Submitted:

31 August 2024

Posted:

03 September 2024

You are already at the latest version

Abstract

The small business sector in Kazakhstan demonstrates dynamic growth, but its sustainable development in modern conditions requires activation from government agencies, society and entrepreneurs themselves

The purpose of the article is to study the development of small entrepreneurship in Kazakhstan and develop a mechanism for sustainable development based on network interaction "business entities - society-state" with the identification of priority areas of development based on a rating approach.

The methods of bibliographic analysis of scientific literature, statistical, correlation analysis, survey, comparative analysis, ranking based on data normalization were used.

The results revealed the need to formalize indicators of sustainable development of the small business sector in strategic development programs; create conditions, support, explain the importance and prospects of investing in sustainable innovations by small businesses; form a balanced strategy for achieving carbon neutrality based on network interaction "business entities - society-state" with the identification of priority areas of development based on a rating approach to ensure transparency and publicity of decisions made.

Conclusions are made about the need to popularize sustainable development among business entities, stimulate investment activity through government participation, legislative regulation of public presentation of non-financial reporting, and assist society in the formation of an ESG culture.

Keywords:

small business

; Kazakhstan

; sustainable development

; ESG

; responsible investment

; network interaction “business entities – society – state”

1. Introduction

The growing relevance of sustainable development is caused by the ongoing climate transformation in the world - extreme meteorological, climatic and hydrological events caused or provoked by anthropogenic factors. This necessitates economic restructuring to achieve carbon neutrality. The small business sector is a driving force in any country with a market economy.

In the development of the ESG agenda, Kazakhstan demonstrates trends typical for most countries. As of 2023, the country ranked 66th out of 163 in the SDG ranking. It was found that an average of 81 percent of state budget funds were allocated to achieve the SDGs, but only 58.6 percent of targets received funding. This indicates a potential mismatch between budget allocation and goal prioritization (UNDP, 2024). And, while the large Kazakhstani entrepreneurship sector demonstrates successful experience in implementing the principles of sustainable development, responsible investment, and public presentation of financial statements, this initiative is not mandatory for the small business sector. At the same time, it cannot be said that insufficient attention is paid to the development of small business in Kazakhstan. The republic has adopted the "Concept for the Development of Small and Medium-Sized Entrepreneurship until 2030". The small and medium-sized enterprise (SME) sector plays a key role in the innovative development of Kazakhstan. Statistical results for the period from 2015 to 2022 indicate stable GDP growth due to the SME sector (Adilet, 2022). The share of SMEs in the structure of Kazakhstan's GDP in 2022 was 33.5% (Adilet, 2022), in 2015 24.9% (Buribaeva et. al., 2020), the increase over the period was 8.6%.

Sustainable development of Kazakhstan's small business should be carried out with close cooperation between the state, business entities and society. Despite the growth of Kazakhstan's indicators in the field of small business development, qualitative changes that take into account social, economic and environmental processes are required to ensure a further positive impact on economic diversification, the realization of export potential and the sustainability of long-term economic growth of the country. The main parameters of the strategic development of Kazakhstan's SMEs are associated with an increase in the number of people employed, an increase in the share of GDP, and an increase in labor productivity and investment. At the same time, building up entrepreneurial potential does not focus on achieving a climate-neutral, resource-efficient and flexible digital economy. Further sustainable development should be carried out on the basis of active network interaction of stakeholders "business entities - society-state".

State support for small businesses should stimulate the implementation of initiatives that contribute to the sustainable development of sectors of the national economy. The limited budget funds and the need to improve the efficiency of their use require support for entrepreneurial initiatives that contribute to sustainable development.

EU countries demonstrate active involvement in the promotion of sustainable development. In the context of sustainable development, the European Union has adopted a number of strategic documents aimed at supporting and developing small and medium-sized businesses. The main principles of SME development in Europe focus on capacity building and supporting the transition to sustainable development and digitalization, reducing the regulatory burden and improving access to finance. The dynamics of the dominant influence of the SME sector are typical for all developed Western countries. 24 million European SMEs represent 99% of all EU enterprises (SMEs in Europe, 2024). In the structure of European GDP, the share of small and medium-sized businesses varies around 60% (EPP group, 2024). The purpose of the article is to study the development of small entrepreneurship in Kazakhstan and to develop a mechanism for sustainable development based on the network interaction of "business entities - society-state" with the identification of priority areas for development based on the rating approach.

Maintaining the trajectory of sustainable growth of small entrepreneurship through the development and establishment of partnerships is aimed at solving the business problem of increasing the efficiency of public investment. Understanding the need to support the sustainable development of SMEs requires the active assistance of all stakeholders. Integration of social, environmental, financial goals in the activities of business entities requires a change in approaches to its management. Socially responsible business becomes a philosophy that forms the architecture of interaction between all stakeholders, with the active participation of society in order to create civil control.

Approaches to doing business require rethinking, the use of state support and promotion measures for the sustainable economic development of small entrepreneurship in the Republic of Kazakhstan.

The structure of the article includes an analysis of regulatory documents on the strategic development of small entrepreneurship in Kazakhstan, identifying key indicators for building entrepreneurial potential within the framework of its sustainable development, the presence of formalized indicators. In order to identify development trends in the small business sector since the adoption of the SDGs in 2015, a chronological assessment of the dynamics of key indicators of small business development in Kazakhstan for 2015-2023 was conducted based on statistical data, including an assessment of costs (investments) in environmental protection. To understand the attitude of small businesses to the ideas of sustainable development, a survey was conducted among individual entrepreneurs, heads of limited liability partnerships, and peasant farms. Achieving the effectiveness of sustainable development is possible with a clear understanding of development priorities by all stakeholders, and the presence of feedback between them. In order to identify significant areas of sustainable development, stakeholders (representatives of business, government, society) were asked within the survey to assess the significance of "forms/directions" of sustainable development that allow for increased efficiency of small businesses. Determining priorities allows for an assessment of the significant areas of each stakeholder; understanding, the presence of disagreements, consistency of views on promoting the concept of sustainable development; implementing (adjusting) the budget of public funds for investing in the sustainable development of small businesses, taking into account network interaction.

2. Literature Review

The concept of sustainable development is a relevant area of modern scientific thought. A current trend in business development is the ESG policy, which involves the implementation and adherence to ESG principles (Divaeva, 2022). The United Nations has formulated 17 Sustainable Development Goals (SDGs), which serve as a guideline for the strategic development of territories. The ESG concept reflects the ideas of sustainable development for building the future of individual countries and the world as a whole.

Compliance with social and environmental SDGs affects compliance with economic SDGs, which supports the efforts that the country makes to comply with such (Del-Aguila-Arcentales et al., 2022). Compliance with economic SDGs affects the competitiveness of the country. In environmental terms, entrepreneurship helps reduce carbon emissions and promotes sustainable business practices (Elmonshid & Sayed, 2024).

To support SMEs, the European Union has developed an SME Strategy for a Sustainable and Digital Europe (Mrochkovskiy, 2022). The key principles of this strategy are: removing regulatory and practical barriers to doing business; improving access to finance; supporting the transition to sustainable development and digitalization.

According to Eurostat, up to 90% of enterprises trading in Europe are small and medium-sized businesses, 70% of which are microenterprises with up to 9 employees. SMEs employ 67% of the employed population in Europe, and the added value they create per year is estimated at 3.9 trillion euros. It is small businesses that create a field for healthy competition, provide jobs and pay taxes (OSDP, 2024).

Some authors note the particular importance of pursuing ESG goals for financial firms, since their business is critically dependent on customer loyalty, which is positively dependent on reputation (Ovechkin, 2021). A study (Gomes & Pinho, 2023) on the commitment of European SMEs to SDG 12 found that SMEs' implementation of resource efficiency actions at the micro level had a positive impact on the adoption of macro-level decarbonization measures. Well-planned strategies of small businesses can address environmental and social issues, and integrating the development of planned and new strategies can enable small firms to align core business goals with sustainable development goals (Luederitz et al., 2021, Ayyagari et al., 2007). Lack of government and organizational support are identified as the main barriers to sustainability practices in SMEs (Kumar, 2022). The environmental management system in Kazakhstan is regulated at three levels - international, national and organizational (Zarubina et al., 2022).

