Submitted:

27 September 2023

Posted:

28 September 2023

You are already at the latest version

Abstract

Thailand has formulated her climate change policy and updated relevant plans and policies to align with the goal of achieving carbon neutrality and net zero GHG emissions. This study investigates the optimal level of GHG mitigation in Thailand, taking into account the marginal abatement cost (MAC) and social cost of carbon (SCC). It evaluates how energy efficiency and renewable energy technologies influence GHG reduction in the power and industrial sector and illustrates policy recommendations that align with the 2020 to 2050 policy and plan period. The findings indicate that there may be instances where GHG mitigation potential is insufficient to reach the national mile-stone. In such cases, it becomes imperative to leverage all technologies within the marginal abatement cost curve (MACC) and also utilization of the social cost of carbon for policy decision making and meeting the desired goals. In certain scenarios, the adoption of additional technologies or measures may be necessary, such as flexible power generation and deploying carbon capture and storage or hydrogen which are high-cost technologies. Furthermore, preparations should be made for multiple levels of climate change policies and plans beyond 2030.

Keywords:

NDC

; Carbon Neutrality

; Optimum Degree

; Marginal Abatement Cost

; Social Cost of Carbon

; Industry Sector

; Power Sector

; Thailand

1. Introduction

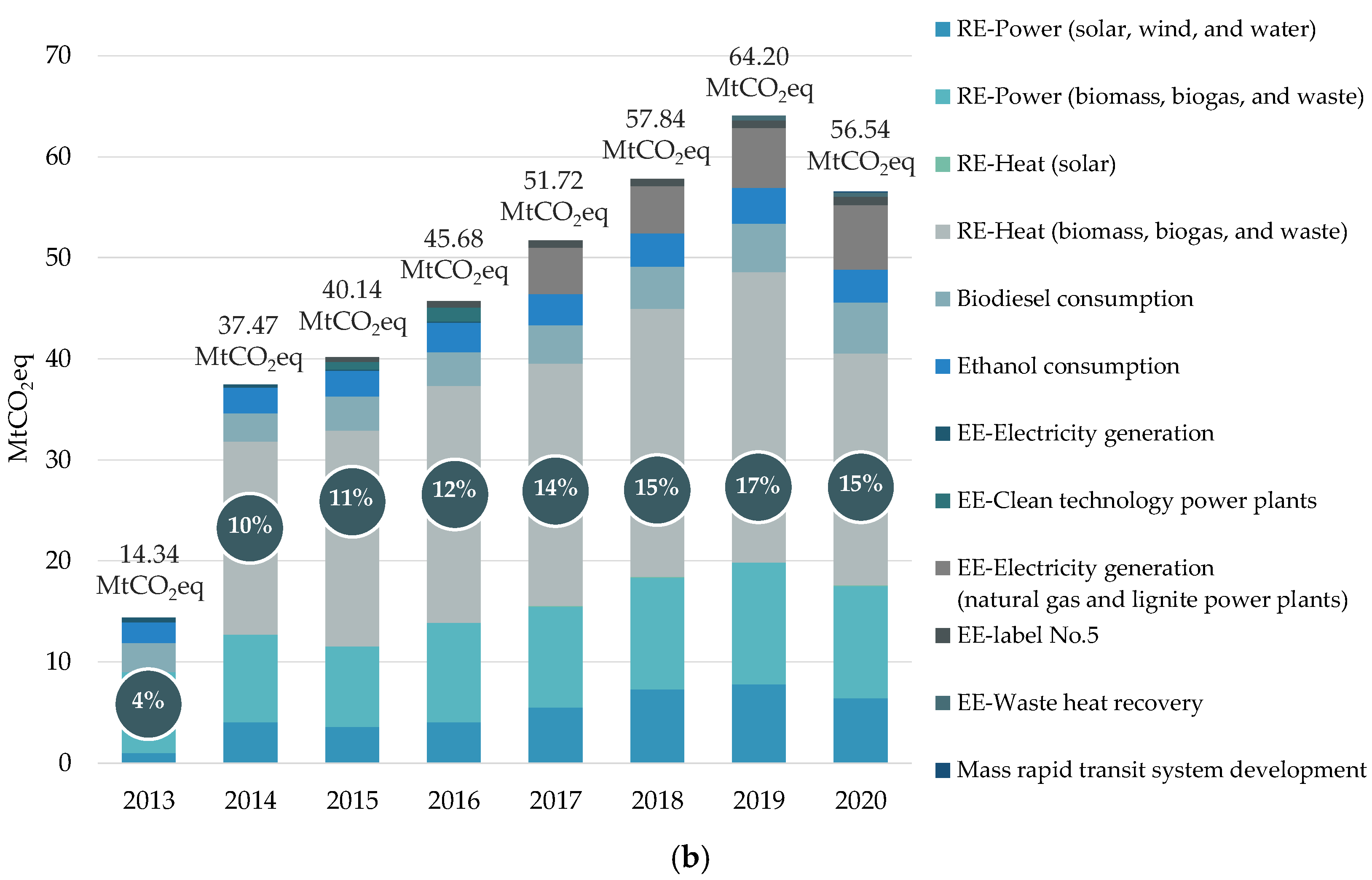

The current climate change poses severe repercussions for global ecosystems and is projected to exacerbate in the future. Thailand, as a nation, is not exempt from the impacts of climate change due to its consistent exposure to climate fluctuations, such as floods and droughts, which have inflicted significant harm on its economy and ecosystems. Despite these daunting challenges, Thailand acknowledges its responsibility as a signatory to the United Nations Framework Convention on Climate Change (UNFCCC) and a participant in the Paris Agreement. To commence, Thailand’s commitment to Nationally Appropriate Mitigation Actions (NAMA) in 2014 pledged voluntary efforts to reduce greenhouse gas (GHG) emissions in the energy and transportation sectors by 7 to 20% below business-as-usual (BAU) levels by 2020. In 2020, Thailand reported a NAMA performance of 56.54 million tonnes of carbon dioxide equivalent (MtCO2eq), constituting approximately 15.40% [1]. Subsequently, Thailand submitted its Nationally Determined Contribution (NDC) to the UNFCCC in 2015, aiming for a 20% reduction in GHG emissions from the BAU level by 2030, with the potential to increase this target to 25% contingent on various international support. This NDC has evolved into the roadmap and then Action Plan for the period of 2021 to 2030, anchored with 2015 as the baseline year, focusing predominantly on mitigation actions within the energy and transport sectors, with a target of 113 MtCO2eq emissions reductions by 2030 [2]. In 2021, during the 26th Conference of the Parties (COP) on Climate Change, Thailand displayed an unwavering commitment to advancing climate change solutions. Thailand’s aspirations encompassed achieving carbon neutrality by 2050, attaining net zero GHG emissions by 2065, and elevating its Nationally Determined Contribution (NDC) target to reduce GHG emissions by 30 to 40% by 2030, surpassing its previous aim of 20 to 25% from usual GHG emissions [3]. In addition to these endeavors, Thailand introduced the Long-term Low Greenhouse Gas Emission Development Strategy (LT-LEDS) as a guiding framework for its long-term national GHG mitigation efforts. This strategy provides clear objectives and guidelines for GHG reduction in the long run [4].

Beyond setting GHG mitigation targets, policies, roadmaps, and action plans for GHG mitigation guidelines, another crucial aspect to contemplate involves the decision-making process for selecting effective policies or measures capable of significantly curbing energy consumption, which affects GHG emissions. Policymakers require access to comprehensive mitigation technology-economic data to inform their deliberations. It’s widely realize that policy decision in the context of climate change rely on two key tools: the marginal abatement cost (MAC) and social cost of carbon (SCC). The MAC considers in terms of GHG mitigation by utilizing the marginal abatement cost results that provide basic data to prioritize low-carbon technologies or measures required to mitigate GHG emissions, usually measured in tonnes of carbon dioxide equivalent. On the other hand, SCC considers as the cost of damages inflicted by rising increments by tonnes of carbon dioxide equivalent that contribute to long term climate change impacts. The combined consideration of MAC and SCC reveals the optimal degree of GHG mitigation required for implementation. The results can serve as support for decision-making regarding technology investments or measures that influence GHG mitigation, along with shaping policies and other financial-economics guidelines. Additionally, both sectors have potentially support the consideration establishment of investment or pricing guidelines, such as carbon taxes or carbon credit trading, including international emission trading in the future to advocate effective policies for achieving GHG mitigation targets across short-term, medium-term, and long-term.

The organization of this paper comprises six sections: (i) introduction, (ii) the details on Thailand’s energy and climate policy and plan, (iii) presentation of materials and methods, (iv) analysis of research findings, (v) conclusion, and (vi) policy recommendations covering both policy and technology implementation. The details are as follows.

2. Thailand’s Energy and Climate Plan and Policy

Thailand has developed strategic, plans and policies relevance to energy and GHG to support all sectors of its economy, with a particular emphasis on the industrial and power sectors.

2.1. Energy Policy

The Ministry of Energy has established the Thailand Integrated Energy Blueprint (TIEB) [5], which constitutes the nation’s comprehensive long-term energy strategy. It comprises five subsidiary plans designed include: (i) the Power Development Plan (PDP), (ii) the Energy Efficiency Plan (EEP), (iii) the Alternative Energy Development Plan (AEDP), (iv) the Gas Plan, and (v) the Oil Plan. Notably, the key important energy plans and policies with relevance to GHG mitigation policies in Thailand are the PDP, EEP, and AEDP. The details of relevant plans can be described in Table 1.

2.2. Climate Policy

The climate policies and plan targeting energy and climate change issues, with a particular emphasis on the industrial and power sectors, that is Thailand’s National Determined Contributions (NDC) and the Net Zero GHG Roadmap. The details of relevant plans can be described in Table 2.

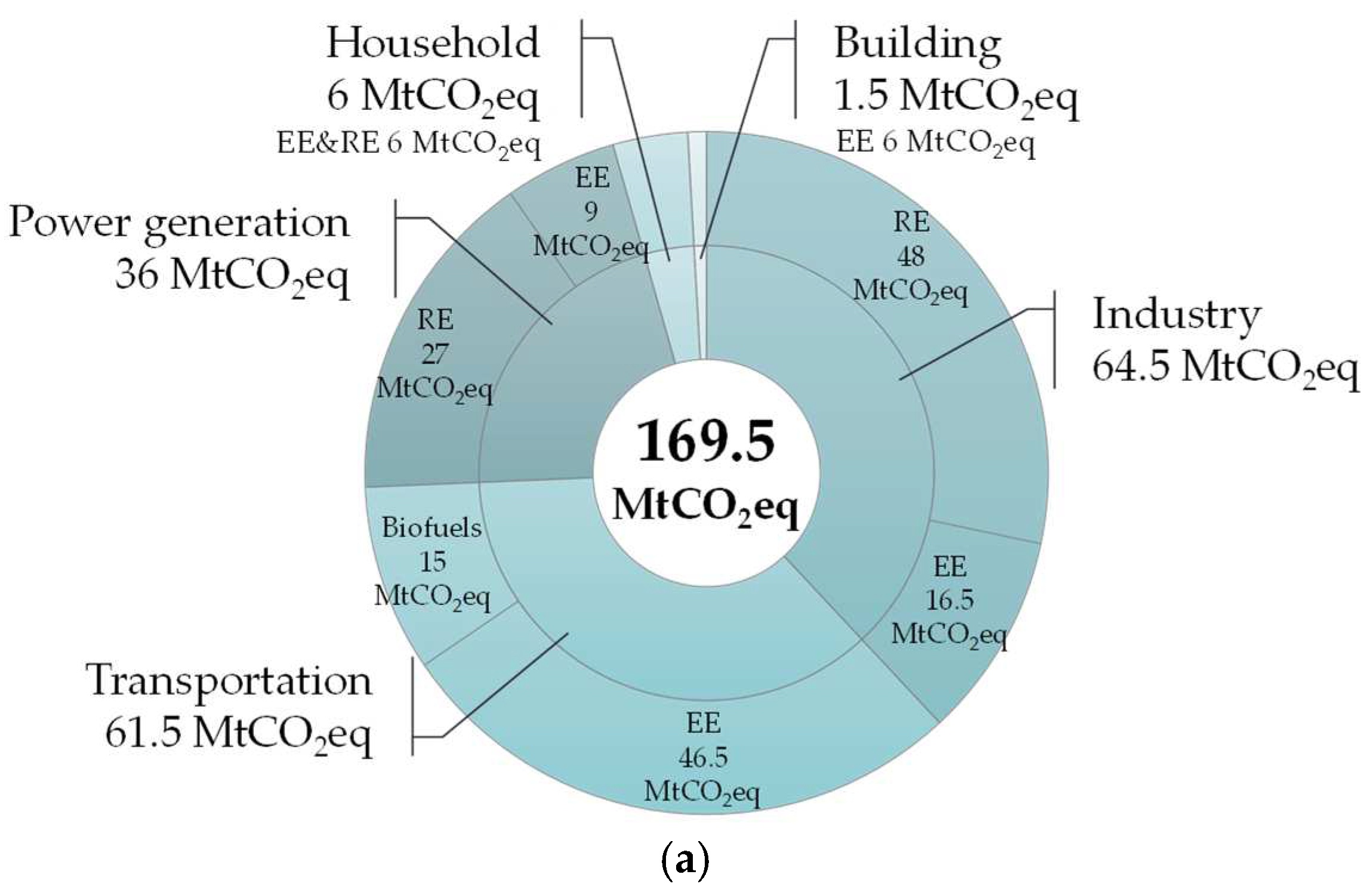

Figure 1.

