Submitted:

22 April 2024

Posted:

22 April 2024

You are already at the latest version

Abstract

This study examines the impact of executives implicated in fraud on firms' investment decisions using AAERs in the US, aiming to address the underexplored aspect of rationalization within the fraud triangle. Executives implicated in fraud often display abnormal attitudes to justify accounting irregularities, prompting an investigation into how abnormal investment decisions are used for rationalizing fraud, given their critical role in a firm's long-term sustainability. Analysis of AAERs spanning from 1981 to 2013 reveals that implicated executives, particularly CEOs and CFOs, tend to make abnormal investment decisions, and that collusive fraud exacerbates this behavior. Notably, such executives lean towards overinvestment, particularly in R&D expenditures, to hide or justify fraud; the duration of fraud amplifies its impact on investment decisions. By shedding light on the rationalization aspect of the fraud triangle, this research contributes valuable insights for investors, regulators, and academia emphasizing the significance of public disclosure of fraud to enhance transparency in capital markets and the importance of ethics-focused education in accounting to prevent corporate fraud.

Keywords:

Fraud

; Implicated Executives

; Colluded Executives

; Firms’ Investment Decisions

; Sustainability

1. Introduction

This study examines the impact of executives implicated in financial reporting fraud (hereafter fraud) on firms’ investment decisions. Also, it investigates how colluded executives in fraud influence investment decisions. We use hand-collected data of fraud cases in which executives are implicated or colluded using publicly disclosed Accounting and Auditing Enforcement Releases (AAERs) of the U.S. Securities and Exchange Commission (SEC). Prior studies suggested that more than half of executives are implicated in fraud, and of these cases, over 60% involve at least two executives [1, 2, 3]. Studies investigating fraud cases where executives are implicated (or colluded) have been limited, mainly due to the challenges of identifying executive involvement in AAERs.

The fraud triangle consists of three elements that underlie a fraudster’s decision to commit fraud: opportunities, incentives, and rationalization [4-6]. Prior studies primarily focused on examining factors related to opportunity and incentives that reflect circumstances [e.g., 7-12]. Rationalization, however, is an internal process within firms , and mainly observable at the individual level analysis. Due to the constraints of generalizable empirical data, research on rationalization in fraud has been limited.

Executives implicated in fraud may display aberrant attitudes to justify obscure accounting irregularities and hide them from investors, regulators, external auditors, and other stakeholders [13]. This study examines the distinct behaviors of executives implicated in or colluded in fraud. Moreover, we focus on internal investment decision-making in firms to explore the fraud rationalization process. To date, there is little research that deals with the relationship between fraud and its effect on internal decision-making. This study fills the void by examining how executives use abnormal investment decisions as a means of rationalizing fraud.

Optimal investments are vital for sustainable firm growth. Underinvestment undermines a firm's growth potential, ultimately resulting in deterioration of the economic base. Conversely, overinvestment beyond an optimal level can strain a firm's cash flows and increase economic costs, thereby impeding firm growth. Overinvestment without commensurate returns can lead to financial constraints, triggering a vicious cycle of subsequent underinvestment. Therefore, investment decision-making is the most critical internal process for a firm's long-term sustainability.

This study relies on AAERs from 1981 to 2013 to create a sample of fraud firms with available investment data. These releases summarize enforcement actions subject to civil lawsuits brought by the SEC in federal court whether a firm’s financial statements were materially misstated; the charges brought against named executives; the year fraud began; the year fraud detected; and the amount of civil penalty if applicable. Recent fraud studies documented that use of AAERs decreases the likelihood of type I errors given that firms undergoing SEC investigations are subject to the most egregious manipulations [3, 11, 12]. A fraud-only analysis allows representation of fraud firms free from hidden bias. AAERs clearly identify fraud firms, names and roles of specific management team members, and what charges were laid against them, which is the core of identification methodology utilized in this study. However, the small sample size resulting from use of AAERs increases the probability of Type II errors, reducing the power of empirical tests and decreasing the generalizability of the results [3, 15]. We utilize bootstrap analysis to address the non-normality of fraud firms in our sample by estimating the resampling distributions. We thus acquire multiple bootstrap samples that represent the fraud population. By employing bootstrap analysis, we expand the sample size from 151 to 1,510 firm-level observations, thereby bolstering the reliability of our statistical analysis without relying on strict assumptions about the underlying distribution of the data.

The first analysis shows that when executives are implicated in fraud cases, it results in abnormal investment decisions. Analyzing Chief Executive Officers (CEOs), Chief Financial Officers (CFOs), and other executives separately, we find that abnormal investment decisions are more prevalent when the CEO or CFO is implicated. The findings indicate that executives implicated in fraud cases are more likely to rationalize their misconduct through over- or underinvestment than those unnamed in fraud cases. We speculate that named executives might perceive that they can compensate for distorted financial information through inappropriate investments. Moreover, to mask their own misdeeds, they may strategically choose to overinvest or underinvest [13].

The second analysis presents evidence that collusive fraud among executives leads to abnormal investment decisions. Analysis according to executive roles indicates that CEO or CFO involvement in collusive fraud intensifies abnormal investment decision-making. Conversely, collusion among other executives than the CEO or CFO has no incremental impact on investment decisions. Li [3] documented that the interconnectedness among top management team members fosters ‘groupthink’, consequently elevating the risk of accounting fraud. Building on Li's findings [3], this study offers additional evidence that groupthink involving high-level C-suite positions in collusive fraud detrimentally influences investment decision-making.

Further analysis disaggregates investment by level (overinvestment, underinvestment) and find that executives involved in fraud generally overinvest rather than underinvest. However, if CEOs or CFOs are implicated or colluding in fraud, they tend to underinvest by not investing in profitable projects. In the next analysis, we disaggregate investment by type (capital expenditures, R&D expenditures, and acquisition expenditures); the results are qualitatively similar to the main results. This shows the robustness of our findings. Among the three investment types, all implicated executives in our sample invested in R&D inefficiently to hide or rationalize fraud. Inefficient investment of the other two investment types (capital expenditure and acquisition expenditures) occurred only when the CEO or CFO was involved. This indirectly suggests that R&D is an easier channel through which to disguise fraud than other investment types. Additionally, our results reveal that the duration of fraud influences the impact of implicated and colluded executives on abnormal investment, with longer durations showing increased impact.

This study contributes to the literature as follows. Firstly, by examining fraud cases involving implicated or colluding executives, this study provides insights into the rationalization element of the fraud triangle, an area that remains relatively unexplored. Secondly, this study offers supplementary empirical evidence to enhance the understanding of the relationship between fraud and investment decision-making initially provided by McNichols and Stubben [13]. They anticipated that executives' awareness of fraud may impact decision-making processes, but their analysis was not differentiated based on this awareness. We verify that executives' awareness of fraud has a detrimental impact on investment decisions. Thirdly, this study expands the findings of Li [3], who illustrated how groupthink negatively influences internal decision-making in firms. Executives who collude in fraud, especially CEOs and CFOs, make abnormal investment decisions through group thinking to conceal their wrongdoing. Fourthly, we discuss the usefulness of public disclosure of executive involvement or collusion via AAERs in the U.S. In firms where executives are implicated or colluded in fraud, there is an increased probability of making inefficient investment decisions, ultimately leading to a decline in the firm's sustainability. Investors can evaluate a firm's sustainability by analyzing the detailed fraud information provided in AAERs. This study underscores the importance of public disclosure of fraud by regulators to alert capital market participants.

This paper is organized as follows: Section 2 reviews prior literature and establishes the rationale behind the hypotheses. Section 3 outlines the sample selection process and research methodology. Section 4 presents the empirical results, while Section 5 reports the findings of additional tests. Finally, Section 6 concludes the study, highlighting its contributions and limitations.

2. Literature Review and Hypothesis Development

2.1. Financial Reporting Fraud and Investment Decision-making

Prior papers presented evidence that fraud occurs in the presence of a fraud triangle –opportunities, incentives, and rationalization [16-18]. To date, research has predominantly focused on determinants of opportunity and incentives [7,8]. Several studies have found a relationship between equity incentives and the probability of financial reporting fraud [9,11,12]. Others identified fraud incentive-related red flags evident in a firm’s financial statements [19]. Fraud opportunity-related studies presented evidence that weak corporate governance, including weak internal controls, unethical tone at the top, and inadequate internal policies and procedures, provide ideal circumstances for management to commit fraud [20-22, 23]. Another primary research focus has been market reactions following fraud detection [e.g., 24,25]. Prior studies showed that firms accused of fraud by the SEC experience a decline in firm value and a significant increase in the cost of capital.

A few studies have shown that high-quality accounting information facilitates efficient investment decision-making [26,27]; however, they provided limited evidence on whether and how fraud may hinder the decision-making process. To our knowledge, the paper of McNichols and Stubben [13] is the only empirical study of the relationship between financial accounting fraud and firms’ investment decisions. In their empirical analysis, McNichols and Stubben [13] classified firms facing SEC enforcement, those undergoing shareholder lawsuits for accounting irregularities, and those requiring financial restatements as firms involved in accounting fraud. In that study, firms in which financial reporting fraud occurred made suboptimal investment decisions.

The following description has been offered of the process by which abnormal investments occur in fraudulent firms. Fraud causes information asymmetry among stakeholders (management, boards of directors, external investors, etc.), thereby fostering inefficient investment [28]. Furthermore, the manipulated accounting information masks underlying trends in revenue and earnings growth, which may distort growth expectations, especially when investment decision-makers are not aware of the misstatement. Then, investment decisions are made by several parties, including the CEO, CFO, boards who monitor the capital budget, and external investors. These stakeholders, who are unaware of underlying misstatements, may inadvertently incentivize or tacitly support management's inefficient investments.

In addition, when CEOs or CFOs, who have substantial sway in investment decisions, are involved in fraud, they may understand the true accounting information but may choose to make suboptimal investment decisions to conceal the firm’s actual performance. Such CEOs and CFOs may persistently engage in overinvestment to maintain the illusion of profit, aiming to avoid detection by regulatory agencies or investors. They may also overinvest in projects with negative net present value to turn around performance. Furthermore, they may refrain from investing in profitable projects to enhance short-term myopic performance because investment expenditures are recognized as expenses on the income statement, which can lead to a decrease in current performance, including reduced operating income. CEOs and CFOs may fall into optimistic bias, leading to inefficient investment decisions with distorted growth trends to meet capital market expectations. While McNichols and Stubben [13] explained the impact of such behavior of CEOs and CFOs on investment decisions, they did not present empirical results regarding executives' involvement in fraud.

Due to available data limitations, few empirical studies on executives implicated in fraud cases have been conducted. However, Davidson [12] noted that executives implicated in fraud have stronger equity incentives than executives who are not implicated in fraud. That study demonstrated that decision-making varies across executive positions, and its fraud analysis at the executive level provided robust empirical results regarding fraud incentives for executives. Davidson [12] also shed light on the personal incentives of executives' involvement in fraud, examining the impact of such incentives on firms’ internal decision-making processes.

As previously mentioned, executives implicated in fraud make suboptimal investment decisions to avoid fraud detection by regulators and investors. From the viewpoint of these executives, revelation of malfeasance can profoundly affect their careers and quality of personal life because upon discovering their involvement in fraud, most firms typically dismiss these executives [1,7]. Thus, they might strategically overinvest by mimicking high-performing peer firms to conceal misconduct [29]. They may expect that the return from overinvestment will offset performance distortion [13]. Moreover, they may curtail investments in profitable projects to avoid incurring investment costs and to enhance short-term performance.

In some cases, executives implicated in fraud may not allow accounting fraud to influence their firms’ investment decisions. However, at least one of the investment decision-makers within such firms may be misled by the distorted accounting information [13]. Because of the complexity of the situations, predicting the impact of executive involvement in fraud on internal investment decision-making is challenging. As there are conflicting views on the impact of executives involved in fraud on investment decision-making, we put forward the following null hypothesis.

Hypothesis 1: Executives implicated in fraud have no impact on abnormal investment.

2.2. Collusive Fraud and Investment Decision-making

Collusion involving two or more executives undermines the effectiveness of corporate governance and internal control systems, which serve as vital monitoring mechanisms for firms [30,31]. Financial reporting is a multifaceted process involving multiple parties, and collusive accounting fraud occurs more frequently than solo fraud [2,32,33]. In the study of Khanna et al. [32], on average, litigation or SEC enforcement actions implicated 4.8 individuals for the period of 1996 and 2006. Studies have found that in over 60% of fraud cases involving implicated executives, collusion involving two or more individuals occurred [1,2]. However, studies investigating fraud cases involving colluding executives have been limited. A few studies show that the executives’ connections with audit committee members, CEOs, and CFOs elevate the likelihood of financial reporting fraud [32,34,35].

Li [3] examines whether firms are more likely to commit fraud in the presence of stronger interconnections among top executives. In the corporate, top executives connected thought social ties are prone to share common perspectives and values. Under certain types of stress, social ties promote groupthink among executives, which, in turn, increases the probability of rationalization about fraud and actual incidences of fraud. Similarly, social psychologists observed that when a group of people share common values and identify themselves as part of the same group, groupthink may develop. This can lead to flawed decision-making processes, particularly under external pressures [36,37].

McNichols and Stubben [13] proved that firms increase capital expenditures to make fraudulent reports appear authentic, suggesting that fraud may involve manipulating real activities; this requires coordination among executives. In the line of context, colluded executives are more likely to rationalize their underhandedness, including exploitation of investment for private benefit, through groupthink. Colluded executives often endeavor to rationalize fraud in a collective manner by exerting pressure on other members to disregard moral values and crucial information during their investment decision-making processes [38-40]. Furthermore, collusion among executives weakens internal governance mechanisms in firms, enabling their misconduct to remain within a closed circle. Consequently, abnormal investment decisions are made because other decision-makers are unaware of the misstatements.

On the other hand, groupthink within firms may have a positive influence on internal decision-making processes. It may lead to information sharing among colluded executives, enhancing the efficiency of investment decisions by fostering a better understanding of undistorted financial information. A cohesive leadership team is more inclined to collaborate towards firm objectives [41]. Strong trust among members of the top management team makes them more inclined to share information and knowledge. Such cohesion diminishes relationship-driven conflicts and enhances investment efficiency [42]. Executives colluding in fraud may even seek alternative strategies to conceal their misconduct, choosing to abstain from exploiting opportunities and making investment decisions for private benefit. They may even make optimal investment decisions considering firm sustainability.