Small and medium-sized enterprises can be a decisive force in the fight against climate change and the promotion of green thinking and sustainable development (Korneeva et al., 2021). Today, ESG is a factor in investment decisions, which contributes to the active participation of the large business sector in promoting the concept of sustainable development.

Government support during the corona crisis for SMEs and the use of government feedback through the mitigation measures applied. provides more support in the form of direct subsidies (Sujová & Kupčák, 2024). Such support helps SMEs overcome financial problems due to reduced sales and liquidity.

The study (Wang et al., 2022) notes that when firms benefiting from tax incentives receive large cash subsidies, these subsidies hinder the expected green innovation activities, thereby creating a “crowding out” effect of tax incentives. Tax incentives promote corporate green innovation, while subsidies have little impact on green innovation.

Research (Das et al., 2019) notes that corporate sustainability is a widely practiced area in large organizations, but social and environmental practices are seriously ignored in small and medium-sized enterprises, especially in emerging markets. Large corporations often have more resources to implement sustainability initiatives. They may have dedicated departments and a significant R&D budget to implement advanced technologies for their sustainability practices. In contrast, such resources are a constraint for SMEs, but they are more flexible in adapting to new changes due to simpler processes (Basit, 2024).

ESG Data Analysis with Machine Learning and Deep Learning Algorithms (Lee et al., 2022) examines the possibility of applying AI algorithms to ESG data sets in a comprehensive approach. Taking into account sustainability factors of business entities should occur at the early stages of product development, which involves the use of tools and methods for developing sustainable products in business decision-making processes (Gomes & Pinho, 2023). The authors studied the impact of investment, financial, administrative and regulatory requirements on the implementation of methods to improve the efficiency of resource use in small and medium-sized enterprises. Researchers (Dellaportas et al., 2012, pp.238) conclude that there is a "relationship between ESG rating and profitability". Successful companies implement social and environmental policies on a larger scale compared to financially unsuccessful enterprises. The concept of sustainable development and green economy, which implies the need to justify the use of new financial instruments (Litvinova et al., 2023). Achieving ESG goals affects improving reputation, improving the quality of management, and attracting qualified personnel, which is reflected in increasing business profitability (Forcadell & Aracil, 2017).

Research (Steyn 2014, Ghoul et al. 2017, Buallay 2019, Becker et al. 2022, Kumar 2022, Atan et al. 2018) has primarily focused on examining the relationship between ESG disclosure and performance of large and publicly listed companies.

Companies should adopt transparent communication practices, providing stakeholders with clear and accurate information about their ESG performance, targets, and progress. Regular reporting and disclosure of ESG performance can help build trust and facilitate constructive dialogue (McKinsey & Company, 2019).

A review of sustainability measurement practices for businesses (Serzante & Khudozhnyk, 2023) found a significant trend towards comprehensive and integrated approaches to sustainability measurement, emphasizing the importance of considering economic, social, and environmental factors in an integrated manner. The researchers note that Asia and Europe have been the most studied regions, with a focus on the secondary sector of enterprises. The network interaction of innovation development of the economy within the framework of the Triple Helix "university-industry-government" is complemented by the Triple Helix "university-state-government" for sustainable development (Zhou & Etzkowitz, 2021). Zhou and Etzkowitz proposed a Triple Helix twin framework for innovation and sustainable development. The roles of government, industry, civil society and academia in knowledge sharing processes are considered in the Quadruple Helix model. The Quadruple Helix (Carayannis & Campbell, 2012) is combined with a public perspective based on media and culture. The Quintuple Helix model of innovation and the SDGs is expanded to consist of political, educational, economic, environmental and social systems. The work (Barcellos-Paula et. al., 2021) presents a Quintuple Helix model and the Sustainable Development Goals for Latin America. The lack of publicity in the activities of small business entities in Kazakhstan, the low correlation between investments in innovation and the share of innovative products in the GDP structure, and limited resources lead to the need to transform the interaction of key stakeholders “business entities - society-state” with the identification of priority areas of development using a rating approach. Over the past fifteen years, Kazakhstan has adopted a number of legislative documents aimed at the sustainable development of the country. These are the Environmental Code (2021), the Corporate Governance Code (2018), the Social Code of the Republic of Kazakhstan (2023), the Strategy for achieving carbon neutrality of the Republic of Kazakhstan until 2060, 2023), and the Green Taxonomy (On approval of the classification (taxonomy) of “green” projects, 2021). All these laws are aimed at the sustainable development of Kazakhstan.

An analysis of a systematic review of the literature on the sustainable development of small and medium-sized businesses (Martins et al., 2022) allowed us to draw conclusions about the insufficient number of studies devoted to reporting in the field of sustainable development of SMEs. Environmental aspects of business have the strongest positive impact on the long-term sustainability of SMEs (Zvarikova, 2024). The results of the study indicate that human resource management, finance and the degree of digitalization of SMEs significantly affect the viability of the business.

The use of domestic developments will reduce the costs of companies for the acquisition and maintenance of foreign digital software (Zarubina et al., 2021).

According to a study by Jusan Analytics, the survival rate of small and medium businesses in Kazakhstan is 18%. Among the problems affecting such a low level of sustainability, industry experts highlight low productivity, inflation, monopolized markets, and the lack of effective public policy instruments (Zakon.kz, 2023). Achieving ESG goals can bring certain benefits that a company can convert into financial results. The level of a company's reputation will increase if such a company demonstrates increased concern for the environment. Conversely, the level of a company's reputation will decrease if such a company is involved in scandals related to a negative impact on environmental safety.

The existing literature mentions that a joint mode of operation, government policy and assistance, as well as a supportive organizational culture can positively affect the sustainability indicators of SMEs and, therefore, improve their financial performance.

Sustainable development is a modern trend, which is confirmed by a significant number of scientific studies around the world. Public and accessible information on the large business sector makes it possible to conduct research in the field of ESG. For the small business sector, conducting research on sustainable development is currently problematic due to the lack of public reporting, including ESG reporting. The presence of gaps in information access, the importance of the small business sector for the innovative development of the country, led us to the need to conduct research on the mechanism for promoting sustainable development for the small business sector. The following research questions were posed within the framework of this study and require consideration:

- −

- Do the parameters of strategic development of Kazakhstani small business reflect its sustainable development?

- −

- What is the understanding of sustainable development by Kazakhstani small business entities?

- −

- What are the significant “forms/directions” of sustainable development that allow for increasing the efficiency of small business entities in Kazakhstan?

- −

- Balanced sustainable development based on network interaction “business entities – society-state” will ensure focusing

