Submitted:

14 May 2024

Posted:

14 May 2024

You are already at the latest version

Abstract

This study aims to analyze various types of pellet fuels used as energy sources in Bulgaria, focusing on their energy characteristics and the consumer preferences. Both standard and specialized methods such as thermogravimetry (TG) and differential scanning calorimetry (DSC) are used for the analyses. The results from TG and DSC indicate that during the drying of the samples, moisture is evaporated from their surface, along with the release of volatile substances. The processes during the analysis are accompanied by energy absorption, with the main stage being combustion, where the primary amount of heat is generated. Standard analysis methods show that wood pellets usually contain about 7.31% moisture, 0.72% ash and have a calorific value of 18.33 kJ/kg, while sunflower pellets contain about 7.62% moisture, 2.42% ash and have a calorific value of 19.63 kJ/kg. Mixed pellets contain about 7.07% moisture, up to 0.69% ash and have a calorific value of 18.05 kJ/kg. A specialized marketing research was conducted to investigate consumer attitudes and preferences toward purchasing different types of solid biomass fuels on Bulgarian market. This study provides information on the quality of pellets as fuel by offering a detailed analysis of their fuel properties and ensuring their effective utilization as an energy source.

Keywords:

marketing research

; consumers

; pellets

; fuels

; energy

; ash content

; moisture content

; calorific value

; TG

; DSC

1. Introduction

Nowadays one of the key aspects related to energy resources is their contribution to energy and environmental preservation. Biomass is known as one of the most effective and sustainable energy sources, providing both renewable fuel and environmental benefits [1,2,3]. Containing a significant amount of carbon, biomass plays a crucial role in balancing greenhouse gases. It serves as an alternative to traditional energy resources [4,5,6,7]. The increasing consumption of pellets for heating and hot water production requires diversity in the raw materials used for fuels [8,9,10,11]. Modern technologies enable the production of renewable fuels from agricultural and industrial waste materials, offering both economic and ecological advantages. The EU and its member states aim to increase the share of energy originating from renewable sources to 34% by 2050 [12,13,14,15]. To achieve this, they promote the use of fuels derived from solid biomass waste materials. These fuels are produced from both agricultural and forestry sectors as well as industry. This is crucial for addressing waste generation issues and their negative impact on the environment. Furthermore, the reuse of these materials allows for increased revenue through the sale of secondarily generated solid biofuels, as well as reducing expenses for energy needs [16,17,18,19].

The energy needs of many people in Bulgaria, especially for heating and warming household water, are often met through the use of wood pellets as fuel. This form of fuel is produced from waste wood originating from forest clearing and the activities of the wood processing industry [20,21,22,23]. The technological steps for producing wood pellets involve initial crushing of the products, followed by drying, fine grinding, pressing without the addition of binding agents and finally cooling the resulting pellets. Proper utilization of solid biofuel in the form of wood pellets ensures an efficient fueling process. The low bulk density of solid biofuels makes them more suitable for local use near production regions. To some extent, this can be compensated by the possibility of packaging and transporting pellets over long distances, but this increases production costs [24,25,26,27,28,29]. Global leaders in the production and use of pellets are primarily the USA and Canada, followed by Europe [29,30,31,32,33].

One of the most important oilseed crops, known to humanity for centuries, is the sunflower [34,35,36,37]. Market leaders in sunflower production are countries from Europe and Asia. After processing, large quantities of waste in the form of stalks and husks are generated following the extraction of oil from the seeds. One of the applications of sunflower husks in energy production is as a raw material for fuel in the form of pellets [38,39,40]. Their production is profitable and they are cheaper than wood pellets in Bulgaria. The biggest drawback of sunflower pellets is their high ash content after combustion.

Wood and sunflower pellets are fuels that can be used for heating residential buildings, industrial buildings and agricultural facilities, as well as for electricity generation through installations that utilize renewable energy sources. This diverse range of applications makes them a key component of strategies to diversify the energy mix and reduce carbon dioxide emissions. Interestingly, around the world, this type of solid biofuel often replaces coal in electricity production [41,42,43,44].

To improve the fuel parameters of produced wood and sunflower pellets, highly specialized scientific methods and technologies are used in accordance with the standards in force in EU countries. These methods involve studying key parameters such as moisture content, ash content and calorific value, as well as applying advanced analytical tools to measure their physical and chemical properties. Techniques such as mass spectroscopy, thermogravimetry, differential scanning calorimetry and others are used for this purpose [45,46]. These techniques provide detailed information about the quality of the pellets and help to better understand their physical and chemical properties, ultimately contributing to their more efficient use as an energy source.

Many scientists are engaged in the analysis of some of the main parameters of pellet fuels from different sources and their influence on the operation of pellet fuel systems around the world. They use a wide variety of data collected from different sources and studies. Currently, in scientific circles, special attention is paid to the study of important parameters such as moisture and ash content and how they affect the efficiency of pellet fuel systems, especially in our country [47,48,49]. This is essential to determine the best ways to use pellet fuels in energy systems and to reduce their environmental footprint.

The focus of this study is the results of a marketing research that centers on consumer opinions regarding the use of wood and sunflower pellets in Bulgaria, with particular attention to their moisture and ash content, as well as their calorific value. Detailed analyses of these properties are conducted using both energetic methods and specialized techniques such as thermogravimetry and differential scanning calorimetry. These methods and techniques enable a scientific investigation into the composition and energy properties of the pellets, contributing to a better understanding of their characteristics and their potential as an energy source.

Understanding consumer preferences is crucial for businesses to tailor their products and marketing strategies effectively. By studying consumer opinions, companies can gain insights into which types of solid biomass fuels consumers prefer and why. This information can help them adjust their product offerings to better meet consumer demand, leading to increased sales and market share. Consumer feedback on moisture and ash content, as well as calorific value, provides valuable insights for product improvement. Companies can use this feedback to refine their manufacturing processes and formulations, ensuring that their pellets meet or exceed consumer expectations in terms of quality and performance. This can enhance customer satisfaction and loyalty in the long run, allowing companies to adjust their marketing strategies and positioning. Understanding consumer preferences and concerns regarding pellet quality can also help companies ensure compliance with regulatory standards and requirements.

2. Materials and Methods

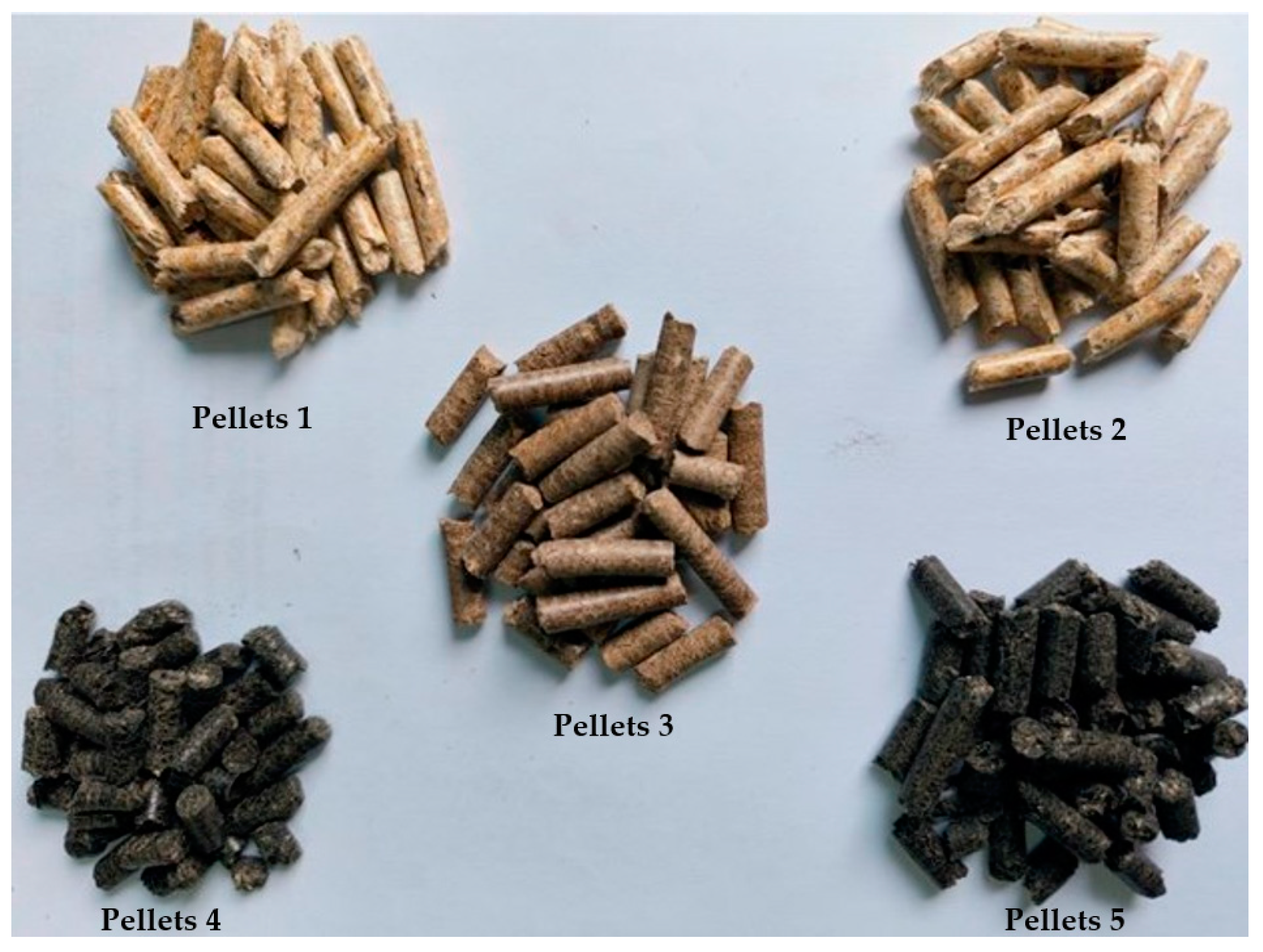

After analyzing the survey data for solid biofuels, two types of wood and sunflower pellet samples from different producers were selected. The third type of pellets are produced after mixing sunflower husks and softwood waste in a ratio of 1:3. Research has been carried out to determine some typical parameters such as calorific value, ash content and moisture. Additionally, their mass loss and thermal properties were measured using TG and DSC.

2.1. Materials

2.2. Research Methods

2.2.1. Determination of Some of the Energy Parameters.

The determination of some of the fuel’s energy parameters such as calorific value, moisture content and ash content is conducted in accordance with European and Bulgarian standards, as per [50,51,52,53]. The pellets are purchased from retail stores and manufacturers. They are packaged in bags weighing 15 kg each. To obtain accurate and correct results, the bags containing the selected pellets are opened prior to the study and quantities of approximately 3 kg are prepared for examination for each type of pellets.

To determine the moisture content, the tested sample must be no less than 300 grams. Before the examination, the material is ground and then the sample is dried in an air environment for a certain time. The process continues until the sample reaches a constant mass, after which the percent water content is calculated as mass loss, according to [50].

Initially, the sample was subjected to drying for approximately one hour at a temperature of about 250°C. The temperature then is increased gradually to about 550°C, at which point the combustion process ends [51,52]. For an accurate recording of the results, it is recommended that the burning time should be at least 2 hours.

To determine the overall calorific value of the tested pellets, a method described in [53] is utilized. The experiments are conducted in a bomb calorimeter by burning benzoic acid at a predetermined temperature of 25°C and constant volume. The higher heating value is determined by correcting the temperature (temperature rise) and subsequently determining the effective heat capacity of the device. This process takes into account the initial energy for ignition, the energy of combustion and the thermal effect of additional reactions. The lower heating value is calculated from the results obtained for the higher heating value, considering the moisture and hydrogen content in the samples.

2.2.2. Thermogravimetric Analysis and Differential Scanning Calorimetry

The thermogravimetric analysis method is used for detailed study of the thermal properties of the pellets. Special equipment [54,55,56,57] is used to conduct the analysis, which allows precise control of the temperature and measurement of the change in the mass of the sample depending on the temperature.

At the beginning of the experiment, the pellets are subjected to gradual heating from room temperature to a certain maximum value, which is pre-determined according to the investigated samples and the interests of the study, in this case 750°C. During heating the change in pellets mass is measured, observing any physicochemical changes that may occur, such as material degradation, oxidation reactions or evolution of gasses.

Differential scanning calorimetry is an analytical method that finds wide application in the study of the thermal properties of various materials, including pellets. This method allows a detailed study of the thermal changes that occur in the samples during controlled heating or cooling at a certain rate. In this case the samples were tested at two rates of 5°C/min and 10°C/min. Thermal changes are recorded by measuring the difference in heat between the sample and the reference material. This process allows precise determination of the temperature limits at which various thermal processes such as degradation of the material or changes in its phase occur.

