Submitted:

29 June 2024

Posted:

01 July 2024

Read the latest preprint version here

Abstract

This article examines the integration of artificial intelligence (AI) and robotic process automation (RPA) in financial accounting and management, underscoring their role in driving the digital transformation of corporate finance. It discusses the shortcomings of traditional financial processes and highlights the potential of AI and RPA technologies to enhance efficiency, accuracy, and cost-effectiveness. The paper also explores the limitations of RPA, such as its challenges in processing unstructured data and handling complex decision-making scenarios. Looking forward, it considers the future trends in AI and RPA, emphasizing the benefits of cloud technology in scaling automated systems and addressing associated challenges.

Keywords:

Artificial intelligence (AI)

; Robotic Process Automation (RPA)

; Intelligent Process Automation (IPA)

; Financial Risk Management

1. INTRODUCTION

With the advent of the era of artificial intelligence, the application of AI is more and more extensive, and the fields of financial accounting and financial management have successively produced application tools such as industry-financial integration software and financial robots. By applying these intelligent products, financial accounting can realise the expansion and extension of traditional accounting work, such as the realisation of manual accounting semi-automation by the computer instead of manual bookkeeping and manual participation only at the beginning and end of the process. [1-3]. At the same time, the original analysis of accounts is carried out according to statements, books, etc.. In the analysis process, the amount of information processed is limited due to people's limited energy. Still, the application of AI technology can achieve extensive data analysis, make the information more diversified, and expand the financial accounting work.

As Internet technology has been popularised in all walks of life, artificial intelligence (AI) has also emerged as a complex and systematic engineering supported by various high-tech technologies. In financial management, robotic process automation (RPA) technology brings a new wave of digital transformation to corporate finance, which can handle repetitive tasks and simulate user actions and interactions. [4-5]. RPA is most likely to make efforts in the two significant aspects of transactional financial processing and internal risk control, such as inventory and cost, asset accounting, and other business processes, which will make the future work in the accounting field more and more automated. Businesses and accountants should be prepared to face the necessary AI in this wave.

2. RELATED WORK

2.1. Traditional Financial Accounting Process

From the 1980s to the modern era, the accounting organisation process has undergone qualitative changes, significantly impacting data storage and the accounting mode. The accounting process can be integrated with automatic control systems to achieve automatic inspection, improve the accuracy and timeliness of accounting, liberate financial personnel from essential accounting work, and promote the automation of the accounting process. In the Internet environment, accounting information can improve the efficiency of economic work and help it conform to the changing market trends. However, because the information from various departments cannot be interactive, the promotion of financial work is limited, affecting the overall management level of enterprises and weakening the industry's core competitiveness. [6,7,8]. Therefore, the innovation of the financial management mode should use a highly integrated system to realise the integrated development of industry and finance.

Enterprise management control requires the close cooperation of various departments and employees, and two modes of centralisation and decentralisation can be used for financial management authority. In centralised enterprises, the decision-making power falls on the head office, which weakens the work enthusiasm of subsidiaries. Under the decentralisation mode, subsidiaries have specific operational decision-making power, and the parent company still supervises and evaluates significant decisions. However, without the support of Internet technology, enterprises will face inevitable management conflicts under any management mode, resulting in the loss of control of the financial management system and limited capital control ability.

Deficiencies of the financial decision support layer: There will be an information island phenomenon if enterprise information cannot be integrated and interworked. [8]. The financial process will not adapt to the current social and economic development law, making the enterprise's organisational structure redundant. Decision-making information needs to be reported layer by layer, affecting the timeliness and accuracy of information, making it difficult to gain a competitive advantage. Therefore, in the Internet environment, enterprises should improve their financial management mode, accurately grasp core information, meet the development goal of maximising corporate value, and promote the mutual integration and communication of corporate financial management information.

2.2. Financial Process Intelligence

The development background of financial process intelligence is diverse and interwoven, involving the following five aspects: First, in terms of technology, with the popularisation and development of technologies such as the Dazhi moving cloud area, the basic technology of process automation is becoming more and more abundant. RPA can handle processes in a way that mimics the user interface and enables more extensive process automation through cloud computing technology. The maturity of AI technology allows IPA, which integrates AI algorithms, to automate processes that can process unstructured data, make complex decisions, and self-learn and optimise based on experience and feedback. Second, in terms of policies, governments and international organisations continue to advocate the development of a digital economy, enterprise digital transformation, and artificial intelligence technology and have introduced relevant policies to support technological innovation and process automation, support R&D [10]. investment, guide enterprises to upgrade information facilities, and cultivate digital talents, and have passed a series of laws and regulations. It emphasises the need to pay attention to data security, privacy protection, and compliance in process automation.

