Submitted:

17 June 2023

Posted:

19 June 2023

You are already at the latest version

Abstract

As a part of the European Green Deal, the Corporate Sustainable Reporting Directive will apply to over 50,000 companies in Europe, meant to advance the quality of sustainability reporting in the EU, and reduce global emissions and emission distribution inequality. Part of the requirements centre around organisational emission quantification, which will bring much attention to the methodological aspects and resulting decision support capability, which calls for synthesis and argues for clarity. Currently, quantifying the emissions embedded in global transactions mostly focus on direct value-chain attributes, and do not consider unintended consequences beyond the scope of assessment. To achieve genuine reductions, estimated emissions must be considered from a systems perspective to accurately reflect their true impact. While emission inventories serve several purposes, incorrect application limits their potential. The CSRD aligns itself with the GHG Protocol, which does not explicitly facilitate this distinction, although new Land Sector and Removals Guidance draft does, in part. With first CSRD reports expected in 2025, and the GHG protocol entering a revisions period, it presents an opportunity to marry systems thinking with carbon literacy, thereby equipping the expected surge of activity with the sufficient tools for an accelerated transition.

Keywords:

climate change mitigation and adaptation

; economic structures

; driving forces

; transitional risks

; consequential attributional

1. Value Chain Emissions and Inequalities

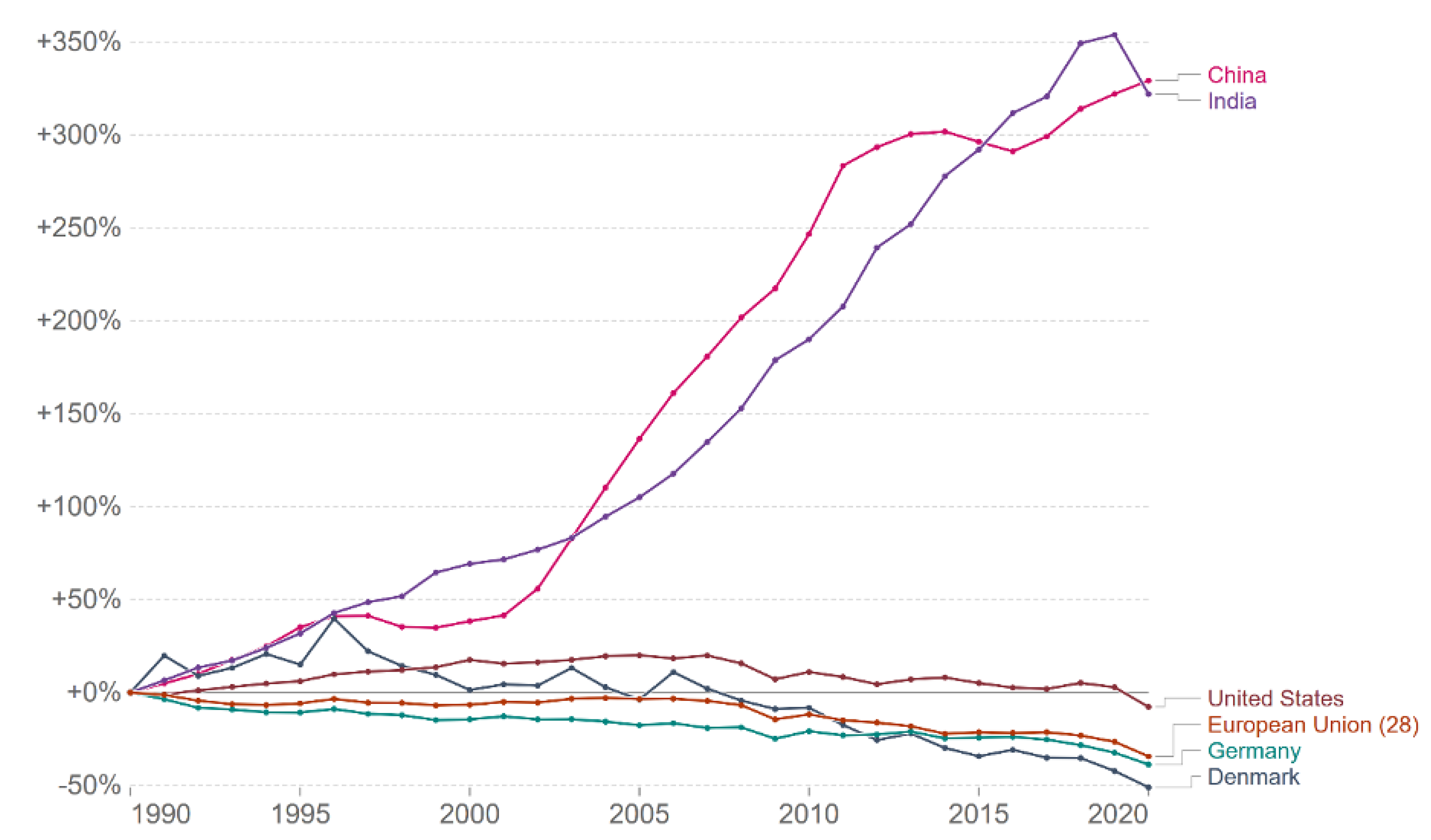

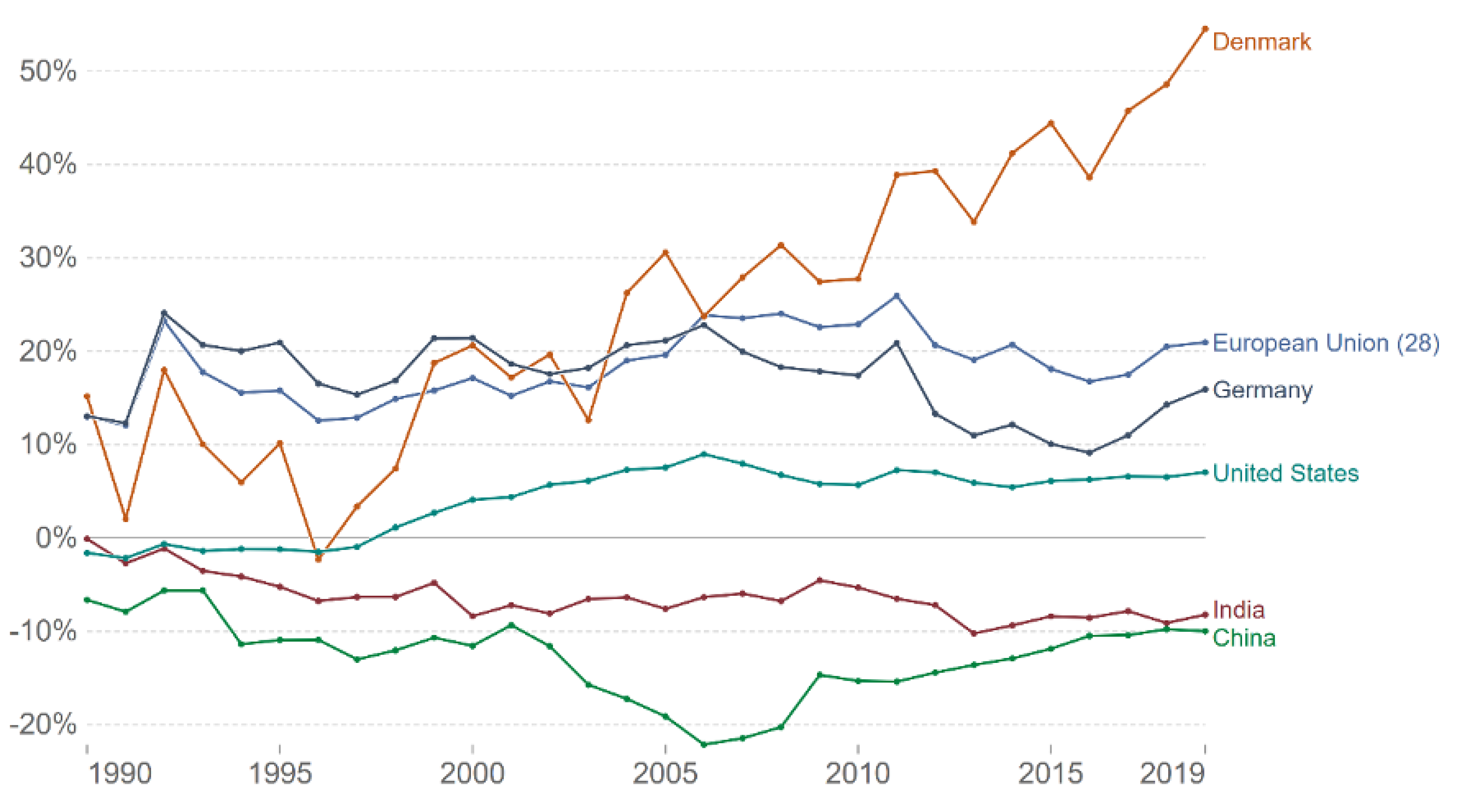

