Submitted:

07 July 2023

Posted:

10 July 2023

You are already at the latest version

Abstract

The purpose of this paper is to propose a tool to measure the performance of a Strategic Asset Management Plan (SAMP) based on a Balanced Scorecard (BSC). The SAMP converts organizational objectives into asset management objectives, also specifies the role of the asset management system and brings support to achieve asset management objectives. The SAMP becomes the heart of the organization and integrates with long-term, medium-term, and short-term financial plans integrated with same term activity plans. In the SAMP, the balance among performance, costs and risks is also taken into consideration in order to achieve the organization’s objectives. On the other side, the SAMP is a guide to set the asset management objectives while describing the role of the Asset Management System (AMS) in meeting those objectives. While SAMP is the central figure of AMS, it is important to measure its performance and needs to be build and improved through an iterative process, what means that is not just a document, it is “the document”, and should be treated as a “living being” that needs to adapt to internal and external changes quickly. The BSC is an excellent tool where, through the appropriate Key Performance Indicators (KPIs), the progress can be measured, and is supported by four perspectives: Financial; Customer; Internal Process; and Learning and Growth.

Keywords:

ISO 5500X

; sustainability

; asset management

; physical assets

; SAMP

; balanced scorecard

; KPI

1. Introduction

1.1. Framework

In our days sustainability has been a major topic, mainly because the demand is growing; as an example Portugal, from 1995 till 2015, the urban area increased 40,2% (Uva, 2015). This growth is the fruit of population demand for new infrastructures (housing, factories, roads, etc.), and this issue is reflected worldwide (Frolking et al., 2013; Y. Liu et al., 2022; Maktav et al., 2005; Seto et al., 2011),; basically this reflects the increase of needed resources.

On the other side, authors link economic sustainability with management of physical assets (Lach et al., 2005), others state that, in many industries, maintenance procedures can significantly contribute to the pursuit of sustainable development (Ghaleb & Taghipour, 2022) thus, the use of assets is linked with sustainability, in order to develop sustainable economies; the benefits of these assets in terms of innovation and knowledge-based technologies are used, thus linking innovation, knowledge, and the environment (X. Wang et al., 2022).

So, it is important to implement strategies that successfully increase the sustainability of the environment based on complementary assets (Sadeghi Dastaki et al., 2022). It might be difficult for decision-makers to maintain an asset's performance in accordance with rational repair strategies, because they may neglect to create suitable maintenance plans or fail to maintain the assets. Organizations face pressure from all over the world to guarantee the sustainability of their assets (Hassan et al., 2022). Concerns about sustainability and safety are raised over whether essential installation maintenance is being sufficiently funded to guarantee long-term viability (Amaechi et al., 2022).

There is industry 4.0 technologies being rapidly incorporated into Asset Life Cycle Management (ALCM) and, in the manufacturing sector, to meet sustainability objectives (Weerasekara et al., 2022), while using industry 4.0 technologies industries look for opportunities of sustainable manufacturing (Jamwal et al., 2021), companies expect, through Industry 4.0 technologies, to achieve sustainable outcomes (Kamble et al., 2018). The use of technologies like Neural Networks for modelling pavement performance in order to improve sustainability (Deng & Shi, 2022), basically companies expect to have the highest production while utilizing the fewest resources. For this to happen, it is important that assets have predictive maintenance policies to increase their availability (A. Martins et al., 2021; A. B. Martins et al., 2020, 2022; J. A. Rodrigues et al., 2021, 2023; J. A. Rodrigues, Farinha, et al., 2022; J. A. Rodrigues, Martins, et al., 2022; Joao Rodrigues et al., 2020; João Rodrigues et al., 2021).

On the other side, the one of the concerns on sustainability is related to global warming and rising sea levels (Shen et al., 2022), while this changes bring more vulnerability to climate disasters, the global water cycle is also growing more intense as a result of climate change, with drier parts becoming drier and wetter ones usually becoming wetter. Nearly, half of the world's population, of around 3.6 billion people, currently reside in places that may be water deficient for at least one month out of the year (Jafari Shalamzari & Zhang, 2018; Khatibi & Arjjumend, 2019; Orimoloye et al., 2021; Procházka et al., 2018). Another scenery that is widely acknowledged that climate change is a reality because of occurrences that have place in 2021, including severe drought in Madagascar, a snowfall in Brazil, and summertime flooding in central Europe (de Almeida Pais et al., 2021). Previous studies have established a connection between climate change and the increase in the temperature due to CO2 emissions (de Almeida Pais et al., 2021).

As an example, Portugal had an extreme drought from January 2022 till September 2022 (IPMA, 2022a) reaching over 60% of the territory of extreme drought and on the other side on December 2022, having the Lisbon precipitation reached values of 17,1 mm/m2 in 10 minutes causing floods all over Lisbon (Figure 1) (IPMA, 2022b).

Drought brings, the need to find other resources of water for all purposes and that requires investment but, when dealing with floods, authors refer to massive economic breakdown, enormous loss of life, destruction in housing and infrastructures, agriculture, and other activities (Arabameri et al., 2020; Kanani-Sadat et al., 2019; Paul et al., 2019; Saha et al., 2022; Szwagrzyk et al., 2018; Tehrany et al., 2015).

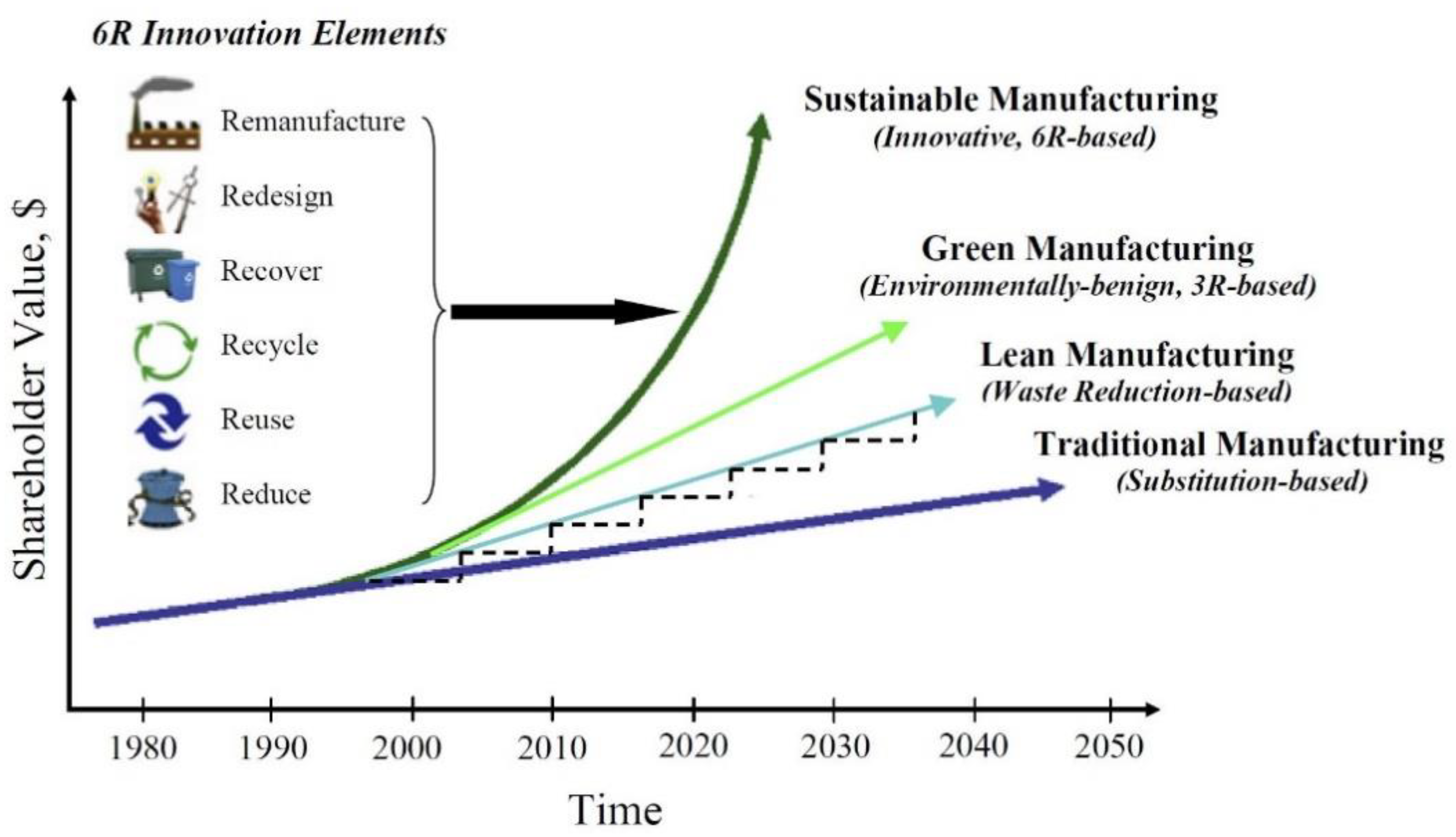

Because the earth natural resources are scarce and finite (Afgan et al., 1998; Coutinho et al., 2016; Dasgupta & Heal, 1974; Desing et al., 2019; Hall & Hall, 1984; Krautkraemer, 2005; Makarova et al., 2016; Mok et al., 2020; Neumayer, 2002; Root et al., 2003; Smith, 1979; Subhoni et al., 2018), there is a need to better manage those resources, some authors claim that the as efficient utilization of natural resource improves results on economic advancement (Digalwar et al., 2022; Padilla-Lozano & Collazzo, 2022; Zhang & Dilanchiev, 2022); other authors reinforce the need to reduce waste and reuse equipment’s in its end life, whether to rebuild similar or others (Saleem et al., 2022; Shylo et al., 2020). At this point it is important to emphasize the importance of Reinforce the reduce; Reuse; Recycle; Recover; Redesign; and Remanufacture (Figure 2). The basic goal is to maximize the life cycle, realize and produce value from the assets, and maintain the value and sustainability of the assets through appropriate management (de Almeida Pais et al., 2021).

According to World Commission on Environment and Development (WCED), “Sustainable development is development that meets the needs of the present without compromising the ability of future generations to meet their own needs” (WCED, 1987).

