Submitted:

16 May 2023

Posted:

17 May 2023

You are already at the latest version

Abstract

This article purposed to examine the impact of integration between Lean accounting (LA) tools & Just in Time (JIT) technique on Cost Reduction (CR) in modern manufacturing environment in Saudi establishments, these two variable moderated by Ethical Standards (ESs). A quantitative methodology was used for realizing the study objectives and answering study questions, the main tool exercised for producing the incipient data was a fully-structured questionnaire with closed ended questions, which was designed and passed around online among a selected sample of (109) managers and accountants in Saudi manufacturing firms. Descriptive and deductive statistics adopted to derive the findings, wherefore the compiled responses analyzed by SPSS & AMOS and the results showed that there is direct and indirect effect of LA tools & JIT technique on CR in Saudi industrial companies, especially when using ESs. These findings could provide decision makers in Saudi manufacturing companies with the acuity of adopting both methods in a combined way to maximize the profits of these firms. The results of this study also suggest that the application of LA tools & JIT technique has a positive effect on the promotion of sustainable manufacture and consequent achievement of high sustainable performance.

Keywords:

Lean Accounting

; Lean Production

; Just In Time

; Ethical Standard

; Cost Reduction

; Sustainable Manufacturing

; Backflush Costing

; & Value Stream

1. Introduction

New technological advancements and environmental alterations that have taken place in modern periods have affected the economic surroundings and remarkably influenced the accounting scope, where an enormous expansion of industrial companies has arisen, which guide to enlarge contesting and complicatedness of customers’ matters [1]. The main purpose of the firm is to maximize the shareholders’ wealth; maximization of shareholders’ wealth indicates increased profits in long run orientation. The only way to guarantee maximizing profits in the long- run orientation has been to implement Cost Reduction (CR) methods. However, in recent years, traditional CR methods have be unable to realize the prospective outcomes [2]. There is a set of criticisms to the conventional management accounting system that restrains it from realizing its goals, some of those criticisms are related to the management accounting system and others are related to the financial accounting system, that these systems were not harmonized well with the requirements of the modern manufacturing environment [3]. These factors and others have led to actuality that there is no existence for traditional companies, due to relying heavily on technology orientation; so many companies tend to integrate with others to block themselves from strong competition. This alteration of standpoint has determined the search of new alternative methods for manufacturing and managing, which encounters the client’s requirements and strengthens the competitive advantage of companies [4].

Due to this manufacturing evolution, new management philosophies appeared, such as total quality management system, Value Stream (VS) system, Lean Production (LP), Just In Time (JIT) technique, et cetera. The appearance of these philosophies had a considerable influence on the structure of manufacturing costs, such as increasing product quality, lower defects & wastage, reducing manufacturing time, reducing inventory cost, et cetera [5]. The observer of the classical management accounting system, which concentrates mightily on the human component, find it inappropriate for the quick growths in contemporary manufacturing systems, which made it requisite for management accounting to go along with these advancements. As a result, some advancements manifested in costing systems, such as activity-based costing systems, target costing systems, product life cycle systems, throughput accounting, Backflush Costing (BC) systems, Lean accounting (LA) tools, et cetera [6].

2. Literature Review

Almaskhor [6] focused on the effect of integration between throughput accounting and LA tools on CR in Saudi industrial establishments; the study deduced that the twain methods are interrelated in their efficiency to minimize manufacturing expenditures. Kadhim et al. [7] discussed the amalgamation of LA tools and activity-based budgeting for upgrading a company’s performance; the study concludes that the conjunction between LA tools and activity-based budgeting leads to reliable financial and non-financial information. Al-Dulemi & Shehadeh [8] Investigated the function of LA tools in lowering manufacturing expenditures in Jordanian industrialization companies, the researchers induced that the implementation of LA tools participate in decreasing manufacturing expenditures. Alobaidy [1] examined the correlation between LA methods and a balanced scorecard to assess the fulfillment of some companies, the study showed that there is a fundamental relation between LA tools and a balanced scorecard perspective. Almusawi et al. [9] concentrated on the impact of LA tools on financial achievement, the researcher noted that the application of VS system encourages directors to differentiate between value-added and non-value-added activities, consequently removing the squandering and economizing the obtainable resource more effectively. Muhammad & Isah [10] condensed on the effect of LA tools on the financial activity of private companies, and the study concludes that LA tools plays an essential role in upgrading the financial performance of these institutions. Airout, & Alhajahmad [11] examined the impact of using LA tools on industrial companies, the researcher found that using the LA tools has a considerable influence on developing the lean planning level in these companies.

Pawlik et al. [12] investigated the implementation of lean tools in industrial remanufacturing processes; the outcomes of these investigations pick out specified lean tools that assist manage the ingrained complication of the remanufacturing processes, and then ameliorate the aggregate productivity. Marques et al. [13] Stated how lean approach might be used to not only upgrade the operational achievement, but also sustainability performance.

According to Singh, & Kumar [14] lean principles are all about reducing waste and maximizing value concerning time, cost, quality, and function. Okolocha, & Anugwu [15] are defined lean as the improvement of the value of products while eliminating it as a management philosophy that frowns at waste and promotes value during production. Muhammad & Isah [10] believed that the prime aim of lean is to eliminate waste and reduce unnecessary costs associated with activities to provide positive returns to the companies. Therefore, LP is a tool company exercise to remove non-value-added activities in their production process to reduce production costs [1]. In the opinion of Ofileanu & Topor [4] the idea of LP is not unprecedented, being a conjunction of the techniques applied in the past and offered in an integrated way, such as JIT production. Therefore, Ghaithan, et al. [16] set some dimensions of LP: provider feedback, JIT, client partnership, pull approach, setup time lowering, complete preventative maintenance, statistical procedure control, and employee participation. Daferighe et al. [2] believed that the efficient implementation of LP principles concentrates on cutting off non-value-added periods and waste costs to upgrade customer service and acquire higher satisfaction scales. Daferighe et al. [2] argued that using the lean idea economically removes dissipation in the inventory management area. Nevertheless, the decrease in inventory volume passively affects the income result and drops out a deceptive effect. Lopez & Santos [17] Showed that operational privilege and waste removal should lead to an advancement in effectiveness, a CR, and ultimately growth in net profit. However, this is not the case; numerous companies find that their accounting techniques are inconsistent with their LP actions and Ethical Standards (ESs). Daferighe et al. [2] also argued that LP introduces methods that are not congruent with traditional costing systems; consequently necessitating the search for appropriate accounting techniques such as LA tools to fill this gap. Elsukova [18] believed that the cost accounting system plays a substantial factor in upgrading the economic situation of companies by supplying advantageous facts for decision-making concerning cost control & product pricing. However, Muhammad & Isah [10] argued that most conventional cost accounting systems do not align with the modern environment’s information needs. Therefore, picking the appropriate cost accounting system has been considered a challenge in most companies because it influences financial performance [19]. Almagtome & Shaker [19] believed that newfangled cost management needs elaborate cost information on the particular element of the production system. To deal with these challenges, managers tend to use the LA tools to eliminate waste, reduce production costs and increase profits [20].

