Submitted:

18 January 2024

Posted:

19 January 2024

You are already at the latest version

Abstract

The efficient and sustainable management of hospitals is an increasingly relevant challenge in the healthcare sector. With limited financial resources, regulatory pressures and increasing demands for quality services, hospitals are faced with the want to approve sound policies to certify financial and operational sustainability. Management accounting is critical in this instance. In Portugal the DL nº 284, of July 26, 1999, allow us to confirm the need to reinforcement of profitability and efficiency in the provision of healthcare. Management accounting is an essential tool for monitoring and controlling costs, making strategic decisions, efficiently allocating resources and evaluating performance in the hospital environment. It allows a comprehensive view of financial and operational aspects, providing valuable information for management and strategic planning. However, the sustainability of hospital management accounting is a critical and complex topic that deserves special attention. Hospitals face several challenges, such as the complexity of hospital costs, the integration of information systems and the measurement of healthcare value. These challenges can compromise the effectiveness of management accounting and its ability to provide relevant and reliable information for decision making. As a result, it is required to address the sustainability of hospital management accounting by identifying the specific challenges faced in this area and exploring opportunities to overcome them. By addressing these challenges and seizing opportunities, hospitals can strengthen their position in the healthcare sector, improve their operational efficiency, optimize resource allocation and ensure the provision of quality services to patients. In this article, the challenges faced by hospital management accounting will be analysed, such as the complexity of costs, the integration of information systems and the measurement of value in healthcare. Additionally, opportunities to improve financial and operational management will be highlighted through the adoption of advanced technologies, an emphasis on value-based management and collaborative partnerships. By exploring these themes, this essay aims to make a contribution. to the advancement of hospital management accounting and the sustainability of hospitals in the current healthcare scenario.

Keywords:

financial sustainability

; management accounting

; sustainable management

; cost control

; hospitals

1. Introduction

The efficient and sustainable management of hospitals is an increasingly relevant challenge in the healthcare sector. With limited financial resources, regulatory pressures and increasing demands for quality services, hospitals are faced with the want to approve sound policies to certify financial and operational sustainability. Management accounting is critical in this instance. In Portugal the DL nº 284, of July 26, 1999, allow us to confirm the need to reinforcement of profitability and efficiency in the provision of healthcare.

Management accounting is an essential tool for monitoring and controlling costs, making strategic decisions, efficiently allocating resources and evaluating performance in the hospital environment. It allows a comprehensive view of financial and operational aspects, providing valuable information for management and strategic planning.

However, the sustainability of hospital management accounting is a critical and complex topic that deserves special attention. Hospitals face several challenges, such as the complexity of hospital costs, the integration of information systems and the measurement of healthcare value. These challenges can compromise the effectiveness of management accounting and its ability to provide relevant and reliable information for decision making.

As a result, it is required to address the sustainability of hospital management accounting by identifying the specific challenges faced in this area and exploring opportunities to overcome them. By addressing these challenges and seizing opportunities, hospitals can strengthen their position in the healthcare sector, improve their operational efficiency, optimize resource allocation and ensure the provision of quality services to patients.

In this article, the challenges faced by hospital management accounting will be analysed, such as the complexity of costs, the integration of information systems and the measurement of value in healthcare. Additionally, opportunities to improve financial and operational management will be highlighted through the adoption of advanced technologies, an emphasis on value-based management and collaborative partnerships. By exploring these themes, this essay aims to make a contribution. to the advancement of hospital management accounting and the sustainability of hospitals in the current healthcare scenario.

2. Review of Literature

2.1. The study's objectives and purpose

2.1.1. Hospital Management Accounting: Concepts and Functions

Hospital management accounting is defined as the accounting of a hospital. to the usual of accounting and financial techniques applied specifically in the hospital environment. It involves the collection, analysis and interpretation of financial and operational evidence relevant to the strategic management of hospitals. Its main objective is to provide data and insights for decision making, performance monitoring and cost control.

Importance of management accounting for hospitals: Management accounting is critical to hospital management's efficiency and sustainability. It allows managers to have a clear view of finances and operations, helping to make decisions based on accurate information. Furthermore, management accounting provides effective cost control and the identification of areas for improvement, contributing to the optimization of resources and the achievement of satisfactory financial results. As a major provider of services and consumer of resources, the public sector has a large influence on national and international progress towards sustainable development. Furthermore, public sector organizations (PSOs) face increasing pressure to lead by example in managing and reporting sustainability issues (GRI, 2004, 2005; GRI FPA, 2012). Due to the critical impact that PSOs have on the environment and society, it has become increasingly important to analyze accounting, reporting and sustainability reporting practices, as well as to conduct research involving policy professionals in the public sector (Bola and Grubnic, 2007; Bola et al., 2014).

Natural resource conservation and emission levels, environmental activities and initiatives, aspects of employment, occupational health and safety, community relations, stakeholder engagement, and the organization's economic impact are all examples of sustainability performance (Hoque and Adams, 2008). The use of sustainability accounting allows for the systematic identification and interconnection of the social, environmental, and economic costs and benefits of organisational policies and actions, as well as their implementation into organisational decision-making (Hopwood et al., 2005).

As a result, the sustainability report serves as “a vehicle for evaluating the economic, environmental and social impacts of the organization's operations, products and services and its overall contribution to sustainable development” (GRI, 2004, p. 20).

According to existing literature, the public sector has implemented sustainability accounting and reporting procedures. To date, the primary research focus has been on sustainability reporting techniques (Gibson and Guthrie, 1995; Goswa-mi and Lodhia, 2014; Guthrie and Farneti, 2008; Leesone et al.,, 2005; William et al.,, 2011; Williams, 2015), drivers of sustainability reports (Farneti and Guthrie, 2009;Lodhia and Jacobs, 2013; Lodhia and et al.,, 2012; Marcuccio and Steccolini, 2005; Mussari and Monfardini, 2010), sustainability accounting (Bola, 2004,2005,2007), accounting for environmental management (qiane et al., 2011) and stakeholder adjustment (Gregoe et al., 2013; Kaur and Lodhia, 2014, 2016, 2017, 2018, 2019). However, there is still a lot to learn about accounting, accountability, and sustainability reporting in the public sector.

Importance of management accounting for hospitals: Management accounting theatres a crucial part in the efficient and sustainable management of hospitals. It allows managers to have a clear view of finances and operations, helping to make decisions based on accurate information. Furthermore, management accounting provides effective cost control and the identification of areas for improvement, contributing to the optimization of resources and the achievement of satisfactory financial results.

Functions of management accounting in the hospital context: Management accounting performs several functions in the hospital context, including:

Cost assessment and control: Management accounting allows for detailed monitoring and control of hospital costs, identifying areas where expenses can be reduced, operational efficiency can be improved and resources can be allocated more effectively.

Strategic decision making: Management accounting provides financial and operational information that supports strategic decision making. It assists in evaluating investments, defining service prices, identifying revenue sources and long-term planning, enabling the implementation of more effective strategies.

Performance evaluation: Management accounting allows the analysis and monitoring of the hospital's performance in several areas, such as patient care, operational efficiency and quality of services. This facilitates the identification of strengths and weaknesses, enabling the implementation of corrective actions to improve overall performance.

Planning and budgeting: Management accounting plays a fundamental role in the hospital's financial and budgetary planning. It assists in revenue projection, cost estimation, definition of financial goals and efficient allocation of available resources, allowing for more accurate strategic planning.

