Submitted:

17 September 2023

Posted:

18 September 2023

You are already at the latest version

Abstract

The objective of this study was to identify the factors determining a company’s corporate governance related to climate change. We analyzed the effect of various sustainability corporate governance variables on the disclosure level of climate change governance. These variables included facts such as having a dedicated sustainability executive and board committee, the mediating effect of female representation on the board of directors, number of reporting years according to TCFD, membership in a sustainability index, MSCI ESG rating, the existence of a corporate climate transition plan, a mention of the UN Global Compact and GRI, company location, as well as company size and profitability.

By adopting a multi-theoretical framework that included stakeholder theory as well the legitimacy and agency theory, the underlying research study used a sample of 100 of the largest global companies by market capitalization and their reporting for the year 2020.

Based on 1,400 observations for fiscal year 2020 and using correlation analysis, univariate and linear multiple regressions, we find a positive association between having a climate transition plan in place, being a leader in sustainability according to MSCI ratings, and being a DJSI constituent and the propensity to disclose information on governance for climate change. In addition, we find a company with a dedicated sustainability executive show an increased tendency to be transparent on climate governance issues. Furthermore, having a company location in a developed country is significantly and positively associated with climate change governance.

Surprisingly, gender diversity in the corporate board or having a sustainability board committee did not show any significant correlation between a higher climate change governance level. The same was true for companies being active in either the extractive or non-extractive sector. Companies referring to the Global Reporting Initiative (GRI) or UN Global Compact also did not score higher in climate change governance. Neither did corporate profitability or size play a significant role.

Our results are robust to variations and provide valuable insights for researchers, academics, executives, practitioners as well as regulators. As more and more companies are shifting towards a climate change reporting framework, it is of paramount importance that we are able to determine the contributing variables that lead to effective climate change corporate governance.

Our results are inconsistent with stakeholder theory and are strongly suggesting that a diversified board and the existence of a sustainability committee that meets often/sufficiently may not necessarily lead to a higher level of transparency/quality regarding climate change. While more research is needed, knowing that a dedicated sustainability executive as well as having a climate plan in place can make a difference in climate change reporting, can be very beneficial to many corporate stakeholders. Given the current urgent climate change situation and the crucial role that corporation play in it, dedicated sustainability positions and committees need to be established. The findings could be useful for managers as well as governmental standards setter and regulators who are interested in improving corporate practices dealing with climate change. This study applies STATA software with various regression models to empirically test the relationship between CG and other variables and corporate climate change reporting.

Keywords:

climate change

; corporate governance

; oversight

; non-financial reporting

; corporate social responsibility (CSR)

; sustainability

; gender diversity

; sustainability board committee

; r

; voluntary disclosure theory

; signaling theory

; Hofstede’s cultural’s dimensions theory

; institutional theory

; Gender socialization theory

; Resource dependence theory

; Upper echelon theory

; social innovation theory

; Carbon emissions

; CSR disclosure

1. Introduction

Just recently, climate change was named as one of the top 6 priority areas in the field of business sustainability [1]. According to a definition by the United Nations, climate change (hereinafter also "climate") refers to long-term shifts in temperatures and weather patterns [2]. Climate change is not a new phenomenon. Since the 18th century, human activity has been a major contributor to climate change, primarily through the burning of fossil fuels such as coal, oil, and gas which creates greenhouse gas emissions that will trap the sun’s heat and increase temperatures [3].

Climate scientists have showed that humans are responsible for virtually all global heating over the last 200 years [4]. Human activities like the ones mentioned above are causing greenhouse gases that are warming the world faster than at any time in at least the last two thousand years [5]. In addition, the past eight years were the warmest on record globally, fueled by ever-rising greenhouse gas concentrations and accumulated heat, according to six leading international temperature datasets consolidated by the World Meteorological Organization [6]. The consequences of climate change now include, among others, intense droughts, water scarcity, severe fires, rising sea levels, flooding, melting polar ice, catastrophic storms, and declining biodiversity [7]. Consequently, climate change has become an urgent global issue that requires immediate action from governments, businesses, as well as individuals [8].

Climate change is often defined as the concept of risks and opportunities for companies related to climate change and investors increasingly demand more concise and clearer ESG disclosure that can be compared between organization to organization [9]. As climate change impacts become increasingly severe, the need for concise and comprehensive reporting has become more important than ever. Efficient climate change reporting helps to increase awareness, facilitate informed decision-making, and drive action to mitigate the impacts of climate change [10]. Overall, climate change reporting is a crucial tool in the fight against climate change. By promoting transparency and accountability, reporting can help to drive action to reduce greenhouse gas emissions, adapt to the impacts of climate change, and build a more sustainable future for all.

Adopted in 2015, the Paris Agreement is a legally binding international treaty on climate change. It was adopted by 196 Parties at the UN Climate Change Conference (COP21) and became effective in November 2016 [11]. Its central objective is to strengthen the global response to climate change by keeping a global temperature rise this century well below 2 degrees Celsius above pre-industrial levels and to pursue efforts to limit the temperature increase even further to 1.5 degrees Celsius [12]. Recently, the need to limit global warming to 1.5°C earlier has been emphasized based on more detailed scientific evidence [13]. Since 2020, the Paris Agreement requires all signatories to submit “nationally determined contributions” (NDCs), including a regular emissions report and national implementation efforts [14].

In 2015, the EC issued its first NDC jointly with its Member States. Importantly, certain Member States have issued their own independent NDCs and plans on how to achieve them. The EU, and its Member States, have jointly committed to a binding target of an "at least 40% reduction in greenhouse gas emissions by 2030 compared to 1990" [15}. In 2019, the European Commission (EC) published new guidelines on reporting climate-related information which are consistent with the requirements of the Non-Financial Reporting Directive and integrate the recommendations of the Task Force on Climate-related Financial Disclosures (TCFD) [16]. The TCFD’s recommendations are voluntary for all member states and do not supersede national disclosure requirements. Several member states have issued their own independent “nationally determined contributions” (NDCs) and plans to achieve them [17].

As climate change is introducing more risks and uncertainties into financial systems, but information failures limit the understanding of financial impacts on organizations. To create transparency regarding these risks, in 2015, the Basel-based Financial Stability Board (FSB) set up an international working group, the Task Force on Climate-related Financial Disclosures (TCFD), with the overall objective to improve climate-related corporate disclosures [18]. More specifically, the TCFD seeks disclosure of companies' governance, strategy, risk management, targets, and metrics for evaluating climate risks and opportunities [19]. The first TCFD recommendations were published in 2017 and the latest update followed in 2021 (TCFD 2023). The TCFD is a global consortium of investors, accountants, and company executives. The TCFD's framework has been endorsed by over 4,000 organizations and 101 jurisdictions globally, including the national governments of Canada, Switzerland, the UK, France, Sweden, New Zealand, and many securities exchange commissions worldwide [20].

In 2022, The United States Securities and Exchange Commission (SEC) rule on mandatory climate risk disclosures was proposed with the objective to make reporting practices consistent and comparable to meet investor demand [21]. The SEC rule is built around the Task Force for Financial Disclosures (TCFD) recommendations addressing topics such as Governance, Strategy, Risk Management, Metrics and Targets, as well as the Greenhouse Gas (GHG) Protocol for emissions reporting. The SEC is planning to finalize the climate change disclosure rule in 2023 [22].

Over the last few years, several other organizations or regulators have voiced the need for a global mandatory and standardized approach to climate change reporting. Therefore, various forms of non-financial reporting have become increasingly common [23,24,25]. Examples for these reports are corporate carbon reporting (which discloses corporate greenhouse gas (GHG) emission.

Another approach to climate reporting has been promoted by the CDP (formerly Climate Disclosure Project), a not-for-profit charity that has been using a global disclosure system for investors, companies, cities, states and regions to manage their environmental impacts for over 20 years [26]. CDP asks the world’s largest organizations to voluntarily disclose information on climate risks and low carbon opportunities by using the CDP disclosure guidelines. Based on the submitted information, CDP scores will then assign a score from A-F on how organizations are doing with respect to their disclosure on climate, water, and forests. CDP is considered the “gold standard for corporate environmental reporting” and is fully aligned with the TCFD recommendations. In 2022, almost 20,000 global organizations disclosed data through CDP, including more than 18,700 companies' worth approximately one half of global market capitalization [27].