According to Yavuz [21] manufacturing companies now have more benefit in lean orientation for several reasons, such as CR, profit maximization, productivity improvement, elasticity improvement, et cetera. Muhammad & Isah [10] showed that the idea of LA tools should be understood as a set of tools that reduce elements that do not add value to a product to satisfy the customers’ needs and create additional gain. Okpala [22] defined LA as applying lean techniques to a firm’s accounting control and measurement procedures to assist lean management in realizing lean philosophy. LA tools primary goals are completely compatible with companies’ purposes in the modernistic surroundings with regard to CR, quality improvement, customer gratification, et cetera [1]. Andinyanga [23] considered that LA tools draw knowledge from such lean tools like continuous improvement, target costing, VS, JIT, & BC, as its tools build up LA.

As LA tools, JIT technique is a manufacturing philosophy that targets removing squandering that does not add value to the product [24]. However, Fonseca & Domingues [25] argued that JIT technique is not about eliminating inventories only, but rationalizing them, so inventory grades must be optimal. Milewski [26] believed that there are benefits and costs related with preserving inventory, in using JIT technique. Therefore, this requires a balance between benefits and costs in implementing this system. Siddiqui [27] showed that JIT technique has manifested that it could save a lot of waste for the company, which leads to more profits; the best method to get these benefits is to concentrate on what is needed and not waste time and money in inventory. Arai [28] showed that companies implementing JIT technique have adopted an accounting system called LA that addresses financial and non-financial measures.

According to Kocamis [29] VS system is a tool exercised by LA tools to ameliorate and improve the decision-making process to identify and eliminate unfruitful activities. Therefore, VS system comes up with understandable and adequate facts for cost management in the company [30]. BC system is a costing system commonly used in JIT technique; according to this system, companies primarily work backward, calculating products cost after they are sold or shipped. Al-Dulemi, & Shehadeh [8] Believed that VS system & BC system tools were used the pull principle, which based on the customer’s request for the product, and then the company; provides raw materials needed for production, so no need for inventory retention, so VS system & BC system tools are used as synonyms in LA tools & JIT technique.

Some dimensions have been identified in previous literature, and it related to study variables. Table 1 shows these dimensions:

3. Methodology

This study investigates the impact of LA tools & JIT technique integration on CR in modern manufacturing environment in Saudi companies. Based on quantitative & empirical study layout, this study used prime and secondary data. To familiarize ourselves with issues connected to the LA tools & JIT technique concept, we have collected secondary data from various sources such as; journals, theses, scientific books, etc. The primary data were produced via questionnaire; questionnaires were circulated randomly for several managers & accountants in KSA manufacturing companies to assess the influence of integration between LA tools & JIT techniques on CR. The study tool was prepared in five reply options of a Likert scale (i.e. strongly agree, agree, neutral, disagree, and strongly disagree).

A quota sampling technique was adopted for this study. The questionnaire was designed based on former literature, which included two sections for a number of closed statements, directed at collecting data on the variables of the study: the first section related to demographic data (age, qualification, job title & experience) and Table 1 shows the frequencies and percentages for the study sample. The second section involves four parts related to the study variables. The first part includes a set of (7) items asking about the first independent variable JIT technique. While the second part inquires about the second independent variable LA tools, which contains (8) items. The third part is connected to the moderator variable ES, which includes of (3) items, and the last part is related to the dependent variable CR, which contains of (4) items.

Competent experts have arbitrated the questionnaire and an experimental test of the questionnaire was achieved to afford high quality and verify the questionnaire’s precision. The outcome of the precision test shows that the designed questionnaire is mightily dependable. This questionnaire was passed around online among a selected sample of (109) directors and accountants in Saudi manufacturing firms. To obtain dependable data, the selected criterion items were translated from English into Arabic to minimize translation mistakes and to appear the veritable sense and Local knowledge, as most respondents have used Arabic.

