Submitted:

18 April 2024

Posted:

22 April 2024

You are already at the latest version

Abstract

EIMIs face the challenge of adapting to the Paris Agreement and the European Green Deal to achieve carbon neutrality. This change is being driven by consumer interest in low-carbon products, regulatory requirements from climate agreements and investors prioritizing sustainability. This pressure is pushing companies to go beyond short-term financial gains and integrate sustainability into their business. The growing awareness of the environmental impact of business models (BM) has fueled the development of Sustainable Business Models (SBMs). This study aims to link the discussion on the role of SBMs in the drivers of decarbonization, to improve the understanding of how the drivers can be integrated and enable new BMs for EIMIs. Based on a structured literature review, semi-structured interviews were conducted in the EIMIs. The study identifies BM-components that are influenced by these drivers and require sustainable business model innovation (SBMI). The results show that decarbonization drivers have a significant impact on all BM components. Experts emphasize the importance of collaborative approaches and cooperation throughout the value chain. This research elaborates on the importance of systematic analysis to understand how companies can effectively manage decarbonization drivers and suggests in-depth exploration within BM-research to uncover potential SBM design options.

Keywords:

decarbonization

; business model

; sustainable transformation

; business model innovation

; survey

1. Introduction

Energy-intensive manufacturing industries face the challenge of becoming climate-neutral in line with the Paris Agreement and the European Green Deal [1,2,3]. The German government defines the term decarbonization as the reduction of carbon dioxide emissions towards a carbon-free economy [4]. The EIMI include the iron and steel industry, the chemical industry, the minerals and materials industry (cement), and the metal industry. These industries produce materials and goods essential to the European economy [5]. EIMI is a very carbon-intensive sector of the economy and is the largest contributor to Germany’s industrial greenhouse gas (GHG emissions). Furthermore, around 80 percent of GHG emissions in the German industrial sector and around 20 percent of total German GHG emissions are caused by EIMI [6]. In addition to technical factors, economic factors such as low profit margins, high capital requirements, and long facility life cycles contribute to the complexity of reducing GHG emissions in the EIMI [7,8,9]. In recent decades, incremental efficiency improvements have already allowed much of the low-hanging fruit for reducing GHG emissions in these industries to be gathered. Further emission reductions to decarbonize the EIMI to mitigate climate change and its consequences are possible but require a combination of solutions beyond incremental efficiency improvements [1,10]. According to [11], significant emission reduction adjustments will be necessary in the coming years to fulfill new regulations, whereas there is not only one solution [11].

The growing interest of consumers towards the carbon footprint of their products, new regulations resulting from political agreements on climate neutrality, and investors reorienting their investment strategies towards sustainability are pushing companies to go beyond short-term financial benefits and integrate sustainability holistically into their organizations and business logic [12,13,14]. As conventional business activities have so far paid little attention to the aspects of sustainability, interest in the connection between sustainability, business models (BM), and innovation has risen sharply [15,16]. The sustainable innovation process is promoted by new or optimized technologies, customer demand, expansion of the positive corporate image, emerging new markets for sustainable products, and markets that are more fragmented with fewer competitors [17,18,19,20,21]. In addition to technological innovations, companies must also develop non-technological innovations. This can include, for example, processes, organizational practices, services, and BMs that proactively respond to changing conditions [22,23]. The growing awareness of the negative environmental impact of conventional BMs has promoted the development of SBMs [24]. A BM is defined as the logic of how organizations create, deliver, and sustain value while considering the interests of various stakeholders, the environment and society. Accordingly, SBMs are instructions that go beyond individual companies and technologies and focus on system-wide sustainability changes [25,26,27,28]. The extent to which the industrial decarbonization of EIMI triggers SBMI has an impact on the environment [5].

Although the importance of decarbonization of the EIMI has increased in research in recent years, there is a lack of industry-specific research [29]. In addition, there is little research that takes into account the combination of decarbonization and business models and examines the interrelationships and correlations between them. Research activities on SBMs have intensified in recent years, focusing on the different types of SBMs [22,24,30,31,32]. Most of the literature from BM or sustainable business model research (BM research) has focused on establishing a circular economy in the form of a circular business model as a solution [25,33,34]. The existing literature on industrial decarbonization has acknowledged the importance of new BM and business model innovation (BMI) in the context of sustainability, but does not systematically analyze when and how BMs need to adapt to the different decarbonization pathways [5,35]. Initial literature already highlights EIMI and industrial decarbonization, but this focuses more on a generic perspective than on the detailed level in terms of the business model component level (BM component) [10,29,31,36]. Research points to a need for research to understand the role of BMI in industrial decarbonization from the perspective of industrial decarbonization research and BM research [5,29]. This can provide a better understanding and conceptualization of the BM and its components for accelerating emissions reduction.

The motivation of this analysis is to strengthen the understanding of the role of SBM in the industrial decarbonization literature with business model theory and literature while opening up the empirical field in the combination of the topics. A deeper understanding of this combination will allow us to understand how decarbonization objectives can be integrated into BM and how they enable new SBMs of EIMI. This paper aims to fill this research gap by answering the following research question: Which BM components are influenced by the drivers of decarbonization targets in EIMI companies and require SBMI? Based on the interviews with 22 industry experts and the falsification of pre-established theses, the core findings were determined. According to this, the drivers of the decarbonization targets (economic, political, and social) require a fundamental transformation of the existing BMs and significantly influence almost all BM components. This study contributes to theory and practice. It identifies the key challenges companies face when decarbonization targets affect their BMs, and an SBMI is initiated to secure their competitiveness and promote long-term growth.

2. Materials and Methods

2.1. Study Design, Sample, and Setting

This research paper presents a study in two parts based on the collection of qualitative data using semi-structured interviews. The study focused on industry-specific drivers and cross-industry patterns. The first part of the study focused on the steel, cement, and chemical industries. The partial results are published in [37]. In the second part, the scope was expanded to include the glass, paper, and metals industries, as well as downstream stakeholders and consulting. As part of the deductive research [38], a structured literature review was first carried out on the drivers of decarbonization targets in the EIMI in Germany [39]. This forms the starting point for identifying and categorizing the drivers of decarbonization targets that promote or inhibit SBMI. Orientation is based on the STEP method [40], which analyses the macroeconomic environment of an object of investigation according to socio-cultural, technological, economic, and political influencing factors, as these represent the main drivers [41]. The microeconomic influencing factors of the categorization according to Osterwalder and Pigneur are also covered below [42].

The theses address specific theses about the drivers and form the basis for the qualitative expert interviews. The interviews were conducted with the aim of gaining an in-depth understanding of the dynamic drivers. An interview guide included open-ended questions and served as a flexible framework for data collection [43,44]. The main questions of the interview are organized according to driver clusters, which include political, economic, and social drivers. Furthermore, there are introductory questions about the person and concluding questions about potential requirements for a methodology. In addition, the questionnaire contains a brief initial situation and objectives as well as relevant definitions of industrial decarbonization and business model theory, which were provided to the experts before the interviews. An excerpt with exemplary questions in the five sections is shown in Table 1.

2.2. Data Collection

The expert interviews were conducted from June 2023 to February 2024. The 45-60 minute semi-structured interviews (via telephone or web-based platforms; teams) were conducted one-on-one in-depth.

A qualitative approach to data collection was chosen, as the research area has not yet been investigated much and experts from the field can provide up-to-date and detailed insights into the research area. The interviews were audio-recorded and transcribed verbatim. After this, all data were anonymized for reporting.

2.3. Study Sample

22 experts took part in the study. Most participants came from the EIMI (see Appendix A for details). In addition, industry-wide insights were gathered through four interviews with experts from associations and management consultancies. The experts reported on experiences within their companies in the context of decarbonization, BMI, and company-specific transformation paths. According to the experts, the economic driver is most important in the companies, while the social driver is considered to the least important. 14 out of 21 companies indicated that their company requires support in the sustainable transformation of their BM.

