Submitted:

05 August 2024

Posted:

06 August 2024

You are already at the latest version

Abstract

The following article analyses the relationship between Non-Performing Loans and innovation systems at a global level. The analysed data were obtained from the World Bank and the Global Innovation Index for the period 2013-2022 for 149 countries. The analysis was conducted using clustering with the k-Means algorithm, optimized with the Silhouette coefficient and the Elbow method. Subsequently, econometric analysis was carried out using panel data with Random Ef-fects and Fixed Effects. The clustering results show that the optimal number of clusters is three. The econometric analysis highlights the positive relationship between Non-Performing Loans, the exports of cultural and creative services, and the Innovation Input Sub-Index. The results also show the negative relationship between Non-Performing Loans, the H-Index, and the exports and imports of ICT services.

Keywords:

Non-Performing Loans

; Banking stability

; Innovation

; k-Means

1. Introduction

Financial stability and innovation are two pillars essential for the economic health and development of nations. However, the interplay between these elements is intricate, with Non-Performing Loans (NPLs) serving as a critical factor influencing both. NPLs, which refer to loans that are in default or close to being in default, are a crucial metric for assessing the health of financial institutions and, by extension, the broader economy. High levels of NPLs indicate potential vulnerabilities within the financial system, reflecting borrowers' inability to meet their debt obligations, which can lead to cascading economic consequences. The significance of NPLs extends beyond their immediate impact on banks' balance sheets. They are also indicative of broader economic conditions and can influence the trajectory of financial innovation. When financial institutions are burdened with high levels of NPLs, their capacity to lend diminishes, leading to a contraction in available credit for businesses and consumers. This contraction can stifle economic growth and inhibit the adoption of innovative financial products and services. Conversely, a stable financial environment with low NPL levels fosters a conducive atmosphere for innovation, allowing financial institutions to take on calculated risks and invest in new technologies and methodologies that drive economic progress (Bolgova et al., 2016; Serrano, 2021).

The relationship between NPLs and financial innovation is multifaceted. On the one hand, financial innovation can lead to an initial increase in NPLs due to the introduction of new, untested products that may pose higher risks. For instance, the subprime mortgage crisis in the United States highlighted how innovative financial products, such as mortgage-backed securities, could lead to significant financial instability when not managed properly. On the other hand, innovation in financial technologies and risk management practices can help mitigate the risks associated with NPLs. Advanced data analytics, Machine Learning, and blockchain technology are examples of innovations that can enhance the accuracy of credit risk assessments, improve loan monitoring, and streamline the resolution of NPLs, thereby contributing to financial stability. The economic implications of NPLs are profound, affecting not only financial institutions but also the broader economy. High levels of NPLs can erode banks' capital bases, reduce profitability, and constrain their ability to provide new loans. This, in turn, can lead to a credit crunch, where businesses, especially small and medium-sized enterprises (SMEs), find it difficult to obtain the financing needed for growth and innovation. In economies heavily reliant on banking sector credit, this can slow down overall economic activity and impede the development of new industries and technologies (Kim and Park, 2017; Ozili, 2019).

Moreover, the management of NPLs is crucial for maintaining financial stability. Effective NPL management strategies include asset quality reviews, the establishment of asset management companies (AMCs), and the development of legal frameworks for insolvency and debt recovery. These measures not only help in cleaning up banks' balance sheets but also restore confidence in the financial system. Countries that have implemented robust NPL management frameworks, such as Italy with its "GACS" scheme (Garanzia Cartolarizzazione Sofferenze), have seen improvements in financial stability and a gradual reduction in NPL levels. Financial stability and innovation are particularly important in the context of achieving sustainable development goals (SDGs). Sustainable development requires a stable financial system that can support long-term investments in infrastructure, renewable energy, and social programs. High NPL levels can divert resources away from these critical areas, undermining efforts to achieve sustainable development. Conversely, financial innovation can play a significant role in advancing sustainable development by creating new financing mechanisms, such as green bonds and social impact bonds, that channel funds into projects with positive environmental and social outcomes (Ma and Fung, 2006; Osuji, 2012).

The role of regulatory frameworks in balancing financial stability and innovation cannot be overstated. Regulatory bodies must ensure that financial institutions maintain adequate capital buffers and adhere to prudent lending practices to prevent the buildup of NPLs. At the same time, regulations should not stifle innovation. A balanced approach is needed, one that encourages the adoption of new technologies and financial products while safeguarding against systemic risks. For example, the Basel III framework, which emphasizes capital adequacy, stress testing, and market liquidity risk, provides a comprehensive approach to managing risks while allowing room for financial innovation. In addition, the global financial landscape is interconnected, meaning that financial instability in one region can have ripple effects worldwide. The 2008 financial crisis demonstrated how interconnected global markets are and how financial innovation, in the form of complex derivatives, could amplify systemic risks. Therefore, international cooperation and coordination in financial regulation are essential for managing the risks associated with NPLs and promoting global financial stability. Institutions such as the International Monetary Fund (IMF) and the Financial Stability Board (FSB) play crucial roles in fostering international dialogue and setting global standards for financial regulation (Iris, 2017; Lumpkin, 2010).

The advent of fintech and digital banking has further complicated the relationship between financial stability and innovation. Fintech companies, with their innovative approaches to financial services, have the potential to significantly reduce NPLs through better credit scoring models and more efficient loan processing systems. However, the rapid growth of fintech also poses regulatory challenges, as traditional regulatory frameworks may not be equipped to address the unique risks associated with digital financial services. Regulators must adapt to these changes and develop new strategies to monitor and manage risks in the fintech sector. Moreover, the role of NPLs in shaping investor sentiment and market confidence is significant. High levels of NPLs can lead to a loss of confidence among investors, resulting in higher funding costs for banks and a potential withdrawal of capital from the financial system. This loss of confidence can exacerbate financial instability and create a vicious cycle where deteriorating financial conditions lead to further increases in NPLs. Therefore, maintaining a low level of NPLs is crucial for sustaining investor confidence and ensuring a stable financial environment conducive to innovation and growth (Pierri and Timmer, 2020; Ismanto et al., 2023).

In conclusion, NPLs are crucial in the relationship between financial stability and innovation. While high levels of NPLs can signal financial distress and hinder economic growth, effective management, and regulatory strategies can mitigate these risks and create a stable environment that fosters innovation. The interplay between NPLs, financial stability, and innovation underscores the need for a balanced approach that promotes economic development while safeguarding against systemic risks. By addressing the challenges associated with NPLs and leveraging the potential of financial innovation, policymakers can ensure a resilient and dynamic financial system that supports sustainable economic growth.

2. Literature Review

Financial Innovation and Stability

This sub-section explores the intricate relationship between financial innovation and stability. Several studies analyzed how innovations in financial products, services, and technologies can both bolster and destabilize financial systems. Financial innovation is relevant in shaping the dynamics of financial stability and economic growth. The nexus among innovation, financial depth, and economic progress is intricate, reflecting both opportunities and risks associated with novel financial products and technologies. Santos-Arteaga et al. (2020) emphasize the critical balance that the European Union (EU) must maintain to foster innovation while ensuring financial stability. They argue that the innovation dynamics in the EU, driven by regulatory frameworks and market demands, have significantly impacted financial stability, particularly in times of economic uncertainty. Priem (2022) discusses the European distributed ledger technology pilot regime, which aims to strike a balance among innovation, investor protection, and financial stability. This regime represents a proactive approach to harnessing the potential of blockchain technology while mitigating associated risks. Similarly, Shapoval (2021) explores the relationship between financial innovation and economic growth, highlighting how advancements in financial technologies can lead to deeper financial markets and, consequently, robust economic growth. However, the author cautions that without proper regulatory oversight, these innovations could pose significant risks to financial stability. Chien et al. (2021) further explore the impact of financial innovation on bankruptcy rates in the information, communication, and technology (ICT) sector, finding that innovative financial instruments can reduce bankruptcy risks by providing more flexible financing options. Lee et al. (2020) investigate the role of institutional environments in facilitating bank growth through financial innovation. Their findings suggest that banks operating in supportive institutional frameworks are more likely to adopt innovative financial products, leading to enhanced growth and stability. Shen et al. (2022) examine the impact of technological finance on financial stability from the perspective of high-quality economic growth, arguing that technological advancements in finance contribute to economic resilience by improving efficiency and reducing systemic risks. Ozili and Iorember (2023) discuss the dual objectives of financial stability and sustainable development, emphasizing that financial innovations must align with broader economic goals to achieve long-term stability. Wijayanto et al. (2023) highlight the importance of uniting innovation and stability for business flexibility, suggesting that firms that successfully integrate innovative practices into their operations are better positioned to adapt to changing market conditions and maintain stability. Jeong et al. (2020) provide a case study of the Korean food industry, illustrating how open innovation practices can enhance a firm's financial sustainability. The research shows that collaborative innovation efforts, such as partnerships and knowledge sharing, can lead to improved financial performance and stability. López-Penabad et al. (2021) analyze the competition and financial stability in European listed banks, finding that competitive pressures can drive banks to innovate, ultimately contributing to financial stability by enhancing operational efficiency and risk management practices. Ihebuluche et al. (2022) examine the relationship between financial innovation and central bank independence in selected OECD countries, arguing that independent central banks are better equipped to regulate innovative financial products and maintain stability. Korepanov et al. (2020) focus on managing the financial stability potential of crisis enterprises, highlighting the role of innovative financial strategies in navigating economic downturns and maintaining solvency. Duong et al. (2022) explore how innovation and ownership concentration affect the financial sustainability of energy enterprises in a transition economy. Their findings indicate that firms with concentrated ownership structures and innovative practices are more likely to achieve financial sustainability. Hassania and Eghdami (2023) investigate the moderating role of corporate governance in the relationship between innovation and financial stability, finding that strong governance frameworks can enhance the stability benefits of financial innovation. Xu et al. (2021) discuss the potential risks and benefits of financial innovation in the context of economic policy uncertainty, suggesting that while innovation can drive economic sustainability, it also introduces new risks that require careful management. Zouari and Abdelmalek (2020) examine the impact of financial innovation on risk management and bank performance, concluding that innovative financial products can enhance banks' risk management capabilities and improve overall performance. Kim et al. (2020) analyze the effects of financial crises on bank diversification and stability in OECD countries, finding that diversified banks are better able to withstand economic shocks and maintain stability. Pernell (2020) discusses the lessons learned from banks' adoption of shareholder value management during financial innovation periods, highlighting the need for balanced approaches to innovation that consider both profitability and stability. Ullah et al. (2023) investigate the impact of intellectual capital efficiency on financial stability in banks, finding that banks that effectively leverage intellectual capital are more likely to achieve stability. Saha and Dutta (2021) explore the nexus of financial inclusion, competition, concentration, and financial stability, providing cross-country empirical evidence that inclusive financial systems and competitive markets contribute to stability. Degl'Innocenti et al. (2018) provide evidence from the Global Financial Crisis, illustrating how banks' innovation capacity can enhance competitiveness and stability. Saydaliev et al. (2022) examine the relationship among financial inclusion, financial innovation, and macroeconomic stability, arguing that inclusive and innovative financial systems are crucial for maintaining stability. Koch (2004) discusses the balance between innovation networking and political dynamics, highlighting the need for stable regulatory environments to support innovation. Fostel et al. (2017) analyze how financial innovation drives capital flows and increases financial instability, suggesting that while innovation can enhance capital allocation efficiency, it also introduces new risks that need to be managed. Aglietta and Scialom (2009) discuss the permanence and innovation in central banking policy for financial stability, emphasizing the need for adaptive policies that can respond to evolving financial landscapes. Lauretta (2018) provides an agent-based modeling approach to understanding the finance-growth nexus, illustrating how financial innovation, such as home mortgage securitization, can impact economic growth and stability. Minto et al. (2017) identify threats to financial stability originating from fintech, suggesting that while fintech offers significant benefits, it also introduces new vulnerabilities that need to be addressed. Borio (2011) emphasizes the need to rediscover the macroeconomic roots of financial stability policy, suggesting that a holistic approach to financial regulation is essential for managing the risks associated with innovation. Azarenkova et al. (2018) examine the influence of financial technologies on global financial system stability, finding that fintech innovations can enhance stability by improving financial inclusion and efficiency.

