Submitted:

03 September 2024

Posted:

04 September 2024

You are already at the latest version

Abstract

The purpose of this paper is to show how the self-exciting threshold autoregressive (SETAR) model could be an appropriate econometric framework for characterizing the dynamics of the U.S. public debt/GDP ratio after the Bretton Woods collapse. Our preferred SETAR specifications are capable in capturing the main stylized facts of the U.S. public debt/GDP ratio between 1974 and 2024. In addition, the estimated SETAR models are consistent with several theoretical frameworks that seek to explain the behavior of the U.S. public debt/GDP ratio before and after the Global Financial Crisis (GFC). Finally, the paper provides some arguments on why the previous studies that use the exponential smooth threshold autoregressive (ESTAR) models, or SETAR-type models for the first differences of the U.S. public debt/GDP ratio, are potentially mis-specified, both on econometric and economic grounds.

Keywords:

SETAR model

; United States

; sovereign debt

; persistence

; non-linear fiscal adjustment

MSC: 62M10; 91B84

1. Introduction

In a comprehensive review on the use of threshold autoregressions (TAR) and self-exciting threshold autoregressions (SETAR) in economics, Hansen (2011) [1] provides an overview of 75 papers that employ (SE)TAR econometric framework in modeling and forecasting output growth, interest rates, prices, stock returns and exchange rates. This paper shows how SETAR methodology can be particularly useful in modeling asymmetries in the dynamics of public debt/GDP ratio. We focus on modeling non-linearities in the U.S. public debt/GDP ratio after the Bretton Woods collapse. Not only that our estimated two-regime and three-regime SETAR specifications are capable in capturing stylized facts of the U.S. public debt/GDP ratio between 1974Q1and 2024Q1, but they are also consistent with several theoretical predictions regarding the behavior of the U.S. public debt, starting, most notably, from the seminal paper by Barro (1979) [2]. Finally, we also show how previous contributions that use the exponential smooth transition autoregression (ESTAR) model and the SETAR model for the first differenced U.S. public debt/GDP ratio are potentially mis-specified on both econometric and economic grounds.

To acquaint the reader with the previous literature on public debt behavior in the case of the United States, we organize the rest of the introductory section by reviewing the literature on potential non-stationarity of the U.S. public debt/GDP ratio first, and then discuss papers that model the non-linearities in the dynamics of the U.S. public debt. As Bec et al. (2004) [3] caution, establishing the stationarity of the time series in question prior to estimating the appropriate SETAR model is essential, since the underlying econometric methods developed in Hansen (1996, 1997, 2017) [4,5,6], González and Gonzalo (1997) [7] and Gonzalo and Pitarakis (2002) [8] rest crucially on the ergodicity and global stationarity assumptions for the stochastic process under investigation.

Persistence

Barro (1979) [2] was the first to claim that there are no underlying economic forces that would cause public debt/GDP ratio to converge to some steady-state target value. In other words, in Barro’s (1979) [2] tax smoothing model, the U.S. public debt behaves like a random walk after World War I. The public debt/GDP ratio exhibits unpredictable movements governed only by transitory government spending (mostly during wars) and countercyclical output shocks (mostly during recessions). There is also no effect of both unanticipated and expected (anticipated) inflation on the public debt/GDP ratio. The stated results do not change regardless of whether one measures public debt at nominal (par) or market values.

Hamilton and Flavin (1986) [9] refute Barro’s (1979) [2] conclusion that the U.S. public debt/GDP ratio exhibits random walk-type behavior, although for a much shorter period spanning from 1960 to 1984. By applying the standard Dickey-Fuller unit root test of Dickey and Fuller (1981) [10], Hamilton and Flavin (1986) [9] reject the unit root non-stationarity hypothesis for the U.S. public debt/GDP ratio at 10% significance level

Kremers (1988) [11], however, shows that the non-stationarity of the U.S. public debt/GDP ratio cannot be rejected in the post-World War II data. Contrary to Hamilton and Flavin (1986) [9], Kremers (1988) [11] implements an augmented Dickey-Fuller unit root test to appropriately model the autocorrelation present in the residual values of the U.S. public debt-to-GDP ratio, and consequently overturns the results of Hamilton and Flavin (1986) [9] by not being able to reject the non-stationarity hypothesis at any critical level of up to 90%. In addition, Kremers (1989) [12] further shows that even for the combined inter- and post-war period one cannot firmly reject the non-stationarity hypothesis in the case of the U.S. public debt/GDP ratio.

Wilcox (1989) [13] argues that the U.S. public indebtedness measure that Hamilton and Flavin (1986) [9] use is inappropriate since it rests on the undiscounted public debt. Contrary to Hamilton and Flavin (1986) [9], Wilcox (1989) [13] calculates the discounted value of the U.S. public debt where the present value of the public debt at a particular point in time is calculated using stochastic real interest rates. Wilcox (1989) [13] uses the discounted value of the U.S. government debt to define a public debt sustainability criterion which states that overall fiscal policy is sustainable if the projected discounted value of the public debt/GDP ratio approaches zero, i.e., if the expected present value of the sum of future primary surpluses equals the current market value of the U.S. public debt. As in Hamilton and Flavin (1986) [9], Wilcox (1989) [13] operationalizes his sustainability criterion by comparing the current market value of the public debt with the sum of expected discounted primary surpluses and denotes the difference between the two as where is the market value of public debt and is the stochastic interest rate measured in real terms. Wilcox (1989) [13] further argues that the behavior of is influenced by the behavior of -if is non-stationary, then is stochastic, and if is stationary, then is constant. The conclusion of Wilcox (1989) [13] is that for the period after 1974, the discounted market value of the U.S. public debt is non-stationary.

Given the inconclusive evidence of previous unit root studies in assessing the sustainability of the U.S. public debt, Bohn (1998, 2007) [14,15] criticizes a unit root-type regressions on two grounds. First, Bohn (1998) [14] argues that unit root test regression suffers from an omitted variable bias since they do not account for the cyclical output changes and transitory government spending. By aiming to explain the variations in the primary fiscal balance as a function of movements in the public debt, output gap and transitory government spending, Bohn (1998) [14] proposes a fiscal reaction function (FRF) regression approach to test for the mean-reversion in the stochastic process for the U.S. public debt. Using the data for the United States between 1916 and 1995, Bohn (1998) [14] concludes that the U.S. public debt/GDP ratio behaves as highly persistent, but overall mean-reverting, stationary stochastic process. Regardless of how interest rates and growth rates compare, a positive response of the primary fiscal balance to public debt movements represents a sufficient condition for public debt sustainability, since any upward movement in public debt/GDP ratio would be reversed with positive primary fiscal balance response.

Second, the sustainability notion of Wilcox (1989) [13], , is always satisfied, since the exponential growth in the denominator asymptotically dominates the polynomial growth in the numerator irrespective of the order of integration for -see Proposition 1 on page 1840 of Bohn (2007) [15] for a detailed proof.

Contrary to Bohn (1998) [14], who estimates a single equation ordinary least squares (OLS) FRF, Cochrane (2020, 2022) [16,17] estimates a vector autoregressive (VAR) model with public debt and primary fiscal surplus and finds a 0.98 value for the first lag debt coefficient. In other words, Cochrane (2020, 2022) [16,17] reaffirms the findings of Bohn (1998) [14] that public debt/GDP ratio is stationary, but highly persistent, near-unit root stochastic process.

