Submitted:

22 December 2023

Posted:

26 December 2023

You are already at the latest version

Abstract

This article delves into the pro-cyclicality of Loan Loss Provisions (LLPs) and earnings management, along with equity management, in Portuguese banks against the backdrop of implementing the IFRS 9's Expected Credit Loss (ECL) model. It concentrates on how LLPs mirror economic cycles and financial management practices, providing valuable insights into the operational dynamics of the Portuguese banking sector, marked by distinct economic and regulatory challengesThe research examined a sample of five Portuguese commercial banks, chosen from a group of seventeen in the Portuguese Banking Association. Data spanning from 2013 to 2022 were manually gathered. A multiple linear regression model was employed to scrutinize the relationship between LLPs and variables indicative of economic cycles and the earnings and equity management. The methodology aligns with the approaches of Araújo et al. (2018), Beatty and Liao (2014), and Casta et al. (2019). The analysis indicates a pro-cyclicality in LLPs within the Portuguese context, with a positive response of LLPs to economic indicators like unemployment. Contrarily, the extent of earnings and equity management under the ECL model was less marked compared to the Incurred Credit Loss (ICL) model, suggesting the impact of more stringent regulatory measures. The research corroborates the pro-cyclicality of LLPs in Portuguese banks under the ECL framework, underscoring the necessity for ongoing monitoring and refinement of models for forecasting and recognizing credit losses. The findings point to an area for improvement in financial management practices, despite regulatory enhancements, to promote transparency and ensure financial stability.

Keywords:

earnings management

; equity management

; pro-cyclicality

; loan loss provision

; IFRS 9

; expected credit loss

1. Introduction

The subprime mortgage crisis, which sparked the 2007 financial crisis, exposed issues in accounting standards that contributed to the loss of confidence in the banking system. One of the primary weaknesses was the insufficient and delayed recognition of LLPs1 arising from the diminished recoverable value of loans and other financial instruments (Bischof et al., 2021). Consequently, the need to modify the credit loss model emerged from the 2007 financial crisis, which precipitated economic crises worldwide, prompting a reevaluation of the approach to financial instruments (Pucci, 2017). In response, the International Accounting Standards Board (IASB) published the International Financial Reporting Standard 9 (IFRS 9) in July 2014, replacing the International Accounting Standard 39 (IAS 39). IFRS 9 was developed based on a logical model for recognizing and measuring financial instruments, introducing the concept of expected losses (Silva, 2017).

The existing model, supported by IAS 39 and known as the ICL, delayed the recognition of LLPs until there were clear and objective indications of impairment (Bushman & Williams, 2015; Casta et al., 2019; Gebhardt & Novotny-Farkas, 2011; Laux, 2012). IAS 39 was formulated by the IASB to restrict companies' ability to constitute impairments without justification, using them as a means of earnings management2 (Beck & Narayanamoorthy, 2013; Camfferman, 2015; Wall & Koch, 2000).

As Harrald and Sandall (2010) point out, discussions about banking regulation aim to ensure the stability of the financial system, considering that the system can amplify the effects of economic expansion and contraction phases. Pro-cyclicality, or the positive correlation between a variable and economic activity, is at the heart of this debate (Bebczuk et al., 2011). For Longbrake and Rossi (2011), the financial system should, instead of amplifying, smooth out economic cycles. Pro-cyclicality can become particularly problematic by exacerbating the impact of a downturn in the economic cycle, exacerbating crises, and compromising stability. It is observed that, at the beginning of a declining economic cycle, banks recognize few LLPs. However, as the crisis deepens, LLPs increase, which harms the banks' financial situation, reducing credit availability precisely when it is most needed in the market (Araújo et al. 2018). Berger and Udell (2004) and Bouvatier and Lepetit (2012) warn that the excessive cyclicality of bank credit can intensify the economic cycle, increase systemic risk, and harm the proper allocation of available resources for loans, highlighting the importance of mitigating the pro-cyclicality of the financial system to achieve economic stability.

In addition to economic cycles, earnings management in dynamic models is also a concern for standard setters, as well as the transparency of financial statements (FASB-IASB, 2009). Compared to the ICL model of IAS 39, the IFRS 9's ECL model exhibits greater subjectivity, particularly in the judgment required for recognizing LLPs (Novotny-Farkas, 2016). On the other hand, the ECL model can contribute to greater banking transparency and more effective market discipline, being fundamental in enhancing financial stability (Onali et al., 2021). Salazar et al. (2023) also confirm the improvement in transparency with IFRS 9 compared to IAS 39, considering the disclosed information on LLP and the new disclosures of phase 2 Loan Loss Allowances (LLAs), providing stakeholders with more information on the anticipation of future risks.

This study aims to analyze the pro-cyclicality of LLPs in Portuguese banks, determining the existence of either a negative or positive relationship with economic cycles, and to assess the presence of earnings management and equity management through their recognition in five Portuguese commercial banks, over the period from 2013 to 2022. The results indicate that there is pro-cyclicality in the ECL model, as well as earnings management and equity management. The methodology used to capture economic cycles, and earnings and equity management, is based on a multiple linear regression model adapted from the studies of Araújo et al. (2018), Beatty and Liao (2014), and Casta et al. (2019).

This research stands out from previous studies by focusing on the impact of LLPs recognition within a single jurisdiction, capturing only the local effects of the ECL model on Portuguese banks. The findings of this study will thus enable regulators and standard-setters to observe whether the ECL model is creating the necessary reserves to face periods of crisis and, simultaneously, if it is being used for earnings and equity management in Portuguese banks. With this approach, the study makes a significant contribution to the literature on the behavior of LLPs recognition through the ECL model under IFRS 9, in economic cycles and its potential use for earnings and equity management.

The study is divided into five chapters. Following this introductory first chapter, there is a chapter on literature review and hypothesis formulation. The third chapter presents the analysis model and the variables used in the empirical study, as well as the sample and methods of data collection and processing. In the fourth chapter, the statistical analysis is carried out, and the results obtained are discussed. Finally, in the fifth chapter, the main conclusions of the study are presented, along with its limitations, and suggestions for future research are identified.

2. Literature Review

2.1. Cyclicality and Pro-Cyclicality of LLPs

2.1.1. Overview

Cyclicality refers to the cyclical nature of the economy, where periods of expansion and recession occur. These economic cycles can affect the quality of a financial institution's assets and, consequently, the LLPs (Longbrake & Rossi, 2011). On the other hand, pro-cyclicality refers to a phenomenon where the policies, practices, or financial instruments adopted by financial institutions, or by regulators, amplify the cyclical fluctuations of the economy instead of smoothing them (Bebczuk et al., 2011). Borio et al. (2001) define pro-cyclicality as the tendency of the financial system to generate booms and financial collapses, more specifically considering the mechanisms that amplify these financial fluctuations. Ozili and Outa (2017), in their literature review study, mention that the term pro-cyclicality is used when banks enter a recession period, leading their managers to decrease credit granting and increase LLPs. This increase, during periods of recession, will further reduce the banks' net interest margin, decreasing profits and deteriorating their situation during the recession. Regarding LLPs, pro-cyclicality occurs when the actions of financial institutions amplify economic movements, increasing risks during periods of expansion and exacerbating recessions (Longbrake & Rossi, 2011).

In summary, cyclicality and pro-cyclicality can be distinguished as follows:

- Cyclicality: Refers to the cyclical nature of the economy, characterized by periods of expansion and recession. Economic cycles impact LLPs due to variations in the financial performance of companies and households.

- Pro-cyclicality: Refers to the tendency of policies, practices, or financial instruments to amplify the cyclical fluctuations of the economy, rather than mitigating them. In the context of LLPs, pro-cyclicality occurs when the actions of financial institutions exacerbate economic movements, increasing risks during periods of expansion and recession.