2. Methodology

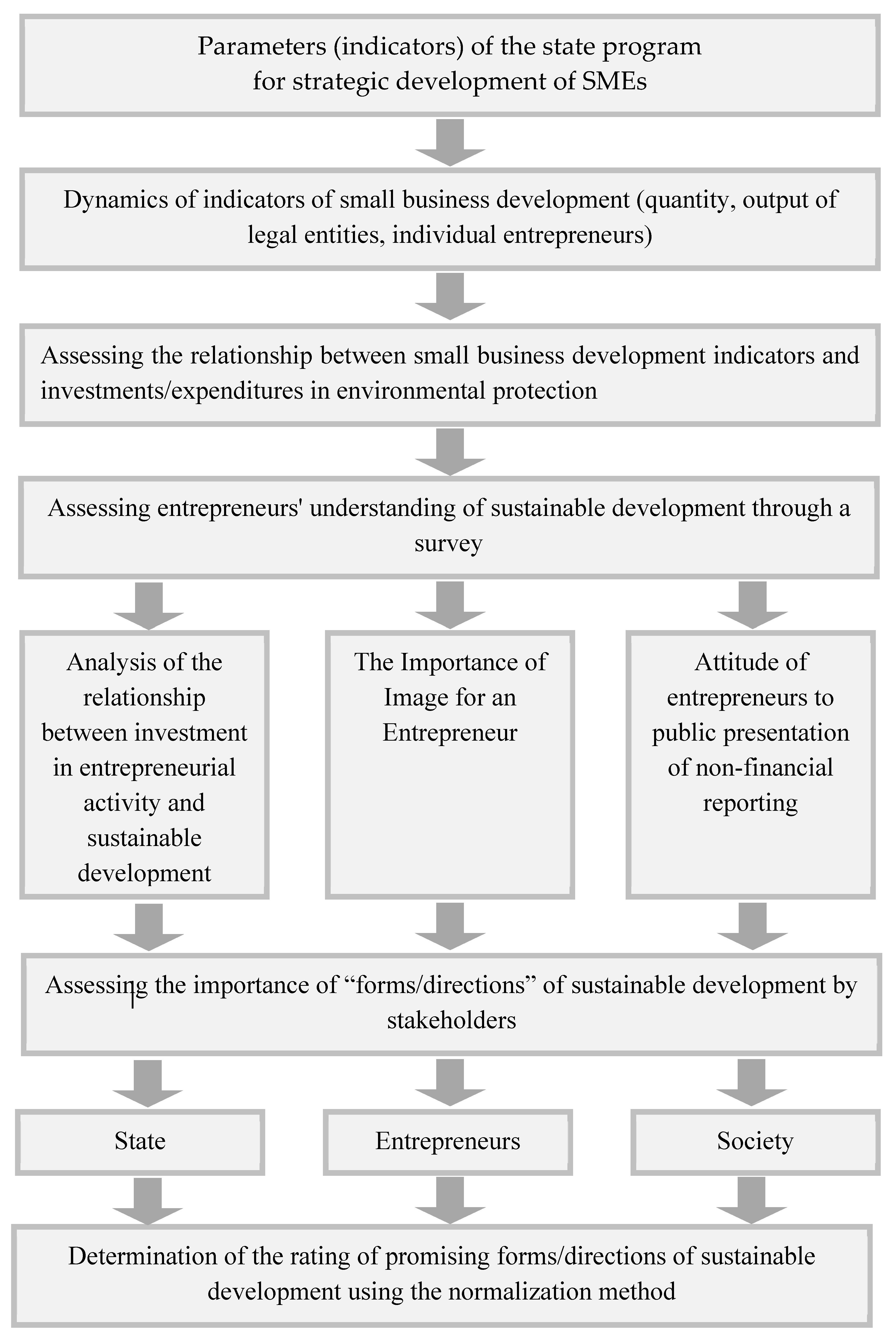

The study of the mechanism for promoting sustainable development for the Kazakhstan small business sector was conducted in several stages. Figure 1 shows a block diagram of the study stages. At the first stage, an analysis of the state strategic program for the development of small and medium entrepreneurship ("Concept for the Development of Small and Medium Entrepreneurship until 2030") was performed, an analysis of the parameters of strategic development (the share of SMEs in GDP, the share of medium-sized companies in GDP, the share of the non-observed economy in GDP, the score of the Republic of Kazakhstan in the index of economic freedoms in the Business Freedom sphere, the score of the Republic of Kazakhstan in the index of economic freedoms in the Monetary Freedom sphere, the score of the Republic of Kazakhstan in the index of economic freedoms in the Trade Freedom sphere, the score of the Republic of Kazakhstan in the index of economic freedoms in the Investment Freedom sphere, the growth of average real labor productivity in medium-sized enterprises (per 1 enterprise), employment (million people) in medium-sized enterprises, the share of investments in fixed capital of medium-sized enterprises in the total volume of investments in fixed capital of all business entities) aimed at the sustainable development of the SME sector.

The analysis of the dynamics of small business development, the relationship between the key indicators of small business development and investments/expenditures in environmental protection was performed. For this purpose, we used statistical data from the Bureau of National Statistics of the Agency for Strategic Planning and Reforms of the Republic of Kazakhstan (Bureau of National Statistics, 2024). The statistical forms "Statistics of enterprises. Small and medium entrepreneurship", "Report on environmental protection costs", "Report on investment activities" were studied. The analysis used data for the period from 2015, when the United Nations adopted the Sustainable Development Goals, to 2023. Based on the data obtained, a correlation analysis of the relationship between the indicators of small business development and investments, expenses in environmental protection was performed.

Also, an analysis was made of the dynamics of legal entities of small businesses, individual entrepreneurs, the output of legal entities of small businesses, the output of legal entities of individual entrepreneurs, the share of innovative products in GDP, the share of domestic R & D costs in GDP. The next step in the study was a survey among small business entities. The questionnaire developed by the authors included 6 closed questions with answer options, which allowed us to quickly conduct a survey of Kazakhstani entrepreneurs.

To conduct the survey, we calculated the sample.

The sample size was determined by the formula (Scanmarket, 2024), when the sample size is comparable to the size of the general population.

where Z – is a coefficient depending on the confidence level chosen by the researcher, Z = 1.96;

N – is the size of the general population;

p – is the proportion of respondents with the feature being studied;

q = 1 - p – is the proportion of respondents who do not have the feature being studied;

Δ – is the maximum sampling error, 10%;

n – is the sample size.

The survey involved individual entrepreneurs, heads of limited liability partnerships, and farms. A total of 99 people took part in the survey.

The survey involved individual entrepreneurs themselves, heads of limited liability partnerships, and farms.

As part of the survey, we were interested in the attitude of entrepreneurs to investing the income received in entrepreneurial activity, in sustainable business development; to the public presentation of non-financial reporting on the results of the organization's activities (environmental protection, social and corporate responsibility), and the image of the organization being formed. We were interested in the issue of using loans in professional activities. The state actively supports the development of small businesses by providing grants and loans with a low interest rate. The mechanism of financial support can be applied to those entities that actively support the implementation of ESG principles.

At the third stage, an assessment of the forms/directions of stakeholder assistance in the development of the concept of sustainable development (state, society, entrepreneurs) was carried out, and a rating of the importance of the identified aspects was determined using the normalization method. The significance of the answers to the proposed forms/directions is ranked in the range from 1 to 3, (1-min, 3-max).

Based on the responses received from the survey, conclusions were made on the need to develop a balanced strategy for achieving carbon neutrality based on network interaction between “business entities – society-state” with the identification of priority areas of development based on a rating approach to ensure transparency and publicity of decisions taken; creation of economic conditions for the implementation of sustainable development principles in the practical activities of business entities.

3. Results

In the innovative development of Kazakhstan, the small and medium-sized enterprise (SME) sector plays a key role. To ensure the continuous development of entrepreneurship at the state level, a program document has been adopted. Monitoring the indicators of small entrepreneurship development for 2015-2023 allows us to draw conclusions about the positive dynamics of its development.

However, the conducted analysis of the main parameters of the strategic development of Kazakhstan's SMEs is associated with an increase in the number of employees, an increase in the share of GDP, an increase in labor productivity, and investment. At the same time, in the strategic document ("Concept for the Development of Small and Medium Entrepreneurship until 2030"), building up entrepreneurial potential does not focus on achieving a climate-neutral, resource-efficient and flexible digital economy. The dominant stakeholder - the "state", within the framework of the strategic document aimed at the development of SMEs, does not formalize the indicators of sustainable development of the SME sector.

The key indicators of the concept are presented in the Table 1.

The indicators of small business development in Kazakhstan for 2015-2023 demonstrate dynamic development (Table 2). Both the number of entrepreneurs and the number, as well as the volume of production, are growing. The volume of production increased for legal entities of small business more than 4 times, for individual entrepreneurs almost 3 times.

The costs and investments in environmental protection for 2015-2023 were also analyzed. In the republic, the growth rate of costs for environmental protection was 2.369. The growth of investments significantly outpaces the growth rate of costs, the growth rate was 3.224.

We have assessed the correlation between the output of small businesses and the costs and investments in environmental protection. The correlation was calculated using the Pearson function in Excel. The pairwise correlation between the output of small business legal entities and the investments directed toward environmental protection is high - 0.854. The pairwise correlation between the output of small business individual entrepreneurs and the investments directed toward environmental protection is average - 0.532.

Table 4.

Correlation between the output of small businesses and costs, investments in environmental protection in the Republic of Kazakhstan.

