Submitted:

18 November 2023

Posted:

22 November 2023

You are already at the latest version

Abstract

Finnish government's carbon neutrality goal by 2035 requires integration of renewable energy sources into the power grid. Considering the stochasticity of these resources, additional sources of flexibility are necessary to balance supply and demand in the power grid. District heating network (DHN) operators in Finland plan to shut down fossil-fuel-based combined heat and power plants and electrify heating systems by deploying heat pumps (HPs) and electric boilers. Techno-economic analysis and optimal operation of DHN-connected HPs and electric boilers in providing ancillary balancing services considering the 15-minute granularity in the balancing markets in Finland were investigated. The objective was to maximize the potential revenue for DHN operators gained from the day-ahead electricity market and frequency containment reserve (FCR) balancing markets. Three inter-connected DHNs in the Helsinki metropolitan area were optimized considering the reference year 2019 and each operator's decarbonization strategies for 2025. HPs could gain the highest profit from FCR-D up-regulation market, while the electric boiler may gain considerable profits from FCR-D down-regulation market. Compared to other balancing markets studied, the FCR-N market had a limited profit margin. Sensitivity analysis indicated that spot electricity prices and CO2 emission allowance prices have a significant impact on the profit from balancing markets.

Keywords:

District heating

; Electrification

; power-to-heat

; Balancing markets

; Techno-economic analysis

; Helsinki metropolitan area

; heat pump

1. Introduction

The Paris Agreement ratified by the world community represents a commitment to work together to mitigate the human-induced greenhouse effect [1]. To decarbonize the energy sector and expand renewable sources of power generation, such as wind and solar power, the European Commission has launched a “European green deal” [2]. At a national level, the Finnish government has committed to achieving carbon neutrality by 2035 [3]. The large integration of intermittent power generation, variable resources with limited controllability, results in power deficits and surpluses that can affect the balance and cause grid frequency, voltage, and power transmission phase angle deviations [4]. As a result, ancillary services are required to respond to an unanticipated deficiency or surplus in power production or consumption in a cost-effective and efficient manner [5]. Recently, the provision of ancillary services from wind and nuclear power has been introduced in Finland. Loviisa nuclear power plant, for example, has joined the frequency containment reserve for disturbance (FCR-D) down-regulation market [6,7]. Balancing markets, operated by national transmission system operators (TSOs), ensure that sufficient electric capacity (i.e., reserve capacity) is always available to supply the required energy flow to preserve the grid frequency [8].

Power-to-heat (P2H) technologies such as heat pumps (HPs), electric boilers, and combined heat and power (CHP) technologies that operate at the interface between the two sectors can provide several benefits to the electrical power system, including increased flexibility and network support, such as reserve provision [9,10,11,12,13], congestion management and voltage control [14]. As a solution to the challenges posed by the stochastic nature of renewable heat sources and the large number of unprofitable biomass boilers in rural district heating, [15] explored the potential for the utilization of HPs in the Austrian electricity market. By participating in the day-ahead and balancing markets, HPs could save energy costs as well as earn additional revenues. District heating networks (DHNs) have large electrical capacities due to existing CHP plants and HPs [16,17]. To decarbonize this sector, which has 50% of market share of space heating in Finland in 2021 [18], operators aim to reduce dependency on fossil fuels by the integration of large-scale HPs and electric boilers, in addition to biomass fuels [19]. Several CHP plants will be shut down before the end of their technical lifetime, and city DH companies are increasing wind power and nuclear power via shareholdership. Most notably, DHNs are natural aggregators of heat demand and can set operating modes that permit the incorporation of higher shares of renewable energy sources without jeopardizing heat consumers’ comfort, utilizing centralized thermal energy storage [20]. Authors in [21] assessed the technical potential of DHNs to contribute to Frequency Containment Reserves (FCR), Automatic and Manual Frequency Restoration Reserves (aFRR and mFRR) markets and estimated the potential at country and EU levels based on appropriate assumptions. A significant degree of flexibility can be provided by DHNs based on the findings of the study. Javanshir et al. [22] conducted a literature and industry review and proposed an optimal operation of an electrified DHN to participate in different electricity and balancing markets for a hypothetical mid-sized city DHN, considering the technical requirements of providing reserve in each market. Results indicated the economic benefits of providing balancing services from HPs in the aFRR market. According to Wang et al [23], CHP plants provide flexibility as a means of reducing wind power curtailment and increasing revenue through ancillary services. Using a case study of optimal dispatch of a CHP plant in Copenhagen, Denmark in the heat market, the study compared the flexibility of different CHP unit types, operation modes, and integration of heat accumulators. Haakana et al. [24] proposed a methodology to optimize the operation of a CHP plant in liberalized energy markets by considering various marketplaces available for heat and electrical power end products, with a focus on electricity reserve market opportunities.

Literature discusses the benefits of DHN-connected P2H units for providing balancing services. In [22], a comprehensive literature review was presented. However, some of the research gaps, to the best knowledge of the authors, remain understudied. The interaction between the operation of a reserve unit in a DHN and other production units that do not participate in the balancing markets is sometimes overlooked in the literature [24]. This is important in the sense that the provision of balancing services from a reserve unit may disrupt the heat demand balance, which is the priority of a DHN operator. The study of major changes in the electricity and balancing markets is another important issue overlooked in the literature. One major upcoming change is the shorter imbalance settlement period (15-minute time resolution), which allows market participants to react easier to changes and the costs of imbalances can be divided more accurately between the participants causing the imbalances. It may also help to enable Europe-wide cross-border intraday and balancing markets [25]. In addition, it may facilitate the emergence of new market opportunities related to demand response and smart grids. In addition, Finland will introduce a single-price model, automated balancing power markets, and a common Nordic and later European FRR market [26]. Currently, all electricity markets in Finland, including the day-ahead, intraday, and balancing markets, not to mention the imbalance settlement, operate via one-hour blocks [27]. There will be a significant reformation to this when all of the above will transform into a shorter, 15-minute time resolution. According to the proposal published by eSett, the imbalance settlement provider [28], the volume fee for imbalances will continue to apply to the net imbalance per hour instead of the imbalance in each specific 15-minute imbalance settlement period. The pricing of imbalances will continue to be based on the hourly price of balancing power. The proposals call for the balancing energy caused by the activation of reserves to be calculated in 15-minute periods following the transition to a 15-minute imbalance settlement period [29]. However, the trading period in the reserve market will continue to be one hour. Hence, further research is needed to address these gaps.

Finland’s installed wind power capacity increased by 74% from 2021 to 2022 to 5677 MW, while the average electricity consumption was 9360 MW [30]. Due to the large-scale integration of wind power into the Finnish electrical power system and the above-mentioned research gaps, this study investigated the feasibility of DH systems in providing balancing services. With the electrification of DH systems in Finland, larger capacities of HPs and electric boilers are available, which could contribute to balancing markets and generate additional revenue, as the DH operators are also losing income from electricity sales when shutting down the CHP plants. Therefore, the possibilities of the Helsinki metropolitan DHN, including the interconnected DHNs of Helsinki, Espoo, and Vantaa cities, when providing FCR balancing services to the electrical power system were examined. This system produced about 11.1 TWh of DH for more than one million people in 2022 [18]. The study also considered the upcoming changes in the market, such as the single-price model and 15-minute resolution in the balancing markets. The studied DHNs were simulated in 2019 and 2025, considering the planned decarbonization pathways of these DHNs.

The remainder of the paper is as follows. In the methods section, subsection 2.1. explains the optimal operation of the case study DHN without considering balancing market participation. In subsection 2.2 the studied balancing markets, their requirements, and the operation of DHN in these markets are explained. The configuration of the case study DHN is explained in subsection 2.3. Results of the simulations and conclusions are placed in sections 3 and 4.

2. Methods

This study examined the possibilities of the Helsinki metropolitan area DHN participating in the Finnish balancing markets. 2019 was used as the base year, as it was the last year with regular electricity prices before Covid and the Ukrainian war [31]. In addition, the plausible changes by the year 2025 were modelled by assuming that the heat generation fleet changes according to the carbon neutrality plans of the cities. In the first subsection, the optimal operation of the studied DHN to provide required heat demand to end-users without providing balancing services is described. The study of the balancing markets and the operation of the DHN in these markets is then presented in subsection 2.2. A summary of the case study DHN and its configuration in the studied years (2019 and 2025) is provided in the last subsection.

2.1. The optimal operation of DHN to provide heat (day-ahead scheduling)

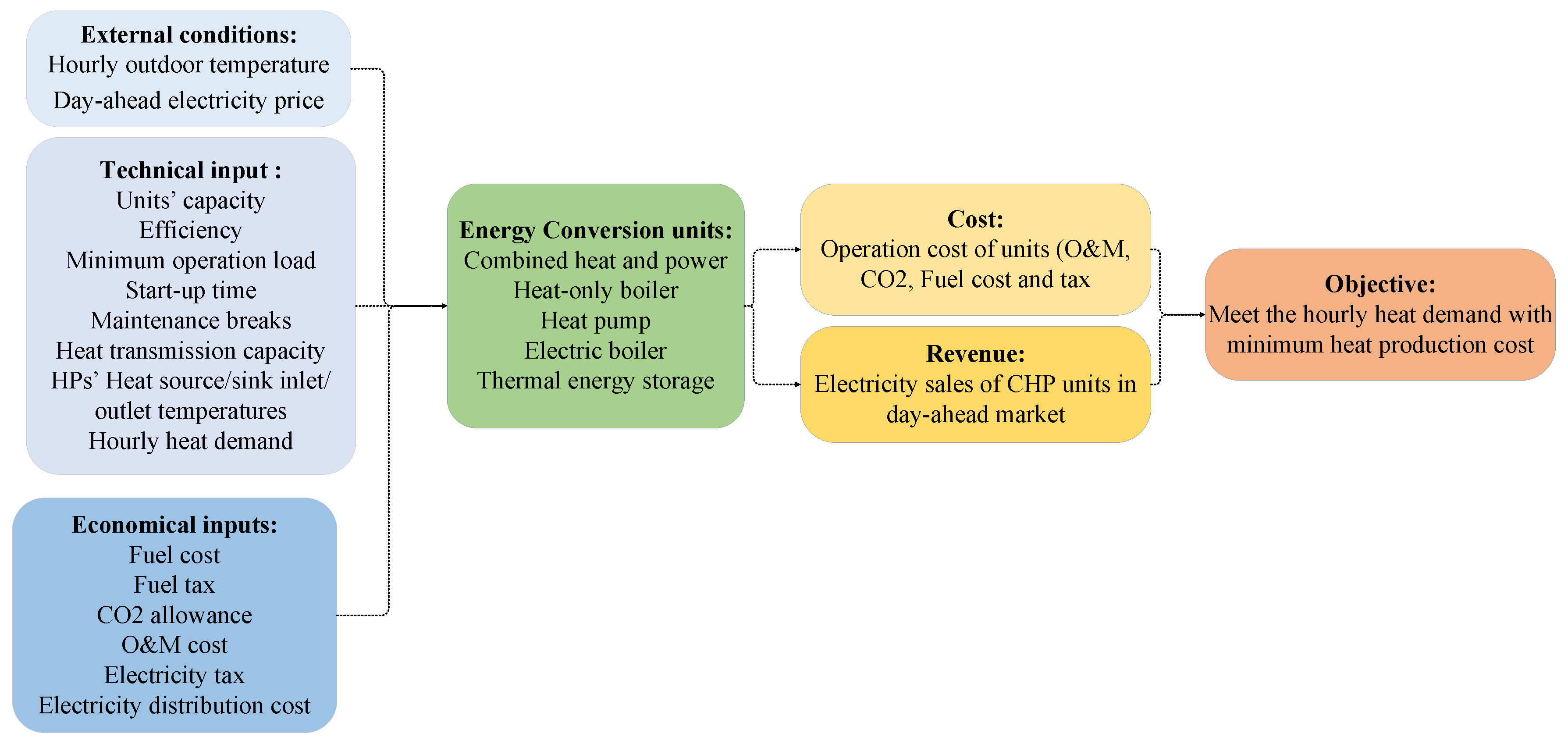

The DHN of Helsinki metropolitan area is simulated and optimized in EnergyPRO software [32,33]. The mechanism of the software is to provide a least-cost solution while ensuring heat demand can be met by the heat supply every hour. The software minimizes the yearly net operating costs of the entire system. The production cost of each unit is calculated by the cost of fuel consumption, fuel tax, operation and maintenance (O&M) costs, as well as CO2 allowance cost of fuels. For HPs and electric boilers, operating costs include electricity consumption and distribution costs, electricity tax, and O&M costs. CHP units gain revenue by selling the produced electricity in the day-ahead electricity market with realized prices. As input to the simulation, historical day-ahead electricity prices [31], fuel prices [34], CO2 allowance prices in the European Union Emission Trading System (EU ETS) [35], weather data [36], and calculated hourly heat demand based on heating degree days for each city [16], as well as annual heating demand, were used. The district heating business in Finland is a natural monopoly, i.e., there is no competitive market for heat, so heat prices are regulated and the revenue from heat sales is not included in the analysis [37].