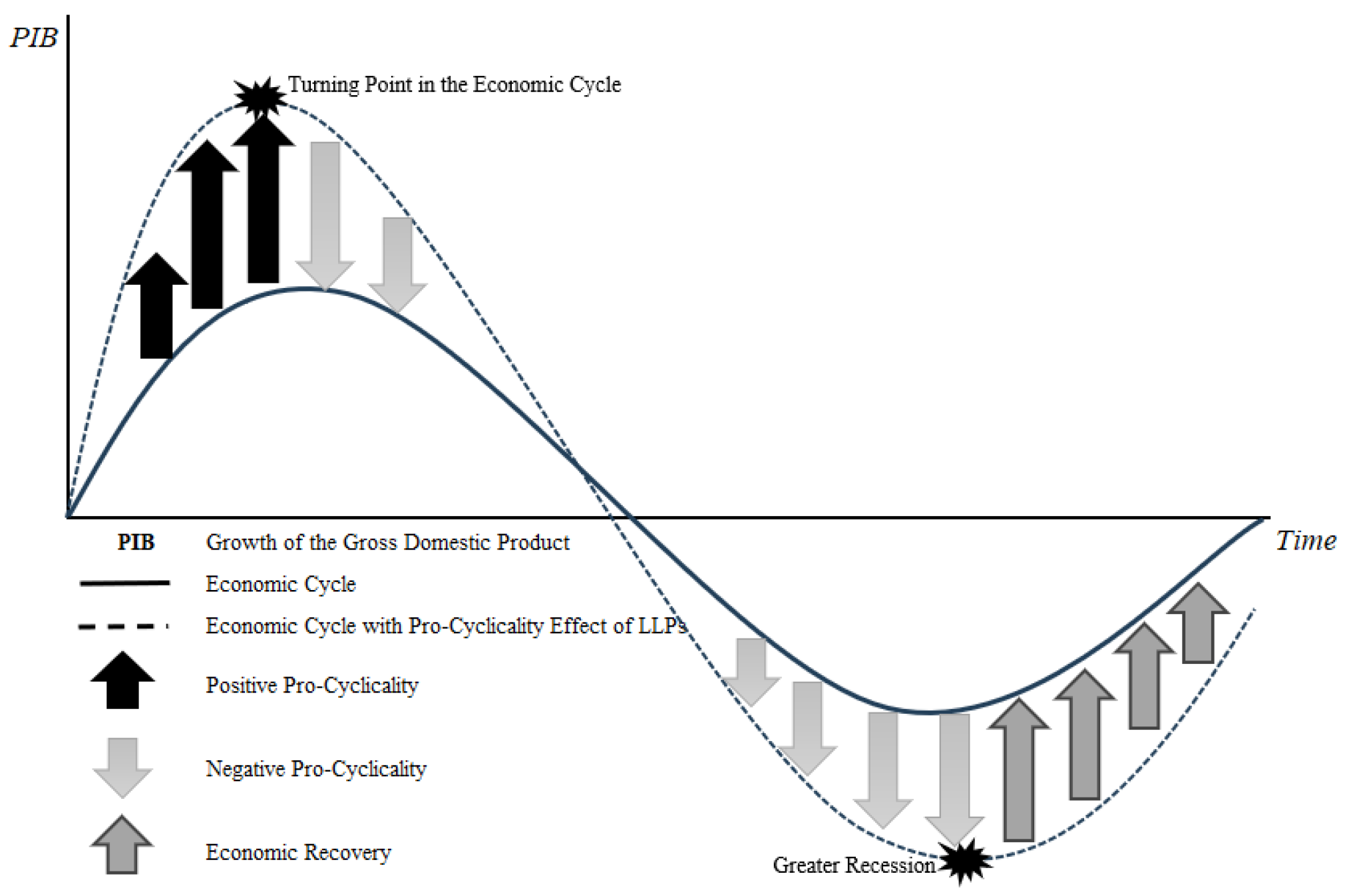

Pro-cyclicality has a positive effect during periods of economic growth (Longbrake & Rossi, 2011), but contributes negatively at the turning point of the economic cycle, as well as during recessions, potentially delaying economic recovery. Furthermore, the actions in recognizing LLPs by financial institutions can also aggravate economic movements, increasing risks during recessions (Chen et al., 2020; Goma et al., 2019; Pastiranová & Witzany, 2021). Some degree of pro-cyclicality is inevitable and inherent in economic activity, but the credit market intensifies the peaks and troughs of this cycle (Bikker & Metzemakers, 2005; Borio et al., 2001).

Figure 1 aims to illustrate the effect of LLP pro-cyclicality on economic cycles as found in the literature (Donelian, 2019; Novotny-Farkas, 2016).

2.1.2. Subsubsection

As depicted in Figure 1, at the onset of an economic downturn, banks recognize few LLPs. However, as the crisis worsens, LLPs increase, deteriorating banks' financial positions, reducing credit issuance (precisely when the market needs it most), intensifying the economic cycle, increasing systemic risk, and impairing the proper allocation of available loan resources (Berger & Udell, 2004; Bouvatier & Lepetit, 2012).

According to the literature (Boutatier & Lepetit 2012; Donelian, 2019; Morrison & White 2010; Novotny-Farkas, 2016; Ozoli & Outa 2017; Pucci 2017), the pro-cyclicality of the credit market can be positive or negative, as follows:

Positive Pro-cyclicality:

- A key variable in credit assessment is the expectation of future cash flows of companies to pay their debts.

- In a booming economic cycle, macroeconomic factors (e.g., consumption, production) significantly favor most companies' projections, such as cash flows and debt repayment capacity.

- With this positive bias, banks' credit assessments are also favored, determining a lower default probability, increasing credit issuance to companies, and thus, their leverage.

- More credit leads to increased production investment and greater infusion of resources into the real economy, further amplifying economic growth (positive pro-cyclicality).

- This assessment can create a vicious cycle, resulting in an economic boom until a specific event occurs or leverage (i.e., risk) increases. This situation is not sustainable and can lead to a reversal of expectations.

Negative Pro-cyclicality:

- Once expectations reverse, the capacity of companies to generate cash flows is questioned and reassessed.

- With this negative bias, there is an increase in credit risk assessed by banks, also increasing the probability of default and reducing (or even ceasing) credit issuance.

- The reduction (or absence) of credit negatively impacts investments and even production, further amplifying the negative effect on the economy (negative pro-cyclicality), potentially creating a vicious cycle and dragging the economy into a recession and possible collapse.

- Unlike the previous reversal, exiting a recession (especially one exacerbated by credit pro-cyclicality) is more costly and time-consuming. The change is slow to alter market perception and, consequently, the financial institutions' credit risk analysis. The resumption of credit issuance is a critical variable for economic recovery.

2.1.2. Cyclicality and Pro-Cyclicality in the ICL Model of IAS 39

Pucci (2017) contends that, at the onset of the 2007 crisis, IAS 39 and its ICL model were culpable for exacerbating the negative effects of the economic downturn by underestimating LLPs, leading various entities to demand significant changes in the credit loss recognition model, including the G20 and the Financial Stability Board. Novotny-Farkas (2016) argues that the accounting of LLPs, following the ICL model approach of IAS 39, amplifies the upward and downward movements of the economic cycle. During periods of economic expansion, banks may recognize the risk premiums included in the interest rates charged on loans but do not account for the corresponding expenses for the expected credit risk.

The lack of timeliness in recognizing LLPs and their impact on capital reserve adequacy led to balance sheet contraction, contributing to increased systemic risk during the financial crisis (Bushman & Williams, 2015; Gebhardt & Novotny-Farkas, 2011; Hoogervorst, 2014; Laux, 2012). In this regard, Laux (2012) suggests that accounting standards and regulation may have contributed to the 2007 financial crisis by allowing various banks to delay their actions. Using data from banks in the United States, which experienced delays in recognizing LLPs during the financial crisis, Bushman and Williams (2015) observed greater balance sheet contraction in these banks, contributing to higher systemic risk. During that crisis, it became evident that restrictive impairment rules allowed banks to even conceal inevitable losses (Gebhardt & Novotny-Farkas, 2011), recognizing them immediately before the loans defaulted (Hoogervorst, 2014).

This delay in recognizing LLPs, as highlighted in the literature, was implicit in paragraphs §58 and §59 of IAS 39, referring to the recognition of impairment loss requiring the occurrence of a loss event that adversely affected the estimated future cash flows (IAS 39, §§58-59). Consequently, banks could not recognize losses due to likely unfavorable future events, even excluding expected LLPs from events occurring after the balance sheet date.

2.1.3. Cyclicality and Pro-Cyclicality in the ICL Model of IAS 39

Following the 2007 financial crisis, the IASB faced a significant and complex challenge in developing a comprehensive standard for financial instruments (Ferreira, 2011). Consequently, new requirements for the recognition and measurement of financial instruments were released in 2009 and 2010, and in 2013, a new hedge accounting model was introduced, culminating in the final publication of IFRS 9 in July 2014. The changes introduced by this new standard include a logical model for recognizing and measuring financial instruments, as well as the incorporation of the expected loss concept (Silva, 2017). The new ECL model of IFRS 9 replaces the former ICL model defined in IAS 39.

The ambition of this new provisioning model is to anticipate future losses by recognizing LLPs, thus avoiding what happened to the financial sector during the 2007 financial crisis with the abrupt recognition of LLPs under the IAS 39's ICL model (Casta et al., 2019). However, the European Banking Authority (EBA, 2021) identifies some limitations in the application of the ECL model, such as a significant increase in credit risk for the entire set of financial assets, making its individual application quite restricted and potentially having a strong impact on the transition to phase 2 of that model. A conservative approach to credit risk might result in delays in recognizing LLPs. Therefore, a good alignment between regulators and standard-setters in defining default of credit losses is crucial to avoid divergences in the application of the ECL model by different institutions, as addressed by the IASB in its 2020 communication3.

The most common method for calculating LLAs4 in the ECL model relies essentially on the probability of default (PD), which translates the likelihood of default, the loss given default (LGD), representing the loss resulting from default, and the exposure at default (EAD), referring to exposure at the time of default (KMPG, 2016; López-Espinosa et al., 2021; Volarevi & Varovic, 2018). The PD estimate is based on the client's risk classification. Using forecasts for key indicators like GDP growth, interest rates, and unemployment, different macroeconomic scenarios such as optimistic, pessimistic, and intermediate are projected. The likelihood of each scenario occurring is calculated and, based on the customer's profile, the PD is assessed for each macroeconomic scenario. The PD is calculated as a weighted average of the values, considering the likelihood of each scenario occurring (López-Espinosa et al., 2021). Therefore, obtaining the PD estimate is challenging for financial institutions as it depends on the estimation of various factors or indicators.