Table 4.

Correlation between the output of small businesses and costs, investments in environmental protection in the Republic of Kazakhstan.

| Indicators | Output of products by legal entities of small businesses | Output of products by individual entrepreneurs | Total costs of environmental protection | Investments aimed at environmental protection |

|---|---|---|---|---|

| Production of products by legal entities of small businesses | 1 | 0,782 | 0,895 | 0,854 |

| Production of products by legal entities of small businesses | 0,782 | 1 | 0,645 | 0,532 |

| Total costs of environmental protection | 0,895 | 0,645 | 1 | 0,99 |

| Investments aimed at environmental protection | 0,864 | 0,532 | 0,99 | 1 |

To assess entrepreneurs' understanding of sustainable development, the need to popularize and implement sustainable development principles in the practical activities of business entities, a survey was conducted among small business entities.

The survey results showed that 39.4% of entrepreneurs use loans in their professional activities, 60.6% of current entrepreneurs use their own funds in the formation and development.

The next question was related to determining the percentage of income invested by a business entity in entrepreneurial activity (an activity aimed at systematically obtaining profit from owning property, selling goods, performing work or providing services), as well as the willingness to invest in sustainable business development.

The results are presented in Table 5.

As the survey results showed, small businesses actively invest their income in entrepreneurial activities. At the same time, they are ready to invest only a small part of their income in sustainable development. The correlation between investing in business and investing in sustainable development is negative - 0.225. This indicates that these business entities are not ready to invest in sustainable development.

According to a survey conducted by the United Nations Global Compact among companies from 160 countries, the majority of small and medium-sized businesses associate ESG programs with unnecessary expenses and do not see their advantages. Less than half of companies with a turnover of up to $ 25 million reported the implementation of sustainable development practices. For comparison: among large companies with a turnover of more than $ 1 billion, the share of those who have relevant practices is 94 (Safronova A., 2023).

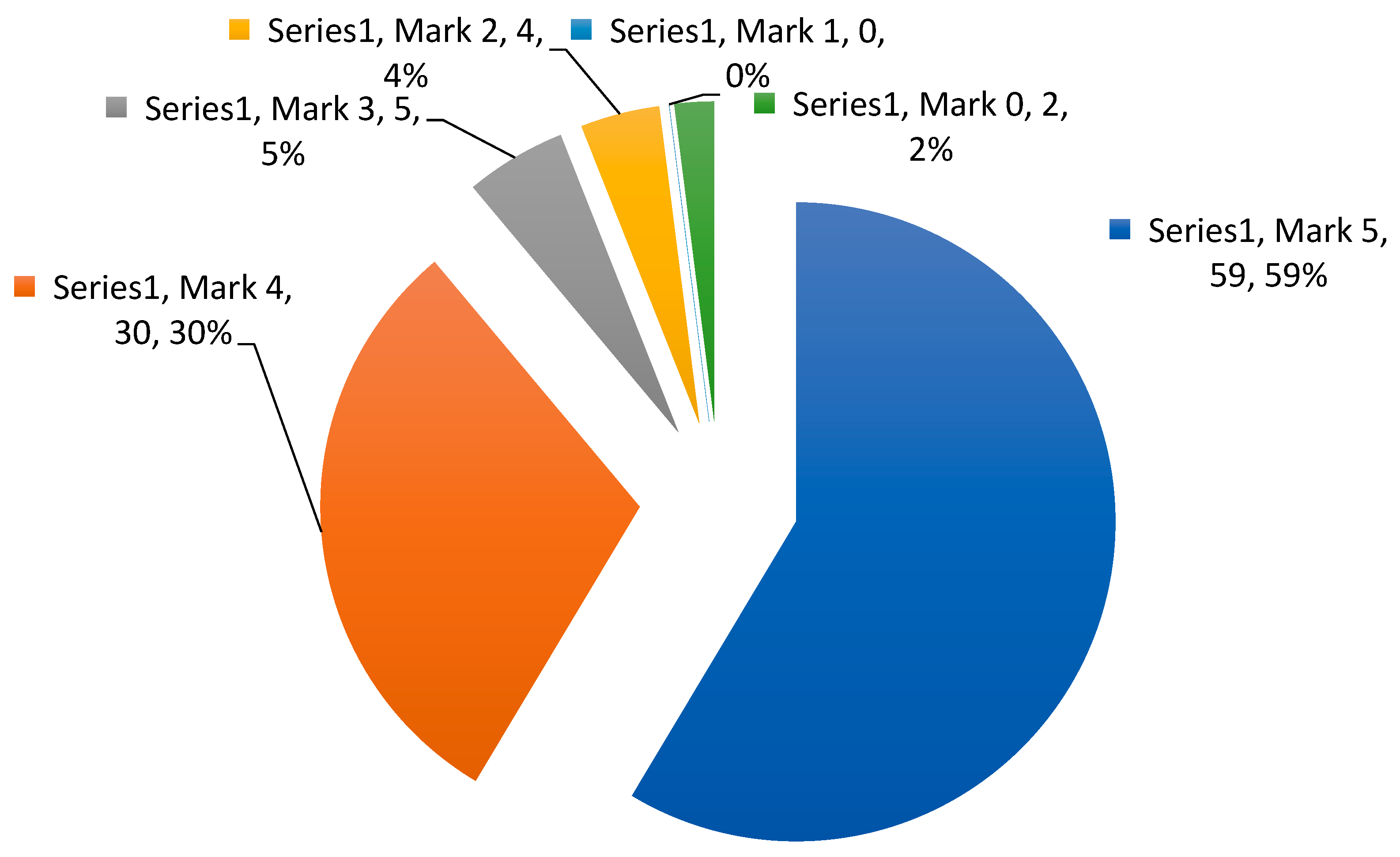

The study was also interested in the attitude of small businesses to the image. Respondents were asked to rate the importance of image on a five-point scale: 5 - maximum, 0 - no importance.

As the survey results showed, image is important for 88.9% of small businesses. Image is formed through active interaction of elements of the internal and external environment. An active stakeholder of the external environment is society. Public opinion analysis allows us to identify consumer preferences and identify new opportunities for the development of a business entity. Environmental image in modern conditions is a system of stable ideas that have developed in society about how a company's activities affect the environment, how environmentally friendly its products are, and how seriously it treats compliance with environmental legislation. Thus, the formation of the image of a business entity occurs through active network interaction "business entity - society".

