Submitted:

13 September 2024

Posted:

16 September 2024

You are already at the latest version

Abstract

As part of the "Indonesia Emas 2045" framework, State-Owned Enterprises (SOEs) in the construction industry are expected to dominate government infrastructure projects. This research conducts an industrial foresight analysis of Indonesia's SOE construction industry to identify future trends and opportunities. The study employs a three-level analysis: macro (using the PESTLE framework), meso (applying Porter's Five Forces), and micro (focusing on organizational scope). Data were collected from seven industry experts from both SOEs and the private sector, supplemented by secondary sources. The qualitative findings were gathered using Delphi method, while expert voting provided the quantitative assessment. The results highlight that focusing on macro-level targets like Net Zero Emissions (NZE) and Sustainable Development Goals (SDGs) is crucial in implementing Environmental, Social, and Governance (ESG) practices. Adoption of advanced technologies such as Construction 4.0 emerges as a top priority, with digital innovations such as predictive analytics, digital control towers, LiDAR, and Building Information Modeling (BIM) enhancing efficiency and risk management. Achieving sustainability and technological advancement requires regulatory certainty, serving as the third pillar at the macro level. At the micro level, strengthening the SOE construction industry's core competencies, resources, and capabilities is essential to accelerate future trends. Competitiveness at the meso level is not a significant concern, as the industry operates with moderate competition.

Keywords:

foresight industry

; industry

; PESTLE

; Porter’s five forces

; SOE

1. Introduction

The main focus of “Indonesia Emas 2045” is sustainable economic development and equitable growth, as reflected in the development of the new capital city (2025-2045) and national strategic projects initiatives. Projections suggest that government infrastructure projects will dominate the period from 2025 to 2034. During this time, State-Owned Enterprises (SOEs) are expected to hold nearly 50 percent of the total market [1]. However, SOEs in the construction industry face poor financial performance, characterized by low profitability, critical liquidity, and high debt ratios. According to Wibowo et al. [2], SOEs in the construction industry are less efficient than private construction companies.

The liquidity crisis experienced by SOE construction companies is marked by a decline in revenue, with a compound annual growth rate (CAGR) of -6 percent from 2018 to 2023, and negative net profit margins of -34.7 percent in 2023. This indicates significant internal financial problems, such as low receivables collectability and rising liabilities, which reached Rp287.03 trillion in Q1/2023 [3]. Moreover, project performance was poor, with only 46 percent of projects completed on time and within budget in 2022. This reflects significant weaknesses in internal management [4,5]. Financial issues are largely driven by internal weaknesses in utilizing and managing existing resources. Improving financial management and operational efficiency is key to strengthening the position of SOE construction companies in Indonesia [6,7].

In response to significant opportunities that SOE construction companies will face in the future, these companies must focus on strengthening their internal factors. External factors, such as regulations that may benefit SOEs, need to align with economic conditions and technological developments to improve company performance. SOEs must develop internal capabilities that are adaptive and responsive to external opportunities and challenges [8]. Fisunenko and Sidorov [9] indicate that government regulations, economic policies, and market pressure can significantly impact the financial security of SOEs construction companies.

Furthermore, technological advancements such as building information modelling (BIM), construction automation, and the use of drones for site surveys has gained increasing importance in the global construction industry. Technological innovation is a major factor which can push or prevent progress in the construction sector [10]. Liu [11] suggests effective investment strategies must consider environmental, economic, political, and social changes through proper market positioning. To remain competitive, SOE construction companies must be prepared to adapt to sustainable innovations and ongoing external changes.

Being responsive to constantly changing external factors is crucial for the future of Indonesia’s construction industry. The construction industry’s success depends on company management’s ability to face these challenges. Most scientific studies related to the construction industry have focused on strengthening internal company aspects. As example, research by Benson & Rahayu [12] analyzed key success factors for improving labor management at SOE construction companies in Indonesia. The research found that factors such as training and skill development, effective communication, and a fair incentive system play an important role in improving labor productivity and manners.

Fatima [13] identified key indicators determining the performance of construction companies in Indonesia. The study found factors such as effective project management, the use of modern technology, and adherence to quality and safety standards are crucial in influencing company performance. Huda et al. [14] examined parameters for improving the performance and competitiveness of construction companies in Indonesia, and revealing innovation in construction technology, efficiency in supply chain management, and the implementation of sustainable business practices are key to enhance competitiveness. However, an ideal approach would integrate internal strengthening with the ability to respond effectively to external dynamics.

Strengthening internal factors without integrating future foresight leaves companies unprepared to face sudden major changes. In developed countries, foresight is used extensively to develop future scenarios that help companies adapt and formulate long-term strategies [15]. Rust and Koen [16] emphasized the importance of utilizing industry foresight, which focuses on identifying key technological trends to improve the efficiency and competitiveness of the construction industry. As highlighted by Alizadeh and Soltanisehat [17], scenario-based methods in industry foresight help plan strategies to address future challenges and maintain competitive advantages.

Within the framework of dynamic capabilities strategic management, a company must adapt, build, and reconfigure its internal and external competencies to face rapid future changes. Foresight plays a key role in sensing opportunities and risks. This becomes an integral part of the company’s long-term strategic foundation [18]. In Indonesia, the use of foresight remains limited and has not yet become a core component of construction companies’ strategies [12,13,14]. This raises concerns about their readiness to face major changes, such as technological shifts or sudden changes in government policy. Compared to other countries, Indonesia faces unique challenges, including frequently changing regulations and suboptimal infrastructure, which must be considered in foresight planning [19].

This research aims to conduct an industrial foresight analysis of Indonesia’s SOE construction industry to identify future trends as an effort to recognize upcoming opportunities. The foresight analysis in this research consists of three levels of analysis: macro, meso, and micro analysis. At the macro level, global trends and external environmental changes are identified, and continue to shape company policies at the meso level. At the micro level, the analysis focuses on individual behavior and small units such as organizations that interact with changes at the meso and macro levels. The micro-meso-macro framework in industrial foresight provides a comprehensive view in efforts to build a solid long-term strategy [20,21,22]. The subsequent sections of this research will address the literature review and methodology, followed by the findings, discussion of their implications, and conclusions.

2. Literature Review

At the end of the 20th century, foresight became an important instrument for addressing long-term issues related to risks and uncertainty as a consequence of unprecedented globalization and technological advancements [23]. Foresight has increasingly become a relevant trend in strategic management. Its emergence and significance are driven by the failure of traditional approaches to respond effectively and decisively in the face of environmental changes [24].

Foresight is defined as the process of analyzing current conditions based on past and present events, while also projecting possible future events. Several practices and techniques have been suggested as essential elements of foresight, such as scenario planning, environmental monitoring, technology road mapping, trend analysis, and real options analysis. These techniques enable companies to reduce uncertainty and improve their ability to understand changes and challenges that may arise in the future and impact the company or the entire industry [25].

Within the framework of dynamic capabilities strategic management, which involves a company’s ability to adapt, build, and reorganize its internal and external competencies to face rapid future changes, foresight is part of the sensing process aimed at recognizing opportunities and risks. By identifying potential trends and changes, companies can be more proactive in developing strategies that respond to market dynamics. This becomes an integral part of the company’s long-term strategic foundation, ensuring that they not only survive but also thrive amidst uncertainty [18].

As foresight becomes increasingly widespread across various companies and industries, careful assessment is required regarding its benefits and contributions to an organization’s long-term performance [26]. The growing complexity and dynamics of the business environment, coupled with the difficulty of making reliable predictions, add to the challenges of shared learning and transferring best foresight practices [27]. As a result, managers can learn which lessons can be transferred from one company (and industry) to another.

In modern management, there is no single approach to foresight. Foresight methodologies encompass several principles and rules, a series of research methods, and procedures for interacting with experts. The level of detail and reliability of foresight depends on the task set and the methods used. Foresight methods for predicting the future can be divided into two groups. The first group is based on quantitative analysis by collecting quantitative data about the current and past situation. The second group uses a qualitative approach or a combination of both [28].

Several studies related to the application of foresight in various industries have been conducted. In the technology industry, Technological foresight plays an important role in formulating science and technology policies, as well as selecting key industries for development. This approach promotes the evolution of regional technology industry clusters [29]. The industry 4.0 era has made technological foresight essential for organizational resilience in the electrical engineering sector. Leading companies and innovation ecosystems use foresight to guide R&D decisions and innovation strategies, with a complementary approach between company-based foresight and ecosystem-based foresight [30].