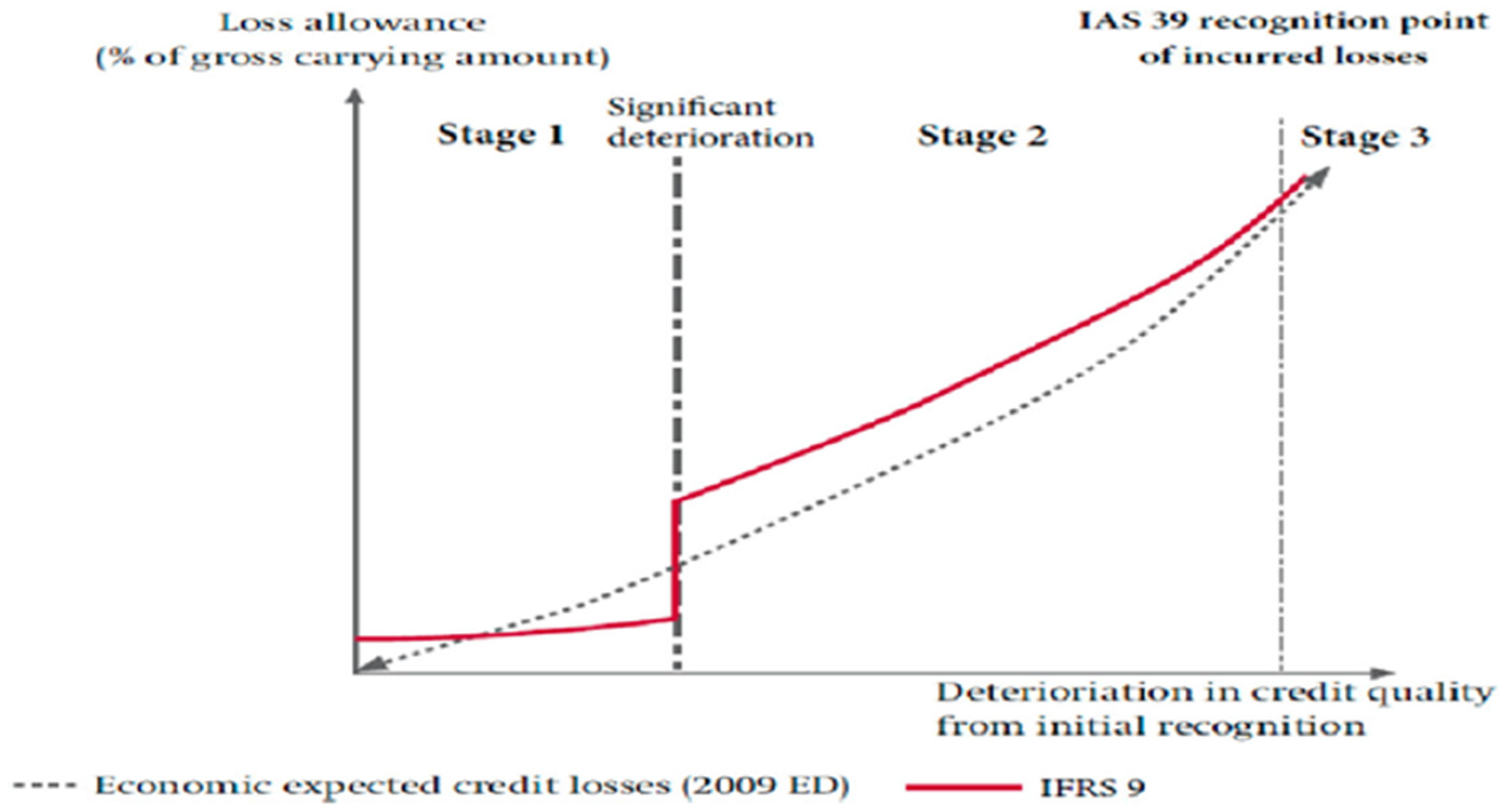

As Novotny-Farkas (2016) notes, all LLPs accounting models that seek to reflect economic conditions are inherently pro-cyclical. In the same study, the author states that the approach of the IFRS 9's ECL model can mitigate concerns about pro-cyclicality. The recognition of 12-month LLPs for phase 1 serves, to some extent, as an adjustment for the credit spread recognized through income, thus resulting in less overstated profits. This will reduce the possibility of distributing overstated profits, in the form of dividends and bonuses, during periods of economic expansion and will result in more capital to support losses during a downturn. Moreover, the more timely recognition of LLPs and their impact on regulatory capital can mitigate excessive loan growth during periods of economic expansion. In fact, as shown in Figure 2, in phase 1, overstated LLAs are expected, having a "buffer effect on regulatory" that increases with the risk of newly granted loans.

Novotny-Farkas (2016) believes that the timelier recognition of LLPs and a higher level of disclosures will promote market discipline. Specifically, providing timely information about credit risk (increases in credit risk) to market participants can reduce financing constraints in times of financial stress. Thus, with a dynamic model, such as the IFRS 9's ECL model, banks are expected to be less susceptible to the pro-cyclical effects of credit risk, as:

- At the peak of the economic cycle, PDs and LGDs are lower, requiring less capital, increasing regulatory capital, and allowing for more credit to be granted for the same amount of available capital. However, in the face of phase 1 of the ECL model, a containment in excessive credit granting is expected, considering economic forecasts.

- At the onset of a potential recession period, the PD and LGD are higher, necessitating more capital, thus reducing regulatory capital and, consequently, the availability to grant more credit. It is expected that the LLAs will be larger, enabling the absorption of future LLPs and maintaining credit provision, contributing to the reversal of the downward economic cycle.

2.2. The Relationship Between LLPs and Economic Cycles

Various authors have focused their studies on the behavior of LLPs during economic cycles, arguing that they are pro-cyclical, as they reinforce the current state of the economy (Agénor & Zilberman, 2015; Bikker & Metzemakers, 2005; Bouvatier & Lepetit, 2012; Olszak et al., 2017). The recognition of LLPs tends to be substantially higher in a downward economic cycle, reflecting the growth of risk (Bikker & Metzemakers, 2005). Bouvatier and Lepetit (2012) analyzed how the rules for recognizing LLPs influence the loan market, concluding that a credit loss system based on past information increases the pro-cyclicality of market fluctuations. According to the authors, in a credit loss system based on predictions of future losses, the problem of pro-cyclicality does not exist. Agénor and Zilberman (2015) also show that in a backward-looking credit loss model, LLPs are pro-cyclical because they are triggered by overdue payments (or non-performing loans), which depend on current economic conditions and the relationship between LLAs and loans. Olszak et al. (2017) found that LLPs in large, publicly-traded commercial banks, as well as in banks reporting consolidated financial statements, are more pro-cyclical. Conversely, they found that the existence of strict capital standards and better investor protection are associated with less pro-cyclicality in LLPs.

Ozili and Outa (2017) questioned to what extent dynamic norms should be applied differently in developed and emerging countries. In Ozili's study (2019), some clues are found, highlighting the role of regulators in the proper application of the standard. In that study, evidence was found that African banks in more corrupt environments tend to smooth their positive results more aggressively, with this smoothing being reduced among African banks in environments with strong investor protection. Thus, in jurisdictions where the environment and incentive for earnings management are greater, regulators will play a key role in the proper application of the standard (Marton & Runesson, 2017). Saurina (2009) emphasizes the importance of regulators' and financial institutions' awareness of pro-cyclicality and the need to adopt measures to mitigate its negative effects, aiming for proper credit risk management and reduction of LLPs, opting for a dynamic system for credit losses to mitigate pro-cyclicality. In 2020, due to the COVID-19 pandemic and its consequences on the real economy, EBA moratorium guidelines were implemented to prevent volatile impairments and safeguard the quality of banking profits. During this period, banks faced significant challenges in determining significant increases in credit risk, which consequently had repercussions on the amounts of the different phases of the ECL model, limiting its impact on LLPs (Salazar et al, 2023). Krüger et al. (2018) also argue that in times of crisis, regulators have the possibility to mitigate the effects of recessions, either by decreasing cyclical buffers or by modifying the approach to LLPs, especially when banking institutions face adversities.

These constant external pressures from various regulators, whether legislative or normative, refer us to Institutional Theory. This theory provides a comprehensive and complex view of organizations, asserting that they are influenced by normative pressures, sometimes from external sources, such as supervisors. Under certain conditions, these pressures lead the organization to be guided by legitimized elements and standardized procedures (Zucker, 1987). According to Meyer and Rowan (1977), organizations are led to adopt practices and procedures defined by standardized concepts of organizational work prevalent and institutionalized in society, regardless of the immediate effectiveness of these practices. Demirguç-Kunt et al. (2008) state that banks that respect the information disclosure principles set forth in the Basel II agreement tend to receive more favorable financial ratings from Moodys. On the other hand, Poghosyan and Čihak (2011) mention that market discipline, considered by the Basel II agreement, allows the identification of weaker banks, enabling preventive measures. Morrison and White (2010) suggest that regulators' observation of weaknesses can stabilize economies, having the potential to prevent systemic risks. In a more recent study, Bischof et al. (2021) reinforce the importance of regulators in protecting the regulatory capital of LLPs, through regulatory adjustments, which can diminish banks' incentives for corrective actions. Barnoussi et al. (2020) confirm this intervention in the EU context, suggesting that banking regulators encouraged banks to minimize the effects of the COVID-19 pandemic, where ECL model provisions should be based on long-term expectations. Thus, it is demonstrated that banking regulators seem more concerned with circumventing the impact of the ECL model, altering its measurement rules, rather than changing the accounting standards.

2.3. Impact of Dynamic Models on Economic Cycles Management

2.3.1. Dynamic Models of LLPs

Evidence that LLPs are pro-cyclical, particularly in Europe and the United States, has led regulators and standard-setters to advocate for an anti-cyclical or dynamic credit loss system to mitigate the pro-cyclicality of LLPs (Ozili & Outa, 2017). A dynamic credit loss system is one where banks report higher LLPs during economic upturns and recognize lower LLPs during recessions, utilizing LLAs built up during good economic times to offset bank credit losses during downturns (Saurina, 2009). Essentially, the goal of a dynamic LLP model is to enhance bank safety and soundness by creating larger LLAs during economic growth, preventing insolvency due to increased LLPs in economic downturns, allowing utilization of these reserves during crisis periods (Balla & McKenna, 2009).

Before IFRS 9 and its ECL model, few countries had adopted a dynamic LLP system, with Spain, Peru, Uruguay, and Chile being examples (Ozili & Outa, 2017). In Spain, the Bank of Spain mandated banks to adopt a dynamic LLP system in 2000 (Saurina, 2009). According to Novotny-Farkas (2016), transitioning to IAS 39 should have led to a reversal of LLAs, as they were inconsistent with the ICL model approach. However, the Bank of Spain encouraged Spanish banks to continue the previous regime, not reversing the LLAs, leading to an accumulation of past reserves alongside LLPs recognized under IAS 39. This process, incompatible with IAS 39 requirements, also made Spanish LLAs less transparent (Gebhardt & Novotny-Farkas, 2011). Novotny-Farkas (2016) argued that these high-cycle reserves could be used by Spanish banks to conceal losses until their complete utilization, making banks appear healthy over the years when they were actually struggling financially. Eventually, several Spanish banks faced difficulties and required bailouts after depleting their LLAs and realizing hidden losses (Bloomberg, 2012).