Heat demand must be met on every time step, which is one hour in this study. The running orders of the production units are calculated for every hour according to the net production costs and revenues (for CHPs), but some technical limitations, such as starting and shut-down times, as well as the limitations in fuel usage were assumed [38], and these have an impact on the running order as well. Instead of calculating the running order chronologically hour by hour, the software ensures the optimal operation strategy by committing the production units to the most favorable periods at first. Figure 1 illustrates the mentioned inputs and outputs used in the model. Because the DH system in this stage only participates in the day-ahead electricity market, by consuming and selling electricity, this stage is called the day-ahead scheduling stage.

2.2. The operation of DHN in the balancing markets (balancing stage)

This study assumed the participation of HPs and electric boilers within the studied DHN, as reserve units, in balancing markets. The following subsections explain the operation of reserve units and the entire network while providing balancing reserves.

2.2.1. Market background

Balancing markets in Finland consist of frequency containment reserves for normal operation (FCR-N), frequency containment reserves for disturbances (FCR-D), fast frequency reserves (FFR), and frequency restoration reserves that can be activated automatically (aFRR) or manually (mFRR) [8]. A detailed description, key characteristics, and requirements of each product, as of 2021, specified by the local Finnish TSO, Fingrid [8], are summarized in [22]. While the focus of the previous study was on aFRR market [22], in this study the provision of balancing services in FCR markets, including FCR-N, FCR-D up-regulation, and FCR-D down-regulation markets is investigated.

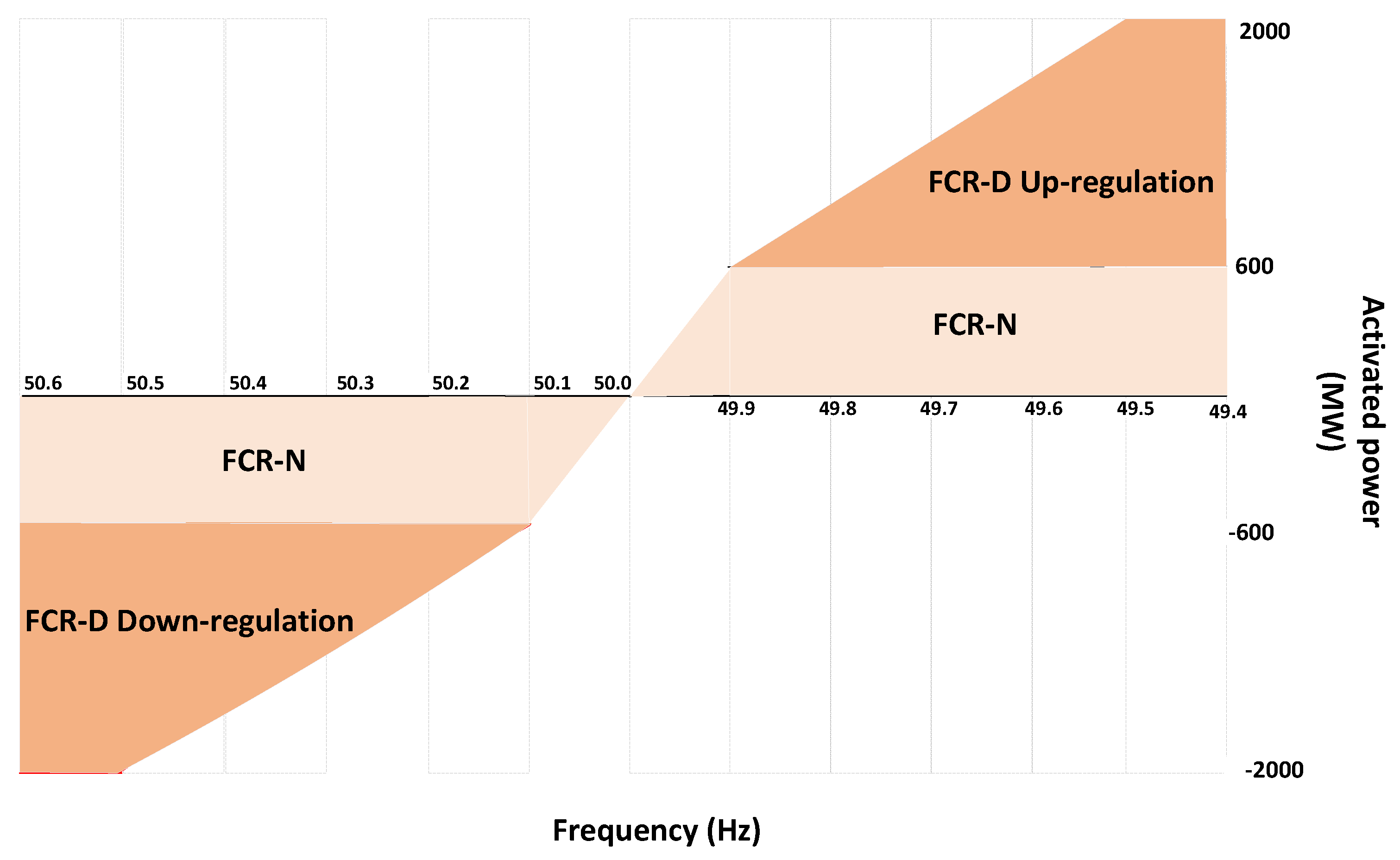

FCR-N and FCR-D are active power reserves automatically controlled based on frequency deviation. During normal operation and disturbances, they control the grid frequency. FCR-N aims to keep the frequency within the standard frequency range of 49.9 Hz to 50.1 Hz [8]. When the frequency deviation exceeds the standard range, FCR-D aims to limit it to 49.5 Hz or 50.5 Hz. As a symmetrical product, FCR-N must have the ability to up and down-regulate. FCR-D is divided into separate up and down-regulation products. In ultimo 2021 the downward regulation of FCR-D will also be implemented in the Nordic synchronous area with requirements mirrored from the upward regulation [8]. 2019 FCR market capacity prices are used in the 2019 and 2025 simulations. FCR markets require a rapid response time of 3 minutes for FCR-N and 30 seconds for FCR-D [8] and HPs are usually not capable of ramping up and down that quickly unless they are equipped with special configurations, as argued following an industry and literature review in [22]. In Copenhagen, Denmark, the FlexHeat HP, a two-stage ammonia heat plant with a thermal capacity of 800 kW, delivers forward temperatures of 60 to 82 ° for district heating, where additional equipment is installed to pre-heat the system, thereby allowing the compressors to ramp up faster and provide FCR products. In this study, it is assumed that HPs in the case study DHN can provide FCR products. Electric boilers are capable of fast ramping and can therefore participate in many balancing markets with fast activation requirements, such as FCR, FFR, and aFRR [39].

2.2.2. Energy analysis

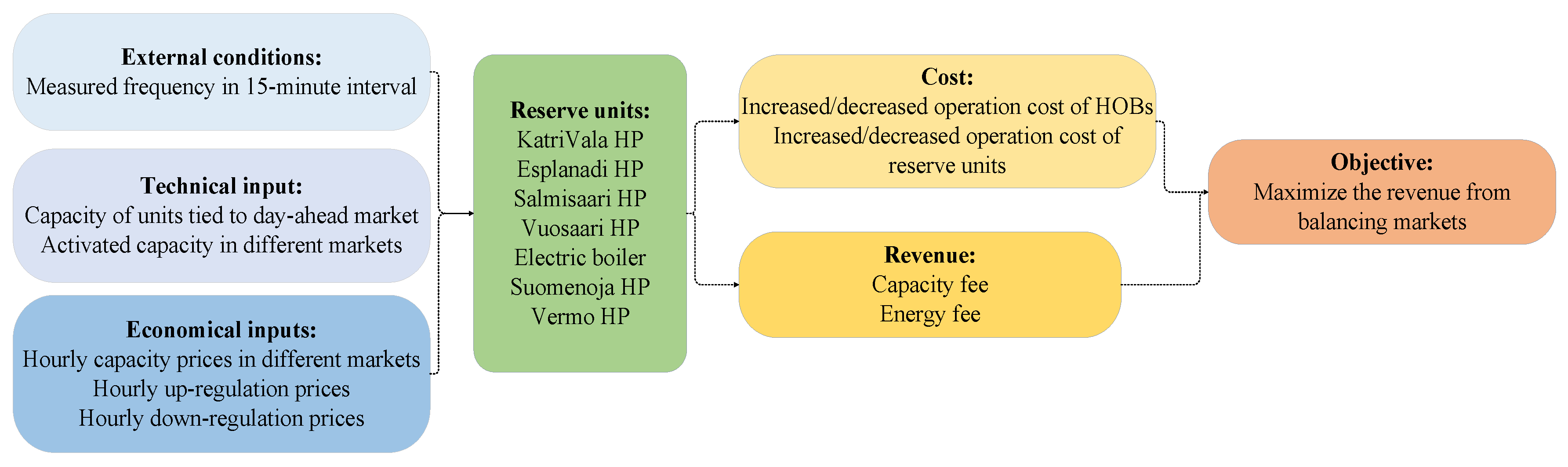

Reserve units offer to receive payment in exchange for allocating capacity to the balancing markets. The objective here is to maximize this revenue by making the optimal use of reserve units’ capacities, without disrupting the heat demand balance. During periods of positive imbalance (demand exceeding supply), reserve units provide downward reserve (down-regulation) by increasing electricity consumption or decreasing electricity production. When there is a negative imbalance, where demand exceeds supply, reserve units provide upward reserve (up-regulation) by reducing electricity consumption or increasing production. As the gate-closure time of the FCR market (18:30 EET time zone in the hourly market one day before the operation day (D-1)) takes place after the day-ahead market trades have been published (14:00 EET time zone in day D-1) [8], it is then known exactly how much of the capacity of a reserve unit has been tied in the day-ahead market (the day-ahead scheduling stage). So, after publishing the day-ahead market results and determining the optimal operation of the units in the day-ahead scheduling, the operator can offer the available capacity of reserve units to FCR-N, FCR-D up-regulation, and FCR-D down-regulation markets separately.