In the energy industry, the rapid depletion of fossil fuels and environmental concerns have made technological foresight a key strategy. Countries and companies use foresight to identify critical future needs and opportunities, with scenario-based analysis guiding strategic decisions [31]. In the rapidly changing UK financial services industry, strategic foresight functions as a learning process within organizations. It involves exploring future possibilities through various mechanisms to maintain organizational coherence and drive continuous innovation [32].

Examples of foresight in the construction and infrastructure industries include a foresight study in South Africa’s construction sector, which emphasized the need for innovation to develop specific technological necessary solutions to provide and maintain economic and social infrastructure. Investment in construction innovation must be based on a review of the current state of construction technology and an analysis of the drivers and trends shaping the future landscape of the industry [16].

The UK’s foresight program focused on increasing investment in research and development, as well as infrastructure for innovation. The program involved various groups to examine issues such as housing, renovation and reuse of facilities, sustainable materials, information and communication technology, business, globalization, and construction safety. The final report recommended nine steps to improve the construction industry, including promoting “smart” buildings and infrastructure, enhancing health and safety, and integrating supply chains [33].

There is also a scenario-based foresight study on green construction technology, assisted by building information modeling (BIM), in the Philippines. This study examined the correlation between green construction and political, economic, social, technological, and environmental factors. The main goal was to promote green construction theory supported by BIM in the Philippines [34]. Infrastructure providers in the Netherlands use various foresight methods, including scenario thinking and quantitative methods for data analysis. Their focus is on linking long-term developments with short-term ones and ensuring that organizations remain flexible in facing an uncertain future [35].

Research on the construction industry sector in Indonesia has been conducted by several researchers with different focuses. Arditi & Mochtar [36] focused on improving productivity in Indonesia’s construction industry. Susilowati & Chrishnawati [37] highlighted the importance of a strategic approach to human resource management in construction companies. Kusumawati et al. [38] examined dominant factors in the implementation of strategic management to improve performance in Indonesia’s SOEs. Research by Yusof et al. [39] studied the strategic management practices of construction companies in Medan, Indonesia, and found that companies using strategic management had better performance.

Sawlani et al. [40] investigated the impact of competitive advantage on company performance in Indonesia’s construction industry, finding that low company competitiveness led to production inefficiency and slowed growth. Other research also showed that debt as a source of capital for financing construction projects caused companies to face significant financial risks, causing lower efficiency compared to private companies. Therefore, efforts are needed to strengthen the position of SOE construction companies in Indonesia [2].

This research addresses a critical gap by highlighting the urgency of understanding foresight implementation within the dynamic capabilities framework in Indonesia’s SOE construction sector. SOEs in Indonesia’s construction sector face significant challenges related to efficiency and competitiveness, further worsened by high debt burdens. A comprehensive future outlook is essential to mitigate uncertainty, which is crucial for achieving sustainability and excellence in the construction industry, particularly for SOEs.

3. Methods

3.1. Research Framework

The foresight analysis in this research consists of three levels: macro, meso, and micro analysis. At the macro level, global trends and external environmental changes are identified, which then shape company policies at the meso level. At the micro level, the analysis focuses on individual behavior and small units, such as organizations, that interact with changes at both the meso and macro levels. The micro-meso-macro framework in industrial foresight provides a comprehensive view in efforts to build a solid long-term strategy [20,21,22].

This research uses several frameworks as the foundation for analysis. At the macro level, PESTLE framework (political, economic, social, technological, legal, environmental) is applied to analyze external factors that can influence the SOE construction industry. Six key factors are analyzed: environmental conditions and sustainability aspects, innovation and technological advancements, political and social stability, national economic and financial conditions, government policies, and regulations. PESTLE helps identify and analyze political factors, such as government policies and political stability, which influence large projects, and economic factors, such as inflation and interest rates, which impact project costs and funding [9].

Social factors, such as demographic changes that affect demand for infrastructure projects, are also analyzed [41]. Additionally, technological factors, for instance the adoption of new technologies including BIM, enhance operational efficiency [10]. Policy factors, such as regulations affecting construction operations, and environmental factors, including the impact of climate change and sustainability policies on project operations, are also considered in the analysis [9].

At the meso level, this research analyzes competition in the construction industry using Porter’s Five Forces framework to forces which are shaping the competitive dynamics. This approach assesses the threat of new entrants by evaluating barriers for new companies to enter the industry, such as high capital requirements or strict regulations, which can protect existing companies from new competition. The bargaining power of suppliers is assessed based on how dependent companies are on specific suppliers and the suppliers’ ability to raise prices or lower product quality. The bargaining power of buyers reflects the ability of buyers, such as governments or large private companies, to push prices down or demand higher quality.

The threat of substitute products or services examines the risk posed by the emergence of more efficient or innovative alternatives that could replace traditional construction services. Lastly, the level of rivalry among existing companies in the industry is analyzed to determine the intensity of competition among major players, which can affect pricing strategies, innovation, and market growth. This approach provides deep insights into the factors influencing the competitiveness of SOEs in the construction industry, enabling them to develop more effective and adaptive strategies to face market challenges [42].

At the micro level, this research analyzes the organizational level, referring to Alexandra & Wyborn [43], who use the organizational context as the smallest level in structuring industry foresight. The organizational level links the resources and capabilities of a company or industry to future challenges. At this level, factors such as employee competence and core company competencies play a key role in shaping the future of construction companies. Employee competence includes the skills, knowledge, and abilities of individuals that can contribute to project success and adaptation to industry changes. Meanwhile, core company competencies encompass strategic advantages and unique capabilities that differentiate a company from its competitors and allow it to remain competitive in the market.

3.2. Analysis Stages

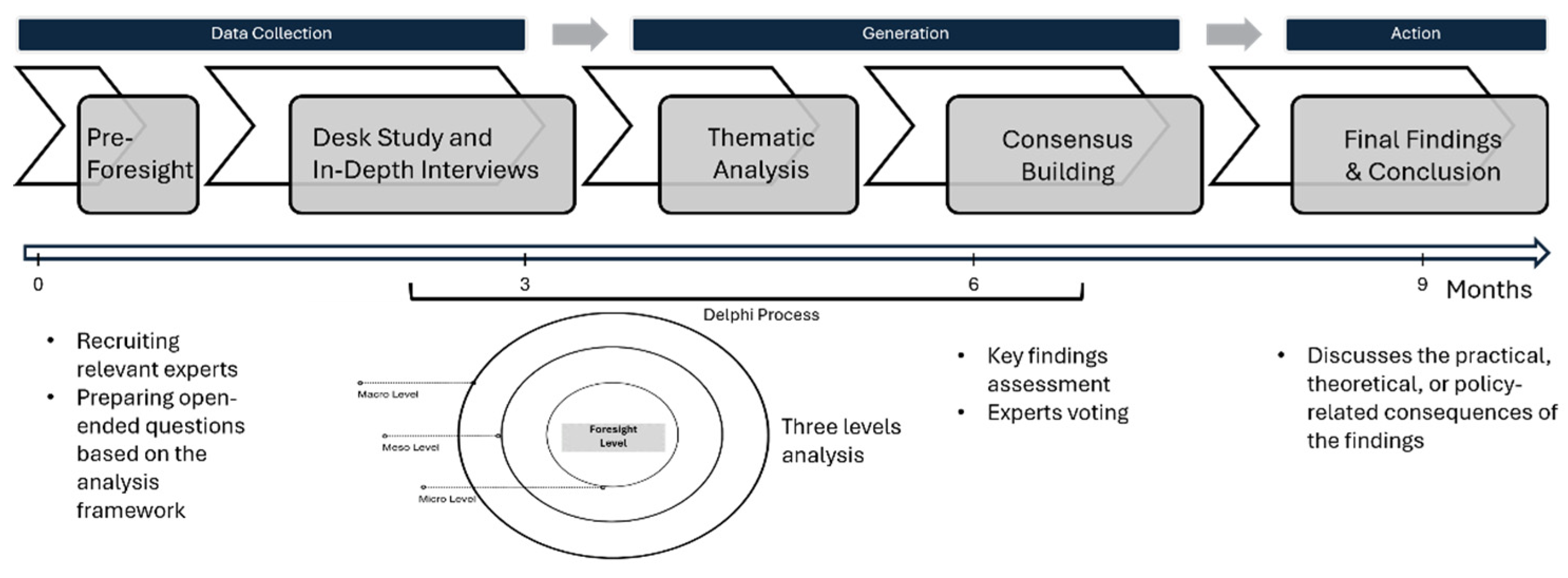

The research data consists of primary data collected through a series of in-depth interviews with eight experts in the construction industry, including practitioners and stakeholders from SOEs. The list of respondents can be found in Table 1. Each respondent was assigned a unique code to facilitate referencing in the analysis results. The research data is also supported by secondary data obtained through a desk study from government publications, SOE annual reports, previous studies, and relevant industry databases. This data is used to understand the historical context and current trends influencing the construction industry in Indonesia.

