Submitted:

26 June 2024

Posted:

27 June 2024

You are already at the latest version

Abstract

Debates regarding human capital disclosure (HCD) emphasise the usefulness of people-related information in stimulating investor confidence and building stakeholder trust. Despite this, human capital (HC) information is interwoven in most international sustainability reporting standards such as the global reporting initiative (GRI), thereby concealing the impact of human resource (HR) practices in shareholder value creation. The aim of this study is to develop a taxonomy to assess HCD in the sustainability reports to capture the true value of HC distinctively. A content analysis-based study with a deductive approach was followed by utilising the GRI standards to isolate and classify people-related information into an HCD sustainability taxonomy. 40% HC metrics were extracted from the GRI standards and subsequently classified into 7 dimensions, namely, human capital allocation, human capital wellbeing, human capital investment, human capital network, human capital governance, human capital risk and human capital earnings. Furthermore, 40 GRI content indexes of the companies listed in the Johannesburg Stock Exchange (JSE) revealed that most disclosures are covered in the human capital governance and human capital earnings categories. HCD sustainability provides investors and HR professionals with a useful tool to assess people-related information from the sustainability reports for isolating the true value of HC.

Keywords:

Sustainability reporting

; human capital disclosure

; GRI reporting standard

; taxonomy development

1. Introduction

Human capital (HC) is a significant element of corporate reporting that builds investor confidence and creates shareholder value, yet the disclosure of this intangible asset is erratic, thereby leads to information asymmetry. In terms of HC theory, improved people’s skills, knowledge, abilities or collectively referred to as competencies, enable them to perform optimally towards business growth [13,31,50], hence the disclosure of this information is considered essential for investor decision-making. [22] applied attribution theory in behavioural finance to confirm that investors use HC information to draw market inferences when buying, holding or selling stocks. Moreover, HC information must clearly be isolated in sustainability reporting instead of being camouflaged in the other disclosure elements. Concealed human capital value (HCV) contributes to increased gap between market to-book-value of the organisation [2,4,23] and denies investors essential information to make profitable decisions.

Human capital disclosure (HCD) is underpinned by stakeholder theory in that information about human resource (HR) practices builds trust between the organisation and interested parties [48]. To address the lack of standardised reporting practices, researchers and business professionals continue to grapple with determining the value HC and disclosing this in a manner that maximises investor returns [6,10,11,12,14,15,37,41,45,47,49]. HCD requirements are interwoven in the global reporting initiative (GRI) and the International Sustainability Standards Board (ISSB) recently undertook a research project aimed at standardising HCD. These standards often create confusion and anxiety on the preparers of the corporate reports, leading to duplicate HCD in integrated and sustainability reports. In fact, the proliferation of standards results in the concealment of HCV, which is often accounted as part of the social (S) and governance (G) elements of sustainability reporting [1,6,12,13,16,23,26,32,34,36]. The standard setters emphasise the disclosure of credible, comparable, and consistent environmental, social and governance [ESG] information [1,6]. To reduce the overlapping effect in sustainability reporting and build investor confidence, it is important to reconcile standards for ensuring that the preparers of corporate reports have uniform guidelines that lead to credible non-financial information disclosure [3,7,35,38,43,52].

Despite the ongoing efforts, there are still no clear HCD guidelines in sustainability reporting demonstrating how the HRM solutions specifically optimise people’s intangible asset in the organisations. For this reason, it is imperative to dissect HC value-relevant information from the “S” and “G” indicators through systematic taxonomy development classifying HR reporting elements into specific domains. Taxonomy development is an evidence-based thematic analysis technique applied to classify and measure the extent of sustainability information in the corporate reports. This approach allows the researcher to identify and code information into specific categories by means of either a deductive or inductive approach taking into consideration the literature survey as well as the regulatory requirements in sustainability reporting [9,17,19,20,27,40]. Currently, no study provides scientific evidence on the development and application of a taxonomy to assess HCD in sustainability reporting using the foundation, general, economic, and social dimensions of the GRI framework. The taxonomy can guide a structured approach for identifying, tracking, and scoring HC disclosures in sustainability reporting.

2. Problem Statement

HCD requirements are integrated in different sustainability reporting standards and treated as part of the “S” and “G” disclosure, leading to the true value of people’s intangible assets being concealed. Also, the HC metrics in most ESG standards are similar, inconsistent, and incomparable, which results in duplicate and omitted people-related information in sustainability reporting.

3. Research Objective

The main objective of the study is to develop a taxonomy to assess the extent of HCD in the sustainability reports by using the GRI standards as a navigation tool. The study was based on the following research sub-objectives (RSOs):

RSO 1: To identify the people-related information in sustainability reporting through the GRI framework.

RSO 2: To classify the people-related information derived through the GRI framework into a taxonomy of key HC reporting categories.

RSO 3: To assess the extent of HC information in sustainability reporting using the HC sustainability reporting taxonomy.

Next, a detailed literature survey is presented to understand the theoretical underpinnings of the study, the relationship between sustainability reporting and HCD as well as to unpack the existing knowledge on the use of taxonomies in corporate disclosure.

4. Literature Review

4.1. Human Capital Disclosure (HCD) Theoretical Perspective

Theoretically, HC is defined as the employees’ quality of competencies that depends on investment, earnings and wellbeing, and if it is harnessed optimally leads to improved productivity [13,31,50]. HC is one of the most critical intangible assets that leads to economic growth and organisational competitive advantage. From a resource-based view (RBV) of the firm, the heterogeneous nature of employees provides the organisations with different options to leverage HC for creating shareholder value, build stakeholder trust and improve investor confidence [13,16]. On the interface between HC and stakeholder theories, the organisations are expected to provide value-relevant information to key stakeholders on approaches utilised to improve the employees’ level of competencies. According to [13] HC value-relevant information required by the stakeholders and investors can cover the employees’ qualification or competence, motivation or commitment, and initiatives to attract, develop and retain skills. The increasing demand for this information implies that the organisations’ HR information systems must be aligned to the markets’ expectations, particularly the sustainability reporting regulations for providing value-relevant HCD. [15] confirmed that internal HR systems must incorporate appropriate metrics on HR practices that contribute towards organisational performance for disclosure in the external market. In terms of applied attribution theory in behavioural finance, it can be concluded that HC information provides key people indicators that investors should consider in resource allocations, and the broader stakeholder fraternity relies on these disclosures to understand the potential economic growth of companies [22]. [48] combined the agency, legitimacy, stakeholder and resource-based view theories in HCD analysis and concluded that the board of directors (BoDs) must observe the disclosure regulations to improve transparent-based relationship with the investment community with focus on reducing the agency costs.

