Submitted:

20 August 2024

Posted:

21 August 2024

You are already at the latest version

Abstract

While financial literacy is crucial in improving the population's financial well-being, its effectiveness can be enhanced by exposure to financial information. This paper investigates the nexus between financial literacy, financial information consumption, and financial well-being in rural Ghana. The study employed cross-sectional data from a survey of 663 rural households using simple random and cluster sampling with reflective-reflective constructs. The data was analyzed using Structural Equation Modelling-Partial Least Squares. The findings reveal that financial literacy and financial information consumption significantly enhance financial well-being among rural households in Ghana. Financial Literacy also promotes Financial Information Consumption. Notably, financial literacy's impact on financial well-being is stronger when mediated by the consumption of financial information. These findings underscore the importance of improving financial literacy and information access to uplift financial well-being in rural areas. Moreover, the study highlights that financial literacy education is crucial as it plays a mediating role; recipients of financial education experience a more substantial impact. Such findings emphasize the importance of acquiring financial knowledge and effectively processing financial information to achieve financial prosperity, particularly in rural areas. These findings should motivate individuals, especially those in rural areas, to process financial information successfully rather than merely acquiring financial knowledge to attain financial prosperity.

Keywords:

Financial Literacy

; fianncial well-being

; financial information

; rural settings

1. Introduction

Financial literacy (FL) involves having a comprehensive understanding of essential financial matters [1]. However, low levels of FL remain a global challenge [2,3]. FL is crucial for enhancing financial well-being (FWB) and has become a major policy priority for developing countries [4,5], as well as for advancing Sustainable Development Goals (SDGs) 3 and 4. Goal 3 focuses on ensuring health and well-being for individuals of all ages, while Goal 4 emphasizes the importance of inclusive and equitable education and promotes lifelong learning opportunities for all. In the past decade, governments, especially in developing countries, have crafted policies and made significant investments to create a financially inclusive and educated society. Despite these efforts, two out of three individuals in the developing world remain financially illiterate [6].

Recently, individuals have been increasingly mandated to manage their retirement funds carefully to ensure their financial well-being both during their working years and after retirement [7,8]. However, the average citizen may lack the necessary knowledge of the financial market’s complexities for effective calculations and planning [9], which might affect people’s FWB [7]. This issue was exemplified during COVID-19 when most people’s FWB was reduced due to loss of employment [10].

Previous studies have documented the link between FL and FWB [10,11,12,13,14,15]. The evidence from these studies suggests a bidirectional relationship between FL and FWB, yet some findings are contradictory[13,16,17,18,19,20,21]. For example, [18] found that financial knowledge did not correlate with projected financial security but did impact current stress levels related to money management. [19] demonstrated that the relationship between financial knowledge and FWB is more indirect than direct. [20] examined FL and FWB in India and found no significant relationship. [22] showed that prudent financial behaviour and subjective financial knowledge predict FWB. [21] also found a direct significant impact of FL on FWB, with financial self-efficacy partially mediating the relationship. This literature suggests that neither subjective nor objective FL alone can fully explain a secure financial future. In light of this, [23] concluded that there is much more to learn about the relationship between FL and FWB. One factor that has not been extensively studied is financial information (FI).

FI is crucial for achieving and maintaining FL to reach desired financial goals [24]. Prior studies have often conflated FL with FI, yet these concepts are distinct [25]. FI pertains to current news about financial market developments, whereas FL encompasses the knowledge one already possesses to leverage these developments. FI is an enabler of FL, which alone might not suffice to ensure sound financial decisions [26]. Conversely, FL enables individuals to unlock doors for individuals to evaluate FI, which is essential for sound decision-making that enhances FWB.

Although past studies have shown that FWB depends on the level of FL [27,28], financial decisions are typically based on both FL and FI. From this perspective, the literature suggests that the informational dimension is critical in determining how FL influences FWB [29]. It further emphasizes that lifetime experience in FI consumption is highly relevant to FWB expectations [30], arguing that the more FI an individual receives, the more likely it will influence beneficial financial decision-making [31,32,33,34]. However, to make good use of FI, one must be financially literate to convert FI into decisions that positively affect FWB [35].

[36] observed that information exerts a more substantial influence on the financial decisions of economic agents when the information consumed is relevant to financial decisions that improve FWB [37]. [38] argues that inadequate FI consumption among the financially literate may lead to inappropriate financial decisions, thereby failing to influence FWB. Therefore, the quality of financial knowledge shapes people’s ability to manage finances [31], which ultimately impacts FWB.

This study employed a multi-theoretical lens to examine the relationship between financial literacy (FL) and financial well-being (FWB). By integrating Prospect Theory with Resource Dependency Theory, the study aims to understand the mediating role of financial information in the relationship. Prospect Theory suggests that FL influences decision-making under uncertainty, thereby impacting FWB [39]. Meanwhile, Resource Dependency Theory emphasizes the critical role of FI as a resource for people to rely on when making financial decisions. FL enhances financial decision-making, increases access to financial resources, and ultimately improves FWB by enhancing one’s capacity to consume FI [40]. Thus, FI mediates the relationship between FL and FWB by serving as a crucial resource for risk management, access to financial opportunities, and well-informed decision-making.

The literature discussed above suggests that FI may act as a mechanism through which FL leads to FWB, as has been noted in previous studies that FL might not lead to FWB unless it passes through a mechanism [13,41]. Consequently, several studies examined mediating variables to explain the mixed evidence in the FL-FWB relationship. Such variables included financial inclusion [4,42,43,44,45,46], financial behaviour [12,47,48] and consumption needs [13].

None of these studies explored the role of FIC. This study seeks to bridge this gap in the literature. In pursuing this analysis, the study seeks to make several other contributions to the current body of knowledge in the area. First, the study focuses on rural areas where financial information has traditionally been low compared to urban settings. The information flow to rural settings has improved with the advent and widespread usage of mobile phones and increased access to the Internet. These changes make rural settings crucial for research to advise on inclusive development policies because rural populations are the most financially vulnerable concerning FL [11]. The dynamics of rural and urban contexts differ regarding information flow, level of education and type of financial products available. The rural context has been less researched, and previous studies have recommended further investigations in these areas [12,49]. Exploring FIC in rural households would be an effective way to understand and improve household living standards.

The rest of the paper is structured as follows: section 2 discusses the methodology for the study, section 3 presents study results, and Section 4 discusses the findings, conclusions, and implications of the study.

2. Research Method

2.1. Study Site/Region

This study was conducted in Ghana’s Upper West Region (UWR). At around 18,478 square kilometres or 12.7% of the country’s total land area, this region is the seventh largest area in the country. It has 11 political districts, with Wa as a regional political and administrative capital. Situated in Ghana’s northwest corner, it borders Burkina Faso to the north, Ivory Coast to the west, the Savanah Region to the south, and the Upper East Region of Ghana to the east. The main economic activity is agriculture, in which 72% of the population is engaged, and it has a long dry season from October to May every year. Because the UWR is classified as the poorest of the poor regions in Ghana [50], there have been many financial education programmes since the 2015 Ghana Statistical Service (GSS) Report [51]. It is a rural region, with 73.6% of its population living in rural areas and a literacy rate of 46% [52]. While there is no reported evidence of the level of financial literacy in UWR of Ghana, a related study on the level of financial inclusion is reported to be 20% household access to formal financial services [53].

