Submitted:

18 June 2024

Posted:

19 June 2024

You are already at the latest version

Abstract

Consumer protection in the financial market has several dimensions. From a formal point of view, consumer rights are guaranteed by law. Market asymmetries are eliminated through the obligation to provide consumers with complete and objective information about financial products and services, honest marketing communication and professional sales practices. Programs are implemented in schools and the media to promote knowledge and responsible use of financial products and services. Despite the efforts made, the number of incorrect and suboptimal financial decisions is so high that the risk of households falling into excessive debt remains significant.

The limited effectiveness of the law led to the claim that only effective education can reduce the risk of suboptimal financial decisions. Unfortunately, the efforts made in this area are not fully satisfactory.

The aim of the article is to review scientific research on the financial knowledge of consumers in Central Europe and compare it to the results of a study conducted in Poland in January 2024.

The results of the analysis could indicate the direction of further research on the possibilities of eliminating suboptimal financial decisions of consumers without limiting - for their better protection - access to financial products.

Keywords:

Financial literacy

; behavioral finance

; consumers' cognitive errors

; responsible lending and borrowing.

1. Introduction

Consumer protection on the financial market has been subjected to extensive academic research and constituted an arena for an array of legislative initiatives since the mid 20th century. Consumer rights on the financial market are regulated in Europe by EU directives (the latest Consumer Credit Directive CCD - Directive (EU) 2023/2225 of the European Parliament and of the Council of 18 October 2023) and local legal systems. Market asymmetries are practically eliminated through the obligation to provide consumers with complete and objective information about financial products and services, honest marketing communication and professional sales practices. Consumer rights are safeguarded by courts, specialized institutions and professional organizations promoting principles of good practices. Campaigns are run in schools and the media to offer knowledge and promote the responsible use of financial products and services (Amagir, 2018).

Conducted research confirms that European consumers, are aware of some basic economic concepts and categories (OECD/INFE: 2016, 2020). However, they are much weaker when it comes to making practical use of their knowledge. Their practical financial behavior often contradicts their declared level of knowledge.

From an academic perspective, financial literacy is one of the most relevant and cutting-edge areas of behavioral finance research. Bandura’s social learning theory posits that behavioral learning occurs not only through reactive and operant conditioning, but also by observing other people’s behavior (Bandura, 1986). A key question here is whether the flaws only indicate a poor level of financial education, which is not focused on building positive behavior patterns, but instead on transferring knowledge of economics and finance. Consumers know economic concepts, but they can interpret them correctly (Rich, 2018). Perhaps a phenomenon that Wagner wrote about in the concept of three states of memory comes into play here: Standard Operational Procedures. Regarding SOP’s, a memory state is possible when it is not modified and its contents do not affect behavior – this is inactive memory (Holmes et al., 2020).

At the opposite extreme stand the supporters of behavioral economics, who refer to the need to discover and accept consumer behavior on the financial market. Level of financial knowledge does not predict consumer behavior in the same indelible manner as behavioral factors related to financial decisions.

2. Literature and Research Explaining the Causes of Suboptimal Financial Decisions Made by Consumers

2.1. Consumers’ Cognitive Biases

When selecting financial products and services, consumers should be guided by the principle of rational choice and consider a range of factors, not just cost in absolute terms. European legal regulations guarantee access to multidimensional information on the features, costs, consumer rights and risks related to a given loan product. Rational credit decisions therefore arise from knowledge, personal experience or are the consequence of seeking financial advice. In practice, however, consumers tend to decide to take on high risks based solely on a spurious comparison of available options or make decisions spontaneously without even a basic analysis. This phenomenon does not pertain to a specific cultural or social group; nor does it only concern selected regions or countries.

In practice, many individual patterns of consumer behavior are repeated, and are noticeably inconsistent with the results of an objective appraisal of the situation. According to Thaler, the source of such phenomena are heuristics and cognitive biases. They are sometimes explained as imitative actions taken by individuals ‘in a hurry’ or based on a possibly skewed understanding of ‘common sense’. In neoclassical economic theory, heuristics and cognitive biases can only be committed randomly, and can be ignored due to their rarity and because they often cancel each other out. However, Thaler’s research showed that there are situations in which errors are not rare and random, but of a systemic nature (Thaler, 2015).

One theoretical explanation may be behavioral prospect theory (Schlinger, 2009), which is related to the framing effect (Tversky & Kahneman, 1981; Mcelroy & Seta, 2003) – how the situational context changes the criteria based on which consumers form their opinions. In theoretical models, the method of presenting a financial offer is irrelevant, because a rational consumer makes a choice only based on known and measurable objective criteria. In practice, however, I am aware that how the offer is presented may influence the choices made. Therefore, the ethics of salespeople and their manner of presentation are crucial when it comes to the actual purchase of financial and investment products.

In the light of rational choice theory (Hausman, 1995), people make decisions in such a way as to maximize their utility. Thaler points out that often supposedly irrelevant factors (Thaler, 2015 [NYT]), previously considered marginal, can significantly affect both the financial decisions made and the level of satisfaction with these decisions. Here, for example, one might cite the disastrous – albeit strongly opinion-forming – impact of unprofessional financial advisors, such as online influencers or sales made by persuasive telemarketers.

At the core of human nature lies loss aversion – we value goods that we own more highly than those with similar features and values but belonging to other people (Kahneman et al., 1990) . Similarly, what they have now is valued higher than what they could potentially have. This is known as the endowment effect and is particularly relevant from the perspective of the financial market (Thaler, 2015).

Mental accounting (Thaler, 2004) is an extremely relevant factor that sways consumers' decisions on the credit market. Whether consciously or subconsciously, when managing their household budget, people make decisions assuming a lack of income flexibility in their household. In circumstances where the level of remuneration is fixed, costs are also allocated in the same way. Therefore, loan offers are analyzed from the perspective of fixed costs and having to then secure enough funds to be able to repay the loan. Therefore, any shift in the cost of credit represents an extraordinary windfall for the consumer (when interest drops) or an unforeseen cost (when it rises).

The overconfidence effect is quite common and here individuals tend to overestimate their own abilities. From the perspective of the financial market, the key here is the ability to appraise the likelihood of future negative outcomes, and a lack of such skill may lead to the underestimation of risk.

2.2. Modern Perception of Financial Literacy and Learning Methods - Conclusions from Research

Seen from the perspective of economics, financial knowledge as a concept includes a few different aspects of personal finance management. It is a key skill that helps individuals make informed financial decisions, plan, and achieve their personal financial goals. The key elements of financial knowledge involve the following: budgeting, investing, using credit, retirement planning, and tax knowledge. When individuals have similar levels of knowledge, a factor that moderates the results obtained is strongly correlated with skill sets: the ability to compare financial products and to negotiate financial contracts

What this means is that financial literacy should enable people to achieve much more than just their financial goals. A study by Burkhauser, Gustman, Laitner, Mitchell and Sonnega explains that older people’s sense of financial well-being does not depend on current income and accumulated assets but in time allocation of consumption opportunities (Burkhauser et al., 2009). In this way, they justify the notion that financial literacy offers greater utility throughout a consumer’s life. According to Lusardi and Hastings, financial knowledge is the ability to avoid unwanted and costly financial experiences (Lusardi, 2008; Hastings & Mitchell, 2018)

Studies have repeatedly shown that poor financial knowledge translates into limited participation on the financial market. Research by van Rooij, Lusardi and Alessie confirmed that people with weak financial knowledge tend not to own shares and stocks (van Rooij et al., 2007). Financial literacy not only increases consumer participation in the financial market, but also means that they may decide to implement well-thought-out and safe investment strategies. Disparities in the level of financial knowledge acquired early in life imply significant wealth inequality in adulthood (Lusardi & Mitchell 2014, 2017).