As there are conflicting views on the impact of colluding executives on investment decision-making, we present the following null hypothesis.

Hypothesis 2: Collusion among executives has no impact on abnormal investment.

3. Sample Selection and Research Design

3.1. Sample Selection

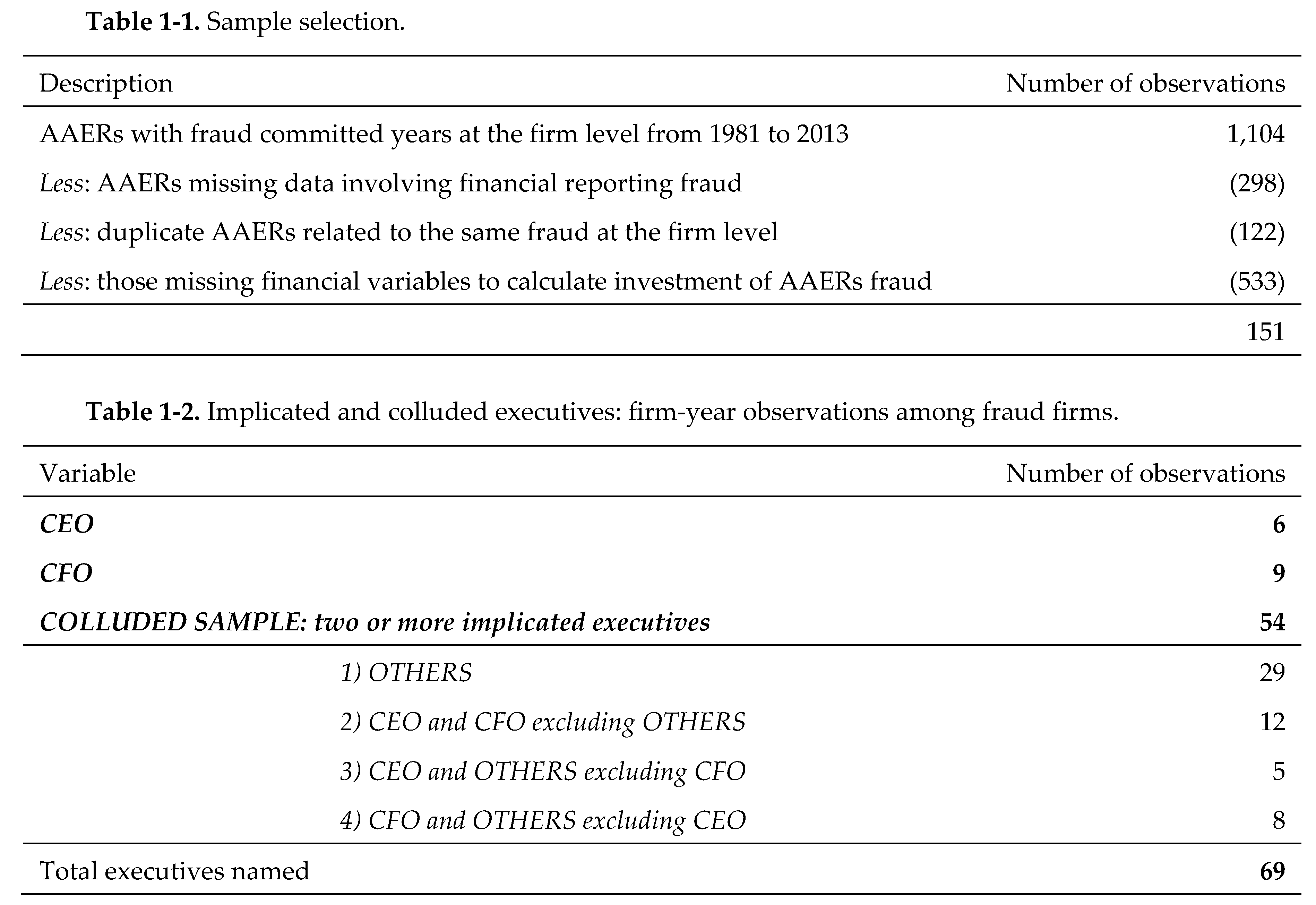

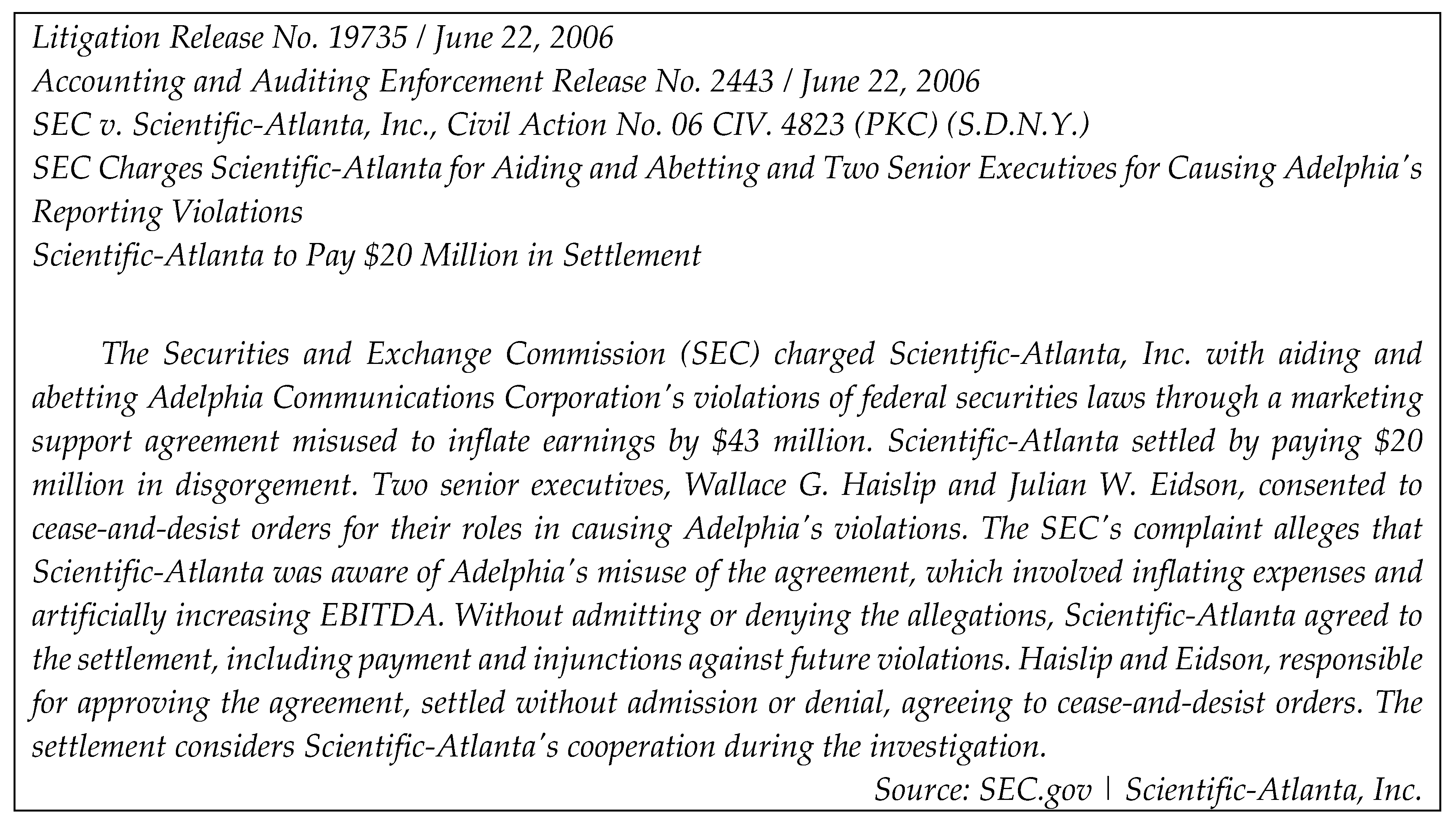

Table 1-1 outlines the sample construction process. To examine the impact of implicated executives and collusive fraud on firms’ investment decisions, we started with a total of 1,104 AAERs from 1981 to 2013. These releases summarize enforcement actions subject to civil lawsuits brought by the SEC in federal court providing the following information: whether the firm’s financial statements were materially misstated; whether charges were brought against named executives; the year fraud began; the year fraud was detected; and the amount of civil penalty, if applicable. Appendix A shows a sample AAER.

Approximately 27% of AAERs (298 observations) did not mention whether the release was associated with financial reporting fraud; these were deleted. In addition, about 11% of AAERs (122 observations) constituted multiple releases against the same firm; these were also eliminated. In nearly 48% of AAERs (533 AAER-observations), CIK, GVKEY, or CUSIP numbers were not available to link to fraud firms’ investment variables from the Compustat database; this also significantly reduced the sample size. As a result, the final sample of firms in which fraud was committed consisted of 151 firm-year observations.

Table 1-2 shows information about executive involvement in fraud. Approximately 45.70% (69 firm-year observations) of out of 151 samples are implicated in financial reporting fraud, and about 78.26% (54 firm-year observations) of 69 sample firms had at least two or more executives colluded; this is similar to percentages reported in prior studies [1-3].

3.2. Abnormal Investment Measure

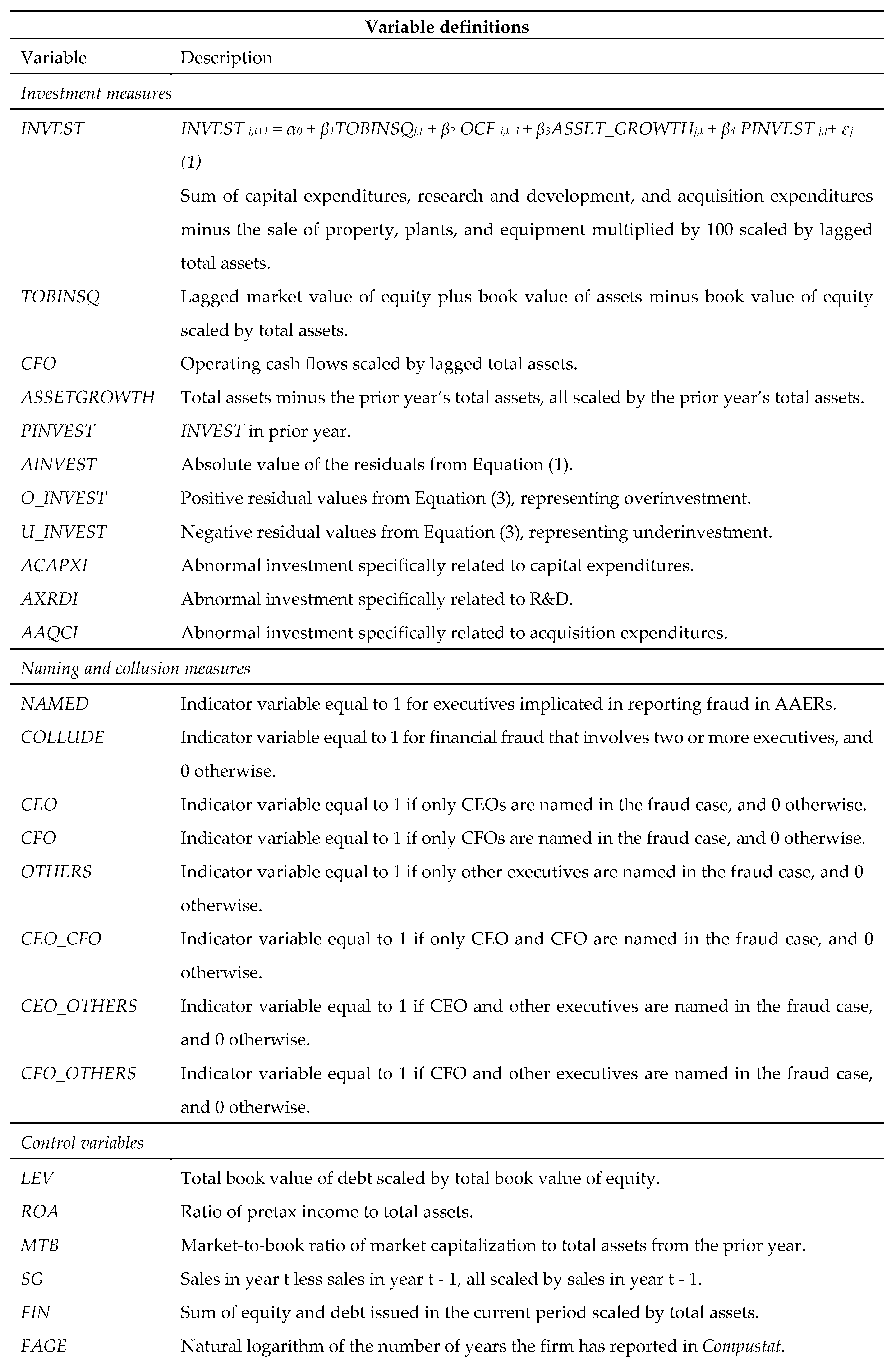

The primary variable representing abnormal investment (AINVEST) is calculated as the difference between firm j’s actual investment (INVEST) and its expected investment. This difference is obtained by taking the absolute value of the residuals from model (1) following prior studies [13,27, 43-45]. A firm’s expected investment is a value estimated based on several factors, including Tobin’s Q (TOBINSQ), current operating cash flows (OCF), asset growth (ASSET_GROWTH), and the prior year’s investments (PINVEST) by industry-year. This estimation is conducted for industries with at least 15 observations per industry [43]. The variable INVEST represents the sum of capital expenditures, R&D expenditures, and acquisition expenditures minus the sale of PP&E. As the absolute value of the residuals increases, a firm’s abnormal investment increases.

INVESTj,t+1 = α0 + β1TOBINSQj,t + β2OCFj,t+1 + β3ASSET_GROWTHj,t + β4 PINVESTj,t+εjt (1)

INVEST = the sum of capital expenditures, research and development, and acquisition expenditures minus the sale of property, plants, and equipment multiplied by 100 scaled by lagged total assets; TOBINSQ = market value of equity plus book value of assets minus book value of equity; OCF = operating cash flows scaled by lagged total assets; ASSET_GROWTH = total assets minus the prior year’s total assets, all scaled by the prior year’s total assets; PINVEST = INVEST in the prior year.

