Submitted:

11 May 2024

Posted:

13 May 2024

You are already at the latest version

Abstract

In this research, the primary goal was to investigate the relationship between strategic planning and organizational performance in Iraq's manufacturing context. The study's primary data sources were 360 manager respondents. The structured questionnaire was used to collect primary data from manufacturing firms located throughout Iraq. To analyze the result, the researcher used descriptive statistics, correlation, and multiple regression analysis. SPSS version 16 software was used to conduct data analysis. The result reveals that the process of strategic planning has a beneficial effect on financial performance. Environmental scanning has a statistically significant positive effect on a company's non-financial performance. Management participation and planning formality positively and statistically significantly affect a business's non-financial performance at the 10 percent level. The domain of strategy and technique has not impacted the company's non-financial performance.

Keywords:

Organization Performance 1

; Manufacturing Sector 2

; Planning Formality 3

; Strategic Techniques 4.

1. Introduction

When we look at this phenomenon's strategic thinking, we notice that it has gone through many phases and has worked its way through different semantic contexts. The word "strategy" has had several meanings throughout the millennium. However, it still maintains the semantic roots of its original meaning. Strategy originally grew out of the practice of commanding or leading armies during war and represented military campaigns. It was first used in war as a tool for success and for claiming victory. It was only afterward applied to other realms and domains of human relations, such as political, economic, and business settings. Although the term "strategy" is widely used, there is no universally accepted definition of the term. Thus, its essence is context- and person-dependent; its meaning varies according to the individual. Sun Tzu's "The Art of War," regarded as the world's oldest military treatise, has been translated by Giles and Tzu (2005)[1]. Alkhafaji & Nelson (2013)[2] note that strategy is a fast and accurate response to environmental changes; it is not a specific action plan. So, many disciplines have started using the term "strategy," including the business management industry. Young (2001)[3] noted that establishing long-term goals and core objectives for an enterprise, deciding courses of action, allocating resources needed to carry out these plans, and so on are crucial to success. They focused on large corporations and how their expansion was addressed by instituting new administrative structures. The study also covered the change in a firm's strategic positioning and how it affects administrative structure adjustments across the various organizations. They have gotten much scholarly attention because of this interpretation, which has helped propel the field forward.

Palia (1979)[4], describing the "nature of the organization," found the "common thread" in organizations' product-market-activities strategies as being the focal point of the organization's operations. The author pointed out two main points: first, a strategy is the "unifying thread" of a given organization, whose main activities align with one another; and second, a strategy is supposed to create differences between competing companies.

Drucker (1954)[5] focused on the concepts that made the most contributions to the literature on strategy and created viral management texts such as Corporate Strategy. William Newman (1951) may have been the first person to use the term "strategy." However, there is some debate about whether Newman originated the term or simply popularized an existing concept. Porter (1996)[6] argues that the firm's strategy tool is needed to separate it from competitors and create and maintain an advantage. Strategy is about being unique and engaging in activities that your competitors are unlikely to have the stomach for. He stated that strategy enables organizations to undertake activities that are dissimilar from those of their competitors.

Fuertes et al. (2020)[7] define strategy as "a plan of action, a set of guidelines to deal with a situation that explains how a firm reaches its desired position from its current state." In the definition of strategy as a pattern, strategy is consistent behavior, even if it's not meant to be that way. Strategy can be defined as the mediating force between an organization and its environment because it positions an organization by locating it in an environment. The strategy is based on long-term targets that a company defines. Strategy is an in-depth plan that provides a path for how an organization can accomplish its mission and goals Plowman & Wilson (2018)[8]. The organization's overall strategy should consider its operational divisions; it should be broad, allowing for high strategic direction, and the plans for each operational division should be compatible. The definition of the strategy being used for this research is taken from Tien (2019)[9].

Joakim Björkdahl (2020)[10] argued that manufacturing has the characteristics of a development engine for growth, a fast return on investment, rapid technological advancement, and an increased return on investment due to growth. While only about 10% of the economy today, Iraq's industrial sector is expected to contribute significantly to the country's earnings from foreign exchange, the development of micro and small businesses, the growth of the domestic product, and employment opportunities.

In this research, the researcher dedicated himself exclusively to privately-owned manufacturing firms that are found in Iraq. Studies often include companies of different sizes, and this study is no exception. The research concentrates on the relationship between the strategic planning domain and the organizational performance domains. The study employs a cross-sectional study design, allowing data to be collected in a single visit. The researcher in this study focused on strategic planning and how it influences manufacturing companies' performance in developing countries, especially in Iraq. As the government hopes to industrialize Iraq, the manufacturing sector's performance is necessary. The study's results will influence both business and government policies to help corporations perform better. Along with the variables that require attention, the study identified potential planning and strategy implementation barriers, making the findings applicable to businesses operating in similar contexts, such as manufacturing, as they demonstrate how to optimize performance. They believed their study's results would help in the making of strategic planning-related policies. Nonfinancial performance, which other researchers have overlooked, will also be examined. So far, this research has aided strategic planning studies and serves as an excellent foundation for future researchers.

2. Literature Review

2.1. Strategic Planning

In this research, strategy implementation is assessed by making the strategic plan happen. There are multiple ways to form strategies, including implicit and explicit. Zerfass et al. (2018)[11] argue that implicit strategy formation is more successful, while other scholars argue that explicit strategy formation is preferable. They claim that there is no official strategic planning within an organization and that strategy should only be developed in exceptional circumstances. While strategies are normally classified as intentional or emergent, there are exceptions to the rule. Emergent strategies are responses to unexpected occurrences that are built without a plan and happen in the middle of strategy implementation Candido & Santos, (2019)[12]. Differences are possible as the designed strategy was not fully implemented, meaning that strategy is dependent not only on design but also on actual action. According to Shu (2017)[13], emergent and deliberate strategies are both successful business strategies that include the component of emergent strategy. A firm's long-term strategy will only benefit if it is developed through an intended strategy. Unplanned strategies, however, are neutral for the company.

Bryson et al. (2018)[14] have carried out their research and found a connection between strategic planning and organizational performance. In their study, Hopkins and Hopkins (1997)[15] used seven components to measure strategic planning and discovered that each component affected the planning process in terms of how the manager emphasized each component in implementing the company's strategy. The study concluded that financial performance increases when strategic planning is implemented. Additionally, the strategic planning process settled how managerial and organizational factors influenced the outcomes. Baker (2003)[16] investigated the connection between planning, its strategic and operational divisions, and business performance with data from the California executives of five food industries. It was found that an organized, strategic planning process was positively correlated with good financial performance.

French et al. (2004)[17] conducted a study on strategic planning in small professional service firms in Australia. The businesses in the study were placed into non-planning, informal planning, formal planning, and sophisticated planning categories, with no discernible differences being found in firms of similar sizes and incomes. A significant relationship emerged, proving the correlation between net profit and informal planning.

Gibson & Cassar (2005)[18] looked at small Australian businesses over a long period to find the connections between planning and success. According to the findings, those who did not use planners (which complemented a firm's strategy) consistently outperformed their counterparts. The researchers theorized that a firm's introduction of planning only follows a period of growth and never precedes it.

