Submitted:

03 June 2024

Posted:

03 June 2024

You are already at the latest version

Abstract

This study analyzes the relevance of governance structure for efficiency in revenue collection by Brazilian Water Utilities (WUs). Data was collected from the National Information System on Sanitation (SNIS) for 127 Brazilian WUs, covering a balanced longitudinal panel from 2018 to 2022. Governance structures evaluated included Ownership (public or private) and Corporatization (publicly traded or not). In scientific databases, we did not find studies on the efficiency of specific WUs in collecting customer bills for services rendered and its relationships with this type of governance; thus, this would be the main innovative contribution of the study to the previous literature. In the first stage, the study utilized the Dynamic Slack Based Model (DSBM) to assess revenue collection efficiency. In the second stage, an econometric model with Generalized Estimating Equations (GEE) to explain the efficiency. The findings revealed a global average inefficiency of 50.47% in revenue collection. Corporatization was linked to higher collection efficiencies, while ownership type was significant, but with lower collection efficiency. Factors such as tariff accessibility, urbanization, and the COVID-19 pandemic also influenced efficiency. The study suggests regulatory bodies should consider these insights to implement policies that prevent inefficiencies from affecting the tariff system for services.

Keywords:

efficiency

; water and wastewater services

; governance structure

; revenue collection

; ownership

1. Introduction

According to [1], taxation is one method through which governments use to generate revenue to fulfill the needs of their citizens. Additionally, the authors state that the purpose of taxation is to gather funds for the armed forces and administrative expenses.

The efficiency of revenue collection measures how effectively a utility can convert its billed revenue into actual cash [2]. Moreover, from a broad perspective public authorities see revenue collection as a way to stimulate and manage the economic and social, aiming the national development [3]. To achieve this objective, it is necessary a high revenue collection performance to promote efficiency in the service provision and a national and organizational economic growth [4].

In 2011, the UN Secretary-General, Ban Ki-moon, emphasized that governments need to recognize that the urban water crisis is a crisis of governance, characterized by weak policies and management, rather than a scarcity problem [5]. Therefore, an important aspect to consider is the tariff revisions and how they affect other areas, such as revenues, with the aim of achieving higher quality services [6].

In the Brazilian context, water supply and sanitation services were primarily managed by public entities. However, this situation has been changing with the increasing number of concessions of these services to private entities [7]. Thus, understanding the organizational structure of the water supply service has been crucial to improving its efficiency [8].

As water supply and sanitation services have been provided by only one utility in each region of the country, a natural monopoly exists. Typically, in markets with this configuration, investments tend to be high, costs very low, and there is little or no rivalry [9]. This leads to a scenario of inefficiency since competitive pressures aimed at maximizing profits are absent [10]. However, the recent update of Law 11.445/07 [11] through the enactment of Law 14.026/20 [12] has brought forth incentives to open up competition, encouraging greater private capital investment in the sector's concessions.

In this context, the present study aims to analyze the association between governance structure and revenue collection efficiency, which is measured by the Intertemporal Dynamic efficiency of revenue collection. Governance structure in this study is related to the control of the utility, which can be private (utilities with mixed capital with private management or private utilities) or public (utilities with mixed capital with public control), and whether the utility is corporatized (with shares on the stock exchange registered with the Brazilian Securities and Exchange Commission) or non-corporatized.

Recent discussions about privatizations have been taking place worldwide in recent years, and the water and sanitation sector is no exception. In this context, this topic has been widely debated [13]. Privatization, as highlighted by the authors, aims to enhance service efficiency through corporate governance. In developed countries, however, a different scenario emerges. A remunicipalization movement is occurring in various regions, particularly in European countries, where the return to public control has been driven by high tariffs imposed without corresponding improvements in service quality by private entities, as well as low transparency [14].

In Brazil, the discussion about the outsourcing and privatization of basic services was prominent in the 1990s and has returned to the political agenda due to the new regulatory framework for the sector, introduced by Provisional Measure 868/18, which amended the regulatory framework for basic sanitation – Law 11.445/2007 [11]. After losing validity, it was replaced by Bill 4.162/2019, which later became Law 14.026/2020 [12]. This new law creates ideal conditions for municipalities to promote the concession of sanitation services to the private sector. In this sense, the privatization of sanitation services contrasts with the global trend of remunicipalizing services [15].

Those who oppose the privatization process, including members of the Brazilian academia, sanitation sector experts, social movements, unions, and political parties, argue that privatization will not achieve the desired objectives. They claim that service improvement is incompatible with profit generation and that peripheral areas will be the most affected. As water becomes a commodity, the most vulnerable consumers will be unable to afford it. Additionally, there will be little investment in sanitation due to its low profitability [15].

According to [13], privatization aims to increase service efficiency through corporate governance. Conversely, [16] argue that the pro-(re)municipalization movement seeks social justice by advocating for lower and more affordable tariffs, defending sustainability through investment in the system network to reduce losses, and promoting democratic management through greater financial transparency.

In this context, to increase efficiency or send a "positive signal" to the market, it is expected that utilities listed on the CVM will present better performance indicators than non-listed utilities. Regarding privatization, despite the global discussion and movement towards remunicipalization in various countries, it is anticipated that services provided by private entities aim to enhance service efficiency [13].

[17] identifies ownership and regulatory mechanisms as key explanatory variables in the governance structure used in water utility benchmark studies. Additionally, other variables are considered, including the number of towns served (output), capital expenditures (input), chemical quality (quality), the region of operation (environmental factors), and gross domestic product (GDP) per capita (macroeconomic factors).

Another significant variable to consider was the peak of the COVID-19 pandemic. According to [18], economies faced a supply and demand shock that triggered a global financial crisis due to pandemic-related factors. The authors also point out that this crisis incorporated the potential impacts of the pandemic, leading to a sharp decline in major stock market indices in March 2020, with values plummeting by nearly one-third within a few weeks.

In this context, this study aims to analyze the relevance of governance structure for efficiency in revenue collection by Brazilian Water Utilities – WUs. In furtherance of this goal, we collected and analyzed data from the National Information System on Sanitation (SNIS). The present work contributes to the scientific area because it brings another point of view of governance structure by focusing on collection performance. The identification of these factors will provide valuable insights and support decision-making by regulators aiming to enhance service efficiency.

2. Literature Review

The new legal framework for sanitation in Brazil, approved by Law 14.026/2020 [12], allowed the participation of the private sector through concession contracts, asset rentals, or management assistance tied to performance targets (efficiency contracts). This has sparked extensive discussions about efficient water management, becoming a key focus in academic and regulatory debates [8]. The authors highlight that control influences the level of investment, financing structure, and associated service costs.

With the framework established by Law 14.026/2020 [12], the Brazilian sanitation system has become quite similar to the French sanitation system in both institutional and regulatory models [19]. However, in the French context, the performance of private utilities did not meet expectations, with progressively increasing tariffs and, in some areas, unsatisfactory service quality, leading to the remunicipalization of water services in 2010 [20].

In that context, accurate billing and appropriate pricing are key to ensuring stable revenue [21], besides [22], point out that Public water utilities may suffer losses due to inefficient tariffs and billing, faulty metering, non-revenue water, and illegal connections.

In Spain, [23] found that privatization leads to higher prices, whereas [24] concluded that prices are lower when services are provided directly by local councils. Conversely, when services are outsourced, prices under public management are higher than those under private management.

In Italy, [25] and [26] found that water and sanitation utilities (WSUs) under public management charge lower tariffs. These findings align with those of [27], who reported higher prices for public-private partnerships in France. [28] also found that in Germany, consumers pay more when utilities are privately managed. Other research supports this, showing that private utilities generally charge more than public ones. For example, in Chile, privatization led to short-term tariff increases [29], and in various developing countries, public-private partnerships resulted in higher tariffs [30].

These findings suggest that private management often results in higher prices, likely due to the focus on cost recovery and profitability. However, an empirical study in Argentina showed that privatization improved productivity and reduced tariffs [31]. Similarly, in Thailand, privatization lowered prices for poorer urban consumers [32], which aligns with Brazilian policies aimed at improving accessibility by reducing tariffs for low-income and low-consumption households [33].

The public inefficiency is linked to the independence of private utilities, as public providers face budgetary constraints. This situation resembles the French case, where significant modernization, such as the replacement of lead pipes and improvement of water quality, occurred in the early stages of the concession period. Despite these investments, which may have improved water quality, the sharp increase in public service tariffs and restricted access for poorer populations contributed to the remunicipalization process [19].

Various factors can influence the efficiency of services provided. [34] identified a positive influence of regulatory incentives on operator efficiency and divergent results concerning privatization, economies of scale, scope, and density. [35] found economies of scale, especially for small utilities, but ambiguous results for privatization. [36] indicated in a meta-regression of 60 articles a high likelihood that in developed countries, it is more common to find diseconomies of scale and scope among larger providers and those with public control. [37] analyzed the impact of privatization and regulation on efficiency.

In this context, findings in Brazil identified only economies of scale [38,39,40]. Regarding private control, results varied. In a survey by [34], 18 studies identified private control as more efficient, 17 found inconclusive results, and 12 indicated public control as more efficient. Additionally, [41] point out that differences in provider efficiency are due to the methods or data sources used.

One of the issues that initiated the privatization debate in Brazil was the poor management and indicators presented by public control. In this regard, [42] asserts that losses and defaults were high.

Despite the empirical literature, three theories support the argument for superior private performance: Property Rights Theory, Public Choice Theory, and Agency Theory [43].

Using [43] theoretical framework, Property Rights Theory argues that under public management, managers cannot claim any generated savings, have no incentives for cost containment or launching new products/services, and thus do not act towards these goals. Public Choice Theory infers that bureaucrats seek to serve their own interests at the expense of common interest, leading to patronage policies and other issues. Finally, Agency Theory suggests that principals (public managers) could exploit informational asymmetry for tariff collection that benefits them.

H1: Privately controlled utilities are more likely to achieve better efficiency in revenue collection.

The informational asymmetry in markets originates from the inherent uncertainty about the quality of products or services provided. According to [44], this uncertainty is the main driver for products and services of varying quality being treated the same, devaluing higher-quality products and overvaluing lower-quality ones.

