Submitted:

14 August 2024

Posted:

15 August 2024

You are already at the latest version

Abstract

Our decisions today are part of an economic thinking which aims to fix problems and increase the efficiency of capital markets. Our economy is still largely approached as a system which is unre-lated to our environment or social returns like community well-being, social cohesion, equitable distribution of resources, etc. To fully incorporate sustainability into cost-benefit analysis, busi-nesses need to change their financial approach, showcasing how long-term thinking impacts prof-its. Money's value is not static and evolves with time and technology. We propose to introduce a variation of cost/benefit and present value calculations. Precise calculations reveal the benefits of long-term strategies over short-term profit focus. As financial systems evolve and technology advances, the accurate calculation of money's time value will continue to play a crucial role in shaping economic landscapes and guiding financial choices. In this article, we demonstrate that updated calculations could be a key enabler to visualize the benefits of long-term thinking or “patient finance” as compared to a short-term focus on profit. We introduce the concept and calculation of a Present Future Value (PFV).

Keywords:

TVM (Time Value of Money)

; Sustainable Prosperity

; Innovation

; CBA (Cost-Benefit Analysis)

; Patient Finance

1. Introduction: Sustainability and Financial Calculations

Our decisions today are part of an economic thinking which aims to address problems and increase efficiency of capital markets. Our thinking is still predominantly based on the idea that money is an endless stock which cannot affect the real variables in life. As a result, our economy is still largely approached as a system which is unrelated to our environment.

The financial calculations of cost-benefit and money time value are embedded within that economic logic. The so-called science of economy is being challenged more and more by alternative perspectives. Such perspectives are being provided by economists such as Stephanie Kelton, Stephen Levitt, Stephen Dubner, or Mariana Mazzucato. These economists are pushing the boundaries as to how we look at those models. They are preparing a shift to an economy that is more in touch with real-life and real-nature situations; an economy that fits within the paradigm of a social capitalism that seeks a fair and regenerative distribution of wealth rather than a capitalism that targets short-term profit maximization.

Economy aims to model the way in which we see the world around us:

- -

- Economy is a social science. It is not an exact science. Economic theories provide us with a frame to look at the world, to try and make sense of it. In the same way as stories try to make us see the world through the eyes of the characters and the context within which a story unravels itself. As part of a system.

- -

- The first writers weren’t poets. They were accountants. The evolution of writing started off with people using a little clay tablet and a reed stylus to mark down who owed what to whom.

- -

- Money is fiction. Interest is fiction. Present and future values are fictions. They are useful made-up concepts which help us to manage supply and demand through an endless stock of money that stores value over time.

If money is fiction and if interest is fiction, then it may be time to revisit the current narrative so that it reflects the way in which we want to see the world. In our view, the missing link between the adaptation of our economic models and its implementation lies partially in the financial formulas which are being used. Hence, we make a proposal to introduce a variation of cost/benefit and present value calculations.

2. Our Proposed Method: Amended Formulas to Integrate Sustainability and Visualize Long-Term Thinking in Finance

2.1. Sustainability: Setting the Scene

Europe is home to a staggering 22.5 million Small to Medium-sized Enterprises (SMEs), which collectively make up a remarkable 99.8% of all enterprises, as per Eurostat data. These SMEs are responsible for generating 53% of the annual value in Europe, significantly outweighing the 47% contributed by the relatively small 0.2% of larger corporations.

However, it is concerning that while 90% of business leaders acknowledge the pivotal role of sustainability in shaping the future of their companies, only two-thirds of them have a concrete sustainability strategy in place [1].

At the current pace, Europe will not achieve its emission reduction targets by 2030, let alone the aspiration of becoming a carbon-neutral continent by 2050.

One of the key obstacles that hinders leaders in embracing sustainability is the widespread misconception that sustainable practices will impede the speed of their operations. Corporate sustainability however not only enhances a business' long-term viability but also bolsters its profitability, attractiveness, and competitiveness.