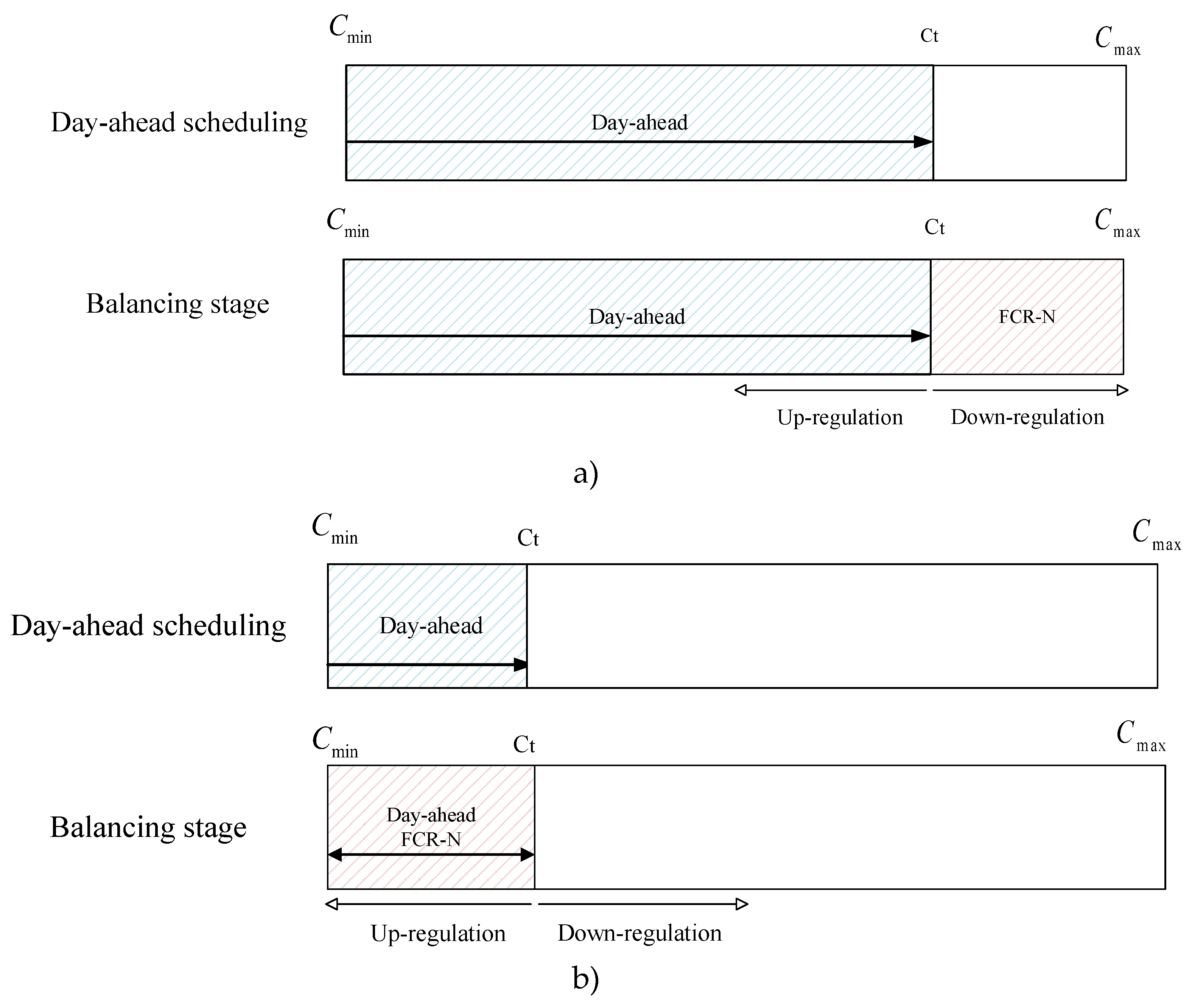

As the FCR-N market requires symmetrical capacity bids, the balancing responsible unit should be able to increase or decrease its electricity consumption simultaneously. Figure 2 illustrates how the available capacity of HP is allocated to FCR-N market after the day-ahead scheduling stage. Figure 2(a) shows a reserve providing HP which more than half of its capacity is tied to the day-ahead market in the day-ahead scheduling stage . In this case, MW of capacity is available for FCR-N market, so that the HP can do up or down-regulation simultaneously. In contrast, Figure 2(b) depicts the case where the HP is operating with less than 50% of the maximum load in the day-ahead scheduling stage. In this case, capacity can be allocated to the market. In this study the minimum load for a large-scale HP is considered 10% of maximum load [40]. If the day-ahead market offer is not accepted, the operator cannot offer capacity to the FCR-N market, because down-regulation is not possible. It is assumed that all the accepted day-ahead bids (CHP production and HP and electric boiler consumption) are accepted with the realized market prices. If the reserve market offers are not accepted, the operator can still procure the required electricity from the intraday market, which closes separately for each hour 15 minutes before the delivery hour on the operation day [41]. Intraday market was excluded in this study as the focus is on balancing and day-ahead markets.

Hence, at each timestep the maximum capacity offered to FCR-N market can be calculated by the following equation, where denotes the maintained capacity in the FCR-N market. and represent maximum and minimum capacities of the HP, whereas is the capacity of the HP at a particular hour. The maximum capacity bid to FCR-N market is 5 MW [8]. The same equation can be applied for the electric boiler.

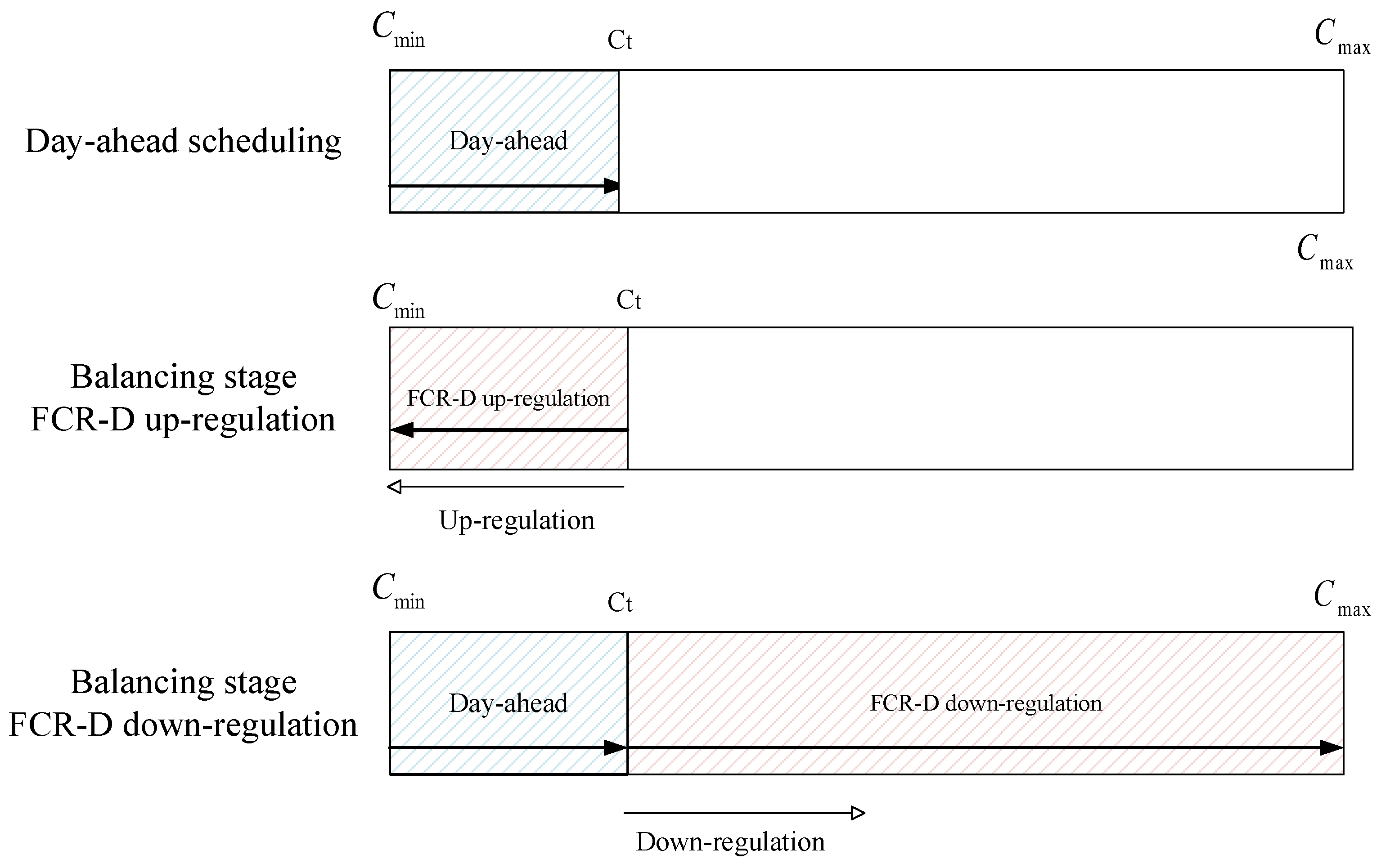

Separate up and down-regulation bids are required for FCR-D up-regulation and FCR-D down-regulation markets, respectively. In order for a HP to be able to provide FCR-D down-regulation reserve at a particular hour, it should be operating in the day-ahead scheduling stage, i.e., not being turned off at that hour because the HP’s starting time is greater than the required time for FCR-D activation. The electric boiler, on the other hand, is assumed to be capable of providing down-regulation reserve even when it is not operating in the day-ahead schedule [22]. Figure 3 illustrates the capacity allocation mechanism for FCR-D down-regulation and FCR-D up-regulation markets.

Equations 2 and 3 express the maximum capacity allocation to FCR-D up-regulation and down-regulation markets, respectively, considering the maximum bid of 10 MW to these markets. and represent the maintenance capacities in the FCR-D up-regulation and down-regulation markets, respectively.

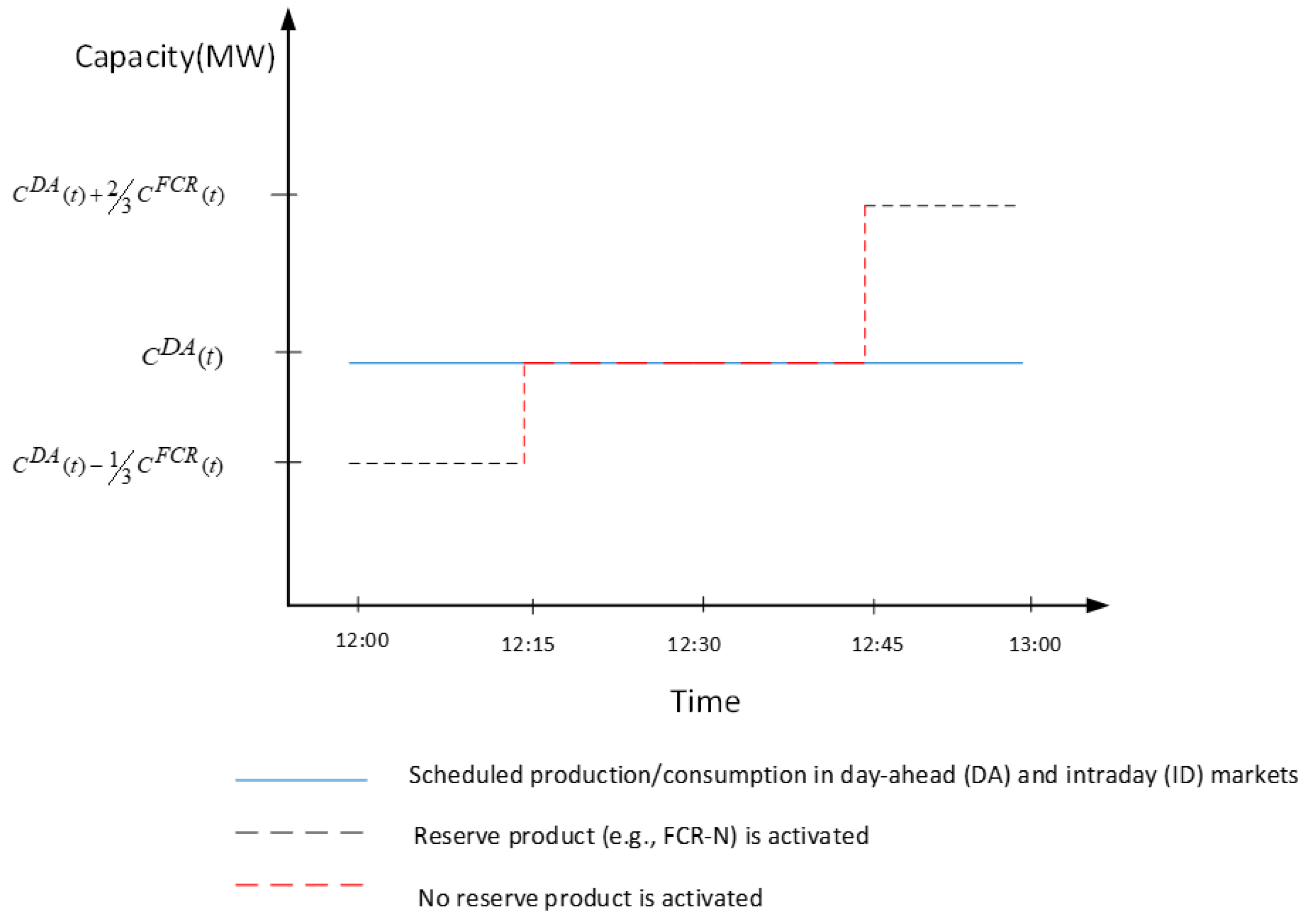

After the closure of FCR-N and FCR-D markets in day D-1, in the operation day (day D), it is possible that the entire or a part of the accepted capacity gets activated. The capacity of a reserve unit in FCR markets is activated linearly based on the local measured frequency, as illustrated in Figure 4 [8]. Linear activation guarantees equal activation for all service providers. The negative sign implies down-regulation, while the positive means up-regulation. The mathematic modeling of the FCR linear activation is expressed in equations 4-6. Historical measured frequency in 2019 is gathered from [8].

indicates the local measured frequency in 15-minute interval [8]. Following the activation of reserve units during the operation day heat imbalances would occur. In the event of up-regulation, the HP or electric boiler should reduce electricity consumption, determined in the day-ahead scheduling stage. As a result, their heat production would also be reduced, and vice versa in the event of down-regulation. In this study, it was assumed that heat-only boilers (HOBs) within each city’s DH system would adjust their production level in the day-ahead scheduling stage, in order to compensate for heat imbalances. Since HOBs are located near end-users and have fast reaction times, they can respond to heat imbalances without compromising the comfort of the end-users. Up-regulation requires reserve units to reduce their electricity consumption. To make up for the reduced heat production from reserve units after activating the reserve capacity, HOBs should increase their heat production. Similarly, the level of heat production of HOBs should be reduced during down-regulation. Increasing or decreasing the production of HOBs also increases or decreases their operational cost, which is taken into account in calculating the profit from balancing markets in the next section.

