Submitted:

18 March 2024

Posted:

18 March 2024

You are already at the latest version

Abstract

Business-to-business (B2B) manufacturing companies are increasingly confronted with transformative trends such as sustainability, digitalization, and servitization. These trends are changing how product portfolios are developed, and value contributions are assessed, and therefore have disruptive potential. Dealing with these disruptive factors in Product Portfolio Management (PPM) is a largely unexplored topic. This study presents an empirical-qualitative exploration that contributes significantly to the field. The aim is to clarify the extent to which disruptive factors influence the evaluation and shaping of the product portfolio in B2B manufacturing companies. The Gioia method was used to evaluate 21 semi-structured interviews with experts from leading B2B manufacturing companies. Eight overarching challenges in PPM resulting from the disruptive factors were identified. Based on the eight overarching challenges and their associated causal relationships, two aggregated dimensions of action were derived: (1) increasing speed and flexibility by using generative artificial intelligence (AI) in a defined PPM process and (2) adjusting the product portfolio evaluation to consider various strategic drivers. These two dimensions of action call for future research to overcome the disruptive factors in PPM.

Keywords:

product portfolio management

; disruption

; digitalization

; sustainability

; servitization

; generative artificial intelligence

; decision-making

; value-oriented

; business model

; b2b

; manufacturing

1. Introduction

Managing product portfolios is a strategic task for manufacturing companies [1]. In the European Economic Area in particular [2], manufacturing companies are facing rising sustainability requirements that challenge their established approaches to product portfolio management [3,4]. The goals set out in the Paris Climate Agreement and European Green Deal for climate neutrality [5] are increasingly transferred to the corporate level, with some companies, such as Henkel [6] and Siemens [7], aiming to achieve carbon neutrality already by 2030. This affects their value chains and product carbon footprint, which is the total amount of greenhouse gas emissions caused by a product or service throughout its lifecycle [8,9].

Faced with increasing sustainability requirements, many manufacturing companies are also experiencing stagnant or even declining product sales. Managing a diversified range of offerings is therefore gaining importance in B2B industries. [1,10,11] Manufacturing companies such as Jungheinrich [12], Trumpf [13], and Heidelberger Druckmaschinen [14] have recognized a growing need for service orientation, also known as servitization [15], as a strategic response to this challenge [16,17,18]. This development is further accelerated by digitalization, which not only opens up additional revenue opportunities [19] through data-based services [14,20] but also promises growing market shares [21,22].

These new market influences are recognized and explored as disruptive factors in this study. Disruptive factors have the potential to fundamentally change and replace established structures and processes. They may require a reassessment of a company's existing products and services, and necessitate the need for strategic realignment or business model innovation. Companies must recognize these disruptive factors and react accordingly to secure or expand their market position. [23,24,25]

Product Portfolio Management (PPM) is a sub-discipline of strategic management that evaluates, optimizes, and controls existing and future product-market activities with a long-term perspective [1,26]. Compared to product management, PPM adopts a higher-level perspective to allocate resources according to their strategic relevance and prioritization of measures. Product managers, in contrast, are more focused on implementing individual product strategies [26,27,28]. In recent publications, PPM also includes services, hybrid product-service bundles, and digital offerings in the context of digitalization [29,30,31,32]. Occasionally it is also referred to as a solution portfolio [33,34]. According to [28], [35] and [31], PPM has three main objectives: (1) maximizing the value of the portfolio, (2) ensuring strategic fit with corporate goals, and (3) balancing short-term profitability with long-term growth opportunities.

Faced with disruptive factors, companies need to expand their core offerings and adapt their product portfolio accordingly [25,36]. Traditional PPM methods, such as the two-dimensional market share/market growth matrix of the Boston Consulting Group or the technology portfolio matrix according to Pfeiffer, are hardly suited to respond to disruptive challenges and increasing complexity [32,37]: According to [38] and [39], managing various business and revenue models in a portfolio, such as one-time sales of physical products and recurring revenue from service-oriented offerings, remains an unexplored area. [40] and [31] argue that focusing solely on individual offerings, such as services or physical products, can lead to a misallocation of resources. Therefore, it is necessary to take a comprehensive approach to the product portfolio throughout its entire life cycle. Other disruptive factors, such as sustainability requirements, are not taken into account in the portfolio alignment according to [41]. This may result in companies not being properly positioned in the context of long-term climate change. Moreover, traditional PPM methods are insufficient in considering the bundling of services, such as product-service systems, or the provision of ecosystem services with partner companies, as stated in [34].

In sum, decision-making processes regarding product portfolio strategy may not sufficiently represent disruptive factors [25,32,36,41,42]. As stated by [43] and [44], uncontrolled expansion of the product portfolio, based on outdated approaches and methods that do not consider disruptive factors, can lead to profit losses.

Therefore, this study aims to identify and specify challenges and best practices in dealing with disruptive factors in PPM. More specifically, we raise the following research question: To what extent do disruptive factors influence the evaluation and shaping of product portfolios in manufacturing B2B companies? Based on surveys with 21 industry experts and employing the Gioia method, eight key challenges and two action plans were identified. This study contributes to both, theory and practice. It highlights key challenges companies face when adapting their PPM to disruptive factors to ensure their competitiveness and promote long-term growth. The results of this study also enhance the understanding of PPM in a transformative environment and provide a starting point for further research in this dynamic field.

2. Materials and Methods

The research design of an empirical-qualitative investigation was chosen for the study to answer the research question and to uncover previously neglected phenomena and interrelationships in managing disruptive factors in PPM [45].

2.1. Preparation and Creation of the Semi-Structured Interview Questionnaire

To create a semi-structured interview questionnaire, initial basic research was conducted, and informal conversations were held with industry experts at the world’s leading industrial trade fair in Hannover in 2023. Against this backdrop, a set of theses was formulated and then incorporated into the interview questionnaire. The questionnaire is divided into four sections: (1) Classification of the experts and current situation of PPM, (2) challenges and influencing factors in PPM, (3) best practices to cope with disruptive factors, and (4) requirements for a new methodology to deal with these challenges. An excerpt with exemplary questions in the four sections is shown in Table 1.

The questionnaire also includes a brief introduction and description of the research objective, as well as relevant definitions of PPM and disruptions provided to the experts before the interviews.

2.2. Data Collection

Upon completing the questionnaire, experts from leading companies in the B2B manufacturing industry were contacted, focusing on strategic decision-makers, executives, or employees in the portfolio or product management field. A total of 21 interviews were conducted between July 2023 and February 2024. The interviews were conducted online via Microsoft Teams, either in German or Englisch, and lasted on average 45 minutes. The interviews were recorded with the experts' consent, and the transcripts were subsequently anonymized. An exception is the last interview, where no real expert was interviewed but the program ChatGPT, as already investigated by [46]. In this case, ChatGPT was instructed to assume the role of a product portfolio manager in a medium-sized B2B manufacturing company. Table 2 provides an overview of the respondents. In addition, two experts organized follow-up workshops to obtain more in-depth knowledge about the PPM in the two companies.

2.3. Data Analysis

The Gioia method [47] was chosen for analyzing the interview transcripts. This method represents a systematic approach to analyzing qualitative data, commonly used in empirical social research, particularly in studies with exploratory character. It enables the identification of patterns and themes from various qualitative data, leading to the development of theoretical insights and models. A major advantage of the Gioia method is its transparency and comprehensibility. It clearly structures the analysis process using a data structure based on first and second-order concepts, and gradually condenses empirical observations into theoretical constructs. [47,48] In this study, the codings of the interview transcripts were first aggregated into primary themes, which were then embedded into overarching second-order challenges. These challenges further led to aggregated third-order dimensions and their associated causal relationships. The Gioia method is described as the most popular and widely accepted template for interpretive qualitative research due to its rigorous analytical process [48]. The interview transcripts were coded using the MAXQDA program. DeepL was used for the translation of German quotes. Parts of the quoted text have been reworded to reduce colloquialisms.

