Submitted:

04 May 2024

Posted:

07 May 2024

You are already at the latest version

Abstract

The integration of commodities into stock exchanges marked a pivotal moment in the analysis of price dynamics. Commodities, essential for both daily sustenance and industrial processes, encompass hard commodities like metals and energy, alongside soft commodities such as agricultural produce. This paper investigates the implications of commodity price volatility on commercial and financial landscapes, recognizing its profound impact on global economies. This study employs a meticulous methodology, delineated into four stages: identification, control, and final selection of academic articles, culminating in their tabulation. Methodologically, a literature review serves as the primary tool for data acquisition, with a focus on existing scientific knowledge to bridge gaps and propose avenues for further inquiry. Drawing from reliable sources, including Google Scholar and Science Direct, the research navigates through a wealth of scholarly discourse on commodity market dynamics. By analyzing trends in academic publications, particularly focusing on the interplay between volatility spillover and gold, this paper provides insights into the evolution of research paradigms over time. Ultimately, this paper not only synthesizes existing knowledge but also identifies lacunae for future investigation, thereby contributing to a deeper understanding of the complexities surrounding commodity markets and their ramifications on global economies.

Keywords:

Volatility Spillover

; Gold

; Aluminum

; Silver

; Copper

; Platinum

; Oil

; Gas

; Soybeans

; Corn

; Wheat

1. Introduction

Humanity uses commodities in a variety of processes, either as raw materials for manufacturing, food, and survival or as parts of a product. At the same time, goods are divided into two basic categories: hard and soft. Specifically, hard commodities include metals and energy, such as gold and natural gas. Additionally, soft goods are agricultural and livestock products such as corn and wheat (United Nations Conference on Trade and Development 2021).

The introduction of commodities to stock exchanges and their characterization as stock market products in 2000 is a milestone in the examination of their price behavior. Considering that these goods exist in the daily life of the population, it is understandable that the volatility of their price affects both commercial and financial levels. For this reason, there has been a strong investor interest in commodities and their investment potential (Basak and Pavlova 2016). However, the percentage of each country's dependence and independence from goods, given its wealth-producing sources, characterizes it in terms of its commercial power. In particular, it is a fact that phenomena such as unemployment and low rates of production processes are directly linked to dependence on goods (United Nations Conference on Trade and Development 2021). Therefore, through the import and export activities of a country, its degree of dependence is understood.

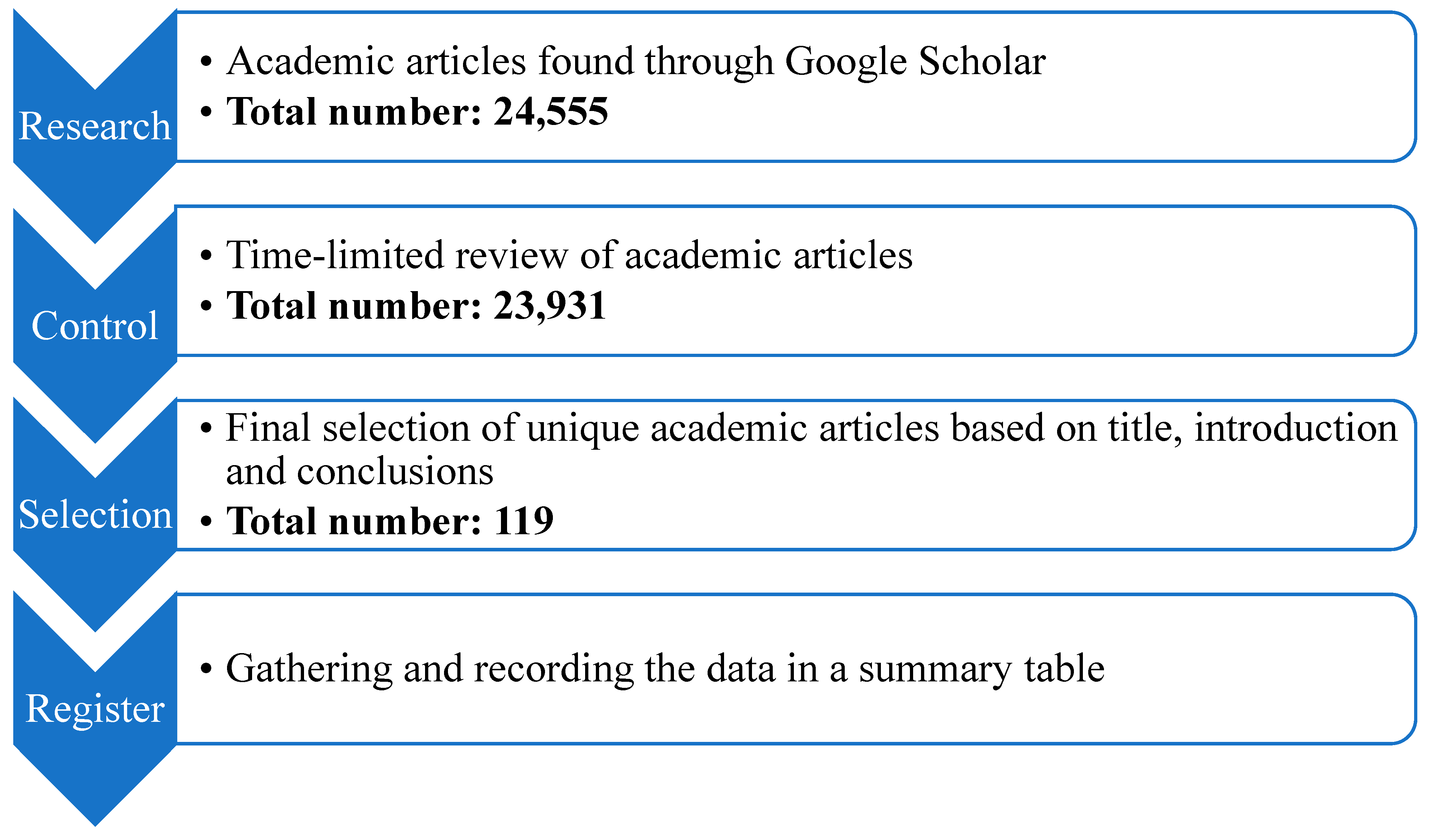

The present study presents the causes as well as the consequences of the above instability following a specific methodology. The steps, which were followed during the research, are four and include the identification, control and final selection of the academic articles as well as their gathering in a table.

2. Methodology

The research was carried out using a specific methodological tool. In particular, methodical research was conducted with the aim of selecting data from reliable sources. This tactic presupposes the definition of specific keywords that are relevant to the subject of the research. In addition, it requires the search and selection of the literature through which the necessary data are retrieved (Saunders et al. 2009). The bibliographic review has as its main axis the critical utilization of the already existing scientific knowledge, aiming to cover the bibliographic gaps (Tranfield et al. 2003). At the same time, the methodological tool in question has the possibility of determining cognitive limitations but also of submitting proposals for further study (Schindler 2021). The choice of the specific method for the present research was made as the contemporary literature uses different tactics. This results in existing data coming from primary research. Thus, this particular study fills the gap by investigating the already existing data.

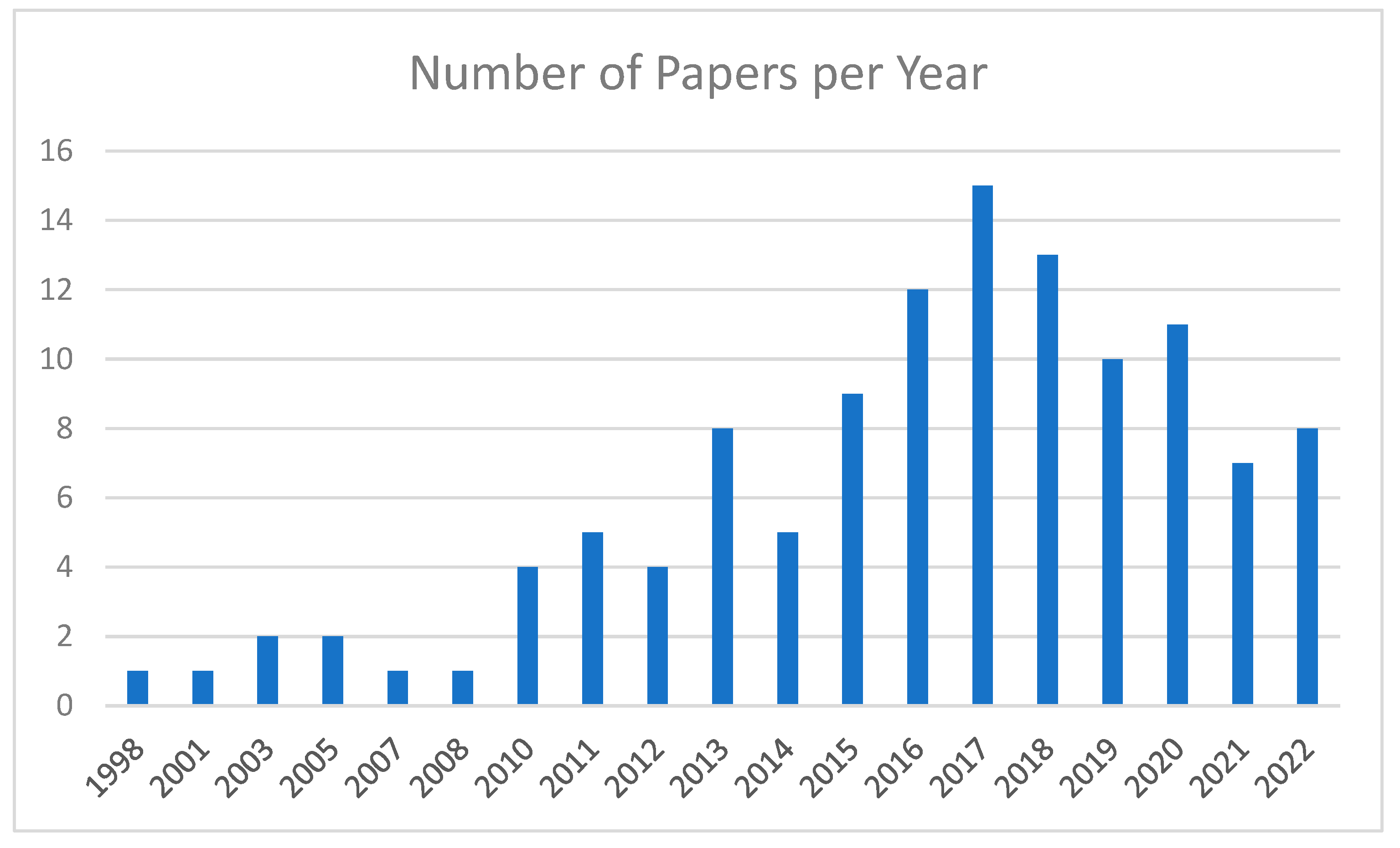

Therefore, the present research uses the literature review as a methodological technique, with the aim of selecting existing data and classifying them according to the content as well as the perspectives for future study. In detail, Figure 1 shows the steps of the method, which include searching the data, checking the relevant publications, selecting the scientific articles and recording them in summary tables. Additionally, Figure 1 graphically displays the number of academic publications per year for the "volatility spillover" and "gold" combination. It is important to note that the main purpose of gathering the data is to record research knowledge on the topic in question clearly and to identify directions for further research.

The data collection for the present study was carried out using two electronic tools, Google Scholar. In particular, Google Scholar is one of the most popular search engines for academic publications, which covers findings of a global scope. In addition, it offers numerous research publications regarding management and finance issues (Amara and Landry 2012). In addition, a variety of academic articles is sourced from Science Direct. In particular, it is considered an online site, which provides academic findings, which are published by the publishing house Elsevier. For this reason, it is a reliable source of data for the business and finance industry (Charoenthammachoke et al., 2020).

2.1. Search of academic articles

The search for the data was carried out using the online tools Google Scholar, while various findings come from publishing houses such as Springer, Elsevier, and Emerald. The search used only published academic articles on the subject. The keywords that were used to search the data are descriptive of the topic and the loads selected to be studied. In particular, these words were "volatility spillover," "gold," "silver," "aluminum," "copper," "platinum," "oil," "natural gas," "soybeans," "corn," and "wheat”. At this point, it is necessary to note that, during the research, combinations of the keyword "volatility spillover" were used with each of the above commodities. Therefore, the total combinations are ten and indicatively have the following form: "volatility spillover" and "gold." In particular, the total number of results when searching for the above combinations in Google Scholar is 24,555. Table 1 presents the search results in detail.

2.2. Review of peer reviewed articles

The results of the initial search include published academic works of various years. Therefore, a selection of articles was then carried out, which were published in the last twenty-five years or so, namely from 1998 to 2022. The number of results is smaller compared to the initial search, as 23,951 appear in Google Scholar. Table 2 shows the results of the relevant publications in detail.

2.3. Selection of academic articles

The initial search based on the general keywords indicated a large number of published articles having “volatility” or “spillover” in their topic. To ensure that each article in this study was relevant to the researched domain, the abstract, key words, and introductory section were manually evaluated by the authors. This allowed us to exclude false positives, i.e. articles that include the terms “volatility” and “spillover” in the title, abstract, or keywords but are unrelated to the domain under study.

In this way, the data of each project was checked thoroughly. Then, the final selection was based on the presence or absence of the keywords in two main parts of the academic works. Thus, it was deemed necessary to have these words in the title and summary of the publications. This resulted in 119 unique articles being isolated from the Google Scholar search. This resulted in the following number of articles as they can be observed in Table 3.

2.4. Data Records

The gathering and recording of them was carried out using Excel, where summary tables were created according to the goods. Specifically, the tables in question contain information related to the selected scientific articles. The author, the year of publication, the title of the article, the name of the scientific journal, the econometric method, the frequency of data collection, the period, the place of interest, and the results of each research are recorded in detail. It is important to note that the data in the scientific articles comes from 1980 to 2022.

As, we can observe from Table 4, the majority of the papers have been published I journals to energy and resources, however due to the econometric approaches that volatility spillover is using researches have also appeared in econometric or financial journals.

Also, as our research has revealed, the matter of volatility spillover has been highly researched over the years as we see a clear increase of publications between 1998 and 2002 in Figure 2.

3. Results

The modern era is characterized by high levels of economic volatility, which is becoming evident both in stock exchanges and in the global economy. The constant change in commodity prices has a direct impact on this volatility. The effects of the volatility of the price of a commodity become evident in the prices of various goods, stock markets, certain indices, stock markets, exchange rates, and a variety of different variables (Chevallier & Ielpo 2013; Gao et al. 2021; Hegerty 2016; Malik & Hammoudeh 2007; Mensi et al. 2017; Sumner et al. 2010). For this reason, there is a frequent preoccupation of researchers with the behavior of prices, the causes of volatility and the factors that are affected.

3.1. Gold

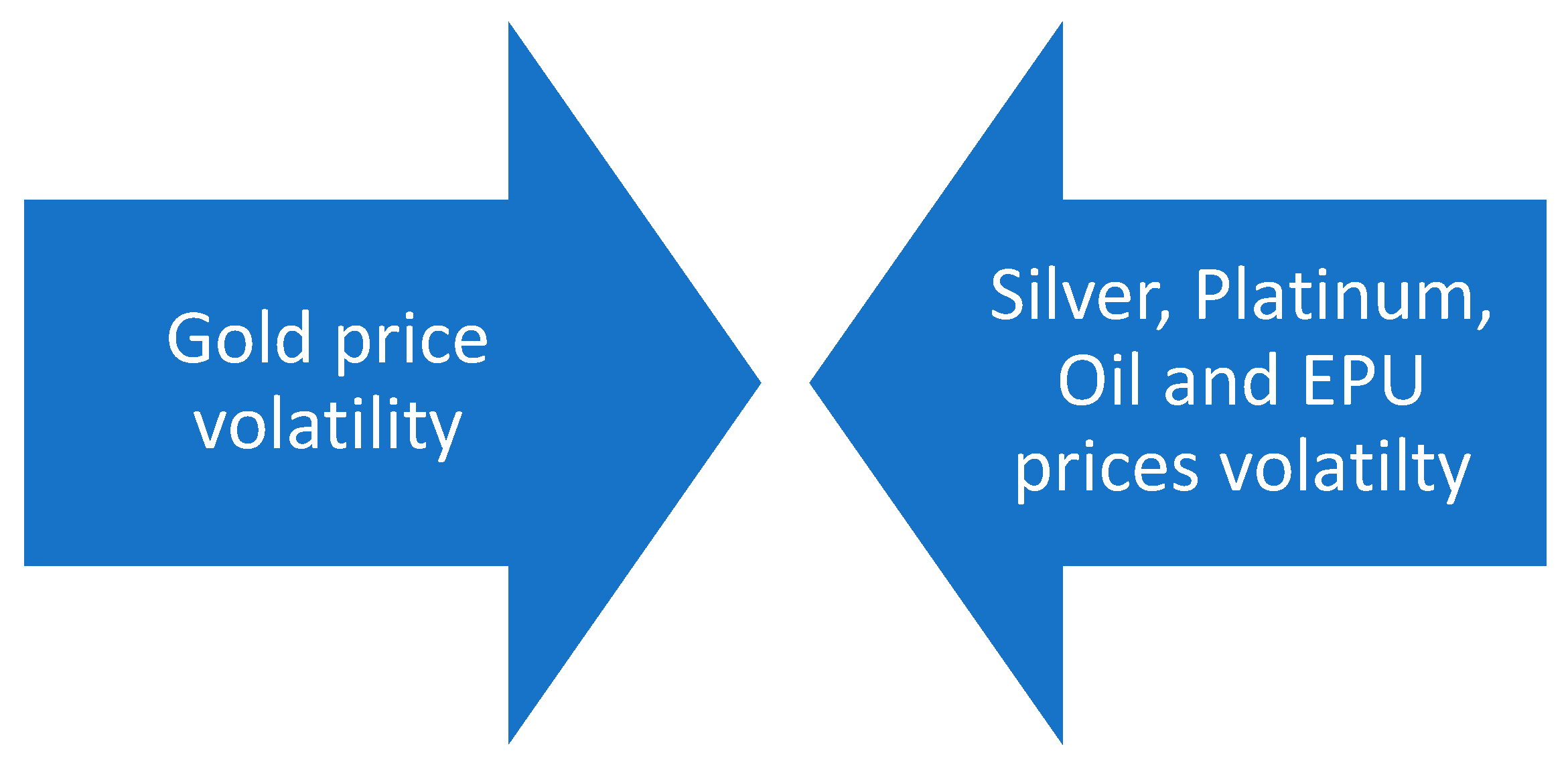

Its market is affected by a variety of factors. In particular, according to Figure 3, precious metals such as silver and platinum have an obvious two-way effect on their price during the period 1999-2016 in global markets (Reboredo and Ugolini 2015; Mensi, Al-Yahyaee et al. 2017; Uddin et al. 2019). At the same time, energy commodities such as oil and natural gas play an important role in their price change at the international level and in a period of 29 years from 1993 to 2022 (Behmiri and Manera 2015; Reboredo and Ugolini 2016; Guhathakurta et al. 2020; Jiang et al. 2022; Arfaoui et al. 2023). Additionally, there is a strong influence of various commodity prices on the volatility of the precious metal in India (Roy and Sinha Roy 2017). At this point, it is necessary to point out that gold prices interact with each other. According to the literature, the New York market exerts a significant influence on gold prices in Asia and, in particular, in Tokyo and Shanghai (Wang et al. 2016).