On the other hand, Campbell et al. (2023) [18] argue that the U.S. public debt/GDP ratio after the World War II must be non-stationary since it has little ability to predict its own dynamics, as well as future fiscal developments in taxes and spending. Campbell et al. (2023) [18] instead propose a stationary government surplus/debt ratio as a useful predictor of future fiscal outcomes.

Finally, although Jiang et al. (2024) [19] find that the U.S. public debt/GDP ratio is persistent, close to a unit root, stochastic process, the authors exclude the possibility that there is an actual unit root in the autoregressive representation for the public debt/GDP ratio on several grounds. First, a non-stationary public debt/GDP would breach any upper bound given an arbitrarily long forecast horizon. Second, a unit root stochastic process would also imply an ever-increasing variance of the public debt/GDP ratio with the passage of time. Third, large increases in the public debt/GDP ratio in the U.S. fiscal history were usually followed by i) discretionary fiscal adjustments; ii) high inflation; iii) financial repression in the form of interest rate caps on government borrowing; or iv) corrections in market prices of government bonds. In sum, Jiang et al. (2024) [19] conclude that the U.S. public debt/GDP ratio exhibits highly persistent, near-unit root, behavior, but more importantly, the authors contribute such autocorrelation profile to the 2007 structural break due to the Global Financial Crisis (GFC). However, as Jiang et al. (2024) [19] acknowledge themselves, the timing of the structural break is exogenous to the dynamics of public debt/GDP ratio.

The reader should note at this point that even if the timing of the 2007 structural break had been endogenous, i.e., explained by the underlying forces that govern the dynamics of public debt/GDP ratio, Carrasco (2002) [20] warns that endogenous structural change tests have no power if the data are generated by a non-linear threshold-type model. Putted differently, the non-linear threshold-type tests for parameter stability have greater power in comparison to tests that deal with structural change in parameters. Consequently, Carrasco (2002) [20] advises that testing the null hypothesis of linearity against a threshold alternative is the most robust approach in detecting parameter instability in macroeconomic and financial time series.

The recommendations of Carrasco (2002) [20] regarding the use of non-linear threshold-type models in economics are crucial from the standpoint of this paper, even more so given the results by Gonzáles and Gonzalo (1997) [7] and Lanne and Saikkonen (2002) [21] who caution about the observational equivalence between the actual unit root stochastic processes and respective non-linear alternatives, especially in small samples. The question is, however, which non-linear threshold alternative is the most suitable one in describing the dynamics of highly persistent near-unit root stochastic processes such as the one governing the dynamics of the U.S. public debt/GDP ratio after the Bretton Woods collapse.

Non-Linearities

One of the first contributions that model the non-linearities in the dynamics of the U.S. public debt/GDP ratio is Sarno (2001) [22]. In particular, Sarno (2001) [22] estimates the ESTAR model of the following form

in which represents the first difference operator, is the ergodic and globally stationary public debt/GDP ratio, and are regime-dependent level shifts, the residuals are , while is the delay parameter. The transition function between the two regimes takes the form where measures the speed of transition between the two regimes and denotes the threshold public debt/GDP ratio. The sum of autoregressive coefficients, , determines the order of autoregression (), while and represent respective regime-dependent autoregressive slope coefficients. Although it is admissible for , the global stationarity condition for the described ESTAR model of Sarno (2001) [22] demands that and .

Sarno (2001) [22] estimates the Equation (1) on a sample spanning from 1916 to 1995 to discover that the U.S. public debt/GDP ratio behaves as a nonlinear mean-reverting ESTAR stochastic process. There are, however, several potential problems with the underlying ESTAR econometric estimates from Sarno (2001) [22].

First, since the Equation (1) of Sarno (2001) [22] from above is parameterized and estimated in first differences and not levels of public debt/GDP ratio, the estimates from (1) might be prone to an omitted variable bias. The Equation (1), in essence, represents a non-linear reaction function of on in which the response of to is regime specific and determined by the estimated values of , and , as well as on the shape of the transition function which, in the case of Sarno (2001) [22], is an exponential transition function. Since is approximately equal to the overall fiscal balance corrected for the potential stock-flow discrepancies, the ESTAR Equation (1) is essentially a non-linear FRF of the overall fiscal balance to regime specific values. To the extent that approximates the dynamics of the U.S. primary fiscal balance, the Equation (1), similarly to the unit root test regressions, also does not incorporate the transitory government spending and cyclical output shocks on its right-hand side. More importantly, Bohn (1998) [14] explicitly states that is a function of both lagged public debt/GDP and non-debt components, most notably the output gap and transitory government spending. In particular, the Equation (4) from Bohn (1998) [14] reads as follows

in which for the real interest rate and the real growth rate , and where represents lagged output gap and transitory government spending, under the realistic assumption that both variables are strictly bounded stochastic processes. In Table 2 (page 956), Bohn (1998) [14] provides estimates of the Equation (2) from above. In addition, when evaluating a nonlinear response of primary fiscal balance to changes in public debt/GDP ratio in Table 3 (page 958), Bohn (1998) [14] explicitly controls for the variations in output gap and transitory government spending. Similar to Bohn (1998) [14], Mendoza and Ostry (2008) [23] and Mauro et al. (2015) [24] also quantify the size of an omitted variable bias for the primary balance FRF coefficient in a wider international and historical context.

Second, a claim of Sarno (2001) [22] on page 120 that “there is growing evidence that governments respond more to primary deficits (surpluses) when public debt is particularly high (low)” is a valid empirical fact in the case of the U.S. for the sample period from 1916 to 1995 which both Bohn (1998) [14] and Sarno (2001) [22] use in their respective studies. However, there is a statistically significant structural shift in the primary balance FRF coefficient after the GFC, as D’Erasmo et al. (2015) [25] document in the case of the U.S. for the period 1791-2014. Using the extended sample period that ends in 2014, D’Erasmo et al. (2015) [25] manage to overturn most of the results originally reported by Bohn (1998) [14]. In particular, due to an unprecedented public debt build up after the 2008 GFC, D’Erasmo et al. (2015) [25] quantify a much lower primary balance FRF coefficient to public debt upward movements. This finding of D’Erasmo et al. (2015) [25] contradicts the statement of Sarno (2001) [22] from page 121 “…that governments react more strongly to primary deficits when the deviation of the debt/GDP ratio from equilibrium is large in absolute size suggests that the larger the deviation from the long-run equilibrium of the debt/GDP ratio, the stronger will be the tendency to move back to equilibrium.”

The reader should also note that the emphasized assertions of Sarno (2001) [22], and the original estimates by Bohn (1998) [14], are inconsistent with the sovereign borrower rational expectations equilibrium model of Ghosh et al. (2013) [26] in which the fiscal behaviour of the sovereign borrower tracks a reduced form FRF with the fiscal fatigue characteristics. The FRF with fiscal fatigue characteristics of Ghosh et al. (2013) [26] implies a cubic relationship between primary fiscal balance and public debt such that at low levels of debt there is no, or even negative, relationship between the primary balance and public debt. With the increase of public debt, the response of the primary balance increases also, but the magnitude of the response eventually weakens and finally decreases at very high levels of debt. In sum, it is unlikely that governments can respond more aggressively to increased primary deficits when public debt/GDP ratio is particularly high, if only because the primary surplus/GDP ratio cannot exceed 100% while interest payments and public debt as % of GDP can.