2.2.3. Economic analysis

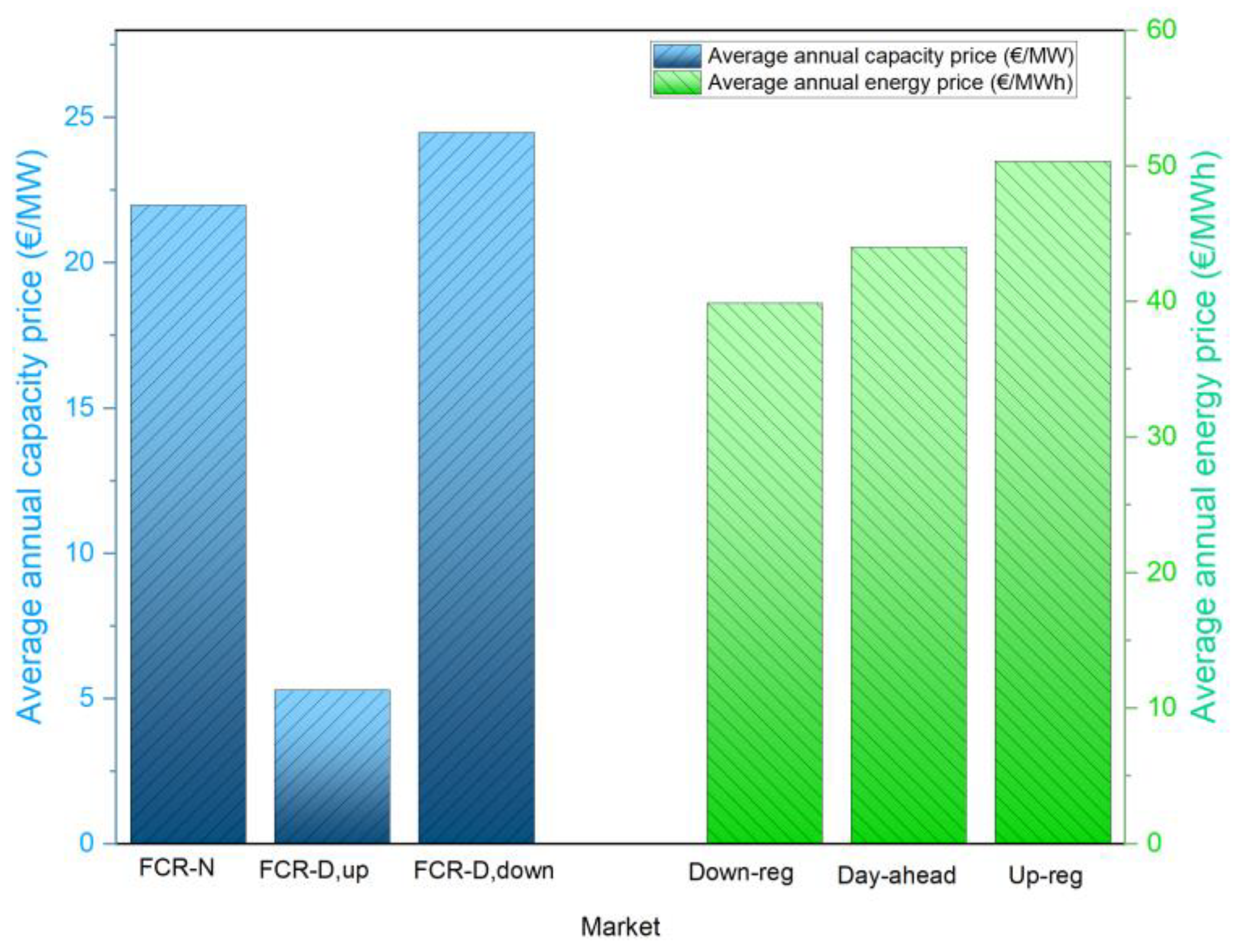

The local TSO pays for the balancing service provider for maintaining the reserve capacity available for activation. This is called capacity payment (capacity fee) which is the product of the accepted capacity in the auction and the realized capacity price of the corresponding hour, gathered from [8]. In addition to the capacity payment, a separate activation payment (energy fee) based on actual activated energy is paid to the provider. The energy payment is considered in the imbalance settlement of the balance responsible party. The energy fee is obtained by multiplying the activated energy in the corresponding balancing market by the upward/downward balancing price according to the one-price system, in which the purchase and sales prices of imbalance energy are identical [8]. According to this model, during an up-regulating hour, the price of imbalance energy is the up-regulating price, and during a down-regulating hour, the price of imbalance energy is the down-regulating price. If no regulations were carried out during an hour, the price of imbalance energy is the Finnish day-ahead price. Table 1 exemplifies the various mechanisms of price systems [8]. The up-regulation price is the price of the most expensive mFRR up-regulation bid ordered; however, at least the price for the bidding area of Finland in the day-ahead market during the hour in question. The down-regulation price is the price of the cheapest mFRR down-regulation bid ordered; however, no more than the price for the bidding area of Finland in the day-ahead market during the hour in question [8]. Figure 5 depicts the average capacity prices in FCR-N and FCR-D hourly markets and the average of down-regulation, up-regulation, and spot prices in 2019 [25,31].

To have a more accurate model, 15-minute granularity in the balancing market was considered in this study. Figure 6 depicts the schematic of a reserve unit when providing, for example, FCR in the market with 15-minute granularity. Local measured frequency in 2019, gathered from [25] was used in 15-minute resolution to model the activation of the reserve units in FCR markets, using equations 4-6 [22].

According to this model and the single-price system, the day-ahead cost, energy, and capacity fees for a reserve unit participating in FCR markets can be calculated as follows:

where is the capacity of a reserve unit tied to day-ahead market (day-ahead scheduling stage) and is the hourly day-ahead prices gathered from Nordpool [27]. , , and are the capacity prices in the corresponding markets [8]. and are the activated up-regulation and down-regulation capacities in each market during 15-minute intervals multiplied by the up-regulation balancing prices of the corresponding hour, , and down-regulation price, , respectively. The net profit for each reserve unit gained from each of the mentioned markets is the sum of capacity and energy fees. The net profit for each city’s DHN operator from participating in the balancing markets was obtained by summing the profits of all reserve units within the city’s DHN and the change in the operation cost of HOBs resulting from increasing or decreasing their production level to compensate for the heat imbalances after activating reserve capacities. Figure 7 summarizes the inputs and outputs used in the simulation during balancing market participation.

2.3. Case Study DHN

The Helsinki metropolitan area consists of three major cities: Helsinki, Espoo, and Vantaa. Each city has a DHN owner which operates the city DH system. Each of these operators has formulated decarbonization strategies and timelines for the transition to clean DH. Several heat exchanger stations allow heat transmission in both directions between the cities, but this region does not have an overall joint DH optimization [18]. The bi-directional heat transmission capacity between Espoo and Helsinki is 120 MW and 130 MW between Vantaa and Helsinki [18]. In this study, the heat transmission between cities was considered cost-free to optimize the entire system as a cohesive in a hypothetical case.

In 2019, Helsinki was mainly dependent on natural gas and coal-fired CHPs and HOBs to meet its heat demand. The DHN operator, Helen, is planning to curb coal usage by 2025 by shutting down two coal-fired CHP units, with the combined thermal output of 720 MW to be replaced with large-scale HPs, electric boilers, and thermal energy storages [19]. Espoo DHN operator Fortum has also decided to discontinue the use of coal in 2025. To achieve this, low-carbon technologies such as heat recovery from datacenters, new HPs as well as biomass-fueled power plants will be introduced [42]. Still, two gas-fired CHPs remain in the DHN of Espoo. For Vantaa, a waste to heat power plant serves the baseload and will be expanded under the decarbonization strategy to phase out the use of coal already in 2022 [43]. The waste used for the process is collected from the whole metropolitan region. Vantaa is also planning the world’s largest underground thermal storage with capacity of 90 GWh and a volume of 1 million m3 [43]. Financial input data including fuel and CO2 allowance prices, and fuel and electricity taxes are listed in Table A1 in the Appendix A. Detailed units within each DHN in 2019 and 2025 are listed in Table A2, Table A3 and Table A4 in the Appendix A.

Due to the uncertainty associated with future fuel and electricity prices, the same historical fuel and electricity prices for 2019 were also used for the simulation of 2025. As capacity prices in different balancing markets have not significantly changed in recent years [8], the same hourly capacity prices were used in the FCR-N and FCR-D up-regulation markets for 2019 and 2025. Due to the introduction of the FCR-D down-regulation market in 2021, 2022 capacity prices for this market were used in both simulations. The increasing EU ETS prices affect fossil fuel costs. While for 2019, the historical EU ETS prices with the annual average of 24.9 €/ton CO2 were used, in 2025 simulations the EU ETS prices of 2022 with the annual average of 80 €/ton CO2 were considered. However, this is not expected to have any significant impact on the electricity market price in Finland, as electricity production will be practically carbon-free in Finland in 2025 and Finland will not be net importer of electricity anymore. It was assumed that all HPs and electric boilers in the DH system can provide balancing services. The minimum load for each HP was considered as 10% of maximum load [36]. Table 2 summarizes the reserve providing units in each DH system in 2019 and 2025. HPs were modeled based on heat source and sink inlet and outlet temperatures [17].

