Submitted:

15 April 2024

Posted:

16 April 2024

You are already at the latest version

Abstract

On the basis of a stocktaking on PVC in Europe and on a current ECHA investigation report, we conclude that regulatory action at EU level is recommended. We support ECHA's regulatory proposals in the main, but come to a more comprehensive proposal for the phasing-out of PVC beyond the area of electrical installations. PVC stored in buildings and infrastructure to date amounts to around 160 million tonnes ("stock") and this mass is still increasing. Parts from the stock have entered the waste management sector for years and their mass is gradually increasing. Neither material, chemical nor energy recovery will be able to absorb these incoming quantities. We therefore come to the conclusion that PVC should be collected separately and disposed of in an infrastructure designed for chlorine recovery. The required infrastructure should be set up and operated by the chemical industry. So, PVC will lose its status as a particularly economically favorable plastic. In view of the constantly increasing stock, we recommend phasing-out the production of virgin PVC as early as possible. In our opinion, this would also be justifiable because the effects of the closed loop recycling announced by VinylPlus ('Vinyl') would go in the same direction.

Keywords:

PVC stock

; material recycling

; chemical recycling

; chlorine cycle

; economy

1. Introduction

As documented in [1], the PVC industry's track record to date of increasing the sustainability of PVC plastic is not convincing. The question therefore arises as to whether the legislator should intervene in Europe or at national level?

Regulatory action must be well justified in each case. PVC differs from all other plastics, as described in [i], due to the high chlorine content in the polymer and the share and characteristics of additives. Various studies and reports have been submitted by the EU Commission in order to prepare for possible regulatory action, particularly with regard to environmental and health questions [2]. In 2022, the EU Commission presented a further report entitled: "The use of PVC (poly vinyl chloride) in the context of a non-toxic environment" [3]. ECHA's recently presented "Investigation Report" is of particular importance [4].

Regulatory areas of action must be considered throughout the entire life cycle of the plastic. They can therefore start with production, address the consumption phase and finally concern waste disposal (post consume).

2. Production

Manufacturing of the monomer VC, the polymer and some additives is subject to the regulations of the chemical industry in Europe. For the marketing of the polymer or compounds, justifications for government intervention only arise from the downstream life cycle phases, which we will discuss below. ECHA takes a rather critical view of a phase-out, in particular because PVC is a low-cost plastic and other plastics [iv] resp. non-plastic alternatives are only available as substitutes at higher prices. This chapter will therefore firstly examine how PVC is priced and how the markets are strategically linked.

2.1. Soda

To understand the economics of PVC, we need to look back a little further into the last century. Sodium carbonate (Na2CO3, "soda", "soda ash" or "washing soda") was and is an important substance for carrying out chemical reactions. Due to its alkaline properties, soda was used for many purposes (paper industry, food production, chemical industry). Soda ash is found in natural minerals (such as salt lakes) and can be obtained from certain incinerator ashes or by chemical conversion of sodium chloride. Over 100 years ago, it was discovered that soda can be made even more reactive (corrosive) through chemical conversion [5]. This is why sodium hydroxide (NaOH) today is still called 'caustic soda' in English. Caustic soda was able to open up even more areas of application than (simple) soda, such as dissolving metals from ores. As a result, soda and caustic soda were, and still are, outstanding bulk chemicals for industry.

In addition to the chemical extraction of caustic soda, an electrolytic process was added end of the 19th century that could also produce caustic soda from salt: the chlor-alkali electrolysis. The chemical and electrolytic processes for the production of caustic soda were in competition with each other. A CIA report from the 1950s on the situation in the USSR and the USA shows the strategic importance of alkali extraction and the competition between the processes [6]. In the following years the electrolytic production of caustic soda gradually became more economically viable than the chemical production (today 65% of the global market) [7].

2.2. Chlorine

Chlor-alkali electrolysis as a co-production process has an economical advantage, it produces stoichiometrically equal amounts of caustic soda (sodium hydroxide, NaOH), chlorine (Cl2) and hydrogen (H2) from common salt (NaCl) [8]. In terms of mass, 1120 kg NaOH (i.e. 2240 kg NaOH (50%)) and 28 kg hydrogen are produced per 1000 kg chlorine [9]. To date, just under 70 chlor-alkali electrolysis plants are in operation in Europe, with a production capacity of a good 11.6 million tonnes chlorine per year [10]. With 15 chlor-alkali electrolysis plants and a production capacity of 5.1 million tonnes, Germany is the largest chlorine producer in Europe. "At the beginning of the 1990s, there was a clear surplus of around 20% of caustic soda, so that chlorine (production in Germany in 1997: 3.5 million tonnes) can be regarded as the volume-determining product of this process" [11], p. 42].

But in the beginning, the market for caustic soda (NaOH) was the driving force behind the success of chlor-alkali electrolysis. For the abundant chlorine, a market had to be found for. Initially, the focus was on inorganic chemicals (chlorides). At the end of the 19th century, chlorine was introduced for drinking water disinfection (Hamburg, 1893) and later as bleaching agent in the pulp and paper industry. During the First World War, some of the chlorine was used from the German side as war gas. Later, organic substances were added. In 1935, mass production of PVC began at the Wolfen and Bitterfeld plants of IG Farben AG [12], and PVC became the most important sales market for chlorine. Globally 35 to 40% of the chlorine from electrolysis is currently used for PVC production [13], in Europe, the latest figure was 31% [vii]. With PVC, chlorine becomes a component of the manufactured product. Chlorine is also used as an agent to produce reactive intermediate products such as propylene chlorohydrin, phosgene or epichlorohydrin. These intermediates are then used in further reactions to produce other plastics, among other things. Here, the chlorine does not appear in the product, but leaves the industrial plant as chloride via waste water or is utilized as hydrochloric acid (HCl).

