Submitted:

11 October 2023

Posted:

11 October 2023

You are already at the latest version

Abstract

The purpose of this study is to elucidate the factors influencing the voluntary adoption of IFRS by examining, analyzing, and synthesizing findings from empirical studies conducted worldwide. The research scrutinizes 185 relevant studies on the voluntary adoption of IFRS published before August 2023. Our assessment reveals that, in prior research, the factors influencing the voluntary adoption of IFRS are categorized into seven main factors, including corporate operations, capital structure, ownership structure, internationalization, financial performance, corporate governance, and several other factors. These studies employ various methodologies, including data surveys, and cross-sectional data, to estimate the relationships between these factors and the voluntary adoption of IFRS. In addition to providing an evaluation of the research in this field, this study can serve as a framework for future researchers to link and compare the results of different studies. We anticipate that this research will be beneficial for future scholars interested in the factors influencing the voluntary adoption of IFRS. Furthermore, the study proposes essential guidance for future research considerations.

Keywords:

IFRS

; Literature review

; Voluntary adoption

1. INTRODUCTION

The European Union adopted regulations to facilitate the preparation of consolidated accounts for EU-listed companies, including insurers and banks, in accordance with the International Financial Reporting Standards (IFRS) from 2005 onwards. Consequently, the International Accounting Standards Board (IASB) introduced IFRS, a set of accounting rules designed to establish a uniform platform for global financial reporting. The widespread adoption of IFRS across the globe is primarily motivated by the evident advantages these standards offer. They promote comparability in financial reporting, enhance investor protection through increased accounting transparency and disclosure, boost capital market liquidity, and contribute positively to global economic growth and development (Soderstrom & Sun, 2007). Moreover, the varying accounting practices adopted in different countries pose a challenge for users of financial statements when it comes to comparing the performance of companies listed on various stock exchanges worldwide (Prather-Kinsey, 2006). Such discrepancies can put certain investors and financial statement users at a disadvantage. Consequently, the adoption of IFRS has seen substantial growth since 2005, establishing IFRS as a universally acknowledged accounting standards framework (De George, Li, & Shivakumar, 2016; Nguyen et al, 2020).

In recent years, several comprehensive studies on the voluntary adoption of IFRS have been conducted. For instance, Soderstrom and Sun (2007) conducted a review of 13 studies that assessed the impact of changing accounting standards and discussed the determinants of accounting quality following the adoption of IFRS. Jamal et al. (2008) provide an overview of research on the transition from GAAP to IFRS. Ramanna (2013) conducts a comprehensive analysis of studies related to IFRS in Canada, China, India, and the US. Păşcan (2015) analyzes the impact of the transition from national accounting standards to IFRS on accounting quality in Europe, based on a review of 18 studies. De George, Li and Shivakumar (2016) present an overview of studies related to IFRS adoption by businesses worldwide. From the above analysis, existing evaluation documents on the voluntary application of IFRS focus on assessing and analyzing the benefits, disadvantages, challenges, or opportunities that businesses receive when applying IFRS. However, very few studies explore the determinants of businesses’ voluntary adoption of IFRS. While many studies assess the transition to IFRS, they often lack in-depth examinations of the factors that influence firms’decisions to voluntarily adopt IFRS. This deficiency served as the primary impetus behind the research review presented in this paper. To guide the rest of our review, we formulated the following research question: “What are the specific factors influencing firms' voluntary adoption of IFRS in the existing literature?”. Research was undertaken to address this question.

The structure of this article is as follows: Section 2 outlines the research methodology. Section 3 offers a comprehensive overview of the literature, summarizing previous studies that analyze the factors influencing the voluntary adoption of IFRS. In Section 4, we categorize these factors affecting the voluntary adoption of IFRS. Subsequently, Section 5 delves into the research findings and draws conclusions. The article concludes in Section 6, where we also provide recommendations for future research.

