Submitted:

16 November 2023

Posted:

17 November 2023

You are already at the latest version

Abstract

The field of CSR has witnessed considerable growth and established itself as a significant subject in family business literature. However, despite previous reviews exploring this topic from various angles, there remains a crucial gap in understanding the influence of diverse regulatory frameworks and cultural values on the development of literature production and research streams across different regions. This gap holds particular significance for comprehending the latest advancements in this dynamic field, particularly in emerging economies, where cultural norms play a substantial role in shaping the relationship between family firms and CSR. To bridge this gap, this paper conducts a comprehensive review of empirical studies focusing on sustainability in family firms. These studies are organized based on the country of study, and our review encompasses 232 articles published between 1996 and 2023. Utilizing bibliometric software, we systematically group these articles into three distinct clusters: North American studies, European studies, and Asian studies, adhering strictly to our inclusion criteria.

Keywords:

bibliometric review

; corporate social responsibility

; family firms

; content analysis

1. Introduction

Over the past decade, sustainability has garnered significant attention across various spheres—media, institutions, policy-making bodies, and both national and international organizations such as the United Nations. Corporate Social Responsibility (CSR) has emerged as a crucial tool in enterprise management, recognized for its pivotal role in tackling social issues [1].

While the exploration of sustainability in management literature traces back to the 1950s [2,3], the literature on CSR has experienced a recent, rapid expansion. CSR is now under investigation within diverse contexts, including state-owned firms [4,5], privately-owned companies [6], and family-owned enterprises [7,8,9]. Understanding how CSR strategies evolve in distinct organizational settings and how sustainability drives competitive advantage and value creation has indeed become a focal point.

Family firms have drawn particular attention from practitioners and academics for several reasons. Firstly, their economic significance is noteworthy since they constitute almost two-thirds of all private businesses globally [10] and contribute significantly to GDP and employment, especially in countries like Brazil, the USA, and Italy, where they account for over 90% of the national economy [10]. Secondly, family firms possess unique characteristics that set them apart from other private entities. The intimate connection between family members and the business significantly influences the firm's culture, operational traits, and social conduct [11], potentially leading to different CSR practices. Moreover, there's a common belief that family-owned enterprises are deeply ingrained in their communities compared to non-family firms, impacting their societal influence.

Literature has extensively explored the relationship between family involvement and sustainability practices, proposing various theoretical frameworks like resource-based view theory, social capital theory, organizational identity theory, socioemotional wealth theory, and inference theory to comprehend the family firm context [12].

Recent contributions have also highlighted the strong influence of cultural norms and regional contexts on the relationship between family firms and CSR, especially in diverse regulatory environments [13,14]. Cultural values and norms significantly shape corporations' roles in addressing societal concerns [15,16] and influence the decision-making process of family owners regarding CSR strategies. Additionally, social pressure on sustainability issues varies across regions, being higher in North American and European countries with a stakeholder orientation and lower in Eastern countries with a pronounced shareholder-oriented culture [17].

The heightened interest and growing research on sustainability in family firms have necessitated comprehensive reviews of the literature to understand current trends. Despite several reviews and contributions [18,19,20,21,22,23], little focus has been placed on the influence of national culture and norms on literature production.

In response, this study aims to bridge this gap by conducting a bibliometric review based on co-citations and co-words, categorizing and analyzing papers according to the country of analysis. This approach sheds light on CSR in family firms, utilizing a dataset of 232 papers from 1996 to 2023.

To our knowledge, this is the first updated bibliometric review delving into national and regional influences on literature production. The article is structured as follows: we start by describing the research methodology used to compile the database. Section 3 presents the findings of the bibliometric review, while Section 4 outlines the key conclusions.

2. Methodology

To answer our research question and to gain insights into the current debate and identify leading trends in the literature, this study employs a combination of bibliometric techniques, such as citations, keyword analysis, and content analysis [24,25]. Bibliometric analysis is a widely used tool for globally analysing existing literature. It involves applying quantitative and statistical analysis to publications and their citations to assess the state of the literature, providing comprehensive data on the activities and impacts of research in a specific field. To gather the necessary data, the study uses the Scopus database, a reliable tool commonly employed in previous bibliometric research [26,27], known for its lack of bias toward publisher and is wide coverage that allows Scopus to be considered particularly appropriate for smaller research areas [28], as in the case of the focus of sustainability research within family firms. Scopus is also widely acknowledged for its greater compatibility in combination with VOS Vieweer and Bibliometrix along with Biblioshiny package in R program [29,30], which we have used as primary tool to comprehend the structure of the literature.

To conduct the bibliometric review, we performed the methodological process summarized in Table 1. In the first step, we developed a keyword search in the Scopus databases and executed it in September 2023. These keywords were identified after a thorough review of the seminal papers in the field of CSR in the family firm’s environment. The resulting search included two set of keywords. The first set dealt with the identification of sustainability-relevant research using: “CSR” or “Environment* social* and governance" or "ESG" or "Corporate* social* responsib*" or social* responsib*" or “corporate social initiative*” or “corporate responsib*” or “ethic”. The second set focused on the literature on family firms: "family firm*" or "family business*" or "family governance" or "family owner*" or "family CEO*" or "family enterprise" or “family control” or “family owned business*” or “family owned compan*" or "family owned firm*" or "family run business*" or "family managed business*" or “family owned enterprise*”. By screening all search results that included both a keyword from the two groups in the title, abstract and author’s keywords we identified 541 studies. In the second step we only included published papers in the English language and belonging to the areas of Business, Management, and Accounting; Economics, Econometrics, and Finance; Social Sciences; Environmental Science. Considering our objective to comprehensively review the entire body of literature and gain insight into the latest developments in a highly dynamic field, our search was not constrained by a specific date. Consequently, we retrieved papers written up to the year 2023. The second step resulted in the identification of 402 papers. The third step consisted of a one-to-one detailed examination of each paper in the dataset by the authors independently in order to remove unrelated and not relevant articles, resulting in a final sample of 232 papers.

We further conducted a comprehensive examination of each paper to determine their research methods, which were categorized as quantitative, qualitative/conceptual, or reviews (bibliometric, systematic, or meta-analyses), and the countries of study. The results, as presented in Table 2, reveal that the majority of papers employed a quantitative approach, while 10% were qualitative or conceptual, and 3% were reviews. Regarding the research-originating study, our analysis indicates that research on corporate social responsibility in family firms encompasses both developed and emerging economies. The most frequently studied countries were the USA (14.4%), followed by China (8.4%), and Spain (6.9%). In terms of macro-regions, Asia featured prominently with 80 studies, followed by Europe with 62 studies, and North America with 35 studies. To address our research question, we compared the entire sample with three distinct clusters of papers that focused on Asia, Europe, and North America.

3. Results

We analyzed the four clusters of papers resulting from our research using VOS Viewer and the R-package Biblioshiny, which provides comprehensive features, including conceptual structure and thematic analysis, as well as various tables and graphs [31].

3.1. Descriptive analysis

As indicated in Table 3, the entire sample of quantitative papers (n = 232) was written by 570 authors and published in 101 journals, spanning from 1996 to 2023. The average citation level per document was 38.3. On average, each document had 2.46 authors, indicating that most articles had at least two authors. This is further supported by the average number of co-authors per document, which was 2.83. Notably, only 28 papers were authored by a single individual, comprising approximately 12% of the total, underscoring a significant level of collaboration in sustainability publications.

When examining the three sub-samples, it becomes apparent that the level of collaboration and the number of international co-authors are notably higher in the European sample. This sub-sample indeed exhibited a much lower percentage of single-authored documents compared to the entire sample.