Falshaw et al. (2006)[19] examined the relationship between formal strategic planning and businesses. On a Likert scale, data for the study was collected from senior employees at various companies. It was found that subjective performance was not connected to the level of organizational planning process formality. Kraus et al. (2006)[20]: Strategic planning in Austrian small businesses the authors believe that proper planning is far more important than other aspects of firm management like time horizon, strategic instruments, and control. Glaister et al. (2008)[21] assessed the impact of formal strategic planning on the performance of Turkey's most prominent manufacturing companies. The study looked at factors such as environmental turbulence, organizational structure, and firm size and their impact on the link between formal strategic planning and performance. It was a conversational approach to plan delivery, with executive decision-making and plan creation left to the executives' discretion. The research concluded that successful strategic planning helps a company's performance.

Kori et al. (2020)[22] tried to determine if strategic planning affects financial and nonfinancial performance in a business. Many empirical studies on the relationship between strategic planning and financial performance (Nambirajan & Prabhu, 2010[23], Wolf & Floyd, 2017[24], George et al., 2019[25]) suggest that the strategic planning construct can be measured as a single dimension, like a formal process.

The literature review favors a relationship between strategic planning and performance. Nearly all the research in this report shows strong evidence that strategic planning boosts company performance. Several studies on various corporate environments and geographic locations were supported, conducted among various organizations and sectors, and across various levels of employees Anwar & Shah, (2021)[26]. Other researchers have discovered beneficial relationships using various financial and environmental indicators, such as success in the financial markets Judge & Douglas, (1998)[27] and employee development Kraus et al., (2006)[20]. Strategic planning is one of the constructs that comprises four dimensions: environmental scanning, management participation, planning formality, and strategic techniques.

2.2. Environmental Scanning

As per Ivancic et al. (2017)[28], "environmental scanning" is the examination, organization, and distribution of external trends. The information gathered from environmental scanning helps people decide whether to enter a market or not. Chang (2018)[29] described environmental scanning as assimilating external factors. Management should begin strategic planning by "scanning the environment, analyzing competitive activity, assessing strengths and weaknesses, and identifying and evaluating alternative courses of action" Aldehayyat & Twaissi (2011)[30].

Ramanujam & Venkatraman (1987)[31] have research on planning system characteristics and planning effectiveness by companies. In this research, a canonical correlation analysis was used to determine the relationship between planning system characteristics and planning effectivenessnonical correlation analysis was used to determine the relationship between planning system characteristics and planning effectiveness. The following are the two characteristics of the organizational context of planning and four internal, external, and functional and technique planning systems characteristics studied. The single respondent from each organization provided the data for the study. They found that how a company's executives were focused on the outside world influenced the planning process. The researcher's report noted that response bias could have been present in individual responses.

The strategic planning process of banks in the United States was examined Hopkins & Hopkins,(1997)[15]. They looked at the effects of environmental factors. The study concluded that environmental factors did not influence the severity of a bank's strategic plan, contrasting the results of other researchers. Their plausible explanation is that environmental concerns played a minor role in strategic planning. Environmental perceptions were so similar that environmental interests had little room to influence bank decisions.

Al Khattab et al. (2012)[32] conducted research on the strategic planning process. Its connection to hotel organizational success was examined using Jordanian hotels as the sample. This study used various dimensions, like internal and external environmental scanning, strategic techniques, management participation, functional coverage, and a time horizon, to measure the latent variable known as strategic planning. They concluded that external environmental scanning was used more than internal scanning in all four- and five-star hotels during the strategic planning process. Many studies on strategic planning have concluded that corporations should include environmental factors in their planning strategy. The current study on internal environmental scanning is important because the internal environment affects strategic planning and a firm's performance.

2.3. Planning Formality

Gkliatis and Koufopoulos (2013)[33] have conducted studies in Greek five-star hotels about the formal strategic planning process. In their studies, the nature and use of the planning process were determined by using the following six items: the formal process used, the existence of an individual or group prime responsible for coordinating planning, the extent to which top management creates a conducive environment, a formal statement about the business's direction, if planning is done with the use of company plans, and how company plans are used to evaluate management performance. The researchers discovered a high level of planning formality, which they believe indicates a manager's desire to follow through on plans regularly.

2.4. Strategic Techniques

Different scholars provide some definitions to clarify the meaning of various strategic tools, as no clear definition exists. Clark (1997)[34] claimed that some decision-making strategies include techniques, analytical frameworks, approaches, and methodologies. The author discovered that the management literature lacks a complete description of strategic management tools. The argument is backed by the fact that fourteen studies have investigated formal strategic planning. The studies reviewed had a significant issue with the planning strategy's description, as described by the author. Finally, the author concluded that "we cannot tell if strategic planning is scientifically valuable unless we know the techniques used" Al-Surmi et al., (2020)[35].

Knott (2006)[36], a strategy tool, describes different methods, ideas, and concepts that can guide strategic thinking and management. Managers find the tools of the strategic management process to be useful guidance and a point of departure. Strategic tools have an impact on an organization's strategic communication because they "drive the emphasis on strategy from external factors, such as competition and environmental uncertainty, to internal factors, such as team motivations and personal histories, allowing leaders to use these tools in their own best interests and thus adding value for the organization" Darvishmotevali et al. (2020)[37].

Phillips and Moutinho (1999)[38] employed analytical methods and five other factors to examine UK hotels' strategic planning outcomes. This method included long-term goals, planned strategy, current operational performance, financial coverage, and strategic planning staff assistance. The study's results led to the creation of a diagnostic tool that aids in hotel planning. A technique in addition to six critical factors was discovered when researching what makes for successful planning.

Gunn & Williams' (2007)[39] investigation into the identification of strategic tools took place at UK companies. A strategic planning study was conducted. The respondents were asked how frequently they utilize each of the various strategic tools. The survey results revealed that SWOT was ranked first by respondents, with benchmarking following closely behind. The researchers concluded that strategists should not use only one strategic tool, as different tools could help look at a broader range of options. Efendioglu & Karabulut (2010)[40] investigated privately owned large Turkish firms to discover if incorporation tools improved business performance. Even though the researchers exposed several relationships between tools and performance, they still did not go beyond claiming that this connection exists at the end of the day. The findings indicate that Turkey, a transitional economy, has seen a noticeable rise in strategic tools and processes. It is unclear whether or not using these tools affects a company's performance.

2.5. Management Participation

Management involvement has been interpreted in various ways. To understand how employees in a firm feel about the development of their organizations, it is specified that the presence of "participation" is when individuals at a higher level in the firm provide visible extra roles or role-expanding opportunities for individuals or groups at a lower level to have a greater voice in the organization Sung & Choi (2018)[41].

Kaur et al. (2018)[42] also looks at middle management's involvement in the planning process for banks and manufacturing companies. Their analysis involves five processes: identifying and setting objectives, suggesting and evaluating options, making operational details, moving forward, and making decisions. Management participation was looked at from many different angles in this research in comparison to other studies. Thus, their findings were that having middle-level managers participate in strategy formulation ensures they comprehend the goals.

There have been efforts to understand the role management plays in the strategic planning process. Elbanna (2008)[43], in his study of an Egyptian company's board members, CEOs, and various middle-level management groups, asked them to rate the degree to which senior management, including boards, CEOs, and various middle-level management groups, were able to influence the strategic planning process. Researchers discovered that manager participation had no effect on business strategy.

Ugboro et al. (2010)[44] conducted research to learn how top-down strategic planning impacts the effectiveness of strategic planning in public transit organizations where a top-down approach is used. The research uncovered that strategic planning was positively linked to top management. This research found that the strategy-development process was positively associated with management's role in strategic planning. Studies on the impact of middle-level management participation in strategic planning show a positive role for them in the process Linder & Sax (2020[45]). Elliott et al. (2020)[46], examining top management's involvement in the strategic planning process along with middle-level management participation, would yield more significant results. Therefore, the evaluation considers management participation from four perspectives: consideration and explanation of strategic issues, creation of strategic proposals, determination of which proposals to pursue, and making choices about strategic proposals.