3. Results

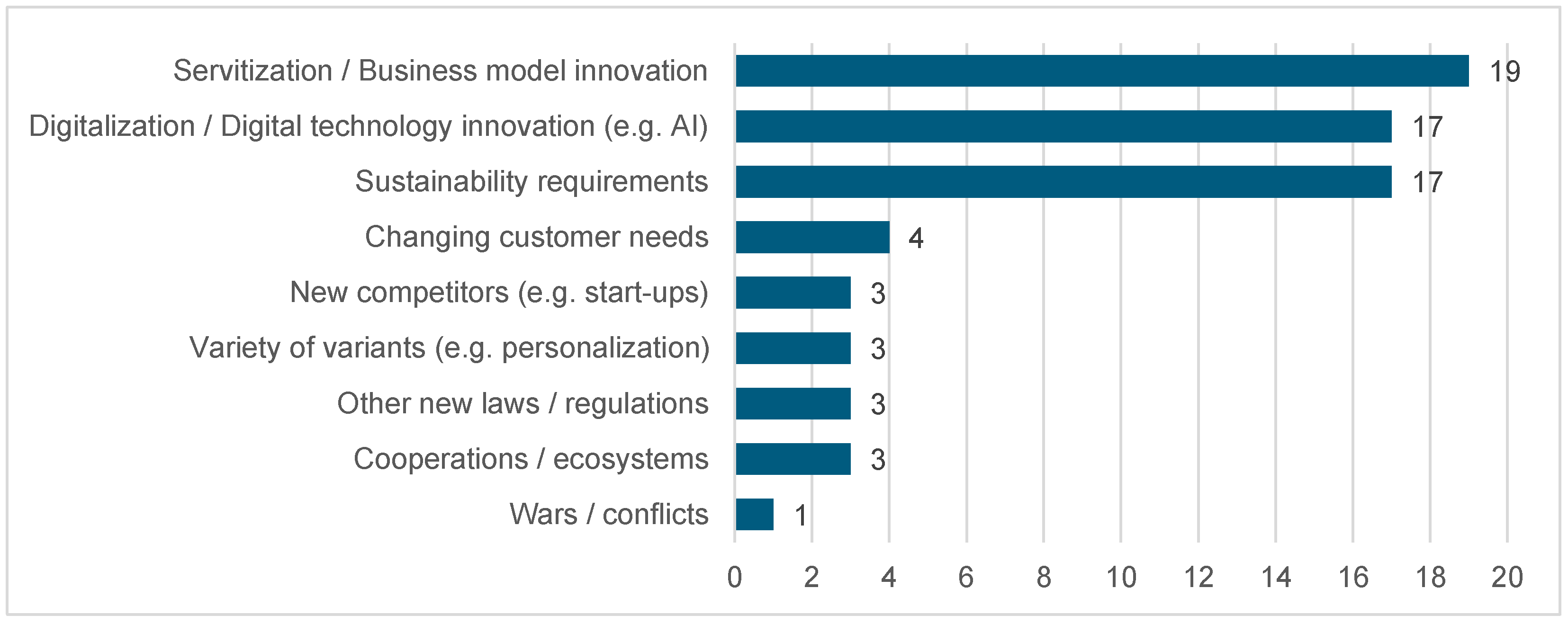

Various factors can have a disruptive effect on the product portfolio and thus lead to new challenges [42]. According to the interviews, the megatrends of sustainability, digitalization, and servitization are among the strongest influencing factors (Figure 1). Nineteen experts identified a stronger service orientation, often together with digitalization, as a driver for new business models such as subscriptions. 17 experts mentioned the regulatory requirements related to sustainability, while another 17 highlighted digitalization as a driver for technological innovations such as AI. Occasionally, additional topics such as changing customer needs (4) or variety through personalization (3) were mentioned. According to an expert, these factors are considered challenging 'evergreens' in PPM (I6).

These disruptive factors lead to eight overarching challenges, discussed in more detail below.

3.1. Eight Second-Order Challenges in PPM Due to Disruptive Factors

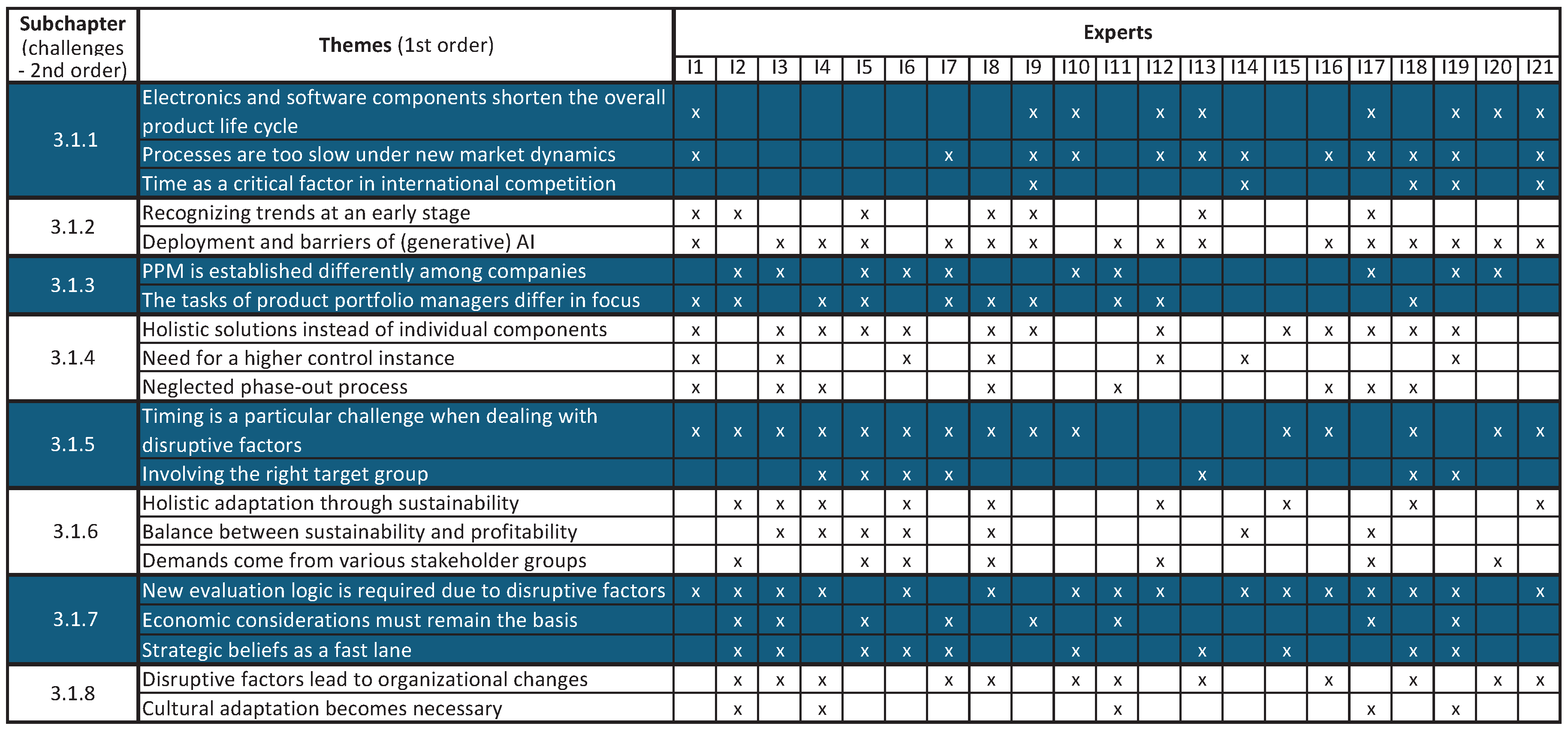

In the following, the eight overarching challenges (2nd order) are described, which, in turn, are made up of different themes (1st order) identified in the expert interviews. Figure 2 outlines wich topics the experts contributed to. It serves as an introduction to the following subsections, representing the eight challenges.

3.1.1. Accelerating Product Life Cycles under Disruptive Market Conditions

Electronics and software components shorten the overall product life cycle: A central challenge in PPM is the emergence of new market dynamics due to shorter product life cycles resulting from the integrated use of electronics and software components (I1, I9, I10, I12, I17, I19). This trend is seen as a direct consequence of digitalization and rapid technological advancements. In the past, products or systems could remain on the market for up to 30 years. Nowadays, companies are forced to renew their products and especially their software components much more frequently, sometimes quarterly, to remain competitive. This creates a tension between the different lifecycles of hardware and software components (I9, I13, I17, I21). In the automotive sector, the challenge is to bring short-cycle software functions to life in the vehicles (I20).

