Submitted:

02 May 2023

Posted:

02 May 2023

You are already at the latest version

Preprints on COVID-19 and SARS-CoV-2

Abstract

This study examines the negative impacts of dark stores on the urban environment from three perspectives: land use, transportation, and streetscape. It is conducted on B-Mart, a representative dark store in South Korea. First, in terms of land use, we find that dark stores that function as logistics facilities conflict with the surrounding land use. Second, by analyzing the location of dark stores and the hourly traffic volume of delivery vehicles, we find that the impact on the surrounding transportation infrastructure and pedestrian traffic is not as significant as previously claimed. However, during the transportation and loading process of the dark store, several problems such as traffic violations, illegal parking, and illegal loading were observed, posing a risk to nearby vehicles and pedestrians. Third, in terms of streetscapes, the location of dark stores on the ground floor of buildings can harm streetscapes. The current urban planning system in South Korea does not clearly define the status and function of dark stores, making it unclear how to manage them. Therefore, it is necessary to clarify their legal definition and introduce urban planning and design guidelines that are consistent with their appropriate location and appearance.

Keywords:

Dark Store

; Micro-Fulfillment Center

; Case Study

; Online Shopping

; COVID-19

1. Introduction

One of the most remarkable changes since the COVID-19 pandemic is that social distancing due to infection concerns has reduced face-to-face activities, and various “contactless” services have appeared [1]. Particularly, the online shopping market has grown explosively since the outbreak of COVID-19. The pandemic has shifted consumer behavior towards a greater reliance on online shopping [2,3,4]. In a survey conducted by UNCTAD [5] with 3,700 consumers in nine countries, more than half of the respondents stated that they had shopped online more often since the COVID-19 pandemic started. The transition from offline to online shopping for groceries is especially significant, as found by several studies [6,7,8,9]. Forbes [10] lists that while 19% of American consumers shopped for groceries online in 2019, 79% did so in 2020.

The shift from offline to online shopping has triggered changes in the urban space. In the context of South Korea, one of the most prominent features in this regard is the rapid growth of a new type of commercial facility called the “dark store.” The term “dark store” refers to a store that only buys and sells goods online, even though it is an offline store. Dark stores played an important role in overcoming the COVID-19 crisis. During the pandemic, companies used them to meet the rapidly increasing demand for online orders and allowed consumers to receive their required products quickly at home without face-to-face transactions.

With the growth of dark stores as a new consumption channel, news articles and reviews have also increased, but academic discussions remain scarce. Sapiro [11] reviewed dark stores from an economic perspective and discussed their impact on consumers, workers, and urban communities. Nobre and Vita [12] assumed their possible negative external effects on the urban environment, such as traffic-flow interference, noise, pollution, saturation of electricity and telephone infrastructure, crime, and devaluation of nearby real estate, and suggested ways to reduce these within the existing legal system. Nevertheless, more systematic analyses and verifications, using objective data from field surveys, are required. Many experts predict that even after the COVID-19 impact neutralizes, dark stores will continue functioning as a new, leading shopping channel in the post-pandemic era. Therefore, it is important to identify this new facility’s effects on the urban environment and prepare institutional devices to address them.

Set against this background, this study assesses existing arguments about dark stores’ negative effects on the urban environment, using various survey data. It discusses the tasks of urban planning, urban design, and architecture that are necessary for the dark store to become a common commercial facility in South Korea in the future.

2. Theoretical Background

2.1. Changes in Commercial Environment and Emergence of Dark Stores in South Korea During COVID-19

Seoul Special City, the target area of this study, has been the capital of South Korea since the Joseon Dynasty (1392–1897) when it was named Hanyang. During the Joseon Dynasty, major commercial districts were named Sijeon. Sijeons have long functioned as centers for commercial activity and have since turned into present-day traditional markets. In addition to these traditional markets, various commercial facilities such as departmental stores, large discount stores, and convenience stores began sprouting up in South Korea in the mid-1980s. Departmental stores were the first modern commercial facilities to be introduced in the 1930s, followed by modern supermarkets, which appeared in the 1960s. Till the 1980s, retail activities were centered on traditional markets. This is because, during the Joseon Dynasty, commercial activities were neglected under the idea of Sa-nong-gong-sang, which emphasized four categories of occupation or people, sa (scholars), nong (farmers), gong (craftsmen), and sang (merchants) as supreme in that order. This made it difficult to develop other commercial facilities except for Sijeon. Further, during the Japanese colonial period, it was difficult to accumulate commercial capital due to the monopoly of Japanese companies [13]. Moreover, in the 1960s after the Korean War, investment in the commercial sector was relatively poor due to export-led economic policies centered around manufacturing.

In the 1990s, large capital, which had been concentrated in the manufacturing industry, was transferred to the retail and distribution industry, and multinational retailers such as Wal-Mart and Carrefour began to enter South Korea. The growth of the distribution industry led to the offline commercial environment in South Korea, which today consists of facilities such as traditional markets, small stores, departmental stores, supermarkets, large discount stores, convenience stores, outlets, and multi-complex shopping malls. According to the Retail Life Cycle, which explains the evolution of the retail industry, departmental stores, supermarkets, and large discount stores are past their maturity, and convenience stores and online shopping are entering maturity. Mobile shopping, which has grown rapidly in recent years, has entered a new growth period [13].

E-commerce, the exchange of goods or services using various electronic media between organizations or individuals, debuted in the 1960s with the Electronic Order Entry System and Electronic Data Interchange that later developed into the Electronic Document Interchange (EDI), Airline Reservation System, and Electronic Fund Transfer [14,15]. Since then, e-commerce has evolved into modern-day online shopping. This was pioneered in the 1990s, with the development of information technology, and more precisely, the Internet [15].

In South Korea, e-commerce began in the 1980s with credit card mail-order sales. The earliest form of online shopping, such as home shopping through personal computer (PC) communication and cable TV, emerged in the 1990s. The current form of online shopping, using the Internet, developed in the 2000s [16]. Later, with the advent of smartphones and simple payment services, the growth of the mobile shopping market accelerated [16].

