Submitted:

06 November 2024

Posted:

07 November 2024

You are already at the latest version

Abstract

As pension benefits from statutory public schemes become less generous and many countries face pension-savings crises, the willingness to participate in supplementary retirement-saving instruments becomes crucial for sustainable financial well-being. The study highlighted factors influencing participation in auto-enrollment and private supplementary pension savings. The study focuses mainly on financial literacy and trust. We used the CAWI method with 867 interviews in Poland - the first country in Central and Eastern Europe to introduce an auto-enrolment pension system. Our study uses multivariable data-mining tools, and several regression models were applied. We used Logistic Regression (LR), Multivariate Linear Regression (MLR), and Factor Analysis of Mixed Data (FAMD) to support the LR analysis. We propose four regression models. Our findings present that: 1. The lower the consumer’s knowledge level, the more their decisions are based on trust. 2. Trust in the state, rather than trust in financial institutions, plays a crucial role for people with low financial literacy, which is a critical factor in choosing the auto-enrolment option for pension savings. 3. Men had higher odds of auto-enrolment pension saving than women. 4. Employees of economic universities and academics had higher odds of participating in capital pension plans than those of general universities and non-academics. Our findings can signal to governments and policymakers about factors influencing the choice of auto-enrolment supplementary retirement savings. These findings strengthen the role of sustainable economic education.

Keywords:

pension

; trust

; financial literacy

; consumer savings

; employee capital plans

; long-term financial security

; survey

; data mining

; auto-enrollment pensions

1. Introduction

Population aging is a characteristic of all contemporary societies, placing significant pressure on national pension savings systems. These demographic changes lead to financial challenges. The main objective of this article is to present how trust and financial literacy influence the choice of supplementary pension savings. In the article we mainly focus on trust and financial literacy in pension savings. We also use some socio-demographic variables such as gender, age, type of research unit (general university or economic university), and position at the universities (academic staff, non-academic staff). The recent decades have witnessed a sharp growth in research on financial literacy and retirement preparation, which shows how important this area of research is [1,2,3,4,5,6,7]. Since the global financial crisis in 2008, financial literacy has come to the forefront of policy agendas aimed at enhancing financial sector stability [6,8]. High financial literacy improves human capital and subsequently enhances people’s ability to make better financial decisions [9]. High financial literacy leads to better economic outcomes and financial well-being, and this is why it is so important nowadays [10]. Understanding the development of trust in pensions and particularly in pension providers (government, pension funds) is of crucial importance for two reasons. First, changes in pension policy are likely to involve losses in trust when the interests of groups are at risk, but the real issue is whether trust can be rebuilt or whether it has been replaced by distrust. When trust is low, pension providers may become more risk averse or more reluctant to undertake the necessary corrective reforms. The second reason why the development of trust over time is an important topic is that changes in trust levels can affect individual decisions about saving, investing, and working over the life course [11].

The scope of the research includes financial literacy, trust and their impact on consumer pension decisions. Statutory and supplementary pension instruments are offered around the world. Statutory pensions are mandatory for all, while supplementary pensions are optional. In our article, we focus on the supplementary (auto—enrolment) pension, which is Employee Capital Plans. Because statutory pension benefits in public sector schemes are becoming less generous and many countries struggle with pension-savings crises, the willingness to participate in newly introduced retirement-saving instruments is essential for consumers’ financial well-being. Some people want to participate in the supplementary system to receive extra retirement money, while others do not. The research question is: What factors influence the willingness to participate in a supplementary pension instrument? The study covers employees of higher education institutions, both academic staff and administrative staff. The article is based on a case study in Poland. The survey was conducted in 2021, when the auto-enrolment pension was established in Poland for the higher education sector. Experience in some EU countries with auto-enrolling workers in pensions indicates that once enrolled, most workers stay enrolled, suggesting that auto-enrolment may be a desirable policy for other countries. However, the experience with auto—enrolment is much different in Poland [12]. In Poland, the participation rate of consumers in auto-enrollment pensions is the lowest [13]. Poland, as the first country in the Central and Eastern Europe region to introduce such a policy, can inspire similar reforms in neighboring countries, adapting them to local needs and conditions. As one of the seven OECD countries that have introduced an auto-enrolment supplementary pension product, Poland can provide some information about the strengths and weaknesses of introducing this product to improve consumers’ financial security.

In this research, we propose four hypotheses. We hypothesized that financial literacy determines the propensity to participate in the auto-enrolment pension savings. We also analysed how the level of trust in the state and financial institutions influences the decision to participate in the auto-enrolment pension savings. The other two hypotheses focus on university staff and their sociodemographic variables. We found that employees of economics universities show a greater willingness to participate in the auto-enrolment pension savings than general university employees. The last hypothesis suggests that academic staff are more likely to enrol in the auto-enrolment pension than non-academic staff.

In our research, when constructing models, we examined multidimensional forms of trust, which make this study stand out from others. This research contributes to the literature on pension savings and retirement consumer decisions. Our research includes trust in the state, Social Insurance Institutions (ZUS), financial institutions (commercial banks, Open Pension Funds (OFE), investment funds), and confidence in other people. We measured how financial literacy and trust play a role in pension consumers’ decisions; the inevitable question is whether they are related. This relationship has been investigated using various quantitative and qualitative methods. Previous approaches have ranged from neoclassical and behavioral models of decision-making [14] to formal models [15] based on different regression estimators and models [16]. With pension benefits based on statutory participation in public pension schemes becoming less generous than before [17], it is important to continue exploring the motivation behind pension consumer decisions to fill all possible gaps in our understanding of the processes leading to individuals’ choices. The current research market does not analyze consumer attitudes toward newly introduced retirement-saving instruments. Our study fills this gap in the literature by using multivariable data-mining tools and examining the participation of academic community members, including highly educated scientific staff and lesser-educated and lower-salaried administration workers, in newly introduced auto-enrolment pension. The study is essential for the economic community because it allows for a better understanding of the factors influencing consumers’ retirement decisions, particularly voluntary auto-enrolment pensions, which can help create more effective public and financial policies. The case of Poland is important for other countries in Central and Eastern Europe and the European Union because many of these countries face similar demographic and economic challenges. The research results can serve as a model for predicting consumer behavior and shaping strategies at the regional and EU levels.

2. Literature Review on Financial Literacy, Trust and Retirement

The article builds on several related studies, including research on financial literacy, trust, and pensions as a sustainable long-term savings. In recent years, there has been a growing interest in the scientific community in the impact of financial literacy on pension decisions resulting from an aging society. The economic importance of financial literacy has been increasingly documented in the empirical literature [3,4,5,7]. Agnew et al. [14] found that financial literacy was an important variable in explaining variations in pension saving behavior and that trust played a role in determining quit rates in automatic enrolment plans. They concluded that complex factors, including neoclassical employee and plan design variables, information or transaction cost problems such as financial literacy, and psychological or behavioral biases such as procrastination and mistrust drive pension savings [18]. Alessie et al. [19] present evidence on financial literacy and retirement preparation in the Netherlands based on two surveys conducted before and after the onset of the financial crisis. Using information on the economic conditions and financial knowledge of relatives, they found a positive effect of financial literacy on retirement preparation. Kalmi and Ruuskanen [20] presented the results of the first financial literacy study in Finland, finding a positive relationship between financial literacy and retirement planning among women. The results indicate that reducing state-guaranteed retirement benefits may challenge the less-educated sections of society. Studies point to the significance of financial literacy in retirement planning [6,21,22]. Our research is focused on university (academic and non-academic) employees in Poland. Some researchers have also recognized university employees as an interesting research subject. Dewi et al. [23] studied Indonesian academic community members and concluded that lecturers must improve their perceived knowledge, skills, and awareness.

Our study also concentrates on trust. First, the choice of focusing on trust was inspired by Fisch and Seligman [16], who demonstrated the importance of trust and financial literacy in accumulating retirement savings through self-directed pension programs. Second, trust is an important factor in pension decisions [16]. Trust, especially in Polish conditions, is a crucial factor. Due to historical events that were not always beneficial for additional retirement security in Poland, Polish society is skeptical about new proposals relating to voluntary retirement savings. This is why we have studied trust in both financial institutions that manage the private savings of Poles and in the state that initiated auto-enrolment pension savings in Poland in the first place. It is also essential to analyze trust in the Social Insurance Institution, a state organization that manages the public retirement system in Poland (collecting contributions and paying out benefits). This institution includes people who create specific solutions for society, such as the PPK. Trust in each other (interpersonal trust), as well as in institutions and organizations (institutional trust) [24], as described above, has also been explored in this article.

The current scholarly literature on pension trust is limited [25]. Trust plays an important role in pension savings [26]. Agnew et al. [14] present that knowledge and trust in financial institutions are strongly correlated with 401(k) savings behavior. In the case of voluntary savings, plan knowledge is important as it determines eventual participation, whereas in the case of automatic enrollment, inappropriate saving behavior often results from low trust in financial institutions. The authors show that trust can be a more significant issue for less-educated and lower-salaried employees. This means that its effects are not always visible in studies of voluntary plans, as respondents meeting these criteria are not numerous. The existing literature lacks studies focusing on the retirement savings of people with low education levels and low income; thus, the authors emphasize the necessity of research in this area. The research market lacks these kinds of studies among employees of public universities, and our study fills this research gap. Koch et al. [27] measured how trust in adults aged 50–70 years in the state of Singapore relates to pension plan participation and withdrawals, life, health, and long-term care insurance purchases, and stock market engagement. The results of their study demonstrated that trust in people is not statistically significantly related to pension behavior. However, trust in financial and governmental representatives is positively associated with not only greater pension wealth balances but also a higher likelihood of having life, health, and long-term care insurance coverage. Koch et al. [27] also showed that trust in financial professionals and government officials is strongly associated with financial literacy scores, employment status, and knowledge of household finances. The results of this study are significant because people aged 50–70 years are becoming a dominant element of society. Moreover, as documented by [28], trust has a positive correlation with knowledge, among other factors. They show that people with higher education, higher income, and younger age are more likely to trust the government. However, what is also important is the information provided to the public on how the government performs. The results of an experimental survey conducted by Alessandro et al. [29] show that the content of the information itself affects the evaluation people make about the government. This information can also be related to finance and long-term savings. Baidoo and Akoto [30] noted that many people in developing countries use informal methods of saving (such as saving at home or with friends or family members) because of their low trust in financial institutions. Baidoo and Akoto [30] studied the effect of trust on individuals’ decisions to save at financial institutions in Ghana, postulating that individuals who have attained some forms of formal education are likely to better understand the operations of financial institutions and are thus likely to have more trust in them. The findings demonstrate that with the rise in individuals’ trust in financial institutions, the likelihood of saving at these institutions also increases and is statistically significant. Similar results were achieved by Beckmann and Mare [26], who used unique survey data across 10 emerging market economies in Central, Eastern, and Southeastern Europe, and showed that trust in the financial system increases the probability of holding formal savings and diversification among formal saving instruments. In addition, the way in which society perceives the public retirement system and the institution that controls it is crucial. In Poland, it is the Social Insurance Institution (pl. Zakład Ubezpieczeń Społecznych—ZUS), which is an institution in the public finances sector. Møness and Høyer [31] point to the broad significance and influence of trust in public-sector institutions. They demonstrated that high trust in one of these institutions positively influences trust in other institutions that play a similar social function.