Some authors assert that dynamic models can improve and mitigate economic downturns, reducing the pro-cyclicality of LLPs (Chan-Lau, 2012; Wezel, 2010). Chan-Lau (2012), analyzing Chilean banks, concluded that dynamic LLP adoption could enhance Chilean bank solvency but did not help reduce LLP pro-cyclicality, suggesting the need for alternative anti-cyclical measures beyond dynamic LLPs, like the countercyclical capital buffers proposed by Basel III or the anti-cyclical LLA rule implemented by Peru in 2008. Wezel (2010) examined Uruguay's dynamic LLP model using a stress-testing methodology and found that LLPs accumulated since 2001 fully absorbed minor impacts, offsetting the additional costs caused by specific LLP increases in economic downturns.

In summary, the appropriate application of the inherently dynamic ECL model depends on various factors to become robust and transparent, with good interplay among all participants. This includes creating measures that promote convergence between normative and regulatory rules, such as establishing buffers (Chan-Lau, 2012) or stress-testing the model (Wezel, 2010), to estimating LLPs and their fiscal and accounting treatment and their impact on bank reserves (Balla & McKenna, 2009; Chan-Lau, 2012). Decision-makers' ability to handle subjectivity and judgment is also crucial for the effective application of the ECL model (Novotny-Farkas, 2016).

2.3.2. Analysis of the IFRS 9 ECL Model

Several authors argue that forward-looking models can trigger strong reactions to changes in the economy (Abad & Suarez, 2017; Bikker & Metzemakers, 2005; Chen et al., 2020; Engelmann & Nguyen, 2023; Gomaa et al., 2019; Pastiranová & Witzany, 2022; Pastiranová & Witzany, 2021; Seitz et al., 2018). Bikker and Metzemakers (2005) share previously mentioned concerns about dynamic models for LLPs, emphasizing their viability only if economic recessions or booms are easily detectable by banks. In practice, detecting the course of economic cycles is challenging due to their unpredictable duration and magnitude (Bikker & Metzemakers, 2005). Therefore, they observed that LLPs were substantially higher when GDP growth was lower, reflecting increased risk during economic downturns. The new ECL model aims to minimize risks through the early recognition of LLPs, enabling financial institutions to mitigate systemic impacts without affecting their continuity. However, the sensitivity to changes in economic conditions of the ECL model under IFRS 9 is higher compared to the ICL model under IAS 39 (Abad & Suarez, 2017). Pastiranová and Witzany (2021) confirm this behavior in their study, analyzing the impact of implementing IFRS 9 in the Czech banking sector, concluding that the increased complexity of the ECL model and changes in macroeconomic expectations lead to greater LLP volatility. Another study by the same authors (Pastiranová & Witzany, 2022) addressed the pro-cyclical behavior of the ECL model from the first quarter of 2015 to the third quarter of 2020 for EU banks, observing the economic cycle dynamics during the economic slowdown caused by the COVID-19 pandemic, not rejecting the hypothesis that the rules of the ECL model are sensitive to changes in economic cycles. Seitz et al. (2018), in a predictive study with historical data, estimated that the ECL model's reserves would likely not result in the increase anticipated by the IASB in anti-cyclical LLP reserves. Chen et al. (2020) reinforce this idea, using a theoretical model for impairment of financial assets, particularly credit cards, according to the new rules in the ECL model under IFRS 9, concluding that these assets need to recognize more LLPs to withstand future risks arising from economic downturns. Engelmann and Nguyen (2023), despite observing a global increase in LLPs, state that banks in Canada, Oceania, and Western Europe are less prepared and will be more affected by a similar credit shock (the same loss in their credit portfolios) than Chinese banks.

The size of banks has also been an explanatory variable for the recognition of LLPs under the ECL model of IFRS 9 (López-Espinosa & Penalva, 2023; Mechelli & Climini, 2021; Onali et al., 2021). Smaller entities and countries with lower regulatory degrees tend to devalue information for investors (Mechelli & Climini, 2021). Conversely, Onali et al. (2021) reinforce these findings, noting that the potential benefits of the ECL model are more evident in larger banks with lower profitability and higher systemic risk, as well as those that received public bailouts, showing a positive reaction to the adoption of the new model. The same study suggests that the ECL model could lead to greater banking transparency and more effective market discipline, essential aspects for improving financial stability. López-Espinosa and Penalva (2023), using a sample of listed Spanish banks, found that the implementation of IFRS 9 facilitated timelier recognition of LLPs, having a negative effect on credit, specifically for smaller banks.

Beyond economic cycles and bank size, earnings management is another important aspect to consider in this new ECL model. Although the replacement of the ICL model with the ECL model facilitates higher reserves, the outcome is less than expected, not compensating for the potentially positive effects of the ECL model through earnings management, leading to the conclusion that the use of forward-looking information may have increased managerial discretion and, consequently, the possibility of greater conservatism (Gomaa et al., 2019). Novotny-Farkas (2016) had already warned of greater subjectivity in this standard compared to IAS 39 in terms of judgment for recognizing LLPs. This new reality may allow bank administrations to manage earnings, as the ECL model is more forward-looking compared to the ICL model. Therefore, standard-setters' concerns might not be safeguarded, as the dynamic provisions present in this new model can potentially promote earnings management, impairing the transparency of financial statements (FASB-IASB, 2009). On the other hand, Du et al. (2023) reveal that bank managers are reluctant to incorporate good news when historical information indicates high default risk and potentially significant credit loss. Their study's results suggest that the observed conservatism could introduce an unintentional bias when managers incorporate forward-looking information into credit loss estimates, potentially reducing bank lending and, thus, their capacity to take on additional risks. As previously mentioned, Onali et al. (2021) suggest that the ECL model could lead to greater banking transparency and more effective market discipline. A recent study by Nnadi et al. (2023) found an increase in earnings management among banks outside the EU following the introduction of IFRS 9, with no evidence of any difference in earnings management behavior for banks within the EU. Conversely, Norouzpour et al. (2023) observed a general increase in earnings and equity management following the adoption of IFRS 9, highlighting that this increase was observed in banks located in countries with low regulation. In contrast, in countries with high regulation, there was no significant change in earnings and equity management following the implementation of IFRS 9.

LLPs play a fundamental role in most of the literature on banking sector accounting. As accruals, LLPs are essential for bank performance and, being estimates, can entail information asymmetries (Beatty & Liao, 2014). Thus, the ECL model under IFRS 9, by incorporating judgments and subjectivity in recognizing LLPs, may cause information asymmetry issues among various stakeholders (Novotny-Farkas, 2016).

In this context, Agency Theory becomes important. This theory offers a comprehensive and complex view of organizations, asserting that they are influenced by normative pressures, sometimes from external sources like supervisors. Under certain conditions, these pressures lead an organization to align with legitimized elements and standardized work procedures (Zucker, 1987). According to Meyer and Rowan (1977), organizations are compelled to adopt practices and procedures defined by standardized concepts of organizational work prevalent and institutionalized in society, regardless of the immediate effectiveness of these practices. Demirgüç-Kunt et al. (2008) state that banks adhering to the information disclosure principles outlined in the Basel II agreement tend to receive more favorable financial ratings from Moody's. Alternatively, Poghosyan and Čihák (2011) note that market discipline, as considered by the Basel II agreement, facilitates the identification of weaker banks, enabling preventive measures. Morrison and White (2010) suggest that regulator observation of weaknesses can stabilize economies, potentially preventing systemic risks. Flannery et al. (2013) reinforce this idea, suggesting that regulators should encourage banks to be more transparent, as this significantly reduces the likelihood of deposit runs during economic downturns.

2.4. Formulation of Hypotheses

Previous studies anticipate the cyclicality of LLPs as a norm, arguing that dynamic models seek to improve their pro-cyclicality, accepting that some inherent pro-cyclicality in economic activity is natural, so that the credit market does not tend to increase the amplitude of the peaks and troughs of economic cycles.

The literature reviewed predicts that the cyclical nature of LLPs is common and that dynamic models attempt to mitigate this pro-cyclicality, recognizing that a certain pro-cyclicality is inherent in economic activity. It is important to prevent the credit market from amplifying the extremes of economic cycles (Agénor & Zilberman, 2015; Bikker & Metzemakers, 2005; Borio et al., 2001; Bouvatier & Lepetit, 2012; Chen et al., 2020; Goma et al., 2019; Morrison & White 2010; Novonty-Farkas 2016; Olszak et al., 2017; Ozoli & Outa, 2017; Pastiranová & Witzany, 2021; Pucci, 2017). Based on these evidences, the first hypothesis to be tested is formulated:

: The recognition of LLPs in Portuguese banks, according to the IFRS 9's ECL model, exhibits pro-cyclicality.

Moreover, the literature review also indicates that the ECL model of IFRS 9 is characterized by greater subjectivity compared to the ICL model of IAS 39, increasing discretionary power in the recognition of LLPs and, consequently, being more permissive to earnings and equity management (Du et al., 2023; Gomaa et al., 2019; Novotny-Farkas, 2016; Ozili & Outa, 2017). Therefore, it is expected that banks reduce (increase) the recognition of LLPs according to the profits obtained and the desired equity. Thus, the second hypothesis to be empirically tested is formulated:

: The recognition of LLPs in Portuguese banks, according to the IFRS 9's ECL model, allows for earnings and equity management.

3. Methodology

3.1. Analysis Model and Variables

To test the formulated hypotheses, the following multiple linear regression model was utilized, which describes the relationship between the dependent variable LLPs (explained variable) and the explanatory variables representative of economic cycles and the management of earnings and equity. This approach follows the methodology adopted in the studies of Araújo et al. (2018), Beatty and Liao (2014), and Casta et al. (2019).

In Table 1, the description of the dependent, independent, and control variables used in the model is presented.