3.3. Firm-clustered Regression Model

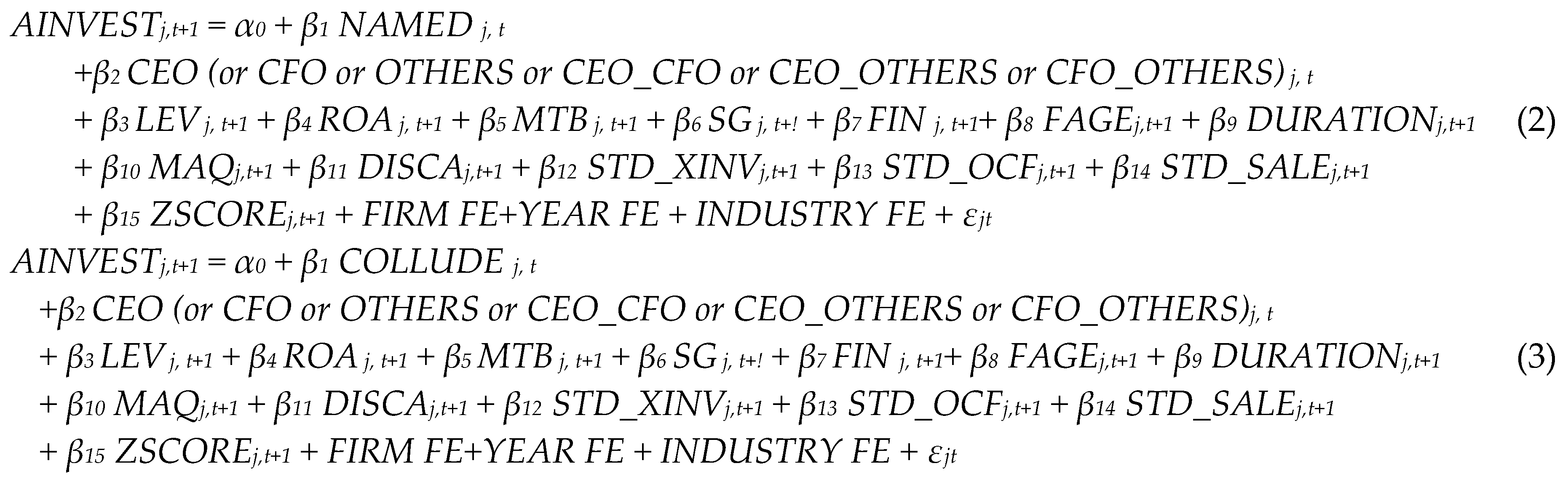

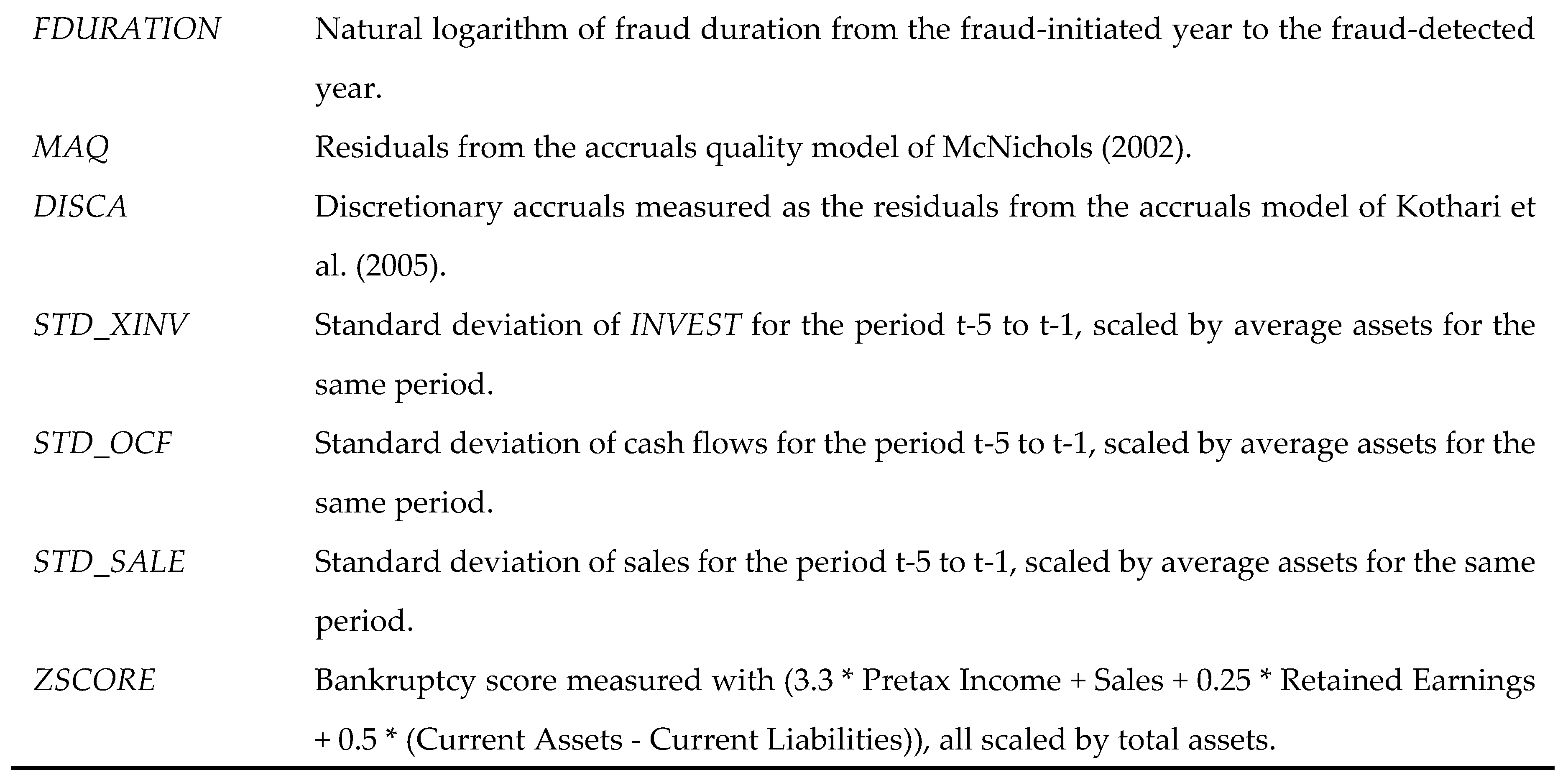

We adopt clustered regression models after applying a bootstrapping procedure (with 10 bootstrapped samples). Model (2) estimates the impact of implicated executives (NAMED) in fraud cases on abnormal investment to test hypothesis 1. To see the incremental effect of specific roles among those executives, we include CEO, CFO, OTHERS, CEO_CFO, CEO_OTHERS, and CFO_OTHERS in model (2). Then, model (3) estimates the impact of colluded executives (COLLUDE) in fraud cases on abnormal investment to test hypothesis 2. We include a set of control variables that directly impact abnormal investment and fraud, following prior studies [12,43]. Leverage (LEV) and return on assets (ROA) are associated with profitability on investment decisions, which is directly related to executives’ incentives to commit fraud. Market-to-book ratio (MTB), sales growth (SG), and financing (FIN) assess firms’ growth potential. Firm age (FAGE) and fraud duration (DURATION) account for the life cycle of firms and fraud incubation period (i.e., from the initiation of fraud to its detection by the SEC). Furthermore, we include a series of financial characteristics that influence firms’ investment decisions. To control for financial reporting quality, we include discretionary accruals (DISCA) and accruals quality (MAQ). We also include the volatilities of investment (STD_XINV), operating cash flows (STD_OCF), and total sales (STD_SALE) for the past five years, as these variables influence current and future investment decisions. Lastly, ZSCORE is included to control for bankruptcy risk. Finally, we include firm, year, and industry fixed effects to control for unobservable factors.

where

where

AINVEST = absolute value of the residuals from Equation (1); NAMED = indicator variable equal to 1 for executives implicated in reporting fraud according to AAERs; COLLUDE = indicator variable equal to 1 for financial fraud that involves two or more executives, and 0 otherwise; CEO = indicator variable equal to 1 for only CEO named in the fraud case, and 0 otherwise; CFO = indicator variable equal to 1 for only CFO named in the fraud case, and 0 otherwise; OTHERS = indicator variable equal to 1 for only other executives named in the fraud case, and 0 otherwise; CEO_CFO = indicator variable equal to 1 for only CEO and CFO named in the fraud case, and 0 otherwise; CEO_OTHERS = indicator variable equal to 1 for CEO and other executives named in the fraud case, and 0 otherwise; CFO_OTHERS = indicator variable equal to 1 for CFO and other executives named in the fraud case, and 0 otherwise; LEV = total book value of debt scaled by total book value of equity; ROA = ratio of pretax income to total assets; MTB = market-to-book ratio of market capitalization to total assets from the prior year; FIN = sum of equity and debt issued in the current period scaled by total assets; FAGE = firm age as the natural logarithm of the number of years the firm has reported in Compustat; DURATION = natural logarithm of fraud duration from the fraud-initiated year to the fraud-detected year; MAQ = residuals from the accruals quality model of McNichols [2002]; DISCA = discretionary accruals measured as the residuals from the accruals model of Kothari et al. [2005]; STD_XINV = standard deviation of INVEST for the period t-5 to t-1, scaled by average assets for the same period; STD_OCF = standard deviation of cash flows for the period t-5 to t-1, scaled by average assets for the same period; STD_SALE = standard deviation of sales for the period t-5 to t-1, scaled by average assets for the same period; ZSCORE = bankruptcy score measured as follows: (3.3 * Pretax Income + Sales + 0.25 * Retained Earnings + 0.5 * (Current Assets - Current Liabilities)), all scaled by total assets.

4. Empirical Results

4.1. Descriptive Statistics

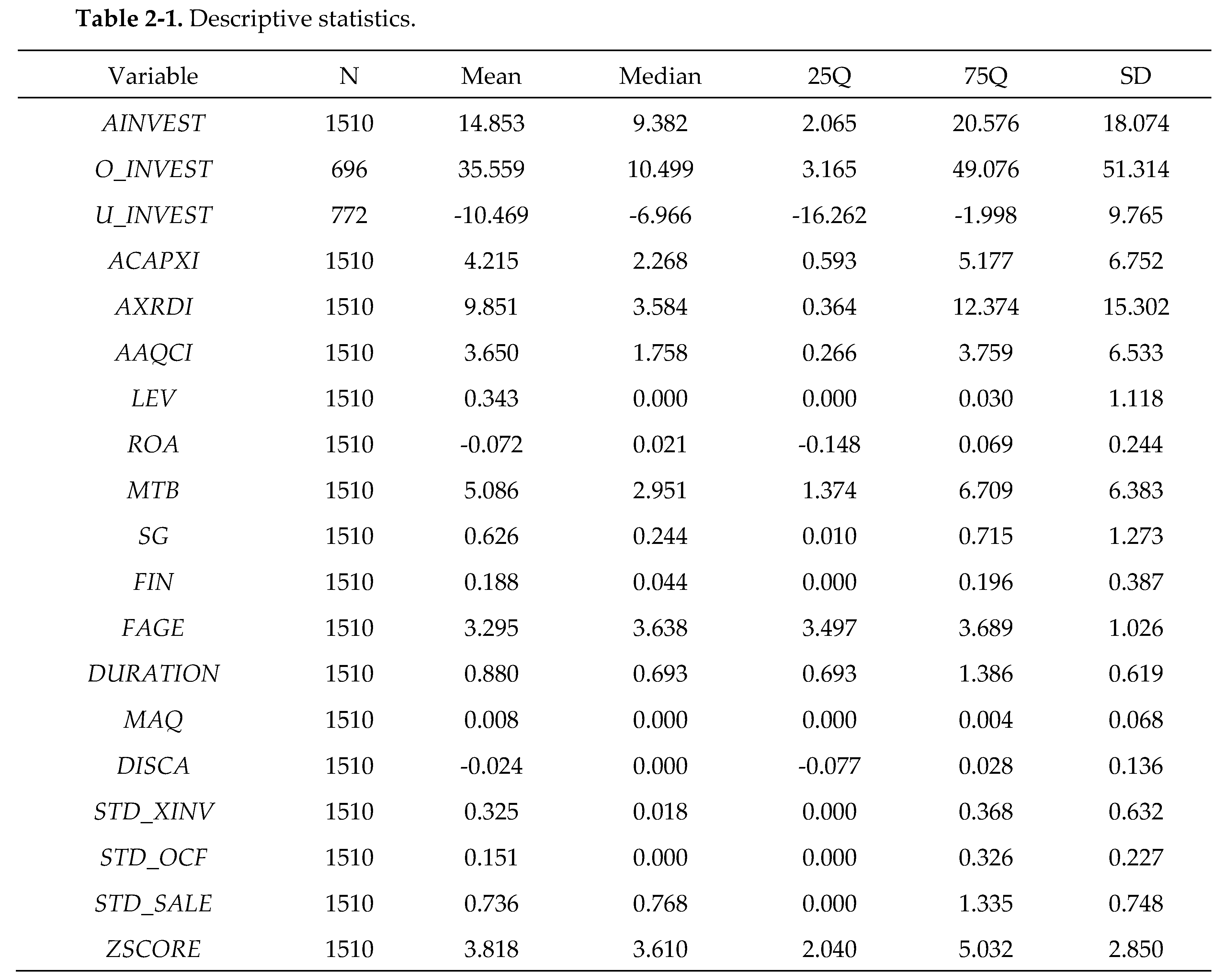

Table 2-1 shows the descriptive statistics for abnormal investment and investment levels (AINVEST, O_INVEST, U_INVEST), disaggregated types (ACAPXI, AXRDI, AAQCI), and control variables (LEV, ROA, MTB, SG, FIN, FAGE, DURATION, MAQ, DISCA, STD_XINV, STD_OCF, STD_SALE, ZSCORE). The mean values of AINVEST, O_INVEST, and U_INVEST are 14.853, 35.559, and -10.469, respectively, suggesting that abnormal investment (AINVEST) is mainly driven by overinvestment (O_INVEST) compared to underinvestment (U_INVEST). The mean values of abnormal investment in capital expenditures (ACAPXI), R&D expenditures (AXRDI), and acquisition expenditures (AAQCI) are 4.215, 9.851, and 3.650, respectively, indicating that abnormal investment in AXRDI is the highest among fraud firms. Moving to control variables, we see that the value for return on assets (ROA) is -0.072, whereas that for the market-to-book ratio (MTB) is 5.086, indicating that on average, fraud firms have low profitability with relatively high market value. This finding is consistent with the descriptive statistics in Davidson [12]. On average, the age (FAGE) of fraud firms is 27 years and fraud duration (DURATION) is 2 years. All continuous variables are winsorized at 1% and 99% to minimize the likelihood that the results are driven by outliers and/or erroneous data.