The demand for caustic soda in Europe is largely taken up by the chemical industry, pulp and paper industry, food industry, alumina and other metals industry. For hydrogen, there are various areas of application, like steam generation, in the chemical industry [vii] and – perspectively – in the field of energy storage [14].

2.3. The Economy of PVC Production

As the price of chlorine (and therefore of PVC) could be kept low through co-production, industry was able to establish PVC as a mass plastic for the construction sector.

Since – as explained in more detail in [i] – PVC can only be made usable by in the first place adding stabilizers, the construction sector is also the ideal area of application for this reason. Stabilization only had to be "extended".

There is really nothing reprehensible about the strategy of looking for a new use for a waste product from a chemical process – on the contrary. This happens in countless processes in the chemical industry. Entire sites such as the one of BASF in Ludwigshafen live this interconnected concept. However, this mainly involves organic substances consisting of carbon, nitrogen, hydrogen and oxygen. PVC is a special case here because chlorine is not otherwise bound into a chemical product to any relevant extent.

As chlorine as a gas or liquid is extremely dangerous (see above: war gas) and can only be stored in small amount to a great expense, the local and timely use of chlorine is a key prerequisite for economic success. Although chlor-alkali electrolysis is financed economically via hydrogen and sodium hydroxide, it is for that controlled by chlorine sales. If sales of chlorine, i.e. PVC, stagnate, technical and economic constraints arise. In this case, chlorine could theoretically be disposed of by converting it to chloride. However, this could not be compensated for economically because the price of electrolytic caustic soda is capped [15]. On the one hand, consumers of electrolytic caustic soda could switch to soda (sodium carbonate, Na2CO3) (substitution) or the market could ramp up or reactivate the remaining capacities for the chemical production of caustic soda [xi]. The faltering sales of chlorine and PVC would therefore force the chlor-alkali industry to reduce capacity and strengthen the soda ash markets and chemical production of caustic soda. But this is not, what they economically want to do. This makes it clear why parts of the chemical industry are fighting so doggedly for this plastic.

All market players are aware that the intricate construct of chlor-alkali electrolysis only works if PVC can be offered at a significantly lower price than polyethylene (PE), for example. As the raw material for all competing plastics is the same – naphtha or the high value chemicals from the hydrocracker the price of chlorine is the decisive factor. This becomes even clearer when comparing PE and PVC from the production side. In each case, the raw material is ethylene from the cracking process, i.e. the same starting material. And the conversion process to the respective polymer is technically more complex for PVC than for PE. So only the price of chlorine makes PVC more attractive than PE, for example.

Let us summarize: Due to the limited storage capacities for chlorine, chlor-alkali electrolysis is generally controlled by chlorine sales [16]. If the PVC market falters, the electrolysis plants are scaled back. This also leads to a loss of revenue for the other linked products (electrolytic caustic soda, hydrogen), which exacerbates the economic problem. PVC sales, which account for around 35 to 40% of chlorine globally [17], are therefore vital for the chlor-alkali industry. The price of PVC is kept strategically low via the price of chlorine, which is possible due to joint production. This explains the economic success of PVC in the production phase. Below we will examine the costs and challenges that PVC poses for the end-of-life phase.

3. Consumption Phase

The authors of a study commissioned by the EU Commission identified various risks, particularly in relation to additives [iii]. However, they considered the data gaps to be so large that there were no recommendations for action. In particular, the question of the extent to which the additives – especially plasticizers – can leak out from the plastic seemed unclear, at least on the basis of the publicly available data. It is undisputed that plasticizers migrate, but the quantities are unclear and therefore the exact risks that must be present for a product ban, too.

The risks for the consumption phase have been known for decades: As early as the 1990s, for example, DEHP levels in Japanese homes were found to be on average 10 times higher than in outdoor air. And measurements in 2000/2001 in about 130 apartments and kindergartens in Germany showed a median DEHP level in house dust just around 1 g/kg [18,19]. These old studies can be "stacked" further [20]: "Children come into contact with DEHP released from a variety of products, including building materials, and flooring and wall coverings. In 2004, researchers in Sweden found that DEHP (and butyl benzyl phthalate) concentrations in dust were associated with PVC flooring and wall materials in their study of 390 homes [21]. In 2014, French researchers evaluated indoor air and dust in 30 French homes; again, phthalates, including DEHP, had the highest concentrations in both air and dust [22]”.

It was therefore consequent to clarify the need for regulation of PVC and PVC additives in more detail. To this end, the EU Commission commissioned the European Chemicals Agency (ECHA) to draw up an "Investigation Report". The report has been available since the end of 2023 [iv]. In it, the ECHA sees the following need for action:

- "Regulatory action is needed to minimize risks from plasticizers, and in particular ortho-phthalates", that have structures that have already shown reproductive toxicity or endocrine effects for related substances.

- "Regulatory action is needed to reduce the risks from the organotin substances."

- "Regulatory action is necessary to ensure minimization of the releases of PVC microparticles and prioritized PVC additives."

The substance-related need for action is based on the possible migration or emissions from plastics. The risks are seen both for the environment and for humans. The need for action can be handled via the respective REACH procedures. It is now up to the EU Commission to trigger mandates.

