Submitted:

19 October 2024

Posted:

21 October 2024

You are already at the latest version

Abstract

The Balanced Scorecard (BSC) is a widely recognized strategic performance metric that has been extensively studied in large corporations but remains underexplored in the context of Small and Medium-sized Enterprises (SMEs). Understanding the effectiveness of BSC in aligning performance metrics with strategic goals and enhancing performance management in SMEs is critical for fostering growth and competitive advantage. This systematic review aims to evaluate the effectiveness of the Balanced Scorecard in measuring performance and strategy execution within SMEs, particularly focusing on financial and non-financial outcomes such as employee motivation, customer satisfaction, and business sustainability. A systematic review was conducted following the PRISMA framework, incorporating 136 studies sourced from Google Scholar, Web of Science, and SCOPUS. Eligibility criteria focused on publications from the last ten years that address the implementation of BSC in SMEs. Quantitative, qualitative, and mixed-method studies were included, with 49.63% of studies using quantitative methods, 26.67% qualitative, and 23.70% mixed-methods. Risk of bias was assessed using the Chrohane tool, revealing high risks in 90 studies due to incomplete outcome data and selective reporting. The review found that 74% of studies adopted a holistic approach by focusing on all four BSC perspectives (Financial, Customer, Internal Processes, and Learning and Growth). ROI emerged as the most frequently discussed key performance indicator, addressed in 36.84% of publications, while customer satisfaction and employee engagement were covered in 26.32% each. Geographic disparities were observed, with most of the research concentrated in Asia and Europe (40%) and only 8% in Africa. Despite positive outcomes such as improved business sustainability and competitive advantage (38.52% of studies), challenges persisted, including poor strategy execution and limited resources, necessitating careful customization of BSC to SME-specific contexts. The Balanced Scorecard demonstrates significant potential in enhancing performance management and strategic execution within SMEs, particularly when tailored to address unique constraints such as resource limitations. This review highlights the need for further research to standardize key performance indicators and explore sector-specific applications. By addressing these gaps, the BSC can be more effectively utilized to drive growth, agility, and long-term competitive advantage in SMEs.

Keywords:

Balanced Scorecard

; performance measurement

; SMEs

; strategy execution

; sustainability

; competitive advantage

; systematic review

1. Introduction

The Balanced Scorecard (BSC) is a renowned strategic management framework that offers a holistic view of organizational performance by incorporating a blend of financial and non-financial measures [,2]. Originally conceptualized by Kaplan and Norton, the BSC seeks to align business activities with an organization's overarching vision and strategy, thereby facilitating enhanced monitoring of performance and more effective strategy execution [3,4]. Although the BSC is widely implemented and rigorously studied within large corporations, its adoption and efficacy in the context of Small and Medium Enterprises (SMEs) remain relatively underexplored [5,6]. SMEs, which are generally defined by the number of employees and annual revenue, vary in size across different countries and sectors [7,8]. Despite their pivotal role in driving economic growth, fostering innovation, and generating employment, SMEs often face distinct challenges that differ significantly from those of larger enterprises [9]. These challenges typically encompass resource limitations, difficulties in strategic execution, and constraints in tracking and managing performance [10,11].

Research focusing on the BSC's application within SMEs is notably limited, particularly concerning its practical implementation and its impact on organizational performance metrics and strategic outcomes [12]. Given the resource constraints that characterize SMEs, there is a tendency to prioritize financial indicators, frequently overlooking the non-financial dimensions that the BSC framework emphasizes [13,14]. This systematic review seeks to bridge this research gap by evaluating the effectiveness of the BSC methodology specifically in SMEs, with an emphasis on how the framework’s four perspectives—financial, customer, internal business processes, and learning and growth—can address the unique challenges SMEs face [15,16]. The motivation for conducting this systematic review arises from the need to deepen the understanding of how SMEs can harness the BSC to enhance strategic execution, improve performance management practices, and achieve long-term sustainability [17,18]. By thoroughly analyzing the existing literature, this paper aims to elucidate both the limitations and advantages of employing the BSC in the SME sector, providing valuable insights into the factors contributing to its successful implementation and identifying potential obstacles to its adoption [19,20]. This focused evaluation contributes to advancing theoretical perspectives and practical applications, thereby enriching the discourse on the role of the BSC in driving SMEs' strategic and operational success.

The comparative analysis of previous literature reviews on the Balanced Scorecard (BSC) implementation in SMEs reveals several gaps and research opportunities, as shown in Table 1. While some studies emphasize the lack of focus on SME-specific BSC applications or cover sustainability integration, others are limited by regional scope or lack of empirical data. The proposed systematic review aims to address these gaps by offering a more comprehensive evaluation of BSC trends in SMEs, with a focus on performance measurement evolution, regional diversity, and sustainability practices. This expanded scope will provide deeper insights into BSC's practical implications for SMEs and contribute to addressing the identified research limitations as shown in Table 1.

Identified gaps suggest the need for further investigation into BSC's role in developing economies, new empirical studies to substantiate theoretical findings, and an expansion of the scope to incorporate diverse industries. The proposed systematic review aims to address these limitations by providing a comprehensive evaluation of BSC applications in SMEs, focusing on trends in performance measurement, integration with sustainability frameworks, and contextual adaptations across various regions.

1.1. Research Questions

The Balanced Scorecard Methodology has been extensively studied and implemented in Small and Medium Enterprises, although a systematic literature review that outlines the application of the BSC in Small and Medium Enterprises or (SMEs) is very critical, and to achieve this, the following research questions have been considered:

- How is customer satisfaction measured and monitored in SMEs using the BSC framework?

- Which role does technology play in implementing an effective BSC in SMEs?

- What is the impact of the BSC on the performance and motivation of employees in SMEs?

- What challenges do SMEs face when integrating the BSC methodology into their existing management practices?

- How do SMEs customize the BSC framework to align with their specific strategic goals as well as operational contexts?

1.2. Research Motivation

The Balanced Scorecard (BSC) methodology, designed to translate organizational strategy into actionable performance metrics, has been extensively adopted and studied within large corporations. Despite its demonstrated effectiveness in strategic alignment and performance enhancement, BSC's application within SMEs remains underexplored. This study aims to bridge this gap by investigating the potential benefits and challenges associated with BSC in the SME context. SMEs, which play a vital role in economic growth, job creation, and innovation, often face resource constraints, smaller workforce sizes, and lower operational scales compared to larger firms. These factors hinder their ability to effectively implement strategic management frameworks such as the BSC. Modern research highlights that SMEs must rapidly adapt to market changes, optimize resource allocation, and sustain competitiveness in volatile economic conditions.

The BSC provides a structured approach for translating strategic objectives into performance measures, offering SMEs a clear framework for strategic alignment and performance evaluation. However, there is a scarcity of research on how SMEs can effectively adapt and implement the BSC framework to address their unique operational constraints and strategic needs. This systematic review addresses this critical gap by evaluating the application of BSC within SMEs, examining its impact on strategy execution and performance metrics, and identifying best practices for overcoming implementation challenges. Understanding how to customize BSC to meet SME-specific requirements is essential for enhancing strategic management practices, contributing to long-term growth, and building organizational resilience.

1.3. Research Contribution

This systematic review provides a comprehensive analysis of the application of the Balanced Scorecard methodology within SMEs, emphasizing its role in performance measurement and strategy execution. By evaluating a wide range of studies from three major academic databases, this review assesses the effectiveness of BSC implementation in SMEs. The findings reveal recent trends in adapting the BSC framework, including integrating digital tools and data analytics for real-time performance monitoring. Additionally, the review highlights the growing emphasis on aligning BSC metrics with sustainable business practices.

Several gaps in the existing literature are identified, such as the absence of standardized metrics tailored to SME-specific challenges and limited research on the impact of BSC on innovation and organizational agility. The review addresses these gaps, providing insights into how SMEs can adapt the BSC methodology effectively. Case studies demonstrating successful adaptations and innovative approaches are also examined, showcasing how SMEs customize BSC frameworks to align with competitive pressures and dynamic market conditions. Furthermore, this review synthesizes empirical evidence across various studies, offering actionable recommendations for SMEs aiming to implement BSC methodologies. It contributes to the literature by presenting a consolidated view of BSC's impact on strategic outcomes and performance improvement in smaller enterprises. Overall, this systematic review not only addresses existing gaps but also provides practical guidance for SMEs seeking to leverage the BSC for enhanced strategic alignment and business performance.

1.4. Research Novelty

This systematic review addresses a crucial gap in the literature by focusing specifically on the Balanced Scorecard's application in SMEs. Previous studies primarily target large corporations, with limited investigation into how the BSC framework operates within the tailored operational challenges of SMEs, such as resource constraints, limited managerial capacity, and informal business processes. This study offers a deeper examination of the four BSC perspectives—financial, customer, internal business processes, and learning and growth—emphasizing their interconnections and customized applicability for SMEs.

The financial perspective in SMEs is often challenged by unstable cash flows and restricted access to capital. This study explores how SMEs can adapt the BSC to focus on financial sustainability through agile financial management. The customer perspective, typically addressed in the context of large-scale customer bases, is revisited to show how SMEs can leverage BSC to closely monitor customer satisfaction, which is often relationship-based in small businesses. For internal business processes, SMEs frequently face inefficiencies and lack formalized processes. This review demonstrates how the BSC can provide a structured method for optimizing internal operations, directly addressing gaps in previous studies that overlooked process improvement in resource-limited environments. The learning and growth perspective, crucial yet underexplored in SMEs, is highlighted in terms of employee development and innovation. By examining these four perspectives, the review fills gaps in the literature and offers a detailed understanding of BSC's role in improving SME performance and strategy execution. The findings suggest that a tailored BSC model, sensitive to the specific needs and contexts of SMEs, can drive competitive advantage, sustainability, and strategic agility.

2. Materials and Methods

In this section, the study presents in full detail the methodology of how information was collected from various sources from different databases, the computer code used to search for research papers, the inclusion and exclusion criteria for the review etc. This includes all the materials and methods used to gather research papers, and the process is as follows: Firstly, the focus is on the eligibility criteria, information sources, search strategy, the process of selection, the process of collecting data, data items, study risk of bias assessment, effect measures, synthesis methods, reporting bias, as well as certainty assessment. This information is provided below:

2.1. Eligibility Criteria

The eligibility criteria for this systematic review were carefully defined to ensure the inclusion of high-quality and relevant studies that focus on the application of the Balanced Scorecard (BSC) methodology within the context of Small and Medium Enterprises (SMEs). The criteria were established with the intention of capturing recent advancements in the field and providing a comprehensive analysis of BSC implementation in SMEs. The selected criteria are described below, followed by a summary of the inclusion and exclusion conditions presented in Table 2. The inclusion of studies published between 2014 and 2024 was chosen to reflect the most recent developments in strategic management tools and methodologies. This period is considered relevant for understanding current trends in BSC application and addressing any evolving challenges that SMEs face. Publications prior to 2014 were excluded to maintain a focus on modern practices and innovations. Additionally, only peer-reviewed journal articles were considered, as peer review serves as a quality control mechanism, ensuring that the studies have undergone rigorous evaluation by experts. This requirement helps maintain the credibility and robustness of the evidence presented in this review. The review specifically targeted studies that discuss the BSC methodology in SMEs, providing insights into how these businesses adapt and implement BSC. General BSC studies not tailored to SMEs were excluded to focus on the unique context and challenges faced by smaller enterprises.

Studies were also required to be published in English to ensure accessibility and consistency in the analysis, despite recognizing the potential limitation of language bias. Finally, studies with unclear methodologies or insufficient data were excluded to uphold the integrity and reliability of the findings. These criteria collectively aim to provide a well-rounded and current analysis of BSC use in SMEs, ensuring that only relevant and high-quality studies are considered. Table 2 summarizes the inclusion and exclusion criteria applied in this review [172,173,174,175,176,177,178,179,180,181,182,183,184,185,186,187].

The eligibility criteria outlined above ensure that the systematic review captures recent evidence, maintains a high standard of quality, and provides meaningful insights into the strategic management practices of SMEs. By narrowing the focus to studies within the defined timeframe and context, the review aims to generate findings that are not only academically rigorous but also practically relevant for business leaders seeking to implement the BSC in their organizations.

2.1. Information Sources

For this systematic review, three primary databases—Google Scholar, SCOPUS, and Web of Science—were selected to ensure a comprehensive and high-quality search of the literature. These databases were chosen based on their distinct advantages and complementary strengths, which provide a balanced approach to the review [172,173,174,175,176,177,178,179,180,181,182,183,184,185,186,187]. Google Scholar is a widely accessible search engine that indexes a broad range of academic content, including journal articles, conference papers, and books. Its inclusion is justified by its extensive coverage, capturing a diverse array of documents related to the Balanced Scorecard methodology across different disciplines and contexts. However, one limitation of Google Scholar is that it does not consistently guarantee the quality of indexed sources. Since its algorithms can include non-peer-reviewed content, variability in the quality of search results may arise. SCOPUS serves as a comprehensive abstract and citation database, known for its wide disciplinary range, particularly in business management and strategic research. It indexes only peer-reviewed journals, book chapters, and conference proceedings, which adds rigor to the search results. SCOPUS's strong citation tracking capabilities help identify highly cited and influential works. However, coverage bias can occur, as the database tends to focus on established journals and publishers, potentially missing research from less conventional sources. Web of Science (WoS) is another premier research database, offering access to a variety of citation indexes across multiple academic disciplines. It is selected for its rigorous indexing standards and detailed bibliometric data, which are essential for tracking citation patterns. The database's emphasis on high-quality publications ensures a reliable review, although it shares the limitation with SCOPUS regarding coverage bias, as it predominantly includes well-established journals.

In choosing these three databases, this review balances scope and quality, ensuring a broad interdisciplinary perspective that covers various facets of the Balanced Scorecard implementation in SMEs. The databases were selected following a five-step process for determining information sources, as illustrated in Figure 1. This multi-step process ensures a systematic approach to capturing high-quality and relevant studies.

2.1. Search Strategy

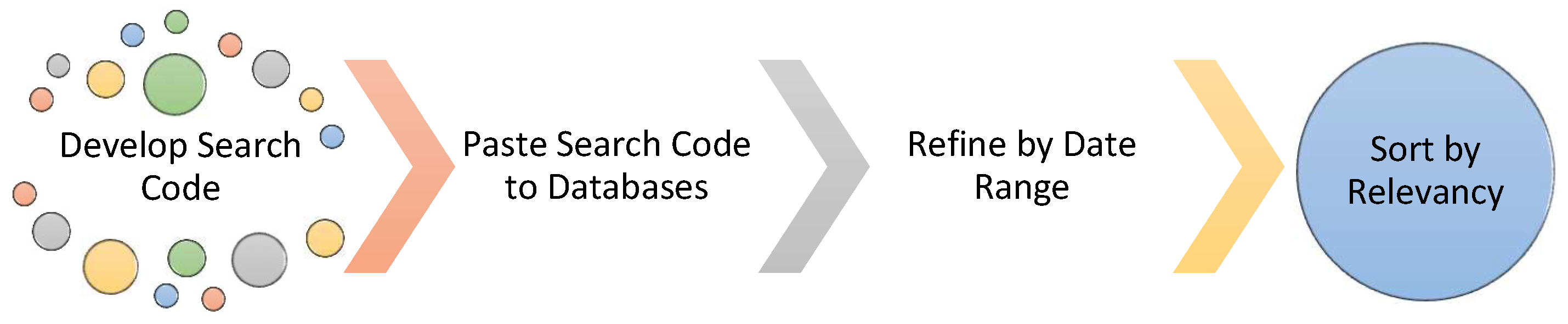

To ensure a thorough and high-quality systematic review, a comprehensive search strategy was employed to identify relevant literature on the Balanced Scorecard (BSC), performance metrics, and strategy execution in Small and Medium Enterprises (SMEs) [172,173,174,175,176,177,178,179,180,181,182,183,184,185,186,187]. This process was designed to capture a diverse range of studies, allowing for a well-rounded exploration of BSC implementation across different contexts and recent developments. By following a structured and iterative approach, as shown in Figure 2, the search strategy aimed to balance inclusivity and rigor, ensuring that only the most pertinent and methodologically sound research articles were included. The search string used, which combined terms like Balanced Scorecard, BSC, performance metrics, strategy execution, and SMEs, aimed to comprehensively capture the application of BSC in SMEs. The search was conducted across three prominent academic databases: Scopus, Web of Science, and Google Scholar. Each database was selected for its distinctive strengths in covering business and management research, particularly in the areas of strategic management and SME-related studies. The time frame of 2014 to 2024 was chosen to include the most current research, reflecting recent trends and methodologies.

The search process encountered challenges, including terminology variations and the need for manual filtering to ensure relevance. Refinements were made to the search string to address these issues, such as using synonyms and alternative phrases to capture studies using different terms for the same concepts. The final selection of studies focused on peer-reviewed journal articles, conference proceedings, and case studies with rigorous methodologies, excluding non-academic sources and studies that lacked sufficient methodological quality. This careful selection process helped ensure the inclusion of high-quality, relevant literature that would provide a solid foundation for understanding BSC implementation in SMEs.