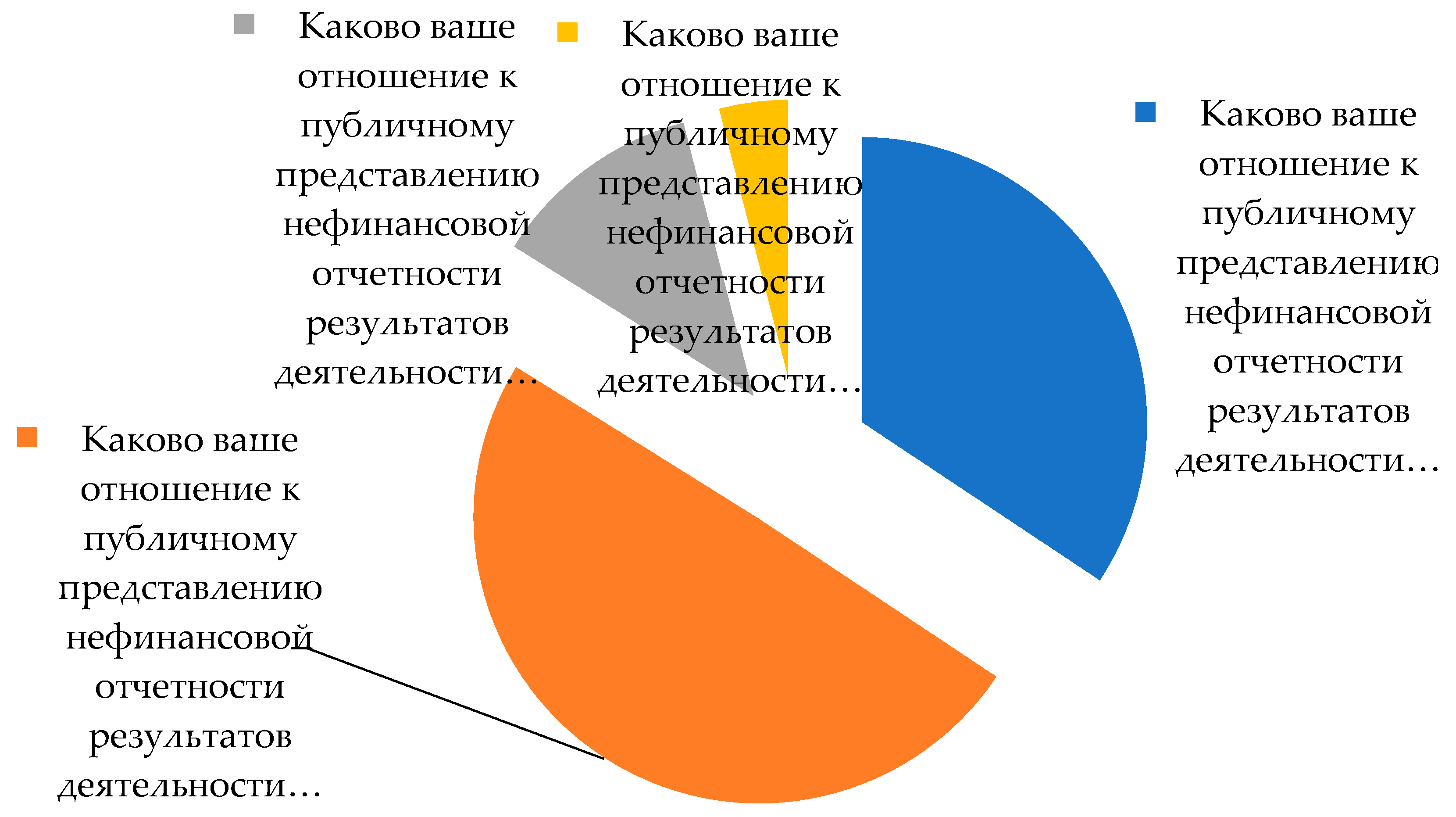

Also, the respondents-entrepreneurs were asked a question regarding their attitude to the public presentation of non-financial reporting on the results of the organization's activities (environmental protection, social and corporate responsibility)? The results of the received answers are presented in Figure 2.

The availability of statistical, financial, tax reporting on individual small business entities in various industries and areas of activity in the Republic of Kazakhstan is not public. The parameters of the efficiency of economic activity can be obtained using the data of management accounting, primary accounting documentation. The lack of public financial and non-financial information on small business entities does not allow monitoring the efficiency of their activities.

The results obtained indicate that only a third of the respondents agreed to the public presentation of non-financial reporting. Almost half of the small business entities surveyed, namely 49.5%, would agree to the public presentation of non-financial reporting only in the case of legislative regulation.

Thus, the survey showed that entrepreneurs try to use their own funds in their activities, ensuring financial independence. Entrepreneurs are not ready to actively invest funds in the sustainable development of their business. At the same time, a positive aspect is concern for the image, as well as active investment in the functioning of the business entity.

Since the main goal of any commercial enterprise is to maximize profits, then an increase in investment should lead to an increase in the economic effect. The use of tax incentives can serve as a tool for tax breaks for those business entities that invest in sustainable development. A comparative analysis of tax regimes for Kazakhstani small businesses is presented in Table 6.

Small businesses can choose either the general tax regime or the simplified one. The object of taxation when applying the general regime is profit, the profit tax rate is 20% for limited liability partnerships and 10% for individual entrepreneurs. When applying the simplified system, there are income restrictions, the tax rate is 3% of income.

Tax incentives promote corporate "green" innovation, while subsidies have little effect on "green" innovation (Wang C. Et al., 2022).

The use of deductions related to investments in sustainable business development will reduce the taxable base for business entities and stimulate responsible investment under the simplified and general tax regime. For individual entrepreneurs operating under the simplified system, whose object of taxation is income, the incentive mechanism may be associated with the use of a reduced tax rate or a zero tax rate. State support for sustainable development of small businesses can be regulatory and incentive. The state can adopt laws and regulations aimed at regulating the activities of companies in accordance with ESG principles. This may include requirements for compliance with environmental standards, social responsibility and corporate governance. The state can support or create standards and certification systems that assess companies' compliance with ESG principles. This can help investors and consumers make more informed decisions when choosing companies to invest in or cooperate with.

The state can also provide incentives for companies that actively implement ESG practices: tax breaks, subsidies and other incentives for organizations operating in accordance with ESG principles.

The formation of a set of measures for the sustainable development of small businesses should occur with the feedback of all stakeholders.

Active network interaction "business entities - society-state" ensures the integration of sustainable development into the activities of business entities.

We asked stakeholders to assess the significance of "forms/directions" of sustainable development that allow for increased efficiency of small businesses.

Each stakeholder was offered evaluation criteria, the significance of which had to be assessed in the range from 1 to 3.

As representatives of government agencies, heads of akimats, tax authorities, and statistics authorities were interviewed.

The assessment of the degree of significance of forms/directions of sustainable development for each of the parties is presented in the Table 6. Using the normalization method, a rating of promising forms/directions of sustainable development for each of the stakeholders was determined.

Table 7.

Criteria for forms/directions of sustainable development.

| Stakeholders | Forms/ Directions |

Significance (1-3) 1-min, 3-max |

Min | Max | (Xi-Xmin)/(Xmax-Xmin) |

|---|---|---|---|---|---|

| State | Investment opportunities: grants | 2,74 | 1,77 | 2,74 | 1,00 |

| Investment opportunities: loans | 1,95 | 1,77 | 2,74 | 0,18 | |

| Investment opportunities: subsidies | 2,59 | 1,77 | 2,74 | 0,84 | |

| Tax preferences | 2,26 | 1,77 | 2,74 | 0,50 | |

| Legislative regulation of public presentation of financial statements | 1,77 | 1,77 | 2,74 | 0,00 | |

| Legislative regulation of public presentation of non-financial reports | 1,79 | 1,77 | 2,74 | 0,03 | |

| Standards and certification systems | 2,36 | 1,79 | 2,74 | 0,59 | |

| Society | Recycling of resources | 2,63 | 2,35 | 2,65 | 0,94 |

| Environmental activism | 2,65 | 2,35 | 2,65 | 1,00 | |

| Use of "green" technologies | 2,63 | 2,35 | 2,65 | 0,94 | |

| Use of "green" technologies | 2,35 | 2,35 | 2,65 | 0,00 | |

| Entrepreneurs | Lean | 2,38 | 1,94 | 2,75 | 0,55 |

| Recycling of used resources | 2,61 | 1,94 | 2,75 | 0,83 | |

| Implementation of sustainable development principles in personnel management | 2,74 | 1,94 | 2,75 | 0,99 | |

| Integration of sustainable development principles into business processes and operational activities | 2,18 | 1,94 | 2,75 | 0,30 | |

| Access to sustainable finance | 2,75 | 1,94 | 2,75 | 1,00 | |

| Formation of non-financial reporting for sustainable development of a business entity | 1,94 | 1,94 | 2,75 | 0,00 |

In the context of sustainable innovative development of industries and sectors of the national economy, focusing on priority areas allows government agencies to concentrate their efforts and budget funds on significant forms of support for small businesses.

Civil society as an element of state and business control in the context of publicity and the formation of a social partnership system determines the priorities of areas for further sustainable development. Increasing the role of civil society in the sustainable development of small businesses is aimed at taking into account its interests as key stakeholders who are consumers of products and services. Small business entities in the implementation of their business strategies in modern conditions also determine priority areas of sustainable development. The priority of areas of sustainable development of small businesses allows identifying key growth points. Transparency, publicity of the selected forms/areas increases the responsibility of stakeholders, as well as balanced sustainable development.

The importance rating of various forms/areas of sustainable development is presented in Table 8.