2.2. Sustainability: An Integrated Perspective

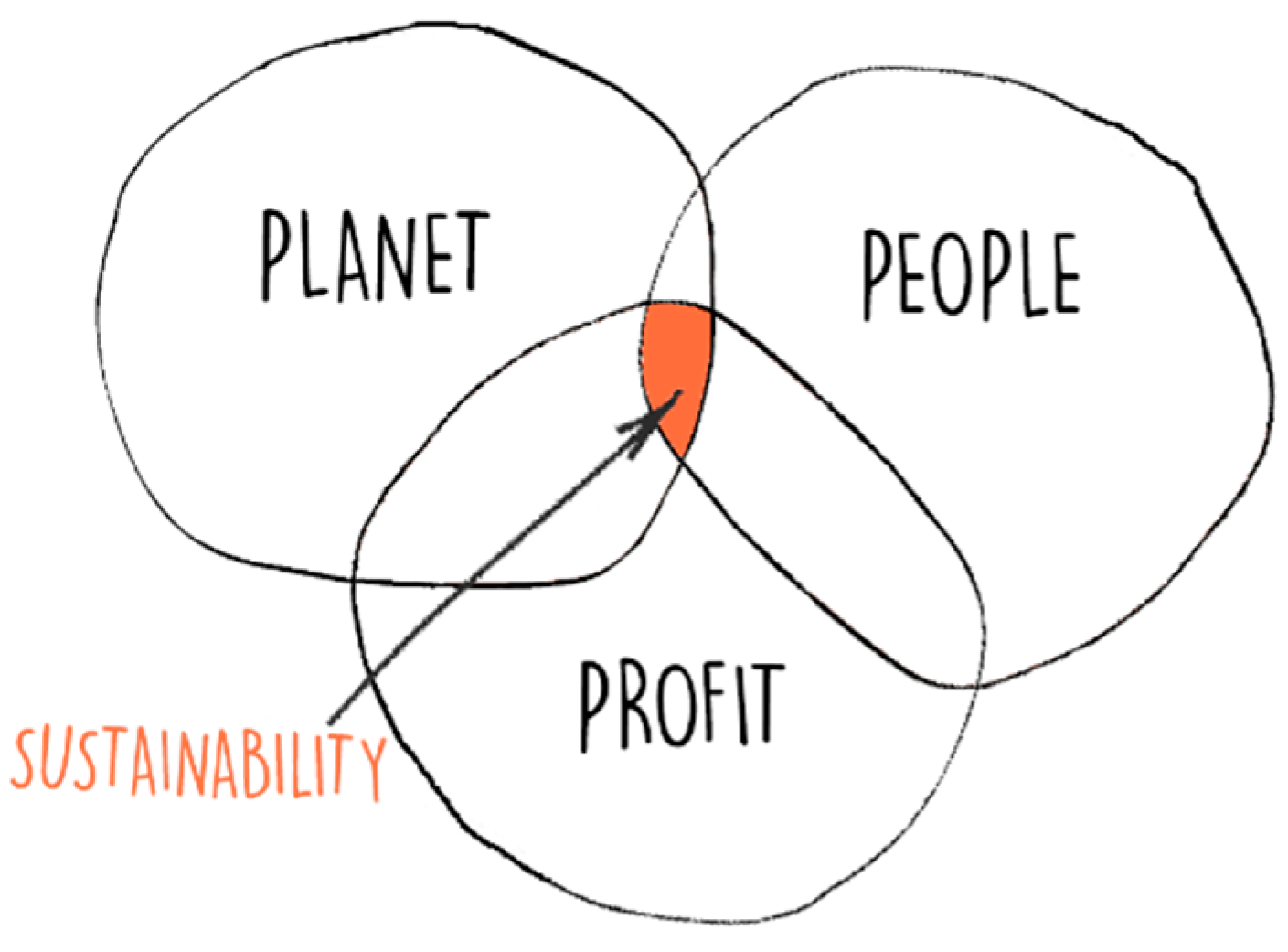

It is important to note that the overarching concept of sustainability, as defined by the United Nations and encapsulated in the 17 Sustainable Development Goals (SDGs). These goals can be summarized as striving to meet the needs of the present without compromising the needs of future generations. When a company incorporates some of these SDGs into its strategy, it is referred to as practicing sustainability. When sustainability is ingrained in a company's strategy, it is commonly referred to as Corporate Social Responsibility or Corporate Sustainability, a framework that encourages businesses to consider the "triple bottom line" – "people, planet, and profit."

