Submitted:

01 March 2023

Posted:

03 March 2023

You are already at the latest version

Abstract

In this age of global warming, academics and policymakers are increasingly concerned about firm environmental sustainability success. Therefore, this study aims to investigate whether Environmental, Social and Governance (ESG) performance impacts sustainability performance through the mediating effect of firm innovation. To this end, Structural Equation Modeling (SEM) was deployed to analyze data collected from the employees of manufacturing industries in an emerging economy like Bangladesh. The results revealed that ESG performance significantly enhances the innovation and sustainability performance of manufacturing industries, indicating that the higher the ESG performance of a firm, the greater its innovation and sustainability performance. Furthermore, the results confirmed that firm innovation performance fully mediates the relationship between ESG initiatives and sustainability performance. The findings of this study provide policymakers and industry authorities with valuable insight into the role of ESG and innovation performance in improving sustainability performance. Specifically, the study sheds knowledge on how firm ESG initiatives and innovation performance impact sustainability performance in the manufacturing sector of an emerging economy like Bangladesh.

Keywords:

Sustainability performance

; Environmental

; Social and Governance (ESG) performance

; Innova-tion performance

; mediating effect

; manufacturing firms

1. Introduction

Traditionally, the performance of business firms was measured based on economic indicators. However, this evaluative approach has now been upgraded to include sustainable performance [1]. As result, firms now prioritize sustainable performance to meet the demand of some notable stakeholders like regulatory bodies, environmentally concerned institutions, society, etc [2]. Sustainable performance is inextricably related to Corporate Social Responsibility (CSR), since it helps firms address the environmental and social interests of their stakeholders [3]. Sustainable performance, indicated by economic, social and environmental indicators, shows the path to solving sustainability challenges, thereby providing organizations with a competitive edge [4]. To manage sustainable challenges, regulators are pressurizing firms to incorporate social and environmental goals into their economic agenda [5]. Moreover, the sustainable performance also aids the achievement of Sustainable Development Goals (SDGs), which primarily focus on economic development, extreme poverty elimination, social trust building and protection of the environment [6].

Many factors contribute to the sustainable practices of business organizations, among which is compliance with ESG principles [7]. ESG principle is considered a prerequisite for sustainable development of the global economy and society [8]. Recent threats to the society and environment due to industrialization along with the COVID-19 pandemic have further aroused global interest in ESG [9]. The three elementary factors of ESG namely environmental, social and governance are considered crucial for investment analysis and decision-making process while evaluating a corporation’s sustainable development [10,11,12,13]. These three factors quantify the sustainable performance and social influence of business practices. Developments based on ESG principles such as ESG disclosure standards, ESG evaluation systems and ESG index systems are constantly promoting a new pattern of sustainable development since the formal inception of ESG principles in 2004 [8]. Owing to the wide adoption of ESG in the practical field, global research interest in ESG has increased.

As a crucial determinant of sustainable business practices, ESG has been investigated from the perspective of developed countries. Hussain, Rigoni [12] analyzed the performance of the triple bottom line to investigate the relationship between corporate governance and Sustainability Performance (SP) in US-based firms; Maali, Rakia [14] analyzed the mediating role of CSR on the relationship between corporate governance and sustainability performance in the UK; Yang, Du [15] investigated the impact of changes in clean energy, green financing and economic practices on sustainability performance through ESG performance in G7 countries; Kocmanová and Šimberová [16] studied the relationship between ESG indicators and sustainability performance in Czech companies; Ye, Song [17] explored the impact of ESG on sustainability performance, reflected as stock return, in EU members countries. Also, remarkable studies have been conducted to measure the impact of ESG performance on sustainability performance in emerging economies like China [9,18,19] , Brazil [20,21], Korea [22], India [23,24], etc. While some studies have also been conducted to address ESG and sustainability performance issues in Bangladesh, an emerging market [25,26,27], less emphasis has been given to exploring such issues in the manufacturing industry. Bangladesh significantly depends on the manufacturing industry, particularly the Ready-Made Garment (RMG) sector, for its forex inflow. It is the 39th largest economy in the world, with a promising manufacturing industry, which currently contributes a Manufacturing Value Added (MVA) of 20.6% to GDP [28].

Sustainable business practice has a huge significance for manufacturing industries, since it facilitates their environmental and social compliance. The manufacturing industry tends to generate more negative outcomes on the environment than the service industry, thus necessitating their adoption of sustainable business practices [12,29]. Some researchers identified factors like institutional pressure [30] and green practice[31] as influencing the sustainability performance of the manufacturing industries in Bangladesh. Earlier studies conducted in developed and emerging economies have demonstrated the influence of ESG principles on sustainable business performance. However, this relationship remained unexplored in the Bangladeshi manufacturing industry, which is known for flaunting its environmental and social requirements. ESG principle could be a panacea for sustainability challenges of the Bangladeshi manufacturing industry, particularly the RMG sector, which is also criticized for the mistreatment of its workers [32]. The sector was also censured for its violation of local and global labor standards and rights, which jeopardize the safety of its workers. The Rana Plaza collapse, causing the death of 1129 workers in 2013, the Spectrum Sweater collapse in 2005 and the Tazreen Garments Fire in 2012 are some of the unforgettable scary evidence of poor workplace safety in Bangladesh [33,34]. Proper compliance with ESG principles could overcome the shortcomings of Bangladeshi manufacturing industries. Thus, this research aims to understand the impact of ESG practices on the sustainable performance of manufacturing industries in Bangladesh. In addition, the study will also examine the mediating impact of innovation performance on the relationship between ESG practice and sustainable performance of the Bangladeshi manufacturing industry, since the adoption of new technologies and development of innovative business models are considered a crucial player in sustainable business development [3]. The scarcity of resources, considered a notable peril towards the sustainability of the business, is also a major concern of ESG principles and could be resolved through green innovation performance [35]. However, innovation strategies should be aligned with sustainability goals to reduce negative impacts on the environment [36]. In addressing the issues identified above, this study will examine the following research questions:

RQ 1: How does ESG performance influence the sustainability performance of the Bangladeshi manufacturing industry?

RQ 2: How does innovation mediates the relationship between ESG initiatives and sustainability performance in the Bangladeshi manufacturing industry?

This study contributes to the existing literature in the following ways. First, most of the research that explores the impact of ESG on sustainability performance were conducted in developed countries, creating a deficit of knowledge on the relationship in the context of developing countries. Therefore, this study attempts to fill this gap by investigating the impact of ESG on the sustainability performance of the Bangladeshi manufacturing industry. Second, prior research recognized the direct and indirect effects of innovation on ESG performance, but no study explores the mediating impact of innovation on the association between ESG and sustainability performance. Hence, this study examines the mediating effect of innovation performance on the relationship between ESG and sustainability performance. Finally, this study will offer worthy insights for owners of Bangladeshi manufacturing industries and policymakers who are deeply concerned about the global acceptability of RMG firms amid their violation of social and environmental interests.

The remainder of the paper is structured as follows: Section 2 review the literature and develops the research hypotheses. In section 3, the study describes the sample, variables, empirical models and method. The results are discussed and interpreted in section 4. Finally, section 5 presents the conclusion and policy implication.

2. Literature review and hypothesis development

2.1. Theoretical Background

Theories of sustainability such as agency theory, stakeholder theory, legitimacy theory, signaling theory and institutional theory demand the adoption of ESG principles for a corporation to be sustainable.

According to the stakeholder theory, a corporation has to focus on the interest of all the related parties. This theory emphasizes the need for firms to be concerned with social and environmental interests while pursuing organizational objectives. Some research works have argued that sustainability performance is achieved through an enhanced stakeholder relationship [10]. In line with the stakeholder theory, Flammer and Kacperczyk [37] found a positive impact of ESG on employee engagement, which is a pre-requisite of sustainability performance. To become sustainable and gain competitive edge, a firm must focus on minimizing the negative impact of their activities on the environment through product innovation and strategy implementation [38]. The establishment of sustainable performance is considered a crucial factor for balancing the interest of all stakeholders [39]. Stakeholder-oriented management theory indicates that an enhanced stakeholder relationship could promote corporate sustainability performance [40]. This theory stresses that firms must address the interests of all stakeholders that are affected by or can influence the company’s performance [10], in agreement with the theory of enlightened value maximization [39]. ESG practices help corporations to maximize long-term value by complying with the social needs and environmental obligations [41]. Corporate shared value theory introduced by Kramer and Porter [42] demands the inclusion of societal interest in a firm’s strategy and operations to gain a competitive edge and achieve a sustainable performance.

Another theory that demonstrates the need for ESG practice to produce sustainable business practice is the legitimacy theory, which opines that a corporation’s social acceptance contributes positively toward its existence and growth [43]. This theory outlines the relationship between society and corporations, claiming that social values, norms and beliefs must be complied with by the companies [13,44]. ESG practices are considered key to enhancing the social acceptability of the corporation. This theory further suggests that firms follow a symbolic approach that involves the expression of behavior that shows their agreement with the norms of the society [45]. To put simply, firms should try and show society that they are conducting their business in compliance with social norms and bounds [46]. Firms should also undertake social and environmental practices and disclosures to attract societal appraisal and be perceived as legitimate by external stakeholders [47,48].

2.2. Sustainability Performance

Elkington [49] introduced the “Triple Bottom Line” as a concept of sustainable performance in which firms incorporate Economic, Environmental and Social (EES) objectives in their business strategy implementation, intending to protect and sustain the environment and society while maximizing their market capitalization. Supporting this concept, Khan, Ahmad [50] and Masud, Rashid [44] referred to sustainability as the alignment of economic growth with social and environmental objectives to create value for the society as well as the corporation. Kamble, Gunasekaran [51] defined sustainable performance as the deployment of strategies that ensure a balance between social enhancement, environmental protection and economic growth. Helleno, de Moraes [52] also defined sustainability performance as a bunch of business actions intended to meet the present needs without compromising future needs. Moktadir, Rahman [53] demonstrated that industries motivated by sustainability performance are redefining their business plans and activities by considering economic, environmental and social impacts.