The regulatory consequences for reducing emissions of PVC microplastics are more difficult. The focus here is particularly on the recycling industry, as high emissions are assumed during processing (shredding). For example, a measurement campaign at a recycling plant in the UK, which was state of the art, showed that around 6% of the plastic waste (4–130 kg/t) was discharged as microplastics with the wastewater [25]. The plant had a high separation efficiency for particles with a size > 40 μm, with the majority of particles with a size of 5-40 μm being separated. Particles with a size < 5 μm were generally not removed by the filtration, but ended up in the wastewater. From their data, the authors concluded that without wastewater filtration, 13% of the plastic throughput would end up in the wastewater. The authors cite two other comparable publications [26,27] and conclude that – taking into account the different analytical methods used to determine the concentrations of microparticles in the process and waste water of the recycling plants – the results of all three available studies are coherent [xviii]. However, the database for this is very small so far. This will certainly need to be investigated further in the near future.

The risks of microplastic emissions, for example for the marine environment, have been scientifically described. PVC microplastic emissions are considered by the ECHA to pose an outstanding risk because PVC contains the highest quantities of problematic additives of all plastics. There are many areas of action for the risk management of microplastic emissions and these include, in particular, European industrial installations legislation [28], where limits could be placed on emissions via the air or water pathways.

Proposals for phasing out PVC itself are considered by ECHA to be socio-economically difficult, partly because PVC as a plastic is generally cheaper (PVC is therefore the cheapest option). A complete ban would therefore have economic disadvantages. ECHA recommends further assessments for a sectoral phase-out of PVC: "When considering which PVC uses contribute most to the environmental risks identified for the priority additives, cable (a soft PVC use) stands out as the only contributor to the releases of priority additives. .... The substitution of PVC with alternative materials in cables would be less costly than for other uses, and therefore a restriction of PVC in cables to minimize the risks of additives seems worth further evaluation" [iv].

4. End-of-Life Phase

PVC leads to problems as soon as PVC products become waste. Leaving aside the legacy additives (see [i, [29]]), most of the problems are related to the chlorine in the polymer molecule.

4.1. PVC Stock

As calculated in [i], around 6 million tons of PVC (compounds) are currently used in the EU every year. In the 1990s, the figure was already 5 million tons [30]. Around 85% of this ends up in the construction sector. Here, products such as pipes, sheets, cables, hoses and profiles have a service life of at least 30 to 50 years and more. This creates a gigantic stockpile, deposited in our buildings etc. By 2010, this stockpile had increased to a total of 270 kg/capita [xxii]. There are no current figures for today's situation. Since the 1990s, the PVC stockpile has grown by around 7 kg/capita per year. With this growth, the current figure would be just under 370 kg/capita, which would correspond to an in-use stock of 160 million tonnes PVC (compounds).

The problem of accumulated PVC stocks in our technical environment is not a new finding; it has been recognized since the 1990s (see Error! Reference source not found.) and [viii, p. 36]), but this development has not been stopped.

