Submitted:

02 May 2024

Posted:

03 May 2024

You are already at the latest version

Abstract

In recent years, ESG (environmental, social, governance) has emerged as a critical investment concept. Its goal is to create value for both shareholders and society, encouraging companies to optimize social value. However, the exploration and research into "the proportion of firms ex-porting and the pathways through which the environmental, social, and governance activities of carbon-intensive firms influence firms' financial performance" remains largely unexplored. This study establishes a research framework within this context, utilizing listed Chinese manufactur-ing companies as the research subjects. Employing a fixed-time, fixed-industry, two-way fixed-effects model methodology, it delves into the relationship between ESG ratings, the pro-portion of firms' exports, and firms' financial performance through panel regression modeling. This study emphasizes the moderating role of carbon-intensive firms in the relationship. Find-ings indicate that both enterprise export proportions and carbon-intensive firms significantly affect the correlation between corporate ESG activities and financial performance. This has im-plications for investors, company management, policymakers, and regulators. Based on these findings, we propose policy recommendations at corporate and governmental levels to enhance ESG significance, strengthen corporate governance, and promote continuous ESG advancement. The study provides micro-level evidence of the interaction among ESG ratings, export ratios, carbon-intensive enterprises, and corporate performance, empowering investors to make in-formed decisions.

Keywords:

ESG ratings

; corporate financial performance

; corporate export ratio

; carbon-intensive firms

; Chinese listed firms

1. Introduction

Global environmental concerns are on the rise, prompting countries to develop sustainable development programs aimed at tackling climate change. In China, as economic transformation progresses, the concept of green development is gaining traction, with enterprises playing a pivotal role in promoting sustainability. In recent years, the Chinese government has implemented a series of policies to promote ecological civilization and green development. In alignment with these efforts, the ESG evaluation system has gained increasing attention. Regulators have issued policies to integrate ESG elements into the oversight of listed companies, encouraging ESG information disclosure and enhancing supervision. Meanwhile, the export ratio of enterprises, a crucial economic indicator, significantly influences corporate performance and long-term development, especially in achieving the 'dual carbon' goal. Given the unique dynamics of the Chinese economy, it is clear that domestic demand is paramount. However, leveraging exports for growth is also indispensable. Thus, factoring in the export rate allows for a holistic assessment of a company's economic robustness and sustainability, offering broader insights for achieving the "double carbon" goal.

Despite numerous empirical studies analyzing the link between ESG and corporate financial performance, findings vary and can be categorized into two main perspectives: one suggests a negative correlation between ESG and corporate financial performance, while the other proposes a positive correlation. ESG is thought to enhance corporate financial performance [1,2,3]. Moreover, ESG initiatives can boost firms' financial performance by bolstering investor confidence and fostering innovation [4]. Different industries place different emphasis on environmental, social and governance ( ESG ) factors. For example, the automotive industry places more emphasis on governance (G) [5], and European firms prioritize social factors (S) [6]. Some studies suggest that prioritizing environmental performance may negatively affect firms, resulting in increased expenditures on disclosing ESG information and decreased financial performance [7]. ESG controversies may somewhat weaken corporate performance [8]. Other studies have found no significant relationship between ESG performance and corporate financial performance, suggesting that ESG policies may have a limited short-term impact on corporate financial performance [9]. Emphasizing environmental factors alone in ESG may not enhance corporate performance. Additionally, the relationship between ESG and financial performance may be insignificant for certain enterprises, such as those not primarily engaged in pollution monitoring or high-tech industries [10]. Many scholars tend to concentrate on the influence of individual ESG factors on firms' financial performance, often overlooking the significance of other interconnected factors. Although the impact of ESG strategies and operations on corporate financial performance has been a hot topic in modern academic and business research, there is still a relative lack of research in the ESG literature on the impact of ESG ratings of carbon-intensive companies on their financial performance. Additionally, the export activities of listed firms play a crucial role in economic development [11]. However, research on firms' export ratios remains limited from this perspective. Carbon-intensive industries play a crucial role in ecological sustainability [12]. Sixteen carbon-intensive industries, including coal, mining, textile, tannery, paper, petrochemical, pharmaceutical, chemical, metallurgy, and thermal power, are categorized as carbon-intensive enterprises [13]. Given the nature of their operations, carbon-intensive listed companies are significant contributors to carbon emissions. Consequently, these companies face stringent regulations and social pressure from environmental protection agencies [14]. Therefore, understanding the correlation between ESG activities and financial performance in carbon-intensive industries is imperative. In summary, the main issues identified in this study are as follows: Do ESG ratings of Chinese listed companies affect their financial performance? Does the ESG rating of Chinese listed companies affect their export ratio? What is the impact of E, S, and G factors on a firm's financial performance? Which factor has the greatest influence? What is the impact of export ratio, a key indicator of corporate development, on company performance? Does the presence of carbon-intensive firms impact financial performance? These questions constitute the focal point of this study. Therefore, the purpose of this paper is to study the impact of ESG rating on corporate financial performance and its specific impact paths, to provide more guidance and practice for Chinese enterprises to create long-term sustainable earnings, and to provide policy reference suggestions for the sustainable development of China's economy. Building on the background, this study focuses on manufacturing enterprises listed on the Shanghai and Shenzhen stock exchanges from 2009 to 2022. Its objective is to delve into the influence of ESG factors on corporate financial performance. The contributions of this paper are outlined below:

This study confirms the influence of ESG performance on corporate financial performance. Unlike previous studies that predominantly examine the impact of individual ESG factors on corporate financial performance, this study explores the independent effects of environmental (E), social (S), and governance (G) factors separately. Furthermore, this study validates the influence of the firm's export ratio as an additional factor, enhancing the understanding of elements affecting firms' financial performance. Lastly, this study examines the moderating effects of significant carbon-intensive firms in China on the relationship between ESG and corporate financial performance. Through these validations, this study aims to provide more guidance and practical experience for Chinese firms to create long-term sustainable profitability, as well as to provide reference suggestions for the formulation of related policies.

The main text is structured as follows: The introductory section provides background information on ESG research and underscores the critical importance of ESG for Chinese manufacturing enterprises. The second part gives a comprehensive introduction to the literature review and then presents the hypotheses of this study. The third part is the research model, variable definitions, and research methodology of this study. The fourth part is the analysis results of the empirical study. Finally, the fifth part, as the conclusion part, summarizes the results of the study and its managerial and theoretical significance, and makes suggestions for future research.

2. Literature Review and Research Hypotheses

- (1)

- ESG ratings and corporate financial performance

ESG is Environmental, Social and Governance and its various sub-factors [15]. ESG is considered to have a significant impact on the sustainability and long-term value of a company by minimizing the negative impacts that a company may have on the environment and society and maximizing the effectiveness of corporate governance [16]. ESG contains a wide range of information related to the environment, society, and dominance structure, and therefore can be an important indicator for firms to consider along with financial results when making decisions [17]. If a firm has a high level of ESG, it can effectively deal with various risks including market, policy and financial risks, which can help to improve its business performance [18]. According to existing studies, there is a close relationship between ESG and firms' financial outcomes [19]. For example, some studies found that firms' non-financial and ESG efforts negatively impacted liquidity and efficiency but ultimately improved profitability and cash generation [18]. Han et al. (2016) analyzed the relationship between ESG ratings and firm performance and confirmed that there was a significant effect between the two [20]. In a study utilizing the ESG index of the Korea Domination Constructing Institute, ESG outcomes and the financial outcomes or corporate value of the firms were largely positively correlated [21]. These studies confirm that there is a close relationship between non-financial and ESG and corporate outcomes or business results.

As listed companies that form the backbone of China's economy, ESG issues are crucial to China's economic development in the national strategy [22]. Listed companies, as leaders of enterprise development, should pay more attention to ESG, reduce environmental, social and governance structure risks through ESG improvement, improve risk response-ability, promote sustainable development, and ultimately improve enterprise efficiency [23]. Therefore, listed companies should pay more attention to ESG rating for sustainable development. From the above perspective, ESG ratings help to reduce the negative impacts of environmental, social and governance structure issues encountered by firms in their business activities, improve operational efficiency, and positively affect corporate performance. Based on this, the following assumptions can be made.

