Submitted:

11 August 2024

Posted:

13 August 2024

You are already at the latest version

Abstract

Jordan is classified as a low- to-middle-income, in which the primary energy sources are imported crude oil and natural gas. The energy expenses represent a high percentage of the country's GDP. Meanwhile, due to its geographical location and its climate, Jordan ranks very high among the world countries with respect to solar energy exploitation potential. Therefore, solar energy is a key resource that can be utilized to significantly improve both the country’s economy and energy security. It has to be highlighted that Jordan focus on a network dedicated to solar energy and it has to be mentioned the Erasmus Plus INNOMED Project based on virtual classrooms, which aims to promote innovative technologies and applications of solar energy in MENA Countries. This paper presents an overview of the solar energy resources in Jordan that includes: the current situation, the potential, and future expectations.

Keywords:

Solar Energy

; PV

; PV regulation

; MENA Countries

1. Introduction

Energy is a necessity for life on earth. Providing people with energy is likely one of the most urgent issues that humanity is now facing. A simple and affordable energy supply is urgently needed, especially in developing nations [1]. Energy consumption among people is directly correlated with their access to healthcare, longevity, and education. A person’s quality of life is affected by these crucial variables [2]. A strong and rapid effort is required to increase access to modern energy facilities in developing nations. Access to energy is essential for promoting social and economic growth, reducing poverty, and advancing global security [3].

The energy sector in Jordan plays a pivotal role in the nation’s economic development and sustainability goals. As of the most recent reports, Jordan’s energy mix is characterized by a diversified portfolio that includes conventional and renewable sources. According to the Minister of Energy and Mineral Resources (MEMR), the primary sources of energy in Jordan include natural gas, oil, and renewable energy [4]. For the future, Jordan is facing two major challenges: on the one hand the growing energy demand and a very limited domestic resource on the other hand. In 2012, the national production of energy – including crude oil, natural gas and renewable energy – was 272 ktoe (thousand tons of oil equivalent), which represents about 5% of the overall energy consumption. Thus, the diversification strategy is aimed at enhancing energy security, reducing dependence on fossil fuels, and mitigating environmental impacts. At that point the, the adoption on the Renewable Energy has increased since then.

Jordan is classified as a low- to middle- income country. As of the date of writing this paper, the country’s population has reached about 11.55 million [5]. Natural resources including water, fossil fuels, and other industrial materials are limited in Jordan. Therefore, Jordan’s primary energy sources are imported crude oil and natural gas from nearby Arab nations. The economy of the nation is largely reliant on tourism and the business services industry, along with a few other sectors including the fertilizer and pharmaceutical industries. In recent years, Jordan’s economy has grown more quickly, which has increased demand for energy in all of its forms. This has coincided with a noticeable trend toward the use of natural gas as the main energy source.

The Jordanian economy is negatively impacted by issues such as the rising demand for energy, the impact of the region’s circumstances on the country, and a shortage of energy sources. These elements heighten the necessity of developing alternate and renewable energy sources through investment.

On the other hand, Jordan has plenty of sunshine. The non-renewable energy technologies developed in recent years have the potential to advance welfare, efficiency, and progress while also generating significant pollution and environmental concerns. Additionally, the rising demand for energy puts pressure on the available resources and imperils sustainability.

A remarkable advancement has occurred in the solar energy sector in Jordan between 2015-2023 that makes the solar energy produced in Jordan covers 26% of the electricity generation. However, because of the economic conditions and a high energy bill of the country on one hand, and the very high potential of solar energy in the country on the other hand, more advancement is demanded.

This paper presents an overview of the solar energy situation in Jordan. The energy landscape in Jordan is described first, in connection to various economic, energy and environmental indicators. The solar resources potential for Jordan is subsequently analyzed based on solar energy indicators. Policies, regulations, installed capacity, investments, and challenges are then presented, to obtain an overview of the current status of solar energy and its exploitation in Jordan. The paper concludes with a future outlook for solar energy in Jordan.

2. Overview of Jordan’s Energy Landscape

2.1. Jordanian Energy Sector in Number

Over 97% of Jordan’s energy requirements are imported. More than 21% of the country’s GDP is spent on the energy bill. Jordan’s energy demand has increased dramatically during the past 20 years, and fossil fuels (crude oil and gas) have been used in order to keep up with it while renewable energy utilization has stayed steady at 1% until 2015. The percentage of renewable energy only began to rise over that level in the last eight years, while the nation’s overall use of renewable energy only slightly grew. However, both in Jordan and globally, the rate of increase in energy consumption continues to outpace the rate of increase in the use of renewable energy sources. [6].

The Jordanian government liberalized its energy market in November 2012, and changed fuel prices in accordance with the international price market. The price of gasoline is currently adjusted each month in accordance with global pricing. Jordan’s decision to stop providing subsidies for fossil fuels promotes the use of renewable energy. The International Energy Agency emphasizes that energy subsidies have a number of detrimental implications. Subsidies promote excessive energy consumption, accelerate the decline of exports, jeopardize energy security by increasing imports, deplete state budgets for importers, discourage investment in energy infrastructure, alter markets, obstruct clean energy investment, increase CO2 emissions and local pollution, counteract the effect of high international prices on decreasing demand, encourage fuel adulteration and smuggling, and unfairly benefit the middle class and the rich [7].

The only hydrocarbon fuel source in Jordan at the moment is the 1987-discovered Risha gas field. In addition to having abundant oil shale deposits, Jordan is also fortunate to have a high potential for solar, wind, geothermal, and biofuel energy sources. These are clean sources that have no harmful effects on the environment. Jordan has a significant solar energy potential due to its location in the sunbelt region. According to [3], the daily average solar irradiance on a horizontal surface range between 5-7 kWh/m2, with the yearly average of solar energy being around 1800 kWh/m2.

Figure 1 summaries the major parameters of the energy sector in Jordan as issued by the [8] of the Minister of Energy and Mineral Resources (MEMR). According to Figure 1, the primary energy consumed in Jordan in 2021 was 8166 ktoe, and the cost of the imported energy was 1.86 million JD (1.86 million or billion?). About 26% of the electricity generation in 2021 was generated from renewable energy, which forms the vast majority of the 28% of the electricity that was generated from local sources. This highlights the importance of developing the renewable energy in Jordan as the only source to achieve energy security.

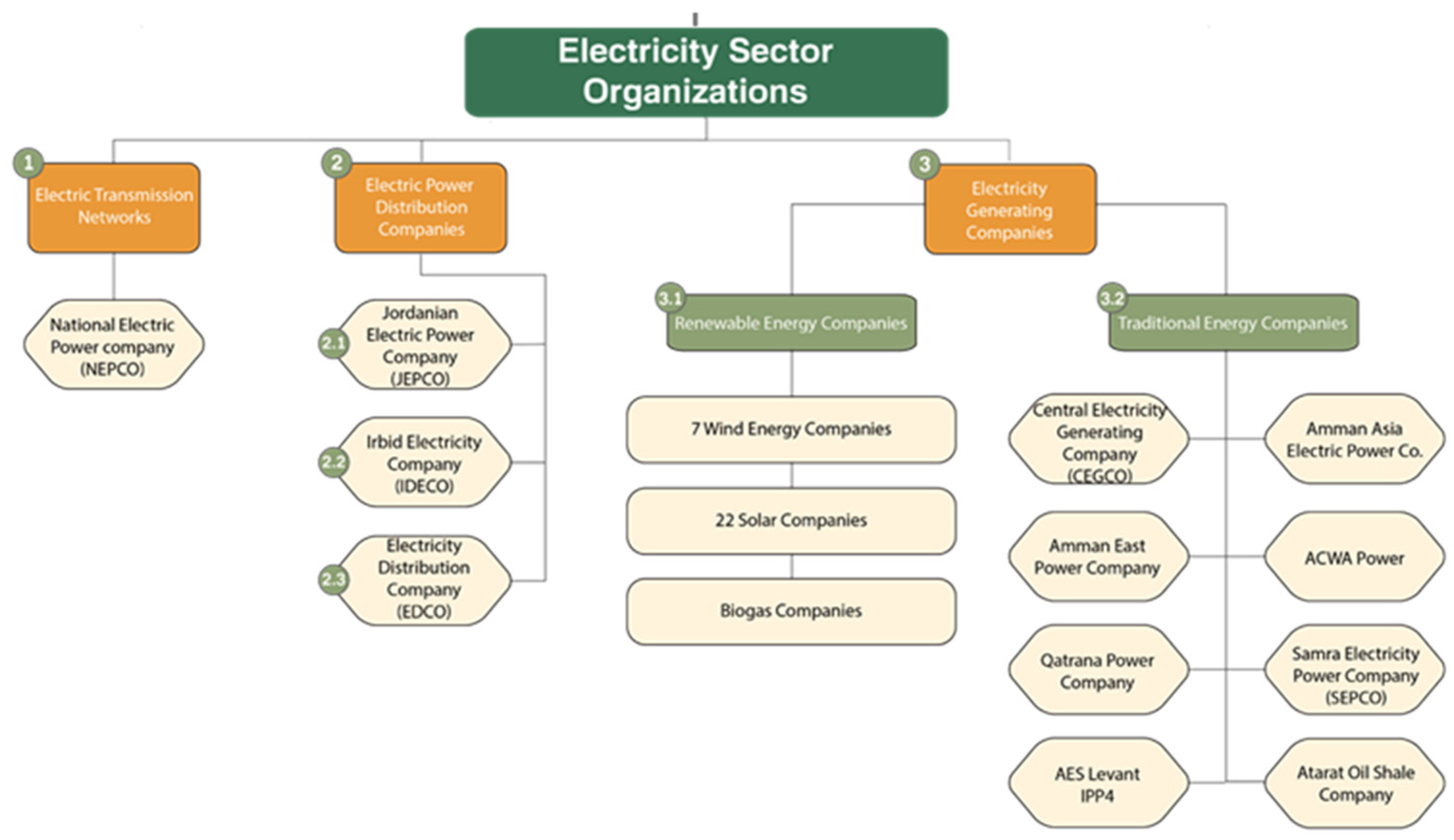

2.2. Electricity Sector Organization

Figure 2 illustrates the electricity sector structure in Jordan. Under this structure, the private sector is substantially responsible for power generation and distribution. The public sector is exclusively in charge of transmission, with a limited involvement in generation. The sector is regulated by an independent Electricity Sector Regulatory Commission (ERC); its main duty is setting electricity tariffs [9].

