Submitted:

30 January 2024

Posted:

31 January 2024

You are already at the latest version

Abstract

Numerous researchers acknowledge that occupational pension protects employees. However, the total occupational pension is shared by employees and employers in China, which is a cost. This study aimed to explore the occupational pension on corporate social responsibility (CSR) and organizational resilience. We drew upon insights from cost-stickiness and resource-based theories to develop a model that illuminates how occupational pension affected firms’ stance toward CSR in the context of the COVID-19 pandemic and how this, in turn, has result organizational resilience. This study categorized CSR into strategic and responsive activities based on cost stickiness. We selected a total of 34,145 observations of Chinese listed companies over the period 2010-2023 as a sample to investigate whether occupational pension changes CSR strategies. The results showed that the cost pressure to contribute to occupational pension drove firms to reduce their responsive CSR and boost their strategic CSR. Moreover, strategic CSR improved organizational resilience, but responsive CSR did not. This relationship between occupational pension and CSR was significantly and negatively moderated by the minimum wage and population aging. Whereas, the relationship between CSR and organizational resilience was significantly and positively moderated by digital transformation and marketing capabilities. This study has implications for decision-making regarding high-quality firm development.

Keywords:

pension insurance

; organizational resilience

; digital transformation

; aging population

; minimum wage

; marketing capability

1. Introduction

Occupational pension is a crucial labor protection system in many countries. In 1984, China introduced an enterprise pension system to partially provide retirement benefits to enterprise workers (Zheng, Lyu, Jia, Hanewald, & Finance, 2023). The occupational pension system became mandatory nationwide in 2011 with the introduction of the Social Security Law in 2010 (Shan & Park, 2023). Under the Social Security Law, both employers and employees are responsible for paying basic occupational pension premiums (H. Wang, Huang, & policy, 2023). As society grows, pension premiums continue to increase, so the cost to the business continues to rise (J. Hu, Stauvermann, Nepal, Zhou, & Health, 2023; H. Wang et al., 2023; Jin Wang, Wang, Long, & Chen, 2023). These cost shocks costs have affected enterprise behavior and investment decisions in various ways, such as increasing tax avoidance (Campbell, Goldman, & Li, 2021), reducing outward investment (Duckett & Change, 2020), inhibiting innovation (W. Gao, Chen, Xu, Lyulyov, & Pimonenko, 2023), and influencing strategic corporate decisions (Agarwal, Pan, & Qian, 2020; Wahyudi, Hasanudin, & Pangestutia, 2020).

Will firms cut or maintain their corporate social responsibility (CSR) investments amid rising pension premiums? Theoretical analyses of the possible mechanisms involved still leave the answer uncertain. CSR refers to the activities of enterprises that incorporate social and environmental issues into their operations and interactions with stakeholders (Van Marrewijk, 2003). According to Porter and Kramer’s (2006) framework for CSR decision-making, CSR can be divided into two categories: responsive and strategic (M. E. Porter & M. R. J. H. b. r. Kramer, 2006). Responsive CSR aims to improve short-term stakeholder relationships and is often viewed as a symbolic impression management activity (Michael E. Porter & Mark R. Kramer, 2006), or short-term investment separate from the organization’s core business (Bansal, Jiang, & Jung, 2015; Muller & Kräussl, 2011). Strategic CSR is an investment with limited short-term returns and requires long-term planning, significant resource investment, and major organizational restructuring (Bansal et al., 2015; Habib & Hasan, 2016; Kang, 2016).

When firms face cost shocks, they must weigh the costs of adjusting CSR, including economic losses (Ibrahim, Ali, Aboelkheir, & Taxation, 2022) and social, contractual, or psychological costs (Costa & Habib, 2023), as well as the loss of intangible assets such as reputational capital (Ibrahim et al., 2022). This understanding is based on cost stickiness theory (Habib & Hasan, 2016; Venieris, Naoum, & Vlismas, 2015). Cost-stickiness theory suggests that certain costs are sticky and increase more with a firm’s business volume rather than decrease when business volume falls asymmetrically (Anderson, Banker, & Janakiraman, 2003; Venieris et al., 2015). Several studies have shown that CSR is a long-term investment with limited short-term returns (Habib & Hasan, 2016; Kang, 2016). The value-creating effect of CSR can only be realized through sustained investment (Habib & Hasan, 2016; Kang, 2016). If firms respond to the labor cost shock of rising occupational pension costs by reducing CSR expenses or adjusting CSR inputs, they will also face higher adjustment costs, which may force them to abandon CSR altogether (Habib & Hasan, 2016; Venieris et al., 2015).

Besides exploring the mechanisms of firms’ adjustment to CSR based on the cost stickiness theory, this study introduces the resource base theory to illustrate how CSR affects organizational resilience. In the wake of the COVID-19 pandemic, organizational resilience has emerged as a critical factor in ensuring sustainable business operations, environmental adaptability, and quality development (Kantur & Say, 2015). The level of organizational resilience indicates how well firms cope with and adapt to turbulent environments (Guo, Kuai, & Liu, 2020; Jiang, Ritchie, & Verreynne, 2019). However, few studies have analyzed the impact of CSR from the perspective of organizational resilience (Torres & Augusto, 2021). Resource-based theory was first proposed by Wernerfelt (1984), who argued that scarce resources acquired by firms can help them improve their competitiveness and performance (Wernerfelt, 1984). Studies have shown that corporate investment in social responsibility leads to more effective advice and greater acquisition of scarce resources for stakeholders (Freeman, Dmytriyev, & Phillips, 2021). This study applied resource-based theory to analyze the impact of CSR on organizational resilience from the perspective of resource acquisition as well as applying insights drawn from stakeholder theory and signaling theory in the analysis.

Additionally, we assessed the moderating role of the macro-social development level. According to China’s fifth national census (2000), the proportion of the population aged 65 years and above at that time was approximately 7%, making China an aging country (Bai & Lei, 2020). As the number and proportion of the aging population increase, the dwindling labor supply poses a long-term threat to business development (Clemens, 2021; Jarzebski et al., 2021). Similar to occupational pension, the minimum wage system plays a role in safeguarding the basic living standards of those on low incomes and in improving income distribution. However, a significant increase in the minimum wage can also result in a labor cost shock (Clemens, 2021).

The moderating role of a firm’s strategic level was also assessed. Digital transformation is driving Chinese enterprises to upgrade to artificial intelligence and informatization, which is likely to significantly improve productivity through the efficient transmission of information and optimal allocation of resources (H. Li, Yang, Jin, & Wang, 2023). This study considered marketing capability as an important indicator for improving enterprise efficiency in acquiring resources (Mishra & Modi, 2016).

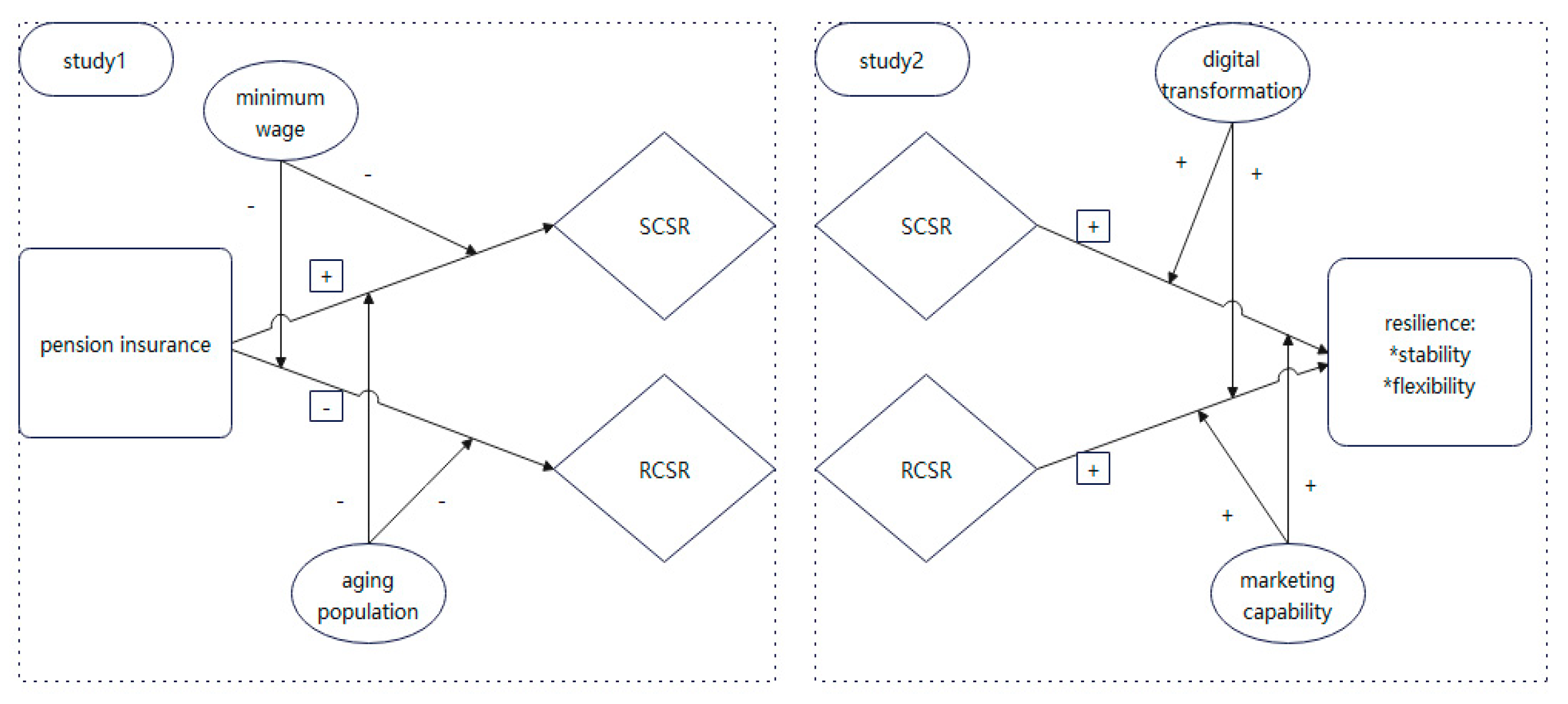

Current research has focused primarily on the positive effects of occupational pension on society and the labor force, while neglecting its cost to firms. Our empirical investigation, which involved Chinese A-share listed firms from 2010 to 2023, aimed to reveal the relationship between occupational pension, CSR, and organizational resilience. The findings of this study are intended to aid policymakers in comprehending and evaluating the extent of the impact of the occupational pension system in China. Additionally, they can help inform corporate managers in relation to more effective strategic decision-making when faced with labor cost shocks. Figure 1 illustrates the theoretical framework of the study.