Third, some novel econometric findings of Heinen et al. (2012) [27] and Buncic (2019) [28] are in contrast with the claims of Sarno (2001) [22] about the desirable properties of the exponential transition function, most notably the properties about its boundedness between 0 and 1 and symmetrically inverse-bell shaped transition function around 0. On page 120, below the Equation (1), Sarno (2001) [22] claims that “these properties are attractive in the present context because they allow symmetric adjustment of d(t) for deviations above and below the equilibrium level.” However, Heinen et al. (2012) [27] argue that one cannot distinguish the transition function in relation to extreme parameter combinations which is especially the case for very small or very large values of the error term variance, or when certain model parameters tend to their limiting values. The consequence of this identification problem are strongly biased estimators in the case of ESTAR model specification.

Similar to Heinen et al. (2012) [27], Buncic (2019) [28] emphasizes an additional identification problem in the case of the ESTAR model which implies observational equivalence between the exponential transition function and the quadratic transition function in cases when the speed of transition parameter takes on relatively small values. On the other hand, for relatively large values of the speed of transition parameter , there is an observational equivalence between the exponential transition function and indicator outlier fitting function. In other words, the exponential transition function acts like a dummy variable which removes the influence of outlier observations. As the simplest possible alternative to the ESTAR model specification, Buncic (2019) [28] recommends the use of (SE)TAR-type threshold models.

Fourth, as Sarno (2001) [22] notes in the footnote number 3 on page 120 of his article, an alternative smooth transition function to the exponential one of the ESTAR process is the logistic transition function of the LSTAR model specification. Sarno (2001) [22] opts for an exponential transition function on statistical grounds and further argues that the LSTAR model “seems relatively less appropriate for modeling the dynamics of the public debt/GDP ratio”, since it implies asymmetric behaviour of public debt/GDP with respect to endogenously estimated threshold. Cochrane (2022) [17], however, claims (page 31) that “the s-shaped surplus/GDP process is a crucial lesson” for the post-World War II fiscal dynamics. In other words, today’s deficits are followed by future surpluses, since the surplus/GDP follows an s-shaped process in a two-variable VAR setting with public debt/GDP and surplus/GDP ratios. But even if the statements of Cochrane (2022) [17] about the s-shaped surplus/GDP process are correct, which Campbell et al. (2023) [18] and Jiang et al. (2024) [19] question on the basis of highly persistent near-unit root process for public debt/GDP, the problem with the LSTAR model specification, as Ekner and Nejstgaard (2013) [29] claim on page 17, is that “a large and imprecise estimate of the speed of transition parameter implies that the LSTAR model is effectively a TAR model.”

Both the recommendations of Buncic (2019) [28] and Ekner and Nejstgaard (2013) [29] show that the (SE)TAR process has more desirable statistical properties in comparison to ESTAR and LSTAR processes, respectively. Gnegne and Jawadi (2013) [30] estimate a two-regime SETAR process for the public debt/GDP ratio in the case of the United States between 1970 and 2009. However, similarly to Sarno (2001) [22], Gnegne and Jawadi (2013) [30] model the non-linear behaviour in the changes, not levels, of the public debt/GDP ratio which effectively implies investigating asymmetries in the stock-flow adjusted overall fiscal balance. The choice of Gnegne and Jawadi (2013) [30] to focus on changes, instead on levels, of the public debt/GDP ratio is governed by the potentially inappropriate choice of respective unit root tests. In particular, Gnegne and Jawadi (2013) [30] assert (Table 1, page 158) that

“According to Table 1, the great majority of unit root tests indicate that public debt/GDP ratio in the case of US is an I(1) stochastic processes. To check the robustness of our findings for the presence of structural breaks, we further apply a ZA unit root test, but the main conclusion about I(1) behaviour remains unchanged.”

Gnegne and Jawadi (2013) [30], hence, use the Zivot-Andrews (ZA) unit root test with single endogenous structural break to strengthen their findings about the I(1) nature of the stochastic process for the U.S. public debt/GDP ratio between 1970-2009. Chortareas et al. (2008) [31], however, caution that the results of unit root tests with structural breaks often do not agree with the results of unit root tests that posit a non-linear stationarity under the alternative hypothesis. In other words, since unit root tests with structural breaks essentially capture the different time series characteristics of the stochastic process in question, one should use them only as complementary tests to the non-linear unit root tests, as Chortareas et al. (2008) [31] recommend.

Since the choice of a particular alternative hypothesis in unit-root tests affects their ability to reject the null hypothesis, one particular testing strategy for attaining the desirable power of unit root testing procedures would be to use an F-test of Enders and Granger (1998) [32] for the null hypothesis of a unit root against an alternative of a stationary two-regime SETAR process. The reader should note, however, that the Monte Carlo simulations of Enders (1998) [33] report that the F-test of Enders and Granger (1998) [32] has lower power than the traditional Dickey-Fuller unit root test of Dickey and Fuller (1981) [10] that ignores the threshold break under the alternative. The problem with the Dickey-Fuller unit root test, on the other hand, is that it has very low power in the case of highly persistent near-unit root AR(1) processes, which is precisely the case for the U.S. public debt/GDP ratio. Since both the F-test of Enders and Granger (1998) [32] and the Dickey-Fuller test of Dickey and Fuller (1981) [10] have low power in the case of the U.S. public debt/GDP ratio, one potential solution is to use the efficient unit root tests of Elliott et al. (1996) [34], since Bec et al. (2022) [35] find that these unit root tests have higher power than traditional unit root tests, single threshold-type unit root tests of Enders and Granger (1998) [32] and two threshold-type unit root tests of Kapetanios and Shin (2006) [36] in the case when AR(1) coefficient is larger than 0.95.

Although Gnegne and Jawadi (2013) [30] do not report the results of efficient unit root tests from Elliott et al. (1996) [34], they present, in line with the recommendations from Bohn (2007) [15], the results of the stationarity KPSS test of Kwiatkowski et al. (1992) [37]. In particular, Bohn (2007) [15] asserts that testing the null hypothesis of stationarity against the alternative of a unit root can be of economic interest, since one can, after concluding that the null hypothesis of stationarity cannot be rejected, proceed to test for potential non-linearities in the stochastic process for public debt. However, Gnegne and Jawadi (2013) [30] present only the results of the stationarity testing with the intercept term without trend, even though the Figure 2 on page 156 of their paper clearly depicts the upward trending behaviour in the U.S. public debt/GDP ratio between 1970 and 2009. The realized value of the KPSS test statistics of 1.44 from Table 1 (page 158) of Gnegne and Jawadi (2013) [30] rejects the null hypothesis of stationarity at the 5% significance level, but the results have to be interpreted with caution since the choice of an intercept term as the only deterministic component can influence the power of the stationarity test of Kwiatkowski et al. (1992) [37].