Hypothesis 1:

ESG ratings have a positive impact on firms' financial performance.

- (2)

- E ratings and corporate financial performance

Increasing environmental pressures and natural deterioration have become a major obstacle for mankind. Sustainable development and environmental issues are increasingly emphasized by the international community, academia and industry, and these issues directly affect the business activities of enterprises and their financial performance [24]. At the same time, research on environmental issues has been actively carried out, and the impact of environmental issues has been explored from different perspectives, such as resource depletion and industrial waste emissions. Different enterprises encounter different environmental problems in their production processes, and therefore the environmental strategies they choose are also diverse. In Europe, firms' environmental strategies play an important role in the regulation of environmental and economic performance, especially for firms adopting shareholder value-oriented strategies [24]. Countries are in the process of developing environmental policies and rules that are appropriate to their circumstances, and China is no exception. China requires firms to manage their production in accordance with established environmental regulations and to publish environmental information on a regular basis [25]. Strict environmental regulations promote competition among firms, which ultimately improves firms' efficiency, encourages lower production costs, and increases consumer satisfaction and sales, thereby improving firms' profitability. Firms with high environmental levels tend to publish environmental information more frequently and with greater transparency. From the standpoint of a company, publishing environmental information about its own company may have an impact on the stock price. Negative news reports related to the environment may have a negative impact on the stock price, while positive reports may have a positive impact [26]. Therefore, to enhance corporate value, companies may comply with environmental laws and regulations, proactively prevent undesirable environmental activities, and proactively publicize environmental information. These environmental efforts may adversely affect corporate effectiveness in the short term, but in the long term, they are more conducive to sustainable development and ultimately improve corporate performance [27].

Existing studies have analyzed the correlation between environmental outcomes and business outcomes. The results show that there is a significant correlation between the environmental investment index and the price-earnings ratio, and there is a close relationship between environmental performance and corporate financial performance [28]. Enterprises with high environmental performance not only significantly improve their external reputation but also increase their business performance. In addition, previous studies have shown that the level of environmental business activities of enterprises has a positive impact on enterprise value [29]. Therefore, the following hypotheses are proposed in this study.

Hypothesis 2:

E ratings have a positive impact on firms' financial performance.

- (3)

- S ratings and corporate financial performance

Corporate social responsibility is a hot topic in current academic research. Academics have launched extensive research on social responsibility. The business objectives of enterprises should pursue both the maximization of a single benefit and the maximization of the overall well-being of stakeholders. From this perspective, social responsibility can be defined as a company's efforts to maximize corporate value by strengthening ethical management [30]. Research confirms that corporate social responsibility positively affects financial performance [31].

By engaging in social responsibility activities, companies can improve their social reputation, increase consumer confidence, attract investors, and ultimately promote sustainable development. Prior studies have shown that in the literature examining the relationship between CSR activities and firm value, there is empirical evidence that excessive corporate social involvement can improve brand image, employee satisfaction, and customer loyalty and positively affect firm performance [32]. In other words, if a company can actively participate in social activities, corporate value and business results will rise. Actively fulfilling social responsibility helps to reduce the adverse social and environmental risks faced by enterprises, reduce negative social impacts, increase social awareness, and avoid some potential lawsuits and industry regulatory issues, thus reducing corporate risks [33]. Employees who work in companies with positive social impacts feel a greater sense of fulfillment, which helps to improve employee performance and creativity. Positive corporate social responsibility often helps to build a favorable corporate image and enhance corporate reputation [34]. These positive images help to build trusting relationships with stakeholders such as shareholders, employees, and customers, which in turn improves the firm's position in the market. Some investors and shareholders are increasingly focusing on corporate social responsibility performance. A high level of social responsibility can attract more socially responsible investors and increase the share price and market value of a company [35].

Listed companies, as an important part of Chinese enterprises, should actively participate in social activities. The active participation of enterprises in social responsibility activities is usually due to their long-term planning for sustainable development. This long-term perspective facilitates enterprises to better cope with changes and uncertainties and improve their long-term performance. That is, the more a firm engages in social activities, the higher the financial results of its operations [36]. Therefore, the following hypothesis is formulated.

Hypothesis 3:

S ratings has a positive impact on firms' financial performance.

- (4)

- G ratings and corporate financial performance

Unstable external factors have a negative impact on business operations. Compared to the uncertainty of the external environment, firms pay more attention to the management and improvement of the internal environment. To reduce the uncertainty of internal environment, firms should strengthen their own control structure [37].

By measuring various factors such as shareholders' rights, board of directors, outside directors, share concentration, public disclosure system, ownership consistency, etc., corporate dominance structure is proved to be a determinant factor affecting the value of the firm [38]. Therefore, firms can mitigate the dominance structure problem by improving various dominance structure subordinate factors such as extra-social director ratio, board size, institutional investor share rate, and operator share rate [39]. Current research on the relationship between corporate governance structure and corporate performance is quite extensive. For example, the results of research on the relationship between corporate dominance structure and firm value show that firm value increases with the increase in the operator's shares, and the higher the rate of out-of-society directorships and the shares of institutional investors, the higher the value of the firm [40]. The dominant structure activities of the firm can increase the transparency of the financial information of the firm [41]. In terms of economic outcomes, higher levels of dominance structure are associated with higher business outcomes [42,43].

In domestic and international studies on the relationship between corporate dominance structure and firm value, Korean scholars utilized the corporate dominance structure index of the Corporate Domination Structure Institute. They found that the higher the dominance structure index, the higher the financial outcome and firm value of the firm. A study of the relationship between dominant structure and firm value in Korea revealed a meaningful positive relationship between the dominant structure index and firm value [44]. A study of the relationship between corporate governance structure and firm performance in the United States measured corporate governance structure indices. It confirmed a positive correlation between the indices and firm value [38]. In addition, using the level of shareholders' equity of the top 1500 firms in the 1990s, the stronger the dominance structure, the better the firm value and operating results [43]. In other words, if firms pursue a better and healthy dominance structure, they can increase firm value and operating results. Previous research on Chinese dominance structure suggests that there is a defined correlation between dominance structure and return on assets for Chinese firms [45]. For Chinese firms, there is a considerably defined relationship between dominance structure and firm value, which proves that for every 1% increase in the level of dominance structure, firm value increases by 0.01%. Based on these findings, this study aims to clarify the relationship between the level of governance and corporate financial performance of listed companies in China and, therefore, proposes the following hypotheses on the basis of previous studies.

Hypothesis 4:

G ratings have a positive impact on firms' financial performance.

- (5)

- ESG ratings, firm export ratios and firm financial performance

More studies are needed on enterprise ESG rating evaluation and enterprise export ratio. As the concept of sustainable development penetrates all aspects of enterprise development, ESG-related concepts and systems are being improved. Most of the existing studies believe that an enterprise's ESG performance can improve its financial performance and operational performance in terms of environment, society, and corporate governance, and from the perspective that ESG performance unilaterally supports exports, thus enhancing the competitive advantage of exporting enterprises in the international market and promoting their exports [46].

Generally speaking, enterprises with high ESG not only have good management ability and financial performance but also pay attention to the sustainable development of the enterprise, which is characterized by solid risk resistance, high credit quality, etc. On the one hand, it reduces the cost of capital acquisition, which can improve the performance of the environment, social responsibility, and corporate governance. On the other hand, it improves the market competitiveness of the enterprise's products through a good reputation, which has a positive exporting impact [47].