Thailand at-a-glance: (a) GHG mitigation target in energy and transport sector; (b) GHG mitigation achievement 2013–2020.

Figure 1.

Thailand at-a-glance: (a) GHG mitigation target in energy and transport sector; (b) GHG mitigation achievement 2013–2020.

The studied related to energy and climate policy in Thailand industrial and power sectors such as the analysis energy demand in the Thailand manufacturing sector [11], energy reduction performance tracking from having Thailand’s eight-step Energy Management System (EnMS) in designated facilties [12], in addition to monitoring past energy consumption reductions that effect directly to GHG, the future energy and GHG emission forecasting is also analyzed by Wongkot.W. [13] using the Integrated model for augur from Thailand’s long-term low carbon energy efficiency and renewable energy plan in industrial and power sectors.

3. Materials and Methods

The conceptual framework of this research is divided into three sections, (i) MAC, (ii) SCC, and (iii) the optimal degrees of abatement. The details are as follows.

3.1. Model Framework

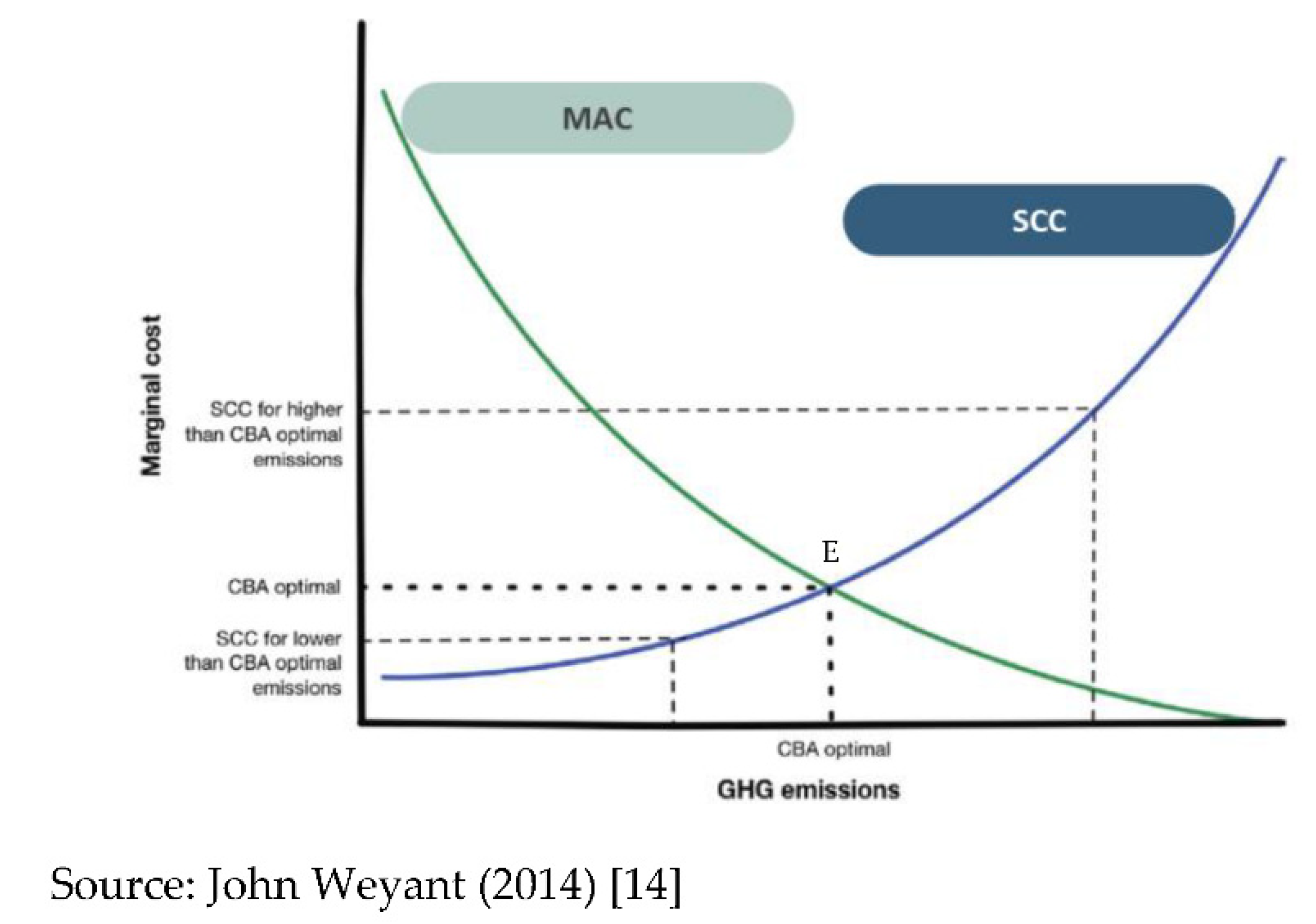

In the analysis of the optimal level of emission, economists will apply the concepts of marginal damage cost (MDC) and marginal abatement cost (MAC) according to the principle of the benefit-cost analysis (BCA). If there are a lot of GHG emissions, the MDC is high, but the MAC is low. On the other hand, if GHG emission is low, the MDC is low, but the MAC is high. The optimal GHG emissions level is point E, that is MAC equal to MDC. The conceptual overview of optimal carbon emissions can be expressed as Figure 2.

3.2. Marginal Abatement Cost

The marginal abatement cost is a crucial tool for evaluating the expenses, encompassing both investment and operation and maintenance (O&M) costs of energy projects or measures. This tool aids policymakers in making economically sound decisions for formulating national-level subsidization schemes and implementing projects. This significance arises because many developing countries face budgetary constraints when supporting climate mitigation projects, necessitating a prioritization balance between cost and emissions reduction goals. To achieve GHG reduction targets, it is imperative to prioritize measures by representing outcomes through MACC, utilizing financial and economic data [15,16,17]. These MACC illustrate the relative significance of measures in the relationship between GHG emission reduction and their associated costs or price, which means the marginal cost of reducing one additional unit of CO2 [18]. Furthermore, policymakers can utilize this prioritization of measures and policies to design and implement appropriate GHG reduction policies, guided by the MACC, which offer users insights into the dimensions or outcomes of MAC and GHG mitigation potential.

There are several studies related to MAC, those on energy efficiency and renewable energy technologies in multitudinous economic sectors and countries. For instance, study the MACC of low carbon technology in energy efficiency and renewable energy i.e., McKinsey&Company [19], Petra Wachter [20], J.F.T. de Souza et al. [21], Xiufeng Yue et al. [22], and Nadine Ibrahim et al. [23]. Calculated the MAC in energy efficiency technologies i.e., K. Promjiraprawat et al. [24], Juan Peng et al. [25], Jiakui Chen et al. [26], Xi Yang et al. [27], and Bei Gao et al. [28]. While He Xiao et al. [29], Govinda R. Timilsina et al. [30], Jan Abrell et al. [31], and Phitsinee Muangjai et al. [32,33] have assessed the MAC of renewable energy technologies. The equation for MAC is expressed as follow.

where: MAC represents the marginal abatement costs (THB/tCO2eq), CPS represents total cost of GHG mitigation technology in policy scenarios (THB/energy unit), CBS represents total cost of baseline technology (THB/energy unit), EPS represents the total amount of GHG in mitigation technology in policy scenarios (tCO2eq/unit), while EBS represents the amount of GHG emission in baseline technology or scenario (tCO2eq/unit).

where: ICPS and ICBS represent the investment cost of technology in policy and baseline scenario, respectively (THB), OMCPS and OMCBS represent the operation and maintenance cost of the technology in policy and baseline scenario, respectively (THB), FCPS and FCBS represent the fuel cost of the technology in policy and baseline scenario, respectively (THB), while A represents amount of energy which is MJ for heat generation, kWh for electricity generation. For the case of energy efficiency improvement, it refers to the amount of energy that can be conserved through the implementation of the new energy efficiency technology (kWh or MJ). The investment cost for heat generation includes the cost of waste-to-energy technology and heat generation while the cost of electricity generation encompasses building construction, land, machinery and equipment, engineering design with consultant and survey costs. The investment cost for increasing energy efficiency relates to the cost of technology (machines or equipment).