Support for value-based management: Hospital management accounting can adopt the value-based management approach, which seeks to evaluate and improve the relationship between the health results achieved and the costs involved. This allows for a more strategic allocation of resources and more effective management of the services provided.

In summary, hospital management accounting is essential for the efficient and sustainable management of hospitals. It provides relevant information for strategic decision making, cost control, performance monitoring and financial planning, contributing to the success of healthcare institutions.

This study aims to expand research in the public sector accounting, accountability, and sustainability reporting. The goal is to expand on current public-sector research programmes and better understand the role of PSOs in advancing the accounting, accountability, and sustainability reporting agenda. The documents demonstrate varied accounting and sustainability reporting techniques of various types of PSOs from various nations. Environmental reports, social reports, and sustainability reports in hybrid PSOs are among the documents included in this special edition, as are integrated reporting (IR) and stakeholder adjustment, as well as the implementation of environmental performance into the Balanced Scorecard (BSC) and performance evaluation systems. The articles employ a variety of investigative methodologies, such as case studies that include interviews and longitudinal content analyses, web content analysis, and quantitative methods such as surveys and linear regression. The studies' backdrop includes hybrid PSOs in Spain and Sweden, the Italian provincial government, the Australian healthcare sector, New Zealand Post, Moroccan public institutions and enterprises, and Malaysian local governments.

Because hybrid PSOs have financial and non-financial objectives, they operate in a complicated business environment, and this complexity impacts sustainability reporting approaches. Argento et al. (2019) Using institutional logics, we investigated the nature of and influences on the sustainability dissemination practices of 45 Swedish state-owned healthcare facilities (SOEs). The authors employed quantitative content analysis to analyse the impact of public ownership, board composition, firm size, and profitability on the substance of sustainability reporting disclosures from state-owned enterprises. The authors demonstrated that just two criteria, "state ownership" and "company size," have a substantial impact on public firms' sustainability disclosures. They discovered that fully public entities reveal less sustainability information than partially state-owned SOEs, while large SOEs release significantly more than small SOEs.

Argento et al. (2019), Andrades and Larrán-Jorge (2019) Examine the disclosure policies of Spanish public corporations, with a focus on mandated non-financial disclosures. The research includes data about the level of mandatory non-financial reports made by Spanish state-owned companies, as well as the factors that influence these reports. The researchers describe a low level of mandated non-financial information disclosure due to uncertainty in Spanish rules and a lack of implementation of New Public Management, resulting in a lack of accountability and effective regulatory enforcement. According to the authors, the extent of disclosures is determined by institutional size, with larger SOEs disclosing greater details than small SOEs.

Internal regulation (IR) in the public sector is another major topic of study. In this regard, Farneti et al. (2019a) Investigate the impact of IR demands and stakeholder information on social disclosures, focusing on the three social capitals identified in the IR framework: intellectual, human, and social and relationship capital. Using an internal organisational perspective, the authors undertake a case study to illustrate changes in disclosures to various stakeholder groups as a result of IR adoption. Adopting the IR framework, the authors discovered, promoted broad stakeholder involvement and a materiality assessment methodology, allowing the case study organisation to minimise the amount of social disclosures and focus on the social issues most significant to interested parties.

Farnetie et al.(2019b) using longitudinal analysis, investigate non-financial disclosures in an Italian provincial government's social reports to establish their significance, contribution, and evolution. They conducted in-depth research using case studies to learn more about the extent and application of voluntary social and environmental disclosures. The authors observed a rise in the level of disclosure throughout the ten-year period, as well as a shift from a descriptive, narrative approach to more detailed disclosures. The organisation, however, chose metrics from the Global Reporting Initiative (GRI). The authors also observe a widespread reduction in interest in the development of autonomous social reports, and that such reports have been prepared only to gain public credibility.

As a result, the authors emphasised the necessity for non-financial information disclosure regulation because the organization's social and environmental disclosures were primarily at its discretion.

Previous research has primarily focused on wealthy countries, and little is known about how the public sector in developing countries maintains and presents non-financial performance metrics. In line with this, Ibrahimi and Naim (2019) studied various aspects influencing the usage of non-financial indicators in Moroccan governmental institutions and firms' performance evaluation systems (MPIE). The authors show, using contingency theory, that the Moroccan MPIE's use of non-financial metrics is determined only by the institution's age. Other organisational variables, such as the size of the institution and the competitive environment, did not stimulate the incorporation of non-financial metrics in performance evaluation systems.

However, Che-Ku-Kassime et al., (2019) Using legitimacy theory, we performed a study to examine the environmental reporting practices of Malaysian local governments and the determinants of such activities.

The authors demonstrated that most Malaysian local governments report environmental information using more than one disclosure average. Annual reports and website announcements are major modes of communication. They also discovered that the primary purpose for environmental reporting is to preserve and improve the organization's image in the eyes of the appropriate audience.

An important area of research is the use of the BSC to specifically incorporate environmental performance in the public sector. Khalide et al., (2019) As a leading provider of healthcare services in Australia, investigate the viability of various BSC models for incorporating environmental performance. Using a case study methodology, the authors offer four viewpoints that can help healthcare organisations include environmental performance into their BSC, including an enlarged model with five perspectives and an integrated model with a separate climate change perspective. The authors believe, however, that the adoption of a specific model is contingent on the organization's environmental vision and strategy.

2.1.2. Challenges in Hospital Management Accounting

Complexity of hospital costs: The complexity of hospital costs is a significant challenge in hospital management accounting. Hospitals deal with a wide range of costs, including medical supplies, employee salaries, advanced medical technology, and medications. Additionally, costs may vary depending on the different departments and services offered by the hospital. Management accounting faces the challenge of capturing, tracking and correctly allocating these costs, ensuring the accuracy and reliability of accounting information.

Integration of information systems: Hospitals generally have fragmented and non-integrated information systems. This means that different departments and areas of the hospital may have their own recording and data management systems, which makes it difficult to obtain consistent and up-to-date data. Management accounting faces the challenge of integrating these systems to obtain a comprehensive and accurate view of accounting information. Lack of integration can lead to gaps in communication and make it difficult to effectively analyze and monitor financial and operational data.

Measuring value in healthcare: Measuring value in healthcare is a complex challenge in hospital management accounting. The assessment of health value involves measuring the results achieved by health services and their relationship with the costs involved. This requires the development of appropriate metrics and indicators to capture the value generated by hospital services, such as improving patients' quality of life, reducing complications and avoidable costs. Management accounting faces the challenge of defining and implementing these metrics in an accurate and relevant way.

Planning and budgeting: Planning and establishing adequate budgets are critical challenges in hospital management accounting. Hospitals face financial constraints and need to balance their revenues with operating costs. Management accounting plays a key role in projecting revenue, estimating costs and setting realistic financial goals. However, the challenge lies in accurately forecasting revenues while considering changes in reimbursement policies, fluctuations in demand for healthcare services, and other unpredictable external factors.

Addressing these challenges in hospital management accounting requires innovative approaches, advanced technologies, interdisciplinary collaboration and continuous improvement of accounting and financial processes. By overcoming these challenges, hospitals can improve operational efficiency, optimize resource allocation, and make more informed decisions to ensure long-term financial and operational sustainability.

2.1.3. Opportunities in Hospital Management Accounting

Use of advanced technologies: Hospital management accounting can benefit from the use of advanced technologies, such as integrated management systems, data analysis and process automation. These technologies allow the integration of data from different systems, real-time monitoring of accounting information and the generation of detailed reports. This facilitates access to accurate and updated information, making decision-making more informed and allowing for more efficient and results-oriented management.