2.3. Hypothesis Development

The earlier section highlights the propositions of different theories, which demonstrate how corporate sustainable performance could be achieved by ESG practices. Several research works have been conducted to help define sustainable business practices and the impact of ESG practices.

2.3.1. Environmental Performance, Innovation Performance, and Sustainability performance

Major environmental concerns include air and water pollution, GHG emissions, waste management, climate change, natural system, changes in land use, loss of biodiversity, renewable energy, etc. [54]. Moreover, depleting natural resources, population growth, slowed economic development and climate change call for conscious efforts from various stakeholders to ensure the sound functioning of the society and economy [55]. Sultana, Zulkifli [25] indicated that corporations with worthy environmental practices could achieve sustainable and viable financial returns while also earning satisfactory environmental compliance ratings. Mousa and Othman [56] found a positive impact of green HRM and a dimension of environmental practice on sustainability performance. Abdul-Rashid, Sakundarini [57] proposes that sustainability performance can be achieved in the manufacturing industry by undertaking environmental initiatives. Ali, Zailani [58] evidenced a positive impact of resource, energy and waste management on the sustainable performance of manufacturing firms. Since the environmental issue is now a concern for environmental pressure groups, regulatory bodies and society, consideration of this issue in business decision-making could help firms, including the Bangladeshi manufacturing industry, achieve a competitive edge, high compliance ratings as well as sustainable performance. Thus, this study postulates the following hypothesis:

H1:

Environmental performance enhances sustainability performance in the Bangladeshi manufacturing Industry.

Ong, Lee [59] highlighted that the implementation of active environmental protection strategies and routines can promote innovations in organizations. Crossan and Apaydin [60] identified organizational capability, generated by the proper implementation of environmental strategies, mission, systems and structures, as the foundation of innovation practices. Cohen and Levinthal [61] claimed that innovation performance is the outcome of a corporation’s absorption capacity, which is reflected by environmental performance. Delmas and Burbano [62] also mentioned dynamic environmental performance as an indicator of a corporation’s ability to identify new dimensions of environmental knowledge and utilize them for importing new business solutions and developing products and processes. Based on a survey of 2000 European manufacturing firms, Wagner [63] observed a positive impact of environmental performance on both product and process innovation. Similarly, Carrión-Flores and Innes [64] identified the positive impact of toxic pollution reduction, an indicator of environmental performance, on environmental innovation quantified by environmental patents. A study on Taiwanese manufacturing firms by Chiou, Chan [65] demonstrated that a crucial outcome of environmental performance is green product innovation. Sezen and Cankaya [66] also demonstrated the positive impact of environmental performance by manufacturing firms on green process innovation. In light of the above, it is assumed that a firm’s greater environmental performance will result in its better environmental innovation. Consequently, the following hypotheses are advanced:

H2:

Environmental performance enhances innovation performance in the Bangladeshi manufacturing industry.

2.3.2. Social Performance, Innovation Performance and Sustainability performance:

Taddese, Durieux [67] defined social performance as the societal impact of business practices on delivered products and services. They describe human rights, health and safety practices and development management as an indicator of social performance. Based on the sustainable assessment theory, Chaim, Muschard [68] stated that long-term sustainability could be achieved through the training and development of employees, which is considered a social contribution. Avery [69] documented that a sustainable corporation must have a mission to contribute to society, considering the direct or indirect relationship between corporate and societal sustainability. Ketprapakorn and Kantabutra [70] highlighted that corporate sustainability depends on four social dimensions, namely leadership, resilient development, stakeholder focus and sharing practices. Chams and García-Blandón [71] argued that sustainable human resource management is necessary to ensure sustainable performance and ultimately attain SDGs. Kim [72] also emphasized the need for social capital for attaining sustainability. Since no remarkable study has been conducted on the impact of societal performance on the sustainability of the Bangladeshi manufacturing industry and in view of the aforesaid, this study assumes the following:

Corporate social performance can be defined as discretionary activities to meet the demand and expectations of society and external stakeholders beyond the interest of shareholders and the firm [73]. Prior studies argued that social performance like external stakeholder relationship management helps corporations access diversified knowledge and information [74,75]. McWilliams and Siegel [76] claimed that access to external knowledge enhances firms’ absorption capacity, which is necessary to promote their innovativeness. Accordingly, MacGregor, Espinach [77], Mahlouji and Anaraki [78] argued that corporations that fail to consider CSR might struggle to innovate. Porter and Kramer [79] also regarded CSR as a potential source of competitive edge and innovation for firms. Bocquet, Le Bas [80] also reiterate that social performance is necessary for process and product innovation. Herrera [81] suggested that management focusing more on social contribution is likely to find and respond to dynamic strategic challenges and opportunities. Li and Liu [82] indicated macro-environment and stakeholder assessment as pre-requisite for successful innovation. A study on 320 Japanese firms by Broadstock, Matousek [83] revealed that CSR activities developed firm’s capacity of innovativeness. Setini, Yasa [84] collected data from 200 women entrepreneurs and found that social capital programs positively impact the creative industry. Based on the responses from 433 Chinese firm, Zhang, Loh [85] also found a positive impact of social performance on innovation performance with a moderating role of corporate governance. Thus, this study concludes that societal performance might facilitate access to stakeholder support to elevate the innovative capacity of Bangladeshi manufacturing industry and posits following:

H3:

Social performance enhances sustainability performance in the Bangladeshi manufacturing Industry.

H4:

Social performance enhances innovation performance in the Bangladeshi manufacturing Industry.

2.3.3. Corporate Governance Performance, Innovation Performance and Sustainability Performance:

Rodrigue, Magnan [86] identified a positive link between corporate governance and environmental disclosure, which is a requirement for sustainable performance. Similarly, Ricart, Rodríguez [87] found a positive impact of the sustainability committee, a corporate governance characteristic, on sustainability performance. Many studies have found a positive relationship between corporate governance and sustainability performance [88,89,90,91,92] but some researchers such as Rodrigue, Magnan [86], Michelon and Parbonetti [93] have reported an insignificant relationship between sustainability committees and sustainability performance. Maali, Rakia [14], however, demonstrated a positive relationship between corporate governance and sustainability performance through the mediating effects of CSR. Considering that good governance ensures corporate compliance with social and environmental standards, Arora and Dharwadkar [94] concluded that corporate governance plays a crucial role in ensuring sustainable performance. Al-Shaer and Zaman [95], Bravo and Reguera-Alvarado [96] and Cruz and Tolentino [97] recognized the positive role of a diversified board on sustainability performance. In the same vein, Carter, D’Souza [98] and Rao and Tilt [99] highlighted the importance of diversified stakeholders in corporate governance structure to ensure sustainable and financial performance. Hussain, Rigoni [12] demonstrated that corporate governance enhances sustainability performance by building stakeholder trust. Furthermore, García Martín and Herrero [100], Shahrier, Ho [101] and Shahrier, Ho [101] identified education background of board of directors, a crucial characteristic of board composition, as generating positive outcomes on sustainability performance. Considering the aforementioned arguments, this study posits following:

Corporate governance entails the implementation of some crucial policy instruments to attain organizational goals; it encompasses control mechanisms, risk management, corporate strategy and coordination [102,103]. A desired corporate governance mechanism promotes better innovation management activities for achieving organizational sustainability. Prior research claimed that the possession of a larger number of boards of directors and an internal governance mechanism promotes firms’ innovation and sustainability performance [104,105,106]. Wang, Abbasi [107] argued that a larger board size would promote firms’ innovation by enabling the convergence of expertise, skills and ideas. However, Suman and Singh [108] and AlHares [109] identified agency conflict and communication gaps due to larger board size as key hindrances to firms’ innovation. Consequently, Fu [110], [111] recommended a positive role of independent directors in innovative performance. Nevertheless, some researchers found that concentrated ownership could facilitate sustainable innovation, since large stockholders have the power and incentive to encourage management toward innovation [112,113]. In view of the foregoing, this research posits the following hypotheses:

H5:

Corporate governance enhances sustainability performance in the Bangladeshi manufacturing industry.

H6:

Corporate governance enhances innovation performance in the Bangladeshi manufacturing industry.

2.3.4. Innovation Performance and Sustainability Performance

Sustainability is defined as a “mother lode of organizational and technological innovations”[114]. Examining the impact of innovation on sustainability performance is crucial to promote the SDG 9. Knowles [115] mentioned that a firm’s ability to innovate positively influences its capability of survival and prospects. Similarly, Varis and Littunen [116] highlighted that the survival, success and growth of corporations tremendously depend on innovation capability irrespective of their size and other attributes. They investigated different dimensions of innovation and found that a firm’s growth was positively influenced by market, product and process innovations, as opposed to organizational innovation. Chen, Liu [117] also identified the crucial role of administrative, product and process innovation on firm sustainability. Bakar and Ahmad [118] demonstrated that innovation capability is crucial for the expansion and growth opportunities of businesses and also their achievement of a competitive edge. Bakhtina [119] acknowledged the contribution of innovation in controlling carbon emissions and climate change. Also, Weihong, Caitao [120] highlighted the role of cultural openness and the learning capability of firms in their attainment of sustainable competitive advantage. Backed by these shreds of evidence, the following hypothesis is advanced:

H7:

Innovation Performance enhances sustainability performance in the Bangladeshi manufacturing industry.