See Appendix B for definitions of variables.

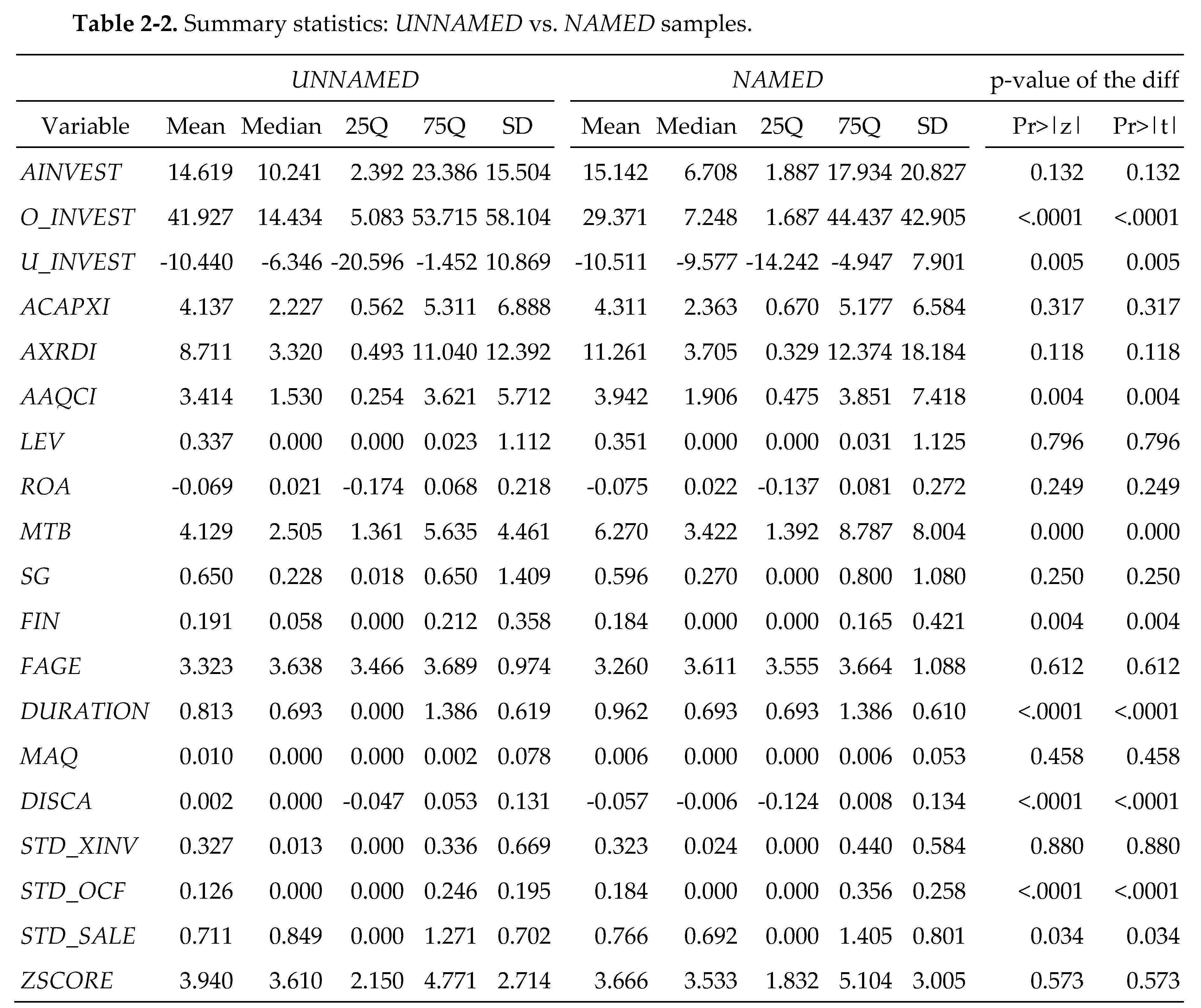

Table 2-2 provides results of the univariate analysis of data for executives who are not implicated (UNNAMED) and those implicated (NAMED) among fraud firms. The results indicate that the mean values of O_INVEST in the UNNAMED (41.927) sample are significantly higher than those in the NAMED (29.371) sample at the 0.001 level, whereas the mean values of U_INVEST in the NAMED (-10.440) sample are significantly lower than those in the UNNAMED (-10.511) sample at the 0.05 level. Significant variations in profitability (MTB), financial reporting quality (DISCA), and volatility in operating cash flows and sales (STD_OCF, STD_SALE) between the UNNAMED and NAMED samples also indicate that the differences between them do not appear to be driven solely by specific variables. Thus, it is necessary to perform a multivariate analysis to verify the differences between the UNNAMED and NAMED samples.

See Appendix B for definitions of variables.

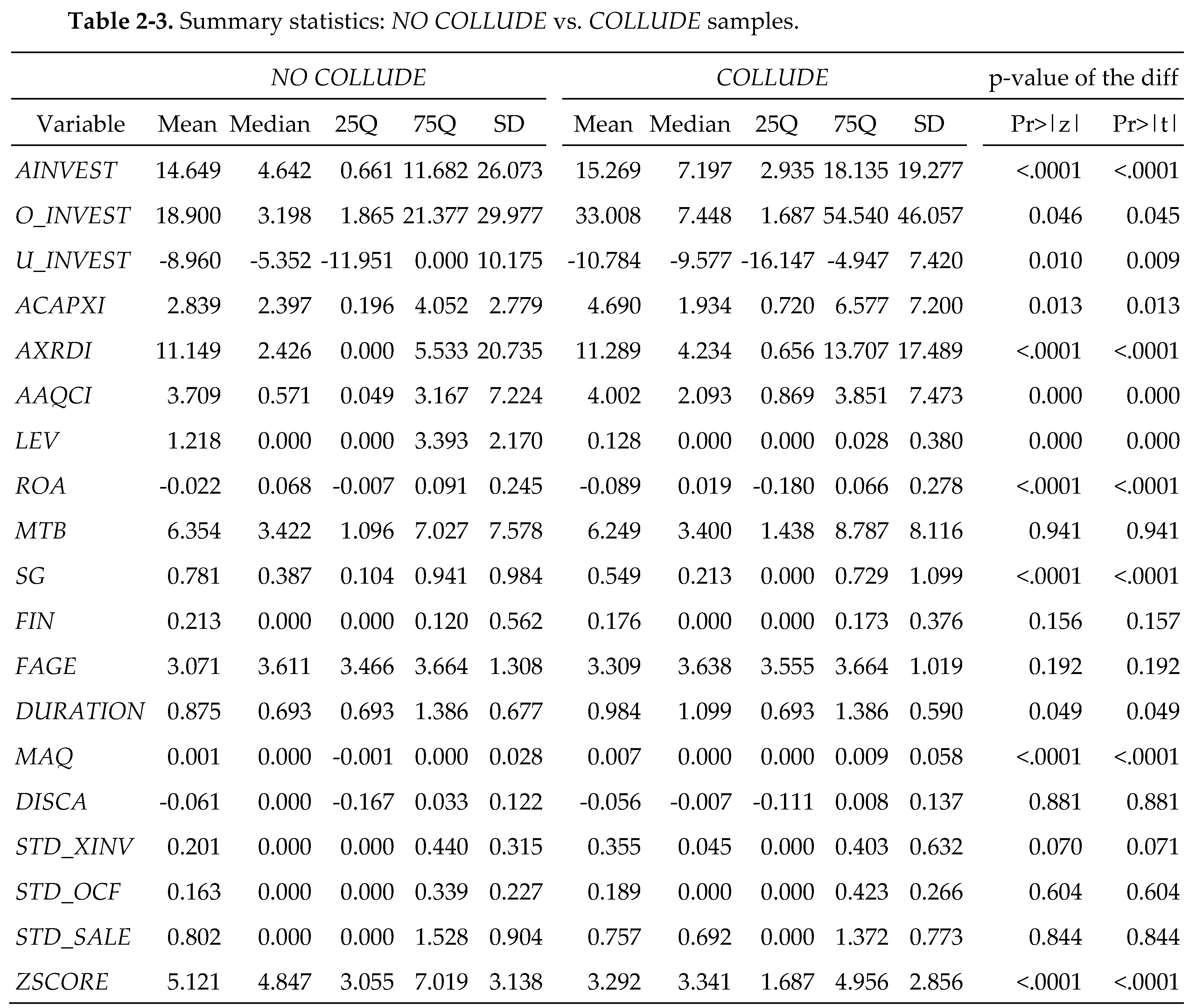

Table 2-3 presents results of the univariate analysis of executives not involved in collusion (NO COLLUDE) and executives involved in collusion (COLLUDE) among fraud firms. The results indicate that the values of investment efficiencies (AINVEST, O_INVEST, U_INVEST, ACAPXI, AXRDI, AAQCI) are consistently and significantly higher in the COLLUDE sample than in the NO COLLUDE sample, indicating that abnormal investment is more prevalent in the former than in the latter. COLLUDE sample firms have lower leverage (LEV), lower ZSCORE, lower growth rate (SG), and higher volatilities of investment (DSTD_XINV). Once again, the differences between NO COLLUDE and COLLUDE do not appear to be driven solely by specific variables, suggesting that it is necessary to perform a multivariate analysis.

See Appendix B for definitions of variables.

4.2. Main Analysis

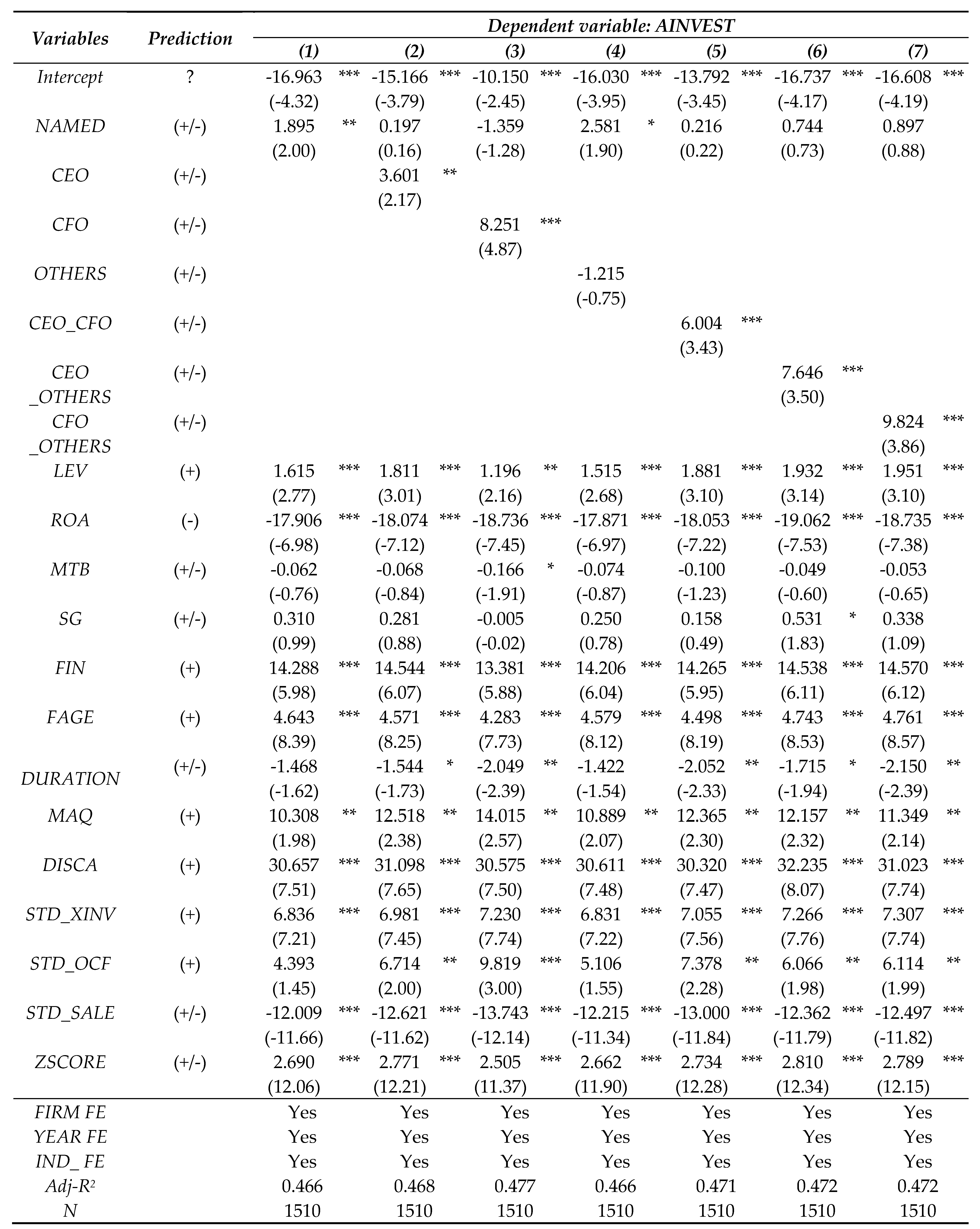

Table 3 shows the main results of estimating model (1). In column (1), the coefficient of NAMED is significant and positive (1.895 with a t-value = 2.00) at the 0.05 level, indicating that implicated executives engage in abnormal investment decisions. This implies that executives implicated in fraud are more likely to either overinvest or underinvest to disguise their misconduct. In columns (2) to (4), upon analyzing CEO, CFO, and OTHERS separately in addition to NAMED, we see that suboptimal investment decisions are more prevalent when CEOs (3.601 with t-value = 2.17) or CFOs (8.251 with a t-value = 4.87) are implicated. Values are not significant when other executives (OTHERS) are implicated, indicating that executives other than CEOs or CFOs may have incentives to conceal their involvement in fraud, but they lack authority in the investment decision-making process. Columns (5), (6), and (7) reconfirm the incremental impact of CEOs and CFOs (6.004 with a t-value 3.43), CEO_OTHERS (7.646 with a t-value = 3.50), and CFO_OTHERS (9.824 with a t-value = 3.86), suggesting that CEO or CFO involvement subsumes that of other executives in terms of making suboptimal investment decisions. Results for other control variables are similar to those in previous studies [12,43].