Transactions see goods or services delivered in exchange for money, of which many include the invisible exchange of embedded emissions yet most fail to disclose. As transactions continue in an unchanged manner, emissions accumulate, further accelerating the trajectory towards 1.5 degrees. In June 2023, the remaining global carbon budget was reduced, further highlighting the need for rapid decarbonization [1] and call for critical conversations of current carbon quantification systems and their application. Companies are expected to play a pivotal role in nations achieving their emission targets by reducing their production related emissions, but emission-oriented policies do not yet address the largest source of embedded emissions, namely the value chain. On a global scale, the disproportionate and inequal distribution of GHG emissions (and along with these, other production related hazardous emissions) between the North and South is the greatest. While industrialized countries have overall reduced their national emissions since 1990, outsourced production related emissions in China and India have increased dramatically (Figure 1) in so called pollution havens [2]. One driver of this inequality is that companies of industrialized countries have increased their net-import of CO2 embedded in trade (Figure 2) [3]. In China for example, intermediate products are identified as the main source of embodied emissions export [4] – in other words, the geographical distribution of companies from industrialized nations’ value chain (scope 3) emissions highlight and perpetuate the inequality of global emission distributions. On an organisational level, who is responsible for the embedded emissions of global value chain transactions? Sanderson (2021) suggests a shared responsibility between buyer and seller that reflect our perceptions of sustainability which lacks in many transactions of today, a sentiment also widely reflected in literature [5,6,7,8,9,10].