In fact, the organisation’s institutional knowledge reflected in its employees’ and the board’s HC plays a critical role in improving sustainability reporting practices [7,26,44]. According to [30] the board’s quality of HC enables the company’s governing body to effectively discharge oversight in the strategic functioning of the organisation. Knowledge-related HC measured in terms of educational attainment of the board members and their experience enable the governing body to use appropriate tone in the disclosure of information in the annual reports [25]. Board composition should reflect the diversity of skills and knowledge to ensure that key structures or committees are capacitated with credible individuals with competence to drive the organisation to greater hights. Board members’ competence improves strategic oversight, effective application of the reporting standards in corporate disclosure and is reflected in the boards’ transparent ethical behaviour [24,25,29]. In can be deduced that the institutional knowledge embedded in the board and employees’ HC is essential for organisational success, moreover this information is disclosed in the sustainability reports through the GRI standard requirements.

4.2. Sustainability Reporting

Sustainability reporting is a strategic communication mechanism providing information on the ESG risks, impacts and opportunities. Companies adopt the GRI standards and align their internal reporting practices to ensure that internal and external stakeholders receive information that demonstrates corporate social investment (CSI), responsible business not only prioritising financial returns, but seeking to improve socio-economic development and preserve the environmental ecosystem [1,6,8,16,21,26,32,34,36,42]. In recent years, there has been a proliferation of international standards aimed at regulating sustainability reporting through effective corporate governance to reduce anxiety to the prepares of the reports, avoid duplication and omission, subsequently provide comparable ESG information. In 2020, the ISSB acting under the auspices of the International Financial Reporting Standards (IFRS) foundation undertook stakeholder consultations with academics, government agencies, practitioners, investors, nongovernmental organizations (NGOs) and social partners to revise the global sustainability disclosure standards [3,5,38,52].

This led to the establishment of the general requirements for companies to report financial materiality and non-financial materiality related information, which is already covered by the GRI. The debate on sustainability standard setting remains contentious and is out of the scope of this study. Although, it is important to note the contradictions and converges of these standards since they carry significant implications for HCD. Thus, the focus is now drawn back to the application of the GRI standards towards the development of a taxonomy to assess HCD in the sustainability reports.

The GRI reporting framework has been adopted for over two decades by most the companies listed on the Johannesburg Stock Exchange (JSE) in South Africa and provide a structured approach to organise sustainability information in the corporate reports, which can seamlessly be located through the content index. The sustainability or integrated reports include a GRI content index that serves as a navigation tool for users to locate information easily [8,28]. GRI Disclosure 102-55 provides the guidelines for compiling a content index to be attached in the corporate reports and this was utilised in this study to trace people related information towards compiling the HC sustainability reporting taxonomy.

4.3. HCD in Sustainability Reporting

A much intriguing question in corporate disclosure is the investigation of the relationship between sustainability and intellectual capital (IC) reporting to determine synergies, similarities, and contradictions regarding the type of information disclosed, taking into consideration the continuously evolving regulatory framework. IC includes HC, structural capital (SC) and relational capital (RC), collectively considered as the organisational intangibles that create value. SC concerns the organisation’s configuration of internal structures, systems, processes in a manner that optimises HC to generate returns, whereas RC is about the company’s corporate image that can be enhanced through stakeholder management and hence this information is disclosed in the sustainability reports [7,8,26,32,34,51]. The current study does not focus on SC and RC, and these aspects will not be explored further. Although, and from an IC synergistic perspective, it must be noted that HCD has implications for SC disclosure and RC disclosure in sustainability reporting. Few studies have investigated the relationship between HCD and sustainability reporting with results signifying the value-relevance of people-related information. Firstly, [34] used the GRI framework to determine the integration of HC indicators in sustainability reporting.

This study confirmed that employment, labour management relations, health and safety, training, and education as well as diversity specific HC metrics are disclosed in sustainability reporting. Later, [8] established that HC information, namely, employees’ characteristics, training, skills wellbeing, and insurance policy was most disclosed in sustainability reporting. Although, the study did not apply the GRI framework, but the HC indicators were extracted through a literature survey and identified in the sustainability reports. Furthermore, [6] utilised the HC items based on GRI framework to assess the disclosure of this information in the sustainability reports and confirmed that more of this information is covered as part of on social disclosures. [39] identified fifteen (15) labour practices and decent work conditions which relate to HCD. Recently, [51] indicated that improved HCD as a component of IC can be attributed to the ongoing debates on the regulation of social information transparency in the sustainability reports. HCD is a critical component in sustainability reporting covered in the governance and social dimensions of the GRI standards.

Therefore, most studies investigated HCD by analysing the social dimension of the GRI framework only, resulting in the omission of other crucial people-related information such as board’s HC in the governance dimension. Moreover, a taxonomy incorporating the board and employees’ information from the foundation, general, economic, and social disclosures of the GRI standards can serve as a useful tool to assess HCD holistically in sustainability reporting.