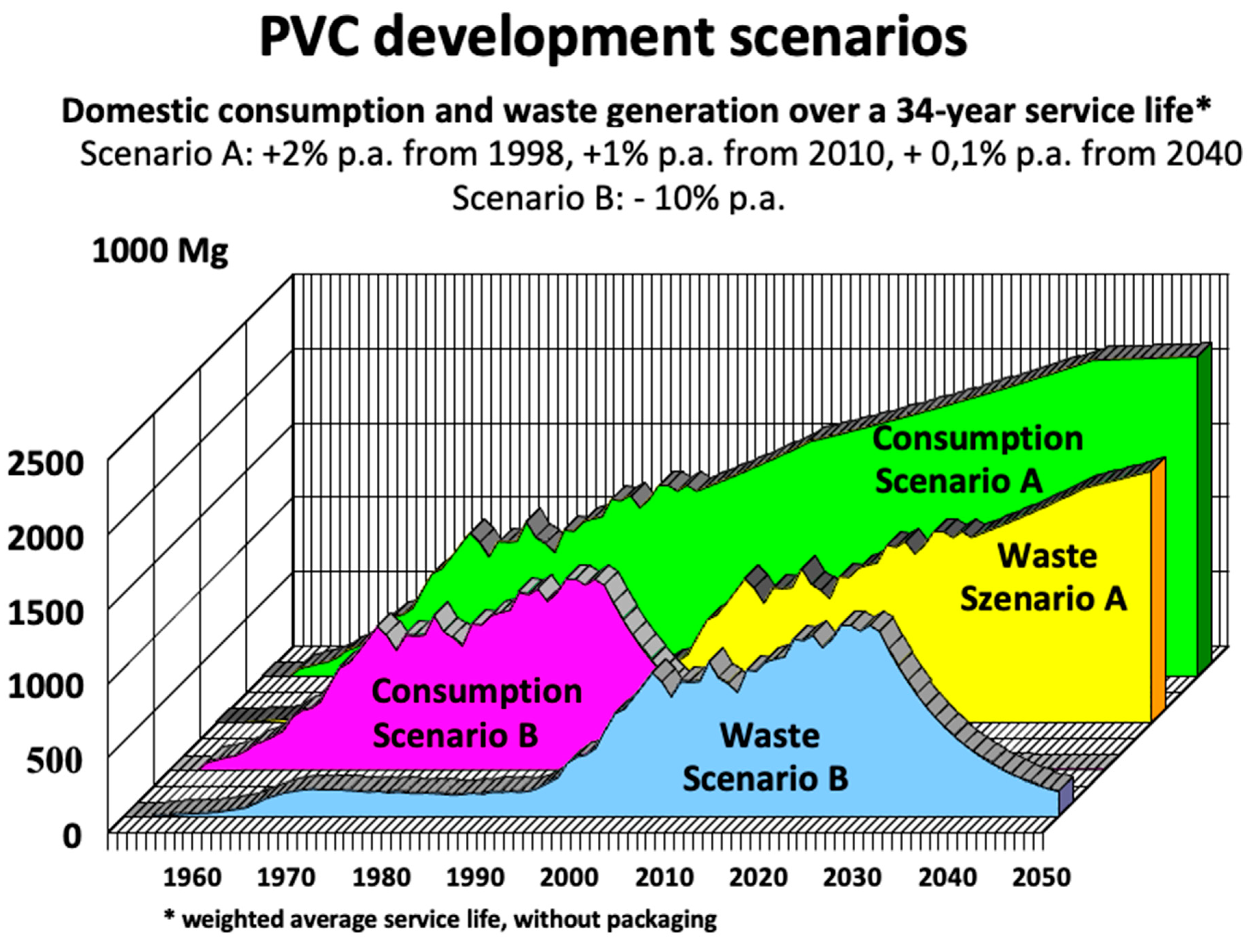

Figure 1.

Scenarios for the consumption of PVC products (compounds, excluding packaging) and subsequent waste generation in Germany; average service life: 34 years, without packaging. Source: [xxiii, xxiv], adapted.

Figure 1.

Scenarios for the consumption of PVC products (compounds, excluding packaging) and subsequent waste generation in Germany; average service life: 34 years, without packaging. Source: [xxiii, xxiv], adapted.

Error! Reference source not found.shows an estimate for Germany (created at the end of the 1990s [31,32]) as to when the PVC waste plastics put into circulation. The different options of the development of the PVC waste were considered in two scenarios. Scenario A assumes a (conservatively) estimated growth rate in new PVC production of 2% p.a. from 1998, plus 1% p.a. from 2010 and plus 0.1% p.a. from 2040. Even though government intervention was not apparent at that time, a phase-out or better conversion scenario was nevertheless presented in scenario B, in which PVC production falls by 6% each year – in relation to 1997 production. According to scenario A, the volume of PVC waste in Germany (excluding packaging) at the beginning of the 2020s was expected to be around 920.000 tonnes. This forecast is really near the data reported by 'Vinyl' [33]: "Compared to 2017, the volume of PVC waste increased by almost 24 percent to 861,000 tonnes in 2021. This increase is determined in particular by the increasing return of durable building products, which have been increasingly installed since the 1960s, 1970s and 1980s." According to [xxii], the amount of PVC waste has increased from around 3 kg per capita per year in the 1990s to just under 5 kg in 2010. Extrapolated to today, we are probably looking at a good 6 kg per capita per year. This is in line with forecasts made by experts in 1990. Assuming that the use of PVC in the construction industry would remain more or less constant, they calculated that from around 2000/2005, around 0.5 million tonnes of PVC residues (equivalent to a good 6 kg/capita) would have to be disposed of from construction waste every year [vi].

In summary, it can be said that solving the stockpiling problem is a matter of urgency, not least because the quantities stockpiled are increasing every year. As shown above, the annual volume of PVC waste is increasing, which the waste management industry has to cope with. Assuming that PVC consumption remains more or less unchanged, but the stock is increasingly transferred to the waste management sector, the growth of the stock slows down. However, according to our estimates, there is still a slight increase in the in-use stock. As the service life of PVC products and buildings is getting on in years, an avalanche of PVC into the waste management sector is to be expected in the coming years. What options does the waste management industry have to absorb this development? We will discuss this in the following.

4.2. Setting up a Chlorine Cycle to Cope with the Stock

Do we need to set up a chlorine cycle to solve the todays and especially the future stock-problem? In Germany, this discussion was held decades ago. Here is a quote from the Enquête Commission of the German Bundestag [34] on the subject [35]: AgPU [36] "expects that in future a capacity of 240,000 tons of PVC mono-incineration plants will be required annually, in which 144,000 tons of HCl will be produced. The increased supply of HCl will lead to a corresponding reduction in electrolysis capacity. ... Assuming a collection rate of 80%, 360,000 tons of HCl would be produced from 600,000 tons of PVC waste."

The PVC industry and AgPU, as mentioned, already advocated closing the chlorine cycle in the 1990s. However, as documented in [i], the use of MSWI (municipal solid waste incineration) for this purpose has so far been without practical success. PVC mono-incineration with separation of HCl would be another option. This HCl could be made available to the chemical industry for oxychlorination for VC production, for example. However, a relevant closure of the chlorine cycle leads to an excess of HCl [xxvi], which industry has to manage.

A relevant chlorine surplus, regardless of the cause, can only be absorbed by closing down electrolysis plants. This would require expensive imports of caustic soda or result in increasing the more expensive chemical causticizing process [xi].

The costs of establishing a chlorine cycle are difficult to estimate. "Initial estimates of the costs for the processes described indicate that they could be in the range of 100 to 400 euros/ton of waste delivered, with the REDOP [37] process tending to be at the lower end and the DOW/BSL [38] process at the upper end" [39].

To summarize: The stock problem could be solved by setting up a suitable technical infrastructure to close the chlorine cycle. However, this would have an impact on the chlor-alkali electrolysis capacities and on the sodium hydroxide supply.