Technological Innovation and Sustainable Development

This sub-section delves into how technological innovations contribute to sustainable development and financial stability. Financial innovation has been recognized as a critical driver of economic growth and stability, particularly in the context of achieving SDGs in emerging economies. Wahab et al. (2022) discuss the role of financial stability, technological innovation, and renewable energy in attaining SDGs in Brazil, Russia, India, China, and South Africa (BRICS) countries, emphasizing the interconnectedness of these elements in fostering sustainable development. They state that financial stability is a prerequisite for the effective implementation of technological innovations and renewable energy initiatives, which in turn contribute to these nations' overall economic stability and growth. In a similar vein, Pan et al. (2019) examine the dynamics of financial development, trade openness, technological innovation, and energy intensity in Bangladesh, highlighting the intricate relationship between these factors. Their findings suggest that technological innovation, when coupled with financial development and trade openness, can significantly reduce energy intensity, thereby promoting a more sustainable economic growth model. The study underscores the importance of integrating financial and technological strategies to achieve long-term sustainability goals. Khalatur et al. (2022) focus on innovation management as a fundamental aspect of digitalization trends and the security of the financial sector. They argue that effective innovation management practices are essential for maintaining the security and stability of financial systems, especially in the face of rapid digitalization. This perspective is further supported by Salleo (2018), who posits that technological innovation is poised to reshape financial regulation, necessitating a re-evaluation of existing regulatory frameworks to accommodate new technological realities. Jeong et al. (2020) explore the concept of open innovation and its impact on the financial sustainability of large firms, using the Korean food industry as a case study. They find that open innovation practices, such as collaborative research & development (R&D) and knowledge sharing, can enhance financial sustainability by fostering a culture of continuous improvement and adaptability. This is particularly relevant in industries characterized by rapid technological advancements and shifting consumer preferences. Michalopoulos et al. (2009) emphasize the role of financial innovation in driving economic growth by enhancing the efficiency of financial markets. Mikhaylov et al. (2023) analyze the potential of open innovation-oriented fintech solutions for financial development in emerging economies. Using an integrated decision-making approach, they demonstrate that fintech innovations can play an important role in enhancing financial inclusion and development, thereby contributing to broader economic stability. Anning-Dorson et al. (2018) investigate how external dynamics, such as market competition and regulatory changes, influence market innovation in financial services. They find that external factors significantly impact the innovation strategies of financial institutions, which in turn affect their competitive advantage and stability. Kolodiziev et al. (2016) further elaborate on the selection of financial innovations based on the financial soundness and life cycle stage of banks. The study suggests that banks should adopt different innovation strategies depending on their financial health and maturity to ensure sustainable growth and stability. Boz and Mendoza (2014) explore the relationship among financial innovation, risk discovery, and the US credit crisis, highlighting the potential risks associated with unregulated financial innovations. They explain that while financial innovation can lead to significant economic benefits, it also introduces new risks that need to be carefully managed to prevent financial crises. Lane (2011) discusses the complexity and innovation dynamics, emphasizing the importance of understanding the intricate interplay between technological change and economic systems. It is suggested that a comprehensive approach to managing innovation dynamics is crucial for maintaining economic stability and growth. Okrah and Hajduk-Stelmachowicz (2020) examine the impact of political stability on innovation in Africa, finding that stable political environments are conducive to fostering innovation and economic development. Jenkinson et al. (2008) address the challenges of financial innovation and regulation, emphasizing the need for adaptive regulatory frameworks to accommodate the evolving landscape of financial markets. Savchuk et al. (2021) propose a matrix model for understanding the innovation imperatives of global financial innovation, suggesting that a structured approach to innovation management can enhance the stability and development of financial systems. An et al. (2021) use an evolutionary game theory model to analyze the inter-relationships between financial regulation and innovation, finding that adaptive regulatory strategies are essential for fostering a balanced and stable financial system. Onyshchenko et al. (2020) explore the impact of innovation and digital technologies on the state's financial security, emphasizing the need for robust regulatory frameworks to manage the risks associated with digitalization. The study highlights the importance of integrating innovation and security strategies to ensure the long-term stability of financial systems. Magazzino et al., (2024) offer a thorough exploration of the relationships between credit markets, economic output, and productivity. This comprehensive review synthesizes various studies to present an overarching view of how credit availability impacts economic growth and productivity. The authors emphasize the significance of well-developed financial systems in fostering economic expansion through investment and innovation facilitation. They also discuss the potential negative consequences of excessive credit, such as financial instability and economic downturns. Their analysis reveals the complexity and context-dependence of the credit-output-productivity relationship, suggesting that policy interventions should be tailored to specific economic environments. Magazzino and Santeramo (2023) explore the dynamic interplay between financial development and economic growth. This article examines how improvements in the financial sector can lead to enhanced productivity and overall economic performance. Through empirical data, the authors demonstrate that financial development significantly contributes to growth by providing more efficient capital allocation and fostering entrepreneurial activities. However, they caution against potential pitfalls, such as the risk of financial bubbles and crises, which can arise from overly rapid financial sector expansion. Their analysis emphasizes the need for balanced financial policies that support growth while mitigating risks. Magazzino et al., (2021b) investigates the specific context of agricultural growth. The authors employ artificial neural networks to analyze how financial development influences agricultural productivity and economic growth. Their findings indicate that financial development positively impacts agricultural output by enabling better access to credit for farmers, thus facilitating investments in advanced technologies and practices. This study highlights the role of financial systems in supporting sector-specific growth and underscores the potential of advanced analytical techniques in economic research. Magazzino et al. (2021a) examine the complex interactions between innovation, logistics performance, and environmental sustainability. Using quantile regression analysis, the authors provide evidence that while innovation and efficient logistics systems are crucial for economic performance, they often come at the cost of environmental degradation. The study suggests that achieving a balance between these three aspects is essential for sustainable development. Policymakers are encouraged to foster innovation and improve logistics efficiency while implementing stringent environmental regulations to mitigate adverse effects. Solangi et al., (2024) focus on the factors driving green innovation and its impact on the adoption of renewable energy technologies. The authors identify key drivers, including government policies, technological advancements, and market incentives, which promote the shift towards renewable energy. They argue that a combination of these factors can significantly accelerate the transition to sustainable energy sources. The study also discusses potential barriers and offers solutions to overcome them, highlighting the importance of a coordinated approach in promoting green innovation. Jianing et al., (2024) investigate how digitalization and technological advancements can contribute to the sustainable exploitation of natural resources. The authors argue that digital technologies, such as the Internet of Things (IoT) and artificial intelligence (AI), can enhance resource management by providing real-time data and optimizing resource use. They present case studies showing that technological innovation can lead to more efficient and sustainable resource extraction practices, thereby reducing environmental impact. The study underscores the potential of digitalization as a tool for achieving sustainable development goals.

Market Dynamics and Competitive Advantage

This sub-section examines how innovation drives market dynamics and competitive advantages across various sectors. The relationship between financial innovation and economic growth is complex, encompassing a range of factors including financial markets, venture capital, and technological advancements. Pradhan et al. (2018) delve into the endogenous dynamics among innovation, financial markets, venture capital, and economic growth in Europe, illustrating how these elements are interlinked and contribute to the overall economic trajectory. The study highlights the importance of a robust financial market and the presence of venture capital as catalysts for innovation and economic growth, suggesting that these factors create a virtuous cycle that drives development. Gubler (2011) provides a theoretical framework for understanding the financial innovation process, emphasizing the stages through which new financial products and services are developed and brought to market. The analysis underscores the role of regulatory environments and market demands in shaping the innovation landscape, suggesting that a conducive regulatory framework is essential for fostering financial innovation. Yun et al. (2018) examine the cyclical dynamics of open innovation in entrepreneurial contexts, highlighting how open innovation practices can enhance the innovation capacity of firms and contribute to economic growth. The study suggests that collaborative efforts and knowledge sharing are critical components of successful innovation strategies, particularly in dynamic and competitive markets. Ülgen (2014) offers a Schumpeterian analysis of economic development and financial innovations, highlighting the conflicting dynamics between creative destruction and economic stability. The study suggests that while financial innovations are essential for economic progress, they also introduce new risks and uncertainties that need to be carefully managed. This is particularly relevant in the context of digitalization and technological advancements. Akbar et al. (2024) explore the role of institutional dynamics in fostering corporate innovation and sustainable development. The findings suggest that strong institutional frameworks and supportive policies are critical for encouraging corporate innovation, which in turn drives sustainable economic growth. This aligns with the work of Pan et al. (2019), who examine the interplay between financial development, trade openness, technological innovation, and energy intensity in Bangladesh. The study highlights the importance of integrating financial and technological strategies to achieve SDGs, suggesting that these elements are mutually reinforcing. Beck (2018) discusses the challenges of regulating financial innovation, emphasizing the need for adaptive and forward-looking regulatory frameworks that can keep pace with rapid technological advancements. The analysis underscores the importance of balancing the benefits of financial innovation with the need to maintain financial stability, suggesting that regulators must be proactive in addressing emerging risks. Jia et al. (2021) investigate the relationship between economic policy uncertainty and financial innovation, finding that uncertainty can significantly impact innovation activities. The study suggests that stable and predictable policy environments are essential for fostering financial innovation and ensuring long-term stability. Wu and Gong (2019) explore the impact of open innovation communities on enterprise innovation performance. Their findings indicate that participation in open innovation communities can enhance the innovation capabilities of firms, leading to improved performance and stability. Nesvetailova (2008) discusses the concept of liquidity illusion in the context of financial innovation and the credit crunch, highlighting the risks associated with complex financial instruments. It is found that financial innovations, while beneficial, can create false perceptions of liquidity and stability, which can lead to financial crises if not properly managed. This underscores the importance of transparency in financial practices, as discussed by Delimatsis (2013), who argues that transparent financial innovation is essential for maintaining investor confidence and ensuring the long-term stability of financial systems, particularly in post-crisis environments.

