Submitted:

08 December 2023

Posted:

12 December 2023

You are already at the latest version

Abstract

Several life contingency agreements are based on the assumption that policyholders have impaired life expectancy attributable to factors such as lifestyle, social class, or preexisting health issues. Quantifying two crucial variables, augmented death probabilities and the discount rate of projected cash flows, is essential for pricing such agreements. Information regarding the correct values of these parameters is subject to vagueness and imprecision, which further intensifies if impairments must be considered. This study proposes modelling mortality and interest rates using a generalization of fuzzy numbers (FNs), known as intuitionistic fuzzy numbers (IFNs). Consequently, this paper extends the literature on life contingency pricing with fuzzy parameters, where uncertainty in variables, such as interest rates and death probabilities, is modelled using FNs. While FNs introduce epistemic uncertainty, the use of IFNs adds bipolarity to the analysis by incorporating both positive and negative information regarding actuarial variables. Our analysis focuses on two agreements involving policyholders with impaired life expectancy: determining the annuity payment in a substandard annuity and pricing a life settlement over a whole life insurance policy. In particular, we emphasize modelling interest rates and survival probabilities using triangular intuitionistic fuzzy numbers (TIFNs) owing to their ease of interpretation and implementation.

Keywords:

substandard annuities

; life settlement pricing

; intuitionistic fuzzy sets

; intuitionistic fuzzy numbers

1. Introduction

Life insurers have traditionally focused on providing standardized life coverages, pricing them primarily based on age and, when permissible, gender (Gatzer & Klozki, 2016). However, since the last decades of the 20th century, a significant trend in the insurance industry has been the customization of services to align with the individual needs of the insured (Tereszkiewicz & Południak-Gierz, 2021). This shift underscores the importance of considering the heterogeneity of life expectancies in the offering and valuation of policies addressing life contingencies, such as life annuities (Olivieri & Pitacco, 2016).

Within the realm of life contingency insurance, two general types can be distinguished: life annuities, covering the contingency of survival, and life insurance, addressing the contingency of death (Promislow, 2014). In both types of insurance contracts, there are agreements in which projected cash flows are performed to individualize the mortality of insured persons. This involves considering the possibility that owing to their particular lifestyle, health, etc., an insured person may have a diminished life expectancy (LE) compared to the expected norm for their age. This study addresses two situations in actuarial pricing linked to life contingencies associated with life insurance coverage: special-rate life annuities and life settlements.

In the domain of life annuities, the use of standard probabilities for evaluation is attractive primarily for healthy individuals but may not be suitable for those with impaired life expectations. Thus, to expand their market, some insurers offer elevated annuity rates to individuals with critical health conditions (Olivieri & Pitacco, 2016). This practice is known as a special rate or substandard annuity.

When a policyholder seeks to liquidate life insurance prematurely, the insurer determines the amount offered, referred to as the surrender value, by valuing it using standard death probabilities. In highly developed life markets, such as those of the United States, there is the option to sell life insurance to third parties—investors in life insurance policies—under agreements known as life settlements (LSs). Through these transactions, policyholders with impaired life expectancies can obtain greater value by selling their policies than surrender value (Brockett et al., 2013) because reduced LEs are associated with higher prices. This is because of the likelihood that investors will pay fewer pending insurance premiums, and the death benefit is expected sooner (Braun & Xu, 2020).

The assessment of life contingencies with heterogeneous life expectancies (LEs) relies on conventional life insurance mathematics, involving the discounted value of expected cash flows with an appropriate interest rate and death probabilities tailored to the specific policyholder. This applies to both special-rate annuities (Pitacco, 2017) and life settlements (LSs) (Braun & Xu, 2020). Adjusting one-year death probabilities suited to the policy of interest is typically done by referencing a standard mortality law corresponding to a large group, representing the mortality behavior of an "average" person, and subsequently adapting it to the particular characteristics of the life contingencies intended for valuation (Olivieri, 2006).

The parameters embedded in life insurance pricing are subject to various types of uncertainty, such as risk, vagueness, and imprecision. Traditionally, the valuation of life contingencies has operated under the assumption of pure risk, wherein the probabilities associated with potential outcomes (e.g., death, survival, or disability) are considered perfectly known. Consequently, the discounted valuation of cash flows typically assumes that the parameters associated with valuation, primarily interest rate and survival probabilities, are quantifiable by real numbers. This holds true for standard life contingencies (Promislow, 2014), special-rate annuities (Pitacco, 2017) and life settlements (Lubovich et al., 2008).

However, in practice, information regarding the precise values of parameters used in life contingency valuation contains various sources of imprecision and uncertainty; thus, employing crisp parameters represents a simplification (Lemaire, 1990). The technical interest rate paid by insurance companies to policyholders and annuitants must align with the risk-free interest rate expected in the economy over the duration of the contracts. This requires making prudent assumptions about the risk-free interest rate in the long term, the knowledge of which is inherently vague (Devolder, 1988; Ryan & Harbin, 1998).

Uncertainty also significantly influences the standard mortality probabilities used in valuation given that the evolution of population mortality over time is not predictable with absolute precision. To address this, dynamic stochastic mortality models have been developed as, for example, that in Lee and Carter (1992). Moreover, considering heterogeneous life expectancies introduces additional sources of uncertainty into mortality probabilities. Many factors influencing life expectancy are inherently imprecise from a medical standpoint (Anderton & Robb, 1998), and policyholders often possess more information about their LEs than evaluators (Bauer et al., 2020). Furthermore, information provided by applicants in medical interviews may be inaccurate, false, or incomplete, often because they have incentives to obtain more favorable prices (Bundock, 2006). Additionally, ongoing advancements in medical technologies have contributed to increasing life expectancies, potentially surpassing the estimates made at the time of valuation based on available information (Xu & Hoesh, 2018).

Fuzzy set theory (FST) provides tools such as fuzzy expert systems, fuzzy numbers, fuzzy random variables, and fuzzy regression, allowing for the treatment of uncertainty. These tools have been in use since the 1980s in financial and actuarial mathematics. While traditional financial methods, such as cash flow discount models or option pricing models, provide a solid analytical foundation, the integration of fuzzy tools can improve the results by addressing additional sources of uncertainty alongside inherent risks (Andrés-Sánchez, 2023).

In the realm of financial and actuarial pricing, seminal works by Kaufmann (1986), Buckley (1987), and Lemaire (1990) proposed modelling uncertain parameters using fuzzy numbers (FNs). In these contributions, FNs must be interpreted as quantification of epistemic uncertainty, capturing vague or incomplete information about the value of the parameter of interest (Dubois & Prade, 2012). Let be a variable (the adequate discount rate). We can define the fuzzy number , interpreted as "the discount rate must be approximately ," by using a possibility distribution that measures the ease in which a value will be equal to. This interpretation of an FN has been widely used in FST for financial and actuarial analyses.

Following Dong & Li (2016), capital budgeting and cash-flow discounting were the initial domains in which uncertainty by means of fuzzy numbers was introduced. This includes the computation of the net present value (Kaufmann, 1986), the internal rate of return (IRR) (Buckley, 1992) and the terminal value of an investment project (Kahraman et al., 2002). Likewise, the application of a fuzzy-random approach to option pricing, both in continuous time and discrete time, has been a burgeoning field in this regard (Muzzioli &de Baets, 2016; Andrés-Sánchez, 2023).

Fuzzy actuarial pricing, both in life insurance (Lemaire, 1990) and nonlife insurance (Cummins and Derrig, 1997), predominantly employs the discounted value of projected cash flows. However, within the realm of life contingency analysis, Anzilli and Fachinetti (2017), Nowak and Romaniuk (2017), and Anzilli et al. (2018) used option-pricing methods with fuzzy parameters. Similarly, Mircea and Covrig (2015) and Ungureanu and Vernic (2015) model the terminal value of an insurance company within a predefined time horizon as the terminal value of its projected cash flows. In the nonlife insurance arena, Apaydin and Baser (2010) and Heberle and Thomas (2014) delve into the development of fuzzy claim reserving. Table 1 provides a deeper overview of studies using FNs to model uncertainty in actuarial pricing.

The concept of intuitionistic fuzzy numbers (IFN) is a tool in the theory of intuitionistic fuzzy sets presented by Atanasov (1986) and Atanasov (1989), which allows the quantification of uncertain quantities. They extend the concept of FNs (Mitchel, 2004) and facilitate the inclusion of bipolar information along with epistemic uncertainty in the quantification of parameters of interest. In this context, bipolarity involves considering both positive information regarding the potential values of the parameter of interest and negative information related to the values that the parameter actually cannot take (Dubois & Prade, 2012).

According to Dubois and Prade (2012), the bipolarity considered in instruments such as IFNs does not introduce additional uncertainty; however, it does provide new information. In the case of IFNs, this entails adding an estimate of values that, with certainty, should be excluded, thus complementing information about the believed possible values of a quantity.

The application of IFN parameters in financial pricing is significantly scarcer than that of conventional fuzzy numbers, especially in finance, and is absent in actuarial pricing. Applications include capital budgeting (Kumar and Bajaj, 2014; Kahraman et al., 2015; Boltürk & Kahraman, 2022; Haktanır & Kahraman, 2023), option pricing (Wu, 2016) and real option pricing (Ersen et al., 2018; Ersen et al., 2023).

Building upon the reflections presented in this introduction, this study expands on the findings of Andrés-Sánchez et al. (2020) in special rate annuities and Aalei (2022) and Andrés-Sánchez and González-Vila (2023) in LSs. These contributions model the uncertainty of LE and adequate discount rates using FNs. This work generalizes these results by considering that information about these parameters is provided by IFNs, with a specific focus on triangular IFNs owing to their higher practical applicability.

The remainder of this paper is organized as follows. The next section introduces the fundamentals of intuitionistic fuzzy numbers and their arithmetic operations. The third section develops elements of life insurance in the presence of heterogeneity in LEs under the hypothesis that discount and mortality rates are estimated by means of IFNs. The fourth section develops substandard life annuities and life-settlement pricing in the presence of intuitionistic information. This study concludes by highlighting the main results and suggesting further research.

2. Intuitionistic fuzzy numbers

2.1. Fuzzy numbers and intuitionistic fuzzy numbers

Definition 1.

A fuzzy set (FS) in a referential set , is defined as (Zadeh, 1965):

where is the so-called membership function.

Definition 2.

Fuzzy set can be represented through level sets or -cuts, , (Zadeh, 1965):

Definition 3.

A fuzzy number (FN), , is a fuzzy subset of the real line (Dubois &Prade, 1993) that:

- i. is normal, i.e.,

- ii. is convex, i.e.,

Remark 1.

As a consequence, the α-cuts of , , are confidence intervals:

where is an increasing function of and is a decreasing function.

Fuzzy set theory commonly represents imprecise quantities and parameters using fuzzy numbers (FNs) (Dubois & Prade, 1993).

Definition 4.

A triangular fuzzy number (TFN) can be symbolized by the triplet , :

being it α-cut representation:

TFNs are very common in practical financial applications within fuzzy set theory (Andrés-Sánchez, 2023). In triangular fuzzy numbers, the grading of the membership level is performed linearly, which is reasonable because it applies the principle of parsimony when dealing with vague information (Jiménez & Rivas, 1998).

Thus, the fuzzy number is interpreted as a value that is "approximately with the lower and upper extreme scenarios denoted as and , respectively. For example, an economic prediction such as "the inflation next year will be approximately 3%, and we do not expect it to be below 2.5% or above 4%" can be represented as (2.5%, 3%, 4%).