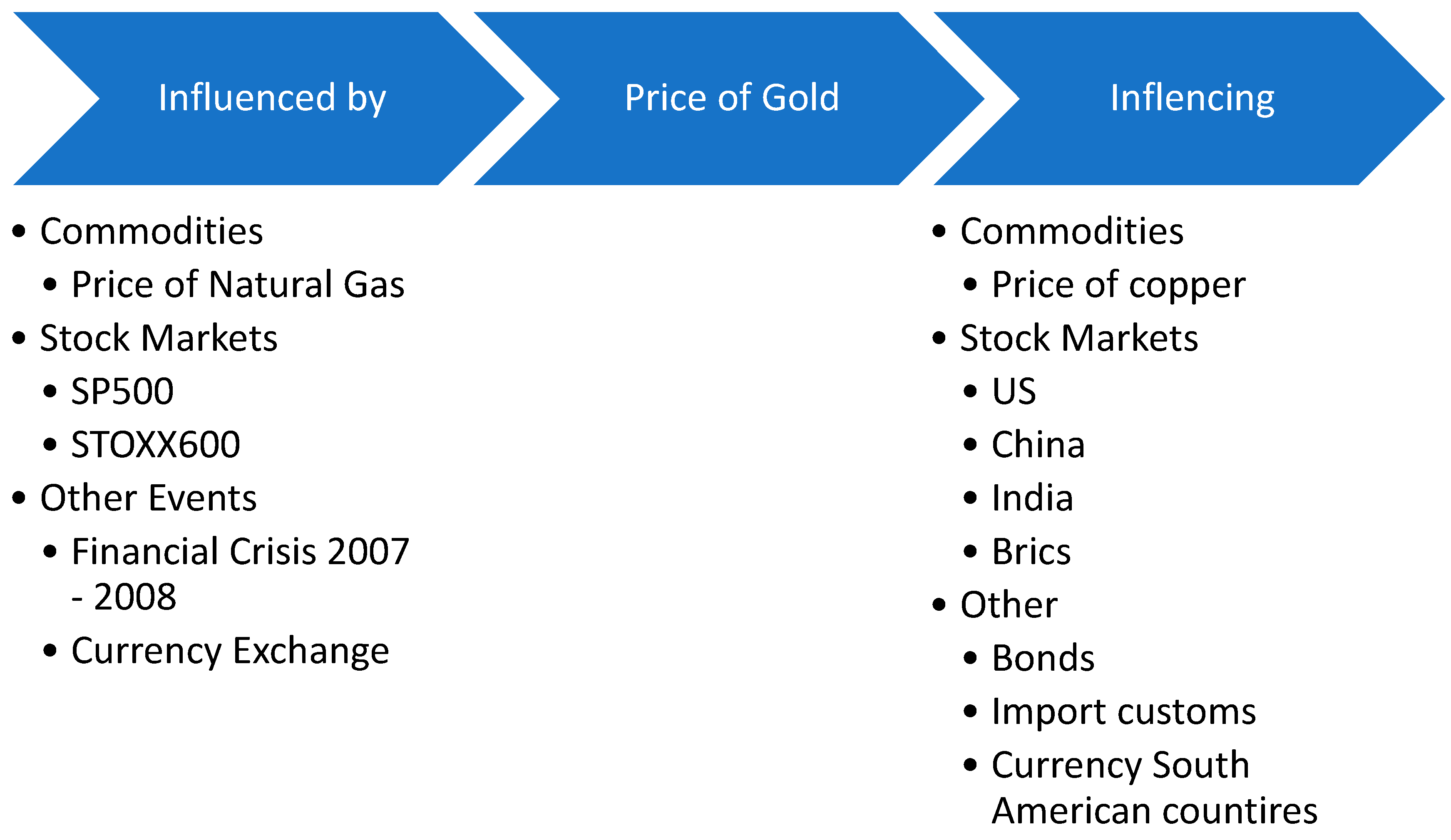

Then, the stock market exerts a significant influence on the volatility of the price of the metal in question, as shown in Figure 4. In particular, during the period 2009-2014, the spot and forward price of gold on the Indian Multi Commodity Exchange showed a significant impact on the market for the precious metal, which in turn increased import duties but also the accuracy of domestic available reserves (Pandey 2014). It is crucial to add that the mobility of the stock market indices shows a significant impact on its price. In particular, the literature with data from 1986 to 2018 reports that volatility is observed in the precious metal market when the S&P 500, STOXX 600, and EPU indices show movements in their prices (Mensi et al. 2013; Mensi, Al-Yahyaee, et al. 2017; Balcilar et al. 2021; Gao et al. 2021).

Modern researchers, when examining the period 1992-2015, observed a strong influence of the international financial crisis of 2007 on various commodities, which resulted in the appearance of a changing price for gold (Chevallier and Ielpo 2013). In addition, another major factor in gold price volatility is exchange rates. It is necessary to note that exchange rate markets interact with each other as well as with the markets of various goods (Hammoudeh et al. 2010; Kumar et al. 2022). Finally, the interest of various scholars has been attracted to the monetary variables and the existence of correlation with the gold market. Thus, the literature shows that there is an effect of monetary variables on the price of the precious metal during the period 1986-2006 (Batten et al. 2010). However, the influence that the volatile price of gold has on different variables is remarkable.

The mobility in the gold market is of particular interest as it affects the economy in various ways, according to Figure 4. For about 50 years, specifically from 1970 to 2018, the researchers reported that the volatility of the price of a specific metal exerts a significant effect on the stock markets internationally (Sumner et al. 2010; Vardar et al. 2018). In particular, gold appears to exert pressure on Chinese stock markets, culminating in the global financial crisis in 2007, whenever the most intense pressure from the international gold market occurs (el Hedi Arouri et al. 2015; He et al. 2020). At the same time, the literature notes that the Indian stock market is particularly affected by the volatility of the gold price from 2009 to 2016 (Bouri et al. 2017). Additionally, the gold market's relationship with the BRICS and US stock exchanges is worth discussing. In particular, the researchers note the existence of the influence of gold on the said markets during the fifteen years 2000-2015 (Raza et al. 2016; Pandey and Vipul 2018), while regarding the United States of America, the pressure appears over time from 2000-2018 (He et al. 2020). In addition, major stock indices such as the EPU and S&P 500 show a close connection with the volatility of the metal price (Gao et al. 2021; Mensi et al. 2022).

It is necessary to present the results regarding the remaining commodities. The literature time limits the effect of gold on other commodities from 1985 to 2022. In particular, the researchers observe a special correlation between the gold market with other precious metals such as silver, platinum, and copper while at the same time, it seems to affect future prices (Antonakakis and Kizys 2015; Kang et al. 2017; Dutta 2018; Oliyide et al. 2021; Umar et al. 2021). At this point, it is necessary to point out that precious metal markets show significant interactions regarding their prices (Batten et al. 2015). Additionally, oil prices are greatly affected whenever gold markets are volatile on the above timeframes (Ewing and Malik 2013; Maghyereh et al. 2017; Tiwari et al. 2021).

More recently, the war between Ukraine and Russia has pushed gold pressure on other commodities, and a separate example of this pressure is wheat price volatility (Wang et al. 2022). During the research of the BRICS markets, the volatility of the gold price affects the South African exchange rate and inflation (Hegerty 2016). In conclusion, the volatility of gold in the US and Japanese markets appears to interact with each other, with the former market appearing to exert a stronger influence (Xu and Fung 2005).

At this point, it is necessary to point out that the research on the behavior of gold was carried out thoroughly and in both directions. Nevertheless, the main proposal of the present study is the future investigation of the gold market in relation to the activity of interested companies that use it as a raw material. Thus, the importance of the effect of the price of the precious metal on the actual operation of an economic unit becomes understandable.

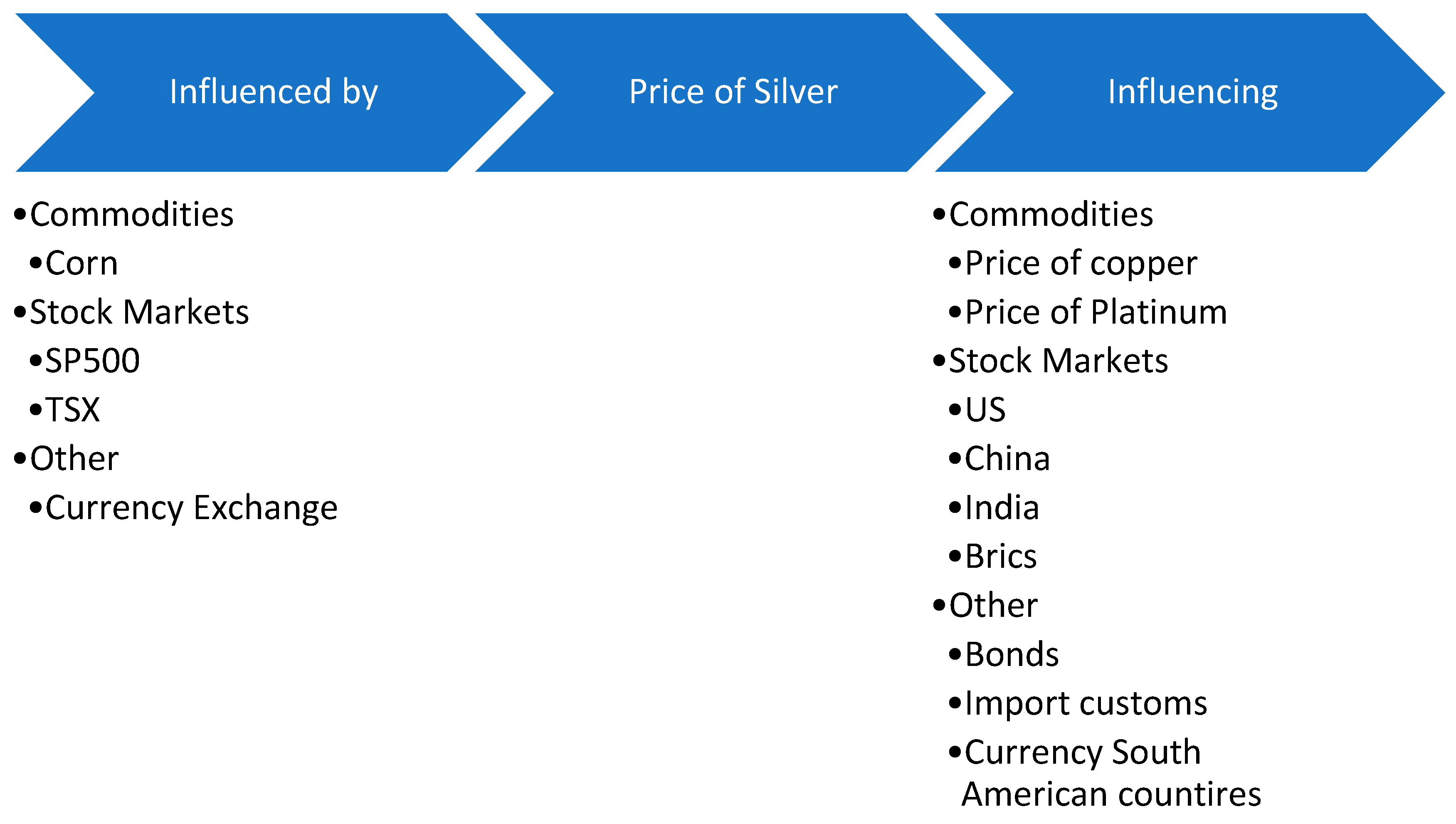

3.2. Silver

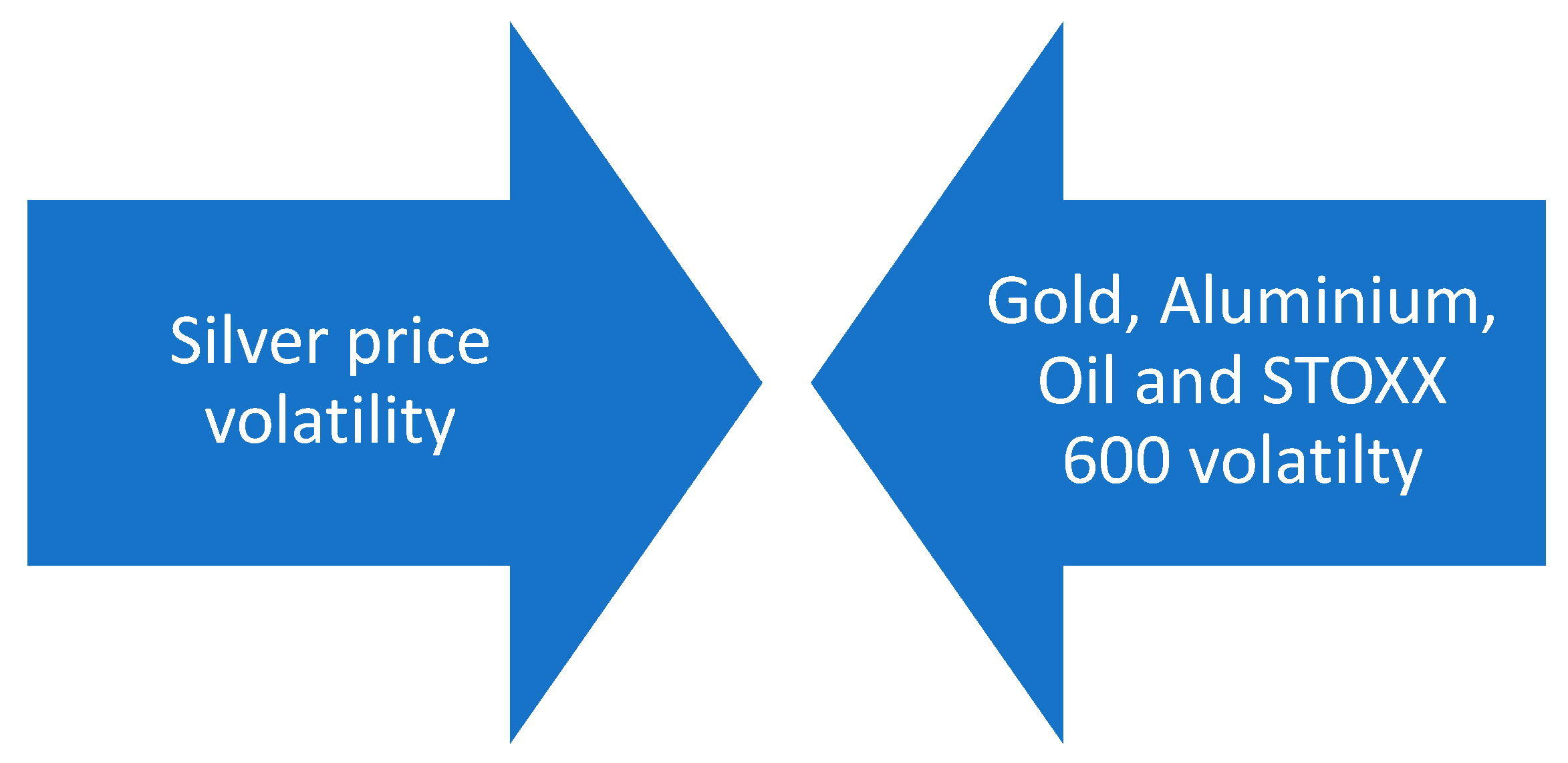

Silver, like any precious metal, exhibits a strong correlation with a variety of commodities, as shown in Figure 5. Of particular importance is the effect of oil on the price of the specific metal. The literature reports that sudden changes in the price of oil have a direct effect on the volatility of the price of silver during the period 1993-2015 in international markets (Behmiri and Manera 2015; Reboredo and Ugolini 2016). Additionally, the relationship of all precious metals to silver is important. In particular, the researchers, when examining the period 1986-2015, noted that almost all metals (Batten et al. 2010; Reboredo and Ugolini 2015) influence silver. However, the strongest interaction appears to exist between gold, aluminum, and silver over the last 30 years or so, as shown in Figure 5 (Chevallier and Ielpo 2013; Antonakakis and Kizys 2015; Dutta 2018; Uddin et al. 2019; Umar et al. et al. 2021). In addition, this precious metal is correlated with the price of an agricultural product, corn. It is reported in the literature that, in the years 1992 to 2015, the volatility of the price of this agricultural product had significant effects on the silver market (Chevallier and Ielpo 2013).

It is necessary to note that various financial indicators heavily influence its market. In particular, the movement of the S&P 500, STOXX 600 and TSX indices approached the interest of the researchers during the period under review from 2000 to 2016. The results of the research show a strong pressure of these indices on the price of silver (Mensi, Al-Yahyaee, et al. 2017). To sum up, the market of precious metals shows a strong connection with the exchange rate. The researchers, examining daily data, concluded that during the decade 1997-2007, the foreign exchange market affected the change in the price of silver (Hammoudeh et al. 2010).

However, it is equally important to analyze the variables, which affect the volatility of silver price. Like any precious metal, silver has a significant impact on hard commodities. In particular, the literature reports that silver affects the price of gold, aluminum, copper, and platinum when examining the period 1982-2019, while this relationship is strongly displayed in the markets of China, Japan, and the USA (Xu and Fung 2005; Chevallier and Ielpo 2013; Batten et al. 2015; Reboredo and Ugolini 2015; Hu et al. 2020; Oliyide et al. 2021). In particular, the researchers point out that there is a relationship between the price volatility of the precious metal and the said energy commodity in the years 1990 to 2017 in the American market (Kang et al. 2017; Tiwari et al. 2021). In addition, the mention of its effect during the war in Ukraine is noteworthy. Contemporary research notes that silver, along with gold, copper, and platinum, are the transmitters of volatility in commodities such as wheat (Wang et al., 2022).

A variety of studies then presents the connectivity of silver market volatility with stock markets and financial indices. The effect of silver is felt in various financial institutions inside and outside Europe, such as in Germany, France, South Korea, India, and the USA. Researchers report that during and after the global crisis, precious metal price volatility pressured financial markets (Vardar et al. 2018; Tiwari et al. 2021). Additionally, the STOXX 600 index is a shining example of the effect of silver on financial variables, especially during the period 2000-2016 (Mensi, Al-Yahyaee, et al. 2017). Research reports that this precious metal has a significant impact on solar energy businesses, specifically in the period 2011-2017 (Dutta 2019).

However, scholarly research on silver market activity is relatively limited compared to that of gold. The basic proposition of this bibliographic study is the future engagement of researchers with the behavior of the price of silver in specific financial institutions around the world. In this way, the gap in the literature regarding the silver market and its correlation with the stock markets is immediately covered.

