Submitted:

02 August 2024

Posted:

02 August 2024

You are already at the latest version

Abstract

Matters relating to preservation of environmental resources and climate change, social inclusion and diversity, and open and sound governance have rapidly gained global attention. However, little is known about the construction industry in meeting the environmental, social and governance (ESG) criteria towards sustainable development. In this study, the purpose is to identify the key ESG indicators for construction development. A systematic literature review was undertaken using data from Scopus, PubMed, Google Scholar, JSTOR, ProQuest, and Web of Science. The results show some of the key ESG indicators as climate resilience and green construction activities (at the project level), and active stakeholder engagement and effective project governance (at the firm level) and meeting environmental and social regulation requirements (industry/national level). The limitation of the article is in the sample size of twenty-six journal articles with future expectation of increment as ESG gain more acceptance in the construction industry. This study will be significant for the design of practice framework and policies on ESG in the construction industry. Comprehensively, this study presents relevant ESG indicators for construction management and presents essential information for future research.

Keywords:

Climate change

; Construction industry

; ESG

; Sustainability

; Literature review

; social diversity

1. Introduction

As stakeholders continue to place a greater focus on environmental protection, social inclusion, as well as open and accountable ESG disclosures have reached a crescendo within the 21st century together with traditional financial disclosures. The construction sector, like any other sector like manufacturing, fashion, retail, and mining is significantly affected by ESG disclosures in a variety of ways. Darnall, et al. [1] and Akomea-Frimpong, et al. [2] mentioned that the built environment emits 30% or more of carbon emissions, and larger than 40% of energy consumption together with 32% of the world's natural resources. These evidences show that the construction industry should be involved in sustainability drive to minimise these challenges in the release of emissions, energy usage and the plundering of natural resources by meeting the ESG targets [3,4]. The goal of ESG in the construction sector is to improve the standards of environmental consciousness and promote more eco-friendly project design and operations [5]. The construction sector is also expected to reduce the amount of waste it produces, maximize recycling, and reuse efforts, and incorporate circular economy principles into its design decisions [6]. Furthermore, construction firms may utilize ESG reports to identify areas of poor implementation of inclusion and diversity policies. Increasingly, there is a policy shift towards a mixture of environmental and social responsibility strategies in the construction sector [7]. According to Heal [8] and [9], by showing commitment to environmental sustainability and social responsibility, construction companies may enhance their reputation among stakeholders. Moreover, the preference among stakeholders to companies with positive ESG policies is high. Thus, firms in the construction sector that prioritise ESG issues are likely to have extended sustainable effects [10]. These firms may attract investors that value ESG elements and develop a reputation for ethical business operations by sharing information about their ESG initiatives. Finally, ESG reporting is increasingly becoming a regulatory requirement in some jurisdictions (countries) [11]. Therefore, contractors may avoid legal fines and reputational damage by complying with these regulations. In the attempt to harvest the above-mentioned benefits from ESG practices and reporting, construction firms may be confronted with unclear ESG criteria (indicators) [12,13]. Without criteria to measure the implementation of ESG in the construction sector, some firms may attempt to present misleading and substandard ESG reports to stakeholders. Some firms may manipulate annual disclosures on ESG to paint a picture of embracing sustainable practices against the backdrop of self-engineered and questionable benchmarks [14]. Therefore, this article aims at identifying the key ESG indicators in the construction industry from existing literature.

The arguments for this paper are as follows. First, the current literature on ESG is skewed to manufacturing, retail, banking and other sectors with very few studies on the construction research field [15]. These industries operate differently from the construction sector. Construction projects go through a lifecycle embracing different stages and stakeholders with diverse and complex interests [16]. There is a dearth of scholarly works on ESG application to resolve these complexities in informing the measurement of ESG in construction activities. Second, practical indicators on ESG towards construction development remains not clearly defined and in some countries and industries not existent on construction sector [17,18]. With the world inching towards more sustainable zero-carbon emission and inclusive construction policies, it is evident the construction industry needs to adapt to changing social, economic, environmental and governance progress [19,20]. The rest of the sections of the study is the following: an overview of the methodology followed by outcomes of the analysis of the data including discussions of the results. Finally, the conclusions, implications, and limitations.

2. Methodology

Literature on ESG in the construction industry were retrieved and analysed following the systematic literature review approach (SLR) [21]. The steps outlined in the SLR include:

2.1. Search Strategy

The first stage involves identifying relevant literature in various bibliographic databases. A systematic search and retrieval of relevant documents were conducted in Scopus, ProQuest, Web of Science, Google Scholar, and PubMed. These databases are prominent depositories for indexing a large number of studies in [22]. The keywords utilised in the search include: “Environmental, social and governance” OR “ESG” OR “ESG disclosures” OR “ESG reporting” OR “ESG report*” OR “ESG disclos*”, AND “construct* industry” OR “building sector” OR “construction sector” OR “Built* Environment”. This search resulted in 531, 426, 5433, 3257 and 132 documents in PubMed, Scopus, ScienceDirect, Web of Science, ProQuest, EBSCOhost, and Google Scholar respectively. Supplementarily, the searches in the databases were supported by checking the citations and reference lists of articles to retrieve additional documents inclusive of grey literature (theses and reports). At this stage, a total of 178 studies were found increasing the number of studies to 9977.

2.2. Eligibility Criteria

The eligibility criteria set for the analysis of the studies identified through Step 2.1 include the following inclusion and exclusion criteria:

- Language: Include studies published in English and exclude articles written in languages other than English [25].

- Full-text accessibility: Include documents available and downloadable in full-text, exclude not-found and not downloadable articles [26].

- Focus: Include articles with coverage of ESG in the construction industry especially ESG indicators [27].

2.3. Selection of Relevant Documents

A total number of 9799 documents were found in Scopus, other documents from Web of Science, EBSCOhost, Google Scholar, ProQuest, and PubMed as explained in Stage 2.1. Additional results of 178 documents from citation (or reference) search and grey literature were added to the 9799 documents. A total of 9977 documents were imported into Endnote to remove duplicates among databases. At this stage, 1572 documents were removed due to duplication. The paper titles and the summary of the abstracts of the remaining 4871 underwent screening. The eligibility criteria set in Section 3.2 was applied to screen the titles and abstracts by all the authors. A total of 4724 documents were removed after this process. Further, the remaining 147 articles were fully read in view of the eligibility criteria. In the end, 26 articles with 121 articles removed because they failed to meet the eligibility criteria.

2.4. Data Extraction and Analysis

Extraction of the relevant data from the selected 26 documents to address the research objective was performed by all the authors. Preferably, Microsoft Excel sheet was utilised to record the data extraction. Data extracted by an author was checked and rechecked by all the other authors. Data extracted includes bibliometric information about the 26 articles including author(s), document type, publishing entity and year, country of origin, the aims/objective/focus of the studies, and research design. In addition, texts and statements on ESG indicators were extracted and recorded in Microsoft Excel after repetitive reading and comparing all the articles. The identified texts, words, phrases and statements were thoroughly analysed and grouped into themes based on similar patterns and purposes [28]. The authors conferred and cross-checked the themes on the ESG indicators. The mean scores of the key groups of the ESG indicators in Table 3 were calculated using the number of articles from which the indicators were identified divided by the total indicators within the four latent variables [29]. The purpose of the calculation is to rank the order of importance of the latent variables (principal ESG indicator groups). The formula for the mean score is:

where is mean sore, is the relevant study from which the indicators are identified and is all the observed variables in a latent variable.