Definition 5.

An intuitionistic fuzzy set (IFS) defined in a referential set is (Atanassov, 1986):

where measures the membership of in and nonmembership. The functions are as follows:

Remark 2.

Note that not necessarily , that is, an element is allowed to avoid belonging to and its complement with a degree of hesitancy, , which is:

Remark 3.

IFS generalizes the concept of FS such that if , is a conventional FS .

Definition 6.

An IFN can be expressed using -levels or -cuts, , (Atanassov, 1986):

Remark 4.

can be decoupled into two level sets (Yuan et al., 2014):

in such a way that:

Definition 7.

Le be a fuzzy subset . Following Burillo and Bustince (1996), IFS can be induced by means of an application by stating and as follows:

- ,

and then:

Definition 8.

An intuitionistic fuzzy number (IFN) is an IFS defined on real numbers (Kahraman et al., 2015), such that

- It is normal, i.e.,

- is convex,

- and is concave:

Remark 5.

The -cuts of , can be decoupled as:

where is an increasing (decreasing) function of and decreases (increases) with respect to .

Remark 6.

Thus, an -level of can be represented:

An IFN is an imprecise quantity that is measured using a real number. If nonmembership is established as , then is an FN.

Remark 7.

Let be an FN that generates an IFN by considering in Definition 7 . Therefore, in this case, and .

Following Mitchell (2004), can be interpreted as the upper distribution function of the uncertain quantity , and can be interpreted as the lower distribution function. In this way, Dubois and Prade (2012) interpreted and as bipolar possibility distribution measurements in such a way that accounts for the potential possibility and accounts for the real possibility of being .

Definition 9.

A triangular intuitionistic fuzzy number (TIFN) can be denoted as , with membership and nonmembership functions (Kumar & Bajaj, 2014):

and,

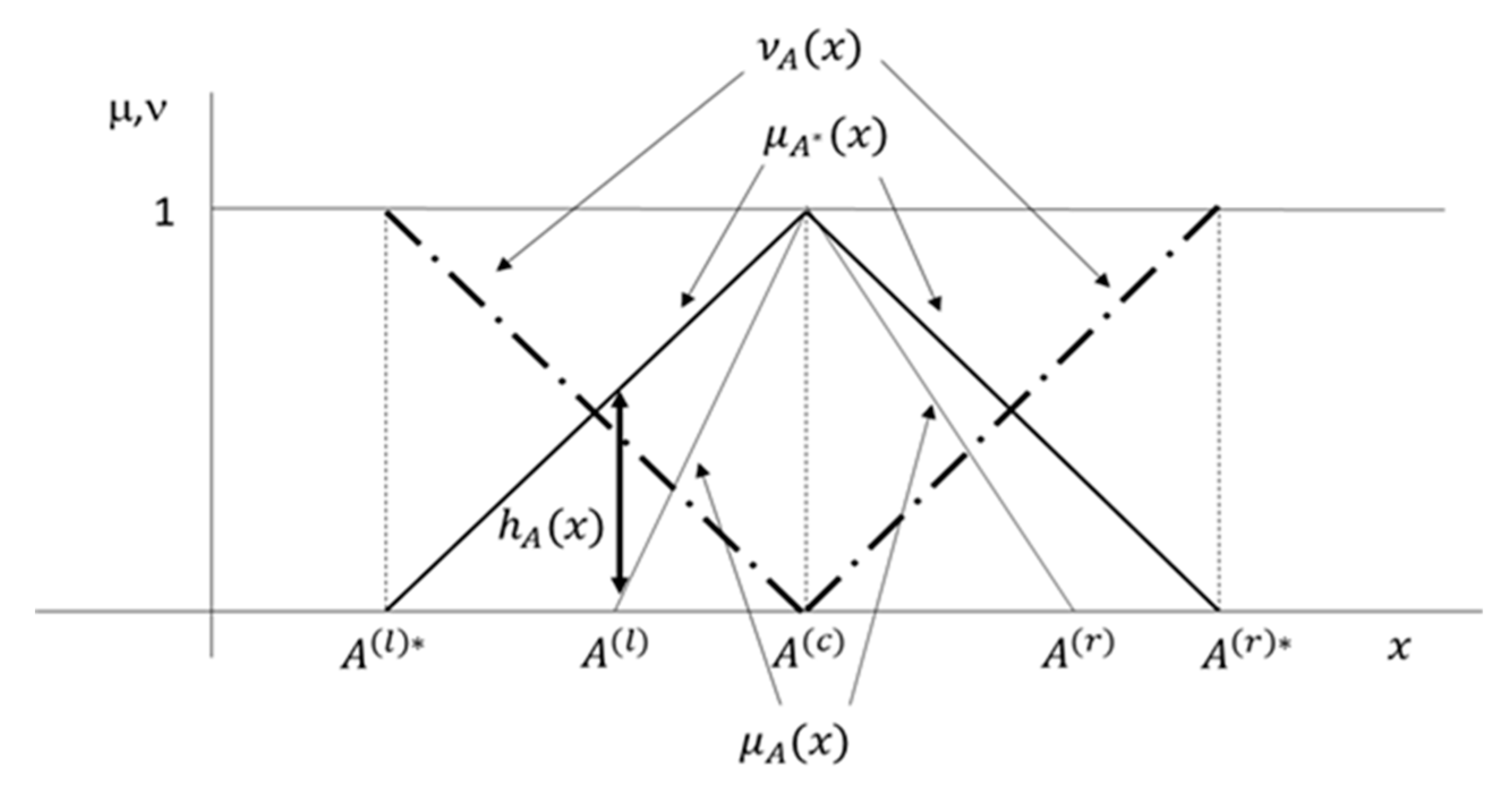

where . Figure 1 depicts the shape of a TIFN and the relationship between the embedded functions , and

Remark 8.

The level sets of a TIFN can be decoupled in:

Thus, TIFNs are an extension of TFNs, such that if and , we deal with a conventional TFN (Kumar & Hussain, 2015). Triangular uncertain parameters are commonly considered in practical applications involving intuitionistic modelling (Mahapatra & Roy, 2013; Kahramam et al., 2015; Kumar & Hussain, 2015; Bhaumik et al., 2017; Rasheed et al., 2021). The argument put forward by Jiménez and Rivas (1998), based on applying the parsimony principle for the use of TFNs, can be extended to the use of TIFNs.

A TIFN adapts very naturally to the way humans make estimations by incorporating more nuances than are necessary to fit a TFN. Once again, we can see that represents the scenario with maximum reliability. Moreover, whereas and are two extreme lower scenarios, and are two extreme upper scenarios. is considerably lower than the central value, and is exceptionally low compared to the possible values of the parameter. For example, in the context of a random variable, could be a reasonably small percentile (e.g., the 5th percentile), and is an exceptionally extreme percentile (e.g., the 0.1 percentile). If 0, meaning that we do not assign a likelihood to parameter taking the value , but express some level of doubt about its nonmembership, because .

Similarly, can be described as a notably high realization of and can be assimilated to a relatively high percentile of a random variable (e.g., the 90th percentile). In contrast, has a potentially extremely high value (e.g., 99.5th percentile).

Note that TIFNs allow modelling estimations of a parameter that, while its knowledge may also be vague and imprecise, contains more nuances than an FN. For instance, a statement such as "inflation is approximately 3%, ranging from 2.5% to 4%. However, it is sure that will not be lower than 2% or higher than 5%" could be quantified as 〈(2.5%,3%,4%)(2%,3%,5%)〉 using TIFNs.

Remark 9.

From Definition 7, a TFN can induce TIFN by stating such that , , and letting Specifically, the hesitancy level is:

2.2. Intuitionistic fuzzy number arithmetic

In the introduction, we highlighted numerous applications of fuzzy subsets in finance and insurence pricing using fuzzy number inputs. In all these cases, the fundamental problem lies in evaluating actuarial functions whose inputs are given via fuzzy numbers. This requires the application of Zadeh's extension principle with max-min operators, typically implemented through functional analysis in alpha-level sets.

Shen and Chen (2012) and Bayeg and Mert (2021) generalize to IFN arithmetic the findings of Nguyen (1978), Deng and Shah (1987), and Buckley and Qu (1990) in their evaluation of functions with fuzzy estimates of variables through alpha cuts.

Let be a continuous and differentiable function , such that the values of the input variables are given the means of IFNs . It generates IFN , , whose characteristic functions and must be obtained by using a convolution of a τ-conorm with a τ-norm. For an extended exposition of the usual combinations of τ-conorms and τ-norms, see Atanassova (2007). Among these combinations, it is common to generalize Zadeh’s principle by using the min-norm and max-conorm as follows (Bayeg & Mert, 2021):

Therefore, if are FNs, it is only necessary to obtain using the usual max-min principle. Therefore, to obtain from , we must implement (Shen and Chen, 2012):

and thus, given that is continuous, the cuts of are:

where:

being,

Therefore, and can be obtained analogously to the -cuts of the conventional fuzzy number functions. To obtain , given that the domain on which is evaluated is convex, as it is a rectangle in , the global optima in the domain , (minimum of ), and (maximum f), well (Deng & Shah, 1987):

- are the local optima at internal points where . Thus, is negative semidefinite if is obtained at and positive semidefinite for .

- If there are no local optima in , the argument that optimizes is found at the vertex of the domain .

Similar considerations are made for the determination of , which requires obtaining and .

Following Buckley and Qu (1990), when monotonically increases with respect to and monotonically decreases in ,, is

By analogy, the β-cuts of are:

The sum and subtraction results of the two TIFNs are also TIFNs. Letting and , we find that:

The multiplication of a TIFN by a scalar is also a TIFN.

The evaluation of nonlinear functions using TIFNs does not produce a TIFN. Despite this limitation, Kreinovich et al. (2020) argue that linear shapes often offer an effective solution to practical issues in the majority of cases. In many instances, straightforward and intuitively clear methods have proven to be the most successful, combining both formulas and intuition. The alignment of the resulting membership function with the original fuzzy concept improved as the characteristic value approached the minimum value. Hence, it is reasonable to consider utilizing functions for alternative fuzzy modelling, where the characteristic value is minimized (Kreinovich et al., 2020).