3.3. Aluminium

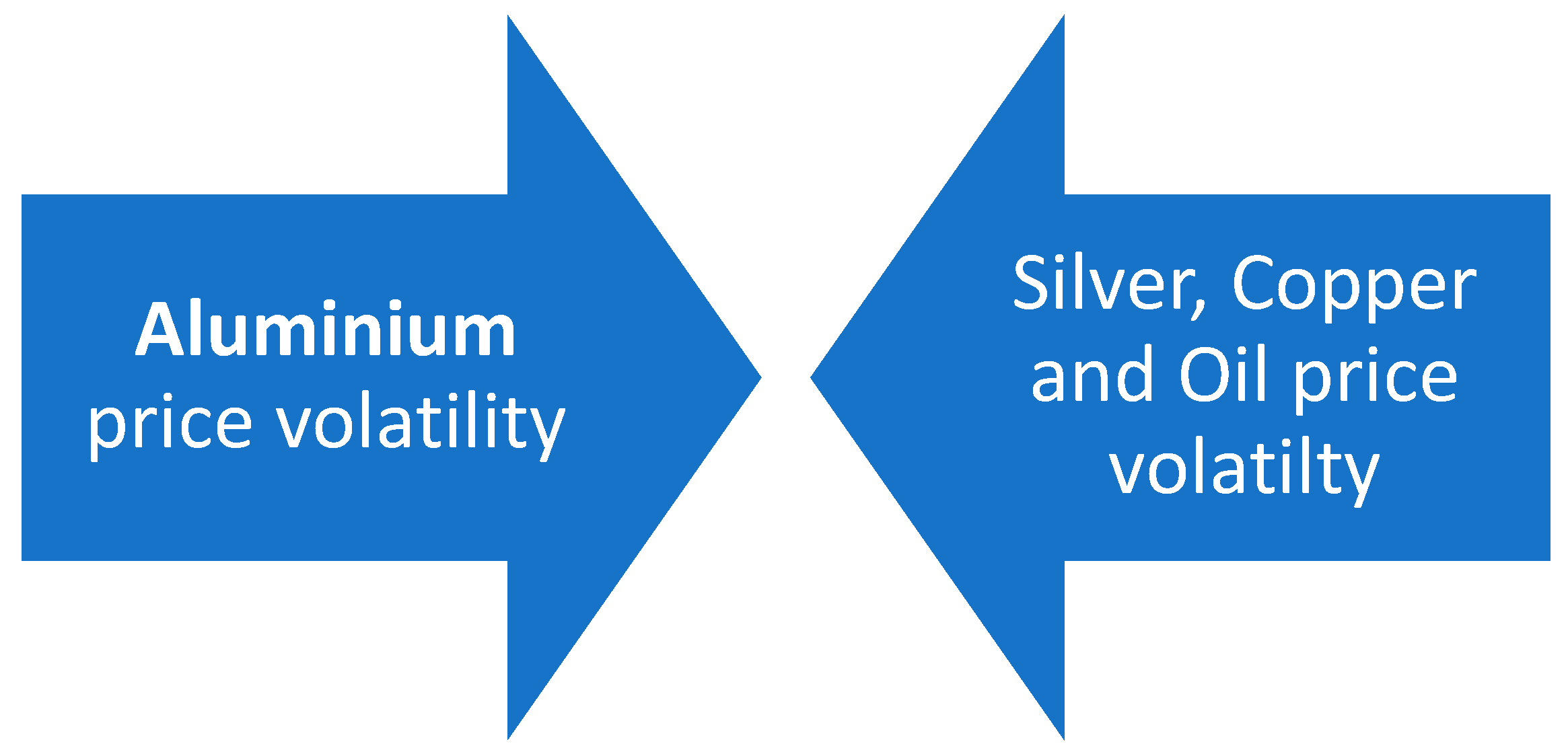

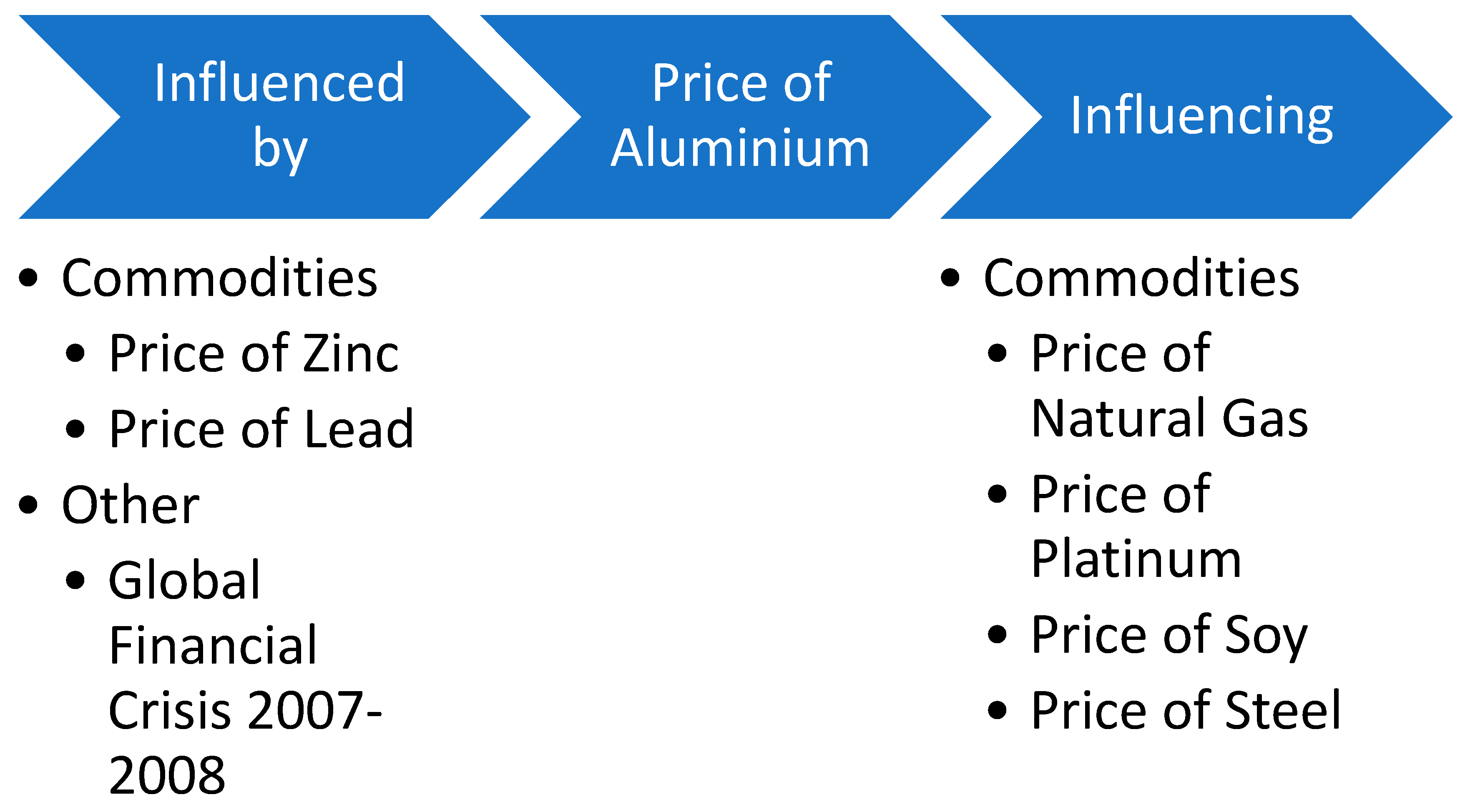

Aluminum, also known as aluminum, shows a weaker interaction with the rest of the commodities, as can be understood from Figure 7. Specifically, according to the literature, this precious metal is under pressure from the volatility of the price of zinc and lead during the period 1993-2019 (Gong et al. 2022). At the same time, according to Figure 7, aluminum has a bidirectional effect with silver and copper. In particular, the researchers present a correlation of these three metals in the years 1985 to 2020 (Chevallier and Ielpo 2013; Oliyide et al. 2021; Umar et al. 2021). However, this relationship is noteworthy in the Chinese market, where the literature states that the specific metals interacted with each other in the period 2009-2017 (Hu et al. 2020).

Additionally, there is a significant correlation between the price of aluminum and the volatility of the oil market. This relationship is also bidirectional and appears stronger from 2004 to 2015, according to Figure 8 (Behmiri and Manera 2015; Reboredo and Ugolini 2016; Zhang and Tu 2016). In addition, the literature notes the significant influence of the 2008 international financial crisis on precious metal prices (Chevallier and Ielpo 2013; Kang and Yoon 2016). This results in the observation of volatility in the price of aluminum in both global and local markets (Kang and Yoon 2019).

However, it is worth noting the variables that are affected by the volatility of the aluminum price. The platinum and steel market is highly volatile, being pressured by the price of aluminum (Chevallier and Ielpo 2013; Hu et al. 2020; Umar et al. 2021). At the same time, the researchers consider it appropriate to examine the relationship between aluminum and natural gas. Thus, they observed that the volatility of the aluminum market directly affects the price of natural gas, especially in the period 1992-2015 (Chevallier and Ielpo 2013). Of particular interest is the influence of aluminum on agricultural products. The literature reports that this particular metal results in wheat and soybean price volatility (Chevallier and Ielpo 2013). Equally important is the effect of the war between Ukraine and Russia. In the survey of the period, aluminum is presented as a transmitter of volatility, directly affecting the prices of various commodities (Wang et al. 2022).

It is necessary to make suggestions regarding the necessity of future investigation of the aluminum market. This precious metal presents various research gaps as its price behavior has been studied to a limited extent. Thus, a primary proposal for research is the relationship of the aluminum market with the stock markets worldwide. These investigations have as a direct result, the understanding of the strong connection of various commodities with financial institutions. At the same time, it is important to study the behavior of the price of aluminum, taking as an impact parameter various stock indices such as the S&P 500. In this way, basic literature gaps are covered regarding the causes and consequences of the volatility of the aluminum market.

3.4. Copper

Continuing with the price behavior of various commodities, copper is worth investigating. The markets of this particular metal worldwide show strong interaction. In particular, the literature notes that during the period 2000-2006, the spot price of copper in the Chinese market interacted with the futures price of the commodity (Liu et al. 2008). At the same time, before the onset of the global crisis in 2007-2008, the volatility of the price of copper on the London Metal Exchange (LME) and the New York-based Commodity Futures Exchange (NYMEX) resulted in the volatility of the copper market. On the Shanghai Metal Exchange (Yin and Han 2013; Kang and Yoon 2016; Lee and Park 2020). However, during the international crisis, while the above effects remain unchanged, it is observed that the Shanghai market (SHFE) affects the LME and NYMEX yield spreads (Lee and Park 2020). After the financial crisis, the SHFE copper price appeared to influence the corresponding market on the London Metal Exchange, while the SHFE copper price appeared to be pressured by NYMEX copper volatility (Yin and Han 2013).

In addition, the volatility of the futures price of copper on the London Metal Exchange has a direct impact on the appearance of volatile futures prices of the metal at the global level. In particular, the researchers report this phenomenon for the US and China market during the period 2003-2019 (Shen and Huang 2022). It is worth noting at this point that the fluctuating copper prices on the LME and NYMEX are affecting the Indian commodity exchange (MCX). Thus, according to the literature, in the decade 2007-2017, the price of copper in MCX showed strong volatility (Manisha 2017).

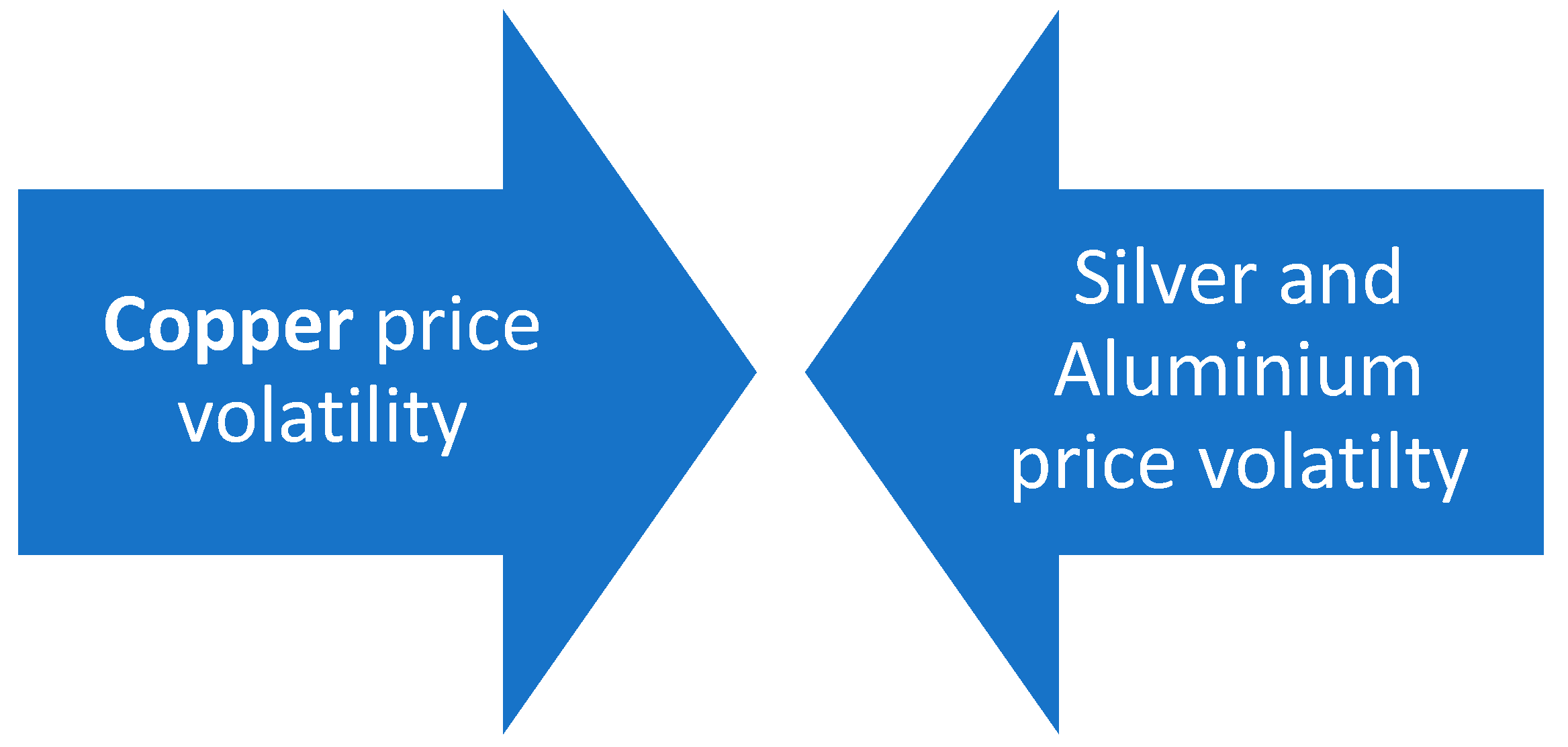

However, the relationship of copper with other commodities is of particular interest. Various researchers have dealt with the effect of the price of various goods on the market volatility of the metal in question. As shown in Figure 8, oil is one of the commodities that obviously affects the price of copper, especially when investigating the period 1993-2015 and the Chinese metal market (Behmiri and Manera 2015; Reboredo and Ugolini 2016; Zhang and Tu 2016). In addition, volatility in the price of copper occurs due to the volatile behavior of the gold market. In particular, the literature notes that for about 30 years, the unstable price of gold worldwide resulted in the volatility of the copper market (Chevallier and Ielpo 2013; Oliyide et al. 2021; Umar et al. 2021). It is necessary to point out that aluminum and silver behave in a bidirectional manner with the specific metal, as shown in Figure 9. In particular, aluminum and copper show a strong interaction when examining the years 1992 until 2015, while silver and copper interacted for 8 years (2009-2017) and mainly in the Chinese market (Chevallier and Ielpo 2013; Hu et al. 2020). At the same time, the volatility of the price of corn has an effect on the price of copper, which seems to change during the investigation of the years 1992-2015 (Chevallier and Ielpo 2013).

Next, it is worth investigating various exogenous variables which directly affect the price of the precious metal. US stock market news is a key driver of volatility in commodity prices, specifically copper. In particular, researchers observed a strong influence of new US financial institutions during the period 1995 to 2001 on the price of copper and especially on the Chinese metal market (Fung et al. 2003). In addition, the global financial crisis in 2007, which saw a sharp downturn in banking systems, also affected commodity prices. Therefore, the price of copper experienced volatility (Kang and Yoon 2016, 2019; Manisha 2017). Then, the interest of scholars was attracted by the gold market in emerging economies such as Brazil and Chile. Research results indicate that the Chilean economy is putting particular pressure on the price of copper (Hegerty 2016).

On the other hand, equally important are the factors that are affected by the change in the price of copper. Thus, the researchers' research regarding the effect of copper on precious metals is particularly important. The literature reports that nickel and tin are directly affected by the volatility of the copper market when examining the period 1993-2019 with daily basis data (Gong et al. 2022). In addition, the researchers note that the price of steel shows strong volatility from 2007 to 2019 due to the corresponding volatility in the copper market in China (Hu et al. 2020). At this point, it is necessary to point out that copper also affects the Chinese economy. In particular, the volatility of international copper prices brings significant consequences to the economic actions of the Asian country (Guo 2018). Concluding with the variables that are affected by the volatility of the copper market, it is important to mention that the volatile price of the precious metal in Brazil and Mexico has affected the exchange rate of these countries for about 35 years (Hegerty 2016).

Nevertheless, it is worth noting that the copper market is suitable for further research as it is of particular interest. Thus, one of the important gaps that arise in this particular literature study is the correlation of the copper market with the volatility of certain indicators. Considering that modern studies deal with the interaction of metal markets, specifically with copper, the existence of a relationship between the price of copper and stock market indices is considered worthy of investigation. In addition, this precious metal is a key raw material for various economic units that deal with electricity, telecommunications, medicine, and IT. Therefore, as can be understood, the volatility of the price of copper directly affects the activity of the above companies. For this reason, it is deemed necessary to carry out relevant, thorough research.