Table 3 further demonstrates that pioneering studies in the late nineties on sustainability in family firms were primarily focused on European and North American countries. This suggests that these regions historically placed more emphasis on sustainability issues compared to their Asian counterparts. Additionally, these studies show a higher number of citations (average of 44.5 and 74.94 for Europe and North America, respectively), suggesting that these papers are generally consulted by researchers investigating the topic.

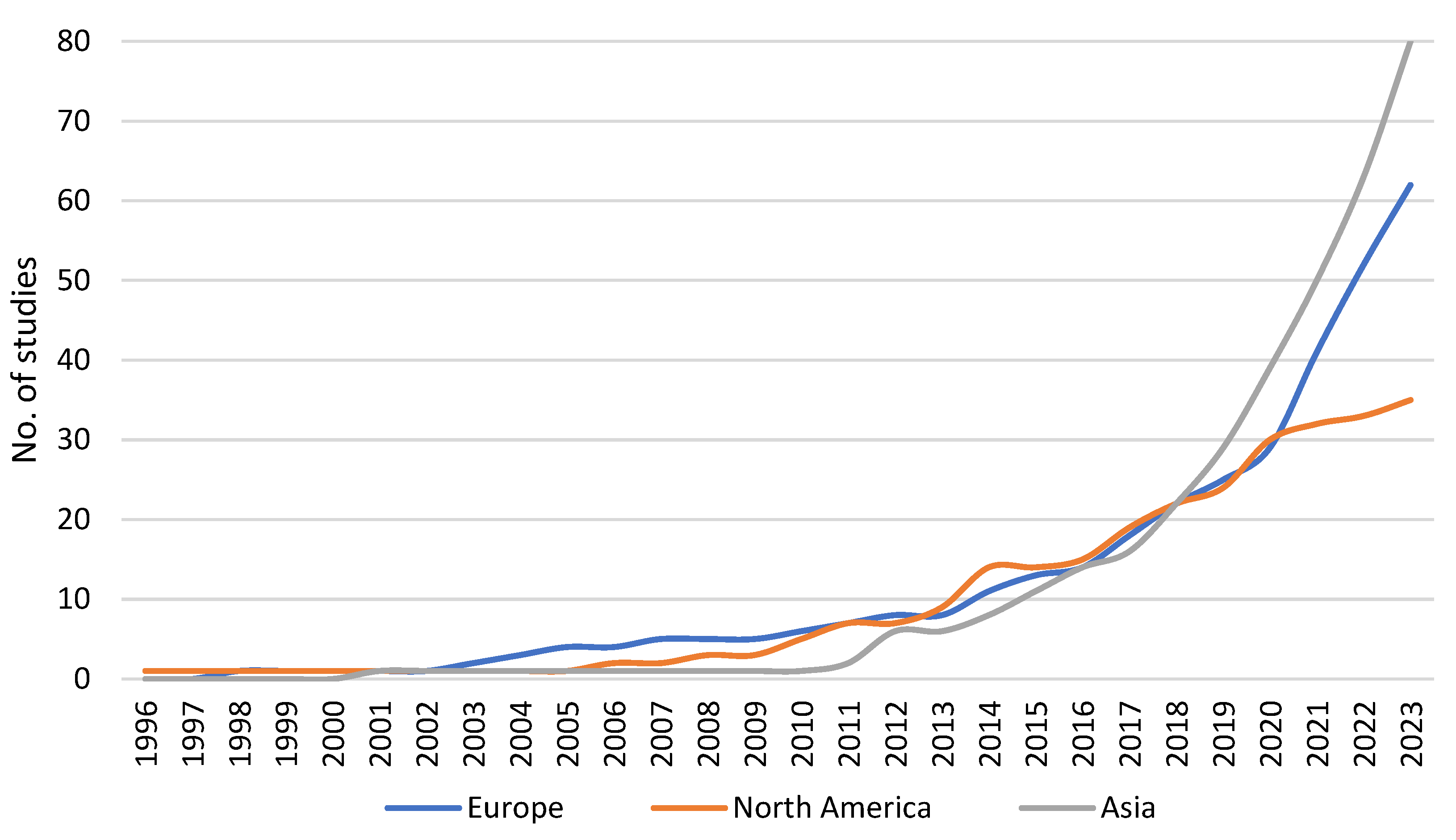

Figure 1 illustrates the evolution of the field in terms of the cumulative number of publications. Literature on sustainability in family firms emerges heterogeneously in the regions under analysis: research on western countries began to grow in the early 2000s, while studies on Asian countries show a delay of about eight years. It is noteworthy that nowadays Asia is becoming increasingly attractive for researchers, with an annual growth rate of 13.74%, compared to 9.65% and 2.6% for Europe and North America, respectively.

The substantial difference in the growth rates of European and North American studies becomes more pronounced after the Covid-19 pandemic. Before the pandemic, studies in the two regions followed a similar pattern. However, after the crisis, the two lines diverged. This behaviour could be explained by significant regulatory interventions by the European legislator, which has implemented various initiatives to strengthen the transparency of sustainability disclosures, develop responsible approaches, and regulate taxonomies and investments towards sustainability.