2.1. Selection Process

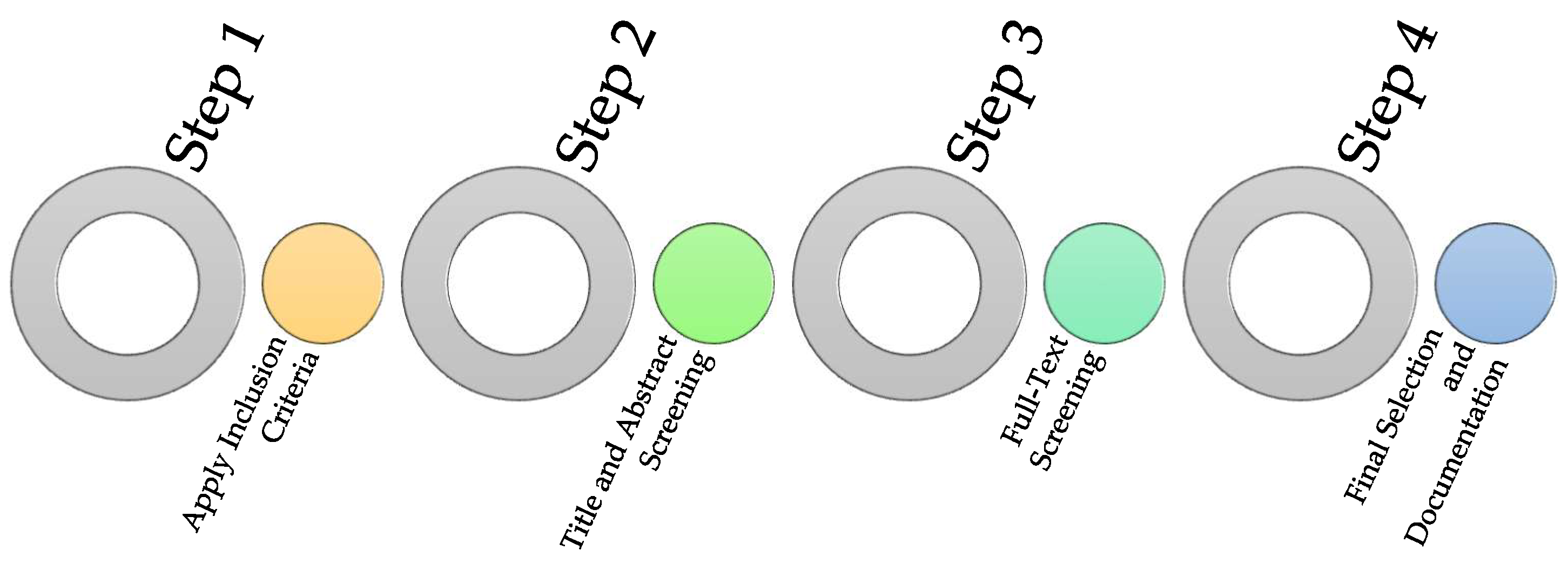

The study selection process for this systematic review was meticulously designed to ensure that only the most relevant and high-quality studies were included [172,173,174,175,176,177,178,179,180,181,182,183,184,185,186,187]. This process was implemented to filter out studies that did not meet the established criteria and to focus on those that would provide the most valuable insights into the implementation of the Balanced Scorecard (BSC) in Small and Medium-sized Enterprises (SMEs). Given the specific focus on BSC applications in the SME context, the selection criteria emphasized factors such as methodological rigor, publication quality, and relevance to the research questions. The selection involved multiple stages to refine the list of eligible studies. Initially, the inclusion criteria were applied to identify potentially relevant studies, followed by systematic screenings of titles, abstracts, and full texts. Each stage was conducted manually by two independent reviewers to ensure consistency and to minimize the risk of bias. In cases where disagreements arose, a consensus was reached through discussion, guaranteeing a thorough evaluation of all potential studies. Figure 3 outlines these steps in detail, depicting the sequential approach taken from the initial application of inclusion criteria to the final documentation of selected studies.

The multi-step selection process ensured a comprehensive review, aligning the chosen studies with the objectives of this systematic review and enabling a robust analysis of the BSC's effectiveness in SMEs. This careful approach, involving manual screening and multiple verification stages, contributed to a high-quality dataset that underpins the findings and recommendations of this review.

2.1. Data Collection Process

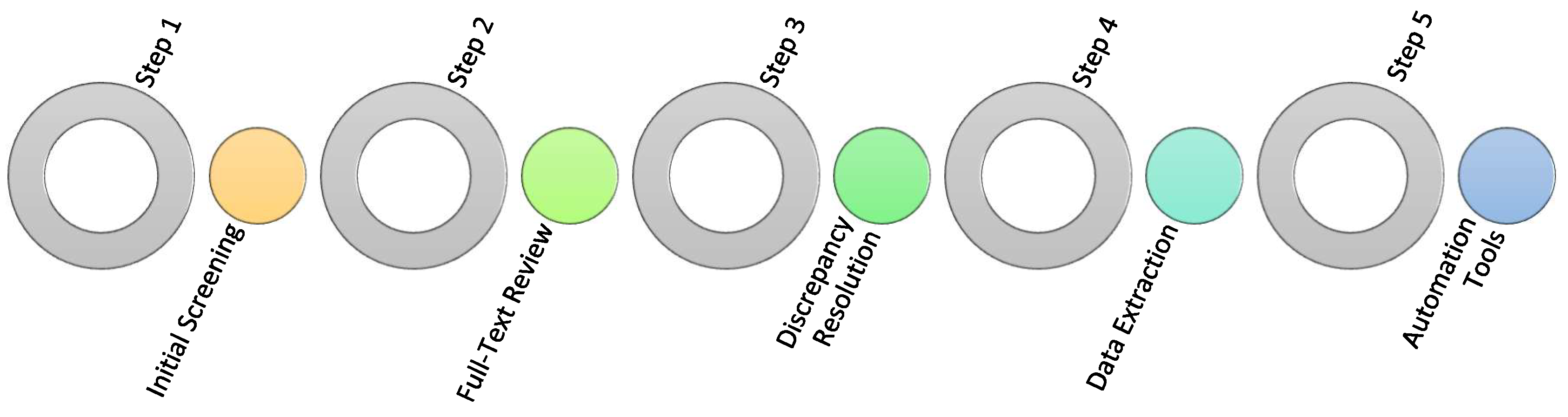

The data collection process for this systematic review was designed to systematically gather information on the implementation of the Balanced Scorecard (BSC) in Small and Medium-sized Enterprises (SMEs). A structured approach was applied to ensure the accuracy and objectivity of the data extracted from peer-reviewed studies [172,173,174,175,176,177,178,179,180,181,182,183,184,185,186,187]. The multi-step process began with identifying relevant studies that focused on the use of the BSC for performance measurement and strategy execution within the SME context. This systematic approach aimed to capture a comprehensive view of the literature, as depicted in Figure 4, which outlines the sequential steps involved in the data collection. Three independent reviewers conducted the data collection to enhance the reliability of the results. The process began with the screening of titles and abstracts, followed by a full-text review to determine the eligibility of each study based on established inclusion criteria. By having reviewers work independently, potential biases were minimized. Discrepancies between reviewers were addressed through discussions to reach a consensus, ensuring the selection of only relevant, high-quality studies.

Throughout the data collection phase, variability in the reporting standards of the studies posed a challenge, particularly in terms of consistency. To mitigate this, a standardized coding scheme was developed to ensure uniformity across the extracted data, encompassing study characteristics, BSC implementation details, performance metrics, and strategic outcomes. This coding scheme facilitated a coherent analysis and synthesis of the findings. The data collection framework involved five key steps: Initial Screening, Full-Text Review, Discrepancy Resolution, Data Extraction, and the use of Automation Tools for quality assurance. These steps collectively ensured the systematic retrieval and verification of data, providing a strong foundation for analysing how SMEs implement the BSC to overcome strategic challenges and drive performance improvements.

2.1. Data Items

The data items selected for this review focused on key performance indicators linked to the Balanced Scorecard (BSC) implementation in SMEs. Metrics were classified into customer satisfaction, employee performance, financial outcomes, and supporting tools [172,173,174,175,176,177,178,179,180,181,182,183,184,185,186,187]. These categories ensured comprehensive coverage of BSC's impact on strategic goals in SMEs. Figure 5 illustrates the data identification process.

Customer satisfaction was assessed through surveys, interviews, and Net Promoter Scores, providing both qualitative and quantitative insights. Employee performance and engagement metrics, including job satisfaction and productivity, were evaluated using surveys and performance reviews. Financial and non-financial outcomes, such as profitability and internal process improvements, were analysed to measure BSC's alignment with strategic goals. Where data was incomplete, decisions were made based on the relevance of available information. The review also examined software and digital tools used in BSC implementation, recognizing their role in execution. When details were missing, industry standards informed assumptions. This categorization aimed to capture BSC's influence on diverse performance metrics across SMEs.

2.1. Study Risk of Bias Assessment

The study risk of bias assessment is a critical step in ensuring the validity and reliability of systematic reviews [172,173,174,175,176,177,178,179,180,181,182,183,184,185,186,187]. For this review on the Balanced Scorecard (BSC) methodology in SMEs, potential biases were thoroughly evaluated using the Cochrane Risk of Bias tool, which helped identify and manage risks associated with selection, performance, detection, and reporting biases. Given that SMEs differ significantly from large corporations, the review specifically tailored the assessment to address the unique operational conditions of smaller enterprises, ensuring the findings are applicable and credible within the context of SME performance evaluation.

A tri-reviewer approach was employed to minimize bias, with two independent reviewers conducting evaluations separately before reaching a consensus through discussion. This process ensured that assessments were unbiased and well-supported. Selection bias was addressed by including only studies specifically focused on SMEs, while performance bias was managed by emphasizing studies using performance metrics appropriate for smaller enterprises. Detection bias was reduced by selecting studies employing robust, SME-specific tools, such as BSC models adapted for the unique needs of SMEs. Additionally, reporting bias was tackled by conducting a broad literature search across multiple databases (SCOPUS, Web of Science, and Google Scholar) to ensure the inclusion of a diverse range of studies, including less frequently cited works. Manual assessment, rather than automation tools, was used to maintain a context-specific approach, as automated processes might miss the nuanced differences in BSC applications between SMEs and larger firms. Figure 6 illustrates the risk of bias assessment process, detailing each step taken to evaluate and mitigate biases at various stages.

This comprehensive assessment aimed to ensure the quality and relevance of the studies included in the review, systematically addressing potential biases. The approach enhanced the reliability of the conclusions by tailoring the evaluation criteria to the specific characteristics of SMEs, making the findings more applicable to this sector. This bias management strategy ensures transparency and rigor in the systematic review process.

2.1. Effect Measures

To address, Effect Measures, this systematic review evaluates multiple metrics to capture the impact of Balanced Scorecard (BSC) implementation in SMEs, specifically focusing on financial and non-financial dimensions. The primary measures employed include customer, employee, and organizational outcomes, each assessed using distinct quantitative indicators. For customer outcomes, metrics such as the Net Promoter Score (NPS) and Customer Satisfaction Index (CSI) were utilized. NPS provides a direct gauge of customer loyalty and likelihood to recommend, while CSI quantifies satisfaction levels through survey-based data, reflecting the effects of BSC on customer experiences before and after implementation [172,173,174,175,176,177,178,179,180,181,182,183,184,185,186,187].

Employee-related metrics include the employee turnover rate and Key Performance Indicators (KPIs) to measure retention, engagement, and productivity shifts post-BSC. These measures illustrate changes in workforce dynamics and internal processes attributable to BSC adoption. For organizational performance, financial metrics such as profitability and revenue growth were analyzed, complemented by non-financial metrics like process innovation and operational efficiency improvements, offering a well-rounded evaluation of BSC's impact on SMEs. The methodological process of selecting and applying these effect measures is visualized in Figure 7, which outlines key steps from identifying relevant metrics to synthesizing results.

2.1. Synthesis Methods

The synthesis methods employed in this systematic review aimed to comprehensively integrate findings related to the implementation of the Balanced Scorecard (BSC) in SMEs [172,173,174,175,176,177,178,179,180,181,182,183,184,185,186,187]. The approach began with a structured search and selection process, ensuring the inclusion of only relevant studies published between 2014 and 2024, written in English, and peer-reviewed. These studies specifically addressed the BSC's role in performance metrics and strategy execution within SMEs, thereby aligning with the objectives of this review. Figure 8 provides a visual representation of the synthesis methods applied throughout the review. During data preparation, steps were taken to address missing or ambiguous data by imputing values when appropriate and ensuring consistency across studies through format standardization. This process involved excluding studies with substantial data limitations and documenting the impact on findings. Microsoft Excel was used for organizing extracted data, facilitating the comparison of variables such as performance metrics, strategy execution, and outcomes related to BSC implementation.

Qualitative synthesis methods played a significant role in analyzing the data, identifying thematic patterns and insights about BSC's impact on performance management and strategy execution in SMEs. While meta-analysis was not conducted due to the heterogeneity of the included studies, subgroup analyses were used to explore differences by industry type, geographic location, and SME size. Sensitivity analyses further strengthened the findings by excluding outlier studies to determine their influence on the conclusions. The synthesis approach allowed for a comprehensive evaluation of both financial and non-financial outcomes of BSC implementation, providing insights into its effectiveness in various SME contexts. This process ensured a robust and detailed analysis of the literature, thereby supporting the validity of the review's conclusions.

2.2. Reporting Bias

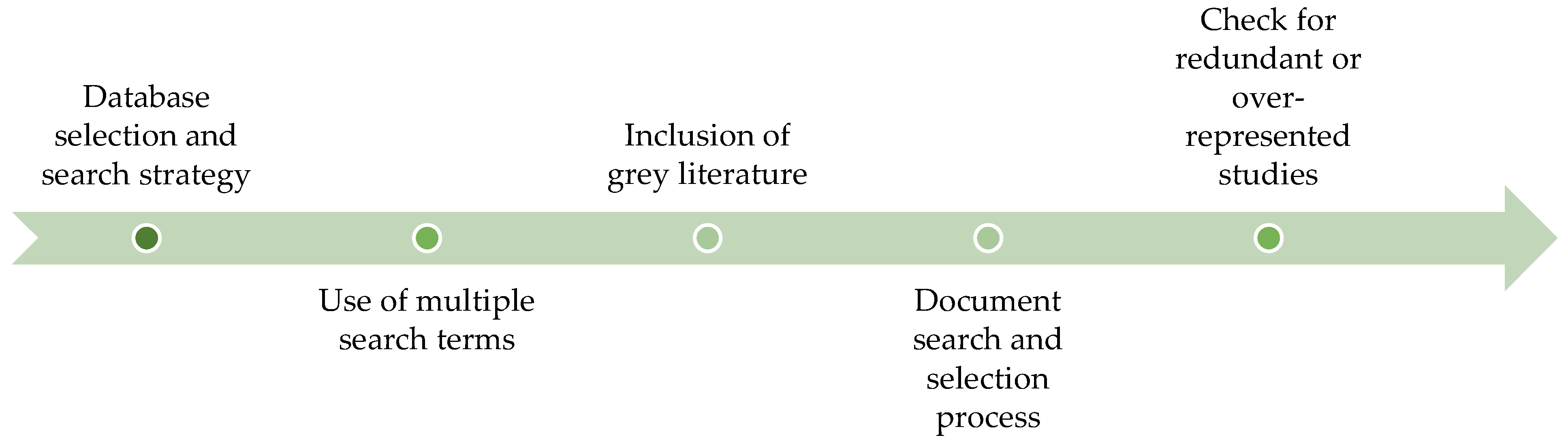

In this systematic review, assessing the risk of reporting bias was critical to ensuring the validity of the findings related to the Balanced Scorecard Methodology in SMEs. The review implemented a multi-step approach to detect potential biases and improve the comprehensiveness of the evidence base. A detailed search was conducted across multiple databases, including SCOPUS, Web of Science, and Google Scholar, which helped minimize publication bias by covering a wide spectrum of research, including grey literature such as case studies, conference papers, and dissertations [172,173,174,175,176,177,178,179,180,181,182,183,184,185,186,187]. By incorporating these diverse sources, the review aimed to avoid selective reporting bias that could arise if only peer-reviewed journal articles were considered. To further reduce the risk of bias, any available research protocols were compared with the results sections of the studies included in the review to identify any inconsistencies or instances of selective outcome reporting. This comparison was essential for ensuring that all relevant findings were accounted for and that no significant results were omitted or selectively highlighted. The overall approach emphasized qualitative synthesis while striving for a balanced and complete representation of the available evidence. The process used to assess and address reporting bias is illustrated in Figure 9, which outlines the steps taken to identify potential issues, including database selection, grey literature inclusion, and checks for redundant or over-represented studies.

This systematic review undertook a rigorous process to address reporting bias by employing a comprehensive search strategy, comparing research protocols to reported results, and including diverse types of literature to provide a more balanced evidence base. These efforts minimized the risk of missing data or selectively reported findings, thereby enhancing the reliability of the conclusions regarding the Balanced Scorecard's application in SMEs.