"We notice that the greater the proportion of electrical and software components, the shorter the product life cycle becomes [...] The question is then to what extent the life cycles of the hardware have to be adapted, if the product life cycle for electrical components is 7 years, and even less for software components, then the mechanics do not have to last for 20-30 years." (I17)

Processes are too slow under new market dynamics: Customer feedback can quickly be gathered in the digital world, but this also means the market changes more rapidly (I13). Twelve respondents recognize the need to adapt quickly to market changes and emphasize the importance of agility and efficient decision-making processes. They noted that traditional, slow process structures and decision-making are no longer sufficient. Instead, decisions must be made quickly based on valid input criteria focusing on industrial suitability (I10).

„The more digital the portfolio becomes, the more dynamic it becomes. In the past, you might have brought out new releases every two years. Nowadays, new releases are sometimes necessary every 12 weeks. As a result, your portfolio has to become smaller, or the processes have to become faster and more efficient." (I12)

Time as a critical factor in international competition: The time for adapting the product portfolio has become a stronger competitive factor and requires appropriate conditions to be internationally competitive (I9, I14). „Time is money, so whoever is fastest on the market, for example, when it comes to AI, will do the business [...] Germany is sometimes relatively slow compared to other countries such as China and the USA in terms of process structures and other hurdles such as more norms. This is a major obstacle to competition.“ (I9) As a result, some experts (I9, I14, I18, I19, I21) call for a change in mindset, advocating faster release and testing of new ideas, such as minimum viable products (MVPs). „The sales department is still used to presenting prototypes that have already been intensively tested.“ (I19)

3.1.2. Difficulties with Technology and Trend Radar as Well as the Use of AI

Recognizing trends at an early stage: Another challenge is detecting (disruptive) trends early and responding quickly to avoid falling behind (I1, I2). However, researching new technologies and trends is often time-consuming and uncertain, especially when technologies reach a relevant level of maturity or a “tipping point” (I2, I13, I17).

„Researching new technologies and trends involves a great deal of effort and usually also a bit of shooting in the dark about when these technologies have reached the tipping point of relevant maturity.“ (I2)

The need to continuously monitor new market influences and adjust the portfolio accordingly has been emphasized to keep the core business attractive (I5). The challenge is to keep up with the speed of trends, especially in an industry such as mechanical engineering, where developments are traditionally time-consuming (I8), although the development speed is currently increasing due to technologies such as AI (I9). To remain competitive, it is necessary to have resources that can screen the market (I13).

„Just observing all the launches by OpenAI shows how incredibly complex it is. It requires multiple individuals who truly understand the impact these trends have on your product.“ (I13)

Deployment and barriers of (generative) AI: In this context, ten interviews proactively addressed the potential of generative AI, particularly in the areas of technology scouting and competitive analysis, to uncover new perspectives and improve reaction time.

„Today, the product manager or portfolio manager collects the data. While there is a wealth of valuable information online, it must be evaluated properly. However, there is certainly room for improvement. I believe that with the help of AI, much more can be done to identify competitors and markets.“ (I1)

Although nine of the surveyed experts already use AI models in their range of smart services, they do not yet have an established management processes with AI support.

„Currently, no AI is in use. However, it is in the pipeline that AI will be used in the future for scenario simulations, for example, to provide decision-making aids or suggestions for portfolio adjustments.“ (I3)

Nevertheless, seven companies reported conducting initial tests with generative AI, such as ChatGPT or various copilots. A major obstacle to the use of AI, which was addressed in the context of prescriptive AI and the data collection, is data quality and overcoming data silos between different business areas. Different systems and data structures are sometimes used, which need to be standardized, for example, to implement a smart monitoring platform for PPM (I3, I7, I12, I18, I19). The use of tools such as ChatGPT has also been criticized. For instance, in small industries with few competitors, ChatGPT answers may originate from the company's own website (I19). In addition, an in-house model may only be used internally, such as for knowledge transfer (I19), due to data security concerns with sensitive information (I16, I19, I20).

3.1.3. Lack of Clarity on PPM Roles and Responsibilities

PPM is established differently among companies: The expert interviews reveal that companies have established different areas of responsibility for PPM. In some companies, PPM is centrally organized and plays a cross-functional role, for example, in incorporating cross-product requirements into the portfolio, which is not possible from the business units due to limitations and local requirements (I2, I3, I6, I7, I20). In other companies, product managers or product management leadership are responsible for PPM (I2, I5, I6, I10, I11, I19). For three respondents, the two aspects are handled differently even within the company (I2, I7, I11).

„From an academic perspective, it is common and also companies with a certain history in portfolio management often have an overarching strategic portfolio level and then the underlying product management level [...] However, in companies that are still on their way there, we see that product management as such is still very strong and also more widespread in general than the portfolio perspective.“ (I6)

Changes to the product portfolio or discontinuations are also organized differently in the companies. Strategic adjustments are typically made through a portfolio board of leaders from various business areas and the C-level management in a semi-annual (I5, I10) or annual (I7, I17) cycle. Operational adjustments are also coordinated on a shorter cycle at a lower hierarchical level (I7, I10, I21).

The tasks of product portfolio managers differ in focus: The focus of product portfolio managers also varies among companies. For some experts, the focus of their tasks is to address sustainabilitye requirements, such as reducing the product carbon footprint (I1, I11, I18). Other companies focus on coordinating the overall solution, such as products with digital components and services, to harmonize cybersecurity or interface requirements, as they affect the portfolio differently in various business areas (I11, I12). In some companies, services and physical products are managed separately (I2, I4, I7, I8, I11), while in others, portfolio managers are responsible for both areas (I5, I9, I12). It is, therefore, not surprising that all interviewed experts report using self-developed analysis tools. These tools are typically based on well-known methods such as the BCG Matrix, Pareto analysis, life cycle analysis, or similar but they are then adjusted to company-specific requirements using utilities like Excel.

„This is actually a customized Excel spreadsheet that provides an assessment based on key information and shows where products are positioned in the portfolio, enabling the corresponding decisions to be made.“ (I18)

3.1.4. Rising Product Portfolio Complexity

Holistic solutions instead of individual components: Traditionally, the product portfolio of manufacturing companies was dominated by physical goods. Twelve experts report that, in the context of digitalization, the service business is increasingly becoming a core part of companies' operations and a differentiating factor.

„We're more part of the chemical industry, which means our main part has been supplying chemicals, physical products. However, as an emerging part of our portfolio, services are now becoming more and more important […] recently, we developed a new digital service which integrates a sensor into this connection and basically you can monitor all of your seals in the plant.“ (I3)

Services are also getting more complex. This is due to the need for new digital services to be compatible with older machines in the company's portfolio (I9) or designed for third-party systems (I16). Furthermore, comprehensive and additional consulting services are now offered, not just 'simple' maintenance work, to improve customer processes (I4, I17, I18). The customer does not have pain points with individual machinery or components but rather with the inflow and outflow of materials, process flows, and logistics processes (I5, I8). Additionally, the shortage of skilled workers has increased the demand for comprehensive solutions and a stronger focus on process optimization among customers (I8).

„This actually has little to do with the actual core business model of selling machines, instead, we solve our customers' problems by understanding their processes.“ (I5)

Need for a higher control instance: The increasing interplay of different areas such as software, services, machines, and automation for the realization of solution offerings requires cross-divisional coordination, standardization, and specification, which also increases the visibility and relevance of PPM within the organization (I1, I3, I8, I14). Megatrends such as digitalization and sustainability have cross-product impacts that require a higher-level authority such as PPM or the consolidation of business areas (I1, I6, I12, I14, I19). The influence of digitalization has led to more interactions between products than in the past with mechanical products (I19).

„Product management in today's world cannot exist without portfolio management. There is always some kind of interplay between different technologies. This has become increasingly important in recent years.” (I14)

Accordingly, portfolio management was newly established only a few years ago for two of the experts interviewed (I1, I8) and has been placed in the focus of top management as the "number one priority" for another expert (I3).

Neglected phase-out process: Portfolio complexity is not only increasing due to new business models and the focus on the service business as a holistic solution for customer processes. Six experts also report that a structured phase-out process is being neglected.