2.6. Organizational Performance

A company's success is built on the outcomes of individual or group efforts within it. Performance is a company's ability to acquire and distribute resources in various manners to obtain a competitive advantage Udriyah et al., (2019)[47]. The use of organizational performance in strategic management studies shows the strength of strategic planning George et al., (2019)[25]; Bu et al., (2020)[45]. Omran et al. (2021)[48] note that there are two types of performance that researchers have noticed: financial performance and non-financial performance. Variables relevant to financial statements will be emphasized in business performance.

2.7. Financial Performance

When used to measure financial performance in larger companies, Lee et al. (2009)[49] discovered that traditional accounting measures focused on financials underperformed. Many experts now argue that this system, which is described in many published works, neglects essential elements of an advantage such as the workforce, innovation, and leadership Reuvers et al., (2008)[50]. It was also never meant to measure the entire organization's success Bucklin & Sengupta, (1993)[51]. Abdel-Basset et al. (2020)[52] say that firms' financial measures are accurate, though easy to obtain.

2.8. Nonfinancial Performance Measures

Nonfinancial performance measures, as opposed to traditional organizational performance metrics, provide more timely information that is less susceptible to manipulation and thus more relevant to the business Davies & Boczko, (2005)[53]. We concentrated on both financial and nonfinancial performances to exploit the benefits of both kinds of measurement. Researchers in strategic planning are staying true to their recommendations despite widespread criticism for recommending only conventional financial performance be studied and leaving out nonfinancial issues. Including non-financial performance metrics was discovered to be worth studying. There is scarce empirical evidence in developing countries, making it challenging to research the issue, which is probably just as important in developed countries. It is discovered that researching the context of developing countries is vital. As Miller (2018)[54] suggested, it is the process of planning that is important, rather than the plan itself. Therefore, this research recommends including the strategic planning process perspective in future studies of strategic planning. Strategic planning procedures have all been scrutinized because they examine the formalities of planning, the management's participation, environmental scanning, and the strategic techniques used to generate company strategies. Thus, this study filled the existing literature gap by resolving several possible causes of conflicting results. to achieve each of the study's research objectives. Is there a link between strategic planning and the company's financial and non-financial performance?

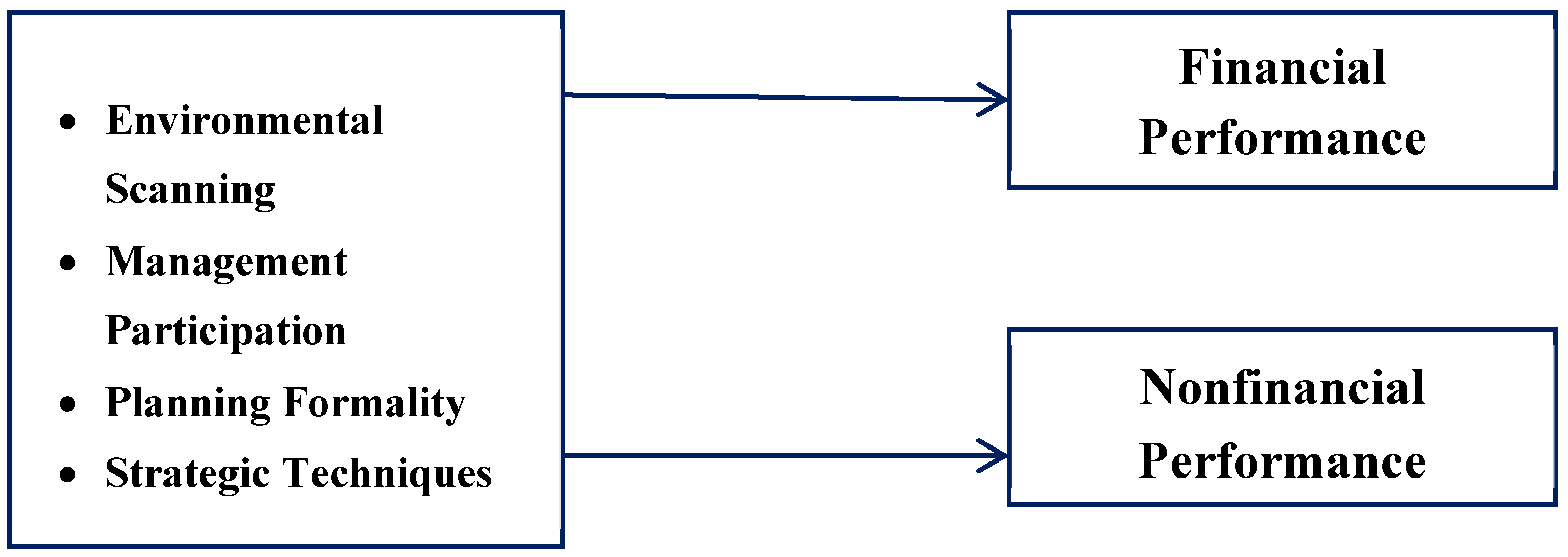

Figure 1.

Conceptual Framework.

Therefore, the four variables displayed on the conceptual framework as independent variables made the study meaningful to evaluate the dependent variable of organizational performance. Moreover, organizational performance was evaluated from both a financial and non-financial perspective, as shown in the above conceptual framework model.

2.9. Objective

The study's overall goal was to look into the link between strategic planning and the performance of manufacturing companies. The study's main objective is to find out the relationship between strategic planning and the performance of financial and non-financial companies. Several scholars have discussed the relationship between strategic planning and organizational performance, but findings are conflicting (Shrader et al.,(1984)[55]; Akinyele & Fasogbon, (2010)[56]; Arasa & Obonyo, (2012)[57]; George et al., (2019)[25]; Zhao et al., (2021)[58]. Strategic planning can improve performance, but it's not a prerequisite; some believe it is just a waste of time. Others believe planning has a minimal effect on performance (Capon et al., 1994). Some see a negative relationship between planning and performance Gibson & Cassar, (2005)[59]. Based on the above literature review, the researcher formulated the hypothesis.

H1:

There is a positive relationship between strategic planning and financial performance.

Another hypothesis of this study was to discover whether there is a correlation between strategic planning and nonfinancial company performance. Based on the existing research, the researcher formulated the hypothesis. In light of that, it is based on a resource-based view when discussing the theoretical framework for the hypothesis that ties strategic planning to nonfinancial performance. A resource-based view considers how a company utilizes its internal assets to obtain an advantage. In meta-analysis, research on strategic management studies has revealed that the resource-based view has emerged as the primary and influential foundation Barney, (1995)[60]; Crook et al., (2008)[61]. The non-financial performance showed a positive relationship Rudd et al., (2008)[62]; Fullerton & Wempe, (2009)[63].

H2:

There is a positive relationship between strategic planning and nonfinancial performance.

3. Research Methodology

3.1. Independent Variables and Their Measurement

To better understand how this model is to be used, experts in the field have thoroughly investigated the concept of strategic planning and divided it into four dimensions: environmental scanning, management participation, level of formality, and techniques employed in the planning. The department's strategic planning process is essential, as it serves as a foundation for implementation. The initial test of its influence on strategic environmental scanning had nine items. In order to know the extent to which strategic planning places emphasis on various topics, the respondents were asked to choose an option between "a lot more emphasis" and "a lot less emphasis" on a scale from 1 to 5. The environmental assessment evaluation was adapted from the original Aldehayyat & Twaissi, (2011)[30].