2.3.4. The Mediating Role of Innovation on the Relationship Between ESG and Sustainability Performance

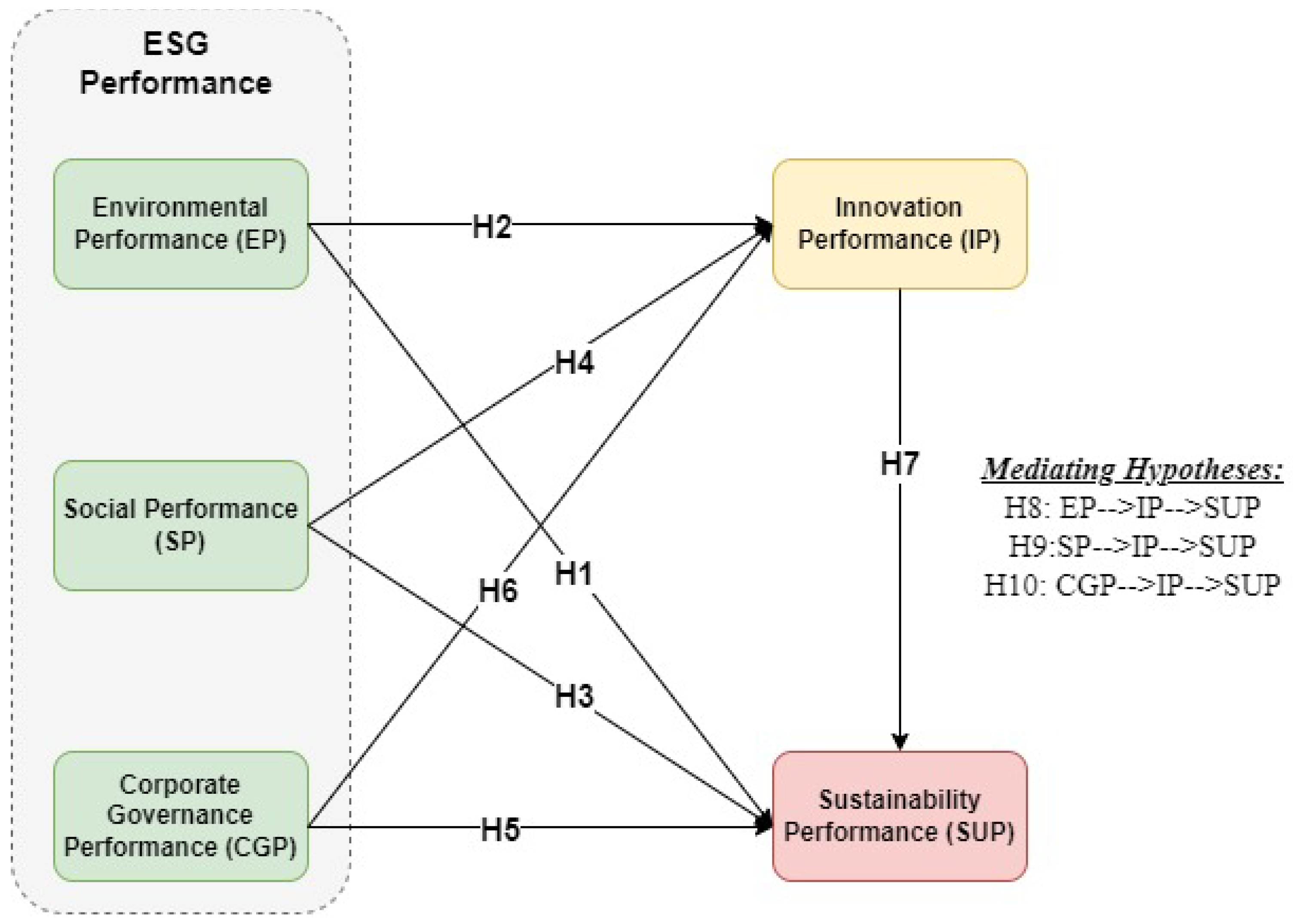

Considering the importance of sustainability, firms, policymakers and societal actors are now searching for innovation to help organizations achieve sustainability [121]. Innovation is considered a key factor in a sustainable manufacturing process [122]. Prior studies described a sustainable manufacturing system as the development of the product while conforming with the global best practices, such as controlling negative environmental consequences, conserving natural resources and energy and ensuring the safety of the workplace [123]. Kanashiro and Rivera [124] demonstrated that sustainability issues could be solved through strategic change, innovation and new strategy implementation. Wong, Tseng [125] highlighted the significance of green innovation in controlling environmental impact and attaining eco-targets. Albort-Morant, Leal-Millán [126], Huang, Hu [127] and Tang, Qiu [128] described green innovation as having a positive impact on the management of internal dynamic dimensions, pressure from market and customers as well as compliance with environmental regulations. Dicuonzo, Donofrio [129] identified a positive relationship between ESG performance and innovation, measured by R&D investment and the number of patents developed by firms. As an innovation, De Santis and Presti [130] suggested that big data could help achieve sustainability. Carayannis, Sindakis [131] described business model innovation and technology as prerequisites for growth and industrialization. Ahmad and Wu [132] also evidenced the role of eco-innovation on ecological sustainability. Du and Li [133] documented that technological innovation promotes total factor carbon productivity. Although several studies have found a positive relationship between innovation and sustainability, some researchers like Du and Li [133], Marsat and Williams [134], and Mithani [135] demonstrated that innovation negatively affects sustainability. These literature works further evidenced that innovation influences ESG practices as well as sustainability, and the impact of ESG on some crucial corporate issues was found to be mediated by innovation. Chouaibi, Chouaibi [11] and Xu, Imran [136] identified mediating role of green innovation on ESG and financial performance. Ge, Xiao [137] demonstrated that innovation input mediates the relationship between ESG and the high-quality development of Chinese enterprises. Yoo, Yeon [138] confirmed the mediating role of technology on CSR and corporate financial performance in the US hospitality industry. Shih [139] also noted that innovation, an outcome of knowledge management, mediates the CSR contribution to promoting corporate’s performance. Wang, He [140] showed that different types of environmental regulation positively influence sustainability performance through the innovation of green technology. Javed, Ali [141] demonstrated that innovation plays significant mediating role between ESG and responsible leadership. The impact of economic, social and environmental performance on different corporate outcome through innovation has been studied extensively, but a significant research gap exists on the mediating role of innovation on the association between ESG and sustainability performance. In light of above-mentioned, this study hypothesizes the following:

H8:

Innovation performance mediates the relationship between environmental performance and sustainability performance.

H9:

Innovation performance mediates the relationship between social performance and sustainability performance.

H10:

Innovation performance mediates the relationship between corporate governance performance and sustainability performance.

Figure 2.

Proposed Model.

3. Materials and Methods

3.1. Sample and Data Collection Procedure

To collect data, a structured close-ended questionnaire was distributed among employees of manufacturing industries in Chattogram, a port city and the site of most Bangladeshi companies. The manufacturing industry has been selected for this study due to the lack of prior studies on the relationship between ESG and sustainability performance in the industry and the developing country, particularly Bangladesh. The manufacturing industry has been selected for this study due to the lack of prior studies on the relationship between ESG and sustainability performance in the industry and the developing country, particularly Bangladesh. The manufacturing industry is a critical part of the economy in Bangladesh, and it is important to understand how ESG and sustainability performance can be improved in this sector. This study will help to fill the gap in the literature and allow for a better understanding of the relationship between ESG and sustainability performance in the manufacturing sector. This study will identify best practices for improving ESG and sustainability performance in the manufacturing sector of Bangladesh, and provide a basis for further research and policy-making. Based on random stratified sampling, a total of 350 questionnaires were served, of which 280 were returned. However, after filtering out the incomplete data, a total of 250 complete responses, indicating a response rate of 71.43%, were retained for further analysis. Studies have suggested that for investigation having three or more indicators per factor, a sample size of 150 is usually considered sufficient for a convergent and proper solution [142]. As a result, respondents demographic information as can be shown in Table 1.

3.2. Measurement Instrument

The respondents were asked to complete a closed-ended structured questionnaire to assess their firm sustainable performance (SUP). The questionnaire employed a seven-point Likert scale ranging from one (strongly disagree) to seven (strongly agree). Items of the questionnaire were adapted from earlier research [10,44,92,143] on ESG practices and sustainable performance. The survey was made up of two segments: demographic and item-related sections. Specifically, the study included twenty-two (22) items with seven (5) latent variables. The items under each construct have been presented in Appendix A.

3.3. Data Analysis Tools

The study used Partial Least Squares – Structural Equation Modelling (PLS-SEM) to examine the hypothesized relationship. Since PLS-SEM enables the estimation of a number of intricate structural relationships between the variables and the investigation of their mediating effects, this method is especially suitable for this model. Furthermore, PLS-SEM can produce reliable results with a small sample size [144]. The PLS-SEM analysis was carried out using SmartPLS 3.3.3 software, and the model was developed from a causal approach [145]. To clarify the complex interactions between one or more predictor factors and one or more dependent variables, this study used a number of statistical approaches, including measurement and structural models. While the structural model investigated the interactions between latent variables, the measurement model focused on the relationships between measurable and latent variables [143].

For the descriptive statistics, the study estimated the mean, standard deviation, skewness and kurtosis. The study also performed Cronbach’s Alpha (CA) coefficient, Average Variance Extracted (AVE) and Composite Reliability (CR) to check the consistency and reliability of the data. Moreover, the study estimated R2 to check the explaining power of the model and conducted the Fornell-Larcker test to check the discriminant validity of the constructs. Also, HTMT correlations were analyzed to check the internal correlations among the variables and multicollinearity issues, and lastly, SEM was performed to examine the significance of the proposed relationships.