2.4. Data Analysis

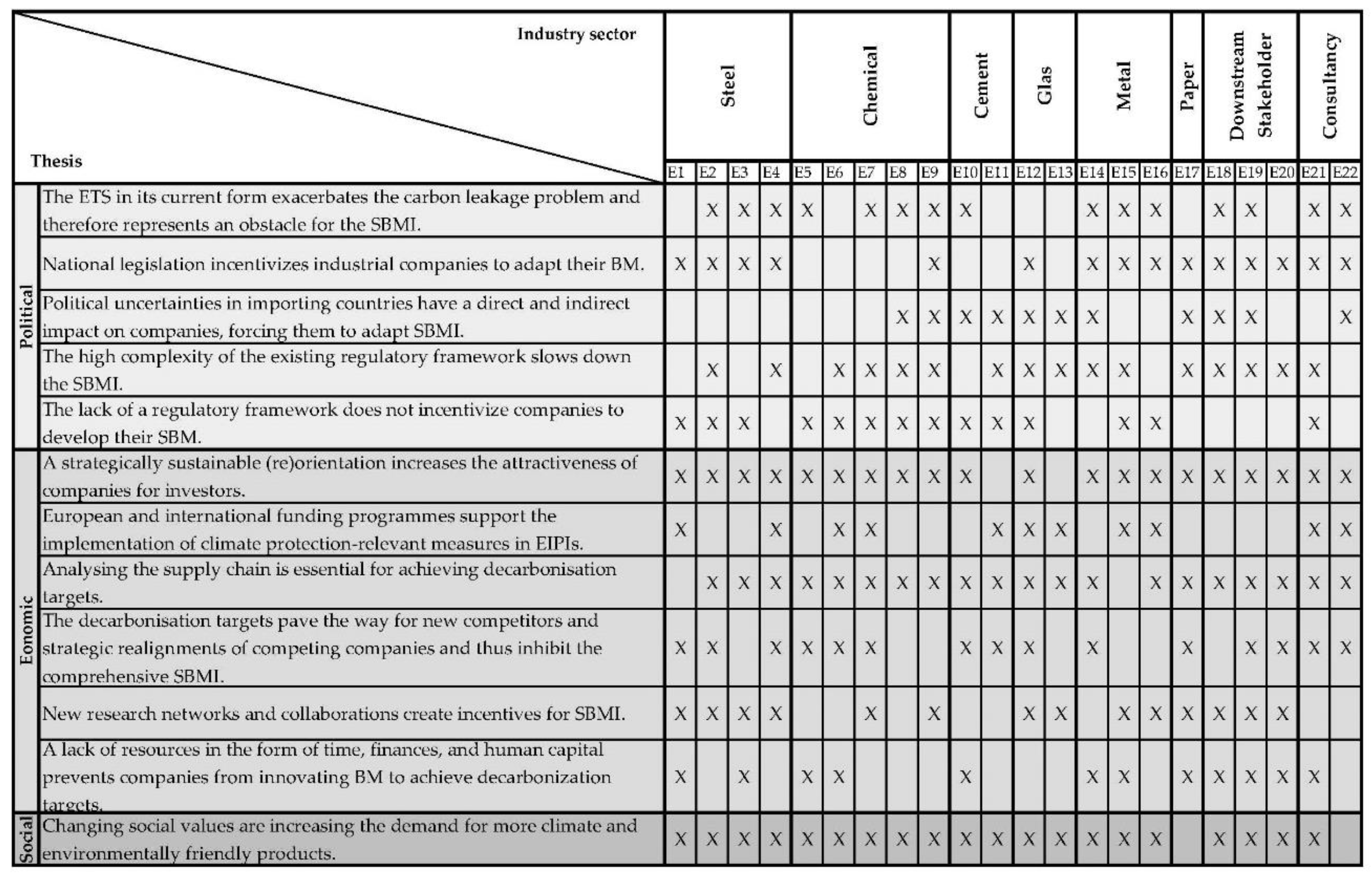

The analysis process consists of coding the transcripts from the expert interviews as a starting point, as well as the interpretation and falsification of the theses. The data analysis was carried out by thematic analysis, in which the transcripts of the interviews were systematically analyzed using specialized analysis software. The video recordings were converted into transcripts using f4x software. The MAXQDA program was used to code the transcripts. The code system comprises three main categories representing the three driver clusters, and the individual theses represent the subcategories. The analysis was case-based. This means that the transcripts were processed individually, one after the other. As part of the coding process, 518 coded elements were grouped into three clusters. The thesis matrix (Figure 1) provides an overview of which expert stated on which thesis.

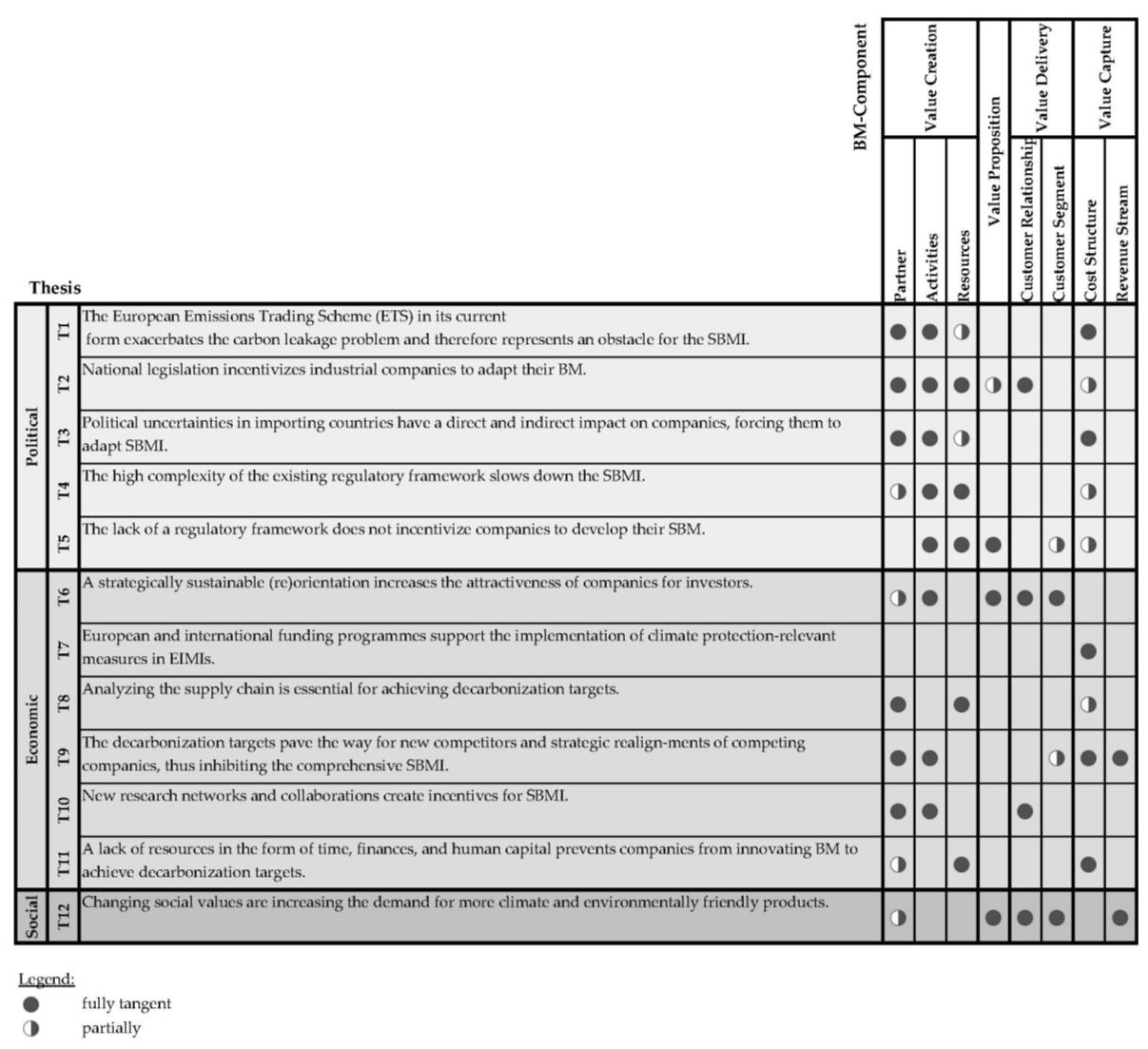

The cross-case evaluation and validation or falsification of the 12 theses were then carried out in line with Döring and Bortz and presented in 3.2 [45]. Paraphrased, anonymized sample quotes from interviewees were selected for publication (see Table 3-5). This was then used to map the theses to the BM components, whereby the Harveyball visualization was selected (Figure 2).

2.5. Rigor and Trustworthiness

All interviews were coded by one researcher (F.M.), whereby a random sub-sample was coded independently by an assistant, and the comparison took place afterwards. The coding framework was designed based on the theses already established. The interview data was analyzed by a researcher (F.M.) and checked by an assistant. Saturation of the sampling, data collection, and analysis was ensured by dividing the study into two parts.

3. Results

3.1. Description of the Theses Derived from the Literature

Below, the theses are described in detail. They were clustered into political, economic, and social theses and identify drivers of decarbonization targets in relation to SBMI.

Table 2.