Emphasis on value-based management: Hospital management accounting can adopt the value-based management approach, which seeks to evaluate and maximize the value generated by the health services provided. This approach emphasizes the relationship between the health outcomes achieved and the costs involved. By measuring and analyzing value in healthcare, management accounting can identify opportunities for improvement, optimize resource allocation and make strategic decisions based on relevant data. This contributes to improving the quality of services and maximizing results for patients and the hospital institution.

Partnerships and interdisciplinary collaboration: Hospital management accounting can benefit from collaboration with other healthcare professionals and areas of hospital management. The partnership between accountants, administrators, doctors, nurses and other professionals can provide a more comprehensive and integrated view of hospital management. This collaboration allows the sharing of knowledge, experiences and perspectives, enriching analysis and decision-making. Furthermore, interdisciplinary collaboration can facilitate the identification of opportunities for improvement, the implementation of effective measures and the promotion of more efficient and sustainable management.

By taking advantage of these opportunities in hospital management accounting, hospitals can improve their operational efficiency, allocate resources more strategically, measure and maximize healthcare value, and promote collaboration between professionals. This contributes to the financial and operational sustainability of hospitals, as well as the delivery of quality services to patients.

2.1.4. Strategies for the Sustainability of Hospital Management Accounting

Improving accounting data integrity and dependability: An important strategy for the sustainability of hospital management accounting is improving accounting data integrity and dependability. This involves implementing strict internal controls, periodic reviews of accounting processes, using advanced technologies to automate repetitive tasks and ensure data integrity. Furthermore, it is essential to establish clear recording and reporting standards, ensuring that all professionals involved have an adequate understanding of accounting practices.

Hospital administration training and professional development accounting: Investing in training and professional development in hospital management accounting is essential for the sustainability of this area. Professionals responsible for accounting must have a solid knowledge of financial and cost accounting, as well as an understanding of the peculiarities and challenges of the healthcare sector. Participation in specific training, courses and workshops can help update and improve professionals' skills, allowing them to perform their roles more efficiently and effectively.

Integration of information systems: The integration of information systems is a crucial strategy for the sustainability of hospital management accounting. This involves implementing a comprehensive and integrated hospital information system that allows real-time collection, storage and sharing of accounting data. Systems integration facilitates communication between different departments and areas of the hospital, avoiding redundancies, errors and rework. Furthermore, an integrated system provides a comprehensive and updated view of accounting information, contributing to more efficient and informed management.

Implementation of relevant performance indicators: Implementation of key performance indicators is fundamental to the sustainability of hospital management accounting. These indicators must be aligned with the hospital's strategic goals and reflect the financial, operational and quality aspects of services. Some examples of indicators may include cost per procedure, bed occupancy rate, patient satisfaction and operational efficiency indices. The definition and monitoring of these indicators allows for a continuous assessment of the hospital's performance, identifying areas for improvement and guiding decision-making.

Continuous assessment and monitoring: Continuous assessment and monitoring are fundamental strategies for the sustainability of hospital management accounting. This involves carrying out internal and external audits, periodic reviews of accounting processes, analysis of deviations and variations, in addition to regular monitoring of performance indicators. Continuous assessment and monitoring allow you to recognise possible problems and conduct remedial actions swiftly, ensuring the efficacy and dependability of accounting procedures.

By adopting these strategies, hospitals can strengthen the sustainability of management accounting, improving the quality of accounting data, training their professionals, integrating information systems, implementing relevant performance indicators and continuously monitoring accounting processes. This contributes to more efficient and informed management, allowing hospitals to face the challenges of the healthcare sector and achieve satisfactory financial and operational results.

3. Methodology

To carry out the Systematic Literature Review on the abovementioned issue. “Sustainability of Accounting in Hospital Management - A Systematic Literature Review”, we used a methodology based on previous research and scientific contributions. In this way, the 5-step methodology of Khan et al (2003) was our reference point for the implementation of this Systematic Literature Review, which in turn, consists of the following structure: (1) Identification of the issue/problem; (2) Sample determination (Identification of relevant works); (Research profile (Assessment of quality of studies (3) and Analysis/summary of evidence (4)); and (5) Interpretation/exposition of results.

3.1. Identifying the issue/problem

The present study addresses the importance of management accounting in the financial and operational sustainability of hospitals. The study highlights how management accounting is a crucial tool for monitoring, cost control, strategic decision-making, efficient resource allocation and performance assessment in the hospital environment.

The issue of sustainability in hospital management accounting is identified as a complex and critical topic, emphasizing the challenges faced by hospitals, such as the complexity of costs, integration of information systems and measurement of value in healthcare. These challenges can negatively impact the effectiveness of management accounting, compromising its ability to provide relevant and reliable information for decision-making.

The document proposes to explore these challenges and identify opportunities to overcome them, emphasizing the need for innovative approaches, the use of advanced technologies and interdisciplinary collaboration. The importance of facing these challenges is highlighted to strengthen the position of hospitals in the health sector, improve operational efficiency, optimize resource allocation and ensure the provision of quality services to patients.

In short, the central issue of the study is the need to sustain and improve hospital management accounting in the face of the challenges and complexities of the sector, with the aim of ensuring the efficiency, effectiveness and financial sustainability of hospitals.

3.2. Sample identification

Given that the study was completely exploratory in nature, we employed two scientific databases for this purpose: Web of Science and Scopus.

In both databases, we considered the following keywords: Financial Sustainability, Management Accounting, Sustainable Management, Cost Control and Hospitals. In the web of Science, we obtained 25 articles. From Scopus, we obtained 14 articles.

To process the information obtained through the Web of Science and Scopus databases, we use bibliometric analysis, applying statistical methods that allow us to analyze scientific performance through the number of citations, collaborations (co-authorship), specialties and research themes and knowledge flow patterns. Additionally, this method is also based on the transparency of data collection and the definition of document selection criteria. To carry out this analysis, we used the R-Studio software – package: Bibliometrix R (version 2023.09.0463, Boston, MA, USA). This procedure generates various matrices that are followed by the normalisation of similarity publications.

After integrating both databases into R-Studio, with a view to joining documents and eliminating duplicate articles, we obtained a representative sample of 37 articles.

3.3. Research profile (Study quality assessment (3) and Evidence analysis/summary (4))

Through the bibliometric analysis carried out, we obtained insights into the overall performance of authors in their research over the years, having evidence of the main publications each year, the trajectory of each author and their works published over time, emphasizing the central topics research and the countries where these studies were carried out. This analysis allows us to provide data on collaboration between institutions, authors and countries over the years. With this information, it is intended that this study contributes significantly to scientific research in these matters – Sustainability of accounting in Hospital Management.