4. Results

4.1. Descriptive Statistics

For descriptive analysis, the study calculated the mean, standard deviation, Kurtosis and Skewness (see Table 2). The mean value of all items was observed to be within the range of 5–6, indicating that most of the respondents moderately agree with items of sustainability performance and its indicators. Moreover, the standard deviations were within 0.5 to 0.7, suggesting that the items are uniformly dispersed. Furthermore, the values of Kurtosis and Skewness were lower than 3 and 10, respectively, thus validating the normality of the data and their suitability for further analysis [146]. Also, the VIF values of all items were less than the threshold of 10, indicating the absence of multicollinearity in the study [147]. Finally, since the predictor and outcome data have been collected with a single technique, the study examined the presence of Common Method Bias (CBM) and confirmed the inexistence of CBM.

4.2. Reflective Measurement Model

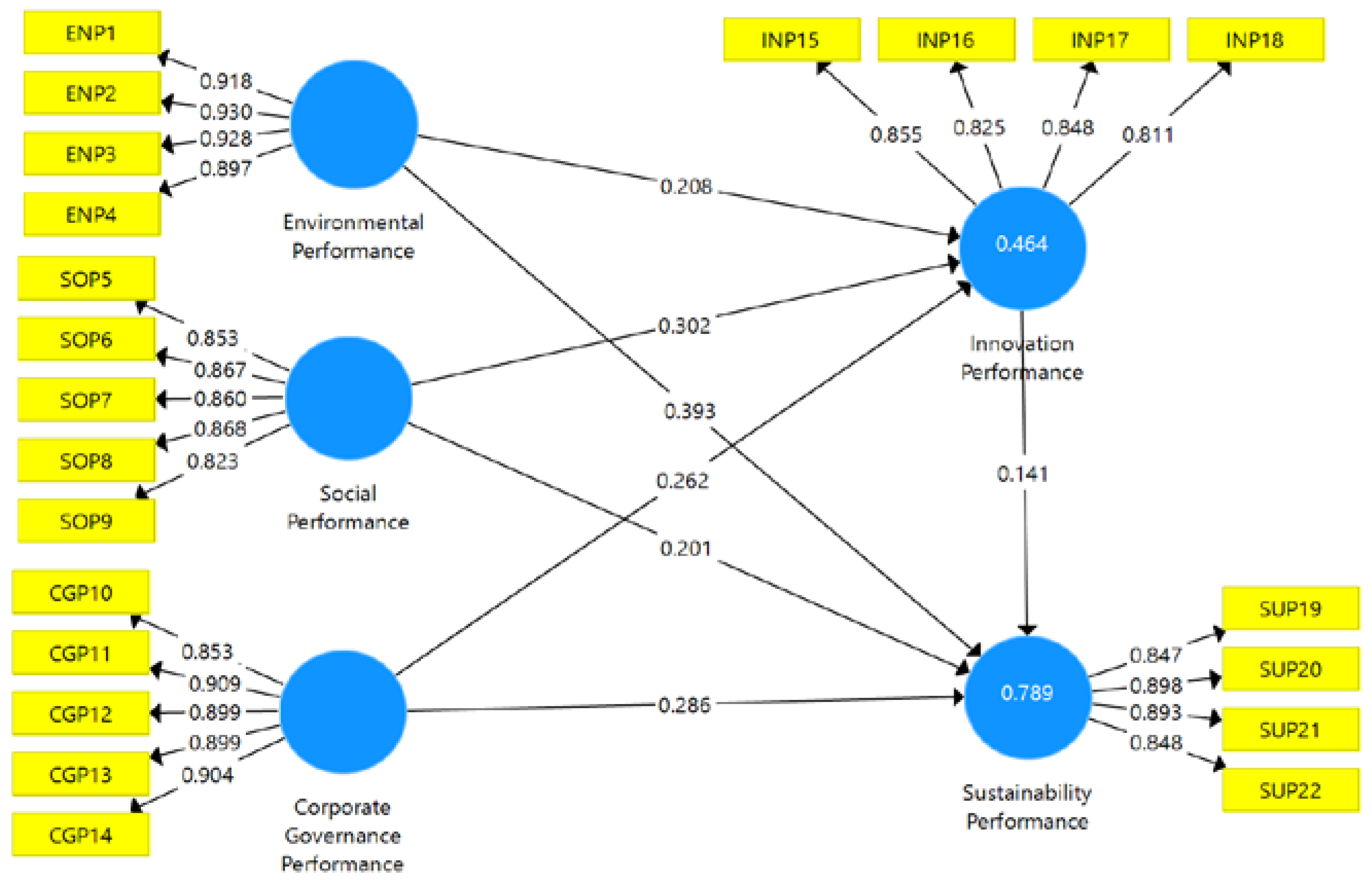

The study validates the measurement of the constructs by undertaking reliability (item and internal consistency) and validity (convergent and discriminant) tests. First, the study examines the loading values of individual items shown in Table 1 and Figure 1 to evaluate the internal consistency. The results revealed that the loading values of all items exceeded the threshold value of 0.70 [148], indicating that items utilized in this study are reliable. Table 3 shows the outcomes of the construct’s reliability and validity. Moreover, the internal reliability of the structures was validated using CA and CR values, and a result greater than 0.70 is considered acceptable [148]. As the CA and CR values for all factors were higher than the recommended value of 0.7 [148], the study satisfies the internal consistency requirement.

Figure 1.

Measurement Model.

Further, the study examines the convergent validity using the AVE. The values of AVE were between 0.697 and 0.843, which exceed the threshold level of 0.05 [148]. Therefore, the research fulfills the criteria of convergent validity. Additionally, the Heterotrait–Monotrait correlation ratio (HTMT) and the Fornell–Larcker criteria were employed to evaluate the discriminant validity of the research constructs. The discriminant validity results, which are displayed in Table 4, showed that each set of variable correlations did not exceed the square root of the AVE. Likewise, all component HTMT values were less than 0.90, proving that discriminant validity is not a problem [149]. In other words, the investigated variables have a strong discriminant validity [150].

4.3. Model Fit Statistics

Table 3 represents the constructs’ predictive power, which also shows how well the model’s explanatory variables predict outcomes. The result showed a predictive power (R2) of 0.789 and 0.464 for innovation performance and sustainability performance, respectively. As per past literature, an R2 value larger than 0.26 [151] is indicative of good predictive power.

The Confirmatory Factor Analysis (CFA) was further performed on the final measurement model to examine the degree of fit of our measuring model. However, the validity of the CFA model is dependent on the good fit of the conceptual model. To check the fitness of the model, the study employed the Standardized Root Mean Square Residual (SRMR), which is an indicator of the difference between the observed correlation and the model-implied correlation matrix. The results revealed an SRMR value of 0.05, which is less than the benchmark of 0.08 [152] and thus confirms the fitness of our proposed model.