Figure 1.

The triple bottom line.

In this article, we choose to use the term CSR to underscore the proactive efforts companies take to not only become more environmentally and socially sustainable, but also to ensure long-term viability and growth.

However, 98% of corporate sustainability initiatives fail, because executives do not have a compelling business case. Executives need compelling ROI information when they assess proposals and that includes non-financial data on sustainability which does not impair the attractiveness of the business case [2].

The P³ calculator invented by Trianon Scientific communication (Trianon) answers that need. It helps executives calculate (statistically) beforehand how much more profitable they could be within 3 years by implementing more sustainable practices in their operations.

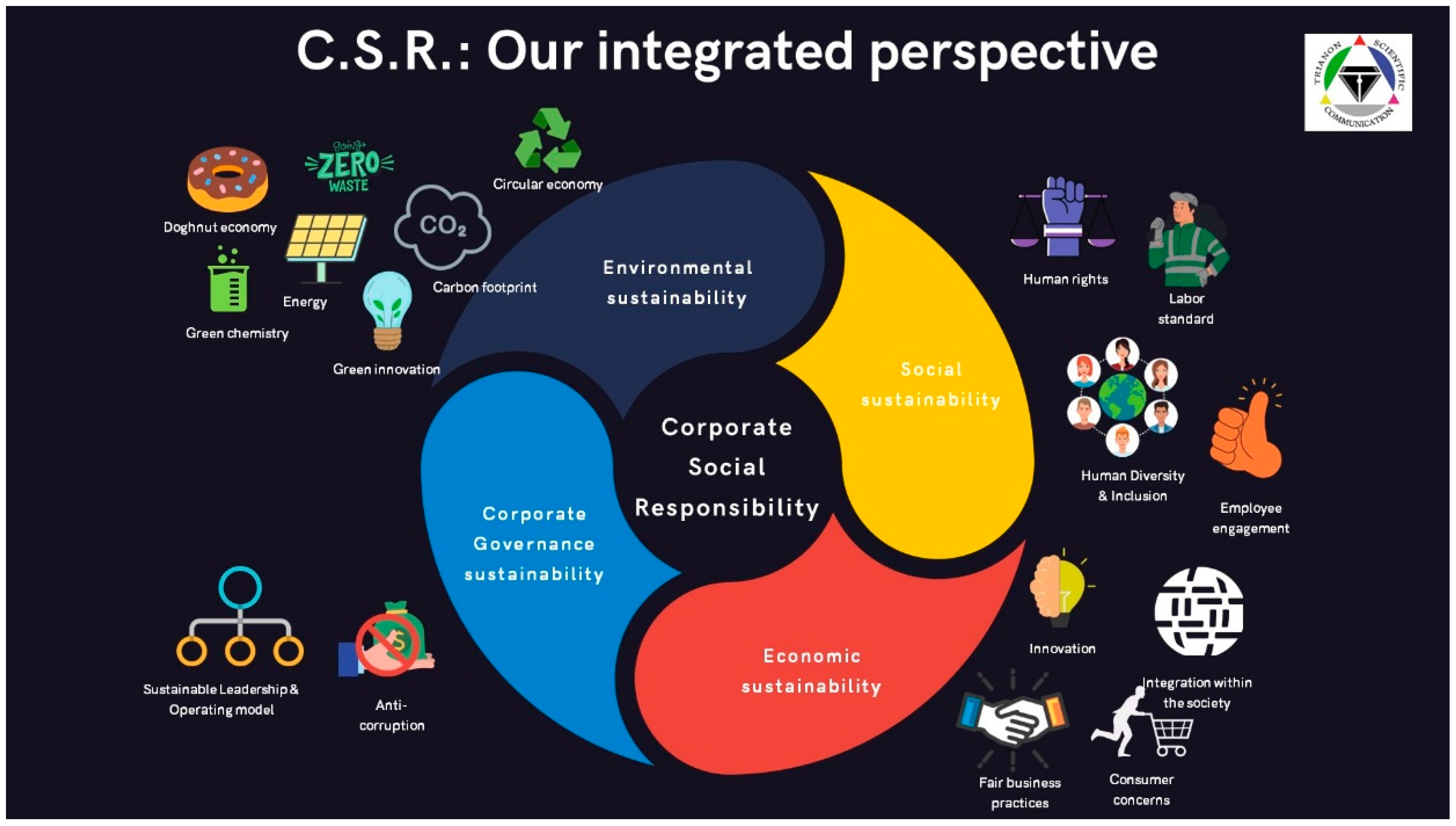

One way sustainability is integrated into cost-benefit calculations, is through the inclusion of externalities. Externalities refer to the costs that are not accounted for in market prices. By considering the environmental and social impacts of an activity, companies can better assess the true costs and benefits of their operations, including potential risks and opportunities.