The institutions responsible for regulating, generating, transmitting and distributing electricity all over the country are divided as:

- National Electric Power company (NEPCO)

NEPCO is a public shareholding company owned by the Jordanian government. Its duties include building, running, and maintaining the transmission systems inside the kingdom’s borders. It also manages the electric transmission network which links the national electrical system to those of the neighboring countries. Additionally, it protects the national energy supply by adding new generation facilities.

- 2.

- Electric Power Distribution Companies that include:

2.1. Jordanian Electric Power Company (JEPCO): a public shareholding corporation in charge of electricity distribution in the governorates of Amman, Zarqa, Ma’daba, and Balqa.

2.2. Irbid District Electricity Company (IDECO): a public shareholding corporation in charge of electricity distribution in the governorates of Irbid, Mafraq, Jerash and Ajloun.

2.3. Electricity Distribution Company (EDCO): a public shareholding corporation in charge of electricity distribution outside of JEPCO and IDECO’s concession areas, specifically in the Southern, Eastern, and Jordan Valley regions.

- 3.

- Electricity Generation Companies:

3.1. Renewable energy companies: That include 7 wind energy companies, 22 solar energy companies, and biogas companies.

3.2. Traditional energy companies. The major ones are:

3.2.1. Central Electricity Generating Company (CEGCO): a 1999-founded public shareholding firm. Its duties include power generation and wholesale sales to the National Electric Power Company. At the end of 2021, the company’s generating capacity was 752 MW [10].

3.2.2. Amman East Power Company: The American AES Company and the Japanese MITSUI Company are the owners of the privately held Amman East Power Project. It was established in 2009 and is in charge of producing and selling electricity to NEPCO. The company was the first privately funded facility in Jordan to produce electricity in East Amman power plant/Al-Manakher, which began producing electricity on May 26, 2009. The company’s generating capacity has reached about 400 MW [11].

3.2.3. Qatrana Electric Power Company (QEPC): a private firm founded in 2010 and is owned by the Saudi XENEL firm and the Korean KEPCO Company. The company’s mission is to produce and supply electricity to NEPCO. the company’s generating capacity is about 450 MW [12].

3.2.4. Samra Electric Power Company (SEPCO): a private shareholding company that was established in 2004 and is entirely owned by the government. The company is tasked with producing power and selling it to NEPCO. the company’s generating capacity is 1241 MW [13].

3. Solar Resources Potential in Jordan

The solar potential is determined by appropriate solar energy potential indicators, such as the direct normal irradiation (DNI), diffuse horizontal irradiation (DHI), global horizontal irradiation (GHI), the specific photovoltaic output (PVOUT) and the seasonality index.

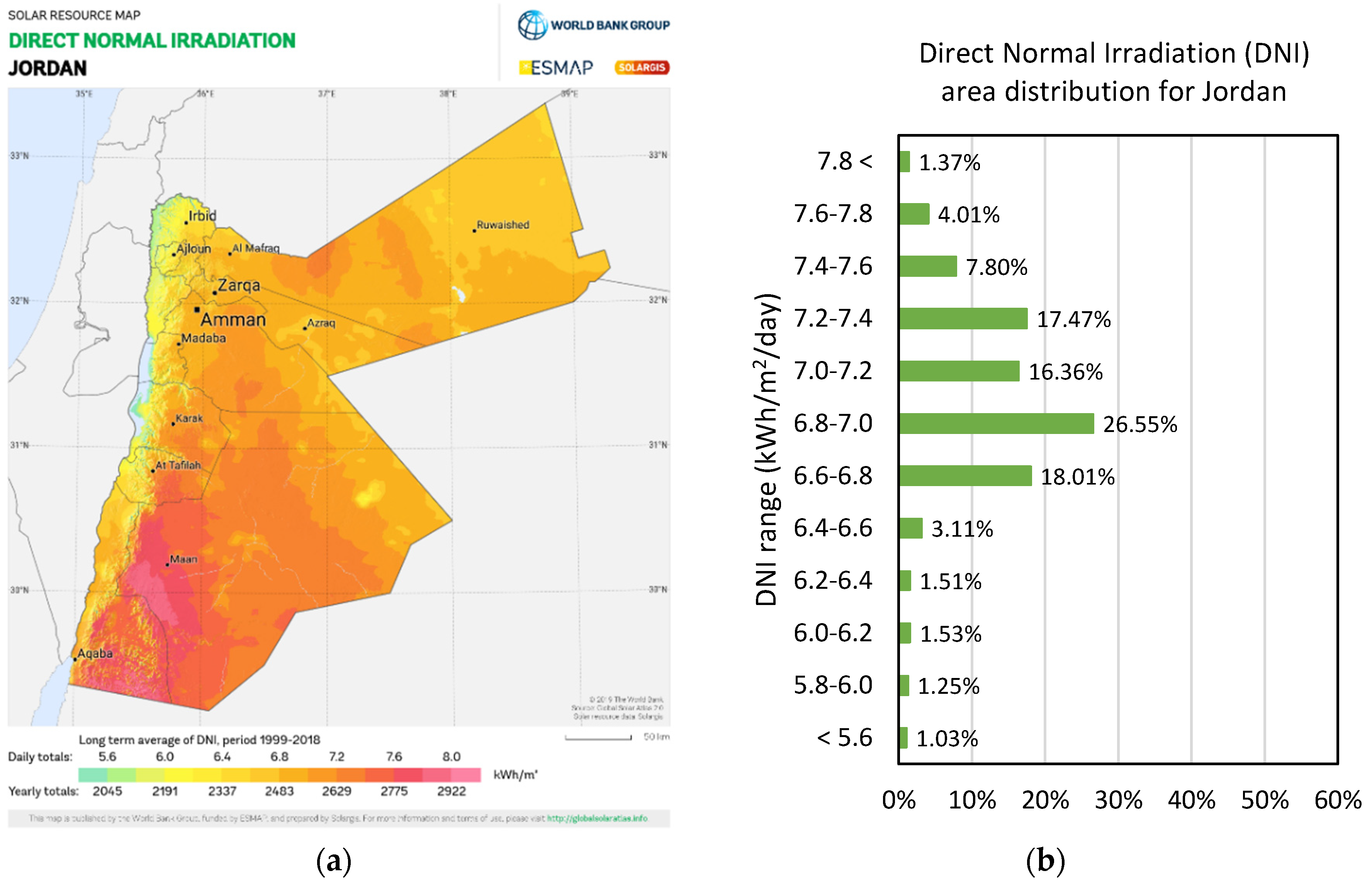

The direct normal irradiation DNI is a term synonymous to “beam radiation” and refers to the amount of solar radiation from the direction of the sun, that is, radiation received by a surface normal to the sun [14,15]. Direct normal irradiation is a very important indicator for the energy yield and the performance assessment of concentrating solar power (CSP) and concentrator solar photovoltaic (CPV) technologies, and for determining the global irradiation received by tilted or sun-tracking photovoltaic modules [16,17].

The diffuse horizontal irradiation DHI is a synonym “diffuse sky radiation” and refers to the radiation received by a horizontal plane from the sun after the direction of radiation has been altered by scattering, excluding circumsolar radiation [14,18]. High DHI values are produced by an unclear atmosphere or cloud reflections.

Global horizontal irradiation GHI refers to the shortwave solar radiation received by a horizontal plane. It results from the combination of direct and diffuse radiation [14,15,16]. Although there is also a radiation component that is due to ground-reflected radiation, its effect is not significant. Hence, the GHI is given by [14] as shown in Equation (1):

where Z is the solar zenith angle.

The units for all irradiation indicators are usually J/m2, MJ/m2 or kWh/m2, that is, incident energy per unit area on a surface. The incident energy is determined by integrating over a specific time period, usually an hour or a day [18,19].

