Submitted:

18 August 2024

Posted:

19 August 2024

You are already at the latest version

Abstract

Scholars in the field of environmental economics have extensively examined the relationship between foreign direct investment (FDI) and economic growth. However, they have often failed to consider the crucial roles played by technological innovation and financial development in determining environmental costs. The rapid economic growth and urbanization witnessed in BRICS countries have led to a substantial increase in energy demands, resulting in significant environmental degradation. This study aims to investigate the impact of financial development (including measures such as broad money, domestic credit to the private sector, FDI, and green technological innovation) on carbon emissions in BRICS countries using data from 2001 to 2023. The results of the study demonstrate a strong cross-sectional dependence among the countries in the panel. The Augmented Mean Group (AMG) estimator reveals a negative and statistically significant long-term relationship between broad money, FDI, green technological innovation, and CO2 emissions. On the other hand, domestic credit to the private sector shows a positive and significant association with carbon emissions. To determine the direction of causality, the study utilizes the Dumitrescu and Hurlin panel causality test. The findings indicate a non-directional long-term causality between financial development and CO2 emissions. However, a unidirectional causality is observed between green technological innovation and carbon emissions. Based on these findings, the study suggests that the development of industries, financial institutions, and technological innovation is crucial for attracting high-quality FDI in BRICS countries. However, it also highlights the significant contribution of these developments to environmental degradation, necessitating urgent policy responses.

Keywords:

Broad Money

; Green technological innovation

; Augmented Mean group

; Environmental Quality

1. Introduction

Environmental quality has become a pressing global issue as nations grapple with the dual challenges of economic development and environmental sustainability. The quest for economic growth has historically been accompanied by increased environmental degradation, manifesting in pollution, resource depletion, and climate change. However, the advent of green technological innovation and the strategic development of financial sectors offer potential pathways to mitigate these adverse impacts while promoting sustainable development. The relationship between economic growth and environmental quality is often described by the Environmental Kuznets Curve (EKC) hypothesis. The EKC suggests an inverted U-shaped relationship between per capita income and environmental degradation: as an economy grows, environmental degradation initially increases, reaches a peak, and then declines as income continues to rise and cleaner technologies are adopted (Grossman & Krueger, 1995). In China, financial development indirectly affects environmental pollution through various pathways, with different impacts in regions of low and high financial development (Xu et al., 2021). In Iran, financial development accelerates environmental degradation, while trade openness reduces environmental damage (Esmaeilpour & Lotfalipour, 2014). However, a global study of 131 countries found that financial development indicators significantly improve environmental quality by reducing ecological footprint (Majeed & Mazhar, 2019). Conversely, research on emerging and growth-leading economies (EAGLEs) demonstrates that overall financial development, including its depth, access, and efficiency dimensions, significantly reduces environmental quality (Khan et al., 2023). These conflicting findings highlight the need for tailored environmental protection policies that consider regional financial development characteristics and the complex interplay between financial development and environmental quality. Recent studies have examined the complex relationships between financial development, economic growth, globalization, and environmental quality. Financial development has been found to have an inverted U-shaped relationship with economic growth, initially promoting growth but potentially slowing it at higher levels (Li et al., 2015). This hypothesis underscores the importance of technological advancement and policy interventions in breaking the link between economic growth and environmental harm. Financial development refers to the growth and maturation of financial institutions, markets, and instruments that facilitate investment and economic activity. A well-developed financial system can influence environmental quality in several ways. Firstly, it provides the necessary capital for investments in environmentally friendly technologies and projects. Secondly, it enhances the efficiency of resource allocation, ensuring that investments are directed towards sustainable and productive uses. Thirdly, financial markets can incentivize firms to adopt greener practices through mechanisms such as green bonds and environmental, social, and governance (ESG) criteria. A burgeoning body of various suggests that financial development can have both positive and negative impacts on environmental quality. On the positive side, access to finance can enable firms to invest in cleaner technologies and adopt sustainable practices (Shahbaz et al., 2016). Conversely, increased financial activity can also lead to higher levels of consumption and industrial activity, which may exacerbate environmental degradation if not properly managed (Zhang, 2011). The net effect of financial development on environmental quality thus depends on a variety of factors, including regulatory frameworks, market incentives, and the overall structure of the financial system. Green technological innovation involves the development and implementation of new technologies that reduce environmental impacts and promote sustainability. These innovations span various sectors, including energy, transportation, manufacturing, and agriculture. Examples include renewable energy technologies, energy-efficient appliances, waste reduction techniques, and sustainable agricultural practices. The role of green technological innovation in enhancing environmental quality is well-documented. Innovations in renewable energy technologies, such as solar and wind power, have significantly reduced greenhouse gas emissions and dependence on fossil fuels (IRENA, 2020). Similarly, advancements in energy efficiency technologies have lowered energy consumption and reduced environmental footprints across industries (Jednak, et. Al., 2020). Moreover, green innovations often lead to cost savings and increased competitiveness for firms, creating a win-win situation for both the economy and the environment. The interaction between financial development and green technological innovation is a critical area of interest for policymakers and researchers alike. Financial development can facilitate green innovation by providing the necessary funding and investment opportunities for research and development (R&D) activities. Furthermore, financial institutions can play a pivotal role in supporting green startups and scaling up environmentally friendly technologies. Conversely, green technological innovation can influence financial markets by creating new investment opportunities and altering risk perceptions. For instance, the rise of green bonds and ESG investing reflects a growing recognition of the financial value of sustainability. Additionally, green technologies can mitigate environmental risks that could otherwise impact financial stability, such as those associated with climate change and resource scarcity. financial development leads to environmental degradation, while others suggest it can improve environmental outcomes through green investments and sustainable practices. For instance, research by (Nguyen, et al., 2024) states that the relationship between financial development and environmental pollution is an inverted U-shape in low-income countries, but not in middle-income countries. (Ruza & Caro-Carretero, 2022) indicates that the relationship between financial development and environmental degradation is non-linear, with financial development initially increasing emissions but then decreasing them after a certain threshold.—The relationship between financial development and different greenhouse gas emissions (CO2, methane, nitrous oxide) varies, with an inverted U-shaped relationship for methane emissions but a U-shaped relationship for CO2 emissions. (Xu, et. al., 2021) clearly states that financial development has different indirect impacts on environmental quality depending on the level of financial development in the region. In regions with poor financial development, financial development can indirectly increase environmental pollution by stimulating economic growth and industrial development. In regions with high financial development, financial development has mixed effects it can both improve and worsen environmental quality through different pathways. This gap underscores the need for more comprehensive studies that consider a broader range of variables and employ sophisticated analytical techniques. The relationship between financial development, green technology innovation and environmental quality has become a focal point of research in recent years, reflecting the growing concerns over the sustainability of economic growth. This research aims to examine how financial development, including metrics such as broad money, domestic credit to the private sector, foreign direct investment (FDI), and green technological innovation, influences carbon emissions in BRICS countries using data from 2001 to 2023. The findings reveal a significant cross-sectional dependence among the countries in the panel. The structure of the paper is as follows: Section 2 reviews the empirical literature on the relationship between financial development and carbon emissions. Section 3 details the research data definitions and the empirical methodologies used in this study. Section 4 presents the empirical results, and Section 5 concludes the paper.

2. Review of Literature

This review of literature aims to synthesize existing research on the impact of financial development and green technological innovation on environmental quality, highlighting key findings, methodologies, and theoretical perspectives.

2.1. Financial Development and Environmental Quality

Environmental sustainability has become an increasingly pressing concern, capturing the attention of scholars. This heightened interest has led to the development of a broader spectrum of empirical research. The ecological footprint (EF) is a popular metric for measuring impact on the environment. Several recent research projects have investigated what causes ecological footprints to grow or shrink. Urbanization, renewable energy, resource extraction, and technical progress are some of the aforementioned variables (Sharif, et al., 2022; Yasin et. al., 2023). The development of new technologies, as well as the creative use of existing technology, are included in technological innovation. Ahmad et al. (2023) state that this entails creating innovative ideas, creating and executing new patents, and altering how things are produced. Technological innovation is thought to be a crucial solution to environmental problems. It can reduce carbon dioxide emissions by using a variety of techniques. These include carbon absorption in photosynthetic processes in biomass systems, carbon storage in fossil fuel infrastructure, and energy storage device use in power production. In addition, there are several ways in which green technology might influence environmental pre-eminence. As technology continues to progress, scientists and policymakers are starting to see the value of technological innovation in reducing CO2 emissions, (Ahmad et al. 2023; Razzaq, et al., 2023). Similarly, Islam et al. (2023) found that TI negative shock can raise CO2 emissions.