4.3. Material Recycling of PVC to Cope with the Stock

The propagated material recycling (post-consumer waste, see [i]) has been stagnating for years at a low level. In our opinion, this is not an inability on the part of recyclers, but has to do with the chemical composition of PVC. Mixed PVC waste cannot be processed into high-quality products due to the different plasticizer types and concentrations (melting point, product homogeneity [40]). And even in the case of separately collected construction products, material recycling is complicated.

And the additives produce also legal problems, which are not solved up today. The content of additives also determines whether the PVC waste must be classified as non-hazardous or hazardous waste. E.g., the amendment to Annex VIII of the Basel Convention inserted a new entry A3210, which clarifies the scope of plastic wastes presumed to be hazardous and therefore subject to the PIC procedure. The new entry became effective as of 1 January 2021 [41]. The classification AC300 [42] resp. A3210 [43] applies – under others – to soft PVC waste containing hazardous stabilizers or phthalates in concentrations such that a hazard-relevant property applies (e.g. DEHP over 0.3% – HP10 toxic to reproduction), such as PVC flooring waste or cable peeling residues from old cables (incl. filter dusts from cable waste processing) [44,45].

In summary, it can be said that material recycling cannot make a relevant contribution to solving the stock problem, particularly because it is questionable whether there is a sense and a need for billions of additional low-quality recycling-products of around more than 100 million tonnes for the EU.

4.4. Chemical Recycling of PVC

Chemical recycling technologies such as pyrolysis, gasification, hydro-cracking or depolymerization are suitable for plastic recycling. Some pyrolysis processes can also tolerate moderate concentration of chlorine in the feedstock. But, to date, not a single plant exists that can chemically recycle relevant quantities of PVC waste [i]. One of the reasons for this is the economy of the chlor-alkali electrolysis, too. Industrial-scale chlorine or chemical recycling plants are likely to be larger than 100,000 t/a if they are to be operated economically. As early as 1994, AgPU stated the demand for plant capacity for chlorine recycling for Germany is at 240,000 tons per year [xxvi]. These plants would produce a lot of chlorine (probably HCl). Customers would have to be found for this. One likely consequence: chloro-alkali electrolysis capacities would have to be reduced, resulting in plant closures and economic losses [xxvi].

4.5. PVC and Co-Incineration to Cope the Stock

Chlorine interferes with energy recovery in cement plants [46]. Taking account of their local raw material situation, many cement plants (in Germany) have always operated bypass systems in order to control the chlorine and alkali balance of their kiln systems [47]. If waste-derived fuels have a higher chlorine content than standard fuels, it may be necessary to set up a bypass in cement plants that have not previously been affected in order to prevent the build-up of a chlorine cycle and the resulting caking. In this case, the energy balance of the process is also affected. For example, the removal of hot raw material and hot gas leads to a higher specific energy consumption of about 6 to 12 MJ/t clinker per percentage point of removed kiln inlet gas [48].

This problem can be solved by limiting the chlorine content in the input [xxxii]. Across Europe, there are quality standards for solid recovered fuels (SRF) that are categorizing SRF into classes focusing on the key properties net calorific value (NCV), content of chlorine (Cl) [49] and mercury (Hg), that are defined by boundary values (e.g. arithmetic mean, median or 80th percentile) [50]. According to general operating experience, the chlorine content should be below 1 % by mass (dry), which causes difficulties for many RDF processors.

Overall, waste co-incineration cannot increase the input of PVC and therefore for the future make a relevant contribution to solving the stock issue.

4.6. Incineration to Cope with the Stock

Today the main route for PVC waste is (municipal solid waste) incineration (see [i]). Within waste incineration, chlorine is converted to hydrogen chloride. HCl has a corrosive effect and increases the costs of flue gas cleaning. In the past, around 50 % of the chlorine input in incineration plants has been attributable to PVC [51]. It is assumed that due to the decline of PVC in the packaging sector and the recycling activities of DSD, the proportion may be lower today [52]. Concrete figures are not available. However, a significant increase in bulky waste is to be expected as discarded PVC building products from the stock are pressing into municipal waste management (see section 0).

So far, today's chlorine problem in the EU incineration plants has essentially been "solved" by dilution. For example, in the various thermal processes in the waste sector, care is taken to ensure that the respective chlorine content in the plant input does not exceed a certain concentration. For this reason, PVC is also specifically regulated in the acceptance conditions of some waste incineration plants (see [i]).

It must also be considered in light of the fact that waste incineration must and will change at latest by 2050. In the EU, municipal waste (MW) incineration will be subject to emissions trading in the future, e.g. already in Germany (German Fuel Emissions Trading Act [53]). In June 2022, the European Parliament approved the inclusion of municipal waste incineration installations in the revised EU Emission Trading System to the EU-ETS Directive, starting in January 2026 [54]. Due to the likelihood that this regulation is on its way, plastics are expected to be partly separated prior to waste incineration. In this Scenario, the operators of waste incineration plants would also attempt to reduce the PVC input in parallel and not increase it.

In this context, many waste incineration plants are also planning to remove CO2 from their waste gas. Today, it is already questionable whether open loop (no replacement of virgin PVC) or downcycling can provide sufficiently high life cycle assessment credits to be superior to energy recovery. Compared to climate-neutral waste incineration plants, life cycle assessment for downcycling would deteriorate further in the future. It is therefore particularly important for the future to include the high-quality recycling quantities in the recycling statistics for the EU and also for 'Vinyl' (replacement of virgin PVC, see [i]).

A further increase in the PVC-Input of the European incineration plants to cope with the PVC- stock would therefore not to be an option.