Research has confirmed that the presentation format of financial information influences the choices made by those with less financial knowledge (Hastings & Mitchell, 2018). Hundtofte and Gladstone also proved that consumers using mobile applications made by loan companies are much more likely to demonstrate impulsive purchasing behavior and are more willing to take out payday loans (Hundtofte & Gladstone, 2017). Another study yielded some interesting findings indicating that financial literacy negatively correlates with investment in cryptocurrencies (Panos et al., 2019). Research by these authors indicates that less financially educated consumers do not understand the sources of risk associated with purchasing cryptocurrency and having succumbed to overconfidence bias, they are more likely to take on excessive investment risk.

Bandura’s social learning theory posits that behavioral learning occurs not only through reactive and operant conditioning, but also by observing other people’s behavior (Bandura, 1986; Skinner, 1957). This theory assumes that new patterns of behavior are acquired via two key mechanisms:

- Learning by consequences, which is like operant conditioning, involves consciously constructing hypotheses regarding what actions, and under what circumstances, have led to desired results.

- Modeling, where behavior is based on the observation of other people’s actions and their consequences.

Both mechanisms proposed by Bandura can be successfully related to financial knowledge, but they are not mechanical in nature. Therefore, they require focus and awareness – we learn from how we interpret events. A classic example of this is a proposal offered by George Moschis and Gilbert Churchill (Moschis & Churchill, 1978), who distinguished three theoretical elements relevant to changes in consumer socialization: initial structural variables, the socialization process and outcome variables. The initial variables include the structural properties of the environment, such as social class, gender and race, and age and place in the life cycle. They stated that the socialization process runs according to learning mechanisms based on observation, imitation and modelling. This basic scheme of the learning process and the socialization factors mentioned by the authors were supplemented with explanations from other theories, such as: Piaget’s theory of cognitive development, Eagle’s theory of social role modelling (Eagly, 1987), Bandura’s learning model or Bronfenbrenner's theory of ecological systems (Bronfenbrenner, 1986).

Supporters of the view that financial education has a key impact on safe and universal access to the financial market refer to the primacy of knowledge and reason over the emotions that go hand in hand with consumption. People with knowledge and established positive behavior patterns should act rationally, make rational choices about financial products and services without falling prey to consumerism. However, in practice, consumer research shows that despite having relatively well-developed financial knowledge, awareness and understanding of economic concepts, a statistically significant number of people do indeed make incorrect financial decisions that are difficult to explain. So, does human nature defy scientific and educational consistency here?

Research related to financial literacy carried out on behalf of the OECD (OECD, 2016, 2020), indicates a gradual improvement in EU countries consumers. For example, in 2020 Polish consumers achieved a score of 13 out of 21 possible points, indicating that 62.1% of the population feels confident in financial matters and is not far behind the leading countries in the ranking. This is an increase from their 2016 score of 11.6 points. Slovenia emerged as the top performer in the 2020 ranking with 14.7 points, where 70% of the population claimed proficiency in financial knowledge and skills. Austria followed closely behind with a score of 14.4 points, and 68% of its population demonstrating financial competence. Conversely, Italy (11.1 points) and Romania (11.2 points) recorded the lowest financial literacy results (Rutecka-Góra, 2020).

Research related to financial literacy has been conducted many times in CEE. Alena Opletalová (2015) outlines the importance of economic and financial literacy in primary and secondary schools in the Czech Republic. Her research findings in the Czech Republic and from the World Bank have shown high levels of household debt while also indicating the need for higher levels of financial education. Young people are characterized by a relatively high level of knowledge about economic concepts and categories, although there is a clear difference resulting from the place of residence (residents of large cities have greater knowledge) and gender (men show greater interest in and understanding of economic concepts). Krechovvská (2015) highlights the important role of financial literacy as one of the factors that ensures sustainable development in society.

The research made by Slovak scientists suggest that the student’s gender, father’s education, family’s financial background, and student’s part-time work experience were important determinants of financial literacy (Bohn et al. 2023). This research showed that students from families with the lowest incomes (up to 1500 €) have a statistically significant lower level of financial literacy by about 5 percentage points compared to wealthier families. Students whose parents’ owned stocks were over 7 percentage points more likely to answer the risk diversification question correctly. Furthermore, students whose parents had retirement savings were 6 percentage points more likely to answer correctly.

Financial education is essential for the public to be able to connect to international financial networks. Hungarian research made by (Hergár, et al.,2024) twere concentrated to capability to manage loans and savings, and to understand the functioning and inherent risks of the financial system. In Hungary development of financial literacy is the joint duty of governments, educational institutions, financial actors, and civil society.

Romanian researchers prepared questionary (34 questions) related to measure individual abilities to manage personal finances, attitudes towards several financial instruments or techniques and financial knowledge. They constructed an index for measuring financial well-being and three difficulty-ranked financial literacy indices (Nitoi et al, 2022). The findings show that only 8.27% of Romanians answered financial literacy questions correctly. The result allows for cross-country comparisons, revealing significant differences compared to advanced economies - Germany (53.20% of correct answers), Switzerland (50.10%), the Nethelands (44.80%), Austria (33.30%), the U.S. (30.20%), France (30.90%), Japan (27%), or Italy (24.90%). Also, the level of financial literacy in Romania is lower, even when compared to that of developing economies such as e.g. Hungary (25.69%), Croatia (27.66%), Poland (29.91%), or Czechia (42.33%).

The study conducted in Ukraine has indicated a lack of financial literacy at both the micro and macro levels, which does not allow for an effective system of income, costs, and savings. If the population income exceeds it expenses, a deficit of funds is created at the level of the government budget formation. If the population in a crisis significantly reduces the amount of loans received in order not to become financially dependent and to pay higher interest rates, then the state, on the contrary, actively attracts the loans (Dudchyk et al. 2023).

Observations and analyses from Poland have been shared by Grzesiuk (Grzesiuk, et al., 2019) and Pawlak, who focused on Polish political views and examined the possible connections between financial knowledge and approach to economic issues (Pawlak, 2020). Jagoda Gola have investigated household financial behavior (Gola & Smyczek, 2019). In 2019, Święcka and her team examined the level of financial knowledge among high school students in Poland (Święcka et al., 2020).

Cwynar (2021) underlines large heterogeneity both in overall financial literacy and its partial scores (i.e., financial knowledge, confidence, attitudes) among CEE countries. His analysis results suggest that financial literacy is differently associated with gender and age in Eastern Europe compared to Western Europe. All these phenomena appear to be the result of different political, social, economic, and culture-related experiences in these two parts of Europe after World War II.

In 2023, as part of the research #JacyPolacy (eng. What Poles), Maison (2023) presented a study involving a representative group of 1,076 consumers (2023). Analysis of responses revealed that many Poles possess accurate financial knowledge, such as understanding the interest rate risks associated with foreign currency loans. However, a discrepancy was observed between older and younger generations, with those over 55 exhibiting the highest levels of financial knowledge.

Analyses have revealed that financial literacy, defined as the understanding of concepts, categories, and financial products and services, is relatively high among consumers. Individuals demonstrate familiarity with major financial concepts. However, when it comes to practical skills, which are crucial in navigating the financial market, people tend to perform less effectively. To validate findings from previous research and assess the current landscape, a survey on the financial knowledge of Polish consumers was conducted in January 2024. The results obtained aim not only to assess the level of consumers' knowledge but also to pinpoint areas where efforts should be intensified in terms of financial education and outreach to enhance understanding of the financial market.