The TG and DSC studies were conducted using a thermal analyzer STA PT 1600 in a laboratory environment [58]. A sample with a mass of about 1 gram is placed in the device, which is determined based on the type of material and the studied parameters. This mass is sufficient to provide the required sample for the analysis. The temperature in the device increases gradually and evenly to 750°C. This range of temperatures was chosen according to the specific requirements of the tested samples and the research objectives.

Two heating speeds are used - 5°C/min and 10°C/min. The choice of heating rate is essential because it can affect the kinetics of the reactions that occur in the material during the analysis. The faster heating can accelerate various thermal processes, while the slower heating can allow a more complete and detailed analysis of the thermal changes.

During the heating and analysis process, changes in the mass of the samples and the difference in heat release or absorption are observed. These observations are crucial for understanding the thermal characteristics of the material and for identifying the various thermal processes that may occur under different conditions of temperature and heating rate.

The data obtained from the analysis are used to create profiles of the curves from thermogravimetric analysis (TGA) and DSC. These profiles provide a visual representation of the thermal changes in the material as a function of temperature and heating rate, which allows detailed study and analysis of their characteristics.

Based on the data obtained from the methods mentioned above and the marketing research of consumer preferences, an analysis can be conducted to determine whether this type of pellets is suitable for sale on the market and to explore their potential applications. First, by examining the moisture and ash content, the quality of the pellets as a fuel and their fuel efficiency can be assessed. High moisture content can reduce their energy value and increase the amount of emitted gases and ash, which may make them less suitable for certain applications such as heating. Then the analysis of calorific value provides insight into their energy value and potential for efficient utilization. Higher calorific value usually indicates better fuel quality and more efficient combustion. TG and DSC help evaluate the stability of the material at different temperatures and combustion conditions. This is important for determining the suitability of the pellets for various heating purposes. Additionally, they can detect potential changes in the chemical composition of the pellets during heating, which is crucial for understanding their fuel properties and efficiency.

2.2.3. Marketing Research of Customer Preferences

In order to explore consumer attitudes and preferences regarding the purchase of various types of solid biomass fuels on Bulgarian market, a specialized marketing research was carried out. The survey spanned from November 2023 to February 2024, encompassing both online and in-store responses. It comprised 9 closed questions exploring diverse facets of pellet types covering aspects like quality, pricing, distribution channels and packaging. The target demographic group included end-users (individuals and households) utilizing pellets for heating in Bulgaria. The survey concluded upon reaching 200 responses. It's worth emphasizing that pellet preferences may significantly fluctuate based on factors such as regional availability and heating requirements.

Understanding consumer behavior through marketing research helps manufacturers tailor their offerings of solid biomass fuels to meet consumer needs and preferences. This insight aids in market segmentation, allowing businesses to target specific consumer groups with tailored strategies. This knowledge also provides a competitive advantage by identifying market gaps and enabling businesses to differentiate themselves. It also optimizes marketing strategies by informing pricing, distribution and promotional activities for maximum impact.

3. Results

Based on the methods outlined above, the averaged results obtained from the research of the five types of pellets are presented.

3.1. Results of Using the Materials and Methods

3.1.1. Results of Determining the Energy Characteristics of the Pellets

Table 2 presents the averaged results obtained from the study of the energy characteristics of the pellets.

The results of the research show that the different types of pellets have different parameters that affect their efficiency as a fuel. Type 2 pellets are characterized by the lowest moisture content, which makes them more suitable for a combustion process, as the lower moisture content provides better combustion and higher efficiency. On the other hand, type 4 pellets have the highest moisture content, which can reduce their efficiency as a fuel. In relation to ash content, type 2 pellets have the lowest ash content, which is preferred for cleaner combustion and less residue formation. Type 5 pellets, on the other hand, have the highest ash content, which can be a challenge to maintain the combustion system. When it comes to calorific value, type 3 pellets are found to have the lowest value, which may mean that they are less efficient in the combustion process. Compared to them, type 4 pellets have the highest calorific value, which makes them preferred for more efficient and strong combustion.