The BRICS nations—Brazil, Russia, India, China, and South Africa—have experienced significant financial growth in recent years. However, this rapid development has bad environmental consequences, mainly in terms of increased carbon emissions. Researchers have been investigating the bond between financial development and carbon emissions in these countries. The Environmental Kuznets Curve (EKC) hypothesis posits that the relationship between financial development and CO2 emissions is characterized by an inverted U-shape (Castiglione, et al., 2012). However, more recent studies suggest that this relationship is more complex and may depend on factors such as a country’s stage of development and its economic structure (Apergis and Payne, 2014). Research indicates that financial development can contribute to higher carbon emissions in BRICS nations. For instance, (Shahbaz et al. 2019) observes that financial development leads to increased carbon emissions in Brazil, Russia, and South Africa. Similarly, (Zhang et al. 2021) observed this relationship in China and India. Because financial development often results in greater energy consumption, industrialization, and economic growth, all of these contribute to higher carbon emissions.

Some studies have revealed a more nuanced relationship between financial development and carbon emissions. For example, (Dong et al. 2019) found that financial development in China can reduce carbon emissions by encouraging clean energy and decreasing energy intensity. Similarly, (Bhattacharya et al. 2019) observed that in India, financial development can lower carbon emissions by promoting sustainable energy and reducing carbon intensity.

Researchers have also examined the impact of carbon emissions on financial development in BRICS countries. (Khan et al. 2020) found that carbon emissions can hinder financial development in Brazil, Russia, and South Africa by slowing economic growth and exacerbating environmental degradation. Conversely, (Li et al. 2020) discovered that in China and India, carbon emissions can actually stimulate financial development by driving investment in clean energy and reducing carbon intensity. There is constant debate among scholars regarding the role of financial development in promoting a low-carbon economy. Some argue that financial development suppresses CO2 emissions, a perspective supported by (Aluko et al. 2020) identify that financial development is inversely correlated with CO2 emissions in 35 sub-Saharan African countries. Their research indicates that a 1% increase in financial development could reduce CO2 emissions by 2.743%. (Nosheen et al. 2020) conducted a study on 11 Asian countries and found that financial development positively impacts economic growth while negatively impacting CO2 emissions. They concluded that financial development helps investors and companies obtain credit for environmentally friendly technologies. (Odhiambo’s 2020) research on 39 sub-Saharan African countries also suggested that financial development reduces CO2 emissions unconditionally on the other hand, some argue that financial development promotes CO2 emissions. (Raghutla et al.2024) found that financial development and technology can help BRICS economies reduce CO2 emissions and improve environmental quality over the long term. (Umar et al.2020) used data from China and found that from 1975 to 1983, financial development significantly reduced CO2 emissions. However, (Nasir et al. 2021) analyzed Australia’s industrialization and concluded that financial development is related to CO2 emissions, with a short-term two-way causal relationship between economic growth and CO2 emissions. They suggested that long-term financial development might positively impact CO2 emissions. Financial development fosters innovation, leading to environmentally sustainable technologies, especially in the energy sector (Álvarez-Herránz et al. 2017; Duque-Grisales et al. 2020; Ozcan et al. 2020). It promotes technological advancements through new products or processes that reduce emissions and energy consumption (Birdsall and Wheeler 1993; Abbasi & Riaz 2016; Law et al. 2018). However, increased investment through financial development can also elevate energy consumption, adversely affecting the environment (Jensen 1996; Ogbeifun&Shobande 2022). Financial and economic growth attracts Foreign Direct Investments (FDI) and Foreign Institutional Investments (FII) to emerging economies like India (Gandhi et al. 2013; Dhingra et al. 2016). FDI enhances technology transfer, expertise, and green technology adoption, reducing carbon footprints (Pantelopoulos 2022). this comprehensive review of literature studies serves as a crucial step in identifying and formulating hypotheses that are well-supported by existing research. These hypotheses can then guide future empirical investigations, contributing to a deeper understanding

2.2. Green Technological Innovation and Environmental Quality

Green technological innovation is pivotal for achieving sustainable environmental outcomes. Innovations in green technology encompass a wide range of developments, including renewable energy technologies, energy-efficient processes, and pollution control mechanisms. The literature consistently highlights the beneficial effects of green technological innovation on environmental quality. For example, Popp (2019) argues that technological advancements in renewable energy significantly reduce greenhouse gas emissions and reliance on fossil fuels. Additionally, Jaffe and Stavins (1995) found that innovations in energy-efficient technologies lead to substantial reductions in energy consumption and pollution levels. The effectiveness of green technological innovation in improving environmental quality can be influenced by various moderating factors. According to Horbach et al. (2012), the regulatory environment plays a critical role in determining the adoption and impact of green technologies. Their study suggests that stringent environmental regulations spur innovation and lead to better environmental outcomes.

The World Bank has long maintained that economic growth increases per capita income, reduces poverty, and enhances environmental quality. Manufacturers with insightful knowledge and recognition invest more in developing environmentally friendly technologies, positively impacting CO2 emissions and reducing environmental contamination (Sun, et. al. 2023). Conversely, economic growth can increase production and consumption, putting more pressure on environmental resources and causing harm (He, et al., 2024; Li, & Li, (2022).), positive innovations in financial systems, such as market expansion, risk minimization, product and process innovations, investment diversification, optimal resource allocation, and increased research in financial systems, have been shown to positively impact the environment (Chishti and Sinha 2022). Numerous studies indicate that capital markets, a key component of financial development, reward firms with higher equity valuations for strong environmental performance (Chishti, et al., 2023). Consequently, countries with well-developed financial markets tend to benefit from better environmental quality (Dasgupta et al. 2001; Zhang 2021; Majeed and Mazhar 2019).

However, there are opposing viewpoints. Increased credit facilities through financial development can lead to higher consumption of automobiles, electronic gadgets, and machinery, which negatively impacts the environment. Additionally, credit provided for business expansion, new technological innovation machinery replacement, or new plant purchases can raise CO2 levels in a country (Zhang, et l., 2021).

The relationship between carbon emissions and financial development in BRICS nations is complex and multifaceted. While financial development can lead to higher carbon emissions, it can also support sustainable energy initiatives and reduce carbon intensity. Similarly, carbon emissions can both hinder financial development and encourage investment in clean energy and environmental improvement. Further research is necessary to fully understand this relationship and to develop policies that support sustainable financial development in BRICS nations. There are many studies that offer a contradictory support about the Environmental Kuznets Curve (EKC) hypothesis, showing both positive and negative relationships among financial expansion and carbon emissions across different settings. For instance, research by (Shahbaz et al. 2019) and (Zhang et al. 2020) suggests that financial development leads to increased carbon emissions in BRICS nations. In contrast, (Dong et al. 2020) and (Bhattacharya et al. 2019) disagree that financial development can actually lead to reduced emissions by promoting technological progress.

Environmental quality in BRICS countries (Brazil, Russia, India, China, and South Africa) has been a focal point in global discussions due to their significant economic growth and substantial environmental footprint. While numerous studies have explored the impact of financial development and green technological innovation on environmental quality individually, there remains a notable gap in integrated research that comprehensively examines their combined effects within these emerging economies. Most existing literature primarily focuses on developed nations or treats financial development and green innovation as isolated factors. Moreover, the interplay between financial systems and green technologies in fostering sustainable development within the unique socio-economic contexts of BRICS countries has not been adequately addressed. The varying stages of economic development, regulatory frameworks, and technological advancements in these countries necessitate a nuanced analysis that captures their distinctive characteristics and interdependencies.

H1.

Financial Development Positively Affects Environmental Quality

H2.