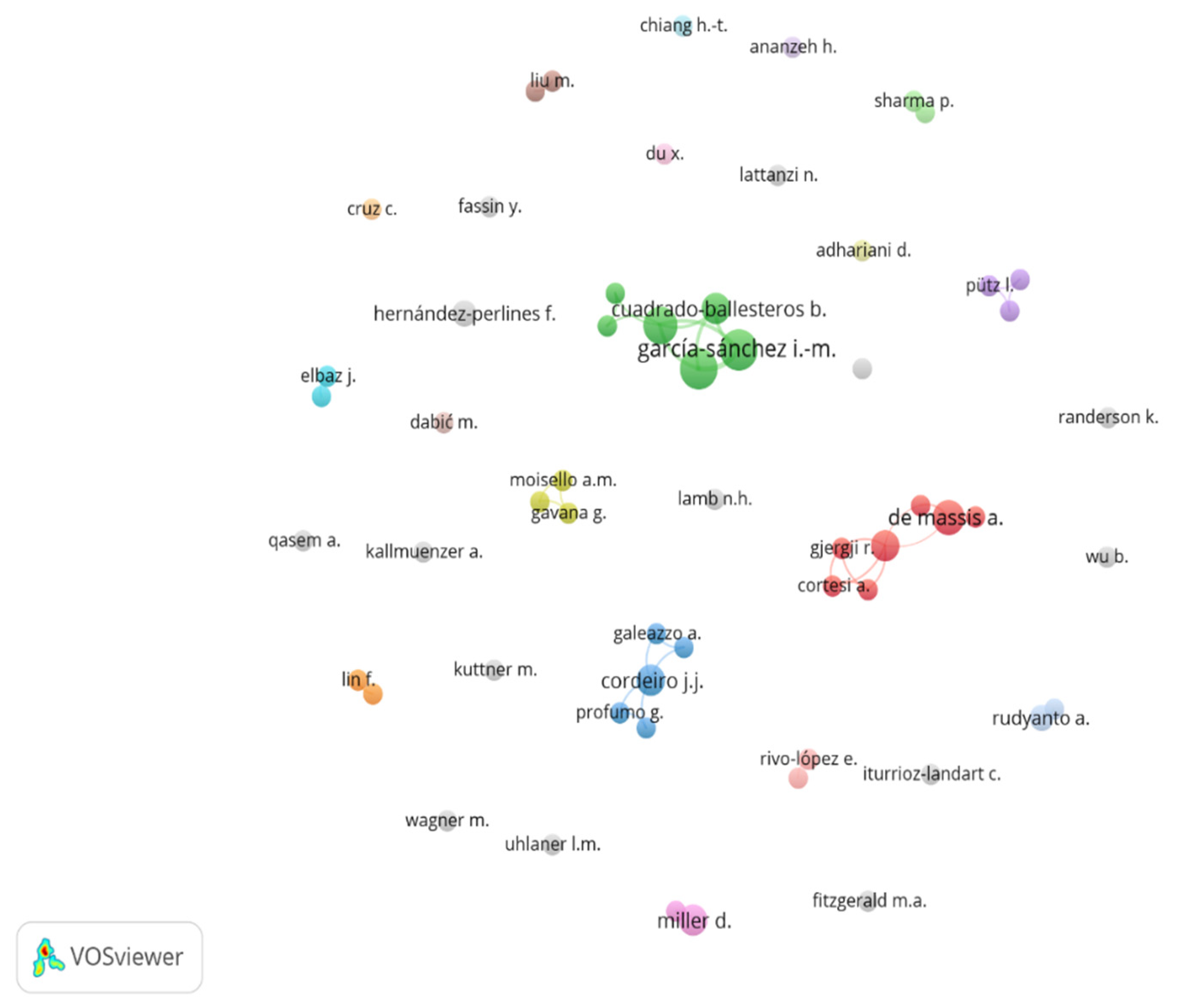

We analyse the network among researchers investigating sustainability in family firms. Figure 2 graphically represents the relationships among authors in the production of papers and the intensity of these relationships. The size of the nodes indicates the number of contributions by an author, and the thickness of the lines specifies the frequency of scientific collaborations in which scholars have worked together. First, the analysis reveals that only ten authors have more than two publications on the topic and that such productive authors work in the same clusters. The most productive author is García-Sánchez I.-M., followed by Rodríguez-Ariza L. and De Massis A. Second, the figure shows a high number of authors with very few weak relationships and limited relevance in terms of citations. This suggests that the majority of authors work in isolation, and there are no leading groups in this area of study. An exception is represented by the green, red, and blue groups, mainly composed of European authors. These results further highlight the intuition that Europe is currently leading research on these topics, particularly in Spain and Italy.

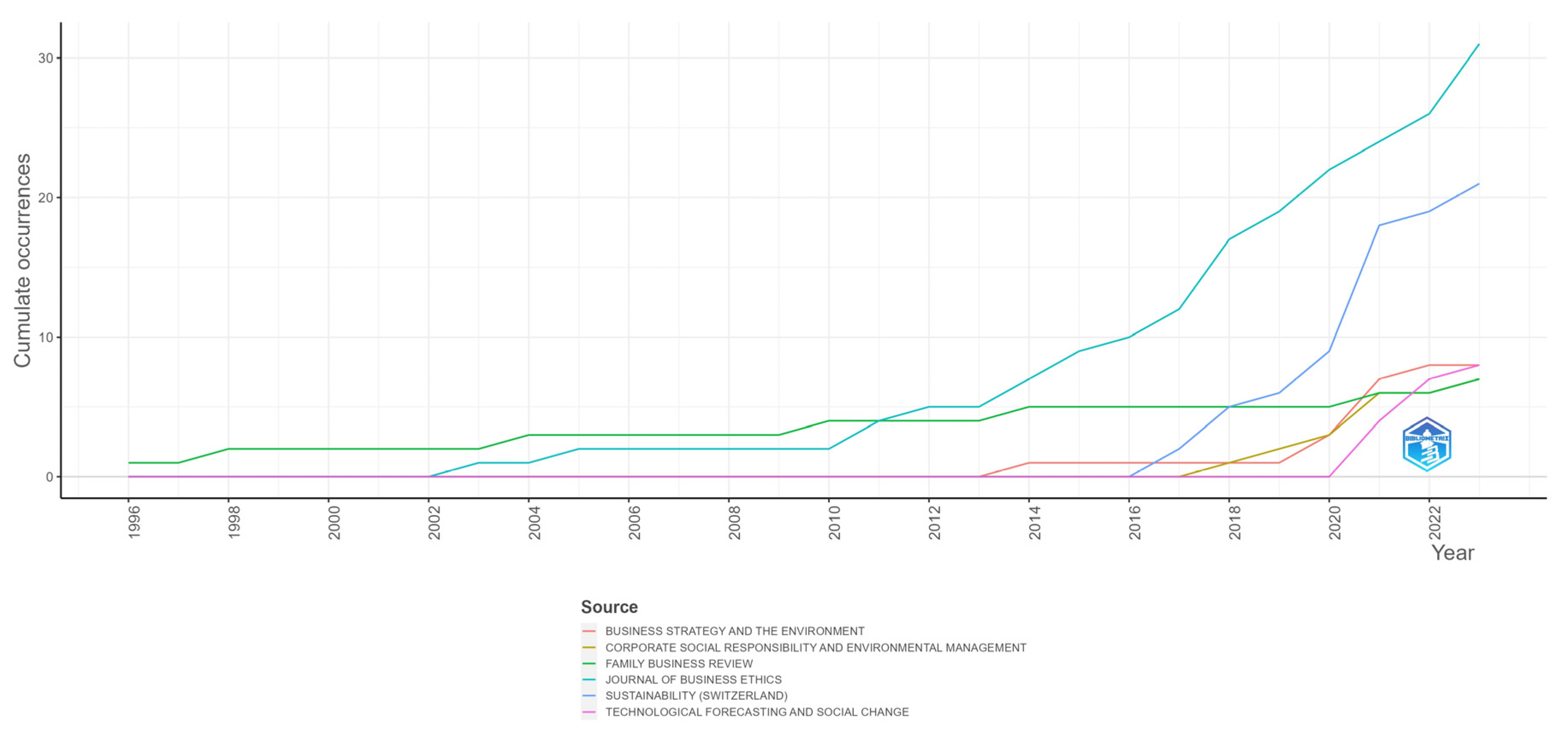

The 232 reviewed studies were published in 101 journals until 2023. Table 4 lists the journals with the highest number of published articles and citations. The table reveals that articles on sustainability in family firms are predominantly featured in journals focused on general management, social responsibility, and ethics. The leading journals in terms of the most publications are the Journal of Business Ethics (31 articles) and Sustainability (21 articles), while other journals exhibit a lower number of published studies. Among the remaining 86 sources, 69 published only one article.

In terms of the number of citations, the Journal of Business Ethics outperforms other sources, covering 23.63% of the citations. The second most cited journal is Entrepreneurship: Theory and Practice. Despite this journal publishing only four articles on CSR in family firms, it hosts the most cited paper on the topic, namely the works by [32] and [33].

Table 4 also indicates a certain degree of concentration among the most recurrent journals, as the first fifteen sources account for 53.88% and 67.59% of the total in terms of the number of articles and citations, respectively.

Figure 3 depicts the cumulative increase in the number of publications by each top journal. Since 2016, the number of publications by the Journal of Business Ethics and Sustainability has seen a significant increase. These journals have recently surpassed more specialized journals such as Family Business Review, which is primarily devoted to the exploration of dynamics of family firms. While Family Business Review was the primary outlet until 2011, in the last decade, Sustainability and the Journal of Business Ethics have emerged as the main sources for studies, becoming fundamentals publications for academics and policymakers focused on sustainability disclosure mandates. This suggests that topics related to family firms are no longer confined to specialized journals but are welcomed in a broader range of sources, indicating the increasing interest among scholars and editors.

Untabulated results show that Sustainability is the preferred output for studies on European countries (14.52%), while Journal of Business Ethic is the main source for Asian and North American research (7,5% and 25.71%, respectively).

