Submitted:

28 September 2024

Posted:

30 September 2024

You are already at the latest version

Abstract

This study, which investigates the impact of foreign bank entry on the efficiency and sustainability of domestic banks in developing countries using a Meta-Frontier analysis to estimate efficiency scores, presents findings of significant importance to banking and finance. By incorporating financial, social, and environmental sustainability proxies—such as efficiency, loan portfolio composition, and macroeconomic conditions—this study assesses whether foreign competition enhances or undermines the long-term stability of domestic banking sectors. The results show that while foreign banks can improve financial efficiency, they may destabilize domestic banks, notably smaller or less capitalized institutions. Additionally, the findings suggest that banks with higher investments in SME lending and green projects demonstrate better social and environmental sustainability. Policymakers and financial institutions must consider these dual effects when promoting foreign bank entry.

Keywords:

foreign banks

; bank efficiency

; sustainability

; financial sustainability

; social sustainability

; environmental sustainability

; meta-frontier analysis

; developing countries

; green lending

; sme lending

; macroeconomic factors

; banking competition

1. Introduction

The global banking environment has undergone significant transformations in the past few decades, with an increasing presence of foreign banks in developing countries. In Central and Eastern Europe, the foreign share of banking sector assets increased dramatically after the 2008 financial crisis, with more than 60% of banking assets in countries like Poland, the Czech Republic, and Hungary being controlled by foreign entities by 2020 (European Central Bank, 2021). Similarly, foreign bank presence in Latin America remained strong, with countries like Argentina and Chile reporting over 40% of total banking assets under foreign control by 2020 (World Bank, 2021). In Asia, while foreign bank penetration remains lower, countries such as Indonesia and Vietnam have seen a steady rise in foreign bank involvement, with foreign-controlled assets reaching around 10% as of 2020 (Bank for International Settlements, 2021). In contrast, Mediterranean countries maintain more conservative levels of foreign bank integration, with foreign-controlled assets still below 20% in most countries in the region (IMF, 2021).

Several factors have contributed to this growing presence of foreign banks. Deregulation and the relaxation of entry barriers in developing countries have been crucial in attracting foreign capital, especially during financial crises. The privatization of inefficient public banks and the desire for more stable capital inflows—compared to volatile portfolio investments—have driven many developing countries to open their banking sectors to foreign investors. For instance, the global financial crisis of 2008 and subsequent economic downturns revealed domestic banking sectors' vulnerabilities, particularly in non-performing loans and weak regulatory frameworks. By 2020, countries like Poland and Romania had drastically reduced their non-performing loan ratios to below 5%, reflecting improved banking sector resilience and more stringent regulations (World Bank, 2021).

In this context, the consequences of foreign bank entry on domestic banks and the financial systems of host countries remain a topic of debate. While some scholars argue that foreign banks enhance the efficiency of local banking sectors by introducing advanced technology and practices (Claessens et al., 2010), others caution that increased foreign competition can undermine the stability and profitability of domestic banks. The empirical evidence is mixed: studies like those of Hermes and Lensink (2014) and Unite and Sullivan (2015) have shown that foreign bank entry can reduce local banks' market share and profitability, especially those operating in less developed regulatory environments. Moreover, the COVID-19 pandemic has further complicated this narrative, as foreign banks in developing countries often faced fewer regulatory constraints and were better positioned to adapt to post-pandemic financial conditions (BIS, 2021).

This paper aims to evaluate the sustainable impact of foreign bank presence on the efficiency and stability of domestic banks in 54 developing countries. It uses a Meta-Frontier analysis to assess variations in efficiency across different technological and institutional environments. Focusing on the post-pandemic recovery and the global trend toward sustainable financial practices, this study contributes to the ongoing debate on whether foreign banks are a stabilizing force in developing markets or pose risks to long-term financial stability.

2. Literature

2.1. Positive Effects

2.1.1. Improving Efficiency

The relaxation of the entry barriers has been greatly encouraged by the expected positive effects on local banks' efficiency. Installing new foreign banks, usually more efficient than local ones, profoundly modifies the structure of local banking markets and could intensify competition in these markets. This new environment could incite local banks to improve their efficiency levels to protect their market share (Chantapong S (2003). They would be forced to align with their foreign counterparts by enhancing the quality of their management and the adoption of new banking techniques. This presence could ensure the transmission of knowledge and banking expertise because of the synergistic effect that this creates (Weill L (2003); Bonaccorsi di Patti E., DC and Hardy (2005)), required for controlling costs, improving the quality of products, expansion of product mix (Abut D., S. Biogio and D. Siller (1999), Berger and De Young (2001); Liu L. (2002b)) and improving their operational performance. Other studies show that severe restrictions on foreign bank's entry only increased overhead costs and reduced the efficiency of the banking sector. S. Claessens and Glaessner (1999); JR Barth, Caprio G. and R. Levine (2001); Agenor P. R. (2001); Kraft et al. (2002) argue that the opening of the domestic financial system to foreign competition can be profitable for domestic banks and lead to profits. Installing new competitors can increase the number of actors in this system and could lead to improved efficiency in the country's financial intermediation process. This improvement may result from decreased costs and excessive profits associated with a monopoly market or the existence of a cartel.

Several studies have empirically shown the positive effect of foreign presence on the efficiency of local banks in developing countries. The most comprehensive study returns to Cleassens S. et al. (2001). These authors confirm that foreign banks are associated with a decrease in financial margin, financial income, and total expenses for domestic banks. They interpreted these effects as a sign of improving local banks' efficiency. Buch CM (1997) also achieved these results for the domestic banks in Central and Eastern Europe, Denizer C. (1999) for the domestic banks in Turkey and Barajas A., and R. Steiner Salazar N. (2000) for the domestic banks in Colombia.

Other authors, such as Detraigache and Gupta (2004), Agenor (2001), and Kroszner (1998), mentioned that the entry of foreign banks could mitigate harmful public control over the activity of local banks. This could reduce the harmful effects of moral hazard, which is primarily due to the risky behavior of domestic banks. This new context would promote better allocation of financial resources, thus improving the operational functioning of domestic banks (Tschoegl AE (2003)).

2.1.2. Improves Stability

As for stability, the foreign presence could improve the stability of the banking sector and make it less vulnerable to crises (Bosco M. (2003), Feldstein (2002); JR Barth, G. Caprio and R. Levine (2001), Levine R (1999), Demirgüç-Kunt, A., and R. Levine HG Min (1998)). In the new environment, which is characterized by the presence of foreign banks, the banking authorities would be obliged to improve regulation and banking supervision to control and supervise the risks inherent either in traditional banking activities or in financial products that would be newly launched in local markets (PM Garber (2000)), or in the wide range of international activities led by financial institutions (DJ Mathieson and Roldós J. (2001)). Foreign presence can ensure the transfer of expertise in selecting credits and could consequently improve credit quality, especially for domestic banks.