Signaling Theory, formulated by [45], posits that an individual's characteristics can be manipulated by the individual. The author suggests that in decision-making environments with uncertainty, these characteristics or parameters can guide decisions, thus acting as potential mitigators of informational asymmetry [46].

According to [46], higher quality companies adopt policies that allow their superiority to be perceived, while lower quality companies tend to adopt policies that conceal their weaknesses. Therefore, presenting better signals with improved revenue collection efficiency indicators can be interpreted by the market as a sign of higher quality service providers.

For [47], revenue evasion (or uncollected receivables) is related to economic efficiency. Thus, corporatized (with shares on the stock exchange) companies aim to present "good signals" (Signaling Theory) to the market, and a high inefficiency of revenue collection may indicate a failure in controls or practices to ensure resource inflows for services rendered. Revenue is crucial because it influences a business's earnings and reflects its performance over a specific period [48]. Several factors impact business profitability. For instance, companies that cannot generate and collect sufficient revenue to cover operational costs may face economic failure [49]. [50] concurred with [49], noting that accelerated revenues are essential for business survival, as they can determine liquidity and profitability. Conversely, declining revenues coupled with rising costs can create a gap that negatively affects business profitability.

H2: Corporatized utilities with shares on the stock exchange are more likely to achieve greater efficiency in revenue collection.

3. Materials and Methods

3.1. Data Collection

The research followed a two-stage scheme. In the first stage, we used the Dynamic Slack Based Model (DSBM) to measure revenue collection efficiency (EFF). In the second stage, we applied EFF as a dependent variable in a Generalized Estimating Equations (GEE) regression to analyze the relation between factors of governance structure of the utilities, the cost of services, the environment, macroeconomic variables and the COVID-19 pandemic.

Our sample selection included public utilities, private utilities, mixed capital utilities with public management, and mixed capital utilities with private management listed in the SNIS database between 2018 and 2022. Initially, 180 utilities were selected. However, due to missing information, the absence of financial reports, and the presence of outliers, we excluded some utilities, resulting in a final sample of 127 utilities and 635 observations of a balanced panel.

The data were collected from the Brazilian sanitation information system or Sistema Nacional de Informações Sobre Saneamento (SNIS) and included variables of demographic and macroeconomic nature. Sections 3.2.2 and 3.3 will detail the methodologies used for collecting each variable, as well as the expected results based on the literature.

3.2. Model Specification for Efficiency Score Model

3.2.1. The Data Envelopment Analysis Model Proposed

Data envelopment analysis (DEA) is widely used, appearing in 68% of the literature on water and sanitation efficiency in developing countries. The majority of studies (9 out of 12) use the variable returns to scale (VRS) approach, which compares operators at the same scale level, whereas the constant returns to scale (CRS) approach assumes that all operators function at an optimal level [41].

To choose between the models with CRS and VRS, we will follow the logic presented by [51], using the t-test for paired samples of two related groups: one group with efficiency scores generated with CRS and the other with scores generated by VRS. If there is a significant difference between the means of the two groups, the VRS model will be selected. However, if the efficiency scores do not exhibit normal distribution behavior, the non-parametric Wilcoxon two–related-sample test will be used.

In addition to the scale choice, more concerns are described by [52], concerning the protocol for Non-homogeneous units and non-homogeneous environment, homogeneity between the units is suggested, as all information involved is from the same public utility service and the recognition and measurement process follows the same accounting regulations. The issue of a Non-homogeneous environment is expected to be verified with the explanatory model. Regarding the protocol of the number of inputs and outputs number of units, there is no restriction, as there are 127 DMUs for one input, one output, and one carry-over, which can be considered as output. Furthermore, correlations will be used to verify factor correlation and isotonicity.

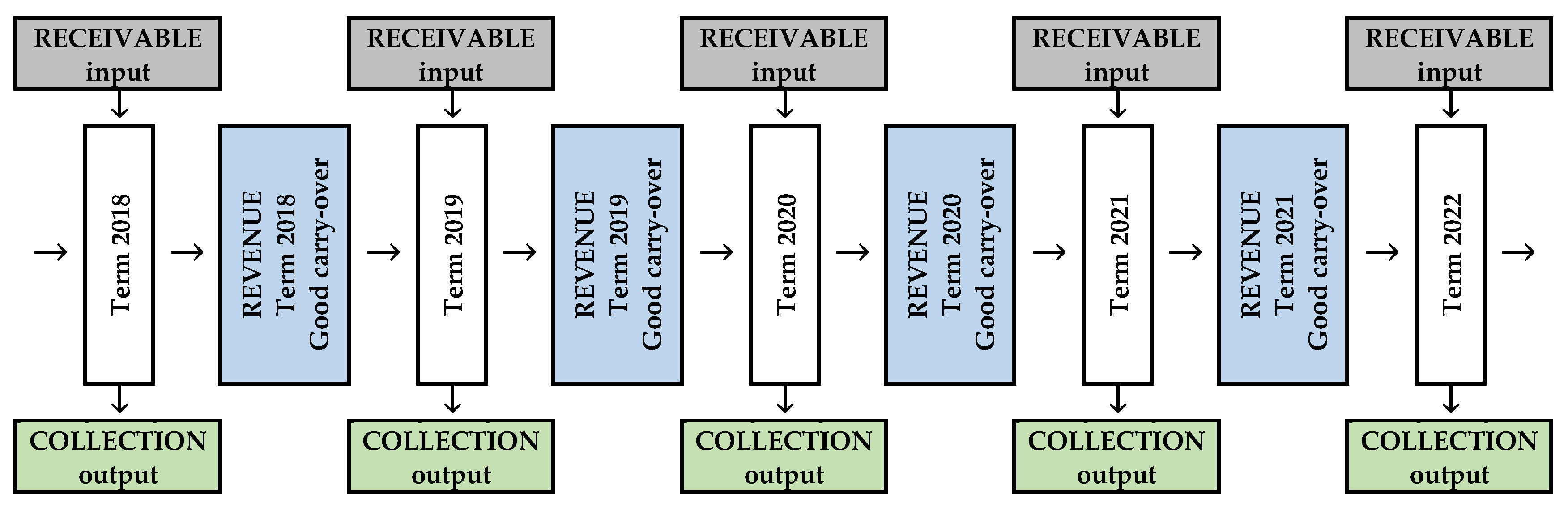

In the Brazilian water and wastewater sector, tariff review processes cover a cycle of 4 to 5 years, often recognizing efficiencies by periods and overall cycles. In this case, an intertemporal dynamic analysis is an interesting proposal, especially when it is necessary to capture the effect of efficiency from one year being carried over to another year. However, traditional DEA models only evaluate period efficiency scores independently. To address this, [53] introduced production frontiers with dynamic DEA. Following this perspective, [54,55,56,57,58,59,60,61,62] expanded the scope of the DEA additive model known as the Slack Based Model (SBM) to a dynamic model capable of estimating the production frontier over several periods: the Dynamic Slack Based Model (DSBM).

Returning to the scope of the sector, some work is being developed concerned with intertemporal effects (dynamic efficiency). [63] aimed to measure efficiency dynamically, incorporating intertemporal capital links within the production function for the water and wastewater sector in England and Wales (1996-2011), concluding that ignoring intertemporal effects can lead to overestimation of allocative inefficiency

Other studies evaluating the efficiency of the water and wastewater sector using dynamic models based on slack include [38], who developed a score for the dynamic efficiency of water and sewerage utilities in Brazil, considering the universal access deficit to services as a bad carry-over, and explained their efficiency through the governance structure. [64] examined the pattern of water use efficiency and its potential relationship with urbanization and foreign direct investment between 2007 and 2016 in 11 West African countries (these two used the DSBM). [65] analyzed the impact of the Brazilian regulatory environment on the efficiency levels of water and sewerage utilities, using the network approach of Tone and [62], DNSBM.

Also concerned with the temporal influence on revenue collection efficiency, the DSBM model is used in this study to observe only dynamic collection efficiency, which involves a small set of variables extracted from financial accounting.

3.2.2. Variable Selection for Efficiency Assessment

In Brazilian water utilities tariff review processes, losses due to uncollectible credits are tariff components and, in some cases, subject to certain regulatory limits. According to Brazilian accounting standards the [66] Pronunciamento Técnico CPC 48 - Instrumentos Financeiros (correlation with International Accounting Standards - IFRS 9), determines that such expected losses may be calculated on accounts receivable from customers using a matrix of accruals. Unfortunately, the SNIS database does not have information on expenditure on losses in accounts receivable from customers, with credit balances in said accounts being the best proxy available in the system.

Customer accounts receivable occupy an important space and substantial representation in current assets and working capital [67]. The cash flow does not necessarily reflect the profit disclosure resulting from increased accounts receivable, and the failure in debt collection processes leads to bad debts and deep economic crises in entities [68], in this sense, Customer Accounts Receivable - RECEIVABLE it is the first variable considered to evaluate efficiency, being classified as “input”.

In the water sector, receivable collection and cost recovery represent critical references for financial sustainability and the continuity of water delivery [69,70]. These factors are especially important for enabling expansion and equity in the provision of services [70]. Low received collection rates result in insufficient cash to meet the challenge of providing water services in the necessary quantity and quality; renewing aging infrastructure; coverage of the growing population and urbanization; impacting human resources; and tariff issues [71]. Efficient receivables collection enhances the financial performance of water providers [72], therefore, the Collection Received from Customers (COLLECTION) variable, which represents the annual value effectively collected from all operational revenues, will be the "output" in the efficiency score assessment.

Considering that the "input" (RECEIVABLE) is working capital from operational revenues billed for services provided to consumers, which have not yet entered the utility's cash flow, and the "output" (COLLECTION) is the result of the same revenues added to the cash flow, regardless of the accrual period of the invoiced amounts. The moment in which such revenues enter the utilities' cash flow is important for evaluating the efficiency of water services calculated by), where represents the delay in accounts receivable (in days equivalent), is the accounts receivable from drinking water at the reference date; , sales revenues during the assessment period; and; the assessment period [73]. For wastewater services, the importance is the same [74] and is calculated similarly, recognizing only revenues and receivables from wastewater services (performance indicator code ).

