Submitted:

03 July 2024

Posted:

06 July 2024

You are already at the latest version

Abstract

The apparel manufacturing industry's growth over recent decades has heightened concerns about its environmental impact, including resource use, energy and water consumption, waste generation, chemical disposal, and greenhouse gas emissions. Companies have responded by initiating environmental actions and enhancing legitimacy through environmental disclosures. This study examines the nature of these disclosures among Sri Lankan apparel manufacturing companies to understand corporate priorities and identify areas for reporting improvement. Publicly available data from web pages and standalone reports were analyzed using content analysis. Findings indicate that only 23% of registered companies disclose environmental performance, while 60% of key industry players provide higher levels of transparency. Disclosures cover greenhouse gas emissions, carbon footprint, renewable energy, energy and water use, waste management, biodiversity, and environmental certifications. Key players offer detailed information on specific areas like carbon footprint, energy use, and waste management. This study highlights the need for more comprehensive and transparent environmental reporting to promote sustainable practices within the Sri Lankan apparel industry.

Keywords:

Environmental Sustainability

; Disclosure

; Apparel Manufacturing

; Sri Lanka

1. Introduction

A growing number of concerns have in place regarding the environmental issues of the apparel manufacturing industry with the rapid growth of the industry such as, use of hazardous chemicals, extensive use of non-renewable resources, generation of waste [1,2,3]. According to the global data in terms of use of hazardous chemicals and materials apparel industry is second dirtiest industry only to the oil. And it consumes half of the cotton production of the world to produce fabrics and generate a bulk of waste [4]. It uses considerable amount of water and generates waste water [5]. The industry also significantly contributes to the carbon emission by using energy for the operations approximately 8% - 10% of global carbon footprint [3,6,7]. The role of organizations as a solution provider is important since they are the drive of economic development owning the resources and capacity to implement the sustainable solutions. Organizations have responsibility on their shoulders to ensure a sustainable world [8,9,10,11].

Contrasting to recent past, the partners in fashion supply chain are required to address the concerns of customers regarding environmental impacts on different areas such as energy, waste, water, pollution and high level of carbon and chemical footprints behind the manufacturing process of their favorite jeans or t-shirt. Ethical consumerism and ethical trading are becoming much popular along with these issues [12,13,14]. These rising concerns are a significant factor influential to ensure both sustainable production and consumption in the long run. Responding to these global concerns, Sri Lankan apparel manufacturing organizations are also engaging in different initiatives to reduce their carbon footprint to zero by 2025 via efficient management of energy, water and waste in manufacturing process [15].

Conversely, implementing environmental sustainability initiatives in apparel manufacturing sector associated with challenges in broader sense. First, absence of a clear and commonly agreed definition for sustainability in the sector. Second the apparel industry supply chain is extremely complex as the supply chain for any large apparel brand often consists of a large number of suppliers, manufacturers, distributors, and retailers. Third there is an increasing trend in apparel industry for moving towards a fast fashion business model [2].

Despite these challenges, companies have put forward diverse actions responding to these environmental concerns and those initiatives have created a competitive advantage for the companies by branding them as environmentally friendly in the global market. Sri Lanka as an assembling country is facing ever increasing competition from the giant players in global market such as China, European Union and India, who own 66.4% of the global apparel market while Sri Lanka owned 1.2%. However, Sri Lanka has created a unique global niche market for apparels with its innovative and environmentally sustainable strategies to design, produce and deliver the apparels. Today, “Made in Sri Lanka” is something more than just apparel in global market due to its branding as environmentally friendly. With approximately USD 4.9 billion of export income and 1.2% of a global market share in year 2023, it has been progressing in branding Sri Lanka as an environmentally sustainable and ethical production destination. Long-term partnership of Sri Lanka with leading brands such as Nike, M&S, Victoria’s Secret, Gap, Tommy Hilfiger and Ralph Lauren have confirmed the country’s capability to cater to the rising mixture of demands in global fashion market [15].

Measuring sustainability performances is important for a proper evaluation of the company’s environmental performance thereby to formulate future goals. Gathering information on environmental performances facilitates the steps taken for controlling and this ensures that the organization will be able to achieve eco-efficiency and sustainability throughout the business process [3,16,17]. Generally large companies tend to use a good number of environmental Key Performance Indicators (KPI) but still they did not fully cover the dimensions suggested by Global Reporting Initiative (GRI) which provide guidelines in reporting environmental performances. Measuring environmental performances using KPIs is lack in small scale companies compared with larger companies mainly because of financial reasons. This put forward that impact and benefits of environmental sustainability are not much clear to organizations.

Companies usually present the information regarding their environmental performances on the areas of energy, water, waste, use of recycled materials, organic materials usage, chemical substances and etc. [16,18]. Also, in many cases organizations start their journey in sustainability focusing on minor actions that can be taken such as matters in energy use or reduction of waste. However, in recent past, environmental indicators are on the rise where organizations concern about matters such as waste production per unit produced [19], emission of CO2 per ton of production output [20,21] or land usage in hectares [22,23]. The way companies are interacting with the natural environment is increasingly considered as an important aspect in corporate agenda. The image that company holds in the eyes of the stakeholders as it would not produce any harmful impact on environment or are not associated with any environmental risk is critical for the company’s success [24]. Environmental sustainability reporting is one way of communicating this information to the stakeholders. If sustainability reporting can convince as the organization as an environmentally friendly before the stakeholders it will reduce the risk and the continuation of the company’s operations [25,26,27].

Global Reporting Initiative as the world’s most widely used corporate sustainability reporting guidelines explained,

“Sustainability reporting helps organizations to set goals, measure performance, and manage change in order to make their operations more sustainable. A sustainability report conveys disclosures on an organization’s impacts (be they positive or negative) on the environment, society and the economy” [28] (p. 3).

Sustainability reporting shares the information about the initiatives and includes both qualitative and quantitative information to the public via different media often through web sites, stand-alone reports, annual reports and integrated reports with financial reports. Organizations communicate their progress on sustainability initiatives through the use of indicators in economic, environmental, and social performance. Moreover, companies disclose their environmental performances via different mechanisms. Global platforms and guidelines are available such as Carbon Disclosure Project (CDP), Sustainable Disclosure Database (SDD), Sustainable Apparel Coalition (SAC) – HIGG Index, United Nations Global Compact – UNGC, Global Reporting Initiative (GRI) for companies to share and benchmark their performances regarding the broader area of sustainability. The Ministry of Mahaweli Development and Environment has introduced the National Green Reporting System (NGRS) specifically for Sri Lanka for reporting sustainability performances. NGRS has been developed adopting the GRI guidelines into Sri Lankan context without deviating the underlying fundamentals.

Though there are plenty of mechanisms available for reporting it is interesting to note that very less number of Sri Lankan companies were participating reporting their environmental performances in global platforms. Nevertheless, the topic of sustainability reporting in Sri Lanka receives relatively less attention in research compared to other parts of the world. Sustainability reporting is not mandatory in Sri Lanka, as with many other countries in the world, thus it is likely that voluntary sustainability reporting by Sri Lankan companies may show structural diversity and disclosures may vary from low to high levels.