Nowadays, circular economy become very important regarding the need to achieve a sustainable development (Stahel, 2016). As the need of reduction, reuse, recovery, and recycling of materials and energy has become a priority. Circular economy obtained a major role in order to achieve those priorities (Halkos & Petrou, 2019; Pais et al., 2019), reinforcing the need of transition from the linear economy that started in the industrial revolution to the circular economy needs to be priority. The biological processes in which nothing is wasted serve as an inspiration for the circular economy. Despite certain misconceptions about the circular economy concept, previous authors (Dutt & King, 2014; J. Henriques et al., 2021, 2022; J. D. Henriques et al., 2022; Kirchherr et al., 2017; Prieto-Sandoval et al., 2018; Rajput & Singh, 2019; Rokicki et al., 2020; Zink & Geyer, 2017) have advocated the necessity of the circular economy to achieve an sustainable development.

Even relaying on every development on our days in order to achieve a sustainable development, we need to use energy in a sustainable way by reducing consumption and find renewable energy sources (Akhkozov et al., 2022; Danilenko et al., 2022; Doroshkevich et al., 2017, 2019; Lyubchyk et al., 2015; Shylo et al., 2022) and low carbon energy sources, while developing low consumption equipment’s and energy efficient projects investors, We will feel more attracted to make investments (Sarmas et al., 2022) and bringing an economic growth (H. Liu et al., 2022).

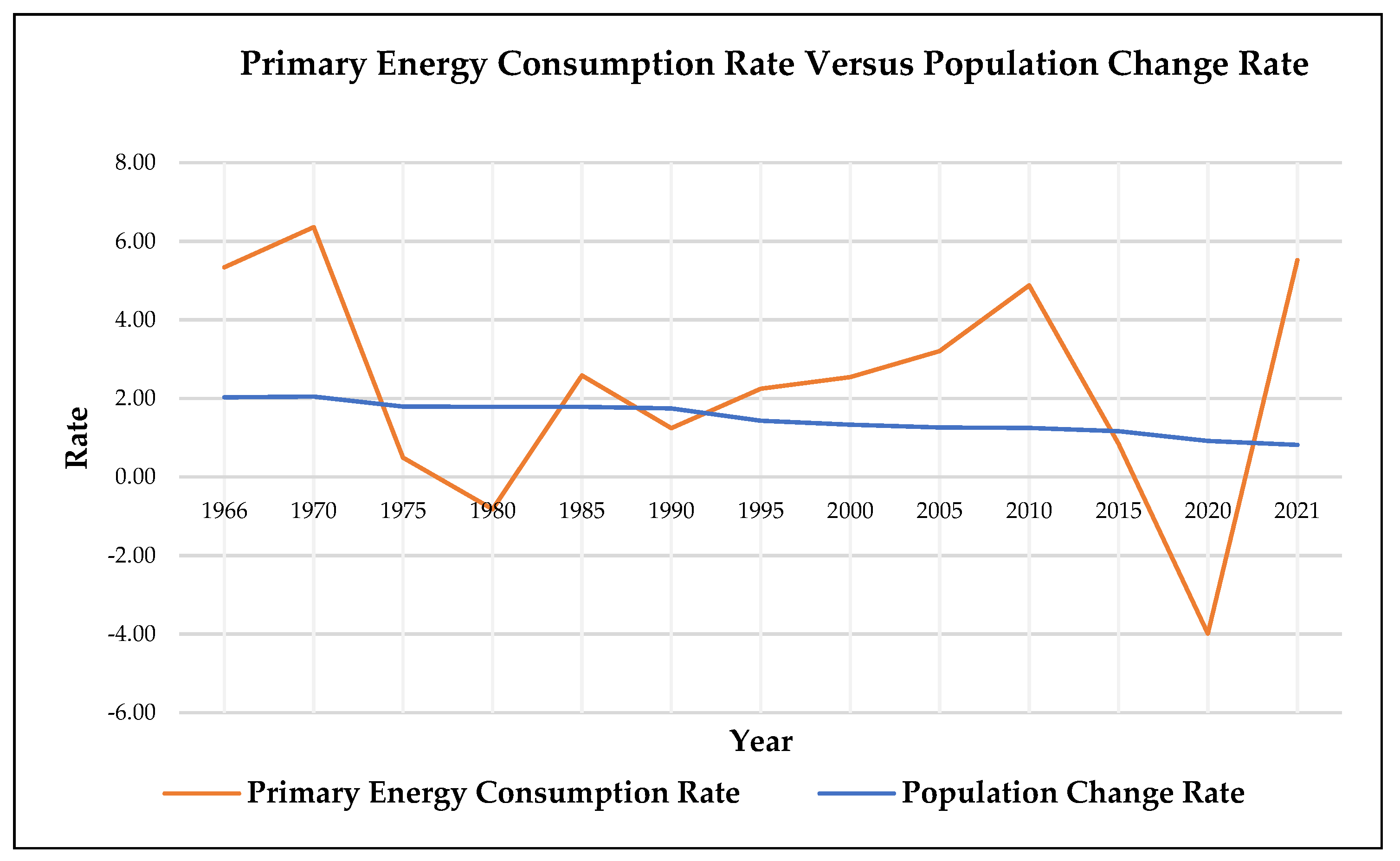

Energy sources have always been crucial to the advancement of human society. Energy has been the primary engine behind the advancement of modern civilization since the industrial revolution (Afgan et al., 1998). While energy consumption growth rate is aligned with economic growth rate, the population growth rate tends to decrease each year (Figure 3).

Other authors state that economic growth is improved by investing in physical assets and energy use, but at the expense of environmental sustainability (I. Khan et al., 2022). Luciani (Luciani, 2020) illustrates how the rate at which renewable energy transitions occur influences whether or not economic growth will be supported; on the one hand, investing in physical assets makes it easier to integrate cutting-edge technologies into the production process which will facilitate the needed transition (Figure 3) (Sinha et al., 2021).

To fulfil the needed transition for Asset Management (AM) will become a great advantage, because makes it easier to train qualified workers, to improve knowledge transfers, to acquire leading alternative management platforms, etc. (I. Khan et al., 2022). This improves not only the transition to renewable energy, but also a sustainable use of energy, what leads to an economic growth (Chakraborty & Mukherjee, 2010; Li et al., 2021). When considering AM, there are some steps to build it: the SAMP is the main document and details the asset management objectives, that explains their relationship to the organizational objectives and the framework required to achieve the asset management objectives (ISO 55002:2018. Asset Management — Management Systems — Guidelines for the Application of ISO 55001, 2018), in order to build a reliable SAMP its needed to have accurate data (Mateus et al., 2023). As the SAMP is the main document it is important to be able to measure its performance and quality - there are not any studies where this issue is studied. In addition, if we want to evaluate the SAMP’s performance we need to measure it, aiming to improve it. With this objective the authors present a new tool to fill that gap.

1.2. Aim and Research Methodology

The aim of this research was to address the limitations of the existing quantitative methods used to measure the performance of a Strategic Asset Management Plan, by offering a new approach. For this purpose, it was used a five steps methodology (K. S. Khan et al., 2003):

- a) Framing questions for a review;

- b) Identifying relevant work;

- c) Assessing the quality of studies;

- d) Summarizing the evidence;

- e) Interpreting the findings.

1.3. Research Questions

- While building an Asset Management System (AMS) is it a core element to measure its performance?

- How can measure the SAMP performance?

- Being the SAMP the central figure in the AMS, how can it be measured?

1.4. Paper Structure

This paper is structured as follows:

- synthesizes relevant literature on Strategic Asset Management Plan performance measuring tools;

- presents the Scorecard;

- presents the Performance Measuring tool of a Strategic Asset Management Plan through a Balanced Scorecard;

- presents a discussion;

- offers the conclusions.

2. Literature Review

When considering asset management, the value must be closely related to the organization's objectives and the asset management objectives compatible with those objectives (De-Almeida-e-Pais et al., 2022). Both these objectives and the results of the actions taken to achieve them should be measurable (Arthur et al., 2016).

Roda & Garetti (Roda & Garetti, 2015) presented the Total Cost of Ownership (TCO) evaluation methodology that is based on a cost model and a performance model, in 9 steps, being the first 6 related with performance evaluation and the last 3 with cost evaluation:

- Process understanding and system’s components identification;

- Identification of failures modes or stop causes of each component;

- Reliability, maintainability and operation data acquisition (TBF and TTR);

- Modelling of the as-is system through Reliability Block Diagram (RBD) logic;

- Simulation (Monte Carlo);

- Technical performance calculation of the system;

- Cost model setting;

- Cost data acquisition;

- Calculation of TCO.

For the modelling and calculation steps from 4 to 6, the model uses software R-MES Project©.

Simões et al. (Simões et al., 2011) conducted an analysis of 345 various performance metrics for maintenance management. This study offers suggestions for creating performance metrics; however, it only examined a portion of the asset management (AM).