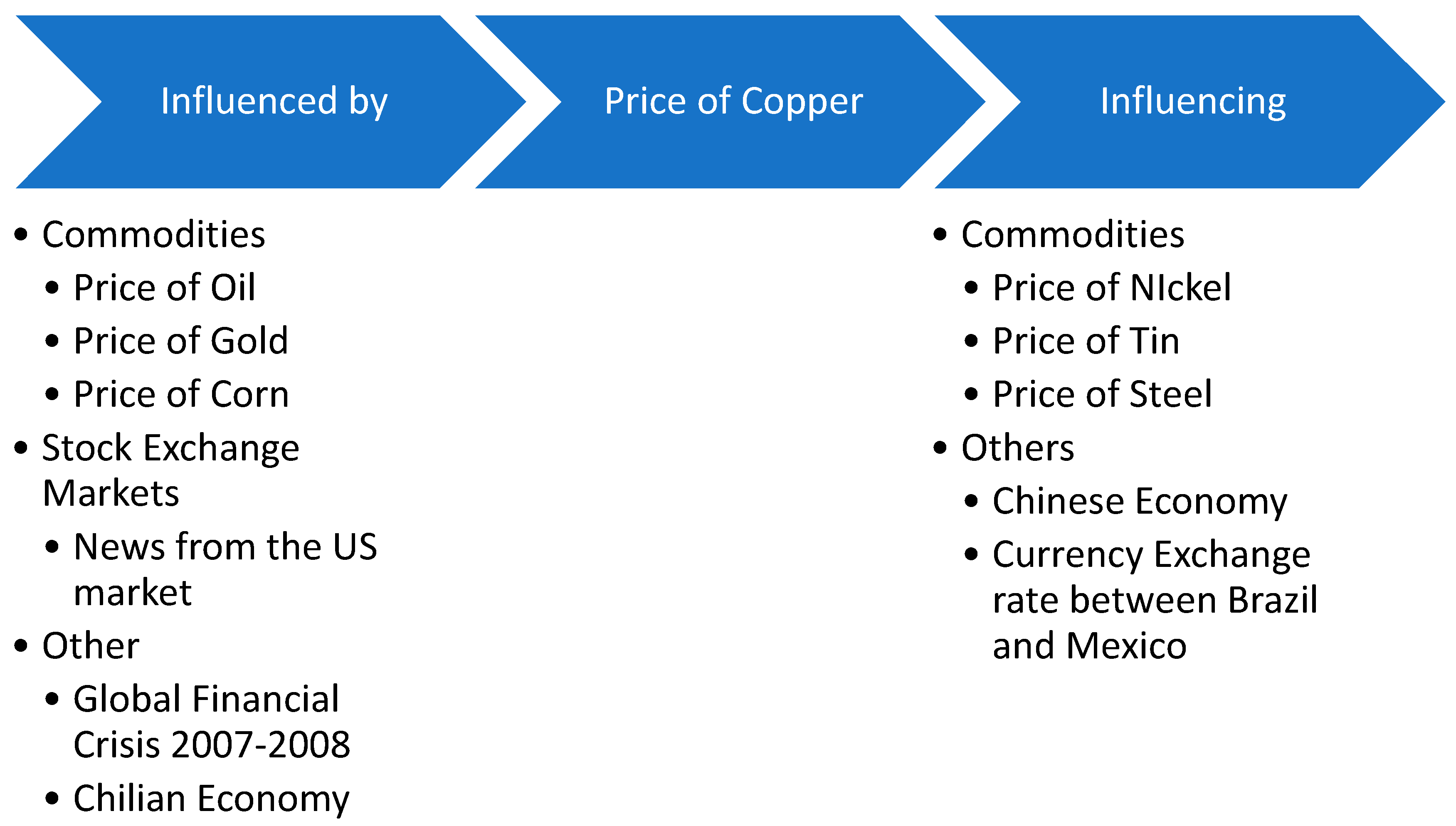

3.5. Platinum

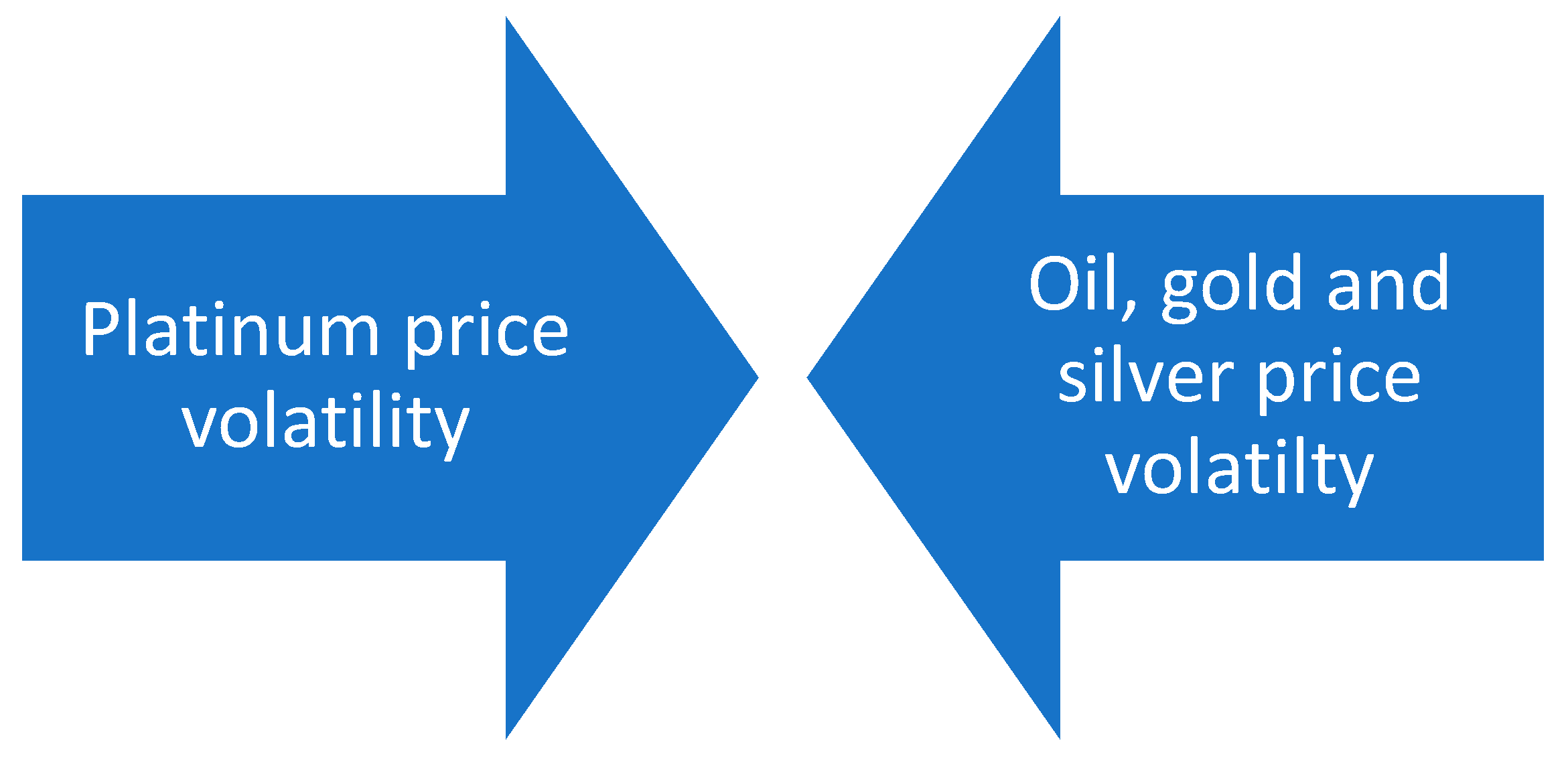

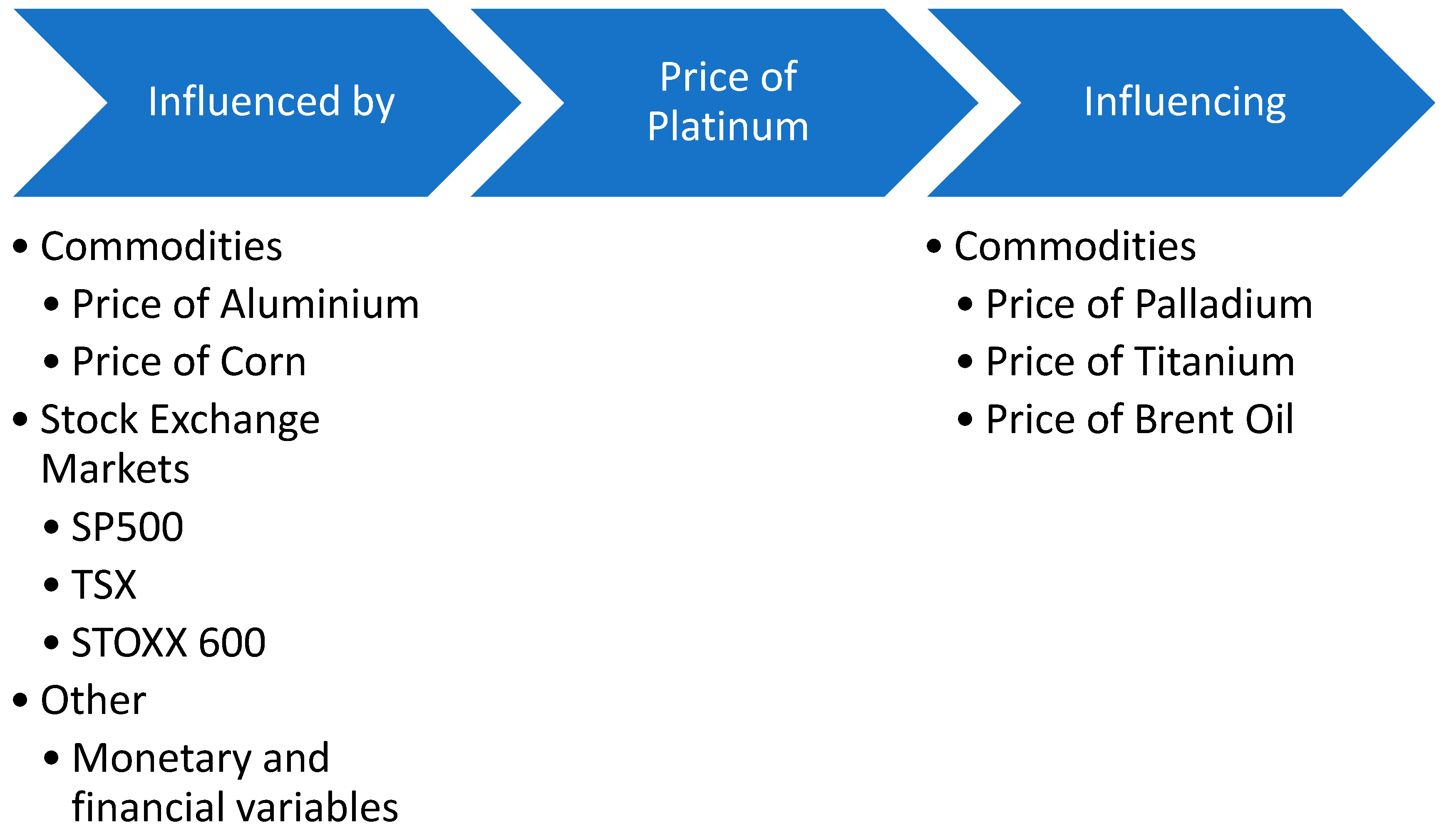

Finishing with the analysis of the behavior of the precious metals market, it is worth investigating the price of platinum. It is characteristic that the platinum market interacts with the price of oil, gold, and silver. Specifically, when analyzing the period 1992-2015, the literature reveals that the platinum and oil markets are affected in both directions, as can be understood from Figure 11 (Behmiri and Manera 2015; Reboredo and Ugolini 2016; Tiwari et al. 2021). Additionally, gold and platinum have a similar relationship. In detail, the volatility of the price of one precious metal results in the volatility of the market of the other. Thus, the researchers analyzing this correlation noticed that for about 30 years, these markets showed strong interaction (Chevallier and Ielpo 2013; Antonakakis and Kizys 2015; Reboredo and Ugolini 2015; Mensi, Al-Yahyaee et al. 2017; Uddin et al. al. 2019; Umar et al. 2021). At the same time, it is worth noting that platinum and silver attracted the interest of various scholars because of the relationship they exhibited. In particular, in the last 20 years, the prices of these precious metals have mutually influenced each other (Reboredo and Ugolini 2015; Uddin et al. 2019). A separate example is the markets of Japan and the USA, which strongly display this relationship (Xu and Fung 2005).

According to Figure 12, the volatility in the platinum price is also caused by the volatility of the aluminum market. More specifically, the literature reports that, when investigating the last 30 years, the fluctuating price of aluminum induces volatility in the platinum market (Chevallier and Ielpo 2013; Umar et al. 2021). Another commodity that affects the price of platinum is corn. Its market shows various fluctuations during the period 1992-2015, an element which is reflected, according to the researchers, in the price of platinum (Chevallier and Ielpo 2013). Despite this, the particular valuable is seriously affected by the prices of some financial indicators. In detail, these indices are the S&P 500, the TSX, and the STOXX 600. Thus, their price movements had an impact on the platinum market for about 15 years, especially from 2000 to 2016 (Mensi, Al-Yahyaee, et al. 2017). Concluding with the factors that influence the price of platinum, various monetary and financial variables have the above capacity. Contemporary literature dates this effect from 1986 to 2006 (Batten et al. 2010).

However, particularly important is the influence exerted by the price of platinum on various commodities. In more detail, the price of palladium shows intense volatility during the period during which it receives pressure from the platinum market. Additionally, the literature reports that both titanium and crude oil are affected by platinum price volatility. At this point it is necessary to underline that these effects appear in the US markets and during the research, which is conducted from 1990 to 2017 (Tiwari et al. 2021).

At this point, the literature approach regarding the platinum market has some things that could be improved. In particular, a research gap is observed when studying the behavior of platinum in relation to the activity of various stock exchanges worldwide. Thus, future actions are deemed necessary, in order to complete the above observation. In addition, this literature review suggests the investigation of the correlation between the platinum market and various exchange rates. It is understood that similar commodities interact with foreign exchange markets. However, there needs to be a clear gap in the literature regarding platinum.

3.6. Oil

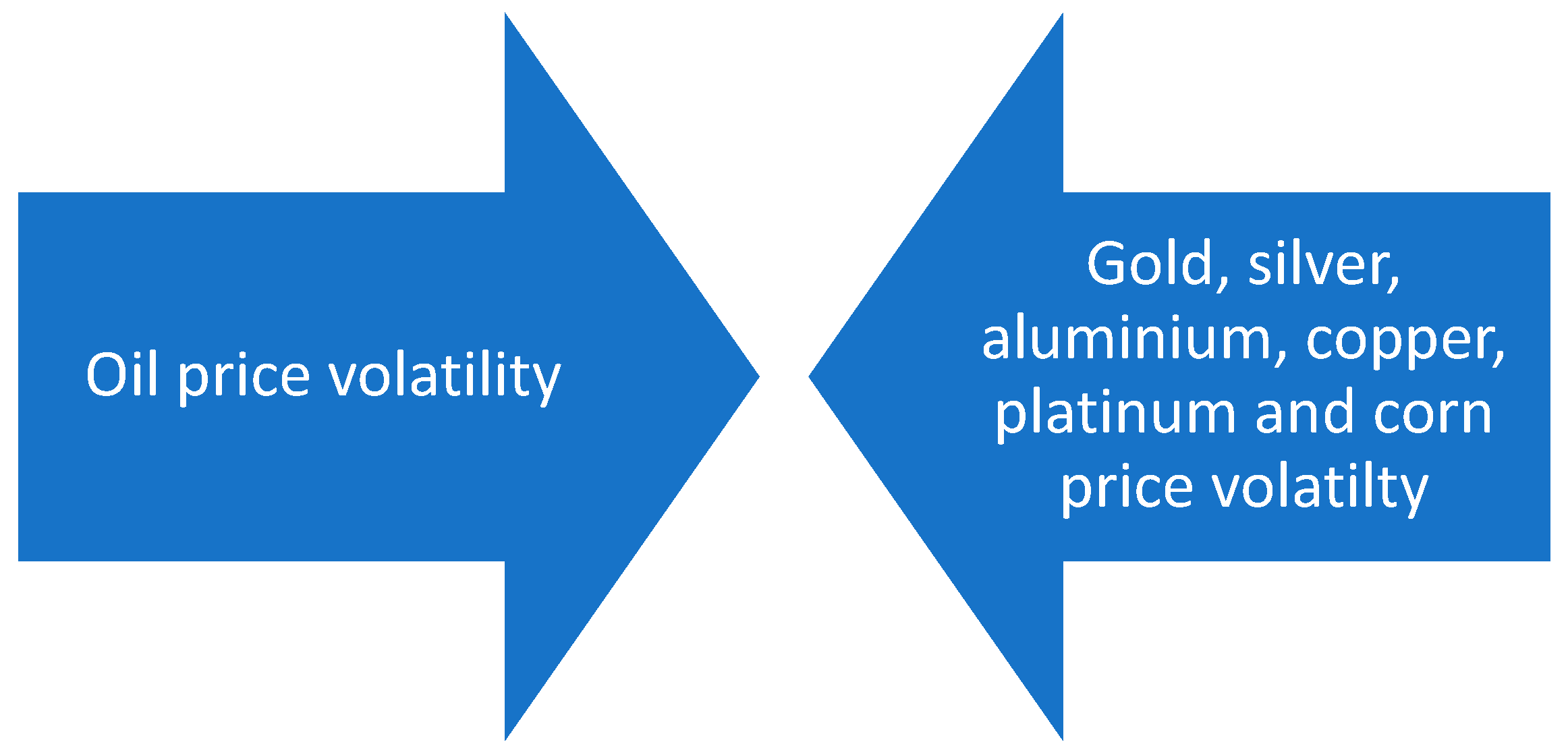

Oil, like gold, is a commodity for which thorough research has been carried out regarding the reaction of their price to various stimuli as well as the impact of their volatility. However, the interaction of the oil market with the prices of precious metals is of particular interest. In particular, it is observed that oil exhibits a stronger interaction with gold than with the rest of the metals under consideration. This correlation appears when investigating the period 1993-2015 and includes markets of global scope, with the European Union, the USA, and the Gulf countries being prominent examples (Chevallier and Ielpo 2013; Ewing and Malik 2013; Antonakakis and Kizys 2015; Maghyereh et al. al. 2017; Guhathakurta et al. 2020; Tiwari et al. 2021). Additionally, as shown in Figure 13, the literature notes that oil market volatility is correlated with silver, aluminum, copper, and platinum prices. The markets in which this interaction is more pronounced are those of China, Japan, the European Union and the USA over fifteen years, i.e. from 2000 to 2015 (Ji and Fan 2012; Chevallier and Ielpo 2013; Antonakakis and Kizys 2015; Behmiri and Manera 2015; Reboredo and Ugolini 2016; Zhang and Tu 2016; Oliyide et al. 2021; Tiwari et al. 2021). Another commodity that has a two-way relationship with the oil market is corn. In particular, the researchers point out that for the decade 2007-2017, the two markets simultaneously acted in the same direction. This has, as a clear result, the existence of a correlation between the volatility of the price of these commodities (Du et al. 2011; Wu et al. 2011; Onour and Sergi 2012; Chevallier and Ielpo 2013; Mensi, Tiwari, et al. 2017; Guhathakurta et al. et al. 2020).

A remarkable finding of the researchers is the interaction that the oil markets present with each other, as shown in Figure 14. In various cases, the international prices of the commodity in question influence and be influenced by the local oil markets. Specifically, when investigating the years 2001-2013 and taking daily data, the researchers note that global oil prices have a major impact on the corresponding Chinese market. Additionally, they report that the relationship is bidirectional, despite the fact that Chinese prices affect international markets with less intensity (Zhang and Wang, 2014). Next, the oil stock markets in Asian countries are of particular interest. In particular, the stock returns of Saudi Arabian and Iraqi financial institutions show a strong interaction during the survey, which was carried out in the period 2009-2018 (Ashfaq et al., 2019). Stock returns in the United Arab Emirates have a similar correlation with oil stock prices in Korea (Ashfaq et al., 2019). The above reactions are justified by the characterization of these countries as exporters and importers of oil. Therefore, commodity prices and stock markets show a direct relationship.

At this point, it is necessary to point out that oil is under strong pressure from the price of West Texas Intermediate (WTI) crude oil. This type of oil is a tool for pricing oil. Therefore, WTI price volatility is a direct result of commodity market volatility (Ji et al., 2018; An et al., 2020; Mensi et al., 2021). However, this relationship has become bidirectional in the Chinese and US markets due to the onset of the 2007 global financial crisis (Xu et al., 2019).

As shown in Figure 14, the oil market interacts with financial institutions in the United States of America. However, the researchers set a specific parameter for the existence of this relationship. When using the data analysis models, specific events are defined, such as a war conflict, and only then the two-way correlation between the price of oil and the US stock markets is shown (Ewing and Malik, 2016; Khalfaoui et al., 2019).

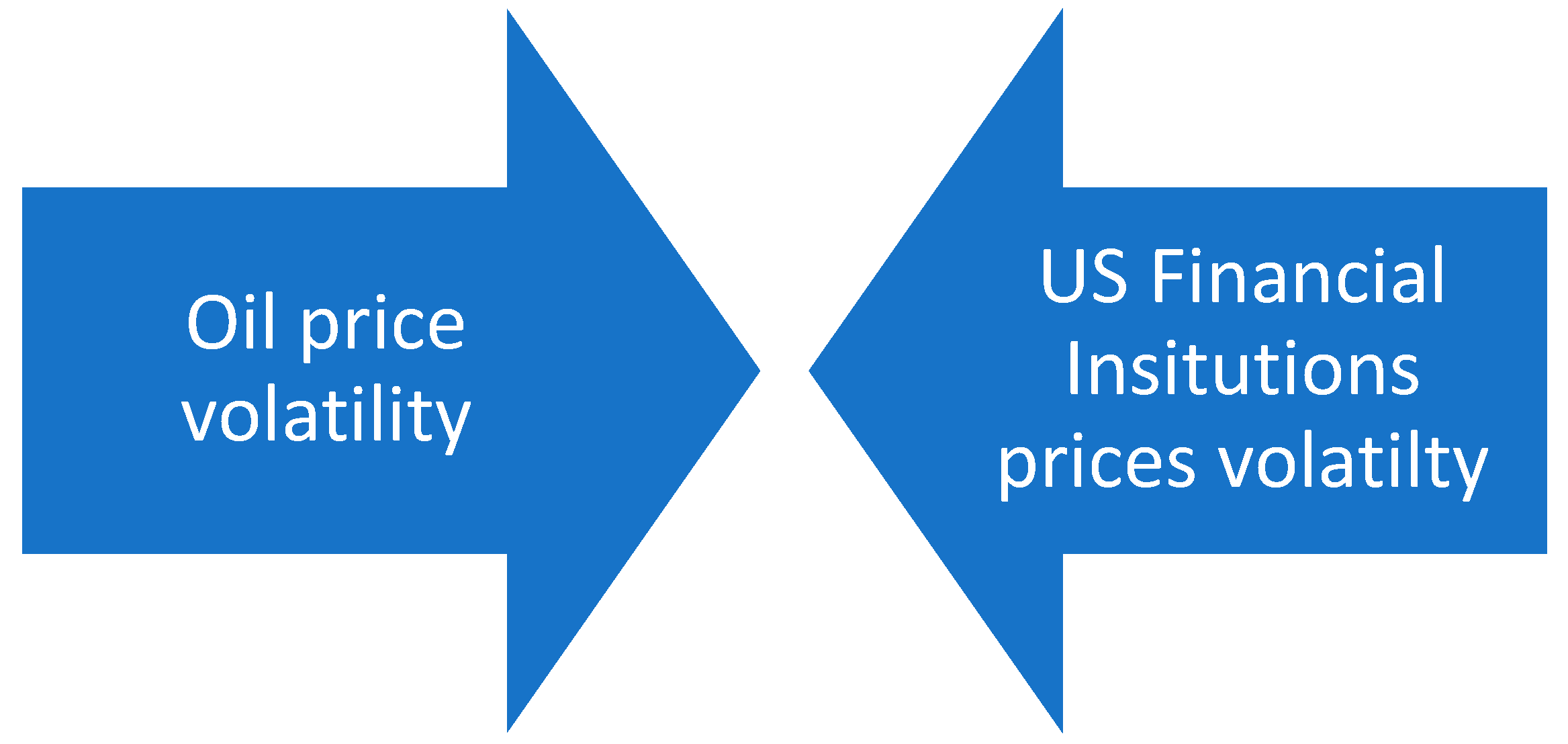

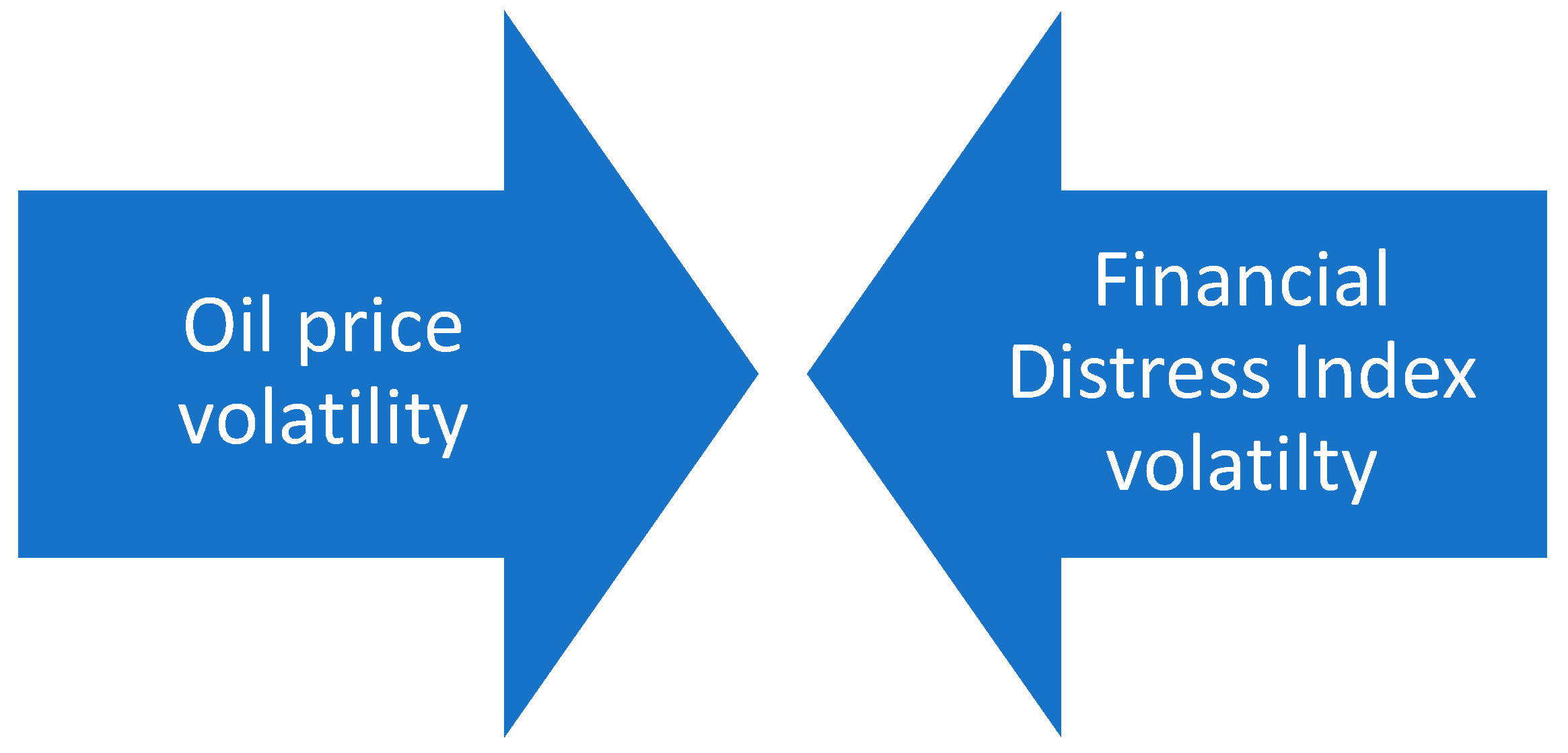

According to Figure 15, the price of oil interacts with the Financial Distress Index. It is noteworthy that researchers delineate their study temporally, taking into account the years before and after the global crisis. Therefore, the results indicate that before the 2007 crisis, the oil market influenced the price of this particular index, whereas after the event, this relationship reversed direction (Nazlioglu et al., 2015).