However, the CDP is not the only reporting framework that corporations are using for their climate reporting. The UN Global Compact, established in 2000, has grown into the world's largest corporate sustainability initiative, with a reach of more than 12,000 companies and 3,000 non-business stakeholders in 160 countries [28]. It applies their “Ten Principles” dealing with human rights, labour, the environment, and anti-corruption as the main driver of corporate sustainability [29]. The UN Global Compact’s strategy focuses on five main issue areas, one of them being Climate Action (Sustainable Development Goal SDG 13) [30]. The Intergovernmental Panel on Climate Change (IPCC), on the other hand, is the United Nations body for assessing the science related to climate change [31]. It most recently published Climate Change 2023 Synthesis Report provides the main scientific input to COP28 and is used by countries to review their progress towards the Paris Agreement goals [32].

The report outlines that humans are responsible for all global heating over the past 200 years leading to an increase in temperature of 1.1°C above pre-industrial levels [33]. The report reminds us that every increment of warming will come with more extreme weather events. In addition, the report outlines that a 1.5°C limit can still be achieved and makes urgent recommendations and outlines specific action items that must take place [34].

The Global Reporting Initiative (GRI) has been dominating ESG reporting since 1997 [35]. Founded by the GRI in 2015, the Global Sustainability Standards Board (GSSB) is responsible for “setting the world’s first globally accepted standards for sustainability reporting” [36]. Established as an independent operating entity under the auspices of GRI, GSSB members represent a range of expertise and multi-stakeholder perspectives on sustainability reporting. Issued in 2016, the GRI Sustainability Reporting Standards (GRI Standards) are designed to be used by organizations to report about on impacts on the economy, the environment, and society [37]. Regarding sustainability reporting, more standards are being developed by other standard setters as well, such as the European Union (EU) which adopted the Corporate Sustainability Reporting Directive (CSRD) in 2022.

With a focus on climate-related disclosure, there are three universal GRI Standards that apply to every organization preparing a sustainability report. The GRI 305 titled “Emissions” is a topic specific GRI Standard which concerns itself with environmental topics ([38]. The organizations are making sure to collaborate and to align their standards or guidelines to improve the consistency and comparability of environmental data and to make reporting more efficient and effective [39]. The TCFD is also well aligned with the CDP. GRI is complementary to TCFD, and many companies use a combination of GRI, CDP, and TCFD [40].

Another prominent standard setter with global reach is the IFRS Foundation, which is a not-for-profit, public interest organisation established to develop high-quality, understandable, enforceable, and globally accepted accounting and sustainability disclosure standards [41]. The IFRS has two boards, the International Accounting Standards Board (IASB) and the International Sustainability Standards Board (ISSB). In 2022, the ISSB started to explore whether and how companies’ financial statements can provide better information about climate-related risks [42}. Shortly after, the ISSB published the Exposure Draft IFRS S2 Climate-related Disclosures which is based on the recommendations of the Task Force on Climate-Related Financial Disclosures (TCFD). After publishing the Exposure Draft and asking for stakeholder feedback, it is expected that an IFRS Sustainability Disclosure Standard will be published in 2023 [43].

Bottom of Form

To date most of the research on carbon reporting has focused on the rationales for and impacts of voluntary disclosures [44] [[45]. Given that in some countries, mandatory reporting is already in place, our analysis also considers responses to mandatory reporting, so as to speak to wider policy questions about the effectiveness of transparency requirements in nudging firms to behave more sustainably [46].

Our study contributes to the current literature in the following ways. First, it adds to the very limited literature on climate-related disclosure for global companies. Secondly, we use a sample comprised of approximately 1,400 observations from a broad representation of 18 countries, representing the major regions of the world. Thirdly, we do not differentiate between mandatory and voluntary disclosure. Finally, we obtain significant results by applying a consistent and simple scoring system for all companies (versus using pre-assessed scores). In addition, we are using social innovation theory, a theory that has not been used int this context. Our topic is especially important since recent studies have shown that non-financial information can reduce information asymmetries [47] [48].

The following section two presents a literature review and the paper's theoretical framework. Afterwards, the research methodology is summarized. Section four presents the sample demographics while section five includes statistical univariate and multivariate analysis. Finally, the sixth section includes the discussion and conclusions.

2. Literature and hypothesis development

The multi-faceted topic of mandatory and voluntary corporate disclosure and its multiple drivers in different contexts have been the subject of many research studies in the past. Just the topic itself, research results have been mixed [49]. Researchers have explored the topic of increase in corporate climate reporting. They also tried to identify the reason why some companies are disclosing voluntary non-financial information and the scope and quality of the provided information. Another approach was to recognize incentives that lead to increased transparency and comparability of such reporting. Typically, there are a few theories on which those studies are based ranging from agency theory, resource dependence theory, upper echelons theory, and voluntary disclosure to legitimacy and stakeholder, signaling theory, and social innovation theory [50] [51].

In 1976, Jensen and Meckling defined an agency relationship as “a contract under which one or more persons (the principal(s)) engage another person (the agent) to perform some service on their behalf which involves delegating some decision-making authority to the agent” [52] (1976, p. 308). Due to the separation of ownership and management, a misalignment of interests is created. Since managers have better access to information than any shareholder or investor, this can lead to misuse of information at the expense of corporate long-term value creation [53] [54}. It can also potentially cause information asymmetry leading to agency costs for the principals (owners) [55] [56]. An efficient corporate governance structure and process can protect shareholders’ interests and thereby reduce or minimize agency costs ([57] [58]. Minimal agency cost results in reduced information asymmetry and this will then lead ultimately to high quality information disclosure ([59] [60].

Since mandatory information disclosure is often considered insufficient, voluntary disclosure is used by managers to provide a fuller picture [61] [62] [63]. In fact, it has been argued that board attributes can directly influence a company’s sustainability strategy [64], oversight of management [65], and reduction of information asymmetry [66], all from the perspective of agency theory.

Legitimacy theory is one of the most often named and applied theories in the area of corporate sustainability disclosure [67] [68]. Simply said, it states that any firm operates under a social contract. In addition, the existence of the organization can only be justified if it provides benefits to society continuously. It has to demonstrate its legitimacy to the public, otherwise it will risk losing the support of the society it operates in [69]. One way to ascertain and maintain such support is voluntary publication of CSR information [70]. By publishing climate change information, the company could gain such societal support and thereby reduce the risk of losing organizational legitimacy [71] [72]. On the other hand, legitimacy theory also applies to poor sustainability performers that tend to “overshare” to either receive social recognition or maintain it [73] [74] [75]. In the context of carbon reporting, the carbon information can be considered mainly private knowledge of the managers ([76] [77]. Hence, there is still information asymmetry regarding the carbon and energy data revealed. Therefore, manager still have an incentive to conceal true carbon information if they are not performing well in this regard [78] [79]. This has also been called the “symbolic legitimation/greenwashing view” ([80].

While the focus of agency theory has primarily been on shareholders, the scope of legitimacy theory goes further, which is especially relevant when considering more organizational stakeholders and increasingly also environmental, ethical, and social matters [81] [82]. Hence, the responsibilities of the board of directors have become wider in scope and include now also ethical, economic, environmental, and social factors in consideration of corporate strategic planning and long-term value creation ([83] [84] [85] [86].

In fact, researchers have found that companies with good corporate governance are embracing their responsibilities to their stakeholders, and this is reflected in more and better corporate disclosure [87].

Another theory that is applicable to our research topic is voluntary disclosure theory. Voluntary disclosure theory predicts that a company with superior sustainability performance voluntarily will disclose information to increase market value [89] [90]. Drawing parallels to legitimacy theory, it can be argued that low-performing companies prefer to voluntarily disclose low-quality information to mask poor sustainability performance while maintaining legitimacy [91] [92].