Description: Study 1 shows that occupational pension increased strategic CSR and decreased responsive CSR. Study 2 showed that strategic and responsive CSR increased organizational resilience.

2. Theory and hypothesis development

2.1. Occupational pension, strategic and responsive CSR

There is a significant contrast between strategic and responsive CSR strategies in terms of cost stickiness (Habib, Hasan, & Research, 2016). Strategic CSR integrates social responsibility with corporate strategies, resources, capabilities, processes, business models, and stakeholder interactions (M. E. Porter & M. R. J. H. b. r. Kramer, 2006). This approach requires long-term planning, significant investments in resources, and major organizational restructuring, particularly in areas such as product and customer responsibilities (Bansal et al., 2015). Therefore, the cost of maintaining strategic CSR activities is significant. Consequently, cutting strategic CSR in response to labor cost shocks from pension premiums can lead to economic losses, social costs, contractual or psychological costs, and losses of intangible assets, such as reputational capital (Y. Chen, Guiping, & Gao, 2023; Habib & Hasan, 2016; Venieris et al., 2015).

Responsive CSR aims to improve stakeholder relations and meet stakeholder demands in the short term, aligned with established norms, expectations, and practices to build legitimacy and gain resource support (M. E. Porter & M. R. J. H. b. r. Kramer, 2006). Some have viewed responsive CSR as a token impression management activity or a short-term investment separate from the organization’s core business (Bansal et al., 2015; Muller & Kräussl, 2011). In China, responsive CSR includes exercising community responsibility through charitable donations and environmental responsibility through environmental protection inputs (Tao & Song, 2020). According to the over-investment hypothesis of agency theory, charitable giving may be viewed as agency behavior that reflects management self-interest. CEOs may be inclined to over-invest in charitable giving, which can negatively affect the interests of shareholders and the overall value of the firm. This over-investment can even become a significant economic burden, constraining firm growth (Barnea & Rubin, 2010; Friedman, 1970). Responsive CSR is a reversible short-term investment that requires fewer resources, incurs lower adjustment costs, and is less susceptible to stickiness. Therefore, we argue that firms can quickly adjust or reduce responsive CSRs when faced with labor cost shocks from pensions (Buslei, Geyer, & Haan, 2023; Jin Wang et al., 2023).

Based on the above analysis, we formulated the following hypotheses:

Hypothesis 1a: Due to high cost stickiness, firms will maintain strategic CSR when facing labor cost shocks from occupational pension.

Hypothesis 1b: Due to low cost stickiness, firms will cut responsive CSR when facing labor cost shocks from occupational pension.

2.2. Strategic, responsive CSR and organizational resilience

Meyer (1982) coined the term ‘organizational resilience’ to describe an organization’s ability to respond to disturbances and restore the previous order (Meyer, 1982). Scholars have summarized the concept of organizational resilience in terms of ability or process. Organizational resilience refers to the dynamic and flexible ability of an organization to combine prediction, stability maintenance, survival, endurance, adaptation, learning, and developmental abilities (Carvalho & Areal, 2016; Ma, Su, Wang, Qiu, & Guo, 2018).

Previous studies have shown the complexity of the factors that influence organizational resilience (Andersson, Cäker, Tengblad, & Wickelgren, 2019). This study primarily examined the mechanisms of organizational resilience from three perspectives: individual, organizational, and environmental. Individual factors influencing resilience include knowledge acquisition, skill training, and ability improvement (Williams, Gruber, Sutcliffe, Shepherd, & Zhao, 2017). In addition, creativity (Manfield & Newey, 2017), employee psychological capital (Linnenluecke, 2017), and leadership (de Oliveira Teixeira & Werther Jr, 2013) are important factors. At the organizational level, the factors with the greatest influence include managing organizational relationships (Kahn et al., 2018) and transferring information within an organization (Bustinza, Vendrell-Herrero, Perez-Arostegui, & Parry, 2019). According to Kahn et al. (2018), based on intergroup relationship theory, when a department is under external pressure, neighboring departments may use approaches such as assistance, adaptation, and integration to enhance the resilience of the department (Y. Gao & Gao, 2023; Jin, Zhang, Ye, Yao, & Song, 2024; G. Liu, Liu, Zhang, Zhu, & Organization, 2021).

Effective communication and engagement with stakeholders can improve a firm’s ability to adapt to environmental changes and reduce negative impacts (M. DesJardine, P. Bansal, & Y. Yang, 2019a; Kahn et al., 2018). By improving communication and contact with stakeholders, firms that actively engage in social responsibility activities can enhance their ability to adapt to environmental changes and reduce negative impacts caused by such changes (M. DesJardine et al., 2019a). However, few studies have examined the factors influencing firms’ organizational resilience during crises, particularly during the COVID-19 pandemic. Furthermore, in the Chinese context, it is necessary to enhance the exploration of socially responsible investments to improve organizational resilience (Lu, Yang, & Yu, 2022; M. Sajko, C. Boone, & T. Buyl, 2021a).

2.2.1. The impact of strategic CSR on organizational resilience

Strategic CSR focuses on stakeholders, such as employees, consumers, and suppliers, who are closely linked to a firm’s development, competition, and strategic changes (Pollman, 2019). For example, employee responsibility can foster loyalty, solidarity, and a positive corporate culture, which can help firms withstand shocks and overcome challenges (Crane & Matten, 2020; Fukuda & Ouchida, 2020; Pollman, 2019). By fulfilling product and consumer responsibilities, firms can develop high-quality products, build an excellent brand image, maintain and attract high-quality customers, and enhance their overall social image (Huang, Chen, & Nguyen, 2020; Michael E Porter & Mark R Kramer, 2006).

According to resource-based theory, firms can improve their competitiveness and prevent crises by integrating resources (Yang, Wang, Jing, Liu, & Niu, 2022). Following understandings derived from resource-based theory and stakeholder theory, firms can effectively strengthen the connection between themselves and strategic stakeholders such as employees, consumers, and suppliers by enhancing their strategic CSR, which will enable them to acquire scarce strategic resources more readily (Yang et al., 2022). Specifically, investing in CSR strengthens the connections between firms and strategic stakeholders, which will enable such firms to obtain scarce resources that are closely related to their core business, thus strengthening their defensive capabilities in the face of crises and enhancing their stability and flexibility (M. DesJardine et al., 2019a; Sajko et al., 2021a; Wieczorek-Kosmala, 2022).

The transmission mechanism of market signals was severely comprised during the COVID-19 pandemic, leading to increased information asymmetry and opacity (S. Li, Wang, Filieri, & Zhu, 2022; Polyzos, Fotiadis, & Samitas, 2021). According to signaling theory, firms can use CSR investments to communicate their stable and positive states to stakeholders, which is likely to increase stakeholder support and investment confidence in such firms, as well as enhance firms’ ability to withstand changes in the external environment (Bebchuk & Fried, 2003; M. R. DesJardine, Marti, & Durand, 2021; Fama, 1980; S. Li et al., 2022; Polyzos et al., 2021). Following understandings derived from signal and stakeholder theories, firms can release strategic CSR-related information to dispel stakeholder doubts and strengthen connections among employees, consumers, suppliers, and other stakeholders (M. R. DesJardine et al., 2021; S. Li et al., 2022).

Based on the above analysis, we proposed the following hypothesis:

Hypothesis 2a: Strategic CSR improves organizational resilience.

2.2.2. The impact of responsive CSR on organizational resilience

According to stakeholder theory, governments and communities are important for CSR as responsive stakeholders (Michael E Porter & Mark R Kramer, 2006). Exercising environmental responsibility is mandatory in China (Elhendy, Tsutsui, O’Leary, Xie, & Porter, 2006; Michael E Porter & Mark R Kramer, 2006). However, this has not been consistently applied in relation to enterprises’ core business and strategic objectives because environmental responsibility has a shorter investment cycle and is more reversible than strategic CSR (Elhendy et al., 2006; Guo et al., 2020; Michael E Porter & Mark R Kramer, 2006). Community responsibility refers to the responsibilities and tasks that enterprises should undertake to maintain public safety and to help realize the public interests of community residents (Jianjun Zhang, Marquis, & Qiao, 2016). In China, autonomous organizations such as neighborhood and village committees are the main bodies that guarantee community safety and deal with emergency affairs. Community responsibility is mostly guaranteed and implemented through meeting state-enforced obligations, whereas enterprises invest in community responsibility to respond to policies and systems and meet legitimacy needs (Jianjun Zhang et al., 2016). However, investment in community responsibility requires a focus away from the core business of enterprises and does not enhance their operational capacity, improve their performance level, or help them recover (Al-Mamun & Seamer, 2021; Jianjun Zhang et al., 2016). Based on understandings derived from resource-based and stakeholder theories, responsive CSR can meet the needs of responsive stakeholders, such as the government and community, but it is difficult to obtain scarce resources related to the core business of enterprises from the government and community. Therefore, allocating resources to exercise responsive CSR may be considered wasteful, and over-investment in this area may hinder business recovery in the post-pandemic era (M. DesJardine et al., 2019a; Sajko et al., 2021a; Wieczorek-Kosmala, 2022).

According to signaling theory, responsive CSR satisfies the needs of responsive stakeholders, such as governments and communities; improves information transparency between governments, communities, and firms; and, to some extent, strengthens government and community support for firms (C.-D. Chen, Su, & Chen, 2022). However, government and community support for firms tends to emerge only after a long period of time. For example, it takes considerable time for supportive policies to be introduced. In addition, policies introduced by the government have a strong macro-regulatory function, making it difficult to influence the internal structure and resource allocation of firms (Ketter, 2022; Sharma, Thomas, & Paul, 2021; Wieczorek-Kosmala, 2022). In summary, responsive CSR makes it difficult to effectively promote firms’ organizational resilience and even impede it. Therefore, this study argues that responsive CSR does not enhance and can even undermine a firm’s organizational resilience.