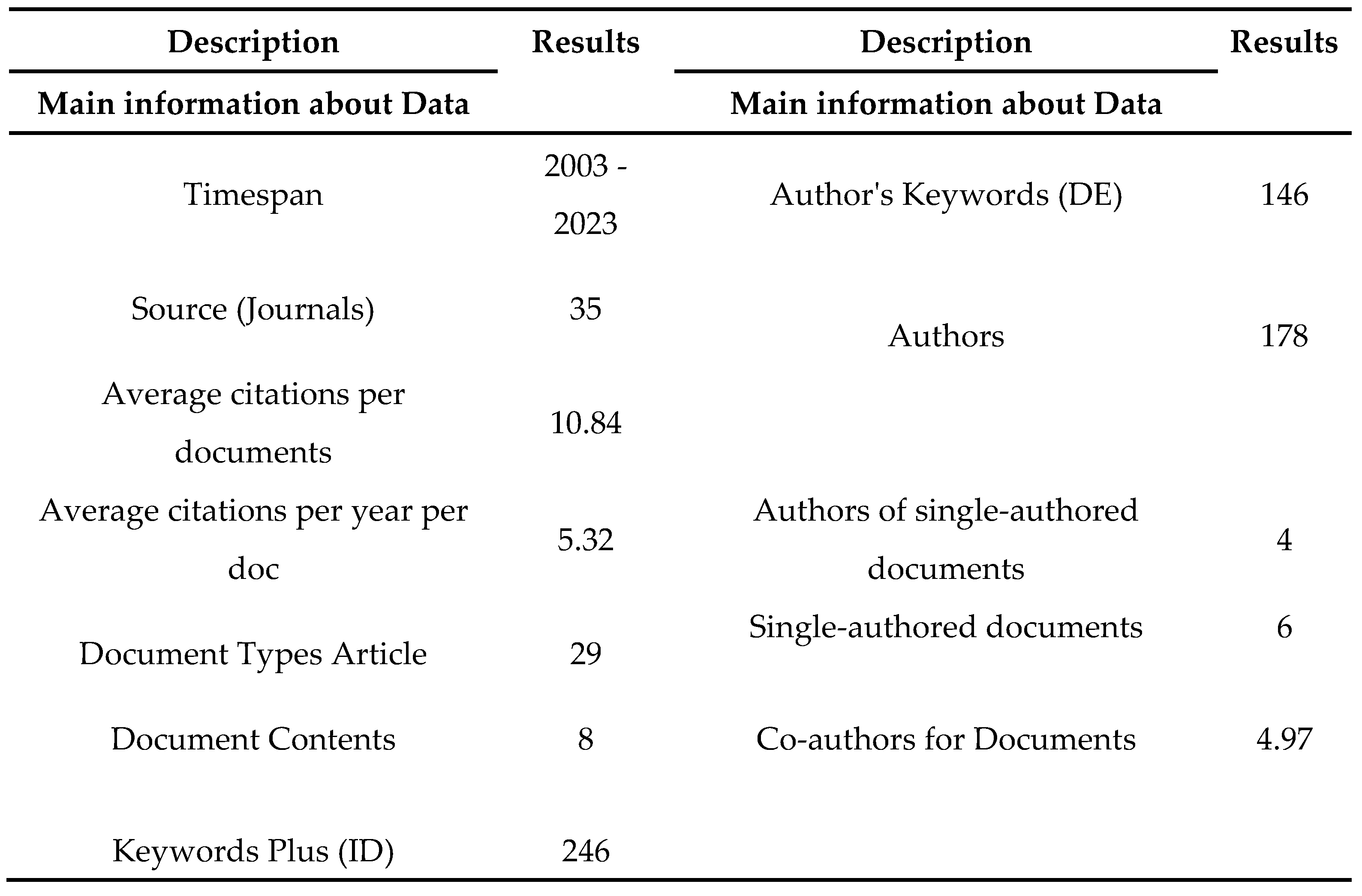

Figure 1 compiles a summary of the Web of Science and Scopus databases, in an integrated way and without duplications. This table offers a global view of recent scientific production. It is important to highlight that, during this period, scientific production included an average of 35 articles by 178 different authors, with an average of approximately 4.97 co-authorships per article.

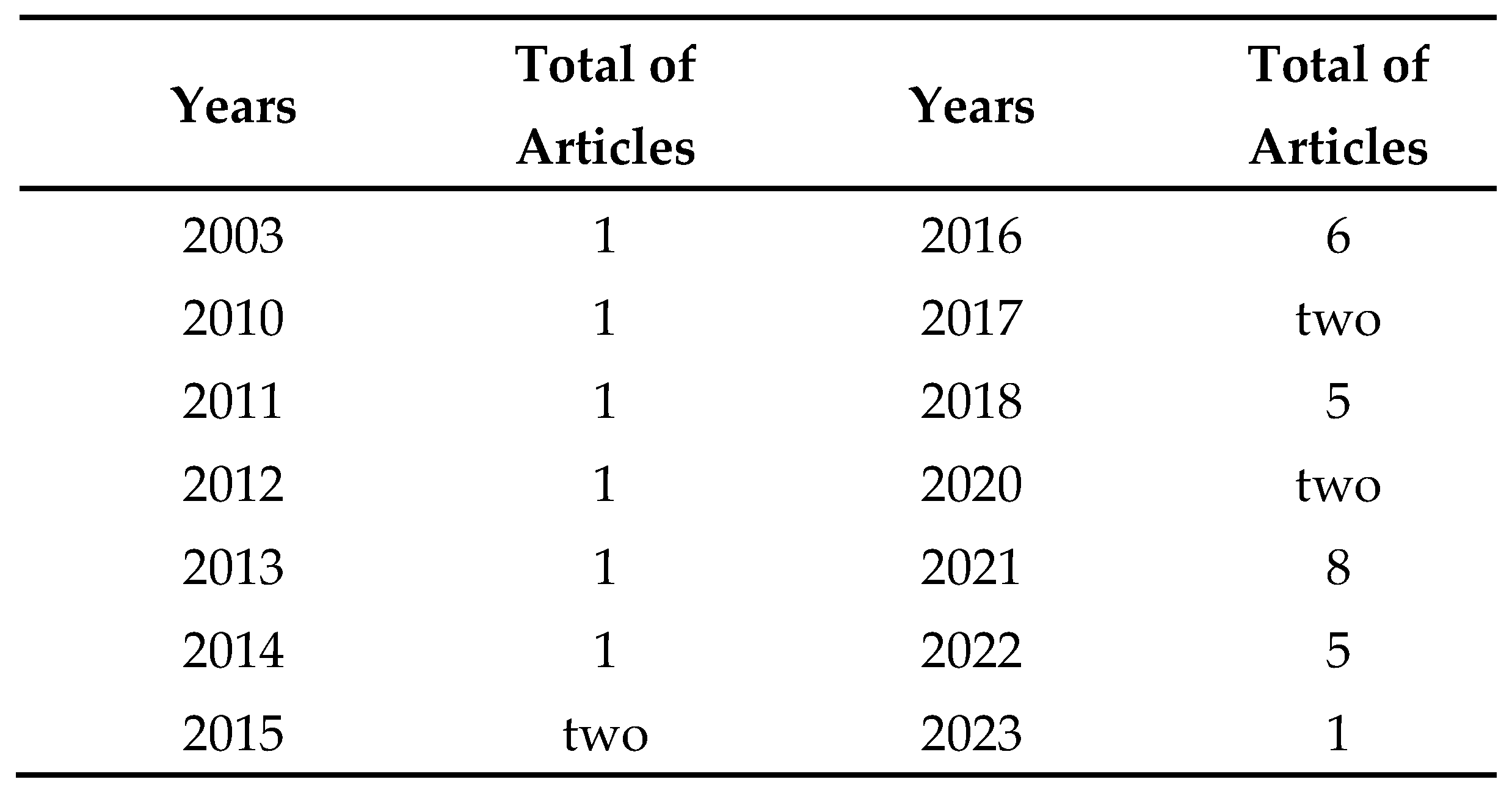

Figure 2 illustrates the progression of the sample that supports the systematic literature review.