Table 1.

A main reviews of research on financial literacy, trust, and pension decisions.

| Authors | Research scope | Research methodology | Conclusions |

|---|---|---|---|

| Bielawska, Turner (2023) [12] | Trust and auto—enrolment in pensions. | A survey of 400 employees was conducted in April/May 2021. Compassion UK and Poland. | Auto—enrolment in pensions in the UK is successful due to inertia, but in Poland, workers distrust future pension benefits, leading to a high opt-out rate. |

| Clark, Pelletier (2022) [32] | Automatic enrollment, age, sex, and income. |

The research participants are South Dakota state and local government employees, including teachers. The authors use regression analysis. |

Authors find that automatic enrollment changes differences in the participation rate by age, sex, and income. We also find that prior to the adoption of auto-enrollment, agencies that ultimately chose to implement this policy had higher participation rates compared to those that did not adopt auto -enrolment. |

| Fisch, Seligman (2021) [16] | Financial literacy, trust and financial market participation. | Data collection and survey development were conducted over three distinct field research periods. 1. In late 2017—an independent financial literacy survey was developed and fielded. 2. spring 2018—selected financial literacy questions integrated with many questions targeting trust. (550 observations). The authors engaged in an analysis estimation to decide on a stopping point for field research. 3. The authors entered data collection (collected 312 observations. Sample sizes -over 700. |

Trust and financial literacy both strongly influence financial market participation, but trust has a more uniform relationship with increased participation, while financial literacy has a u-shaped relationship with reduced participation and increased participation. Trust in financial institutions increases the propensity to save and invest, which is crucial for accumulating capital for retirement. |

| Koh, Mitchell, Fong, (2019) [27] | Pensions savings, trust in financial and public-sector | The study draws on the Singapore Life Panel (SLP®), a high-frequency internet survey of people aged 50-70, to assess how trust ties to older respondents’ pension plan participation and others | Trust in financial and public-sector representatives is positively associated with pension savings, investments, and insurance purchases, while trust in people is uncorrelated with retirement preparedness behaviors. |

| Ricci and Caratelli (2015) [33] | The study is about the complex relationship between financial literacy, retirement planning, and trust in financial institutions. | The authors use data from the 2010 Bank of Italy Household Income and Wealth Survey. The impact of financial literacy on retirement planning is a well-established issue in the existing empirical literature. | Financial literacy positively impacts retirement planning and private pension decisions, while trust in financial institutions positively influences both entry into private pension schemes and devoting severance pay to private pension schemes. |

| Agnew, Szykman, Utkus, (2012) [14] | Financial knowledge, trust in financial institution, auto-enrolment, | The author assesses the relationship between the employee auto-enrolment participation decision using several probit regressions relating an employee’s plan participation decision to various demographic measures and our trust and plan knowledge indicators | Knowledge and trust in financial institutions strongly correlate to pension savings behavior based on auto-enrolment. In supplementary pension plans, knowledge and demographic characteristics are related to participation in auto-enrolment plans. In automatic enrollment settings, trust in financial institutions and knowledge of an available plan match are related to participation. Although this study cannot prove causality of the relationships, it does extend our understanding of the complex factors underlying savings choices. Policy implications are discussed. |

3. Research Framework and Hypotheses

3.2. Employee Capital Plans (PPK) in Pension Schemes

Many countries are struggling with pension-savings crises. There is a risk that funds will be insufficient to help maintain a healthy lifestyle after retirement [17]. The answer to this problem may be to join the Employee Capital Plans (Pracownicze Plany Kapitałowe—PPK) as an auto-enrolment, long-term savings program. Retirement pensions in Poland are paid to each person who are part of a retirement scheme. Retirement pensions are paid out by the Social Insurance Institution. They are financed by the employer and employee contributions made by the employer on behalf of the employee. The conditions for obtaining retirement pensions and determining the amount depend on which age group the person belongs to. Certain occupational groups have different rules for granting retirement pensions (e.g.; miners, uniformed services). The pension system in Poland has two schemes [34]: statutory and supplementary pension schemes.

Statutory pension schemes are public systems involve managers payment of contributions by employees and/or employers on behalf of employees, manager by the Social Insurance Institution and, in the case of farmers, the Agricultural Social Insurance Fund. In this pillar, everyone is obliged to pay pension insurance contributions. Since 1 October 2017, the general retirement age has been 60 years for women and 65 years for men. The statutory pension system is financed from contributions (19.52% of gross salary) paid in equal shares by employees and employers. Overall, social insurance coverage is high in Poland. At the end of 2022, the population of Poland was 37.767 million. At the end of 2022, there were 22.2 million people of working age (220 thousand less than a year ago), which constituted approximately 58.7% of the total population (compared to 59.1% in 2021, 64.4% in 2010, and 60.8% in 2000). People of post-working age accounted for over 8.6 million, and the share of this group in the population increased to 22.8% (from 22.5% in 2021, 16.8% in 2010, and 14.8% in 2000) [35]. According to OECD forecasts, by 2075, Poland’s demographic burden ratio will be one of the highest in the entire organization (after Korea, Portugal, Japan, and Greece, among others) [35].

Supplementary pension schemes.

Supplementary pension schemes are created by employers and consist of accounts in Employee Capital Plans. In summary was introduced to only 2.6% of the working-age population, which is 4.0% of socially insured people [36]. In June 2024, there were 881.38 thousand Individual Pension Accounts (3.6% or 5.4% of the working-age and socially insured population, respectively) and 526.28 thousand Individual Pension Security Accounts (2.3% and 3.4%, respectively). In 2019, payments were made into only around 40% of these accounts. This indicates that these schemes play a negligible role in the current retirement income provision. Most of the income of pensioners comes from the public, statutory pension provision [37]. In principle, the auto-enrolment savings contribution is funded by employers (1.5% of the salary, plus up to 2.5% voluntarily) and employees (2.0% of the salary, plus up to 2% voluntarily). Additionally, participants receive a welcome fee from the state and a surcharge at the end of each year (PLN 250, or about 50 euros, as a welcome contribution, plus 48 euros every year). Employee Capital Plans savings are designed to supplement benefits from the public and statutory pension system: a person who does not agree to join the new program must opt out. For many, this was a completely new topic, especially for those who were not closely involved in finance or keenly interested in personal finance, including retirement security.

Employees from the private sector (48.1%) are almost twice as likely to participate in Employee Capital Plans than those from the public sector (24.9%). Employees of the largest entities were most willing to join PPK through auto-enrolment — participation in companies employing over 250 people was 67%. When it comes to the age range, there is a clear dominance of employees aged 25–34 and 35–44. They constitute 34.2% and 33.3% of the participants, respectively. People over 60 years of age are the least willing to join the program (0.5%). The average age of a PPK participant is 39 years. There are slightly more men (51.8%) than women (48.2%) in the program. Additionally, 4.9% of participants are people of nationalities other than Polish. Only 50.7% of contributions to PPK (PLN 7.5 billion) are made by employees. The second largest amount is contributions from employers (38.5%, PLN 5.7 billion), followed by state subsidies (10.9%, PLN 1.6 billion) (PPK, 2023). However, pension savings play a significant role in total savings [38]. Generally, savings for retirement in Poland are not a strong point. Polish society does not have much experience in supplementary savings due to two reasons: 1. Supplementary retirement savings have a short history, and consumers do not have much experience in this area. For a long time, there was only the public system. Supplementary pensions are new, with PPK, the key focus of this article, introduced in 2021. 2. Some consumers do not have enough budget to save for supplementary retirement, and there is insufficient financial knowledge about future retirement possibilities. Poles usually save only in the short term, which is less effective.

Since 2009, old-age pensions in Poland have been granted predominantly according to new system rules based on the defined-contribution (DC) principle. The new system offers less generous benefits. As a result, the risk of poverty has increased but remains close to the EU average. In the future, an increase in the risk of poverty can be expected, as replacement rates decline further. Between 2017 and 2019, an increased inflow of newly granted pensions was observed (around 1 million new pensions in three years). This was because of lowering pensionable ages to 60 for women and 65 for men. At the same time, the rise in the employment rate of people aged 55-64 stagnated and the number of working pensioners increased. This increased the pension system dependency rate. The new supplementary occupational Employee Capital Plans with auto-enrolment may improve future adequacy, if people decide to use their savings for annuity payments. However, participation in supplementary savings, including the PPKs, is lower than expected. To improve the adequacy of future pensions it is important to promote longer working lives, including working beyond the pensionable age, combined with increased savings in occupational and supplementary plans; in the longer run, a return to a higher pensionable age is recommended [34].