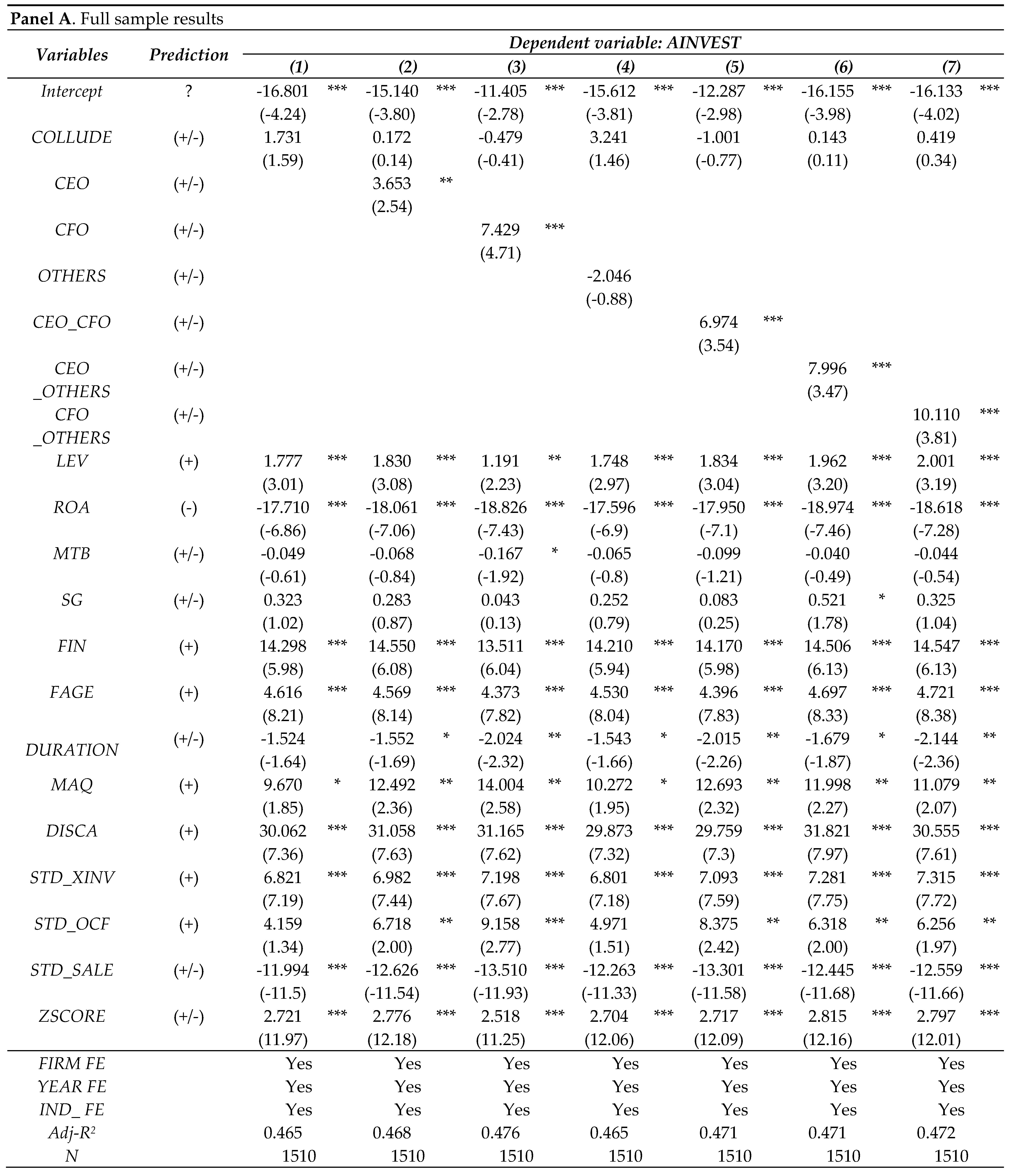

Table 4 presents the main results of estimating model (3). Panel A tests the pooled sample of 1,510 firm-level observations, including UNNAMED observations, to determine the overall impact of colluded executives on abnormal investment, whereas Panel B tests the subsample of 675 firm-level observations, excluding UNNAMED observations, to specifically examine the impact of collusion among executives on abnormal investment among those implicated. Panels A and B are qualitatively similar; thus, we herein focus on the results of Panel B. In Table 4, Panel B, column (1) shows that the coefficient of COLLUDE is significant and positive (4.483 with a t-value = 2.23) at the 0.05 level, indicating that colluded executives are more likely to make abnormal investment decisions. The results extend those of Li [3] by showing that groupthink in fraudulent firms leads to abnormal investment decisions. Executives colluded in fraud are more likely to use groupthink to rationalize fraud and to conceal their misconduct. In particular, investment decision-making is a multifaceted internal process that requires group effort among executives to justify financial results. In column (4), upon analyzing the role of colluded OTHERS, we see that the result for suboptimal investment decisions is not significant. In contrast, columns (5), (6), and (7) reconfirm the incremental impact of CEO_CFO (20.182 with a t-value = 7.45), CEO_OTHERS (15.079 with a t-value = 3.86), and CFO_OTHERS (19.730 with a t-value = 2.59) on AINVEST at the 0.001 level, indicating that the involvement of CEOs and CFOs strengthens the propensity of misallocating resources compared to other executives given their higher decision-making power.

5. Results of Additional Analyses

5.1. Additional Analysis 1: Overinvestment vs. Underinvestment

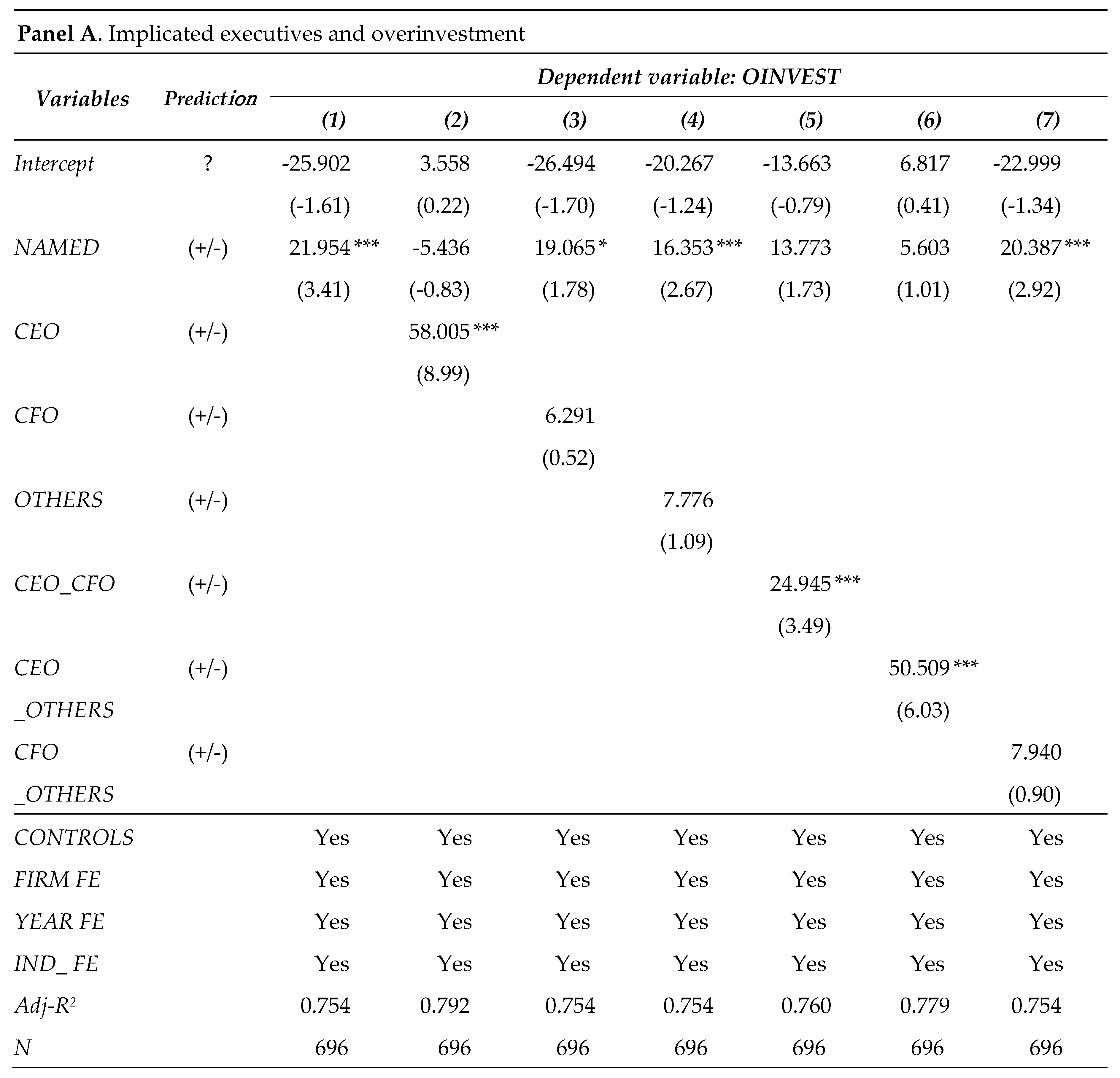

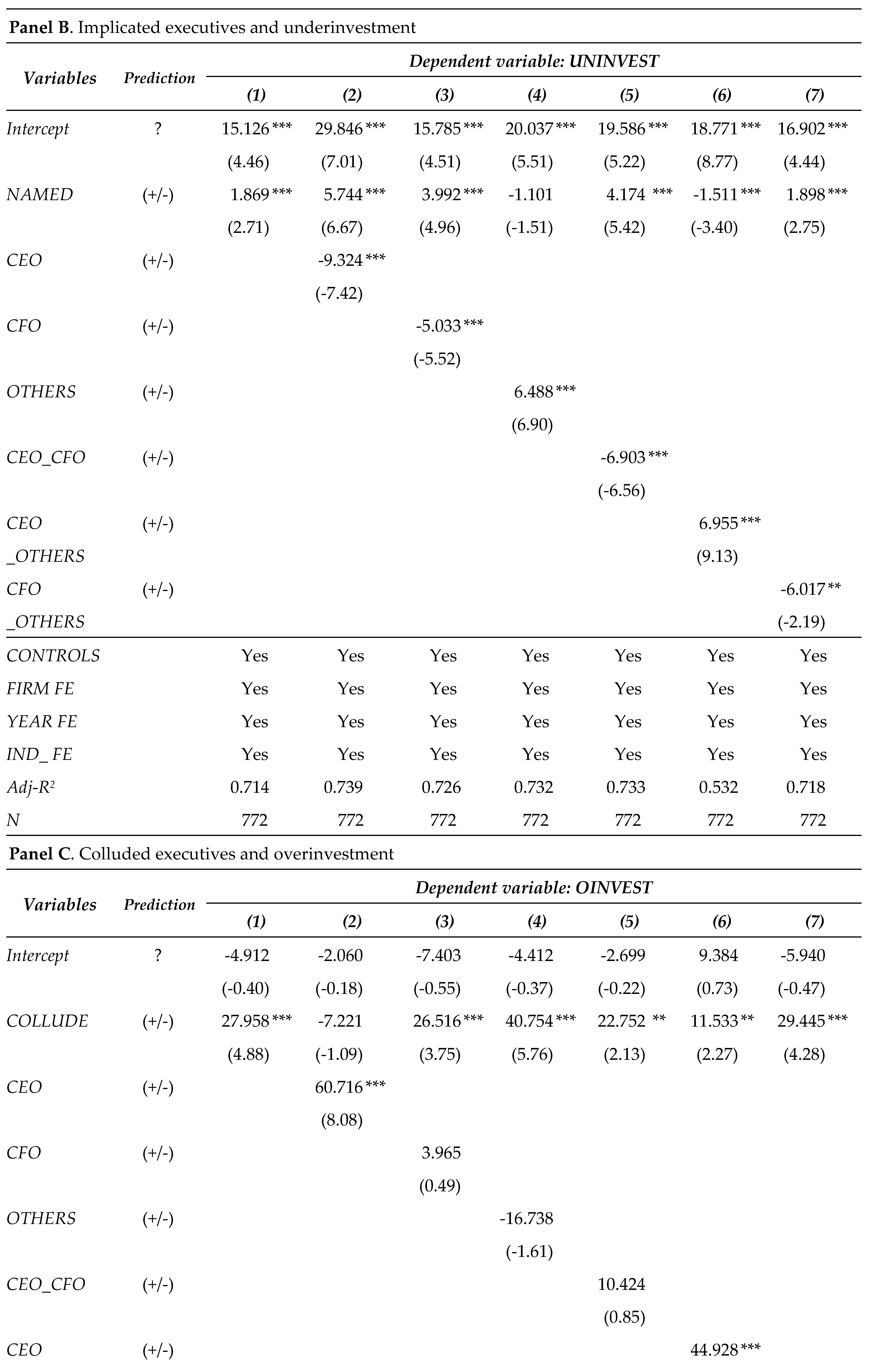

We next examine the impact of executives implicated in fraud on abnormal investments by disaggregating investment levels: overinvestment (O_INVEST) versus underinvestment (U_INVEST). Table 5, Panel A presents the results for the impact of executives on O_INVEST. In column (1), the coefficient of NAMED is significant and positive (21.954 with a t-value = 3.41) at the 0.001 level, indicating that implicated executives are prone to overinvest. Similarly, the coefficients of NAMED are generally positive and significant across the board except for in columns (2), (5), and (6), in which the significance of NAMED is absorbed by the CEO effect, which indirectly confirms that CEOs drive overinvestment decision-making among implicated executives. With respect to U_INVEST, Panel B in Table 5 shows the effect of named executives on underinvestment. In column (1), NAMED is positive and significant (1.869 with a t-value = 2.71), indicating that executives involved in fraud do not underinvest. However, when CEOs or CFOs are involved, as shown in columns (2), (3), (5), and (7), respectively, the coefficients of CEO, CFO, CEO_OTHERS, and CFO_OTHERS are negative and significant, suggesting that C-suite executives implicated in fraud may choose to underinvest to hide their misconduct.