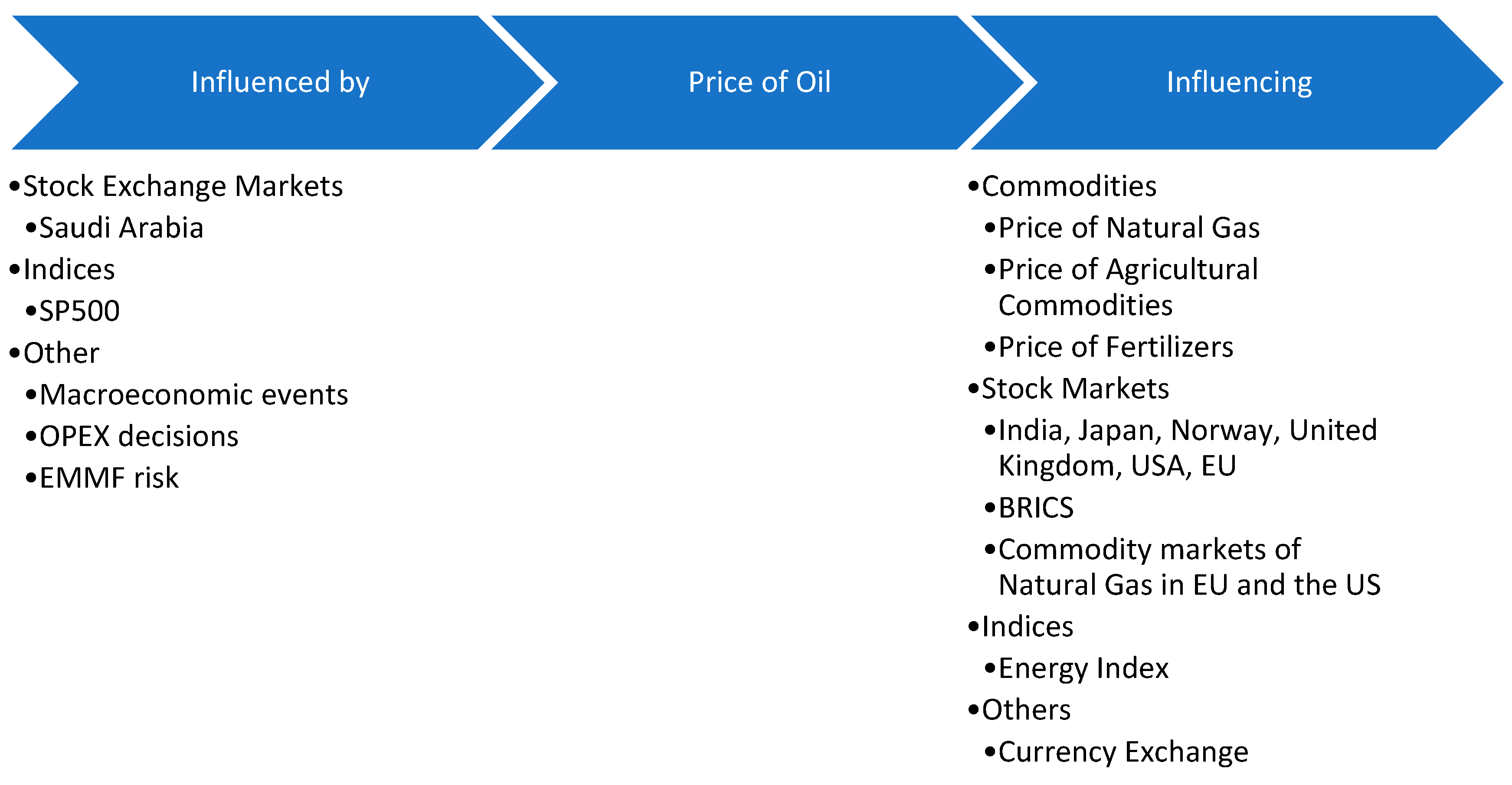

At this point, it is necessary to examine the factors which are responsible for the change in the price of oil, as presented in Figure 16. The Saudi Arabian stock market influences the price of merchandise. When investigating the period 1994-2001, the literature notes that the volatility of the global oil market occurs due to the effect of shares in the stock markets of the Arab country (Malik and Hammoudeh 2007). Additionally, scholars cite the effect of S&P 500 stock index volatility on the price of "black gold." In particular, this index shows a strong influence on the global oil market from 2000 to 2011 (Mensi et al. 2013; Xu et al. 2019).

It is necessary to note that this particular market is highly sensitive to various political and economic events. Some examples of such situations are the global financial crisis of 2007 and the terrorist attack of September 11 in America. The effects of these actions become evident in both commodity prices and stock markets (Singh et al. 2011; Xu et al. 2019). At the same time, the Organization of Petroleum Exporting Countries has attracted the interest of researchers regarding its ability to influence oil prices. Thus, in a study, which was carried out from 2000 to 2003 with daily data, the conclusions state that the organization's production decisions significantly affect the oil market (Mensi et al. 2014). In conclusion, the literature links the price volatility of this commodity to the risk of EMMFs in the period before 2008. However, after the global crisis, this effect weakens (Ewing et al. 2018).

On the other hand, there is a variety of variables where the impact of oil price volatility becomes apparent. Natural gas is one of the commodities that react to the volatile "black gold" market. In particular, the price of natural gas shows strong volatility during the research period 1992-2015 in global markets (Chevallier and Ielpo 2013; Karali and Ramirez 2014; Zhu et al. 2018; Zhong et al. 2019). A notable event is the "Shale Gas Revolution" in the USA, which was a transmitter of instability from oil prices in the European natural gas market. However, researchers note that prior to the above incident, the oil market was influencing natural gas prices in North America (Lin and Li 2015; Geng et al. 2016). In addition, the volatility of the oil market carries its effects on agricultural commodities. Commodities under investigation include wheat, barley, cereals, corn, and soybeans. Various scholars thoroughly investigated the relationship between oil and these products over 32 years, i.e., from 1986 to 2018 (Du et al. 2011; Onour and Sergi 2012; Nazlioglu et al. 2013; Mensi et al. 2014; Saghaian et al. al. 2018; Dahl et al. 2020; Guhathakurta et al. 2020; Yip et al. 2020). It is worth pointing out that the relationship above is strongly presented in China and the USA during the period 2006-2015 (Siami-Namini and Hudson 2017; Luo and Ji 2018).

It is necessary to mention its effect on stock exchanges. In summary, the countries in which these exchanges are located are Japan, Norway, the United Kingdom, the USA, and Europe. In particular, the studies time limit the influence of the oil market on institutions over 30 years, i.e., from 1985 to 2015 (Ågren 2006; El Hedi Arouri et al. 2011; Arouri et al. 2012; Perifanis and Dagoumas 2018; Zhang et al. et al. 2020). In addition, the literature cites that the volatile oil market has serious effects on the stock markets of the BRICS countries (Brazil, Russia, India, China, and South Africa). Findings regarding the Indian financial market indicate that this pressure appeared in 2009 and lasted for 7 years (Bouri et al. 2017; Kumar et al. 2019). At the same time, for the rest of the countries of the BRICS organization, the duration of this influence has a starting year in 2000 and a fifteen-year duration (Raza et al. 2016; Pandey and Vipul 2018).

At the level of stock market indices, the price of oil has a significant effect on the electricity index. The above phenomenon was more pronounced between Turkey and the USA for 4 years, namely from 2003 to 2007 (Soytas and Oran 2011). In addition, the effect of the oil market on the fertilizer market is particularly important. In particular, food commodities, the price of oil, sudden events in the energy market, and changes in the prices of edible goods have a direct effect on the volatile fertilizer market. Thus, a change is also observed in the prices of wheat and corn (Onour and Sergi 2012). Concluding with the effects of the volatility of the oil market, it is worth noting that this action affects the exchange rate around the world. The literature points out that this effect has been researched from 2005 to 2020 and is due to the close connection of exchange rates with various commodities (Nekhili et al. 2021).

However, the research process on oil prices has some gaps. The present bibliographic study proposes, as a future action, the investigation of the behavior of the specific energy commodity with regard to sustainable development. Considering that this concept is related to the environment and economic development, it is worth noting its relationship with oil. Additionally, another suggestion for future research is energy storage and the ways in which the price of oil can be changed with this process.

3.7. Natural Gas

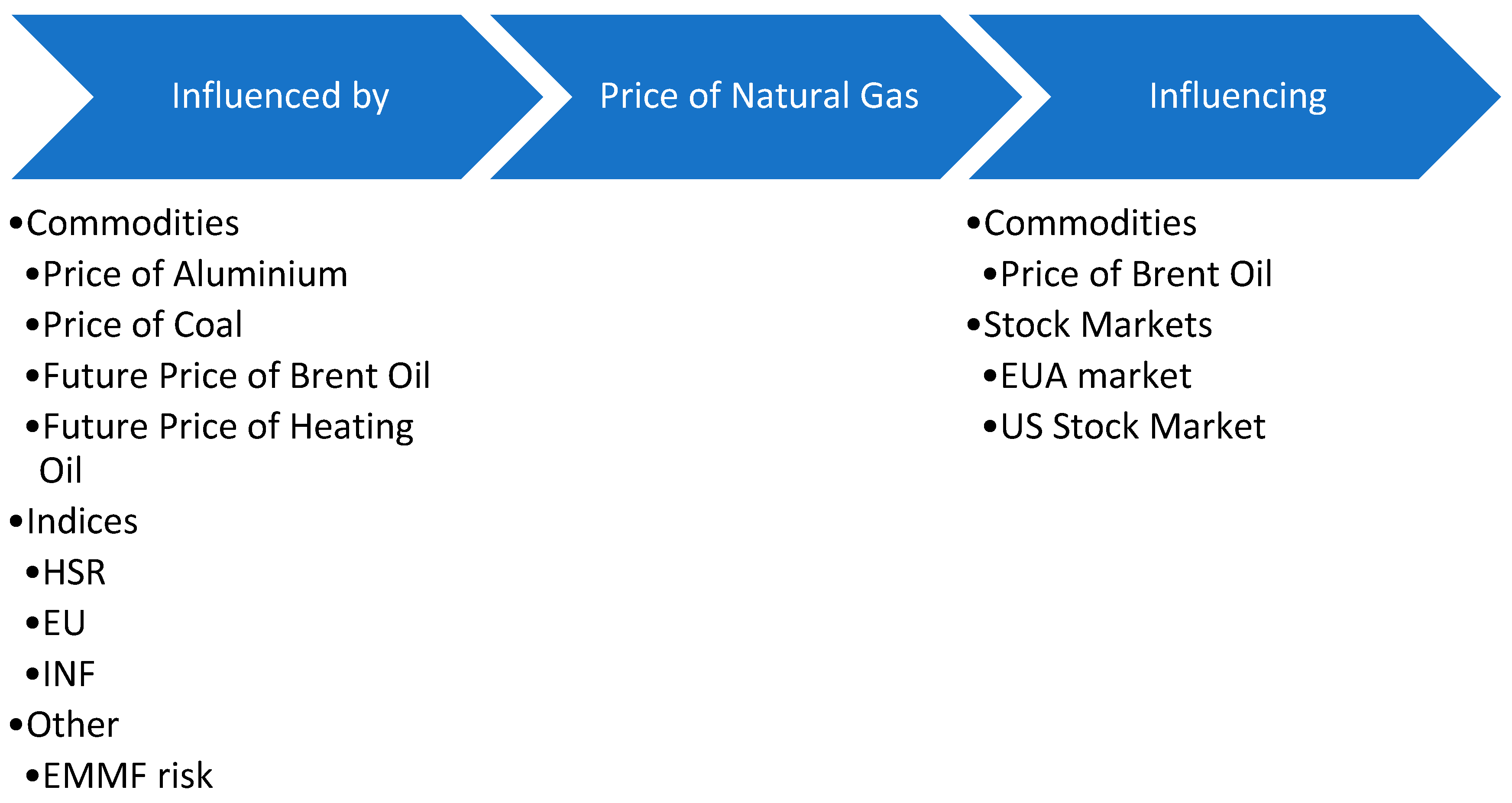

Another important energy commodity that is worth investigating in terms of its price behavior is natural gas. As shown in Figure 17, the price of this commodity is affected by precious metals, namely aluminum and coal. In the case of aluminum, literature findings indicate that this effect occurs when investigating the period 1992-2015, taking daily data (Chevallier and Ielpo 2013). At the same time, coal showed a strong influence on the price of natural gas in the European markets from 2008 to 2019. At this point, it is necessary to point out that the volatility of the coal price comes from the occurrence of volatility in the coal market (Zhang and Sun 2016; Wu et al. 2020).

It is important to investigate the effect of stock prices on the commodity market. In particular, the literature notes that the future prices of crude oil and heating oil affect the natural gas market during the survey of the years 2005-2019 (Sehgal et al. 2013; Gong et al. 2021). In addition, another important factor in the occurrence of volatility in the price of natural gas is the pressure of the stock market indices. The volatile energy commodity market is a result of the volatility in the price of the CNI HSR, CNI EU, and CNI INF indices, which appeared during the 2010-2021 research period (Dai and Zhu 2022). In conclusion, scholars associate natural gas market volatility with the risk of EMMFs before the onset of the global financial crisis in 2007. However, after 2008, there was a decline in this relationship (Ewing et al. 2018).

Nevertheless, the price of natural gas, in turn, has important consequences on a variety of variables. Specifically, researchers present the effect of volatility in the price of natural gas as a cause for the volatility of the crude oil market during the period 1994-2011 (Karali and Ramirez 2014).

In addition, there is a spillover of natural gas price volatility into the EUA markets. Literature findings indicate that natural gas, coal, and Brent oil exert significant pressures on the EUA markets when investigating the years 2005-2015 (Dhamija et al. 2018; Chen et al. 2019). Next, it is worth noting that the price of the specific energy commodity and the American stock markets show a short-term correlation. Natural gas market volatility is transferred to financial institutions with heterogeneous behavior from 2013 to 2019 (Geng et al. 2020).

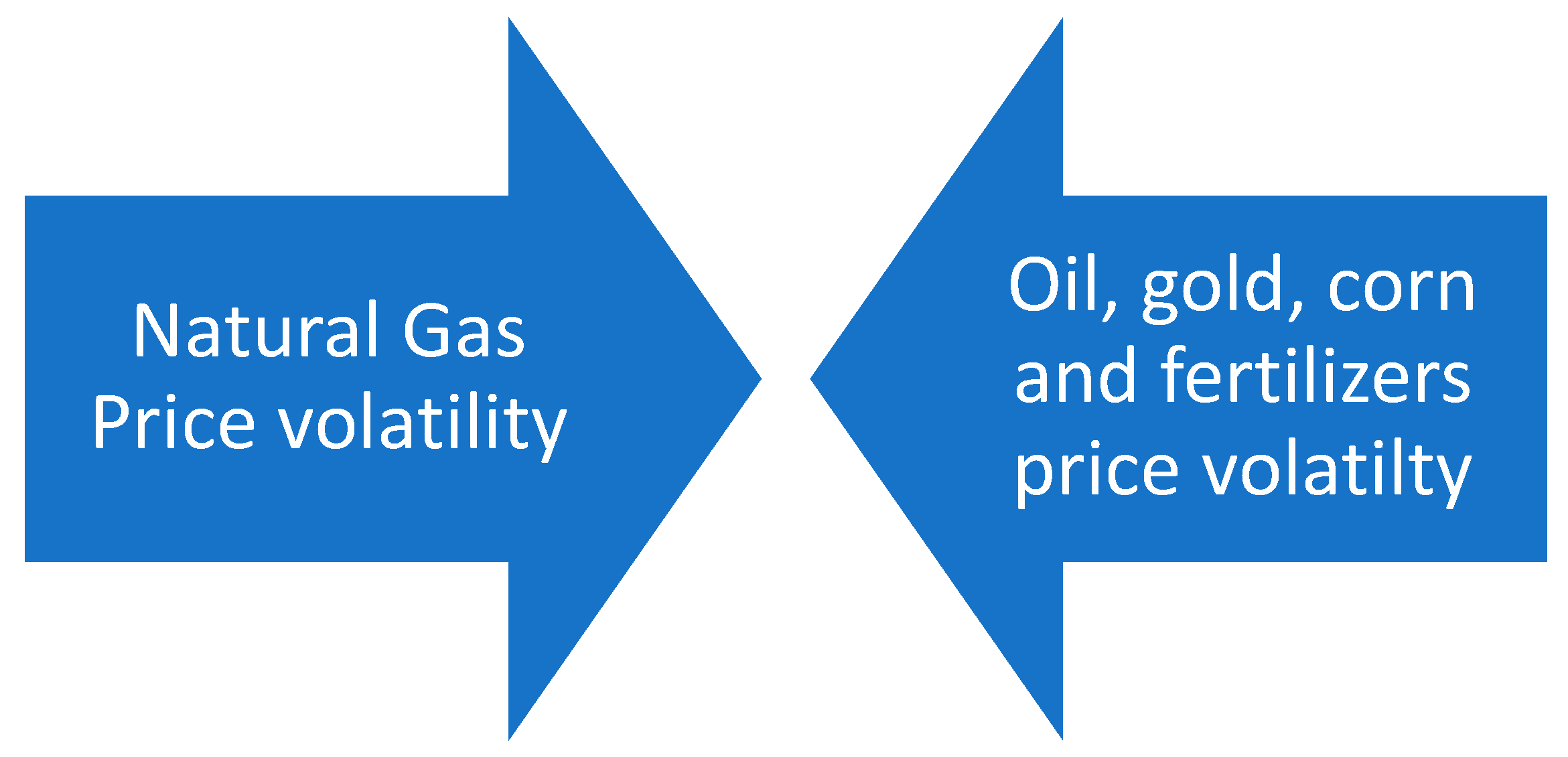

It is also noteworthy the fact of interaction, which the natural gas market exhibits with oil, gold and corn, as shown in Figure 18. More in detail, the markets of the two energy commodities show a strong interaction when examining the years 1992 -2015 both in terms of spot and forward prices (Chevallier and Ielpo 2013; Zhu et al. 2018; Gong et al. 2021). At the same time, researchers researching the period 1992-2022 observed a strong correlation between the prices of natural gas and gold. It is necessary to note that, during the COVID-19 era, this relationship is characterized as stronger (Chevallier and Ielpo 2013; Kumar et al. 2022; Arfaoui et al. 2023). The last commodity with which the price of natural gas seems to interact is corn. The direction of the correlation of their markets is characterized as bidirectional and appears strongly from 1994 to 2015 (Chevallier and Ielpo 2013; Etienne et al. 2016).