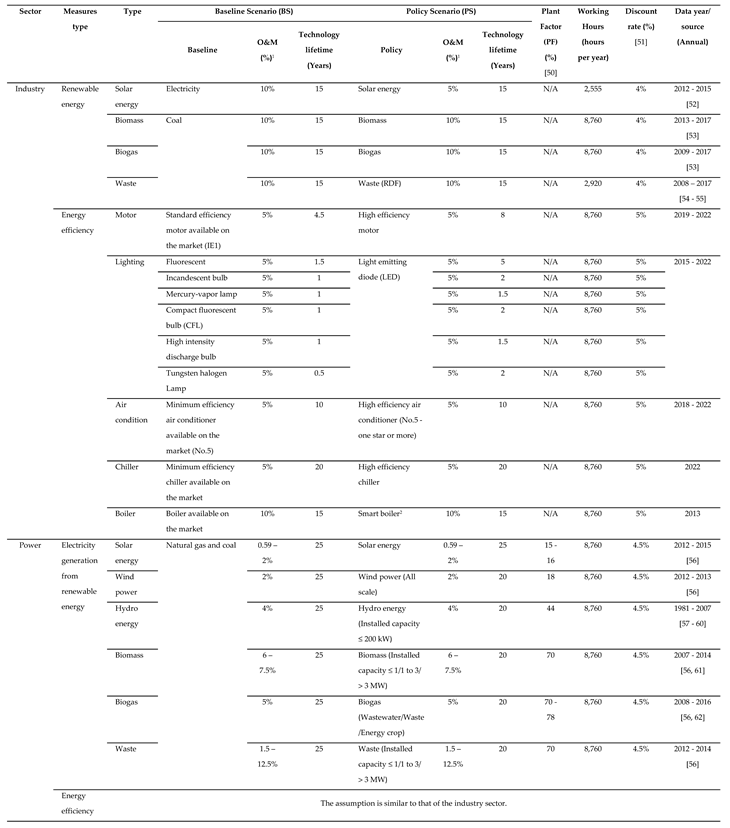

3.2.1. Economic Data and Key Assumptions

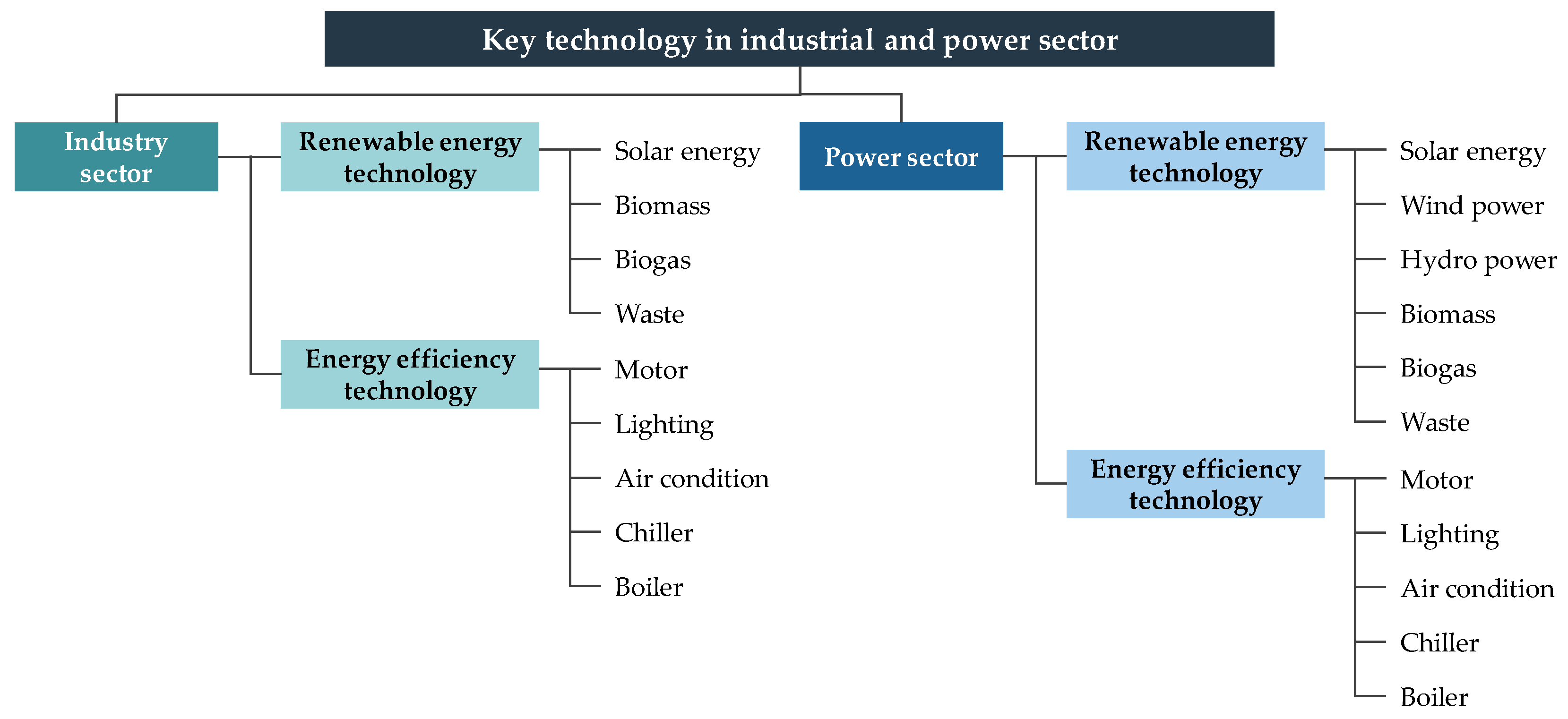

The data on the total cost were comprised of two components: the investment cost and the operation and maintenance (O&M) cost over the technology’s lifetime. The methodology for collecting cost data involved two main approaches: (i) conducting interviews and distributing questionnaires to persons with relevant data, and (ii) gathering pertinent information from public reports, websites, and research documents disseminated by government agencies and private sectors. The collected data solely pertains to the investment costs. Consequently, hypotheses were formulated regarding the percentage of the O&M cost and other related factors to estimate the overall costs over the technology’s lifetime. Detailed assumptions are provided in Appendix A. The total cost data were converted into monetary values and adjusted by using the reference NDC 2015 base year of Bank of Thailand’s Consumer Price Index (CPI) [34]. The key technology list can be express as Figure 3.

3.3. Social Cost of Carbon

The social cost of carbon is a tool for measuring the value of broad economic harm caused by climate change resulting from prolonged carbon dioxide emissions. The economic damage values stem from the release of GHG into the atmosphere and the subsequent alterations in GHG concentrations, leading to shifts in global average temperatures. Notably, the value of SCC escalates over time, as the persistence of GHGs contributes increasing to the atmosphere, causing more damage to increase. This assessment considers the cost per unit of carbon dioxide emissions or its equivalent (if other GHGs are covertly considered). It provides policymakers with insights into the economic impact of their decisions when crafting GHG reduction policies or action plans. Typically, the valuation of SCC is widely reflected in carbon price, such as carbon taxes, emissions trading. The SCC equation is presented as Equation (4) [35].

where: SCC represents the social cost of carbon (USD/tCO2eq), S* represents the stock of CO2 in the atmosphere (tCO2eq), D’(S*) represents the flow of marginal damages at each point in time, r represents a discount rate (%), and “φ” represents the decay rate of the stock of CO2 in the atmosphere (%).

Richard B. Howarth et al. [36], J.C.J.M. van den Bergh et al. [37], and Pu Yang et al. [38], have conducted reviews of the SCC and estimated it using various models. Additionally, Mojtaba Khastar et al. [39] and Krishna Teja Malladi et al. [40] have scrutinized the implications of SCC to emission reduction and other related issues. In this study, SCC values derived from prior research were employed, with consideration given to adapting the data to align with the nation’s climate change policy and plan. This research revealed significant variability in SCC values, stemming from estimations based on different discount rates, that is commonly used discount rates include 5%, 3%, and 2.5%.

3.4. Optimal Degrees of Abatement

The optimal level of abatement when implementing a GHG reduction policy in Thailand requires consideration of two key facets: MAC and SCC. Additionally, it necessitates thoughtful deliberation regarding the GHG emission targets.

The aim of the study regarding GHG emission target assess and project GHG emissions in the industrial and power sectors, encompassing emissions under business-as-usual (BAU) and net zero targets leading to emission mitigation targets projection from 2020 to 2050. The GHG emissions forecast for Thailand under the BAU scenario from 2020 to 2050 in this study was based on historical GHG emissions data from 2000 to 2018, sourced from the Office of Natural Resources and Environmental Policy and Planning [41,42,43,44] and comprises of four distinct scenarios as outlined below.

Table 3.

Scenario and assumption in this study.

| Scenario | Details (covering from 2020 to 2050) |

|---|---|

| 1 | Forecasts the forthcoming GHG emissions, within 2030 at 555 MtCO2eq in accordance with existing national assumption [45]. |

| 2 | GHG emissions were projected based on the 2.37% annual average growth rate (AAGR) from the year 2000 to 2018. |

| 3 | Using time series regression methodologies with data spanning from 2000 to 2018 for GHG forecast. This approach yielded a forecast of future GHG emissions, reflecting an AAGR of 1.32%. |

| 4 | Future GHG emissions were forecasted by establishing a growth rate in 2019 of 1.11% per year, derived from the AAGR between 2013 to 2018, which aligns with the NAMA’s AAGR. This growth rate was then plus by an incremental annual growth rate following the same trend as the growth rate in Scenario 3. |

Figure 4.

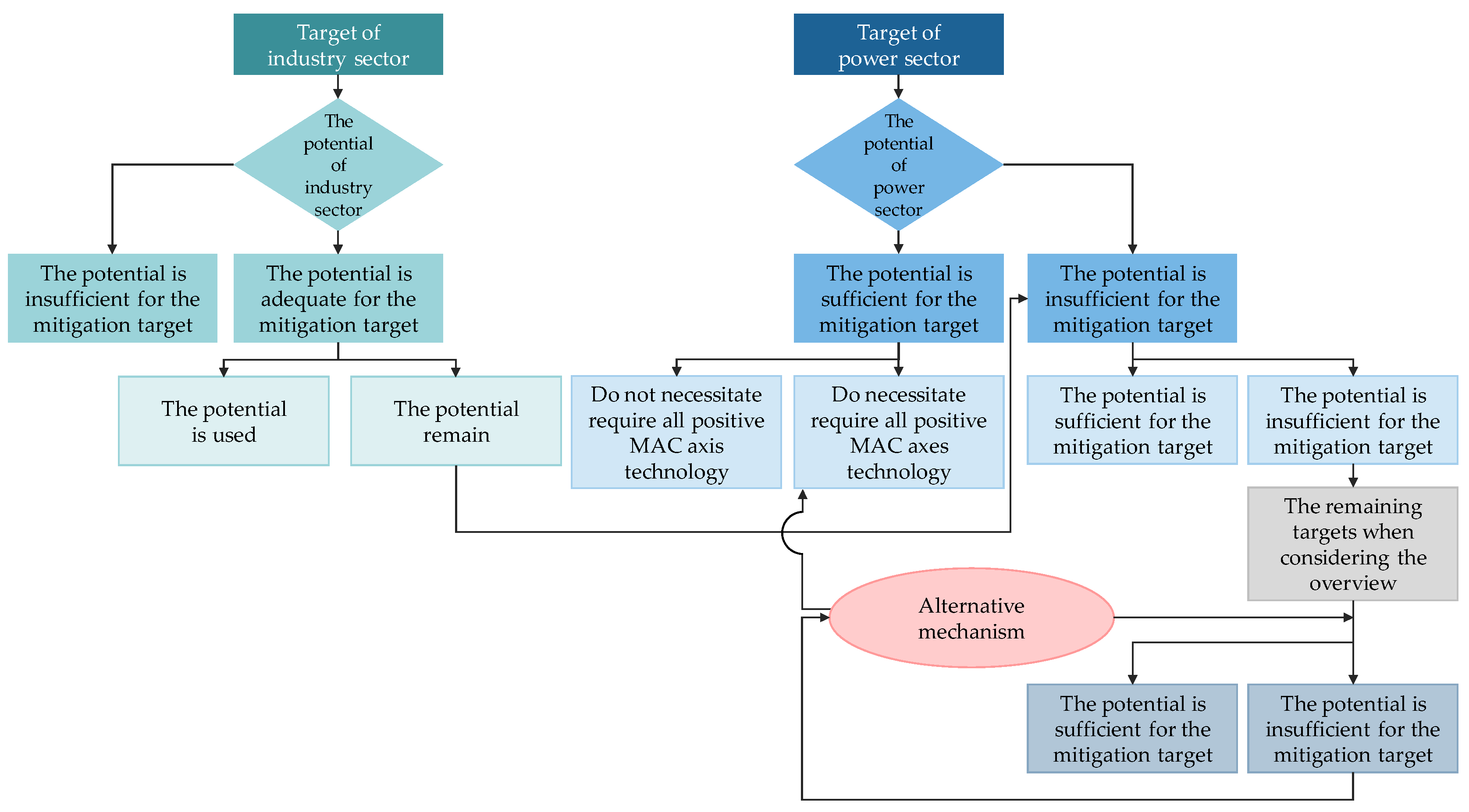

Decision tree for analyzing the optimal level of abatement.

4. Results

4.1. Marginal Abatement Cost and Mitigation Potential

The MAC and mitigation potential assessments results of energy efficiency improvement and renewable energy technologies within the power and industrial sector. The results are elucidated as follows.