According to Spence’s signaling theory, market signals are attributes of one party that can assist other parties make better investment decisions [93]. This positive link between market signals by disclosing voluntary information and company market value has been identified in prior studies in various contexts [94] [95] [96].

So far, we have identified corporate value creating theories, however, other theories can also be applied in the context of voluntary sustainability as well as climate-relate information disclosure. A theory that is increasingly mentioned in the CSR context, is stakeholder theory. Stakeholder theory states that an organization is responsible not only to its shareholders and creditors but to various degrees all its stakeholders [97] [98] [99]. In addition, especially regarding environmental reporting, Van der Laan Smith, Joyce, et al. (2005) [100] argue that differences across cultures influence CSR disclosure quality and quantity. Stakeholder theory states that the directors must ensure that the information needs of shareholders and other stakeholders are balanced when publishing non-mandatory information [101]. Furthermore, when adopting a stakeholder view, the presence of a sustainability or similarly named committee clearly indicates the commitment of an organization to its stakeholders [102] [103]. These committees and their members, when appointed right, are acutely aware of the importance of sustainability as part of the overall business strategy. This increasingly also includes concerns from relevant stakeholders for the impacts of corporate strategy and actions on climate change [104] [105]. Transparency and accountability are of growing importance when identifying the pathway to a lower corporate carbon footprint. This includes but is not limited to developing and adopting an efficient carbon governance system.

Ideologically closely related to stakeholder theory, institutional theory describes how market actors adapt to their institutional settings [106] [107] [108]. More specifically, researchers have also investigated the relationships between CSR disclosures and corporate attributes and industries [109] [110] [111] [112]. Moreover, it has been suggested that the corporate social disclosure in annual financial reports is closely related to the role of an organization within its society [113].

So far, researchers interested in institutional theory and the environment focused heavily on environmental practices. Climate change goes hand in hand with institutional ideology [114] [115]. According to Tjernström and Tietenberg (2008) [116], different countries exhibit institutional differences when dealing with the topic of climate change. For example, there are differences across Europe in attitudes towards climate citizenship, including climate concern, perceived responsibility, and willingness to support and take climate action [117].

Unlike agency theory that is concerned with the board’s monitoring role, resource dependence theory relates to its advising and unique resource providing role [118] [119] [120] [121] [122] . A diverse board of directors will typically also have a diverse set of qualifications and skills. Regarding board characteristics, the one attribute that has probably been explored the most is gender. It is often assumed and has been empirically proven that female directors show a different approach to some issues which can be beneficial when dealing with complicated board matters. More specifically, female board members have been described as being more humane, socially adapt, creative, and open-minded [123] [124] [125]. From the resource dependence theory's perspective, these characteristics lead to inclusion of climate change mitigation and issues into corporate strategies development [126] [127] [128].

Geert Hofstede’s study on different dimensions of cultures identifies the dimension Masculism and Feminism as two opposites on a cultural spectrum [129]. Although his critics repeatedly have claimed that the results are dated and things have changed, it cannot be denied that certain aspects still hold true in almost all our societies but especially in developing countries.

Similarly, according to gender socialization theory, women and men have different perspectives towards environmental issues due to differences in their education [130] [131]. Women have been raised and educated to nurture and care about others [132]. Thus, compared to their male counterparts, female directors are more aware about environmental issues [133] [134] and even have higher ethical standards [135]. Accordingly, they will promote more proactive environmental strategies [136] [137] [138]. Moreover, female directors will embrace a longer-term stakeholder orientation compared to their male peers [139), which results in initiating and supporting climate change initiatives.

A third theory alluding to differences in behaviour due to gender is the upper echelons theory. It was first described by Hambrick & Mason in 1984. The theory is based on the assumption that demographic characteristics and experiences influence people’s values and behaviours which leads to differences in decision-making and leadership styles [140]. Thus, in the language of upper echelons theory, female directors’ distinctive backgrounds might increase the board's diversity, enabling to recognize and embrace environmental innovations faster than their male colleagues [141] [142]. Due to this, the board is more inclined to invest in climate change [143] [144] [145].

Lastly, a theory that has not been given much credit as of now in the context of climate change, is social innovation theory which has developed from entrepreneurial as well as academic literature [146]. Logue argues that that the concept of social innovation has been around for a very long time.

According to social innovation theory, economic progress cannot be disassociated from social progress or with the urgent need to do the “right things at the right time”. The idea of social innovation is based on three main pillars: social value creation, capture, and distribution; cross-sector collaborations and networks; and a relentless pursuit of institutional change [147]. Like any other polysemous concept, it offers opportunity to analyze the current situation and urgent need for action of different players in the climate change scenario.

| Theories | Explanations | Hypothesis/Variable affected |

| Agency theory | Theorizes that investors (principles) delegate the task of running a firm to the company's managers. Efficient corporate governance can minimize resulting agency costs |

CSR Committee CSR Executive BoD female percentage |

| Legitimacy theory | Predicts that to get resources and be accepted,organization has to comply with its social contract. Argues that companies employ sustainability disclosure to improve the public perception of their sustainability performance. Poorly performing companies use sustainability disclosure as a legitimation strategy to influence public perceptions of their sustainability performance |

GRI standards DJSI constituent TCFD reports UN Global Compact CSR Committee CSR Executive |

| Signaling theory | Predicts that companies publish information to influence potential shareholders |

GRI standards TCFD reports UN Global Compact Climate transition plan DJSI constituent |

| Stakeholder theory | Predicts that companies publish information to influence/inform stakeholders |

GRI standards UN Global Compact Climate transition plan CSR Committee DJSI constituent TCFD reports |

| Institutional theory | Theorizes that company is part of social system/structure and has to act a certain way to be accepted |

Developed vs. emerging country Climate transition plan ESG reporting CSR Committee CSR Executive |

| Voluntary disclosure theory | Predicts that a company with good performance is incentivized to disclose information regarding its performance to increase its market value; bad performers try to greenwash |

GRI standards UN Global Compact Climate transition plan CSR Committee CSR Executive DJSI constituent TCFD reports MSCI ESG ranking |

| Geert Hofstede’s Cultural Dimensions theory | Predicts differences between different cultures as well as between developments statuses of countries |

Developed vs emerging country BoD female percentage CSR Executive |

| Gender socialization theory | Predicts that females behave differently, also in context as board member | BoD female percentage |

| Resource dependence theory | Predicts that board of directors provides firms unique resources and capabilities | BoD female percentage |

| Upper echelon theory | Predicts that directors’ demographic characteristics and experiences shape their values and behaviours→females behave differently | BoD female percentage |

| Social Innovation theory | Predicts that organizations distribute value and collective impact to address social problems. | Developed vs emerging country |

| Research-based | ||

| Not based on theory |

Research results suggest that factor “size” is significant determinant of companies’ CSR disclosure practices [148] [149]. Kup et al. [150] examined Chinese companies' CSR and sustainability reports, demonstrating that larger firms are likely to disclose more CE information to meet stakeholders' expectations. |

Size |

| Research results suggest that factor “industry” is significant determinants of companies’ CSR disclosure practices [151] [152] [153]. | Extractive vs Non-extractive Industry | |

| Research results suggest that ratio of “female directors” influence climate change innovation mainly through their involvement in management as executive directors, rather than through the monitoring and advisory roles that characterize independent directors [154]. | BoD female percentage | |

| Research results suggest that factors such as legitimacy concerns are significant determinants of companies’ CSR disclosure practices [155] [156] [157] [158] [159] [160]. |

MSCI ESG ranking Indirectly: DJSI constituent TCFD reports UN Global Compact |

|

As much as the individual theories can contribute to the corporate social accounting framework (coined by [161], we must accept that many of them together play a role in the CSR disclosure phenomena. While it has often been claimed that the theories do not have anything in common, several researchers have considered them as being complimentary and not competing as it is claimed that the issue at hand is analyzed from different angles and will provide “the bigger picture” ([162] [163] [164]. Especially in the context of corporate governance, the broader viewpoint of legitimacy theory has proven to be more and more acceptable [165] [166] [167] [168} [169]. In the spirit of this, our study also adopts a broader theoretical framework that combines the idea of above-mentioned theories when examining corporate governance and its influence on climate-related information disclosure [170] [171] [172]. By adopting a multi-theoretical framework that includes above mentioned theories, our study used a sample of 100 large global companies belonging to several industries and sectors.