The presence of foreign banks, characterized by good diversification of their financial resources, can support economic activity in the host countries (Chantapong S. 2003 L. Weill 2003 Crystal JS et al. 2002). These banks can help local companies in difficulties to recapitalize. Liu L. (2002a) (2002b), Goldberg (2001), and R. Levine (1996) argue that the presence of foreign banks could assist host countries hit by banking crises to restructure their financial systems. It would facilitate the influx of foreign capital needed to finance the restructuring program. The United Nations (2007) states that the decision to permit foreign banks to enter local banking systems in Asia and Latin America is largely motivated by the insufficient capital of internal financial sources. These banks can provide the necessary funds to ensure stability in funding economic activities even during economic recession. They can be considered an excellent way to diversify risks when the internal economic situation is terrible and to protect national savings against massive capital flight away, which can destabilize the whole financial sector. Crystal JS, Dages BG and L. Goldberg (2002), L. Goldberg, BG Dages and D. Kinney (2000) argue that foreign banks had not reduced their credit activities during the Chile, Colombia, Argentina, and Mexico crises. The credit growth rate granted by these banks was higher and more stable than domestic banks during even the post-crisis period. Peek and Rosengren (2000b) also confirm these results for Argentina, Brazil, and Mexico. Aziz et al. (2002) state that the crisis, which seriously affected Indonesia's interest rates and exchange rates, didn't have the same consequences for domestic and foreign banks. Foreign banks, which didn't undergo the same capital losses that domestic banks, had continued their activities to compensate for the decrease in the volume of loans granted by domestic banks. They played a significant role in stabilizing the situation during the crisis period. Foreign banks could thus complement the banking environment of host countries and would not replace existing domestic banks.

2.2. Negative Effects

2.2.1. Active Impact

The presence of foreign banks could reduce the share of local banks' credit market. These banks may set competitive lending rates compared to those offered by domestic banks. The domestic banks, which are handicapped by their high restructuring costs due to the low level of operational efficiency and a large volume of non-performing loans inherited from the protectionism period, may be unable to provide appropriate means to face a new, more competitive environment. They might suffer a decline in their market share and place themselves in an uncomfortable situation, especially when the performance gap with their foreign counterparts would be very significant. The current state of the banking sector in developing countries confirms this result; the share of the credit market for foreign banks has increased significantly and even reached more than 50% of the local market in countries such as Argentina (Goldberg and L. al 2000).

Increased competition in the credit market can incline domestic banks to undertake risky projects. Foreign banks, beneficiaries of a more developed risk management than domestic banks and an ability to attract the least risky customers would tend to select and "cherry-pick" the best and most profitable customers in the local market, including the most creditworthy corporate and wealthy individuals. Domestic banks may be unable to provide better conditions than those offered by foreign banks, and they would be obliged to serve and finance riskier projects that foreign banks have refused funding. In other words, the decline in profits in the banking sector, which can be driven by increased competition, can lead domestic banks to reposition themselves on niche businesses abandoned by foreign banks to generate the minimum profit needed to cover overhead costs. Leaving domestic banks to serve the riskiest customers is considered a misallocation of financial resources, and it may deteriorate the quality of domestic banks' portfolios.

Barajas A., R. Steiner, and Salazar N. (2000) studied the effect of the entry of foreign banks into Colombia's banking sector. They used a representative sample of the banking system comprising 32 banks for the 1985-1998 period. They conclude that the decrease in the financial margin, induced by increased competition following the entry of foreign banks, has increased the volume of non-performing loans and has deteriorated, therefore, the quality of the domestic bank's credit portfolio. Foreign banks, having an efficiency advantage, gained a significant share in the retail and consumer lending market; they finance the least risky projects while leaving the riskiest projects and the worst consumers financed by the domestic banks. The result proved by Unite A. et M. Sullivan (2003) for the Philippine banking sector.

Bosco G (2003) also confirms this result for transition countries and the Southern Mediterranean. He demonstrates that the level of bank efficiency greatly affects its ability to select good customers. The most efficient banks are the best able to choose profitable projects and decrease credit risk accordingly. The efficiency gap between foreign banks and domestic banks can lead domestic banks to finance "risky clients" and have a loan portfolio characterized by a large volume of non-performing loans.

2.2.2. Passive Impact

Also, in the new competitive environment, local banks can not attempt to increase the deposit rates to save and retain depositors. These banks, which are generally characterized by relatively high operations costs against foreign banks, are not able to increase fluency in the remuneration of deposits to satisfy their depositors and, thus, may be unable to manage increased competition in the deposit market. Their efficient foreign counterparts would rather be able to set more attractive deposit rates to attract depositors and consequently gain a significant deposit market share. The decrease in deposit market share may have two negative effects. The first is that the decrease in deposits can be interpreted as a bad signal by the capital market, and the depositor may lose confidence in their local banks. The second effect is that domestic banks, to face the new context, would be forced to resort to other, more expensive modes of financing to fund their financial intermediation activities and to ensure the balance between assets, liabilities, and equities.

Intensifying price competition may lead banks to reduce their financial intermediation margins to ensure their survival. This decrease can attenuate the financial income and cash flow if banks find themselves unable to reduce the costs of borrowed funds or control overheads in parallel. Various studies have come to confirm that the change in the market structure following the entry of new banks, more efficient than domestic banks in developing countries, can lead to an unfavorable change in the profitability of domestic banks (Cleassens et al 2001, Clarke G. et al. 1999 and Buch CM 1997). To face this context and ensure the stability of their financial income, these banks may be forced to grant more credits to offset the loss caused by lower pricing and increased funding costs. In other words, they may be forced to give a greater volume of loans with low financial margins. They could thus compensate for the decrease in the financial margin (price effect) by increasing the volume of loans granted (quantity effect). This strategic choice aimed at expanding the market share to offset the margin decline can lead to over-indebtedness of customers, and this can lead to an increase in the counterparty risk, especially in unfavorable economic conditions. Banks no longer comply with the prudential rules, they would tend to preserve, by all means, their market shares, even neglecting the risk that such a decision could lead to a deterioration in the quality of their assets. Dietsch (1996) and Keeton W.R (1999) reported that increased credit volume could lead to an increase in bad loans if the increase is justified only by a change in the policy of granting loans and not by the existence of profitable investment opportunities.

2.3. Hypothesis

The increase in the volume of non-performing loans to banks could cause the banks to bear high operating costs. According to Berger A.N and R. Deyoung (1997), any delay in payment would cause the bank to deploy additional costly managerial efforts to manage unpaid. The costs borne by banks are mainly the cost of the extra controls on borrowing and assessment of their pledges, the cost of attachment of pledge if other defaults occur, the costs related to any operation that aims to defend the stability and image vis authorities of banking supervisory and market participants, the cost of additional precautionary aimed at preserving the quality of loans already granted and which may be of major interest to the bank in a financial position perilous and sales control costs (securitization). Unpaid payments also increase the bank's financial expenses. The use of additional funds to reward the registered capital loss would bear the banks an additional risk premium and thus increase the deposit rates. In this case, the unfavorable change in interest rates would lead to an increase in financial expenses that would negatively impact the financial margin, especially when banks can not increase lending rates simultaneously.

Increasing costs following the appearance of credit problems could affect the efficiency level of banks (Berger A.N and R. Deyoung 1997). Empirical studies demonstrate the existence of a negative relationship between efficiency and non-performing loans to failing banks; an increase in the volume of non-performing loans would promote a deterioration in the level of cost efficiency. Deyoung R. and G. Whalen (1994) state that a deterioration in cost efficiency would precede the increase in lost credits. Similarly, a low level of efficiency would lead to a deterioration of the credit portfolio quality, and this would mitigate more efficient banks.