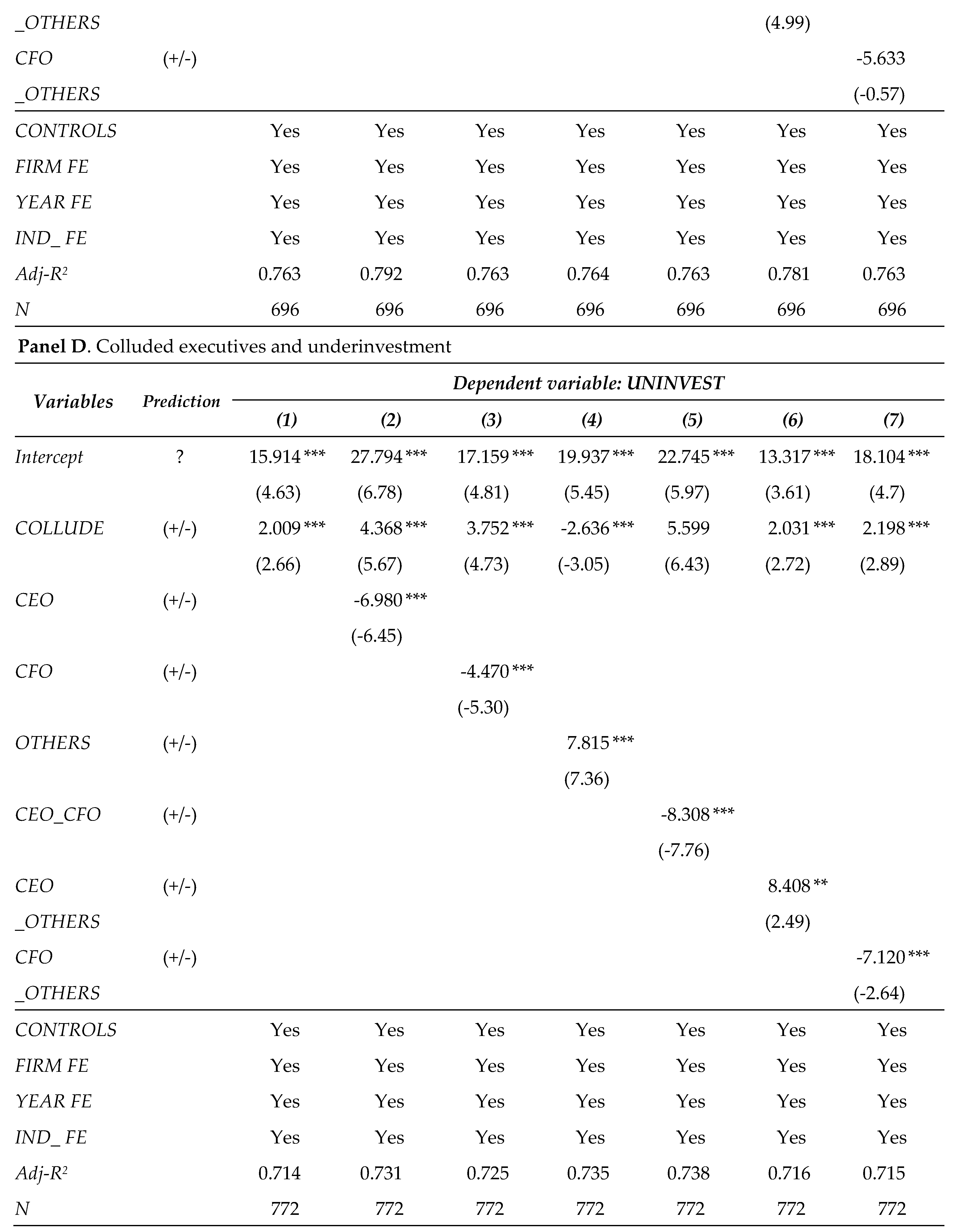

In Panels C and D in Table 5, we examine the impact of colluded executives on abnormal investments by disaggregating investment levels: overinvestment (O_INVEST) versus underinvestment (U_INVEST). Panel C in Table 5 presents the results of testing for the impact of executives colluding in fraud on O_INVEST. In column (1), the coefficient of COLLUDE is significant and positive (27.958 with a t-value = 4.88) at the 0.001 level, indicating that colluded executives are prone to overinvest. With respect to U_INVEST, Panel D in Table 5, column (1) shows a significant positive coefficient (2.009 with a t-value = 2.66), indicating that collusion among executives reduces underinvestment. However, columns (5) and (7), respectively, show that the coefficients of CEO_CFO and CFO_OTHERS are significant and negative. This suggests that collusion with the CFO is associated with a tendency to underinvest. In summary, executives involved in fraud in our sample generally overinvested rather than underinvesting during the study period. However, if the CEO or CFO was implicated or colluded, they tended to underinvest by not investing in profitable projects.