Hypothesis development

Extant studies have confirmed the complexity of the issue by finding several indicators that influence climate change corporate governance. According to the previous literature, we posit 13 hypotheses, whose development is as follows. Since the association with gender diversity of the board of directors and various factors has been explored the most extensive by previous research empirical studies, we will start with this corporate governance characteristic.

Females and males have long been identified as having different social and personality traits {173] [174]. Women, on average, are considered more diligent and committed than men [175] Moreover, women are also considered more democratic, open to collaboration and harmony oriented than their male counterparts [176] [177]. Ultimately, female directors will balance the board’s dynamic, enhance its independence and the quality of monitoring [178] [179].

The results of previous research studies have shown that an increase in female directors can improve board governance in general [180] [181]. Interestingly enough, it was also found that board gender diversity has a positive effect on innovation in general [182] [183] [184] [185]]. The researchers explained the findings by the fact that female directors have different skill sets, perspectives, capabilities, and knowledge, all of which will lead to innovation and increased creativity [186] [187] [188] [189]. Other researchers agree that diversity in an organisation improves problem-solving, leadership effectiveness and global collaborations [190] [191] [192] [193].

In the past, researchers have also documented general positive association between gender diversity of the board of directors and sustainability or CSR [194] [195] [196]. The authors offered the explanations that female directors are more environmentally sensitive and proactive compared to their male colleagues [197] [198] [199] [200] [201] [202]. It has also been assumed that an increased level of board development activities and decreased level of conflict led to a better outcome.

According to Velte (2015), gender diversity has been taken into account more frequently recently when analyzing its impact on CSR reporting [203]. More academics found increased female board representation to have a positive influence on CSR reporting quality [204] [205] [206 [207] [208].

The majority of studies found a positive association between gender diversity and CSR disclosure [209] [210] [211]; environmental disclosure [212] [213] and ESG disclosure [214] [215]. Other authors document a positive relationship between board gender diversity and voluntary disclosure of climate change information [216] [217] [218] [219] [220].

Therefore, we expect that female supervisory board members will also have an impact on CSR reporting.

Regarding the impact of female gender on eco-innovation, studies such as [221], [222], [223]), [224, [225], [226], [227] and [228]] found a positive relationship between female board members and eco-innovation. In addition, Atif et al. (2021) [229] showed a positive relationship between gender board diversity and renewable energy consumption whereas Gull et al. (2023) [230] found a positive influence on waste management. Garcia-Sanchez et al. (2023)’s [231] findings showed that the level of climate change innovation is positively associated with both the percentage as well as the number of female board members. With regard to carbon emissions, [232] Haque (2017) identified a positive impact of female directors on the company's efforts in reducing emissions, and [García Martín and Herrero (2020) [233] and Konadu et al. (2022) [234] even noted a negative relationship between board gender diversity and carbon emissions.

Thus, the theoretical predictions that female board members will increase climate change awareness and incorporation of climate change considerations into business and corporate strategies are consistent with previous empirical evidence. In summary, the overall empirical evidence suggests that gender-diverse boards are more likely to disclose information on climate change corporate governance.

Hence, in line with stakeholder theory as well as prior empirical results, our first hypothesis is as follows:

H1. There is a positive association between boardgender diversity and climate change corporate governance disclosure.

A sustainability or CSR (or similar) committee can be considered a sub-commission with members that are specialists in the area of managing and reporting social, economic and environmental issues [235] [236] [237]. Datt et al. (2019) [238] state that the existence of a sustainability committee, a climate change or environmental committee or similar suggests that a company has committed to its sustainability ambitions strategy and tries to implement strategic goals and objectives with CSR in mind. Members of this committee will often prioritize resources to achieve reduction targets and monitor carbon reduction performance [239]. Past empirical studies, for example, found a significant positive relationship between the existence of an CSR committee and environmental disclosure [240] or carbon disclosure ([241] [242].

A sustainability committee is often considered an important and useful resource for a company as the specific non-financial background provided by its committee members allows the company to incorporate sustainability issues into its strategic plan and actions [243]. Therefore, such a committee can play an important role in monitoring the legitimacy of the firm’s operations and its relationships with its different stakeholder groups [244] [245].

Empirically, academic literature converged on detecting a positive impact of the presence of a CSR/sustainability committee on: CSR or sustainability disclosure [246] [247] [248] [249]; carbon disclosure [250]; and ESG disclosure [251]; [252]. Other empirical evidence shows that the existence of a specific Corporate Social Responsibility (CSR)/ sustainability committee constitutes a positive driver of utilities’ overall ESG disclosure levels ([253]. Haque (2017) [254] also reports a positive relationship between a CSR committee and carbon mitigation initiatives for UK companies. Just recently, Córdova et al., (2021) [255] also found a positive relation between the existence of a CSR committee and environmental disclosure in South American companies.

Thus, from the stakeholder perspective, firms that have a sustainability or CSR committee are more likely to engage to address stakeholder needs and engage in climate change activities and corporate governance disclosure.

We apply the above arguments tocorporate governance disclosure and make a similar prediction.Therefore, based on the broad theoretical and previous empirical evidence, the following hypothesis is posited:

H2. There is a positive association between the presence of a board CSR/sustainability committee andand climate change corporate governance disclosure.

Not much literature has been dedicated to the relatively new role of corporate sustainability officer (CSO). This is especially true for empirical research studies. Typically, we hear about CSR activities that improve relationships with stakeholders, thereby mitigate the firm's business risk [256]. In addition, CSR can help corporations in gaining access to a larger talent pool, and lower capital cost, which in turn significantly reduces the risk of failure and enhances organizational performance [257]. It has been argued that creating specialized executive sustainability positions represents a big change in the structure of top management teams (TMTs) and how sustainability is dealt with [258] [259]. It has been argued that CSOs have been appointed due to external stakeholder pressure. Therefore, CSO appointments have been looked at rather symbolic than transformative for the company [260].

Similarly, Peters et al. (2018) analyzed some of these CSO appointments and their association with subsequent sustainability performance [261]. It was found that overall, CSOs are either not statistically related or negatively related to changes in firm performance. Their results indicate that the creation of a CSO position may represent more of a symbolic versus substantive governance mechanism. We did not differentiate between the position of a CSO and a sustainability executive. Given the competing propositions, we state the following null hypothesis:

H3: There is no association between having a dedicated sustainability executive officer or CSO andclimate change corporate governance disclosure.

As confirmed by 2022 research conducted by KPMG, the GRI Standards remain the most widely used sustainability reporting standards globally [262]. The first version of what was then the GRI Guidelines (G1) published in 2000 by the Global Reporting Initiative, an independent not for profit institution, now located in the Netherlands. In 2016, GRI transitioned from providing guidelines to setting the first global standards for sustainability reporting – the GRI Standards [263]. GRI standards are not only used by large global corporations but also by governments, small and medium enterprises, non-governmental organizations (NGOs), and industry groups in more than 90 countries. These globally applicable standards enable organizations to voluntarily disclose the environmental, social, and economic dimensions of their organizational activities to a level equivalent to that of generally accepted accounting principles for financial reporting in terms of rigor, comparability, auditability, and general acceptance [264] [265] [266}. Luo and Tang (2022) also argue that organization that adopt GRI standards show their commitment to information transparency on the topic of environment and climate change. In addition, GRI standards stand for standardization and comparability of ESG information.