Third, in terms of application, process automation technology has gradually penetrated all walks of life, including finance, medical care, manufacturing, retail, logistics, public utilities, and other industries, explicitly involving finance, human resources, customer service, supply chain management, manufacturing and other fields of business processes. [11]. Organisations dramatically increase productivity, reduce labour costs, and allow employees to engage in more creative work by automating back-office processes such as administration, finance, and IT support. Fourth, regarding ecology, several software service providers and platforms specialising in process Automation solutions have emerged in the market, such as UiPath, Automation Anywhere, Blue Prism, Lai Ye Technology, Yisaiqi, Daguan Data, etc. [12]. They have built an ecosystem of products and services, including software development tools, APIs (Application Programming interfaces), training courses, and community support. They have gradually integrated closely with various enterprise management software and AI service platforms. The result is a much larger technological ecosystem.

This process is designed to replace or assist human beings in completing various daily tasks through computer software, hardware, and artificial intelligence, improving work efficiency, reducing error rates, saving costs, and improving business response speed. Process automation includes related concepts such as RPA, IPA, and super automation. [10,11]. RPA is a process automation technology that utilises software to simulate and perform repetitive, regular, and predictable tasks that humans perform in everyday business processes. The core of RPA is to replace human beings in performing repetitive, rule-based computer tasks, which often include data entry, form filling, file transfer, email sending, and receiving. IPA combines AI, automation, and other cutting-edge technologies applied to process automation. [13]. IPA focuses on simple automation and mimicking human activities and can also learn to improve and optimise these activities continuously. IPA is a new technology derived from RPA and represents a more intelligent process automation technology. Super automation is a broad and deep application of automation strategies and technologies that aims to go beyond traditional automation methods and automate processes on a larger and more profound scale by integrating multiple advanced technologies and tools. Super automation not only supports a single automation task but also covers all aspects of the automation life cycle, from identifying processes that can be automated to continuously optimising them, including process discovery, analysis, design, automation implementation, performance measurement, monitoring, and periodic reevaluation.

2.3. Limitations of RPA Technology

Although RPA can effectively solve problems with the characteristics of "process, clear rules, repetitive trivial" and reduce the error rate of business operations, its use is also expanding across industries, across regions, and on a large scale, RPA has many development bottlenecks or technical limitations relative to the needs of more intelligent process automation.