Hence, the multiplication and division of two TIFNs does not result in TIFNs, as indicated by the exact membership function expressions in Mahapatra and Roy (2013). However, it is worth noting that they allow expressions similar to those presented for the product and division of TFNs in Kaufmann (1986), which are widely used in practical applications. Thus, the triangular approximation of the product of two TIFN and that are strictly nonnegative, that is, and :

Similarly, the triangular approximation of the division of two TIFN and when and is

It is well known that there are many financial functions that, despite not being linear, when they are evaluated, the result is well approximated by a TFN that maintains the same support (the 0-cut) and core (the 1-cut). This encompasses the present value of a set of cash flows (Kaufmann, 1986), the final value of a pension plan (Jiménez & Rivas, 1998), or the internal rate of return (Terceño et al., 2003). In the actuarial field, this involves the estimation of claim reserves (Heberle & Thomas, 2014), asymptotic probabilities of the number of claims in a bonus-malus system (Villacorta et al., 2021), payment of an immediate annuity (Andrés-Sánchez et al., 2020), and price of LSs (Andrés-Sánchez and González-Vila, 2023). Following the same philosophy, Kumar and Bajaj (2014) postulate that the net present value function, when cash flows and the discount rate are estimated using TIFNs, can be approximated through a TIFN with the same <0,1>-cut and <1,0>-cut. Therefore, in this study, when the initial data are estimated by TIFNs , the approximate TIFN is considered:

in such a way that if is continuous and monotonically increasing with respect to the m first variables and monotonically decreasing with respect to the last n-m:

By analogy with the error measurement in the triangular approximation of fuzzy numbers in Andrés-Sánchez and González-Vila (2023), the quality of the relative error measurement in the bounds of calculated with (2a)-(2d) by those of its triangular approximation, (5a)-(5f), is, in

and for

Therefore, to measure the average relative deviations, we use the weights of (6a) and (6b). In the case of belonging to a greater -level, it implies a larger reliability. Therefore, we define the weighted average errors for the approximation of :

On the other hand, in , a greater nonmembership degree supposes lower reliability. Therefore, we define the weighted average errors for the approximation of :

3. An intuitionistic fuzzy framework to evaluate life contingencies for heterogeneous life expectancies

3.1. Modelling one-year death probabilities with intuitionistic fuzzy numbers

The consideration of heterogeneity in mortality involves obtaining death probabilities or instantaneous mortality rates appropriate for the particular for whom life contingencies are being priced (Olivieri, 2006). When the cause of substandard LE is common to a wide group of people, such as smoking, specific mortality tables can be developed. However, in many cases, this is not possible either because there are very specific causes of impairment (e.g., a rare disease) or because the cause of impairment is a combination of risk factors (Pitacco, 2019). Thus, a common alternative is to take as a reference standard death probability, symbolized as for a person aged to fit the actual probability The probabilities consider common conditions affecting a large group, such as climate, pollution, healthcare system, gender, and smoking status.

Subsequently, must be transformed to obtain specific probabilities , that is, , by introducing individual characteristics that shape the specificity of the evaluated person's LE, such as the presence of any preexisting disability (Olivieri, 2006).

There are numerous ways to obtain from in practice (Pitacco, 2019). One of the most common methodologies considered in this study involves setting a parameter , the so-called mortality multiplier, such that:

where if , we have a substandard LE; if , it is a preferred risk; and if , it is a standard risk (Pitacco, 2019). It is clear that .

Standard mortality probabilities can be derived from either a static or a dynamic survival table. In the latter scenario, as seen in the works of Koissi and Shapiro (2006), Andres-Sánchez and González-Vila (2019), and Szymański and Rossa (2021), future survival probabilities are estimated as FNs using fuzzy regression methods and the analytical groundwork of Lee-Carter (1992). The fuzziness of standard probabilities in the context of static mortality tables is used, for example, in Lemaire (1990). Thus, we suppose that the set of one-year death probabilities is given by IFNs, :

We also assume that the mortality multiplier, , will be estimated with IFN , whose -cut is denoted as

Several clarifications can be made regarding the justification of using an IFN mortality multiplier:

- A widely used method for determining is the numerical rating system (Kita, 1988), which is particularly prevalent in the life settlement market (Xu, 2020). With this method, , where represents a percentage increase in the death probability associated with the jth factor, that is, it is a so-called debit. Conversely, implies a decrease in the death probability as the factor increases LE, that is, it is a credit. The debits and credits can be precisely estimated (Werth, 1995) or expressed imprecisely using fluctuation bands instead of clear values; in this last case, IFNs could be suitable to model them. According to Xu and Hoesch (2018), medical underwriting for life settlements is inherently imprecise due to several factors. Base mortality tables inherited from the life insurance market introduce inaccuracies in mortality rates for elderly populations because data for these age groups are scarce (Braun & Xu, 2020). Other factors also contribute to biased and imprecise information fitting for debits and credit. These include false application of information, lack of critical information, and incorporation of irrelevant and false information. These factors emphasize the need to assess life settlement prices by introducing variability bands in mortality multipliers when calculating LS prices of LSs (Xu & Hoesch, 2018).

- Lim and Shyamalkumar (2022) indicate that to fit the mortality multiplier, unreported deaths must be considered, whose knowledge is inherently vague because data on this issue in practice are incomplete. They outline that a commonly agreed estimate is "approximately 5%" and seniors ranging from "5-7%,". Note that these statements are vague and imprecise and are therefore susceptible to being modelled with a TIFN whose base TFN may be (5%, 5,5%, 7%).

- Goodwin et al. (2004) recommend that, in tariffing involving older people with impairments, seeking the judgment of a professional gerontologist is advisable. Fuzzy-set instruments can naturally model subjective information from experts (Shapiro, 2004).

- Evaluating not only central values but also extreme mortality scenarios is common practice in insurance markets. Richards (2008) provided an example in the context of life annuities, and Xu and Boesch (2018) expressed extreme scenarios in the 5th and 95th percentiles. In Andrés-Sánchez and González-Vila (2023), the use of a fuzzy triangular number is justified to shape the mortality multiplier that can be considered "most reliable" and two extreme scenarios below and above this central value. The use of TIFNs generalizes the use of TFNs involving a central scenario and two pairs of extreme scenarios, below and above this central value. In these pairs, while one scenario might be factually extreme (e.g., percentiles 10 and 90), the other could be potentially extreme (e.g., comparable to percentiles 0.5 and 99.5).

- In the life settlement market, reliable values of life expectancy and, consequently, the mortality multiplier are typically expressed not by a crisp parameter but with a set of crisp estimates. This is because the LE of the insured is often reported by at least two independent medical underwriters (Xu, 2020). Therefore, for a given policy, if the set of multipliers by LE providers is , it seems reliable to give a fuzzy quantification to the mortality multiplier, as “it must be approximately and it may fluctuate in margins depending on (Andrés-Sánchez & González-Vila, 2023).

- The derivation of the sensitivity of death probability to risk factors through regression methods, as developed by Meyricke and Sherris (2013), assumes that the estimation of death probabilities and coefficients involves probabilistic confidence intervals. The results of Couso et al. (2001), Dubois et al. (2004), and Sfiris and Papadopoulos (2014) facilitate the inference of fuzzy numbers using probabilistic confidence intervals. These findings were employed in a regression framework by Adjenughwure and Papadopoulos (2020) and Al-Kandari et al. (2021), where the variables of interest were predicted by fuzzy numbers induced from probabilistic confidence interval estimates derived from statistical regression. From Remark 6, we can induce a TIFN from the estimated TFN.

- Of course, fuzzy one-year standard mortality probabilities may consider an impairment cause common to a wide proportion of the population, for which the evaluator has developed mortality tables ad hoc (Drinkwater et al., 2006). An example of this is the mortality tables for smokers. If a person has no other cause of impairment,

Under our assumptions, the one-year death probability of the assessed life contingency can be obtained as IFN . The probability can be fitted by its -cut by evaluating (7) using rules (2a)–(2d), (8), and (9). So,

where

3.2. Modelling the probabilities of survival and the curtate life expectancy with intuitionistic fuzzy numbers

The survival probability in years for people with impaired life expectancy of age x years, , and LE , is obtained from adjusted one-year death probabilities. Therefore, and are functions of the multiplier and the vector of standard death probabilities that serve as a baseline, which we denote as . Thus, we can obtain life probabilities as

and curtate life expectation as,

where ≤0.

From the -cuts of in (8), we refer to as the path with the lowest death probabilities of and as that of the upper probabilities. Therefore, for , the lower path of the standard death probabilities is , and the upper path is .

If the mortality multiplier is IFN (9) and the standard death probabilities are defined as (8), the probability of survival years at age , , is also an IFN whose -cut can be denoted as

Therefore, considering that in relationship (11), the probability of survival is an inverse function of the mortality multiplier and the baseline probabilities of death, we obtain using (2a)–(2d):

Under the hypothesis of intuitionistic parameters, LE, , is fitted through its -cut:

which is obtained by evaluating (12) with life probabilities (13a)-(13b):

If , the parameters , and can be approximated using TIFN (1a)–(1d). By denoting , , , and and considering (5a)–(5f) and (11), survival probabilities can be approximated as:

where:

For LE, , because it can be obtained using (12) and then by rule (3a):

Example 1.

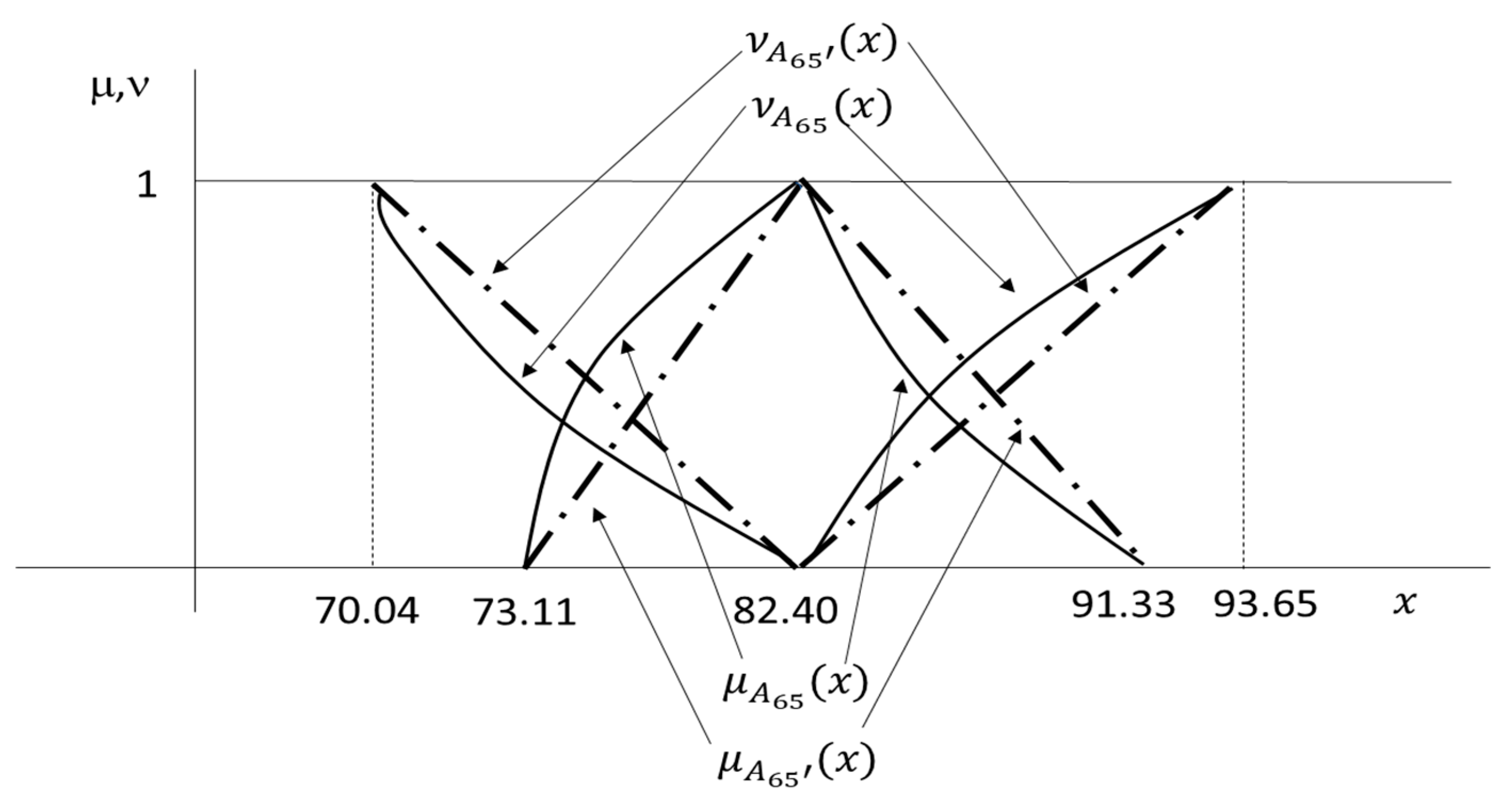

To develop the numerical applications of this study, we used survival tables for the Spanish population for 2019 from the Human Mortality Database (https://www.mortality.org/). Therefore, is indeed a crisp probability. We also assume a mortality multiplier . Table 2 shows for a person aged =65, the <,1−>cuts, where =0,0.25,0.5,0.75, of and their triangular approximations and . Table 2 also shows the errors by and calculated using (6a)–(6d).