Overall, the literature highlights the intricate and multifaceted relationship between financial innovation, economic growth, and financial stability. Financial innovations have the potential to drive economic development and enhance financial stability by improving efficiency, inclusivity, and adaptability. However, these benefits come with inherent risks that must be carefully managed through effective regulatory frameworks and innovation management practices. The studies reviewed underscore the importance of aligning innovation strategies with institutional policies, ensuring transparency in financial practices, and adopting adaptive regulatory approaches to mitigate the risks associated with financial innovations. By balancing these elements, it is possible to harness the benefits of financial innovation while maintaining the stability and sustainability of financial systems.

A summary of the literature reviewed is given in Table 1 below.

3. Data

Below, the variables used for the regression metric analysis and clustering are analyzed in a synthetic way. The sources used for the construction of the database used for the analysis are also identified. The description of the variables is given in Table 2.

4. Clusterization with k-Means algorithms

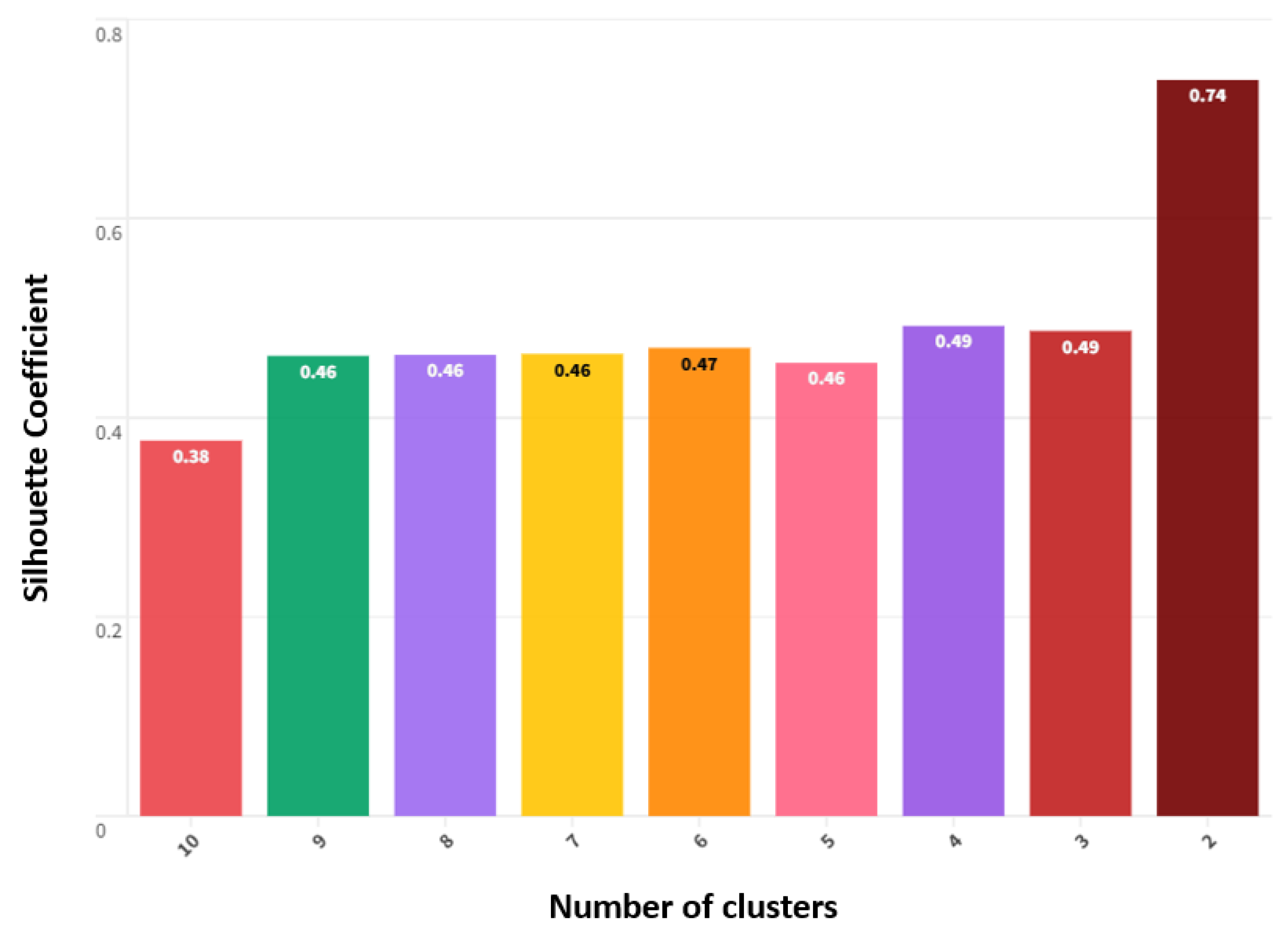

In what follows a clustering with the k-Means algorithm is shown. Since the k-Means algorithm is an unsupervised Machine Learning (ML) algorithm, it is necessary to find tools to help identify the optimal number of clusters. In this case, we compare the results of clusterization using the Silhouette coefficient using the Elbow method. Clustering with the k-Means algorithm optimized with the Silhouette coefficient involves assigning a number to each cluster. This number ranges from -1 to 1. The closer the value is to 1, the more efficient the clustering is (Yuan and Yang, 2019; Punhani et al., 2022). Therefore, we calculate the Silhouette coefficient value for k values between 2 and 10. The number of clusters that maximize the Silhouette coefficient occurs at k=2 (see Figure 1).

The cluster analysis, based on the percentage of bank NPLs to total gross loans, uncovers a striking contrast between countries grouped in Cluster 1 (C1) and Cluster 2 (C2). Countries in C2 show significantly higher levels of NPLs compared to those in C1, sparking our curiosity to explore the underlying economic, political, and financial factors contributing to such differences. The complete list of countries for each cluster is given in the Appendix. C1 countries demonstrate greater economic resilience compared to C2, as evidenced by their ability to withstand external shocks and maintain financial stability. The economic structures in C1 are more diversified, reducing the reliance on a single sector and spreading the risk across various industries. In contrast, C2 countries often have undiversified economies, heavily dependent on a few sectors like agriculture or natural resources, which are more vulnerable to economic fluctuations.

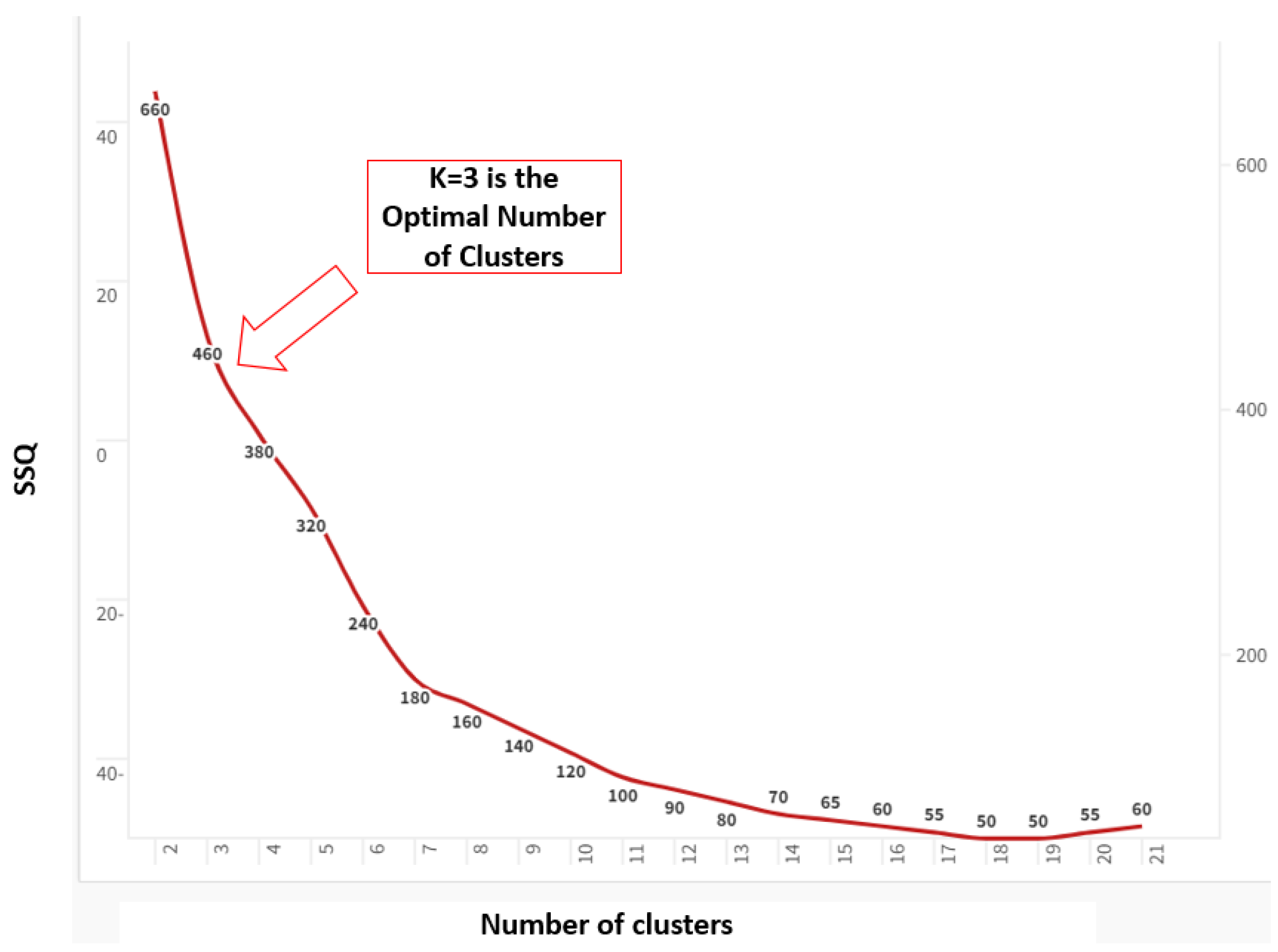

However, the clustering performed with the k-Means algorithm optimized with the Silhouette coefficient is not without its challenges. It results in a significant polarization of the countries, with most of them grouped in C1 and C2 being completely marginal. This imbalance in the distribution of the countries within the different clusters highlights the inefficiency of the clustering analysis. To address this, we turn to the Elbow method for the optimization of the clustering with the k-Means algorithm (see Figure 2). The Elbow method provides a robust approach to ensure a more balanced distribution of countries across clusters, enhancing the reliability of our analysis.