5.2. Additional Analysis 2: Disaggregated Investment by Type

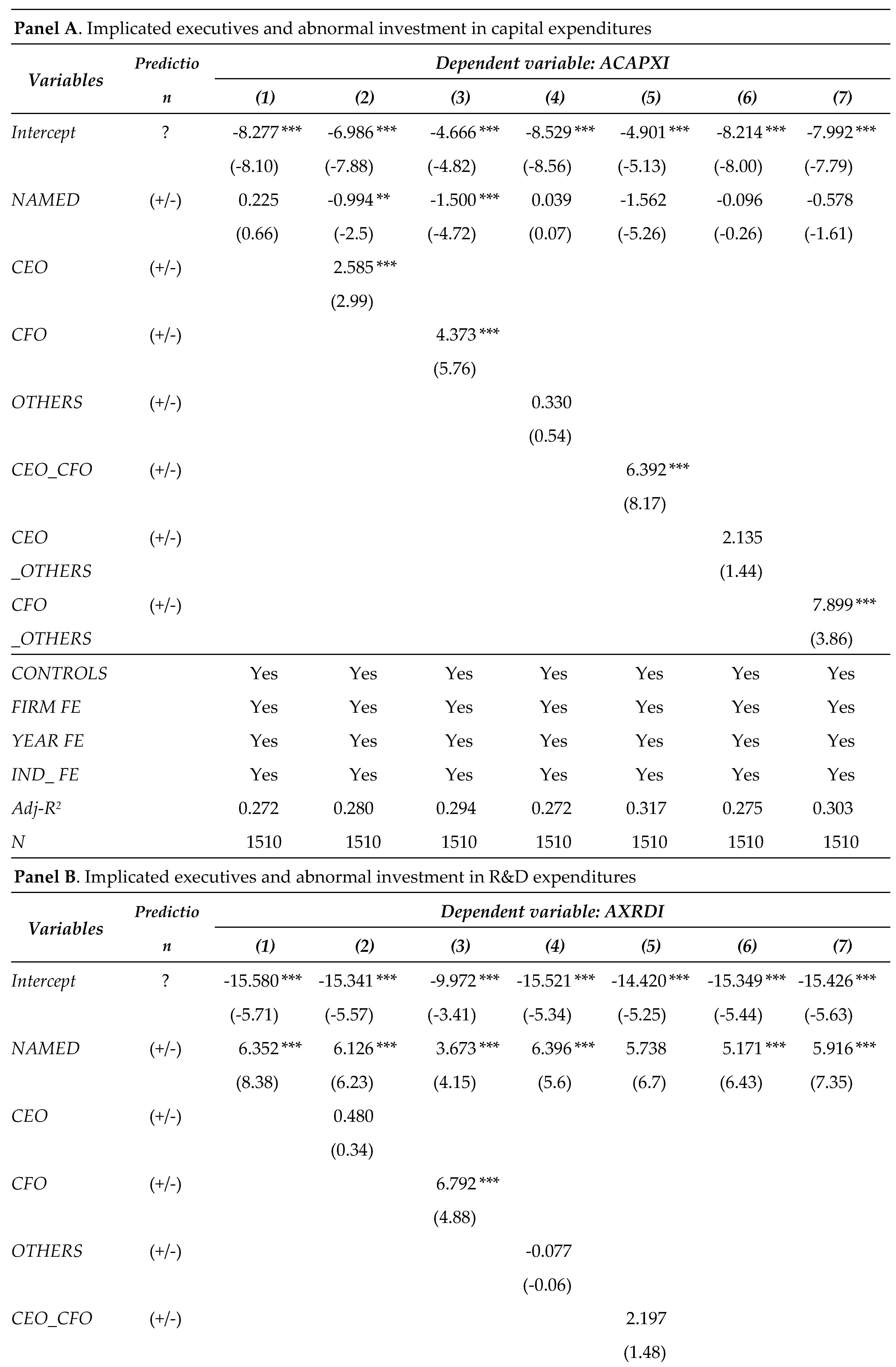

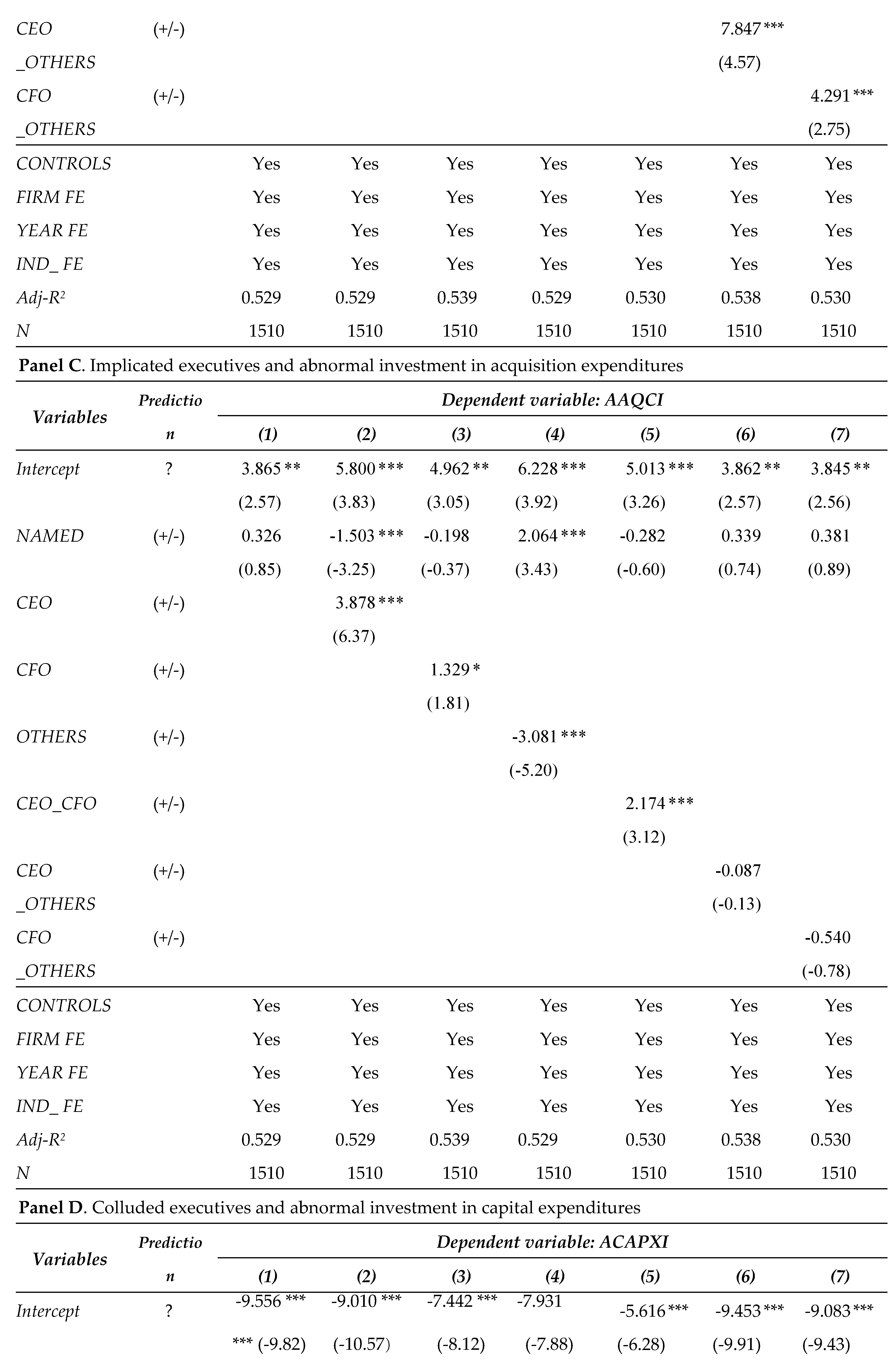

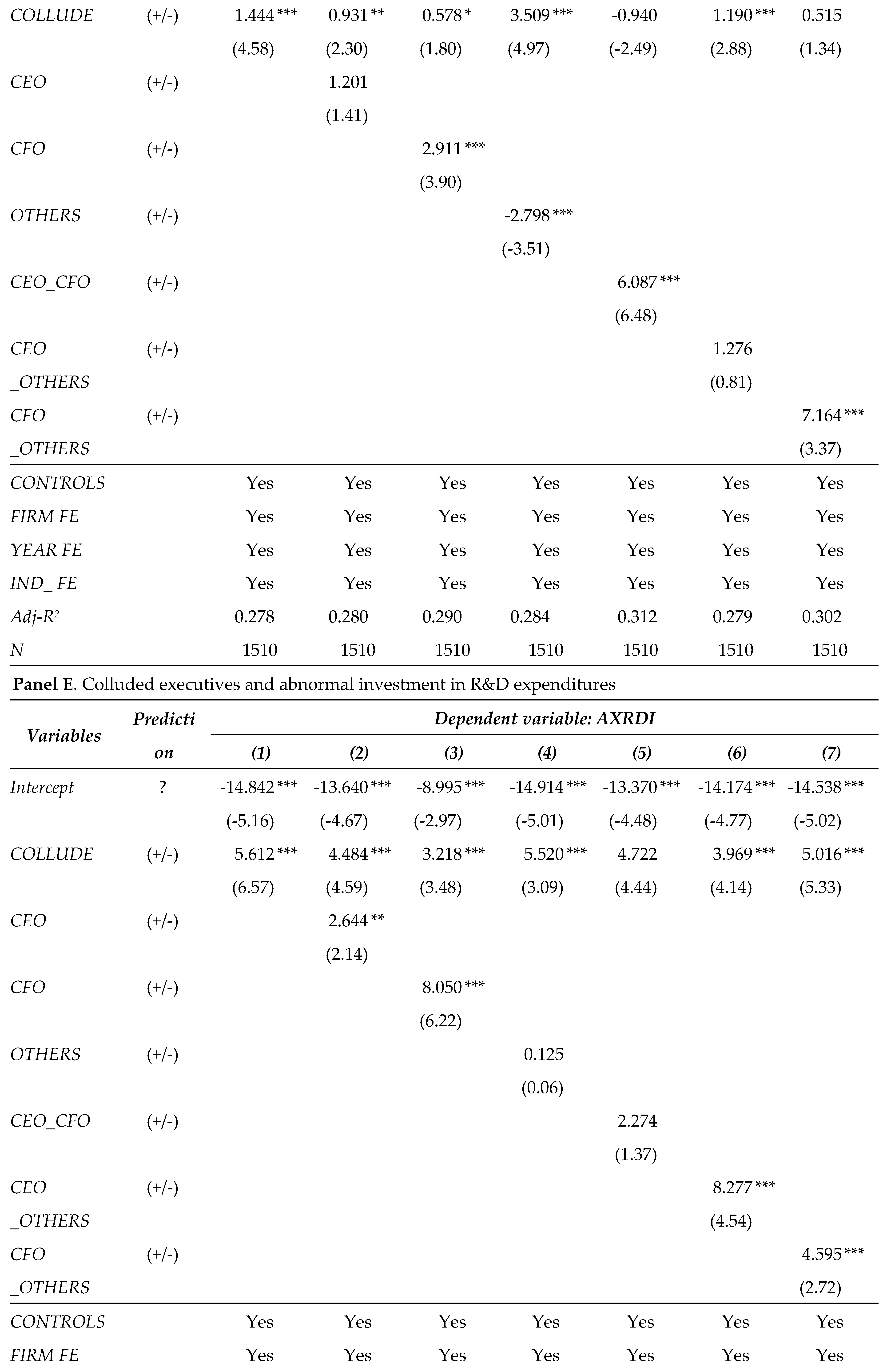

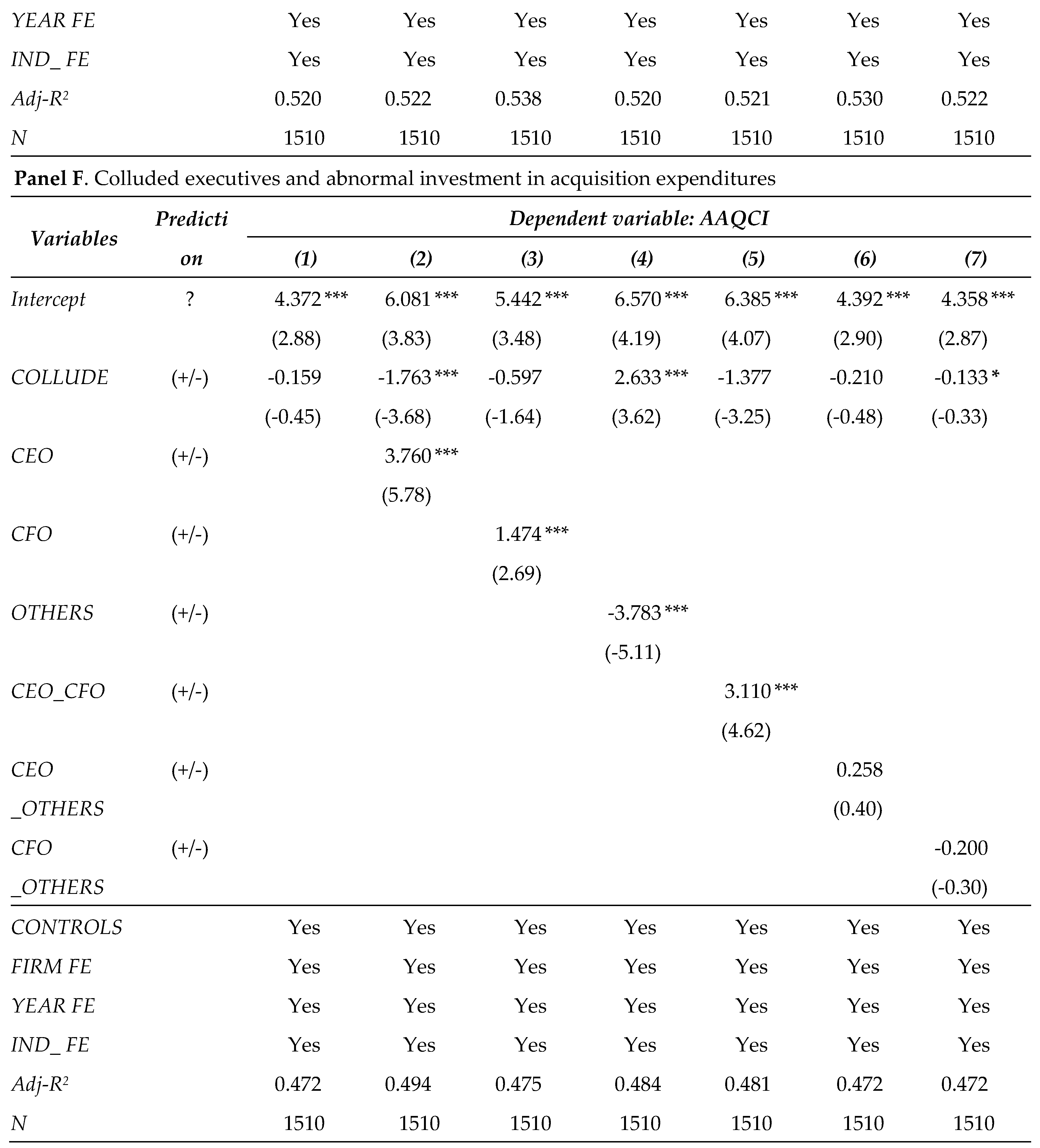

In the next analysis, we examine the impact of implicated executives on abnormal investments by disaggregating investment types, as follows: capital expenditures (ACAPXI), R&D expenditures (AXRDI), and acquisition expenditures (AAQCI) (Table 6). Panels A, B, and C present the results of testing for the impact of executives implicated in fraud on ACAPXI, AXRDI, and AAQCI, respectively. Collectively, the coefficient of NAMED is significant and positive in relation to AXRDI (6.352 with a t-value = 8.38) as shown in Panel B, whereas the coefficient of NAMED is not significant in relation to ACAPXI or AAQCI in Panels A and C. The results suggest that executives implicated in fraud tend to make the most abnormal investments in R&D among the three investment types to hide or rationalize fraud. Inefficient investment of the other two investment types (capital expenditure and acquisition expenditures) occurs when the CEO or CFO is involved. This indirectly suggests that R&D is an easier channel through which to disguise fraud than other investment types.

Panels D, E, and F in Table 6 exhibit the results of testing for the impact of colluded executives on ACAPXI, AXRDI, and AAQCI, respectively. In the case of collusion, the coefficient of COLLUDE is significant and positive in relation to ACPAXI in Panel D (1.444 with a t-value = 4.58) as well as in relation to AXRDI in Panel E (5.612 with a t-value = 6.57), suggesting that collusive fraud significantly deteriorates efficient resource allocation in terms of both capital expenditures and R&D. Abnormal investments in the form of acquisition expenditures are made when the CEO is involved. This indirectly confirms the CEO effect in relation to fraud via acquisition expenditures. Taken together, the results show that executives colluding in fraud choose capital expenditures and R&D as venues for rationalizing their misconduct.

5.3. Additional Analysis 3: Impact of Fraud Duration

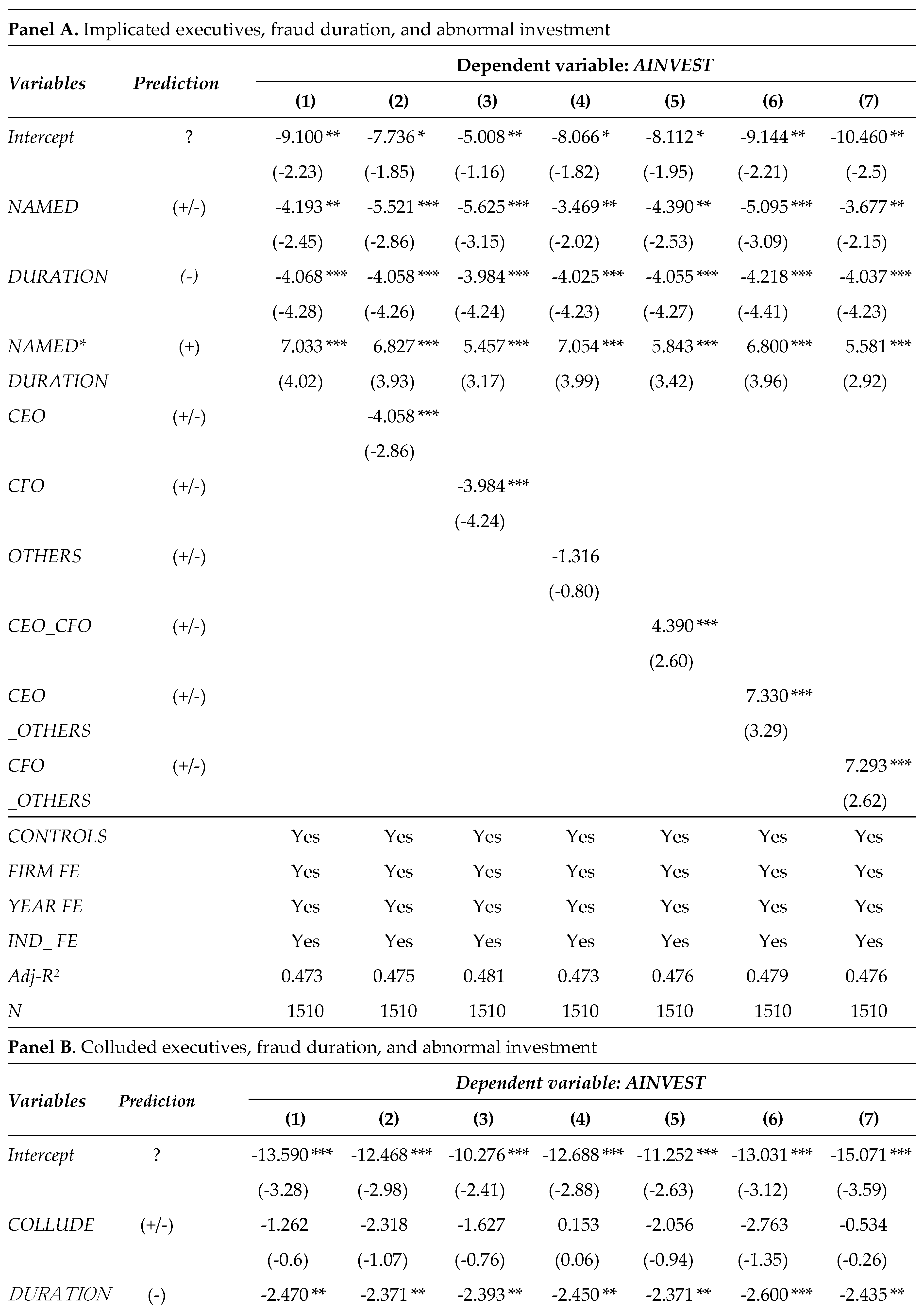

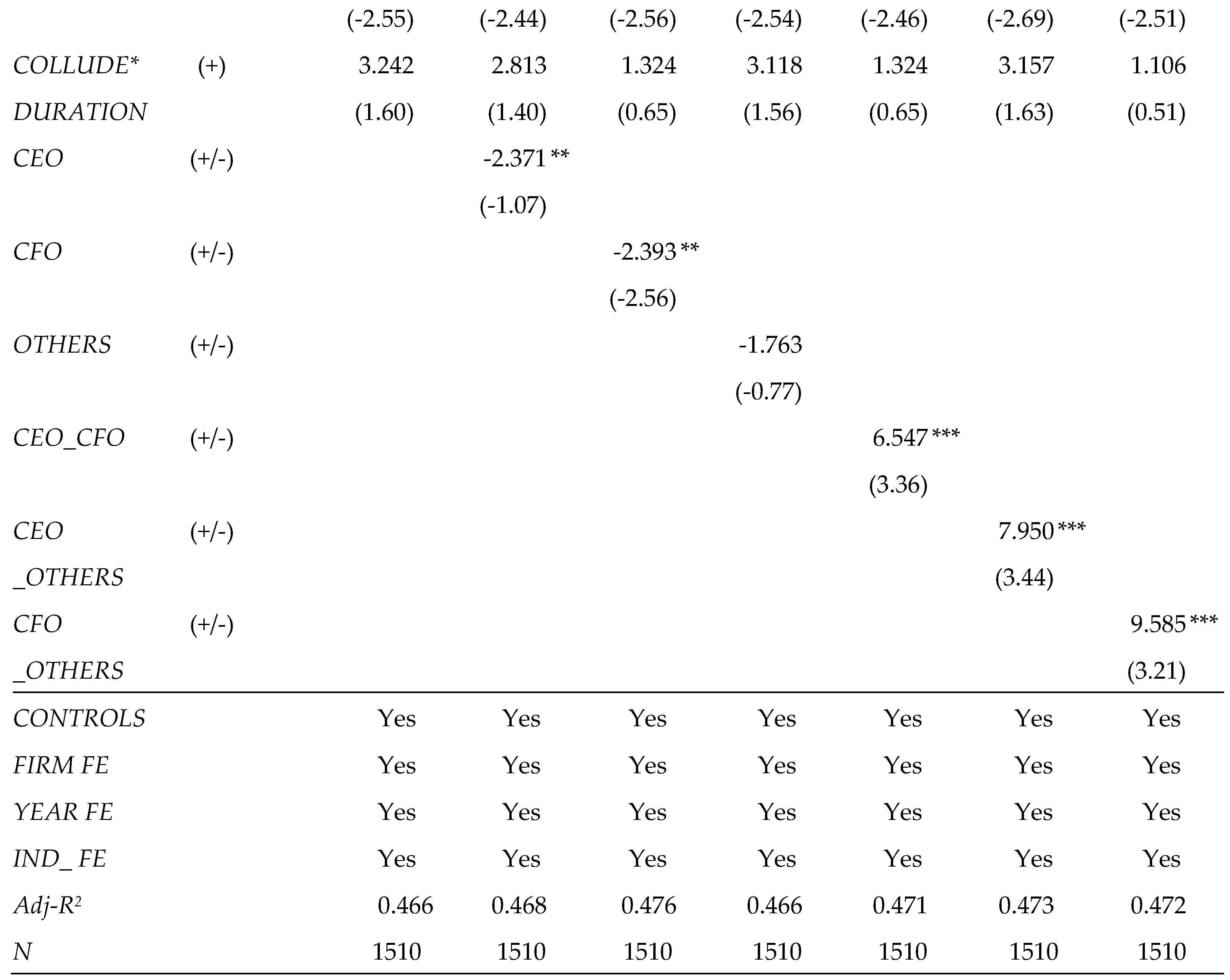

Despite the high confidence level of financial misstatement identified by the SEC (low type I error), it takes a long time to detect corporate fraud based on evidence-based approaches. Thus, in the last analysis, we examine whether and how fraud duration influences the impact of implicated executives and those colluded in fraud on abnormal investments. Table 7, Panel A shows the impact of fraud duration (DURATION) in the relationship between implicated executives and abnormal investment. The results present evidence that longer DURATION significantly exacerbates the impact of executives implicated in abnormal investment at the 0.001 level.

