Submitted:

01 December 2023

Posted:

04 December 2023

You are already at the latest version

Abstract

The objectives of this article are to examine whether the application of digitalization in enterprise budgeting affects the fulfilment of budgeting functions and their qualitative characteristics, and to investigate whether the realization of budgeting functions brings benefits. The research was conducted from the perspective of contingency theory, both internal and external conditions. The study used an online survey targeting company budgeting staff. Structural Equation Modelling was utilized to validate the structural model (PLS-SEM technique). The conclusions confirm that the application of digitalization, which particularly pertains to ERP, Business Intelligence systems and accounting systems with budgeting solutions, positively impacts the fulfilment of budgeting functions and most of their qualitative characteristics, while Blockchain makes a minor contribution. Our research suggests that contingency variables, particularly internal ones such as company size, the quality of the organizational structure, and support for competitive strategy, continue to affect budgeting implementation even with the participation of digitalization in budgeting. Budgeting functions and their qualitative aspects are notably correlated with the advantages derived from budgeting, including financial performance, sustainable development and budget task execution.

Keywords:

budgeting

; digitalization

; budgeting functions

; company performance

; management accounting

1. Introduction

This article aims to explore the influence of digitalization on the evaluation of budgeting functions, encompassing planning, motivation, performance appraisal/control, and their qualitative attributes. Grounded in the principles of contingency theory, the study also considers the effect of various factors that condition the impact of digitalization on the assessment of budgeting functions. These factors include firm size, environmental uncertainty, technological advancement, organizational culture, competition, as well as corporate goals and strategy. Moreover, the research delves into the interplay between the evaluation of budgeting functions and digitalization, examining their joint effect on the accomplishment of budgetary tasks and overall organizational performance, spanning financial outcomes and sustainable development endeavors.

Within the scholarly discourse, extensive research has been conducted on the influence of specific contingent variables on budgeting functions. These variables include firm size [1], [2], organizational structure [3] environmental uncertainty [4], [5], [6], [7], technological sophistication [8], [9], [10], organizational culture [11], [12], competition [13], as well as corporate goals and strategies [14], [15] However, these studies notably lack any references to the impact of digitalization on budgeting and its functions.

Within the existing literature, extensive investigations have been conducted to explore the impact of digitalization on the practice of management accounting solutions in enterprises. Noteworthy studies conducted by Rikhardsson and Yigitbasioglu (2018) [16], Garanina et al. (2022) [17], Kostić and Sedej (2022) [18], Granlund and Malmi (2002) [19], Martin et al. (2016) [20], Yigitbasioglu (2019) [21], and Möller et al. (2020) [22] have provided valuable insights in this area. This article highlights the preliminary nature of most investigations in the domain, primarily focusing on the realm of management accounting, rather than specifically delving into budgeting, its functions, and qualitative attributes. While studies conducted by Bhimani (2020) [23] and Bhimani and Willcocks (2014) [24] have contributed substantially, empirical research remains scarce in this area. Moreover, the research at hand addresses a critical void as it pertains to the comprehensive evaluation of the influence of digitalization on budgeting functions, their qualitative characteristics, and the resultant impact on organizational achievements, including financial performance and sustainable development goals. Selected studies, namely Baumöl and Perscheid (2019) [25], Bergmann et al. (2020) [10], Dillerup et al. (2019) [26], Duh et al. (2006) [27], Kappes and Klehr (2021) [28], and Nasca et al. (2018) [29], touch upon certain qualitative aspects of budgeting. However, they fall short of providing a holistic assessment of digitalization’s implications on budgeting functions, their qualitative features, and the outcomes in terms of organizational performance. Bergmann et al. (2020) [10] found a positive correlation between data infrastructure refinement and the use of business analytics in budgeting. They also discovered that organizations emphasizing budgeting functions were more likely to adopt business analytics in budgeting, leading to higher satisfaction with the budgeting process. However, the study only focused on the impact of one digitalization tool, business analytics.

Studies consistently indicate that the implementation of digitalization has a positive impact on enterprise performance, including financial achievements [30], [31], [32], [33], [34], [35], [36] and a company’s sustainable development goals [37], [38], [39]. However, these studies predominantly focus on the effects of digitalization in the operational aspects of the enterprise, with limited attention given to supporting (managerial) processes, particularly budgeting and budgetary control. Furthermore, the role of budgeting in supporting the achievement of a company’s sustainable development goals has primarily been analyzed through the lens of project budgeting rather than comprehensive budgeting (master budget).

From the analysis of previous studies, it becomes evident that there exist research gaps, particularly in the following areas: the impact of digitalization on the execution of budgeting functions, consideration of the effect of contingent variables in this relationship (such as firm size, environmental uncertainty, competition, technology, etc.), establishing correlations between the execution of budgeting functions and the assessment of budgetary task achievements, the financial outcomes of budgeting, and achievements in sustainable development in the context of implementing digitalization in budgeting.

The study used a survey, conducted online and anonymously, targeting company budgeting staff around the world. It was distributed through social media and survey platforms, as well as directly to companies from the EMIS database. Structural Equation Modelling (SEM) was utilized for measurement validation and to evaluate the structural model. The PLS-SEM technique was used to assess the complex relationships among multiple variables, and the mixed model was employed (both reflective and formative).

The article consists of six sections, including the introduction. Section 2 presents prior research on the determinants of budgeting function execution, the impact of digitalization on firm performance, the consequences of digitalization in managerial accounting systems and budgeting, and the formulation of the research hypotheses. Section 3 describes the data sources and research methodology. Section 4 contains the research results. In Section 5, a discussion is conducted in light of the research findings resulting in final conclusions (Section 6).

2. Prior research and hypothesis development

2.1. Budgeting functions and the determinants of their execution

Budgets can be defined as numerically or quantitatively expressed plans of a company’s activities. It is not possible to present action plans more precisely than numerically, but precise planning can only be done within a relatively short time horizon. As a result, budgets are plans with a relatively short time horizon, typically not extending beyond the following year, and are usually divided into monthly segments [40]. Barret and Fraser [41] identify two groups of budgeting functions: core functions (planning, motivating, establishing performance benchmarks, and working with teams of individuals); and supporting functions (coordinating and learning).

In this article, we examine the impact of digitalization on budgeting functions in light of contingency theory. According to contingency theory in management, the effectiveness of an organization primarily relies on a specific set of environmental variables, with technology being a significant component, along with managerial and resource variables [42]. The design of an organization and its subsystems should be integrated with the surrounding environment and able to adapt to diverse organizational circumstances. While early studies in contingency theory emphasized the internal and external contingencies of organizations, current literature highlights the importance of organizational knowledge creation within this framework [43]. Contingency theory has remained a valuable framework for analyzing specific situational factors. The theory proposes that contextual factors have an impact on the organizational structure of a business unit, and that in turn, the organizational structure influences the performance of the company. Consequently, specific ways of organizing a business unit are more likely to yield favorable performance outcomes when aligned with specific contextual factors, creating a concept known as a “good fit” [44]. The primary factors influencing the outcomes can be categorized into two groups: external and internal contingencies [45]. The frequently analyzed external contingencies consist of technology, market rivalry or antagonism, environmental unpredictability, and national culture. Meanwhile, the principal internal factors encompass organizational size, structure and strategy, remuneration arrangements, information systems, psychological aspects (e.g., tolerance for ambiguity), employee participation in control mechanisms, market position, product life-cycle stage, and changes in systems. The following contingencies can be identified as particularly influential in the implementation of budgeting functions (the symbols for these contingencies in brackets are used further in the study):

- a)

- Organizational size (S). A relationship was identified between budget emphasis and factors such as size, decentralization, and interdependence within organizations [1]. The size of an organization can impact budgeting processes, as larger organizations may require more complex and extensive budgeting systems to manage their operations effectively [2].

- b)

- Organizational structure (SQ). The level of decentralization including participation in budgeting (OS). In highly structured organizations, individuals perceive themselves as having greater influence and thus actively participate in budget planning. They also express satisfaction with budget-related activities [3]. Managers in organizations characterized by concentrated authority are typically responsible for fewer variables and experience higher levels of pressure from superiors. Bruns and Waterhouse (1975) found that individuals view budgets as less beneficial and constraining their adaptability; however, they still indicate contentment with how their superiors employ budgets [3].

- c)

- Environmental uncertainty (EU). Participative budgeting is considered highly significant for both planning and control purposes, particularly in terms of vertical information sharing and coordinating interdependence. Additionally, specific reasons for implementing participative budgeting are found to be correlated with factors that precede it - environmental and task uncertainty, task interdependence, and superior-subordinate information asymmetry [5]. The level of uncertainty in the external environment, such as market volatility or regulatory changes, can affect budgeting practices. Organizations operating in highly uncertain environments may need to adopt flexible/rolling budgeting approaches as complementary to traditional annual budgets in order to adapt to changing conditions [6], [7].

- d)

- Technological sophistication (TS). The impact of technology on budgeting functions can be both indirect (influence of technology applied in operational activities) and direct (systems used in budgeting). According to published research, the implementation of emerging technology necessitates adjustments in both cost structures and the information required for effective management. This includes expanding the utilization of management accounting systems and methodologies [8], [9]. The level of technological advancement within an organization can directly impact budgeting processes [10].

- e)

- Organizational culture (OC). The findings from research into means and cultural factor analysis provide compelling evidence for the presence of a distinct organizational culture, indicating a high level of shared beliefs among managers. Collectively, these analyses confirm the impact of organizational culture on budget-related behavior (BRB) [11]. For example, when distinguishing between two types of organizational culture, namely humanist and managerialist, the impact of the specific type of organizational culture on BRB was noted. Under the humanist culture, a participative budgeting style is observed, while the managerial culture aligns with a managerial budgeting style. The managerialist approach involves budget manipulation, substantial time investment in budgeting, flexibility within the budget for innovation, and recognition of the budget’s value in the managerial role. The findings indicate that the effectiveness of budget participation in reducing role ambiguity can be influenced by organizational culture [12].

- f)

- Leadership style (PE). The leadership style within an organization can influence how budgeting functions are approached. In terms of leadership, leaders who demonstrate a considerate leadership style are more inclined to encourage subordinate involvement in the budgeting process. Expanding on this discovery, the participation of subordinates in budgeting activities may act as a mediator between leadership style and workplace outcomes, such as job satisfaction. Furthermore, the results suggest that superiors tend to promote subordinate participation when evaluating them based on budgetary goals [46]. The leadership style influences subordinates’ approach to achieving budgetary tasks [47].

- g)

- Industry, including competition (CP). Libby and Waterhouse (1996) found that in environments with intense competition, organizations tended to adopt a wider range of management accounting systems [48]. Managers’ perception of a high level of competition positively influenced their understanding of budgeting [13].