For the use of the DSBM model is required to identify the connection components of the efficiency (carry-over), which carry the efficiency from one period to another, according to their characteristics. So, it is possible to identify four categories of carry-overs: good carry-over (desirable and behavior similar to that of an output), bad carry-over (undesirable and behavior similar to that of an input), free carry-over (discretionary and freely controlled by the DMU) and fixed carry-over (non-discretionary and outside the control of the DMU) [62].

The collections for a period do not correspond to the same revenue period, considering that consumers will be charged at different due dates, others delay payments (for a long or short time), or even fail to make them. To capture this phenomenon in the efficiency score, operating revenues are weighted considering the delay period and will be a good carry-over (REVENUE), as its increase is related to the increase in revenue collections within the existing receivables conditions. Considering that each utility has its own billing and recognition policy for probable losses. Furthermore, the hypothesis of a constant currency based on an inflationary index also requires careful consideration so that collections are more closely linked to the inflationary processes of their respective revenues.

Due to the limitation of data before 2017 (since the longitudinal panel began in 2018, there are collections billed in 2017, for example) for all DMUs studied, we set the maximum delay period at 2 years.

If the delay is less than or equal to 365 days, the REVENUE values will be those of the same COLLECTION period. If the delay is greater than or equal to 730 days, revenue from the immediate previous year will be considered. If they do not fit into any of these situations, REVENUE will be the result of the weighted average between the operating revenues of the reference period and the immediately previous period, according to the time that exceeds 365 days, given by: : (1) , where is the invoiced value of utility j in year t (term of DSBM) arising from the utility's core activities and corresponds to the sum of direct and indirect operating revenue from water and wastewater services (FN005 of SNIS), and is the delay in accounts receivable from utility j in period t, calculated according to [73,74]. This measurement procedure is justified because, in the sector, it is common for consumer debts to be paid in installments, sometimes over up to 24 months, and recorded in the accounts as receivables from noncurrent assets.

The efficiency model studied focuses on the effort to increase revenue collection, considering the level of customer receivables observed for each utility (DMU). Therefore, the orientation of the data envelopment model is towards output. All values are measured in BR (Reais) and were adjusted to the constant currency of the year 2022, based on the Brazilian inflationary correction measured by the Índice Nacional de Preços ao Consumidor Amplo (IPCA) released by the Instituto Brasileiro de Geografia e Estatística (IBGE), accumulated retroactively up to each year. Figure 1 and Table 1 present the structure and description of the variables used in calculating efficiency based on DSBM, respectively. In [62], the DSBM is described extensively and in detail using 27 mathematical notations. The DSBM specification column of Table 1 presents the descriptions of the variables observed in these notations (see the paper for more details).

3.3. Econometric Model Construction and Variables Measurement

To analyze these variables, we employed the Generalized Estimating Equations (GEE) regression, an extension of generalized linear models (GLM) suitable for longitudinal panel data [75]. This method was chosen due to the time-dependent nature of the dependent variable.

In GEE models, it is necessary to choose the distribution family (the random component for the response variable, which follows a distribution from the exponential family), the link function (the connection between the random component and the systematic component), and the within-group correlation structure or working correlation matrix (exchangeable, independent, autoregressive, stationary, and unstructured). The model with the smallest Quasi-likelihood under the Independence Model Criterion (QIC) is suggested as the most robust choice in GEE [76].

The econometric model has assumed that the option family follows a binomial distribution, where the results can only be grouped into two categories: inside and below the optimal efficiency frontier, as explained in [38]. For DSBM scores, two link functions will be considered: identity and logit. In this sense, we will use the lowest QIC criterion for a more robust link and correlation matrix choice.

The following panel data model is constructed to analyze the association between governance structure and efficiency:

Table A1 (Appendix A) describes all variables of the explanatory econometric model. The dependent variable was obtained from DSBM efficiency. The independent variables included in the study model were corporatization (CORP) and ownership (OWN), both of which are dummy variables. The first variable was assigned a value of 1 for utilities listed (with shares on the stock exchange) on the Comissão de Valores Mobiliários (CVM) and 0 for non-listed utilities. The second variable was assigned a value of 1 for utilities with private control (mixed capital utilities with private control or private utilities) and 0 for utilities with public control (mixed capital utilities with public control). The corporatization variable was manually collected from the CVM website, while the ownership variable was collected from the SNIS using the Juridical Nature (Natureza Jurídica) data.

The control variables included in the model were: customers’ representative (REPCUST), network density (DENSITY), tariff affordability (AFFOR), provider size (SIZECUST), urban population served (URB), utilities working with both services water and wastewater (JOINT) and the COVID-19 pandemic period.

The tariff affordability variable (AFFOR) was added to capture the effect of elasticity on the payment of fees. It was derived from three variables: two collected from the SNIS and one from the IBGE database. The first two variables did not require specific treatment. However, the variable obtained from the IBGE database needed to be processed as follows. The GDP per municipality was obtained from the platform, as well as the population it served. The GDP per municipality was summed by the utility responsible for the supply to find the GDP per municipality per utility. This value was then divided by the total population served by the utility to obtain the GDP per capita per utility, which was finally updated using the IPCA index.

According to the findings of [38], performance and GDP have a negative relationship. However, [77] found a positive impact of GDP on operator efficiency, while [78] did not identify any statistical significance. Regarding tariffs, [40] found that tariffs have a negative relationship with productivity.

Additionally, [33] pointed out that affordability presents a critical issue, as lower-income families spend a higher percentage of their monthly budget on water supply and sanitation services compared to higher-income families. The author noted that families earning up to two minimum wages spent 1.46% of their monthly budget on these services, whereas families earning more than 30 minimum wages spent only 0.29% of their monthly budget on the same services.

The variable for the share of residential connections (REPCUST) was collected from the SNIS database. The treatment performed to obtain this variable involved summing the residential water and sewage connections and dividing by the total water connections plus the total sewage connections, to determine the share of residential connections in relation to the whole. Another variable included to capture the share of a specific stratum of the total was the urban population share (URB), obtained by the ratio of the urban population served by water and sewage treatment divided by the total water and sewage connections.

In this context, according to the findings of [79], less populous cities exhibit better relative performance. [80] indicated that the number of measured consumers is negatively associated with performance, while [81] suggested that rural operators have higher productivity values.

The density variable was also collected from the SNIS platform and was included in the model to measure the extent of water and sewage connections divided by the total population served. The literature indicates that increasing network density enhances the efficiency of providers by reducing costs [82].

A single variable was included in the model to capture the type of service, which was treated as a dummy variable. Utilities providing both water and sewage services were coded as 1, while utilities providing either water or sewage services were coded as 0. In developing countries, the presence of economies of scope has yielded different results. While [83] and [38] found evidence of economies of scope, [84] and [80] and did not. The former found no significant results, and the latter found diseconomies of scope.

Economies of scope relate to the provision of two services or the production of two products that, when produced or provided together, reduce the associated costs, thereby making businesses more efficient or productive.

The last variable inputted was a dummy variable to categorize the COVID-19 pandemic period from 2020 onwards.

3. Results and Discussion

3.1. Revenue Collection Efficiency Assessment

Table 3 presents the descriptive statistics of the variables established to evaluate the efficiency of revenue collections by panel year. Notably, the average value of collections was higher in 2022, while the average receivables from consumers were the lowest, signaling possible general improvements in collections in that year. This understanding is strengthened by the observation that average revenues and receivables in 2019 were higher than in 2022, while average collections were lower, indicating lower cash conversion in 2019.

Regarding isotonicity, all efficiency variables in all years rejected the possibility of normal distribution in the Kolmogorov-Smirnov and Shapiro-Wilk tests. Therefore, the correlation test used was the non-parametric Kendall's tau-b test. Table 4 shows all correlation coefficients between revenue collection efficiency variables significant at 1%, with 0.821 being the lowest among all coefficients. This proves that the isotonicity verification protocol was followed and that a proportional increase in inputs generates a proportional increase in outputs.

Considering that the output orientation had already been defined, the return to scale issue was decided by the Wilcoxon two–related-sample test, which rejected the hypothesis of equality of means between the efficiency scores reproduced under the premise of CRS and VRS. Therefore, VRS was chosen, following the understanding of [51]. Table B1 (Appendix B) and Table 5 present the results of the efficiency scores in revenue collection using the DSBM model, input-oriented and variable return to scale.

The results revealed an overall average efficiency in revenue collection for all years of 49.53% (Overall Score), indicating a general average inefficiency of 50.47%. In the annual observation, the least inefficient period was 2020, with a global average inefficiency of 45.92%, and 2018 was the worst year in the panel with 55.07% inefficiency. Only 4 utilities were efficient across the entire panel. In 2022, 4 fewer utilities reached the efficiency frontier compared to 2021, which also slightly increased overall inefficiency.

In the analysis of inefficiencies by clusters (classified according to Tukey's Hinges without the efficient ones in the sample): Extreme inefficiencies, High inefficiencies, and 25% with the lowest inefficiencies, it is possible to observe that 30 utilities were classified as such in the overall score, with 2018 being the worst year, showing 32.28% of utilities in the extreme inefficiency zone.

Considering the overall score, the following utilities are efficient: 35503000-SABESP; 43149000-CORSAN; 51055811-AMA; 51083011-AUS. The most critical inefficiencies were identified in the following utilities: 11001812-APB; 11002000-CAERD; 11004512-ABU; 13026000-COSAMA; 13026011-MA; 15013012-ASF; 15061312-BRK; 21075012-BRK; 21112012-BRK; 21113000-CAEMA 22110000-AGESPISA; 23042011-SAAEC; 27043000-CASAL; 28003000-DESO; 29307711-EMSAE; 33018511-FSSG; 33045511-FABZO; 51027911-AGUASCAR; 51033511-ACO; 51035012-ADI; 51049011-SBJ; 51050011-AJ; 51060011-ANOR; 51063012-APA; 51063711-SBPP; 51065011-APO; 51067511-APL 51068211-APE 51073011-ASJ 51085011-AVE.