In contrast, the question raise that the environmental sustainability initiatives might have been implemented by apparel manufacturing organizations as a superficial and misleading adaption which is called as “Green washing” rather aiming at the end result of positive effect to reduce the impact [19]. As well it is argued that these actions might be measured and disclosed to the public to create an affirmative impression about the organization’s activities but without any association of real changes in operations which can be called as “Symbolism” rather communicating about how the operational changes have impacted which are more reliable with the expectations of the society [25,26]. Accuracy of the claims of reporting is questionable due to lack of standardization, verification, and the voluntary nature of sustainability disclosures [29,30]. Previous studies have failed to provide a global view in sustainability reporting as they were often based on specific regions or country-specific [31]. Few studies are currently available which explore the nature of sustainability reporting specifically in environmental performances of apparel manufacturing industry in Sri Lanka [32,33,34]. And this will be the very first study to cover the whole apparel manufacturing industry in Sri Lanka to examine the environmental sustainability reporting. Given the fact, it is an important need to examine the nature of the disclosures in environmental performances for better understanding of the priorities of companies and to where reporting may possibly be improved. Therefore, this paper investigates the nature and the level of public disclosure of environmental performances of the apparel manufacturing companies in Sri Lanka.

2. Materials and Methods

2.1. Study Approach

The study focusing on examined public disclosures of environmental performances of apparel manufacturing companies in Sri Lanka. The recent period of the disclosures or recent issue of the stand-alone sustainability reports was considered.

2.2. Selection of Sample

Apparel manufacturing can be classified into few key areas as manufacturing textiles, garments, and accessories etc. The companies who manufacture wearable apparel were considered as the population of the study. The name list of registered companies in the category of “Apparels” was extracted from the Export Development Board web page as it was the most reliable information available to obtain a complete list of apparel manufacturing companies in Sri Lanka. The total number of companies was 226 however it includes many different types of companies which is not directly linked with manufacturing wearable apparels. Therefore, 68% the companies (153) who produce wearable apparels were selected after careful analysis from the total list.

2.3. Data Collection

Key environmental performances disclosures of selected companies were identified through the preliminary investigation. And the disclosed environmental performances areas; GHG emissions, waste, water, chemical usage and any other relevant environmental performances information was extracted from the relevant company web page, latest standalone sustainability reports issued by the companies, and global reporting information were extracted from the Communication on Progress (COP) reports submitted to United Nations Global Compact (UNGC) and Carbon Disclosure Project (CDP) web page as secondary sources to identify the level and the nature of disclosures in environmental performances. Extraction of data from the web sites was conducted accessing the web pages during the period of January to April 2024. The available COP reports were downloaded from the UNGC web page through https://www.unglobalcompact.org/.

2.4. Data Analysis and Presentation

First, content analysis was performed to analyze the nature of public disclosures of environmental performances utilizing the information from relevant web pages, stand-alone reports. The publicly available information of all companies was extracted and detail analysis was conducted to examine the nature of the public disclosures of environmental performances of apparel manufacturing companies in Sri Lanka. Frequency tables were developed based on the information extracted to calculate the reporting frequencies and graphs were used to show the results of the findings as appropriate.

3. Results

3.1. Industry Categorization of Companies

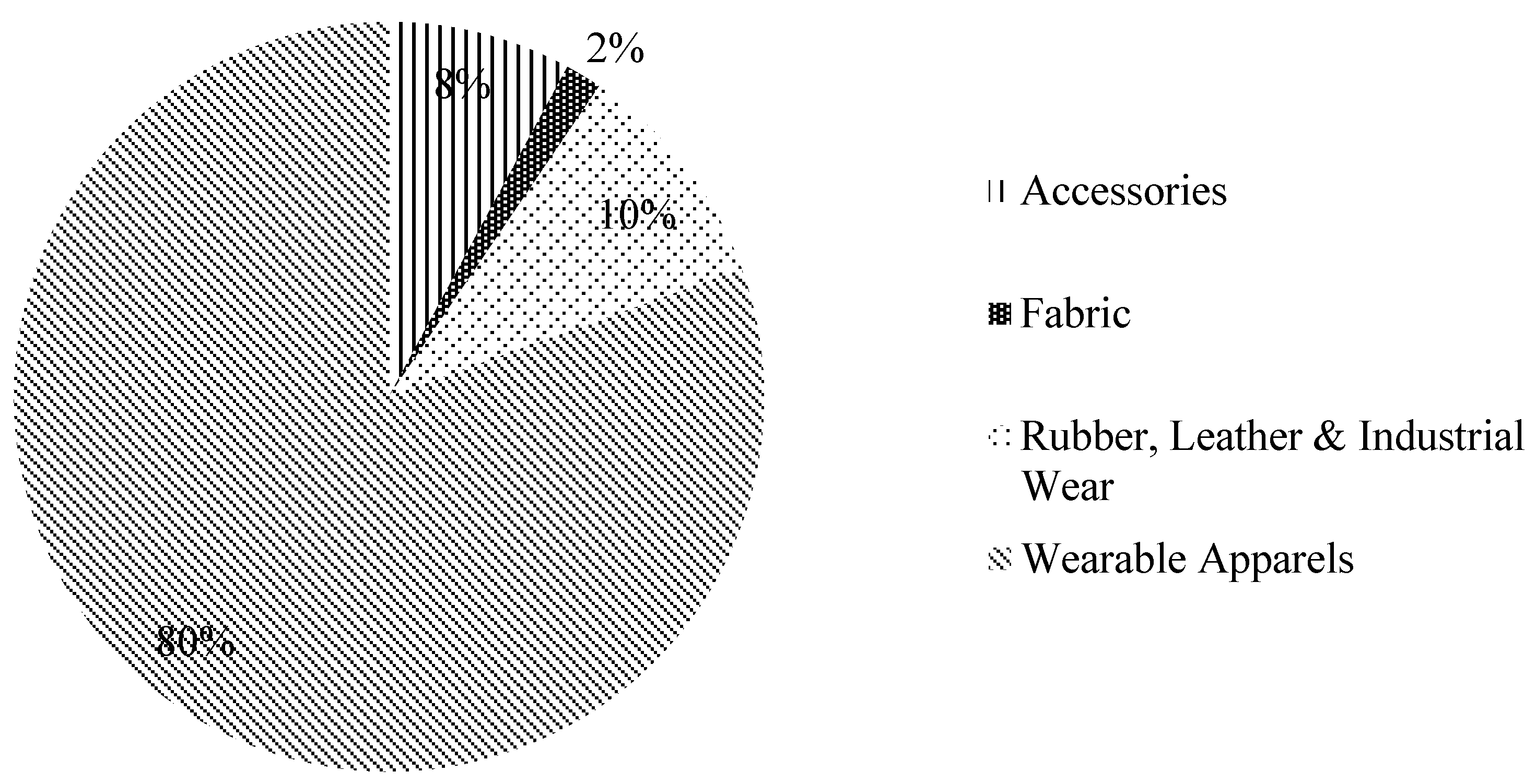

Relevant information of the companies registered under the Export Development Board [EDB] in Sri Lanka were extracted from the web. The total number of companies registered in EDB is 226. The categorization of the companies based on their operation is shown in Figure 1.