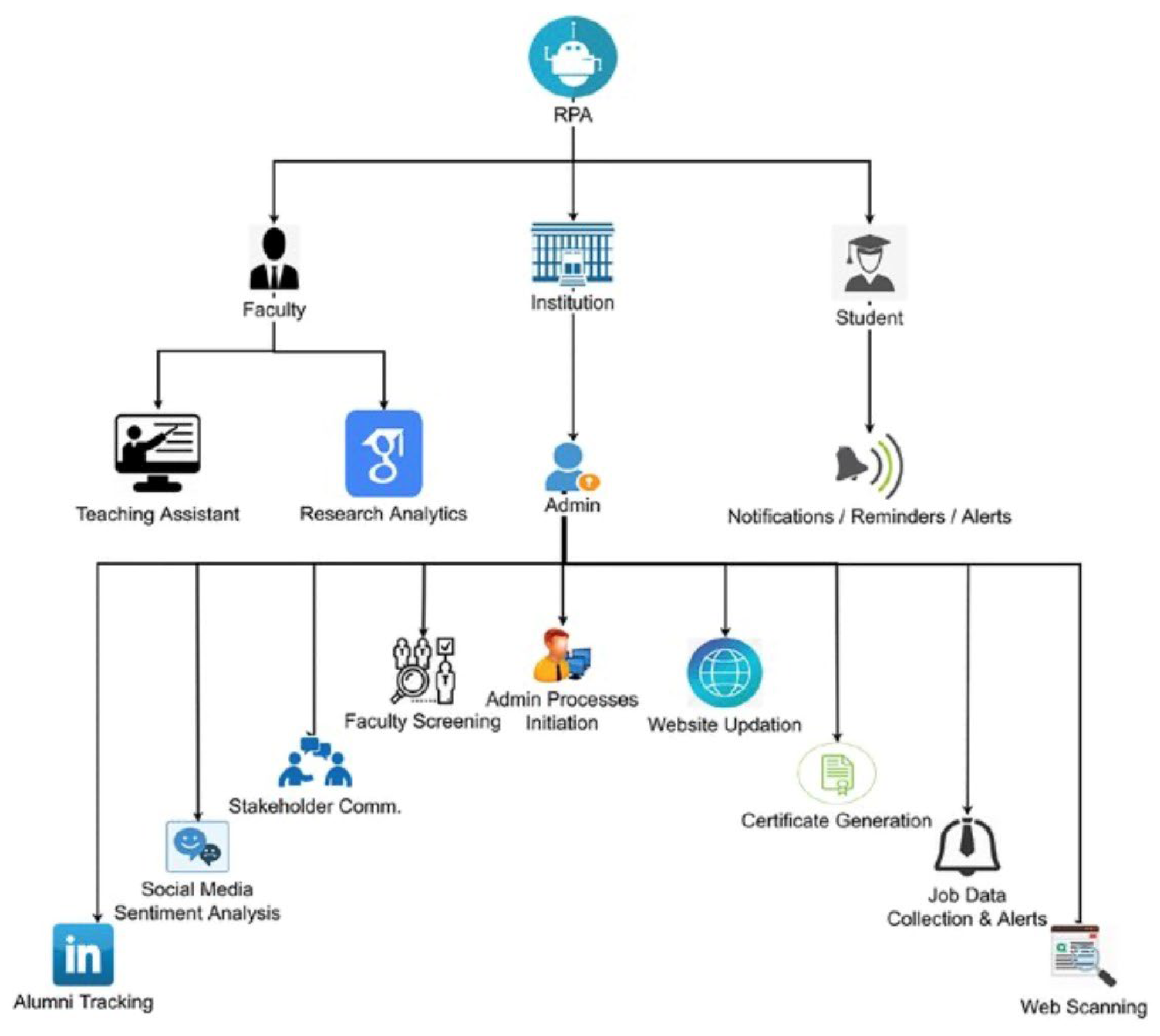

Figure 1.

RPA financial management working principle framework.

(1) RPA technology mainly suits structured data and process processing with clear rules. It cannot process unstructured data like free-form text, images, voice, handwritten documents, and other information[13]. . For example, traditional RPA systems usually only process structured invoice data in the financial field. If invoices are received in handwritten or complex formats, manual intervention may be required to transcribe and process them.

(2) RPA follows preset rules and logic and cannot cope with complex decisions and abnormal situations. For example, in the financial field, RPA usually handles reconciliation and reimbursement processes according to predefined rules and may need help to make proper judgments in exceptional cases, such as complex cost-sharing rules or non-standard contract terms.

(3) When RPA encounters business process changes, it must often be reconfigured and debugged. For example, when the menu position and field name change[14,15,16]. , RPA may fail due to the failure to find the expected user interface elements. Especially in the automation scenario of complex processes, such as changes in national tax policies that result in changes in calculation methods, RPA may need to be manually reconfigured.

(4) RPA is suitable for simple, repetitive, and regular processes and cannot be processed for processes involving multiple judgments, multi-step logical derivation, or requiring consideration of numerous complex conditions. For example, due to the complexity of the logic, it is difficult for RPA to predict the future cash flow or evaluate the potential financial risks by itself.

(5) RPA is not sufficiently responsive to unforeseen external factors. When faced with user interface changes, system upgrades, etc., especially in the face of constantly evolving system login authentication methods, such as difficult-to-recognize character verification codes, SMS verification codes, mobile app verification codes, fingerprint and iris recognition, the operation of traditional RPA may fail.

(6) RPA is limited in handling tasks requiring advanced human language understanding and emotion recognition. For example, in accepting financial counselling, when customers call to express strong dissatisfaction or complaints, although they can answer questions according to the preset script, they cannot understand customers' anger, anxiety, or satisfaction, nor can they make emotional feedback and decisions in real time[17]. .

The above limitations of RPA will bring about many problems, such as limited process adaptability, lack of complex decision-making ability, reduced system compatibility and stability, increased system maintenance costs, limited scalability and flexibility, etc. Therefore, the applicability of RPA technology should be carefully evaluated when designing process automation schemes, and the possibility of combining it with other advanced technologies should be fully considered.