2.2. Certainty Assessment

A robust search strategy was employed to gather studies that are relevant. Multiple academic databases have been searched, including SCOPUS, Google Scholar, and Web of Science, using the following search code: Balanced Scorecard OR BSC AND SMEs OR Small and Medium-sized enterprises OR Small and Medium enterprises [172,173,174,175,176,177,178,179,180,181,182,183,184,185,186,187]. The initial search yielded 10 000 articles. These articles were subjected to a screening process: Articles were assessed based on their titles and abstracts to determine their eligibility and relevance. Studies that did not meet the eligibility criteria were excluded. The remaining articles were reviewed in full to evaluate their methodology as well as relevance. Inclusion criteria was applied to ensure studies specifically addressing the BSC in SMEs were selected. Two independent reviewers from colleagues working on the same project, which is creating a journal, conducted the screening and selection. All disagreements were resolved through discussion. Clear, predefined inclusion and exclusion criteria were utilized consistently to ensure decision-making that is objective. These measures were implemented to reduce bias.

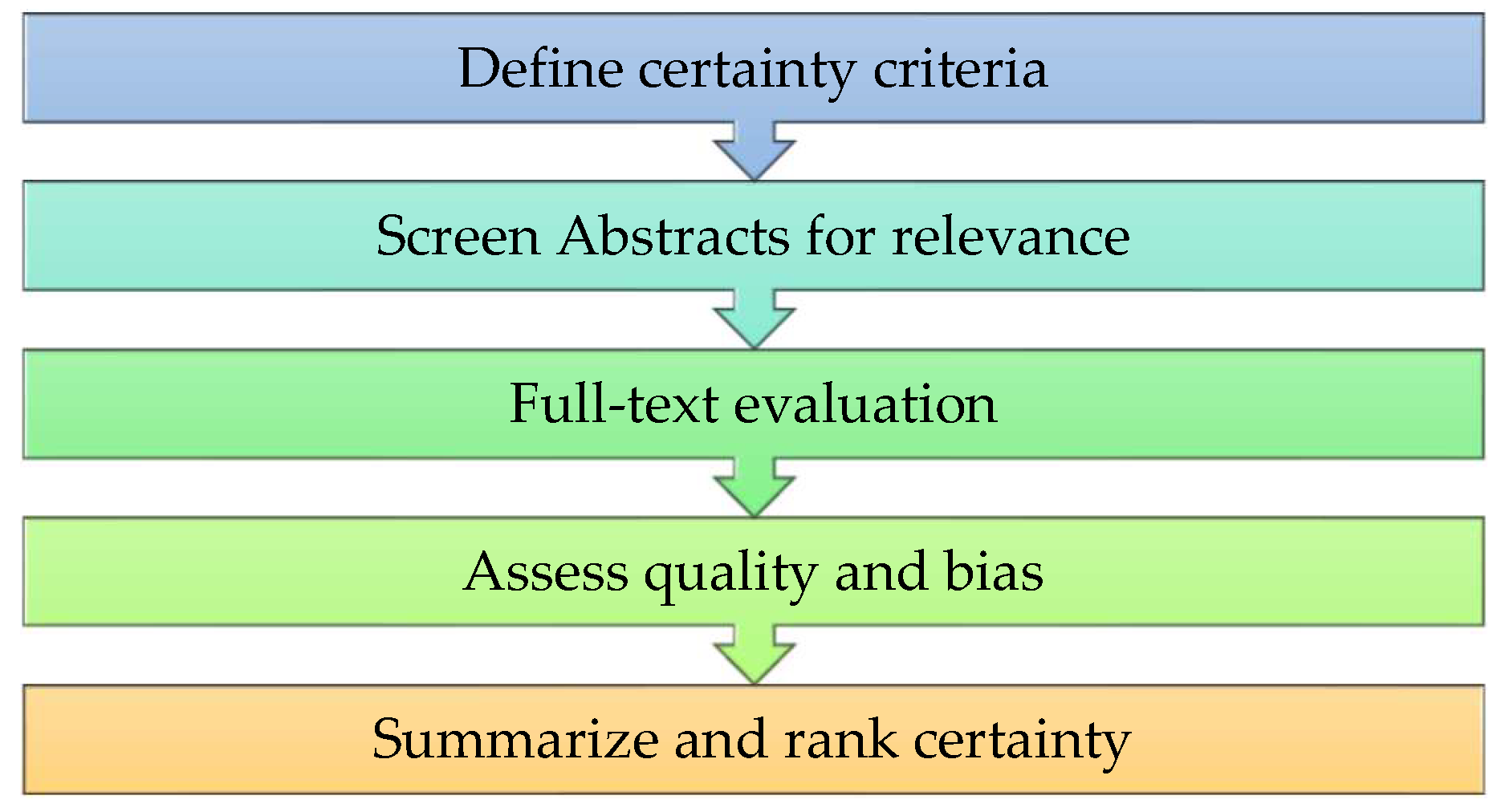

Figure 10 outlines the steps taken to ensure the credibility of this systematic review: Define Certainty Criteria – Criteria were established for the evaluation of the relevance as well as quality of studies. Screen Abstracts for Relevance – Abstracts were initially screened to exclude or filter out studies that are irrelevant. Full-Text Evaluation – Selected articles were reviewed in full to assess whether they meet the required standard, as well as to assess their quality and applicability.

Assess Quality and Bias – Studies were evaluated for potential biases and methodological quality. Summarize and Rank Certainty – The findings were summarized, and the studies were graded based on the certainty of their contributions to this systematic review. This visual aid provides clarity on the review process, and it supports the presentation of results. By adhering to these methodological procedures, this review aims to deliver a comprehensive as well as an unbiased analysis of the BSC methodology in SMEs, which contributes valuable insights to the field. Figure 10 shows the steps followed for the certainty of assessment.

3. Results

This section is divided by subheadings, and it provides a concise and precise description of the experimental results, their interpretation, as well as the experimental conclusions drawn.

3.1. Study Selection

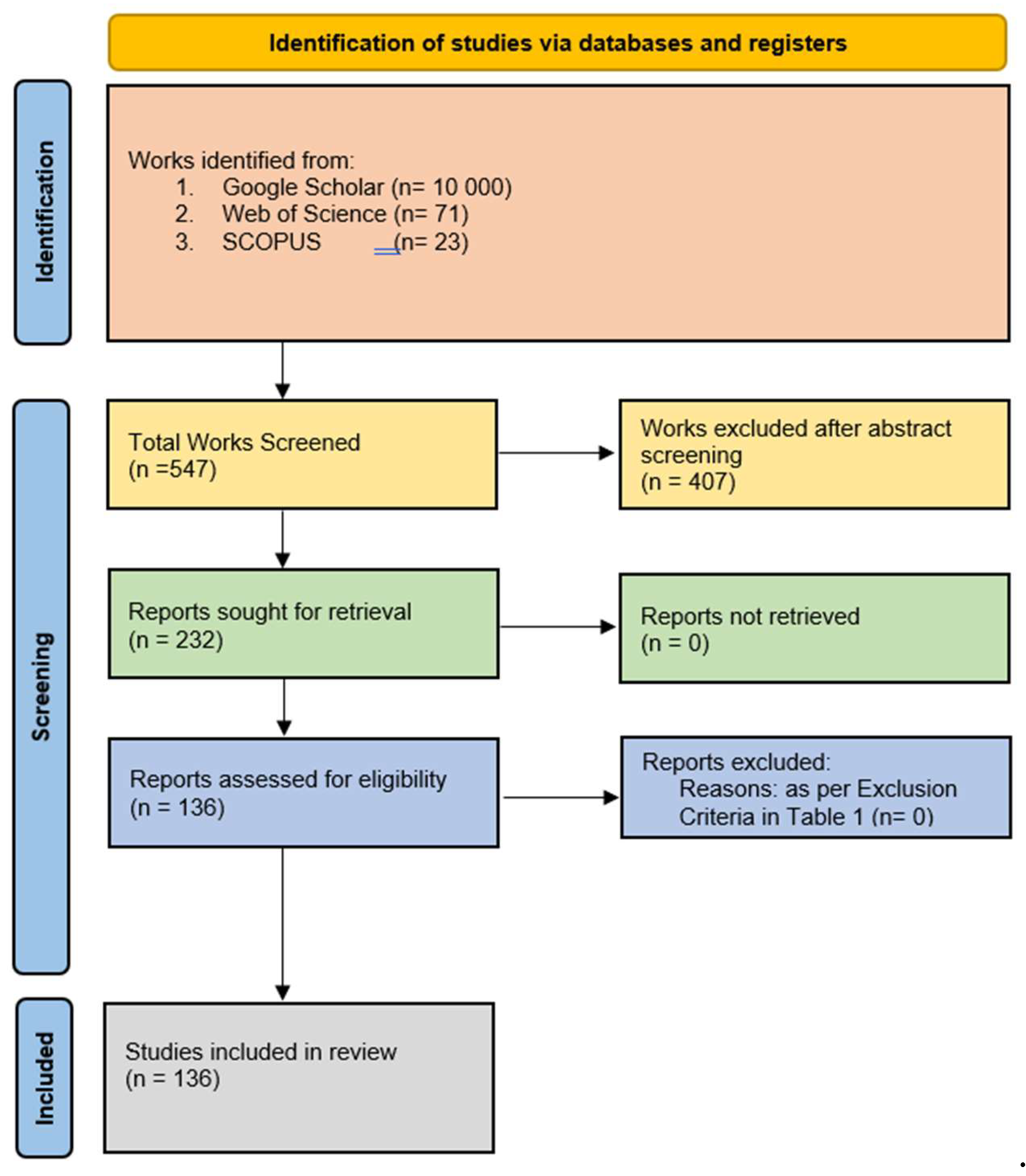

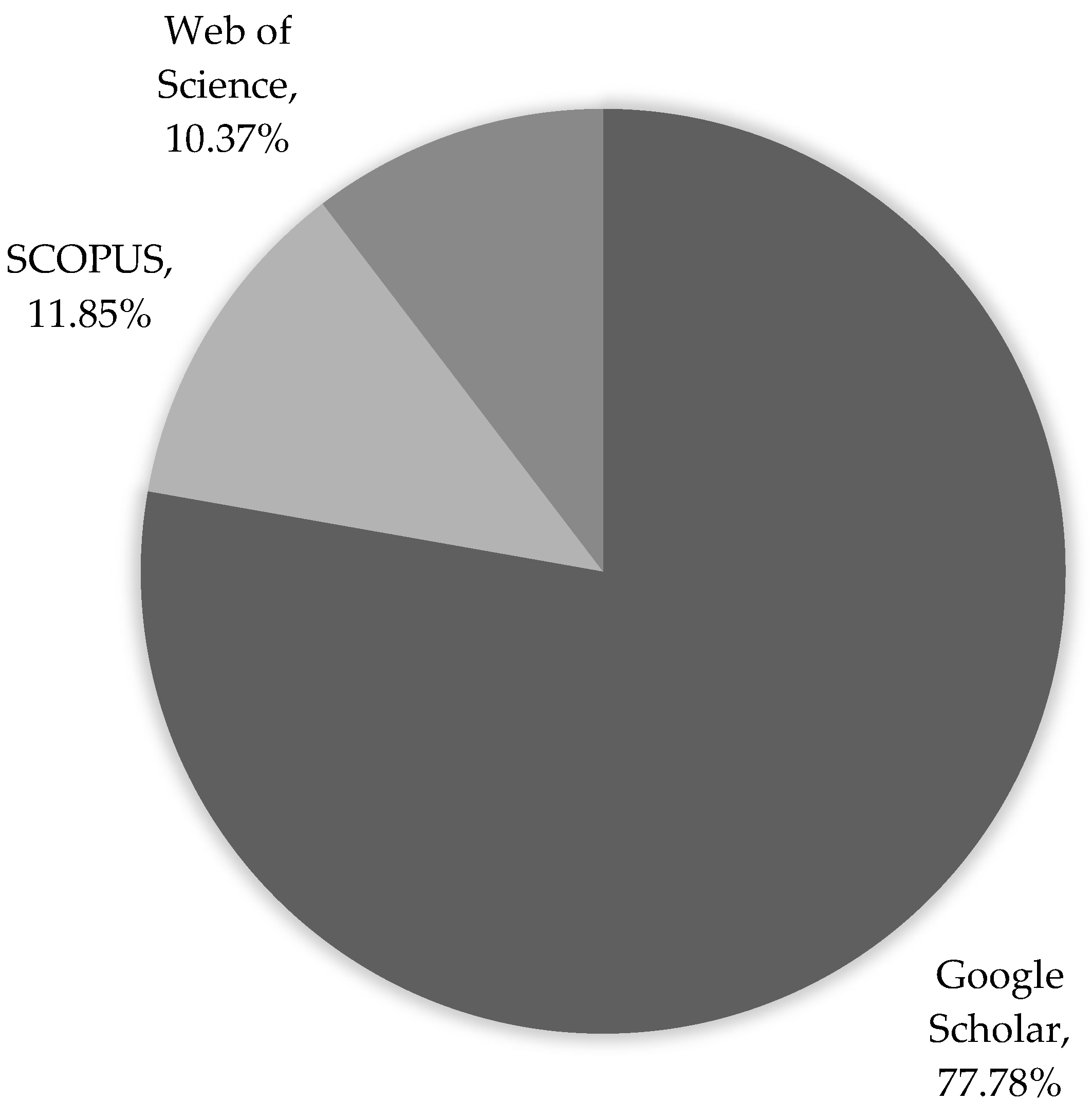

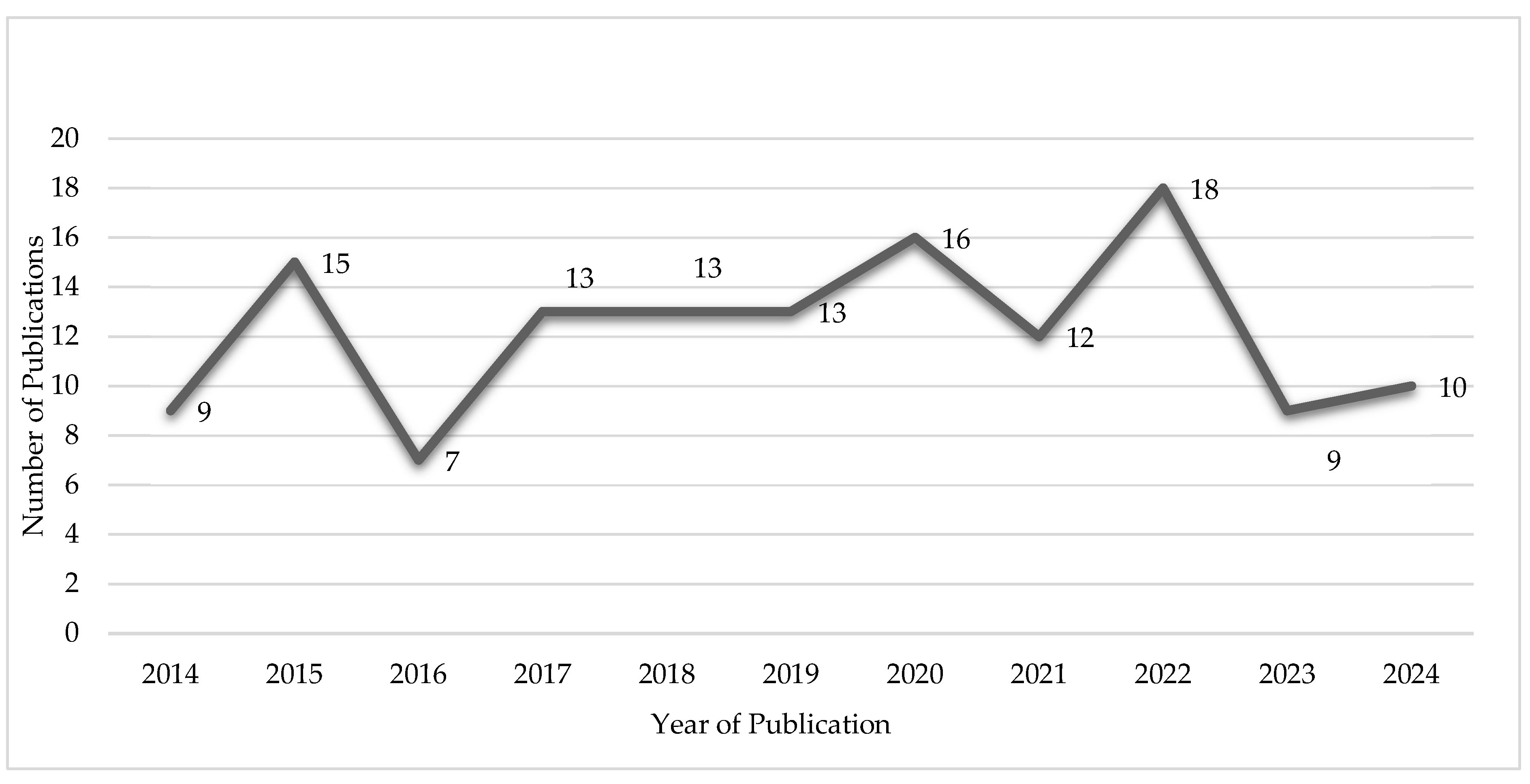

This study selection process followed the process shown in Figure 11. The research papers were extracted from the databases: Google Scholar, Web of Science, and SCOPUS, using the keyword search mentioned in section 2.3. Search strategy. The research papers were collected based on the inclusion and exclusion criteria mentioned in section 2.1. Eligibility criteria, and 10 000 papers appeared, and the papers were filtered using the inclusion and exclusion criteria, and the most relevant papers were selected. The selected papers are 136 papers. Out of 136 papers, 109 were from Google Scholar, 14 were from Web of Science, and 16 were from SCOPUS, and this is demonstrated in Figure 12. Out of the collected 136 papers, there were book chapters, conference papers, dissertations, and journal articles. All the 136 papers were eligible for full-text review and were integrated into this process of systematic analysis. Figure 13 shows the distribution of online databases, and many papers were collected from Google Scholar. Table 3 shows the publications of research papers associated with the Balanced Scorecard Methodology Performance Metrics and Strategy Execution in SMEs. Over the past 10 years, the table shows that the number of publications of research papers associated with this study increased, and this shows that there is a growing interest in the implementation of BSC in SMEs. Figure 13 shows the number of publications for different years in the past 10 years.