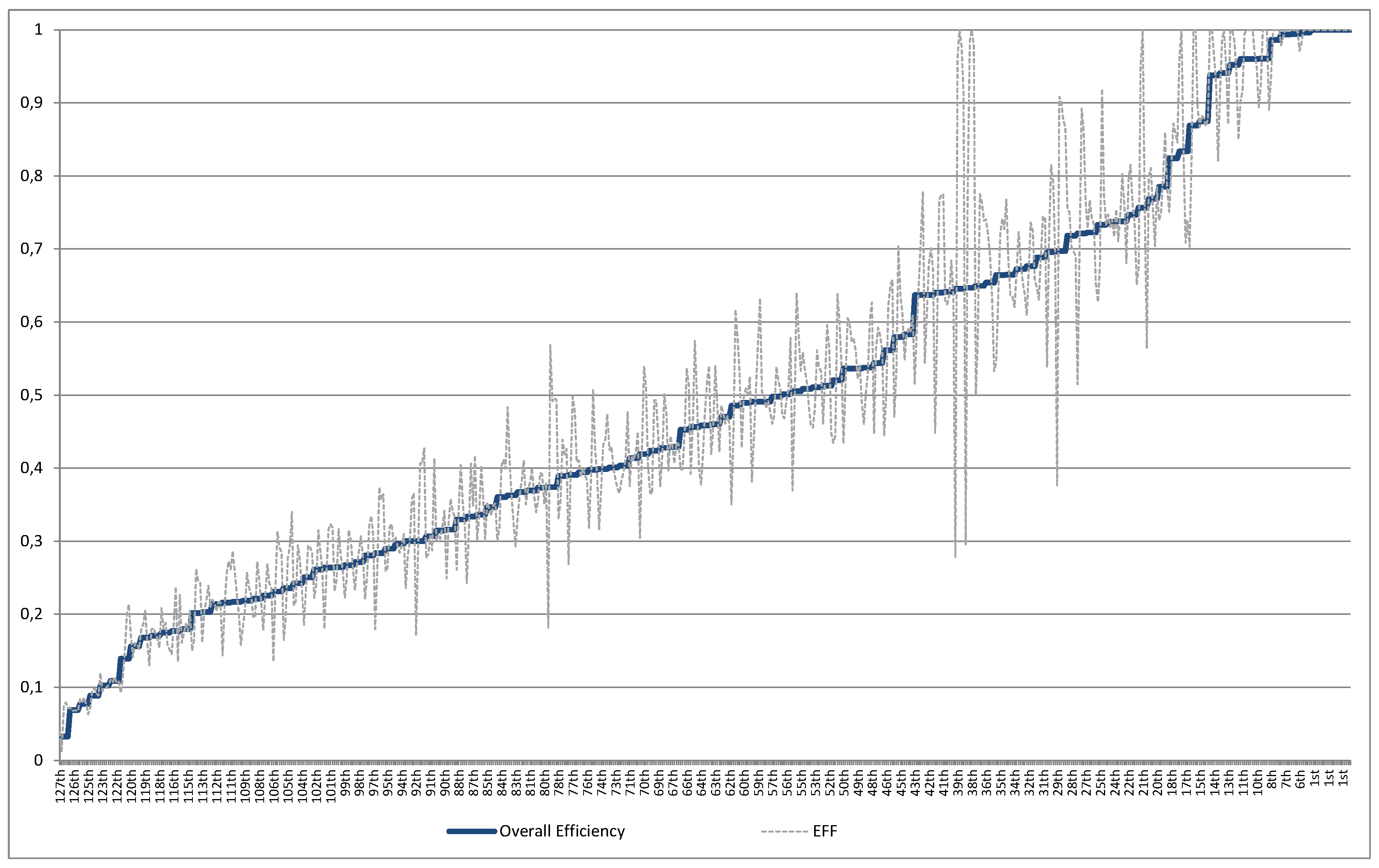

The dispersions reproduced by the different efficiency scores obtained by each utility over the years of the panel can be seen in Graph 1.

The Graph 1 illustrates how the revenue collection efficiencies of utilities fluctuate from year to year, indicating a certain level of independence in scores from one year to the next. These fluctuations highlight significant gains and losses in efficiency for various utilities over different years. The next section will present the results of the explanatory model.

3.2. Econometric Explanatory Model

3.2.1. Descriptive Statistic

Table 6 presents the descriptive statistics of the variables analyzed. For the dependent variable, we observe a mean revenue collection efficiency of 50% with a standard deviation of 26%.

Regarding the variables of interest in the study, the sample shows that, on average, 11%% of the utilities are corporatized and 74% are controlled by private agents. Other factors analyzed indicate that 47% of utilities are listed on the stock market, while 53% are not; 52% of concessionaries provide both water and wastewater services; and 60% of the period analyzed includes the pandemic period.

It is worth noting that the sample studied represents, over the panel, averages of 73% of active water connections, 72% of active sewage connections, 76% of revenue from services, and 77% of the revenue collection of all Brazilian utilities registered in the SNIS database. This includes those considered direct provision, where municipalities themselves, through government agencies or their own government departments (usually infrastructure departments), manage the services. These were not considered within the scope of our study due to the lack of corporatization characteristics.

3.3. Explanatory Econometric Analysis

Table 7 shows that the Variance Inflation Factor (VIF) is low, ruling out the possibility of multicollinearity. Among the combinations of link functions (logit and identity) and within-group correlation structures, the models with stationary and unstructured structures did not converge. Among the remaining combinations (exchangeable, independent, and autoregressive), the model with the identity link function and independent correlation structure obtained the lowest QIC, making it the most robust and therefore selected for explanatory analyses

In terms of ownership public or private, the results showed that being controlled by private owners is associated with lower revenue collection efficiency. Some studies have observed that private utilities tend to lead to higher prices, such as in Chile [29] and in various developing countries with public-private partnerships that have increased tariffs [30], possibly aiming to recover costs and enhance profitability.

In this sense, hypothesis H1 is rejected. It is worth noting that the only model that presented this significant result at the 5% level was the identity-independent model; all the others were not significant. Another possible explanation may be based on the findings of [7], which suggest tariffs for private utilities 27.97% higher.

Regarding corporatization, the results revealed that utilities listed on the Brazilian stock exchange are more efficient in collecting revenue. Therefore, hypothesis H2 cannot be rejected. This is possibly due to stricter enforcement of service cutoffs for late payments, making these utilities more efficient in revenue collection.

A theoretical argument supporting this is Signaling Theory, formulated by [45], which posits that individuals can manipulate their characteristics to guide decision-making in uncertain environments. These characteristics can mitigate informational asymmetry [46]. Furthermore, according to this author, higher quality utilities adopt policies to showcase their superiority, while lower quality utilities conceal their weaknesses. Therefore, presenting better signals through improved revenue collection efficiency can be interpreted by the market as an indicator of higher quality service providers.

The urbanization factor is associated with lower efficiency, likely because in rural areas a cheaper tariff, known as the “social tariff [7], is commonly applied, making it easier for people to pay. The findings also align with [81], who indicated that rural operators are more productive.

The tariff affordability variable (AFFOR) was added to capture the effect of elasticity on the payment of fees. The findings can be explained by the behavior of public institutions, which have high consumption but also high rates of default on payments. It is very common for Brazilian utilities to mention difficulties in collecting revenue from public consumers in their integrated reports. For example, [86], reports a high number of uncollected bills linked to public consumers

The last significant variable was the COVID-19 pandemic. At first glance, it may seem strange to observe better revenue collection efficiency during a crisis period. However, various social policies were implemented to protect and support informal workers with financial aid during this time. The most significant policy was the emergency aid established by Law 13.982/2020 [85]. This law provided a fixed amount of money to help individuals, with an additional amount and three times more for women who are the primary breadwinners of their households.

4. Conclusions

Generally, studies related to the efficiency of Water Utilities (WUs) are focused on investigating the relationships between governance (ownership, regulation, etc.) and the technical and economic efficiencies of the sector, mainly those involving costs. This work focused on analyzing a more specific problem, which would be the relevance of governance structure for efficiency in revenue collection for these utilities in the Brazilian scenario, which is an innovative contribution in relation to previous literature.

Focusing on the evaluation of efficiency, the results showed an overall average inefficiency in revenue collection of 50.47%, which has been decreasing slowly over the years with small oscillations of increase and decrease. The year the COVID-19 pandemic began was noted as having the lowest inefficiencies. On an annual basis, at least 17% of utilities are extremely inefficient, with many fluctuating from year to year, showing improvements and deteriorations in efficiency. In other words, there is a significant gap in inefficiencies within the sector that needs to be addressed with systemic productivity gains in collection efficiency year after year

In the second stage, the explanatory econometric model was applied to explain the findings. The results indicate that private management is associated negatively with revenue collection efficiency. Contrary to the predominant research paradigm that suggests productivity and efficiency are superior in private management over public management (H1), we find evidence that this efficiency does not extend to revenue collection performance. This can be explained and corroborated by studies showing that private utilities often result in higher prices, as evidenced in Chile [29] and in developing countries with public-private partnerships that have led to increased tariffs [30].

Additionally, being corporatized (publicly listed) is positively associated with revenue collection efficiency. This reinforces the presented framework and supports the hypothesis (H2). In summary, it can be pointed out that publicly listed utilities generally implement policies that showcase their strengths, whereas lower quality utilities often employ strategies to hide their shortcomings [46].

Some variables presented a strong association with revenue collection efficiency: URB, AFFOR, and COVID19. The first variable supported the existing framework, which indicated that rural operators are more productive and that urban utilities tend to apply more expensive tariffs compared to rural operators. The second variable showed that affordability is negatively related to collection performance, as public institutions with high bills also tend to have high default rates. The third variable indicated that the pandemic period was associated with better efficiency. Contrary to common sense, this crisis period may have resulted in more efficiency, possibly due to government political aid in Brazil, especially the emergency aid. Other factors investigated didn’t present evidence of association with revenue collection efficiency, REPCUST, DENSITY, SIZECUST, JOINT.