- h)

- Strategic goals and objectives (BS): Research findings indicate that when managers have an understanding of their budget goals, and when those goals are challenging, this tends to have beneficial effects on their attitudes towards their jobs and the budget. In addition, the level of difficulty associated with budget goals was found to impact the performance of managers in managing their budgets. Furthermore, both the difficulty and clarity of budget goals contribute to increasing the motivation of managers to meet their budgetary targets [14]. Budgeting processes are also greatly influenced by the competitive strategies adopted in SBUs (Strategic Business Units), portfolio strategies [15], and the product life cycle [49].

Undoubtedly, a critical aspect that deserves considerable attention is the influence of budgeting on the overall performance of an enterprise. The findings indicate that diagnostic and/or interactive use of the budget has an impact on both organizational commitment and managerial performance. This suggests that the effects of budget utilization on managerial performance are only observed when managers demonstrate commitment to the organization [50]. This appears to show that when individuals actively participate in budgeting, it has a positive impact on their managerial performance [51], [52]. Prior research indicates that companies that adopt operating budgets at a faster pace are typically associated with faster growth rates [53]. The research also emphasizes the role of budgeting in achieving sustainable development goals. Moreno-Monsalve et al. (2023) conducted a study which showed that sustainable development-oriented projects tend to create value, with four key dimensions - impact, relevance, effectiveness, and efficiency - playing a significant role in explaining their success [37]. The strategic priorities related to sustainability are of high importance and urgency, and research showed that the prudent allocation of investment can enhance the sustainability and long-term viability of the shipping industry [38]. Furthermore, research demonstrates that the implementation of smart contracts improves procurement efficiency in terms of cost, time, and quality, while at the same time providing sustainable competitive advantages [39]. The incorporation of sustainability-focused requirements and budgets streamlines the prioritization of design decisions by assessing their impact on diverse environmental factors [54]. Research outcomes suggest that Environmental Management Systems act as a mediator in the link between Sustainability Management Accounting and Organizational Performance within the Indonesian manufacturing sector [55].

2.2. Digitalization, its instruments, and its impact on company performance

Digitalization refers to the utilization of diverse technologies, such as cloud technologies, sensors, big data, and 3D printing, to develop new products, digital services, and innovative business models [56]. The instruments of digitalization encompass a wide range of solutions, including Management Information systems (MIS), Enterprise Resource Planning (ERP) systems, cloud computing (CC), Big Data Analytics (BDA), Customer Relationship Management (CRM) systems, Robotic Process Automation (RPA), the Internet of Things (IoT), Artificial Intelligence/Machine Learning (AI/ML), Digital Collaboration Tools (DCC), E-commerce platforms, and Blockchain technology (BC) [57], [58], [59], [60], [61], [62], [63], [64], [65], [66], [67], [68].

The existing literature highlights the positive impact of digitalization on financial performance through multiple pathways. Implementing digitalization leads to cost-efficient actions, increased profitability, and enhanced productivity [69]. The influence of digitalization on company performance is closely tied to technological advancements and modifications [30]. By implementing the Industry 4.0 concept, companies can achieve enhanced performance through cost reduction, improved product quality, customization, prompt delivery, and the introduction of new products [31]. Moreover, digitalization can reduce transaction costs, further augmenting financial performance [70]. The combination of digitalization and servitization also contributes to improved financial results [34]. Furthermore, the implementation of big data positively influences financial performance [35], as does the active use of social networks [36]. These benefits extend not only to regular enterprises but also to financial institutions [71], [72]. Several studies underscore the positive impact of digitalization on financial performance. Customer engagement and technology strategy significantly influence service innovation, thereby affecting both financial and non-financial performance [73]. In the context of SMEs, digitalization positively impacts financial outcomes and depends on information technology, employee skills, and digital strategy [74].

Research studies have investigated the indirect links between digital technology adoption and financial success, emphasizing the role of strategies, resources, and capabilities [75]. Additionally, product innovation plays a vital role in shaping the relationship between digitalization and performance [76]. Combining digitalization with a distinct innovation strategy is deemed essential [77]. Furthermore, a positive link between digitalization and firm performance is evident in the context of servitization [78], [20].

Nevertheless, the literature reveals a paradox concerning the financial consequences of using digital platforms, with a potential reduction in the sale of goods accompanied by an increase in services [79]. Additionally, investments in data analytics in the banking sector may increase productivity, but they also lead to a reduction in return on equity and return on assets [80]. The relationship between digitalization and financial performance may follow an inverted U-shaped curve, with dynamic capability positively influencing this link [81].

Digitalization can lead to improved processes, added value generation, and enhanced customer experience [82]. Its positive impact on financial performance is observed in various aspects, such as in the value chain by vendors and clients, the assistance of core capabilities, and the adoption of e-purchasing systems [83], [84], [85]. Internal barriers significantly influence the development of digitalization processes, and the Industry 4.0 concept has a positive impact on organizational performance [86]. The attitude towards digitalization and the identification of barriers plays a crucial role in harnessing the potential of digitalization [87], [88]. Leadership also plays a pivotal role in effectively controlling digital conversion [89], [89], while a positive attitude towards digitalization influences the intention to use digital tools [90].

2.3. The impact of digitalization on management accounting and budgeting

In the literature, it is emphasized that digitalization affects methodological approaches in management accounting [91]. Bhimani and Willcocks (2014) maintain that changes in information technology unavoidably transform information gathering and investigation with regard to management and control functions [24]. However, the results of research on the impact of digitalization on managerial accounting are quite modest, and even more so in the case of the impact of digitalization on budgeting. Rikhardsson and Yigitbasioglu (2018), based on analysis of the literature on the subject, showed that there is relatively little interest among researchers in investigating the relationship between management accounting and Business Intelligence (BI) and Business Analytics (BA). However, they also pointed to significant gaps in this respect, including the role of prediction with the use of BI/BA in management accounting tasks, and the correction the role and competence of accountants in connection with the application of BI/BA in management accounting [16].

Arnaboldi et al. (2017) worked on research into the relationship between technology-enabled networks and accounting functions. They indicated three areas of future investigations: performance indicators, governance of information resources, and modification of information and the process of adoption of decisions [92]. According to Flyverbom (2022), the first shift to digital architecture visibility requires broadening the extent of analysis so as to catch the elements and outlines of digital architectures. The second shift digs down into the inward mechanism of digital architectures by enunciating how concepts about digital figures and visibility management can be employed to comprehend data retrieval processes, algorithmic classification, and logic [93]. Knudsen (2020) analyzed how digitalization influenced accounting practice, and indicated the impacts on the boundaries of accounting, power relations, and the production of knowledge for decision-making. According to Korhonen et al. (2020), digitalization can signify the automation of analytical work, however, professionals should not endeavor to program nonprogrammable processes [64].

Previous scientific studies have more frequently focused on the impact of individual digitalization tools on managerial accounting. Garanina et al. (2022) analyzed the impact of blockchain on the accounting profession, indicating the future higher-profile advisory role of accountants [17]. Kostić and Sedej (2022) found four areas of management accounting that may be impacted by blockchain technology: collaboration, trust, inter-organizational control, and information exchange [18]. Other research results indicate that ERP systems have a limited impact on management accounting and control procedures [19]. There is also a proposal that the importance of big data be included in the accounting curriculum [94]. Kellogg et al. (2020) showed that the use of algorithmic technologies develops important but also contentious control instruments, for example by hiding the working methods used by employees, as well as the important results they achieve [95]. Vasarhelyi et al. (2015) maintain that big data changes the sources of information in accounting and auditing [96].

Prior research has also explored the integration of digitalization into managerial accounting, and considers its consequences and conditions. Specific attention is devoted to analyzing the effective impact of digitalization on managerial accounting solutions [97]. In their findings, Moll and Yigitbasioglu (2019) suggest that technology facilitates a novel exchange of information, thereby improving financial and management accounting, but that this enhancement necessitates accountants to expand their skill sets [21]. A study conducted by Möller et al. (2020) demonstrates the role of digitalization, data analytics, and automated prediction technologies, which employ time-series methods, machine learning, and simulation [22]. Bergmann et al. (2020) discovered a favorable link between the refinement of data infrastructure and the utilization of business analytics (BA) in budgeting. They also established a positive correlation between the significance of an organization’s budgeting function and the utilization of BA, leading to higher satisfaction with budgeting [10]. Quattrone (2016) maintains that the unworkability of achieving excellent information and rational decision-making in data-controlled organizations represents the initial stage in restoring the proper role of management accounting [98]. Quinn et al. (2014) emphasize the collaborative role of management accountants with technical experts and cloud service providers in providing accurate information. They propose that cloud technology can be efficiently employed to communicate information to managers [99]. Raisch and Krakowski (2020) stress that automation and augmentation (humans operating together with machines to carry out a task) are essentially complementary, rather than dissociable and contradictory [100]. Taipaleenmäki and Ikäheimo (2013) find that developments in information technology facilitate the convergence of management accounting and financial accounting. Moreover, the utilization of technology also influences the behavioral and organizational sphere, affecting accounting processes and the role of accountants [101]. Buhmann et al. (2019) analyze the accountability process of algorithms and identify three interconnected capacities: reputational concerns, engagement strategies, and discourse principles [102].

The outcomes obtained from an investigation aimed at German companies validate the positive correlation between the intricacy of data infrastructure and the incorporation of BA within budgetary protocols, as established by Bergmann et al. in 2020 [10]. Furthermore, an intensified emphasis on strategic planning aligns with an increased integration of BA into the budgeting framework. However, no analogous association is discerned for the evaluative aspect. Encouragingly, their study establishes a favorable nexus between the utilization of BA and the satisfaction derived from the budgeting process. This underscores the potential of analytics in alleviating discontentment arising from conventional budgeting methodologies.

Digitalization has various impacts on the qualitative characteristics of budgeting processes, including efficiently evaluating and interpreting large amounts of data [25], streamlining budgeting through BA with favorable outcomes [10], and addressing challenges such as quicker changes, digital business models, incorporating external data, and effective data management [26]. Utilizing IT tools for planning positively correlates with overall performance, but hindrances such as inadequate education and staff resistance can impact their effectiveness [27]. The research results indicate a positive role of digitalization in budgeting for the achievement of sustainable development goals within enterprises, specifically at the project management level [39]. Additionally, digitalization enables more automated, detailed, and adaptable budgeting [28], improves accuracy and flexibility in planning [103], enhances communication, collaboration, and coordination [104], simplifies budgeting processes [29], and integrates budgeting with other information systems (ERP, CRM, SCM) [105].

2.4. Hypothesis development

Analysis of prior studies indicates that various authors have considered the impact of budgeting contingencies, such as the size of the enterprise, its organizational structure, the level of environmental uncertainty, technology, organizational culture, leadership style, competition, unit objectives and strategy, on the execution of budgeting functions. However, these studies lack answers to the question of how these conditions/contingencies relate to digitalization in budgeting, especially considering the fact that emerging technologies in budgeting are becoming more prominent. On the other hand, research on the impact of digitalization on budgeting only minimally addresses the above-mentioned contingencies of enterprise activities.