Not reacting to these inequalities on an organisational level will perpetuate the global distribution, leaving pollution havens of the world to bear the unfair emissions burden of global transactions. However, when considering this it is important to note how one determines who is responsible for what. The notion of shared responsibility is linked to the value chain, but as we will return to, there are compelling arguments for linking the responsibility to changes of flows in response to decisions, which may be both in and outside the value or supply chain [11]. This opens for important discussions of what determines the changes in emissions as depicted in Figure 1 and Figure 2, and what actions are needed to control these.

2. Organisational Inventories and Their Potential

On a global level companies can voluntarily disclose their organisational footprints and carbon management strategies e.g., via CDP (formerly the Carbon Disclosure Project) and Science Based Targets (SBTi). In Europe, organisational emission disclosure is a component of the broader obligations for companies complying with the Corporate Sustainability Reporting Directive (CSRD), a reporting policy that will initially be applicable to larger companies (estimated over 50,000) and gradually extended to smaller companies [12]. The dominant language for how to estimate organisational emissions follow the Greenhouse Gas Protocol (GHGP), which define three scopes that company emission sources can be allocated to, and how to navigate varying qualities of data required to estimate them. Organisational inventory requirements of the CSRD align to this framework for easier adoption. For the majority of companies, the most significant portion of their emissions are in scope 3, both up and down the value-chain [13]. Including scope 3 emissions therefore becomes necessary for a climate-just greenhouse gas (GHG) inventory when considering our perceptions of justice and fairness in relation to who is responsible for the emissions, and in turn the global emission distribution. The most significant scope 3 categories reported by companies today are currently voluntary by the GHGP, where incomplete and incomparable activity and emissions data coupled with limited accountability hinder progress. Demand for data supporting scope 3 assessments is expected to increase however as value chain emissions are required in CSRD compliant reports. As emission disclosure is becoming recognized as a must-have in seller/buyer transactions for companies who openly engage with and promote sustainability, it promotes carbon literacy among both parties and quantifies the transaction’s invisible cost for organisational GHG inventories. For widespread use and sufficient application however, there remains a need for complete and transparent emission quantification, supported by sound data.

Emission accounting at a firm level serve several purposes but require separate methods and data to answer different questions. An understanding of the emissions arising from company activities (both direct and indirect, and within and beyond the scope of analysis) act to inform true decarbonisation decisions through hotspot identification. If the goal is to reduce global emissions, a systems view is required to ensure unintended emissions do not occur outside of the assessment boundaries. Such assessments are well suited for decision support and can be considered for internal use. Alternatively, the assessment can be used as a communication tool to indicate that the firm is engaging with and aware of their impacts, setting and tracking targets, allocating ownership, and eventually showing the achieved reductions. Such assessments report attributes allocated to the products or services and are not concerned with consequences beyond the boundaries of the supply chain and does not include system effects captured when applying system-expansion. In organisational inventories, they represent the activities of the reporting firm alone, and are by current consensus acknowledged for external use i.e., with reference to the GHGP. Instead, we recommend using an approach that explicitly takes systemwide impacts into consideration. These distinctions are well documented in the literature but not yet widely adopted, as called for by the problem at hand [11,14,15,16,17]. It is vital to note that different models answer different questions.

Organisations and frameworks such as CDP, SBTi, and the CSRD require and assess disclosure of climate impacts and climate plans, but risks pointing the internal tool outwards, aimed at stakeholders such as investors. Climate responsible investors are expected to represent a substantial portion of the €1 trillion that EU Green Deal plans to mobilize over the next decade [18]. Investor actions will be in part based on assessments and reports underpinned by company disclosures from organisations and frameworks such as CDP, SBTi and the CSRD, where incorrect application of an organisational inventory may have detrimental consequences for the reporting firm. For reporting companies, determining what a relevant and useful assessment is present uncertainties that embody the transitional climate risks presented by the Task Force for Climate Related Non-Financial Disclosure [19]. However, if a company is supported with the correct climate related information and possess the carbon literacy to ask the correct questions of their data, they can harness the benefits of both internal and external inventories, which in turn reduces their climate related transitional risks (and present opportunities). Central to managing such transitional risks are sound, robust, and quantitative assessment of risks, which is supported through accurate and transparent climate related information [20]. Further, if the internal inventory is to provide adequate decision support the methods used to estimate emissions need to represent the true impact i.e., by including all relevant activities considered from a systems perspective. Understanding and applying these concepts in the 50,000 CSRD compliant companies presents a formidable task of ensuring an accessible, usable, and informing data foundation.

3. Assessing Emissions Related to Activity

There are many standards that describe the methods for determining and disclosing the environmental impact of products, such as the PAS 2050, the GHG Protocol, and the European PEF Guide, all referring to the canonical ISO 14040 series. The series defines the most appropriate way to navigate the many decisions that go into conducting a Life Cycle Assessment (LCA) – constituting how to build an emissions inventory that relates activities to emissions both in the foreground system, mostly representing activities with scope 1 and 2 emissions, and the background system, mostly representing activities with scope 3 emissions. An essential support for the practitioner is the availability of databases supplying background data. There are various paid and free databases connecting activities to emission intensities 1, (EI) and they are widely accessible, although some, especially the free databases lack the variety and detail that companies with diverse supply-chains need for a climate just emissions inventory. A significant difference between available databases is the openness in terms of possibility to track combined productions, i.e. the availability of connected unit processes or conflated system processes. Furthermore, the majority of databases are ‘calculated’ according to often diverging modelling principles, using system expansion or various allocation procedures i.e. mass allocation, value allocation, or exergy allocation [17].