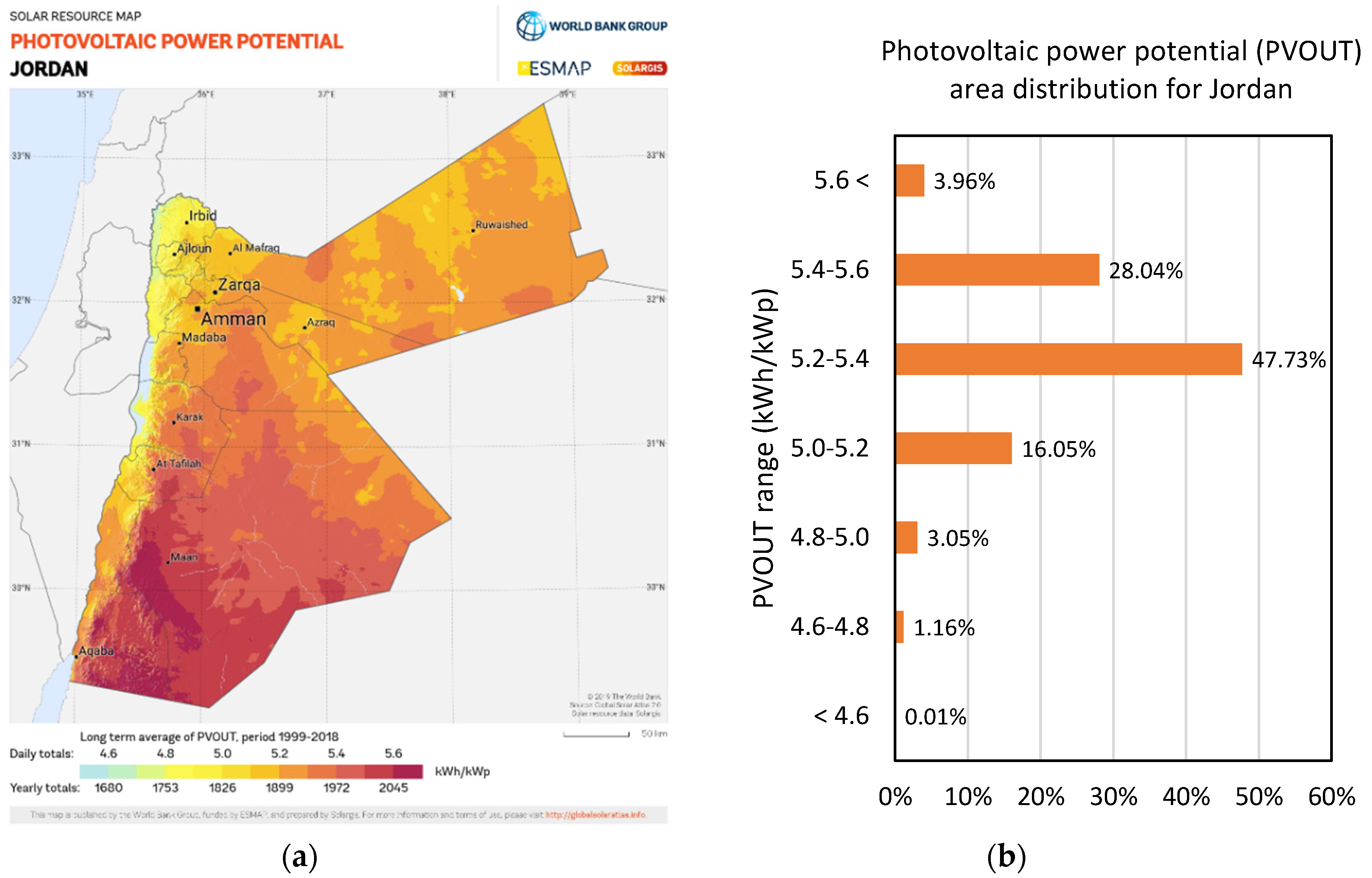

Another indicator, which is a measure of photovoltaic power potential, is the specific photovoltaic output (PVOUT) in kWh/kWpeak, that is, photovoltaic electricity (AC) delivered by a PV system, normalized to 1 kWp of installed capacity. It represents long-term yearly average of daily totals of potential electricity production from a 1 kW-peak grid-connected solar photovoltaic (PV) power plant [15,16,19,20].

Apart from the aforementioned indicators that are related to solar energy potential and electricity production, another significant indicator is the “seasonality index”, defined as the ratio of the highest and the lowest average monthly PVOUT values in an average year [15]. A high seasonality index reflects a country or region with a high seasonal variability in electricity production through photovoltaic modules. Low values of the seasonality index are desirable for a stable solar energy exploitation.

The values of selected indicators for Jordan are shown in Table 1 along with the world rank of Jordan for each indicator.

According to Table 1, Jordan ranks 19th among 209 countries in the world, with a GHI of 6.02 kWh/m2/day, the highest being 6.47 kWh/m2/day for the Republic of Yemen and the lowest being 2.53 kWh/m2/day for Ireland [21]. However, Jordan ranks 3rd in terms of PVOUT with a value of 5.32 kWh/kWp/day, following Chile (5.36 kWh/kWp/day) and Namibia (5.38 kWh/kWp/day). The lowest value is that of Ireland (2.51 kWh/kWp/day). Although the seasonality index ranks Jordan in the 110th place, its value is 1.41, which is relatively low, considering that the lowest seasonality index is 1.15 (Haiti) and the highest 14.97 (Norway). This indicates that the photovoltaic potential in Jordan varies by about 40% around the year.

In Figure 3, Figure 4, Figure 5 and Figure 6 the area distribution of solar energy indicators is presented for Jordan. The direct normal irradiation shown in Figure 3 ranges from 5.66-7.89 kWh/m2/day with an average of 7 kWh/m2/day [20]. More than half of the area presents DNI values between 6.8-7.4 kWh/m2/day. Figure 4 shows the long-term averages of daily and yearly totals of global horizontal irradiation kWh/m2/day or year. This indicator varies within the range 5.5-6.4 kWh/m2/day with an average value of 6.02 kWh/m2/day. Approximately 70% of the area has a GHI value between 5.8-6.2 kWh/m2/day. While the GHI represents theoretical potential, the practical potential is represented by the photovoltaic potential (PVOUT). The average value of PVOUT is 5.32 kWh/kWp, its minimum value is 4.74kWh/kWp and its maximum value is 5.7 kWh/kWp [20]. Almost half of the area presents a PVOUT values between 5.2-5.4 kWh.kWp.

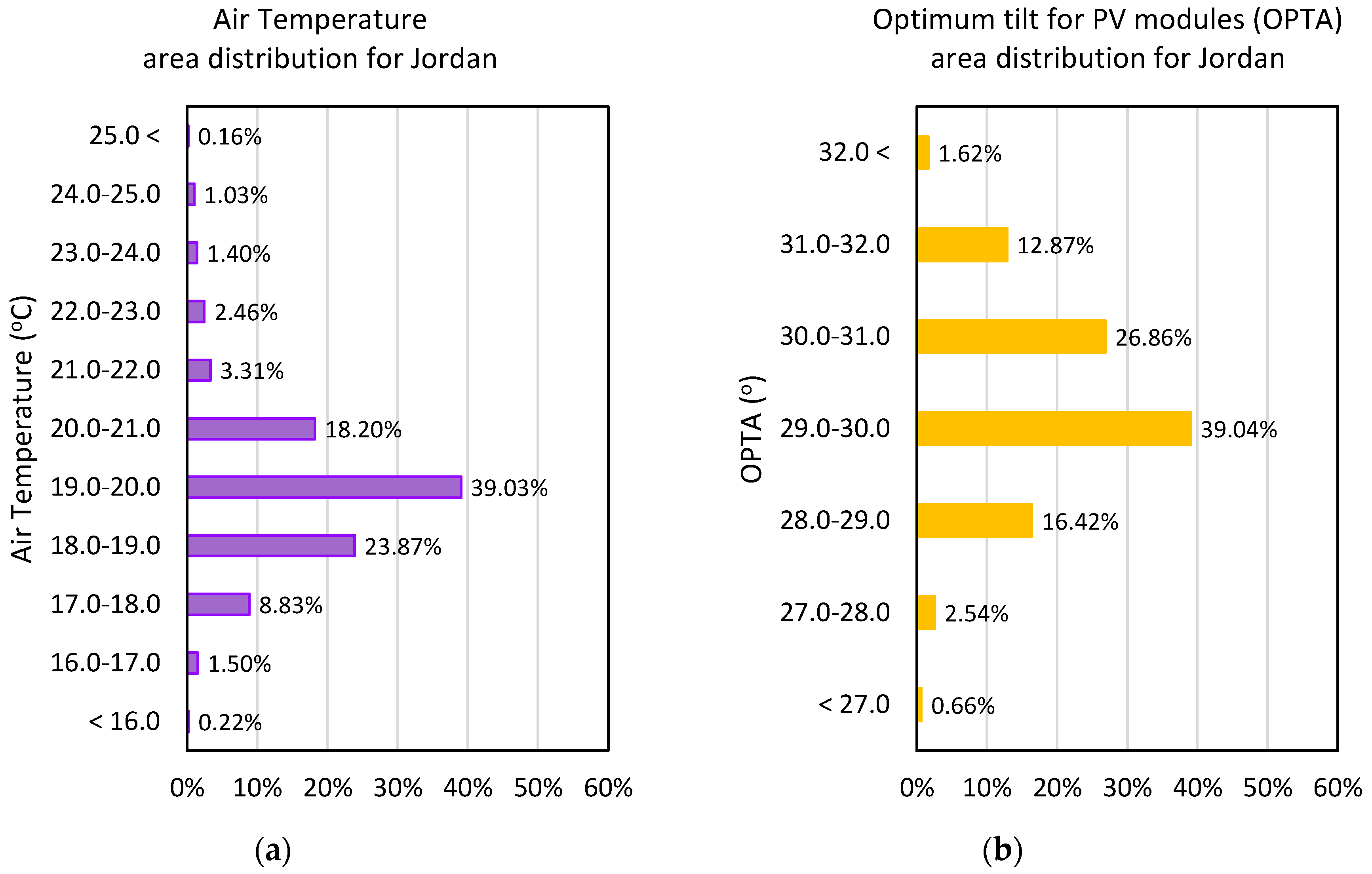

In Figure 6a the distribution of the average air temperature is shown. This refers to 2 m above ground. Most of the area presents an average air temperature between 18-20 oC. The highest average air temperature is 24.6 oC and the lowest is 16.3 oC, while the average value is 19.5 oC. Figure 6b shows the optimum tilt angle (OPTA) for a PV module. This ranges between 27-33o, with an average value of 30°C [20]. For the 80% of the area the OPTA is between 28-31°C.