Many authors have examined the relationships between digitalization and the performance of enterprises, including their financial achievements and the achievement of sustainable development goals. However, the results of studies on the impact of the digitalization of budgeting on budget task execution and overall enterprise performance, including financial achievements and sustainability goals, are weak. Additionally, there is insufficient knowledge regarding the factors that shape enterprise performance as a result of digitalizing budgeting processes.

Analysis of previous studies enables the formulation of the following hypotheses:

H1: The implementation of digitalization in budgeting enhances the execution of budgeting functions (including planning, motivation, control, coordination, and learning functions), as well as the qualitative characteristics of budgeting, but this improvement is contingent upon various budgeting conditions such as the size of the enterprise, its organizational structure, the level of environmental uncertainty, technology, organizational culture, leadership style, competition, unit objectives, and strategy.

H2: The enhancement of budgeting functions is accompanied by improved budget task execution, better assessment of the financial benefits stemming from digitalization, higher financial performance of the enterprise, and support for the achievement of the company’s sustainable development goals. The use of digitalization in budgeting is correlated with higher ratings in terms of budget task performance, the financial benefits resulting from budgeting, the company’s financial situation, and its sustainable development goals.

3. Data and methodology

The research was conducted based on a survey study. The survey instruments were developed in combination with a literature review. The data for the questionnaire was collected through the use of a non-interventional, anonymized, self-administered, web-based survey to be completed by individuals involved in budgeting within their company (management, chief accountants, and accounting specialists) between August and November 2023. The survey was distributed using social media and groups devoted to survey exchanges, as well as via the online research platforms Survey Swap and Survey Circle. Moreover, the links to surveys were sent by email to 37600 companies, whose email addresses were identified from the EMIS database. Ultimately, 319 responses were received, which represents a 0.85% response rate. The dominant part of the operational activities of the companies studied were conducted in a range of countries, namely: Argentina, Armenia, Australia, Austria, the Bahamas, Bahrain, Bangladesh, Belgium, Bhutan, Bulgaria, Canada, China, Costa Rica, Croatia, Cyprus, Denmark, Egypt, Finland, France, Georgia, Germany, Greece, Hungary, India, Ireland, Israel, Italy, Jordan, Malaysia, Malta, Mauritius, Mexico, Morocco, the Netherlands, Pakistan, Poland, Portugal, Romania, Saudi Arabia, the Seychelles, Singapore, Slovenia, South Africa, Spain, Switzerland, Thailand, the United Arab Emirates, the United Kingdom, the United States of America, and Vietnam.

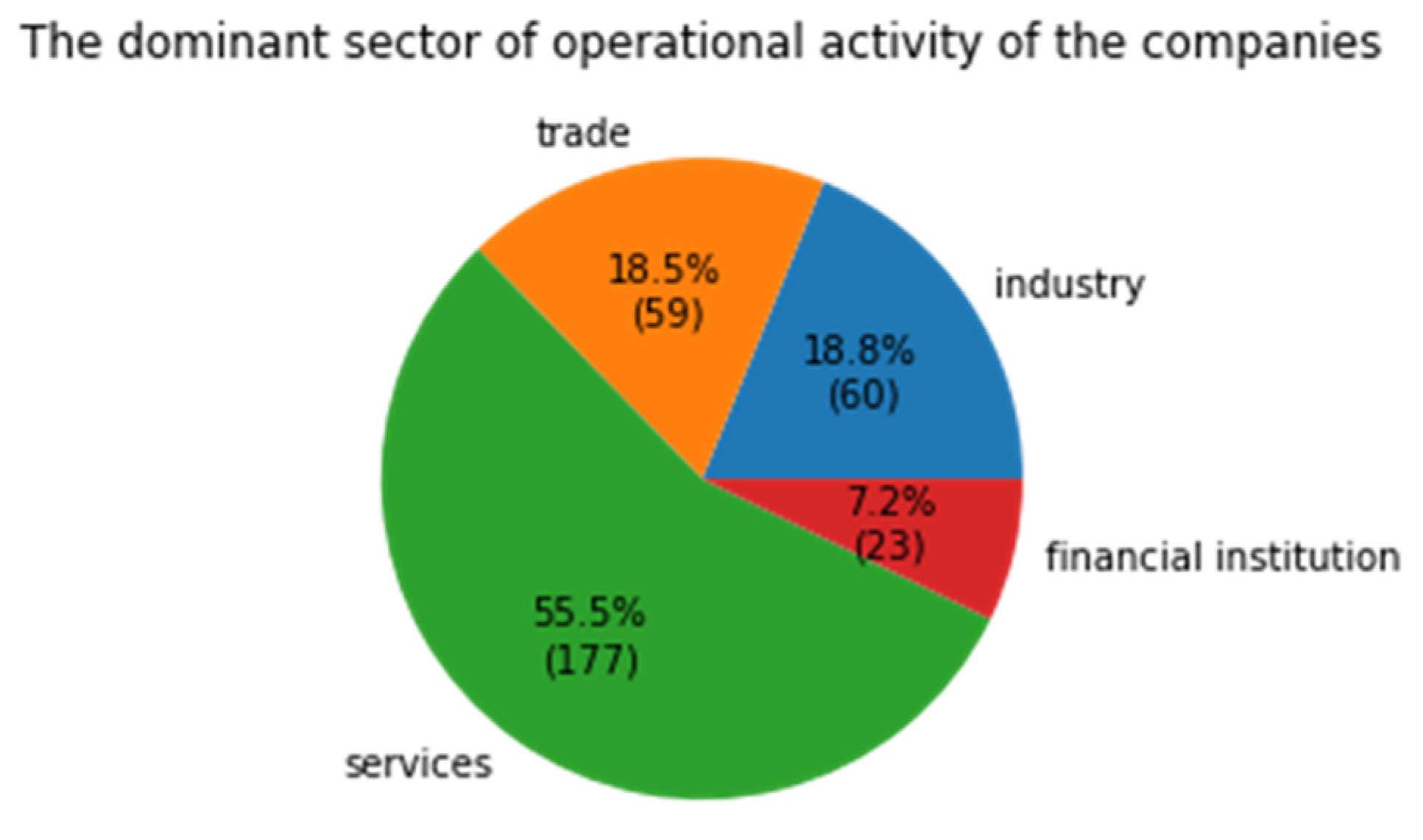

The dominant sector of operational activity of the companies studied is presented in Figure 1.

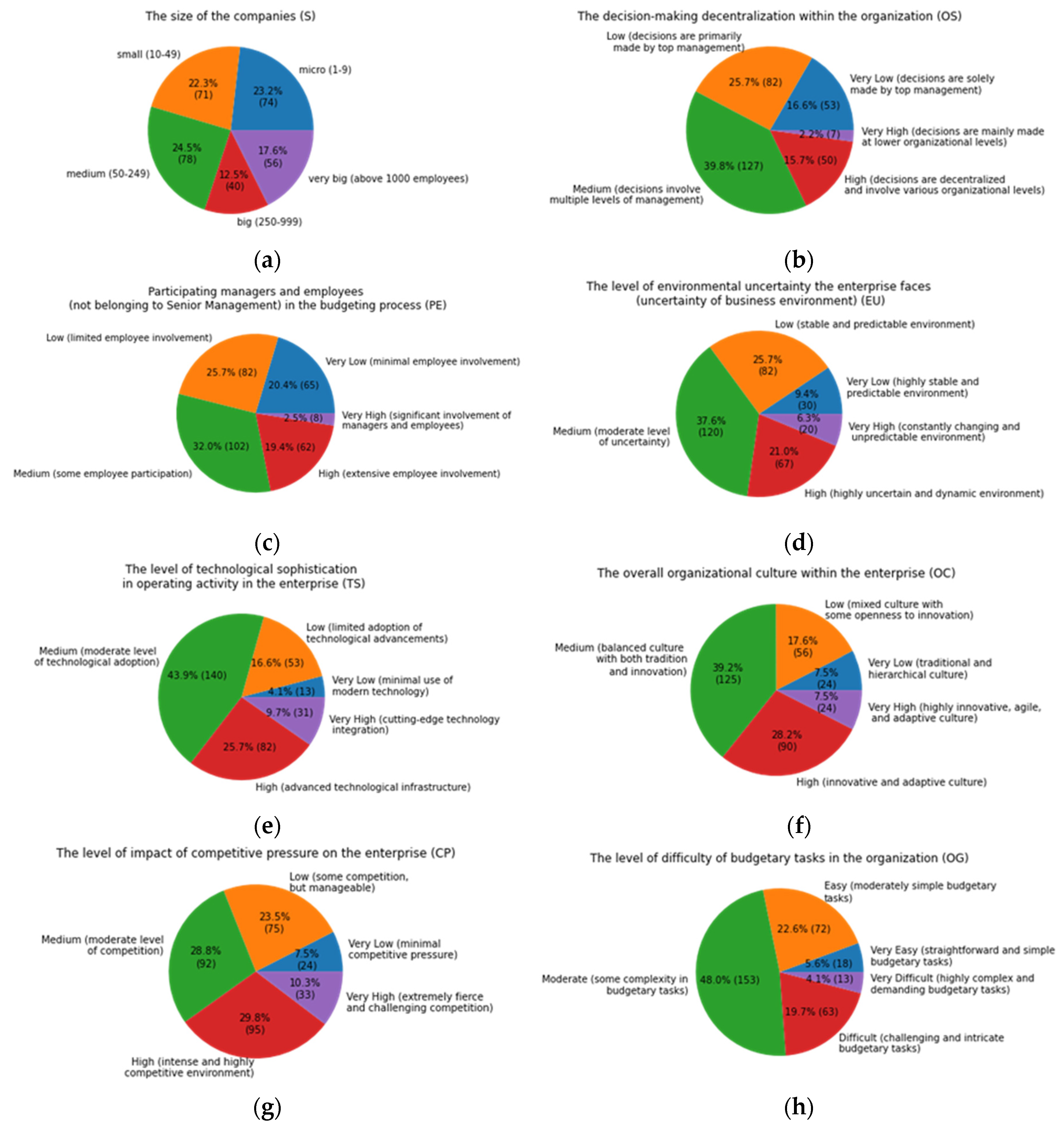

The first part of the questionnaire was related to budgeting contingencies. The following contingencies were analyzed:

- size of enterprise (S),

- decision-making decentralization (OS),

- participation of managers and employees (not belonging to Senior Management) in budgeting (PE),

