Submitted:

25 March 2024

Posted:

26 March 2024

You are already at the latest version

Abstract

The oil and gas industry in Nigeria, a vital contributor to the nation's economy, has long been associated with significant environmental challenges. Pollution, habitat destruction, and greenhouse gas emissions have raised global concerns about sustainability and corporate responsibility. This empirical study explores the relationship between environmental accounting practices and the financial performance of listed oil and gas companies in Nigeria. We investigated eight oil and gas companies that are publicly traded on the Nigerian Stock Exchange Market (NGX) as of January 17, 2022, from 2011 to 2022. The study employs Driscoll-Kraay standard errors and reveals that environmental accounting had significant effects on returns on assets, earnings per share, and liquidity ratio. The study revealed that the implementation of environmental accounting practices had diverse effects on the performance of oil and gas companies in Nigeria. The findings encourage policymakers and stakeholders in the sector to utilise the insights and design more effective regulations and incentives that promote environmental corporate responsibility. Also, valuable insights into the potential benefits and challenges associated with adopting environmental accounting practices, and influencing the decision-making processes of corporate stakeholders were provided to ensure sustainability in terms of improved financial performance of the oil and gas sector in Nigeria.

Keywords:

environmental accounting

; financial performance

; oil and gas companies

; Nigeria

; Driscoll-Kraay standard errors

1. Introduction

Climate change, global warming, ozone layer depletion, pollution, and ocean acidification are some of the key environmental issues the world currently experiences. These key issues are direct consequences of business, organizations, companies and firms not being mindful of the effect of their business operations on the environment, society, and economy. For many years, stakeholders have been clamoring for organizations to be held responsible for the impact of their activities on the environment because of the imbalances in the environmental system. The environmental system is imbalanced, and stakeholders have been demanding that organisations be held responsible for their activities’ effects on the environment for a long time [1,2]. The success of every business organization is largely dependent on revenue and the benefits to the environment, society, and economy.

Concern and attention are growing among countries and organisations regarding the necessity of environmental accounting. This has emerged as an essential issue for business organisations and nations due to the critical role that the environment plays in the progress and growth of both entities [1]. Environmental accounting as an aspect of corporate social responsibility is a crucial phenomenon that is very vital to the life of any business organization. With the increase in the awareness of stakeholders about the impact of corporate organisations’ activities on the environment, organizations must adapt to the expectations and demands of stakeholders [2]. According to [3], businesses, particularly those whose operations have an impact on the environment, ought to be transparent about their financial commitments to improving the environment. This is especially true for businesses whose operations involve pollution and other environmental hazards. Environmental disclosure in yearly reports is still a current problem in research. [4] claims that non-financial reporting is expanding because of increased awareness among businesses, stakeholders, and shareholders about how these problems ultimately impact a company’s long-term performance.

In a developing economy like Nigeria, there is no definite accounting standard or guideline that requires organizations to report the impact of their activities in their annual reports. Environmental concerns in Nigeria and elsewhere reduce life expectancy. Thus, the Companies and Allied Matters Act (CAMA), International Accounting Standards (IAS), and International Financial Reporting Standards (IFRS) do not require quantitative or qualitative disclosure of (financial) environmental accounting information in annual reports. There is no mandatory Stock Exchange listing requirement for Nigerian companies to disclose environmental accounting information, but the Nigerian Stock Exchange’s 2018 sustainability reporting Guideline advised corporations to disclose environmental events. Thus, Nigerian environmental accounting disclosure is voluntary, which discourages it [1,5].

The oil and gas sector, as one of the major contributors to the emission of greenhouse gases, has come under public scrutiny and is expected to act and reduce its negative impact on the environment. The oil and gas sector plays a vital role in the growth and development of the Nigerian economy and the achievement of sustainable development goals. Oil and gas companies are profit-oriented enterprises like other companies and strive to improve their financial performance. Every company that makes a profit strives to improve its corporate financial performance, which is used to gauge the productivity and effectiveness of its managers. Every company can benefit from a healthy, long-lasting competitive advantage if it can devote its people and resources to strategic tasks that improve organizational performance while adhering to moral and ethical standards [5,6]. Any organization’s performance will be continuously evaluated, resulting in the timely and important information that managers need to make decisions that will advance the organization and enhance their operations [6]. The major methods of financial analysis are used to value a company’s overall financial performance. To forecast a company’s future growth, stability, and health, financial analysis is used. Based on the intended application, timing, and nature of the information resources, the best financial analysis approach should be chosen [2,7].

Numerous elements, which may be divided into micro and macro factors, influence how well organizations operate financially. Additionally, they exert a substantial influence on the valuation of a company’s financial performance [8]. Financial performance is typically measured by return on assets, earnings per share, return on equity, and net profit margin. Factors such as liquidity, ownership, age and size of the firm, leverage, productivity, solvency, and restrictions in the available resources are affected by micro factors, while macro factors encompass exogenous factors that exert an influence on the financial state of companies [8]. An imbalance in business, the economy, and the world might result from financial crises [7].

In the global community, corporate entities are confronted with economic, social, and environmental responsibilities, duties, and functions. Businesses face significant obstacles in the current economic climate when attempting to strike a balance between financial performance and corporate sustainability. The global development, growth, and survival of corporations are predominantly contingent upon the financial performance and operational efficacy of their management [9]. Companies in Nigeria voluntarily provide information about their environmental responsibility efforts in their financial reports. Many organizations include qualitative or quantitative information about their efforts to uphold environmental stewardship in their financial reports. The effectiveness of management in managing people and resources in any organization is very tactical in contributing to the synergy between social and environmental accounting information and a company’s financial performance. This study is therefore aimed at determining the effect of environmental accounting on the performance of listed oil and gas companies in Nigeria.

Conceptually, Performance is an inclusive term that encompasses any aspect or the entirety of an organization’s activities over a period of time, typically evaluated in relation to past or anticipated cost effectiveness, managerial responsibility, or liability [9]. [10] define performance as a collection of financial and non-financial indicators that furnish all stakeholders with insight into the organization’s management’s capability to accomplish the predetermined goals for the fiscal period. Financial performance evaluates the effectiveness with which a company converts its primary business assets into profit, in addition to identifying the financial consequences of its operational strategies and procedures [11]. According to [7], financial performance pertains to the degree to which an organisation has achieved its financial objectives. Financial performance is an inherently subjective metric that assesses the efficiency with which an organisation utilises its core business assets to produce income. It provides an indication of the overall health and actual financial standing of a company [12].

The phrase “green” or “environmental accounting” might signify different things to different people. A common understanding is that “green accounting” refers to the practice of tracking and reporting expenses that have an impact on the environment [13]. Providing objective evidence of environmental circumstances, environmental accounting focuses on a firm’s environmental performance statistics [4]. Financial and non-financial information are both included. Additionally, green accounting is defined by [6] as a way to economically measure an organization’s performance regarding the environment. Information regarding the operational performance of the company in relation to environmental protection is the aim. Shareholders and bondholders are the only parties who can use conventional accounting to make decisions based on financial data. The goal of “green accounting” is to include in the monetary impact on the environment when calculating business profits. There is a common understanding that environmental accounting is a collection of activities undertaken by organisations to track and report on how well they are doing in terms of protecting the environment [14].