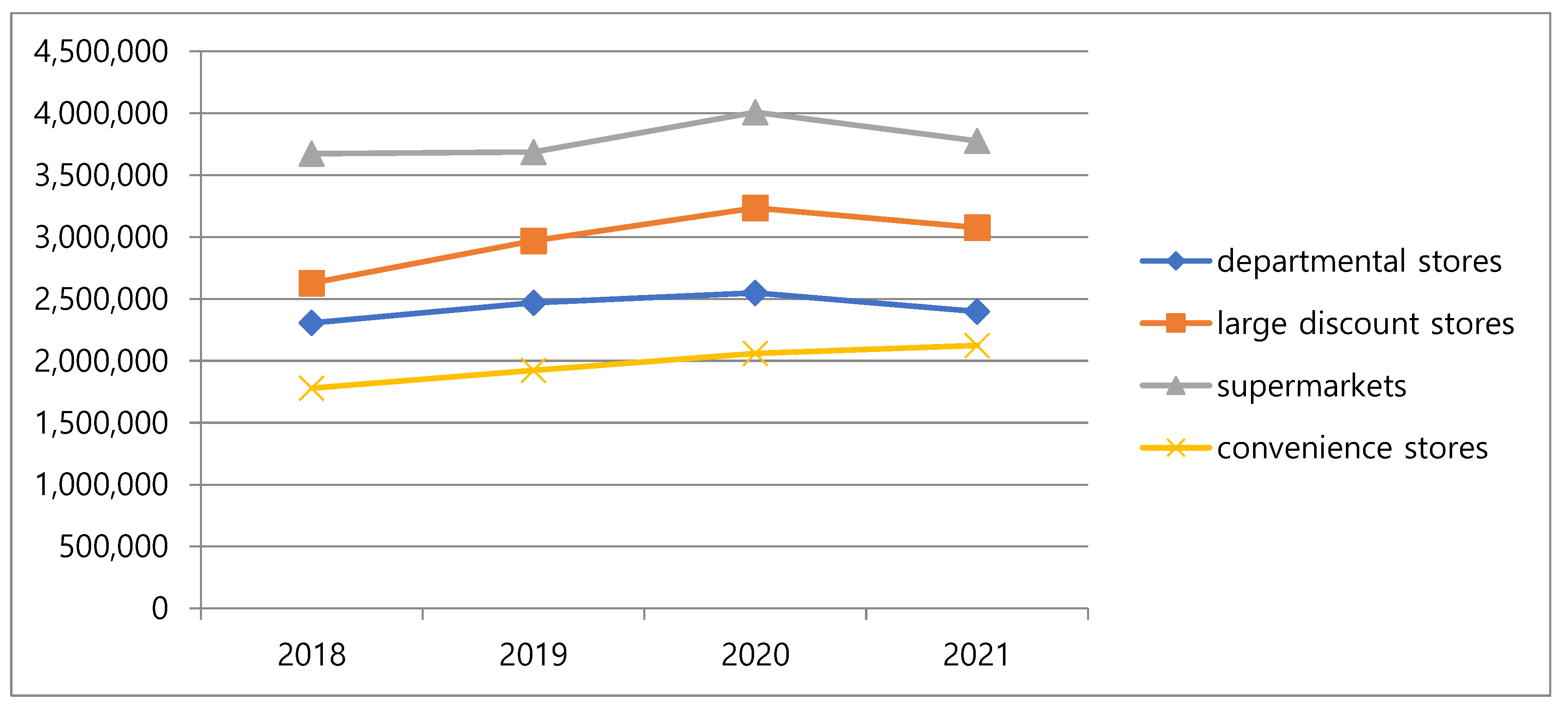

The shift from offline to online shopping became more rapid during the pandemic. To prevent the spread of COVID-19, the South Korean government implemented one of the strongest social distancing policies in the world, restricting access to certain frequently-visited facilities. As a result, as presented in Figure 1, sales at departmental stores, supermarkets, and large discount stores decreased for around a year, starting in January 2020, when COVID-19 was first detected. However, sales at convenience stores increased slightly. This shows that due to the pandemic, the site of consumption changed from a large commercial facility to an easily accessible local store near a house that would not be crowded with people.

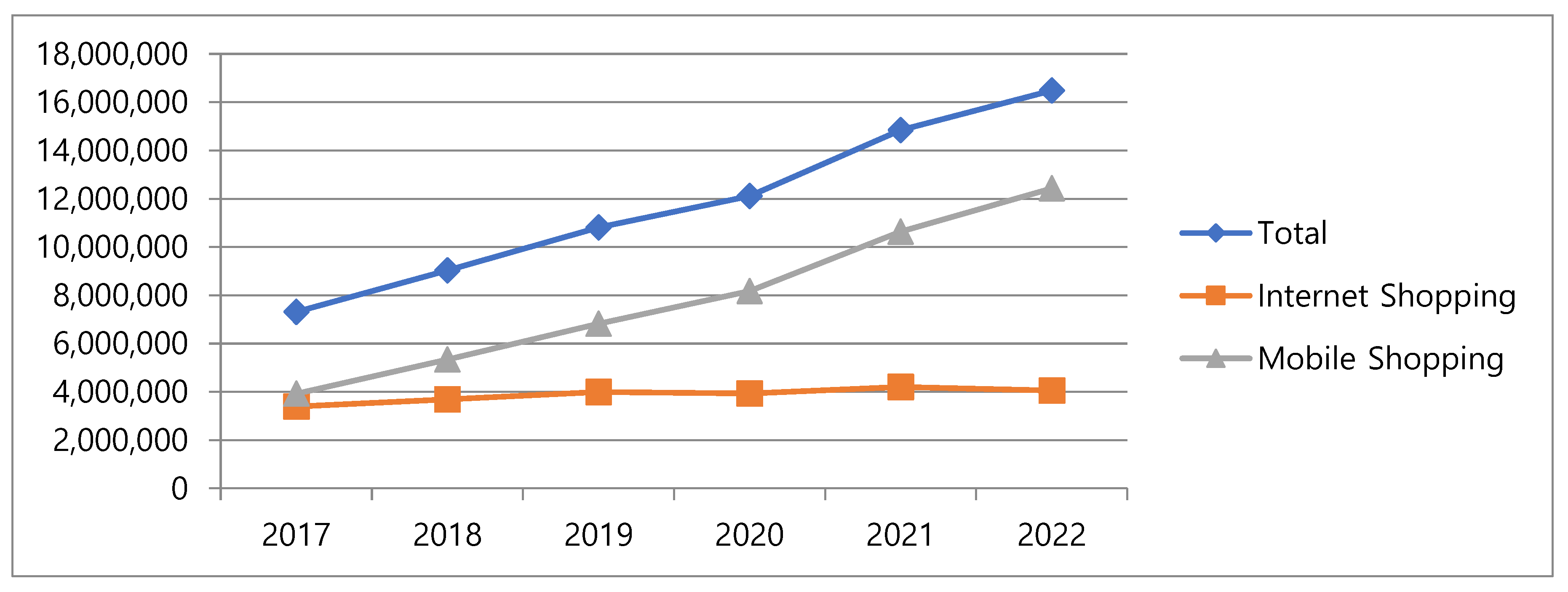

On the contrary, the size of the online market grew more rapidly during the pandemic, which is supported by considerable data [17,18]. According to the Korea Information Society Agency’s survey results [19,20,21], the proportion of online shoppers aged 12 and older showed a moderate increase, accounting for 57.4% in 2016, 59.6% in 2017, 62.0% in 2018, and 64.1% in 2019. However, after COVID-19, the proportion increased sharply to 69.9% in 2020 and reached 73.7% in 2021. Additionally, the average monthly frequency of Internet shopping per person increased from 3.3 times in 2019, to more than 5.0 times from 2020 onwards (Table 1). In particular, mobile shopping has grown rapidly (Figure 2).

Older consumers have had a significant impact on the growth of the online market. COVID-19 has encouraged older people who did not previously engage in online shopping to try it [4]. According to the National Information Society Agency [19,20,21], the Internet shopping usage rates in people’s 50s, 60s, and 70s increased from 44.1% to 67.8%, 20.8% to 41.2%, and 15.4% to 23.0%, respectively, between 2019 and 2021 in South Korea. Moreover, Kim [22], analyzed credit card big data and confirmed that online consumption increased by more than 17% among those who were in their 60s and older.

The impact of COVID-19 is also evident in the changes to items traded online. Especially concerning daily necessities, strong social distancing policies lead even those consumers who were previously passive towards online shopping to partake in it. As dining at restaurants and purchasing groceries at offline stores became replaced by food delivery services and online grocery shopping, the proportion of groceries and food items in online shopping increased from 35.0% in 2019 to 57.1% in 2021 [21]. Additionally, specific items that had to be kept fresh, such as livestock, agricultural, and marine products, were purchased online more often than other items [23,24].

The increase in online shopping for certain items, such as household goods and groceries, has led to significant changes in the offline physical commercial environment. According to a service industry survey by the National Statistical Office, the volume of business at departmental stores, large discount stores, and supermarkets has decreased, and those of Internet-based and home-shopping sites has increased. Simultaneously, a new type of commercial facility called the “dark store” has emerged.

A “dark store” literally means a store with its lights off. The term comes from the store’s characteristic of actually existing in the real physical world but not being visited by consumers to purchase goods, unlike in traditional physical stores where sellers and consumers conduct face-to-face transactions. Orders and payments for goods are made only online and dark stores store goods for shipment, package them as soon as they are ordered, and deliver them quickly to the destination set by the consumer. As a prototype of the dark store, the concept of a “special offline store” for dealing with online products was introduced by Sainsbury, a British supermarket chain in the early 2000s, which later shut down due to poor business [25]. Later, in 2009, U.K.-based Tesco first used the term “dark store,” which then spread to France, Russia, and the United States. For instance, in 2020, GORILLAS, a German on-demand grocery delivery company that assures a 10-minute delivery service, was founded and has been growing rapidly, having expanded to 55 European cities in little more than a year. Before COVID-19, large retailers were leaders in South Korea’s offline and online markets. However, during COVID-19, South Korea’s specific commercial environment, the development of online shopping and related technologies, and the pandemic situation increased the online demand for groceries, which consequently placed more importance on fast delivery. This accelerated participation of not only the existing large retailers, but also start-ups, thereby promoting the introduction and growth of dark stores.