4. Current State of Solar Energy in Jordan

4.1. Policies and Regulations

Jordan is a Middle Eastern country that has faced several energy-related challenges, including growing energy demand, dependence on fossil fuels, and the need to develop sustainable energy sources. The Jordanian government has undertaken various initiatives to address these challenges and promote energy sustainability.

The legal and institutional framework includes several key laws and regulatory bodies:

Ministry of Energy and Mineral Resources (MEMR): MEMR is the main government body responsible for formulating and implementing energy policies. It has worked to promote energy efficiency, diversify energy production, and develop new energy projects.

Energy Regulatory Authority (ERA): The ERA is the independent regulatory body responsible for monitoring and regulating the energy sector. The ERA plays a crucial role in approving energy tariffs and ensuring transparency and fairness in energy markets.

Renewable Energy Law of 2012 (Renewable Energy and Energy Efficiency Law (REEEL)—Law No. 13 for the year 2012): This law was an important step toward promoting renewable energy in Jordan. It provided tax incentives, feed-in tariffs, and facilities for investment in renewable energy and in particular in solar and wind energy.

Jordan Energy Strategy (JES): JES is the strategic document edited by the MEMR to design the main objectives and strategies to improve the energy program of Jordan for the decade 2020-2030. It was developed and released in June 2020.

National Energy Efficiency Action Plan (NEEAP): NEEAP is a document adopted in Jordan in 2014 to promote the optimal use of energy in different economic and non-economic sectors.

Jordan Renewable Energy & Energy Efficiency Fund (JREEEF): JREEEF is a public fund created by Bylaw No. 49/2015 which helps farmers, households, industries, hotels, mosques, churches, schools and communities to optimize their energy consumptions and to use more renewable energy.

International Renewable Energy Agency (IRENA): IRENA is an intergovernmental organization that supports countries in their transition to a sustainable energy future and serves as the principal platform for international cooperation, a center of excellence and a repository of policy, technology, resources and financial knowledge on renewable energy.

Jordan has set clear energy goals to address energy challenges and promote sustainability:

- Increasing Renewable Energy: Jordan has an ambitious goal to increase the share of renewable energy in its overall generation. This includes the implementation of large-scale solar and wind power projects.

- Reducing Dependence on Fossil Fuels: The country aims to reduce its dependence on fossil fuels through the diversification of energy sources.

- Energy Efficiency: Promoting energy efficiency in various sectors, such as industrial, residential and commercial, is a priority to reduce overall energy consumption.

Jordan has made significant progress in the development of solar and wind energy. Several key projects have been implemented in these areas. The 2012 Renewable Energy Law established feed-in tariffs for solar and wind energy, incentivizing investment in these sectors.

It is worth to mention several bylaws and regulations that have been released for the implementation of the REEEL:

- Bylaw No. 50 of 2015 and its amendment in 2016 (conditions and procedures of the renewable energy direct proposal submission and connection to the grid).

- Instructions for costs of connecting renewable energy sources to the distribution system in the cases of competitive bidding and direct proposals related to Article 9/B of the REEEL.

- Instructions for the sale of electrical energy generated from renewable energy systems related to Article 10/B of the REEEL (net metering system).

- Instructions governing electricity wheeling for energy generated from renewable energy sources, for consumption purposes and not for sale to others (electricity wheeling) and for wheeling charges (costs of the electricity wheeling).

- Bylaw No. 49/2015 (JREEEF).

- Bylaw No. 10 of 2013, amended in 2015, 2017 and 2018 (tax exemptions for renewable energy and energy efficiency systems and equipment).

- Intermittent Renewable Resources Distribution Connection Code at Medium Voltage.

- Guidelines for interconnection of renewable energy sources on distribution and transmission grids as well as on electric meters for net metering apply to both distribution and transmission grids.

The Jordanian government has been actively promoting energy efficiency in various sectors. This includes awareness programs, incentives for the adoption of energy-efficient technologies, and regulations to improve energy management.

Jordan has partnered with international organizations and donors to obtain funding and technical support for renewable energy and energy sustainability projects. These partnerships have played a significant role in achieving the country’s energy goals.

It is important to note that the Middle East region faces unique challenges, including political tensions and instability. These factors can affect energy planning and energy supply security.

Jordan has made significant progress in the energy sector, with the goal of reducing dependence on fossil fuels and increasing the use of renewable energy sources. The energy regulations and policies adopted have created a favorable environment for investment in the energy sector, particularly in solar and wind energy. However, regional instability and other ongoing challenges require careful management to ensure a reliable and sustainable energy supply. Collaboration with international organizations has played a significant role in achieving the country’s energy goals.

The author in [24] made a picture of the status of investment and development of RERs in Jordan in 2020. They started their analysis with the point that in the year 2020, Jordan imported around 94% of the total fossil fuels from other countries for the internal national energy demand. This weakness exposed the national economy to fuel price variations impacting different economy sectors. In their work, they highlight that the national energy demand is growing at an average rate of 3% per year (aligned to Countries with similar economies) which has led the national government to fix the goal of covering 10% of the energy demand from RERs. The main RERs in Jordan are solar, wind and biomass energy and they found that the contribution of clean energy in 2020 was not enough (7% of total energy demand).

Moreover, the author in [25], based on the same starting points of [24], pointed out that the instability and conflicts of the geographical and political region are the main issues to face to guarantee stability of the energy market and production, in particular for Jordan, which has the weakness of scarcity of energy resources. Despite the favorable natural conditions for solar energy exploitation, Jordan’s energy mix is still dominated by imported fossil fuels and natural gas. They concluded that Jordan and the authorities have to work to design new and advanced strategies towards a more sustainable energy sector in the next few years.

The researchers in [26,27] concluded that the reduction of importing energy is one of the key factors to let Jordan be less sensitive to regional conflicts and political instability. In this vision the redefinition of the national energy mix is one of the solutions, improving the RERs and in particular solar energy. It was also concluded that the negative consequences of a regional conflict should have reduced impacts in the medium and long term if a rational and sustainable policy is adopted by the Jordan Government.

In the recent study by [28], it is outlined that the Jordan government is working on energy policy towards the attainment of Sustainable Development Goals (SDGs) by leveraging technology to promote economic growth while preserving the environment. Among their results, they highlighted that the development and adoption of advanced technologies should be given top priority by the policymakers in Jordan to create a sustainable economic development.

On the other hand, [29] showed that this topic is currently dominated by economic considerations in Jordanian society that derive from concerns about electricity costs, supported by safety problems during the operation and maintenance of electricity generation power plants. Another factor highlighted by their work is the strong will of all the stakeholders to have the opportunity to be involved in decision-making processes on energy transition rather than purely to compensate local communities for the installation of electricity generation and transmission technologies.

The work in [30] carried out a strategic analysis of the potentiality of the development and implementation of an action plan for the renewable energy resources in Jordan that is a detailed and useful tool for all the stakeholders.

As reported in the document by [31], in 2020 Jordan launched the Jordan Energy Strategy (JES) for the decade 2020-2030. It is an ambitious plan, which aims to ensure energy security, affordability and sustainability, along with increased use of domestic energy resources and improving the energy mix in a relatively short time. Starting from considering different scenarios for 2030, the plan has been conceived to promote the energy independence of the Country and thus to reach broader strategic objectives: diversifying the energy sources, boosting the use of domestic energy resources, increasing energy efficiency and reducing energy costs throughout the national economy, and continuing to develop the Jordanian energy system. One of the main goals is to increase energy production by renewable resources up to 31% of power generation share by 2030.