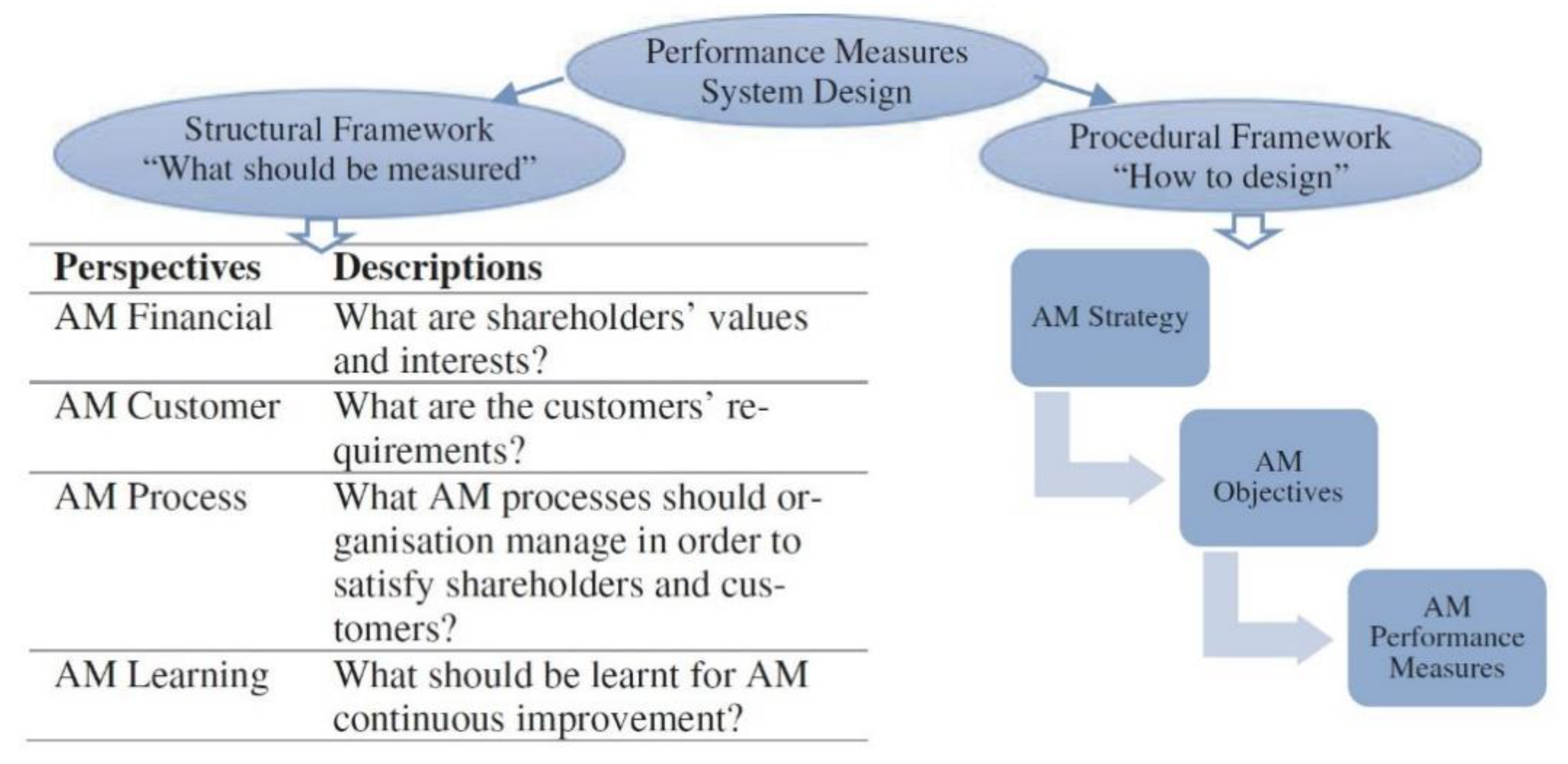

Wang et al. (J. Wang et al., 2016) developed performance measures for AM; they adapted the Balanced Scorecard (BSC) saying that it is important to combine Asset Management with a BSC. The authors presented a framework for designing performance measures (Figure 4). While using a BSC combined with AM, establishing objectives and performance measures and descriptions, they present a lack of numerical elements that can be quantified.

Arthur et al. (Arthur et al., 2016) seek the need to create a “line of sight”, while using a Balance Scorecard (BSC), in order to achieve that the following phases were selected:

- 1. Develop the AM strategy and identify AM objectives;

- 2. Select performance indicators;

- 3. Test for alignment or line of sight;

- 4. Reflect on the process and outcome.

They also selected performance indicators and the need of those to have a “line of sight” to the Asset Management objectives.

While using the BSC approach, Arthur et al. (Arthur et al., 2016) developed their own top-down strategy map for creating performance measures. But this novel strategy failed to solve engineering asset management systems integrative complexity, because it needed performance measures design from multiple perspectives.

Abdul-Nour et al. (Abdul-Nour et al., 2021), about Performance Measurement (PM), stats that PM in Asset Management Systems is typically studied from a maintenance viewpoint rather than a global perspective supporting their affirmation on Kumar et al. (Kumar et al., 2013), Simões et al. (Simões et al., 2011), and Maletič et al. (Maletič et al., 2014).

Regarding measuring Asset Performance, Wijnia (Wijnia, 2022) says that “what gets measures gets done”, but the author concerns is the value to deliver, and the validity of the indicators. In order to evaluate asset performance, the author considers a pragmatic solution, but gives two questions:

- 1. Is it really only about delivering an absolute amount, like the produced volume, the availability of an asset or staying within budget limits?

- 2. Or is it more about assuring that the available resources are used in the most effective and efficient way, like driving towards the best value per unit of cost or the lowest cost per unit of production?

Wijnia (Wijnia, 2022) considers the second more aligned with continual improvement, but his conclusion considers, while setting targets, a common practice, considered a difficult track, and considers the use of ratio indicators an easier way; in other way, he considers that may cross international boundaries while under your control, contravening the standards for reliable indications.

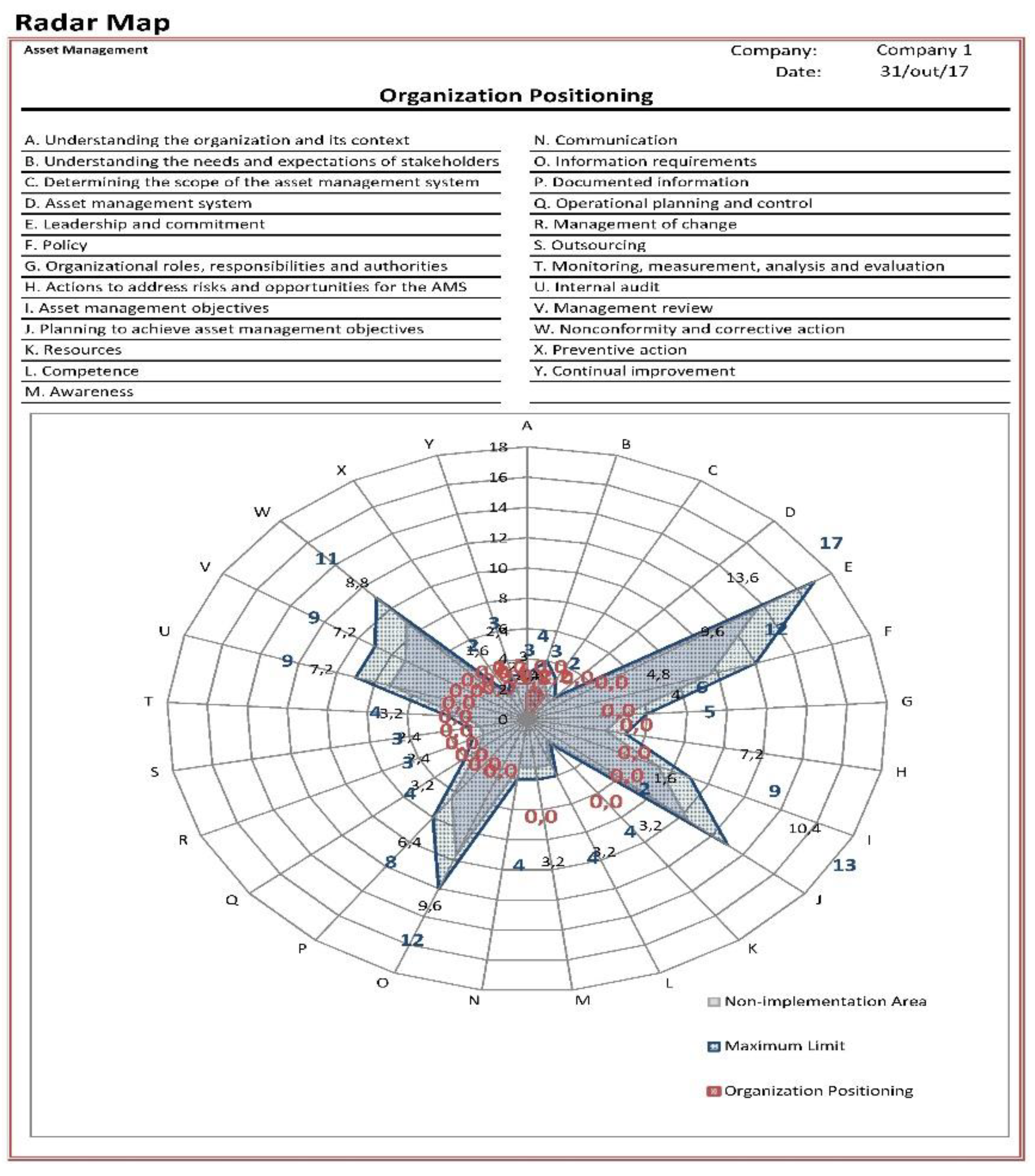

Pais et al. (Pais et al., 2019) presented a model to Diagnosis the Organization’s State in order to apply ISO 55001 the same model as a tool to help implementing and continuous improvement on ISO 55001; the model has 25 surveys and a total of 154 questions, being the results presented on a radar map (Figure 5).