Overview of the thesis.

| No. | Thesis | Source |

|---|---|---|

| Political | ||

| 1 | The European Emissions Trading Scheme (ETS) in its current form exacerbates the carbon leakage problem and therefore represents an obstacle for the SBMI. | [46,47,48,49,50,51] |

| 2 | National legislation incentivizes industrial companies to adapt their BM. | [10,52,53,54,55,56] |

| 3 | Political uncertainties in importing countries have a direct and indirect impact on companies, forcing them to adapt SBMI. | [57,58,59,60,61] |

| 4 | The high complexity of the existing regulatory framework slows down the SBMI. | [18,62,63,64] |

| 5 | The lack of a regulatory framework does not incentivize companies to develop their SBM. | [11,18,63,64,65,66,67,68,69,70] |

| Economical | ||

| 6 | A strategically sustainable (re)orientation increases the attractiveness of companies for investors. | [10,18,19,58,62,72,73,74] |

| 7 | European and international funding programs support the implementation of climate protection-relevant measures in EIMIs. | [53,62,75,76,77,78,79] |

| 8 | Analyzing the supply chain is essential for achieving decarbonization targets. | [29,71,81,82,83,84,85] |

| 9 | The decarbonization targets pave the way for new competitors and strategic realignments of competing companies, thus inhibiting the comprehensive SBMI. | [12,58,74,84,86,87,89] |

| 10 | New research networks and collaborations create incentives for SBMI. | [29,90,91,92] |

| 11 | A lack of resources in the form of time, finances, and human capital prevents companies from innovating BM to achieve decarbonization targets. | [75,86,93] |

| Social | ||

| 12 | Changing social values are increasing the demand for more climate and environmentally friendly products. | [12,18,71,73,74,94,95] |

- T1: The European Emissions Trading Scheme (ETS) in its current form exacerbates the carbon leakage problem and therefore represents an obstacle to SBMI.

Outsourcing industrial companies to countries outside the emissions trading system (ETS) is favored by the less stringent regulations regarding emission limits and penalties that prevail there [46,47]. Regulations such as the ETS significantly impact BM and can create a need for transformation [41,48]. The outsourcing of production steps in the course of BMI induces significant adjustments in key activities and cost structures as well as in the network of business partners [49]. In addition, there is a risk of increased imports of emission-intensive raw materials, semi-finished, or finished products instead of domestic production. Due to the lack of import regulations that provide for emissions regulation, imported products can be purchased at lower costs [47]. The ETS can thus hinder SBMI by promoting BMI that are not sustainable. This will remain the case until instruments to prevent carbon leakage, such as the border carbon adjustment mechanism (CBAM), are effectively implemented [50,51].

- T2: National legislation incentivizes industrial companies to adapt their BM.

Political framework conditions, including legislative initiatives by the federal government, are crucial for the development of BMI [10,41,52]. Furthermore, commitment at the political level is essential for promoting SBMI, along with other factors. [53] The Federal Climate Protection Act, which defines precise emission reduction targets for various economic sectors as well as sanction mechanisms, is intended to encourage companies to develop SBM [54]. Based on this, companies implement climate protection-relevant processes in their production facilities and evaluate the carbon footprints of resources, products, and supply chains [55,56]. This initiates an SBMI that integrates key resources, partners, and activities and generates a differentiated value proposition for customer segments.

- T3: Political uncertainties in importing countries have a direct and indirect impact on companies, forcing them to adapt SBMI.

The stability of political systems both in countries where governments are based and in countries where corporate goods are imported represents a political factor contributing to BMI [41,57]. A BM is significantly influenced by the surrounding competitive environment, including the presence of substitute goods and the role of suppliers [58]. Imports from non-European countries often face reliability issues and direct risks down the supply chain, which can lead to material shortages and fluctuations in energy prices due to political instability [59]. The worldwide activities have highlighted this dependency and led to short-term adjustments in national energy policy, which, in turn, had a significant impact on the corporate landscape [60]. In addition, anticipating future political developments in relevant countries is essential. Companies are required to rely more heavily on domestic suppliers (key partners) or adapt internal processes (key activities) to minimize the risk of supply disruptions [61].

- T4: The high complexity of the existing regulatory framework slows down the SBMI.

The increasing number and complexity of regulatory requirements at the national or EU level leads to an increased effort in fulfilling these regulations, thereby increasing compliance costs for companies [18,62]. Regulations, especially those relating to fees, taxes, and charges on electricity consumption, can differ considerably depending on the industrial sector and are often characterized by a high degree of complexity. For companies operating in different industries, it is, therefore, essential to understand these complex regulatory requirements and to align strategic management decisions in line with them [62,63,64]. This requires effective knowledge management within the company and with partners [63]. Elements such as key partners, resources, and activities are particularly affected by these requirements.

- T5: The lack of a regulatory framework does not incentivize companies to develop their SBM.

The European Union has laid the foundation for the decarbonization of the European economy with the introduction of the Green Deal [65]. Nevertheless, there is a lack of willingness on the part of many companies in the member states to commit to this goal and the associated sustainable transformation [64,66,67]. Another obstacle is the lack of harmonized standards [18,68], for example, in the classification of different types of hydrogen, which makes it increasingly difficult for customers to understand the GHG emissions associated with each feedstock [69]. Clear labeling of products with lower CO2 emissions, such as steel or cement, could highlight their CO2 efficiency and thus create a competitive advantage for more sustainable products [11,70]. This would allow companies to better target their value proposition to the needs of customer segments [63,71]. The lack of regulation in these areas particularly affects companies' key resources, customers, cost structure, and value proposition.

- T6: A strategically sustainable (re)orientation increases the attractiveness of companies for investors.

Integrating environmental, social, and governance (ESG) criteria into the BM is increasingly decisive for a company’sthe long-term competitiveness and future viability [58,72]. Investors are increasingly taking ESG criteria into account in their investment strategies, which can give companies that position themselves as sustainable at an early stage a so-called first or early mover advantage [10,62,73]. This makes it possible to attract targeted investors who act as key partners. In addition, existing investors in capital market-oriented companies can also push for compliance with ESG criteria [19]. The strategic review and adaptation of BM components, in particular, the development and communication of a new value proposition based on ESG criteria, are crucia l to meet the requirements and expectations of investors [18,74].

- T7: European and international funding programs support the implementation of climate protection-relevant measures in EIMIs.

Government funding programs provide industrial companies with financial support for sustainability projects to introduce innovations to the market and increase their competitiveness [75]. This helps EIMI companies to reduce the high investment costs for decarbonization projects and the associated financial risks of radical innovation. For example, the BMWK supports research, development, pilot projects, and investments in climate-friendly plants with its "Decarbonization in Industry" program [76]. In the future, public funding is expected to be increasingly focused on supporting SBM and innovation. Energy-intensive companies profit, in particular, from funding for measures to reduce process-related CO2 emissions [53]. Investments in production facilities that rely on low-emission processes or bridging technologies, as well as research and development projects, can be funded [77]. In addition, contracts for a fixed CO2 price [78,79], such as Contracts for Difference (CCfD) [79], offer incentives through improved forecasting and the compensation of higher operating costs for climate protection investments, regardless of the fluctuating prices for ETS certificates [62].

- T8: Analyzing the supply chain is essential for achieving decarbonization targets.

The focus on creating shared value within partnerships makes a detailed analysis of the value chain essential for the further development of the BM [29,81]. This careful examination of the supply chain is crucial to achieve decarbonization goals effectively. It enables companies to identify the main sources of GHG emissions by capturing both direct emissions caused by production processes (key resources) and indirect emissions caused by the transport and procurement of materials [82]. This understanding allows companies, especially in the EIMI, to use resources in a targeted manner where they can make the greatest contribution to reducing emissions [83,84]. The transparency generated by the analysis is essential for taking responsibility for environmental impacts and communicate them openly [71,85].

- T9: The decarbonization targets pave the way for new competitors and strategic realignments of competing companies, thus inhibiting the comprehensive SBMI.

The increasing focus of political decisions on the reduction of GHG emissions in order to achieve the 1.5-degree target and the resulting changes in market conditions are forcing companies to organize their BM sustainably way [12,86]. As a result of this development, companies within the same industry increasingly try to position themselves through the unique selling point of sustainability [74]. The challenge is intensified when new market participants with innovative BM or providers of substitute products enter the market. This threat from new competitors can make it more difficult to differentiate the BM but also hinder the further development of a company's BM [58,84]. In addition, the availability of key resources can be restricted [12,87]. For example, primary steel manufacturers in the steel industry [88] see themselves threatened by secondary manufacturers offering lower CO2 products made from steel scrap. In the cement industry, producers of substitutes for cement clinker, such as slag, granulated blast furnace slag, or fly ash [89], pose a challenge to traditional manufacturers.

- T10: New research networks and collaborations create incentives for SBMI.

The BM of an organization includes not only how value is created, delivered, and captured but also the development of strategic networks and the establishment of collaborations and partnerships [28,81]. These partnerships play a crucial role in shaping the BM [41,90]. Participation in national and international research networks facilitates the exchange between science and industry and keeps companies informed about the latest state of the art. In addition, networks enable a critical review and adaptation of value chains, paving the way for new business relationships [41,91]. The aim is to collect ideas and suggestions for innovative BM and to promote their successful implementation [92].

- T11: A lack of resources in the form of time, finances and human capital prevens companies from innovating BM to achieve decarbonization targets.

Resources, whether tangible or intangible, play a central role in the functioning and development of a BM, as they are directly or indirectly involved in its performance [41]. The BMI is realized through processes that take place within a time frame and are influenced, among other things, by employees and financial resources. A lack of resources such as time, finance, and human capital can significantly limit a company's capacity to carry out BMI, especially in achieving decarbonization goals [75]. Financial constraints can prevent companies from making necessary investments in low-carbon technologies or processes [93]. In addition, a lack of qualified personnel can hinder the necessary interdisciplinary collaboration and integration of different disciplines that are essential for developing and implementing advanced decarbonization strategies [75,86].