Green Technological Innovation Positively Affects Environmental Quality

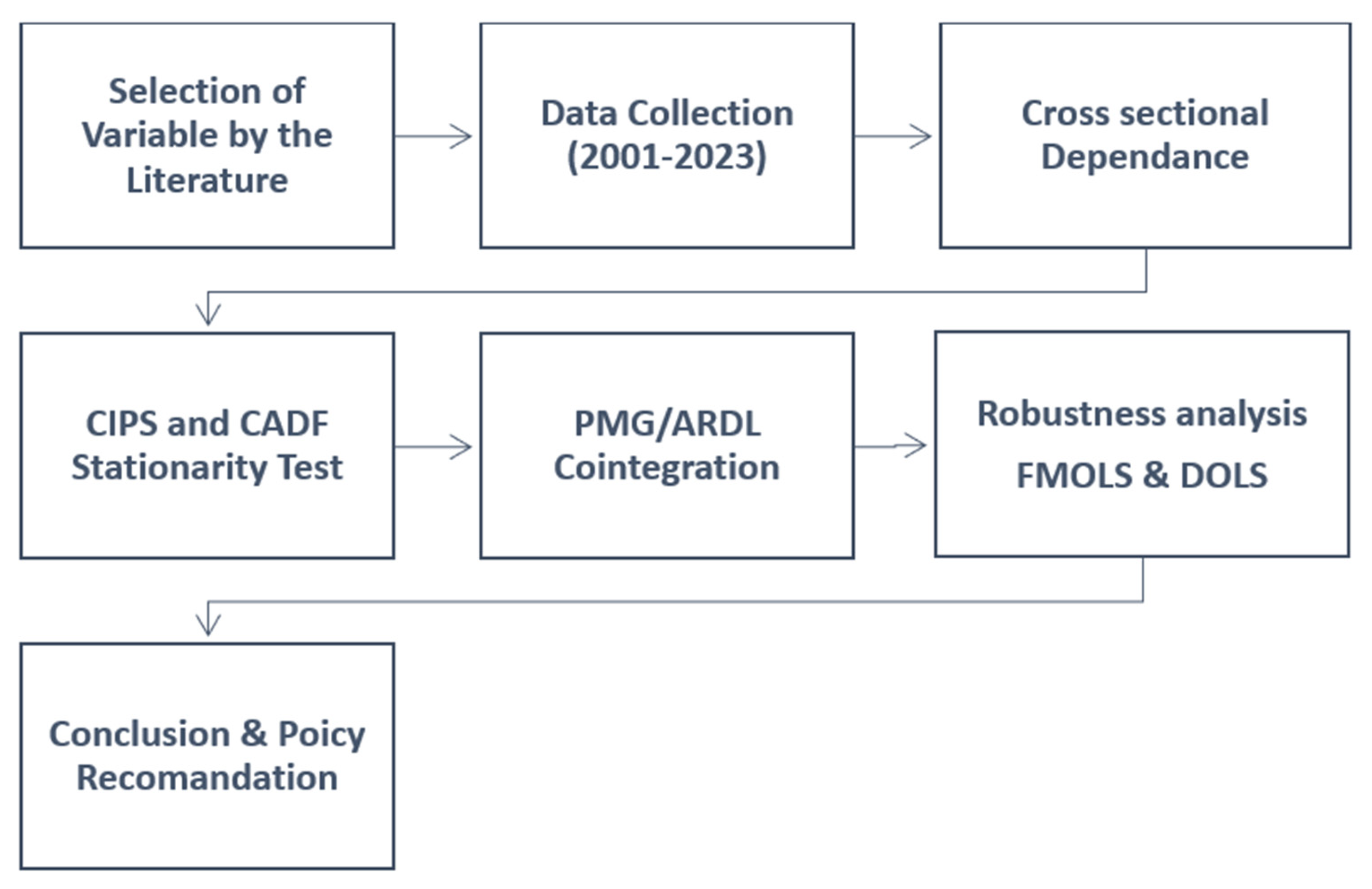

3. Research Methodology

3.1. Data

The objective of this research endeavour is to examine the relationship and how financial development and green technology adoption, collectively influence the carbon emissions of the BRICS countries. The empirical investigation utilized panel data spanning from 2001 to 2023 and employed robust econometric methodologies. A detailed analysis of the data is presented in Table 1 below

3.2. Empirical Model

The relationship between how financial development and green technology adoption, collectively influence the carbon emissions of the BRICS countries can be expressed in a functional form in Equation (1) as follows.

Initially, we calculate the multiple linear regression models, which can be represented as follows.

Equation (2) represents the multiple linear regression model, where CO2 denotes the Carbon emission, BM stands for Broad money, DCPS, domestic credit to private sector FDI represents the Foreign direct investment, and GTI, stand for green technological innovation. The coefficients of control variables are represented by the symbol α, whereas signifies the error term. As ARDL serves as the final estimation strategy, Equation (2) can be re-expressed as:

Equation (3) employs the “Δ” symbol to signify the difference operator. The coefficients α1 to α3 pertain to explanatory variables, while β1 to β4 represent control variables in the long term. Additionally, in the ARDL framework, coefficients are estimated for the short run as well. Thus, γ1 to γ3 denote the short-run estimation coefficients for explanatory variables.

3.3. Econometric Methodology

The aims of this paper are to explore the how financial development and green technology adoption, collectively influence the carbon emissions of the BRICS countries. The paper used linear and nonlinear autoregressive distributed lag (ARDL) approaches to explore these associations. The results of the Westerlund co-integration show long-run co-integration between the load capacity factor and the independent variables. The investigation focuses on BRICS countries over the period spanning from 2001 to 2023. The research methodology involves several steps: first, assessing the homogeneity of slopes; second, examining cross-sectional dependence in panel data; and third, applying a panel co-integration test. Subsequently, based on the outcomes of these tests, the study selected the econometric model and estimation approach, leading to an analysis of the long-term causal relationships among the variables.

3.3.1. The Slope Homogeneity Test

The issue of varying slopes holds significant relevance in panel data econometrics. We examine slope heterogeneity by employing the Pesaran, & Yamagata (2008) to address this concern. This test assesses slope heterogeneity by analysing the dispersion of the weighted slope for each individual. The test statistics are determined through the following equations.

3.3.2. The Cross-Section Dependence Test

To assess cross-sectional dependence, we utilized the CD test Pesaran, (2015). The test statistics are presented as follows:

3.3.3. Unit Root Test

The well-known first-generation unit root tests such as the Augmented Dickey-Fuller (ADF), Phillips-Perron, Breitung, Maddala, and Hadri tests are widely utilized in econometrics. However, they are not suitable when dealing with issues like (CSD) and (SH) in the data. These problems can undermine the reliability of the results obtained from these traditional tests.

In light of these challenges, a second-generation unit root test known as the Cross-Sectional (CIPS) and the Cross-Sectional (CADF) test, as proposed by (Pesaran, 2007), come into play. These advanced tests are designed to assess the stationarity of variables in panel data, even in the presence of Cross-Sectional Dependence and Slope Heterogeneity. Equation (5) outlines a crucial step in the CIPS test, which involves calculating the cross-sectional mean of “ti.” This mean calculation is a fundamental component of the CIPS test, serving as part of the procedure to determine the stationarity of variables while accounting for the challenges posed by Cross-Sectional Dependence and Slope Heterogeneity.

The Cross-Sectional Augmented Dickey-Fuller (CIPS) test has been gaining appeal in the academic sphere due to its effectiveness in addressing issues related to Cross-Sectional Dependence (CSD) and heterogeneity. In this method, the baseline hypothesis revolves around the unit-root test. If test indicates the variable exhibits stationarity at I (I), it signals the need to proceed with a cointegration test before delving into parameter estimation. To facilitate the CIPS test, the Cross-Sectional Augmented Dickey-Fuller (CADF) method is employed to calculate the necessary statistics. Conversely, Equation (6) for CADF, which stands for Cross-Augmented Dickey-Fuller, can be expressed as follows:

This equation forms the foundation for the Cross-Sectional Augmented Dickey-Fuller Test method, enabling researchers to obtain the essential statistics used in the CIPS test, where Yt-1 and ΔYit-1 are at level (I (0)) and first difference (I (I) of each cross-sectional series.

3.3.4. Co-Integration Test

The examination of cointegration holds significant importance in econometric literature, given that many assumptions in economic theories pertain to long-run implications. Consequently, this study explores the existence of a long-run relationship among integrated series. Given the presence of cross-sectional dependency, the Westerlund, (2008) is employed due to its capability to yield robust and reliable results, as indicated by Pesaran, (2015). The Westerlund cointegration test outperforms conventional cointegration tests by effectively addressing cross-sectional dependence. One notable advantage of this test lies in its utilization of the bootstrap approach technique, which is particularly effective in accommodating cross-sectional dependence. The second-generation Pesaran, (2015), typically comprises four eqations, represented as Equations (7)–(10). These equations serve as the foundation for conducting cointegration analysis in scenarios where panel data exhibits complex characteristics such as cross-sectional dependence, heterogeneity, and non-stationarity.

In the realm of statistical analysis for panel data, there are several sorts of group means statistics represented as Gt and Ga, as well as panel means statistics denoted as Pt and Pa. Each of these statistical measures serves specific purposes and is abbreviated accordingly. When we assume that the model variables are independent, often called the “null” hypothesis, and the alternative hypothesis suggests the existence of co-integration among the variables, we calculate test statistics for this purpose. These statistics help us determine whether the data provides evidence for the presence of these co-integrating relationships or if the null hypothesis of no relationship between the variables holds. Essentially, these statistics are essential for assessing the strength and significance of potential co-integration among the variables being studied.

In this research, the robustness of the estimation outcomes obtained through the ARDL method was verified by conducting FMOLS and DOLS tests. Additionally, panel causality testing was conducted to explore the causal relationships among the variables. For this purpose, the DHC test was employed, which is a variation of the Granger causality test specifically designed for heterogeneous panel datasets with fixed coefficients (Ahmed et al., 2022). The DHC test utilizes the Zbar test to assess normal distribution and the Wbar test to evaluate the mean (Dumitrescu and Hurlin, 2012). It is represented by the following equation:”

where j represents the lag length and represents the autoregressive parameters.