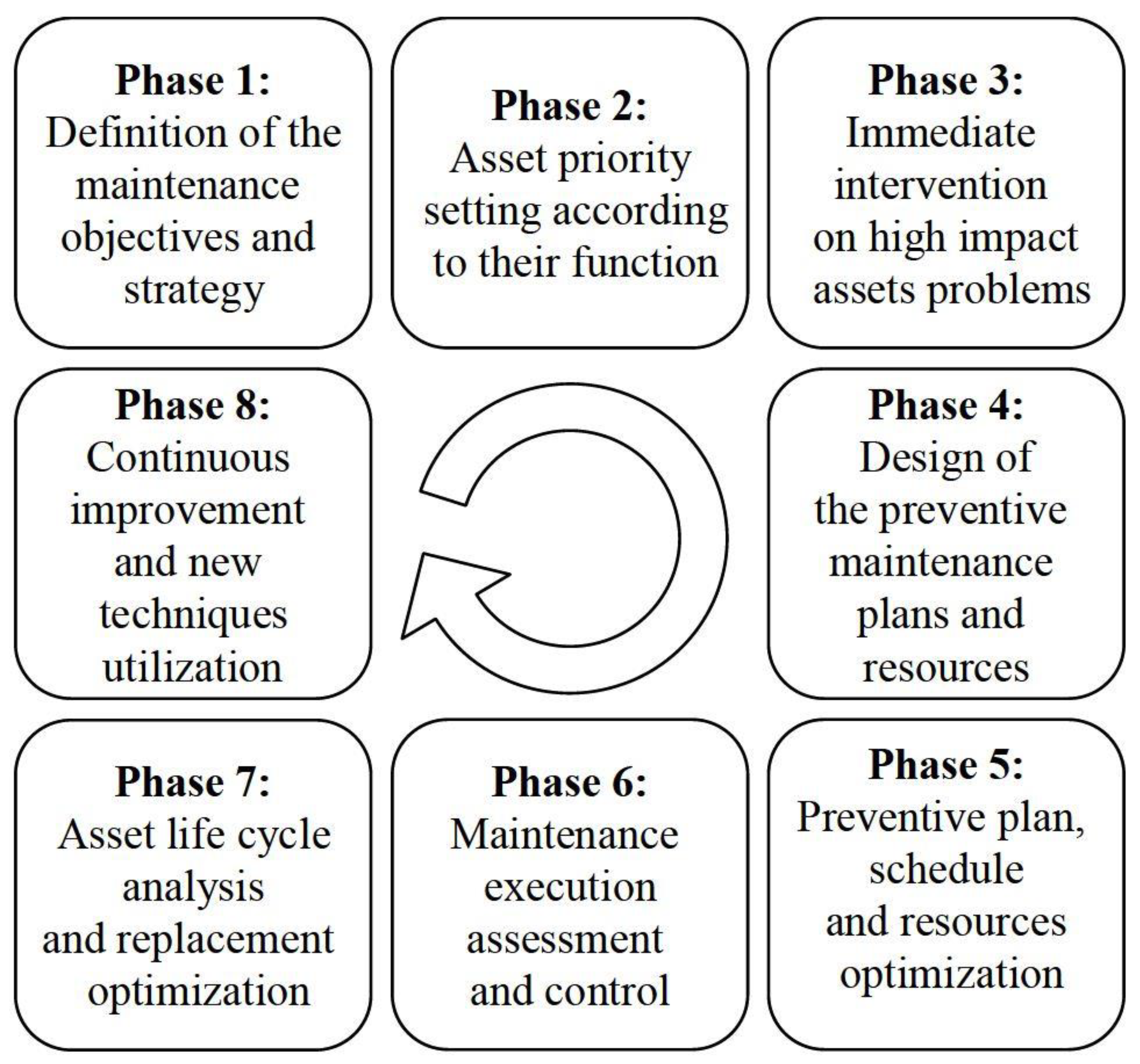

In 2007 Crespo presented a Maintenance Management Model (Figure 6) (Márquez, 2007); based on that model, Parra et al. (Parra et al., 2021) present an audit tool for Asset Management, Operational Reliability & Maintenance Survey (AMORMS).

The AMORMS is an audit that pretends to help the management process of ISO 55001; the evaluated areas are eight:

- 1. Definition of the maintenance objectives and KPI’s;

- 2. Asset priority and maintenance strategy definition;

- 3. Immediate intervention on high impact weak point;

- 4. Design of the preventive maintenance plans and resources;

- 5. Preventive plan, Schedule, and resources optimization;

- 6. Maintenance execution assessment and control;

- 7. Asset life cycle analysis and replacement optimization;

- 8. Continuous Improvement and new tech.

From these eight areas it results 150 questions survey, being the result a radar map. This model also gives support tools to help process management.

Another model for audits presented by the same author is the Asset Management Survey ISO 55001 (AMS-ISO 55001), that is based on the asset management norm ISO55001 (Duque et al., n.d.); it is focused on auditing the processes of life cycle of assets managing according to ISO 550001, and is based on the ISO 55001 requirements:

- 1. Context of the organization;

- 2. Leadership;

- 3. Planning;

- 4. Support;

- 5. Operation;

- 6. Performance evaluation;

- 7. Improvement.

In order to measure performance (PM), Folan & Browne (Folan & Browne, 2005) divide it in two core areas:

- 1. Recommendations for performance measures;

- 2. Recommendations and issues for PM framework and system design.

The first one place emphasis on good performance measures and the second focus on recommendations regarding design and development of PM and suggest the use of BSC.

Regarding measuring the performance of a document such as the Strategic Asset Management Plan (SAMP) there is not any study, report or research directly about it. Then, it is very important to contribute to fill this gap in order to help the organizations evaluate their SAMP as the central document in the AMS.

3. Balanced Scorecard

The first research question (While building an Asset Management System (AMS) is it a core element to measure its performance?) is answered by the SAMP itself, as the main document that details the Asset Management objectives; it is clear its importance and the central figure in the Asset Management System (AMS). Its purpose is to provide a precise framework for a strategic asset decision-making which is aligned with the organizational performance targets. This is demonstrated in this section.

The Balance Scorecard (BSC) have been introduced in 1992 by Robert S. Kaplan and David P. Norton (Kaplan , R. S. & Norton, 1992), as they presented the BSC, they started with a strong statement, that was widely used today: “What you measure is what you get”. Recently, Robert S. Kaplan in a book chapter entitled “Conceptual Foundations of the Balanced Scorecard” (Kaplan, 2009), cited Lord Kelvin (1883):

“I often say that when you can measure what you are speaking about, and express it in numbers, you know something about it; but when you cannot measure it, when you cannot express it in numbers, your knowledge is of a meagre and unsatisfactory kind.

If you cannot measure it, you cannot improve it.”

In the same book chapter, the author explains why he and David P. Norton introduced the BSC, saying that they held the opinion that managers need measurement just as much as scientists did. Companies have to incorporate the measurement of intangible assets into their management systems if they wanted to improve the management of their intangible assets (Kaplan, 2009).

The BSC translates vision and strategy into four perspectives: Financial; Customer; Internal Business Process; and Learning Growth. Each one of these perspectives has their own objectives, measures, targets, and initiatives (Figure 7). This tool was inspired in a project developed in the 1950s, by the corporate staff of General Electric (GE) to create performance metrics for the company's decentralized business units (Lewis, 1955).

The GE team come with one financial and seven nonfinancial metrics to measure performance:

- 1. profitability (measured by residual income);

- 2. market share;

- 3. productivity;

- 4. product leadership;

- 5. public responsibility (legal and ethical behaviour and responsibility to stakeholders including shareholders, vendors, dealers, distributors and communities);

- 6. personnel development;

- 7. employee attitudes;

- 8. balance between short-range and long-range objectives.

The roots of the BSC are found in these eight objectives. In the eighth objective, the balance between short-range and long-range objectives can be complex, the example of GE as their management asserting that business pressure for quick profits caused them to forsake long-term goals and their civic duties.

Other management tools such as Peter with his classic book from 1954, “The Practice of Management”, introducing the management by objectives where the employees should have personal performance goals that are closely aligned with the business plan (Drucker, 1954). In the mid-1960s, Robert Anthony build upon earlier researches (H. Simon et al., 1954; H. A. Simon, 1963), offered a thorough framework for systems of planning and control. Anthony distinguished three sorts of systems: operational control; managerial control; and strategic planning.

In the 1970s and 1980s other movement arise, such as the Japanese Management Movement bringing advancements in just-in-time production and quality (Vaszkun & Tsutsui, 2012). In 2008 Punniyamoorthy & Murali (Punniyamoorthy & Murali, 2008) introduced the Balanced Score that is based on BSC and is used as a benchmarking tool.

According to Scopus (Scopus, n.d.), 5,035 studies were published under the topic Balanced Scorecard. The BSC has been a tool widely used in research, where improving sparked intense interest worldwide (Nørreklit, 2003), the Balanced Scorecard has been used by 60% of Fortune 1,000 organizations in the USA (Silk, 1998). Anand et al. (Anand et al., 2005) claim that is inventive method for raising strategic awareness within the firm is through the use of the Balanced Scorecard.

Yet the BSC establish a comprehensive framework that connects individual accomplishments and efforts to business-unit goals reinforcing a holistic model (Johanson et al., 2006),

According to the BSC collaborative, there are four barriers to strategic implementation (Punniyamoorthy & Murali, 2008):

- Vision barrier - No one in the organization understands the strategies of the organization.

- People barrier - Most people have objectives that are not linked to the strategy of the organization.

- Resource barrier - Time, energy, and money are not allocated to those things that are critical to the organization. For example, budgets are not linked to strategy, resulting in wasted resources.

- Management barrier - Management spends too little time on strategy and too much time on short-term tactical decision making.

Even if the BSC concept has been widely embraced and applied in the corporate sector (Ahn, 2001; Aidemark, 2001; Pink, G H; McKillop I, Schraa, EG; Preyra, C; Montgomery, C; Baker, 2001), in areas such as education, did not occur with such significance (Karathanos & Karathanos, 2005), despite short use in education, there are some studies and implementations (Beard, 2009; Cullen et al., 2003; Karathanos & Karathanos, 2005; Kiriri, 2022; O’Neil et al., 1999; Sharaf-Addin & Fazel, 2021; Stewart, A. C.; Carpenter-Hubin, 2001; Walter et al., 2001).

Researches made were the BSC is used to evaluate the performance of the SAMP do not exist. There are some studies and implementations of performance measures of the Asset Management System (AMS) that emphasizes the results (Hatcher et al., 2012; Mizusawa D.; McNeil S., 2005; Posavljak et al., 2013) to measure the system and, in specific the SAMP and its performance, in order to understand if he complies with ISO 55001 requirements.

Based on the preceding, it is clear the importance of measuring the SAMP performance while a core element of the AMS. By doing this, the AMS is also being measured and can be improved and taken in the organizational objectives direction.

4. Balanced Scorecard in a Strategic Asset Management Plan

This section tries to answer to the second and third research question. It starts with the second question (How can measure the SAMP performance?).

The Balance Scorecard (BSC) is tailored to the organization for which it is established and enables the development of Key Performance Indicators (KPIs) for tracking maintenance management performance in line with the strategic goals of the business (Crespo Márquez et al., 2012). Contrary to traditional metrics, which are control-oriented, the Balanced Scorecard prioritizes attaining performance goals while putting overarching strategy and vision at the forefront (Duffuaa, 2000).

As stated by Kaplan & Norton (Kaplan , R. S. & Norton, 1992), “What you measure is what you get”, it is clear the importance to measure the SAMP. So, it is needed to set a parallel between ISO 55001 Requirements and the BSC perspectives (Table 1); in this table, the BSC perspectives are indicated and for each one the authors introduced the questions related, measurements pretended, the physical assets intervention related, ISO 55001 requirements and, finally, the KPI’s to measure performance.

The KPI’s used (Table 2) were chosen taking into consideration the measurements pretended concerning specific ISO 55001 requirements.

The grounding for the chosen KPI’s is presented in Table 3.

The data needed in order to calculate the KPI’s are presented in Table 4.

By the preceding it is demonstrated how the KPIs based on a BSC may help to measure the SAMP performance.

The last question to answer is: “Being the SAMP the central figure in the AMS, how can it be measured?”. There can be other ways and tools to be used in order to measure the SAMP. The authors proposed a model based on the BSC and its perspectives, mainly because it is a document that sets the strategy to achieve assets goals focused on the organization objectives and also measuring the decision-making criteria.

The calculated KPI’s are presented in Table 5. To obtain a value between 0 and 100 a coefficient was introduced in each KPI; in this way, the KPI was limited to 100, that is the maximum value expected. The KPI’s, such as ROI, EPS and RG, are unlikely to achieve the value of 100, as can be seen in Table 5; those KPI’s are the ones with values under 100 but, at same time, are the values expected for the respective KPI.