2. RESEARCH METHOD

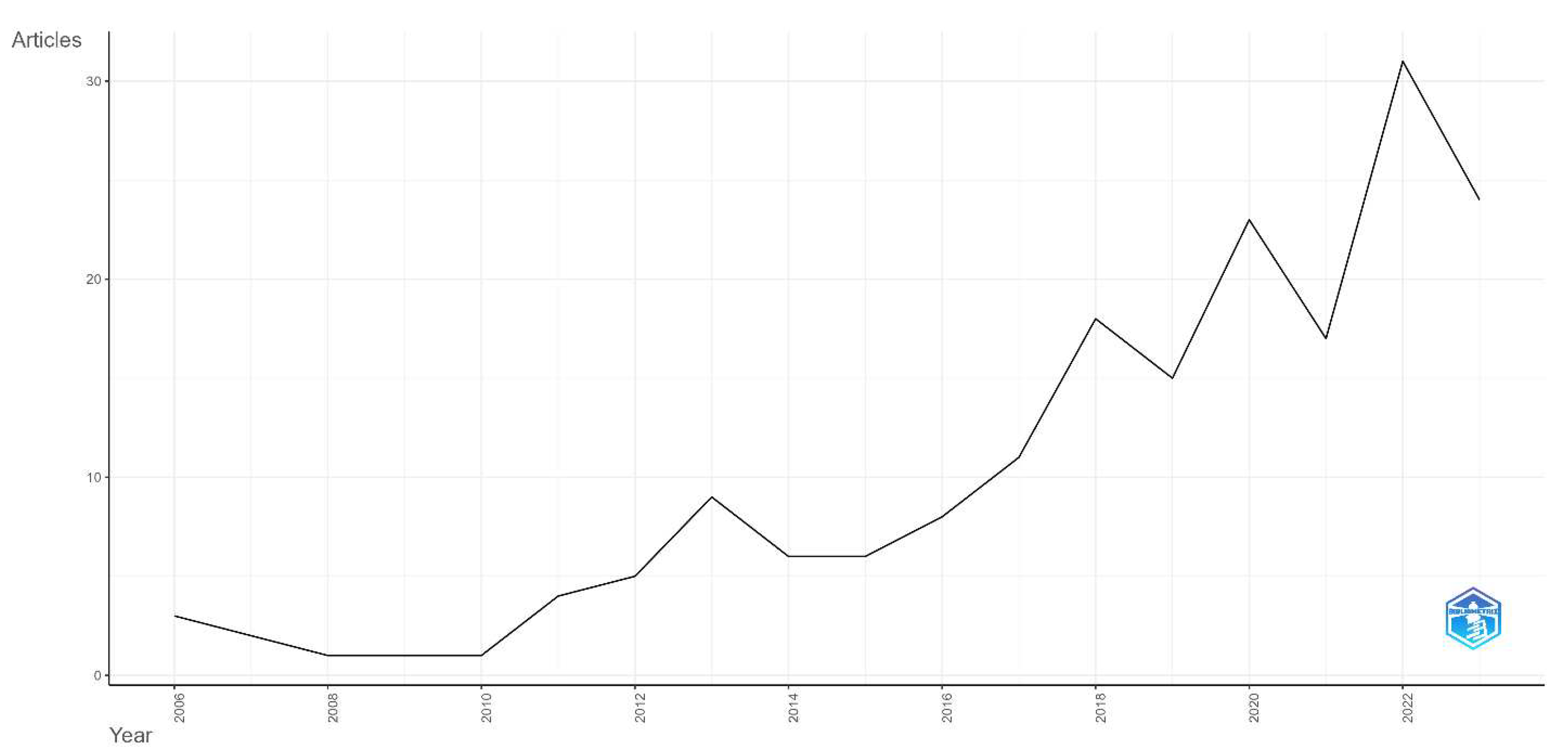

This study employs a literature review to investigate studies relating to determinants of IFRS application voluntary. This study considered the scope of the reviewed research through following criteria: (i) Studies published before August 2023, (ii) Studies published in peer-reviewed research journals, and (iii) Studies written in English. Databases were used to find out previous empirical evidence, including Scopus and Google Scholar. Keywords searched in the title/abstract/keyword field in the selected database included: “Voluntary IFRS”, “Voluntary International financial reporting standards”, “Voluntary adoption of IFRS”, and “Voluntary adoption of International financial reporting standards”. As a result, a total of 185 relevant studies were found (Refer to Figure 1). After eliminating duplicate studies and studies unrelated to the research topic, we analyzed the content of the studies.

Based on the search results of related studies, we have identified the ten most cited studies by scholars on Scopus and Google Scholar, as presented in Table 1. One such study is by Van Tendeloo and Vanstraelen (2005), who analyzed the impact of voluntary adoption of IFRS on earnings management using data from 212 listed companies in Germany. Another notable study is by Christensen et al. (2015), which examined changes in accounting quality resulting from the voluntary adoption of IFRS, with data collected from 310 companies headquartered in Germany.

3. LITERATURE SUMMARY BY THEORETICAL FRAMEWORK

Previous studies investigating the voluntary adoption of IFRS have employed various theoretical frameworks, such as positive accounting theory, institutional theory, agency theory, and several other relevant theories.

3.1. Positive accounting theory

Positive accounting theory, initially proposed by Watts and Zimmerman in 1990, offers insights into the rationale behind the selection of specific accounting policies. This theory aims to elucidate and forecast the decision-making process regarding accounting policies (Watts & Zimmerman, 1990). It posits several predictions regarding managerial behavior, suggesting that firms disclose information tailored to their financial requirements (Fields, Lys, & Vincent, 2001). According to positive accounting theory, voluntary information disclosure signifies their pursuit of optimal actions, thereby enhancing financial reporting quality and serving the interests of investors (Fields, Lys, & Vincent, 2001). This choice to share voluntary information serves as a positive signal to investors, instilling confidence in the accuracy and verifiability of financial statements (Lambert, 2001). As a result, numerous studies investigating the voluntary adoption of IFRS have drawn upon positive accounting theory as a foundational framework (Emmanuel Iatridis, 2012; Matonti & Iuliano, 2012; Pichler, Cordazzo, & Rossi, 2018; Tran et al, 2019).

3.2. Institutional theory

Institutional theory delves into the influence of various entities, including government bodies, professional organizations, and societal groups, on the behavior of businesses. Scott (2004) contends that companies often find themselves constrained by government policies, especially when the government implements IFRS. Meyer and Rowan (1977) have demonstrated that these institutional pressures manifest through societal norms and governmental regulations. Guerreiro, Rodrigues and Craig (2012) utilize institutional theory to elucidate the motives behind voluntary IFRS adoption, emphasizing the interests, identities, values, and assumptions of both individuals and organizations. Companies, whether parent organizations or subsidiaries, often choose to implement IFRS to facilitate the preparation of more comparable financial statements (Guerreiro, Rodrigues, & Craig, 2012). Institutional theory provides a valuable framework for understanding how organizations respond to external regulatory pressures, as it posits that internal dynamics, interests, and agency play pivotal roles in determining organizational adaptations (Dillard, Rigsby, & Goodman, 2004; Greenwood & Hinings, 1996; Oliver, 1991). Several studies have employed institutional theory to investigate the voluntary adoption of IFRS (Guerreiro, Rodrigues, & Craig, 2012; Thien & Hung, 2021).

3.3. Agency theory

Agency theory is a fundamental concept focused on information disclosure within organizations. This theory views a firm as the central hub of agency relationships involving various individuals (Jensen & Meckling, 1976). At its core, agency theory elucidates the prevalence of corporate governance mechanisms, primarily built upon the assumption of conflicts between owners and managers (Clarke, 2004). As proposed by Mizruchi (2004), the separation of ownership and control arises from the structural framework and professional management model adopted by modern corporations. Muth and Donaldson (1998) contend that this separation enhances managerial power, often leading to decisions that prioritize managers’ interests at the expense of shareholders (Muth & Donaldson, 1998). Consequently, effective corporate governance mechanisms, including robust boards of directors and monitoring mechanisms, become imperative to represent shareholder interests and oversee managerial actions. These mechanisms, in turn, incentivize managers to disclose comprehensive information, thus addressing the information requirements of financial report users (Alanezi & Albuloushi, 2011). Furthermore, agency theory underscores the vital role of a company’s board of directors as a critical oversight mechanism, aimed at mitigating information asymmetry by providing high-quality information, ultimately enhancing corporate reputation (Ahmad-Zaluki & Nordin Wan-Hussin, 2010). Several studies have applied agency theory to elucidate the rationale behind the voluntary adoption of IFRS (Alanezi & Albuloushi, 2011; Di Fabio, 2018; Hlel & Nafti, 2019; Pichler, Cordazzo, & Rossi, 2018).