Regarding the explained (dependent) variable, most models that address the relationship between the recognition of LLPs, economic cycles, and earnings management use the variable LLP_it as the dependent variable (Araújo et al., 2018; López-Espinosa et al., 2021; Pastiranová & Witzany, 2022).

As for the explanatory variables, the variables and are used to study the effects of economic cycles on the recognition of LLPs, and the variables and are used to study earnings management and equity management in the recognition of LLPs. Control variables include bank size (), accounting standard used (), LLAs (), and the amount and variation of loans granted ().

Table 2 succinctly presents the expected results regarding the behavior and sign of the coefficients associated with the explanatory and control variables, considering the formulated hypotheses. In other words, it summarizes the theoretical or expected predictions, based on the literature review, for the impact of independent and control variables on the dependent variable.

To more thoroughly assess the impacts on LLPs and validate the two formulated hypotheses, the model will be estimated separately for two periods: from 2013 to 2017, corresponding to the application period of the ICL model; and from 2018 to 2022, corresponding to the application period of the ECL model. Dividing the sample into two distinct periods will allow for an analysis of the behavior of the explanatory variables in relation to the dependent variable, verifying the consistency of the main model's results. This detailed approach is essential to better understand the impacts of LLPs under both models (ICL and ECL) over the periods of their application.

3.2. Sample and Data

The sample for this study was defined using the database of the Portuguese Banking Association, which, as of April 2023, listed 17 banks with consolidated reports and accounts available for the semesters of 2012 to 2022, from which all necessary data was manually collected to construct the variables. Twelve banks were excluded from the study, specifically: BES, BESI, Banif, Sant Consumer, CBI, BBVA, Itaú, and Barclays, for not being present throughout the entire study period and for having ceased to exist or no longer being part of the database; Invest and Crédito Agrícola, due to structural changes during the analysis period; and BIG and Finantia, due to the unavailability of all the necessary data for the study. Therefore, the final sample consists of 5 commercial banks.

Table 3 presents the banks included in the sample, ordered by decreasing total assets as of 31-12-2022. As can be seen, on the last day of the year 2022, the total accumulated assets on the balance sheet of all the banks in the sample amounted to 309 billion euros.

CGD, being a public bank with significant market presence, stands out for having the highest asset value compared to other banks in the sample (33.44% of the total sample). CGD is followed by BCP (29.31%), Santander (18.32%), BPI (12.69%), and Montepio (6.23%). Regarding net LLPs, CGD and Santander show negative values, suggesting that these banks recognized reversals of LLPs exceeding the LLPs recognized in 2022. This fact indicates improvements in asset quality (i.e., the customer portfolio) or the general economic situation, changes in accounting policy, or earnings management. The value of net LLPs varies among banks, with CGD showing a negative value of -5,300 million euros, BCP with 300,829 million euros, Santander with -11,943 million euros, BPI with 66,334 million euros, and Montepio with 13,371 million euros.

The ratio of earnings before taxes and LLPs over the total assets of the banks is used to study earnings management, considering LLPs as an instrument for managing results when the increase in earnings before taxes and LLPs leads to a higher level of LLPs. This indicator varies among the banks in the sample, with Santander having the highest value of 1.50%, followed by BPI with 1.35%, CGD with 1.10%, Montepio with 0.49%, and BCP with 0.47%.

Regarding LLAs, CGD shows the highest value both in absolute terms and relative to total assets. The other banks follow the order of their magnitude in the values presented in LLAs, both in absolute and relative terms, except for Montepio. Montepio, in absolute terms, has the lowest LLAs value but, in proportion to its assets, has the second highest value. This result could have various interpretations, ranging from a high risk in the loan portfolio to overvalued reserves.

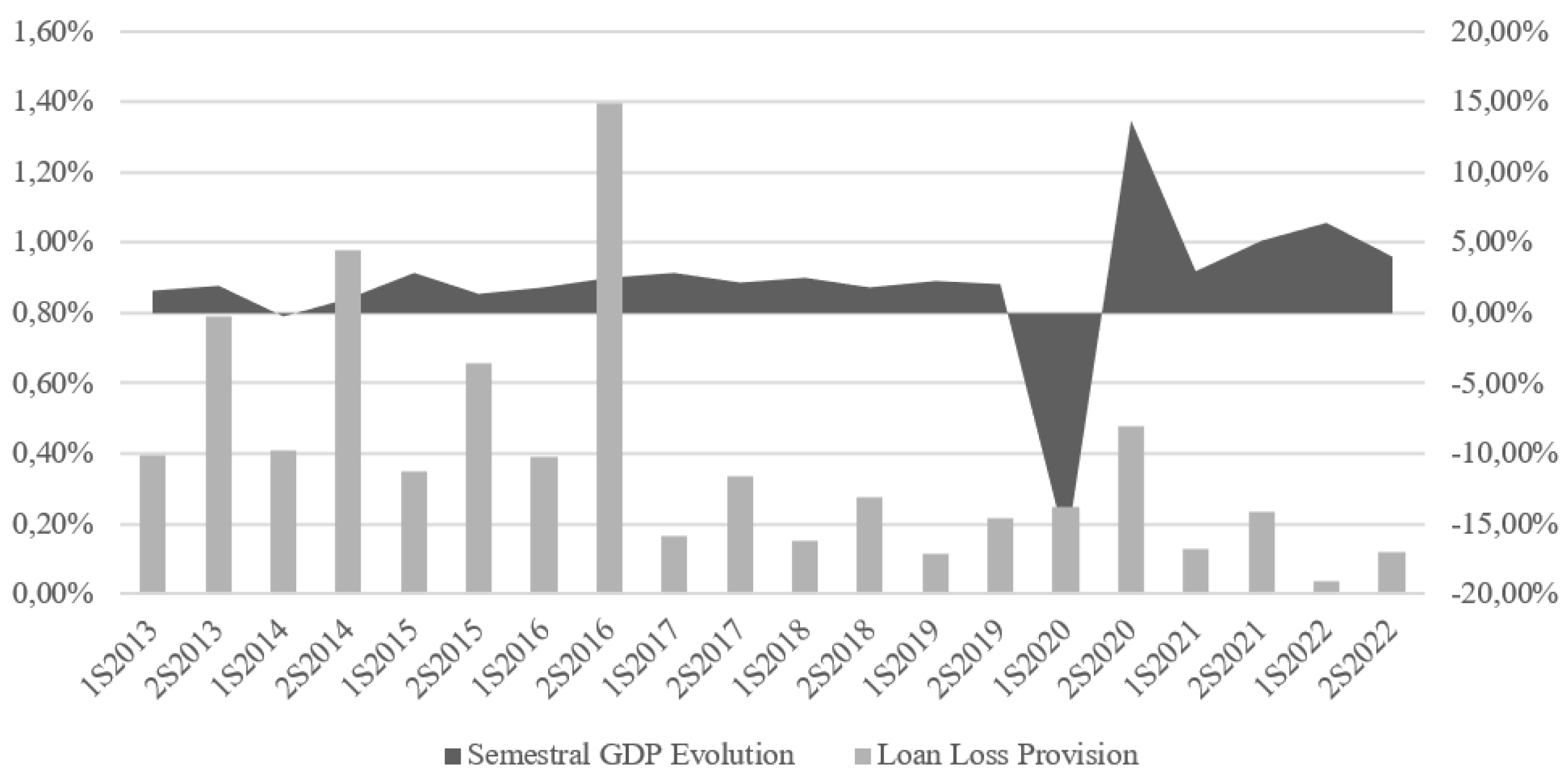

Semestral GDP Evolution | Net LLP over Total Assets of Banks

As evident in Figure 3, the GDP showed fluctuations throughout the period analyzed. Initially, there was a growth of 1.62% in the first semester of 2013, followed by a slightly higher increase of 1.94% in the second semester of the same year. However, in the first semester of 2014, there was a decline of -0.27% in GDP, followed by a recovery in the second semester, with a growth of 1.02%. These variations indicate changes in economic activity during that period. In the following years, GDP continued to show moderate growth, with rates varying between 1.32% and 2.92% in different semesters between 2015 and 2018. However, in 2020, the COVID-19 pandemic significantly impacted the Portuguese economy, resulting in a sharp GDP decline of -16.57% in the first semester. Nevertheless, a remarkable recovery of 13.67% was recorded in the second semester of the same year. The economic recovery continued in 2021 and 2022, with positive growth rates but slowing down in the second semester of 2022 (3.98%).

Regarding LLPs, they remained relatively stable throughout the analyzed period, varying between 0.03% and 1.40%. This stability may indicate a consistent environment in terms of credit risk over time, not showing a possible pro-cyclical behavior in the recognition of LLPs by Portuguese banks. This stability could be attributed to the legislative action of the Portuguese State, which implemented and maintained moratoriums for a considerable part of the credits granted to households and companies. Additionally, the IASB also intervened, limiting the recognition and increase of LLPs for phase 2 (significant risk increase) through a communication that altered the accounting policy of the ECL model (IASB, 2020). These measures likely played a fundamental role in avoiding significant fluctuations in LLP recognition during the crisis period and the consequent impact on banks' equity, providing greater stability in the financial sector.

4. Results

4.1. Descriptive Statistics

Table 4 presents the descriptive statistics of the variables under study, providing an overview of the basic characteristics of the data, including measures of central tendency such as mean and median, and measures of dispersion like the standard deviation.

The dependent variable has a total number of observations equal to 100, just like all other variables in the study. Observing the descriptive statistics, the variation in the minimum and maximum values of each variable becomes evident. For example, the dependent variable varies between -0.002 and 0.026, meaning the observed minimum value is -0.002 and the maximum value is 0.026. The average of impairments is 0.004, while the median is 0.003. The standard deviation is 0.005. The negative minimum values indicate that some banks in the sample could reverse impairments, reflecting improvements in credit risk or recovery of loans previously considered impaired. Furthermore, the low standard deviation points to little dispersion in the data, indicating low variation in impairments and possible stability in the credit conditions of the banks in the sample for the studied period.