Empirically, many academics are interested in the empirical effects of environmental accounting on performance, but their studies have led to diverse findings. A study by [15] examined the relationship between environmental accounting disclosure and return on assets. The study focused on the financial performance of food and beverage enterprises in Nigeria. Listed Nigerian oil and gas businesses’ financial performance was studied by [16] in relation to green environmental accounting. The research concluded that the chosen oil and gas businesses’ financial performance was positively impacted by green environmental accounting. The findings of [9,17] are in agreement with this conclusion. [18] employed a basic linear regression method for analysis and data from companies’ publicly available annual financial records for two oil and gas companies listed on the Nigerian Stock Exchange (from 2010 to 2014). The results showed that CSR significantly and positively affects profits, and concluded that corporate social responsibility impacted their earnings.

Moreover, extant studies [1,2,19] have also looked at how social and environmental disclosures affect the performance of consumer goods and manufacturing companies. Based on the results, [19] found that the impact of social and environmental disclosure on return on assets was unaffected by firm size or age, but that it did significantly affect earnings per share. The Nigerian oil and gas firms’ CSR initiatives and earnings per share were studied by [1]. Their research showed that oil and gas companies’ profits were unaffected by their CSR initiatives. An investigation into the effect of CSR on energy companies’ bottom lines was conducted by [2] in Lithuania. Corporate social responsibility and financial performance were shown to have no relationship, according to the study. [5,6,8,20] were among the papers that found that social and environmental accounting significantly affected the profitability of financial institutions. According to research by [20], listed Nigerian family-owned businesses’ financial performance suffered due to environmental accounting. Environmental accounting information has a substantial effect on the financial performance of manufacturing enterprises, according to [5]. Environmental CSR, business performance, and partnership restructuring were found to be positively correlated by [6], who established a link between the two. In addition, the results showed that the connection between environmental CSR and partnership restructuring was decreased by industrial power and dysfunctional competition.

The novelty of this study is depicted in addressing the pitfalls of environmental practices and disclosure patterns concerning the financial performance of Nigeria’s oil and gas sector, which is a sector that is actively involved in the exploration of natural resources and the destruction of the environment, and which should ordinarily be responsible to the environment and society in return. Also, most studies on environmental, social, and governance (ESG) practices and financial performance have been accomplished in developed economies, with limited attention given to emerging markets, particularly Nigeria, where ESG practices differ significantly due to regulatory, cultural, and socioeconomic factors. Research is needed to understand how specific variations in ESG practices, especially environments, affect the financial performance of oil and gas companies, particularly in Nigeria. Also, much of the existing literature tends to focus on individual ESG factors, such as environmental performance or social responsibility, rather than examining the holistic impact of ESG practices on financial performance. There is a need for studies that analyze the combined effects of various ESG factors on financial outcomes, especially in the context of the oil and gas industry. Lastly, there is ongoing debate regarding the appropriate methodologies and metrics for measuring ESG performance and its relationship with financial outcomes. Many existing studies rely on self-reported data, which is largely subject to biases and inaccuracies. Standardized metrics for ESG, like the Global Reporting Initiative (GRI), are needed to facilitate comparability and enhance the validity of findings across studies. In addition, more robust methodologies such as Driscoll-Kraay standard errors, which are robust to serial correlation and provide reliable estimates even in the presence of heteroscedasticity (which is often a cross-section issue), are appropriate in the presence of short time-series or limited cross-sectional observations such as this present study.

The remaining sections of the paper are structured as follows: Section 1 is an introduction and identifies gaps in the literature; Section 2 presents the data measurements and sources; In Section 3, we discuss theory development and hypotheses. Section 4 gives a summary of the methods and data sources, including modeling techniques, variable measurement, and empirical strategy employed in the study; Section 5 explores the empirical findings and goes into detail about the results and discussions; and Section 6 concludes and discusses policy implications.

2. Data and Measures

2.1. Performance Measures

Companies’ performance can be measured in a number of ways. The most popular approaches used by academics and researchers to assess financial performance are those based on market indicators and accounting measures. Scholars agree that accounting-based measures, or market-based indicators, are the best ways to assess financial success [21]. Commonly used accounting-based metrics include net profit margin, return on equity, return on sales, return on capital utilised, and return on asset. Although they are frequently employed, market-based metrics such as price-book ratio, dividend yield, earnings per share, and dividend per share, Tobin’s Q, and earnings yield. For this study, the accounting-based measures used were return on assets and liquidity, while the market-based measure used was earnings per share.

[15] assert that return on assets is a comprehensive indicator of operational efficiency. Return on assets (ROA) is a crucial number used by shareholders to evaluate the effectiveness of management in utilising the average amount of investment in the company’s assets, regardless of whether the investment comes from investors or creditors. The ROA indicator is a highly effective metric for evaluating the financial robustness and operational effectiveness of a company. This ratio is crucial for management to assess the performance of enterprise assets in relation to planned business objectives and market rivals [22]. [23] contend that liquidity is a crucial indicator of a company’s capacity to meet its financial obligations promptly. Liquidity ratios demonstrate the capacity of a business to fulfil its immediate financial obligations. If these ratios reflect weakness, it suggests that the organisation may encounter challenges in meeting its short-term financial liabilities. According to [24], earnings per share is a ratio that measures the effectiveness of management in generating profits for shareholders. It displays the portion of a company’s net profit that is allocated to all shareholders of the company. Earnings per share (EPS) is a financial metric that quantifies a company’s capacity to earn net profits per share [25].