This analysis categorizes countries into three clusters (C1, C2, and C3) based on the percentage of NPLs to total gross loans. C2 has the highest level of NPLs, followed by C1 and C3. The complete list of countries for each cluster is given in the Appendix.

C1 comprises a group of 50 countries from various regions and different levels of economic development, which exhibit a moderate level of NPLs. This cluster includes countries. Many African countries face challenges such as political instability, economic diversification issues, and lower financial inclusion, contributing to moderate NPL levels. For Asia, countries such as Afghanistan, Bangladesh, Bhutan, and India are included. These nations are characterized by rapidly growing economies but also face structural challenges in their banking sectors, including regulatory and supervision weaknesses. Moreover, this cluster includes Eastern European countries – such as Albania, Belarus, Bosnia and Herzegovina, Bulgaria, Croatia, Hungary, and Romania – which often deal with legacy NPL issues from past financial crises and ongoing economic transitions. For the Middle East, Iraq and Lebanon are included. Political instability and economic volatility in these countries contribute to moderate NPL levels. For Latin America and the Caribbean, the presence of countries like Barbados, Curacao, Dominica, and St. Vincent and the Grenadines indicates a region with a mix of economic resilience and vulnerabilities impacting their banking sectors (Molochko, 2001; Tmava et al., 2018; Smits and Permanyer, 2019).

C2 represents countries with the highest levels of NPLs. In Europe, Greece and Cyprus stand out due to their well-documented financial crises. Both countries underwent severe banking sector distress, leading to significant accumulations of NPLs. The economic recovery in these nations has been slow, and the banking sectors continue to deal with the fallout. In the post-Soviet states, Ukraine and Tajikistan face economic challenges, including conflict, political instability, and weak institutional frameworks, contributing to high levels of NPLs. In Africa, countries like Comoros, Chad, Central African Republic, and Equatorial Guinea are characterized by fragile economies, political instability, and low financial sector development. These factors significantly impact the quality of the loan portfolios of banks. Small nations, such as St. Kitts and Nevis and San Marino, represent small economies with unique challenges. St. Kitts and Nevis, while having a relatively small banking sector, faces vulnerabilities typical of small island economies, including exposure to external economic shocks. San Marino, despite being a high-income economy, has seen its banking sector struggle with legacy NPLs (Klein, 2013; Škarica, 2014; Dimitrios et al., 2016; Katsampoxakis and Basdekis et., 2022; Msoni, 2022).

Cluster C3 includes a broad array of different countries, totalling over 80. These countries have the lowest levels of NPLs, indicating healthier banking sectors relative to clusters C1 and C2. Many high-income and stable economies, such as Austria, Belgium, France, Germany, and the United States, are placed here. These countries typically have robust financial regulatory frameworks, diversified economies, and strong institutional capacities that contribute to lower NPL ratios. Argentina, Brazil, China, and India represent significant emerging markets with diverse economic bases and strong growth trajectories. While challenges exist, the banking sectors in these countries are relatively better positioned to manage loan portfolios. Countries such as Chile, Colombia, Costa Rica, and Malaysia are characterized by growing economies, improving financial infrastructure, and regulatory improvements that help maintain lower NPL levels. Countries like Fiji, Iceland, and Luxembourg show that smaller economies can maintain low NPL levels through sound economic policies and effective financial sector management (Jenkins, 2001; Balkaran, 2007; Rubini and Wang, 2020).

The categorization of countries into clusters C1, C2, and C3 highlights significant differences in the health of their banking sectors. Countries in C2, with the highest levels of NPLs, face systemic risks that require comprehensive policy responses, including financial sector reforms, improved regulatory oversight, and measures to address broader economic vulnerabilities. Countries in C1, with moderate NPL levels, also need to strengthen their financial systems. These nations should focus on structural reforms, improving governance in the banking sector, and fostering economic stability to prevent an escalation of NPL levels. Countries in C3, with the lowest NPL levels, provide models for effective banking sector management. The stability in these countries can be attributed to sound regulatory practices, diversified economies, and strong institutional frameworks. However, continuous vigilance is necessary to maintain this stability, especially in the face of global economic uncertainties. For C2 countries, immediate policy actions are necessary to stabilize the banking sector. This includes measures like bank recapitalization, enhancing regulatory and supervisory frameworks, and addressing macroeconomic instability. The international community can play a supportive role through financial assistance and technical support. For C1 countries, policies should focus on preemptive measures to avoid slipping into higher NPL categories. This involves improving credit risk management practices, strengthening regulatory oversight, and fostering economic growth that can support healthy banking sector development. For C3 countries, maintaining the status quo requires ongoing reforms and adaptations to new economic challenges. These countries should continue to innovate in financial regulation, enhance risk management frameworks, and promote economic policies that sustain growth and stability. The analysis of NPLs across these clusters provides valuable insights into the health of banking sectors worldwide. Countries in C2 face the most significant challenges and require urgent and comprehensive policy interventions. C1 countries need to strengthen their financial systems to avoid deterioration, while C3 countries, despite their relative stability, must continue to adapt and reform to maintain their low NPL levels. This clustering based on NPL ratios not only highlights the varying degrees of banking sector health but also underscores the importance of targeted policy measures to ensure financial stability and economic growth (Thaci, 2013; Çifter, 2015; Huljak et al., 2015; Aiyar et al., 2015).

Therefore, the comparison between clustering with the k-Means algorithm using the Silhouette coefficient and the Elbow method highlights a greater efficiency of the second one due to its ability to provide a representation of country groups that is closer to the complexity of the phenomenon at a global level.

Regarding the regression analysis, the following equation is estimated:

where i=149 and t=[2013;2022]. The results are given in Table 3.