The null hypothesis and the alternative hypothesis of this test are as follows:

In this analysis, we utilize the panel ARDL model to estimate the regression. The choice of employing the panel ARDL as an estimation strategy steps from preliminary statistical assessments, particularly testing of unit root, to check the stationarity of the selected series. This study conducts unit root tests including the Im, Pesaran, and Shin W-stat (Im et al., 2003), as well as Augmented Dickey-Fuller (ADF) test, which is introduced by Dickey & Fuller, (1979), and present the results in Table 5. The statistical analysis reveals a mixed trend of stationarity, with some series exhibiting stationarity at level I(0) while others show stationarity at the first difference I(1). Given this mixed trend of stationarity, we opt for the panel ARDL approach for regression analysis. The ARDL model is well-suited to handle different levels of stationarity, cointegration, and endogeneity. Additionally, (Farooq, et al. 2024) demonstrates that the panel ARDL model can provide efficient estimates even with small sample sizes. By incorporating lags, the ARDL model effectively mitigates endogeneity issues. This modelling approach has also been utilized by (Khan et al. 2022) in examining similar sets of variables.

Furthermore, to certify the robustness of the findings, this study employs the fully modified OLS and dynamic OLS models which is used in earlier studies by (Shahbaz, 2009; Priyankara, 2018; Khan et al., 2019; Olofin et. al., 2019; Olorogun, 2023; Ramirez, 2023) These models also facilitate long-run estimation of coefficients, thereby enhancing the reliability of our findings.

Figure 1.

Framework of analysis.

4. Results and Discussion

4.1. Descriptive Statistics on Study Variables

The Table 2 provided outlines various statistical measures for five variables: LCO2 (likely referring to log-transformed CO2 emissions), LBM (log-transformed broad money), LDCPS (log-transformed domestic credit to the private sector), LFDI (log-transformed foreign direct investment), and LGTI (log-transformed green technology innovation). Key metrics include the mean, median, maximum, minimum, standard deviation, skewness, and kurtosis. The mean values show LCO2 at -1.55, indicating an overall negative average, while the other variables have positive means, with LGTI highest at 9.45. Medians are close to their means, indicating relatively symmetric distributions. However, LCO2 is negatively skewed, suggesting a longer left tail, while LGTI shows positive skewness, indicating a longer right tail. Kurtosis values around 3 indicate that the variables are fairly close to a normal distribution, though LCO2 shows lower kurtosis at 2.09.

4.2. Correlation between Variables

The correlation matrix reveals positive correlations between LCO2 and both LBM and LDCPS, with values of 0.55 and 0.56, respectively. Conversely, LCO2 has a negative correlation with LFDI at -0.45. LBM and LDCPS are highly correlated at 0.93, suggesting a strong relationship between biomass and domestic credit. The Figure 2 suggests that while CO2 emissions are linked to broad money and domestic credit to private sector, they inversely relate to foreign investment, highlighting complex interdependencies among economic and environmental factors.

4.3. The Slope of Heterogeneity Test

Table 3 shows the results of the slope homogeneity test, which follows the methodology outlined.The test results reveal a problem with heterogeneity in the model, meaning that the coefficients are not consistent and vary across different countries. This variability in slopes indicates that the relationship between the variables differs from one country to another.

By rejecting the assumption that slopes are homogeneous (i.e., consistent across all countries), the findings suggest that applying a panel causality analysis under the assumption of homogeneous slopes could lead to incorrect conclusions. In other words, assuming that the effect of the independent variable on the dependent variable is the same for all countries may not be accurate and could result in misleading interpretations of the data. This highlights the importance of accounting for these differences to ensure more accurate and reliable analysis.

Table 4 displays the results of the Pesaran (2015) CD test, which checks for cross-sectional dependence in panel data. The results show that cross-sectional dependence exists, meaning that the data points across different sections (e.g., countries) are correlated and not independent of each other. Given the presence of both slope heterogeneity (as identified in Table 3) and cross-sectional dependence, it is crucial to use analytical methods that address these issues. To properly analyze the data, we will utilize second-generation panel unit root tests and cointegration methods. These advanced methods are designed to handle the complexities introduced by both varying slopes and interdependencies across different sections of the panel data, ensuring more accurate and robust results.

The next phase of the research involves ensuring the proper sequence for integrating multiple datasets. Table 5 shows the results from the CIPS, CADF, and Levin panel unit root tests. These tests reveal that some variables are stationary at their levels, indicated as I(0), while others are stationary only after first differencing, indicated as I(1). Due to the mixed integration properties of the variables, where some are I(0) and others are I(1), we use both linear and nonlinear ARDL (Autoregressive Distributed Lag) cointegration methods. These methods allow us to accurately analyze the relationships between the variables despite their different levels of integration, ensuring robust and reliable results in our analysis.

Table 5.

Unit Root Test.

| Cross Section ally Augmented IPS (CIPS) | |||||

| Level | First Difference | ||||

| Variable | Statistics | Prob. | Statistics | Prob. | Decision |

| LCO2 | 1.58 | 0.94 | -3.37*** | 0.00 | I(0) |

| LBM | 0.11 | 0.54 | -8.26*** | 0.00 | I(I) |

| LDCPS | -1.73** | 0.04 | -10.99*** | 0.00 | I(0) |

| LFDI | -2.20 | 0.01 | -6.96*** | 0.00 | I(I) |

| LGTI | 1.21 | 0.11 | -3.91*** | 0.00 | I(I) |

| Cross Section ally Augmented CADF (CADF) | |||||

| Level | First Difference | ||||

| Variable | Statistics | Prob. | Statistics | Prob. | Decision |

| LCO2 | 3.55 | 0.96 | 31.20*** | 0.00 | I(0) |

| LBM | 9.20 | 0.90 | 92.51*** | 0.00 | I(I) |

| LDCPS | 22.93 | 0.01 | 35.11*** | 0.00 | I(0) |

| LFDI | 20.86 | 0.02 | 60.77*** | 0.00 | I(I) |

| LGTI | 15.60 | 0.10 | 37.21*** | 0.00 | I(I) |

| Cross Section Levin et al. (2002) | |||||

| Level | First Difference | ||||

| Variable | Statistics | Prob. | Statistics | Prob. | Decision |

| LCO2 | 0.69 | 0.75 | -2.43*** | 0.00 | I(I) |

| LBM | -1.84 | 0.03 | -5.09*** | 0.00 | I(I) |

| LDCPS | -2.95** | 0.00 | -4.91*** | 0.00 | I(0) |

| LFDI | -1.38 | 0.08 | -3.55*** | 0.00 | I(I) |

| LGTI | -3.74 | 0.00 | -2.85*** | 0.00 | I(I) |

The panel unit root test was performed under the null hypothesis wherein the variables are homogeneous non-stationary. ***, **, and * denote statistical signifcance level at 1%, 5%, and 10%, respectively.

After completing the unit root tests, the next step is to examine if the variables exhibit a long-term co-integration relationship. Table 6 presents the results from the co-integration assessments using the Westerlund (2007) approach.

The outcomes of the Westerlund panel co-integration test indicate that the statistics lead to rejecting the hypothesis of non-cointegration more frequently at the panel level compared to the individual level. This implies that there is a significant long-term relationship between two or more variables across the panel data. In other words, the variables move together over the long run, confirming the presence of co-integration.