36 companies were identified which cannot be placed into either category as they are not directly relevant to the industry (Ex: Retail, Wood Items, Logistics, etc) or sufficient information was not available for a proper identification of the category. Hence, those have been removed from the analysis. 153 companies belong to the category of manufacturing wearable cloth which accounts for 80%. The rest of 37 companies were identified in manufacturing of accessories (8%), Manufacturing of fabric (2%) and Rubber, Leather & Industrial Wear (10%). Therefore, study revealed that majority of the companies in apparel manufacturing industry in Sri Lanka engages in producing wearable clothes. This finding is in line with the global classification of the apparel industry where Sri Lanka has been identified as an assembly country [35,36].

3.2. Availability of Public Disclosures of Environmental Performances of Apparel Manufacturing Companies

The information availability of the relevant web pages of the company were considered as the initial stage to analyze the availability of public disclosures of environmental performances due to the fact that web page is a basic media that almost any organization is uses to reach to the general public in today’s digitalizing society. Out of the study sample only 62% companies have a web page and only 64% of those web sites were in active status.

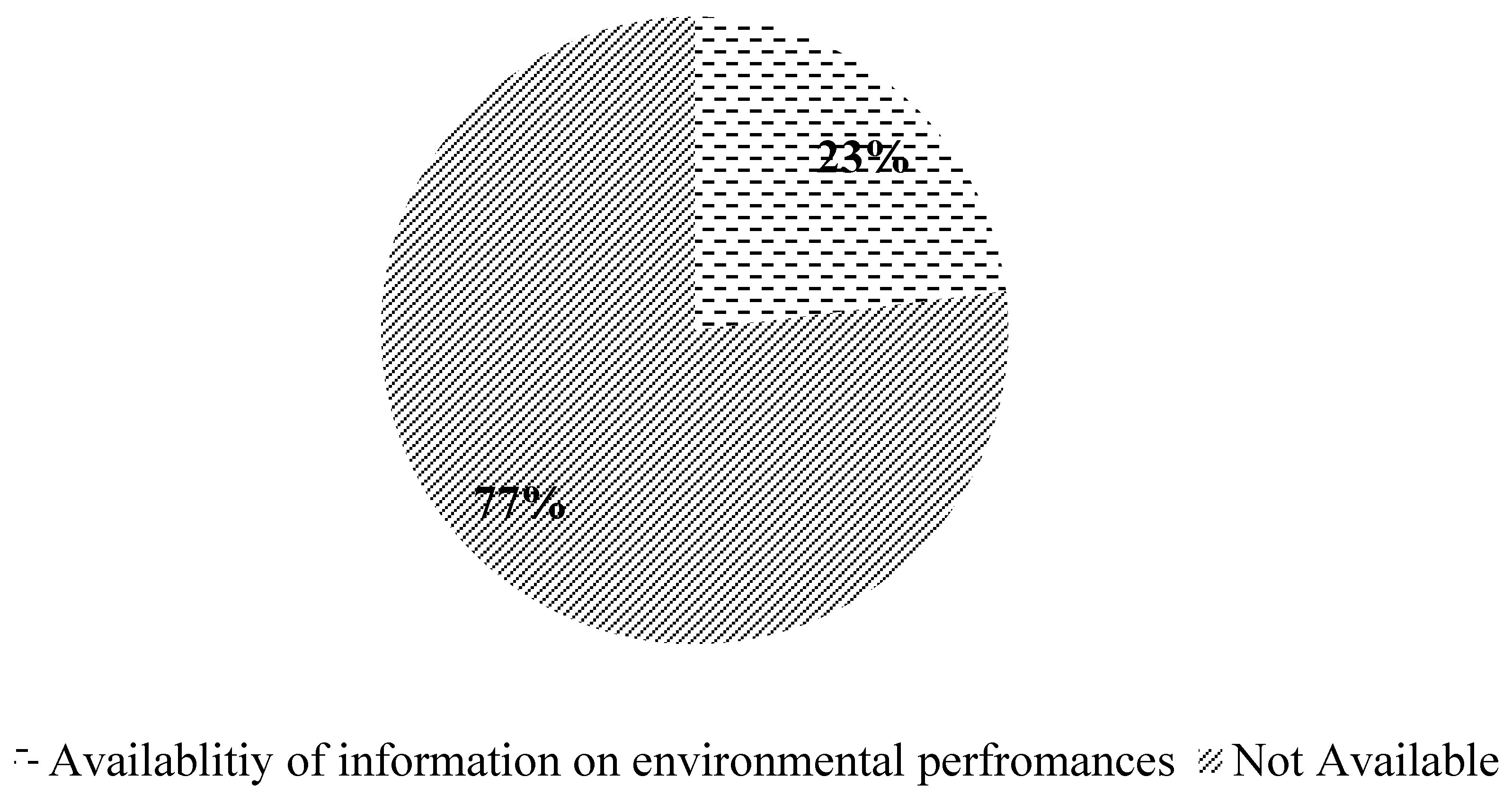

Apart from the web page the SDD database, Stand-alone sustainability reports and any other means of information that was publicly available were considered. The following Figure 2 shows the availability of public disclosures regarding any environmental related performances information of the apparel manufacturing companies.

The availability of the environmental performance related information was in a minimal level which accounts only for 23%. However, it is important to note that this availability includes any kind of information regarding the environmental performances of the company which was not adequately presented any detail information. The 77% of the rest do not report any kind of information regarding their environmental performances in public domains.

