Submitted:

17 May 2023

Posted:

18 May 2023

You are already at the latest version

Abstract

This study investigates the impact of governance variables on the earnings quality based on the industry the firm is in. it has been identified that earnings management have been practised differently by different industries. Most of the research under earnings management have focussed on holistic impacts of corporate governance variables on discretionary accruals while this study has categorised the firms based on what industry they fall on while identifying the impacts of the variables of corporate governance on discretionary accruals. Initially, this paper has studied the estimation of the value of discretionary accruals and identified that performance matched discretionary accruals as the best model as per the explanatory power of the model is higher than other models. Hence, the estimation of the earnings management has been calculated based on performance matched discretionary accruals in this research. This research has studied the impacts of the governance attributes on the earnings management categorising the firms based on the industry they are in; hence, the value of earnings management has been categorically separated; hereafter, the impact of the corporate governance factors on the value of categorically separated earnings management have been statistically analysed. This study has considered the descriptive study to compare the means, medians and standard deviations of the earnings management of various industries. Moreover, Pearson correlations and Spearman rank correlation have been used as a research tool to examine the correlation coefficients.

Keywords:

Corporate Governance

; Earnings Management

; Industry-wise

1. Introduction

Financial fraud has become one of the key issues discussed in relevant circles for theoretical and practical perspectives. Many enterprises create fake profits by manipulating earnings management to mislead investors who may invest more in the company once they believe its good performance. Meanwhile, there are some enterprises that modify the financial reports with a shrunk profit to avoid tax by increasing the cost expenses of the company.

The value of discretionary accruals can be basically shaped by the type of industry they fall in. Hence, the corporations are categorised according to their industries. The researchers Dopuch et al, (2005); Gul et al, (2009); and Craswell et al, (1995), Ware (2015), Kumara (2021) have recommended that the firms perform the earnings management practices as per the industry they are in. They suggested that the estimation of discretionary accruals can be noisy and biased when there are no homogenous conditions, hence, suggested that the firms have to be separated with respective industries. Hence, industry analysis removes such concerns and examine of the previous result is different from the results those get obtained from industry type.

This researcher has conducted the statistical test by following the model of Frankel et al (2002) and Srinidhi and Gul, (2007), Kumara (2021) who have separated the firm industry-wise and run the regression analysis. The industries are categorised as Engineering and consultancy, Distribution and Supplier, Food Services, Home and Building services, Hospitality Industry, IT Company, Manufacturing Company, Oil and Gas Company, Pharmaceutical Company, Retail Industry, Support Industry, Trading and Mining Company. As per the recommendation by Carcello et al, (2002) and Abbott et al, (2006), this study has created the dummy variables. The selected industry is considered as 1, otherwise, it is zero.

The main aim of the research is to investigate the effectiveness of the governance in controlling the practices of earnings management industry-wise.

The objectives of the this research to estimate industry-wise earnings management of the FTSE350 companies of the UK. This research also analyses the effectiveness of various factors of corporate governance in terms of controlling the industry-wise practices of earnings management.

2. Hypothesis Development

This study has uniquely presented the idea of studying the relationship between corporate governance and earnings management assuming that the practice of earnings management could be driven by the industry type the firm operates. Recent studies by Jia & Zhang (2013), Wu et al (2018) based on the impact of governance and discretionary accruals illustrate that the inferences drawn by the research including heterogenous firms may be noisy and biased. Therefore, this study is carried out to reflect the results of the effectiveness of the corporate governance on industry-wise earnings management.

In reference to the research carried out by Frankel et al. (2002) and Srinidhi and Gul, (2007), this study continues to identify the industry-wise analysis in terms of governance factors and earnings management based on the listed firms in the UK. This study includes the eleven largest industries where more than 70% of the sample have been included. Moreover, Consistent with Carcello et al. (2002) and Abbott et al. (2006), this study includes an industry dummy variable for each one of these industries. Dummy variables take the value of one if the firm belongs to that particular industry, and zero otherwise.

H1: The factors of corporate governance have negative impacts on industry-wise earnings management.

3. Literature Review

Around the last decade 20th century and first decade of the 21st century, the practice of the aggressive accounting became so much popular due to which many largest corporations of the various countries have faced the audit failures and got collapsed from the market. Manipulative financial reporting has negative consequences, including loss of confidence in financial statements, degradation of corporate governance, bankruptcy, and reduced efficiency of financial markets and the economy (Zhang et al, 2018).

This failures included the United States, Europe, and Asia; there are few larger companies like Xerox, Enron, WorldCom, Health South, Parmalat, Vivendi, Satyam Computer Services, Sino-Forest, etc. who have seen such market failures. These scandals often involve accounting manipulations ranging from creative shaping of financial results to fraudulent or misrepresented financial statements (Sharmila, 2020).

The purpose of the earnings manipulation is to shaping financial statements to deceive financial statement users, gain benefits or bonuses, fulfil loan requests, and meet external expectations. Inaccurate valuation of balance sheet positions can lead to false balance sheets, hidden financial results, latent reserves, and losses. Corporate governance aims to encourage the efficient use of resources and accountability for the stewardship of those resources, aligning the interests of individuals, corporations, and society (Lee & Chou, 2020).