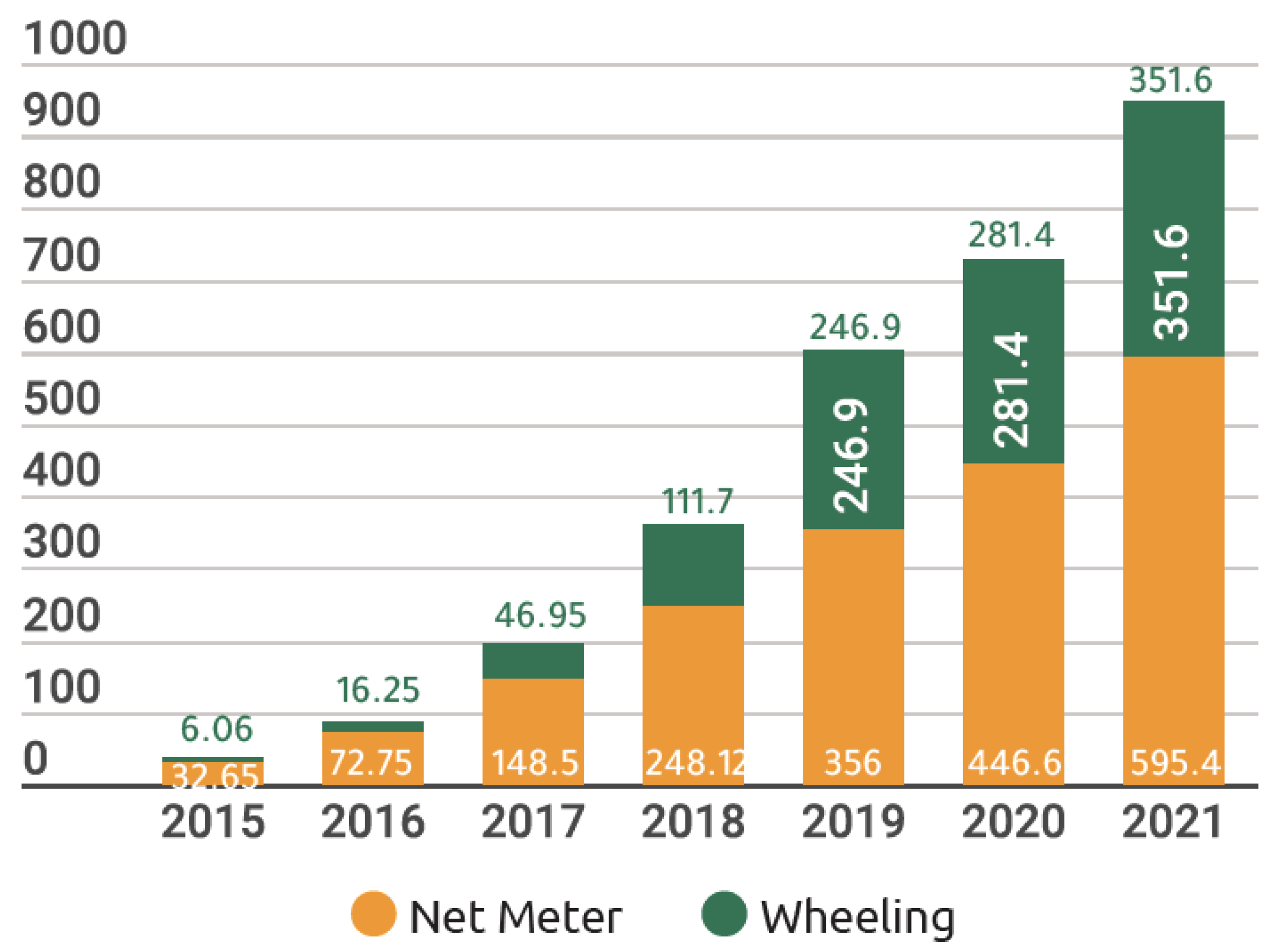

4.2. Installed Capacity

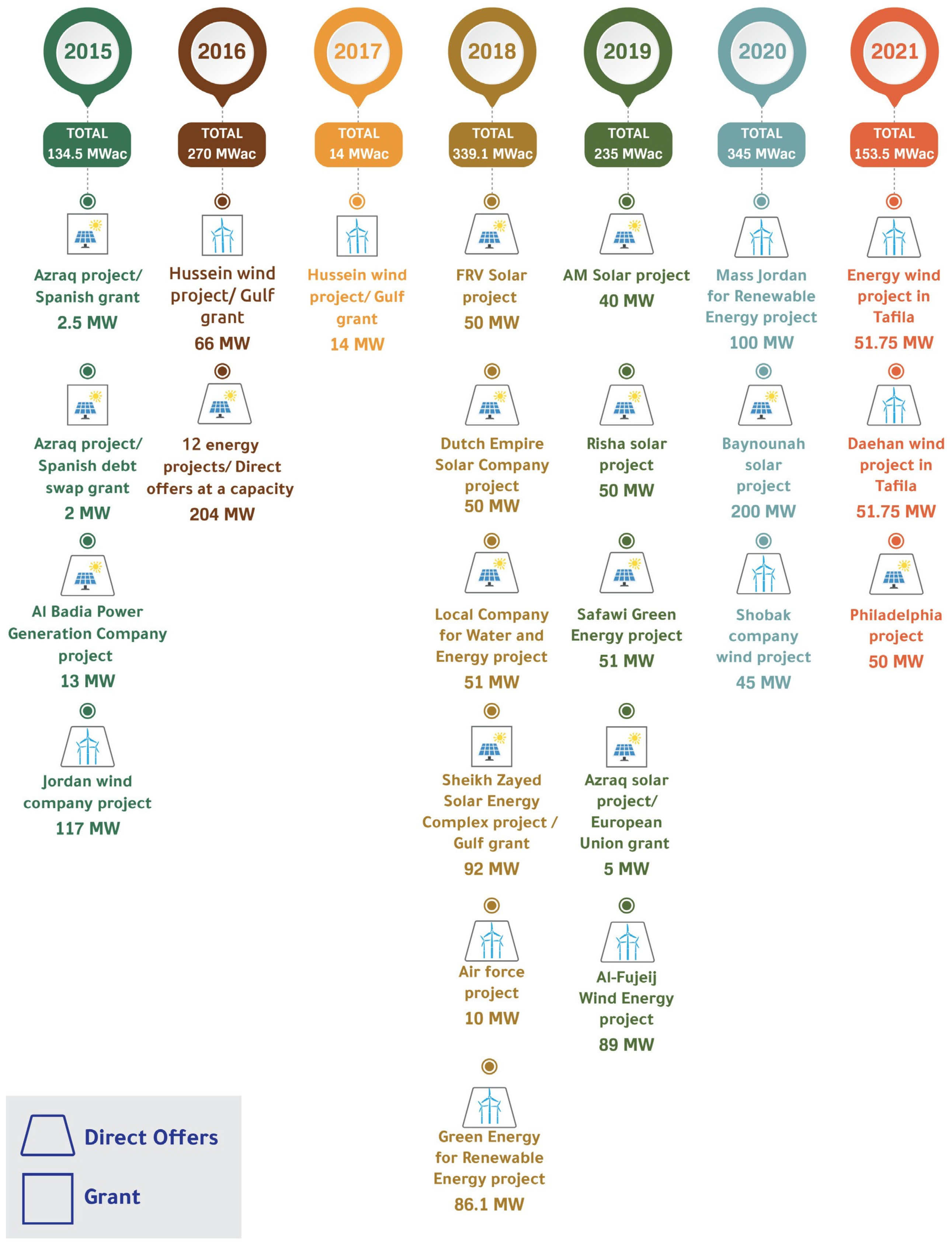

Up to 2021, the total installed capacity of projects using renewable energy to produce electric power has exceeded 2445.7 MW, which includes: 947.6 MW of renewable energy projects owned by subscribers to cover their consumption by using net metering and wheeling schemes, and 1498.1 MW projects where the electric power generated is sold to the electric companies. Figure 7 shows the increased capacity over the years 2015-2021 of the first type of the projects (The majority of this type is electricity generated by PV panels), while Figure 8 shows the main renewable energy projects of the second type that were established between 2015-2021. The figure shows that the vast majority of the projects are solar energy or wind energy projects.

4.3. Investment and Funding

aJordan is a country that has recognized the importance of renewable energy sources for its energy security and economic growth. Among the renewable energy sources, solar energy has emerged as a key area of focus for Jordan, given its abundant sunshine and potential for cost-effective power generation. In recent years, Jordan has made significant strides in developing its solar energy sector, with the support of both government and private sector investments.

Government Support for Solar Energy in Jordan:

Jordan’s approach to solar energy is comprehensive, involving capacity expansion, policy implementation, financial support programs, and the development of both large and small-scale projects. This strategy positions solar energy as a crucial component of Jordan’s energy mix and a key factor in reducing its carbon footprint and dependency on fossil fuels. Here are the key aspects of this support:

- Increase in Solar Energy Capacity: Jordan is expected to increase its solar energy capacity from 1.7 GW in 2020 to 2.7 gigawatts (GW) by 2023. This significant expansion is part of the country’s strategy to reduce its reliance on imported fossil fuels [32].

-Renewable Energy Encouragement and Energy Efficiency Fund (JREEEF): The Jordanian Ministry of Energy’s Renewable Energy Encouragement and Energy Efficiency Fund has completed the second phase of its support program for solar cell systems in households. This initiative indicates the government’s commitment to promoting solar energy at the household level, although the subsidy program was suspended after reaching the target number of beneficiaries and exhausting the allocated budget.

-Renewable Energy Target: By 2030, Jordan aims to derive 50% of its energy from renewable sources. This ambitious goal underscores the country’s commitment to transitioning to renewable energy.

-Investment in Sustainable Energy in Public Buildings: The government is also focusing on sustainable energy investment in public buildings, with national plans supporting this initiative. The 2023–24 period is seen as a critical window for developing practical strategies to achieve this goal.

-Policies and International Agreements: The Jordanian government introduced a feed-in tariff system in 2012, offering a fixed rate for solar energy producers to sell their electricity to the grid. This policy has attracted investments and led to the development of large-scale solar projects. Furthermore, Jordan has signed agreements with international organizations and foreign governments, such as a 2018 agreement with the IFC to support the development of a 200 MW solar project.