3.3. Disclosing Areas of Environmental Performances of the Companies

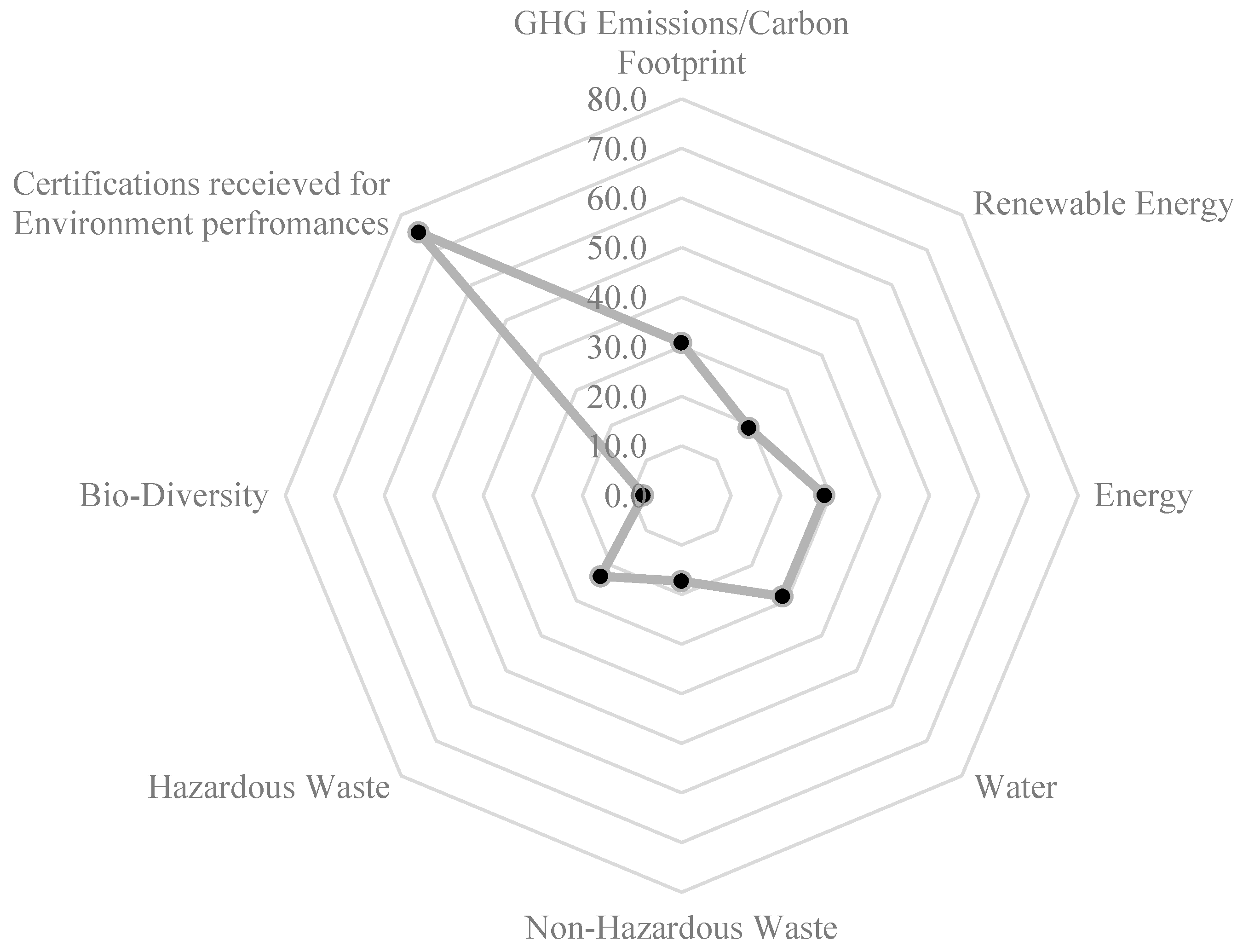

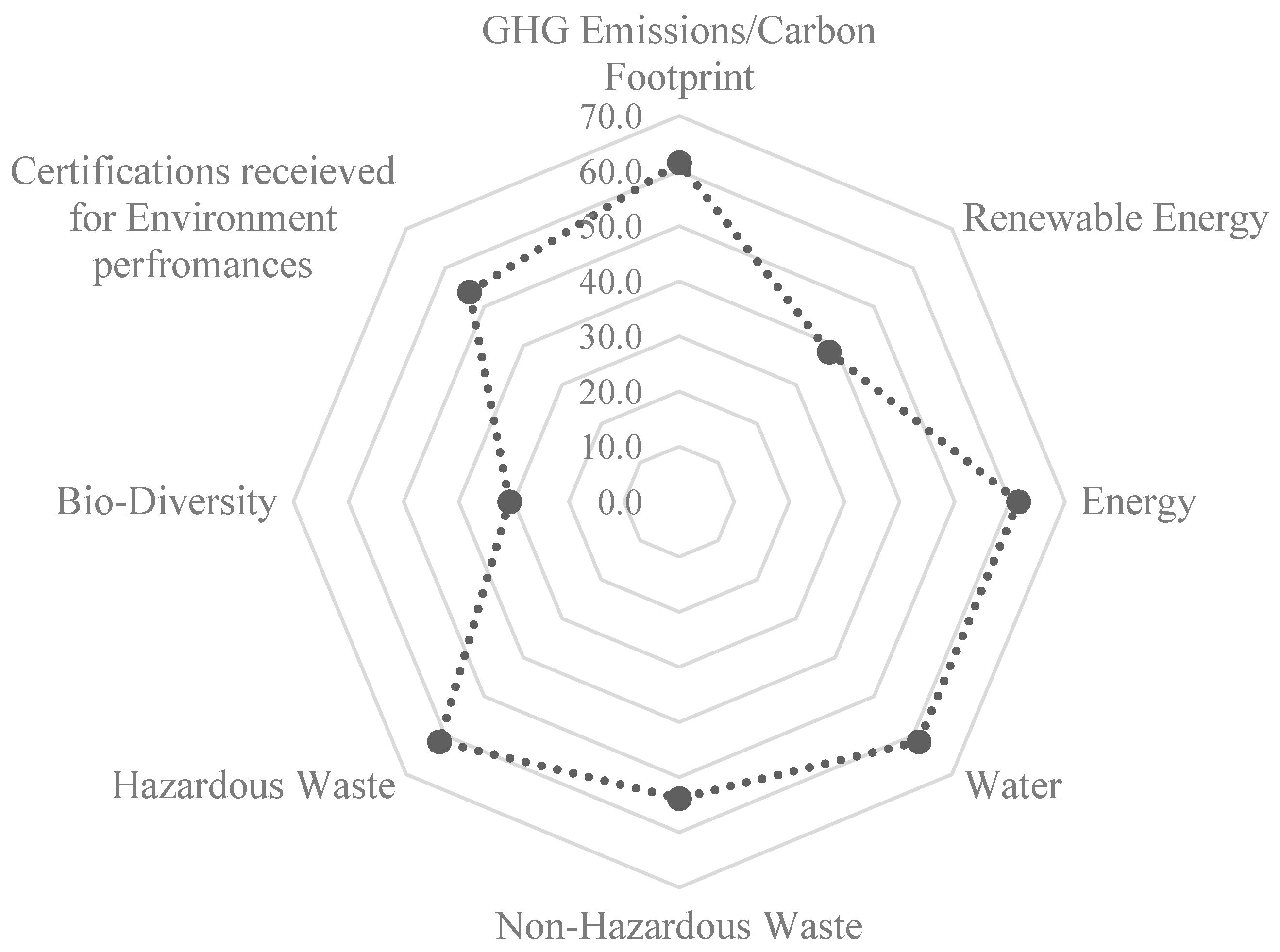

The disclosed information about the environmental performances were pooled into eight different areas: GHG Emissions/Carbon Footprint, Renewable Energy, Energy, Water, Non-Hazardous Waste, Hazardous Waste, Bio-Diversity, and Certifications received for Environmental/sustainability performances. These areas were decided based on the GRI indicators. Figure 3 illustrate the environment performance reporting areas with their strength.

Many companies disclosed their certifications received for different environmental/sustainability performances which represented the highest reporting area. This consists 27 different certifications obtained by the apparel manufacturing companies. The Table 1 below depicts the detail illustration of the certifications of apparel manufacturing companies.