The Organisation of Economic Cooperation and Development (OECD, 1999) defines corporate governance as the system that directs and controls business corporations, specifying the distribution of rights and responsibilities among various stakeholders and providing the structure through which company objectives are set and performance is monitored (Zhang & Jia, 2013).

First, we contribute to literature by providing evidence of industry effects on firms’ earnings management decisions. Firms in the same industry face similar market conditions and (growth) prospects. Prior studies provide evidence that these industry prospects affect firms’ financial decisions. Harford (2005) finds that merger waves occur in response to specific industry shocks that require largescale reallocation of assets. Mackay and Phillips (2005) find that industry and group factors are important to firms’ capital structure decisions.

In relation to the above arguments about the influence of the industry valuation on the costs and the benefits of earnings management, as well as the likelihood of earnings management being detected, we predict that the incentives to engage in earnings management vary across time and are associated with aggregate levels of industry valuations: earnings management is expected to occur more frequently when industry valuation is high. Therefore, our main hypothesis is that industry valuation has a positive impact on the degree of earnings management in that industry (Zhang et al, 2017).

4. Data and Method

This section has encompassed the method of forecasting earnings management. This part also presents how different industries practices discretionary earnings management differently. Moreover, this further clarifies that how corporate governance can responsibly be involved in controlling aggressive accounting manipulation. The factors of industry-wise earnings management and the attributes of the corporate governance have been demonstrated and identified how significantly the factors of corporate governance can control the practice of earnings management.

4.1. Earnings management Variables

In this empirical research, two main factors have been included to examine the impact of corporate governance on earnings management. Firstly, earnings management has been estimated by using performance matched discretionary accruals which considers numerous variables as below:

Healy (1985) and Jones (1991) have used balance sheet approach, as mentioned in equation (v), to calculate total accruals in which following formula has been used. This can be mentioned as below:

Where,

= Change in current assets in year t;

= Change in cash in year t;

= Change in current liability in year t;

= Change in current maturities of long term debt and other short term debt included in current liabilities between current year t and previous year t-1;

= Depreciation and amortisation expense in year t.

Further, The first stage uses balance sheet approach to calculate total accruals as mentioned above while the second stage is used to compute non-discretionary accruals as below:

The heteroscedasticity in this model could be the problem because of the variables involved in the regression analysis due to which the original variables are deflated by total asset at (t-1). Additionally, many researchers (Chen & Zhang, 2012; Greene, 2014) admit that variables used in performance matched discretionary accruals models are deflated by average total assets to lessen heteroscedasticity.

Thirdly, discretionary accruals are computed by

While calculating the value of discretionary accruals, this research has not paid attention on the particular event and concentrate on the values of the earnings management. It does not consider the signs while making regression analysis. Hence, the absolute value of the discretionary accruals has been created for the analysis; the reason behind this is because the manipulation can be done in both positive and negative ways to meet the contractual obligations (Warfield et al, 1995; Klein; 2002). Estimates of the firm specific parameters are generated using the performance matched discretionary accruals model in the estimation period.

4.2. Industry-wise Corporate Governance and Earnings Management

This papers basically deals with testing hypothesis by considering OLS analysis (e.g., Elamer et al., 2017; Elghuweel et al., 2017; Ghosh et al., 2010) to identify the impact of corporate governance on earnings quality.

Hence, the empirical model is formed as below:

= Discretionary Accruals (for firm i during the time t) in its absolute value based on performance matched discretionary accruals Model; where discretionary accruals has been considered as a proxy of earnings management. Further, this paper presents the empirical analyses, comprising the descriptive statistics, bivariate correlations & multivariate regression.

The interpretation of other variables have been made as follow:

Boardsize: The total number of directors in the board committee.

Boardind: The independence of the board is measured dividing total board members by independent non-executive members.

Brdmeet: the number of meetings held in an accounting period by the board members.

Chairmanind: This has been created as dummy variable. The value is taken as 1 if the chairman in independent otherwise it is 0.

Remcommind: This is also dummy variable, which considers one if the members of the committee are entirely independent; and zero otherwise.

Femaleboard: The percentage of female presence in the board.

Noncommind: The presence of Non-executive directors in the board in the form of proportion.

NonEXMeet: This is considered as dummy variables if the non-executive directors meet in absence of chairman, zero otherwise.

NEDFee: The total amount in a year paid to each Non-executive director.

Manown: managerial ownership is calculated as the percentage of shares held by executives out of the total number of shares.

Instown: The percentage of shares outstanding owned by institutional owners.

Blockholder: This is regarded as a dummy variable. The value one is considered when the external stockholder owned 10% and more; zero otherwise.

Leverage: This is ratio between the long-term debt and total asset.

CFO: This is calculated by considering cash flow from operating activities and value of total asset of the beginning of the accounting year.

ROA: return on asset.

Indspec: Industrial Special which is dummy variable. This considers the value 1 for the relative industry and 0 for other industries.

5. Findings/Results

This section comprises the outcome of the research which has been conducted by deploying the univariate and multivariate methods. The univariate methods have been followed by the multivariate methods where the former deals with descriptive statistics while the latter deals with hypothesis testing. As per the nature of the data, this research has not considered the ordinary least square method, instead, has considered general least square method to avoid the misinterpretations those may arise due to the consequences of not meeting the conditions for ordinary least square method.