It can be verified that the triangular approximation calculated with (15)–(16) to the original IFNs, which were previously calculated throughout (13a)–(13b) in the case of and with (14) in the case of , works well. The endpoints of the -cuts in the case where the largest errors occurred, which were placed in , never exceeded 1%.

3.3. Pricing immediate whole life annuities and immediate whole life insurances with intuitionistic fuzzy parameters

Life contingency pricing requires establishing not only an adequate rating of covered contingencies but also an adequate discount rate for linked cash flow. A clear distinction can be drawn between an insurer's liability-pricing setting and the sale of policies to third parties, as in the case of life settlements. In the first case, the interest rate is the so-called technical interest rate. In this context, the insurer's projection should align with the anticipated profitability of the portfolio in which premiums are invested, often comprising a substantial portion of public debt bonds (Ryan & Harbin, 1998). Conversely, when pricing an LS, the discount rate, also referred to as the internal rate of return (IRR), is higher. This is because it is obtained by adding a premium to the risk-free interest rate to reward the risks assumed by the policy buyer, such as those linked to longevity and liquidity (Braun & Xu, 2020) and asymmetric information (Bauer et al., 2020).

Whether in one situation or the other, denoting the discount rate as , the unitary pricing of immediate whole annuities and immediate whole insurance is determined as follows.

In this regard, it is easy to check that 0 and

Let us now price life contingencies with an IFN , whose-cut is symbolized as

The representation of interest rates through an IFN is an extension of how the fuzzy actuarial literature in Table 1 proposes quantifying uncertainty in discount rates, that is, using FNs. From the intuitionistic interest rate and life probabilities, we obtain IFNs present values of whole life immediate annuities and whole life immediate insurance, denoted as and , respectively. Thus, the -cut of the annuity

is obtained throughout and by considering that the present value of annuity (17) decreases with respect to the interest rate and increases with respect to survival probabilities. Using (2a)–(2d) and (13a)-(13d) in (17), we obtain

The -cut of the entire life insurance is obtained by considering that (18) is an increasing function of the mortality multiplier and standard death probability and decreasing with respect to the interest rate. Therefore, to obtain

We evaluate (18) by applying rules (2a)-(2d) and using (10a)-(10b) and (13a)-(13d):

If we use a TIFN to model , , and the discount rate is also a TIFN , the value of the whole life annuity can be approximated by TIFN :

where from (17) and (5a)-(5f):

In the case of whole life insurance , the TIFN approximate is:

being, from (18) and (5a)-(5f):

Example 2.

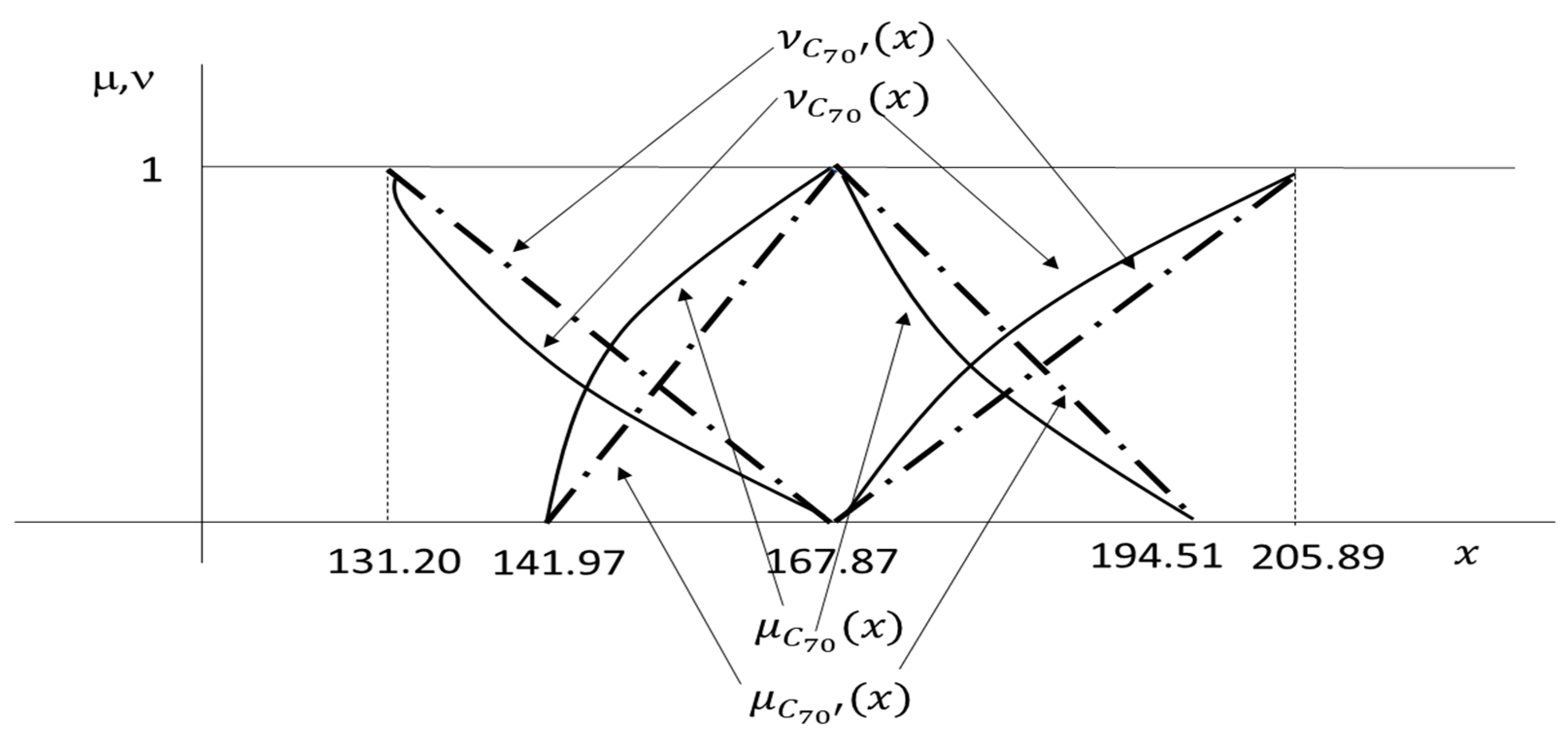

We price a whole life annuity and whole life insurance for a person aged 𝑥=65 with the same baseline death probabilities and mortality multiplier as in example 1. Likewise, we use a discount rate 𝑖=<(0.01, 0.02, 0.03) (0.0075, 0.02, 0.0325)>. Table 3 shows the <𝛼, 1-𝛼 >-cuts, 𝛼=0, 0.25, 0.5. 0.75, 1 for 65 and·65 and their TIFN approximate 65′ and 65′ in (21) and (22). The errors caused by the approximations were calculated using (6a) and (6d). It can be checked that if the input data are given by the TIFN, approximating the price of life contingencies with a linear shape provides reliable results. Note that the errors obtained by approximating TIFN were quite small. The greatest errors are produced in 65∗𝛽=65∗𝛽,65∗𝛽, in which the average error is not larger than 0.6%. Figure 2 shows the shape of 65 calculated using (20a)–(20d) and the triangular approximation (22).

4. Pricing special rate annuities and life settlements with intuitionistic fuzzy parameters

4.1. Obtaining the periodical payment of a substandard annuity with intuitionistic fuzzy number parameters

Special-rate or substandard annuities are immediate annuities that, at the commencement of the contract, consider additional pricing factors along with the policyholder's age and gender (if permissible). These factors result in the augmentation of annuity payments because of diminished life expectancy (Gatzer & Kotzki, 2016).

In accordance with Pitacco and Tabakova (2022), based on the severity of impairment (ranging from minor to major), we can distinguish enhanced life annuities, impaired annuities and care annuities. An enhanced life annuity disburses income to an individual with a slightly reduced life expectancy attributable to concrete circumstances such as smoking or adverse sociodemographic status (Drinkwater et al., 2015). The augmentation in annuity benefits (in comparison to a standard-rate life annuity with the same premium) arises predominantly from the utilization of a higher mortality assumption in specific life tables. Conversely, an impaired-life annuity yields a higher income than an enhanced life annuity, reflecting health conditions that significantly curtail the annuitant's LE (e.g., diabetes, chronic asthma, and cancer). Finally, care annuities target individuals, typically those of advanced age, with severe impairments, or individuals already in a state of senescent disability (or long-term care).

Therefore, for a whole-life substandard annuity that is underwritten with a single premium by a person with age , the annual payment is

and so

The interpretation of the discount rate as a technical interest rate, which is how it should be understood in the context of substandard annuities, is seen as a financial return assured by the company to the policyholder in the long term (Devolder, 1988). Ryan and Harbin (1998) suggest that a prudent prediction of the discount rate must be made, especially for maturities exceeding 30 years, for which there are no investment instruments ensuring an interest rate. Note that the statement provides very vague information, both in regard to the interest rate, which is simply "prudent," and the lack of knowledge that may exist about the evolution of risk-free interest rates over such long periods. In this sense, Lemaire (1990) justifies the use of a fuzzified interest rate as a "partial measure of our ignorance" of the behavior of interest rates throughout the duration of policies.

In a pension funding setting, Betzuen et al. (1997) propose, as is common practice, using Fisher's relationship between the nominal interest rate, real interest rate, and anticipated inflation to fit a fuzzy interest rate. In this regard, Devolder (1988) indicates that the real interest rate must be quantified "between 2% and 3%" and that anticipated inflation "must be reasonable in the long term." Although Devolder did not aim to justify the use of fuzzy sets when estimating interest rates, these rules represent imprecisely defined real interest rates and vague anticipated inflation rates.

Thus, let be the same single premium to buy an enhanced annuity for a person aged and IFNs death probabilities , mortality multiplier and technical interest . Function (23) and the intuitionistic fuzzy parameters used to evaluate it induce an intuitionistic payment with -cuts:

Note that the annuity payment increases with the discount rate, mortality multiplier, and standard mortality probability. Thus, is obtained by evaluating (23) using rules (2a)–(2d).

In the case where the standard one-year death probabilities, mortality multiplier, and discount rate are estimated by TIFN, allows a linear approximation (1a)–(1d):

Notice that the premium can be considered a TIFN and that in (22). Thus, by applying (4b),

Example 3.

We fit the intuitionistic fuzzy number of the annuity payment for two individuals aged years and a single premium . We use the same baseline mortality table, mortality multiplier, and technical interest rate as in example 2. Table 4 displays the <1->-cuts, =0, 0.25, 0.5, 0.75, and 1 for and and their TIFN approximate and . It can be verified that if the initial data are expressed by means of TIFNs, the approximation to , provides a practically perfect fit. The greatest errors were obtained over and , which, in any case, were on average only 0.05%. Figure 3 depicts the shape of calculated using (24a)–(24b) and its linear approximate (25), .

