Submitted:

02 May 2024

Posted:

06 May 2024

You are already at the latest version

Abstract

Oracles have been suggested as a vital piece of infrastructure necessary to allow blockchain-based smart contracts to reach their full potential by interacting with real-world data. This paper begins by providing an approachable entry point to the oracle problem and the current landscape of existing solutions. From there, we provide an overview of published research to narrow down unexplored research directions and derive questions for interviews. Finally, the results of 15 unstructured expert interviews are presented and discussed. The focus here is the industry landscape of oracle projects, opportunities for innovation, and challenges needing to be overcome.

Keywords:

smart contracts

; automation

; fintech

; oracles

; process optimization

; web3

1. Introduction

As blockchain technology matures, the need for reliable and efficient methods to integrate real-world data into decentralized applications becomes increasingly vital. Blockchain oracles serve as intermediaries facilitating this crucial information flow from off-chain sources to on-chain smart contracts. This paper aims to contribute to current research on blockchain oracles, hybrid smart contracts, and the interplay between off-chain and on-chain elements. The paper is positioned to provide easy access to readers who may be unfamiliar with the topic while offering insights with respect to potential future extractable value.

1.1. Blockchain: A Trust Machine

For years now, blockchain technology has been making waves. At times, being proclaimed a key driver for the next industrial revolution [1,2]. At others, condemned as nothing more than a useless gimmick powering a gigantic Ponzi scheme [3]. Regardless of the public and market sentiment toward the technology, there are certainly reasons it has received so much attention beyond speculation.

In its most simplified form, a public blockchain is a shared append-only ledger that enforces certain rules while allowing anyone read and write access. This distributed digital ledger allows users to deterministically achieve consensus on a common reality without the need for centralized parties to keep records and govern the process [4]. Blockchain technology was first introduced in Bitcoin, though the term “Blockchain” was never explicitly mentioned in the original whitepaper by Nakamoto [5]. Bitcoin was designed to function as a peer-to-peer electronic cash system with a native, independent currency and monetary system tied to participation in the maintenance of the network and processing of transactions [5]. For the first time in history, there was a globally standardized currency that anyone could use, but nobody could monopolize control over due to the fundamental design of blockchain consensus protocols.

While this in itself is a historic achievement, researchers interested in the technology quickly realized other potential use cases in which such a system might yield significant benefits and potentially revolutionize how we transact, exchange value, and keep records. Early examples mentioned by Tapscott [6] include the standardized recording of land titles, providing financial services to all regardless of factors such as location and access to legal documents, decentralized sharing economy platforms, self-sovereign digital identity, automated royalty payments for digital content, and even technology-enabled systems to support and improve governmental functions. In general, blockchain technology primarily enables two functions: (1) digital scarcity enabling value transfer and (2) decentralized processing and validation of transactions immutably stored in a chronologic ledger; the emphasis concerning more advanced applications beyond basic party-to-party asset transfer is on the latter. While digital scarcity certainly plays a role, decentralized computation and execution of transactions can be used to create systems and protocols for various use cases. The innovation here is that neither trust among participants nor the involvement of a central governing party is necessary for anyone to participate in a system or use an application.

Decentralized computation via a smart contract network allows for guaranteed neutral execution of pre-defined logic. This is useful as it removes the need for trust when engaging in even complex transactions. Decentralized computation is practical when building so-called Decentralized Applications (dApps). User-facing applications utilizing a blockchain in its back-end. Currently, the primary use for dApps is in finance, primarily on the Ethereum blockchain [7]. Decentralized finance (DeFi) is an umbrella term for decentralized exchanges, lending protocols, derivatives, insurance, and more. All logic for such applications is written ahead of time in the form of a smart contract and published on a blockchain. Once published, the code cannot be changed but it can be audited by all parties. The logic outlined in the contract is executed when a party interacts with the contract [7]. This allows parties to engage in complex transactions without the need to trust one another - the operation is trustless [8]. There is no need for a bank, a government, a notary, an escrow agent, or any other middleman whose role traditionally is to help overcome issues of trust. This has the potential to drastically streamline and disintermediate a wide variety of transactions, even beyond finance.

Before going further into detail about the blockchain’s role as a trust machine, it is essential to understand decentralization and how it is achieved and maintained. At the foundation of every blockchain is the consensus protocol - in other words, how network participants agree on a common truth to be immutably recorded on the ledger [9]. Depending on whether the blockchain is public, allowing anyone to participate in consensus, private, allowing only allowlisted nodes to participate, or a hybrid system, different methods are used to ensure network integrity. Underlying these different approaches is the need for Byzantine fault tolerance.

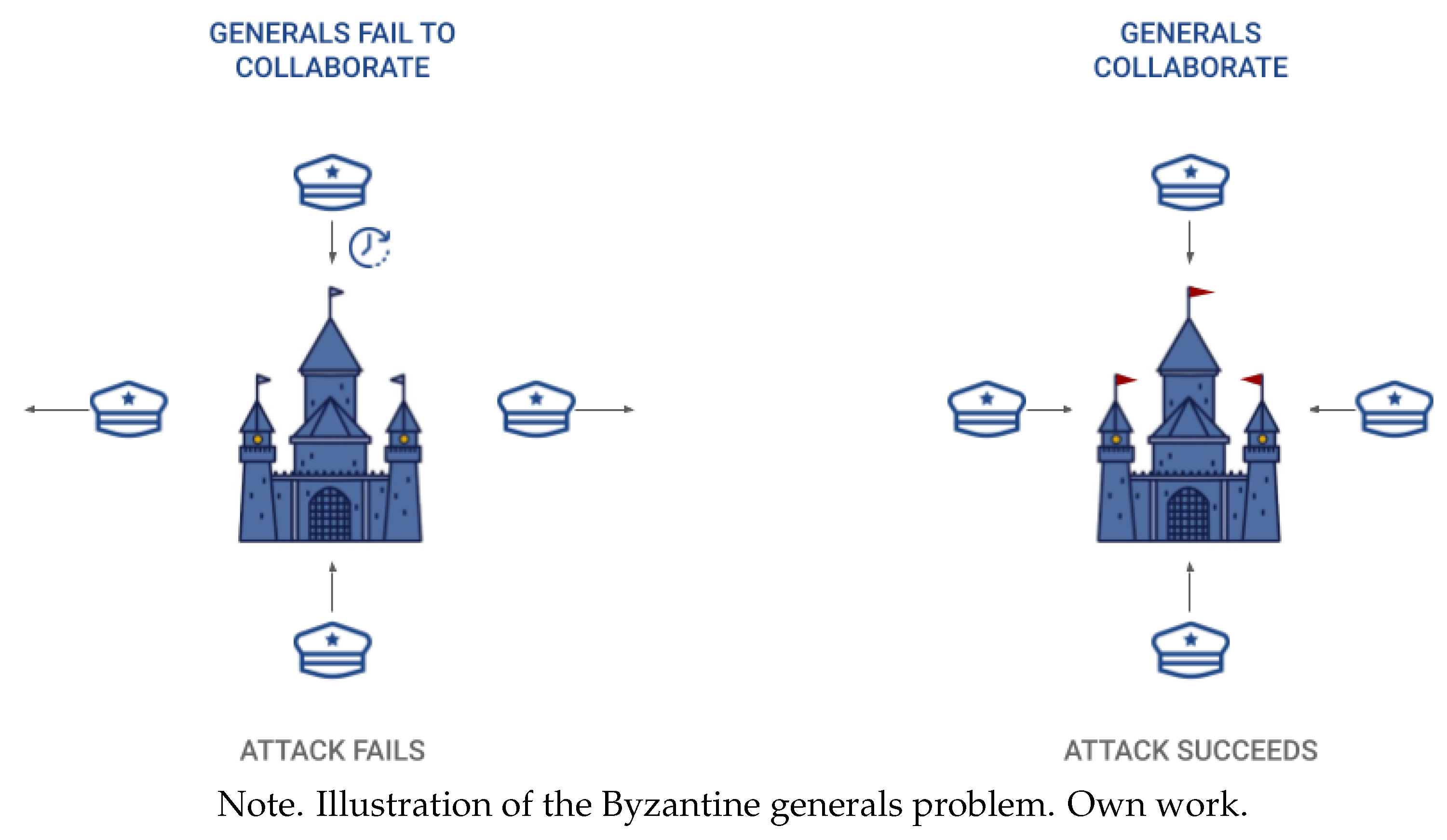

The term Byzantine fault comes from the so-called Byzantine Generals Problem, an allegory describing the fundamental challenge of ensuring a certain minimum percentage of actors behave as expected. The analogy used to describe this problem involves multiple generals planning to attack a fortress. The battle is won if all generals coordinate the attack and follow through. If, however, certain generals fail to participate in the coordinated attack or retreat instead of attacking, the battle is lost. Generals cannot be expected with absolute certainty to communicate honestly. Messengers between them may be intercepted, the other party may inject false messengers, and generals may outright lie [10].

Figure 1.

Byzantine Generals Problem.

The two leading permissionless consensus protocols, meaning anyone can participate and participants cannot inherently be trusted, used in public blockchains to overcome this issue are proof of work (PoW) and proof of stake (PoS). In proof of work, network participants use computing power to solve hash-puzzles [11] while in competition with each other. Economic incentives ensure that participants use their computing power to secure the network rather than attack it [5]. Proof of stake works very similarly, though it does not use computational power but rather direct financial incentives. Participants in PoS consensus commit funds as collateral to contribute to transaction validation. These foundational protocols ensure the network’s neutrality or decentralization [12]. There are other approaches to consensus, some of which build on a certain element of trust achieved by only allowing known actors to participate, also known as permissioned blockchains. This, of course, also creates a limited network that may be easier to target [13].