4.4. Classification of HC-Based Sustainability Information

As outlined in the preceding sections, HCV is obscured, camouflaged, and largely concealed in the sustainability reports. This can be overcome by the development of an HCD taxonomy with clearly describes HR technical domains and related metrics derived from the GRI standards to guide the seamless retrieval of information about HC decision-making. Several taxonomies have been developed and tested in corporate disclosure studies including sustainability reporting. To reflect, [40] constructed a taxonomy to assess social and environmental disclosures in the annual reports through schema of classifications to improve understandability and comparability of this information. The study derived key indicators, namely, profile, policies, external relations, management performance, occupational health and safety, product performance and sustainability as the main categories of the taxonomy. The taxonomy can be used by the stakeholders to navigate and retrieve customised information in the integrated reports. Also, [9] conducted a systematic literature review and supplemented it with thematic content analysis of 300 web pages of the companies’ websites to construct a taxonomy classifying the sustainability communication topics into four dimensions, namely, planet, people, profit and governance for enabling key stakeholders to source related information optimally. To address the lack of agreed methodology to assess integrated reporting, [20] developed a taxonomy for assessing integrated reports by analysing the sustainability narratives and classified this information into form and content constructs. [19] validated these constructs using capital market data and the multivariate statistics confirmed that the form of sustainability reporting contributes more explanatory information than the content. Lastly, [39] classified fifteen (15) GRI standards related to labour practices and decent work into a designated framework to assess the adoption of the EU Directive 2014/95. The preceding literature survey indicate that sustainable finance taxonomies are implemented to provide the stakeholders and investors with ESG performance information reflecting the company’s assets and economic activities [27]. Based on this, this study applied the GRI standards to develop a HC sustainability reporting taxonomy.

5. Research Method

A content analysis-based deductive approach was followed using the GRI content index containing approximately 163 sustainability standards to identify and describe HC information. The adoption of this bottom–up procedure with predefined categories can guide the subsequent classification of emerging themes and organise related items of measurement into a taxonomy [6, 9, 34, 46). Objectivity and consistency are important for classifying information into emerging themes based on predefined categories [6].

Furthermore, a descriptive data analysis was conducted from a sample of 40 GRI content indexes of the JSE listed companies to assess the extent of HC information in sustainability reporting based on taxonomy. Therefore, the HC metrics and people-related information were extracted from the foundation, general, economic, and social dimensions of the GRI standards. This information focused specially on employee-related and boards’ HC disclosures. Five themes from the employee and board specific disclosures emerged and these provides a theoretical framework for assessing HC in the sustainability reports. In terms of ethical considerations and before secondary data was extracted from the sustainability reports, the study was approved by the university’s ethics committee with project number IPSY-2022-26066.

6. Results

After carefully reviewing the GRI standards using the bottom–up procedure, HC information of the BoDs and employees was identified. As shown in Table 1, this information was coded BHCD if it relates to the board’s HC, EHCD for employee specific information and N/A is it was not found applicable to either the BoDs or employees:

It was found that approximately 40% HC metrics and people-related disclosures are accounted in sustainability reporting, of which moderate represents the boards HC, whereas more pertain to employee-related information while less represents both cohorts. Secondly, and after determining a number of the GRI-based HC metrics as presented in Table 1, the next step was to classify these measures into the HR dimensions related to the attraction, sourcing, development, wellbeing, engagement and retention of employees. This top-down approach allows the researcher to identify items related to predefined categories and subsequently construct these into a new classification [9,46]. The use of the GRI standards including the description and metrics made the identification of HC related items seamless. Therefore, the following themes and subthemes in Table 2 were generated:

The themes represent HC information in the GRI standards focusing on the boards and employee disclosures. Finally, Table 3 below provides the association of the emergent themes with EHCD and BHCD linked to the GRI standard numbers as indicated in Table 1.