In the analysis process, this research employs a combined qualitative and quantitative method over a period of nine months. The qualitative method used is the Delphi method, aimed at reaching a consensus among experts regarding future trends in the SOE construction industry. The interview questions were designed to be open-ended (in-depth interviews) to allow respondents to provide deep and reflective insights [44]. Meanwhile, the quantitative method used a simple approach, namely expert voting on the significance of key findings. The analysis flow can be seen in Figure 1.

The initial stage of the research involved the selection of experts and the scheduling of time with them, as well as the preparation of the questionnaire based on the predetermined analytical framework (Subsection 3.1). The first round of interviews with the experts aimed to identify key themes across the three levels of analysis through open-ended responses. The next stage measured frequency or intensity of the occurrence of certain themes or terms in the responses, which were further elaborated using secondary data; this process was known as thematic analysis. The results revealed key findings from the research at the three levels of analysis. The following step involved reaching a consensus to ensure agreement among the experts on these key findings, in order to refine the results. Final step involved assessing the impact of key findings by conducting a vote among experts to select the most significant findings. The research concluded with a literature review to examine the discourse and implications of these findings.

4. Results

4.1. Analysis of Key Findings

4.1.1. Macro Level

The macro-level analysis using the PESTLE framework resulted in six key findings related to external factors that could shape the future conditions of the construction industry. The six key findings at the macro level are as follows.

- 1.

- Environmental Conditions and Sustainability

The deteriorating environmental conditions due to climate change have become a frequently considered factor globally in recent decades. The Sustainable Development Goals (SDGs), adopted by 193 countries, including Indonesia, and the United Nations Climate Change Conference (COP21) in Paris, which led to the Paris Agreement, set targets for carbon emission reductions to keep global temperature rises below 2°C, with efforts to limit them to 1.5°C. This target requires a 45% reduction in emissions by 2030 to achieve net zero emissions (NZE) by 2050. The Indonesian government has committed to this target through the enactment of Law No. 16 of 2016 on the Ratification of the Paris Agreement to the United Nations Framework Convention on Climate Change.

As a result, various policies related to the environment have been established in the construction sector, including in Indonesia. Green infrastructure, through the Green Building Concept (BGH), is regulated by Government Regulation No. 16 of 2021 concerning the Implementation of Law No. 28 of 2002 on Buildings, supporting the commitment to reducing gas emissions. Furthermore, environmental management in the road sector is governed by Directive No. 28 of 2023 on Guidelines for Environmental Management in the Road Sector, issued by the Ministry of Public Works and Public Housing (PUPR). The financial sector also supports this by promoting financing for projects transitioning from high-carbon-emitting activities to more environmentally friendly ones, known as green financing.

The application of ESG (Environmental, Social, and Governance) principles, which serve as a framework for evaluating how a company or organization manages its environmental impact, social responsibility, and corporate governance, has become highly important. According to interview results, companies that implement ESG are preferred by investors (R1, R2, R3, R4, R5, R6, R7). As a result, projects that apply ESG principles receive greater attention. In Malaysia, financing for sustainable projects, such as energy efficiency projects, receives a 2% discount on interest/profit per year for the first seven years, with 60% government guarantees. In Indonesia, green financing schemes are still under development and are expected to be launched in Q2 2024 and take effect in early 2025 [45].

This demonstrates the emergence of a sustainability megatrend not only in Indonesia but worldwide. In line with these trends, data from Infrastructure Monitor [46] shows that private investment in the renewable energy sector, as well as energy storage, transmission, and distribution, continued to grow in 2022, totaling nearly $180 billion globally. This sector attracted the highest investment compared to others. Moreover, there has been a shift in investment from biomass to hydrogen, which is a much cleaner energy source with high potential for efficient energy production. Since 2020, investment in hydrogen has increased sharply, peaking in 2022 at $6 billion. This aligns with expert interviews, where investors indicated a preference for companies that implement ESG and aim for sustainability, not only economically but also socially and environmentally. Therefore, sustainability will shape the construction industry moving forward.

- 2.

- Innovation and Technological Advancements

Technological advancements driven by changing environmental conditions are pushing the construction industry to continuously innovate and adapt. New markets, such as power generation and transmission, oil and gas, as well as mining and metals, present challenges for the construction industry to develop new technologies and enhance the technical capabilities of its workforce in conducting business activities. The construction of buildings and roads, emphasizing the “green building” principles, also demands the use of environmentally friendly materials. Rapid technological advancements, such as modular construction, automation, and the application of digital technologies, have increasingly become necessities.

Based on the interviews, three out of eight respondents explained that predictive tools for project scheduling, digital control towers, Light Detection and Ranging (LiDAR) for topographic mapping and pre-construction survey, Building Information Modelling (BIM), which provides accurate building model designs up to 8D, drive the greatest value in project execution, allowing projects to be completed on time and within budget (R3, R5, R6). The aggressive competition between domestic construction companies and foreign construction firms, which possess more advanced technical capabilities, has resulted in the erosion of new, higher-margin markets. Therefore, the construction industry must continue to innovate, develop technology end-to-end, and enhance the technical skills of its workforce to remain competitive and keep up with technological advancements. Companies that continuously innovate and adopt technological advancements will endure the volatility that occurs.

Additionally, Sawhney et al. [47] introduced the concept of Construction 4.0 (C4), which envisions the future of the construction industry. C4 has key components consisting of the Internet of Things, Data, and Services (IoS), Cyber-Physical Production Systems (CPPS), Cyber-Physical Systems (CPS), and the Internet of Things (IoT). This includes BIM, which provides modelling and simulation features as a core component of the C4 framework, and the cloud-based Common Data Environment (CDE), which acts as a repository to store all data related to construction projects throughout their lifecycle. The development of technology and the Construction 4.0 concept in the construction industry is predicted to become a future priority (R6).

- 3.

- Political and Social Stability

The current global economy is heavily influenced by the geopolitical conflict between Russia and Ukraine, which began with Russia’s military intervention in February 2022. Russia, as the world’s third-largest oil producer and exporter, with a production of 11.26 million barrels per day, plays a significant role in global oil trade. This intervention caused a supply shock in Russian oil trade, leading to rising prices in the global market, including in Indonesia. The increase in oil prices has resulted in higher material and operational costs for companies, making political stability a crucial factor for the construction industry to consider.

From a social perspective, factors such as Indonesia’s population growth rate of 1.13 percent in 2023 [48] and the trend of migration to urban areas present opportunities for the construction industry. Additionally, according to interview results, the demand for affordable housing is one of the key opportunities that can be tapped into by considering the characteristics of the current market. One respondent explained, “Buildings with a modular concept can meet the demand for affordable housing. Moreover, this concept creates efficiency in terms of both time and cost” (R6). Therefore, changing consumer preferences and behaviours will shape the construction industry moving forward.

- 4.

- National Economic and Financial Conditions

Fluctuations in national economic and financial conditions, driven by global economic changes such as Gross Domestic Product (GDP) growth rates, the benchmark interest rate (BI Rate), and exchange rates, significantly impact company performance. Indonesia’s GDP growth rate contracted by 2.07 percent in 2020 due to the Covid-19 pandemic, which resulted in delays in infrastructure projects and weakened corporate financial performance [48]. Over time, the economy began to recover, with GDP growth reaching 5.31 percent in 2022, although it dropped slightly to 5.05 percent in 2023. This economic growth was accompanied by rising inflation, which peaked at 5.95 percent in September 2022 [49].

The increase in inflation prompted Bank Indonesia to raise the benchmark interest rate from 3.5 percent in July 2022 to 6 percent in January 2024 [49], leading to higher bank loan interest rates. Based on interview results, three out of seven respondents stated that construction companies relying on bank loans for project financing are burdened by high interest rates (R2, R3, R4). This is reflected in the financial condition of SOE construction companies in recent years. The fluctuating exchange rate of the rupiah against the US dollar has also increased, reaching Rp15,673 in February 2024 [50], indicating the weakening of the rupiah. This condition affects companies that borrow from international financial institutions. Economic and financial fluctuations will be a crucial consideration for the construction industry moving forward.

- 5.

- Regulations/Law

At the macro level, due to the impact of climate change, various standards related to the construction industry have been established. Based on the interview results, all respondents emphasized the importance of complying with existing standards or regulations (R1, R2, R3, R4, R5, R6, R7). Examples include Leadership in Energy and Environmental Design (LEED), a green building certification adopted by various countries, and Greenship certification as the Green Building Council Indonesia (GBCI), which is more commonly applied in Indonesia. Additionally, one respondent highlighted the International Labour Organization (ILO) standards for workplace safety, which set international labour standards (R1). From an anti-corruption regulation perspective, the United Nations Convention Against Corruption (UNCAC) is an international treaty aimed at combating corruption worldwide.