Based on the above analysis, we proposed the following hypothesis:

Hypothesis 2b: Responsive CSR weakens organizational resilience.

2.3. The moderating role of minimum wage

Increases in the minimum wage create an incentive effect according to efficiency wage theory, which postulates a positive relationship between a worker’s income and his or her efficiency, and that higher wages increase productivity due to increased effort at work and motivation (especially for low-skilled workers) to upgrade and train (Clemens, 2021; Kong, Wang, & Zhang, 2020; Starr, 2019). However, minimum wages trigger negative effects when the increases exceed certain thresholds (Akee, Zhao, & Zhao, 2019; Fieseler, Bucher, & Hoffmann, 2019; Pancieri et al., 2022). According to the relevant provisions of the Labor Contract Law, firms are required to pay compensation for the dismissal of employees, the amount of which is directly linked to the minimum wage standard (Akee et al., 2019). Minimum wages reduce the cost of employee advocacy, increase the cost of dismissal, and increase job stability. Firms cannot easily fire even poorly performing employees, which dampens the motivation of others (Akee et al., 2019; Cooper, Gong, & Yan, 2018). Firms cannot easily fire employees, even poorly performing employees, which reduces the motivation of other employees (Q. Li, Zhao, Chen, & Trade, 2023). To some extent, the minimum wage increases firms’ cost burden.

Based on the above analysis, we proposed the following hypothesis:

Hypothesis 3a: Higher minimum-wage levels exacerbate decreases in responsive CSR related to occupational pension.

Hypothesis 3b: Higher minimum-wage levels mitigate increases in strategic CSR related to occupational pension.

2.4. The moderating role of population aging

The impact of population ageing on the world economy has been thoroughly analyzed in the existing literature (Nadkarni & Prügl, 2021). However, in contrast, the process of population ageing in China is complex. This is because population ageing in China is taking place in the context of “ageing before wealth” (JQ Zhang & He, 2022). Economic growth has been crucial in strengthening resources for old age, but China is now facing downward pressure on its economy (JQ Zhang & He, 2022). With its population aging faster than middle-income countries can normally sustain, China’s per capita income level has yet to reach the world’s high level (Ren, Hu, Tang, & Chadee, 2023). The challenge is how to provide the country with resources for old age (Ren et al., 2023). Population aging disrupts China’s labor market and increases recruitment costs for companies (Ding & Ran, 2021; Maestas, Mullen, & Powell, 2023). At the same time, the aging population also increases the cost of pension contributions, thus significantly increasing the operating costs of enterprises (Ding & Ran, 2021; Maestas et al., 2023).

Based on the above analysis, we proposed the following hypothesis:

Hypothesis 4a: Higher population-aging levels exacerbate decreases in responsive CSR related to occupational pension.

Hypothesis 4b: Higher population-aging levels mitigate increases in strategic CSR related to occupational pension.

2.5. The moderating role of digital transformation

The digital economy has generated new business models in areas such as the Internet (Russell, 2013), big data (Watts & Feltus, 2017), cloud computing (Wu, Pellegrini, Gao, Casale, & Systems, 2019), artificial intelligence (Barta, Görcsi, & Research, 2021), and the Internet of Things (IoT) (Y. d. Gao et al., 2021). These technologies have become increasingly integrated into various sectors of the economy and society, playing an important role in creating employment, stimulating consumption, and driving investment (Pandey & Pal, 2020).

The COVID-19 pandemic has further highlighted the importance of network effects and new business models in the digital economy, which has attracted widespread academic attention (Pandey & Pal, 2020). The impact of digital transformation extends beyond macroeconomic and production spheres, with significant effects on firms’ internal and external environments, providing a strong impetus for high-quality development, transformation, and upgrading (Watts & Feltus, 2017; Wei et al., 2019). Digitally transformed firms have fewer barriers to information transfer (Lanzolla et al., 2020; Moi, Cabiddu, & Governance, 2021). In addition, digital transformation makes it easier for firms to fully absorb resources (S. Chen, Zhang, & Finance, 2021; Feyen, Frost, Gambacorta, Natarajan, & Saal, 2021).

Based on the above analysis, we proposed the following hypothesis:

Hypothesis 5a: Digital transformation mitigates decreases in responsive CSR related to occupational pension.

Hypothesis 5b: Digital transformation exacerbates increases in strategic CSR related to occupational pension.

2.6. The moderating role of marketing capability

Marketing capabilities can play a moderating role in terms of facilitating transformation of a firm’s resources into products (Mishra & Modi, 2016). Specifically, the impact of marketing capabilities on firm resilience can be categorized into two aspects. First, based on signaling and stakeholder theories, high marketing capability provides more convenient signaling channels for firms, which improves the efficiency of information transmission (Mishra & Modi, 2016). Therefore, enterprises with high marketing capabilities can appropriately signal social responsibility to stakeholders (Mishra & Modi, 2016).

Second, based on resource base theory and stakeholder theory, marketing capability refers to a firm’s ability to understand the preferences and needs of stakeholders, such as employees, consumers, products, communities, and the environment. A high marketing capability can increase the efficiency of resource transformation (Xiong & Bharadwaj, 2013). CSR investment enables firms to obtain scarce resources, and firms with high marketing capabilities can increase the effectiveness of socially responsible investments. Marketing capabilities enhance the impact of CSR and make it easier for firms to transform socially responsible resources into output and value, thereby increasing their resilience to risks (Mishra & Modi, 2016; Morgan, 2012).

In summary, this study argues that marketing capabilities facilitate the transformation of strategic CSR investments into organizational resilience by improving the efficiency of information and resource transformation. Although responsive CSR focuses on stakeholders not involved with a firm’s core business, marketing capabilities allow for this to some extent by improving the efficiency of information and resource transformations. Thus, marketing capabilities mitigate the damaging or inhibiting effects of responsive CSR on organizational resilience.

Based on the above analysis, we proposed the following hypothesis:

Hypothesis 6a: Marketing capability promotes the transformation of strategic CSR into organizational resilience in firms.

Hypothesis 6b: Marketing capability mitigates the inhibitory effect of responsive CSR on organizational resilience in firms.

3. Methodology

Our main study is divided into two parts: study 1 examines the effect of occupational pension on CSR, and study 2 examines the effect of CSR on organizational resilience.

3.1. Sample

Our sample consists of data from 2010 to 2023 for a sample of listed companies in China. The final sample consists of 34,145 observations. All continuous variables were logged in this study. To minimize the effect of outliers, all continuous variables are winnowed at the 1% and 99% levels.

3.2. Measures

occupational pension. Based on previous studies (Shan & Park, 2023; Zheng et al., 2023), we use the amount of occupational pension (LPensions) in the annual reports of listed companies. In the robustness test, we use the DID enacted by the 2010 Social Security Law to measure it.

Strategic and responsive CSR. Learning from previous methods, strategic CSR (LSCSR) is the sum of employee responsibility, consumer responsibility and product responsibility, responsive CSR (LRCSR) is the sum of environmental responsibility and community responsibility (Michael E Porter & Mark R Kramer, 2006; Porter & Kramer, 2011). This part of data in the benchmark regression comes from the social responsibility report of listed firms disclosed by Hexun.com (Gu, Liu, & Peng, 2022; Nwagbara & Reid, 2013; Michael E Porter & Mark R Kramer, 2006).

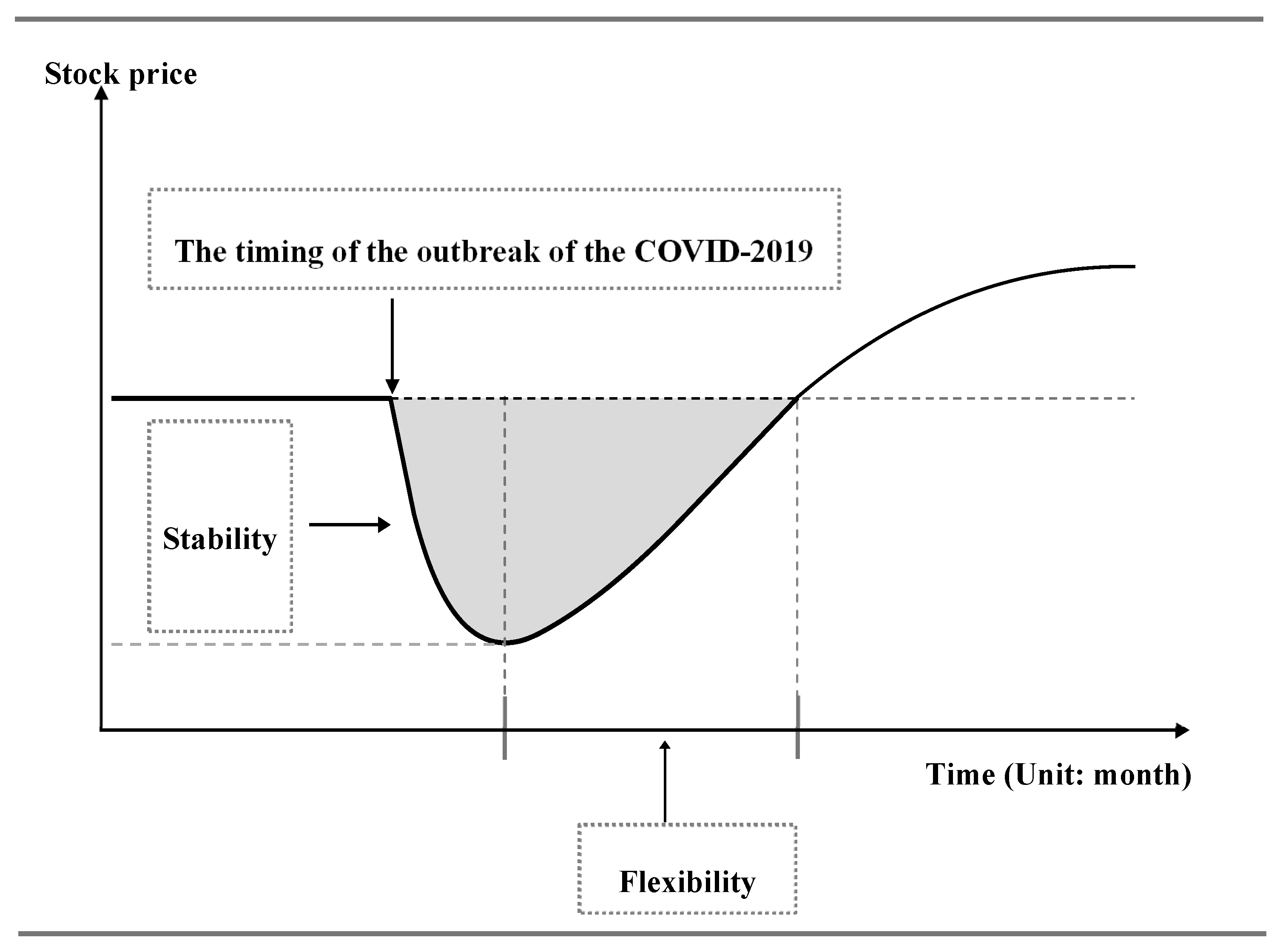

Organizational resilience. We categorized resilience into stability and flexibility, as outlined by DesJardine et al (M. DesJardine, P. Bansal, & Y. J. J. o. M. Yang, 2019b; M. Sajko, C. Boone, & T. J. J. o. M. Buyl, 2021b). LStability refers to the maximum loss in stock price. To make the final result more accurate and objective, we used the relative value of the maximum loss. To illustrate this conclusion, this study introduced the reverse coding method of Fan et al. (2001), to measure stability. LFlexibility refers to the time taken for stock price to recover from the lowest point to 30% of the initial efficiency level, as measured using the reverse coding method. Data are from the Wind database.