Even though Carbon Footprint (GHG Emission) was a main area of the environmental performances yet the public disclosure of the GHG emissions of the companies was very low where only 30.8% companies have reported about CFP. However, out of that 25% of the sample has presented detail information regarding their CFP with numerical facts and figures, actions taken on CFP while the other 5.8% just mentioned that they concern about the CFP without any specific detail regarding CFP. Interestingly when looking at the ownership of the companies it was identified that these 25% of the sample of companies were owned by three groups of companies which holds a larger market share in the Sri Lankan apparel manufacturing industry at present.

3.4. Environmental performances information disclosure of key players of the apparel manufacturing industry

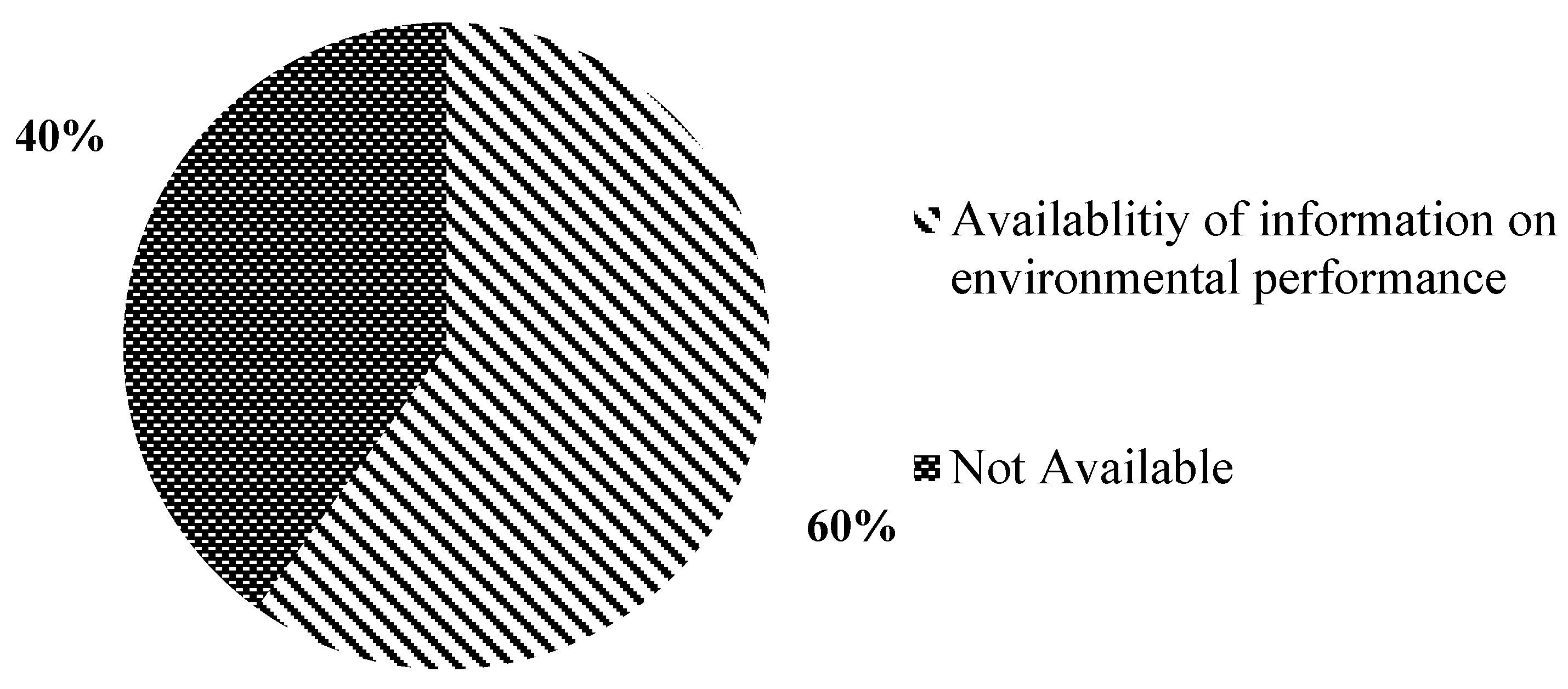

The EDB has listed thirteen apparel manufacturing companies as key players in the latest industry capability report in 2023. The following Figure 4 represents the availability of public disclosures in environmental performances of those key players.

Majority of the companies among key players report their environmental performances information to the public which accounts for 60% of the sample. Thus, it was a good indicator that the public disclosures of environmental performances of the apparel manufacturing industry is in a good level since these key players owns a larger market share in the total apparel manufacturing industry in Sri Lanka.

In addition to availability of the public disclosures in environmental performances, the same analysis was conducted to identify the reporting areas with their strengths of the key players in the apparel manufacturing industry and the results presented in the Figure 5 below.

This analysis (Figure 5) have revealed differing results in how key industry players are reporting their environmental sustainability performances to the public compared to the previous analysis (Figure 3) of the environmental sustainability performances reporting of all apparel manufacturing companies in the industry. The highest reporting areas were identified as GHG Emission (Carbon Footprint), Energy, Water and Hazardous Waste with equal strength and the second highest categories were Non-Hazardous waste, and Certifications received for environmental performances. The least reporting area in this category was Bio-Diversity. Carbon Footprint (GHG Emission) was a prominent area in public disclosures among the key players of the industry.