3. Empirical Verification of Cognitive Errors Made by Consumers on the Financial Market.

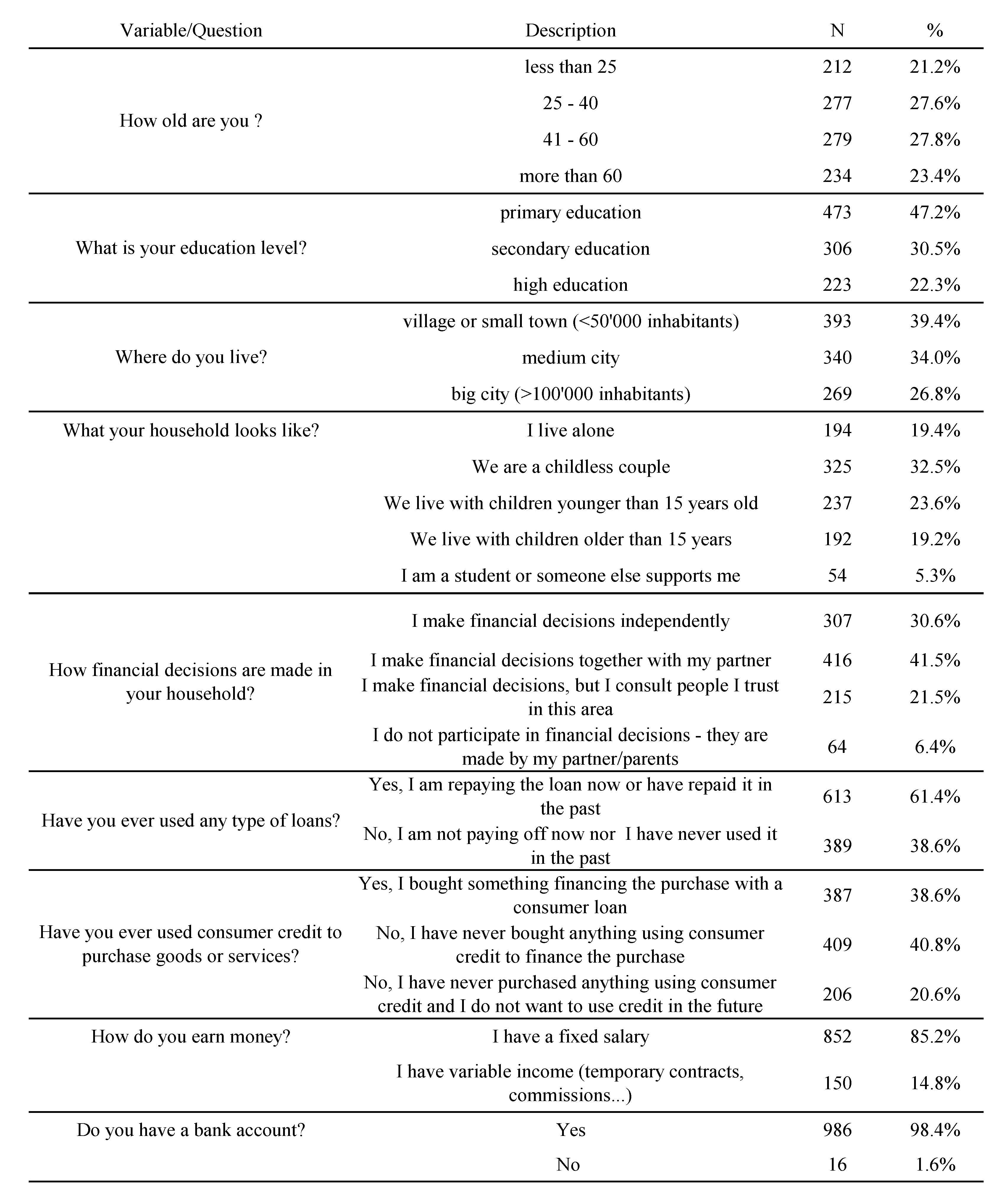

In January 2023, a survey was conducted by PAPI & CAWI on the financial knowledge of consumers in Poland. N = 1,002 people took part in the study and the statistical distribution of the research group was maintained in accordance with the demographic profile from the National Census conducted in 2021.

Table 1.

Distribution and characteristics of the sample (N = 1002).

Source: Gebski (2024) Financial literacy - own research.

4. Methodology

IBM® SPSS® Statistics 29.0.0. software was used to analyze dependencies and their strength.

The following statistical tests were used:

Pearson's χ2 test (a non-parametric test) used to examine the relationship between two variables measured on a qualitative scale.

The formula:

Where V is between 0 and 1 and the closer it is to 0, the more independent variables we are in.

- n is the number of observations,

- r is the number of levels of one variable,

- k is the number of levels of the second variable.

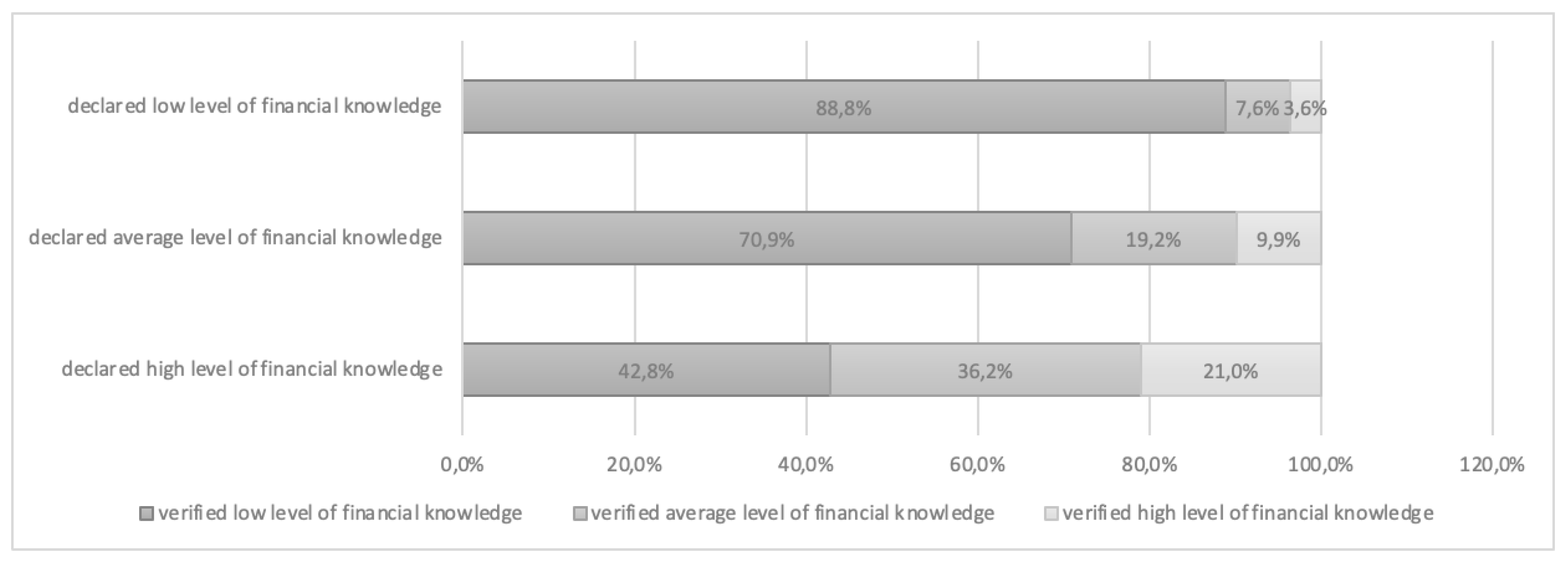

- Kendall's tau correlation analysis (a non-parametric method) for examining the relationship between two variables measured on an ordinal scale. Unlike Pearson correlation, Kendall’s Tau doesn’t rely on the assumption of linearity, making it useful for ordinal data. The study examined the relationship between consumers' self-assessment of their knowledge and the results obtained when answering verification questions (Graph 1).

Kendall's tau correlation value can range from -1 to 1, where values closer to -1 mean a strong negative correlation and values closer to 1 mean a strong positive correlation.