4.4. SEM Hypotheses Testing

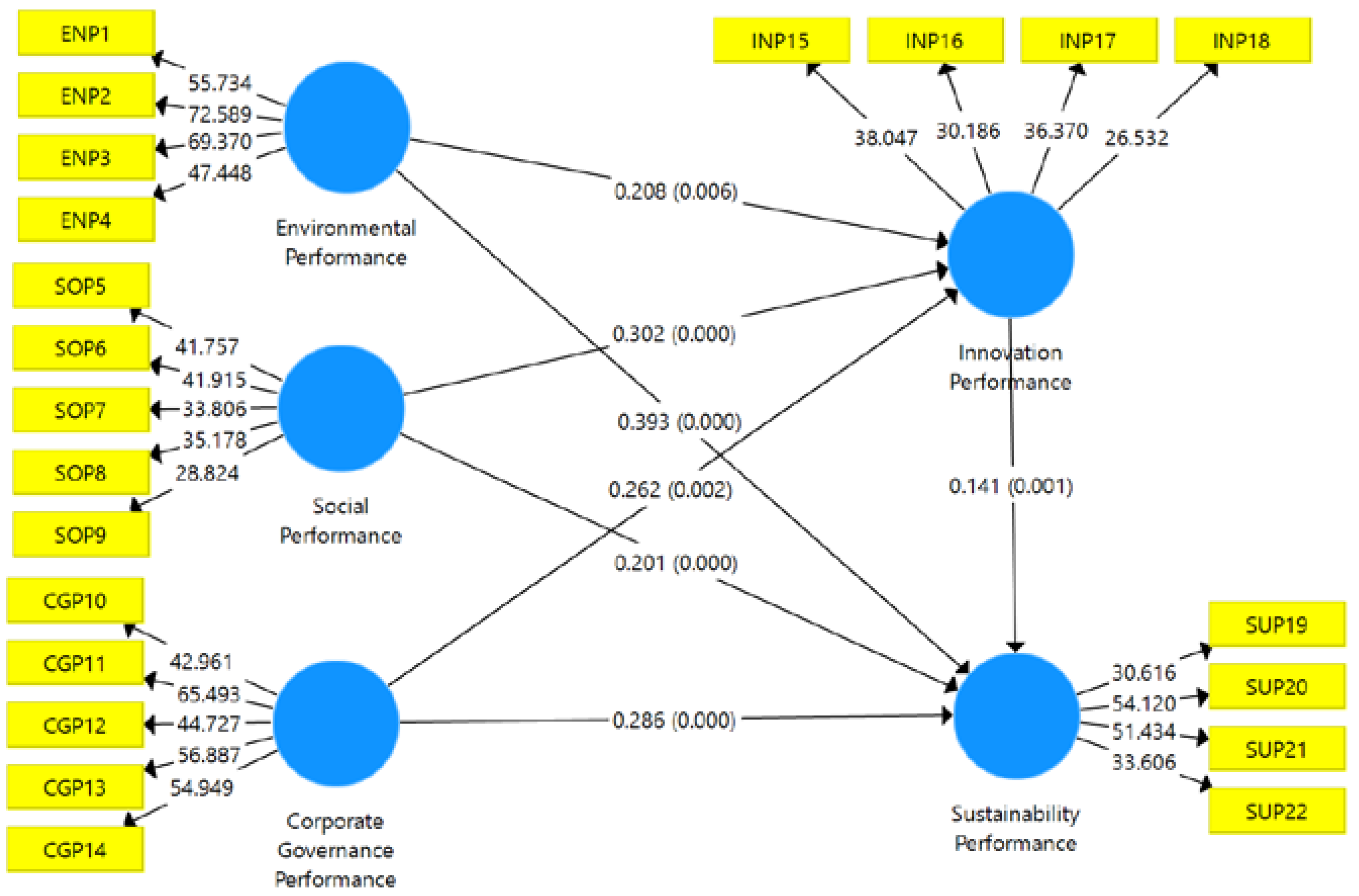

To test the proposed hypotheses, the study applied the SEM method, a popular multivariate statistical tool for validating the relationship between latent variables [149]. Additionally, the SEM method is more suitable for both complex and simple models [145], and its result show the paths, beta values (coefficients), t-statistics and p-values. The SEM results are presented in Table 5 and showed that environmental performance (EP) significantly impacts sustainability performance (SUP) (β1 = 0.393, p = 0.001), thus supporting H1. The coefficient value indicates that a 1% change in EP results in a 0.392% change in SUP. Similarly, EP was observed to significantly impact innovation performance (IP) (β1 = 0.208, p = 0.007), thus validating H2. The results also revealed that a 1% change in EP leads to a 0.208% change in IP. The social performance (SOP) was found to enhance both SUP (β1 = 0.201, p = 0.000) and IP (β1 = 0.302, p = 0.000) at the 1% level of significance, supporting H3 and H4. The results indicated that a 1% rise in SOP would enhance the SUP and IP by 0.20% and 0.30%, respectively. Moreover, Table 5 also shows that corporate governance performance (CGP) positively and significantly impacts the SUP (β1 = 0.286, p = 0.000) and IP (β1 = 0.262, p = 0.002) in the Bangladeshi manufacturing industry, thus affirming H5 and H6, respectively. The results further indicated that if the governance performance is raised by 1%, the SUP and IP will be increased by 0.286% and 0.262%, respectively. The result of the direct relationship between the mediating variables (IP and SUP) supported the H7 of a significant positive effect of IP on SUP (β1 = 0.141, p = 0.002) at the 1% level of significance.

Figure 2.

SEM outputs.

Further, the SEM hypotheses results showed that IP fully mediates the relationship between ESG and firm SUP at the 5% significance level. More specifically, IP has a significant positive influence on the effects of EP, SOP and CGP on SUP. Therefore, the results supported H8, H9 and H10, and further indicated that a 1% increase in EP, SOP and CGP would enhance the SUP by 0.029%, 0.043% and 0.037% respectively, via IP.

5. Discussion and Conclusion

The study examines whether ESG performance impacts sustainability performance through the mediating effect of firm innovation in Bangladeshi manufacturing industries. The results revealed that the higher the ESG performance of a firm, the greater its sustainability and innovation performance. Moreover, innovation fully mediates the relationship between ESG initiatives and sustainability performance, indicating that if a firm enhances its innovation performance, its ESG will accelerate sustainability performance.

As exhibited in Table 2 and Figure 2, a positive relationship exists between environmental performance, innovation and sustainability performance. The empirical results support hypotheses H1 and H2 and are consistent with the findings of prior literature [56,57,58]. The finding implies that the higher the environmental performance of manufacturing industries, the greater their sustainability performance. In other words, if firms ensure the reduction of air emissions, hazardous and harmful material consumption and frequent environmental accidents through proper resource, energy and waste management, their environmental performance will increase. Moreover, environmental performance enhances firms’ ability to identify the new dimension of environmental knowledge and innovation and use it for providing innovative business solutions and developing products and processes [62]. Thus, the study evidenced that environmental performance plays a crucial role in making manufacturing firms in Bangladesh more sustainable and innovative.

Similarly, a significant positive relationship was observed between social performance, innovation and sustainability performance, supporting hypotheses, H3 and H4. The result agrees with the studies of Chaim, Muschard [68], Chams and García-Blandón [71] and Kim [72]. The result indicates that if firms improve their human rights, health and safety within their business practices, their social performance will be enhanced [67]. This advises that firms take necessary initiatives such as the provision of employee training and development, promotion of occupational health and safety, and maintenance of commitment to employee job security and satisfaction as well as community and societal satisfaction to enhance their social performance and in turn achieve long-term sustainability performance. Moreover, social performance enhances firms’ capacity of innovativeness [83] and creativity [84]. Therefore, the study documented that social performance plays a significant role in the firms’ achievement of sustainability and innovation performance.

Moreover, the study found a significant positive association between corporate governance performance, innovation performance and sustainability performance, thereby supporting H5 and H6 as well as the findings of prior studies [88,89,90,91]. As good governance encourages firms to prioritize social and environmental issues, corporate governance can be said to be a determinant of sustainability performance [94]. The findings suggest that regulatory bodies should monitor the conformance of firms with environmental and social standards to promote sustainable practices. Also, strong corporate governance demands that the board of directors and investors should not only focus on financial performance but also ensure ESG compliance to enhance sustainability performance. The board of directors should also ensure transparency and accountability at all organizational level while promoting environmental compliance to build good governance and ultimately accelerate sustainability performance. Additionally, concentrated ownership could facilitate sustainable innovation, since large stockholders have the power and incentive to encourage management toward innovation [112,113]. The findings also suggest that the management of the manufacturing sectors exercise caution when deciding which risk-control tools to implement.

As indicated in the result, a significant positive relationship was observed between innovation performance and sustainability performance, thus validating H7. The survival, success and growth of a firm are highly dependent on its innovation capacity, firm market, and product and process innovation, all of which also contribute to the firm’s sustainability performance [116,117]. Moreover, innovation performance provides firms with a more competitive edge in expanding their business operation [118]. Therefore, firms need to focus on product design and development to satisfy the customers and consequently enhance their sustainability.

Further, the results revealed that innovation performance fully mediates the relationship between ESG and sustainability performance, thus supporting H8, H9 and H10. The study found that ESG performance, directly and indirectly, influences innovation performance, which in turn generates a positive impact on sustainability performance. The findings indicate that if a firm’s ESG performance increases, its innovation performance will improve. Firm innovation is, therefore, considered a crucial factor in ensuring sustainability performance, as it also mediates the effect of ESG performance on firm performance [136] and other corporate issues [11]. Through innovation performance, the firm can develop products and sustainable manufacturing processes. Moreover, innovation performance encourages organizational change to achieve sustainability [121] by controlling negative environmental consequences, conserving natural resources and energy, and ensuring the safety of the workplace [123]. Innovation performance also helps firms’ management to comply with environmental, social and governance regulations. Due to innovation performance, products are developed and designed in a way that enables their recycling, reuse and decomposition. Additionally, innovation in green technology increases firms’ capacity to satisfy customers with newly designed products, which in turn enhances their competitiveness in the global market. This not only reduces energy consumption and production cost but also enhance firm productivity and financial performance. Therefore, firms should focus on improving their innovation performance to enhance the effect of ESG performance on their sustainability performance.

6. Theoretical and Practical Implications of the Study

The findings of this study have several implications for the policymakers, the industries’ authorities, firm managers, regulatory bodies and other stakeholders. The study provides valuable insight into actions necessary to ensure better sustainability performance through ESG and innovation performance. Since environmental issues are a great concern for environmental pressure groups, regulatory bodies and society, the study suggests that firms consider ESG performance while making a business decision. Firms’ prioritization of ESG not only help them achieve a competitive edge and high compliance rating but also ensure their attainment of better sustainability performance. In this era of globalization, researchers, economists, and government and non-government organizations are now concentrating on pro-environmental and social initiatives, including the development of green production processes, reduction of air emissions and solid waste, promotion of employees and society’s welfare, and encouragement of green behavior among the general public. Therefore, this study highlights some policy implications that are relevant to social and environmental issues of manufacturing industries. First, the study provides academics with a new conceptual model on how firm innovation plays a crucial mediating role in the relationship between ESG performance and sustainability performance. Second, the study advises firms’ managers to adopt new technology and strategies and consider eco-friendly projects while developing their products. The adoption of innovation in product design help firms not only to satisfy their customers but also to help minimize their eco-unfriendly actions, such as the generation of greenhouse gases and solid wastes. Third, to enhance their reputation, firms should take the necessary initiatives to develop their employees, ensure occupational health and safety, enhance job security and remunerations, and address the concerns of the community and other stakeholders. Fourth, the regulatory bodies in conjunction with stakeholders at different levels should monitor the compliance of industries with environmental rules and regulations to promote green innovation and sustainable performance and ultimately protect the environment [153]. Finally, the research offers insights into how the government, local community, corporate organizations and other stakeholders may work together to successfully attain sustainable performance in various industries. This includes the establishment of a set of corporate rules and regulations that guarantee that all manufacturing industries manage environmental resources, ensure high-quality production processes, manage waste and make socially responsible contributions. Additionally, industry management could emphasize the importance of sustainable development and conservation of the environment for future generations by raising public awareness about green performance.