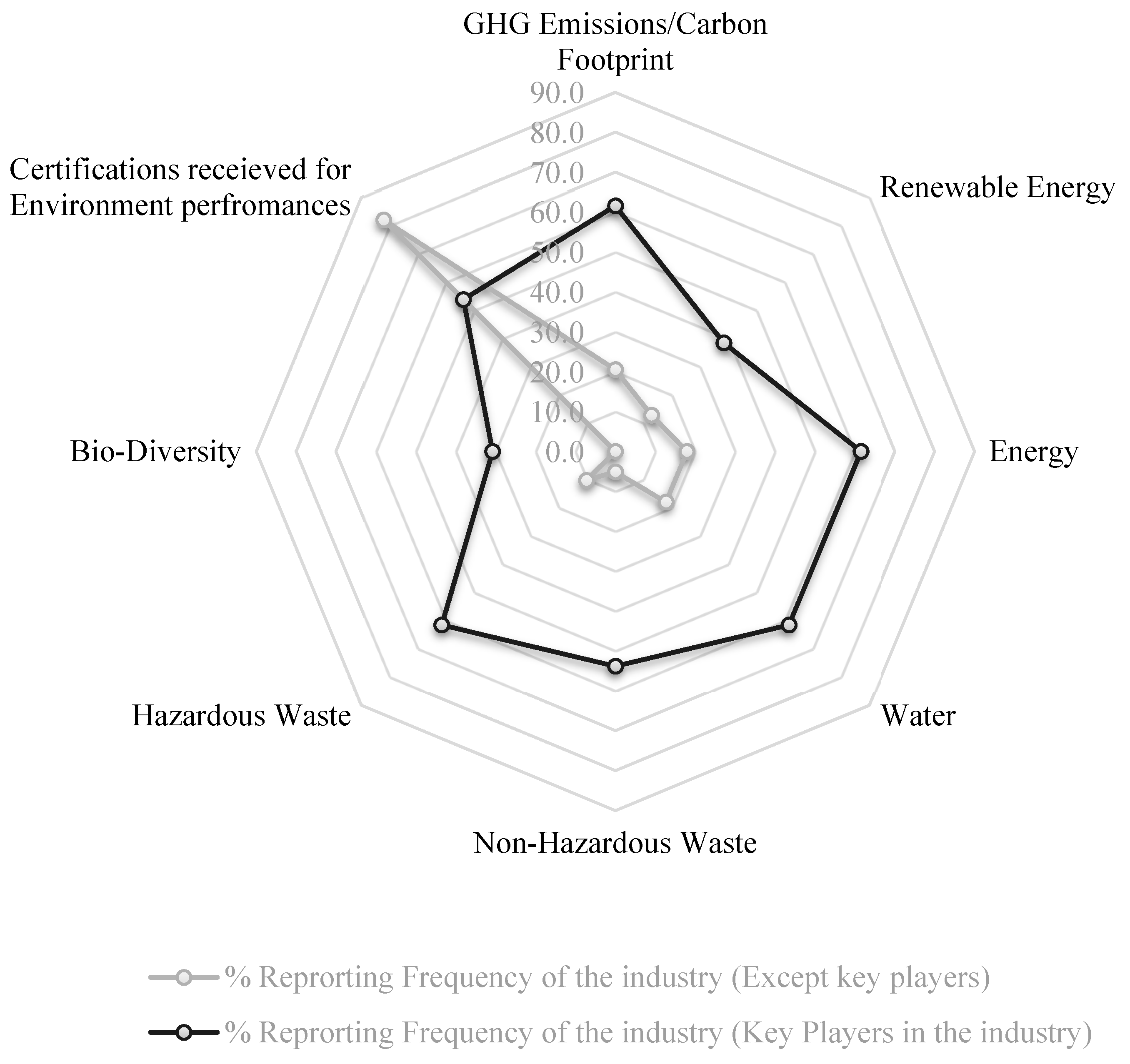

3.5. Comparison of the Public Disclosures of Environmental Performances in the Industry

The percentage comparison of public disclosures of environmental performance between the key players in the industry and the rest of the companies was presented in Figure 6 below. All reporting areas were high in the industry key players except the certifications received for environmental performance.

4. Discussion

The findings from this study highlight several important trends and gaps. The overall availability of environmental performance information is quite limited, with only 23% of companies disclosing any such information. This lack of transparency is concerning, as it reflects a broader issue within the industry regarding inadequate environmental reporting. A significant 77% of companies do not provide any environmental performance data in public domains, which restricts stakeholders' ability to assess and compare the environmental impacts and sustainability initiatives of these companies.

One positive aspect identified is the reporting of certifications received for environmental and sustainability performances. This area represents the highest reporting category, with 27 different certifications documented by the apparel manufacturing companies. This suggests that while general environmental performance data may be lacking, companies still strive to achieve and showcase third-party validation of their efforts. Certifications can serve as a useful benchmark for sustainability practices, providing some level of assurance to stakeholders about the companies' environmental responsibility. Certifications and third-party validations are commonly used by companies to enhance their credibility and demonstrate a commitment to sustainability [37].

Carbon Footprint (GHG Emission) reporting is another critical area of environmental performance. However, the public disclosure of GHG emissions is significantly low, with only 30.8% of companies reporting on this metric. Furthermore, detailed information about Carbon Footprints, including numerical data and actions taken, is presented by just 25% of the sample. Interestingly, these detailed reports come from companies owned by three major groups that hold a significant market share in the Sri Lankan apparel industry. This indicates that larger companies with greater market influence may have more resources and incentives to disclose comprehensive environmental data.

The analysis also reveals that key industry players are more inclined to report on environmental sustainability performance compared to the general industry trend. Among these leading companies, the highest reporting areas include GHG Emissions (Carbon Footprint), Energy, Water, and Hazardous Waste, indicating a more balanced and comprehensive approach to environmental reporting. Non-Hazardous Waste and Certifications for environmental performance follow closely, while Bio-Diversity remains the least reported area. The focus on Carbon Footprint among key players underscores its importance as a critical environmental metric. These findings align with existing literature on corporate environmental reporting. The extent and quality of sustainability reporting are often influenced by company size and stakeholder pressure. Larger companies with more resources are more likely to engage in detailed reporting due to increased scrutiny from stakeholders and the need to maintain a positive public image [29,38].

Furthermore, the low level of detailed GHG emission reporting is consistent with findings by [39], who suggest that while companies may recognize the importance of carbon footprint disclosures, they often lack the detailed strategies and actions needed to report comprehensively. This highlights the need for improved frameworks and guidelines to support companies in their environmental reporting efforts.

In conclusion, while there is some progress in environmental sustainability reporting within the Sri Lankan apparel manufacturing industry, significant gaps remain. The overall low level of transparency and the lack of detailed information from the majority of companies indicate a need for improved reporting practices. Encouragingly, key industry players are leading the way with more comprehensive disclosures, particularly in critical areas such as GHG emissions. Moving forward, increased stakeholder pressure and the adoption of standardized reporting frameworks could help elevate the overall quality and extent of environmental sustainability reporting in the industry.

When comparing the publicly reported environmental performances information of the selected apparel manufacturing data it was identified that there is a huge variability and inconsistency in what firms are publicly reporting about their environmental performances between the companies and with the same company over time periods. The information varies from just only referring to the statements like “we care for the environment” to a detail disclosure of the environmental performances with numerical facts and figures including carbon foot print. Notably the variability in reporting made comparison more difficult between companies. Further appropriate guidelines are necessary to promote reporting that results in the provision of comparable and relevant data across firms and over time. Early researches have also confirmed this by suggesting introducing more standardized forms of corporate emissions accounting, monitoring and disclosure. This in turn feeds into the debate on the limitations of voluntary reporting of corporate environmental performance and on the potential benefits of standardized, mandatory reporting [40,41]. The complete and more consistent are the data about environmental performances, the easier it will be for stakeholders (including those within the corporations themselves) to monitor progress, to compare performance, and to exert influence. However, even if a mandatory reporting requirement were introduced, it is likely that this would only be a partial solution. Evidence from other mandatory schemes suggests that corporations could retain significant flexibility in the ways they measure and report their emissions [42]. Furthermore, in the absence of a global agreement on corporate environmental performances, differences between national schemes will make it difficult to compare the data produced from different jurisdictions [42].