4.4. Pooled Mean Group Autoregressive Distributed Lag (PMG- ARDL) Analysis

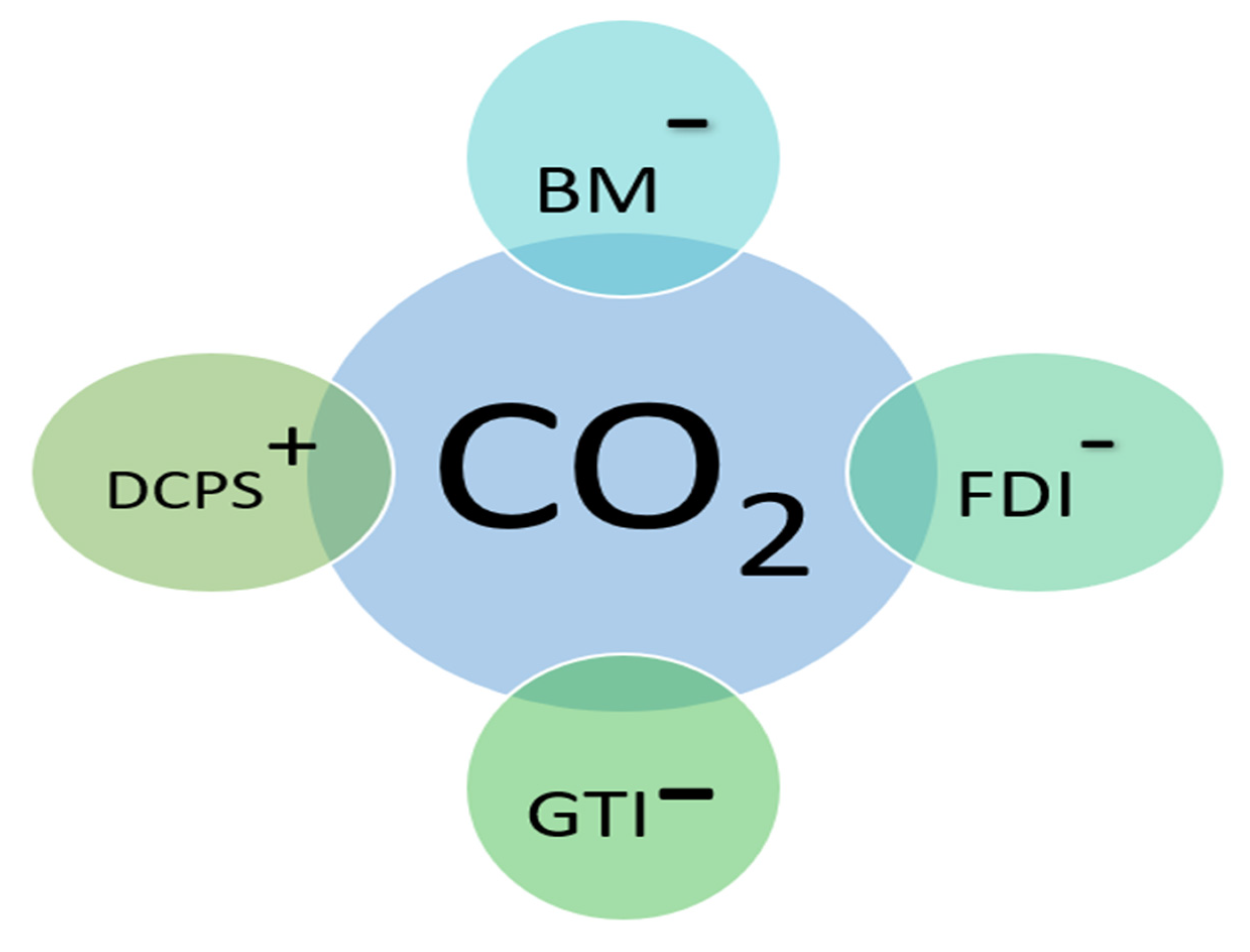

In Table 7, the analysis reveals that broad money (LBM) significantly reduces CO2 emissions in the long term, with a 2.88% decrease in emissions in BRICS countries linked to increased LBM. This reduction is due to broad money facilitating investments in green technologies, lowering financing costs, enhancing financial stability, encouraging sustainable practices, ensuring regulatory compliance, and fostering eco-friendly innovations (Batool et al., 2020; Gök, 2020; Neog & Yadava, 2020). These results align with recent studies indicating that financial development improves environmental quality and reduces CO2 emissions in BRICS economies.

Conversely, the analysis shows that LDCPS (domestic credit to the private sector) has a positive and statistically significant impact on carbon emissions, meaning a 1% increase in LDCPS leads to higher emissions. Studies by Ali et al. (2020) and Jianguo et al. (2022) have found that financial development and stock market growth can expand financing options, lower costs, reduce risks, and promote investments, which in turn increase energy consumption and emissions.

However, foreign sector development shows a negative but statistically insignificant impact on carbon emissions, indicating that a 1% increase results in a 0.74% decrease in emissions. FDI can reduce carbon emissions by introducing advanced, energy-efficient technologies and environmentally friendly practices to the host country (Zhu, et al., 2023). Foreign firms often adhere to stricter environmental regulations from their home countries, thereby improving environmental standards and lowering emissions in the host country (Pao & Tsai, 2011). Additionally, FDI can stimulate economic growth, enhancing the host country’s capacity and willingness to invest in environmental protection and sustainable practices (Cole, et al., 2021). On the other hand, FDI can have negative impacts on carbon emissions. It may be directed toward countries with lax environmental regulations, leading to higher emissions as companies exploit these lenient policies (Hoffmann et al., 2005). FDI can also lead to increased industrial production and energy consumption, particularly in carbon-intensive industries, thereby raising emissions (Shahbaz et al., 2015). Moreover, FDI can drive the exploitation of natural resources, resulting in deforestation, land degradation, and higher emissions (Tang & Tan, 2015).

Similarly, green technology innovation (GTI) benefits BRICS countries by reducing carbon emissions. A 1% increase in GTI corresponds to a 0.29% decline in emissions, indicating an adverse relationship between GTI and CO2 emissions. The negative coefficient of GTI suggests that higher levels of GTI can decrease CO2 emissions. Therefore, policies promoting innovation are crucial for minimizing emissions. This is because GTI: (i) Improves operational capabilities while reducing environmental impact, addressing the economic-environmental issue, (ii) Enhances resource use efficiency, encourages sustainable energy development and use, and lowers environmental pollution, (iii)Through advanced technology, efficient energy usage reduces consumption and improves financial development and environmental quality by decreasing CO2 emissions. To create a greener society and improve environmental quality in BRICS economies, it is essential to promote green economic growth and finance strategies, facilitate technology transfer for green investments and trade, focus on R&D, ICT, biotechnology, and nanotechnology, and implement policies that reinforce green innovation in global markets. Technological innovation is also critical in OECD economies for reducing emissions and environmental degradation, consistent with recent research by Guo et al. (2021) and Shan et al. (2021), which found that GTI positively impacts CO2 emissions. Zhao et al. (2022) revealed that GTI mitigates CO2 emissions by improving technological innovation, similar to findings by Bakhsh et al. (2021) that investing in technology innovation helps reduce CO2 emissions. To ensure the reliability of these findings, FMOLS and DOLS tests were conducted, with results presented in Table 8. Figure 2 offers a concise overview of the study’s key findings and insights, providing a clear and efficient summary. Examining Figure 2 will give a comprehensive understanding of the research outcomes. Figure 3 summarizes the model.

The study’s findings are consistent and reliable, as indicated by the results from various estimation methods. The fixed effects model and DOLS (Dynamic Ordinary Least Squares) produced results similar to those obtained through AMG (Augmented Mean Group) and FMOLS (Fully Modified Ordinary Least Squares), despite having different coefficient values. This consistency across multiple methods suggests that the study’s conclusions are robust and dependable.

Table 9.

Results of Dumitrescu Hurlin (DH) panel causality tests.

| Null hypothesis | W-Stat | Zbar-Stat. | Prob. | Direction of causality |

| LBM LCO2 | 7.91 | 4.76 | 2.01 | Non-directional causality between REC and LGDP |

| LCO2 LBM | 1.78 | -0.42 | 0.67 | |

| LDCPS LCO2 | 2.55 | 0.22 | 0.82 | Non -directional causality between TI and GDP |

| LCO2 LDCPS | 7.74 | 4.62 | 4.E | |

| LFDI LCO2 | 2.01 | -0.23 | 0.93 | Non -directional causality between GDP and ED |

| LCO2 LFDI | 1.95** | -028 | 0.02 | |

| LGTI LCO2 | 5.38 | 2.62 | 1.23 | Uni-directional causality between FS and GDP |

| LCO2 LGTI | 2.32 | 0.03 | 0.97 |

Notes: 1. Asterisk(s) ***, **, * represent(s) the rejection of the null hypothesis at 1%, 5% and 10% significance levels. 2. The symbol ≠ implies does not homogeneously cause.

4.5. Panel Causality Test Results

We used the D-H causality estimation method to analyze the causal relationships among the study variables. The findings, presented in Table 11, indicate that there is only one unidirectional causality: from green technology innovation (lGTI) to carbon emissions. Additionally, there are non-directional causal relationships among broad money (lBM), domestic credit to the private sector (LDCPS), and foreign direct investment (LFDI). This means that, for the most part, the variables do not show a specific directional causality with each other.

Conclusions and Policy Recommendation

The primary goal of this study is to evaluate the influence of financial development and green technological innovation on environmental quality in BRICS countries from 2001 to 2023. Recognizing the potential cross-country dependencies (CD), various econometric techniques are employed, confirming CD among the panel countries. The study uses the Augmented Mean Group (AMG) estimator and robustness tests such as Fully Modified Ordinary Least Squares (FMOLS) and Dynamic Ordinary Least Squares (DOLS). The findings indicate that broad money (BM), foreign direct investment (FDI), and green technological innovation (GTI) significantly reduce carbon emissions, whereas domestic credit to the private sector (DCPS) has an insignificant positive impact on emissions.

Results from the DOLS and fixed effects models align with those from FMOLS and AMG, although coefficient values vary. Additionally, there is unidirectional causality between GTI and carbon emissions, while BM, DCPS, and FDI exhibit non-directional causal relationships with carbon emissions. These outcomes suggest that financial development and green technological innovation generally enhance environmental quality, except for the impact of domestic credit to the private sector.

Empirical evidence confirms that FDI helps reduce CO2 emissions. This indicates that FDI, combined with green technology transfer and improved labor and environmental management, can assist BRICS countries in achieving sustainable development goals. Financial development is essential for promoting environmental transparency in these nations. The study provides recommendations for fostering financial development and green technological innovation in an environmentally friendly manner.