First, according to stakeholder theory, high ESG performance of enterprises is more likely to attract the attention of relevant stakeholders in the market, so that export enterprises can benefit from the advantages of low cost and high market share [48].; second, for the government, the government and relevant administrative units can introduce ESG-related policies and guiding measures, so that enterprises pay attention to the green development and the concept of sustainable development, which is conducive to the good and stable development of the whole economy. Enterprises with strong business management ability and high social influence are important handholds for the government to promote ESG development. Enterprises with high ESG performance are more likely to establish a good relationship with the government and obtain a better development environment. As the government plays an important resource allocation role in economic development, enterprises with high ESG performance can play a "leading role" and enjoy corresponding financial support and policy preferences, which is conducive to promoting exports and giving exporters more advantages in terms of policies and costs [49]. Third, from the perspective of consumers, enterprises with high ESG performance have high levels of business management and produce high quality products [50]. Through effective communication and active social participation, consumers' awareness and satisfaction with products can be increased, making them more inclined to purchase products from firms with high ESG performance [51]. On the other hand, firms with high ESG performance indicate that the firms are performing well in environmental protection and corporate social responsibility, and since environmental protection awareness is deeply rooted in people's minds, firms with high ESG performance can attract environmentalist consumers to buy the products they produce [52]. Therefore, high ESG performance can increase a firm's operating profit and market share, and positively affect the firm's exports. Based on this, we propose the following hypothesis.

Hypothesis 5:

ESG ratings have a positive impact on firm export ratios.

Hypothesis 6:

Firm export ratios will mediate the relationship between ESG ratings and firms' financial performance.

- (6)

- The Moderating Role of Carbon Intensive Firms

The "double carbon" goal is an inherent requirement for China to achieve high-quality and sustainable development, and China's time to achieve the "double carbon" goal is tight and the task is heavy, and the high-carbon enterprises in the eight industries of iron and steel, petroleum, electric power, and chemical industry are not only important industries for China's economic development, but also have become the focus and difficulty of China's realization of the "double carbon" goal that cannot be ignored, and it has great significance for promoting the green transformation of enterprises and realizing sustainable development [53]. According to previous studies, 1,755 listed companies disclosed ESG-related reports in 2022, accounting for 34.32%, which also fully indicates that ESG plays the role of "booster" in the green development of enterprises [54].

From a sustainable development perspective, ESG performance enhances enterprises' risk tolerance, boosts long-term financial performance, and increases organizational flexibility. However, listed companies, as key players in the capital market's high-quality development, may also impact the environment negatively while extracting resources for value creation [55], with carbon-intensive enterprises being the most representative. To actively and steadily promote the realization of the "dual carbon" goal and strengthen enterprises' environmental awareness and green behaviors, local governments have introduced a series of environmental regulatory policies. Carbon-intensive enterprises with high ESG performance can timely avoid various policy barriers brought about by environmental regulation, effectively respond to the improvement of product and production standards, improve domestic and international ESG performance, reduce the risks and economic losses caused by environmental issues, and improve the long-term performance of enterprises and enhance organizational flexibility [56]. In addition, the development of ESG requires companies to improve their production processes and replace energy-intensive technologies with green and low-carbon technologies, which obviously puts higher demands on carbon-intensive companies. High-carbon enterprises that actively improve their ESG performance have more experience in green development, which can effectively reduce the risks caused by poor management, improve organizational flexibility, and promote corporate financial performance.

From the perspective of the enterprise's own environmental pollution, carbon-intensive enterprises generally pay more attention to environmental protection and take more green sustainable development measures [57], which not only help reduce the enterprise's operating costs such as energy and resource use, but also reduce the negative impact on the environment. Carbon-intensive enterprises optimize their production processes and use clean energy, which not only reduces environmental risks but also establishes an environmentally friendly image, which has a positive impact on financial performance.

Hypothesis 7:

Carbon-intensive enterprises will moderate the relationship between ESG ratings and firms' financial performance.

3. Research Design

3.1. Sample Selection and Data Sources

This study analyzes the impact of corporate ESG ratings on corporate financial performance based on a sample of manufacturing enterprises listed on China's Shanghai and Shenzhen stock exchanges with 14 years of data from 2009 to 2022. The financial data and export ratios of listed enterprises were gathered from the Wind Financial Terminal and CSMAR database, while corporate ESG ratings were obtained from Huazheng ESG in Shanghai. To mitigate the impact of outliers, the main variables in the data were adjusted by 1% above and below. A total of 18,650 individual observations of listed Chinese manufacturing companies were collected.

3.2. Variable Setting

- (1)

- Corporate financial performance (ROA)

The explained variable is corporate financial performance. There are various measures of corporate financial performance in existing studies, such as ROE value and Tobin Q. In this paper, ROA is chosen as the indicator for the following reasons: ROA reflects a firm's capacity to generate net profit from its total assets and is commonly utilized across diverse industries and firm types. Moreover, it is unaffected by a firm's size, making it suitable for assessing both profitability and asset utilization efficiency [58,59,60].

- (2)

- ESG Ratings (ESG)

In this paper, the HuazhengESG rating index is chosen as the explanatory variable to measure the ESG performance of enterprises. The Huazheng Index has assessed the ESG performance of Chinese listed companies since 2009, primarily emphasizing financial significance. Data are predominantly sourced from enterprise disclosures, ensuring high reliability and alignment with China's national context. Widely cited by researchers, this index provides a solid foundation [59,61]. Building on previous research, this paper integrates Huazheng ESG scores with corporate panel data in a one-to-one matching process. The independent variables used in this study include the overall ESG rating level and the respective rating levels of E, S and G. The ESG rating levels of the firms in this study are determined based on panel data. These ratings are derived from the ESG rating levels of listed Chinese firms reported by the Shanghai Huazheng Index from 2009 to 2022 (January, April, July, and October), representing annual averages. To ensure precision in the empirical analyses, we assign nine grades as follows: AAA (9), AA (8), A (7), BBB (6), BB (5), B (4), CCC (3), CC (2), and C (1). The average of the ESG rank levels reported in April and October from 2009 to 2022 is utilized for each respective E, S, and G rank level.

- (3)

- Mediating variable

Export: An enterprise's export ratio is the revenue it earns from the sale of goods or the provision of services to foreign markets, reflecting its competitiveness and ability to expand its business in the global marketplace. This indicator is crucial for assessing the scale and effectiveness of an enterprise's international operations, especially for those reliant on global markets to drive sales and profits. In this paper, the export value includes the export of products and services, so it is not limited to specific industries, and the logarithm of the export value of enterprises is taken to calculate the export ratio of enterprises [10].

- (4)

- Moderating variable

Carbon-intensive enterprises (Carbon_Intensity): In this paper, carbon-intensive enterprises are used as the moderating variable, and the moderating variable of carbon-intensive enterprises is set to 1 and other enterprises are set to 0 to verify the moderating effect.

- (5)

- Control variables

To prevent bias in the model estimation results due to the omission of variables and to examine better the correlation between ESG rating and firms' financial performance, it is necessary to control for other variables that affect firms' financial performance [62,63,64,65]. Therefore, this study collates the control variables used in previous studies in the relevant literature and selects equity concentration (Top1), enterprise size (Size), growth capacity (Tagr), liquidity ratio (Cr), cash ratio (Cash ratio), and book-to-market ratio (Mb ratio) as the control variables. In addition, we control the year and industry. The definitions of the relevant variables are detailed in Table 1.

3.3. Research Model

To avoid endogeneity problems as much as possible and to reduce the interference of missing variables, a two-way fixed effects model is used in this paper to control for individuals and years. This method is usually used for panel data.

To investigate the effect of ESG ratings on firms' financial performance, model (1) is constructed:

Meanwhile, to study the impact mechanism of ESG ratings on corporate financial performance, this paper adopts the mediation effect test method to introduce mediating variables to construct a model2,3:

To delve into the influence of carbon-intensive firms on the correlation between ESG ratings and firms' financial performance, we introduced the interaction term into Model (1) to derive Model (4).

where is the explanatory variable of this paper, is the explanatory variable of this paper, is the export ratio of enterprises, which represents the mediator variable of this paper, stands for carbon intensive enterprises, represents the control variable, denotes the time fixed effect, denotes the individual fixed effect, and is the random disturbance term. In this model, individual fixed effects and time fixed effects are introduced to control the effects of individual characteristics that do not vary over time and time characteristics that do not vary over time on the dependent variables, to reduce the omitted variable bias and improve the accuracy of the model estimation.