5. Conclusions

This study reveals that environmental performance disclosure among apparel manufacturing companies in Sri Lanka is significantly lacking, with only 23% of companies providing any public information, and a mere 5.7% offering detailed, analyzable data. The reported areas are limited to GHG Emissions/Carbon Footprint, Energy, Water, Non-Hazardous Waste, Hazardous Waste, and Bio-Diversity, with a strong emphasis on certifications obtained for different environmental or sustainability aspects. The voluntary nature of these disclosures, due to the absence of legal mandates, contributes to the inconsistency and incomparability of the reported data. However, key industry players, who hold substantial market shares and cater to prominent buyers, show a markedly higher level of disclosure at 60%, particularly in Carbon Footprint reporting, which stands at 61.5%. This indicates that market influence and stakeholder pressure can drive better transparency and sustainability practices within the industry. To enhance overall environmental performance reporting, there is a need for standardized frameworks and potential regulatory requirements in Sri Lanka.

Author Contributions

Conceptualization, AWT and WMPSB; methodology, AWT and WMPSB; formal analysis, AWT.; writing—original draft preparation, AWT.; writing—review and editing, WMPSB.; supervision, WMPSB.; All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding.

Data Availability Statement

These data were derived from the following resources available in the public domain (Stand Alone reports, web pages, etc).

Conflicts of Interest

The authors declare no conflicts of interest.

References

- Allwood, J.M.; Laursen, S.E.; Malvido de Rodríguez, C.; Bocken, N.M. Well Dressed? The Present and Future Sustainability of Clothing and Textiles in the United Kingdom, University of Cambridge Institute for Manufacturing, Cambridge. 2006.

- Fletcher, K. ‘Sustainable Fashion and Textiles’, Earthscan, London, UK. 2008. [Google Scholar]

- Grazzini, L.; Acuti, D.; Aiello, G. Solving the puzzle of sustainable fashion consumption: The role of consumers’ implicit attitudes and perceived warmth. Journal of Cleaner Production 2021, 287, 125579. [Google Scholar] [CrossRef]

- Chan, H.-L.; Wei, X.; Guo, S.; Leung, W.-H. Corporate social responsibility (CSR) in fashion supply chains: A multi-methodological study. Transportation Research Part E: Logistics and Transportation Review, 2020, 142, 102063. [Google Scholar] [CrossRef]

- Paździor, K.; Wrębiak, J.; Klepacz-Smółka, A.; Gmurek, M.; Bilińska, L.; Kos, L.; Sójka-Ledakowicz, J.; Ledakowicz, S. Infuence of ozonation and biodegradation on toxicity of industrial textile wastewater. Journal of Environmental Management, 2017, 195, 166–173. [Google Scholar] [CrossRef] [PubMed]

- Quantis, Measuring Fashion: Environmental Impact of the Global Apparel and Footwear Industries Study Full report and methodological considerations, 2018.

- Shrivastava, A.; Jain, G.; Kamble, S.S.; Belhadi, A. Sustainability through online renting clothing: Circular fashion fueled by instagram micro-celebrities. Journal of Cleaner Production. 2021, 278, 123772. [Google Scholar] [CrossRef]

- Hawken, P. The Ecology of Commerce: A Declaration of Sustainability. New York: HarperCollins Publisher, 1993.

- Shrivastava, P. The role of corporations in achieving corporate sustainability, Academy of Management Review, 1995, Vol. 20 No. 4, pp. 936-960.

- Tuppura, A.; Arminen, H.; Patari, S.; Jantunen, A. Corporate social and financial performance in different industry contexts: the chicken or the egg?, Social Responsibility Journal, 2016, Vol. 12 Issue 4, pp. 672-686. [CrossRef]

- Bubicz, M.E.; Dias Barbosa-Póvoa AP, F.; Carvalho, A. Social sustainability management in the apparel supply chains. Journal of Cleaner Production, 2021, 280, 124214. [Google Scholar] [CrossRef]

- Goworek, H. Social and environmental sustainability in the clothing industry: a case study of a fair-trade retailer, Social Responsibility Journal, 2011, Vol. 7 Issue: 1, pp.74-86. [CrossRef]

- Islam, M.M.; Perry, P.; Gill, S. Mapping environmentally sustainable practices in textiles, apparel and fashion industries: A systematic literature review. Journal of Fashion Marketing and Management. 2020, 1361–2026. [Google Scholar] [CrossRef]

- Kabir SM, F.; Chakraborty, S.; Hoque SM, A.; Mathur, K. Sustainability assessment of cotton-based textile wet processing. Clean Technologies, 2019, 1, 232–246. [Google Scholar] [CrossRef]

- Export Development Board. Industry Capability Report. 2017.

- Kozlowski, A.; Searcy, C.; Bardecki, M. Corporate sustainability reporting in the apparel industry: An analysis of indicators disclosed, International Journal of Productivity and Performance Management, 2015, Vol. 64 Issue: 3, pp.377-397. [CrossRef]

- Muñoz-Torres, M.J.; Fernández-Izquierdo M, Á.; Rivera-Lirio, J.M.; Ferrero-Ferrero, I.; EscrigOlmedo, E. Sustainable supply chain management in a global context: A consistency analysis in the textile industry between environmental management practices at company level and sectoral and global environmental challenges. Environment, Development and Sustainability, 2021, 23, 3883–3916. [Google Scholar] [CrossRef]

- Turker, D.; Altuntas, C. Sustainable supply chain management in the fast fashion industry: An analysis of corporate reports, European Management Journal, 2014, Volume 32, Issue 5, 837-849.

- Testa, F.; Boiral, O.; Iraldo, F.J. Internalization of environmental Practices and Institutional Complexity: Can stakeholders Pressures Encourage Greenwashing?, Journal of Business Ethics, 2018, Volume 147, Issue 2, pp 287–307. [CrossRef]

- Validi, S.; Bhattacharya, A.; Byrne, P.J. A case analysis of a sustainable food supply chain distribution system: a multi-objective approach, International Journal of Production Economics, 2014, Vol. 152 No. 1, pp. 71-87.

- Wiedmann, T.O.; Lenzen, M.; Barrett, J.R. Companies on the scale, Journal of Industrial Ecology, 2009, Vol. 13 No. 3, pp. 361-383.

- Ewing, B.R.; Hawkins, T.R.; Wiedmann, T.O.; Galli, A.; Ercin, A.E.; Weinzettel, J.; Steen-Olsen, K. Integrating ecological and water footprint accounting in a multi-regional input–output framework, Ecological Indicators, 2012, Vol. 23 No. 1, pp. 1-8.

- Abbate, S.; Centobelli, P.; Cerchione, R. Sustainability trends and gaps in the textile, apparel and fashion industries. Environment, Development, Sustainability 2024, 26, 2837–2864. [Google Scholar] [CrossRef] [PubMed]

- Weidstam, E. Sustainability Passion in Fashion: Challenges and Opportunities for Small and Medium-Sized Swedish Apparel Brands when Working with Corporate Social Responsibility in their Global Supply Chain. Master’s Thesis, Stockholm University, Sweden, September 2014. https://ieeexplore-ieee-org.ezproxy.lb.polyu.edu.hk/document/5997938/.

- Kim, J., Bach, S. Clelland, I. Symbolic or behavioural management? Corporate reputation in high-emission industries, Corporate Reputation Review, 2007, Vol. 10 No. 2, pp. 77-98.