Before presenting the methodological econometric framework in the next section of the paper, it would be useful to summarize main points regarding the time series properties of the U.S. public debt/GDP ratio after the Bretton Woods collapse. First, the U.S. public debt/GDP ratio can be best characterized as the near-unit root stochastic process with a first lag autocorrelation coefficient higher than 0.95. Second, in determining the order of integration of the U.S. public debt/GDP ratio, one should place emphasis on efficient unit root tests from Elliott et al. (1996) [34] and stationarity test from Kwiatkowski et al. (1992) [37] using both the intercept and linear time trend as deterministic components in testing regressions. Third, to model threshold non-linearities in the dynamics of the U.S. public debt/GDP ratio one should opt for the SETAR model specification instead of ESTAR or LSTAR model specifications. Fourth, the SETAR model should be estimated in levels, not first differences, of the U.S. public debt/GDP ratio since i) the first differenced public debt/GDP approximates the overall fiscal balance corrected for the stock-flow adjustments and consequently has an alternative economic interpretation with respect to the public debt/GDP ratio measured in levels; and ii) bond investors, credit rating agencies, policy makers and international financial institutions are primarily interested in monitoring and forecasting public debt/GDP ratio in levels, not first differences.

2. Methods

Tsay (1989) [38] is an early contribution in detecting the number and location of thresholds using an intuitive graphical approach on the residuals from the arranged linear AR(p) autoregression. More recently, Hansen (1996, 1997, 2017) [4,5,6] develops an asymptotic p-value based approach that supports testing, estimation and inference for general two-regime SETAR type models of order p. Following closely, almost verbatim, the exposition in Hansen (1997) [5], this section acquaints the reader with the theoretical econometric background on which the empirical estimates from Section 3 are based.

Following Hansen (1996, 1997, & 2017) [4,5,6], a two-regime SETAR model with an autoregressive order has the following form

in which denotes the indicator function, is the threshold variable with the delay parameter set equal to one (, and is the value of the threshold. The parameters are autoregressive slopes for the lower regime () while are autoregressive slopes for the upper regime . The error , potentially heteroscedastic, is martingale difference sequence.

We present only the case for the delay parameter set equal to one ( since i) the partial autocorrelation function of the U.S. public debt/GDP ratio points to an AR(1) process for the U.S. public debt/GDP ratio for the period in question and since ii) by definition, we have where takes on discrete values only. Note that the estimation problem in the case of still implies super consistent least squares (LS) estimate of , since the parameter space over which one must conduct the grid search for would be discrete.

To estimate the threshold parameter and slope coefficients, Hansen (1997) [5] introduces the following notation

and

yields the following representation for Equation (3)

or

where

Hansen (1997) [5] estimates the parameters of Equation (7), and , with the conditional LS estimator. In particular, for a given value of , the LS estimate of is

with residuals

and residual variance

The LS estimate of is the value that minimizes the right-hand side of Equation (10)

where describes the lower () and the upper () percentiles of the probability distribution of the ordered threshold variable.

Hansen (1997) [5] solves the minimization problem from Equation (11) using direct search. The reader should note that the residual variance from Equation (10), , takes on at most distinct values when is varied, and these values correspond to , Consequently, to find the LS estimate of Equation (11), Hansen (1997) [5] estimates the ordinary least squares (OLS) regressions of the form setting for each which amounts to slightly less than regressions. For each regression, Hansen (1997) [5] calculates the residual variance and concentrates on the value of that corresponds to the smallest variance

Hansen (1997) [5] finds the LS estimate of as , while the LS residuals are equal to with sample variance

To construct asymptotically valid confidence intervals for , Hansen (1997) [5] recommends the use of the following likelihood ratio statistics

for which is the likelihood ratio statistic to test the null hypothesis , and for which, trivially, for . Hansen (1997) [5] further denotes the -level critical value for as in which is the random variable with the following probability density function

and for which the 95% critical value equals 7.35 (see the second row of Table 1 in Hansen (1997) [5]). To find the 95% confidence interval for , Hansen (1997) [5] sets

which can be found graphically by plotting the likelihood ratio sequence against and drawing a flat line at 7.35, i.e., at the 95% critical value for . Since the set can be disjoint in practice, it is possible to perform a threshold search over a convexified region where Γnd . Hansen (1997) [5] provides Monte Carlo evidence in favour of using over .

Hansen (1997) [5] also shows how to construct a -level confidence intervals for the slope parameters of the SETAR model in question. If is the -level critical value for the normal distribution and if is the standard error for , then the -level confidence interval for , conditional on being fixed, is

When is known, and equals , Equation (16) trivially becomes . Since is a consistent estimator of at a fast rate, Hansen (1997) [5] proceeds as if and use as an asymptotically valid confidence interval for . However, since in small samples might not be estimated precisely, this sampling error would also affect the precision of estimates. To reduce the sampling error, Hansen (1997) [5] proposes to first construct a -level, , confidence interval for , and for each in this -level confidence interval, calculates a confidence interval for , and then form the union of all these sets. More formally, if represents a confidence interval for for a given asymptotic coverage , , and if, for each , one can construct the confidence interval as in Equation (16) and denote the union of these sets to

so it is possible to reduce the sampling error of the slope parameter estimates, as Hansen’s (1997) [5] Monte Carlo experiment shows. As Hansen (1997) [5] notes, by construction, increases with in the sense that for . In addition, the smallest member of this class is , the confidence interval formed by ignoring the sampling variation in , so that is by construction larger than for any .

3. Results

This section consists of two subsections. Section 3.1. presents main stylized facts for the U.S. public debt/GDP ratio for the period 1974Q1-2024Q1. Section 3.2. presents econometric estimates of single and double threshold SETAR specifications.