Panel B shows the impact of fraud duration (DURATION) in the relationship between colluded executives and abnormal investment. The results present evidence that longer DURATION does not aggravate the impact of colluded executives on abnormal investment, suggesting that DURATION does not necessarily influence the relationship between collusion among executives and their abnormal investment decisions. In summary, the results suggest that executives implicated in fraud cases are more likely to rationalize abnormal investment decisions to hide accounting irregularities from investors, regulators, external auditors, and other stakeholders [13] as fraud duration increases.

6. Discussion and Conclusion

This study investigates the impact of executives involved in fraud on firms' investment decisions utilizing AAERs in the U.S. While previous studies primarily examined factors related to opportunity and incentives within the fraud triangle, rationalization has received limited attention due to data constraints. Executives implicated in fraud often show aberrant attitudes to rationalize accounting irregularities. This study fills the gap by exploring how executives use abnormal investment decisions as a means of rationalizing fraud in light of the critical role of investment decisions in a firm's long-term sustainability.

Analysis of AAERs from 1981 to 2013 reveals that executives implicated in fraud cases tend to make abnormal investment decisions, particularly CEOs and CFOs. Collusive fraud among executives exacerbates abnormal investment decision-making. The results also indicate that such executives generally tend to overinvest rather than underinvest, particularly in R&D expenditures, to conceal or rationalize fraud. The duration of fraud further amplifies the impact of implicated executives on abnormal investment.

By shedding light on the rationalization element of the fraud triangle and offering insights into the detrimental impact of fraud on investment decisions, this research can help investors, regulators, and academics. Investors may be able to evaluate a firm's sustainability by analyzing the detailed fraud information available in AAERs, in which information about fraud cases is continuously updated. Furthermore, this study underscores the importance and urgency of public disclosure of fraud by regulators to alert capital market participants. Lastly, academics interested in ethics-focused education in accounting departments will find this study useful. When students recognize how abnormal investment decisions can be made at the expense of curtailed growth or innovation due to fraud, increased awareness of ethical decision-making will be a preventive control over corporate fraud.

Author Contributions

Moon Kyung Cho established the initial research design and provided interpretation of the analysis results. Minjung Kang extensively reviewed prior studies, outlined the reasoning behind the hypothesis, reviewed the research design, and provided comments. Both authors co-wrote and revised the manuscript and confirmed the final submission.

Acknowledgments

Moon Kyung Cho confirms that this is an original research topic based on her proposal submitted to the Association of Certified Fraud Examiners Foundation (hereafter “Foundation”) in March 2023 with a contract agreement to conduct the study between July 2023 and July 2024. We are grateful to the Foundation for providing hand-collected data. Minjung Kang acknowledges financial support provided by an Incheon National University Research Grant in 2021.

Conflicts of Interest

The authors declare no conflict of interest.

Appendix A. Title: U.S. SECURITIES AND EXCHANGE COMMISSION

Appendix B

References

- Beasley, M.; Carcello, J.; Hermanson, D.; Neal, T. Fraudulent Financial Reporting 1998-2007, an Analysis of U.S. Public Companies. Association Sections, Divisions, Boards Teams 2010. 453 Available at: "Fraudulent financial reporting: 1998-2007: An analysis of U.S. public companies" by Mark S. Beasley, Dana R. Hermanson et al. (olemiss.edu).

- Free, C.; Murphy, P.R. The ties that bind: The decision to co-offend in fraud. Contemporary Accounting Research 2015, 32, 18–54. [Google Scholar] [CrossRef]

- Li, V. Groupthink tendencies in top management teams and financial reporting fraud. Accounting and Business Research 2023, 54, 255–277. [Google Scholar] [CrossRef]

- Rezaee, Z. Causes, consequences, and deterrence of financial statement fraud. Critical Perspectives on Accounting 2005, 16, 277–298. [Google Scholar] [CrossRef]

- Hogan, C.E.; Rezaee, Z.; Riley, R.A.; Velury, U. Financial statement fraud: Insights from the academic literature. Auditing: A Journal of Practice and Theory 2008, 27, 231–252. [Google Scholar] [CrossRef]

- Trompeter, G.; Carpenter, T.; Desai, N.; Jones, K.; Riley, R. A synthesis of fraud related research. Auditing: A Journal of Practice and Theory. [CrossRef]

- Feroz, E.; Park, K.; Pastena, V. The financial and market effects of the SEC’s accounting and auditing enforcement releases. Journal of Accounting Research 1991, 29, 107–142. [Google Scholar] [CrossRef]

- Dechow, P.M.; Sloan, R.G.; Sweeney, A.P. Causes and consequences of earnings manipulation: An analysis of firms subject to enforcement actions by the SEC. Contemporary Accounting Research 1996, 13, 1–36. [Google Scholar] [CrossRef]

- Efendi, J.; Srivastava, A.; Swanson, P. Why do corporate managers misstate financial statements? The role of option compensation and other factors. Journal of Financial Economics 2007, 85, 667–708. [Google Scholar] [CrossRef]

- Schrand, C.; Zechman, S. Executive overconfidence and the slippery slope to financial misreporting. Journal of Accounting and Economics 2012, 53, 311–329. [Google Scholar] [CrossRef]

- Armstrong, C.; Larcker, D.; Ormazabal, G.; Taylor, D. The relation between equity incentives and misreporting: The role of risk-taking incentives. Journal of Financial Economics 2013, 109, 327–350. [Google Scholar] [CrossRef]

- Davidson, R.H. Who did it matters: Executive equity compensation and financial reporting fraud. Journal of Accounting and Economics 2022, 73, 1–24. [Google Scholar] [CrossRef]

- McNichols, M.F.; Stubben, S.R. Does earnings management affect firms’ investment decisions? The Accounting Review 2008, 83, 1571–1603; [Google Scholar] [CrossRef]

- Amiram, D.; Bozanic, Z.; Cox, J.D.; Dupont, Q.; Karpoff, J.M.; Sloan, R. Financial reporting fraud and other forms of misconduct: A multidisciplinary review of the literature. Review of Accounting Studies 2018, 23, 732–783. [Google Scholar] [CrossRef]

- Clatworthy, M.A.; David, A.P.; Peter, F.P. Evaluating the properties of analysts’ forecasts: A bootstrap approach. The British Accounting Review 2007, 39, 3–13. [Google Scholar] [CrossRef]

- American Institute of Certified Public Accountants (AICPA). SAS No. 99: Consideration of Fraud. New York: AICPA, 1988.

- International Auditing and Assurance Standards Board (IAASB). International standard on auditing 240: The auditor’s responsibilities relating to fraud in an audit of financial statements, 2006. Available at: http://www.ifac.org/.

- Bell, T.B.; Carcello, J.V. A decision aid for assessing the likelihood of fraudulent financial reporting. Auditing: A Journal of Practice and Theory 2000, 19, 169–184. [Google Scholar] [CrossRef]

- Lee, T.A.; Ingram, R.W.; Howard, T.P. The difference between earnings and operating cash flow as an indicator of financial reporting fraud. Contemporary Accounting Research 1999, 16, 749–786. [Google Scholar] [CrossRef]

- Farber, D. Restoring trust after fraud: Does corporate governance matter? The Accounting Review 2005, 80, 539–561. [Google Scholar] [CrossRef]

- Beasley, M. An empirical analysis of the relation between Board of Director composition and financial statement fraud. The Accounting Review 1996, 71, 443–465. [Google Scholar]

- Beasley, M.S.; Carcello, J.V.; Hermanson, D.R.; Lapides, P.D. Fraudulent financial reporting: Consideration of industry traits and corporate governance mechanisms. Accounting Horizon 2000, 14, 441–454. [Google Scholar] [CrossRef]

- Uzen, H.; Szewczyk, S.H.; Varma, R. Board composition and corporate fraud. Financial Analysts Journal 2004, 60, 33–43. [Google Scholar] [CrossRef]

- Nourayi, M.M. Stock price responses to the SEC's enforcement actions. Journal of Accounting and Public Policy 1994, 13, 333–347. [Google Scholar] [CrossRef]

- Silvers, R. The valuation impact of SEC enforcement actions on nontarget foreign firms. Journal of Accounting Research 2016, 54, 187–234. [Google Scholar] [CrossRef]

- Biddle, G.; Hilary, G. Accounting quality and firm-level capital investment. The Accounting Review 2006, 81, 963–982. [Google Scholar] [CrossRef]

- Biddle, G.; Hilary, G.; Verdi, R.S. How does financial reporting quality relate to investment efficiency? Journal of Accounting and Economics 2009, 48, 112–131. [Google Scholar] [CrossRef]

- Bar-Gill, O.; Bebchuk, L. Misreporting corporate performance (working paper). Harvard University, 2003. [CrossRef]

- Kedia, S.; Philippon, T. The economics of fraudulent accounting. Review of Financial Studies 2009, 22, 2169–2199. [Google Scholar] [CrossRef]

- International Auditing and Assurance Standards Board (IAASB). International standard on auditing 200: Overall objectives of the independent auditor and the conduct of an audit in accordance with International Standards on Auditing, 2006. Available at: http://www.ifac.org/.

- International Auditing and Assurance Standards Board (IAASB). International standard on auditing 315: Identifying and assessing the risks of material misstatement through understanding the entity and its environment, 2006. Available at: http://www.ifac.org/.

- Khanna, V.; Kim, E.H.; Lu, Y. CEO connectedness and corporate fraud. The Journal of Finance 2015, 70, 1203–1252. [Google Scholar] [CrossRef]

- Robson, K.; Young, J.; Power, M. Themed section on financial accounting as social and organizational practice: Exploring the work of financial reporting. Accounting, Organizations and Society 2017, 56, 35–37. [Google Scholar] [CrossRef]

- Bruynseels, L.; Cardinaels, E. The audit committee: Management watchdog or personal friend of the CEO? The Accounting Review 2014, 89, 113–145. [Google Scholar] [CrossRef]

- Kuang, Y.F.; Liu, X.K.; Paruchuri, S.; Qin, B. CFO social ties to non-CEO senior managers and financial restatements. Accounting and Business Research 2020, 52, 115–149. [Google Scholar] [CrossRef]

- Janis, I.L. Groupthink: Psychological Studies of Policy Decisions and Fiascos (2nd ed.). Boston, MA: Houghton Mifflin, 1982.

- Moorhead, G.; Neck, C.P.; West, M.S. The tendency toward defective decision making within self-managing teams: The relevance of groupthink for the 21st century. Organizational Behavior and Human Decision Processes 1998, 73, 327–351. [Google Scholar] [CrossRef]

- Hogg, M.A.; Hains, S.C. Friendship and group identification: A new look at the role of cohesiveness in groupthink. European Journal of Social Psychology 1998, 28, 323–341. [Google Scholar] [CrossRef]

- Tetlock, P.E. Identifying victims of groupthink from public statements of decision makers. Journal of Personality and Social Psychology 1979, 37, 1314–1324. [Google Scholar] [CrossRef]

- Ntayi, J.M.; Byabashaija, W.; Eyaa, S.; Ngoma, M.; Muliira, A. Social cohesion, groupthink and ethical behavior of public procurement officers. Journal of Public Procurement 2010, 10, 68–92. [Google Scholar] [CrossRef]

- Weick, K.E.; Roberts, K.H. Collective mind in organizations: Heedful interrelating on flight decks. Administrative Science Quarterly 1993, 38, 357–381. [Google Scholar] [CrossRef]

- Jehn, K. A multimethod examination of the benefits and detriments of intragroup conflict. Administrative Science Quarterly 1995, 40, 256–557. [Google Scholar] [CrossRef]

- Abernathy, J.L.; Beyer, B.; Downes, J.F.; Rapley, E.T. High-quality information technology and capital investment decisions. Journal of Information Systems 2020, 34, 1–29. [Google Scholar] [CrossRef]

- Goodman, T.H.; Neamtiu, M.; Shroff, N.; White, H.D. Management forecast quality and capital investment decisions. The Accounting Review 2014, 89, 331–365. [Google Scholar] [CrossRef]

- Koh, P.-S.; Reeb, D.M. Missing R&D. Journal of Accounting and Economics 2015, 60, 73–94. [Google Scholar] [CrossRef]

Table 3.

Implicated executives and abnormal investment (H1).

|

***, **, and * denote significance at the 1%, 5%, and 10% levels, respectively, based on a two-tailed test. All variables are described in Appendix B.

Table 4.

Colluded executives and abnormal investment (H2).

|

***, **, and * denote significance at the 1%, 5%, and 10% levels, respectively, based on a two-tailed test. All variables are described in Appendix B.

Table 5.

Additional analysis 1: disaggregated investment.

|

***, **, and * denote significance at the 1%, 5%, and 10% levels, respectively, based on a two-tailed test. All variables are described in Appendix B.

Table 6.

Additional analysis 2: disaggregated investment types.

|

***, **, and * denote significance at the 1%, 5%, and 10% levels, respectively, based on a two-tailed test. All variables are described in Appendix B.

Table 7.

Additional analysis 3: fraud duration.

|

***, **, and * denote significance at the 1%, 5%, and 10% levels, respectively, based on a two-tailed test. All variables are described in Appendix B.

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Copyright: This open access article is published under a Creative Commons CC BY 4.0 license, which permit the free download, distribution, and reuse, provided that the author and preprint are cited in any reuse.