2.4. Data privacy and security considerations

Data privacy and security are important issues that cannot be ignored while driving the transformation of financial enterprises to automated processing. Especially when large amounts of customer data and sensitive corporate information are involved, protecting data security and compliance with regulatory requirements is critical.

First, strict data protection measures must be implemented during automated processing to protect customer data from unauthorised access and disclosure. [18,19]. ]. Technically, encrypting data storage and transmission through encryption technology, limiting data access rights, and implementing multiple authentication and other measures can effectively prevent data leakage and abuse. In addition, a sound access control and audit mechanism is established to monitor and record data access activities and promptly detect and respond to potential security threats.

Second, financial companies must comply with relevant laws, regulations, and industry standards when implementing automated processing and develop and enforce best practices that meet compliance requirements. For example, it ensures the legality and transparency of data collection, processing, and storage per regulations such as the Personal Information Protection Act and GDPR[20]. . It also provides appropriate protection measures for the rights of data subjects, such as access, correction, and deletion. In addition, through regular compliance reviews and employee training, we ensure that all data processing activities comply with the latest regulations and privacy protection requirements.

By combining data protection technologies and compliance practices, financial firms can effectively address data privacy and security challenges while driving automation, ensuring that customer and corporate data is handled and protected safely and lawfully.

3. Process Automation System Architecture

Robotic Process Automation (RPA) is a technology that uses robotic software to simulate and perform repetitive, regular tasks humans perform on computers. These tasks typically include data entry, form filling, file transfer, email sending and receiving, etc.

The core technologies related to traditional RPA mainly include three aspects: the core basic technology related to automation, the technology related to data acquisition, and the related technology for decision judgment[21]. . Core underlying technologies related to automation include screen capture, mouse and keyboard simulation, email automation, interface integration with Windows and Office software, and workflow technology to control and manage the automatic delivery of documents across different systems. The technologies related to data acquisition include sensor data acquisition technology, web crawler technology, database query technology, OCR technology, and NLP technology. The relevant technologies for decision judgment include various business rule engines, knowledge base systems, data-based decision-making, and so on.

3.1. RPA System

The RPA editor is a companion development tool for designing, developing, debugging, and deploying robot scripts. RPA editor usually provides a visual control drag and edit function, automatic script recording function, automatic script hierarchical design function, workflow editor function, robot remote configuration function, and interface integration ability. [22]. An RPA operator is a robot that performs automated execution operations. RPA runner uses mouse and keyboard event simulation techniques, screen capture techniques, and workflow techniques described above to simulate human operations to complete complex business process operation activities. RPA controller refers to the management program for the whole life cycle of the robot, which is a supporting tool for operation and maintenance personnel to monitor, maintain, and manage the running state of the robot. The RPA controller provides a centralised control centre to monitor the operating status of multiple robots and provides remote maintenance and technical support. [23,24,25]. The controller has security management and control functions, automatic task assignment, queue management, and failure recovery functions.

Some vendors further divide the RPA system into a user interface layer, development and design layer, automation execution layer, task scheduling and management layer, data integration and processing layer, underlying technical support and infrastructure layer, and security and compliance component layer, but the core is still the above three components.

3.2. How RPA Works in the Financial Field

The reconciliation process in the financial field can significantly improve efficiency and accuracy. The following is a typical RPA financial reconciliation process:

1. Automatic data acquisition: RPA financial robots can automatically log in to various economic systems, banking systems, or other relevant data sources to obtain data that needs to be reconciled. This data may include bank account information, transaction records, invoices, bills, etc.

2. Data preprocessing: [26]. The RPA financial robot will clean, organise, classify, and format the acquired data according to preset rules for subsequent reconciliation operations.

3. Automatic reconciliation: [27]. According to preset reconciliation rules, the RPA financial robot will automatically check bank statements and internal accounts. This may include initial reconciling (comparing the closing balance on the bank statement with the bank balance on the company's internal books) and detail reconciling (checking the bank statement and the company's internal books one by one to check that each transaction is accurate).

4. Exception handling: In the reconciliation process, if the RPA [28,29,30,31]. financial robot finds any abnormal or inconsistent situation, such as unreached accounts, duplicate records, missing records, etc., it will mark these abnormal situations and generate corresponding reports or notices for further processing by financial personnel.