- environmental uncertainty (EU),

- technologically sophisticated operating activity (TS),

- organizational culture (OC),

- competitive pressure (CP),

- difficulty of budgetary tasks (OG),

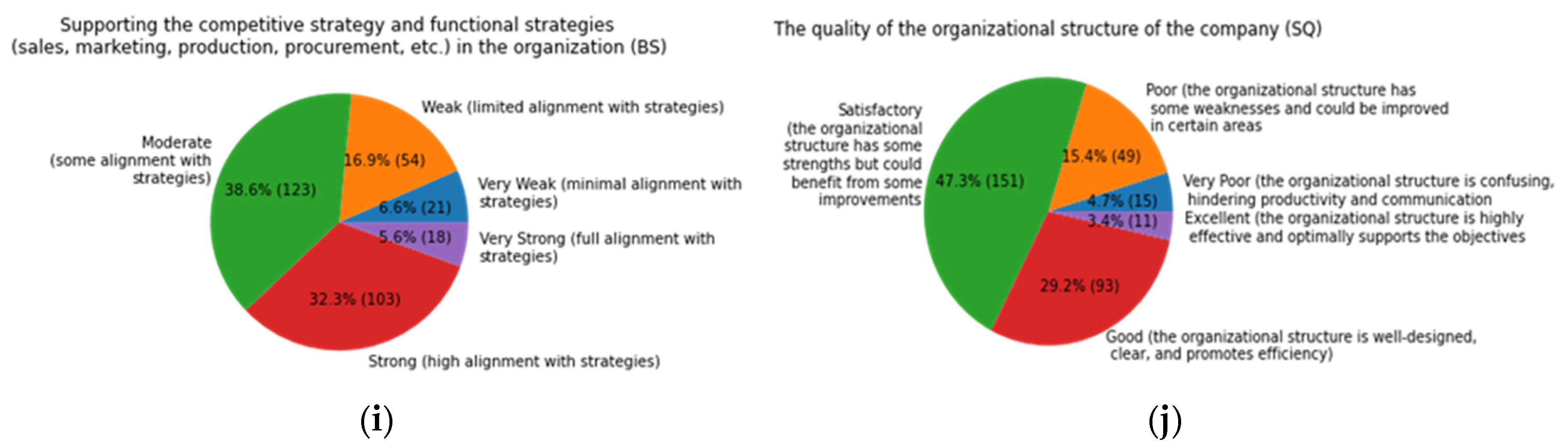

- support of competitive strategy and functional strategies (sales, marketing, production, procurement, etc.) (BS),

- quality of the organizational structure (SQ).

All the variables in the questionnaire were rated on a five-point Likert scale. The responses are coded as follows: 1 – the lowest level of a particular contingency, 2 - low level, 3 – medium level, 4 – high level, 5 – the highest level. The responses are presented in Figure 2, whilst the statistics are displayed in Table 1.

Following this, questions were asked regarding the application of the following digitalization solutions in budgeting. The following technologies were analyzed: Integrated MIS - in particular ERP systems (MIS/ERP), cloud computing (CC), Big Data Analytics (BDA), business intelligence tools (BI), Customer Relationship Management systems (CRM), Robotic Process Automation (RPA), Artificial Intelligence/Machine Learning (AI/ML), the Internet of Things (IoT), digital collaboration and communication tools (DCC), dedicated information systems for budgeting and control (IBS), Accounting Information Systems with budgeting solutions (AIS), Blockchain technology (BC), and Excel/Access (E/A). The intensity of the use of specific digitalization solutions in budgeting was evaluated by respondents using the following possible responses: no implementation (1), planned implementation within the next 3 years (2), partial implementation (3), moderate implementation (4), and high level of implementation (5). The responses and statistics are presented in Table 2.

The results indicated that the implementation of modern technologies in the budgeting processes is in its infancy. The technologies usually employed in budgeting solutions are based on Excel/Access (mode = 5, median = 4). Emerging sophisticated technologies such as Machine Learning/Artificial Intelligence, Robotic Process Automation, and the Internet of Things were used to a small extent (mode = 1, median = 2), especially Blockchain (median and mode = 1).

The respondents were subsequently asked about budgeting functions and the qualitative characteristics of budgeting in their companies. The following functions were investigated:

- planning – contribution to creating a financial plan outlining future goals, expenses, and revenues for the organization (EP),

- motivating – budgets serve as targets for teams and individuals, motivating them to achieve budgetary tasks, in particular through incentivizing (EM),

- controlling – establishing performance benchmarks and working with teams of individuals (EV),

- coordinating – fostering coordination, communication, and collaboration among different departments within the organization (EC),

- learning from past experiences and adapting to changing circumstances through budgeting (EL),

- simplicity of budgeting (EG),

- flexibility of budgeting (EF),

- efficiency of budgeting (EE),

- level of integration of budgeting with other information systems (ERP, PMS, CRM, HMR, P2P, and others) (EI),

- level of detail and completeness of information required in budgeting (ED),

- level of adaptation to new circumstances resulting from budgeting (EA).

Responses were coded using a scale from 1 (very low rating), 2 (low rating), 3 (moderate rating), 4 (high rating) to 5 (very high rating). The results are presented in Table 3.

In the next step, questions were asked regarding the benefits of budgeting. In this stage of the research, we verified whether perceived budget task execution (TE), perceived financial benefits from budgeting (FP1), perceived financial performance of the enterprise (FP2), and evaluation of supporting the company’s sustainable development (SD) were positively correlated with the evaluation of budgeting functions and the qualitative characteristics of budgeting. Variable TA was measured by indicating the level of execution of budget tasks (from 1 – very low, to 5 – very high). Variable FP1 encompassed the assessment of perceived financial benefits from budgeting and was measured on a scale from 1 (very poor financial benefits) to 5 (very significant financial benefits). Variable FP2 reflected the assessment of the company’s financial performance on a scale from 1 (very poor financial results) to 5 (very good financial results). The respondents rated to what extent budgeting in the company supported the company’s sustainable development (variable SD) on a scale from 1 (budgeting does not support the company’s sustainable development) to 5 (budgeting fully and actively promotes the company’s sustainable development). The results and statistics are presented in Table 4.

Following this, Structural Equation Modeling (SEM) was employed to validate the measurements and to assess the structural model. First-generation multivariate data analysis techniques, for example multiple and logistic regression and analysis of variance (ANOVA), have crucial limitations, namely: a simple model structure involving one layer of dependent and independent variables, that all variables should be considered observable, and the assumption that variables are measured without error [106]. These limitations can be overcome by using second-generation techniques, namely SEM, which are increasingly popular in academia. The modeling uses the interrelationships between latent constructs involved in the analysis and allows for the assessment of complex relationships among multiple variables. Generally, there are two types of SEM techniques: CB-SEM and PLS-SEM. CB-SEM is used for existing theory testing and confirmation, while for prediction and theory development, the appropriate method is PLS-SEM [106]. Moreover, PLS-SEM is the preferred approach for formative measurement models [106]. In this study, due to the theory development, PLS-SEM was employed to validate the measurements and asses the structural model.

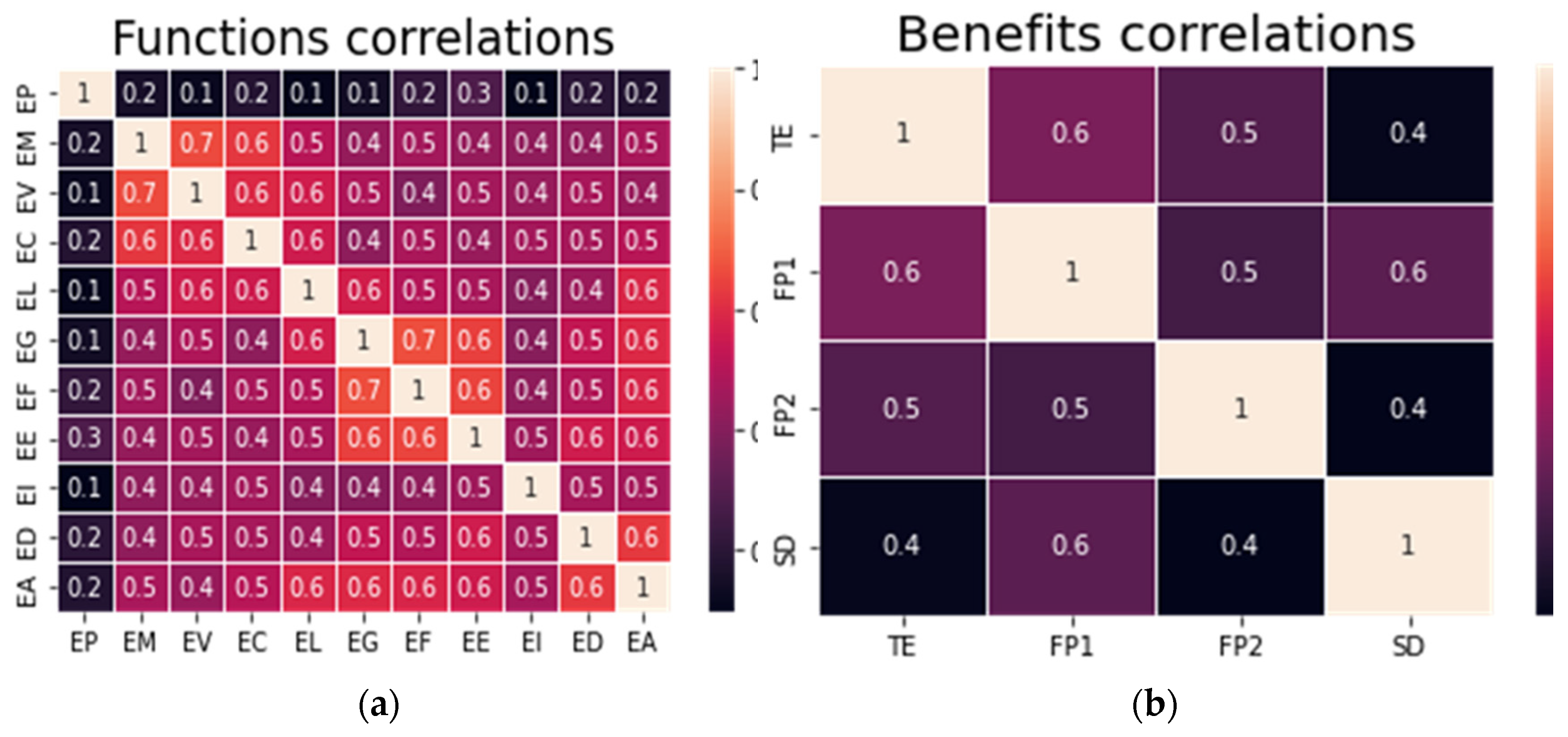

There are two conceptual approaches to measurement: reflective and formative. In the reflective measurement model, the indicators are considered to be manifestations of the construct, which means that the relationships go from the construct to the indicators, while in the formative measurement model, the indicators define and form the construct [107], so a change in the indicators results in a change in the construct. In this study, taking into account theoretical considerations such as the nature of the latent constructs, the direction of causality between the indicators and latent constructs, and the characteristics of the items used to measure the constructs [108], a mixed model was employed (both reflective and formative). The formative model was used for c constructs Contingencies and Digitalization because each indicator contributes a specific meaning to the latent variable. Meanwhile, the indicators manifested by the constructs Functions and Benefits share a common theme, are interchangeable, and are highly correlated. The correlation was confirmed using heat maps (Figure 3). The heat maps display the correlation between multiple indicators for the variables Functions and Benefits as a color-coded matrix and the Pearson correlation coefficient. Accordingly, the latent variables Functions and Benefits are reflective in nature.