3.2. Study Characteristics

In this section, studies are included as well as the characteristics of each study. The characteristics of these research papers are reporting the details of the studies, and this is their applicability. The table shown below presents the research papers as well as citations, title, sample size, subject area, perspectives of Balanced Scorecard, and key performance indicators. Only 20 papers were used for the study characteristics, and this is shown in Table 3.

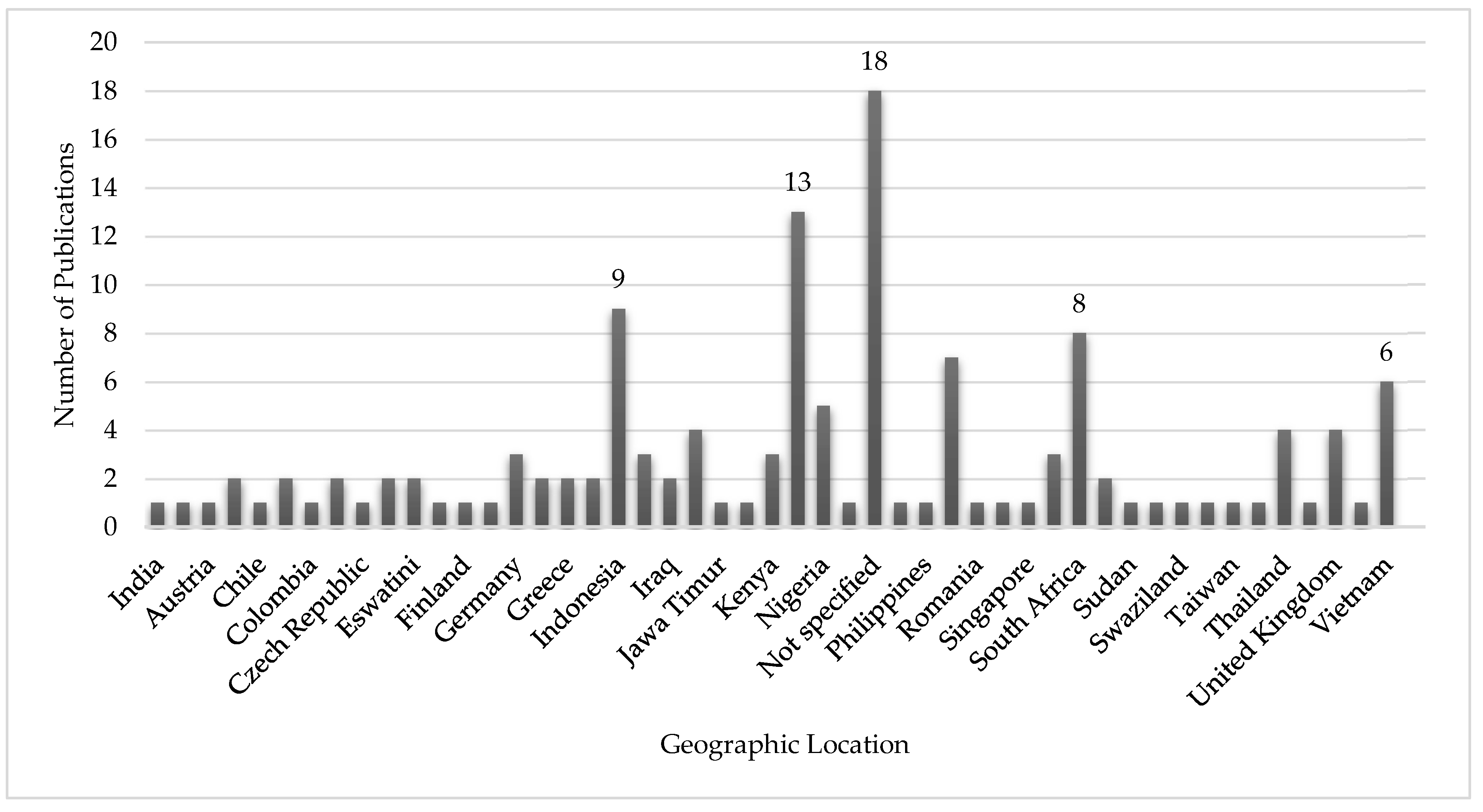

The distribution of publications on the Balanced Scorecard across various geographic locations is revealed in Figure 14. Asia and Europe have the largest number of publications, with Asia (including countries like: Vietnam, Malaysia, and Indonesia) leading with 13, 6, and 9 publications. Europe follows with significant contributions from individual countries such as Italy= 4 and United Kingdom=4. Other regions with substantial contributions include South Africa which stands at 8 publications as well as Portugal with 7 publications. Some research papers did not specify their geographic locations, and they amount to 18. Overall, the results tell us that while research on the BSC is globally distributed, there is a significant concentration in Europe and Asia, with notable contributions from countries like South Africa and Portugal. This geographic distribution highlights the global interest in the Balance Scorecard but underscores certain regions as more prominent in this research field.

The results suggest that the BSC is more extensively researched and more effectively implemented in certain regions. The very high volume of publications in Asia, particularly in Indonesia, Vietnam, and Malaysia, reflect a strategic focus on enhancing performance metrics within rapidly growing economies. This rising trend correlates with broader economic shifts in these regions, such as increasing emphasis on performance management as well as strategic alignment in SMEs. Overall, the geographic distribution of BSC research highlights regional differences in interest and implementation, suggesting that further investigation must be done into the factors driving these discrepancies could offer valuable insights into the effectiveness and adoption of the BSC methodology in various contexts.

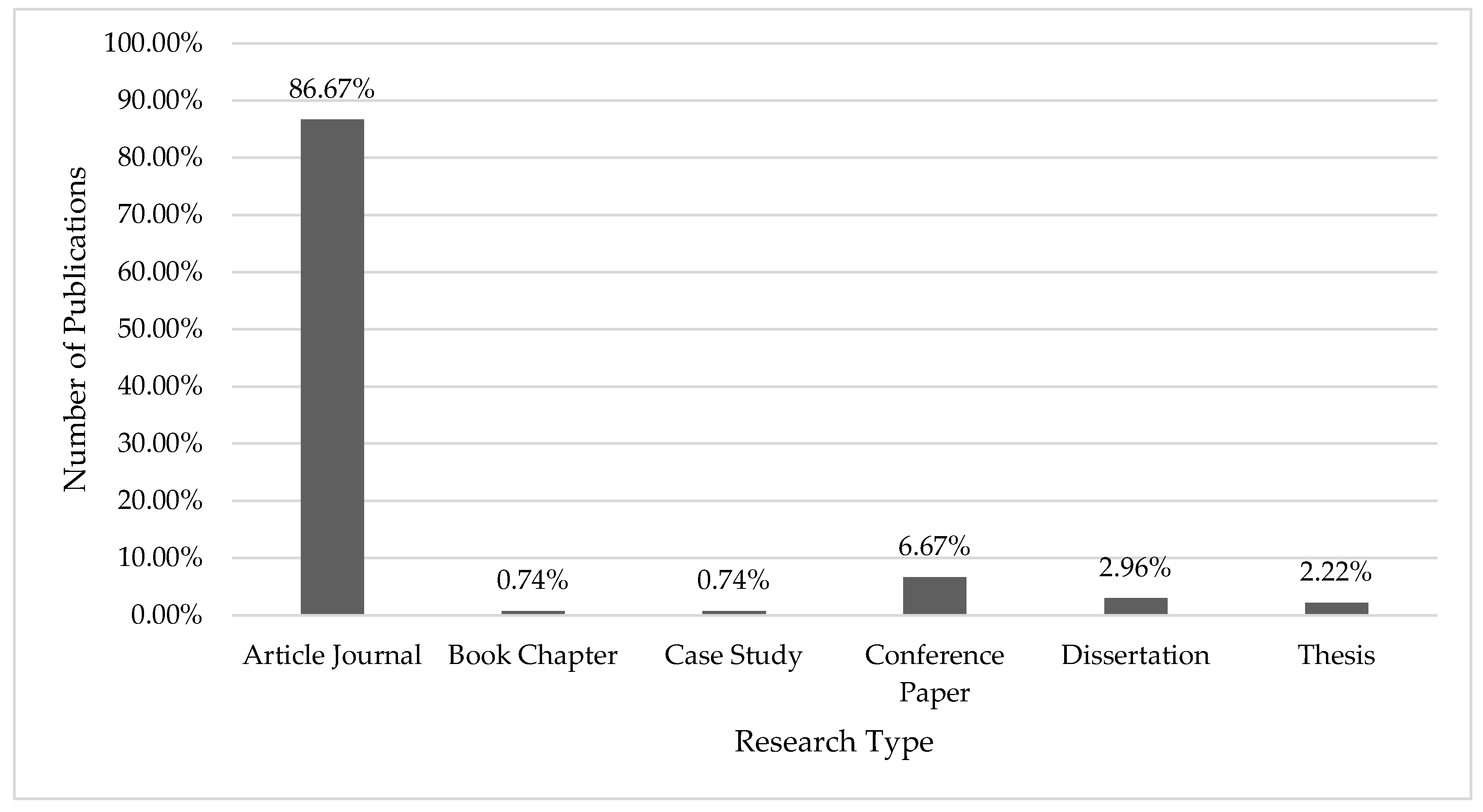

Figure 15 illustrates the distribution of different types of research outputs related to the BSC. Many publications, 86.67%, are Journal Articles, and this reflects a strong preference for this format for distributing research outcomes. Conference Papers follow with 6.67%, indicating a lesser focus on presenting findings at academic conferences. Dissertations and Theses collectively make 5.18%. Case Studies and Book Chapters, each contribute 0.74%. This distribution shows that while journal articles are dominant in the publication landscape for Balanced Scorecard research, there is also some engagement with other types of studies such as conference presentations as well as academic theses. Overall, the minimal representation of other formats tells us that journal articles are the primary medium for disseminating research in this field.

The dominance of journal articles in the dissemination of BSC research highlights their role as the primary medium for stringent, peer-reviewed studies. This high percentage signifies that journal articles are the preferred format for presenting comprehensive analyses and validated findings on the implementation of BSC and effectiveness in SMEs. The sparse contribution from case studies and book chapters means that these methods are less used in the current BSC research framework. This distribution indicates a concentration of research efforts in producing journal articles that are detailed, peer-reviewed, which may possibly reflect a preference for well-established, empirical evidence over exploratory studies. Future research might benefit from diversifying publication formats and methodologies to enrich understanding as well as the application of BSC in SMEs.

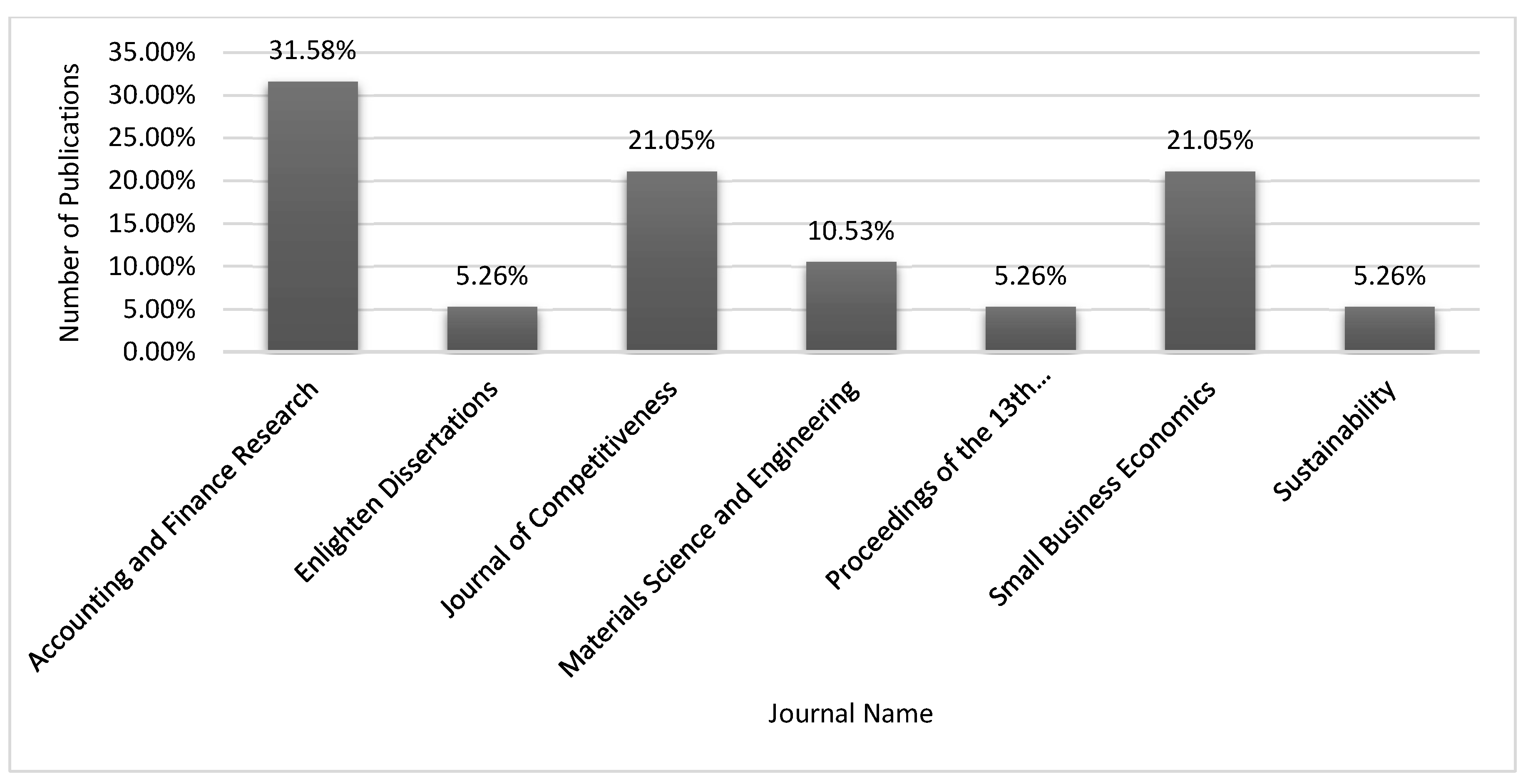

The results illustrate how the publications related to the Balanced Scorecard methodology across various journals are distributed. The Accounting and Finance Research Journal has the highest proportion of publications which is 31.6%, which indicates that this journal is a prominent source for research on Balanced Scorecard within the context of financial and accounting studies. The Small Business Economics, as well as the Journal of Competitiveness, each contribute approximately 21% of the publications, reflecting a strong interest in BSC’s impact on the economic aspects as well as competitive strategies within SMEs. Materials Science and Engineering Journal, and Proceedings of the 13th European Conference on Innovation and Entrepreneurship, both account for the 5.3%, this suggests that BSC research is less in these areas, this indicates a niche or less direct application. Similarly, Sustainability represents 5.3%, showing that while BSC’s role in sustainability is recognized, it is less emphasized when compared to other fields. This distribution underscores that the primary focus of the BSC research is on financial management and competitiveness in SMEs, with different degrees of interest in other disciplines. This information is shown in Figure 16.

The distribution of publications across these journals notifies that the BSC methodology is largely explored through the view of financial management and competitive strategy within SMEs. The high proportion of articles in accounting and finance journals highlight the important role that financial performance measurement plays in BSC research. The substantial representation in journals focused on small business economics and competitiveness further shows the impact of the methodology on strategic decision-making and competitive positioning in SMEs. The lower representation in other journals, such as those focused on sustainability and materials science, suggests these areas are less prioritized in the context of BSC research. This distribution of journals points to a high interest in how BSC can improve financial and strategic outcomes in SMEs, while indicating future research opportunities to explore its application in other emerging fields.