4. Results

4.1. Descriptive Statistics

As can be seen from Table 2, the sample of this study totaled 18,424. The maximum value of corporate financial performance (ROA) from 2009 to 2022 was 0.202, the minimum value was -0.199, and the mean value was 0.043, which did not produce a deviation. The majority of the enterprises were profitable and cheerful, but there were still loss-making enterprises. The maximum value of ESG grade (ESG) of listed enterprises is 7.750, the minimum value is 1.000, and the mean value is 4.173. The mean value of ESG grade of listed enterprises is in the range of B~BB, which also reflects that listed enterprises have invested a lot in ESG, and a few of them do not pay enough attention to it. Most of the book-to-market ratio is lower than 1, indicating that there is a general problem with the overvaluation of listed companies in China. The control variables, such as Enterprise size, are also within a reasonable range.

According to related studies, the existence of multicollinearity independent and control variables was verified by the variance inflation factor. As shown in Table 3, the VIF value of the primary variable is less than 5, and the average VIF value is less than 2. This suggests that the selected variables in this paper are not affected by multicollinearity.

4.2. Integated ESG Model

Table 4 presents the results of the empirical multiple regression analysis testing Hypothesis 1, which examines the impact of ESG rating evaluation results on corporate financial performance. Based on the analysis results, both column (1) and column (2) exhibit significant coefficients for ESG_score at the 1% confidence level before and after the inclusion of control variables. Precisely, an increase of 1 unit in ESG_score corresponds to a positive impact of 0.0035 units on the enterprise's ROA. The findings suggest a positive relationship between ESG_score and enterprise ROA. As the ESG_score increases, so does the enterprise's ROA, implying that higher ESG performance correlates with better financial performance. The enhancement of enterprise ESG ratings contributes to improved financial outcomes, thus supporting hypothesis 1.

4.3. Individual ESG Model

Table 5 shows the results of empirical multiple regression analysis of the impact of E, S and G ratings on corporate financial performance (ROA), respectively. According to the results of the empirical multiple regression analysis of the impact of E-rating on corporate financial performance hypothesis 2, columns (1) and (2) are the regression results before and after adding control variables; it can be seen that before and after the addition of control variables coefficients of the independent variable E-score are significant at the 1% confidence level, and every one-unit increase in the E-score has a 0.0004-unit negative impact on the corporate ROA, and the hypothesis 2 does not hold. Companies may face increased costs when implementing environmental protection measures, such as investing in cleaner technologies, upgrading waste treatment systems, and complying with stricter environmental regulations. Consequently, this could lead to a decline in the company's financial performance. Consequently, these expenses can temporarily dent a firm's profitability. Based on the empirical multiple regression analysis investigating hypothesis 3 concerning the influence of S-level evaluation on corporate financial performance, the coefficients of the independent variable S-score remain significant at the 1% confidence level both before and after integrating control variables. Specifically, for every one-unit rise in the S-score, there is a positive impact of 0.0002 units on the enterprise's ROA. As the S-score rises, corporate ROA also increases, thereby supporting hypothesis 3. Corporate social scores encompass aspects such as employee welfare, labor standards, safety management, consumer protection, and community involvement. These metrics underscore the significant role that corporations play in promoting social welfare and upholding stakeholder rights. Investing in employee welfare, health, safety, and training not only boosts employee satisfaction and loyalty but also minimizes turnover. Consequently, this enhances the productivity and profitability of the firm. The empirical multiple regression analysis for hypothesis 4, exploring the impact of G-rating on enterprise financial performance, reveals a significant positive coefficient for the variable G-score at the 1% confidence level. Precisely, each one-unit increase in the G-score corresponds to a positive effect of 0.0006 units on the enterprise's ROA. Hypothesis 4 is supported. Among the influences of environmental, social, and corporate governance on firms' financial outcomes, corporate governance (G) emerges as the variable with the most significant impact on financial performance. The dominant structure encompasses a firm's operational framework, policies, and influence on corporate decisions and stakeholders. This includes aspects such as leadership structure, board diversity and independence, monitoring procedures, internal controls, shareholder rights, and transparency. Sound corporate governance norms, such as transparent decision-making processes and robust internal control and compliance systems, assist companies in identifying and managing risks, thus averting financial and reputational setbacks.

4.4. Mediating Model

Table 6 illustrates the mediating effect of firms' exports. The regression results indicate a significant positive relationship between ESG ratings and firms' exports, with a coefficient of 0.0236, which is significant at the 5% level. In column (3), the coefficient for firms' exports is significantly positive at the 1% level. Moreover, for every unit increase in a firm's ESG score, its financial performance improves by 0.0034 units. Firms' export ratio mediates the effect of ESG ratings on firms' financial performance, confirming hypotheses 5 and 6.

Despite the significance of all core coefficients, this study further validated the mediating variables by employing the Sobel test. As depicted in Table 7, the Z value of the Sobel test is 3.126, significantly surpassing the threshold of 2.58, with a corresponding p-value of less than 0.01, thereby passing the Sobel test.

4.5. Moderating Model

The analysis results in Table 8 indicate that the post-regression interaction term coefficient of ESG_score x Carbon_intensity in column (2) exhibits a significant positive effect at the 10% level. This indicates that the effect of ESG scores on firms' financial performance is more pronounced in heavily polluting firms. Hypothesis 7 is supported. ESG scores exert a more substantial influence on the financial performance of highly carbon-intensive firms compared to those with lower carbon intensity. This is attributed to the heightened environmental regulations, increased social responsibility expectations, and the presence of sustainability-focused investors within these firms. The business decisions of carbon-intensive firms are intricately linked to the critical issue of environmental impact. This amplifies the effects of ESG improvements or deficiencies, directly influencing firms' compliance costs, market acceptance, and investment appeal.