Each model consists of two sub-models: inner or structural, which links together the latent variables (constructs), and the outer or measurement sub-model which explains the relationships between the latent variable and its indicator variables [106].

The development of the model and the calculations, as well as testing the hypotheses, were conducted with the use of SmartPLS 4.0 software [109].

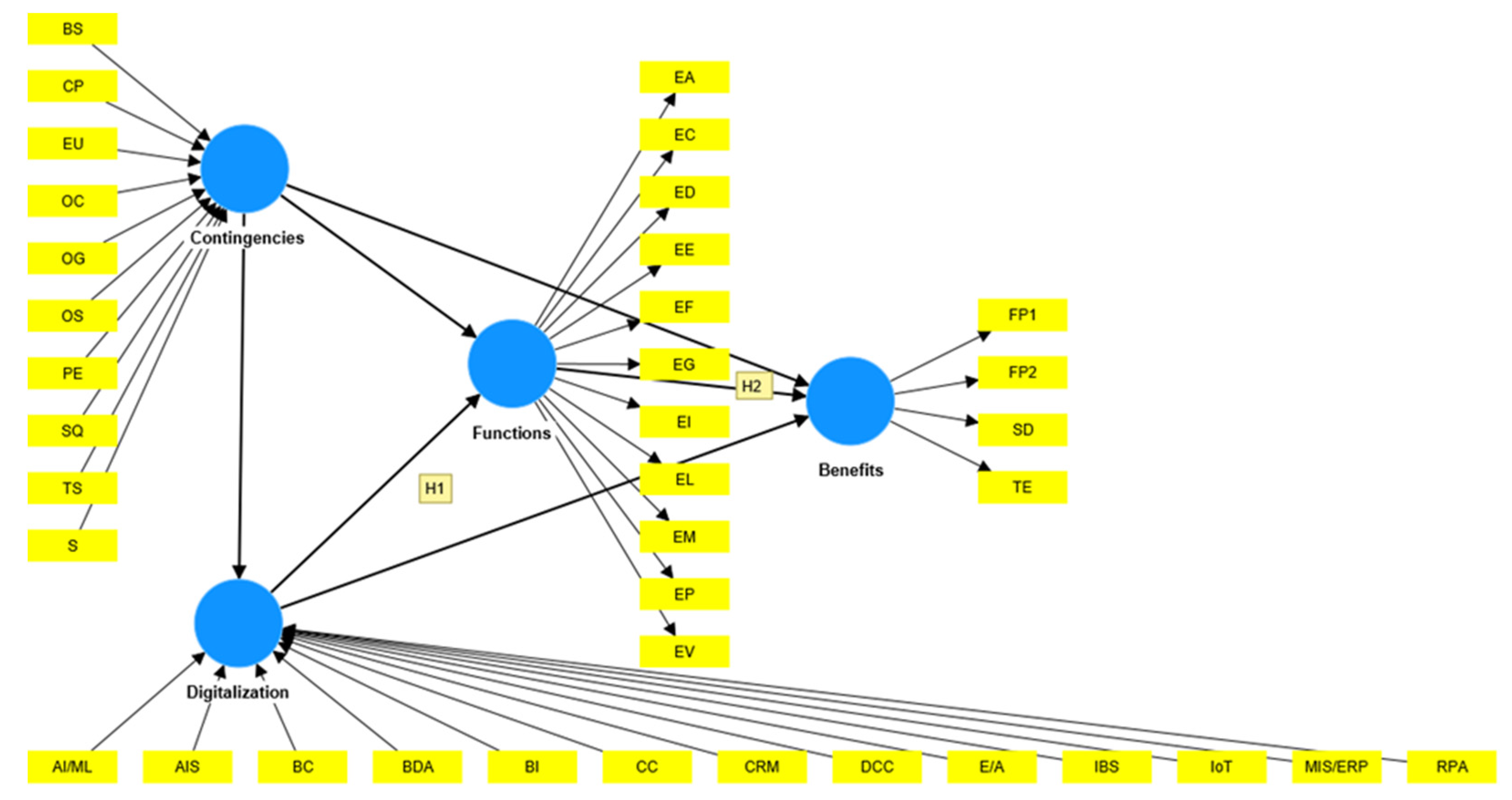

The study model is shown in Figure 4.

The model contains four latent constructs depicted in the ovals: Contingencies, Digitalization, Functions, and Benefits. The indicators are presented in rectangles. The construct Contingencies is formed from the indicators presented in Table 2, while Table 3 shows the indicators of Digitalization, and respectively Table 4 and Table 5 Functions and Benefits. The single-headed arrows point in the direction that represents the directional relationship [106].

The study model consists of two mediator variables Digitalization and Functions. The mediators are intermediate variables that increase or decrease the effect of the independent variables on the dependent variable [110], which means that a third mediator variable intervenes between the two other related constructs. In the study model, Functions mediates the relationships between Contingencies and Benefits as well as Digitalization and Benefits, whereas Digitalization intervenes between Contingencies, Functions, and Benefits.

The model was calculated using 3000 iterations and a 10-7 stop criterion to determine the path coefficients, outer weights and loadings. In the further stage, the bootstrapping procedure was employed to determine the significance of the estimated path analysis. In this non-parametric procedure, a large number of samples are drawn from the original sample with replacement [106]. In this research, 5000 bootstrap samples were used and the procedure was conducted with a 95% confidence level. The study model is presented in Figure 5. The analysis of the formative models focuses on the outer weights, while the reflective models take into account the outer loadings.

4. Results

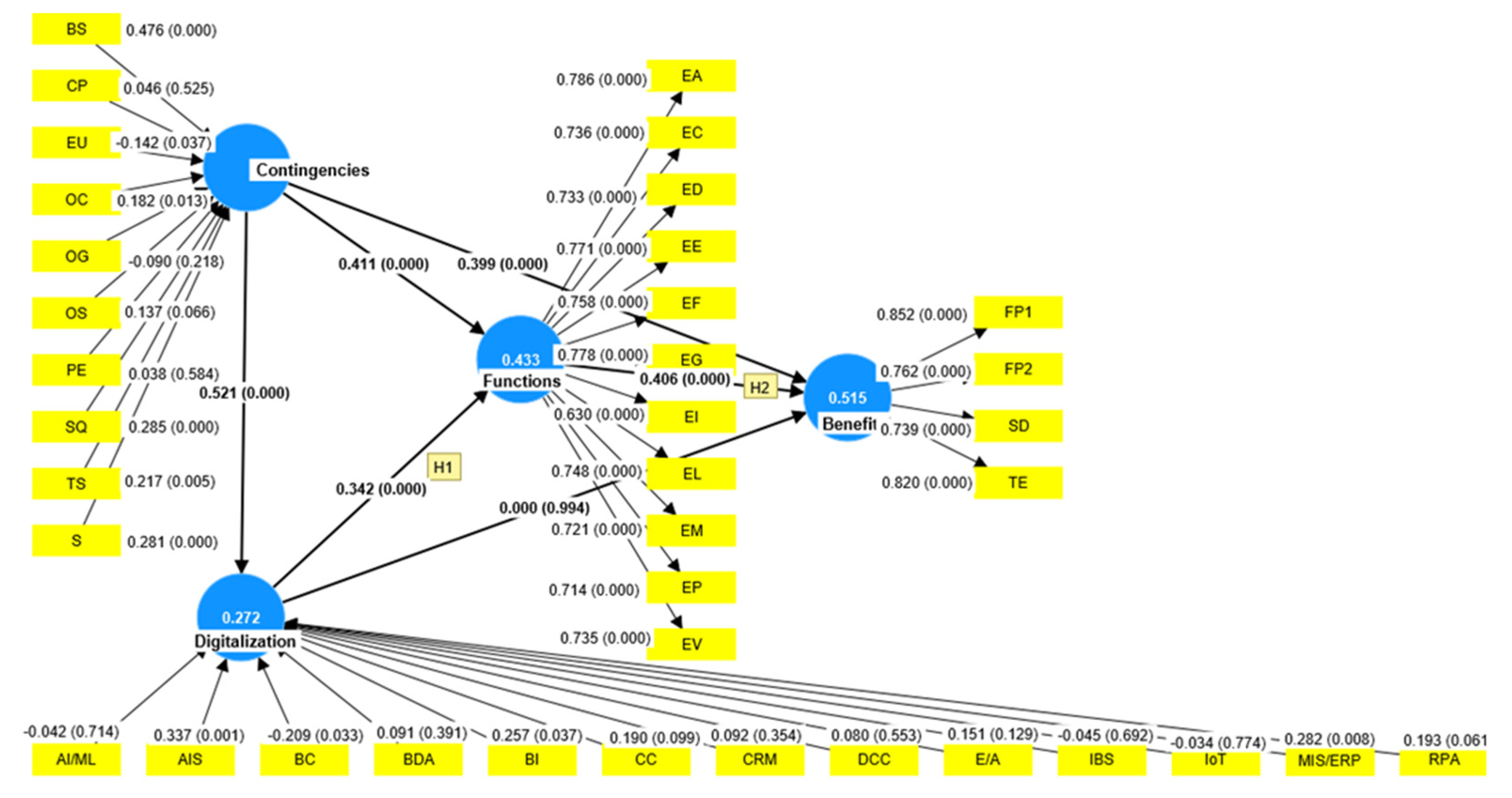

In Figure 5, the results of PLS-SEM modeling are presented in accordance with the structure described in Figure 4. In the inner model, the path coefficients and p-value are displayed, while in the outer model – the outer weights or loadings and the p-value. Additionally, the R-square (R2) was calculated for the constructs and is presented in the ovals.

The determination of R2 for the constructs demonstrates a moderate fit of the model for the variables Functions and Benefits, and a weak fit for Digitalization [110]. The R2 for Digitalization is 0.272, which means that the proposed model explains 27.7% variance of the variable, while respectively for the variables Functions it is 43.3% and Benefits 51.5%.

Analysis of mediators indicated that the path coefficients are positive and significant (p<0.05) for Digitalization -> Functions -> Benefits, Contingencies -> Functions -> Benefits, Contingencies -> Digitalization -> Functions with medium partial positive effect, for the path: Contingencies -> Digitalization -> Functions -> Benefits – with a small partial positive effect, and no effect for Contingencies -> Digitalization -> Benefits. (Table 6).