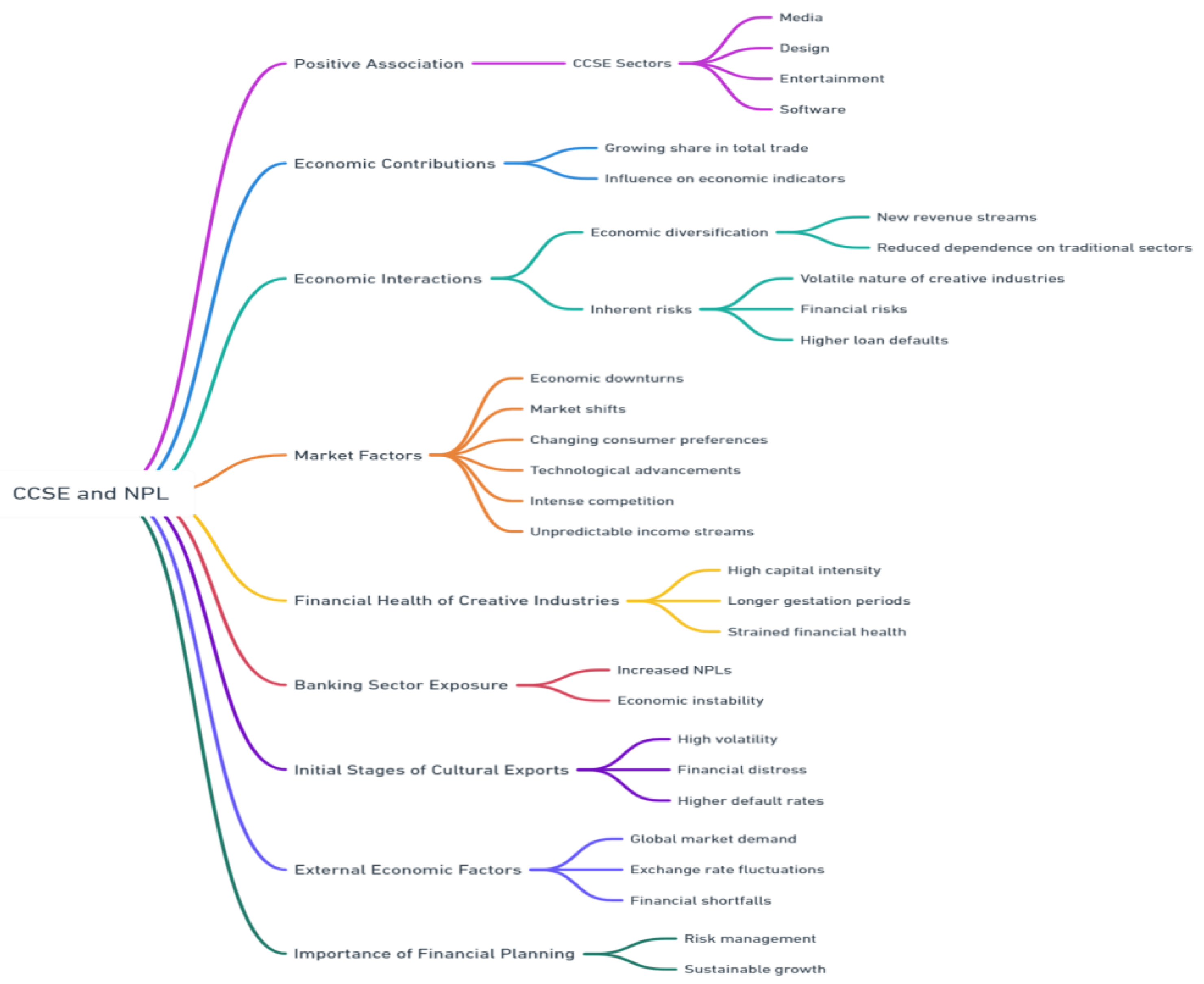

According to the panel data regression results, the level of NPL is positively associated with CCSE, encompassing sectors like media, design, entertainment, and software, which are increasingly recognized as vital components of modern economies. As these sectors grow and contribute a larger share to total trade, they influence various economic indicators, including the NPL ratio in the banking sector. Understanding why these two variables might rise together requires analyzing their underlying economic interactions. Economic diversification through an increase in cultural and creative services exports can have a dual effect. While it provides new revenue streams and reduces dependence on traditional sectors, it also involves inherent risks due to the volatile nature of creative industries. The financial risks associated with funding these innovative but uncertain ventures can lead to higher loan defaults, increasing the NPL ratio (Gouvea and Vora, 2018). This risk is particularly acute during economic downturns or market shifts that disproportionately affect the creative sectors. The creative industries often face significant market fluctuations due to changing consumer preferences, technological advancements, and intense competition. These fluctuations can result in unpredictable income streams for businesses in this sector, making them more prone to defaulting on loans. Banks exposed to these sectors might see an increase in NPLs as businesses struggle to maintain consistent revenue, especially during periods of economic instability (Berger and DeYoung, 1997). The cultural and creative sectors often require substantial upfront investments in technology, talent, and infrastructure. The high capital intensity and longer gestation periods before seeing returns can strain the financial health of companies within these industries. As banks extend credit to support these investments, the likelihood of defaults increases if the expected returns are not realized in a timely manner, thereby raising the NPL ratio (Gouvea and Vora, 2016). While cultural and creative exports can offer stable long-term earnings, their initial stages are often marked by high volatility. The uncertainty in achieving stable earnings can lead to financial distress among businesses, resulting in higher default rates on loans. This trend is exacerbated in economies that heavily invest in boosting their cultural exports without adequate financial safeguards. External economic factors, such as global market demand and exchange rate fluctuations, can significantly impact the earnings from cultural and creative services exports. Adverse changes in these factors can lead to unexpected financial shortfalls for businesses, increasing their risk of loan defaults. This external volatility is transmitted to the banking sector, resulting in a higher NPL ratio (Dash and Parida, 2012). The growth of cultural and creative services exports as a percentage of total trade can lead to an increase in the NPL ratio due to the high volatility, substantial investment requirements, and market uncertainties inherent in these industries. While these exports contribute positively to economic diversification and innovation, their financial instability and associated risks can strain the banking sector, leading to higher loan defaults. Understanding this relationship underscores the need for careful financial planning and risk management to support sustainable growth in both the creative industries and the broader economy (see Figure 3).

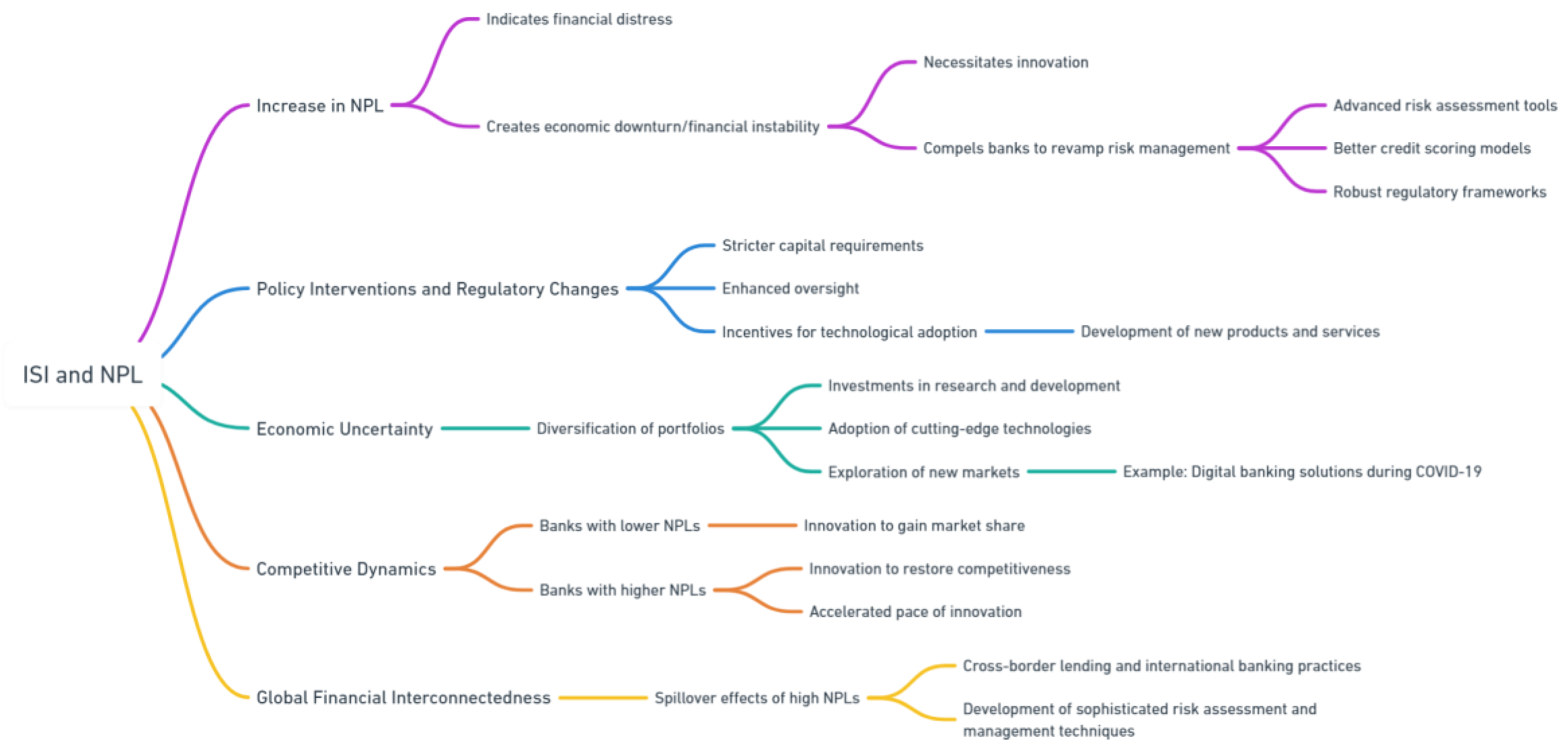

In addition, it is found that the increase in ISI increases NPL as well, which can be explained through several interconnected mechanisms. This relationship may initially appear counterintuitive, as high levels of NPLs generally indicate financial distress. However, upon closer examination, the dynamic interplay between financial stress and innovation reveals a more complex narrative. Firstly, NPLs often signify periods of economic downturn or financial instability, which create an environment that necessitates innovation. During such periods, banks and financial institutions are compelled to rethink and revamp their risk management strategies and lending practices. The need to mitigate future risks and recover from financial losses drives these institutions to adopt innovative approaches and technologies. For instance, the aftermath of financial crises has historically led to the development and implementation of advanced risk assessment tools, better credit scoring models, and more robust regulatory frameworks (Próchniak and Wasiak, 2016). Moreover, the presence of high NPLs can trigger policy interventions and regulatory changes that foster innovation. Governments and regulatory bodies, in response to rising NPLs, may introduce measures aimed at improving financial stability and encouraging sustainable lending practices. These measures can include stricter capital requirements, enhanced oversight, and incentives for technological adoption in the banking sector. Such regulatory changes can act as catalysts for innovation, pushing banks to develop new products and services that align with the revised regulations and market needs (Alandeani and Asutay, 2017). Economic uncertainty, often reflected by high NPL ratios, also plays a crucial role in fostering a culture of innovation. During uncertain times, both businesses and financial institutions seek to diversify their portfolios and reduce dependency on traditional revenue streams. This diversification often leads to investments in research and development, the adoption of cutting-edge technologies, and the exploration of new markets. For example, during the COVID-19 pandemic, many banks increased their investment in digital banking solutions to cater to the changing needs of consumers and ensure continuity of services (Park and Shin, 2020). Furthermore, high levels of NPLs can influence the competitive dynamics within the banking sector. Banks with lower levels of NPLs may capitalize on their stronger financial position to innovate and gain market share, while those with higher NPLs may be driven to innovate out of necessity to restore their competitiveness. This competitive pressure can accelerate the pace of innovation across the sector, as banks strive to improve their offerings and operational efficiency (Laryea et al., 2016). Additionally, the interconnectedness of global financial markets means that high NPLs in one region can have spillover effects on other regions, prompting a global response that includes innovative financial solutions. For instance, cross-border lending and international banking practices may evolve in response to rising NPLs in emerging markets, leading to the development of more sophisticated risk assessment and management techniques on a global scale (Rosenkranz and Lee, 2019). In conclusion, while high levels of NPLs indicate financial stress and potential economic downturns, they also create a fertile ground for innovation. The necessity to mitigate risks, adapt to new regulations, compete effectively, and respond to global financial dynamics drives banks and financial institutions to adopt innovative practices and technologies. This complex interplay ultimately contributes to the increase in the ISI despite the rise in NPLs, highlighting the resilience and adaptability of the financial sector in the face of challenges (see Figure 4).

