Submitted:

23 August 2023

Posted:

24 August 2023

You are already at the latest version

Abstract

In this work, optimal consumption and investment strategies are derived for risk-averse investors under the 4/2 stochastic volatility class of models. We work under an expected utility (EUT) framework and consider a Constant Relative Risk Aversion (CRRA) investor, who might also be ambiguity-averse. The corresponding Hamilton-Jacobi-Bellman (HJB) and HJB-Isaacs (HJBI) equations are solved in closed-form for a subset of the parametric space and under some restrictions on the portfolio setting, for complete markets. Conditions for proper changes of measure and well defined solutions are provided. These are the first analytical solutions for the 4/2 stochastic volatility model and the embedded 3/2 model for the type of excess returns established in .

Keywords:

4/2 stochastic volatility model

; CRRA utility

; optimal portfolio choice and consumption

; Heston’s process

; 3/2 process

1. Introduction

Dating back to the 1980s, in the seminal work of [1] (equations II.1–II.8), the excess return of a security, also known as its risk premium, has been prescribed as proportional to powers of the volatility. Specifically, three models were proposed, all presented in terms of the market price of risk (MPR) —that is, technically the ratio of the excess return and the volatility of the security. The first model, type I, assumed a MPR proportional to volatility (i.e., power ). This model implies that each risk factor earns a risk premium that is proportional to the variance of the factor’s return. The second and the third models (types II and III) postulate constant MPR (i.e., power 0 on variance) and constant excess return (i.e., power on variance, inversely proportional to volatility), respectively. These models have been widely used in the literature; see [2,3,4] for examples involving stochastic volatility (SV), stochastic interest, and jumps.

The specification of MPRs play a very important role in expected utility portfolio optimization. In this context, [5] solved the portfolio optimization problem for MPR of types I and II, in a setting of CRRA (power) utility, in an incomplete market with finite horizon for the Heston model (aka the 1/2 model). [6] considered the optimal investment and consumption problem in an incomplete market for the 3/2 model of [7] with Epstein-Zin-Weil recursive utility and an infinite horizon, which implies a value function independent of time. In particular, the authors considered two forms of excess return —constant and linear in the variance (i.e., the MPRs of types I and III). Nevertheless, the exact solution is only available when the agent’s elasticity of intertemporal substitution is one with constant excess return (type III). For all other cases, the solutions are approximations.

Our paper presents the very first closed-form analysis for type I MPR on the recently proposed 4/2 model (see [8]) with a finite horizon, consumption, and complete markets. This leads, as a by-product, to the first analysis of type I MPR on the 3/2 model. We incorporate several ingredients of interest to practitioners in an EUT setting: complete markets1, consumption and terminal wealth, and ambiguity aversion.

Two recent studies have been conducted on the 4/2 model under MPRs outside of the settings in [1], while excluding consumption in their analyses. First, [9] explored the optimal investment problem for a risk-averse investor in both incomplete and complete market in the absence of consumption. The authors employed the same MPR for the 1/2 and 3/2 components —proportional to , the driver of variance. This means the Heston component follows the type II MPR in [5], whereas the 3/2 component follows type I MPR in [6]. Second, the work of [10] considered an investor that is not only risk-averse, but also ambiguity-averse.

Solving the optimal consumption and asset allocation with the advanced 4/2 model for a type I MPR is challenging. The fact that our closed-form solutions are non-affine is proof of this challenge and an important departure from the exiting literature. When the MPR is proportional to a 4/2-structured volatility, the risk premium/excess return is proportional to the variance, . This means there are nonlinear elements in the drift of the equity, which jeopardizes affine solutions and the solvability of the implied partial differential equations (PDEs) in the corresponding Hamilton-Jacobi-Bellman (HJB) and HJB Isaacs (HJBI) equations.

The contributions of our work are as follows:

- We conduct the first risk-averse, expected utility analysis in the presence of consumption for the non-affine class of SV models known as 4/2, under the preferable setting of MPR proportional to variance (type I). Our closed-form solutions, see Propositions 2, are of a non-affine nature, requiring confluent hypergeometric functions. As a byproduct, we produce the very first closed-form portfolio analysis for the 3/2 model for finite horizons.

- We extend the solutions described above to an ambiguity-averse investor, leading to the very first related analyses for the 4/2 and 3/2 models, see Proposition 3. In all cases, we consider complete markets, providing conditions for well-defined solutions under the assumption of existence, and proper changes of measure.

-

For a risk-averse investor, in a complete market, we illustrate the differences between the 4/2 model and the popular embedded cases of the 1/2 (Heston) and 3/2 models. On the one hand, the 4/2 and 1/2 models recommend similar levels of consumption and exposure. On the other hand, the 3/2 leads to 20% or higher levels of consumption and absolute exposures (see Figure 1, Figure 2, Figure 3, Figure 4, Figure 5 and Figure 6).The difference in terms of exposures is exacerbated when considering an ambiguity-averse investor in a complete market. In such case, the 3/2 model performance could double absolute exposures compare to the 1/2 and 4/2 models (see Figure 12).

The paper is structured as follows. Section 2 describes the 4/2 model under consideration and the derivatives needed in the portfolio. Section 3 presents and solves the consumption and terminal wealth expected utility problem for a risk-averse investor. Section 3.1 focuses on the complete market case. Section 4 then extends the problematic to an ambiguity-averse investor, with a section on complete markets (Section 4.1). Section 5 studies and implements the top three main cases numerically. First, Section 5.1 analyses a risk-averse investor in a complete market with consumption. Second, Section 5.2 studies an ambiguity-averse complete market investor with no consumption. Finally, Section 6 concludes the paper. All proofs are provided with details in a complementary Appendix A.

2. Model formulation

We assume the stochastic processes describing the financial market are defined on a complete probability space with a right-continuous filtration . The price process of the risky asset follows the so-called 4/2 model:

where is the variance driver, which follows a CIR with mean-reversion rate , long-run mean , and volatility of volatility . The Feller condition (i.e., ) is also imposed to keep the process strictly positive. The standard Brownian motions (BM) in dynamic of risky asset and in the dynamic of variance driver are correlated with parameter . Thus, we will write , where is another standard BM, independent of . The variance, denoted by is given as follows:

This setting implies market prices of risk with the following representation:

where , a and b are positive constants, and are constant. is the market price of variance risk, and is the market price of stock risk. Moreover, can be interpreted as the market price of stock idiosyncratic risk (i.e., with respect to ). Note that in this form of market price of risk, the excess return of the risky asset is proportional to its variance as recommended in the economics literature; see [1] equation (II.6), type I. As for the market price of variance risk , we use Ito’s lemma to create the process of the variance:

Hence our choice of market price of variance risk is: . That is, it is proportional to the volatility of the asset. This is similar to the proposal in [2].

As pointed out by [8], a risk-neutral measure may not exist in the 4/2 model, which is a feature inherited from having the 3/2 model [11]. This failure causes the discounted asset price process may be a strict -local martingale, and not a true -martingale that equivalent to the historical measure . Thus, we explore the feasibility of changing measure under the market price of risk introduced in Equation (4).

In the next proposition we identify the parametric conditions needed for the existence of a valid risk-neutral measure , which follows [9,12]. These conditions will be assumed throughout the paper.

Proposition 1.

The change of measure is well defined for pricing purposes under the following conditions:

See Appendix A.1 for the complete proof.

Furthermore, we assume the investor can also allocate on a financial derivative on the underlying. Let denote the price of the option. It can be shown that the option price evolves with the stochastic differential equation (SDE):

where , and denote the partial derivatives of option price function m with respect to and . Equations (1), (2), and (7) are considered as the reference model.

3. Portfolio optimization under EUT

We consider the investor exhibits CRRA utility for both intermediate consumption and terminal wealth with the same risk-aversion level . That is, we define the utility functions for consumption and for terminal wealth (abusing notation slightly):

where coefficients and are non-negative. The ratio indicates the relative importance of intermediate consumption and terminal wealth, and it thus affects decision-making (optimal strategy). Without loss of generality, we can set , and let determine the relative importance ratio.

The objective of the investor is to maximize their utility from intermediate consumption and terminal wealth ; therefore the reward functional for the investor is defined as follows:

where is a discount rate, is a control variable to be clarified in the next section, and the goal is

where is the value function and the space of admissible controls with , , is the set of feedback strategies that satisfy standard conditions (see [13]).

3.1. Complete market analysis

Let be the fraction of wealth invested in the stock, be the fraction of wealth invested in the option that follows dynamic (7), be the remaining portion of wealth invested in the money account, and the consumption at time t. The wealth of the investor follows the SDE:

where we have assumed the money market account evolves as , and

For simplicity of presentation, we will drop the subindex t in .

Under Bellman principle, the value function satisfies the HJB equation:

with boundary condition . Here , , , , , and are the first and second partial derivatives of function with respect to t, x, and v.

We conjecture our value function can be represented as follows:

where for all v. This conjecture leads to the following PDE for h:

where , : ×⟶ are measurable functions, and

Details of this calculation can be found in Appendix A.2. Next, we provide the solution to the HJB equation.

Proposition 2

(4/2 model in complete market).Let us define

If the parameters satisfy 1 and the following three conditions:

See proof in Appendix A.2.

It should be noted that in case of no consumption, we can assume a simpler value function representation:

and solving the maximization problem in (13), we obtain

Nonetheless, as , the nonlinear term cannot be eliminated in the PDE for , thus rendering a closed-form solution impossible under the 4/2 SV model. Moreover, a closed-form solution is available in [14] (Example 1) for stock prices following the 1/2 SV model in a complete market without ambiguity.

4. Robust consumption portfolio optimization under EUT

Assume the investor is uncertain about the probability distribution for the reference model and consider a set of plausible, alternative models when making investment decisions. Specifically, the investor is uncertain about the distribution of and .

Let be an -valued -progressively measurable process and define the Radon-Nikodym derivative process by

According to Girsanov’s theorem, the process

is a Wiener process under probability measure . Let denote the set of all -progressively measurable processes such that the process (25) is a well-defined Radon-Nikodym derivative process. This formulation of incorporating investor’s model uncertainty is actually allowing uncertainty on the drift of diffusion risk factors of the stock and its variance’s driver (i.e., and , respectively).

The alternative model then follows:

The reward functional can be defined as in the previous section for a given probability measure :

In the presence of a preference for robustness, the investor’s objective is to minimize the penalty term and maximize his utility from intermediate consumption and terminal wealth :

where is the value function, and the last two terms serves as the penalty term for deviating too far from the reference model. The space of -adapted process , is the set of perturbations; the space of admissible controls (i.e., , ) is the set of feedback admissible strategies. The perturbations and in the penalty term are scaled by and , respectively. That is, the larger the values of and , the smaller the penalties for deviating from the reference model, which implies that the investor is more uncertain about the model. Following [15], we assume

where denotes the ambiguity-aversion parameters. In this specification, the optimal strategy would be independent of the current wealth level for a power utility investor, namely homothetic robustness in [15]. Further, can be interpreted as ambiguity aversion regarding the volatility driver, while represents ambiguity about the stock process.