3.1. Stylized Facts

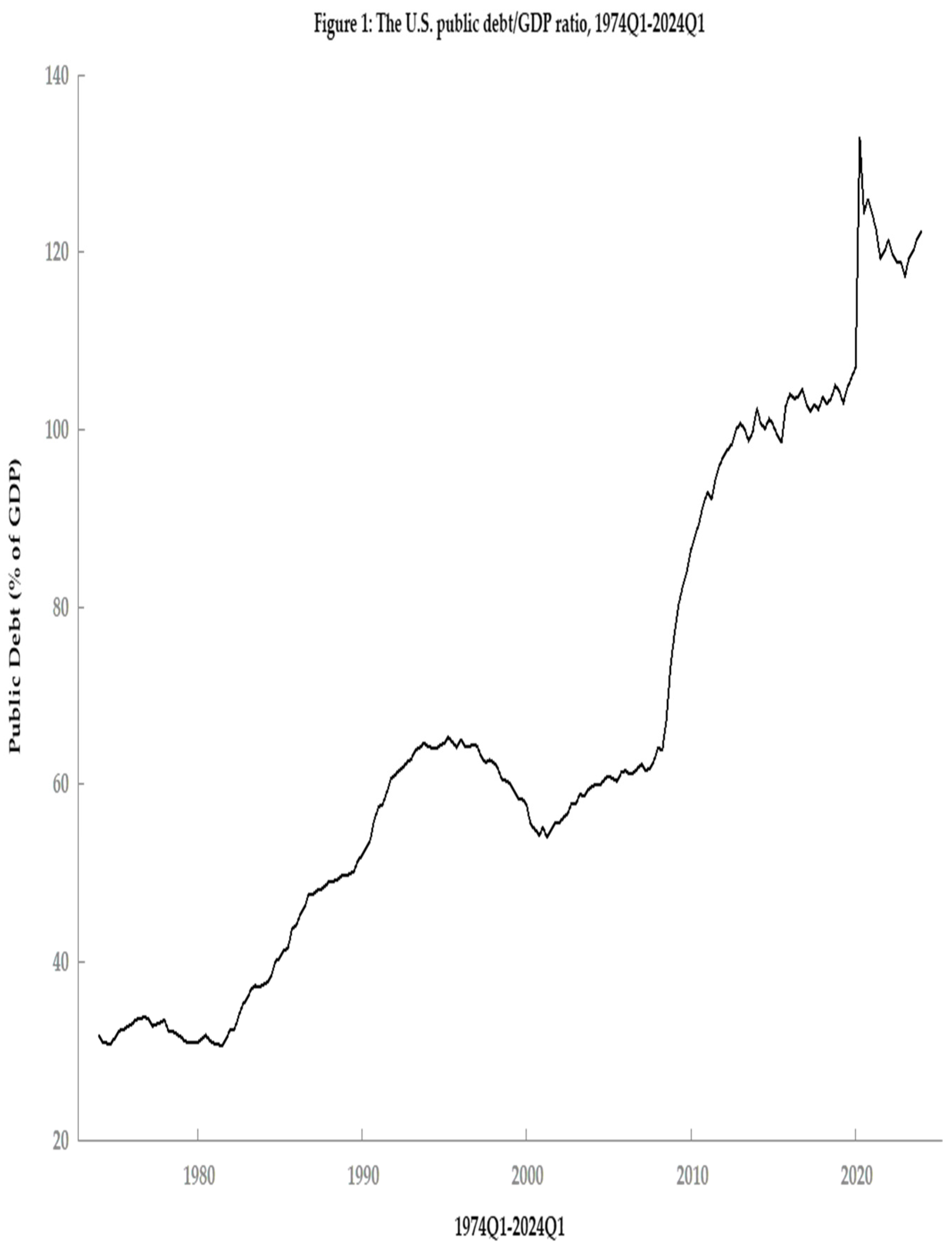

Figure 1 plots the dynamics of the seasonally adjusted federal U.S. public debt as % of GDP for the period 1974Q1-2024Q1. Following Acalin and Ball (2024) [39], we use the data from the U.S. Office of Management and Budget. The data can be downloaded from the Federal Reserve Bank of St. Louis website under the code number GFDEGDQ188S.

Since the U.S. public debt/GDP ratio between 1946 and 1974 fell by 23 percentage points, primarily due to FED’s interest rate pegging policy between 1942 and 1951 and unanticipated inflation during the 1960s, as Acalin and Ball (2024) [39] document in great detail, the sample starts at 1974Q1. In addition, the beginning of the sample in 1974 enable us to investigate non-linearities in the dynamics of the U.S. public debt/GDP ratio for a relatively homogeneous period of flexible exchange rates after the Bretton Woods collapse. The end of the sample, 2024Q1, corresponds to the last publicly availabe data point on the 23rd of July when we downloaded the data from the FRED website.

Following the advice of Bohn (2005) [40], we measure public indebtedness as % of GDP, since unscaled time series for the federal U.S. public debt exhibits non-stationary variance. In addition, we opt for the par, instead of market, value of the federal U.S. public debt, since Jiang et al. (2022) [41] report that market value and par value of the outstanding U.S. federal debt move closely for the period under scrutiny.

As Figure 1 shows, the dynamics of the U.S. public debt/GDP ratio is highly persisitent with the first lag autocorrelation coefficient of 0.98. The realized value of the Elliott-Rothenberg-Stock (ERS) point optimal unit root test statistics from Elliott et al. (1996) [34] equals 28.59, and it is statistically significant at 1% significance level. On the other hand, the realized value of the DF GLS unit root test statistics from Elliott et al. (1996) [34] is only -1.11, so we cannot reject the unit root null at any meaningful level of significance. Finally, when we appply a KPSS statioanarity test with quadratic spectral kernel and Andrews’s bandwidth, we obtain the realized value of the KPSS test statistics of 0.18, which is consistent with the non-rejection of the null hypothesis of stationarity at the 1% significance level. In sum, the results, available from the authors upon request, support the notion of stationary public debt/GDP ratio in the case of the U.S. between 1974Q1 and 202Q1. In all tests, we use both an intercept and a linear time trend as deterministic components, and choose the number of lags in test regressions according to the modified Akaike criterion (MAIC) of Ng and Perron (2001) [42], given that we fix the the maximum number of lags to four due to quarterly business cycle data frequency.

Apart from depicting a highly persistent dynamics of the U.S. public debt/GDP ratio, Figure 1 also documents that the U.S. public debt/GDP ratio exhibits a non-linear behaviour with several potential thresholds situated around the mid-1990s, around 2008, most probably due to the GFC, and around the end of 2014 when the FED stopped with its quantitative easing program. We resort to estimating potential thresholds from Figure 1 in the subsection that follows.

3.2. Econometric Estimates

Table 1 presents the conditional LS estimates of Equation (3) for the case. The estimated value of the threshold for the one quarter lagged U.S. public debt/GDP ratio is 65% of GDP and corresponds to the second quarter of 1995, 1995Q2. All estimated coefficients, except the intercept term in the lower regime (), are statistically significant at the 1% significance level. We do not use the heteroscedasticity consistent standard errors since White’s heteroscedasticity test does not detect the presence of heteroscedasticity in the residual values of the U.S. public debt/GDP ratio from the estimated AR(1) linear autoregression. In terms of the statistical significance of the estimated coefficient values, the results do not change, however, even if use heteroscedasticity corrected standard errors. The residuals from the estimated two-regime SETAR model are not normally distributed due to a single 25 percentage points COVID-19 outlier in the second quarter of 2020, 2020Q2. In spite of the detected COVID-19 outlier, the coefficient stability tests based on recursive residuals report that the estimated coefficients are stable.

Note that both AR(1) slope coefficients are highly persistent: the AR(1) slope coefficient in the lower regime () equals 0.99 with the 95% confidence interval of , while the AR(1) slope coefficient in the upper regime () equals 0.92 with the 95% confidence interval of . Although both AR(1) slope coefficients are highly persistent, the Wald coefficient restriction test rejects the null hypothesis of their equality-the realized value of the chi-squared test statistics with one degree of freedom, , equals 6.29 with an associated p-value of 0.01. In other words, the AR(1) slope coefficient in the lower regime is not statistically different from one, according to the results of the Wald coefficient restriction test (, while the AR(1) coefficient in the upper regime is statistically different from one, according to the results of the Wald coefficient restriction test (. Even though the lower regime AR(1) slope coefficient exhibits potential partial unit root behaviour, note that the use of the LS estimator is justifiable, i.e., the LS estimates are consistent and asymptotically normal, as shown in González and Gonzalo (1997) [7].