“The problem is at a certain point the incremental growth of profits is so low and the impact from complexity on your supply chain is so high that you may have a negative effect on your company […] that's really one of the biggest problems of companies like ours with a very complex portfolio because maintaining this can be quite a challenge.” (I3)

By acquiring companies with their own portfolios that have grown differently over time, duplicates with similar customer benefits are created in some cases, and central PPM tasks become more relevant to bundle and strategically align the portfolio (I1, I3, I8, I16). Internal costs arise not only from the expansion of the number of products and variants but also from the additional complexity of storage locations and supply chains (I3).

“If there is no structured phase-out process for years, acceptance and understanding must first be created within the company that not all products can always be kept in the portfolio and that customers must be convinced to switch to other products in the portfolio.” (I8)

The experts with an established phase-out process attempt to keep the number of variants constant (I4, I8, I11, I18).

„For physical products, limits are defined for the sales volume that must be achieved. There are only a few exceptions that can be afforded because they have important interactions [...] We try to maintain a portfolio of around 4,000 items that still generates sales growth.“ (I4)

3.1.5. Timing and Engaging the Relevant Audiences Is a Substantial Hurdle

Timing is a particular challenge when dealing with disruptive factors: One significant obstacle in PPM is timing the handling of disruptive influences. This includes the transition from analog to digital products, as exemplified in measurement technology (I1), the introduction of innovative sales structures such as transaction platforms (I5, I7), the transformation of traditional business models from single sales to subscription-based approaches (I2), as well as the focus on sustainable product lines (I2, I3). One difficulty here is the short-cycle assessment of the maturity of technologies or trends, that was previously described (chapter 3.1.2) as a challenge (I2, I20). In addition, customers in conservative industries often struggle with significant changes, even when they are technologically superior (I4).

„Customers prefer to stick with the proven.“ (I4)

Therefore, the customer requires a retraining process (I10). According to seven experts, an essential success factor for the timing of introducing disruptive services lies in actively involving and understanding the target audience. When market readiness is uncertain, companies should develop a flexible approach that can be adapted to specific needs (I15, I21). It is essential to test innovations through low-threshold offers, such as MVPs, and observe the customer's response (I6, I18). This can also be done through separate innovation portfolios (I6) or by collaborating with startups to respond quickly and flexibly to market requirements (I5, I6). Furthermore, testing smart services in one's own production can help identify optimization potential and lead to success (I16). An expert also reports on sustainability, stating that in the first step, their own organization was enabled and intensively engaged with the topic, to demonstrate better know-how in external perception (I18). Two experts report that disruptive approaches also require perseverance (I8, I9) and that the failure of new ideas is also part of it (I7). „You also have to be brave enough to fail. 9 out of 10 good ideas will fail.“ (I7)

In order to minimize the risk of timing for market entry, some experts rely on co-innovations with their own key accounts, for example (I7, I8, I21). Innovations are tested together and then used as a reference when offering them to the broader market (I7).

Involving the right target group: Involving the relevant target groups for successful timing poses a particular challenge. The target group should be involved early in an initial phase (I13, I19) and then transition into a continuous feedback cycle (I13). Companies need to identify the people who are particularly open to new services or disruptive innovations (I4, I6). When developing new business models like "as-a-service" offerings, it is crucial to address the right stakeholders, such as those who are interested in improving overall performance and can benefit directly from the offering (I4). This can be particularly challenging in multi-level sales structures (I4, I5). Successful timing depends not only on direct customers but also on the customers and suppliers of the customer (I5).

„It doesn't really depend on the primary target group [...] there are hundreds of arguments [...], but the process chains on the outside always kill the whole idea.“ (I5)

However, due to fear of neglecting direct customers, communication and coordination may not always take place (I5). Alternative options include seeking input from communities and trusted stakeholder networks (I4, I6, I18). It is, therefore, industry-specific to identify the relevant target audience and the appropriate contact person within the company (I7).

„This is an important sales process, understanding who the players are and who makes the decision.“ (I7)

3.1.6. Sustainability-Oriented Alignment of the Product Portfolio

Holistic adaptation through sustainability: The increasing focus on sustainability and stricter environmental regulations drive companies to develop more environmentally friendly products and production processes. This requires investment in research and development and the revision of existing product lines (I3, I4, I6, I21).

„If I would tell one big trend which require changes in our portfolio, it would be sustainability.“ (I3)

Two experts report that all activities in the companies are already designed and tested for sustainability (I18, I12).

„We no longer use fossil fuels in production [...] we are ISO 14001 environmentally certified [...] the entire life cycle is designed to be sustainable in order to reduce CO2 emissions - from raw materials and production processes through to recycling or use [...] supplier data on the carbon footprint is also requested and taken into account when selecting suppliers.“ (I18)

In some cases, this also has a strong impact on the technologies and core competencies used by companies. For example, some companies are implementing new business areas in the field of hydrogen (I1, I16) or electrification (I8). Advising customers on how to achieve their sustainability goals (I12) or developing smart services for CO2 balancing or extending product life cycles (I2, I16) also represents a new business in the context of sustainability.

„In addition, expanded sustainability approaches are gaining importance, including design principles for the circular economy, innovative modularization, shortening product life cycles and research into upgrade opportunities within the circular economy.“ (I6)

Balance between sustainability and profitability: Although these topics are receiving increasing attention, some companies are observing rather than actively shaping these developments. This is often due to cost considerations having priority in operational business (I6, I17). Even though experts are aware of the sustainability trend, some report that they currently receive few specific customer requirements (I5, I8, I17) or that they are only relevant in certain markets such as Europe (I14).

“Companies that want to make their portfolio more sustainable are not doing so because of a short-term need or a quick return on investment but because they want to be strategically well-positioned for the long-term.“ (I6)

In order to maintain long-term competitiveness in the field of sustainability, portfolio management must create the necessary framework early on (I14). For example, at a company in the Adhesive Solutions sector, all products in the portfolio are checked for climate neutrality, and the revenue loss resulting from the discontinuation of non-sustainable offerings by the target year for climate neutrality is calculated (I3). An optimal balance must be struck between current cash cow products and future sustainable growth products (I2, I3). Resources allocated to sustainability aspects are therefore no longer available for other technological innovations (I8).

Demands come from various stakeholder groups: Although some experts see few specific customer requirements (I5, I8, I17) and new product development should be based on customer pain points (I14), sustainability is also strongly driven by society and politics (I12). Shareholders and investors pressure publicly traded companies to act sustainably or at least develop a strategy in that direction (I2, I5, I12).

„Portfolio management is also important for visibility in the capital market. It is crucial to invest in things that make one investable.“ (I5)

When these guidelines are integrated into the corporate goals of large companies such as automakers, it affects the supply chain and leads to adjustments in the product portfolio of suppliers (I6, I20).

3.1.7. Outdated Evaluation Logic and KPIs Must be Adapted for Disruptive Innovations

New evaluation logic is required due to disruptive factors: Disruptive factors such as the sustainability shift, digital transformation, and servitization can lead companies to change their business models and require a new valuation logic. To assess the products’ potential, estimation based on existing business can be used (I15). However, when evaluating the potential of innovations in sustainability or digital solutions, existing methods may not suffice (I2, I15, I21).

„If you want to move away from a linear business model and act more circularly, you will need a new or adapted metrics system because the classic linear revenue from the new machine perspective will gradually decline. Ultimately, this will shift to retrofits, repair actions, and module integration of components that extend the lifecycle. All of this requires a different metrics system.“ (I2)

While financial KPIs are important, they alone are not sufficient to capture the potential of disruptive innovations or the strategic significance of products and services for the company's future viability.

„Especially when introducing new products, technologies, or disruptive initiatives, I will need to consider softer evaluations to determine if they offer long-term benefits.“ (I2)

Accordingly, 15 of the surveyed experts call for an adjustment and expansion of metrics for a new evaluation logic. One requirement is a quantitative comparability of customer benefits based on objective evaluation criteria (I15). An adapted evaluation logic should connect the software and hardware worlds and be able to compare them reasonably without becoming too complex and no longer suitable for the industry (I10). The value contribution to the customer should be the focus of the assessment (I1, I10, I14, I15, I19).

„ We manage ourselves according to value contribution [...] In terms of sustainability, we must also consider the benefits it provides to the customer. “ (I14)

Economic considerations must remain the basis: Various metrics can play a relevant role in the value-oriented alignment of the product portfolio and quantification of customer benefits. Although 15 of the surveyed experts confirmed that a purely financial evaluation of the product portfolio is no longer sufficient, the financial perspective should still form the foundation of the evaluation (I3, I5, I7, I9, I17).