Companies operating dark stores in South Korea include established large retailers such as E-Mart, Lotte Mart, and Homeplus, as well as newer and rapidly growing startups such as B-Mart, Coupang Eats Mart, and Curly. Among them, retailers such as E-Mart, Lotte Mart, and Homeplus, which have been operating large offline stores for the past 20 to 30 years, have been operating dark stores in parallel by utilizing the basement spaces of their existing stores in response to the rapid decline in offline customers and the surge in online orders since the COVID-19 pandemic. In contrast, B-Mart, Coupang Eatsmart, and Curly operate solely as dark stores.

Among them, B-Mart is a pioneer in the Korean dark store market. It is a grocery online shopping and delivery service provided by Korea’s leading delivery application, “Delivery Nation,” which was launched in 2010. Since launching the service in November 2019, the number of dark stores in the Seoul metropolitan area has increased to more than 30 within a year. In particular, product sales in 2020 were KRW 218.8 billion, more than four times higher than in 2019, and sales in August 2020 increased by 963.3% year-on-year.

The wayB-Mart works is as follows: picking, packing, and delivery. When an order is placed online, employees in the warehouse (dark store) retrieve the items from shelves, pack them in white bags and place them in a locker at the entrance. A delivery driver who accepted the delivery task moves to the dark store at the designated time and waits briefly. When the packing is complete, a delivery order number is displayed on a monitor. The driver confirms the number, picks up the bags and delivers them to the customer’s home. Orders can be placed 24 hours a day and, in addition to instant delivery, you can also schedule a delivery at a time of your choosing. You can purchase a wide variety of products, from food to basic household items. B-Mart offers about 7,000 items, including over 200 varieties of fruits and vegetables, such as strawberries, grapes, and mangoes.

The main concepts of dark stores like B-Mart are “ultra-small quantities” and “immediate delivery.” B-Mart is an online grocery service that delivers within 30 minutes to an hour, no matter how small the order is; this is termed “quick commerce.” B-Mart is spreading to areas near its customers. In particular, unlike other dark stores, most delivery workers are not employees of B-Mart, but people who work part-time in their free time. As of 2019, only 3,000 of B-Mart’s 17,000 delivery workers were employees of B-Mart; the remaining 14,000 were temporary part-time workers. This labor mobility has also been a driving force behind the rapid growth of B-Mart.

2.2. Possible Changes to the Urban Environment Caused by Dark Stores

A dark store is a retail store that sells goods, but operates on a completely different basis than a traditional brick-and-mortar retail store. In a dark store, consumers do not walk around the store to browse and purchase goods, so there are no facilities for displaying goods or spaces for customer convenience. Shapiro [11] explains that dark stores are more of a logistics than commercial facility because they are only responsible for storing, packaging, and shipping goods. Nevertheless, dark stores are distinctly different from traditional logistics facilities in some ways. They rely on fast delivery as the key to their success. Unlike conventional online shopping, where it can take a day or more to receive an order, the time between ordering and receiving an item at a dark store is between 30 minutes and an hour. To make this possible, dark stores are located in urban centers, very close to consumers. Therefore, dark stores are perceived as something that has never been done before.

The emergence of new facilities that combine the characteristics of different facilities has implications for the urban environment. For example, the negative impacts of Airbnb, which has characteristics of both housing and accommodation, have been widely discussed, because it essentially places hotels in residential areas. Gurran and Phibbs [26] note that the influx of tourists into residential neighborhoods can lead to problems such as noise, disturbance, traffic congestion, parking difficulties, litter, and crime; Sheppard and Udell [27] explain that, to the extent that these problems are concentrated in a community, they can lead to a decrease in property value. Other studies have found that Airbnb can harm the hotel industry [28,29] or cause a shortage in residential housing and an increase in housing prices [30,31]. Based on these studies, major cities in the United States and Europe have adopted a variety of institutional arrangements to regulate Airbnb [32].

Similar to Airbnb, dark stores have the potential to create a variety of impacts on the urban environment due to their heterogeneous nature as commercial and logistics facilities. Vehicles that are used to deliver goods can cause congestion in urban centers and increase the risk of accidents for pedestrians. In particular, these negative effects are expected to be stronger when dark stores are located near residential neighborhoods with many narrow side streets.

Because dark stores are, as their name implies, unlit, they are not only aesthetically unpleasant from a landscape perspective, but can also increase the perception of crime on the street by creating a sense of isolation and lack of maintenance. As a result, the areas where they are located may be avoided by pedestrians, which can lead to a decrease in street vitality.

Nevertheless, there is still no institutional means to manage dark stores. Even though they can generate traffic that exceeds infrastructure capacity and adversely affects the pedestrian environment, their impact has not been evaluated during the introduction process. They are also excluded from mandatory closures and business hour restrictions that apply to existing Korean large discount stores and corporate supermarkets, even though they can cause significant damage to small local stores in residential areas.

3. Methods

This study targets Seoul Special City, the capital city of South Korea. The administrative divisions of South Korea consist of nine provinces and seven metropolitan cities. Seoul Special City has the highest population density and the most workers and businesses among all provinces and metropolitan cities, making it a center for various consumption activities with high purchasing power (see Table 2).

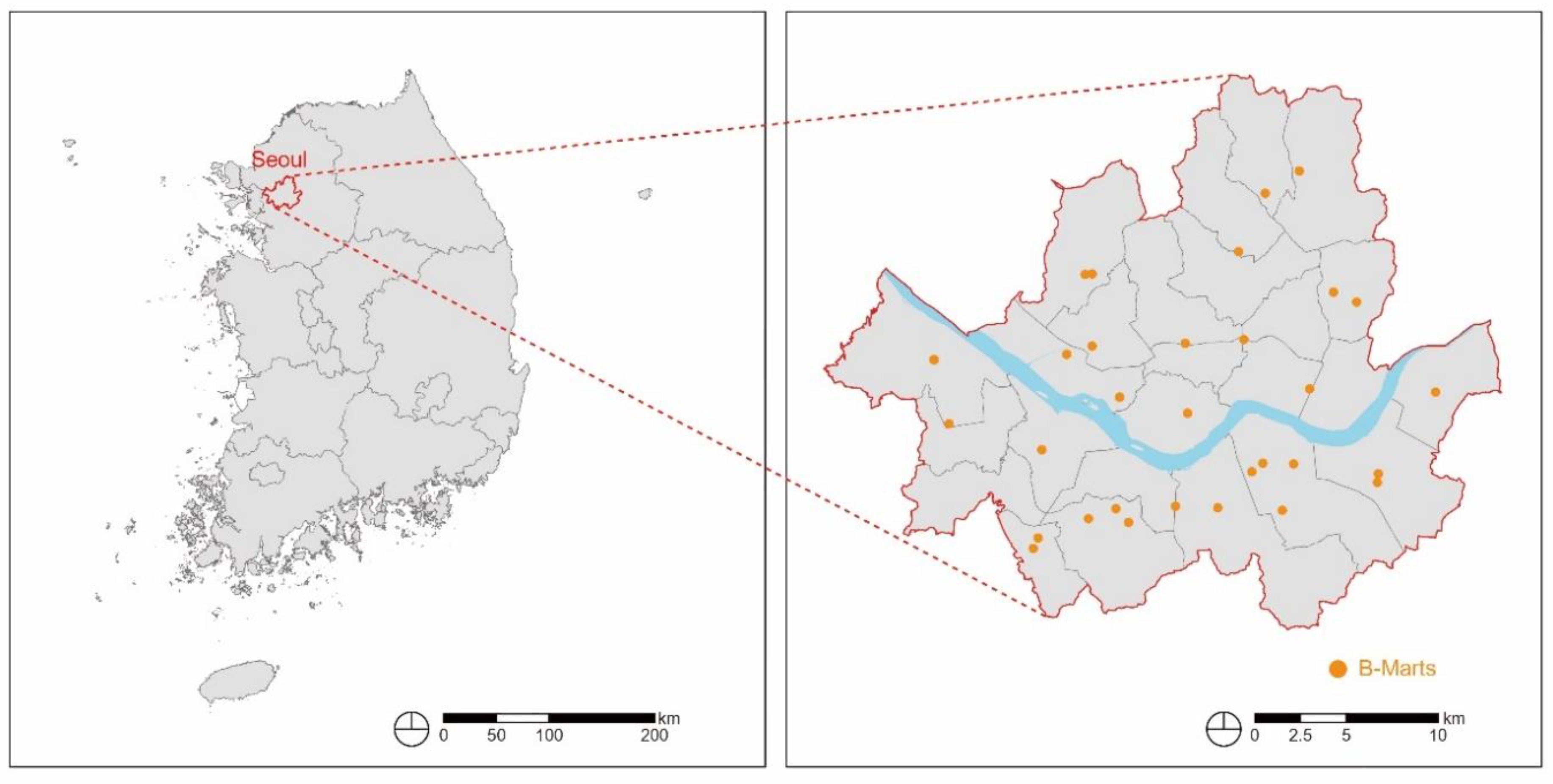

As seen in Figure 3, as of July 2021, there were 32 operating B-Marts in Seoul Special City that could be searched through Naver Map, one of the most prominent online maps in South Korea. All 32 are analyzed in this study.