7. Limitations and Directions for Future Studies

Like many other studies, the present study has several flaws. First, the study collected data from employees of manufacturing industries, while neglecting other significant players in the manufacturing industries; hence, the findings may be biased. Due to the employees’ reluctance to contribute to the data and the industries’ restrictions on access to the workers, the sample size was modest. Therefore, the results of the current research could be strengthened by increasing the sample size and considering other stakeholders in the manufacturing sector, including investors, customers and top-level managers. Future research can also investigate similar hypotheses among other industries operating in Bangladesh (e.g., financial and non-financial sectors). Second, to strengthen the findings, future studies could investigate the impact of ESG performance on sustainability and economic performance through the mediating effect of green innovation practices. Finally, because the study was carried out in Bangladesh, a developing nation, its conclusions may not be generalizable. Thus, future researchers could carry out a cross-country investigation and a study of similar objectives but on other industries.

Ethics approval and consent to participate

Ethical review and approval were waived for this study due to the fact that there is no institutional review board or committee in Bangladesh. Besides, the study was conducted as per the guidelines of the Declaration of Helsinki. The research questionnaire was anonymous, and no personal information was gathered.

Informed Consent Statement

Oral consent was obtained from all individuals involved in this study.

Availability of data and materials

The data that support the findings of this study are available from the corresponding authors upon reasonable request.

Competing interests

The authors declare no conflict of interest.

Author Contributions

Conceptualization, ShuKang Zhou; Formal analysis, Shah Asadullah Mohd. Zobair; Funding acquisition, ShuKang Zhou; Investigation, ShuKang Zhou, Md. Harun Ur Rashid and Shah Asadullah Mohd. Zobair; Methodology, Shah Asadullah Mohd. Zobair; Project administration, Md. Harun Ur Rashid and Farid Sobhani; Resources, Md. Harun Ur Rashid and Abu Bakkar Siddik; Software, ShuKang Zhou; Supervision, Farid Sobhani; Validation, Md. Harun Ur Rashid and Abu Bakkar Siddik; Visualization, Shah Asadullah Mohd. Zobair, Farid Sobhani and Abu Bakkar Siddik; Writing – original draft, ShuKang Zhou and Md. Harun Ur Rashid; Writing – review & editing, Shah Asadullah Mohd. Zobair, Farid Sobhani and Abu Bakkar Siddik.

Funding

This study has not received any external funding.

Acknowledgments

The researchers would like to express their gratitude to the anonymous re-viewers for their efforts to improve the quality of this paper.

Appendix A

Table A1.

Survey Items.

| Item code | Descriptions | Sources |

| Environmental Performance (ENP) | ||

| ENP1 | Reduction of air emissions. | [143] |

| ENP2 | Minimization of effluent/ solid waste. | |

| ENP3 | Less consumption of hazardous/harmful/toxic materials. | |

| ENP4 | Reduced the frequency of environmental accidents. | |

| Social Performance (SOP) | ||

| SOP5 | Training and development of employee | [25] |

| SOP6 | Promotion of employee occupational health and safety | |

| SOP7 | Employee job security and satisfaction | |

| SOP8 | Commitment to community and society satisfaction | |

| SOP9 | Supplier commitment and initiative | |

| Corporate governance performance (CGP) | ||

| CGP10 | Compliance with the set standards | [44] |

| CGP11 | Improvement of environmental compliance | |

| CGP12 | Improved the set of rules and regulations | |

| CGP13 | Enhancement of risk control mechanism | |

| CGP14 | Promotion of transparency and accountability | |

| Innovation performance (INP) | ||

| INP15 | Improvement of the level of customer satisfaction with product design and development. | [92] |

| INP16 | Development of products that are easy to recycle, reuse and decompose. | |

| INP17 | Improved continual introduction of new product ideas into the production process. | |

| INP18 | Improved market success of new products being tested. | |

| Sustainability performance (SUP) | ||

| SUP19 | Reduction of the rate of energy consumption and enhancement of economic development | [51,52] |

| SUP20 | Strengthening of the capacity for innovation in green technology and enhancement of competitiveness in the global arena | |

| SUP21 | Promotion of sustainable development and preservation of the environment for future generations | |

| SUP22 | Promotion of best practices and public awareness of the GP. | |

References

- Chin, T.A., H.H. Tat, and Z. Sulaiman, Green supply chain management, environmental collaboration and sustainability performance. Procedia Cirp, 2015. 26: p. 695-699. [CrossRef]

- Acciaro, M., et al., Environmental sustainability in seaports: a framework for successful innovation. Maritime Policy & Management, 2014. 41(5): p. 480-500. [CrossRef]

- Iqbal, Q., N.H. Ahmad, and H.A. Halim, Insights on entrepreneurial bricolage and frugal innovation for sustainable performance. Business Strategy & Development, 2021. 4(3): p. 237-245. [CrossRef]

- Niroumand, M., et al., Frugal innovation enablers: a comprehensive framework. International Journal of Innovation Science, 2020. [CrossRef]

- Iqbal, Q., N.H. Ahmad, and B. Ahmad, Enhancing sustainable performance through job characteristics via workplace spirituality: A study on SMEs. Journal of Science and Technology Policy Management, 2018.

- Holden, E., et al., The imperatives of sustainable development: needs, justice, limits. 2017: Routledge.

- Xu, J., F. Liu, and Y. Shang, R&D investment, ESG performance and green innovation performance: Evidence from China. Kybernetes, 2020. [CrossRef]

- Li, T.-T., et al., ESG: Research progress and future prospects. Sustainability, 2021. 13(21): p. 11663. [CrossRef]

- Broadstock, D.C., et al., The role of ESG performance during times of financial crisis: Evidence from COVID-19 in China. Finance research letters, 2021. 38: p. 101716. [CrossRef]

- Alsayegh, M.F., R. Abdul Rahman, and S. Homayoun, Corporate economic, environmental, and social sustainability performance transformation through ESG disclosure. Sustainability, 2020. 12(9): p. 3910. [CrossRef]

- Chouaibi, S., J. Chouaibi, and M. Rossi, ESG and corporate financial performance: the mediating role of green innovation: UK common law versus Germany civil law. EuroMed Journal of Business, 2021. [CrossRef]

- Hussain, N., U. Rigoni, and R.P. Orij, Corporate governance and sustainability performance: Analysis of triple bottom line performance. Journal of business ethics, 2018. 149(2): p. 411-432. [CrossRef]

- Deegan, C., Introduction: The legitimising effect of social and environmental disclosures–a theoretical foundation. Accounting, auditing & accountability journal, 2002.

- Maali, K., R. Rakia, and M. Khaireddine, How corporate social responsibility mediates the relationship between corporate governance and sustainability performance in UK: a multiple mediator analysis. Society and Business Review, 2021. [CrossRef]

- Yang, Q., et al., How volatility in green financing, clean energy, and green economic practices derive sustainable performance through ESG indicators? A sectoral study of G7 countries. Resources Policy, 2022. 75: p. 102526. [CrossRef]

- Kocmanová, A. and I. Šimberová, Determination of environmental, social and corporate governance indicators: framework in the measurement of sustainable performance. Journal of Business Economics and Management, 2014. 15(5): p. 1017-1033. [CrossRef]

- Ye, C., X. Song, and Y. Liang, Corporate sustainability performance, stock returns, and ESG indicators: fresh insights from EU member states. Environmental Science and Pollution Research, 2022. 29(58): p. 87680-87691. [CrossRef]

- Zhang, X., X. Zhao, and Y. He, Does it pay to be responsible? The performance of ESG investing in China. Emerging Markets Finance and Trade, 2022: p. 1-28. [CrossRef]

- Niesten, E., et al., Sustainable collaboration: The impact of governance and institutions on sustainable performance. Journal of cleaner production, 2017. 155: p. 1-6. [CrossRef]

- Crisóstomo, V.L., F. de Souza Freire, and M.R.D.O. Freitas, Determinants of corporate sustainability performance–evidence from Brazilian panel data. Social Responsibility Journal, 2019. [CrossRef]

- Miralles-Quirós, M.M., J.L. Miralles-Quirós, and L.M. Valente Gonçalves, The value relevance of environmental, social, and governance performance: The Brazilian case. Sustainability, 2018. 10(3): p. 574. [CrossRef]

- Yoon, B., J.H. Lee, and R. Byun, Does ESG performance enhance firm value? Evidence from Korea. Sustainability, 2018. 10(10): p. 3635. [CrossRef]

- Garcia, A.S., W. Mendes-Da-Silva, and R.J. Orsato, Corporate sustainability, capital markets, and ESG performance, in Individual behaviors and technologies for financial innovations. 2019, Springer. p. 287-309.

- Rajesh, R., Exploring the sustainability performances of firms using environmental, social, and governance scores. Journal of Cleaner Production, 2020. 247: p. 119600. [CrossRef]

- Sultana, S., N. Zulkifli, and D. Zainal, Environmental, social and governance (ESG) and investment decision in Bangladesh. Sustainability, 2018. 10(6): p. 1831. [CrossRef]

- Zheng, G.-W., et al., Factors affecting the sustainability performance of financial institutions in Bangladesh: the role of green finance. Sustainability, 2021. 13(18): p. 10165. [CrossRef]

- FAKIR, A. and R. JUSOH, Board gender diversity and corporate sustainability performance: Mediating role of enterprise risk management. The Journal of Asian Finance, Economics and Business, 2020. 7(6): p. 351-363. [CrossRef]

- Tribune, D., Is Bangladesh’s manufacturing sector fit to compete? 2022. https://www.dhakatribune.com/business/2022/10/11/is-bangladeshs-manufacturing-sector-fit-to-compete.

- Zaid, A.A., A.A. Jaaron, and A.T. Bon, The impact of green human resource management and green supply chain management practices on sustainable performance: An empirical study. Journal of cleaner production, 2018. 204: p. 965-979.