The adopted level of statistical significance was p < 0.05, marked as *, as well as additional more precise levels of p < 0.01, marked as ** and p < 0.001, marked as ***.

5. Financial Literacy & Financial Behavior – Observations

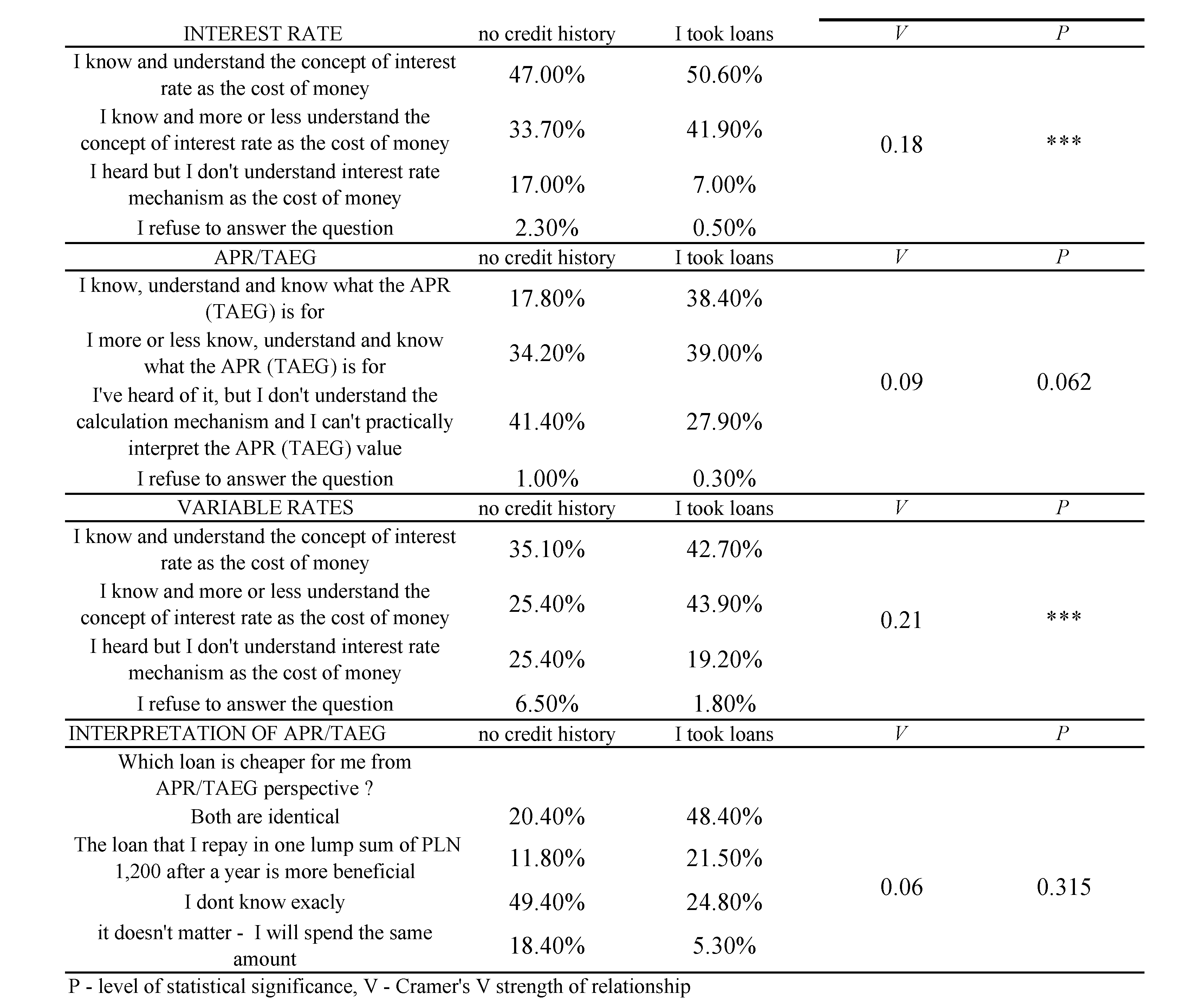

Declared by respondents’ level of financial knowledge was objectively high – 87.9% claimed that they know and at least more or less understand the concept of interest rate as cost of money (see Table 2). More than half (56.7%) also declared some awareness of the concept of APR/TAEG. From the perspective of Central European Countries (EU members) where mortgage loans are still granted to consumers at variable interest rates, it is encouraging that 74.7% of respondents declared that they understand how the variable interest rate loan mechanism works as well as the possible consequences for borrowers.

Consumers stated that they are aware of the risk of excessive household debt – for 88.7% of respondents, it is a situation where their current income is not sufficient to repay their loans on time. For 50.6%, debt significantly burdening household budgets is a danger sign. Only 25% believe that excessive debt requires new loans to be taken out to repay previous loans (a credit trap).

Consumer bankruptcy in the CEE region is perceived as shameful (41.1% of responses) and a consequence of irresponsible budget management and excessive debt (55.9% of responses). For more than half of the respondents (56.2%), undergoing a court bankruptcy procedure represents an opportunity to eradicate debt and have a ‘fresh start’. Tellingly, nearly one third of those for whom consumer bankruptcy would present an opportunity for debt relief do not believe that it will in any sense require the liquidation of part of their assets to repay the debt – they only expect the lenders to reduce the debt.

Practical financial behavior were tested by some questions were asked regarding a hypothetical instalment loan taken out to finance the purchase of a laptop (see Table 3). The testing questions were intended to verify the actual level of knowledge - in most studies preceding our research, the authors limited themselves to consumer self-assessment. Intuitive distrust was confirmed by the results of the study.

To simplify the calculations, the loan was to be free of charge (zero interest, commission, or additional insurance) and granted for 12 months. The respondents were invited to compare two loan repayment options:

- a one-off repayment of the entire amount after one year (PLN 1,200)

- repayment of the loan in 12 equal monthly instalments of PLN 100 each

When asked about their repayment preferences, consumers agreed that repayment in 12 monthly instalments was easier from their perspective (74.4% of respondents). 13.3% of respondents preferred to postpone the repayment, while 12.3% did not notice any difference between the two options. The above is justified and is a practical reflection of the subconscious use of mental accounting.

Questions that asked for a comparison of both repayment options from the perspective of APR/TAEG along with the time value of money yielded some interesting answers. Nearly 1/3 of the respondents (31%) did not understand the concept of time value of money and compared the available credit options solely from a cash perspective (actual expense). An additional 25% of respondents gave the wrong answer (repayment in 12 monthly instalments), suggesting and a budget and liquidity approach should take precedent when comparing financial products. This means that these answers were also given by some who had previously declared in the first part of the survey that they were aware of and understood financial concepts (the economics students, most of whom (95%) marked the correct answer, improved the overall score for this question).

The third question in this regard concerned a comparison of both available loan options from an APR/TEAG perspective, which in this case was the same in both cases. Only 25% of respondents gave the correct answer. Significantly more respondents evaded the question here (48% said they did not really know what the answer was).

To avoid eroding the respondents’ self-confidence[1], the verification questions, due to their similar content, were not placed one after the other, but were spread throughout the survey.