4.7. Landfilling of PVC

In the past, PVC's high concentration of additives, particularly plasticizers, led to pollution of seepage water and the surrounding area. There is still no landfill ban in the EU. According to the European Landfill Directive, member states may continue to landfill waste; this will only be limited to a maximum of 10% of the municipal waste generated from 2035 onwards. In some European countries (Germany, Austria, Switzerland (no EU member state)), the landfilling of high-calorific or other organic materials has been prohibited for years. The revision of the European Waste Framework Directive and the Landfill Directive in 2024 could provide the regulatory framework for a landfill ban by 2030.

Technically, PVC can be landfilled in large quantities. Even though this is prohibited in many European countries, these landfills can only be avoided in the long term if there is another option for solving the problem and this is also implemented.

5. Conclusion

The question of regulatory requirements must be answered separately for the different stages of the life cycle of PVC. The most pressing problems and therefore also the priority need for regulation exist, as shown above, for the end-of-life phase.

5.1. End-of-Life Phase

Obviously, none of the waste disposal processes currently in use (recycling, energy recovery) have sufficient capabilities to absorb the additional quantities of PVC from the stock. Therefore, the only solution to the today PVC-waste and the stock problem or the "PVC avalanche" that is heading towards the waste management sector is to dispose of PVC separately.

From a regulatory perspective, it should be discussed whether the few large polymer manufacturers in the EU should be obliged to take back PVC waste and convert it into HCl. This would create a plant infrastructure with which also the stock of PVC could be processed stepwise. This would relieve the other parts of the waste management sector of chlorine. However, this would, as we have described, result in the closure of chlor-alkali electrolysis capacities.

As shown above, ECHA rejects a phasing out of PVC especially with the socio-economic argument of the low costs of PVC compared to alternative plastics/materials [iv]. However, this argument is only applicable if the additional costs of the post-consumer phase – for the disposal of chlorine and the management of the PVC stock – are not taken into account. If included, PVC becomes an expensive plastic and a year by year-increasing legacy that necessitates phase-out soon.

5.2. Production

The regulatory requirements for the production phase are, in our opinion, sufficiently defined to ensure the protection of employees and consumers. The environmental organizations point out that several additives in PVC are not regulated e.g. by REACH; due to bottlenecks of resources and data availability the regulation of further PVC additives has not progressed further yet. The papers of the European Commission [iii] and ECHA [iv] fail – to their opinion – to address aspects that would justify or necessitate a corresponding need for regulation, such as quoting an authorization to be in place as a risk management measure does not consider the not unusual cases of non-compliance. Also, accidents during transport like the East Palestine, Ohio train Derailment on February 3, 2023, where vinyl chloride was one of the primary chemicals of concern involved in the derailment [55] are not or not sufficiently addressed up to today.

The economics of chlorine production make it clear why PVC is a cost-effective plastic. The economic effects of a "ban" and a closed cycle of PVC for chlor-alkali electrolysis are similar.

5.3. Consumption Phase

For the consumption phase of PVC, there are a whole series of requirements for chemical legislation, both with regard to the plastic itself and in particular the additives used. The ECHA has drawn up a comprehensive catalogue of requirements in its Investigation Report, which we support.

References

- Lahl, U.; Zeschmar-Lahl, B. (2024): Over 30 years of PVC recycling – a critical inventory. Submitted for publication.

- European Commission (2000): GREEN PAPER: Environmental issues of PVC. Brussels, 26.7.2000, COM(2000) 469 final https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=LEGISSUM%3Al28110 (https://eur-lex.europa.eu/legal-content/EN/TXT/PDF/?uri=CELEX:52000DC0469).

- European Commission, Directorate-General for Environment (2022): The use of PVC (poly vinyl chloride) in the context of a non-toxic environment – Final report. Publications Office of the European Union https://data.europa.eu/doi/10.2779/375357 (https://op.europa.eu/en/publication-detail/-/publication/e9e7684a-906b-11ec-b4e4-01aa75ed71a1).

- ECHA (2023): INVESTIGATION REPORT ON PVC AND PVC ADDITIVES. VERSION NUMBER: 1.0 (Final), DATE: 22/11/2023 https://echa.europa.eu/documents/10162/17233/rest_pvc_investigation_report_en.pdf.

- For example, through the so-called soda-lime process, using naturally occurring calcium carbonate (limestone) and sodium carbonate (e.g. natron from soda lakes).

- Economic Intelligence Report: The soda ash and chemical caustic soda industry in the USSR. CIA/RR 29, CRR Project 22.4.1 https://www.cia.gov/readingroom/docs/DOC_0000316347.pdf.

- However, chemical production maintained in medium-sized form, particularly in emerging markets.

- 2 NaCl + 2 H2O → H2 + Cl2 + 2 NaOH.

- Tötsch, W., Gaensslen, H. (1990): Polyvinylchlorid – Zur Umweltrelevanz eines Standardkunststoffes. Verlag TÜV Rheinland GmbH, Köln, 1990.

- Euro Chlor/Cefic (2023): Chlor-alkali industry review 2022/2023 https://www.eurochlor.org/wp-content/uploads/2023/10/Chlor-Alkali-Industry-Review_CORRECTED-2023-10-06.pdf.

- Umweltbundesamt (1999): Handlungsfelder und Kriterien für eine vorsorgende und nachhaltige Stoffpolitik am Beispiel PVC. Umweltbundesamt (Ed.), Erich Schmidt Verlag, Berlin, 1999.

