. International Journal of Business and Management 2013, 8, 102–112. [Google Scholar]

- Jia, L.; Hall, D.; Sun, S. (2014). The effect of technology usage habits on consumers’ intention to continue to use mobile payments. Twentieth Americans Conference on Information Systems (pp. 1–12). Savannah; pp. 1–12.

- Karjaluoto, H.; Leppaniemi, M.; Standing, C.; Kajalo, S.; Merisavo, M.; Virtanen, V.; Salmenkivi, S. Individual differences in the use of mobile services among Finnish consumers. International Journal of Mobile Marketing 2006, 1, 4–10. [Google Scholar]

- Kımıloğlu, H.; Aslıhan Nasır, V.A.; Nasır, S. Discovering behavioral segments in the mobile phone market. Journal of Consumer Marketing 2010, 27, 401–413. [Google Scholar] [CrossRef]

- Kiwanuka, A. Acceptance process: The missing link between UTAUT and diffusion of innovation theory. American Journal of Information Systems 2015, 3, 40–44. [Google Scholar]

- Lee, Y.-K.; Park, J.-H.; Chung, N.; Blakeney, A. A unified perspective on the factors influencing usage intention toward mobile financial services. Journal of Business Research 2012, 65, 1590–1599. [Google Scholar] [CrossRef]

- Liao, Z.; Shi, X.; Wong, W.-K. Consumer perceptions of the smartcard in retailing: An empirical study. Journal of International Consumer Marketing 2012, 24, 252–262. [Google Scholar] [CrossRef]

- Liébana-Cabanillas, F.; De Luna, I.R.; Montoro-Ríos, F.J. User behaviour in QR mobile-payment system: The QR payment acceptance model. Technology Analysis & Strategic Management 2015, 27, 1031–1049. [Google Scholar]

- Lin, C.-H.; Shih, H.-Y.; Sher, P.J. Integrating technology readiness into technology accep-tance: The TRAM model. Psychology & Marketing 2007, 24, 641–657. [Google Scholar]

- Hair, F.H.; Black, W.C.; Babin, B.J.; Anderson, R.E.; Tatham, R.L. (2006). Multivariate data analysis (6th ed.). Upper Saddle River, NJ: Pearson-Prentice Hall.

- Herzberg, A. Payments and banking with mobile personal devices. Communications of the ACM 2003, 46, 53–58. [Google Scholar] [CrossRef]

- Hooper, D.; Coughlan, J.; Mullen, M. Structural-equation modelling: Guidelines for determining model fit. Electronic Journal of Business Research Methods 2008, 6, 53–60. [Google Scholar]

- Mallat, N. Exploring consumer adoption of mobile payments – A qualitative study. The Journal of Strategic Information Systems 2007, 16, 413–432. [Google Scholar] [CrossRef]

- Changsu Kim, Mir obit Mirusmonov, In Lee, An empirical examination of factors influencing the intention to use mobile payment, Computers in Human Behavior, Volume 26, Issue 3,2010,Pages 310-322,ISSN 0747-5632. [CrossRef]

- Bilińska-Reformat, K.; Kieżel, M. (2016). Retail banks and retail chains cooperation for the promotion of the cashless payments in Poland. Twentieth Americans Conference on Information Systems (pp. 1–12). Savannah, Venice, Poland.

- Krüger, M.; Seitz, F. (2014). Costs and benefits of cash and cashless payment instruments: Overview and initial estimates. Study commissioned by the Deutsche Bundesbank. Frankfurt,Germany.

- World Payment Report (2020). Non-cash payments volume. Available online: https://worldpa ymentsreport.com/non-cash-payments-volume-2/ (accessed on 11 September 2020).

- Golobal Trade (2020). Toward a global cashless economy. Available online: https://www. globaltrademag.com/toward-a-global-cashless-economy/.

- Research and Market (2020). Global cards & payments market insights, 2015–2019 & 2019–2023. Available online: https://www.globenewswire.com/news-release/2020/04/ 16/2017151/0/en/Global-Cards-Payments-Market-Insights-2015-2019-2019-2023. Html.

- Pikri, E. (2019). How cashless is Malaysia right now? 1996. Available online: https:// fintechnews.my/19964/payments-remittance-malaysia/cashless-malaysia-credit-debitca rd-e-wallet-money/ (accessed on 10 July 2019).

- Bank Negara Malaysia (2019). Malaysia's payment statistics. Available online: http://www.bnm.gov.my/index.php?ch=ps&pg=ps_stats&lang=en.

- Mering, R. (2019). Survey: More Malaysians prefer cashless payment with debit cards, online banking. Retrieved 11 July 2019. Available online: https://www.malaymail.com/news/money/ 2019/01/17/survey-more-malaysians-prefer-cashless-payment-with-debit-cards-onlinebank/1713682.