Furthermore, in line with Indonesia’s government policies on infrastructure development, various policy packages and regulations have been issued. These include presidential regulations (perpres), fiscal policies, and institutional developments. For instance, in 2014, Perpres No. 75, which was later revised to Perpres No. 122 of 2016, initiated the establishment of the Committee for the Acceleration of Priority Infrastructure Provision (KPPIP). KPPIP was formed by the President to promote Priority Infrastructure Projects (PIP). The committee is led by the coordinating minister for Economic Affairs and includes members such as the Minister of Finance, the Minister of National Development Planning, the Minister of Agrarian Affairs and Spatial Planning, and the Minister of Environment and Forestry.

The economic policy package issued in 2015 aimed to reform regulations hindering economic growth, streamline bureaucracy, and provide initiatives to strengthen Indonesia’s investment climate and economy. Fiscal policies such as the Ministry of Finance Regulation No. 260/PMK.08/2016 regulate the payment mechanisms for availability payments in Public-Private Partnership (PPP) projects. This policy is expected to enhance project feasibility, attracting investor interest by offering periodic payments to implementing entities for infrastructure services that meet the quality standards specified in PPP agreements. Ministry of Finance Regulation No. 189/PMK.08/2015 governs the procedures for providing and implementing government guarantees for infrastructure financing through direct loans from international financial institutions to SOEs, supporting SOEs’ ability to secure direct loans to accelerate infrastructure provision (credit enhancement).

The government also injected capital into PT Sarana Multi Infrastruktur (PT SMI) through Ministry of Finance Regulation No. 232/PMK.06/2015, converting the Government Investment Center into State Capital Participation (PMN) in PT SMI, amounting to Rp18.4 trillion. PT SMI, as the center for infrastructure financing, is fully capitalized by the Republic of Indonesia under the Ministry of Finance and regulated by Ministry of Finance Regulation No. 100/PMK.010/2009. PT SMI operates across eight sectors: roads and bridges, transportation, oil and gas, telecommunications, waste management, electricity, irrigation, and water supply.

Additionally, the government expanded the role of PT Penjaminan Infrastruktur Indonesia (PT PII) through presidential regulation (Perpres) No. 82 of 2015, which provides central government guarantees for infrastructure financing through direct loans from international financial institutions to SOEs. It also offers guarantees to SOEs tasked with specific projects as outlined in Presidential Regulations. Government support and the existing standards through various regulations in the construction sector create both opportunities and challenges for the industry in the future.

- 6.

- Government Policies

Along with the growing global trend toward sustainability, including the shift in investment supporting energy efficiency, various government policies have been implemented to support this transition. In Indonesia, infrastructure development occurs across various sectors, including roads, bridges, waterways, and sanitation in the infrastructure sector; power plants and transmission in the energy sector; and oil, gas, mining, and metals in the industrial sector [1]. Moving forward, infrastructure development in the energy sector will become a priority for National Strategic Projects (PSN) in Indonesia. According to the latest developments outlined in Coordinating Minister for Economic Affairs Regulation No. 7 of 2023, there are 211 projects and 13 programs, including the development of the National Capital City (IKN) area, on the PSN list, with an estimated total investment of Rp6,445 trillion. Of this total, Rp2,385 trillion comes from the state budget (APBN), Rp1,353 trillion from SOEs, and Rp2,707 trillion from private enterprises [51]. The government collaborates with private enterprises, including SOE construction companies, under a scheme known as Public-Private Partnership (KPBU) to carry out infrastructure development.

In executing government projects under the KPBU scheme, companies often need to secure independent financing, which typically involves external project financing, such as debt, to fund the investment. According to interview results, one respondent explained that external financing through debt is seen as carrying lower risk compared to internal financing. This is because debt financing tends to have lower costs compared to internal financing, which typically comes from retained earnings or company equity (R3). As seen with companies in eight developing African countries, Caglayan & Machokoto [52] found that fixed investment spending is more sensitive to external funds, particularly debt, than internal funds. This indicates that external funds are used more frequently for investments due to their lower risk. However, inadequate debt management and debt burden, if not accompanied by an increase in revenue or operational efficiency, will lead to poor financial performance for the company. Additionally, two respondents stated that when working on government projects, companies often use a tender system that prioritizes the lowest cost. This environment forces construction companies to undercut each other in order to win project contracts, which results in minimal profit margins (R3, R5).

4.1.2. Meso Level

The meso-level analysis using Porter’s Five Forces framework to assess competition within the industry is as follows.

- 1.

- Threat of New Entrants

Government regulations and policies for the development of construction industry have potential to encourage the growth of new companies in the construction sector. Through national strategic projects, investments in infrastructure development—such as toll roads, bridges, airports, and power plants—have been the main drivers of growth in this sector. However, new entrants may face significant challenges in becoming leaders in the construction industry due to the substantial capital requirements to enter the industry. In addition, new entrants need experience and must demonstrate good performance to build a solid company reputation. New companies must put in more effort to acquire loyal customers. Beyond customer loyalty, the reputation of new companies will also affect their ability to access capital through bank loans.

According to the interview results, five respondents stated that the main threat of new entrants to domestic construction companies comes from foreign construction firms (R1, R2, R3, R4, R6). The level of product differentiation in the domestic construction industry tends to be low, and new entrants with innovative foreign products have the potential to capture the domestic market. The construction industry, both globally and domestically, is increasingly shifting towards sustainable development. Currently, trends in construction projects are focusing more on factors such as energy efficiency, waste management, and the use of environmentally friendly materials. As a result, projects in these sectors are often taken over by foreign companies.

By sector, according to interview results, two respondents stated that the threat of new entrants in the infrastructure sector tends to be low, as infrastructure is a basic product and a core competency of established companies. The threat arises in the building construction sector and the mining and energy sectors, where new entrants (including foreign companies) can offer innovative breakthroughs, especially in work methods. These sectors are expected to become priority sectors in the future (R3, R6). Therefore, the threat of new entrants in the building and energy construction sectors is considered to be moderate to high.

Table 2.

Threat of New Entrants.

| No | Threat of New Entrants |

| 1 | Government support through regulations and policies for the development of the construction industry has the potential to give rise to new companies in the construction sector. |

| 2 | New entrants require substantial capital to enter the construction industry, and significant investment is needed to reach an economic scale. |

| 3 | New entrants face difficulty gaining loyal customers because they need extensive experience and strong performance to build a reputation, affecting customers more likely to trust established players. |

| 4 | New entrants find it difficult to secure bank credit due to the need for proven experience and strong performance. |

| 5 | The level of product differentiation in the construction industry tends to be low, allowing new entrants with innovative foreign products to potentially capture the domestic market. |

- 2.

- Bargaining Power of Buyers

The market in Indonesia’s construction industry consists of both government and private sectors. SOE construction companies primarily serve government buyers, especially for infrastructure projects, while private companies tend to appoint foreign or private contractors to carry out their projects. The reliance of SOE construction companies on the government as their main buyer results in high bargaining power for the government. According to interview results, one respondent explained that, since the primary client of SOE construction companies is the government, which enforces the Construction Services Law requiring the lowest possible price, the government has high bargaining power (R3).

The government, as a buyer, is sensitive to the prices offered by construction companies. The pricing for the services provided is adjusted according to the government’s financial conditions. Additionally, buyers have high bargaining power because they possess extensive knowledge of the products being offered. Information on operational processes and tariff calculations is already available in the Construction Project Bidding Documents, allowing buyers to negotiate for lower prices. Construction companies must be cautious in their project execution, as failure to demonstrate strong performance can result in penalties or even blacklisting.

Moreover, the products offered by SOE construction companies tend to be standardized, with a low level of differentiation. Due to the standard nature of the products, the buyer switching cost tends to be low, enabling buyers to easily switch from one company to another. The above explanation demonstrates that the bargaining power of buyers in Indonesia’s construction industry is high. The domestic market is limited to certain buyers, but moving forward, it is expected that SOE construction companies can capture a greater share of the private sector and even international markets.

Table 3.

Threat of New Entrants.

| No | Bargaining Power of Buyers |

| 1 | High dependence on the government as the buyer |

| 2 | Buyers are sensitive to the prices offered |

| 3 | Companies will face consequences if performance is poor |

| 4 | Buyers have extensive knowledge of the products |

| 5 | Low buyer switching costs |

| 6 | The products offered are standardized |

| 7 | Limited number of buyers, particularly in the Indonesian market |

- 3.