Given the results of different empirical studies, there is no clear answer as to the positive effect of this presence; there are supporters and detractors. The decision to open the banking sector to foreign competition that would help improve efficiency presents very expensive costs for those countries. Empirical studies that have interpreted the decrease in profitability as a good sign of the presence of foreign banks have ignored the negative effect of this decline on the stability of banks. Analysis of recent banking crises shows that the decrease in profitability could encourage the adoption of risky strategies and promote the emergence of crises. The negative effects of the presence can dominate its positive effects and can lead to serious consequences for domestic banks. Williamson and Mahar (1998) report that excessive risk-taking can neutralize the positive effects that can result from financial liberalization and thus lead to a financial crisis. The decrease in the volume of deposits and loans to local banks can lead to their bankruptcy.

Thus, opening in a period marked by the fragility of local banks could promote the degradation and not the improvement of their efficiency levels and their stability. To fill the literature, this work refers to the differential efficiency hypothesis developed by Demsetz (1973) and to the results of Berger and R. Deyoung AN (1997), which demonstrated the negative impact of the poor quality of loan portfolios on the efficiency of banks, to test the following research hypothesis:

Hypothesis: The presence of foreign banks in developing countries could negatively affect domestic banks' efficiency level.

3. Methodology

3.1. Modeling

The model used is inspired by previous works such as Detragiache et al. (2006), Hermes and Lensink (2004), and Claessens et al. (2001). These studies explain bank profitability and efficiency based on bank-specific characteristics and the macroeconomic environment in which banks operate. Our model assesses the impact of foreign bank entry on the efficiency of domestic banks in developing countries using sustainability proxies related to efficiency, bank characteristics, and macroeconomic factors.

Our model is specified as follows:

where b, t, and p, respectively, reflect the bank b in year t and the country p;

Ybtp = α + ξ Presencetp + φβ Bbtp + δ Mtp + γ Inter + εbtp.

b = 1, .. ..., n, t = 1, ...., T and p = 1, .. ..., P.

Ybtp: Efficiency of domestic banks; serving as the proxy for financial sustainability.

Presencetp represents the "presence of foreign banks" (measured by the proportion of foreign-controlled assets), which serves as a proxy for their influence on financial stability and sustainability.

Btp: includes bank characteristics, such as size (total assets), capital adequacy ratio, and loan portfolio composition (e.g., proportion of green or SME loans), which reflect financial, social, and environmental sustainability.

Mtp includes macroeconomic variables like GDP growth, inflation rate, and interest rate, which affect banks' overall financial sustainability.

Inter: includes interaction terms (Presence * Performance Gap between domestic and foreign banks) to measure the moderating effect of foreign bank presence on domestic bank characteristics, allowing us to test how competition influences sustainability.

εbtp: The stochastic component of the error is assumed to be uncorrelated with the explanatory variables and follows the normal distribution N (0, σε). It is independent and identically distributed (iid).

This study uses two different methods to measure each bank's efficiency level. The first is to calculate the intermediation margin ratio, which has been widely used in the literature to assess the effect of the entry of foreign banks on the efficiency of local banks in developing countries. The second method is based on the estimated efficiency level by the "Meta frontier approach." This approach calculates the technical efficiency of banks operating different production technologies, and they are subject to different environmental conditions (economic, political, social ... etc.). It provides a measure of the efficiency level of banks operating in different countries while considering the existing technological gap between these countries.

Suppose we have "P" in different countries, and each country 'p' contains Np banks that face the same input prices and pursue the goal of cost minimization given the output level. The stochastic cost frontier model for each bank "b" of the country "p" at the time "t" can be formulated as follows:

where CTbt(p) is the total cost, Xbt (p) is the vector of output and input prices. φ (p) is the vector of unknown parameters to be estimated. Vbt (p) is the usual error term that follows the normal distribution N (0, σ2); it is independent of Ubt(p). It is a white noise used to control measurement errors and determinants of costs beyond the control of managers. The term also captures the luck (bad) of the bank having experienced a favorable (unfavorable) exogenous shock that (increases) decreases the total cost of the bank. Ubt(p) is the deviation of the cost of the firm b compared to the efficiency frontier. It serves as an approximation of technical and allocative inefficiency. It is positively defined with an independent distribution Vbt(p).

To facilitate the equation (2-29), it can be formulated as follows:

Following Battese et al. (2004), this model assumes that for each country, there is only one data generation process for banks that use a given technology.

Therefore, this model is applied to each country to assess its stochastic frontier cost. Meta-frontier takes the same functional form as an individual stochastic frontier for each country. Thus, the function of the Meta-cost frontier that envelops the frontiers of specific costs for each country can be formulated as follows:

Is the optimal expense for the bank "b" at the time "t" required to produce the given output amount under exogenous input price conditions?

Is the vector of parameters associated with the Meta-frontier cost function that satisfies the condition (C1) below:

Meta-frontier is the deterministic function parameter that envelops the deterministic part of the individual cost frontiers. Its values must be less or equal to the deterministic components of the estimated stochastic cost frontier for each country. The cost Meta-frontier function can reflect the minimum production cost to produce a given output level. This is the minimum cost associated with the technique of more efficient production. The inequality constraint given by equation (C1) must be satisfied for all countries throughout the period. Meta-frontier is considered the curve enveloping the individual frontier cost countries.

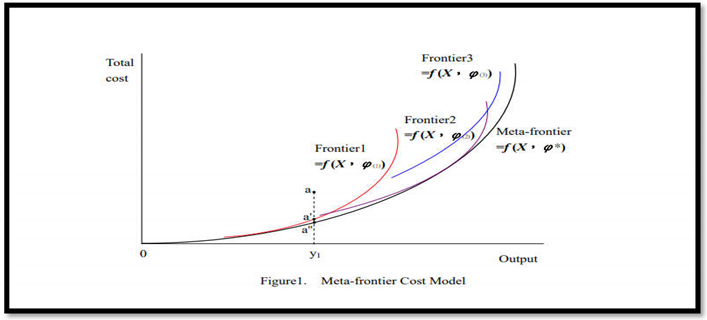

Figure 1 illustrates how the Meta-frontier cost envelops the stochastic frontiers function of different countries in the case of a single output.

In this figure, the frontier 1, 2, and 3 represent four stochastic frontiers for 3 countries. The cost of the Meta-frontier function that encompasses the three stochastic frontiers indicates the possibility of producing at a total cost below the deterministic costs correlated with the stochastic cost frontiers of the four countries. Frontiers 1 and 2 are arbitrarily chosen to be tangent to the Meta-frontier, and frontier 3 is not. Thus, as the stochastic cost frontiers 1 and 2 are closest to the Meta-frontier, we can say that banks in countries 1 and 2 adopt more production technology developed than those in the third country.

3.2. The Efficiency Score and the Technology Gap Ratio "TGR"

A company's cost efficiency is evaluated by the minimum cost (taken from the frontier) to the observed current cost for the same given production and conditions price. It is a measure of cost deviation versus best performance.

The Meta-frontier cost efficiency."" of a bank "b" in a year "t" in the country "p" can be estimated using the Meta-frontier model, as specified in equation (5) :

Integrate the equation (3) into equation (5):

where the first term on the right reflects the level of technical efficiency (EC) on the stochastic cost frontier of the country "p."1

It must be between 0 and 1 because It is considered a non-negative random variable.

For the second term, it is the technology gap ratio "TGR."

The ratio "" measures the technology gap for country "p" where production technology adopted by its firms is less developed than that available for all countries. It is obtained from the Meta-frontier cost function.

According to the constraint (C1), this measurement is between 0 and 1. A country's high value of the ratio "TGR" reflects its adoption of advanced production technology.