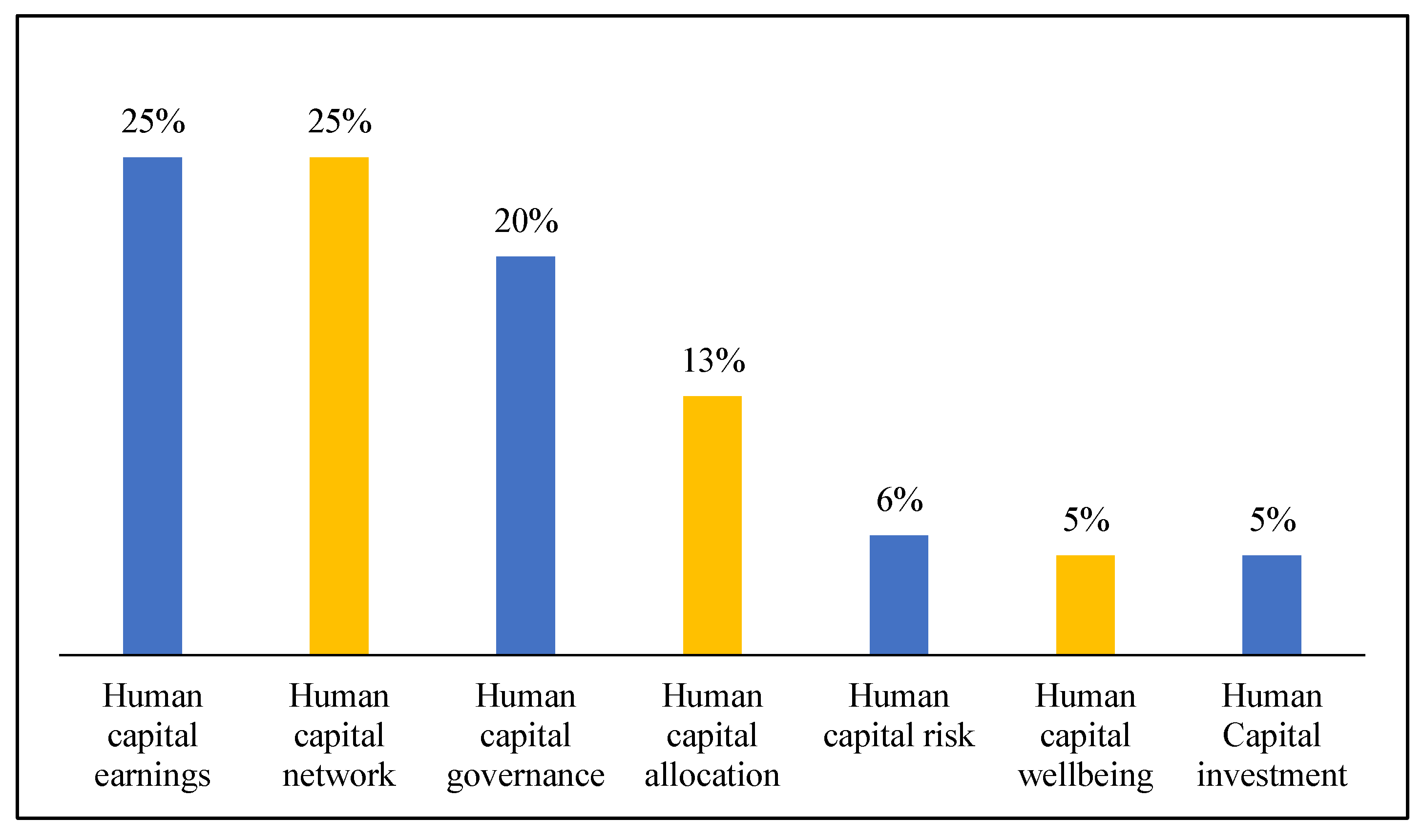

The codes can facilitate traceability of HC information in sustainability reports and can be useful in assessing quality disclosure. The table shows that HCN and HCG cover most people related GRI standards, whereas HCA, HCI, and HCR contain the second highest. Boards’ HC is covered more in HCG where the governing body provides information reflecting how their collective knowledge, skills and abilities translate into effective corporate governance. HCG has significant implications for employee behaviour and performance although no specific standards relate to this dimension. HCN reflects the role of the board in terms of promoting internal and external stakeholder engagement, while at the same time encourage upward communication from employees to management. HCA, HCW, HCI, HCR and HCE cover more GRI standards for employee HCD implying that the internal HR information system must be well configured to provide timely and accurate information for sustainability reporting. It can be concluded that the isolated GRI-people related standards into this taxonomy provide a useful tool for the investment community and HR professionals to assess HC sustainability reporting. Therefore, to illustrate the use of this taxonomy, Figure 1 shows the results of HC sustainability disclosure based on a sample of 40 GRI content indexes of the JSE listed companies.

According to the results, information about HCD was mostly disclosed in respect of policies and processes used to determine remuneration, incentive pay and employee benefits. HCN was also mostly disclosed with information regarding the companies’ efforts to improve internal stakeholder engagement. Information on HCG was disclosed on the governance structure and committees responsible for decision-making as well as performance evaluation of the boards. This was followed by HCA with information on employee and board demographics including diversity statistics. The most highly disclosed information relates to mandatory or regulatory requirements. Least disclosures in HCR, HCW and HCI are concerning in that this creates information asymmetry. Perhaps the lack of disclosure in these dimensions can be attributed to the sensitivity of some information in the market and hence it is withheld. Also, some of this information is considered voluntary disclosures and the board is not compelled to make such information available in the public. These results substantiate that isolating HR information from the GRI standards can enable the investment community and HR Professionals to evaluate the people management initiatives that add shareholder value and improve HC sustainability reporting.

7. Discussion

HC information is duplicated and scattered in the sustainability and integrated reports. This unstandardised reporting leads to lack of transparency, preferential voluntary disclosure and creates imbalanced information that negatively affects the investment process. The development of the HC sustainability disclosure taxonomy followed a rigorous process where the people related GRI standards were isolated and classified into key 7 HR dimensions. This top-down procedure enables researchers to apply the existing framework in identifying the appropriate categories and associated items. The HCD taxonomy can serve as useful blueprint to decide on the disclosure of people-related information to improve sustainability report taking into consideration the GRI standards. Through this taxonomy, researchers can efficiently locate HC information in corporate reports using the GRI content index. This information can be help in statistical analysis, benchmarking and improving the quality of reporting. The study confirms that isolating HR information from the GRI standards can enable the investment community and HR Professionals to evaluate the impact of HC on the business using the sustainability reports.

8. Conclusions

The study sought to develop a taxonomy for assessing HC information in the sustainability reports. The GRI standards were utilised to isolate people-related information which were subsequently classified into 7 dimensions, namely, human capital allocation, human capital wellbeing, human capital investment, human capital network, human capital governance, human capital risk and human capital earnings. These dimensions represent 40% HC metrics in the GRI standards, and the results revealed that most disclosures are covered in the HCG and HCE categories. This taxonomy provides practical guidelines on how to identify, track, and score people-related information in the sustainability reports to isolate the value of HC. The taxonomy is based on the existing GRI standards and may nullify the ongoing attempts to implement the international HR reporting guidelines. While this point serves a significant implication, the taxonomy did not consider a comparative analysis of the GRI standards with the other international HR reporting guidelines to identify similarities and inconsistencies for building an integrated classification. Further research can be conducted with the application of the taxonomy to assess HC sustainability disclosure through cross-sectional and panel data analysis using a larger sample of listed companies.

Author Contributions

Writing—original draft preparation; methodology; writing—review and editing, M.D. Magau.

Funding

This research received no funding.

Institutional Review Board Statement

Not applicable in that there was no involvement of humans or animals in the study.

Informed Consent Statement

Not applicable in that there was no involvement of humans or animals in the study.

Data Availability Statement

Secondary data was extracted from the GRI content indexes of the JSE listed companies and is contained in the article.

Conflicts of Interest

The author declares no conflict of interest.