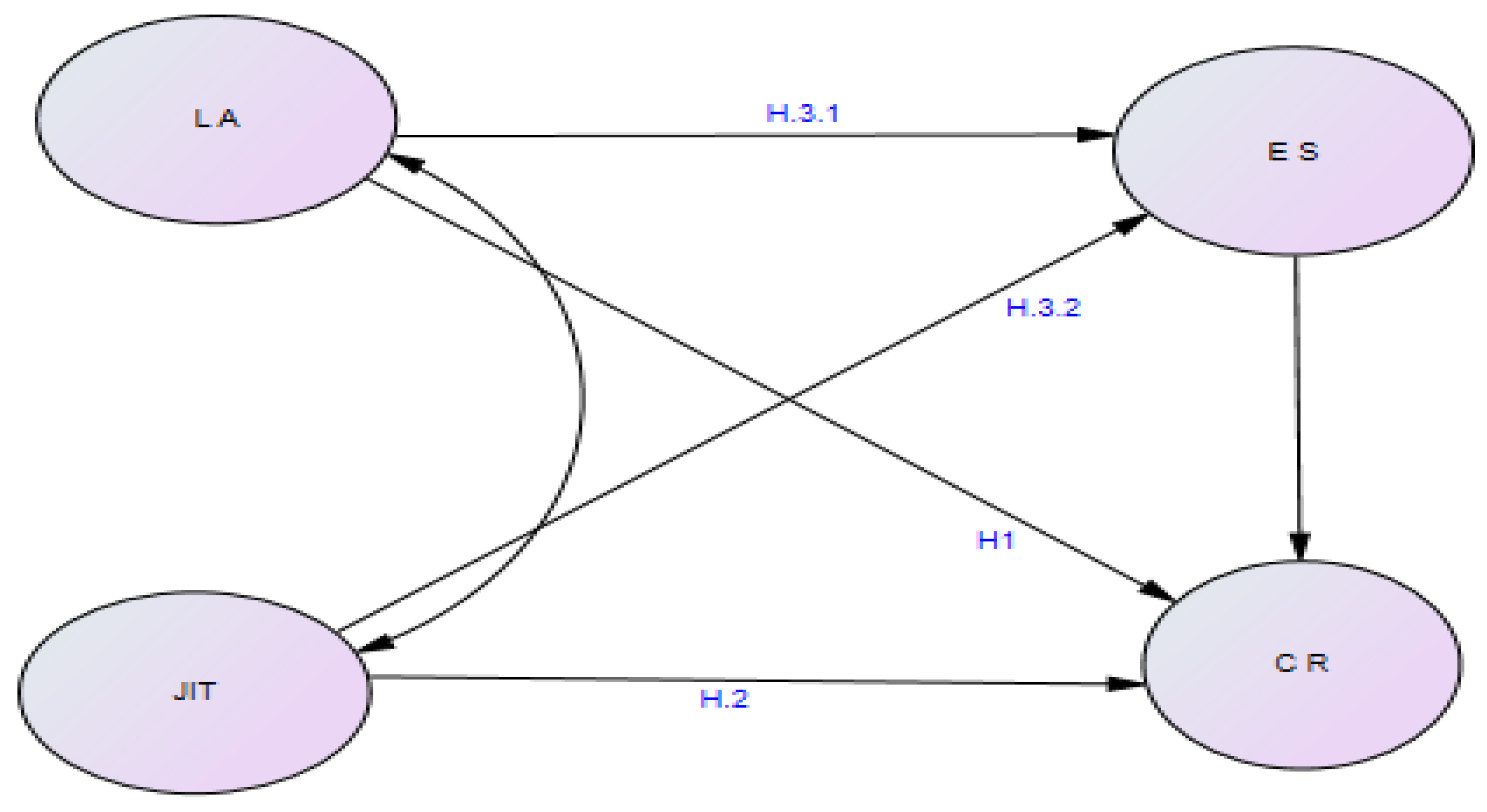

Following the discussions in introduction and literature review, the framework shown in Figure 1, was developed to assess the direct & indirect impact of integration between LA tools & JIT technique on CR in the modern manufacturing environment in Saudi companies. This assessment can be carried out by formulating the following six hypotheses:

H.1:There is a significant effect of using LA tools on CR: In this hypothesis, we discuss the relations between LA tools & CR, we believe that LA tools have a direct effect on CR; this can be realized by concentrating on reducing elements that not add value to the product, and hence reducing production cost.

H.2:There is a significant effect of using JIT technique on CR: We begin our hypothesis discussion by developing the relations between JIT technique & CR; we believe that JIT technique contributes in removing squandering that not adding value to the product, by doing this, reducing production cost. Additionally, according to JIT technique, there is no need for inventory procedures, so this reduces production cost.

H.3.1:ESs moderate the effect of using LA tools on CR: In this hypothesis, we believe that ESs play an essential role in applying LA as a vital tool in CR. Managers sometimes concentrate on CR unethically to gain self-interest.

H.3.2:ESs moderate the effect of using JIT on CR: In this hypothesis, also we believe that ESs play an important role for applying JIT as a vital technique in CR, because managers sometimes concentrate on CR by using unethical ways to obtain self-interest. In addition, we discuss to what extent there an integration between LA tools & JIT technique reducing production cost, especially by using VS system & BC system.

4. Study Results

4.1. The Demographic Data

The demographic data of the study sample in Table 1 above presents that the specimen comprises of two types of workforce of industrial companies in Saudi Arabia, which are accountants by percentage of (60.6%) and managers (production manager, financial manager, industrial engineer) by ratio of (39.4%). However, the most shared in this study was age section below 40 years old with a ratio of (76.1%), followed by (22.9%) of individuals from 40 to 55 years old, and lastly (0.9%) of individuals aged is older than 55 years. The majority of the study participants were well educated, having a Bachelor’s degree (67%), a higher diploma with a ratio of (21.1%), a master’s degree with a ratio of (7.3%) & a Ph.D. with a ratio of (4.6%). With regard to experience, the analysis shows that employees of 5 to 10 years of experience are highly sore (47.7%), followed by employees with less than 5 years of experience (26.6%), followed by employees of 11 to 20 years of experience (18.3%), and lastly employees more than 20 years’ experience (7.3%), which indicates that the study participants were included a highly qualified people who know the study field, and this presents their capability to answer the study questions with high reliability.