- Hrasky, S. Carbon footprints and legitimation strategies: symbolism or action?, Accounting, Auditing & Accountability Journal, 2011, Vol. 25 Issue: 1, pp.174-198. [CrossRef]

- Sheehy, B. Farneti, F. Corporate Social Responsibility, Sustainability and Corporate Sustainability: What is the difference and does it matter? 2020, Vol 13, 5965 Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3549577.

- GRI, G4 Sustainability Reporting Guidelines. Reporting Principles and Standard Disclosures, Global Reporting Initiative, Amsterdam, 2013.

- Adams, C.A. Frost, G.R. Integrating sustainability reporting into management practices, Accounting Forum, 2008, Vol. 32 No. 4, pp. 288-302.

- Davis, G. Searcy, C. A review of Canadian corporate sustainable development reports, Journal of Global Responsibility, 2010, Vol. 1 No. 2, pp. 316-329.

- Feng, P.; Ngai, C.S. Doing More on the Corporate Sustainability Front: A Longitudinal Analysis of CSR Reporting of Global Fashion Companies. Sustainability 2020, 12, 2477. [Google Scholar] [CrossRef]

- Dissanayake, D., Tilt, C., Xydias-Lobo, M. Sustainability reporting by publicly listed companies in Sri Lanka, Journal of Cleaner Production, 2016, 1-14. [CrossRef]

- Dissanayake, D., Tilt, C., Qian, W. Factors influencing sustainability reporting by Sri Lankan companies, Pacific Accounting Review, 2019, Vol. 31 Issue: 1, pp.84-109. [CrossRef]

- Peiris, N., Anise, R. Corporate Sustainability Reporting: An Empirical Study on Social & Environmental Reporting among Sri Lankan Public Listed Companies in the Hotel and Travel Industry, Colombo Journal of Advanced Research, 2019, Vol. 1, No. 1; 2019.

- World Bank Group – Trade and Competitiveness, Apparel GVC Analysis Industry-Specific Global Value Chains, (N.D).

- Athukorala, P. Ekanayake, R. Repositioning in the Global Apparel Value Chain in the Post-MFA Era: Strategic Issues and Evidence from Sri Lanka. Development Policy Review, 2017, Vol. 36. 10.1111/dpr.12226. [CrossRef]

- Kolk, A., Pinkse, J. Business Responses to Climate Change: Identifying Emergent Strategies, California Management Review, 2005, Volume: 47 issue: 3, 6-20.

- Nuskiya, M.N.F. , Ekanayake, A., Beddewela, E., Meftah Gerged, A. Determinants of corporate environmental disclosures in Sri Lanka: the role of corporate governance, Journal of Accounting in Emerging Economies, 2021, Vol. 11 No. 3, pp. 367-394. [CrossRef]

- Prado-Lorenzo, J., Isabel G., Sánchez, I.M.G. Stakeholder Engagement and Corporate Social Responsibility Reporting: The ownership Structure Effect. Corporate Social Responsibility and Environmental Management. 2009, 16. 94. [CrossRef]

- Kolk, A.; Levy, D.; Pinkse, J. Corporate responses in an emerging climate regime: The institutionalization and commensuration of carbon disclosure. European Accounting Review, 2008, 17: 719–745.

- Sullivan, R.; Gouldson, A. Does voluntary carbon reporting meet investors’ needs?’, Journal of Cleaner Production, 2012, 36: 60–67.

- Sullivan, R.; Gouldson, A. Pollutant release and transfer registers: Examining the value of government-led reporting on corporate environmental performance. Corporate Social Responsibility and Environmental Management, 2007, 14: 263–273.

Figure 1.

Industry categorization of apparel manufacturing companies in Sri Lanka based on the operation.

Figure 1.

Industry categorization of apparel manufacturing companies in Sri Lanka based on the operation.

Figure 2.

Availability of public disclosures in environmental information of apparel manufacturing companies in Sri Lanka.

Figure 2.

Availability of public disclosures in environmental information of apparel manufacturing companies in Sri Lanka.

Figure 3.

Public disclosure areas of environmental sustainability information of wearable apparel manufacturing companies.

Figure 3.

Public disclosure areas of environmental sustainability information of wearable apparel manufacturing companies.

Figure 4.

Availability of public disclosures in environmental information of key players in the apparel industry.

Figure 4.

Availability of public disclosures in environmental information of key players in the apparel industry.

Figure 5.

Public disclosure areas of Environmental Sustainability Information of key players in apparel manufacturing industry in Sri Lanka.

Figure 5.

Public disclosure areas of Environmental Sustainability Information of key players in apparel manufacturing industry in Sri Lanka.

Figure 6.

Comparison of the public disclosures areas of environmental information between key players in the industry and the rest of the companies.

Figure 6.

Comparison of the public disclosures areas of environmental information between key players in the industry and the rest of the companies.

Table 1.

Summary of certifications obtained by apparel manufacturing companies in Sri Lanka.

| S/N | Certification Type | Total No of Companies Certified |

|---|---|---|

| 1 | WRAP - Worldwide Responsible Accredited Production | 44 |

| 2 | ISO 14001 - Environmental Management Systems | 32 |

| 3 | OHSAS 18001 - Occupational Health and Safety Assessment Series | 15 |

| 4 | Responsible Care | 14 |

| 5 | BSCI - Business Social Compliance Initiative | 13 |

| 6 | ETI - Ethical Trading Initiative | 13 |

| 7 | GOTS - Global Organic Textiles Standards | 13 |

| 8 | Sedex - Supplier Ethical Data Exchange Database | 12 |

| 9 | LEED - Leadership in Energy and Environmental Design | 11 |

| 10 | Organic 100 content standard | 11 |

| 11 | CTPAT - Customs Trade Partnership Against Terrorism | 9 |

| 12 | Fair Trade USA | 9 |

| 13 | ISO 9001:2015 - Quality Management Systems | 9 |

| 14 | RCS - Recycled Claim Standard | 8 |

| 15 | Confidence in Textiles (Tested for harmful substances) / OEKO TEX | 8 |

| 16 | GRS - Global Recycled Standard | 7 |

| 17 | GSV - Global Security Verification | 6 |

| 18 | Net Zero Carbon Certified | 6 |

| 19 | Sri Lanka apparel garment without guilt | 5 |

| 20 | BCI - Better Cotton Initiative | 5 |

| 21 | ISO 14064-3-2006 - Greenhouse Gases - Part 3 | 4 |

| 22 | ISO 50001 - Energy Management | 4 |

| 23 | Organic blended Content standard | 4 |

| 24 | GMP - Good Manufacturing Practice | 2 |

| 25 | WCA - Workplace Condition Assessment | 1 |

| 26 | Zero Waste To Landfill Certificate | 1 |

| 27 | Carbon Neutral | 1 |

WRAP - Worldwide Responsible Accredited Production, ISO 14001 - Environmental Management Systems, OHSAS 18001 - Occupational Health and Safety Assessment Series were the certifications reported in highest frequency.

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Copyright: This open access article is published under a Creative Commons CC BY 4.0 license, which permit the free download, distribution, and reuse, provided that the author and preprint are cited in any reuse.