3. Findings and Discussions

3.1. Description of Selected Studies

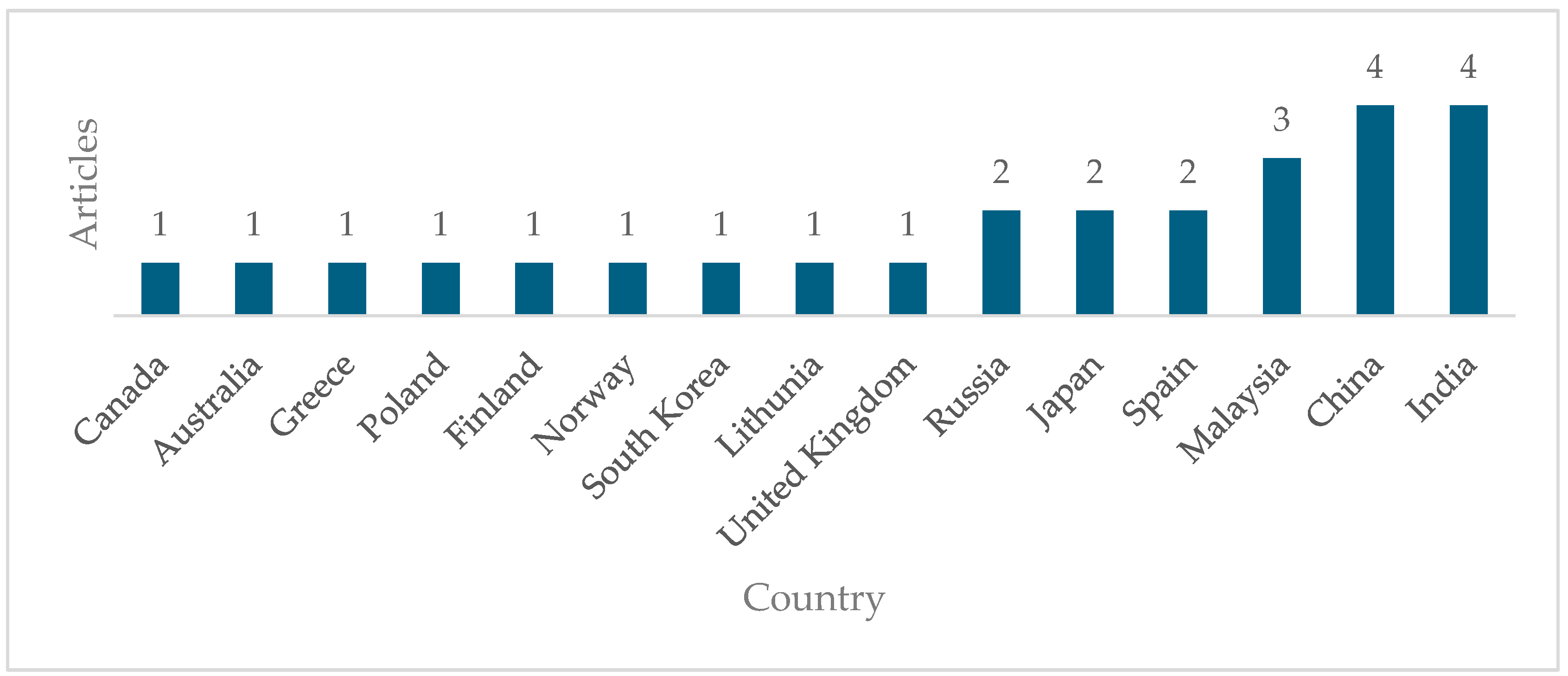

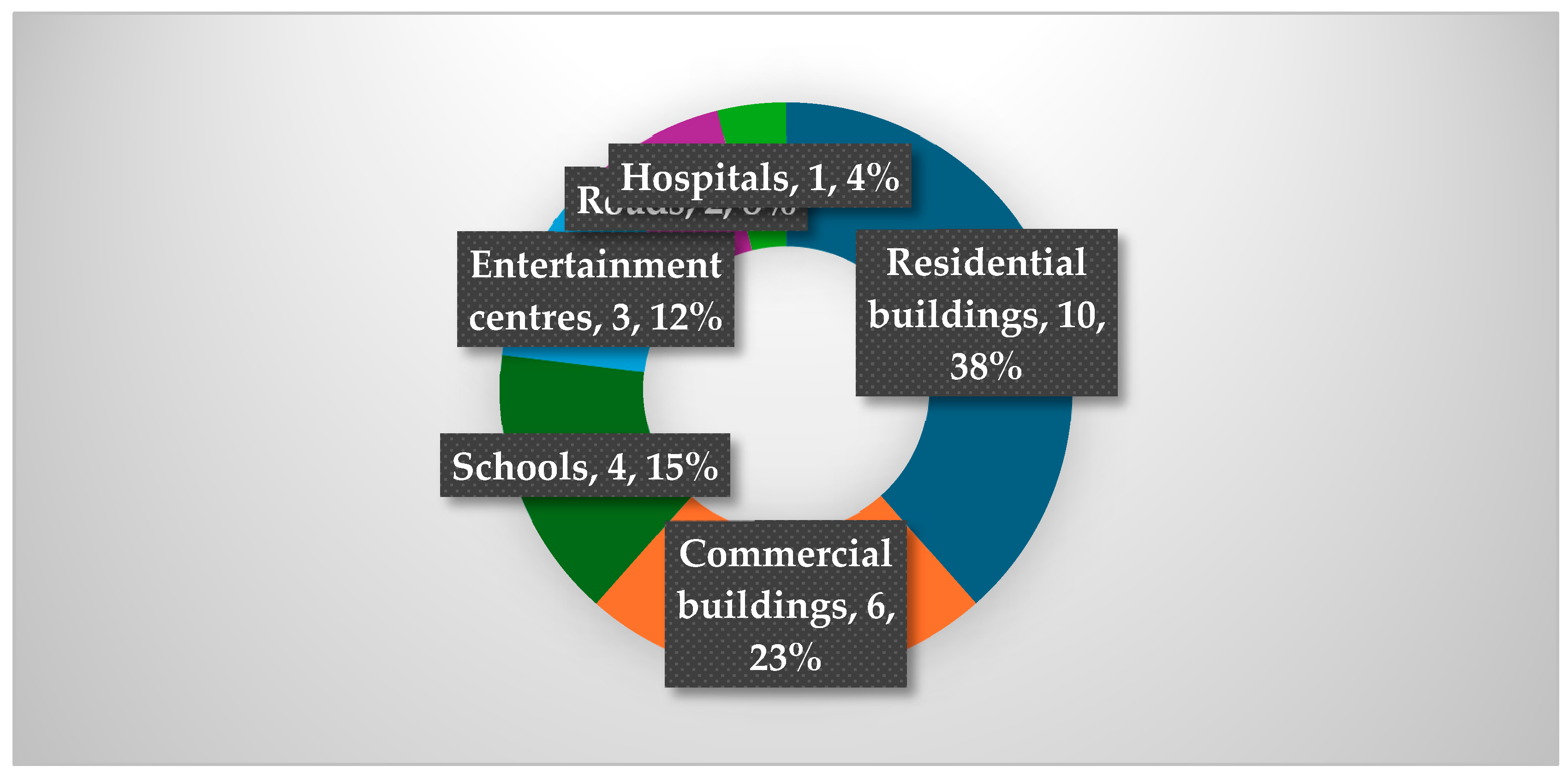

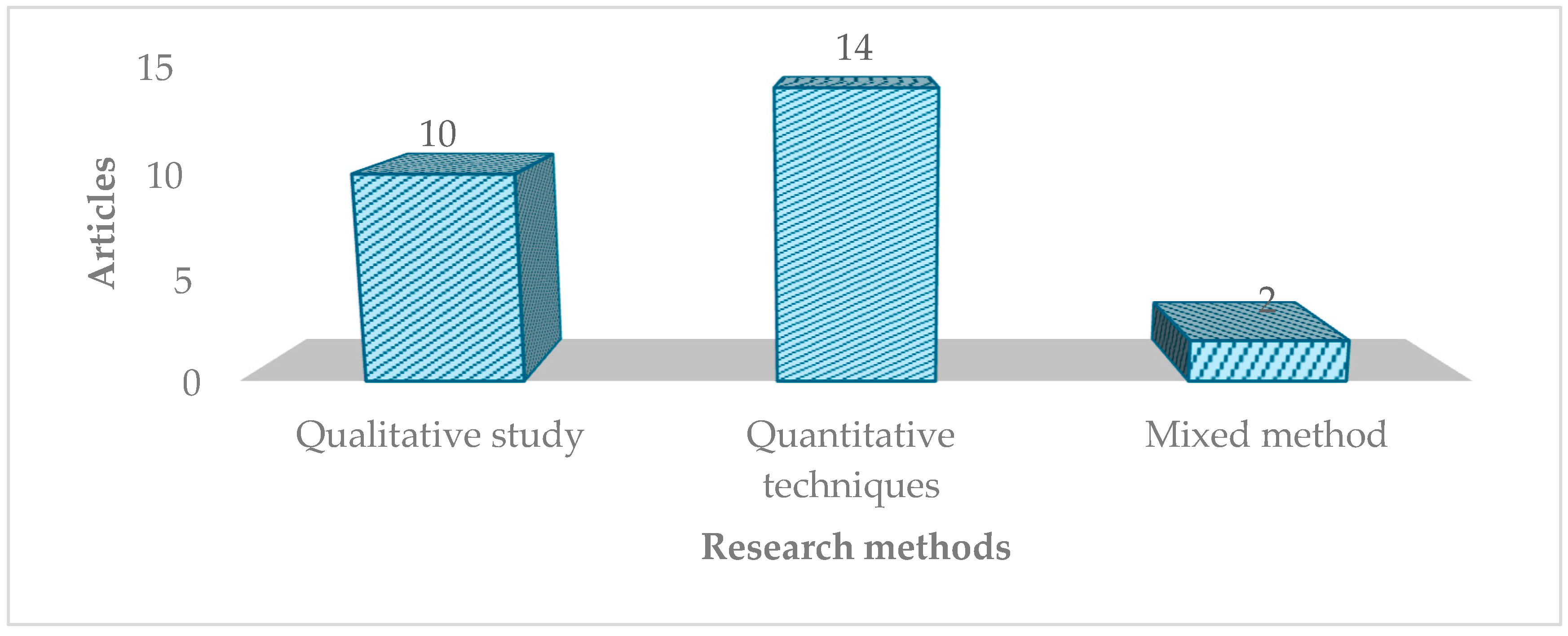

As demonstrated in Figure 1, Figure 2 and Figure 3, the studies included in this analysis were made up of peer-reviewed journal articles (26 articles). The peer-reviewed journal articles are scholarly works assessed by scholars in the same field of construction management and published by academic journals such as “Sustainability, Journal of Cleaner Production and Journal of Management in Engineering” [30]. With the exception of Mukhlisin, et al. [31] and Siew, et al. [32], all the studies were published after 2015 which is after the implementation of the UNSDGs which promote environmental, social and governance practices [33]. Studies were conducted in highly developed countries including Australia, Canada, United Kingdom, Finland, Japan, United States, Russia, and Spain. China and India are exceptions, developing nations that recorded eight studies. In these developing countries, there is an increasing interest in ESG-related issues to preserve the environment, minimise climate change risks, and support projects towards attaining the net-zero emission targets [34]. While most of the studies covered general construction projects together with specific focus on buildings and infrastructure projects such as sports complex and entertainment centres.