Byzantine fault tolerance of blockchains allows for a provably fair and independent network able to store and process data without the need for a central authority. In short, blockchains are useful when trust between two parties wishing to transact does not exist, which is quite common in a digital economy.

1.2. The Oracle Problem

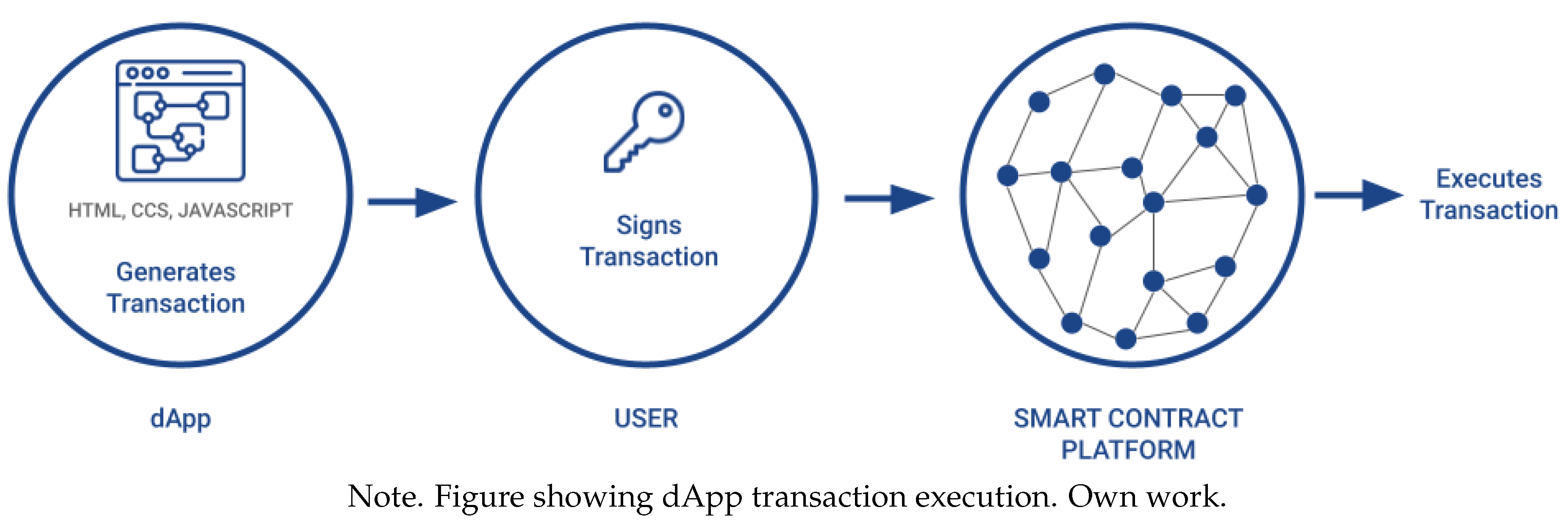

Bitcoin was originally designed as a decentralized peer-to-peer cash system able to not only execute transactions between parties but also to utilize a native currency with automated monetary policy [5]. While extreme price volatility [14] and high transaction fees [15] have hindered Bitcoin’s adoption as a digital cash system, as demonstrated when Steam removed Bitcoin as payment method in 2017 [16], some argue Bitcoin has found use as a form of “digital gold” - a relatively uncorrelated digital commodity [17]. With Bitcoin’s continued proof that a decentralized blockchain system can reliably secure value, new projects began emerging. Ethereum, for example, took the concept further by adding Turing completeness - the ability to execute computer code [18]. At Devcon1 in 2015, Ethereum co-founder Vitalik Buterin used the allegory of Ethereum being a smartphone on which Bitcoin is merely one single application [19]. This type of Turing complete Blockchain is also sometimes called a smart contract platform. Smart contract platforms have the ability to execute series of “if-then” statements, allowing for logic to be written onto the network. Using a traditional web front-end and connection to a smart contract platform, developers have the ability to build applications with decentralized execution [20]. Such applications have the potential to offer a tremendous amount of value as they replace the need for trust with cryptographic guarantees.

Figure 2.

dApp Architecture.

Blockchains have been operational for around 15 years now, and while the promise of a world with a reduced need for intermediaries has attracted some attention, mainstream adoption, and real-world use cases are still few and far between, at least when compared to the full potential of the technology. While this may largely be attributable to scaling problems found in many blockchain networks, difficult user experience journeys, and an inherent lack of understanding of the technology [21], an argument could also be made that decentralized applications that could make a real positive difference in every day life have not yet been built. Whereas simple decentralized applications are already available and quite successful by some metrics, for example, decentralized peer-to-peer lending platforms and decentralized exchanges [22], more advanced applications that would offer value in the daily life of most average people are not. When developing smart contracts, there is a limit as to what can be done natively within a certain blockchain network. Such networks are isolated systems by design. This provides excellent levels of security and reliability. However, it also makes the development of smart contracts that rely on external data challenging to build. The potential of decentralized execution is limited without the ability to observe and interact with off-chain systems. Hence, the question of how developers may provide data access to their smart contracts without potentially introducing major security vulnerabilities arises. Is there a way to minimize centralization and maximize data integrity in data provision? This challenge is sometimes called the oracle problem [23]. Consequently, third-party services that enable data availability are referred to as oracles.

Figure 3.

The Oracle Problem.