Therefore, when a firm conducts a GHG inventory, it becomes essential to ask where the emissions data is coming from, and the level of data quality required. As the majority of a company’s emissions are in scope 3, they are by definition and in part, another company’s direct scope 1 and 2 emissions. Engaging suppliers on such topics may provide advantageous reductions in a producer’s carbon intensities and add an environmental layer to buyer/seller dialogue on how to further find mutual data driven benefits in their partnership. For example, a clothing company may ask for emissions data and suggest low carbon intensive energy solutions to their textile supplier which will “contribute” less emissions to the final delivered product, reducing the product intensity and lowering the operation emissions. By extending the requirement of quantification, customers requesting the emission intensity of the products they purchase can be satisfied by conducting an LCA. However, as emissions are not yet a normal part of transactions, customers often refer to LCA or EI databases in place of supplier specific data.

The GHGP has a set of recommendations that suggests how to navigate the variability between supplier specific and average data EIs (see table 1), starting with the most desirable – supplier specific. Here suppliers can present a detailed account of the emission intensities underlying the product transaction, however while the green transition is still evolving, this is not yet commonplace. Least desirable in the GHGP is the spend based method, which uses e.g. Environmentally Extended Input/Output (EEIO) models, that produce results based on spend using sector average data. The GHGP suggests that mixing these methods is acceptable, where for example, scope 3.1 Purchased Goods may be calculated using an EEIO, and scope 3.6 Business Travel emissions using a process-based, or supplier specific approach [21].

This section may be divided by subheadings. It should provide a concise and precise description of the experimental results, their interpretation, as well as the experimental conclusions that can be drawn.

Table 1.

Greenhouse Gas Protocol Data Hierarchy taken from the GHGP [21].

Table 1.

Greenhouse Gas Protocol Data Hierarchy taken from the GHGP [21].

| Calculation Method | Upstream Production Emissions | Supplier’s Scope 1 and 2 Emissions |

|---|---|---|

| Supplier Specific | Supplier Specific Data | Supplier Specific Data |

| Hybrid Method | Supplier Specific Data or average data, or a combination of both | Supplier Specific Data |

| Average Data Method | Average Data | Average Data |

| Spend Based Method | Average Data | Average Data |

4. Consequential and Attributional LCA

An important distinction to make when it comes to LCA’s, and the subsequent EIs used in GHG inventories, is that there are two main trains of thought that are defined by asking different questions of the same data: Consequential LCA (cLCA) and Attributional LCA (aLCA). As the names suggest, aLCA considers the product-specific attributes that define the impacts from producing, consumption, and disposal of a product, asking the question: what was the impact of this product? The method applies normative attributional allocation of coproduction or partitioning of unit processes, in the attempt to model the supply chain or the value chain, by using partitioning according to mass or value [17].

Consequential LCA provides information on the consequences or relative change of impact at system level as a result of the production, consumption, and disposal of a product, both in and outside of the product supply chain. cLCA avoids allocation by using substitution, or systems expansion as it is called in the ISO 14040 series, where it also is stated that “wherever possible, allocation should be avoided” [22]. Therefore, cLCA asks the question: what will the system-wide impact be of additional purchase (consuming and disposing of) this product?

Under both approaches, the impact can be determined per unit of specific product, such as a L of milk, or a kWh of electricity. However, since cLCA methodology includes effects beyond the boundaries set in the supply or the value chain, it relies on modelling which productions respond to the increased demand and delineates the effect of these changes by considering market effects and marginal suppliers, including considerations of public regulations and other market external constraints [11,23,24,25]. For adequate comparison between aLCA results, methodology must share characteristics such as allocation method, which is mostly determined by value- or supply-chain characteristics. This is described by ISO as the partitioning of in/output flows of a process and can be done via economic allocation or mass allocation. Partial substitution is also seen, especially in modelling end-of-life processes, such as in the PAS2050 standard. In short, aLCA does not aim to quantify the total change caused by the decision in question, which Plevin and Wenzel argue is information essential for overall emission reductions [26,27]. The literature has many real life and hypothetical examples showcasing these characteristics, for a non-exhaustive list see: Sandén and Karlström 2007; Thomassen et al. 2008; Weidema et al. 2018, 2020; Brander et al. 2019; Ekvall 2020; Schaubroeck et al. 2021b; Brander 2022; Brander and Bjørn 2022; Løkke and Madsen 2022 [11,14,15,16,17,28,29,30,31,32].

The LCA literature agrees that uncritically mixing the two methods in a single analysis opens for misleading interpretations [17,30] as they ask different questions they can result in different outcomes and should therefore be avoided [17,33,34]. Using data from both methods in the same assessment is possible, however the problems arise when different data sources (implying different data collection principles) are vertically integrated, i.e., using a tiered approach or partial disaggregation. Brander suggests an application for both, where aLCA is be used for allocating responsibility, setting targets and tracking progress (the external inventory), however actions intended to reduce emissions are checked with a cLCA method to prevent undesirable effects outside of the inventory boundary (the internal inventory) – a common consensus in the literature [16,35]. The central discussion here is whether the transaction needs both methods. This has been discussed between Weidema et al. and Brander et al. [11,31,36], who agree regarding the importance of applying consequential LCA to avoid suboptimized decisions but disagree regarding the need of applying both methods. Our point is that in principle, consequential modelling provides the essential answers for guiding decisions, and that the attributional modelling is best substituted with traceable supply chain management, that partly enables accounting, and partly enables relevant modelling of the consequences of the system (Løkke & Madsen 2022). However, the aLCA approach is seen in so many company level efforts on presenting sustainability, through baseline emission inventories and net zero pledges, that it is unthinkable to abruptly change the systems. Furthermore, the transition will in reality require a massive learning process in terms of deeper understanding of what questions the two modelling approaches answer, and for that reason, a parallel combination of aLCA and cLCA may be needed.