The independent variable shows a minimum value of -0.224 and a maximum of 0.452. The average is -0.053, and the median is -0.080, with a standard deviation of 0.145. Considering the average and median, it is observed that, in general, variables like , , , , and show close values, suggesting a symmetric or approximately symmetric distribution. However, there are exceptions, such as the variable , which has an average of -0.053 and a median of -0.080, indicating an asymmetry in the distribution of the data, confirmed by its higher standard deviation.

In fact, the standard deviation is a relevant measure as it indicates the dispersion of data around the mean. Higher values of standard deviation, as observed in the variable (0.145) and (0.576), suggest greater variability in the data.

The variable is a dummy variable, for which it is important to note that there are 50 observations corresponding to the value 0, indicating the use of the IAS 39 standard in the period from 2013 to 2017, and 50 observations corresponding to the value 1, i.e., the use of the IFRS 9 standard in the period from 2018 to 2022.

In Table 5, descriptive statistics for the variables tested in the two hypotheses of the study are presented, divided into two sub-samples corresponding to the following two sub-periods: ICL Model (2013-2017); and ECL Model (2018-2022).

Table 5 shows notable differences in the descriptive statistics for the two analyzed sub-periods. For example, the variable shows distinct minimum values in the ICL and ECL models. However, it's important to consider that between 2018 to 2022, there was a significant drop in this indicator due to the COVID-19 pandemic, which influences the values presented for this period. The means of the explanatory variables also differ between models, which may indicate a more significant impact of these variables on LLPs under the IFRS 9's ECL model. Similar observations are made for the maximum values and standard deviations of the variables and , indicating changes in the magnitude and dispersion of the data between the accounting models.

In the ICL model, the variable presents higher minimum, maximum, and mean values compared to the ECL model, indicating larger reserves in the previous model. This is despite the economic performance deteriorating in the ECL model period (2018 to 2022) compared to the ICL model period (2013 to 2017), with greater instability and unpredictability in the economy. Despite this, the variable shows greater stability under the ECL model, not anticipating some pro-cyclicality attributed to a dynamic model in the literature review. This fact could be a sign of earnings management by the banks in the sample.

These disparities between the two sub-periods could be attributed to differences in accounting policies and criteria for recognizing LLPs between the ICL and ECL models. The data indicates that the choice of accounting model can affect how financial and control variables relate and are reflected in the banks' LLPs, particularly in this study, in Portuguese banks.

4.2. Analysis and Discussion of Results

To test the first hypothesis (H1: The recognition of LLPs in Portuguese banks, according to the IFRS 9's ECL model, exhibits pro-cyclicality) and the second hypothesis (H2: The recognition of LLPs in Portuguese banks, according to the IFRS 9's ECL model, allows for earnings and equity management), a multiple linear regression model was utilized. This model describes the relationship between the dependent variable LLP (explained variable) and the explanatory variables representative of economic cycles and the management of earnings and equity, following the methodology adopted in the studies of Araújo et al. (2018), Beatty and Liao (2014), and Casta et al. (2019).

Before proceeding with the correlation analysis of the variables, their normality was tested to decide between the Pearson and Spearman tests for analyzing the correlations among the various model variables. From the analysis conducted, it was concluded that the variables , and follow a normal distribution, and the remaining variables do not. Therefore, the Spearman correlation matrix was chosen, as presented in Table 6.

The Spearman correlation matrix in Table 6 reveals several significant associations among the variables used in the model. There is a strong negative correlation between and , suggesting that banks with higher equity tend to recognize fewer LLPs. A strong negative correlation is also observed between Portugal's GDP and the LLPs recognized by the banks in the sample, indicating potential pro-cyclicality in LLP recognition. The moderate positive correlations with control variables and were expected, as the data in these variables are related. The variable shows correlations with various variables, except for and . In summary, the results from the Spearman test provide important preliminary trends and have aided in the selection of variables for the regression model.

Although these correlations are an important basis for model construction, it is essential to perform a more thorough analysis when using a multiple linear regression, which requires verifying the assumptions that validate the model used (Laureano, 2020, p. 236). To analyze the presence of autocorrelation among the regression residuals, the Durbin-Watson test was conducted, yielding a result of 1.52, which indicates that the assumption of error independence is verified. The normal distribution of errors was tested using the Kolmogorov-Smirnov normal distribution adherence test, with the null hypothesis of error normality being rejected (p-value <0.01). However, in large samples (n>30), as in this study (n≥100), regression results can be considered in a linear regression model (Laureano, 2020). Multicollinearity was tested in all variables, and the assumption of its absence was verified. Additionally, the F-test (ANOVA) was conducted to verify the global significance of the model, allowing for statistical inference. This test confirmed that the model is adequate for explaining the relationship between the dependent variable and the independent variables, being statistically significant (p-value <0.05).

In Table 7, the results of the model estimation are presented for the entire sample (2013-2022) and for the sub-periods corresponding to the use of the ICL (2013-2017) and ECL (2018-2022) models.

An R² above 50% is a good indicator for the model's performance and acceptance, as well as the F-test (ANOVA) for the global significance of the model (Lauriano, 2020). In the main model, a determination coefficient (R²) of 0.502 was observed, indicating that 50.2% of the variation in the dependent variable was explained by the independent variables. Regarding the F-test, both the main model and the subperiod models are adequate for explaining the relationship between the dependent and independent variables, being statistically significant (p-value <0.05).

Among the variables studied in the main model, and are statistically significant, with showing a positive relationship and a negative relationship with the dependent variable, both behaviors being expected. On the other hand, , , , , and do not show statistical significance, indicating that they do not have a statistically significant impact on the dependent variable . The control variable proved to be statistically significant, showing a positive influence on the dependent variable , as expected (Agénor & Zilberman, 2015). With the subperiod models, an attempt was made to separately analyze the impact on the dependent variable over two distinct periods: the ICL model (2013 to 2017) and the ECL model (2018 to 2022). In the ICL model, the variables , , , , and had statistically significant impacts on the dependent variable , with the variables , and showing a negative relationship and the other statistically significant variables showing a positive relationship. In the ECL model, the variables , , , , and have statistically significant impacts on the dependent variable . The variable , and _itshow a positive relationship and the other statistically significant variables show a negative relationship with the dependent variable . It is noteworthy that the variable is statistically significant in both models, which is not the case in the main model, although with opposite signs.

According to the results presented in the subperiod models, it is possible to validate the first hypothesis with the variable (H1: The recognition of LLPs in Portuguese banks, according to the IFRS 9's ECL model, exhibits pro-cyclicality) showing, in the subperiod of the ECL model, a positive relationship with the dependent variable , meeting the initial expectations that a dynamic model reacts positively to individual economic conditions (unemployment), recognizing more LLP (Chan-Lau, 2012; Novotny-Farkas, 2016; Wezel, 2010).

Although the variable is not statistically significant for the ECL model (p-value = 0.138), it is closer to being significant compared to the ICL model (p-value = 0.769). This is typical of a dynamic model, where LLP recognition occurs not at the moment of default, but when economic conditions show negative signs (Bushman & Williams, 2015; Casta et al., 2019; Gebhardt & Novotny-Farkas, 2011; Laux, 2012). Thus, regarding the first hypothesis (H1), the expected pro-cyclicality was evidenced, as reviewed in various studies, for the Portuguese context (Agénor & Zilberman, 2015; Bikker & Metzemakers, 2005; Bouvatier & Lepetit, 2012; Borio et al., 2001; Chen et al., 2020; Goma et al., 2019; Morrison & White, 2010; Novonty-Farkas, 2016; Olszak et al., 2017; Ozoli & Outa, 2017; Pastiranová & Witzany, 2021; Pucci, 2017). This result is consistent with some studies suggesting potential difficulties for managers in incorporating indicators and implementing countercyclical reserves (Du et al., 2023; Seitz et al., 2018), as well as failing to reveal economic factors, as happened during the COVID-19 pandemic (Barnoussi et al., 2020). These results may also be influenced by the specific behavior of Portuguese banks, which, due to the history of financial crises (the most recent in 2011 with a new financial bailout), have become more restrained in recognizing LLP. Furthermore, ongoing assistance from the Portuguese state to banks, businesses, and families (e.g., state guarantees in moratoriums granted during the COVID-19 pandemic) may have delayed the emergence of defaults, or increased credit risk. Another possible explanation is related to the restraint in recognizing LLP during the COVID-19 pandemic and regulators' concerns about banks' regulatory capital (Barnoussi et al., 2020; Bischof et al., 2021). This conservative approach to credit risk, already signaled, could result in delays in recognizing LLP (EBA, 2021).

Regarding hypothesis 2 (H2: The recognition of LLPs in Portuguese banks, according to the IFRS 9's ECL model, allows for earnings and equity management), evidence of a significant relationship for the two explanatory variables ( and ) in the ECL model was also found, meeting the initial expectations (Du et al., 2023; Gomaa et al., 2019; Novotny-Farkas, 2016; Ozili & Outa, 2017). However, this statistical relevance is stronger in the ICL model (p-value < 0.05) than in the new ECL model (p-value < 0.10). This statistically more significant relevance in the previous ICL model, regarding the management of earnings and equity by Portuguese banks in the recognition of LLP, aligns with studies reporting delays in recognizing LLP in the ICL model of IAS 39 and even hiding inevitable losses (Gebhard & Novotny-Farkas, 2011; Hoogervorst, 2014). The unified European regulation, through the EBA, may have minimized the impact of LLP recognition on earnings management in the ECL model compared to ICL (Nnadi et al., 2023), thereby demonstrating that regulation is important in minimizing the possibility of earnings management, providing discipline and transparency to the market (Onali et al., 2021).

This article also confirmed the positive influence of LLAs on LLPs recognition in both models, demonstrating that LLPs are recognized considering existing LLAs. This result corroborates the empirical evidence previously found in the literature review, that the positive relationship between LLAs and LLPs recognition (Agénor & Zilberman, 2015) reduces the ability of bank managers to increase loans to existing risk clients, in both ECL and ICL models (Du et al., 2023).