References

- Abeysekera, I. A framework for sustainability reporting. Sus. Account. Manag. Pol. J. 2022, 13, 1386–1409. [Google Scholar] [CrossRef]

- Abdolmohammadi, M.J. Intellectual capital disclosure and market capitalization. J. Intell. Cap. 2005, 6, 397–416. [Google Scholar] [CrossRef]

- Afolabi, H.; Ram, R.; Rimmel, G. Influence and behaviour of the new standard setters in the sustainability reporting arena: implications for the Global Reporting Initiative’s current position. Sus. Account. Manag. Pol. J. 2023, 14, 743–775. [Google Scholar] [CrossRef]

- Alfraih, M.M. (2018). Intellectual capital reporting and its relation to market and financial performance. Int. J. Eth. Sys. 2023, 34, 266–281. [Google Scholar] [CrossRef]

- Ali, I.; Fukofuka, P.T.; Narayan, A.K. Critical reflections on sustainability reporting standard setting. Sus. Account. Manag. Pol. J. 2023, 14, 776–791. [Google Scholar] [CrossRef]

- Alvarez, A. Corporate response to human resource disclosure recommendations. Soc. Resp. J. 2015, 11, 306–323. [Google Scholar] [CrossRef]

- Bananuka, J.; Tauringana, V.; Tumwebaze, Z. Intellectual capital and sustainability reporting practices in Uganda. J. Intell. Cap. 2023, 24, 487–508. [Google Scholar] [CrossRef]

- Cinquini, L.; Passetti, E.; Tenucci, A.; Frey, M. Analyzing intellectual capital information in sustainability reports: some empirical evidence. J. Intell. Cap. 2012, 13, 531–561. [Google Scholar] [CrossRef]

- Confetto, M.G.; Covucci, C. A taxonomy of sustainability topics: a guide to set the corporate sustainability content on the web. The TQM J. 2021, 33, 106–130. [Google Scholar] [CrossRef]

- Di Vaio, A.; Palladino, R.; Hassan, R.; Alvino, F. Human resources disclosure in the EU Directive 2014/95/EU perspective: A systematic literature review. J. Clean. Produ. 2020, 257, 120509. [Google Scholar] [CrossRef]

- Ehnert, I.; Parsa, S.; Roper, I.; Wagner, M.; Muller-Camen, M. Reporting on sustainability and HRM: A comparative study of sustainability reporting practices by the world's largest companies. The Int. J. HRM., 2016, 27, 88–108. [Google Scholar] [CrossRef]

- Farneti, F.; Casonato, F.; Montecalvo, M.; de Villiers, C. The influence of integrated reporting and stakeholder information needs on the disclosure of social information in a state-owned enterprise. Meditari Account. Res. 2019, 27, 556–579. [Google Scholar] [CrossRef]

- Frangieh, G.C.; Yaacoub, H.K. Socially responsible human resource practices: disclosures of the world’s best multinational workplaces. Soc. Responsib. J. 2019, 15, 277–295. [Google Scholar] [CrossRef]

- Gamerschlag, R. Value relevance of human capital information. J. Intell. Cap. 2013, 14, 325–345. [Google Scholar] [CrossRef]

- Grassmann, M.; Fuhrmann, S.; Guenther, T.W. Drivers of the disclosed “connectivity of the capitals”: evidence from integrated reports. Sus. Account. Manag. Pol. J. 2019, 10 877‐908.

- Lajili, K. Human capital disclosure and the contingency view. Pers. Rev. 2022, Vol. ahead-of-print No. ahead-of-print.

- Lim, H.J.; Mali, D. A comparative analysis of human capital information opaqueness in South Korea and the UK. J. Intell. Cap. 2022, 23, 1296–1327. [Google Scholar] [CrossRef]

- La Torre, M.; Valentinetti, D.; Dumay, J.; Rea, M.A. Improving corporate disclosure through XBRL: An evidence-based taxonomy structure for integrated reporting. J. Intell. Cap. 2018, 19, 338–366. [Google Scholar] [CrossRef]

- León, R.; Salesa, A. Is sustainability reporting disclosing what is relevant? Assessing materiality accuracy in the Spanish telecommunication industry. Environ. Dev. Sus. 2023, 1–28. [Google Scholar]

- Lueg, R. Constructs for assessing integrated reports—Testing the predictive validity of a taxonomy for organisation size, industry, and performance. Sus. 2022, 14, 7206. [Google Scholar]

- Lueg, K.; Lueg, R. Deconstructing corporate sustainability narratives: A taxonomy for critical assessment of integrated reporting types. Corp. Soc. Resp. Env. Manag. 2021, 28, 1785–1800. [Google Scholar] [CrossRef]

- Maione, G. An energy company's journey toward standardized sustainability reporting: addressing governance challenges. Transf. Govt. Ppl, Proc. Pol 2023, Vol. ahead‐of‐print No. ahead‐of‐print.

- Mariappanadar, S.; Kairouz, A. Influence of human resource capital information disclosure on investors’ share investment intentions: An Australian study. Pers. Rev. 2017, 46, 551–571. [Google Scholar] [CrossRef]

- Marzo, G. The market-to-book value gap and the accounting fallacy. J. Intell. Cap. 2013, 14, 564–581. [Google Scholar] [CrossRef]

- Martikainen, M.; Kinnunen, J.; Miihkinen, A.; Troberg, P. Board’s financial incentives, competence, and firm risk disclosure: Evidence from Finnish index listed companies. J. Appl. Account. Res. 2015, 16, 333–358. [Google Scholar] [CrossRef]

- Martikainen, M.; Miihkinen, A.; Watson, L. Board characteristics and negative disclosure tone. J. Account. Lit. 2023, 45, 100–129. [Google Scholar] [CrossRef]

- Massaro, M.; Dumay, J.; Garlatti, A.; Dal Mas, F. Practitioners’ views on intellectual capital and sustainability: From a performance-based to a worth-based perspective. J. Intell. Cap. 2018, 19, 367–386. [Google Scholar] [CrossRef]

- Moneva, J.J.; Scarpellini, S.; Aranda-Usón, A.; Etxeberria, I.A. Sustainability reporting in view of the European sustainable finance taxonomy: Is the financial sector ready to disclose circular economy? Corp. Soc. Resp. Env. Manag. 2022, 30, 1336–1347. [Google Scholar] [CrossRef]