The following questions were designed to discover how actively managers were involved in department planning. They were asked to place on a five-point Likert scale, ranging from "strongly participating" to "not participating at all," their assessment of the amount of time and effort top management would put into producing a strategic plan. The framework for measuring senior management's involvement came from Aldehayyat and Twaissi (2011)[30].

The third round of questions examined the formality of the planning. Participants were also requested to evaluate how formally strategic planning is executed as described by various categories such as consensus, "deep, iterative, and timely exploration of issues," identifying complex dependencies, constructing coherent scenarios, and making sound investments and planning" on a five-point Likert scale ranging from strongly agree to strongly disagree Glaister et al., (2008)[21].

The last group of questions pertains to the planning-process tactics utilized by companies. On a five-point Likert scale, ranging from "extremely important" to "not familiar with," the respondents were asked to identify how important possible strategy techniques are. This scale was based on previously published works like Elbanna (2010)[64] and Aldehayyat & Twaissi (2011)[30].

3.2. Dependent Variables and Their Measurement

The financial performance evaluation included a numerical, subjective measurement of four items. ROA, ROE, annual sales, and the number of employees, including long-term employees, from the past three years the companies each supplied data for the performance measurement. Consequently, the researcher has chosen to gauge the firms' financial results using the top and upper-middle management's assessment of the situation used in creating the scale Hornsby, (2002)[65].

Subsequently, the respondents were asked to provide a subjective, numerical evaluation of the company's nonfinancial performance on ten performance measurement items because the traditional financial-based evaluation is recognized as an important practice to support. Respondents were asked how each company performed in nonfinancial terms. The questionnaire utilized the Elbanna (2010)[64] Balanced Scorecard scale, which allowed participants to check off their corporate opinion on a 5-point Likert scale consisting of 10 items (including the categories of customer, internal business, and learning and growth perspectives). "Excellent" is at one end of the scale, while "very poor" is at the other.

3.3. Research Design and Methodology

This research centered on private manufacturing firms situated in the Kurdish part of the country. The study included a range of manufacturing businesses, from small to large. The study had respondents among both top-level managers and upper-middle-level managers. In this research, almost nine out of ten people (87.8%) returned their questionnaires to us, which we can use for our analysis. Therefore, the 360 participants will be able to provide relevant results with the various multivariate analysis types that are being used to fulfill the research's objective. Based on the experience required to participate in the study, participants must have worked in a managerial position for four years or more. To accomplish the goals of the research, the researcher collected data using a quantitative method.

A survey developed by the researchers and administered to department managers and top-level managers of manufacturing companies in Iraq was made up of both open-ended and closed-ended questions. It was also possible to clear up any confusion the respondents had because the researcher could present herself to them in person to help answer their questions. The questionnaire included four sections to provide comprehensive data in order to answer the research's primary research question. Section A included basic demographic information; Section B was dedicated to strategic planning; Section C dealt with questionnaires that measured the manufacturing companies' subjective financial performance; and Section D focused on how well they perform on a nonfinancial level. The appropriate parametric statistical techniques were used to analyze and process the previously classified and gathered information. The researcher utilized descriptives, test reliability, correlation, and multiple regression to complete their statistical findings.

Multiple linear regression analysis is used to solve estimation problems that have three or more variables. We use the Ordinary Least Squares method to solve this problem (OLS). The relationship between a dependent variable and a set of independent variables can be estimated using this model.

The model created for this problem is shown in the equations below.

Organizational Performance = α0+ β1 Environmental Scanning + β2 Management Participation + β3Planning Formality+ β4Strategy Technique +ε ……………………. (1)

Were

α0 represents intercept

β1, β2, β3,……… βn represent the parameters to be estimated

ε represent the error term

β1, β2, β3,……… βn represent the parameters to be estimated

ε represent the error term

For statistical analysis, the researcher used SPSS version 16.

3.3. Analysis

This section aims to measure the relationship between manufacturing companies' strategic planning and organizational performance in Iraq. The study's research model defines strategic planning as one of its dimensions, and that is because the research model includes environmental scanning, management participation, planning formality, and strategic techniques. It refers to the departments of a company on which external factors may have an impact on the company's performance. Measures of management participation determine the involvement of upper-level management in department planning, and planning formality investigates the formality of the planning process. The techniques used to form the strategic plan are found in the strategic tool.

3.4. Reliability Test

The degree to which a measurement of a phenomenon produces a stable and consistent result is referred to as its reliability Carmines and Zeller, (1979)[66]. Reliability is also concerned with the ability to reproduce results. A scale or test is said to be reliable if it consistently produces the same result when repeated measurements are taken under the same conditions Moser and Kalton, (1989)[67]. Testing for reliability is necessary because it refers to the consistency of a measuring instrument's performance across its various components Taherdoost, (2016)[68]. When using Likert scales, it is generally considered to be the most appropriate measure of reliability to use Whitley & Kite (2012)[69]. In this research work, the researcher applied a reliability test to measure the internal consistency of the strategic planning and organizational performance constructs shown in the table below.

Table 1.

Cronbach’s Alpha value for Strategic Planning constructs.

| Sl. No | Constructs | Cronbach's Alpha if Item Deleted | Cronbach’s alpha Value |

|---|---|---|---|

| Environmental Scanning | |||

| 1 | Examining previous results | .834 | .849 |

| 2 | Examining the causes of previous failures | .836 | |

| 3 | Trends in customer/end user behavior are examined. | .838 | |

| 4 | Internal Capabilities Assessment | .834 | |

| 5 | Trends in supplier analysis | .830 | |

| 6 | An examination of global competitive trends | .834 | |

| 7 | Economic and commercial situations in general | .828 | |

| 8 | Trends in technology analysis | .831 | |

| 9 | Information system for management | .833 | |

| Management Participation | |||

| 1 | Examining and elaborating strategic concerns | .706 | .712 |

| 2 | Strategic proposals are created. | .711 | |

| 3 | Strategic proposals are assessed. | .636 | |

| 4 | Selecting strategic options | .619 | |

| Planning Formality | |||

| 1 | Strategic planning is done on a need-to-know basis. | .826 | |

| 2 | Strategic planning receives as much attention as is required. | .807 | |

| 3 | Informal presentations are the most common means of communicating with the target audience. | .809 | |

| 4 | Decision makers are in charge of strategic planning. | .802 | .836 |

| 5 | Strategic planning is done in an open discourse with the staff. | .801 | |

| 6 | Planning decisions are discretionary. | .806 | |

| 7 | Strategic planning is a result-driven process, not a procedure-driven one. | .811 | |

| 8 | Random progress reviews, not progress reviews, are conducted on the strategic plan. | .805 | |

| 9 | Strategic planning is regarded as having a low level of responsibility. | .810 | |

| Strategic Techniques | |||

| 1 | Analysis of Porter's Five Forces model | .848 | .857 |

| 2 | A financial evaluation | .849 | |

| 3 | Analyze the value chain | .850 | |

| 4 | Analysis of core capabilities and competencies | .845 | |

| 5 | A study of human resources | .848 | |

| 6 | Organizational culture analysis | .852 | |

| 7 | Analysis of PEST (Political, Economic, Social, and Technological) elements | .842 | |

| 8 | An examination of the most important (essential) success factors | .845 | |

| 9 | Analyze your competitors | .845 | |

| 10 | SWOT Analyze | .842 | |

| 11 | Analysis of Stakeholders | .846 | |

| 12 | Models for economic forecasting | .851 | |

| 13 | Other companies' exceptional performers are used as a benchmark. | .849 | |

The Cronbach's alpha coefficient, a widely used measure of how consistent data is across items, was used by the researchers to determine the reliability of their findings. According to Hair et al. (2009)[70], a reliable coefficient value should be at least 0.60. In this research work, the strategic planning constructs produced a coefficient value greater than 0.712, which was deemed acceptable by the researchers.