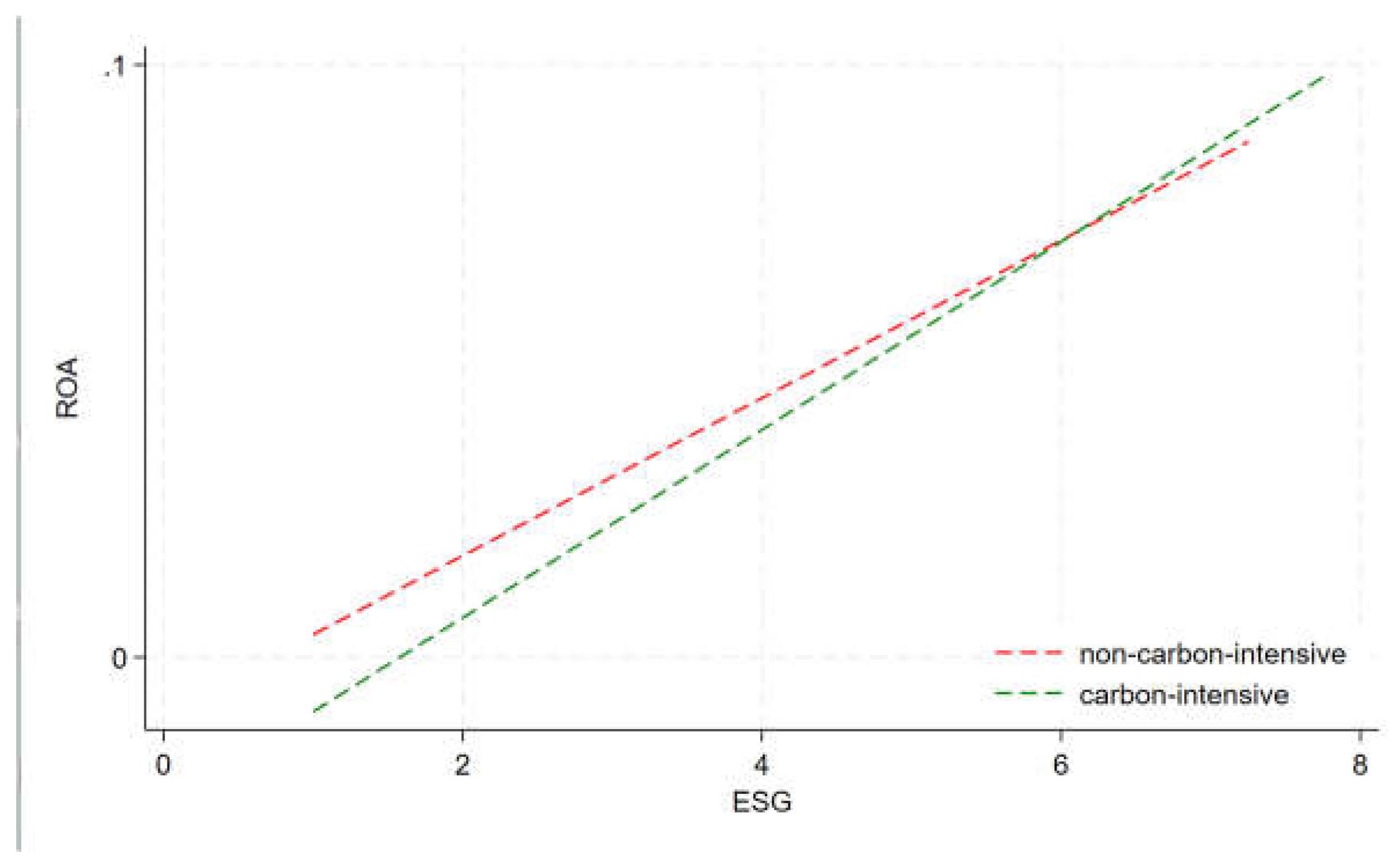

To assess the moderating role between carbon-intensive and non-carbon-intensive firms, this study constructs fitted plots to test potential heterogeneity in the impact of environmental, social, and corporate governance on the ROI of both types of firms. The plot indicates positive slopes for both types of firms, with steeper slopes observed for carbon-intensive firms. This implies that the positive influence of ESG scores on ROI is more pronounced among carbon-intensive firms. This conclusion is confirmed.

Figure 1.

Mechanism of ESG's impact on ROA. Carbon-intensive versus non-carbon-intensive firms.

5. Conclusion

5.1. Summary

Based on the data of Chinese A-share-listed manufacturing firms from 2009 to 2022, we evaluate the impact of ESG ratings on firms' financial performance. The results of this study indicate that ESG ratings have a positive impact on the improvement of firms' financial performance. This finding reinforces the conclusions drawn from prior academic studies, which predominantly suggest a positive correlation between ESG factors and financial performance [66,67]. This study enriches our understanding of the impact of ESG ratings on financial performance, focusing on listed firms and those with substantial carbon footprints in developing nations. It addresses the urgent need for these firms to transform and provides a rationale for investing in ESG initiatives. This study also reveals that E rating negatively affects firms' financial performance, diverging from previous findings. The necessity for firms to enhance environmental governance and decrease carbon emissions to meet environmental regulations might explain the adverse effect on financial performance. This could lead to increased operational expenses for the enterprise, potentially impacting financial performance negatively. S and G ratings positively influence firms' financial performance, with G rating exerting the most significant impact among E, S, and G ratings. Firstly, effective governance practices assist firms in managing risks, enhancing operational efficiency, and fostering transparency, thereby directly improving financial performance. Secondly, as investors increasingly favor firms with solid governance and social responsibility practices, these companies often attract more investment, leading to higher share prices and, consequently, improved financial performance indirectly. The firm's export ratio acts as a mediator, playing a crucial role in the link between ESG ratings and corporate performance. High ESG performance can elevate the corporate export ratio, thereby fostering sustainable development and enhancing the company's value. The moderating effect test conducted on carbon-intensive enterprises confirms their role in moderating the relationship between ESG ratings and corporate performance. Specifically, it suggests that the impact of ESG ratings on corporate financial performance is more significant for carbon-intensive enterprises. Carbon-intensive firms experience a more significant impact on financial performance from their ESG ratings than low-carbon firms. This is primarily attributed to the heightened environmental regulations, increased social responsibility expectations, and a sustainability-focused investor base unique to carbon-intensive industries. Operational and strategic decisions of carbon-intensive firms are intricately tied to environmental impacts. As such, any enhancements or deficiencies in ESG practices are amplified, directly affecting the firm's compliance costs, market acceptance, and investment appeal.

5.2. Theoretical Implication

This study's findings offer empirical evidence of the correlation between listed companies' ESG ratings and their financial performance, illuminating the pathways through which this relationship unfolds. This understanding holds significant theoretical implications for the evolution of businesses among listed companies and the promotion of sustainable economic development. In addition to validating composite ESG ratings, this study contributes to the literature on ESG and financial performance by examining the individual impacts of environmental (E), social (S), and governance (G) factors. Additionally, by integrating mediating effects to investigate how environmental, social, and governance (ESG) factors influence financial performance through diverse pathways, this study enhances our comprehension of the factors impacting ESG ratings and corporate financial performance. It furnishes theoretical underpinnings and insights for scholarly inquiry in this domain, fostering theoretical advancement in associated fields. By considering contingent factors such as carbon intensity, this study broadens the scope of the research. These theoretical implications argue for the development of targeted ESG policies and standards, especially for carbon-intensive firms, and highlight the importance of optimizing ESG ratings for listed companies.

5.3. Practical Implication

Government departments should promote the establishment of robust ESG rating systems and long-term rating mechanisms among listed companies. This entails incorporating international best practices and aligning them with local contexts to develop standardized ESG rating criteria for companies. Encouraging companies to establish robust ESG rating information proactively helps mitigate information asymmetry and safeguards investors' rights and interests. Furthermore, governments can incentivize enterprises to embrace social responsibility and boost investments in environmental protection proactively. This can be achieved through mechanisms such as tax incentives, environmental rewards, and other supportive measures. Such initiatives aim to encourage enterprises to shift their development paradigms towards sustainability.

Embracing ESG practices positively influences corporate performance. Decision-makers within corporations should prioritize ESG investments in their long-term development strategies. This includes enhancing environmental protection efforts, fulfilling social responsibilities, and improving corporate governance practices. Low-carbon and carbon-intensive enterprises can significantly boost their economic performance by actively embracing ESG responsibilities. Thus, enterprises must adopt a paradigm shift, integrating ESG principles into their strategic frameworks, enhancing stakeholder communication, and diligently fulfilling social obligations. These actions not only pave the way for sustainable corporate development but also contribute to the advancement of social, ecological, and economic prosperity. Simultaneously, companies must bolster internal oversight and penalties for environmental violations to mitigate environmental pollution and ecological harm. Instituting a long-term ESG rating mechanism will enable companies to showcase favorable ESG ratings, bolster investor confidence, and drive ongoing enhancement of corporate performance standards.

5.4. Limitations and Future Research

This study has limitations. Firstly, it focuses solely on the manufacturing industry of Chinese listed firms, which restricts its scope to a specific sector and may only partially capture the characteristics of Chinese firms overall. Future research could broaden the study's scope by selecting additional samples from various industries to gather more comprehensive and diverse data. In this study, we solely employ short-term indicators (ROA) to gauge firms' financial performance, overlooking the potential influence of ESG ratings on long-term performance. Hence, future research could refine this aspect further and continually optimize the current research framework in line with the Chinese context. This approach minimizes redundant data collection and analysis, fostering a deeper grasp of ESG activities' actual impact on long-term corporate performance.

Author Contributions

Conceptualization, H.D. and W.L.; data curation, H.D. and W.L.; formal analysis, H.D.; investigation, H.D. and W.L.; methodology, H.D.; project administration, W.L.; resources, H.D. and W.L.; software, H.D. and W.L.; supervision, W.L.; validation, H.D.; visualization, W.L.; writing—original draft, H.D. and W.L.; writing—review and editing, H.D. and W.L. All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding.