To compare to other countries, we also present the situation of auto-enrolment pensions in OECD and other countries. The number of OECD countries operating an automatic enrolment scheme in a retirement savings plan at the national level is increasing. By the end of 2023, seven OECD countries had implemented auto-enrolment programs with an opt-out option at the national level: Italy (since 2007), Lithuania (since 2019), New Zealand (since 2007), Poland (since 2019), Türkiye (since 2017), the United Kingdom (since 2012), and the Slovak Republic (since 2023) [13]. The USA has also implemented such a scheme since 2018 [39]. New Zealand has achieved a participation rate above 80% in the “KiwiSaver” scheme. In the United Kingdom, which initiated its auto-enrolment program more recently than New Zealand, 50% of the working-age population was participating in an employer-sponsored pension plan in 2022. In Italy, since 2007, the severance pay provision of private-sector employees is automatically paid into an occupational pension plan unless the employee makes an explicit choice to remain in the TFR regime. However, a vast majority of workers have chosen to do so, and only 13% of the working-age population is now participating in an occupational pension plan. Poland and Türkiye also have a relatively low participation rate in plans with automatic enrolment (13% and 15%, respectively), potentially due to the recent introduction of the program and a potential lack of trust in it. By contrast, Lithuania already has a relatively high participation rate in the second pension pillar (over 75%), despite the recent introduction of its auto-enrolment program in 2019. The second pillar already existed prior to 2019, and employees joining the scheme voluntarily could not leave it afterwards. Automatic enrolment is also encouraged by regulation in Canada and the United States but at the firm level. In Germany, automatic enrolment can be implemented in occupational defined contribution pension plans for private-sector employees in the case of deferred compensation, but it needs to be specified in collective agreements. [13].

Many recent pension reforms require individuals to be proactive in their decision-making regarding long-term savings as a form of retirement security. In this study, we present the results of the first survey on the PPK among employees of public universities in Poland and examine their connections to financial literacy and trust. We use three core financial literacy questions [2,6], not for the student cohort, but for university employees.

This study presents data from research conducted in Poland between May and July 2021 on a representative sample of 857 university employees, including both academic and non-academic workers. These universities were chosen because of their obligation to participate in the new PPK program and the high diversity of education levels among the employees, ranging from highly educated scientific staff to lesser-educated and lower-salaried administrative workers.

Furthermore, the universities selected to participate in the study were chosen from two groups. Half were general universities with a wide range of faculties, such as biology, medicine, physics, mathematics, earth sciences, and computer science. The remaining four were economics-focused universities, educating students and teaching economics and finance only. This study introduces several data-mining methods to consider the role of trust and financial literacy in employees’ participation in PPK as the primary research problem. The following research hypotheses are proposed:

Hypothesis 1.

Financial literacy determines the propensity to participate in the PPK.

Hypothesis 2.

Employees of economics universities show a greater willingness to participate in the PPK than general university employees.

Hypothesis 3.

Academic staff are more likely to enroll in the PPK thannon-academic staff.

Hypothesis 4.

The level of trust in the state and financial institutions influences the decision to participate in the PPK.

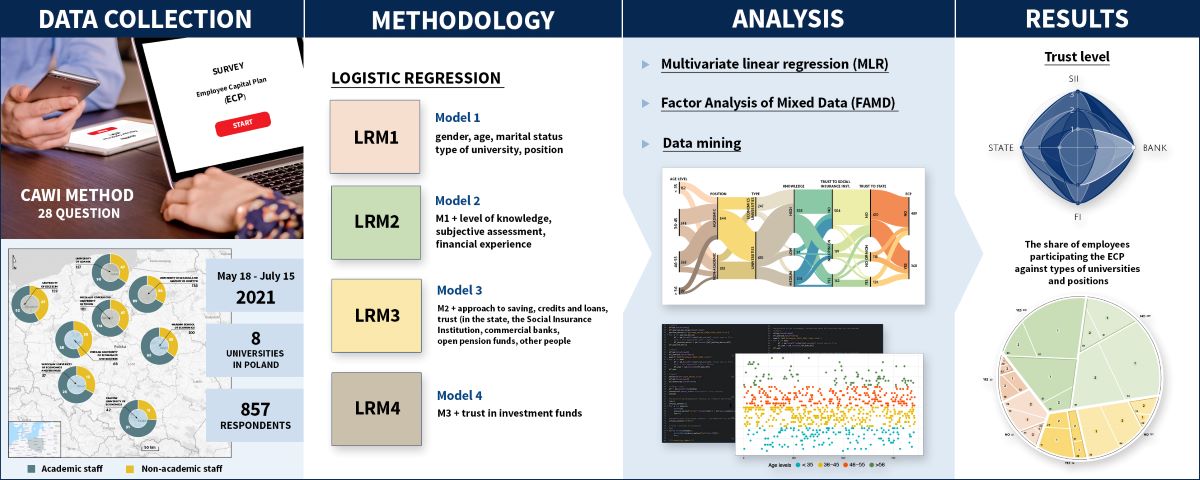

4. Data and Research Methods

4.2. Data Collection

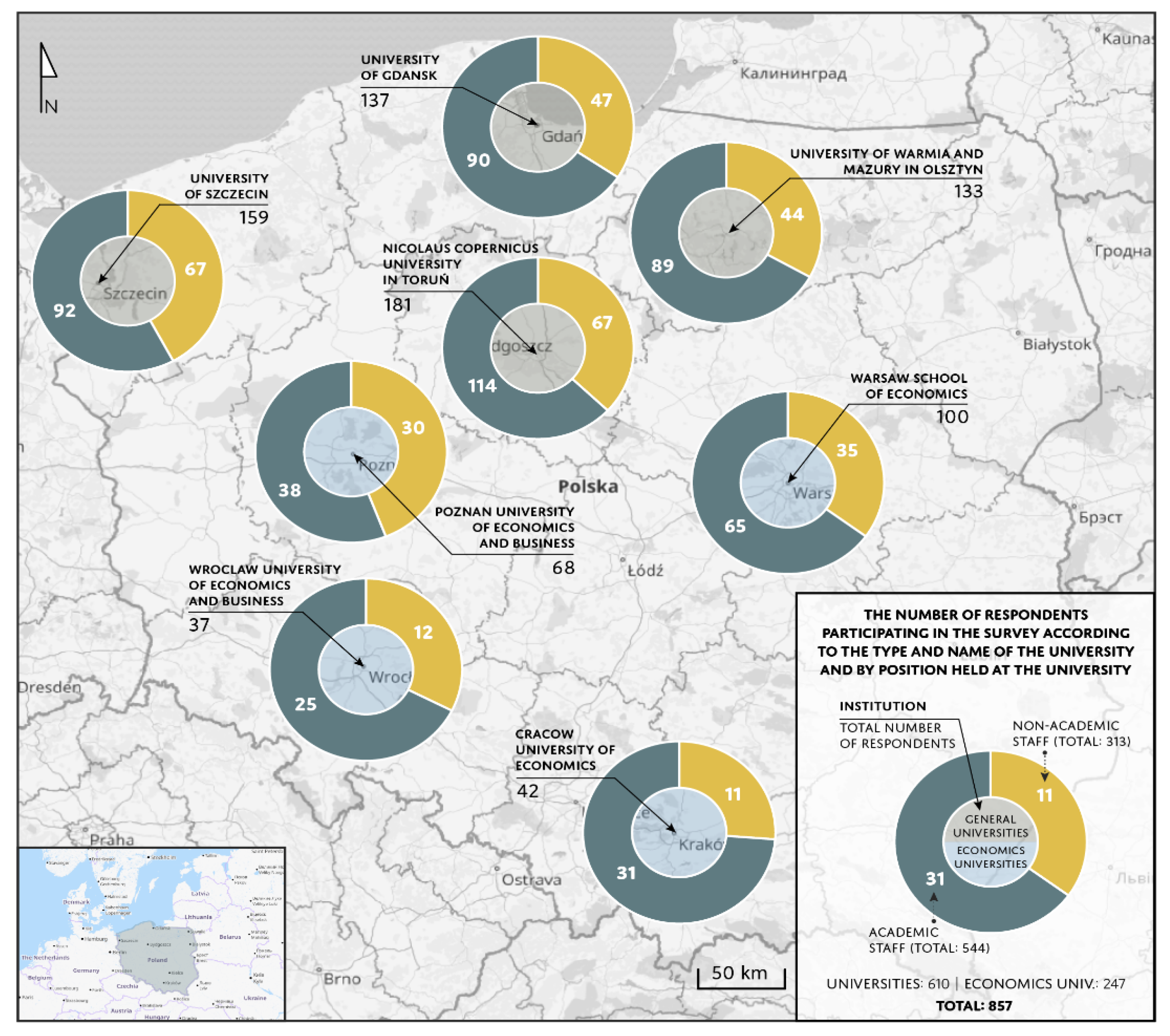

The survey was conducted in Poland in 2021 using a Computer-Assisted Web Interview (CAWI) method and a questionnaire consisting of 28 questions. The analysis was conducted as part of the research project entitled ‘Employee Capital Plans in Polish Public Universities’, launched in October 2020, a few months before the introduction of the PPK to budgetary units in Poland, including universities. Eight universities (Figure 1) participated in this project, including four general universities and four economics universities. The questionnaires were sent via email. The 867 correctly completed questionnaires were divided into the following two categories: academic universities with a wide range of faculties and economics universities with scope-limited faculties and economic and financial profiles. The electronic version of the questionnaire was available online from May 18 to July 15, 2021. The relatively long period of questionnaire availability was due to the fact thatthe timing of PPK implementation differed according to university.

The study respondents were divided into two categories: academic and non-academic staff (i.e.; administrators, conservators, porters, housekeepers and others). Academic staff were further divided into the following three main groups based on the Act on Higher Education in Poland: (1) research, (2) research and teaching staff, and (3) teaching staff. Research workers were solely concerned with science and research. Research and teaching staff consisted of employees with the following three areas of responsibility: research, teaching, and organisational activities. The teaching staff were only involved in teaching and organisational activities (Figure 1).

In this survey, we considered financial literacy and trust levels. Following a widely implemented methodology, financial literacy was measured to capture three basic economic concepts: compound interest, inflation, and risk diversification [6,8]. For trust analysis, individuals declared their confidence in various institutions, including the state, the Social Insurance Institution, financial institutions (commercial banks, Open Pension Funds, investment funds), and trust in other people. Finally, the dependent variable was generated based on the request, ‘Please select the statement reflecting your knowledge and position regarding membership of the auto-enrolment pension savings (PPK)’ Many choices were provided to answer this question and ultimately, the following seven options were considered.