As the voluntary adoption of the GRI standards is widely considered a step towards higher quality sustainability reports [267] [268] (Adams, 2004; Luo and Tang, 2022), we expect that it will also have an effect on disclosure on carbon corporate governance. Therefore, based on the broad theoretical and previous empirical evidence, the following hypothesis is posited:

H4. There is a positive association between the adoption of GRI guidelines or standards andand climate change corporate governance.

Each year, the Dow Jones Sustainability™ Index (DJSI Index) uses an assessment (Corporate Sustainability Assessment) to identify global sustainability leaders [269]. These DJSI constituents represents approximately the top 10% of the biggest 2,500 companies based on long-term economic, environmental, and social criteria [270] [271] [272]. The DJSI indicators are based on a thorough analysis of corporate economic, environmental, and social performance, assessing issues such as corporate governance, risk management, strategic planning, branding, climate change mitigation, supply chain standards and labor practices [273].

Consistent with legitimacy theory, Cordeiro and Tewari (2015), by using an event study to capture the investor reaction to Green Rankings in September 2009, found that, for the sample of the largest 500 US firms, investors reacted positively to the rankings of green performance in terms of both short-term and longer-term (up to 12 months) returns [274]. In addition, other empirical research studies suggest that factors such as legitimacy concerns are significant determinants of disclosure of sustainability practices for companies [275] [276] [277] [278] [279] [280].

Consistent with voluntary disclosure and signaling theory, another study concluded that superior sustainability performers choose to disclose high-quality sustainability information to signal their superior performance to the market and its stakeholders. In addition, based on legitimacy theory, the authors stated that poor sustainability performers prefer low-quality sustainability disclosure to disguise their true performance to simultaneously protect their reputation and legitimacy [281]. Also referring to signaling theory, Searcy and Elkhawas (2012) [282] provide insights through the results of a survey, in which Canadian corporations use the Dow Jones Sustainability Index (DJSI) as signal for reputable reasons [283].

Therefore, drawing on legitimacy, stakeholder, voluntary and signaling theory as well as previous research, we develop our fifth hypotheses:

H5: There is a positive association between being a DJSI constituent andand climate change corporate governance disclosure.

Increased sustainability information disclosure can reduce information asymmetry between organization and stakeholders and among stakeholders [284] [285]. In addition, it facilitates stakeholders' understanding of the company's carbon risk profile and its relative performance and standing compared to its competitors [286]. It is no secret that companies that perform better than their peers get rewarded by stakeholders, getting better and more contracts, lower cost of capital, better talent, etc. [287]. On the other hand, stakeholders might deprive socially and/or environmentally irresponsible companies of much needed resources ([288]. Therefore, organization will have a great incentive to actively engage in climate change information disclosure to sustain their competitive advantage. Similar to the reasoning outlined above regarding the variable UN Global Compact above, stakeholder, signaling theory and voluntary disclosure theory also apply here.

Ever since financial benchmark developers have been active in developing ESG indices for analysts, investors, and asset managers as Environmental, Social and Governance (ESG) ratings have been becoming an integral part of financial, business and consumption decisions ([289]. MSCI has been one of the financial providers in driving ESG and climate transparency to help provide their customers with information of the value of ESG data and ratings and raise awareness on the financial impact of climate change [290].

The publicly available MSCI ESG Ratings & Climate Corporate search tool allows anyone to search over 2,900 companies that are constituents of the MSCI All Country World Index. Information that is available is: ESG and climate risks and opportunities, including Implied Temperature Rise, Decarbonization Targets, ESG Ratings, ESG Controversies, Business Involvement Screens and SDG Net Alignment [291]. The difference of the MSCI rating tool is that it provides a rating also to the low performers, in contrasts to the DJSI, for example. Therefore, it provides a more intricate picture on how the companies are doing with regard to their ESG compared with each other.

Accordingly, based on legitimacy, stakeholder, signaling, and voluntary disclosure theory and empirical evidence, we formulate the following hypothesis:

H6: There is a positive association between companies ranked as ESG leaders compared to their competitors (MSCI) andclimate change corporate governance disclosure.

The UN Global Compact is often called the world’s largest global corporate sustainability initiative [292]. Its inception was announced in 1999 at the World Economic Forum, a broad framework providing guidelines to implement social practices [293]. It is based on ten principles addressing issues in many important areas. The United Nations Global Compact (UNGC) is one of the most important corporate social responsibility voluntary initiatives aimed at aligning companies' strategies and operations with principles that involve human rights, labor, environment, and anti-corruption [294] [295] [296].

Currently, more than 16,000 companies and 3,800 non-business participants operating in more than 170 countries have committed to the UN Global Compact [297]. Companies that want to become UNGC participants are required to prepare a Letter of Commitment expressing adherence to the ten principles. The commitment includes a pledge to operate responsibly, take actions that support society, commit to the effort from the organization’s highest level, pushing sustainability deep into the organizational DNA and engage locally. A commitment from the chief executive (or equivalent, for non-business entities) – with support from the Board is required, as well as financial contributions [298]. While this is a very elaborate commitment, the potential outcomes of UNGC are numerous and include enhanced reputation, improved social and environmental performance, and increased attractiveness for investors [299].

According to Orzes et al. (2020), literature on the topic of UNGC is still strongly conceptual. They regard this as a major limitation of this field of research, and others agree [300] [301]. To formulate our research hypotheses, we rely on stakeholder, signaling theory and voluntary disclosure theory. For example, in a research study using a sample of 175 global firms, the authors find support to the theory for joining the UN Global Compact [302]. Basing their hypothesis on signaling theory, they concluded that the UNGC certification can be seen as a signal to the market to provide value to the customers.

It is assumed that companies that show such commitment to the UN Global Compact membership, they will also be committed when disclosing information on their climate change corporate governance. Hence, in line with theory and prior empirical results, our seventh hypothesis is as follows:

H7: There is a positive association between the application of the UN Global Compact andand climate change corporate governance disclosure.

For the most part, regulations for carbon reduction are still not in place or not enforced yet in most countries, federally or state or province-wide, even though this has been met with growing resistance by many stakeholders [303] [304]. Several previous research studies concluded that companies approach this situation in many ways. On the one side of the spectrum, we see that organizations are waiting for the governments to implement regulations and policies whereas other are proactively finding trailblazing ways to be leaders in their industry [305]. This can be in the way how they measure and report their emissions, how they invest in low-carbon technologies and innovate products, etc. [306]. On the other hand, when revealing a company's poor carbon performance, this can create very negative publicity and damage the company’s reputation [307].

It has to be noted that as of late, there has been a push towards regulation by several governments or agencies that committed to mandating companies to report climate-related financial risks. As a result, we’ve seen several regulatory developments in the EU, UK, Canada, and the US, and ISSB, for example, that draw on the Task Force on Climate-related Financial Disclosures TCFD framework [308].

Based on institutional and stakeholder theory, voluntary disclosure theory and signaling theory, we argue that proactive organization that had already made efforts towards making a climate transition plan will disclose and communicate the information on who will govern their climate change journey. With a climate transition plan in place that is communicated properly to relevant stakeholders, their carbon actions are transparent and credible. By doing so, the company differentiates itself from its peers.

Accordingly, we state our prediction in the eighth hypothesis here:

H8: There is a positive association between being having a climate transition plan andand climate change corporate governance disclosure.

Researchers around the world have started to analyze sustainability, CSR, circular economy (CE) and climate reports. When Kuo and Chang (2021) analyzed the sustainability reports of Chinese companies, they found that more environmentally sensitive firms are likely to disclose more circular economy information [309]. García-Sánchez et al. (2023) examined Spanish CSR reports and corporate websites and found that sectors sensitive to institutional pressures show a higher likelihood to disclose problems as well as solutions related to their projects [310]. Roberts et al. (2022) analysed the financial and sustainability reports of 28 global companies in three different sectors [311]. They concluded that companies in the automotive industry are particularly committed to disclosing CE-related information compared with companies operating in the defense, transportation and aerospace sectors.