This study examines the negative impacts of B-Marts on the urban environment from three perspectives: land use, transportation, and landscape. First, we analyze the zoning of the land where B-Marts are located and the use of the building; based on this, we examine whether there is a possibility of conflict with adjacent land uses, given the actual function of the B-Mart. Second, the study examines the B-Mart stores’ possible negative impact on traffic. To do so, we analyze the number of facilities frequently used by pedestrians, such as bus stops, subway stations, and parks, as well as the number of residents who are considered vulnerable groups for traffic safety problems, such as older adults and youth within a 500-meter radius around the center of the B-Marts, which corresponds to the walking area. We then conducted a t-test to confirm whether the location characteristics of B-Marts differ from those of large discount stores, a typical existing large commercial facility that generates intensive vehicle traffic. This allows us to analyze whether B-Marts may have a greater negative effect by being located in more pedestrianized areas than large discount stores. Additionally, we investigate the number and size of roads bordering the site where B-Marts are located. For a specific case surrounded by particularly poor roads, we conduct a field survey to analyze the operating characteristics of delivery vehicles. In this case, the B-Mart is located in a residential area and is only connected by a 7-meter-wide side street, so the impact on traffic and pedestrian movement can be relatively large. The fieldwork was conducted over a nine-hour period, from 11 am to 8 pm on Sunday, August 22, 2021, and Monday, August 9, 2021. Further, we verify the impact of B-Marts on safety by identifying the illegal parking and driving of delivery vehicles and illegal loading of goods. Third, the visual characteristics of B-Marts are examined to confirm the adverse effects on the streetscape.

4. Results

4.1. Do B-Marts Negatively Affect Land Use?

South Korea’s zoning system guides land use in a way that is economical and efficient and promotes public welfare by establishing the functions of land by law. One of the key roles of the zoning system is to spatially separate conflicting land uses and link complementary land uses by stipulating permitted and prohibited building uses for each zoning district. Therefore, it is important to look at the zoning districts in which B-Marts are currently located.

In South Korea, B-Marts are classified as storage facilities, which means that they are considered intermediate storagefacilities for fast delivery rather than commercial facilities, which is why they are also called micro-fulfillment centers (MFC).

However, in addition to warehouse function, B-Marts can also be considered commercial facilities in that they essentially sell various products to consumers. Simultaneously, considering the number of logistics sold and delivered in B-Marts, they also function as logistics facilities. Since the various characteristics of B-Marts are not limited to one facility under the existing urban planning facility classification system, the question remains as to which urban planning standards or architectural standards should be applied. This means that the various characteristics of B-Marts may cause unexpected dissonance in the existing land use. Therefore, it is essential to discuss what institutional arrangements should be put in place to effectively resolve them.

The results of investigating zoning in the areas where the 32 B-Marts are located in Seoul Special City are shown in Table 3. The general residential and commercial areas had 11 (34.38%) and 10 (31.25%) stores, respectively. The semi-industrial area had five stores (15.63%). The semi-residential and second general residential areas each had three stores (9.38%).

Table 4 shows the building uses allowed by zoning on the land where B-Marts have been introduced. As mentioned above, B-Marts are currently recognized as storage facilities, and some of these are located in residential areas. However, according to the zoning code, warehousing facilities cannot be located in residential areas in principle. The location of warehouses in semi-residential, general commercial, and semi-industrial areas are allowed by land zoning. Semi-residential areas focus on residential functions that are supplemented by some supportive commercial and business functions. The general commercial area oversees general commercial and business functions. The semi-industrial area is where residential, commercial, and business functions are supplemented with light industrial functions. According to the zoning codes, warehouses cannot be located in the second and third general residential areas, as these are designed to be pleasant residential environments, with mid- and high-rise houses. The Seoul Metropolitan Government allows warehouses under a certain size (less than 1,000 m2) within residential areas, and B-Mart follows this standard. However, if a B-Mart needs to load, store, and distribute more goods than can be handled in this area, problems may arise.

In addition to its function as a warehouse, B-Marts also sell goods. As such, they may compete with stores in the local neighborhood. According to a report from the Korea Institute of Industrial Economics, retail sales in areas where B-Marts have opened have declined by 8−10%. More specifically, convenience stores dropped by 8.4%, large supermarkets by 9.2%, and cafes by 10.6%.

In South Korea, large discount and department stores are subject to regulations, such as mandatory holidays and location restrictions, to mitigate the impact on local business owners. However, because B-Marts are classified as warehouses, they are exempt from these regulations. In fact, merchants near B-Marts point out that “B-Marts were virtually no different from offline stores in terms of being located in close proximity to consumers like existing large discount stores. Yet, they were exempt from distribution law regulations,” and that “the growth of quick commerce such as B-Mart posed a major threat to small business owners in alleyways as face-to-face transactions have decreased significantly since COVID-19.”

B-Marts also function as logistics facilities that support order processing, inventory management, packaging, and delivery of goods. Since logistics facilities require a larger area than warehouses and increase the traffic volume of vehicles for delivery, Seoul Metropolitan Government does not allow logistics facilities to be built in residential areas. Therefore, negative impacts on traffic, safety, and landscape can be expected from B-Marts located in residential areas, due to the high traffic volume and large-scale land use.

The primary uses of the buildings where B-Marts are located are as follows: Commercial and business buildings are the most common, with 22 (68.75%), followed by neighborhood or convenience facilities in apartment complexes, and residential buildings, with four (12.5%) each. In addition, although extremely rare, there is one (3.125%) case of a B-Mart being located in an educational research facility and one (3.125%) case of a partial space in a townhouse being used as a B-Mart. As such, dark stores are likely to conflict with surrounding land uses because they share the characteristics of multiple facilities.

4.2. Do B-Marts Negatively Affect Traffic?

Traffic due to delivery vehicles, such as motorcycles and personal vehicles, is common around B-Marts. Thus, B-Marts located in areas with high pedestrian populations are likely to negatively impact traffic. Table 5 shows the average value of 32 B-Marts and 64 large discount stores, for each of the five attributes. In Seoul Special City, B-Marts tend to be located in neighborhoods having a higher number of older adults compared to large discount stores. Conversely, neighborhoods where B-Marts are located are more likely to have fewer children, fewer public transportation facilities, and smaller park areas. However, the differences between these attributes are not statistically significant (Table 6). This suggests that the impact of B-Marts on pedestrians is not as great as that of traditional retail at the neighborhood level.

There may not be a significant impact on pedestrians at the neighborhood level, but delivery vehicles may cause congestion on the roads around B-Marts. This may depend on the capacity of the roads and type and number of delivery vehicles. Table 4 shows the results of the connectivity study for all 32 cases.

Table 7 shows that most of the stores (18; 56.25%) were connected by two roads, and seven (21.88%) were connected by three roads. This shows that most B-Marts are located in places with relatively good road connectivity, suggesting that the burden on the surrounding roads of B-Marts may not be as severe as claimed in existing media articles. However, although their numbers are small, four stores are connected by only one road, and three are connected by back roads that are less than 10 meters wide. In these cases, delivery vehicles are likely to cause traffic congestion.