The price of natural gas was also investigated thoroughly in terms of its relationship with the fertilizer market. Additionally, researchers note that these two markets influenced each other over twenty years, specifically from 1994 to 2014 (Etienne et al. 2016). In addition, natural gas markets around the world exhibit significant interdependence. In particular, the energy commodity's spot and futures prices, as well as the US and UK ETF markets, were highly correlated from the start of the global crisis of 2007 to 2016 (Chang et al. 2018; Zhang and Liu 2018). It is necessary to note that according to the literature, its markets at the European level are strongly connected (Broadstock et al. 2020).

At this point, it is necessary to underline those studies on the natural gas market that have literature gaps. For this reason, it is appropriate to list some suggestions for future study. In particular, the price of natural gas is worth investigating in relation to the course of energy utilities. Thus, the importance of the energy commodity in relation to the supply of electricity becomes understandable. At the same time, the relationship between the price of natural gas and the energy sector of the S&P 500 index is worthy of investigation. In this way, the influence of the index on the formation of the natural gas market and the activity of the companies concerned is perceived.

3.8. Soy

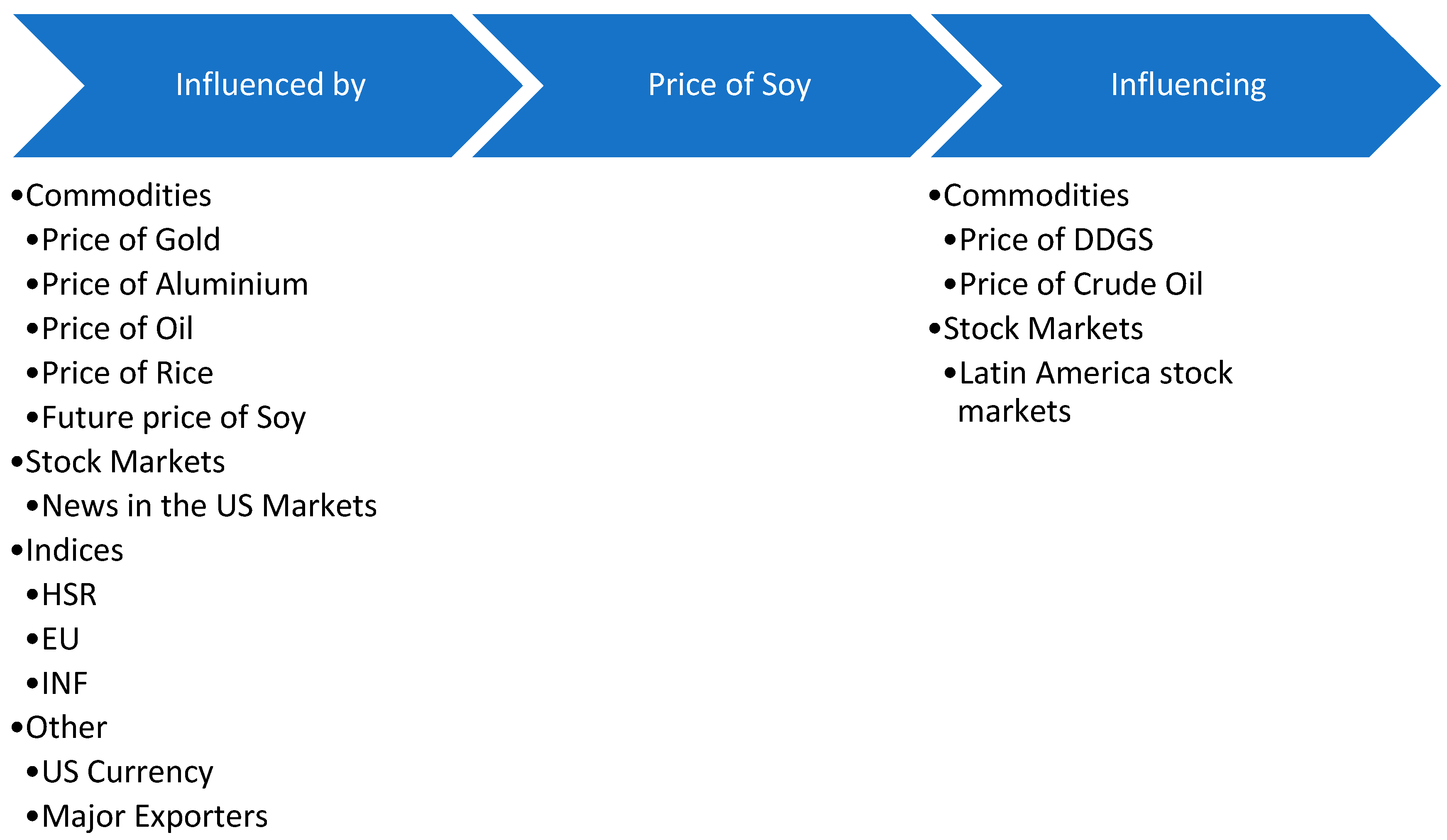

The last category of goods, which is investigated, is agricultural products. According to Figure 19, soybeans are strongly correlated with a variety of commodities, stock markets around the world, and various variables. Precious metals that affect the soybean market are gold and aluminum. Scholars, using daily data, observe this effect when investigating the period 1992-2015 in global markets (Chevallier and Ielpo 2013). Additionally, the literature highlights that soybean price volatility is a result of the pressure exerted by the oil market. In particular, in the last 30 years or so, i.e., from 1986 to 2018, the price of soybeans shown unstable behavior when linked to oil (Nazlioglu et al. 2013; Guhathakurta et al. 2020; Yip et al. 2020). Another commodity, which has a significant impact on the soybean market, is rice. The literature notes that the price of rice from 1992 to 2015 has a strong influence on the soybean market, making it volatile (Chevallier and Ielpo 2013).

Next, the effect that the stock market has on the price of soybeans is notable. The researchers note that the international futures prices of the agricultural commodity in question have a direct effect on the appearance of volatility in the price of imported soybeans in China. The above influence is shown from 2011 to 2016 by taking daily data (Zhao et al. 2010; Ma and Diao 2017; Sanjuán-López and Dawson 2017). At the same time, the news of the American financial institutions is a main cause of volatility in the price of soybeans. In more detail, scholars present the influence of these youth on Chinese agricultural markets when examining the years 1995-2001 (Fung et al. 2003).

It is also notable that the price of soybeans is volatile as a variety of variables pressure it. Specifically, after the global financial crisis of 2007, the exchange rate of the US dollar and its unstable price had a great impact on the international soybean market (Siami-Namini and Hudson 2017). In addition, soybeans in the local Chinese market are showing strong volatility, which comes from the dominant agricultural exporters. The above occurs as these producers can adjust pricing (Zhao and Goodwin 2011).

However, the soy market, in turn, affects certain commodities and stock exchanges. In particular, the volatility of the soybean market has a severe impact on the price of DDGS wheat, an animal feed commodity. The literature spans this relationship from 2000 to 2016, observing markets weekly (Etienne et al. 2017). In addition, spillover of soybean price volatility is present in the crude oil market. After the end of the global crisis of 2007, agricultural commodities significantly affected the price of this type of oil in global markets (Dahl et al. 2020). Concluding with the consequences of the volatile soybean price, it is worth noting that Latin American financial institutions are significantly affected. Examining the years 1986-2011, researchers show that negative changes in agricultural commodity prices can exert severe pressure on Latin American stock markets (Candela and Farace 2018).

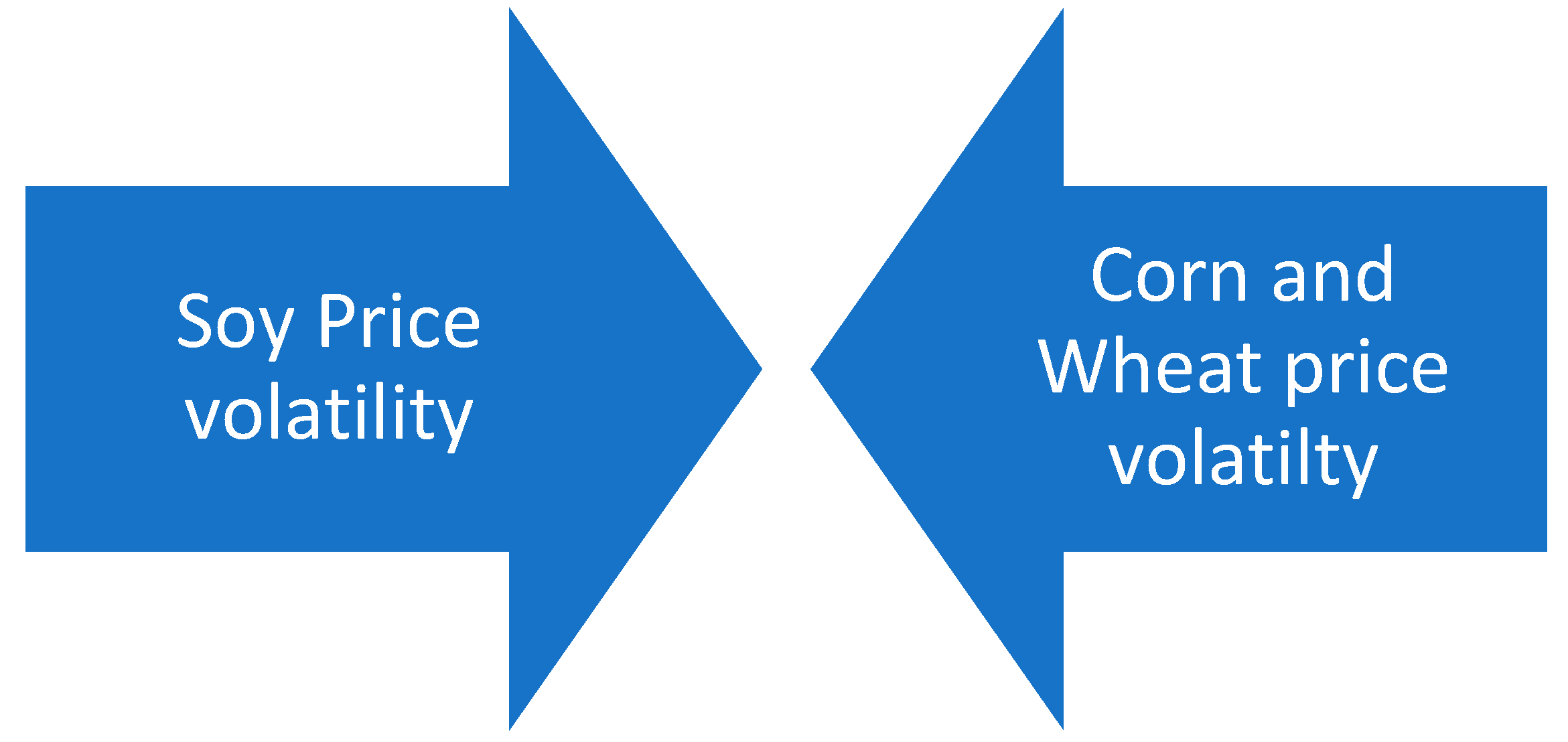

Of particular interest are the two-way relationships of the soybean market with different commodities. As shown in Figure 20, soybean interacts with two agricultural products, corn and wheat. The literature findings highlight that the correlation of soybean market volatility with corn is mainly found in the US and during the period 1992-2015 (Zhao and Goodwin 2011; Chevallier and Ielpo 2013; Hamadi et al. 2017). In the case of soybeans and wheat, scholars report that volatility spillovers between markets existed from 1999 to 2016. Notably, this correlation is strongly found in US agricultural markets (Bernhardt 2017; Hamadi et al. 2017).

However, the soybean price literature presents some research gaps. For this reason, the present study lists below suggestions for future research processes. First, it is worth investigating the relationship of the soybean price to the S&P GSCI Soybeans Index. In this way, a check is made on the effect of the stock market index on the soybean price and vice versa. Additionally, one more indicator that needs to be researched in terms of its relationship with the soybean market is the Producer Price Index (PPI). This index provides information on various agricultural commodities and varies according to the prices producers receive for their goods. Thus, the connection of this index with the price of soybeans is examined.