Finally, the findings of this work may indicate some practical implications, such as alerting regulatory bodies about the importance of imposing regulatory limits for recognizing losses with uncollectible receivables, putting pressure on utilities to improve collection practices with a focus on reducing losses, providing fairer tariffs under an efficiency regime.

Author Contributions

For research articles with several authors, a short paragraph specifying their individual contributions must be provided. The following statements should be used “Conceptualization, A.B. and F.A.S.M.; methodology, A.B. and F.A.S.M; software, A.B.; validation, A.B., F.A.S.M. and P.S.; formal analysis, A.B. and F.A.S.M.; investigation, A.B. and F.A.S.M.; resources, A.B and P.S.; data curation, A.B., F.A.S.M. and P.S.; writing—original draft preparation, A.B. and F.A.S.M.; writing—review and editing, A.B., F.A.S.M. and P.S.; visualization, P.S.; supervision, P.S.; project administration, A.B.; funding acquisition, A.B. All authors have read and agreed to the published version of the manuscript.”

Funding

This research was funded by Agreement 002/2021-ARSBAN/UFRN (Convênio 002/2021 – ARSBAN/UFRN) - Applied Research and Technical-Scientific Studies on Regulatory Topics Involving the Performance (Efficiency, Productivity and Quality) of Water Supply and Sanitation Services Provided in the Municipality of Natal.

Data Availability Statement

Publicly available datasets were analyzed in this study. This data can be found here: [http://app4.mdr.gov.br/serieHistorica/]; [https://www.ibge.gov.br/estatisticas/economicas/precos-e-custos/9256-indice-nacional-de-precos-ao-consumidor-amplo.html?edicao=37613&t=downloads]; [https://cvmweb.cvm.gov.br/SWB/Sistemas/SCW/CPublica/CiaAb/FormBuscaCiaAb.aspx?TipoConsult=c] and [https://www.ibge.gov.br/estatisticas/economicas/contas-nacionais/9088-produto-interno-bruto-dos-municipios.html?=&t=resultados]

Conflicts of Interest

The authors declare no conflicts of interest.

Appendix A

Table A1.

Description of the model's explanatory variables.

| Variable | Description | Expectation a priori and hypothesis |

|---|---|---|

| Revenue collection efficiency score of utility j in year t, calculated using the DSBM model under the premises of VRS and input-oriented, considering customer accounts receivables (input), revenue collections (output), and revenue (good carry-over). Source: DSBM Score | Dependent Variable | |

| Corporatization of utility j in year t. This variable captures whether a utility is publicly listed. 1 for utilities listed with the CVM, 0 otherwise. Source: CVM | - (H2) | |

| Ownership structure of utility j in year t. Was collected through SNIS platform, using the information of “Natureza juridica”. 1 for utilities with private control (“Empresa Privada” and “Sociedade de economia mista com gestão privada”), 0 for utilities with public control (“Empresa Pública” and “Sociedade de economia mista com gestão pública”). | -/+ (H1) | |

| Proportion of residential customers per economies of utility j in year t. Thus, the number of active residential water (AG013 of the SNIS) and wastewater (ES008 of the SNIS) units that were fully operational on the last day of the reference year proportional to active water (AG003 of the SNIS) and wastewater (ES003 of the SNIS) economies refer to the number of units connected to the water supply network and provided with water for user consumption in the reference year. | + | |

| Density of the service area of utility j in year t. Therefore, the total population served with water (AG001 of the SNIS) and wastewater (ES001 of the SNIS) services by the service provider on the last day of the reference year proportional to active water (AG003 of the SNIS) and wastewater (ES003 of the SNIS) economies refer to the number of units connected to the water supply network and provided with water for user consumption in the reference year. | -/+ | |

| Average per Capita Consumption (IN022 from the SNIS) * Average Applied Tariff (IN004) proportional of water services relative to GDP per capita. On this portal, the GDP per municipality, the population attended per municipality, and the GDP per capita per municipality can be found. For this work, the GDPs per municipality were summed to calculate the GDP per company. Then, the GDP per capita per company was obtained by dividing this total by the sum of the total population served per company. Average Tariff and GDP adjusted using the Brazilian price index IPCA/IBGE. | - | |

| Size of utility j in year t. Total assets relative to the number of economies served. So, The annual value of the sum of Current Assets, Long-Term Receivables, and Permanent Assets (BL002 of the SNIS) proportional to active water (AG003 of the SNIS) and wastewater (ES003 of the SNIS) economies refer to the number of units connected to the water supply network and provided with water for user consumption in the reference year and then adjusted using the Brazilian price index IPCA/IBGE (measured in BR/Econ). | - | |

| Proportion of the urban population served in relation to the total active economies of utility j in year t. It represents the value of the urban population served with water supply by the service provider on the last day of the reference year, in proportion to the total population served with water (AG001 from the SNIS) and wastewater (ES001 from the SNIS) services by the service provider on the last day of the reference year. | + | |

| Joint provision of water and wastewater of utility j in year t. Was collected through SNIS platform, using the information of “Tipo de serviço”.1 for utilities providing both water and wastewater services (“Água e Esgoto”), 0 for utilities providing either water or wastewater services (“Água”; “Esgoto”). | -/+ | |

| Effect of COVID-19 on utility j in year t 2020 onwards. | -/+ |

Appendix B

Table B1.

– DSBM Efficiencies scores.

| DMU | Overall Score | 2018 | 2019 | 2020 | 2021 | 2022 | DMU | Overall Score | 2018 | 2019 | 2020 | 2021 | 2022 |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 11000212-AA | 0,284 | 0,180 | 0,261 | 0,374 | 0,357 | 0,364 | 35334011-CODEN | 0,961 | 0,925 | 1,000 | 1,000 | 1,000 | 0,891 |

| 11001812-APB | 0,271 | 0,233 | 0,266 | 0,287 | 0,307 | 0,275 | 35350011-ESAP | 0,505 | 0,370 | 0,493 | 0,640 | 0,581 | 0,533 |

| 11002000-CAERD | 0,170 | 0,179 | 0,181 | 0,174 | 0,167 | 0,154 | 35356012-CAEPA | 0,721 | 0,515 | 0,714 | 0,892 | 0,864 | 0,763 |

| 11002812-ARM | 0,300 | 0,172 | 0,279 | 0,407 | 0,406 | 0,427 | 35385011-AP | 0,419 | 0,305 | 0,424 | 0,539 | 0,512 | 0,404 |

| 11004512-ABU | 0,139 | 0,092 | 0,114 | 0,152 | 0,200 | 0,214 | 35407011-BRK | 0,428 | 0,375 | 0,418 | 0,501 | 0,474 | 0,395 |

| 13026000-COSAMA | 0,033 | 0,039 | 0,012 | 0,075 | 0,079 | 0,072 | 35452012-SANESALTO | 0,733 | 0,627 | 0,678 | 0,919 | 0,773 | 0,732 |

| 13026011-MA | 0,180 | 0,161 | 0,174 | 0,187 | 0,177 | 0,205 | 35467011-BRK | 0,424 | 0,366 | 0,364 | 0,493 | 0,493 | 0,443 |

| 14001000-CAER | 0,637 | 0,515 | 0,594 | 0,653 | 0,710 | 0,779 | 35475012-COMASA | 0,869 | 0,703 | 0,826 | 1,000 | 1,000 | 0,892 |

| 15013012-ASF | 0,236 | 0,165 | 0,194 | 0,277 | 0,291 | 0,340 | 35503000-SABESP | 1,000 | 1,000 | 1,000 | 1,000 | 1,000 | 1,000 |

| 15014000-COSANPA | 0,307 | 0,277 | 0,283 | 0,307 | 0,287 | 0,413 | 35524012-BRK | 0,508 | 0,559 | 0,536 | 0,516 | 0,484 | 0,459 |

| 15050311-PMNP/ANP | 0,281 | 0,221 | 0,254 | 0,320 | 0,335 | 0,307 | 35570011-CAV | 0,677 | 0,609 | 0,672 | 0,736 | 0,725 | 0,657 |

| 15061312-BRK | 0,217 | 0,287 | 0,257 | 0,228 | 0,202 | 0,158 | 41069000-SANEPAR | 0,960 | 1,000 | 1,000 | 0,968 | 0,949 | 0,894 |

| 17210000-SANEATINS | 0,941 | 0,912 | 0,987 | 1,000 | 0,947 | 0,871 | 41182011-PS | 0,401 | 0,425 | 0,430 | 0,400 | 0,385 | 0,372 |

| 21075012-BRK | 0,089 | 0,073 | 0,096 | 0,099 | 0,092 | 0,089 | 42020712-GS | 0,646 | 0,279 | 0,961 | 1,000 | 0,978 | 0,913 |

| 21112012-BRK | 0,156 | 0,169 | 0,141 | 0,161 | 0,159 | 0,152 | 42024012-BRK | 0,785 | 0,739 | 0,749 | 0,803 | 0,860 | 0,786 |

| 21113000-CAEMA | 0,077 | 0,084 | 0,080 | 0,086 | 0,077 | 0,063 | 42024511-AB | 0,458 | 0,378 | 0,420 | 0,477 | 0,519 | 0,540 |

| 21122013-AT | 0,373 | 0,355 | 0,393 | 0,392 | 0,351 | 0,381 | 42032012-AC | 0,561 | 0,445 | 0,502 | 0,622 | 0,650 | 0,658 |

| 22110000-AGESPISA | 0,102 | 0,120 | 0,095 | 0,098 | 0,099 | 0,103 | 42054000-CASAN | 0,737 | 0,747 | 0,730 | 0,740 | 0,717 | 0,754 |

| 22110011-AT | 0,489 | 0,428 | 0,496 | 0,509 | 0,501 | 0,525 | 42062012-GS | 0,697 | 0,375 | 0,908 | 0,902 | 0,876 | 0,867 |

| 23042011-SAAEC | 0,203 | 0,161 | 0,205 | 0,218 | 0,239 | 0,210 | 42083011-CIA de Águas | 0,501 | 0,472 | 0,468 | 0,493 | 0,509 | 0,578 |