3. Results

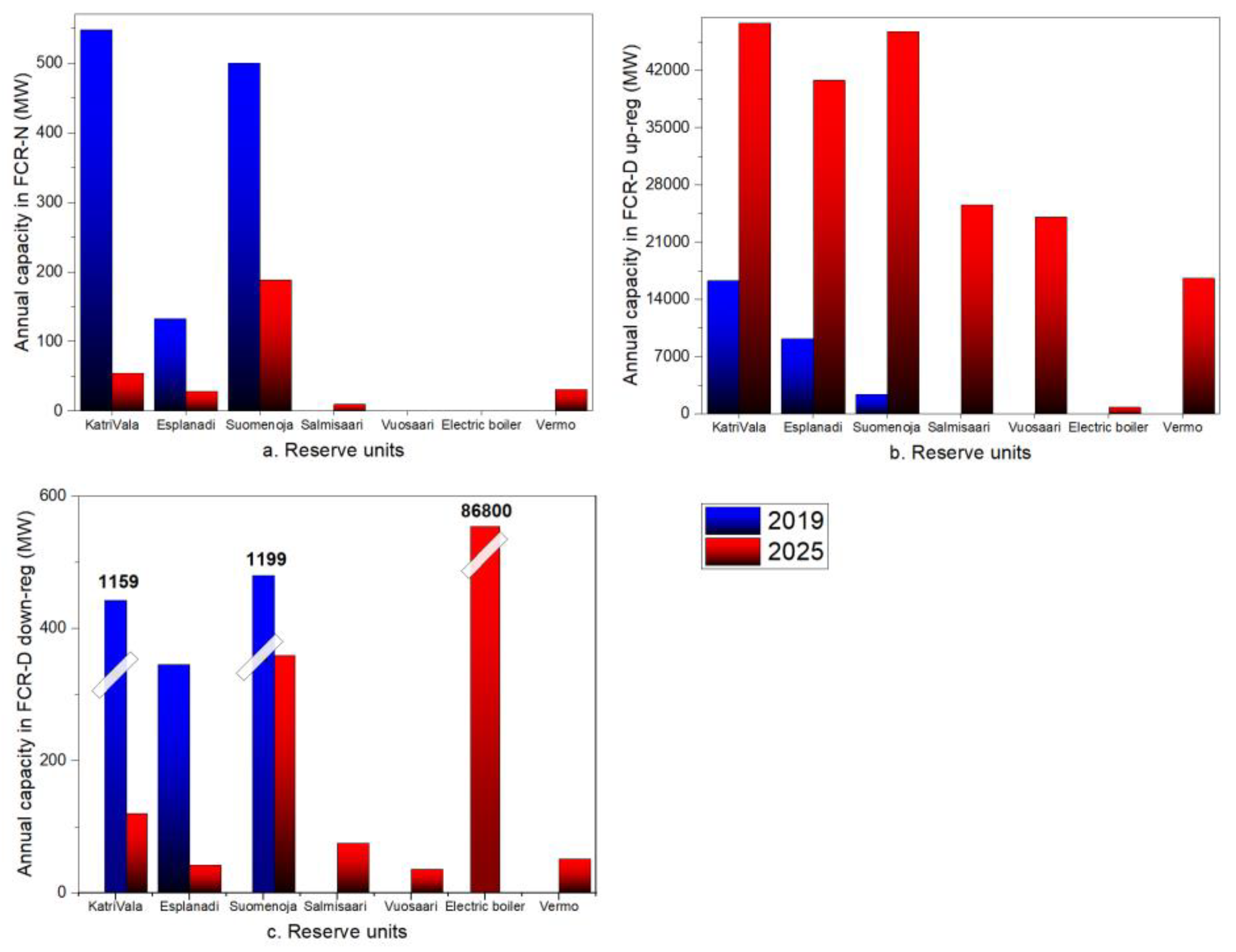

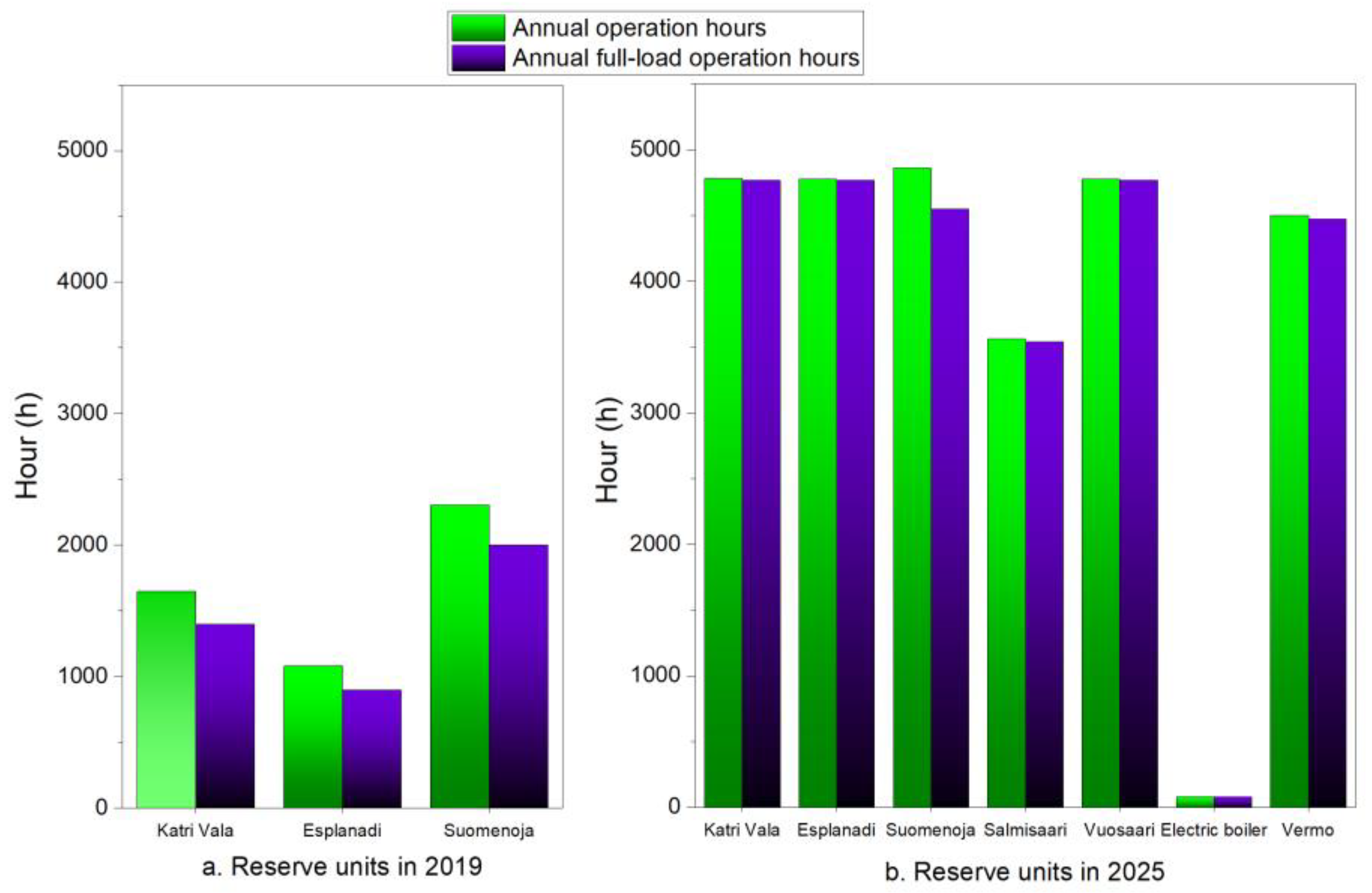

This section summarizes the findings of the simulations of the Helsinki metropolitan area DHN with the configurations of 2019 and 2025 in FCR-N, FCR-D up-regulation, and FCR-D down-regulation markets. The case study was calibrated against the actual fuel consumption of each DH system for the year 2019, as gathered from the annual reports [19,42,43]. Table A2 in the Appendix A summarizes the numerical results. While Figure 8, Figure 9 and Figure 10 illustrate the results for the individual reserve units in the studied balancing markets, Figure 11 presents the city-level results for Helsinki and Espoo cities. Figure 8 illustrates the annual operation hours and annual full-load operation hours of HPs and the electric boiler in the optimal operation of the DHN in the day-ahead market to meet heat demand (day-ahead scheduling stage) in 2019 and 2025. Compared to 2019, HPs will be more cost-effective in 2025 because of higher EU ETS prices and thus higher fossil fuel costs, resulting in higher operating hours of HPs in 2025, as depicted in Figure 8. Recently, electric boilers have been introduced into DH systems in Nordic countries, where they are mainly used during periods of very low or negative electricity prices. In the simulation, the electric boiler was only used during very few hours in 2025, but always at full capacity as can be seen from the figure.

Figure 9 shows the sum of available hourly reserve capacity from each reserve unit in the studied balancing markets, calculated with equations 1-3, over the entire 2019 and 2025. In the optimal operation of the DH system in the day-ahead scheduling stage (operation based on spot prices), during hours that a HP or an electric boiler is in operation with the maximum capacity to meet heat demand, the unit cannot offer any capacity to FCR-N or FCR-D down-regulation market for that hour. This is because the unit cannot do down-regulation, i.e., increase electricity consumption while operating at full capacity. This can be seen from Figure 8 and Figure 9 where the Katri Vala, Esplanadi, and Suomenoja HPs have a higher ratio of annual full-load hours to their total operation hours in 2025 compared to 2019 (Figure 8). This results in lower total available reserve capacity from these units in FCR-N and FCR-D down-regulation markets in 2025, as illustrated in Figure 9(a) and Figure 9(b).

Accordingly, the Vuosaari, Salmisaari, and Vermo HPs in 2025 will be operating at their maximum capacity when they operate within the day-ahead scheduling model (Figure 8(b)). Thus, there is a negligible amount of reserve capacity available from these units for the FCR-N and FCR-D down-regulation markets. The electric boiler can provide down-regulation even when it is not in operation in the day-ahead scheduling, as opposed to HPs which cannot ramp-up (provide down-regulation) when they are not in use [22]. In the simulations, HPs were assumed to be able to provide down-regulation only when they are operating in the day-ahead scheduling during that hour (at least with their minimum capacity, which is assumed to be 10% of their maximum capacity). Based on Figure 8 and Figure 9, it can be seen that the electric boiler’s annual available reserve capacity for FCR-N and FCR-D upregulation is relatively small, while it can provide significant reserve capacity for the FCR-D down-regulation market since most of the year the unit is not scheduled for the optimal operation on a day-ahead basis, see Figure 8(b). Unlike the FCR-N and FCR-D down-regulation markets, where a higher ratio of full load hours to total operating hours of a unit in the day-ahead scheduling means a lower reserve capacity available to the markets, the higher ratio results in a larger available reserve capacity for the up-regulating FCR-D market, as shown in Figure 8 and Figure 9. In comparison with 2019, the Katri Vala, Esplanadi, and Suomenoja HPs will have a greater capacity available in FCR-D up-regulation in 2025.

Figure 9.

(a). The sum of available capacity from each reserve unit in FCR-N market in 2019 and 2025. (b). The sum of available capacity from each reserve unit in FCR-D up-regulation market in 2019 and 2025. (c). The sum of available capacity from each reserve unit in FCR-D down-regulation market in 2019 and 2025. The sums are calculated as the available capacity in each hour and then integrated over the whole year.

Figure 9.

(a). The sum of available capacity from each reserve unit in FCR-N market in 2019 and 2025. (b). The sum of available capacity from each reserve unit in FCR-D up-regulation market in 2019 and 2025. (c). The sum of available capacity from each reserve unit in FCR-D down-regulation market in 2019 and 2025. The sums are calculated as the available capacity in each hour and then integrated over the whole year.

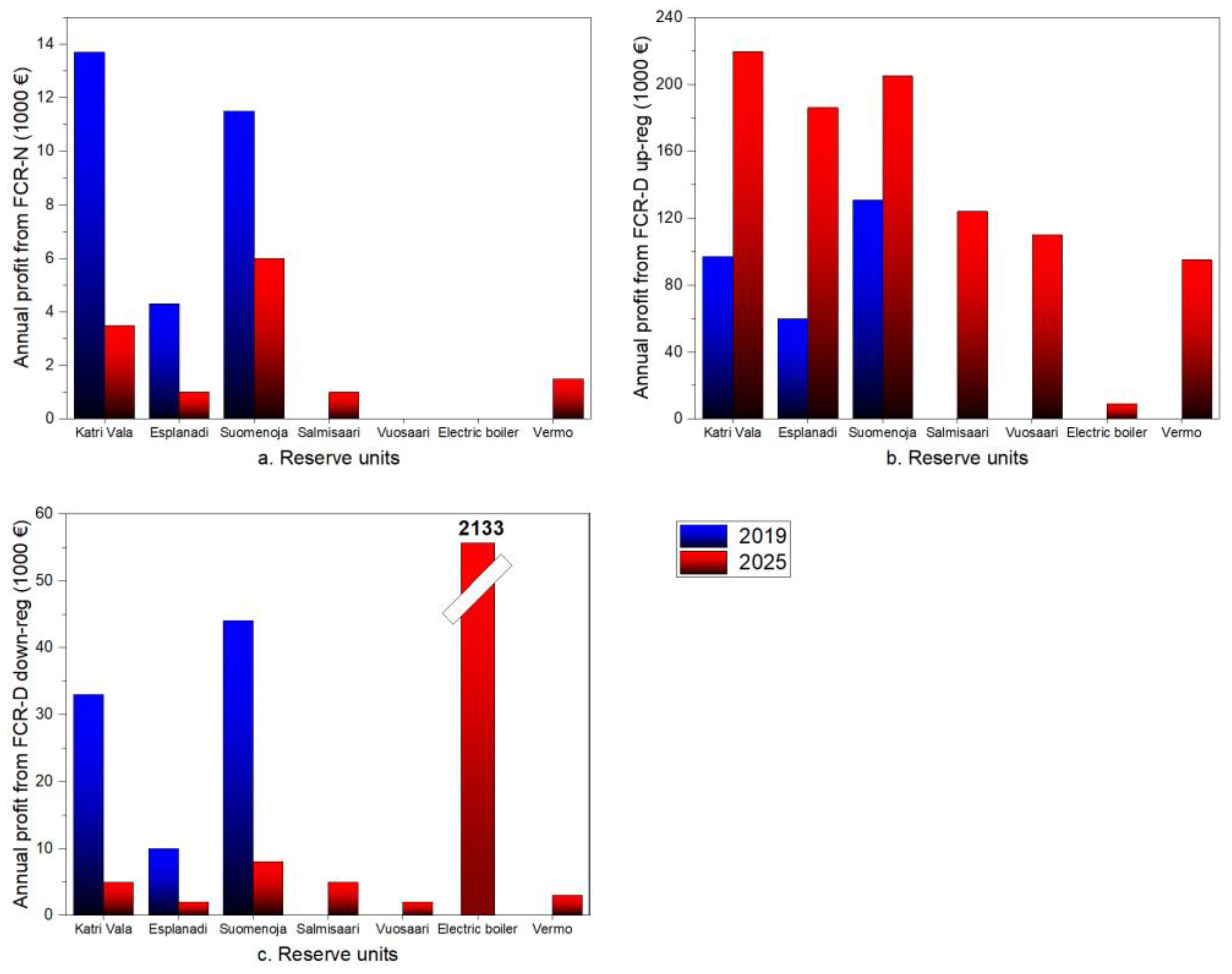

Figure 10 shows the annual net profit gained by each reserve unit in 2019 and 2025 from providing reserve capacity to the studied balancing markets. As discussed in section 2.2.3, the annual net profit was calculated as the sum of capacity and energy fees received from each market during the year. In calculating the net profit, the increase or decrease in the operating costs of the reserve unit, i.e., the variable O&M cost, was also taken into account. As the total available reserve capacities of HPs in the FCR-N and FCR-D down-regulation markets would decrease in 2025, as indicated in Figure 9, the revenue from these markets is expected to decrease, which is depicted in Figures 10(a) and (c). On the other hand, more revenue from FCR-D up-regulation would be gained in 2025. The highest revenue is for the electric boiler in the FCR-D down-regulation market.

Figure 10.

(a). The annual net profit of each reserve unit gained from FCR-N market in 2019 and 2025. (b). The annual net profit of each reserve unit gained from FCR-D up-regulation market in 2019 and 2025. (c). The annual net profit of each reserve unit gained from FCR-D down-regulation market in 2019 and 2025.

Figure 10.

(a). The annual net profit of each reserve unit gained from FCR-N market in 2019 and 2025. (b). The annual net profit of each reserve unit gained from FCR-D up-regulation market in 2019 and 2025. (c). The annual net profit of each reserve unit gained from FCR-D down-regulation market in 2019 and 2025.