„Soft factors are important [...], but economic feasibility must always be considered first.“ (I9)

However, changes are necessary even in financial KPIs to compare, for example, the potential of one-time sales and recurring revenue (I2, I11, I19).

„The traditional KPI is still revenue, but this may not work for different revenue models. Subscription-based models may generate more revenue over time, but they may initially perform worse than one-time sales.“ (I19)

Additional KPIs, such as "orders received" or "initial contract length", could be included to take better account of recurring income (I19). Another possible solution in the financial valuation method could be discounting and annuities (I11).

Strategic beliefs as a fast lane: Besides the financial perspective, some companies take additional strategic assessments into account, which can also lead to a prioritization of products with lower economic attractiveness (I3, I6, I7).

„It was clear that purely financial numbers don’t cover the whole strategic context.“ (I3) „In some companies, we observe a kind of fast lane when the business case fundamentally fits [...] even if it may be worse than other products but is still focused on due to strategic beliefs.“ (I6)

One respondent's company defined eight non-financial or semi-financial factors in addition to financial considerations included in product and portfolio evaluation, including factors related to sustainability impact or innovation level (I3). In this case, the innovation level reflects the status of the product life cycle (I3) and could be an indicator for growth potential (I5). Relevant sustainability metrics include carbon footprint, energy and material consumption, according to the experts (I2, I3, I5, I18). Additionally, cross-selling and cannibalization effects within a portfolio should be considered (I2, I7, I10).

In the context of digitalization, further metrics become relevant and feasible. For example, smart services can be used to collect customer data that can enhance the company's products or to identify optimization potential for customers (I2). In this context, follow-up business potential, such as spare parts sales, is also a relevant metric (I19). Digital services also enable tracking the number of transactions or click-bait, which are considered more relevant for the business-to-customer sector due to higher user numbers (I13). Moreover, a competitive perspective can also be relevant in evaluating products and services in the portfolio to consider whether the competition can adapt the offering or whether market shares can be secured. (I2, I5).

3.1.8. Disruptive Factors Require Organizational and Cultural Adjustments

Disruptive factors lead to organizational changes: The impact of disruptive factors requires significant organizational adaptations. In response, companies have established specialized departments such as Digitalization (I3, I13, I16), Sustainability (I3, I18), and Service Innovation (I2, I4, I7, I8, I11), depending on their strategic priorities (I6, I21). It allows these functions to be more prominent within the organizational structure. For example, a dedicated service department can more effectively focus on developing innovative revenue models, such as subscription models, than possible within the scope of traditional product development (I11). Furthermore, companies are exploring new business models by founding start-ups or investing in start-ups, which can lead to creating subsidiaries with focused and more agile structures in the digital sector (I3, I13, I16). Some of these spin-offs have experienced significant growth to several hundred employees within a few years (I13, I16). In the context of these developments, PPM is essential to ensure a coherent alignment between the various business units and departments (I8, I10, I19, I20, I21).

Cultural adaptation becomes necessary: Dealing with disruptive factors requires not only organizational adjustments but also an adapted corporate culture that promotes openness and innovation (I2, I4, I17, I19).

„This is where you really need a few mavericks who can see the opportunities and the potential without being tied to the status quo.“ (I4).

This also requires different skills throughout the organization, especially in sales (I2, I4, I17, I19), for example, to "understand the customer's problems holistically and not just negotiate prices" (I19). A new incentive system to redefine responsibility and distribution for revenue growth among the various areas of the company is also necessary (I11).

„To expand my service area, I could introduce recurring payment models. However, this may result in a reduction of revenue from one-time product sales.“ (I11)

As a result, distribution heavily depends on the underlying logic of incentivization (I2, I19).

„The new machine business is currently better intensified than perhaps the service that will come in the future. Therefore, a reevaluation is necessary.“ (I2)

A change in mindset and a diversified approach are also necessary in decision-making boards, which are often staffed with similar personality types from C-level management. The perception and evaluation of disruptive factors, such as sustainability and digitalization, vary among individuals, so decision-making boards should be heterogeneously staffed with a variety of perspectives (I19).

3.2 Aggregated Dimensions of Action (3rd Order)

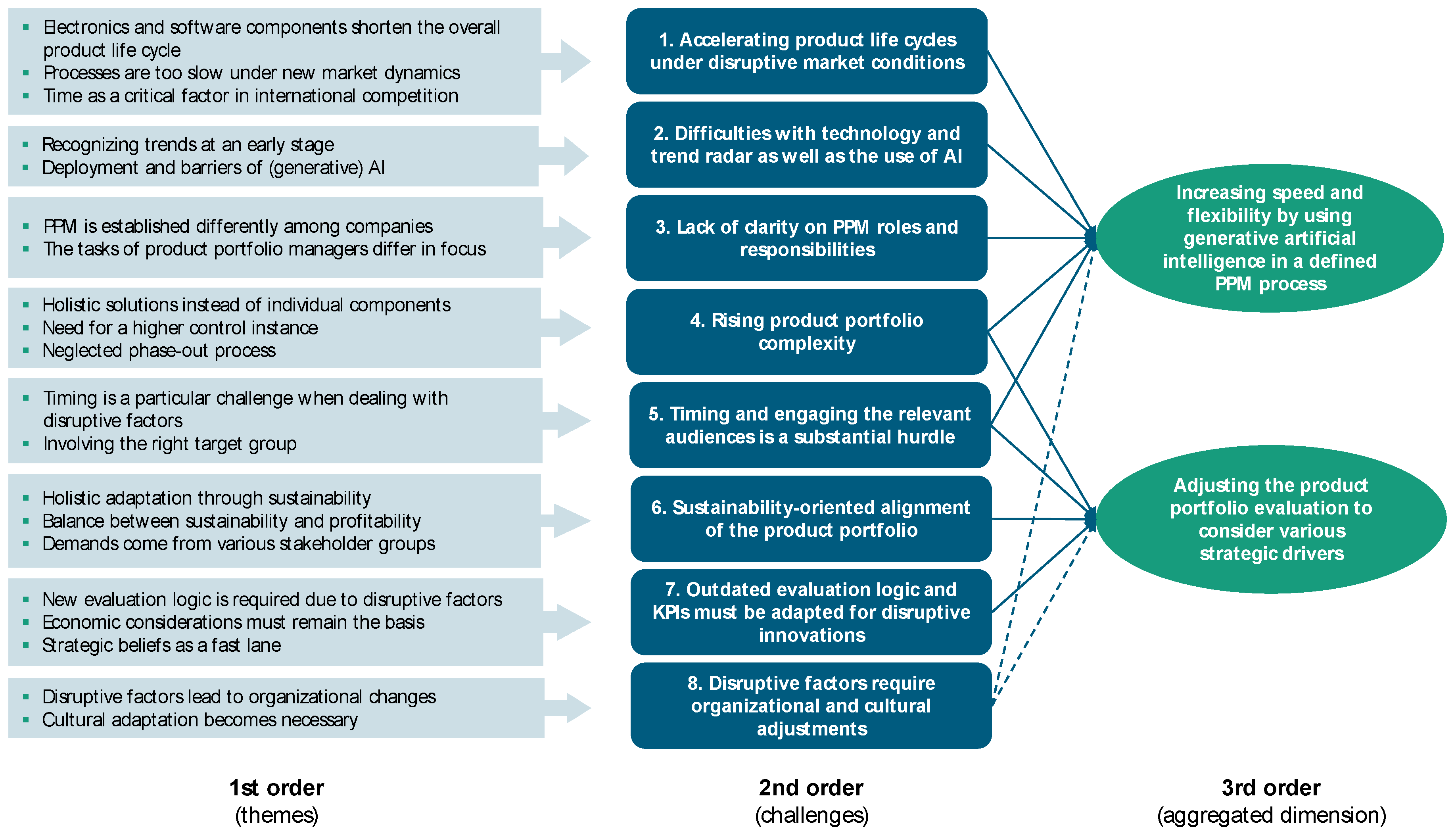

Based on the challenges described, two essential dimensions of action can be derived for PPM in the B2B area of manufacturing. These two dimensions bundle specific second-order challenges and address common requirements that represent the need for further research. Figure 3 shows the data structure according to the Gioia method [47] of the empirical-qualitative exploration as an overview of the results. It visualizes the themes of the first order, the overarching challenges of the second order, and the dimensions derived from them with their interrelationships.