By the preceding it is demonstrated how the KPIs based on a BSC result on values that permit to measure the SAMP performance.

5. Discussion

The use of Balanced Score Card (BSC) brings to an upper level regarding the measuring of the SAMP performance and, easily can quantify each perspective and each standard requirement, while helping to see which requirements need to be improved and what is necessary to be done to improve it.

The perspectives described on the BSC (Table 1) can be complemented with goals. The organizations, while checking were they are, can also set where they want to be; this can be made by setting goals and objectives for each perspective, being these goals individuals and focused in each organization.

The results obtained in (Table 5) for a specific organization can vary from activities or country, focusing on the organization used to test the model, the results show that their SAMP is on the right path.

Analysing the results, the obtained values are in the average of this specific activity but, KPI such as Net Promoter Score (NPS), Repeat Purchase Rate (RPR), Customer Satisfaction Score (CSAT), and Employee Skills Rate (ESR) can be improved, thus showing that the SAMP isn’t yet build correctly or isn’t known for the company, then changes must be made to improve those KPI results.

As an example, the CSAT obtained the value of 47,55%, which is low for this organization; questions like the following ones must be placed: the customers complain are being addressed? Measures were taken to correct or lessen the nonconformities? There is a follow up with costumers concerning the nonconformities? Tools like the Deming Cycle (PDCA) are well known and of simple use to a continuous improvement that can be used to correct the nonconformities that took the costumer to give a bad review.

Principles such as Economic Rationality (ER), Strategic Management (SM) or Sustainable Development Goals (SDGs) are aligned with AM and within the SAMP.

Those principles can be applied and are related with the KPI presented and discussed. The proposed SAMP measuring tool was validated by using data from waters companies and the results were validated by the stakeholders, recognizing the improvement on the described areas.

6. Conclusions

The Asset Management (AM) is a great tool on these days, helping with topics such as sustainability, circular economy, industrial symbiosis, business continuity and others. The method presented in this paper can help and improve the use of AM. While using AM, the Strategic Asset Management Plan (SAMP) plays a very important role so, it is important to have a robust SAMP, that can be only achieved if we are able to measure the performance that it provides; the use of Balanced Score Card (BSC) brings the capability to measure the SAMP performance and can easily be evaluated.

After the evaluation is made, the tool presented also helps to correct the nonconformities in order to have a SAMP aligned with the organization objectives; the use of tools such as PDCA cycle will help to correct systematically the nonconformities and achieve the excellence in AM. The use of a Balanced Scorecard (BSC) to measure the performance of a Strategic Asset Management Plan (SAMP) improves the SAMP and an allows an overall improvement of the AMS. This results in improving sustainability and business continuity risk. By other side, principles such as economic rationality can also be used aiming to improve employee’s behaviour. At the end, the main question for all could be, what planet do we want to leave for the posterity?

Author Contributions

Conceptualization, E.P., J.T.F. and H.R.; methodology, E.P., J.T.F. and H.R.; formal analysis, J.T.F. and H.R.; investigation, E.P.; resources, J.T.F., H.R. and A.J.M.C.; writing—original draft preparation, E.P.; writing—review and editing, J.T.F., H.R. and Se.L.; project administration, J.T.F., A.J.M.C. and Sv.L.; funding acquisition, J.T.F. and A.J.M.C. All authors have read and agreed to the published version of the manuscript.

Funding

The research leading to these results has received funding from the European Union’s Horizon 2020 research and innovation programme, under the Marie Sklodowvska-Curie grant agreement 871284 project SSHARE, the European Regional Development Fund (ERDF) through the Operational Programme for Competitiveness and Internationalization (COMPETE 2020), under Project POCI-01-0145-FEDER-029494, and by the Portuguese Foundation for Science and Technology (FCT) under Projects UIDB/04131/2020 and UIDP/04131/2020.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

Restrictions apply to the availability of these data.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Abdul-Nour, G., Gauthier, F., Diallo, I., Komljenovic, D., Vaillancourt, R., & Côté, A. (2021). Development of a Resilience Management Framework Adapted to Complex Asset Systems: Hydro-Québec Research Chair on Asset Management. In Lecture Notes in Mechanical Engineering (pp. 126–136). [CrossRef]

- Afgan, N. H. , Gobaisi, D. Al, Carvalho, M. G., & Cumo, M. Sustainable energy development. Renewable and Sustainable Energy Reviews 1998, 2, 235–286. [Google Scholar] [CrossRef]

- Ahn, H. Applying the Balanced Scorecard Concept: An Experience Report. Long Range Planning 2001, 34, 441–461. [Google Scholar] [CrossRef]

- Aidemark, L.-G. The Meaning of Balanced Scorecards in the Health Care Organisation. Financial Accountability and Management 2001, 17, 23–40. [Google Scholar] [CrossRef]

- Akhkozov, L., Danilenko, I., Podhurska, V., Shylo, A., Vasyliv, B., Ostash, O., & Lyubchyk, A. Zirconia-based materials in alternative energy devices - A strategy for improving material properties by optimizing the characteristics of initial powders. International Journal of Hydrogen Energy 2022, 47, 41359–41371. [CrossRef]

- Amaechi, C. V., Reda, A., Kgosiemang, I. M., Ja’e, I. A., Oyetunji, A. K., Olukolajo, M. A., & Igwe, I. B. Guidelines on Asset Management of Offshore Facilities for Monitoring, Sustainable Maintenance, and Safety Practices. Sensors 2022, 22, 7270. [CrossRef]

- Anand, M., Sahay, B. S., & Saha, S. Balanced Scorecard in Indian Companies. Vikalpa: The Journal for Decision Makers 2005, 30, 11–26. [CrossRef]

- Arabameri, A., Saha, S., Chen, W., Roy, J., Pradhan, B., & Bui, D. T. Flash flood susceptibility modelling using functional tree and hybrid ensemble techniques. Journal of Hydrology 2020, 587, 125007. [CrossRef]

- Arthur, D., Schoenmaker, R., Hodkiewicz, M., & Muruvan, S. (2016). Asset Planning Performance Measurement (pp. 79–95). [CrossRef]

- Beard, D. F. Successful Applications of the Balanced Scorecard in Higher Education. Journal of Education for Business 2009, 84, 275–282. [Google Scholar] [CrossRef]

- BP. (2022). Statistical Review of World Energy. https://www.bp.com/en/global/corporate/energy-economics/statistical-review-of-world-energy.html.

- Chakraborty, D., & Mukherjee, S. The Relationship between Trade, Investment and Environment. Foreign Trade Review 2010, 45, 3–37. [CrossRef]

- Coutinho, M. L., Miller, A. Z., Rogerio-Candelera, M. A., Mirão, J., Cerqueira Alves, L., Veiga, J. P., Águas, H., Pereira, S., Lyubchyk, A., & Macedo, M. F. An integrated approach for assessing the bioreceptivity of glazed tiles to phototrophic microorganisms. Biofouling 2016, 32, 243–259. [CrossRef]

- Crespo Márquez, A., Parra Márquez, C., Gómez Fernández, J. F., López Campos, M., & González-Prida Díaz, V. (2012). Life cycle cost analysis. In T. Van der Lei, P. Herder, & Y. Wijnia (Eds.), Asset Management: The State of the Art in Europe from a Life Cycle Perspective (Vol. 9789400727, pp. 81–99). Springer Netherlands. [CrossRef]

- Cullen, J., Joyce, J., Hassall, T., & Broadbent, M. Quality in higher education: from monitoring to management. Quality Assurance in Education 2003, 11, 5–14. [CrossRef]

- Danilenko, I., Gorban, O., Shylo, A., Volkova, G., Yaremov, P., Konstantinova, T., Doroshkevych, O., & Lyubchyk, A. Humidity to electricity converter based on oxide nanoparticles. Journal of Materials Science 2022, 57, 8367–8380. [CrossRef]

- Dasgupta, P., & Heal, G. The Optimal Depletion of Exhaustible Resources. The Review of Economic Studies 1974, 41, 3. [CrossRef]

- De-Almeida-e-Pais, J. E., Cardoso, A. J.., Farinha, J. T., & Raposo, H. (2022). ISO 55001 - A Proposal For a Strategic Asset Management Plan. In J. F. Silva & S. A. Meguid (Eds.), Proseeding M2D2022 - 9th International Conference on Mechanics and Materials in Design (Issue July, pp. 577–590). https://paginas.fe.up.pt/~m2d/proceedings_m2d2022/.

- de Almeida Pais, J. E., Raposo, H. D. N., Farinha, J. T., Cardoso, A. J. M., & Marques, P. A. Optimizing the Life Cycle of Physical Assets through an Integrated Life Cycle Assessment Method. Energies 2021, 14, 6128. [CrossRef]

- Deng, Y., & Shi, X. An Accurate, Reproducible and Robust Model to Predict the Rutting of Asphalt Pavement: Neural Networks Coupled With Particle Swarm Optimization. IEEE Transactions on Intelligent Transportation Systems 2022, 23, 22063–22072. [CrossRef]

- Department of Economic and Social Affairs - United Nations. (2022). World Population Prospects 2022. https://population.un.org/wpp/.

- Desing, H., Widmer, R., Beloin-Saint-Pierre, D., Hischier, R., & Wäger, P. Powering a sustainable and circular economy—an engineering approach to estimating renewable energy potentials within earth system boundaries. Energies 2019, 12. [CrossRef]

- Digalwar, A. K., Saraswat, S. K., Rastogi, A., & Thomas, R. G. A comprehensive framework for analysis and evaluation of factors responsible for sustainable growth of electric vehicles in India. Journal of Cleaner Production 2022, 378, 134601. [CrossRef]

- Doroshkevich, A. S., Asgerov, E. B., Shylo, A. V., Lyubchyk, A. I., Logunov, A. I., Glazunova, V. A., Islamov, A. K., Turchenko, V. A., Almasan, V., Lazar, D., Balasoiu, M., Doroshkevich, V. S., Madadzada, A. I., Kholmurodov, K. T., Bodnarchuk, V. I., & Oksengendler, B. L. Direct conversion of the water adsorption energy to electricity on the surface of zirconia nanoparticles. Applied Nanoscience 2019, 9, 1603–1609. [CrossRef]

- Doroshkevich, A. S., Lyubchyk, A. I., Shilo, A. V., Zelenyak, T. Y., Glazunova, V. A., Burhovetskiy, V. V., Saprykina, A. V., Holmurodov, K. T., Nosolev, I. K., Doroshkevich, V. S., Volkova, G. K., Konstantinova, T. E., Bodnarchuk, V. I., Gladyshev, P. P., Turchenko, V. A., & Sinyakina, S. A. Chemical-electric energy conversion effect in zirconia nanopowder systems. Journal of Surface Investigation: X-Ray, Synchrotron and Neutron Techniques 2017, 11, 523–529. [CrossRef]

- Drucker, P. (1954). The Practice of Management. HarperCollins.