4.2. Exploratory Factor Analysis (EFA) & Confirmatory Factor Analysis (CFA)

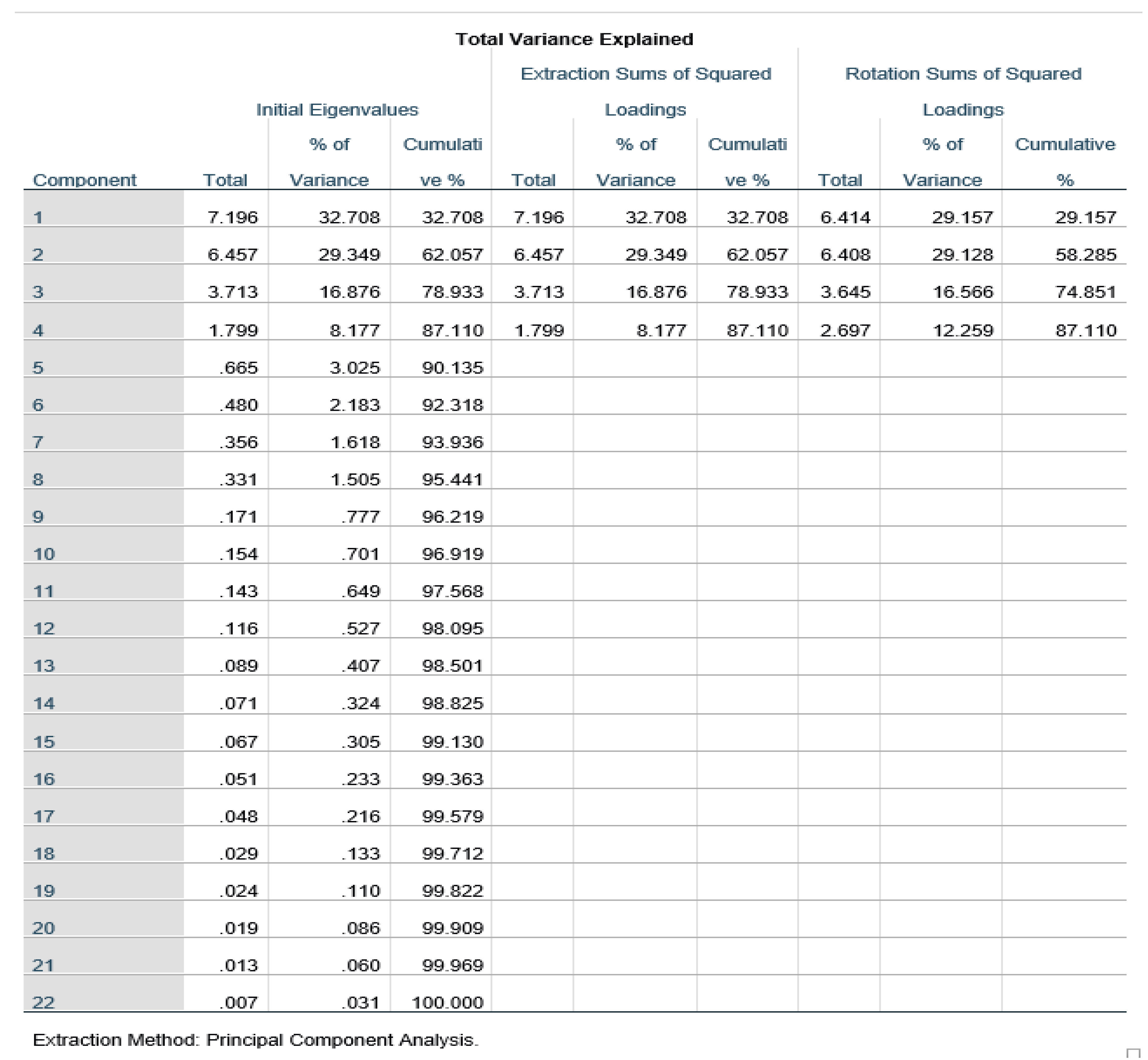

EFA identifies implicit variables and loads each implicit variable with a set of questionnaire statements. The study concluded that the questionnaire form statements were loaded with underlying factors over than 70%. As shown in this Table 2, the KMO measured 0.813 (Table 2). This is suitable because the KMO value is over than 0.60, and the extracted value is higher than the value determined by Hair, Anderson, Tatham, & William [35]. Thus, the sample is congruent with the study, and the CFA was used to ascertain the plausibility of the factor frame generated by the EFA. After the statistical analysis results, it was confirmed that 22 indicators of four latent variables JIT, LA, ES, and CR. According to study analysis, Eigenvalues for all four variables JIT, LA, ES, and CR are more than one, (7.20, 6.46, 4.71, and 1.80, respectively). According to study analysis, also, variance explained for all four variables JIT, LA, ES, and CR indicated good results (32.71, 29.35, 16.88, and 8.18, respectively), with cumulative value of (87.11), this means that there is no dominant variable means, and all reduction in costs is related to these variables, the remaining value (12.89) for other variables, as shown in Table 4 and Table 5, In addition to Figure 2.

Table 2.

Demographic data.

| Data | Frequency | Percent % | |

|---|---|---|---|

| Age | less than 25 | 19 | 17.4 |

| 25 to 39 | 64 | 58.7 | |

| 40 to 55 | 25 | 22.9 | |

| over 55 | 1 | 0.9 | |

| Total | 109 | 100% | |

| Qualification | Bachelor | 73 | 67 |

| Higher Diploma | 23 | 21.1 | |

| Master | 8 | 7.3 | |

| PhD | 5 | 4.6 | |

| Total | 109 | 100% | |

| Job Title | Accountant | 66 | 60.6 |

| Production Manager | 12 | 11 | |

| Financial Manager | 14 | 12.8 | |

| Industrial Engineer | 17 | 15.6 | |

| Total | 109 | 100% | |

| Experience | Less than 5 years | 29 | 26.6 |

| 5 to 10 | 52 | 47.7 | |

| 11 to 20 | 20 | 18.3 | |

| More than 20 | 8 | 7.3 | |

| Total | 109 | 100% |

Table 3.

KMO and Bartlett’s Test.

| Kaiser-Meyer-Olkin Measure of Sampling Adequacy. | .813 | |

|---|---|---|

| Bartlett’s Test of Sphericity | Approx. Chi-Square | 3970.614 |

| Df | 253 | |

| Sig. | .000 | |

Table 4.