3.2. Co-occurrence network

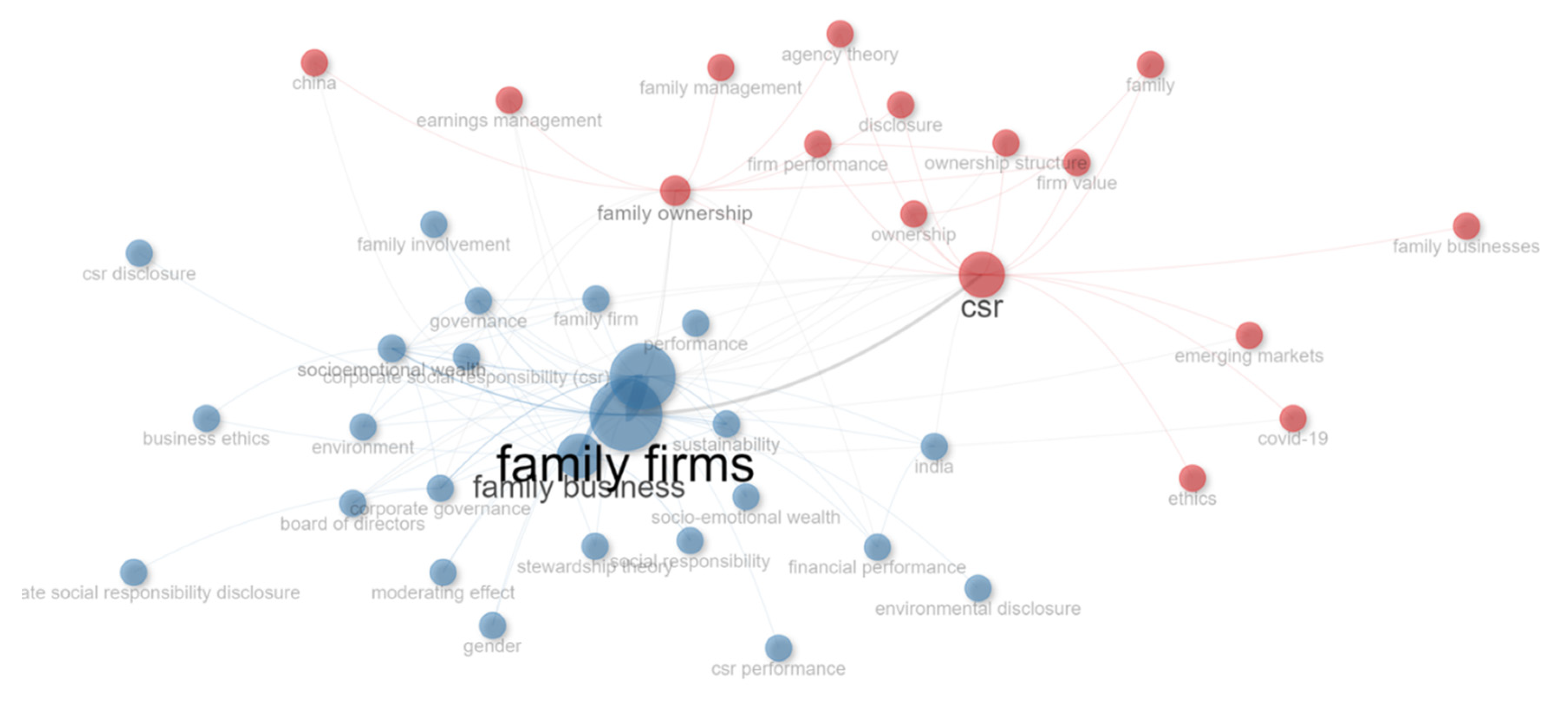

Main topics and main research streams are related to the words included in the research strategy. So, they also are the consequence of the decisions initially assumed in sample definition. We included the most important words and also their similarities both to maximize the composition of the sample to be analyzed and the coverage of our analysis.

The aggregate representation of co-occurrence network, as in Figure 4, suggests that two research streams are put into evidence. The first word or statement highlighted is, as expected, “family firms” and “family business”. This network connects a lot of other words or statements, that mainly come from the input of the research. As a consequence, this network is the largest. Within this network, we can observe some relevant focuses. The first one is about family firms’ governance, family involvement and the role of board of directors. These analyses are mainly related to the development of the business, with a clear focus on strategies and organization. Family firms are characterized by specific challenges, as for example the family involvement and the generational succession, towards the future of the business. A second focus is about performance. This cluster is large, as it encompasses both papers analyzing social and environmental performance, within the broad area of Corporate Social Responsibility (CSR), but also the economic performance. The relationship between CSR and economic performance has become increasingly closed over time, as the non-financial performance gained in importance. So, regardless of the firms’ size and business model, the integration of the performance’s analysis related both to economic and non-financial contents offers a comprehensive overview of the firm, its governance and its business. According to the increasing spread of the integrated report, we may expect the importance of this stream will grow in next years, also for family firms.

The third main focus is related to disclosure. Disclosure is declined according to different points of view: CSR disclosure and environmental disclosure are the most common. The quality and the depth of the information provided to the financial markets, to the social communities and to all the categories of shareholders are expected to increase over time, to enhance the quality of social and economic reporting. As a consequence, the markets’ evaluation will be related to a full and large dataset of data and qualitative information about firms’ business.

The second largest network is built around “Corporate Social Responsibility” (and sometimes even just the acronym). A quite large set of keywords is related to CSR. Among all, family ownership, ownership structure, family management are the most cited. Moreover, some focuses on firms’ performance and value are into evidence too.

Among the untabulated results, we have that the cluster of the European studies highlights two main research streams. The first one related to “family business”, with a prevalence of keywords related to the distinguish characteristics of the small business, with regards to corporate governance and entrepreneurship. The second one mainly focuses on the linkage between “family firms” and “corporate social responsibility”, where firms’ performance and disclosure are put into evidence. Asian studies can be represented thanks to two large sets of keywords, “family firms/CSR” and “corporate social responsibility/family ownership”. Even if most cited keywords are similar to the rest of the sample, Asian studies – that are, on average, relatively newer – offer some specific focuses on socioemotional wealth theory, institutional voids and the role of family business within emerging markets. American studies are focused on two major research streams, that are in line with motor themes and two broad keywords that deal with “family firms” and “csr/corporate social responsibility”.