4.2. Pricing life settlements with intuitionistic fuzzy number parameters

In a life settlement, policyholders sell their life-contingent insurance payments to investors as lump sums. The price is determined through an individualized estimation of survival probabilities by the life insurance provider, along with a specific IRR (Braun & Xu, 2020). All else being equal, a life settlement company offers a higher payment for life insurance policy with a shorter estimated LE. This is because, on average, survival-contingent premiums must be paid for a shorter period, whereas the death benefit is disbursed sooner (Bauer et al., 2020).

Within the concept of life settlement, it is essential to distinguish between viatical settlements associated with terminal illness and those in which the policyholder does not necessarily suffer from an excessively severe impairment (Gatzer, 2010). Engaging in these types of transactions is beneficial for all participants. Policyholders with impaired LE receive a higher price than the surrender value in the early cancellation of their policies. Investors, through LSs and the bonds derived from their securitization, have alternative assets to invest in, whose returns are uncorrelated to those of conventional financial assets such as stocks and bonds. Finally, from the insurance companies’ perspective, investing in LSs can cover the longevity risk associated with life insurance contract liabilities (Kung et al., 2021).

The price of a life settlement on whole life insurance for a policyholder aged , , comes from the difference between the expected value of the death benefit and stream of premiums. In this regard, among the existing approaches to price-life settlements, the most common is the probabilistic method, which uses conventional actuarial life mathematics (Brockett et al., 2013):

where and is the death benefit if the insured person died at age =1,2,…,. ∞ and is the premium payable at age . Thus, if and are constant amounts, and , we find that

and notice that and

Establishing an IRR in the valuation of LSs requires setting an interest rate much higher than the technical interest rate at which the insurer would value the policy. This interest rate is obtained by augmenting the risk-free interest rate by adding a premium to the inversor’s assumed risk. According to an empirical study of the US life settlement market by Braun and Xu (2020), this premium can be decomposed into longevity risk (approximately 75%), premium risk (approximately 10%), and default risk (over 6%). One way to estimate this interest rate is to use recently concluded LSs with similar characteristics as a reference. This is the so-called neighborhood method (AA-Partners Ltd., 2015). While AA-Partners Ltd. (2015) reduced the set of IRRs used as a benchmark to a crisp value, Andrés-Sánchez and González-Vila (2023) proposed quantifying this set of crisp points as a TFN that retains more information than a single real value.

A common approach used to obtain IRR involves adjusting the yield spread using regression methods, which depend on proxy variables for the risks faced by investors in life insurance policies (Braun & Xu, 2020; Kung et al., 2021). The analytical frameworks provided by these regression models can be leveraged to implement fuzzy regression. This tool has been applied in other actuarial contexts, such as adjusting the term structure of interest rates (Andrés-Sánchez & Terceño, 2003; Shapiro, 2005) or adjusting mortality laws (Koissi & Shapiro, 2006; Szymański & Rossa, 2021) and claim reserving (Apaydin & Baser, 2010; Woundjiagué et al., 2019). Of course, these would yield fuzzy predictions for yield spread. Alternatively, the original econometric models of Braun and Xu (2020) and Kung et al. (2021) produce predictions through probabilistic confidence intervals that can be used to fit an FN representation by means of a probability-possibility transformation (Adjenughwure & Papadopoulos, 2020; Al-Kandari et al., 2021), which may be the basis for inducing intuitionistic quantifications by Definition 7 and Remark 7.

In the case of life settlements, if they are evaluated as IFN , and , the price for a policyholder aged years is an IFN whose cuts are denoted as:

that in the case of variable death benefits and periodical premiums can be obtained from (26) by using rules (2a)–(2d) and considering that the price of an LS decreases with respect to the discount rate and increases with respect to the one-year death probabilities and the mortality multiplier:

In the case of constant benefit and pending premiums (27), (28a)–(28d) become:

Suppose that and are TIFNs. The estimated price of life insurance policy has a linear shape:

where by applying (5a)-(5f) in relation (26):

Example 4.

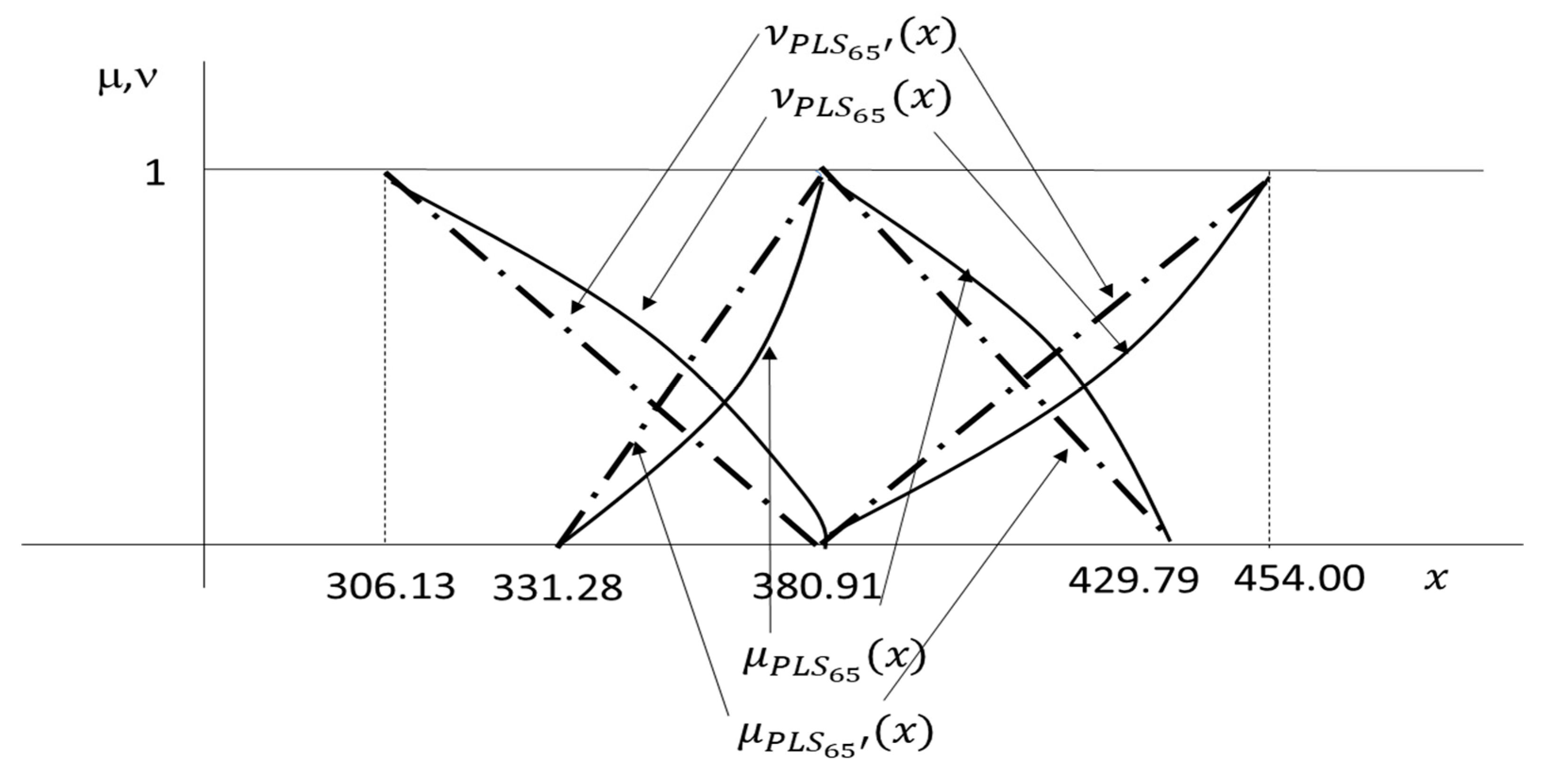

We determined the price of a life settlement for two persons aged 65 and 75 years with the same baseline death probabilities and mortality multiplier <(5, 6, 7) (4.5, 6, 7.5)>, as in the above numerical applications. The IRR is <(0.11, 0.12, 0.13) (0.105, 0.12, 0.135)>. In both cases, the death benefit is C=1000 monetary units, pending annual premiums of 14.78 monetary units. Table 5 displays -cuts for < , 1->, =0, 0.25, 0.5. 0.75, 1 of and and their TIFN approximates and . Again, we can verify that if the input data are expressed by means of TIFNs, a linear shape approximation to , provides a practically perfect fit. In all cases, the deviations are less than 0.2%. Figure 4 depicts the shape of calculated using (29a)–(29b) and its linear approximate (30), .

5. Conclusions and further research

The parameters necessary for the actuarial pricing of life contingencies, such as mortality and discount rate, are subject to several sources of imprecision and vagueness. This fact has motivated several studies that introduce these sources of uncertainty using fuzzy numbers (FNs). FNs have been applied to model uncertain variables in the field of life insurance (Lemaire, 1990; Andrés-Sánchez & González-Vila, 2012; Anzilli et al., 2018) as well as in nonlife insurance (Cummins and Derrig, 1997; Shapiro, 2004). In a more specific context of valuing life contingencies linked to impaired life expectancies (LEs), Andrés-Sánchez et al. (2020) contributed to the field of special-rate annuities, and Aalaei (2022) and Andrés-Sánchez and González-Vila (2023) did so in a life settlement setting.

Our work extends the results related to the valuation of life contingencies, especially those associated with substandard LEs, under the assumption that information on discount rates and mortality is provided by intuitionistic fuzzy numbers (IFNs). It is worth noting that to the best of our knowledge, the application of life insurance pricing using parameters estimated through IFNs is novel. Thus, the developments of Kumar and Bajaj (2014), Kahraman et al. (2015), Ersen et al. (2023), and Haktanır and Kahraman (2023) in a capital budgeting setting are extended to actuarial analysis.

The use of FNs in the context of actuarial and financial pricing allows for the introduction of epistemic uncertainty, that is, the perceived reliability of the possible values of the parameters of interest (Dubois & Prade, 2012). Therefore, FNs only allow the introduction of positive information about the feasible values of the parameter. The IFNs permit bipolatity to be added by introducing both positive and negative information regarding variables of interest. In other words, it involves not only using estimated reliable values of the variable but also their unfeasible values (Dubois & Prade, 2012).

We focused on the use of input variables estimated by triangular IFNs (TIFNs) and the approximation of the results obtained with linear shapes. Thus, as indicated by Kreinovich et al. (2020), linear shapes often provide an effective resolution for practical applications of fuzzy set theory. The interpretability of results by end users who may not necessarily have knowledge of fuzzy logic (Andrés-Sánchez & González-Vila, 2017a; Kreinovich et al., 2020) is a desirable property of using TIFNs. The calculation of the present value of life contingencies with TIFN parameters can be implemented with a very low error by evaluating five scenarios: one considered as the maximum reliability and two pairs of extreme positive and negative scenarios. Thus, the results obtained are consistent with those obtained with the application of FNs in financial-actuarial analysis. Although the actuarial functions are nonlinear, the results provide a good triangular approximation in accordance with the literature on fuzzy financial mathematics (Kaufmann, 1986; Jiménez & Rivas, 1998; Terceño et al., 2003; Heberle & Thomas, 2014; Villacorta et al., 2021; Andrés-Sánchez & González-Vila, 2023).