- T12: Changing social values are increasing the demand for more climate and environmentally friendly products.

The increasing decarbonization targets reflect a social trend towards greater sustainability awareness, resulting in a future increase in demand [73,86] for more climate-friendly products and services in all sectors - from basic material production to the end consumer stage [74,94,95]. The carbon footprint of products and services is thus becoming a decisive factor that not only influences private purchasing decisions but also plays a role in corporate procurement strategies and supplier selection [63,96]. This development has an impact on almost all elements of a company's business model [12], as it requires a comprehensive consideration of sustainability aspects in product development, marketing [18], procurement, and production [71].

Figure 1 shows the categorization of the theses into the three clusters and indicates which expert contributed to which thesis, which, in turn, are clustered into sectors.

3.2. Falsification of the Results

The falsification is presented in three sections. In the first section, the political theses T1 - T5 are falsified, followed by the falsification of the theses in relation to economic drivers (T6 - T11). The final section is the social thesis T12.

Political (T1 – T5):

Table 3 illustrates the experts' statements on the political theses (T1 – T5) with selected quotations.

- T1: The majority of experts (13 out of 22) from the EIMI confirm that the ETS in its current form exacerbates the carbon leakage problem and represents an obstacle for the SBMI, but at the same time, recognize considerable potential in this instrument for promoting sustainable innovation, which, however, requires significant adjustments.

Experts 16, 18, 21, and 22 highlight that the CBAM can make a targeted contribution to mitigating the carbon leakage problem exacerbated by the ETS and thus remove an obstacle to SBMI. They highlight the need for international regulatory instruments to ensure a fair competitive environment, and experts 16 and 21 point out that the cost structures of the BMs and key activities (E21, E22), such as production and purchasing, can be influenced by the CBAM. In addition, the selection of key partners, specifically suppliers, based on their CO2 emissions in the context of CBAM is also highlighted as a relevant factor (E18). The majority of experts 2, 3, 5, 7, 9, and 10 from various sectors underline the urgency of a protection system against unfair competition from outside in order to effectively counter the challenges of carbon leakage.

According to expert opinions 15, 16, and 18, the ETS significantly influences access to raw materials and supply chains, which requires a re-assessment of supplier structures (E16) and burdens the cost structure (E15) due to rising raw material prices (E10). For example, these challenges for globally operating EIMI companies are intensified by competition for regional raw materials and competition with more emission-intensive but cheaper products on international markets (E7).

The experts agree that the ETS has no direct impact on location decisions, outsourcing, or investment decisions (E4, E8, E10, E14, E18, E21, E22). For example, other factors, such as market conditions, dominate in the steel and chemical industries (E4, E8), and energy costs have always been decisive in the cement industry, without any specific influence from the ETS (E10). Increased costs for CO2 certificates also play a minor role in investment decisions (E21, E22).

Experts 12, 15, and 16 highlight the significant role of the national electricity price in the context of the ETS. The initially low CO2 prices (E12, E18) undermined the effectiveness of the ETS in the initial phase. Experts 3 and 9 see an increasing importance of the ETS for make-or-buy decisions, especially for companies that produce in Europe and have to adapt to rising CO2 prices by 2030. Companies at the beginning of the value chain will therefore be more affected by the ETS in the future (E12, E22), which emphasizes the need for a strategic transformation.

- T2: 18 out of 22 experts confirm the thesis that national legislation incentivizes EIMI SBMI.

Implementating the Corporate Sustainability Reporting Directive (CSRD) and the EU taxonomy through national legislation incentivizes industrial companies to adapt their BM to sustainability criteria. Experts 14, 18, 19 and 22 highlight that these regulatory measures strengthen the stakeholder relationship through improved sustainability reporting and facilitate access to sources of capital, such as green bonds (E18). Expert 16 emphasizes the increased responsibility towards key partners, especially suppliers, which is incentivized by the sustainability reports within the supply chains.

Experts from the steel (E2) and chemical (E9) industries highlight the role of national policy as a signal for the sustainable transformation of companies. This concerns the adaptation of key resources, partners, and activities, which leads to a new value proposition. An example is the promotion of electromobility, which has initiated increased production of relevant battery chemicals in the chemical industry and led to a reassessment of product portfolios and partnerships, emphasizing the importance of comprehensive regulation as a driver for sustainable business development (E9).

Expert 7 notes that regulatory requirements make investments in Germany less attractive than other European countries. In contrast, the five experts from the glass and metals industry rate the influence of national laws on the decarbonization of their BM as low. Expert 12 sees decarbonization as the result of a combination of regulatory requirements and pressure from consumers and customers, while expert 14 emphasizes that other factors, such as customer requirements, play a more important role beyond legal regulations.

- T3: 10 out of 22 experts emphasize the direct impact of political uncertainty on supply chains, such as the diversion of shipping routes due to conflicts in the Middle East, while others point to indirect consequences, such as delays in procurement and equipment or rising costs for renewable energy.

Experts 12,13,16,17, and 22 discuss the direct impact of political uncertainties on supply chains and emphasize the importance of regional supply routes as an opportunity to overcome these challenges. Focusing on regional value chains enables companies to react flexibly to political instability and minimize the associated risks. Experts 14 and 22 highlight the fact that compliance requirements are also easier to fulfill. Despite global networking and the potential impact of worldwide political developments (E17), the influence of political uncertainties in the cement industry is estimated to be low due to the regional nature of the product (E10, E11) (Table 3).

Political risks in importing countries affect purchasing and, thus, the cost structures of companies, as confirmed by experts 13, 14, 16, and 18. The procurement of equipment for sustainability projects (E13) is particularly challenging, highlighting the importance of secondary materials (E14). The chemical industry, for example, procures many raw materials internationally (E9); therefore it faces particular challenges that require purchasing strategies to be adapted in order to tackle political uncertainties effectively.

The direct effects of political uncertainties on supply chains require adapted risk management strategies in companies, as expert 22 points out. This requirement is also supported by experts 13, 14, and 19, who have implemented corresponding risk management decisions in their companies. These decisions concern key activities such as investments and production and are essential in order to be able to react to dynamic global political developments and strengthen corporate resilience.

- T4: The experts (14 out of 22) confirm that the high complexity of the regulatory framework represents a barrier for SBMI.

The high level of complexity represents a significant barrier for SBMI by using valuable resources and impairing the core business (E12, E13, E15). Expert 13 reports that regulatory requirements not only hinder innovative approaches but also require a comprehensive allocation of resources that could otherwise be used for developing and implementing innovations. In response to these challenges, companies are intensifying the exchange and cooperation within their networks in order to find joint solutions for overcoming regulatory complexity and thus strengthen knowledge management and the ability to innovate. In addition, representatives of the chemical and cement industries (E6, E7, E9, E11) argue that a more flexible and open regulatory design that actively incorporates the competencies and problem-solving potential of companies is essential to minimize the commitment of resources caused by regulatory requirements and at the same time pave the way for sustainable innovation. The complexity of legislation means that companies are reluctant to invest in new technologies (E15, E16, E22). Expert 16 emphasizes that the lack of a market for certain technologies hinder key activities, which makes the development and introduction of sustainable technologies more difficult.

Increased bureaucracy in Germany inhibits the change of BM and impairs planning security (E7, E17, E19, E21), which leads to cost increases (E17). Investments are affected by bureaucratic hurdles and could, therefore, be outsourced abroad (E21). Experts 17 and 20 point out that regulatory complexity delays the introduction of innovative systems and sustainable practices.

- T5: 10 out of 22 experts confirm that the lack of a regulatory framework will hinder SBMI. No generally valid falsification is possible for this thesis.

Expert 12 refers to the uncertainty surrounding the development of electricity-based, decarbonized production facilities, which is intensified by inadequate regulation. Expert 21 supports the call for mandatory decarbonization targets for manufacturing companies increase price pressure and create a competitive regulatory environment that could incentivize sustainable development. Experts 15, 16, and 21 underline the need for an appropriate regulatory framework to promote investment and innovation in the area of decarbonization. They point out the importance of financial and material resources for the development and commercialization of environmentally friendly technologies.

In the chemical industry (E6) and the cement industry (E11), the lack of a regulatory framework is seen as an obstacle to introducing sustainable products and practices. The need to meet market requirements with adequate regulations in a timely manner is emphasized, as are the challenges of introducing new, sustainable input products and balancing their emissions. In the steel sector (E13), innovative plants are put into operation later than abroad due to the lack of a standardized definition of hydrogen and end products. In addition, the definition of green steel in connection with products from the secondary route (E14) would also be an issue. Furthermore, experts 13 and 18 criticize framework conditions for CO2 capture technologies by. The use of sustainable or recycled building materials concerns waste, environmental, product, and disposal legislation, and this regulatory complexity leads to delays in the implementation of innovations (E20).