The effect size can be interpreted based on the path coefficient, with the values indicating mediating effect sizes of 0.01 for a small effect, 0.09 for a medium effect, and 0.25 for a large effect [111]. In the further analyses, the total effect was investigated (equivalent to the direct and indirect effects of the constructs through mediation).

The findings from the bootstrapping, including the mean from the original sample (O), the mean in bootstrapping, i.e., the average coefficient over all bootstrapping runs (M), the standard deviation (STDEV), the t-values, and p-values, as well as the confidence intervals, are presented in Table 7.

The path coefficient can be interpreted in the following way: if Digitalization changes by one standard deviation, Functions changes by 0.342 standard deviations. As we hypothesized, digitalization positively affects budgeting functions (path coefficient = 0.342, p < 0.001), supporting H1. Furthermore, if the variable Functions changes by one standard deviation, the variable Benefits increases by 0.406 standard deviations. Budgeting functions are significantly related to the benefits of budgeting (path coefficient 0.406, p < 0.001), which provides empirical support for H2.

The next stage is evaluating the quality of the measurement model. Assessment of the reflective measurement model involves indicator reliability, internal consistency reliability, convergent validity, and discriminant validity [106].

Indicator reliability is first assessed by observing the factor loadings and examining how much of each indicator’s variance is explained by its construct, which is indicative of indicator reliability (Table 8). The outer loading, which constitutes the absolute correlations between a construct and each of its manifest variables, should be higher than 0.7 [112], while above 0.708 is recommended as such a value indicates that the construct explains more than 50% of the indicator’s variance [106].

The results show that for the latent variable Functions, all factor loadings are above 0.708 except for EI (i.e., the level of integration of budgeting with other information systems), for which the loading is 0.630. Furthermore, all indicator loadings of the construct Benefits are high, above the recommended value. Moreover, the results are significant.

Internal consistency reliability involves an examination of the extent to which indicators measuring the same construct are associated with each other using the following metrics: Cronbach’s alpha, composite reliability (rho_a), and composite reliability (rho_c), whose recommended values are between 0.70 and 0.90, whereas a result above 0.95 indicates redundancy [106]. The results, as shown in Table 9, are acceptable.

The next step involves the assessment of convergent validity based on the average variance extracted (AVE), which measures the extent to which the construct converges to explain the variance of its indicators. The results are also satisfactory since the average variance extracted (AVE) value for each construct in Table 9 is no less than the recommended threshold value of 0.50.

The fourth step is measurement discriminant validity. Hair et al. suggest using the heterotrait-monotrait ratio (HTMT), which for conceptually different constructs should be less than 0.85 [106]. The result is acceptable since HTMT for the variables Functions <-> Benefits is equal to 0.739.

As our PLS-SEM model includes both formative and reflective constructs, it is essential to evaluate the formatively specified constructs. The three key steps for evaluating formative models include the assessment of convergent validity, the indicator of collinearity (VIF, variance inflation factor), statistical significance, and the relevance of the indicator weights [106].

Convergent validity in the formative measurement model involves each latent variable using global single-item measurements in the research questionnaire with generic assessments of the concepts that capture the essence of the constructs. Then, to do a convergent validity test, the global single-item measurements can be employed in the redundancy analyses and the correlation between the formative construct and the single-item measurement should be greater than 0.708 [113]. In the case of a lack of such global single-item measurement, the best solution is to use a reflective measurement model of the same model, as was applied in this study.

To assess the level of collinearity, the variance inflation of factor (VIF) values was evaluated (Table 10). The results indicate that VIF < 3 for all variables, hence collinearity is not a problematic issue [106].

The last step in the evaluation of the formative measurement models comprises the examination of the statistical significance and relevance of the indicator weights [106]. Table 11 presents the outer weights.

An outer weight close to 0 means a weak relationship, a weight close to 1 indicates a strong positive relationship, and a weight close to -1 shows a strong negative relationship [114].

Based on the results presented in Table 11, it is evident that several key indicators play a significant role for the construct Contingencies. These include internal contingencies such as BS (strategy), SQ (structure), and S (size), as well as external contingencies such as EU (environmental uncertainty), OC (culture), and TS (technology). Interpretation of the indicator weight is based on its absolute and relative size. This means that support of competitive strategy and functional strategies (sales, marketing, production, procurement), the size of the company, organizational culture and technological sophistication imply a positive contribution, while respectively environmental uncertainty has a relatively negative contribution to the construct.

Meanwhile, for construct Digitalization the following indicators are significant: AIS, BC, BI, MIS/ERP. Therefore, such technologies as Integrated MIS in particular Enterprise Resource Planning systems (MIS/ERP), business intelligence tools (BI), and Accounting Information Systems with budgeting solutions (AIS) indicate a higher relative contribution to the construct, while Blockchain (BC) has a negative contribution. Although the remaining indicators are not statistically significant, it is uncommon for them be removed from the model, as formative measurement theory requires all indicators in order to fully capture the domain of the latent variable [114].

5. Discussion

The research aimed to investigate the impact on budgeting functions of digitalization used in budgeting, on the grounds of contingency theory. As technology continues to change the world in many ways, it also influences budgeting processing in enterprises and the role of controllers. A literature review was carried out in order to propose a model related to the implementation of technologies in budgeting processes, and its impact on the functions, qualitative characteristics and benefits arising from budgeting, taking into account company contingencies. In its theoretical perspective, the model and its constructs, as well as the indicators were based on prior literature. Our PLS-SEM model includes both formative and reflective constructs. The construct validity and reliability of the model were conducted according to criteria for both measurement theories: formative and reflective. The assessment of the model is satisfactory since it meets all the requirements.

The findings indicate that the current state of digitalization in budgeting is rather low, and that the adoption of technologies is still limited, except for Excel and Access. The findings are convergent with the conclusions of the report prepared by IGC (International Group of Controlling) [115].

The research results confirm both hypotheses. Digitalization positively affects budgeting functions and the qualitative characteristics of budgeting (path coefficient =0.342, p<0.001), supporting hypothesis H1. In this regard, the results of our research expand the research approaches and results obtained by other authors: (Moll and Yigitbasioglu [21], Möller et al. [22], Bergmann et al. [10], as well as Raisch and Krakowski [100], however our research results pertain to a broader spectrum of digitalization tools used in budgeting. Additionally, analysis of the mediation models reveals a medium partial positive effect, (0.179, p<0.001) for the path Contingencies - Digitalization (of budgeting) - Functions of budgeting (and qualitative characteristics of budgeting). This means that the adoption of digitalization strengthens the effect of contingencies on budgeting functions. We confirm that budgeting functions and their qualitative characteristics (incorporating: planning, motivating, controlling, coordinating, learning from past experiences and adapting to changing circumstances through budgeting, simplicity of budgeting, flexibility of budgeting, and efficiency of budgeting) are significantly related to the benefits of budgeting. The path coefficient for Functions (of budgeting and the quantitative characteristics of budgeting) - Benefits (arising from budgeting) is equal to 0.406, p<0.001, with the outer weights of the indicators positive and statistically significant, which provides empirical support for H2.

We have provided evidence that selected internal company contingencies, i.e., support of competitive strategy and functional strategies, size of the company, quality of the organizational structure and support of competitive strategy, as well as external contingencies, i.e., technological sophistication and organizational culture, have a positive contribution. Meanwhile, the next external contingency, i.e., environmental uncertainty, has a relatively negative contribution to the construct. The findings of our research indicate that, even with the incorporation of digitalization in budgeting, the impact of contingency variables on the implementation of budgeting functions remains significant, especially as regards internal contingencies. These variables, whose importance has previously been demonstrated by other authors, were identified without considering the aspect of digitalization in budgeting: [1], [2], [3], [8], [9], [10], [11], and [15]. At the level of significance of individual contingencies, our research did not confirm the importance of competition, which is inconsistent with some research findings [48], [13]. It is noteworthy that according to our research findings, the level of environmental uncertainty is negatively correlated with the assessment of budgeting function execution. This may be the result of budgeting methods not being adequately adapted by companies to conditions of higher environmental uncertainty [3], [6], [7], however it certainly requires more detailed investigation.

The digitalization technologies used in budgeting: integrated MIS in particular Enterprise Resource Planning systems (MIS/ERP), business intelligence tools (BI), and accounting information systems with budgeting solutions (AIS) indicate a higher relative contribution to the construct, while Blockchain (BC) has a negative relative contribution, which addresses the research gap identified by Rikhardsson and Yigitbasioglu [16]. The findings of our research indicate that the use of ERP systems in budgeting is a significant factor in enhancing the execution of budgeting functions, which contradicts the results described by Granlund and Malmi [19]. In the context of BI systems, our research findings confirm the positive role of their application in budgeting, in agreement with Bergmann et al. [10]. Although the remaining indicators for digitalization are not statistically significant as individual variables, they are required in order to fully capture the domain of the latent variable (Digitalization), indirectly indicating their role as digitalization tools enhancing budgeting functions and the qualitative characteristics of budgeting. Our research findings confirm the impact of digitalization in budgeting on selected qualitative characteristics of budgeting, including simplicity of budgeting (confirming the findings of Ghobakhloo [29]), flexibility of budgeting (in accordance with Koch et al. [103]), efficiency of budgeting (relating to Duh et al. [27]), the level of detail and completeness of information required in budgeting (corresponding with Amann [104]), and the level of adaptation to new circumstances resulting from budgeting (with reference to Kappes and Klehr [28]).

The findings demonstrate that for the latent variable Functions (functions of budgeting and the qualitative characteristics of budgeting), all the factor loadings are high above 0.708, except for EI (level of integration of budgeting with other information systems), for which the loading is 0.630. Furthermore, all the indicator loadings of the construct Benefits (of budgeting) are also high, above the recommended value. Consequently, the constructs explain more than 50% of the indicator’s variance. The significant benefits arising from budgeting include: perceived budget task execution, perceived financial benefits from budgeting, perceived financial performance of the enterprise, and evaluation of support for the company’s sustainable development. Our research further confirms a small positive indirect impact in the relationship: Contingencies - Digitalization - Functions – Benefits (O = 0.073, p = 0.000). This aligns with the more simplified research findings that indicate a positive correlation between digitalization of budgeting and corporate achievements: financial performance [69], [30], [31], [35] (but our findings relate to supporting and managerial processes), and support for company’s sustainable development [37], [38], [39] (however, our findings relate to the overall budgeting system, not project budgeting). These research findings contribute to theory and practice in several ways. Firstly, we contribute to the literature on digitalization in budgeting by developing an understanding of the impact of emerging technologies and tools on budgeting functions and the qualitative characteristics of budgeting, as well as the benefits arising from budgeting, especially on the grounds of contingency theory. Although the benefits of the adoption of modern technologies have been indicated and confirmed in prior studies, there is still little conceptual understanding and empirical evidence to validate these assertions, especially using second-generation analyzing data techniques such as PLS-SEM. This study fills the research gap in this area.