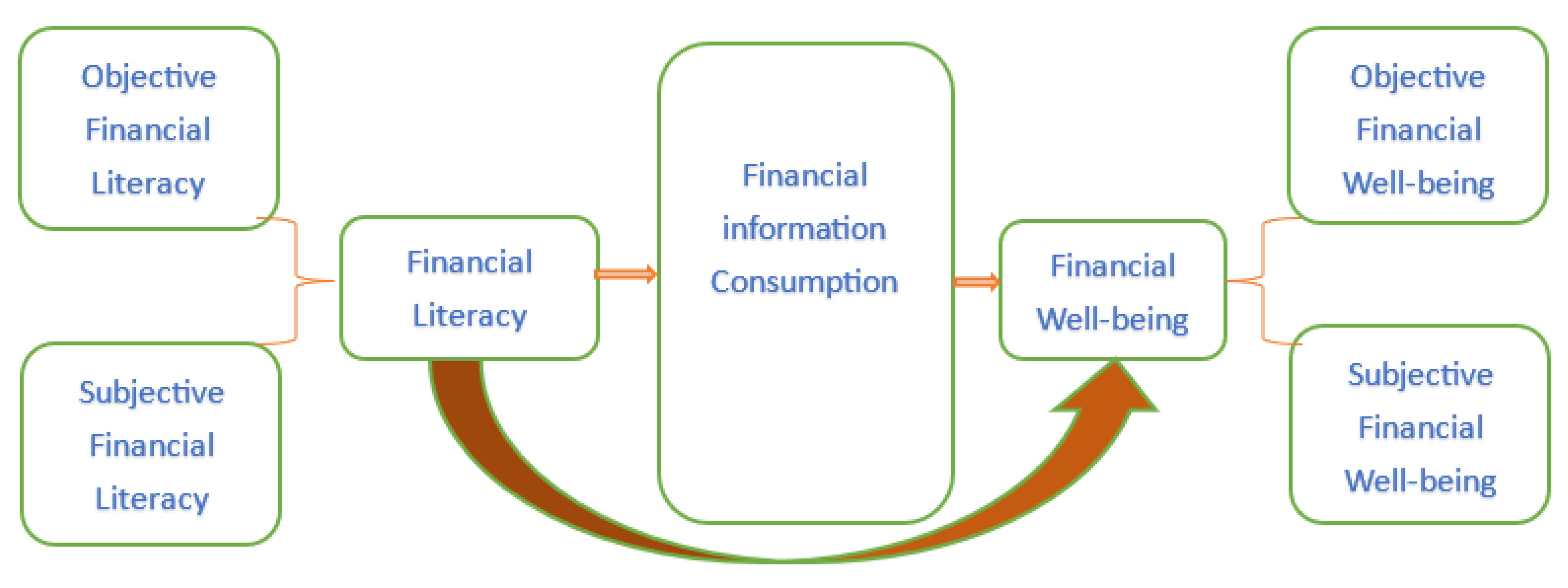

The characteristics of the region and its policy-maker interests make it relevant for a dedicated study to understand the interplay between FIC and FWB in the region’s rural context. The current study uses structural equation modelling to this effect. Figure 1 depicts the core of the investigation, i.e. the role of FIC in the relationship between FL and FWB. The key hypothesis is that financial information consumption mediates the relationship between FL and FWB (hypothesis H4).

The structural equation modelling analysis also makes it possible to delve deeper into the analysis by exploring jointly hypotheses depicting other relationships. In this perspective, the study hypothesizes first that FL has a significantly positive relationship with rural households’ FI consumption(H1); second, that FI consumption has a significantly positive relationship with FWB (H2); third, that FL is positively related to FWB(H3); fourth, that FIC mediation is stronger amongst financially literate than amongst financially illiterate (H5).

2.2. Study Design

A cross-section research design was employed, with a well-structured questionnaire to gather data for hypothesis testing. The study focused on rural households in Ghana with specific reference to the Upper West Region. Following the Housing and Population Census 2021, the region had 134,487 households. Heads of the household in the region participated in the study.

Using an online sample calculator (www.suveyststem.com), the minimum sample size for this population was 598 households, but 663 households were analyzed. The study used cluster sampling to cover the entire population. Within each cluster, simple random sampling was used to select communities and households where participants reside. The study used a random sampling method to sample clusters, communities within a cluster, and households within a community. A community’s sample size target was based on its total population. A simple random sampling technique gave everybody an equal chance to participate in the study. Heads of the households selected and agreed to participate were enrolled in the study. Otherwise, the next random household was approached until the community’s target sample size was achieved.

A repeated two-stage reflective-reflective HOC approach was used to test hypotheses and conduct one multigroup analysis to establish significant differences in the mediating role. This method’s implementation necessitates developing and estimating the model indicators that link each low-order construct (LOC). The output score of LOC became the input for modelling the HOC and assessing the hypotheses under investigation. The structural equation model partial least square (SEM-PLS) with percentile bootstrap was the method used for analysis. According to Hair, Risher [54], SEM-PLS is the appropriate analysis tool because it can estimate complex relational models with multiple constructs, indicator variables, and structural routes without requiring distributional assumptions on the data. This study also followed a standard diagnostic approach to validate the measurement model for the structural analysis, as suggested [54]. The statistical output of the measurement and structural model was estimated using SmartPLS version 4.

2.3. FL Measurement

The construct is extracted from literature related to FL. To measure FL objectively, this study follows [55] and [56] with seven financial knowledge and skill questions. Similarly, to measure FL subjectively, the approach of [56] was followed by eight statements/questions. While the objective measure is a Multiple-choice answer, the subjective measure is a Likert scale. The measurements adopted were modified to fit the context of the study.

2.4. FWB Measurement

To measure FWB objectively, this study follows [57] with modification while employing the measurement scale by [58] for subjective measurement. Eight questions are on subjective measures, and four are on objective measures. Respondents score from 1-10 depending on the answer selected for subjective, while multiple choice is provided for the objective measure. Some indicators were modified to fit the context of the study.

2.5. FIC Measurement

This study follows [13,25,59], approach to measuring financial information consumption with modification. Various questions/statements are adopted and modified to measure financial information consumption with a 7-point Likert scale. Respondents rate how satisfied they are with the sufficiency of financial information consumption.

3. Result and Data Analysis

Table 1 above shows that most household heads respondents were male, accounting for 95.6%, while the remaining 4.4% were females. This suggests a significant gender imbalance in the household leadership role in rural settings. The result indicates that the most extensive age distribution falls within the age bracket of 30-39, followed by 60+, accounting for 25.3% and 18.3%, respectively. It needs to be noted that 81.7% are within the active labour force age bracket. This information could help target specific age brackets for policies and services offered to people in household leadership roles. More than four-fifths of the respondents were not retirees, indicating an active labour force among heads of household.

Additionally, 70.4% of the heads of household are married, with the remaining 29.6% representing divorced, separated, single, and windowed. Information from this demographic can be valuable to tailoring services to marital statuses in rural settings. Besides, the data indicates that a significant portion of the rural household heads are self-employed, representing 85.7%. This gives us an understanding of the distribution of different working sectors in rural settings, which can help design targeted financial services and products. Almost half of the respondents have once received FL education before. This finding suggests an awakening of interest among the heads of households in rural settings about obtaining financial knowledge that could affect financial decision-making and changing financial behaviour.

3.1. Measurement Model Assessment –Lower Order Construct (LOC)

3.2. Indicator Loadings

The first step for SEM-PLS analysis in the measurement model is to evaluate the indicator reliability. For an indicator of a construct to be reliable, it is suggested to have a factor loading of 0.7 or more [54,60]. However, for an indicator to be deleted from a construct, such an indicator should significantly impact the reliability and validity of the construct [54] from Table 2 above. Even though the ability to identify the cost of taking credit (subjective financial literacy indicator), encountering payment problems monthly (objective financial well-being indicator) and living paycheck to paycheck (subjective financial well-being indicator), showed loading below 0.70, these indicators were maintained in the constructs as they did not significantly influence the construct’s reliability and validity (see details below).

3.3. Construct Reliability

According to [61], the Cronbach alpha test has been employed to establish the reliability of a construct in most prior studies. Table 2 displays the results of the alpha reliability. The present study’s construct Cronbach alpha ranges from 0.880 to 0.944, indicating that the construct reliability is well above the threshold of 0.6, as recommended [62,63]. The composite reliability (CR) outcome, as indicated in Table 2 above, is indifferent from the alpha value, confirming the construct reliability of the measurement model.

3.4. Convergent Validity

Aside from the construct reliability, convergent validity is an essential element in the measurement model. This validity is established when the Average variance extracted (AVE) value is 0.5 or greater [64]. This confirms that the concepts in use should be related to each other. From Table 2 above, all the constructs have AVE values above 0.50, which range between 0.697 and 0.750, indicating that all the constructs carry convergent validity.