3.1.2. Results of the TG and DSC of the Pellets

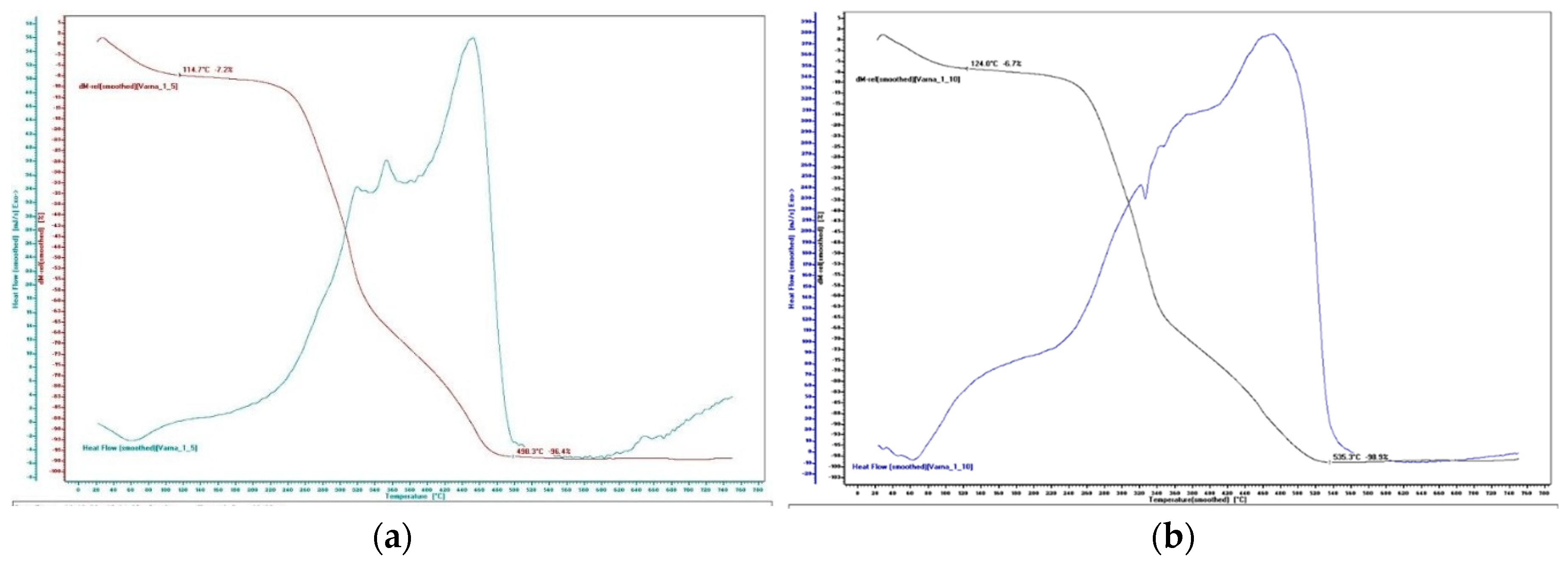

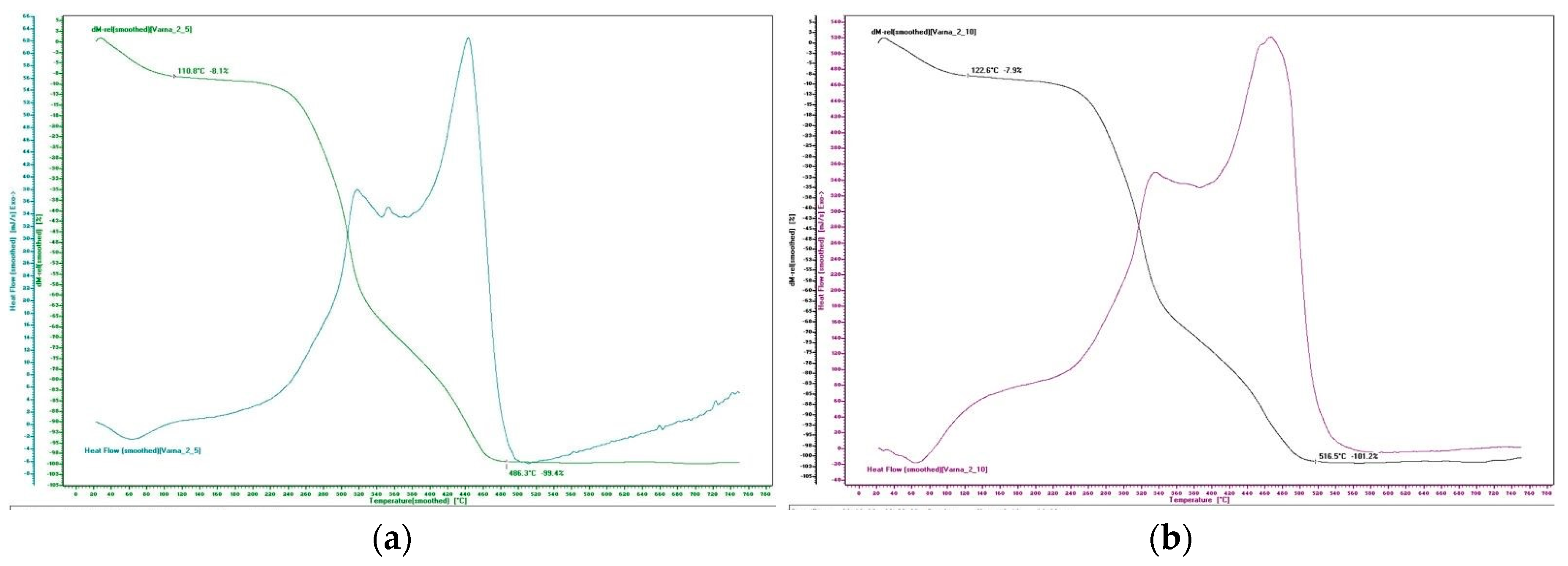

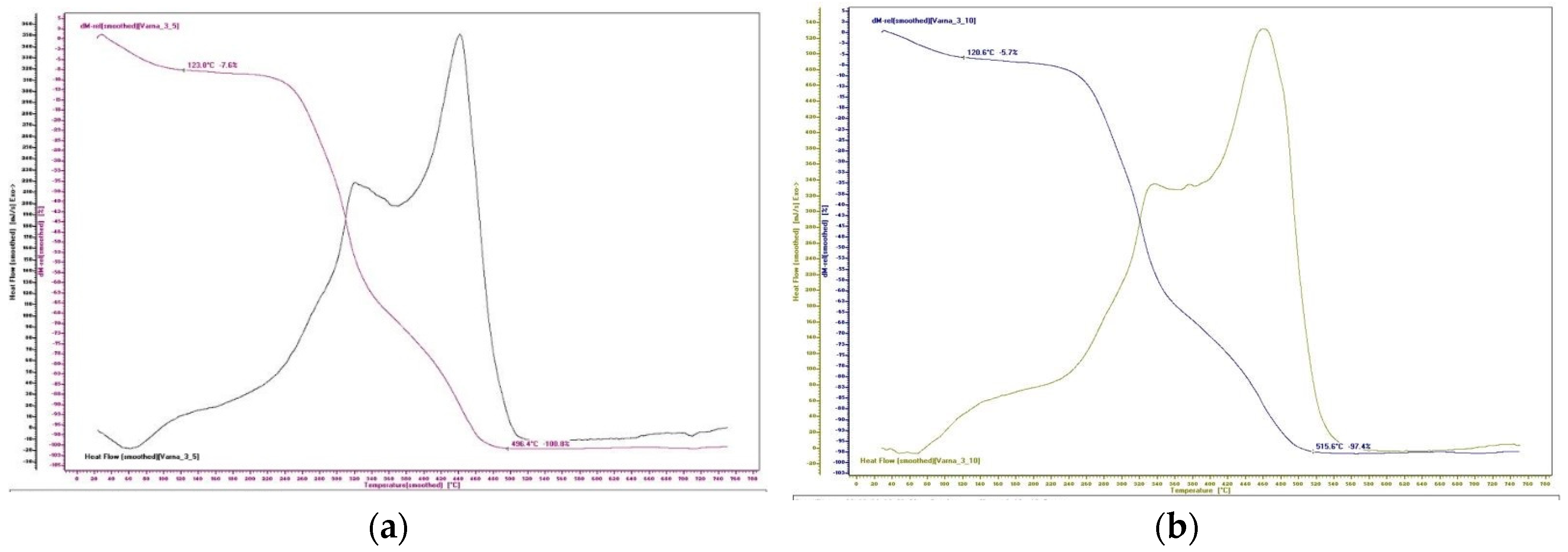

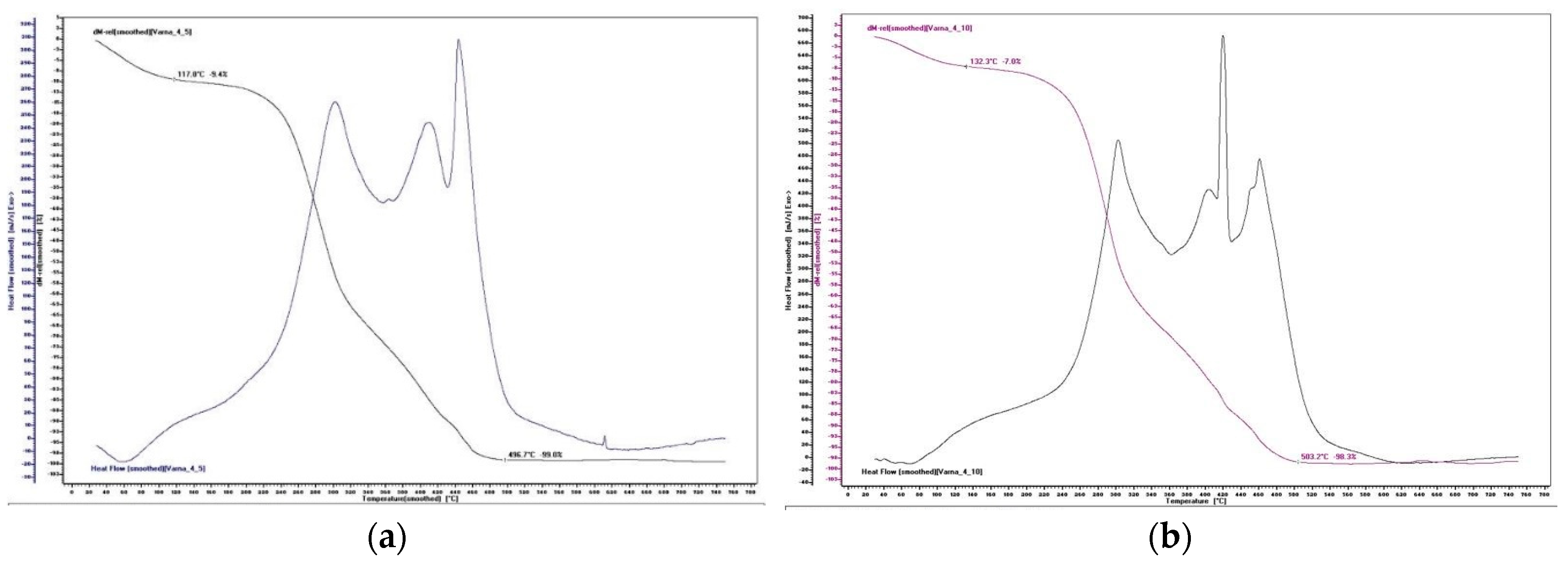

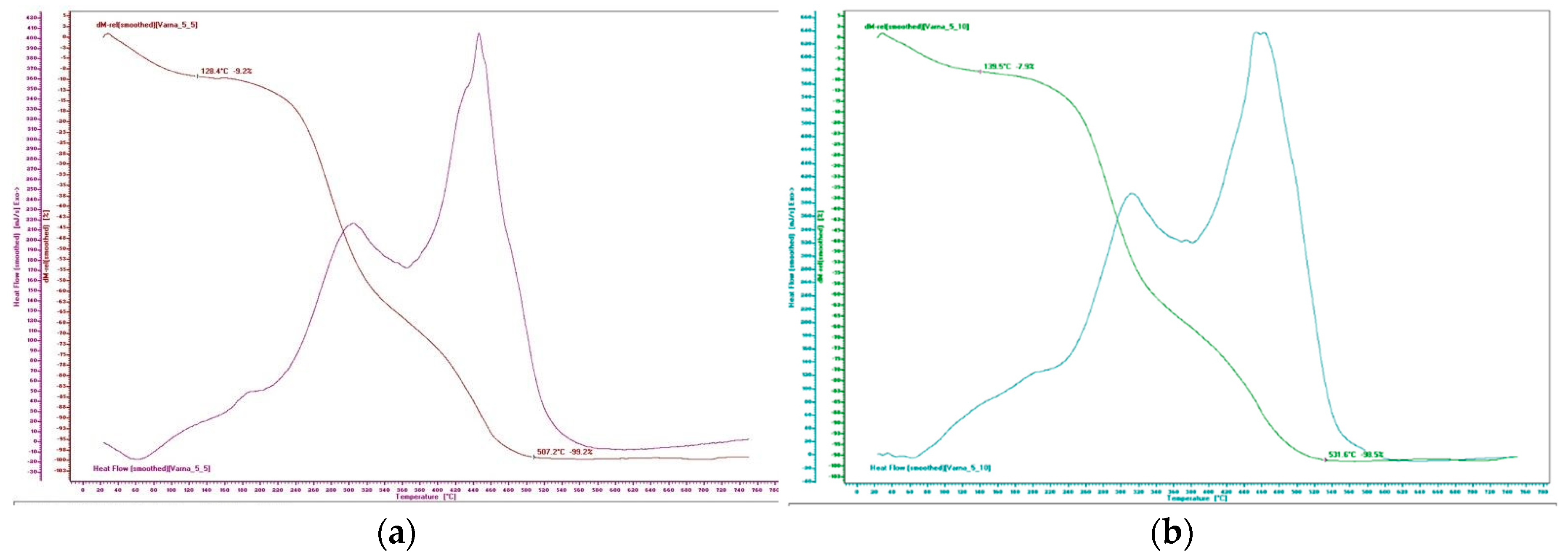

Figure 2, Figure 3, Figure 4, Figure 5 and Figure 6 show TG and DSC results at different heating rates of 5℃/min and 10℃/min up to a temperature of 750°C. These figures illustrate the curves of TGA and DSC at different heating rates, as described above. According to the results obtained from the thermogravimetric analysis, the results can be conditionally divided into three stages. The first stage represents the drying process and the release of light volatile substances. The second stage is the main stage of the process, where the combustion process takes place and the main separation of volatile substances occurs. The third stage is when the smoldering process takes place.

During the drying stage, moisture evaporates from the surface of the samples and simultaneously with that volatile substances are released. The processes that occur during the examination of the samples are carried out during the absorption of energy. During the main stage of the process, combustion takes place, where with the temperature increase, the main amount of heat is formed as a reaction to the process. The intensity of the combustion process increases the rate of release of volatile substances, which in turn increases the amplitude of the temperature peaks in the heat load curve. For each type of pellets, the observed exothermic peaks at 5℃/min and 10℃/min have approximately the same values.

The results in Table 3 show that the maximum temperatures of the combustion process for all tests are observed between 400℃ and 500℃, where significant amounts of heat are released. After reaching the temperature of about 440℃, the combustion process is almost complete and the observed mass losses are greatly reduced. At this point, the third stage of the process begins - smoldering, which develops in the residual material. Smoldering ends when the residual heat is removed from the system.

Table 4 presents the temperature ranges of the thermal decomposition stages of the studied biofuels.

The results of the tests in Table 4 show that in all experiments with different types of pellets almost complete combustion was achieved, where the loss of the total mass was over 99%. The average value of the residual mass for all trials and samples is about 0.1% and this value is primarily related to the ash content of the tested pellet samples.

Table 5 shows the maximum total mass losses observed during the thermal decomposition of biofuels.

The TGA results from Table 5 show that until reaching temperatures between 111℃-129℃ (at a rate of 5℃/min) and 121℃-140℃ (at a rate of 10℃/min), during the drying stage of samples, no major mass loss was observed. At both test rates, the mass loss varies between 7-9% depending on the type of pellets. Slightly higher mass losses (10-15%) for all pellets were observed in the range of 220-240℃ at 5℃/min and 230-275℃ at 10℃/min. That is where the increase in heat flow begins. By the end of the combustion process of each type of pellets, according to the thermogravimetric curves, losses between 85% and 95% can be reported. After reaching an average temperature of about 458℃ at a rate of 5℃/min and 476℃ at a rate of 10℃/min, the rate of mass loss is reduced until complete combustion is reached.

3.2. Results of the Marketing Research of Customer Preferences for Solid Biomass Fuels Usage in Bulgaria

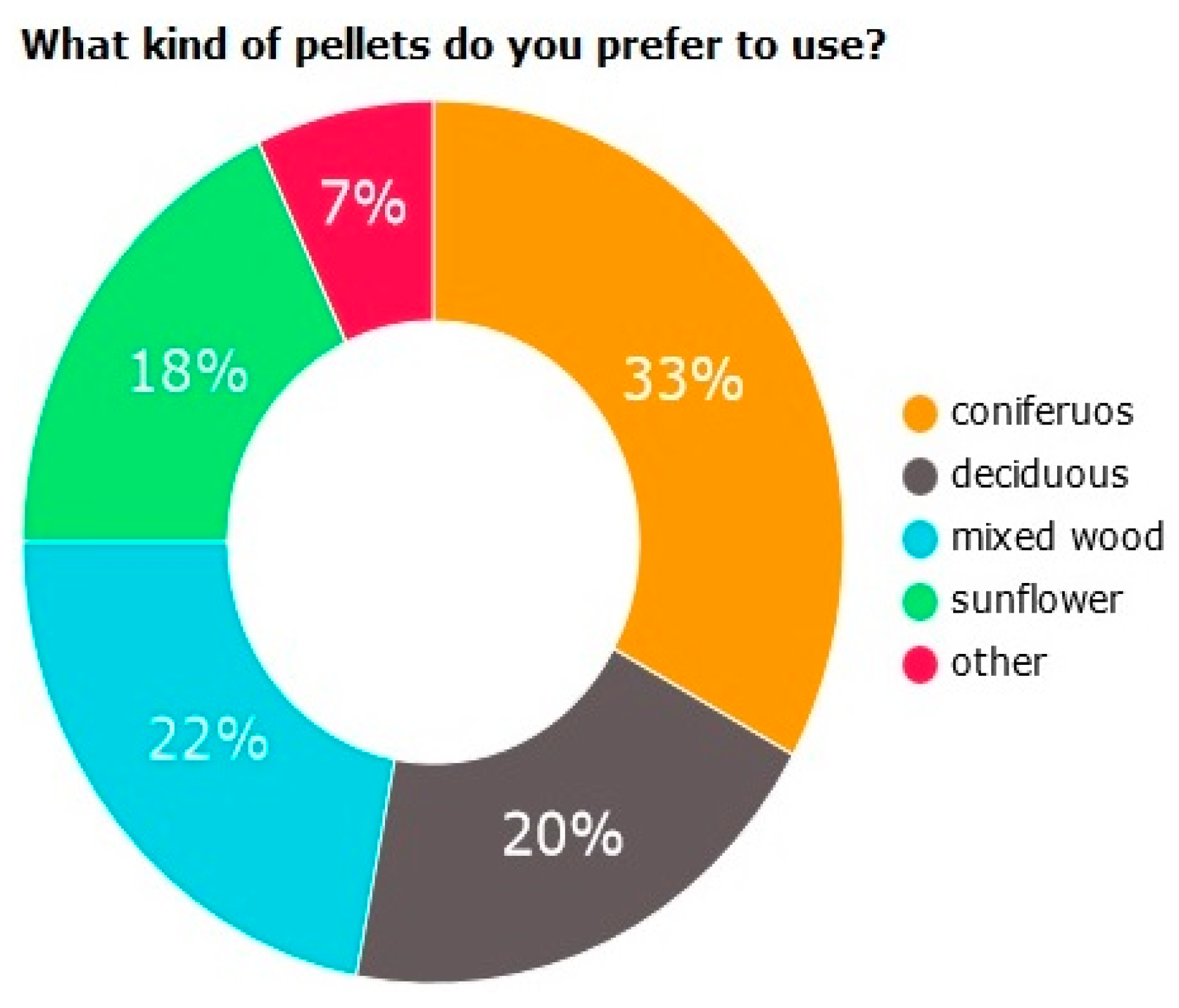

The data collected from the marketing research indicates a diverse range of preferences among respondents, with coniferous pellets and mixed wood pellets being the most popular purchase choices of solid biomass fuels, respectively 33% and 22%, followed by deciduous pellets (20%) and sunflower pellets (18%) (see Figure 7).