5. Decisions for Improving Decision Support

Certainly, the debates in this space will have an impact on the future of GHG accounting, with important steps achieved in defining both a/cLCA and describing their characteristics and modelling limitations [17]. However, this still leaves common companies with the dilemma of how to navigate today’s economic and environmental transactions. The amount of carbon quantification we see today is not sufficient. The reluctant adoption of this technology is of course a complex issue, but the fact remains that most transactions occur absent of emission disclosure, which presents an opportunity for intervention. Without, those firms communicating results are faced with choices that don’t have very many repercussions, yet: On the one hand a more comprehensive assessment yields higher emission intensities, which despite providing more decision support, risk climate-shaming the reporter in the short term, and on the other hand is an immediately “green” marketable product boasting low emissions which lacks accountability and restricts the potential for meaningful betterments and emission reductions in the future. Intentional or unintentional misleading constatations and suboptimal application of carbon management tools will result in false successes, and a lateral green transition rather than one that drives reductions. This requires systems thinking and carbon literacy of the company to identify and decide on which information to use for decision support. Greenwashing is a pervasive risk in this process, with some countries introducing policies to combat it. For example, the European Green Deal describes that greenwashing is reduced when reliable, comparable, and verifiable information is presented to buyers, and that “companies making ‘green claims’ should substantiate these against a standard methodology to assess their impact on the environment” [37], and the Danish Consumer Ombudsman can fine companies for such misleading communication [38].

Still, the marketability of emission disclosure is not lost on engaged producers, as it presents a competitive metric that can be evaluated. In 2020, an 866-product carbon footprint database was published using CDP data, all of which follow aLCA methodology (Meinrenken et al., 2020), adding to the growing list of attributional EI databases available. This is partly due to a range of influences, such as the institutional inertia supporting aLCA methods (the GHGP suggests using aLCA for organisational inventories), the intuitive structure, or the market advantage of communicating on specific products, which may be perceived by the customer as more precise as it reflects precise supply chain data and proprietary information. However, precise supply chain data, and thereby precise emission estimates within the supply chain is not in contradiction to cLCA methodology – the difference lies in the interpretation of the data (Løkke and Madsen, 2022). There is still need for a greater data foundation for public cLCA databases, which should be prioritized as decision support functions of inventories grow. One example is The Great Climate Database focusing on food products, which draws on Exiobase 3, an EEIO database [39]. The major EEIO database Exiobase 3 is freely available for download [40] and is being used to develop a disaggregated open access database covering all global regions [41].

Emission quantification will receive more attention after policies such as the CSRD, and brings to question how accurate and relevant the disclosed emissions are, and what purpose they serve? They must answer the right question which is often related to why one conducts an emissions inventory in the first place. The environmentally conscious company will likely point to global emission reductions as a main reason, suggesting cLCA. But as we have discussed above, the risks of not disclosing are growing amidst an increasingly concerned market and present opportunities for proactive firms, however hasty adoption may result in suboptimal outcomes if suppliers are unable to match their methods to those of their customers. Accuracy and relevance are two of five core principles of a GHGP inventory to ensure usefulness of the exercise but assumes consistent methods of buyer and seller. As a result, the outcome of an externally aimed inventory risks being interpreted as internal decision support material. However responsible decision support must adopt a consequential approach, referring to a system perspective that reflects the consequences of decisions if the intention is to reduce global emissions [11]. The current GHGP framework does not explicitly facilitate this on the level where buyers and sellers disclose emissions, although the World Resource Institute suggest using consequential modelling when providing decision support or determining product emissions against a counterfactual baseline scenario [35]. Weidema shows how three different perspectives are used to describe the impacts and responsibilities related to an activity, i.e., a product or a service: value chain responsibility, supply chain responsibility and consequential responsibility, where they argue only the consequential is indispensable in terms of linking actions to changes in the state of the earth [11]. The GHGP Policy and Action Standard and recently in its Land Sector and Removals Guideline draft (currently in pilot testing phase) address the consequential perspective. They conclude that intervention-based accounting (the consequential perspective) should be used to determine the impacts of corporate actions but should be reported outside of a GHG inventory [42,43].

6. Promoting Systems Thinking

To remain relevant through a green transition and minimize their transitional risks, companies must direct informed initiatives to reduce their emissions, and disclose their progress. If we are to achieve significant reductions widespread adoption must be seen, however true decision support via carbon quantification is unintuitive compared to aLCA and presents potentially conflicting messages to the common company. Regardless, to be compliant with frameworks such as CDP, SBTi and the CSRD, a consumption-based inventory is required by including scope 3 emissions. As the majority of a traditional firm’s emissions lie with their suppliers, often times overseas, and the GHGP’s data hierarchy prioritises supplier specific data, companies (especially ones with complex supply chains) are then tasked with tracking the quality and characteristics of their available supplier data, using databases that match their supplier’s data, or committing to consistent use of a specific database. For CSRD compliant companies, access to the carbon literacy required for such critical evaluation of supplier or database data can be achieved through new personnel or purchased through consultants. However, cascading effects will place onus on smaller suppliers of CSRD compliant firms as they follow the GHGP and prioritize supplier specific data. Those with sufficient data availability on their products and services will gain market advantage, in turn progressing the green transition – but at what pace? 50,000 companies present a sizeable increase in the application of LCA and emission quantification, as well as a risk of companies using the same inventories to guide decarbonisation. First round CSRD submission is planned for 2025, which presents a window of opportunity for the LCA community to shift attention to the superior decision support capabilities of cLCA and accelerate the decision-making capability of users.