3.5. Discriminant Validity

Hair, Risher [54] note that one way to assess measurement model discriminant validity was Heterotriat-Monotriat (HTMT), aside from Fornell and Larker’s Criterion and cross-loading. Discriminant construct validity indicates the extent to which a construct is genuinely different from the other constructs in a model [64,65]. Even though there are many means of testing, HTMT is suggested in empirical studies to have superior outcomes over others [66]; hence, it is dominant in contemporary studies. To establish discriminant validity, all pair constructs should be below 0.90 [54]. Table 3 below shows that all pair values are below the recommended value of less than 0.90; hence, discriminant validity was maintained.

The study also used Fornell and Larker’s Criterion to complement HTMT. This approach compares AVE’s square root with the correlation between the latent variables. According to [64], the construct should be able to explain the variance of its indicator than it does with the other constructs. Therefore, for discriminant validity to be confirmed, the square root of AVE should produce a more excellent value than the correlation with other constructs. Table 4 below demonstrates Fornell and Larker’s Criterion, which confirmed the discriminant validity established in Table 3 of HTMT.

3.6. Assessment of Measurement Model –Higher Order Construct (HOC)

FL and FWB are both higher-order reflective-reflective constructs derived from subjective and objective measurements of LOC. To validate these HOCs, the same procedure used for evaluating LOC was applied. This involved assessing the constructs’ reliability (both indicator reliability and internal consistency) as well as their validity (convergent and discriminant validity). Table 5 below presents the results of the measurement assessment for these higher-order constructs.

Table 5 above confirms the reliability and convergent validity of the HOCs. The measurement models demonstrate satisfactory reliability and validity, with indicators reliability values exceeding the recommended threshold of 0.70 and Cronbach’s alpha and composite reliability both surpassing the 0.60 benchmarks. In Table 6, the discriminant validity is adequately supported by both the Heterotrait-Monotrait ratio (HTMT) and Fornell and Larker’s Criterion (FLC). HTMT values fall below the recommended cut-off of 0.90, while the FLC approach, which compares AVE’s square root with the correlation between the latent variables, yields values greater than the correlations with other constructs, as shown in Table 6 below.

The HOC results provide a solid foundation for testing the study’s structural model. Consequently, the items used to measure the constructs in this study are validated and appropriate for assessing and estimating structural model parameters.

3.7. Assessment of Structural Model and Hypotheses Testing

The structural model examines the inter-relationship between FL, FIC and FWB. Table 7 below shows the results of the direct relationships.

Table 7 presents the result of the model’s direct effects. In line with hypothesis H1, the relationship between FL and FIC was examined using path analysis. The result indicates a significant positive relationship between FL and FIC (β=0.387; p<0.001; t=10.980), confirming the hypothesis both in terms of direction and significance. Another hypothesis, H2, explored the direct impacts of FIC on FWB. The analysis reveals that FIC significantly and positively influences FWB (β=0.550; p<0.001; t=18.573), consistent with the proposed hypothesis H2. Additionally, the study examined whether the relationship between FL and FWB remains significant when FIC is included in the model. The results show a significant relationship (β=0.162; p<0.001; t=5.011), aligning with hypothesis H3.

In addition to the complete data analysis, a multigroup analysis was conducted to explore the relationships between heads of households receiving education and those not receiving it. Table 7 shows that both groups exhibited a significant positive relationship between FL and FIC (β=0.480; p<0.001; t=10.385) for those who received FL education and (β=0.596; p<0.001; t=16.385) for those who did not. Similarly, the relationship between FIC and FWB was found to be positively and significant for both groups (β=0.519; p<0.001; t=12.238) for those who received FL education and (β=0.207; p<0.001; t=3.645) for those who did not. Additionally, the direct relationship between FL and FWB was significant for both groups (β=0.286; p<0.001; t=6.011) for the FL-educated group and (β=0.105; p<0.05; t=2.397) for FL-non-educated group. The multigroup analysis, as shown in Table 7, indicates that the findings from both groups are largely consistent with the results from complete data analysis. However, the impact of FL on FIC is stronger among those who never received FL education than those who have. Conversely, for the other relationships, the results favour those who have received FL education, underscoring the significance of FL education in influencing these inter-relationships.

In SEM-PLS output, the significance of the specific indirect effect is crucial for establishing mediation. Mediation cannot be claimed if the specific indirect effects are not significant. Additionally, further examination of the direct effect in the presence of the mediator(s) is necessary to determine the type of mediation when the indirect effect is significant. If the direct effect remains significant alongside the mediator, partial mediation is established; otherwise, full mediation is indicated. Another method of determining mediation is using Variance Accounted For (VAF). Full mediation is confirmed if the calculated VAF is 80% or greater; partial mediation is present if the indirect effect is significant, but VAF is less than 80%. Partial mediation can be complementary or competitive: a positive effect indicates complementary mediation, while a negative relationship suggests competitive mediation.

Given the critical role of FIC, it is conceptualized as a mediator between FL and FWB. Therefore, a mediation analysis was conducted to test the role of FIC in the relationship. As shown in Table 8 above, the study reveals a significant indirect positive relationship between FL and FWB through FIC (β=0.213; p<0.001; t=9.726) based on the specific indirect effect from the complete data. Additionally, multigroup analysis indicates that both ever-received, and never-received FL education groups show significant mediation effects, with the impact of FIC being stronger for those who have received FL education (β=0.249; p<0.001; t=8.262) compared to those who have not (β=0.123; p<0.001; t=3.564). The findings are consistent across complete data and group analysis.

Comparing the specific indirect effects of FIC on the FL-FWB relationship against the direct effects of FL and FWB Table 8, it is evident that for the complete data and the never-received FL education group, the impact on FWB is strengthened when mediated by FIC. The complete data analysis suggests that FL education enhances FWB, with the impact being almost double for those who have received FL education compared to those who have not. Notably, while FL directly influences FWB (β=0.162), this effect is amplified when mediated by FIC (β=0.213), indicating that FIC enhances the influence of FL on FWB better. However, for those who have received FL education, the direct effect is stronger than the mediated effects, while for those who have never received FL education, the opposite is true. This could imply that consuming financial information (FI) beyond an optimal level may impair effective decision-making.

An analysis of Table 8 was conducted to determine the type of mediation. The results show that both direct and specific indirect effects are significantly positive across all cases. Additionally, Variance Accounted For (VAF) was computed as the ratio of indirect effect to total effect. The VAF for FIC is 56.8% for the complete data (0.213/0.375=0.568), 46.5% for the ever-received FL education group (0.249/0.535=0.465) and 53.9% for the never-received FL education group (0.123/0.228=0.539).

Given that both direct and indirect effects are significantly positive and the VAF value is below 80% across all cases, the mediation role is determined to be partial, with the mediation role being complementary due to positive relationships. Therefore, FL and FIC jointly and positively influence FWB, and hypothesis H4 is accepted.

3.8. Multigroup Analysis

One of the study hypotheses tested was to examine the relationships in multigroup to see if there was a significant difference between the groups. This was conducted between those who ever received and never received FL education. Bootstrapping multigroup analysis was therefore conducted to see if the differences are significant. Table 9 below shows the outcome of the multigroup analysis.

These findings indicate that the outcome significantly differs between ever-received and never-received FL education in all analysis fronts. This implies that ever-received and never-received FL education significantly differed in how FL by itself and via FIC affect FWB. The above analysis showed significant differences and positive coefficients, indicating that the pathway appears firmer for those who received FL education except for the FIC effect on FWB. The magnitude favours those who never received an FL education. Additionally, there is a statistically significant difference (p<0.05) in the indirect effect of FL through FIC to FWB, with a positive difference of 0.126. Hence, H5 is accordingly supported. The negative statistical difference does exist in favour of those who never had an FL education. This suggests the effect is more pronounced in favour of those who never had an FL education than those who ever received an FL education.

Wong [67] argued that the assessment coefficient of determination (R2) is significant in structural model evaluation. Thus, the structural model explanatory power was evaluated by assessing the R2. The R2 value indicates the degree of variance in the endogenous construct(s) explained by the exogenous construct(s) [54]. Based on the acceptable fit recommended by Chin [68], R2 values of 0.19, 0.33, and 0.67 are considered weak, moderate, and strong, respectively. From Table 10 above, the result indicates that FL can explain 15% of the variance in FIC, while FL and FIC jointly explain 39.8% of the variance in FWB.