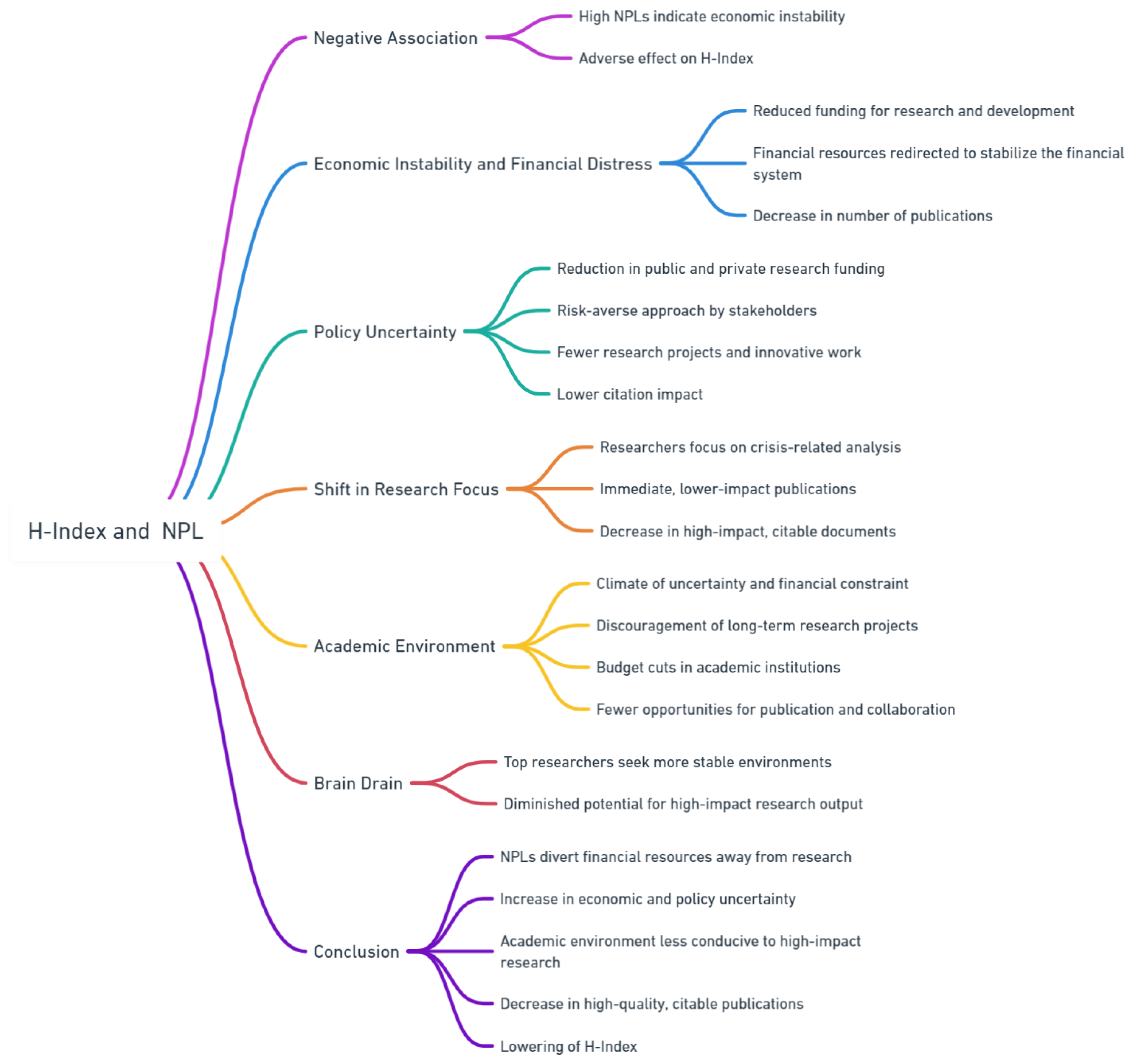

The empirical findings also highlight that NPL is negatively associated with the H-Index. This relationship is a complex issue rooted in the dynamics of economic instability, financial sector health, and the subsequent impact on academic productivity and citation impact. The H-Index measures both the productivity and citation impact of a researcher, institution, or journal, focusing on citable documents such as articles, reviews, and conference papers. When NPLs increase, it often reflects broader economic and financial stress that can adversely affect this index. Firstly, high levels of NPLs are indicative of economic instability and financial distress within the banking sector. This instability can lead to reduced funding for research and development activities, as financial resources are redirected towards stabilizing the financial system and addressing the immediate crises caused by rising NPLs. For instance, during periods of economic downturns and increased NPLs, banks and other financial institutions may cut back on investments in academic and research institutions, leading to a decrease in the number of publications and a subsequent drop in the H-Index (Park and Shin, 2020). Moreover, economic policy uncertainty, which often accompanies rising NPLs, can further exacerbate the decline in academic productivity. Increased policy uncertainty can lead to a reduction in both public and private research funding as stakeholders adopt a more risk-averse approach. This reduction in funding translates to fewer research projects being undertaken, less innovative work being published, and consequently, a lower citation impact as reflected in the H-Index (Ashraf and Shen, 2019). Furthermore, the academic community is not immune to the broader economic conditions that affect the financial sector. Researchers, particularly those in economics and finance, may shift their focus from innovative research to more immediate, crisis-related analysis and publications. While this shift is critical for addressing the pressing issues of the time, it may not lead to high-impact, citable documents that contribute significantly to the H-Index. The urgency to address the financial crises can result in a proliferation of lower-impact publications that do not receive the same level of citations as more innovative, groundbreaking research (Bouheni et al., 2021). Additionally, high levels of NPLs can influence the overall academic environment by creating a climate of uncertainty and financial constraint. This environment can discourage long-term research projects and collaborations that are often necessary for producing high-quality, citable research. Academic institutions may face budget cuts, leading to fewer opportunities for researchers to publish their work and engage in collaborative projects that enhance citation impact. The stress on financial systems due to high NPLs can also lead to a brain drain, where top researchers and academics seek more stable environments, further diminishing the potential for high-impact research output (Laryea et al., 2016). In conclusion, the increase in bank NPLs to total gross loans (%) negatively impacts the Citable documents H-Index by diverting financial resources away from research and development, increasing economic and policy uncertainty, and creating an academic environment less conducive to high-impact research. These factors collectively lead to a decrease in the number of high-quality, citable publications, thereby lowering the H-Index. Addressing the underlying causes of high NPLs and stabilizing the financial sector are crucial for maintaining robust academic productivity and citation impact (see Figure 5).

Moreover, NPL decreases with the increase of ICTEXP due to several interconnected economic and financial factors that impede the overall efficiency and competitiveness of the ICT sector. Firstly, high levels of NPLs are indicative of financial instability and economic distress within a country. When banks accumulate a significant proportion of NPLs, it reflects poor financial health and heightened credit risk, which necessitates banks to divert their resources and focus on managing these nonperforming assets rather than extending credit to other sectors, including ICT. This reallocation of resources can result in reduced availability of credit for businesses in the ICT sector, hampering their ability to invest in infrastructure, innovation, and expansion activities essential for competing in international markets (Park and Shin, 2020). Secondly, economic uncertainty and instability, which are often associated with high NPL ratios, can deter both domestic and foreign investment in the ICT sector. Investors tend to be risk-averse during periods of financial instability, leading to a reduction in capital inflows necessary for developing ICT services. The decrease in investment can impede the growth and modernization of ICT infrastructure, thereby limiting the sector's ability to offer competitive services in the global market (Ashraf and Shen, 2019). Moreover, the banking sector's health is closely linked to the overall economic environment, which in turn affects the ICT sector. A financially unstable banking system due to high NPLs can lead to higher borrowing costs and stricter lending criteria. These conditions can stifle entrepreneurial activities and innovation within the ICT sector, as firms face higher hurdles in securing necessary funding for development and export activities. The increased cost of capital and reduced access to credit can significantly impede the growth of ICT services exports (Bouheni et al., 2021). Additionally, high NPLs can lead to a broader economic slowdown, which impacts consumer demand for ICT services both domestically and internationally. As economic conditions deteriorate, businesses and consumers may cut back on spending, including on ICT services, which reduces the overall demand and, consequently, the export potential of these services. This demand reduction can have a cascading effect on the ICT sector, leading to decreased revenues and a lower contribution to total trade (Najeeb, 2022). Furthermore, the correlation between financial health and trade performance is also reflected in the competitiveness of the ICT sector on a global scale. Countries with stable financial systems and low NPL ratios tend to have better-developed ICT infrastructures and more robust export strategies. In contrast, countries struggling with high NPL ratios may lack the necessary financial stability to support their ICT services' continuous development and competitiveness in the international market. The lack of a supportive financial environment can hinder the ability of ICT firms to innovate, scale, and compete globally (Goswami et al., 2011). In conclusion, the decrease in NPL with the increase of ICTEXP can be attributed to the financial instability and economic uncertainty that high NPL ratios bring. These conditions reduce the availability of credit, deter investment, increase borrowing costs, and ultimately stifle the growth and competitiveness of the ICT sector in the global market. Addressing the underlying issues of high NPLs is crucial for fostering a stable financial environment conducive to ICT services' growth and export potential (see Figure 6).