4.1. Complete market analysis

Let be the fraction of wealth invested in the stock, be the fraction of wealth invested in the option, and be the remaining portion of wealth invested in the money account, while is consumption at time t. The wealth of the investor follows

where

That is, if we can find wealth exposures and to the fundamental risk factors and , the corresponding wealth weights and can also be obtained. The value function satisfies the HJBI (robust) equation:

with boundary condition . Similarly to Section 3.1, after solving the first order conditions, we conjecture a value function as follows:

where for all v. This leads to the following PDE for :

Details of this calculation can be found in Appendix A.3. In order to find a solution we need to eliminate the term ; this means:

By setting , and rearranging terms we obtain

where

Next, we present the main result of the section.

Proposition 3

(4/2 model in complete market, robustness).Let

and (condition (37)). Assume , μ, and ν satisfy conditions (18) and 1. Then, the solution of the HJBI Equation (33) is , and solves the PDE in Equation (37) and admits the representation:

where , and follows from Equation (21) with associated m, D, β, and K.

Moreover, the optimal consumption-wealth ratio, and variance-stock exposures are given by

The worst case measure is determined by

See proof in Appendix A.3.

The previous result can be seen as a generalization of Proposition 2 by setting . It should be noted that the closed-form solution does not support ambiguity-aversion or uncertainty on the variance driver (i.e., must be zero). Next, conditions on the parametric space are provided to ensure that the optimal change of measure is well-defined in the complete market.

Proposition 4.

For the optimal Radon-Nikodym in the complete market to be a well-defined density, parameters should satisfy the following condition:

where , and .

See proof in Appendix A.4.

Important solutions can be produced in the absence of consumption. In this case, the candidate for the solution of HJBI Equation (33) is , where solves the PDE

with

The main result is reflected in the next corollary.

Corollary 5

(4/2 model in complete market, robustness, no consumption). Let

Assume , and

while μ, and ν satisfy conditions (18) and 1. Then , and has the representation:

where , and is the same as Equation (21) with associated m, D, β, and K.

Moreover, the optimal variance-stock exposures are given by

The worst case measure is determined by

See proof in Appendix A.5.

In contrast to a solution in the presence of consumption (Proposition 3), here we can entertain non zero ambiguity-aversion on variance () and stock (), which provides a window into the impact of ambiguity-aversion in general.

5. Numerical analysis

This section is divided in three subsections corresponding to the two most important contributions of the paper. First, Section 5.1 presents the findings of closed-form solutions to a complete market with consumption (from Section 3.1). Second, Section 5.2 presents the solution to complete markets for ambiguity-averse investors (from Section 4.1).

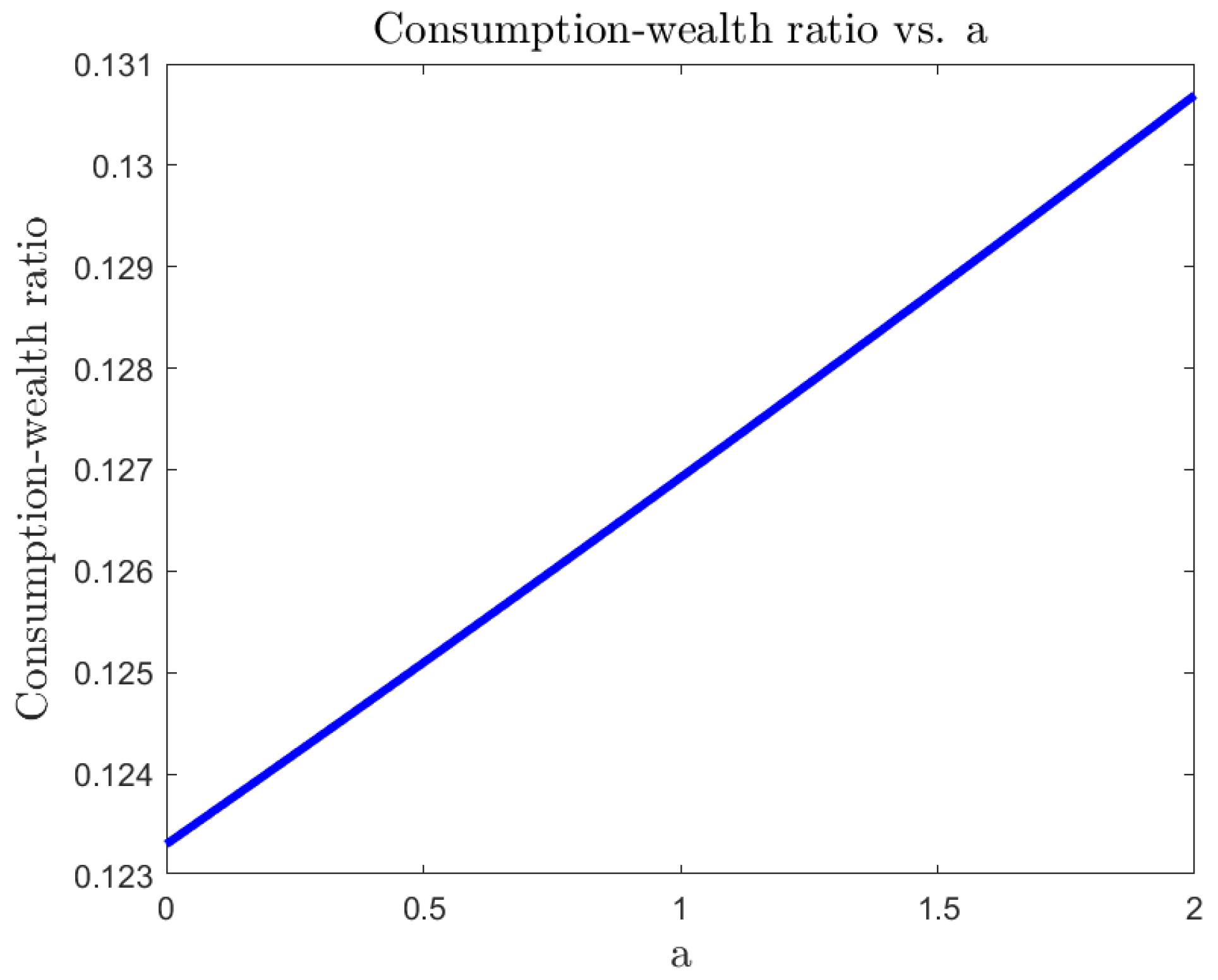

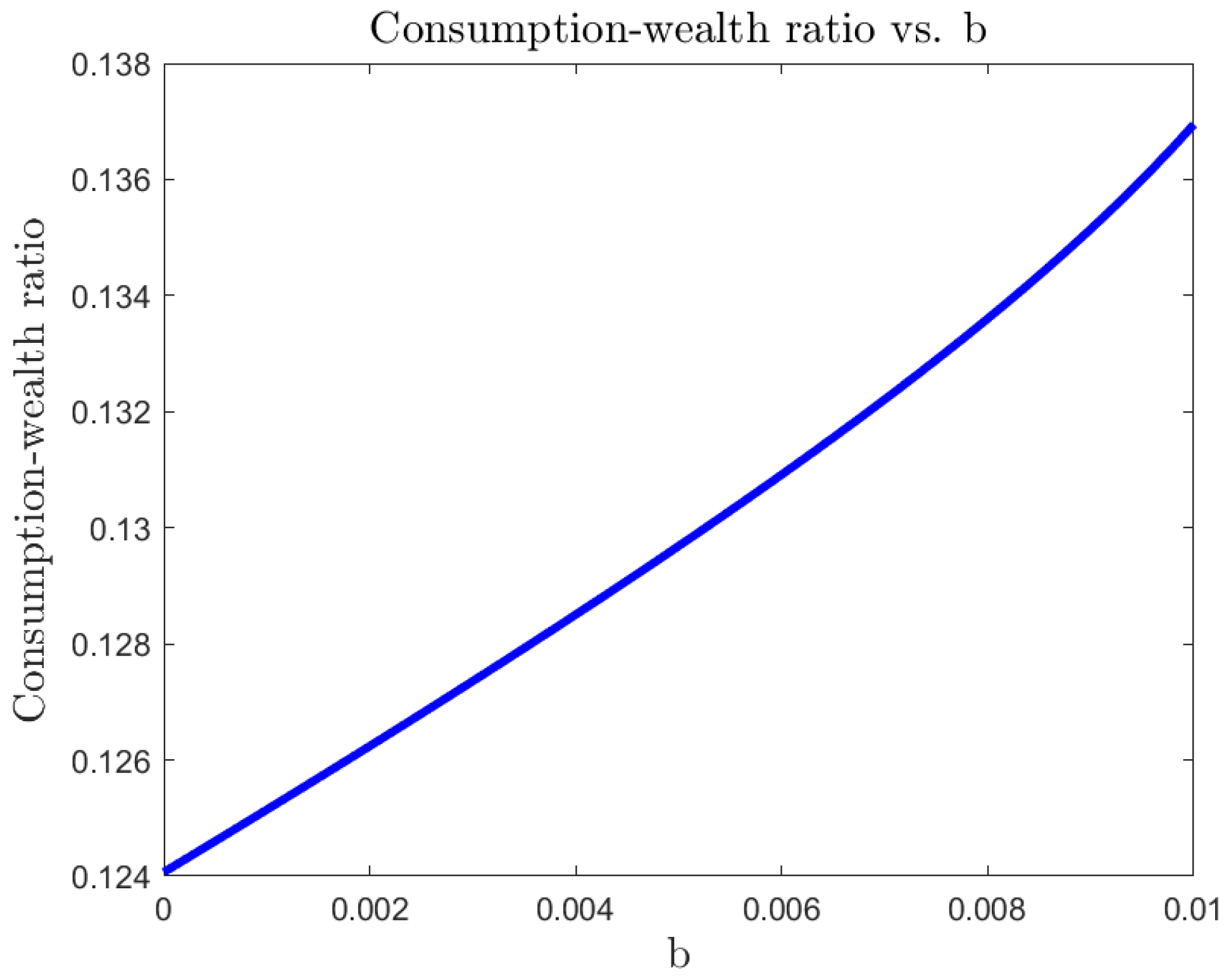

Note that, we cannot use the estimation results of the “drift group" from [9] because of the new choice of MPR for 4/2 and 3/2 models. To accommodate to our choice of MPR, we re-estimate the rate of market price of risk for each model by fixing the excess return at (long-term value), in line with [9]. Then, we follow the procedure of [9] and substitute into the regression to update for each model. The estimation results and the other baseline parameters are presented in Table 1 and Table 2, respectively. In this section, we set , and solve for for each model according to the relationship .