The greatest potential for small businesses is in such forms of investment as grants and subsidies for business development. Representatives of the public consider it necessary to be active in the field of environmental protection, recycling of resources, and the use of "green technologies" to ensure sustainable development. Small businesses focus on access to sustainable financing, the introduction of sustainable development principles into personnel management, and the recycling of resources used. Balanced sustainable development based on network interaction "business entities - society-state" will ensure focus on priority areas for stakeholders, transparency, publicity of decisions made, the possibility of taking corrective actions taking into account the opinions of all stakeholders.

The presence of a correlation between priority forms/directions in achieving sustainable development indicates that all stakeholders understand and share promising directions of sustainable development at the macro and micro levels. In the absence of a correlation between the opinions of stakeholders, the key role of the coordinator (the state) is to form a sustainable development vector, identify the causes of disagreements and, if necessary, make corrective actions, discuss and provide investment support for promising projects.

4. Discussion

The conducted research allowed us to identify a number of problems. First of all, it is necessary to define parameters and indicators aimed at developing small businesses in the context of sustainable development, active use of green, resource-efficient technologies at the level of state strategic programs and documents.

The growth of small business competitiveness should primarily occur through the production of sustainable innovative products and services using digital and green technologies. The state will be able to provide incentives for companies that actively implement ESG practices: grants, subsidies, tax breaks and other incentives for organizations operating in accordance with ESG principles.

The state will be able to adopt laws and regulations aimed at regulating the activities of companies in accordance with ESG principles.

Currently, Kazakhstani small businesses are not ready to actively invest in sustainable development. This indicates the need to create conditions, support, explain the importance and prospects of investing in sustainable innovation. Investing in sustainable innovation requires legislative support in the form of grant funding, project subsidies, and preferences.

Active network interaction between the state and entrepreneurs can be carried out taking into account the rating of priority areas in achieving sustainable development. This approach will ensure the definition of significant elements in the implementation of the carbon neutrality strategy. In conditions of limited resources, the budget of allocated public funds can focus on the most promising areas. And the choice of such priority areas should be carried out with the direct participation of society.

The presence of feedback between entrepreneurs and the public will ensure publicity and transparency of activities.

The study identified the following issues that require further resolution. Firstly, in order to create favorable social conditions and protect the environment of small businesses, it is necessary to develop ESG standards. Secondly, non-financial reporting, including indicators of environmental protection, social and corporate responsibility, requires legislative regulation. Thirdly, it is necessary to carry out further work to determine private and integrated indicators of non-financial reporting that allow determining the degree of compliance of the business entity with sustainable development.

Such steps will allow public monitoring of the environmental, social, and management profile of the entrepreneur.

5. Conclusions

Sustainable development of Kazakhstan's small business should be carried out with close cooperation between the state, business entities and society. Strategic indicators of small business development provided for in the state program should correlate with sustainable development, active use of green, resource-efficient technologies, which currently requires adjustment. The dominant stakeholder - the "state", within the framework of a strategic document aimed at the development of SMEs, does not formalize the indicators of sustainable development of the SME sector.

Network interaction "business entities - society-state" will allow introducing the concept of sustainable development to business entities with the support of government agencies and the active participation of society.

In the context of sustainable innovative development of industries and spheres of the national economy, focusing on priority areas allows government agencies to concentrate efforts, budget funds on significant forms of support for small businesses.

At the moment, Kazakhstan's small business entities are not ready to actively invest in sustainable development. This indicates the need to create conditions, support, explain the importance and prospects of investing in sustainable innovations.

Active network interaction between the state and entrepreneurs can be carried out taking into account the rating of priority areas in achieving sustainable development. In conditions of limited resources, the budget of allocated public funds can focus on the most promising areas. Civil society as an element of control of the state and business in the conditions of publicity and the formation of a system of social partnership determines the priorities of areas for further sustainable development. Increasing the role of civil society in the sustainable development of small entrepreneurship is aimed at taking into account its interests as key stakeholders who are consumers of products and services. This approach will ensure the definition of significant elements in the implementation of a balanced strategy for achieving carbon neutrality, transparency, and publicity of decisions made.

Author Contributions

Conceptualization, Zarubina Venera , Mikhail Zarubin.; methodology Zarubina Venera , Mikhail Zarubin; formal analysis Zhaukhar Yessenkulova; Meimankulova Zhuldyz; research Gumarova Tursyngul, Daulbayeva Almira, Kurmangalieva Aizhan, Meimankulova Zhuldyz; visualization Daulbayeva Almira, Kurmangalieva Aizhan; writing — original draft preparation, Zarubina Venera , Zhaukhar Yessenkulova; writing — review and editing, Mikhail Zarubin. All authors have read and agreed to the published version of the manuscript.

References

- Atan, Ruhaya & Alam, Md. Mahmudul & Said, Jamaliah & Zamri, Mohamed. (2018). The Impacts of Environmental, Social, and Governance Factors on Firm Performance: Panel Study on Malaysian Companies. Management of Environmental Quality An International Journal. 29. 182-194. [CrossRef]

- Ayyagari, M., Beck, T., & Demirguc-Kunt, A. (2007). Small and medium enterprises across the globe. Small Business Economics, 29(4), 415–434. [CrossRef]

- Barcellos-Paula, L.; De la Vega, I.; Gil-Lafuente, A.M. The Quintuple Helix of Innovation Model and the SDGs: Latin-American Countries’ Case and Its Forgotten Effects. Mathematics 2021, 9, 416. [CrossRef]

- Basit, Shoaib & Gharleghi, Behrooz & Batool, Khadija & Hassan, Sohaib & Afshar Jahanshahi, Asghar & Kliem, Mujde. (2024). Review of Enablers and Barriers of Sustainable Business Practices in SMEs. Journal of Economy and Technology. 2. [CrossRef]

- Becker, Martin G. & Martin, Fabio & Walter, Andreas, 2022. "The power of ESG transparency: The effect of the new SFDR sustainability labels on mutual funds and individual investors," Finance Research Letters, Elsevier, vol. 47(PB).

- Buallay, Amina. (2019). Between cost and value: Investigating the effects of sustainability reporting on a firm’s performance. Journal of Applied Accounting Research. 20. [CrossRef]

- Bureau of National Statistics of the Republic of Kazakhstan. Available online: https://stat.gov.kz/ru/ (accessed on 22 june 2024).

- Buribaeva G., Sarsekeev F., Ospanov A., Imashev B. Report on the state of development of small and medium-sized enterprises in Kazakhstan and its regions. - Nur-Sultan, 2021, issue No. 13. 100 p. Available online: https://damu.kz/upload/iblock/cae/xqhsqdrqgmhk90la0cicsr434otz3k54/%D0%94%D0%90%D0%9C%D0%A3%20_%20%D0%BE%D1%82%D1%87%D0%B5%D1%82%20%D0%9C%D0%A1%D0%9F%20_%20%D1%80%D1%83%D1%81.pdf (accessed on 12 july 2024).

- Carayannis, Elias & Campbell, David. (2012). Triple Helix, Quadruple Helix and Quintuple Helix and How Do Knowledge, Innovation and the Environment Relate To Each Other?. International Journal of Social Ecology and Sustainable Development. 1. 41-69. [CrossRef]

- Code of the Republic of Kazakhstan dated December 25, 2017 No. 120-VI “On taxes and other obligatory payments to the budget (Tax Code)” (with amendments and additions as of July 21, 2024). Available online: https://online.zakon.kz/Document/?doc_id=36148637 (accessed on 12 july 2024).

- Code of the Republic of Kazakhstan dated January 2, 2021 No. 400-VI “Ecological Code of the Republic of Kazakhstan” (with amendments and additions as of July 22, 2024.). Available online: https://online.zakon.kz/Document/?doc_id=39768520 (accessed on 12 july 2024).

- Das, Maitreyee & Krish, Rangarajan & Dutta, Gautam. (2019). Corporate sustainability in small and medium-sized enterprises: a literature analysis and road ahead. Journal of Indian Business Research. ahead-of-print. [CrossRef]

- Decree of the President of the Republic of Kazakhstan dated February 2, 2023 No. 121 “On approval of the Strategy for achieving carbon neutrality of the Republic of Kazakhstan until 2060.”. Available online: https://adilet.zan.kz/rus/docs/U2300000121/info (accessed on 10 july 2024).