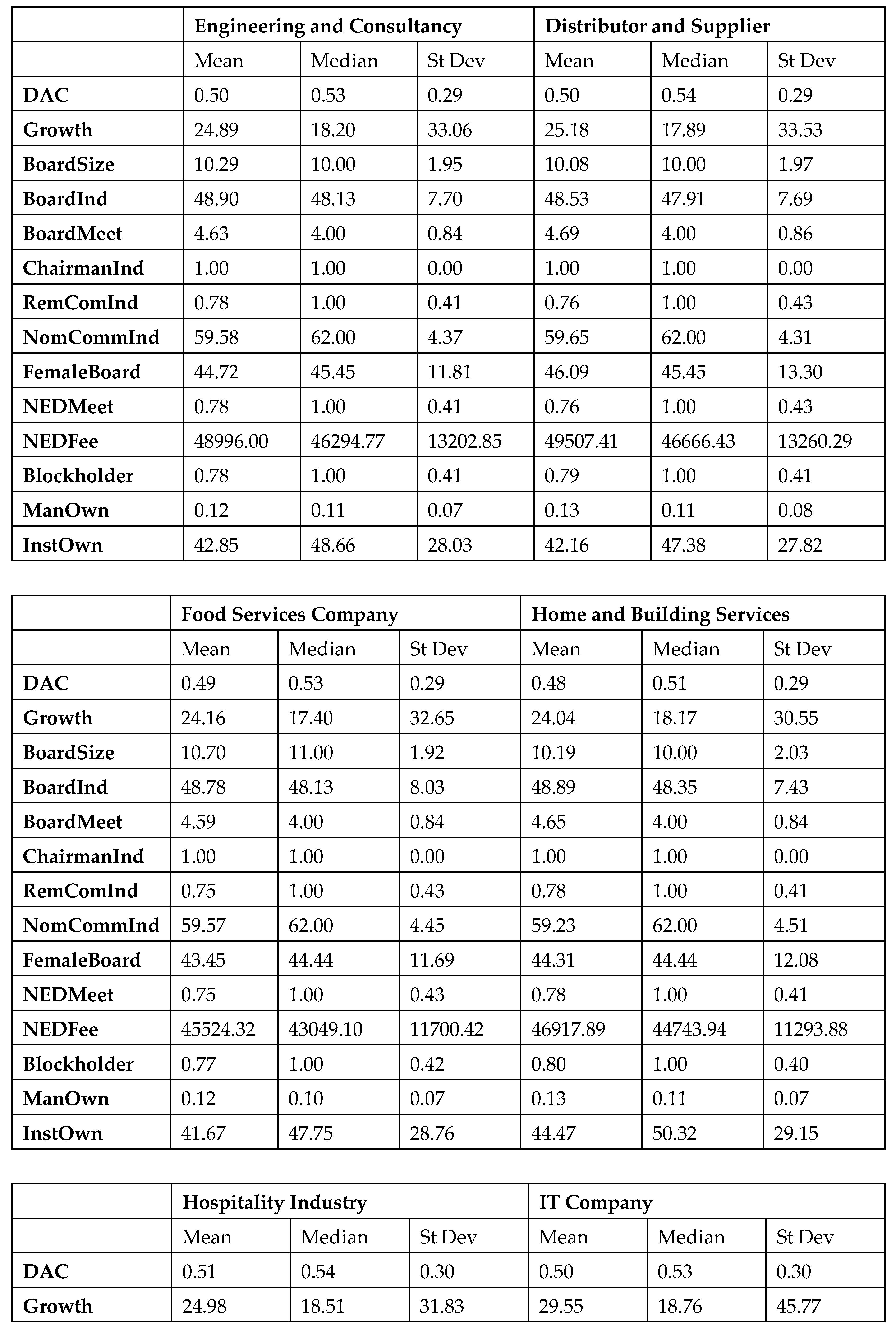

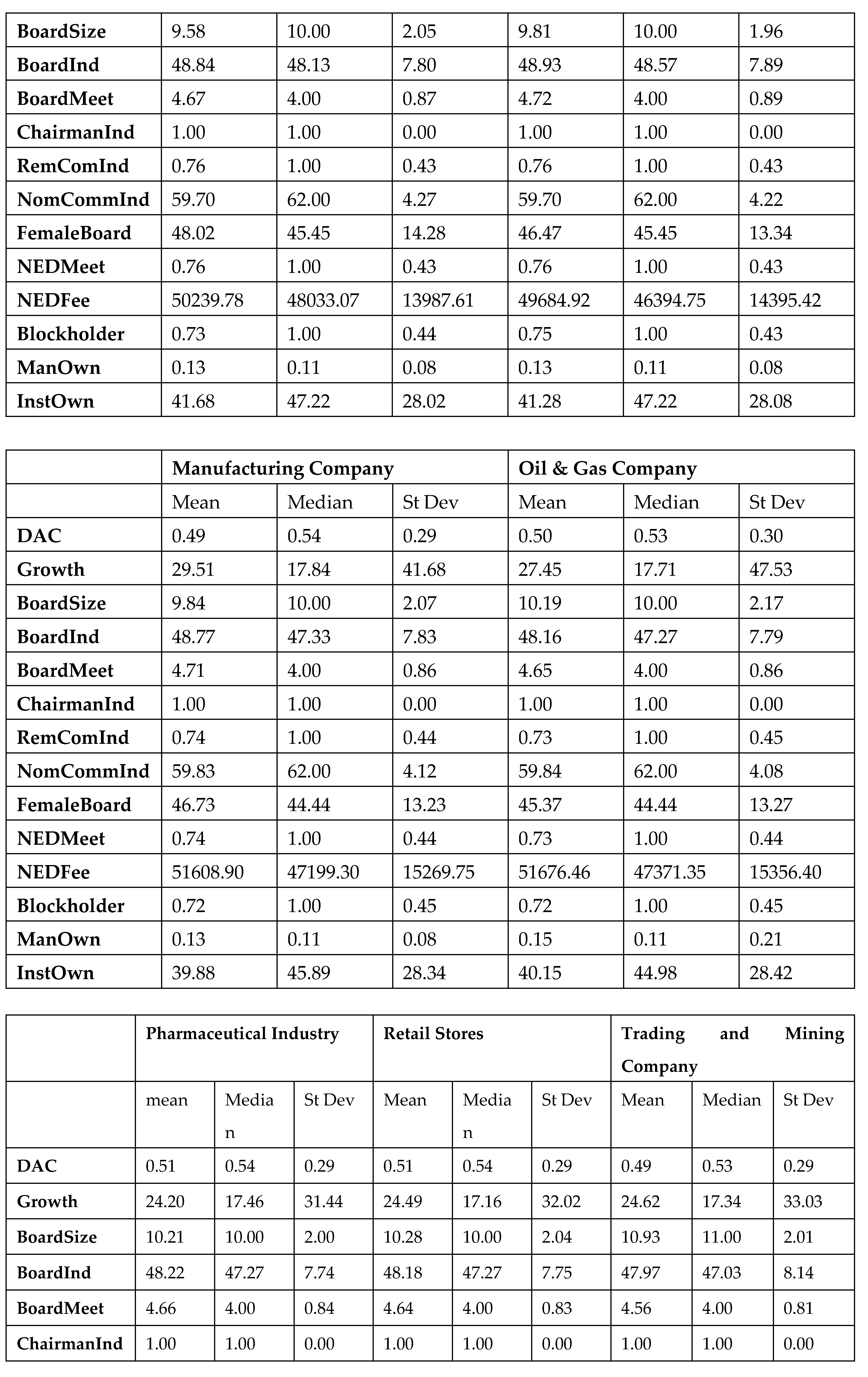

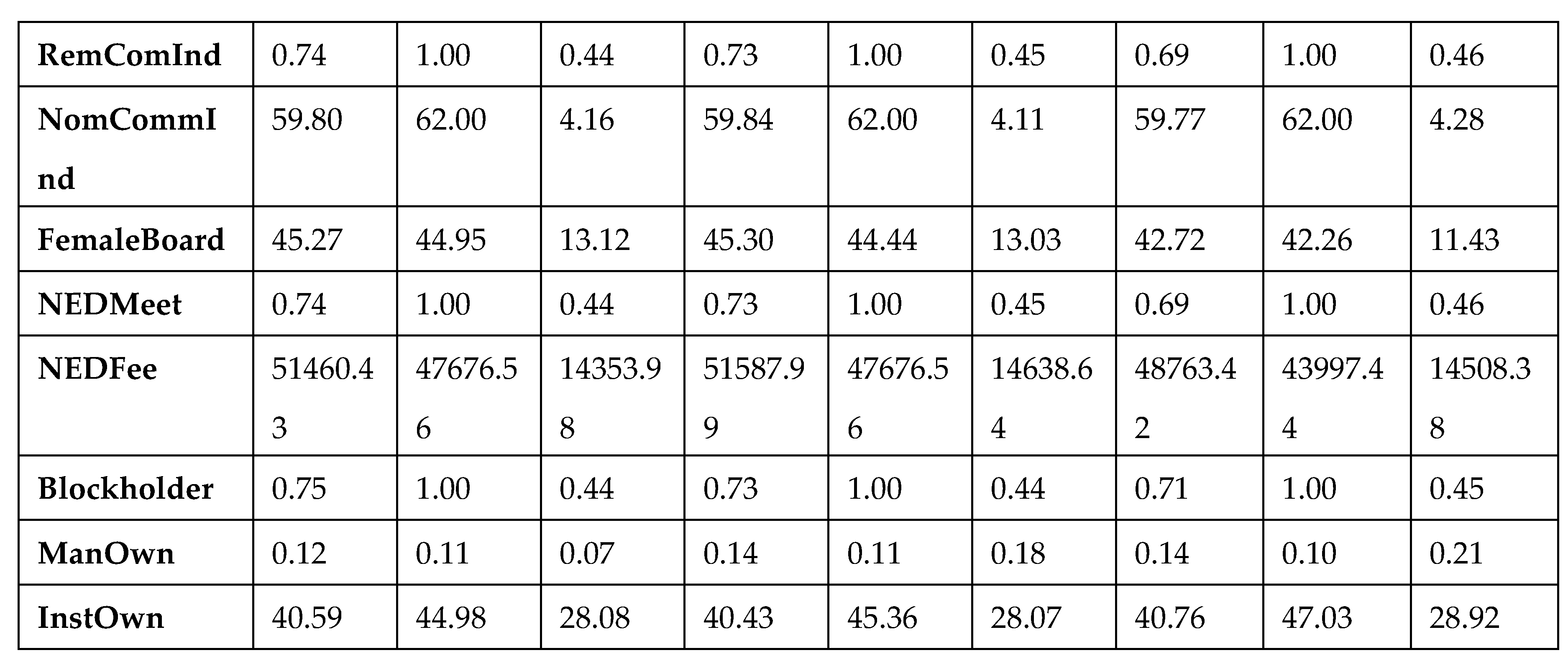

5.1. Descriptive Study: industry wise Analysis of Discretionary Accruals

The practice of earnings management may have been done differently as per the types of the industry they are in. The performance of the earnings management based on the industry may be similar or maybe not. This study investigates the impact of same variables of first model and second by categorising the samples in respective industry on the earnings quality.

There are some researchers Frankel et al (2002) and Srinidhi and Gul, (2007), Maurya, (2009), Zermi et al (2012) who have studied the performance of earnings management industry-wise and the impact of corporate governance on the earnings quality. In their research they have collected the data from six largest industries. Following those research, this study has included 11 largest industries from FTSE350 index based on the UK. These industry has included 70.41% of the sampled firms.

The industries are categorised as Engineering and consultancy (Eng&Con), Distributor and Supplier (dist & Sup), Food Services (FoodServ), Home and Building services (Hom&Build), Hospitality Industry (Hot&Rest), IT Company (IT Comp), Manufacturing Company (Manu Comp), Oil and Gas Company (oil & Gas), Pharmaceutical Company (pherm Com), Retail Industry (Retail), Trading and Mining Company (trading & Mining).

The presentation of the variables in the Table 5.1; in the Appendix section, demonstrates the industry-wise mean, median and standard deviation of variables. The average value of discretionary accruals is presented in terms of each industry. The value of discretionary accruals varies from industry to industry. This study has identified that the value of discretionary accruals in Engineering and Consultancy is different from the value of Food services and Home and Building Services.