3.2. ESG Indicators in Construction Industry

In Table 1, a total of 96 indicators of ESG on performance in the construction industry are presented. These ESG indicators are relevant benchmarks in assessing responsible and sustainable practices [1,35]. ESG indicators seen in Table 2 go beyond traditional financial metrics to provide a more complete understanding of the construction industry’s environmental, social, and governance policies and practices [36]. The prominent ESG indicators in Table 2 include the attainment of low or zero carbon emission from construction activities. This indicator measures the level of greenhouse gases emitted by a construction project, aiding in the assessment of project’s environmental impact and efforts to mitigate climate change [37]. This indicator encourages project managers to incorporate eco-friendly and sustainable project measures and smart technologies for net-zero carbon emission targets [38,39]. Employee wellbeing and turnover rate is another term for the rate at which construction workers and construction professionals are treated as well as leaving a construction firm over a given period. This ESG indicator presents the critical results of a firm’s ability to attract and retain talent. A high employee turnover rate may indicate problems with employee satisfaction, work culture, or management practices, which can have long-term consequences for the company's success and sustainability. Another important indicator is community engagement, which measures a company's level of involvement and impact in the communities in which it operates [18]. It assesses a construction firm's efforts to foster positive relationships within communities where projects are constructed and operated in the built environment. This indicator takes philanthropic activities, employee volunteerism, and community investments into account [40]. To provide a summary of the rest of the ESG performance indicators in Table 2, the explanations are in three forms of ESG: environmental dimension, social inclusion, accountability and transparency in governance. The environmental dimension evaluates the construction industry's environmental impact [15].

In addition, construction firms are assessed based on their environmental initiatives, such as the implementation of environmentally-friendly energies, net-zero greenhouse gas emissions, and sustainable supply chains [41]. Climate change policy, water management, pollution prevention, biodiversity impacts, and green building practices are some examples from Table 1.

The Social dimension of ESG indicators examine the construction industry’s social impact, including its interactions with employees, users of construction projects, communities, and other stakeholders [42]. The performance indicators in Table 2 that depict the social dimensions of ESG include the treatment of construction workers, the construction firm’s dedication to employee well-being, diversity and inclusion policies and practices, labour standards, high score of user satisfaction, community engagement, and philanthropic activities [43]. The Governance indicators assess the project management practices and structures within the construction industry. It entails evaluating a firm's leadership, project steering committees and board structures, executive compensation, transparency in decision-making processes, and adherence to ethical and legal requirements [44]. Internal systems, leadership ethics, transparency, executive compensation, board diversity, corruption policies, and shareholder rights are all evaluation criteria of ESG in the built environment. To support the various findings, several studies within and outside the construction industry have confirmed the importance of ESG framed within the performance indicators of construction firms, and an instance is the field of socially responsible investment (SRI) [45]. ESG-induced performance indicators were used as a proxy for sustainability performance in the SRI market [6]. By reporting these ESG indicators, the authors mentioned that it caused an increment in the share value of the companies, and it enhanced the priorities of societal progression, good governance, and preservation of the environment. In the built environment, Musarat, Alaloul, Irfan, Sreenivasan and Rabbani [37], posited that improved ESG performance benchmarks is seen in the climate resilience and low risks of investments. In addition, Kim and Lee [46], argued for the importance of benchmarks and ratings on ESG for the construction firms can learn from to develop project related ESG performance indicators. Using multiple firms from different industries, Hayashi, Hiyama and Kubo [16], established that companies should develop and implement risk-inspired ESG scores to assess the financial investments in construction projects. Further, it was explained in the articles that the implementation of ESG guiding framework relates and involves stakeholders in performance management. However, during times of crisis, such as the coronavirus crisis, the application, and effects ESG practices vary depending on the project and organisational policies and practices. Deamer, et al. [47] found that the coronavirus pandemic impacted the finances of firms negatively but firms with enhanced ESG practices had better performance outcomes.

The use of ESG indicators is growing in popularity in all industries inclusive of the construction industry. Well-established and holistic ESG performance indicators are helpful in assisting organisations to identify areas for improvement, manage risks, and improve corporate reputation and long-term value [35]. ESG indictors also provide useful information for financiers to make informed decisions and allocate capital to green construction projects with the focus on sustainable development [48]. However, there are some drawbacks to using ESG indicators. Studies have pointed lack of transparency and convergence to these metrics as different organisations and projects demand different ESG indicators. Different rating agencies also assess ESG performance using different methods and criteria, resulting in a lack of agreement on definition and measurement [4]. Because of these disparities, different opinions and ratings abound on the best ESG performance benchmarks for projects [18]. Furthermore, concerns have been raised on the ethical dimensions ESG indicators and inadequate integration of all the UN SDGs. ESG rating agencies pick and choose biased standards to measure sustainable practices of construction firms [45,49]. Such ratings are heavily influenced by the project managers. Critics of ESG indicators and its disclosures especially the extreme right-wing politicians in the United States, for instance, see ESG incorporation into public projects as a waste of money and “woke” capitalism. [50] Supported by corporate allies and fossil fuel lobbyists, these right-wing politicians have initiated bills and reviewed project contracts to avoid the disclosure of ESG indicators in public projects.

3.3. Conceptualising the Review Findings

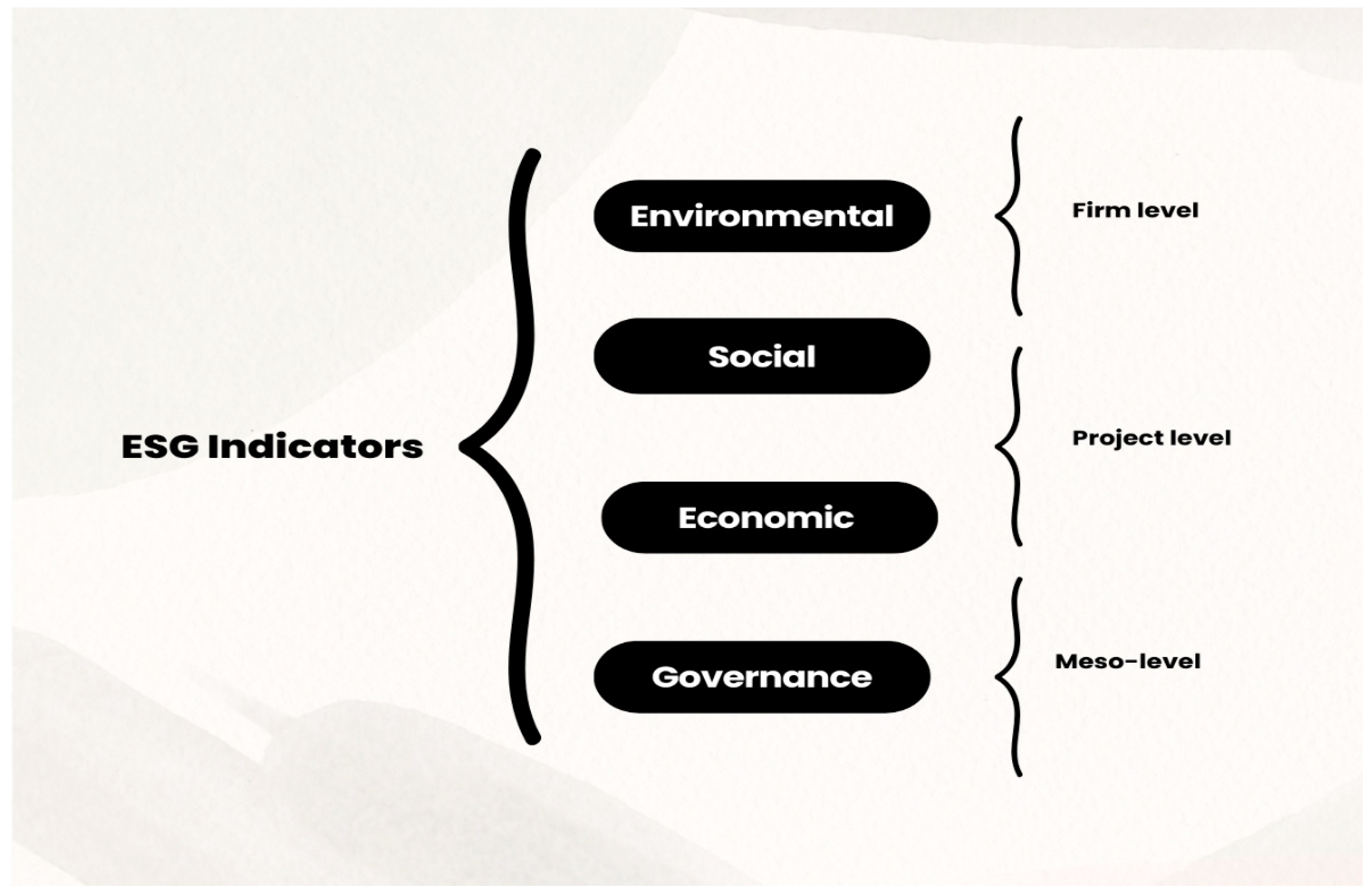

In Table 2 and Figure 4, the ESG indicators from Table 1 have been classified using the three baselines of sustainability (social, economic and environmental) together with a fourth pillar of “governance” in the reference to existing literature [51]. Bose [4] argued that ESG establishes the financial, social and ecological balance in the construction projects. Moreover, ESG is also an avenue for stakeholders to realise the social responsibility and contribution of construction firms to societies [52]. Stakeholders in the construction sector pursue long-term investment and social capital development through ESG with strong support from environmental protection and governance policies. ESG is also a prime indicator of sustainability for construction stakeholder’s investment and ensures the promotion of net-zero principles [53].

Similarly, continual disclosure of ESG indicators and practices serves as an image enhancing strategy to attract responsible investors, and manage long-term sustainability into construction development [17]. Further, the importance of the four basic pillars of ESG are investment analysis and decision-making strategies in the construction industry were ranked in the order of importance in Table 3 putting on the environment indicators (1st), social progress (2nd), and governance (3rd) and economic prosperity (4th).