Based on data from our sample, made up of 37 articles, it is observed that scientific research has focused on topics related to the Sustainability of Accounting in Hospital Management since 2003. There is a growing trend in the volume of investigations, with a peak in the last five years, namely in 2018 and 2021. However, in 2020, due to the COVID-19 pandemic, there was a reduction in investigations, which is understandable considering the exceptional circumstances of that year, especially in the health sector, which was the most affected. On the other hand, in 2021, there was a recovery with the publication of 8 articles, compared to just 2 in 2020. Other notable years were 2016 and 2018, with 6 articles each, and also 2019 with 15 articles, 2022 with 7 and 2022 with 5 articles. Although there has been significant progress over time, it is clear that the topic is still recent and has room for further development. This growth trend demonstrates the importance of overcoming the challenges faced by the health sector on a global scale, with the aim of promoting a quality life for the population.

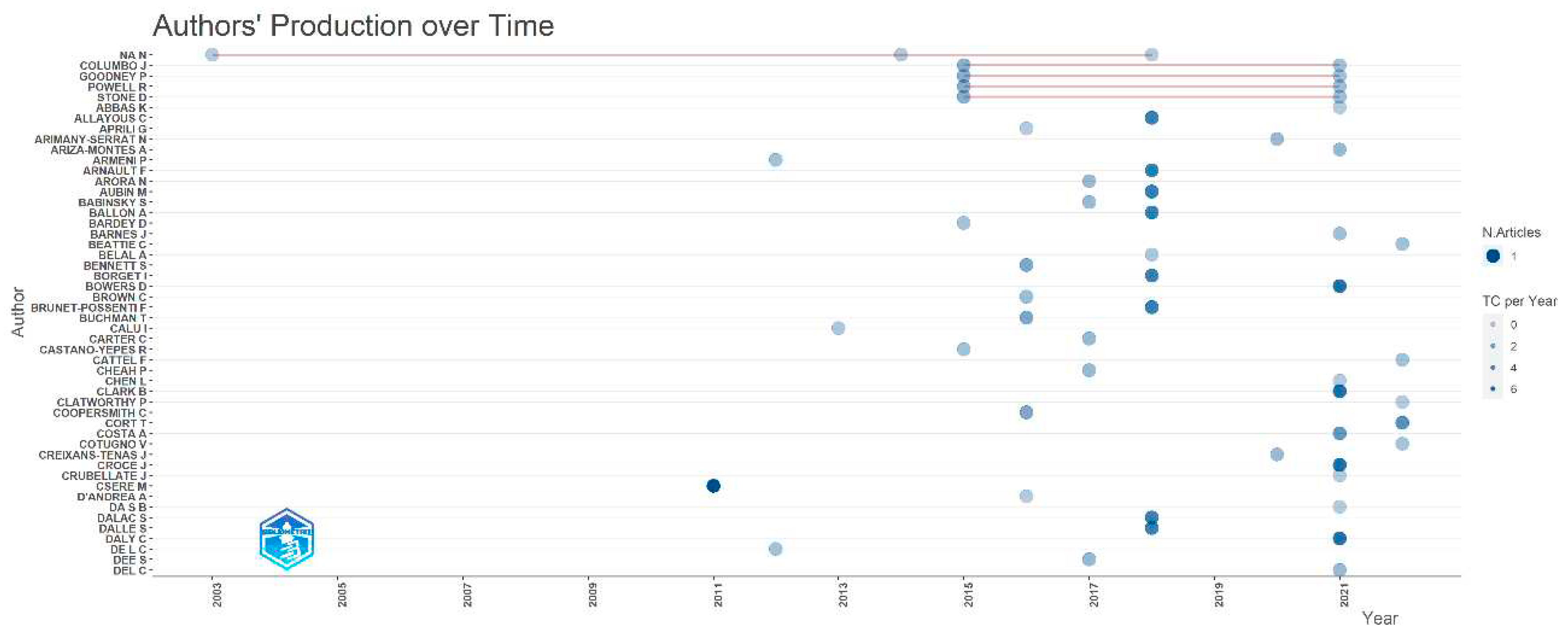

Figure 3 Authors Production over Time", shows the publication productivity of different authors over time. On the vertical axis, we have the list of authors, and on the horizontal axis, the years of publication, extending from approximately 2003 to after 2021.

Individual publications are represented by circles, with the size of the circle denoting the total number of citations (TC) each article received in that specific year, as evidenced by the legend "TC per Year".

At the top of the graph, we see that there is a line with multiple circles aligned horizontally, this means that an author has a significant number of articles published over the years, with each circle representing an article. The frequency of circles along the line indicates the consistency of publications over time.

The number of circles per author varies, with some authors having only one or two circles (indicating few publications) and others having several circles over several years, showing a longer publication history.

Another point identified was the evolution of the density of circles over the years, having been noticed essentially in more recent years, which indicates an increase in publication activity or in the author database over time. For authors who have larger circles, it means that their articles have been cited more.

It should be noted that this graph represents only a fraction of the authors in the main database (50 authors), so the trends observed in this analysis may not completely reflect the publication activity of the entire database. However, it offers insights into the production of the authors included in this study.