The following two sections describe the aggregated dimensions and interrelationships with the second-order challenges. The eighth challenge, “Disruptive factors require organizational and cultural adjustments", encompasses the entire corporate culture and organization and is not specific to the product portfolio. Therefore, this challenge plays only an indirect role in the aggregated dimensions and is not explored in depth. Approaches to organizational change in response to disruptive influences are described by [49].

The dimension of “Increasing speed and flexibility by using generative AI in a defined PPM process” aims to address challenges 1-5 effectively. According to experts, new market dynamics, due to disruptive influences, shorten product life cycles, especially for digital components. Shorter product life cycles require faster and more efficient decision-making and development processes within companies [50,51]. In addition, experts describe the early detection of trends and new technological developments as a challenge, as it requires substantial time investment and personnel resources. In this context, the need for using generative AI has already been mentioned by experts. Generative AI could accelerate individual process steps in PPM, reduce resource requirements, and thus optimize the handling of shorter product life cycles. Research by [52] and [53] shows that the use of generative AI can increase productivity in individual process steps in related areas by more than 50%. A framework could be used to investigate the application and potential of generative AI in PPM and provide guidance to companies. To address the requirements for clearer differentiation of tasks and responsibilities, the framework for the use of generative AI could be based on a defined PPM process with clear task packages. This would also promote the establishment of PPM as a central control instance [54,55]. Furthermore, trend and technology radar, the definition of actions for a consistent phase-out process, and the early involvement of relevant target groups to mitigate risks in terms of the right timing can be integrated into the framework as integral process elements to cope with further identified challenges.

With the second dimension “Adjusting the product portfolio evaluation to consider various strategic drivers", challenges 4-7 are primarily addressed. The increasing complexity of the product portfolio, driven by the integration of services and digital offerings presents new requirements for portfolio evaluation. A strategically adaptive evaluation system must be developed to consider this complexity and enable a holistic assessment. This includes evaluating physical products, services, and digital offerings, and requires expanding evaluation criteria to adequately capture the strategic significance and value contribution for the relevant target groups. [42,56,57]

The increasing importance of sustainability in product development and portfolio management requires the integration of sustainability criteria into the evaluation logic. This includes, for example, the assessment of the product carbon footprint or energy efficiency to ensure that the portfolio meets the growing demands for environmental compatibility.[56] Adjusting valuation logic and KPIs based on values is crucial to ensure the companies’ long-term competitiveness and future viability [36,42].

4. Discussion

The presented study examines the effects of disruptive factors on the evaluation and shaping of product portfolios in manufacturing companies in the B2B sector. The research question is answered with empirical data collected and analyzed with the help of the Gioia method, which contributes to and extends the current state of research. The study identifies eight challenges that arise from disruptive factors in PPM. The findings have been further specified, and the need for the developed dimensions of action has been clearly demonstrated. These dimensions of action include (1) increasing speed and flexibility by using generative AI in a defined PPM process and (2) adjusting the product portfolio evaluation to consider various strategic drivers. Both dimensions of action emphasize the relevance and necessity for companies to adjust their PPM practices to remain competitive in disruptive changes [32,36,42].

Existing approaches partially address the need for increased speed and flexibility in PPM. [37] proposed a prescriptive data analysis approach for product portfolio control. However, experts surveyed consider the short-term potential of prescriptive methods to be limited, since data quality and the overcoming of data silos between different corporate divisions represent a major hurdle (Section 3.1.2). The use of generative AI has been explored in related disciplines, such as the framework proposed by [58], the study conducted by [59] in the field of product management, and the approach taken by [60] in the area of business model innovation. A framework for PPM for generative AI does not yet exist and thus represents a further opportunity for research and industry [52,58,59,60]. Some surveyed companies are already testing generative AI with in-house models to avoid sharing data with third-party companies or other countries (Chapter 3.1.2). Therefore, a framework for PPM should also outline the requirements for each process step, indicating whether public or in-house software can be used, as shown in the model by [61] for the financial sector.

A clearly defined PPM process was not listed as a separate dimension, as foundational works have already outlined PPM processes [1,26,62]. Nevertheless, adaptating to disruptive trends may be useful, such as the framework for PPM in digital transformation [30]. This can enable clearer delimitation and more agility with further challenges addressed through detailed and self-contained tasks (work packages) [54,55].

Similarly, the adaptation of portfolio valuation to take account of various value-oriented strategic factors is also being partly addressed by initial approaches in research. [33] present a concept to enable portfolio management for solution providers with physical products, services, and digital components, often in combination with new business models. At the same time, they also represent the need for further detailing their methodology, the consideration of interactions within the portfolio, and the integration of sustainability aspects. [56] presents an approach to support manufacturing companies in integrating sustainability criteria into their product portfolios. Here, further development of methods as well as the adaptation to different company contexts and the empirical validation are described as further research needs. Additionally, [42] present a method for managing disruptive innovation in portfolio planning. However, they demonstrate that further research is necessary to establish and prioritize evaluation criteria for handling disruptive innovations in a corporate context, in addition to the primarily used financial methods.

Both identified dimensions of action demonstrate that there are research gaps, more specifically with regard to the integration of generative AI into PPM and the development of an adaptive evaluation system with new value-oriented KPIs. Future research should aim to develop specific frameworks and methods to help companies effectively adapt their product portfolios to the challenges of a disruptive environment. This also includes the empirical evaluation of the effectiveness of such approaches in an industrial context.

As a side project, ChatGPT was also used as an interview partner in the study, as previously investigated by [46]. From ChatGPT as an interviewee, some of the identified challenges were mentioned, such as the increasing complexity of product portfolios, the need to integrate sustainability criteria, and the increasing demands for higher dynamics. However, the feedback provided was rather generic and lacked specific examples from companies as described by the experts. Despite this, the responses were a good reflection of the general sentiment among the experts. Therefore, [46] suggests using large language models such as ChatGPT to explore different perspectives on research topics but recommends caution due to the unpredictable results.

In conclusion, the discussion reveals that PPM in manufacturing B2B companies faces significant challenges due to disruptive factors. The development and implementation of adaptive management practices that consider generative AI to increase speed and the integration of further strategic evaluation criteria are critical to ensure resilience and competitiveness in a transformative business environment.

Author Contributions

T.G. worked on the conceptualization, the investigation of the research subject, the design of the methodology, the development of the general structure, and writing of the manuscript. T.B. and A.E. supervised the work and provided critical feedback to shape the research, analysis, and manuscript. All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding.

Acknowledgments

We would like to thank all the participating experts who were available for interviews and whose insights made a valuable contribution to this study.

Conflicts of Interest

The authors declare no conflicts of interest.

References

- Dunst, K.H. Portfolio Management: Konzeption für die strategische Unternehmensplanung. Zugl.: Darmstadt, Techn. Hochsch., Diss. u.d.T.: Dunst, Klaus H.: Entwicklung einer Portfolio-Management-Konzeption für die strategische Planung in Multiprodukt-Unternehmen, 2., verb. Aufl.; de Gruyter: Berlin, 1983; ISBN 3-11-008876-2. [Google Scholar]

- European Commission. A Clean Planet for all: A European strategic long-term vision for a prosperous, modern, competitive and climate neutral economy. Available online: https://eur-lex.europa.eu/legal-content/EN/TXT/PDF/?uri=CELEX:52018DC0773.

- Axelson, M.; Oberthür, S.; Nilsson, L.J. Emission reduction strategies in the EU steel industry: Implications for business model innovation. J of Industrial Ecology 2021, 25, 390–402. [Google Scholar] [CrossRef]

- Wyns, T.; Khandekar, G.; Axelson, M.; Sartor, O.; Neuhoff, K. Industrial Transformation 2050: Towards an Industrial strategy for a Climate Neutral Europe, 2019. Available online: ies.be.

- 5. European Commission. Der europäische Grüne Deal, b: online: https://eur-lex.europa.eu/resource.html?uri=cellar, 0021.

- Henkel. Henkel treibt Nachhaltigkeitsziele voran – mit Fortschritten bei Klimaschutz und sozialem Engagement. Available online: https://www.henkel.de/presse-und-medien/presseinformationen-und-pressemappen/2023-03-07-henkel-treibt-nachhaltigkeitsziele-voran-mit-fortschritten-bei-klimaschutz-und-sozialem-engagement-1807096 (accessed on 29 February 2024).