Table 2.

Cronbach's Alpha value for Organizational Performance constructs.

| Sl. No | Constructs | Cronbach's Alpha if Item Deleted | Cronbach’s alpha Value |

|---|---|---|---|

| Financial Performance | |||

| 1 | Growth is outpacing those of our competitors. | .873 | .909 |

| 2 | In comparison to our competitors, our total sales tax return is | .874 | |

| 3 | Our financial performance is superior than that of our competitors. | .883 | |

| 4 | In comparison to our competitors, our total asset tax return is | .894 | |

| Nonfinancial Performance | |||

| 1 | Our company's operational efficiency is high. | .859 | .874 |

| 2 | Our company's assets are put to good use. | .856 | |

| 3 | Our company's product/service quality | .866 | |

| 4 | Our company's employee satisfaction rate is high. | .860 | |

| 5 | Our company's new product/service development is in full swing. | .858 | |

| 6 | Our company's employee development is a priority. | .868 | |

| 7 | Our company's employee talent is | .861 | |

| 8 | Our company's management quality is excellent. | .860 | |

| 9 | Our company's customer satisfaction rate is high. | .865 | |

| 10 | Our company's social responsibilities are as follows: | .869 | |

Researchers turned to the Cronbach's alpha coefficient to measure reliability, a widely used measurement for how consistent data is across items. The reliable coefficient value should be at least 0.60, as Hair et al. (2009)[70] defined. The organizational performance constructs and instruments in the preceding table produced a coefficient value greater than.874, which was deemed acceptable.

3.5. Correlation of Constructs

To understand the link between the two constraints, we examined the correlation of each of the domains with a Pearson correlation coefficient. To further the correlation between strategic planning and organizational performance constraints, a correlation matrix is established below.

The correlation between the strategic planning and financial performance constructs is displayed in Table 3. Each decimal value in the table represents the correlation. The correlation coefficients are shown to be all positive and significant. A correlation between domains can range from low (0.429) to high (0.621).

In Table 4, each decimal value represents the correlation between the strategic planning and nonfinancial performance constructs. The constructs are labeled in the label row and column of Table 4. It shows the correlation coefficients were all positive and statistically significant. Strategic planning and nonfinancial performance constructs have a correlation value that ranges from 0.339 to 0.461.

3.6. Result of Strategic Planning on the Financial Performance

Multiple regression analysis was found to be a good way to figure out how each of the four predictors of strategic planning affects the financial performance of the companies. This is shown in the table below.

The Durbin-Watson test was used to check for autocorrelation. It came out to be 1.446, which means that the model has no autocorrelation. We can see from Table 5 that R2 is 0.485 for the companies' strategic planning and financial performance. It can be inferred that financial performance can be explained by 48.5% of predictors.

A multiple regression analysis was used to study the relationship between strategic planning constraints and financial performance. In this study, environmental scanning, management participation, planning formality, and strategy technique are all considered independent variables, and financial performance is considered the dependent variable. A multiple regression analysis was therefore done to see if the variables could be brought together.

Financial Performance = 1.554+ 0. 253 Environmental Scanning + 0.108 Management Participation + 0.315 Planning Formality+ 0.596 Strategy Technique

Therefore, from the above equation formulated based on the regression analysis result, strategy technique has a greater effect on financial performance than planning formality, environmental scanning, and management participation. The researcher's theory was proven correct. It showed a clear correlation between strategic planning and financial performance (F = 83.619, p = 0.000), which means the researcher's hypothesis was accepted.

The regression analysis results show that strategy techniques have a positive impact on company financial performance (B =.596, P < 0.000). The regression analysis result shows that the strategy technique most affects financial performance, environmental scanning, management participation, and planning formality. The results reveal that hypothesis (H1) accepted a positive relationship between strategic planning and financial performance. In the context of this research, the new study supports previous studies. A study conducted on the largest manufacturing companies found that the relationship between planning and performance was positive and strong Glaister et al., (2008)[21]. In the context of this investigation, the new study supports previous hotels that found a solid and positive relationship between strategic planning and firm performance (Aldehayyat & Al Khattab, (2012)[30]. Banking institutions that work on a strategic planning process directly affect financial issues Glaister et al., (2008)[21]. Hopkins (1997)[15], in his study, found there is no relationship between the formal planning process and financial performance.

3.7. Result of Strategic Planning on the Nonfinancial Performance

According to the studies, multiple regression analysis is a good way to figure out how each of the four predictors of strategic planning affects the non-financial performance of the companies, as shown in the table below.

Durbin-Watson statistics tests were used to determine autocorrelation. The test result was 1.361, indicating that the model does not have a problem with autocorrelation. In addition, as shown in Table 7, the R square for strategic planning is 0.227. The table result reveals that the predictor variables explained 22.7 percent of nonfinancial performance, a significant amount.

Nonfinancial Performance = 2.208+ 0.462Environmental Scanning + 0.095Management Participation + 0.099Planning Formality

The above equation was formulated based on the regression analysis result. The multiple regression analysis is an appropriate method for determining the impact of the strategic planning domain on nonfinancial performance. From the above Table 8, the four domains of environmental scanning, management participation, planning formality, and strategy technique are used to predict the company's nonfinancial performance. Based on the above results, it appears that environmental scanning has the greatest impact on nonfinancial performance, followed by management participation and planning formality. Table 8 and the above equation reveal that the environmental scanning construct has a positive and statistically significant effect on the company's nonfinancial performance at the one percent level (B =.462, P 0.000). The level of management participation and planning formality has a positive and statistically significant impact on the company's nonfinancial performance at the 10 percent level. The strategy-technique construct has had no significant impact on the nonfinancial performance of the company. The results reveal that the hypothesis (H2) that there is a positive relationship between strategic planning and nonfinancial performance was partially accepted.

4. Conclusion

In this study, a positive correlation was exposed between strategic planning and organizational performance. The strategic planning process of departments that employs domains such as environmental scanning, management participation, planning formality, and strategy technique helps manufacturing companies improve their financial and nonfinancial performance. Furthermore, the process of strategic planning has a positive impact on the financial performance of a company. When it comes to the company's nonfinancial performance, environmental scanning has a positive and statistically significant impact. The level of management participation and planning formality has a positive and statistically significant impact on the company's nonfinancial performance at the 10 percent level. The domain of strategy and technique has had no significant impact on the nonfinancial performance of the company. Based on the result, the researcher can conclude that it is important to pay careful attention to and put resources towards things like setting long-term goals, making goals each year achievable, brainstorming potential strategic alternatives, and evaluating departmental progress on strategic endeavors.