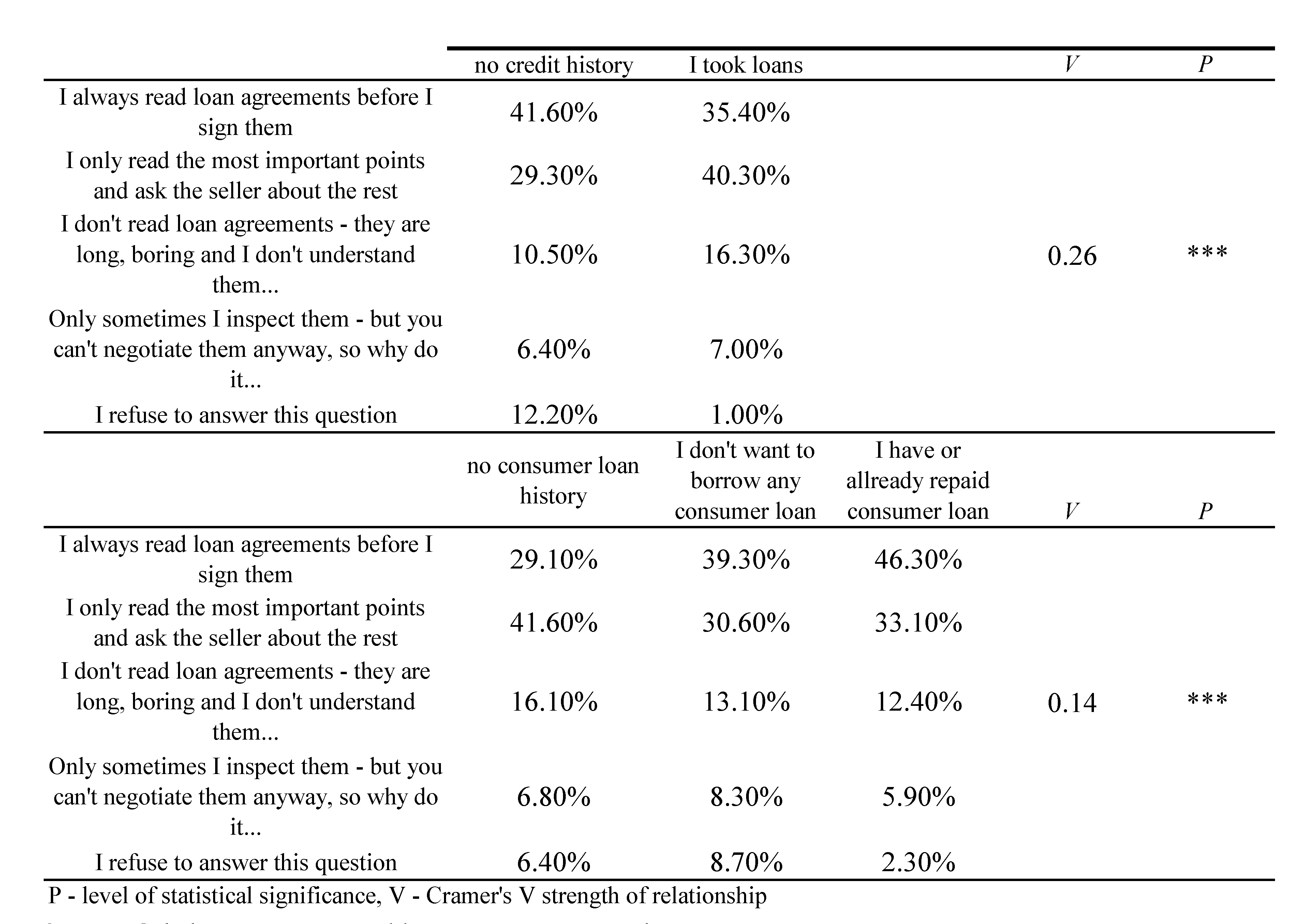

Some interesting observations were elicited by the question regarding the approach taken to signing loan agreements. Only 37.8% of respondents confirmed that they always read financial agreements carefully before signing them. More than 1/3 of the respondents (36%) do so superficially and, most importantly, they trust the salesperson enormously, relying solely on his or her opinions and advice. A further 14% do not analyze the content of agreements, considering them boring and, most importantly, not worth bothering about due to the inability to negotiate them anyway. In this case, the phenomena described as irrelevant factors and overconfidence, consisting in uncritical acceptance of the seller's recommendations, became very visible.

6. Results and Discussions by Topic and Globally

The obtained results allowed for an in-depth analysis of the statistical relationships between individual demographic sections and the responses obtained.

Researchers first examined the relationship between the use of loans and the level of financial knowledge of consumers (Table 4) and the fact of having previous experience with financing household needs in the form of a bank loan (Table 5). The relationship between demographic and social categories and the practice of concluding loan agreements was subject to an in-depth analysis (Table 6). The perception of consumer bankruptcy from a demographic perspective was verified in Table 7. The observation regarding consumers' interest in and their awareness of the cost of credit on a credit card account was also interesting (Table 8).

6.1. Examined Relationships

Previous experience in using loans should influence positively consumers' level of financial knowledge. As expected, analyses using Pearson's χ2 tests for the relationship between the use of loans and financial knowledge confirmed the influence of consumers’ personal experiences of financial products with declared financial knowledge. The analysis of the results presented in Table 4 shows that there is a statistically significant relationship between the overall use of loans and declared knowledge of the cost of money V = 0,18; p < 0,01 and variable interest rates V = 0,21; p < 0,001. People who have taken out loans tended to claim knowledge and understanding of concepts such as the cost of money and variable interest rates. However, it was not demonstrated by the study group that taking out loans had a statistically significant impact on knowledge of other financial concepts.

Loan agreements were more carefully read by people who admitted that they did not use loans in general, as well as by people who have taken out consumer/instalment loans (see. Table 5).