Factor Analysis Matrix.

| Factor | Component | ||||

|---|---|---|---|---|---|

| Code | 1 | 2 | 3 | 4 | |

| Value-Added Activity (VAA) | JIT1 | .985 | |||

| Setup Time Reduction (STR) | JIT2 | .967 | |||

| Inventory Level (IL) | JIT3 | .966 | |||

| Defect Products (DP) | JIT4 | .964 | |||

| Supplier Development (SD) | JIT5 | .933 | |||

| Resources Utilization (RU) | JIT6 | .921 | |||

| Competitive Advantage (CA) | JIT7 | .884 | |||

| Value-Added Activity (VAA) | LA4 | .923 | |||

| Setup Time Reduction (STR) | LA1 | .910 | |||

| Inventory Level (IL) | LA3 | .892 | |||

| Defect Products (DP) | LA2 | .891 | |||

| Resources Utilization (RU) | LA5 | .879 | |||

| Competitive Advantage (CA) | LA6 | .855 | |||

| Continuous Flow (CF) | LA7 | .826 | |||

| Customer Involvement (CI) | LA8 | .817 | |||

| Operating Hours Cost (OHC) | CR1 | .967 | |||

| Product Design Cost (DDC) | CR2 | .961 | |||

| Inventory Cost (IC) | C63 | .935 | |||

| Defects Cost (DC) | CR4 | .791 | |||

| Truthful Information (TI) | ES2 | .906 | |||

| Safety Products (SP) | ES1 | .899 | |||

| Transparency (T) | ES3 | .747 | |||

Table 5.

Eigenvalues & variance explained.

4.3. The Hypotheses Test

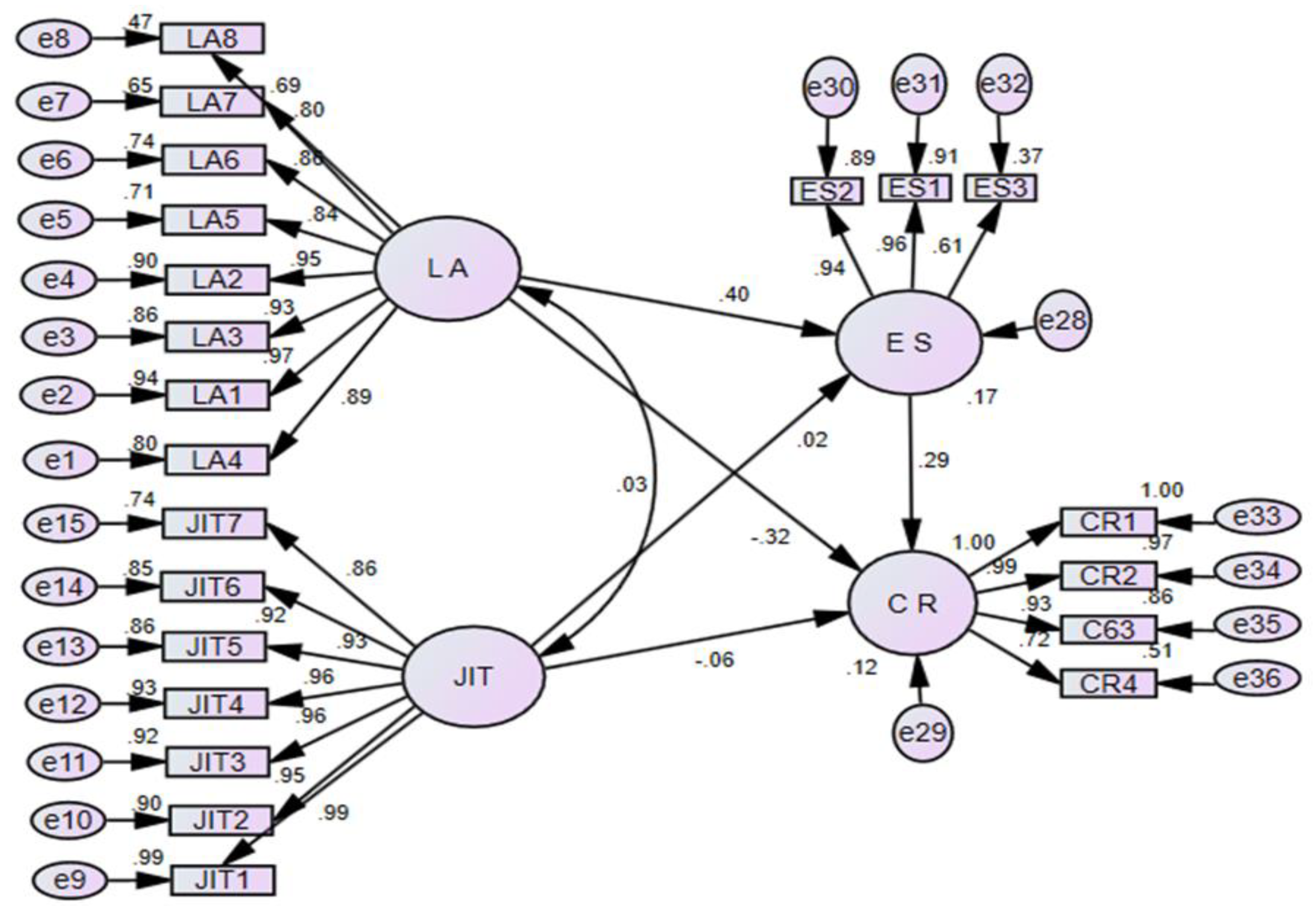

The study examined the direct and indirect impact of integration between LA tools & JIT technique on CR. Path analysis (PA) was used to test the hypotheses as one of the structural equation modeling methods (SEM), as shown in Figure 2 and Table 5, Table 6 and Table 7, where it was found that: By using AMOS software version 24, & SPSS software version 24 for data analysis there is a statistical effect at the level of significance of 0.05 for the LA on CR, with factor analysis of 0.32, which confirms acceptance (H.1: There is a significant effect of using LA tools on CR). There is no statistical effect for the JIT technique on CR, with factor analysis of 0.06, which indicates the rejection of (H.2: There is a significant effect of using JIT technique on CR). There is indirect effect at the level of significance of 0.05 for the LA on CR throw ESs, with factor analysis of 0.40, which confirms acceptance (H.3.1: ESs moderate the effect of using LA tools on CR). There is indirect effect at the level of significance of 0.05 for the JIT technique on CR throw ESs, with factor analysis of 0.20, which confirms acceptance (H.3.2: ESs moderate the effect of using JIT on CR).