-Large-Scale and Small-Scale Solar Projects: The growth in solar energy is partly due to the development of large-scale projects, including the 800 MW Al-Dhafra project and the 400 MW Al-Risha project. Additionally, there is significant potential for small-scale solar installations like rooftop systems, which could account for up to 1.4 GW of solar energy capacity by 2030 [32].

Private Sector Investment in Solar Energy in Jordan

Private sector investment in solar energy in Jordan has been significant and is a vital component of the country’s shift towards renewable energy.

- Baynouna Solar Energy Project: The Baynouna Solar Energy Company, a joint venture between Abu Dhabi’s clean energy company Masdar and Finnish investment and asset management group Taaleri, operates Jordan’s largest clean energy project with a 200 megawatt (MW) capacity. The Baynouna Solar Park, developed through a power purchase agreement between Masdar and National Electric Power Company (NEPCO), Jordan’s state electricity provider, produces over 560 gigawatt-hours (GWh) of power annually. This project plays a crucial role in contributing to Jordan’s climate targets, providing clean energy access, creating jobs, and promoting economic growth [33].

- International Support: The project has garnered support from various international financial institutions, including the International Finance Corporation (IFC), the Opec Fund for International Development, the KfW Group’s DEG, and the Japan International Cooperation Agency. Masdar is active in more than 40 countries and has committed to investing in projects worth over $30 billion, to expand its renewable energy capacity to at least 100 GW by 2030. Additionally, Masdar signed a preliminary agreement with the Jordanian Ministry of Energy and Mineral Resources to explore the development of a further 2 GW of renewable energy projects in Jordan [33].

- Largest Private-to-Private Solar Project: The Climate Investment Funds (CIF), the European Bank for Reconstruction and Development (EBRD), and several multi-sector partners have financed Jordan’s largest private-to-private solar facility. This facility is expected to produce 70 GWh of energy annually and reduce carbon emissions by 41,500 tons every year. Jordan’s solar power capacity has seen a remarkable rise, jumping from around 20 MW in 2012 to over 1,000 MW, with an additional 1.2 GW under construction or development [34].

- Public-Private Partnerships (PPPs): Jordan has a history of using PPPs in the Mena region, financing key infrastructure, including renewable energy projects, through these partnerships. These PPPs are an essential part of Jordan’s Economic Modernization Vision 2023-33, which aims to attract a total capital investment of 41.4 billion JD (58.3 billion$) and achieve annual economic growth of 5.6 percent. The government is aiming to catalyze new PPPS worth 10 billion JD, with the private sector expected to contribute 73% of the funds.[35]

- Institutional Support and Investment Environment: To address challenges in PPPs, Jordan established the Project Preparation Development Facility with the help of the IFC. This facility aims to build government capacity for more informed decisions about PPPs and develop a pipeline of bankable projects. Additionally, in 2021, Jordan established a dedicated Ministry of Investment and introduced the Investment Environment Law.

4.4. Main Challenges and Barriers

Jordan’s solar energy sector, while making significant strides, is confronted with several challenges and barriers:

-High Project Costs and Regulatory Challenges: The primary challenges in the development of renewable energy projects in Jordan include high project costs, primarily due to high taxes and extensive regulatory procedures required for new projects. These factors can deter investment and slow down the development of new renewable energy initiatives. Solutions proposed include the reduction of taxes and customs for targeted renewable energy projects to make the sector more appealing to businesses.

-Energy Surplus and Storage: One of the major challenges Jordan faces is managing an energy surplus generated from renewable sources, including solar. This issue underscores the need for high technology storage solutions to effectively store energy produced from solar and wind sources. Without adequate storage capabilities, the sector cannot fully realize its potential.

-Grid Capacity and Expansion Struggles: The Jordanian renewable energy network is facing struggles in its expansion due to several factors. These include the grid’s limited capacity to absorb renewable energy, the inherent intermittent nature of renewable energy sources, and challenges related to the storage of generated electricity. Addressing these issues is critical for the expansion and efficiency of the renewable energy network.

-Private Sector Development: In response to these challenges, Jordan has turned its focus towards private sector development. The private sector is expected to play a crucial role in delivering new projects across various domains, including renewable energy. This shift is part of the country’s broader strategy to address energy needs amidst challenges like rapid population growth, water scarcity, and the impact of regional instability and major supply disruptions.

-Renewable Energy Law and Private Sector Participation: The Renewable Energy and Efficiency Law passed by the Jordanian government in 2012 and amended in 2015 marked a significant shift in the development of renewables. It enabled greater flexibility in site selection and technical specifications for renewable projects, facilitating private sector participation. This law was a response to the previously rigid and slow framework that limited renewable energy development.[36]

-Lack of Public Awareness: Another challenge facing the adoption of solar energy in Jordan is the lack of public awareness about the benefits of renewable energy. While there has been some progress in recent years in terms of raising awareness, many people in Jordan still do not fully understand the potential of solar energy.

To address this challenge, it is important for the government and other stakeholders to continue to educate the public about the benefits of solar energy. This could involve targeted marketing campaigns, public outreach initiatives, and other efforts to raise awareness about the potential of renewable energy.

-Limited Technical Capacity: A final challenge that we will mention in this paper is the limited technical capacity in the country. While there are a number of experienced solar energy companies operating in Jordan, there is still a shortage of skilled professionals and technicians who can design, install, and maintain solar energy systems.

These challenges highlight the complex nature of transitioning to renewable energy sources in Jordan. Addressing these issues will require a coordinated approach involving technological advancements, regulatory reforms, and robust government support. To address this challenge, the government and other stakeholders need to invest in building the technical capacity in the country. This could involve providing training and education programs to help develop new skills and expertise, and it could also involve partnering with international organizations and companies.