The 95% confidence interval for the estimated threshold break is . Note that the upper value of the threshold of in the case of the 95% confidence interval corresponds to the third quarter of 2008, 2008Q3, when the macro and fiscal effects of the GFC in the United States started to unravel. Figure 1 shows the estimated threshold break with an associated 95% critical value and the 95% confidence interval for the threshold break.

Since Figure 2 also depicts a potential second threhold break at 100.5% public debt/GDP ratio, we also estimate a three-regime SETAR model using the sequential LS estimator of Gonzalo and Pitarakis (2002) [8]. We present the estimates of a three-regime SETAR model in Table 2. All estimated coefficients, except the intercept term in the lower () regime, are statistically significant at 1% significance level. Note, however, that there is little difference between the estimated coefficient values in the middle ( and the upper () regime implying that the two-regime SETAR model from Table 1 is probably a better characterization of non-linearities and asymmetries in the dynamics of the U.S. public debt/GDP ratio between 1974Q1 and 2024Q1. In the discussion section below, we, hence, put greater emphasis in discussing the results from the two-regime SETAR model presented in Table 1.

4. Discussion

As shown in previous section, the AR(1) slope coefficient for one quarter lagged public debt/GDP ratio, , in the lower regime (), equals 0.99, i.e., it exhibits a (near) unit root behaviour. This finding is in line with the seminal tax smoothing model of Barro (1979) [2] briefly reviewed in the introduction of the paper. In other words, it could be the case that the dynamics of U.S. public debt/GDP ratio below 65.31% threshold behaves randomly due to unanticipated shocks in output gap and transitory government spending. In addition, Aiyagari et al. (2020) [43] further argue that the high persistence of public debt is due to market incompleteness which implies that the government cannot issue state-contingent debt, i.e., it can only issue risk-free debt. In a more general model of incomplete markets than the one presented in Aiyagari et al. (2020) [43], Bhandari et al. (2017) [44] reaffirm the findings of Aiyagari et al. (2020) [43] regarding the behaviour of the U.S. public debt/GDP ratio. In particular, Bhandari et al. (2017) [44] show that the public debt/GDP ratio has an invariant stationary probability distribution, but with a very slow mean-reversion (a half-life of almost 250 years).

The AR(1) slope coefficient for one quarter lagged public debt/GDP ratio in the upper regime () equals 0.92., i.e., it exhibits highly persistent, but not unit root, behaviour. If one closely inspects the data for the U.S. public debt/GDP ratio, it becomes evident that public debt/GDP ratio in the case of the United States trends above the 65.31% threshold after 2008Q3. In fact, if one disregards the 2008Q3-2024Q1 subsample, the only quarter when the public debt/GDP ratio is higher or equal than the 65.31% endogenous threshold is 1995Q2. This finding, hence, confirms that our endogenously estimated threshold corresponds to an exogenously imposed 2007 structural break in Jiang et al. (2024) [44]. In other words, our result show that Jiang et al. (2024) [44] were correct to place the structural break in the U.S. public debt dynamics in 2007. In addition, this finding is also consistent with the FRF estimates of D’Erasmo et al. (2015) [25] who quantify the absence of mean reversion in the U.S. public debt/GDP ratio since the GFC due to a structural shift in the primary balance FRF coefficient.

More importantly, the estimated persistent AR(1) slope coefficient for the upper regime of 0.92 is also in line with several theoretical conjectures and predictions from Jiang et al. (2024) [44,45,46,47]. In particular, Jiang et al. (2024) [44,45,46,47] argue that persistent behaviour of the U.S. public debt/GDP after the GFC is due to: i) biased subjective expectations and beliefs on the part of bond investors; ii) FED’s inelastic demand for the U.S. Treasurys after 2008 through its quantitative easing programs; and iii) the perception of foreign investors that the U.S. Treasurys represent a risk-free asset, i.e., that the U.S. government is a supplier of safe assets; iv) strucutural break in the U.S. fiscal policy.

As already noted, D’Erasmo et al. (2015) [25] were among the first to document a structural break in the U.S. fiscal policy after the GFC. Jiang et al. (2024) [45] further support the findings of D’Erasmo et al. (2015) [25] by estimating a time-varying FRF which exhibits decreasing, and even negative, response of the primary fiscal balance to debt build-up after 2008. The unresponsiveness of the U.S. primary fiscal balance to debt accumulation essentially implies the absence of mean-reversion in the dynamics of the U.S. public debt/GDP ratio. In other words, the behaviour of fiscal policy in the U.S. after the GFC is characterized by the characteristics of fiscal fatigue, as Ghosh et al. (2013) [25] predict.

Jiang et al. (2024) [46] further argue that there is a perception in international investment community that the U.S. government is a supplier of risk-free government bonds. This exorbitant privilege enables the U.S. government to counter-cyclically issue a risk-free debt at low interest rates further exacerbating the persistency in the autocorrelation profile of the U.S. public debt/GDP ratio. In other words, the inelastic foreign demand for the U.S. Treasurys implies that, contrary to other economies around the world, the U.S. government can issue new debt even in “bad” times, and hence “insure” the U.S. taxpayers in short-to-medium run by not raising taxes or cutting spending to cover the pro-cyclical increase in fiscal deficit due to an aggregate recession shock.

The foreign investment community is not the only inelastic buyer of the U.S. Treasurys. The FED, through its quantitative easing programs, managed to acquire large shares of the U.S. government debt. In fact, from 2008Q3 to 2024Q1, the amount of the U.S. federal debt held by the FED as % of GDP increased by approximately 14 percentage points, from 3.2 % of GDP in 2008Q3 to 17.6% of GDP in 2024Q1, as readers can see by themselves from the chart under the ticket code HBFRGDQ188S at the official website of the Federal Reserve Bank of St. Louis. Note that the 14 percentage points increase in the FED’s holdings of the U.S. public debt/GDP ratio since 2008Q3 is remarkably close to the intercept level shift between the two regimes of our preffered SETAR model from Table 1. In particular, while in the lower () regime the intercept is not statisitcally significant, the 95% confidence interval for the intercept in the upper () regime is , capturing potentially the level-shift in FED’s asset purchases.

The likelihood that the FED would prevent a default of the U.S. government might also influence the subjective beliefs of bond investors. In other words, the investors in U.S. Treasurys might continue to buy the U.S. federal debt, if they have optimistic expectations about the future fiscal outlook in the United States. These overly optimistic expectations, supported by the FED’s actions, can induce highly persistent shocks in the U.S. public debt/GDP ratio after the GFC.

Finally, our three regime SETAR model from Table 2 is to, a certain extent, consistent with theoretical model of Elenev et al. (2024) [48]. Elenev et al. (2024) [48] construct a dynamic stochastic general equilibrium model (DSGE) for the U.S. economy with a novel feature that fiscal policy in the United States does not respond continuously, but discretely to the movements in the public debt/GDP ratio. Furthermore, Elenev et al. (2024) [48] calibrate that in “normal times”, when only productivity shocks govern the economic dynamics and monetary policy is “conventional”, the upper austerity threshold for the U.S. public debt/GDP ratio equals 115%, while the lower profligacy threshold equals 47.5%. Elenev et al. (2024) [48] determine the austerity and profligacy thresholds endogenously to keep the public debt/GDP ratio risk-free and stationary. Our respective endogenously estimated thresholds of 65.31% and 100.5% could potentially correspond to calibrated threshold values of Elenev et al. (2024) [48].