Similarly, the Q2 values indicate how well the path model can predict the original observed data values [69]. Q2 > 0 is needed to confirm predictive relevance [54,70]. Table 10 provides the Q2 value of the endogenous variables. Following Table 10, Q2 values were more significant than zero; thus, the predictive relevance of the model was confirmed. Finally, the effect size (f2) suggests that the effect size of FL on FWB and FIC is smaller than the effect emanating from FIC to FWB.

4. Discussion

Financial literacy (FL) policy remains central in enhancing inclusive and sustainable development because it improves individuals’ FWB. While research has informed policy-makers, the factors influencing FL’s impact and the interplay between these factors and FWB are poorly understood. This paper focused on understanding FI consumption and its linkage with FL and FWB, specifically in rural Ghana, a developing country. The emphasis on rural areas was motivated by the fact that most studies have overlooked these settings. With the advent and widespread use of mobile phones and the Internet, rural areas now have more access to financial news. It is important to explore how this affects finances and the interplay between FI consumption, FL, and FWB.

The study aimed to answer whether FL influences FWB, whether FIC influences FWB, and whether FIC mediates the effect of FL on FWB. Empirical analysis showed that FL influenced FIC, supporting the hypothesis that increasing FL enhances FI consumption in rural settings (H1). Second, the results of this study revealed that the relationship between FIC and FWB is positive and statistically significant in the rural setting. This was expected since adequate consumption of financial information empowers and enriches individual financial decision-making, and it implied an effect on FWB (H2). Additionally, FL was found to be significantly and positively related to FWB, demonstrating that FL is a key determinant of FWB in rural settings. Achieving FL allows individuals to pursue long-term objectives, maintain financial flexibility, and experience financial satisfaction, supporting the hypothesis that increased FL leads to increased FWB (H3).

Furthermore, the study found that FIC mediates the relationship between FL and FWB, demonstrating complementary partial mediation. This suggests that growing FIC is crucial for FL to significantly affect FWB. The findings indicated that obtaining FL is beneficial, but FI consumption is necessary to improve FWB (H4). Multigroup analysis showed that the impact of FI consumption is greater for those who have received FL education compared to those who have not, highlighting the importance of FL education in enhancing FI consumption and, consequently, FWB(H5)

Prior studies have shown a positive relationship between FL and consumption behaviour [71,72]. For example, Fariana, Surindra [71], analyzing the link between FL and consumption behaviour in Indonesia using multiple linear regression, found that FL positively influenced consumptive behaviour, while Koomson, Villano [72] found similar results assessing FL training programmes on household consumption in Ghana employing ordinary least squares. Since consumption depends on information, the finding supports the notion that FL is responsible for FI-seeking behaviour on financial products [25]. Similarly, our study finds that the relationship between FL and FIC is positively related.[73], examining information transparency and FWB in Colombia using multiple regression, found that information transparency improves FWB. Like [73], our study found a significant positive relationship between FIC and FWB using SEM-PLS in rural settings. Our findings support the claim that lack of information consumption affects individuals’ and households’ ability to save to secure a better financial life [27]. The present and prior study’s findings underscore the significance of maintaining awareness of FIC in financial decision-making. The empirical results of our study align with findings from other developing and emerging economies, such as [10] in Nigeria, [12] in India, [4] in South Africa, [74] and [43] in Ghana. All these studies found significant positive relationships between FL and FWB. Additionally, studies like [13] and [43] found that the presence of mediating factors did not distort the significant effect of FL on FWB, consistent with our finding that FI consumption mediates the FL-FWB relationship without distorting it.

The call for increasing the intensity of FL in developing countries is justified [75], especially in rural settings. The empirical results demonstrate that FL alone can improve FWB, but FIC makes it more significant and relevant. The empirical results demonstrate that while FL alone can improve FWB, FI consumption makes this improvement more significant and relevant. This study highlights the criticality of the indirect effect of FI consumption, which is more potent than the direct effect of FL on FWB. This importance confirms the usefulness of interpreting other mediating variables previously identified in prior studies, such as consumption patterns [13], financial behaviour [12], and access to financial services[43]. [13], employing actual pattern consumption as a mediator in Australia using ordered logistic regression, found a consumption pattern to partially mediate the relationship. [12], using financial behaviour as a mediator in India by employing SEM-PLS, found the partial mediating role of financial behaviour in the relationship. [43] used access to financial services to examine the relationship between FL and household income in Ghana by employing a process macro model, and they also found partial mediation. Our findings are also consistent with prior studies. We found partial mediation using FIC as a mediator in the relationship between FL and FWB. Thus affirming [76] conclusion that the relationship between FL and FWB is better for those with regular access to FI. Just as FL can help smooth consumption patterns to reap the benefit of FWB [13], FL helps smoothen FIC to achieve the desired goal of FWB of rural households. The disaggregated data into ever and never-received FL education findings further demonstrated the importance of financial education. The magnitude of impact for those who had ever received FL education was more than twice that of those who had never received FL education before. Hence, the recent calls for government and development partners to increase investment in FL education further strengthen the situation [77].

In contrast, [78] analysis, using information source preference and FL in Malaysia, found that information consumption through media and family & peers showed a negative relationship with FL. This finding deviates from current and prior studies to the extent that they found a negative significant relationship. They argued that family & peers are suboptimal options for financial information, and the ineffective nature of FI transmission in the media would have accounted for this. They concluded that consumers should be careful about their financial information sources. Similarly, [79] analysis in the USA using National Financial Capability Study data by employed objective financial literacy and financial satisfaction evidence showed that objective financial knowledge negatively impacted financial satisfaction. Their measurement lacks multidimensionality as the concepts, which might have occasioned this relationship.

On the contrary, this study accounted for multidimensionality and thus showed a positive relationship supporting theory. Like other direct relationships, the difference in effect in the relationship between FIC and FWB favours never received. This outcome could be deduced that overconfidence in FIC on the part that ever-received FL education might have exceeded the optimal level, and the excessive flow of FI may have affected judgement. Hence, the impact of FL education on the relationship is weakened. This finding agrees with the conclusion by [7] that having some level of financial ignorance is optimal in financial decision-making.

5. Study Summary, Implication and Recommendations

5.1. Summary

This study explored the role of financial information consumption (FIC) in the relationship between financial literacy (FL) and financial well-being (FWB) in rural Ghana. Using a structural equation model, the study illuminated the importance of FL and FIC as key determinants of FWB in rural contexts. It found that FL enhances FWB both directly and through its interaction with FIC. However, FL alone is insufficient; FIC plays a crucial role, and receiving FL education significantly mediates the link between FL and FWB. The findings imply that rural individuals must combine FL with FIC to improve their FWB effectively. Financially literate individuals benefit from consuming financial information to set realistic financial goals and make informed decisions. FIC supports overall well-being by helping individuals stay on track and make necessary adjustments to achieve their financial objectives. Thus, both FL and FIC are essential for assessing and improving FWB in rural settings.

5.2. Study Implications

The study highlights that receiving FL education is vital for mediating the FL-FWB relationship in rural areas. Rural residents who have received FL education are better at utilizing their financial knowledge to consume FI and enhance their FWB. Financial educators and advisors should emphasize the role of FIC in improving FWB and integrate it into financial education programs. Regular seminars, workshops, and training sessions organized by NGOs, governments, and financial institutions can help raise awareness and optimize the use of FI. Governments should support these educational efforts to align with the Sustainable Development Goals (SDGs).

5.3. Recommendations for Further Research

Future studies should investigate additional characteristics of financial information, such as consumption patterns, sources, and quality, to understand their impact on FWB. Researchers should also consider modeling multiple dimensions of financial information as higher-order constructs (HOC) to capture a broader perspective and enhance understanding.

Author Contributions

This article’s development and writing have benefited greatly from the contributions of each listed author.

Funding

No organization provided the authors with funding support for the paper submitted.

Inform Consent Statement

Informed consent was obtained from all subjects involved in the study.