Experts 1, 2, and 3 see potential in public procurement and other regulated markets to accelerate the sustainable transformation by incentivizing green materials.

Economical (T6 – T11):

Table 4 illustrates the experts' statements on the economical theses (T6 – T11) with selected quotations.

- T6: The expert statements significantly confirm the thesis, with 17 out of 22 experts believing that a sustainable (re)orientation increases a company’s attractiveness.

The rise in investment in green assets, as observed by experts 15, 16, and 22, emphasizes the need for companies to position themselves in the area of sustainability (E6). This is particularly highlighted in the glass industry (E12), where a reorientation with regard to CO2 emissions is seen as essential for investor attractiveness. The increasing importance of sustainability aspects in investment decisions is highlighted by the interest of major financial players such as the Allianz Group, various banks (E15), and BlackRock as illustrative examples by experts 12, 19, 22. The demand for concrete measures, such as the implementation of science-based targets (E5, E6, E7) and participation in Climate Action 100+ (E5, E8), shows the expectations that investors have of companies.

Pressure from customers and other stakeholders forces companies to make strategic changes that increase their attractiveness. The increasing demand for sustainable products (E17, E18, E19, E20, E21) and the expansion of the product portfolio to include such products are clear indicators of market trends. Companies that focus on sustainability at an early stage position themselves for long-term growth and minimize potential risks.

Implementing a sustainability strategy, often driven by investment requirements (E17, E18, E21), is not only a response to external requests but also serves as a competitive advantage and driver of innovation. This proactive attitude is particularly valued by investors and makes companies more attractive to investors (E12, E14, E18). Despite different requirements for listed compared to privately managed companies (E18, E21, E22), the fundamental change towards more sustainability is a development that ultimately comes from the companies themselves (E22).

- T7: According to the experts (7 out of 22), the number of instruments and the total amount of funding from global and European funding programs is sufficient, but implementation has a significant negative impact on the EIMI's SBMI. The hypothesis is, therefore, refuted.

Experts point out that despite the availability of funding, the application processes are complex, and companies often have to bear a considerable share of the financing themselves (E21). The need for long-term planning and the high level of competition in European calls for funding also make it difficult to implement sector-specific projects (E12), which calls into question the effectiveness of the funding programs.

The importance of incentives for establishing innovative technologies on the market is emphasized by experts 15 and 16 from the metals industry. Support and funding are essential to drive innovation, minimize financial risks, and reduce climate-damaging emissions in the long term. However, time-consuming official approval processes hinder the utilization of funding instruments, and European funding pots remain unused (E3, E5).

The framework conditions of European funding instruments, which stipulate that no project steps may be carried out before an application is submitted, penalize projects that are already underway (E5). This limits the opportunities to become competitive through funding. Although new funding models such as CCfD are welcomed (E6), the question remains whether SBMs can be realized without continuous funding.

Despite the challenges mentioned, expert 10 from the cement industry sees subsidies as an important incentive that signals the necessary transformation path. This highlights the role of funding programs as a signpost for the industry, even if practical implementation and accessibility need to be improved in order to fully exploit the potential.

- T8: The requirement to analyze the supply chain in the context of achieving decarbonization targets requires an industry-specific approach within the EIMI. Particularly in scenarios in which the supply chains consist primarily of small and medium-sized enterprises, such an analysis proves impractical due to an insufficient database or the limited number of suppliers for whom switching is impossible.

The importance of partnerships and well-considered supplier selection is highlighted by experts from various sectors (E1, E2, E3, E4). They emphasize that there are challenges, particularly in the precious metals and paper industry and with smaller suppliers, that make it difficult to implement sustainability standards without sufficient capacity or the necessary knowledge (E14, E16, E17, E20). In this case, the targeted use of resources to promote and support suppliers is crucial in order to jointly achieve sustainability goals (E18, E19, E22). The targeted support of actors who pay high costs for reducing emissions is another important aspect. Strategic resource allocation allows higher end prices to be distributed across the value chain and holistic decarbonization to be achieved (E7, E8). This also includes the involvement of energy suppliers, users, and product disposal companies.

The pressure for decarbonization within the value chain, especially from key partners such as the automotive industry (E21), makes an in-depth analysis of the supply chain necessary (E18, E21, E22). This analysis serves as a basis for the targeted allocation of resources to establish effective partnerships and drive decarbonization forward. The challenges of data consistency and the accounting of emissions in the upstream and downstream supply chain require a targeted allocation of resources in order to achieve the necessary transparency and precision. This is particularly relevant in value chains characterized by SMEs (E4). The use of resources for energy-related material flow management and the selection of innovative suppliers are decisive steps towards reducing emissions in the upstream and downstream supply chain (E5, E6, E7, E9).

- T9: The thesis that decarbonization targets inhibit SBMI through new competitors and strategic realignments cannot be clearly confirmed due to differing expert opinions and industry-specific differences. While some sectors are dominated by first movers, others are focused on replacement.

Experts 14, 17, and 20 emphasize the need to closely monitor the activities of competitors in order to keep pace with the changes brought about by decarbonization. The use of renewable energies by some competitors places pressure on the entire industry to follow and develop its own decarbonization strategies.

Expert 12 points out that decarbonization is currently creating financial disadvantages (cost structure, sources of income), which could give companies that do not actively participate a short-term competitive advantage. In the context of the chemical industry, expert 12 points out that eliminating certain products with a high carbon footprint from the product portfolio creates space for other companies willing to continue manufacturing these products and gain market share. This illustrates how decarbonization targets can influence market dynamics and favor new competitors. Innovation is crucial to survive in the competitive environment changed by decarbonization in the long term (E19). Companies that invest in sustainable innovations (E1, E2, E3, E6, E7) aim to play a pioneering role to achieve price premiums and set themselves above the competition.

The importance of cooperation and joint initiatives (E21, E22) in the EIMI is emphasized. By working together, challenges can be tackled more effectively, and industry-wide solutions can be developed, which increases the intensity of competition in procurement markets for more sustainable raw materials (E6, E7).

- T10: According to 15 out of 22 experts, new research networks and collaborations create incentives for SBMI.

There is a positive general opinion of such networks and cooperations across all sectors, particularly in the steel and chemical industries (E1, E2, E3, E4, E6, E7, E9). According to expert 16, collaboration with external parties is essential to intensify research and development activities and accelerate innovation. Expert 15 emphasizes the importance of cooperation within the industry and with innovation hubs to develop new technologies and promote knowledge transfer, which forms the basis for SBMI.

For example, research networks in the glass industry make a significant contribution to research that focuses on closing recycling loops (E12, E13). Through the development of innovative technologies, specific waste streams, such as glass fragments, can be effectively reused, which significantly increases the sustainability of production.

Research partnerships, including competitors and industry associations, enable a valuable exchange of experience and learning from the best practices of other companies (E2, E4, E18). This enables companies to learn from each other and to jointly develop and implement sustainable innovations. Such cooperative approaches not only promote the development of SBMI, but also help to move the entire industry towards sustainability.

- T11: The thesis is confirmed by 12 of the 22 experts, with the lack of financial and human capital resources taking center stage.

While there is a growing interest among young people in sustainability issues, there is a lack of the necessary expertise and experience (E20). Expert 21 underlines the difficulties in recruiting qualified personnel and the associated high costs. Expert 15, on the other hand, reports no recruitment problems, which could indicate industry- or company-specific differences.

The financial challenges, in particular, the cost structures and the need to take economic aspects into account when implementing sustainability goals, are identified as further barriers (E15, E20). The trade-off between costs and sustainability goals confronts many companies with major challenges. The experts agree that climate protection measures and production costs are high (resource-intensive) and that the demand for sustainable products is still too low to achieve broad market penetration. This inhibits the willingness to innovate, as the products are not yet competitive (E1, E2, E5, E9, E11).

Social (T12):

Table 5 illustrates the experts' statements on the social theses (T12) with selected quotations.

- T12: Although more than half of the experts believe that changing social values increase the demand for climate and environmentally friendly products, some point to the influence of the supply chain and the lack of a significant increase in demand, which limits the overall validity of the thesis.

The shift in social values towards greater environmental awareness is reflected in an increasing demand for climate and environmentally friendly products, which presents companies with the challenge of adapting their BM accordingly. This development is confirmed by 8 out of 22 experts (E13, E14, E15, E16, E18, E20, E21, E22), who emphasize the growing pressure from end customers on the entire value chain. In particular, the increased demand for recycling, re-manufacturing, and the circular economy (E18) illustrates this trend.

In some sectors, such as the steel (E1) and chemical industries (E6, E7), there is a slowly increasing demand for sustainable solutions. Experts 12 and 13 from the glass industry perceive price competition in the market despite the increased demand for climate-friendly products. This makes the supply of environmentally friendly glass more difficult, as competitors who do not decarbonize can offer their products more cheaply.