3.4. Several other relevant theories

Signaling theory, originally formulated by Spence in 1973 to address information asymmetry (Spence, 1973), found further application when Ross (1977) employed it to elucidate voluntary information disclosure. Verrecchia (1983) delves into corporate behavior, highlighting how companies strategically opt for voluntary information disclosure, such as earnings forecasts, to distinguish themselves in the market and enhance their market value. Ajinkya and Gift (1984) emphasize the reliability and relevance of management forecasts as valuable information for investors, given their association with stock price adjustments. In the context of IFRS adoption, signaling theory posits that it serves as a credible signal indicating enhanced quality, transparency in financial reporting, and reduced information asymmetry, primarily through the improvement of forecast accuracy (Masoud, 2017). Numerous studies have employed signaling theory to shed light on the motivations behind the voluntary adoption of IFRS (Alanezi & Albuloushi, 2011; Hlel & Nafti, 2019).

The foundation of Decision Usefulness Theory is rooted in the fundamental purpose of accounting: to provide information that aids users in making informed decisions (Hitz, 2007). This theory underscores that financial statements should not only assist users in assessing a company’s historical performance but also enable them to make informed projections about its future prospects. Consequently, it becomes imperative to present accounting information with honesty and fairness, accurately reflecting the underlying economic transactions (Dandago & Hassan, 2013; Hitz, 2007). Decision Usefulness Theory finds application in the work of Thien and Hung (2021), who utilize it to elucidate the rationale behind the voluntary adoption of IFRS.

Legitimacy theory posits that companies should operate in compliance with relevant laws and regulations in the countries where they conduct business (Suchman, 1995). Under the framework of legitimacy theory, companies are incentivized to make decisions that align with established standards, thereby enabling a deeper understanding of the factors within legitimacy theory that influence these corporate choices (De Luca & Prather-Kinsey, 2018). Several studies have applied legitimacy theory to elucidate the perspectives of accountants, scholars, chief accountants, financial directors, and managers regarding the voluntary adoption of IFRS (Phan, Joshi, & Mascitelli, 2018; Phan, 2014; Thien & Hung, 2021).

Economic theory argues that a firm’s commitment to enhanced information disclosure can mitigate information asymmetry among investors and curb adverse selection in capital markets. This, in turn, leads to increased market liquidity, reduced capital costs, and an overall enhancement of company value (Verrecchia, 2001). Information asymmetry often fosters adverse selection among investors, resulting in decreased market liquidity (Verrecchia, 2001). In less liquid markets, heightened information disclosure levels serve to alleviate information asymmetry, subsequently lowering equity issuance prices and the cost of capital (Baiman & Verrecchia, 1996). Given the assumption that the adoption of IFRS leads to improved disclosure, enhanced quality, and comparability in financial reporting practices, businesses voluntarily embracing IFRS can reap the aforementioned benefits (Sato & Takeda, 2017). Sato and Takeda (2017) employ economic theory to investigate the voluntary adoption of IFRS by businesses.

Expectancy theory, as proposed by Vroom in 1964, posits that firms are driven by the anticipation of rewards to enhance their performance. According to this theory, when individuals highly value a specific reward, they are more inclined to enhance their performance in pursuit of that reward (Vroom, 1964). On one hand, IFRS voluntary application can lead to improved accounting quality, primarily through enhanced financial statement comparability. Conversely, it may also result in lower accounting quality due to increased complexity, although this aspect lacks experimental verification (Gu, 2021). Gu (2021) contends that the voluntary adoption of IFRS by listed companies can indeed enhance accounting quality, and it identifies Expectancy Theory as a suitable framework for explaining managerial behavior in this context.

4. LITERATURE SUMMARY BY PREDITOR VARIABLES

The voluntary adoption of IFRS by businesses is influenced by a multitude of factors, which can be categorized into several key groups: (i) Corporate operations, (ii) Capital structure, (iii) Ownership structure, (iv) Internationalization, (v) Financial performance, (vi) Corporate governance, and (vii) Several other factors.

4.1. Corporate operations

The voluntary adoption of IFRS is significantly influenced by their corporate operations. The scale of a company’s operations is often quantified by metrics such as the logarithm of total assets, the number of subsidiaries and the number of years it has been in business (as shown in Table 2). Previous research has established that the scale of operations plays a pivotal role in explaining accounting choices during the transition from GAAP to IFRS (Kvaal & Nobes, 2010). However, Sato and Takeda (2017) and Chung and Park (2017) have presented evidence indicating that a longer history of business operations has a detrimental impact on the voluntary adoption of IFRS.

4.2. Capital structure

Capital structure is a recognized factor that influences the voluntary adoption of IFRS. Capital structure can be assessed through various indicators, including increases in debt capital, increases in equity capital, total liabilities, and financial leverage (as illustrated in Table 3). Most factors related to capital structure exert a positive influence on the voluntary adoption of IFRS by listed enterprises. However, research by Sato and Takeda (2017) and Chung and Park (2017) has demonstrated that financial leverage has a negative impact on the voluntary adoption of IFRS. Furthermore, a defining characteristic of businesses that choose to adopt IFRS voluntarily may be their relatively low capital intensity (André, Walton, & Yang, 2012). Consequently, they predict and confirm that companies primarily investing their assets in fixed assets are less inclined to adopt IFRS.

4.3. Ownership structure

Ownership structure has been found to be a factor related to firms’ voluntary adoption of IFRS. Ownership structure encompasses various factors, including the overall ownership composition, foreign ownership ratio, and the presence of family members on the company’s board (as displayed in Table 4). Notably, Renders and Gaeremynck (2007) demonstrated a negative influence of ownership structure on the voluntary adoption of IFRS. Similarly, Alanezi and Albuloushi (2011) revealed that the presence of family members on the board of directors has a detrimental impact on the voluntary adoption of IFRS. Conversely, Sato and Takeda (2017) found a positive relationship between the foreign ownership ratio and the voluntary adoption of IFRS by listed firms. In contrast, Matonti and Iuliano (2012) presented evidence showing that foreign ownership is negatively associated with the voluntary adoption of IFRS. Foreign shareholders, seeking to minimize the costs of obtaining reliable financial information, are more likely to favor firms that report in accordance with IFRS (Matonti & Iuliano, 2012).