I have submitted a declaration of leaving the auto-enrolment pension savings (PPK) before collecting the contribution.

I have submitted a declaration of leaving the auto-enrolment pension savings (PPK) after collecting the contribution.

I have been automatically enrolled in the auto-enrolment pension savings (PPK), I have not submitted a declaration of ceasing to pay contributions to the auto-enrolment pension savings (PPK), and I am not going to do it.

I have been automatically enrolled in the auto-enrolment pension savings (PPK), I have not submitted a declaration of ceasing to pay contributions, and I am going to do it.

I am out of the auto-enrolment age, but I voluntarily signed up for the auto-enrolment pension savings (PPK).

I am out of auto-enrolment age, and I will not sign up for the auto-enrolment pension savings (PPK).

I do not know if I belong to the auto-enrolment pension savings (PPK).

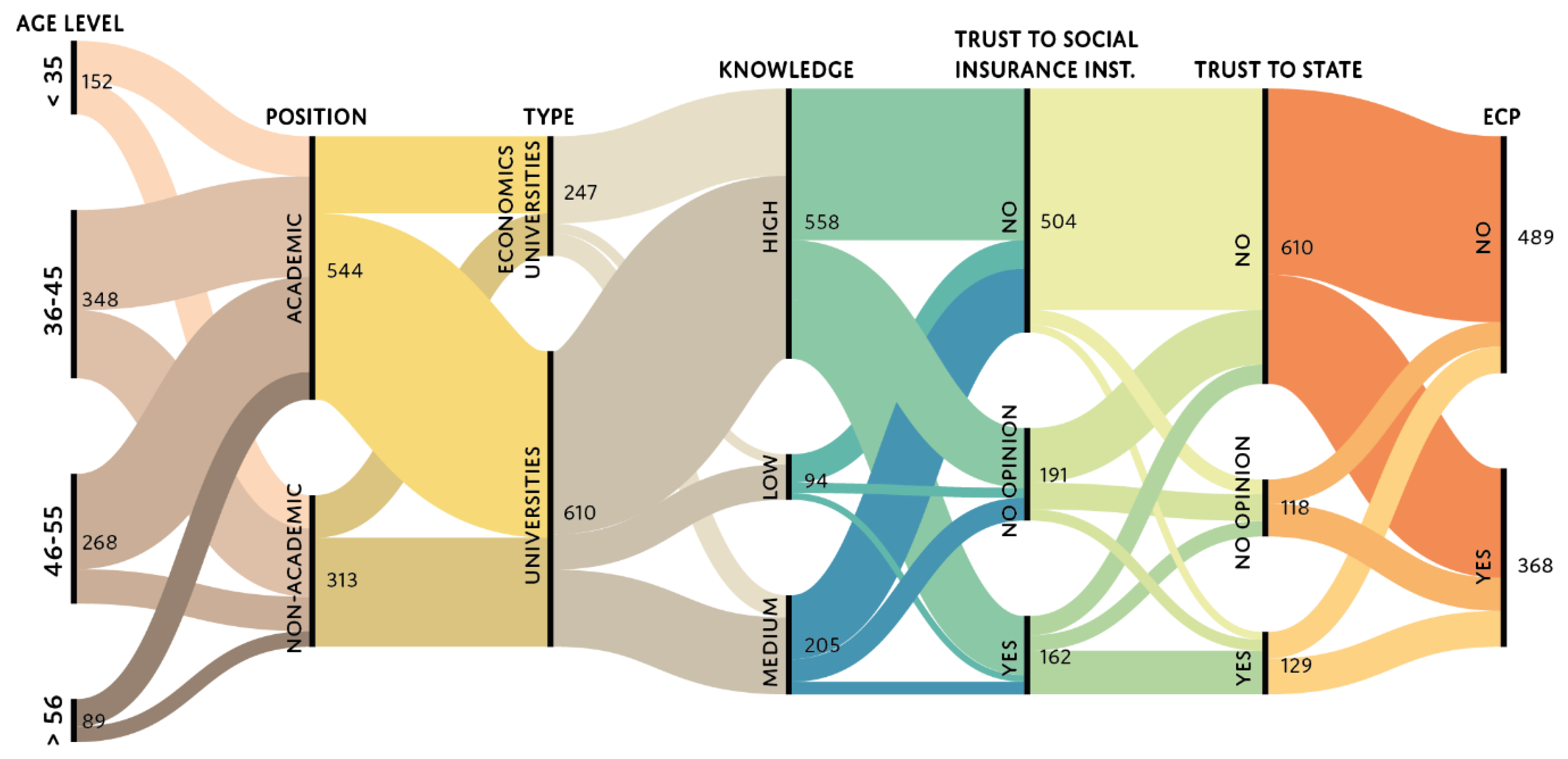

Thus, the people who did and did not join the Employee Capital Plan were distinguished. The first group (‘yes’ for participation) included people who chose options 3, 4, or 5, and the second group (‘no’ for participation) included people who chose 1, 2, or 6. People who chose option 7 (i.e.; they did not know if they belonged to the PPK) were excluded from further analyses. The final number consisted of 857 samples, which were used for further analysis. Quantitative representation of answers and data structural changes in the selected variables are visualised and represented using an alluvial graph (Figure 2).

4.2. Methodology

Powerful data-mining methods play an important role in the study of economic development, support, and decision-making analysis [2,3,40,41]. In this study, data-mining technology was used to identify the knowledge and key factors in consumers’ pension decision-making processes. The implemented methods extracted from the data samples the relationships among financial literacy, trust, and individuals’ retirement planning.

First, the chi-square test of independence was used to test whether there was a statistically significant relationship between objective and subjective knowledge, trust in the analysed institutions, type of university, and position held. Furthermore, the Mann-Whitney U test was used to check whether the level of knowledge significantly differed between academic and non-academic employees, as well as between general and economics university employees. The Mann-Whitney U test also verified that the level of trust significantly differs between academic and non-academic employees, as well as between general university and economics university staff.

Logistic regression (LR) was used to investigate the relationships between one or more independent variables. This is a widely implemented multidimensional method for modelling dichotomous data [2,3,4,42,43,44]. Four Logistic Regression Models (LRM) were built. Depending on the set of potential explanatories (independent) variables, they were either qualitative or quantitative. In each subsequent model, variables constituting the basis for the construction of the previous model were included in the analysis.

LRM1—Model 1 (M1): Considered respondents’ records, that is, gender, age, marital status, type of university they work at, and their position at the university.

LRM2—Model 2 (M2): Considered all potential variables used to build M1 and knowledge-related questions, that is, the level of objective knowledge, subjective assessment of the level of knowledge, skills in the field of personal finance, and the degree to which respondents’ knowledge and financial experience influenced their decision to participate in the PPK.

LRM3—Model 3 (M3): Considered all potential variables used to build M2. Additionally, the analysis also considered the approach towards saving and using credit and loans in the respondent’s households. It also considered questions regarding trust in the state, social insurance institutions, commercial banks, open pension funds, and other people.

LRM4—Model 4 (M4): Considered all potential variables used to build M3 and trust in investment funds. Thus, in constructing M4, we used a set of all potential explanatory variables.

To support the LR analysis, the following two alternative methods were used: (a) Multivariate Linear Regression (MLR) and (b) Factor Analysis of Mixed Data (FAMD). These methods were applied to define the most important factors in structuring consumers’ pension decisions. While MLR is one of the most popular and widely used statistical techniques for analysing multiple variables estimating a single regression model with more than one outcome variable, the FAMD is more sophisticated principal component method for analysing datasets containing both quantitative and qualitative variables [2,45].

5. Results

5.1. General Descriptive Results

According to the analysis, there is a statistically significant correlation between position (academic and non-academic) and the level of financial knowledge. The chi-square test showed that the relation is statistically significant (ꭓ2=41.19, p<0.001, Cramer’s V=0.219). Financial literacy significantly differs between academic and non-academic employees as well as between general and economics university staff. Therefore, the Mann-Whitney U test was used because of the lack of a normal distribution in each group. The resulting value of the test probability, p<0.001, demonstrated that the difference between the average levels of academic and non-academic employees’ knowledge was statistically significant.

ANALYSING the responses regarding compound interest, inflation, and risk diversification, the average number of correct answers was 2.63 for the academic group and 2.28 for the non-academic group. Similarly, in the second case, the calculated probability of p=0.00127 shows that the difference between the average knowledge levels of academic and non-academic employees was statistically significant. However, in the economics university group, 72.9% of the respondents gave correct answers to all knowledge-testing questions, whereas in the general university group, only 62.0% answered correctly.

Concerning subjective financial literacy, only 10.0% of the respondents showed very high levels of knowledge, 35.2% showed high knowledge, 37.7% had medium/average knowledge, 12.5% had low levels of knowledge, and 4.6% had very low levels of knowledge. Furthermore, the relationship between the standing answers given by respondents to the knowledge-testing questions and their subjective financial literacy showed a statistically significant relation (ꭓ2=123.819, p<0.001, Cramer’s V=0.219). Respondents who demonstrated higher objective financial literacy also reported subjective financial literacy and personal finance skills at a higher level than those who had worse results on the objective financial literacy test.