Environmental Indicators

In the wake of the explosion of the ESG concept in construction industry discussions, ESG disclosures/reporting is a frequently used to acknowledge the project and firm performance reports beyond the conventional financial statements [20]. Environmental reporting involves construction corporations revealing the impacts of their activities on safeguarding the environment, climate and biodiversity [1]. ESG reporting comprises a comprehensive publication of the firm's ESG actions, including the initiatives and elements of ESG performance outside the influence of management [45]. Erkens, Paugam and Stolowy [7] recounted that typically, environmental disclosure of construction firms is voluntary, and the process is not well-defined and standardised for all firms. Environmental reports advocates and increases the availability of ESG data to researchers and practitioners, and encourages construction firms to adjust their actions and conducts to minimise carbon emissions [18]. These requirements maybe project specific or requirements from the industry and currently the European Union. Bose [4] claims that, external stakeholders such as the European Union and environmental pressures groups are increasingly demanding the disclosure of non-financial environmental information beyond what is typically accessible in financial statements on construction activities. ESG reporting is viewed as a prerequisite for environmental responsibility wooing investment funding for sustainable construction activities.

Social Indicators

Brogi, Lagasio and Porretta [18] and Chen, Wang, He and Zhang [40] claimed the relevance of social ESG indicators and the possibility of substituting the bluewashing of these key metrics of progress from contractors. These behaviours of construction firms are demonstrated in the misleading information on transitioning to inclusive construction project practices. According to Lokuwaduge and De Silva [54], these deceptive practices in disclosing social sustainability practices in construction projects are common in attracting the support of traditional authorities and the public at large to execute projects. EY [55] reported that contractors within the construction sector overstate a project’s inclusion strategies with false and creative financial reporting methodologies to present diversity, equity and inclusion (DEI) metrics. The report continued that construction firms sometimes publish vague or unverifiable social claims on projects with the aim of attracting financial investments and court public support. Heal [8] also stated that construction firms are prone to using irrelevant corporate social responsibility claims to distract the public from significant and harmful environmental impacts of projects. A critical institutional account of decoupling these false claims, according to Erkens, Paugam and Stolowy [7], is to develop a well-planned and coordinated organisational strategies to promote the transition of sustainable, inclusive and green project practices. Construction firms and project management professionals should be trained to meeting stakeholder expectations on zero-carbon emissions without really altering project practices. The construction industry is heavily reliant on fossil fuel products such as coal and petroleum to support projects that have adverse impacts on the environment and future generations [56]. Project managers and project steering committees should support realistic and justifiable projects without having enough and sustainable finance to support green project development.

Governance Indicators

The rising concerns on undefined disclosing indicators of governance malpractices of firms highlight the diversion from sustainable reporting standards increase the risks of information asymmetry [57,58]. Stakeholders are misled to believe that every activity and transaction has been reported but in reality things have been hidden to the detriment of the well-being of the stakeholders concerning adhering to project and firm level regulations. Hadro, et al. [59] mentioned that poor governance systems on construction transactions are subtle authorisation of fraud and misleading reporting from the top management of construction firms. Galvin [60] and Eisenkopf, Juranek and Walz [35] revealed the commitments from the management emphasise on the genuineness of firms efforts to improve the state of the organisational and project structures for sustainable construction development. To continue to ensure continuous improvement in the governance framework, regulations and government support should be available to fine dishonest disclosures of organisations and measures to fight climate change [44,61].

Economic Indicators (4th Rank)

Construction firms should be the source of economic prosperity as projects built by this industry form the foundation of societal development [62,63].So, construction firms should present the contribution the industry has made towards the economic development of societies in their reportage [44,62]. Construction companies should desist from exclusively presenting only positive news and omit negative news related to their economic activities that are detrimental to the society. Corporate deceptions and manipulations in the process of financial reporting their environmental activities be checked with the established indicators [54]. Contractors should be wary of legitimising unethical behaviours on presentation of fraudulent financial reports to enhance their image and annual performance [40]. Investors into projects should be equipped with ESG ratings to woo public praise and private investments [46,62].

Table 3.

Computation and ranking of the principal ESG indicators.

| Environmental indicators | Economic indicators | Governance indicators | Social indicators | |

|---|---|---|---|---|

| 4 | 3 | 1 | 2 | |

| 2 | 2 | 2 | 4 | |

| 5 | 3 | 3 | 3 | |

| 2 | 1 | 3 | 2 | |

| 1 | 2 | 2 | 1 | |

| 3 | 3 | 5 | 1 | |

| 1 | 2 | 2 | 4 | |

| 4 | 2 | 2 | 3 | |

| 3 | 2 | 3 | 3 | |

| 1 | 1 | 2 | 4 | |

| 2 | 2 | 3 | 3 | |

| 2 | 1 | 1 | 1 | |

| 1 | 1 | 4 | 4 | |

| 5 | 1 | 3 | 1 | |

| 6 | 2 | 4 | ||

| 5 | 3 | 1 | ||

| 3 | 2 | 3 | ||

| 2 | 2 | 3 | ||

| 3 | 1 | 5 | ||

| 1 | 3 | 4 | ||

| 4 | 2 | 2 | ||

| 3 | 4 | 2 | ||

| 3 | 3 | 3 | ||

| 2 | 3 | 1 | ||

| 3 | 3 | 3 | ||

| 3 | 2 | |||

| 1 | 3 | |||

| 4 | 2 | |||

| 3 | ||||

| Sum | 79 | 26 | 64 | 77 |

| Mean score | 2.82 | 1.86 | 2.56 | 2.66 |

| Ranking | 1st | 4th | 3rd | 2nd |

5. Implications of the Study

The findings of this research are relevant for the promotion of awareness and integration of ESG indicators in sustainable practices in the construction industry. These indicators will be relevant in ESG reporting on construction activities to investors, clients, and the public [64]. With comprehensive ESG disclosure indicators, construction professionals can confidentially regularly disclose information about their environmental and social performance against measured metrics. This will help improve the image of the construction firms and the performance of projects. Construction companies may develop risk mitigation strategies that consider ESG factors, ultimately reducing project-related risks [54]. This study will again draw the attention of the contractor to the ethical cost they will incur for their improper actions. This will make the private contractor realize the importance of ethical responsibilities in construction. Financial investors in the construction of projects will be drawn to consider social, ethical, ecological, governance and sustainable priorities in their investment decisions [13]. The integration of social and economic blind supervision will effectively curb contractor fraudulent environmental behaviour [37]. However, at present, the studies on ESG have focused largely on firm specific variables with limited focus on specific projects at the project level, extremely little is known about ESG practices comparative to firm-level measures on social, governance and environmental responsibilities. Therefore, it is essential to expand ESG models and practices on project specific indicators [44]. Projects such as sanitation, water, airports and ports and education have not received ESG-related practice models. Hence this study calls for the consideration of distinct ESG-inspired project management practices that ensures disparities between regions and project sizes.

From the results of this study, it is expected that advanced research may be considered to develop a framework for ESG reporting and disclosure [60,65]. This will ease the exercise of the firms in disclosing information regarding their environmental, social, and economic performance, to determine which firm is doing well as far as ESG is concerned and which components of the construction firms needs to be improved to meet the ESG standards. Also, the study is expected to influence the following issues relating to ESG that have received fewer investigations, and development of practice models from construction researchers. Future studies can focus on these, to include: deciphering how ESG connects with the construction industry; managing ESG risks; ESG-inspired supply chain and procurement; measuring, monitoring, and reporting ESG performance [45]. Additional topics for study include the rating, tracking, and planning of ESG indicators, use and misuse of ESG disclosures; firm culture, diversity, inclusion, and leadership changes; GHG emissions and social equity dimensions for the construction industry [10]. Moreover, the list of further research areas can embrace leadership and managerial aspects of implementing ESG; smart technologies on blockchain, digitization, and artificial intelligence for ESG implementation; insurance costs and impacts on small to medium-sized construction companies.

The outcomes of this study promote the inclusion of societal changes and social fabric within construction organisations and communities in which projects are constructed. As the world gravitates towards diversity and inclusive policies, project practices and performance evaluation will be shaped by ESG indicators [18,38]. Diversity and social inclusion policies in the construction industry will ensure everyone including communities and cultures is respected and integrated into the project management. Emphasis on reduction of wage losses, unemployment, improved education and better health and safety care are implemented within the construction sector. Greenwashing stands against societal ethics and regulations, and it is crucial that construction firms develop frameworks to address these ethical problems. The study has provided checklists for contractors to be aware and implement measures to mitigate them.

6. Conclusions

This study identified the major ESG indicators within the construction sector. The findings from this study based on past literature highlights the various ESG indicators in construction projects that aim at reaching sustainability targets in the construction industry. The results were classified into project, firm and industry (and/or national) indicators of ESG. Key indicators on ESG at these levels include lowest pollution and waste and green biodiversity (project level), present of ESG oversight and inclusive policies at the firm level, and robust regulations on climate change and government support at the industry and national levels. With respect to the four classified ESG pillars, the dominant indicators include climate resilient and green project practices (environmental indicators), high return investment and maximum current asset ratio (economic indicators), community involvement and stakeholder support (social indicators), and effective project governance and equitable labour laws (governance indicators). As explained in Section 4, these findings have significant implications for the policies, practice, society, the environment, and future studies. However, this study has inherent limitations. The main limitations of this study are the lack of application of these identified ESG indicators to practical project, firm and industry cases in construction project management. Theoretically, inadequate journal articles exist on the ESG indicators in the construction industry, and this is evident in the 26 articles used for this study. It is suggested that more studies should be conducted to deepen the theoretical underpinning of the concepts of ESG in the construction industry together with validation of empirical real-life project and firm data.