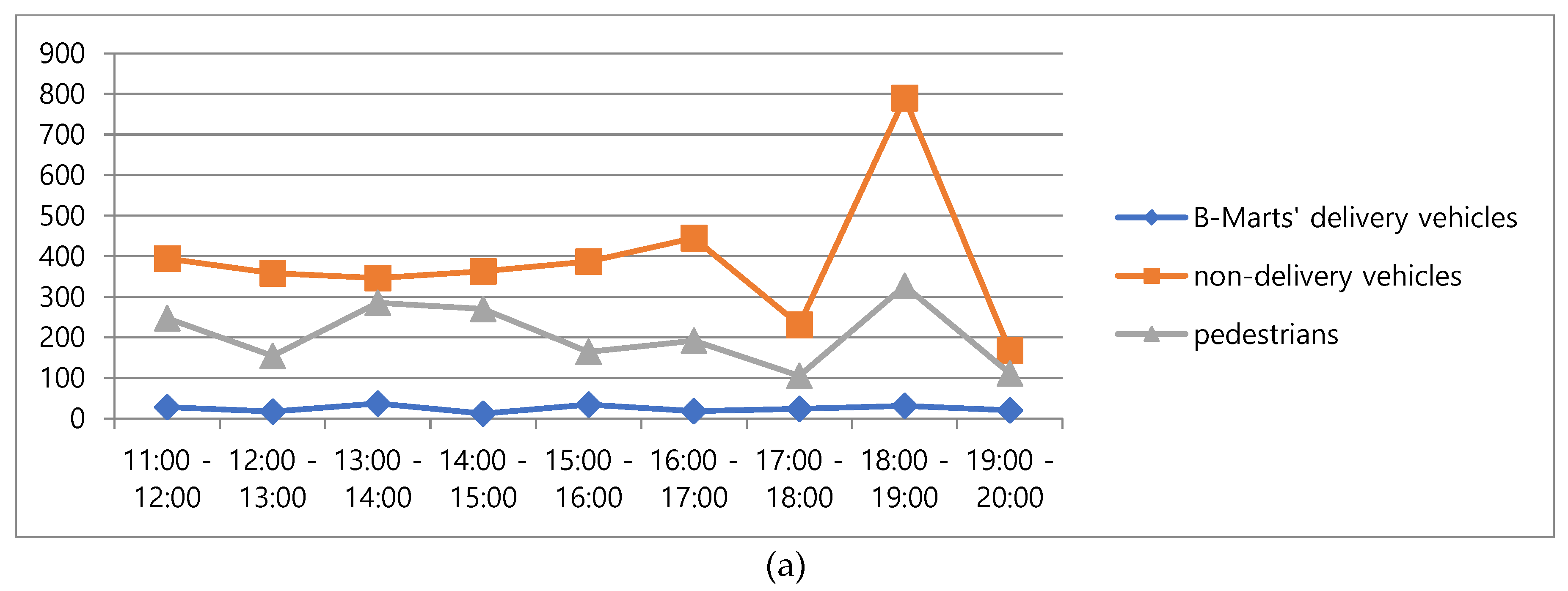

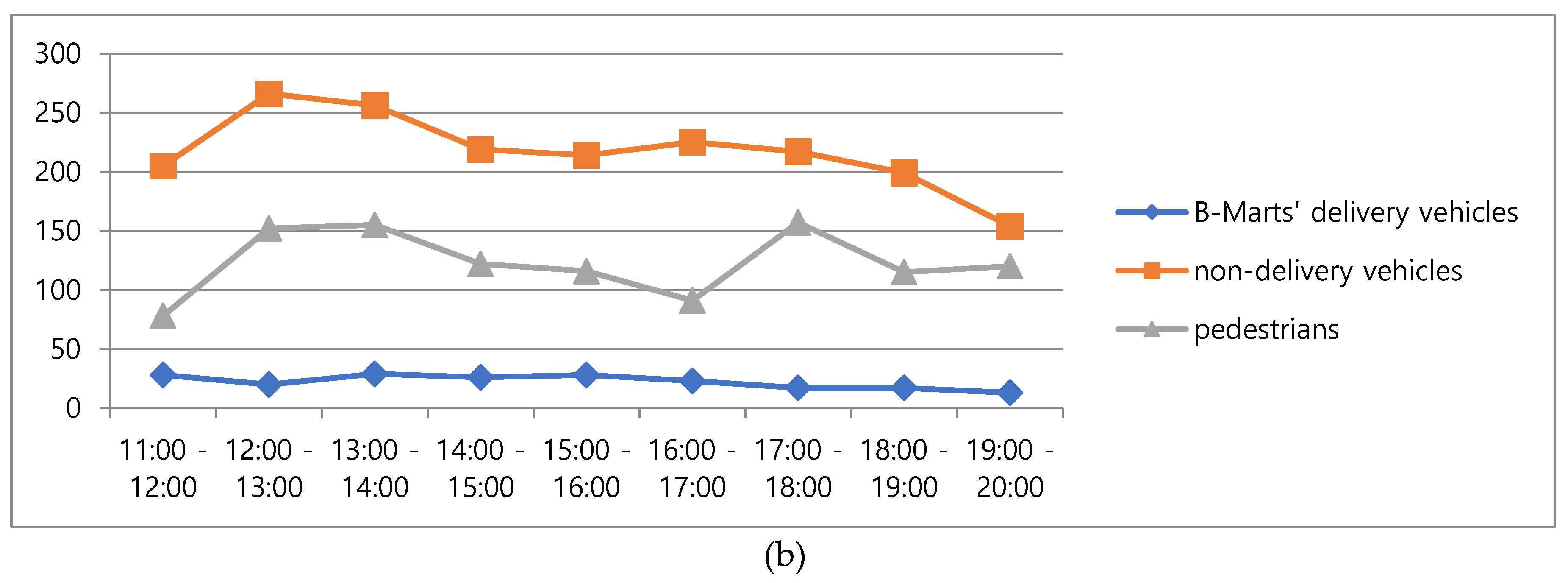

The operating characteristics of delivery vehicles are presented in Table 8. First, the ratio by type of delivery vehicle reveals that 89.81% of deliveries were made on motorcycles, followed by bicycles, personal mobility, and other vehicles, in that order. Next, we analyzed the number of delivery vehicles, non-delivery vehicles, and pedestrians on the roads near the B-Mart by time of day. As shown in Figure 4, the amount of traffic generated by B-Mart’s delivery vehicles are relatively small compared to non-delivery vehicles and pedestrians. However, there is a risk of accidents occurring during peak hours when the number of vehicles and pedestrians increase.