5. Conclusions

5.1. Discussion

The study values the impact of integration between LA tools & JIT technique on CR in the modern manufacturing environment in Saudi companies. This study mostly focused on investigating the direct and indirect impact of LA tools & JIT technique on CR and the integrated impact of LA tools & JIT technique on CR in chosen companies. The findings of this study displayed that there is a direct effect of LA tools (0.3) on CR (H.1); this result is in line with previous studies that claimed the direct and positive impact of LA tools on CR & performance (4, 6, 7, 9, 10). However, the findings of this study also showed that there is no direct effect of JIT technique (0.03) on CR (H.1), despite of previous studies that claimed the direct effect of JIT technique on CR (27, 28). The results of this study also showed that there is an indirect effect of LA tools (0.29) on CR throw ESs (H.3.1). This study indicated that there is an indirect effect of JIT technique (0.29) on CR throw ESs (H.3.2); this means that ESs play a marvelous role for the application of LA tools & JIT technique as significant factors in CR especially cost that related to operating hours cost (0.967), design cost (0.961), inventory cost, (0.935) & defects cost (0.791), the reason for that: managers concentrate sometimes on CR by using unethical ways to obtain self-interests, therefore in these cases, company need to use some ESs when it applies LA tools & JIT technique, especially standards that related to: truthful information (0.906), safety products (0.899), and transparency (0.747).

With regard to integration between LA tools & JIT technique on production cost, the two applications were agreed in some dimensions:

Value-Added Activity (VAA): The two applications concentrates on VAA to remove non-value added activities in production process in order to reduce production costs, the factor analysis for JIT technique & LA tools of this dimension was (0.985) & (0.923) respectively.

Setup Time (ST): Both applications try to reduce ST from purchasing raw materials to delivering production to the customer in order to reduce production costs, the factor analysis for JIT technique & LA tools of this dimension was (0.967) & (0.910) respectively.

Inventory Level (IL): Jointly the two applications try to decrease the IL, only a minimal or nil inventory should be maintained in order to reduce production costs, the factor analysis for JIT technique & LA tools of this dimension was (0.966) & (0.892) respectively.

Defect Products (DP): Cooperatively both applications try to reduce DP that occur during production in order to meet the customer’s needs and hence reduce production costs, the factor analysis for JIT technique & LA tools of this dimension was (0.964) & (0.891) respectively.

Resources Utilization (RU): The two applications try to make optimal use of available resources, by doing this the company utilize its resources in a more effective way and hence reducing costs, the factor analysis for JIT technique & LA tools of this dimension was (0.921) & (0.879) respectively.

Competitive Advantage (CA): The both applications try to increase the CA; this factor allows the company to generate more sales than its market rivals, the factor analysis for JIT technique & LA tools was (0.884) & (0.855) respectively.

According to this analysis, both applications play important role in CR by eliminating waste and reduce unnecessary costs associated with activities such as; removing non-value added activities, maintaining lower inventory, producing non-defective product, and realizing optimal use of available resources, therefore by doing the companies ensure sustainable consumption and production patterns, this is one of Sustainable Development Goals (SDGs). The results suggest that the application of LA tools & JIT technique has a positive effect on the promotion of sustainable manufacture and consequent achievement of high sustainable performance. This result is in line with previous studies that claimed the direct and positive impact of these applications on realizing sustainable performance (36, 37, 38).

5.2. The Study Implication

These findings could provide decision makers in Saudi manufacturing companies with the shrewdness into the momentousness of adopting both LA tools & JIT technique in their firms in a combined way to reduce cost and maximize the profits of these firms. Moreover, the study findings help decision-makers in these companies to concentrate on factors that contribute to profit maximization, especially factors related to LA tools & JIT technique such as value-added activity (0.985, 0.923), setup time reduction (0.967, 0.910), inventory level (0.966, 0.892), defect products (0.964, 0.891), resources utilization (0.921, 0.879), and competitive advantage (0.884, 0.855).

5.3. Limitations & Future Directions of Study

The first limitation of this study concerns the difficulty in generalizing study results, this study was applied only on manufacturing companies in Saudi Arabia, therefore, it is difficult to generalize these results to industrial companies in other countries. The second limitation concerns the sample size of the study; this study was concentrated on small number of managers and accountants in manufacturing companies in Saudi Arabia. Another limitation of this study is the study did not include service establishments in Saudi Arabia environment; the study was concentrated on manufacturing companies and Service facilities were ignored. Some presuppositions made in this study require extra future study. For example, JIT technique is relatively new to Saudi Arabia environment, may be the majority of Saudi manufacturing companies have not yet implemented both LA tools & JIT technique, so the respondents’ background on these applications is limited; thus the respondent’s answer to this field might not be inaccurate. Therefore, we recommended examining the level of integration of both applications in Saudi Arabian industries, especially with regard to other variables contradictory variables found in this study, that effect integration between LA tools & JIT technique on CR, these variables lead to CR (12.89%) as shown in Table 5. We therefore recommended to examine the level of integration of both researching the relationship between VS system & BC system as a tool used in LA tools & JIT technique.

Author Contributions

the author did all work in this article.

Funding

This study was funded by deputyship for study & innovation, ministry of education in Saudi Arabia.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

Not applicable.

Acknowledgments

The author extend his appreciation to the Deputyship for Research & Innovation, Ministry of Education in Saudi Arabia For Funding this Research work through the project number (2022/01/22182).

Conflicts of Interest

The authors declare no conflict of interest.