Finally, the cost efficiency relative to the Meta-frontier as measured by the equation (5) can then be formulated as follows:

The vector It is obtained after solving the following optimization problem:

As all deviations are positive according to the constraint (C2), all the absolute differences are equal to the differences. Using equations (3) and (4), we can convert the optimization problem above (10, C2) to a linear programming problem "LP" :

The functional form of the cost function adopted for calculating the level of efficiency is the type of translog cost function; it is as follows:

where (Ln CT) is the natural logarithm of the total cost of the bth bank in the period t, (Ln wi bt) is the natural logarithm of its ith input prices, (Ln yk) represents the natural logarithm of its kth output, (Ln F) denotes its capitalization ratio used to control observable heterogeneity among banks.

where (Ln CT) is the natural logarithm of the total cost of the bth bank in the period t, (Ln wi bt) is the natural logarithm of its ith input prices, (Ln yk) represents the natural logarithm of its kth output, (Ln F) denotes its capitalization ratio used to control observable heterogeneity among banks.

where (Ln CT) is the natural logarithm of the total cost of the bth bank in the period t, (Ln wi bt) is the natural logarithm of its ith input prices, (Ln yk) represents the natural logarithm of its kth output, (Ln F) denotes its capitalization ratio used to control observable heterogeneity among banks.Technical inefficiency, due to the excessive use of inputs to produce a given volume of output resulting from the choice of the wrong combination of inputs given their relative prices in the market, would be captured by the inefficiency term Ubt. The term Vbt is used to control measurement errors and determinants of costs beyond the control of managers. This term also captures the (bad) luck of the bank having experienced an exogenous shock (unfavorable) favorable that (increases) decreases the total cost of the bank.

To be consistent with the economic theory, the cost function should be: (i) non-negative, (ii) twice continuously differentiable in its domain, (iii) symmetric, (iv) linear homogeneous in input prices, (v) monotonically increasing in input prices and outputs, (vi) concave in input prices. The parameters need to satisfy the following restrictions :

φij = φji, γkm = γmk ⇒ pour que la fonction de coût soit symétrique

φi = 1, φij = 0, λik = 0, ψfi = 0 ∀ i

In this work, we refer to the intermediation approach to define the inputs and outputs bank.

The independent variables included in the model reflect the characteristics of the banks and the environment in which they operate. We select variables that can be measured for all banks in different countries.

3.3. Sample and Database

The database exploited in this research covers 1993-2001, including 1799 operated banks active in 54 developing countries (Table 1).

The results illustrated in Table 2 confirm that the choice of the model is appropriate. The p-value of the χ2 test (Prob> χ2) is zero in all regressions. This proves that the model is statistically significant. Table 2 illustrates interesting results of environmental variables on the efficiency of banks.

The choice of these large samples is motivated by two main reasons. The database available allows us to appreciate the impact of foreign bank entry on the efficiency of domestic banks in several countries. The achieved results are more conclusive. And secondly, this presence is not the same intensity for different countries. For example, in 1999, the total assets of foreign banks in Argentina were almost 48.6% of the total assets of the entire banking sector, and that of Poland was 52.5%, while for other countries such as Egypt, the presence was almost 4% in 1998. These various examples enable us to appreciate the real contribution of the presence of foreign banks in those countries.

4. Results

The results of the estimation of the model (1) are shown in the Table below (Table 1). The dependent variable is the bank efficiency level measured by the "Meta frontier approach." The model estimated is the Tobit model because the variable "cost efficiency" is very special; its value is between 0 and 1.

4.1. Variable Concentration "Conc"

The variable coefficient concentration (Conc) is significantly positive in all regressions. The concentration, therefore, positively affects the level of efficiency of banks. The more concentrated the market, the more banks could benefit. In a context characterized by a low number of players, the information asymmetry would not be intense, and information on the quality of borrowers would not be too dispersed. Banks, in this case, would, at low cost, have good information in quantity and quality on the ability of borrowers to meet their funding commitments. These interpretations can be supported by Detragaiache et al. (2006), who argue that good information on debtors could help banks reduce their operating costs.

The most important conclusion we can draw from the positive sign of this variable is that it confirms the efficiency differential hypothesis developed by Demsetz (1973). This sign would mean that the concentration is due to differential efficiency and that the most efficient banks dominate the least efficient banks. The dominant position of some banks reflects greater efficiency, not the exercise of market power or barriers to entry.

4.2. The Variable Presence of Foreign Banks "Presence":

The estimated coefficient of our key variable, "Presence of Foreign Banks (Presence)," is significantly negative in all regressions. This implies that an increase in the level of foreign bank presence may result in a loss of efficiency for domestic banks due to an increase in total costs not justified by the increase in production volume (output) or factor prices production (inputs). Thus, the presence of foreign banks is most important; the loss would be more serious in terms of cost control.

The entry of foreign banks would thus have negative effects on local banks. The increased competition fostered by the entry of new foreign units, which perform better than local banks, would lead the latter to (i) pursue risky strategies and (ii) use more expensive funding.

In addition, high restructuring costs can deteriorate the level of efficiency of local banks. The entry of foreign banks can encourage their local counterparts to make new investments in the banking technologies and techniques adopted and improve the managerial capacity of their staff to face the new competitive environment. Restructuring costs can be high, which can increase the total costs of local banks and deteriorate their efficiency levels, even in the short and medium term.

Our results contradict those from studies by N. Hermes and R. Lensink (2004); Unite A. and M. J. Sullivan (2003); Drakos K. (2003); Classes S. et al. (2001); Barajas et al. (2000); Denizer (1999); Demirgüç-Kunt, Huizinga (1999). These studies conclude that the presence of foreign banks improves the efficiency of local banks. However, this result would remain very relative; it would largely depend on the proxy taken to assess the efficiency improvement. In these works, authors considered the decrease in the financial margin as an important sign confirming the positive effect of the presence of foreign banks. However, in our opinion, this is a biased interpretation of the margin decline and should not always be interpreted as a good sign that reflects an improvement in the efficiency of local banks. This decrease has been seen as one of the determining factors in the onset of the most recent banking crises. Indeed, a decrease in investment margin can destabilize the banking industry, especially when it is not accompanied by effective cost control, and this is also the case in developing countries. The limits of financial ratios in evaluating the level of efficiency have contributed to these results; the current state of banking sectors, clearly marked by a strong presence of foreign banks, proves that the foreign presence has not led to improved efficiency of domestic banks in developing countries. Also, the choice of their samples may bias their results, Hermes N. and R. Lensink (2004); Classes S. et al. (2001). For example, even if they have operated a very large sample, they neglected the country effect in their regressions. The dependent variable in their models is that domestic banks operate in developed and developing countries. This choice is highly disputed; the sample is not homogeneous.

Our result is consistent with Daniel Ofori-Sasu et al. (2018) and Haiyan Yin et al. (2020). Using data from 25s banks in Ghana over a 6-year period (2010–2015), Daniel Ofori-Sasu et al. (2018) prove that an immediate and a short-term entry of foreign banks has a consistent negative relationship with both technical- and cost-efficiency scores. In contrast, the long-term entry of foreign banks shows an inconsistent relationship with the banking efficiency scores. Using unbalanced panel data (banks from 126 countries from 1995-2013), Haiyan Yin et al. (2020) show that foreign bank numbers are positively associated with both cost inefficiency and overhead costs, suggesting that foreign bank presence increases cost inefficiency.