4.1.1. Industry Sector

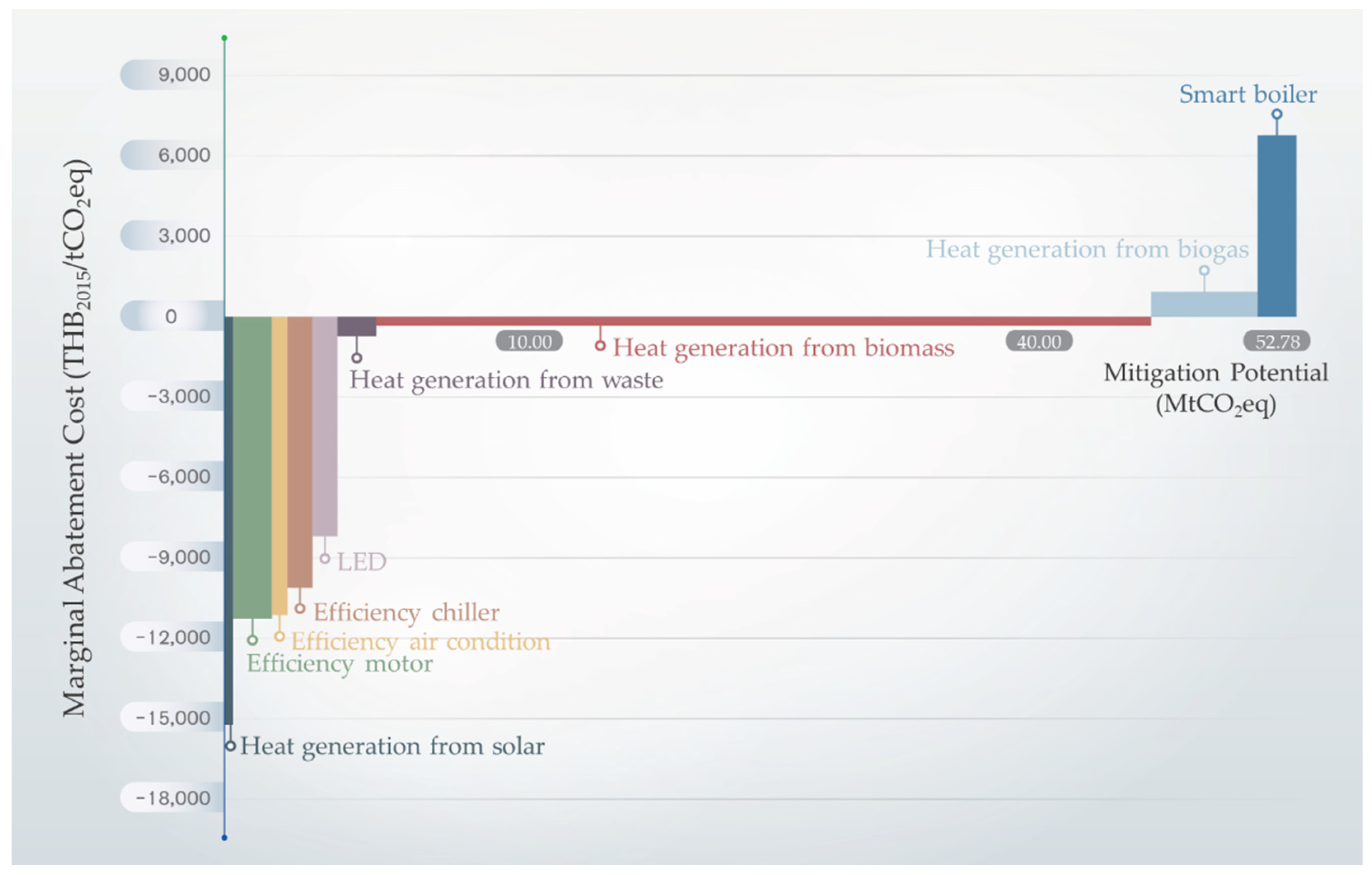

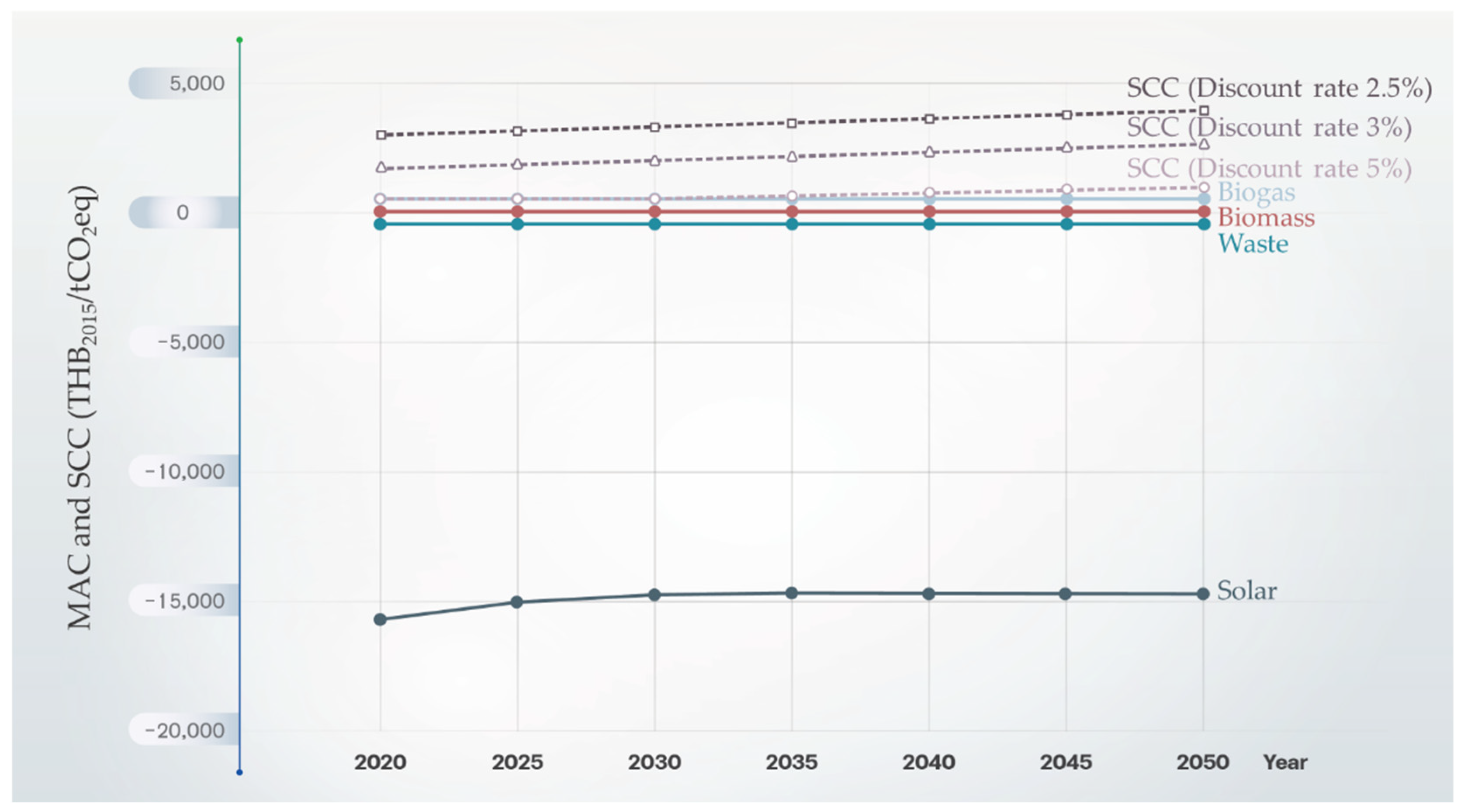

For the industrial sector, the MAC results encompassing heat generation from renewable energy and energy efficiency improvement technologies in electricity and thermal energy, spanning from 2020 to 2050, are presented in Table 4. The MACC for solar energy is positioned on the negative axis, indicating that the MAC for heat generation from solar technologies is lower than from electricity. Biomass and waste technologies also fall within the negative axis, signifying that in terms of heat generation cost, biomass and waste are more cost-effective options compared to coal. In the context of GHG mitigation, this implies that biomass and waste to heat energy generation technology investment would entail minimal or no incremental costs for these technologies. This suggests that the utilization of bio-based renewable energy, particularly biomass, holds significant potential for reducing GHG emissions. However, in the case of heat generation from biogas, the MAC indicates a positive value, meaning the MAC from using biogas is high compared to coal. The mitigation potential for heat generation from renewable energy technologies tends to increase by an average of 4.69% from the year 2020 to 2050. Heat generation from biogas technologies contributes to GHG mitigation progress but is associated with a higher MAC, implying that substantial investment would be necessary to implement these GHG mitigation measures. Nevertheless, if policymakers believe in the high efficiency of this technology, the investment might be justified.

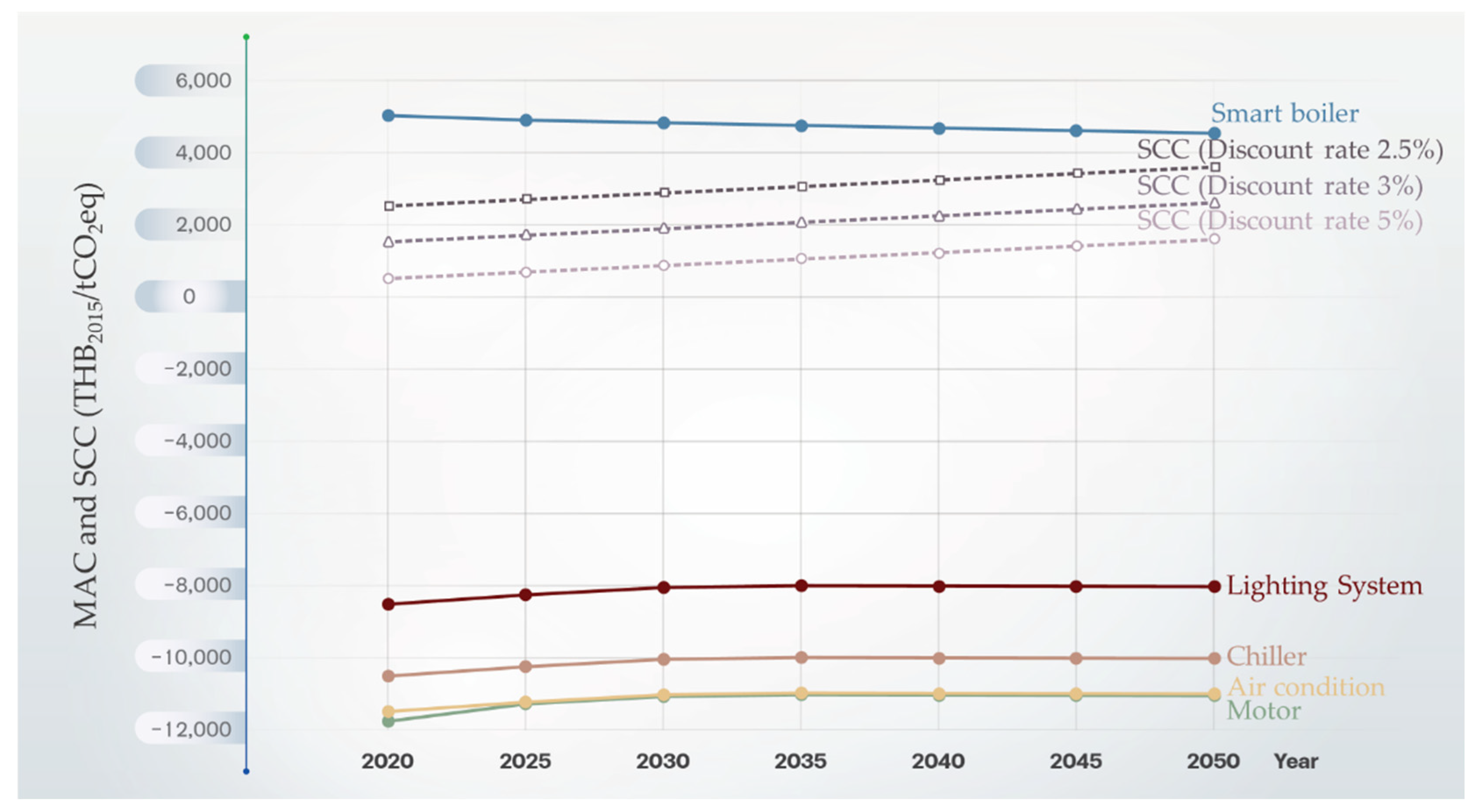

Furthermore, high efficiency technologies in electricity exhibit a MAC positioned on the negative axis, implying that high efficiency measures/technologies incur lower costs compared to the base cases. This suggests that industries could implement these technologies on their own, with limited support or intervention from public agencies. On average, the GHG mitigation potential tends to increase by 6.01%. However, it’s worth noting that the MAC for utilizing a smart boiler system instead of a standard boiler is in positive value due to its high initial cost. Nevertheless, this technology still leads to a GHG mitigation potential increase averaging 5.87%.