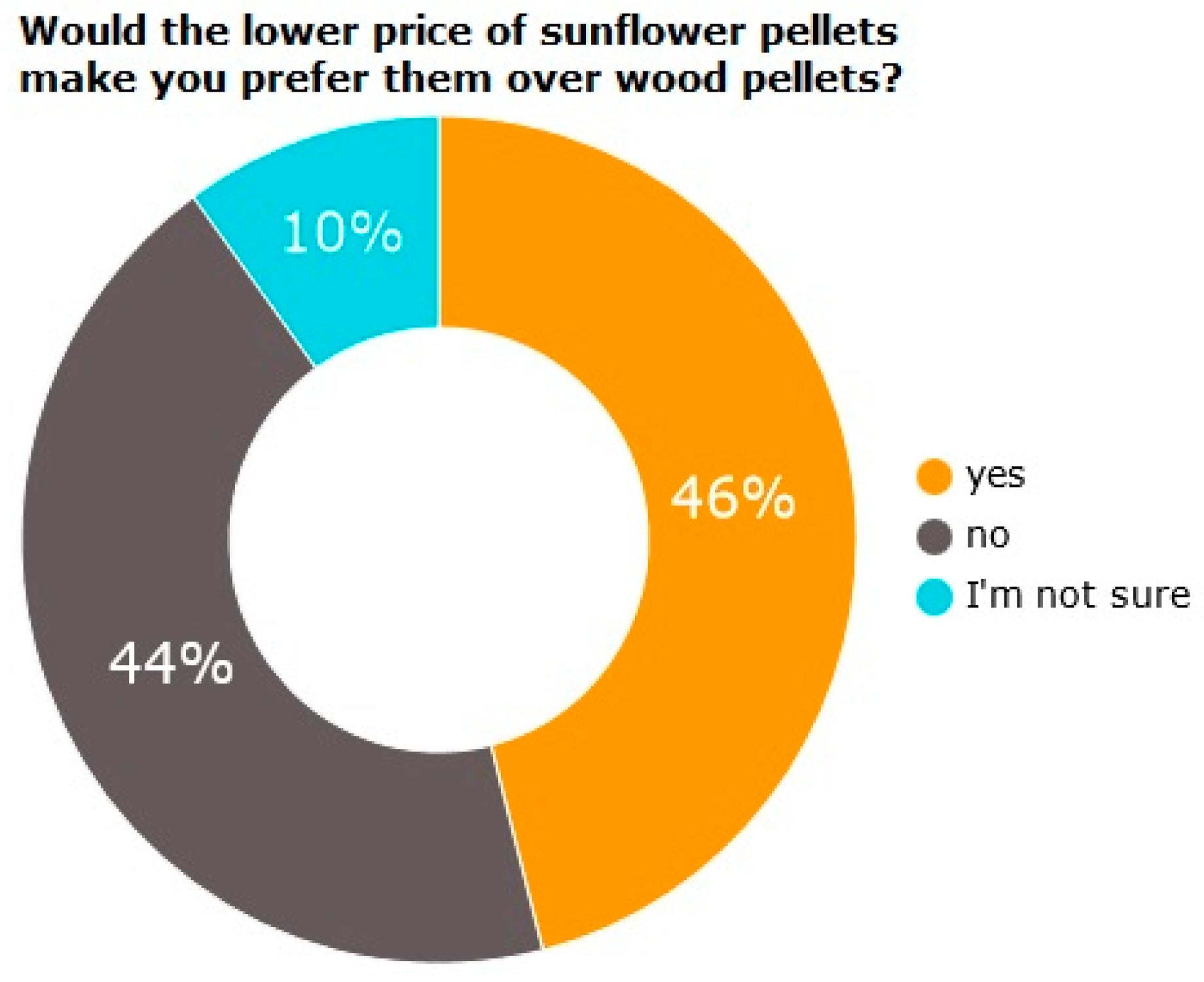

The second survey question (see Figure 8) aims to understand the influence of price on customers’ preferences for sunflower pellets over wood pellets. The results indicate that a slight majority (46%) would prefer sunflower pellets due to their lower price, while a significant portion (44%) would not be swayed by the lower price and still prefer wood pellets. Additionally, 10% of the respondents are uncertain about their preference, indicating some level of indecision or lack of strong preference.

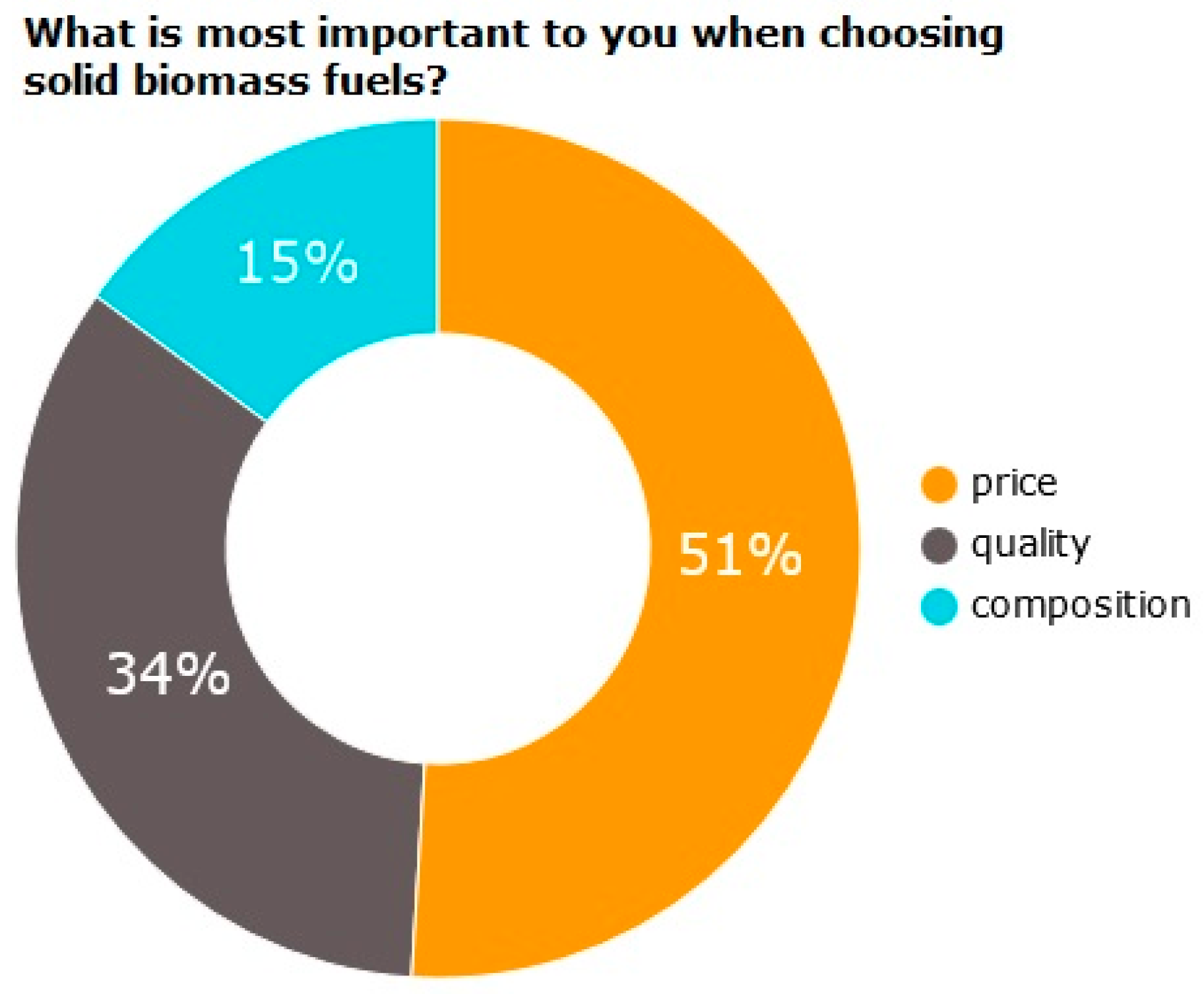

The third question from the survey uncovers what factors are most important to costumers when choosing solid biomass fuels (see Figure 9). The findings reveal that the majority (51% of the respondents) prioritize price, indicating that affordability plays a crucial role in their decision-making process. Following price considerations, 34% of the respondents place importance on quality, suggesting that many customers are willing to invest more in pellets of superior quality, potentially driven by factors such as enhanced efficiency, cleanliness or environmental sustainability. Only 15% of the respondents prioritize composition, implying that while some consumers may have concerns about the specific ingredients or additives in the solid biomass fuels, it is not a significant consideration compared to price and quality for most respondents.

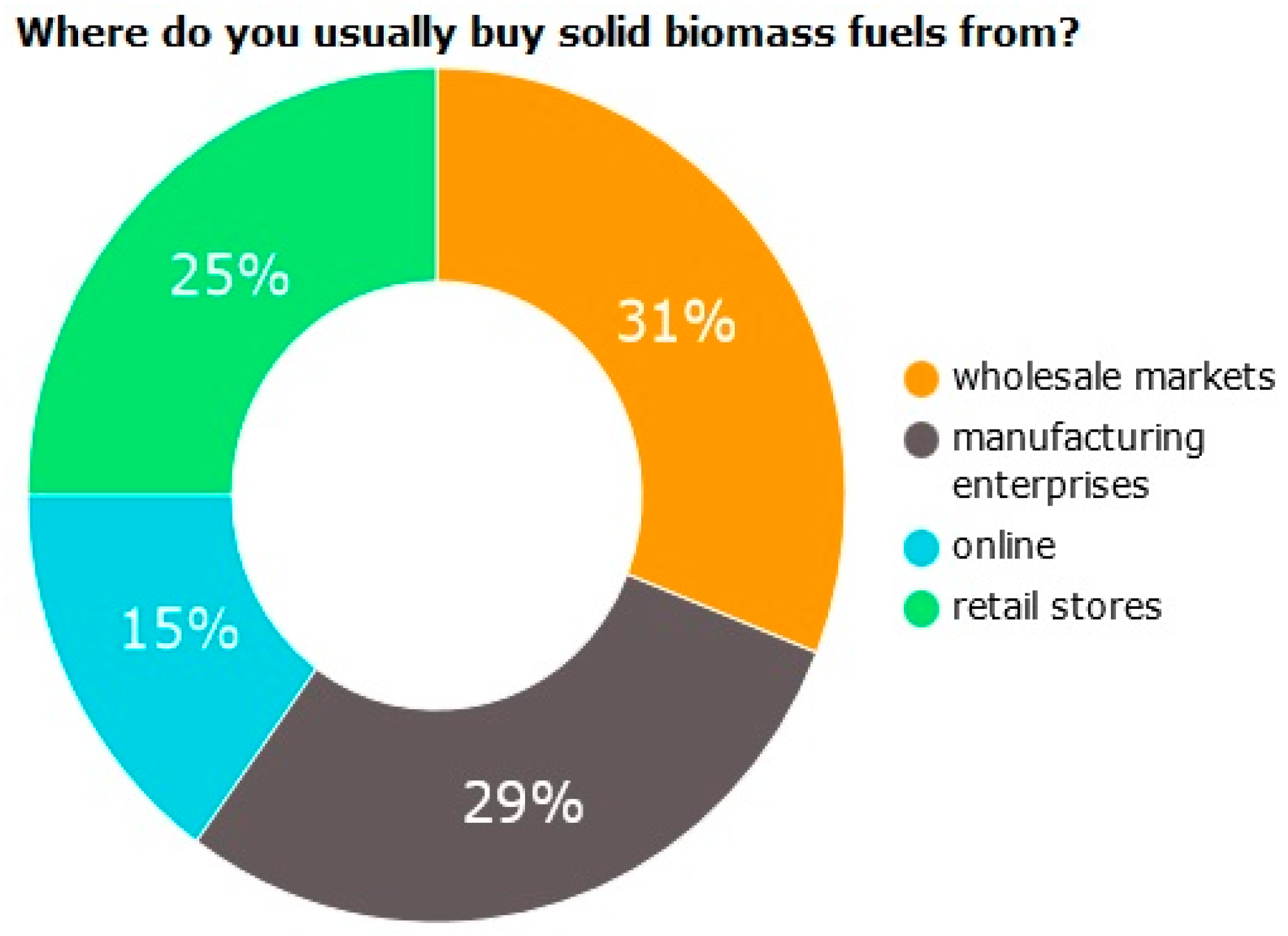

The objective of the next survey question (see Figure 10) is to gain insight into costumers' purchasing habits regarding solid biomass fuels, specifically inquiring about their preferred purchasing channels. A significant portion of the respondents (31%) prefer to purchase pellets from wholesale markets, suggesting that a notable portion of consumers may be purchasing pellets in large quantities or for commercial purposes. Factors such as pricing, availability and convenience likely influence this choice.

The fact that nearly a third of the respondents buy pellets directly from manufacturing enterprises (29%) suggests a preference for obtaining products directly from the source. This choice may be influenced by factors such as trust in product quality, direct access to fresher products and potentially better pricing due to bypassing intermediaries. The proportion of respondents buying pellets online is lower than those opting for wholesale markets and manufacturing enterprises. Nevertheless, online purchases (15%) still constitute a significant segment of the market. Convenience, diverse product options and possibly competitive pricing are key motivators behind this preference. Also factors like delivery choices and the ease of comparing products may further encourage consumers to choose online shopping. While not the majority, a significant portion of the respondents still prefer purchasing pellets from retail stores (25%).