2.2. Environmental Measures

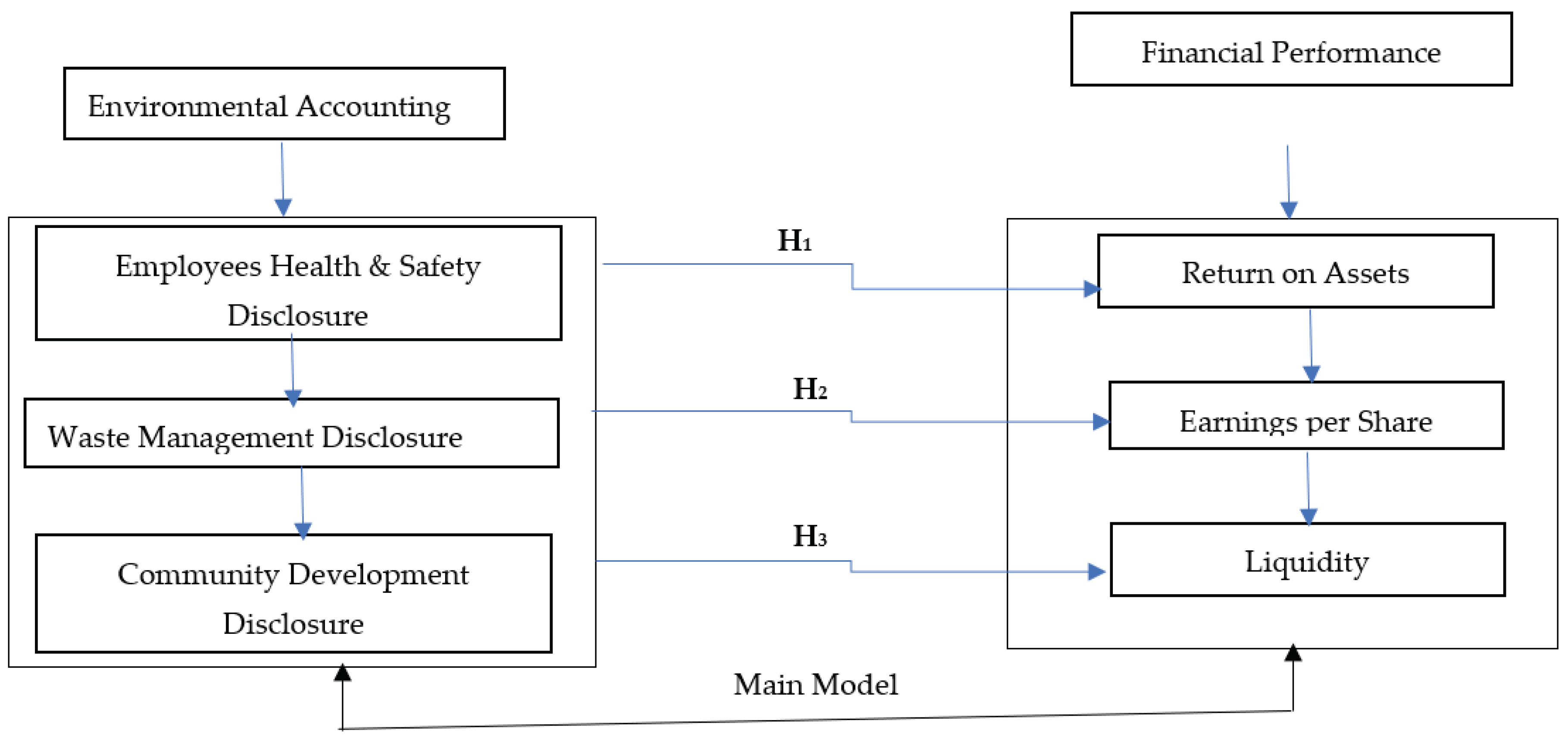

Studies on environmental accounting have been surrounded by diverse measurements such as environmental disclosure score, ESG score, Global Reporting Index (GRI), Fortune magazine reputation index, MSC KLD 400 social index, Vigeo Index and Dow Jones Sustainability Index, as well as content analysis and definitions based on researchers’ methodologies, research approaches, and the scope of their studies. One of the best measures, according to recent literature [5,14,20,26], that captures several aspects of ESG is the GRI. In this study, the GRI framework was employed to assess environmental accounting, as only a limited number of studies have utilised this index in the literature. Environmental accounting was evaluated through the utilisation of waste management disclosure (WMD), community development disclosure (CDD), and employees’ health and safety disclosure (EHSD). [26] defined employee health and safety disclosures as reports or programmes designed to safeguard employees against the actions of organisations.

For WMD, [5] argue that WMD is the disclosure of a company’s physical management of waste, reduction of waste generation, and promotion of reuse and recycling. [14] opine that WMD is a measure introduced by organizations to avoid or reduce waste. It covers the cost of the treatment of waste, management of waste, pollution, reparation, resourcing, and conservation. Regarding CDD, a company’s relationship with its host community can be managed by disclosing its environmental and social initiatives. This creates a stable business climate free from protest or conflict and is affected by important stakeholders. [20] define CDD as costs incurred by organizations for the good of society and a clean environment for communities.

3. Theory Development and Hypotheses

This study is anchored on the signaling theory. Michael Spence introduced the signaling theory in 1973. This concept posits that business directors engage in voluntary disclosure, which includes the disclosure of social responsibility and the manipulation of market asymmetry to convey precise signals to the market demonstrating the favourable performance of their organisations. The signaling theory provides clarity on how companies employ diverse boards to convey their commitment to social values to a variety of organisations. Information asymmetry occurs when people get different information. Signaling theory helps reduce information asymmetry and ensures all stakeholders get the same information, which will aid in making sound decisions.

The hypotheses provided in the null form, depicted in the conceptual framework in Figure 1, are to be tested to examine the effect of environmental accounting on the financial performance of oil and gas companies in Nigeria:

4. Materials and Methods

In empirical research that involves time-series and cross-sectional data with potential correlation and heteroscedasticity, using appropriate standard errors is crucial to making accurate statistical inferences [27]. In the context of this study that investigates the relationship between environmental accounting and the financial performance of listed oil and gas companies in Nigeria, the Driscoll-Kraay (DK) standard errors offer several justifications by addressing serial correlation which often a characteristic of time-series data where observations at different time points are correlated. The presence of serial correlation can lead to biased estimates and inefficient standard errors if not properly accounted for. Driscoll-Kraay standard errors are robust to serial correlation and provide reliable estimates even in the presence of autocorrelation [27,28]; by handling heteroscedasticity which is often a cross-section issue. In financial data and other economic time series, heteroscedasticity (unequal variance of errors) is a common issue. Heteroscedasticity can result in standard errors that are biased and can lead to erroneous statistical inferences. Driscoll-Kraay standard errors are robust to heteroscedasticity, ensuring accurate estimates of coefficients and valid hypothesis tests [27,29].

Also, the Driscoll-Kraay standard errors are especially appropriate in the presence of short time series or limited cross-sectional observations such as this present study. The flexibility in modeling and robustness to misspecification are other desirable features of the Driscoll-Kraay standard errors. It does not require strict assumptions about the underlying data distribution. The model specifications can be linear or non-linear models, making them suitable for various empirical analyses [27,30]. Its robustness to certain forms of model misspecification enhances the validity of results in case of model uncertainty [27]. Lastly, Driscoll-Kraay standard errors are particularly suitable for panel data models, offering advantages over traditional standard errors (pooled OLS, fixed-effect, and random effect) in dealing with correlation and heteroscedasticity in this context [27]. Since this study focuses on listed oil and gas companies in Nigeria which involves panel data with repeated observations for each firm over time, the likelihood of one form of spatial dependence or others in the panel sample would produce inconsistent standard errors. Hence, the usual ordinary least square (OLS), fixed effect, and random effect standard errors become ineffective.