- Mohua, M.J. and W.F.W. Yusoff. Are Institutional Pressures Influencing on Sustainable Business Performance in the RMG Industries of Bangladesh? in Business Innovation and Engineering Conference 2020 (BIEC 2020). 2021. Atlantis Press.

- Rashid, M.H.U., et al., Factors influencing green performance in manufacturing industries. International Journal of Financial Research, 2019. 10(6): p. 159-173.

- Hossan, C.G., M.A.R. Sarker, and R. Afroze, Recent unrest in the RMG sector of Bangladesh: Is this an outcome of poor labour practices? International Journal of Business and Management, 2012. 7(3): p. 206.

- Ansary, M.A. and U. Barua, Workplace safety compliance of RMG industry in Bangladesh: Structural assessment of RMG factory buildings. International Journal of Disaster Risk Reduction, 2015. 14: p. 424-437. [CrossRef]

- Butler, S., Bangladeshi factory deaths spark action among high-street clothing chains. The Guardian, 2013. 23.

- Wang, C. and J. Li, The evaluation and promotion path of green innovation performance in Chinese pollution-intensive industry. Sustainability, 2020. 12(10): p. 4198. [CrossRef]

- Tariq, A., Y. Badir, and S. Chonglerttham, Green innovation and performance: moderation analyses from Thailand. European Journal of Innovation Management, 2019. [CrossRef]

- Flammer, C. and A. Kacperczyk, Corporate social responsibility as a defense against knowledge spillovers: Evidence from the inevitable disclosure doctrine. Strategic Management Journal, 2019. 40(8): p. 1243-1267. [CrossRef]

- Atan, R., et al., The impacts of environmental, social, and governance factors on firm performance: Panel study of Malaysian companies. Management of Environmental Quality: An International Journal, 2018.

- Ashrafi, M., et al., Understanding the conceptual evolutionary path and theoretical underpinnings of corporate social responsibility and corporate sustainability. Sustainability, 2020. 12(3): p. 760. [CrossRef]

- Freeman, R.E. and S. Dmytriyev, Corporate social responsibility and stakeholder theory: Learning from each other. Symphonya. Emerging Issues in Management, 2017(1): p. 7-15. [CrossRef]

- Rezaee, Z., Business sustainability research: A theoretical and integrated perspective. Journal of Accounting literature, 2016. [CrossRef]

- Kramer, M.R. and M. Porter, Creating shared value. Vol. 17. 2011: FSG Boston, MA, USA.

- Guthrie, J. and L.D. Parker, Corporate social reporting: a rebuttal of legitimacy theory. Accounting and business research, 1989. 19(76): p. 343-352. [CrossRef]

- Masud, M.A.K., et al., Organizational strategy and corporate social responsibility: The mediating effect of triple bottom line. International journal of environmental research and public health, 2019. 16(22): p. 4559.

- Michelon, G., S. Pilonato, and F. Ricceri, CSR reporting practices and the quality of disclosure: An empirical analysis. Critical perspectives on accounting, 2015. 33: p. 59-78. [CrossRef]

- Deegan, C., EBOOK: Financial Accounting Theory: European Edition. 2011: McGraw Hill.

- Deephouse, D.L., Does isomorphism legitimate? Academy of management journal, 1996. 39(4): p. 1024-1039.

- Eliwa, Y., A. Aboud, and A. Saleh, ESG practices and the cost of debt: Evidence from EU countries. Critical Perspectives on Accounting, 2021. 79: p. 102097. [CrossRef]

- Elkington, J., Partnerships from cannibals with forks: The triple bottom line of 21st-century business. Environmental quality management, 1998. 8(1): p. 37-51. [CrossRef]

- Khan, I.S., M.O. Ahmad, and J. Majava, Industry 4.0 and sustainable development: A systematic mapping of triple bottom line, Circular Economy and Sustainable Business Models perspectives. Journal of Cleaner Production, 2021. 297: p. 126655. [CrossRef]

- Kamble, S.S., A. Gunasekaran, and S.A. Gawankar, Achieving sustainable performance in a data-driven agriculture supply chain: A review for research and applications. International Journal of Production Economics, 2020. 219: p. 179-194. [CrossRef]

- Helleno, A.L., A.J.I. de Moraes, and A.T. Simon, Integrating sustainability indicators and Lean Manufacturing to assess manufacturing processes: Application case studies in Brazilian industry. Journal of cleaner production, 2017. 153: p. 405-416. [CrossRef]

- Moktadir, M.A., et al., Drivers to sustainable manufacturing practices and circular economy: A perspective of leather industries in Bangladesh. Journal of Cleaner Production, 2018. 174: p. 1366-1380.

- Fernando, J., UN Principles for Responsible Investment (PRI). Investopedia, 2022. https://www.investopedia.com/terms/u/un-principles-responsible-investment-pri.asp.

- Zhu, D., Research from global Sustainable Development Goals (SDGs) to sustainability science based on the object-subject-process framework. Chinese Journal of Population Resources and Environment, 2017. 15(1): p. 8-20. [CrossRef]

- Mousa, S.K. and M. Othman, The impact of green human resource management practices on sustainable performance in healthcare organisations: A conceptual framework. Journal of Cleaner Production, 2020. 243: p. 118595.

- Abdul-Rashid, S.H., et al., The impact of sustainable manufacturing practices on sustainability performance: Empirical evidence from Malaysia. International Journal of Operations & Production Management, 2017.

- Ali, M.H., et al., Impacts of environmental factors on waste, energy, and resource management and sustainable performance. Sustainability, 2019. 11(8): p. 2443. [CrossRef]

- Ong, T.S., et al., Environmental innovation, environmental performance and financial performance: Evidence from Malaysian environmental proactive firms. Sustainability, 2019. 11(12): p. 3494. [CrossRef]

- Crossan, M.M. and M. Apaydin, A multi-dimensional framework of organizational innovation: A systematic review of the literature. Journal of management studies, 2010. 47(6): p. 1154-1191. [CrossRef]

- Cohen, W.M. and D.A. Levinthal, Absorptive capacity: A new perspective on learning and innovation. Administrative science quarterly, 1990: p. 128-152. [CrossRef]

- Delmas, M.A. and V.C. Burbano, The drivers of greenwashing. California management review, 2011. 54(1): p. 64-87.

- Wagner, M., Innovation and competitive advantages from the integration of strategic aspects with social and environmental management in European firms. Business Strategy and the Environment, 2009. 18(5): p. 291-306. [CrossRef]

- Carrión-Flores, C.E. and R. Innes, Environmental innovation and environmental performance. Journal of Environmental Economics and Management, 2010. 59(1): p. 27-42. [CrossRef]

- Chiou, T.-Y., et al., The influence of greening the suppliers and green innovation on environmental performance and competitive advantage in Taiwan. Transportation Research Part E: Logistics and Transportation Review, 2011. 47(6): p. 822-836. [CrossRef]

- Sezen, B. and S.Y. Cankaya, Effects of green manufacturing and eco-innovation on sustainability performance. Procedia-Social and Behavioral Sciences, 2013. 99: p. 154-163. [CrossRef]

- Taddese, G., S. Durieux, and E. Duc, Sustainability performance indicators for additive manufacturing: a literature review based on product life cycle studies. The International Journal of Advanced Manufacturing Technology, 2020. 107(7): p. 3109-3134. [CrossRef]

- Chaim, O., et al., Insertion of sustainability performance indicators in an industry 4.0 virtual learning environment. Procedia Manufacturing, 2018. 21: p. 446-453. [CrossRef]

- Avery, G., Leadership for sustainable futures: Achieving success in a competitive world. 2005: Edward Elgar Publishing.

- Ketprapakorn, N. and S. Kantabutra, Sustainable social enterprise model: Relationships and consequences. Sustainability, 2019. 11(14): p. 3772. [CrossRef]

- Chams, N. and J. García-Blandón, On the importance of sustainable human resource management for the adoption of sustainable development goals. Resources, Conservation and Recycling, 2019. 141: p. 109-122. [CrossRef]

- Kim, J., Social dimension of sustainability: From community to social capital. Journal of Global Scholars of Marketing Science, 2018. 28(2): p. 175-181. [CrossRef]

- Duque-Grisales, E. and J. Aguilera-Caracuel, Environmental, social and governance (ESG) scores and financial performance of multilatinas: Moderating effects of geographic international diversification and financial slack. Journal of Business Ethics, 2021. 168(2): p. 315-334. [CrossRef]

- Choi, J. and H. Wang, Stakeholder relations and the persistence of corporate financial performance. Strategic management journal, 2009. 30(8): p. 895-907. [CrossRef]

- Costa, C., L.F. Lages, and P. Hortinha, The bright and dark side of CSR in export markets: Its impact on innovation and performance. International Business Review, 2015. 24(5): p. 749-757. [CrossRef]

- McWilliams, A. and D. Siegel, Corporate social responsibility and financial performance: correlation or misspecification? Strategic management journal, 2000. 21(5): p. 603-609.

- MacGregor, S.P., X. Espinach, and J. Fontrodona. Social innovation: Using design to generate business value through corporate social responsibility. in DS 42: Proceedings of ICED 2007, the 16th International Conference on Engineering Design, Paris, France, 28.-31.07. 2007. 2007.

- Mahlouji, H. and N.K. Anaraki, Corporate social responsibility towards social responsible innovation: A dynamic capability approach. International Review of Business Research Papers, 2009. 5(6): p. 185-194.

- Porter, M. and M. Kramer, Creating Shared Value. Harvard Business Review, 89 (1/2): 62-77. 2011.