- Duffuaa, S. O. Duffuaa, S. O. (2000). Mathematical Models in Maintenance Planning and Scheduling. In Maintenance, Modeling and Optimization (pp. 39–53). Springer US. [CrossRef]

- Duque, P., Parra, C., Pizarro, F., Aránguiz, A., & Vega. (n.d.). Audit models for asset management, maintenance and reliability processes: A case study applied to the copper mining sector.

- Dutt, N., & King, A. A. The judgment of garbage: End-of-pipe treatment and waste reduction. Management Science 2014, 60, 1812–1828. [CrossRef]

- Expresso. (2022). Mau tempo provoca uma morte, mais de 100 deslocados e 10 desalojados. https://expresso.pt/sociedade/2022-12-08-Mau-tempo-provoca-uma-morte-mais-de-100-deslocados-e-10-desalojados.-Houve-47-resgatados-de-veiculos-0c87fd50 . 2022.

- Folan, P., & Browne, J. A review of performance measurement: Towards performance management. Computers in Industry 2005, 56, 663–680. [CrossRef]

- Frolking, S., Milliman, T., Seto, K. C., & Friedl, M. A. A global fingerprint of macro-scale changes in urban structure from 1999 to 2009. Environmental Research Letters 2013, 8, 024004. [CrossRef]

- Ghaleb, M., & Taghipour, S. Assessing the impact of maintenance practices on asset’s sustainability. Reliability Engineering & System Safety 2022, 228, 108810. [CrossRef]

- Halkos, G., & Petrou, K. N. Analysing the Energy Efficiency of EU Member States: The Potential of Energy Recovery from Waste in the Circular Economy. Energies 2019, 12, 3718. [CrossRef]

- Hall, D. C., & Hall, J. V. Concepts and measures of natural resource scarcity with a summary of recent trends. Journal of Environmental Economics and Management 1984, 11, 363–379. [CrossRef]

- Hassan, A. M., Adel, K., Elhakeem, A., & Elmasry, M. I. S. Condition Prediction for Existing Educational Facilities Using Artificial Neural Networks and Regression Analysis. Buildings 2022, 12, 1520. [CrossRef]

- Hatcher, W. E. ., Whittlestone, A. P. ., Sivorn, J. ., & Arrowsmith, R. A service framework for highway asset management. IET & IAM Asset Management Conference 2012 2012, 91–91. [CrossRef]

- Henriques, J. D., Azevedo, J., Dias, R., Estrela, M., Ascenço, C., Vladimirova, D., & Miller, K. Implementing Industrial Symbiosis Incentives: an Applied Assessment Framework for Risk Mitigation. Circular Economy and Sustainability 2022, 2, 669–692. [CrossRef]

- Henriques, J., Ferrão, P., Castro, R., & Azevedo, J. Industrial Symbiosis: A Sectoral Analysis on Enablers and Barriers. Sustainability 2021, 13, 1723. [CrossRef]

- Henriques, J., Ferrão, P., & Iten, M. Policies and Strategic Incentives for Circular Economy and Industrial Symbiosis in Portugal: A Future Perspective. Sustainability 2022, 14, 6888. [CrossRef]

- ISO 55002:2018. Asset management — Management systems — Guidelines for the application of ISO 55001, (2018) (testimony of International Organization for Standardization).

- IPMA. (2022a). Indice PDSI (Palmer Drought Severity Index). https://www.ipma.pt/pt/oclima/observatorio.secas/.

- IPMA. (2022b). Precipitação forte na região Lisboa. https://www.ipma.pt/pt/media/noticias/documentos/2022/Precipitacao-intensa-lisboa_vrs1.pdf.

- Jafari Shalamzari, M., & Zhang, W. Assessing Water Scarcity Using the Water Poverty Index (WPI) in Golestan Province of Iran. Water 2018, 10, 1079. [CrossRef]

- Jamwal, A., Agrawal, R., Sharma, M., Manupati, V. K., & Patidar, A. (2021). Industry 4.0 and Sustainable Manufacturing: A Bibliometric Based Review (pp. 1–11). [CrossRef]

- Johanson, U., Skoog, M., Backlund, A., & Almqvist, R. Balancing dilemmas of the balanced scorecard. Accounting, Auditing & Accountability Journal 2006, 19, 842–857. [CrossRef]

- Kamble, S. S., Gunasekaran, A., & Gawankar, S. A. Sustainable Industry 4.0 framework: A systematic literature review identifying the current trends and future perspectives. Process Safety and Environmental Protection 2018, 117, 408–425. [CrossRef]

- Kanani-Sadat, Y., Arabsheibani, R., Karimipour, F., & Nasseri, M. A new approach to flood susceptibility assessment in data-scarce and ungauged regions based on GIS-based hybrid multi criteria decision-making method. Journal of Hydrology 2019, 572, 17–31. [CrossRef]

- K, *!!! REPLACE !!!*. Kaplan , R. S. & Norton, D. P. The Balanced Scorecard: measures that drive performance. Harvard Business Review, January–February 1992, 71–79. 19 February.

- Kaplan, R. S. (2009). Conceptual Foundations of the Balanced Scorecard. In M. D. Chapman, Christopher S.; Hopwood, Anthony G. and Shields (Ed.), Handbook of Management Accounting Research (pp. 1253–1269). Elsevier Ltd. [CrossRef]

- Karathanos, D., & Karathanos, P. Applying the Balanced Scorecard to Education. Journal of Education for Business 2005, 80, 222–230. [CrossRef]

- Khan, I., Zakari, A., Dagar, V., & Singh, S. World energy trilemma and transformative energy developments as determinants of economic growth amid environmental sustainability. Energy Economics 2022, 108, 105884. [CrossRef]

- Khan, K. S., Kunz, R., Kleijnen, J., & Antes, G. Five steps to conducting a systematic review. JRSM 2003, 96, 118–121. [CrossRef]

- Khatibi, S., & Arjjumend, H. Water Crisis in Making in Iran. Grassroots Journal of Natural Resources 2019, 2, 45–54. [CrossRef]

- Kirchherr, J. Kirchherr, J., Reike, D., & Hekkert, M. Conceptualizing the circular economy: An analysis of 114 definitions. Resources, Conservation and Recycling 2017, 127(September), 221–232. [CrossRef]

- Kiriri, P. N.. Management of Performance in Higher Education Institutions: The Application of the Balanced Scorecard (BSC). European Journal of Education 2022, 5, 141–154. [CrossRef]

- Krautkraemer, J. A. (2005). Economics of Natural Resource Scarcity: The State of the Debate. Resources for the Future. Resources for the Future. [CrossRef]

- Kumar, U., Galar, D., Parida, A., Stenström, C., & Berges, L. Maintenance performance metrics: a state-of-the-art review. Journal of Quality in Maintenance Engineering 2013, 19, 233–277. [CrossRef]

- Lach, D., Rayner, S., & Ingram, H. Taming the waters: strategies to domesticate the wicked problems of water resource management. International Journal of Water 2005, 3, 1. [CrossRef]

- ., *!!! REPLACE !!!*. Lewis, R. W. (1955). Measuring, reporting and appraising results of operations with reference to goals, plans and budgets. Planning, Managing and Measuring the Business: A case study of management planning and control at General Electric Company. Controllership Foundation.

- Li, W., Elheddad, M., & Doytch, N. The impact of innovation on environmental quality: Evidence for the non-linear relationship of patents and CO2 emissions in China. Journal of Environmental Management 2021, 292, 112781. [CrossRef]

- Liu, H., Khan, I., Zakari, A., & Alharthi, M. Roles of trilemma in the world energy sector and transition towards sustainable energy: A study of economic growth and the environment. Energy Policy 2022, 170, 113238. [CrossRef]

- Liu, Y., Xu, W., Hong, Z., Wang, L., Ou, G., & Lu, N. Assessment of Spatial-Temporal Changes of Landscape Ecological Risk in Xishuangbanna, China from 1990 to 2019. Sustainability 2022, 14, 10645. [CrossRef]

- Liyanage, J. P., Badurdeen, F., & Ratnayake, R. M. C. Industrial asset maintenance and sustainability performance: Economical, environmental, and societal implications. Handbook of Maintenance Management and Engineering 2009, 665–693. [CrossRef]

- Luciani, G. (2020). The Impacts of the Energy Transition on Growth and Income Distribution (pp. 305–318). [CrossRef]

- Lyubchyk, A., Filonovich, S. A., Mateus, T., Mendes, M. J., Vicente, A., Leitão, J. P., Falcão, B. P., Fortunato, E., Águas, H., & Martins, R. Nanocrystalline thin film silicon solar cells: A deeper look into p/i interface formation. Thin Solid Films 2015, 591, 25–31. [CrossRef]

- Makarova, T. L., Zakharchuk, I., Geydt, P., Lahderanta, E., Komlev, A. A., Zyrianova, A. A., Lyubchyk, A., Kanygin, M. A., Sedelnikova, O. V., Kurenya, A. G., Bulusheva, L. G., & Okotrub, A. V. Assessing carbon nanotube arrangement in polystyrene matrix by magnetic susceptibility measurements. Carbon 2016, 96, 1077–1083. [CrossRef]

- Maktav, D., Erbek, F. S., & Jürgens, C. Remote sensing of urban areas. International Journal of Remote Sensing 2005, 26, 655–659. [CrossRef]

- Maletič, D., Maletič, M., Al-Najjar, B., & Gomišček, B. The role of maintenance in improving company’s competitiveness and profitability. Journal of Manufacturing Technology Management 2014, 25, 441–456. [CrossRef]

- Márquez, A. C. (2007). The Maintenance Management Framework. Springer London. [CrossRef]

- Martins, A. B., Farinha, J. T., & Cardoso, A. M. Calibration and certification of industrial sensors – a global review. WSEAS Transactions on Systems and Control 2020, 15, 394–416. [CrossRef]

- Martins, A. B., Fonseca, I., Farinha, J. T., Reis, J., & Marques Cardoso, A. J. (2022). Prediction Maintenance Based on Vibration Analysis and Deep Learning – a Case Study of a Drying Press Supported on a Hidden Markov Model. SSRN Electronic Journal. [CrossRef]

- Martins, A., Fonseca, I., Farinha, J. T., Reis, J., & Cardoso, A. J. M. Maintenance Prediction through Sensing Using Hidden Markov Models—A Case Study. Applied Sciences 2021, 11, 7685. [CrossRef]

- Mateus, B., Mendes, M., Farinha, J. T., Martins, A. B., & Cardoso, A. M. (2023). Data Analysis for Predictive Maintenance Using Time Series and Deep Learning Models—A Case Study in a Pulp Paper Industry (pp. 11–25). [CrossRef]

- Mizusawa D.; McNeil S. (2005). Trinitiy in transportation planning: Strategic planning, asset management, and performance measures. Annual Conference - Canadian Society for Civil Engineering (Vol. 2005).