5.1. Complete market analysis with consumption

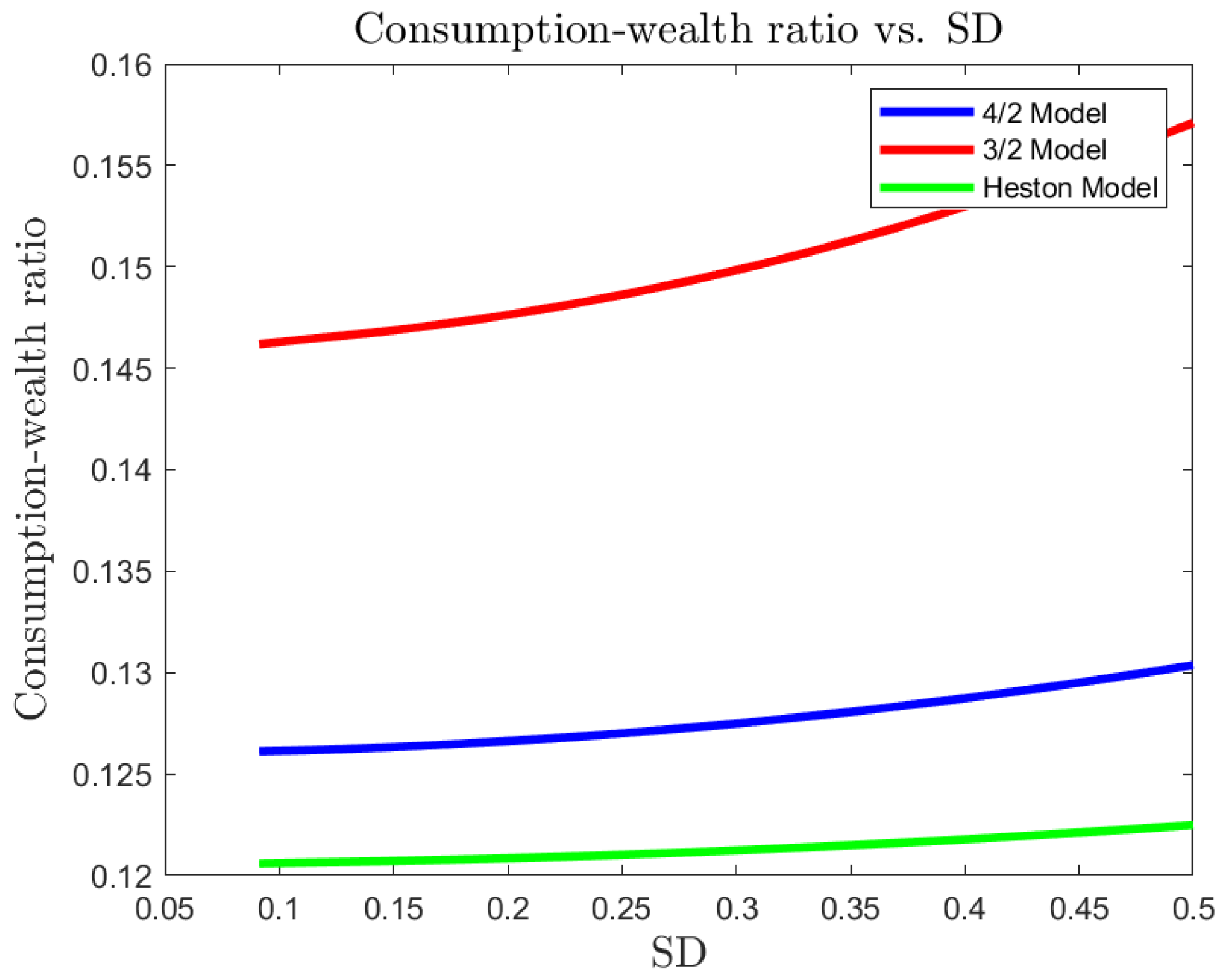

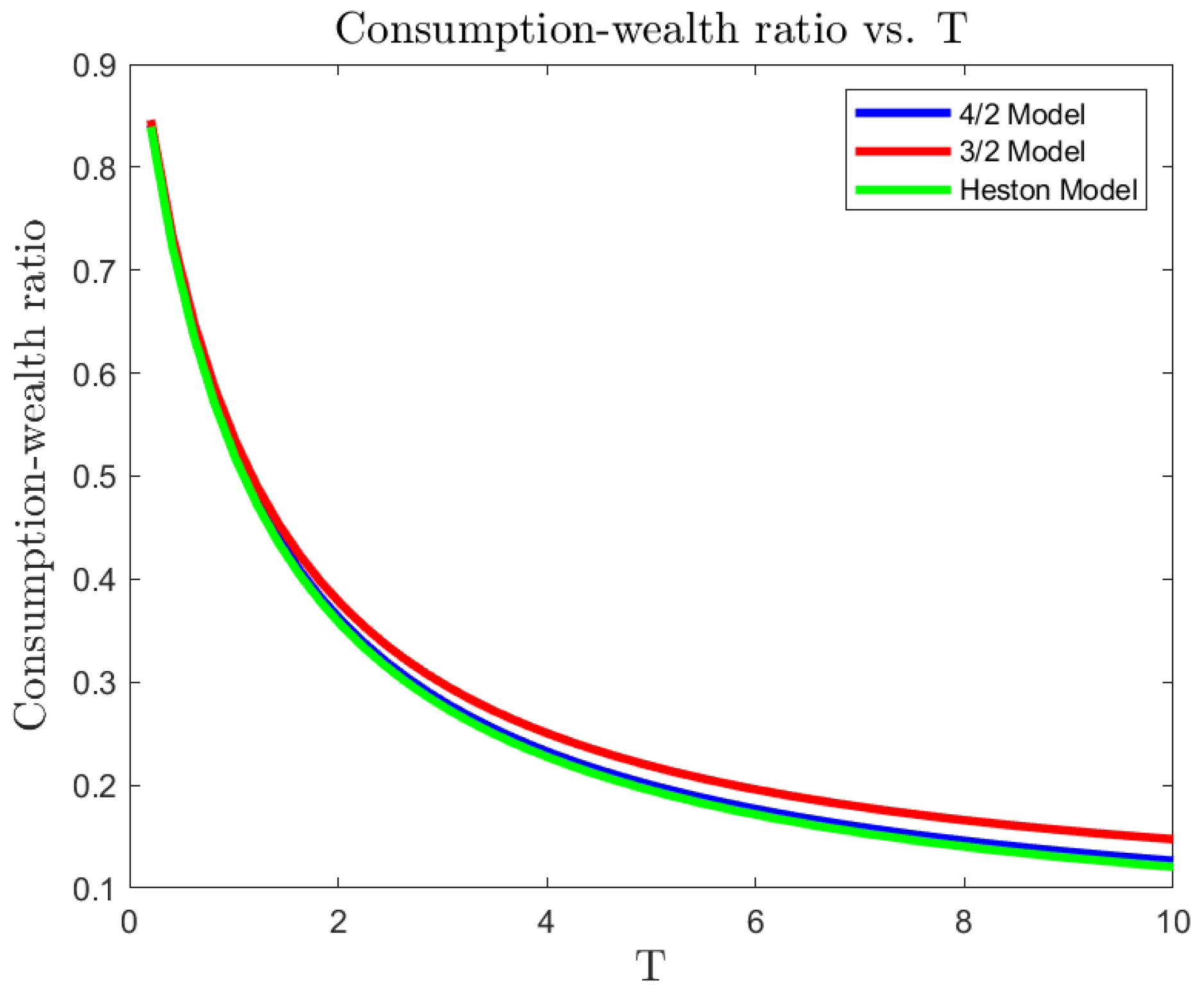

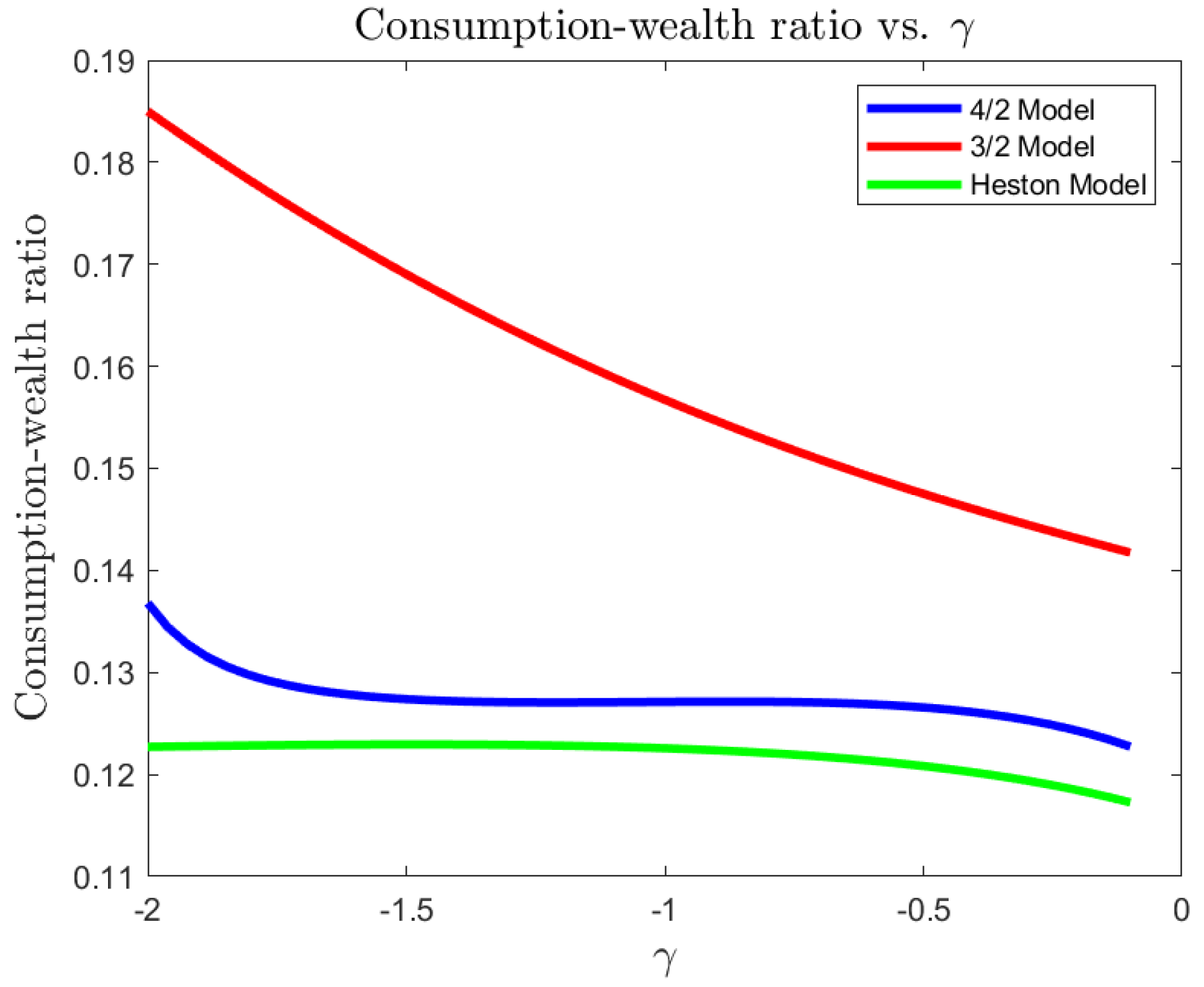

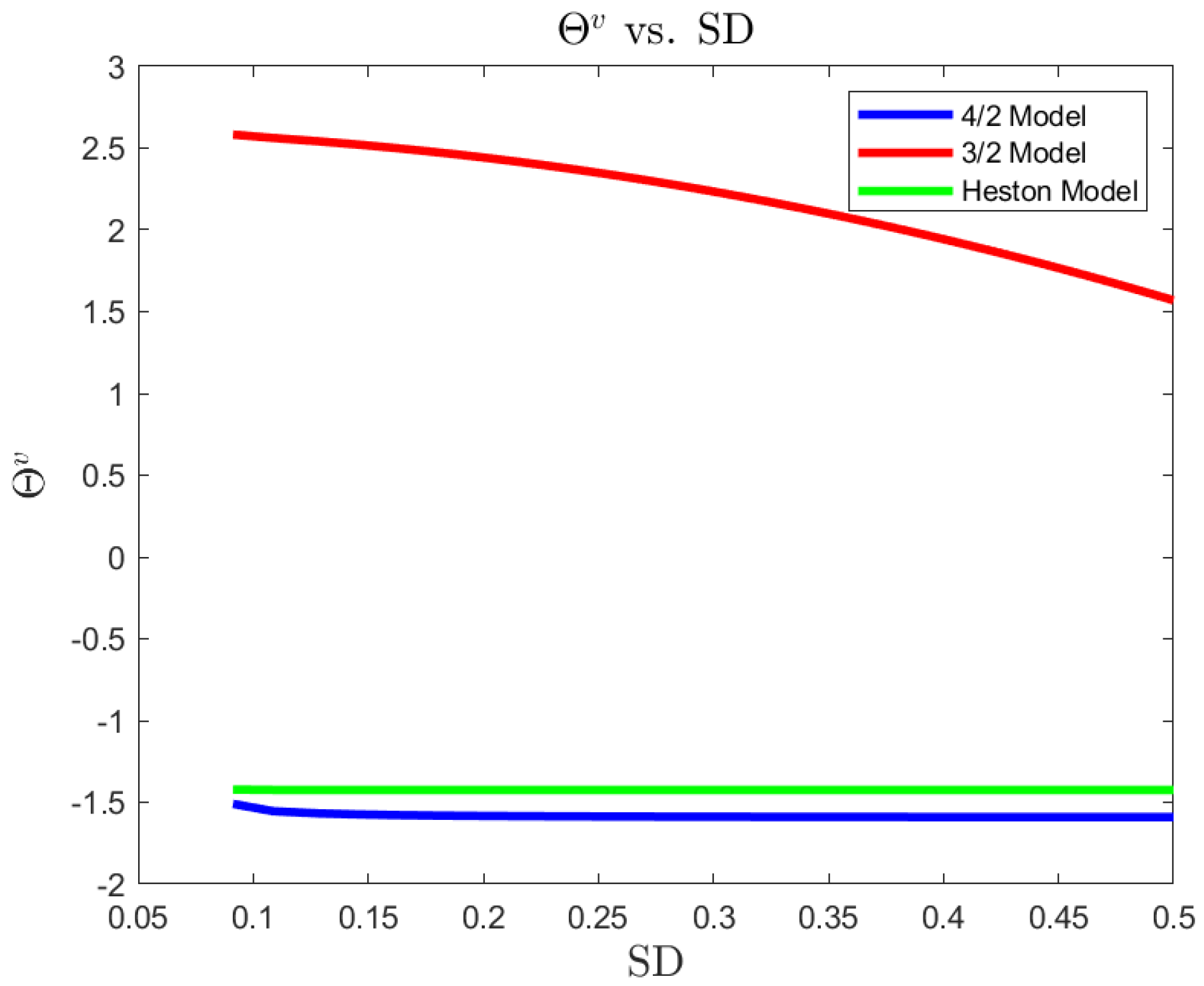

Figure 1, Figure 2 and Figure 3 present the optimal consumption-wealth ratio as a function of standard deviation (SD), investment horizon T, and risk-averse level , respectively. Intuitively, the optimal consumption-wealth ratio is related to the state of the economy. All models recommend an increase in consumption in a highly volatile economic state. In particular, the 4/2 model slightly recommends more consumption than the Heston model, while the 3/2 model suggests at least 20% more consumption. This behaviour of the 3/2 model may be explained by its excess return (i.e., ), which decreases with the increase of . That is, the more volatile the market, the less excess return the 3/2 investor would get from investing in a risky asset. As a result, the investor would allocate his wealth into consumption to get higher utility.

On the other hand, both Heston and 4/2 model compensate the investor with higher excess return if the market becomes more risky. Hence, only a small portion of wealth is shifted from investing in risk assets into consumption. In general, the 3/2 model always implies the most wealth exposures, while the 4/2 model lies in between, closer to the conservative Heston model but with higher sensitivity to the changes in market conditions (SD), and risk-averse level .