Further, there are other industries Hospitality Industry, Manufacturing Company, Pharmaceutical Company, Retail Stores and Trading and Mining Company have different level of earnings management (closely equal to 0.51). The average value of earnings management (closely equal to 0.50) is almost equal to Engineering and Consultancy; Distributor and Supplier, IT Company, Oil and Gas Company. Similarly, there are some other industries like Food Services, Home and building services has equal amount (closely equal to 0.48) earnings management.

In this study, it has been paid proper attention to the earnings management industry-wise and identified that the performance of earnings management varies as the industry varies. The Hospitality Industry has shown closely higher level of performance of earnings management than other industries where it shows that the value of discretionary accrual is 0.5135 where Home and Building Services shows the lower level of earnings management which is about 0.479.

Hospitality Industry, Pharmaceutical Industry and Trading and Mining Company have slightly higher level of earnings management out of other industries for the Samples of FTSE350 companies of the UK. This practice of manipulation in such industries is because these industries are more complex in nature; hence, these companies have higher interest in manipulating earnings quality due to their motives and scopes in compare to other industries.

Hospitality industries are more complex because of their seasonality. The revenue in certain periods of the year are produced really high whereas in quiet months of the year the revenue goes to slow. Due to which the earnings manipulation is very prevalent in hospitality industry to smooth the bottom line of the organisation.

On the other hand, the pharmaceutical companies incorporate the firms those have issues in revenue recognition as too many research and development activities takes place. The research and development in this sector is a lot more severe than any other industry, hence, these is higher chance of manipulation on earnings quality. Similar issues have been found in trading and mining company due to the complex nature of such business.

The results of the study have been supported by the researcher Beasley, (1996); Jayola et al, (2017) which have admitted the variations of earnings management level as the industry varies. According to them, the fraudulences activities are of different nature in different types of industries.