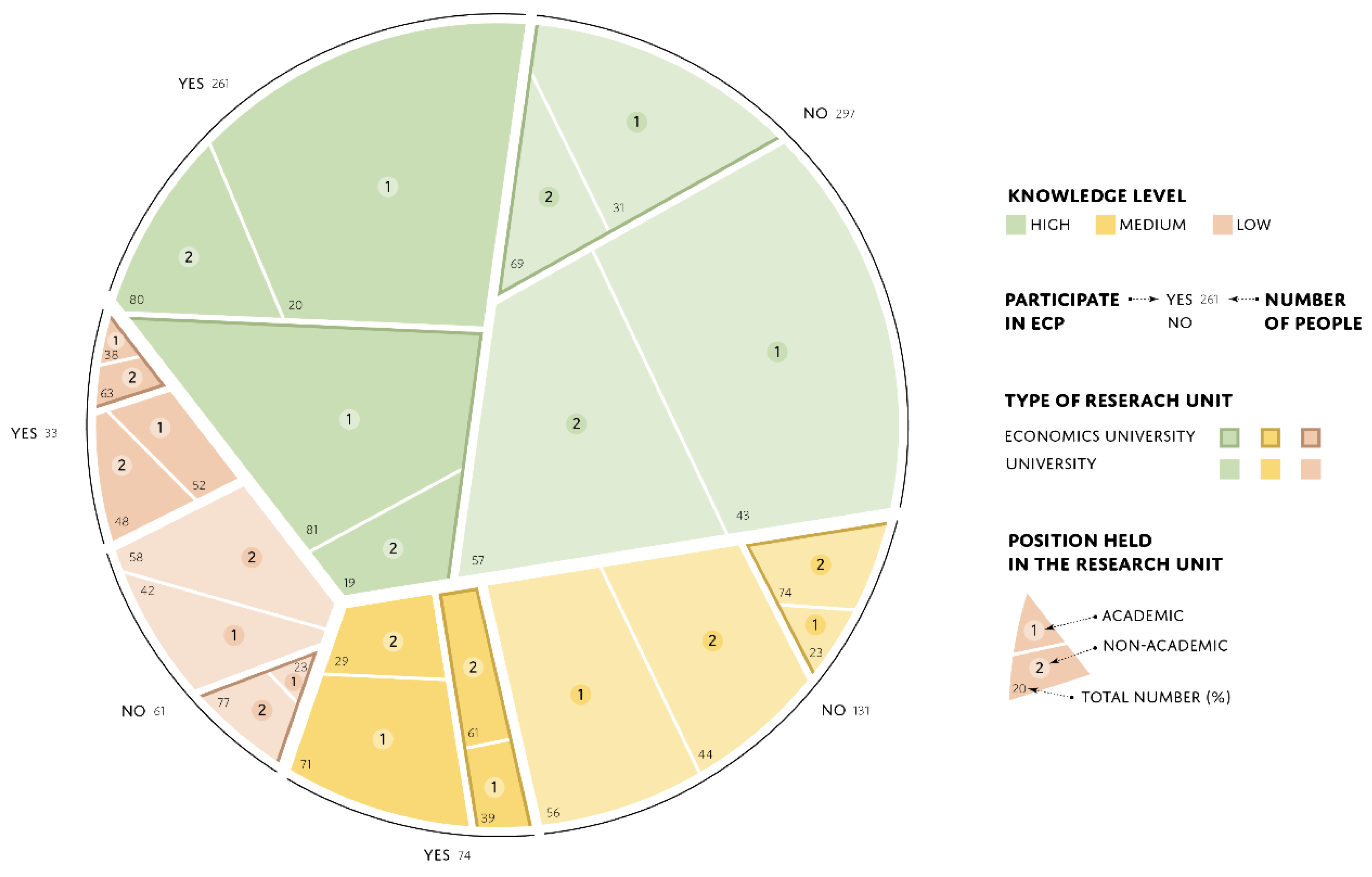

Based on the descriptive analysis, a clear connection was seen between financial knowledge level and participation in the PPK. Respondents characterised by high levels of knowledge were more likely to join the PPK. While this conclusion is clear, the proportions of those who participated and those who resigned, especially for positions held in the research units and the university type, suggest that other variables came into play. For both types of universities, 80% of the respondents who had decided to participate in the new pension reform and joined the PPK program represented the academic group; the remaining 20% were non-academic (Figure 3). This is the only similarity that was captured in employees’ behaviours across both university types. The first significant difference was observed among those who resigned. In general universities, there are 57% academic workers and 43% non-academic workers, whereas for economic universities, these figures are 69% and 31%, respectively. Furthermore, inequalities exacerbate the creation of two different behavioural pathways. For general universities, the percentage of employees who decided to participate in PPK was always higher in the academic group, regardless of the knowledge level; the percentage difference slowly reduced from medium to low knowledge levels. However, within the group of those who decided to resign, the proportions were quite stable at all levels. For economic university types, a dynamic change in pension decisions was observed between knowledge levels. While a very high dominance of participation in PPK was observed in the academic group for high education level, the situation was totally different for medium and low levels, in which many participants of the program represented non-academic staff (Figure 3).

Regarding trust, high diversity was observed depending on the type of institution; however, one general rule was noted. There existed a very low level of trust among academic employees. This distrust was mainly directed towards the state, but was also visible for all financial institutions, including commercial banks, open pension funds, and investment funds. Respondents who did not trust the state constituted 61.3% of the academic group, whereas this figure was 38.7% for non-academic employees. Similar differences were observed for academic and non-academic staff based on their trust in banks, which reached 68.8% and 31.2%, respectively. A noticeable difference was visible between the trust of employees from economics and general universities. In the first group, the value representing trust in banks slightly exceeded 40%, while in the second group, it was 33.6%.

A majority (52.6 %) of the respondents did not trust open pension funds, 29.2% did not have an opinion, and 18.2% trusted these institutions. The structure of the responses to the questions regarding open pension funds was almost identical for both the groups. Moreover, their responses were very similar in this regard. Under Poland’s compulsory retirement system, trust in the SII is crucial. An analysis of the responses shows that almost 60% of general university employees and 56.3% of economics university employees did not trust the SII. In terms of position, 64.9% of non-academic employees did not trust SII, whereas 55.3% of the academic staff declared a lack of trust in SII. Considering that the SII is responsible for paying out the benefits of the compulsory parts of social insurance, such a low level of trust should contribute to a higher readiness to undertake other forms of retirement coverage managed by private companies. However, in the case of the PPK, this situation does not occur, as 64.0% of respondents who did not participate in the PPK showed a lack of trust the SII; moreover, as many as 78.5% of respondents did not trust the state.

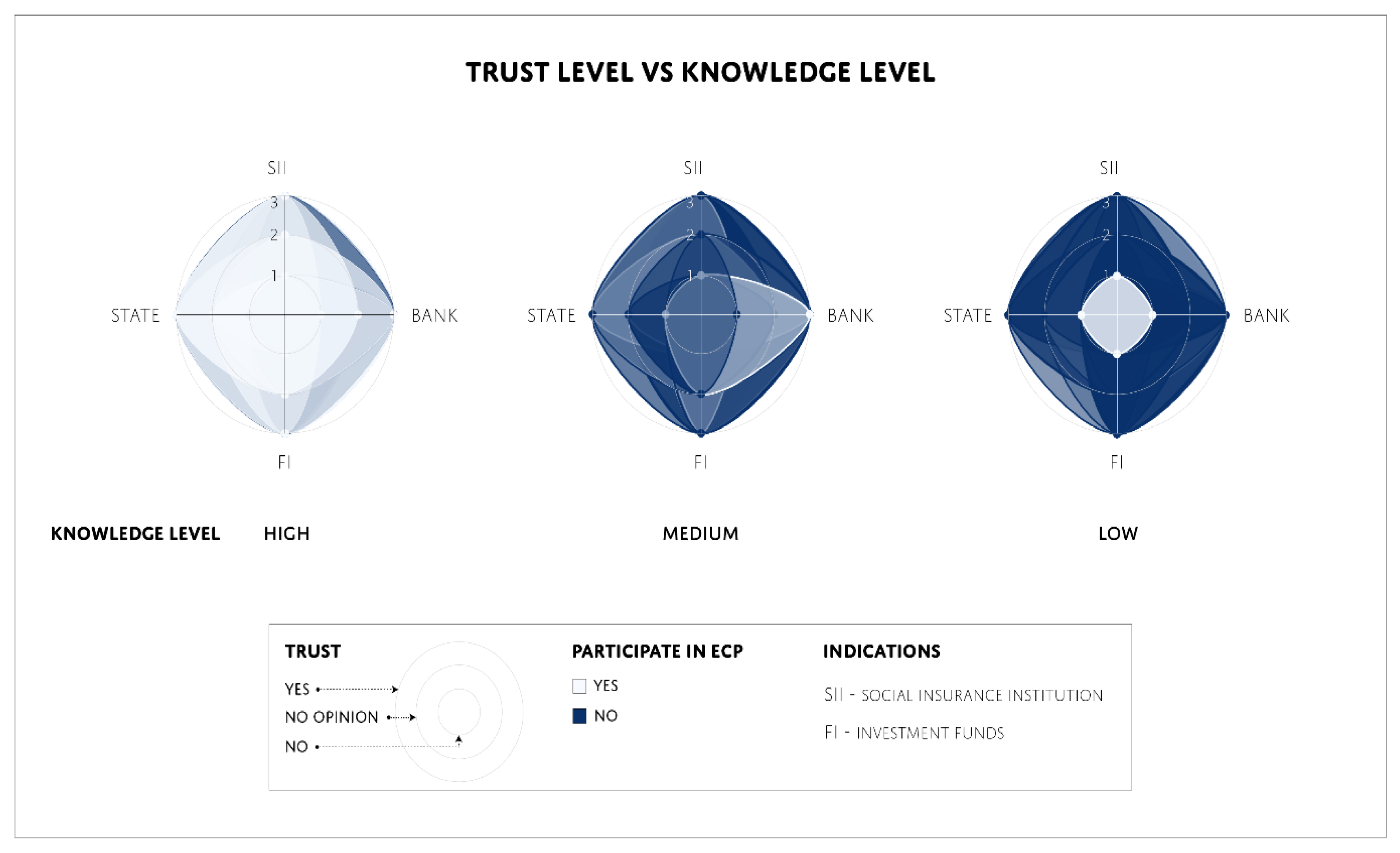

Comparing trust levels with financial literacy levels and participation in the PPK revealed a progressive trend, indicating an increase in the importance of trust in the pension consumer decision-making process. The lower the knowledge level, the more important trust was. Generally, for the group characterized by a high knowledge level, trust could be ignored, which confirms the earlier results. However, for the group with the lowest financial literacy, trust in social insurance institutions and investment funds appeared to be a major determinant of pension decision-making (Figure 4).