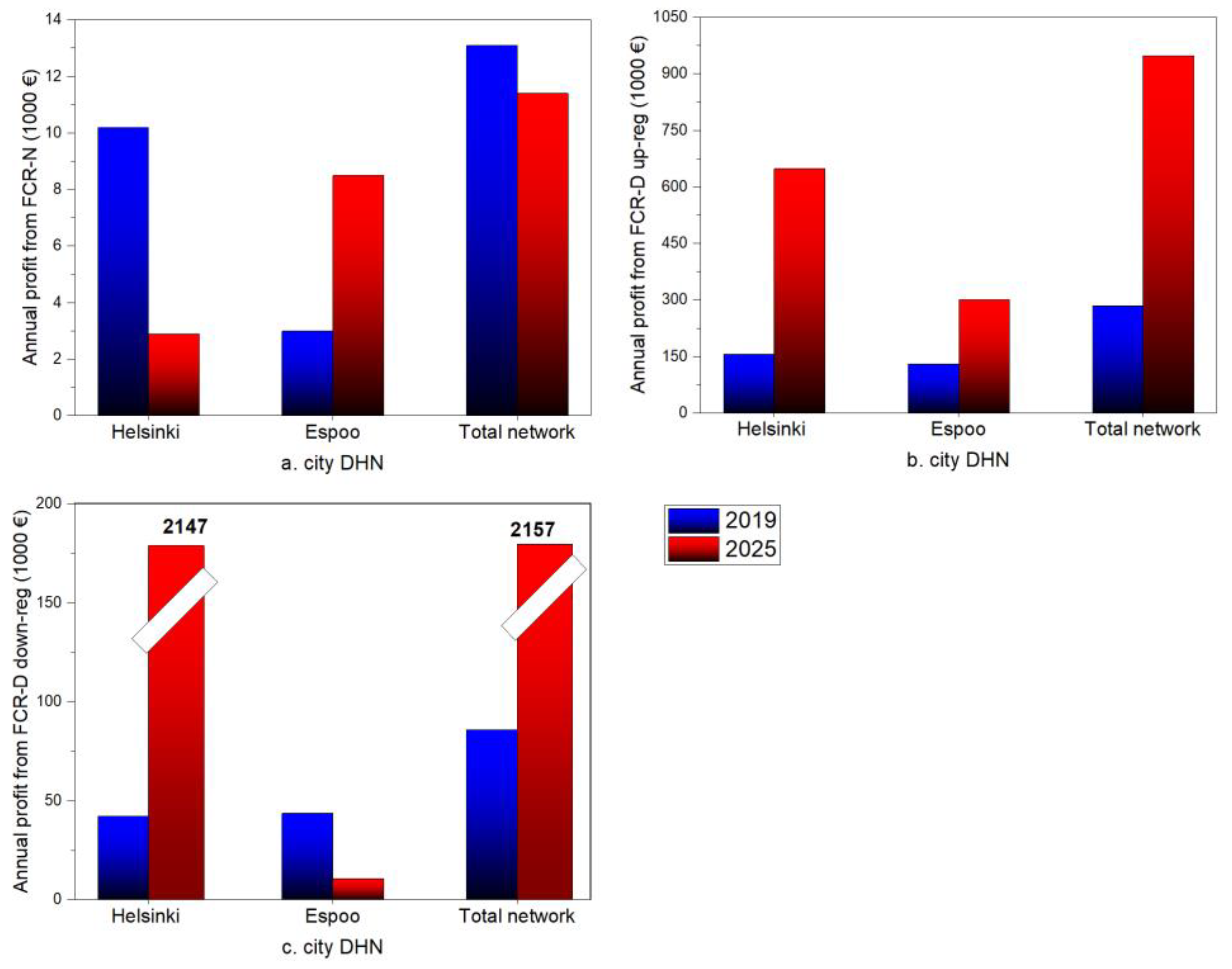

Figure 11 illustrates the annual net profit for each city DH system and the entire case study DH system, i.e., Espoo, Helsinki, and Vantaa. In the situation of 2019, Helsinki DH had significantly more profit from the FCR-N market than Espoo DH; however, with the heat generation fleet 2025, Helsinki DH’s profit from this market would be lower than Espoo DH’s, despite the increased capacities of HPs in Helsinki DH. Figure 8 and Figure 9(a) show that the Katri Vala and Esplanadi HPs within Helsinki DH would have considerably lower reserve capacities in FCR-N in 2025 than the Suomenoja HP, which belongs to Espoo DHN. Figure 8(b) illustrates how shutting down large capacities of CHP units in the Helsinki DH system would result in increased full-load operation hours for HPs with day-ahead schedules. As a result of increased operating hours of HPs in the day-ahead scheduling in 2025, illustrated in Figure 8, both cities can earn more from the FCR-D up-regulation market. The electric boiler could provide significant profit from the FCR-D down-regulation market for Helsinki DH in 2025.

Figure 11.

(a). The annual net profit for each city DHN from FCR-N market in 2019 and 2025. (b). The annual net profit for each city DHN from FCR-D up-regulation market in 2019 and 2025. (c). The annual net profit for each city DHN from FCR-D down-regulation market in 2019 and 2025.

Figure 11.

(a). The annual net profit for each city DHN from FCR-N market in 2019 and 2025. (b). The annual net profit for each city DHN from FCR-D up-regulation market in 2019 and 2025. (c). The annual net profit for each city DHN from FCR-D down-regulation market in 2019 and 2025.

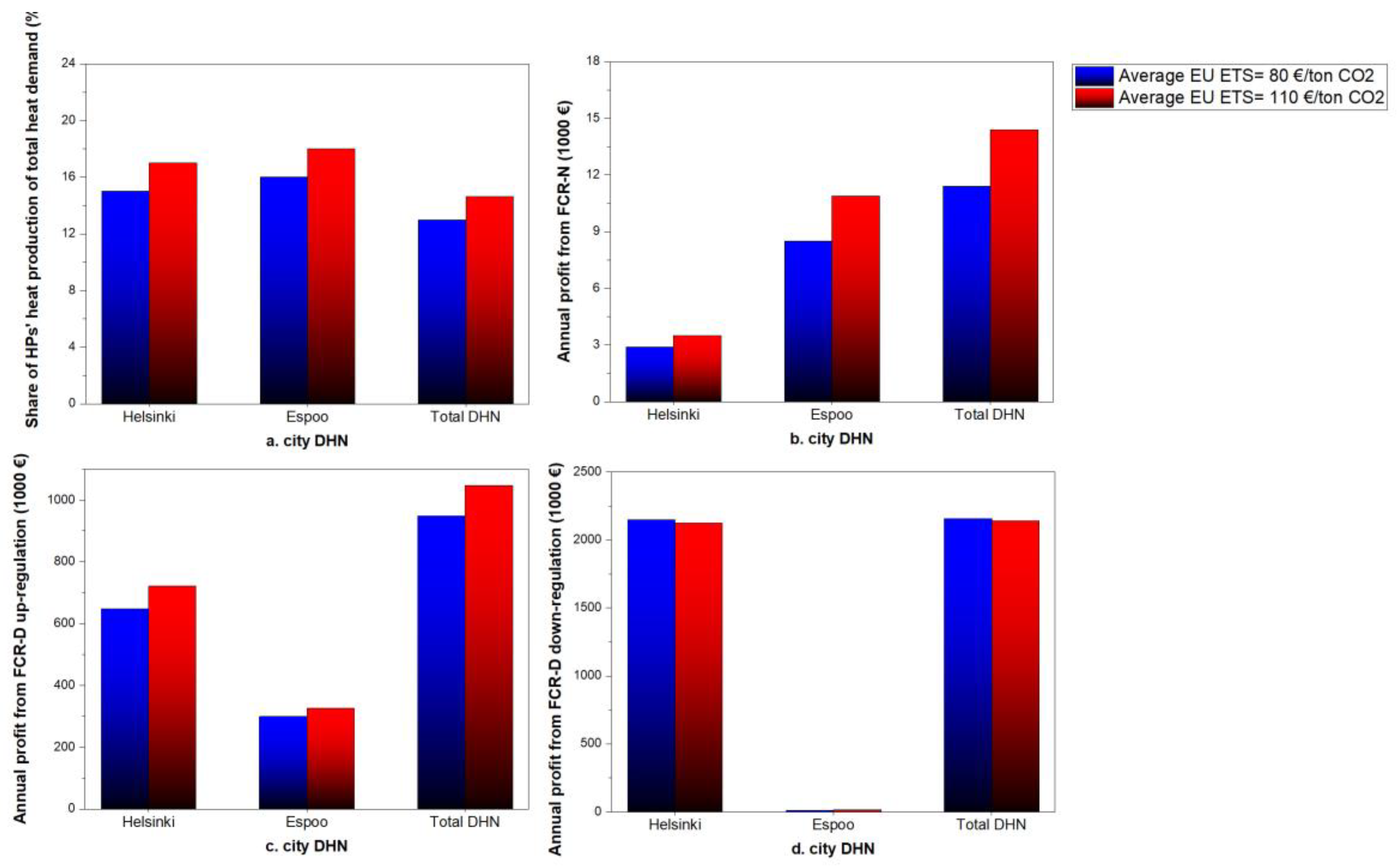

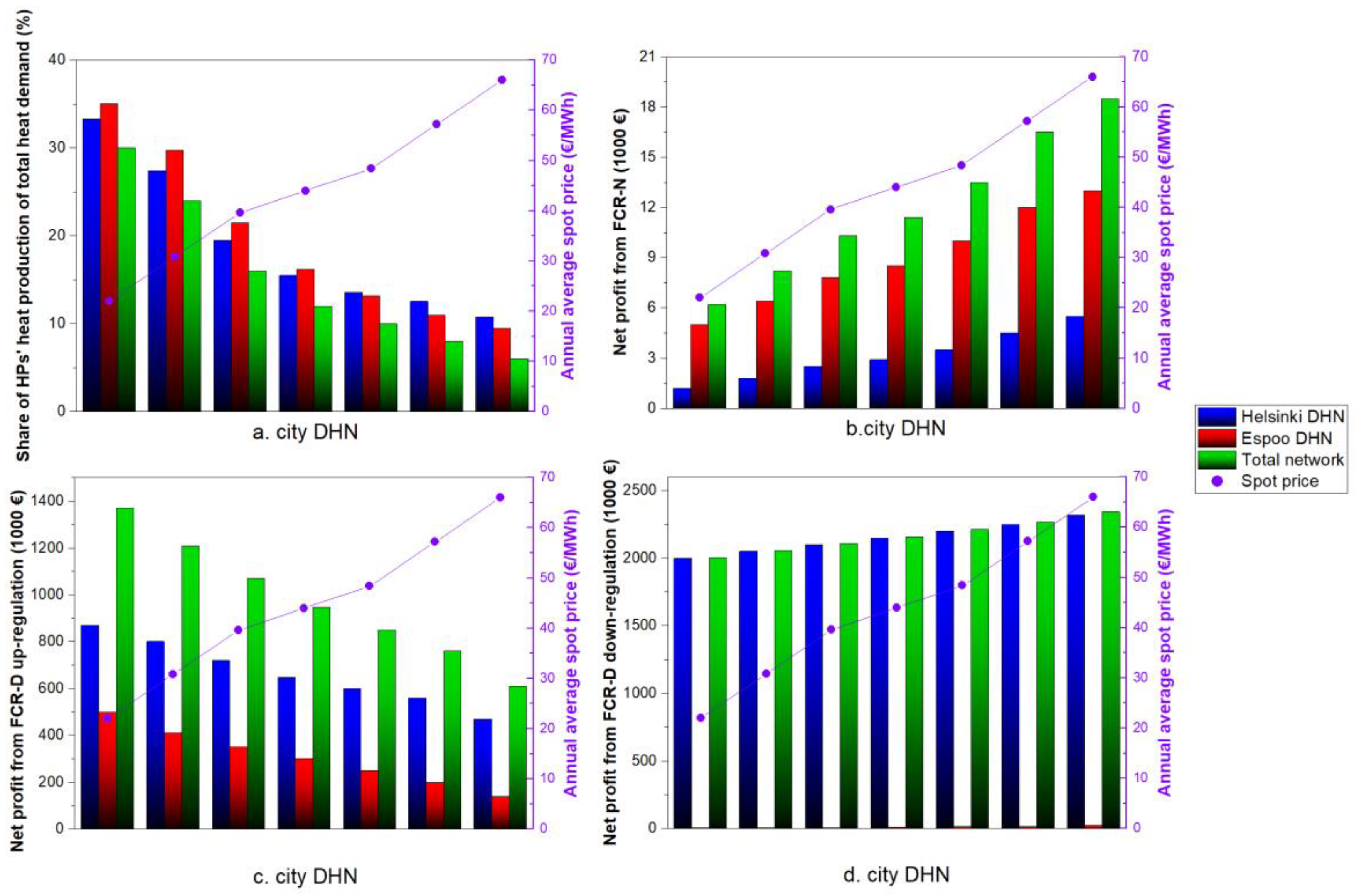

Given the complexity and uncertainty surrounding future market development, it is critical to identify the primary factors affecting the results. The most important unpredictable factors are electricity prices and fuel costs. Especially, increasing EU ETS prices significantly affect fuel costs for power plant operators [35]. Hence, a sensitivity analysis of the electricity prices and EU ETS prices was conducted for the year 2025 simulation. Figure 12 illustrates the results for the case study DHN with the 2025 generation fleet using the assumed historical EU ETS prices of 2022, with the annual average of 80 €/tonCO2, as well as the projected prices for 2025, with the annual average of 110 €/tonCO2 [35]. Figure 12(a) illustrates the share of heat produced annually by HPs within each city DHN in comparison to its annual heat demand. As a result of the increase in EU ETS prices, fuel prices increase, CHP production decreases, and HP production rises. Figure 12(b), Figure 12(c), and Figure 12(d) illustrate the annual net profit for each market based on different EU ETS prices. With higher EU ETS prices, revenues from all markets, except for the FCR-D down-regulation market, would increase. Due to the higher operating hours of the electric boiler in the day-ahead scheduling system, a lower reserve capacity is available in this market, thereby decreasing the achievable total net profit with the higher EU ETS prices. As the operation hours of the CHPs decrease due to higher EU ETS prices, HPs should run more to offset the heat demand, increasing the capacity for the FCR-D upregulation market, illustrated in Figure 12(c).