Appendix: Retrieved Articles for the Analysis

| Article (Authors, Year) |

| 1. Li, et al. [66] |

| 2. Mukhlisin, Ibrahim, Jaafar and Razali [31] |

| 3. Li, et al. [67] |

| 4. Baabou, Bjørn and Bulle [6] |

| 5. Wang, Zeng, Xia, Wu and Xia [36] |

| 6. Siew, Balatbat and Carmichael [32] |

| 7. Chastas, Theodosiou, Kontoleon and Bikas [39] |

| 8. Barykin, Strimovskaya, Sergeev, Borisoglebskaya, Dedyukhina, Srklyarov, Sklyarova and Saychenko [49] |

| 9. Hayashi, Hiyama and Kubo [16] |

| 10. Chen, Wang, He and Zhang [40] |

| 11. Musarat, Alaloul, Irfan, Sreenivasan and Rabbani [37] |

| 12. Lin and Zhang [68] |

| 13. Hadro, Fijałkowska, Daszyńska-Żygadło, Zumente and Mjakuškina [59] |

| 14. Siew [11] |

| 15. Aksenova, Kiviniemi, Kocaturk and Lejeune [5] |

| 16. De Castro, Pacheco and González [64] |

| 17. Norang, Støre-Valen, Kvale and Temeljotov-Salaj [9] |

| 18. Park, Kim, Lee, Kim and Kong [10] |

| 19. Apanaviciene, Daugeliene, Baltramonaitis and Maliene [38] |

| 20. Kempeneer, Peeters and Compernolle [13] |

| 21. Adewumi, et al. [69] |

| 22. Balon, et al. [70] |

| 23. Srivastava, et al. [71] |

| 24. Zhang, et al. [72] |

| 25. Singh and Kumar [73] |

| 26. Halder and Batra [74] |

Author Contributions

Conceptualization of the paper, literature review, methodology, data collection, cleaning and analysis, writing all done by all the authors: supervision and review of article Isaac Akomea-Frimpong. All authors have consented to the article by reading and agreeing to the manuscript.

Funding

This research has no funding support.

Data Availability Statement

Data for this article will be available upon request from the corresponding author.

Acknowledgments

Thank you for all comments from anonymous reviewers and editors in making this article rich.

Conflicts of Interest

The authors declare no conflicts of interest.

References

- Darnall, N.; Ji, H.; Iwata, K.; Arimura, T.H. Do ESG reporting guidelines and verifications enhance firms' information disclosure? Corporate Social Responsibility and Environmental Management 2022, 29, 1214–1230. [Google Scholar] [CrossRef]

- Akomea-Frimpong, I.; Agyekum, A.K.; Amoakwa, A.B.; Babon-Ayeng, P.; Pariafsai, F. Toward the attainment of climate-smart PPP infrastructure projects: a critical review and recommendations. Environment, Development and Sustainability 2023. [Google Scholar] [CrossRef]

- Chastas, P.; Theodosiou, T.; Kontoleon, K.J.; Bikas, D. The Effect of Embodied Impact on the Cost-Optimal Levels of Nearly Zero Energy Buildings: A Case Study of a Residential Building in Thessaloniki, Greece. Energies 2017, 10. [Google Scholar] [CrossRef]

- Bose, S. Evolution of ESG reporting frameworks. Values at Work: Sustainable Investing and ESG Reporting 2020, 13–33. [Google Scholar]

- Aksenova, G.; Kiviniemi, A.; Kocaturk, T.; Lejeune, A. From Finnish AEC knowledge ecosystem to business ecosystem: lessons learned from the national deployment of BIM. Construction management and economics 2019, 37, 317–335. [Google Scholar] [CrossRef]

- Baabou, W.; Bjørn, A.; Bulle, C. Absolute Environmental Sustainability of Materials Dissipation: Application for Construction Sector. Resources 2022, 11, 76. [Google Scholar] [CrossRef]

- Erkens, M.; Paugam, L.; Stolowy, H. Non-financial information: State of the art and research perspectives based on a bibliometric study. Comptabilité-Contrôle-Audit 2015, 21, 15–92. [Google Scholar] [CrossRef]

- Heal, M. Sustainability in Construction Practices as Emphasis on Environmental Investing in ESG Model Grows. 2022. [Google Scholar]

- Norang, H.; Støre-Valen, M.; Kvale, N.; Temeljotov-Salaj, A. Norwegian stakeholder's attitudes towards EU taxonomy. Facilities 2023, 41, 407–433. [Google Scholar] [CrossRef]

- Park, E.; Kim, Y.; Lee, A.; Kim, J.; Kong, H. Study on the Global Sustainability of the Korean Construction Industry Based on the GRI Standards. International Journal of Environmental Research and Public Health 2023, 20. [Google Scholar] [CrossRef]

- Siew, R.Y.J. Critical evaluation of environmental, social and governance disclosures of Malaysian property and construction companies. Construction Economics and Building 2017, 17, 81–91. [Google Scholar] [CrossRef]

- Yu, E.P.-y.; Van Luu, B.; Chen, C.H. Greenwashing in environmental, social and governance disclosures. Research in International Business and Finance 2020, 52, 101192. [Google Scholar] [CrossRef]

- Kempeneer, S.; Peeters, M.; Compernolle, T. Bringing the user Back in the building: an analysis of ESG in real estate and a behavioral framework to guide future research. Sustainability 2021, 13, 3239. [Google Scholar] [CrossRef]

- Zhao, E.; May, E.; Walker, P.D.; Surawski, N.C. Emissions life cycle assessment of charging infrastructures for electric buses. Sustain. Energy Technol. Assess. 2021, 48, 14. [Google Scholar] [CrossRef]

- Ebolor, A.; Agarwal, N.; Brem, A. Sustainable development in the construction industry: The role of frugal innovation. Journal of Cleaner Production 2022, 380. [Google Scholar] [CrossRef]

- Hayashi, T.; Hiyama, K.; Kubo, R. CASBEE-Wellness Office: An objective measure of the building potential for a healthily built environment. Japan Architectural Review 2021, 4, 233–240. [Google Scholar] [CrossRef]

- Chen, G.; Wei, B.; Dai, L. Can ESG-responsible investing attract sovereign wealth funds’ investments? Evidence from Chinese listed firms. Frontiers in Environmental Science 2022, 10, 935466. [Google Scholar] [CrossRef]

- Brogi, M.; Lagasio, V.; Porretta, P. Be good to be wise: Environmental, Social, and Governance awareness as a potential credit risk mitigation factor. Journal of International Financial Management & Accounting 2022, 33, 522–547. [Google Scholar]

- Clementino, E.; Perkins, R. How do companies respond to environmental, social and governance (ESG) ratings? Evidence from Italy. Journal of Business Ethics 2021, 171, 379–397. [Google Scholar] [CrossRef]

- Buniamin, S.; Nik Ahmad, N.N. An integrative perspective of environmental, social and governance (ESG) reporting: A conceptual paper. 2015. [Google Scholar]

- Page, M.J.; McKenzie, J.E.; Bossuyt, P.M.; Boutron, I.; Hoffmann, T.C.; Mulrow, C.D.; Shamseer, L.; Tetzlaff, J.M.; Akl, E.A.; Brennan, S.E. The PRISMA 2020 statement: an updated guideline for reporting systematic reviews. International Journal of Surgery 2021, 88, 105906. [Google Scholar] [CrossRef]

- Kukah, A.S.; Akomea-Frimpong, I.; Jin, X.; Osei-Kyei, R. Emotional intelligence (EI) research in the construction industry: a review and future directions. Engineering, Construction and Architectural Management, 2021; ahead-of-print. [Google Scholar]

- Jandrić, P. A peer-reviewed scholarly article. Postdigital Science and Education 2021, 3, 36–47. [Google Scholar] [CrossRef]

- Mahood, Q.; Van Eerd, D.; Irvin, E. Searching for grey literature for systematic reviews: challenges and benefits. Research synthesis methods 2014, 5, 221–234. [Google Scholar] [CrossRef] [PubMed]

- Brenya, R.; Akomea-Frimpong, I.; Ofosu, D.; Adeabah, D. Barriers to sustainable agribusiness: a systematic review and conceptual framework. Journal of Agribusiness in Developing and Emerging Economies 2022. [Google Scholar] [CrossRef]

- Panic, N.; Leoncini, E.; De Belvis, G.; Ricciardi, W.; Boccia, S. Evaluation of the endorsement of the preferred reporting items for systematic reviews and meta-analysis (PRISMA) statement on the quality of published systematic review and meta-analyses. PloS one 2013, 8, e83138. [Google Scholar] [CrossRef] [PubMed]

- Kukah, A.S.; Akomea-Frimpong, I.; Jin, X.; Osei-Kyei, R. Emotional intelligence (EI) research in the construction industry: a review and future directions. Engineering, Construction and Architectural Management 2022, 29, 4267–4286. [Google Scholar]

- Kennedy, R.A.; McKenzie, G.; Holmes, C.; Shields, N. Social support initiatives that facilitate exercise participation in community gyms for people with disability: a scoping review. International Journal of Environmental Research and Public Health 2022, 20, 699. [Google Scholar] [CrossRef] [PubMed]

- Chan, A.P.; Nwaogu, J.M.; Naslund, J.A. Mental ill-health risk factors in the construction industry: systematic review. Journal of construction engineering and management 2020, 146, 04020004. [Google Scholar] [CrossRef]

- Björk, B.-C.; Solomon, D. The publishing delay in scholarly peer-reviewed journals. Journal of informetrics 2013, 7, 914–923. [Google Scholar] [CrossRef]

- Mukhlisin, M.; Ibrahim, A.; Jaafar, O.; Razali, S.F.M. Electrochemical assessment of water quality as an effect of construction. Int.J.Electrochem.Sci. 2012, 7, 5467–5483. [Google Scholar] [CrossRef]

- Siew, R.Y.; Balatbat, M.C.; Carmichael, D.G. The relationship between sustainability practices and financial performance of construction companies. Smart Sustain. Built Environ. 2013, 2, 6–27. [Google Scholar] [CrossRef]

- Akomea-Frimpong, I.; Jin, X.; Osei-Kyei, R.; Kukah, A.S. Public–private partnerships for sustainable infrastructure development in Ghana: a systematic review and recommendations. Smart Sustain. Built Environ. 2023, 12, 237–257. [Google Scholar] [CrossRef]