The study highlights the importance of promoting FDI, financial development, and green technological progress to lower CO2 emissions. For instance, advancements in green technology and improvements in energy efficiency can enhance the environmental well-being of BRICS countries. Financial growth can boost environmental quality by encouraging investments in eco-friendly technologies. Governments should prioritize investments in such technologies.

Policies that encourage financial openness and liberalization to attract FDI related to research and development can help mitigate environmental degradation. Regulations should require foreign investment companies to adopt green technologies. Energy consumption programs should shift from non-renewable to renewable energy sources, and policies supporting renewable energy production and use will positively and sustainably impact economic growth. Efforts to control CO2 emissions and related policy recommendations should be tailored to each country’s specific emission levels.

While this study focuses on FDI inflows, future research could explore the roles of international trade and technological innovation in assessing pollution levels using both the Environmental Kuznets Curve (EKC) and the pollution haven hypothesis. This would provide further insights into the factors influencing the shape of the EKC.

References

- Grossman, Gene M., and Alan B. Krueger. “Economic growth and the environment.” The quarterly journal of economics 110.2 (1995): 353-377. [CrossRef]

- Xu, X., Huang, S., Haizhong, A., Vigne, S., & Lucey, B. M. (2021). The influence pathways of financial development on environmental quality: New evidence from smooth transition regression models. In SSRN Electronic Journal. Elsevier BV. [CrossRef]

- Moghadam, H. E., & Lotfalipour, M. R. (2014). The environmental issues and forecasting threshold of income and pollution emissions in Iran economy. International Journal of Resistive Economics, 2(2), 72..

- Majeed, M. T., & Mazhar, M. (2019). Financial development and ecological footprint: a global panel data analysis. Pakistan Journal of Commerce and Social Sciences (PJCSS), 13(2), 487-514.

- Khan, H., Dong, Y., Nuţă, F. M., & Khan, I. (2023). Eco-innovations, green growth, and environmental taxes in EU countries: A panel quantile regression approach. Environmental Science and Pollution Research, 30(49), 108005-108022. [CrossRef]

- Li, L., Zhai, Z., Liu, J., & Hu, J. (2015). Estimating industrial and domestic environmental releases of perfluorooctanoic acid and its salts in China from 2004 to 2012. Chemosphere, 129, 100-109. [CrossRef]

- Shahbaz, M., Shahzad, S. J. H., Ahmad, N., & Alam, S. (2016). Financial development and environmental quality: the way forward. Energy policy, 98, 353-364. [CrossRef]

- Zhang, Y. J. (2011). The impact of financial development on carbon emissions: An empirical analysis in China. Energy policy, 39(4), 2197-2203. [CrossRef]

- International Renewable Energy Agency (IRENA). (2020). Renewable Power Generation Costs in 2019. Retrieved from https://www.irena.org/publications/2020/Jun/Renewable-Power-Generation-Costs-in-2019.

- Jednak, S., Minović, J., & Kragulj, D. (2020). A review of economic and environment indicators and energy efficiency: Evidence from the EU and Serbia. Economic themes, 58(4), 459-477. [CrossRef]

- Nguyen, T. K. L., Ngo, H. H., Guo, W., Nghiem, L. D., Qian, G., Liu, Q., ... & Mainali, B. (2021). Assessing the environmental impacts and greenhouse gas emissions from the common municipal wastewater treatment systems. Science of the Total Environment, 801, 149676. [CrossRef]

- Ruza, C., & Caro-Carretero, R. (2022). The non-linear impact of financial development on environmental quality and sustainability: evidence from G7 countries. International Journal of Environmental Research and Public Health, 19(14), 8382. [CrossRef]

- Xu, W., Xie, Y., Cai, Y., Ji, L., Wang, B., & Yang, Z. (2021). Environmentally-extended input-output and ecological network analysis for Energy-Water-CO2 metabolic system in China. Science of the Total Environment, 758, 143931. [CrossRef]

- Sharif, T., Uddin, M. M. M., & Alexiou, C. (2022). Testing the moderating role of trade openness on the environmental Kuznets curve hypothesis: a novel approach. Annals of Operations Research, 1-39. [CrossRef]

- Yasin, I., Aslam, A., Siddik, A. B., Abbass, K., & Murshed, M. (2023). Offshoring the scarring causes and effects of environmental challenges faced by the advanced world: an empirical evidence. Environmental Science and Pollution Research, 30(32), 79335-79345. [CrossRef]

- Ahmed, N., Hamid, Z., Rehman, K. U., Senkus, P., Khan, N. A., Wysokińska-Senkus, A., & Hadryjańska, B. (2023). Environmental regulation, fiscal decentralization, and agricultural carbon intensity: a challenge to ecological sustainability policies in the United States. Sustainability, 15(6), 5145. [CrossRef]

- Razzaq, A., Fatima, T., & Murshed, M. (2023). Asymmetric effects of tourism development and green innovation on economic growth and carbon emissions in Top 10 GDP Countries. Journal of Environmental Planning and Management, 66(3), 471-500. [CrossRef]

- Islam, M. M., Shahbaz, M., Sultana, T., Wang, Z., Sohag, K., & Abbas, S. (2023). Changes in environmental degradation parameters in Bangladesh: the role of net savings, natural resource depletion, technological innovation, and democracy. Journal of Environmental Management, 343, 118-190. [CrossRef]

- Castiglione, C., Infante, D., & Smirnova, J. (2012). Rule of law and the environmental Kuznets curve: evidence for carbon emissions. International Journal of Sustainable Economy, 4(3), 254-269. [CrossRef]

- Apergis, N., & Payne, J. E. (2017). Per capita carbon dioxide emissions across US states by sector and fossil fuel source: evidence from club convergence tests. Energy Economics, 63, 365-372. [CrossRef]

- Shahbaz, M., Haouas, I., & Van Hoang, T. H. (2019). Economic growth and environmental degradation in Vietnam: is the environmental Kuznets curve a complete picture?. Emerging Markets Review, 38, 197-218. [CrossRef]

- Zhang, Y., Sun, M., Yang, R., Li, X., Zhang, L., & Li, M. (2021). Decoupling water environment pressures from economic growth in the Yangtze River Economic Belt, China. Ecological Indicators, 122, 107314. [CrossRef]

- Dong, L., Tong, X., Li, X., Zhou, J., Wang, S., & Liu, B. (2019). Some developments and new insights of environmental problems and deep mining strategy for cleaner production in mines. Journal of Cleaner Production, 210, 1562-1578. [CrossRef]

- Bhattacharyya, A. (2019). Corporate environmental performance evaluation: A cross-country appraisal. Journal of cleaner production, 237, 117607. [CrossRef]

- Khan, A., Muhammad, F., Chenggang, Y., Hussain, J., Bano, S., & Khan, M. A. (2020). The impression of technological innovations and natural resources in energy-growth-environment nexus: a new look into BRICS economies. Science of The Total Environment, 727, 138265. [CrossRef]

- Li, J., Pei, Y., Zhao, S., Xiao, R., Sang, X., & Zhang, C. (2020). A review of remote sensing for environmental monitoring in China. Remote Sensing, 12(7), 1130. [CrossRef]

- Aluko, O. A., & Obalade, A. A. (2020). Financial development and environmental quality in sub-Saharan Africa: Is there a technology effect?. Science of the Total Environment, 747, 141515. [CrossRef]

- Nosheen, F., Imran, M., Anjum, S., & Kouser, R. (2021). Economic growth, environmental efficiency, and industrial transfer demonstration zones of China: A way forward for CPEC. Review of Applied Management and Social Sciences, 4(2), 357-370. [CrossRef]

- Odhiambo, N. M. (2020). Financial development, income inequality and carbon emissions in Sub-Saharan African countries: a panel data analysis. Energy Exploration & Exploitation, 38(5), 1914-1931. [CrossRef]

- Raghutla, C., Malik, M. N., Hameed, A., & Chittedi, K. R. (2024). Impact of public-private partnerships investment and FDI on CO2 emissions: A study of six global investment countries. Journal of Environmental Management, 360, 121213. [CrossRef]

- Umar, M., Ji, X., Kirikkaleli, D., & Xu, Q. (2020). COP21 Roadmap: Do innovation, financial development, and transportation infrastructure matter for environmental sustainability in China?. Journal of environmental management, 271, 111026. [CrossRef]

- Nasir, M. A., Canh, N. P., & Le, T. N. L. (2021). Environmental degradation & role of financialisation, economic development, industrialisation and trade liberalisation. Journal of environmental management, 277, 111471. [CrossRef]

- Álvarez-Herránz, A., Balsalobre, D., Cantos, J. M., & Shahbaz, M. (2017). Energy innovations-GHG emissions nexus: fresh empirical evidence from OECD countries. Energy Policy, 101, 90-100. [CrossRef]

- Duque-Grisales, E., Aguilera-Caracuel, J., Guerrero-Villegas, J., & García-Sánchez, E. (2020). Can proactive environmental strategy improve Multilatinas’ level of internationalization? The moderating role of board independence. Business Strategy and the Environment, 29(1), 291-305. [CrossRef]

- Ozcan, B., Tzeremes, P. G., & Tzeremes, N. G. (2020). Energy consumption, economic growth and environmental degradation in OECD countries. Economic Modelling, 84, 203-213. [CrossRef]

- Birdsall, N., & Wheeler, D. (1993). Trade policy and industrial pollution in Latin America: where are the pollution havens?. The Journal of Environment & Development, 2(1), 137-149. [CrossRef]

- Abbasi, F., & Riaz, K. (2016). CO2 emissions and financial development in an emerging economy: an augmented VAR approach. Energy policy, 90, 102-114. [CrossRef]

- Law, B. E., Hudiburg, T. W., Berner, L. T., Kent, J. J., Buotte, P. C., & Harmon, M. E. (2018). Land use strategies to mitigate climate change in carbon dense temperate forests. Proceedings of the National Academy of Sciences, 115(14), 3663-3668. [CrossRef]

- Jensen, J. (1996). Chlorophenols in the terrestrial environment. Reviews of Environmental Contamination and Toxicology: Continuation of Residue Reviews, 25-51.