4.3. Variable Financial Disintermediation "Disinter," Actual Interest Rate "RealInterate" and Economic Development "GDP per Capita":

Internal factors could promote the efficiency of domestic banks in developing countries. The coefficients of "Financial Disintermediation (Disinter)" and "Real Interest Rate (RealInterate)" are positive in sign and statistically significant in all regressions.

Thus, the higher the financial disintermediation ratio, the greater the efficiency level would be improved. This result shows that direct market financing and banks would be complementary, not substitutes. The increased competition between these two modes of financing may encourage banks to make more effort in monitoring and controlling their cost structures, forcing them to lower their lending rates and provide favorable conditions for agents in need of financing.

The sign of the coefficient of the environmental variable (Real Interest Rate " RealInterate "), which is positive and significant at the 1% level, suggests that an increase in the real interest rate can positively affect the efficiency of banks in developing countries. The plausible explanation we can advance is that the transition from an economy characterized by financial repression to a market economy can help improve the efficiency of banks.

The setting of interest rates by the banking authorities tends to restrict the development of financial intermediation, especially when it is accompanied by framing credit policy. Banks would be required, in this case, to finance productive sectors and low-yield activities through very low interest rates, often known as preferential interest rates. The intervention of the state in financing the economic circuit can increase the cost of the process of financial intermediation and foster the misallocation of national savings; loan decisions would be guided rather by political factors by profitability and efficiency considerations.

Finally, the value taken by the coefficient of the last environmental variable, "GDP/per capita," is significantly positive at 1%. This implies that economic growth can promote a higher standard of bank efficiency. Thus, a favorable economic environment can positively affect the demand and supply of banking services and reduce the volume of non-performing loans. The portfolio's credit quality would improve, and the cost of managing non-performing loans would be low.

4.4. Effects of Specific Variables to Banks on Their Efficiency Levels

Next, we present the results of estimating the coefficients of different variables that characterize specific banks.

All coefficients of environmental variables have kept the same signs and meanings even with the inclusion of two new variables: Size (Ln size) and other Non-productive Assets (OtherNProAssets). This would support the absence of multicollinearity between the explanatory variables.

The estimated coefficient of the variable "Size" is a positive and significant sign confirming the presence of economies of scale in banking activity. An increase in the size and degree of integration into the economic circuit would allow the bank to amortize its operating costs over a large number of operations and set prices competitively. Banks are interested in increasing the volume of their activities to achieve economies of scale.

Thus, we can conclude that banks in developing countries suffer from the size problem. Their sizes would not allow them to invest in new banking technologies and techniques to diversify their risks and reduce costs. The size would be a factor that can prevent domestic banks from competing with foreign banks.

4.4.1. Other Non-Performing Assets "OtherNProAssets"

For the variable "Other non-performing assets " OtherNProAssets, "the coefficient is negative and not significant. These banks assets2 Are associated with different costs, especially financial costs related to their pay and sometimes high opportunity costs, which are due primarily to idle capital that could be exploited in financing activities generating added value (granting loans and holdings of securities). Thus, for a given bank, if the part of these assets increases, its total cost will increase, and its efficiency level will deteriorate further.

4.4.2. The Variable Net Loans/Total Assets "Net Loans) in%":

The included variable "Net loans/total assets (Net loans)" coefficient in the fourth regression is significantly positive at 5%. Thus, the more managers take care of granting low-risk loans, the more the bank's total cost will decrease, and its efficiency level will improve. This indicates that decreasing nonperforming loans would also decrease the bank's cost. To improve its efficiency level, the bank has to ensure good ex-ante credit risk and control of the borrower's behavior once funding is granted to overcome adverse selection and moral hazard problems that may emerge and deteriorate the bank's position. We join then Berger A.N. and R. Deyoung (1997) to argue that a large volume of non-performing loans can be considered a source of inefficiency for banks.

Foreign banks' entry can affect domestic banks' efficiency through non-performing loans. Thus, since our results suggest that foreign banks' entry has negative effects on the efficiency of domestic banks in developing countries, we can conclude that the relaxation of entry barriers could alter the quality of domestic banks' credit portfolios through a remarkable increase in the volume of non-performing loans.3 Foreign banks would monopolize the most profitable market share and force their local counterparts to finance the segment of the market characterized by a high proportion of high-risk clients. Foreign banks can overcome the information asymmetry problem by their expertise or even by gradually acquiring domestic banks' capital and could thus provide a database necessary for assessing the quality of local borrowers.

4.4.3. The Variable "Income Ratio (Coeffiexplo)":

For the variable "income ratio (Coeffiexplo)," the coefficient is significantly negative at 10%. Thus, the greater the share of NBI (Net Banking Income) absorbed by the structure costs, the more the banks' efficiency level deteriorates. To improve its efficiency and ability to face the new competitive environment, the bank must exert more effort in controlling the cost structure to minimize the operating cost of each monetary unit produced.

4.5. Interaction Terms:

The table below (Table 2) presents the results of estimating our model (Equation 1). We introduce the interaction terms. We remark that the signs and significance of the coefficients of the different variables do not change following the model's estimation (6) and (7).

The results illustrated in Table 2 are very important and confirm the conclusions that we have just stated. The presence of foreign banks may deteriorate the efficiency of domestic banks in developing countries.

The result relating to the interaction term between "the degree of presence of foreign banks" and "efficiency gap between the average efficiency level of foreign banks and the efficiency of each bank b (denoted PDEB)" well confirms our research hypothesis. The coefficient of this term, which is significant and has a negative sign at 1%, indicates that the presence of foreign banks can have a significant negative impact on the efficiency of domestic banks, especially when the difference in efficiency between banks - Foreign and Domestic - is significant. The magnitude of this effect is greater than that of the variable "presence of foreign banks" considered separately in all other estimates (1, 2, 3, 4, 5, 6, and 7). The result of the seventh estimate confirms the hypothesis advanced. The sign of the coefficient of the interaction terms "presence" and "efficiency gap between foreign banks and domestic banks" (noted PDEM) is also negative. According to the results illustrated in Table 3, the magnitude of this effect is also greater than the effect of the variable "presence of foreign banks' taken separately in the other estimates.

Overall, the estimates reported in all the tables above indicate that the relaxation of barriers to entry can not be regarded as an appropriate solution for developing countries. The literature has unanimously argued that foreign banks are generally more efficient than domestic banks. Our results also support this thesis; the level of technical efficiency estimated by the Meta-frontier approach proves that foreign banks have an efficiency advantage when entering developing countries. And this advantage is also the determining factor in relaxing barriers to entry in these countries. Banking authorities in these countries seek, through their decisions, a synergistic effect that can result from the presence of more efficient entities. The intensification of competition would encourage local banks to improve their levels of production efficiency to ensure their survival. However, the result can be disappointing; this difference would not favor an improvement but rather a deterioration in efficiency. Local banks could not withstand fierce competition from more efficient foreign banks. The most efficient banks would be able to attract undoubted customers and gain an attractive market share. This would confirm the differential efficiency hypothesis advanced by Demsetz (1973). Thus, the greater the efficiency gap between foreign and domestic banks, the more the deterioration in the efficiency level of local banks would further worsen and even lead to a market largely dominated by foreign financial institutions. In this case, the banking authorities would lose control over the banking sector and, therefore, the means of financing their economy. Finally, the efficiency gap between the two banks can greatly reduce the viability of the less efficient banks and condition the future structure of the local banking system in developing countries.