Secondly, the findings may be useful for financial professionals and trainees, as well as managers, in understanding the benefits of budgeting digitalization and the conditions that influence the implementation of modern techniques and instruments. According to Ulrich and Rieg (2022), the main obstacles to digitalization are a lack of knowledge and insufficient abilities [115]. By conceptualizing the impact of digitalization on budgeting functions and benefits, our study directs attention toward the necessity to adopt emerging technologies in enterprises, and hence ensure that employees involved in budgeting processes acquire and improve digital competencies.

The findings of the study must be interpreted in light of certain limitations. Firstly, the literature research method concerns only papers that correspond to particular search criteria, so there is a risk of omitting some research. Secondly, we used a small sample size – only 319 respondents. Finally, the questionnaire was based on a data collection method from which some variables could have been omitted due to the closed questions and their lower validity rate. Also, the questionnaire only examines limited budgeting contingencies, functions and benefits, as well as technologies; therefore, the results cannot be generalized and may not reflect findings in other areas and circumstances.

Despite these limitations, we believe our study offers opportunities for future research. Firstly, the understanding of digitalization and its impact on budgeting functions and benefits could be further advanced by conducting more context-specific investigations, for example in a particular industry or SME sector. Secondly, the study provides an important basis for further studies aimed at investigating the digital competencies required by employees involved in budgeting processes in a changing environment.

6. Conclusions

The research conclusions confirm that the application of digitalization in budgeting positively impacts the fulfilment of budgeting functions and most of its qualitative characteristics. Specifically, this pertains to digitalization tools such as: ERP, business intelligence tools (BI), and accounting information systems that include budgeting solutions, however Blockchain contributes negatively to budgeting. Our research suggests that despite digitalization in budgeting, contingency variables, particularly internal ones, continue to significantly affect budgeting implementation. Budgeting functions and their qualitative aspects, notably encompassing planning, motivation, control, coordination, learning from past experiences, adapting to changes through budgeting, along with simplicity, flexibility, and efficiency of budgeting, are notably correlated with the advantages derived from budgeting. These benefits encompass the following achievements: perceived execution of budget tasks, perceived financial benefits from budgeting, perceived financial performance of the enterprise, and evaluation of support for the company’s sustainable development.

Author Contributions

For research articles with several authors, a short paragraph specifying their individual contributions must be provided. The following statements should be used “Conceptualization, A.P.; methodology, A.K.; software, A.K.; formal analysis, A.P.; investigation, A.K.; resources, A.P.; data curation, A.K.; writing—original draft preparation, A.P.; writing—review and editing, A.P.; visualization, A.K.; supervision, A.P.; project administration, A.P.; funding acquisition, A.P. All authors have read and agreed to the published version of the manuscript.” Please turn to the CRediT taxonomy for the term explanation. Authorship must be limited to those who have contributed substantially to the work reported.

Funding

This article is financed as part of the research tasks of the University of Economics in Katowice under the title: Accounting changes due to the Covid-19 pandemic (stage II).

Conflicts of Interest

The authors declare no conflict of interest. The funders had no role in the design of the study; in the collection, analyses, or interpretation of data; in the writing of the manuscript; or in the decision to publish the results.

References

- Sandalgaard, N.; Nielsen, C. Budget emphasis in small and medium-sized enterprises: evidence from Denmark. J. Appl. Account. Res. 2018, 19, 351–364. [Google Scholar] [CrossRef]

- Brownell, P. Participation in Budgeting, Locus of Control and Organizational Effectiveness. Particip. Budg. Account. Rev. 1981, 56, 844–860. [Google Scholar]

- Bruns, W.J.; Waterhouse, J.H. Budgetary Control and Organization Structure. J. Account. Res. 1975, 13, 177. [Google Scholar] [CrossRef]

- Hong, K.K.; Kim, Y.G. The critical success factors for ERP implementation: an organizational fit perspective. Inf. Manag. 2002, 40, 25–40. [Google Scholar] [CrossRef]

- Sheilds, J.; Sheilds, M. Antecedents of participative budgeting. Accounting, Organ. Soc. 1998, 23, 49–76. [Google Scholar] [CrossRef]

- Ekholm, B.G.; Wallin, J. The impact of uncertainty and strategy on the perceived usefulness of fixed and flexible budgets. J. Bus. Financ. Account. 2011, 38, 145–164. [Google Scholar] [CrossRef]

- Leon, L. De; Rafferty, P.D.; Herschel, R. Replacing the Annual Budget with Business Intelligence Driver-Based Forecasts. Intell. Inf. Manag. 2012, 04, 6–12. [Google Scholar] [CrossRef]

- Chenhall, R.H. Management control systems design within its organizational context: Findings from contingency-based research and directions for the future. Accounting, Organ. Soc. 2003, 28, 127–168. [Google Scholar] [CrossRef]

- Shields, M.D. Management accounting practices in Europe: A perspective from the States. Manag. Account. Res. 1998, 9, 501–513. [Google Scholar] [CrossRef]

- Bergmann, M.; Brück, C.; Knauer, T.; Schwering, A. Digitization of the budgeting process: determinants of the use of business analytics and its effect on satisfaction with the budgeting process. J. Manag. Control 2020, 31, 25–54. [Google Scholar] [CrossRef]

- Goddard, A. Organisational culture and budgetary control in a UK local government organisation. Account. Bus. Res. 1997, 27, 111–123. [Google Scholar] [CrossRef]

- Ng O’Connor The Influence of Organizational Culture on the Usefulness of Budget Participation by Singaporean-Chinese Managers. Account. Organ. Soc. 1995, 20, 383–403. [CrossRef]

- Hoque, Z.; Hopper, T. Political and industrial relations turbulence, competition and budgeting in the nationalised jute mills of Bangladesh. Account. Bus. Res. 1997, 27, 125–143. [Google Scholar] [CrossRef]

- Li, W.; Nan, X.; Mo, Z. Effects of budgetary goal characteristics on managerial attitudes and performance. 2010 Int. Conf. Manag. Serv. Sci. MASS 2010 2010. [Google Scholar] [CrossRef]

- Govindarajan, J.K.; Shank, V. Strategic cost management -The new tool for competitive advantage.pdf. Free Press, 1993; 271. [Google Scholar]

- Rikhardsson, P.; Yigitbasioglu, O. Business intelligence & analytics in management accounting research: Status and future focus. Int. J. Account. Inf. Syst. 2018, 29, 37–58. [Google Scholar] [CrossRef]

- Garanina, T.; Ranta, M.; Dumay, J. Blockchain in accounting research: current trends and emerging topics. Accounting, Audit. Account. J. 2022, 35, 1507–1533. [Google Scholar] [CrossRef]

- Kostić, N.; Sedej, T. Blockchain Technology, Inter-Organizational Relationships, and Management Accounting: A Synthesis and a Research Agenda. Account. Horizons 2022, 36, 123–141. [Google Scholar] [CrossRef]

- Granlund, M.; Malmi, T. Moderate impact of ERPS on management accounting: A lag or permanent outcome? Manag. Account. Res. 2002, 13, 299–321. [Google Scholar] [CrossRef]

- Martín-Peña, M.L.; Sánchez-López, J.M.; Díaz-Garrido, E. Servitization and digitalization in manufacturing: the influence on firm performance. J. Bus. Ind. Mark. 2020, 35, 564–574. [Google Scholar] [CrossRef]

- Moll, J.; Yigitbasioglu, O. The role of internet-related technologies in shaping the work of accountants: New directions for accounting research. Br. Account. Rev. 2019, 51, 100833. [Google Scholar] [CrossRef]

- Möller, K.; Schäffer, U.; Verbeeten, F. Digitalization in management accounting and control: an editorial. J. Manag. Control 2020, 31. [Google Scholar] [CrossRef] [PubMed]

- Bhahimani, A. Digital data and management accounting: why we need to rethink research methods. J. Manag. Control 2020, 31, 9–23. [Google Scholar] [CrossRef]

- Bhimani, A.; Willcocks, L. Digitisation, Big Data and the transformation of accounting information. Account. Bus. Res. 2014, 44, 469–490. [Google Scholar] [CrossRef]

- Baumöl, U.; Perscheid, G. Der Weg ist das Ziel: wie Sie mithilfe von adaptiven Planungsverfahren und innovativen IT-Lösungen den Datenberg erklimmen. Control. Zeitschrift für erfolgsorientierte Unternehmenssteuerung 2019, 31, 34–38. [Google Scholar] [CrossRef]

- Dillerup, R.; Witzemann, T.; Schacht, S.; Schaller, L. Planung im digitalen Zeitalter. Control. Manag. Rev. 2019, 63, 46–53. [Google Scholar] [CrossRef]

- Duh, R.R.; Chow, C.W.; Chen, H. Strategy, IT applications for planning and control, and firm performance: The impact of impediments to IT implementation. Inf. Manag. 2006, 43, 939–949. [Google Scholar] [CrossRef]

- Kappes, M.; Klehr, D. Simulation und Szenarien-Modellierung – und deren Einsatz in der Unternehmenssteuerung an einem Beispiel. Controll. Mag. 2021, 64–69. [Google Scholar]

- Nasca, D.; Munck, J.C.; Wald, A.; Gleich, R. Wie die digitale Transformation zum Erfolgsfaktor der “Modernen Budgetierung” wird - Ergebnisse einer empirischen Studie und Best-Practice-Beispiele. Controlling 2018, 30, 37–46. [Google Scholar]

- Ghobakhloo, M. The future of manufacturing industry: a strategic roadmap toward Industry 4.0. J. Manuf. Technol. Manag. 2018, 29, 910–936. [Google Scholar] [CrossRef]

- Moeuf, A.; Pellerin, R.; Lamouri, S.; Tamayo-Giraldo, S.; Barbaray, R. The industrial management of SMEs in the era of Industry 4.0. Int. J. Prod. Res. 2018, 56, 1118–1136. [Google Scholar] [CrossRef]

- Westerman, G.; Bonnet, D.; McAfee, A. Leading Digital: Turning Technology into Business Transformation 2014, Volume 52.