Institutional Review Board Statement

Not applicable.

Data Availability Statement

The data presented in this study are available on request from the corresponding author.

Acknowledgments

Special thanks are given to those who participated in the writing of this paper.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Velte, P. Does ESG performance have an impact on financial performance? Evidence from Germany. J. Glob. Responsib. 2017, 8, 169–178. [Google Scholar] [CrossRef]

- Alareeni, B.A.; Hamdan, A. ESG impact on performance of US S&P 500-listed firms. Corporate Governance: The International Journal of Business in Society 2020, 20, 1409–1428. [Google Scholar]

- Habib, A.M. Does real earnings management affect a firm's environmental, social, and governance (ESG), financial performance, and total value? A moderated mediation analysis. Environment, Development and Sustainability 2023, 1–30. [Google Scholar] [CrossRef]

- Tang, H.; Xiong, L.; Peng, R. The mediating role of investor confidence on ESG performance and firm value: Evidence from Chinese listed firms. Finance Res. Lett. 2024, 61. [Google Scholar] [CrossRef]

- Aydoğmuş, M.; Gülay, G.; Ergun, K. Impact of ESG performance on firm value and profitability. Borsa Istanb. Rev. 2022, 22, S119–S127. [Google Scholar] [CrossRef]

- Tahmid, T.; Hoque, M.N.; Said, J.; Saona, P.; Azad, A.K. Does ESG initiatives yield greater firm value and performance? New evidence from European firms. Cogent Bus. Manag. 2022, 9. [Google Scholar] [CrossRef]

- Pulino, S.C.; Ciaburri, M.; Magnanelli, B.S.; Nasta, L. Does ESG Disclosure Influence Firm Performance? Sustainability 2022, 14, 7595. [Google Scholar] [CrossRef]

- DasGupta, R. Financial performance shortfall, ESG controversies, and ESG performance: Evidence from firms around the world. Finance Res. Lett. 2022, 46. [Google Scholar] [CrossRef]

- Nirino, N.; Santoro, G.; Miglietta, N.; Quaglia, R. Corporate controversies and company's financial performance: Exploring the moderating role of ESG practices. Technological Forecasting and Social Change 2021, 162, 120341. [Google Scholar] [CrossRef]

- Wu, K.S.; Chang, B.G. The concave–convex effects of environmental, social and governance on high-tech firm value: Quantile regression approach. Corporate Social Responsibility and Environmental Management 2022, 29, 1527–1545. [Google Scholar] [CrossRef]

- Zhou, F.; Wen, H. Trade policy uncertainty, development strategy, and export behavior: Evidence from listed industrial companies in China. J. Asian Econ. 2022, 82. [Google Scholar] [CrossRef]

- Hou, J.; Teo, T.S.H.; Zhou, F.; Lim, M.K.; Chen, H. Does industrial green transformation successfully facilitate a decrease in carbon intensity in China? An environmental regulation perspective. J. Clean. Prod. 2018, 184, 1060–1071. [Google Scholar] [CrossRef]

- Zhao, X.; Liu, C.; Yang, M. The effects of environmental regulation on China's total factor productivity: An empirical study of carbon-intensive industries. Journal of Cleaner Production 2018, 179, 325–334. [Google Scholar] [CrossRef]

- Elsayih, J.; Datt, R.; Tang, Q. Corporate governance and carbon emissions performance: Empirical evidence from Australia. Australas. J. Environ. Manag. 2021, 28, 433–459. [Google Scholar] [CrossRef]

- Ersoy, E.; Swiecka, B.; Grima, S.; Özen, E.; Romanova, I. The Impact of ESG Scores on Bank Market Value? Evidence from the U.S. Banking Industry. Sustainability 2022, 14, 9527. [Google Scholar] [CrossRef]

- Alsayegh, M.F.; Rahman, R.A.; Homayoun, S. Corporate Economic, Environmental, and Social Sustainability Performance Transformation through ESG Disclosure. Sustainability 2020, 12, 3910. [Google Scholar] [CrossRef]

- Bassen, A.; Kovács, A.M. Environmental, social and governance key performance indicators from a capital market perspective; Springer Fachmedien Wiesbaden, 2000; pp. 809–820. [Google Scholar]

- Sassen, R.; Hinze, A.-K.; Hardeck, I. Impact of ESG factors on firm risk in Europe. J. Bus. Econ. 2016, 86, 867–904. [Google Scholar] [CrossRef]

- Ellili, N.O.D. Impact of ESG disclosure and financial reporting quality on investment efficiency. Corp. Governance: Int. J. Bus. Soc. 2022, 22, 1094–1111. [Google Scholar] [CrossRef]

- Han, J.-J.; Kim, H.J.; Yu, J. Empirical study on relationship between corporate social responsibility and financial performance in Korea. Asian J. Sustain. Soc. Responsib. 2016, 1, 61–76. [Google Scholar] [CrossRef]

- Luo, W.; Tian, Z.; Fang, X.; Deng, M. Can good ESG performance reduce stock price crash risk? Evidence from Chinese listed companies. Corp. Soc. Responsib. Environ. Manag. 2023, 31, 1469–1492. [Google Scholar] [CrossRef]

- Arvidsson, S.; Dumay, J. Corporate ESG reporting quantity, quality and performance: Where to now for environmental policy and practice? Bus. Strat. Environ. 2021, 31, 1091–1110. [Google Scholar] [CrossRef]

- Ding, H.; Su, W.; Hahn, J. How Green Transformational Leadership Affects Employee Individual Green Performance—A Multilevel Moderated Mediation Model. Behav. Sci. 2023, 13, 887. [Google Scholar] [CrossRef] [PubMed]

- López-Gamero, M.D.; Molina-Azorín, J.F.; Claver-Cortés, E. The whole relationship between environmental variables and firm performance: Competitive advantage and firm resources as mediator variables. J. Environ. Manag. 2009, 90, 3110–3121. [Google Scholar] [CrossRef] [PubMed]

- Liu, Y.; Kim, C.Y.; Lee, E.H.; Yoo, J.W. Relationship between Sustainable Management Activities and Financial Performance: Mediating Effects of Non-Financial Performance and Moderating Effects of Institutional Environment. Sustainability 2022, 14, 1168. [Google Scholar] [CrossRef]

- Dong, X.; Wen, X.; Wang, K.; Cai, C. Can negative media coverage be positive? When negative news coverage improves firm financial performance. Journal of Business & Industrial Marketing 2022, 37, 1338–1355. [Google Scholar]

- Zhou, G.; Liu, L.; Luo, S. Sustainable development, ESG performance and company market value: Mediating effect of financial performance. Bus. Strat. Environ. 2022, 31, 3371–3387. [Google Scholar] [CrossRef]

- Hang, M.; Geyer-Klingeberg, J.; Rathgeber, A.W. It is merely a matter of time: A meta-analysis of the causality between environmental performance and financial performance. Bus. Strat. Environ. 2018, 28, 257–273. [Google Scholar] [CrossRef]

- Li, Z.; Liao, G.; Albitar, K. Does corporate environmental responsibility engagement affect firm value? The mediating role of corporate innovation. Bus. Strategy Environ. 2020, 29, 1045–1055. [Google Scholar] [CrossRef]

- Nave, A.; Ferreira, J. Corporate social responsibility strategies: Past research and future challenges. Corp. Soc. Responsib. Environ. Manag. 2019, 26, 885–901. [Google Scholar] [CrossRef]

- Giannarakis, G.; Konteos, G.; Zafeiriou, E.; Partalidou, X. The impact of corporate social responsibility on financial performance. Invest. Manag. Financial Innov. 2016, 13, 171–182. [Google Scholar] [CrossRef]

- Jo, H.; Harjoto, M.A. Corporate Governance and Firm Value: The Impact of Corporate Social Responsibility. J. Bus. Ethic- 2011, 103, 351–383. [Google Scholar] [CrossRef]