Some customers are prepared to pay a higher price for sustainability (E22), which makes it easier for companies to achieve their climate targets. Social debates, such as those of Fridays for Future, are leading to a rethink of corporate strategy (E19), whereby the adaptation of strategy is essential to effectively integrate sustainability into the BM (E16, E19). One major challenge is the lack of labeling and transparency of CO2-reduced products, which makes it difficult for end customers to distinguish between sustainable and less sustainable products. This applies, in particular, to products whose sustainability aspect is not immediately recognizable, such as vehicles made of green steel or climate-neutral paint (E3, E5, E9).

Despite the social pressure for greater sustainability, experts point out that many customers are unwilling to bear the additional costs for sustainable products (E3, E5, E7, E9, E11). The shift in social values towards greater environmental awareness is reflected in an increasing demand for climate and environmentally friendly products, which presents companies with the challenge of adapting their BM accordingly. This development is confirmed by 8 out of 22 experts (E13, E14, E15, E16, E18, E20, E21, E22), who emphasise the growing pressure from end customers on the entire value chain. In particular, the increased demand for recycling, re-manufacturing and the circular economy (E18) illustrates this trend.

3.3. Analysis of the Influence of the Drivers (T1-T12) on the Business Model Components

The influence matrix presented below (Figure 2) shows which drivers (T1 - T12) affect a company’s BM components. The Harvey ball representation was selected to show how much a driver affects a BM component. A filled circle shows that a BM component is completely tangent to a thesis, or - half-filled - is partially tangent to it.

The analysis of the ETS (T1) shows its far-reaching impact on BM components, in particular on the cost structure, key partners, and activities, which are completely affected by the need for a protection system for fair competitive conditions and the influence of the CBAM. The ETS significantly influences access to raw materials, and their CO2 emissions triggers a reassessment of the supplier structure, thus influencing the cost structure. At the same time, the CO2 price has an indirect effect on make-or-buy decisions, which has a comprehensive impact on the cost structure. Resources are partially affected, as the selection and accessibility of suppliers based on their CO2 emissions can directly influence the availability and costs of resources.

When evaluating the impact of national legislation (T2) on EIMI's SBMI, it becomes apparent that legal incentives comprehensively influence the BM components. These reports strengthen the customer relationship through increased transparency and responsibility and positively influence the relationship with partners. Evaluating the carbon footprint of products and reviewing supply chains leads to a necessary adjustment of resources, partners, and activities, generating a new value proposition. Regulatory requirements can also stimulate a BMI that causes companies to rethink their investment strategies, influencing the cost structure. Thus, partners, activities, resources, and customer relationship are fully affected while the cost structure and value proposition are only partially affected.

An analysis of the impact of political uncertainties in importing countries (T3) on companies highlights that both direct and indirect effects force an SBMI. The impact on supply chains is considerable, in particular, the importance of regional supply routes is emphasized, which requires a re-evaluation of procurement strategies. These uncertainties significantly affect the cost structure, especially when companies highly dependend on the international sourcing of raw materials. In addition, political uncertainties require adjusting risk management strategies that directly affect business activities. As a result, activities, partners, and the cost structure are fully affected, while resources are only partially affected.

Investigating the impact of the existing complex regulatory framework (T4) on the slowdown of SBMI reveals that complexity binds resources, as employees are needed to understand the regulations and process company-specific. Complexity also encourages joint dialogue between companies and their partners. The activities of companies are restricted by the uncertainty regarding investments in new technologies or innovations. This means that activities and resources are completely affected, while the involvement of partners and cost structure are only partially affected.

The examination of the impact of the lack of a regulatory framework (T5) on SBMI shows that the uncertainties resulting from the lack of standards hinder investments in sustainable innovations and technologies (see T4), which directly affects the cost structure. The lack of markets for sustainable, CO2-free products and the lack of labeling of such products delay the development of new value propositions and indirectly affect the customer segment that could be addressed with sustainable products. In addition, resources are not being utilized due to the lack of a political framework. This leads to a complete disruption of activities, resource utilization, and value propositions, while the cost structure and customer segment are only partially affected.

Responding to the increasing demand for sustainable products through a strategic reorientation (T6) leads to an adapted value proposition for customers, increasing the companies’ attractiveness for investors. Companies that rely on the first-mover advantage and expand their portfolio to include sustainable products can tap into new customer segments and also improve customer relationships by responding to customer inquiries for such products. The value proposition, key activities, and the customer relationship and segments are thus fully affected, while partners are only partially affected.

The complexity of the application processes makes it difficult to use European and global funding programs (T7). These factors directly affect the cost structure of companies by causing additional financial burdens and reducing the efficiency of funding allocation.

Overcoming challenges together in the context of decarbonization requires targeted knowledge and sufficient capacity, which presupposes the focused use of resources along the entire value chain. An effective allocation of resources makes it possible to distribute some of the costs arising from higher end prices along the value chain, which affects the cost structure of the companies involved. In addition, the pressure within the value chain leads to an in-depth analysis (T8) and the establishment of partnerships. Partners and resources are fully affected, while the cost structure is only partially affected.

The analysis of the impact of decarbonization targets on BM components shows that activities, partners, revenue sources, and cost structures are fully tangent, as companies are forced to adapt their strategies to keep pace with the changes caused by decarbonization and remain competitive (T9). Customer segments are affected to some extent, as there is a need to adapt to changing customer preferences and, at the same time, recognize new market opportunities arising from the strategic realignment of competing companies.

The involvement of external partners and the integration of customers in development processes are key factors promoted by new research networks and cooperations (T10). This dynamic leads to a complete influence on key partners and activities through the need to strengthen cooperations and develop joint initiatives. At the same time, the customer relationship is fully affected, as the direct involvement of customers in the innovation process enables closer engagement and a deeper understanding of customer needs.

In achieving decarbonization goals, companies face an acute shortage of specific expertise, financial resources, and skilled personnel (T11). This problem can be tackled by entering into new partnerships. The lack of financial resources has a direct and extensive impact on the companies’ cost structure by exacerbating the trade-off between the need to achieve sustainability goals and the associated costs.

The shift in social values (T12) towards greater climate and environmental awareness induces an increased demand for ecologically sustainable products, which requires a complete reorganization of the value proposition of companies. This dynamic intensifies price competition and significantly influences revenue by forcing companies to develop differentiated pricing strategies. By integrating customers, for example, companies can develop sustainable products and thus address new customer segments with higher price willingness.

4. Discussion

4.1. Statement of Principal Findings

This study used a qualitative empirical approach to systematically analyze the drivers of the decarbonization targets on the BM components and thus demonstrated an understanding of the influences [24]. The decarbonization of the EIMI represents a complex challenge that requires a fundamental transformation of the existing BM [97]. The analysis of the various drivers - from sustainability-oriented investment strategies of investors to national legislation and changes in social values - makes it clear that almost all BM components, from the cost structure and key activities to value propositions and customer relationships, are significantly influenced. Based on the findings of [24] regarding the need to understand the dynamics of national policies, SBM, and the transition process towards a sustainable economy, there is a clear need for in-depth research within business model theory. The aim is to decipher the complex interactions between the drivers of decarbonization and the components of BM. In particular, the identification of design options for SBM that promote both ecological and economic sustainability is the focus of research interest. In this context, reference is made to the work of [28], which explores new BM options in the EIMI.

In addition, models are to be developed that contribute to overcoming the drivers and support SBMI. These models must focus on reducing the complexity of the various drivers of decarbonization and promoting proactive SBMI so that companies can not only meet regulatory requirements but also tap into new market opportunities and secure long-term competitive advantages. A particular focus can be placed here on the research call of [28], whereby the influence of decision-making processes on SBMI in the EIPI should be considered.

Promoting cooperation between companies, research institutions, and end customers can accelerate the development and implementation of SBMI. In particular, involving external partners in the innovation process [98] opens up new perspectives for sustainable business practices and promotes the development of BMs that support the transition to environmentally friendly practices without neglecting economic viability [99,100,101]. Accordingly, following on from [71], the influence of openness in the context of sustainable transformation, or SBMI, should be highlighted as a future research need.

This study makes a significant contribution to understanding the role of SBM and SBMI in industrial decarbonization and provides essential insights for scientific research and business practice.

4.2. Strengths and Limitations

The sample size of the study (n=22) was sufficient to explore the research objectives and ensure adequate data completeness. A key strength of this study was the positions of the interviewees, which allowed for in-depth insights into the BM of companies in the domain of sustainability. The adaptation of the STEP method made it possible to present the key factors of the business environment from a macro perspective and to analyze how various influencing factors affect the BM and SBMI in the context of decarbonization targets. However, it should be noted that beyond the specifically focused driver clusters, it is possible that other driver clusters also have an influence. By extending the scope of the study to the entire EIMI and not just the selected industries, the results of the study were enriched by a more comprehensive analysis.

5. Conclusions

In summary, this study shows that the decarbonization of the EIMI requires a profound and holistic adaptation of the BM. Implementing SBMI is a complex but essential task that requires close collaboration between all stakeholders. The results of this study provide important insights for understanding SBMI in the context of meeting decarbonization targets and offer a starting point for further research in the field of SBM.