Ethical Approval and Data Availability Statement

The paper literature used previously published works that were properly cited, and the raw data was gathered per ethical clearance obtained from the University of Kwa Zulu Natal Research Ethical Board with approval number HSSREC/00006314/2023. The ethical requirements guided the data availability and are available from the corresponding author [Peter Kwame Kuutol] on request.

Conflict of Interest

The authors declare no conflict of interest.

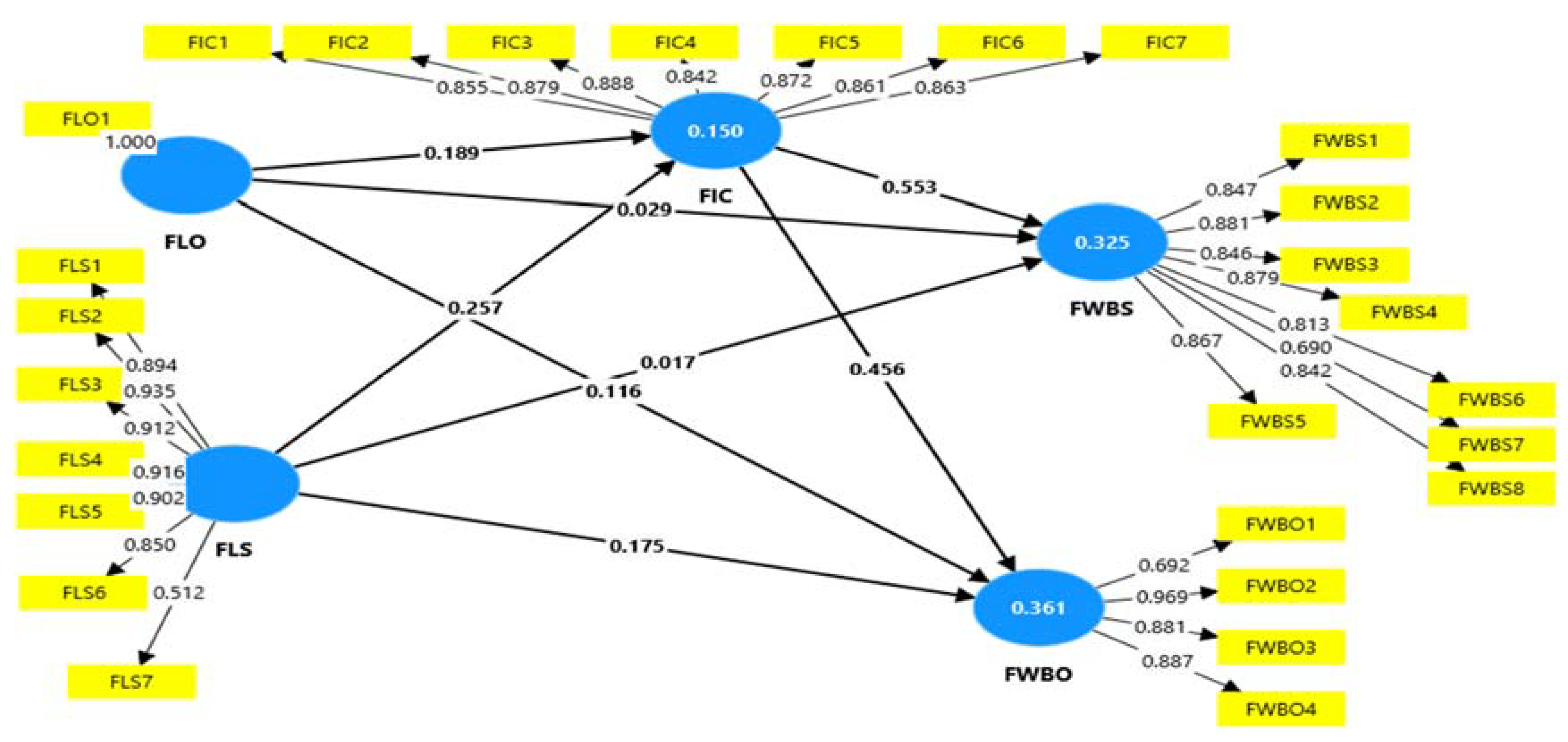

Appendix 1: Path model for the LOC of this study.

Figure 2.

Path Model Used for LOC- SEM-PLS.

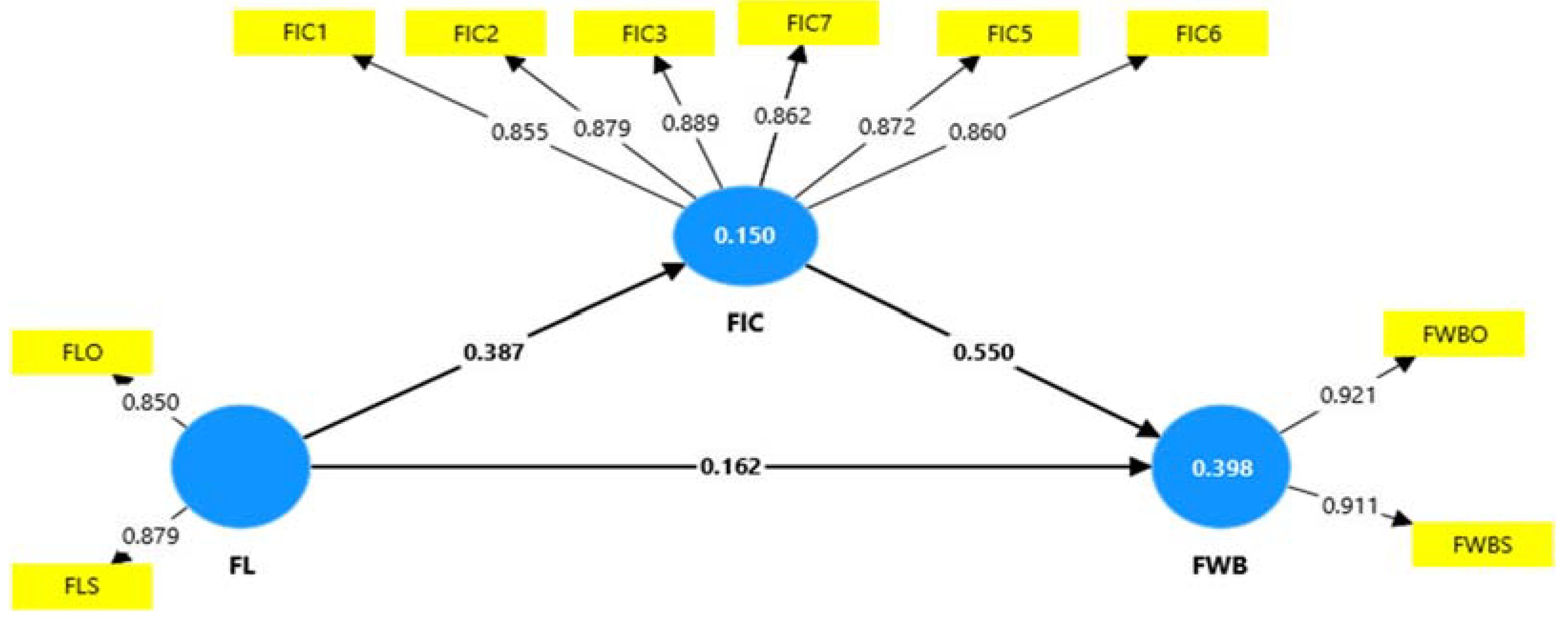

Appendix 2: Path Model Used for HOC- SEM-PLS

Figure 3.

Path Model Used for HOC- SEM-PLS.