- Mok, W. K., Tan, Y. X., & Chen, W. N. Technology innovations for food security in Singapore: A case study of future food systems for an increasingly natural resource-scarce world. Trends in Food Science & Technology 2020, 102, 155–168. [CrossRef]

- Neumayer, E. Scarce or Abundant? The Economics of Natural Resource Availability. Journal of Economic Surveys 2002, 14, 307–335. [Google Scholar] [CrossRef]

- Nørreklit, H. The Balanced Scorecard: what is the score? A rhetorical analysis of the Balanced Scorecard. Accounting, Organizations and Society 2003, 28, 591–619. [Google Scholar] [CrossRef]

- O’Neil, H. F., Bensimon, E. M., Diamond, M. A., & Moore, M. R. Designing and Implementing an Academic Scorecard. Change: The Magazine of Higher Learning 1999, 31, 32–40. [CrossRef]

- Orimoloye, I. R., Belle, J. A., Olusola, A. O., Busayo, E. T., & Ololade, O. O. Spatial assessment of drought disasters, vulnerability, severity and water shortages: a potential drought disaster mitigation strategy. Natural Hazards 2021, 105, 2735–2754. [CrossRef]

- Padilla-Lozano, C. P., & Collazzo, P. Corporate social responsibility, green innovation and competitiveness – causality in manufacturing. Competitiveness Review: An International Business Journal 2022, 32, 21–39. [CrossRef]

- Pais, E., Raposo, H., Meireles, A., & Farinha, J. T. ISO 55001 – A Strategic Tool for the Circular Economy – Diagnosis of the Organization’s State. Journal of Industrial Engineering and Management Science 2019, 2018, 89–108. [CrossRef]

- Parra, C., Viveros, P., Kristjanpoller, F., & Marquez, A. C. (2021). TÉCNICAS DE AUDITORÍA PARA LOS PROCESOS DE: MANTENIMIENTO, FIABILIDAD OPERACIONAL Y GESTIÓN DE ACTIVOS (AMORMS & AMS-ISO 55001) (Issue March). Universidad de Sevilla, Universidad Técnica Federico Santa María.

- Paul, G. C., Saha, S., & Hembram, T. K. Application of the GIS-Based Probabilistic Models for Mapping the Flood Susceptibility in Bansloi Sub-basin of Ganga-Bhagirathi River and Their Comparison. Remote Sensing in Earth Systems Sciences 2019, 2(2–3), 120–146. [CrossRef]

- Pink, G H; McKillop I, Schraa, EG; Preyra, C; Montgomery, C; Baker, G. R. Creating a balanced scorecard for a hospital system. Journal of Health Care Finance 2001, 27, 1–20.

- Posavljak, M., Tighe, S. L., & Godin, J. W. Strategic Total Highway Asset Management Integration. Transportation Research Record: Journal of the Transportation Research Board 2013, 2354, 107–114. [CrossRef]

- Prieto-Sandoval, V., Jaca, C., & Ormazabal, M. Towards a consensus on the circular economy. Journal of Cleaner Production 2018, 179, 605–615. [CrossRef]

- Procházka, P., Hönig, V., Maitah, M., Pljučarská, I., & Kleindienst, J. Evaluation of Water Scarcity in Selected Countries of the Middle East. Water 2018, 10, 1482. [CrossRef]

- Punniyamoorthy, M., & Murali, R. Balanced score for the balanced scorecard: a benchmarking tool. Benchmarking: An International Journal 2008, 15, 420–443. [CrossRef]

- Rajput, S., & Singh, S. P. Connecting circular economy and industry 4.0. P. Connecting circular economy and industry 4.0. International Journal of Information Management 2019, 49(November 2018), 98–113. [CrossRef]

- Roda, I., & Garetti, M. (2015). Application of a Performance-driven Total Cost of Ownership (TCO) Evaluation Model for Physical Asset Management. In 9th WCEAM Research Papers - Volume 1 Proceedings of 2014 World Congress on Engineering Asset Management (pp. 11–23). Springer International Publishing. [CrossRef]

- ., *!!! REPLACE !!!*. Rodrigues, J. A., Farinha, J. T., Cardoso, A. M., Mendes, M., & Mateus, R. (2023). Prediction of Sensor Values in Paper Pulp Industry Using Neural Networks (pp. 281–291). [CrossRef]

- Rodrigues, J. A., Farinha, J. T., Mendes, M., Mateus, R., & Cardoso, A. Short and long forecast to implement predictive maintenance in a pulp industry. Eksploatacja i Niezawodnosc - Maintenance and Reliability 2021, 24, 33–41. [CrossRef]

- Rodrigues, J. A., Farinha, J. T., Mendes, M., Mateus, R. J. G., & Cardoso, A. J. M. Comparison of Different Features and Neural Networks for Predicting Industrial Paper Press Condition. Energies 2022, 15, 6308. [CrossRef]

- Rodrigues, J. A., Martins, A., Mendes, M., Farinha, J. T., Mateus, R. J. G., & Cardoso, A. J. M. Automatic Risk Assessment for an Industrial Asset Using Unsupervised and Supervised Learning. Energies 2022, 15, 9387. [CrossRef]

- Rodrigues, Joao, Costa, I, Farinha, J., Mendes, M., & Margalho, L. Predicting motor oil condition using artificial neural networks and principal component analysis. Eksploatacja i Niezawodność – Maintenance and Reliability 2020, 22, 440–448. [CrossRef]

- Rodrigues, João, Farinha, J. M. T., & Cardoso, A. M. Predictive maintenance tools – a global survey. WSEAS Transactions on Systems and Control 2021, 16, 96–109. [CrossRef]

- Rokicki, T., Perkowska, A., Klepacki, B., Szczepaniuk, H., Szczepaniuk, E. K., Bereziński, S., & Ziółkowska, P. The importance of higher education in the EU countries in achieving the objectives of the circular economy in the energy sector. Energies 2020, 13. [CrossRef]

- Root, T. L., Price, J. T., Hall, K. R., Schneider, S. H., Rosenzweig, C., & Pounds, J. A. Fingerprints of global warming on wild animals and plants. Nature 2003, 421, 57–60. [CrossRef]

- Sadeghi Dastaki, M., Afrazeh, A., & Mahootchi, M. A two-phase decision-making model for product development based on a product-oriented knowledge inventory model. Journal of Knowledge Management 2022, 26, 943–971. [CrossRef]

- Saha, S., Gayen, A., & Bayen, B. Deep learning algorithms to develop Flood susceptibility map in Data-Scarce and Ungauged River Basin in India. Stochastic Environmental Research and Risk Assessment 2022, 36, 3295–3310. [CrossRef]

- Saleem, H., Khosravi, M., Maroufi, S., Sahajwalla, V., & O’Mullane, A. P. Repurposing metal containing wastes and mass-produced materials as electrocatalysts for water electrolysis. Sustainable Energy & Fuels 2022, 6, 4829–4844. [CrossRef]

- Sarmas, E., Marinakis, V., & Doukas, H. A data-driven multicriteria decision making tool for assessing investments in energy efficiency. Operational Research 2022, 22, 5597–5616. [CrossRef]

- Scopus. (n.d.). Scopus. Retrieved December 23, 2022, from https://www.scopus.com/. /: https, 23 December.

- Seto, K. C., Fragkias, M., Güneralp, B., & Reilly, M. K. A Meta-Analysis of Global Urban Land Expansion. PLoS ONE 2011, 6, e23777. [CrossRef]

- Sharaf-Addin, H. H., & Fazel, H. Balanced Scorecard Development as a Performance Management System in Saudi Public Universities: A Case Study Approach. Asia-Pacific Journal of Management Research and Innovation 2021, 17(1–2), 57–70. [CrossRef]

- Shen, S., Chang, R. H., Kim, K., & Julian, M. Challenges to maintaining disaster relief supply chains in island communities: disaster preparedness and response in Honolulu, Hawai’i. Natural Hazards 2022, 114, 1829–1855. [CrossRef]

- Shylo, A., Danilenko, I., Gorban, O., Doroshkevich, O., Nosolev, I., Konstantinova, T., & Lyubchyk, A. Hydrated zirconia nanoparticles as media for electrical charge accumulation. Journal of Nanoparticle Research 2022, 24, 18. [CrossRef]

- Shylo, A., Doroshkevich, A., Lyubchyk, A., Bacherikov, Y., Balasoiu, M., & Konstantinova, T. Electrophysical properties of hydrated porous dispersed system based on zirconia nanopowders. Applied Nanoscience 2020, 10, 4395–4402. [CrossRef]

- Silk, S. Automating the Balanced Scorecard. Management Accounting 1998, 79, 38–44. [Google Scholar]

- Simões, J. M., Gomes, C. F., & Yasin, M. M. A literature review of maintenance performance measurement. Journal of Quality in Maintenance Engineering 2011, 17, 116–137. [CrossRef]

- Simon, H. A. A Framework for Decision Making. Proceedings of a Symposium on Decision Theory 1963, 1– 9 , 22–28. 9.

- Simon, H., Guetzkow, H., Kozmetsky, G., & Tyndall, G. (1954). Centralization vs. Decentralization in Organizing the Controller’s Department. Controllership Foundation Scholars Book Co.

- Sinha, A., Mishra, S., Sharif, A., & Yarovaya, L. Does green financing help to improve environmental & social responsibility? Designing SDG framework through advanced quantile modelling. Journal of Environmental Management 2021, 292, 112751. [CrossRef]

- Smith, V. K. Natural Resource Scarcity: A Statistical Analysis. The Review of Economics and Statistics 1979, 61, 423. [Google Scholar] [CrossRef]

- Stahel, W. R. Circular economy. Nature 2016, 531, 435–438. [Google Scholar] [CrossRef] [PubMed]

- Stewart, A. C.; Carpenter-Hubin, J. Stewart, A. C.; Carpenter-Hubin, J. (2001). The balanced scorecard. Planning for higher education. 37–42.