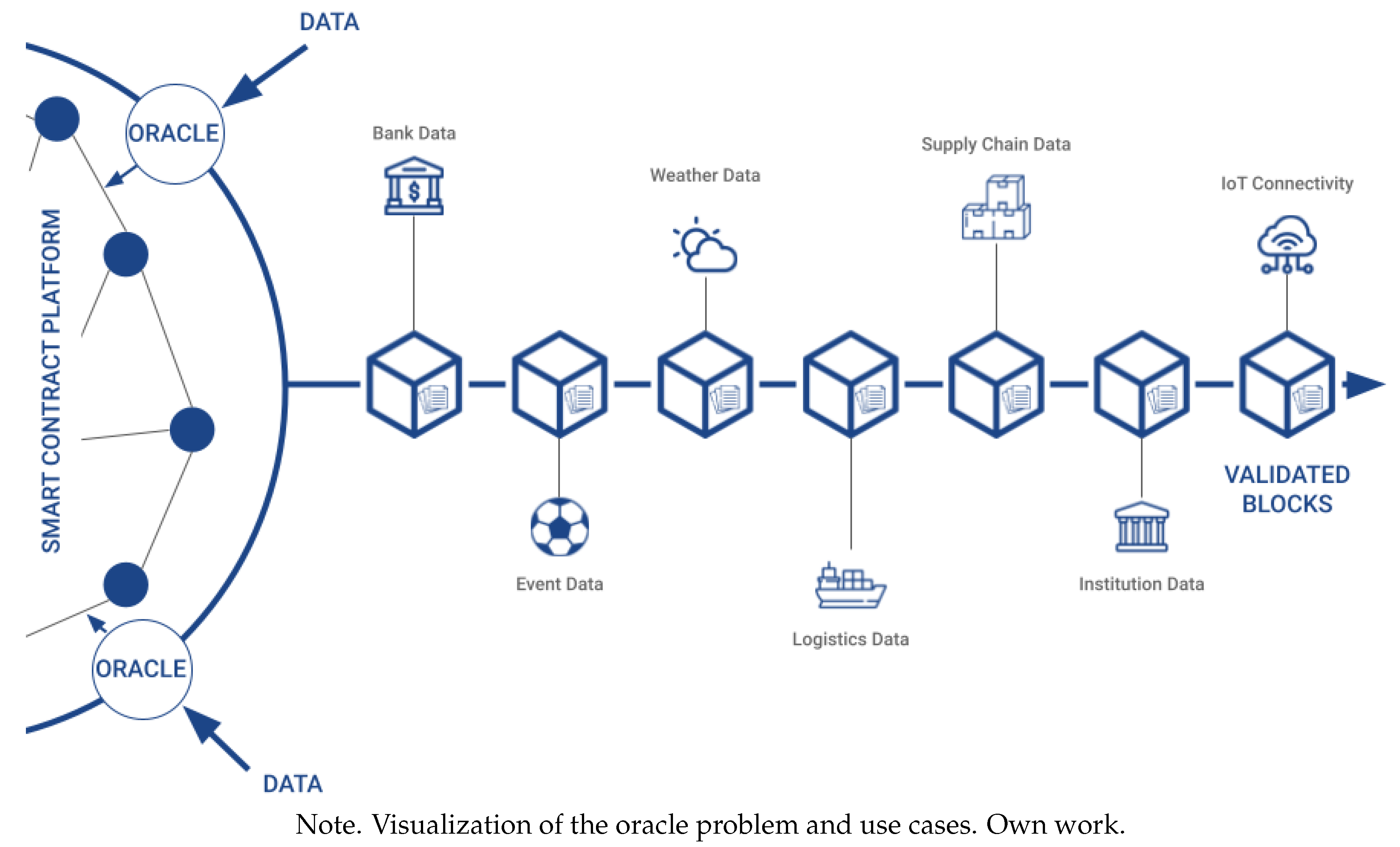

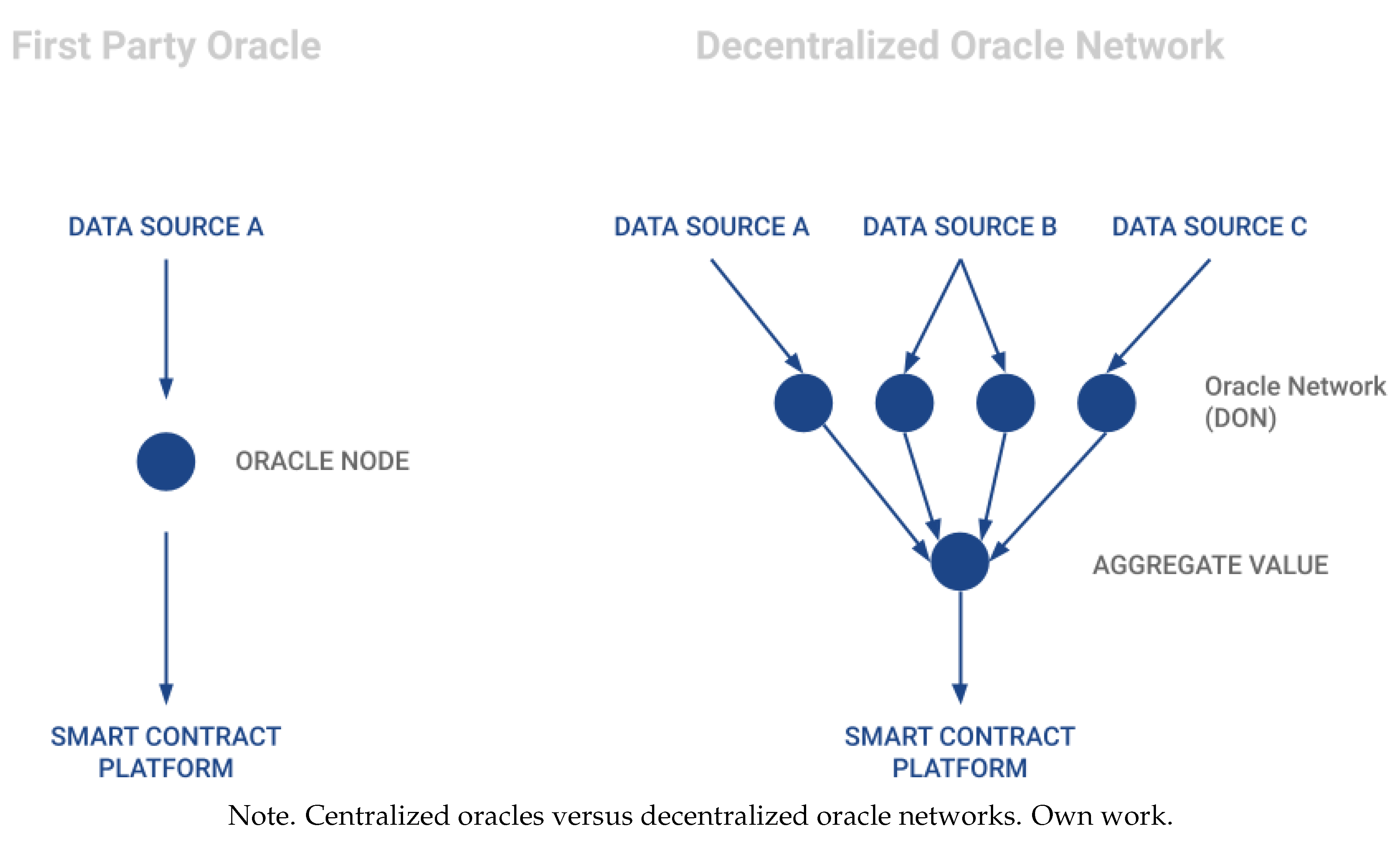

Currently, there are several approaches to allow smart contracts to access blockchain-external data. The most primitive way to enable data access are centralized oracles. Centralized oracles provide data from a single external source and are operated by a single entity. Such oracles are very easy to implement and often purpose-built. However, being centralized, they also present a single point of failure. If the data is corrupted or manipulated, it may lead to significant ramifications [24]. Alternatively, several projects are working on implementing decentralized oracles. Decentralized oracle implementations are the focus of this paper. Among them are Chainlink, Band Protocol, API3, and many others. A brief summary of how these projects tackle the Oracle problem follows.

Chainlink is considered the industry leader, going by various metrics, including the total number of integrations [25]. Chainlink is focused on third-party oracles. Theoretically, anyone can set up and operate a node that makes data available on-chain. Node operators are not automatically considered trusted. Economic considerations are used to create trust, with dishonest node operators being punished. A very similar approach is used by Band Protocol (Band, n.d.-b), though using their own blockchain network. API3, on the other hand, relies on trusted first-party oracles to solve the oracle problem (API3, n.d.). Whereas Chainlink and Band Protocol rely on a network of nodes to fetch data from external data sources, e.g., APIs, API3 enables API providers to operate their own oracle node directly. There are, of course, many other approaches to solving the oracle problem. While this paper primarily focuses on decentralized third-party oracle networks, particularly Chainlink’s implementation, all approaches will be taken into consideration.

Third-party-based oracle systems approach to overcoming the oracle problem is called a decentralized oracle network, DON for short. As briefly explained above, a decentralized oracle network comprises a committee of nodes [26]. DONs ingest data through a connection between the oracle node and an Application Programming Interface (API) provided by one of many data providers. Different nodes within a single DON gather data from multiple independent sources, and a median of all the different data reported by the various nodes is made available to the smart contract.

Figure 4.

Decentralized Oracle Network Data Aggregation.

Aggregation and the ability for anyone to operate a node within a DON or to create a new DON, provide a high level of reliability, redundancy, and a degree of decentralization. Nodes also sign the data sent to the network, proving which node was the one to send it. Even though the data is aggregated off-chain, these signatures remain attached to the data and are also sent on-chain. Since this signature is stored on a blockchain, there is a transparent and permanent historical record of the performance of a certain node. Reputation systems allow smart contract developers to filter nodes by certain metrics [26]. This introduces competition for node operators and is an additional incentive to keep nodes honest. In addition to data sourcing and delivery, oracle networks may offer various services, such as trustlessly triggering actions in a smart contract, creating and providing a source of randomness, and more. Oracle functions are discussed in part V of Theory.

1.3. Research Direction

After the introduction, the theory section delves into the importance of data in both Web2 and Web3. It explores the potential applications of hybrid smart contracts and their technical foundations. Additionally, it presents a comprehensive overview of the predominant oracle protocols in use today, along with their functions and key stakeholders. The theory chapter aims to provide readers unfamiliar with smart contracts and oracles with the necessary foundational information.

The overarching goal of this paper is to contribute to the available research surrounding blockchain oracles by providing insight regarding the following three guiding research questions. (1) How do stakeholders position themselves within the competitive landscape, and what are the criticisms and advantages of their approaches? (2) How mature is the industry in its current usage, and what is its future outlook? (3) What opportunities are enabled by the industry, and what tangential businesses arise from it? These questions will be further refined and positioned to fill gaps in current research identified in the literature review section of this paper. Following the literature review and the methodology chapter, the insights gained through 15 expert interviews are presented.

2. Theory

In 2006, British mathematician Clive Humby said, "Data is the new oil.” [27]. In the years since then, huge companies with data as a core part of their business model have climbed up the market capitalization rankings of major stock markets worldwide. The internet has enabled new possibilities for data sourcing, transfer, and use cases involving data. With new technologies such as AI and blockchain, the significance of data is posed to only increase. Decentralized computation and digital currency promise to enable a wide variety of new use cases in the same way the internet has, potentially reshaping the entire data industry. This section aims to explore the data economy of today, provide an in-depth summary of how oracles work, why this topic is significant, as well as the current state of the technology. Furthermore, the landscape of oracle protocols and stakeholders in oracle systems are explained.

2.1. Data Economy

The importance of data in business has increased considerably in recent years, fundamentally changing how businesses function and generate value. For organizations to succeed in the modern digital era and acquire a competitive edge, data has long been considered a crucial strategic asset [28]. Data is being used by businesses to improve customer experiences, streamline operations, spur innovation, and make optimal decisions [29]. The digital economy runs on data, which enables businesses to open up new income sources and provide value for their consumers and shareholders. Using services and exchanging goods produces information that is stored, transferred, and used. This subchapter will examine the present situation in today’s data economy, as well as highlight the current value of data as a strategic asset.

Considering that some of the largest companies in the world by market capitalization are technology companies with a strong emphasis on data in their business models, data is clearly of high strategic importance. Apple, Microsoft, Alphabet, Amazon, and Meta, in particular, would likely never have reached their current dominant positions without the strategic integration of big data in their business models. Be it generating and monetizing data by selling it to advertisers, or using data to increase revenue in some other way, for example, by up- and cross-selling, or using data as a competitive advantage by creating walled garden ecosystems surrounding it. This phenomenon is nothing new and has been clearly identified for many years now. According to a study by Davenport and Harris [30], businesses that effectively leverage data are more likely to achieve superior performance than those that do not. The study found that data-driven companies outperformed their competitors in terms of profitability, productivity, and market valuation. In addition to technology companies, businesses across all industries are recognizing the importance of data in the context of their operations. They leverage data to optimize processes, improve customer experiences, and make informed decisions. For instance, retail companies use data to personalize their marketing efforts and increase customer loyalty [31], while healthcare providers use data to improve patient outcomes and reduce costs [32]. Even Netflix’s popular television series "House of Cards" was originally greenlit based on data analysis that revealed viewers of the original BBC version of the drama, also like films starring Kevin Spacey or produced by David Fincher [33]. Netflix knew the show would be a hit without seeing a single scene.