- Bargaining Power of Suppliers

Suppliers in the construction industry consist of material suppliers and subcontractors. One respondent explained that the construction industry has a significant dependency on material suppliers because construction heavily relies on the equipment and materials provided by suppliers, which enables suppliers to maximize their profits (R3). SOE construction companies have a large number of suppliers, meaning the dominance of individual suppliers tends to be low. However, some suppliers offer unique and high-quality products, making it difficult to replace them with other suppliers.

Additionally, subcontractors play a crucial role. One respondent mentioned that experienced subcontractors working on construction projects in collaboration with the main contractor have the potential to acquire the knowledge and capabilities to transition into main contractors (forward integration) (R3). Subcontractors may acquire or merge with the businesses they serve while retaining control over their original operations. This can create competition between contractors and subcontractors. Therefore, construction service companies need specific strategies to maintain supplier loyalty and avoid competition with them. It can be concluded that the bargaining power of suppliers in the construction industry is medium.

Table 4.

Bargaining Power of Suppliers.

| No | Bargaining Power of Suppliers |

| 1 | The construction industry is dependent on suppliers (subcontractors, material suppliers) |

| 2 | The dominance of suppliers is low |

| 3 | The dominance of subcontractors is medium |

| 4 | Suppliers’ knowledge and capabilities may enable them to become main contractors (forward integration) |

| 5 | Suppliers’ wage levels |

| 6 | Switching costs between suppliers |

- 4.

- Threat of Substitute Products

The products offered by domestic construction companies, including SOE construction companies, tend to be standardized. This business climate leads to price competition among companies operating in the same sector. Four out of seven respondents stated that the threat comes from competitors who can offer substitute products with better quality and more affordable prices (R2, R3, R4, R6).

The creation of substitute products with better quality is driven by technological advancements. Based on the interview results, one respondent explained that compared to domestic companies, SOE construction products are superior, and several innovations have already been implemented. For example, modular buildings, which are more efficient in terms of both time and cost, are available, although their prices are higher (R6). In Indonesia, the modular concept is predominantly owned by SOE construction companies, while most competitors have not yet entered this field, which creates difficulties for buyers in finding substitute products. Therefore, the threat of substitute products is considered low.

Table 5.

Bargaining Power of Suppliers.

| No | Threat of Substitute Products |

| 1 | Substitute products are more expensive |

| 2 | Buyers tend to have difficulty finding substitute products |

| 3 | SOE construction companies offer superior substitute products compared to domestic competitors, but at higher prices |

| 4 | Technological advancements can create better substitute products |

- 5.

- Rivalry Among Similar Competitors

The construction industry is expected to grow by 7.5% by 2029 [53]. SOE construction companies, as market leaders in the construction sector in Indonesia, play a significant role in shaping competition within the country’s construction industry. Currently, 69 construction companies are listed on the Indonesia Stock Exchange [54]. The primary clients of SOE construction companies include the government and SOEs, as well as regionally owned enterprises (BUMD), which typically involve high-value projects. According to interview results, four respondents stated that SOE construction companies outperform domestic competitors in the same category. However, they lag behind foreign companies, which possess higher levels of technology and competence (R2, R3, R4, R6). Therefore, the level of competition among domestic competitors is considered medium, while competition with foreign companies is considered high.

Additionally, it is difficult for construction companies, especially SOE construction companies, to exit the industry due to the assets they have acquired. This situation underscores the need for companies to enhance their competitiveness to address increasing complexity.

Table 6.

Rivalry Among Similar Competitors.

| No | Rivalry Among Existing Competitors |

| 1 | The construction industry is projected to grow by 7.5% by 2029. |

| 2 | There are 69 construction companies listed on the Indonesia Stock Exchange (IDX). |

| 3 | Rivalry among similar domestic competitors is considered medium, while it is high among foreign competitors. The number of construction projects is increasing, but the size of the projects, especially government assignments, is often too large. |

| 4 | There are significant barriers to exiting the construction industry. |

Referring to the industry competitiveness categorization by Indrarathne et al. [55], based on the five forces analyzed, the threat of new entrants is considered medium to high, the bargaining power of buyers is high, the bargaining power of suppliers is medium, the threat of substitute products is low, and the level of rivalry among similar competitors is medium. Therefore, it can be concluded that the overall level of competition in the construction industry falls within the medium to high category.

4.1.3. Micro Level

At the organizational level, factors such as resources, capabilities, and core competencies will shape the future of construction companies. In terms of core competencies, according to interview results, five respondents explained that the core competency of construction companies is solely in building activities (R2, R3, R4, R5, R6). However, with market developments and project offerings featuring various schemes—such as Build, Operate, and Transfer (BOT); Public-Private-Partnership (PPP) or Kerjasama Pemerintah dan Badan Usaha (KPBU), which encompasses Design, Build, Finance, Operate, and Maintenance (DBFOM); Joint Venture (JV); Joint Operation (JO) or Kerjasama Operational (KSO); and the off-taker market has affected the business activities of companies have become increasingly complex and less focused on their core competencies.

In terms of capabilities, based on interview results, two respondents noted that managing projects across various sectors and schemes on an end-to-end basis contributes to the company’s burden (R3, R5). For example, the concession project for the Light Rail Transit (LRT) can create new business opportunities, such as the development of properties around LRT stations. This opportunity in the property business requires the company to engage in end-to-end business activities, from design, build, finance, operate, and maintain—especially investments in finance, this investment activity has reduced the company’s profits due to high short-term interest expenses or the implementation of projects with an Operation Cooperation (KSO) scheme for the constructed hotel, which requires the company to be involved in the operation or management of the asset. This has led to a decline in the company’s profits if the revenue generated is lower than the operational costs. These end-to-end business activities outside of the company’s core competencies increase the company’s burden. In the future, as the market becomes more volatile and project complexity rises, SOE construction companies will need to adapt to these developments.

From a resource perspective, as the company takes on more projects and schemes, the number of resources or assets owned by the company grows—whether in terms of human resources; tangible assets such as toll roads, railways, property, equipment, and so on; or intangible assets like intellectual property rights, licenses, and software. One respondent explained that the increase in resources has not been matched by proper management and utilization (R3). For example, applying the KSO scheme to hotels, apartments, or other commercial assets recorded as tangible assets owned by the company can lead to increased operational costs. This occurs particularly when there is a lack of sufficient marketing activities, which may result in the assets not generating revenue. Moreover, employee’s integrity and work culture also emerge as critical issues. The acquisition of fixed assets, such as land that is non-marketable, legally questionable, financially unviable, or technically impracticable, constitutes fraud and contributes to the deterioration of the company’s cash flow (R3). Therefore, it can be concluded that the core competency of the company lies solely in building activities, while its capability to manage projects outside of its core competency is insufficient, and the utilization of company resources remains suboptimal. These factors form the root of the problems faced by SOE construction companies for now. As a result, SOE construction companies must be able to transform in order to handle the complexities of both the present and the future at macro, meso, and micro levels.

4.1.4. Key Findings

Based on the foresight analysis at the macro, meso, and micro levels, several key findings can be outlined, as seen in Table 7.