While observing industry-wise data, mainly, in terms of Board Independence, the mean value is about 49% and the average of Board meeting is 5 times a year as per the sampled data collected from FTSE350 UK. Moreover, the board size in average in case of all industries, most of them have about 10 members but food services has average value of 11 members. These values are quite higher than previous results where Maurya, (2009) and Al-shaer and Zaman (2021) have reported that board independence is about 40% and meetings, in average, were 3 times.

While observing the impact of board composition and earnings management closely, it is found that the presence of higher independence of the directors in the board has negative impact on earnings management. In engineering and Consultancy, the average value of earnings management is 0.496 while the board size is 10.288 and board independence is 49.898. In Distributor and Supplier, the average value of board size is 10.07 and board independence is 48.53. This data presents that while the value of board independence and board size are slightly increased, the value of earnings management has been reduced with significant amount. This concludes that the presence of board independence and board size is negatively associated while observing this relationship industry-wise.

Moreover, similar type of relationship can be identified while observing the relationship between board independence and board size with earnings management in terms if IT companies and Manufacturing Companies. While observing the data of Pharmaceutical industry and Retail Industry, this also approves the negative relationship between the board composition and earnings management. However, this kind of relationship does not exist in terms of other industries; food services; home and building services.

The sampled data of this study, in terms of nomination committee, the average value of nomination committee in all types of industries are same. This is because the organisations have to follow the nation’s regulations, however; while observing the data in comparison to the average value of earnings management, it does not reject the null hypothesis.