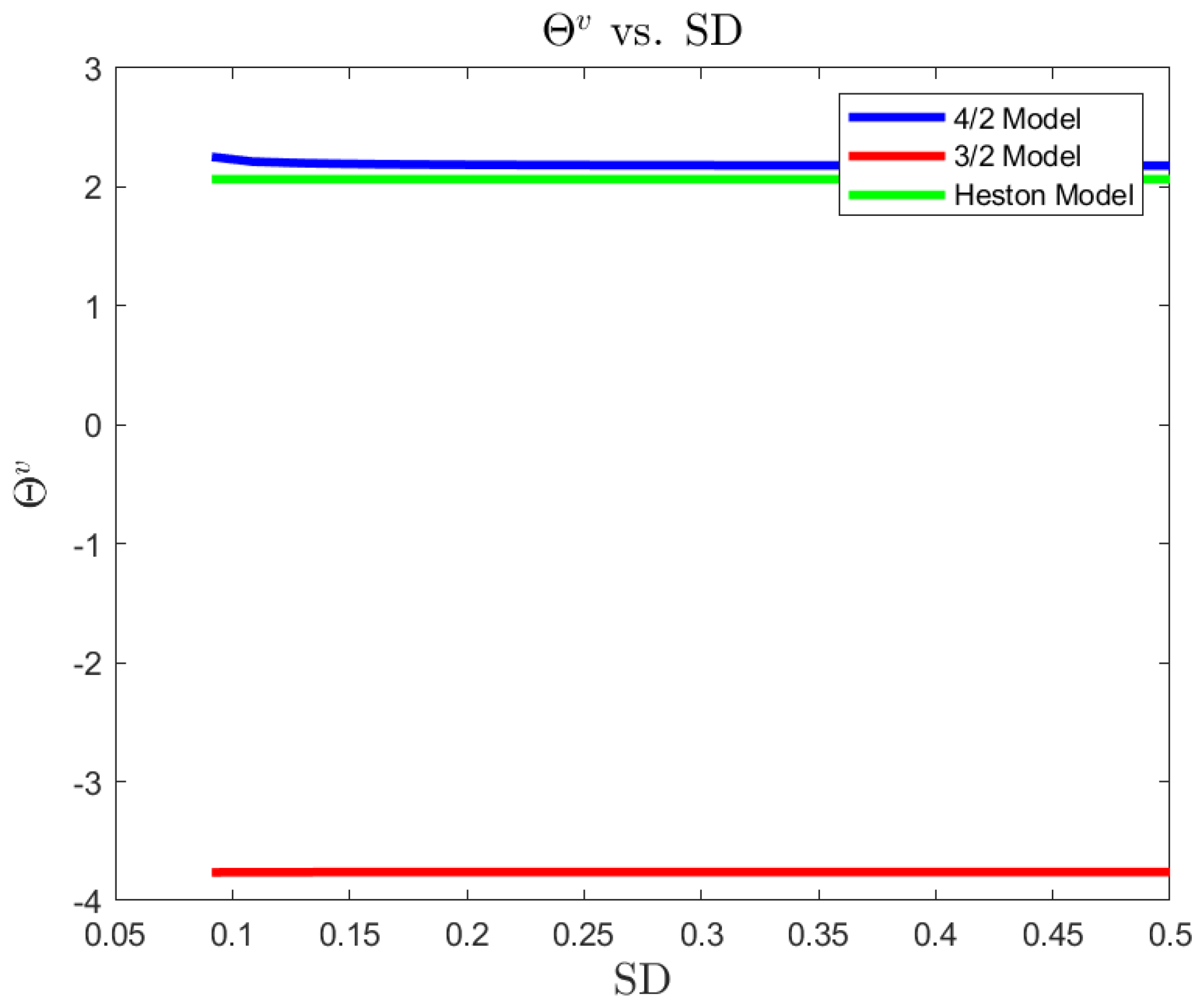

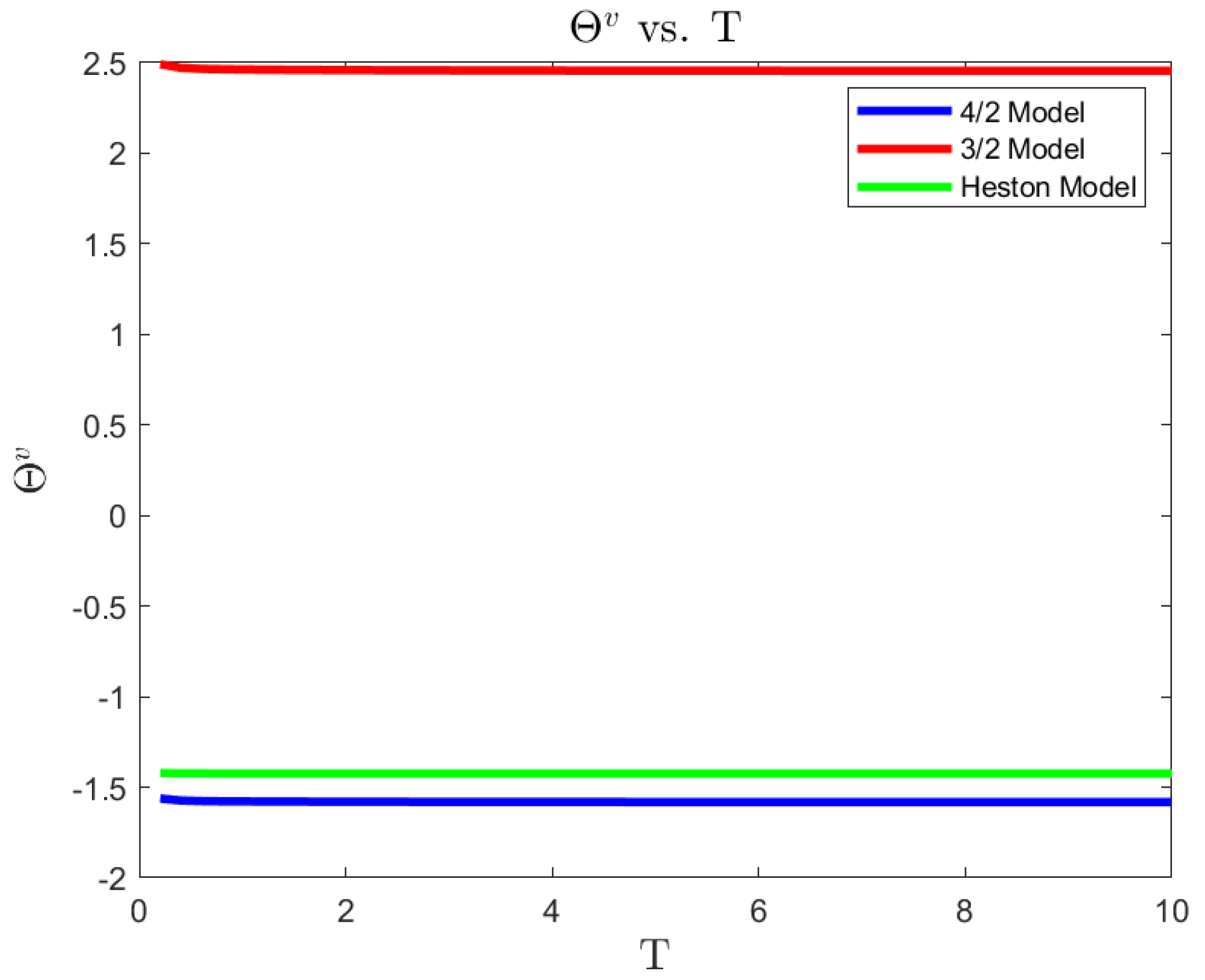

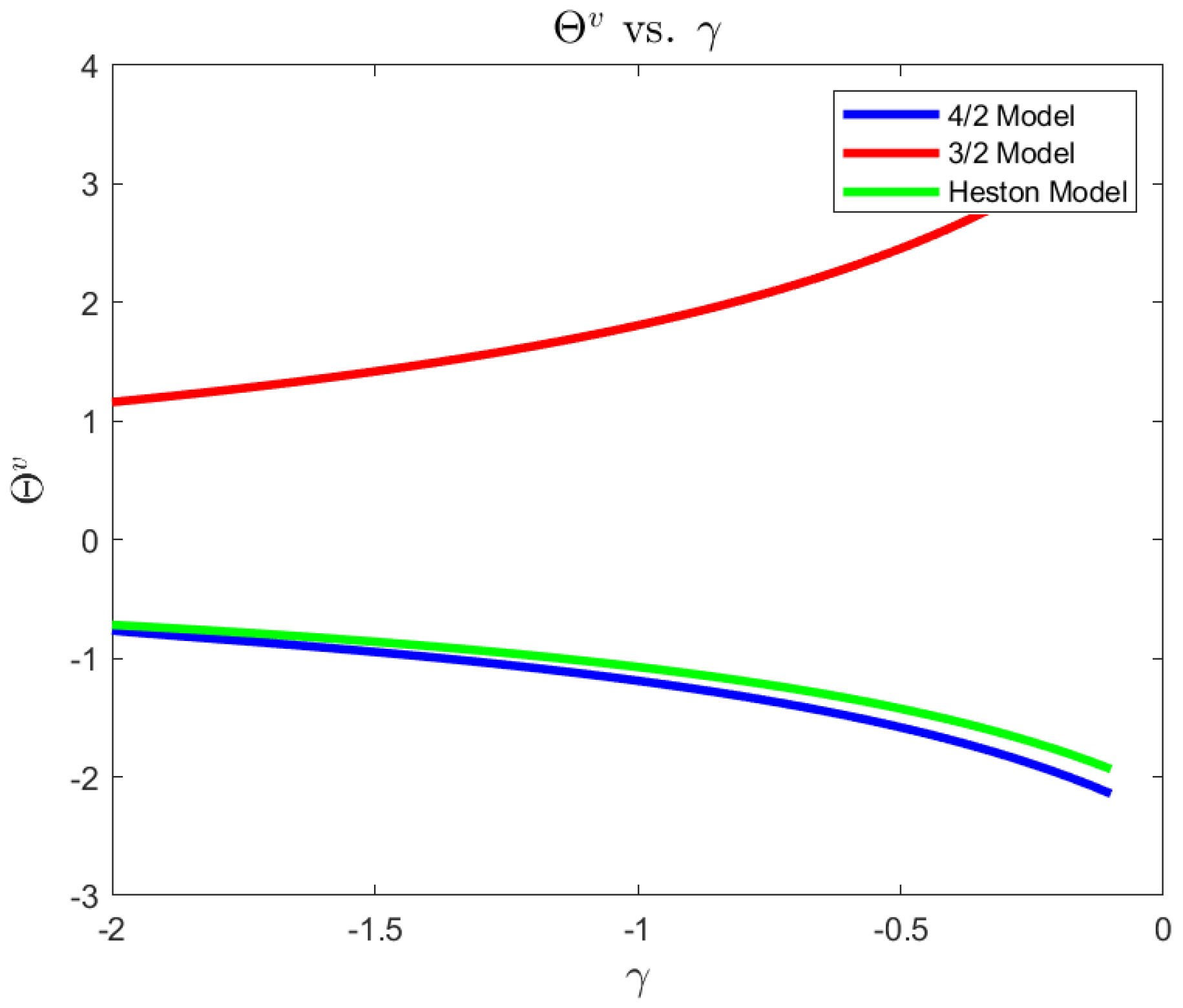

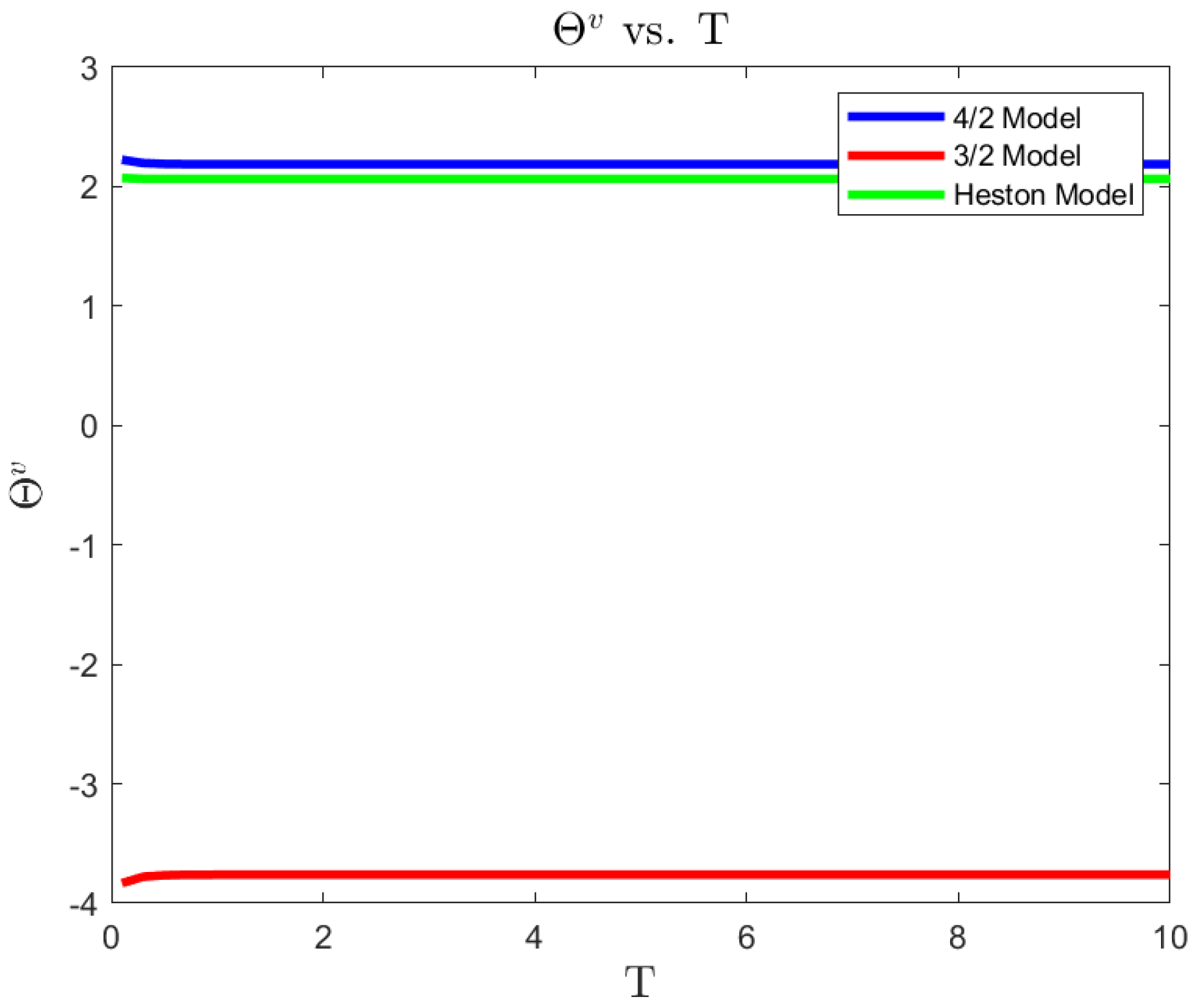

Figure 4, Figure 5 and Figure 6 present the plots of the optimal wealth exposure to variance driver’s risk as a function of SD, investment horizon T, and risk-averse level , respectively. In contrast to the 3/2 model, the exposures to variance driver’s risk under Heston and 4/2 model are insensitive to the changes in market conditions. That is, both Heston and 4/2 model suggest a constant level of total wealth exposure to variance risk. However, the 3/2 model disinvests the risk of variance driver as the market gets into a highly volatile state, which can be understood as decreasing the holding on the asset associated with less excess return.