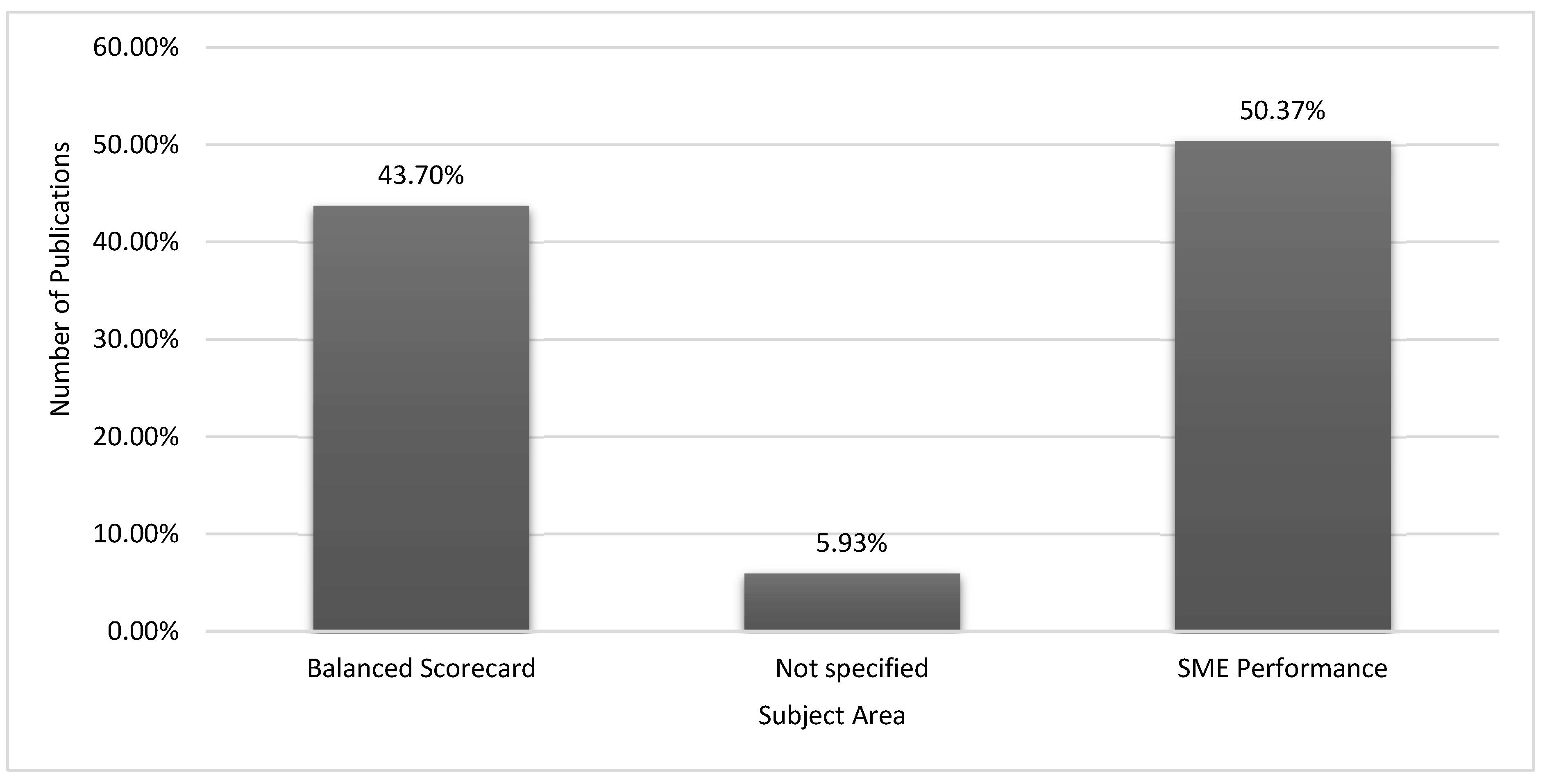

Figure 17 illustrates the distribution of publications within the subject areas relevant to this systematic review. It reveals that a substantial proportion of the literature: 43.70% sorely focuses on the Balanced Scorecard. This indicates that there is a strong interest in how the BSC framework is applied and analyzed in diverse contexts. The area of SME Performance, which is very important for this review, constitutes the largest segment, which is 50.37%, indicating its significant emphasis in literature. On the other hand, 5.93% of the publications are not specified, suggesting a minor proportion of the literature remains unspecific. Overall, these results underscore a prominent focus on both the BSC methodology and SME performance, aligning well with the objectives of this systematic review to explore the application as well as the impact of BSC in SMEs.

The data underscores a clear trend towards a concentrated focus on the performance of SMEs and the BSC methodology within the literature. The significant emphasis on the performance of SMEs suggests that researchers are specifically interested in evaluating how the BSC framework impacts performance metrics in SMEs, aligning well with the objectives of this review to understand the practical implications of BSC in improving SME performance. The considerable proportion of publications dedicated to the BSC methodology reveal ongoing scholarly engagement with refining and expanding the theoretical as well as the practical applications of the framework. The small percentage of unspecified publications indicate that there is emerging areas of research or gaps in the literature classification. This distribution reveals that while there is a very strong focus on theoretical underpinnings and practical applications of BSC in SMEs, there is also a need for more comprehensive categorization as well as exploration of emerging topics. Future research will benefit from addressing these gaps and expanding the focus to include the less explored areas related to the BSC methodology.

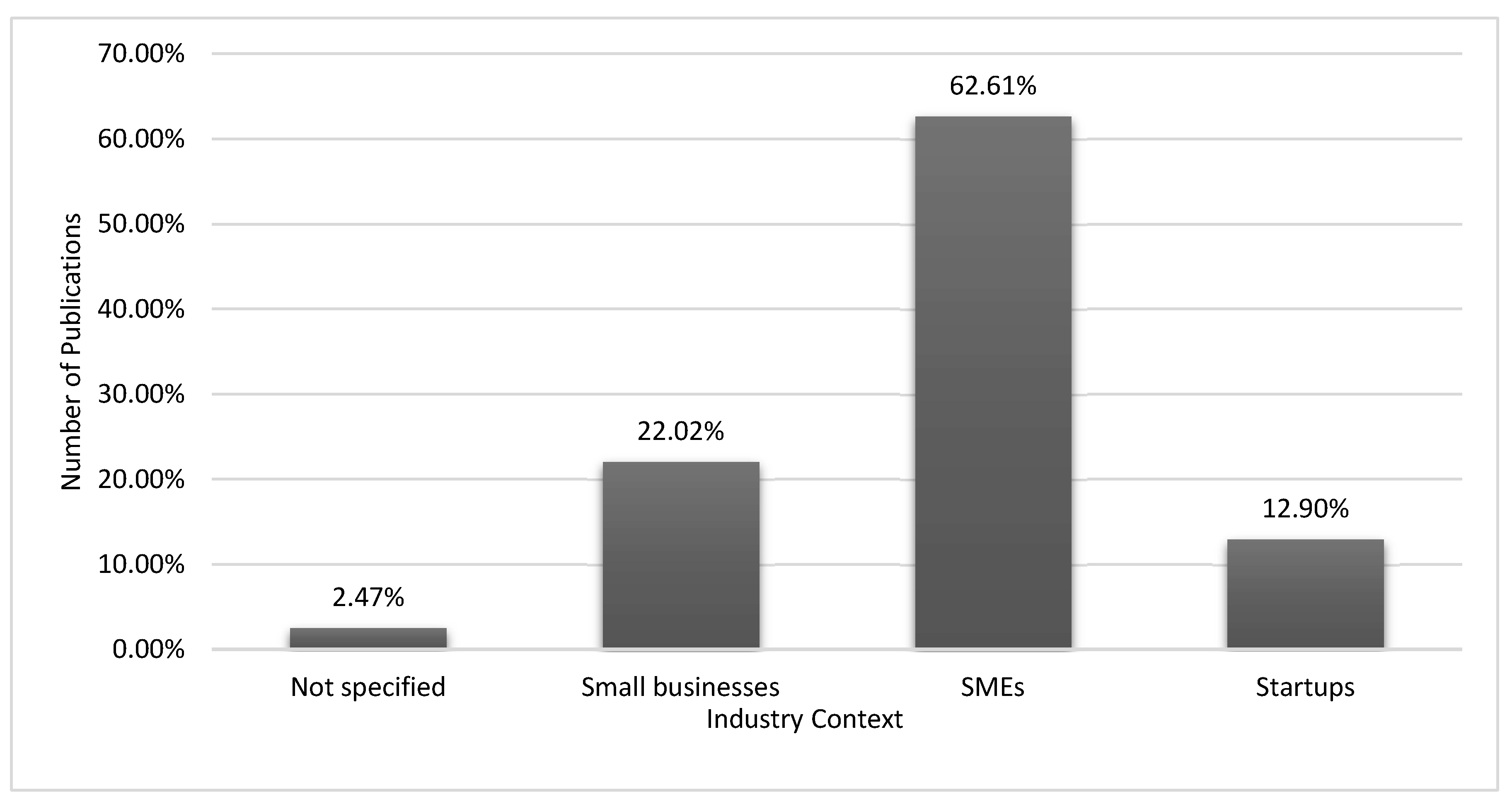

Figure 18 shows the distribution of publications according to their industry context, focusing on SMEs, startups, and small businesses. Most of the literature, comprising 62.61%, specifically approaches SMEs, underscoring a strong emphasis on this sector, which is central to this review. Small businesses contribute 22.02% of the publications, presenting a significant but smaller body of research compared to SMEs. Startups offer 12.90% of the publications, indicating a average level of interest in this area. Additionally, 2.47% of the publications do not specify the industry context. These results propose that while there is notable research focused on SMEs, there is less focus on startups and small businesses, aligning well with the review’s objective of investigating the Balanced Scorecard’s impact within SMEs.

The predominance of publications focusing on SMEs underscores a clear research priority in understanding how the Balanced Scorecard methodology is applied and its effectiveness in this sector. This high concentration reveals the relevance and significance of BSC in addressing the unique challenges and opportunities faced by SMEs, hence aligning with the aim of the review to explore its impact in this context. The comparatively smaller focus on small businesses and startups means that while these areas are acknowledged, they are under explored compared to SMEs. This could suggest that there is a potential gap in the literature regarding how BSC might be adapted in startups and small businesses, which could be valuable for future research. There is a very low rating of unspecified industry contexts, which could reflect emerging areas of study or limitations in the available data, this suggests that new research directions might be needed. Overall, the results highlight a concentrated effort on SMEs, but also underscore opportunities for further investigation into the applicability of BSC across the different types of business contexts.

3.3. Risk of Bias in Studies

In this section, each study assessed the risk of bias by using the Chrohane risk tool. This tool assessed each study by evaluating their random sequence generation, allocation concealment, blinding of participants and personnel, blinding of outcomes, incomplete outcome data, selective reporting, other bias and overall risk of bias. Table 4 represents each study’s assessment by showing if the headings are UNCLEAR, LOW OR HIGH as a summary.

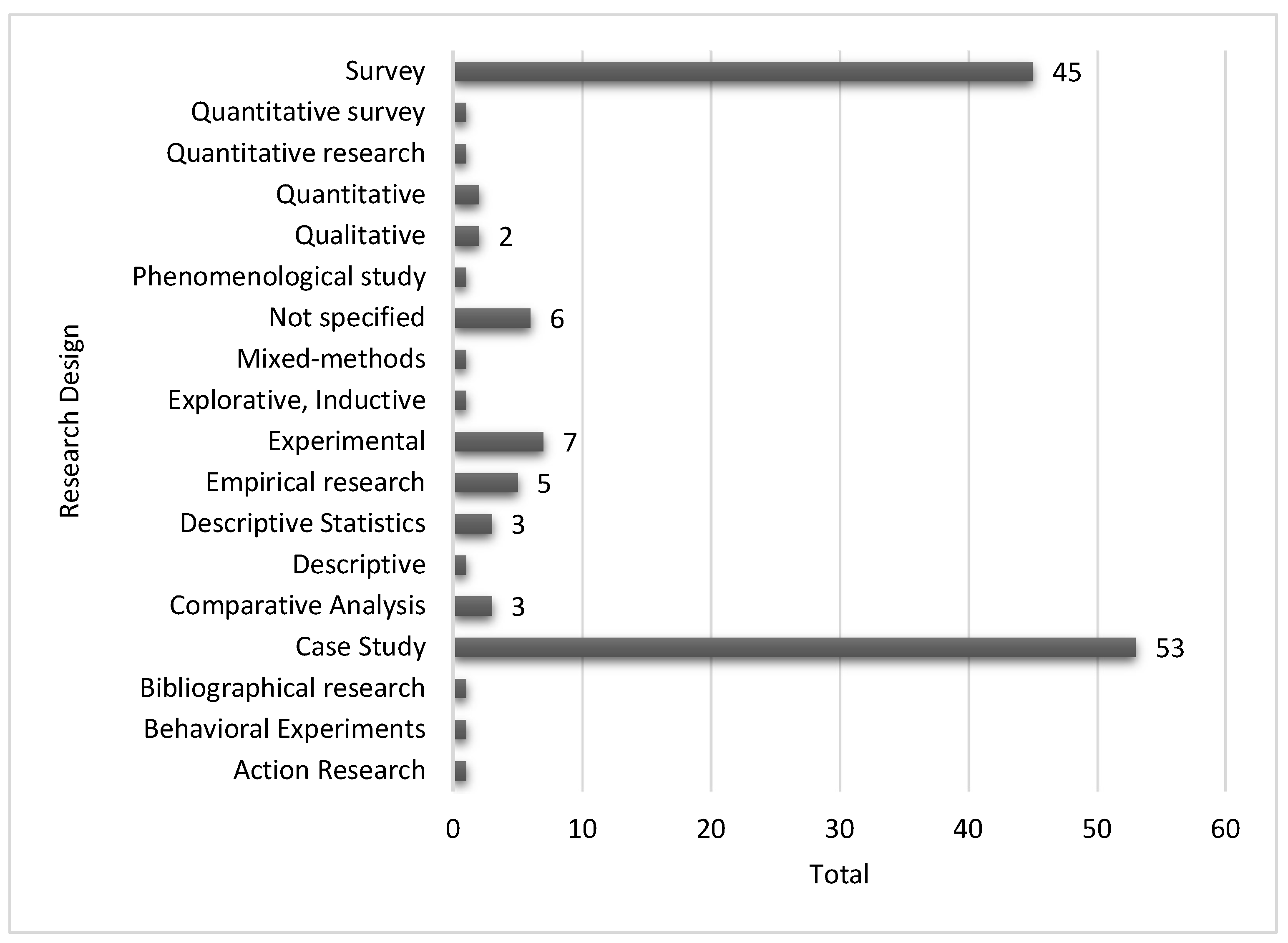

Figure 19 underscores that case studies and surveys are the predominant methods, with 53 and 45 publications respectively. This indicates a strong focus on detailed, real-world investigations and data collection from various SMEs to assess the effectiveness of the Balanced Scorecard (BSC). The significant number of experimental (7) and empirical research (5) studies suggests that some research efforts involved controlled experiments or data-driven insights to evaluate BSC applications. Meanwhile, less common research designs such as action research, behavioral experiments, and phenomenological studies reflect approaches to exploring BSC. The presence of diverse methodologies including mixed methods, qualitative, and quantitative approaches represents a comprehensive effort to capture different facets of BSC's impact. The small number of publications with unspecified research designs (6) points to some void in methodological clarity. Overall, the distribution highlights a strong emphasis on practical and applied research methods to understand BSC in SMEs.

The supremacy of case studies and surveys in the reviewed literature implies that practitioners and researchers alike prioritize real-world applicability and broad data collection when assessing the Balanced Scorecard's (BSC) effectiveness in SMEs. Case studies offer deep insights into individual organizations, while surveys offer a broader overview of BSC implementation across various SMEs. The relatively small number of experimental and empirical research studies shows that while some researchers attempt to control variables and derive data-driven conclusions, the field largely depends on observational methods. This reliance could suggest a potential gap in understanding causality and the direct impact of BSC on performance metrics. The different range of methodologies, including action research and phenomenological studies, highlights an acknowledgment of the BSC’s multifaceted nature and the need to investigate its implementation from various perspectives. The presence of mixed methods shows an effort to integrate qualitative and quantitative data to offer a more comprehensive view. However, the six studies with unspecified research designs implies an area for improvement in methodological rigor. The overall analysis underscores a strong engagement with practical aspects of BSC implementation, yet it also highlights a need for more experimental and thoroughly defined research approaches to better elucidate the direct effects of BSC on SME performance outcomes.

3.4. Results of Individual Studies

Table 5 summarizes the findings from several studies that explore the implementation and impact of the Balanced Scorecard (BSC) within small and medium-sized enterprises (SMEs) across different countries and industries. Each study assesses key performance dimensions, including customer perspective, internal processes, financial outcomes, and long-term organizational impacts. These studies collectively provide insights into how the Balanced Scorecard has influenced business efficiency, strategic management, and performance outcomes in SMEs. The findings highlight variations in the sample sizes, the extent of BSC adoption, and the nature of organizational improvements, particularly in relation to financial and non-financial performance indicators. The data presented offers a comprehensive look into the short- and long-term benefits observed, including improvements in strategic alignment, communication, competitive advantage, and resource management. Additionally, these studies show how the Balanced Scorecard has been integrated with other performance measurement tools, such as lean practices and management competence frameworks, to enhance overall business performance.