Figure 2.

An integrated perspective.

2.3. A Practical Example: Interface

There is reliable evidence that quantifies the value of a company integrating CSR and sustainability into its corporate DNA [3]. Interface, a global carpet manufacturing company based in Atlanta (USA) and employing 5000 people, is a good example that profitability and environmental sustainability can go hand in hand. Since 1996, Interface has made remarkable strides in reducing its carbon footprint (74% reduction). They have also managed to minimize greenhouse gas (GHG) emissions at their carpet manufacturing sites by 96% since 1996. An impressive 75% of the energy consumed at their manufacturing sites comes from renewable sources.

Another remarkable aspect of Interface's sustainability efforts lies in their materials sourcing. An impressive 60% of the materials used in Interface carpet tile products come from recycled or bio-based sources.

This commitment to sustainability has been accompanied by great profitability. Only 4 years after starting its sustainability journey, the company witnessed a 66% increase in sales, and a doubling of profits. By successfully reducing waste by 40%, Interface achieved cost savings amounting to $76 million. These cost-saving measures continued to be effective, and the company achieved annual savings of $185.4 million [4].

More is needed, however, to embed and apply the ’sustainability rationale' into the current financial and business logic, considering the IPCC predictions of having 7 years left before the ’point of no return’ will be reached.

To have impact at scale, we see value in challenging (1) the prevalent economic model on which current financial and accounting narratives are based, as well as (2) some of the formulas which are prevalent in our calculations of profit. Our proposed amendments aim to illustrate that it is possible to integrate the 3Ps (People, Planet, Profit) into existing ways of calculating profit, without a complete overhaul.

2.4. Sustainability: A Key Element in Cost/Benefit Calculations

In companies using sustainability approaches, profits improve by up to 80% within 3 to 5 years, just by applying good practices already proven to be efficient in other businesses. The consequences can be seen in:

For each of the categories, depending on the business, there are several ways of capturing savings. Imagine how far a little innovation could take businesses and the economy as a whole!

If companies are not proactively improving their social and environmental impact, the costs will progressively increase, and their profits will decrease by 16 % to 36%.

2.5. Sustainability: 2 Case Studies of Companies That TRIANON Has Worked with

A shoe producer lost money every day because of the amount of waste produced, waste that could be avoided if used more efficiently. Improving the efficiency of the production has brought significant profit. Increasing layout6 optimization thanks to a dedicated software allowed to increase efficiency by more than 10%, save 8% materials, and reduce waste by (70%).

A food company contacted TRIANON because their profits were impeded by the high percentage of products not passing quality control. TRIANON proposed to handle this challenge in a long-lasting way by investing in hiring people from more diverse backgrounds in the production chain. By increasing the inherent (e.g. gender) and acquired (e.g. background, culture) diversity by 15% at every level, the number of products passing quality control increased by 20% in 3 months.

In the first case, the company invested in new software, and training its employees. In the second case, they invested in hiring more diverse workforce. Both did not happen overnight. But putting environmental and social sustainability into the growth strategy of their company brought benefits that persist several years later. It is important to note that the decision to use more environmentally or social practices was directly linked to the company’s existing priorities.

2.6. Sustainability: The Role of Corporate Governance

Corporate governance encompasses the rules, relationships, and practices guiding an organization's direction and control. According to the OECD, it plays a crucial role in enhancing efficiency, fostering growth, and bolstering investor confidence within a company.

Defining corporate governance as the process of decision-making and subsequent implementation, it is obvious that the two above companies have effective governance as they made multiple stakeholders collaborate to find solutions that benefit their respective business success.