The positiveness of the wealth exposures among models may be explained by the correlation between the risk factors of asset price and its variance driver for each model. Moreover, all three models recommend a constant level of wealth exposure in terms of investment horizon, as shown in Figure 5. Further, if the investor is less risk-averse, all the three model suggest more aggressive wealth exposure in the absolute sense.

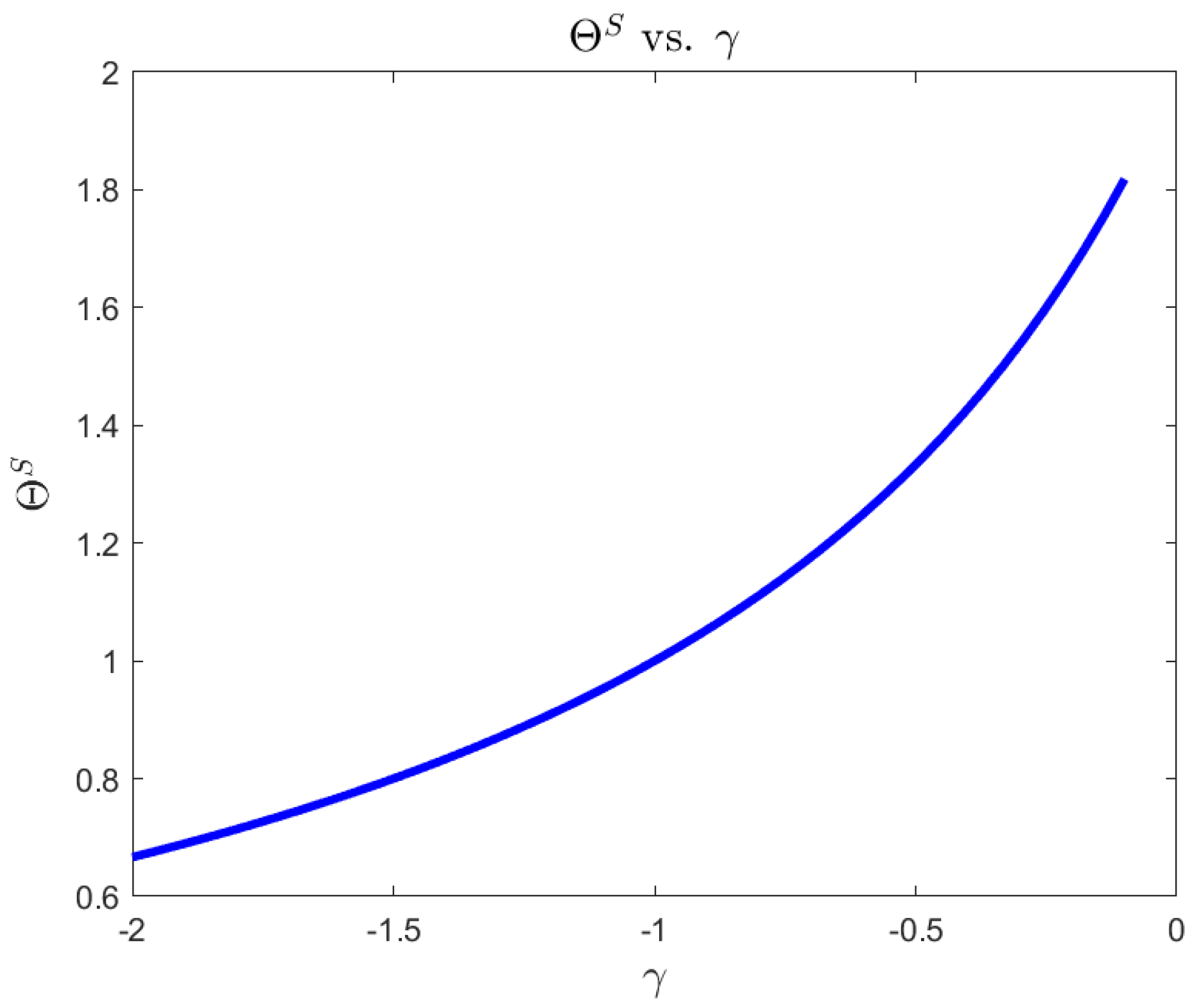

The plot of optimal wealth exposure to stock’s risk versus risk-averse level is given in Figure 7. As we expect, less risk-averse investors allocate more wealth to stocks.

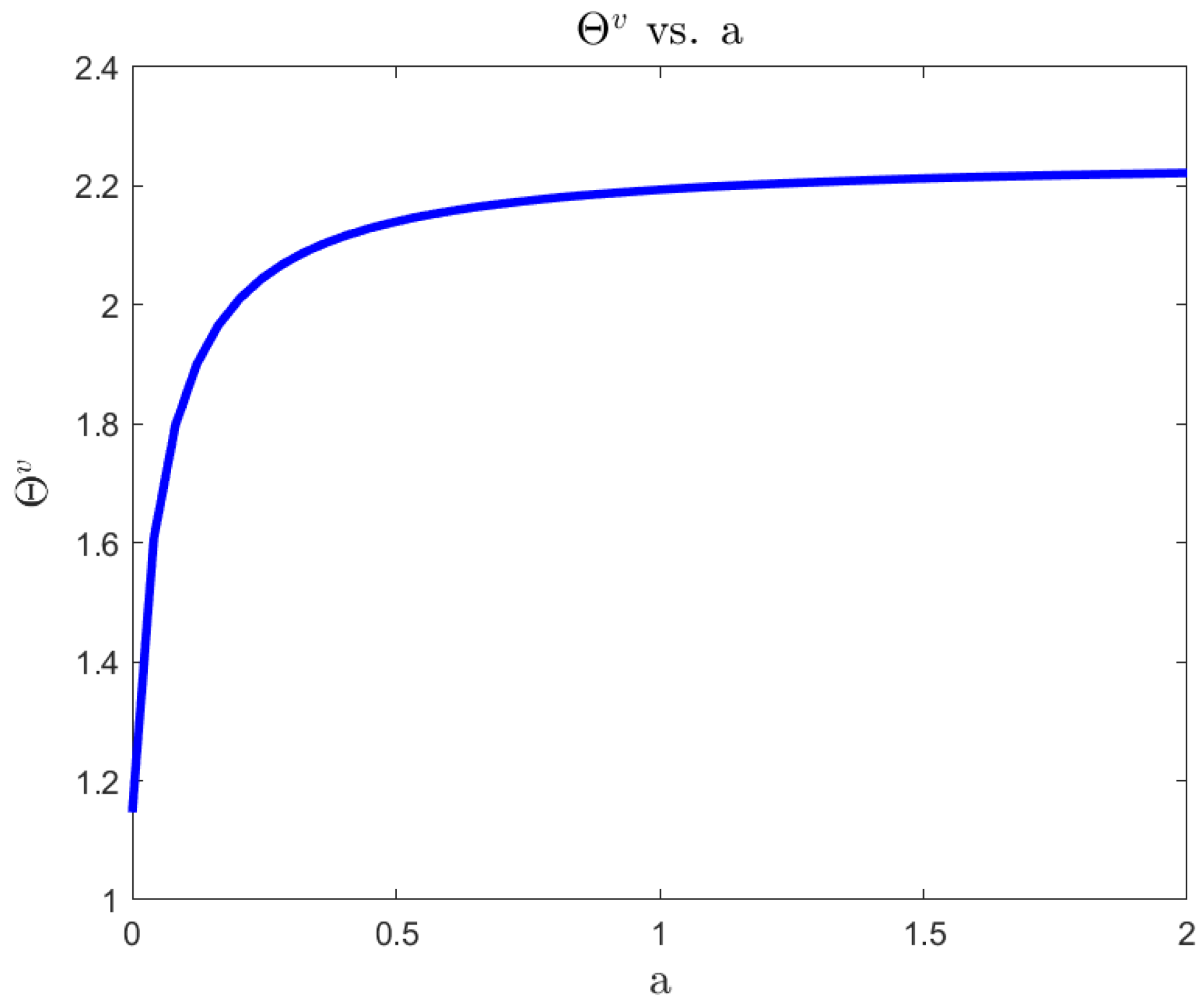

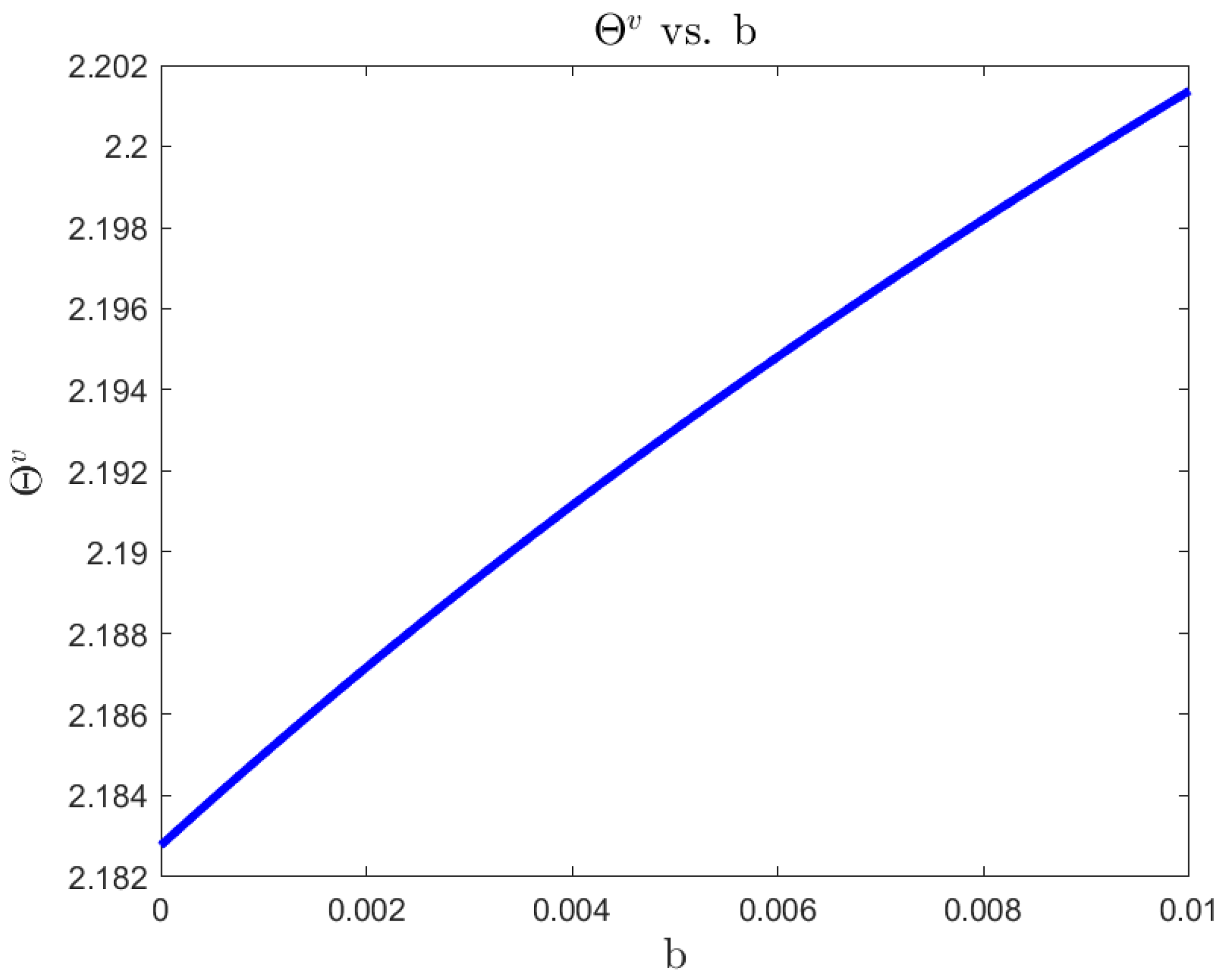

The sensitivity analysis of parameters a, b on optimal consumption-wealth ratio and optimal wealth exposure with 4/2 model are explored in Figure 8, Figure 9, Figure 10 and Figure 11 respectively. Although the 3/2 model behaves differently from the Heston model from our previous observation, the consumption-wealth ratio trends seem dominated by b (i.e., more sensitivity to b), while the wealth exposure is dominated by the 1/2 component (i.e., more sensible to changes in a).