One of the things that will help the company realize its goals is to be sure its strategic plan can get it there. However, this plan can be foiled if some problems that crop up in putting it into practice are not taken care of. The strategy will never work unless the barriers found in the study are eliminated. Managers, specifically department managers, must communicate the strategy via their appropriate channels (written and oral) to be involved in the planning process, with particular attention to employee participation in strategy making. This is beneficial because it is more likely to be successful when everyone works on the strategy. Department managers should get their employees to accept the significance and importance of the strategy before introducing it. To do this, they must discuss and convince their staff members beforehand.

Strategic planning is critical to helping large manufacturing firms excel in both financial and nonfinancial performance. In order to effectively maximize the performance of their company, managers should devote enough effort to the strategic planning process. They are using SWOT analysis, cost-benefit analysis, competitive and critical success factor analysis, and internal environment scanning (past performance evaluation, customer trend analysis, and the reasons for the analysis of past failures). In this study, the researcher also has limitations. This study focuses solely on the manufacturing sector. However, it would have been broader if all business and community sectors in the area had been included. This study examined the relationships between strategic planning (the independent variable) and the four constructs only. For upcoming research in the future, other research could be done to study the relationship between strategic planning and intervention strategies by adding extra dimensions to each of the ideas above. For the study, the data was collected at one time. However, the study's issue represents complicated activities that call for longitudinal data because firm causal relationships exist between the constructs or dimensions of the study. This means that it is necessary to show that firms' financial and nonfinancial performance is due to planning and related activities undertaken previously, not just in the present. The conclusions should be confirmed using a long-term study.

Funding

This study is performed as a part of Ph.D., work and received no funding from any funding agency or institution.

Data Availability Statement

The data used to support the findings of this study are available from the corresponding author upon request.

Conflicts of Interest

The authors declare that, there is no conflict of interest in publication of this article.

References

- S. Tzu, “The Art of War,” Article, 2005, Accessed: May 08, 2024. [Online]. Available: www.gutenberg.org.

- A. F. Alkhafaji, “Strategic Management,” 2013.

- D. R. Young, “Organizational identity in nonprofit organizations: Strategic and structural implications,” Nonprofit Manag Leadersh, vol. 12, no. 2, pp. 139–157, 2001. [CrossRef]

- K. A. Palia, “AN EXPLORATORY ANALYSIS OF THE RELATIVE STRATEGIC SIGNIFICANCE OF DIFFERENT ORGANIZATIONAL FUNCTIONS IN INDUSTRIAL FIRMS PURSUING DIFFERENT GRAND CORPORATE STRATEGIES,” 1979. Accessed: May 08, 2024. [Online]. Available: https://www.proquest.com/docview/303004595?pq-origsite=gscholar&fromopenview=true&sourcetype=Dissertations%20&%20Theses.

- P. Drucker, “The practice of management.” Accessed: May 08, 2024. [Online]. Available: https://search.worldcat.org/title/859708498.

- D. G. Porter, “Environmental Change and Security Project Report,” article. Accessed: May 08, 2024. [Online]. Available: https://books.google.com.cy/books?hl=tr&lr=&id=mpK5AAAAIAAJ&oi=fnd&pg=PA61&dq=Porter,+D.+G.+(1996).+security+risk,+that+they+have+environmental+threats,+but+sible.%22+10+Here+Levy+displays+his+own&ots=AI7SUnbqT-&sig=eXTT7YuxRtN6DY0ueZlqELe7oQs&redir_esc=y#v=onepage&q&f=false.

- G. Fuertes, M. Alfaro, M. Vargas, S. Gutierrez, R. Ternero, and J. Sabattin, “Conceptual Framework for the Strategic Management: A Literature Review - Descriptive,” Journal of Engineering (United Kingdom), vol. 2020. Hindawi Limited, 2020. [CrossRef]

- K. D. Plowman and C. Wilson, “Strategy and Tactics in Strategic Communication: Examining their Intersection with Social Media Use,” International Journal of Strategic Communication, vol. 12, no. 2, pp. 125–144, Mar. 2018. [CrossRef]

- H.-T. Nguyen, International Economics Business and Management Strategy. 2019. [Online]. Available: https://www.researchgate.net/publication/338570555.

- J. Björkdahl, “Strategies for Digitalization in Manufacturing Firms,”. 62, no. 4, pp. 17–36, May 2020. [CrossRef]

- A. Zerfass, D. Verčič, H. Nothhaft, and K. P. Werder, “Strategic Communication: Defining the Field and its Contribution to Research and Practice,” International Journal of Strategic Communication, vol. 12, no. 4, pp. 487–505, Aug. 2018. [CrossRef]

- C. J. F. Cândido and S. P. Santos, “Implementation obstacles and strategy implementation failure,” Baltic Journal of Management, vol. 14, no. 1, pp. 39–57, Jan. 2019. [CrossRef]

- E. (Emily) Shu, “Emergent strategy in an entrepreneurial firm: the case of Lenovo in its formative years,” International Journal of Emerging Markets, vol. 12, no. 3, pp. 625–636, 2017. [CrossRef]

- J. M. Bryson, L. H. Edwards, and D. M. Van Slyke, “Getting strategic about strategic planning research,” Public Management Review, vol. 20, no. 3. Taylor and Francis Ltd., pp. 317–339, Mar. 04, 2018. [CrossRef]

- W. E. Hopkins and S. A. Hopkins, “STRATEGIC PLANNING-FINANCIAL PERFORMANCE RELATIONSHIPS IN BANKS: A CAUSAL EXAMINATION,” Strategic Management Journal, vol. 18, pp. 635–652, 1997. [CrossRef]

- G. A. Baker, “Strategic Planning and Financial Performance in the Food Processing Sector,” Review of Agricultural Economics, vol. 25, no. 2, pp. 470–482, Dec. 2003. [CrossRef]

- S. J. French, S. J. Kelly, and J. L. Harrison, “The role of strategic planning in the performance of small, professional service firms. A research note,” Journal of Management Development, vol. 23, no. 8, pp. 765–776, 2004. [CrossRef]

- B. Gibson and G. Cassar, “Longitudinal analysis of relationships between planning and performance in small firms,” Small Business Economics, vol. 25, no. 3, pp. 207–222, Oct. 2005. [CrossRef]

- J. R. Falshaw, K. W. Glaister, and E. Tatoglu, “Evidence on formal strategic planning and company performance,” Management Decision, vol. 44, no. 1. pp. 9–30, 2006. [CrossRef]

- S. Kraus, R. Harms, and E. J. Schwarz, “Strategic planning in smaller enterprises – new empirical findings,” Management Research News, vol. 29, no. 6, pp. 334–344, 2006. [CrossRef]

- M. Glaister et al., “Caffeine supplementation and multiple sprint running performance,” 2008. Accessed: May 08, 2024. [Online]. Available: https://research.stmarys.ac.uk/id/eprint/111/1/Glaister-Caffeine-Supplementation.pdf.

- B. W. Kori, S. M. A. Muathe, and S. M. Maina, “Financial and Non-Financial Measures in Evaluating Performance: The Role of Strategic Intelligence in the Context of Commercial Banks in Kenya,” International Business Research, vol. 13, no. 10, p. 130, Sep. 2020. [CrossRef]

- T. Nambirajan and M. Prabhu, “COMPETITIVENESS OF MANUFACTURING INDUSTRIES IN UNION TERRITORY OF PUDUCHERRY (INDIA): A CRITICAL ANALYSIS,” 2010. Accessed: May 08, 2024. [Online]. Available: https://research.stmarys.ac.uk/id/eprint/111/1/Glaister-Caffeine-Supplementation.pdf.