Regarding the size of banks, it was expected that it would positively affect LLP recognition - the larger the bank, the higher the level of LLP recognition (Mechelli & Climini, 2021; Onali et al., 2021). However, the study's results indicate that, with the ECL model of IFRS 9, the size of Portuguese banks negatively affects LLP recognition. This intriguing result in the context of the Portuguese reality diverges from the reviewed literature. Containment in recognizing LLP, as analyzed, can be considered one of the possible causes for this result. Moreover, it is important to note that three of the four largest banks in the sample underwent public recapitalization through the issuance of Contingent Convertible Bonds (CoCos) in June 2012 (BCP, BPI, and CGD), which may have negatively impacted LLP recognition in subsequent years.

5. Conclusions

This article represents a pioneering approach in analyzing the pro-cyclicality of LLPs in Portuguese banks, as well as the management of earnings and equity through their recognition. The financial sector is crucial for any country, especially in a scenario of rising interest rates, potentially playing a significant role in managing an impending economic and/or financial crisis. In Portugal, a country that recently sought external assistance, the financial sector gains particular relevance since, in an overly leveraged economy, the adequacy of banks' reserves is fundamental to overcoming an economic recession scenario.

This article study aimed to analyze the pro-cyclicality of LLPs in Portuguese banks, as well as the existence of earnings and equity management through their recognition, over a time frame from 2013 to 2022. The study focused on five Portuguese commercial banks, selected from a base of seventeen banks from the Portuguese Banking Association, excluding twelve due to the lack of data. A multiple linear regression model was used, identifying how LLPs react to the behavior of explanatory variables, economic cycles, and the management of earnings and equity, over an extended period of 10 years (2013 to 2022), following the methodology adopted by Araújo et al. (2018), Beatty and Liao (2014), and Casta et al. (2019).

The results confirm the pro-cyclicality in the recognition of LLPs in Portuguese banks, in line with the first hypothesis (H1: The recognition of LLPs in Portuguese banks, according to the IFRS 9's ECL model, exhibits pro-cyclicality), where the ECL model of IFRS 9 responds positively to economic indicators like unemployment, even though GDP did not show statistical significance. This pro-cyclicality reflects the ECL model's reaction to adverse economic contexts, corroborating the literature in the Portuguese context.

Regarding the second hypothesis (H2: The recognition of LLPs in Portuguese banks, according to the IFRS 9's ECL model, allows for earnings and equity management), a significant relationship in the management of earnings and equity in the ECL model is verified, although less pronounced compared to the previous ICL model. This evidence suggests that despite the EBA regulation and the new accounting model potentially attenuating earnings management, it continues to be a practice in LLP recognition, albeit less intensively, highlighting the importance of regulation to ensure discipline and transparency in the financial market.

This article makes significant contributions to the literature on understanding the impact of the ECL model of IFRS 9 on Portuguese banks. The results validate the hypothesis of pro-cyclicality in the ECL model of IFRS 9, showing that it is more sensitive to economic conditions compared to the ICL model of IAS 39, confirming expectations from Abad and Suarez (2017). However, given the current macroeconomic conditions, such as the conflict in Ukraine, inflation, rising interest rates, and weak growth in Europe, the ECL model of IFRS 9 seems not to be anticipating the recognition of LLPs, suggesting it may not be performing as expected by Portuguese banks, i.e., creating adequate countercyclical reserves (LLAs) to face future crises. One possible cause for this could be the systematic intervention of the state, which is not creating incentives for Portuguese banks to reflect macroeconomic conditions (), focusing only on microeconomic conditions (), i.e., financing efforts and defaults of families and businesses. These events should have timely influenced the increase in reserves, which did not happen, potentially leading to restraint in recognizing LLPs. This study also brings contributions to practice, particularly for regulators and professionals in the field, as the expected increase in recognizing LLAs, anticipating adverse economic conditions, was not observed, alerting to the existence of earnings and equity management by Portuguese banks. However, earnings and equity management is less pronounced in the ECL model compared to the old ICL model, indicating that greater transparency and better European regulatory mechanisms by the EBA may have attenuated this behavior.

Like any scientific study, this one also has limitations. Firstly, the study focused solely on Portuguese banks, limiting the generalization of the results to other jurisdictions. Moreover, the sample does not cover all financial institutions in Portugal due to the limitations mentioned in the sample definition, being a reduced sample of banks, a consequence of the intention to study in depth a single jurisdiction, Portugal. Another limitation refers to the analysis period, which may not encompass all relevant economic variations over time. Lastly, the study focused on quantitative analysis, leaving out possible qualitative explanations that could enrich the understanding of the phenomena under study.

In future studies, it would be important to analyze and compare the impact of government policies and financial assistance on the pro-cyclicality in recognizing LLPs in the ECL model. Additionally, it is relevant to investigate whether the reserves of the ECL model in Portuguese banks are adequate to face a financial crisis similar to the last high-risk mortgage credit crisis (subprime). Although the study points to an anticipation in recognizing LLPs, they may not be sufficient for a large-scale crisis. Another interesting line of research would be to study the behavior of the ECL model over a more extended period, using estimated models developed in some studies on this area. Finally, it would be important to estimate the impact of LLPs on Portuguese banks' equity and regulatory capital if there had been no government assistance and recommendations, like the one from IASB (2020), for restraint in recognizing LLPs.

Author Contributions

Conceptualization, M.R.; methodology, M.R.; validation, C.C. and C.C.; formal analysis, M.R.; investigation, M.R.; writing—original draft preparation, M.R.; writing—review and editing, C.C. and C.C.. All authors have read and agreed to the published version of the manuscript.

Data Availability Statement

Publicly available datasets were analyzed in this study with sources as outlined in 3.2. Sample and Data.

Conflicts of Interest

The authors declare no conflict of interest.

| 1 | In the specialized literature on the subject, it is common to encounter the terms Loan Loss Provisions (LLPs) and Loan Loss Allowances (LLAs) to designate credit impairment losses. For the sake of uniformity in the terminology used in studies, this research will use the abbreviation LLP to express credit impairment losses recognized in the period, and LLA for the accumulated credit impairment losses, following the approach of Salazar et al. (2023). |

| 2 | In this study, the term earnings management is used to describe deliberate intervention by managers through the recognition of LLP and its impact on the banks' results and equity. According to Schipper (1989), this manipulation is an intentional intervention in financial information to obtain specific benefits, particularly through the selection of accounting practices that align more closely with the interests of managers or the company. Similarly, Healy and Wahlen (1999) note that earnings management occurs when managers use their judgment to alter financial reports to influence stakeholders' perception or meet specific contractual clauses. |

| 3 | During the COVID-19 pandemic, the IASB intervened, limiting the recognition and increase of LLPs for phase 2 (significant increase in risk) through a communication that altered the accounting policy of the ECL model. In this note, the IASB indicates that the impact on loans due to moratoriums, when backed by the states, should not be interpreted as a significant increase in risk. |

| 4 | "LLA = EAD × PD × LGD" |

References

- Abad, J. , & Suarez, J. (2017). Assessing the cyclical implications of IFRS9: A recursive model. European Systemic Risk Board. [CrossRef]

- Agénor, P. R., & Zilberman, R. (2015). Loan loss provisioning rules, procyclicality, and financial volatility. Journal of Banking and Finance, 61, 301–315. [CrossRef]

- Araújo, A. M. H. , Lustosa, P. R. B., & Dantas, J. A. (2018). A Ciclicidade da Provisão para Créditos de Liquidação Duvidosa nos Bancos Comerciais do Brasil. Brazilian Business Review, 15(3), 246–261. [CrossRef]

- Balla, E., & Mckenna, A. (2009). Countercyclical tool for. Convergence, 95(4), 383–418.

- Barnoussi, A. , Howieson, B., & van Beest, F. (2020). Prudential application of IFRS 9: (Un)fair reporting in COVID-19 crisis for banks worldwide?!. Australian Accounting Review, 30(3), 178–192. [CrossRef]

- Beatty, A. , & Liao, S. (2014). Financial accounting in the banking industry: A review of the empirical literature. Journal of Accounting and Economics, 58(2–3), 339–383. [CrossRef]

- Bebczuk, R. , Burdisso, T., Carrera, J., & Sangiácomo, M. (2011). A new look into credit procyclicality: International panel evidence. BCRA Working Paper, (55), 1–40.

- Beck, P. J. , & Narayanamoorthy, G. S. (2013). Did the SEC impact banks’ loan loss reserve policies and their informativeness? Journal of Accounting and Economics, 56(2–3), 42–65. [CrossRef]

- Berger, A. N., & Udell, G. F. (2004). The institutional memory hypothesis and the procyclicality of bank lending behavior. Journal of Financial Intermediation, 13(4), 458–495. [CrossRef]

- Bikker, J. A. , & Metzemakers, P. A. J. (2005). Bank provisioning behaviour and procyclicality. Journal of International Financial Markets, Institutions and Money, 15(2), 141–157. [CrossRef]

- Bischof, J. , Laux, C., & Leuz, C. (2021). Accounting for financial stability: Bank disclosure and loss recognition in the financial crisis. Journal of Financial Economics, 141(3), 1188–1217. [CrossRef]

- Bloomberg. (2012). The EU smiled while Spain’s banks cooked the books - Bloomberg. Retrieved from http://www.bloomberg.com/news/2012-06-14/the-eu-smiled-while-spain-s-banks-cooked-the-books.html.

- Borio, C. , Furfine, C., & Lowe, P. (2001). Procyclicality of the financial system and financial stability: Issues and policy options. BIS Papers Chapters, 01(1), 1–57. Retrieved from http://ideas.repec.org/h/bis/bisbpc/01-01.html.