Following several studies on the link between environmental accounting disclosures and financial performance [1,5,8,9,19,20], the functional model is specified as:

where is a vector of indicators of financial performance of Oil and Gas sector at time, t and firm i, while represents a vector of variables of environmental accounting disclosure at time, t and firm i. The financial performance (PER) of Oil and Gas sector is measured by Returns on assets (ROA), Earning per share (EPS), and liquidity (LIQ) while environmental accounting disclosures were measured using waste management disclosure (WMD), community development disclosure (CDD), and employees’ health and safety disclosure (EHSD). Thus, the empirical model is specified as:

where is a vector financial performance (proxied by Returns on assets (ROA), Earning per share (EPS), and liquidity (LIQ)) at time, t and firm i, and represents employees’ health and safety disclosure at time, t and firm i; represents waste management disclosure at time, t and firm i; represents community development disclosure at time, and firm while is the firm specific disturbance term while . Table 1 and Table 2 present the variable definition/measurements and the list of selected eight (8) oil & gas companies listed on the NGX as of 17th January 2022 respectively.

5. Results and Discussion

5.1. Descriptive Statistics and Correlation Analysis

To give background knowledge on the variables, it is crucial to talk about the descriptive statistics of the ones used in the study. Table 3 displays the descriptive statistics, whereas Table 4 displays the correlation matrix of the variables used in the study. The average of 17.16 return on asset implies that 17.16% is the proportion of the return generated per naira of total asset utilized; while the average of earnings per share shows that the reported earnings of equity share are 4.60 kobo, while 1.01 of liquidity indicates that on average of Oil & Gas Companies can pay short term debts immediately. The average of 0.96 of Employees’ Health and Safety Disclosure (EHSD) indicates that on average seven (7) Oil and Gas companies reported employees’ health and safety disclosure in their annual report, 0.10 of Waste Management Disclosure (WMD) indicates that on average one (1) company reported about WMD in its annual report; while 0.49 of Community Development Disclosure (CDD) indicates that on average three (3) companies reported about CDD in their annual report. The minimum values of ROA, EPS, and LIQ indicate that there are periods of reported losses by the selected companies. The Employees Health & Safety Disclosure (EHSD), Waste Management Disclosure (WMD), and Community Development Disclosure (CDD) each have a minimum value of 0.00, indicating that some firms have various levels of Environmental Accounting practices proxies among themselves. However, the result presented in Table 3 revealed that Return on Asset (ROA) and Earnings per Share (EPS) exhibited the greatest degree of dispersion from the mean at 75.3% and 8.49%, respectively. In contrast, Liquidity (LQ), Employees Health & Safety Disclosure (EHSD), Waste Management Disclosure (WMD), and Community Development Disclosure (CDD) displayed standard deviations of 0.82%, 0.50%, 0.31%, and 0.21%, respectively. These values suggest that there were fluctuations within the dataset under consideration.

The correlation matrix presents the level of multicollinearity among the independent variables of the research in Table 4. The findings revealed that the correlation between EHSD and WMD was 8.2%, whereas the correlation between CDD and EHSD was 21.3%. Neither of these correlations exceeded the 80% threshold for multicollinearity proposed by [31]. Therefore, the research concluded that the issue of multicollinearity among the independent variables does not arise. Furthermore, the findings presented in Table 4, including the Variance-Inflation Factor (VIF), corroborated the conclusions drawn from the correlation matrix that multicollinearity is not an issue among the independent variables. This is supported by the variables’ mean VIF value of 1.78, which is below the recommended thresholds of 5 or 10 as proposed by [32].

5.2. Stationarity and Cross-Sectional Dependence Tests

One major observation in the model is the assumption of interdependence among the oil and gas companies. Environmental disclosures tend to ensure collective sustainability decision-making for the companies since this is one of the requirements of global environmental management. Built on this argument, this work adopts tests for cross-sectional dependence among the companies using the cross-sectional unit root test and cross-sectional dependence test. These tests determine whether series are heterogeneous. Table 5 contains the outcomes of the unit root test conducted on the variables. At each level, the results indicate that every variable is stationary. Hence, it can be concluded that the variables adopted in the models do not lead to spurious regression. Moreover, to check for cross-sectional dependence among the oil and gas companies, we adopt three cross-sectional tests (Perasan, Frees, and Friedman tests). The results, in Table 6, show that the models exercise a high cross-sectional dependency as shown by the significance levels. All three methods reported cross-sectional dependence among the oil and gas companies.

5.3. Effect of Environmental Accounting on Financial Performance

Table 6 presents the outcomes of the cross-sectional dependence tests, which indicate the presence of cross-sectional dependence among companies. Consequently, the conventional ordinary least square (OLS), fixed effect, and random effect standard errors are rendered inapplicable, rendering their interpretations superfluous. In order to address the challenges associated with cross-sectional dependence, correlation, and heteroscedasticity in the panel of oil and gas companies, the Driscoll-Kraay standard errors presented in Table 7 are interpreted. The findings presented in Table 7 indicate that Employees Health & Safety Disclosure (EHSD) has a statistically significant adverse impact on the performance of publicly traded Oils and Gas firms, as measured by Returns on Assets (ROA) (= -85.77, p<0.05). However, it has a significant positive influence on the performance of such firms as measured by Earnings per Share (EPS) (= 3.166, p<0.05), and on the performance of publicly traded Oils and Gas companies as measured by Liquidity (= 0.831, p<0.05). Based on this result, a one-unit increase in EHSD is associated with an 85.77 unit decline in ROA, while EPS and LIQ increase by 3.166 and 0.831 units, respectively, for the selected oil and gas corporations in Nigeria. The results in Table 7 also reveal that Waste Management Disclosure (WMD) has a significant negative effect on the performance of listed Oils and Gas companies measured by Returns on Assets (ROA) (= -2.039, p<0.05); but it has a significant positive effect on the performance of listed Oils and Gas companies measured by Earnings per Share (EPS) (= 0.155, p>0.05) and Liquidity Ratio (LIQ) (= 0.292, p<0.05). This result implies that a unit increase in WMD would lead to a 2.039 unit decrease in ROA; leading to 0.155 and 0.292 unit increases in EPS and LIQ respectively for the selected Oils and Gas companies in Nigeria. A negative effect of Waste Management Disclosure (WMD) on the financial performance of listed oil and gas companies

The findings presented in Table 7 indicate that Waste Management Disclosure (WMD) has a statistically significant adverse impact on the performance of listed Oils and Gas firms, as evaluated by Returns on Assets (ROA) (= -2.039, p<0.05). However, it has a statistically significant positive influence on Earnings per Share (EPS) and Liquidity Ratio (LIQ) (= 0.155, p>0.05) and (= 0.292, p<0.05) respectively. Based on the findings, it can be inferred that a one unit increase in WMD would result in a 2.039 unit reduction in ROA. In contrast, the Oils and Gas companies in Nigeria would experience increases of 0.155 units in EPS and 0.292 units in LIQ. The results in Table 7 and Table 8 show that Community Development Disclosure (CDD) has a significant negative effect on the performance of listed Oils and Gas companies measured by Returns on Assets (ROA) (= -36.71, p<0.05), Earnings per Share (EPS) (= -0.0449, p>0.05) and Liquidity Ratio (LIQ) (= -0.119, p<0.05). This result implies that a unit increase in CDD would lead to a 36.71 unit decrease in ROA; a 0.0449 unit decrease in EPS, and a 0.119 unit decrease in LIQ respectively for the selected Oils and Gas companies in Nigeria.