Another strand of studies focuses on sustainability information disclosure topics such as carbon, GHG, climate change and biodiversity [312]. For example, Bahari et al. (2016) investigated Chinese, East Indian, and Japanese electricity-generating companies and observed a general resistance to disclose carbon-related information [313]. Talbot and Boiral (2018), on the other hand, investigated the impression management strategies used by energy-sector companies to conceal or justify evidence about their climate performance [314]. Finally, Matsumura et al. (2014) found a higher likelihood of carbon emission disclosures by firms that are more environmentally proactive in general [315].

Therefore, based on legitimacy, stakeholder, signaling, and voluntary disclosure theory and empirical evidence, we posit the following hypothesis:

H9: There is a positive association between being in the extractive industry (higher carbon risks) andand climate change corporate governance disclosure.

It has long been noted that, empirically, there are many significant differences between CSR reporting and disclosure across countries [316]. This also applies to the same organizations even with locations in different regions. For example, Eccles et al. (2012) note that a few independent agencies such as Domini (KLD), Bloomberg and Reuters corporations based on their CSR performance and that these ratings and rankings vary across both firms and countries [317].

Therefore, based on institutional theory, Hofstede cultural dimensions’ theory, and social innovation theory and empirical evidence, we posit the following hypothesis:

H10: There is a positive association between being located in a developed country andand climate change corporate governance disclosure.

After the creation of the Basel-based Financial Stability Board (FSB) whose role is to promote international financial stability, it created the Task Force on Climate-Related Financial Disclosures (TCFD) in 2015 [318]. The TCFD's main focus is to improve and increase reporting of climate-related financial information ([319]. In 2020, The World Economic Forum’s (WEF) International Business Council issued a report proposing a set of ESG metrics including disclosures for its members to align their mainstream reporting [320]. CFD-aligned reporting was recommended as the template for climate risk reporting under the “Planet” reporting pillar [321].

Its latest recommendations were published in 2017 and since then, in their lates status report, published in 2022, the Task Force has seen significant momentum around adoption of and support for its recommendations as detailed in previous status reports as well as in this report [322].

TCFD supporters have increased to more than 3,800 companies that have continued their TCFD-aligned reporting, and there have been important actions by regulators, jurisdictions, and international standard-setters to use the TCFD recommendations in developing climate-related reporting requirements and standards — including but not limited to proposals released by the U.S. Securities and Exchange Commission, the International Sustainability Standards Board (ISSB), and the European Financial Reporting Advisory Group [323].

Considering the fact that the TCFD recommendations have not been around for a long time yet and mostly they have not been implemented as guidelines or standards, not much research has been conducted as of yet. In 2017, Eccles and Krzus (2018) conducted what they called a “field experiment” to evaluate how difficult it will be for companies to implement the recommendations of the Task Force on Climate-related Financial Disclosures (TCFD) by analyzing the disclosures of 15 of the biggest US oil & gas companies [324]. This was even before the TCFD’s recommendations were published.

They found large variation across companies, with most making some disclosures but some being quite progressive. Interestingly, and contrary to TCFD’s recommendations, they found that most of the disclosures were published in non-mandatory sustainability reports and not in the mandatory annual financial reports. The authors’ conclusion was that companies seemed to be able to follow the TCFD’s recommendations if they had to.

A more recent study, set in Italy, found that there are many factors that play an important role when it comes to the decision if a company will use the TCFD guidelines or not [325]. Our assumption is that when a company is showing commitment to climate-related information disclosure by using the TCFD recommendation framework, there will also be climate-change corporate governance system in place.

Finally, based on legitimacy, stakeholder, signaling, and voluntary disclosure theory and empirical evidence, we posit our last hypothesis:

H11: There is a positive association between the number of years a company has been preparing a report according to TCFD guidelines andand climate change corporate governance disclosure.

As control variables, we recognized three company-, and corporate governance-specific variables that extant literature has shown to be associated with corporate governance quality [326]).

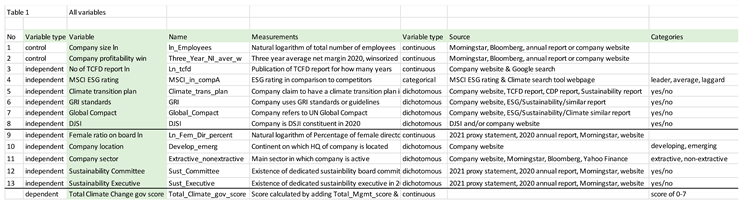

All variables are presented in Table 1 with detailed explanations.

3. Research methodology and data

3.1. Sample

In this demographics section, we describe the dependents and independent variables. Then we detail how the sample was prepared followed by the methodology used.

The main goal of this paper is to analyse the sustainable profile of Fintech and Insurtech companies. We can approximate this profile by three different dimensions: (i) CO2 emissions; (ii) obtaining green certificates and sustainability rankings; (iii) alignment with SDG. In this way, we compute different panel data models depending on the dimension to be analysed.

As sample, the 100 largest companies in the world by market capitalization in 2021 (in billion U.S. dollars) according to Forbes were used (Forbes, 2021). The financial data were obtained from the Bloomberg, Morningstar and Yahoo Finance database.

Table 1 describes the variables used to explain how actively companies promote sustainability. They include economic-financial attributes of companies and related corporate information. The source of information is also shown. In addition, to control the impact of possible macro-economic or legislative events that could influence the company's ability to promote sustainability, dichotomous year variables are included.

Table 1.

Descriptive variables, names, measurements, types, source, categories.

|

We are using the fact of being a constituent in the Dow Jones Sustainability Index (DJSI) as a proxy for sustainability performance [327]. The variable DJSI assumes the value of one if a company belongs to the DJSI in 2020 and zero otherwise.

As dependent variable, a score based on TFCD’s criteria consisting of two main categories which are board-related and management-related were developed. The board-related oversight score consists of three individual scores. The first one assesses processes and frequency by which the board and/or board committees (e.g., audit, risk, or other committees) are informed about climate-related issues. The second assesses whether the board and/or board committees consider climate-related issues when reviewing and guiding strategy, major plans of action, risk management policies, annual budgets, and business plans as well as setting the organization’s performance objectives, monitoring implementation and performance, and overseeing major capital expenditures, acquisitions, and divestitures. Finally, the third score measures how the board monitors and oversees progress against goals and targets for addressing climate-related issues. The maximum score is 3 points.

For the management-related score, four scores are used. The first one measures whether the organization has assigned climate-related responsibilities to management-level positions or committees; and, if so, whether such management positions or committees report to the board or a committee of the board and whether those responsibilities include assessing and/or managing climate-related issues. The second sub score is assigned if the company provides a description of the associated organizational structure(s) whereas the third sub score measures if processes by which management is informed about climate-related issues are in place. The fourth sub score is based on how management (through specific positions and/or management committees) monitors climate-related issues. The maximum score is 4 points.

Therefore, a total maximum score of 7 can be achieved. The scoring was done by gathering information based on company annual financial reports, 10K reports, proxy statements, appendices, environment progress reports, sustainability reports, integrated reports, climate change transition (resilience) reports, CDP reports, TFCD-based reports, ESG reports, Carbon neutrality reports, corporate citizen reports, company websites, company sustainability charter, Climate risk and resiliency summary, Governance report, GC web pages, board committee charters, Climate risk management (TCFD) report, Sustainability Data book, CG report, TCFD content index, Impact report, GC charter, Business responsibility (BRR) report, TCFD content index, etc.

In our analysis, we use our construct for the voluntary carbon governance disclosure score as a proxy for the quality of a firm's carbon disclosure which is very similar to the TCFD guidelines and the CDP scoring. It has, however, the advantage, to get a score for companies that have not used neither TCFD nor CDP but have provided other information.

The scoring was conducted by one main scorer and a second scorer conducted blind spot checks on batches of 5 companies. If the spot check rate was off by 10%, the whole batch needed to be re-checked and reconciled. This happened twice.

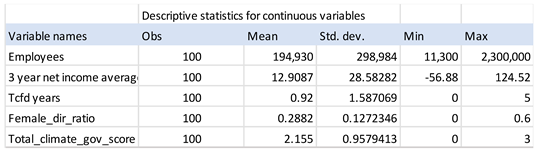

Table 2A.