- Del-Aguila-Arcentales, S.; Alvarez-Risco, A.; Jaramillo-Arévalo, M.; De-la-Cruz-Diaz, M.; Anderson-Seminario, M.d.l.M. Influence of Social, Environmental and Economic Sustainable Development Goals (SDGs) over Continuation of Entrepreneurship and Competitiveness. J. Open Innov. Technol. Mark. Complex. 2022, 8, 73. [CrossRef]

- Dellaportas, Steven & Langton, Jonathan & West, Brian. (2012). Governance and accountability in Australian charitable organisations: Perceptions from CFOs. International Journal of Accounting and Information Management. 20. 238-254. [CrossRef]

- Divaeva E.A.(2022). Conditions for transformation of ESG principles: economic and social aspects // Innovations and investments. 2022. No. 1. Available online: https://cyberleninka.ru/article/n/usloviya-transformatsii-esg-printsipov (accessed on 25 june 2024).

- Elmonshid, L.B.E.; Sayed, O.A. The Relationship between Entrepreneurship and Sustainable Development in Saudi Arabia: A Comprehensive Perspective. Economies 2024, 12, 198. [CrossRef]

- EPP group. Available online: https://www.eppgroup.eu/what-we-stand-for/our-priorities/helping-small-business-to-thrive (accessed on 22 june 2024).

- ESG for SMEs: obligation, option or opportunity? Available online: https://www.zakon.kz/ekonomika-biznes/6401861-ESG-dlya-malogo-i-srednego-biznesa-obyazatelstvo-optsiya-ili-vozmozhnost.html (accessed on 12 july 2024).

- Forcadell, Francisco & Aracil, Elisa. (2017). European Banks' Reputation for Corporate Social Responsibility: European Banks' Reputation. Corporate Social Responsibility and Environmental Management. 24. 1-14. [CrossRef]

- Ghoul, S. E., Guedhami, O., & Kim, Y. (2017). Country-level institutions, firm value, and the role of corporate social responsibility initiatives. Journal of International Business Studies, 48(3), 360–385. [CrossRef]

- Gomes, S., & Pinho, M. (2023). Can we count on the commitment of European SMEs to achieve SGD12? An exploratory study of business sustainability. Journal of Cleaner Production, 425, 139016, 1-9. Gomes, S., & Pinho, M. (2023). Can we count on the commitment of European SMEs to achieve SGD12? An exploratory study of business sustainability. Journal of Cleaner Production, 425, 139016, 1-9. [CrossRef]

- Janáková Sujová, Andrea, and Václav Kupčák. (2024). "Changes in SME Business Due to COVID-19—Survey in Slovakia and the Czech Republic" Economies 12, no. 1: 17. [CrossRef]

- Korneeva, Elena & Skornichenko, Natalia & Oruch, Tatiana. (2021). Small business and its place in promoting sustainable development. E3S Web of Conferences. 250. 06007. [CrossRef]

- Kumar, Praveen & Firoz, Mohammad. (2022). Does Accounting-based Financial Performance Value Environmental, Social and Governance (ESG) Disclosures? A detailed note on a corporate sustainability perspective. Australasian Business, Accounting and Finance Journal. 16. 41-72. [CrossRef]

- Kumar, S., Raut, R. D., Aktas, E., Narkhede, B. E., & Gedam, V. V. (2022). Barriers to adoption of industry 4.0 and sustainability: a case study with SMEs. International Journal of Computer Integrated Manufacturing, 36(5), 657–677. [CrossRef]

- Lee, O.; Joo, H.; Choi, H.; Cheon, M. Proposing an Integrated Approach to Analyzing ESG Data via Machine Learning and Deep Learning Algorithms. Sustainability 2022, 14, 8745. https://doi.org/10.3390/su14148745Lee, O.; Joo, H.; Choi, H.; Cheon, M. Proposing an Integrated Approach to Analyzing ESG Data via Machine Learning and Deep Learning Algorithms. Sustainability 2022, 14, 8745. [CrossRef]

- Luederitz, Christopher & Caniglia, Guido & Colbert, Barry & Burch, Sarah. (2021). How do small businesses pursue sustainability? The role of collective agency for integrating planned and emergent strategy making. Business Strategy and the Environment. [CrossRef]

- Martins, A.; Branco, M.C.; Melo, P.N.; Machado, C. Sustainability in Small and Medium-Sized Enterprises: A Systematic Literature Review and Future Research Agenda. Sustainability 2022, 14, 6493. [CrossRef]

- McKinsey & Company. (2019, November 14). Five ways that ESG creates value. Available online: https://www.mckinsey.com/capabilities/strategy-and-corporate-finance/our-insights/five-ways-that-esg-creates-value (accessed on 25 june 2024).

- Mrochkovskiy N.S. Conditions of Sustainable Development for Sme Entities in the Course of COVID-19 Pandemic. Vestnik of the Plekhanov Russian University of Economics. 2022;(1):109-113. (In Russ. [CrossRef]

- On approval of the classification (taxonomy) of “green” projects subject to financing through “green” bonds and “green” loans, Resolution of the Government of the Republic of Kazakhstan dated December 31, 2021 No. 996. Available online: https://adilet.zan.kz/rus/docs/P2100000996 (accessed on 10 july 2024).

- On approval of the Concept for the development of small and medium entrepreneurship in the Republic of Kazakhstan until 2030 Resolution of the Government of the Republic of Kazakhstan dated April 27, 2022 No. 250. Available online: https://adilet.zan.kz/rus/docs/P2200000250 (accessed on 10 july 2024).

- On approval of the Model Code of Corporate Governance in state-controlled joint stock companies, with the exception of the National Welfare Fund (Order of the Minister of National Economy of the Republic of Kazakhstan dated October 5, 2018 No. 21. Registered with the Ministry of Justice of the Republic of Kazakhstan on November 12, 2018 No. 17726 // Official website of the Ministry of Justice Republic of Kazakhstan. Available online: https://adilet.zan.kz/rus/docs/V1800017726 (accessed on 10 july 2024).

- Ovechkin D.V. (2021). Responsible investments: the impact of ESG rating on firm profitability and expected return on the stock market. Scientific journal of NRU ITMO. Economics and Environmental Management Series, (1), 43-53.

- Safronova A. (2023). Research: what small and medium-sized businesses in Russia know about sustainable development. Available online: https://www.forbes.ru/forbeslife/491162-issledovanie-cto-malyj-i-srednij-biznes-v-rossii-znaet-pro-ustojcivoe-razvitie (accessed on 12 july 2024).

- Scanmarket. Available online: https://scanmarket.ru/blog/vyborka-razmer-ne-glavnoe-ili-glavnoe (accessed on 12 july 2024).

- SDG Platform for Central Asia. Available online: https://www.undp.org/ru/kazakhstan/stories (accessed on 12 august 2024).

- Serzante, M. & Khudozhnyk, A.(2023). Reviewing Sustainability Measurement Methods for Enterprises. Sustainability. 15, 15514. [CrossRef]

- SMEs in Europe. Available online: https://www.consilium.europa.eu/en/policies/support-to-small-and-medium-sized-enterprises (accessed on 12 june 2024).

- Social Code of the Republic of Kazakhstan (Code of the Republic of Kazakhstan dated April 20, 2023 No. 224-VII ZRK) // Official website of the Ministry of Justice of the Republic of Kazakhstan. Available online: https://adilet.zan.kz/rus/docs/K2300000224 (accessed on 10 july 2024).

- Steyn, Maxi. (2014). Organisational benefits and implementation challenges of mandatory integrated reporting: Perspectives of senior executives at South African listed companies. Sustainability Accounting, Management and Policy Journal. 5. 476-503. [CrossRef]

- Svetlana A. Litvinova & Olga B. Ivanova & Oksana S. Chernobay & Venera R. Zarubina, 2023. "Green Mortgage as the Key to Energy-Efficient and Resource-Saving Real Estate," World Scientific Book Chapters, in: Elena G Popkova & Natalia G Vovchenko & Olga V Andreeva (ed.), Climate-Smart Innovation Social Entrepreneurship and Sustainable Development in the Environmental Economy, chapter 17, pages 269-284, World Scientific Publishing Co. Pte. Ltd.