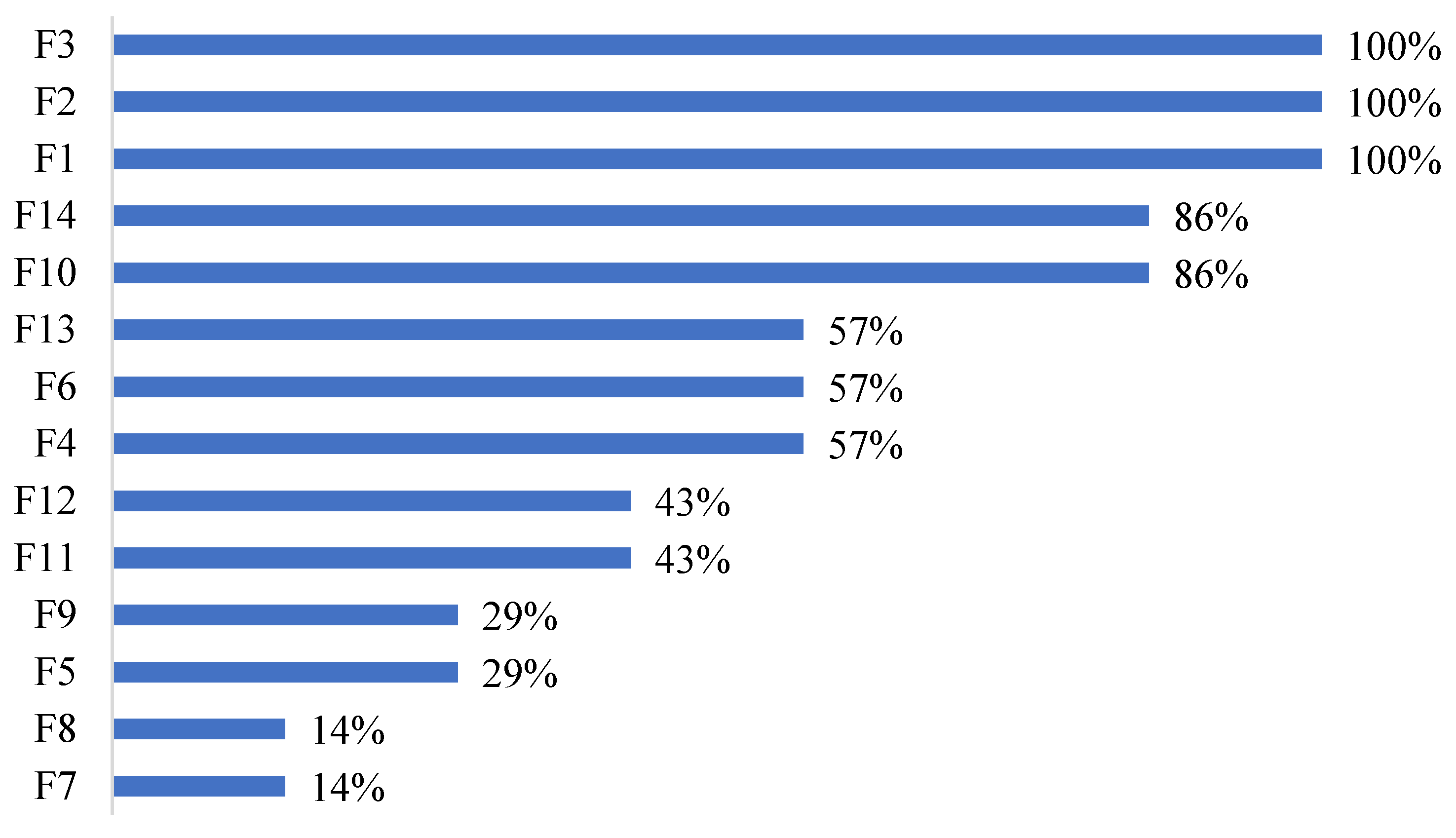

4.2. Significance of Key Findings

This research identifies 16 key findings considered to be important factors in forming future trends in the construction industry. Experts have assessed that the targets for net zero emissions (NZE), sustainable development goals (SDGs), and environmental, social, and governance (ESG) should serve as guidelines for all stakeholders, including those in the construction industry. Other important findings highlight that technological advancements and the Construction 4.0 concept will be top priorities for the construction industry in the future, and these are viewed as the most significant factors for the industry’s future. This indicates that, at the macro level, environmental conditions, sustainability aspects, innovation, and technological advancements are the key drivers of future success in the construction industry. Strengthening legal certainty is also required at the macro level.

At the micro level, there is a consensus that core competencies, resources, and capabilities must be enhanced to effectively address future challenges. At the meso level, the importance is considered less significant compared to the other two levels, as the industry is characterized by medium competitiveness. Further details can be found in below.

Codes of key findings from Figure 2 are described as follows.

| F1: | NZE and SDG targets serve as guidelines for all stakeholders to implement ESG, including in the construction industry. |

| F2: | Companies that implement ESG are more attractive to investors. |

| F3: | Technological advancements and the Construction 4.0 concept are becoming a priority for the construction industry. For example, the use of predictive analytics for project scheduling, digital control towers, LiDAR, and BIM is driving the greatest value in project execution, ensuring projects are on time and on budget. |

| F4: | Changes in consumer preferences regarding construction products. |

| F5: | Foreign political instability affects price/exchange rate fluctuations and impacts companies’ operational costs. |

| F6: | High interest rates and price fluctuations affect project financing and investment. |

| F7: | Occupational safety regulations. |

| F8: | Global green building regulations such as LEED. |

| F9: | Anti-corruption regulations (UNCAC), with implications that continued corrupt practices would reduce investor confidence in companies. |

| F10: | The implementation of various policy packages and regulations, including Presidential Regulations (Perpres), fiscal policies, and institutional development to support infrastructure development in Indonesia. |

| F11: | Unhealthy competition due to the lack of regulations related to cost and fees (tender system). |

| F12: | National infrastructure development requires significant investment, leading companies to rely on external debt financing. |

| F13: | The overall level of competition in the construction industry is medium to high. |

| F14: | The core competency of companies is limited to building. Their capability to handle projects beyond their core competency is inadequate, and the suboptimal management of resources is the root cause of the issues faced by SOE construction companies. |

5. Discussions

Key findings must be the primary focus for all stakeholders in Indonesia’s SOE construction industry. These findings represent future opportunities to excel in securing National Strategic Projects (PSN). Internal strategies need to be elaborated by considering key findings as the most important and influential external factors on the industry. Through this foresight analysis, all stakeholders are expected to be alert and responsive, aligned with the dynamic capabilities’ framework, which refers to a company’s ability to adapt to future changes. This capability includes sensing, aimed at recognizing future opportunities and risks as a foundation for developing long-term strategies [18].

This research reveals that NZE targets and sustainable development goals (SDGs) should be guidelines for all stakeholders in implementing ESG. Investor preferences for companies applying ESG principles align with several studies that show companies with strong ESG performance tend to attract more investment. This is linked to increased awareness of sustainability and environmental responsibility among investors, identified as a key driver of the construction industry’s transformation towards a more sustainable future [11,56,57,58]. The implementation of ESG in the construction industry not only enhances the company’s reputation and trust but also plays a crucial role in the long-term sustainability of this industry, especially in the context of tightening regulations and market expectations.

It should be noted that the concept of sustainability is not entirely free from criticism. The adoption of ESG practices in developing countries often faces significant challenges, including a lack of accurate data, limited infrastructure, and inadequate political support [59]. An unbalanced ESG approach that fails to consider local conditions in emerging markets can hinder economic growth and disrupt the development of effective and relevant sustainability strategies. It is essential to develop a more flexible and contextual approach to ESG implementation to support sustainable development across different economic environments [60].

Another important finding reveals that technological advancements and the Construction 4.0 concept should also be prioritized. The application of advanced technologies such as predictive analytics, digital control towers, LiDAR, and BIM in the construction industry has been proven to increase project efficiency, ensuring projects are completed on time and within budget. The integration of these technologies significantly improves project management, reduces risks, and enhances accuracy in planning and executing construction projects [61,62]. The adoption of digital technologies like BIM has been identified as one of the key factors for success in addressing the growing complexity of projects, enabling better management of the various variables affecting the success of construction projects [63]. The implementation of these technologies not only improves operational efficiency but also has a significantly positive impact on project sustainability by reducing construction waste and improving resource use efficiency [64].

Another equally important key finding is the role of regulations through fair legal certainty, along with strengthening the organizational level by reviewing core competencies, resources, and company capabilities. In terms of regulation, legal certainty is an essential foundation for the development of the construction industry in any country, especially for government construction companies. Legal certainty not only boosts investor confidence and facilitates strategic decision-making but also helps minimize legal risks that may arise during project execution. Consistent and transparent law enforcement can strengthen the operational stability of construction companies, allowing them to plan and execute projects more efficiently [65].

The factors of resources, capabilities, and core competencies are also key determinants of the future of the construction industry. Core competencies focused solely on construction activities (build) are becoming less relevant, given the market complexity and project schemes that require companies to operate end-to-end. Current capabilities have proven insufficient, as evidenced by the increased burden due to diversification into other sectors, such as property development around the LRT project in Indonesia. Furthermore, the increase in company resources has not been matched by effective utilization, leading to high operational costs without corresponding revenue growth [66,67,68]. Future challenges, such as sustainability and technological advancement, must be addressed through transformation and adaptation at the micro level. This can be achieved by improving the utilization of resources, capabilities, and core competencies to ensure competitiveness and sustainability in the future.

The key findings from this research illustrate the future priorities of the industry, emphasizing the importance of a policy foundation that combines sustainability and technology as the main pillars in advancing Indonesia’s SOE construction industry. This foresight scenario is designed to achieve the “Indonesia Emas 2045” vision and support the success of SOEs in dominating the majority of the infrastructure development market in Indonesia. This study has several limitations, such as subjectivity and openness in the qualitative research process, as well as variations in participants’ interpretations that may affect the consistency of the results. On the other hand, qualitative research allows for a deep understanding of the phenomena being studied, flexibility in adapting data collection and analysis techniques, and the ability to capture the complexity of expert opinions [69,70]. The analysis at the micro or organizational level could be developed more comprehensively by applying a more in-depth framework, such as VRIO (value, rarity, imitability, organization) [71].