5. Difference analysis: If there are reconciliation differences, RPA financial robots can assist financial personnel in analysing and finding the reasons for the differences, such as accounting errors, bank processing lag, etc., and preparing the corresponding adjustment entries.

6. Current payment confirmation: The RPA financial robot can also assist financial personnel in verifying the accounts receivable and accounts payable of the enterprise and check the current statement with the customer to ensure the consistency of the accounts of the two sides.

Generate reports: [32]. According to the reconciliation results, the RPA financial robot can automatically generate detailed reconciliation reports, including reconciliation time, reconciliation objects, reconciliation content, existing differences, processing results, etc. These reports can be reviewed and confirmed by the finance staff.

3.3. RPA financial application advantages

The application of RPA in the financial field is the application of advanced technologies such as artificial intelligence and machine learning. There are many application scenarios. The following are some typical examples. First, regarding accounts receivable management, the RPA system forecasts the possibility and time of accounts receivable recovery by integrating CRM [33]. and ERP [34]. system data, combining customer credit ratings, historical payment records, industry trends, and macroeconomic indicators. When there is a late payment, the system can automatically send a reminder and adjust the lousy debt reserve according to the forecast results, reducing the uncertainty of the financial statements.

Regarding automated cash flow forecasting, RPA can integrate multiple financial data sources, such as bank statements, sales orders, purchase contracts, etc., and apply time series analysis or other forecasting models to predict future cash flows. In the face of uncertainties such as market changes and seasonal effects, RPA can quickly recalculate expected cash inflows and outflows to help decision-makers make capital arrangements and liquidity management in advance. [35]. Secondly, regarding intelligent cost accounting, factors such as raw material price fluctuations and exchange rate fluctuations in production cost estimation will lead to cost uncertainty. By capturing market price data in real-time, using complex event processing techniques to track material cost changes, and automatically updating product costing, RPA enables management to react quickly, adjust pricing strategies, or find alternative supply sources.

Regarding dynamic budget adjustment, in the budget preparation stage, RPA can simulate the financial performance under different business scenarios, such as slowing sales growth and rising costs, and help enterprises develop flexible budget plans through hypothesis analysis and sensitivity testing. In the implementation process, once the actual performance deviates from the budget target, the IPA can give real-time warnings and recommend adjustments to budget allocation to achieve optimal allocation of resources[36]. .

For example, by combining machine learning algorithms, RPA can enable more accurate cash flow predictions. Traditional cash flow forecasting models may be limited by static rules and historical data, and it is difficult to capture complex market changes and economic fluctuations. However, machine learning techniques are able to analyze large amounts of real-time data, identify potential market trends, and make dynamic adjustments based on these data to improve forecast accuracy and flexibility.

In addition, machine learning can also play an important role in cost calculation and budget adjustment. Faced with uncertainties such as fluctuations in raw material prices or changes in exchange rates, machine learning can capture market price data in real time and apply complex event processing techniques to optimize product costing. In this way, companies are able to react more quickly[37]. , adjust pricing strategies or find alternative supply channels to meet the challenges of market changes and economic fluctuations. The application of these machine learning algorithms not only expands the application scenarios of RPA in the field of finance, but also improves the intelligence level of automated systems, making them better able to adapt to complex business environments and changing market conditions.

There are also some typical solutions for RPA in response to changes in the system login verification code, which are implemented using intelligent technology[38,39]. . One is the use of OCR technology solutions. If the captcha is text-based, the RPA program can recognise and extract characters from the image by integrating OCR technology. When the verification code is refreshed, the OCR module will automatically capture and identify the new verification code image. The second is the use of image recognition and machine learning technology solutions. For complex or distorted captCHA, RPA can use deep learning and neural networks for image recognition and improve the recognition accuracy by training the model. If the captcha pattern changes frequently, the model must have some generalisation ability to adapt to the emerging style.

Conclusion

With the continuous development of AI technology, RPA is expected to combine more powerful AI technologies in the future, such as general AI technology represented by large models. RPA links AIGC, and the two interact to form a more advanced IPA technology, further improving the human-machine interaction capability of process automation technology. At the same time, the self-learning and self-optimization capabilities of RPA robots will be qualitatively improved, and they will be able to understand and process unstructured data better to optimise more complex business processes and meet the needs of diversified business scenarios. With the support of technologies such as large AI models, RPA will enhance understanding and learning capabilities, evolve into agents with greater autonomy, improve human-computer interaction capabilities, extend the life cycle of RPA, and significantly expand the scope of use in various industries. At the same time, technologies such as large models can also bring challenges such as accuracy, interpretability, data quality, team capabilities, computing costs, and data privacy security.