References

- Alobaidy, R.J.A.E. Integration of lean accounting techniques and balanced scorecard to evaluate the performance of economic units; an exploratory or applied study in Iraq. Period. Eng. Nat. Sci. 2019, 7, 1812–1820. [Google Scholar] [CrossRef]

- Daferighe, E.E.; James, E.E.; Offiong, P.E. Lean Accounting and Waste Management in Brewery Industry in Nigeria. Advances in Research 2018, 15, 40484. [Google Scholar] [CrossRef]

- Ali, S.B.; Khan, Z.S.; Ashah, Z.; Ahmad, M. Lean Accounting System: Importance and Successful Implementation. J. Contemp. Issues Bus. Gov. 2021, 27, 2388–2398. [Google Scholar] [CrossRef]

- Ofileanu, D.; Topor, D.I. Lean Accounting an Ingenious Solution for Cost Optimization, International J. Acad. Res. Bus. Soc. Sci. 2014, 4, 342–352. [Google Scholar] [CrossRef]

- Mohamed, A.F.; Mwanyota, M.J. Effects of selected lean management practices on financial performance of private hospitals in Mombasa County, Kenya. Int. J. Supply Chain Manag. 2018, 3, 1–21, Available online: iprjb.org/journals/index.php/IJSCM/article/view/717. [Google Scholar]

- Almashkor, I.A.S. The Effect of Integration between Throughput Accounting and Lean Accounting on Cost Reduction. J. Manag. Inf. Decis. Sci. 2021, 24, 1–14. [Google Scholar]

- Kadhim, H.K.; Kadhim, A.A.H.; Azeez, K.A. The Integration of Lean Accounting and Activity-Based Public Budgeting for improving a firm’s Performance. Int. J. Innov. Creat. Change 2020, 11, 555–567, Available online: https://www.ijicc.net/. [Google Scholar]

- Al-Dulemi, K.; Shehadeh. M. A. Role of lean accounting in reduction production costs in Jordanian Manufacturing Corporation. Res. J. Financ. Account. 2018, 9, 2222–1697, Available online: https://iiste.org/Journals/index.php/RJFA/article/view/43837. [Google Scholar]

- Almusawi, E.; Almagtome, A.; Shaker, A.S. Impact of lean accounting information on the financial performance of healthcare institutions: A Case Study. J. Eng. Appl. Sci. 2019, 14, 589–599, https://www.researchgate.net/publication/340264004. [Google Scholar] [CrossRef]

- Muhammad, L.; Isah, A.I. Impact of Lean Accounting on Financial Performance of Private Hospitals in Kaduna State. Sokoto J. Manag. Stud. 2020, 22, 121–136. [Google Scholar]

- Airout, R.M.; Alhajahmad, F.B. The Impact of Using the Lean Accounting Tools on Improving the Lean Planning Level in the Jordanian Industrial Public Shareholding Companies. Int. J. Econ. Manag. Syst. 2022, 7, 211–227. [Google Scholar]

- Pawlik, E.; Ijomah, W.; Corney, J.; Powell, D. Exploring the Application of Lean Best Practices in Remanufacturing: Empirical Insights into the Benefits and Barriers. Sustainability 2022, 14, 149. [Google Scholar] [CrossRef]

- Marques, P.A.; Carvalho, A.M.; Santos, J.O. Improving Operational and Sustainability Performance in a Retail Fresh Food Market Using Lean: A Portuguese Case Study. Sustainability 2022, 14, 403. [Google Scholar] [CrossRef]

- Singh, S.; Kumar, K. A study of lean construction and visual management tools through cluster analysis. Ain Shams Eng. J. 2021, 12, 1153–1162. [Google Scholar] [CrossRef]

- Okolocha, C.B.; Anugwu, C.C. Lean Manufacturing Approach and Operational Efficiency of Nigerian Pharmaceutical Companies in Anambra State. Saudi J. Bus. Manag. Stud. 2022, 7, 94–99. [Google Scholar] [CrossRef]

- Ghaithan, A.; Khan, M.; Mohammed, A.; Hadidi, L. Impact of Industry 4.0 and Lean Manufacturing on the Sustainability Performance of Plastic and Petrochemical Organizations in Saudi Arabia. Sustainability 2021, 13, 11252. [Google Scholar] [CrossRef]

- Lopez, P.R.A.; Santos, J.F. An accounting system to support process improvements: Transition to lean accounting. J. Ind. Eng. Manag. 2010, 3, 576–602. [Google Scholar] [CrossRef]

- Elsukova, T.V. Lean Accounting and Throughput Accounting: An Integrated Approach. Mediterr. J. Soc. Sci. 2015, 6, 3. [Google Scholar] [CrossRef]

- Almagtome, A.; Shaker, A.S. Impact of lean accounting information on the financial performance of healthcare institutions. J. Eng. Appl. Sci. 2019, 14, 589–599. [Google Scholar] [CrossRef]

- Aziz, K.; Awais. M.; Rahat, Q.; Ul Hasnain, S.S.; Shahzadi, I. Impact of outsourcing on lean operations in Pakistani healthcare industry. Int. J. Eng. Inf. Syst. 2017, 1, 116–123. [Google Scholar]

- Yavuz, O. Profitability by selling below the average unit cost: Lean cost accounting and a real application. Int. J. Manag. Sci. 2017, 4, 56–59, Available online: https://www.researchgate.net/publication/339435193. [Google Scholar]

- Okpala, K.E. Lean accounting and lean business philosophy in Nigeria: An exploratory research. Int. J. Econ. Financ. Manag. 2013, 2, 508–515, Available online: https://www.researchgate.net/publication/259621522. [Google Scholar]

- Andinyanga, U.S. Implementation Effect of Lean Accounting Practices on Financial Performance of Listed Industrial Goods Firms in Nigeria: A Literature Review. BUJAB 2022, 7, 486–496, Available online: http://35.188.205.12:8080/xmlui/handle/123456789/796. [Google Scholar]

- Madanhire, I.; Kagande, L.; Chidziva, C. Application of Just In Time (JIT) Manufacturing Concept in Aluminium Foundry Industry in Zimbabwe. Int. J. Sci. Res. 2013, 2, 334–347, https://www.ijsr.net/archive/v2i2/IJSROFF2013037.pdf. [Google Scholar]

- Fonseca, L.M.; Domingues, J.P. The best of both worlds? Use of Kaizen and other continuous improvement methodologies within Portuguese ISO 9001 certified organizations. TQM J. 2018, 30, 321–334. [Google Scholar] [CrossRef]

- Milewski, D. Managerial and Economical Aspects of the Just-In-Time System: Lean Management in the Time of Pandemic. Sustainability 2022, 14, 1204. [Google Scholar] [CrossRef]