Sample distributions/ descriptive statistics for continuous variables.

|

Tables 2A-2C provide an overview of the descriptive statistics for the variables that are included in the study (2C in Appendix). Initially, there were 100 companies in our sample from 10 different sectors. The mean for employees was 194,930. The smallest company by employees had 11,300 and the largest employed 2,300,000. The 3-year net income average was US 12.91 million with a minimum of US -56.88 million and a maximum of US 124.52 million. The number of years that companies used the TCFD guidelines on average was 0.92 years with a minimum of 0 and a maximum of 5 (since 2017).

The mean of the female directors on the board was 28%. It ranged from 13% to 60%. The data shows that the Total Voluntary carbon governance score ranged from 0 to 7 with an average of 4.97.

Table 2B.

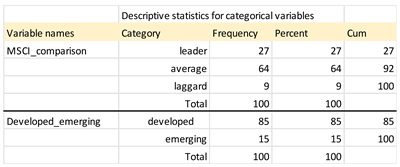

Sample distributions/ descriptive statistics for categorical variables.

|

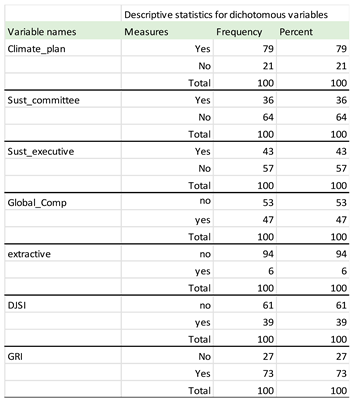

As for the categorical variables, 27% of companies were categorized as “leaders” according to MSCI ESG criteria whereas 64% were “average” and 9% were considered “laggards”. 85% of companies were headquartered in developed countries and the remaining 15% in emerging countries.

Referring to Table 2C in the Appendix, 6% of companies were active in the extractive industry. 36% reported having a sustainability or equivalent committee and 43% had a sustainability executive. 79% had a climate transition plan in place. 47% of the sample companies were using the UN Global Compact, while 39% were DJSI constituents. And 73 of all companies were referring to the Global Reporting Initiative (GRI).

Regarding firm-level controls, company size was measured as the natural logarithm of total number of employees at the end of the financial year (Ln_Employees). The natural logarithm was also used for the ratio of the female directors on the board (Ln_Precent_fem_dir) and the years the company has used the TCFD guidelines (Ln_tcfd). For our profitability variable, we used the winsorized three year-over-year net income average.

3.2. Empirical Model

To test our eleven hypotheses, we estimate equation (1) using ordinary least squares regression with robust standard errors:

Total_Climate_Gov_Scorei,t+1 = β0 + β1 ln_Fem_Dir_Percenti,t + β2 ln_EmployeesI,t + β3 Three_Year_NI_averi,t + β4 Ln_Tcfdi,t + β5 Sust_Committeei,t + β6 Sust_Executivei,t + β7 MSCI_in_compA,t + β8 Climate_trans_plani,t + β9 GRIi,t + β10 Global_Compacti,t + β11DJSIi,t + β12 Develop_Emergi,t + β13 Extractive_nonextractivei,t + ui + ei,t

Where β = , μ = , ε = , i = company, t = time

𝜀𝑖𝑡 = 𝜗𝑖𝑡 is the random error term for company i in moment t

All the analyses were performed with the Stata 17 software.

Please note that the voluntary carbon corporate governance disclosure score is measured at year t + 1, whereas all independent and control variables are measured at year t. This research design aims to alleviate endogeneity concerns caused by simultaneity or a reverse causal concern [328].

4. Results

4.1. Correlation analysis

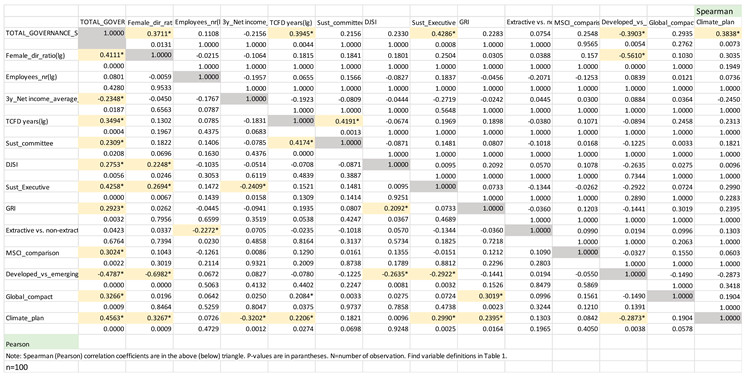

Table 4.1 presents the pairwise Pearson/Spearman correlation matrix for the dependent, independent, and the control variables. In general, Pearson correlation is most appropriate for measurements taken from an interval scale, while the Spearman is more appropriate for measurements taken from ordinal scales ([329].

Total_climate_gov_score: Total Climate Corporate Governance Score, Ln_Employees: Company size, Female_Dir_percent: Female directors on board percentage ln, Three_Year_NI_aver: Company profitability winsorized, Ln_tcfd: No of TCFD report years ln, Sust_Committee: Sustainability Committee Y/N, Sust_Executive: Sustainability Executive Y/N, MSCI_in_compA: MSCI ESG rating leader, average or laggard, Climate_trans_plan:Climate transition plan Y/N, GRI: GRI Standards Y/N, Global_Compact: Global Compact Y/N, Develop_Emerg: Developmental status of country where HQ is, Extractive_Nonextractive: Company in high-carbon sector Y/N

*correlation is significant at the 0.05 level (2-tailed); ** correlation is significant at the 0.01 level (2-tailed)

When examining the Pearson correlation values, the variables Ln_Female_Dir_ratio and Ln_TCFD correlate positively and significantly with our dependent variable Total_Climate_Gov_Score. Hence, we find a correlation between the independent variables and the dependent variable that could support our study’s hypotheses. Using Spearman correlation values, we observe a positive and significant correlation for the variables Sustainability_Executuve and Climate_transition_plan with the dependent variable at the 0.05 significance level. In addition to this, profitability correlates negatively and significantly with Total_Climate_Gov_Score at the 5% level.

The highest pairwise correlation coefficient is between the variables Developing_Emerging and Female_Dir_Percent (-0.6982). [Fidell and Tabachnick (2003) suggest that multicollinearity could be a problem when the correlation between the independent variables is higher than 0.90 [330]. The variance inflation factors (VIF) mean for our regression model is 3.62 while the highest VIF is 7.73. Since none of the variables has a VIF value over 10, multicollinearity is not considered a problem when interpreting the regression results [331].

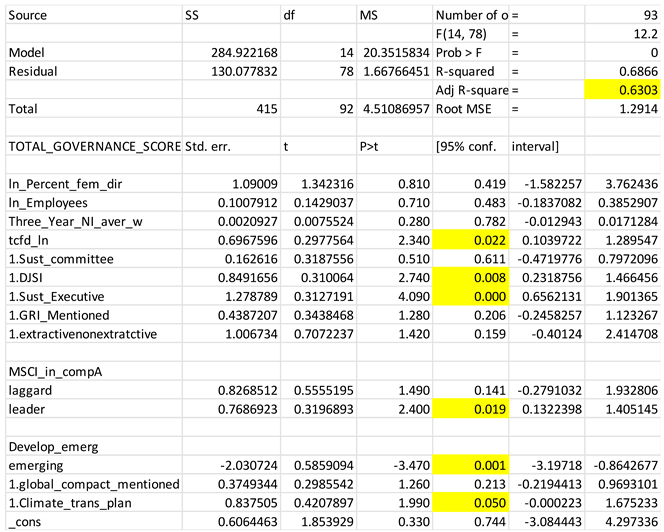

4.3. Multivariate results

The results of the multiple regression analysis are presented in Table 4.2. The model is highly significant (F =12.2 and p < 0) and has very good explanatory power (adjusted R2 = 0.63). We conducted regression diagnostics to make sure the assumption of linearity between the predictors and the outcome variable, normal distribution of errors, homoscedasticity and independence of errors were in place. However, only a very rare data set will meet all assumptions perfectly.