The ability to collect and analyze vast amounts of data has opened up new opportunities for businesses to create value and gain a competitive edge in the market. While this is hardly surprising, and the term “big data” is commonly used, there are many different ways for companies to participate in and profit from the data economy. The following briefly summarizes some of the largest stakeholders and their activities.

2.1.1. Infrastructure

The most basic layer of the data economy is infrastructure. This layer’s stakeholders are primarily large technology companies, including Amazon, Google [34], Microsoft, IBM, and Oracle, among others. These companies offer a range of products and services that help organizations manage and analyze their data effectively. AWS, a part of Amazon that offers cloud-based computing and storage services, brought in $80 billion in revenue in 2022, a large percentage of which came from data-related services, including data warehousing, analytics, and machine learning [35]. The Cloud business of Google, which provides comparable services, produced $26.2 billion in revenue in 2022 [34]. The Azure cloud platform, which offers various data-related services like data analytics, machine learning, and artificial intelligence, contributed significantly to Microsoft’s $198 billion in sales in 2022 [36], making it another prominent player in the big data market. The cloud division of Oracle, which provides data-related services, including database management, analytics, and machine learning, generated over $10 billion in revenue in 2022 [37]. These companies provide the backbone for the data economy, primarily storing and processing vast quantities of data.

2.1.2. Data Brokers & Aggregators

Companies that collect and sell data are often called data brokers or aggregators. These companies specialize in collecting, analyzing, and selling large amounts of data. Many of these companies focus on different types of data [38]. In general, they can be separated into companies focused on personal data, and companies focused on non-personal data. Some of the largest data aggregators focused primarily on personal data include Acxiom, Experian, Equifax, TransUnion, Oracle Data Cloud, and Neustar, among others [39]. These companies collect data from various sources, including public records, social media, online activity, and consumer transactions, among others. They then package this data into profiles or segments, which are sold to other companies for targeted advertising, lead generation, and other marketing purposes. On the non-personal data side, companies such as Bloomberg and Thomson Reuters specialize in collecting and selling financial data, including market data, news, and analytics, to financial institutions, investors, and other businesses. Other companies, such as IHS Markit, specialize in collecting and selling data related to industries such as energy, automotive, and technology. In addition, some companies specialize in collecting and analyzing sensor data from devices such as Internet of Things (IoT) sensors, smart home devices, and industrial equipment. These companies include firms such as Intel, IBM, and Siemens, among others. They collect and analyze sensor data to help businesses optimize their operations, improve efficiency, and identify new business opportunities.

2.1.3. Data Users

Finally, there are the companies and organizations that purchase the generated data. The key customers in the data economy who purchase data from brokers can vary depending on the type of data being sold and the specific industry involved. Different organizations, with different strategic objectives, purchase different types of data. Commonly quoted examples include marketers and advertisers, using consumer data to identify potential customers and create targeted advertising campaigns [40], healthcare companies, which purchase data including patient demographics, medical history, and clinical results in an effort to improve patient outcomes and reduce costs [32], government agencies, and researchers, to name a few.

More interestingly in the scope of this paper is the use of data by financial institutions. These organizations use data to assess risk, prevent fraud, and optimize investment portfolios, among other things. One concrete example of this is BlackRock’s Aladdin. Short for Asset, Liability, and Debt and Derivative Investment Network [41], Aladdin is a technology platform that ingests data and provides investment management, risk management, and operational tools to institutional investors [42]. As of 2020, Aladdin managed $21.6 trillion in assets [43]. In order to power Aladdin’s capabilities, BlackRock purchases a variety of data from different sources. Some examples of data that is purchased for Aladdin include market data, for example, market prices, trading volumes, and other indicators, economic data, including indicators such as GPD, inflation, and employment, fundamental data on individual companies, such as financial statements, earning reports, and analyst estimates. Other purchased data types include satellite imagery, social media sentiment analysis, and credit card transaction data [44]. This data is used to gain insights into specific industries or companies and to identify potential investment opportunities. Once acquired, the data is processed and analyzed using machine learning and other quantitative methods.

AI and machine learning is an industry with great promise that relies on large quantities of data to train and improve their models. The more data that is available, the better the AI [45]. Machine learning has made tremendous progress in recent years in the areas of autonomous navigation [46], generation of media [47], efficiency improvements in industry, and more, promising to disrupt a plethora of different sectors, creating a tremendous amount of value in the process. However, some issues related to the data economy are highlighted particularly well in this area of generative AI. An example of such an issue is the question of copyright in generative AI. When an AI model is trained with images from certain artists and learns to replicate their style and patterns, should the artist who created the source material be rewarded, and to what extent? Other issues in the data economy relate to privacy, security, the monopolization of data, and more. Ultimately, advancements in the area of artificial intelligence have the potential to transform the way we work, live, and conduct business, largely through automation. Not just in manufacturing and industry but also in finance, digital technology, and much more. Spanning industries and trillions of dollars of economic activity. As such, it is important to approach this technology thoughtfully and responsibly.

While data has become a vital resource in almost any type of industry, we may be only just scratching the surface. Data is critical in automation, especially in combination with other technological advancements such as additive manufacturing, blockchain, IoT, and others. Important in the scope of this paper is the overlap between data and decentralized computation and value settlement.

2.2. Data in Web3

In 1997, computer scientist, legal scholar, and cryptographer Nick Szabo published a paper titled “The God Protocols” (1999). In this paper, he describes his vision for decentralized, cryptographically guaranteed fair systems that are more efficient and secure than traditional systems - Mathematically Trustworthy Protocols. The use cases for such protocols proposed by Szabo include decentralized currency systems, dispute resolution, contract enforcement, identity, and voting [48]. Such systems, in theory, have the potential to reshape large parts of the economy by increasing efficiency and reducing the need for centralized authorities and intermediaries. In 1998, Szabo proposed a decentralized currency system named Bit gold [49]. The basic idea behind Bit gold was to create a decentralized system for creating and managing a scarce digital asset, which could be used as a medium of exchange and store of value without relying on a central authority. However, Bit gold was never implemented (Van Wirrum, 2018). Over the years, many projects have attempted to fill the various proposed functions of a god protocol. Some specialized in one functionality, others in universality, composability, and interoperability. Most notably Bitcoin, which began operating in 2009 [50]. Bitcoin was originally designed as a peer-to-peer cash system, including a decentralized currency and settlement network [5]. In July of 2023, Bitcoin is currently the decentralized network with the most nodes [51] and has a market capitalization of over $500 billion [52]. Bitcoin proved that such a decentralized protocol is possible in practice. With one of the proposed use cases of such a god protocol achieving at least some success, developers became inspired to find ways to build even more capable systems.

Today, there are thousands of protocols. Nonetheless, Szabo’s vision of the potential of a god protocol has not yet been fulfilled. That is not to say that no progress has been made. Smart contract platforms, such as Ethereum, have the fundamental functionalities necessary to implement decentralized contract enforcement, dispute resolution, identity systems, voting systems, and more [53].

Ethereum, for example, is not simply a decentralized ledger that stores account balances but is instead more fittingly described as a distributed state machine [54] as explained in the Ethereum developer documentation:

Ethereum’s state is a large data structure that holds not only all accounts and balances, but a machine state, which can change from block to block according to a predefined set of rules, and which can execute arbitrary machine code.

This combination of memory and executive capabilities is often also summarized as the Ethereum Virtual Machine or EVM for short. The EVM functions as a decentralized computer composed of a worldwide network of participants able to execute arbitrary functions [54]. In practice, it is already possible to build decentralized financial service applications, organizational structures governed by voting, identity and reputation protocols, and much more. However, one limiting factor to Ethereum’s functionality is data availability. While developers have a toolset of functions, Ethereum is an isolated system that does not natively allow for outside connections. While this separation is essential for security and stability, it limits the type of applications for which the EVM may be used.

This is a problem since much of digital innovation is combinatorial in nature. On one hand, the open-source ideals found in the blockchain space are a tremendous advantage. On the other hand, new services often rely on data feeds in the form of Application Program interfaces and Micro Services that integrate specific functionalities not available within the closed system of the Ethereum Virtual Machine. In Web2, this is not an issue. Organizations may easily leverage external APIs. Ridesharing applications, such as Uber for example, do not use infrastructure built from the ground up, instead using pre-built APIs. Often a GPS API for location data (e.g., MapBox), an SMS API for messaging (e.g., Twilio), and a currency API (e.g., BrainTree) for payment processing [55]. These are external services not maintained by or directly accessible by organizations; an interface is necessary. It is no different regarding applications built to utilize a decentralized network for computation. The problem regarding connectivity and reliability that arises in decentralized systems is often referred to as the oracle problem.

2.3. Significance

In order for applications built to run on a decentralized computation network to reach their true potential, they need to be aware of and able to communicate with external systems [56]. Being able to ingest real-world data, such as market prices, allows smart contracts to use them as triggers for an “if-then” statement on-chain. Having the ability to send messages from on-chain to blockchain external systems would allow them to trigger events such as sending payments off-chain or sending instructions to physical devices, to name just a few examples. In order to enable this type of functionality a piece of middleware is needed. This piece of infrastructure is referred to as an oracle [56]. Smart contracts that use oracles for their processes are also called hybrid smart contracts since they combine off-chain and on-chain data and computation [57].