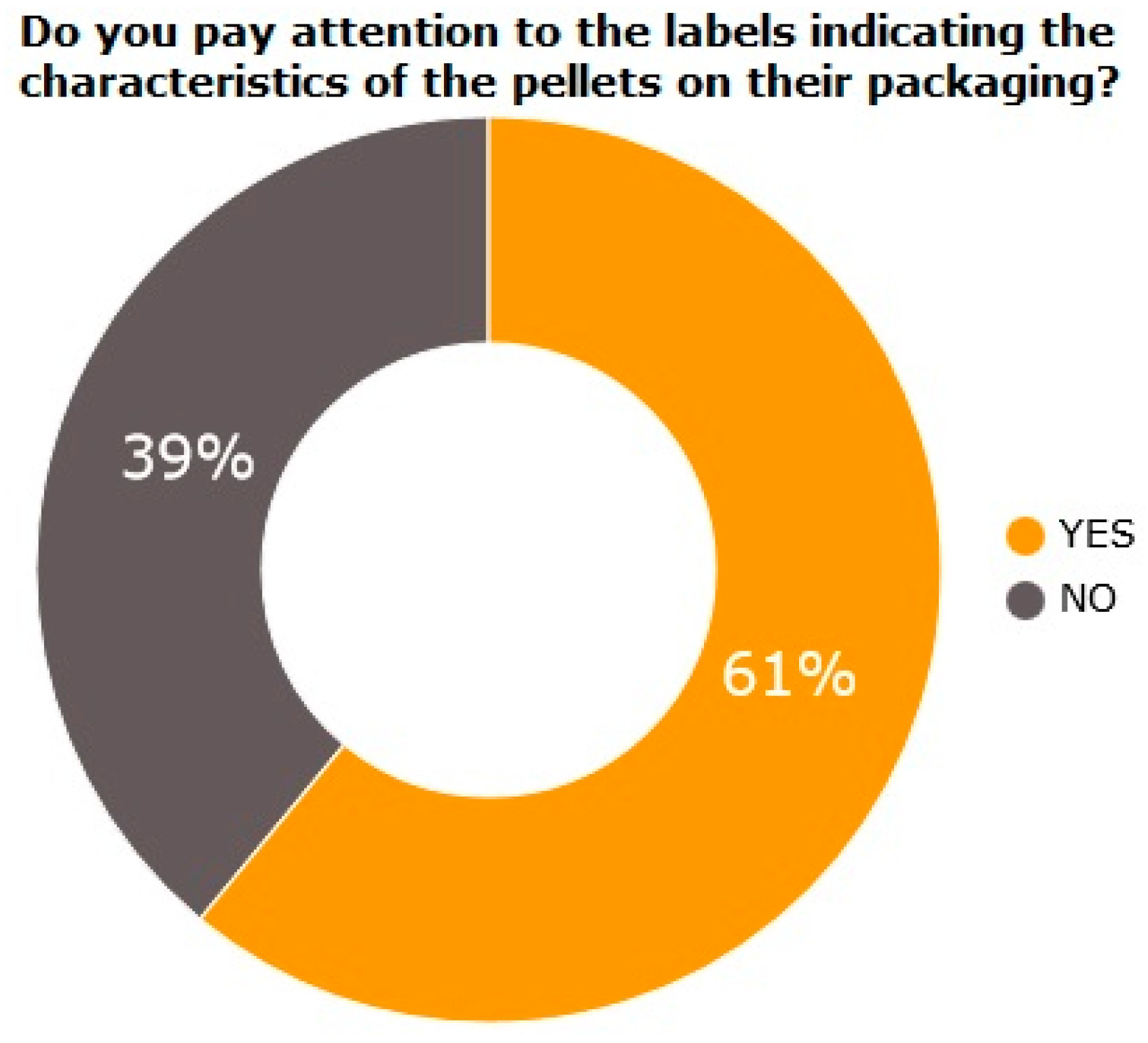

The marketing research results highlight the significance of clear and informative pellet labeling (see Figure 11). Marketers can utilize this insight to optimize label design and content, meeting the preferences of the majority who prioritize this aspect of packaging. Additionally, efforts can be made to understand and potentially address the reasons behind the minority of consumers who do not pay attention to labels, ensuring that important information reaches all consumer segments effectively.

61% of the respondents indicate that they pay attention to the labels on pellet packages regarding their characteristics. This suggests that a significant part of the costumers value the information provided on product labels. Reasons for this could include concerns about product quality, safety, environmental impact or meeting specific requirements for their intended use. Additionally, consumers may perceive labels as indicators of transparency and trustworthiness from the manufacturer or brand. A smaller proportion, 9% of the respondents admit to not paying attention to the labels on pellet packages regarding their characteristics. This minority group may have various reasons for disregarding labels, such as preconceived notions about the product, previous satisfactory experiences with similar products or a lack of interest in product details.

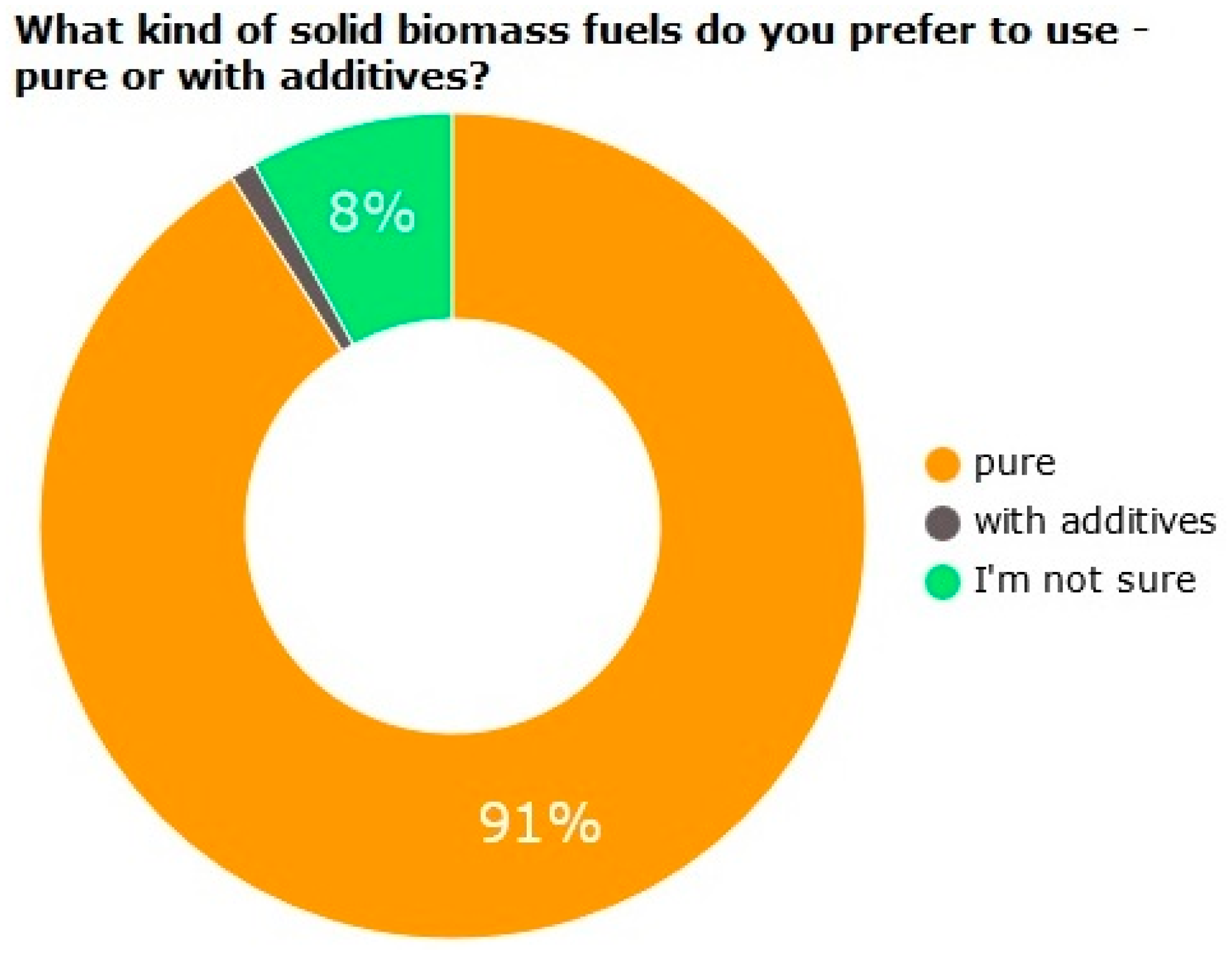

The survey results further reveal a clear consumer preference for pure solid biomass fuels, with a minority favoring fuels with additives. Moreover, a notable portion of the respondents are unsure about their preference, providing marketers with an opportunity to educate and clarify any doubts. This understanding of preferences can guide product development, marketing strategies and messaging to effectively meet consumer needs and preferences in the pellet market (see Figure 12). The vast majority (91% of the respondents) indicate a preference for pure solid biomass fuels. This strong inclination suggests that consumers prioritize simplicity and purity in their pellet choices. Reasons for this preference may include concerns about potential negative impacts of additives on health, the environment or pellet performance. Also consumers may perceive pure pellets as more authentic and natural, aligning with preferences for minimally processed or organic products.

A very small fraction, only 1% of the respondents, express a preference for pellets containing additives. Consumers who favor solid biomass fuels with additives may prioritize specific benefits offered by the additives, such as enhanced performance, flavor or nutritional value. However, the low percentage indicates that this segment is not substantial compared to those favoring pure pellets. 8% of the respondents express uncertainty regarding their preference for either pure or additive-containing pellets. This uncertainty may stem from a lack of information about the differences between pure and additive-containing solid biomass fuels, indecision about personal preferences or a need for more information to form a preference.

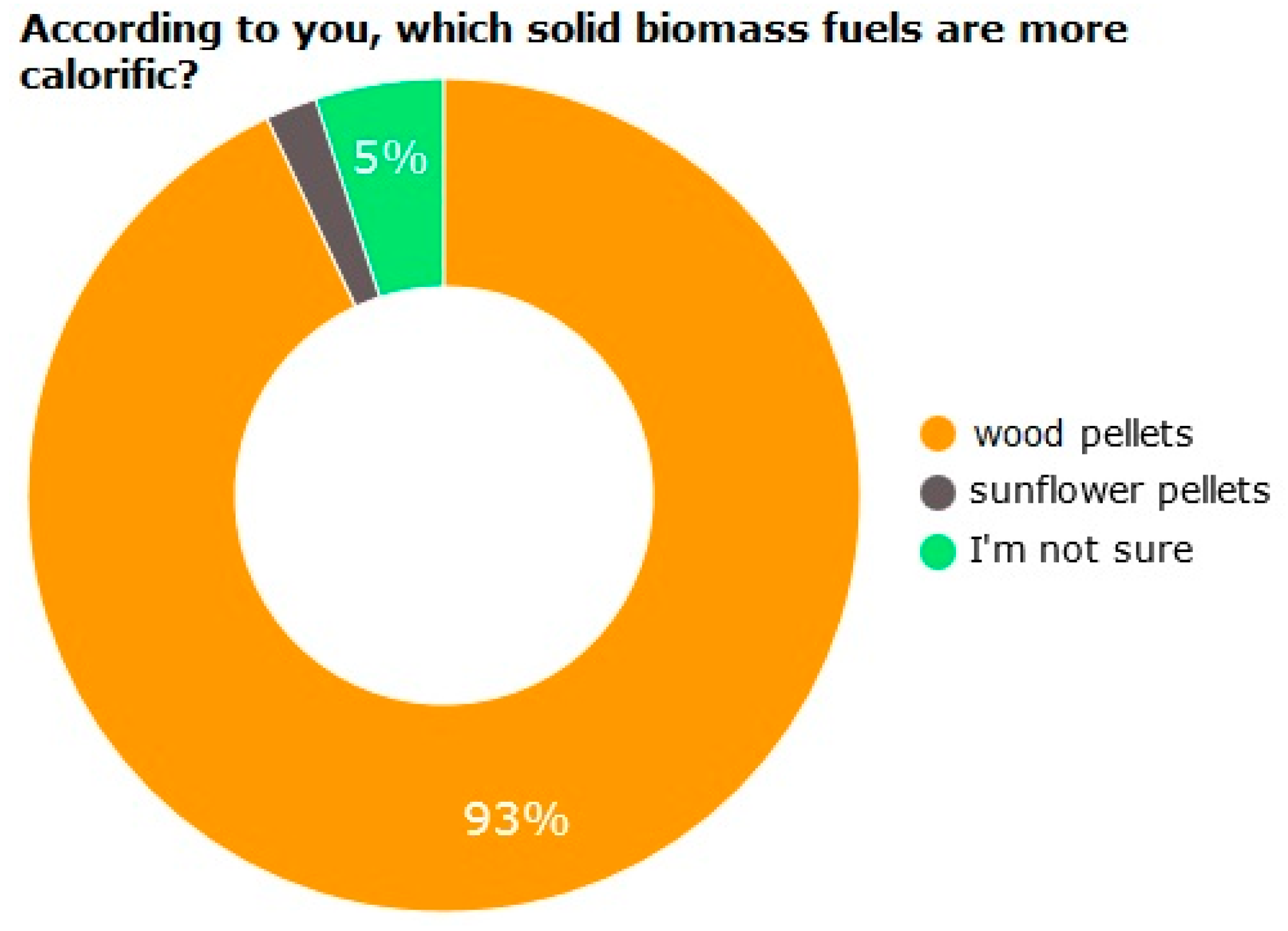

The survey data indicates a strong belief among Bulgarian customers that wood pellets are more calorific compared to sunflower pellets (see Figure 13). The vast majority, comprising 93% of the respondents, believe that wood pellets are more calorific. This preference likely reflects the widespread use and familiarity of wood pellets as an efficient heating fuel in Bulgaria, as well as their reputation for efficient energy production. Only a tiny fraction, just 2% of the respondents, believe that sunflower pellets are more calorific.