5.2. Complete market analysis without consumption for ambiguity-averse investors

In this case, we have a constraint in the level of ambiguity-aversion and risk-aversion allowed to produce closed-form solutions, see Equation (48), which is

In this section, we continue using the baseline parameters, with , and we further set in this section. The plots of optimal wealth exposures to variance driver’s risk versus SD and investment horizon T are displayed in Figure 12 and Figure 13. It can be seen that all the three models are quite insensitive to changes in the state of volatility and investment horizon, whereas the 3/2 model is apparently more aggressive than Heston and 4/2 model by suggesting an almost double exposure to wealth.

Figure 12.

vs. SD.

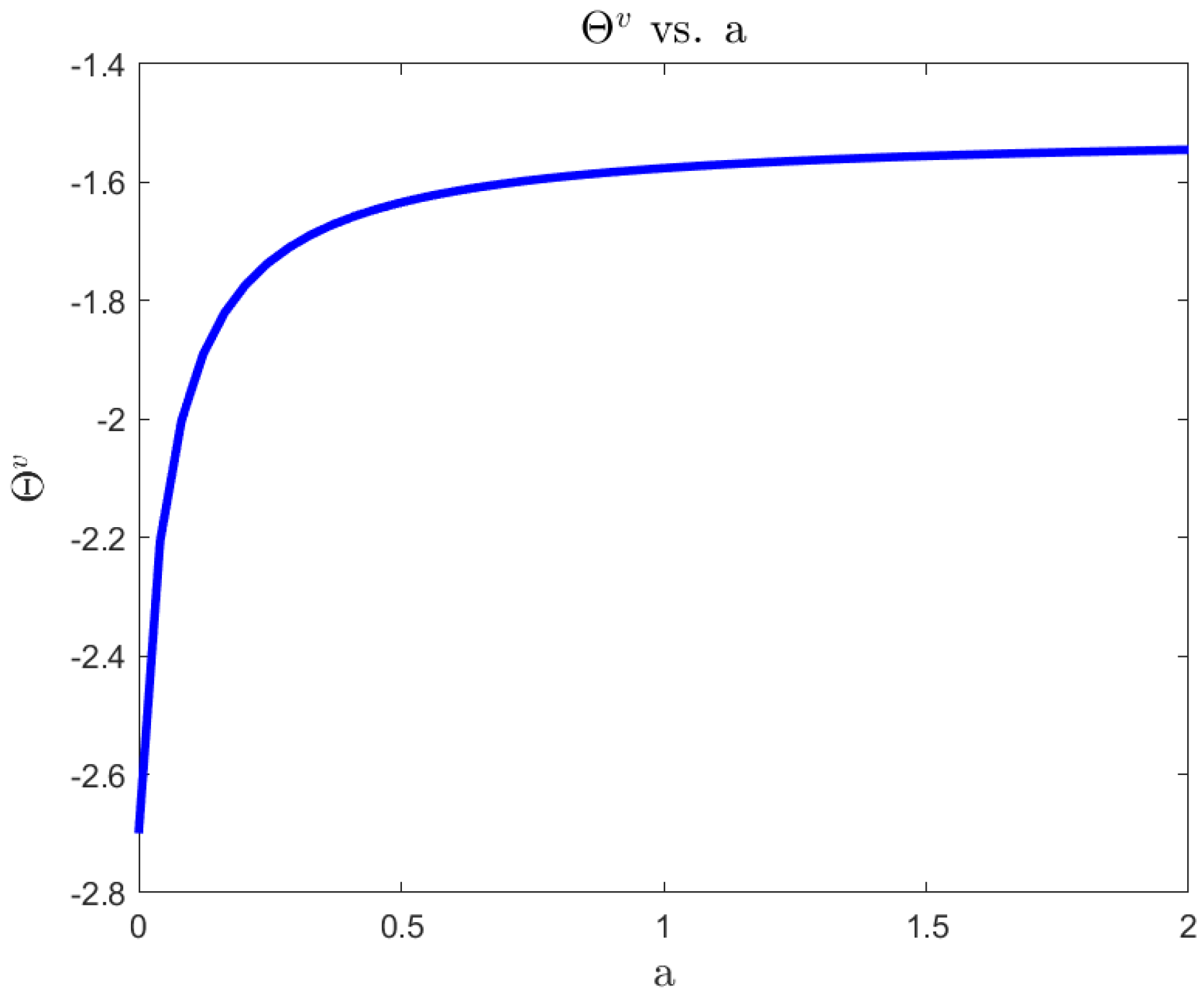

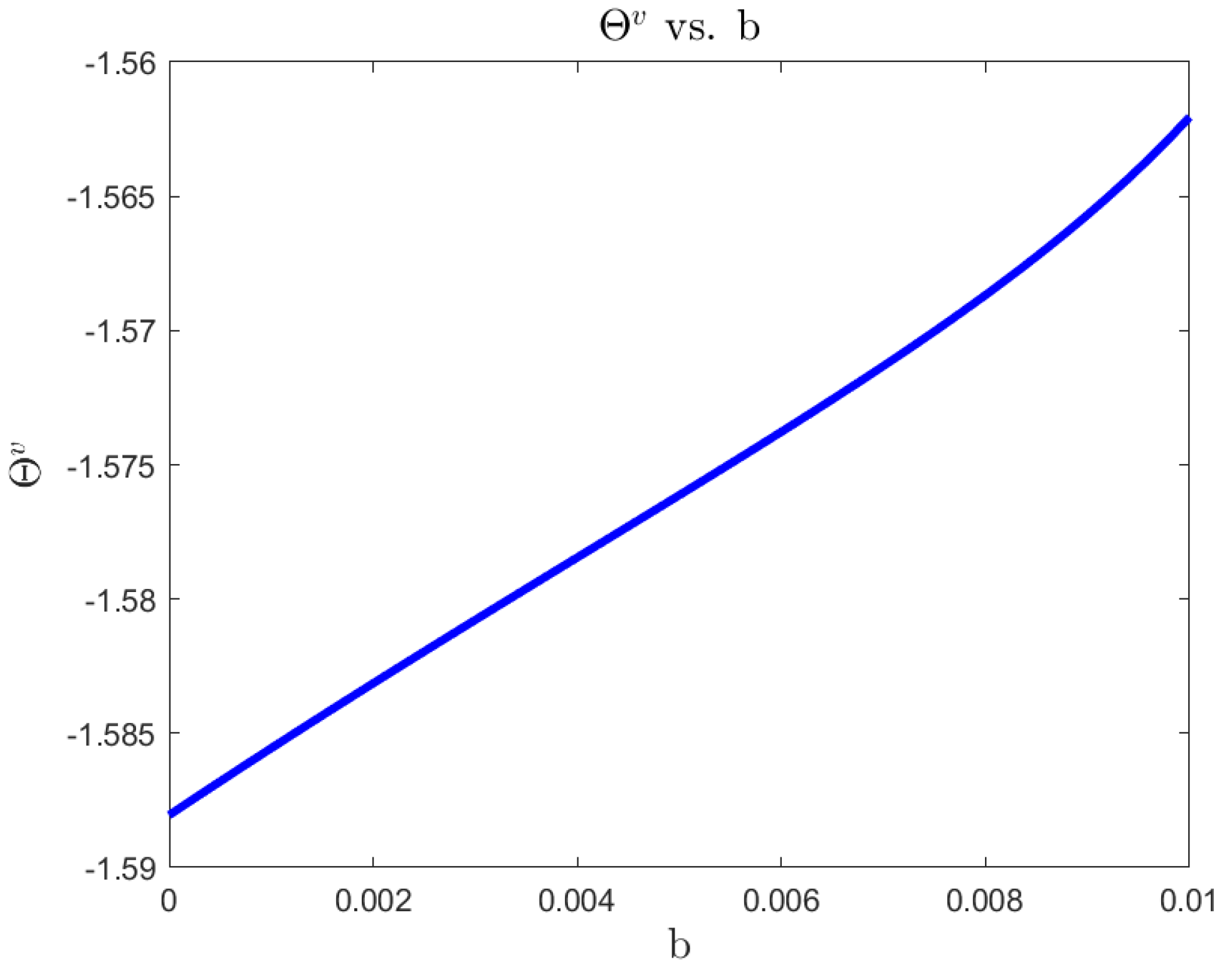

The impact of parameters a, b on wealth exposure with the 4/2 model can be found in Figure 14 and Figure 15, respectively. The marginal effect of the 1/2 component decreases dramatically when a is greater than 0.5, while the 3/2 component b suggests a slightly increase in the exposure of wealth to variance driver’s risk.

6. Conclusion

In this paper, an optimal investment problem for a risk-averse investor under the 4/2 SV model and a 4/2-structured MPR is considered by combining with various elements of interest to scholars and practitioners. These elements include market completeness, terminal wealth with consumption, and ambiguity-aversion. By employing a corresponding derivative to complete the market, taking consumption into account, and allowing for different levels of uncertainty with respect to different risk factors, we orient our setting more close to real world, which implies the importance in finding a closed-form solution. Although, the non-affine nature of the 4/2 volatility and the 4/2-structured MPR is challenging, we found closed-form solution for the case of complete market with consumption, and for all the other interesting cases under certain conditions.