5. Conclusions

This study has examined the impact of foreign bank entry on the efficiency and sustainability of domestic banks in 54 developing countries, employing a Meta-Frontier analysis to assess the efficiency of domestic banks in comparison to their foreign counterparts. The results reveal that while foreign banks often enhance the financial efficiency of domestic banks by introducing advanced technology and management practices, they also introduce challenges in terms of increased competition and potential market destabilization for local institutions.

These findings align with the conclusions of Claessens et al. (2010) and Levine (2001), who argue that foreign bank entry tends to improve efficiency in local markets by raising the competitive bar. However, similar to the work of Hermes and Lensink (2014) and Unite and Sullivan (2015), this study also highlights the risks posed to financial sustainability in countries with weaker regulatory frameworks. In such contexts, domestic banks may struggle to maintain their market position and financial health, especially when competing against better-capitalized foreign institutions. Thus, the results suggest a dual effect: while foreign banks contribute to short-term efficiency improvements, they may simultaneously undermine the long-term financial stability of local banks, particularly smaller or less-capitalized ones.

In contrast to studies that emphasize the purely positive effects of foreign bank entry, such as Bhattacharya (1993) and Terrell (1986), this study presents a more nuanced view. It shows that social and environmental sustainability are also critical factors in determining the overall impact of foreign bank presence. Domestic banks that focus on socially responsible lending, such as SME financing, tend to exhibit more robust performance and greater resilience under the pressures of foreign competition. Similarly, those who prioritize green lending demonstrate stronger environmental sustainability, reflecting a growing trend toward sustainable finance. This adds a new dimension to the literature by incorporating sustainability proxies, such as loan portfolio composition, into the analysis of foreign bank entry.

Moreover, the results suggest that while foreign banks tend to perform better in terms of financial efficiency, domestic banks that adopt sustainable finance practices are more likely to achieve long-term resilience. This highlights the need for policymakers to foster an environment where domestic banks can strengthen their social and environmental sustainability, enabling them to compete more effectively with foreign entrants.

Policymakers must carefully consider the dual impact of foreign bank entry on both the efficiency and sustainability of domestic banks. While foreign banks introduce operational improvements, their presence may undermine the financial stability of domestic institutions without adequate regulatory support. To ensure a sustainable financial ecosystem, domestic banks should be encouraged to adopt socially responsible and environmentally conscious lending practices, such as SME lending and green finance initiatives, to enhance their competitiveness in an increasingly globalized banking environment.

Future research should further explore the long-term effects of foreign bank presence on the financial stability, social inclusion, and environmental impact of banking sectors in developing economies. This is particularly relevant in the context of global challenges such as climate change, economic inequality, and the push for more inclusive financial systems.

Appendix A

Table A1.

Number of domestic and foreign banks in domestic banking sector :1993-2001.

| Number of domestic and foreign banks in domestic banking sector | ||||

|---|---|---|---|---|

| Continent | countries | Total Number of Commercial Banks* | Number of Domestic Banks** | Number of Foreign Banks*** |

| Argentina | 98 | 80 | 18 | |

| Bolivia | 16 | 14 | 2 | |

| Brazil | 159 | 130 | 29 | |

| Chile | 34 | 25 | 9 | |

| Colombia | 30 | 24 | 6 | |

| Latin America | Costa Rica | 27 | 26 | 1 |

| (13 countries) | Écuador | 40 | 39 | 1 |

| Jamaica | 12 | 9 | 3 | |

| Mexico | 40 | 25 | 15 | |

| Paraguay | 27 | 21 | 6 | |

| Peru | 27 | 20 | 7 | |

| Uruguay | 21 | 9 | 12 | |

| Venezuela | 46 | 41 | 5 | |

| Algeria | 6 | 5 | 1 | |

| Botswana | 6 | 1 | 5 | |

| Africa | Egypt | 30 | 23 | 7 |

| (8 countries) | Marocco | 13 | 9 | 4 |

| Nigeria | 46 | 42 | 4 | |

| South Africa | 33 | 26 | 7 | |

| Tunisia | 12 | 7 | 5 | |

| Zimbabwe | 9 | 5 | 4 | |

| Armenia | 7 | 6 | 1 | |

| Austria | 33 | 22 | 11 | |

| Bulgaria | 18 | 12 | 6 | |

| Croatia | 40 | 28 | 12 | |

| Cyrus | 17 | 12 | 5 | |

| Estonia | 8 | 5 | 3 | |

| Hungary | 34 | 10 | 24 | |

| Latvia | 25 | 18 | 7 | |

| Lithuania | 15 | 7 | 8 | |

| Malta | 10 | 5 | 5 | |

| Europe | Polond | 59 | 23 | 36 |

| (16 countries) | Russia | 112 | 103 | 9 |

| Slovakia | 21 | 14 | 7 | |

| Slovenia | 23 | 20 | 3 | |

| Turkey | 61 | 59 | 2 | |

| Ukraine | 38 | 32 | 6 | |

|

Asia (17 countries) |

Bahrain | 9 | 5 | 4 |

| China | 41 | 39 | 2 | |

| India | 63 | 60 | 3 | |

| Indonesia | 105 | 82 | 23 | |

| Jordan | 11 | 9 | 2 | |

| Lebanon | 70 | 55 | 15 | |

| Malaysia | 52 | 40 | 12 | |

| Nepal | 9 | 7 | 2 | |

| Pakistan | 23 | 23 | 0 | |

| Philippines | 41 | 34 | 7 | |

| Qatar | 5 | 5 | 0 | |

| Saudi Arabia | 10 | 7 | 3 | |

| Singapore | 21 | 16 | 5 | |

| South Korea | 53 | 49 | 4 | |

| Syria | 1 | 1 | 0 | |

| Thailand | 16 | 10 | 6 | |

| Vietnam | 16 | 15 | 1 | |

References

- Abut D., S. Bigio et D.A. Siller, 1999. The independent local bank in Latin America. Goldman Sachs Investment Research. November 23.

- Agénor P., 2001. Benefits and costs of international financial integration: Theory and Facts. Paper prepared for the conference on Financial Globalization: Issues and Challenges for Small States (Saint Kitts, March 27-28, 2001), organized by the Word Bank Institute in collaboration with the Malta Institute for Small States and the Eastern Caribbean Central Bank.

- Angbazo L.,1997. Commercial bank net interest margins, default risk, interest-rate risk, and off-balance sheet banking. Journal of Banking and Finance, (21), pp 55-87.

- Atkinson S.E., et C. Cornwell, 1993. Measuring technical efficiency with panel data: A dual approach. Journal of Econometrics 59, pp 257-261. [CrossRef]

- Aziz I., W. Bailey, C.X. Mao, F. Siddik et W. Thorbecke, 2002. Firm behavior, economic vulnerability, and the credit crunch: an analysis of micro-macro interactions, mimeo. Asian Development Bank Institute.

- Barajas A, R. Steiner, et N. Salazar, 2000. The impact of liberalization and foreign investment in Colombia’s financial sector, Journal of Development Economics, Vol 63, pp 157–196. [CrossRef]

- Barth J. R, G. Caprio et R. Levine, 2001. The regulation and supervision of banks around the world a new data base, The world banks.