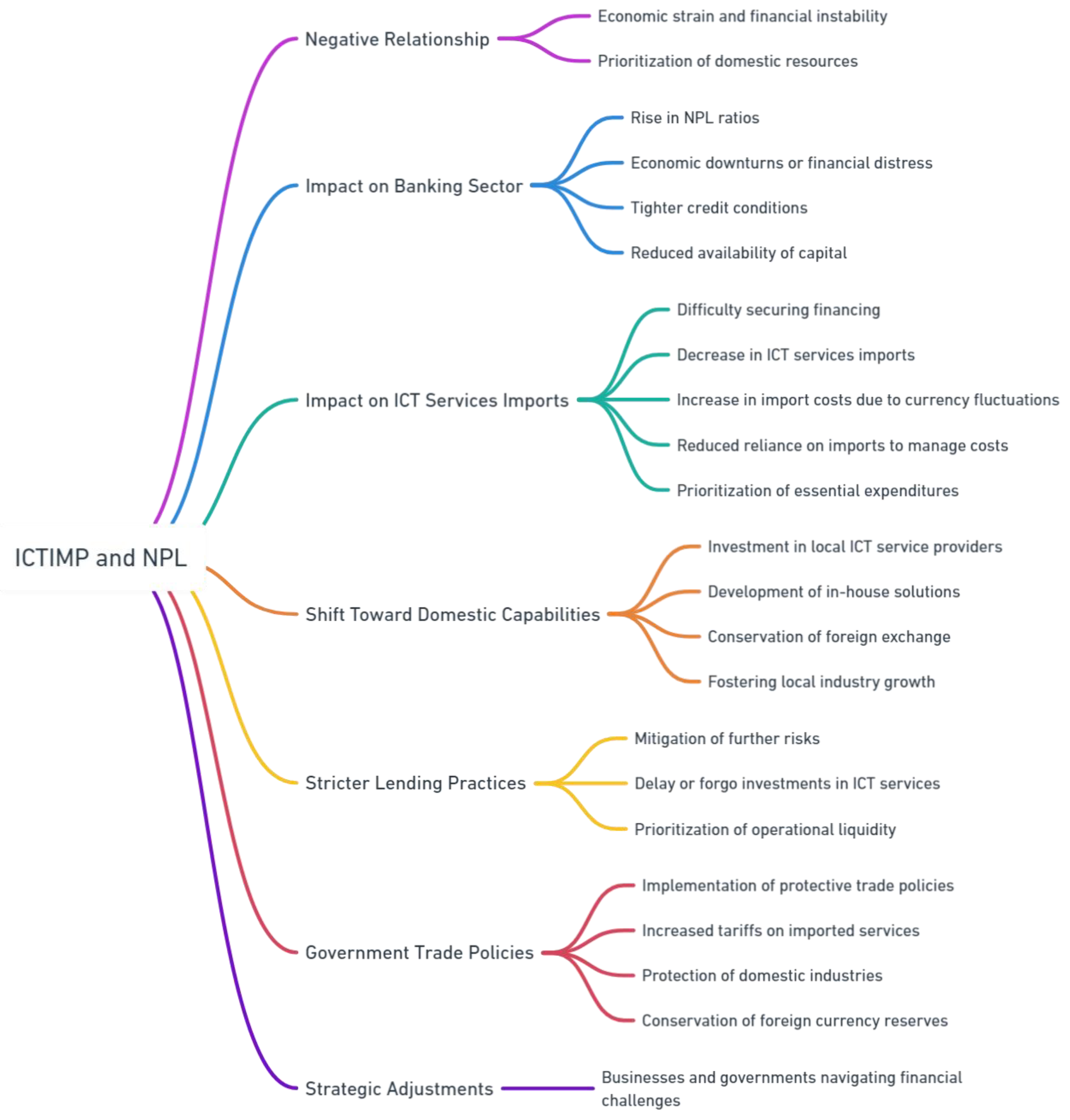

The negative relationship between ICTIMP and NPL can be understood through a combination of economic strain, financial instability, and prioritization of domestic resources. This relationship highlights how the health of the banking sector can directly impact the import behaviors of an economy, particularly in sectors as vital as ICT services. ICT services imports encompass various critical components such as software, IT consulting, data processing, and telecommunication services. These imports are essential for maintaining and advancing technological infrastructure, supporting business operations, and fostering innovation. However, when the banking sector experiences a rise in NPL ratios, it signals broader economic and financial instability that can curtail the ability and willingness of a country to import such services. When the NPL ratio increases, it reflects a deteriorating financial situation within the banking sector, often due to borrowers’ inability to repay loans. This scenario typically arises during economic downturns or periods of financial distress. As banks struggle with higher NPLs, they become more risk-averse, leading to tighter credit conditions and reduced availability of capital for businesses and consumers. Consequently, companies, especially those in need of ICT services, may find it challenging to secure financing for imports, leading to a decrease in ICT services imports (Lee and Rosenkranz, 2019). High NPL ratios can undermine confidence in the financial system, leading to broader economic instability. This instability can result in significant currency fluctuations, making imports more expensive. As the cost of importing ICT services rises, businesses may reduce their reliance on these imports to manage costs, further decreasing the percentage of ICT services in total trade. Financial instability often forces businesses to prioritize essential expenditures, sidelining investments in ICT services that might be deemed non-critical during economic hardships (Berger and DeYoung, 1997). In response to rising NPL ratios and the associated financial strain, governments and businesses may shift their focus toward strengthening domestic capabilities. This shift can involve investing in local ICT service providers or developing in-house solutions to reduce dependency on costly imports. Such strategies are aimed at conserving foreign exchange and fostering local industry growth, which becomes more pronounced when the banking sector is under stress and external borrowing or investment is less viable (Ali et al., 2014). High NPL ratios lead to stricter lending practices, as banks seek to mitigate further risks. Companies facing credit constraints may delay or forgo investments in ICT services, which are often seen as capital-intensive. Instead, they might prioritize maintaining operational liquidity and addressing immediate financial obligations. This shift in investment priorities reduces the demand for ICT services imports, reflecting a broader trend of scaling back on expenditures perceived as less urgent (Bouheni et al., 2021). Governments facing high levels of NPLs may implement protective trade policies to stabilize the economy. These policies could include increased tariffs on imported services, including ICT, to protect domestic industries and conserve foreign currency reserves. Such measures directly reduce the import levels of ICT services, as higher costs deter businesses from procuring services from abroad (Warue, 2013). These factors collectively discourage the import of ICT services, reflecting a strategic adjustment by both businesses and governments to navigate financial challenges (Figure 7).

Finally, the level of NPL decreases with the increase in ICT due to several interrelated factors that undermine economic stability, financial resource allocation, and overall confidence in the banking sector. High levels of NPLs indicate financial distress within banks, which has a ripple effect on the broader economy, including ICT infrastructure and investments. This relationship can be dissected into a few key areas. Firstly, high NPLs signify poor financial health of banks, which in turn constrains their ability to extend credit to various sectors, including ICT. When banks face a high proportion of bad loans, they need to allocate more resources to cover potential losses, leading to tightened lending standards and reduced availability of credit. This credit crunch affects businesses across the economy, including those in the ICT sector, which rely heavily on continuous investments for infrastructure development, technological advancements, and innovation (Park and Shin, 2020). Secondly, economic instability, which often accompanies rising NPLs, can deter both domestic and foreign investment. Investors seek stable environments where the risk of financial loss is minimized. High NPLs signal financial instability and increased risk, causing investors to become cautious or withdraw their investments altogether. This reduction in investment particularly affects capital-intensive sectors like ICT, which require substantial and ongoing financial inputs to maintain and upgrade infrastructure, adopt new technologies, and support innovation activities (Ashraf and Shen, 2019). Additionally, financial instability reflected by high NPLs can lead to an overall economic downturn. In such periods, both businesses and consumers may cut back on spending, including ICT services and products. The decreased demand can limit the revenue streams for ICT companies, making it challenging for them to sustain operations, invest in new technologies, or expand their services. This slowdown directly impacts the ICT sector’s contribution to the GII (Bouheni, et al. 2021). Moreover, the banking sector’s focus shifts significantly when dealing with high levels of NPLs. Banks need to manage these bad loans, which often involves restructuring, recovering bad debts, and dealing with legal issues. This diversion of focus and resources means that banks have less capacity to support ICT projects through loans or other financial services. This lack of support can stifle the growth and development of the ICT sector, as it depends heavily on bank financing for both operational and capital expenditures (Laryea et al. 2016). Furthermore, the presence of high NPLs can also undermine the trust and confidence in the financial system. A banking sector plagued with bad loans can erode confidence among businesses and consumers alike, leading to decreased economic activity. When trust in the financial system wanes, it can result in a lower rate of adoption and integration of ICT solutions, as both individuals and businesses might be reluctant to invest in new technologies or digital transformations that require significant upfront costs and rely on a stable financial environment (Goswami et al., 2012). In conclusion, the negative relationship between ICT and NPLs can be attributed to the financial strain on banks, reduced investments, economic instability, decreased demand, and a shift in banking priorities. These factors collectively hinder the growth and development of ICT infrastructure and services, ultimately affecting the country's overall innovation capacity (see Figure 8).

5. Policy Implications

Following the empirical results, countries with high NPL ratios should consider adopting international banking standards such as Basel III, which emphasizes capital adequacy, stress testing, and market liquidity risk management. These standards can help stabilize financial institutions by ensuring they maintain sufficient capital buffers and manage risks more effectively. For example, Greece and Cyprus, which have faced significant financial crises, could benefit from stricter adherence to Basel III standards to prevent future banking sector distress. In addition to adopting international standards, enhancing regulatory frameworks is crucial. Strengthening regulatory oversight ensures that banks adhere to prudent lending practices and maintain healthy loan portfolios. Regulatory bodies should be empowered to enforce stringent loan classification and provisioning guidelines. For instance, implementing robust regulatory frameworks in the Central African Republic and Chad could improve banking practices and reduce NPL ratios (Illy and Ouedraogo, 2020; Obadire et al., 2022).

Reducing sectoral dependence is essential for countries with high NPLs, which often rely heavily on a few sectors, making them vulnerable to economic shocks. Promoting diversification can mitigate this risk by encouraging investment in various sectors, including manufacturing, services, and technology. Countries like Equatorial Guinea and Chad, which depend heavily on oil, should invest in other industries to stabilize their economies. Supporting SMEs and entrepreneurship can drive economic diversification and innovation. Policies that provide financial support, tax incentives, and technical assistance to SMEs can foster a more resilient economy. For example, initiatives like microfinance programs in Bangladesh have successfully supported SMEs, contributing to economic growth and stability (Wolde and Geta, 2015; López-Cálix, 2020). Promoting good governance is critical for economic growth and financial stability. Efforts to reduce corruption, enhance transparency, and strengthen legal frameworks are essential. For instance, Ukraine and Chad should focus on improving governance and reducing political instability to create a conducive environment for economic activities. Strengthening institutions that uphold property rights, enforce contracts, and provide reliable legal recourse is foundational to a healthy banking sector. Improving institutional quality in countries like the Central African Republic can help build trust in the financial system and reduce NPLs (McFerson, 2009; Kossele and Shan, 2018).

Investing in ICT infrastructure is vital for innovation. Governments should invest in ICT infrastructure to support digital transformation and enhance productivity. Countries like Kenya and India have made significant investments in ICT, boosting innovation and economic growth. Increased funding for R&D can drive innovation and economic diversification. Public and private sector collaboration in R&D should be encouraged. For example, China's significant investment in R&D has positioned it as a global leader in innovation (Holden, 2013; Lui and Xia, 2018). Financial inclusion initiatives can ensure that individuals and businesses have access to necessary financial services, reducing the risk of loan defaults. Policies should promote the availability of affordable credit, savings, and insurance products. India's financial inclusion programs, such as the Pradhan Mantri Jan Dhan Yojana, have increased access to banking services for millions of people. Enhancing financial literacy programs can educate borrowers on prudent financial management, reducing the likelihood of loan defaults. Financial education campaigns in countries like Brazil have improved financial literacy, contributing to better loan repayment rates (Nimbrayan et al., 2018).