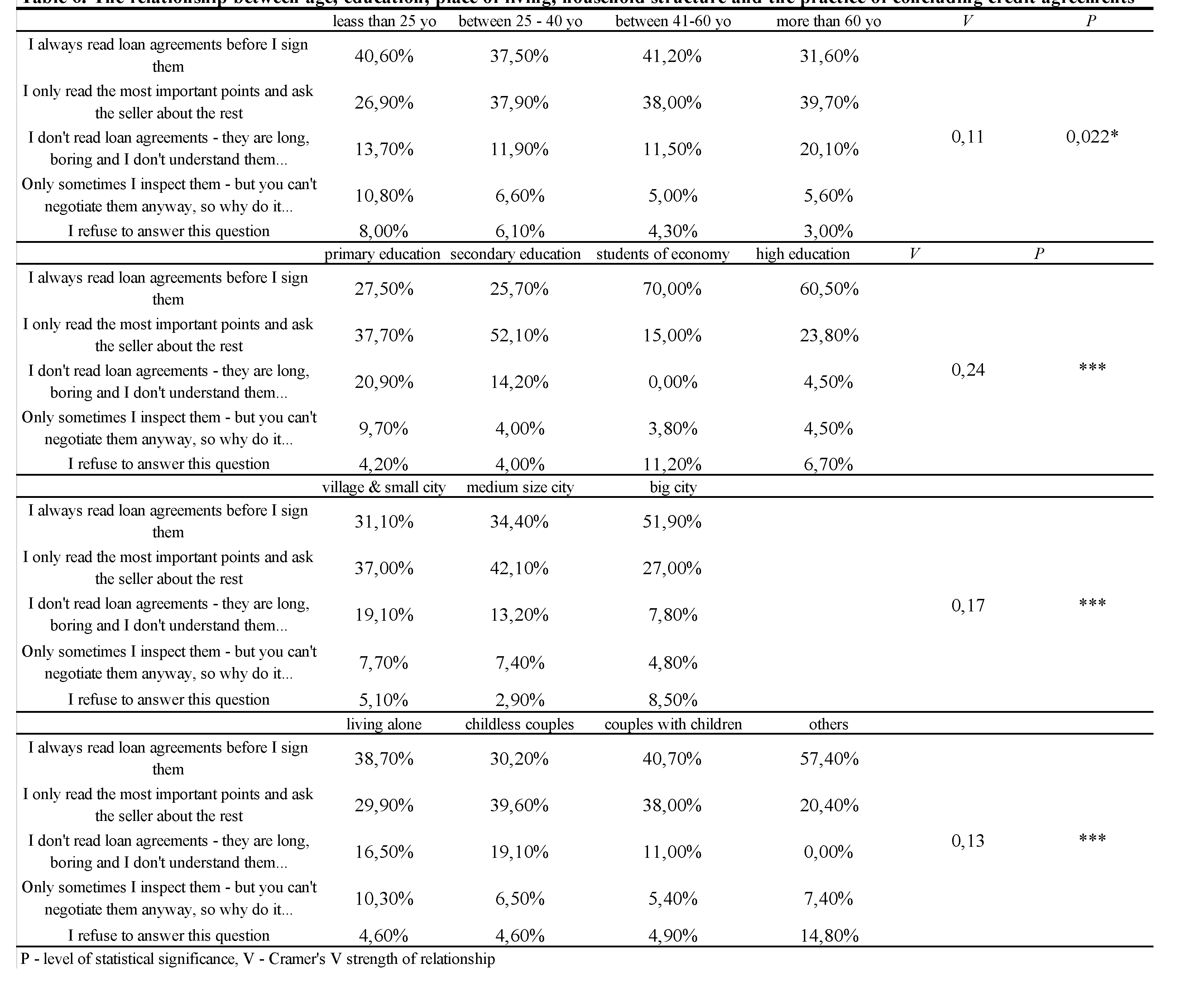

The approach taken in terms of reading financial contracts before signing them indicated a few significant correlations – relationships between age, place of residence, education and the structure of the consumer household (see Table 6):

- Those who claimed that they carefully read loan agreements tended to be young people up to 25 years of age, as well as those with higher education.

- there was a statistically significant relationship between approach taken to signing consumer loans and place of residence and household. Those living in large cities and raising children or were themselves dependent on someone else were more likely to carefully read credit agreements.

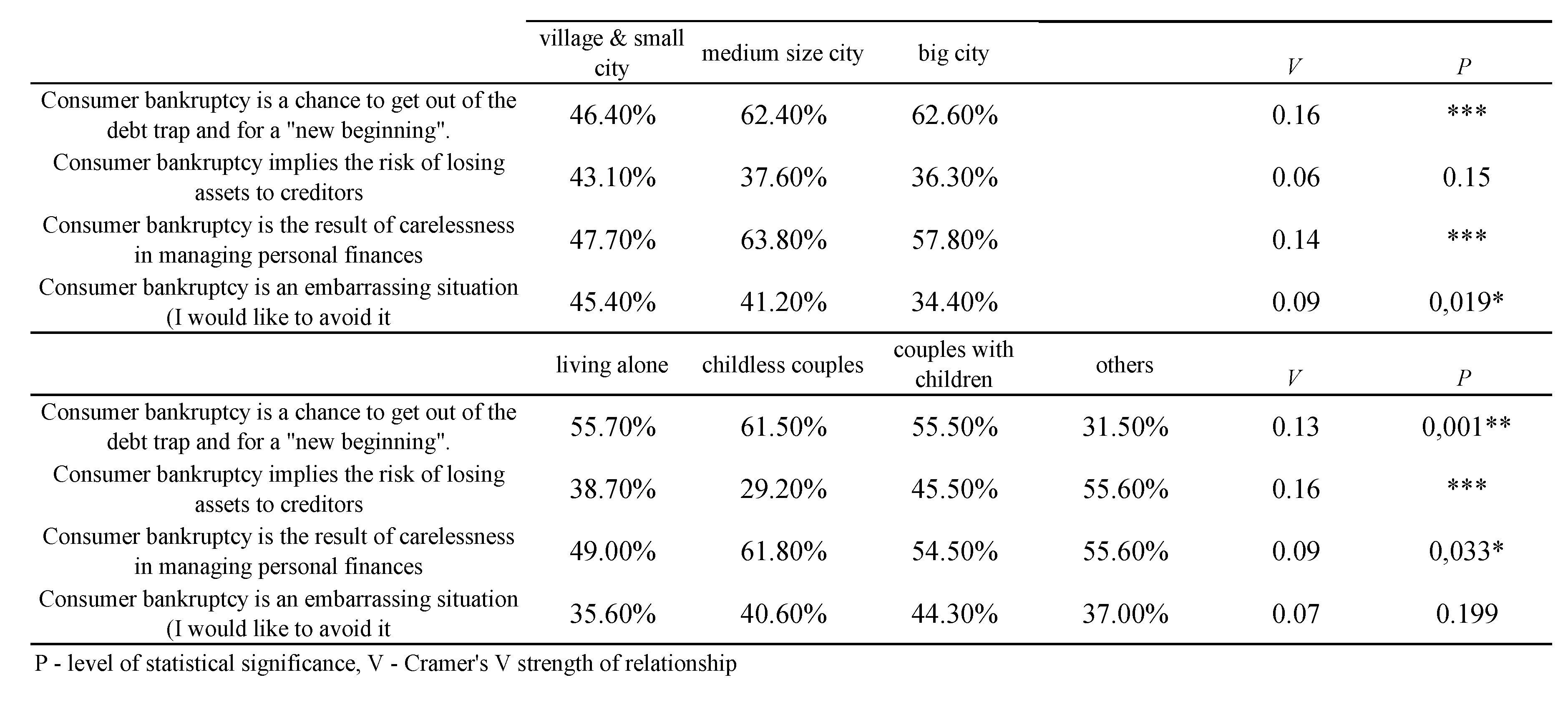

Table 7 presents the findings for the relationship between age and education and the perception of consumer bankruptcy. One may observe that people over 40 years of age more often perceived consumer bankruptcy as an opportunity to escape the debt trap and make a ‘fresh start’. It was also demonstrated that people with only primary education were more likely to appraise consumer bankruptcy as an opportunity to climb out of the debt trap and make a ‘new start’, or as an embarrassing situation, while for people with secondary or higher education, consumer bankruptcy tended to imply the risk of losing property to creditors.