- CHIA. An ESG Reporting Standard for Australian Community Housing; Community Housing Industry Association, 2023. [Google Scholar]

- Eisenkopf, J.; Juranek, S.; Walz, U. Responsible Investment and Stock Market Shocks: Short-Term Insurance without Persistence. British Journal of Management 2023, 34, 1420–1439. [Google Scholar] [CrossRef]

- Wang, G.; Zeng, S.; Xia, B.; Wu, G.; Xia, D. Influence of financial conditions on the environmental information disclosure of construction firms. Journal of Management in Engineering 2022, 38, 04021078. [Google Scholar] [CrossRef]

- Musarat, M.A.; Alaloul, W.S.; Irfan, M.; Sreenivasan, P.; Rabbani, M.B.A. Health and safety improvement through Industrial Revolution 4.0: Malaysian construction industry case. Sustainability 2022, 15, 201. [Google Scholar] [CrossRef]

- Apanaviciene, R.; Daugeliene, A.; Baltramonaitis, T.; Maliene, V. Sustainability Aspects of Real Estate Development: Lithuanian Case Study of Sports and Entertainment Arenas. Sustainability 2015, 7, 6497–6522. [Google Scholar] [CrossRef]

- Chastas, P.; Theodosiou, T.; Kontoleon, K.J.; Bikas, D. The effect of embodied impact on the cost-optimal levels of nearly zero energy buildings: A case study of a residential building in Thessaloniki, Greece. Energies 2017, 10, 740. [Google Scholar] [CrossRef]

- Chen, Y.; Wang, G.; He, Y.; Zhang, H. Greenwashing behaviors in construction projects: there is an elephant in the room! Environmental Science and Pollution Research 2022, 29, 64597–64621. [Google Scholar] [CrossRef] [PubMed]

- Emmitt, S.; Ruikar, K. Collaborative design management; Routledge, 2013. [Google Scholar]

- Huang, R.; Huang, Y. Does internal control contribute to a firm’s green information disclosure? Evidence from China. Sustainability 2020, 12, 3197. [Google Scholar] [CrossRef]

- Paganin, G. Sustainable finance and the construction industry: New paradigms for design development. Techne 2021, 22, 79–85. [Google Scholar] [CrossRef]

- He, Q.; Wang, Z.; Wang, G.; Zuo, J.; Wu, G.; Liu, B. To be green or not to be: How environmental regulations shape contractor greenwashing behaviors in construction projects. Sustainable Cities and Society 2020, 63, 102462. [Google Scholar] [CrossRef]

- Friedman, H.L.; Heinle, M.S.; Luneva, I.M. A theoretical framework for ESG reporting to investors. Available at SSRN 3932689 2021. [Google Scholar]

- Kim, J.; Lee, Y. Association between Earnings Announcement Behaviors and ESG Performances. Sustainability 2023, 15, 7733. [Google Scholar] [CrossRef]

- Deamer, L.; Lee, J.; Mulheron, M.; De Waele, J. Building sustainability impacts from the bottom up: Identifying sustainability impacts throughout a geotechnical company. Sustainability (Switzerland) 2021, 13. [Google Scholar] [CrossRef]

- Cao, Y.; Xu, C.; Kamaruzzaman, S.N.; Aziz, N.M. A systematic review of green building development in China: Advantages, challenges and future directions. Sustainability 2022, 14, 12293. [Google Scholar] [CrossRef]

- Barykin, S.E.; Strimovskaya, A.V.; Sergeev, S.M.; Borisoglebskaya, L.N.; Dedyukhina, N.; Srklyarov, I.; Sklyarova, J.; Saychenko, L. Smart City Logistics on the Basis of Digital Tools for ESG Goals Achievement. Sustainability 2023, 15, 5507. [Google Scholar] [CrossRef]

- Gillan, S.L.; Koch, A.; Starks, L.T. Firms and social responsibility: A review of ESG and CSR research in corporate finance. Journal of Corporate Finance 2021, 66, 101889. [Google Scholar] [CrossRef]

- Yue, X.; Han, Y.; Teresiene, D.; Merkyte, J.; Liu, W. Sustainable funds’ performance evaluation. Sustainability 2020, 12, 8034. [Google Scholar] [CrossRef]

- Giamporcaro, S.; Gond, J.-P.; O’Sullivan, N. Orchestrating governmental corporate social responsibility interventions through financial markets: The case of French socially responsible investment. Business Ethics Quarterly 2020, 30, 288–334. [Google Scholar] [CrossRef]

- Brice, J.; Cusworth, G.; Lorimer, J.; Garnett, T. Immaterial animals and financialized forests: Asset manager capitalism, ESG integration and the politics of livestock. Environment and Planning A: Economy and Space 2022, 54, 1551–1568. [Google Scholar] [CrossRef]

- Lokuwaduge, C.S.; De Silva, K.M. ESG risk disclosure and the risk of green washing. Australasian Accounting, Business and Finance Journal 2022, 16, 146–159. [Google Scholar] [CrossRef]

- EY. The current state of ESG reporting in the engineering and construction industry; 2021. [Google Scholar]

- Gałecka-Drozda, A.; Wilkaniec, A.; Szczepańska, M.; Świerk, D. Potential nature-based solutions and greenwashing to generate green spaces: Developers’ claims versus reality in new housing offers. Urban Forestry & Urban Greening 2021, 65, 127345. [Google Scholar]

- Akerlof, G.A. The market for “lemons”: Quality uncertainty and the market mechanism. In Uncertainty in economics; Elsevier, 1978; pp. 235–251. [Google Scholar]

- Zhang, K.; Pan, Z.; Janardhanan, M.; Patel, I. Relationship analysis between greenwashing and environmental performance. Environment, Development and Sustainability 2023, 25, 7927–7957. [Google Scholar] [CrossRef]

- Hadro, D.; Fijałkowska, J.; Daszyńska-Żygadło, K.; Zumente, I.; Mjakuškina, S. What do stakeholders in the construction industry look for in non-financial disclosure and what do they get? Meditari Accountancy Research 2022, 30, 762–785. [Google Scholar] [CrossRef]

- Galvin, P. Building Blocks of the Future Our Story: How My Company Developed Modular Construction with Recycled Shipping Containers is Advancing Solutions to the Affordable Housing Crisis and Environmental Sustainability. Real Estate Issues 2020, 44, 1–8. [Google Scholar]

- Siano, A.; Vollero, A.; Conte, F.; Amabile, S. “More than words”: Expanding the taxonomy of greenwashing after the Volkswagen scandal. Journal of Business Research 2017, 71, 27–37. [Google Scholar] [CrossRef]

- Lyon, T.P.; Maxwell, J.W. Greenwash: Corporate environmental disclosure under threat of audit. Journal of economics & management strategy 2011, 20, 3–41. [Google Scholar]

- Marquis, C.; Toffel, M.W.; Zhou, Y. Scrutiny, norms, and selective disclosure: A global study of greenwashing. Organization Science 2016, 27, 483–504. [Google Scholar] [CrossRef]

- De Castro, A.V.; Pacheco, G.R.; González, F.J.N. Holistic approach to the sustainable commercial property business: analysis of the main existing sustainability certifications. International Journal of Strategic Property Management 2020, 24, 251–268. [Google Scholar] [CrossRef]

- Willan, C.; Janda, K.B.; Kenington, D. Seeking the Pressure Points: Catalysing Low Carbon Changes from the Middle-Out in Offices and Schools. Energies 2021, 14, 8087. [Google Scholar] [CrossRef]

- Li, R.Y.M.; Li, B.; Zhu, X.; Zhao, J.; Pu, R.; Song, L. Modularity clustering of economic development and ESG attributes in prefabricated building research. Frontiers in Environmental Science 2022, 10, 977887. [Google Scholar] [CrossRef]

- Li, X.; Huang, Y.; Li, X.; Liu, X.; Li, J.; He, J.; Dai, J. How does the Belt and Road policy affect the level of green development? A quasi-natural experimental study considering the CO2 emission intensity of construction enterprises. Humanities & Social Sciences Communications 2022, 9. [Google Scholar] [CrossRef]

- Lin, Y.-H.; Zhang, H. Impact of contractual governance and guanxi on contractors’ environmental behaviors: The mediating role of trust. Journal of Cleaner Production 2023, 382, 135277. [Google Scholar] [CrossRef]

- Adewumi, A.S.; Opoku, A.; Dangana, Z. Sustainability assessment frameworks for delivering Environmental, Social, and Governance (ESG) targets: A case of Building Research Establishment Environmental Assessment Method (BREEAM) UK New Construction. Corporate Social Responsibility and Environmental Management 2024. [Google Scholar] [CrossRef]

- Balon, V.; Bagul, A.; Kumar, R. Green construction supply chain barriers assessment: Evidence from Indian construction industry. Global Business Review 2024, 09721509241231107. [Google Scholar] [CrossRef]

- Srivastava, S.; Iyer-Raniga, U.; Misra, S. Integrated approach for sustainability assessment and reporting for civil infrastructures projects: Delivering the UN SDGs. Journal of Cleaner Production 2024, 459, 142400. [Google Scholar] [CrossRef]

- Zhang, F.; Liu, B.; An, G. Do Government Subsidies Induce Green Transition of Construction Industry? Evidence from Listed Firms in China. Buildings 2024, 14, 1261. [Google Scholar] [CrossRef]

- Singh, A.K.; Kumar, V.P. Establishing the relationship between the strategic factors influencing blockchain technology deployment for achieving SDG and ESG objectives during infrastructure development: an ISM-MICMAC approach. Smart Sustain. Built Environ. 2024, 13, 711–736. [Google Scholar] [CrossRef]

- Halder, A.; Batra, S. Navigating the Ethical Discourse in Construction: A State-of-the-Art Review of Relevant Literature. Journal of Construction Engineering and Management 2024, 150, 03124001. [Google Scholar] [CrossRef]

Figure 1.