Figure 13 illustrates the simulation results for the 2025 generation fleet under different electricity prices. It is important to note that up-regulation and down-regulation prices are cleared following the day-ahead prices, as shown in Table 1. Thus, changing day-ahead prices in the sensitivity analysis implies simultaneously changing up-regulation and down-regulation prices. Figure 13(a) illustrates the share of HPs’ heat production within each city DHN to its annual heat demand along with the annual average of spot prices in the right y axis, while figures (c) to (d) show the annual net profit for each city DH system and the entire network from FCR-N, FCR-D up-regulation, and FCR-D down-regulation markets, respectively. Increasing spot prices results in more revenue gained from electricity sales of CHP units in the day-ahead market. Thus, CHPs’ operation rates increase, while HPs would have lower hours of operation in the day-ahead scheduling, as illustrated in figure 13(a). As there is no HP or electric boiler in Vantaa DHN, increasing electricity prices do not affect CHP operation and Vantaa’s CHP units are not illustrated in the figure. Lower operation of HPs and the electric boiler in the day-ahead scheduling results in higher income from FCR-N and FCR-D down-regulation. In contrast, FCR-D up-regulation would yield lower profit in the higher electricity prices.

4. Conclusions

Towards carbon neutrality by 2035, district heating network (DHN) operators in Finland intend to decarbonize their systems by closing down fossil-fueled combined heat and power plants (CHPs) and installing large-scale heat pumps (HPs) and electric boilers. As a result of decommissioning CHP units, the benefits of simultaneous electricity and heat production are lost, which would have been especially advantageous in high electricity market price situations. Thus, it is important to investigate new income possibilities with electrified heat production units from other markets, such as balancing markets. Furthermore, the need for alternative balancing providers is greater than ever as wind power production is increasingly integrated into the Finnish electrical power system, the installed wind power capacity in Finland being already more than 60% of the average electricity demand in 2022 [30]. This study investigated the techno-economic analysis and economic feasibility of providing ancillary balancing services from HPs and electric boilers operating within a large and electrified DHN to the Finnish electrical power system. The three interconnected DHNs in the Helsinki metropolitan area including DHNs of Helsinki, Espoo, and Vantaa cities serving a total 11.1 TWh of heat to nearly 1.1 million people in 2022 were simulated and optimized. Additionally, this study examined frequency containment reserve (FCR) markets, which include frequency containment reserve markets for normal operation (FCR-N), frequency containment reserve markets for disturbances, up-regulation (FCR-D up-regulation), and down-regulation (FCR-D down-regulation). An important upcoming change in the balancing market, the 15-minute block, was considered in this study. The DHN was simulated and optimized in 2019 based on historical data and in 2025 based on the planned decarbonization pathways of each operator. The most important conclusions of this study are as follows:

- Among the studied markets, the FCR-D up-regulation market is expected to be the most profitable balancing market for large HPs. In total, HPs’ achievable net profit could be 285,000 € and 940,000 € in the analyzed cases of 2019 and 2025 DHNs from this market. In both cases studied, the FCR-N market was the least profitable for HPs and electric boilers.

- Electric boilers, which have recently been introduced into Finnish DH systems, are being used during very low or negative day-ahead electricity prices. While the electric boiler in the case study DHN would be in operation only 1% of hours of 2025 in the day-ahead scheduling, it could provide a net profit of nearly 2.2 million € for the Helsinki DH system from FCR-D down-regulation market, yielding the largest individual benefits from the ancillary services markets studied.

- Higher CO2 emission allowance prices (EU ETS prices) increase the net profit from FCR-N and FCR-D up-regulation markets. Considering the increasing trend of CO2 emission allowance prices in recent years, an increasing profit from these markets is expected in the upcoming years. The profit from FCR-D down-regulation market was found to decrease marginally with higher ETS prices.

Author Contributions

Conceptualization, Nima Javanshir; methodology, Nima Javanshir; software, Nima Javanshir; validation, Nima Javanshir; formal analysis, Nima Javanshir; data curation, Nima Javanshir; writing—original draft preparation, Nima Javanshir; writing—review and editing, Sanna Syri; visualization, Nima Javanshir; supervision, Sanna Syri; project administration, Sanna Syri; funding acquisition, Sanna Syri. All authors have read and agreed to the published version of the manuscript.

Funding

This work has been supported by Doctoral research funding of Aalto University School of Engineering.

Conflicts of Interest

The authors declare no conflict of interests. This is an academic contribution based on data from open sources and does not represent the official view or the actual operation of any organization.

| Nomenclature | |||

| Indices | Abbreviations | ||

| Time | aFRR | Automatic frequency restoration reserve | |

| COP | Coefficient of performance | ||

| Parameters | CHP | Combined heat and power unit | |

| Measured frequency (HZ) | DHN | District heating network | |

| FCR-N Capacity Hourly Market Prices | EU ETS | European union emission trading system | |

| FCR-D Capacity Hourly Market Prices | FCR | Frequency containment reserve | |

| Down-Regulation Balancing Market Price | FCR-N | Frequency containment reserve for normal operation | |

| Up-Regulation Balancing Market Price | FCR-D | Frequency containment reserve for disturbances | |

| Electricity spot prices | FFR | Fast frequency reserve | |

| FLH | Full-load hour | ||

| Variables | HOB | Heat-only boiler | |

| Current setting of a reserve unit | HP | Heat pump | |

| Maximum electrical capacity | mFRR | Manual frequency restoration reserve | |

| Minimum electrical capacity | O&M | Operation and maintenance cost (€) | |

| Maintained capacity in FCR-N market | P2H | Power-to-heat | |

| Maintained capacity in FCR-D up-regulation market | TSO | Transmission system operator | |

| Maintained capacity in FCR-D down-regulation market | |||

| Maintained capacity in day-ahead market | |||

| Activated FCR-N capacity during 15-minute block | |||

| Activated down-ward capacity during 15-minute block | |||

| Activated up-ward capacity during 15-minute block | |||

Appendix A

Table A1.

Financial parameters used in simulations in 2019 and 2025.

| Parameter | Value (€/MWh) | |

|---|---|---|

| Fuel tax [44,45] | ||

| Coal | HOB | 29.2 |

| CHP | 21.5 | |

| Natural gas (NG) | HOB | 20.6 |

| CHP | 13.0 | |

| Light fuel oil (LFO) | - | 27.5 |

| Heavy fuel oil (HFO) | - | 24.5 |

| Fuel cost [34] | ||

| Coal | 7.8* | |

| NG | 23.2 * | |

| HFO | 54.1 * | |

| LFO | 76.2 * | |

| Bio-oil | 67.0 | |

| Wood pellet | 46.7 | |

| Forest chips | 22.2 | |

| Waste | -7.95 | |

| Electricity costs | ||

| Electricity spot price [31] | 44.0 ** | |

| Distribution cost | Helsinki [38] | 32.80 |

| Espoo [46] | 31.40 | |

| Electricity tax [44] | 6.9 | |

| CO2 price [47] (€/tonCO2) | 25 (2019) / 80 (2025) *** |

* While average monthly values of fuel prices are used in the simulation, the value in the tables refers to the yearly average value. ** Hourly values of spot price in used in the simulation, while this refers to the yearly average value. *** Hourly values of CO2 allowance prices are used in the simulations.

Table A2.

Production units in the Helsinki DHN in 2019 and 2025 [19].

Table A2.

Production units in the Helsinki DHN in 2019 and 2025 [19].

| Unit | Fuel | Thermal output (MW) |

|---|---|---|

| Existing | ||

| HOB | LFO | 136 |

| HOB | HFO | 873 |

| HOB | Coal | 170 |

| HOB | NG | 912 |

| HOB | Wood pellet | 92 |

| HP Katri Vala | Wastewater | 105 |

| HP Esplanadi | Wastewater | 22 |

| Hanasaari CHP | Mix (coal and biomass) | 420 |

| Salmisaari CHP | Mix (coal and biomass) | 300 |

| Vuosaari CHPs | NG | 587 |

| Thermal storage | - | 45000 m3 * |

| To be decommissioned by 2025 | ||

| HOB | Coal | 170 |

| Salmisaari CHP | Coal | 300 |

| Hanasaari CHP | Coal | 420 |

| To be deployed/expanded after 2019 | ||

| Vuosaari HOB | Biomass | 260 |

| Salmisaari HOB | Wood pellet | 150 |

| HP Salmisaari | Ambient air | 20 |

| HP Vuosaari | Sea water | 13 |

| HP Katri Vala | Wastewater | 155 |

| Electric boiler | Electricity | 280 |

| Thermal storage | - | 260000 m3 |

* The combined volume of two thermal storages within the Helsinki DHN.

Table A3.

Production units in the Espoo DHN in 2019 and 2025 [48].

Table A3.

Production units in the Espoo DHN in 2019 and 2025 [48].

| Unit | Fuel | Thermal output (MW) |

| Existing | ||

| Suomenoja HPs (3, 4) | Wastewater | 70 |

| Vermo HOB | Bio-oil | 35 |

| Kivenlahti HOB | Wood pellets | 90 |

| HOB | LFO | 85 |

| HOB | NG | 456 |

| HOB | Coal | 80 |

| Thermal storage | - | 18000 m3 |

| Suomenoja 1 CHP | Coal | 160 |

| Suomenoja 2 CHP | NG | 214 |

| Suomenoja 6 CHP | NG | 80 |

| To be decommissioned by 2025 | ||

| Suomenoja 1 CHP | Coal | 160 |

| To be deployed/expanded after 2019 | ||

| Vermo HP | Ambient air | 11 |

| Kivenlahti HOB | Woodchips | 52 |

| Espoo Datacenter | Datacenter | 100 |

Table A4.

Production units in the Vantaa DHN in 2019 and 2025 [43].

Table A4.

Production units in the Vantaa DHN in 2019 and 2025 [43].

| Unit | Fuel | Thermal output (MW) |

| Existing | ||

| HOB | NG | 427 |

| HOB | LFO | 92 |

| Martinlaakso 1 CHP | Wood chips | 100 |

| Jätevoimala CHP waste | Waste | 140 |

| Martinlaakso 2 CHP | Wood chips | 135 |

| Martinlaakso 4 CHP | NG | 90 |

| To be deployed/ expanded after 2019 | ||

| Thermal storage | - | 1,000,000 m3 |

| Martinlaakso CHP | Wood chips | 22.5 |

| HOB | Waste | 64 |

Table A5.

Comparison of fuel consumption from simulations versus the real case study in 2019.

| Fuel consumption (GWh) | Helsinki DHN | Espoo DHN | Vantaa DHN | |||

|---|---|---|---|---|---|---|

| Real situation | Simulation | Real situation | Simulation | Real situation | Simulation | |

| Coal | 6500 | 5500 | 2042 | 1800 | 60, | 850 |

| Natural Gas | 5000 | 6800 | 729 | 1300 | 245 | 350 |

| Oil | 106 | 0 | 4.6 | 1.0 | 1.5 | 0.9 |

| Bio | 226 | 350 | 244 | 150 | 533 | 680 |

| Waste | 0 | 0 | 0 | 0 | 1120 | 1137 |

| Electricity | 133.6 | 95 | 180 | 55 | 0 | 0 |

| Total | 11965 | 12745 | 3200 | 3306 | 2500 | 2247 |

References

- United Nations, Climate Change: The Paris Agreement | UNFCCC n.d. https://unfccc.int/process-and-meetings/the-paris-agreement/the-paris-agreement (accessed June 22, 2021).