- Lin, F.J.; Lin, Y.H. The effect of network relationship on the performance of SMEs. J. Bus. Res. 2016, 69, 1780–1784. [Google Scholar] [CrossRef]

- Abou-foul, M.; Ruiz-Alba, J.L.; Soares, A. The impact of digitalization and servitization on the financial performance of a firm: an empirical analysis. Prod. Plan. Control 2021, 32, 975–989. [Google Scholar] [CrossRef]

- Sambrani, V.N.; Jayadatta, S. Significant indicators of company performance by impact of big data, sustainability and digitalization measures. Srusti Manag. Rev. 2020, 13, 54–63. [Google Scholar]

- Ribeiro-Navarrete, S.; Botella-Carrubi, D.; Palacios-Marqués, D.; Orero-Blat, M. The effect of digitalization on business performance: An applied study of KIBS. J. Bus. Res. 2021, 126, 319–326. [Google Scholar] [CrossRef]

- Moreno-Monsalve, N.; Delgado-Ortiz, M.; Rueda-Varón, M.; Fajardo-Moreno, W.S. Sustainable Development and Value Creation, an Approach from the Perspective of Project Management. Sustain. 2023, 15. [Google Scholar] [CrossRef]

- Ahn, Y.G.; Kim, T.; Kim, B.R.; Lee, M.K. A Study on the Development Priority of Smart Shipping Items—Focusing on the Expert Survey. Sustain. 2022, 14. [Google Scholar] [CrossRef]

- Özkan, E.; Azizi, N.; Haass, O. Leveraging smart contract in project procurement through dlt to gain sustainable competitive advantages. Sustain. 2021, 13. [Google Scholar] [CrossRef]

- Koontz, H.; Weihrich, H. Management; Management, 1988. [Google Scholar]

- Barret, M.E.; Fraser, L.B. Conflicting roles in budgeting for operations. Harv. Bus. Rev. 1977, 55, 137–146. [Google Scholar]

- Luthans, F.; Stewart, T.I. A General Contingency Theory of Management. Acad. Manag. Rev. 1977, 2, 181. [Google Scholar] [CrossRef]

- Petrovska, E.; Berzins, G. Use and Development of Contingency Theory. New Challenges Econ. Bus. Dev. 2020, 380–389. [Google Scholar]

- Romero-Silva, R.; Santos, J.; Hurtado, M. A note on defining organisational systems for contingency theory in OM. Prod. Plan. Control 2018, 29, 1343–1348. [Google Scholar] [CrossRef]

- Otley, D. The contingency theory of management accounting and control: 1980-2014. Manag. Account. Res. 2016, 31, 45–62. [Google Scholar] [CrossRef]

- Kyj, L.; Parker, R.J. Antecedents of budget participation: Leadership style, information asymmetry, and evaluative use of budget. Abacus 2008, 44, 423–442. [Google Scholar] [CrossRef]

- Collins, F.; Munter, P.; Finn, D.W. The Budgeting Games People Play. Account. Rev. 1987, 62, 29–49. [Google Scholar]

- Waterhouse, J.H.; Libby, T. Predicting change in management accounting systems. J. Manag. Account. Res. 1996, 8, 137–150. [Google Scholar]

- Ward, K. Strategic Management Accounting; Butterworth-Heinemann: Oxford, 1993; ISBN 0750624159. [Google Scholar]

- Kaveski, I.D.S.; Beuren, I.M.; Gomes, T.; Lavarda, C.E.F. Influence of the diagnostic and interactive use of the budget on managerial performance mediated by organizational commitment. Brazilian Bus. Rev. 2021, 18, 82–100. [Google Scholar] [CrossRef]

- Tarigan, J. ; Devie The Influence of Budgeting Participation on Managerial Performance in Service Companies : An Evidence from Indonesia. J. Account. Financ. 2015, 15, 95–106. [Google Scholar]

- Zonatto, V.C.d.S.; Nascimento, J.C.; Lunardi, M.A.; Degenhart, L. Effects of Budgetary Participation on Managerial Attitudes, Satisfaction, and Managerial Performance. Rev. Adm. Contemp. 2020, 24, 532–549. [Google Scholar] [CrossRef]

- Davila, A.; Foster, G. Management accounting systems adoption decisions: Evidence and performance implications from early-stage/startup companies. Account. Rev. 2005, 80, 1039–1068. [Google Scholar] [CrossRef]

- Haanstra, W.; Martinetti, A.; Braaksma, J.; van Dongen, L. Design of a framework for integrating environmentally sustainable design principles and requirements in train modernization projects. Sustain. 2020, 12. [Google Scholar] [CrossRef]

- Pramono, A.J.; Suwarno, *!!! REPLACE !!!*; Amyar, F; Friska, R. Sustainability Management Accounting in Achieving Sustainable Development Goals: The Role of Performance Auditing in the Manufacturing Sector. Sustain. 2023, 15. [Google Scholar] [CrossRef]

- Vendrell-Herrero, F.; Bustinza, O.F.; Parry, G.; Georgantzis, N. Servitization, digitization and supply chain interdependency. Ind. Mark. Manag. 2017, 60, 69–81. [Google Scholar] [CrossRef]

- Lucks, K. Industry 4.0 from An Entrepreneurial Transformation and Financing Perspective. Sci 2022, 4. [Google Scholar] [CrossRef]

- Stoica, R.; Stefan, V. The Role of Computerized Solutions in Consolidating Financial Results from the European and Anglo-Saxon Accounting Systems. Valahian J. Econ. Stud. 2018, 9, 83–94. [Google Scholar] [CrossRef]

- Chen, Y.; Li, C.; Wang, H. Big Data and Predictive Analytics for Business Intelligence: A Bibliographic Study (2000–2021). Forecasting 2022, 4, 767–786. [Google Scholar] [CrossRef]

- Gil-Gomez, H.; Guerola-Navarro, V.; Oltra-Badenes, R.; Lozano-Quilis, J.A. Customer relationship management: digital transformation and sustainable business model innovation. Econ. Res. Istraz. 2020, 33, 2733–2750. [Google Scholar] [CrossRef]

- Klimkeit, D.; Reihlen, M. No longer second-class citizens: Redefining organizational identity as a response to digitalization in accounting shared services. J. Prof. Organ. 2022, 9, 115–138. [Google Scholar] [CrossRef]

- Simion, C.P.; Verdeș, C.A.; Mironescu, A.A.; Anghel, F.G. Digitalization in Energy Production, Distribution, and Consumption: A Systematic Literature Review. Energies 2023, 16. [Google Scholar] [CrossRef]

- D’Almeida, A.L.; Bergiante, N.C.R.; de Souza Ferreira, G.; Leta, F.R.; de Campos Lima, C.B.; Lima, G.B.A. Digital transformation: a review on artificial intelligence techniques in drilling and production applications. Int. J. Adv. Manuf. Technol. 2022, 119, 5553–5582. [Google Scholar] [CrossRef]

- Korhonen, T.; Selos, E.; Laine, T.; Suomala, P. Exploring the programmability of management accounting work for increasing automation: an interventionist case study. Accounting, Audit. Account. J. 2021, 34, 253–280. [Google Scholar] [CrossRef]

- Forsstrom, J. Technology Streamlines and Improves Recruitment -- and Institutional Performance. New Engl. J. High. Educ. 2008, 23, 28. [Google Scholar]

- Lee, D.; Wan, C. The Impact of Mukbang Live Streaming Commerce on Consumers’ Overconsumption Behavior. J. Interact. Mark. 2023, 58, 198–221. [Google Scholar] [CrossRef]

- Gong, Q.; Ban, M.; Zhang, Y. Blockchain, Enterprise Digitalization, and Supply Chain Finance Innovation. China Econ. Transit. 2022, 5, 131–158. [Google Scholar] [CrossRef]

- Halilovic, S.; Cicic, M. Understanding determinants of information systems users behaviour: A comparison of two models in the context of integrated accounting and budgeting software. Behav. Inf. Technol. 2013, 32, 1280–1291. [Google Scholar] [CrossRef]

- Kindström, D.; Kowalkowski, C. Service innovation in product-centric firms: A multidimensional business model perspective. J. Bus. Ind. Mark. 2014, 29. [Google Scholar] [CrossRef]

- Li, M.; Zheng, X.; Zhuang, G. Information technology-enabled interactions, mutual monitoring, and supplier-buyer cooperation: A network perspective. J. Bus. Res. 2017, 78, 268–276. [Google Scholar] [CrossRef]

- Wadesango, N.; Magaya, B. The impact of digital banking services on performance of commercial banks. J. Manag. Inf. Decis. Sci. 2020, 23, 343–353. [Google Scholar]

- Paulet, E.; Mavoori, H. Conventional banks and Fintechs: how digitization has transformed both models. J. Bus. Strategy 2020, 41, 19–29. [Google Scholar] [CrossRef]

- Smania, G.S.; Mendes, G.H.d.S.; Lizarelli, F.L.; Favoretto, C. Service innovation in medical device manufacturers: does the digitalization matter? J. Bus. Ind. Mark. 2022, 37, 578–593. [Google Scholar] [CrossRef]

- Eller, R.; Alford, P.; Kallmünzer, A.; Peters, M. Antecedents, consequences, and challenges of small and medium-sized enterprise digitalization. J. Bus. Res. 2020, 112, 119–127. [Google Scholar] [CrossRef]

- Oliver, J.J. Strategic transformations in the media. J. Media Bus. Stud. 2018, 15, 278–299. [Google Scholar] [CrossRef]

- Popović-Pantić, S.; Semenčenko, D.; Vasilić, N. Digital technologies and the financial performance of female smes in Serbia: The mediating role of innovation. Econ. Ann. 2020, 65, 53–81. [Google Scholar] [CrossRef]

- Fernández-Portillo, A.; Almodóvar-González, M.; Sánchez-Escobedo, M.C.; Coca-Pérez, J.L. The role of innovation in the relationship between digitalisation and economic and financial performance. A company-level research. Eur. Res. Manag. Bus. Econ. 2022, 28. [Google Scholar] [CrossRef]

- Ricci, F.; Scafarto, V.; Ferri, S.; Tron, A. Value relevance of digitalization: The moderating role of corporate sustainability. An empirical study of Italian listed companies. J. Clean. Prod. 2020, 276. [Google Scholar] [CrossRef]

- Hänninen, M.; Smedlund, A. Same Old Song with a Different Melody: The Paradox of Market Reach and Financial Performance on Digital Platforms. J. Manag. Stud. 2021, 58, 1832–1868. [Google Scholar] [CrossRef]

- Gul, R.; Ellahi, N. The nexus between data analytics and firm performance. Cogent Bus. Manag. 2021, 8. [Google Scholar] [CrossRef]

- Yu, F.; Jiang, D.; Zhang, Y.; Du, H. Enterprise digitalisation and financial performance: the moderating role of dynamic capability. Technol. Anal. Strateg. Manag. 2023, 35, 704–720. [Google Scholar] [CrossRef]

- Verhoef, P.; Broekhuizen, T.; Bart, Y.; Bhattacharya, A.; Dong, J.Q.; Fabian, N.; Haenlein, M. Digital transformation: A multidisciplinary reflection and research agenda. J. Bus. Res. 2021, 122, 889–901. [Google Scholar] [CrossRef]

- Barua, A.; Konana, P.; Whinston, A.B.; Yin, F. An empirical investigation of net-enabled business value. MIS Q. Manag. Inf. Syst. 2004, 28, 585–620. [Google Scholar] [CrossRef]