While observing industry-wise, 73% of the sampled firms have managed to hold the meeting without presence of executive directors. In comparison to this, the board meetings are held quite a lot of times which is about 5 times a year. This study finds that the meetings seem to have been decreased from past practices as Maurya, (2009) reports that the board meeting used to be held in average of 8 times a year by each industry of FTSE350 companies.

Further, this study finds that the average fee of non-executive directors is about £26,341 per year. The industry which pay the highest amount to the non-executive directors is Retail industry which is about £51,588 per year. This amount is quite higher from the lowest amount paid about £45,524 by Food and Services Industry. The relationship with earnings management in terms of pay to the non-executive directors does not show the significant results in this study. The lowest amount is paid by Food and Services Industry; also, the average earnings management value is also found low in this industry.

While observing the data, regarding ownership, this study finds that the low average value of managerial ownership is 0.124% in Engineering and Consultancy Industry while the block holders and institutional ownership are far more than managerial ownership. These value has exceeded the standard assumption (10%) in each industry. The managerial ownership is low; this may be because the external stake holder like institutional owners and block holders exerts the pressure to have ownership of the organisation.

The value of discretionary accruals can be basically shaped by the type of industry they fall in. Hence, the corporations are categorised according to their industries. The researchers Dopuch et al., (2005); Gul et al., (2009); and Craswell et al., (1995), Ware (2015), Kumara (2021) have recommended that the firms perform the earnings management practices as per the industry they are in. They suggested that the estimation of discretionary accruals can be noisy and biased when there are no homogenous conditions, hence, suggested that the firms have to be separated with respective industries. Hence, industry analysis removes such concerns and examine of the previous result is different from the results those get obtained from industry type.

This research is conducted through the statistical test by following the model of Frankel et al. (2002) and Srinidhi and Gul, (2007), Kumara (2021) who have separated the firm industry-wise and run the regression analysis. The industries are categorised as Engineering and consultancy, Distribution and Supplier, Food Services, Home and Building services, Hospitality Industry, IT Company, Manufacturing Company, Oil and Gas Company, Pharmaceutical Company, Retail Industry, Support Industry, Trading and Mining Company. As per the recommendation by Carcello et al., (2002) and Abbott et al., (2006), this study has created the dummy variables. The selected industry is considered as 1, otherwise, it is zero.