Thus, good corporate governance and good CSR strategies are linked. Good corporate governance is essentially built on: economic progress, social development, and environmental improvements. Good governance ultimately fosters sustainability and creates sustainable values. Companies also realize long-term benefits, including risk reduction, attracting new investors and shareholders, and increased equity.

The pursuit of corporate sustainability continually refines and strengthens the principles of good corporate governance. Assessing profitability solely through monthly or quarterly KPIs cannot capture the sustainability ethos in business. Sustainability efforts must be evaluated over the medium to long term for a comprehensive understanding. Investing in sustainability is a long-term investment. The financial balance sheet (the economic bottom line) is only one of the 3 bottom lines (i.e., economic, environmental, and social) that must be considered to have a truly sustainable business. However, balance sheets provide only a snapshot of a company’s financial health. While profitability is essential for the long-term survival and growth of any organization, it alone cannot guarantee sustainability. By focusing solely on financial performance, businesses may overlook their impacts on the environment and society, leading to potential risks and missed opportunities.

Shortism, i.e. focusing on immediate gains while disregarding long-term consequences, poses a significant threat to sustainability. Decision-makers prioritizing short-term profits over the long-term well-being of society and the environment contribute to the depletion of natural resources, exacerbate climate change, and perpetuate social inequalities. To address this issue, financial instruments that embed long-term ESG considerations such as the European Long-Term Investment Fund play a pivotal role, as they embed long-termism and encourage investments that not only generate profits but also create lasting positive impacts. It is crucial that investors find their way to this type of financial instruments in the capital markets. While ESG labels and standards are valuable, we argue below that more could be done to favour long-term prosperity over short-term profitability.

3. Time Value Calculations Can Offer a Different Perspective on Profit

The basis for today's financial decision-making, spanning spending, saving, and investing, stems from centuries-old mathematical formulas, with key contributions by mathematicians like Isaac Newton or Richard Price. The concept of the time-value of money has emerged in the 17th and 18th-centuries and underpins modern financial calculations.

3.1. Proposed Amendment

In the current future-value formula,

where FV denotes “Future-Value”, PV denotes “Present-Value”, “I” means interest rate, and “n” is time. It is thus a method of calculating how much the present value of an asset will be worth at a specific time in the future. The FV is the PV discounted by an interest rate thus equating the buying power in the future with the present.

FV = PV x (1+i)n,

The above formula mainly considers the notion of “interest accruing over time” to determine the value of an investment. No factor in this formula integrates whether the investment will be detrimental to the environment or not.

We find this approach no longer sustainable. Hence, we would like to propose an updated concept; one that mirrors the way in which our language verbalizes the world around us through the past, present, and future tenses of verbs and through its derived form that range from imperfectum to perfectum. From incomplete to complete states of future where you only achieve the desired future outcome by translating that outcome into concrete actions today.

What then is our desired outcome when discussing future value? As our planetary resources are limited, we need to somehow limit our unlimited notion of money, to derive a “present-future-value” (PFV) which allows a comparison between monetary profit and sustainable planetary prosperity, and which somehow takes into account the valid conditions to allow regeneration of our planetary resources.

This is our proposed formula for a present future value:

where  represents the connectivity coefficient which (for the sake of this article) takes values between 0 and 2. 5. There is at present no established mathematical symbol specifically for Urania, hence our suggestion to develop one for the expression of a connectivity coefficient.

represents the connectivity coefficient which (for the sake of this article) takes values between 0 and 2. 5. There is at present no established mathematical symbol specifically for Urania, hence our suggestion to develop one for the expression of a connectivity coefficient.

PFV = [PV x (1+i)n ] x,

,

represents the connectivity coefficient which (for the sake of this article) takes values between 0 and 2. 5. There is at present no established mathematical symbol specifically for Urania, hence our suggestion to develop one for the expression of a connectivity coefficient.3.2. Explanation

The value for should represent the degree to which a company contributes to prosperity. Being value-based, it allows to visualize the change towards sustainability. The connectivity coefficient should also reflect the sincerity of and the trust in the company. This can be reflected through various measures such as: is there a clear and feasible strategy, translated in strategic objectives, a roadmap, KRIs, KPIs, changed processes, monitoring & reporting? Did the required culture shift happen? Is the reporting on strategy, latest position, plans for coming years fully transparent? Are adverse impacts accounted for? Are the numbers auditable and audited, both internally and externally? In such way, a small change in the formula might prove a giant step towards the design of tools that explicitly help achieve directionality with a purpose.