These extreme scenarios can be interpreted within the concept of bipolar possibility as outlined by Dubois and Prade (2012). While the extreme scenarios associated with the values considered in the membership function can be understood as reasonable extreme scenarios, those originating from the nonmembership function admit an interpretation of potential extreme situations. The developments presented can be seamlessly extended to consider a couple of values for maximum reliability scenarios instead of just one using trapezoidal IFN.

A natural continuation of this work is the introduction of uncertainty in the analysis of nonlife insurance, extending the results obtained with FN parameters to obtain claim provisions (Andrés-Sánchez, 2012; Heberle & Thomas, 2016), the discounted value of nonlife insurance liabilities (Cummins & Derrig, 1997), and the terminal value of an insurance company (Ungureanu & Vernic, 2015) using parameters estimated with IFNs instead of FNs.

The ability to represent gradualness and ontological uncertainty by fuzzy subsets (Dubois & Prade, 2012) is also susceptible to its application in life insurance pricing and insurance decision-making (Lemaire, 1990; Ostaszewki, 2003; Shapiro, 2004; Shapiro, 2013). Heterogeneity in annuities is commonly introduced by dividing policyholders into relatively broad groups based on generic impairment levels (Anderton & Robb, 1998; Olivieri & Pitacco, 2016). The use of instruments such as expert systems (Andrés-Sánchez and Gonzáles-Vila, 2020) allows consideration of the simultaneous membership of a policyholder in more than one group, assigning a level of membership to each of them. For example, if the group of annuitants with standard LE is established for those for whom =1, being the next group annuitants "slightly impaired" LE (=1.1), an annuitant with =1.01 essentially belongs to the standard annuitants' group but must have some membership degree in the "slightly impaired" group.

Author Contributions

The paper has only one author.

Funding

This research has benefited from the Research Project of the Spanish Science and Technology Ministry "Sostenibilidad, digitalizacion e innovacion: nuevos retos en el derecho del seguro" (PID2020- 117169GB-I00).

Data Availability Statement

Data on the mortality of the Spanish population are publicly available in the Human Mortality Database (https://www.mortality.org/).

Ethics Statement

Does not apply.

Conflicts of Interest

The authors declare no conflicts of interest.

References

- Aalaei, M. (2022). Pricing life settlements in the secondary market using fuzzy internal rate of return. Journal of Mathematics and Modelling in Finance, 2(2), 53-62. [CrossRef]

- AA-Partners Ltd. (2017). AAP Life Settlement Valuation. Available online: https://www.aa-partners.ch/fileadmin/files/Valuation/AAP_Life_Settlement_Valuation_-_Manual_V6.0.pdf (accessed on 10 September 2022).

- Adjenughwure, K.; Papadopoulos, B. Fuzzy-statistical prediction intervals from crisp regression models. Evol. Syst. 2020, 11, 201–213. [Google Scholar] [CrossRef]

- Al-Kandari, M.; Adjenughwure, K.; Papadopoulos, K. A Fuzzy-Statistical Tolerance Interval from Residuals of Crisp Linear Regression Models. Mathematics 2020, 8, 1422. [Google Scholar] [CrossRef]

- Anderton, W. N., & Robb, G. H. (1998). Impaired Lives Annuities. In Medical Selection of Life Risks (pp. 169-171). London: Palgrave Macmillan UK.

- Andrés Sánchez, J. D., & Gonzalez-Vila, L. (2019). A fuzzy-random extension of the Lee-Carter mortality prediction model. International Journal Of Computational Intelligence Systems, 12, 2, 775-794. [CrossRef]

- Andrés-Sanchez, J., & Gómez, A.T. (2003). Applications of fuzzy regression in actuarial analysis. Journal of Risk and Insurance, 70(4), 665-699. [CrossRef]

- Andrés-Sanchez, D., & Gonzalez-Vila, L. (2017a). Some computational results for the fuzzy random value of life actuarial liabilities. Iranian Journal of Fuzzy Systems, 14(4), 1-25. [CrossRef]

- Andrés-Sánchez, J., & Gonzalez-Vila, L. G. V. (2017b). The valuation of life contingencies: A symmetrical triangular fuzzy approximation. Insurance: Mathematics and Economics, 72, 83-94. [CrossRef]

- Andrés-Sánchez, J. (2012). Claim reserving with fuzzy regression and the two ways of ANOVA. Applied Soft Computing, 12(8), 2435-2441. [CrossRef]

- Andrés-Sánchez, J. (2014). Fuzzy claim reserving in nonlife insurance. Comput. Sci. Inf. Syst., 11(2), 825-838. [CrossRef]

- Andrés-Sánchez, J. D. (2023). Fuzzy Random Option Pricing in Continuous Time: A Systematic Review and an Extension of Vasicek’s Equilibrium Model of the Term Structure. Mathematics, 11(11), 2455. [CrossRef]

- Andrés-Sánchez, J., & Puchades, L. G. V. (2012). Using fuzzy random variables in life annuities pricing. Fuzzy sets and Systems, 188(1), 27-44. [CrossRef]

- Andrés-Sánchez, J., & Puchades, L. G. V. (2023). Life settlement pricing with fuzzy parameters. Applied Soft Computing, 148, 110924. [CrossRef]

- Andrés-Sánchez, J., Puchades, L. G. V., & Zhang, A. (2020). Incorporating fuzzy information in pricing substandard annuities. Computers & Industrial Engineering, 145, 106475. [CrossRef]

- Anzilli, L., & Facchinetti, G. (2017). New definitions of mean value and variance of fuzzy numbers: An application to the pricing of life insurance policies and real options. International Journal of Approximate Reasoning, 91, 96–113. [CrossRef]

- Anzilli, L., Facchinetti, G., & Pirotti, T. (2018). Pricing of minimum guarantees in life insurance contracts with fuzzy volatility. Information Sciences, 460, 578–593. [CrossRef]

- Apaydin A. and Baser, F. (2010). Hybrid fuzzy least-squares regression analysis in claims reserving with geometric separation method. Insur. Math. Econ., 47, 113–122. [CrossRef]

- Atanassov, K. T. (1986). Intuitionistic fuzzy sets. Fuzzy sets and Systems, 20(1), 87-96. [CrossRef]

- Atanassov, K. T. (1989). More on intuitionistic fuzzy sets. Fuzzy sets and systems, 33(1), 37-45. [CrossRef]

- Atanassova, L. (2006). On intuitionistic fuzzy versions of L. Zadeh’s extension principle. Notes on Intuitionistic Fuzzy Sets, 13(3), 33-36. Available online: https://ifigenia.org/images/b/bc/NIFS-13-3-33-36.pdf.

- Bauer, D., Russ, J., & Zhu, N. (2020). Asymmetric information in secondary insurance markets: Evidence from the life settlements market. Quantitative Economics, 11(3), 1143-1175. [CrossRef]

- Bayeg, S., & Mert, R. (2021). On intuitionistic fuzzy version of Zadeh’s extension principle. Notes on Intuitionistic Fuzzy Sets. 27, 3, 9-17. [CrossRef]

- Betzuen, A., López, M. J., & Rivas, J. A. (1997). Actuarial mathematics with fuzzy parameters: An application to collective pension plans. Fuzzy economic review, 2(2), 4. [CrossRef]

- Bhaumik, A., Roy, S.K., & Li, D.F. (2017). Analysis of triangular intuitionistic fuzzy matrix games using robust ranking. Journal of Intelligent & Fuzzy Systems, 33(1), 327-336. [CrossRef]

- Boltürk, E., & Kahraman, C. (2022). Interval-valued and circular intuitionistic fuzzy present worth analyses. Informatica, 33(4), 693-711. [CrossRef]

- Braun, A., Xu, J. (2020). Fair value measurement in the life settlement market. The Journal of Fixed Income, 29 (4), 100-123. [CrossRef]

- Brockett, P.L., Chuang, S.-L., Deng, Y., MacMinn, R.D. (2013). Incorporating longevity risk and medical information into life settlement pricing. Journal of Risk and Insurance, 80 (3), 799-826. [CrossRef]

- Buckley, J. J. (1987). The fuzzy mathematics of finance. Fuzzy sets and systems, 21(3), 257-273. [CrossRef]

- Buckley, J. J. (1992). Solving fuzzy equations in economics and finance. Fuzzy Sets and Systems, 48(3), 289-296. [CrossRef]

- Buckley, J.J., & Qu, Y. (1990). On using α-cuts to evaluate fuzzy equations. Fuzzy Sets and Systems, 38, 3, 309–312. [CrossRef]

- Bundock, G. (2006). Application Processing. In: Brackenridge, R.D.C., Croxson, R.S., MacKenzie, R. (eds) Brackenridge’s Medical Selection of Life Risks. Palgrave Macmillan, London. [CrossRef]

- Burillo, P., & Bustince, H. (1996). Construction theorems for intuitionistic fuzzy sets. Fuzzy Sets and Systems, 84(3), 271-281. [CrossRef]

- Cassú C., Planas, P., Ferrer, J. C., & Bonet, J. (1996). Accumulated capital for the retirement plans in fuzzy finance mathematics. Fuzzy economic review, 1(1), 5. [CrossRef]

- Couso, I.; Montes, S.; Gil, P. The necessity of the strong α-cuts of a fuzzy set. Int. J. Uncertain. Fuzziness Knowl.-Based Syst. 2001, 9, 249–262. [Google Scholar] [CrossRef]

- Cummins, D.J., & Derrig, R. A. (1997). Fuzzy financial pricing of property-liability insurance. North American Actuarial Journal, 1(4), 21-40. [CrossRef]

- Dębicka, J., Heilpern, S., & Marciniuk, A. (2022). Modelling Marital Reverse Annuity Contract in a Stochastic Economic Environment. Statistika: Statistics & Economy Journal, 102(3). [CrossRef]

- Derrig, R. A., & Ostaszewski, K. M. (1997). Managing the tax liability of a property-liability insurance company. Journal of Risk and Insurance, 695-711. [CrossRef]

- Devolder, P. (1988). Le taux d'actualization en assurance. Geneva Papers on Risk and Insurance, 13, 265-272. Available online: https://link.springer.com/content/pdf/10.1057/gpp.1988.20.pdf.

- Dong, W., & Shah, H. C. (1987). Vertex method for computing functions of fuzzy variables. Fuzzy sets and Systems, 24(1), 65-78. [CrossRef]

- Dong, M. G., & Li, S. Y. (2016). Project investment decision making with fuzzy information: A literature review of methodologies based on taxonomy. Journal of Intelligent & Fuzzy Systems, 30(6), 3239-3252. [CrossRef]

- Dubois, D., & Prade, H. (1993). Fuzzy numbers: an overview. Readings in Fuzzy Sets for Intelligent Systems, 112-148.

- Dubois, D., & Prade, H. (2012). Gradualness, uncertainty and bipolarity: making sense of fuzzy sets. Fuzzy sets and Systems, 192, 3-24. [CrossRef]

- Dubois, D.; Folloy, L.; Mauris, G.; Prade, H. (2004). Probability–possibility transformations, triangular fuzzy sets, and probabilistic inequalities. Reliab. Comput., 10, 273–297. Available online: https://www.irit.fr/~Henri.Prade/Papers/DFoulMauP.pdf.