- Siddiqui, A. The Importance of Just in Time Methodology and its Advantages in Health Care Quality Management Business. Biomed. J. Sci. Tech. Res. 2022, 42. [Google Scholar] [CrossRef]

- Arai, K. Lean Manufacturing and Performance Measures: Evidence from Japanese Factories. IUP J. Oper. Manag. 2021, 20, 7–34. [Google Scholar] [CrossRef]

- Kocamis, T.U. Lean Accounting Method for Reduction in Production Costs in Companies. Int. J. Bus. Soc. Sci. 2015, 6, 7–13, Available online: file:///C:/Users/a.ismael/Downloads/LeanAccountingMethodforReductioninProductionCostsinCompanies.pdf. [Google Scholar]

- Maskell, B.H.; Baggaley, B.; Grasso, L. Practical Lean Accounting: A Proven System for Measuring and Managing the Lean Enterprise, 2nd ed.; Taylor & Francis Group: New York, 2017; p. 475. [Google Scholar] [CrossRef]

- Sahoo, S. Lean manufacturing practices and performance: The role of social and technical factors. International J. Qual. Reliab. Manag. 2020, 37, 732–754. [Google Scholar] [CrossRef]

- Woehrle, S. Using dynamic value stream mapping and lean accounting box scores to support lean implementation. Am. J. Bus. Educ. 2010, 3, 67–75. [Google Scholar] [CrossRef]

- Sila, I.; Ebrahimpour, M. Critical linkages among TQM factors and business results. Int. J. Oper. Prod. Manag. 2005, 25, 1123–1155. [Google Scholar] [CrossRef]

- Shaqour, E.N. The impact of adopting lean construction in Egypt: Level of knowledge, application, and benefits. Shams Eng. J. 2022, 101551. [Google Scholar] [CrossRef]

- Hair, J.F.; Anderson, R.E.; Tatham, R.L.; William, C. Multivariate Data Analysis, 5th ed.; Upper Saddle River: Prentice Hall, NJ, USA, 1998; Available online: https://www.ijsr.net/archive/v2i2/IJSROFF2013037.pdf. [Google Scholar]

- Yin, L.; Liu, J. Impact of Environmental Economic Transformation Based on Sustainable Development on Financial Eco-Efficiency. Sustainability 2023, 15, 856. [Google Scholar] [CrossRef]

- : Mao, H.-Y.; Lu, W.-M.; Shieh, H.-Y. Exploring the Influence of Environmental Investment on Multinational Enterprises’ Performance from the Sustainability and Marketability Efficiency Perspectives. Sustainability 2023, 15, 7779. [Google Scholar] [CrossRef]

- Chen, P.-K.; Lujan-Blanco, I.; Fortuny-Santos, J.; Ruiz-de-Arbulo-López, P. Lean Manufacturing and Environmental Sustainability: The Effects of Employee Involvement, Stakeholder Pressure and ISO 14001. Sustainability 2020, 12, 7258. [Google Scholar] [CrossRef]

Figure 1.

The study model with reference to study hypotheses and variables.

Figure 2.

The model fit.

Table 1.

Dimensions Description.

| Dimension | Description |

|---|---|

| Value-Added Activity (VAA) | This dimension is refers to any activity that increases the product value. It directly contributes to meeting customer needs, and customers are willing to pay for it [5]. |

| Setup Time Reduction (STR) | This element is crucial point that determines the pliability of a manufacturing arrangement such that it can readily accommodate diversification in the resource and programs. STR assess how much setup period can be minimized before production. [16]. |

| Inventory Level (IL) | Inventory costs money for storage & management, so inventory increases the financial risks. Only a minimal or nil inventory should be maintained. |

| Defect Product (DP) | This dimension is refers to a product that fails to meet the customer’s needs. It is be necessary to design a product that contributes to realizing a competitive advantage for the company [16]. |

| Supplier Development (SD) | This mensuration explores the continuous advancement of suppliers’ achievement by measuring supplier competencies and addressing basic interests [31]. |

| Resources Utilization (RU) | This dimension is refers to how much of the available resources are currently used by the company. This helps the company to plan how to utilize its resources in a more effective way [32]. |

| Competitive Advantage (CA) | This dimension refers to factor allowing a company to produce products better than its competitors. This factor allow the company to generate more sales than its market rivals [10]. |

| Continuous Flow (CF) | CF evaluates if there is a gradual permanents flow on the manufacturing floor, ensuring no big downtime [16]. |

| Customer Involvement (CI) | CI is fundamental measurement that describes whether client needs have been met and their gratification has been realized. This measure inspects the narrow relation between the company and client [33]. |

| Truthful Information (TI) | Information is truthful if it reflects reality. Information may be disclosed in a way that is contrary to actual position [34]. |

| Safety Products (SP) | This dimension refers to a product that provides a low risk, taking into account the reasonably foreseeable use of the product and the need to maintain a high level of protection for consumers [16]. |

| Transparency (T) | This dimension is refers to the basic democratic principle that obliges state agencies to publish information of public interest and make it accessible [34]. |

Table 6.

Regression Weights (Direct Effects).

| Variable | Estimate | S.E. | C.R. | P-value | Result | ||

|---|---|---|---|---|---|---|---|

| CR | <--- | LA | -.304 | .098 | -3.107 | .002* | Accept |

| CR | <--- | JIT | -.058 | .085 | -.684 | .494 | Reject |

Note **, p-value < 0.05; ***, p-value < 0.001. Significant at the 0.05 level. Source. Amos Results.

Table 7.

Regression Weights (Indirect Effects).

| Hypothesis | P-value | Result |

|---|---|---|

| CR <--- ES <--- LA | *** | Accept |

| CR <--- ES <--- JIT | *** | Accept |

Note **, p-value < 0.05; ***, p-value < 0.001. Significant at the 0.05 level. Source. Amos Results.

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Copyright: This open access article is published under a Creative Commons CC BY 4.0 license, which permit the free download, distribution, and reuse, provided that the author and preprint are cited in any reuse.