Source: Review results.

4.4. Internationalization

The level of internationalization is also recognized as a significant factor influencing the voluntary adoption of IFRS. This includes three key factors: internationalization, enterprises engaged in trade with foreign markets, and cross-listing on foreign exchanges (as indicated in Table 5). According to Bassemir (2018), research indicates that businesses with numerous subsidiaries, and significant international transactions tend to prefer IFRS adoption. The role of international business orientation in IFRS adoption aligns with the notion that companies operating at the international level are more inclined to perceive the need for adopting a reporting strategy that enables effective communication with a diverse set of stakeholders, including international constituents and customers (André, Walton, & Yang, 2012). Additionally, internationally oriented companies often face heightened complexity in information processing and may choose to address these needs through IFRS adoption (Bassemir, 2018). Most factors related to internationalization have a positive impact on enhancing to voluntary adoption of IFRS.

4.5. Financial performance

Financial performance factors have also been shown to be related to the voluntary adoption of IFRS by enterprises. Financial performance encompasses factors such as profit, market capitalization, and growth rate (as displayed in Table 6). Specifically, market capitalization is positively correlated with the voluntary adoption of IFRS (Emmanuel Iatridis, 2012). In contrast, Alanezi and Albuloushi (2011) argue that profits have a negative impact on the voluntary adoption of IFRS by listed enterprises.

4.6. Corporate governance

Corporate governance activities play a significant role in influencing the voluntary adoption of IFRS. Factors related to corporate governance activities encompass governance practices, internal governance, management changes preceding the adoption of IFRS, the engagement of Big4 audit firms, and the presence of an audit committee (as shown in Table 7). Most factors associated with corporate governance activities exhibit a positive correlation with the voluntary adoption of IFRS. Companies audited by prominent audit firms may demonstrate a higher level of compliance and familiarity with IFRS requirements (Street & Gray, 2002). Consequently, companies audited by large audit firms (Big 4) are more likely to provide voluntary IFRS information prior to adopting IFRS (Tarca, 2004).

4.7. Several other factors

Various factors influencing the voluntary adoption of IFRS are primarily documented and assessed by professionals such as employees, accountants, chief accountants, auditors, and financial directors. For instance, Guerreiro, Rodrigues and Craig (2012) conducted a survey among financial managers and accountants representing 474 large unlisted companies in Portugal to analyze patterns of voluntary IFRS adoption. Thien and Hung (2021), building upon the work of Guerreiro, Rodrigues, and Craig (2012), conducted an analysis of the impact of institutional pressure, legal considerations, risk factors, and uncertainties on the voluntary adoption of IFRS by SMEs. Their analysis was based on a survey involving 272 auditors, financial directors, and chief accountants. Phan, Joshi and Mascitelli (2018) conducted a survey involving 728 participants, including auditors, accountants, and accounting scholars, to investigate the patterns of voluntary IFRS adoption behavior.

Refer to Table 8 for details.

5. CONCLUSIONS AND DISCUSSIONS

The objective of this study is to conduct a comprehensive review of the existing literature concerning the determinants of voluntary IFRS adoption. The review reveals that prior research has extensively utilized various theoretical frameworks, including positive accounting theory, institutional theory, agency theory, and several other pertinent theories. Additionally, the findings from the examination of factors influencing the voluntary adoption of IFRS are categorized into seven primary groups.

The majority of studies have been conducted in developed countries with early IFRS adoption roadmaps, such as EU countries, which constitute a significant portion of the research (Bertrand, de Brebisson, & Burietz, 2021; Li, 2010; Renders & Gaeremynck, 2007). Additionally, several other countries have been considered for evaluation, including England (André, Walton, & Yang, 2012; Muller, Riedl, & Sellhorn, 2008), Brazil (Almeida & Rodrigues, 2017), Canada (Ledoux & Cormier, 2013), Portugal (Guerreiro, Rodrigues, & Craig, 2008, 2012), the Czech Republic (Procházka, 2011), Germany (Moya & Oliveras, 2006; Van Tendeloo & Vanstraelen, 2005), South Korea (Kim & Choi, 2014), China (Liu et al., 2011), Israel (Chen, Gavious, & Lev, 2017), Japan (Giner et al., 2019), France (de La Bruslerie & Gabteni, 2014), Turkey (Aksu & Espahbodi, 2016), Italy (Matonti & Iuliano, 2012), and Vietnam (Nguyen, 2022; Thien & Hung, 2021). Moreover, the reviewed studies predominantly employ quantitative methods to examine the factors influencing the voluntary adoption of IFRS. These studies are characterized by empirical testing and retesting of theoretical models related to the benefits of voluntary IFRS adoption, with the primary quantitative methods being multivariate regression, descriptive statistics, and linear structural models.

Research on the voluntary adoption of IFRS worldwide primarily employs two main approaches. The first approach revolves around firm characteristics assessments, with studies focusing on analyzing the determinants influencing the voluntary adoption of IFRS by companies. For instance, Procházka (2011) utilized data from unlisted firms in the Czech Republic to scrutinize voluntary IFRS adoption behavior. André, Walton and Yang (2012) conducted an extensive analysis of the factors impacting the voluntary adoption of IFRS among 8,417 medium and large non-listed companies in the UK. Matonti and Iuliano (2012) examined a sample of 206 private companies in Italy to investigate the factors affecting their voluntary adoption of IFRS. Yang (2014) explored the factors influencing voluntary IFRS adoption and conducted a comparative study between the UK and Germany, drawing upon survey data from medium and large enterprises. Additionally, Sakawa, Watanabel and Gu (2021) conducted research on the voluntary adoption of IFRS by small and medium-sized enterprises in Japan. The second approach involves assessments from various professionals, including employees, accountants, chief accountants, auditors, and financial directors. Noteworthy studies following this approach include Guerreiro, Rodrigues and Craig (2012), Thien and Hung (2021), and Phan, Joshi and Mascitelli (2018).