- Venera Zarubina, Mikhail Zarubin, Olga Andreeva, Darkhan Akhmetov and Ekaterina Gutnova (2021). Web-service promotion of SaaS service for mining design. Innovative Marketing, 17(4), 49-61. [CrossRef]

- Wang C, Chen P, Hao Y and Dagestani AA (2022). Tax incentives and green innovation—The mediating role of financing constraints and the moderating role of subsidies. Front. Environ. Sci. 10:1067534. [CrossRef]

- Why is small and medium business not developing in Kazakhstan? Available online: https://osdp.kz/ru/statya/pochemu-v-kazahstane-ne-razvivaetsya-malyj-i-srednij-biznes (accessed on 25 june 2024).

- Zarubina, Venera & Zarubin, Mikhail & Yessenkulova, Zhaukhar & Salimbayeva, Rassima & Satbaeva, Gulbarshyn & Kenzhebekova, Dina. (2022). Promotion of the EIA Subsystem of the 3D-Quarry Web Application. Environmental and Climate Technologies. 26. 883-897. [CrossRef]

- Zhou, C.; Etzkowitz, H. Triple Helix Twins: A Framework for Achieving Innovation and UN Sustainable Development Goals. Sustainability 2021, 13, 6535. [CrossRef]

- Zvarikova, K., Dvorsky, J., Belas, J. J., & Metzker, Z. (2024). Model of sustainability of SMEs in V4 countries. Journal of Business Economics and Management, 25(2), 226–245. [CrossRef]

Figure 1.

Flow chart of the study results.

Figure 2.

Results of responses to the question “What is the importance of the organization’s image for you?”.

Figure 2.

Results of responses to the question “What is the importance of the organization’s image for you?”.

Figure 3.

What is your attitude towards public presentation of non-financial reporting on the organization's performance (environmental protection, social and corporate responsibility)?

Figure 3.

What is your attitude towards public presentation of non-financial reporting on the organization's performance (environmental protection, social and corporate responsibility)?

Table 1.

Key indicators of the Concept for the Development of SMEs in Kazakhstan until 2030.

| Indicator | Meaning |

|---|---|

| Share of SMEs in GDP | 40% |

| Share of medium-sized companies in GDP | 20% |

| Employment (million people) in medium-sized enterprises | 5 |

| Growth of average real labor productivity in medium-sized enterprises (per enterprise) | 50% |

| The share of investments in fixed capital of medium-sized enterprises in the total volume of investments in fixed capital of all business entities | 15% |

| Source: On approval of the Concept for the development of small and medium entrepreneurship in the Republic of Kazakhstan until 2030 Resolution of the Government of the Republic of Kazakhstan dated April 27, 2022 No. 250. Available online: https://adilet.zan.kz/rus/docs/P2200000250 | |

Table 2.

Indicators of small business development in Kazakhstan for 2015-2023.

| Index | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | 2021 | 2022 | 2023 | Growth rate 2023/2015 |

|

|---|---|---|---|---|---|---|---|---|---|---|---|

| Legal entities of small business, units | 175 679 | 189 637 | 208 742 | 231 325 | 258 365 | 280 200 | 299 737 | 416 080 |

438 403 |

2,495 | |

| Individual entrepreneurs, units | 882 849 | 736 121 | 747 107 | 809 115 | 855 920 | 857 910 | 907 722 | 104 4 252 |

133 6 490 |

1,514 | |

| Small business legal entities, thousand people | 1 185,2 | 1 249,3 | 1 301,8 | 1 351,9 | 1 408,2 | 1 462,4 | 1 488,8 | 3 125,1 |

1 728,8 |

1,458 | |

| Individual entrepreneurs, thousand people |

1 360,3 | 1 288,2 | 1 240,9 | 1 315,2 | 1 378,9 | 1 353,8 | 1 367,1 | 1 367, 14 |

1 678, 5 |

1,234 | |

| Output of products by legal entities of small businesses, thousand tenge | 10200061 | 13568530 | 16488047 | 18272335 | 22947233 | 23401108 | 28446662 | 2945 2215 |

4206 9312 |

4,12 | |

| Output of products by individual entrepreneurs, thousand tenge | 1 518 237 | 1 511 733 | 1 554 704 | 1 764 985 | 1 902 754 | 1 729 842 | 3 401 450 | 3404 453 |

4468 161 |

2,94 | |

| Share of innovative products in GDP,% | 0,92 | 0,95 | 1,55 | 1,72 | 1,60 | 2,43 | 1,71 | 1,81 | 1,99 | 2,16 | |

| Share of domestic R&D expenditure in GDP, % | 0,17 | 0,14 | 0,13 | 0,12 | 0,12 | 0,13 | 0,13 | 0,12 | 0,25 | 1,47 | |

| Source: Bureau of National Statistics of the Republic of Kazakhstan https://stat.gov.kz/ru | |||||||||||

Table 3.

Costs and investments in environmental protection for 2015-2023.

| Indicator | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | 2021 | 2022 | 2023 | Growth rate 2023/2015 |

| Total costs for environmental protection, million tenge | 257 533 | 196 143 | 262 407 | 302 177 | 420 392 | 384 016 | 416 956 | 444514 | 610285 | 2,369 |

| Investments aimed at environmental protection, million tenge | 82 883 | 43 937 | 86 962 | 111 161 | 198 722 | 173 619 | 171 165 | 159661 | 267261 | 3,224 |

| Source: Bureau of National Statistics of the Republic of Kazakhstan https://stat.gov.kz/ru | ||||||||||

Table 5.

Survey results.

| Question | Percent | I do not invest | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Less than 10 | 10-20 | 20-30 | 30-40 | 40-50 | 50-60 | 60-70 | 70-80 | All income received | ||

| The percentage of income invested by a business entity in entrepreneurial activity | 2 | 8,1 | 18,2 | 20,2 | 14,1 | 12,1 | 10,1 | 3 | 11,1 | 2 |

| The percentage of income that a business entity is willing to invest in sustainable business development | 32,3 | 31,3 | 12,1 | 3 | 5,1 | 1 | 0 | 1 | 1 | 13,1 |

| Correlation | -0,225 | |||||||||

Table 6.

Comparative analysis of the general and simplified taxation regimes in the Republic of Kazakhstan.

Table 6.

Comparative analysis of the general and simplified taxation regimes in the Republic of Kazakhstan.

| Criterion | Taxation regimes | |

|---|---|---|

| Generally established | Simplified | |

| Taxable object | Profit | Actual income |

| Limits on numbers | 100 | 30 |

| Cash register machine | mandatory application | mandatory application |

| Turnover restrictions | absent | 24038 minimum calculation indicator |

| Restrictions on types of activities | In accordance with Article 683 of the Tax Code of the Republic of Kazakhstan | Limited list |

| Tax rate | 20% of profit for LLC, 10% for individual entrepreneurs | 3% of income |

| Source: Tax Code of Kazakhstan, 2024, https://online.zakon.kz/Document/?doc_id=36148637 | ||

Table 8.

Rating of priority forms/directions in achieving sustainable development of stakeholders.

| Rank | State | Society | Entrepreneurs |

|---|---|---|---|

| 1 | Investment opportunities: grants | Environmental activism | Access to sustainable finance |

| 2 | Investment opportunities: subsidies | Recycling of resources | Implementation of sustainable development principles in personnel management |

| 3 | Standards and certification systems | Use of "green" technologies | Recycling of used resources |

| 4 | Tax preferences | Innovation and digital technologies | Lean |

| 5 | Investment opportunities: loans | - | Integration of sustainable development principles into business processes and operational activities |

| 6 | Legislative regulation of public presentation of non-financial, financial reporting | - | Formation of non-financial reporting for sustainable development of a business entity |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Copyright: This open access article is published under a Creative Commons CC BY 4.0 license, which permit the free download, distribution, and reuse, provided that the author and preprint are cited in any reuse.