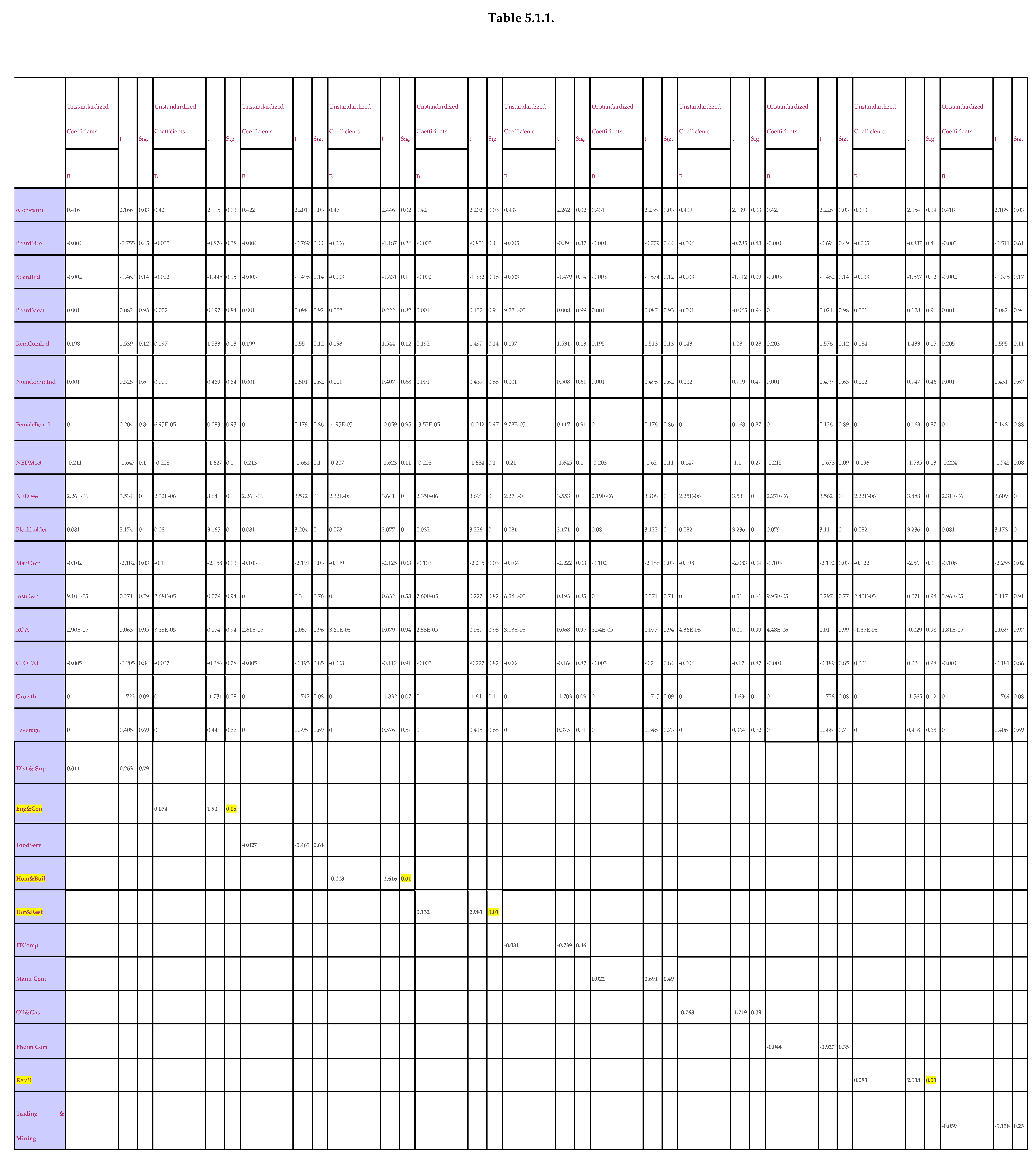

5.1.1. Multivariate Analysis: Industry-wise Analysis

The researchers Jones (1991), Ahmed-Zaluki (2011), Cimini (2015) has concluded that parametric tests are considered as the most relevant tools in a situation when the conditions of OLS are fulfilled but in a situation, where the conditions of ordinary least square are violated, non-parametric tests are more relevant and powerful. Non-parametric test does not demand the conditions of normal distribution and homogeneity of variance to be met. Hence, based on the discussion made in above, this study uses non-parametric tests, so, general least square is being considered in place of ordinary least square in the multivariate test.

The statistical calculation from Table 5.1.1., it presents that there are 11 different industries. The data has been organised in the form of dummy variable. This study has identified that out of 11 industries, five industries have the significant results which shows significant changes from earlier studies. Maurya (2009) has presented that out of six industries only one industry has positive significant results. The industry in his research was construction and building material. This industry followed the income-increasing approach and the relationship was significant.

Both engineering, and hotel and restaurant industries are very complex sectors, hence, there are more parties involved and may exerts pressure to management and compel them to practice earnings management. These both types of industries have different way of contracting methods while negotiating the job; therefore, their way of recognising revenue may have various type of complexities. This result is similar to the result of Beasley et al. (2000), Bhattacharya et al. (2003) and Tang (2017) who have argued that the nature of fraudulences activities depends on the type of industry. Both engineering, and hotel and restaurant industries are very complex sectors, hence, there are more parties involved and may exerts pressure to management and compel them to practice earnings management. These both types of industries have different way of contracting methods while negotiating the job; therefore, their way of recognising revenue may have various type of complexities. This result is similar to the result of Beasley et al. (2000), Bhattacharya et al. (2003) and Tang (2017) who have argued that the nature of fraudulences activities depends on the type of industry.

The statistical calculation from Table 5.1.1, it presents that there are 11 different industries. The data has been organised in the form of dummy variable. This study has identified that out of 11 industries, five industries have the significant results which shows significant changes from earlier studies. Maurya, (2009) has presented that out of six industries only one industry has positive significant results. The industry in his research was construction and building material. This industry followed the income-increasing approach and the relationship was significant.

This study has identified oil and gas company; and home and building company have practised income-decreasing approach whereas engineering and consulting, hotel and restaurant; and retail industry have followed income-increasing approach. As presented above in the Table 5.1.1, the β= 0.074 and P-value =0.050 have been found while investigating the impact of engineering and consulting industry on earnings management. Similarly, hotel and restaurant industry presents that β= 0.132 and P-value =0.003. These both industries have positive relationship at significant level.

Both engineering, and hotel and restaurant industries are very complex sectors, hence, there are more parties involved and may exerts pressure to management and compel them to practice earnings management. These both types of industries have different way of contracting methods while negotiating the job; therefore, their way of recognising revenue may have various type of complexities. This result is similar to the result of Beasley et al. (2000), Bhattacharya et al. (2003) and Tang (2017) who have argued that the nature of fraudulences activities depends on the type of industry.

Further, retail industry has also followed income increasing approach of earnings management where the β= 0.083 and P-value =0.033. Mostly, retail industry handles too many transactions, inventories and cash transactions in daily basis. This is very different area of the industries out of other in the business sector. Hence, the corporate governance in such industry may not be able to control each fraudulence activity. This result is consistent with the recommendation made by Beasley et al. (2000) who have investigated that the fraudulences activities occurs with different nature in different types of industry.

Moreover, home and building, and oil and gas company have followed the income decreasing practice of earnings management. From the statistical calculation it has been identified that the β= -0.0118 and P-value =0.009 in terms of home and building industries whereas oil and gas company presents the β= -0.068 and P-value =0.086. They both are negatively associated with earnings management at significant level.

6. Conclusion

The analysis has considered two important statistical tests; univariate and multivariate. The univariate tests have considered the descriptive statistics while multivariate tests have considered the regression analysis. In general, it is identified that the variables of the corporate governance are found as active attributes to control the practice of the earnings management.

This study has identified oil and gas company; and home and building company have practised income-decreasing approach whereas engineering and consulting, hotel and restaurant; and retail industry have followed income-increasing approach. As presented above in the Table 5.1.1, β= 0.074 and P-value =0.050 have been found while investigating the impact of engineering and consulting industry on earnings management. Similarly, it has been identified that hotel and restaurant industry has β-value = 0.132 and P-value =0.003. These both industries have positive relationship and are at significant level.