5.2. Regression Analysis

To investigate the relationship between participation in the PPK and different driving forces, such as the respondents’ financial literacy, trust in the state and financial institutions, and dependence on demographic attributes, several regression models were applied. MLR and FAMD were performed for the entire set of variables; however, a LR model was applied in the form of a building analysis process. First, it was used to analyse the impact of only independent variables, such as demographic variables (gender, age, and marital status) and those related to the professional profile of the respondents (type of research unit and position at the research unit) on the dependent variable (LRM1). In the next stages, the model was successively extended to include additional potential variables determining participation in PPKs (LRM2, LRM3 and LRM4). Table 1 reports the results, presenting only the variables that were statistically significant in at least one LR model.

Table 2.

Logistic regression models for participation in the auto-enrolment pension savings.

| Variables | LRM1 | LRM2 | LRM3 | LRM4 |

|---|---|---|---|---|

| Gender (ref. woman) Age (ref. < 35 years old) 36–45 years old 46–55 years old 55 years old or older Type of research unit (ref. general university) Position at the research unit (ref. academic staff) Level of knowledge My own knowledge and financial experience Trust in the state (ref. no) I have no opinion / neither yes nor no Yes Trust in commercial banks (ref. no) I have no opinion / neither yes nor no Yes Trust in open pension funds (ref. no) I have no opinion / neither yes nor no Yes Trust in investment funds (ref. no) I have no opinion / neither yes nor no Yes Constant Cox–Snell’s R-squared Nagelkerke’s R-squared Hosmer-Lemeshow (p-value) Log likelihood Observations Gender (ref. woman) Age (ref. < 35 years old) 36–45 years old 46–55 years old 55 years old or older Type of research unit (ref. general university) Position at the research unit (ref. academic staff) Level of knowledge My own knowledge and financial experience Trust in the state (ref. no) I have no opinion / neither yes nor no Yes Trust in commercial banks (ref. no) I have no opinion / neither yes nor no Yes Trust in open pension funds (ref. no) I have no opinion / neither yes nor no Yes Trust in investment funds (ref. no) I have no opinion / neither yes nor no Yes Constant Cox–Snell’s R-squared Nagelkerke’s R-squared Hosmer-Lemeshow (p-value) Log likelihood Observations Gender (ref. woman) Age (ref. < 35 years old) 36–45 years old 46–55 years old 55 years old or older Type of research unit (ref. general university) Position at the research unit (ref. academic staff) Level of knowledge My own knowledge and financial experience Trust in the state (ref. no) I have no opinion / neither yes nor no Yes Trust in commercial banks (ref. no) I have no opinion / neither yes nor no Yes Trust in open pension funds (ref. no) I have no opinion / neither yes nor no Yes Trust in investment funds (ref. no) I have no opinion / neither yes nor no Yes Constant Cox–Snell’s R-squared Nagelkerke’s R-squared Hosmer-Lemeshow (p-value) Log likelihood Observations |

- - - - - 2.180*** .445*** .793* .062 .083 .972 1,116.374 857 |

1.433* - - - - 2.256*** .456*** 1.283* .625*** 1.909* .139 .187 .977 1,042.303 857 |

1.408* * .620* .905 .501* 2.325*** .463*** 1.257* .637*** *** 1.992** 2.214*** - - - ** 1.749** 1.293 1.605 .178 .239 .157 1,002.585 857 |

1.504* * .646* .922 .502* 2.479*** .425*** - .654*** *** 2.075*** 2.327** * .553** .652 ** 1.829** 1.143 ** 1.578* 2.061** 2.433** .189 .253 .784 991.743 857 |

| - - - - - 2.180*** .445*** .793* .062 .083 .972 1,116.374 857 |

1.433* - - - - 2.256*** .456*** 1.283* .625*** 1.909* .139 .187 .977 1,042.303 857 |

1.408* * .620* .905 .501* 2.325*** .463*** 1.257* .637*** *** 1.992** 2.214*** - - - ** 1.749** 1.293 1.605 .178 .239 .157 1,002.585 857 |

1.504* * .646* .922 .502* 2.479*** .425*** - .654*** *** 2.075*** 2.327** * .553** .652 ** 1.829** 1.143 ** 1.578* 2.061** 2.433** .189 .253 .784 991.743 857 |

|

| - - - - - 2.180*** .445*** .793* .062 .083 .972 1,116.374 857 |

1.433* - - - - 2.256*** .456*** 1.283* .625*** 1.909* .139 .187 .977 1,042.303 857 |

1.408* * .620* .905 .501* 2.325*** .463*** 1.257* .637*** *** 1.992** 2.214*** - - - ** 1.749** 1.293 1.605 .178 .239 .157 1,002.585 857 |

1.504* * .646* .922 .502* 2.479*** .425*** - .654*** *** 2.075*** 2.327** * .553** .652 ** 1.829** 1.143 ** 1.578* 2.061** 2.433** .189 .253 .784 991.743 857 |

Note: Significant individual coefficients are indicated by ***p<0.001, **p<0.01 and *p<0.05.

Within LRM1, only two variables appeared to be strongly significant. Economics university employees had approximately 2.2% higher odds of conducting savings through PPK than general universities’ employees. Therefore, employees of economic universities were more willing to save for old age than general universities’ employees. Moreover, these odds were approximately 55% lower for non-academic staff than for academic staff. Thus, research employees and research and teaching staff were more likely to declare their participation in capital plans in the workplace. A significantly high correlation was found between university types and positions held (academic/non-academic). Moreover, this correlation was confirmed using MLR and FAMD.

Both MLR and FAMD underlined financial knowledge and experience as major factors influencing decisions regarding participation in PPK. The role of the level of financial literacy (objective knowledge, graded on a four-point scale) as determined by the respondents (subjective knowledge graded on a five-point scale) was added to all potential variables used to build the first logistic regression model (LRM1). This led to the creation of the second model (LRM2). This helped analyse the impacts of demographic variables and those related to respondents’ knowledge on the accumulation of funds in the capital plan. The second model demonstrated that financial literacy has a positive and statistically significant effect on auto-enrolment pension savings participation, confirming that the level of financial literacy determines the willingness to participate in auto-enrolment pension savings (Table 1). Furthermore, a unit increase in financial literacy was associated with an approximately 28% increase in capital plan participation. Thus, respondents with higher levels of financial literacy may be more likely to accumulate wealth.

Additionally, LRM2 and FAMD showed a positive and statistically significant effect of gender. Men had approximately 43% higher odds of saving in PPK than women. Like LRM1, the type of university in which a respondent worked, and their position held were statistically significant. Employees of economic universities and academics had higher odds of participating in capital pension plans than the employees of general universities and non-academics (by approximately 125% and 55%, respectively). While the level of respondents’ knowledge and skills in the field of personal finance, objective knowledge, and financial experience appeared to be very important in pension decision behaviour, subjective knowledge (self-indicated level of knowledge) did not affect wealth accumulation under the PPK (it was statistically insignificant). Moreover, based on both regressions (LRM2 and MLR), self-confidence in financial knowledge had a statistically significant negative correlation with wealth accumulation in capital plans. With the increasing importance of knowledge and financial experience, the chances of auto-enrolment pension savings participation may decrease (by 38%).

The third logistic regression model (LRM3) reran participation in the PPK regression, adding trust variables to all earlier explanatory features, such as trust in selected institutions and people, as well as the attempt to save and use credit and loans. The regression results, like earlier models, underlined objective knowledge as positively significant. A unit increase in the level of knowledge raised the odds of participating in the PPK by approximately 26%. Similarly, the significance of gender, age, type of research unit, and position was confirmed. According to the analysis, most men saved using the PPK (40% more likely than women) and so did young people (up to 35 years of age) (twice as often as people over 55). Finally, the new variables implemented in the LRM3 played an important role in explaining the respondents’ behaviour. One major feature was trust in the state. Considering that employers are obligated to create such a plan for their employees, they must subsidise it from the budget in the form of welcome and annual payments to the employee’s account. The importance of this variable seemed reasonable. The results indicated that respondents who trusted the state were 2.2 times more likely to participate in the PPK. Similarly, trust in open pension funds was statistically significant. People who trusted OFE were 1.8 times more likely to participate in the PPK than people who did not trust OFE. However, in this model, trust in banks and other people as well as the approach to saving and using credit and loans turned out to be statistically insignificant.

Finally, when building the overall logistic regression model (LRM4), we included trust in investment funds as the last independent variable. Assets accumulated in the PPK account are mostly managed by investment fund companies and invested in funds with a different risk profile adjusted for the age of the participant (called the defined-date funds), which was the reason for adding this variable in the final model composition. We found that, like the LRM3 and FAMD, when trust was included in the analysis, men, people up to 35 years of age, and employees of economic universities and academics showed higher odds of saving in the PPK. However, in contrast to the LR, MLR, and FAMD, the level of objective knowledge was found to be statistically insignificant. Considering trust in the analysed institutions and people, apart from trust in the state and open pension funds, trust in commercial banks and investment funds was found to be important. Respondents who trusted investment funds were approximately 140% more likely to auto-enrolment pension savings. Therefore, it can be concluded that when trust in institutions managing funds is analysed, it is particularly important to build trust in investment funds; however, the financial knowledge of the respondents can be ignored.

6. Discussion

A positive effect of financial literacy on retirement is evident [4,5,19,46]. Numerous studies [16,20] show that financially knowledgeable people accumulate more retirement wealth and decide to have pension savings [32,47,48]. Most studies point to the significance of financial literacy in retirement planning [1,6,21]. However, research in New Zealand does not support the overall trend. Crossan et al. [49] analysed the level of financial literacy in New Zealand and found that financial literacy is not significantly related to retirement decisions. This may reflect the dominant role of New Zealand’s public pension system in providing retirement income security. According to Goda et al. (2020), auto-enrolment pension plans increase savings primarily among those with low financial literacy. The scientific literature examining the relationship between financial literacy and retirement in general is clear and mainly has a positive influence. However, it is no longer so obvious when we add trust and combine it with participation in auto-enrolment. In our research, financial literacy positively impacts pension decisions regarding auto-enrolment choosing. We supported H1. Our research agrees with the main direction of the previous studies.