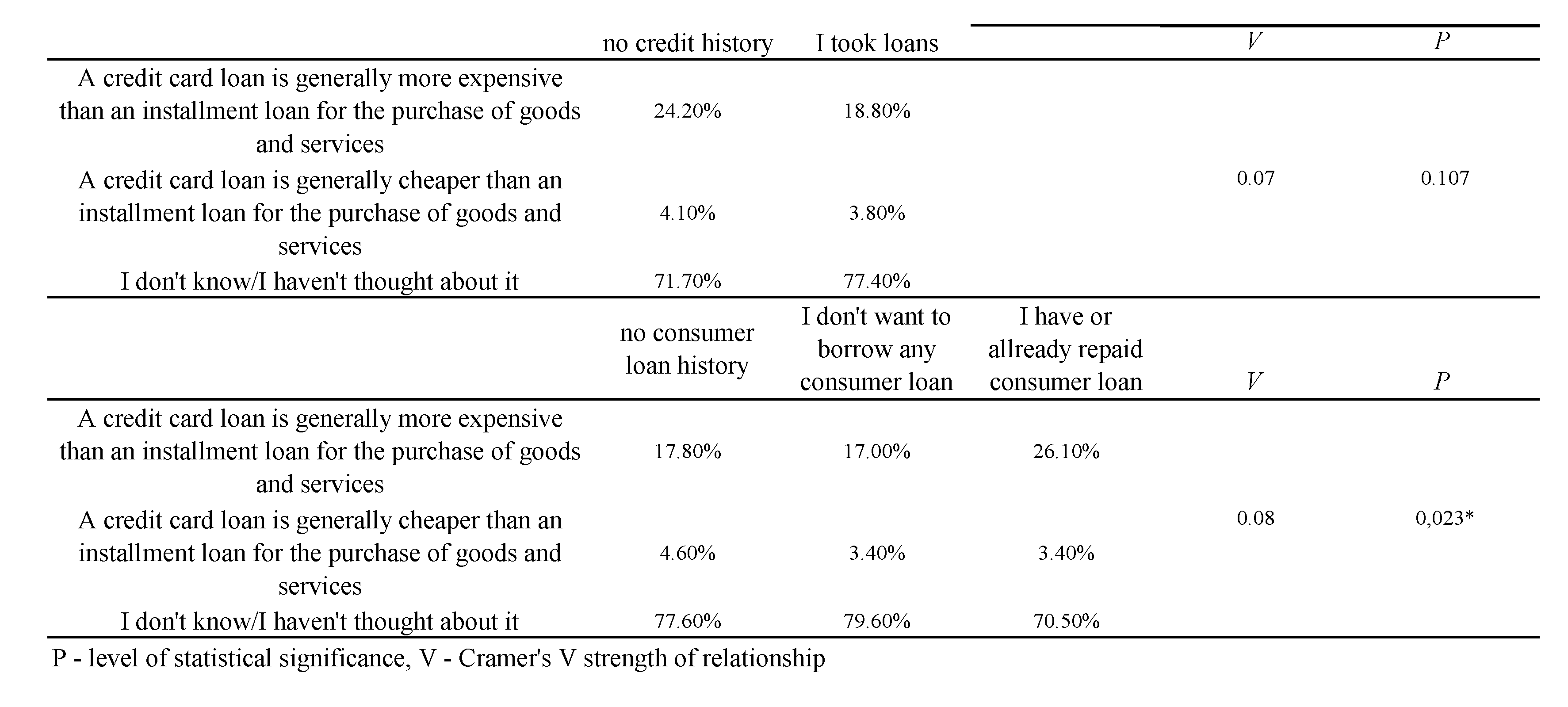

People with experience of consumer loans were usually aware that a credit card loan is generally more expensive than an instalment loan for purchasing goods and services, but this relationship was not strong(see Table 8). However, ignorance and lack of interest in comparing the cost of a loan in a credit card account was common – 46.7% of respondents indicated that they did not know and had never been interested in this issue. Only 21.5% of respondents answered that, to the best of their knowledge, this type of loan is generally more expensive than an instalment loan offered at a point of sale for goods and services.

6.2. Overall Financial Literacy

An analysis of the findings of the consumer survey yields several interesting observations leading to the following conclusions regarding the nominal financial knowledge of the respondents and their behavior in practice on the financial market. The influence of behavioral factors such as heuristics and cognitive errors on how consumers behave when choosing and evaluating financial products and services is particularly tangible.

The study confirms that consumers overestimate their level of financial knowledge and are uncritical towards their own shortcomings when it comes to the responsible use of financial products and services (see Graph 1). The analysis was based on a comparison of declared knowledge of financial concepts and categories with answers to questions checking actual knowledge (declination to answer a question or an admission to not knowing the right answer were treated in the same way as incorrect answers).

This proves consumers’ superficial knowledge, limited to financial concepts simply defined. Therefore, one may justify formulating a thesis about the drastically insufficient level of financial education and the practical ineffectiveness of teaching programs in this area.

The study also revealed that accurate evaluations and decisions are much more strongly correlated with personal experience, observation, and intuition than with the declared level of financial knowledge – consumers with experience in taking out consumer loans read contracts and much more accurately interpret items such as APR/TEAG and the value of money over time. Secondly, the respondents showed some susceptibility to the significant influence of behavioral factors conducive to making suboptimal financial decisions:

- nearly 36% of the respondents elect not to personally verify the terms of a loan agreement, relying on the salesperson’s opinions and recommendations. Such people are significantly exposed to the framing effect and possible consequences of information asymmetry.

- analysis of preferences regarding the method of loan repayment (one-off or instalments) revealed that mental accounting strongly influences consumers’ credit decisions, which is justifiable and rational from the perspective of consumer households. Subconsciously, consumers assume that their household budgets lack income flexibility and prefer solutions that ensure ongoing liquidity for the household.

- At the same time, when choosing a product or service, consumers are influenced by supposedly irrelevant factors such as the advisor’s suggestions, peer pressure or opinions commonly repeated on social media. This applies to young people especially (<25 years old) and those who have cash – in the questionnaire they tended to answer that they were indifferent to the choice of repayment method or preferred to pay ‘as late as possible’;

- the ease with which respondents treated consumer bankruptcy as an opportunity for a ‘fresh start’, while ignoring the costs of restructuring (involving one’s own assets to repay part of the debt) is an example of hyperbolic discounting.

Therefore, the picture of consumer knowledge blurs in the light of the conducted research. The knowledge possessed is quite broad, yet superficial, and when subjected to practical verification it turns out that it is not reflected in the financial decisions made in practice or the answers given to the verification questions.

7. Conclusions

The results of the study do not differ significantly from those obtained by other researchers. However, the special feature of this study was a much deeper verification of consumers' actual knowledge. In the studies by Maison (2023), Opletalova (2015) and Hergár, et al. (2020). he analysis and description of the results were limited to “diagnosos”. In this study, the structure of the questions assumed the desire to verify actual knowledge and therefore the questions were mixed in such a way that the respondents were not influenced by their previous answers.

In this way, practical confirmation of the suggestions of researchers comparing the level of knowledge in different EU countries was obtained. Even if consumers know economic concepts and categories, they cannot verify them. For example, they do not distinguish TAEG from APR - they cannot interpret the result or the content of the task. Poles uncritically believe advisors and are not interested in the real (financial) cost of the loan, assessing it only through the prism of the amount spent.

It would be extremely interesting to compare experimentally whether the problem with the practical use of financial knowledge occurs mainly in CEE economies, or whether similar problems also affect consumers in highly developed countries.

To what extent are the intensity of cognitive biases and problems with correct attribution correlated with the level of market development, or are they a common problem in households? Such knowledge can shed new light on the problem of the effectiveness of consumer protection, shifting the burden from the concept of empowered customer, which is the basis of European regulations, towards the American total regulation and the average customer, which is its subject.

The methodology applied in this article can contribute to the question of financial regulation by also looking at FinTech and especially financial Blockchain technology. In particular, the issue of virtual currencies (Bitcoin, Ethereum, Ripple, Litecoin...) can be a direction for research in the CEE countries or the EU.

References

- Amagir, A. , Groot, W., Maassen van den Brink, H., & Wilschut, A., A review of financial-literacy education programs for children and adolescents. Citizenship, Social and Economics Education. [CrossRef]

- Bandura, A. , (1986). Social foundations of thought and action: A social cognitive theory, National Inst of Mental Health, Prentice-Hall, Inc.

- Böhm, P. , Böhmová, G., Gazdíková, J., & Šimková, V. Determinants of financial literacy: Analysis of the impact of family and socioeconomic variables on undergraduate students in the slovak republic. Journal of Risk and Financial Management 2023, 16, 252. [Google Scholar]

- Bronfenbrenner, U. , Ecology of the family as a context for human development: Research perspectives. Developmental Psychology 1986, 22, 723–742. [Google Scholar] [CrossRef]

- Burkhauser, R. , Gustman, A., Laitner, J., Mitchell, O., Sonnega, A. (2009), Social Security Research at the Michigan Retirement Research Center, 69 Social Security Research Bulletin 51.

- Cwynar, A. (2021). Financial literacy and financial education in Eastern Europe. The Routledge Handbook of Financial Literacy, 400-419.

- Dudchyk, O. , Matvijchuk, I., Kovinia, M., Salnykova, T., & Tubolets, I. (2023). Financial literacy in Ukraine: from micro to macro level.

- Eagly, A. , (1987), Sex differences in social behaviour: A social-role interpretation, Hillsdale, NJ: Erlbaum.

- Frame, W. S. , Wall L., i White, L. J., (2019) Technological Change and Financial Innovation in Banking: Some Implications for FinTech, (in) Oxford Handbook of Banking, 3rd ed., edited by A. Berger, P. Molyneux, and J. O. S. Wilson, s. 262–284, Oxford University Press.