- Raihan, T.; Al Karim, R. CSR and employee job satisfaction: A case from MNCS Bangladesh. Global Journal of Human Resource Management 2017, 5, 26–39. [Google Scholar]

- Arikan, E.; Kantur, D.; Maden, C.; Telci, E.E. Investigating the mediating role of corporate reputation on the relationship between corporate social responsibility and multiple stakeholder outcomes. Qual. Quant. 2014, 50, 129–149. [Google Scholar] [CrossRef]

- Flammer, C. Corporate Social Responsibility and Shareholder Reaction: The Environmental Awareness of Investors. Acad. Manag. J. 2013, 56, 758–781. [Google Scholar] [CrossRef]

- Barauskaite, G.; Streimikiene, D. Corporate social responsibility and financial performance of companies: The puzzle of concepts, definitions and assessment methods. Corp. Soc. Responsib. Environ. Manag. 2020, 28, 278–287. [Google Scholar] [CrossRef]

- Beiner, S.; Drobetz, W.; Schmid, M.M.; Zimmermann, H. An Integrated Framework of Corporate Governance and Firm Valuation. Eur. Financial Manag. 2006, 12, 249–283. [Google Scholar] [CrossRef]

- Black, B.S.; Jang, H.; Kim, W. Does Corporate Governance Predict Firms' Market Values? Evidence from Korea. J. Law, Econ. Organ. 2006, 22, 366–413. [Google Scholar] [CrossRef]

- Yeh, C.M. The influence of foreign institutional investors, institutional directors, and the share pledge ratio of directors on financial performance of tourism firms. Tour. Econ. 2019, 26, 179–201. [Google Scholar] [CrossRef]

- Saci, F.; Jasimuddin, S.M. Does the research done by the institutional investors affect the cost of equity capital? Finance Res. Lett. 2020, 41, 101834. [Google Scholar] [CrossRef]

- Caputo, F.; Pizzi, S.; Ligorio, L.; Leopizzi, R. Enhancing environmental information transparency through corporate social responsibility reporting regulation. Bus. Strat. Environ. 2021, 30, 3470–3484. [Google Scholar] [CrossRef]

- Brown, L.D.; Caylor, M.L. Corporate governance and firm performance. Available at SSRN 586423. 2004.

- Gompers, P.; Ishii, J.; Metrick, A. Corporate Governance and Equity Prices. Q. J. Econ. 2003, 118, 107–156. [Google Scholar] [CrossRef]

- Black, B.; Kim, W. The effect of board structure on firm value: A multiple identification strategies approach using Korean data. J. Financial Econ. 2012, 104, 203–226. [Google Scholar] [CrossRef]

- Li, K.; Yue, H.; Zhao, L. Ownership, institutions, and capital structure: Evidence from China. J. Comp. Econ. 2009, 37, 471–490. [Google Scholar] [CrossRef]

- Chen, Y.; Xu, Z.; Wang, X.; Yang, Y. How does green credit policy improve corporate social responsibility in China? An analysis based on carbon-intensive listed firms. Corp. Soc. Responsib. Environ. Manag. 2022, 30, 889–904. [Google Scholar] [CrossRef]

- Tang, H. The Effect of ESG Performance on Corporate Innovation in China: The Mediating Role of Financial Constraints and Agency Cost. Sustainability 2022, 14, 3769. [Google Scholar] [CrossRef]

- Ionescu, G.H.; Firoiu, D.; Pirvu, R.; Vilag, R.D. THE IMPACT OF ESG FACTORS ON MARKET VALUE OF COMPANIES FROM TRAVEL AND TOURISM INDUSTRY. Technol. Econ. Dev. Econ. 2019, 25, 820–849. [Google Scholar] [CrossRef]

- Wu, Q.; Chen, G.; Han, J.; Wu, L. Does Corporate ESG Performance Improve Export Intensity? Evidence from Chinese Listed Firms. Sustainability 2022, 14, 12981. [Google Scholar] [CrossRef]

- Pinheiro, A.B.; dos Santos, J.I.A.S.; Cherobim, A.P.M.S.; Segatto, A.P. What drives environmental, social and governance (ESG) performance? The role of institutional quality. Manag. Environ. Qual. Int. J. 2023, 35, 427–444. [Google Scholar] [CrossRef]

- Li, Y.; Li, J. The Relationship between Environmental, Social, Governance, and Export Performance in Manufacturing Companies: A Literature Review. Theor. Pr. Res. Econ. Fields 2023, 14, 345–356. [Google Scholar] [CrossRef]

- Yang, O.-S.; Han, J.-H. Assessing the Effect of Corporate ESG Management on Corporate Financial & Market Performance and Export. Sustainability 2023, 15, 2316. [Google Scholar] [CrossRef]

- Huang, Y.; Zhang, Y. Digitalization, positioning in global value chain and carbon emissions embodied in exports: Evidence from global manufacturing production-based emissions. Ecol. Econ. 2023, 205. [Google Scholar] [CrossRef]

- Wang, Z.; Chu, E.; Hao, Y. Towards sustainable development: How does ESG performance promotes corporate green transformation. Int. Rev. Financial Anal. 2023, 91. [Google Scholar] [CrossRef]

- Huang, R.; Chen, D. Does Environmental Information Disclosure Benefit Waste Discharge Reduction? Evidence from China. J. Bus. Ethic- 2014, 129, 535–552. [Google Scholar] [CrossRef]

- Wang, K.; Zhang, X. The effect of media coverage on disciplining firms’ pollution behaviors: Evidence from Chinese heavy polluting listed companies. J. Clean. Prod. 2020, 280, 123035. [Google Scholar] [CrossRef]

- Zhao, X.; Liu, C.; Sun, C.; Yang, M. Does stringent environmental regulation lead to a carbon haven effect? Evidence from carbon-intensive industries in China. Energy Econ. 2019, 86, 104631. [Google Scholar] [CrossRef]

- Weng, P.S.; Chen, W.Y. Doing good or choosing well? Corporate reputation, CEO reputation, and corporate financial performance. The North American Journal of Economics and Finance 2017, 39, 223–240. [Google Scholar] [CrossRef]

- Xu, Y.; Zhu, N. The Effect of Environmental, Social, and Governance (ESG) Performance on Corporate Financial Performance in China: Based on the Perspective of Innovation and Financial Constraints. Sustainability 2024, 16, 3329. [Google Scholar] [CrossRef]

- Zhang, Y.; Wang, X.; Guo, W.; Guo, X.; Wang, Q.; Tan, X. Does ESG Performance Affect the Enterprise Value of China’s Heavily Polluting Listed Companies? Sustainability 2024, 16, 2826. [Google Scholar] [CrossRef]

- Lin, Y.; Fu, X.; Fu, X. Varieties in state capitalism and corporate innovation: Evidence from an emerging economy. Journal of Corporate Finance 2021, 67, 101919. [Google Scholar] [CrossRef]

- Zeng, L.; Jiang, X. ESG and Corporate Performance: Evidence from Agriculture and Forestry Listed Companies. Sustainability 2023, 15, 6723. [Google Scholar] [CrossRef]

- Gao, S.; Meng, F.; Wang, W.; Chen, W. Does ESG always improve corporate performance? Evidence from firm life cycle perspective. Front. Environ. Sci. 2023, 11. [Google Scholar] [CrossRef]

- Chouaibi, S.; Chouaibi, J.; Rossi, M. ESG and corporate financial performance: The mediating role of green innovation: UK common law versus Germany civil law. EuroMed J. Bus. 2021, 17, 46–71. [Google Scholar] [CrossRef]

- Qu, W.; Zhang, J. Environmental, Social, and Corporate Governance (ESG), Life Cycle, and Firm Performance: Evidence from China. Sustainability 2023, 15, 14011. [Google Scholar] [CrossRef]

- Alshehhi, A.; Nobanee, H.; Khare, N. The Impact of Sustainability Practices on Corporate Financial Performance: Literature Trends and Future Research Potential. Sustainability 2018, 10, 494. [Google Scholar] [CrossRef]

- Friede, G.; Busch, T.; Bassen, A. ESG and financial performance: Aggregated evidence from more than 2000 empirical studies. J. Sustain. Finance Invest. 2015, 5, 210–233. [Google Scholar] [CrossRef]

Table 1.