6. Conclusions

The foresight analysis of Indonesia’s SOE construction industry highlights several key findings, with a primary focus on identifying future opportunities. The construction industry’s success heavily depends on integrating internal and external company factors, such as focusing on macro-level targets like Net Zero Emissions (NZE) and the Sustainable Development Goals (SDGs) in implementing Environmental, Social, and Governance (ESG) practices. Additionally, the adoption of advanced technologies like Construction 4.0 has become a top priority, with digital innovations such as predictive analytics, digital control towers, LiDAR, and Building Information Modeling (BIM) enhancing project efficiency and strengthening risk management. However, achieving sustainability and technological advancement presents challenges due to weaknesses in regulatory certainty—which serves as the third pillar at the macro level—and organizational limitations in core competencies, resources, and current capabilities at the micro level. At the micro level, strengthening the SOE construction industry’s core competencies, resources, and capabilities is essential to accelerate future trends. Competitiveness at the meso level is not a significant concern, as the industry operates with moderate competition.

References

- Bappenas Rencana Pembangunan Jangka Panjang Nasional 2025-2045.; 2021;

- Wibowo, F.A.; Satria, A.; Gaol, S.L.; Indrawan, D. Financial Risk, Debt, and Efficiency in Indonesia’s Construction Industry: A Comparative Study of SOEs and Private Companies. Journal of Risk and Financial Management 2024, 17, 303. [CrossRef]

- Chih, Y.-Y.; Hsiao, C.Y.-L. Brace for Another Crisis: Empirical Evidence from US Construction Industry and Firm Performance during and after 2007–2009 Global Financial Crisis. Journal of Management in Engineering 2023, 39, 04022069. [CrossRef]

- Bajjou, M.S.; Chafi, A. Identifying and Managing Critical Waste Factors for Lean Construction Projects. Engineering Management Journal 2020, 32, 2–13. [CrossRef]

- Mahamid, I. Impact of Rework on Material Waste in Building Construction Projects. International Journal of Construction Management 2022, 22, 1500–1507. [CrossRef]

- Fadhillah, M.R.; Riantini, L.S.; Latief, Y. Objective Identification from Every Success Factors or Clause of the Integration Process Management System to Increase the Performance Efficiency of State-Owned Construction Services Organization in Indonesia. IOP Conference Series: Earth and Environmental Science 2020, 426, 012025. [CrossRef]

- Vidiola, J. Increasing Investment Effectiveness In State-Owned Companies In Indonesia By Implementing Measurable And Careful Risk Management. Asian Journal of Social and Humanities 2023, 1, 484–495. [CrossRef]

- Fehan, H.; Aigbogun, O. Impact of External Environmental Factors on Construction Firms’ Performance, Mediated By Institutional Pressures. Civil Engineering Journal 2022. [CrossRef]

- Fisunenko, N.; Sidorov, O. THE IMPACT OF ENVIRONMENTAL FACTORS ON THE ECONOMIC SECURITY OF THE CONSTRUCTION COMPANIES. Eastern Europe: economy, business and management 2021. [CrossRef]

- Blayse, A.M.; Manley, K. Key Influences on Construction Innovation. Construction Innovation: Information, Process, Management 2004, 4, 143–154. [CrossRef]

- Liu, W. A Case Study of Market Strategy in Foreign Direct Investment in Kenya’s Construction Industry. American Journal of Industrial and Business Management 2023, 13, 761–777. [CrossRef]

- Benson; Rahayu, S.A. Analysis of Factors Shaping Project Portfolio Management at Indonesia Construction Public State-Owned Enterprise to Increase Workforce Management. International Journal of Scientific and Research Publications (IJSRP) 2021, 11, 324–329. [CrossRef]

- Fatima, I. Main Performance Indicators for A Construction Company in Indonesia. Asia Pacific Journal of Advanced Business and Social Studies 2017, 3. [CrossRef]

- Huda, M.; Soepriyono; Siswoyo Study of Parameters for Improving Performance and Competitiveness of Construction Companies in Indonesia 2019.

- Adeleke, A.; Bahaudin, A.; Kamaruddeen, A.M.; Bamgbade, J.; Salimon, M.G.; Khan, M.; Sorooshian, S. The Influence of Organizational External Factors on Construction Risk Management among Nigerian Construction Companies. Safety and Health at Work 2017, 9, 115–124. [CrossRef]

- Rust, F.; Koen, R. Positioning Technology Development in the South African Construction Industry: A Technology Foresight Study. Journal of the South African Institution of Civil Engineering 2011, 53, 02–08.

- Alizadeh, R.; Soltanisehat, L. Stay Competitive in 2035: A Scenario-Based Method to Foresight in the Design and Manufacturing Industry. foresight 2020, 22, 309–330. [CrossRef]

- Teece, D.; Pisano, G. The Dynamic Capabilities of Firms; Springer, 2003;

- Sandee, H. Improving Connectivity in Indonesia: The Challenges of Better Infrastructure, Better Regulations, and Better Coordination. Emerging Markets Economics: Industrial Policy & Regulation eJournal 2016. [CrossRef]

- Dopfer, K.; Foster, J.; Potts, J. Micro-Meso-Macro. Journal of Evolutionary Economics 2004, 14, 263–279. [CrossRef]

- Roberts, A. Bridging Levels of Public Administration: How Macro Shapes Meso and Micro. Administration & Society 2019, 52, 631–656. [CrossRef]

- Serpa, S.; Ferreira, C. Micro, Meso and Macro Levels of Social Analysis. International Journal of Social Science Studies 2019. [CrossRef]

- Bourgeois, R.; Sette, C. The State of Foresight in Food and Agriculture: Challenges for Impact and Participation. Futures 2017, 93, 115–131. [CrossRef]

- Vecchiato, R. Creating Value through Foresight: First Mover Advantages and Strategic Agility. Technological Forecasting and Social Change 2015, 101, 25–36. [CrossRef]

- Amer, M.; Daim, T.U.; Jetter, A. A Review of Scenario Planning. Futures 2013, 46, 23–40. [CrossRef]

- Vecchiato, R.; Favato, G.; Di Maddaloni, F.; Do, H. Foresight, Cognition, and Long-term Performance: Insights from the Automotive Industry and Opportunities for Future Research. FUTURES & FORESIGHT SCIENCE 2020, 2, e25. [CrossRef]

- Rohrbeck, R.; Battistella, C.; Huizingh, E. Corporate Foresight: An Emerging Field with a Rich Tradition. Technological Forecasting and Social Change 2015, 101, 1–9. [CrossRef]

- Petrenko, Y.; Denisov, I.; Metsik, O. Foresight Management of National Oil and Gas Industry Development. Energies 2022, 15, 491. [CrossRef]

- Xiang-fang, M. Application of Technology Foresight in Leading High-Tech Industries. Science-technology and Management 2008.

- Danko, T.; Shyriaieva, N. Industry 4.0 Technology Foresight in Electrical Engineering Sector. In Proceedings of the 2023 IEEE 4th KhPI Week on Advanced Technology (KhPIWeek); IEEE: Kharkiv, Ukraine, October 2023; pp. 1–6.

- Haiyan, L. Technology Foresight in Energy Industries. Journal of Chemical Industry and Engineering 2006.

- Costanzo, L.A. Strategic Foresight in a High-Speed Environment. Futures 2004, 36, 219–235. [CrossRef]

- Broyd, T.W. Constructing the Future. In Advances in Building Technology; Elsevier, 2002; pp. 1519–1526 ISBN 978-0-08-044100-9.

- David, J.P.; Imbang, G.A.; Cruz-Arreza, J.F.; Belbes, J.L.; Capa, K.; Caparas, J.F.; Vera, D.D.; Mabuti, M.; Maristela, C.M.; Ramos, J.B.; et al. Scenario-Driven Technology Foresight For BIM-Assisted Green Construction Technology. 2020, 241, 235–245. [CrossRef]

- Van Der Duin, P.; Ligtvoet, A. Defending the Delta: Practices of Foresight at Dutch Infrastructure Providers. In Futures Thinking and Organizational Policy; Schreiber, D.A., Berge, Z.L., Eds.; Springer International Publishing: Cham, 2019; pp. 71–90 ISBN 978-3-319-94922-2.