- Ersen, H. Y., Tas, O., & Kahraman, C. (2018). Intuitionistic fuzzy real-options theory and its application to solar energy investment projects. Engineering Economics, 29(2), 140-150. [CrossRef]

- Ersen, H. Y., Tas, O., & Ugurlu, U. (2022). Solar Energy Investment Valuation With Intuitionistic Fuzzy Trinomial Lattice Real Option Model. IEEE Transactions on Engineering Management.). [CrossRef]

- Gatzert, N., & Klotzki, U. (2016). Enhanced annuities: Drivers of and barriers to supply and demand. The Geneva Papers on Risk and Insurance-Issues and Practice, 41, 53-77. [CrossRef]

- Gatzert, N. (2010). The secondary market for life insurance in the UnitedKingdom, Germany, and the United States: Comparison and overview. Risk Management and Insurance Review, 13 (2), 279-301. [CrossRef]

- Haktanır, E., & Kahraman, C. (2023). Intuitionistic fuzzy risk adjusted discount rate and certainty equivalent methods for risky projects. International Journal of Production Economics, 257, 108757. [CrossRef]

- Heberle, J., & Thomas, A. (2014). Combining chain-ladder claims reserving with fuzzy numbers. Insurance: Mathematics and Economics, 55, 96-104. [CrossRef]

- Heberle, J., & Thomas, A. (2016). The fuzzy Bornhuetter–Ferguson method: an approach with fuzzy numbers. Annals of Actuarial Science, 10(2), 303-321. [CrossRef]

- Jiménez, M., & Rivas, J. A. (1998). Fuzzy number approximation. International Journal of Uncertainty, Fuzziness and Knowledge-Based Systems, 6(01), 69-78. [CrossRef]

- Kahraman, C., Çevik Onar, S., & Öztayşi, B. (2015). Engineering economic analyses using intuitionistic and hesitant fuzzy sets. Journal of Intelligent & Fuzzy Systems, 29(3), 1151-1168. [CrossRef]

- Kahraman, C., Ruan, D., & Tolga, E. (2002). Capital budgeting techniques using discounted fuzzy versus probabilistic cash flows. Information Sciences, 142(1-4), 57-76. [CrossRef]

- Kaufmann, A.: (1986) Fuzzy subsets applications in OR and management. In: Jones, A., Kaufmann, A., Zimmermann, H.J. (eds.) Fuzzy sets theory and applications, pp. 257–300. Springer, Netherlands.

- Kita, M. W. (1988). The rating of substandard lives. In Medical Selection of Life Risks (pp. 61-88). London: Palgrave Macmillan UK.

- Koissi, M. C., & Shapiro, A. F. (2006). Fuzzy formulation of the Lee–Carter model for mortality forecasting. Insurance: Mathematics and Economics, 39(3), 287-309. [CrossRef]

- Kreinovich, V., Kosheleva, O., Shahbazova, S.N. (2020). Why Triangular and Trapezoid Membership Functions: A Simple Explanation. In: Shahbazova, S., Sugeno, M., Kacprzyk, J. (eds) Recent Developments in Fuzzy Logic and Fuzzy Sets. Studies in Fuzziness and Soft Computing, vol 391. Springer, Cham. [CrossRef]

- Kumar, G., & Bajaj, R. K. (2014). Implementation of intuitionistic fuzzy approach in maximizing net present value. International Journal of Mathematical and Computational Sciences, 8(7), 1069-1073.

- Kumar, P. S., & Hussain, R. J. (2015). A method for solving unbalanced intuitionistic fuzzy transportation problems. Notes on Intuitionistic Fuzzy Sets, 21(3), 54-65.

- Kung, K. L., Hsieh, M. H., Peng, J. L., Tsai, C. J., & Wang, J. L. (2021). Explaining the risk premiums of life settlements. Pacific-Basin Finance Journal, 68, 101574. [CrossRef]

- Lee, R. D., & Carter, L. R. (1992). Modelling and forecasting US mortality. Journal of the American statistical association, 87(419), 659-671. [CrossRef]

- Lemaire, J. (1990). Fuzzy insurance. ASTIN Bulletin: The Journal of the IAA, 20(1), 33-55.

- Lim, H. B., & Shyamalkumar, N. D. (2022). Evaluating Medical Underwriters in Life Settlements: Problem of Unreported Deaths. North American Actuarial Journal, 26(2), 298-322. [CrossRef]

- Lubovich, J., Sabes, J., & Siegert, P. (2008). Introduction to Methodologies Used to Price Life Insurance Policies in Life Settlement Transactions. [CrossRef]

- Mahapatra, G. S., & Roy, T. K. (2013). Intuitionistic fuzzy number and its arithmetic operation with application on system failure. Journal of uncertain systems, 7(2), 92-107. Available online: https://www.researchgate.net/publication/286377011_Intuitionistic_fuzzy_number_and_its_arithmetic_operation_with_application_on_system_failure.

- Meyricke, R., & Sherris, M. (2013). The determinants of mortality heterogeneity and implications for pricing annuities. Insurance: Mathematics and Economics, 53(2), 379-387. [CrossRef]

- Mircea, I., & Covrig, M. (2015). A discrete time insurance model with reinvested surplus and a fuzzy number interest rate. Procedia Economics and Finance, 32, 1005-1011. [CrossRef]

- Mitchell, H. B. (2004). Ranking-intuitionistic fuzzy numbers. International Journal of Uncertainty, Fuzziness and Knowledge-Based Systems, 12(03), 377-386. [CrossRef]

- Muzzioli, S., & De Baets, B. (2016). Fuzzy approaches to option price modeling. IEEE Transactions on Fuzzy Systems, 25(2), 392-401. [CrossRef]

- Nguyen, H.T. (1978). A note on the extension principle for fuzzy sets, J. of Mathematical Analysis and Aplications 64 (1978) 369-380. [CrossRef]

- Nowak, P., & Romaniuk, M. (2017). Catastrophe bond pricing for the two-factor Vasicek interest rate model with automatized fuzzy decision making. Soft Computing, 21, 2575-2597. [CrossRef]

- Olivieri, A. (2006). Heterogeneity in survival models. Applications to pensions and life annuities. Belgian Actuarial Bulletin, 6(1), 23–39. [CrossRef]

- Olivieri, A., & Pitacco, E. (2016). Frailty and risk classification for life annuity portfolios. Risks, 4(4), 39. [CrossRef]

- Pitacco, E. (2017). Life Annuities. Products, Guarantees, Basic Actuarial Models. Available online: https://ssrn.com/abstract=2887359. [CrossRef]

- Pitacco, E. (2019). Heterogeneity in mortality: a survey with an actuarial focus. European Actuarial Journal, 9, 3-30. [CrossRef]

- Pitacco, E., & Tabakova, D. Y. (2022). Special-rate life annuities: analysis of portfolio risk profiles. Risks, 10(3), 65. [CrossRef]

- Promislow, S. D. (2014). Fundamentals of actuarial mathematics. John Wiley & Sons.

- Rasheed, F., Kousar, S., Shabbir, J., Kausar, N., Pamucar, D., & Gaba, Y. U. (2021). Use of intuitionistic fuzzy numbers in survey sampling analysis with application in electronic data interchange. Complexity, 2021, 1-12. [CrossRef]

- Richards, S. J. (2008). Applying survival models to pensioner mortality data. British Actuarial Journal, 14(2), 257-303. [CrossRef]

- Ryan Jr, J. A., & Harbin, R. F. (1998). Structured settlements. In Medical Selection of Life Risks (pp. 173-180). London: Palgrave Macmillan UK.

- Sfiris, D.S.; Papadopoulos, B.K. Nonasymptotic fuzzy estimators based on confidence intervals. Inf. Sci. 2014, 279, 446–459. [Google Scholar] [CrossRef]

- Shapiro, A. F. (2004). Fuzzy logic in insurance. Insurance: Mathematics and Economics, 35(2), 399-424. [CrossRef]

- Shapiro, A. F. (2005). Fuzzy regression models. Article of Penn State University, 102(2), 373-383.

- Shapiro, A. F. (2013). Modelling future lifetime as a fuzzy random variable. Insurance: Mathematics and Economics, 53(3), 864-870. [CrossRef]

- Shen, Y., & Chen, W. (2012). Multivariate extension principle and algebraic operations of intuitionistic fuzzy sets. Journal of Applied Mathematics. Article ID 845090. [CrossRef]

- Szymański, A., & Rossa, A. (2021). The modified fuzzy mortality model based on the algebra of ordered fuzzy numbers. Biometrical Journal, 63(3), 671-689. [CrossRef]

- Terceño, A., Andrés-Sánchez, J., Barberà, G., & Lorenzana, T. (2003). Using fuzzy set theory to analyse investments and select portfolios of tangible investments in uncertain environments. International Journal of Uncertainty, Fuzziness and Knowledge-Based Systems, 11(03), 263-281. [CrossRef]

- Tereszkiewicz, P., & Południak-Gierz, K. (2021). Liability for incorrect client personalization in the distribution of consumer insurance. Risks, 9(5), 83. [CrossRef]

- Terceno, A., Andrés-Sánchez, J., Belvis, C., & Barbera, G. (1996). Fuzzy methods incorporated to the study of personal insurances. In 1st International Symposium on Neuro-Fuzzy Systems, AT'96. Conference Report (pp. 187-202). IEEE.

- Ungureanu, D., & Vernic, R. (2015). On a fuzzy cash flow model with insurance applications. Decisions in Economics and Finance, 38, 39-54. [CrossRef]

- Villacorta, P. J., González-Vila Puchades, L., & de Andrés-Sánchez, J. (2021). Fuzzy Markovian Bonus-Malus Systems in Nonlife Insurance. Mathematics, 9(4), 347. [CrossRef]

- Woundjiagué, A.; Bidima, M.L.D.M.; Mwangi, R.W. (2019). A fuzzy least-squares estimation of a hybrid log-poisson regression and its goodness of fit for optimal loss reserves in insurance. International Journal of Fuzzy Systems, 21, 930-944. [CrossRef]

- Wu, L., Liu, J. F., Wang, J. T., & Zhuang, Y. M. (2016). Pricing for a basket of LCDS under fuzzy environments. SpringerPlus, 5(1), 1-12. [CrossRef]

- Zadeh, L. A. (1965). Fuzzy sets. Information and control, 8(3), 338-353. [CrossRef]

- Xu, J. (2020) Dating death: An empirical comparison of medical underwriters in the US life settlement market, North Am. Actuar. J. 24 (1) 36–56. [CrossRef]

- Xu, J., Hoesch, A. (2018) Predicting longevity: An analysis of potential alternatives to life expectancy reports, J. Invest. 27 (supplement) 65–79. 79. [CrossRef]

Figure 1.

Triangular intuitionistic fuzzy number.

Figure 2.

Shapes of and its triangular approximate .

Figure 3.

Shapes of and its triangular approximate .

Figure 4.

Shapes of and its triangular approximate .

Table 1.