- IG Farben was formed 1925 from the merger of eight German companies – Agfa, BASF, Bayer, Cassella, Chemische Fabrik Griesheim-Elektron, Chemische Fabrik vorm. Weiler-ter Meer, Hoechst and Chemische Fabrik Kalle.

- Vinyl Council Australia (undated): Chlorine https://www.vinyl.org.au/chlorine (5.3.2024).

- Lahl, U. (2023): Chemische Energien. In: Hermann, W. (Hrsg.): Antriebswende. Strategien, Positionen und Meinungen zur neuen Mobilität, 53–82 https://www.bzl-gmbh.de/antriebswende-chemische-energien-2023/.

- Wesnæs, M., Weidema, B.P. (2006): Long-term market reactions to changes in demand for NaOH. Study for Novozymes. Copenhagen: 2.-0 LCA consultants. https://lca-net.com/files/naoh.pdf.

- "Since chlorine cannot be stored, chlor-alkali plants are operated in line with demand for chlorine, itself highly influenced by the demand for PVC" [ix].

- "Worldwide about 35-40 per cent of the chlorine manufactured is used to make PVC" [ix].

- Median: 703 mg/kg; range: 31–1763 mg/kg.

- The European Council of Vinyl Manufacturers – ECVM (2024): Health concerns about indoor air quality https://pvc.org/about-pvc/pvc-additives/plasticisers/health-concerns-about-indoor-air-quality/ (11.03.2024).

- Health Care Without Harm – HCWH (2021): The polyvinyl chloride debate: Why PVC remains problematic material. June 2021 https://noharm-europe.org/sites/default/files/documents-files/6807/2021-06-23-PVC-briefing-FINAL.pdf.

- Bornehag, C.-G.; Sundell, J.; Weschler, C.J.; Sigsgaard, T.; Lundgren, B.; Hasselgren, M.; Hägerhed-Engman, L. (2004): The Association between Asthma and Allergic Symptoms in Children and Phthalates in House Dust: A Nested Case-Control Study Environmental Health Perspectives Volume 112, Issue 14, 1393–1397. [CrossRef]

- Blanchard, O.; Glorennec, P.; Mercier, F.; Bonvallot, N.; Chevrier, C.; Ramalho, O.; Mandin, C.; Le Bot, B. (2014): Semivolatile Organic Compounds in Indoor Air and Settled Dust in 30 French Dwellings. Environmental Science & Technology 2014 48 (7), 3959–3969. [CrossRef]

- ECHA (2023): ECHA identifies certain brominated flame retardants as candidates for restriction. ECHA/NR/23/07, Helsinki, 15 March 2023 https://echa.europa.eu/de/-/echa-identifies-certain-brominated-flame-retardants-as-candidates-for-restriction.

- ECHA (2023): Regulatory strategy for flame retardants. March 2023 https://echa.europa.eu/documents/10162/2082415/flame_retardants_strategy_en.pdf.

- Brown, E.; MacDonald, A.; Allen, S.; Allen, D. (2023): The potential for a plastic recycling facility to release microplastic pollution and possible filtration remediation effectiveness. Journal of Hazardous Materials Advances, Volume 10, 2023, 100309, (https://www.sciencedirect.com/science/article/pii/S2772416623000803). [CrossRef]

- Guo, Y.; Xia, X.; Ruan, J.; Wang, Y.; Zhang, J. Guo, Y.; Xia, X.; Ruan, J.; Wang, Y.; Zhang, J.; LeBlanc; G.A.; An, L. (2022): Ignored microplastic sources from plastic bottle recycling. Sci. Total Environ. 838 (2), 156038 https://www.sciencedirect.com/science/article/abs/pii/S0048969722031357. [CrossRef]

- Suzuki, G.; Uchida, N.; Tuyen, L.H.; Tanaka, K.; Matsukami, H.; Kunisue, T.; Takahashi, S.; Viet, P.H.; Kuramochi, H.; Osako, M. (2022): Mechanical recycling of plastic waste as a point source of microplastic pollution. Environ. Pollut. 303, 119114 https://www.sciencedirect.com/science/article/abs/pii/S0269749122003281. [CrossRef]

- Industrial Emissions Directive (IED), Best Available Technique (BAT), BAT Reference documents (BREFs).

- ECHA (2023): INVESTIGATION REPORT ON PVC AND PVC ADDITIVES. Appendix F – Legacy additives in PVC https://echa.europa.eu/documents/10162/17233/rest_pvc_investigation_report_appendix_f_en.pdf.

- Ciacci, L.; Passarini, F.; Vassura, I. (2017): The European PVC cycle: In-use stock and flows. Resources, Conservation and Recycling, Volume 123, 108–116. https://www.sciencedirect.com/science/article/pii/S0921344916302002. [CrossRef]

- Lahl, U.; Zeschmar-Lahl, B. (1997): PVC-Recycling: Anspruch und Wirklichkeit. Hrsg.: GREENPEACE Deutschland, 1997.

- Lahl, U.; Zeschmar-Lahl, B. (1998): Recycling von PVC-Kunststoffen. Müll-Handbuch, Kz. 8625.2, Lfg. 9/1998.

- VinylPlus (undated): Industry uses significantly more recyclates. https://www.pvcrecyclingfinder.de/en/pvc-recycling-in-deutschland/ (12.3.3024).

- Deutscher Bundestag (1994): Bericht der Enquête-Kommission „Schutz des Menschen und der Umwelt – Bewertungskriterien und Perspektiven für umweltverträgliche Stoffkreisläufe in der Industriegesellschaft". 12. Wahlperiode, Drucksache 12/8260, 12.07.94 https://dserver.bundestag.de/btd/12/082/1208260.pdf.