Geographical location of the studies.

Figure 2.

Different projects identified in the papers.

Figure 3.

Methods of research used in the articles.

Figure 4.

Principal ESG indicators.

Table 1.

ESG indicators for the construction industry.

| S/N | ESG indicator | Explanation | Source (refer to Table 1) |

|---|---|---|---|

| ESG1 | Climate resilient | Ability of projects to cope with changing weather conditions | [1,2,3,8,10,14,26] |

| ESG2 | Ecological adaptation score | High survival of organisms in an area where a project is built | [1,9,20,22] |

| ESG3 | Efficient project resource management | Maximum and efficient usage of project resources which includes the protection of the environment | [4,7,8,9,11,18,19,21] |

| ESG4 | Affordability and Security measure | Affordable houses for low-income earners | [1,3,16,23] |

| ESG5 | Resident Voice | Concerns of residents and communities are incorporated in ESG framework | [1,11,22,24] |

| ESG6 | Resident Support | Initiatives from builders are supported by the residents and the community. | [7,9,21,25] |

| ESG7 | Collaborative placemaking | More emphasis on the needs of the people who will use the building space | [6,9,13,21,26] |

| ESG8 | Effective corporate systems and controls on governance | The overall structure and approach to governance on ESG implementation | [1,4,6,7,13,14,21,23] |

| ESG9 | Reliable supply chain of construction materials | The housing provider procures responsibly, considering supplier diversity and screening and sustainable procurement practices | [4,8,11,21,25] |

| ESG10 | Environment Management Systems | The practices and established systems to mitigate the environment impact of projects | [3,9,10,19,20] |

| ESG11 | Stakeholder Engagement/ Collaboration | Getting stakeholders to be part of ESG conversation and implementation | [3,4,7,11,14,15] |

| ESG12 | Diversity and inclusion | An open and inclusive work culture | [3,5,9,13] |

| ESG13 | Green biodiversity | This involves developing natural land by restricting some operations to protect plant and animal life | [2,7,9,10,15,17] |

| ESG14 | Lowest waste and Pollution | Few records of wastes and hazardous air pollution | [1,3,4,5,9,12,15,16,17,19,20] |

| ESG15 | Charity and Community Engagement/ Volunteering and Probono Work | This could be in a form of donations and support to various charitable and education-related organisations on a pro-bono basis. | [5,7,9,12] |

| ESG16 | Additional Employment/ Local jobs creation | Providing job opportunities for locals where projects are developed | [1,2,9,10,14,19] |

| ESG17 | Enhancement of professional social and skill development | Continuous training and development of project team members on ESG | [2,14,15,22,25] |

| ESG18 | Positive health status of project teams | Active consideration of the health and wellbeing of project staff including managers and construction workers | [1,2,3,4,5,6,7,8,9,10,22] |

| ESG19 | Minimum carbon emissions | This involves reducing the overall carbon footprint of projects | [1,2,5,7,8,19,24] |

| ESG20 | Robust policies and guidance documentation | These documents govern business activities | [1,2,3,15] |

| ESG21 | Energy consumption/saving rate | Total amount of energy needed for a given process measured in MWh | [3,5,6,7,9,11,12,17,19,20] |

| ESG22 | Least greenhouse gas effects | Minimum of carbon emissions into the environment | [2,5,7,9,12,13,14,16,17,18,19,20] |

| ESG23 | Compliance with environmental regulations and standards | The extent to which the environmental regulations and standards are adhered to by firms | [7,9,21,25] |

| ESG24 | Voluntary environmental practices beyond compliance | Projects should have environment impact levels below the standard limits | [8,10,11,19,21] |

| ESG25 | Level of environmental awareness training and programs | Construction workers and connected stakeholders are trained and influenced by sustainable environmental practices | [6,7,9,12,13,23] |

| ESG26 | Environmental information disclosure score | The level at which environmental information of a project is disclosed against the ESG global standards considered relevant in the industry | [3,7,10,20,25] |

| ESG27 | High return on investment | High ratio between the net income of projects and investments | [8,10,14,21,26] |

| ESG28 | Current assets to liabilities score | Dividing total present assets by recent liabilities incurred | [8,14,16,20,21] |

| ESG29 | Summary of the stakes in the firms | Percentage of ownership of the firm’s green assets | [7,9,16,25] |

| ESG30 | Total assets of the firm | Gross assets of a firm inclusive of environmental and social capital | 13, 14, 20, 15, 10] |

| ESG31 | Longevity of firm existence | The length of firm inception to present | [7,14,15,21] |

| ESG32 | Cost-benefit analysis score | A score to assess the economic viability of methodologies used in projects | [7,11,17,18,19,20,23,25] |

| ESG33 | Firm procurement decisions | The choices made by firms when procuring services affect the environment | [6,11,13,24] |

| ESG34 | Anti-discrimination and equal opportunity | Avoiding the distinction between employees to disadvantage some and advantage others | [6,17,18,21] |

| ESG35 | Gender balance | Percentage of full-time employment, contractor and consultant positions held by women | [3,6,19,20,25] |

| ESG36 | Risk and credit rating score | The potential risks associated with a project and the possible benefits of a project | [1,3,4,7,8,13,20] |

| ESG37 | Level of employee engagement | The degree to which employees identify with the goals and values of the organization | [5,7,10,23] |

| ESG38 | Extent of community investment | The measure of how much is invested into communities enduring the impacts of activities from firms | [5,7,10,19,26] |

| ESG39 | Board independence | Availability of independent directors to avoid being unduly influenced by a vested interest | [1,3,5,14,20] |

| ESG40 | Executive compensation | Commendable cash and non-financial benefits to top leaders who are committed to implementation of ESG in project management | [1,5,9,13,17] |

| ESG41 | Ethics and compliance training | Training to educate employees about the rules, regulations, and new policies they should adhere to | [3,5,7,8,10,18,22,25] |

| ESG42 | Count of data privacy and security breaches | Measure of the rate at which unauthorized parties gain access to sensitive data of a firm | [5,9,12,20] |

| ESG43 | Supplier audits | Availability of deliberate plans and controls on purchasing and supply risks | [5,8,14,15,21] |

| ESG44 | Sustainable growth rate | The measure of maximum rate of growth that a company can sustain without additional debt | [4,6,11,14,26] |

| ESG45 | Environmental efficiency | Reducing environmental destruction as much as possible while providing the expected deliverables | [10,14,17,20] |

| ESG46 | Recycled greenhouse gas | This involves capturing more greenhouse gases than releasing | [2,7,9,15,21] |

| ESG47 | Level of drainage contamination | How projects lead to the contamination drainage systems in the communities | [1,6,15,26] |

| ESG48 | Application of circular economy scores | Circular Economy Score considers several parameters for each of the 5 pillars, and the outcome is a value between 0 and 100 | [4,11,15,25] |

| ESG49 | Extent of accountability | The level at which responsibility is accepted for honest and ethical conduct towards others by the firm | [1,2,7,15,20] |

| ESG50 | Lifecycle rating of projects | Rating the projects across the various stages of the project lifecycle phases | [9,15,16,21] |

| ESG51 | Green development | Incorporation of green construction practices into project development. | [16,17,18,19,22] |

| ESG52 | Labour productivity | The total volume of output per unit labour of a firm | [2,4,6,16] |

| ESG53 | Process improvement | Regular upward improvement in processes towards the achievement ESG goals | [1,5,7,16] |

| ESG54 | Achievable project goals | These are stipulated project goals which are specific and achievable | [2,5,7,16] |

| ESG55 | Use of renewable energies | The use of renewable energies in place of fossil fuels during and after project delivery | [7,11,17,19] |

| ESG56 | Promotion of basic human rights | Enforcing and ensuring fundamental rights of employees and stakeholders | [3,5,6,7,9,16] |

| ESG57 | Food security | The measure of the ability of Individuals to access nutritious and sufficient food | [4,10,17,22] |

| ESG58 | Eradication of modern slavery | Avoiding the exploitation of employees and individuals in the community for commercial gains of the project | [7,12,19] |

| ESG59 | Sustainable infrastructure | Undertaking projects which considers the social, economic, and environmental implications | [2,7,15,20] |

| ESG60 | LEED-certified projects | Green construction activities on projects happen within the requirements of LEED framework. | [2,7,9,16] |

| ESG61 | Disaster recovery and response | The rate at which a firm recovers from a disaster or manages a disaster for minimum negative impacts | [1,5,7,25] |

| ESG62 | Smart engineering and technology solutions | A method, processes, and IT tools to design and develop innovative infrastructure | [4,6,7,8,18] |

| ESG63 | Employee attraction and retention | Finding the right kind of people that fit into your company ethos while creating structure, processes, and procedures that keep your employees engaged and working for your firm | [2,8,18,23,26] |

| ESG64 | Presence of ESG Oversight | Regulatory compliance; formal ESG oversight structures; reporting and transparency | [1,6,8,9,11,15] |

| ESG65 | Minimum records of greenwashing (behaviour) | Greenwashing is the overstatement of the environmental and social credentials of an organisation or product | [1,2,4,6,16] |

| ESG66 | Innovation | This could be in a form of embracing new technologies in the industry | [4,5,7,10,19] |

| ESG67 | Balance ecosystem | Provision of projects that support a natural habitat which is sustainable and where there is interdependency | [5,8,11,17] |

| ESG68 | Preserve cultural heritage | Keeping the artifacts and traditions of a community intact while projects are developed | [2,3,6,18] |

| ESG69 | Economic prosperity | The measure of the economic growth, economic security, and economic competitiveness of a firm | [2,7,8,22,25] |