| 23044000-CAGECE | 0,429 | 0,444 | 0,430 | 0,407 | 0,436 | 0,433 | 42084512-IS | 0,650 | 0,500 | 0,574 | 0,775 | 0,765 | 0,739 |

| 24081000-CAERN | 0,938 | 1,000 | 1,000 | 0,967 | 0,926 | 0,821 | 42091012-CAJ | 0,641 | 0,629 | 0,624 | 0,637 | 0,684 | 0,635 |

| 25075000-CAGEPA | 0,347 | 0,353 | 0,345 | 0,336 | 0,349 | 0,352 | 42125012-AP | 0,403 | 0,366 | 0,384 | 0,395 | 0,413 | 0,477 |

| 26116000-COMPESA | 0,470 | 0,486 | 0,474 | 0,461 | 0,471 | 0,460 | 42162012-ASFS | 0,538 | 0,460 | 0,503 | 0,530 | 0,606 | 0,627 |

| 27043000-CASAL | 0,168 | 0,178 | 0,187 | 0,205 | 0,162 | 0,130 | 42187012-TBSSA | 0,300 | 0,236 | 0,282 | 0,299 | 0,358 | 0,366 |

| 28003000-DESO | 0,214 | 0,220 | 0,215 | 0,204 | 0,217 | 0,216 | 43149000-CORSAN | 1,000 | 1,000 | 1,000 | 1,000 | 1,000 | 1,000 |

| 29148011-EMASA | 0,696 | 0,538 | 0,723 | 0,815 | 0,791 | 0,688 | 43224011-BRK | 0,394 | 0,411 | 0,388 | 0,400 | 0,391 | 0,383 |

| 29274000-EMBASA | 0,718 | 0,756 | 0,750 | 0,702 | 0,697 | 0,691 | 50027000-SANESUL | 0,723 | 0,728 | 0,767 | 0,742 | 0,734 | 0,653 |

| 29307711-EMSAE | 0,202 | 0,150 | 0,164 | 0,262 | 0,245 | 0,243 | 50027011-AG | 0,414 | 0,376 | 0,417 | 0,410 | 0,423 | 0,450 |

| 31039011-SANARJ | 0,391 | 0,269 | 0,396 | 0,497 | 0,479 | 0,408 | 51002511-AAF | 0,360 | 0,300 | 0,320 | 0,403 | 0,412 | 0,399 |

| 31062000-COPASA | 0,994 | 0,979 | 0,990 | 1,000 | 1,000 | 1,000 | 51013011-AA | 0,996 | 0,982 | 1,000 | 1,000 | 1,000 | 1,000 |

| 31367011-CESAMA | 0,654 | 0,740 | 0,720 | 0,691 | 0,632 | 0,533 | 51018012-ABG | 0,498 | 0,461 | 0,472 | 0,539 | 0,520 | 0,507 |

| 31471011-CAPAM | 0,664 | 0,545 | 0,631 | 0,722 | 0,742 | 0,727 | 51026711-ACV | 0,399 | 0,317 | 0,374 | 0,432 | 0,439 | 0,474 |

| 31472011-COSÁGUA | 0,580 | 0,470 | 0,535 | 0,704 | 0,635 | 0,612 | 51027011-AC | 0,641 | 0,448 | 0,592 | 0,767 | 0,774 | 0,775 |

| 32012011-BRK | 0,537 | 0,577 | 0,561 | 0,522 | 0,541 | 0,490 | 51027911-AGUASCAR | 0,231 | 0,135 | 0,244 | 0,313 | 0,291 | 0,284 |

| 32053000-CESAN | 0,875 | 0,867 | 0,883 | 0,879 | 0,868 | 0,878 | 51030511-AC | 0,316 | 0,249 | 0,325 | 0,358 | 0,342 | 0,333 |

| 33002011-CAJ | 0,689 | 0,647 | 0,631 | 0,693 | 0,744 | 0,744 | 51032011-AC | 0,511 | 0,455 | 0,482 | 0,561 | 0,538 | 0,532 |

| 33007011-PROLAGOS | 0,314 | 0,300 | 0,309 | 0,303 | 0,321 | 0,342 | 51033011-AC | 0,486 | 0,350 | 0,455 | 0,617 | 0,577 | 0,530 |

| 33010011-CAP | 0,491 | 0,504 | 0,501 | 0,482 | 0,492 | 0,478 | 51033511-ACO | 0,264 | 0,180 | 0,252 | 0,316 | 0,323 | 0,319 |

| 33018511-FSSG | 0,175 | 0,208 | 0,181 | 0,188 | 0,158 | 0,152 | 51034011-CBA | 0,297 | 0,305 | 0,292 | 0,284 | 0,293 | 0,310 |

| 33024012-BRK | 0,374 | 0,181 | 0,569 | 0,492 | 0,497 | 0,493 | 51035012-ADI | 0,242 | 0,212 | 0,218 | 0,294 | 0,275 | 0,233 |

| 33033011-CAN | 0,986 | 0,935 | 1,000 | 1,000 | 1,000 | 1,000 | 51041011-AG | 0,389 | 0,330 | 0,356 | 0,439 | 0,419 | 0,426 |

| 33034011-CANF | 0,952 | 1,000 | 1,000 | 0,985 | 0,943 | 0,850 | 51049011-SBJ | 0,226 | 0,178 | 0,225 | 0,268 | 0,243 | 0,235 |

| 33038011-CAPY | 0,367 | 0,337 | 0,362 | 0,385 | 0,410 | 0,351 | 51050011-AJ | 0,216 | 0,144 | 0,210 | 0,256 | 0,273 | 0,262 |

| 33039011-CAI | 0,747 | 0,794 | 0,815 | 0,760 | 0,737 | 0,651 | 51055811-AMA | 1,000 | 1,000 | 1,000 | 1,000 | 1,000 | 1,000 |

| 33042011-CAAN | 0,824 | 0,751 | 0,805 | 0,872 | 0,860 | 0,846 | 51056011-AM | 0,334 | 0,243 | 0,318 | 0,406 | 0,349 | 0,417 |

| 33045511-FABZO | 0,069 | 0,072 | 0,068 | 0,069 | 0,068 | 0,068 | 51060011-ANOR | 0,109 | 0,110 | 0,107 | 0,114 | 0,106 | 0,108 |

| 35021011-AA | 0,513 | 0,461 | 0,527 | 0,596 | 0,564 | 0,448 | 51062511-SETAE | 0,994 | 1,000 | 1,000 | 1,000 | 1,000 | 0,971 |

| 35028011-SAMAR | 0,738 | 0,711 | 0,749 | 0,802 | 0,758 | 0,681 | 51063012-APA | 0,222 | 0,197 | 0,195 | 0,272 | 0,248 | 0,214 |

| 35029011-CAA | 0,520 | 0,435 | 0,445 | 0,638 | 0,603 | 0,546 | 51063711-SBPP | 0,264 | 0,231 | 0,247 | 0,317 | 0,280 | 0,261 |

| 35095011-SANASA | 0,769 | 0,799 | 0,811 | 0,756 | 0,704 | 0,784 | 51064211-APA | 0,330 | 0,261 | 0,342 | 0,406 | 0,353 | 0,322 |

| 35110011-EAC | 0,337 | 0,302 | 0,334 | 0,403 | 0,361 | 0,303 | 51065011-APO | 0,219 | 0,181 | 0,206 | 0,257 | 0,237 | 0,227 |

| 35144011-EMDAEP | 0,756 | 0,676 | 0,951 | 1,000 | 0,764 | 0,565 | 51067511-APL | 0,267 | 0,223 | 0,250 | 0,315 | 0,302 | 0,265 |

| 35177011-GUARA | 0,398 | 0,318 | 0,390 | 0,508 | 0,428 | 0,390 | 51068211-APE | 0,177 | 0,145 | 0,188 | 0,237 | 0,135 | 0,227 |

| 35184011-SAEG | 0,834 | 0,958 | 1,000 | 0,840 | 0,709 | 0,739 | 51070411-APL | 0,370 | 0,371 | 0,380 | 0,401 | 0,363 | 0,340 |

| 35190512-AH | 0,544 | 0,448 | 0,563 | 0,592 | 0,582 | 0,562 | 51072411-ASC | 0,647 | 0,295 | 0,770 | 0,985 | 1,000 | 0,978 |

| 35253012-CAJA | 0,637 | 0,544 | 0,615 | 0,681 | 0,701 | 0,671 | 51073011-ASJ | 0,261 | 0,222 | 0,240 | 0,315 | 0,287 | 0,262 |

| 35259011-DAE Jundiaí | 0,583 | 0,548 | 0,582 | 0,592 | 0,587 | 0,609 | 51079011-AS | 0,491 | 0,382 | 0,445 | 0,508 | 0,568 | 0,632 |

| 35269011-BRKL | 0,665 | 0,768 | 0,686 | 0,636 | 0,635 | 0,620 | 51079211-AS | 0,536 | 0,433 | 0,512 | 0,605 | 0,599 | 0,574 |

| 35284011-SM | 0,453 | 0,399 | 0,398 | 0,452 | 0,536 | 0,513 | 51083011-AUS | 1,000 | 1,000 | 1,000 | 1,000 | 1,000 | 1,000 |

| 35293011-AM | 0,290 | 0,259 | 0,262 | 0,319 | 0,324 | 0,299 | 51085011-AVE | 0,250 | 0,185 | 0,237 | 0,295 | 0,292 | 0,284 |

| 35294012-BRK | 0,363 | 0,483 | 0,411 | 0,362 | 0,323 | 0,293 | 52087000-SANEAGO | 0,960 | 0,901 | 0,916 | 0,994 | 1,000 | 1,000 |

| 35298011-AMT | 0,457 | 0,392 | 0,463 | 0,574 | 0,499 | 0,400 | 53001000-CAESB | 0,673 | 0,667 | 0,723 | 0,685 | 0,655 | 0,639 |

| 35303011-SANESSOL | 0,460 | 0,418 | 0,453 | 0,540 | 0,489 | 0,423 |

References

- Olaoye, Clement Olatunji; Atilola, Oluseyi Olabanji. Effect of e-tax payment on revenue generation in Nigeria. 2018, 4, 56-65.