- Mori Junior, R.; Best, P. GRI G4 content index: Does it improve credibility and change the expectation-performance gap of GRI-assured sustainability reports? Sus. Account. Manag. Pol. J. 2017, 8, 571–594. [Google Scholar] [CrossRef]

- Ngu, S.B.; Amran, A. The impact of sustainable board capital on sustainability reporting. Strat. Dir. 2019, 35, 8–11. [Google Scholar] [CrossRef]

- Nicholson, G.J.; Kiel, G.C. Breakthrough board performance: how to harness your board’s intellectual capital. Corp. Gov. 2004, 4, 5–23. [Google Scholar] [CrossRef]

- Nkundabanyanga, S.K.; Balunywa, W.; Tauringana, V.; Ntayi, J.M. Board role performance in service organisations: the importance of human capital in the context of a developing country. Soc. Resp. J. 2014, 10, 646–673. [Google Scholar] [CrossRef]

- Oliveira, L.; Lima Rodrigues, L.; Craig, R. Intellectual capital reporting in sustainability reports. J. Intell. Cap. 2010, 11, 575–594. [Google Scholar] [CrossRef]

- Pandit, G. M. First look at the human capital disclosures on Form 10-K. Analyzing the SEC mandate and comparing it to SASB and EU standards. CPA J. 2021, 52. [Google Scholar]

- Pedrini, M. Human capital convergences in intellectual capital and sustainability reports. J. Intell. Cap. 2007, 8, 346–366. [Google Scholar] [CrossRef]

- Perera-Aldama, L. GRI and materiality: discussions and challenges. Sus. Account. Manag. Pol. J. 2023. 14, 884–903. [CrossRef]

- Petcharat, N.; Zaman, M. Sustainability reporting and integrated reporting perspectives of Thai-listed companies. J. Fin. Rep. Account. 2019, 17, 671–694. [Google Scholar] [CrossRef]

- Pigatto, G.; Cinquini, L.; Tenucci, A.; Dumay, J. Disclosing value creation in integrated reports according to the six capitals: a holistic approach for a holistic instrument. Sus. Account. Manag. Pol. J. 2023, 2023. 14, 90–123. [Google Scholar] [CrossRef]

- Pizzi, S.; Principale, S.; de Nuccio, E. Material sustainability information and reporting standards. Exploring the differences between GRI and SASB. Meditari Account. Res. 2022, Vol. ahead-of-print No. ahead-of-print.

- Posadas, S.C.; Tarquinio, L. Assessing the effects of Directive 2014/95/EU on nonfinancial information reporting: Evidence from Italian and Spanish listed companies. Adm. Sci. 2021, 11, 89. [Google Scholar] [CrossRef]

- Raar, J. Reported social and environmental taxonomies: a longer-term glimpse. Manag. Audit. J. 2007, 22 840-860.

- Raimo, N.; Ricciardelli, A.; Rubino, M.; Vitolla, F. Factors affecting human capital disclosure in an integrated reporting perspective. Meas. Bus. Excell. 2020, 24, 575–592. [Google Scholar] [CrossRef]

- Ramona, Z.; Askarany. D. Sustainability reporting and organisational factors. J. Risk Financ. Manag. 2023, 16, 163–1‐18. [Google Scholar]

- Rowbottom, N. Orchestration and consolidation in corporate sustainability reporting. The legacy of the Corporate Reporting Dialogue. Account. Audit. Account. J. 2023, 36, 885–912. [Google Scholar] [CrossRef]

- Saha, R.; Maji, S.G. Board human capital diversity and firm performance: evidence from top listed Indian firms. JIBR. 2022, 14, 382–402. [Google Scholar] [CrossRef]

- Salvi, A.; Raimo, N.; Petruzzella, F.; Vitolla, F. The financial consequences of human capital disclosure as part of integrated reporting. J. Intell. Cap. 2022, 23, 1221–1245. [Google Scholar] [CrossRef]

- Sujatha, R.; Bandaru, R.; Rao, R. Taxonomy construction techniques–issues and challenges. IJCSE. 2011, 2, 661–671. [Google Scholar]

- Sürdü, F.B.; Çalışkan, A.Ö.; Esen, E. Human resource disclosures in corporate annual reports of insurance companies: A case of developing country. Sus. 2020, 12, 1–20. [Google Scholar]

- Tejedo-Romero, F.; Araujo, J.F.F.E. The influence of corporate governance characteristics on human capital disclosure: the moderating role of managerial ownership. J. Intell. Cap. 2022, 23, 342–374. [Google Scholar] [CrossRef]

- Terblanche, W.; De Villiers, C. The influence of integrated reporting and internationalisation on intellectual capital disclosures. J. Intell. Cap. 2019, 20, 40–59. [Google Scholar] [CrossRef]

- Valenti, A.; Horner, S.V. Leveraging board talent for innovation strategy. J. Bus. Strat. 2020, 41, 11–18. [Google Scholar] [CrossRef]

- Van der Zahn, J.L.W.M. Sustainability reporting regime transition and the impact on intellectual capital reporting. J. Appl. Account. Res. 2023, 24, 544–582. [Google Scholar] [CrossRef]

- Zaid, M.A.A.; Issa, A. A roadmap for triggering the convergence of global ESG disclosure standards: lessons from the IFRS foundation and stakeholder engagement. Corp. Gov 2023, Vol. ahead‐of‐print No. ahead‐of‐print.

Figure 1.

Human capital disclosure taxonomy for assessing sustainability reporting.

Table 1.