| ESG70 | Enough economic capital | Ensuring that the amount of capital that needed to survive any risks that the firm takes is adequate | [1,7,8,14] |

| ESG71 | Gender pays ratio | Median male salary to median female salary | [2,5,6,23,24] |

| ESG72 | Temporary worker rate | Percentage of full-time positions held by part-time/contract/temporary workers. | [6,15,23,25] |

| ESG73 | Non-discrimination records | This ensures that no one is denied their rights because of certain factors like race and gender | [1,3,13,22] |

| ESG74 | Incentivized pay to construction workers | Additional compensation awarded to construction workers for results they achieved | [1,3,5,17,24] |

| ESG75 | Fair labour practices | Practices that guarantee the equitable and unbiased protection of both employers and employees | [2,3,4,7,21] |

| ESG76 | Supplier code of conduct | Eco-friendly supply chain channels together with respectful and fair workplace for employees. | [3,8,13] |

| ESG77 | Robust internal systems against corruption | There are explicit codes of ethics and governance structures against corruption of all forms | [3,7,10,12] |

| ESG78 | Regular sustainability reports | Regular reporting on the environmental, social, and economic risks and opportunities of a firm | [3,7,9,11,17,18,19,26] |

| ESG79 | External stakeholder assurance | Ensure the interests of different stakeholders are satisfied | [3,4,15,16,21] |

| ESG80 | Effective management and supervision | Measure of the output of employees based on direction, guidance, and control of the working force by management | [2,4,10,11,13] |

| ESG81 | Requirements on ESG are clearly transparent | Open disclosure of ESG requirements for construction firms to follow | [3,4,7,23] |

| ESG82 | Overall firm performance | The total performance of a firm inters of profits, growth, customer satisfaction and sustainability | [2,8,13,18] |

| ESG83 | User satisfaction ratings | This measures a customer's satisfaction with an organization | [1,4,6,18,24] |

| ESG84 | Increased quality of life | The level of satisfaction of employees across all aspects of their lives and well-being | [1,4,9,18,19] |

| ESG85 | Acceptable level of heat and the cooling of indoors of the projects | The acceptable level of heating and the cooling of the building for minimum environmental impacts | [6,7,8,20] |

| ESG86 | Reduction of economic and social disparities between regions | Reducing the unequal distribution of income and opportunity between different groups in society | [2,5,12,19,20] |

| ESG87 | Decreasing rate of poverty | Reducing the ratio of the number of people in each community whose income falls below the poverty line | [1,4,8,19,25] |

| ESG88 | Social inclusion and cohesion | A measure of how all groups have a sense of belonging, participation, inclusion, recognition, and legitimacy. | [2,3,8,19,24] |

| ESG89 | Sustainable property investment | Investing in projects which are sustainable and environmentally friendly both during construction and in use | [1,6,17,19,24] |

| ESG90 | Regulation and compliance requirements | A construction firm adheres to council regulations and local practices | [2,9,10,15,25] |

| ESG91 | Rate of client cancellations and delays | The rate at which projects are delayed by firms and the potential of project cancellation by clients | [1,3,7,10,15] |

| ESG92 | Technological readiness | The proclivity of employees to embrace and use new technologies for sustainable projects | [2,9,12,18,23] |

| ESG93 | Social innovativeness | Design and implementation of modern solutions to enhance the wellbeing and welfare of communities | [2,18,19,23] |

| ESG94 | Green carbon-neutral badge | Application of environmentally conscious technologies and software platforms to monitor ESG performance and LEED compliance in projects. | [1,12,14] |

| ESG95 | Fair and equitable compensation to workers. | Employees are remunerated fairly. | [1,2,5,7,8] |

| ESG96 | Government involvement and advocacy | litigation, lobbying, and public education on ESG by government | [1,3,21] |

Table 2.

Classification of the ESG indicators at different levels of analysis.

| Principal variable | S/N | Specific variable | Level of analysis | ||

|---|---|---|---|---|---|

| Project level | Firm level | Meso-macro level | |||

| Environmental indicators | ESGE | ||||

| ESG1 | Climate resilient | X | |||

| ESG2 | Ecological adaptation score | X | |||

| ESG9 | Reliable supply chain of construction materials | X | |||

| ESG10 | Environment Management Systems | X | X | ||

| ESG13 | Green biodiversity | X | |||

| ESG14 | Lowest waste and Pollution | X | |||

| ESG19 | Minimum carbon emissions | X | |||

| ESG21 | Energy consumption/saving rate | X | |||

| ESG22 | Least greenhouse gas effects | X | |||

| ESG23 | Compliance with environmental regulations and standards | X | X | ||

| ESG24 | Voluntary environmental practices beyond compliance | X | X | ||

| ESG25 | Level of environmental awareness training and programs | X | |||

| ESG26 | Environmental information disclosure score | X | |||

| ESG43 | Supplier audits | X | |||

| ESG44 | Sustainable growth rate | X | X | ||

| ESG45 | Environmental efficiency | X | X | ||

| ESG46 | Recycled greenhouse gas | X | |||

| ESG47 | Level of drainage contamination | X | |||

| ESG51 | Green development | X | X | ||

| ESG55 | Use of renewable energies | X | |||

| ESG57 | Food security | X | |||

| ESG60 | LEED-certified projects | X | |||

| ESG61 | Disaster recovery and response | X | X | ||

| ESG62 | Smart engineering and technology solutions | X | X | ||

| ESG67 | Balance ecosystem | X | X | ||

| ESG76 | Supplier code of conduct | X | |||

| ESG85 | Acceptable level of heating and the cooling of the building | X | |||

| ESG94 | Green carbon-neutral badge | X | |||

| Economic indicators | ESGEc | ||||

| ESG27 | High return on investment | X | X | ||

| ESG28 | Current assets to liabilities score | X | |||

| ESG29 | Summary of the stakes in the firms | X | |||

| ESG30 | Total assets of the firm | X | |||

| ESG31 | Longevity of firm existence | X | |||

| ESG32 | Cost-benefit analysis score | X | X | ||

| ESG52 | Labour productivity | X | X | ||

| ESG69 | Economic prosperity | X | |||

| ESG70 | Enough economic capital | X | X | ||

| ESG74 | Incentivized pay to construction workers | X | |||

| ESG86 | Reduction of economic and social disparities between regions | X | |||

| ESG87 | Decreasing rate of poverty | X | |||

| ESG89 | Sustainable property investment | X | |||

| ESG95 | Fair and equitable compensation to workers | X | |||

| Governance indicators | ESGG | ||||

| ESG3 | Efficient project resource management | X | |||

| ESG8 | Effective corporate systems and controls on governance | X | |||

| ESG20 | Robust policies and guidance documentation | X | X | ||

| ESG33 | Firm procurement decisions | X | |||

| ESG36 | Risk and credit rating score | X | X | ||

| ESG39 | Board independence | X | |||

| ESG40 | Executive compensation | X | |||

| ESG41 | Ethics and compliance training | X | X | ||

| ESG42 | Count of data privacy and security breaches | X | X | ||

| ESG48 | Application of circular economy scores | X | |||

| ESG49 | Extent of accountability | X | |||

| ESG50 | Lifecycle rating of projects | X | |||

| ESG53 | Process improvement | X | X | ||

| ESG54 | Achievable project goals | X | |||

| ESG64 | Presence of ESG oversight | X | X | ||

| ESG65 | Minimum records of greenwashing (behaviour) | X | |||

| ESG66 | Innovation | X | X | ||

| ESG77 | Robust internal systems against corruption | X | |||

| ESG78 | Regular sustainability reports | X | X | ||

| ESG80 | Effective management and supervision | X | |||

| ESG81 | Requirements on ESG are clearly transparent | X | X | ||

| ESG82 | Overall firm performance | X | |||

| ESG90 | Regulation and compliance requirements | X | X | X | |

| ESG92 | Technological readiness | X | X | ||

| ESG96 | Government involvement and advocacy | X | |||

| Social indicators | ESGS | ||||

| ESG4 | Affordability and Security measure | X | |||

| ESG5 | Resident Voice | X | |||

| ESG6 | Resident Support | X | |||

| ESG7 | Collaborative placemaking | X | X | ||

| ESG11 | Stakeholder Engagement/ Collaboration | X | X | ||

| ESG12 | Diversity and inclusion | X | X | ||

| ESG15 | Charity and Community Engagement/ Volunteering and Probono Work | X | X | ||

| ESG16 | Additional Employment/ Local jobs creation | X | |||

| ESG17 | Enhancement of professional social and skill development | X | X | ||

| ESG18 | Positive health status of project teams | X | |||

| ESG34 | Anti-discrimination and equal opportunity | X | |||

| ESG35 | Gender balance | X | |||

| ESG37 | Level of employee engagement | X | X | ||

| ESG38 | Extent of community investment | X | X | ||

| ESG56 | Promotion of basic human rights | X | X | ||

| ESG58 | Eradication of modern slavery | X | |||

| ESG59 | Sustainable infrastructure | X | X | ||

| ESG63 | Employee attraction and retention | X | X | ||

| ESG68 | Preserve cultural heritage | X | X | ||

| ESG71 | Gender pays ratio | X | |||

| ESG72 | Temporary worker rate | X | X | ||

| ESG73 | Non-discrimination records | X | |||

| ESG75 | Fair labour practices | X | X | ||

| ESG79 | External stakeholder assurance | X | |||

| ESG83 | User satisfaction ratings | X | |||

| ESG84 | Increased quality of life | X | |||

| ESG88 | Social inclusion and cohesion | X | |||

| ESG91 | Rate of client cancellations and delays | X | |||

| ESG93 | Social innovativeness | X | X | ||

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Copyright: This open access article is published under a Creative Commons CC BY 4.0 license, which permit the free download, distribution, and reuse, provided that the author and preprint are cited in any reuse.