While use cases of blockchain oracles are very diverse and found across many different industries, a commonly cited example is that of parametric insurance, as it highlights not only the functional significance of oracles but also the benefits of cryptographic guarantees and decentralization. Functionally, a decentralized parametric insurance application consists of a smart contract containing the insurance logic and a set of oracles providing the necessary data to evaluate and enforce claims [58]. The case of parametric flight-delay insurance is an excellent example: the insured pays a given fee into a smart contract to insure against the cancellation or delay of a specified flight. At a certain point in time, an oracle is used to query details about the flight, and depending on predefined conditions, the claim is automatically settled. The entire process is automated and executed according to the smart contract. Neither the insured nor the insurer need to trust each other since no one can interfere with the execution [59]. The insured benefits from transparency, immutability, and speed. So long as the oracle reports the correct data, there is no way for either party not to complete the agreement as outlined in the smart contract. Settlement is automated and happens instantly [58]. The other side also benefits from efficiency gains. Rather than relying on third-party insurers, airlines could directly integrate such an application into existing systems and processes, potentially boosting efficiency, reducing potential legal liabilities, and increasing transparency. While it is possible to employ parametric insurance without smart contracts, decentralized implementations benefit from cryptographically guaranteed execution. Once the hybrid smart contract is active, the agreement will be immutably executed as specified therein [60], making trust and legal protection superfluous.

Flight insurance is just one rudimentary example of a decentralized parametric insurance application. The example of crop insurance better highlights the potential of decentralized parametric insurance. Decentralized parametric crop insurance allows farmers around the world access to standardized insurance against specific weather events threatening their crops. If the oracle reports that there was less than a certain amount of rain where the insured are located, they are automatically paid out drought insurance compensation. This simple concept increases the availability of insurance as the insured need only a cheap phone and internet access to enter into contracts. There is no need for extensive documentation or regional insurance providers [58]. This is significant because in LEDCs, formal agricultural insurance is often not available at all [61], and these regions are also the most vulnerable to extreme weather events; exacerbated by global warming [62]. Furthermore, these regions are also more likely to rely on subsistence farming to support local populations [63], further emphasizing the importance of insurance. In other words, these already vulnerable regions are hit the hardest and hurt the most [62]. According to a prediction by the Intergovernmental Panel on Climate Change, the increasing frequency and extent of extreme weather events, such as heatwaves and droughts, will cut agricultural productivity in Africa by up to 50 percent [64]. Already, agricultural productivity has declined by 34 percent since 1961 due to climate change [64]. Access to modern financial services such as insurance is highly important for LEDCs. Many financial products do not exist for speculative reasons but rather to allow people and businesses to mitigate risks and hedge against unfavorable situations [65]. The scalability, security, and transparency provided through hybrid smart contracts has the potential to allow anyone anywhere access to reliable financial services.

Beyond being better for customers, cryptographically guaranteed self-executing contracts lead to significant efficiency gains for companies through automation, allowing for increased profits or reduced prices for customers. The extent of these efficiency gains cannot be understated. A tangentially related example of the impact of this type of technology can be found in the reinsurance industry. According to a report by PwC, the reinsurance industry alone stands to reduce its expenses by 15% to 25% by automating settlement using smart contracts amounting to $5-10 billion saved yearly (2016).

The insurance sector is far from the only industry likely to be disrupted by implementing hybrid smart contracts. Other examples of where potential use cases are to be found include the financial sector as a whole, supply chain management, gaming, marketing, government, mobility, and manufacturing [66,67,68]. Everywhere conventionally a middleman or additional process has been needed to establish trust there is potential for disruption [69]. In the financial industry alone, there are countless potential use cases for hybrid smart contracts, as many industry subsections exist purely to facilitate transactions between parties and enable hedging against risk.

While critics might say that cryptographic guarantees and decentralized networks replacing centralized authorities is unnecessary as regulation makes these intermediaries reliable, some cases prove otherwise, underscoring how imperfect a system relying on centralized trusted authorities to function can be, no matter the level of regulation. In the lead-up to the subprime mortgage crisis of 2008, one specific middleman played a significant role: ratings agencies (Bush, 2022). Since 1936, US banks have been legally required to act only on “recognized ratings manuals” regarding the buying and selling of bonds. “Recognized ratings manuals” refers to the information published by the rating agencies, typically one of the big three agencies: Moody’s, Standard & Poor’s, or Fitch. In the leadup to the financial crisis, rating agencies gave mortgage-backed securities overly high ratings. When the subprime mortgage market began collapsing, many highly rated securities turned out to be far riskier than investors had been led to think (White, 2010). Some researchers have highlighted the fact that since rating agencies were paid by the companies issuing the securities, they had the incentive to offer high ratings [70]. The 2008 financial crisis led to a total loss of over $2 trillion in global economic growth [71], millions of jobs, and billions in income. All in large part attributable to the failure of a trusted middleman to remain unbiased. An interesting question to look into is which examples of intermediaries we rely on today pose a particularly high risk and whether automating their functions via a hybrid smart contract would be feasible.

2.4. Use Cases

While parametric insurance is a great example case that highlights both the capabilities and significance of oracle-enabled hybrid smart contracts, the benefits apply to various industries. This chapter summarizes prominent use cases, especially those highlighted in academic publications. This is not an exhaustive list; instead, it is a collection of use cases considered especially significant in current discourse and research. It also provides examples of experimental use case implementations from smaller projects and hackathons.

2.4.1. Interoperability, Real World Assets, Perpetuals

One of the most anticipated use cases for oracles is direct interoperability when moving assets from blockchain to blockchain or between off-chain bank accounts and a blockchain. The potential benefits of blockchain interoperability have been the focus of research for several years now [72]. Different methods to enable blockchains to communicate with one another have been developed, though some implementations fall short, as demonstrated by the wormhole platform hack in early 2022 in which an attacker stole around $300M worth of crypto assets from the aforementioned cross-chain protocol [73]. Certain tokens may be natively available on multiple smart contract platforms with a dApp that allows bridging by burning a token on one chain and issuing it on another. Such tokens are in the minority, with one example being USDC issued by Circle [74]. The majority of tokens require workarounds, such as AMM systems or wrapped tokens. AMM systems essentially allow the trustless exchange of tokens, in some cases including tokens across different blockchains, through linked liquidity pools. This process has potential issues concerning security and attracting and efficiently allocating liquidity. Wrapped tokens are created by locking up any crypto assets on one chain and issuing a new token representative of the collateral on another chain. An example is WBTC, a bitcoin pegged token on the Ethereum blockchain. While in some cases, wrapped tokens are an effective solution, they are seen as a workaround rather than a complete solution [72].

Chainlink Labs recently launched its Cross-Chain Interoperability Protocol (CCIP), a standardized protocol for cross-chain communications. CCIP combines the burning of tokens on one chain and minting them on another for tokens that natively have that function, such as USD; for other tokens, it uses a lock and burn function - essentially creating a wrapped token via an oracle node. Theoretically, oracle nodes can potentially make wrapped tokens more secure and trustless. In addition to tokens, CCIP allows the transfer of arbitrary data between chains. An oracle node receives and forwards the data to the destination chain [75]. While CCIP is still very new, it will be exciting to see whether it finds adoption.

Another missing link that may be solved via oracles is the connection of traditional financial intermediaries to smart contract platforms. In June 2023, Swift, “the most prominent standards body in the global banking community [76]” announced that it was exploring connectivity between permissioned blockchains, as may be used by traditional financial intermediaries and the public Ethereum blockchain via Chainlink oracle nodes [77]. The ability to transfer tokenized assets from a permissioned blockchain to public blockchains would open the door for a significant increase in liquidity on public blockchains.

While tokenization, the process of digitizing real assets, is still in its infancy, it promises to “help create universally accessible, fast, liquid, and transparent investment and financial systems” [78], and potentially enable entirely new types of digital securities. “A Security Token’ is a digital and tokenized version of traditional security, and its value depends on the value of the asset, i.e., the value of the ownership that the token represents [79].” Security tokens are particularly relevant when it comes to ownership rights. The benefits of tokenized assets include the ability to raise capital and liquidity benefits due to fractionalization and theoretical global ease of access [78].

Complementary to digital assets tokenized via collateralization, perpetual futures, often referred to as perpetuals or perps, which follow the price movement of specific assets without being collateralized by that asset, have been gaining popularity. Perpetuals are a derivative providing investors with long or short exposure to an asset without needing to hold a specific asset. Perpetuals use fees to incentivize traders to close the gap between future and spot prices. At the moment, perpetuals are almost exclusively used to represent crypto futures but may well be used to provide exposure to off-chain assets in the future [80]. In order to do this, perpetuals protocols must only be able to access off-chain data pertaining to the spot prices of the assets being traded.

2.4.2. Supply Chain

One specific use case thoroughly discussed in current research is in the supply chain field. It has been hypothesized for years now, that the field of supply chain is ripe for disruption by blockchain-based applications [81]. While there have been some experimental implementations of on-chain supply chain tracking applications, none have had the type of disruptive success that some may have expected. One example is Walmart’s blockchain-tracked supply chains for Mangos and Pork [82]. These were implemented in 2018 and discontinued in late 2022 [83]. One main problem that is present in on-chain supply chain management applications is that while the blockchain is an immutable way to store and make data accessible if the information that is put into the system is incorrect, there is no added value of using such a system. As Caldarelli [84] point out:

As information on the blockchain is immutable but not necessarily true, without a trusted third party to verify the data to be inserted, the details provided should not be considered any more trustworthy than those contained in a legacy database.

Additional barriers to adoption may be found in cost and caused by supply chain fragmentation and outsourcing. Nonetheless, experts agree that adopting blockchain-based oracle-supported supply chain tracking applications can lead to more efficient, sustainable, and transparent supply chains [56].