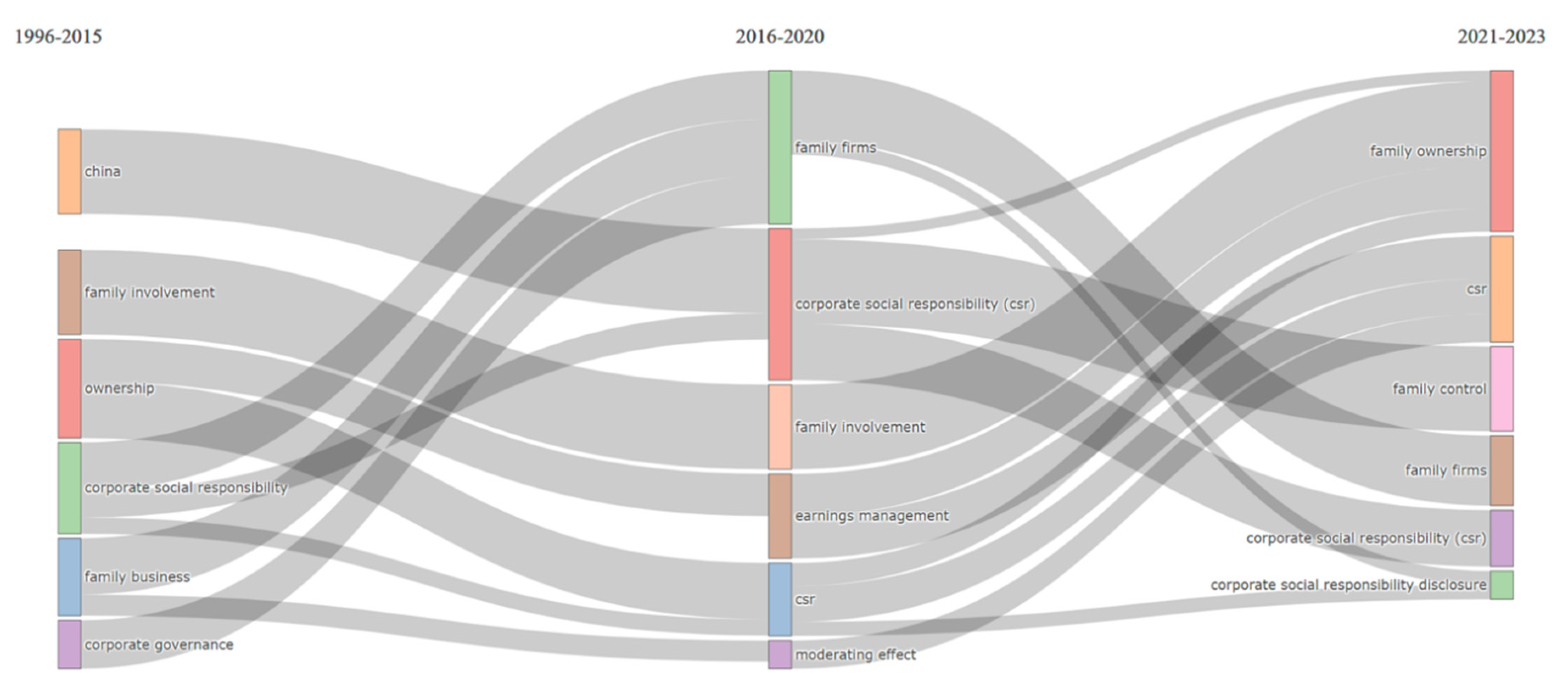

3.3. Thematic evolution

As often reported in other similar studies, Figure 5 summarizes the evolution of research and the history of themes over time, using authors’ keywords. In order to analyze the differences in keywords’ relevance over time, we split the overall time horizon (1996-2023) into three segments: the first period, the longest one, takes from 1996 to 2015, the second one is in the range 2016-2020, while the last one encompasses the last three years (2021-2023). We also tried different time limits, but we noticed small differences. The final version, that refers to the above-mentioned “time windows”, moreover, can be explained with the relevance of some key dates. In 2015, for example the Paris Climate Agreement was signed and also the 17 SDGs were adopted by the United Nations; in 2020 we had the outbreak of the COVID-19 pandemic. We can expect that these milestones have pushed firms to devote higher attention to the relationship between CSR and performance, as well as to the analysis of their business, in terms of risks, efficiency, and sustainability.

Moreover, it’s worthy to mention that in recent years the number of contributions largely increased: these topics had a growing interest by researchers. Also, the geographical heterogeneity increased, with a higher number of papers coming from Asian countries or based on Asian firms.

In the first stage (1996-2015), among the most cited authors’ keywords we have family involvement, ownership, corporate social responsibility, and family business. As noted, the main focus is on “basic” themes that refer to firms’ management. The studies about CSR increased their importance over time and, actually, in the second stage (2016-2020) this keyword regained importance. Solid and basic profiles, however, are still relevant, i.e., the management of family firms and strategic decisions about family involvement and earning management. In the final stage (2021-23), the words’ distribution has remained similar. The family ownership is the most cited item, while the corporate social responsibility (its acronym) confirms its relevance. During the pandemic, global economies faced severe recession and firms had to face new challenges: new economic equilibria are required to face new risks. Sustainability is more and more included in firms’ strategies, as confirmed by the importance of CSR, family control and disclosure among the most cited items within this last time segment.

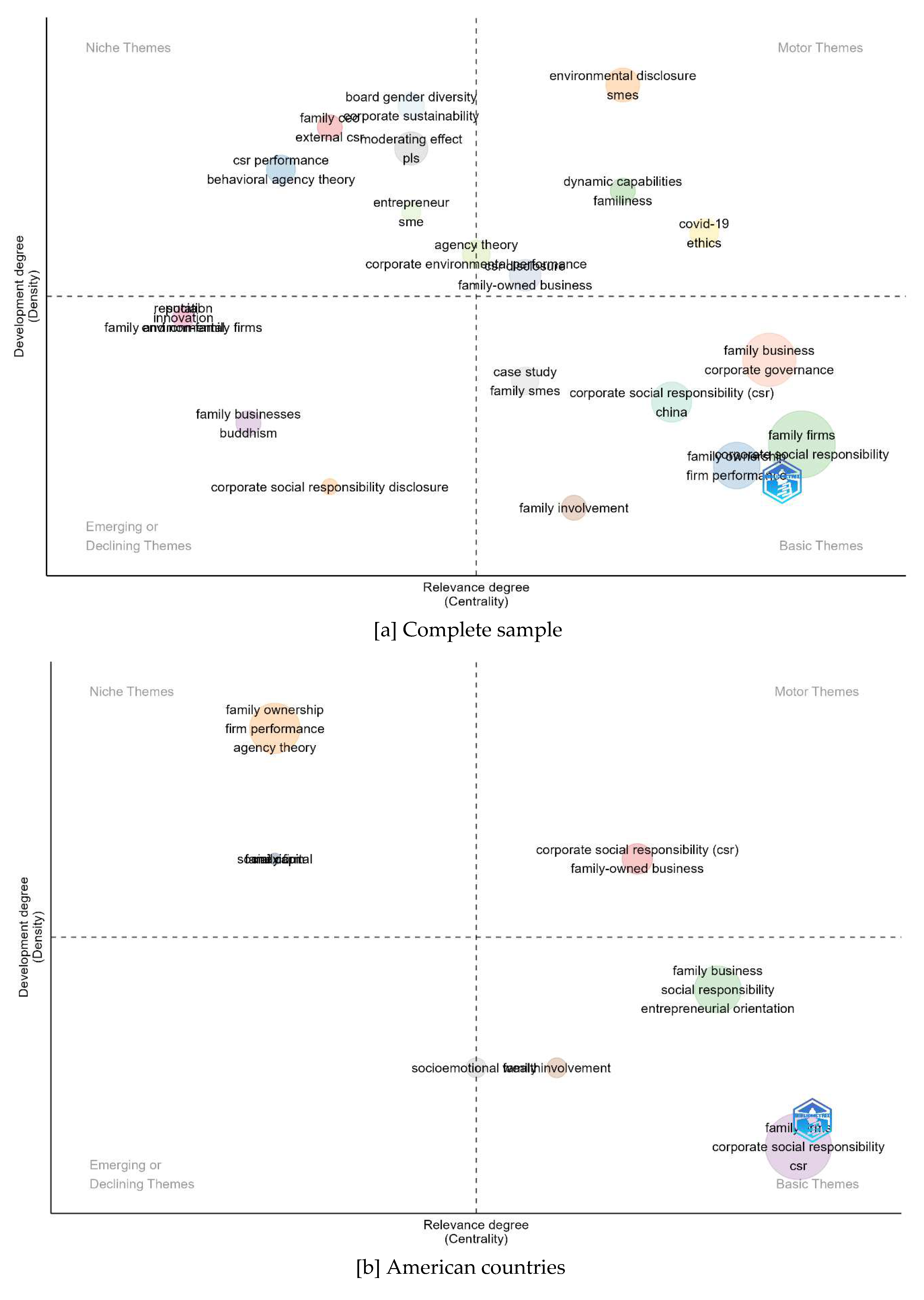

3.4. Thematic maps

Figure 6 that summarizes the relevance degree (centrality) and the development degree (density) suggests four macrotypes of themes to be analyzed: “motor themes” are characterized by high centrality and density, while – at the opposite – we have “emerging or declining themes”. Intermediate sections encompass both themes that are central but with a low level of development (“basic themes”), and themes well developed butess central (“niche themes”). Some remarks worth a mention.