We clearly represent the measurement dimensions of resilience in Figure 2.

Aging population. One of the moderating variables of this paper is the degree of aging (LAging). Referring to previous studies, this paper used the percentage of the population over 65 years old in each city from China Statistical Yearbook data to measure this variable (Bellino et al., 2020; B. Hu, Peng, Zhang, Yu, & Health, 2020).

Minimum wage. Minimum wage is one of the moderating variables in this paper (LMiwage). Referring to previous studies, this paper searched the official government websites, such as the provincial human resources and social security departments. It manually organized the data of minimum wage standards in the local areas (Du & Wang, 2020).

Digital transformation. The dependent variable of this paper is the degree of digitalization (LDigitaltrans). Concerning previous studies, this paper adopted the Digital Transformation Index of Chinese Listed Companies, jointly published by the National Finance Team of Guangdong Institute of Finance and the Editorial Board of Research in Financial Economics, to measure the degree of digital transformation (LDigitaltrans) (H. Liu, Wang, Liang, & Wang, 2022; Jingyong Wang, Song, & Xue, 2023). The larger the value of the Digital indicator, the higher the enterprise’s digital transformation degree.

Marketing capability. The moderating variable in this paper is marketing capability (LCmkt). In this paper, the stochastic frontier model (SFA) is used to measure the marketing capability. The stochastic frontier production function reflects the functional relationship between the input mix and the maximum output under the specific technical conditions and the given combination of production factors (Mishra & Modi, 2016). In this paper, sales revenue is taken as the output index, and sales expenses, intangible assets and customer relationship management are taken as the input index of marketing capability (Mishra & Modi, 2016). Among them, sales expense reflects marketing expenditure; Intangible assets reflect brand effect, intellectual property and goodwill, etc. The level of customer relationship management reflects sales from repeat customers (Mishra & Modi, 2016). Based on the above analysis, this paper builds a stochastic frontier model of marketing capability: sales revenue =f (sales expenses, intangible assets, customer relationship management). Then, through the regression analysis of the above model, the non-negative inefficiency item in the model is calculated, and then the exponential operation is carried out to obtain the value of marketing capability.

Controls. Referring to previous studies (M. DesJardine et al., 2019b; Sajko et al., 2021b), to control for the influence of other factors, this study chose enterprise size (LSize), asset-liability ratio (LLev), return on assets (LROA), cash flows (LCashflow), shareholding concentration (LTop5), age of business (LListAge) and growth capacity (LRevenue) as the control variables. The data were obtained from the CSMAR (China Economic and Financial Research Database) database.

4. Methodology

4.1. Descriptive statistics

Table 1 showed descriptive statistics of variables.

4.2. Correlation analysis

This paper reported and observed the correlation coefficient matrix between the two variables to test whether there is a strong correlation between the variables. It was easy to find that the correlation between the explained variables and the explanatory variables in Table 2 was significant, which initially confirmed the rationality of the main regression. Moreover, the absolute values of correlation coefficients among independent variable, dependent variables, and mediating variables were all less than 0.7, so a strong correlation between variables is excluded, indicating that there is no severe correlation between variables (Ali, Nawab, Abbas, Zulkiffal, & Sajjad, 2009).

4.3. Study1: Impact of occupational pension on CSRs

In Table 3, the coefficient of Lpensions in Model 1 is significantly positive, indicating that firms’ occupational pension expenditures are positively related to strategic CSR, which verifies Hypothesis 1a. In Model 2, the coefficient of Lpensions is significantly negative, indicating that firms’ occupational pension expenditures are negatively related to responsive CSR, which verifies Hypothesis 1b. From the regression results of Models 1 and 2, it can be seen that firms do not adjust all types of CSR downward in response to the cost of occupational pension expenditures, but selectively increase strategic CSR and decrease responsive CSR.

4.4. Study2: Impact of CSRs on Organizational Resilience

In Table 4, the coefficients of SCSR are significantly positive in both Model 1 and Model 3, indicating that strategic CSR increases organizational resilience, verifying Hypothesis 2a.In Model 2 and Model 4, the coefficients of RCSR are significantly negative, indicating that responsive CSR decreases organizational resilience, verifying Hypothesis 2b. From the above regression results, it is clear that strategic CSR increases resilience and responsive CSR does not.

4.5. Robustness tests

4.5.1. DID tests for the relationship between occupational pension and CSRs

In this study, the difference-in-difference model is used for the robustness test (Etinzock, Kollamparambil, & Sciences, 2019). The difference-in- difference model can effectively solve the problem of endogeneity among variables (Shen, Zheng, & Yang, 2020). The difference-in-difference method is often used in policy evaluation models (Encina, 2013). Therefore, we constructed a difference-in-difference model to evaluate the occupational pension policy. For the treatment of the policy object (Treat), we take the average value of occupational pension expenditure as the standard, with enterprises above this average taking the value of 1, and enterprises below or equal to this average taking the value of 2. For the treatment of the policy object (Treat), we take the average value of occupational pension expenditure as the standard, with enterprises above this average taking the value of 1, and enterprises below or equal to this average taking the value of 0. And, for the treatment of the policy time variable (Time), this study takes the value of 1 for the year after the year in which the Social Security Law was enacted, and 0 for the year before the enactment of the Law.We take the value of 1 for the year after the year in which the Law was enacted, and 0 for the year before the enactment of the Law. We define Treat*Time as the effect of the passage of the Social Security Law (DID) to test the robustness of the relationship between occupational pension and CSRs.

In Table 5, the coefficient of DID in Model 1 is significantly positive, indicating that the enactment of the Social Security Act positively affects strategic CSR, verifying Hypothesis 1a. The coefficient of DID in Model 2 is significantly negative, indicating that the enactment of the Social Security Act negatively affects responsive CSR, verifying Hypothesis 1b. The coefficient of DID in Model 2 is significantly negative, indicating that the enactment of the Social Security Act negatively affects responsive CSR, verifying Hypothesis 1b.The regression results of both Models 1 and 2 indicate that the results of Hypotheses 1a and 1b are robust.

4.5.2. Changing the measurement of the dependent variable for the relationship between CSRs and organizational resilience

We replaced the measure of organizational resilience with a robustness test. We replace stability and flexibility with the degree of growth and volatility of the firm’s stock value. In Table 6, the coefficients of SCSR are significantly positive in Model 1 and significantly negative in Model 3. This indicates that strategic CSR will increase organizational resilience, verifying Hypothesis 2a. the coefficients of RCSR are all significantly negative in Model 2, and the coefficients of RCSR are all significantly positive in Model 4, verifying Hypothesis 2b. from the above regression results, it can be seen that strategic CSR increases resilience, whereas responsive CSR does not. This proves that the original results are robust.

5. Further studies

5.1. The moderating effects tests

Table 6 Robust test for CSRs on Organizational Resilience

Further research has been conducted to explore the moderating role of the relationship between occupational pension, CSR and organizational resilience.

As shown in Table 7, Models 1 and 3, the coefficient of Lmiwage*Lpensions is significantly negative, indicating that the minimum wage system mitigates the positive correlation between Lpensions and SCSR and exacerbates the negative correlation between Lpensions and RCSR, thus proving Hypotheses 3a and 3b. In Models 2 and 4, the coefficient of Laging* is significantly negative, indicating that population aging mitigates the positive correlation between Lpensions and SCSR and exacerbates the negative correlation between Lpensions and RCSR, proving Hypotheses 4a and 4b.

As shown in Table 8, in Models 1, 2, 5 and 6, the coefficients of LDigitaltrans*LSCSR and LDigitaltrans*LRCSR are significantly positive, indicating that Digital Transformation exacerbates the positive correlation between SCSR and Organizational Resilience, and Digital Transformation mitigates the negative correlation between RCSR and Organizational Resilience, proving Hypotheses 5a and 5b. In Models 3, 4, 7 and 8, the coefficients of LCmkt*LSCSR and LCmkt*LRCSR are significantly positive, indicating that marketing capability facilitates the positive correlation between LSCSR and Organizational Resilience and indicating that marketing capability mitigates the negative correlation between LRCSR and Organizational Resilience, proving Hypotheses 6a and Hypotheses 6b.

6. Conclusions and Discussions

The main purpose of our study is to investigate the impact of occupational pension on CSR, as well as the impact of CSR on organizational resilience. The findings of this study suggest that depending on the cost stickiness of CSR, occupational pension induces firms to reduce responsive CSR investments and increase strategic CSR under the cost stickiness effect of occupational pension premiums. Moreover, strategic CSR increases organizational resilience and responsive responsibility decreases organizational resilience. In addition, this study explores the moderating effects of population aging, minimum wage, digital transformation, and marketing capabilities on the above relationships.