- Bocquet, R., et al., Are firms with different CSR profiles equally innovative? Empirical analysis with survey data. European Management Journal, 2013. 31(6): p. 642-654. [CrossRef]

- Herrera, M.E.B., Creating competitive advantage by institutionalizing corporate social innovation. Journal of business research, 2015. 68(7): p. 1468-1474. [CrossRef]

- Li, D.-y. and J. Liu, Dynamic capabilities, environmental dynamism, and competitive advantage: Evidence from China. Journal of business research, 2014. 67(1): p. 2793-2799. [CrossRef]

- Broadstock, D.C., et al., Does corporate social responsibility impact firms’ innovation capacity? The indirect link between environmental & social governance implementation and innovation performance. Journal of Business Research, 2020. 119: p. 99-110. [CrossRef]

- Setini, M., et al., The passway of women entrepreneurship: Starting from social capital with open innovation, through to knowledge sharing and innovative performance. Journal of Open Innovation: Technology, Market, and Complexity, 2020. 6(2): p. 25. [CrossRef]

- Zhang, Q., L. Loh, and W. Wu, How do environmental, social and governance initiatives affect innovative performance for corporate sustainability? Sustainability, 2020. 12(8): p. 3380.

- Rodrigue, M., M. Magnan, and C.H. Cho, Is environmental governance substantive or symbolic? An empirical investigation. Journal of Business Ethics, 2013. 114(1): p. 107-129. [CrossRef]

- Ricart, J.E., M.Á. Rodríguez, and P. Sanchez, Sustainability in the boardroom: An empirical examination of Dow Jones Sustainability World Index leaders. Corporate Governance: the international journal of business in society, 2005. 5(3): p. 24-41.

- Spitzeck, H., The development of governance structures for corporate responsibility. Corporate Governance: The international journal of business in society, 2009.

- Liao, L., L. Luo, and Q. Tang, Gender diversity, board independence, environmental committee and greenhouse gas disclosure. The British accounting review, 2015. 47(4): p. 409-424. [CrossRef]

- Amran, A., S.P. Lee, and S.S. Devi, The influence of governance structure and strategic corporate social responsibility toward sustainability reporting quality. Business Strategy and the Environment, 2014. 23(4): p. 217-235. [CrossRef]

- Arena, C., S. Bozzolan, and G. Michelon, Environmental reporting: Transparency to stakeholders or stakeholder manipulation? An analysis of disclosure tone and the role of the board of directors. Corporate Social Responsibility and Environmental Management, 2015. 22(6): p. 346-361. [CrossRef]

- Rashid, M.H.U. and M.A. Hamid, Measurement of CSR Performance in Manufacturing Industries: A SEM Approach. International Journal of Social Ecology and Sustainable Development (IJSESD), 2022. 13(6): p. 1-18.

- Michelon, G. and A. Parbonetti, The effect of corporate governance on sustainability disclosure. Journal of management & governance, 2012. 16(3): p. 477-509. [CrossRef]

- Arora, P. and R. Dharwadkar, Corporate governance and corporate social responsibility (CSR): The moderating roles of attainment discrepancy and organization slack. Corporate governance: an international review, 2011. 19(2): p. 136-152. [CrossRef]

- Al-Shaer, H. and M. Zaman, Board gender diversity and sustainability reporting quality. Journal of Contemporary Accounting & Economics, 2016. 12(3): p. 210-222. [CrossRef]

- Bravo, F. and N. Reguera-Alvarado, Sustainable development disclosure: Environmental, social, and governance reporting and gender diversity in the audit committee. Business Strategy and the Environment, 2019. 28(2): p. 418-429. [CrossRef]

- Cruz, C. and C. Tolentino, Gender, social recognition, and political influence. 2019, Working Paper.

- Carter, D.A., et al., The gender and ethnic diversity of US boards and board committees and firm financial performance. Corporate Governance: An International Review, 2010. 18(5): p. 396-414. [CrossRef]

- Rao, K. and C. Tilt, Board composition and corporate social responsibility: The role of diversity, gender, strategy and decision making. Journal of Business Ethics, 2016. 138(2): p. 327-347. [CrossRef]

- García Martín, C.J. and B. Herrero, Do board characteristics affect environmental performance? A study of EU firms. Corporate Social Responsibility and Environmental Management, 2020. 27(1): p. 74-94. [CrossRef]

- Shahrier, N.A., J.S.Y. Ho, and S.S. Gaur, Ownership concentration, board characteristics and firm performance among Shariah-compliant companies. Journal of Management and Governance, 2020. 24(2): p. 365-388. [CrossRef]

- Sahar, E., N. Zulkifli, and Z. Zakaria, Corporate governance integration with sustainability: a systematic literature review. Corporate Governance: The international journal of business in society, 2018. [CrossRef]

- Kusi, B.A., et al., Does corporate governance structures promote shareholders or stakeholders value maximization? Evidence from African banks. Corporate Governance: The international journal of business in society, 2018. [CrossRef]

- Merendino, A. and R. Melville, The board of directors and firm performance: empirical evidence from listed companies. Corporate Governance: The international journal of business in society, 2019. [CrossRef]

- Gutiérrez-Martínez, I. and F. Duhamel, Translating sustainability into competitive advantage: the case of Mexico’s hospitality industry. Corporate Governance: The International Journal of Business in Society, 2019. [CrossRef]

- Rodriguez-Fernandez, M., Social responsibility and financial performance: The role of good corporate governance. BRQ Business Research Quarterly, 2016. 19(2): p. 137-151. [CrossRef]

- Wang, Y., et al., Corporate governance mechanisms and firm performance: evidence from the emerging market following the revised CG code. Corporate Governance: The international journal of business in society, 2019. [CrossRef]

- Suman, S. and S. Singh, Corporate governance mechanisms and corporate investments: evidence from India. International Journal of Productivity and Performance Management, 2020. 70(3): p. 635-656. [CrossRef]

- AlHares, A., Corporate governance mechanisms and R&D intensity in OECD courtiers. Corporate Governance: The International Journal of Business in Society, 2020. 20(5): p. 863-885.

- Fu, Y., Independent directors, CEO career concerns, and firm innovation: Evidence from China. The North American Journal of Economics and Finance, 2019. 50: p. 101037.

- Lu, J. and W. Wang, Managerial conservatism, board independence and corporate innovation. Journal of Corporate Finance, 2018. 48: p. 1-16.

- Omri, W., A. Becuwe, and J.-C. Mathe, Ownership structure and innovative behavior: Testing the mediatory role of board composition. Journal of Accounting in Emerging Economies, 2014.

- Asni, N. and D. Agustia, Does corporate governance induce green innovation? An emerging market evidence. Corporate Governance: The International Journal of Business in Society, 2022(ahead-of-print). [CrossRef]

- Nidumolu, R., C.K. Prahalad, and M.R. Rangaswami, Why sustainability is now the key driver of innovation. Harvard business review, 2009. 87(9): p. 56-64.

- Knowles, C.D., Measuring innovativeness in the North American softwood sawmilling industry. 2007: Oregon State University.

- Varis, M. and H. Littunen, Types of innovation, sources of information and performance in entrepreneurial SMEs. European Journal of Innovation Management, 2010. [CrossRef]

- Chen, J., Z.-C. Liu, and N.-Q. Wu. Relationships between organizational learning, innovation and performance: an empirical examination. in 2009 International Conference on Information Management, Innovation Management and Industrial Engineering. 2009. IEEE.

- Bakar, L.J.A. and H. Ahmad, Assessing the relationship between firm resources and product innovation performance: A resource-based view. Business Process Management Journal, 2010.

- Bakhtina, V.A., Innovation and its potential in the context of the ecological component of sustainable development. Sustainability Accounting, Management and Policy Journal, 2011. [CrossRef]

- Weihong, X., S. Caitao, and Y. Dan. A study on the relationships between organizational culture, organizational learning, technological innovation and sustainable competitive advantage. in 2008 international conference on computer science and software engineering. 2008. IEEE.

- Ivanaj, S., et al., Multinational Enterprises’ strategic dynamics and climate change: drivers, barriers and impacts of necessary organisational change. Journal of Cleaner Production, 2015. 30: p. 1e4. [CrossRef]

- Faulkner, W. and F. Badurdeen, Sustainable Value Stream Mapping (Sus-VSM): methodology to visualize and assess manufacturing sustainability performance. Journal of cleaner production, 2014. 85: p. 8-18. [CrossRef]

- Commerce, T., The US Department of The International Trade Administration and The US Department of Commerce’s definition for Sustainable Manufacturing. The US Department of Commerce, 2010.

- Kanashiro, P. and J. Rivera, Do chief sustainability officers make companies greener? The moderating role of regulatory pressures. Journal of Business Ethics, 2019. 155(3): p. 687-701. [CrossRef]

- Wong, W.P., M.-L. Tseng, and K.H. Tan, A business process management capabilities perspective on organisation performance. Total Quality Management & Business Excellence, 2014. 25(5-6): p. 602-617. [CrossRef]

- Albort-Morant, G., A. Leal-Millán, and G. Cepeda-Carrión, The antecedents of green innovation performance: A model of learning and capabilities. Journal of Business Research, 2016. 69(11): p. 4912-4917. [CrossRef]

- Huang, X.-x., et al., The relationships between regulatory and customer pressure, green organizational responses, and green innovation performance. Journal of Cleaner Production, 2016. 112: p. 3423-3433. [CrossRef]

- Tang, K., Y. Qiu, and D. Zhou, Does command-and-control regulation promote green innovation performance? Evidence from China’s industrial enterprises. Science of the Total Environment, 2020. 712: p. 136362.

- Dicuonzo, G., et al., The effect of innovation on environmental, social and governance (ESG) practices. Meditari Accountancy Research, 2022(ahead-of-print). [CrossRef]