Author Contributions

F.M. worked on the conceptualization, the investigation of the research subject, the design of the methodology, the development of the general structure, and the writing of the manuscript. T.B. supervised the work and provided critical feedback to shape the research, analysis, and manuscript. All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding.

Acknowledgments

We would like to thank all the participating experts who were available for interviews and whose insights made a valuable contribution to this study.

Conflicts of Interest

The authors declare no conflicts of interest.

Appendix A

The following is a list of the experts interviewed and their branch and position, including the numbering used in the text.

Table A1.

Overview of the experts surveyed and their positions.

| No. | Position | Industry |

|---|---|---|

| 1 | Senior ESG Manager | Steel |

| 2 | Project spokesperson for a million euro decarbonization project | Steel |

| 3 | Head of Public and Regulatory Affairs | Steel |

| 4 | Head of Competence Center Climate and Energy | Steel |

| 5 | Corporate Sustainability Manager | Chemical |

| 6 | Head of Sustainability Business Integration | Chemical |

| 7 | Head of Corporate Sustainability | Chemical |

| 8 | Senior Manager Sustainability Reporting | Chemical |

| 9 | Head of Corporate Strategy | Chemical |

| 10 | Senior engineer in the areas of climate protection, environment and operational technology | Cement |

| 11 | Test center manager in concrete and application technology | Cement |

| 12 | Global Affairs Manager | Glas |

| 13 | Sustainability Director | Glas |

| 14 | Sustainability Manager | Metal |

| 15 | Member of Board | Metal |

| 16 | Head of Decarbonization | Metal |

| 17 | Manager Sustainability & Energy | Paper |

| 18 | Sustainability Manager | Downstream Stakeholder |

| 19 | Sustainability Manager | Downstream Stakeholder |

| 20 | Sustainability Manager | Downstream Stakeholder |

| 21 | Partner Strategy & Transactions | Consultancy |

| 22 | Senior Manager Strategy & Transactions | Consultancy |

References

- European Commission. A clean planet for all - A European long-term strategic vision for a prosperous, modern, competitive and climate neutral economy. 2018. Available online: https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX%3A52018DC0773 (accessed on 10.01.2024).

- Wyns, T.G.; Khandekar, G.A.; Axelson, M.; Sartor, O.; Neuhoff, K. Industrial Transformation 2050 - Towards an Industrial strategy for a Climate Neutral Europe.; Institute for European Studies Vrije Universiteit Brussel: Brussel, Belgium, 2019; Available online: https://www.ies.be/files/Industrial_Transformation_2050_0.pdf (accessed on 10.01.2024).

- Europäische Kommission. Der europäische Grüne Deal. 2023. Available online: https://eur-lex.europa.eu/resource.html?uri=cellar:b828d165-1c22-11ea-8c1f-01aa75ed71a1.0021.02/DOC_2&format=PDF (accessed on 10.01.2024).

- BMUB. Klimaschutzplan 2050 - Klimapolitische Grundsätze und Ziele der Bundesregierung. 2016. Available online: https://www.bmwk.de/Redaktion/DE/Publikationen/Industrie/klimaschutzplan-2050.pdf?__blob=publicationFile&v=1 (accessed on 23.02.2023).

- Axelson, M.; Oberthür, S.; Nilsson, L.J. Emission reduction strategies in the EU steel industry: Implications for business model innovation. Journal of Industrial Ecology 2021, 25, 390–402. [Google Scholar] [CrossRef]

- Statistisches Bundesamt (Destatis). Anthropogene Luftemissionen - 2000 bis 2019. 2021. Available online: https://www.destatis.de/DE/Themen/Gesellschaft-Umwelt/Umwelt/UGR/energiefluesse-emissionen/Publikationen/Downloads/anthropogene-luftemissionen-5851103197004.html (accessed on 20.12.2023).

- Gross, S. The challenge of decarbonizing heavy industry. 2021. Available online: https://www.brookings.edu/articles/the-challenge-of-decarbonizing-heavy-industry/ (accessed on 08.2023).

- Agora Energiewende, Wuppertalinstitute. Klimaneutrale Industrie: Schlüsseltechnologien und Politikoptionen für Stahl, Chemie und Zement. 2019. Available online: https://epub.wupperinst.org/frontdoor/index/index/docId/7675 (accessed on 30.11.2023).

- Wesseling, J.H.; Lechtenböhmer, S.; Åhman, M.; Nilsson, L.J.; Worrell, E.; Coenen, L. The transition of energy intensive processing industries towards deep decarbonization: Characteristics and implications for future research. Renewable and Sustainable Energy Review 2017, 79, 1303–1313. [Google Scholar] [CrossRef]

- Wyns, T.; Axelson, M. Decarbonising Europe's Energy Intensive Industries. The Final Frontier.; Institute for European Studies Vrije Universiteit Brussel: Brussel, Belgium, 2016; Available online: https://carbonmarketwatch.org/wp/wp-content/uploads/2016/05/Final-Frontier-Innovation-Report-Web-Version.pdf (accessed on 30.11.2023).

- Mobarakeh, M.R.; Kienberger, T. Climate neutrality strategies for energy-intensive industries: An Austrian case study. Cleaner Engineering and Technology 2022, 10, 100545. [Google Scholar] [CrossRef]

- Evans, S.; Vladimirova, D.; Holgado, M.; Van Fossen, K.; Yang, M.; Silva, E.A.; Barlow, C.Y. Business Model Innovation for Sustainability: Towards a Unified Perspective for Creation of Sustainable Business Models. Business Strategy and the Environment 2017, 26, 597–608. [Google Scholar] [CrossRef]

- Rosato, P.F.; Caputo, A.; Valente, D.; Pizzi, S. 2030 Agenda and sustainable business models in toursim: A bibliometric analysis. Ecological Indicators 2021, 121, 106978. [Google Scholar] [CrossRef]

- Sinkovics, N.; Gunaratne, D.; Sinkovics, R.R.; Molina-Castillo, F.-J. Sustainable Business Model Innovation: An Umbrella Review. Sustainability 2021, 13, 7266. [Google Scholar] [CrossRef]

- Galvão, G.D.; Evans, S.; Ferrer, P.S.; de Carvalho, M.M. Circular business modell: Breaking down barriers towards sustainable development. Business Strategy and the Environment 2022, 31, 1504–1524. [Google Scholar] [CrossRef]

- Reinhardt, R.; Christodoulou, I.; Gassó-Domingo, S.; Gracía, B.A. Towards sustainable business models for electric vehicle battery second use: A critical review. Journal of Environmental Management 2019, 245, 432–446. [Google Scholar] [CrossRef]

- Rennings, K. Redefining innovation - eco-innovation research and the contribution from ecological economics. Ecological Economics 2000, 32, 319–332. [Google Scholar] [CrossRef]

- Asswad, J.; Hake, G.; Gómez, J.M. Overcoming the Barriers of Sustainable Business Model Innovations by Integrating Open Innovation. In Business Information System, 1st ed.; Abramowicz, W., Alt, R., Franczyk, B., Eds.; Springer: Cham, 2016; Volume 255, pp. 302–314. [Google Scholar] [CrossRef]

- Rahman, H.U.; Zahid, M.; Al-Faryan, M.A. ESG and firm performance: The rarely explored moderation of sustainability strategy and top management commitment. Journal of Cleaner Production 2023, 404, 136859. [Google Scholar] [CrossRef]

- Alshehhi, A.; Nobanee, H.; Khare, N. The Impact of Sustainability Practices on Corporate Financial Performance: Literature Trends and Future Research Potential. Sustainability 2018, 10, 494. [Google Scholar] [CrossRef]

- Pulino, S.C.; Ciaburri, M.; Magnanelli, B.S.; Nasta, L. Does ESG disclosure Influence Firm Performance? Sustainability 2022, 14, 7595. [Google Scholar] [CrossRef]

- Stubbs, W.; Cocklin, C. Conceptualizing a "Sustainability Business Model". Organization & Environment 2008, 21, 103–127. [Google Scholar] [CrossRef]

- Upward, A.; Jones, P. An Ontology for Strongly Sustainable Business Models: Defining an Enterprise Framework Compatible with Natural and Social Science. Organization & Environment 2016, 29, 97–123. [Google Scholar] [CrossRef]

- Hernández-Chea, R.; Jain, A.; Bocken, N.M.; Gurtoo, A. The Business Model in Sustainability Transition: A Conceptualization. Sustainability 2021, 13, 5763. [Google Scholar] [CrossRef]

- Geissdoerfer, M. Sustainable Business Model Innovation: Process, challenge and implementation. Procedia Manufacturing 2019, 8, 262–269. [Google Scholar] [CrossRef]

- Bocken, N.; Short, S.; Rana, P.; Evans, S. A literature and practice review to develop sustainable business model archetypes. Journal of Cleaner Production 2014, 65, 42–56. [Google Scholar] [CrossRef]

- Teece, D.J. Business Models, Business Strategy and Innovation. Long Range Planning 2010, 43, 172–194. [Google Scholar] [CrossRef]