References

- Lusardi, A. and O. S. Mitchell, How ordinary consumers make complex economic decisions: Financial literacy and retirement readiness. Quarterly Journal of Finance 2017, 7, 1750008. [Google Scholar] [CrossRef]

- Klapper, L. and A. Lusardi, Financial literacy and financial resilience: Evidence from around the world. Financial Management 2020, 49, 589–614. [Google Scholar] [CrossRef]

- Chabaefe, N.N. and A. Qutieshat, Financial Literacy, Financial Education and Financial Experience: Conceptual Framework. International Journal of Economics and Financial Issues 2024, 14, 44–55. [Google Scholar] [CrossRef]

- Akande, J. , et al., Financial literacy and inclusion for rural agrarian change and sustainable livelihood in the Eastern Cape, South Africa. Heliyon 2023, 9. [Google Scholar] [CrossRef] [PubMed]

- Koomson, I. , et al., Effect of financial literacy on poverty reduction across Kenya, Tanzania, and Uganda. Global Social Welfare 2023, 10, 93–103. [Google Scholar] [CrossRef]

- De Beckker, K., K. De Witte, and G. Van Campenhout, Identifying financially illiterate groups: An international comparison. International Journal of Consumer Studies 2019, 43, 490–501. [Google Scholar] [CrossRef]

- Lusardi, A., P. -C. Michaud, and O.S. Mitchell, Optimal financial knowledge and wealth inequality. Journal of political Economy 2017, 125, 431–477. [Google Scholar] [CrossRef]

- Sousa-Ribeiro, M. , et al. , To work after retirement: a qualitative study among mental health nursing assistants. Nordic Psychology 2024, 1–27. [Google Scholar] [CrossRef]

- Español, R.D., J. T. Miñoza, and L. Zosa, Financial literacy and entrepreneurial behavior of Junior high school students: Basis for TLE management plan. Ho Chi Minh City Open University Journal of Science-Economics and business Administration 2024, 14. [Google Scholar] [CrossRef]

- Sajuyigbe, A.S. , et al., The interplay of financial literacy on the financial behavior and well-being of young adults: Evidence from Nigeria. Jurnal Ilmu Ekonomi Terapan Vol 2024, 9, 120–136. [Google Scholar] [CrossRef]

- Lusardi, A. and F. -A. Messy, The importance of financial literacy and its impact on financial wellbeing. Journal of Financial Literacy and Wellbeing 2023, 1, 1–11. [Google Scholar]

- Sehrawat, K., M. Vij, and G. Talan, Understanding the path toward financial well-being: evidence from India. Frontiers in psychology 2021, 12, 638408. [Google Scholar] [CrossRef]

- Xue, R. , et al., Financial well-being amongst elderly Australians: the role of consumption patterns and financial literacy. Accounting & Finance 2020, 60, 4361–4386. [Google Scholar] [CrossRef]

- Matey, J. , Financial Literacy and Consumer Financial Well-being in Ghana: Any Nexus with Economic Stability? International Journal of Arts and Humanities Studies (IJAHS) 2021, 1, 14–22. [Google Scholar] [CrossRef]

- Niţoi, M. , et al., Financial Well-Being and Financial Literacy in Romania. Institute for World Economy Working Paper, 2022.

- Riitsalu, L. , et al. , From security to Freedom—The meaning of Financial Well-being changes with age. Journal of family and economic issues 2024, 45, 56–69. [Google Scholar] [CrossRef]

- Schmidtke, K.A. , et al. , A Randomized Controlled Trial to Evaluate Interventions Designed to Improve University Students’ Subjective Financial Wellness in the United Kingdom. Journal of Financial Counseling and Planning 2020, 31, 296–312. [Google Scholar]

- Ponchio, M.C., R. A. Cordeiro, and V.N. Gonçalves, Personal factors as antecedents of perceived financial well-being: evidence from Brazil. International Journal of Bank Marketing 2019, 37, 1004–1024. [Google Scholar] [CrossRef]

- Richards, D.W., A. D. Ahmed, and M.S. Tahir, Addressing the Challenge of Problematic Debt: Australia and Eurozone. 2019.

- Utkarsh, et al. , Catch them young: Impact of financial socialization, financial literacy and attitude towards money on financial well-being of young adults. International Journal of Consumer Studies 2020, 44, 531–541. [CrossRef]

- Lone, U.M. and S.A. Bhat, Impact of financial literacy on financial well-being: a mediational role of financial self-efficacy. Journal of Financial Services Marketing 2024, 122–137. [Google Scholar] [CrossRef]

- Riitsalu, L. and R. Murakas, Subjective financial knowledge, prudent behaviour and income: The predictors of financial well-being in Estonia. International Journal of Bank Marketing 2019, 37, 934–950. [Google Scholar] [CrossRef]

- Nanda, A.P. and R. Banerjee, Consumer’s subjective financial well-being: A systematic review and research agenda. International Journal of Consumer Studies 2021, 45, 750–776. [Google Scholar] [CrossRef]

- Pahlevan Sharif, S. and N. Naghavi, Family financial socialization, financial information seeking behavior and financial literacy among youth. Asia-Pacific Journal of Business Administration 2020, 12, 163–181. [Google Scholar] [CrossRef]

- Barbić, D., A. Lučić, and J. M. Chen, Measuring responsible financial consumption behaviour. International journal of consumer studies 2019, 43, 102–112. [Google Scholar] [CrossRef]

- Mian, T.S. , Examining the level of financial literacy among Saudi Investors and its impact on Financial Decisions. International Journal of Accounting and Financial Reporting 2014, 4, 312–328. [Google Scholar] [CrossRef]

- Lusardi, A. , Household saving behavior: The role of financial literacy, information, and financial education programs. 2008c, National Bureau of Economic Research. [CrossRef]

- Yeh, T.-m. , An empirical study on how financial literacy contributes to preparation for retirement. Journal of Pension Economics & Finance 2022, 21, 237–259. [Google Scholar]

- Kienzler, M., D. Västfjäll, and G. Tinghög, Individual differences in susceptibility to financial bullshit. Journal of Behavioral and Experimental Finance 2022, 34, 100655. [Google Scholar] [CrossRef]

- Keister, L.A. and L. Wei, Chinese Wealth Inequality: Housing, Financial Assets, and the Emergence of a Wealthy Elite, in SOCIAL INEQUALITY IN CHINA. 2023, World Scientific. p. 283-315. [CrossRef]

- Zia-ur-Rehman, M. , et al. , How perceived information transparency and psychological attitude impact on the financial well-being: mediating role of financial self-efficacy. Business Process Management Journal 2021. [Google Scholar] [CrossRef]

- Asandimitra, N. and A. Kautsar, The influence of financial information, financial self efficacy, and emotional intelligence to financial management behavior of female lecturer. Humanities & Social Sciences Reviews 2019, 7, 1112–1124. [Google Scholar] [CrossRef]

- Lusardi, A. , Financial literacy and the need for financial education: evidence and implications. Swiss Journal of Economics and Statistics 2019, 155, 1–8. [Google Scholar] [CrossRef]

- Bottazzi, L. and A. Lusardi, Stereotypes in financial literacy: Evidence from PISA. Journal of Corporate Finance 2021, 71, 101831. [Google Scholar] [CrossRef]

- Lusardi, A., A. Hasler, and P.J. Yakoboski, Building up financial literacy and financial resilience. Mind & Society 2021, 20, 181–187. [Google Scholar] [CrossRef]

- Conrad, C., Z. Enders, and A. Glas, The role of information and experience for households’ inflation expectations. European Economic Review 2022, 143, 104015. [Google Scholar] [CrossRef]

- Tolchah, M. and M.A. Mu’ammar, Islamic Education in the Globalization Era. Humanities & Social Sciences Reviews 2019, 7, 1031–1037. [Google Scholar]

- Tchamyou, V.S. , The role of information sharing in modulating the effect of financial access on inequality. Journal of African Business 2019, 20, 317–338. [Google Scholar] [CrossRef]

- Bianchi, M. , Financial literacy and portfolio dynamics. The Journal of Finance 2018, 73, 831–859. [Google Scholar] [CrossRef]

- Lusardi, A. and O.S. Mitchell, The economic importance of financial literacy: Theory and evidence. Journal of economic literature 2014, 52, 5–44. [Google Scholar] [CrossRef]

- Limbu, Y.B. and S. Sato, Credit card literacy and financial well-being of college students: A moderated mediation model of self-efficacy and credit card number. International Journal of Bank Marketing 2019, 37, 991–1003. [Google Scholar] [CrossRef]

- Greenberg, A.E. and H.E. Hershfield, Financial decision making. Consumer Psychology Review 2019, 2, 17–29. [Google Scholar] [CrossRef]

- Twumasi, M.A. , et al., The Mediating Role of Access to Financial Services in the Effect of Financial Literacy on Household Income: The Case of Rural Ghana. Sage Open 2022, 12, 21582440221079921. [Google Scholar] [CrossRef]

- Selvia, G. , et al., The Effect of Financial Knowledge, Financial Behavior and Financial Inclusion on Financial Well-being. 2021.