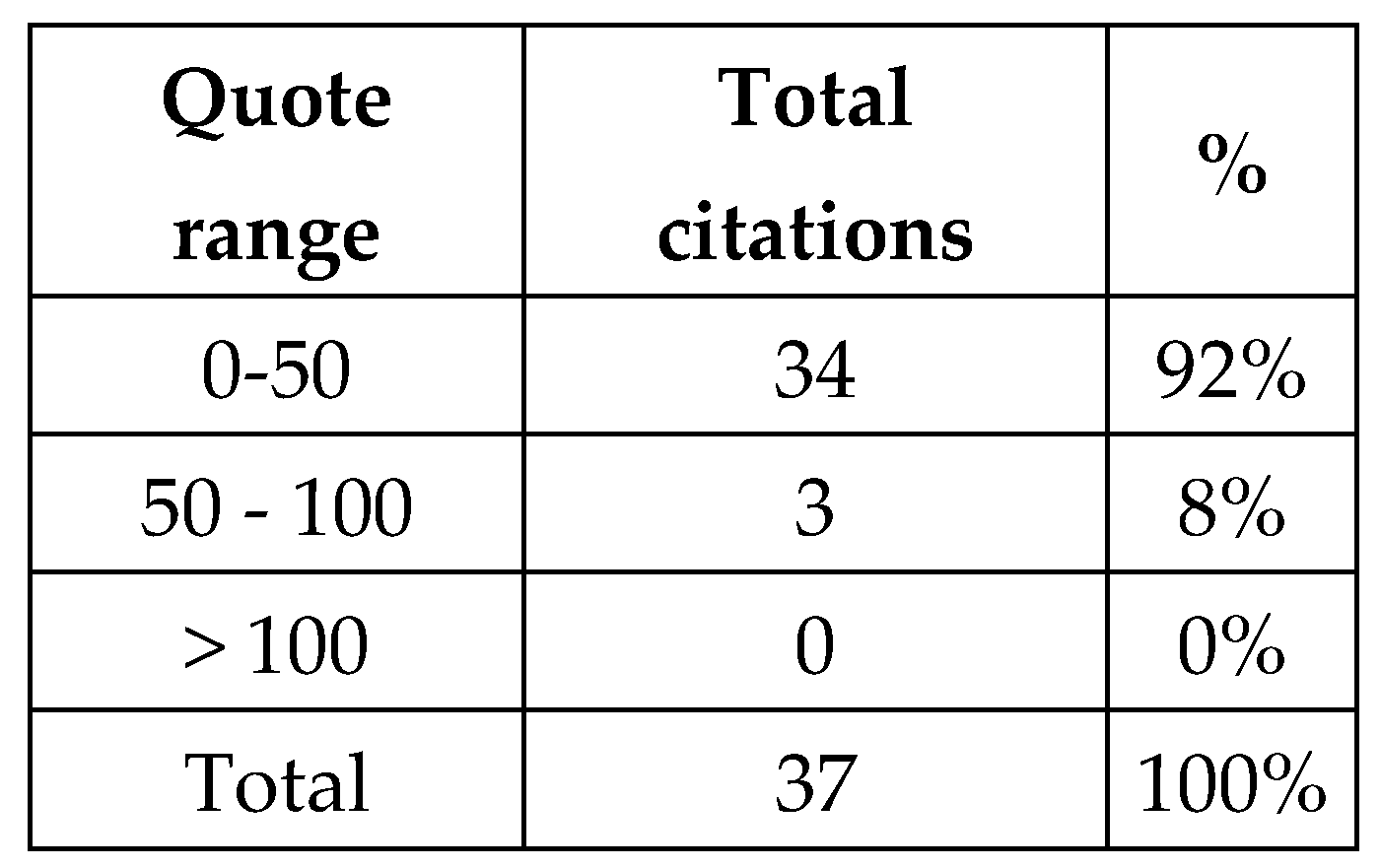

Based on our analysis of Figure 4, it was found that the articles included in our sample had, on average, 10.84 annual citations. It was found that approximately 95% of articles were cited between 0 and 50 times; 5% received between 50 and 100 citations and around 0% exceeded 100 citations. Notably, the most cited works are also the most recent equivalent to the last 5 years with publications from 2011 to 2023 receiving between 42 to 92 citations. This trend highlights the growing importance of exploring these matters and transposing them to the present, especially when we are faced with structurally inefficient systems, where the investigation of strategic methodologies must play a crucial role in the improvement and organizational success of these institutions.

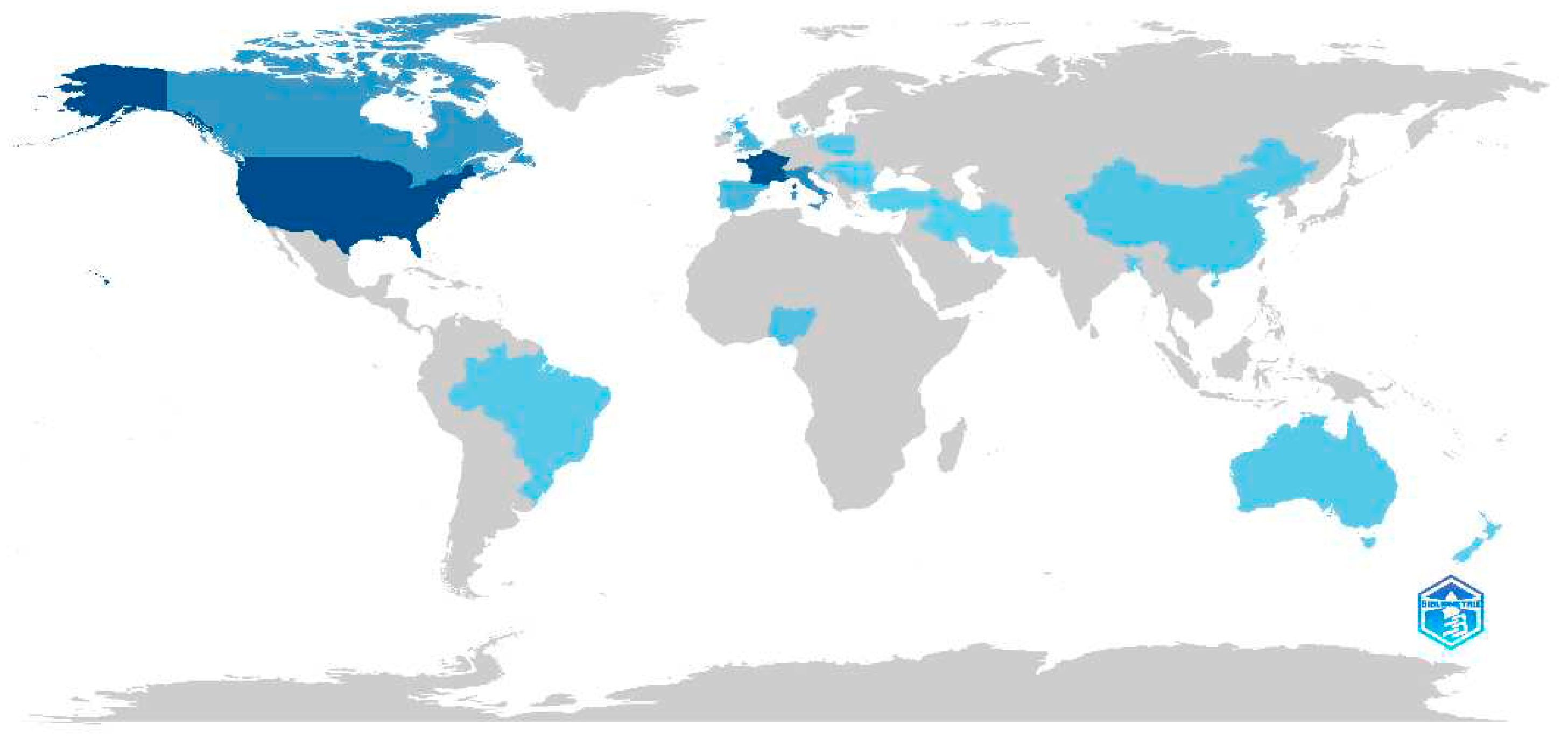

Figure 5 Country Scientific Production is a collopic map that shows scientific production by each country. The different shades of blue represented in each country indicate the level of scientific production, where darker tones suggest greater scientific production and lighter tones indicate lower scientific production.

In this sense, we see that the United States has a darker tone, which suggests that in relation to this topic they are the country with the greatest scientific production. We also found that other countries, such as Australia, Brazil, China, India and some in Europe (for example Italy), also show scientific production high regarding these themes, although less intense than in the United States.

3.4. Interpretation and presentation of results

In the context of interpreting and presenting the results, the article highlights the crucial role of the sustainability of hospital management accounting in the effective administration of hospitals. The study highlights the relevance of management accounting in terms of financial supervision, cost control, strategic decision-making, performance evaluation and financial planning.

The article also addresses the obstacles encountered in hospital management accounting, such as the complexity of hospital costs, the integration of information systems and the assessment of value in healthcare. To overcome such challenges, innovations, investments in technology and a collaborative effort between subjects are necessary.

At the same time, the study identifies opportunities for progress in hospital management accounting, emphasizing the use of advanced technologies, management focused on added value and interdisciplinary cooperation. The implementation of technologies such as integrated management systems and data analysis can increase efficiency and precision in hospital management. Furthermore, value-oriented management provides better assessment and optimization of costs in relation to health outcomes. Collaboration between accountants, administrators and healthcare professionals provides a more complete and unified perspective of hospital management.

In order to promote advances in hospital management accounting, it is imperative to deepen the accuracy and reliability of accounting data, encourage the professional development of those involved, integrate information systems, implement relevant performance indicators and cultivate a culture of continuous evaluation and monitoring.