This research is an empirical study on the influence of corporate governance and on controlling manipulation of the earnings quality industry-wise. Various attributes of the corporate governance monitoring tools have been deployed and identified the controlling measures of them in terms of earnings management; as per the category of the industry the firm lies.

Appendix

Table 5.1.

Industry-wise Descriptive Statistics.

|

References

- Abbott, L.J., Parker, S. & Peters, G.F. (2014). Audit Committee Characteristics and Restatements. Auditing: A Journal of Practice & Theory, 23(1) 69-87.

- Al-Shaer, H. and Zaman, M. (2021), "Audit committee disclosure tone and earnings management", Journal of Applied Accounting Research, 5(2): 25-47.

- B. Sharmila (2020) “Study of improved Mandarin (Citrus Reticulate Blanco) orchard management practices in mid hills of Gandaki province, Nepal,” Malaysian Journal of Sustainable Agriculture, vol. 4, no. 2, pp. 49–53. [CrossRef]

- Beasley, M. S. (1996). An empirical analysis of the relation between the board of director composition and financial statement fraud. The Accounting Review, 71(4), 443–465.

- Bhattacharya, U., H. Daouk, and Welker, M. (2003) The World Price of Earnings Opacity. Accounting Review, 78 (3): 641–678. [CrossRef]

- Chia-Hao Lee & Pei-I Chou. (2020) Industry competition, earnings management and leader–follower effects, Applied Economics, 52:4, 388-399. [CrossRef]

- Craswell, A.T., Francis, J.R., and Taylor, S.L. (1995). Auditor Brand Name Reputations and Industry Specializations. Journal of Accounting and Economics, Vol. 5(4): pp. 297-322. [CrossRef]

- Frankel, R. M., Johnson, M. F., and Nelson, K. K. (2002). The Relation between Auditors’ Fees for Non Audit Services and Earnings Management. The Accounting Review, Vol. 77, pp. 71–105.

- Greene, W. (2014). Econometric Analysis. 7th ed. New York: Pearson Education Ltd.

- Gul, F.A., Yu Kit Fung, S., and Bikki, J. (2009). Earnings Quality: Some Evidence on the Role of Auditor Tenure and Auditors’ Industry Expertise. Journal of Accounting and Economics, Vol. 47: pp. 265– 287. [CrossRef]

- H. Wu, W. Wang, C. Wen, and Z. Li, (2018) “Game theoretical security detection strategy for networked systems,” Information Sciences, vol. 453, pp. 346–363. [CrossRef]

- Healy, P.M. (1985). The effect of bonus schemes on accounting decisions. Journal of Accounting and Economics, 7(1-3), 85-107. [CrossRef]

- Jaggi, B., Leung, S., and Gul, F. (2009). Family Control, Board Independence and Earnings Management: Evidence Based on Hong Kong Firms. Journal of Accounting and Public Policy, Vol. 28: pp. 281– 300. [CrossRef]

- Jones, J. (1991). Earnings Management During Import Relief Investigations. Journal of Accounting Research, 29(2), 193-228.

- Klein, I. (2012). The impact of changing stock ownership patterns in the United States: Theoretical implications and some evidence. Revue deconomie Industrielle, 82(4), 39–54.

- Kumara, E.S. (2021), Does Corporate Governance enhance Financial Distress Prediction? South Asian Journal of Business Insights, 1(1), 78-114. [CrossRef]

- Zhang, X., Yang, and Ke, L. (2017) “The evolutionary game simulation on Technology innovation between government and small and medium-sized enterprises,” Science and Technology Management Research, vol. 37, no. 12, pp. 15–23.

- Lim, N., Dopuch, N. and Pincus, M. (2008). Evidence on the choice of inventory accounting methods: LIFO versus FIFO. Journal of Accounting Research, 28-59. [CrossRef]

- Maurya, H. (2009). Corporate environmental disclosure, corporate governance and earnings management. Emerald Group Publishing Limited, 13(2), 7- 20.

- Tang, J. (2017). CEO Duality and Firm Performance: The Moderating Roles of Other Executives and Block holding Outside Directors. European Management Journal, 35 (3), 362–372. [CrossRef]

- Ware, S. J. (2015). Debt, Poverty, and Personal “Financial Distress”. American Bankruptcy Law Journal, 89 (3), 493–510.

- Warfield, T., and Wild, J. (1995). Managerial Ownership, Accounting Choices, and Informativeness of Earnings. Journal of Accounting and Economics, Vol. 20: pp. 61-91. [CrossRef]

- Jia, Y., and Zhang, S. (2013) “Analysis of quality evolutionary games in dairy industry based on industry growth--the evolutionary direction, speed and innovative strategy,” Soft Science, vol. 27, no. 12, pp. 11–16.

- Zermi, M., Elina, H., Jarvinen, T., & Niemi, L. (2012). Do joint audits improve audit quality? Evidence from voluntary joint audits. European Accounting Review, 21 (4), 731-765. [CrossRef]

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Copyright: This open access article is published under a Creative Commons CC BY 4.0 license, which permit the free download, distribution, and reuse, provided that the author and preprint are cited in any reuse.