This minimal preference indicates that the perception of sunflower pellets as a highly calorific fuel is not widely held among Bulgarian customers. Sunflower pellets may not be as commonly used or as well-known for their heating properties compared to wood pellets, leading to a lower level of confidence in their calorific value. However, there remains a small percentage of consumers (5%) who are uncertain about this comparison of wood pellets versus sunflower pellets, suggesting an opportunity for further education and clarification on the calorific properties of different pellet types.

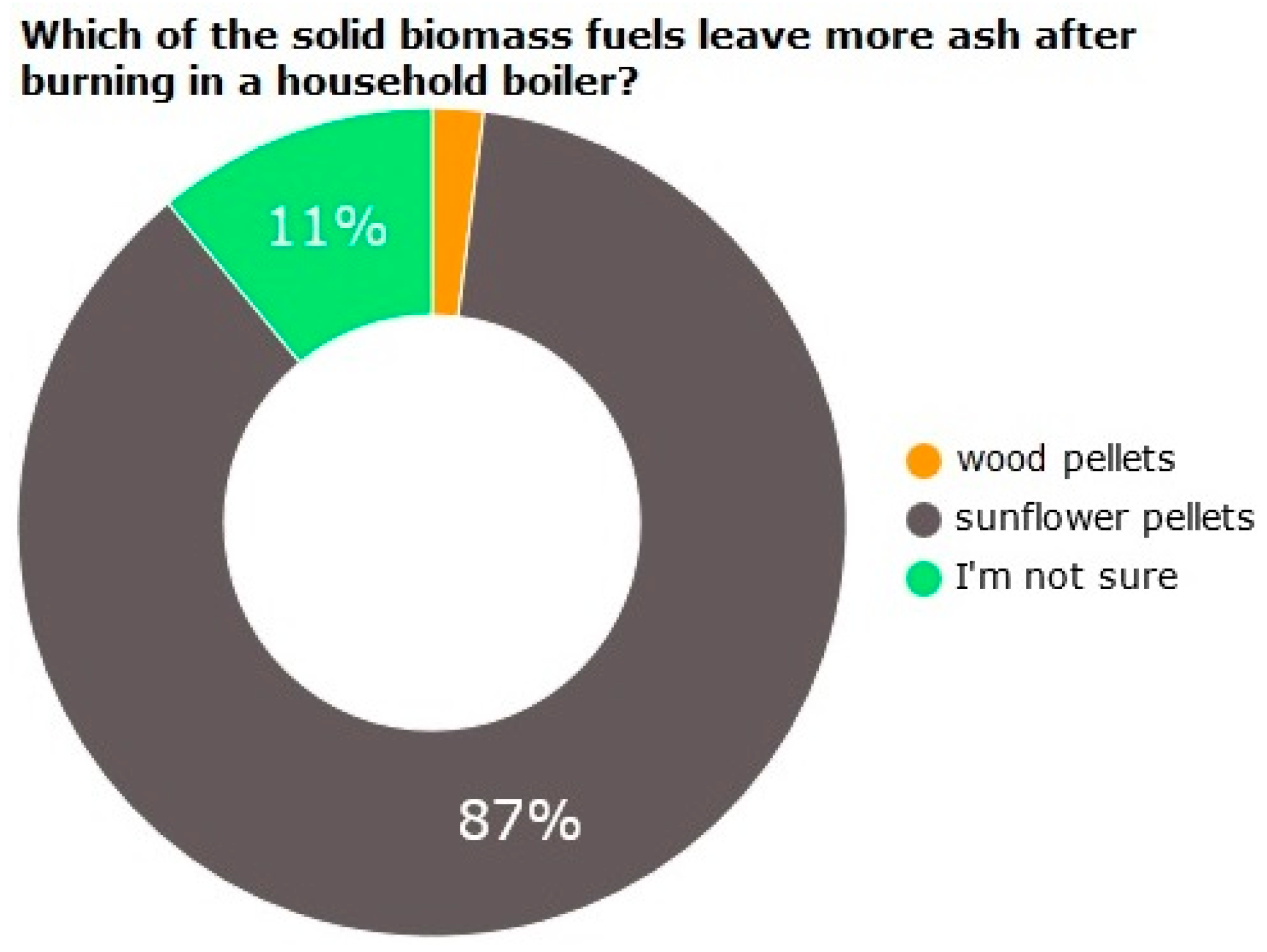

According to the marketing research results, there is a widespread belief among Bulgarian customers that sunflower pellets leave more ash after burning in a household boiler compared to wood pellets. While there is a minimal percentage of respondents who believe otherwise, a notable portion also express uncertainty about this comparison, suggesting an opportunity for clarification and education on the ash-producing characteristics of different pellet types (see Figure 14).

The overwhelming majority, comprising 87% of the respondents, believe that sunflower pellets leave more ash after burning in a household boiler. This strong preference suggests a widespread perception among Bulgarian customers that sunflower pellets result in higher ash residue compared to other types, such as wood pellets. This preference may stem from personal experiences or observations of higher ash content when using sunflower pellets, leading to a general consensus among consumers. Only a very small group, representing 2% of the respondents, believe that wood pellets leave more ash after burning. This minor preference suggests that there is minimal belief among Bulgarian customers that wood pellets produce higher ash residue. This could be due to wood pellets being perceived as a cleaner-burning fuel compared to sunflower pellets, with lower ash content as a result. 11% of the respondents express uncertainty regarding which type of pellets leaves more ash after burning. This uncertainty may arise from a lack of firsthand experience or knowledge about the ash-producing properties of different pellet types.

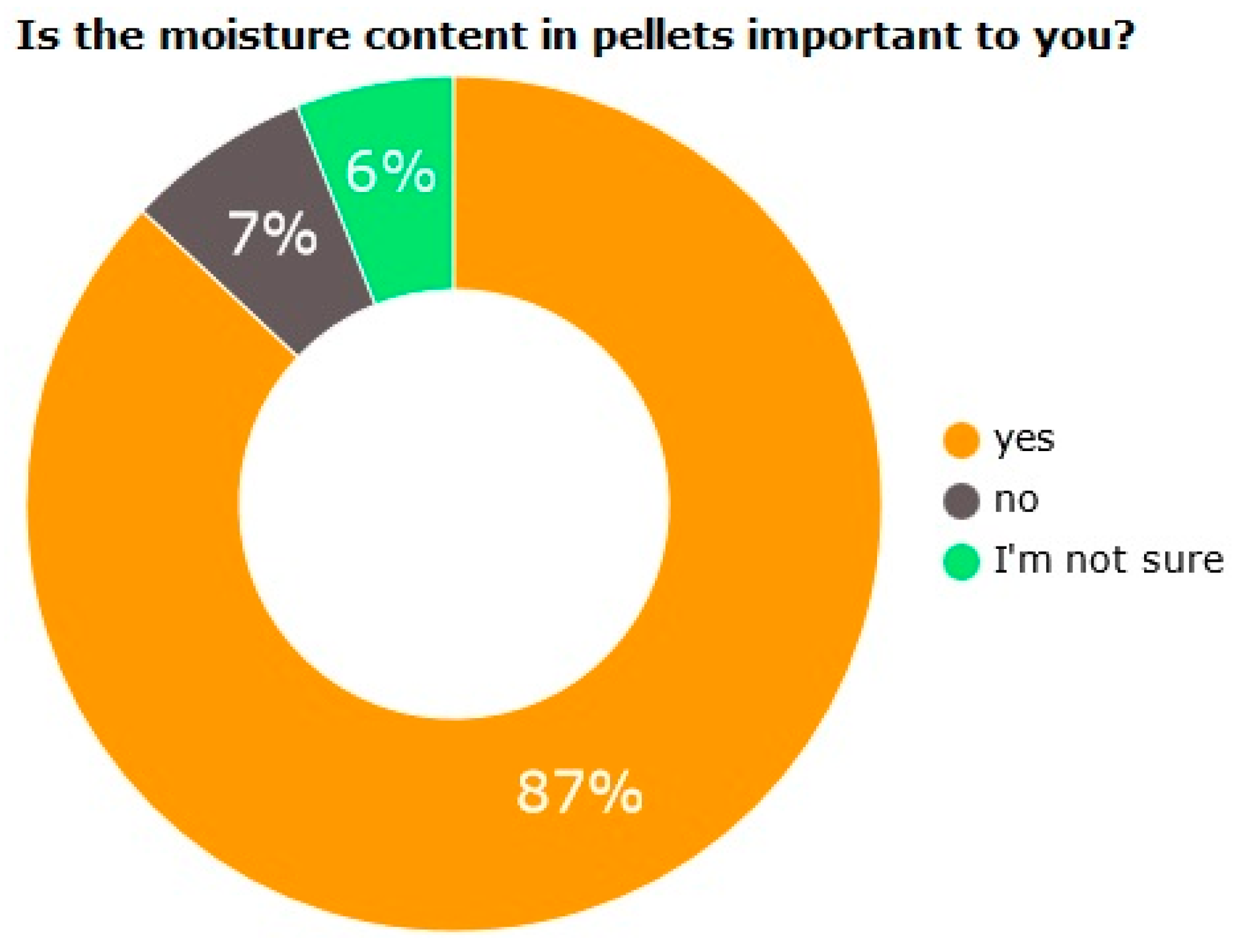

The marketing research results also highlight a strong consensus among the respondents regarding the significance of moisture content in pellets, with the majority considering it a critical factor in their purchasing decisions. There are smaller segments of consumers who either do not prioritize moisture content or are uncertain about its importance. Addressing these perspectives and providing clarity on the role of moisture content could assist consumers in making more informed choices when selecting pellets (see Figure 15).

The majority of the respondents (87%) acknowledge the importance of moisture content in pellets. The significance attributed to moisture content likely stems from its crucial role in the efficiency and performance of pellet-fueled appliances, such as boilers or stoves. Maintaining appropriate moisture levels is essential for achieving efficient combustion and maximizing heat output. Hence, consumers value pellets with suitable moisture content to ensure optimal performance and energy efficiency. A small minority, comprising 7% of the respondents, express that moisture content in pellets is not a critical factor for them. This viewpoint suggests that some customers prioritize other factors, such as price or availability, over moisture content when making pellet purchases. Alternatively, they may not fully grasp the impact of moisture content on pellet performance or may not view it as a primary consideration in their decision-making process. Another 6% of the respondents convey uncertainty regarding the importance of moisture content in pellets, which may arise from a lack of knowledge or understanding regarding the role of moisture content in pellet performance.

4. Discussion

The obtained results from the marketing research suggest that while price is a factor for many Bulgarian customers, there are still a considerable number of individuals who value other factors such as quality or convenience over price when choosing between the different solid biomass fuel types.

The data highlights the diverse range of purchasing channels preferred by Bulgarian customers when it comes to buying pellets. Factors such as pricing, convenience, product availability and trust in product quality likely play significant roles in shaping these preferences. Additionally, the distribution of preferences across different channels underscores the importance for pellet suppliers and marketers to maintain a strong presence across various biomass fuel sales channels to effectively cater to different consumer segments and their preferences. This indicates that conventional physical retail stores remain influential in Bulgarian market. Factors such as accessibility, in-person assistance and immediate availability of products may influence customers to choose retail stores for their pellet purchases.

For marketers, addressing customers’ uncertainty regarding their preference for either pure or additive-containing solid biomass fuels could involve providing clear and informative product descriptions, emphasizing the benefits of each option and addressing any consumer concerns about additives. Marketers must also delve into the motivations behind consumer behavior, to correct misconceptions and enhance the effectiveness of the labeling of solid biomass fuels packaging ultimately ensuring a better understanding of consumer preferences and needs.

The analysis of the energy characteristics from the research leads to the improvement of the combustion process when using pellet fuels and achieving a more efficient and sustainable use of energy. The research results in [59] almost overlap those obtained for some of the parameters and provide information about the quality and efficiency of sunflower and wood pellets and their use in the combustion process. The studies presented in reference [60] emphasize the importance of pellets as fuel produced from agricultural and forestry waste and their significant role in optimizing the combustion process. Analysis of the TG results shows that the resulting curves are very similar to each other. However, there are some significant differences in the temperature peaks and in the curves of the heat flow. These differences are mainly due to the different composition of the materials used for the production of biomass pellets. The cited authors in reference [61] conduct a detailed research analysis on the method of thermogravimetry and the theoretically assumed forms of the curve obtained after analyzing the data resulting from the tests. Their analytical approach includes studying various physicochemical characteristics of the materials and their reactions, which is crucial for better understanding and optimization of processes in the field of fuel technologies. In study [62,63], a thermogravimetric analysis is conducted focusing on the characteristics of five different types of biomass that have the potential to be used as fuel materials. The analysis of the results from previous studies by other authors, as well as from the current research, underscores the importance of using thermogravimetric analysis in combination with differential scanning calorimetry to assess the thermal properties of pellets. Conducting studies on the combustion process of pellets produced by mixing different types of biomass opens perspectives for future research and for developing new types of pellets meeting the needs of the energy market.