- European Climate Law n.d. https://ec.europa.eu/clima/eu-action/european-green-deal/european-climate-law_en (accessed December 4, 2021).

- Finland’s Integrated Energy and Climate Plan. työ- ja elinkeinoministeriö; 2019.

- Cramton P. Electricity market design. Oxf Rev Econ Policy 2017;33:589–612. [CrossRef]

- van der Veen RAC, Hakvoort RA. The electricity balancing market: Exploring the design challenge. Util Policy 2016;43:186–94. [CrossRef]

- Nuclear power to the reserve market - ePressi n.d. https://www.epressi.com/tiedotteet/energia/ydinvoima-mukaan-reservimarkkinoille.html (accessed May 15, 2023).

- Hae Tuulivoima reservimarkkinoille -pilottiin 16.1.2023 mennessä - ePressi n.d. https://www.epressi.com/tiedotteet/energia/hae-tuulivoima-reservimarkkinoille-pilottiin-16.1.2023-mennessa.html (accessed May 15, 2023).

- Fingrid-Reserves and balancing power n.d. https://www.fingrid.fi/en/electricity-market/reserves_and_balancing/ (accessed December 5, 2021).

- Pudjianto D, Djapic P, Aunedi M, Gan CK, Strbac G, Huang S, et al. Smart control for minimizing distribution network reinforcement cost due to electrification. Energy Policy 2013;52:76–84. [CrossRef]

- Baeten B, Rogiers F, Helsen L. Reduction of heat pump induced peak electricity use and required generation capacity through thermal energy storage and demand response. Appl Energy 2017;195:184–95. [CrossRef]

- Vanhoudt D, Geysen D, Claessens B, Leemans F, Jespers L, van Bael J. An actively controlled residential heat pump: Potential on peak shaving and maximization of self-consumption of renewable energy. Renew Energy 2014;63:531–43. [CrossRef]

- Cooper SJG, Hammond GP, McManus MC, Rogers JG. Impact on energy requirements and emissions of heat pumps and micro-cogenerators participating in demand side management. Appl Therm Eng 2014;71:872–81. [CrossRef]

- Melsas R, Rosin A, Drovtar I. Value Stream Mapping for Evaluation of Load Scheduling Possibilities in a District Heating Plant. Transactions on Environment and Electrical Engineering 2016;1:62–7. [CrossRef]

- Meesenburg W, Ommen T, Elmegaard B. Dynamic exergoeconomic analysis of a heat pump system used for ancillary services in an integrated energy system. Energy 2018;152:154–65. [CrossRef]

- Terreros O, Spreitzhofer J, Basciotti D, Schmidt RR, Esterl T, Pober M, et al. Electricity market options for heat pumps in rural district heating networks in Austria. Energy 2020;196:116875. [CrossRef]

- Javanshir N, Hiltunen P, Syri S. Is Electrified Low-Carbon District Heating Able to Manage Electricity Price Shocks? International Conference on the European Energy Market, EEM 2022;2022-September. [CrossRef]

- Javanshir N, Syri S, Teräsvirta A, Olkkonen V. Abandoning peat in a city district heat system with wind power, heat pumps, and heat storage. Energy Reports 2022;8:3051–62. [CrossRef]

- Finnish energy. District heating statistics n.d. https://energia.fi/en/newsroom/publications/district_heating_statistics.html#material-view (accessed February 18, 2022).

- Power plants | Helen n.d. https://www.helen.fi/en/company/energy/energy-production/power-plants (accessed February 1, 2023).

- Tomita K, Ito M, Hayashi Y, Yagi T, Tsukada T. Electricity Adjustment by Aggregation Control of Multiple District Heating and Cooling Systems. Energy Procedia 2018;149:317–26. [CrossRef]

- Boldrini A, Jiménez Navarro JP, Crijns-Graus WHJ, van den Broek MA. The role of district heating systems to provide balancing services in the European Union. Renewable and Sustainable Energy Reviews 2022;154:111853. [CrossRef]

- Javanshir N, Syri S, Tervo S, Rosin A. Operation of district heat network in electricity and balancing markets with the power-to-heat sector coupling. Energy 2023;266:126423. [CrossRef]

- Wang J, You S, Zong Y, Traeholt C, Zhou Y, Mu S. Optimal dispatch of combined heat and power plant in integrated energy system: A state of the art review and case study of Copenhagen. Energy Procedia 2019;158:2794–9. [CrossRef]

- Haakana J, Tikka V, Lassila J, Partanen J. Methodology to analyze combined heat and power plant operation considering electricity reserve market opportunities. Energy 2017;127:408–18. [CrossRef]

- Fingrid n.d. https://www.fingridlehti.fi/en/finland-switching-to-15-minute-imbalance-settlement/#e2892316 (accessed February 21, 2023).

- Jaakamo N. Impact of the 15-Minute Imbalance Settlement Period and Electricity Storage on an Independent Wind Power Producer 2020.

- Nordpool. Day-Ahead Prices n.d. https://www.nordpoolgroup.com/Market-data1/#/nordic/table (accessed April 12, 2021).

- eSett in Brief | Nordic Imbalance Settlement | eSett n.d. https://www.esett.com/about/esett-in-brief/ (accessed February 21, 2023).

- eSett’s 15 min ISP Commissioning Plan has been published - eSett n.d. https://www.esett.com/news/esetts-15-min-isp-commissioning-plan-has-been-published/ (accessed February 21, 2023).

- Energy Year 2022 - Electricity - Energiateollisuus n.d. https://energia.fi/en/newsroom/publications/energy_year_2022_-_electricity.html#material-view (accessed May 16, 2023).

- Nordpool, Day-ahead market n.d. https://www.nordpoolgroup.com/the-power-market/Day-ahead-market/ (accessed December 4, 2021).

- EMD International A/S, EnergyPRO n.d. https://www.emd.dk/energypro/ (accessed March 23, 2020).

- Østergaard PA, Andersen AN, Sorknæs P. The business-economic energy system modelling tool energyPRO. Energy 2022;257:124792. [CrossRef]

- Statistics Finland- Energy prices n.d. https://www.stat.fi/til/ehi/kuv_en.html (accessed March 23, 2022).

- EU Emissions Trading System (EU ETS) | Climate Action n.d. https://ec.europa.eu/clima/policies/ets_en (accessed March 23, 2021).

- Finnish Meteorological Institute. Weather Data n.d. https://en.ilmatieteenlaitos.fi/ (accessed April 12, 2021).

- Patronen J, Kaura E, Torvestad C. Nordic heating and cooling. Nordic Council of Ministers; 2017. [CrossRef]

- Su Y, Hiltunen P, Syri S, Khatiwada D. Decarbonization strategies of Helsinki metropolitan area district heat companies. Renewable and Sustainable Energy Reviews 2022;160:112274. [CrossRef]

- Energinet Elsystemansvar A/S Document type 2019.

- Technology Data. Danish Energy Agency 2016. https://ens.dk/en/our-services/projections-and-models/technology-data (accessed April 12, 2021).

- Nordpool-Intraday market n.d. https://www.nordpoolgroup.com/the-power-market/Intraday-market/ (accessed December 5, 2021).

- Fortum n.d. https://www.fortum.com/files/fortum-sustainability-2020/download (accessed March 23, 2022).

- Vantaan Energia n.d. https://www.vantaanenergia.fi/ (accessed February 1, 2023).

- Tax rates on electricity and fuels - vero.fi n.d. https://www.vero.fi/en/businesses-and-corporations/taxes-and-charges/excise-taxation/sahkovero/Tax-rates-on-electricity-and-certain-fuels/ (accessed March 23, 2022).

- Electricity production and in combined production of heat and electricity - vero.fi n.d. https://www.vero.fi/en/businesses-and-corporations/taxes-and-charges/excise-taxation/excise-duty-refunds/electricity-production-and-in-combined-production-of-heat-and-electricity/ (accessed April 12, 2022).

- Caruna Oy-Network service and connection fee rates for the high-voltage distribution network n.d.

- Carbon Price Viewer - Ember n.d. https://ember-climate.org/data/carbon-price-viewer/ (accessed June 13, 2021).

- Espoo Clean Heat | Fortum n.d. https://www.fortum.com/products-and-services/heating-cooling/espoo-clean-heat (accessed February 1, 2023).

Figure 1.

Input and output parameters used in the model in the day-ahead scheduling stage.

Figure 2.

(a). The capacity allocation of a HP or an electric boiler to FCR-N market when the HP is in operation with more than 50% of its maximum capacity in the day-ahead scheduling stage. (b). The capacity allocation of a HP or an electric boiler to FCR-N market when the HP is in operation with less than 50% of its maximum capacity in the day-ahead scheduling stage.

Figure 2.

(a). The capacity allocation of a HP or an electric boiler to FCR-N market when the HP is in operation with more than 50% of its maximum capacity in the day-ahead scheduling stage. (b). The capacity allocation of a HP or an electric boiler to FCR-N market when the HP is in operation with less than 50% of its maximum capacity in the day-ahead scheduling stage.

Figure 3.

Capacity allocation of a HP or an electric boiler to FCR-D up-regulation and down-regulation markets.

Figure 3.

Capacity allocation of a HP or an electric boiler to FCR-D up-regulation and down-regulation markets.

Figure 4.

Activation of a reserve unit as a function of frequency in FCR markets [8].

Figure 4.

Activation of a reserve unit as a function of frequency in FCR markets [8].

Figure 5.

Annual average capacity and energy prices in 2019.

Figure 6.

The schematic of 15-minutes granularity in the balancing stage.

Figure 7.

Input and output parameters used in the model during balancing markets participation (balancing stage).

Figure 7.

Input and output parameters used in the model during balancing markets participation (balancing stage).

Figure 8.

Annual operation hours and annual full-load operation hours of the reserve units in the day-ahead scheduling in 2019 and 2025.

Figure 8.

Annual operation hours and annual full-load operation hours of the reserve units in the day-ahead scheduling in 2019 and 2025.

Figure 12.

(a). The share of annual heat production by each city’s HPs to its annual heat demand. (b) the annual net profit for each city DHN from FCR-N market, (c) the annual net profit for each city DHN from FCR-D up-regulation market and (d) the annual net profit for each city DHN from the FCR-D down-regulation market.

Figure 12.

(a). The share of annual heat production by each city’s HPs to its annual heat demand. (b) the annual net profit for each city DHN from FCR-N market, (c) the annual net profit for each city DHN from FCR-D up-regulation market and (d) the annual net profit for each city DHN from the FCR-D down-regulation market.

Figure 13.

(a). The share of annual heat production by each city’s HPs to its annual heat demand in different electricity spot price. (b). the annual net profit for each city DHN from FCR-N market. (c). The annual net profit for each city DHN from FCR-D up-regulation market. (d). The annual net profit for each city DHN from FCR-D down-regulation market.

Figure 13.

(a). The share of annual heat production by each city’s HPs to its annual heat demand in different electricity spot price. (b). the annual net profit for each city DHN from FCR-N market. (c). The annual net profit for each city DHN from FCR-D up-regulation market. (d). The annual net profit for each city DHN from FCR-D down-regulation market.

Table 1.

Various price systems models in the balancing markets [8].

Table 1.

Various price systems models in the balancing markets [8].

| Up-Regulation | No Regulations | Down-Regulation | |

| Up-regulation price | 80 | 70 | 90 |

| Day-ahead price | 70 | 70 | 90 |

| Down-regulation price | 70 | 70 | 60 |

| Purchase/sales price for imbalance energy | 80 | 70 | 60 |

* All Prices are in €/MWh and are just for exemplification of the case.

| Unit | Heat source | COP 2019/2025 |

Electrical capacity (MW) 2019/2025 |

|---|---|---|---|

| Helsinki | |||

| Katri Vala HP | Waste heat | 2.4 / 2.3 | 43 / 67 |

| Salmisaari HP | Ambient air | - / 2.1 | 0 / 8 |

| Vuosaari HP | Sea water | - / 2.3 | 0 / 5.5 |

| Esplanadi HP | Waste heat | 2.2 / 2.3 | 9.8 / 9.8 |

| Electric Boiler | - | 99 % | 0 / 280 |

| Espoo | |||

| Suomenoja 3 and 4 HPs | Wastewater | 2.5 / 2.2 | 18/30 |

| Vermo HP | Air | - / 2.0 | 0 / 4.5 |

1 The COPs in this table are average actual COPs (different from design COP which is a constant value) calculated based on heat source and sinks’ inlet and outlet temperautres during a year. 2 Efficiency of the electric boiler.

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Copyright: This open access article is published under a Creative Commons CC BY 4.0 license, which permit the free download, distribution, and reuse, provided that the author and preprint are cited in any reuse.