6. Discussion

As measured by Returns on Assets (ROA), the adverse impact of Employees Health & Safety Disclosure (EHSD) on the financial performance of publicly traded oil and gas companies is multifaceted. Accidents, infections, and injuries among personnel may ensue due to substandard health and safety protocols, which may ultimately cause operational disruptions and diminished productivity. This aligns with the findings of previous studies [1,2,5,10,12], that EHSD can have a significant impact on the company’s capacity to produce returns on its assets, as periods of inactivity and lower efficiency can lead to decreased output and revenues. Having a negative EHSD can harm the reputation of oil and gas companies, resulting in reduced trust and confidence among stakeholders such as investors, customers, and the public [2,12].

Moreover, positive EPS impacts suggest that the company is producing increased earnings in comparison to the outstanding shares. This increases shareholder value by distributing earnings across a reduced number of shares, resulting in increased dividends per share or possible share price growth. According to [6], a positive EHSD reflects the company’s prioritization of its employees’ well-being, thereby boosting investors’ trust. Investors may view these companies as well-managed and socially responsible, thus impacting their investment choices in a good way. This may result in decreased operational interruptions, reduced insurance expenses, and potentially decreased legal responsibilities, all of which can enhance financial performance and increase EPS. Also, a positive effect of EHSD on the liquidity ratio indicates that the oil and gas companies possess enough current assets to meet their short-term obligations. The findings conform to [6], [8], and [9] by concluding that financial stability decreases the chances of insolvency or liquidity issues, which can harm the companies’ operations and reputation. Higher liquidity ratios indicate the company’s ability to readily fulfill its immediate financial responsibilities, including bill payments, debt repayments, and operational costs [5,8]. This boosts the company’s financial adaptability and decreases the chances of default, perhaps resulting in enhanced creditworthiness and reduced borrowing expenses. High liquidity ratios suggest that the company has surplus funds that can be used for investing in growth possibilities like capital expenditures, acquisitions, or research and development. This allows the corporation to undertake strategic initiatives that can improve long-term profitability and competitiveness in the oil and gas industry.

An adverse impact of Waste Management Disclosure (WMD) on the financial performance of quoted oil and gas companies measured by Returns on Assets (ROA) could lead to increased operational costs, environmental liabilities, reputational damage, regulatory compliance costs, litigation risk, loss of social license to operate, and long-term sustainability concerns. Addressing waste management issues proactively is essential for mitigating these risks and improving financial performance, measured by ROA in the long run. This finding supports the conclusion from extant studies [9,10,33] that poor waste management practices can lead to higher operational costs for oil and gas companies. This can include expenses related to waste disposal, remediation of environmental damage, regulatory compliance, and fines for violations.

Higher costs reduce profitability and negatively impact ROA. Inadequate waste management may result in environmental liabilities for the company, such as cleanup costs, legal fees, and penalties for environmental violations [33]. As revealed by the positive effects of WMD on EPS and liquidity ratio, effective waste management practices can lead to cost savings for oil and gas companies. By minimizing waste generation, optimizing resource utilization, and implementing efficient waste disposal methods, companies can reduce operating expenses and improve profitability [1,6,12]. Higher earnings translate to an increased EPS, while improved liquidity ratios indicate better cash management and resource allocation, further enhancing financial performance. Also, transparent disclosure of waste management efforts demonstrates the companies’ commitment to sustainability and regulatory compliance, which can enhance investor confidence and attract socially responsible investors. Increased investor interest and support can contribute to higher EPS and liquidity ratios as demand for the company’s shares grows [5,7]. According to [2], by complying with waste management regulations and implementing best practices, companies can mitigate the risk of fines, penalties, and legal liabilities associated with non-compliance. Thus, reduced risk exposure improves financial stability, lowers the cost of capital, and enhances EPS and liquidity ratios.

The negative effect of CDD practices may lead to reputational damage for the company. If the company is perceived as neglecting its social responsibility or failing to address community needs, it can erode trust and credibility among stakeholders, including investors, customers, and regulators [9,10]. Also, poor community development practices can lead to increased operational costs for oil and gas companies. The finding is in line with previous studies [5,8,9,10] that negative CDD practices may expose the company to regulatory and legal risks. Failure to meet community expectations or comply with relevant regulations can result in fines, penalties, and legal liabilities for the company. These increased costs reduce profitability, lower EPS, and negatively impact liquidity ratios. This can result in decreased investor confidence, reduced market demand for the company’s shares, and potential boycotts by customers, ultimately impacting ROA, EPS, and liquidity ratios.

7. Conclusions and Policy Recommendations

The incorporation of environmental accounting metrics into the annual reports of companies has been the subject of numerous research studies, as it is widely believed that such information can enhance the financial performance of such organisations. The study examined the impact of environmental accounting practices on the financial performance of eight (8) listed oil and gas firms in Nigeria for the period of 2011 to 2022. As measured by return on assets (ROA), the initial hypothesis investigated the impact of environmental accounting on the financial performance of listed oil and gas companies in Nigeria. At the 5% and 10% levels of significance, employee health and safety disclosure (EHSD) and community development disclosure (CDD) were found to have statistically significant adverse effects on return on assets (ROA), respectively. On the other hand, waste management disclosure (WMD) had a negative but insignificant impact on ROA for listed oil and gas companies. The impact of environmental accounting on the financial performance of listed oil and gas corporations in Nigeria, as measured by earnings per share (EPS), was the subject of the second hypothesis. The findings indicate that Earnings per Share (EPS) is positively impacted by EHSD and WMD, while the impact of WMD is statistically insignificant. Additionally, it was disclosed that the impact of CDD on the Earnings per Share (EPS) of listed oil and gas companies in Nigeria is marginally negative. The third hypothesis examined the impact of environmental accounting on the liquidity ratio (LIQ), a metric used to represent the financial performance of listed oil and gas companies in Nigeria. The findings indicate that EHSD and WMD have a statistically significant positive impact on the liquidity ratio of listed oil and gas companies in Nigeria. Conversely, CDD exhibits a statistically significant negative influence on the liquidity ratio.

The results show that, overall, listed oil and gas businesses in Nigeria see considerable improvements in their financial performance due to EHSD and WMD, but CDD causes these companies’ financial performance to suffer. According to the study’s findings, environmental accounting can help Nigerian oil and gas businesses improve their financial performance in a number of ways. The study’s conclusions exhort governments and corporate players operating in Nigeria’s oil and gas industry to apply the knowledge gained to create more sensible rules and incentives that support environmental stewardship. In order to enhance the financial performance of Nigeria’s oil and gas industry, significant insights into the possible advantages and difficulties of implementing environmental accounting standards were also given. These insights would ultimately have an impact on the decision-making processes of corporate stakeholders.