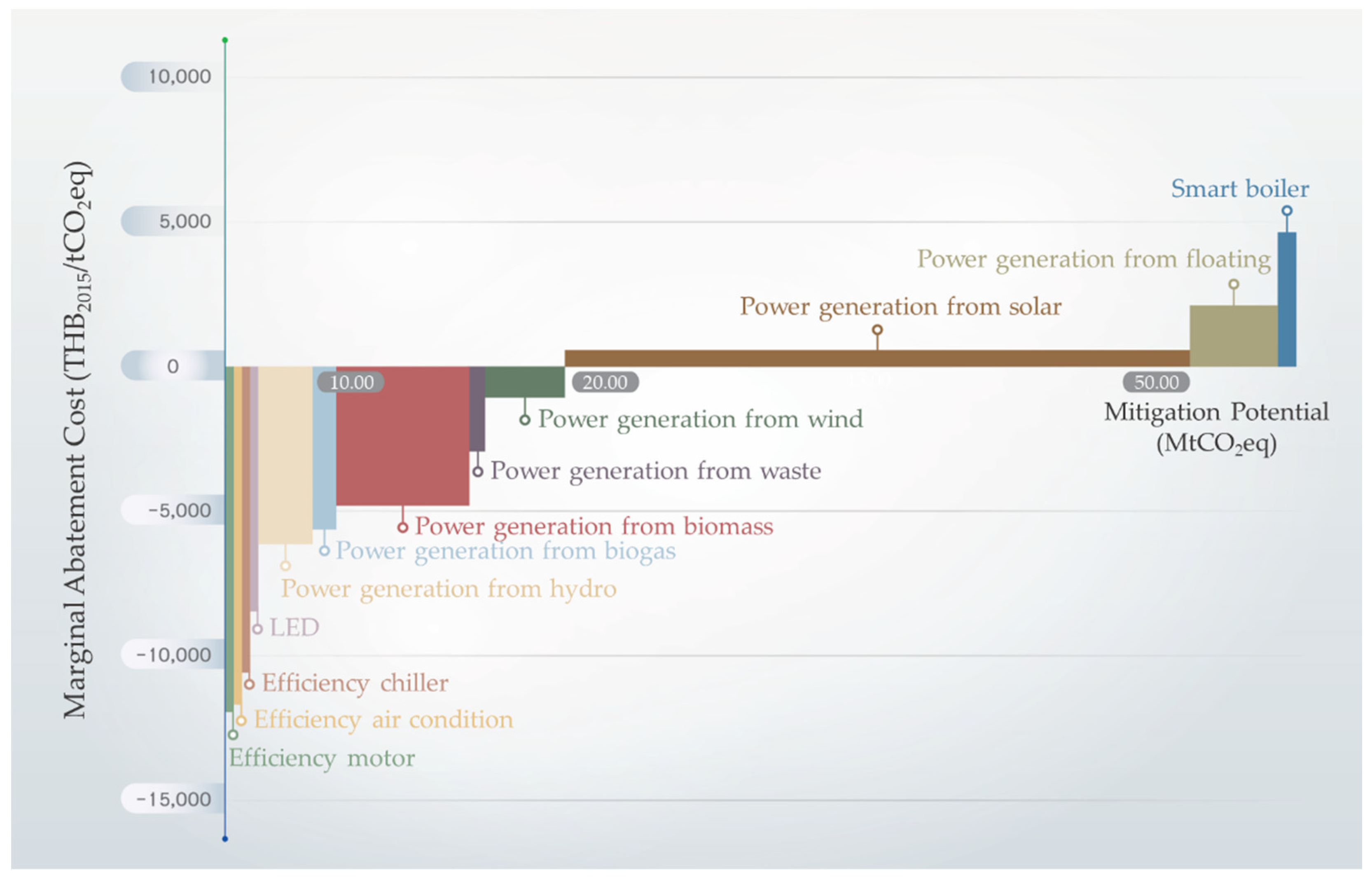

Figure 5.

Marginal abatement cost curve of GHG technology in industry sector in 2030.

4.1.2. Power Sector

Regarding the power sector, the technologies under consideration are electricity generation from renewable sources and high efficiency technologies in electricity and heat. The MAC results from 2020 to 2050 are presented in Table 5. The MAC values of hydro energy, biomass, biogas, and waste are negative, indicating that their costs are lower compared to the base case. However, solar energy and solar floating technologies exhibit positive MAC values, which later turn negative as time progresses due to technological advancements and market mechanisms. In contrast, technologies i.e., smart boilers, CCS, and BECCS maintain consistently positive and relatively high MAC values. Hence, if public agencies or stakeholders anticipate the implementation of technologies with positive MAC values before self-transition, it is crucial to utilize SCC to establish and consider appropriate mechanisms The MAC for electricity generation from renewable energy can vary significantly, influenced by factors such as plant factors, electricity generation costs, technology, geographical location, and scale (economies of scale). On average, the GHG mitigation potential from electricity generation using renewable energy sources between 2020 to 2050 is trending to increase by 8.91%.

The MAC for high efficiency technologies in electricity and heat within the power sector similar to the industrial sector. However, the GHG mitigation potential from increasing energy consumption efficiency of these technologies differs from the industrial sector where the GHG mitigation potential of high efficiency technologies in electricity and heat tends to increase by 5.93% and 6.08% on average, respectively.

Figure 6.

Marginal abatement cost curve of GHG technology in power sector in 2030.

4.2. Social Cost of Carbon

In this study, we applied SCC values from previous research, and considered using this data to suit the nation’s climate change policy and plan. Most research studies related to SCC relied on Integrated Assessment Models (IAMs), with commonly used models including DICE, PAGE, and FUND. Upon the gathered SCC values, it became evident that these values varied significantly and exhibited great diversity. This variation in values can be explained by different discount rates, with rates being 5%, 3%, and 2.5%, respectively. Discount rates play a crucial role in SCC estimation as they enable the conversion of estimates of future climate change damages into present values. They also reflect the importance of present and future consequences. The assumptions of difference in the discount rate, with high discount rates having a low significant effect on future consequences compared to the present, while low discount rates determine the future effect will closely resemble the current one [47]. Because the damages from GHG emissions have global repercussions rather than being limited to a specific area or country, it is essential to select a global SCC for Thailand in this study. The SCC values employed in this study were sourced from the Interagency Working Group on the Social Cost of Greenhouse Gases [48]. These values were initially estimated in USD in the year 2007 but were adjusted the inflated to 2017 USD values. Subsequently, these values were converted from USD to THB based on the average exchange rate provided by the Bank of Thailand [49] in 2017, which was 33.94 THB/USD. These values were adjusted with time at the base year of 2015 where the headline Consumer Price Index from the Bank of Thailand was applied as a reference for these adjustments [34]. The SCC values in THB/tCO2eq units from 2020 to 2050 are detailed in Table 6. It is important to note that these values tend to increase over time as GHG emissions accumulate continuously. Consequently, as time progresses, the anticipated damages from climate change are expected to grow larger in the future.

4.3. Optimal Degrees of Greenhouse Gas Mitigation

The results of optimal degrees of GHG mitigation consist of two sections, (i) GHG emission mitigation target and (ii) optimal degrees of abatement. The details are as follows.

4.3.1. Emission Mitigation Target

The estimation of GHG emission mitigation targets for the industry and power sectors from 2020 to 2050 is calculated from the differences between the forecasted GHG emissions in a business-as-usual scenario and a net zero emission scenario within each sector. The average growth rates for emission mitigation targets in each sector can be summarized as follows: In Scenario 1, the power sector has a 3.38% growth rate, while the industry sector has a 3.07% growth rate. In Scenario 2, the power sector has a 3.46% growth rate, with the industry sector having a 3.12% growth rate. In Scenario 3, the power sector has a 3.55% growth rate, whereas the industry sector has a 2.97% growth rate. Lastly, in Scenario 4, the power sector has a 3.86% growth rate, and the industry sector has a 2.21% growth rate. The GHG mitigation target could be estimated as shown in Table 7.

4.3.2. Optimal Degrees of Abatement

The results concerning the GHG mitigation targets and potentials for each scenario within both the power and industrial sectors, including a comparison of the mitigation targets and potentials under implemented technologies or policies, can be shown in Table 7. In Scenario 1, the GHG mitigation potential of the power sector from 2020 to 2025 can be achieved for the target. However, from 2030 to 2045, the GHG mitigation potential will be lower than the target, but in 2050 it is sufficient for the target. For the industrial sector, the GHG mitigation potential remains sufficient for 2020 to 2050 target. Based on the analysis of both sectors in Scenario 1, it appears that the GHG mitigation potential is adequate for the mitigation target. In Scenario 2, it becomes evident that the mitigation potential of both the power and industrial sectors is sufficient for the mitigation target every year. In the overview of the two sectors, the GHG mitigation potential is sufficient with the mitigation target. In Scenario 3, the GHG mitigation potential of both the power and industrial sectors remains sufficient for the mitigation target. Finally, in Scenario 4, the GHG mitigation potential of the two sectors is sufficient for the mitigation target. When examining the results from all scenarios in both sectors, the analysis yields two cases:

- Case 1: GHG mitigation potential surpasses or is sufficient to meet the GHG mitigation target. In this situation, the prioritization of GHG mitigation can arrange technologies can applied based on MACC. Consequently, there is no need to utilize all technologies or fully their potential to achieve GHG mitigation.

- Case 2: GHG mitigation potential below the mitigation target. In this situation, GHG mitigation efforts must encompass the utilization of all available technologies. Additionally, it becomes necessary to introduce supplementary technologies or measures, accompanied by the consideration of setting alternative mechanisms in various forms, including the utilization of SCC in decision making processes aimed at attaining the mitigation target.

If the GHG mitigation potential is insufficient for the mitigation target, as observed in Scenario 1 (2030 to 2045) for the power sector, the utilization of all technologies in the MACC becomes necessary. Furthermore, the implementation of additional technologies or measures is required to achieve the GHG mitigation target. Additionally, it’s essential to consider other mechanisms in various forms using SCC for adopting the specific policy, such as emissions trading systems or carbon taxes to drive investment decisions in GHG mitigation technologies in alignment with the MACC.