- Ferrada, L.M. and V. Montaña, Inclusion and financial literacy: The case of higher education student workers in Los Lagos, Chile. Estudios Gerenciales 2022, 38, 211–221. [Google Scholar] [CrossRef]

- Fu, J. , Ability or opportunity to act: What shapes financial well-being? World Development 2020, 128, 104843. [Google Scholar] [CrossRef]

- Grable, J.E. and S.-H. Joo, A snapshot view of the help-seeking market. Journal of Financial planning 2003, 16, 88. [Google Scholar]

- Hasibuan, B.K., Y. M. Lubis, and W.A. HR. Financial literacy and financial behavior as a measure of financial satisfaction. in 1st Economics and Business International Conference 2017 (EBIC 2017). 2018. Atlantis Press. [CrossRef]

- Kaur, G., M. Singh, and S. Gupta, Analysis of key factors influencing individual financial well-being using ISM and MICMAC approach. Quality & Quantity 2023, 57, 1533–1559. [Google Scholar]

- Service, G.S. , Ghana Living Standards Survey Round 6 (GLSS 6). 2015, Ghana Statistical Serivce: Accra:Ghana.

- Koomson, I., R. A. Villano, and D. Hadley, The role of financial literacy in households’ asset accumulation process: evidence from Ghana. Review of Economics of the Household 2022, 1-24. [CrossRef]

- Service, G.S. Ghana 2021 Population and Housing Census: Prelimenary Report. 2021, Ghana Statistical Service: Accra:Ghana.

- Service, G.S. , Ghana Living Standards Survey Report (GLSS 7). G: 2020, Ghana Statistical Service: Accra:Ghana, 2020. [Google Scholar]

- Hair, J.F. , et al. , When to use and how to report the results of PLS-SEM. European business review 2019, 31, 2–24. [Google Scholar] [CrossRef]

- Lusardi, A. and O. S. Mitchell, Financial literacy around the world: an overview. Journal of pension economics & finance 2011, 10, 497–508. [Google Scholar] [CrossRef]

- Vieira, K.M. , Júnior, F.; Potrich, A.C.G. Measuring financial literacy: Proposition of an instrument based on the Item Response Theory. Ciência E Nat 2020, 42, 38. [Google Scholar] [CrossRef]

- Comerton-Forde, C. , et al., Measuring financial wellbeing with self-reported and bank record data. Economic Record 2022, 98, 133–151. [Google Scholar] [CrossRef]

- Prawitz, A. , et al. InCharge financial distress/financial well-being scale: Development, administration, and score interpretation. Journal of Financial Counseling and Planning 2006, 17. [Google Scholar]

- Higgins, T.; Roberts, S. Financial wellbeing, actions and concerns-preliminary findings from a survey of elderly Australians. in Sydney, ON: Institute of Actuaries of Australia Biennial Convention. 2011. Citeseer.

- Hair, J.; Alamer, A. Partial least squares structural equation modeling (PLS-SEM) in second language and education research: Guidelines using an applied example. Research Methods in Applied Linguistics 2022, 1, 100027. [Google Scholar] [CrossRef]

- Latif, K.F.; Baloch, Q.B. Role of Internal Service Quality (ISQ) in the relationship between Internal Marketing and Organizational Performance. Abasyn University Journal of Social Sciences 2015, 8. [Google Scholar]

- Van Griethuijsen, R.A. , et al. Global patterns in students’ views of science and interest in science. Research in science education 2015, 45, 581–603. [Google Scholar] [CrossRef]

- Priyatno, D. Independent learning data analysis with SPSS; Bandung: MediaKom, 2013. [Google Scholar]

- Fornell, C.; Larcker, D.F. , Evaluating structural equation models with unobservable variables and measurement error. Journal of marketing research 1981, 18, 39–50. [Google Scholar] [CrossRef]

- Chin, W.W. , How to write up and report PLS analyses, in Handbook of partial least squares: Concepts, methods and applications. 2009, Springer. p. 655-690.

- Henseler, J. , Ringle, C.M.; Sarstedt, M. A new criterion for assessing discriminant validity in variance-based structural equation modeling. Journal of the academy of marketing science 2015, 43, 115–135. [Google Scholar] [CrossRef]

- Wong, K.K.-K. Mediation analysis, categorical moderation analysis, and higher-order constructs modeling in Partial Least Squares Structural Equation Modeling (PLS-SEM): A B2B Example using SmartPLS. Marketing Bulletin 2016, 26, 1–22. [Google Scholar]

- Chin, W.W. The partial least squares approach to structural equation modeling. Modern methods for business research 1998, 295, 295–336. [Google Scholar]

- Akter, S.; D’ambra, J.; Ray, P. An evaluation of PLS based complex models: the roles of power analysis, predictive relevance and GoF index. in Seventeenth Americas Conference on Information Systems. 2011. Detroit, Michigan.

- Henseler, J., C. M. Ringle, and R.R. Sinkovics, The use of partial least squares path modeling in international marketing, in New challenges to international marketing. 2009, Emerald Group Publishing Limited. p. 277-319.

- Fariana, R.E. , Surindra, B. ; Arifin, Z. The influence of financial literacy, lifestyle and self-control on the consumption behavior of economic education student. International Journal of Research and Review 2021, 8, 496–503. [Google Scholar] [CrossRef]

- Koomson, I. ,Villano, R.A.; Hadley, D. Accelerating the impact of financial literacy training programmes on household consumption by empowering women. Applied Economics 2021, 53, 3359–3376. [Google Scholar] [CrossRef]

- Losada-Otálora, M. and L.Alkire, Investigating the transformative impact of bank transparency on consumers’ financial well-being. International Journal of Bank Marketing 2019, 37, 1062–1079. [Google Scholar] [CrossRef]

- Adam, A.M. , Frimpong, S. ; Boadu, M.O. Financial literacy and financial planning: Implication for financial well-being of retirees. Business & Economic Horizons 2017, 13, 224–236. [Google Scholar]

- Karakurum-Ozdemir, K., M. Kokkizil, and G. Uysal, Financial literacy in developing countries. Social Indicators Research 2019, 143, 325–353. [Google Scholar] [CrossRef]

- Huston, S.J. Measuring financial literacy. Journal of consumer affairs 2010, 44, 296–316. [Google Scholar] [CrossRef]

- Blay, M.W. , et al., Determinants of Financial Literacy and its Effect on Stock Market Participation among University Students in Ghana. International Journal of Economics and Financial Issues 2024, 14, 15–25. [Google Scholar] [CrossRef]

- Sabri, M.F. and E.C.-X. Aw, Financial literacy and related outcomes: The role of financial information sources. International journal of business and society 2019, 20, 286–298. [Google Scholar]

- Robb, C.A. , et al. The influence of student loan debt on financial satisfaction. Journal of Family and Economic Issues 2019, 40, 51–73. [Google Scholar] [CrossRef]

Figure 1.

Analytical Framework. Source: Own Compilation.

Table 1.

Descriptive Statistics of Respondents.

| Category | Frequency | Percent (%) | |

|---|---|---|---|

| Gender | Female | 29 | 4.4 |

| Male | 634 | 95.6 | |

| Age bracket | 18-19 | 26 | 3.9 |

| 20-29 | 152 | 22.9 | |

| 30-39 | 168 | 25.3 | |

| 40-49 | 115 | 17.3 | |

| 50-59 | 81 | 12.2 | |

| 60+ | 121 | 18.3 | |

| Retiree | No | 534 | 80.5 |

| Yes | 129 | 19.5 | |

| Marital Status | Single | 64 | 9.7 |

| Married | 467 | 70.4 | |

| Divorced | 41 | 6.2 | |

| Separated | 40 | 6.0 | |

| Window/widower | 51 | 7.7 | |

| Working Sector | Agric-Self employed | 489 | 73.8 |

| Trading-self employed | 79 | 11.9 | |

| Formal Sector-Public | 33 | 5.0 | |

| Formal Sector-Private | 9 | 1.4 | |

| Unemployed | 53 | 8.0 | |

| Accommodation Status’ | A rented Residence | 110 | 16.6 |

| My own Residence | 302 | 45.6 | |

| My parents’ Residence | 222 | 33.5 | |

| Institution provided Residence | 29 | 4.4 | |

| Receive financial literacy education | No | 356 | 53.7 |

| Yes | 307 | 46.3 | |

Table 2.