In conclusion, the sustainability of hospital management accounting is fundamental to ensuring the operational efficiency and financial viability of hospitals, enabling them to provide informed and strategic management, in order to achieve continuous improvement and innovation in the area.

4. Conclusion

The sustainability of hospital management accounting plays a fundamental role in the efficient and effective management of hospitals. Throughout this article, we discuss the concepts and functions of hospital management accounting, highlighting its importance in financial monitoring, cost control, strategic decision making, performance evaluation and financial planning.

However, we also address the challenges faced in hospital management accounting, such as the complexity of hospital costs, the integration of information systems and the measurement of healthcare value. These challenges require innovative approaches, investments in technology and interdisciplinary collaboration to overcome them.

At the same time, we identify opportunities to advance hospital management accounting, such as the use of advanced technologies, a focus on value-based management and interdisciplinary collaboration. The adoption of advanced technologies, such as integrated management systems and data analytics, offers the opportunity to improve the efficiency and accuracy of hospital management accounting. Value-based management allows you to evaluate and optimize the relationship between health outcomes and the costs involved. Furthermore, interdisciplinary collaboration between accountants, administrators and healthcare professionals enables a more comprehensive and integrated view of hospital management.

To further advance in the area of hospital management accounting, it is necessary to invest in improving the accuracy and reliability of accounting data, promote the training and professional development of those involved, seek the integration of information systems, implement relevant performance indicators and establish a culture of continuous evaluation and monitoring.

In short, the sustainability of hospital management accounting is essential to guarantee the efficiency, effectiveness and financial sustainability of hospitals. By facing the challenges and taking advantage of the opportunities mentioned, hospitals will be prepared for more informed and strategic management, constantly seeking improvements and advances in the area of hospital management accounting.

5. Perspectives for future studies

From the start, and there is still much more to be discovered in this field. Because the United Nations produced the 2030 Agenda for Sustainable Development, the following subjects are still being researched. Let us go over some examples:

- Public-sector sustainability reporting framework development: Investigate and create public-sector sustainability reporting frameworks, taking into account the characteristics and peculiarities of this sector, to provide comprehensive information on social, environmental and economic dimensions

- Assessment of the quality and relevance of public sustainability reports sector: Investigate the quality of sustainability reports produced by public sector entities, considering the reliability, transparency, integrity and relevance of the information presented.

- Evaluation of the influence of sustainability reports in government: Analyze the impact of sustainability reports on decision-making, accountability to society and management practices of public sector entities, identifying changes and improvements resulting from these reports.

- Comparative analysis of public sector sustainability reporting methods: Carry out comparative studies between different public sector entities, at local, regional and national levels, to identify good practices and sustainability reporting standards, seeking to understand the differences and similarities between approaches adopted.

- Development of specific sustainability indicators for the public sector: Develop sustainable performance indicators that are relevant and appropriate for the public sector, considering the particularities of the activities and responsibilities of this sector, allowing a more accurate and comprehensive assessment of sustainable performance.

- Integration of environmental cost accounting in the public sector: Investigate ways to integrate environmental cost accounting into public sector accounting practices, allowing the measurement and monitoring of costs associated with the environmental impacts of government activities.

- Analysis of barriers and challenges in implementing accounting, reporting and sustainability reporting in the public sector: Identify the main barriers and challenges faced by public sector entities in implementing accounting practices and sustainability reporting, such as lack of resources, organizational resistance and knowledge gaps.

- Assessing stakeholders' Role in Accounting, accountability and sustainability reporting in the public sector: Analyze the involvement and influence of stakeholders, such as citizens, local communities, civil society organizations and regulatory bodies, in accounting, accountability and sustainability reporting in the public sector.

- Impact of legislation and regulation on environmental accounting and reporting in the public sector: Investigate the impact of laws and regulations related to sustainability accounting and reporting in the public sector, considering how these policies influence accountability and transparency practices.

- Explore the use of modern technologies in public sector sustainability accounting and reporting: Investigate the potential and benefits of leveraging technologies such as artificial intelligence, big data, and blockchain in public sector sustainability accounting and reporting, with the goal of improving information accuracy, efficiency, and reliability.

The theme of this article expanded accounting, accountability, and sustainability reporting in the public sector literature. The articles in this special issue provide an excellent starting point for the growing need for context-specific studies that provide more information about accounting, accountability, and sustainability reporting in the public sector.

6. Study limitations

The constraints identified in hospital management accounting, according to the document, include:

- Complexity of Hospital Costs: Hospitals deal with a variety of costs, such as medical supplies, salaries, advanced medical technology, and medications. These costs vary between departments and services, and management accounting faces the challenge of capturing, tracking and allocating these costs accurately and reliably.

- Integration of Information Systems: Hospitals often have fragmented and unintegrated information systems. This creates difficulties in obtaining consistent and updated data, in addition to creating gaps in communication and difficulties in effectively analyzing and monitoring financial and operational data.

- Measuring Value in Health: Assessing value in health is complex and involves measuring the results achieved by health services and their relationship with costs. Developing appropriate metrics and indicators to capture the value generated by hospital services is a significant challenge.

- Planning and Budgeting: Hospitals face the challenge of balancing revenues with operating costs under financial constraints. Management accounting is critical in projecting revenue, estimating costs, and setting realistic financial goals, but it is challenging to accurately forecast revenue considering changes in reimbursement policies, fluctuations in demand for healthcare services, and other unpredictable external factors.

To overcome these challenges, innovative approaches, advanced technologies, interdisciplinary collaboration and continuous improvement of accounting and financial processes are required.

Author Contributions

We certify that we have participated and contributed sufficiently for the completion of the manuscript and have agreed to have our name listed as a contributor. We believe that the manuscript represents valid and credible work. Neither the content of this manuscript nor any other unified content with substantially similar or comparable substance under our creation or authority has been considered for publication elsewhere. We certify that complete data regarding the study is proclaimed in this manuscript and no data from the study has been published solely or separately. we attest that, we will cooperate in providing any required information related to the study during peer review by the editor or their assignees. Any direct or indirect financial interests or conflicts that exist or may be perceived to exist have been disclosed in the cover letter. Sources of external support for this work are mentioned in the cover letter. All persons who have made substantial and significant contributions to this work, but are not contributors, are mentioned in the acknowledgment with the written permission of the contributors to include their name. If there is no acknowledgment part in the manuscript, that means we have not received any contributions and also, no contributor has been omitted.

Declaration of interests

The authors declare that we have no known competing financial interests or personal relationships that could have appeared to influence the work reported in this paper. The authors declare the following financial interests/personal relationships which may be considered as potential competing interests: Paula Cristina de Almeida Marques reports a relationship with PhD student of Universidade do Minho, Portugal that includes board membership. Paulo Alexandre Teixeira Faria Pereira de Oliveira reports a relationship with PhD student of Universidade do Minho, Portugal that includes board membership. Sofia Nair Meneses Pacheco Barbosa reports a relationship with PhD student of Universidade Portucalense Infante D. Henrique, Portugal that includes Financial Auditor.

References

- Andrades, J. and Larrán-Jorge, M. (2019), “Examination of the amount of mandatory non-financial contributions information disclosed by Spanish state-owned companies and their potential variables.

- influential”, Meditari Pesquisa Contábil.