2.4.3. Other

Additional cases of applications relying on verifiable data inputs to smart contracts can be found across a variety of sectors. In healthcare, for example, there is the potential to share data, such as patient records, between healthcare service providers, leading to efficiency improvements and likely also improved medical outcomes for patients. Additionally, blockchain-based prescriptions may reduce fraud compared to legacy methods [85]. However, health care is rife with sensitive data, and any mistakes may be disastrous. As in the supply chain field, the critical point is inputting reliable, verifiable data into the blockchain-based system while addressing additional privacy concerns. This trend continues when looking into academia, where privacy and reliability are paramount, for example, when storing academic credentials and transcripts on-chain [72]. Beyond this, examples of value-adding applications have been identified in IoT integrations [86], real estate [87], and beyond. The following chapter will take a closer look at some of the functionalities mentioned that are enabled by oracle protocols. Verifiable oracle data feeds, multiparty computation, and zero-knowledge proofs have been identified as crucial elements in hypothetical blockchain-based applications [86].

2.5. Oracle Implementations & Functions

This section focuses on oracle solutions available today. First, a comparison of different oracle protocol implementations is presented. Next, a closer look at data feeds, inputs, and functionalities that allow for the cryptographically guaranteed automation of various services. An overview of a hybrid smart contract developers toolbox, so to speak.

2.5.1. Oracle Risks

This section aims to explain the current industry standards when implementing oracles. While a centralized oracle is easy to establish for each use case, such implementations introduce vulnerabilities. Smart contracts take the data received from oracles as it is presented. Even if the information is clearly false, it is used as instructed. Hence, while hybrid smart contracts themselves will always predictably act as they are programmed to, the contract will not act as it should if the data source used is corrupted or manipulated; the contract will not act as it should. When using a single centralized oracle there is a high risk of this happening [88]. An example can be found when looking at the decentralized lending platform Compound. In 2020, Compound was sourcing data regarding the market value of assets from a centralized oracle run by Coinbase [89]. Compound allows users to borrow on-chain assets so long as they put up other on-chain assets as collateral. If users are unable to maintain a certain minimum percentage of collateralization, their position is liquidated. On November 26th, the oracle reporting the price of DAI, a US Dollar stablecoin, falsely reported the price of DAI as having spiked to $1.30. As a result, some users were now deemed undercollateralized, and over $89 million ended up being erroneously liquidated [90]. Had multiple oracles connected to different exchanges been used to provide the smart contracts with a median price, this situation could have been prevented. Ultimately, this case highlights the need for a degree of decentralization and redundancy with regard to data provision. Decentralized oracle networks are made up of multiple different independent nodes, all independently incentivized to act honestly. Using decentralized oracle networks instead of single centralized oracles has become the state of the art when building decentralized applications.

2.5.2. Oracle Implementations

Many different projects are working on making data accessible to smart contract developers. The following is a summary of some of the most prominent such projects.

Table 1.

Oracle Protocols: Overview.

| Protocol | Architecture | Networks | Token | Launch | Team |

|---|---|---|---|---|---|

| Chainlink | Multiplea | 11 | Yes | May 2019 | 400+ |

| Band | Algorithmic | 18 | Yes | Sept 2021b | 32 |

| API3 | 1st Party | 10 | Yes | July 2021 | 33 |

| Pyth | 1st Party | 20 | Yes | Aug 2021 | 25 |

| RedStone | Algorithmic | 39 | Planned | Jan 2022 | 14 |

| Tellor | Optimistic | 6 | Yes | Aug 2019 | 12 |

| Witnet | Algorithmic | 25 | Yes | Nov 2020 | 10 |

| DIA | Algorithmic | 8 | Yes | 2018c | 25 |

| Supra | Algorithmic | N/ad | Planned | N/ad | 90 |

| UMA | Optimistic | 2 | Yes | May 2021 | 136 |

aAlgorithmic & 1st Party; bLaunch of current version; cUnclear whether this is start of development or mainnet launch; dData Feeds not yet live.

Chainlink

Chainlink is the apparent market leader for oracles by crucial metrics such as the number of integrations, value secured, number of DONs, and several others [25]. Chainlink was the first oracle project launching on the Ethereum main net in May 2019 [91]. Currently, Chainlink DONs are integrated into over 1600 projects, they have delivered over 5.8 billion data points to smart contracts enabling over $6.9 trillion in transactions associated with these smart contracts across 11 different smart contract platforms, including Ethereum, Polygon, Arbitrum, and others [25]. Chainlink DONs are used by many prominent protocols, such as the lending platforms Aave and Compound, the insurance protocols Nexus Mutual and Etherisc, and the Loopring exchange [92]. Chainlink DONs comprise several nodes, each using different data sources. There is a minimum number of nodes that can be set for the data to be used and a maximum deviation from the mean that each node should not surpass. Chainlink employs a combination of a reputation system and staking to ensure nodes act as they should [93]. Chainlink DONs are used to bridge off-chain data and provide off-chain computation.

The team behind Chainlink is the largest in the oracle space, currently consisting of over 400 people [75]. The team is supported by advisors such as Ari Juels (professor at Cornell Tech), Tom Gonser (founder of DocuSign), Eric Schmidt (former CEO of Google), Jeff Weiner ( former CEO of Linkedin), Balaji Srinivasan (former CTO of Coinbase) and Dan Boneh (professor at Stanford University and the head of its Applied Cryptography Group) [55].

Band Protocol

Band Protocol was launched on the Ethereum main net in 2020. However, this first version received little attention from developers, and the team abandoned the initial design to build Band v2. Band v2 relies on its own blockchain, where node operators also act as validators for this chain’s consensus protocol. Nodes combine data retrieved from external APIs to provide data on-chain. However, the types of APIs that can be connected are limited to freely accessible feeds. Password-protected or paid APIs can currently either not be connected or require the cooperation of API providers [94]. Some off-chain computation features are built natively into the protocol. Band protocol currently has limited adoption and is struggling to take advantage of network effects. The team behind Band Protocol consists of roughly 32 people [95].

API3

API3 was launched in July 2021. Included in the founding team are several former Chainlink employees. API3 hopes to disrupt the oracle space by allowing Web2 API providers to make their data available directly to on-chain applications. Rather than using oracle nodes to collect data from various data sources, API3 focuses on first-party oracle nodes. While this design offers some potential advantages, such as transparency of data sources and vastly lower latency [96], it could be argued that this approach brings some of the concerns of centralized oracles. While the need to maintain reputation will likely deter node operators in this system from acting dishonestly, relying on single centralized parties as data sources may introduce certain risks. Currently, API3 is available on ten smart contract networks. Any API can be made available on-chain via the API3-developed middleware Airnode [96]. The team behind API3 currently consists of roughly 33 people [97]. API3DAO, the decentralized autonomous organization used in some governance functions, currently comprises 6538 members [98].

Pyth

Similar to API3, Pyth has taken a first-party oracle approach focusing on low latency, high confidence market data, primarily price data of currencies, crypto assets, and publically traded equities [99]. Currently, Pyth serves over 250 data feeds across over 20 blockchains. Data is served directly by trading firms, cryptocurrency exchanges, and other financial services providers such as Jane Street Capital, Gemini, Cboe Global Markets, and roughly 80 others [100]. Data providers operate a fork of the Solana blockchain named Pythnet. On this chain, data is aggregated and made available to other networks [100]. Having launched in August of 2021, Pyth is on the newer side of oracle platforms. Prominent users of the Pyth network include the synthetic assets platform Synthetix and Tradingview [100]. Pyth currently has around nine employees [101]. Pyth does not currently have an associated token but is planning to launch one for certain governance functions [99].

RedStone

RedStone primarily provides price data regarding cryptocurrencies, stocks, currencies, and commodities, though this platform offers flexibility regarding data types. For example, there is an oracle reporting the number of Refugees leaving Ukraine, the floor price of certain NFTs, and the prices of grains and livestock. Data is primarily sourced from cryptocurrency exchanges and publicly available APIs [102]. RedStone is focusing on both push and pull-based oracles. In push-based oracles, nodes must “push data onto the chain in certain intervals [103]. In pull-based oracles, data is not continuously delivered on-chain but only when requested. Data is stored on the decentralized storage protocol Arweave and is delivered on a specific blockchain by a network of nodes upon request. These oracles are available on over 39 Blockchains [103]. The protocol was launched in January of 2022 [104], currently has around 17 employees [105], and has 1190 different data feeds [102].

Tellor

Tellor is taking an open approach to oracles. A user can request that any data be reported on-chain for a small payment. Data reporters then compete to provide the requested data to claim the tip. Any holder of the token associated with Tellor may lock tokens in order to be able to dispute data reports. When a dispute is opened, the community has two days to vote on the correctness of the report. If the user who opened the dispute correctly flagged the data, the node that supplied the data is penalized. Otherwise, the user who supplied the data receives the locked tokens of the user who opened the dispute. While the dispute is ongoing, a new value is reported to the requester [106]. Tellor is live on the six most prominent EVM main net blockchains, currently has around 12 employees [107], and initially launched in August 2019 [108].

Witnet

The Witnet oracle operates on its own blockchain secured by a decentralized network of nodes that earn WIT from fulfilling requests for data and participating in consensus. Developers may use Witnet for its cryptocurrency price feeds, as a source of randomness, or to connect to external APIs. There are 248 price feeds to 25 smart contract platforms [109]. Witnet originally launched in November 2020 [110] and currently has around 10 team members (Witnet, n.d.-b). Currently, Witnet fulfills around 10,000 to 15,000 data requests per week, according to figures published by the Witnet Foundation. By relying on its own blockchain, Witner Oracles benefits from increased efficiency since the Witnet blockchain is able to communicate data to all other integrated EVM chains without needing a separate decentralized network of node operators for each one [110].