6.1. Main Conclusions

First, the study’s main findings are as follows: occupational pension reduces reactive CSR and increases strategic CSR investment based on the cost stickiness theory. The cost stickiness of strategic CSR cost stickiness is high. Enterprises are reluctant to pay high adjustment costs under the cost pressure of paying for occupational pension. Instead, they increase strategic CSR to obtain additional benefits. The cost stickiness of responsive CSR is low, so under the cost pressure of paying for occupational pension, enterprises are willing to pay lower adjustment costs to reduce the costs caused by responsive CSR investment.

Second, different CSR inputs have varying effects on organizational resilience. Strategic CSR inputs promote the formation of organizational resilience, while responsive CSR inputs inhibit it. As a long-term corporate investment, strategic CSR aims to strengthen a company’s core business and create an intersection of interests between the company and its strategic stakeholders. This increases the stability and flexibility of the company and promotes the formation of organizational resilience. On the other hand, responsive CSR may prioritize short-term benefits, which can hinder efforts to improve the core business of the enterprise, negatively impact its stability and flexibility, and impede the development of organizational resilience.

Third, the minimum wage moderates the relationship between occupational pension and CSR. Our research shows that the minimum wage and occupational pension share similarities. Both are forms of labor protection that increase the burden on firms. The cost effect of minimum wage is similar to the effect of firms’ contributions to occupational pension. Therefore, we conclude that the minimum wage worsens the negative relationship between occupational pension and responsive CSR. The study shows that the minimum wage negatively moderates the positive correlation between occupational pension and strategic CSR. Additionally, the study finds that population aging has a moderating effect on the relationship between occupational pension and CSR. Population aging shocks the labor market and increases the cost of hiring employees for firms, which in turn increases the burden on companies. Therefore, population aging exacerbates the negative relationship between occupational pension and responsive CSR. Furthermore, population aging mitigates the positive relationship between occupational pension and strategic CSR.

Forth, our study shows that digital transformation moderates the relationship between CSR and organizational resilience. It enables firms to access information quickly and accelerates their efficiency in absorbing resources, facilitating the transformation of strategic CSR into organizational resilience. Additionally, digital transformation mitigates the reduction of responsive CSR to organizational resilience. Marketing capabilities moderate the relationship between CSR and organizational resilience. Our study shows that marketing capabilities help deliver intra-firm messages to stakeholders more effectively. Additionally, firms with higher marketing capabilities accelerate stakeholder support for the firm, which facilitates the transformation of strategic CSR into organizational resilience. Similarly, companies with greater marketing capabilities can reduce the negative impact of responsive CSR on organizational resilience.

6.2. Theoretical Contributions

First, to clarify the controversy surrounding the motivation of Chinese firms to fulfill their CSR from the integrated perspective of the cost stickiness theory. This study categorizes CSR into responsive and strategic, based on the cost stickiness theory (M. E. Porter & M. R. J. H. b. r. Kramer, 2006), and examines how the dynamic balance between the responsive and strategic institutional fit is achieved in the process of CSR fulfillment (M. E. Porter & M. R. J. H. b. r. Kramer, 2006). The study’s findings offer a theoretical framework for why companies adopt CSR, enriching the application of cost stickiness theory and stakeholder theory.

Second, This study contributes to the existing literature on enhancing organizational resilience processes from a CSR perspective, based on the context of COVID-19. Previous literature has primarily focused on the capability view of organizational resilience, which emphasizes resilience as an organizational characteristic (M. DesJardine et al., 2019b; Do, Budhwar, Shipton, Nguyen, & Nguyen, 2022; Hillmann & Guenther, 2021; Sajko et al., 2021b). This study examines the relationship between CSR and organizational resilience from the perspectives of stakeholder theory, resource-based theory, and signaling theory. The findings indicate that strategic CSR enhances organizational resilience, while responsive CSR inhibits organizational resilience. This study explains how to enhance organizational resilience in the context of COVID-19. It expands research understanding of CSR and organizational resilience and enriches the application of stakeholder theory, resource-based theory, and signaling theory.

Finally, this study offers a unique contribution to the marketing literature by considering the moderating role of marketing capabilities in the relationship between CSR and organizational resilience. The incorporation of marketing capabilities into a model of the relationship between CSR investments and organizational resilience sheds further light on the boundary mechanisms of the impact of CSR on organizational resilience. Compared to previous studies (Mishra & Modi, 2016), this study analyzed the moderating effect of marketing capabilities on the relationship between CSR and organizational resilience. The findings suggest that firms with higher marketing capabilities contribute more to organizational resilience through strategic CSR. Additionally, it was found that responsive CSR had a weaker inhibitory effect on organizational resilience for firms with higher levels of marketing capabilities. Firms with high levels of marketing capability can effectively correct the degree of deviation between responsive CSR and the firm’s core business. This study enriches and expands the explanatory scope of stakeholder theory, resource base theory, and signaling theory from the perspective of marketing capability.

6.3. Management Implications

The study’s findings aid policy makers in comprehending and evaluating the precise effects and extent of influence of the occupational pension system. Additionally, the study’s results assist corporate managers in determining the direction of optimization for CSR investment strategies when confronted with labor cost shocks, and in enhancing the organization’s risk-resistant capability while fulfilling social responsibility practices. In times of peace, managers should be prepared for potential risks, predict changes in the external environment, proactively adapt to market fluctuations, continuously acquire high-quality resources, and make timely adjustments to their corporate development strategies to improve the organizational resilience of their enterprises.

First, companies should increase their investment in strategic CSR, such as product responsibility and consumer responsibility. Strengthening customer relationship management can effectively improve the organizational resilience of enterprises and promote high-quality development and sustainable operation (Ntounis, Parker, Skinner, Steadman, & Warnaby, 2022; Wieczorek-Kosmala, 2022). Simultaneously, improving awareness of product innovation and avoiding product homogenization are also important for enhancing the organizational resilience of enterprises (J. Liu, Yue, Yu, & Tong, 2022). In the process of business practice, enterprises should accelerate digital transformation and upgrading to improve the efficiency of scarce resource acquisition and information transfer.

Secondly, enterprises should invest in responsive CSR moderately. This is because over-investment in responsive CSR, after satisfying the conditions of legitimacy and consistency, can divert resources from a firm’s core business, which is not conducive to organizational resilience and sustainable operations (Barnea & Rubin, 2010; Friedman, 1970). Companies should evaluate and measure their investment in responsive CSR in a timely manner and manage it appropriately to maintain a balance between strategic and responsive CSR.

Thirdly, improving marketing capabilities can enhance the corporate brand image, promote resource transformation and information transfer efficiency, and improve the quality of corporate development (Mishra & Modi, 2016). Marketing competence helps firms fulfill the process of strategic CSR, improves their organizational resilience, and avoids the consumption and destruction of firms’ strategic resources due to over-investment in responsive CSR.

Author Contributions

Conceptualization, Hao Wang and Tao Zhang; methodology, Hao Wang, Tao Zhang and Xi Wang; software, Hao Wang and Xi Wang; validation, Hao Wang, Tao Zhang and Xi Wang; formal analysis, Hao Wang and Tao Zhang; investigation, Hao Wang; resources, Xi Wang; data curation, Hao Wang and Xi Wang; writing—original draft preparation, Hao Wang; writing—review and editing, Hao Wang; visualization, Tao Zhang and Jiansong Zheng; supervision, Hao Wang and Jiansong Zheng; project administration, Hao Wang and Jiansong Zheng; funding acquisition, Tao Zhang All authors have read and agreed to the published version of the manuscript.

Funding

This study is supported by the Research Project of Macao Polytechnic University (RP/ESCHS-04/2020).

Data Availability Statement

The data that support the findings of this study are available from Hexun Evaluation of Corporate Social Responsibility Reports of A-share Listed Companies, China Stock Market & Accounting Research database (CSMAR), Annual financial statements of listed companies, but restrictions apply to the availability of these data, which were used under license for the current study, and so are not publicly available. Data are however available from the authors upon reasonable request and with permission of Beijing Hexun Online Information Consulting Service Company Limited (Hexun Evaluation of Corporate Social Responsibility Reports of A-share Listed Companies), Shenzhen CSMAR Data Technology Company Limited (CSMAR), Listed on the official website of the year (Annual financial statements of listed companies).

Acknowledgments

The authors are grateful to all research staff that contributed to the data collection required for this study.

Conflicts of Interest

We have no conflicts of interest to disclose.

Declarations: We confirm that this work is original and has not been published elsewhere, nor is it currently under consideration for publication elsewhere. We have no conflicts of interest to disclose. We confirm that all authors have approved the manuscript for submission.

References

- Agarwal, S., Pan, J., & Qian, W. J. M. S. (2020). Age of decision: Pension savings withdrawal and consumption and debt response. 66(1), 43-69. [CrossRef]

- Akee, R., Zhao, L., & Zhao, Z. J. C. E. R. (2019). Unintended consequences of China’s new labor contract law on unemployment and welfare loss of the workers. 53, 87-105. [CrossRef]

- Al-Mamun, A., & Seamer, M. (2021). Board of director attributes and CSR engagement in emerging economy firms: Evidence from across Asia. Emerging Markets Review, 46. [CrossRef]

- Ali, M. A., Nawab, N. N., Abbas, A., Zulkiffal, M., & Sajjad, M. J. A. J. o. C. S. (2009). Evaluation of selection criteria in Cicer arietinum L. using correlation coefficients and path analysis. 3(2), 65.