- Ogbeifun, L., & Shobande, O. A. (2022). A reevaluation of human capital accumulation and economic growth in OECD. Journal of Public Affairs, 22(4), e2602. [CrossRef]

- Singhania, M., & Gandhi, G. (2015). Social and environmental disclosure index: Perspectives from Indian corporate sector. Journal of Advances in Management Research, 12(2), 192-208. [CrossRef]

- Dhingra, V. S. (2023). Financial development, economic growth, globalisation and environmental quality in BRICS economies: evidence from ARDL bounds test approach. Economic Change and Restructuring, 56(3), 1651-1682. [CrossRef]

- Pantelopoulos, G. (2023). Human capital, gender equality and foreign direct investment: Evidence from OECD countries. Journal of the Knowledge Economy, 1-17. [CrossRef]

- Popp, D. (2019). Environmental policy and innovation: A decade of research. Environmental and Resource Economics. https://www.nber.org/system/files/working_papers/w25631/w25631.pdf.

- Jaffe, A. B., & Stavins, R. N. (1995). Dynamic incentives of environmental regulations: The effects of alternative policy instruments on technology diffusion. Journal of environmental economics and management, 29(3), S43-S63. [CrossRef]

- Horbach, J. (2016). Empirical determinants of eco-innovation in European countries using the community innovation survey. Environmental Innovation and Societal Transitions, 19, 1-14. [CrossRef]

- Sun, Y., Gao, P., Tian, W., & Guan, W. (2023). Green innovation for resource efficiency and sustainability: Empirical analysis and policy. Resources Policy, 81, 103369. [CrossRef]

- He, W., & Wang, B. (2024). Environmental jurisdiction and energy efficiency: Evidence from China’s establishment of environmental courts. Energy Economics, 131, 107358. [CrossRef]

- Li, L., & Li, W. (2022). The promoting effect of green technology innovations on sustainable supply chain development: evidence from China’s transport sector. Sustainability, 14(8), 4673. [CrossRef]

- Chishti, M. Z., & Sinha, A. (2022). Do the shocks in technological and financial innovation influence the environmental quality? Evidence from BRICS economies. Technology in Society, 68, 101828. [CrossRef]

- Chishti, M. Z., Arfaoui, N., & Cheong, C. W. (2023). Exploring the time-varying asymmetric effects of environmental regulation policies and human capital on sustainable development efficiency: a province level evidence from China. Energy Economics, 126, 106922. [CrossRef]

- Dasgupta, S., Mody, A., Roy, S., & Wheeler, D. (2001). Environmental regulation and development: A cross-country empirical analysis. Oxford development studies, 29(2), 173-187.

- Zhang, J., Ouyang, Y., Ballesteros-Pérez, P., Li, H., Philbin, S. P., Li, Z., & Skitmore, M. (2021). Understanding the impact of environmental regulations on green technology innovation efficiency in the construction industry. Sustainable Cities and Society, 65, 102647. [CrossRef]

- Majeed, M. T., & Mazhar, M. (2019). Financial development and ecological footprint: a global panel data analysis. Pakistan Journal of Commerce and Social Sciences (PJCSS), 13(2), 487-514.

- Shahbaz, M., Haouas, I., & Van Hoang, T. H. (2019). Economic growth and environmental degradation in Vietnam: is the environmental Kuznets curve a complete picture?. Emerging Markets Review, 38, 197-218. [CrossRef]

- Zhang, W., & Li, G. (2020). Environmental decentralization, environmental protection investment, and green technology innovation. Environmental Science and Pollution Research, 1-16.

- Dong, Z., He, Y., Wang, H., & Wang, L. (2020). Is there a ripple effect in environmental regulation in China?–Evidence from the local-neighborhood green technology innovation perspective. Ecological Indicators, 118, 106773. [CrossRef]

- Bhattacharya, A., Nand, A., & Castka, P. (2019). Lean-green integration and its impact on sustainability performance: A critical review. Journal of Cleaner Production, 236, 117697. [CrossRef]

- Pesaran, M. H., & Yamagata, T. (2008). Testing slope homogeneity in large panels. Journal of econometrics, 142(1), 50-93. [CrossRef]

- Pesaran, M. H. (2007). A simple panel unit root test in the presence of cross-section dependence. Journal of applied econometrics, 22(2), 265-312. [CrossRef]

- Westerlund, J. (2008). Panel cointegration tests of the Fisher effect. Journal of applied econometrics, 23(2), 193-233. [CrossRef]

- Ahmed, Z., Ahmad, M., Rjoub, H., Kalugina, O. A., & Hussain, N. (2022). Economic growth, renewable energy consumption, and ecological footprint: Exploring the role of environmental regulations and democracy in sustainable development. Sustainable Development, 30(4), 595-605. [CrossRef]

- Dumitrescu, E. I., & Hurlin, C. (2012). Testing for Granger non-causality in heterogeneous panels. Economic modelling, 29(4), 1450-1460. [CrossRef]

- Im, K. S., Pesaran, M. H., & Shin, Y. (2003). Testing for unit roots in heterogeneous panels. Journal of econometrics, 115(1), 53-74. [CrossRef]

- Dickey, D. A., & Fuller, W. A. (1979). Distribution of the estimators for autoregressive time series with a unit root. Journal of the American statistical association, 74(366a), 427-431.

- Farooq, S. A., Mukhtar, S. H., Raina, A., Haq, M. I. U., Siddiqui, M. I. H., Naveed, N., & Dobrota, D. (2024). Effect of TiB2 on the mechanical and tribological properties of marine grade Aluminum Alloy 5052: An experimental investigation. Journal of Materials Research and Technology, 29, 3749-3758. [CrossRef]

- Shahbaz, M. (2009). A reassessment of finance-growth nexus for Pakistan: under the investigation of FMOLS and DOLS techniques. IUP Journal of Applied Economics, 8(1), 65.

- Priyankara, H. P. R., Luo, F., Saeed, A., Nubuor, S. A., & Jayasuriya, M. P. F. (2018). How does leader’s support for environment promote organizational citizenship behaviour for environment? A multi-theory perspective. Sustainability, 10(1), 271. [CrossRef]

- Khan, I., Saeed, K., & Khan, I. (2019). Nanoparticles: Properties, applications and toxicities. Arabian journal of chemistry, 12(7), 908-931.

- Olofin, R. E. (2019). Strengthening civil-military relations in Nigeria for improved national security: Lessons from the field. Deepening Civil Military Relations for Effective Peacebuilding and Democratic Governance in Nigeria. Ni.

- Olorogun, L. A. (2023). Modelling Financial Development in the Private Sector, FDI, and Sustainable Economic Growth in sub-Saharan Africa: ARDL Bound Test-FMOLS, DOLS Robust Analysis. Journal of the Knowledge Economy, 1-19. [CrossRef]

- Ramirez, J., Carrico, R., Wilde, A., Junkins, A., Furmanek, S., Chandler, T., ... & Begier, E. (2023). Diagnosis of respiratory syncytial virus in adults substantially increases when adding sputum, saliva, and serology testing to nasopharyngeal swab RT–PCR. Infectious Diseases and Therapy, 12(6), 1593-1603. [CrossRef]

- Westerlund, J., & Hosseinkouchack, M. (2016). Modified CADF and CIPS panel unit root statistics with standard chi-squared and normal limiting distributions. Oxford Bulletin of Economics and Statistics, 78(3), 347-364. [CrossRef]

- Batool, M., Jehan, Y., & Hayat, N. (2020). Effect of financial development and institutional quality on the environmental degradation in developed and developing countries. Int J Hum Capital Urban Manage, 5(2), 111-124.