Previous research has identified that the factors influencing the voluntary adoption of IFRS primarily stem from within the enterprise. However, the consideration of external factors believed to impact the voluntary adoption of IFRS remains limited, with a notable focus on the internationalization factor (Emmanuel Iatridis, 2012; Giner et al., 2019; Kim & Shi, 2012a, 2012b; Nguyen, 2022; Sakawa, Watanabel, & Gu, 2021). Especially in countries following a roadmap to prepare for the implementation of IFRS, prior studies have focused on examining factors related to institutional pressures and the perceived benefits and challenges faced by businesses in their prospective adoption of IFRS (Guerreiro, Rodrigues, & Craig, 2012; Phan, Joshi, & Mascitelli, 2018; Thien & Hung, 2021).

Moreover, most factors tend to positively influence the voluntary adoption of IFRS. However, few empirical studies still yield varying conclusions relative to some factors' positive or negative effects on the voluntary adoption of IFRS. For instance, Nguyen (2022) demonstrated a positive relationship between financial leverage and voluntary adoption of IFRS. Di Fabio (2018) suggested that companies in Italy using higher financial leverage are more inclined to voluntarily apply IFRS. Conversely, Sato and Takeda (2017) and Chung and Park (2017) contended that financial leverage has a negative impact on the voluntary adoption of IFRS. Similarly, two other factors, foreign ownership and corporate profits, present contrasting findings in their influence on the voluntary adoption of IFRS.

The research findings contribute to a comprehensive understanding of the factors influencing the voluntary adoption of IFRS by businesses in various contexts, based on a systematic review of 185 articles. These results can be valuable for managers when making decisions related to the voluntary adoption of IFRS. Nonetheless, there are two main limitations to this study. Firstly, this study does not explore variations in findings under different economic and cultural conditions. Secondly, this study does not address the role of moderating variables influencing voluntary adoption of IFRS.

6. DIRECTIONS FOR RESEARCH FUTURE

In terms of theory, previous studies have employed various theoretical frameworks to elucidate the factors influencing the voluntary adoption of IFRS by businesses. Nevertheless, there are limited studies that combine theories to examine the role of corporate managers in relation to internal factors and their influence on the voluntary adoption of IFRS. Consequently, future research should delve into this relationship and offer novel theoretical insights.

With regard to research methods, the majority of previous studies have employed quantitative research approaches. Consequently, future research should consider employing a combination of quantitative and qualitative methods to gain a more comprehensive understanding of the factors that influence the voluntary adoption of IFRS in diverse economic, cultural, and social contexts across various societies.

While previous empirical studies have underscored the influence of managers and business owners in the voluntary adoption of IFRS, there remains a dearth of empirical evidence within the specific context of countries having an IFRS implementation roadmap. Therefore, future research should consider the effect of ownership structure on IFRS adoption in these nations. This inquiry becomes particularly significant in countries harboring numerous state-owned enterprises characterized by distinct attributes—does the voluntary adoption of IFRS differ significantly for these enterprises compared to others?

Moreover, there is controversy surrounding the conclusions drawn from studies regarding the impact of factors on the voluntary adoption of IFRS. Such discrepancies can potentially result in inaccurate assessments and judgments regarding the factors that influence the voluntary adoption of IFRS. Therefore, future research should aim to elucidate these disparities by investigating whether a nonlinear impact of these factors exists on the voluntary adoption of IFRS.

Finally, the majority of prior studies have concentrated on investigating internal factors that influence the voluntary adoption of IFRS, with minimal attention given to external factors. Consequently, future research should explore and incorporate new external factors that may influence the voluntary adoption of IFRS.

References

- Ahmad-Zaluki, N. A., & Nordin Wan-Hussin, W. (2010). Corporate governance and earnings forecasts accuracy. Asian Review of Accounting, 18(1), 50-67. 1. [CrossRef]

- Ajinkya, B. B., & Gift, M. J. (1984). Corporate managers' earnings forecasts and symmetrical adjustments of market expectations. Journal of Accounting Research, 22(2), 425-444. [CrossRef]

- Aksu, M., & Espahbodi, H. (2016). The impact of IFRS adoption and corporate governance principles on transparency and disclosure: the case of Borsa Istanbul. Emerging Markets Finance and Trade, 52(4), 1013-1028. [CrossRef]

- Alanezi, F. S., & Albuloushi, S. S. (2011). Does the existence of voluntary audit committees really affect IFRS-required disclosure? The Kuwaiti evidence. International Journal of Disclosure and Governance, 8(2), 148-173. [CrossRef]

- Almeida, J. E. F. D., & Rodrigues, H. S. (2017). Effects of IFRS, analysts, and ADR on voluntary disclosure of Brazilian public companies. Journal of International Accounting Research, 16(1), 21-35.

- André, P., Walton, P. J., & Yang, D. (2012). Voluntary adoption of IFRS: A study of determinants for UK non-listed firms. In Comptabilités et Innovation. http://papers.ssrn.com/sol3/papers.cfm?abstract_id=1978986.

- Baiman, S., & Verrecchia, R. E. (1996). The relation among capital markets, financial disclosure, production efficiency, and insider trading. Journal of accounting research, 34(1), 1-22.

- Barth, M. E., Landsman, W. R., Lang, M. H., & Williams, C. D. (2013). Effects on Comparability and Capital Market Benefits of Voluntary Adoption of IFRS by US Firms: Insights from Voluntary Adoption of IFRS by Non-US Firms. https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2196247.

- Bassemir, M. (2018). Why do private firms adopt IFRS? Accounting and Business Research, 48(3), 237-263.

- Bertrand, J., de Brebisson, H., & Burietz, A. (2021). Why choosing IFRS? Benefits of voluntary adoption by European private companies. International Review of Law and Economics, 65, 105968–. https://www.sciencedirect.com/science/article/pii/S0144818820301812. [CrossRef]

- Chen, E., Gavious, I., & Lev, B. (2017). The positive externalities of IFRS R&D capitalization: enhanced voluntary disclosure. Review of Accounting Studies, 22, 677-714. [CrossRef]

- Christensen, H. B., Lee, E., Walker, M., & Zeng, C. (2015). Incentives or standards: What determines accounting quality changes around IFRS adoption? European Accounting Review, 24(1), 31-61.