One way this can be done is by revisiting the GHGP. The first GHGP was published in 2001 and is now entering a revision period, and its new Land Sector and Removals Guidance is in its pilot phase. We see this as a step towards making system thinking more commonplace in the emission inventory, leading to truer decision support, but also recognize the need for correct and transparent data. We suggest that future guidance emphasizes decision support with systems thinking and for it to become a cornerstone for users of the GHGP to facilitate an understanding of both their own system and the related global impacts. There is potential for misleading results when overlaying the a/cLCA methodologies with the GHGP data hierarchy, and we therefore suggest introducing systematic clarity to what the GHG inventory can and cannot be used for, what characteristics such accounting methods would need to have, and by extension, increasing carbon and industrial ecology literacy through clearer understanding of how organisation supply chains interact with surrounding systems using consequential modelling principles. Fast-tracking such academic debates to limit interpretations in the GHGP could reduce the risks of greenwashing and add to a swifter and more effective green transition.

Our takeaway is this: It is important for companies to go beyond their externally aimed normative aLCA inventory for decision support to avoid counterproductive outcomes. If this is not purposely done, companies using the GHGP as guidance for conducting GHG inventories risk not seeing important aspects of the production system and therefore risk making suboptimal decisions with global repercussions. Companies should therefore possess the carbon literacy and systems thinking to flip the hierarchy and make critical decisions, and as a part of the process gain sufficient system understanding to make the counterintuitive become intuitive. Alternatively, we altogether skip aLCA and establish cLCA as the norm. There is no reason that CSRD compliant inventories cannot have a systems thinking foundation, which equally applies to supplier specific data. cLCA logically fulfils requirements of both the internal and the external assessment. Why are we so entrenched in aLCA, when our accelerated deadlines cannot afford false or half successes? CSRD compliance will be a sought-after certificate, and while companies are adopting new structures with designated sustainability roles and personnel, many are not yet financially or structurally prepared for such additions with limited available resources for these tasks. Replacing the external (aLCA) with the cLCA reduces the number of modelling-approaches, streamlines implementation, and accelerates access to decision support. Furthermore, different questions asked with a cLCA approach will naturally give different but internally consistent answers [32]. A first step is integrating this mode of thinking into the standards the CSRD aligns itself to. However, in practice a prerequisite and barrier is data foundation. cLCA data is growing, but as carbon footprints are becoming an increasingly marketable parameter, there is need for an ontology with transparency and provenance which enables preservation of both decision support ability and proprietary information [44,45] such that suppliers can showcase their market-aligned characteristics. Rearranging the existing structures to enable this will only become more difficult the more entrenched aLCA becomes, unless there is greater adoption of systems thinking. With the expected increase of firms adopting carbon quantification practices, there should also be a heightened scrutiny of methods. As a result, LCA must undergo testing to assess fitness for purpose. LCA is currently reserved for experts although made more accessible through public databases, however with the boom of AI and semantic web it is only a question of how long before there is available decision support through such sources. Still, as with the above, this requires that users understand the ways they impact the larger systems they are a part of. Regardless of how quantification will develop, the need for both carbon and industrial ecology literacy are paramount to critically assess the greater systems and use LCA in its most optimal form for decarbonisation.

Author Contributions

Conceptualization, H.S., T.S., and S.L..; writing—original draft preparation, T.S.; writing—review and editing, T.S., H.S., and S.L.; supervision, H.S.; All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding

Data Availability Statement

No new data were created.

Acknowledgments

This work builds upon and reflects the consensus work initiated by Danish Universities on how to account for and assess university climate performance. We would also like to thank Michael Gillenwater and Timen Mattheüs Boeve for discussions leading up to this communication.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Forster, P.M.; Smith, C.J.; Walsh, T.; Lamb, W.F.; Lamboll, R.; Hauser, M.; Ribes, A.; Rosen, D.; Gillett, N.; Palmer, M.D.; et al. Indicators of Global Climate Change 2022: Annual Update of Large-Scale Indicators of the State of the Climate System and Human Influence. Earth Syst. Sci. Data 2023, 15, 2295–2327. [Google Scholar] [CrossRef]

- Taylor, M.S. Advances in Economic Analysis & Policy Unbundling the Pollution Haven Hypothesis. B.E. J. Econ. Anal. Policy Adv. Econ. Anal. Policy 2004, 4, 1–28. [Google Scholar]

- Ritchie, H.; Roser, M.; Rosado, P. CO₂ and Greenhouse Gas Emissions. Our World Data 2020.