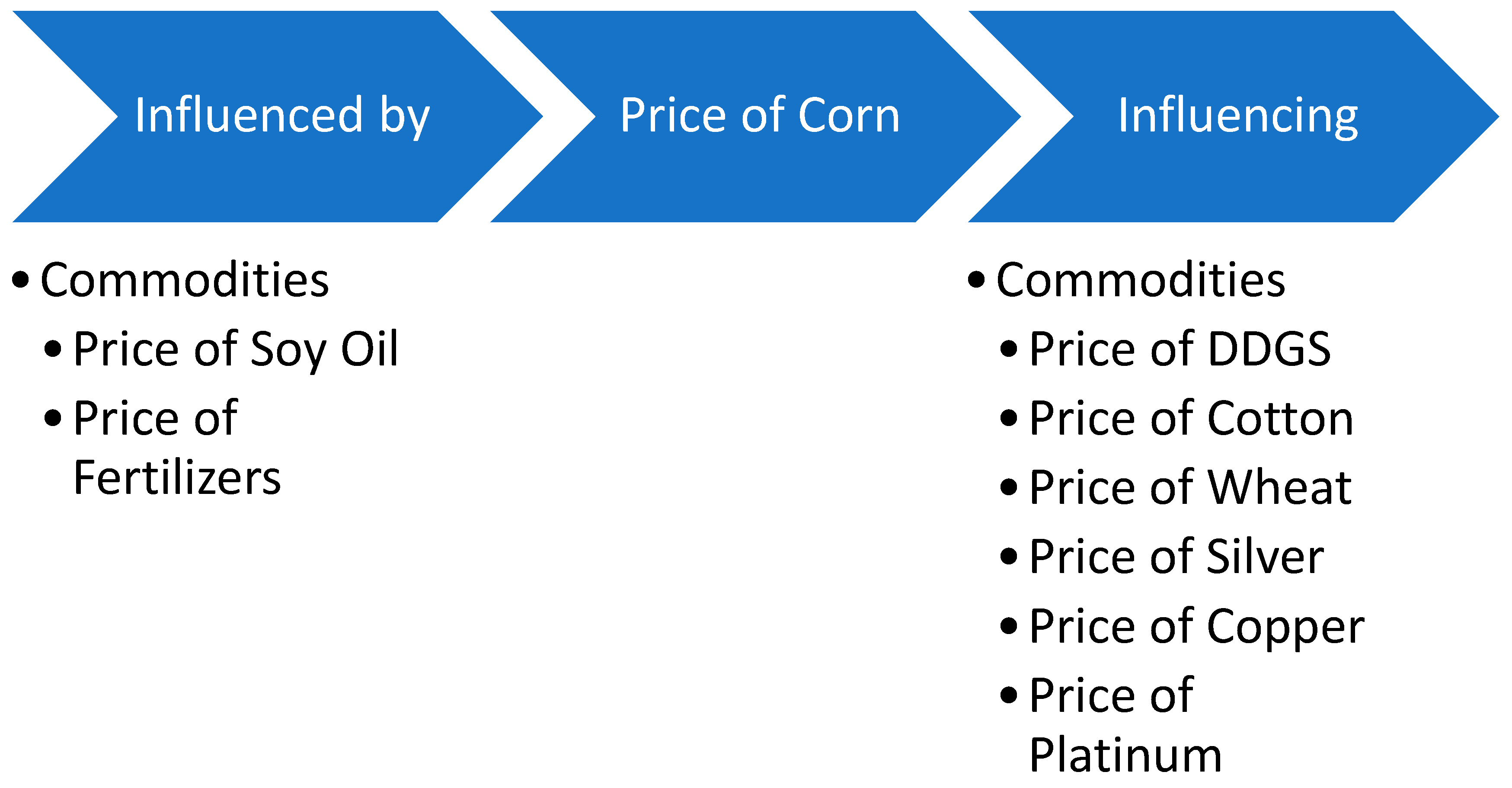

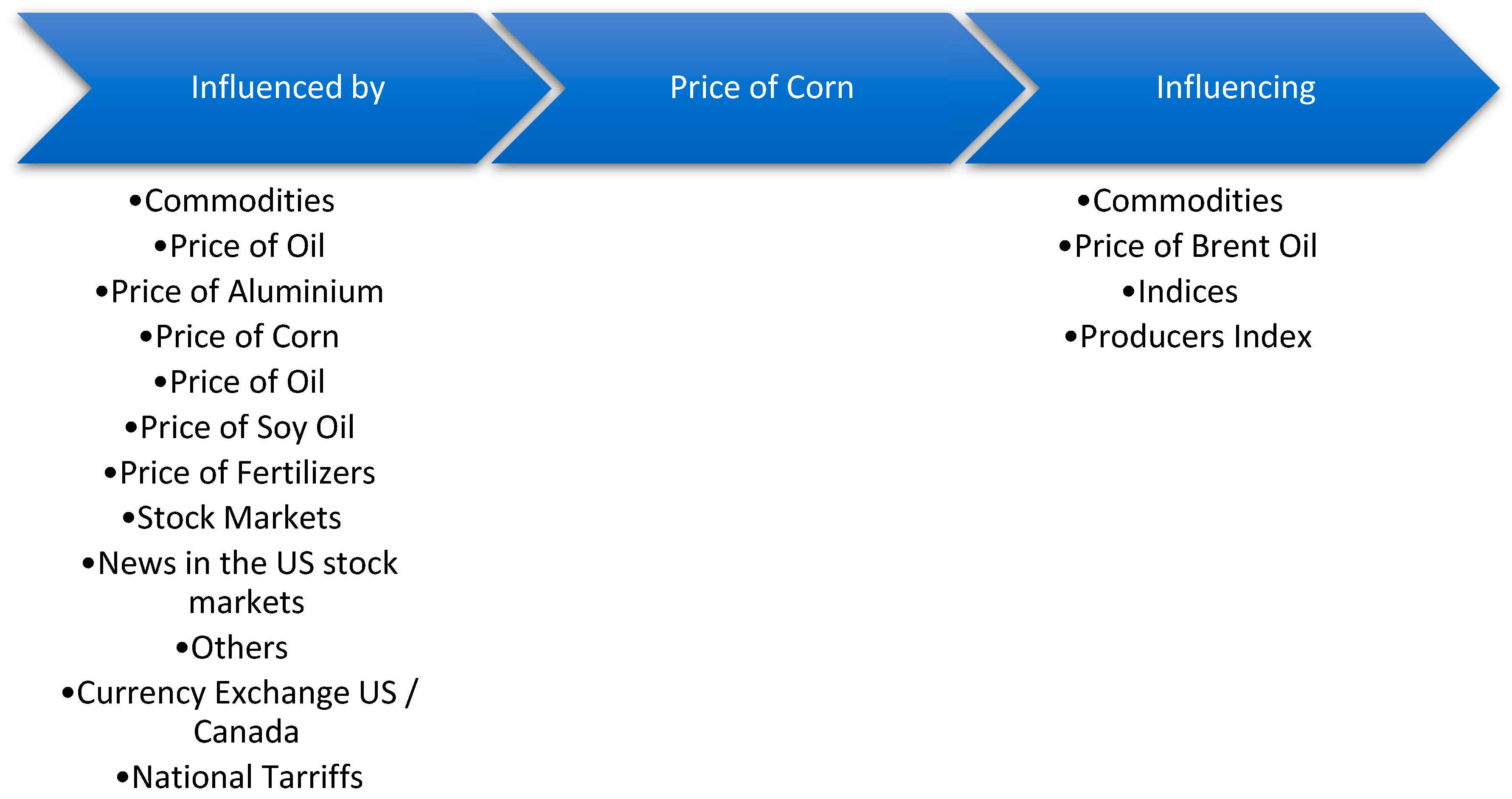

3.9. Corn

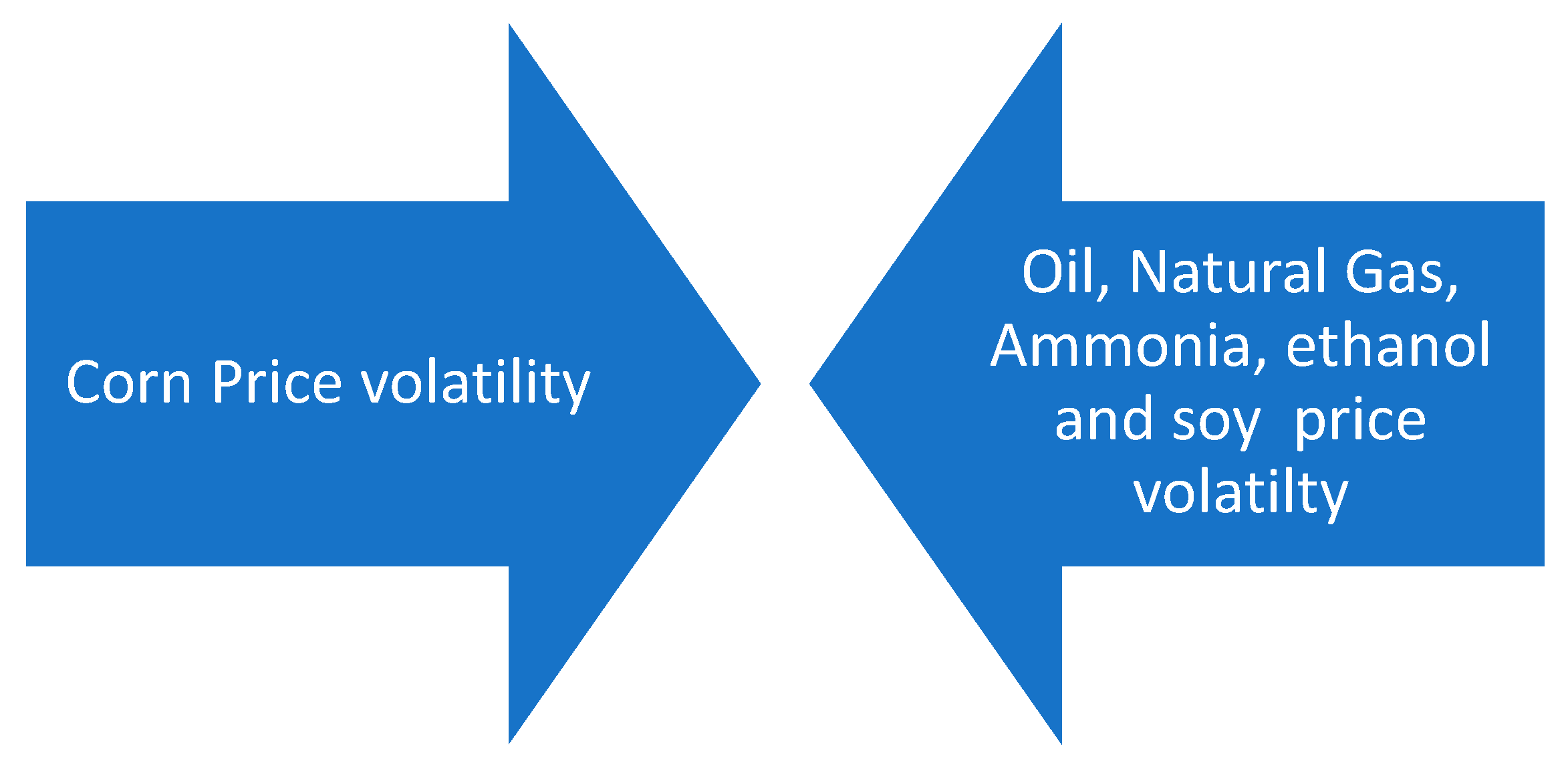

The next agricultural commodity, which is of particular interest in terms of its volatility, is corn. As shown in Figure 21, maize exhibits a strong interaction with a variety of variables. The researchers emphasize that the variable prices of oil and corn are directly linked. For this reason, their findings indicate that the markets of the specific commodities are affected both ways for 26 years, i.e. from 1992 to 2018, and mainly in the USA (Du et al. 2011; Onour and Sergi 2012; Chevallier and Ielpo 2013; Nazlioglu et al. 2013; Mensi, Tiwari, et al. 2017; Guhathakurta et al. 2020; Yip et al. 2020). In addition, corn and natural gas show a similar relationship. According to the literature, the prices of these commodities show volatility when considered simultaneously from 1992 to 2014 (Chevallier and Ielpo 2013; Etienne et al. 2016; Yang et al. 2022). Then, there is a particular correlation between the price of corn and crude oil, especially in the US and China. The results of the studies note that this two-way energy appeared in 1992 and lasted until 2014 in the Chinese and American markets (Wu et al. 2011; Trujillo-Barrera et al. 2012; Haixia and Shiping 2013; Jiang et al. 2015; Luo and Ji 2018; Saghaian et al. 2018).

It is worth noting that the ammonia and corn markets show interaction. Scholars' interest was attracted by the twenty years 1994-2014, whenever product prices had a two-way effect, resulting in their volatility (Etienne et al. 2016). Additionally, there is a strong interaction between corn and ethanol prices. The volatility of these goods is shown when investigating the period 2007-2020 mainly in the markets of China, USA, and Brazil (Trujillo-Barrera et al. 2012; Saghaian et al. 2018; Yosthongngam et al. 2022). The last commodity, whose price moves depending on the corn market, is soybeans. The literature reports that the prices of the two agricultural goods show a strong interaction from 1992 to 2015 in the American markets (Zhao and Goodwin 2011; Chevallier and Ielpo 2013; Hamadi et al. 2017).

The corn market, as shown in Figure 22, is affected by a few variables. In particular, the literature highlights that the price of corn is volatile as the soybean oil market pressures it during the investigation of the years 1999-2015 in the USA (Hamadi et al. 2017). At the same time, the price of the specific agricultural good shows variability due to the purchase of fertilizers. In more detail, fertilizer prices adjust the corn market for about 20 years internationally (Onour and Sergi 2012; Etienne et al. 2016).

On the other hand, the volatile price of corn has the potential to cause a variety of consequences. In particular, one of the products that is under pressure from the volatility of the corn market is cotton. From 2000 to 2012, researchers reported that the price of cotton moved according to the market mobility of the agricultural commodity (Beckmann and Czudaj 2014). Additionally, the fluctuating price of corn has a significant impact on the wheat market. Researchers have been interested in the twenty years 1992-2012 when the strongest influence on the price of wheat appeared at the international level (Chevallier and Ielpo 2013; Lahiani et al. 2013; Beckmann and Czudaj 2014).

It is necessary to point out that a variety of precious metals is seeing a spillover of this volatility. In particular, the metals are silver, copper, and platinum, while the literature reports that the influence appears mainly from 1992 to 2015 (Chevallier and Ielpo 2013). Finally, another commodity heavily impacted by the corn market is DDGS wheat. This product is a component of animal feed and adjusts its price proportionally to that of corn (Etienne et al. 2017). At this point, it is necessary to mention the existence of research gaps on corn market behavior. Therefore, the present bibliographic study proposes as a future action the investigation of the relationship between the stock markets and the price of agricultural goods. In this way, the ability of stock exchanges to shape the prices of various commodities is understood. Additionally, as a suggestion for future research, it is the engagement of scholars regarding the influence of exports on the corn market. It is necessary to point out that relevant research has been carried out on the effect of China's dominant export sectors and the price of soybeans.

3.10. Wheat

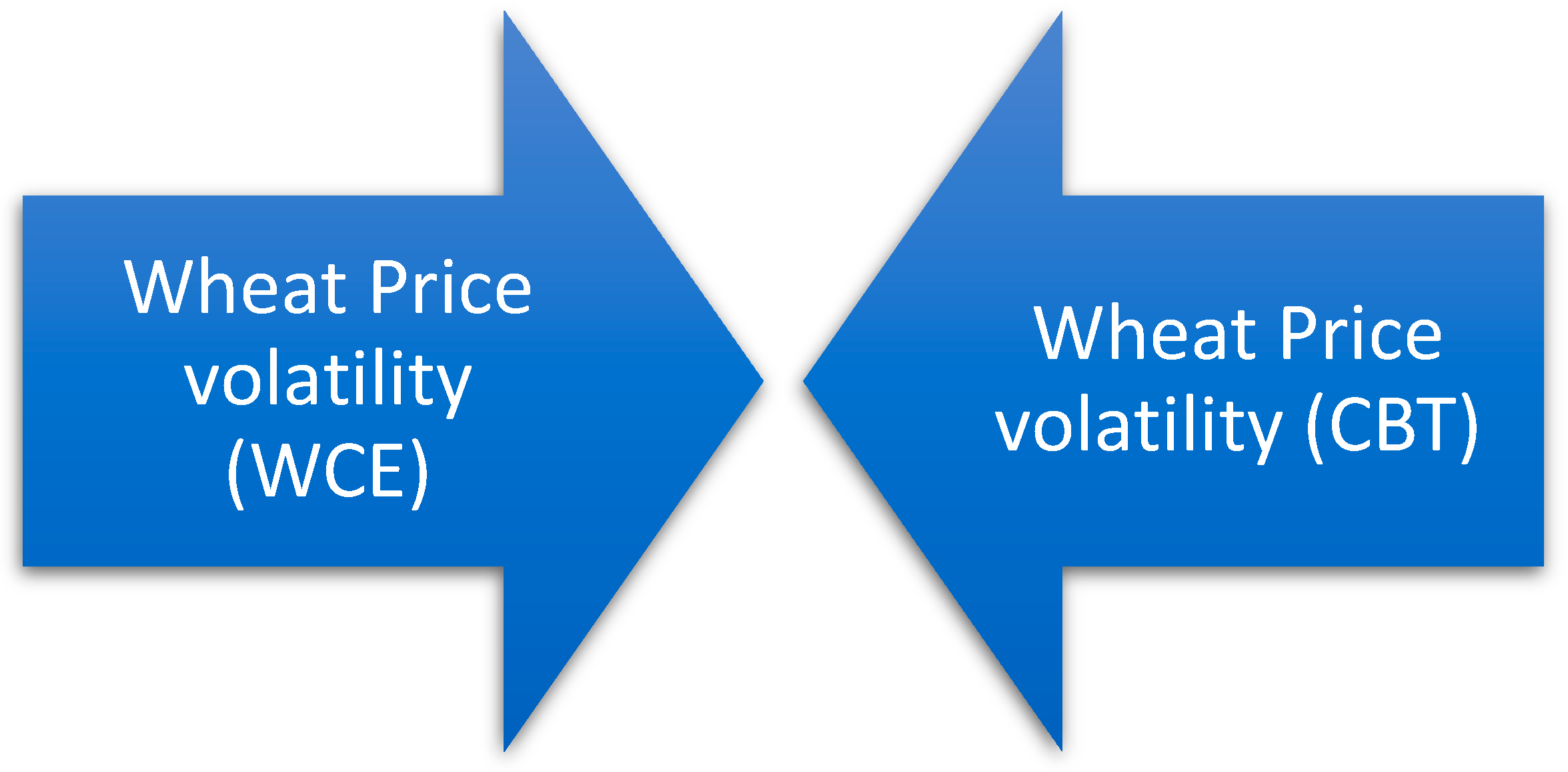

The last under-investigated commodity of the present bibliographic study is wheat. This specific agricultural good is of particular interest as its various markets interact with each other. As Figure 23 shows, wheat prices on the Winnipeg Commodity Exchange (WCE) and Chicago SRW Wheat Futures (CBOT) are affected both ways. The above markets are located in Canada and the USA, respectively, while this relationship takes place from 1980 to 1994 (Booth et al. 1998).

Figure 23.

Wheat price markets volatility and their inter-relationship.

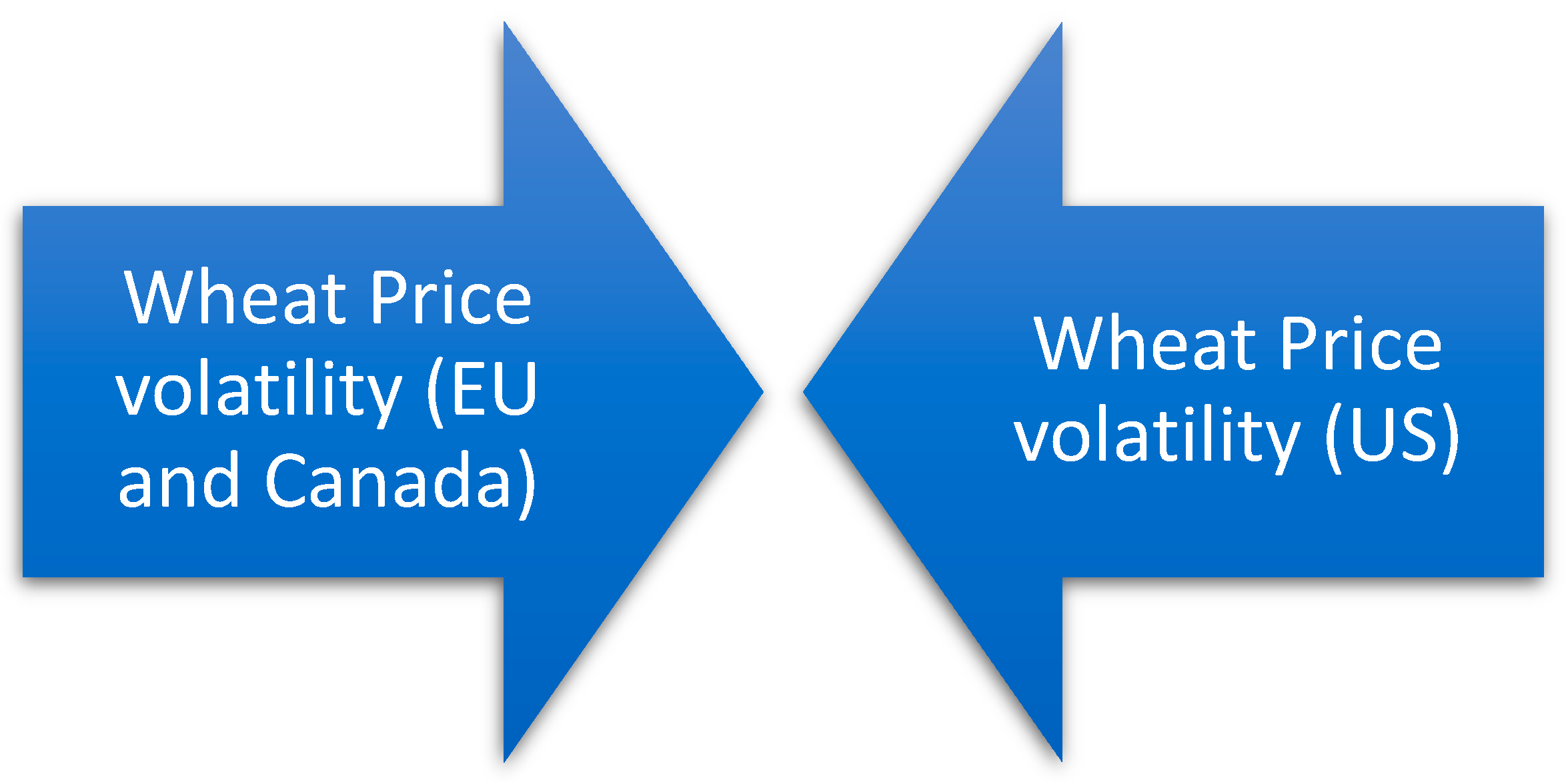

Figure 24.

Wheat price markets volatility and their inter-relationship across the globe.

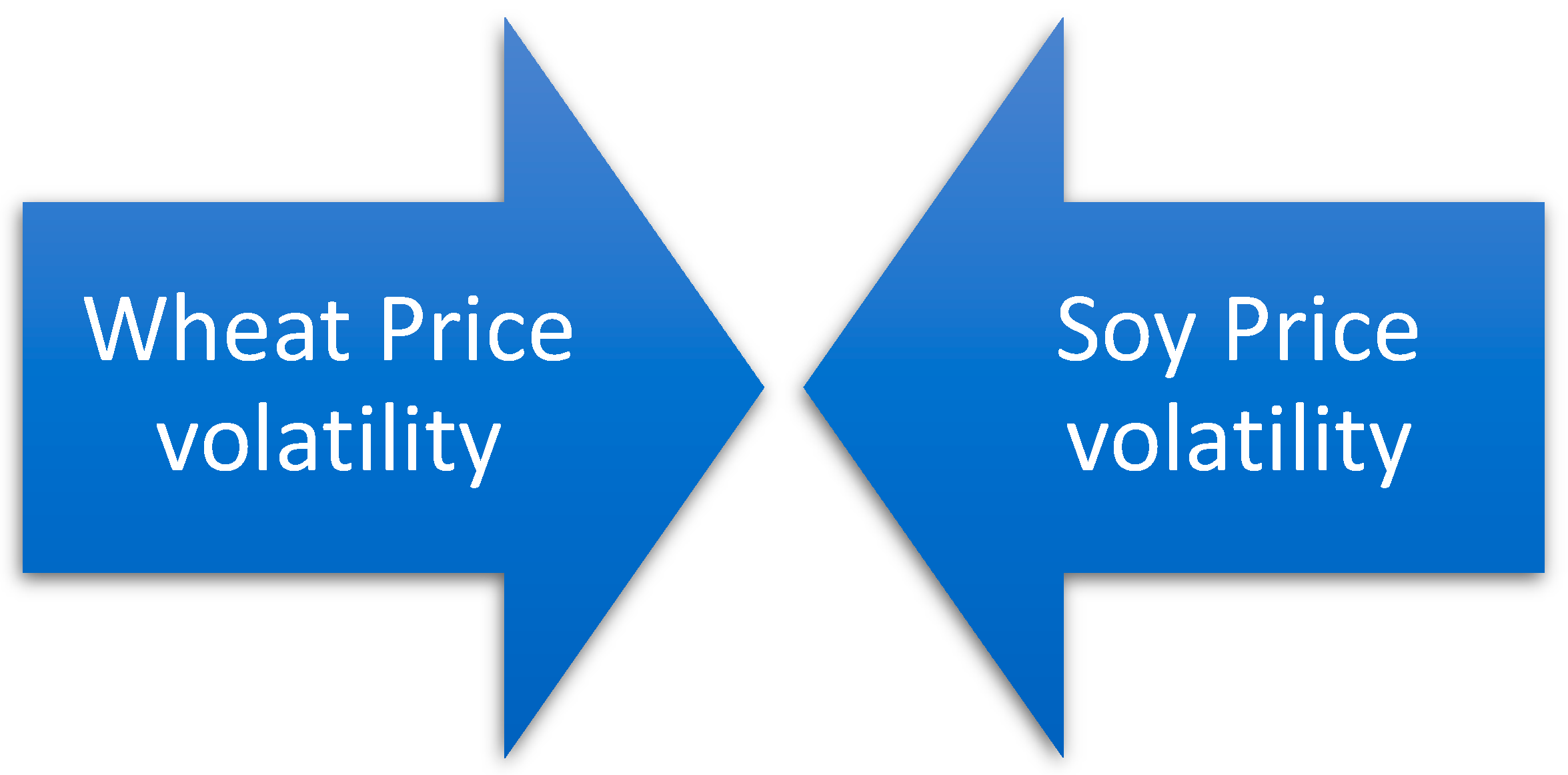

Figure 25.

Wheat Price volatility and its inter-relationship with the prices of other commodities.

The above correlation of Canadian and US wheat prices is changing. In particular, as can be understood from Figure 26, volatility spillover is now taking place from the European and Canadian markets to the US. At this point, it is important to note that the researchers detect this relationship only two years after the end of the above two-way effect, and it lasts for 6 years (Yang et al. 2003).

Additionally, Figure 24 illustrates the correlation shown by the wheat and soybean markets. The two specific agricultural products show a two-way relationship regarding their prices. In more detail, the researchers trace the above effect over time from 1999 to 2016, taking daily data (Bernhardt 2017; Hamadi et al. 2017).

Next, the relationship of wheat with certain precious metals is of particular importance. As shown in Figure 25, the price of gold and aluminum affects the wheat market. The literature dates this influence from 1992 to 2015 in global markets (Chevallier and Ielpo 2013). In addition, a significant cause of wheat price volatility is the mobility of the corn market. Specifically, various studies identify the effect of corn price on wheat, resulting in its volatility when examining the period 1992-2015 (Onour and Sergi 2012; Chevallier and Ielpo 2013; Lahiani et al. 2013; Beckmann and Czudaj 2014).

Another case of volatility spillover is seen from oil to wheat. In more detail, the volatile price of oil has a direct impact on the wheat market, while studies report that this process takes place for 32 years, i.e., from 1986 to 2018 (Du et al. 2011; Nazlioglu et al. 2013; Guhathakurta et al. . 2020; Yip et al. 2020). In addition, the effect of soybean oil on the price of wheat is noteworthy. In particular, the volatile price of the agricultural commodity due to the volatility of the oil market is strongly presented in the American markets. Scholars observe the above diffusion when investigating the period 1999-2015 (Hamadi et al. 2017).