“Basic themes” section shows high concentration of relevant topics, that characterize many contributions. The most important keywords refer to family business, corporate governance, firms’ performance and corporate social responsibility. These topics have remained central over time, and they are useful to build the general framework to analyze firms’ strategies with regards to CSR and sustainability. The basic themes are studied extensively in our sample.

“Niche themes” show low centrality and high level of development: this cluster seems to be quite diversified, as including – among others – board diversity, behavioral agency theory, and moderating effect. “Motor themes”, with high density and centrality, revealed the role of recent studies about COVID-19 pandemic and the rise of environmental disclosure’s issue. “Emerging or declining themes” diffusion is quite limited, as suggested by the small size of the bubble. Innovation and CSR disclosure are cited.

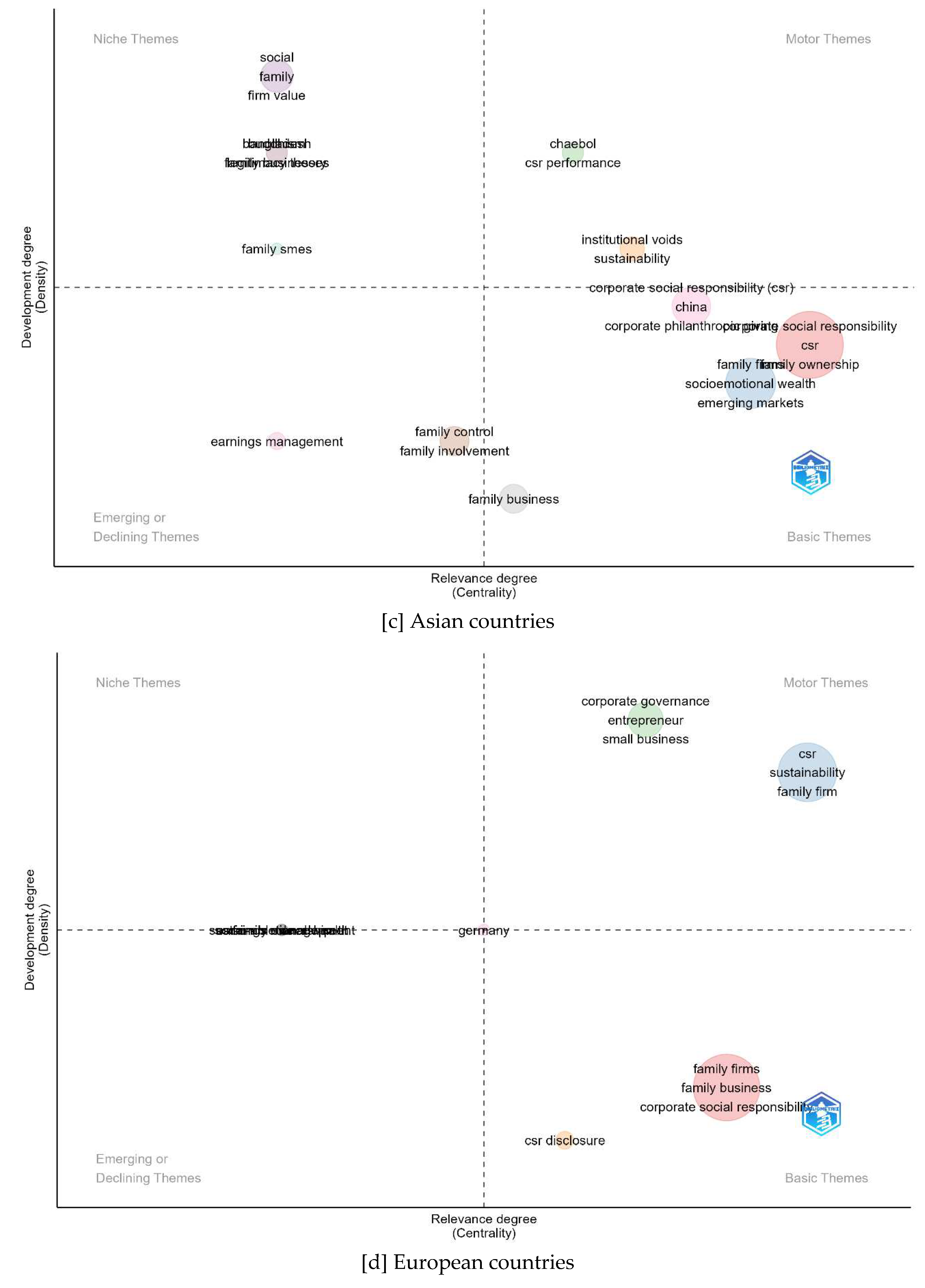

The interpretation of the thematic map of the subsamples offers some intuitions. Asian contributions highlight the relevance of the institutional voids as a “motor theme”, suggesting the necessity of a deeper regulatory intervention on sustainability issues which is still today mainly driven by initiatives of individual companies which are now using CSR to signal to foreign investors that they have more governance structures than other regional competitors [34].

European studies exhibit a slight overlap, primarily centered on CSR, sustainability, and family firms/business. This observation encompasses the most cited broader authors' keywords, reflecting the extensive exploration of these themes. Unlike the other two sub-samples, European studies notably emphasize the significance of disclosure and transparency concerning investors. This keyword is indeed strongly associated with a dimension of high relevance in European studies.

American studies demonstrate a strong central focus on fundamental themes surrounding family business, the historical evolution of corporate social responsibility, and its impact on firm performance. These studies particularly emphasize the relationship between sustainability performance and financial performance, underscoring a heightened focus on this correlation.

3.5. Word cloud

The word cloud depicted in Figure 7 is generated from the Keyword Plus, derived from the entire sample of selected studies. The size of the font corresponds to the frequency of appearance of a specific keyword in the literature. Predominant research streams are centered around corporate social responsibility, sustainability, business, and sustainable development. Notably, there is substantial emphasis on studies related to family business and family firms, as indicated by the significant weight of these keywords.

Regarding specific geographical clusters, the literature has identified several noteworthy keywords. European studies, in particular, demonstrate a focus on familiar themes such as corporate social responsibility and sustainability. However, there is also an emergence of "new" keywords related to governance approaches, decision-making processes, and environmental issues. Notably, environmental management has become a pivotal element within the European context due to the significant emphasis placed on it by regulators.

Asian literature, besides the similar set of most common keywords, identified sever other keywords, including firm ownership, firm size, innovation, and religion, which may suggest a greater attention by researchers.

American studies highlight a huge set of most common keywords (CSR/corporate social responsibility, family firms, family business), but also great attention to some specific keywords, more specific and “niche themes”, as issues about firms’ performance, family involvement and socioemotional wealth.

Upon comparison of the three clusters, it becomes apparent that Europe stands out as the primary driver of the environmental revolution. This distinction arises from the relatively lesser importance attributed to this issue in the other two clusters, where the frequency of this topic is notably low.