- Muriithi, J. M.; Ochieng, I.; Nzioki, Paul M. The Effect Of Improved Revenue-Collection Efficiency Strategy On The Performance Of Wsps In Kenya: A Case Nyahururu Water And Sanitation Company, Nyahururu, Kenya. The Strategic Journal of Business & Change Management 2019, 6, p. 1335-1341.

- Ngotho, Joyce; Kerongo, Francis. Determinants of revenue collection in developing countries: Kenya’s tax collection perspective. Journal of management and business administration 2014, 1, 1-9.

- Nekemia, Ampiire; Atukunda, Gershom; Nuwagaba, Arthur. On-spot billing system, cost of water, revenue collection mechanism & revenue collection performance of public utility entities evidence from NWSC Mbarara Centre. Journal of development, education & technology 2023, 1, 29-54.

- Brazil. Conselho Nacional do Ministério Público. Revista do CNMP: água, vida e direitos humanos / Conselho Nacional do Ministério Público. – n. 7 (2018). – Brasília: CNMP, 2018. Available in: <https://www.cnmp.mp.br/portal/images/revista_final.pdf>.

- Nauges, Celine; Whittington, Dale. Evaluating the performance of alternative municipal water tariff designs: Quantifying the tradeoffs between equity, economic efficiency, and cost recovery. World Development 2017, 91, 125-143.

- Barbosa, Alexandro; Brusca, Isabel. Governance structures and their impact on tariff levels of Brazilian water and sanitation corporations. Utilities Policy 2015, 34, 94–105. [CrossRef]

- Romano, Giulia; Guerrini, Andrea; Vernizzi, Silvia. Ownership, investment policies and funding choices of Italian water utilities: an empirical analysis. Water resources management 2013, 27, 3409-3419.

- Pereira, J. M. Defesa da concorrência e regulação econômica no Brasil. RAM. Revista de Administração Mackenzie 2022, 5, 35-55.

- Leibenstein, Harvey. Allocative efficiency vs." X-efficiency". The American economic review 1966, 56, 392-415.

- Brazil. Lei nº. 11.445, de 5 de janeiro de 2007. Diário Oficial da União, Brasília, DF. 5 jan. 2007. Available in: < https://www.planalto.gov.br/ccivil_03/_ato2007-2010/2007/lei/l11445.htm>.

- Brazil. Lei n. 14.026, de 15 de julho DE 2020. Diário Oficial da União, 16 de julho de 2020. Available in: < https://www.planalto.gov.br/ccivil_03/_ato2019-2022/2020/lei/l14026.htm#:~:text=%E2%80%9CEstabelece%20as%20diretrizes%20nacionais%20para,11%20de%20maio%20de%201978.%E2%80%9D>.

- Estrin, Saul; Pelletier, Adeline. Privatization in developing countries: what are the lessons of recent experience? The World Bank Research Observer 2018, 33, 65–102. [CrossRef]

- Gonçalves, Mariana Berardinelli Vieira Braz. Privatização da Cedae: Na Contramão do Movimento Mundial de Remunicipalização dos Serviços de Saneamento. Geo UERJ 2017, 31, 81-103.

- Ferreira, José Gomes; Gomes, Matheus Fortunato Barbosa; Dantas, Maria Wagna de Araújo. Challenges and controversies of the new legal framework for basic sanitation in Brazil. Brazilian Journal of Development 2021, 7, 65449–65468. [CrossRef]

- Kishimoto, Satoko; Petitjean, Olivier. Cómo ciudades y ciudadanía están escribiendo el futuro de los servicios públicos. The Transnational Institute. Available in: <https://www.tni.org/es/publicaci%C3%B3n/remunicipalizacion-el-futuro-de-los-servicios-p%C3%BAblicos>.

- Berg, Sanford. Water utility benchmarking: measurement, methodologies and performance incentives, v. 9; International Water Association Publishing: London, United Kingdom, 2010.

- Baker, S. R., Bloom, N., Davis, S. J., & Terry, S. J. Covid-induced economic uncertainty. National Bureau of Economic Research 2020.

- Oliveira, Gesner; Marcato, Fernando S.; Scazufca, Pedro; Ferreira, Artur Villela. Estudo técnico: Remunicipalização dos serviços de saneamento básico. estudos de caso e debate. 2018. Available at: https://goassociados.com.br/wpcontent/uploads/2018/11/Parecer-remunicipaliza%C3%A7%C3%A3o-saneamento.pdf>. [CrossRef]

- Vieira, A. C. O direito Humano à água. Imprenta: Arraes Belo Horizonte; Brazil. 2016. pp. 1-128.

- Wichman, C. J. Perceived price in residential water demand: Evidence from natural experiment. Journal of Economic Behavior & Organization 2014, 107, 308–323. [Google Scholar] [CrossRef]

- Namaliya, Nicholas Gracious. Strategies for maximizing revenue collection in public water utility companies. Walden Dissertations and Doctoral Studies. Walden University, 2017.

- Martínez-Espiñeira, Roberto; García-Valiñas, María A.; González-Gómez, Francisco. Does private management of water supply services really increase prices? An empirical analysis in Spain. Urban Studies 2009, 46, 923–945. [CrossRef]

- García-Valiñas, María De Los Ángeles; González-Gómez, Francisco; Picazo-Tadeo, Andres J. Is the price of water for residential use related to provider ownership? Empirical evidence from Spain. Utilities Policy 2013, 24, 59–69. [CrossRef]

- Guerrini, Andrea; Romano, Giulia; Campedelli, Bettina. Factors affecting the performance of water utility companies. International Journal of Public Sector Management 2011, 24, 543–566.

- Romano, Giulia; Guerrini, Andrea; Masserini, Lucio. Endogenous and environmental determinants of water pricing policy in Italy. 2013. Available at: SSRN: < https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2331391>.

- Chong, E.; Huet, F.; Saussier, S.; Steiner, F. Public-private partnerships and prices: Evidence from water distribution in France. Review of Industrial Organization 2006, 29, 149–169. [Google Scholar] [CrossRef]

- Ruester, Sophia; Zschille, Michael. The impact of governance structure on firm performance: An application to the German water distribution sector. Utilities Policy 2010, 18, 154-162.

- Bitrán, Gabriel A.; Valenzuela, Eduardo P. Water services in Chile: comparing private and public performance. 2003. Available at: <https://documents1.worldbank.org/curated/pt/455861468769468006/pdf/261260viewpoint.pdf>.

- Marin, Philippe. Public private partnerships for urban water utilities: A review of experiences in developing countries, nº 8, The world Bank, United States, 2009; pp. 1-177.

- Estache, Antonio; Trujillo, Lourdes. Efficiency effects of “privatization” in argentina’s water and sanitation services. Water policy 2003, 5, 369-380.

- Zaki, Saeed; Nurul Amin, A. T. M. Does basic services privatisation benefit the urban poor? Some evidence from water supply privatisation in Thailand. Urban Studies 2009, 46, 2301–2327. [CrossRef]

- Oliveira, Andre R. Private provision of water service in Brazil: Impacts on access and affordability. MPRA paper 11149 2008. University Library of Munich, Germany. Available at: <https://mpra.ub.uni-muenchen.de/11149/1/MPRA_paper_11149.pdf>.

- Berg, Sanford; Marques, R. C. Quantitative studies of water and sanitation utilities: a benchmarking literature survey. Water Policy 2011, 13, 591-606.

- ABBOTT, Malcolm; COHEN, Bruce. Productivity and efficiency in the water industry. Utilities Policy 2009, 17, 233–244. [CrossRef]

- Carvalho, Pedro; Marques, Rui Cunha; Berg, Sanford. A meta-regression analysis of benchmarking studies on water utilities market structure. Utilities Policy 2012, 21, 40-49.

- Worthington, A. C. A review of frontier approaches to efficiency and productivity measurement in urban water utilities. Urban Water Journal 2014, 11, 55–73. [Google Scholar] [CrossRef]

- Barbosa, Alexandro; De Lima, Severino Cesário; Brusca, Isabel. Governance and efficiency in the Brazilian water utilities: A dynamic analysis in the process of universal access. Utilities Policy 2016, 43, 82-96.

- Sabbioni, Guillermo. Efficiency in the Brazilian sanitation sector. Utilities Policy 2008, 16, 11–20. [CrossRef]

- Motta, Ronaldo Seroa; Moreira, Ajax. Efficiency and regulation in the sanitation sector in Brazil. Utilities Policy 2006, 14, 185–195. [CrossRef]

- Cetrulo, Tiago Balieiro; Marques, Rui Cunha; Malheiros, Tadeu Fabrício. An analytical review of the efficiency of water and sanitation utilities in developing countries. Water research 2019, 161, 372–380. [CrossRef]

- Mello, Marina Figueira. Privatização do setor de saneamento no Brasil: quatro experiências e muitas lições. Econ. Apl. 2005, Ribeirão Preto, 9, 495-517.

- Vining, Aidan R.; Boardman, Anthony E. Ownership versus competition: Efficiency in public enterprise. Public choice 1992, 73, 205-239.

- Akerlof, G. A. The Market for ‘Lemons’: Quality Uncertainty and the Market for Lemons. The Quarterly Journal of Economics 1970, 84, 488–500. [Google Scholar] [CrossRef]

- Spence, Michael. Job Market Signaling. In: Uncertainty in economics. Academic Press 1978, 281-306.

- Morris, Richard D. Signalling, agency theory and accounting policy choice. Accounting and business Research 1987, 18, 47-56.

- Sato, Ivone Dias. Gestão econômica em serviços: procedimento de cobrança para recuperação de receita em núcleos de baixa renda. Masters Degree. Universidade Nove de Julho, São Paulo, 2013.