- C. Wolf and S. W. Floyd, “Strategic Planning Research: Toward a Theory-Driven Agenda,” J Manage, vol. 43, no. 6, pp. 1754–1788, Jul. 2017. [CrossRef]

- B. George, R. M. Walker, and J. Monster, “Does Strategic Planning Improve Organizational Performance? A Meta-Analysis,” Public Adm Rev, vol. 79, no. 6, pp. 810–819, Nov. 2019. [CrossRef]

- M. Anwar and S. Z. A. Shah, “Entrepreneurial orientation and generic competitive strategies for emerging SMEs: Financial and nonfinancial performance perspective,” J Public Aff, vol. 21, no. 1, Feb. 2021. [CrossRef]

- W. Q. Judge and T. J. Douglas, “Performance implications of incorporating natural environmental issues into the strategic planning process: An empirical assessment,” Journal of Management Studies, vol. 35, no. 2, pp. 241–262, 1998. [CrossRef]

- V. Ivančić, I. Mencer, L. Jelenc, and Ž. Dulčić, “STRATEGY IMPLEMENTATION-EXTERNAL ENVIRONMENT ALIGNMENT,” 2017. Accessed: May 08, 2024. [Online]. Available: https://hrcak.srce.hr/file/280822.

- C. H. Chang, “How to enhance green service and green product innovation performance? The roles of inward and outward capabilities,” Corp Soc Responsib Environ Manag, vol. 25, no. 4, pp. 411–425, Jul. 2018. [CrossRef]

- J. Aldehayyat and N. Twaissi, “Strategic Planning and Corporate Performance Relationship in Small Business Firms: Evidence from a Middle East Country Context,” International Journal of Business and Management, vol. 6, no. 8, Aug. 2011. [CrossRef]

- V. Ramanujam and N. Venkatraman, “Planning System Characteristics and Planning Effectiveness,” Strategic Management, 1987. Accessed: May 08, 2024. [Online]. Available: https://www.jstor.org/stable/pdf/2486233.pdf?casa_token=dskopwfokv8AAAAA:6jhISvr05SdmPIApErSPEWDmHRdv-ZMU9yVmBQH58Q0CXXLCBWxcFm6cB-viNV5jt1pYQmc0oJ1Urh4No0QA18g9TK5QT5ohTJHWISjkVeMFuU_F2g.

- A. al Khattab, J. Aldehayyat, M. Alrawad, S. AlYatama, and S. al Khattab, “Executives’ perception of political-legal business environment in international projects,” International Journal of Commerce and Management, vol. 22, no. 3, pp. 168–181, Aug. 2012. [CrossRef]

- I. P. Gkliatis and D. N. Koufopoulos, “Strategic planning practices in the Greek hospitality industry,” European Business Review, vol. 25, no. 6, pp. 571–587, Oct. 2013. [CrossRef]

- A. E. Clark, “LABOUR ECONOMICS Job satisfaction and gender: Why are women so happy at work?,” 1997.

- A. Al-Surmi, G. Cao, and Y. Duan, “The impact of aligning business, IT, and marketing strategies on firm performance,” Industrial Marketing Management, vol. 84, pp. 39–49, Jan. 2020. [CrossRef]

- P. Knott, “A typology of strategy tool applications,” Management Decision, vol. 44, no. 8, pp. 1090–1105, 2006. [CrossRef]

- M. Darvishmotevali, L. Altinay, and M. A. Köseoglu, “The link between environmental uncertainty, organizational agility, and organizational creativity in the hotel industry,” Int J Hosp Manag, vol. 87, May 2020. [CrossRef]

- P. A. Phillips, “Measuring strategic planning effectiveness in hotels,” 1999. [Online]. Available: http://www.emerald-library.com.

- R. Gunn and W. Williams, “Strategic tools: an empirical investigation into strategy in practice in the UK,” Strategic Change, vol. 16, no. 5, pp. 201–216, Aug. 2007. [CrossRef]

- A. M. Efendioglu and T. Karabulut, “Impact of Strategic Planning on Financial Performance of Companies in Turkey,” International Journal of Business and Management, vol. 5, no. 4, Mar. 2010. [CrossRef]

- S. Y. Sung and J. N. Choi, “Effects of training and development on employee outcomes and firm innovative performance: Moderating roles of voluntary participation and evaluation,” Hum Resour Manage, vol. 57, no. 6, pp. 1339–1353, Nov. 2018. [CrossRef]

- J. Kaur, R. Sidhu, A. Awasthi, S. Chauhan, and S. Goyal, “A DEMATEL based approach for investigating barriers in green supply chain management in Canadian manufacturing firms,” Int J Prod Res, vol. 56, no. 1–2, pp. 312–332, Jan. 2018. [CrossRef]

- S. Elbanna, “Planning and participation as determinants of strategic planning effectiveness: Evidence from the Arabic context,” Management Decision, vol. 46, no. 5, pp. 779–796, 2008. [CrossRef]

- I. O. Ugboro, K. Obeng, and O. Spann, “Strategic Planning As an Effective Tool of Strategic Management in Public Sector Organizations,”. vol. 43, no. 1, pp. 87–123, Dec. 2010. [CrossRef]

- S. Linder and J. Sax, “Fostering Strategic Responsiveness: The Role of Middle Manager Involvement and Strategic Planning,” Adapting to Environmental Challenges: New Research in Strategy and International Business, pp. 35–63, Jul. 2020. [CrossRef]

- G. Elliott, M. Day, and S. Lichtenstein, “Strategic planning activity, middle manager divergent thinking, external stakeholder salience, and organizational performance: a study of English and Welsh police forces,” Public Management Review, vol. 22, no. 11, pp. 1581–1602, Nov. 2020. [CrossRef]

- Udriyah, J. Tham, and S. M. Ferdous Azam, “The effects of market orientation and innovation on competitive advantage and business performance of textile smes,” Management Science Letters, vol. 9, no. 9, pp. 1419–1428, 2019. [CrossRef]

- M. Omran, A. Khallaf, K. Gleason, and Y. Tahat, “Non-financial performance measures disclosure, quality strategy, and organizational financial performance: a mediating model,” Total Quality Management and Business Excellence, vol. 32, no. 5–6, pp. 652–675, 2021. [CrossRef]

- D. D. Lee et al., “Revisiting the Vexing Question: Does Superior Corporate Social Performance Lead to Improved Financial Performance?,” 2009.

- M. Reuvers, M. L. Van Engen, C. J. Vinkenburg, and E. Wilson-Evered, “Transformational leadership and innovative work behaviour: Exploring the relevance of gender differences,” Creativity and Innovation Management, vol. 17, no. 3, pp. 227–244, 2008. [CrossRef]

- L. P. Bucklin and S. Sengupta, “Organizing Successful Co-Marketing Alliances,” 1993.

- M. Abdel-Basset, W. Ding, R. Mohamed, and N. Metawa, “An integrated plithogenic MCDM approach for financial performance evaluation of manufacturing industries,” Risk Management, vol. 22, no. 3, pp. 192–218, Sep. 2020. [CrossRef]

- Tony. Davies and Tony. Boczko, “Financial accounting : an introduction,” p. 454, 2005.

- L. N. Miller, “What is Helpful (and Not) in the Strategic Planning Process? An Exploratory Survey and Literature Review,” 2018. Accessed: May 08, 2024. [Online]. Available: file:///C:/Users/phonex/Downloads/tclifford,+LL&M+-+Newton+Miller+-+copyedited+version%20(3).pdf.