Another important factor in changing the price of wheat is the news from the stock markets of America. Specifically, the literature reports that the wheat market in China is strongly pressured by news of financial institutions in the US when examining the years 1995-2001 (Fung et al. 2003). The exchange rate of the Canadian dollar (CAD) plays an important role in the volatility of the price of wheat. Researchers trace the above relationship from 2005 to 2020 (Nekhili et al. 2021). In addition, the fertilizer market has had a great influence on the price of the agricultural commodity from 1992 to 2011. In particular, fertilizers are considered essential tools in agricultural activity and, for this reason, possess the ability to shape the pricing policy of wheat as a product (Onour and Sergi 2012). Finally, government decisions regarding export procedures in Ukraine seriously affect wheat prices around the world. Therefore, the established restrictions of the state lead to the instability of the market of the specific good (An et al. 2016).

In conclusion, wheat price volatility affects some variables. However, as shown in Figure 26, the effects become apparent in very few cases. In more detail, the volatility spillover from the wheat market is shown in the price of crude oil. The literature highlights that the above energy was examined from 1985 to 2005 and from 2006 to 2016. However, the findings indicate that the price of wheat significantly depressed the market for the energy commodity after 2006 (Dahl et al. 2020). Additionally, at the stock market index level, the volatile wheat market can shape the producer price index. Specifically, researchers report that international wheat prices affect the producer price index when examining the years 2000-2011 (Hassouneh et al. 2017).

At this point, the research process on the behavior of the price of wheat presents some gaps. For this reason, the present bibliographic study proposes specific proposals for future research. In particular, it is worth studying the influence that the price of wheat may have on the DDGS product market. The product in question is used as an ingredient in animal feed and is based on wheat. For this reason, the investigation of this influence is considered necessary. In addition, the relationship of wheat with the S&P GSCI Wheat index is of particular interest. Thus, a check is made on the correlation of the stock market index to the price of wheat and vice versa.

4. Conclusion

The purpose of the present bibliographic study is to determine the causes and consequences of the volatility, which is presented by the prices of the goods of bulk ships. It is characteristic that there is a wealth of research on the behavior of the price of each product in international markets and long-term examination periods. The method of this particular investigation includes four steps. In more detail, these are the search, checking, and selection of academic articles and then recording the data in a table.

The results of the above research are clear and cover, to a high degree, the overall picture of commodity price volatility. Specifically, the relationship of the products under investigation with different goods, stock markets, and financial indicators is presented. Additionally, emphasis is placed on various political and economic events, which can change prices. It is also important to note that there are numerous variables, such as the exchange rate, the economic situation of a place, and the producing countries, which have a great correlation with the pricing of goods. Nevertheless, serious scientific gaps are highlighted when examining commodity price behavior. For this reason, suggestions for future research on each commodity are listed above.

References

- Ågren, M. Does Oil Price Uncertainty Transmit to Stock Markets? Uppsala University, Department of Economics: Uppsala, 2006. [Google Scholar]

- Amara, N.; Landry, R. Counting citations in the field of business and management: Why use Google Scholar rather than the Web of Science. Scientometrics 2012, 93, 553–581. [Google Scholar] [CrossRef]

- An, H.; Qiu, F.; Zheng, Y. How do export controls affect price transmission and volatility spillovers in the Ukrainian wheat and flour markets? Food Policy 2016, 62, 142–150. [Google Scholar] [CrossRef]

- An, S.; Gao, X.; An, H.; An, F.; Sun, Q.; Liu, S. Windowed volatility spillover effects among crude oil prices. Energy 2020, 200, 1–15. [Google Scholar] [CrossRef]

- Antonakakis, N.; Kizys, R. Dynamic spillovers between commodity and currency markets. International Review of Financial Analysis 2015, 41, 303–319. [Google Scholar] [CrossRef]

- Arfaoui, N.; Yousaf, I.; Jareño, F. Return and volatility connectedness between gold and energy markets: Evidence from the pre-and post-COVID vaccination phases. Economic Analysis and Policy 2023, 77, 617–634. [Google Scholar] [CrossRef]

- Arouri, M.E.H.; Jouini, J.; Nguyen, D.K. On the impacts of oil price fluctuations on European equity markets: Volatility spillover and hedging effectiveness. Energy Economics 2012, 34, 611–617. [Google Scholar] [CrossRef]

- Ashfaq, S.; Tang, Y.; Maqbool, R. Volatility spillover impact of world oil prices on leading Asian energy exporting and importing economies’ stock returns. Energy 2019, 188. [Google Scholar] [CrossRef]

- Balcilar, M.; Ozdemir, Z.A.; Ozdemir, H. Dynamic return and volatility spillovers among S&P 500, crude oil, and gold. International Journal of Finance and Economics 2021, 26, 153–170. [Google Scholar]

- Basak, S.; Pavlova, A. A Model of Financialization of Commodities. Journal of Finance 2016, 71, 1511–1556. [Google Scholar] [CrossRef]

- Batten, J.A.; Ciner, C.; Lucey, B.M. The macroeconomic determinants of volatility in precious metals markets. Resources Policy 2010, 35, 65–71. [Google Scholar] [CrossRef]

- Batten, J.A.; Ciner, C.; Lucey, B.M. Which precious metals spill over on which, when, and why? Some evidence. Applied Economics Letters 2015, 22, 466–473. [Google Scholar] [CrossRef]

- Beckmann, J.; Czudaj, R. Volatility transmission in agricultural futures markets. Economic Modelling 2014, 36, 541–546. [Google Scholar] [CrossRef]

- Behmiri, N.B.; Manera, M. The role of outliers and oil price shocks on volatility of metal prices. Resources Policy 2015, 46, 139–150. [Google Scholar] [CrossRef]

- Bernhardt, M. 2017. Return and Volatility Spillover Effects in Agricultural Commodity Markets. Salzburg, No. 2017–03.

- Booth, G.G.; Brockman, P.; Tse, Y. The relationship between US and Canadian wheat futures. Applied Financial Economics 1998, 8, 73–80. [Google Scholar] [CrossRef]

- Bouri, E.; Jain, A.; Biswal, P.C.; Roubaud, D. Cointegration and nonlinear causality amongst gold, oil, and the Indian stock market: Evidence from implied volatility indices. Resources Policy 2017, 52, 201–206. [Google Scholar] [CrossRef]

- Broadstock, D.C.; Li, R.; Wang, L. Integration reforms in the European natural gas market: A rolling-window spillover analysis. Energy Economics 2020, 92. [Google Scholar] [CrossRef]

- Candila, V.; Farace, S. On the volatility spillover between agricultural commodities and Latin American stock markets. Risks 2018, 6. [Google Scholar] [CrossRef]

- Chang, C.L.; Mcaleer, M.; Wang, Y. Testing Co-Volatility spillovers for natural gas spot, futures, and ETF spot using dynamic conditional covariances. Energy 2018, 151, 984–997. [Google Scholar] [CrossRef]

- Charoenthammachoke, K.; Leelawat, N.; Tang, J.; Kodaka, A. Business continuity management: A preliminary systematic literature review based on ScienceDirect database. Journal of Disaster Research 2020. [Google Scholar] [CrossRef]

- Chen, Y.; Qu, F.; Li, W.; Chen, M. Volatility spillover and dynamic correlation between the carbon market and energy markets. Journal of Business Economics and Management 2019, 20, 979–999. [Google Scholar] [CrossRef]

- Chevallier, J.; Ielpo, F. Volatility spillovers in commodity markets. Applied Economics Letters 2013, 20, 1211–1227. [Google Scholar] [CrossRef]

- Dahl, R.E.; Oglend, A.; Yahya, M. Dynamics of volatility spillover in commodity markets: Linking crude oil to agriculture. Journal of Commodity Markets 2020, 20. [Google Scholar] [CrossRef]

- Dai, Z.; Zhu, H. Time-varying spillover effects and investment strategies between WTI crude oil, natural gas, and Chinese stock markets related to the Belt and Road initiative. Energy Economics 2022, 108. [Google Scholar] [CrossRef]

- Dhamija, A.K.; Yadav, S.S.; Jain, P. Volatility spillover of energy markets into EUA markets under EU ETS: a multi-phase study. Environmental Economics and Policy Studies 2018, 20, 561–591. [Google Scholar] [CrossRef]

- Du, X.; Yu, C.L.; Hayes, D.J. Speculation and volatility spillover in the crude oil and agricultural commodity markets: A Bayesian analysis. Energy Economics 2011, 33, 497–503. [Google Scholar] [CrossRef]

- Dutta, A. A note on the implied volatility spillovers between gold and silver markets. Resources Policy 2018, 55, 192–195. [Google Scholar] [CrossRef]

- Dutta, A. Impact of silver price uncertainty on solar energy firms. Journal of Cleaner Production 2019, 225, 1044–1051. [Google Scholar] [CrossRef]

- Etienne, X.L.; Trujillo-Barrera, A.; Hoffman, L.A. Volatility spillover and time-varying conditional correlation between DDGS, corn, and soybean meal markets. Agricultural and Resource Economics Review 2017, 46, 529–554. [Google Scholar] [CrossRef]

- Etienne, X.L.; Trujillo-Barrera, A.; Wiggins, S. Price and Volatility Transmissions between Natural Gas, Fertilizer, and Corn Markets. Agricultural Finance Review 2016, 76, 151–171. [Google Scholar] [CrossRef]

- Ewing, B.T.; Gormus, A.; Soytas, U. Risk Transmission from Oil and Natural Gas Futures to Emerging Market Mutual Funds. Emerging Markets Finance and Trade 2018, 54, 1828–1837. [Google Scholar] [CrossRef]

- Ewing, B.T.; Malik, F. Volatility transmission between gold and oil futures under structural breaks. International Review of Economics and Finance 2013, 25, 113–121. [Google Scholar] [CrossRef]

- Ewing, B.T.; Malik, F. Volatility spillovers between oil prices and the stock market under structural breaks. Global Finance Journal 2016, 29, 12–23. [Google Scholar] [CrossRef]

- Fung, H.G.; Leung, W.K.; Xu, X.E. Information Flows Between the U.S. and China Commodity Futures Trading. Review of Quantitative Finance and Accounting 2003. [Google Scholar] [CrossRef]

- Gao, R.; Zhao, Y.; Zhang, B. The spillover effects of economic policy uncertainty on the oil, gold, and stock markets: Evidence from China. International Journal of Finance and Economics 2021, 26, 2134–2141. [Google Scholar] [CrossRef]

- Geng, J.B.; Ji, Q.; Fan, Y. How regional natural gas markets have reacted to oil price shocks before and since the shale gas revolution: A multi-scale perspective. Journal of Natural Gas Science and Engineering 2016, 36, 734–746. [Google Scholar] [CrossRef]

- Geng, J.B.; Xu, X.Y.; Ji, Q. The time-frequency impacts of natural gas prices on US economic activity. Energy 2020, 205. [Google Scholar] [CrossRef]

- Gong, X.; Liu, Y.; Wang, X. Dynamic volatility spillovers across the oil and natural gas futures markets based on a time-varying spillover method. International Review of Financial Analysis 2021, 76. [Google Scholar] [CrossRef]

- Gong, X.; Xu, J.; Liu, T.; Zhou, Z. Dynamic volatility connectedness between industrial metal markets. North American Journal of Economics and Finance 2022, 63. [Google Scholar] [CrossRef]

- Guhathakurta, K.; Dash, S.R.; Maitra, D. Period-specific volatility spillover-based connectedness between oil and other commodity prices and their portfolio implications. Energy Economics 2020, 85. [Google Scholar] [CrossRef]

- Guo, J. Co-movement of international copper prices, China’s economic activity, and stock returns: Structural breaks and volatility dynamics. Global Finance Journal 2018, 36, 62–77. [Google Scholar] [CrossRef]

- Haixia, W.; Shiping, L. Volatility spillovers in China's crude oil, corn, and fuel ethanol markets. Energy Policy 2013, 62, 878–886. [Google Scholar] [CrossRef]

- Hamadi, H.; Bassil, C.; Nehme, T. News surprises and volatility spillover among agricultural commodities: The case of corn, wheat, soybean, and soybean oil. Research in International Business and Finance 2017, 41, 148–157. [Google Scholar] [CrossRef]

- Hammoudeh, S.M.; Yuan, Y.; Mcaleer, M.; Thompson, M.A. Precious metals-exchange rate volatility transmissions and hedging strategies. International Review of Economics and Finance 2010, 19, 633–647. [Google Scholar] [CrossRef]

- Hassouneh, I.; Serra, T.; Bojnec, Š.; Gil, J.M. Modeling price transmission and volatility spillover in the Slovenian wheat market. Applied Economics 2017, 49, 4116–4126. [Google Scholar] [CrossRef]

- He, X.; Takiguchi, T.; Nakajima, T.; Hamori, S. Spillover effects between energies, gold, and stock: the United States versus China. Energy and Environment 2020, 31, 1416–1447. [Google Scholar] [CrossRef]

- El Hedi Arouri, M.; Jouini, J.; Nguyen, D.K. Volatility spillovers between oil prices and stock sector return Implications for portfolio management. Journal of International Money and Finance 2011, 30, 1387–1405. [Google Scholar] [CrossRef]

- El Hedi Arouri, M.; Lahiani, A.; Nguyen, D.K. World gold prices and stock returns in China: Insights for hedging and diversification strategies. Economic Modelling 2015, 44, 273–282. [Google Scholar] [CrossRef]

- Hegerty, S.W. Commodity-price volatility and macroeconomic spillovers: Evidence from nine emerging markets. North American Journal of Economics and Finance 2016, 35, 23–37. [Google Scholar] [CrossRef]

- Hu, H.; Chen, D.; Sui, B.; Zhang, L.; Wang, Y. Price volatility spillovers between supply chain and innovation of financial pledges in China. Economic Modelling 2020, 89, 397–413. [Google Scholar] [CrossRef]

- Ji, Q.; Fan, Y. How does oil price volatility affect non-energy commodity markets? Applied Energy 2012, 89, 273–280. [Google Scholar] [CrossRef]

- Ji, Q.; Geng, J.B.; Tiwari, A.K. Information spillovers and connectedness networks in the oil and gas markets. Energy Economics 2018, 75, 71–84. [Google Scholar] [CrossRef]

- Jiang, J.; Marsh, T.L.; Tozer, P.R. Policy induced price volatility transmission: Linking the U.S. crude oil, corn, and plastics markets. Energy Economics 2015, 52, 217–227. [Google Scholar] [CrossRef]

- Jiang, S.; Li, Y.; Lu, Q.; Wang, S.; Wei, Y. Volatility communicator or receiver? Investigating volatility spillover mechanisms among Bitcoin and other financial markets. Research in International Business and Finance 2022, 59. [Google Scholar] [CrossRef]

- Kang, S.H.; Mciver, R.; Yoon, S.M. Dynamic spillover effects among crude oil, precious metal, and agricultural commodity futures markets. Energy Economics 2017, 62, 19–32. [Google Scholar] [CrossRef]

- Kang, S.H.; Yoon, S.M. Dynamic spillovers between Shanghai and London nonferrous metal futures markets. Finance Research Letters 2016, 19, 181–188. [Google Scholar] [CrossRef]

- Kang, S.H.; Yoon, S.M. Financial crises and dynamic spillovers among Chinese stock and commodity futures markets. Physica A: Statistical Mechanics and its Applications 2019, 531. [Google Scholar] [CrossRef]

- Karali, B.; Ramirez, O.A. Macro determinants of volatility and volatility spillover in energy markets. Energy Economics 2014, 46, 413–421. [Google Scholar] [CrossRef]

- Khalfaoui, R.; Sarwar, S.; Tiwari, A.K. Analyzing volatility spillover between the oil market and the stock market in oil-importing and oil-exporting countries: Implications on portfolio management. Resources Policy 2019, 62, 22–32. [Google Scholar] [CrossRef]

- Kumar, S.; Pradhan, A.K.; Tiwari, A.K.; Kang, S.H. Correlations and volatility spillovers between oil, natural gas, and stock prices in India. Resources Policy 2019, 62, 282–291. [Google Scholar] [CrossRef]

- Kumar, S.; Singh, G.; Kumar, A. Volatility spillover among prices of crude oil, natural gas, exchange rate, gold, and stock market: Fresh evidence from exponential generalized autoregressive conditional heteroscedastic model analysis. Journal of Public Affairs 2022, 22. [Google Scholar] [CrossRef]

- Lahiani, A.; Khuong Nguyen, D.; Vo, T. Understanding Return And Volatility Spillovers Among Major Agricultural Commodities. The Journal of Applied Business Research 2013, 29, 1781–1790. [Google Scholar] [CrossRef]

- Lee, H.B.; Park, C.H. Spillover effects in the global copper futures markets: asymmetric multivariate GARCH approaches. Applied Economics 2020, 52, 5909–5920. [Google Scholar] [CrossRef]

- Lin, B.; Li, J. The spillover effects across natural gas and oil markets: Based on the VEC-MGARCH framework. Applied Energy 2015, 155, 229–241. [Google Scholar] [CrossRef]

- Liu, X.; Cheng, S.; Wang, S.; Hong, Y.; Li, Y. An empirical study on information spillover effects between the Chinese copper futures market and spot market. Physica A: Statistical Mechanics and its Applications 2008, 387, 899–914. [Google Scholar] [CrossRef]

- Luo, J.; Ji, Q. High-frequency volatility connectedness between the US crude oil market and China’s agricultural commodity markets. Energy Economics 2018, 76, 424–438. [Google Scholar] [CrossRef]

- Ma, K.; Diao, G. Study on Spillover Effect between International Soybean Market and China’s Domestic Soybean Market. Ensayos Sobre Politica Economica 2017, 35, 260–266. [Google Scholar] [CrossRef]

- Maghyereh, A.I.; Awartani, B.; Tziogkidis, P. Volatility spillovers and cross-hedging between gold, oil, and equities: Evidence from the Gulf Cooperation Council countries. Energy Economics 2017, 68, 440–453. [Google Scholar] [CrossRef]

- Malik, F.; Hammoudeh, S. Shock and volatility transmission in the oil, US, and Gulf equity markets. International Review of Economics and Finance 2007, 16, 357–368. [Google Scholar] [CrossRef]

- Manisha, D. Study in Copper Price Linkage Between International and Indian Commodity Market. International Journal on Recent Trends in Business and Tourism 2017, 1, 49–53. [Google Scholar]

- Mensi, W.; Al-Yahyaee, K.H.; Hoon Kang, S. Time-varying volatility spillovers between stock and precious metal markets with portfolio implications. Resources Policy 2017, 53, 88–102. [Google Scholar] [CrossRef]

- Mensi, W.; Beljid, M.; Boubaker, A.; Managi, S. Correlations and volatility spillovers across commodity and stock markets: Linking energies, food, and gold. Economic Modelling 2013, 32, 15–22. [Google Scholar] [CrossRef]

- Mensi, W.; Hammoudeh, S.; Nguyen, D.K.; Yoon, S.M. Dynamic spillovers among major energy and cereal commodity prices. Energy Economics 2014, 43, 225–243. [Google Scholar] [CrossRef]

- Mensi, W.; Rehman, M.U.; Vo, X.V. Dynamic frequency relationships and volatility spillovers in natural gas, crude oil, gas oil, gasoline, and heating oil markets: Implications for portfolio management. Resources Policy 2021, 73. [Google Scholar] [CrossRef]

- Mensi, W.; Tiwari, A.; Bouri, E.; Roubaud, D.; Al-Yahyaee, K.H. The dependence structure across oil, wheat, and corn: A wavelet-based copula approach using implied volatility indexes. Energy Economics 2017, 66, 122–139. [Google Scholar] [CrossRef]

- Mensi, W.; Vo, X.V.; Kang, S.H. COVID-19 pandemic’s impact on intraday volatility spillover between oil, gold, and stock markets. Economic Analysis and Policy 2022, 74, 702–715. [Google Scholar] [CrossRef] [PubMed]

- Moher, D.; Liberati, A.; Tetzlaff, J.; Altman, D.G.; PRISMA Group. Preferred reporting items for systematic reviews and meta-analyses: the PRISMA statement. Annals of internal medicine 2009, 151, 264–269. [Google Scholar] [CrossRef] [PubMed]

- Nazlioglu, S.; Erdem, C.; Soytas, U. Volatility spillover between oil and agricultural commodity markets. Energy Economics 2013, 36, 658–665. [Google Scholar] [CrossRef]

- Nazlioglu, S.; Soytas, U.; Gupta, R. Oil prices and financial stress: A volatility spillover analysis. Energy Policy 2015, 82, 278–288. [Google Scholar] [CrossRef]

- Nekhili, R.; Mensi, W.; Vo, X.V. Multiscale spillovers and connectedness between gold, copper, oil, wheat, and currency markets. Resources Policy 2021, 74. [Google Scholar] [CrossRef]

- Oliyide, J.A.; Adekoya, O.B.; Khan, M.A. Economic policy uncertainty and the volatility connectedness between oil shocks and metal market: An extension. International Economics 2021, 167, 136–150. [Google Scholar] [CrossRef]