In conclusion, with the scalability and flexibility of the cloud, enterprises will be able to deploy and manage their process automation systems more efficiently. This will enable businesses to use the latest RPA and IPA technologies without investing in expensive in-house infrastructure. Using cloud-based solutions has two benefits for enterprises. On the one hand, enterprises can scale up or down as needed without additional hardware or infrastructure, which makes it easier for enterprises to respond to changes in business needs and make their operations more agile. On the other hand, the cost of ownership can be reduced, and by using cloud technology, enterprises can eliminate the upfront costs associated with purchasing and maintaining hardware and infrastructure, which helps reduce the overall cost of implementing RPA, making it easier for SMEs to adopt.

Beyond enhancing operational efficiency and process automation, artificial intelligence (AI) is revolutionising risk management within corporate finance. AI-powered algorithms are increasingly deployed to analyse vast datasets, enabling real-time identification of potential financial risks. By leveraging machine learning models, financial institutions can swiftly detect anomalies, predict market trends, and offer actionable insights for optimising risk management strategies. For instance, AI-driven systems can monitor market fluctuations, customer behaviors, and regulatory changes, providing proactive risk assessments and recommendations. This capability enhances decision-making agility and fortifies enterprises against emerging threats in an evolving economic landscape. As AI continues to evolve, its integration with robotic process automation (RPA) promises even greater sophistication in managing financial risks, ensuring businesses remain resilient and adaptive in the face of uncertainty.

Acknowledgments

At the end of this article, I would like to express my sincere thanks to authors such as Han, Wang and others for their research. Their article [1]. "ROBO-ADVISORS: REVOLUTIONIZING WEALTH MANAGEMENT THROUGH THE INTEGRATION OF BIG DATA AND ARTIFICIAL INTELLIGENCE IN ALGORITHMIC TRADING "STRATEGIES" not only provides valuable inspiration for this article, but also delves into the integration of artificial intelligence in algorithmic trading strategies and its important applications in wealth management. In particular, their research presents the concept of Robo-Advisors and analyzes in detail their impact on financial risk management and investment strategy optimization. Through reading the articles of Han, Wang et al., I have a better understanding of the potential and value of intelligent investment technology in the modern financial field. We thank them again for their outstanding contributions and look forward to further discussions in this important field in the future. in addition, thanks to Bai, Xinzhu, Wei Jiang and Jiahao Xu for their research [7]. "Development Trends in AI-Based Financial Risk Monitoring Technologies". Their in-depth analysis and insights provide valuable insights into the trends in AI-based financial risk monitoring technology for this article. In particular, their research explores in detail recent advances in the application of AI in the financial sector, supporting my discussion of AI technology in financial risk management in this article. By reading the work of Bai, Xinzhu, Wei Jiang and Jiahao Xu, I was able to further understand the application prospects and challenges of AI technology in modern financial management. Thank you again for their excellent research and look forward to continuing to draw inspiration and insights from their work in the future.

References

- Han, Wang, et al. "ROBO-ADVISORS: REVOLUTIONIZING WEALTH MANAGEMENT THROUGH THE INTEGRATION OF BIG DATA AND ARTIFICIAL INTELLIGENCE IN ALGORITHMIC TRADING STRATEGIES." Journal of Knowledge Learning and Science Technology ISSN: 2959-6386 (online) 3.3 (2024): 33-45. [CrossRef]

- Xu, Jiahao, et al. "AI-BASED RISK PREDICTION AND MONITORING IN FINANCIAL FUTURES AND SECURITIES MARKETS." The 13th International scientific and practical conference “Information and innovative technologies in the development of society”(April 02–05, 2024) Athens, Greece. International Science Group. 2024. 321 p.. 2024.

- Wang, Yong, et al. "Machine Learning-Based Facial Recognition for Financial Fraud Prevention." Journal of Computer Technology and Applied Mathematics 1.1 (2024): 77-84. [CrossRef]

- Li, H., Wang, X., Feng, Y., Qi, Y., & Tian, J. (2024). Driving Intelligent IoT Monitoring and Control through Cloud Computing and Machine Learning.arXiv preprint. arXiv:2403.18100.