- Fei, R.; Pan, A.; Wu, X.; Xie, Q. How GVC Division Affects Embodied Carbon Emissions in China’s Exports? Environ. Sci. Pollut. Res. 2020, 27, 36605–36620. [Google Scholar] [CrossRef]

- Munksgaard, J.; Pedersen, K.A. CO2 Accounts for Open Economies: Producer or Consumer Responsibility? Energy Policy 2001, 29, 327–334. [Google Scholar] [CrossRef]

- Peters, G.P.; Hertwich, E.G. CO2 Embodied in International Trade with Implications for Global Climate Policy. Environ. Sci. Technol. 2008, 42, 1401–1407. [Google Scholar] [CrossRef]

- Peters, G.P.; Hertwich, E.G. Post-Kyoto Greenhouse Gas Inventories: Production versus Consumption. Clim. Change 2008, 86, 51–66. [Google Scholar] [CrossRef]

- Kondo, Y.; Moriguchi, Y.; Shimizu, H. CO2 Emissions in Japan: Influences of Imports and Exports. Appl. Energy 1998, 59, 163–174. [Google Scholar] [CrossRef]

- Eder, P.; Narodoslawsky, M. What Environmental Pressures Are a Region’s Industries Responsible for? A Method of Analysis with Descriptive Indices and Input-Output Models. Ecol. Econ. 1999, 29, 359–374. [Google Scholar] [CrossRef]

- Le Quéré, C.; Andrew, R.M.; Canadell, J.G.; Sitch, S.; Ivar Korsbakken, J.; Peters, G.P.; Manning, A.C.; Boden, T.A.; Tans, P.P.; Houghton, R.A.; et al. Global Carbon Budget 2016. Earth Syst. Sci. Data 2016, 8, 605–649. [Google Scholar] [CrossRef]

- Weidema, B.P.; Pizzol, M.; Schmidt, J.; Thoma, G. Attributional or Consequential Life Cycle Assessment: A Matter of Social Responsibility. J. Clean. Prod. 2018, 174, 305–314. [Google Scholar] [CrossRef]

- European Commission Corporate Sustainability Reporting Directive . Available online: https://finance.ec.europa.eu/capital-markets-union-and-financial-markets/company-reporting-and-auditing/company-reporting/corporate-sustainability-reporting_en (accessed on 31 August 2022).

- Sanderson, H. Who Is Responsible for Embodied CO2? Climate 2021, 9, 1–5. [Google Scholar] [CrossRef]

- Ekvall, T. Attributional and Consequential Life Cycle Assessment. In Sustainability Assessment at the 21st Century; 2020; p. 42 ISBN 0000957720.

- Brander, M.; Bjørn, A. Principles for Accurate Corporate GHG Inventories and Options for Market-Based Accounting – Working Paper; 2022;

- Brander, M. The Most Important GHG Accounting Concept You May Not Have Heard of: The Attributional-Consequential Distinction. Carbon Manag. 2022, 13, 337–339. [Google Scholar] [CrossRef]

- Schaubroeck, T.; Schaubroeck, S.; Heijungs, R.; Zamagni, A.; Brandão, M.; Benetto, E. Attributional & Consequential Life Cycle Assessment: Definitions, Conceptual Characteristics and Modelling Restrictions. Sustain. 2021, 13, 1–47. [Google Scholar] [CrossRef]

- European Commission The European Green Deal Investment Plan and JTM Explained. Available online: https://ec.europa.eu/commission/presscorner/detail/en/qanda_20_24 (accessed on 19 September 2022).

- TCFD Task Force on Climate-Related Financial Disclosures . Available online: https://www.fsb-tcfd.org/ (accessed on 2 June 2023).

- Sanderson, H.; Stridsland, T. Cascading Transitional Climate Risks in the Private Sector—Risks and Opportunities; Springer International Publishing, 2022; ISBN 9783030862114.

- WRI and WBCSD GHG Protocol | A Corporate Accounting and Reporting Standard; 2004 .

- ISO ISO 14044:2006 - Environmental Management — Life Cycle Assessment — Requirements and Guidelines. Available online: https://www.iso.org/standard/38498.html (accessed on 25 October 2022).

- Weidema, B.P.; Frees, N.; Nielsen, A.M. Marginal Production Technologies for Life Cycle Inventories. Int. J. Life Cycle Assess. 1999, 4, 48–56. [Google Scholar] [CrossRef]

- Weidema, B.P. Avoiding Co-Product Allocation in Life-Cycle Assessment. 2001, 4.

- Brander, M.; Tipper, R.; Hutchison, C.; Davis, G. Consequential and Attributional Approaches to LCA: A Guide to Policy Makers with Specific Reference to Greenhouse Gas LCA of Biofuels. 2008.

- Wenzel, H. Application Dependency of LCA Methodology: Key Variables and Their Mode of Influencing the Method. Int. J. Life Cycle Assess. 1998, 3, 281–288. [Google Scholar] [CrossRef]

- Plevin, R.; Delucchi, M.; Creutzig, F. Response to Comments on “Using Attributional Life Cycle Assessment to Estimate Climate-Change Mitigation. ” J. Ind. Ecol. 2014, 18, 468–470. [Google Scholar] [CrossRef]

- Weidema, B.P.; Simas, M.S.; Schmidt, J.; Pizzol, M.; Løkke, S.; Brancoli, P.L. Relevance of Attributional and Consequential Information for Environmental Product Labelling. Int. J. Life Cycle Assess. 2020, 25, 900–904. [Google Scholar] [CrossRef]