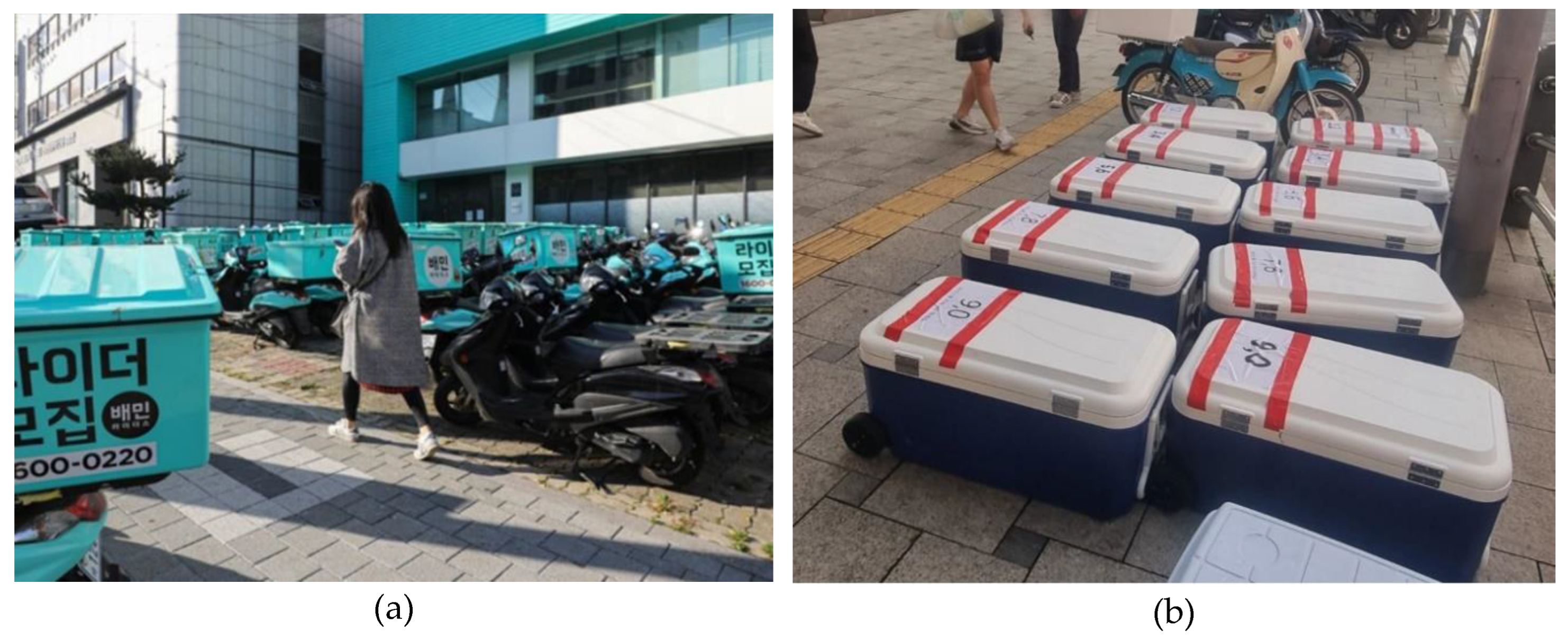

The B-Marts had an average of 197.3 motorcycles for delivery on a weekday and 223 on a weekend. As most B-Marts are located in shopping centers, there is insufficient space to park many motorcycles. As a result, almost all B-Marts park delivery vehicles (including motorcycles) illegally in front of their buildings, causing great inconvenience to pedestrians and risking accidents during peak hours (Figure 5). Since B-Mart provides fast delivery services, there is a high risk of accidents due to delivery drivers speeding, making illegal right and left turns, running red lights, and driving on sidewalks.

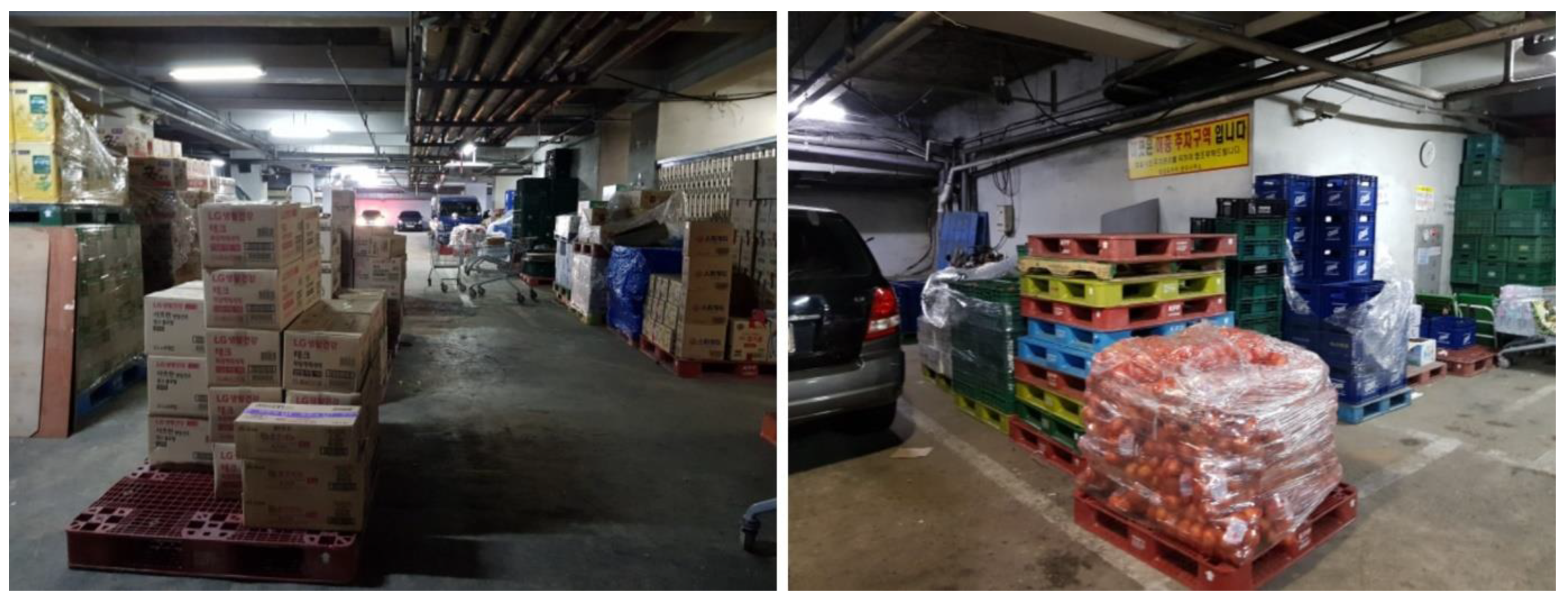

Due to the limited space around most B-Marts, illegal loading on sidewalks, roads, and parking lots is common, which can cause accidents between pedestrians and other vehicles. For example, a B-Mart located in Gangnam, one of Seoul Special City’s busiest neighborhoods, has many iceboxes placed on the sidewalk to allow motorcycles to pick up deliveries quickly during the morning hours when deliveries are at their peak (Figure 5). This greatly reduces the space available for pedestrians, causing sidewalk congestion. In another B-Mart located in the basement of a commercial building, many deliveries are illegally stacked in the underground parking lot (Figure 6). This not only infringes on other vehicles’ parking spaces, but also increases the risk of accidents.

4.3. Does B-Mart Negatively Affect the Streetscape?

Out of 32 B-Marts, 13 (43.33%) are located underground. Since they are not visible from the outside, their negative impact on the streetscape is insignificant in this regard. However, they often affect the streetscape due to the illegal parking of delivery vehicles and illegal loading of delivery items in front of the building. Next, there are seven (23.33%) B-Marts located on the first floor of buildings directly facing pedestrians, which significantly impairs the streetscape. Unlike other commercial buildings, the buildings where B-Marts are located have no signage, are dark inside, and are heavily loaded, which affects the landscape (Figure 7). Additionally, a B-Mart, that occupies the entire first floor of the building in an area with frequent pedestrian traffic has covered all its windows with dark film and illegally parks motorcycles in front of the building; this causes great inconvenience to pedestrians.

In the case of ten B-Marts (33.2%) located on the second and third floors, there were no signage or information signs, and the windows were darkened. Therefore, the negative impact on the streetscape is likely to be more severe if B-Marts are located in areas with many residents and pedestrians. In other words, considering that the vitality of a building is enhanced when the street and interior spaces of a building visually and physically communicate, B-Marts may negatively impact the landscape by blocking this communication and undermining the context of its surroundings.

5. Conclusion

Throughout human history, crises caused by epidemics have been major driving forces in the development of urban structures and systems. In response to health and sanitation challenges such as diseases, cities have constantly evolved to create healthier and safer environments [35,36,37]. After the Black Death in the 14th century, Leonardo da Vinci proposed ideas for future cities that emphasized aesthetics and cleanliness in filthy medieval cities. In the mid-19th century, Britain laid the groundwork for modern urban planning by enacting public health laws to combat crises like cholera, separating residences from factories, installing water supplies, and setting standards for safe ventilation and lighting.

Today, the COVID-19 pandemic has brought about new changes in many areas of urban life [38] and is acting as a turning point in human history, catalyzing rapid changes in cities. In particular, the online shopping market is growing rapidly due to the increasing demand for contactless services. This is even more evident in South Korea. The growth of online shopping is coupled with the expansion of various distribution channels, and a unique phenomenon that has emerged in this process is the unprecedented rise of “dark stores."

A dark store can be considered a commercial facility because it is a store that sells goods. In response to the decline in sales due to COVID-19, large discount stores, a typical retail facility, have converted all or part of their existing facilities into dark stores. Dark stores can also be considered logistics facilities because their main function is to store, package, and deliver goods. Unlike traditional infrastructure classification, the boundaries of dark stores are vague, and the urban planning standards that apply to them are unclear. The introduction of dark stores without a clear institutional basis can negatively impact the surrounding environment in a variety of ways, yet there is little research on them.

This study identifies the possible adverse impacts of B-Marts, a representative dark store in South Korea, from three aspects: land use, transportation, and landscape, through a literature review and field research. First, we found that whether B-Marts are allowed to exist within the current zoning system depends on how they are interpreted as facilities. If they are viewed as a warehouse that collects, stores, packages, and delivers goods, they cannot be located within the current zoning system. Second, our study of delivery vehicles showed that they can negatively impact non-delivery vehicles and pedestrians during certain hours. It was also confirmed that delivery vehicles can cause accidents due to frequent illegal parking and stopping, illegal loading of goods, and so on. Third, it was found that when a B-Mart is located on the ground floor of a building that is visible from the outside, it damages the landscape.