DIA

DIA oracles are focused on providing market data. They currently have around 70 data sources, of which around 45 originate on various blockchains, while 25 are off-chain data sources. Data feeds include prices of various crypto assets, non-fungible tokens (NFTs), and liquid staked derivatives (LSDs). This data is sourced from centralized exchanges, decentralized exchanges, and NFT marketplaces. In addition to price feeds, DIA offers functionality for verifiable randomness on eight smart contract networks, including Polygon, Moonbeam, Fuse, and others [111]. DIA consists of three layers: data collection, data storage and processing, and data publishing. All layers run on a Kubernetes cluster hosted on the IBM cloud [112]. DIA launched in 2018 [113]. The DIA Association currently has around 25 employees [114], and the DIA DAO currently receives between 10 and 30 votes on recent proposals, indicating a rather small community.

Supra

The oracle protocol implementation created by Supra is called Distributed Oracle Agreement (DORA). DORA is made up of a decentralized network of nodes that is itself made up of smaller, periodically randomized networks of nodes [115]. This provides a high level of security in transferring data on-chain. As of July 2023, Supra has not yet launched its oracle protocol on mainnet and is only live as a beta testnet, making it difficult to evaluate further factors. In addition to its oracle protocol, Supra offers randomness services separately from data feeds; this feature is live on several blockchain networks. Supra oracles participated in accelerator programs run by the University of California, Berkeley, and Mastercard [116] (Supra, n.d.-a). Currently, their team consists of roughly 90 people [117].

UMA

UMA employs a so-called optimistic oracle. Anyone can request a specific piece of data such as “What was the mean temperature in July?” or “Who won the World Cup in 2021?”. Users then post a bond and provide an answer to receive a reward. In most cases, the result is assumed to be valid and accepted. In case the information provided is untrue it can be disputed. In this case, the data provider may lose the collateral they deposited. This approach is relatively novel and specializes in delivering a wide variety of data types. It is unsuitable to serve frequently updating data feeds instead posting individual answers to specific questions. UMA is currently primarily used to resolve outcomes in the prediction market “Polymarket” [118]. UMA currently has 136 team members [119]. As of August 2023, UMA has settled 5700 requests since launching on mainnet in May 2021 [120]. An interesting use case of optimistic oracles is using them as triggers in case some external event is observed, e.g., a protocol getting hacked. One downside of this implementation is responsiveness, as oracles must be given a dispute period before being used in a smart contract.

Kleros

Kleros, “The Justice Protocol”, is an oracle focused on determining the truth in subjective cases using crypto-economic incentives and a decentralized network of arbitrators rather than digital data links to objective sources. Kleros focuses on disputes, for example, regarding freelancing, e-commerce, content moderation, etc. [121]. Anyone may become a Juror by staking a certain value. Jurors are presented with cases per their indicated areas of expertise and decide based on voting. Game theoretical models incentivize honest behavior and disincentivize malicious behavior [121]. While this approach differs greatly from the objective raw data-based approach of the oracle platforms mentioned previously, it attempts to fill an important niche in operationally necessary on-chain data. Kleros won the European Commission’s Blockchains for Social Good prize and a grant from the French bank BPI France [122]. Today, Kleros has a team of around 32 people [123].

Augur

Augur takes a completely different approach to oracles than the platforms mentioned previously. It is an oracle and a platform for prediction markets. Users may create prediction markets for future events, such as who will win the upcoming presidential election, users may then bet on the outcome of the event using the US Dollar stablecoin DAI. After a certain deadline, the outcome is determined by allowing users to vote. Correct voters are rewarded, while incorrect voters are penalized [124]. In theory, this method not only provides real-world data on-chain but also provides data on the likelihood of future events. Augur was one of the first dApps to launch on the Ethereum smart contract platform in July 2018 (Blockchains could breathe new life into prediction markets, 2018). In November of 2021, control of Augur was handed over to a newly created Decentralized Autonomous Organization (DAO). The DAO, in theory, is meant to democratize and decentralize ownership and decision-making power over the platform by allowing members to vote on actions and fund allocation of funds. The latest completed prediction market listed on their dApp was completed in July of 2021 with no currently running markets. Recently, a new similar dApp called Polymarket has been gaining attention [125].

The Graph

The Graph indexes and serves data from various smart contract platforms via APIs. Rather than bringing off-chain data on-chain, they are focused on doing the opposite in a way that is easy to integrate for Web2 developers [126]. The Graph offers a lot of flexibility regarding data types going far beyond price feeds.

While Chainlink is currently the industry leader and, in many cases, considered the industry standard, there are many relevant approaches to solving the oracle problem. Some specialize in only one function, while others focus on offering a wide toolbox. In this paper, Chainlink’s terminology and examples of their implementation will, at times, be used; however, the scope of this paper remains project-agnostic.

2.5.3. Inputs and Functions

The inputs made available to smart contract developers by oracles can be split into two main categories: data and off-chain computation. Data may refer to making off-chain data or data from other smart contract platforms that are not natively interoperable available on a specific platform. Computation refers to secure data generation or processing outside of a blockchain or smart contract network to fulfill needs for functions that are not possible or prohibitively expensive when done natively within a smart contract network.

2Data

With regard to the former category, data, there is a wide variety of feeds and categories of data that are made available to smart contract developers. In practice, market data is currently by far the most in-demand data category, as this is necessary for many DeFi applications such as exchanges, lending, and derivatives platforms to operate [127]. The market data category can range from simple spot prices of various on-chain crypto assets to liquidity and volume data of commodities and foreign exchange markets. Various oracle projects support different types of this data. While Chainlink provides great flexibility and supports almost all kinds of such data, other, newer oracle platforms have seen the already maturing market for price feeds and focus exclusively on them, Pyth being an example. Market data availability is a key driver of the decentralized finance (DeFi) ecosystem [127]. DeFi is an umbrella term for decentralized applications offering financial services without relying on intermediaries, such as decentralized exchanges, lending platforms, stablecoin protocols, derivatives, and more [128]. MakerDAO, for example, is a protocol allowing users to lock up various crypto assets to mint the US Dollar stablecoin DAI. The locked value must be higher than the amount of DAI minted and if the value of locked assets drops beneath a set liquidation threshold relative to the outstanding DAI, locked assets may be liquidated. All of this is executed by smart contracts (MakerDAO, 2020). Since smart contracts do not natively know the current value of the US Dollar and relevant crypto assets oracles are needed to provide this information. DeFi has multiplied from roughly 720M USD TVL (Total Value Locked - the value of assets deposited in DeFi protocols) at the beginning of 2019 to a peak of roughly 178B USD at the end of 2021. Currently, TVL hovers between 40B and 45B USD [129]. As mentioned earlier, the rapid growth of this sector has led to many oracle protocols building products targeted specifically to serve DeFi applications.

Another related type of data presently in frequent use is “proof of reserves” data. Stablecoins pegged to currencies, commodities, assets, and their derivatives, are commonly collateralized by assets held off-chain or on another blockchain. In this subcategory, oracles query data sources such as an API made available by a regulated custodian holding funds or assets off-chain or the API of blockchain explorers to verify the amount of funds held by a wallet on another chain [130]. The GBPT stablecoin, for example, is backed by British Pounds (GBP) held in an account at Bank Frick, which provides an API to the nodes of a Chainlink DON. The oracle network pushes new data on-chain every 24 hours or when a deviation of over 2% is reported by the nodes. The oracle network for this PoR (Proof of Reserves) feed currently consists of 16 nodes operated by independent organizations such as Blocksize Capital, Deutsche Telekom MMS, NorthWest Nodes, among others [131].

Aside from finance, there are many custom types of data being made available through oracles. This subcategory is largely made up of less mature data types that rely on rather primitive oracle implementations. The functionality of many oracle protocols to source data from traditional APIs allows developers to easily source many types of data they may need. Chainlink, for example, calls this functionality “External Adapters” [132], while API3 calls it “Airnode” [96]. While often not optimized for decentralization and trust minimization due to the use of a single data source, it offers accessibility and easy implementation. This category of oracle feed enables some of the most innovative use cases by allowing the integration of sensor and satellite data, among other direct data sources. The example of parametric insurance mentioned previously relies on satellite and weather data to determine whether a claim will be paid out [133]. Another example showing an innovative use case of a direct data feed is the Chainlink hackathon project “Link My Ride” which built an external adapter allowing a smart contract to interface with a Tesla vehicle. This interface was used to offer automated rental functionality, including payment and unlocking the car doors for the renter [134]. While this example was highly experimental, it demonstrates the potential of hybrid smart contracts.

The final subcategory of data feeds is cross-chain interfacing. Here oracles are used to read data on one blockchain and provide that data to a smart contract on another blockchain. Beyond crypto stablecoins, in theory, this allows for blockchain interoperability, such as transferring a token from one chain to another, as discussed in Chapter IV a.

Computation & Functions

The second main category of smart contract inputs provided via oracles is computation and functions. In this category, oracles are used to perform functions that are not natively possible or efficient to do on-chain and provide the output for on-chain use without necessarily using data from any external source [130]. The following is a brief summary of various functions currently in use. While many of these functions have different names depending on the oracle platform being used, we will use the terminology used by Chainlink for simplicity.