Reliability and Validity of Indicators and Constructs.

| Indicators | Loadings | Alpha | CR | AVE |

|---|---|---|---|---|

| Compare Price of goods <- FLS | 0.894 | |||

| Money management expectation <- SFLS | 0.935 | 0.934 | 0.940 | 0.735 |

| Check ability to pay <- FLS | 0.912 | |||

| Save to reach financial goal <- FLS | 0.916 | |||

| Have enough reserve for monthly expenses <- FLS | 0.902 | |||

| Consider options for financial decisions <- FLS | 0.850 | |||

| Ability to identify the cost for taking credit <- FLS | 0.512 | |||

| Encountered payment problems monthly <- FWBO | 0.692 | 0.880 | 0.885 | 0.745 |

| Lack of money to spend <- FWBO | 0.969 | |||

| Excess spending over income <- FWBO | 0.881 | |||

| Sufficient savings for period <- FWBO | 0.887 | |||

| Level of financial distress <- SFWB | 0.847 | 0.937 | 0.945 | 0.697 |

| Satisfaction with present financial situation <- FWBS | 0.881 | |||

| Feeling about current financial situation <- FWBS | 0.846 | |||

| Ability to meet monthly expense <- FWBS | 0.879 | |||

| Confident to meet financial situation <- FWBS | 0.867 | |||

| Ability to afford socialization cost <- FWBS | 0.813 | |||

| Living paycheck to paycheck <- FWBS | 0.690 | |||

| Stress on personal finances <- FWBS | 0.842 | |||

| Have sufficient financial information <- FIC | 0.855 | 0.944 | 0.947 | 0.750 |

| Have information to plan income and expenses <- FIC | 0.879 | |||

| Have information for financial possibilities <- FIC | 0.888 | |||

| Look for relevant information on buying decisions <- FIC | 0.842 | |||

| Seek person financial management information <- FIC | 0.872 | |||

| Follow financial information that affects daily life <- FIC | 0.861 | |||

| Availability of financial information is easy to understand <- FIC | 0.863 | |||

| FLO= Objective Financial Literacy, FLS= Subjective Financial Literacy, FWBO = Objective Financial Well-Being, FWBS = Subjective Financial Well-Being, and FIC = Financial Information Consumption | ||||

Table 3.

Heterotriat-Monotriat (HTMT) for Discriminant Validity.

| Constructs | FIC | FLS | FWBO | FWBS |

|---|---|---|---|---|

| FIC | ||||

| FLS | 0.362 | |||

| FWBO | 0.597 | 0.426 | ||

| FWBS | 0.596 | 0.231 | 0.723 |

Table 4.

Fornell and Larker’s Criterion (FLC) for Discriminant Validity.

| Construct | FIC | FLS | FWBO | FWBS |

| FIC | 0.866 | |||

| FLS | 0.351 | 0.857 | ||

| FWBO | 0.554 | 0.392 | 0.863 | |

| FWBS | 0.569 | 0.226 | 0.679 | 0.835 |

Table 5.

Reliability and Construct Validity.

| Indicator | Loadings | Alpha | CR | AVE |

| Objective Financial Literacy (FLO) <- FL | 0.850 | 0.664 | 0.668 | 0.748 |

| Subjective Financial Literacy (FLS) <- FL | 0.879 | |||

| Objective Financial Well-being (FWBO) <- FWB | 0.921 | 0.808 | 0.810 | 0.839 |

| Subjective Financial Well-being (FWBS) <- FWB | 0.911 | |||

| Have sufficient financial information <- FIC | 0.855 | 0.944 | 0.947 | 0.750 |

| Have information to plan income and expenses <- FIC | 0.879 | |||

| Have information for financial possibilities <- FIC | 0.889 | |||

| Look for relevant information on buying decisions <- FIC | 0.841 | |||

| Seek person financial management information <- FIC | 0.872 | |||

| Follow financial information that affects daily life <- FIC | 0.860 | |||

| Availability of financial information is easy to understand <- FIC | 0.862 | |||

| FL= Financial Literacy, FWB = Financial Well-Being, and FIC = Financial Information Consumption | ||||

Table 6.

Discriminant Validity.

| HTMT | FLC | |||||

|---|---|---|---|---|---|---|

| Indicator | FIC | FL | FWB | FIC | FL | FWB |

| FIC | 0.866 | |||||

| FL | 0.484 | 0.387 | 0.865 | |||

| FWB | 0.698 | 0.507 | 0.613 | 0.375 | 0.916 | |

Table 7.

Direct Relationship.

| Hypotheses | Decision | Coef | T stat | P values | Percentile Bootstrap 95% Confidence Interval | |

| Complete | Lower | Upper | ||||

| H1: FL -> FIC | Accepted | 0.387 | 10.980 | 0.000 | 0.330 | 0.446 |

| H2: FIC -> FWB | Accepted | 0.550 | 18.573 | 0.000 | 0.501 | 0.599 |

| H3: FL -> FWB | Accepted | 0.162 | 5.011 | 0.000 | 0.110 | 0.216 |

| Ever-Received FL Education | ||||||

| H1: FL -> FIC | Accepted | 0.480 | 10.385 | 0.000 | 0.403 | 0.555 |

| H2: FIC -> FWB | Accepted | 0.519 | 12.238 | 0.000 | 0.448 | 0.588 |

| H3: FL -> FWB | Accepted | 0.286 | 6.011 | 0.000 | 0.208 | 0.364 |

| Never-Received FL Education | ||||||

| H1: FL -> FIC | Accepted | 0.596 | 16.385 | 0.000 | 0.536 | 0.656 |

| H2: FIC -> FWB | Accepted | 0.207 | 3.645 | 0.000 | 0.119 | 0.303 |

| H3: FL -> FWB | Accepted | 0.105 | 2.397 | 0.008 | 0.035 | 0.177 |

Table 8.

Mediating role of financial information Consumption.

| Complete | Ever-Received FL Education | Never-Received FL Education | |||||||

| hypotheses | Coef | T stat |

P values | Coef | T stat |

P values | Coef | T stat |

P values |

| Specific Indirect Effect | |||||||||

| H4: FL -> FIC -> FWB | 0.213 | 9.726 | 0.000 | 0.249 | 8.262 | 0.000 | 0.123 | 3.564 | 0.000 |

| Direct Effect | |||||||||

| FL -> FWB | 0.162 | 5.011 | 0.000 | 0.286 | 6.011 | 0.000 | 0.105 | 2.397 | 0.008 |

| Total Effect | |||||||||

| FL -> FWB | 0.375 | 10.772 | 0.000 | 0.535 | 12.468 | 0.000 | 0.228 | 4.286 | 0.000 |

Table 9.

Multigroup Analysis.

| Hypothesis | Difference | p-Value | |

| Decision | (Ever Received-Never Received) | ||

| H5: FL -> FIC -> FWB | Accepted | 0.126 | 0.003* |

| FIC -> FWB | -0.116 | 0.024* | |

| FL -> FIC | 0.312 | 0.000* | |

| FL -> FWB | 0.181 | 0.003* |

Note: *The differences are significant in the relationship between the two groups (p<0.05).

Table 10.

Coefficient of Determination (R2), Predictive Relevance (Q2) and Effect size (f2).

| R2 | R2 Adjusted | Q2 | f2 | ||

| FIC | FWB | ||||

| FIC | 0.150 | 0.148 | 0.145 | 0.427 | |

| FWB | 0.398 | 0.396 | 0.136 | ||

| FL | 0.176 | 0.037 | |||

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Copyright: This open access article is published under a Creative Commons CC BY 4.0 license, which permit the free download, distribution, and reuse, provided that the author and preprint are cited in any reuse.