The second main factor in our research is trust. In previous research, trust was primarily examined in relation to financial institutions [14,16,33] and state and public institutions [29]. Our article contains multidimensional forms of trust, including the state, Social Insurance Institutions, financial institutions (commercial banks, Open Pension Funds, investment funds), and trust in other people. According to previous research [14,26,30], trust in the financial system increases the probability of holding formal savings and diversifying among formal saving instruments instead of using informal methods of saving (such as keeping money at home or with friends or family members). Trust processes can have an avalanche effect where high trust in public-sector institutions positively influences trust in other institutions that play a similar social function [31]. Our finding is that the level of trust in the state and financial institutions influences the decision to participate in the auto-enrolment pension (supporting H4). Koch et al. [27] studied interpersonal trust and found that it is not significantly related to pension behavior. Our findings agree with their results.

Our research is focused on university employees, which can be a limitation but also fills a gap. Our respondents are academic employees (masters, doctors, assistant professors, professors, those involved in scientific and teaching activities) and non-academic employees (office staff, technical workers, etc.). We supported H3, which shows that academic staff are more likely to enrol than non-academic staff. Our research also presents data from two kinds of universities: general (which have faculties of economics, mathematics, biology, chemistry, and others) and economics-focused, which focus only on the economic aspect of research and teaching. Our study supported H2, which shows that employees of economics universities are more willing to participate in the auto-enrolment pension than general university employees. The research has some limitations. Respondents were limited to university employees. On the other hand, this enabled the realization of research in a group of respondents with extremely diverse education levels. These groups included employees of economic universities, generally highly educated research staff of traditional universities, and lesser-educated and lower-salaried administrative workers. Analysis of financial literacy and trust in the context of supplementary pension decisions indicates a direction for future research: conducting the same analysis but in a group of consumers with low financial literacy. Interestingly, the literature review by Reuter [50] shows that adopting automatic enrolment has significantly increased participation rates in supplementary pension systems. However, the long-run effects on savings are smaller than the short-run effects, with some savings financed via debt. This conclusion suggests, as a future research direction, that auto-enrolment pension savings should be studied over a longer period.

7. Conclusions

The study highlighted the factors that influence participation in the auto-enrolment supplementary pension scheme. This research represents the first study on auto-enrolment pension system in Poland, which is the first country in Central and Eastern Europe which introduced an auto-enrolment pension system. The study focuses mainly on financial literacy and trust. Financial literacy and trust have been proven to be related to employees’ participation in the supplementary pension system. These findings strengthen the role of economic education in the future. Data used in the article comes from a survey that was conducted in Poland in 2021 using a Computer-Assisted Web Interview (CAWI) method and a questionnaire consisting of 28 questions with 867 interviews. The analysis was conducted as part of the research project entitled ‘Employee Capital Plans in Polish Public Universities,’ launched in October 2020, a few months before the introduction on the market. We used interviews as primary research to show how important trust and financial literacy are in accumulating auto-enrolment retirement savings. Our study uses multivariable data-mining tools, and several regression models were applied. We employed Logistic Regression (LR) and utilized Multivariate Linear Regression (MLR) and Factor Analysis of Mixed Data (FAMD) to support the LR analysis.

This research is part of a global research trend and is the first study in the field of PPK in Poland. In line with the results of studies in many countries around the world [5,16,51,52,53], our research showed that financial literacy has a positive effect on wealth accumulation and pensions, greatly influencing the chances of long-term savings in capital plans. The main contribution of this study is the results from the primary survey, which allow us to build four regression models. Our main finding is that financial literacy is associated with participation in supplementary pensions, impacting not only retirement planning but also the decisions to enter a private pension scheme. The added value of the article is also the inclusion of a wide range of trust factors. Our findings show that a high level of financial literacy greatly influences the chances of long-term savings, and the lower the consumer’s knowledge level, the more their decisions are based on trust. Moreover, our findings indicate that trust in the state, rather than trust in financial institutions, plays a crucial role for people with low financial literacy, which is a key factor in choosing auto-enrolment, complementary option for pension savings. The results of the primary survey showed a positive and statistically significant effect of gender: men had higher odds of auto-enrolment pension savings than women. The type of university where a respondent worked, and the position held were also statistically significant. Employees of economic universities and academics had higher odds of participating in capital pension plans than those of general universities and non-academics. Our findings serve as a strong signal for governments, policymakers, and financial institutions to prepare for financial challenges and effectively improve financial literacy to ensure adequate retirement savings.

The results allowed for the verification of H1, confirming that the level of financial literacy determines the propensity to participate in the auto-enrolment pension savings. This was confirmed using different data-mining tools. H4 also found strong support and significant statistical correlations with consumers’ pension decisions. Our findings indicate that the level of trust in the state and financial institutions influences the decision to participate in the auto-enrolment pension savings, which means that H4 was supported. The analysis also supports H2 and H3: regardless of the university type, academic staff showed higher financial literacy and enrolment than non-academic staff. When financial literacy decreases, the role of trust increases. Thus, PPK can be crucial to achieving social and economic goals. The Polish pension system is currently in a transitional phase. In summary, we can describe a general rule indicating that the lower the consumer’s financial literacy, the more their decisions are based on trust. Such conclusions strongly signal to governments, policymakers, education systems, and financial institutions the need to diversify marketing tools and educational instruments depending on social groups. These results can serve as a platform to provide directions for conducting similar studies in other groups of consumers and other countries, and at different stages of establishing supplementary pension schemes, which could be the subject of in-depth comparative analyses.

Because Poland was the first country in Central and Eastern Europe to introduce an auto-enrolment pension, other countries can observe and draw conclusions by examining this solution’s strengths and weaknesses. In 2022, the participation rate in auto-enrolment in all seven OECD countries that introduced such schemes was higher than in Poland: New Zealand, 83.7%; Lithuania, 76.7%; Great Britain, 50%; Turkey, 14.8%; and Poland, 13.1% [13]. It is essential to improve communication about the benefits and security of pension plans to increase public trust. This article suggests policy implications for enhancing financial literacy, building trust in institutions, diversifying financial education, and developing effective communication strategies. The Polish government introduced a National Strategy for Financial Education in 2024, which we hope will help strengthen the future pension system. It’s worth referring to the research findings on financial education. According to Harvey et al. [54], required financial education in high school has a limited impact on retirement accounts. The authors of this study find no evidence that education increases the likelihood of having a retirement account. Therefore, policymakers who are encouraged to invest in financial education activities must improve the quality of financial education. Appropriately profiled and tested financial education could lead to better retirement planning and greater participation in supplementary pension schemes. Our research suggests that trust in both the state and financial institutions significantly affect participation in pension plans, especially among individuals with lower financial literacy. Therefore, policymakers should consider building public trust in these institutions through transparency and reliable management of pension funds. Tailored programs targeting groups with lower trust in financial institutions may help increase their participation in retirement savings plans. We recommend that the government (Ministry of Education) and educators prioritize personal finance content that is immediately relevant to people’s long-term savings.

The research has some limitations, primarily in the selection of respondents who are university employees. For future research, we recommend conducting a study in groups with lower financial literacy to fill a gap in the literature.

Author Contributions

For research articles with several authors, a short paragraph specifying their individual contributions must be provided. The following statements should be used Conceptualization, B.S., P.K-R; S.P., methodology, B.S., P.K-R; S.P. software, B.S., P.K-R; S.P., validation, B.S., P.K-R; S.P., J.Ś., P.T., formal analysis, B.S., P.K-R; S.P., J.Ś; P.T., investigation, B.S., P.K-R; S.P., J.Ś; P.T., resources, B.S., P.K-R; S.P., J.Ś., P.T., data curation, B.S., P.K-R., S.P., J.Ś; P.T., writing—original draft preparation, B.S., P.K-R; S.P., writing—review and editing, B.S., visualization, J.Ś; P.T., supervision, B.S., P.K-R; S.P., J.Ś; P.T., project administration, B.S., P.K-R; S.P., J.Ś; P.T., funding acquisition, P.T.

Funding

Cofinanced by the Minister of Science under the “Regional Excellence Initiative” Program for 2024-2027 (RID/SP/0045/2024/01).

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Acknowledgments

The analysis was conducted as part of the research project entitled ‘Employee Capital Plans in Polish Public Universities,’ launched in October 2020.

Conflicts of Interest

The authors declare no conflicts of interest.

Link to the data

https://data.mendeley.com/datasets/yj4wf4w4ym/1 (DOI: 10.17632/yj4wf4w4ym.1).

References

- Safari, K.; Njoka, C. Munkwa, M. G. Financial literacy and personal retirement planning: a socioeconomic approach, Journal of Business and Socio-economic Development 2021, 1, 121–134. [Google Scholar] [CrossRef]

- Meir, A.; Mugerman, Y.; Sade, O. Financial literacy and retirement planning. Evidence from Israel, Israel Economic Review, Bank of Israel 2016, 14, 75–95. [Google Scholar]

- Hastings, J.S.; Madrian, B.C.; Skimmyhorn, W.L. Financial literacy, financial education, and economic outcomes. Annual Review of Economics 2013, 5, 347–373. [Google Scholar] [CrossRef] [PubMed]

- Kaiser, T.; Lusardi, A.; Menkhoff, L.; Urban, C. Financial education affects financial knowledge and downstream behaviors. Journal of Financial Economics 2022, 145, 255–272. [Google Scholar] [CrossRef]

- Lusardi, A.; Michaud, P.C.; Mitchell, O.S. Optimal financial knowledge and wealth inequality. Journal of Political Economy 2017, 125, 431–477. [Google Scholar] [CrossRef] [PubMed]

- Lusardi, A.; Mitchell, O.S. Financial literacy around the world: An overview. Journal of Pension Economics and Finance 2011, 10, 479–508. [Google Scholar] [CrossRef]

- Lusardi, A.; Mitchell, O.S. The economic importance of financial literacy: Theory and evidence. Journal of Economic Literature 2014, 52, 5–44. [Google Scholar] [CrossRef]

- Brown, M.; Graf, R. Financial Literacy and Retirement Planning in Switzerland. Numeracy 2013, 6, 1–21. [Google Scholar] [CrossRef]

- Bialowolski, P.; Cwynar, A.; Xiao, J.J.; Weziak-Bialowolska, D. Consumer financial literacy and the efficiency of mortgage-related decisions: New evidence from the Panel Study of Income dynamics. International Journal of Consumer Studies 2022, 46, 88–101. [Google Scholar] [CrossRef]

- Chu, Z.; Wang, Z.; Xiao, J.J.; Zhang, W. Financial Literacy, Portfolio Choice and Financial Well-Being. Social Indicators Research 2017, 132, 799–820. [Google Scholar] [CrossRef]

- van Dalen, H.P.; Henkens, K. Trust and distrust in pension providers in times of decline and reform. Analysis of survey data 2004–2021. De Economist 2022, 170, 401–433. [Google Scholar] [CrossRef] [PubMed]

- Bielawska, K.; Turner, J. Trust and the behavioral economics of automatic enrolment in pensions: a comparison of the UK and Poland. Journal of Economic Policy Reform 2023, 26, 216–237. [Google Scholar] [CrossRef]

- OECD. Pensions at a Glance 2023: OECD and G20 Indicators, OECD Publishing, 2023, Paris, 1-236. [CrossRef]

- Agnew, J.R.; Szykman, L.R.; Utkus, S.P.; Young, J.A. Trust, plan knowledge and 401(k) savings behavior. Journal of Pension Economics and Finance 2012, 11, 1–20. [Google Scholar] [CrossRef]

- Georgarakos, D.; Inderst, R. Financial Advice and Stock Market Participation, 2014 CEPR Discussion Paper No. DP9922. Available online: https://ssrn.com/abstract=2444945.