should represent the degree to which a company contributes to prosperity. Being value-based, it allows to visualize the change towards sustainability. The connectivity coefficient should also reflect the sincerity of and the trust in the company. This can be reflected through various measures such as: is there a clear and feasible strategy, translated in strategic objectives, a roadmap, KRIs, KPIs, changed processes, monitoring & reporting? Did the required culture shift happen? Is the reporting on strategy, latest position, plans for coming years fully transparent? Are adverse impacts accounted for? Are the numbers auditable and audited, both internally and externally? In such way, a small change in the formula might prove a giant step towards the design of tools that explicitly help achieve directionality with a purpose.A connectivity coefficient could be described as a new evaluation criterion which is flexible and dynamic rather than a static Cost-Benefit Analysis. Such connectivity coefficients should reflect the company’s expected future positive impact, based on the choices it makes today. ESG elements that ‘drive up’ the connectivity coefficient will become part of the investment process itself. There may be more than one type of connectivity coefficient depending on the type of the desired change. As we would like to support a re-imagination of current formulas, we will limit ourselves to two important streams where we believe connectivity coefficients could have a significant impact: green transition and digitalization. We acknowledge however that more elaborate research and modelling is required to make this proposed conceptual approach implementable. Research is required to identify (1) all possible scenarios where connectivity coefficients could have a positive impact, (2) all possible features that connectivity coefficients should have and (3) all possible values that such coefficients could take. Here we will limit ourselves to 5 possible values of : 0; 0.5; 1; 1.5; 2.

: 0; 0.5; 1; 1.5; 2.3.3. Potential Areas of Application

- -

- Green transition: The connectivity coefficient could be a score which is derived from a company’s ESG rating. A similar logic was applied in the food industry where scores have become ubiquitous to create transparency for consumers regarding the nutritional value of their purchases. A connectivity coefficient of 0 or 0.5 shows that the investment is likely not to generate the desired profit and to even actively contribute to degeneration. A connectivity coefficient of 1 will be neutral. A coefficient between 1 and 2 will visualize the regenerative effect the investment will ultimately produce. Thus, investors will be encouraged to invest in ‘patient financial instruments’, while companies will be motivated to maximize their positive impact.

- -

- Digitalization: Some technologies or investment decisions with regards to technology have a bigger potential to create real-life and sustainable connections than others, hence the type of technology a company is investing in could be a predictor of sustainable profits. This would also relate to deployment of best practices e.g. fostering financial digital inclusion, literacy, or even mental well-being. Companies that make positive and transparent choices in this regard will have a higher PFVs than others and will create not only stable annuity streams for investors, but also a sustainable contribution to prosperity in a mutually beneficial way.

3.4. An Applied Example of the Connectivity Coefficient

Consider this simplified example:

Company A wants to scale up and therefore seeks capital. Company A’s mission is to transform plastic waste into environmental, social, and economic opportunities in Sub-Saharan Africa. As the market leader, this company has successfully developed a plastic recycling and valorization chain. The recycled waste is sold locally and internationally. They create jobs and thus cleaner and safer local communities. In response to growing demand, the company intends to increase its collection capacity. To finance their growth, they recently issued a fixed-interest corporate bond at 8% with a duration of 5 years. For the sake of this example, we assume that Company A has a connectivity coefficient of 1.5. Note that we have yet to determine a calculation method, even though this is the next step to facilitate practical usage of connectivity coefficients.

For an investment of €15,000 with an interest of 8% for 60 months, this will result in a sum / future value (FV) of €22,347.69 and a total interest of €7,347.69.