Research Model.

| Variable | Symbol | Definition |

|---|---|---|

| Explained variable | Corporate financial performance (ROA) | Net Profit / Total Assets |

| Explanatory variable | ESG Ratings (ESG) | Huazheng ESG ratings range from C to AAA, and the nine ratings are assigned from 1 to 9 by the assignment method |

| Mediating variable | Export | Taking the logarithm of firms' exports |

| Moderating variable | Carbon-intensive enterprises (Carbon_Intensity) | Carbon-intensive firms' moderator variable set to 1, other firms set to 0 |

| Control variable | Equity concentration (Top1) | Shareholding ratio of the largest shareholder |

| Cash ratio (Cash ratio) | Cash/current liabilities | |

| Liquidity ratio (Cr) | Current assets/current liabilities | |

| Book-to-market ratio (Mb ratio) | (Total assets - total liabilities)/total assets | |

| Growth capacity (Tagr) | (Current main operating income - Prior main operating income)/Current main operating income )*100% | |

| Enterprise size (Size) | Natural logarithm of total corporate assets |

Table 2.

Descriptive statistics of major variables.

| Variable | N | Mean | SD | Min | Max |

|---|---|---|---|---|---|

| ROA | 18424 | 0.043 | 0.058 | -0.199 | 0.202 |

| ESG_score | 18424 | 4.173 | 0.984 | 1 | 7.750 |

| Enterprise size | 18424 | 22.07 | 1.193 | 20.05 | 25.74 |

| Equity concentration | 18424 | 33.48 | 14.02 | 8.770 | 71.92 |

| Growth capacity | 18424 | 0.200 | 0.345 | -0.260 | 2.015 |

| Liquidity ratio | 18424 | 0.589 | 0.163 | 0.207 | 0.916 |

| Book-to-market ratio | 18424 | 0.597 | 0.228 | 0.130 | 1.137 |

| Cash ratio | 18424 | 0.857 | 1.353 | 0.027 | 8.748 |

Table 3.

Multicollinearity analysis.

| Variable | VIF | 1/VIF |

|---|---|---|

| Enterprise size | 1.36 | 0.734270 |

| Book-to-market ratio | 1.23 | 0.810117 |

| Cash ratio | 1.23 | 0.813763 |

| Liquidity ratio | 1.16 | 0.860666 |

| Growth capacity | 1.10 | 0.910285 |

| ESG_score | 1.07 | 0.938280 |

| Equity concentration | 1.03 | 0.975401 |

| Mean VIF | 1.17 |

Table 4.

Regression results of ESG ratings and financial performance. .

| (1) | (2) | |

| VARIABLES | ROA | ROA |

| ESG_score | 0.0054*** | 0.0035*** |

| (0.00) | (0.00) | |

| Enterprise size | 0.0075*** | |

| (0.00) | ||

| Equity concentration | 0.0008*** | |

| (0.00) | ||

| Growth capacity | 0.0267*** | |

| (0.00) | ||

| Liquidity ratio | 0.0760*** | |

| (0.01) | ||

| Book-to-market ratio | -0.0777*** | |

| (0.00) | ||

| Cash ratio | 0.0015*** | |

| (0.00) | ||

| Observations | 18,424 | 18,424 |

| R-squared | 0.497 | 0.558 |

| Control | NO | YES |

| Company fixed effect | YES | YES |

| Year fixed effect | YES | YES |

Table 5.

Regression results of E,S,G ratings and financial performance.

| (1) | (2) | |

| VARIABLES | ROA | ROA |

| E | -0.0003*** | -0.0004*** |

| (0.00) | (0.00) | |

| S | 0.0003*** | 0.0002*** |

| (0.00) | (0.00) | |

| G | 0.0009*** | 0.0006*** |

| (0.00) | (0.00) | |

| Enterprise size | 0.0079*** | |

| (0.00) | ||

| Equity concentration | 0.0008*** | |

| (0.00) | ||

| Growth capacity | 0.0267*** | |

| (0.00) | ||

| Liquidity ratio | 0.0753*** | |

| (0.01) | ||

| Book-to-market ratio | -0.0767*** | |

| (0.00) | ||

| Cash ratio | 0.0015*** | |

| (0.00) | ||

| Observations | 18,424 | 18,424 |

| R-squared | 0.500 | 0.560 |

| Control | NO | YES |

| Company fixed effect | YES | YES |

| Year fixed effect | YES | YES |

Robust standard errors in parentheses*** p<0.01, ** p<0.05, * p<0.1.

Table 6.

Mediating effects of export ratios.

| (1) | (2) | (3) | |

| VARIABLES | ROA | export | ROA |

| Export | 0.0026*** | ||

| (0.00) | |||

| ESG_score | 0.0035*** | 0.0236** | 0.0034*** |

| (0.00) | (0.01) | (0.00) | |

| Enterprise size | 0.0075*** | 0.9635*** | 0.0050*** |

| (0.00) | (0.03) | (0.00) | |

| Equity concentration | 0.0008*** | -0.0003 | 0.0008*** |

| (0.00) | (0.00) | (0.00) | |

| Growth capacity | 0.0267*** | -0.2954*** | 0.0274*** |

| (0.00) | (0.03) | (0.00) | |

| Liquidity ratio | 0.0760*** | 0.2147* | 0.0755*** |

| (0.01) | (0.11) | (0.01) | |

| Book-to-market ratio | -0.0777*** | -0.0039 | -0.0777*** |

| (0.00) | (0.06) | (0.00) | |

| Cash ratio | 0.0015*** | -0.0505*** | 0.0016*** |

| (0.00) | (0.01) | (0.00) | |

| Observations | 18,424 | 18,424 | 18,424 |

| R-squared | 0.558 | 0.872 | 0.559 |

| Control | YES | YES | YES |

| Company fixed effect | YES | YES | YES |

| Year fixed effect | YES | YES | YES |

Robust standard errors in parentheses*** p<0.01, ** p<0.05, * p<0.1.

Table 7.

Testing of the mediating effects.

| Coef | Std Err | Z | P>Z | ||

|---|---|---|---|---|---|

| Sobel | .00008436 | .00002699 | 3.126 | .00177216 | |

| Goodman-1 | (Aroian) | .00008436 | .00002714 | 3.108 | .00188207 |

| Goodman-2 | .00008436 | .00002683 | 3.144 | .00166643 |

Table 8.

Testing of the moderating effects.

| (1) | (2) | |

| VARIABLES | ROA | ROA |

| ESG_score x Carbon_intensity | 0.0012* | |

| (0.00) | ||

| ESG_score | 0.0035*** | 0.0030*** |

| (0.00) | (0.00) | |

| Enterprise size | 0.0075*** | 0.0076*** |

| (0.00) | (0.00) | |

| Equity concentration | 0.0008*** | 0.0008*** |

| (0.00) | (0.00) | |

| Growth capacity | 0.0267*** | 0.0266*** |

| (0.00) | (0.00) | |

| Liquidity ratio | 0.0760*** | 0.0763*** |

| (0.01) | (0.00) | |

| Book-to-market ratio | -0.0777*** | -0.0778*** |

| (0.00) | (0.00) | |

| Cash ratio | 0.0015*** | 0.0015*** |

| (0.00) | (0.00) | |

| Observations | 18,424 | 18,424 |

| R-squared | 0.558 | 0.558 |

| Control | YES | YES |

| Company fixed effect | YES | YES |

| Year fixed effect | YES | YES |

Robust standard errors in parentheses*** p<0.01, ** p<0.05, * p<0.1.

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Copyright: This open access article is published under a Creative Commons CC BY 4.0 license, which permit the free download, distribution, and reuse, provided that the author and preprint are cited in any reuse.