- Argento, D. Grossi, G. Persson, K. and Vingren, T. (2019), “Explaining sustainability disclosures of hybrid organizations: the case of Swedish state-owned companies”, Meditari Pesquisa Contábil. 502.

- Ball, A. (2002), “Sustainability accounting in UK local government, an agenda for research”, CCA Research Report, No. 78, Association of Chartered Certified Accountants, London.

- Ball, A. (2004), “A sustainability accounting project for the UK local government sector? testing the.

- process of mapping social theory and locating a frame of reference”. Critical Perspectives on Accounting, Vol. 15 No. 8, pp. 1009-1035.

- Che-Ku-Kassim, CKH, Ahmad, S., Mohd-Nasir, NE, Wan-Mohd-Nori, WMN and Mod Arifin, NN (2019), “Environmental Reporting by Malaysian Local Governments”, Meditari Accounting Research.

- Decree-Law no. 284, of 26th July 1999, published in Official Gazette no. 172, series 1-A.

- Drury, C. (2013). Management and cost accounting. Cengage Learning.

- Farneti, F. and Guthrie, J. (2009), “Sustainability reporting by Australian public sector organizations: why they blow the whistle”, Accounting Forum, Vol. 33 No. 2, pp. 89-98.

- Farneti, F. Casonato, F. Montecalvo, M. and de Villiers, C. (2019a), “The influence of integrating reporting and information needs of stakeholders on the disclosure of social information in a state-owned company”, Meditari Pesquisa Contábil.

- Farneti, F. Guthrie, J. and Canetto, M. (2019b), “Social reporting of an Italian provincial government: a longitudinal analysis”, Meditari Pesquisa Contábil.

- Gibson, R. and Guthrie, J. (1995), “Recent environmental disclosures in annual reports of Australian public and private sector organisations”, Accounting Forum, Vol. 19 Nos. 2/3, p. 111127.

- Goswami, K. and Lodhia, S. (2014), “Sustainability disclosure standards of South Australian local councils: a case study”, Public Money and Management, Vol. 34 No. 4, pp. 273-280.

- GRI (2004), Public Agency Sustainability Reporting: A GRI Resource Document in Support of the Public Agency Sector Supplement, Global Reporting Initiative, Amsterdam.

- GRI (2005), Sector Supplement for Public Bodies, Global Reporting Initiative, Amsterdam.

- GRI FPA (2012), Integrating Sustainability into Reporting - An Australian Public Sector Perspective, GRI Focal Point Australia (FPA), Sydney.

- Guthrie, J. and Farneti, F. (2008), “GRI sustainability report of Australian public sector organizations”, Public Money and Management, Vol. 28 No. 6, pp. 361-366.

- Hansen, D. R. , & Mowen, M. M. (2018). Cost management: Accounting and control. Cengage Learning.

- Hopwood, B. , Mellor, M. and O'Brien, G. (2005), “Sustainable development: mapping different approaches”, Sustainable Development, Vol. 13 No. 1, pp. 38-52.

- Hoque, Z. and Adams, C. (2008), Measuring Public Sector Performance: A Study of Government Departments in Australia, CPA Australia, Melbourne.

- Ibrahimi, M. and Naym, S. (2019), “The contingency of performance measurement systems in Moroccan institutions and public companies”, Management Accounting Research.

- Kaplan, R. S. , & Norton, D. P. (1992). The balanced scorecard: Measures that drive performance. Harvard Business Review, 70(1), 71-79.

- Kaur, A. and Lodhia, S. (2014), “The state of disclosures about stakeholder engagement in sustainability reporting in Australian local councils”, Pacific Accounting Review, Vol. 26 Nos. 1/2, pp. 54-74.

- Kaur, A. and Lodhia, S. (2016), “Influences on stakeholder engagement in sustainability accounting and reporting: a study of Australian local councils”, Corporate Responsibility and Stakeholders, Emerald Group Publishing, Bingley, pp. 105-129.

- Kaur, A. and Lodhia, S. (2017), “The extent of stakeholder involvement in sustainability accounting and reporting: Does stakeholder empowerment really exist?”, Organizational Governance. Moderna, Emerald Publishing, Bingley, pp. 129-145.

- Kaur, A. and Lodhia, S. (2018), “Stakeholder engagement in sustainability accounting and reporting: a study of Australian local councils”, Journal of Accounting, Auditing and Accountability, Vol. 31 No. 1, pp. 338-368.

- Kaur, A. and Lodhia, S. (2019), “Key issues and challenges in stakeholder engagement in sustainability reporting: a study of Australian local councils”, Pacific Accounting Review, Vol. 31 No. 1, pp. 2-18.

- Khalid, S. Beattie, C. Sands, J. and Hampson, B. (2019), “Incorporating the environmental dimension into the Balanced Scorecard: a case study in the healthcare area”, Meditari Pesquisa Contábil.

- Leeson, R. , Ivers, J. and Dickinson, D. (2005), “Public sector sustainability reporting: driving changes in practice, acceptance and reporting by public bodies”, Accountability Forum, Vol. 8 No. 12 /21.

- Lodhia, S. , Jacobs, K. and Park, Y.J. (2012), “Conducting public sector environmental reporting: the disclosure practices of Australian community departments”, Public Management Review, Vol. 14 No. 5, pp. 631-647.

- Lodhia, S. and Jacobs, K. (2013), “The practice turn in environmental reporting: a study of practices in two Australian Commonwealth departments”, Journal of Accounting, Auditing and Accountability, Vol. 26 No. 4, pp. 595-615.

- Lodhia, S. (2018), “Is the medium the message? Advancing the research agenda on the role of the media in sustainability reporting”, Meditari Pesquisa Contábil, Vol. 26 No. 1, pp. 2-12.

- Marcuccio, M. and Steccolini, I. (2005), “Social and environmental reporting in local authorities: a new Italian fashion?”, Public Management Review, Vol. 7 No. 2, pp. 155-176.

- Mussari, R. and Monfardini, P. (2010), “Social accounting practices in the public sector and non-profit organizations: an Italian perspective”, Public Management Review, Vol. 12 nº 4, p. 487492.

- Qian, W. , Burritt, R. and Monroe, G. (2011), “Environmental management accounting in local government: a waste management case”, Journal of Accounting, Auditing and Accountability, Vol. 24 No. 1, pp. 93-128.

- United Nations (UN) (2015), Transforming Our World: The 2030 Agenda for Sustainable Development, United Nations, New York, NY.

- Porter, M. E. (2010). What is value in health care? New England Journal of Medicine, 363(26), 2477-2481.

- Williams, B. , Wilmshurst, T. and Clift, R. (2011), “Sustainability reporting by local government in Australia: current and future perspectives”, Accounting Forum, Vol. 35 No. 3, pp. 176-186.

- Williams, BR (2015), “Reporting on sustainability by Australian boards – a communication perspective”, Asian Accounting Review, Vol. 23 No. 2, pp. 186-203.

- Trotta, P. (2016). Implementing strategic management accounting in hospitals: A case study. International Journal of Business and Management, 11(10), 43-51.

Figure 1.

Database description.

Figure 2.

Annual publication of the source article (Accounting Sustainability in Hospital Management).

Figure 2.

Annual publication of the source article (Accounting Sustainability in Hospital Management).

Figure 3.

Authors production over Time.

Figure 4.

Quote Range.

Figure 5.

- Countries Collaboration World Map.

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Copyright: This open access article is published under a Creative Commons CC BY 4.0 license, which permit the free download, distribution, and reuse, provided that the author and preprint are cited in any reuse.