4.5. Future Outlook of Solar Energy in Jordan

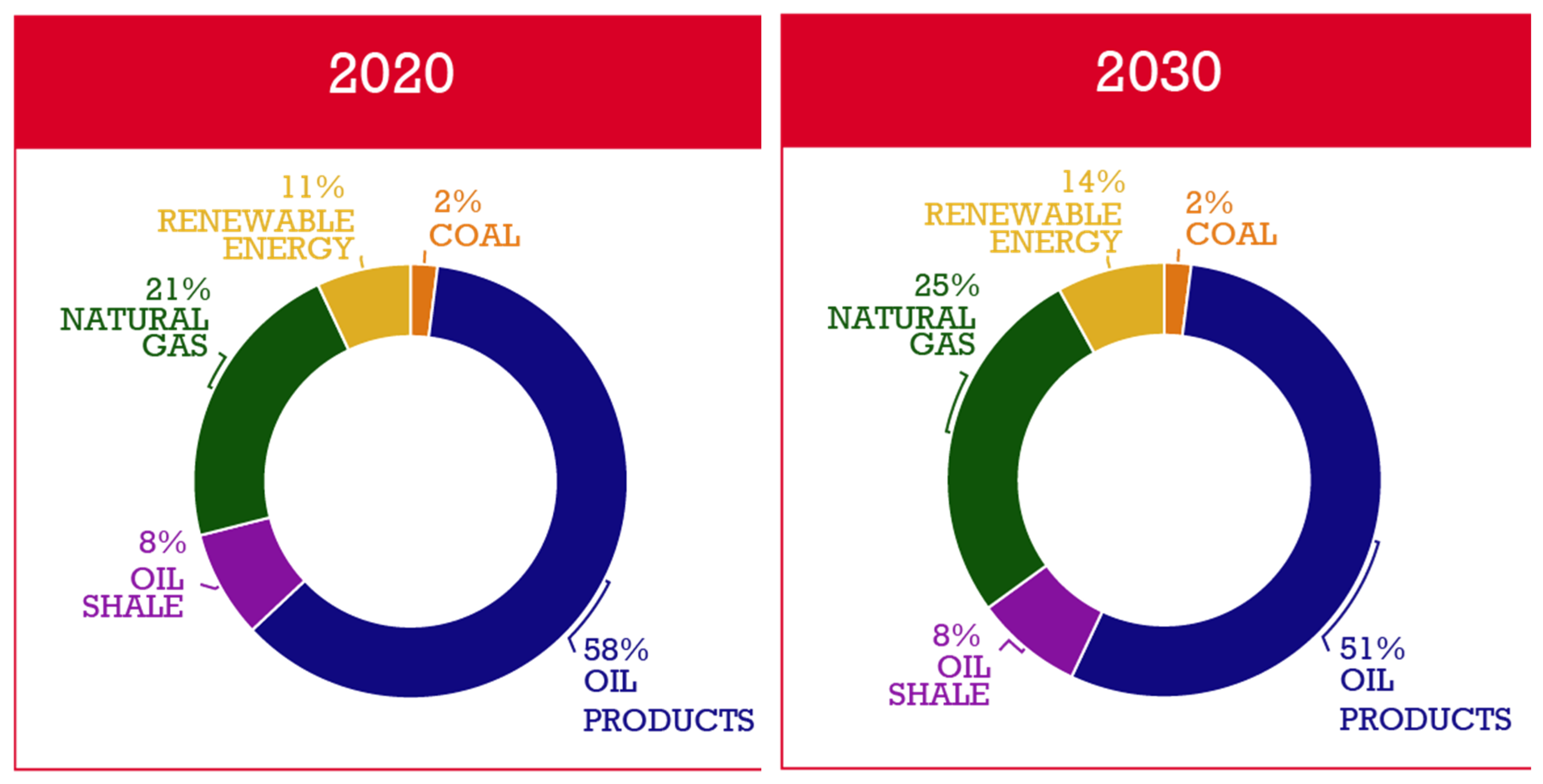

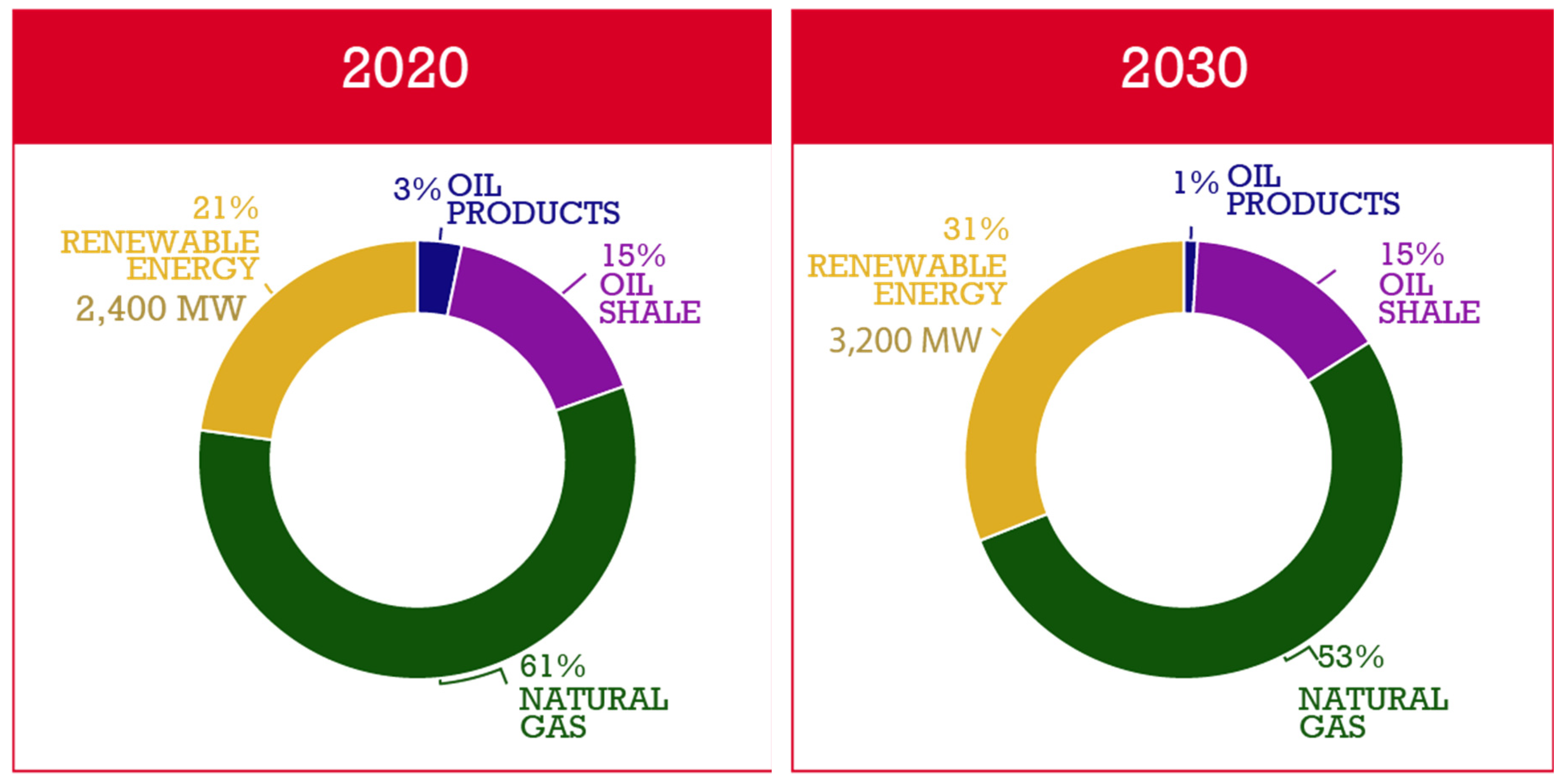

Table 2 shows the forecast of the primary energy demand in Jordan for the period 2020-2030, while Table 3 shows the forecast of the electricity generation for the same decade. Figure 9 shows that the forecast is that the ratio of the renewable energy for the total energy sector in Jordan will increase from 11% in 2020 to 14% in 2030. Figure 10 concentrates on the electricity generation and shows that the generation of electricity from the renewable energy will increase from 2400 MW in 2020 to 3200 MW in 2030 which will increase its contribution in the total electricity generation from 21% to 31%.

The main assumptions used to predict the future numbers in the tables and figures are related to the following parameters:

1. The dependency of GDP growth on the current state of circumstances.

2. The renewable energy projects that are under construction.

3. The National Energy Efficiency Action Plan (NEEAP), which aims to improve energy efficiency in the water sector and cut final energy demand by 15% up to 2025, using 2018 as a base year.

4. The estimated amount of oil that oil shale retorting projects will generate.

5. Increase the Risha gas field’s output.

6. Technical guidelines for power system operation based on the National Electric Power Company’s (NEPCO) plans and agreements.

5. Conclusion

Currently, the electricity generation in energy relies heavily on fossil fuels, particularly natural gas. Merely ¼ of the electricity generation is covered by renewable sources. Since the imported energy cost is high, it is important to further increase the renewable energy penetration in Jordan in order to achieve energy security and economic benefits. The geographic location and climate of Jordan places the country 3rd worldwide in photovoltaic power potential and 19th in terms of global horizontal irradiation, with a favorable seasonal variability.

Jordan has set clear energy goals to address energy challenges and promote sustainability, namely increase the share of renewables in energy generation, reduce fossil fuels dependence, and increase energy efficiency. The main challenges towards these goals are high renewable energy project costs, primarily due to high taxes and extensive regulatory procedures, managing the energy surplus generated from renewable sources, including solar, the grid’s limited capacity to absorb renewable energy, the inherent intermittent nature of renewable energy sources, and challenges related to the storage of generated electricity.

To face these challenges Jordan has turned its focus towards private sector development. The private sector is expected to play a crucial role in delivering new projects across various domains, including renewable energy. The 2012 Renewable Energy and Efficiency Law, along with its amendment in 2015, marked a significant shift in the development of renewables. However, to do so, more investments are required, some policies are needed to be modified, the challenges must be addressed.

6. Acknowledgment

This paper was supported by European Union’s ERASMUS-2022 programm for education, training, youth and sport, Project Number 101092041, project INNOMED (Boosting Innovative Solar Energy Technologies and Applications in Mediterranean Countries Education).

INNOMED is a Project based on virtual classrooms, which aims at promote innovative technologies and applications of solar energy in MENA Countries. INNOMED is an Erasmus Plus Project funded by the European Union which brings together the University of Jordan, Cyprus, Morocco, Austria, Italy and Greece. The synergistic collaboration between the Project Partners is scheduled with a precise to do list of frequent online meetings and periodic face-to-face meetings which involve, every time, all the Countries that are part on the project.

References

- Boutammachte, N., & Knorr, J. “Field-test of a solar low delta-T Stirling engine.” Solar energy 86, no. 6 (2012): 1849-1856. [CrossRef]

- Dascomb, J. “Low-cost concentrating solar collector for steam generation.” (2009).

- Al-Salaymeh, A. “Modelling of global daily solar radiation on horizontal surfaces for Amman city.” Emirates Journal for Engineering Research 11.1 (2006): 49-56.

- Summary of Jordan Energy Strategy 2020-2030 StrategyEN2020.pdf (memr.gov.jo).

- Department of Statistics- Jordan https://dosweb.dos.gov.jo/.

- Al-Salaymeh, A., Abu-Jeries, A., Spetan, K., Mahmoud, M. Elkhayat, M. “A Guide to Renewable Energy in Egypt and Jordan: Current Situation and Future Potentials”. Friedrich-Ebert-Stiftung Jordan & Iraq (2016).

- Jalilvand, D. R. “Renewable energy for the Middle East and North Africa. Policies for a successful transition.” (2012).

- Jordanian Ministry of Energy and Mineral Resources (MEMR) Annual Report 2021 https://www.memr.gov.jo/ebv4.0/root_storage/en/eb_list_page/annual_report_2021_en.pdf.

- World Bank Group. ESMAP (Energy Sector Management Assistance Program), “Power Sector Financial Vulnerability Assessment, Impact of the Credit Crisis on Investments in the Power Sector, Hashemite Kingdom of Jordan”. https://www.esmap.org/sites/esmap.org/files/P116206_Jordan_Power%20Sector%20Financial%20Vulnerability%20Assessment-Impact%20of%20the%20Credit%20Crisis%20on%20Investments%20in%20the%20Power%20Sector_Chavapricha.pdf.

- Central Electricity Generating Company (CEGCO) Annual Report 2021 https://www.cegco.com.jo/Admin_Site/Files/PDF/2a970f31-781f-4d70-93b7-ee0fd1edba34.pdf.

- Amman East Power Company website https://www.aesjordan.com.jo/about-us/ (accessed March 16, 2024).