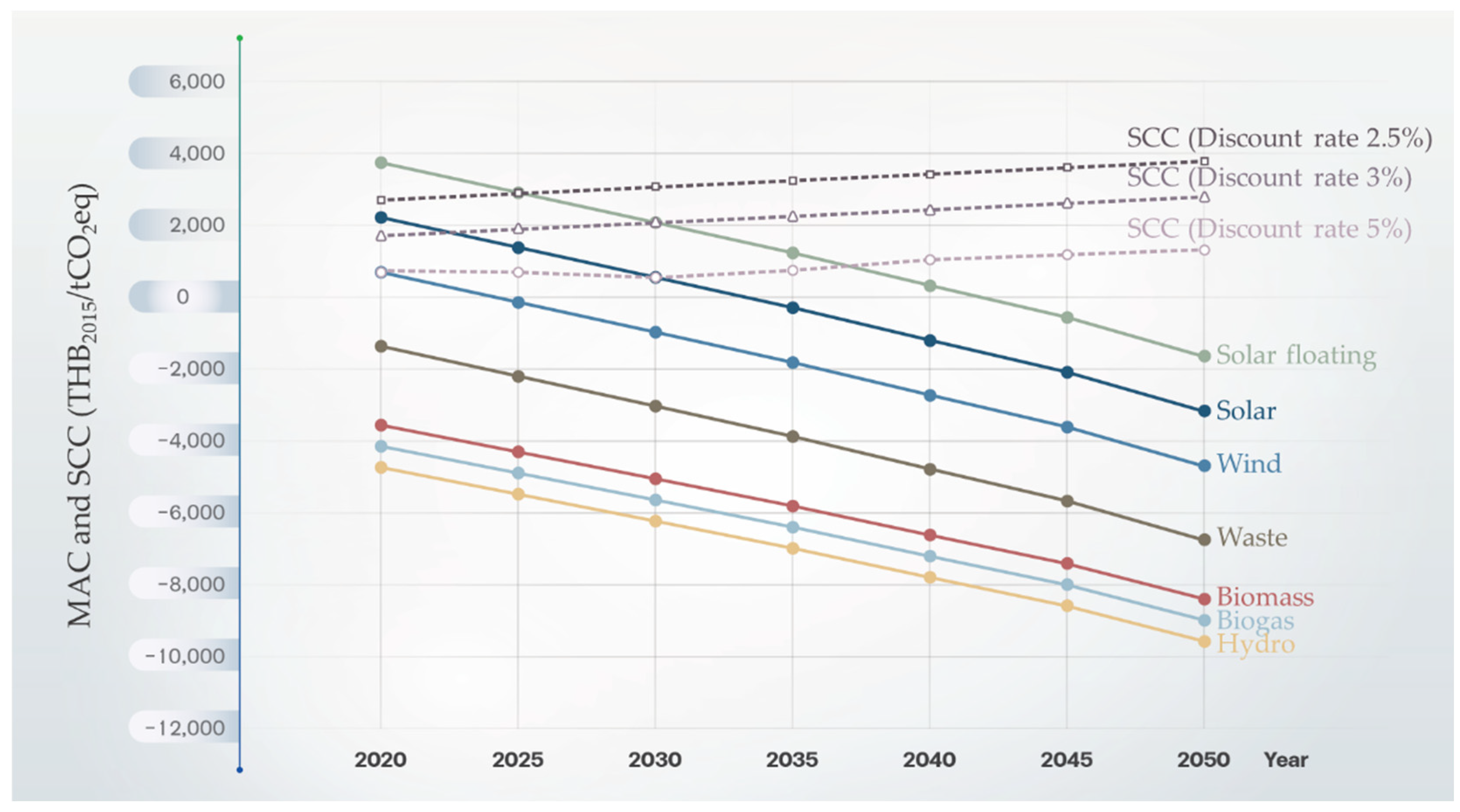

Figure 7, Figure 8 and Figure 9 illustrate the optimal degrees of abatement technology deployment in the power sector. It is evident that in 2030, certain technologies exhibit positive MAC values, including electricity generation from solar PV and farm, solar floating, and smart boiler. Between 2035 to 2040, electricity generation from solar floating and smart boiler maintained positive MAC values, while in 2045, smart boiler, CCS, and BECCS also had positive MAC values. In the power sector, the MAC values of some technologies initially in the positive range gradually transition to negative values over time due to technological advancements and market mechanisms. For example, wind power follows this trend, except for smart boilers, CCS, and BECCS, which remain on the positive axis due to their higher costs. If policymakers intend to implement these technologies before they reach break-even through market mechanisms, they should also take SCC into account as a crucial factor.

For electricity generation from solar energy, the point at which the investment breaks even with the cost of climate change damage occurs in 2023. This signifies that delaying investment beyond this year would result in more severe climate change-related damage. It should be value set an appropriate SCC at approximately 1,882 THB2015/tCO2eq (3% discount rate). Regarding electricity generation from solar floating, the optimal time for implementation is around 2025, at which point the SCC value should be set at approximately 2,806 THB2015/tCO2eq (2.5% discount rate).

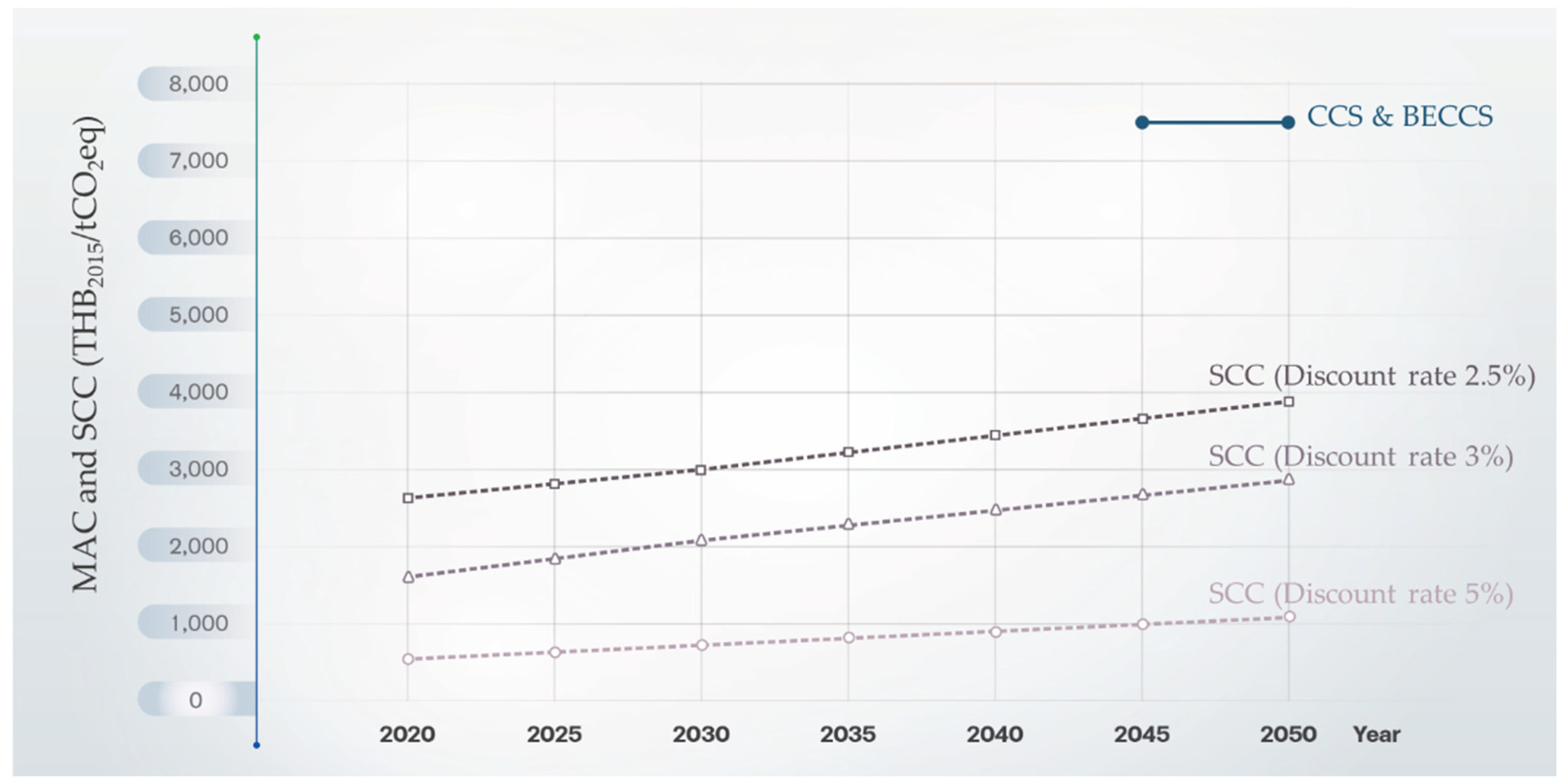

When considering smart boilers, CCS, and BECCS, the SCC should surpass the MAC value for all three technologies, with an approximate value of 5,000 THB2015/tCO2eq for smart boilers and 7,500 THB2015/tCO2eq for CCS and BECCS. Alternatively, supplementary mechanisms may be required apart from SCC, tailored to specific sectors or subsectors.

While the SCC mechanism has been effective in driving investment in certain GHG reducing technologies to meet the country’s emissions targets, the power sector still faces challenges in reducing GHG emissions. To address this, the power sector needs to take further actions, such as transitioning from fossil fuel power generation to natural gas or renewable energy sources as soon as possible. Additionally, there’s a need for grid-flexible power generation and an increased focus on generating electricity from renewable sources beyond the country’s current plan. Alternatively, if the energy type for electricity generation remains unchanged, implementing CCS and BECCS, despite their high investment costs, becomes necessary to achieve the national emissions targets. This might also include considering the adoption of hydrogen technology after 2030.

In contrast, the industrial sector has sufficient GHG mitigation potential to meet its targets, and some technologies may not need to be fully implemented as initially estimated. However, in certain power sector scenarios, the GHG mitigation potential is insufficient for the target. To compensate for this, industrial sector technologies not originally chosen can be considered, particularly those in the positive axis of the MACC, such as heat generation from biogas and smart boilers, which represent around 7.81% and 2.58% of all implementable technologies in the industrial sector. These could help compensate for the missing ones in the power sector.

Figure 10 depicts the optimal degrees of renewable energy technology in the industrial sector, while energy efficiency technology, including CCS and BECCS, can be seen in Figure 8 and Figure 9. Likewise with the power sector, if the industrial sector intends to implement technologies from the positive axis of the MACC, SCC should be taken into account. For instance, the optimal degrees of abatement for heat generation from biogas technology are projected to occur around 2027, with an SCC value set at approximately 650 THB2015/tCO2eq (5% discount rate). However, the initiation implementation of smart boiler technologies would require an SCC higher than the MAC of smart boilers, around 5,000 THB2015/tCO2eq, and approximately 7,500 THB2015/tCO2eq for CCS and BECCS or use alternative mechanisms beyond SCC for specific sectors or subsectors.

5. Conclusions

Despite employing the SCC mechanism to incentivize investments in potential technologies capable of GHG reduction to meet national mitigation targets, the power sector still grapples with challenges in curbing and mitigating GHG emissions. Further addressing this issue necessitates a transition to grid-flexible power generation and an intensified focus on generating electricity from renewable sources more than the current country’s national plan has specified. Alternatively, if the electricity generation remains unchanged, the installation of CCS and BECCS becomes imperative, despite their substantial initial investment costs, such measures are essential to achieve the country’s mitigation targets and may even involve the operating of hydrogen technology post-2030.

The industrial sector has sufficient GHG mitigation potential to meet its target. However, in scenario 1 of the power sector, there are some years with GHG mitigation potential below the target. To compensate for this deficit and ensure the country’s overall target is met, additional measures are necessary for implementation from the industry sector. This entails considering the SCC mechanism to incentivize investments in the required technologies or implementing other energy-in-transition technologies which are CCS, BE-CCS, and hydrogen.

6. Policy Recommendation

6.1. Policy and Plan

-

The restructuring of ministerial administrative agencies associated with climate change under ONEP.

- Short-term: Monitoring and control agencies should be encouraged to expand structures from division based to department based while remaining under the MONRE. Additionally, it is essential to grant legal authority to these departments, enabling them to access relevant data from other relevant agencies.

- Long-term: The Department of Climate Change and Environment (DCCE) should consider transfer to be under The Prime Minister’s Office for GHG data access from multi-agencies, as well as for agility of the implementation.

- Disseminate knowledge among agencies to align ministerial policies and plans with national climate change policies and strategies, ensuring that agencies not only prioritize cost-effectiveness but also comprehend and emphasize investment considerations.

- Resetting the new target in industry and power sectors to balance between the mitigation target and potential.

- The fundamental mandatory driving for GHG mitigation could be established through the enactment of a climate change act, specifying sector-specific targets, with a particular emphasis on the industry and power sectors, which is the sector was high emissions and mitigation potential.

6.2. Technology and Implementation

- Setting additional financial support mechanisms, e.g., carbon tax collection or carbon credit for important technologies such as smart boilers, CCS, and hydrogen.