- Qi, Y., Wang, X., Li, H., & Tian, J. (2024). Leveraging Federated Learning and Edge Computing for Recommendation Systems within Cloud Computing Networks. arXiv preprint. arXiv:2403.03165.

- Song, Jintong, et al. "LSTM-Based Deep Learning Model for Financial Market Stock Price Prediction." Journal of Economic Theory and Business Management 1.2 (2024): 43-50. [CrossRef]

- Bai, Xinzhu, Wei Jiang, and Jiahao Xu. "Development Trends in AI-Based Financial Risk Monitoring Technologies." Journal of Economic Theory and Business Management 1.2 (2024): 58-63. [CrossRef]

- Qi, Y., Feng, Y., Tian, J., Wang, X., & Li, H. (2024). Application of AI-based Data Analysis and Processing Technology in Process Industry. Journal of Computer Technology and Applied Mathematics,1(1), 54-62. [CrossRef]

- Tian, J., Qi, Y., Li, H., Feng, Y., & Wang, X. (2024). Deep Learning Algorithms Based on Computer Vision Technology and Large-Scale Image Data. Journal of Computer Technology and Applied Mathematics,1(1), 109-115. [CrossRef]

- Qian, K., Fan, C., Li, Z., Zhou, H., & Ding, W. (2024). Implementation of Artificial Intelligence in Investment Decision-making in the Chinese A-share Market. Journal of Economic Theory and Business Management, 1(2), 36-42. [CrossRef]

- Li, Zihan, et al. "Robot Navigation and Map Construction Based on SLAM Technology." (2024). [CrossRef]

- Fan, C., Ding, W., Qian, K., Tan, H., & Li, Z. (2024). Cueing Flight Object Trajectory and Safety Prediction Based on SLAM Technology. Journal of Theory and Practice of Engineering Science, 4(05), 1-8. [CrossRef]

- Fan, C., Li, Z., Ding, W., Zhou, H., & Qian, K. Integrating Artificial Intelligence with SLAM Technology for Robotic Navigation and Localization in Unknown Environments.

- Wang, X., Tian, J., Qi, Y., Li, H., & Feng, Y. (2024). Short-Term Passenger Flow Prediction for Urban Rail Transit Based on Machine Learning. Journal of Computer Technology and Applied Mathematics,1(1), 63-69.

- Jiang, W., Yang, T., Li, A., Lin, Y., & Bai, X. (2024). The Application of Generative Artificial Intelligence in Virtual Financial Advisor and Capital Market Analysis. Academic Journal of Sociology and Management, 2(3), 40-46. [CrossRef]

- Feng, Y., Li, H., Wang, X., Tian, J., & Qi, Y. (2024). Application of Machine Learning Decision Tree Algorithm Based on Big Data in Intelligent Procurement. [CrossRef]

- Tian, J., Li, H., Qi, Y., Wang, X., & Feng, Y. Intelligent Medical Detection and Diagnosis Assisted by Deep Learning.

- Ding, W., Zhou, H., Tan, H., Li, Z., & Fan, C. (2024). Automated Compatibility Testing Method for Distributed Software Systems in Cloud Computing. [CrossRef]

- Lin, Tinglan, and Jin Cao. "Touch Interactive System Design with Intelligent Vase of Psychotherapy for Alzheimer’s Disease." Designs 4, no. 3 (2020): 28. [CrossRef]

- Ding, W., Tan, H., Zhou, H., Li, Z., & Fan, C. Immediate Traffic Flow Monitoring and Management Based on Multimodal Data in Cloud Computing. [CrossRef]

- Li, Huixiang, et al. "AI Face Recognition and Processing Technology Based on GPU Computing." Journal of Theory and Practice of Engineering Science 4.05 (2024): 9-16. [CrossRef]

- Yuan, J., Lin, Y., Shi, Y., Yang, T., & Li, A. (2024). Applications of Artificial Intelligence Generative Adversarial Techniques in the Financial Sector. Academic Journal of Sociology and Management, 2(3), 59-66. [CrossRef]