- Gök, A. (2020). The role of financial development on carbon emissions: a meta regression analysis. Environmental Science and Pollution Research, 27(11), 11618-11636. [CrossRef]

- Neog, Y., & Yadava, A. K. (2020). Nexus among CO2 emissions, remittances, and financial development: a NARDL approach for India. Environmental Science and Pollution Research, 27(35), 44470-44481. [CrossRef]

- Ali, M., Raza, S. A. A., Puah, C. H., & Samdani, S. (2021). How financial development and economic growth influence human capital in low-income countries. International Journal of Social Economics, 48(10), 1393-1407. [CrossRef]

- Jianguo, D., Ali, K., Alnori, F., & Ullah, S. (2022). The nexus of financial development, technological innovation, institutional quality, and environmental quality: evidence from OECD economies. Environmental Science and Pollution Research, 29(38), 58179-58200. [CrossRef]

- Zhu, C., Zhang, F., & Zhang, Y. (2023). Revisiting financial opening and financial development: A regulation heterogeneity perspective. Economic Analysis and Policy, 80, 181-197. [CrossRef]

- Pao, H. T., & Tsai, C. M. (2011). Multivariate Granger causality between CO2 emissions, energy consumption, FDI (foreign direct investment) and GDP (gross domestic product): evidence from a panel of BRIC (Brazil, Russian Federation, India, and China) countries. Energy, 36(1), 685-693. [CrossRef]

- Cole, M. A., Elliott, R. J., Okubo, T., & Zhang, L. (2021). Importing, outsourcing and pollution offshoring. Energy Economics, 103, 105562. [CrossRef]

- Hoffman, P. T., Postel-Vinay, G., & Rosenthal, J. L. (2015). Entry, information, and financial development: A century of competition between French banks and notaries. Explorations in Economic History, 55, 39-57. [CrossRef]

- Shahbaz, M., Rehman, I. U., & Muzaffar, A. T. (2015). Re-Visiting Financial Development and Economic Growth Nexus: The Role of Capitalization in B angladesh. South African Journal of Economics, 83(3), 452-471.

- Tang, C. F., & Tan, B. W. (2014). The linkages among energy consumption, economic growth, relative price, foreign direct investment, and financial development in Malaysia. Quality & Quantity, 48, 781-797. [CrossRef]

- Guo, Y. (2021). [Retracted] Financial Development and Carbon Emissions: Analyzing the Role of Financial Risk, Renewable Energy Electricity, and Human Capital for China. Discrete Dynamics in Nature and Society, 2021(1), 1025669.

- Shan, S., Ahmad, M., Tan, Z., Adebayo, T. S., Li, R. Y. M., & Kirikkaleli, D. (2021). The role of energy prices and non-linear fiscal decentralization in limiting carbon emissions: tracking environmental sustainability. Energy, 234, 121243. [CrossRef]

- Zhao, X., Shang, Y., Ma, X., Xia, P., & Shahzad, U. (2022). Does carbon trading lead to green technology innovation: recent evidence from Chinese companies in resource-based industries. IEEE Transactions on Engineering Management, 71, 2506-2523. [CrossRef]

- Bakhsh, S., Yin, H., & Shabir, M. (2021). Foreign investment and CO2 emissions: do technological innovation and institutional quality matter? Evidence from system GMM approach. Environmental Science and Pollution Research, 28(15), 19424-19438. [CrossRef]

Figure 2.

summary of model.

Table 1.

Variables of study.

| Types | Acronym | Variable Titles | Measurements and Data Sources | Data Availability |

| Outcome | CO2 | Corbon Emission | CO2 emissions (kg per 2021 PPP $ of GDP) | 2001-2023 |

| Input | FSD | Broad Money | Broad money (% of GDP) | 2001-2023 |

| DCPS | Domestic Credit to private Sector | Domestic credit to private sector (% of GDP) | 2001-2023 | |

| FDI | Foreign Direct Investment | Foreign direct investment, net inflows (% of GDP) | 2001-2023 | |

|

GTI |

Green Technological Innovation | Green technological Innovation Patent applications, (residents & non-resident) | 2001-2023 |

Note: This table shows the measurement and source of variables. Source: Previous studies.

Table 2.

Summary statistics and correlation statistics.

| LCO2 | LBM | LDCPS | LFDI | LGTI | |

| Mean | -1.55 | 4.38 | 4.09 | 0.42 | 9.45 |

| Median | -1.35 | 4.29 | 4.04 | 0.51 | 9.13 |

| Maximum | -0.32 | 5.43 | 5.27 | 2.27 | 14.17 |

| Minimum | -3.91 | 3.17 | 2.82 | -1.58 | 6.30 |

| Std. Dev. | 0.97 | 0.48 | 0.51 | 0.72 | 2.14 |

| Skewness | -0.54 | 0.41 | 0.33 | -0.32 | 0.68 |

| Kurtosis | 2.09 | 3.02 | 3.17 | 2.72 | 2.85 |

| Correlation | |||||

| LCO2 | LBM | LDCPS | LFDI | LGTI | |

| LCO2 | 1 | 0.55 | 0.56 | -0.45 | -0.01 |

| LBM | 0.55 | 1.00 | 0.93 | -0.27 | 0.63 |

| LDCPS | 0.56 | 0.93 | 1.00 | -0.31 | 0.58 |

| LFDI | -0.45 | -0.27 | -0.31 | 1.00 | -0.17 |

| LGTI | -0.01 | 0.63 | 0.58 | -0.17 | 1.00 |

Table 3.

The Slope of Heterogeneity Test.

| Test statistics | Statistics | p-value |

| ∆test | 2.13** | 0.00 |

| ∆ adj | 4.11** | 0.00 |

symbols *, **, and ***, respectively, describe the levels of significance at 10%, 5%, and 1%, whereas the values in parenthesis contain the p-values.

Table 4.

Cross-Sectional Dependence.

| Variables | CD statistics | p-value | Decisions |

| LCO2 | 5.13*** | 0.00 | Cross sectional dependency |

| LBM | 13.02*** | 0.00 | Cross sectional dependency |

| LDCPS | 7.93*** | 0.00 | Cross sectional dependency |

| LFDI | 1.75*** | 0.07 | Cross sectional dependency |

| LGTI | 1.63*** | 0.10 | Cross sectional dependency |

symbols *, **, and ***, respectively, describe the levels of significance at 10%, 5%, and 1%, whereas the values in parenthesis contain the p-values.

Table 6.

Westerlund (2007) Co-Integration Test.

| Statistics | Value | Z-value | P- Value | Outcomes |

| Gt | 4.02*** | 3.05*** | 0.00 | Co-integration |

| Ga | -2.04*** | -3.60** | 0.05 | Co-integration |

| Pt | -3.12*** | -4.32*** | 0.00 | Co-integration |

| Pa | -1.08** | -1.40* | 0.09 | Co-integration |

The Gt and Ga statistics test cointegration for each cross-section, and Pt and Pa test cointegration in the panel under the null hypothesis of no cointegration. ***, **, and * denote statistical significance level at 1%, 5%, and 10%, level, respectively.

Table 7.

Pooled Mean Group Autoregressive Distributed Lag (PMG- ARDL) Analysis.

| Long Run Equation | Short Run Equation | |||||||

| Variable | Coefficient | Std. Error | t-Statistic | Prob.* | Coefficient | Std. Error | t-Statistic | Prob.* |

| LBM | -2.88 | 1.33 | -2.17 | 0.03 | -0.15 | 0.09 | -1.63 | 0.11 |

| LDCPS | 3.53 | 1.86 | 1.90 | 0.06 | -0.10 | 0.08 | -1.34 | 0.18 |

| LFDI | -0.74 | 0.29 | -2.53 | 0.01 | -0.01 | 0.02 | -0.51 | 0.61 |

| LGTI | -0.29 | 0.24 | -1.20 | 0.23 | 0.08 | 0.04 | 1.86 | 0.07 |

| COINTEQ01 | -0.02 | 0.01 | -1.53 | 0.13 | ||||

The CD statistic test is standard normally distributed under the null of hypothesis of weak cross-sectional dependence. ***, **, and * denote statistical significance level at 1%, 5%, and 10%, respectively.

Table 8.

FMOLS and DOLS robustness test results.

| FOLS | DOLS | |||||||

| Variable | Coefficient | Std. Error | t-Statistic | Prob. | Coefficient | Std. Error | t-Statistic | Prob. |

| LBM | -0.26 | 0.00 | -66.03 | 0.00 | -0.86 | 0.58 | -1.49 | 0.14 |

| LDCPS | 0.41 | 0.01 | 73.80 | 0.00 | 0.96 | 0.55 | 1.76 | 0.09 |

| LFDI | -0.72 | 0.00 | -194.40 | 0.00 | -0.69 | 0.17 | -4.13 | 0.00 |

| LGTI | -0.22 | 0.00 | -53.98 | 0.00 | -0.14 | 0.08 | -1.69 | 0.10 |

Note: ***, **, * report the significance level at 1%, 5%, and 10%, relatively.

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Copyright: This open access article is published under a Creative Commons CC BY 4.0 license, which permit the free download, distribution, and reuse, provided that the author and preprint are cited in any reuse.