- Hastings, J. , and Mitchell, O. S., (2018), How Financial Literacy and Impatience Shape Retirement Wealth and Investment Behaviors, Wharton Pension Research Council Working Papers, Number 13.

- Hausman, D.M. Rational Choice and Social Theory: A Comment. Journal of Philosophy 1995, 92, 96–102. [Google Scholar] [CrossRef]

- Hergár, E, Kovács, L and Németh, E., (2024) The Status and Development of Financial Literacy in Hungary. Financial and Economic Review, 23 (1). pp. 5–28. ISSN 2415-9271.

- Holmes, N. M. , Chan, Y. Y., & Westbrook, R. F. An application of Wagner’s Standard Operating Procedures or Sometimes Opponent Processes (SOP) model to experimental extinction. Journal of Experimental Psychology 2020, 46, 215–234. [Google Scholar] [CrossRef] [PubMed]

- Hundtofte, S. , Gladstone J., (2017), Who Uses a Smartphone for Financial Services? Evidence of a Selection for Impulsiveness from the Introduction of a Mobile FinTech App, Federal Reserve Bank of New York Working Paper.

- Kahneman D, Ketsch J and Thaler R <italic>Journal of Political Economy</italic>. <bold>1990</bold>, <italic>98</italic>, 1325–1348.

- Krechovská, M. (2015). Financial literacy as a path to sustainability, Publisched online 2015, https://fek.zcu.cz/tvp/doc/2015-2. 20 May.

- Lusardi, A., (2008), Financial Literacy: An Essential Tool for Informed Consumer Choice, Working Paper No 14084, National Bureau of Economic Research, https://www.nber.org/papers/w14084 (accessed on December 2023).

- Lusardi, A. , & Mitchell, O. S., (2014), The economic importance of financial literacy: Theory and evidence, Journal of Economic Literature, 52(1), s.5–44. [CrossRef]

- Lusardi, A. , Michaud P. C., i Mitchell O. S. Optimal Financial Knowledge and Wealth Inequality. Journal of Political Economy 2017, 127, 431–477. [Google Scholar] [CrossRef] [PubMed]

- Lusardi, A. , Mitchell, O.S., (2013) The Economic Importance of Financial Literacy: Theory and Evidence, Discussion Paper Netspar.

- Maison D., (2023). https://www.linkedin.com/posts/dominika-maison_wiedza-ekonomiczna-polaków-activity-7155467065988898816-eYFN/?originalSubdomain=pl (dostęp luty 2024).

- Mcelroy, T. , & Seta, J., (2003), Framing Effects: An Analytic-Holistic Perspective, Journal of Experimental Social Psychology, 39, 610-617. [CrossRef]

- Moschis, G. P. , Churchill, G. A. Consumer socialization. A theoretical and empirical analysis. Journal of Marketing Research 1978, 15, 599–611. [Google Scholar] [CrossRef]

- Nitoi, M., Clichici, D., Zeldea, C., Pochea, M., Ciocirlan C (2022), Financial well-being and financial literacy in Romania: A survey dataset, Data in Brief, 43 , 108413, https://www.sciencedirect.com/ science/article/pii/S2352340922006102.

- OECD/INFE (2016). International Survey of Adult Financial Literacy Competencies.

- OECD/INFE (2020). International Survey of Adult Financial Literacy.

- Opletalová, A (2016), Financial Education and Financial Literacy in the Czech Education System, Procedia - Social and Behavioral Sciences, 171,1176-1184, https://www.sciencedirect.com/science /article/pii/S1877042815002591?

- Panos, G. A. Karkkainen, T. i Atkinson, A., (2019), Financial Literacy and Attitudes to Cryptocurrencies, Working Papers in Responsible Banking & Finance 2019, WP Nº 20-002,. [CrossRef]

- Rich, A. S. , & Gureckis, T. M., (2018), The limits of learning: Exploration, generalization, and the development of learning traps, Journal of Experimental Psychology: General, 147(11).

- Rose, G. , Dalakas, V., Kropp, F. Consumer socialization and parental style across cultures: Findings from Australia, Greece, and India. Journal of Consumer Psychology 2003, 13, 366–376. [Google Scholar] [CrossRef]

- Rusek, J. , (2022), Analiza efektu odwrócenia preferencji w procesie dyskontowania społecznego, Warsaw University Press, https://ornak.icm.edu.pl/bitstream/handle/item/4509/0000-DR-172069-praca.pdf?sequence=1. (accessed on 13 December 2023).

- Schlinger, D. H. , (2009), Theory of Mind: An Overview and Behavioral Perspective. The Psychological Record, 59, 435-448. [CrossRef]

- Skinner, B.F., (1957), Verbal behaviour, Appleton-Century-Crofts. [CrossRef]

- Thaler, R. H. (2004), Mental Accounting Matters, (in) Camerer, C. F., Loewentein, G., & Rabin M., (Eds.), Advances in Behavioral Economics (pp. 75–103). Princeton University Press. [CrossRef]

- Thaler, R. H. , (2015), Misbehaving: The making of behavioural economics, W W Norton & Co.

- Thaler, R. H. , (2015), Unless You Are Spock, Irrelevant Things Matter in Economic Behavior, The New York Times, 08/05/2015. https://www.nytimes.com/2015/05/10/upshot/unless-you-are-spock-irrelevant-things-matter-in-economic-behaviour.html?smid=url-share. (accessed on 12 February 2024).

- Tversky, A. , & Kahneman, D. The framing of decisions and therationality of choice. Science 1981, 221, 453–458. [Google Scholar]

- van Rooij, M., Lusardi, A., Alessie, R., (2007), Financial Literacy and Stock Market Participation, Working Paper No 13565, National Bureau of Economic Research, https://www.nber.org/papers/w13565 (accessed on December 2023).

Graph 1.

The relationship between the declared level of financial knowledge and actual knowledge (tested using Kendall’s Tau). Source: Gebski L., (2024) Financial literacy - own research.

Graph 1.

The relationship between the declared level of financial knowledge and actual knowledge (tested using Kendall’s Tau). Source: Gebski L., (2024) Financial literacy - own research.

Table 2.

Knowledge and understanding of principal financial concepts.

Source: Gebski (2024) Financial literacy - own research.

Table 3.

Consumer behavior on the financial market - verification questions.

Source: Gebski (2024) Financial literacy - own research.

Table 4.

The relationship between credit use and financial knowledge.

Source: Gebski (2024) Financial literacy - own research.

Table 5.

The relationship between credit use and financial behavior.

Source: Gebski (2024) Financial literacy - own research.

Table 6.

The relationship between age, education, place of living, household structure and the practice of concluding credit agreements.

Table 6.

The relationship between age, education, place of living, household structure and the practice of concluding credit agreements.

Source: Gebski (2024) Financial literacy - own research.

Table 7.

The relationship between place of residence and household structure with the perception of consumer bankruptcy.

Table 7.

The relationship between place of residence and household structure with the perception of consumer bankruptcy.

Source: Gebski (2024) Financial literacy - own research.

Table 8.

The relationship between the use of credit and knowledge about the cost of credit card loan.

Table 8.

The relationship between the use of credit and knowledge about the cost of credit card loan.

Source: Gebski (2024) Financial literacy - own research.

| 1 | The structure of the test may lead to some incorrect answers. In an experiment I conducted in 2021 on a group of 70 economics students during a colloquium, the test was arranged in such a way that only ‘A’ answers were correct (the students had 4 options ranging from A to D). Even the best in the group made a lot of mistakes by selecting different answers, thinking that the test could not possibly only have correct ‘A’ answers. |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Copyright: This open access article is published under a Creative Commons CC BY 4.0 license, which permit the free download, distribution, and reuse, provided that the author and preprint are cited in any reuse.