- Update MAC and SCC data frequently, and Thailand should estimate her own SCC for more precise evaluation.

- Technology selection should be based on MAC, focusing on mitigation potential and urgency to drive the country towards carbon neutrality and net zero GHG emissions.

Supplementary Materials

The following supporting information can be downloaded at the website of this paper posted on Preprints.org, Figure S1: Marginal abatement cost curve of GHG technology in industry sector in 2020; Figure S2: Marginal abatement cost curve of GHG technology in industry sector in 2025; Figure S3: Marginal abatement cost curve of GHG technology in industry sector in 2030; Figure S4: Marginal abatement cost curve of GHG technology in industry sector in 2035; Figure S5: Marginal abatement cost curve of GHG technology in industry sector in 2040; Figure S6: Marginal abatement cost curve of GHG technology in industry sector in 2045; Figure S7: Marginal abatement cost curve of GHG technology in industry sector in 2050; Figure S8: Marginal abatement cost curve of GHG technology in power sector in 2020; Figure S9: Marginal abatement cost curve of GHG technology in power sector in 2025; Figure S10: Marginal abatement cost curve of GHG technology in power sector in 2030; Figure S11: Marginal abatement cost curve of GHG technology in power sector in 2035; Figure S12: Marginal abatement cost curve of GHG technology in power sector in 2040; Figure S13: Marginal abatement cost curve of GHG technology in power sector in 2045; Figure S14: Marginal abatement cost curve of GHG technology in power sector in 2050.

Author Contributions

Conceptualization, P.M. and W.W.; methodology, P.M. and W.W.; software, P.M.; validation, P.M., W.W., T.J. and C.R.; formal analysis, P.M.; investigation, P.M.; resources, P.M., S.D. and W.T.; data curation, P.M.; writing—original draft preparation, P.M.; writing—review and editing, P.M. and W.W.; visualization, P.M.; supervision, W.W; project administration, P.M. All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

The data used to support the findings of this study are included within the article.

Acknowledgments

The authors would like to thank all relevant agencies for information. We remain culpable for any remaining errors. This research work was partially supported by Chiang Mai University.

Conflicts of Interest

The authors declare no conflict of interest.

Appendix A

Table A1.

The relevant assumptions.

|

1 Operation and maintenance cost was estimated as a percentage of investment cost. 2 Smart boiler in this study, also known as, central heating boiler with smart controls and smart heating controls, to give factory precisely control over the boiler operation, e.g., temperature, pressure, and mass flow rate of the steam.

References

- The Office of Natural Resources and Environmental Policy and Planning (ONEP), Ministry of Natural Resources and Environment. Thailand fourth National Communication (NC4); Publisher: Thailand, 2022.

- The Office of Natural Resources and Environmental Policy and Planning (ONEP), Ministry of Natural Resources and Environment. Thailand’s Nationally Determined Contribution Roadmap on Mitigation (NDC Roadmap); Publisher: Thailand, 2017.

- Thailand Greenhouse Gas Management Organization (Public Organization) (TGO). Available online: https://shorturl.asia/wFBfT (2 December 2022).

- The Office of Natural Resources and Environmental Policy and Planning (ONEP), Ministry of Natural Resources and Environment, Thailand’s Long-term Low Greenhouse Gas Emission Development Strategy. Available online: chrome-extension://efaidnbmnnnibpcajpcglclefindmkaj/https://unfccc.int/sites/default/files/resource/Thailand%20LT-LEDS%20%28Revised%20Versi on%29_08Nov2022.pdf (30 September 2022).

- Energy Policy and Planning Office (EPPO), Ministry of Energy, Thailand Integrated Energy Blueprint (TIEB). Available online: https://www.eppo.go.th/index.php/en/component/k2/item/11449-faq1 (30 September 2022).

- Energy Policy and Planning Office (EPPO), Ministry of Energy. Power Development Plan 2018-2037 (PDP2018), 2020.

- Department of Alternative Energy Development and Efficiency (DEDE), Ministry of Energy. Energy Efficiency Plan 2018-2037 (EEP2018), 2020.

- Department of Alternative Energy Development and Efficiency (DEDE), Ministry of Energy. Alternative Energy Development Plan 2018-2037 (AEDP2018), 2020.

- Department of National Park Wildlife and Plant Conservation, Paris Agreement. Available online: http://reddplus.dnp.go.th/?p=2239 (29 October 2020).

- Thailand Greenhouse Gas Management Organization (Public Organization) (TGO). Nationally Appropriate Mitigation Action (NAMA), 2015.

- Songwut, P.; Wongkot W. The demand for energy in the manufacturing sector of Thailand. The technology and innovation for sustainable development conference, Khon Kaen, Thailand, 2008.

- Wongkot, W. Performance Tracking of Thailand’s Energy Management System under Energy Conservation Promotion Act. Energy Procedia 2016, 100, 448-451.

- Wongkot, W.; Chaichan, R.; Jakapong P. Integrated model for energy and CO2 emissions analysis from Thailand’s long-term low carbon energy efficiency and renewable energy plan. Energy Procedia 2016, 100, 492-495.

- John, W. Integrated assessment of climate change: state of the literature. Journal of Benefit Cost Analysis 2014, 5(3), 377-409. [CrossRef]

- Moran, D.; et al. UK marginal abatement cost curves for the agriculture and land use, land-use change and forestry sectors out to 2022, with qualitative analysis of options to 2050; Publisher: Scottish Agricultural College Commercial, Edinburgh, 2008.

- Jose, L. P.-T.; Andrea, V. P.-H.; Alejandro, S.-B. The problem of ranking CO2 abatement measures: A methodological proposal. Sustainable Cities and Society 2016, 26, 306-317.

- Isacs, L.; Finnveden, G.; Dahllöf, L.; Hakansson, C.; Petersson, L.; et al. Choosing a monetary value of greenhouse gases in assessment tools. Journal of Cleaner Production 2016, 127, 37-48. [CrossRef]

- Fei, T.; Xin, W.; Xunzhang, P.; Xi, Y. Understanding marginal abatement cost curves in energy-intensive industries in China: insights from comparison of different models. Energy Procedia 2014, 318-322. [CrossRef]

- McKinsey&Company. Pathways to a low carbon economy version 2 of the global greenhouse gas abatement cost curve, 2007.

- Petra, W. The Usefulness of Marginal CO2-e Abatement Cost Curves in Austria. Energy Policy 2013, 61, 1116-1126. [CrossRef]

- J.F.T., de S.; B.P., de O.; J.T.V., F.; S.A., P. Industrial low carbon futures: A regional marginal abatement cost curve for Sao Paulo, Brazil. Journal of Cleaner Production 2018, 200, 680-686. [CrossRef]

- Xiufeng, Y.; et al. Identifying decarbonisation opportunities using marginal abatement cost curves and energy system scenario ensembles. Applied Energy 2020, 276, 115456. [CrossRef]

- Nadine, I.; Christopher, K. A Methodology for Constructing Marginal Abatement Cost Curves for Climate Action in Cities. Energies 2016, 9, 227. [CrossRef]

- Kamphol, P.; Pornphimol, W.; Bundit, L.; Toshihiko, M.; Tatsuya, H.; Yuzuru, M. CO2 mitigation potential and marginal abatement costs in Thai residential and building sectors. Energy and Buildings 2014, 80, 631-639. [CrossRef]

- Juan, P.; Bi-Ying, Y.; Hua, L.; Yi-Ming, W. Marginal abatement costs of CO2 emissions in the thermal power sector: A regional empirical analysis from China. Journal of Cleaner Production 2018, 171, 163-174.

- Jiakui, C.; Dong, X. Carbon efficiency and carbon abatement costs of coal-fired power enterprises: A case of Shanghai, China. Journal of Cleaner Production 2019, 206, 452-459. [CrossRef]

- Xi, Y.; Xiaoqian, X.; Shan, G.; Wanqi, L.; Xiangzhao, F. Carbon Mitigation Pathway Evaluation and Environmental Benefit Analysis of Mitigation Technologies in China’s Petrochemical and Chemical Industry. Energies 2018, 11, 3331. [CrossRef]

- Bei, G.; Zuoren, S. Marginal CO2 and SO2 Abatement Costs and Determinants of Coal-Fired Power Plants in China: Considering a Two-Stage Production System with Different Emission Reduction Approaches. Energies 2023, 16, 3488. [CrossRef]

- He, X.; Qingpeng, W.; Hailin, W. Marginal abatement cost and carbon reduction potential outlook of key energy efficiency technologies in China’s building sector to 2030. Energy Policy 2014, 69, 92-105. [CrossRef]

- Govinda, R. T.; Anna, S.; Eduard, K.; Suren, S. Development of marginal abatement cost curves for the building sector in Armenia and Georgia. Energy Policy 2017, 108, 29-43. [CrossRef]

- Jan, A.; Mirjam, K.; Sebastian, R. Carbon abatement with renewable: Evaluating wind and solar subsidies in Germany and Spain. Journal of Public Economics 2019, 169, 172-202. [CrossRef]

- Phitsinee, M.; Wongkot, W.; Rongphet, B.; Neeracha, T.; Det, D.; Chaichan, R. Marginal Abatement Cost of Electricity Generation from Renewable Energy in Thailand. Energy Reports 2020, 767-773. [CrossRef]

- Phitsinee, M.; Wongkot, W.; Rongphet, B.; Neeracha, T.; Chaichan, R.; Det, D. Assessment of Carbon Reduction Costs in Renewable Energy Technologies for Heat Generation in Thailand. Energy Reports 2021, 7, 366-373. [CrossRef]

- Bank of Thailand (BOT), Headline consumer price index. Available online: https://www.bot.or.th/App/BTWS_STAT/statistics/BOTWEBSTAT.aspx?reportID=409&language=ENG (28 September 2022).

- The social cost of carbon. Available online: https://www.oecd-ilibrary.org/sites/9789264085169-17-en/index.html?itemId=/content/component/9789264085169-17-en#fig14.1 (28 September 2022).

- Richard, B.; Howarth,; et al. Risk mitigation and the social cost of carbon Global Environmental Change 2014, 24, 123-131. [CrossRef]

- J.C.J.M., van den B.; W.J.W., B. Monetary valuation of the social cost of CO2 emissions: A critical survey. Ecological Economics 2015, 114, 33-46.

- Pu, Y.; et al. Social cost of carbon under shared socioeconomic pathways. Global Environmental Change 2018, 53, 225-232. [CrossRef]

- Mojtaba, K.; et al. How does carbon tax affect social welfare and emission reduction in Finland? Energy Reports 2020, 6, 736-744. [CrossRef]

- Krishna, T. M.; et al. Impact of carbon pricing policies on the cost and emission of the biomass supply chain: Optimization models and a case study. Applied Energy 2020, 267, 115069. [CrossRef]

- The Office of Natural Resources and Environmental Policy and Planning (ONEP), Ministry of Natural Resources and Environment. Thailand’s Third Biennial Update Report (BUR); Publisher: Thailand, 2020.

- The Office of Natural Resources and Environmental Policy and Planning (ONEP), Ministry of Natural Resources and Environment. Thailand’s First Biennial Update Report (BUR); Publisher: Thailand, 2015.

- The Office of Natural Resources and Environmental Policy and Planning (ONEP), Ministry of Natural Resources and Environment. Thailand’s Second Biennial Update Report (BUR); Publisher: Thailand, 2018.

- The Office of Natural Resources and Environmental Policy and Planning (ONEP), Ministry of Natural Resources and Environment. Thailand’s Forth Biennial Update Report (BUR); Publisher: Thailand, 2022.

- The Office of Natural Resources and Environmental Policy and Planning (ONEP), Greenhouse gas reduction. Available online: https://climate.onep.go.th/th/topic/database/migation-measures/ (30 September 2022).

- The Intergovernmental Panel on Climate Change, The Sixth Assessment Report (AR6). Available online: https://www.ipcc.ch/meeting-doc/ipcc-wgiii-14-and-ipcc-56/ (16 December 2022).