- Subhoni, M., Kholmurodov, K., Doroshkevich, A., Asgerov, E., Yamamoto, T., Lyubchyk, A., Almasan, V., & Madadzada, A. Density functional theory calculations of the water interactions with ZrO 2 nanoparticles Y 2 O 3 doped. Journal of Physics: Conference Series 2018, 994, 012013. [CrossRef]

- Szwagrzyk, M., Kaim, D., Price, B., Wypych, A., Grabska, E., & Kozak, J. Impact of forecasted land use changes on flood risk in the Polish Carpathians. Natural Hazards 2018, 94, 227–240. [CrossRef]

- Tehrany, M. S., Pradhan, B., & Jebur, M. N. Flood susceptibility analysis and its verification using a novel ensemble support vector machine and frequency ratio method. Stochastic Environmental Research and Risk Assessment 2015, 29, 1149–1165. [CrossRef]

- Uva, J. S. 6.o Inventário Florestal Nacional (IFN6). https://www.icnf.pt/api/file/doc/c8cc40b3b7ec8541. 8541.

- Vaszkun, B., & Tsutsui, W. M. (2012). A modern history of Japanese management thought. Journal of Management History 2015, 18, 368–385. [CrossRef]

- Walter, F. Walter, F., Gasparetto, V., & Neto, F. J. K. (2001). THE BUILDING OF THE BALANCED SCORECARD FOR ACADEMICAL ENVIRONMENTS: APPLICATION IN A GERMAN ACADEMIC UNIT THE BUILDING OF THE BALANCED SCORECARD FOR ACADEMICAL ENVIRONMENTS: APPLICATION IN A GERMAN ACADEMIC UNIT. VIII Congresso Brasileiro de Custos.

- Wang, J., Z., & Parlikad, A. (2016). Designing Performance Measures for Asset Management Systems in Asset-Intensive Manufacturing Companies: A Case Study. In H. Koskinen, Kari T.; Kortelainen, T. Aaltonen, Jussi; Uusitalo, & J. Komonen, Kari; Mathew, Joseph; Laitinen (Eds.), Proceedings of the 10th World Congress on Engineering Asset Management (WCEAM 2015) (pp.; pp. 655–662. [CrossRef]

- Wang, X., Xu, Z., Qin, Y., & Skare, M. Innovation, the knowledge economy, and green growth: Is knowledge-intensive growth really environmentally friendly? Energy Economics 2022, 115, 106331. [CrossRef]

- WCED. (1987). Report of the World Commission on Environment and Development : Our Common Future Acronyms and Note on Terminology Chairman ’ s Foreword. Report of the World Commission on Environment and Development: Our Common Future.

- Weerasekara, S., Lu, Z., Ozek, B., Isaacs, J., & Kamarthi, S. Trends in Adopting Industry 4.0 for Asset Life Cycle Management for Sustainability: A Keyword Co-Occurrence Network Review and Analysis. Sustainability 2022, 14, 12233. [CrossRef]

- Wijnia, Y. (2022). Pragmatic Performance Management: Aligning Objectives Across Different Asset Portfolios. In Lecture Notes in Mechanical Engineering (pp. 163–172). [CrossRef]

- Zhang, Y., & Dilanchiev, A. Economic recovery, industrial structure and natural resource utilization efficiency in China: Effect on green economic recovery. Resources Policy 2022, 79, 102958. [CrossRef]

- Zink, T., & Geyer, R. Circular Economy Rebound. Journal of Industrial Ecology 2017, 21, 593–602. [CrossRef]

Figure 1.

Floods in Lisbon December 2022 (Source: (Expresso, 2022)).

Figure 2.

Sustainable manufacturing for the twenty-first century (Source: (Liyanage et al., 2009)).

Figure 3.

Primary Energy consumption Rate Versus Population Change Rate (Adapted from: (BP, 2022; Department of Economic and Social Affairs - United Nations, 2022)).

Figure 3.

Primary Energy consumption Rate Versus Population Change Rate (Adapted from: (BP, 2022; Department of Economic and Social Affairs - United Nations, 2022)).

Figure 4.

Frameworks for designing performance measures (Adapted from: (J. Wang et al., 2016)).

Figure 5.

Radar Map (Adapted from: (Pais et al., 2019)).

Figure 6.

Maintenance Management Model (Adapted from: (Márquez, 2007)).

Figure 7.

Translating vision and strategy: four perspectives (Source: (Kaplan, 2009)).

Table 1.

Balanced Scorecard in SAMP.

| Perspectives | Questions | Measurements | Physical Assets Intervention | ISO 55001 Requirements | KPI |

|---|---|---|---|---|---|

| Financial Perspective | How to reduce costs? | Revenue, Expenses, ROI, Net Income | Maintenance policies; Availability vs Production | 6.2.1; 6.2.2 | ROI, EPS, RG |

| How to increase profitability? | |||||

| How to increase revenue? | |||||

| Customer Perspective | What are the customer’s needs? | Customer Satisfaction, Customer Retention | Quality level related to Physical Assets performance | 4.1; 4.3; 5.3 | NPS, RPR, RC, CSAT |

| What stakeholders expect? | |||||

| What interested parts expect? | |||||

| Internal Business Process Perspective | What are my assets? | Inventory; Quality Control, Product Lead Time | Physical Assets Life-Cycle vs SAMP | 4.4; 5.3; 6.2.1; 6.2.2 | IQI, QCR, PLTF |

| What is the value of my assets? | |||||

| My assets are in line with the organization's objectives? | |||||

| What assets will focus on? | |||||

| How to extend the life-cycle of the assets? | |||||

| What are the non-core assets for the organization? | |||||

| What new assets are needed? | |||||

| How to dispose old assets? | |||||

| How to manage risk? | |||||

| Innovation Learning & Growth Perspective | Increase availability | Employee Skills, Employee Training, Employee Retention, Employee Satisfaction | Maintenance policies vs TPM | 6.2.1; 6.2.2 | ESR, ETR, ERR, ESI |

| Improve reliability |

Table 2.

The Key Performance Indicators.

| KPI | Description |

|---|---|

| ROI | Return on Investment |

| EPS | Earnings per Share |

| RG | Revenue Growth |

| NPS | Net Promoter Score |

| RPR | Repeat Purchase Rate |

| RC | Revenue Concentration |

| CSAT | Customer Satisfaction Score |

| QCR | Quality Control Rate |

| IQI | Inventory Quality Index |

| PLTF | Product Lead Time Forecast |

| ESR | Employee Skills Rate |

| ETR | Employee Training Rate |

| ERR | Employee Retention Rate |

| ESI | Employee satisfaction index |

Table 3.

KPI’s Grounding.

| KPI | Grounding |

|---|---|

| ROI | Measures the return on investment |

| EPS | Presents the profit increase |

| RG | Presents the revenue increase |

| NPS | Measures customer experience |

| RPR | Measures the customers retention |

| RC | Measures the revenue generated from the highest paying client |

| CSAT | Measures the happiness of the costumer with a product or service |

| QCR | Measures the product / service quality |

| IQI | Measures the Inventory Quality |

| PLTF | Measures the time it takes to create a product and deliver it to a consumer |

| ESR | Measures the skills that employees have |

| ETR | Measures the training that employees have |

| ERR | Measures the retention on employees |

| ESI | Measures the employees satisfaction |

Table 4.

Data needed to calculate KPI’s.

| KPI | Data |

|---|---|

| ROI | Current Value of Investment |

| Cost of Investment | |

| EPS | Net Income |

| Preferred Dividends | |

| End-of-Period Common Shares Outstanding | |

| RG | Initial Revenue |

| Final Revenue | |

| NPS | Percentage of Promoters |

| Percentage of Passives | |

| Percentage of Detractors | |

| RPR | Number of customers who made a repeat purchase |

| Number of customers | |

| RC | Amount of revenue that your business earned from the best customer |

| Amount by your business’s total revenue | |

| CSAT | Number of satisfied customers |

| Total customers asked | |

| QCR | Number of good products produced |

| Total of product produced | |

| IQI | Number of assets correctly inventoried |

| Total of assets | |

| PLTF | Estimated total time |

| Real total time | |

| ESR | Number of employees with skills to their work |

| Total number of employees | |

| ETR | Number of hours in training |

| Number of hours planned for training | |

| ERR | Total of new employees retained |

| Total of new employees | |

| ESI | How satisfied are you with your job? |

| How well does your job meet your expectations? | |

| How close is your workplace to your ideal job? |

Table 5.

Calculated KPI’s.

| KPI | Data | Value | KPI Value | Unit |

|---|---|---|---|---|

| ROI | Current Value of Investment | 22,36 | 11,78 | % |

| Cost of Investment | 20,00 | |||

| EPS | Net Income | 106,05 | 6,88 | € |

| Preferred Dividends | 0,43 | |||

| End-of-Period Common Shares Outstanding | 15 | |||

| RG | Initial Revenue | 5,36 | 17,91 | % |

| Final Revenue | 6,32 | |||

| NPS | Percentage of Promoters | 85% | 62,00 | % |

| Percentage of Passives | 25% | |||

| Percentage of Detractors | 23% | |||

| RPR | Number of customers who made a repeat purchase | 86 | 68,25 | % |

| Number of customers | 126 | |||

| RC | Amount of revenue that your business earned from the best customer | 2,35 | 72,31 | % |

| Amount by your business’s total revenue | 3,25 | |||

| CSAT | Number of satisfied customers | 126 | 47,55 | % |

| Total customers asked | 265 | |||

| QCR | Number of good product produced | 12,69 | 88,37 | % |

| Total of product produced | 14,36 | |||

| IQI | Number of assets correctly inventoried | 64 | 77,11 | % |

| Total of assets | 83 | |||

| PLTF | Estimated total time | 54,00 | 90,00 | % |

| Real total time | 60,00 | |||

| ESR | Number of employees with skills to their work | 20 | 76,92 | % |

| Total number of employees | 26 | |||

| ETR | Number of hours in training | 58,00 | 100,00 | % |

| Number of hours planned for training | 50,00 | |||

| ERR | Total of new employees retained | 7 | 77,78 | % |

| Total of new employees | 9 | |||

| ESI | How satisfied are you with your job? | 9 | 85,19 | % |

| How well does your job meet your expectations? | 8 | |||

| How close is your workplace to your ideal job? | 9 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Copyright: This open access article is published under a Creative Commons CC BY 4.0 license, which permit the free download, distribution, and reuse, provided that the author and preprint are cited in any reuse.