First, the negative effect of environmental accounting disclosures (EHSD, WMD, and CDD) can significantly influence the company’s financial performance, potentially leading to stakeholders withdrawing investment, boycotting products, or taking other actions that could impact profitability. An adverse EHSD can impact employee morale and satisfaction, resulting in elevated turnover rates and higher recruitment and training expenses. High employee turnover can cause disruptions in operations and reduce efficiency, ultimately affecting the company’s financial performance and ROA. The negative effect of EHSD on financial performance can result in higher operational costs, reduced productivity, harm to reputation, increased regulatory compliance expenses, heightened litigation risks, and worries regarding long-term sustainability. The study recommends adherence to health and safety regulations that typically involve a substantial investment in training, equipment, and infrastructure, which may impact profitability and ROA positively.

Second, the desirable impact of environmental accounting disclosures, especially EHSD and WMD on earnings per share implies that a workplace that is safe and conducive to good health at work can enhance employee morale, productivity, and retention rates. When employees feel appreciated and secure, they are more inclined to be motivated and involved in their work, resulting in enhanced efficiency and effectiveness, which can subsequently have a beneficial effect on the company’s profitability and earnings per share (EPS). The study thus recommends an implementation of efficient health and safety as well as waste management protocols which lead to financial savings for the firm. This encompasses lowered healthcare expenses, fewer rates of absenteeism, and reduced costs associated with occupational injuries and accidents. The cost savings can directly lead to increased earnings and, subsequently, increased earnings per share (EPS). Positive EHSD and WMD practices lead to increased investor confidence, decreased operational risks, enhanced employee productivity, cost savings, improved reputation, and regulatory compliance. These ultimately result in higher earnings per share (EPS) and overall business prosperity.

Moreover, the oil and gas sector are susceptible to variations in commodity prices, regulatory modifications, geopolitical uncertainties, and other external influences that might affect cash flows. The positive impact of environmental accounting disclosures, especially EHSD and WMD on liquidity ratio ensures sufficient liquidity which enables oil and gas companies to efficiently handle unforeseen obstacles or economic downturns. During a crisis, having enough cash and assets that can be quickly converted into cash can assist reduce risks, keep companies running, and take advantage of opportunities that may surface while competitors face difficulties. High liquidity ratios indicate strong financial health and prudent management practices, which can enhance stakeholder trust. Stakeholders are more inclined to trust and back organizations with robust liquidity situations, potentially resulting in heightened investment, advantageous lending terms, and enhanced commercial partnerships. Thus, we recommended that businesses, firms, and companies particularly those whose operations have an impact on the environment, publish their financial commitments to the improvement of the environment. Making environmental accounting disclosure necessary for firms and businesses, especially oil and gas companies is important since they are actively involved in the exploration of natural resources and the destruction of the environment. Policymakers and accounting organizations should create a framework to assist businesses account for the effects of their operations on society and the environment. Governments should put systems in place to make sure businesses strictly abide by all environmental rules.

Author Contributions

Afolabi, A.R.; Agbor, M.N.: Conceptualization, Methodology, Software, Formal Analysis, Investigation, Data curation, Writing - original draft. Amosun, O.O.; Okunade, S.O: Conceptualization, Methodology, Supervision, Validation, Writing - original draft, Writing - review & editing.

Funding

This research received no external funding.

Institutional Review Board Statement

This study was conducted in accordance with the Declaration and Research Ethics of Chrisland Centre for Research and Statistics (CREST), and approved by the Council, Chrisland University, Abeokuta (11 May 2019).

Data Availability Statement

Data would be made available on request.

Acknowledgments

The authors would like to extend their sincere appreciation to the African Scholars Mentorship Network (ASMN), which is a programme run by the DePECOS Institutions and Development Research Centre (DIaDeRC) in Nigeria, for the invaluable insights it has provided. This mentorship programme greatly aided in the development of the publication. The opinions stated are those of the writers.

Conflicts of Interest

The authors declare no conflicts of interest.

References

- Owolabi, S.A.; Odunlade, O.A.; Amosun, O.O. Corporate Social Responsibility and Earnings Per Share of Oil and Gas Companies in Nigeria. Int. J. Accounting, Finance Risk Manag. 2022, 7, 56. [Google Scholar] [CrossRef]

- Adamkaite, J.; Streimikiene, D.; Rudzioniene, K. The impact of social responsibility on corporate financial performance in the energy sector: Evidence from Lithuania. Corp. Soc. Responsib. Environ. Manag. 2022, 30, 91–104. [Google Scholar] [CrossRef]

- Ohidoa, T.; Omokhudu, O.O.; Oserogho, I. A. F. Determinants of environmental disclosure. Int. J. of Adv. Acad. Res. 2016, 2(8), 49–58. [Google Scholar]

- Ordu, P.; Amah, C. Sustainability accounting and financial performance of oil and gas companies in Nigeria. Int. J. of Innov. Fin. and Econ. Res. 2021, 9(1), 182–197. [Google Scholar]

- Osaloni, B.O.; Oso, O.O. An evaluation of environmental accounting information and financial performance of listed manufacturing firms in Nigeria. Int. J. of Adv. Multidisc. Res. and Stud. 2023, 3(2), 1055–1064. [Google Scholar]

- Makhdoom, Z.H.; Gao, Y.; Song, X.; Khoso, W.M.; Baloch, Z.A. Linking environmental corporate social responsibility to firm performance: The role of partnership restructure. Environ. Sci. Pollut. Res. 2023, 30, 48323–48338. [Google Scholar] [CrossRef]

- Pham, D.C.; Do, T.N.A.; Doan, T.N.; Nguyen, T.X.H.; Pham, T.K.Y. The impact of sustainability practices on financial performance: empirical evidence from Sweden. Cogent Bus. Manag. 2021, 8, 1912526. [Google Scholar] [CrossRef]

- Amosun, O.O.; Owolabi, S.A.; Odunlade, O.A. Social and Environmental Accounting and Performance of Banking Companies Quoted in Nigeria. J. Finance Account. 2022, 10, 160. [Google Scholar] [CrossRef]

- Anselm, C.; Okoye, J. Environmental cost and financial performance of oil and gas companies in Nigeria. Int. J. Adv. Acad. Res. 2015, 1–24. [Google Scholar] [CrossRef]

- Ehioghiren, E. E.; Eneh, O. Corporate social responsibility accounting and financial performance of insurance companies in Nigeria. Int. J. of Acad. Acct., Fin. & Mgt. Res. 2019, 3(5), 16–25.

- Al-Waeli, A.; Khalid, A.; Ismail, Z.; Idan, H. The relationship between environmental disclosure and financial performance of industrial companies with using a new theory: Literature review. J. of Cont. Iss. in Bus. & Govt. 2021, 27(2), 3846-3868.

- Eze, E. Green accounting reporting and financial performance of manufacturing firms in Nigeria. Amer. J. of Hum. & Soc. Sci. Res. 2021, 5(7), 179–187.