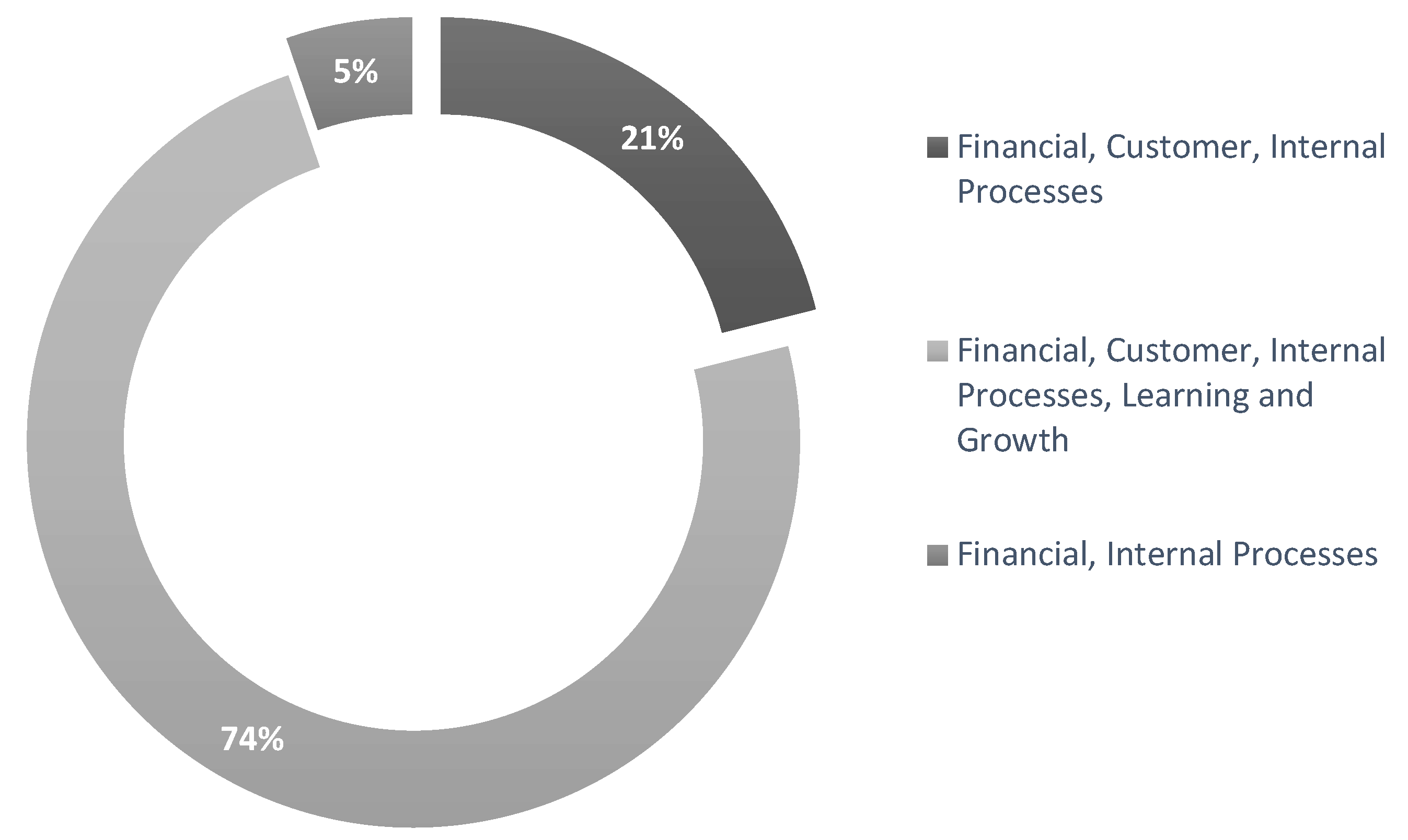

Figure 20 provides a breakdown of publications that focus on different perspectives of the Balanced Scorecard (BSC). The largest segment of the pie chart is 74%, which encompasses studies that address all the four perspectives of BSC: (Financial, Customer, Internal Processes, and Learning and Growth). This shows a strong emphasis on comprehensive analyses that consider all the four BSC’s dimensions (Financial, Customer, Internal Processes, and Learning and Growth). 21% of publications focus on the combination of the three metrics which are: Financial, Customer, and Internal Processes, suggesting a significant but less inclusive approach compared to the model that focuses on all the four metrics. The smallest segment, which is 5%, covers only the Financial as well as the Internal Processes perspectives, underscoring a more limited focus on specific aspects of BSC. Overall, the results show that many of research adopts a holistic view of BSC, integrating all the perspectives to provide a well-rounded analysis of performance metrics of the BSC.

The results uncover a pronounced preference for a holistic approach to the Balanced Scorecard (BSC) methodology in SMEs, with 74% of publications focusing on all four perspectives: Financial, Customer, Internal Processes, and Learning and Growth. This implies a regular trend towards adopting the BSC in its entirety, reflecting an understanding of its potential to offer a comprehensive view of organizational performance. The significant focus on all four perspectives implies that SMEs often pursue a balanced evaluation of various performance dimensions to align with strategic goals. In contrast, the 21% of studies that focus only three perspectives (excluding Learning and Growth) shows a preference for a somewhat simplified version of the BSC, possibly due to practical constraints or a focus on more immediate performance metrics. The minimal focus on just the Financial and Internal Processes perspectives (5%) underscores a niche approach that may reflect specific organizational needs or limitations in implementing a full BSC. This distribution of focus across various BSC perspectives highlights the flexibility of the methodology, but also points to potential voids in the integration of the Learning and Growth dimension. Overall, the findings propose that while the comprehensive BSC approach is widely adopted, there is room for further investigation into how the exclusion of certain perspectives might impact the effectiveness of performance management in SMEs. This analysis emphasizes the need for further research to study the implications of partial versus full implementation of the BSC in various SME contexts.

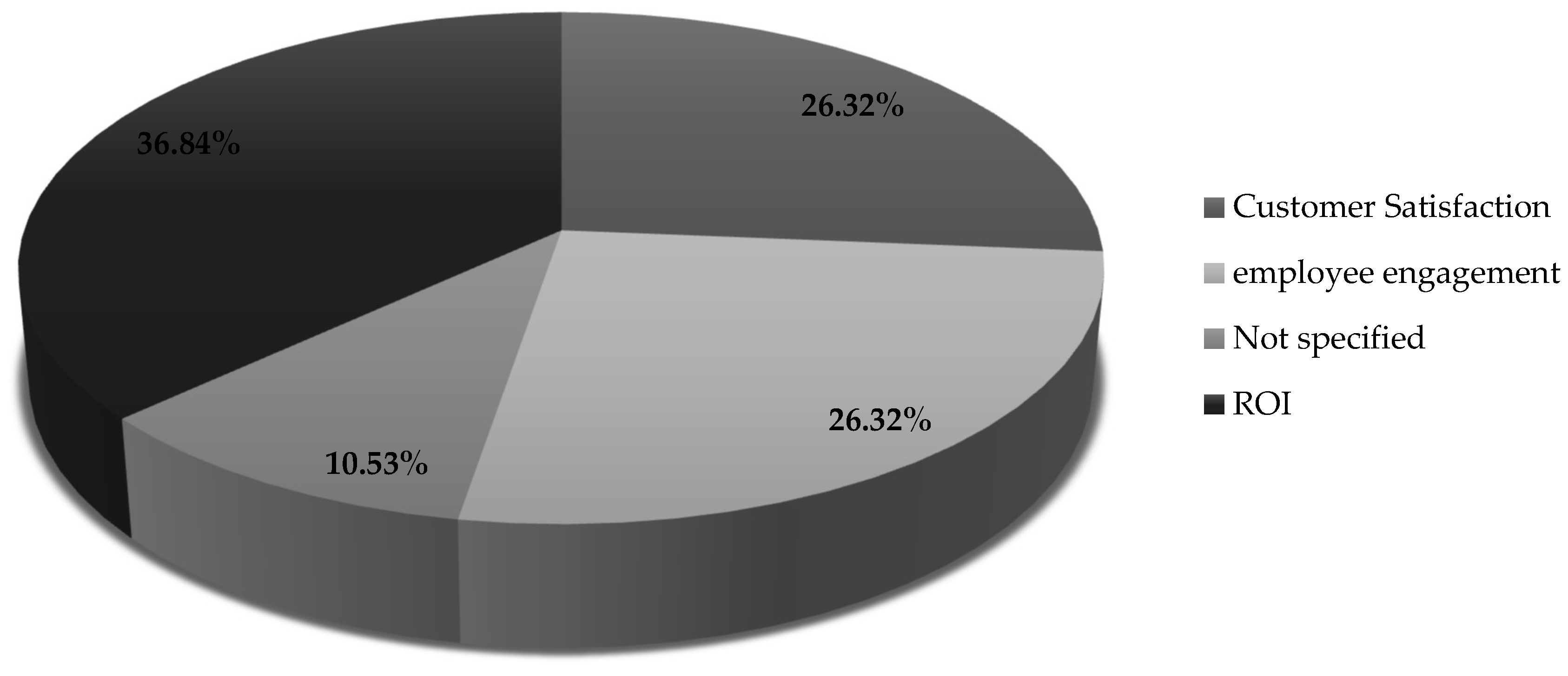

Figure 21 shows how the key performance indicators (KPIs) addressed in the publications reviewed are distributed for the systematic review on the Balanced Scorecard in SMEs. The data shows that Return on Investment or (ROI) is the most frequently discussed KPI, standing at 36.84% of the publications, underscoring its significant role in the evaluation of financial performance and effectiveness. Customer satisfaction as well as employee engagement are equally emphasized, featured in 26.32% of the publications, and this indicates their importance in understanding non-financial performance as well as organizational health. 10.53% of the publications do not specify which KPIs are measured, and this suggests some variability in reporting. This distribution highlights the focus on financial and employee-centric metrics while also pointing to a potential area that requires a more detailed reporting on KPI specifics in future research.

The distribution of key performance indicators (KPIs) emphasized in the publications reflects a nuanced understanding of the Balanced Scorecard (BSC) methodology in SMEs. The domination of Return on Investment (ROI) at 36.84% propose a robust emphasis on financial metrics, underscoring the importance placed on quantifiable financial outcomes within SMEs. This focus on ROI aligns with the requirement for SMEs to indicate clear financial performance and effectiveness, which is critical for securing investment and sustaining operations. In contrast, the same emphasis on customer satisfaction and employee engagement (26.32% each) points to a balanced approach in evaluating non-financial aspects of performance, critical for understanding broader organizational health and strategy execution. The 10.53% of publications that did not specify KPIs show a gap in standardization and reporting, which may vague a comprehensive assessment of BSC effectiveness. This variability suggests that future research should aim for more detailed and consistent KPI reporting to optimize the reliability of findings. Overall, the results propose that while SMEs are increasingly acknowledging the value of both financial and non-financial metrics, there remains a need for greater clarity and uniformity in KPI reporting to fully leverage the Balanced Scorecard methodology for strategic execution.

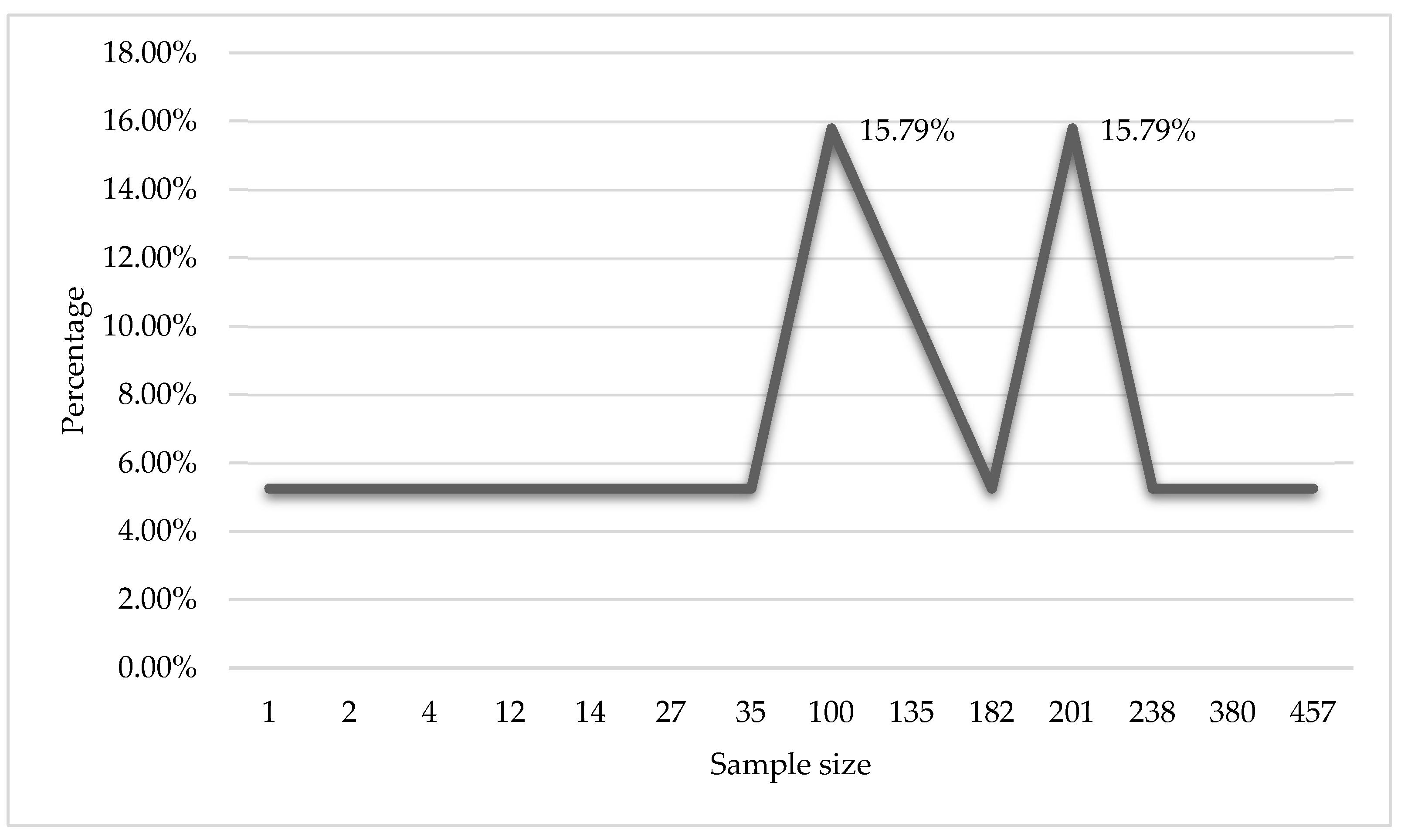

Figure 22 represents a wide variation in the number of participants analyzed. Most papers gathered have relatively small sample sizes, with each category (1, 2, 4, 12, 14, 27, and 35 participants) contributing 5.26% of the total publications. The small sample sizes show how much of the research on the Balanced Scorecard (BSC) in SMEs focus more on detailed, case-specific analysis rather than large-scale surveys or broad statistical studies. This may indicate the unique and context-dependent nature of BSC implementation in SMEs, where customized case studies or small-group analyses are more common for capturing specific organizational dynamics, performance impacts, and strategy execution challenges. However, the small sample sizes also suggest potential limitations in the applicability of findings, as wider trends might not be fully documented in studies with limited participant numbers.

The reliance on small sample sizes may show the complex and context-dependent nature of BSC implementation in SMEs. This approach allows for a refined understanding of how BSC frameworks are adapted and executed within varying organizational environments. However, this focus on case-specific studies could also restrict the generalizability of findings. The lack of larger-scale studies may impede the ability to identify wider trends or overarching patterns in BSC effectiveness across different SMEs. Therefore, while detailed insights are gained from individual case studies, the overall applicability of the results to a wider population of SMEs may be constrained. To optimize the strength of BSC research in SMEs, future studies could benefit from incorporating larger sample sizes or combining case studies with broader surveys to provide a more holistic view of the BSC methodology’s impact and effectiveness.