- Chung, H., & Park, S. O. (2017). Voluntary adoption of the IFRS and industry-level comparability: evidence from Korean unlisted firms. Emerging Markets Finance and Trade, 53(7), 1654-1666. [CrossRef]

- Clarke, T. (2004). Theories of corporate governance. The Philosophical Foundations of Corporate Governance, Oxon, 12(4), 244-266.

- Dandago, K. I., & Hassan, N. I. B. (2013). Decision usefulness approach to financial reporting: A case for Malaysian Inland Revenue Board. Asian Economic and Financial Review, 3(6), 772-784.

- De George, E. T., Li, X., & Shivakumar, L. (2016). A review of the IFRS adoption literature. Review of Accounting Studies, 21, 898-1004. 21, 898–1004. [CrossRef]

- de La Bruslerie, H., & Gabteni, H. (2014). Voluntary disclosure of financial information by French firms: Does the introduction of IFRS matter? Advances in Accounting, 30(2), 367-380.

- De Luca, F., & Prather-Kinsey, J. (2018). Legitimacy theory may explain the failure of global adoption of IFRS: the case of Europe and the US. Journal of Management and Governance, 22, 501-534. [CrossRef]

- Di Fabio, C. (2018). Voluntary application of IFRS by unlisted companies: evidence from the Italian context. International Journal of Disclosure and Governance, 15, 73-86. [CrossRef]

- Dillard, J. F., Rigsby, J. T., & Goodman, C. (2004). The making and remaking of organization context: duality and the institutionalization process. Accounting, Auditing & Accountability Journal, 17(4), 506-542.

- Emmanuel Iatridis, G. (2012). Voluntary IFRS disclosures: evidence from the transition from UK GAAP to IFRSs. Managerial Auditing Journal, 27(6), 573-597. [CrossRef]

- Fields, T. D., Lys, T. Z., & Vincent, L. (2001). Empirical research on accounting choice. Journal of Accounting and Economics, 31(1-3), 255-307.

- Giner, B., Merello, P., Nakamura, M., & Pardo, F. (2019). Implementation of IFRS in Japan: An Analysis of Voluntary Adoption by Listed Firms. Available at SSRN 3542995. https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3542995.

- Greenwood, R., & Hinings, C. R. (1996). Understanding radical organizational change: Bringing together the old and the new institutionalism. Academy of Management Review, 21(4), 1022-1054.

- Gu, J. (2021). Voluntary IFRS adoption and accounting quality: Evidence from Japan. Economic Research-Ekonomska Istraživanja, 34(1), 1985-2012. [CrossRef]

- Guerreiro, M. S., Rodrigues, L. L., & Craig, R. (2008). The preparedness of companies to adopt International Financial Reporting Standards: Portuguese evidence. Accounting Forum, 32(2008), 75-88. [CrossRef]

- Guerreiro, M. S., Rodrigues, L. L., & Craig, R. (2012). Voluntary adoption of International Financial Reporting Standards by large unlisted companies in Portugal–Institutional logics and strategic responses. Accounting, Organizations and Society, 37(7), 482-499. [CrossRef]

- Hitz, J. M. (2007). The decision usefulness of fair value accounting–a theoretical perspective. European Accounting Review, 16(2), 323-362. [CrossRef]

- Hlel, K., & Nafti, I. K. (2019). Board characteristics, IFRS adoption and voluntary disclosure: evidence from management forecasts accuracy in France. International Journal of Management and Enterprise Development, 18(1-2), 41-62.

- Jamal, K., Benston, G., Carmichael, D., Christensen, T., Colson, R., Moehrle, S., Rajgopal, S., Stober, T., Sunder, S., & Watts, R. (2008). A perspective on the SEC’s proposal to accept financial statements prepared in accordance with international financial reporting standards (IFRS) without reconciliation to U.S. GAAP. Accounting Horizons, 22(2), 241-248. [CrossRef]

- Jensen, M. C., & Meckling, W. H. (1976). Theory of firm: managerial behavior, agency costs and ownership structure. Journal of Financial Economics, 3(4), 304-360. [CrossRef]

- Kim, J. A., & Choi, J. S. (2014). The association between the voluntary adoption of K-IFRS by unlisted firms and earnings management. Korean Accounting Review, 39(4), 77-129.

- Kim, J. B., & Shi, H. (2012a). IFRS reporting, firm-specific information flows, and institutional environments: International evidence. Review of Accounting Studies, 17, 474-517. [CrossRef]

- Kim, J. B., & Shi, H. (2012b). Voluntary IFRS adoption, analyst coverage, and information quality: International evidence. Journal of International Accounting Research, 11(1), 45-76.

- Kim, J. B., Tsui, J. S., & Yi, C. H. (2011). The voluntary adoption of International Financial Reporting Standards and loan contracting around the world. Review of Accounting Studies, 16, 779-811. [CrossRef]

- Kvaal, E., & Nobes, C. (2010). International differences in IFRS policy choice: a research note. Accounting and business research, 40(2), 173-187. [CrossRef]

- Nguyen, T. M. H., Nguyen, N. T., Nguyen, H. T. (2020). Factors Affecting Voluntary Information Disclosure on Annual Reports: Listed Companies in Ho Chi Minh City Stock Exchange, The Journal of Asian Finance, Economics, and Business, 7(3), 53-62. [CrossRef]

- Lambert, R. A. (2001). Contracting theory and accounting. Journal of accounting and economics, 32(1-3), 3-87.

- Ledoux, M. J., & Cormier, D. (2013). Market assessment of intangibles and voluntary disclosure about innovation: the incidence of IFRS. Review of Accounting and Finance, 12(3), 286-304. [CrossRef]

- Li, S. (2010). Does mandatory adoption of International Financial Reporting Standards in the European Union reduce the cost of equity capital? The Accounting Review, 85(2), 607-636.