A nice profit, however, the result will be the exact same profit for investing that amount in ‘Company B’ that cuts trees in tropical rainforests. We assume that Company B does some investments in re-forestation, however, these have thus far provided limited off-setting. Hence, Company B has a connectivity coefficient of 0.5. Calculating PFVs for both companies yields:

PFV of €15,000 for Company A = (22,347.69 x 1.5) = 33,521.535

PFV of €15,000 for Company B = (22,347.69 x 0.5) = 11,173.845

This provides dramatically different results. The PFV reflects that Company A provides the better investment in the long run, regardless of its scale-up nature. By deliberately including prosperity into the equation of time-money value calculations, the degenerating nature of certain investments becomes visible and can be expected to lead to more long-term thinking in financial decisions.

4. Public-Private Partnerships to Increase the Speed of Triple Bottom Line Implementation Strategies in Businesses

4.1. A Mission-Oriented Approach through PPPs

Governments and policy makers are gradually moving away from the narrative to “fix problems or market inefficiencies” to a mission-oriented approach. It means asking what kind of markets we want, rather than what problem in the market needs to be fixed. This is fundamentally different from the market failure theory of Vilfredo Pareto, where government has a limited or even no roll at all in value creation.

A mission-oriented approach requires both the private and the public sector to concentrate attention on the outcome rather than on the scale of the challenge. Missions require long-term thinking and patient finance. Hence, all stakeholders need to focus on what needs doing (rather than what needs fixing) and on how to structure budgets accordingly. In our view, public-private partnerships (PPPs) are essential to organize such “mission thinking” as they represent open, symbiotic, and mutualistic partnerships.

PPPs offer a unique platform for collaboration between government entities, private enterprises, and other stakeholders, pooling their expertise, resources and networks to address complex challenges that extend beyond the traditional financial balance sheet. By engaging in PPPs, companies gain access to a broader range of perspectives and expertise, enabling them to adopt a more holistic approach to decision-making. This broader outlook prompts businesses to consider the long-term consequences of their actions and investments, considering not only immediate financial gains but also the social and environmental implications of their endeavors.

Furthermore, PPPs play a crucial role in reshaping investor perspectives by promoting a more comprehensive evaluation of companies. By integrating the principles of the triple bottom line into their operations and investment strategies, companies and investors can actively contribute to the achievement of the UN SDGs.

One notable example of a mission-oriented approach that exemplifies the power of PPPs is NASA's journey to the moon. During the Apollo missions, NASA collaborated with various private companies to achieve that ambitious goal. Similarly, important IT developments like the internet and successful IT companies like Apple and Microsoft have benefited significantly from public-private partnerships.

4.2. Implementation through the IFRS Standards in Analogy with Food Health Labels

There are already various PPPs where both public and private sector stakeholders co-operate on topics like sustainability disclosures. Especially within corporations, audit and accounting have key roles to steer changes into the corporate governance of a firm in all relevant business practices.

Recently, the International Sustainability Standards Board (ISSB) has proposed to create an International Financial Reporting Standards (IFRS) ‘digital’ Sustainability Disclosure taxonomy.

We propose deriving a connectivity coefficient from the IFRS Accounting Standards and/or Sustainability Disclosure Standards. The approach for a connectivity coefficient could be inspired by the EU’s approach for food health labels. such labels and their corresponding easy-to-interpret values ensure that complex sets of information reach the end-consumer in an easily understood form. In the same way, a connectivity coefficient could appear as an easy-to-interpret value to assess the long-term effects of sustainability-related risks and opportunities. At the same time, an auditable connectivity coefficient would ensure the relevant elements are considered to measure the long-term prosperity of a firm’s investments. Taking it one step further, connectivity coefficients could form an industry basis. There would need to be regulation to ensure that industries do not go beyond their “allowed” connectivity coefficient. Such a practical approach could significantly and rapidly increase our chances of success, as it introduces the desired care into the investment process right at its start.

5. Conclusions

Corporate sustainability is more than a ‘nice to have’. It is an essential way of saving costs, increasing revenues and of making money in a regenerative manner. While the financial balance sheet is undoubtedly a crucial metric for assessing business performance, it is only one piece of the puzzle. To have a truly sustainable business, organizations must embrace the triple bottom line approach, which considers the economic, environmental and social impacts of their operations.

Most business leaders agree that sustainability is key for the future of their company. Nevertheless, in practice, it remains difficult to justify the investment cost based on the current financial metrices. Current CBA or net present value calculations are likely to limit the enthusiasm of any innovative mission. At this pace, Europe will not decrease it emissions by half by 2030 and becoming a continent carbon neutral by 2050 seems less and less reachable.