- Thomassen, M.A.; Dalgaard, R.; Heijungs, R.; de Boer, I. Attributional and Consequential LCA of Milk Production. Int. J. Life Cycle Assess. 2008, 13, 339–349. [Google Scholar] [CrossRef]

- Sandén, B.A.; Karlström, M. Positive and Negative Feedback in Consequential Life-Cycle Assessment. J. Clean. Prod. 2007, 15, 1469–1481. [Google Scholar] [CrossRef]

- Brander, M.; Burritt, R.L.; Christ, K.L. Coupling Attributional and Consequential Life Cycle Assessment: A Matter of Social Responsibility. J. Clean. Prod. 2019, 215, 514–521. [Google Scholar] [CrossRef]

- Løkke, S.; Madsen, O. Making The Future of Smart Production for SMEs SMEs and the Sustainability Challenge : Enabling Smart Decision Making. In The Future of Smart Production for SMEs; 2022; pp. 281–295 ISBN 9783031154287.

- Schaubroeck, T.; Gibon, T.; Igos, E.; Benetto, E. Sustainability Assessment of Circular Economy over Time: Modelling of Finite and Variable Loops & Impact Distribution among Related Products. Resour. Conserv. Recycl. 2021, 168, 105319. [Google Scholar] [CrossRef]

- Weidema, B.P. Estimation of the Size of Error Introduced into Consequential Models by Using Attributional Background Datasets. Int. J. Life Cycle Assess. 2017, 22, 1241–1246. [Google Scholar] [CrossRef]

- Russell, S. Estimating and Reporting the Comparative Emissions Impacts of Products. World Resour. Inst. Work. Pap. 2019, 26. [Google Scholar]

- Weidema, B.P.; Pizzol, M.; Schmidt, J.; Thoma, G. Social Responsibility Is Always Consequential — Rebuttal to Brander, Burritt and Christ (2019): Coupling Attributional and Consequential Life Cycle Assessment: A Matter of Social Responsibility. J. Clean. Prod. 2019, 223, 12–13. [Google Scholar] [CrossRef]

- EU European Green Deal. Available online: https://ec.europa.eu/info/strategy/priorities-2019-2024/european-green-deal_en (accessed on 5 August 2022).

- Forbrugerombudsmanden Ny Kvikguide Skal Hjælpe Virksomheder Med ”grøn” Markedsføring Available online:. Available online: https://www.forbrugerombudsmanden.dk/nyheder/forbrugerombudsmanden/pressemeddelelser/2021/ny-kvikguide-skal-hjaelpe-virksomheder-med-groen-markedsfoering/ (accessed on 12 June 2023).

- CONCITO The Big Climate Database, Version 1. Available online: https://denstoreklimadatabase.dk/en (accessed on 30 August 2022).

- Stadler, K.; Wood, R.; Bulavskaya, T.; Södersten, C.J.; Simas, M.; Schmidt, S.; Usubiaga, A.; Acosta-Fernández, J.; Kuenen, J.; Bruckner, M.; et al. EXIOBASE 3: Developing a Time Series of Detailed Environmentally Extended Multi-Regional Input-Output Tables. J. Ind. Ecol. 2018, 22, 502–515. [Google Scholar] [CrossRef]

- AAU Getting the Data Right: About the Project. Available online: https://www.en.plan.aau.dk/getting-the-data-right/about-the-project (accessed on 27 October 2022).

- GHGP Policy and Action Standard; 2011;

- GHGP Draft for Pilot Testing and Review, September 2022; 2022;

- Hansen, E.R.; Lissandrini, M.; Ghose, A.; Løkke, S.; Thomsen, C.; Hose, K. Transparent Integration and Sharing of Life Cycle Sustainability Data with Provenance. In The Semantic Web; Pan, J.Z., Tamma, V., D’Amato, C., Janowicz, K., Fu, B., Polleres, A., Seneviratne, O., Kagal, L., Eds.; Springer International Publishing: Cham, 2020; ISBN 978-3-030-62466-8. pp. 378–394. [Google Scholar]

- Ghose, A.; Lissandrini, M.; Hansen, E.R.; Weidema, B.P. A Core Ontology for Modeling Life Cycle Sustainability Assessment on the Semantic Web. J. Ind. Ecol. 2022, 26, 731–747. [Google Scholar] [CrossRef]

| 1 | Emission intensity (EI) is often mixed up with Emission Factor (EF), which by the IPPC is reserved to describe the amount of GHG’s i.e. emitted when combusting a fossil fuel. EFs are used as a component when determining EIs describing emission intensities of products or activities. |

Figure 1.

1990 to 2020 change in annual CO2e emissions from fossil fuels and industry. It should be noted that the increase in India and China reflects production to both foreign and domestic consumption. Land use change is not included [3].

Figure 1.

1990 to 2020 change in annual CO2e emissions from fossil fuels and industry. It should be noted that the increase in India and China reflects production to both foreign and domestic consumption. Land use change is not included [3].

Figure 2.

1990 to 2019 change of CO2e emissions embedded in trade measured as emissions exported or imported as the percentage of domestic production emissions [3].

Figure 2.

1990 to 2019 change of CO2e emissions embedded in trade measured as emissions exported or imported as the percentage of domestic production emissions [3].

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Copyright: This open access article is published under a Creative Commons CC BY 4.0 license, which permit the free download, distribution, and reuse, provided that the author and preprint are cited in any reuse.