- Anderson, M. C., Banker, R. D., & Janakiraman, S. N. (2003). Are Selling, General, and Administrative Costs “Sticky”? Journal of Accounting Research, 41(1), 47-63. [CrossRef]

- Andersson, T., Cäker, M., Tengblad, S., & Wickelgren, M. (2019). Building traits for organizational resilience through balancing organizational structures. Scandinavian Journal of Management, 35(1), 36-45. [CrossRef]

- Bai, C., & Lei, X. J. C. E. J. (2020). New trends in population aging and challenges for China’s sustainable development. 13(1), 3-23. [CrossRef]

- Bansal, P., Jiang, G. F., & Jung, J. C. (2015). Managing Responsibly in Tough Economic Times: Strategic and Tactical CSR During the 2008–2009 Global Recession. Long Range Planning, 48(2), 69-79. [CrossRef]

- Barnea, A., & Rubin, A. (2010). Corporate Social Responsibility as a Conflict Between Shareholders. Journal of Business Ethics, 97(1), 71-86. [CrossRef]

- Barta, G., Görcsi, G. J. I. J. o. E., & Research, B. (2021). Risk management considerations for artificial intelligence business applications. 21(1), 87-106. [CrossRef]

- Bebchuk, L. A., & Fried, J. M. (2003). Executive compensation as an agency problem. Journal of economic perspectives, 17(3), 71-92. [CrossRef]

- Bellino, S., Punzo, O., Rota, M. C., Del Manso, M., Urdiales, A. M., Andrianou, X., . . . Riccardo, F. J. P. (2020). COVID-19 disease severity risk factors for pediatric patients in Italy. 146(4). [CrossRef]

- Buslei, H., Geyer, J., & Haan, P. J. D. W. R. (2023). Midijob reform: Increased redistribution in occupational pension-noticeable costs, relief not well targeted. 13(7), 63-70. [CrossRef]

- Bustinza, O. F., Vendrell-Herrero, F., Perez-Arostegui, M. N., & Parry, G. (2019). Technological capabilities, resilience capabilities and organizational effectiveness. The International Journal of Human Resource Management, 30(8), 1370-1392. [CrossRef]

- Campbell, J. L., Goldman, N. C., & Li, B. J. C. A. R. (2021). Do financing constraints lead to incremental tax planning? Evidence from the Pension Protection Act of 2006. 38(3), 1961-1999. [CrossRef]

- Carvalho, A., & Areal, N. (2016). Great places to work®: Resilience in times of crisis. Human Resource Management, 55(3), 479-498. [CrossRef]

- Chen, C.-D., Su, C.-H. J., & Chen, M.-H. (2022). Are ESG-committed hotels financially resilient to the COVID-19 pandemic? An autoregressive jump intensity trend model. Tourism Management, 93, 104581. [CrossRef]

- Chen, S., Zhang, H. J. I. R. o. E., & Finance. (2021). Does digital finance promote manufacturing servitization: Micro evidence from China. 76, 856-869. [CrossRef]

- Chen, Y., Guiping, L., & Gao, W. J. E. R.-E. I. (2023). Is occupational pension a barrier to entrepreneurship? New evidence from China. 36(3), 2155207. [CrossRef]

- Clemens, J. J. J. o. E. P. (2021). How do firms respond to minimum wage increases? understanding the relevance of non-employment margins. 35(1), 51-72. [CrossRef]

- Cooper, R., Gong, G., & Yan, P. J. T. E. J. (2018). Costly labour adjustment: general equilibrium effects of China’s employment regulations and financial reforms. 128(613), 1879-1922. [CrossRef]

- Costa, M. D., & Habib, A. J. J. o. M. C. (2023). Cost stickiness and firm value. 34(2), 235-273. [CrossRef]

- Crane, A., & Matten, D. (2020). COVID-19 and the Future of CSR Research. Journal of Management Studies, 58(1), 280-284. [CrossRef]

- de Oliveira Teixeira, E., & Werther Jr, W. B. (2013). Resilience: Continuous renewal of competitive advantages. Business Horizons, 56(3), 333-342. [CrossRef]

- DesJardine, M., Bansal, P., & Yang, Y. (2019a). Bouncing back: Building resilience through social and environmental practices in the context of the 2008 global financial crisis. Journal of management, 45(4), 1434-1460. [CrossRef]

- DesJardine, M., Bansal, P., & Yang, Y. J. J. o. M. (2019b). Bouncing back: Building resilience through social and environmental practices in the context of the 2008 global financial crisis. 45(4), 1434-1460. [CrossRef]

- DesJardine, M. R., Marti, E., & Durand, R. (2021). Why activist hedge funds target socially responsible firms: The reaction costs of signaling corporate social responsibility. Academy of Management Journal, 64(3), 851-872. [CrossRef]

- Ding, X., & Ran, M. (2021). Research on the application of role theory in active aging education service system design. Paper presented at the HCI International 2021-Late Breaking Papers: Cognition, Inclusion, Learning, and Culture: 23rd HCI International Conference, HCII 2021, Virtual Event, July 24–29, 2021, Proceedings 23. [CrossRef]

- Do, H., Budhwar, P., Shipton, H., Nguyen, H.-D., & Nguyen, B. J. J. o. B. R. (2022). Building organizational resilience, innovation through resource-based management initiatives, organizational learning and environmental dynamism. 141, 808-821. [CrossRef]

- Du, P., & Wang, S. J. E. M. (2020). The effect of minimum wage on firm markup: Evidence from China. 86, 241-250. [CrossRef]

- Duckett, J. J. D., & Change. (2020). Neoliberalism, authoritarian politics and social policy in China. 51(2), 523-539. [CrossRef]

- Elhendy, A., Tsutsui, J. M., O’Leary, E. L., Xie, F., & Porter, T. R. (2006). Noninvasive Diagnosis of Coronary Artery Bypass Graft Disease by Dobutamine Stress Real-time Myocardial Contrast Perfusion Imaging. Journal of the American Society of Echocardiography, 19(12). [CrossRef]

- Encina, J. J. E. d. e. (2013). Pension reform in Chile: A difference in difference matching estimation. 40(1), 81-95. [CrossRef]

- Etinzock, M. N., Kollamparambil, U. J. S. A. J. o. E., & Sciences, M. (2019). Subjective well-being impact of old age pension in South Africa: A difference in difference analysis across the gender divide. 22(1), 1-12. [CrossRef]

- Fama, E. F. (1980). Agency problems and the theory of the firm. Journal of political Economy, 88(2), 288-307. [CrossRef]

- Feyen, E., Frost, J., Gambacorta, L., Natarajan, H., & Saal, M. J. B. P. (2021). Fintech and the digital transformation of financial services: implications for market structure and public policy.

- Fieseler, C., Bucher, E., & Hoffmann, C. P. J. J. o. B. E. (2019). Unfairness by design? The perceived fairness of digital labor on crowdworking platforms. 156, 987-1005. [CrossRef]

- Freeman, R. E., Dmytriyev, S. D., & Phillips, R. A. J. J. o. M. (2021). Stakeholder theory and the resource-based view of the firm. 47(7), 1757-1770. [CrossRef]

- Friedman, M. (1970). The Social Responsibility of Business is to Increase its Profits. New York Times Magazine. [CrossRef]

- Fukuda, K., & Ouchida, Y. (2020). Corporate social responsibility (CSR) and the environment: Does CSR increase emissions? Energy Economics, 92. [CrossRef]

- Gao, W., Chen, Y., Xu, S., Lyulyov, O., & Pimonenko, T. J. S. O. (2023). The Role of Population Aging in High-Quality Economic Development: Mediating Role of Technological Innovation. 13(4), 21582440231202385. [CrossRef]

- Gao, Y., & Gao, J. J. E. M. (2023). Employee protection and trade credit: Learning from China’s social insurance law. 127, 106486. [CrossRef]

- Gao, Y. d., Ding, M., Dong, X., Zhang, J. j., Kursat Azkur, A., Azkur, D., . . . Li, W. J. A. (2021). Risk factors for severe and critically ill COVID-19 patients: a review. 76(2), 428-455. [CrossRef]

- Gu, L., Liu, J., & Peng, Y. (2022). Locality stereotype, CEO trustworthiness and stock price crash risk: Evidence from China. Journal of Business Ethics, 1-25. [CrossRef]

- Guo, M., Kuai, Y., & Liu, X. (2020). Stock market response to environmental policies: Evidence from heavily polluting firms in China. Economic Modelling, 86, 306-316. [CrossRef]

- Habib, A., & Hasan, M. M. (2016). Corporate Social Responsibility and Cost Stickiness. Business & society, 58(3), 453-492. [CrossRef]

- Habib, A., Hasan, M. M. J. A., & Research, B. (2016). Auditor-provided tax services and stock price crash risk. 46(1), 51-82. [CrossRef]

- Hillmann, J., & Guenther, E. J. I. J. o. M. R. (2021). Organizational resilience: a valuable construct for management research? , 23(1), 7-44. [CrossRef]

- Hu, B., Peng, D., Zhang, Y., Yu, J. J. I. J. o. E. R., & Health, P. (2020). Rural population aging and the hospital utilization in cities: the rise of medical tourism in China. 17(13), 4790. [CrossRef]

- Hu, J., Stauvermann, P.-J., Nepal, S., Zhou, Y. J. I. J. o. E. R., & Health, P. (2023). Can the Policy of Increasing Retirement Age Raise Pension Revenue in China—A Case Study of Anhui Province. 20(2), 1096. [CrossRef]

- Huang, W., Chen, S., & Nguyen, L. T. (2020). Corporate social responsibility and organizational resilience to COVID-19 crisis: An empirical study of Chinese firms. Sustainability, 12(21), 8970. [CrossRef]

- Ibrahim, A. E. A., Ali, H., Aboelkheir, H. J. J. o. I. A., Auditing, & Taxation. (2022). Cost stickiness: A systematic literature review of 27 years of research and a future research agenda. 46, 100439. [CrossRef]

- Jarzebski, M. P., Elmqvist, T., Gasparatos, A., Fukushi, K., Eckersten, S., Haase, D., . . . Takeuchi, K. J. N. U. S. (2021). Ageing and population shrinking: Implications for sustainability in the urban century. 1(1), 17. [CrossRef]

- Jiang, Y., Ritchie, B. W., & Verreynne, M. L. (2019). Building tourism organizational resilience to crises and disasters: A dynamic capabilities view. International Journal of Tourism Research, 21(6), 882-900. [CrossRef]

- Jin, G., Zhang, J., Ye, Y., Yao, S., & Song, J. J. E. M. (2024). Social insurance law and firm markup in China. 106645. [CrossRef]

- Kahn, W. A., Barton, M. A., Fisher, C. M., Heaphy, E. D., Reid, E. M., & Rouse, E. D. (2018). The geography of strain: Organizational resilience as a function of intergroup relations. Academy of management review, 43(3), 509-529. [CrossRef]

- Kang, J. (2016). Labor market evaluation versus legacy conservation: What factors determine retiring CEOs’ decisions about long-term investment? Strategic Management Journal, 37(2), 389-405. [CrossRef]

- Kantur, D., & Say, A. I. (2015). Measuring organizational resilience: A scale development. Journal of Business Economics and Finance, 4(3). [CrossRef]