- Osterwalder, A.; Pigneur, Y.; Tucci, C.L. Clarifying Business Models: Origins, Present, and Future of the Concept. Communications of the Association for Information Systems 2005, 16. [Google Scholar] [CrossRef]

- van Delft, S.; Zhao, Y. Business models in process industries: Emerging trends and future research. Technovation 2021, 105, 102195. [Google Scholar] [CrossRef]

- Lüdeke-Freund, F.; Carroux, S.; Joyce, A.; Massa, L.; Breuer, H. The sustainable business model pattern taxonomy - 45 patterns to support sustainability-oriented business model innovation. Sustainable Production and Consumption 2018, 15, 145–162. [Google Scholar] [CrossRef]

- Trapp, C.T.; Kanbach, D.K. Green entrepreneurship and business models: Deriving green technology business model archetypes. Journal of Cleaner Production 2021, 297, 126694. [Google Scholar] [CrossRef]

- Boons, F.; Lüdeke-Freund, F. Business models for sustainable innovation: state-of-the-art and steps towards a research agenda. Journal of Cleaner Production 2013, 45, 9–19. [Google Scholar] [CrossRef]

- Bocken, N.; Schuit, C.; Kraaijenhagen, C. Experimenting with a circular business model: Lessons from eight cases. Environmental Innovation and Societal Transitions 2018, 28, 79–95. [Google Scholar] [CrossRef]

- Mangold, H.; van Vacano, B. The Frontier of Plastics Recycling: Rethinking Waste as a Resource for High-V2160alue Applications. Macromolecular Chemistry and Physics 2022, 223, 2100488. [Google Scholar] [CrossRef]

- Vernay, A.-L.; Cartel, M.; Pinkse, J. Mainstreaming Business Models for Sustainability in Mature Industries: Leveraging Alternative Institutional Logics for Optimal Distinctiveness. Organization & Environment 2022, 35, 414–445. [Google Scholar] [CrossRef]

- Geissdoerfer, M.; Weerdmeester, R. Managing business model innovation for relocalization in the process and manufacturing industry. Journal of Business Chemistry 2019, 16, 11–25. [Google Scholar] [CrossRef]

- Mais, F.; Schmitt, L.; Bauernhansl, T. Treiber der nachhaltigen Geschäftsmodellinnovation. Zeitschrift für wirtschaftlichen Fabrikbetrieb 2023, 113, 525–530. [Google Scholar] [CrossRef]

- Meinhold, M.-L. Methodologie. In Die Wissensnutzung und ihre Hindernisse, Gabler Edition Wissenschaft; Deutscher Universitätsverlag: Wiesbaden, Germany, 2001; p. 125. [Google Scholar] [CrossRef]

- Moher, D.; Liberati, A.; Tetzlaff, J.; Altman, D.G.; PRISMA Group. Preferred Reporting Items for Systematic Review and Meta-Analyses: The PRISMA Statement. Annals of Internal Medicine 2009, 151, 264–269. [Google Scholar] [CrossRef]

- Fahey, L.; Narayanan, V.K. Macroenvironmental analysis for strategic management, 1st ed.; South-Western, 1986. [Google Scholar]

- Schallmo, D.R. Geschäftsmodelle erfolgreich entwickeln und implementieren - Mit Aufgaben, Kontrollfragen und Tamplates, 2nd ed.; Springer Gabler: Berlin, Heidelberg, Germany, 2013. [Google Scholar] [CrossRef]

- Osterwalder, A.; Pigneur, Y. Business Model Generation: A Handbook for Visionaries, Game Changers, and Challengers, 1st ed.; John Wiley & Sons: Hoboken, United States, 2010. [Google Scholar]

- Helfferich, C. Die Qualität qualitativer Daten, 4th ed.; VS Verlag für Sozialwissenschaften: Wiesbaden, Germany, 2011. [Google Scholar] [CrossRef]

- Bogner, A.; Littig, B.; Menz, W. Das Experteninterview: Theorie, Methode, Anwendung, 1st. ed.; VS Verlag für Sozialwissenschaften: Wiesbaden, Germany, 2002. [Google Scholar] [CrossRef]

- Döring, N.; Bortz, J. Forschungsmethoden und Evaluation in den Sozial- und Humanwissenschaften, 5th ed.; Springer: Berlin, Heidelberg, Germany, 2016. [Google Scholar] [CrossRef]

- aus dem Moore, N.; Großkurth, P.; Themann, M. Multinational corporations and the EU Emissions Trading System: the specter of asset erosion and creeping deindustralization. Journal of Environmental Economics and Management 2019, 94, 7–9. [Google Scholar] [CrossRef]

- Graichen, V.; Förster, H.; Graichen, J.; Healy, S.; Repenning, J.; Schumacher, K.; Duscha, V.; Friedrichsen, N.; Lehmann, S.; Erdogmus, G.; Haug, I.; Kim, S.; Zaklan, A.; Diekmann, J. Evaluierung und Weiterentwicklung des EU-Emissionshandels aus ökonomischer Perspektive für die Zeit nach 2020 (EU-ETS-7). 2019. Available online: https://www.umweltbundesamt.de/publikationen/evaluierung-weiterentwicklung-des-eu-0 (accessed on: 30.11.2023).

- FUTURIST.; PIK.; Bain & Company. Wie Deutschlands CEOs ihre Unternehmen auf Nachhaltigkeitskurs bringen.2021. Available online: https://www.bain.com/de/insights/nachhaltigkeitsstudie-von-haltung-zu-handlung/ (accessed on: 30.11.2023).

- Åhman, M.; Nilsson, L.J.; Johansson, B. Global climate policy and deep decarbonization of energy-intensive industries. Climate Policy 2017, 17, 634–649. [Google Scholar] [CrossRef]

- Europäische Kommission. Klimaneutral werden. Empfehlung einer Expertengruppe sollen energieintensive Industriezweige bei der Erreichung des EU-Ziels 2050 unterstützen. 2019. Available online: https://ec.europa.eu/commis-sion/presscorner/detail/de/IP_19_6353 (accessed on 16.06.2023).

- Umweltbundesamt. Der Europäische Emissionshandel. 2023. Available online: https://www.umweltbundesamt.de/daten/klima/der-europaeische-emissionshandel#teilnehmer-prinzip-und-umsetzung-des-europaischen-emissionshandels (accessed on: 30.11.2023).

- Nilsson, L.J.; Bauer, F.; Åhman, M.; Andersson, F.N.; Bataille, C.; de la Rue du, Can; Ericsson, K.; Hansen, T.; Johansson, B.; Lechtenböhmer, S.; von Sluiseved, M.; Vogl, V. An industrial policy framework for transforming energy and emissions intensive industries towards zero emissions. Climate Policy 2021, 21, 1053–1065. [Google Scholar] [CrossRef]

- Filho, W.L. Aktuelle Ansätze zur Umsetzung der UN-Nachhaltigkeitsziele, 1st ed.; Springer Spektrum: Berlin, Heidelberg, Germany, 2019. [Google Scholar] [CrossRef]

- Die Bundesregierung. Generationenvertrag für das Klima: Klimaschutzgesetz. 2022. Available online: https://www.bundesregierung.de/breg-de/schwerpunkte/klimaschutz/klimaschutzgesetz-2021-1913672 (accessed on 30.11.2023).

- Hansson, A.M.; Pedersen, E.; Karlsson, N.P.; Weisner, S.E. Barriers and drivers for sustainable business model innovation based on a radical farmland change scenario. Environmental, Development and Sustainability 2023, 25, 8097. [Google Scholar] [CrossRef]

- Long, T.B.; Looijen, A.; Blok, V. Critical success factors for the transition to business models for sustainability in the food and beverage industry in the Netherlands. Journal of Cleaner Production 2018, 175, 82–95. [Google Scholar] [CrossRef]

- Fremery, M.; Gerards Iglesias, S. Abhängigkeit - Was bedeutet sie und wo besteht sie? - Ein Überblick über wirtschaftliche und politische Abhängigkeiten. 2022. Available online: https://www.iwkoeln.de/fileadmin/user_upload/Studien/Report/PDF/2022/IW-Report_2022-Abh%C3%A4ngigkeit.pdf (accessed on 30.11.2023).

- Zollenkop, M. Charakteristika von Geschäftsmodellen und Geschäftsinnovationen. In Geschäftsmodellinnovationen; Gabler Verlag: Wiesbaden, Germany, 2006; p. 114. [Google Scholar] [CrossRef]

- Hermwille, L.; Lechtenböhmer, S.; Åhman, M.; van Asselt, H.; Bataille, C.; Kronshage, S.; Tönjes, A.; Fischedick, M.; Oberthür, S.; Garg, A.; Hall, C.; Jochem, P.; Schneider, C.; Cui, R.; Obergassel, W.; Fragkos, P.; Vishwanathan, S.S.; Trollip, H. A climate club to decarbonize the global steel industry. Nature Climate Change 2022, 12, 494–496. [Google Scholar] [CrossRef]