Hence, more is needed to help companies to visualize the long-term expected benefits of such mission-oriented investments and to support investors in identifying investments that will lead to long-term prosperity. This article provides examples of the former, based on TSC’s experience and its P³ calculator. On the latter, an amendment of time value calculations is being put forward.

Concretely, a new coefficient is introduced in the formula for present value calculations. A so-called “connectivity coefficient” could be described as an evaluation criterion which is flexible and dynamic, and which should help to reflect the company’s expected future positive impact, based on the choices it makes today. The connectivity coefficient could be a key enabler to visualize the benefits of long-term thinking or “patient finance” as compared to a short-term focus on profit. Hence, we introduce the concept and calculation of a Present Future Value (PFV).

Finally, the value of public-private-partnerships is put forward as a key enabler of mission-oriented thinking. Especially in accounting and reporting standards, we believe that a connectivity coefficient could help to demystify complex ESG-related data towards investors, while at the same time providing business leaders with the relevant factor to evidence a compelling ROI on their ESG-related investments.

Let us be clear, being more sustainable is an investment. Have you seen any worthwhile investment giving a return over a short period? So why would you expect sustainability initiatives to do so?

Funding

This article received no external funding.

Institutional Review Board Statement

Not applicable.

Acknowledgments

We would like to thank the following contributors and reviewers of this article:

- -

- John Bendermacher, President of the European Confederation of Institutes of Internal Auditing, Chief Internal Auditor at Euroclear

- -

- Pascale Vandenbussche, Secretary General of the European Confederation of Institutes of Internal Auditing

- -

- Prof.Dr.Mark Coeckelbergh, Professor of Philosophy of Media and Technology at the University of Vienna

- -

- Younes Ouassini, Data Analytics Expert at Euroclear, European Executive MBA student at Vlerick Business School

- -

- Tino Chibebe, MSc, International and Sustainable Finance, Founder of Azteq, Board Member of #SheDIDIT

The thoughts expressed in this article are entirely our own. Any resemblance with existing work is coincidental, although we explicitly acknowledge and thank the authors of below works as sources of inspiration:

- -

- Coeckelbergh, M. (2022). Self-improvement. Technologies of the soul in the age of artificial intelligence. Columbia University Press, New York.

- -

- Goldstein, J. (2021). From Bronze to Bitcoin, the True Story of a Made-up Thing. Atlantic Books London.

- -

- Gorissen, L. (2020). Building the Future of Innovation on million years of Natural Intelligence. StudioTransitio.

- -

- Levitt, S.D., & Dubner, S.J. (2006). Freakonomics. Harper Trophy.

- -

- Mazzucato, M. (2021 ). Mission Economy: a moonshot guide to changing capitalism. Allen Lane.

- -

- Raworth, K. (2017). Doughnut Economics. Seven Ways to Think Like a 21st-Century Economist. Random House.

Conflicts of Interest

The authors declare no conflicts of interest.

References

- Travelperk.com. 60+ Business sustainability statistics (relevant in 2024). Available online: https://www.travelperk.com/blog/business-sustainability-statistics/ (accessed on 8 June 2024).

- Bain.com. Achieving Breakthrough Results in Sustainability. Available online: https://www.bain.com/insights/achieving-breakthrough-results-in-sustainability (accessed on 8 June 2024).

- Hung-Yu Chen, Ming-Chin Lin & Zong-Han Lin (2024) Do corporate social responsibility activities enhance firm value? An empirical evidence from Taiwan, Cogent Economics & Finance, 12:1, 2344228. [CrossRef]

- United Nations Climate Change. Unfcc.com. From Mission Zero to Climate Take Back: How Interface is Transforming its Business to Have Zero Negative Impact | Global. Available online: https://unfccc.int/climate-action/momentum-for-change/climate-neutral-now/interface (accessed on 8 June 2024).

- Average numbers from Trianon Scientific Communication for companies (6-4000 FTE) having a revenue from 1M€ - 500,000,000 M€.

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Copyright: This open access article is published under a Creative Commons CC BY 4.0 license, which permit the free download, distribution, and reuse, provided that the author and preprint are cited in any reuse.