Sustainability reporting-based on HC metrics and people-related information.

| GRI No. | Human capital metrics and people-related information | Linked HCD Codes | |

|---|---|---|---|

| BHCD | EHCD | ||

| 102-7 | Total number of employees based on business operations. | N/A | EHCD-1 |

| 102-8 | Total of employees per employment contract type, gender, geographic location and fulltime employees perform a significant portion of activities. | N/A | EHCD-2 |

| 102-16 | Regular training provided to the board members and employees on values, principles, standards, and norms of behaviour. | BHCD-3 | EHCD-3 |

| 102-17 | Communication and training provided to employees regarding ethics. | N/A | EHCD-4 |

| 102-18 | Structuring of the board and related committees, and roles are allocated for decision-making on ESG. | BHCD-5 | N/A |

| 102-19 | Delegation of authority for ESG topics from the board to senior executives and other employees. | BHCD-6 | N/A |

| 102-20 | Appointment of the executive team members to perform the ESG roles. | BHCD-7 | N/A |

| 102-21 | Board stakeholder consultation on ESG matters. | BHCD-8 | N/A |

| 102-22 | Structuring of the board and related committees in respect of gender independence, tenure, other commitments, ESG competencies. | BHCD-9 | N/A |

| 102-23 | Role of the chairperson of the board and distinction of whether he / she functions within the organisation. | BHCD-10 | N/A |

| 102-24 | Selection process and criteria for the appointment of the board and its committees, diversity consideration, independence ESG expertise. | BHCD-11 | N/A |

| 102-25 | Board responsibility regarding conflicts of interest and measures for employees to consider. | BHCD-12 | EHCD-12 |

| 102-26 | Board and executive leadership responsibility in developing, approving, and updating the strategic direction, and goals related to ESG. | BHCD-13 | N/A |

| 102-27 | Measures taken to develop and enhance the board’s collective knowledge of ESG. | BHCD-14 | N/A |

| 102-28 | Board’s performance evaluation processes in respect of ESG and actions in response of the feedback. | BHCD-15 | N/A |

| 102-29 | Board’s role in identifying and managing ESG material impacts, risks and opportunities, and if there are stakeholder consultation processes on these issues. | BHCD-16 | N/A |

| 102-30 | Board’s role in reviewing the effectiveness of the organisation’s risk management processes for ESG. | BHCD-17 | N/A |

| 102-31 | Frequency of the board engaging on the review of ESG matters and their impacts, risks, and opportunities. | BHCD-18 | N/A |

| 102-32 | Review and approval of sustainability report by the appropriate committees ensuring that ESG material topics are covered. | BHCD-19 | N/A |

| 102-33 | Communication process regarding critical concerns to the board. | BHCD-20 | EHCD-20 |

| 102-35 | Remuneration policies for the board and senior executives in terms of fixed pay and variable pay criteria for achieving the ESG. | BHCD-21 | N/A |

| 102-36 | Consultative processes in determining remuneration. | BHCD-22 | N/A |

| 102-37 | Stakeholder engagement on determining remuneration as well as voting procedures regarding the remuneration policies and proposals. | BHCD-23 | EHCD-23 |

| 102-38 | Ratio of the annual total compensation for the organisation’s employees. | N/A | EHCD-24 |

| 102-39 | Ratio of the % increase in annual total compensation for the organisation’s employees. | N/A | EHCD-25 |

| 102-40 | A list of stakeholder groups including employees and trade unions engaged by the organisation. | N/A | EHCD-26 |

| 102-41 | % of total employees covered by collective the bargaining agreements. | N/A | EHCD-27 |

| 102-42 | The basis for identifying and selecting stakeholders such as trade unions engaged by the organisation. | BHCD-28 | EHCD-28 |

| 102-43 | Stakeholder engagement approach specifically with the trade union, including frequency of engagement. | BHCD-29 | N/A |

| 102-44 | Employee-related issues, concerns raised through stakeholder engagement with the trade union. | N/A | EHCD-30 |

| 103-2 | The total number of employee grievances, the number of grievances that were addressed (or reviewed) and resolved during the reporting period. | N/A | EHCD-31 |

| 201-1 | Direct economic value generated and distributed (EVG&D) in terms of employee wages and benefits. | N/A | EHCD 32 |

| 201-3 | Defined benefit plan, liabilities and how these are met, and the estimated value of those liabilities. Pension contributions and employee participation. | BHCD-33 | EHCD-33 |

| 202-1 | Relevant ratio of the entry level wage by gender at significant locations of operation to the minimum wage. | N/A | EHCD-34 |

| 202-2 | Appointment of senior management from the local community. | BHCD-35 | N/A |

| 205-2 | Communication of anti-corruption policies and procedures to the board members by region, and employees per category and region. | BHCD-36 | EHCD-36 |

| Training of anti-corruption policies and procedures to the board members by region, and employees per category and region. | BHCD-37 | EHCD-37 | |

| 206-1 | Number of legal actions pending or completed regarding anti-competitive behaviour and violations of anti-trust by the board, executive and employees. | BHCD-38 | EHCD-38 |

| The role of board and executive leadership team in formally reviewing and approving the tax strategy, and the frequency of this review. | BHCD-39 | N/A | |

| 207-2 | Accountability of the board and executive leadership team on tax strategy and measures taken about unethical or unlawful behaviour. | BHCD-40 | EHCD-40 |

| 207-4 | Tax calculation for employees based on remuneration and taxes withheld and paid on behalf of employees. | BHCD-41 | EHCD-41 |

| 401-1 | Sourcing and rate of recruitment of new number and rate of new employee age group, gender, and region. | N/A | EHCD-42 |

| Total number and rate of employee turnover by age group, gender and region. | N/A | EHCD-43 | |

| 401-2 | Benefits which are standard for full-time employees but are not provided to temporary or part-time employees, by significant locations of operation. | N/A | EHCD-44 |

| 401-3 | Total number of employees that were entitled to parental leave, by gender, leave provision by gender, leave returnees by gender | N/A | EHCD-45 |

| 402-1 | Weeks’ notice provided to employees and their representatives in respect of organisation restructuring. | N/A | EHCD-46 |

| Specific provisions of notice period in the collective agreements following the consultation and negotiation process. | N/A | EHCD-47 | |

| 403-1 | Implementation of the occupational health and safety system including the scope of workers covered. | BHCD-48 | EHCD-48 |

| 403-2 | Processes used to identify work-related hazards and assess risks on a routine and non-routine basis. | BHCD-49 | EHCD-49 |