- Lin, Y., Li, A., Li, H., Shi, Y., & Zhan, X. (2024). GPU-Optimized Image Processing and Generation Based on Deep Learning and Computer Vision. Journal of Artificial Intelligence General science (JAIGS) ISSN: 3006-4023, 5(1), 39-49. [CrossRef]

- Xu, J., Wang, H., Zhong, Y., Qin, L., & Cheng, Q. (2024). Predict and Optimize Financial Services Risk Using AI-driven Technology. Academic Journal of Science and Technology, 10(1), 299-304. [CrossRef]

- Yang, L., Wang, H., Zheng, J., Duan, X., & Cheng, Q. (2024). Research and Application of Visual Object Recognition System Based on Deep Learning and Neural Morphological Computation. International Journal of Computer Science and Information Technology, 2(1), 10-17. [CrossRef]

- Zhan, T.; Shi, C.; Shi, Y.; Li, H.; Lin, Y. Optimization techniques for sentiment analysis based on LLM (GPT-3). Appl. Comput. Eng. 2024, 67, 41–47. [CrossRef]

- Huo, Mingda, et al. "JPX Tokyo Stock Exchange Prediction with LightGBM." Proceedings of the 2nd International Conference on Bigdata Blockchain and Economy Management, ICBBEM 2023, May 19–21, 2023, Hangzhou, China. 2023.

- Wang, H., Bao, Q., Shui, Z., Li, L., & Ji, H. (2024). A Novel Approach to Credit Card Security with Generative Adversarial Networks and Security Assessment. [CrossRef]

- Xu, X., Xu, Z., Ling, Z., Jin, Z., & Du, S. (2024). Emerging Synergies Between Large Language Models and Machine Learning in Ecommerce Recommendations. arXiv preprint. arXiv:2403.02760.

- Liang, P.; Song, B.; Zhan, X.; Chen, Z.; Yuan, J. Automating the training and deployment of models in MLOps by integrating systems with machine learning. Appl. Comput. Eng. 2024, 67, 1–7. [CrossRef]

- Cheng, Qishuo, et al. "Monetary Policy and Wealth Growth: AI-Enhanced Analysis of Dual Equilibrium in Product and Money Markets within Central and Commercial Banking." Journal of Computer Technology and Applied Mathematics 1.1 (2024): 85-92. [CrossRef]

- Shi, Y., Li, L., Li, H., Li, A., & Lin, Y. (2024). Aspect-Level Sentiment Analysis of Customer Reviews Based on Neural Multi-task Learning. Journal of Theory and Practice of Engineering Science, 4(04), 1-8. [CrossRef]

- Shi, Y.; Yuan, J.; Yang, P.; Wang, Y.; Chen, Z. Implementing intelligent predictive models for patient disease risk in cloud data warehousing. Appl. Comput. Eng. 2024, 67, 34–40. [CrossRef]

- Zhan, T.; Shi, C.; Shi, Y.; Li, H.; Lin, Y. Optimization techniques for sentiment analysis based on LLM (GPT-3). Appl. Comput. Eng. 2024, 67, 41–47. [CrossRef]

- Qin, L., Zhong, Y., Wang, H., Cheng, Q., & Xu, J. (2024). Machine Learning-Driven Digital Identity Verification for Fraud Prevention in Digital Payment Technologies. [CrossRef]

- Wu, B.; Gong, Y.; Zheng, H.; Zhang, Y.; Huang, J.; Xu, J. Enterprise cloud resource optimization and management based on cloud operations. Appl. Comput. Eng. 2024, 67, 8–14. [CrossRef]

- Zhong, Y., Cheng, Q., Qin, L., Xu, J., & Wang, H. (2024). Hybrid Deep Learning for AI-Based Financial Time Series Prediction. Journal of Economic Theory and Business Management, 1(2), 27-35. [CrossRef]

- Zhan, X.; Shi, C.; Li, L.; Xu, K.; Zheng, H. Aspect category sentiment analysis based on multiple attention mechanisms and pre-trained models. Appl. Comput. Eng. 2024, 71, 21–26. [CrossRef]

- Xiang, A., Qi, Z., Wang, H., Yang, Q., & Ma, D. (2024). A Multimodal Fusion Network For Student Emotion Recognition Based on Transformer and Tensor Product. arXiv preprint. arXiv:2403.08511.

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Copyright: This open access article is published under a Creative Commons CC BY 4.0 license, which permit the free download, distribution, and reuse, provided that the author and preprint are cited in any reuse.