- Arditi, D.; Mochtar, K. Productivity Improvement in the Indonesian Construction Industry. Construction Management and Economics 1996, 14, 13–24. [CrossRef]

- Susilowati, F.; Chrishnawati, Y. Strategic Approach in Human Resource Management at Construction Companies in Indonesia. IOP Conference Series: Earth and Environmental Science 2021, 832, 012067. [CrossRef]

- Kusumawati, Q.A.; Pranjoto, R.G.H. Pengaruh Likuiditas, Profitabilitas, Dan Leverage Terhadap Pertumbuhan Laba Dengan Ukuran Perusahaan Sebagai Variabel Moderating Pada Perusahaan SubSektor Kontruksi Dan Bangunan Yang Terdaftar Di Bursa Efek Indonesia Periode 2018-2022. Jurnal Kajian Ilmu Manajemen (JKIM) 2023, 3.

- Yusof, M.N.; Indah Yunitasari; Bakar, A.H.A. Strategic Management In Construction Industry: Case Study In Indonesia. 2008. [CrossRef]

- Sawlani, D.K.; So, I.G.; Furinto, A.; Hamsal, M. The Effect of Competitive Advantage on Company Performance in the Construction Industry Sector in Indonesia. Psychology and Education Journal 2021, 58.

- Musa, M.M.; Amirudin, R.; Sofield, T.; Musa, M.A. Influence of External Environmental Factors on the Success of Public Housing Projects in Developing Countries. Australasian Journal of Construction Economics and Building 2015, 15, 30–44. [CrossRef]

- Porter, M.E. Competitive Advantage: Creating and Sustaining Superior Performance; simon and schuster, 2008;

- Alexandra, C.; Wyborn, C. Foresight in Natural Resource Management: A Case Study in Australia. Futures 2023, 154, 103259. [CrossRef]

- Cuhls, K. The Delphi Method: An Introduction. In Delphi Methods In The Social And Health Sciences; Niederberger, M., Renn, O., Eds.; Springer Fachmedien Wiesbaden: Wiesbaden, 2023; pp. 3–27 ISBN 978-3-658-38861-4.

- Keuangan, O.J. Roadmap Keuangan Berkelanjutan Tahap II (2021-2025) Sustainable Finance Roadmap Phase II (2021-2025) the Future of Finance 2020.

- Permani, R.; Sadicon, M.F.; Mahyassari, R.K. Identifying Opportunities in the Midst of Global Megatrends: A Tool for Policymakers. Global Megatrends: Implications for the ASEAN Economic Community. Jakarta: Association of Southeast Asian Nations 2017.

- Sawhney, A.; Riley, M.; Irizarry, J.; Riley, M. Construction 4.0. Sawhney, A., Riley, M., Irizarry, J., Eds 2020.

- Badan Pusat Statistik [BPS] Laju Pertumbuhan Penduduk 2023.

- Lidyah, R.; Hartini, T.; Krisdayanti, H.; others The Effect on Inflation, Exchange and BI Rate on Third Party Funds With Equivalent Rate (Er) as an Intervening Variable in Shariah Commercial Banks in Indonesia. In Proceedings of the Proceeding International Conference on Islamic Economics and Business (ICIEB); 2024; Vol. 3, pp. 74–93.

- Perdagangan, K. Nilai Tukar Mata Uang Asing Terhadap Rupiah. Satudata. Kemendag. Go. Id 2022.

- Hermawan, Y.P. G20, Indonesia and the Quest for Parameters of Sustainable Infrastructure. 2017.

- Caglayan, M.; Machokoto, M. The Sensitivity of Investment to Internal and External Funds: New Emerging Market Evidence. Research in International Business and Finance 2024, 67, 102099. [CrossRef]

- Mordor Intelligence Indonesia Construction Market 2024.

- Bursa Efek Indonesia [BEI] Daftar Saham 2024.

- Indrarathne, P.; Ranadewa, K.; Shanika, V. Impact of Competitive Forces to the Contractors in Sri Lanka: An Industry Analysis Using Porter’s Five Forces. 2020.

- Jeong, J.-W.; Lee, J.-H. ESG Factors and Their Impact on the Corporate Performance of Construction Firms. Sustainability 2020, 12, 4070.

- Khan, M.; Serafeim, G.; Yoon, A. Corporate Sustainability: First Evidence on Materiality. The Accounting Review 2020, 91, 1697–1724.

- Pizzi, S.; Rosati, F.; Venturelli, A. ESG in the Construction Industry: A Literature Review and Future Research Agenda. Journal of Cleaner Production 2021, 281, 125357.

- Li, J.; Li, Y. Literature Study of ESG in Corporate Investment and ESG Rating Status. Advances in Economics, Management and Political Sciences 2023. [CrossRef]

- Markopoulos, E.; Ramonda, M.B. An ESG-SDGs Alignment and Execution Model Based on the Ocean Strategies Transition in Emerging Markets. Creativity, Innovation and Entrepreneurship 2022. [CrossRef]

- Hossain, A.; Chua, D.K.H.; Yang, Y. Enhancing Construction Project Outcomes through Predictive Analytics and Technology Integration. Automation in Construction 2022, 136, 104184.

- Smith, P.; Tardif, M. The Impact of Digital Technology on Project Delivery in the Construction Industry. Journal of Construction Engineering and Management 2021, 147, 04021038.

- Zhao, Z.; Kwon, O.; Li, H. The Role of Employee Competence in Addressing Increasing Project Complexity in Construction. International Journal of Project Management 2019, 37, 527–539.

- Wang, L.; Zhang, Y.; Chen, F. Sustainable Construction: The Role of Digital Technologies in Enhancing Resource Efficiency and Reducing Waste. Journal of Cleaner Production 2022, 368, 133028.

- Smith, J.; Jones, M.; Brown, C. Advancing Managerial Evolution and Resource Management in Contemporary Business Landscapes. Journal of Management Studies 2020, 58, 1–25.

- Choi, J.-H.; Kim, Y.-S. An Analysis of Core Competency of Construction Field Engineer for Cost Management. Korean Journal of Construction Engineering and Management 2013, 14, 26–34. [CrossRef]

- Haan, J.D.; Voordijk, H.; Joosten, G. Market Strategies and Core Capabilities in the Building Industry. Construction Management and Economics 2002, 20, 109–118. [CrossRef]

- McAdam, R.; Miller, K.; McMacken, N.; Davies, J. The Development of Absorptive Capacity-Based Innovation in a Construction SME. The International Journal of Entrepreneurship and Innovation 2010, 11, 231–244. [CrossRef]

- Creswell, J.W.; Poth, C.N. Qualitative Inquiry and Research Design: Choosing among Five Approaches; Sage publications, 2016;

- Denzin, N.K.; Lincoln, Y.S. The Sage Handbook of Qualitative Research; sage, 2011;

- Putri, R.N.; Syarief, R.; Asnawi, Y.H. Core Competence Development Strategy to Achieve Competitive Advantage (Case Study: Dawoon Tea). Indonesian Journal of Business and Entrepreneurship (IJBE) 2023, 9, 1–1.

Figure 1.

Flowchart of foresight process.

Figure 2.

Influence of key findings (sum of answers exceeds 100% as multiple options are possible).

Table 1.

List of Construction Industry Experts.

| Code | Position | Type of Institution |

| R1 | Director of Human Capital Management | SOE |

| R2 | President Director (2020-2022) | SOE |

| R3 | Vice President of Operation Control | SOE |

| R4 | Director | SOE |

| R5 | Head of Operations | Private |

| R6 | Manager of Research and Development | SOE |

| R7 | SOE Investor | - |

Table 7.

Summary of key findings.

| Factors | Key Finding |

| Macro Levels | |

| Environmental Conditions and Sustainability |

|

| Innovation and Technological Advancements | The development of technology and the Construction 4.0 concept is becoming a priority for the construction industry. For example, the use of predictive analytics for project scheduling, digital control towers, LiDAR, and BIM drives significant value in project execution, ensuring on-time and on-budget completion (F3). |

| Political and Social Stability |

|

| National Economic and Financial Conditions | High interest rates and price fluctuations influence project financing and investment (F6). |

| Regulations and Legal Framework |

|

| Government Policy |

|

| Meso Level | |

| Threat of New Entrants |

|

| Bargaining Power of Buyers |

|

| Bargaining Power of Suppliers |

|

| Threat of Substitute Products |

|

| Rivalry Among Similar Competitors |

|

| Micro Level | |

| Organization | The core competency of companies is limited to building. Their capability to manage projects outside their core competencies is insufficient, and the management of company resources remains suboptimal. This is the root of the problems faced by SOE construction companies (F14). |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Copyright: This open access article is published under a Creative Commons CC BY 4.0 license, which permit the free download, distribution, and reuse, provided that the author and preprint are cited in any reuse.