In the numerical part, we present and compare the portfolio strategies recommended by the 4/2, 3/2, and 1/2 models for an investor who either cares about consumption or concerns about mis-specification of the model in a complete market using real-data parameters. The 4/2 and 1/2 models generally behave similarly in wealth exposures compared to that of 3/2 model. The 4/2 model behaves like an average by lying in-between Heston and 3/2 models in consumption in a complete market.

Appendix A. Proofs

Appendix A.1. Proof of conditions on change of measure

Proof.

The first step is to ensure the change of measure is well-defined and for this we use Novikov’s condition, i.e., generically for i = 1,2

From [8], in order for this expectation to exist, we need two conditions:

The latter condition in Equation (A1) implies, in particular, that our volatility processes satisfy Feller’s condition under and ; in other words, it ensures all our CIR processes stay away from zero under both measures. That is,

The second step is to ensure the drift of the asset price equal to the short rate under , which is obviously satisfied here.

The third step ensures the discounted asset price process, , is a true -martingale and not just a local -martingale, therefore it does not concern the change from to but rather the martingale properties of the asset price under (see [8], section 2 for a similar situation). This step follows closely the step 3 in proof A.1 of [9], where we test the martingale property using the Feller nonexplosion test for volatilities under the measure that takes asset price as numeraire, measure and measure , and it leads to

These together lead to conditions in Proposition 1.

□

Appendix A.2. Proof of Proposition 2 (Complete Market, No Robustness, Consumption)

Proof.

Solving the maximization problem for intermediate consumption:

That is,

where risk averse parameter .

Solving the maximization problem for wealth exposures:

That is,

Under the conjecture of the value function in (14):

where for all v, we compute partial derivatives and substitute into the candidates of optimal consumption wealth ratio from Equation (A4), wealth exposures in Equation (A6), and the PDE (13), we have

It can be seen that there is no nonlinear term in the PDE, thereby, no parameter condition is needed to find explicit solution for .

For clarity we divide both sides of the equation by so that the coefficient of is 1:

where and are defined as follow:

with , , and and can be found in Equation (16).

We aim at an expected value representation of h where v stands for a convenient stochastic process. This is an application of Feynman-Kac formula, therefore the coefficients in (15) must satisfy the conditions of Theorem 1 and Lemmas 2 and 3 in [16].

In the notation of [16] we have: , , , , , , , , and . The process should follow the SDE: .

Using the same arguments as in their section 2.1 (an application on the Heston model), we can conclude that admits the Feynman-Kac representation:

Moreover, we have hence we can apply Tonelli’s Theorem to exchange integral and expectation on the first term:

Here, , and can be rewritten as

with parameters

Note that the conditional expectation in is taken under probability measure such that has drift in Equation (15) instead of . The Feller condition is assumed to be satisfied by the new drift, hence we have:

Furthermore, the function of (A12) can be solved explicitly by [8]’s result for all where :

with

Further, if , , , and in Equation (A13) satisfy following conditions,

Moreover, the optimal wealth exposures and consumption-wealth ratio are given by

□

Appendix A.3. Proof of Proposition 3 (Complete Market, Robustness, Consumption)

Proof.

Solving the minimization problem in (33) first, we obtain:

Substituting the values of and from Equation (A19) into the robust HJB equation, i.e., Equation (33), we obtain the following equation that function has to satisfy. after canceling and recombining terms we get:

Solving the maximization problem for intermediate consumption:

That is,

where risk averse parameter .

We conjecture the following representation of the value function:

where for all v. Substituting the partial derivatives into the candidates of optimal consumption wealth ratio from Equation (A22) and wealth exposures in Equation (A24), we have

Next, we substitute the above expressions of , , and into Equation (A20) to eliminate , divide term , and regroup and simplify leading to:

In order to find a solution we need to eliminate the term , this means:

Then we have a linear PDE,

Further, in order to apply Feynman-Kac formula, we divide both sides of the equation by so that the coefficient of is 1:

This is an application of Feynman-Kac formula, therefore the coefficients in (37) must satisfy the conditions of Theorem 1 and Lemmas 2 and 3 in [16].

In the notation of [16] we have: , , , , , , , , and . The process should follow the SDE: .

Using the same arguments as in their section 2.1 (an application on the Heston model), we can conclude that admits the Feynman-Kac representation:

Moreover, given that : ×⟶ is a measurable function, and then we can apply Tonelli’s Theorem to the first term:

Here, and can be rewritten as

with parameters

Note that the conditional expectation in is taken under probability measure such that has drift in Equation (37) instead of . The Feller condition is assumed to be satisfied by the new drift:

Further, if , , , and satisfy conditions in Equation (A17), then can be solved explicitly by [8]’s result in Equation (21) with associated m, D, , and K like Equation (22). Note that the last two conditions for are satisfied directly. Thus, the dependence of function on and can be omitted. Moreover, the optimal wealth exposures and consumption-wealth ratio with are given by

The worst case measure is determined by

Note that the setting of Proposition 2 can be seen as a particular case of the robust analysis here by enforcing a zero ambiguity aversion, i.e. hence .

□

Appendix A.4. Proof of Proposition 4

Proof.

For this condition, we show the optimal Radon-Nikodym derivative of with respect to in the complete market, such that

is a -martingale to ensure a well-defined . We thus consider sufficient conditions based on Novikov’s equation as follows:

where the optimal perturbations are given in equation (43):

We then consider the process defined as

where , , and .

Hence, the Novikov’s condition of the Radon-Nikodym derivative becomes

For this expectation to exist, by [8], we need

□

Appendix A.5. Proof of Corollary 5 (Complete Market, Robustness, No Consumption)

Proof.

In the case of no intermediate consumption, we conjecture our value function follows

where for all v. Substituting the partial derivatives into the optimal exposures , from Equation (A24), and then into Equation (A20) to eliminate :

Simplifying and substituting , and leads to:

Simplifying, dividing each term by and regrouping leads to:

Simplifying leads to,

In order to eliminate the non-linear term, we need

Thereby, we have a linear PDE

Further, the coefficients of the above PDE satisfy the conditions of [16] as per the previous proposition, then admits the Feynman-Kac representation:

with parameters

Note that the conditional expectation is taken under probability measure such that has drift . The Feller condition is assumed to be satisfied by the new drift:

Further, if , , , and satisfy conditions (A17), can be solved explicitly by [8]’s result like Equation (21) with associated m, D, , and K like Equation (22). Note that the last two conditions for are satisfied directly. Thus, the dependence of function on and can be omitted. Moreover, the optimal wealth exposures with are given by

The worst case measure is determined by

□

References

- Merton, R.C. On estimating the expected return on the market: An exploratory investigation. Journal of financial economics 1980, 8, 323–361. [Google Scholar] [CrossRef]

- Heston, S.L. A closed-form solution for options with stochastic volatility with applications to bond and currency options. The review of financial studies 1993, 6, 327–343. [Google Scholar] [CrossRef]

- Bakshi, G.; Cao, C.; Chen, Z. Empirical performance of alternative option pricing models. The Journal of finance 1997, 52, 2003–2049. [Google Scholar] [CrossRef]

- Bates, D.S. Post-’87 crash fears in the S&P 500 futures option market. Journal of econometrics 2000, 94, 181–238. [Google Scholar]

- Kraft, H. Optimal portfolios and Heston’s stochastic volatility model: an explicit solution for power utility. Quantitative Finance 2005, 5, 303–313. [Google Scholar] [CrossRef]

- Chacko, G.; Viceira, L.M. Dynamic consumption and portfolio choice with stochastic volatility in incomplete markets. The Review of Financial Studies 2005, 18, 1369–1402. [Google Scholar] [CrossRef]

- Heston, S.L. A simple new formula for options with stochastic volatility 1997.

- Grasselli, M. The 4/2 stochastic volatility model: a unified approach for the Heston and the 3/2 model. Mathematical Finance 2017, 27, 1013–1034. [Google Scholar] [CrossRef]

- Cheng, Y.; Escobar-Anel, M. Optimal investment strategy in the family of 4/2 stochastic volatility models. Quantitative Finance 2021. [Google Scholar] [CrossRef]

- Cheng, Y.; Escobar-Anel, M. Robust portfolio choice under the 4/2 stochastic volatility model. IMA Journal of Management Mathematics 2021, 00, 0–36. [Google Scholar] [CrossRef]

- Lewis, A. Option Valuation under Stochastic Volatility. Technical report, Finance Press, 2000.

- Cheng, Y.; Escobar-Anel, M.; Gong, Z. Generalized Mean-Reverting 4/2 Factor Model. Journal of Risk and Financial Management 2019, 12, 159. [Google Scholar] [CrossRef]

- Escobar, M.; Ferrando, S.; Rubtsov, A. Robust portfolio choice with derivative trading under stochastic volatility. Journal of Banking & Finance 2015, 61, 142–157. [Google Scholar]

- Liu, J.; Pan, J. Dynamic derivative strategies. Journal of Financial Economics 2003, 69, 401–430. [Google Scholar] [CrossRef]

- Maenhout, P.J. Robust portfolio rules and asset pricing. Review of financial studies 2004, 17, 951–983. [Google Scholar] [CrossRef]

- Heath, D.; Schweizer, M. Martingales versus PDEs in finance: an equivalence result with examples. Journal of Applied Probability 2000, 947–957. [Google Scholar] [CrossRef]

| 1 | incomplete market solutions follow trivially from our setting |

Figure 1.

vs. SD.

Figure 2.

vs. T.

Figure 3.

vs. .

Figure 4.

vs. SD.

Figure 5.

vs. T.

Figure 6.

vs. .

Figure 7.

vs. .

Figure 8.

vs. a.

Figure 9.

vs. b.

Figure 10.

vs. a.

Figure 11.

vs. b.

Figure 13.

vs. T.

Figure 14.

vs. a.

Figure 15.

vs. b.

Table 1.

Estimates among the various models.

| 4/2 Model | 3/2 Model | Heston | |

|---|---|---|---|

| 7.3479 | 6.9884 | 14.6290 | |

| 0.0328 | 0.0323 | 0.0315 | |

| 0.6612 | 0.3760 | 0.5210 | |

| 0.9051 | 0 | 1 | |

| 0.0023 | 0.0268 | 0 | |

| -0.7689 | 0.7910 | -0.8129 | |

| 3.0176 | 4.2973 | 2.8689 | |

| Theoretical leverage () | -0.7689 | -0.7910 | -0.8129 |

Table 2.

Baseline parameters.

| r | t | T | |||||

|---|---|---|---|---|---|---|---|

| 0.05 | 0.02 | -0.5 | 0.04 | 0 | 10 | 1 | 0.04 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Copyright: This open access article is published under a Creative Commons CC BY 4.0 license, which permit the free download, distribution, and reuse, provided that the author and preprint are cited in any reuse.