Contributions to the financial-actuarial valuation of the arithmetic of fuzzy numbers and.

| Issue | Papers |

|---|---|

| Life insurance pricing (cash-flow discounting) | Lemaire (1990), Ostaszewski (1993), Terceño et al. (1996), Andrés-Sánchez and Terceño (2003), Shapiro (2004), Andrés-Sánchez and González-Vila (2012), Andrés-Sánchez and González-Vila (2017a), Andrés-Sánchez and González-Vila (2017b), Andrés-Sánchez et al. (2020), Aalaei (2022), Dębicka et al. (2022), Andrés-Sánchez and González-Vila (2023). |

| Life insurance pricing (final value) |

Cassú et al. (1996), Betzuen et al. (1997), |

| Insurance pricing (option pricing) |

Anzilli and Fachinetti (2017), Nowak & Romaniuk (2017), Anzilli et al. (2018). |

| Nonlife insurance (cash-flow discounting) |

Derrig and Ostazewski (1997), Cummins and Derrig (1997), Andrés-Sánchez and Terceño (2003), Andrés-Sánchez (2014), |

| Nonlife insurance (terminal value) |

Mircea and Covrig (2015), Ungureanu and Vernic (2015), |

| Claim reserving | Andrés-Sánchez and Terceño (2003), Shapiro (2004), Apaydin and Baser (2010), Andrés-Sánchez (2012), Heberle and Thomas (2014), Heberle and Thomas (2016), Woundjiagué et al. (2019). |

Table 2.

-cuts of and , their triangular approximations and and the measurement of the approximation errors.

Table 2.

-cuts of and , their triangular approximations and and the measurement of the approximation errors.

| 10-year life probability for x=65 | Life expectancy for x=65 | ||||||||

|---|---|---|---|---|---|---|---|---|---|

| α | β | ||||||||

| 1 | 0 | 0.4592 | 0.4592 | 0.4592 | 0.4592 | 9.10 | 9.10 | 9.10 | 9.10 |

| 0.75 | 0.25 | 0.4439 | 0.4749 | 0.4364 | 0.4830 | 8.87 | 9.34 | 8.77 | 9.47 |

| 0.5 | 0.5 | 0.4290 | 0.4912 | 0.4146 | 0.5079 | 8.66 | 9.59 | 8.45 | 9.86 |

| 0.25 | 0.75 | 0.4146 | 0.5079 | 0.3938 | 0.5340 | 8.45 | 9.86 | 8.16 | 10.29 |

| 0 | 1 | 0.4007 | 0.5252 | 0.3740 | 0.5612 | 8.26 | 10.15 | 7.89 | 10.77 |

| α | β | ||||||||

| 1 | 0 | 0.4592 | 0.4592 | 0.4592 | 0.4592 | 9.10 | 9.10 | 9.10 | 9.10 |

| 0.75 | 0.25 | 0.4445 | 0.4757 | 0.4379 | 0.4847 | 8.89 | 9.36 | 8.80 | 9.52 |

| 0.5 | 0.5 | 0.4299 | 0.4922 | 0.4166 | 0.5102 | 8.68 | 9.62 | 8.50 | 9.94 |

| 0.25 | 0.75 | 0.4153 | 0.5087 | 0.3953 | 0.5357 | 8.47 | 9.88 | 8.19 | 10.35 |

| 0 | 1 | 0.4007 | 0.5252 | 0.3740 | 0.5612 | 8.26 | 10.15 | 7.89 | 10.77 |

| α | β | ||||||||

| 1 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| 0.75 | 0.25 | 0.0015 | 0.0015 | 0.0034 | 0.0035 | 0.002 | 0.002 | 0.004 | 0.006 |

| 0.5 | 0.5 | 0.0021 | 0.0020 | 0.0047 | 0.0045 | 0.002 | 0.003 | 0.005 | 0.008 |

| 0.25 | 0.75 | 0.0016 | 0.0015 | 0.0037 | 0.0033 | 0.002 | 0.002 | 0.004 | 0.006 |

| 0 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

|

0.0017 =0.0017 0.0017 |

0.0039 =0.0038 0.0038 |

0.0020 =0.0026 =0.0023 |

0.0043 0.0062 0.0053 |

||||||

Note: the errors are expressed over unity by using (6a)-(6d).

Table 3.

-cuts of and , their triangular approximations and and the measurement of the approximation errors.

Table 3.

-cuts of and , their triangular approximations and and the measurement of the approximation errors.

| Whole life annuity | Whole life insurance | ||||||||

|---|---|---|---|---|---|---|---|---|---|

| α | β | ||||||||

| 1 | 0 | 797.57 | 797.57 | 797.57 | 797.57 | 82.40 | 82.40 | 82.40 | 82.40 |

| 0.75 | 0.25 | 767.44 | 829.95 | 756.02 | 843.58 | 80.12 | 84.66 | 79.43 | 85.30 |

| 0.5 | 0.5 | 739.34 | 864.85 | 718.32 | 894.83 | 77.81 | 86.91 | 76.39 | 88.14 |

| 0.25 | 0.75 | 713.06 | 902.56 | 683.94 | 952.27 | 75.47 | 89.13 | 73.26 | 90.92 |

| 0 | 1 | 688.45 | 943.44 | 652.47 | 1017.14 | 73.11 | 91.33 | 70.04 | 93.65 |

| α | β | ||||||||

| 1 | 0 | 797.57 | 797.57 | 797.57 | 797.57 | 82.40 | 82.40 | 82.40 | 82.40 |

| 0.75 | 0.25 | 770.29 | 834.04 | 761.30 | 852.46 | 80.08 | 84.63 | 79.31 | 85.21 |

| 0.5 | 0.5 | 743.01 | 870.51 | 725.02 | 907.35 | 77.75 | 86.87 | 76.22 | 88.02 |

| 0.25 | 0.75 | 715.73 | 906.97 | 688.74 | 962.25 | 75.43 | 89.10 | 73.13 | 90.83 |

| 0 | 1 | 688.45 | 943.44 | 652.47 | 1017.14 | 73.11 | 91.33 | 70.04 | 93.65 |

| α | β | ||||||||

| 1 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| 0.75 | 0.25 | 0.0037 | 0.0049 | 0.0070 | 0.0105 | 0.0005 | 0.0003 | 0.0015 | 0.0010 |

| 0.5 | 0.5 | 0.0050 | 0.0065 | 0.0093 | 0.0140 | 0.0007 | 0.0004 | 0.0022 | 0.0013 |

| 0.25 | 0.75 | 0.0037 | 0.0049 | 0.0070 | 0.0105 | 0.0005 | 0.0003 | 0.0018 | 0.0009 |

| 0 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

|

= 0.00248 =0.00327 =0.00288 |

=0.00466 =0.00700 0.00583 |

=0.00082 =0.00056 =0.00069 |

=0.00271 =0.00166 =0.00218 |

||||||

Note: The present values are expressed in over 100 monetary units, y, and the measure of errors over unity using (6a)–(6d).

Table 4.

-cuts of and , their triangular approximations and and the measurement of the approximation errors.

Table 4.

-cuts of and , their triangular approximations and and the measurement of the approximation errors.

| α | β | ||||||||

| 1 | 0 | 125.38 | 125.38 | 125.38 | 125.38 | 167.87 | 167.87 | 167.87 | 167.87 |

| 0.75 | 0.25 | 120.49 | 130.30 | 118.54 | 132.27 | 161.33 | 174.46 | 158.59 | 177.24 |

| 0.5 | 0.5 | 115.63 | 135.26 | 111.75 | 139.21 | 154.83 | 181.09 | 149.39 | 186.69 |

| 0.25 | 0,75 | 110.80 | 140.24 | 105.01 | 146.21 | 148.38 | 187.78 | 140.26 | 196.24 |

| 0 | 1 | 106.00 | 145.25 | 98.32 | 153.26 | 141.97 | 194.51 | 131.20 | 205.89 |

| α | β | ||||||||

| 1 | 0 | 125.38 | 125.38 | 125.38 | 125.38 | 167.87 | 167.87 | 167.87 | 167.87 |

| 0.75 | 0.25 | 120.53 | 130.35 | 118.61 | 132.35 | 161.39 | 174.53 | 158.70 | 177.37 |

| 0.5 | 0.5 | 115.69 | 135.32 | 111.85 | 139.32 | 154.92 | 181.19 | 149.54 | 186.88 |

| 0.25 | 0.75 | 110.84 | 140.29 | 105.08 | 146.29 | 148.44 | 187.85 | 140.37 | 196.38 |

| 0 | 1 | 106.00 | 145.25 | 98.32 | 153.26 | 141.97 | 194.51 | 131.20 | 205.89 |

| α | β | ||||||||

| 1 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| 0.75 | 0.25 | 0.00038 | 0.00035 | 0.00061 | 0.00061 | 0.00041 | 0.00041 | 0.00073 | 0.00077 |

| 0.5 | 0.5 | 0.00052 | 0.00045 | 0.00085 | 0.00078 | 0.00057 | 0.00052 | 0.00101 | 0.00099 |

| 0.25 | 0.75 | 0.00041 | 0.00033 | 0.00066 | 0.00056 | 0.00044 | 0.00038 | 0.00078 | 0.00071 |

| 0 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

|

= 0.00026 = 0.00023 = 0.00024 |

= 0.00042 = 0.00040 0.00041 |

= 0.00028 = 0.00027 = 0.00027 |

= 0.00050 = 0.00050 0.00050 |

||||||

Note: The annuity payment is calculated using a pure premium of 1000 monetary units and errors over unity and using (6a)–(6d).

Table 5.

-cuts of and , their triangular approximations and and the measurement of the approximation errors. The benefit of life insurance is , and the annual constant premiums

Table 5.

-cuts of and , their triangular approximations and and the measurement of the approximation errors. The benefit of life insurance is , and the annual constant premiums

| α | β | ||||||||

| 1 | 0 | 380.91 | 380.91 | 380.91 | 380.91 | 597.07 | 597.07 | 597.07 | 597.07 |

| 0.75 | 0.25 | 368.58 | 393.19 | 362.39 | 399.32 | 585.46 | 608.44 | 579.56 | 614.05 |

| 0.5 | 0.5 | 356.20 | 405.43 | 343.77 | 417.63 | 573.60 | 619.59 | 561.48 | 630.52 |

| 0.25 | 0.75 | 343.77 | 417.63 | 325.02 | 435.86 | 561.48 | 630.52 | 542.79 | 646.53 |

| 0 | 1 | 331.28 | 429.79 | 306.13 | 454.00 | 549.09 | 641.25 | 523.44 | 662.09 |

| α | β | ||||||||

| 1 | 0 | 380.91 | 380.91 | 380.91 | 380.91 | 597.07 | 597.07 | 597.07 | 597.07 |

| 0.75 | 0.25 | 368.50 | 393.13 | 362.21 | 399.18 | 585.07 | 608.11 | 578.66 | 613.33 |

| 0.5 | 0.5 | 356.09 | 405.35 | 343.52 | 417.45 | 573.08 | 619.16 | 560.26 | 629.58 |

| 0.25 | 0.75 | 343.69 | 417.57 | 324.82 | 435.73 | 561.08 | 630.20 | 541.85 | 645.84 |

| 0 | 1 | 331.28 | 429.79 | 306.13 | 454.00 | 549.09 | 641.25 | 523.44 | 662.09 |

| α | β | ||||||||

| 1 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| 0.75 | 0.25 | 0.00021 | 0.00016 | 0.00050 | 0.00034 | 0.0007 | 0.0005 | 0.0015 | 0.0012 |

| 0.5 | 0.5 | 0.00029 | 0.00021 | 0.00072 | 0.00043 | 0.0009 | 0.0007 | 0.0022 | 0.0015 |

| 0.25 | 0.75 | 0.00023 | 0.00015 | 0.00059 | 0.00030 | 0.0007 | 0.0005 | 0.0017 | 0.0011 |

| 0 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

|

= 0.00014 = 0.00011 = 0.00012 |

= 0.00035 = 0.00022 0.00029 |