| 403-3 | A description of the occupational health services’ functions that contribute to the identification and elimination of hazards and minimization of risks. | BHCD-50 | EHCD-50 |

| 403-4 | Processes for worker participation and consultation in the on occupational health and safety management system. | BHCD-51 | EHCD-51 |

| 403-5 | Occupational health and safety training provided to workers, including training on specific work-related hazards, hazardous activities / situations. | N/A | EHCD-52 |

| 403-6 | Workers’ access to non-occupational medical and healthcare services, and the scope of access provided. | N/A | EHCD-53 |

| 403-8 | Number and % of all employees and workers who are not employees but covered by the health and safety management system. | N/A | EHCD-54 |

| 403-9 | Work-related injuries including fatalities and hours worked. | N/A | EHCD-55 |

| 403-10 | Work-related ill heath including fatalities. | N/A | EHCD-56 |

| 404-1 | Average hours of training that the organisation’s employees by gender and employee category. | N/A | EHCD-57 |

| 404-2 | Type and scope of programmes implemented, and assistance provided to upgrade employee skills and facilitate continued employability. | N/A | EHCD-58 |

| 404-3 | Percentage of total employees by gender and by employee category who received a regular performance and career development review. | N/A | EHCD-59 |

| 405-1 | Diversity statistics of individuals board and employees per category in terms of gender; age group, other indicators of diversity | BHCD-60 | EHCD-60 |

| 405-2 | Ratio of the basic salary and remuneration of women to men for each employee category, by significant locations of operation. | N/A | EHCD-61 |

| 406-1 | Total number of incidents of discrimination and remediation plans being implemented. | N/A | EHCD-62 |

| 407-1 | Operations and suppliers in which workers’ rights to exercise freedom of association or collective bargaining may be violated or at significant risk. | N/A | EHCD-63 |

| 408-1 | Risk for incidents of child labour, young workers exposed to hazardous work. | N/A | EHCD-64 |

| 409-1 | Risk for incidents of forced or compulsory labour. | N/A | EHCD-65 |

| 410-1 | Percentage of security personnel who have received formal training in the organisation’s human rights policies or specific procedures. | N/A | EHCD-66 |

| 411-1 | Total number of identified incidents of violations involving the rights of indigenous peoples where workers performed the organisation’s activities | N/A | EHCD-67 |

| 412-2 | Training on human rights policies or procedures concerning aspects of human rights that are relevant to operations. | N/A | EHCD 68 |

BHCD = Board human capital disclosure, EHCD = Employee human capital disclosure, N/A = Not applicable.

Table 2.

Emerging HC sustainability disclosure themes.

| Themes and definitions | Sub-themes |

|---|---|

| Human capital allocation (HCA): Information regarding the methods and initiatives taken to attract and source talent into the organisation. |

|

| Human capital wellbeing (HCW): Information regarding the programmes and initiatives to secure the health and safety of employees. |

|

| Human capital investment (HCI): Information regarding the financial and non-financial resources utilised to optimise people’s skills for improving performance. |

|

| Human capital network (HCN): Companies’ engagement with internal, and external stakeholders through its employees. |

|

| Human capital governance (HCG): Information regarding the organisations’ structure, key roles, and processes to improve corporate governance. |

|

| Human capital risk (HCR): Information regarding the organisations’ events or occurrences negatively affecting employees, and the employees’ unethical behaviour negatively affecting the organisation. |

|

| Human capital earnings (HCE): Information regarding paid remuneration, benefits and incentives to employees and the board. |

|

Table 3.

Human capital disclosure taxonomy for assessing sustainability reporting.

| Emergent HC sustainability disclosure themes | HCD disclosure codes linked to the GRI Standards | |||||

|---|---|---|---|---|---|---|

| Human capital allocation (HCA) | EHCD-1 | EHCD-2 | EHCD-4 | BHCD-7 | BHCD-35 | EHCD-42 |

| EHCD-43 | EHCD-45 | EHCD-46 | BHCD-60 | EHC-60 | ||

| Human capital wellbeing (HCW) | EHCD-48 | EHCD-49 | EHCD-50 | EHCD-53 | EHCD-54 | |

| Human capital investment (HCI) | EHCD-3 | BHCD-3 | BHCD-14 | BHCD-37 | EHCD-37 | EHCD-52 |

| EHCD-57 | EHCD-58 | EHCD-59 | EHCD-66 | EHCD-68 | ||

| Human capital network (HCN) | BHCD-8 | BHCD-20 | EHCD-20 | BHCD-22 | BHCD-23 | EHCD-23 |

| EHCD-26 | EHCD-27 | EHCD-28 | EHCD-29 | EHCD-30 | BHCD-36 | |

| EHCD-36 | EHCD-47 | BHCD-51 | EHCD-51 | |||

| Human capital governance (HCG) | BHCD-5 | BHCD-6 | BHCD-9 | BHCD-10 | BHCD-11 | BHCD-12 |

| BHCD-13 | BHCD-15 | BHCD-16 | BHCD-17 | BHCD-18 | BHCD-19 | |

| BHCD-39 | BHCD-40 | BHCD-48 | BHCD-49 | BHCD-50 | ||

| Human capital risk (HCR) | EHCD-31 | BHCD-38 | EHCD-38 | EHCD-40 | EHCD-55 | EHCD-56 |

| EHCD-62 | EHCD-63 | EHCD-64 | EHCD-65 | EHCD-67 | ||

| Human capital earnings (HCE) | BHCD-21 | EHCD-24 | EHCD-25 | EHCD-32 | EHCD-33 | BHCD-33 |

| EHCD-34 | EHCD-41 | EHCD-44 | EHCD-61 | |||

BHCD = Board human capital disclosure, EHCD = Employee human capital disclosure.

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Copyright: This open access article is published under a Creative Commons CC BY 4.0 license, which permit the free download, distribution, and reuse, provided that the author and preprint are cited in any reuse.