- Nkwoji, N. Environmental accounting and profitability of selected quoted oil and gas companies in Nigeria. J. of Acct. and Fin. Mgt. 2021, 7(3), 24–38. [Google Scholar]

- Adegbie, F.F.; Ogidan, A.A.; Siyanbola, T.T.; Adebayo, A.S. Environmental accounting practices and share value of food and beverages manufacturing companies quoted in Nigeria. J. of Crit. Rev. 2020, 7(13), 2256–2264. [Google Scholar]

- Ezeagba, C.E.; Rachael, J.-A.C.; Chiamaka, U. Environmental Accounting Disclosures and Financial Performance: A Study of selected Food and Beverage Companies in Nigeria (2006-2015). Int. J. Acad. Res. Bus. Soc. Sci. 2017, 7. [Google Scholar] [CrossRef]

- Benson, N.C.; Asuquo, A.I.; Inyang, E.O.; Adesola, F.A. Effect Of Green Accounting On Financial Performance Of Oil And Gas Companies In Nigeria. J. Univ. Shanghai Sci. Technol. 2021, 23, 166–190. [Google Scholar] [CrossRef] [PubMed]

- Polycarp, S.U. Environmental Accounting and Financial Performance of Oil and Gas Companies in Nigeria. 10. [CrossRef]

- Eze, J.; Nweze, A.; Enekwe, C. The effects of environmental accounting on a developing nation: Nigerian experience. Europ. J. of Acct, Aud. & Fin. Res. 2016, 4(1), 17-27.

- Emuebie, E.; Olaoye, S.A.; Ogundajo, G.O. Effect of Social and Environmental Disclosure on the Performance of Listed Consumer Goods Producing Companies in Nigeria. Int. J. Appl. Econ. Finance Account. 2021, 11, 35–47. [Google Scholar] [CrossRef]

- Ilelaboye, C.S.; Alade, M.E. Environmental Accounting and Financial Performance of Listed Family-Owned Companies in Nigeria. Int. Rev. Bus. Econ. 2022, 6, 71–82. [Google Scholar] [CrossRef]

- Achim, M.-V.; Borlea, S.N. Environmental performance - Way to boost the financial performance of companies. Environ. Eng. Manag. J. 2014, 13, 991–1004. [Google Scholar] [CrossRef]

- Diaz, J.F.; Pandey, R. Factors affecting return on assets of US technology and financial corporations. J. Manaj. dan Kewirausahaan 2019, 21, 134–144. [Google Scholar] [CrossRef]

- Lalithchandra, E.A.B. Liquidity Ratio: An Important Financial Metrics. Turk. J. Comput. Math. Educ. (TURCOMAT) 2021, 12, 1113–1114. [Google Scholar] [CrossRef]

- Choiriyah, C.; Fatimah, F.; Agustina, S.; Ulfa, U. The Effect Of Return On Assets, Return On Equity, Net Profit Margin, Earning Per Share, And Operating Profit Margin On Stock Prices Of Banking Companies In Indonesia Stock Exchange. Int. J. Finance Res. 2020, 1, 103–123. [Google Scholar] [CrossRef]

- Sudirman, Kamaruddin, & Possumah, B. The influence of net profit margin, debt to equity ratio, return on equity, and earning per share on the share prices of consumer goods industry companies in Indonesia. Int. J. of Adv. Sci. and Tech. 2020, 29(7), 13428- 13440.

- Oti, P.; Mbu-Ogar, G. Analysis of environmental and social disclosure and financial performance of selected quoted oil and gas companies in Nigeria (2012-2016). J. Acct. and Fin. Mgt. 2018, 4(2), 23–37. [Google Scholar]

- Driscoll, J.C.; Kraay, A.C. Consistent Covariance Matrix Estimation with Spatially Dependent Panel Data. Rev. Econ. Stat. 1998, 80, 549–560. [Google Scholar] [CrossRef]

- Joshi, J.M.; Dalei, N.N.; Mehta, P. Estimation of gross refining margin of Indian petroleum refineries using Driscoll-Kraay standard error estimator. Energy Policy 2021, 150, 112148. [Google Scholar] [CrossRef]

- Iheonu, C.; Asongu, S.; Odo, O.P. Financial sector development and investment in selected ECOWAS countries: Empirical evidence using heterogeneous panel data method. MPRA No 107102, 2020. https://mpra.ub.uni-muenchen. 1071. [Google Scholar]

- Khan, A.B.; Siriphan, T.; Mookda, R.; Kongnun, T.; Rattanapong, S.; Omanee, Y.; Thonghom, P. Impact of global financial crisis 2008-09 and global oil prices on the economic growth of Asean countries: An evidence from Driscoll-Kraay Standard Errors Regression. Acad. of Acct. & Fin. Stud. J. 2021, 25(6), 1-11.

- Baltagi, B. Solution Manual for Econometrics, 3rd ed.; Springer, Berlin, 2015.

- James, G.; Witten, D.; Hastie, T.; Tibshirani, R. An introduction to statistical learning with applications in R. Springer, Berlin, 2017.

- Činčalová, S.; Hedija, V. Firm Characteristics and Corporate Social Responsibility: The Case of Czech Transportation and Storage Industry. Sustainability 2020, 12, 1992. [Google Scholar] [CrossRef]

Figure 1.

Conceptual Framework.

Table 1.

Variable Definition and Measurements.

| Variable | Measurement | Justification |

|---|---|---|

| Return on Asset (ROA) | [19] et al. (2021), [22] & Pandey (2019) | |

| Earnings per Share (EPS) | (Earnings available to ordinary shares)/(weighted ordinary shares in issues) x 100 | [19] et al. (2021), [24] et al., (2020), [25] et al., (2020), [17] (2019) |

| Liquidity Ratio (LIQ) | [23] & Rajendhiran (2021), [19] et al. (2021), [17] (2019) | |

| Employees Health & Safety Disclosure (EHSD) | GRI Index | [20] & Alade (2022), [14] et al. (2020), Oti & Mbu (2018) |

| Waste Management Disclosure (WMD) | GRI Index | [14] et al. (2020), Nwaimo (2020), Oti & Mbu (2018). |

| Community Development Disclosure (CDD) | GRI Index | GRI (2021) Oti & Mbu (2018), [14] et al. (2020), Nwaimo (2020), [20] & Alade (2022). |

Source: Researchers’ Compilation.

Table 2.

List of Oil & Gas Companies Listed on the NGX as of 17th January 2022.

| S/N | Companies | Primary Business | Exchange Sector |

|---|---|---|---|

| 1 | 11 Plc | Petroleum Station | Oil and Gas |

| 2 | Ardova Plc (Forte Oil) | Integrated Oil and Gas | Oil and Gas |

| 3 | Conoil Plc | Oil and Gas Refining and Marketing | Oil and Gas |

| 4 | Eterna Plc | Oil and Gas Refining and Marketing | Oil and Gas |

| 5 | Japaul Gold& Ventures Plc | Oil and Gas Refining and Marketing | Oil and Gas |

| 6 | Mrs Oil Nigeria Plc | Oil and Gas Refining and Marketing | Oil and Gas |

| 7 | Oando Plc | Integrated Oil and Gas | Oil and Gas |

| 8 | Total Energies Marketing Nigeria Plc | Oil and Gas Refining and Marketing | Oil and Gas |

Table 3.