- Teo, A.C.; Tan, G.W.; Ooi, K.B.; Hew, T.S.; Yew, K.T. The effects of convenience and speed in m-payment. Industrial Management and Data Systems 2015, 115, 311–331. [Google Scholar] [CrossRef]

- Thomas, H.; Jain, A.; Angus, M. (2013). Measuring progress toward a cashless society. MasterCard advisors (pp. 1–5) Retrived 11 July 2019. 11 July. Available online: https://newsroom.mastercard. com/wp-content/uploads/2014/08/MasterCardAdvisors-CashlessSociety-July-20146.pdf.

- Nagdev, K.; Rajesh, A.; Misra, R. (2021). The mediating impact of demonetisation on customer acceptance for IT-enabled banking services. International Journal of Emerging Markets. [CrossRef]

- Yang, M.; Al Mamun, A.; Mohiuddin, M.; Nawi, N.C.; Zainol, N.R. (2021). Cashless transactions: A study on intention and adoption of e-wallets. Sustainability (Switzerland). [CrossRef]

Figure 1.

Cashless Society Acceptance (CSA) model.

Figure 2.

Cashless Society Acceptance (CSA) Framework.

Table 1.

Operational definitions for all the variables.

| Factors | Model/References | Description |

|---|---|---|

| Drivers | ||

| Perceived Usefulness | UTAUT2 | It is a degree to which a person believes that using a particular system would enhance his/her job performance |

| Perceived Ease of Use | UTAUT2 | The extent to which using a digital payment service is easy. |

| Innovativeness | TRI 2.0 | Inclination of an individual to try out any new information systems |

| Optimism | TRI 2.0 | Positive view of digital payment technology and a belief that it offers people increased control, flexibility, and efficiency in their lives |

| Compatibility | Wiese, M. (2017). | Consistency between digital payment technology and its values, experiences and the needs of potential adopters. |

| Status Symbol | Rena, Z., Salehuddin, M., Zahari, M., & Rosmini, I. (2013)). | The extent to which using digital payment services is deemed as a status symbol |

| Enjoyment | UTAUT 2 | The extent to which using the digital payment services is considered fun |

| Inhibitors | ||

| Lack of Awareness | Oliveria, T. Thomas M., Baptista, G., & Campos, F. (2017). | The failure to be alert of new digital payment technologies. |

| Perceived Risk | TRI 2.0 | The extent to which using the digital payment service incurs costs to the customer |

| Discomfort | TRI 2.0 | Perceived lack of control over digital payment technology and a feeling of being overwhelmed by it |

| Dependent variable | ||

| Cashless Acceptance | The level of acceptance to use cashless payment services | Redefined from TRI 2.0, UTAUT2 and External Factors |

Table 2.

Demographic Profile Results.

| Sample Characteristic | Frequency | Percent (%) |

|---|---|---|

| Gender | ||

| Female | 246 | 56.7 |

| Male | 188 | 43.3 |

| Age | ||

| Less than 25 | 76 | 17.5 |

| 25 - 50 | 335 | 77.2 |

| More than 51 | 23 | 5.3 |

| Education | ||

| High school | 4 | 0.9 |

| Tertiary | 276 | 63.6 |

| Post-Graduate | 154 | 35.5 |

| Income | ||

| < 3,000 (MYR (< 714 USD) | 110 | 25.3 |

| 3,000 - 10,000 (MYR)(714 – 2380 USD) | 270 | 62.2 |

| > 10,000 (MYR)(> 2380 USD) | 54 | 12.4 |

| Use of Digital Payment | ||

| No | 33 | 7.6 |

| Yes | 401 | 92.4 |

| Frequency (weekly) | ||

| 4 – 9 times | 186 | 42.9 |

| < 3 times | 178 | 41.0 |

| >10 times | 70 | 16.1 |

| Services (apps) | ||

| GrabPay | 211 | 48.6 |

| JomPay | 135 | 31.1 |

| Maybank QR Pay | 144 | 33.1 |

| Boost | 112 | 25.8 |

| More than one | 157 | 36.1 |

Table 3.

Factor Loadings and Items.

| Factors | Items | Loading |

|---|---|---|

| Perceived Ease of Use (A1-A3) | I find it easy to use digital payments | A1: 0.91 |

| I find it easy to learn to use digital payments | A2: 0.74 | |

| I find it easy to install digital payment application | A3: 0.82 | |

| Perceived Usefulness (B1 – B3) | Using digital payment would help me to manage my expenses better | B1: 0.61 |

| It is convenient to pay digitally | B2: 0.81 | |

| Digital payment enables me to make payment efficiently | B3: 0.87 | |

| Innovativeness (C1-C3) | I am interested in keeping up with the latest digital payment application. | C1: 1.01 |

| I am interested in using latest digital payment application | C2: 0.67 | |

| I don’t mind trying digital payment application that is new to the market | C3: 0.37 | |

| Optimism (D1-D3) | I belief payments can be successfully completed using digital payments | D1: 0.77 |