- Wagenhofer, A. The role of revenue recognition in performance reporting. Accounting and Business Research 2014, 44, 349–379. [Google Scholar] [CrossRef]

- Oghoghomeh, T.; Anthony, O. Entrepreneur‘s nightmare—Corporate failure: Consequences and probable solutions. Research Journal of Finance and Accounting 2013, 4(19), 45–53. [Google Scholar]

- Boyle, C. E. Adapting to change: Water utility financial practices in the early twenty-first century. American Water Works Association 2014, 106, E1–E9. [Google Scholar] [CrossRef]

- Zhu, Joe. Multi-factor performance measure model with an application to Fortune 500 companies. European Journal of Operational Research 2000, 123, 105–124. [CrossRef]

- Dyson, R.G.; Allen , R.; Camanho , A.S.; Podinovski , V.V.; Sarrico , C.S.; Shale , E.A.Pitfalls and protocols in DEA, European Journal of Operational Research, v. 132, Issue 2, 2001, Pg. 245-259. [CrossRef]

- Färe, R.; Grosskopf, S. Intertemporal Production Frontiers: with Dynamic DEA, 1st ed.; Kluwer Academic Publishers: Boston, US, 1996; 202 pp.

- Nemoto, Jiro; Goto, Mika. Dynamic data envelopment analysis: modeling intertemporal behavior of a firm in the presence of productive inefficiencies. Economics Letters 1999, 64, 51-56.

- Nemoto, Jiro; Goto, Mika. Measurement of Dynamic Efficiency in Production: An Application of Data Envelopment Analysis to Japanese Electric Utilities. Journal of Productivity Analysis 2003, 19, 191-210.

- Sengupta, Jati K. A dynamic efficiency model using data envelopment analysis. International Journal of Production Economics 1999, 62, 209–218. [CrossRef]

- Sengupta, Jati K. Nonparametric efficiency analysis under uncertainty using data envelopment analysis. International Journal of Production Economics 2005, 95, 39–49. [CrossRef]

- Sengupta, Jati K. Persistence of dynamic efficiency in Farrell models. Applied Economics 2010, 29, 665- 671.

- Wang, Mei-Hu; Huang, Tai-Hsin. A study on the persistence of Farrell’s efficiency measure under a dynamic framework. European Journal of Operational Research 2007, 180, 1302-1316.

- Geymueller, Von, P. Static versus dynamic DEA in electricity regulation: the case of US transmission system operators. Cent Eur J Oper Res 2009, 17, 397–413. [CrossRef]

- Chen, Chien-Ming; Dalen, Jan van. Measuring dynamic efficiency: Theories and an integrated methodology. European Journal of Operational Research 2010, 203, 749-760.

- Tone, K., Tsutsui, M. Dynamic DEA:Aslacks-based measure approach. Omega 2010, 38, 145-156.

- Pointon, Charlotte; Matthews, Kent. Dynamic Efficiency in the English and Welsh Water and Sewerage Industry. Omega 2015, 58, 86–96. [CrossRef]

- Addae, E.A.; Sun, D.; Abban, O.J. Evaluating the effect of urbanization and foreign direct investment on water use efficiency in West Africa: application of the dynamic slacks-based model and the common correlated effects mean group estimator. Environ Dev Sustain 2023, 25, 5867–5897. [Google Scholar] [CrossRef]

- Carvalho, Anne Emília Costa; Sampaio, Raquel Menezes Bezerra; Sampaio, Luciano Menezes Bezerra. The impact of regulation on the Brazilian water and sewerage companies’ efficiency. Socio-Economic Planning Sciences 2023, 87, 101537.

- Pronunciamento Técnico CPC 48 Instrumentos Financeiros, Correlação às Normas Internacionais de Contabilidade – IFRS 9. (2016, 04 de novembro). Brasília, DF: Comitê de Pronunciamentos Contábeis. Available at: http://static.cpc.aatb.com.br/Documentos/530_CPC_48.pdf.

- Azhar, Syed; Zeeshan, Khudisya. Receivables Management: A Study of Select State Owned Power Distribution Utilities in India. Finance India 2021, 35, 1173.

- Wejer, Małgorzata; Patterson, Robert. Selected reasons for payment delays and its financial consequences from Polish perspective. Zeszyty Naukowe Wyższej Szkoły Ekonomii i Informatyki w Krakowie 2015, 11, 207-220.

- Murrar, Abdullah; Batra, Madan; Rodger, James. Service quality and customer satisfaction as antecedents of financial sustainability of the water service providers. The TQM Journal 2021, 33, 1867–1885. [CrossRef]

- World Bank. Performance Improvement Planning: Developing Effective Billing and Collection Practices (April 1, 2008). World Bank Policy Research Working Paper No. 44119, Available at SSRN: https://ssrn.com/abstract=1149069.

- Carteado-fatima, E. F.; Vermersch-michel. Non-Revenue Water and Revenue Collection Ratio: Review, Assessment and Recommendations 2016. Available at: https://mcast.edu.mt/wp-content/uploads/New-Appendix-6-Non-Revenue-Water-and-Revenue-Collection-Ratio-Review-Assessment-and-Recommendations.-Carteado.pdf.

- Murrar, Abdullah; Paz, V.; Yerger, D.; Batra, M. Enhancing financial efficiency and receivable collection in the water sector: Insights from structural equation modeling. Utilities Policy 2024, 87, 101723.

- Alegre, H.; Baptista, J. M.; Cabrera Jr, E.; Cubillo, F.; Duarte, P.; Hirner; Merkel, W.; Parena, R. Performance indicators for water supply services. IWA publishing 2010.

- Matos, R., Cardoso, A., Ashley, R. M., Duarte, P., Molinari, A., & Schulz, A. (Eds.). Performance indicators for wastewater services. IWA publishing 2003.

- Liang, Kung-Yee; Zeger, Scott L. Longitudinal data analysis using generalized linear models. Biometrika, 1986; 73, 13–22.

- Hardin, J., Hilbe, J. Generalized linear model and extensions. 2nd ed, Stata Press Publication 2007.

- Mbuvi, Dorcas; Witte, Kristof; Perelman, Sergio. Urban water sector performance in Africa: A step-wise bias-corrected efficiency and effectiveness analysis. Utilities Policy 2012, 22, 31-40.

- See, Kok Fong. Exploring and analysing sources of technical efficiency in water supply services: some evidence from Southeast Asian public water utilities. Water Resources and Economics 2015, 9, 23-44.

- Gupta, Shreekant; Kumar, Surender; Sarangi, Gopal K. Measuring the performance of water service providers in urban India: implications for managing water utilities. Water Policy 2012, 14, p. 391-408.

- Ferro, Gustavo; Romero, Carlos A.; Covelli, María Paula. Regulation and performance: A production frontier estimate for the Latin American water and sanitation sector. Utilities Policy 2011, 19, 211-217.

- Marques, Rui Cunha. Measuring the total factor productivity of the Portuguese water and sewerage services. Economia Aplicada 2008, 12, 215–237.

- Souza, Geraldo Da Silva; Faria, Ricardo Coelho De; Moreira, Tito Belchior S. Efficiency of Brazilian public and private water utilities. Estudos Econômicos (São Paulo) 2008, 38, 905-917.

- Carvalho, Anne Emília Costa; Sampaio, Luciano Menezes Bezerra. Paths to universalize water and sewage services in Brazil: The role of regulatory authorities in promoting efficient service. Utilities Policy 2015, 34, 1-10.

- Nauges, Céline; Van Den Berg, Caroline. Economies of density, scale and scope in the water supply and sewerage sector: a study of four developing and transition economies. Journal of Regulatory Economics 2008, 34, 144-163.

- Brazil. Lei nº. 13.982, de 2 de abril de 2020. Diário Oficial da União, Brasília, DF. 2 abr. 2020. Available in: < https://www.planalto.gov.br/ccivil_03/_ato2019-2022/2020/lei/l13982.htm>.

- Companhia de Água e Esgotos do Rio Grande do Norte (CAERN). 2023 Relatório Integrado de Gestão. Available in: < https://arquivos-transparencia.caern.com.br/s/OUb6QbzywOcNeAe>.

Figure 1.

DSBM structure for the revenue collection efficiency.

.Graph 1.

Spatial representation of revenue collection efficiency.

Table 1.

DSBM variables for the revenue collection efficiency assessment.

| Variable | Description | DSBM Specification |

|

|---|---|---|---|

| Accumulated gross balance of amounts receivable from utility j in year t, considering the last day of the reference year, as a result of billing for direct and indirect water and wastewater services (FN008 of the SNIS), adjusted using the Brazilian price index IPCA/IBGE (measured in BR). |

|

||

| Value effectively collected from all operating revenues of utility j in year t (FN006 of the SNIS), adjusted using the Brazilian price index IPCA/IBGE (measured in BR). |

|

||

| Value of revenue from the direct and indirect provision of water and wastewater services proportional to the delay in accounts receivable of utility j in year t. Adjusted using the Brazilian price index IPCA/IBGE (measured in BR). |

|

||

Table 3.

Panel descriptive statistics of DSBM variables for the revenue collection efficiency assessment.

Table 3.

Panel descriptive statistics of DSBM variables for the revenue collection efficiency assessment.

| Variable | Obs. | Mean | Std. Dev. | Min | Max | |

|---|---|---|---|---|---|---|

| RECEIVABLE (Input) | 2018 | 127 | 165.869.467,21 | 657.283.064,94 | 74.646,46 | 6.897.348.366,50 |

| 2019 | 167.374.566,76 | 561.457.858,19 | 30.585,57 | 5.530.197.982,14 | ||

| 2020 | 158.014.639,85 | 491.273.835,81 | 79.843,79 | 4.591.003.333,72 | ||

| 2021 | 157.639.908,21 | 504.144.089,44 | 124.037,10 | 4.810.883.363,14 | ||

| 2022 | 163.443.068,09 | 533.186.618,26 | 15.745,76 | 5.071.957.155,28 | ||

| COLLECTION (Output) | 2018 | 127 | 471.691.116,07 | 1.749.687.069,82 | 692.011,06 | 17.226.245.956,49 |

| 2019 | 492.783.587,21 | 1.806.613.058,97 | 731.916,37 | 17.697.395.904,04 | ||

| 2020 | 488.928.181,88 | 1.777.387.685,86 | 781.831,46 | 17.223.734.191,47 | ||

| 2021 | 471.055.305,68 | 1.692.515.241,82 | 738.760,91 | 16.353.129.233,29 | ||