- Siemens. Siemens will bis 2030 klimaneutral sein. Available online: https://press.siemens.com/global/de/pressemitteilung/siemens-will-bis-2030-klimaneutral-seinhttps://press.siemens.com/global/de/pressemitteilung/siemens-will-bis-2030-klimaneutral-sein (accessed on 29 February 2024).

- Alvarez, S.; Rubio, A. Carbon footprint in Green Public Procurement: a case study in the services sector. Journal of Cleaner Production 2015, 93, 159–166. [Google Scholar] [CrossRef]

- Special types of life cycle assessment; Finkbeiner, M. , Ed.; Springer: Dordrecht, 2016; ISBN 978-94-017-7608-0. [Google Scholar]

- PwC. Wachstumsstrategien für das B2B Service-Geschäft, 2023. Available online: https://www.pwc.de/de/im-fokus/customer-transformation/wachstumsstrategien-fuer-das-b2b-service-geschaeft.pdf (accessed on 29 February 2024).

- Deloitte. Der zweite Frühling für den Maschinenbau, 2020. Available online: https://www2.deloitte.com/content/dam/Deloitte/ch/Documents/energy-resources/deloitte-ch-digitale-services-maschinenbau-DE_KS8.pdf (accessed on 29 February 2024).

- Menter, M.; Göcke, L.; Zeeb, C. The Organizational Impact of Business Model Innovation: Assessing the Person-Organization Fit. J Management Studies 2022. [Google Scholar] [CrossRef]

- Trumpf. Pay-per-part: TRUMPF offers new business model to utilize spare machine capacity. Available online: https://www.trumpf.com/en_INT/newsroom/global-press-releases/press-release-detail-page/release/pay-per-part-trumpf-offers-new-business-model-to-utilize-spare-machine-capacity/ (accessed on 29 February 2024).

- Rix, C.; Leiting, T.; Holst, L. Herausforderungen der Preisbildung datenbasierter Geschäftsmodelle in der produzierenden Industrie. In Datenwirtschaft und Datentechnologie; Rohde, M., Bürger, M., Peneva, K., Mock, J., Eds.; Springer Berlin Heidelberg, 2022; pp 49–69, ISBN 978-3-662-65231-2.

- Vandermerwe, S.; Rada, J. Servitization of business: Adding value by adding services. European Management Journal 1988, 6, 314–324. [Google Scholar] [CrossRef]

- Stich, V.; Schumann, J.H.; Beverungen, D.; Gudergan, G.; Jussen, P. Digitale Dienstleistungsinnovationen; Springer Berlin Heidelberg, 2019, ISBN 978-3-662-59516-9.

- Linde, L.; Frishammar, J.; Parida, V. Revenue Models for Digital Servitization: A Value Capture Framework for Designing, Developing, and Scaling Digital Services. IEEE Trans. Eng. Manage. 2023, 70, 82–97. [Google Scholar] [CrossRef]

- Eggert, A.; Hogreve, J.; Ulaga, W.; Muenkhoff, E. Revenue and Profit Implications of Industrial Service Strategies. Journal of Service Research 2014, 17, 23–39. [Google Scholar] [CrossRef]

- McKinsey. Five digital and analytics battlegrounds for B2B aftermarket growth, 2022. Available online: https://www.mckinsey.com/capabilities/operations/our-insights/five-digital-and-analytics-battlegrounds-for-b2b-aftermarket-growth (accessed on 29 February 2024).

- Raddats, C.; Kowalkowski, C.; Benedettini, O.; Burton, J.; Gebauer, H. Servitization: A contemporary thematic review of four major research streams. Industrial Marketing Management 2019, 83, 207–223. [Google Scholar] [CrossRef]

- Altenfelder, K.; Schönfeld, D.; Krenkler, W. Services Management und digitale Transformation; Springer Fachmedien Wiesbaden, 2021, ISBN 978-3-658-33974-6.

- Business Fortune Insights. Market Research Report: Software as a Service - Market Size & Growth FBI102222, 2023. Available online: https://www.fortunebusinessinsights.com/software-as-a-service-saas-market-102222 (accessed on 29 February 2024).

- Christensen, C.; Raynor, M.; McDonald, R. What Is Disruptive Innovation? Harvard Business Review 2015. [Google Scholar]

- Kleinaltenkamp, M.; Gabriel, L.; Morgen, J.; Nguyen, M. Marketing und Innovation in disruptiven Zeiten – Eine Einführung und eine Einordnung der Beiträge dieses Buches. In Marketing und Innovation in disruptiven Zeiten; Kleinaltenkamp, M., Gabriel, L., Morgen, J., Nguyen, M., Eds.; Springer Fachmedien Wiesbaden: Wiesbaden, 2023; ISBN 978-3-658-38571-2. [Google Scholar]

- Rauch, S. Strategisches Management technologischer Wandlungsprozesse; Dr. Hut: München, 2024; ISBN 978-3-8439-5410-5. [Google Scholar]

- Wendt, S. Strategisches Portfoliomanagement in dynamischen Technologiemärkten; Gabler Verlag: Wiesbaden, 2013; ISBN 978-3-8349-4272-2. [Google Scholar]

- Homburg, C. Marketingmanagement; Springer Fachmedien Wiesbaden: Wiesbaden, 2020; ISBN 978-3-658-29635-3. [Google Scholar]

- Cooper, R.G.; Edgett, S.J.; Kleinschmidt, E.J. New Product Portfolio Management: Practices and Performance. J of Product Innov Manag 1999, 16, 333–351. [Google Scholar] [CrossRef]

- Kohlborn, T.; Fielt, E.; Korthaus, A.; Rosemann, M.; Davern, M. ; Scheepers. Towards a service portfolio management framework. Proceedings of the twentieth Australasian Conference on Information Systems Understanding shared services: an exploration of the IS literature 2009.

- Schicker, G.; Strassl, J. Produkportfolio-Management im Zeitalter der Digitalisierung, Weiden i.d. OPf., 2019.

- Tolonen, A.; Shahmarichatghieh, M.; Harkonen, J.; Haapasalo, H. Product portfolio management – Targets and key performance indicators for product portfolio renewal over life cycle. International Journal of Production Economics 2015, 170, 468–477. [Google Scholar] [CrossRef]

- Eckert, T.; Hüsig, S. Innovation portfolio management: a systematic review and research agenda in regards to digital service innovations. Manag Rev Q 2022, 72, 187–230. [Google Scholar] [CrossRef]

- Riesener, M.; Kuhn, M.; Boβmann, C.; Schuh, G. Concept for the Portfolio Management of Industrial Solution Providers in Machinery and Plant Engineering. Procedia CIRP 2023, 119, 1152–1157. [Google Scholar] [CrossRef]

- Boßmann, C.; Kuhn, M.; Riesener, M.; Schuh, G. Planning of Hybrid Portfolios for Industrial Solution Providers in Machinery Engineering. In Production at the Leading Edge of Technology; Bauernhansl, T., Verl, A., Liewald, M., Möhring, H.-C., Eds.; Springer Nature Switzerland: Cham, 2024; ISBN 978-3-031-47393-7. [Google Scholar]

- Mikkola, J.H. Portfolio management of R&D projects: implications for innovation management. Technovation 2001, 21, 423–435. [Google Scholar] [CrossRef]

- Gross, E.; Schrader, P.; Gramberg, T.; Schneider, M.; Bauernhansl, T. Identifikation und Auswahl von digitalen Services/Identification and selection of digital services. wt 2023, 113, 376–381. [Google Scholar] [CrossRef]

- Jank, M.-H. Produktportfoliosteuerung mittels präskriptiver Datenanalyseverfahren, 1st ed.; Apprimus Wissenschaftsverlag: Aachen, 2021; ISBN 978-3-86359-963-8. [Google Scholar]

- Li, F. The digital transformation of business models in the creative industries: A holistic framework and emerging trends. Technovation 2020, 92-93, 102012. [Google Scholar] [CrossRef]

- Söllner, C. Methode zur Planung eines zukunftsfähigen Produktportfolios. Dissertation; Heinz Nixdorf Institut.