5. Conclusions

This paper presented estimates from a two-regime and three-regime SETAR specifications to model the non-linear quarterly dynamics of the U.S. public debt/GDP ratio between 1974 and 2024. It would be interesting to supplement the results of this paper with the estimates of Markov-switching models such as those estimated by Davig (2005) [49]. Davig (2005) [49], building on the work of Wilcox (1989) [13], estimates a Markov-switching model for the real discounted U.S. public debt in which the real stochastic risk-free rate serves as a discount factor. The Markov-switching framework of Davig (2005) [49] for the real discounted public debt allows for the tests of both global and local fiscal sustainability. Two extensions of the work by Davig (2005) [49] are possible. First, one can use the average real interest rate adjusted for the risk premium for determining the real discounted value of the U.S. public debt, as Jiang et al. (2024a) [50] do in calculating the discounted value of future primary surpluses. Second, because the average risk-adjusted discount rate on government debt is higher than the growth rate of the U.S. economy, as Jiang et al. (2024a) [50] document, the transversality condition (TVC) is unlikely to be violated in the case of the United States. In other words, since the TVC implies that for the sufficiently long forecast horizon, the discounted value of the U.S. public debt converges to zero, it would be of interest to redefine the global fiscal sustainability conditions of Wilcox (1989) [13] and Davig (2005) [49].

Supplementary Materials

The following supporting zip file containing data, figures, tables, GRETL and STATA codes for reproducing the results from this paper and can be downloaded at: Preprints.org.

Author Contributions

V.A., D.B. and M.D.: investigation and conceptualization; V.A.: methodology and software; V.A.: writing—original draft preparation; D.B. and M.D.: writing—review and editing. All authors have read and agreed to the published version of the manuscript.

Funding

This research was funded by the Ministry of Science, Technological Development and Innovation of the Republic of Serbia under the contract number 451-03-47/2023-01/200005.

Data Availability Statement

The data used in this study are from the U.S. Office of Management and Budget and Federal Reserve Bank of St. Louis, Federal Debt: Total Public Debt as Percent of Gross Domestic Product [GFDEGDQ188S], retrieved from FRED, Federal Reserve Bank of St. Louis; https://fred.stlouisfed.org/series/GFDEGDQ188S, July 23, 2024.

Conflicts of Interest

The authors declare no conflicts of interest. The funders had no role in the design of the study; in the collection, analyses, or interpretation of data; in the writing of the manuscript; or in the decision to publish the results.

References

- Hansen, B. E. Threshold autoregression in economics. Stat. Interface. 2011, 4, 123–127. [Google Scholar] [CrossRef]

- Barro, R. J. On the determination of the public debt. J. Polit. Econ. 1979, 87, 940–971. [Google Scholar] [CrossRef]

- Bec, F.; Ben Salem, M.; Carrasco, M. Tests for unit-root versus threshold specification with an application to the purchasing power parity relationship. J. Bus. Econ. Stat. 2004, 22, 382–395. [Google Scholar] [CrossRef]

- Hansen, B. E. Inference when a nuisance parameter is not identified under the null hypothesis. Econometrica. 1996, 64, 413–430. [Google Scholar] [CrossRef]

- Hansen, B. E. Inference in TAR models. Stud. Nonlinear Dyn. Econometrics. 1997, 2, 1–14. [Google Scholar] [CrossRef]

- Hansen, B. E. Regression kink with an unknown threshold. J. Bus. Econ. Stat. 2017, 35, 228–240. [Google Scholar] [CrossRef]

- González, M.; Gonzalo, J. Threshold Unit Root Models; DES - Working Papers, Statistics and Econometrics, WS 6214; Universidad Carlos III de Madrid, Departamento de Estadística: Madrid, 1997.

- Gonzalo, J.; Pitarakis, J. Estimation and model selection-based inference in single and multiple threshold models. J. Econometrics. 2002, 110, 319–352. [Google Scholar] [CrossRef]

- Hamilton, J. D.; Flavin, M. A. On the limitations of government borrowing: A framework for empirical testing. Am. Econ. Rev. 1986, 76, 808–819. [Google Scholar]

- Dickey, D. A.; Fuller, W. A. Likelihood ratio statistics for autoregressive time series with a unit root. Econometrica. 1981, 49, 1057–1072. [Google Scholar] [CrossRef]

- Kremers, J. J. Long-run limits on the U.S. federal debt. Econ. Lett. 1988, 28, 259–262. [Google Scholar] [CrossRef]

- Kremers, J. J. U.S. federal indebtedness and the conduct of fiscal policy. J. Monet. Econ. 1989, 23, 219–238. [Google Scholar] [CrossRef]

- Wilcox, D. W. The sustainability of government deficits: Implications of the present-value borrowing constraint. J. Money Credit Bank. 1989, 21, 291–306. [Google Scholar] [CrossRef]

- Bohn, H. The behavior of U.S. public debt and deficits. Q. J. Econ. 1998, 113, 949–963. [Google Scholar] [CrossRef]

- Bohn, H. Are stationarity and cointegration restrictions really necessary for the intertemporal budget constraint? J. Monet. Econ. 2007, 54, 1837–1847. [Google Scholar] [CrossRef]

- Cochrane, J. H. The Value of Government Debt; NBER Working Papers 26090; National Bureau of Economic Research, Inc.: Cambridge, MA, 2019.

- Cochrane, J. H. The fiscal roots of inflation. Rev. Econ. Dyn. 2022, 45, 22–40. [Google Scholar] [CrossRef]

- Campbell, J. Y.; Gao, C.; Martin, I. W. R. Debt and Deficits: Fiscal Analysis with Stationary Ratios; Swiss Finance Institute Research Paper No. 23-101; October 23, 2023.

- Jiang, Z.; Lustig, H.; Van Nieuwerburgh, S.; Xiaolan, M. What drives variation in the U.S. debt-to-output ratio: The dogs that did not bark. J. Finance. 2024, 79, 2603–2665. [Google Scholar] [CrossRef]

- Carrasco, M. Misspecified structural change, threshold, and Markov-switching models. J. Econometrics. 2002, 109, 239–273. [Google Scholar] [CrossRef]

- Lanne, M.; Saikkonen, P. Threshold autoregression for strongly autocorrelated time series. J. Bus. Econ. Stat. 2002, 20, 282–289. [Google Scholar] [CrossRef]

- Sarno, L. The behavior of U. S. public debt: A nonlinear perspective. Econ. Lett. 2001, 74, 119–125. [Google Scholar]

- Mendoza, E. G.; Ostry, J. D. International evidence on fiscal solvency: Is fiscal policy responsible? J. Monet. Econ. 2008, 55, 1080–1094. [Google Scholar] [CrossRef]

- Mauro, P.; Romeu, R.; Binder, A.; Zaman, A. A modern history of fiscal prudence and profligacy. J. Monet. Econ. 2015, 76, 55–70. [Google Scholar] [CrossRef]

- D’Erasmo, P.; Mendoza, E.; Zhang, J. What is a Sustainable Public Debt?; PIER Working Paper Archive 15-033; Penn Institute for Economic Research, Department of Economics, University of Pennsylvania: Philadelphia, PA, revised April 16, 2015.