4. Conclusions, contributions and limitations

The family business holds significant importance within society and economic operators and has been extensively studied. Our bibliometric analysis spanned from 1996 to 2023, specifically focusing on sustainability within the context of family firms. We categorized our research sample into papers centered on European, North American, and Asian countries, aiming to assess the potential influence of diverse regulatory frameworks and cultural norms on literature production.

Our systematic literature review unveiled that Corporate Social Responsibility (CSR) remains relatively young within family firm research but is steadily gaining prominence. While early contributions date back to 1996, interest in CSR within family firms significantly expanded after 2000, notably evident in European and North American literature. On the other side, Asian studies exhibit an approximate eight-year lag. Nevertheless, sustainability issues are rapidly increasing their relevance in Chinese and other emerging Asian markets, signifying a global spread of sustainability awareness.

The analysis highlights the pivotal role of the COVID-19 pandemic, prompting significant regulatory interventions by the European legislator. These interventions aimed to enhance transparency in sustainability disclosures, foster responsible approaches, and regulate taxonomies and investments towards sustainability. Accordingly, European studies particularly emphasize disclosure matters, which may significantly influence firm management.

In contrast, studies in Asian countries often emphasize philanthropy and religious aspects, suggesting that family enterprises in these regions traditionally engage in philanthropic activities aligned with cultural norms. However, there's an increasing interest in CSR among firms and investors, calling for deeper regulatory intervention to signal better governance structures to foreign investors compared to regional competitors.

Overall, the subject has garnered substantial attention, diversifying thematically and geographically. While CSR and governance remain fundamental, emerging topics like disclosure and environmental concerns, especially in the European context, are gaining prominence within the broader scope of corporate responsibility.

Acknowledging limitations, diverse definitions of family firms pose challenges in drawing conclusions with external validity. Additionally, focusing on narrative and bibliometric aspects suggests future meta-analyses across various countries and regions for confirmation. Furthermore, limited sample sizes, particularly in the American subsample, limit comprehensive overviews and specific tests for robust results on thematic evolutions.

Funding

This work was supported by the Ministry of University and Research through the PRIN project Fin4Green - Finance for a Sustainable, Green and Resilient Society (M.E.D.G., A.T.). This work is part of the project NODES which has received funding from the MUR – M4C2 1.5 of PNRR with grant agreement no. ECS00000036.

Data Availability Statement

No new data were created or analyzed in this study. Data sharing is not applicable to this article.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Barnett, M.L. The Business Case for Corporate Social Responsibility. Bus Soc 2019, 58, 167–190. [Google Scholar] [CrossRef]

- Bowen, H. Social Responsibilities of the Businessman; University of Iowa Press, 1953.

- Carroll, A.B. Corporate Social Responsibility. Bus Soc 1999, 38, 268–295. [Google Scholar] [CrossRef]

- Tan, D.; Bilal; Gao, S.; Komal, B. Impact of Carbon Emission Trading System Participation and Level of Internal Control on Quality of Carbon Emission Disclosures: Insights from Chinese State-Owned Electricity Companies. Sustainability 2020, 12, 1788. [CrossRef]

- Komal, B.; Bilal; Ezeani, E.; Shahzad, A.; Usman, M.; Sun, J. Age Diversity of Audit Committee Financial Experts, Ownership Structure and Earnings Management: Evidence from China. International Journal of Finance & Economics 2023, 28, 2664–2682. [CrossRef]

- Liu, Q.; Bilal; Komal, B. A Corpus-Based Comparison of the Chief Executive Officer Statements in Annual Reports and Corporate Social Responsibility Reports. Front Psychol 2022, 13. [CrossRef]

- Payne, G.T.; Brigham, K.H.; Broberg, J.C.; Moss, T.W.; Short, J.C. Organizational Virtue Orientation and Family Firms. Business Ethics Quarterly 2011, 21, 257–285. [Google Scholar] [CrossRef]

- Breton-Miller, I. Le; Miller, D. Family Firms and Practices of Sustainability: A Contingency View. Journal of Family Business Strategy 2016, 7, 26–33. [Google Scholar] [CrossRef]

- Chen, J.; Liu, L. Family Firms, National Culture and Corporate Social Performance: A Meta-Analysis. Cross Cultural & Strategic Management 2022, 29, 379–402. [Google Scholar] [CrossRef]

- IFERA Family Businesses Dominate. Family Business Review 2003, 16, 235–240. [CrossRef]

- Daspit, J.J.; Chrisman, J.J.; Ashton, T.; Evangelopoulos, N. Family Firm Heterogeneity: A Definition, Common Themes, Scholarly Progress, and Directions Forward. Family Business Review 2021, 34, 296–322. [Google Scholar] [CrossRef]

- Bargoni, A.; Alon, I.; Ferraris, A. A Systematic Review of Family Business and Consumer Behaviour. J Bus Res 2023, 158, 113698. [Google Scholar] [CrossRef]

- Chapple, W.; Moon, J. Corporate Social Responsibility (CSR) in Asia. Bus Soc 2005, 44, 415–441. [Google Scholar] [CrossRef]

- Witt, M.A.; Stahl, G.K. Foundations of Responsible Leadership: Asian Versus Western Executive Responsibility Orientations Toward Key Stakeholders. Journal of Business Ethics 2016, 136, 623–638. [Google Scholar] [CrossRef]

- Gelfand, M.J.; Nishii, L.H.; Raver, J.L. On the Nature and Importance of Cultural Tightness-Looseness. Journal of Applied Psychology 2006, 91, 1225–1244. [Google Scholar] [CrossRef]

- Garcia-Sanchez, I.-M.; Cuadrado-Ballesteros, B.; Frias-Aceituno, J.-V. Impact of the Institutional Macro Context on the Voluntary Disclosure of CSR Information. Long Range Plann 2016, 49, 15–35. [Google Scholar] [CrossRef]

- Welford, R. Corporate Governance and Corporate Social Responsibility: Issues for Asia. Corp Soc Responsib Environ Manag 2007, 14, 42–51. [Google Scholar] [CrossRef]

- Chalkasra, L.S.P.S.; Rivera, J.P.R.; Basuil, D.A.T. A Review of Theoretical Perspectives on CSR Among Family Enterprises. Vision: The Journal of Business Perspective 2019, 23, 225–233. [Google Scholar] [CrossRef]

- de las Heras-Rosas, C.; Herrera, J. Family Firms and Sustainability. A Longitudinal Analysis. Sustainability 2020, 12, 5477. [Google Scholar] [CrossRef]

- Stock, C.; Pütz, L.; Schell, S.; Werner, A. Corporate Social Responsibility in Family Firms: Status and Future Directions of a Research Field. Journal of Business Ethics 2023. [Google Scholar] [CrossRef]

- Curado, C.; Mota, A. A Systematic Literature Review on Sustainability in Family Firms. Sustainability 2021, 13, 3824. [Google Scholar] [CrossRef]

- Ferreira, J.J.; Fernandes, C.I.; Schiavone, F.; Mahto, R. V. Sustainability in Family Business – A Bibliometric Study and a Research Agenda. Technol Forecast Soc Change 2021, 173, 121077. [Google Scholar] [CrossRef]

- Ramos-Hidalgo, E.; Orta-Pérez, M.; Agustí, M.A. Ethics and Social Responsibility in Family Firms. Research Domain and Future Research Trends from a Bibliometric Perspective. Sustainability 2021, 13, 14009. [Google Scholar] [CrossRef]

- Stanley, T.D. Wheat From Chaff: Meta-Analysis As Quantitative Literature Review. Journal of Economic Perspectives 2001, 15, 131–150. [Google Scholar] [CrossRef]