- "Seitens der AgPU wird damit gerechnet, dass zukünftig eine Kapazität an Monoverbrennungsanlagen von 240 000 t PVC jährlich benötigt wird, in denen 144.000 t HCl anfallen. Das erhöhte Angebot an HCl führt zu einer entsprechenden Rückführung der Elektrolysekapazität. … Eine Erfassungsquote von 80 % vorausgesetzt, würden aus 600.000 t PVC-Abfällen 360.000 t HCl entstehen.".

- Arbeitsgemeinschaft PVC und Umwelt (= Working Group on PVC and Environment).

- Reduction of iron ore by plastics in blast furnace plants.

- DOW/BSL rotary kiln process.

- Bühl, R. (2003): Progress in PVC feedstock recycling. POLIMERY 2003, 48 (4), 263–267 https://ichp.vot.pl/index.php/p/article/download/1861/1816.

- Ait-Touchente, Z.; Khellaf, M.; Raffin., G.; Lebaz, N.; Elaissari, A. (2024): Recent advances in polyvinyl chloride (PVC) recycling. Polym Adv Technol. 2024;35. [CrossRef]

- Basel Convention (2019): Plastic Waste Amendments. https://www.basel.int/Implementation/Plasticwaste/Amendments/Overview/tabid/8426/Default.aspx.

- Notification required for shipments within the EU or between OECD countries.

- Hazardous plastic waste imported from non-OECD countries; waste with code A3210 may not be exported to non-OECD countries.

- Bundesministerium Klimaschutz (BMK), Österreich (2022): Nationale Klarstellungen und Ergänzungen zu den EU-Anlaufstellen-Leitlinien Nr. 12 zur Einstufung von Kunststoffabfällen bei der grenzüberschreitenden Verbringung. Wien, 13. Juni 2022 https://www.bmk.gv.at/dam/jcr:07c4d9f6-99d8-490e-86dd-364bfc8aba6f/Nationale-Klarstellungen-Ergaenzungen_20220613.pdf.

- Löw, S. (2023): Österreichs Position zum Thema Kabelrecycling & Kabelschälreste. Juni 2023.

- Zeschmar-Lahl, B. , Schönberger, H., Waltisberg, J. (2020): Abfallmitverbrennung in Zementwerken. Sachverständigengutachten im Auftrag des Umweltbundesamtes, UBA-Texte 202/2020. https://www.umweltbundesamt.de/sites/default/files/medien/5750/publikationen/2020_11_05_texte_202_2020_abfallverbrennung_zementwerke_1.pdf.

- VDZ (2007): Activity Report 2005–2007 https://www.vdz-online.de/fileadmin/wissensportal/publikationen/basiswissen/taetigkeitsberichte/VDZ_Activity_Report_2005-2007.pdf.

- European Commission (2013): COMMISSION IMPLEMENTING DECISION of 26 March 2013 establishing the best available techniques (BAT) conclusions under Directive 2010/75/EU of the European Parliament and of the Council on industrial emissions for the production of cement, lime and magnesium oxide (notified under document C(2013) 1728) (2013/163/EU) https://eur-lex.europa.eu/legal-content/EN/TXT/PDF/?uri=CELEX:32013D0163&from=EN.

- Chlorine (% in mass (d)): Class 1: ≤ 0.2; class 2: ≤ 0.6; class 3: ≤ 1.0; class 4: ≤ 1.5; class 5: ≤ 3.

- International Organization for Standardization – ISO (2021): Solid recovered fuels – Specifications and classes (ISO 21640:2021) https://www.iso.org/standard/71309.html.

- European Commission (2000): Green Paper – Environmental issues of PVC. Brussels, 26.7.2000, COM(2000) 469 final https://eur-lex.europa.eu/legal-content/EN/TXT/PDF/?uri=CELEX:52000DC0469.

- KRV Wissensportal (2024): Die ökologische Rolle von PVC in Müllverbrennungsanlagen. https://www.krv.de/wissen/energetische-verwertung (8.4.2024).

- Gesetz über einen nationalen Zertifikatehandel für Brennstoffemissionen (Brennstoffemissionshandelsgesetz – BEHG), vom 12. Dezember 2019. Bundesgesetzblatt 2019 Teil I Nr. 50, 19. Dezember 2019 http://www.bgbl.de/xaver/bgbl/start.xav?startbk=Bundesanzeiger_BGBl&jumpTo=bgbl119s2728.pdf.

- European Parliament (2022): Amendments adopted by the European Parliament on 22 June 2022 on the proposal for a directive of the European Parliament and of the Council amending Directive 2003/87/EC establishing a system for greenhouse gas emission allowance trading within the Union, Decision (EU) 2015/1814 concerning the establishment and operation of a market stability reserve for the Union greenhouse gas emission trading scheme and Regulation (EU) 2015/757 (COM(2021)0551 – C9-0318/2021 – 2021/0211(COD))(1) https://www.europarl.europa.eu/doceo/document/TA-9-2022-06-22_EN.html (https://www.europarl.europa.eu/doceo/document/TA-9-2022-0246_EN.pdf).

- EPA (2024): East Palestine, Ohio Train Derailment: Background. Last updated on April 3, 2024 https://www.epa.gov/east-palestine-oh-train-derailment/background (11.4.2024).

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Copyright: This open access article is published under a Creative Commons CC BY 4.0 license, which permit the free download, distribution, and reuse, provided that the author and preprint are cited in any reuse.