- Leitner, C.; Ganz, W.; Satterfield, D.; Bassano, C. Advances in the Human Side of Service Engineering; Springer International Publishing: Cham, 2021; ISBN 978-3-030-80839-6. [Google Scholar]

- Villamil, C.; Hallstedt, S. Sustainabilty integration in product portfolio for sustainable development: Findings from the industry. Bus Strat Env 2021, 30, 388–403. [Google Scholar] [CrossRef]

- Weinreich, S.; Şahin, T.; Karig, M.; Vietor, T. Methodology for Managing Disruptive Innovation by Value-Oriented Portfolio Planning. Journal of Open Innovation: Technology, Market, and Complexity 2022, 8, 48. [Google Scholar] [CrossRef]

- Cenamor, J.; Rönnberg Sjödin, D.; Parida, V. Adopting a platform approach in servitization: Leveraging the value of digitalization. International Journal of Production Economics 2017, 192, 54–65. [Google Scholar] [CrossRef]

- Kowalkowski, C.; Gebauer, H.; Kamp, B.; Parry, G. Servitization and deservitization: Overview, concepts, and definitions. Industrial Marketing Management 2017, 60, 4–10. [Google Scholar] [CrossRef]

- Bortz, J.; Döring, N. Forschungsmethoden und Evaluation: In den Sozial- und Humanwissenschaften, 5. Aufl.; Springer-Verlag: Berlin, 2016; ISBN 978-3-540-33305-0. [Google Scholar]

- Dengel, A.; Gehrlein, R.; Fernes, D.; Görlich, S.; Maurer, J.; Pham, H.H.; Großmann, G.; Eisermann, N.D.g. Qualitative Research Methods for Large Language Models: Conducting Semi-Structured Interviews with ChatGPT and BARD on Computer Science Education. Informatics 2023, 10, 78. [Google Scholar] [CrossRef]

- Gioia, D.A.; Corley, K.G.; Hamilton, A.L. Seeking Qualitative Rigor in Inductive Research. Organizational Research Methods 2013, 16, 15–31. [Google Scholar] [CrossRef]

- Mees-Buss, J.; Welch, C.; Piekkari, R. From Templates to Heuristics: How and Why to Move Beyond the Gioia Methodology. Organizational Research Methods 2022, 25, 405–429. [Google Scholar] [CrossRef]

- Schrader, P.; Gross, E.; Bauernhansl, T.; Hoeborn, G. Digitale und nachhaltige Organisationen/Systematic literature review on modes of organizational ambidexterity – Digital and sustainable organizations. wt 2023, 113, 518–524. [Google Scholar] [CrossRef]

- Seifert, R.W.; Tancrez, J.-S.; Biçer, I. Dynamic product portfolio management with life cycle considerations. International Journal of Production Economics 2016, 171, 71–83. [Google Scholar] [CrossRef]

- Cooper, R.G.; Sommer, A.F. New-Product Portfolio Management with Agile. Research-Technology Management 2020, 63, 29–38. [Google Scholar] [CrossRef]

- McAfee, A.; Rock, D.; Brynjolfsson, E. Der ultimative Leitfaden für KI-Pioniere: Wie lässt sich das Potenzial von KI nutzen. Harvard Business manager 2024, 19–28. [Google Scholar]

- Preetham, F. Product Management will be taken over by AI in 5 years. Available online: https://medium.com/the-simulacrum/product-management-will-be-taken-over-by-ai-in-5-years-780d1302fefc.

- Stettina, C.J.; Hörz, J. Agile portfolio management: An empirical perspective on the practice in use. International Journal of Project Management 2015, 33, 140–152. [Google Scholar] [CrossRef]

- Horlach, B.; Schirmer, I.; Drews, P. Agile Portfolio Management: Desgin Goals and Principles. Proceedings of the 27th European Conference on Information Systems (ECIS) 2019. [Google Scholar]

- Villamil Velasquez, C. Guidance in developing a sustainability product portfolio in manufacturing companies; Blekinge Tekniska Högskola: Karlskrona, 2023; ISBN 978-91-7295-448-9. [Google Scholar]

- Hakanen, T.; Jähi, M. Central activities of solution portfolio management. IJSTM 2021, 27, 104. [Google Scholar] [CrossRef]

- Huang, G.; Huang, K. ChatGPT in Product Management. In Beyond AI; Huang, K., Wang, Y., Zhu, F., Chen, X., Xing, C., Eds.; Springer Nature Switzerland: Cham, 2023; ISBN 978-3-031-45281-9. [Google Scholar]

- Pradhan, D.; Dash, B.; Sharma, P.; Ullah, S. The Impact of Generative AI on Product Management in SMEs 2023.

- Kanbach, D.K.; Heiduk, L.; Blueher, G.; Schreiter, M.; Lahmann, A. The GenAI is out of the bottle: generative artificial intelligence from a business model innovation perspective. Rev Manag Sci 2023. [Google Scholar] [CrossRef]

- Li, Y.; Wang, S.; Ding, H.; Chen, H. Large Language Models in Finance: A Survey. In 4th ACM International Conference on AI in Finance. ICAIF '23: 4th ACM International Conference on AI in Finance, Brooklyn NY USA, 27 11 2023 29 11 2023; ACM: New York, NY, USA, 2023; ISBN 9798400702402. [Google Scholar]

- Paletta, M. Overview of Product Portfolio Management; Cuvillier Verlag: Göttingen, 2019; ISBN 9783736989450. [Google Scholar]

Figure 1.

Disruptive factors affecting the product portfolio, according to experts surveyed.

Figure 2.

Expert contribution to the identified themes (1st order).

Figure 3.

Identified challenges and new action dimensions according to Gioia’s data structure [47].

Figure 3.

Identified challenges and new action dimensions according to Gioia’s data structure [47].

Table 1.

Excerpt from the interview questionnaire.

| Categories in questionnaire |

Sample questions for the categories of the questionnaire |

|---|---|

| Classification of the experts and current situation of PPM |

|

| Challenges and influencing factors in PPM |

|

| Best practice approaches to coping with disruptive influencing factors |

|

| Requirements for a new methodology to cope with challenges |

|

|

Table 2.

Overview of the interview participants.

| No. | Position | Core business of the company or the relevant business unit | Company size(revenue) | ||

|---|---|---|---|---|---|

| I1 | Product Portfolio Manager | Measurement and control technology | 1-5 bn € | ||

| I2 | Director of Future Portfolio Management and Strategy |

System provider for the food, beverage and pharmaceutical industries | 5-10 bn € | ||

| I3* | Director Global Product & Technology Management |

Adhesive technologies | >20 bn € | ||

| I4 | Vice President Product Portfolio Management |

Panel building and switchgear manufacturing | 1-5 bn € | ||

| I5 | Senior Manager Corporate Strategy and Development |

Printing machine manufacturing | 1-5 bn € | ||

| I6 | Head of research group for Product / Portfolio Management |

Research institution | n/a | ||

| I7 | Head of Portfolio Management | Machine tools and laser technology | 5-10 bn € | ||

| I8 | Head of Product Management | Hydraulic components and systems | 100-499 mio € | ||

| I9 | Product Portfolio Manager | Diverse technology solutions | >20 bn € | ||

| I10 | Vice President Product Management and Segment Markeitng |

Automation technology | 500-999 mio € | ||

| I11 | Head of Product Management | Machine tools and laser technology | 5-10 bn € | ||

| I12* | Head of Solution and Service Portfolio Management |

Diverse technology solutions | >20 bn € | ||

| I13 | Product Consultant (former Product Manager) |

IT and strategy consulting | <100 mio € | ||

| I14 | Product Portfolio Manager | Machine tools and laser technology | 5-10 bn € | ||

| I15 | Global Product Manager | Connection technology | 500-999 mio € | ||

| I16 | Product Manager Digital Service |

Plant engineering for steelworks | 5-10 bn € | ||

| I17 | Director Central Marketing and Product Management | Woodworking machinery | 500-999 mio € | ||

| I18 | Head of Product Management | Labeling solutions | < 100 mio € | ||

| I19 | Global Product Manager | Machine and plant construction | 5-10 bn € | ||

| I20 | Partner | Strategy Consulting | n/a | ||

| I21 | ChatGPT in the role of Product Portfolio Manager in a medium sized B2B manufacturing company. | ||||

* Discussions with these experts continued beyond the interviews to gain deeper insights into the companies' PPM.

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Copyright: This open access article is published under a Creative Commons CC BY 4.0 license, which permit the free download, distribution, and reuse, provided that the author and preprint are cited in any reuse.