It could be argued that there are not enough dark stores at this point to create a significant negative impact on the urban environment. However, the low number of dark stores also means that their use might be overly concentrated around a small number of facilities, which can disproportionately exacerbate the negative impacts of dark stores on adjacent neighborhoods. Moreover, one cannot ignore that the number of dark stores will increase in the future due to the increasing demand for them. In this context, this study is significant in that it provides a more systematic examination of the negative impacts of dark stores based on field research, which have been discussed only in a few studies in the context of limited academic research on dark stores.

However, this study has several limitations. Statistical analysis using various quantitative data is necessary to demonstrate the impact of B-Marts on land use, traffic, and landscape, but it was not possible to conduct a quantitative study because B-Marts and other dark stores have been introduced only recently and are scarce. Nevertheless, this study evaluated whether dark stores can be established as a long-term facility by considering the side effects that may occur due to their establishment. In this respect, this study provides a basis for the establishment of an institutional device to solve the problems of dark stores.

Author Contributions

Conceptualization, Y.-J.K.; methodology, Y.-J.K. and J.-H.H.; formal analysis, Y.-J.K. and J.-H.H.; writing—original draft preparation, Y.-J.K. and J.-H.H.; writing—review and editing, J.-H.H.; visualization, J.-H.H.; supervision, J.-H.H.; funding acquisition, Y.-J.K. All authors have read and agreed to the published version of the manuscript.

Funding

This work was supported by the National Research Foundation of Korea (NRF) grant funded by the Korea government (MSIT) [No. 2021R1I1A3043148].

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Acknowledgments

Not applicable.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Pantic, M., Cilliers, J., Cimadomo, G., Montano, F., Olufemi, O., Mallma, S. T., Berg, J. Challenges and opportunities for public participation in urban and regional planning during the COVID-19 pandemic- Lessons learned for the future. Land 2021, 10(12), 1–19.

- Hashem, T. Examining the influence of COVID 19 pandemic in changing customers' orientation towards e-shopping. Mod Appl Sci 2020, 14(8), 59–76. [CrossRef]

- Pantano, E., Pizzi, G., Scarpi, D., Dennis, C. Competing during a pandemic? Retailers’ ups and downs during the COVID-19 outbreak. J Bus Res 2020, 116, 209-213. [CrossRef]

- Eger, L., Komárková, L., Egerová, D., Mičík, M. The effect of COVID-19 on consumer shopping behaviour: Generational cohort perspective. J Retail Cons Serv 2020, 61, 1 –11. [CrossRef]

- UNCTAD. COVID-19 and E-commerce: findings from a survey of online consumers in 9 countries. 2020. Retrieved from https://digitallibrary.un.org/record/3886558/. Accessed December 21, 2022.

- Jensen, K. L., Yenerall, J., Chen, X., Yu, T. E. US consumers’ online shopping behaviors and intentions during and after the COVID-19 pandemic. J Agricul Appl Econ 2021, 53(3), 416434. [CrossRef]

- Music, J., Charlebois, S., Toole, V., Large, C. Telecommuting and food E-commerce: Socially sustainable practices during the COVID-19 pandemic in Canada. Transpt Res Interdiscip Perspect 2022, 13, 100513. [CrossRef]

- Shen, H., Namdarpour, F., Lin, J. Investigation of online grocery shopping and delivery preference before, during, and after COVID-19. Transp Res Interdiscip Perspect 2022, 14, 100580. [CrossRef]

- Tyrväinen, O., & Karjaluoto, H. Online grocery shopping before and during the COVID-19 Pandemic: A meta-analytical review. Telematics Informatics 2022, 71, 13101839. [CrossRef]

- Forbes. Lasting changes to grocery shopping after Covid-19? 2020. Retrieved from https://www.forbes.com/sites/blakemorgan/2020/12/14/3-lasting-changes-to-grocery-shopping-after-covid-19/?sh=2af98f5e54e7 Accessed September 2, 2022.

- Shapiro, A. Platform urbanism in a pandemic: Dark stores, ghost kitchens, and the logistical-urban frontier. J Consum Cult 2022, 23, 168–187. [CrossRef]

- Nobre, J. M. N., Vita, J. B. Analysis of the dark store from the perspective of urban law. Revista de Direito da Cidade 2021, 13(3), 13731392.

- Ahn, K. H., Cho, J. W., Han, S. Introduction to Marketing Channel Management. Hakhyunsa, 2019.

- Lee, C. Analysis on Critical Success Factors on Electronic Commerce –with Internet Shopping Mall-. [Unpublished Master’s Thesis]. Hanyang University, 2000.

- Santos, V. F., Sabino, L. R., Morais, G. M., Goncalves, C. A. E-Commerce: A short history follow-up on possible trends. Int J Bus Admin 2017, 8(7), 130–138. [CrossRef]

- Kang, D. Expansion of online shopping and changes in retail structure. Labor Rev 2021, 191, 719.

- Choe, Y., Lee, J. K., Kim, J. Changes in the distribution industry environment due to COVID-19 and the prospect of distribution regulations. J Law Econ Reg 2021, 14(2), 60 –86.

- Kim, J. T. Changes in the retail industry during the COVID-19 Era. Food Industry and Nutrition 2021, 26(10), 911.

- National Information Society Agency. 2019: A survey on Internet use. Daegu, South Korea, 2020.

- National Information Society Agency. 2020: A survey on Internet use. Daegu, South Korea, 2021.

- National Information Society Agency. 2021: A survey on Internet use. Daegu, South Korea, 2022.

- Kim, M. “So many deliveries”. Even a street icebox. Korea Herald (2021, July 21). Retrieved December 22, 2022, from https://mbiz.heraldcorp.com/view.php?ud=20210721001010.

- Back, S. W., Kim, S. H. Post-COVID-19, directions and challenges of agri-food distribution. Kor J Organ Agri 2021, 29(1), 1–23.

- Jung, Y. B. Post-COVID-19, changes in consumption structure by distribution channels of major livestock products - Based on the results of animal products distribution information survey in the second quarter of 2020. Kor Soc Food Sci Animal Res 2020, 9(2), 74–81.

- Wikipedia. Dark store. Retrieved from https://en.wikipedia.org/wiki/Dark_store/. 2022. Accessed December 21, 2022.

- Gurran, N., Phibbs, P. When tourists move in: How should urban planners respond to Airbnb? J Am Plan Ass 2017, 83(1), 80 –92. [CrossRef]

- Sheppard, S., Udell, A. Do Airbnb properties affect house prices? 2016. Retrieved from https://web.williams.edu/Economics/wp/SheppardUdellAirbnbAffectHousePrices.pdf. Accessed January 6, 2023.

- Zervas, G., Proserpio, D., Byers, J. W. The impact of the sharing economy on the hotel industry: Evidence from Airbnb's entry into the Texas Market. In EC ‘15 Proceedings of the Sixteenth ACM Conference on Economics and Computation, Portland, Oregon. 2015. [CrossRef]

- Choi, K. H., Jung, J., Ryu, S., Kim, S. D., Yoon, S. M. The relationship between Airbnb and the hotel revenue: In the case of Korea. Ind J Sci Tech 2015, 8(26), 1–8.

- Horton, T. Reducing affordability: The impact of Airbnb on the vacancy rate and affordability of the Toronto rental market. [Unpublished Master’s Thesis]. University of Ottawa, 2016.

- Lee, D. How Airbnb short-term rentals exacerbate Los Angeles’s affordable housing crisis: Analysis and policy recommendations. Harvard Law Pol Rev 2016, 10, 229–253.

- Jefferson-Jones, J. Can short-term rental arrangements increase home values?: A case for Airbnb and other home sharing arrangements. Cornell Real Est Rev 2015, 13, 10–19.

- Yoon, J. "Coupang It's Mart" chasing after B Mart. Competition for the delivery app "Quick Commerce" is in full swing. Voice of the people (2021, November 17). Retrieved December 22, 2022, from https://www.vop.co.kr/A00001602941.html.

- Kwon, Y. B Mart in Wongok-dong, Ansan-si, "Controversy" over lawlessness such as illegal landfills. Kmaeil (2020, February 13). Retrieved December 22, 2022, from https://www.kmaeil.com/news/articleView.html?idxno=211239.