5. Conclusions

In conclusion, the comprehensive marketing research findings offer valuable insights for manufacturers and marketers of solid biomass fuels, enabling them to gain a deeper understanding of consumer preferences. By leveraging these insights, they can adapt their products and communication strategies to better align with customer demands, ultimately enhancing their competitiveness and effectiveness in Bulgarian market.

Based on the analysis of the research results on the energy characteristics of biofuels from waste wood (Pellets 1 and 2), sunflower husks (Pellets 4 and 5), and mixed pellets (Pellets 3), it is found that Pellets 4 and Pellets 5 are rated as the highest due to their better energy qualities compared to wood pellets. However, a high ash content is observed in sunflower pellets. The highest total moisture content is recorded in Pellets 4 (7.82%), while the lowest is in Pellets 3 (7.07%).

The analysis of the results from TG and DSC shows that the combustion of the pellets proceeds through three main stages: drying (Stage 1), burning (Stage 2) and smoldering (Stage 3). At temperatures between 111°C and 129°C (at a rate of 5°C/min) and 121°C and 140°C (at a rate of 10°C/min) the drying stage of the samples does not cause significant mass loss. However, the subsequent burning stages lead to more significant mass losses, ranging between 7% and 9% at both investigation rates. At higher temperatures from 220°C to 240°C at a rate of 5°C/min and from 230°C to 275°C at a rate of 10°C/min, an increase in heat flow is observed and the burning process concludes with mass losses ranging between 85% and 95%.

Combining the results from the marketing research of customers’ preferences, the energy analyses and the studies with thermogravimetry and differential scanning calorimetry, forms a closed cycle that reveals important aspects about public opinion regarding the use of biofuels, as well as about the characteristics and energy potential of various types of pellet fuels. These data are of significant importance for developing more efficient methods for utilizing biomass as fuel.

Author Contributions

Conceptualization, P.Z. and M.M.; methodology, P.Z.; formal analysis, N.M. and M.M.; investigation, M.M. and N.M.; resources, P.Z.; data curation, M.M. and N.M.; writing—original draft preparation, M.M. and N.M.; writing—review and editing, P.Z.; visualization, N.M. and M.M.; supervision, P.Z. All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding.

Data Availability Statement

Data are contained within the article.

Acknowledgments

The authors would like to thank to the consumers who participated in the surveys, the retail stores and the manufacturers who kindly provided the pellet fuels, as well as to the laboratories that provided their equipment for conducting the research.

Conflicts of Interest

The authors declare no conflicts of interest.

References

- Nunes, L.J.R. The Rising Threat of Atmospheric CO2: A Review on the Causes, Impacts, and Mitigation Strategies. Environments 2023, 10, 66. [Google Scholar] [CrossRef]

- Strielkowski, W.; Civín, L.; Tarkhanova, E.; Tvaronavičienė, M.; Petrenko, Y. Renewable Energy in the Sustainable Development of Electrical Power Sector: A Review. Energies 2021, 14, 8240. [Google Scholar] [CrossRef]

- Alsarhan, L.M.; Alayyar, A.S.; Alqahtani, N.B.; Khdary, N.H. Circular Carbon Economy (CCE): A Way to Invest CO2 and Protect the Environment, a Review. Sustainability 2021, 13, 11625. [Google Scholar] [CrossRef]

- Mostafaeipour, A.; Bidokhti, A.; Fakhrzad, M.-B.; Sadegheih, A.; Mehrjerdi, Y.Z. A new model for the use of renewable electricity to reduce carbon dioxide emissions. Energy 2021, 238, 121602. [Google Scholar] [CrossRef]

- Voumik, L.C.; Islam, A.; Ray, S.; Yusop, N.Y.M.; Ridzuan, A.R. CO2 Emissions from Renewable and Non-Renewable Electricity Generation Sources in the G7 Countries: Static and Dynamic Panel Assessment. Energies 2023, 16, 1044. [Google Scholar] [CrossRef]

- Nunes, L.J.R. The Rising Threat of Atmospheric CO2: A Review on the Causes, Impacts, and Mitigation Strategies. Environments 2023, 10, 66. [Google Scholar] [CrossRef]

- Cieśliński, R.; Kubiak-Wójcicka, K. Use of the Gas Emission Site Type Method in the Evaluation of the CO2 Emissions in Raised Bogs. Water 2024, 16, 1069. [Google Scholar] [CrossRef]

- Jozay, M.; Zarei, H.; Khorasaninejad, S.; Miri, T. Maximising CO2 Sequestration in the City: The Role of Green Walls in Sustainable Urban Development. Pollutants 2024, 4, 91–116. [Google Scholar] [CrossRef]

- Abakumov, E.; Makarova, M.; Paramonova, N.; Ivakhov, V.; Nizamutdinov, T.; Polyakov, V. Carbon Fluxes from Soils of “Ladoga” Carbon Monitoring Site Leningrad Region, Russia. Atmosphere 2024, 15, 360. [Google Scholar] [CrossRef]

- Bougma, P.-T.C.; Bondé, L.; Yaro, V.S.O.; Gebremichael, A.W.; Ouédraogo, O. Assessing Carbon Emissions from Biomass Burning in Croplands in Burkina Faso, West Africa. Fire 2023, 6, 402. [Google Scholar] [CrossRef]

- Ning, J.; Zhang, C.; Hu, M.; Sun, T. Accounting for Greenhouse Gas Emissions in the Agricultural System of China Based on the Life Cycle Assessment Method. Sustainability 2024, 16, 2594. [Google Scholar] [CrossRef]

- Peng, C.; Li, H.; Yang, N.; Lu, M. A Comparison of Greenhouse Gas Emission Patterns in Different Water Levels in Peatlands. Water 2024, 16, 985. [Google Scholar] [CrossRef]

- Mathur, S.; Waswani, H.; Singh, D.; Ranjan, R. Alternative Fuels for Agriculture Sustainability: Carbon Footprint and Economic Feasibility. Agriengineering 2022, 4, 993–1015. [Google Scholar] [CrossRef]

- Rahmanta, M.A.; Aprilana, A. ; Ruly; Cahyo, N. ; Hapsari, T.W.D.; Supriyanto, E. Techno-Economic and Environmental Impact of Biomass Co-Firing with Carbon Capture and Storage in Indonesian Power Plants. Sustainability 2024, 16, 3423. [Google Scholar]

- Holechek, J.L.; Geli, H.M.E.; Sawalhah, M.N.; Valdez, R. A Global Assessment: Can Renewable Energy Replace Fossil Fuels by 2050? Sustainability 2022, 14, 4792. [Google Scholar] [CrossRef]

- Kalak, T. Potential Use of Industrial Biomass Waste as a Sustainable Energy Source in the Future. Energies 2023, 16, 1783. [Google Scholar] [CrossRef]

- Wieruszewski, M.; Górna, A.; Stanula, Z.; Adamowicz, K. Energy Use of Woody Biomass in Poland: Its Resources and Harvesting Form. Energies 2022, 15, 6812. [Google Scholar] [CrossRef]

- Chlebnikovas, A.; Paliulis, D.; Kilikevičius, A.; Selech, J.; Matijošius, J.; Kilikevičienė, K.; Vainorius, D. Possibilities and Generated Emissions of Using Wood and Lignin Biofuel for Heat Production. Energies 2021, 14, 8471. [Google Scholar] [CrossRef]

- Janiszewska, D.; Ossowska, L. The Role of Agricultural Biomass as a Renewable Energy Source in European Union Countries. Energies 2022, 15, 6756. [Google Scholar] [CrossRef]

- Božič, J.T.; Fric, U.; Čikić, A.; Muhič, S. Life Cycle Assessment of Using Firewood and Wood Pellets in Slovenia as Two Primary Wood-Based Heating Systems and Their Environmental Impact. Sustainability 2024, 16, 1687. [Google Scholar] [CrossRef]

- Halkos, G.E.; Aslanidis, P.-S.C. Addressing Multidimensional Energy Poverty Implications on Achieving Sustainable Development. Energies 2023, 16, 3805. [Google Scholar] [CrossRef]

- IEA. Available online: https://www.iea.org/countries/bulgaria (accessed on 21 April 2024).

- EEA. Available online: https://eea.innovationnorway.com/article/bulgaria:-green-biomass-energy (accessed on 22 April 2024).

- Butler, J.W.; Skrivan, W.; Lotfi, S. Identification of Optimal Binders for Torrefied Biomass Pellets. Energies 2023, 16, 3390. [Google Scholar] [CrossRef]

- Saletnik, B.; Saletnik, A.; Zaguła, G.; Bajcar, M.; Puchalski, C. The Use of Wood Pellets in the Production of High Quality Biocarbon Materials. Materials 2022, 15, 4404. [Google Scholar] [CrossRef] [PubMed]

- Ilari, A.; Pedretti, E.F.; De Francesco, C.; Duca, D. Pellet Production from Residual Biomass of Greenery Maintenance in a Small-Scale Company to Improve Sustainability. Resources 2021, 10, 122. [Google Scholar] [CrossRef]

- Hassan, M.; Usman, N.; Hussain, M.; Yousaf, A.; Khattak, M.A.; Yousaf, S.; Mishr, R.S.; Ahmad, S.; Rehman, F.; Rashedi, A. Environmental and Socio-Economic Assessment of Biomass Pellets Biofuel in Hazara Division, Pakistan. Sustainability 2023, 15, 12089. [Google Scholar] [CrossRef]

- Kogabayev, T.; Põder, A.; Barth, H.; Värnik, R. Prospects for Wood Pellet Production in Kazakhstan: A Case Study on Business Model Adjustment. Energies 2023, 16, 5838. [Google Scholar] [CrossRef]

- Bochniak, A.; Stoma, M. Estimating the Optimal Location for the Storage of Pellet Surplus. Energies 2021, 14, 6657. [Google Scholar] [CrossRef]

- Bosona, T.; Gebresenbet, G. Evaluating Logistics Performances of Agricultural Prunings for Energy Production: A Logistics Audit Analysis Approach. Logistics 2018, 2, 19. [Google Scholar] [CrossRef]

- Kline, K.L.; Dale, V.H.; Rose, E.; Tonn, B. Effects of Production of Woody Pellets in the Southeastern United States on the Sustainable Development Goals. Sustainability 2021, 13, 821. [Google Scholar] [CrossRef]

- Milewska, B.; Milewski, D. Implications of Increasing Fuel Costs for Supply Chain Strategy. Energies 2022, 15, 6934. [Google Scholar] [CrossRef]

- Ter-Mikaelian, M.T.; Chen, J.; Desjardins, S.M.; Colombo, S.J. Can Wood Pellets from Canada’s Boreal Forest Reduce Net Greenhouse Gas Emissions from Energy Generation in the UK? Forests 2023, 14, 1090. [Google Scholar] [CrossRef]

- Giannini, V.; Maucieri, C.; Vamerali, T.; Zanin, G.; Schiavon, S.; Pettenella, D.M.; Bona, S.; Borin, M. Sunflower: From Cortuso’s Description (1585) to Current Agronomy, Uses and Perspectives. Agriculture 2022, 12, 1978. [Google Scholar] [CrossRef]

- Puttha, R.; Venkatachalam, K.; Hanpakdeesakul, S.; Wongsa, J.; Parametthanuwat, T.; Srean, P.; Pakeechai, K.; Charoenphun, N. Exploring the Potential of Sunflowers: Agronomy, Applications, and Opportunities within Bio-Circular-Green Economy. Horticulturae 2023, 9, 1079. [Google Scholar] [CrossRef]

- Nakonechna, K.; Ilko, V.; Berčíková, M.; Vietoris, V.; Panovská, Z.; Doležal, M. Nutritional, Utility, and Sensory Quality and Safety of Sunflower Oil on the Central European Market. Agriculture 2024, 14, 536. [Google Scholar] [CrossRef]

- Mabuza, L.M.; Mchunu, N.P.; Crampton, B.G.; Swanevelder, D.Z.H. Accelerated Breeding for Helianthus annuus (Sunflower) through Doubled Haploidy: An Insight on Past and Future Prospects in the Era of Genome Editing. Plants 2023, 12, 485. [Google Scholar] [CrossRef]

- Puttha, R.; Venkatachalam, K.; Hanpakdeesakul, S.; Wongsa, J.; Parametthanuwat, T.; Srean, P.; Pakeechai, K.; Charoenphun, N. Exploring the Potential of Sunflowers: Agronomy, Applications, and Opportunities within Bio-Circular-Green Economy. Horticulturae 2023, 9, 1079. [Google Scholar] [CrossRef]