- Ketter, E. (2022). Bouncing back or bouncing forward? Tourism destinations’ crisis resilience and crisis management tactics. European Journal of Tourism Research, 31, 3103-3103. [CrossRef]

- Kong, D., Wang, Y., & Zhang, J. J. J. o. C. F. (2020). Efficiency wages as gift exchange: Evidence from corporate innovation in China. 65, 101725. [CrossRef]

- Lanzolla, G., Lorenz, A., Miron-Spektor, E., Schilling, M., Solinas, G., & Tucci, C. L. J. A. o. M. D. (2020). Digital transformation: What is new if anything? Emerging patterns and management research. In (Vol. 6, pp. 341-350): Academy of Management Briarcliff Manor, NY. [CrossRef]

- Li, H., Yang, Z., Jin, C., & Wang, J. J. J. o. K. M. (2023). How an industrial internet platform empowers the digital transformation of SMEs: theoretical mechanism and business model. 27(1), 105-120. [CrossRef]

- Li, Q., Zhao, Z., Chen, T. J. E. M. F., & Trade. (2023). Social Insurance Contribution Rate Reduction Policy and Enterprise Innovation: Evidence from China. 59(4), 1012-1024. [CrossRef]

- Li, S., Wang, Y., Filieri, R., & Zhu, Y. (2022). Eliciting positive emotion through strategic responses to COVID-19 crisis: Evidence from the tourism sector. Tourism Management, 90, 104485. [CrossRef]

- Linnenluecke, M. K. (2017). Resilience in business and management research: A review of influential publications and a research agenda. International Journal of Management Reviews, 19(1), 4-30. [CrossRef]

- Liu, G., Liu, Y., Zhang, C., Zhu, Y. J. J. o. E. B., & Organization. (2021). Social insurance law and corporate financing decisions in China. 190, 816-837. [CrossRef]

- Liu, H., Wang, X., Liang, H., & Wang, L. (2022). Research on Hot Topics and Development Trend of Digital Transformation from the Perspective of Bibliometrics: ——Based on the analysis of CSSCI. Paper presented at the Proceedings of the 3rd International Conference on Industrial Control Network and System Engineering Research. [CrossRef]

- Liu, J., Yue, M., Yu, F., & Tong, Y. (2022). The contribution of tourism mobility to tourism economic growth in China. PLoS One, 17(10), e0275605. [CrossRef]

- Lu, Q., Yang, Y., & Yu, M. (2022). Can SMEs’ quality management promote supply chain financing performance? An explanation based on signalling theory. International Journal of Emerging Markets(ahead-of-print). [CrossRef]

- Ma, S., Su, L., Wang, Z., Qiu, F., & Guo, G. (2018). Resilience enhancement of distribution grids against extreme weather events. IEEE Transactions on Power Systems, 33(5), 4842-4853. [CrossRef]

- Maestas, N., Mullen, K. J., & Powell, D. J. A. E. J. M. (2023). The Effect of Population Aging on Economic Growth, the Labor Force, and Productivity. 15(2), 306-332. [CrossRef]

- Manfield, R. C., & Newey, L. R. (2017). Resilience as an entrepreneurial capability: integrating insights from a cross-disciplinary comparison. International Journal of Entrepreneurial Behavior & Research. [CrossRef]

- Meyer, A. D. (1982). How ideologies supplant formal structures and shape responses to environments. Journal of Management Studies, 19(1), 45-61. [CrossRef]

- Mishra, S., & Modi, S. B. (2016). Corporate social responsibility and shareholder wealth: The role of marketing capability. Journal of Marketing, 80(1), 26-46. [CrossRef]

- Moi, L., Cabiddu, F. J. J. o. M., & Governance. (2021). Leading digital transformation through an Agile Marketing Capability: The case of Spotahome. 25(4), 1145-1177. [CrossRef]

- Morgan, N. A. (2012). Marketing and business performance. Journal of the Academy of Marketing science, 40, 102-119. [CrossRef]

- Muller, A., & Kräussl, R. (2011). Doing good deeds in times of need: a strategic perspective on corporate disaster donations. Strategic Management Journal, 32(9), 911-929. [CrossRef]

- Nadkarni, S., & Prügl, R. J. M. R. Q. (2021). Digital transformation: a review, synthesis and opportunities for future research. 71, 233-341. [CrossRef]

- Ntounis, N., Parker, C., Skinner, H., Steadman, C., & Warnaby, G. (2022). Tourism and Hospitality industry resilience during the Covid-19 pandemic: Evidence from England. Current Issues in Tourism, 25(1), 46-59. [CrossRef]

- Nwagbara, U., & Reid, P. (2013). Corporate Social Responsibility (CSR) and Management Trends: Changing Times and Changing Strategies. Economic Insights-Trends & Challenges, 65(2).

- Pancieri, L., Silva, R. M., Wernet, M., Fonseca, L. M., Hameed, S., & Mello, D. F. J. J. o. C. H. C. (2022). Safe care for premature babies at home: Parenting and stimulating development. 13674935221089450. [CrossRef]

- Pandey, N., & Pal, A. J. I. j. o. i. m. (2020). Impact of digital surge during Covid-19 pandemic: A viewpoint on research and practice. 55, 102171. [CrossRef]

- Pollman, E. (2019). Corporate social responsibility, ESG, and compliance. Forthcoming, Cambridge Handbook of Compliance (D. Daniel Sokol & Benjamin van Rooij eds.), Loyola Law School, Los Angeles Legal Studies Research Paper(2019-35). [CrossRef]

- Polyzos, E., Fotiadis, A., & Samitas, A. (2021). COVID-19 tourism recovery in the ASEAN and East Asia region: asymmetric patterns and implications. ERIA Discussion Paper Series, Paper(379).

- Porter, M. E., & Kramer, M. R. (2006). The link between competitive advantage and corporate social responsibility. Harvard Business Review, 84(12), 78-92.

- Porter, M. E., & Kramer, M. R. (2006). Strategy and society: the link between competitive advantage and corporate social responsibility. Harvard Business Review, 84(12), 78-92, 163.

- Porter, M. E., & Kramer, M. R. (2011). The Big Idea: Creating Shared Value. CFA Digest, 41(1), 12-13.

- Porter, M. E., & Kramer, M. R. J. H. b. r. (2006). The link between competitive advantage and corporate social responsibility. 84(12), 78-92.

- Ren, S., Hu, J., Tang, G., & Chadee, D. J. P. P. (2023). Digital connectivity for work after hours: Its curvilinear relationship with employee job performance. 76(3), 731-757. [CrossRef]

- Russell, A. L. J. I. S. (2013). The internet that wasn’t. 50(8), 39-43. [CrossRef]

- Sajko, M., Boone, C., & Buyl, T. (2021a). CEO greed, corporate social responsibility, and organizational resilience to systemic shocks. Journal of Management, 47(4), 957-992. [CrossRef]

- Sajko, M., Boone, C., & Buyl, T. J. J. o. M. (2021b). CEO greed, corporate social responsibility, and organizational resilience to systemic shocks. 47(4), 957-992. [CrossRef]

- Shan, X., & Park, A. J. J. o. H. R. (2023). Access to pensions, old-age support, and child investment in china. [CrossRef]

- Sharma, G. D., Thomas, A., & Paul, J. (2021). Reviving tourism industry post-COVID-19: A resilience-based framework. Tourism Management Perspectives, 37, 100786. [CrossRef]

- Shen, Z., Zheng, X., & Yang, H. J. P. o. (2020). The fertility effects of public pension: Evidence from the new rural pension scheme in China. 15(6), e0234657. [CrossRef]

- Starr, E. J. I. R. (2019). Consider this: Training, wages, and the enforceability of covenants not to compete. 72(4), 783-817. [CrossRef]

- Tao, W., & Song, B. J. P. R. R. (2020). The interplay between post-crisis response strategy and pre-crisis corporate associations in the context of CSR crises. 46(2), 101883. [CrossRef]

- Torres, P., & Augusto, M. (2021). Attention to social issues and CEO duality as enablers of resilience to exogenous shocks in the tourism industry. Tourism Management, 87, 104400. [CrossRef]

- Van Marrewijk, M. J. J. o. b. e. (2003). Concepts and definitions of CSR and corporate sustainability: Between agency and communion. 44, 95-105. [CrossRef]

- Venieris, G., Naoum, V. C., & Vlismas, O. (2015). Organisation capital and sticky behaviour of selling, general and administrative expenses. Management Accounting Research, 26, 54-82. [CrossRef]

- Wahyudi, S., Hasanudin, H., & Pangestutia, I. J. A. (2020). Asset allocation and strategies on investment portfolio performance: A study on the implementation of employee pension fund in Indonesia. 6(5), 839-850. [CrossRef]

- Wang, H., Huang, J. J. J. o. a., & policy, s. (2023). How Can China’s Recent Pension Reform Reduce Pension Inequality? , 35(1), 37-51. [CrossRef]

- Wang, J., Song, Z., & Xue, L. J. A. S. (2023). Digital technology for good: path and influence—based on the study of ESG performance of listed companies in China. 13(5), 2862. [CrossRef]

- Wang, J., Wang, D., Long, H., & Chen, Y. J. S. A. J. o. B. M. (2023). Do firms’ pension contributions decrease their investment efficiency in Chinese context? , 54(1), 13. [CrossRef]

- Watts, N. A., & Feltus, F. A. J. B. (2017). Big Data Smart Socket (BDSS): a system that abstracts data transfer habits from end users. 33(4), 627-628. [CrossRef]

- Wei, Q., Li, X., Liang, C., Zhang, Z., Guo, J., Hong, G., . . . Huang, W. J. A. O. M. (2019). Recent progress in metal halide perovskite micro-and nanolasers. 7(17), 1900080. [CrossRef]

- Wernerfelt, B. (1984). A resource-based view of the firm. Strategic Management Journal, 5(2), 171-180. [CrossRef]

- Wieczorek-Kosmala, M. (2022). A study of the tourism industry’s cash-driven resilience capabilities for responding to the COVID-19 shock. Tourism Management, 88, 104396. [CrossRef]

- Williams, T. A., Gruber, D. A., Sutcliffe, K. M., Shepherd, D. A., & Zhao, E. Y. (2017). Organizational response to adversity: Fusing crisis management and resilience research streams. Academy of Management Annals, 11(2), 733-769. [CrossRef]

- Wu, X., Pellegrini, F. D., Gao, G., Casale, G. J. A. T. o. M., & Systems, P. E. o. C. (2019). A framework for allocating server time to spot and on-demand services in cloud computing. 4(4), 1-31. [CrossRef]

- Xiong, G., & Bharadwaj, S. (2013). Asymmetric roles of advertising and marketing capability in financial returns to news: Turning bad into good and good into great. Journal of Marketing Research, 50(6), 706-724. [CrossRef]

- Yang, M., Wang, J., Jing, Z., Liu, B., & Niu, H. (2022). Evaluation and regulation of resource-based city resilience: Evidence from Shanxi Province, China. International Journal of Disaster Risk Reduction, 81, 103256. [CrossRef]

- Zhang, J., & He, Y. J. A. J. B. M. (2022). Research on the impact of population aging on the development of digital economy. 4, 107-115. [CrossRef]

- Zhang, J., Marquis, C., & Qiao, K. (2016). Do political connections buffer firms from or bind firms to the government? A study of corporate charitable donations of Chinese firms. Organization Science, 27(5), 1307-1324. [CrossRef]

- Zheng, W., Lyu, Y., Jia, R., Hanewald, K. J. J. o. P. E., & Finance. (2023). The impact of expected pensions on consumption: Evidence from China. 22(1), 69-87. [CrossRef]

Figure 1.