- Bereitschaft, B., Scheller, D. How Might the COVID-19 Pandemic Affect 21st Century Urban Design, Planning, and Development?. Urban Sci 2020, 4(4), 1-22. [CrossRef]

- Eltarabily, S., Elgheznawy, D. Post-Pandemic Cities – The Impact of COVID-19 on Cities and Urban Design. Archit Res 2020, 10(3), 75-84. [CrossRef]

- Martínez, L., Short, J. R. The Pandemic City: Urban Issues in the Time of COVID-19. Sustainability 2021, 13(6), 1-10. [CrossRef]

- Banai, R. Pandemic and the Planning of resilient cities and regions. Cities 2020, 106, 1-6. [CrossRef]

Figure 1.

Recent changes in sales at major offline commercial facilities in South Korea (KRW 1 million).

Figure 1.

Recent changes in sales at major offline commercial facilities in South Korea (KRW 1 million).

Figure 2.

Current trends in Internet and mobile shopping in South Korea (KRW 1 million).

Figure 3.

Location of B-Marts in Seoul Special City.

Figure 4.

Delivery vehicle traffic on (a) weekdays and (b) weekends, according to time.

Figure 6.

Illegal loading inside buildings [34].

Figure 6.

Illegal loading inside buildings [34].

Figure 7.

Streetscape of B-Marts.

Table 1.

Current trends in South Korean Internet shopping.

| Year | 2016 | 2017 | 2018 | 2019 | 2020 | 2021 |

|---|---|---|---|---|---|---|

| Percentage of Internet shopping users among Internet users (%) | 57.4 | 59.6 | 62.0 | 64.1 | 69.9 | 73.7 |

| Average monthly Internet shopping frequency per person (N) | 2.3 | 2.7 | 3.0 | 3.3 | 5.0 | 5.1 |

Table 2.

Number of residents, workers, and businesses in the provinces and cities of South Korea.

| Provinces / Metropolitan Cities | Residents | Population Density | Workers | Businesses | |||

|---|---|---|---|---|---|---|---|

| N | % | N/km2 | N | % | N | % | |

| Seoul Special City | 9,911,088 | 18.71 | 15,839.00 | 5,226,997 | 23.00 | 823,624 | 19.72 |

| Busan Metropolitan City | 3,438,710 | 6.49 | 4,348.90 | 1,465,433 | 6.45 | 290,357 | 6.95 |

| Daegu Metropolitan City | 2,446,144 | 4.62 | 2,728.60 | 967,934 | 4.26 | 210,944 | 5.05 |

| Incheon Metropolitan City | 3,010,476 | 5.68 | 2,765.10 | 1,092,494 | 4.81 | 206,244 | 4.94 |

| Gwangju Metropolitan City | 1,471,385 | 2.78 | 2,948.50 | 631,876 | 2.78 | 123,706 | 2.96 |

| Daejeon Metropolitan City | 1,480,777 | 2.79 | 2,758.10 | 633,418 | 2.79 | 119,628 | 2.86 |

| Ulsan Metropolitan City | 1,153,901 | 2.18 | 1,069.00 | 533,187 | 2.35 | 87,054 | 2.08 |

| Sejong Special Self-governing City | 360,907 | 0.68 | 761.3 | 125,410 | 0.55 | 18,041 | 0.43 |

| Gyeonggi Province | 13,807,158 | 26.06 | 1,325.30 | 5,302,740 | 23.34 | 934,349 | 22.37 |

| Gangwon Province | 1,560,172 | 2.94 | 90.4 | 670,247 | 2.95 | 146,815 | 3.52 |

| Chungcheongnam Province | 1,637,897 | 3.09 | 220.3 | 741,452 | 3.26 | 133,522 | 3.20 |

| Chungcheongbuk Province | 2,185,575 | 4.13 | 264 | 973,944 | 4.29 | 176,643 | 4.23 |

| Jeollanam Province | 1,835,392 | 3.46 | 223.4 | 720,052 | 3.17 | 154,082 | 3.69 |

| Jeollabuk Province | 1,884,455 | 3.56 | 144.9 | 774,294 | 3.41 | 161,883 | 3.88 |

| Gyeongsangnam Province | 2,691,891 | 5.08 | 138.9 | 1,150,047 | 5.06 | 236,807 | 5.67 |

| Gyeongsangbuk Province | 3,407,455 | 6.43 | 316.2 | 1,427,443 | 6.28 | 286,752 | 6.87 |

| Jeju Special Self-governing Province | 697,578 | 1.32 | 362.6 | 286,304 | 1.26 | 66,098 | 1.58 |

| Total | 52,980,961 | 100.00 | 516.2 | 22,723,272 | 100.00 | 4,176,549 | 100.00 |

Table 3.

Number and proportion of B-Marts as per zoning.

| Zoning | Number (N) | Ratio (%) | |

|---|---|---|---|

| Residential Area | 2nd General Residential Area | 3 | 9.38 |

| 3rd General Residential Area | 11 | 34.38 | |

| Semi-Residential Area | 3 | 9.38 | |

| Commercial Area | General Commercial Area | 10 | 31.25 |

| Industrial Area | Semi-Industrial Area | 5 | 15.63 |

| Total | 32 | 100.00 | |

Table 4.

Permissible building uses according to zoning.

| Zoning | Building Usage | |||

|---|---|---|---|---|

| Storage | Warehouse | Distribution Center | ||

| Residential Area | 2nd General Residential Area | Allowed | Not Allowed (Seoul: Conditional Allowance) |

Not Allowed |

| 3rd General Residential Area | Allowed | Not Allowed (Seoul: Conditional Allowance) |

Not Allowed | |

| Semi-Residential Area | Allowed | Allowed | Allowed (Seoul: Not Allowed) |

|

| Commercial Area | General Commercial Area | Allowed | Allowed | Allowed |

| Industrial Area | Semi-Industrial Area | Allowed | Allowed | Allowed |

Table 5.

Neighborhood characteristics of B-Marts and large discount stores.

| Attributes | Facilities | N | Mean | Std. |

|---|---|---|---|---|

| Number of older adults | B-Marts | 32 | 4,472.88 | 444.69 |

| Large discount stores | 64 | 4,214.77 | 252.87 | |

| Number of children | B-Marts | 32 | 1,870.97 | 237.38 |

| Large discount stores | 64 | 2,009.08 | 156.18 | |

| Number of bus stops | B-Marts | 32 | 21.53 | 1.45 |

| Large discount stores | 64 | 22/50 | 1.35 | |

| Number of subway stations | B-Marts | 32 | 1.06 | 0.17 |

| Large discount stores | 64 | 1.19 | 0.10 | |

| Area of parks | B-Marts | 32 | 27,339.98 | 6,580.43 |

| Large discount stores | 64 | 55,120.47 | 19,225.81 |

Table 6.

Results of t-test.

| Attributes | t-value | Degree of freedom | p-value |

|---|---|---|---|

| Number of older adults | 0.505 | 51.632 | 0.308 |

| Number of children | -0.498 | 94 | 0.310 |

| Number of bus stops | -0.447 | 94 | 0.328 |

| Number of subway stations | -0.671 | 94 | 0.252 |

| Area of parks | -1.005 | 94 | 0.159 |

Table 7.

Number and ratio of B-Marts as per characteristics of surrounding roads.

| Attributes | Number of Roads Surrounding B-Mart | |||||

|---|---|---|---|---|---|---|

| 1 | 2 | 3 | 4 | Total | ||

| Number of B-Marts | 4 | 18 | 7 | 3 | 32 | |

| Ratio (%) | 12.50 | 56.25 | 21.88 | 9.38 | 100.00 | |

| Maximum Width of Road (m) | Mean | 14.25 | 28.78 | 26.86 | 30.67 | 26.72 |

| Std | 15.86 | 12.18 | 11.55 | 26.63 | 14.19 | |

Table 8.

Number of delivery vehicles.

| Delivery Vehicle | Car | Motorcycle | Bicycle | PM |

|---|---|---|---|---|

| Number (N) | 6 | 379 | 27 | 10 |

| Ratio (%) | 1.42 | 89.81 | 6.40 | 2.37 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Copyright: This open access article is published under a Creative Commons CC BY 4.0 license, which permit the free download, distribution, and reuse, provided that the author and preprint are cited in any reuse.