- Li, X., & Yang, H. I. (2016). Mandatory financial reporting and voluntary disclosure: The effect of mandatory IFRS adoption on management forecasts. The Accounting Review, 91(3), 933-953. [CrossRef]

- Liu, C., Yao, L. J., Hu, N., & Liu, L. (2011). The impact of IFRS on accounting quality in a regulated market: An empirical study of China. Journal of Accounting, Auditing & Finance, 26(4), 659-676.

- Masoud, N. (2017). The effects of mandatory IFRS adoption on financial analysts’ forecast: Evidence from Jordan. Cogent business & management, 4(1), 1290331. [CrossRef]

- Matonti, G., & Iuliano, G. (2012). Voluntary adoption of IFRS by Italian private firms: A study of the determinants. Eurasian Business Review, 2, 43-70. [CrossRef]

- Meyer, J. W., & Rowan, B. (1977). Institutionalized organizations: Formal structure as myth and ceremony. American journal of sociology, 83(2), 340-363. [CrossRef]

- Mizruchi, M. S. (2004). Berle and Means revisited: The governance and power of large US corporations. Theory and Society, 33, 579-617.

- Moya, S., & Oliveras, E. (2006). Voluntary adoption of IFRS in Germany: a regulatory impact study. Corporate Ownership & Control, 3(3), 138-147. [CrossRef]

- Muller, K. A., Riedl, E. J., & Sellhorn, T. (2008). Consequences of voluntary and mandatory fair value accounting: Evidence surrounding IFRS adoption in the EU real estate industry (No. 09-033). Boston, MA: Harvard Business School.

- Muth, M., & Donaldson, L. (1998). Stewardship theory and board structure: A contingency approach. Corporate Governance: An International Review, 6(1), 5-28. [CrossRef]

- Nguyen, T. H. (2022). The willingness to voluntarily apply international financial reporting standards in Vietnam: Empirical evidence from listed parent companies. Cogent business & management, 9(1), 2116802. [CrossRef]

- Oliver, C. (1991). Strategic responses to institutional processes. Academy of Management Review, 16(1), 145-179.

- Păşcan, I. D. (2015). Measuring the effects of IFRS adoption on accounting quality: A review. Procedia Economics and Finance, 32, 580-587. [CrossRef]

- Phan, D., Joshi, M., & Mascitelli, B. (2018). What influences the willingness of Vietnamese accountants to adopt International Financial Reporting Standards (IFRS) by 2025? Asian Review of Accounting, 26(2), 225-247.

- Phan, D. H. T. (2014). What factors are perceived to influence consideration of IFRS adoption by Vietnamese policymakers? Journal of Contemporary Issues in Business and Government, 20(1), 27-40.

- Pichler, S., Cordazzo, M., & Rossi, P. (2018). An analysis of the firms-specific determinants influencing the voluntary IFRS adoption: evidence from Italian private firms. International Journal of Accounting, Auditing and Performance Evaluation, 14(1), 85-104.

- Prather-Kinsey, J. (2006). Developing countries converging with developed-country accounting standards: Evidence from South Africa and Mexico. The International Journal of Accounting, 41(2), 141-162. [CrossRef]

- Procházka, D. (2011). Readiness for the voluntary adoption of the IFRS by non-listed companies: a Czech perspective. Recent Res Appl Econ WSEAS, 3, 81-86.

- Ramanna, K. (2013). The international politics of IFRS harmonization. Accounting, Economics and Law, 3(2), 1-46. [CrossRef]

- Renders, A., & Gaeremynck, A. (2007). The impact of legal and voluntary investor protection on the early adoption of International Financial Reporting Standards (IFRS). De Economist, 155(1), 49-72. [CrossRef]

- Ross, S. A. (1977). The determination of financial structure: the incentive-signalling approach. The Bell Journal of Economics, 8, 23-40. [CrossRef]

- Sakawa, H., Watanabel, N., & Gu, J. (2021). The internationalization and voluntary adoption of international accounting standards by Japanese MNEs. Management International Review, 61, 713-744. [CrossRef]

- Sato, S., & Takeda, F. (2017). IFRS adoption and stock prices of Japanese firms in governance system transition. The International Journal of Accounting, 52(4), 319-337. [CrossRef]

- Scott, W. R. (2004). Institutional theory. Encyclopedia of social theory, 11, 408-414.

- Soderstrom, N. S., & Sun, K. J. (2007). IFRS adoption and accounting quality: a review. European Accounting Review, 16(4), 675-702.

- Spence, M. (1973). Job market signaling. Quarterly Journal of Economics, 87(3), 355-374.

- Street, D. L., & Gray, S. J. (2002). Factors influencing the extent of corporate compliance with International Accounting Standards: summary of a research monograph. Journal of International Accounting, Auditing and Taxation, 11(1), 51-76. [CrossRef]

- Suchman, M. C. (1995). Managing legitimacy: Strategic and institutional approaches. Academy of Management Review, 20(3), 571-610.

- Tarca, A. (2004). International convergence of accounting practices: Choosing between IAS and US GAAP. Journal of International Financial Management & Accounting, 15(1), 60-91. [CrossRef]

- Thien, T. H., & Hung, N. X. (2021). Institutional pressures, legitimacy, risks, uncertainty and voluntary adoption of IFRS for SMEs in Vietnam. Journal of Eastern European and Central Asian Research, 8(4), 495-510. [CrossRef]

- Tran, T., Ha, X., Le, T & Nguyen, N. (2019). Factors affecting IFRS adoption in listed companies: Evidence from Vietnam.Management Science Letters , 9(13), 2169-2180. [CrossRef]

- Van Tendeloo, B., & Vanstraelen, A. (2005). Earnings management under German GAAP versus IFRS. European Accounting Review, 14(1), 155-180. [CrossRef]

- Verrecchia, R. E. (1983). Discretionary disclosure. Journal of accounting and economics, 5, 179-194.

- Verrecchia, R. E. (2001). Essays on disclosure. Journal of accounting and economics, 32(1-397-180).

- Verriest, A., Gaeremynck, A., & Thornton, D. B. (2013). The impact of corporate governance on IFRS adoption choices. European Accounting Review, 22(1), 39-77. [CrossRef]

- Vroom, V. H. (1964). Work and Motivation. John Wiley and Sons.