We checked for unusual data statistically and graphically with both large residuals and large leverages and decided that we had 7 observations in our sample that were substantially different from all other observations, and we removed them as they were too much of a concern for us.

Table 4.2.

Multiple regression results.

|

Surprisingly, gender diversity in the corporate board (Hypothesis 1) did not show any statistically significant correlation with a higher climate change governance disclosure level. Neither did having a sustainability board committee (Hypothesis 2). Both of these variables were found often significant in previous research related to sustainability.

The same was true for companies being active in either the extractive or non-extractive sector (Hypothesis 9). Against our legitimacy-theoretical foundation and in contrast to Hypothesis 4, companies using the Global Reporting Initiative (GRI) or UN Global Compact also did not have a significant relationship with a higher level of climate change governance disclosure (Hypothesis 7).

We find a company with a dedicated sustainability executive or chief sustainability officer (CFO) show an increased tendency to be transparent on climate governance issues (Hypothesis 3). From an agency standpoint, this affirms that having this extra in place seems to make a big difference when it comes to corporate governance and climate change.

Furthermore, having a company location in a developed country is significantly and positively associated with climate change governance (Hypothesis 10).

The same positive and significant relationship can also be observed for DJSI constituents ((β = 2.74, p-value<0.008) which is in line with our hypothesis 5. In line with hypothesis 8, we find a positive and statistically significant association between having a climate transition plan in place. With regard to hypothesis 11, a positive and statistically significant relationship exists between Total Climate Governance Score and Years of TCFD Reporting (β = 2.34, p-value<0.022).

We also used several control variables to account for the confounding effects of company- and location specific characteristics that may affect climate change disclosure. Consistent with prior studies [332] [333] [334], we control several company characteristics, including firm size and profitability.

4.4. Data Robustness

In order to ensure the robustness of our data, we ran a few extra regressions. Due to the fact that the majority of our sample data came from US companies, we ran our analysis without the US companies. We also ran our analysis using total assets as an alternative proxy for size. Furthermore, we ran our analysis after trimming (instead of winsorizing) the data set to analyze additional effects of size data. Finally, we ran our analysis using ranked values for all variables. We also replaced the natural logarithm of total employees with the total employees number, the natural logarithm of TCFD year number with the TCFD number and the natural logarithm of Female_Director_Percentage with the Female_Director_Percentage. Ultimately, the results were qualitatively very similar to those previously run.

The same is true for variations of the regression itself. We receive the same regression results for our date if we use the hetregress and regress, robust option. The Stata regress command includes a robust option for estimating the standard errors using the Huber-White sandwich estimators. Such robust standard errors can deal with a collection of minor concerns about failure to meet assumptions, such as minor problems about normality, heteroscedasticity, or some observations that exhibit large residuals, leverage or influence. For such minor problems, the robust option may effectively deal with these concerns ([335].

5. Discussion & Conclusion

As pointed out, our results are robust to variations and hopefully can provide valuable insights for researchers, academics, educators, executives, practitioners as well as standard setters. As more and more companies, organization of all sizes as well as governments are shifting towards a climate change reporting framework, it is of paramount importance that we are able to determine the contributing variables that lead to effective climate change corporate governance.

Some of our results are inconsistent with stakeholder, legitimacy and stakeholder theory and are suggesting that a “more diverse” board and a sustainability committee that meets often/sufficiently may not necessarily lead to a higher level of transparency/quality regarding climate change. While more research is needed, knowing that a dedicated sustainability executive as well as having a climate transition plan in place can make a difference in climate change reporting can be very beneficial to many corporate stakeholders.

Our results are inconsistent with some prior research [336] [337] [338] [339], but align with the evidence by Prado- Lorenzo and Garcia-Sanchez (2010) who found that gender diversity had an insignificant or even negative effect when investigating the role of governance on sustainability disclosure [340]. A few other studies had the same results in another sustainability disclosure context and setting [341] [342].

As mentioned previously, not many research studies have been conducted specifically on this topic. Especially the subject of sustainability executive or Chief sustainability officer (CSO) has not been explored much empirically. The fact that there is a statistically significant positive relationship between a sustainability executive and climate change disclosure points towards a needed change in the governance structure to accommodate and enforce changes that will potentially be legislated soon in many countries/jurisdictions by implementing climate-related financial disclosure frameworks.

Our study is not without limitations. Our collection was data included the use of several databases and therefore, the general the limitations of secondary data apply. We used the Fortune 100 Global companies as sample. By doing that, we chose to examine the largest companies in the world, and generalizing any results to small- and medium-sized companies needs to be done cautiously. It is recommended to conduct future research studies to examine how differently sized organizations are disclosing their climate information. In addition, there is also a need for rigorous studies aimed at analyzing different countries and sectors.

Another limitation is the time horizon of the analysis, which is only one year. It is therefore recommended to conduct further research for several time periods to explore the evolutions of corporate climate change disclosure. Another limitation is the limited number of attributes of the board of directors. Future research could address this by adding other characteristics of the board of directors, such as duality, age, nationality, tenure, independence sustainability and/or climate change expertise, etc.

As some of our findings are not in line with prior sustainability studies and theories, we need to explore the reasons for the results. As increasingly, external stakeholders ask for a higher percentage of female directors, for example, multiple stakeholder information disclosure needs need to be served appropriately.

Our results add to the growing empirical evidence in the literature that questions the effectiveness of the current board structures in serving the wider needs of stakeholders and in addressing the relevant issues of climate change, corporate governance, and disclosure. This study has important implications not only for future research but also for stakeholders, investors, analysts, business practitioners, and regulatory bodies. The overall growing awareness of environmental and climate-related issues is most likely only to increase further due to current European and possibly US and Canadian and other countries’ interest on climate change disclosure regulations. Rightfully so as we are on a ticking clock if we want to achieve climate neutrality by 2050.

Conflicts of Interest

The authors declare no conflict of interest.

Appendix

Table 2.

C Sample distributions/ descriptive statistics for dichotomous variables.

|

References

- Boyd, Natasha. “Top Business Sustainability Issues of 2023 .” Network for Business Sustainability (NBS), 29 Apr. 2023, www.nbs.net/top-business-sustainability-issues-of-2023/?utm_source=Master%2BList&utm_campaign=9a17aa531e-EMAIL_CAMPAIGN_2020_01_22_06_29_COPY_01&utm_medium=email&utm_term=0_44e73b0e1c-9a17aa531e-52185613.

- “What Is Climate Change?” United Nations, www.un.org/en/climatechange/what-is-climate-change. Accessed 25 Apr. 2023.

- See 2.

- “Past Eight Years Confirmed to Be the Eight Warmest on Record.” World Meteorological Organization, 12 Jan. 2023, www.public.wmo.int/en/media/press-release/past-eight-years-confirmed-be-eight-warmest-record.

- “Climate Change 2023.” AR6 Synthesis Report, www.ipcc.ch/report/ar6/syr/. Accessed 25 Apr. 2023.

- See 4.

- See 5.

- “Raising Awareness on Climate Change and Health.” World Health Organization (WHO), www.who.int/europe/activities/raising-awareness-on-climate-change-and-health. Accessed 25 Apr. 2023.

- Nagy, D. M., & Williams, C. A. (2022, March 25). ESG and climate change blind spots: Turning the corner on SEC disclosure. SSRN. https://papers.ssrn.com/sol3/papers.cfm?abstract_id=4049878.

- “Homepage: UN Global Compact.” Homepage | UN Global Compact, www.unglobalcompact.org/ Accessed 25 Apr. 2023.

- See 2.

- See 2.

- See 5.

- See 2.

- European Council of the European Union. (n.d.). Paris agreement on climate change. Coliseum. https://www.consilium.europa.eu/en/policies/climate-change/paris-agreement/ Accessed 14 Sep. 2023.