Establishing Asset Management Companies (AMCs) can help banks offload NPLs, clean their balance sheets, and focus on new lending. Malaysia's Danaharta and Korea's KAMCO are successful examples of AMCs that managed NPLs effectively post-crisis. Loan restructuring programs can provide relief to distressed borrowers while helping banks recover some value from NPLs. Italy's "GACS" scheme, which guarantees securitized NPLs, has been effective in reducing NPL ratios. International financial institutions like the IMF and World Bank can provide financial assistance and technical support to countries struggling with high NPLs. Greece received substantial support from the IMF and EU during its financial crisis, which helped stabilize its banking sector. Countries can benefit from sharing knowledge and best practices on NPL management and innovation promotion. Regular forums and workshops organized by international bodies can facilitate this exchange of ideas and strategies (He, 2004; Cerruti and Neyens, 2016). Promoting green financing can drive investments in sustainable projects, reducing economic volatility and fostering long-term growth. The European Union's Green Deal includes financial mechanisms to support sustainable development, which can also help stabilize the financial sector. Encouraging corporate social responsibility (CSR) among banks can lead to more responsible lending practices, reducing the risk of NPLs. Banks that integrate CSR into their operations tend to focus on long-term sustainability, improving overall financial stability. Continuous monitoring of banks' financial health through regular assessments and stress tests can pre-emptively identify risks. The European Central Bank conducts regular stress tests on European banks to ensure financial stability. Policymakers should utilize data and analytics to inform decisions on NPL management and innovation promotion. Countries like Singapore use advanced data analytics to monitor financial sector health and guide policy interventions (Gutiérrez-López and Abad-González, 2020; Brühl, 2021).

The analysis of NPLs and their impact on innovation systems provides valuable insights into the health of banking sectors worldwide. Addressing high NPL ratios requires comprehensive policy interventions focused on strengthening financial regulation, promoting economic diversification, ensuring political stability, enhancing innovation, improving financial inclusion, and fostering international cooperation. By implementing these policy recommendations, countries can manage NPLs effectively and create robust innovation systems that drive sustainable economic growth.

6. Conclusions

This research tried to isolate the role of NPLs in the nexus between financial stability and innovation technology. The empirical analysis used clustering methods (k-Means) together with panel data regressions. The findings highlight that NPLs play a key role in the delicate balance between financial stability and innovation. These loans, which are in default or close to default, are a critical indicator of financial distress within banking institutions and the broader economy. High levels of NPLs signify underlying economic problems, such as poor credit risk management and economic downturns, which can lead to significant financial instability. However, these challenging circumstances also drive the necessity for financial institutions to innovate in their risk management and lending practices. Financial institutions, faced with the pressure of managing high NPL levels, are compelled to adopt advanced technologies and develop innovative strategies to mitigate these risks. Effective management of NPLs is crucial for maintaining financial stability. Mechanisms such as asset quality reviews, which involve comprehensive assessments of the value and performance of a bank’s assets, are vital for identifying and addressing problematic loans. Additionally, the establishment of AMCs can facilitate the resolution of NPLs by buying and restructuring these distressed assets, thus cleaning up banks' balance sheets. Robust legal frameworks for insolvency and debt recovery are also essential, providing clear guidelines and processes for managing defaults and recovering assets. These measures not only help in cleaning up banks' balance sheets but also restore confidence in the financial system. Restoring confidence is critical for fostering an environment conducive to innovation, as it encourages investment and the development of new financial products and services.

Moreover, financial innovation can contribute significantly to reducing NPLs by improving credit assessment processes. Innovations in data analytics and Artificial intelligence can enhance the accuracy of credit scoring models, allowing banks to better assess the creditworthiness of borrowers and reduce the likelihood of defaults. Enhanced monitoring systems, utilizing technologies such as blockchain and real-time data analysis, enable more effective tracking of loan performance and early identification of potential issues. Additionally, providing flexible financing options, such as variable repayment schedules and tailored loan products, can help borrowers manage their debt more effectively and reduce the risk of default. However, the rapid growth of financial technologies and the fintech sector presents new challenges that require adaptive regulatory frameworks to manage associated risks. Fintech companies, with their innovative approaches to financial services, have the potential to disrupt traditional banking models and introduce new risks into the financial system. Regulators must develop strategies to oversee these new entities, ensuring that they adhere to sound risk management practices and do not contribute to financial instability. This includes updating existing regulations to address the unique risks posed by digital financial services and ensuring that fintech companies are subject to the same scrutiny as traditional banks. The interplay between NPLs, financial stability, and innovation highlights the need for a balanced regulatory approach that encourages technological advancements while mitigating potential systemic risks. Policymakers must strike a delicate balance between promoting innovation and maintaining a stable financial environment. This involves supporting the development and adoption of new technologies and ensuring that these innovations do not introduce new vulnerabilities into the financial system. Effective regulation should be forward-looking, anticipating future challenges and adapting to the evolving financial landscape. Ultimately, by addressing the challenges associated with NPLs and leveraging the potential of financial innovation, policymakers can ensure a stable and resilient financial system that supports sustainable economic growth and development. This requires a coordinated effort between regulators, financial institutions, and fintech companies to create an environment where innovation can thrive without compromising financial stability. By fostering a culture of innovation and prudence, the financial system can become more robust and better equipped to support long-term economic development.

Appendix

Clustering results applying the k-Means algorithm optimized with the Silhouette coefficient:

- C1= Afghanistan, Albania, Algeria, Angola, Antigua and Barbuda, Argentina, Armenia, Australia, Austria, Bangladesh, Barbados, Belarus, Belgium, Bhutan, Bolivia, Bosnia and Herzegovina, Botswana, Brazil, Brunei Darussalam, Bulgaria, Cambodia, Cameroon, Canada, Chile, China, Colombia, Congo Dem. Rep., Congo Rep., Costa Rica, Croatia, Curacao, Czechia, Denmark, Djibouti, Dominica, Dominican Republic, Ecuador, El Salvador, Estonia, Eswatini, Ethiopia, Fiji, Finland, France, Gabon, Gambia, Georgia, Germany, Ghana, Grenada, Guatemala, Guinea, Honduras, Hong Kong SAR, Hungary, Iceland, India, Indonesia, Iraq, Ireland, Israel, Italy, Jordan, Kazakhstan, Kenya, Korea Rep., Kosovo, Kuwait, Kyrgyz Republic, Latvia, Lebanon, Lesotho, Lithuania, Luxembourg, Macao SAR, China, Madagascar, Malawi, Malaysia, Maldives, Malta, Mauritius, Mexico, Micronesia Fed. States, Moldova, Monaco, Montenegro, Mozambique, Namibia, Nepal, Netherlands, Nicaragua, Nigeria, North Macedonia, Norway, Pakistan, Panama, Papua New Guinea, Paraguay, Peru, Philippines, Poland, Portugal, Romania, Russian Federation, Rwanda, Samoa, Saudi Arabia, Seychelles, Singapore, Sint Maarten (Dutch part), Slovak Republic, Slovenia, Solomon Islands, South Africa, Spain, Sri Lanka, St. Lucia, St. Vincent and the Grenadines, Sweden, Switzerland, Tanzania, Thailand, Tonga, Trinidad and Tobago, Turkey, Uganda, United Arab Emirates, United Kingdom, United States, Uruguay, Uzbekistan, Viet Nam, West Bank and Gaza, Zambia.

- C2 = Central African Republic, Chad, Comoros, Cyprus, Equatorial Guinea, Greece, San Marino, St. Kitts and Nevis, Tajikistan, Ukraine.

Clustering results applying the Elbow method to the k-Means algorithm:

- C1: Afghanistan, Albania, Algeria, Angola, Antigua and Barbuda, Bangladesh, Barbados, Belarus, Bhutan, Bosnia and Herzegovina, Bulgaria, Cameroon, Congo, Rep., Croatia, Curacao, Djibouti, Dominica, Eswatini, Gabon, Gambia, The, Ghana, Guinea, Hungary, India, Iraq, Ireland, Italy, Kazakhstan, Kenya, Kyrgyz Republic, Lebanon, Madagascar, Malawi, Maldives, St. Vincent and the Grenadines, Mozambique, Moldova, St. Lucia, Portugal, Slovenia, Romania, Nigeria, Pakistan, Tanzania, Sint Maarten (Dutch part), Russian Federation, Zambia, Solomon Islands, Montenegro, North Macedonia.

- C2: Ukraine, Greece, Tajikistan, Comoros, Cyprus, Chad, St. Kitts and Nevis, Central African Republic, Equatorial Guinea, San Marino.

- C3: Austria, Argentina, Armenia, Belgium, Australia, Guatemala, Fiji, Brunei Darussalam, Cambodia, Colombia, France, Congo, Dem. Rep., Honduras, Denmark, Grenada, Brazil, Ecuador, Hong Kong SAR, Jordan, Dominican Republic, El Salvador, Iceland, Costa Rica, Finland, Estonia, Czechia, Canada, China, Israel, Bolivia, Germany, Botswana, Ethiopia, Georgia, Indonesia, Chile, South Africa, Malta, Micronesia, Fed. Sts., Saudi Arabia, Poland, Lithuania, Panama, Luxembourg, Philippines, Latvia, Peru, Spain, Kuwait, Paraguay, Norway, Macao SAR, China, Netherlands, Samoa, Lesotho, Nepal, Rwanda, Mauritius, Namibia, Nicaragua, Papua New Guinea, Malaysia, Slovak Republic, Mexico, Kosovo, Singapore, Seychelles, Monaco, Korea, Rep., Uruguay, United Kingdom, West Bank and Gaza, Uzbekistan, Trinidad and Tobago, United Arab Emirates, Switzerland, Sri Lanka, Turkey, United States, Uganda, Thailand, Tonga, Viet Nam, Sweden.

Abbreviations

| Abbreviation | Definition |

| NPL | Non-Performing Loans |

| AMCs | Asset Management Companies |

| CSR | Corporate Social Responsability |

| EU | European Union |

| IMF | International Monetary Fund |

| FSB | Financial Stability Board |

| GACS | Garanzia Cartolarizzazione Sofferenze |

| R&D | Research and Development |

| SMEs | Small and Medium Enterprises |

| GII | Global Innovation Index |

| SSQ | SSQ |

| CCSE | Cultural and creative services exports, % total trade |

| ICTEXP | ICT services exports, % total trade |

| ICTIMP | ICT services imports, % total trade |

| ICT | Information and communication technologies (ICTs) |

| SDGs | Sustainable Development Goals |

| BRICS | Brazil, Russia, India, China, South Africa |

| OECD | Organisation for Economic Co-operation and Development |

References

- Aglietta, M., & Scialom, L. (2009). Permanence and innovation in central banking policy for financial stability. In Financial Institutions and Markets: 2007–2008—The Year of Crisis (pp. 187-211). New York: Palgrave Macmillan US.

- Aiyar, M. S., Bergthaler, M. W., Garrido, J. M., Ilyina, M. A., Jobst, A., Kang, M. K. H., ... & Moretti, M. M. (2015). A strategy for resolving Europe's problem loans. International Monetary Fund.