- Ghosh, A. R.; Kim, J. I.; Mendoza, E. G.; Ostry, J. D.; Qureshi, M. S. Fiscal fatigue, fiscal space and debt sustainability in advanced economies. Econ. J. 2013, 123, F4–F30. [Google Scholar] [CrossRef]

- Heinen, A.; Michael, J.; Sibbertsen, P. Weak identification in the ESTAR model and a new model. J. Time Ser. Anal. 2013, 34, 238–261. [Google Scholar] [CrossRef]

- Buncic, D. Identification and estimation issues in exponential smooth transition autoregressive models. Oxf. Bull. Econ. Stat. 2019, 81, 667–685. [Google Scholar] [CrossRef]

- Ekner, L. E.; Nejstgaard, E. Parameter Identification in the Logistic STAR Model; Discussion Papers 13-07; University of Copenhagen, Department of Economics: Copenhagen, 2013.

- Gnegne, Y.; Jawadi, F. Boundedness and nonlinearities in public debt dynamics: A TAR assessment. Econ. Modell. 2013, 34, 154–160. [Google Scholar] [CrossRef]

- Chortareas, G.; Kapetanios, G.; Uctum, M. Nonlinear alternatives to unit root tests and public finance sustainability: Some evidence from Latin American and Caribbean countries. Oxf. Bull. Econ. Stat. 2008, 70, 645–663. [Google Scholar] [CrossRef]

- Enders, W.; Granger, C. W. J. Unit-root tests and asymmetric adjustment with an example using the term structure of interest rates. J. Bus. Econ. Stat. 1998, 16, 304–311. [Google Scholar] [CrossRef]

- Enders, W. Improved critical values for the Enders-Granger unit-root test. App. Econ. Lett. 2001, 8, 257–261. [Google Scholar] [CrossRef]

- Elliott, G.; Rothenberg, T. J.; Stock, J. H. Efficient tests for an autoregressive unit root. Econometrica. 1996, 64, 813–836. [Google Scholar] [CrossRef]

- Bec, F.; Guay, A.; Bohn Nielsen, H.; Saïdi, S. Power of Unit Root Tests against Nonlinear and Noncausal Alternatives; THEMA Working Papers 2022-14; THEMA (THéorie Economique, Modélisation et Applications), Université de Cergy-Pontoise: Cergy-Pontoise, 2022.

- Kapetanios, G.; Shin, Y. Unit root tests in three-regime SETAR models. Econometrics J. 2006, 9, 252–278. [Google Scholar] [CrossRef]

- Kwiatkowski, D.; Phillips, P. C. B.; Schmidt, P.; Shin, Y. Testing the null hypothesis of stationarity against the alternative of a unit root. J. Econometrics. 1992, 54, 159–178. [Google Scholar] [CrossRef]

- Tsay, R. S. Testing and modeling threshold autoregressive processes. J. Am. Stat. Assoc. 1989, 84, 231–240. [Google Scholar] [CrossRef]

- Acalin, J.; Ball, L. M. Did the U.S. Really Grow Out of its World War II Debt?; NBER Working Paper No. w31577; August 2023.

- Bohn, H. The Sustainability of Fiscal Policy in the United States; CESifo Working Paper Series 1446; CESifo: Munich, 2005.

- Jiang, Z.; Lustig, H.; Van Nieuwerburgh, S.; Xiaolan, M. Z. Measuring U.S. Fiscal Capacity Using Discounted Cash Flow Analysis; Brookings Papers on Economic Activity. 2022, Fall, 157–209.

- Ng, S.; Perron, P. Lag length selection and the construction of unit root tests with good size and power. Econometrica. 2001, 69, 1519–1554. [Google Scholar] [CrossRef]

- Aiyagari, S. R.; Marcet, A.; Sargent, T. J.; Seppala, J. Optimal taxation without state-contingent debt. J. Polit. Econ. 2002, 110, 1220–1254. [Google Scholar] [CrossRef]

- Bhandari, A.; Evans, J.; Golosov, M.; Sargent, T. J. Fiscal policy and debt management with incomplete markets. Q. J. Econ. 2017, 132, 617–663. [Google Scholar] [CrossRef]

- Jiang, Z.; Lustig, H.; Van Nieuwerburgh, S.; Xiaolan, M. Z. Quantifying U.S. Treasury Investor Optimism; Columbia Business School Research; January 19, 2021.

- Van Nieuwerburgh, S.; Jiang, Z.; Lustig, H.; Xiaolan, M. Manufacturing Risk-free Government Debt; CEPR Discussion Papers 16304; C.E.P.R.: London, 2021.

- Jiang, Z.; Lustig, H.; Van Nieuwerburgh, S.; Xiaolan, M. Fiscal capacity: An asset pricing perspective. Annu. Rev. Financ. Econ. 2023, 15, 197–219. [Google Scholar] [CrossRef]

- Elenev, V.; Landvoigt, T.; Shultz, P. J.; Van Nieuwerburgh, S. Can Monetary Policy Create Fiscal Capacity?; NBER Working Papers 29129; National Bureau of Economic Research, Inc.: Cambridge, MA, 2021.

- Davig, T. Periodically expanding discounted debt: A threat to fiscal policy sustainability. J. Appl. Econ. 2005, 20, 829–840. [Google Scholar] [CrossRef]

- Jiang, Z.; Lustig, H.; Van Nieuwerburgh, S.; Xiaolan, M. Z. The U.S. Public Debt Valuation Puzzle; NBER Working Papers 26583; National Bureau of Economic Research, Inc.: Cambridge, MA, 2019.

Figure 1.

Source: Authors’ calculations.

Figure 2.

Source: Authors’ calculations.

Table 1.

Two-regime SETAR model for the U.S. public debt/GDP ratio, 1974Q1-2024Q1.

| 0.37 | 0.74 | ||

| 0.99*** | 0.01 | ||

| 9.47*** | 2.10 | ||

| 0.92*** | 0.02 | ||

Notes: *** 1% significance level, ** 5% significance level, * 10% significance level. : dependent variable (public debt/GDP ratio). : threshold variable (15% trimming percentage for threshold search with ordinary standard errors and 1000 bootstrap repetitions).

Table 2.

Three-regime SETAR model for the U.S. public debt/GDP ratio, 1974Q1-2024Q1.

| 0.37 | 0.74 | ||

| 0.99*** | 0.01 | ||

| 12.69*** | 4.25 | ||

| 0.88*** | 0.05 | ||

| 11.64*** | 4.11 | ||

| 0.90*** | 0.04 | ||

Notes: *** 1% significance level, ** 5% significance level, * 10% significance level. : dependent variable (public debt/GDP ratio). : threshold variable (15% trimming percentage for threshold search with ordinary standard errors and 1000 bootstrap replications).

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Copyright: This open access article is published under a Creative Commons CC BY 4.0 license, which permit the free download, distribution, and reuse, provided that the author and preprint are cited in any reuse.