- Watts, R. L., & Zimmerman, J. L. (1990). Positive accounting theory: a ten year perspective. The Accounting Review, 131-156.

- Yang, D. (2014). Exploring the determinants of voluntary adoption of IFRS by unlisted firms: A comparative study between the UK and Germany. China Journal of Accounting Studies, 2(2), 118-136. [CrossRef]

Figure 1.

Number of published articles. Source: Review results.

Table 1.

Summary of studies most cited on Scopus and Google Scholar.

| Scopus | Google Scholar | |||

|---|---|---|---|---|

| No. | Studies | Number of citations | Studies | Number of citations |

| 1 | Van Tendeloo and Vanstraelen (2005) | 296 | Van Tendeloo and Vanstraelen (2005) | 1115 |

| 2 | Christensen et al. (2015) | 193 | Christensen et al. (2015) | 931 |

| 3 | Kim and Shi (2012a) | 105 | Kim and Shi (2012a) | 242 |

| 4 | Kim, Tsui and Yi (2011) | 99 | Kim, Tsui and Yi (2011) | 242 |

| 5 | Li and Yang (2016) | 90 | Li and Yang (2016) | 215 |

| 6 | Guerreiro, Rodrigues and Craig (2012) | 75 | Guerreiro, Rodrigues and Craig (2012) | 213 |

| 7 | Kim and Shi (2012b) | 47 | Renders and Gaeremynck (2007) | 154 |

| 8 | Renders and Gaeremynck (2007) | 40 | Kim and Shi (2012b) | 106 |

| 9 | Chen, Gavious and Lev (2017) | 31 | Barth (2013) | 85 |

| 10 | Alanezi and Albuloushi (2011) | 21 | Muller, Riedl and Sellhorn (2008) | 78 |

Source: Review results.

Table 2.

Studies using corporate operations as an independent variable.

| Variable | Studies |

|---|---|

| Firm size | Kim and Shi (2012b), Kim and Shi (2012a), Emmanuel Iatridis (2012), Renders and Gaeremynck (2007), Sato and Takeda (2017), Giner et al. (2019), Di Fabio (2018), Nguyen (2022) |

| Firm age | Sato and Takeda (2017), Giner et al. (2019), Chung and Park (2017) |

| Number of subsidiaries | André, Walton and Yang (2012) |

Source: Review results.

Table 3.

Studies using capital structure as an independent variable.

| Variable | Studies |

|---|---|

| Debt capital | Emmanuel Iatridis (2012) |

| Equity capital | Emmanuel Iatridis (2012) |

| Total liabilities | Emmanuel Iatridis (2012) |

| Financial leverage | Alanezi and Albuloushi (2011), Sato and Takeda (2017), André, Walton and Yang (2012), Yang (2014), Chung and Park (2017), Matonti and Iuliano (2012), Di Fabio (2018), Nguyen (2022) |

Source: Review results.

Table 4.

Studies using ownership structure as an independent variable.

| Variable | Studies |

|---|---|

| Ownership composition | Renders and Gaeremynck (2007), Pichler, Cordazzo and Rossi (2018) |

| Foreign ownership ratio | Sato and Takeda (2017), Sakawa, Watanabel and Gu (2021), Matonti and Iuliano (2012), Nguyen (2022) |

| The presence of family members on the company’s board | Alanezi and Albuloushi (2011) |

Table 5.

Studies using Internationalization as an independent variable.

| Variable | Studies |

|---|---|

| Internationalization | Giner et al. (2019), Sakawa, Watanabel and Gu (2021) |

| Enterprises engaged in trade with foreign markets | Kim and Shi (2012b), Kim and Shi (2012a), Emmanuel Iatridis (2012), Nguyen (2022) |

| Cross-listing on foreign exchanges | Kim and Shi (2012b), Kim and Shi (2012a), Emmanuel Iatridis (2012) |

Source: Review results.

Table 6.

Studies using financial performance as an independent variable.

| Variable | Studies |

|---|---|

| Profits | Alanezi and Albuloushi (2011), Giner et al. (2019), Yang (2014) |

| Market capitalization | Emmanuel Iatridis (2012), Verriest, Gaeremynck and Thornton (2013) |

| Growth rate | Chung and Park (2017) |

Source: Review results.

Table 7.

Studies using corporate governance as an independent variable.

| Variable | Studies |

|---|---|

| Governance practices | Verriest, Gaeremynck and Thornton (2013), Giner et al. (2019) |

| Internal governance | Sato and Takeda (2017) |

| Management changes preceding the adoption of IFRS | Emmanuel Iatridis (2012) |

| Big4 audit firms | Emmanuel Iatridis (2012), Renders and Gaeremynck (2007), Sato and Takeda (2017), André, Walton and Yang (2012), Chung and Park (2017), Pichler, Cordazzo and Rossi (2018), Nguyen (2022) |

| Audit committee | Alanezi and Albuloushi (2011) |

Source: Review results.

Table 8.

Studies using several other factors as an independent variable.

| Variable | Studies |

|---|---|

| Legitimacy | Guerreiro, Rodrigues and Craig (2012), Thien and Hung (2021) |

| Dependence | Guerreiro, Rodrigues and Craig (2012), Thien and Hung (2021) |

| Consistency | Guerreiro, Rodrigues and Craig (2012), Thien and Hung (2021) |

| Constraint | Guerreiro, Rodrigues and Craig (2012) |

| Uncertainy | Guerreiro, Rodrigues and Craig (2012), Thien and Hung (2021) |

| Interconnectedness | Guerreiro, Rodrigues and Craig (2012) |

| Financial risks | Thien and Hung (2021) |

| Operational risks | Thien and Hung (2021) |

| Flexibility | Thien and Hung (2021) |

| Trade | Thien and Hung (2021) |

| Time | Thien and Hung (2021) |

| Industry | Thien and Hung (2021) |

| Perceived benefits | Phan, Joshi and Mascitelli (2018) |

| Perceived challenges | Phan, Joshi and Mascitelli (2018) |

Source: Review results.

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Copyright: This open access article is published under a Creative Commons CC BY 4.0 license, which permit the free download, distribution, and reuse, provided that the author and preprint are cited in any reuse.