| I feel that digital payment is the lead towards the future. | D2: 0.80 | |

| I belief that digital payment provides flexibility | D3: 0.76 | |

| Compatibility (E1-E2) | My lifestyle fits digital payment | E1: 0.80 |

| I have the means to use digital payment (e.g. smartphones) | E2: 0.70 | |

| Enjoyment (F1-F3) | I find it fun using digital payment | F1: 0.70 |

| I enjoy using digital payment in my daily life | F2 0.87 | |

| It gives me satisfaction in making payments using digital payments | F3: 0.84 | |

| Status Symbol(G1-G4) | Digital payments enhance my status | G1: 0.85 |

| Digital payment makes me look professional | G2: 0.85 | |

| Digital payment enhances my confidence | G3: 0.93 | |

| I find it cool in using digital payment | G4: 0.81 | |

| Perceived Risk (H1-H4) | I don’t feel secure in using digital payment | H1: 0.60 |

| I am concerned about my online privacy | H2: 0.24 | |

| I feel uncomfortable as there are too many security breaches lately. | H3: 0.62 | |

| I just don’t trust any online payment mechanism | H4: 0.63 | |

| Lack of Awareness(I1-I3) | I don’t know where I can use digital payments (e.g. restaurant) | I1: 0.82 |

| I am not aware of digital payments available | I2: 0.86 | |

| I don’t know when I can use digital payment | I3: 0.93 | |

| Discomfort (J1-J4) | I find it tedious in always maintaining my credit balance. | J1: 0.75 |

| I find it tedious in setting up digital payment | J2: 0.86 | |

| I find it uncomfortable in carrying my technology device around (e.g. laptop, smart phones) | J3: 0.94 | |

| There are too many hassles in carrying around digital payment (e.g. forgetting to carry around mobile phones, battery dead) | J4: 0.83 |

Table 4.

Construct Reliability Evaluation.

| Construct | Items Description | Items and Factor Loading | Cronbach’s alpha (CA) | Average Variance Extracted (AVE) | Composite Reliability (CR) |

|---|---|---|---|---|---|

| Perceived Ease of Use | I find it easy to use digital payments | A1: 0.91 | 0.826 | 0.69 | 0.82 |

| I find it easy to learn to use digital payments | A2: 0.74 | ||||

| I find it easy to install digital payment application | A3: 0.82 | ||||

| Perceived Usefulness | It is convenient to pay digitally | B2: 0.81 | 0.815 | 0.70 | 0.77 |

| Digital payment enables me to make payment efficiently | B3: 0.87 | ||||

| Optimism | I belief payments can be successfully completed using digital payments | D1: 0.77 | 0.861 | 0.60 | 0.73 |

| I feel that digital payment is the lead towards the future. | D2: 0.80 | ||||

| I belief that digital payment provides flexibility | D3: 0.76 | ||||

| Compatibility | My lifestyle fits digital payment | E1: 0.80 | 0.717 | 0.60 | 0.72 |

| I have the means to use digital payment (e.g. smartphones) | E2: 0.70 | ||||

| Enjoyment | I find it fun using digital payment | F1: 0.70 | 0.863 | 0.60 | 0.73 |

| I enjoy using digital payment in my daily life | F2 0.87 | ||||

| It gives me satisfaction in making payments using digital payments | F3: 0.84 | ||||

| Status Symbol | Digital payments enhance my status | G1: 0.85 | 0.911 | 0.74 | 0.89 |

| Digital payment makes me look professional | G2: 0.85 | ||||

| Digital payment enhances my confidence | G3: 0.93 | ||||

| I find it cool in using digital payment | G4: 0.81 | ||||

| Lack of Awareness | I don’t know where I can use digital payments (e.g. restaurant) | I1: 0.82 | 0.903 | 0.76 | 0.88 |

| I am not aware of digital payments available | I2: 0.86 | ||||

| I don’t know when I can use digital payment | I3: 0.93 | ||||

| Discomfort | I find it tedious in always maintaining my credit balance. | J1: 0.75 | 0.892 | 0.72 | 0.88 |

| I find it tedious in setting up digital payment | J2: 0.86 | ||||

| I find it uncomfortable in carrying my technology device around (e.g. laptop, smart phones) | J3: 0.94 | ||||

| There are too many hassles in carrying around digital payment (e.g. forgetting to carry around mobile phones, battery dead) | J4: 0.83 |

Table 5.

Hypothesis Results.

| Construct | p-value | Hypothesis and Remark |

|---|---|---|

| Perceived Ease of Use | 0.005 | H1 Supported |

| Perceived Usefulness | 0.004 | H2 Supported |

| Optimism | 0.465 | H3 Not Supported |

| Compatibility | 0.505 | H4 Not Supported |

| Enjoyment | 0.254 | H5 Not Supported |

| Status Symbol | 0.118 | H6 Not Supported |

| Lack of Awareness | 0.127 | H8 Not Supported |

| Discomfort | 0.012 | H9 Supported |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Copyright: This open access article is published under a Creative Commons CC BY 4.0 license, which permit the free download, distribution, and reuse, provided that the author and preprint are cited in any reuse.