A process model for our proposed framework.

Figure 2.

Measurement of the resilience.

Table 1.

Descriptive statistics.

| Variable | Obs | Mean | Std.dev. | Min | Max |

|---|---|---|---|---|---|

| LPensions | 34,145 | 13.307 | 1.955 | 6.962 | 17.751 |

| DID | 34,145 | 0.374 | 0.484 | 0.000 | 1.000 |

| LStability | 34,145 | -8.36e-09 | 2.07e-08 | -5.96e-08 | 0.000 |

| LFlexibility | 34,145 | 3.527 | 0.041 | 3.332 | 3.584 |

| LMiwage | 34,145 | 7.416 | 0.235 | 6.721 | 7.816 |

| LAging | 34,145 | -1.745 | 0.318 | -3.103 | -1.047 |

| LDigitaltrans | 34,145 | 0.439 | 0.520 | -0.715 | 1.599 |

| LCmkt | 34,145 | -1.483 | 0.127 | -1.836 | -1.012 |

| LSCSR | 34,145 | 1.593 | 0.407 | 0.000 | 2.079 |

| LRCSR | 34,145 | 1.514 | 0.748 | -1.609 | 3.315 |

| LGrowth | 34,145 | 2.502 | 1.228 | -1.648 | 6.102 |

| LVolatility | 34,145 | -2.138 | 0.359 | -3.085 | -1.074 |

| LSize | 34,145 | 3.098 | 0.043 | 2.997 | 3.255 |

| LLev | 34,145 | -1.015 | 0.464 | -2.726 | -0.140 |

| LROA | 34,145 | -3.248 | 0.732 | -6.133 | -1.619 |

| LCashflow | 34,145 | -2.929 | 0.634 | -5.818 | -1.507 |

| LRevenue | 34,145 | -1.880 | 0.733 | -5.084 | 0.528 |

| LTop5 | 34,145 | -0.670 | 0.244 | -1.525 | -0.139 |

| LListAge | 34,145 | 0.701 | 0.356 | -0.367 | 1.193 |

Table 2.

Correlation coefficient matrix.

| LPensions | DID | LSCSR | LRCSR | LStability | LFlexibility | LMiwage | LAging | LDigitaltrans | LCmkt | LGrowth | LVolatility | LSize | LLev | LROA | LCashflow | LRevenues | LTop5 | LListAge | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| LPensions | 1 | ||||||||||||||||||

| DID | 0.648*** | 1 | |||||||||||||||||

| LSCSR | 0.156*** | 0.095*** | 1 | ||||||||||||||||

| LRCSR | 0.120*** | 0.108*** | 0.058*** | 1 | |||||||||||||||

| LStability | 0.020*** | 0.006 | 0.023*** | 0.013** | 1 | ||||||||||||||

| LFlexibility | 0.021*** | 0.027*** | 0.051*** | -0.005 | 0.011** | 1 | |||||||||||||

| LMiwage | -0.524*** | -0.296*** | -0.157*** | -0.126*** | 0.002 | -0.016*** | 1 | ||||||||||||

| LAging | -0.170*** | -0.077*** | -0.058*** | -0.037*** | -0.012** | 0.010* | 0.358*** | 1 | |||||||||||

| LDigitaltrans | -0.267*** | -0.139*** | -0.103*** | -0.021*** | -0.027*** | -0.017*** | 0.442*** | 0.193*** | 1 | ||||||||||

| LCmkt | 0.095*** | 0.056*** | 0.073*** | 0.083*** | 0.052*** | -0.001 | -0.064*** | -0.036*** | -0.108*** | 1 | |||||||||

| LGrowth | 0.199*** | 0.149*** | 0.088*** | 0.063*** | 0.005 | -0.009* | -0.077*** | 0.038*** | -0.088*** | 0.323*** | 1 | ||||||||

| LVolatility | -0.042*** | -0.079*** | -0.052*** | -0.050*** | 0.007 | 0.042*** | -0.011** | -0.148*** | -0.011** | -0.041*** | -0.056*** | 1 | |||||||

| LSize | 0.186*** | 0.188*** | -0.006 | 0.131*** | 0.012** | 0.038*** | 0.019*** | 0.037*** | -0.017*** | 0.308*** | 0.369*** | -0.121*** | 1 | ||||||

| LLev | 0.082*** | 0.104*** | -0.168*** | 0.058*** | 0.005 | -0.004 | -0.023*** | -0.010* | -0.039*** | 0.201*** | 0.169*** | -0.029*** | 0.479*** | 1 | |||||

| LROA | -0.026*** | -0.026*** | 0.149*** | -0.077*** | 0.017*** | 0.032*** | 0.070*** | 0.012** | 0.069*** | 0.053*** | 0.074*** | 0.028*** | -0.135*** | -0.340*** | 1 | ||||

| LCashflow | -0.004 | 0.004 | 0.057*** | 0.032*** | 0.021*** | 0.019*** | 0.043*** | 0.009* | 0.015*** | 0.087*** | 0.018*** | 0.001 | 0.001 | -0.111*** | 0.297*** | 1 | |||

| LRevenues | -0.036*** | -0.018*** | -0.003 | -0.028*** | 0.006 | 0.004 | 0.014*** | 0.010** | 0.025*** | 0.046*** | 0.099*** | 0.077*** | -0.023*** | 0.013** | 0.116*** | -0.008 | 1 | ||

| LTop5 | 0.040*** | 0.020*** | 0.135*** | 0.032*** | 0.009 | -0.014*** | 0.011** | -0.014*** | -0.037*** | 0.132*** | 0.138*** | -0.029*** | 0.024*** | -0.090*** | 0.162*** | 0.092*** | 0.006 | 1 | |

| LListAge | 0.056*** | 0.058*** | -0.096*** | 0.110*** | 0.016*** | 0.024*** | -0.032*** | 0.001 | -0.039*** | 0.028*** | -0.067*** | -0.085*** | 0.438*** | 0.292*** | -0.227*** | -0.039*** | -0.096*** | -0.311*** | 1 |

Table 3.

Study1: The Impact of Pensions on Strategic and Responsive CSR.

| Model | (1) | (2) |

|---|---|---|

| LSCSR | LRCSR | |

| LPensions | 0.0094*** | -0.0153*** |

| (0.0029) | (0.0045) | |

| LSize | 0.4798*** | -0.4795** |

| (0.1368) | (0.2146) | |

| LLev | -0.1120*** | -0.0172 |

| (0.0108) | (0.0162) | |

| LROA | 0.0421*** | -0.0911*** |

| (0.0055) | (0.0088) | |

| LCashflow | -0.0067 | 0.0294*** |

| (0.0051) | (0.0081) | |

| LRevenue | 0.0047 | 0.0123** |

| (0.0038) | (0.0063) | |

| LTop5 | 0.1693*** | 0.0737** |

| (0.0226) | (0.0342) | |

| LListAge | -0.0409*** | -0.0268* |

| (0.0102) | (0.0158) | |

| Firm_fixed effects | YES | YES |

| Year_fixed effects | YES | YES |

| _cons | 0.2680 | 3.2501*** |

| (0.4166) | (0.6606) | |

| N | 34145.0000 | 34145.0000 |

| r2 | 0.1389 | 0.0495 |

Table 4.

Study2: The Impact of CSR on Organizational Resilience.

| Models | (1) | (2) | (3) | (4) |

|---|---|---|---|---|

| LStability | LStability | LFlexibility | LFlexibility | |

| LSCSR | 0.0011*** | 0.0048*** | ||

| (0.0003) | (0.0007) | |||

| LRCSR | 0.0003* | -0.0006* | ||

| (0.0002) | (0.0003) | |||

| LSize | -0.0016 | -0.0008 | 0.0406*** | 0.0474*** |

| (0.0033) | (0.0033) | (0.0067) | (0.0067) | |

| LLev | 0.0005* | 0.0004 | -0.0010* | -0.0017*** |

| (0.0003) | (0.0003) | (0.0006) | (0.0006) | |

| LROA | 0.0005*** | 0.0005*** | 0.0017*** | 0.0019*** |

| (0.0002) | (0.0002) | (0.0003) | (0.0003) | |

| LCashflow | 0.0006*** | 0.0006*** | 0.0005 | 0.0006* |

| (0.0002) | (0.0002) | (0.0004) | (0.0004) | |

| LRevenue | 0.0002 | 0.0002 | 0.0002 | 0.0001 |

| (0.0002) | (0.0002) | (0.0003) | (0.0003) | |

| LTop5 | 0.0009* | 0.0009* | -0.0041*** | -0.0033*** |

| (0.0005) | (0.0005) | (0.0010) | (0.0010) | |

| LListAge | 0.0014*** | 0.0013*** | 0.0015** | 0.0014* |

| (0.0004) | (0.0004) | (0.0008) | (0.0008) | |

| Firm_fixed effects | YES | YES | YES | YES |

| Year_fixed effects | YES | YES | YES | YES |