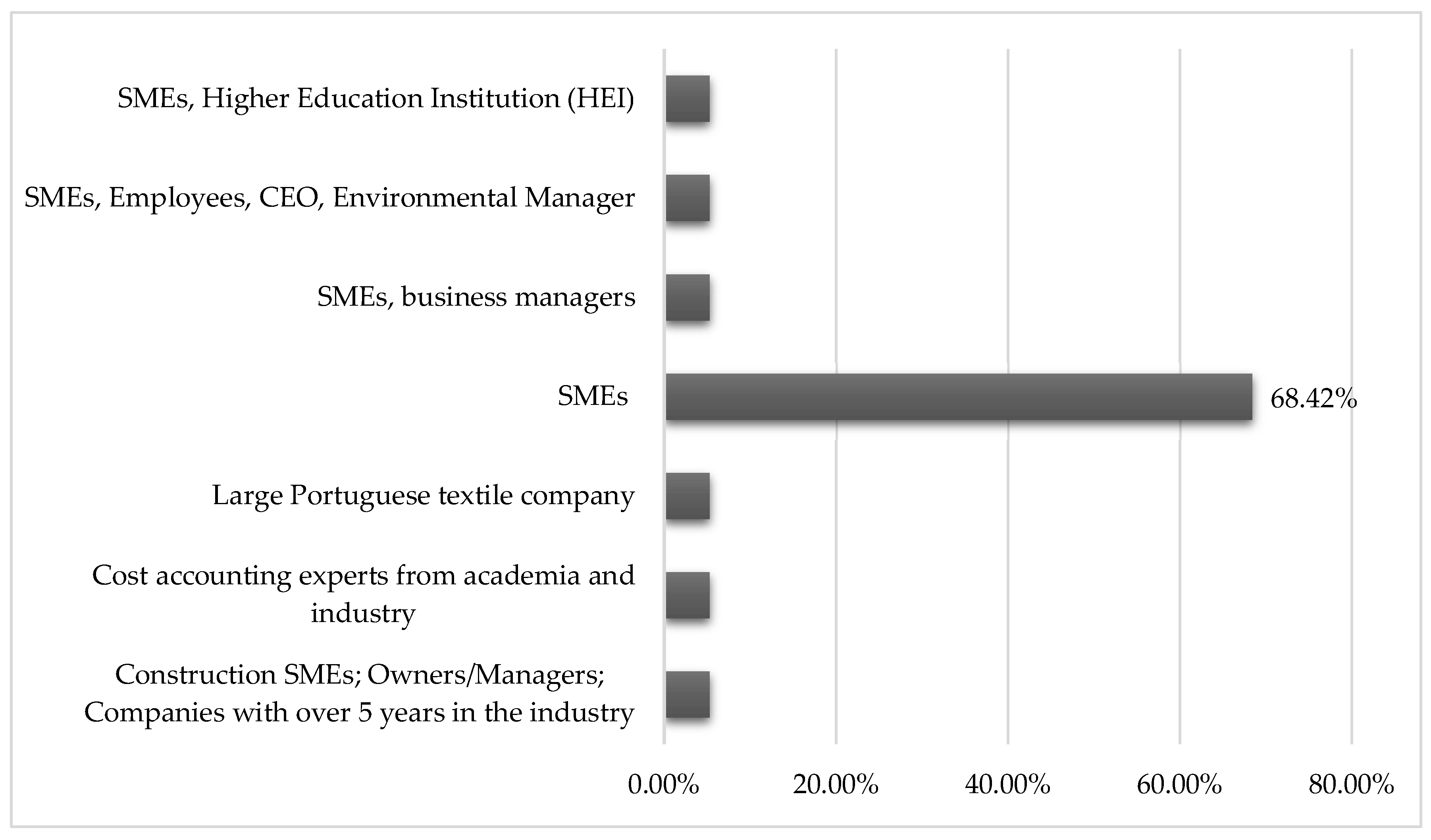

Figure 23 reflects that most studies (68.42%) focus on SMEs as their primary sample, reflecting the central theme of the review—evaluation of Balanced Scorecard (BSC) in the context of small and medium-sized enterprises (SMEs). A smaller portion of studies (5.26% each) involves subgroups within SMEs, such as business managers, employees, CEOs, and environmental managers, highlighting the BSC’s impact across various organizational roles. Additionally, some studies feature specific participants like cost accounting experts or focus on tailored sectors like a large Portuguese textile company or construction SMEs, indicating a diverse range of industries and expertise being explored. This distribution underscores the importance of understanding BSC implementation across various SME contexts, particularly in terms of managerial perspectives and sector-specific challenges. The involvement of academia and higher education institutions (HEIs) in a few studies suggests an interdisciplinary approach, blending practical business insights with academic research. Overall, the results indicate a strong emphasis on SMEs as the focus of the research, with additional consideration given to the roles and expertise of individuals involved in BSC implementation.

The concentration of studies on SMEs underscores a significant focus on how the Balanced Scorecard (BSC) is employed and adapted within this sector. This predominant focus proposes a recognition of the unique challenges encountered by SMEs in performance management and strategy execution. The limited involvement of specific roles such as business managers and environmental managers in some studies may show a narrower scope of investigation into the broader organizational impacts of BSC. However, the presence of studies targeting distinct sectors and roles shows an attempt to tackle these variations and the BSC's adaptability to different contexts. The various range of industries and expertise investigated in the reviewed studies proposes that while the BSC methodology is widely applicable, its implementation and effectiveness can differ significantly based on sector-specific and managerial factors. This variability highlights the need for more distinct analysis within future research, particularly focusing on how sectoral differences influence BSC outcomes. By integrating academic perspectives with practical applications, the studies contribute to a richer understanding of how BSC can be effectively customized to the needs of SMEs, contributing valuable insights into optimizing its strategic impact.

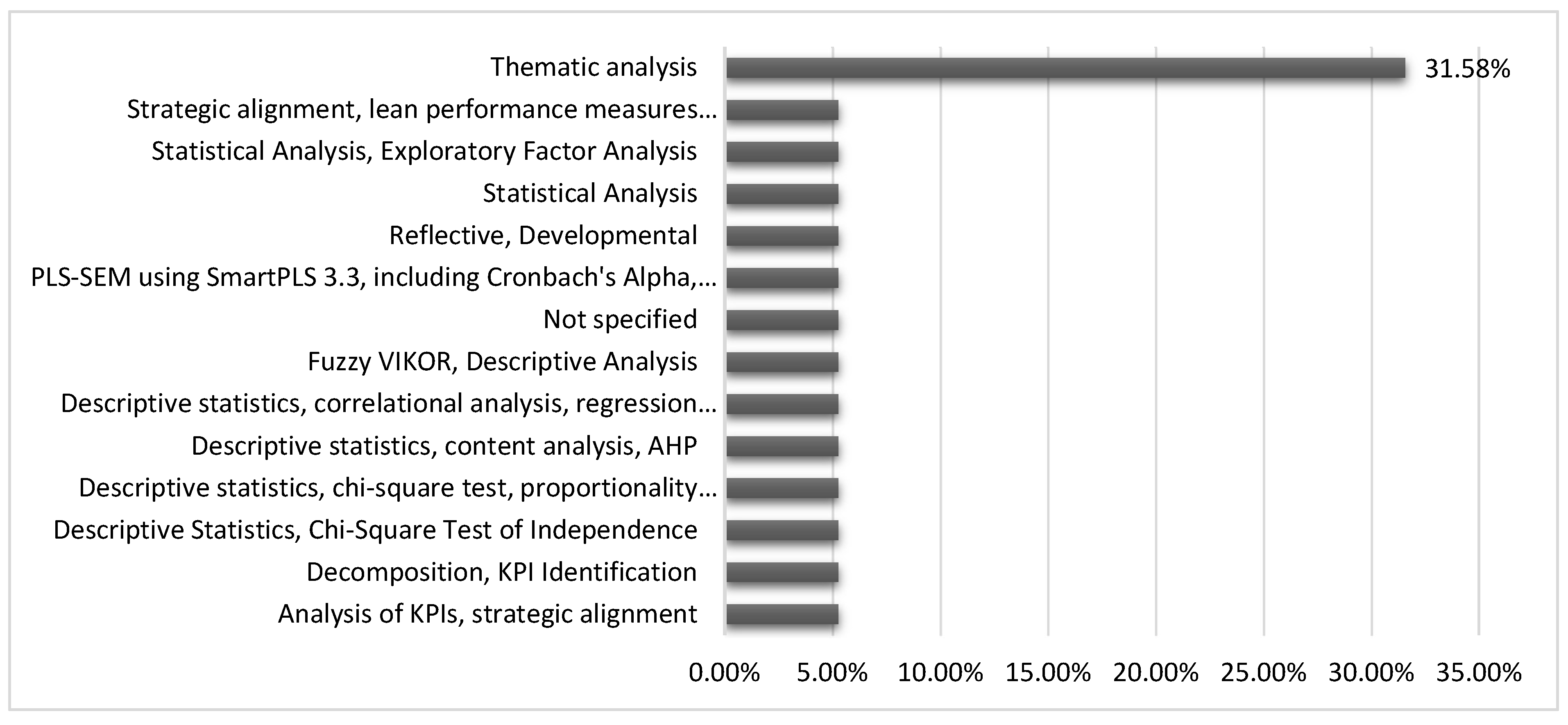

Figure 24 reveals a variety of methods applied to evaluate the effectiveness of the Balanced Scorecard (BSC) in SMEs. Thematic analysis is the most common, accounting for 31.58% of the techniques, highlighting its use in qualitative analysis to explore themes like strategy execution and performance alignment. The remaining techniques, each representing 5.26%, suggest a strong presence of quantitative methods such as descriptive statistics, chi-square tests, regression analysis, and statistical analysis, which reflect the efforts to measure performance using key performance indicators (KPIs) and validate models like PLS-SEM. This diversity of methods implies that studies take both qualitative and quantitative approaches to assess the Balanced Scorecard, providing a holistic view of its impact on SMEs. Thematic analysis dominance may also indicate a focus on understanding subjective factors like employee motivation and customer satisfaction.

The various use of data analytics techniques across the studies highlights the multifaceted approach researchers have taken to evaluate the Balanced Scorecard (BSC) in SMEs. The prevalence of thematic analysis (31.58%) proposes that many studies prioritize investigating qualitative dimensions such as strategy execution and performance alignment, which can contribute insights into how SMEs perceive and implement BSC. This focus might reflect an understanding that the success of BSC in SMEs is not solely reliant on numerical metrics but also on subjective factors like organizational culture and employee engagement. Conversely, the significant presence of quantitative methods, including descriptive statistics, chi-square tests, regression analysis, and PLS-SEM (5.26% each), points to a strong effort to validate the BSC’s impact through empirical measures. This contribution of qualitative and quantitative methods reflects the complexity of evaluating BSC’s effectiveness and suggests that a comprehensive evaluation involves both understanding organizational dynamics and measuring performance metrics. Such a methodological diversity proposes that while the BSC’s effectiveness in SMEs is being rigorously tested, there is also a recognition of the need to interpret results in the context of organizational and strategic nuances.

3.5. Results of Syntheses

The studies that were included in this paper are article journal, conference paper, book chapter, dissertation and thesis that are qualitative studies, quantitative studies or both methods. The participants that were involved in this review ranges from 1 SME to 2000 SMEs. From the participants (SMEs), managers, employees, customers and financial documents were used to keep track of the outcomes and long-term impacts of the BSC implemented in SMEs. These studies were conducted around the world in SMEs. The outcomes that were measured are financial and non-financial indicators (customers, business process, and learning and growth). There are 50 quantitative studies, 90 qualitative and 10 mixed-method studies. These types of study have 20000 participants in SMES that implemented balanced scorecard. 20 studies were low risk of bias, 10 were unclear risk of bias and 90 studies had high risk of lack of blinding and allocation. 10 studies had high overall risk of bias, and 50 studies had unclear incomplete outcome data. These 130 studies were pooled, as they each identified an implementation of BSC method on SMEs within the past 10 years and were not literature reviews.

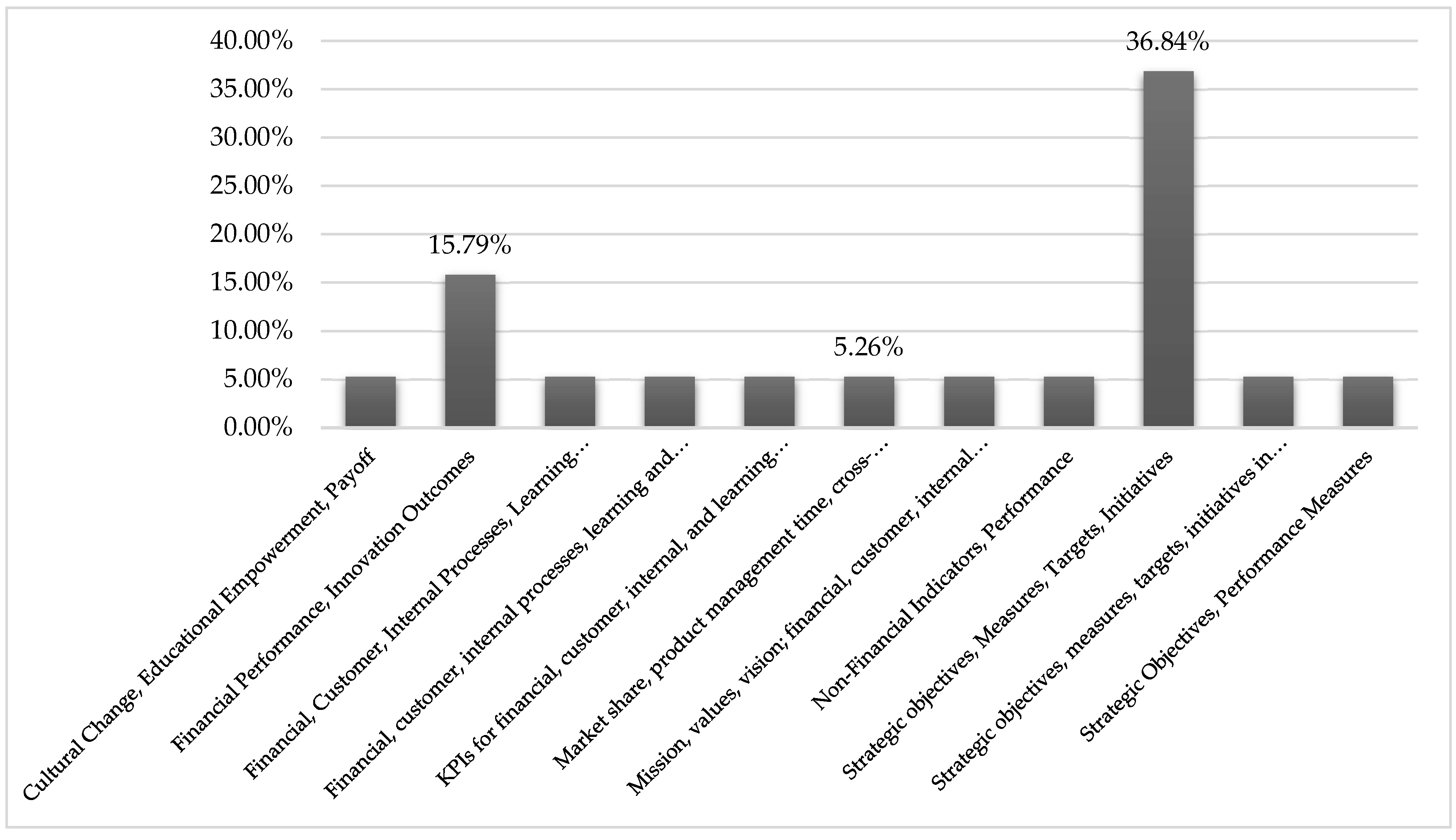

Figure 25 reveals that many studies (36.84%) focus on the core elements of BSC: strategic objectives, measures, targets, and initiatives. This reflects a strong emphasis on the fundamental purpose of the BSC—aligning strategy with measurable outcomes to drive performance improvement. Other studies, comprising 15.79%, also prioritize financial performance and innovation outcomes, highlighting the BSC's role in fostering innovation and financial growth, key concerns for SMEs aiming to stay competitive. Some studies (5.26% each) examine more comprehensive frameworks, integrating financial, customer, internal processes, and learning and growth perspectives, which align with the traditional four BSC perspectives. Additionally, metrics like market share, product management time, and profit comparison point to sector-specific performance indicators, suggesting that some studies customize the BSC framework to reflect the unique needs of specific industries. The inclusion of cultural change, educational empowerment, and knowledge sharing in a few studies indicates that the BSC is also used to track non-financial outcomes like organizational culture and knowledge transfer. This broad mix of financial and non-financial metrics underscores the versatility of the BSC in addressing both tangible and intangible aspects of SME performance, with a clear emphasis on strategic alignment

The data that is presented in Figure 25 shows a diverse application of BSC metrics across different studies, highlighting the adaptability of the framework in addressing various dimensions of SME performance. The dominant focus on core BSC elements depicts a strong preference for using BSC to directly align strategic goals with measurable outcomes, which is important for improving performance in SMEs. The significant attention to financial performance and innovation underscores the role of BSC in driving competitive advantage through both financial growth and fostering innovative practices. The examination of comprehensive frameworks integrating all the four traditional BSC perspectives (5.26% each) indicates a balanced approach to performance measurement, this ensures that all critical areas of business performance are addressed. The inclusion of sector-specific metrics and non-financial outcomes reflects an evolving understanding of the application of BSC beyond traditional measures, showing its flexibility in adjusting and adapting to the unique needs of various industries. These findings suggest that while the core focus remains on strategic alignment and measurable outcomes, there is a growing recognition of the significance of incorporating both financial and non-financial indicators to provide a more holistic view of SME performance. Future research could further explore how these various applications of BSC metrics impact the overall effectiveness and provide insights into optimizing the framework for different business contexts.

Figure 26 illustrates that employee satisfaction and customer satisfaction are the most regularly reported results, including 26.32% of the publications. This highlights a clear focus on how the Balanced Scorecard (BSC) positively influences employee well-being and customer relations in SMEs, which are crucial for sustaining long-term business success. Other results, such as employee motivation, training participation, customer loyalty, and innovation, are also analyzed but to a lesser extent, each having 5.26% of the publications. These results reflect how BSC can enhance employee engagement, alignment with organizational goals, and service quality. Some studies also emphasize improvements in communication, decision-making, and strategic management, showing that the BSC assists SMEs not only to align their staff but also improve operational processes and management strategies. Interestingly, 10.53% of studies did not specify the results, hinting a void in clear documentation of how BSC impacts organizational dynamics. Overall, the results imply that while SMEs benefit from a variety of organizational improvements through BSC, the strongest focus stays on the satisfaction of employees and customers as key drivers of success.

The data in Figure 26 reflects that the Balanced Scorecard is predominantly associated with improving employee and customer satisfaction. This indicates a clear recognition of the effectiveness of BSC in fostering crucial elements for SME success, such as customer relations and employee well-being. The secondary focus on metrics such as employee motivation, training participation, as well as customer loyalty suggests that while these aspects are considered, they are not too central to the impact of BSC in current literature. The fact that some studies report enhancements in communication, decision making, and strategic management underscores a broader role of BSC in refining internal processes and management strategies. However, the unspecified results point to a lack of detailed documentation and possibly a lack of standardized metrics in evaluating the effectiveness of BSC, which could mean potential gaps in the research or imply variations in how outcomes are measured and reported. Overall, these findings suggest that while the BSC framework is treasured for its impact on employee and customer satisfaction, there is a need for a more comprehensive and consistent reporting on its broader organizational impacts as well as effectiveness across different.