- C. B. Shrader, L. Taylor, and D. R. Dalton, “Strategic Planning and Organizational Performance: A Critical Appraisal,” J Manage, vol. 10, no. 2, pp. 149–171, 1984. [CrossRef]

- A. S. Taiwo and F. O. Idunnu, “Impact of Strategic Planning on Organizational Performance and Survival,” Research Journal of Business Management, vol. 1, no. 1, pp. 62–71, Dec. 2010. [CrossRef]

- R. Arasa and P. K’obonyo, “The Relationship between Strategic Planning and Firm Performance,” 2012. [Online]. Available: www.ijhssnet.com.

- Y. Zhao, M. Prabhu, R. R. Ahmed, and A. K. Sahu, “Research Trends and Performance of IIoT Communication Network-Architectural Layers of Petrochemical Industry 4.0 for Coping with Circular Economy,” Wirel Commun Mob Comput, vol. 2021, 2021. [CrossRef]

- N. Capon, J. U. Farley, and J. M. Hulbert, “STRATEGIC PLANNING AND FINANCIAL PERFORMANCE: MORE EVIDENCE*,” 1994.

- J. B. Barney, “Looking inside for competitive advantage. Academy of Management Perspectives, 9(4), 49-61.,” book, Academy of Management Perspectives, 9(4), 49-61., 1995, Accessed: May 08, 2024. [Online]. Available: https://www.ryanhoskin.com/school/MGT%20235/Looking_Inside_for_Competitive_Advantage.pdf.

- T. R. Crook, D. J. Ketchen, J. G. Combs, and S. Y. Todd, “Strategic resources and performance: A meta-analysis,” Strategic Management Journal, vol. 29, no. 11, pp. 1141–1154, Nov. 2008. [CrossRef]

- J. M. Rudd, G. E. Greenley, A. T. Beatson, and I. N. Lings, “Strategic planning and performance: Extending the debate,” J Bus Res, vol. 61, no. 2, pp. 99–108, Feb. 2008. [CrossRef]

- R. R. Fullerton and W. F. Wempe, “Lean manufacturing, non-financial performance measures, and financial performance,” International Journal of Operations and Production Management, vol. 29, no. 3, pp. 214–240, 2009. [CrossRef]

- S. Elbanna, “Strategic planning in the united arab emirates,” International Journal of Commerce and Management, vol. 20, no. 1, pp. 26–40, Mar. 2010. [CrossRef]

- J. S. Hornsby, D. F. Kuratko, and S. A. Zahra, “Middle managers’ perception of the internal environment for corporate entrepreneurship: assessing a measurement scale,” 2002. Accessed: May 08, 2024. [Online].

- E. G. , & Z. Carmines, “Reliability and Validity Assessment,” article,17, 37-49. Accessed: May 08, 2024. [Online]. Available: https://books.google.com.cy/books?hl=tr&lr=&id=o5x1AwAAQBAJ&oi=fnd&pg=PA5&dq=17.%09Carmines,+E.+G.,+%26+Zeller,+R.+A.+(1979).+Assessing+reliability.+Assessing+Reliability:+Reliability+and+Validity+Assessment,+17,+37-49.&ots=2M2IhuGFG0&sig=JkOuGVukUmT1yRqTPWNDqjbEI8g&redir_esc=y#v=onepage&q&f=false.

- C. A. , & K. G. Moser, “Survey Methods in Social Investigation,” 1979. Accessed: May 08, 2024. [Online]. Available: https://www.taylorfrancis.com/books/mono/10.4324/9781315241999/survey-methods-social-investigation-moser-kalton.

- A. Hamed Taherdoost and K. Lumpur, “Validity and Reliability of the Research Instrument; How to Test the Validation of a Questionnaire/Survey in a Research,” 2016. [Online]. Available: https://hal.science/hal-02546799.

- B. E. , & K. M. E. Whitley Jr, “Principles of research in behavioral science. Routledge.,” 2012.

- J. Hair, “Multivariate Data Analysis,” Faculty and Research Publications, Feb. 2009, Accessed: May 08, 2024. [Online]. Available: https://digitalcommons.kennesaw.edu/facpubs/2925.

Table 3.

Correlation between strategic planning and financial performance constructs.

| Correlations | Financial Performance | Environmental Scanning | Management Participation | Planning Formality | Strategy Technique |

|---|---|---|---|---|---|

| Financial Performance | 1.000 | ||||

| Environmental Scanning | .621 | 1.000 | |||

| Management Participation | .486 | .218 | 1.000 | ||

| Planning Formality | .429 | .206 | .268 | 1.000 | .010 |

| Strategy Technique | .529 | .088 | .034 | .010 | 1.000 |

Table 4.

Correlation between strategic planning and nonfinancial performance constructs.

| Correlations | Nonfinancial Performance | Environmental Scanning | Management Participation | Planning Formality | Strategy Technique |

|---|---|---|---|---|---|

| Nonfinancial Performance | 1 | ||||

| Environmental Scanning | .461 | 1 | |||

| Management Participation | .339 | .235 | 1 | ||

| Planning Formality | .370 | .240 | .241 | 1 | |

| Strategy Technique | .410 | .079 | .016 | .003 | 1 |

Table 5.

Model Summary Multiple Regression Analysis.

| Model | R | R Square | Adjusted R Square | Std. Error of the Estimate | Durbin-Watson | F | Sig. |

|---|---|---|---|---|---|---|---|

| 1 | .697 | .485 | .479 | .56911 | 1.446 | 83.619 | .000 |

Table 6.

Coefficient Summary of the strategic planning on the financial performance.

| Model | Unstandardized Coefficients | Standardized Coefficients | T | Sig. | |

|---|---|---|---|---|---|

| B | Std. Error | Beta | |||

| (Constant) | 1.554 | .250 | 6.219 | .000 | |

| Environmental Scanning | .300 | .054 | .253 | 5.588 | .000 |

| Management Participation | .111 | .044 | .108 | 2.521 | .012 |

| Planning Formality | .364 | .050 | .315 | 7.296 | .000 |

| Strategy Technique | .755 | .048 | .596 | 15.592 | .000 |

| Dependent Variable: Financial Performance | |||||

Table 7.

Model Summary Multiple Regression Analysis.

| Model | R | R Square | Adjusted R Square | Std. Error of the Estimate | Durbin-Watson | F | Sig. |

|---|---|---|---|---|---|---|---|

| 1 | .476 | .227 | .218 | .56149 | 1.361 | 26.059 | .000 |

Table 8.

Coefficient Summary of the strategic planning on the nonfinancial performance.

| Model | Unstandardized Coefficients | Standardized Coefficients | T | Sig. | |

|---|---|---|---|---|---|

| B | Std. Error | Beta | |||

| (Constant) | 2.208 | .247 | 8.955 | .000 | |

| Environmental Scanning | .441 | .053 | .462 | 8.338 | .000 |

| Management Participation | .078 | .043 | .095 | 1.796 | .073 |

| Planning Formality | .092 | .049 | .099 | 1.876 | .061 |

| Strategy Technique | .046 | .048 | .046 | 0.971 | .332 |

| a. Dependent Variable: Nonfinancial Performance | |||||

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Copyright: This open access article is published under a Creative Commons CC BY 4.0 license, which permit the free download, distribution, and reuse, provided that the author and preprint are cited in any reuse.