Descriptive Statistics of the variables.

| Variable | Obs. | Mean | Std. Dev. | Min. | Max. |

|---|---|---|---|---|---|

| ROA | 96 | 17.02163 | 75.32424 | -55.75645 | 545.408 |

| EPS | 96 | 4.600182 | 8.487763 | -20.23 | 43.58 |

| LIQ | 96 | 1.014055 | 0.8161189 | -1.15851 | 6.364849 |

| EHSD | 96 | 0.9545455 | 0.2094926 | 0 | 1 |

| WMD | 96 | 0.1022727 | 0.3047431 | 0 | 1 |

| CDD | 96 | 0.4886364 | 0.5027355 | 0 | 1 |

Note: ROA, EPS, LIQ, CDD, WMD, EHSD represent Returns on assets, Earning per share, liquidity, Community development disclosure, Waste management disclosure, and Employees’ health and safety disclosure respectively.

Table 4.

Correlation Analysis for Oil & Gas Companies.

| Correlation Matrix | Variance-Inflation Factor (VIF) | ||||

|---|---|---|---|---|---|

| EHSD | WMD | CDD | VIF | 1/VIF | |

| EHSD | 1.0000 | 1.05 | 0.948089 | ||

| WMD | 0.0737 | 1.0000 | 1.01 | 0.992401 | |

| CDD | 0.2133 | -0.0298 | 1.0000 | 1.05 | 0.952411 |

| Mean VIF = 1.04 | |||||

Note: CDD, WMD, EHSD represent Community development disclosure, Waste management disclosure, and Employees’ health and safety disclosure respectively.

Table 5.

Cross-sectional augmented Im, Pesaran, and Shin (CIPS) Unit Root Test.

| Variables | CIPS Values | Decision |

|---|---|---|

| ROA | -2.155** | I(1) |

| EPS | -3.901*** | I(1) |

| LIQ | -5.215*** | I(1) |

| EHSD | -5.279*** | I(1) |

| WMD | -4.923*** | I(1) |

| CDD | -2.123** | I(1) |

Notes: ***, ** and * indicate 1%, 5% and 10% significant levels respectively.

Table 6.

Cross-Sectional Dependence Tests.

| Tests/Models | ROA Model | EPS Model | LIQ Model | Overall Model |

|---|---|---|---|---|

| Pesaran | 8.358*** | 13.214** | 5.551** | 7.118*** |

| Friedman | 113.518** | 121.265*** | 102.511*** | 112.025*** |

| Frees | 1.6694** | 1.892** | 1.501** | 1.708*** |

Notes: ***, ** and * indicate 1%, 5% and 10% significant levels respectively.

Table 7.

Regression Results on Effect of Environmental Accounting on Financial Performance of Nigerian Oil and Gas sector: Driscoll-Kraay Standard Error Method.

Table 7.

Regression Results on Effect of Environmental Accounting on Financial Performance of Nigerian Oil and Gas sector: Driscoll-Kraay Standard Error Method.

| Return on Asset (ROA) | Earnings per Share (EPS) | Liquidity Ratio (LIQ) | |||||||

|---|---|---|---|---|---|---|---|---|---|

| Variable | Fixed Effect | Random Effect | Driscoll-Kraay FE | Fixed Effect | Random Effect | Driscoll-Kraay FE | Fixed Effect | Random Effect | Driscoll-Kraay FE |

| EHSD | -85.77** | 89.56** | -85.77** | 3.166 | 3.178 | 3.166** | 0.831** | 0.779** | 0.831*** |

| (37.73) | (37.19) | (14.3) | (3.214) | (3.159) | (1.060) | (0.335) | (0.336) | (0.247) | |

| WMD | -2.039 | -12.23 | -2.039 | 0.155 | -0.737 | 0.155 | 0.292 | 0.157 | 0.292*** |

| (54.15) | (33.97) | (12.78) | (4.614) | (4.196) | (0.220) | (0.481) | (0.406) | (0.0329) | |

| CDD | -36.71* | -24.35 | -36.71* | -0.0449 | -0.123 | -0.0449 | -0.119 | -0.166 | -0.119*** |

| (18.74) | (17.03) | (17.97) | (1.597) | (1.554) | (1.814) | (0.166) | (0.163) | (0.0368) | |

| Constant | 117.0*** | 115.7*** | 117.0 | 1.585 | 1.702 | 1.585* | 0.249 | 0.336 | 0.249 |

| (36.92) | (36.90) | (123.1) | (3.146) | (4.230) | (0.719) | (0.328) | (0.378) | (0.241) | |

| R-squared | 0.422 | 0.413 | 0.507 | ||||||

| Adj. R-squared | 0.401 | 0.399 | 0.472 | ||||||

| F-Stat (Prob.) | 3.55** (0.0181) |

5.82** (0.0145) |

44.08*** (0.0000) |

||||||

| No of id | 8 | 8 | 8 | 8 | 8 | 8 | 8 | 8 | 8 |

| Obs. | 88 | 88 | 88 | 88 | 88 | 88 | 88 | 88 | 88 |

Standard errors in parentheses. *** p<0.01, ** p<0.05, * p<0.1.

Table 8.

Regression Results on Effect of Environmental Accounting on Financial Performance of Nigerian Oil and Gas sector: Driscoll-Kraay Standard Error Method.

Table 8.

Regression Results on Effect of Environmental Accounting on Financial Performance of Nigerian Oil and Gas sector: Driscoll-Kraay Standard Error Method.

| Dependent Variable: PERF | Fixed Effect | Random Effect | Driscoll-Kraay FE |

| Ehsd | 0.661* | -0.643* | 0.661* |

| (0.386) | (0.381) | (0.348) | |

| Wmd | 0.247 | 0.262 | 0.247*** |

| (0.554) | (0.508) | (0.0322) | |

| Cdd | -0.0222 | -0.0364 | -0.0222 |

| (0.192) | (0.187) | (0.145) | |

| Constant | 0.637* | 0.614 | 0.637** |

| (0.378) | (0.516) | (0.283) | |

| Observations | 88 | 88 | 88 |

| R-squared | 0.392 | ||

| Adj. R-squared | 0.359 | ||

| F-Stat (Prob.) |

37.03*** (0.000) |

||

| Number of id | 8 | 8 | 8 |

Standard errors in parentheses. *** p<0.01, ** p<0.05, * p<0.1.

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Copyright: This open access article is published under a Creative Commons CC BY 4.0 license, which permit the free download, distribution, and reuse, provided that the author and preprint are cited in any reuse.