- Resources for the future, Social Cost of Carbon 101. Available online: https://www.rff.org/publications/explainers/social-cost-carbon-101/ (2 November 2022).

- Interagency Working Group on Social Cost of Carbon, United States Government. Technical Support Document: Social Cost of Carbon for Regulatory Impact Analysis; Publisher: 2010.

- Bank of Thailand (BOT), Rates of exchange. Available online: https://www.bot.or.th/App/BTWS_STAT/statistics/ReportPage.aspx?reportID=123&language=eng (28 September 2022).

- Energy Policy and Planning Office (EPPO), Ministry of Energy. Power Development Plan 2015-2036 (PDP2015), 2015.

- Thailand Greenhouse Gas Management Organization (Public Organization) (TGO). A project to study the appropriate discount rate determination for assessing the GHG reduction potential at the measure level, 2020.

- Electricity Generating Authority of Thailand (EGAT). Available online: http://www4.egat.co.th/re/egat_business/egat_heater/heater_price.htm (30 September 2020).

- Department of Alternative Energy Development and Efficiency (DEDE), Ministry of Energy. Study project of Renewable Heat Incentive (RHI) to promote the use of renewable energy, 2013.

- Department of Alternative Energy Development and Efficiency (DEDE), Ministry of Energy. Research project and development on Refuse Derived Fuel (RDF), 2008.

- The survey from RDF production company and seminar with related stakeholder.

- Energy Policy and Planning Office (EPPO), Ministry of Energy. Final report in the project support for the review of the cost of electricity purchase in the form of Feed-in tariff. 2015.

- Clean Development Mechanism (CDM), UNFCCC. Available online: https://cdm.unfccc.int/Projects/DB/RWTUV1355821731.47/view (30 September 2022).

- Clean Development Mechanism (CDM), UNFCCC. Available online: https://cdm.unfccc.int/Projects/DB/RWTUV1359566248.84/view (30 September 2022).

- Clean Development Mechanism (CDM), UNFCCC. Available online: https://cdm.unfccc.int/Projects/DB/RWTUV1359567174.34/view (30 September 2022).

- The survey from hydro power plant and seminar with related stakeholder.

- The survey from biomass power plant and seminar with related stakeholder.

- The survey from biogas power plant and seminar with related stakeholder.

Figure 2.

The conceptual overview of optimal carbon emissions policy.

Figure 3.

Key technology list in industrial and power sector in this study.

Figure 7.

Optimal degrees of renewable energy in power sector between MAC and SCC.

Figure 8.

Optimal degrees of energy efficiency improvement in power sector between MAC and SCC.

Figure 9.

Optimal degrees of CCS and BECCS in power sector between MAC and SCC.

Figure 10.

Optimal degrees of renewable energy in industry sector.

Table 1.

The details of energy plan in Thailand.

| Energy Plan | Objectives | Targets |

|---|---|---|

| PDP2018 (2018–2037) is a national long-term electricity generation and supply [6]. | The net amount of power generation at the end of 2037 is 77,211 MW. | |

| EEP2018 (2018–2037) is used for driving energy conservation and supporting future energy technology change [7]. | To reduce energy intensity by 30% in 2037 when comparing with 2010. | The commercial energy consumption must be reduced to 49,064 ktoe of the total final energy consumption in 2037. |

| AEDP2018 (2018–2037) is a national renewable and alternative energy supply and consumption plan [8]. | To increase the proportion of renewable energy consumption in the forms of electricity, heat, and biofuels at 30% of final energy consumption in 2037. | The consumption of renewable energy is 38,284 ktoe.

|

Table 2.

The details of climate plan in Thailand.

| Climate Plan | Objectives | Targets |

|---|---|---|

| National Determined Contributions (2020–2030) is a target and a guideline on national implementation of GHG mitigation [9]. |

|

The GHG mitigation potential of energy and transport sector at 169.5 MtCO2eq.

|

| Net Zero Roadmap 2065 is a framework to implement national GHG mitigation in the long run for clearer targets and guidelines on GHG mitigation [10]. | Carbon neutrality and Net zero GHG emissions: GHG emission does not exceed 120 MtCO2eq. |

Table 4.

Marginal abatement cost of the technology for industry sector.

| Technology | Marginal Abatement Cost (THB2015/tCO2eq) | |||

|---|---|---|---|---|

| 2020 | 2030 | 2040 | 2050 | |

| Solar energy | (15,563) | (14,740) | (14,539) | (14,469) |

| Biomass | (105) | (99) | (98) | (97) |

| Biogas1 | 638 | 604 | 596 | 593 |

| Waste | (651) | (617) | (608) | (605) |

| Energy Efficiency | ||||

| Motor | ||||

| Replacing standard efficiency motor with high efficiency motor | (11,736) | (11,143) | (11,018) | (10,992) |

| Lighting (Average) | (8,480) | (8,116) | (8,029) | (8,005) |

| Replacing fluorescent with LED | (8,122) | (7,725) | (7,634) | (7,613) |

| Replacing incandescent with LED bulb | (8,603) | (8,416) | (8,348) | (8,316) |

| Replacing mercury-vapor lamp with LED | (7,956) | (7,572) | (7,482) | (7,460) |

| Replacing compact fluorescent bulb with LED bulb | (8,705) | (8,237) | (8,169) | (8,166) |

| Replacing high intensity discharge bulb with LED | (9,238) | (8,856) | (8,747) | (8,710) |

| Replacing tungsten halogen lamp with LED bulb | (8,257) | (7,888) | (7,791) | (7,762) |

| Air condition | ||||

| Using high efficiency air condition | (11,432) | (11,084) | (10,967) | (10,917) |

| Chiller (Average) | (10,528) | (9,969) | (9,913) | (9,920) |

| Screw Air Cooled Chiller (VSD) | (10,268) | (9,723) | (9,669) | (9,675) |

| Screw Water Cooled Chiller (VSD) | (10,631) | (10,067) | (10,011) | (10,018) |

| Centrifugal Water-Cooled Chiller (VSD) | (10,710) | (10,142) | (10,085) | (10,092) |

| Boiler | ||||

| Using smart boiler | 5,043 | 4,770 | 4,698 | 4,669 |

| Carbon Capture | ||||

| CCS and BECCS | - | - | - | 7,5002 |

1 The MAC related to heat generation from biogas encompasses various systems and diverse industrial sectors. 2 References for CCS and BECCS are drawn from The Sixth Assessment Report (AR6) from Intergovernmental Panel on Climate Change [46].

Table 5.

Marginal abatement cost of the technology for power sector.

| Technology | Marginal Abatement Cost (THB2015/tCO2eq) | |||

|---|---|---|---|---|

| 2020 | 2030 | 2040 | 2050 | |

| Solar energy | 2,231 | 583 | (1,123) | (3,105) |

| Solar floating | 3,699 | 1,998 | 273 | (1,715) |

| Wind power | 471 | (1,000) | (2,660) | (4,627) |

| Hydro energy | (4,782) | (6,190) | (7,817) | (9,763) |

| Biomass | (3,509) | (4,861) | (6,475) | (8,420) |

| Biogas | (4,054) | (5,499) | (7,134) | (9,082) |

| Waste | (1,457) | (2,966) | (4,630) | (6,595) |

| Energy Efficiency | The marginal abatement cost in the power sector were similar to the industry sector | |||

| Carbon Capture | ||||

| CCS and BECCS | - | - | - | 7,5001 |

1 References for CCS and BECCS are drawn from The Intergovernmental Panel on Climate Change, The Sixth Assessment Report (AR6) [46]. Thailand plan to implement CCS and BECCS from 2045.

Table 6.

Social cost of carbon (THB2015/tCO2eq) between 2020 to 2050.

| Discount rate | Social Cost of Carbon (THB2015/tCO2eq) | |||

|---|---|---|---|---|

| 2020 | 2030 | 2040 | 2050 | |

| 5% | 479 | 650 | 855 | 1,061 |

| 3% | 1,711 | 2,053 | 2,464 | 2,840 |

| 2.5% | 2,532 | 3,011 | 3,456 | 3,901 |

Table 7.

Greenhouse gas mitigation target and potential covering from 2020 to 2050.

| Year | Mitigation Target (MtCO2eq) |

Mitigation Potential (MtCO2eq) |

The Target to Potential ratio (%) |

||||

|---|---|---|---|---|---|---|---|

| Power | Industry | Total | Power | Industry | Total | ||

| Scenario 1 | |||||||

| 2020 | 0.00 | 5.48 | 5.48 | 15.13 | 24.88 | 40.01 | 13.70% |

| 2025 | 11.79 | 7.70 | 19.49 | 24.71 | 39.08 | 63.79 | 30.56% |

| 2030 | 63.35 | 26.29 | 89.64 | 60.45 | 52.78 | 113.23 | 79.17% |

| 2035 | 103.49 | 24.77 | 128.26 | 102.75 | 59.26 | 162.01 | 79.17% |

| 2040 | 134.58 | 34.71 | 169.29 | 123.29 | 68.91 | 192.20 | 88.08% |

| 2045 | 160.92 | 46.21 | 207.14 | 151.31 | 84.66 | 235.97 | 87.78% |

| 2050 | 175.19 | 70.04 | 245.24 | 182.62 | 100.26 | 282.89 | 86.69% |

| Scenario 2 | |||||||

| 2020 | 0.00 | 3.78 | 3.78 | 15.13 | 24.88 | 40.01 | 9.45% |

| 2025 | 1.57 | 2.23 | 3.80 | 24.71 | 39.08 | 63.79 | 5.95% |

| 2030 | 47.62 | 17.87 | 65.48 | 60.45 | 52.78 | 113.23 | 57.83% |

| 2035 | 83.97 | 14.32 | 98.29 | 102.75 | 59.26 | 162.01 | 60.67% |

| 2040 | 113.21 | 23.27 | 136.48 | 123.29 | 68.91 | 192.20 | 71.01% |

| 2045 | 139.89 | 34.95 | 174.83 | 151.31 | 84.66 | 235.97 | 74.09% |

| 2050 | 156.93 | 60.26 | 217.20 | 182.62 | 100.26 | 282.89 | 76.78% |

| Scenario 3 | |||||||

| 2020 | 0.00 | 3.36 | 3.36 | 15.13 | 24.88 | 40.01 | 8.41% |

| 2025 | 0.00 | 0.00 | 0.00 | 24.71 | 39.08 | 63.79 | 0.00% |

| 2030 | 36.31 | 11.81 | 48.11 | 60.45 | 52.78 | 113.23 | 42.49% |

| 2035 | 64.90 | 4.11 | 69.01 | 102.75 | 59.26 | 162.01 | 42.59% |

| 2040 | 84.45 | 7.86 | 92.31 | 123.29 | 68.91 | 192.20 | 48.03% |

| 2045 | 99.25 | 13.18 | 112.43 | 151.31 | 84.66 | 235.97 | 47.65% |

| 2050 | 101.97 | 30.83 | 132.80 | 182.62 | 100.26 | 282.89 | 46.94% |

| Scenario 4 | |||||||

| 2020 | 0.00 | 2.11 | 2.11 | 15.13 | 24.88 | 40.01 | 5.29% |

| 2025 | 0.00 | 0.00 | 0.00 | 24.71 | 39.08 | 63.79 | 0.00% |

| 2030 | 20.96 | 3.59 | 24.56 | 60.45 | 52.78 | 113.23 | 21.69% |

| 2035 | 42.33 | 0.00 | 42.33 | 102.75 | 59.26 | 162.01 | 26.13% |

| 2040 | 54.22 | 0.00 | 54.22 | 123.29 | 68.91 | 192.20 | 28.21% |

| 2045 | 61.22 | 0.00 | 61.22 | 151.31 | 84.66 | 235.97 | 25.94% |

| 2050 | 56.14 | 6.28 | 62.42 | 182.62 | 100.26 | 282.89 | 22.07% |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Copyright: This open access article is published under a Creative Commons CC BY 4.0 license, which permit the free download, distribution, and reuse, provided that the author and preprint are cited in any reuse.