Automation

In order for a smart contract to execute a certain function, that function needs to be called. In most user-facing smart contracts, this is of no issue as the smart contract only needs to perform an action when interacted with by a user [130]. This is the case with most DeFi apps, for example, exchanges, which execute a function when a user initiates a transaction. Not all smart contracts, however, function in this way. An example includes a smart contract that is supposed to check a condition every 24 hours [130]. Doing this manually or incentivizing users to do this is not usually efficient or reliable. Oracle networks can be used to trustlessly interact with a smart contract in a specified way. Chainlink’s automation, formerly Chainlink Keepers, uses a DON to send a predefined transaction based on a trigger condition. By using a decentralized oracle network, this method offers high reliability and redundancy and incentivizes honest behavior. One example use case for automation mentioned in Chainlink’s documentation is a defi yield harvester that withdraws and reallocates capital, generating yield in a defi protocol, allowing for compounding and the employment of advanced strategies [130].

Randomness

Verifiable randomness is currently one of the most prominent use cases for oracles. Computers have two methods to generate randomness: (1) true random number generators (TRNGs) and (2) pseudo-random number generators (PRNGs). PRNGs use a pre-defined algorithm to emulate randomness, whereas TRNGs employ a software-external phenomenon as a source of entropy for randomness generation. Since this external phenomenon cannot be predicted, it may be used to generate a truly random and unpredictable output. In traditional computers, common things used to generate entropy are, for example, the RPM a certain fan in the computer is spinning, current CPU temperature, mouse movements, etc. [135]. Since Blockchains are composed of thousands of computers contributing to an isolated system, this is not natively possible on most contemporary smart contract platforms. Instead, Verified Randomness Functions (VRF) employ oracle nodes to fill this gap. Chainlink’s VRF, for example, works by “combining block data that is still unknown when the request is made with the oracle node’s pre-committed private key to generate both a random number and a cryptographic proof” [75]. Since both the randomness and the cryptographic proof are generated together, the output provided on-chain can be checked before making it available for use by a smart contract. Due to this verification step, nodes are unable to provide biased or manipulated outputs, as the cryptographic check would fail. This function is currently primarily used in the generation of NFT attributes, gambling, and blockchain-enabled games [136].

Scalability & Off-Chain Computations

While smart contract platforms are essentially distributed computers, they trade computational performance for decentralization. The trade-off between scalability, decentralization, and security in the context of blockchain networks is known as the scalability trilemma [137]. Certain blockchain platforms maintain a high level of decentralization but are limited in computational ability, while others focus on scalability over security. For computationally intensive operations, it makes sense to move execution to smart contract platforms optimized for scalability or to a secure off-chain environment. Using oracles and cryptographic guarantees, the computation can trustlessly be outsourced from blockchain networks with low scalability and high security to those with high scalability, returning only the result of the computation [138].

Privacy & Security

One common criticism of smart contract platforms is radical transparency, to the point of potential privacy issues [139]. Blockchains are pseudonymous, not anonymous - while it is possible to remain anonymous, patterns and behaviors may be used to identify users, their behaviors, and holdings. This presents a significant issue for institutional users who may need to protect trade secrets, such as the identities of stakeholders in their supply chain [140]. Oracles can be used to deploy privacy-enabling add-ons to smart contracts. While these add-ons are both plentiful and modular, with new ones continuously being built, there are currently three primary applications: zero-knowledge proofs used to confidentially yet verifiably share the outputs of computations (DECO), trusted hardware connections (Town Crier) [141], and the decorrelation of smart contract execution and settlement (e.g. Mixicles) [142].

Zero-knowledge proof integrations via oracles, such as DECO, allow users to verifiably share a piece of data without revealing its full context [132]. For example, a user may prove that their credit score is above a certain number via a direct connection from an oracle node to the credit score provider. The oracle node obtains the relevant number and transmits only it, no other details, in a cryptographically reliable way. This simple mechanic has a wide variety of applicable use cases and could become an integral part of next-generation smart contracts. Examples include age verification, creditworthiness, insurance premium calculations, Sybil resistance, fraud prevention, and more. DECO was purchased by Chainlink from Cornell University in 2020 [143].

Trusted hardware connections allow smart contracts to access temperproof and confidential oracle inputs via just a single node. This means sensitive information, such as passwords, and personal data may be securely stored and made accessible when needed [142]. An example mentioned in “Town Crier: An Authenticated Data Feed for Smart Contracts” by Zhang et al. [141] is parametric on-chain flight insurance. In order to verify and pay out a claim, the smart contract must be able to access the claimant’s travel details. If the claimant were to submit his travel details directly to the smart contract, this information would be publicly accessible, infringing on their privacy. Instead, the data could be stored on-chain in an encrypted format. In this case, oracle nodes would be needed to decrypt and verify the information, potentially allowing the node operators to access the information. Using a trusted execution environment (TEE) solves this. The TEE acts as a black box decrypting and verifying the information and transmitting the result, was the flight delayed or not, to the smart contract [141]. Use cases for this technology may be found in health care, cyber security, and beyond.

Mixicles allow users to detach the outcome of a smart contract from a payment output. Consider a smart contract based on a binary query, e.g., “Was flight X on time?”, “Was the price of Apple shares above X at time Y?”, “Did Candidate X win the election?”. Based on these inputs, an oracle network can tell a smart contract to transfer funds held in a smart contract to any predefined address [55]. By using newly generated addresses, users may conceal the financial outcome of that smart contract, creating a disconnect between the smart contract and their associated transactions [142].

Beyond these functions, there are those built to remedy specific problems appearing across smart contract platforms, such as Fair Sequencing Services (FSS), which protect from front-running exploits in DeFI [144], Off-Chain Reporting (OCF) which enable batching of oracle network responses to save gas costs [130], and many other, at times custom-built, functions. All in all, oracles act not only as secure data adapters but also as a toolbox, adding functionalities to blockchain networks that are not natively possible. Not all oracle implementations support all functions at once. Some may specialize in a single function.

2.6. Stakeholders & Economics

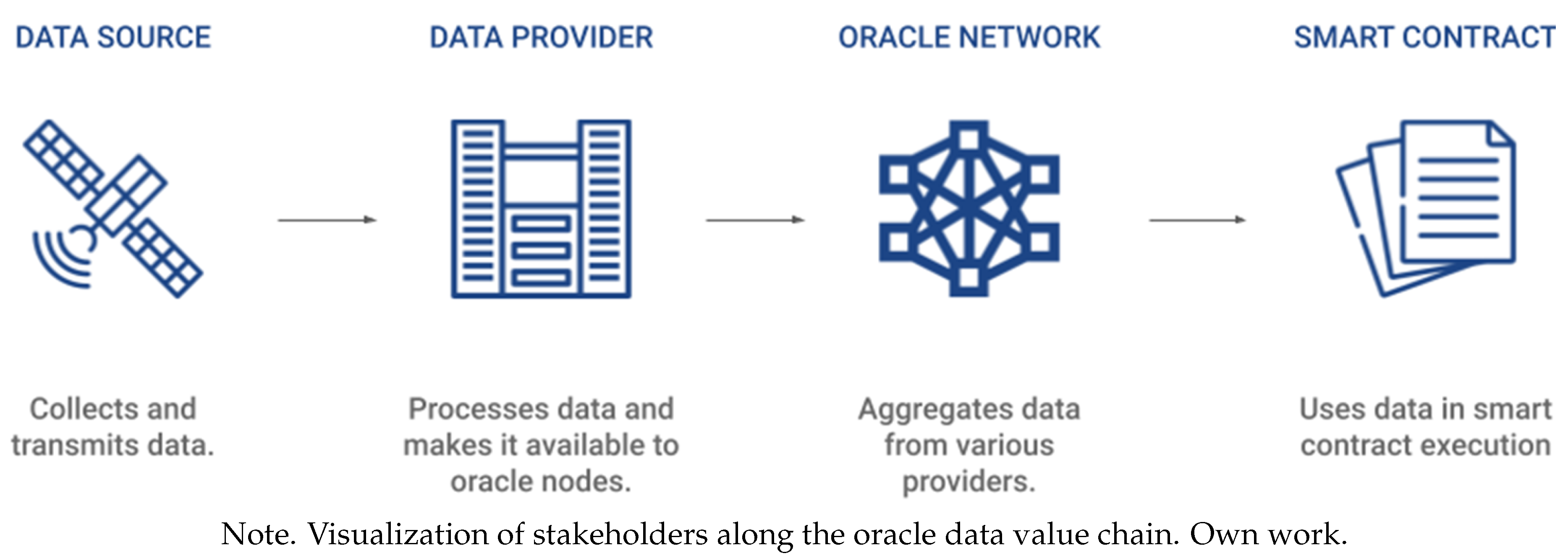

This section explains the stakeholders typically involved, from data sourcing to data delivery across various use cases mentioned in the previous chapter using Chainlink’s implementation. The optimal fundamental constellation of stakeholders is a variety of node operators, typically 10-30, sourcing relevant data from a selection of publicly available data feeds [26]. In the case of market data, e.g., cryptocurrency spot trading data, data sources include price aggregators such as coinmarketcap and coingecko, and exchanges such as Binance and Kraken [92]. Data providers for a specific feed are currently curated and allowlisted by Chainlink Labs [93]. Node operators can then choose a data provider to connect to [130]. The network of nodes aggregates this data, and when a trigger condition is met, one node is selected to transmit the data on-chain [26].

Figure 5.

Oracle Data Value Chain.

The above structure pertains primarily to data feeds with sufficient reputable data sources. Newer and more niche data feeds may need to rely on a single data source either due to uncertain demand, e.g., in the case of highly specific satellite imagery, or there simply not being multiple parties who can access and provide specific data, e.g. in the case of bank account balances. Other functions, such as computation, do not require an off-chain data provider, while others, such as Town crier, do not require a network of nodes. In the following, we will go over the major stakeholders in the sourcing and delivery of data on the chain.

2.6.1. Data Providers