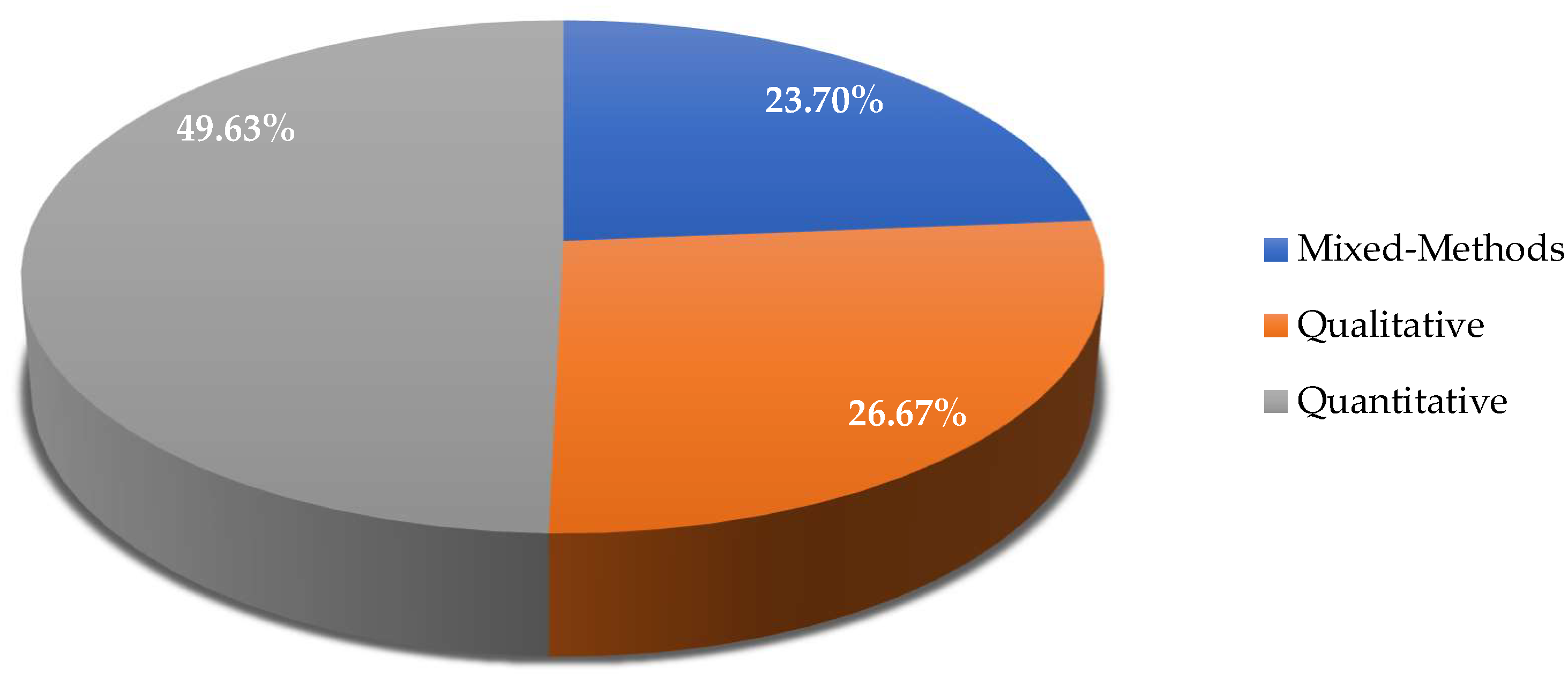

Figure 27 shows that nearly half (49.63%) of the studies employ a quantitative approach, indicating a strong focus on measurable, data-driven performance metrics and outcomes in Balanced Scorecard (BSC) research related to SMEs. Qualitative studies make up 26.67%, highlighting the importance of contextual, in-depth exploration of how BSC is implemented and its impact on strategy execution, employee motivation, and organizational culture in SMEs. Mixed-methods studies represent 23.70%, reflecting a balanced integration of both qualitative and quantitative insights, suggesting that researchers recognize the need to assess both the measurable outcomes, sand the underlying processes or experiences associated with BSC implementation in SMEs. Overall, this distribution suggests a healthy blend of methodologies, with a slight emphasis on quantitative studies, possibly because of the tangible nature of performance metrics tied to BSC frameworks.

The distribution of study types shown in Figure 27 gives valuable insights into the methodological trends in BSC research within SMEs. The dominance of quantitative studies highlights a significant interest in analyzing objective, measurable aspects of BSC, like performance metrics and outcomes. This focus on quantitative data aligns with the emphasis of BSC on tracking and enhancing measurable performance indicators. The substantial proportion of qualitative studies underscores an equally important emphasis on understanding the contextual as well as experiential dimensions of the implementation of BSC, including its effects on employee motivation and organizational culture. The presence of mixed-methods studies means that there is a growing recognition of the value in combining quantitative rigor with qualitative depth to capture a more comprehensive view of the impact of BSC. This methodological diversity reveals a nuanced approach to evaluating BSC, indicating that researchers are also interested in the processes and perceptions that contribute to the effectiveness of the framework. The overall methodological blend indicates a robust research landscape that treasures both empirical measurement as well as contextual understanding, providing a well-rounded perspective on the effectiveness of BSC in SMEs.

Figure 28 papers shows a strong emphasis on business sustainability and competitive advantage, with the latter being mentioned in 38.52% of the publications. This shows that a huge portion of the studies underscore how the Balanced Scorecard (BSC) contributes to long-term strategic benefits for SMEs, such as maintaining a competitive edge and ensuring sustainability. While other impacts such as business growth, improved performance monitoring, and risk management are not frequently mentioned, they still show important areas where BSC is seen to influence long-term outcomes. The broad range of impacts covered, including market consolidation, economic development, and enhanced decision-making, highlights the diverse ways in which BSC is observed to affect SME performance. The percentage of not specified contributes (5.19%) suggests that some studies did not clearly detail the long-term outcomes of BSC implementation. Overall, the results point to a prevailing view that BSC is integral to achieving sustainable competitive advantage and enhancing long-term business performance in SMEs.

The data show a distinct trend towards the Balanced Scorecard's role in enhancing competitive advantage and sustainability, implying that SMEs perceive BSC as an important tool for achieving long-term strategic goals. The high percentage of studies highlighting competitive advantage shows that SMEs mainly value BSC for its ability to assist them outperform competitors over time. Despite the diverse impacts reported, such as improved decision-making and market consolidation, the relatively lower emphasis on business growth and risk management may reflect a research bias towards more clear and immediate benefits. 5.19% of studies with unspecified long-term impacts further proposes a need for more holistic reporting in future research. By integrating these findings, while BSC offers varied benefits, its strategic importance in sustaining a competitive edge and driving sustainability is consistently recognized across studies. This comprehensive understanding underscores the Balanced Scorecard's value not just as a performance measurement tool, but as a strategic framework crucial for long-term success in SMEs

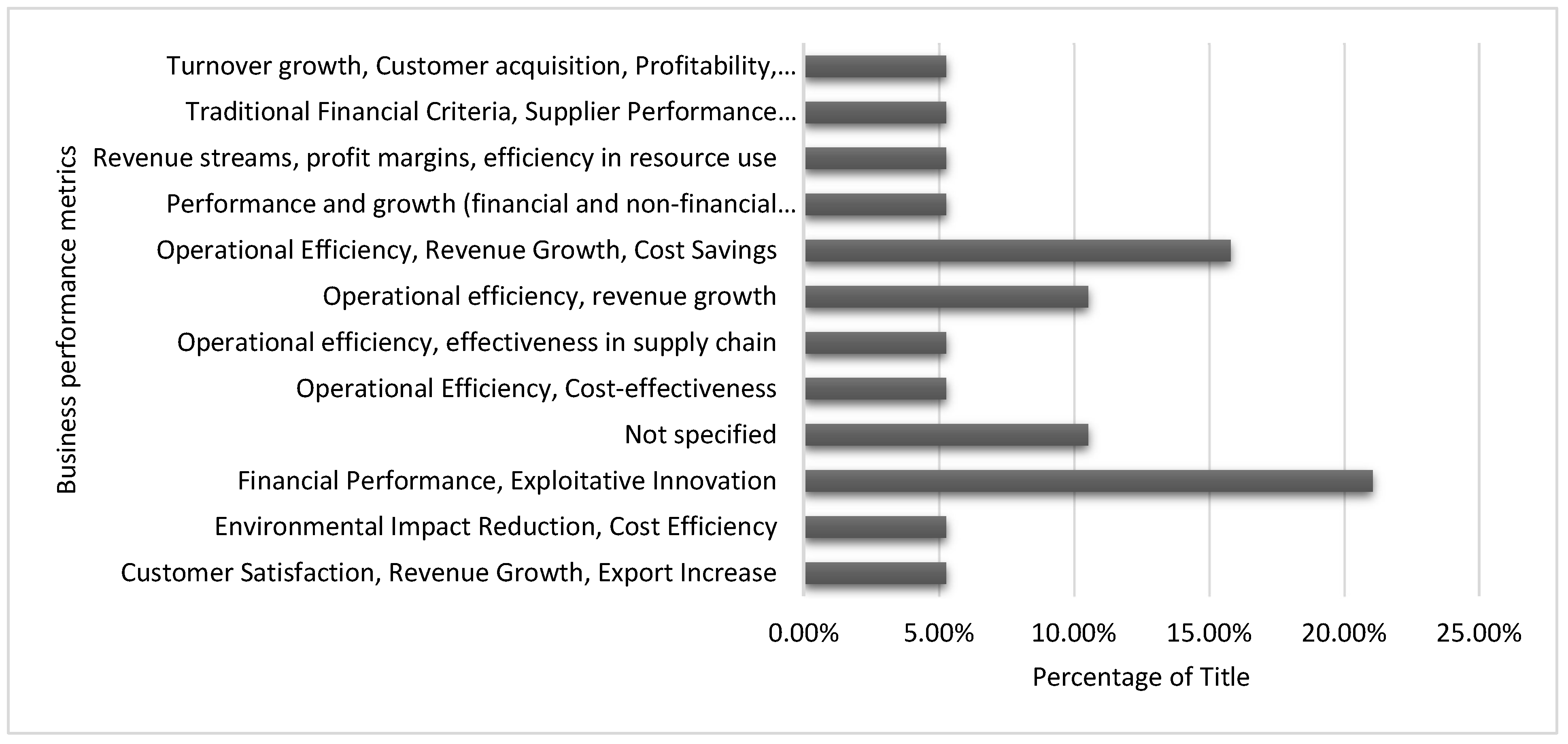

Figure 29 shows key trends in how SMEs measure the impact of the Balanced Scorecard (BSC). The most studied metrics are financial performance and exploitative innovation, accounting for 21.05% of the publications. This proposes that SMEs prioritize evaluating the BSC's role in driving revenue growth and innovation aimed at improving current products or services. Metrics such as customer satisfaction, revenue growth, and export increase (5.26%) and environmental impact reduction combined with cost efficiency (5.26%) are less explored, showing a narrower focus on sustainability and cost-related outcomes.

Notably, 10.53% of studies did not specify performance metrics, which may underscore a void in the literature where the BSC's impact is discussed more generally without detailed metric analysis. These results reflect a significant emphasis on financial outcomes, with less focus on non-financial metrics like environmental sustainability or customer-focused performance. To assess the risk of bias due to missing results or reporting biases in this systematic review on The Balanced Scorecard Methodology: Performance Metrics and Strategy Execution in SMEs, multiple strategies were used. A comprehensive search across databases (Scopus, Web of Science, and Google Scholar), was implemented to minimize publication bias, ensuring that a wide range of studies, both published and unpublished, were collected. Grey literature, conference proceedings, and dissertations were included, to avoid selective reporting biases. Additionally, where research protocols were available, they were compared with the results sections of the included studies to detect any selective outcome reporting. Although the review is primarily qualitative, these strategies ensure that the findings are based on a complete and balanced synthesis of available evidence, reducing the risk of missing data due to reporting biases.

The results highlight a prominent emphasis on financial metrics and exploitative innovation in SMEs' application of the Balanced Scorecard (BSC), proposing that these enterprises predominantly view BSC through the lens of revenue growth and incremental improvements to existing products. This trend shows that while SMEs notice the BSC’s potential to motivate financial performance, there is a relative neglect of other vital dimensions such as customer satisfaction and environmental impact. The lower frequency of studies addressing these non-financial metrics, such as environmental impact reduction and cost efficiency, underscores a potential gap in how SMEs evaluate their strategic performance and sustainability efforts. The 10.53% of studies that overlook specific performance metrics further imply a need for more rigorous reporting standards in the literature. These gaps may point to a broader issue where the comprehensive benefits of the BSC are not fully investigated or captured. Consequently, while SMEs leverage BSC to optimize financial outcomes, a more holistic adoption that includes non-financial metrics could provide a more balanced view of performance and strategic alignment. This analysis presents that to fully realize the BSC's potential, future research should focus on integrating diverse performance metrics and addressing the identified gaps to promote a more complete understanding of its impact on SMEs.

3.6. Reporting Biases

In this systematic review, a thorough evaluation of potential reporting biases as well as missing results that could impact the validity and reliability of our findings was undertaken. The approach used to assess the risk of bias, the used tools, as well as the results of our sensitivity analyses is outlined in this section.

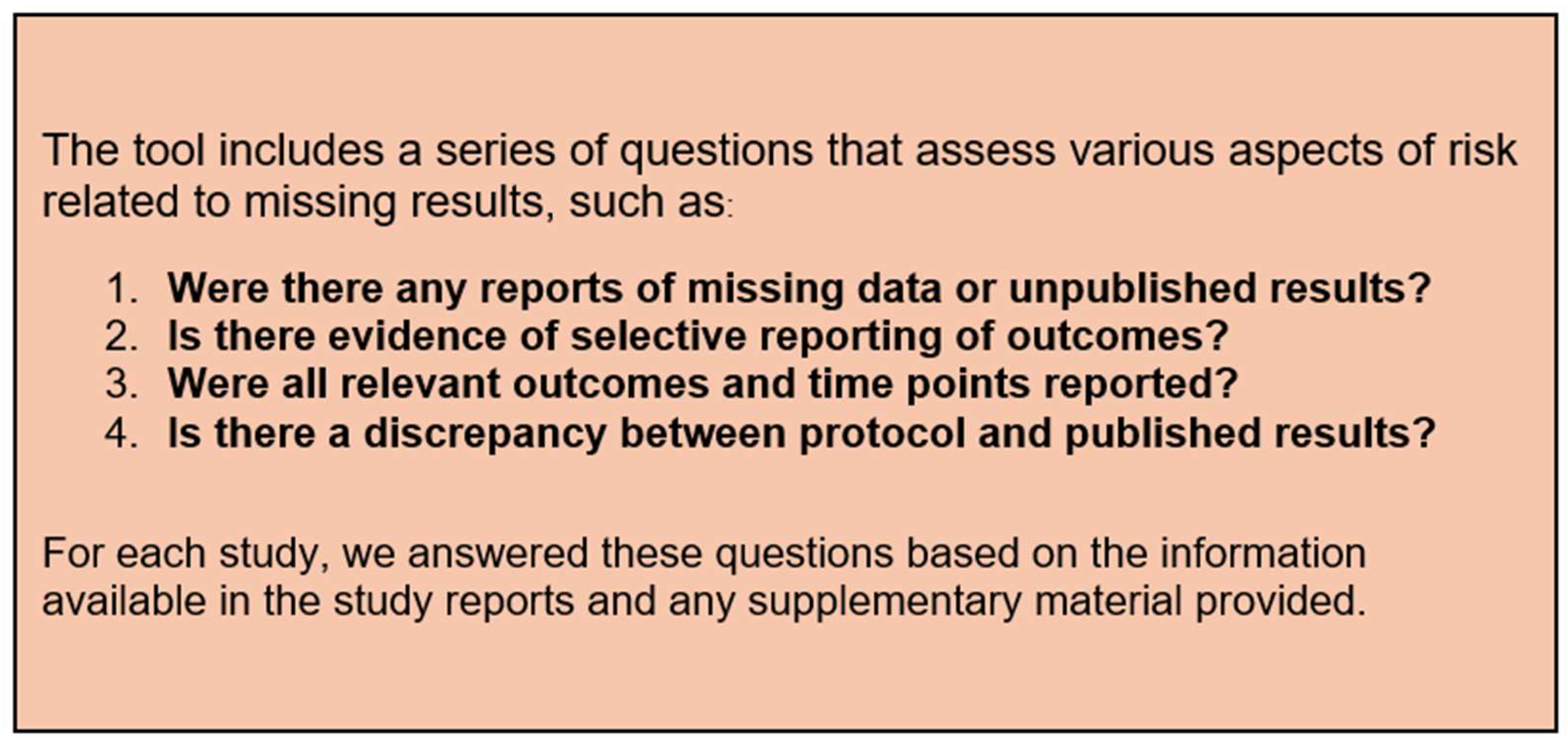

3.6.1. Assessment of Risk Bias