- Bouvatier, V. , & Lepetit, L. (2012). Provisioning rules and bank lending: A theoretical model. Journal of Financial Stability, 8(1), 25–31. [CrossRef]

- Bushman, R. M. , & Williams, C.D. (2015). Delayed expected loss recognition and the risk profile of banks. Journal of Accounting Research, 53(3), 511–553. [CrossRef]

- Camfferman, K. (2015). The emergence of the ‘incurred-loss’ model for credit losses in IAS 39. Accounting in Europe, 12(1), 1–35. [CrossRef]

- Casta, J. F. , Lejard, C., & Paget-Blanc, E., (2019, August). The implementation of the IFRS 9 in banking industry. EUFIN 2019: The 15th Workshop on European Financial Reporting, Vienne, Austria. hal-02405140.

- Chan-Lau, J. A. (2012). Do dynamic provisions enhance bank solvency and reduce credit procyclicality? A study of the Chilean banking system. Journal of Banking Regulation, 13, 178-188. [CrossRef]

- Chen, Y., Yang, C., & Zhang, C. (2020). Study on the influence of IFRS 9 on the impairment of commercial bank credit card. Applied Economics Letters, 29(1), 35–40. [CrossRef] [PubMed]

- Demirgüç-Kunt, A. , Detragiache, E., & Tressel, T. (2008). Banking on the principles: Compliance with Basel core principles and bank soundness. Journal of Financial Intermediation, 17(4), 511–542. [CrossRef]

- Donelian, M. S. (2019). Os efeitos colaterais do IFRS9: O aumento da prociclicidade do crédito na economia real. Retrieved July 17, 2023, from https://www.linkedin.com/pulse/os-efeitos-colaterais-do-ifrs9-o-aumentoda-crédito-na-donelian/?trk=pulse-article&originalSubdomain=pt.

- Du, N. , Allini, A., & Maffei, M. (2023). How do bank managers forecast the future in the shadow of the past? An examination of expected credit losses under IFRS 9. Accounting and Business Research, 53(6), 699-722. [CrossRef]

- EBA. (2021). IFRS 9 implementation by EU institutions: Monitoring report. European Banking Authority. [CrossRef]

- Engelmann, B. , & Lam Nguyen, T. T. (2023). Global assessment of the COVID-19 impact on IFRS 9 loan loss provisions. Asian Review of Accounting, 31(1), 26–41. [CrossRef]

- Ferreira, D. (2011). Instrumentos Financeiros. Rei dos Livros.

- Flannery, M. J. , Kwan, S. H., & Nimalendran, M. (2013). The 2007-2009 financial crisis and bank opaqueness. Journal of Financial Intermediation, 22(1), 55–84. [CrossRef]

- FASB-IASB (2009, March). Information for observers: Spanish provisions under IFRS (Agenda paper 7C), IASB-FASB Meeting, London.

- Gebhardt, G. , & Novotny-Farkas, Z. (2011). Mandatory IFRS adoption and accounting quality of European banks. Journal of Business Finance and Accounting, 38(3–4), 289–333. [CrossRef]

- Gomaa, M. , Kanagaretnam, K., Mestelman, S., & Shehata, M. (2019). Testing the efficacy of replacing the incurred credit loss model with the expected credit loss model. European Accounting Review, 28(2), 309–334. [CrossRef]

- Harrald, P. , & Sandall, T. (2010). Tackling pro-cyclicality in banking regulation. Retrieved from https://www.risk.net/regulation/1800392/tackling-pro-cyclicality-banking-regulation.

- Healy, P. M., & Wahlen, J. (1999). A review of the earnings management literature and its implications for standard settings. Accounting Horizons, 13(4), 365-383. [CrossRef]

- Hoogervorst, H. (2014). Closing the accounting chapter of the financial crisis [Speech]. Asia-Oceania Regional Policy Forum, (April), 1–5. Retrieved from https://cdn.ifrs.org/content/dam/ifrs/news/speeches/2014/hans-hoogervorst-march-2014.pdf.

- IASB. (2020). IFRS 9 and Covid-19. Retrieved from https://cdn.ifrs.org/-/media/feature/supporting-implementation/ifrs-9/ifrs-9-ecl-and- coronavirus.pdf?la=en.

- KPMG. (2016). IFRS 9 Instrumentos Financeiros: Novas regras sobre a classificação e mensuração de ativos financeiros, incluindo a redução no valor recuperável. Retrieved from https://assets.kpmg/content/dam/kpmg/pdf/2016/04/ifrs-em-destaque-01-16.pdf.

- Krüger, S., Rösch, D., & Scheule, H. (2018). The impact of loan loss provisioning on bank capital requirements. Journal of Financial Stability, 36, 114–129. [CrossRef]

- Laureano, R. M. S. (2020). Testes de hipóteses e regressão: O meu manual de consulta rápida. Edições Sílabo.

- Laux, C. (2012). Financial instruments, financial reporting, and financial stability. Accounting and Business Research, 42(3), 239–260. [CrossRef]

- Longbrake, W. A. , & Rossi, C. V. (2011). Procyclical versus countercyclical policy effects on financial services. The Financial Services Roundtable.

- López-Espinosa, G. , Ormazabal, G., & Sakasai, Y. (2021). Switching from incurred to expected loan loss provisioning: Early evidence. Journal of Accounting Research, 59(3), 757–804. [CrossRef]

- López-Espinosa, G. , & Penalva, F. (2023). Evidence from the adoption of IFRS 9 and the impact of COVID-19 on lending and regulatory capital on Spanish banks. Journal of Accounting and Public Policy, 42. [CrossRef]

- Marton, J. , & Runesson, E. (2017). The predictive ability of loan loss provisions in banks: Effects of accounting standards, enforcement and incentives. British Accounting Review, 49(2), 162–180. [CrossRef]

- Mechelli, A. , & Cimini, R. (2021). The effect of corporate governance and investor protection environments on the value relevance of new accounting standards: The case of IFRS 9 and IAS 39. Journal of Management and Governance, 25(4), 1241–1266. [CrossRef]

- Meyer, J. W., & Rowan, B. (1977). Institutional theory and strategic management. The American Journal of Sociology, 83(2), 340–363. [CrossRef]

- Morrison, A. D. , & White, L. (2010). Reputational contagion and optimal regulatory forbearance. ECB Working Paper Series 1196.

- Nnadi, M. , Keskudee, A., & Amaewhule, W. (2023). IFRS 9 and earnings management: The case of European commercial banks. International Journal of Accounting and Information Management, 31(3), 504–527. [CrossRef]

- Norouzpour, M., Nikulin, E., & Downing, J. (2023). IFRS 9, earnings management and capital management by European banks. Journal of Financial Reporting and Accounting, 31(3), 504-527. [CrossRef]

- Novotny-Farkas, Z. (2016). The interaction of the IFRS 9 expected loss approach with supervisory rules and implications for financial stability. Accounting in Europe, 13(2), 197–227. [CrossRef]

- Olszak, M., Pipień, M., Kowalska, I., & Roszkowska, S. (2017). What drives heterogeneity of cyclicality of loan-loss provisions in the EU? Journal of Financial Services Research, 51(1), 55–96. [CrossRef]

- Onali, E. , Ginesti, G., Cardillo, G., & Torluccio, G. (2021). Market reaction to the expected loss model in banks. Journal of Financial Stability, 100884. [CrossRef]

- Ozili, P. K. (2019). Bank income smoothing, institutions and corruption. Research in International Business and Finance, 49(February), 82–99. [CrossRef]

- Ozili, P. K. , & Outa, E. (2017). Bank loan loss provisions research: A review. Borsa Istanbul Review, 17(3), 144–163. [CrossRef]

- Pastiranová, O. , & Witzany, J. (2022). IFRS 9 and its behavior in the cycle: The evidence on EU countries. Journal of International Financial Management and Accounting, 33(1), 5–17. [CrossRef]

- Pastiranová, O., & Witzany, J. (2021). Impact of implementation of IFRS 9 on Czech banking sector. Prague Economic Papers, 30(4), 449–469. [CrossRef]

- Poghosyan, T. , & Čihak, M. (2011). Determinants of bank distress in Europe: Evidence from a new data set. Journal of Financial Services Research, 40(3), 163–184. [CrossRef]

- Pucci, R. (2017). Accounting for financial instruments in an uncertain world: Controversies in IFRS in the aftermath of the 2008 financial crisis [Doctoral Thesis]. Copenhagen Business School. Retrieved from http://openarchive.cbs.dk/xmlui/bitstream/handle/10398/9477/Richard Pucci.pdf?sequence=1#page=108.

- Salazar, Y. , Merello, P., & Zorio-Grima, A. (2023). IFRS 9, banking risk and COVID-19: Evidence from Europe. Finance Research Letters, 56(June), 104130. [CrossRef]

- Saurina, J. (2009). Dynamic Provisioning. Crisis Response No.7. World Bank. Retrieved from http://hdl.handle.net/10986/10241.

- Schipper, K. (1989). Commentary on earnings management. Accounting Horizons, 3(4), 91-102.

- Seitz, B. , Dinh, T., & Rathgeber, A. (2018). Understanding loan loss reserves under IFRS 9: A simulation-based approach. Advances in Quantitative Analysis of Finance and Accounting, 16, 311–375.

- Silva, E. S. (2017). IFRS 9 - Instrumentos Financeiros - Introdução às regras de reconhecimento e mensuração. Vida Económica.

- Volarević, H. , & Varović, M. (2018). Internal model for IFRS 9: Expected credit losses calculation. Ekonomski Pregled, 69(3), 269–297. [CrossRef]

- Wall, L. D. , & Koch, T. W. (2000). Bank loan-loss accounting: A review of theoretical and empirical evidence. Economic Review, (Q2), 1–20. Retrieved from http://ideas.repec.org/a/fip/fedaer/y2000iq2p1-20nv.85no.2.html.

- Wezel, T. (2010). Dynamic loan loss provisions in Uruguay: Properties, shock absorption capacity and simulations using alternative formulas. IMF Working Papers, 10(125), 1. [CrossRef]

- Zucker, L. G. (1987). Institutional theories of organization. Annual Review of Sociology. Vol. 13, 443–464. [CrossRef]

Figure 1.