- Berger A. N., et R. DeYoung, 2001. The effects of geographic expansion on bank efficiency, Journal of Financial Services Research, Vol 19, N° 2-3, pp 163-184. [CrossRef]

- Berger A.N., et R. Deyoung, 1997. Problem loans and cost efficiency in commercial banks, Journal of Banking and Finance 21 N 6, pp 849-870.

- Berger A.N., et T.H. Hannan, 1998. The Efficiency cost of market power in the banking industry: A test of the « Quiet Life » and related hypotheses, The Review of Economics and Statistics, Vol 80, No.3, pp 454-465. [CrossRef]

- Bhattacharya J., 1993. The role of foreign banks in developing countries: A survey of evidence, Unpublished manuscript, Cornell University.

- Bonaccorsi di Patti E., et D.C. Hardy, 2005. Financial sector liberalization, bank privatization, and efficiency: Evidence from Pakistan, Journal of Banking & Finance 29, pp 2381–2406. [CrossRef]

- Bosco M.G., 2003. Are foreign banks more efficient than domestic banks? An empirical study of transition and MED countries, Proceedings of the Global economic Modelling Network, International Conference on Policy Modelling, July 2003.

- Buch C.M., 1997. Opening up for foreign banks: how central and Eastern Europe can benefit, Economics of Transition, Vol 5 (2), pp 339-366. [CrossRef]

- Cao M., et S. Shi, 2000. Screening, bidding, and the loan market, Queen S. University, mimeo.

- Chantapong S., 2003. Comparative study of domestic and foreign bank performance in Thailand: The regression Analysis, Economic Change and Restructuring, Vol 38, N° 1, pp 63-83. [CrossRef]

- Claessens S., A. Demirgüç-Kunt et H. Huizinga, 2001. How does foreign entry affect the domestic banking market? Journal of Banking and Finance 25, pp 891-911.

- Claessens S., et M. Jansen, 2000. The internationalization of financial services: Issues and lessons for developing countries: overview, In The internationalization of financial services: issues and lessons for developing countries, Kluwer law international, The Hague.

- Claessens S., et T. Glaessner, 1999. Internationalization of financial services in Asia In Hanson, J. and S. Kathuria (eds.), India: A Financial Sector For the Twenty-First Century. Washington, D.C.: World Bank, New York, Oxford University Press.

- Clarke G., R. Cull, L. D’Amato et A. Molinari, 1999. The effect of foreign entry on Argentina’s domestic banking sector, The World Bank Series: Policy Research Working Paper Series Number 2158.

- Clarke G., R. Cull, M. Martinez Peria et S.M. Sanchez, 2001. Foreign bank entry: experience, implication for developing countries, and agenda for further research, The World Bank in its series, Policy Research Working Paper Series, N° 2698.

- CNB, 1998. Banking supervision in the Czech Republic, Czech National Bank, Prague.

- Crystal J.S, G.B. Dages et L.S. Goldberg, 2002. Has foreign bank entry led to sounder banks in Latin America, Current Issues in Economics and Finance, Federal Reserve Bank of New York, V 8, N° 1, pp 1-6.

- Daniel Ofori-Sasu, L. Mensah, J.K. Akuma et| I. Doku 2019. Banking efficiency in emerging economies: Does foreign banks entry matter in the Ghanaian context? International Journal of Finance & Economics, vol 24, Issue 3, pp 1091-1108. [CrossRef]

- Dell’Ariccia G., 2000. Learning by lending, competition, and screening incentives in the banking industry, International Monetary Fund, mimeo.

- Demirguç-Kunt A., et H. Huizinga, 1999. Determinants of commercial bank interest margins and profitability: some international evidence, The World Bank Economic Review, vol. 13, Nº 2, pp 379-408. [CrossRef]

- Demirgüç-Kunt A., R. Levine et H.G. Min 1998. Opening to foreign banks: issues of stability, efficiency, and growth, In Proceedings of the Bank of Korea Conference on the Implications of Globalization of World Financial Markets, pp 83-105.

- Demsetz H., 1973. Industry structure, market rivalry, and public policy, Journal of Law and Economics, 16, pp 1-9.

- Denizer C., 1999. Foreign entry in Turkeys banking sector, 1980–1997 The World Bank.

- Detragiache E. et P. Gupta, 2004. Foreign banks in emerging market crises: Evidence from Malaysia, IMF Working Paper.

- Detragiache E., T. Tressel, et P. Gupta, 2006. Foreign Banks in Poor Countries: Theory and Evidence, IMF Working Paper, WP/06/18. [CrossRef]

- Deyoung R., et G. Whalen, 1994. Is a consolidated banking industry a more efficient banking industry?, Office of The Comptroller of The Currency, Quarterly Journal, Vol 13, N° 3, pp 11-21.

- Dietsch M., 1996. Efficience et prise de risque dans les banques en France , Revue économique, Vol47, N 3, pp 745 – 754.

- Drakos K., 2003. Assessing the success of reform in transition banking 10 years later: an interest margins analysis, Journal of Policy Modelling, (25), pp 309–317. [CrossRef]

- Esho N., 2001. The determinants of cost efficiency in cooperative financial institution: Australian evidence, Journal of Banking and Finance, V 25, N 35, pp 941-964. [CrossRef]

- Feldstein M., 2002. Economic and financial crises in emerging markets economies: overview of prevention and management, NBER Working paper.

- Fries S., et A. Taci, 2005. Cost efficiency of banks in Transition: Evidence From 289 Banks in 15 Post-Communist Countries, Journal of Banking and Finance, Vol 29, pp 55-81. [CrossRef]

- Garber P.M., 2000. What you see vs. what you get: derivatives in international capital flows, paper prepared for World Bank–Brookings–IMF Financial Markets and Development Conference on “Emerging Markets in the New Financial System: Managing Financial and Corporate Distress,” Florham Park, New Jersey, March 30–31.

- Goldberg L., 2001. When is U.S. bank lending to emerging markets volatile? Federal Reserve Bank of New York, Mimeo.

- Goldberg L., B.G. Dages et D. Kinney, 2000. Foreign and domestic bank participation in emerging markets: lessons from Mexico and Argentina, FRBNY Economic Policy Review, 6 (3), pp 17-36.

- Hainz C., et M. Schnitzer, 2001. “The development of the banking sector in Eastern Europe : the next decade”, In: Winkler, Adalbert (Hrsg.): Banking and Monetary Policy in Eastern Europe – The First Ten Years, Palgrave, Houndsmills/Basingstoke, pp 205–216.

- Haiyan Yina, J. Yangb et Xing Lu 2020. Bank globalization and efficiency: Host- and home-country effects. Research in Internaional Business and Finance, Vol 54.

- Hermes N., et R. Lensink, 2004. The short–term effects of foreign bank entry on domestic bank behavior: does economic development matter?, Journal of banking and finance, vol 28, pp 553-568. [CrossRef]

- Huang T.H., et T.L. Kao, 2006. Joint estimation of technical efficiency and production risk for multi-output banks under a panel data cost frontier model, Journal of Productivity Analysis, 26, pp 87–102. [CrossRef]

- Kaminsky G., et C. M. Reinhart., 1999. The twin crises: the causes of banking and balance of payments problems, American Economic Review; 89(3), pp 473-500.

- Keeton W.R., 1999. Does faster loan growth lead to higher loan losses? Federal Reserve Bank of Kansas City Economic Review, 84 (2), pp 57-75.

- Kraft E., R. Hofler et J. Payne, 2002. Privatization foreign bank entry and bank efficiency in croatia A fourier-flexible function stochastic cost frontier analysis, Working Paper: The Croatian National Bank.