- Power Technology, “Power plant profile: Al Qatrana IPP 2 Combined Cycle Power Project, Jordan”. https://www.power-technology.com/data-insights/power-plant-profile-al-qatrana-ipp-2-combined-cycle-power-project-jordan/ (accessed March 16, 2024).

- Samra Electric Power Company (SEPCO) website https://www.sepco.com.jo/en (accessed March 16, 2024).

- Solar Resource Glossary n.d. https://www.nrel.gov/grid/solar-resource/solar-glossary.html (accessed March 16, 2024).

- Suri M, Betak J, Rosina K, Chrkavy D, Suriova N, Cebecauer T, et al. Global Photovoltaic Power Potential by Country. World Bank 2020. https://documents.worldbank.org/en/publication/documents-reports/documentdetail/466331592817725242/Global-Photovoltaic-Power-Potential-by-Country (accessed March 16, 2024).

- Solar radiation modeling n.d. https://solargis.com/docs/methodology/solar-radiation-modeling (accessed March 16, 2024).

- Tech Specs n.d. https://solargis.com/maps-and-gis-data/tech-specs (accessed March 16, 2024).

- Duffie, J. A., Beckman, W. A., & Blair, N. Solar engineering of thermal processes. 2nd ed. New York: Wiley; 1991.

- Global Solar Atlas 2.0 : Technical Report. World Bank 2019. https://documents.worldbank.org/en/publication/documents-reports/documentdetail/529431592893043403/Global-Solar-Atlas-2-0-Technical-Report (accessed March 16, 2024).

- Global Solar Atlas n.d. https://globalsolaratlas.info/map?c=31.302022,37.144775,7&r=JOR (accessed March 16, 2024).

- Global Photovoltaic Power Potential by Country | Data Catalog n.d. https://datacatalog.worldbank.org/search/dataset/0038379 (accessed March 16, 2024).

- Global Solar Atlas n.d. https://globalsolaratlas.info/download/jordan (accessed March 16, 2024).

- [Data/information/map] obtained from the “Global Solar Atlas 2.0, a free, web-based application is developed and operated by the company Solargis s.r.o. on behalf of the World Bank Group, utilizing Solargis data, with funding provided by the Energy Sector Management Assistance Program (ESMAP). For additional information: n.d. https://globalsolaratlas.info (accessed March 16, 2024).

- Abu-Rumman, G., Khdair, A. I., & Khdair, S. I. “Current status and future investment potential in renewable energy in Jordan: An overview.” Heliyon 6, no. 2 (2020). [CrossRef]

- Sandri, S., Hussein, H., & Alshyab, N. (2020). Sustainability of the energy sector in Jordan: Challenges and opportunities. Sustainability, 12(24), 10465. [CrossRef]

- Alshwawra, A., & Almuhtady, A. (2020). Impact of regional conflicts on energy security in Jordan. International Journal of Energy Economics and Policy, 10(3), 45-50. [CrossRef]

- Alshwawra, A., Almuhtady, A., & Sakhrieh, A. (2023). Electricity system security in Jordan: A response for arab uprising. Heliyon, 9(5). [CrossRef]

- Fraihat, B. A. M., Ahmad, A. Y. B., Alaa, A. A., Alhawamdeh, A. M., Soumadi, M. M., Aln’emi, E. A. S., & Alkhawaldeh, B. Y. S. (2023). Evaluating Technology Improvement in Sustainable Development Goals by Analysing Financial Development and Energy Consumption in Jordan. International Journal of Energy Economics and Policy, 13(4), 348. [CrossRef]

- Danielson, M., Ekenberg, L., Komendantova, N., Al-Salaymeh, A., & Marashdeh, L. (2022). A participatory MCDA approach to energy transition policy formation. In Multicriteria and Optimization Models for Risk, Reliability, and Maintenance Decision Analysis: Recent Advances (pp. 79-110). Cham: Springer International Publishing.

- Ahmad A. Salah, Mohammad M. Shalby & Firas Basim Ismail (2023) The status and potential of renewable energy development in Jordan: exploring challenges and opportunities, Sustainability: Science, Practice and Policy, 19:1, 2212517.

- IRENA (2021), Renewable Readiness Assessment: The Hashemite Kingdom of Jordan, International Renewable Energy Agency, Abu Dhabi. ISBN: 978-92-9260-277-2.

- Solarquarter, “The Future Looks Bright for Solar Energy in Jordan: A 2023 Outlook”. https://solarquarter.com/2023/02/25/the-future-looks-bright-for-solar-energy-in-jordan-a-2023-outlook/ (accessed March 16, 2024).

- The national news, “Masdar opens Jordan’s largest solar project with 200MW capacity”. https://www.thenationalnews.com/business/energy/2023/02/25/masdar-opens-jordans-largest-solar-project-with-200mw-capacity/ (accessed March 16, 2024).

- Climate investment funds, “CIF, EBRD FINANCE LARGEST PRIVATE-TO-PRIVATE SOLAR PROJECT IN JORDAN”. https://cif.org/news/cif-ebrd-finance-largest-private-private-solar-project-jordan (accessed March 16, 2024).

- Arabian Gulf Business Insight, “PPP pioneer has all the right moves – now it needs new partners”. https://www.agbi.com/articles/jordan-special-report-public-private-partnerships/ (accessed March 16, 2024).

- Oxford business group, “Jordan’s energy sector turns focus to private development and renewable resources”. https://oxfordbusinessgroup.com/reports/jordan/2018-report/economy/energising-new-tactics-the-sector-is-increasingly-turning-to-private-development-and-renewable-sources-to-power-the-nation (accessed March 16, 2024).

Figure 1.

The Jordanian energy sector in 2021 in number. Source: [8].

Figure 1.

The Jordanian energy sector in 2021 in number. Source: [8].

Figure 2.

Electricity Sector Organizations in Jordan. Source: [5].

Figure 2.

Electricity Sector Organizations in Jordan. Source: [5].

Figure 3.

(a) Map of long-term averages of daily an yearly totals of direct normal irradiation (DNI) in kWh/m2 for Jordan [22] (b) Area distribution of DNI (daily totals) for Jordan. Source: Ref. [23].

Figure 5.

(a) Map of long-term averages of daily an yearly totals of photovoltaic power output (PVOUT) in kWh/m2 for Jordan [22] (b) Area distribution of PVOUT (daily totals) for Jordan. Source: Ref. [23].

Figure 6.

Jordan area distribution of (a) average temperature in oC at 2 m above ground and (b) optimum tilt angle for PV modules (OPTA) in degrees. Source: Ref. [23].

Figure 6.

Jordan area distribution of (a) average temperature in oC at 2 m above ground and (b) optimum tilt angle for PV modules (OPTA) in degrees. Source: Ref. [23].

Figure 7.

Added capacity for renewable energy systems with the purpose of covering the consumption of subscribers in Jordan during 2015–2021. Source: [8].

Figure 7.

Added capacity for renewable energy systems with the purpose of covering the consumption of subscribers in Jordan during 2015–2021. Source: [8].

Figure 8.

Electricity generation projects using renewable energy established in Jordan during the period 2015-2021. Source: [8].

Figure 8.

Electricity generation projects using renewable energy established in Jordan during the period 2015-2021. Source: [8].

Figure 9.

The ratio of fuel contribution to the total primary energy mix (2030 -2020). Source: [5].

Figure 9.

The ratio of fuel contribution to the total primary energy mix (2030 -2020). Source: [5].

Figure 10.

The ratio of fuel contribution to electricity generation (2030 -2020). Source: [5].

Figure 10.

The ratio of fuel contribution to electricity generation (2030 -2020). Source: [5].

Table 1.

Jordan world rankings in terms of global horizontal irradiation (GHI), specific photovoltaic output (PVOUT) and seasonality index [21].

Table 1.

Jordan world rankings in terms of global horizontal irradiation (GHI), specific photovoltaic output (PVOUT) and seasonality index [21].

| Indicator | World (209 countries) |

Jordan | Jordan world rank | |

|---|---|---|---|---|

| Highest | Lowest | |||

| GHI (kWh/m2/day) | 6.47 | 2.53 | 6.02 | 19 |

| PVOUT (kWh/kWp/day) | 5.38 | 2.51 | 5.32 | 3 |

| Seasonality Index (-) | 14.97 | 1.15 | 1.41 | 110 |

Table 2.

Primary Energy Demand Forecast for (2020-2030) in Jordan. Source: [5].

Table 2.

Primary Energy Demand Forecast for (2020-2030) in Jordan. Source: [5].

| Year | Primary Energy Demand (Overall domestic consumption) (toe) |

| 2020 | 10,039 |

| 2021 | 10,267 |

| 2022 | 10,420 |

| 2023 | 10,595 |

| 2024 | 10,668 |

| 2025 | 10,967 |

| 2030 | 11,760 |

Table 3.

Electricity Demand Forecast for (2020-2030) in Jordan. Source: [5].

Table 3.

Electricity Demand Forecast for (2020-2030) in Jordan. Source: [5].

| Year | Electricity Demand Gigawatt hour (GWh) |

| 2020 | 17,672 |

| 2021 | 17,831 |

| 2022 | 17,860 |

| 2023 | 17,950 |

| 2024 | 17,958 |

| 2025 | 18,686 |

| 2030 | 19,701 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Copyright: This open access article is published under a Creative Commons CC BY 4.0 license, which permit the free download, distribution, and reuse, provided that the author and preprint are cited in any reuse.