- Havrysh, V.; Kalinichenko, A.; Pysarenko, P.; Samojlik, M. Sunflower Residues-Based Biorefinery: Circular Economy Indicators. Processes 2023, 11, 630. [Google Scholar] [CrossRef]

- Stoicea, P.; Chiurciu, I.A.; Soare, E.; Iorga, A.M.; Dinu, T.A.; Tudor, V.C.; Gîdea, M.; David, L. Impact of Reducing Fertilizers and Pesticides on Sunflower Production in Romania versus EU Countries. Sustainability 2022, 14, 8334. [Google Scholar] [CrossRef]

- Božič, J.T.; Fric, U.; Čikić, A.; Muhič, S. Life Cycle Assessment of Using Firewood and Wood Pellets in Slovenia as Two Primary Wood-Based Heating Systems and Their Environmental Impact. Sustainability 2024, 16, 1687. [Google Scholar] [CrossRef]

- Matula, T.; Labaj, J.; Vadasz, P.; Plešingerová, B.; Smalcerz, A.; Blacha, L. Application of Sunflower Husk Pellet as a Reducer in Metallurgical Processes. Materials 2023, 16, 6790. [Google Scholar] [CrossRef]

- Turzyński, T.; Kluska, J.; Ochnio, M.; Kardaś, D. Comparative Analysis of Pelletized and Unpelletized Sunflower Husks Combustion Process in a Batch-Type Reactor. Materials 2021, 14, 2484. [Google Scholar] [CrossRef] [PubMed]

- Reyes, F.; Vasquez, Y.; Gramsch, E.; Oyola, P.; Rappenglück, B.; Rubio, M.A. Photooxidation of Emissions from Firewood and Pellet Combustion Using a Photochemical Chamber. Atmosphere 2019, 10, 575. [Google Scholar] [CrossRef]

- Mašán, V.; Burg, P.; Souček, J.; Slaný, V.; Vaštík, L. Energy Potential of Urban Green Waste and the Possibility of Its Pelletization. Sustainability 2023, 15, 16489. [Google Scholar] [CrossRef]

- Jasinskas, A.; Kleiza, V.; Streikus, D.; Domeika, R.; Vaiciukevičius, E.; Gramauskas, G.; Valentin, M.T. Assessment of Quality Indicators of Pressed Biofuel Produced from Coarse Herbaceous Plants and Determination of the Influence of Moisture on the Properties of Pellets. Sustainability 2022, 14, 1068. [Google Scholar] [CrossRef]

- Petlickaitė, R.; Jasinskas, A.; Domeika, R.; Pedišius, N.; Lemanas, E.; Praspaliauskas, M.; Kukharets, S. Evaluation of the Processing of Multi-Crop Plants into Pelletized Biofuel and Its Use for Energy Conversion. Processes 2023, 11, 421. [Google Scholar] [CrossRef]

- Rupasinghe, R.L.; Perera, P.; Bandara, R.; Amarasekera, H.; Vlosky, R. Insights into Properties of Biomass Energy Pellets Made from Mixtures of Woody and Non-Woody Biomass: A Meta-Analysis. Energies 2023, 17, 54. [Google Scholar] [CrossRef]

- Kamperidou, V. Quality Analysis of Commercially Available Wood Pellets and Correlations between Pellets Characteristics. Energies 2022, 15, 2865. [Google Scholar] [CrossRef]

- BDS. Available online: https://bds-bg.org/bg/project/show/bds:proj:101406 (accessed on 25 April 2024).

- BDS. Available online: https://bds-bg.org/bg/project/show/bds:proj:119539 (accessed on 25 April 2024).

- BDS. Available online: https://bds-bg.org/bg/project/show/bds:proj:100349 (accessed on 25 April 2024).

- BDS. Available online: https://bds-bg.org/bg/project/show/bds:proj:99910 (accessed on 25 April 2024).

- Civitarese, V.; Acampora, A.; Sperandio, G.; Bassotti, B.; Latterini, F.; Picchio, R. A Comparison of the Qualitative Characteristics of Pellets Made from Different Types of Raw Materials. Forests 2023, 14, 2025. [Google Scholar] [CrossRef]

- Jia, G. Combustion Characteristics and Kinetic Analysis of Biomass Pellet Fuel Using Thermogravimetric Analysis. Processes 2021, 9, 868. [Google Scholar] [CrossRef]

- Silva, J.; Teixeira, S.; Teixeira, J. A Review of Biomass Thermal Analysis, Kinetics and Product Distribution for Combustion Modeling: From the Micro to Macro Perspective. Energies 2023, 16, 6705. [Google Scholar] [CrossRef]

- Dong, L.; Huang, X.; Ren, J.; Deng, L.; Da, Y. Thermogravimetric Assessment and Differential Thermal Analysis of Blended Fuels of Coal, Biomass and Oil Sludge. Appl. Sci. 2023, 13, 11058. [Google Scholar] [CrossRef]

- Linseis. Available online: https://www.linseis.com/en/products/simultaneous-thermal-analyzer-tga-dsc/sta-pt-1600 (accessed on 28 April 2024).

- Szymajda, A.; Łaska, G. The Effect of Moisture and Ash on the Calorific Value of Cow Dung Biomass. Proceedings 2019, 16, 4. [Google Scholar] [CrossRef]

- Zafar, U.; Sarwar, A.; Safdar, M.; Sabir, R.M.; Majeed, M.D.; Raza, A. Development and Characterization of Biomass Pellets Using Yard Waste. Eng. Proc. 2023, 56, 323. [Google Scholar] [CrossRef]

- Almusafir, R.; Smith, J.D. Thermal Decomposition and Kinetic Parameters of Three Biomass Feedstocks for the Performance of the Gasification Process Using a Thermogravimetric Analyzer. Energies 2024, 17, 396. [Google Scholar] [CrossRef]

- Fraga, L.G.; Silva, J.; Teixeira, S.; Soares, D.; Ferreira, M.; Teixeira, J. Influence of Operating Conditions on the Thermal Behavior and Kinetics of Pine Wood Particles Using Thermogravimetric Analysis. Energies 2020, 13, 2756. [Google Scholar] [CrossRef]

- Wilczkowska), E.M.I. (.; Nietrzeba, U.; Pietras, M.; Marciniak, A.; Głuski, G.; Hupka, J.; Szymajda, M.; Kamiński, J.; Szerewicz, C.; Goździk, A.; et al. Possible Options for Utilization of EU Biomass Waste: Pyrolysis Char, Calorific Value and Ash Content. Materials 2024, 17, 226. [Google Scholar] [CrossRef]

Figure 1.

Researched waste raw materials.

Figure 2.

TGA and DSC results for Pellets 1: (a) at a heating rate of 5℃/min; (b) at a heating rate of 10℃/min.

Figure 2.

TGA and DSC results for Pellets 1: (a) at a heating rate of 5℃/min; (b) at a heating rate of 10℃/min.

Figure 3.

TGA and DSC results for Pellets 2: (a) at heating rate 5℃/min; (b) at heating rate 10℃/min.

Figure 3.

TGA and DSC results for Pellets 2: (a) at heating rate 5℃/min; (b) at heating rate 10℃/min.

Figure 4.

TGA and DSC results for Pellet 3: (a) at heating rate 5℃/min; (b) at heating rate 10℃/min.

Figure 4.

TGA and DSC results for Pellet 3: (a) at heating rate 5℃/min; (b) at heating rate 10℃/min.

Figure 5.

TGA and DSC results for Pellets 4: (a) at heating rate 5℃/min; (b) at heating rate 10℃/min.

Figure 5.

TGA and DSC results for Pellets 4: (a) at heating rate 5℃/min; (b) at heating rate 10℃/min.

Figure 6.

TGA and DSC results for Pellets 5 : (a) at heating rate 5℃/min; (b) at heating rate 10℃/min.

Figure 6.

TGA and DSC results for Pellets 5 : (a) at heating rate 5℃/min; (b) at heating rate 10℃/min.

Figure 7.

Customers’ Preferences for Buying Different Types of Solid Biomass Fuels.

Figure 8.

The Price as a Determining Factor for Purchasing Sunflower Pellets.

Figure 9.

Main Decision-Making Factors for Purchasing Solid Biomass Fuels.

Figure 10.

Customers’ Favored Avenues for Purchase.

Figure 11.

Attention to Labels on the Pellets Packaging.

Figure 12.

Customers’ Preferences for Pure Pellets or Pellets with Additives.

Figure 13.

Customers’ Opinion about the Calorific Value of the Different Types of Solid Biomass Fuels.

Figure 13.

Customers’ Opinion about the Calorific Value of the Different Types of Solid Biomass Fuels.

Figure 14.

Customers’ Opinion About the Calorific Value of the Different Types of Solid Biomass Fuels.

Figure 14.

Customers’ Opinion About the Calorific Value of the Different Types of Solid Biomass Fuels.

Figure 15.

Customers’ Opinion about the Importance of Moisture in the Pellets.

Table 1.

Types of raw materials for research.

| Samples | Pellets 1 | Pellets 2 | Pellets 3 | Pellets 4 | Pellets 5 |

|---|---|---|---|---|---|

| type | wood | wood | wood and sunflower | sunflower | sunflower |

| material | CW+DW | CW+DW | CW+SH | SH | SH |

Table 2.

Averaged results from the examining of the energy parameters.

| Indicator | Units | Pellets 1 | Pellets 2 | Pellets 3 | Pellets 4 | Pellets 5 |

|---|---|---|---|---|---|---|

| Total moisture content | % | 7,47±0,20 | 7,14±0,20 | 7,07±0,20 | 7,82±0,20 | 7,42±0,20 |

| Ash content (in dry condition) |

% | 0,79±0,21 | 0,72±0,21 | 0,74±0,21 | 2,57±0,21 | 2,67±0,21 |

| Ash content (in operational condition) |

% | 0,73±0,21 | 0,70±0,21 | 0,69±0,21 | 2,37±0,21 | 2,47±0,21 |

| Calorific value (higher, in dry condition) |

kJ/kg | 19,57±1,8 | 19,96±1,8 | 19,42±1,8 | 21,37±1,8 | 21,07±1,8 |

| Calorific value higher, in operational condition |

kJ/kg | 18,11±1,8 | 18,53±1,8 | 18,05±1,8 | 19,70±1,8 | 19,51±1,8 |

| Calorific value (lower, in dry condition) |

kJ/kg | 18,31±1,8 | 18,69±1,8 | 18,16±1,8 | 20,14±1,8 | 19,85±1,8 |

| Calorific value lower, in operational condition |

kJ/kg | 16,77±1,8 | 17,19±1,8 | 16,71±1,8 | 18,39±1,8 | 18,20±1,8 |

Table 3.

Values of exothermic peaks obtained in the combustion.

| Exothermic peaks observed | ||

|---|---|---|

| 5℃/min | 10℃/min | |

| Pellets 1 | 320℃, 360℃ and 460℃ | 330℃, 350℃, 380℃ and 480℃ |

| Pellets 2 | 320℃ and 460℃ | 340℃ and 480℃ |

| Pellets 3 | 320℃, 360℃ and 460℃ | 340℃, 380℃ and 480℃ |

| Pellets 4 | 310℃, 420℃ and 460℃ | 310℃, 420℃ and 470℃ |

| Pellets 5 | 310℃ and 460℃ | 320℃ and 480℃ |

Table 4.

Stages of thermal decomposition of biofuels.

| Temperature range, ℃ | |||

|---|---|---|---|

| Stage 1 | Stage 2 | Stage 3 | |

| Pellets 1 | 20-115*/ 20-125** | 115-460* / 125-480** | 460-750* / 480-750** |

| Pellets 2 | 20-111* / 20-123** | 111-460* / 123-480** | 450-750* / 480-750** |

| Pellets 3 | 20-123* / 20-121** | 123-460* / 121-470** | 460-750* / 470-750** |

| Pellets 4 | 20-117* / 20-132** | 117-460* / 132-470** | 460-750* / 470-750** |

| Pellets 5 | 20-129* / 20-140** | 129-460* / 140-480** | 460-750* / 480-750** |

* Observed results at a heating rate of 5℃/min. ** Observed results at a heating rate of 10℃/min.

Table 5.

Mass losses during the thermal decomposition of biofuels.

| Losses from the total mass, % | |||

|---|---|---|---|

| Stage 1 | Stage 2 | Stage 3 | |

| Pellets 1 | 7,2* / 7** | 95* / 94** | 1,4* / 4,9** |

| Pellets 2 | 8,1* / 7,9** | 93* / 92** | 6,4* / 8,2** |

| Pellets 3 | 7,6* / 5,7** | 90* / 84** | 10* / 13,4** |

| Pellets 4 | 9,4* / 7** | 89* / 90** | 10* / 8,3** |

| Pellets 5 | 9,2* / 7,9** | 85* / 92** | 14,2*/ 6,5** |

* Observed results at a heating rate of 5℃/min. ** Observed results at a heating rate of 10℃/min.

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Copyright: This open access article is published under a Creative Commons CC BY 4.0 license, which permit the free download, distribution, and reuse, provided that the author and preprint are cited in any reuse.