- Kroszner R., 1998. On the political economy of banking and financial regulatory reform in emerging markets, CRSP Working Paper, N° 472.

- Leightner J.E., et C.C. Knox Lovell, 1998. The Impact of financial liberalization on the performance of Thai banks, Journal of Economic and Business, (50), pp 115-131. [CrossRef]

- Levine R, 1996. Foreign banks, financial development, and economic growth, In: Claude, E., Barfied, (eds), International Financial Markets. AEi Press, Washington, DC.

- Levine.R, 1999. Foreign bank entry and capital control liberalization: effects on growth and stability, mimeo. University of Minnesota.

- Liu L., 2002a. Beyond sequencing: A risk management approach to financial liberalization, ADB Institute.

- Liu L., 2002b. Sequencing PRC.s banking sector reform after the WTO: options and strategy ADB Institute.

- Mathieson D., et J. Roldos, 2001. The role of foreign banks in emerging markets, Paper prepared for the FMI-World Bank-Brookings institution Conference on Financial Markets and Development, 19-21 April, New York.

- Mc Fadden C., 1994. Foreign banks in Australia, The World Bank.

- Montgomery H., 2003. The role of foreign banks in Post-crisis Asia: The importance of method of entry, Asian Development Bank Institute, Research Paper, N° 51.

- Nikiel E.M., et T.P. Opiela, 2002. Customer type and bank efficiency in Poland: implication for emerging market banking, Comptemporary Economic Policy, Vol 20, N° 3, pp 255-271. [CrossRef]

- Palinski A., 1999. Evaluation of bank debt restructuring in 1992-1998 for selected polish bank’s, Bank and Credit, National Bank of Poland, 12.

- Peek J., et E. Rosengren, 2000b. Implications of the globalization of the banking sector: the Latin American experience, Federal Reserve Bank of Boston New England Economic Review September/October 2000.

- Rojas-Suarez L., 1998. Early warning indication of banking crises: what works for emerging markets? With Application to Latin America, Deutsche Bank Securities Working paper.

- Shaffer S., 1998. The winner curse in banking, Journal of Financial Intermediation, 7, pp 359-92. [CrossRef]

- Tschoegl A.E., 2003. Financial crises and the presence of foreign banks, Paper presented at the World Bank conference on Systemic financial distress: containment and resolution, 7-8 October 2003.

- Unite A., et M. Sullivan, 2003. The effect of foreign entry and ownership structure on the Philippine domestic banking market Journal of Banking & Finance 27, pp 2323–2345. [CrossRef]

- Weill L., 2003. Banking efficiency in transition economies the role of foreign ownership Economic of Transition :September 2003, Vol 11, N° 3, pp 569-592. [CrossRef]

- Weller C.E, et A.S. Hersh, 2002. Increased competition from large foreign lenders threaten domestic banks, raises financial instability, Economic Policy Institute, Issue Brief N° 178.

- Weller C.E., 2000a. Financial liberalization, multinational banks and credit supply: the case of Poland”, International review of Applied Economics, Vol 14, N° 2, pp 193-211. [CrossRef]

- Williams B., 1998. Factors affecting the performance of foreign owned banks in Australia: a cross sectional study, Journal of Banking and Finance, (22), pp197-219. [CrossRef]

- Williams B., 2003. Domestic and international determinants of bank profits: foreign banks in Australia, Journal of Banking and Finance, V 27, N° 6, pp 1185-1210. [CrossRef]

- Williamson J., et M. Mahar, 1998. A survey of financial liberalization, Princeton Essays in International Finance, N° 211, November.

Table 1.

Regression Results of the model (1) abc .

| Dependant variable explained: Cost efficiency score. | |||||

|---|---|---|---|---|---|

| Independent variables | (1) | (2) | (3) | (4) | (5) |

| Const | *0.7992599 (0.0421056) | -*0.4680112 (0.0256124) | *0.5229906 (.0130909) | *0.5172407 (0.0100529) | *0.5280572 (0.0092751) |

| Conc | *0.8763611 (0.0653141) | **0.3859111 (0.0218795) | *0.0734156 (0.0283208) | *0.0660494 (0.0172164) | *0.0715238 (0.0170773) |

| Presence | *-0.3802425 (0.1080383) | **-0.3650454 (0.0204817) | *-0.113541 (0.0243711) | **-0.0303685 (0.0149334) | *-0.0311921 (0.0150435) |

| Disinter | *0.0940121 (0.0261897) | *0.029934 (0.0072396) | *0.0267736 (0.0071825) | ||

| RealInterate | *0.0001677 (0.0000174) |

*0.0000486 (9.49 e-06) |

|||

| Ln size | **0.0180043 (0.001847) | ||||

| GDP PER CAPITA |

**0.0000771 (1.46e-06) |

||||

| OthrNProAssets | -0.0003637 (0.0066004) | ||||

| Coeffiexplo | ***-0.000068 (0.0000422) | ||||

| Net loans | **0.0003007 (0.0001422) | ||||

| χ2 | 362.9 (DF = 4) | 3486.28 (DF = 4) | 62.77 (DF = 4) | 32.32 (DF =4) | 26.52 (DF= 4) |

| Prob > χ2 | 0.000 | 0.000 | 0.0000 | 0.0000 | 0.000 |

| Log-likelihood | 362.9 | -4182.6669 | -1434.2935 | -2760.2958 | -2790.2618 |

| a: Dependant variables: adjusted efficiency score obtained following the Meta-frontier approach b: The results take into account data relating to domestic banks only c: The values in parentheses are standard deviations. DF: Degree of freedom * Variable significant at 1%. ** Variables significant at 5%. *** Variable significant at 10%. | |||||

Table 2.

Regression results, including interaction terms.

| Dependant variable explained: Cost efficiency Score. |

||

|---|---|---|

| Independent variables | (6) | (7) |

| Const | *0.4527751 (0.0065672) | *0.6285067 (0.0475267) |

| Conc | *-0.0773446 (0.0125335) | *0.8723656 (0.0698601) |

| Presence | *-0.2303344 (0.0090853) | **-0.2018692 (0.0942831) |

| Disinter | *0.0201269 (0.0046199) | *0.0967843 (0.0252428) |

| Intereel | *0.0000213 (2.85e-06) | *0.0001658 (0.0000181) |

| PDEb | *-0.9304168 (0.0553807) | |

| PDEM | -0.6013531 (0.6188838) | |

| χ2 | 1179.16 (DL = 5) | 323.3 (DL = 5) |

| Prob > χ2 | 0.000 | 0.000 |

| Log-likelihood | 2428.453 | -6447.5456 |

| a: Dependant variables: adjusted efficiency score obtained following the Meta-frontier approach b: The results take into account data relating to domestic banks only c: The values in parentheses are standard deviations. DF: Degree of freedom * Variable significant at 1%. ** Variables significant at 5%. | ||

| 1 | For more details, see Atkinson et Cornwell (1994) and Huang et Kao (2006)). |

| 2 | This variable includes cash and assets that banks are required to hold with the central bank as reserve requirements. |

| 3 | Result confirmed by Unite A and M.J.Sullivan (2003); Cleassens.S et al (2001); Barajas et al (2000). |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Copyright: This open access article is published under a Creative Commons CC BY 4.0 license, which permit the free download, distribution, and reuse, provided that the author and preprint are cited in any reuse.