- Christofi, M.; Pereira, V.; Vrontis, D.; Tarba, S.; Thrassou, A. Agility and Flexibility in International Business Research: A Comprehensive Review and Future Research Directions. Journal of World Business 2021, 56, 101194. [Google Scholar] [CrossRef]

- Pham, H.-H.; Dong, T.-K.-T.; Vuong, Q.-H.; Luong, D.-H.; Nguyen, T.-T.; Dinh, V.-H.; Ho, M.-T. A Bibliometric Review of Research on International Student Mobilities in Asia with Scopus Dataset between 1984 and 2019. Scientometrics 2021, 126, 5201–5224. [Google Scholar] [CrossRef]

- Khan, M.A. ESG Disclosure and Firm Performance: A Bibliometric and Meta Analysis. Res Int Bus Finance 2022, 61, 101668. [Google Scholar] [CrossRef]

- Bretas, V.P.G.; Alon, I. Franchising Research on Emerging Markets: Bibliometric and Content Analyses. J Bus Res 2021, 133, 51–65. [Google Scholar] [CrossRef]

- Derviş, H. Bibliometric Analysis Using Bibliometrix an R Package. Journal of Scientometric Research 2020, 8, 156–160. [Google Scholar] [CrossRef]

- Aria, M.; Cuccurullo, C. Bibliometrix : An R-Tool for Comprehensive Science Mapping Analysis. J Informetr 2017, 11, 959–975. [Google Scholar] [CrossRef]

- Jalal, R.N.-U.-D.; Alon, I.; Paltrinieri, A. A Bibliometric Review of Cryptocurrencies as a Financial Asset. Technol Anal Strateg Manag 2021, 1–16. [Google Scholar] [CrossRef]

- Dyer, W.G.; Whetten, D.A. Family Firms and Social Responsibility: Preliminary Evidence from the S&P 500. Entrepreneurship Theory and Practice 2006, 30, 785–802. [Google Scholar] [CrossRef]

- Cruz, C.; Larraza–Kintana, M.; Garcés–Galdeano, L.; Berrone, P. Are Family Firms Really More Socially Responsible? Entrepreneurship Theory and Practice 2014, 38, 1295–1316. [Google Scholar] [CrossRef]

- Cordeiro, J.J.; Galeazzo, A.; Shaw, T.S.; Veliyath, R.; Nandakumar, M.K. Ownership Influences on Corporate Social Responsibility in the Indian Context. Asia Pacific Journal of Management 2018, 35, 1107–1136. [Google Scholar] [CrossRef]

Figure 1.

Cumulative frequency of published documents.

Figure 2.

Authors networks by normalised citations.

Figure 3.

Cumulative source growth by total number of published documents.

Figure 4.

Topics’ relevance as analyzed in the co-occurrence network.

Figure 5.

Thematic evolution.

Figure 6.

Thematic maps.

Figure 7.

Words cloud.

Table 1.

Methodological process and results.

| Steps | Description | Number of Articles |

|---|---|---|

| Step 1 | Keyword search in the Scopus Database | 541 |

| Step 2 | Application of the following filter: Peer-reviewed articles, English language, Subject areas (Business, Management, and Accounting; Economics, Econometrics, and Finance; Social Sciences and Environmental Science) | 402 |

| Step 3 | Examination of papers by the authors to remove unrelated articles | 232 |

Table 2.

Sample description.

| Research method | # of Articles | % of Articles |

|---|---|---|

| Quantitative | 202 | 87.1% |

| Qualitative/Conceptual | 23 | 9.9% |

| Review | 7 | 3.0% |

| Countries | ||

| USA | 29 | 14.4% |

| China | 19 | 9.4% |

| International sample | 17 | 8.4% |

| Spain | 14 | 6.9% |

| Italy | 13 | 6.4% |

| India | 12 | 5.9% |

| Indonesia | 8 | 4.0% |

| Taiwan | 8 | 4.0% |

| Germany | 7 | 3.5% |

| Regions | ||

| Asia | 80 | 39.6% |

| Europe | 62 | 30.7% |

| North America | 35 | 17.3% |

| International sample | 17 | 8.4% |

| Others | 8 | 4.0% |

Table 3.

Summary of Articles.

| Results | ||||

|---|---|---|---|---|

| Description | Complete sample | Europe | North America | Asia |

| MAIN INFORMATION | ||||

| Timespan | 1996:2023 | 1998:2023 | 1996:2023 | 2001:2023 |

| Sources (Journals, Books, etc) | 101 | 33 | 21 | 53 |

| Documents | 232 | 62 | 35 | 80 |

| Annual Growth Rate % | 14.53 | 9.65 | 2.6 | 13.74 |

| Document Average Age | 4.52 | 4.63 | 7.17 | 3.45 |

| Average citations per doc | 38.29 | 44.45 | 74.94 | 19 |

| References | 17322 | 5609 | 2733 | 5834 |

| DOCUMENT CONTENTS | ||||

| Keywords Plus (ID) | 284 | 119 | 13 | 111 |

| Author's Keywords (DE) | 537 | 188 | 106 | 226 |

| AUTHORS | ||||

| Authors | 570 | 183 | 88 | 203 |

| Authors per doc | 2.46 | 2.95 | 2.51 | 2.54 |

| Authors of single-authored docs | 26 | 3 | 6 | 12 |

| AUTHORS COLLABORATION | ||||

| Single-authored docs (no.) | 28 | 3 | 6 | 13 |

| Single-authored docs (%) | 12.07 | 4.84 | 17.14 | 16.25 |

| Co-Authors per doc | 2.83 | 3.16 | 2.74 | 2.71 |

| International co-authorships % | 32.76 | 37.1 | 34.29 | 31.25 |

Source: Authors’ elaboration using Biblioshiny package in R.

Table 4.

Most influential Journals.

| # | Journal | Number of Articles | Number of Citations | ||

|---|---|---|---|---|---|

| 1 | Journal of Business Ethics | 31 | 13.36% | 2063 | 23.63% |

| 2 | Sustainability | 21 | 9.05% | 321 | 3.68% |

| 3 | Business Strategy and the Environment | 8 | 3.45% | 439 | 5.03% |

| 4 | Technological Forecasting and Social Change | 8 | 3.45% | 220 | 2.52% |

| 5 | Corporate Social Responsibility and Environmental Management | 7 | 3.02% | 162 | 1.86% |

| 6 | Family Business Review | 7 | 3.02% | 486 | 5.57% |

| 7 | Journal of Business Research | 6 | 2.59% | 293 | 3.36% |

| 8 | Journal of Family Business Management | 6 | 2.59% | 39 | 0.45% |

| 9 | Journal of Family Business Strategy | 6 | 2.59% | 311 | 3.56% |

| 10 | Social Responsibility Journal | 6 | 2.59% | 100 | 1.15% |

| 11 | Journal of Cleaner Production | 5 | 2.16% | 163 | 1.87% |

| 12 | Corporate Ownership and Control | 4 | 1.72% | 48 | 0.55% |

| 13 | Entrepreneurship: Theory and Practice | 4 | 1.72% | 1114 | 12.76% |

| 14 | Asia Pacific Journal of Management | 3 | 1.29% | 96 | 1.10% |

| 15 | Asian Business and Management | 3 | 1.29% | 46 | 0.53% |

| Total | 125 | 53.88% | 5901 | 67.59% | |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Copyright: This open access article is published under a Creative Commons CC BY 4.0 license, which permit the free download, distribution, and reuse, provided that the author and preprint are cited in any reuse.