- Fisch, J.E.; Seligman, J.S. Trust, financial literacy, and financial market participation. Journal of Pension Economics and Finance 2022, 21, 634–664. [Google Scholar] [CrossRef]

- EC. The 2018 Pension Adequacy Report: current and future income adequacy in old age in the EU. 2018. Available online: https://ec.europa.eu/info/publications/economy-finance/2018-ageing-report-underlying-assumptions-and-projection-.

- Vickerstaff, S.; Macvarish, J.; Taylor-Gooby, P.; Loretto, W.; Harrison, T. Trust and confidence in pensions: A literature review. Working Paper 2012, 108, Department for Work and Pensions, 1-55. Available online: https://assets.publishing.service.gov.uk/media/5a7cbaf5ed915d63cc65c81d/WP108.pdf.

- Alessie, R.; Van Rooij, M.; Lusardi, A. Financial literacy and retirement preparation in the Netherlands. Journal of Pension Economics and Finance 2011, 10, 527–545. [Google Scholar] [CrossRef]

- Kalmi, P.; Ruuskanen, O.P. Financial literacy and retirement planning in Finland. Journal of Pension Economics and Finance 2019, 17, 335–362. [Google Scholar] [CrossRef]

- Prast, H.; Van Soest, A. Financial literacy and preparation for retirement. Intereconomics 2016, 51, 113–118. [Google Scholar] [CrossRef]

- Fornero, E.; Monticone, C. Financial literacy and pension plan participation in Italy. Journal of Pension Economics and Finance 2011, 10, 547–564. [Google Scholar] [CrossRef]

- Dewi, V.I.; Febrian, E.; Effendi, N.; Anwar, M.; Nidar, S.R. Financial Literacy and Its Variables: The Evidence from Indonesia. Economics and Sociology 2020, 13, 133–154. [Google Scholar] [CrossRef]

- Kwon, O.Y. Social trust and economic development. Edward Elgar Publishing 2019, 16629. [Google Scholar] [CrossRef]

- Van der Cruijsen, C.; de Haan, J.; Roerink, R. Financial knowledge and trust in financial institutions. Journal of Consumer Affairs 2021, 55, 680–714. [Google Scholar] [CrossRef]

- Beckmann, E.; Mare, D.S. Formal and Informal Household Savings: How Does Trust in Financial Institutions Influence the Choice of Saving Instruments? SSRN Electronic Journal 2017, 1–38. [Google Scholar] [CrossRef]

- Koh, B.S.K.; Mitchell, O.S.; Fong, J.H. Trust and retirement preparedness: Evidence from Singapore. Journal of the Economics of Ageing 2021, 18, 100283. [Google Scholar] [CrossRef]

- Zhao, D.; Hu, W. Determinants of public trust in government: empirical evidence from urban China. International Review of Administrative Sciences 2017, 83, 365–384. [Google Scholar] [CrossRef]

- Alessandro, M.; Cardinale Lagomarsino, B.; Scartascini, C.; Streb, J.; Torrealday, J. Transparency and trust in government evidence from a survey experiment. World Development 2021, 138, 105223. [Google Scholar] [CrossRef]

- Baidoo, S.T.; Akoto, L. Does trust in financial institutions drive formal saving? Empirical evidence from Ghana. International Social Science Journal 2019, 69, 63–78. [Google Scholar] [CrossRef]

- Høyer, H.C.; Mønness, E. Trust in public institutions—spillover and bandwidth. Journal of Trust Research 2016, 6, 151–166. [Google Scholar] [CrossRef]

- Clark, R.; Pelletier, D. Impact of defaults on participation in state supplemental retirement savings plans. Journal of Pension Economics and Finance 2022, 21, 22–37. [Google Scholar] [CrossRef]

- Ricci, O.; Caratelli, M. Financial literacy, trust and retirement planning. Journal of Pension Economics and Finance 2017, 16, 43–64. [Google Scholar] [CrossRef]

- European Comission. The 2021 Pension Adequacy Report: current and future income adequacy in old age in the European Union. Country profile, 2021, Volume II. Social Protection Committee, European Commission, Brussels. Available online: https://ec.europa.eu/social/main.jsp?catId=738&langId=en&pubId=8397&preview=cHJldkVtcGxQb3J0YWwhMjAxMjAyMTVwcmV2aWV3.

- Central Statistical Office. US Poland in numbers, Central Statistical Office, 2023. Warsaw. https://stat.gov.pl.

- PPK. Biuletyn Pracowniczych Planów Kapitałowych (Employee Capital Plans Bulletin), 2024. Available online: https://www.mojeppk.pl/aktualnosci/ponad-160-proc-zysku-dla-uczestnikow-ppk-032024.html.

- KNF Raport o stanie rynku emerytalnego w Polsce na koniec czerwca 2024 r.; Komisja Nadzoru Finansowego, Warszawa. (Report on the state of the pension market in Poland at the end of June 2024, Warsaw, Polish Financial Supervision Authority, Warsaw), 2024. Available online: https://www.knf.gov.pl/knf/pl/komponenty/img/Raport_o_stanie_rynku_emerytalnego_w_Polsce_na_koniec%202023_roku.pdf.

- OECD. OECD Pensions Outlook 2020. OECD Publishing, 2020, Paris, 1-210. [CrossRef]

- Beshears, J.; Choi, J.; Laibson, D.; Madrian, B.; Skimmyhorn, W. Borrowing to save? The impact of automatic enrollment on debt. Journal of Finance 2022, 77, 403–447. [Google Scholar] [CrossRef]

- Kim, J. .; Oh, J..; Woo, S. An introduction of new time series forecasting model for oil cargo volume. Journal of Korea Port Economic Association 2018, 34, 81–98. [Google Scholar] [CrossRef]

- Yang, J. Prediction model of regional economic development potential based on data mining technology. Engineering Reports 2023, 5, 1–13. [Google Scholar] [CrossRef]

- Kuswanto, H.; Asfihani, A.; Sarumaha, Y.; Ohwada, H. Logistic regression ensemble for predicting customer defection with very large sample size. Procedia Computer Science 2015, 72, 86–93. [Google Scholar] [CrossRef]

- Strzelecka, A.; Kurdys-Kujawska, A.; Zawadzka, D. Application of logistic regression models to assess household financial decisions regarding debt. Procedia Computer Science 2020, 176, 3418–3427. [Google Scholar] [CrossRef]

- Wang, Y.; Qin, J. Analysis of financial product purchases based on logistic regression. Journal of Physics: Conference Series 2021, 1848, 1–6. [Google Scholar] [CrossRef]

- Pages, J. Analyse factorielle de données mixtes. Revue de Statistique Appliquée 2004, 52, 93–111. Available online: http://www.numdam.org/article/RSA_2004__52_4_93_0.pdf.

- Bucher-Koenen, T.; Lusardi, A. Financial literacy and retirement planning in Germany. Journal of Pension Economics and Finance 2011, 10, 565–584. [Google Scholar] [CrossRef]

- Nguyen, T.A.N.; Polách, J.; Vozňáková, I. The role of financial literacy in retirement investment choice. Equilibrium. Quarterly Journal of Economics and Economic Policy 2019, 14, 569–589. [Google Scholar] [CrossRef]

- Almenberg, J.; Säve-Söderbergh, J. Financial literacy and retirement planning in Sweden. Journal of Pension Economics and Finance 2011, 10, 585–598. [Google Scholar] [CrossRef]

- Crossan, D.; Feslier, D.; Hurnard, R. Financial literacy and retirement planning in New Zealand. Journal of Pension Economics and Finance 2011, 10, 619–635. [Google Scholar] [CrossRef]

- Reuter, J. Plan design and participant behavior in defined contribution retirement plans: Past, present, and future. NBER Working Paper 2024, 32653, 1–45. [Google Scholar]

- Ameriks, J.; Caplin, A.; Leahy, J. Wealth accumulation and the propensity to plan. In Quarterly Journal of Economics 2003, 118, 1007–1047. [Google Scholar] [CrossRef]

- van Rooij, M.C.J.; Lusardi, A.; Alessie, R.J.M. Financial literacy and retirement planning in the Netherlands. Journal of Economic Psychology 2011, 32, 593–608. [Google Scholar] [CrossRef]

- van Rooij, M.C.J.; Lusardi, A.; Alessie, R.J.M. Financial literacy, retirement planning and household wealth. Economic Journal 2012, 122, 449–478. [Google Scholar] [CrossRef]

- Harvey, M.; Urban, C. Does financial education affect retirement savings? The Journal of the Economics of Ageing 2023, 24, 100446. [Google Scholar] [CrossRef]

Figure 1.

Location and type of the universities and number of respondents participating in the survey according to positions held in the research unit.

Figure 1.